Market-based env policy in Latin America J Acquatella

195

MARKET–BASED ENVIRONMENTAL POLICY IN LATIN AMERICA: THEORY AND REALITY A Thesis Presented to the Faculty Of The Fletcher School of Law and Diplomacy By Jean José Acquatella Corrales In partial fulfillment of the requirements for the Degree of Doctor of Philosophy December 2009 Dissertation Committee Prof. William Moomaw, Chair Prof. Katrina Burgess Prof. Ann Helwege

Transcript of Market-based env policy in Latin America J Acquatella

MARKET –BASED ENVIRONMENTAL POLICY IN LATIN AMERICA : THEORY AND REALITY

A Thesis

Presented to the Faculty

Of

The Fletcher School of Law and Diplomacy

By

Jean José Acquatella Corrales

In partial fulfillment of the requirements for the

Degree of Doctor of Philosophy

December 2009

Dissertation Committee

Prof. William Moomaw, Chair

Prof. Katrina Burgess

Prof. Ann Helwege

Jean José Acquatella Corrales

Oficial de Asuntos Económicos CEPAL, Naciones Unidas Unidad de Energía y Recursos Naturales División Recursos Naturales e Infraestructura DRNI Casilla 179-D, Santiago, Chile Tel: +562 210 2153 [email protected] Fax: + 562 208 0484

EDUCATION

THE FLETCHER SCHOOL. Tufts University Ph.D. candidate International Environment and Natural Resource Policy Doctoral fields: international environmental policy, development economics, environmental economics. Dissertation: “Market based environmental policy in Latin America: theory vs. implementation outcomes”. M.A.L.D Master of Arts. Fletcher School 1996 Thesis: "Triggering the implementation of pollution management policies: case study Mexico". Urban and Environmental Policy Department. Tufts University Medford, MA M.A . Master in Urban and Environmental Policy. 1996

UNIVERSIDAD METROPOLITANA ( U.M ) Caracas, Venezuela E.E Electrical Engineer. cum laude 1988 STANFORD UNIVERSITY Palo Alto, CA Engineering and English 1982

EXPERIENCE U.N ECLAC 1999–2010 United Nations Economic Commission for Latin America and the Caribbean Santiago, Chile Economic Affairs Officer Energy and Natural Resources Unit 2006 - 2010 Natural Resources and Infrastructure Division � Regional energy policy analysis and project development in the areas of energy efficiency, renewable

energy, biofuel sector development, and climate change energy policy responses. Sustainable Development Division 1999-2005 � Regional environmental policy analysis and project development in the areas of fiscal-environmental

policy coordination, public finance and economic instruments for environment and natural resource sectors.

� Coordinator ECLAC/IMF/OECD annual Workshop on Fiscal Policy and Environment 2002-2004 � Executive Coordinator ECLAC/UNDP project Application of Economic Instruments for Environmental

Management in Latin America and the Caribbean � Academic Director ECLAC/ASDI/World Bank Institute capacity building program and annual course

on “Market Based Instruments and Financing Sources for Sustainable Development”. � Member Int’l Working Group on Economic Instruments, UNEP Economics and Trade Unit Geneva,

2000-2002 � Coordinator ECLAC/World Bank National Climate Change Strategy Studies (NSS) Regional

Workshop (2001) HIID Harvard Institute for International Development Cambridge, MA Teaching Fellow, Environmental Economics & Policy Analysis Workshop 1998 IAE International Academy of the Environment Geneva, Switzerland Research Fellow, Climate Change and the Global Economy Research Program 1998 UNITAR United Nations Institute for Training and Research Geneva, Switzerland Special Fellow (1996-97) and Consultant (1994-95)

PUBLICATIONS Acquatella Jean and Hugo Altomonte. “Policies for energy access in Latin America and the Caribbean”. Regional contribution to Knowledge Module 23 Energy Access Policies. IIASA / UNIDO Global Energy Assessment (GEA), Vienna, Austria forthcoming 2010. Acquatella, Jean. Energía y Cambio Climático: oportunidades para una política integrada en América Latina y el Caribe. CEPAL / GTZ, LC/W 218. Santiago, Chile 2008. Acquatella, Jean y Alicia Bárcena eds. Política Fiscal y Medio Ambiente: bases para una agenda común. Libro de la CEPAL No. 85, Santiago, Chile 2005. Acquatella, Jean. “ Integración de Políticas Fiscal y Ambiental: análisis y desafíos pendientes”. Introducción y Capítulo 1 en Acquatella y Bárcena eds. Política Fiscal y Medio Ambiente: bases para una agenda común. Libro de la CEPAL No. 85, Santiago, Chile 2005. Lerda, Juan Carlos, Jean Acquatella, José Gomez. “Integración, coherencia y coordinación de Políticas Públicas Sectoriales: reflexiones para el caso de las políticas fiscal y ambiental”. CEPAL, Serie Medio Ambiente y Desarrollo No. 76, noviembre 2003. Acquatella, Jean. “Fundamentos Económicos de los Mecanismos de Flexibilidad para la reducción internacional de emisiones en el marco de la Convención de Cambio Climático (UNFCCC)”, CEPAL, Serie Medio Ambiente y Desarrollo No. 38, julio 2001. Acquatella, Jean. “Aplicación de Instrumentos Económicos en la Gestión Ambiental de América Latina y el Caribe: Desafíos y Factores Condicionantes”. CEPAL/PNUD, Serie Medio Ambiente y Desarrollo No. 31, enero 2001.

Acquatella, Jean. “Financing Carbon Offset Projects: Implications for the design of the Clean Development Mechanism”. International Academy of the Environment (IAE) working paper. Geneva 1998.

Acquatella, Jean ed. “Globalización y Sostenibilidad Ambiental”, capítulo 9 en Globalización y Desarrollo.

CEPAL, Libro institucional para el IXXX Período de Sesiones de la CEPAL, Brasilia 2002. Acquatella, Jean ed. “Consolidar los Espacios del Desarrollo Sostenible”, capítulo 13 en Equidad,

desarrollo y ciudadanía. CEPAL, Libro institucional para el XXVIII Período de Sesiones de la CEPAL, México 2000.

AcLorenzo Eguren. Analysis of the present situation and future prospects of the Clean Development

Mechanism (CDM) in FEALAC member countries. CEPAL – Ministry of Foreign Affairs (MOFA) Government of Japan. May 2006.

Report commissioned by the Government of Japan for the occasion of the Forum of East Asia and Latin American Countries (FEALAC) meeting in Tokyo, 2006.

ADDITIONAL INFORMATION - Bilingual in English and Spanish, basic French. - Nationality: Venezuelan and U.K., one daughter. - International professional experience in most Latin American countries, Europe and USA. - Outdoor sports enthusiast and organizer of nature and cultural expeditions.

ABSTRACT

The dissertation assesses the implementation of “market-based” environmental policy instruments in Latin

America and the Caribbean. National surveys were undertaken in 13 countries to assess implementation

outcomes and instrument choice, 81 instruments in 13 countries were documented in our dataset. Each

record is a mini case-study of the implementation history for one “market-based” instrument (MBI). The

analysis determined the extent of MBIs implementation in practice, the instrument choices made, and the

outcomes obtained by environmental authorities attempting to incorporate MBIs into the regulatory mix.

We find that in a third of all cases documented (25 in 81 or 32%) implementation was either not completed,

or derailed, due to a variety of factors. Furthermore, among 56 cases where implementation took place, 12

instruments ( 21%) were found to be no longer operating or not enforced in practice; and a further 9 (16%)

were operating only partially.

Plausible independent variables associated with these outcomes were identified across cases.

Approximately half of all cases (38 in 81, 47%) indicated poor cooperation by fiscal authorities as a major

barrier to successful implementation outcomes. A third of all cases (26 in 81, 32%) indicated transaction

costs implicit in coordinating MBI operation across bureaucratic boundaries (fiscal–environmental

authorities), and between levels of government, as another barrier behind poor outcomes. Case data

suggests that structural features of the political/institutional context in which environmental authorities

operate condition implementation outcomes. A typology of key interactions identified point to the fiscal-

environmental policy interface, and the public finance–infrastructure policy interface, as key areas where

policy coordination is required for successful implementation.

Integrating MBIs into existing fiscal and sectoral policy structures (agriculture, energy, transport, water) is

often difficult, and sometimes impossible under political/institutional constrains. Political leadership and

governance innovation is required to overcome existing policy biases, and ensure coherent incentives biz-a-

biz high inertia fiscal and public finance bureaucracies. These Latin American findings are a sobering

reminder that there are no easy and quick policy solutions. While increased use of MBIs remains an

important element, any integrated policy response that hopes to tackle the complex environmental

challenges facing this region (and emerging global ones like climate change) will have to emphasize a

much broader set of public interventions.

Dedication

A Angelique (21 Agosto 1994) y mis padres Profesores Harry Acquatella M.D y Greta Corrales de

Acquatella M.D por su amor, y apoyo durante toda esta aventura que empezó en 1993.

To Professor Bill Moomaw in gratitude for his leadership, constant motivation, and encouragement

throughout all these years.

Acknowledgment

En reconocimiento y agradecimiento al Profesor Juan Carlos Lerda, por su amistad y estimulo intelectual

(de las discusiones compartidas surgieron muchos de los conceptos que explora este trabajo); y a mi jefe,

Profesor Hugo Altomonte, por su generoso apoyo para terminar este trabajo, y su amistad y liderazgo que

han sido muy importantes para hacer de mi trabajo en CEPAL una experiencia grata y con sentido.

A big thank you to Professors Ann Helwege, Ann Rappaport, Katrina Burgess and the Tufts UEP and

Fletcher community for their generosity and intellectual stimulus.

In gratitude to the Albert Schweitzer Foundation, and the Tufts – Albert Schweitzer Environmental grant

which supported the origin of this research project; and to the United Nations Economic Commission for

Latin America and the Caribbean (U.N ECLAC) which enabled its conclusion.

Contents

Chapter 1. INTRODUCTION .................................................................................................................................... 1 1.1 Market-based instruments in environmental policy................................................................................. 5 1.2 Motivation of Research............................................................................................................................ 9 1.3 Statement of research objectives............................................................................................................ 14 1.4 Research questions................................................................................................................................. 15 1.5 Overview of dissertation contents and main results............................................................................... 15 CHAPTER 2. LITERATURE REVIEW ................................................................................................................ 18 2.1 Taxonomy of “market-based” instruments in environmental policy .............................................. 18

Environmental taxes .............................................................................................................................. 20 Charges..................................................................................................................................................20 Tradable permit systems........................................................................................................................ 21 Deposit-reimbursement schemes........................................................................................................... 23 Fines for non-compliance with standards.............................................................................................. 23 Environmental performance bonds........................................................................................................ 23 Financial compensation for environmental damages on the basis of legal responsibility ..................... 24 Subsidies for activities related to environmental protection.................................................................. 24 Environmental disclosure and other demand-side information instruments.......................................... 25

2.2 Normative theory ................................................................................................................................. 27

The theory of externalities and normative environmental policy .......................................................... 27 Property rights and the Coasian approach to the internalization of externalities................................... 29 Incomplete information: measuring cost and benefits in the presence of externalities. ........................ 29 Tax interaction effects vs. the “double dividend” ................................................................................. 30 Changes in energy subsidies and other taxes in under fiscal-neutrality. ............................................... 31 Cost-efficiency in normative environmental policy .............................................................................. 32 Instrument design issues under uncertainty: prices vs. quantities ......................................................... 33 Distributive properties........................................................................................................................... 33

2.3 Policy literature on the application of “market-based” instruments .............................................. 35

Environmentally related taxation in OECD countries........................................................................... 35 The political economy of environmentally related taxation. ................................................................. 37 Political economy in implementation of economic instruments in Latin America................................ 39

Public finance: budgetary deficiencies, earmarking of environmental revenue, fiscal competition and perverse incentives. ............................................................................................................................... 41

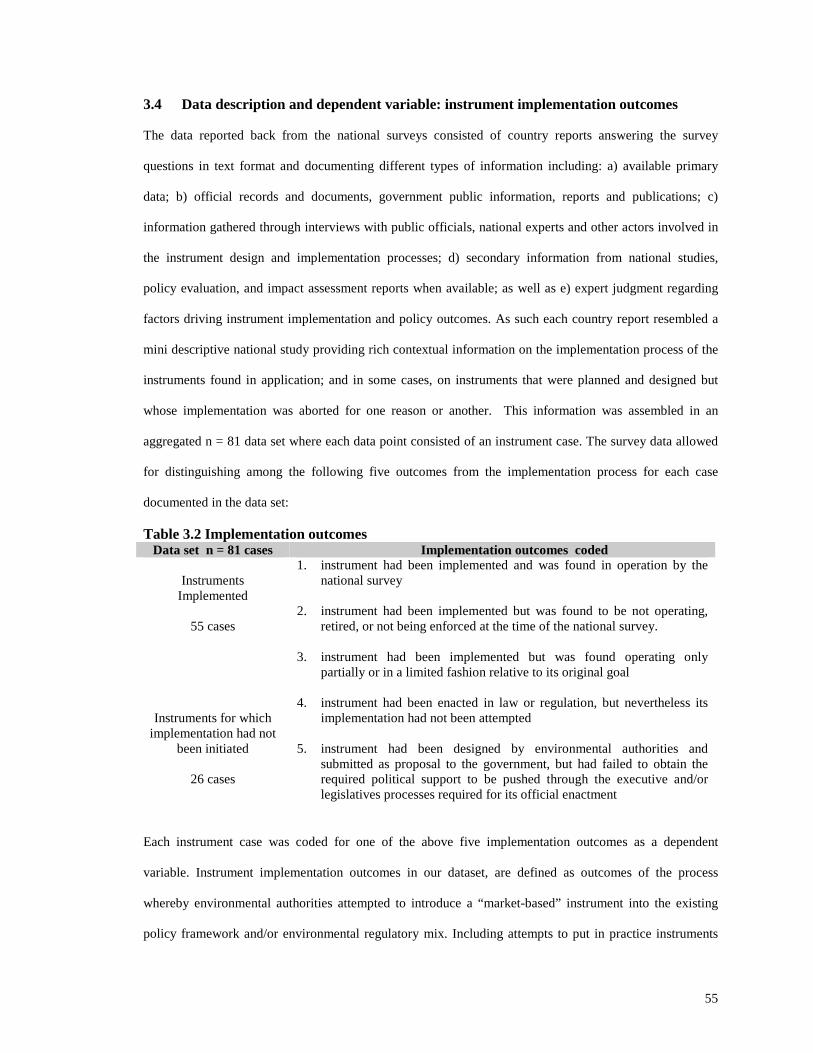

CHAPTER 3 METHODS and DATA .................................................................................................................. 44 3.1 Methodology overview.......................................................................................................................... 44 3.2 National surveys and research scope ..................................................................................................... 46 3.3 Types of environmental policy instruments surveyed ........................................................................... 51 3.4 Data description and dependent variable: instrument implementation outcomes .................................. 54 3.5 Coding of implementation outcomes..................................................................................................... 60 3.6 Process tracing and identification of independent variables .................................................................. 61 3.7 Coding of independent variables associated with observed implementation outcomes......................... 64 3.8 Development of working hypothesis ..................................................................................................... 67 3.9 Framing the analysis of instrument case data ........................................................................................ 68 3.10 Illustrative case studies. ......................................................................................................................... 69

CHAPTER 4. ANALYSIS ........................................................................................................................ 75 4.1 Analysis of the extent of implementation............................................................................ 75

Instruments not – implemented: A closer look at the 25 cases that did not reach the implementation stage (30% of data set). ............................................................................ 79

Main patterns preventing instrument implementation........................................................ 85

Instruments implemented but retired/not enforced/partially operating: A closer look at these 12 cases ( 21% of those implemented). ..........................................89

Main patterns associated with retired / not-enforced / partial operation outcomes. ........... 94

Summary findings on the extent of implementation...................................................101 4.2 Analysis of Instrument Choice........................................................................................... 104

Instrument choice: types of “market-based” environmental instruments implemented ... 104 Positive incentive instruments: Environmental subsidies, tax credits, fiscal transfers and other incentives. ............................................................................................................... 105

Environmental taxes and charges linked to pollution externalities. ................................. 109 User charges for water and municipal service provision.................................................. 113 Other instruments in the data set: tradable permits, deposit-refund, certification............ 118 Instrument choice: summary of findings.......................................................................... 119

4.3 Identifying variables associated observed implementation outcomes. ........................... 123

4.4 Main analytical conclusions from chapter........................................................................ 125 4.5 APPENDIX Ch. 4: Comparing the extent of implementation found with previous studies . 135 CHAPTER 5 CASE STUDY: Colombia’s water pollution charge...................................................136 5.1 Background........................................................................................................................... 136 5.2 Water pollution in Colombia ................................................................................................ 137 5.3 Colombia’s decentralized institutional framework for environmental management ............ 139 5.4 Water pollution control......................................................................................................... 140 5.5 Law 99 economic instruments .............................................................................................. 142 5.6 Design of the Pollution Charge instrument “ Tasa Retributiva” ........................................... 142 5.7 Implementation of the Pollution Charge instrument............................................................. 145

Description of the implementation process during the first three years 1997-2000......... 145 Early successes and environmental effectiveness ........................................................... 148 Problems of implementation at the national level. ........................................................... 154

5.8 Differing assessments ........................................................................................................... 156 5.9 Concluding comments on the “Tasa Retributiva” case study ............................................... 159 5.10 Appendix Ch. 5: Fiscal and environmental decentralization: CAR revenue sources.......... 161 CHAPTER 6 DISCUSSION of FINDINGS and CONCLUSION ..................................................... 165 CONCLUSION…………………………………………………………...……………………………....176 BIBLIOGRAPHY …………………………………………………………………………………...…...178

1

Chapter 1. INTRODUCTION The primary goal of this dissertation is to assess the extent of implementation of “market-based”

environmental policy instruments in Latin America and the Caribbean. National surveys were undertaken in

thirteen countries to assess the implementation of this type of instruments applied towards environmental

objectives in the region. A total of 81 cases from 13 countries were documented. The first part of the

dissertation is focused on the analysis and findings of this survey data to determine the extent of application

of these policy instruments in the region, the instrument choices made, and the outcomes from their

implementation process in this n=81 data set. A secondary goal was to characterize the political and

institutional context in which “market-oriented” environmental policy instruments take place in Latin

America to better understand the nature of the constraints faced by environmental authorities trying to

incorporate this type of instruments into the regulatory mix. This involved the identification of plausible

independent variables or factors associated with the implementation outcomes observed in the data set. The

patterns identified are illustrated with examples from the cases documented for this dissertation and

findings are contrasted with relevant literature in the analysis and discussion chapters.

Findings indicate that, although there has been a considerable extent of incorporation of these instruments

into law or regulations and experimentation with their application (81 cases were documented in thirteen

countries), environmental authorities in Latin American and Caribbean countries have faced significant

difficulties in their attempts to incorporate “market-based” instruments into existing regulation. Contrary to

expectations that the introduction of “market-based” instruments in environmental policy could achieve

rapid improvements in policy outcomes, their actual implementation in Latin America seems to have been

mired in a variety of factors exogenous to environmental policy. The cases in this dissertation illustrate that,

rather than any intrinsic failing with “market-based” instrument design or lack of competence by

environmental authorities, the factors generally associated with poor outcomes point to interactions with

other pre-existing government policies, and poor cooperation by fiscal bureaucracies at various levels of

government as key factors conditioning the implementation outcomes observed. The implementation of

“market-based” environmental instruments interacts with, and across, a number of policy interfaces outside

the strict domain of environmental authorities. The cases in our data set indicate key policy interactions

2

with: a) existing tax policy structures in environmentally sensitive sectors (i.e. agriculture, energy, natural

resources etc.); b) national infrastructure policies and their public finance, in particular for municipal

water/sanitation infrastructure; and c) the interaction between national environmental mandates and the

realities of fiscal decentralization and resource transfers between various levels of government (i.e. federal,

state/provinces, municipal ), among others. Neither private industry opposition to the introduction of

“market-based” environmental instruments, nor weak capacity of environmental authorities featured

prominently in the Latin American cases. These findings are contrary to the emphasis given in the literature

from OECD and developing countries to opposition by industry interest groups, and weak capacity of

environmental authorities respectively, as the major factors determining poor outcomes from new

environmental regulatory initiatives.

The difficulty of introducing “market-based” instruments into the policy mix is illustrated by the fact that in

approximately half of the eighty one cases examined in Latin America and the Caribbean, the obstacles

faced resulted in failure or derailment of the implementation process. The barriers were such that in these

cases, instrument implementation either could not be initiated, or was initiated but the instrument was later

retired and found no longer being applied in practice at the time of the national surveys undertaken. Among

the cases where implementation was achieved and instruments were found in application, over one third

reported obtaining only partial results relative to their intended design goals.

Our thesis is that the observed outcomes from the implementation of “market-based” instruments that have

taken place in Latin American countries since the 1990s, have been conditioned to a great extent by

structural features of the political and institutional context in which environmental authorities operate in

these countries. Most cases where instruments in law or regulation were never implemented point to

particular features of the interaction between traditional fiscal bureaucracies, and recently formed

environmental authorities within the same government, as a major stumbling block in enabling the

incorporation of “market-based” environmental instruments into the existing regulatory mix.

3

Lack of cooperation by fiscal authorities was cited in most cases where the introduction of environmental

charges, fees and/or taxes (i.e. pollution charges, water effluent charges, water use charges etc.) required

accommodation of invoicing and payment collection mechanisms, as well as revenue administration and

allocation channels. In a number of countries fiscal authorities outright opposed any proposal from

environmental authorities involving the introduction of selective environmental taxation or charges. In the

two countries that attempted to introduce “market-based” environmental instruments at the national level

(water pollution charge in Colombia, and payment for environmental services in Costa Rica) environmental

authorities found more resistance in recouping charges from public entities (municipal sewerage authorities

in Colombia, and the public electric utility in Costa Rica) than from private industry and individual users.

The barriers faced by environmental authorities vs. uncooperative fiscal bureaucracies, and other public

entities within the same government in these Latin American cases, illustrate a different dynamic than the

traditional government vs. industry opposition to the introduction of environmental charges highlighted in

the literature.

This thesis is compared with alternative hypotheses advanced in the literature assessing the performance of

“market-based” environmental policy in Latin America, in particular to explain poor implementation

outcomes1. One hypothesis which has been emphasized in this literature attributes poor environmental

policy outcomes to weak technical, financial, and enforcement capacities of environmental authorities in

the region, noting the large asymmetries between mandates and the public resources allocated. A common

theme found in the empirical literature that has looked at developing countries’ experience with the use of

economic instruments in environmental policy, points to the lack of capacity and institutional weakness of

environmental authorities2.

This literature ascribes the poor results in experiences with economic instruments to the weak institutional

capacity of environmental agencies, frequently mentioning lack of technical capacities, weak monitoring

1 Richard Huber, Ronaldo Seroa da Motta, Jack Ruitenbeek. “Market Based Instruments for Environmental Policy Making in Latin America and the Caribbean: lessons from eleven countries”, World Bank Discussion Paper 381. World Bank. Washington DC 1998. 2 An alternative statement of this “weak institutional capacity” hypothesis is that environmental policy is not a priority in a region faced with unmet challenges in poverty reduction and the reversal of a highly skewed distribution of income, and hence insufficient resources are allocated to environmental mandates

4

and enforcement practices, insufficient budgets and trained staff. The data collected for this dissertation

indicate that this diagnosis might be “too narrow” in pointing only to the institutional weakness of

environmental authorities to explain poor environmental policy outcomes. It implies that if only

environmental authorities were allocated more financial and technical resources to increase their

institutional capacity and political bargaining power then we would see a reversal of the disappointing

policy outcomes observed.

Approximately half of all cases in our data set point to the nature of the interaction between traditional

fiscal bureaucracies and more recently established environmental authorities, as a major stumbling block in

the implementation of “market-based” environmental instruments. Lack of cooperation by fiscal authorities

was cited in most cases where the introduction of environmental charges, fees and/or taxes (i.e. pollution

charges, water effluent charges, water use charges etc.) required accommodation of invoicing and payment

collection mechanisms, as well as revenue administration and allocation channels. In a number of countries

fiscal authorities outright opposed any proposal from environmental authorities involving the introduction

of selective environmental taxation or charges. In the two countries that attempted to introduce “market-

based” environmental instruments at the national level (water pollution charge in Colombia, and payment

for environmental services in Costa Rica) environmental authorities found more resistance in recouping

charges from public entities (municipal sewerage authorities in Colombia, and the public electric utility in

Costa Rica) than from private industry and individual users.

The barriers faced by environmental authorities vs. uncooperative fiscal bureaucracies, and other public

entities within the same government in these Latin American cases, illustrate a different dynamic than the

traditional government vs. industry opposition to the introduction of environmental charges highlighted in

the literature. The detailed case studies in this dissertation show that Latin American environmental

authorities have been highly creative in working within existing constraints in the State apparatus, and the

high administrative coordination and information requirements involved in operating any system of

environmental policy instruments.

5

1.1 Market-based instruments in environmental policy The literature has noted the divergence between normative theory prescriptions for greater use of economic

instruments in environmental policy and actual policy practice in the U.S., the European Union and other

OECD countries. That observation has also motivated the growth of a fertile literature in the political

economy of environmental policy3, both in the U.S and Europe, rooted in several theoretical traditions that

attempt to explain social choices of regulation. These include rational choice, public choice (median voter

models), regulatory capture4, interest group competition for political influence5, among others.

More recently and particularly in the U.S, that literature has addressed the political interaction between

government and interest groups to explain environmental regulation and instrument choices, such as the

setting of standards, bureaucratic and industry preferences for direct regulation over taxation, state-level

regulatory choices in the U.S Federal context (i.e. environmental federalism) etc. The empirical literature in

the U.S and Europe has found evidence supporting the notion in these models that political interactions are

often an important determinant of environmental regulatory and policy instrument choices. Oates and

Portney6 point out the diverging paths this trend has taken in both side of the Atlantic, with Europe (in

particular Scandinavian countries, Germany, The Netherlands and Britain) turning first to environmental

taxes, and the U.S towards tradable emissions allowance systems for the control of SO2; arguing that the

reasons are not clear but might be related to the extreme aversion to new forms of taxation in the U.S. The

literature exploring topics of political economy of environmental regulation and instrument choice in the

context of developing countries is relatively scarce. In our opinion this approach is of more practical

interest and policy relevance to developing countries, than the theoretical debate on the direct regulation vs.

“market-based” instruments dichotomy that occupied wide attention during the 1990s.

3 For a comprehensive survey of this literature see reference by Wallace E. Oates and Paul R. Portney “The Political Economy of Environmental Policy”, in Handbook of Environmental Economics. Volume 1, eds. Karl Goran Maler, Jeffrey Vincent (Elsevier, 2003). 4 George J. Stigler, “The Theory of Economic Regulation,” Bell Journal of Economics and Management Science, vol. 2 (1971). 5 Gary Becker, “A Theory of Competition among Pressure Groups for Political Influence.” Quarterly Journal of Economics no 98 (1983). 6 Wallace E. Oates and Paul R. Portney “The Political Economy of Environmental Policy”, in Handbook of Environmental Economics. Volume 1, eds. Karl Goran Maler, Jeffrey Vincent (Elsevier, 2003).

6

For the purpose of this dissertation we use the broad definitions of economic and/or “market-based”

instruments as categorized by Theodore Panayotou and Robert Stavins respectively, both authors have

systematized in their publications the broad repertoire of these instruments as used in environmental policy.

According to Stavins: “Market-based environmental policy instruments are regulations that encourage

behavior through market signals rather than through explicit directives regarding the specific level of

pollution control or methods that the regulated agents must comply with”.7

Earlier Panayotou defined economic instruments for environmental policy even more broadly: “Any

instrument that aims to induce a change in behavior of economic agents by internalizing environmental or

depletion cost through a change in the incentive structure that these agents face (rather than mandating a

standard or a technology) qualifies as an economic instrument”.8

For our purposes the terms “market-based” instruments, and “economic” instruments are equivalent and are

used interchangeably in the text. Pollution charges and tradable permits are the stereotypical examples of

market-based instruments. When properly designed and implemented they create economic incentives at

the margin that encourage firms and/or individuals to undertake pollution control efforts in their own

interest, and that in the aggregate also contribute to meet social environmental policy goals at reduced

collective costs. The above authors’ categorizations include pollution taxes/charges, tradable permits and

cap-and-trade systems, effluent charges, deposit-refund systems, user charges, insurance premium taxes,

sales taxes, administrative charges, and tax differentiation systems which includes credit, tax cuts and

subsidies for environmentally desirable behavior. Robert Stavins’ categorization of “market-based”

instruments also includes market creation (establishment of water rights markets, and restructuring of

electric power markets with environmental impacts), information programs (labeling/certification,

environmental performance reporting/disclosure), liability rules, and reduction of government subsidies for

activities with adverse environmental impacts. The first section of the literature review in Chapter 2,

7 Robert Stavins. “Market-Based Environmental Policies”, in: Public Policies for Environmental Protection, P. Portney and R. Stavins, eds., Resources for the Future, Washington D.C (2000). 8 Theodore Panayotou. Instruments of Change: motivating and financing sustainable development, UNEP, (UK: Earthscan publications, 1998).

7

explains these instruments in detail, as well as their applications in environmental policy. Table 3.1 in the

methodology Chapter 3, provides a detailed taxonomy of the instruments included in the scope of the

national surveys undertaken for this dissertation.

The theoretical promise of “market-based” instruments is based on the fact that regulatory flexibility across

heterogeneous agents is required for cost-efficient achievement of social environmental goals. In general

environmental regulation proceeds in practice by authorities first establishing a certain policy goal (such as

for example achieving a certain ambient air quality standard, or reducing annual pollutant emissions by a

specific amount etc.), and then appropriate instruments must be designed and applied in practice to attain

the established policy goals at reasonable costs to society. Herein lies the attractiveness of greater reliance

on “market-based” environmental policy for its cost minimizing properties. In theory the flexibility

introduced by “market-based” instruments should enable the attainment of the established environmental

goal at the least possible aggregate cost, by allocating the overall burden across agents in the most efficient

manner. It is perhaps these cost-efficient properties, rather than theoretical welfare maximization through

internalization of externalities, that make “market-based” environmental policy relevant.

Providing increased flexibility is particularly important when aggregate environmental goals must be

attained through collective efforts by highly heterogeneous economic agents and sectors, each confronting

widely different marginal cost structures for pollution abatement. This is the case for example of CO2

emissions reduction in the context of climate change mitigation. Achieving an aggregate national goal of

reducing “X” amount of CO2 emissions at the least possible cost, requires that those agents facing lower

costs per ton of CO2 emissions reduction undertake more abatement, than other agents facing higher per

unit costs. In this context, a cap and trade system could be used to establish the aggregate CO2 emissions

cap and enable economic agents to buy and sell their CO2 emission allowances depending on whether their

own marginal CO2 abatement costs are below or above the market price for emission allowances. Firms

with lower CO2 abatement costs have an incentive to reduce emissions as much as possible and sell their

excess allowances for profit. The demand in this market for CO2 emission allowances is provided by firms

8

facing the opposite marginal cost situation, where it is cheaper to purchase CO2 emission allowances to

comply with the regulation than undertaking costly emission reductions.

The same flexibility can also be introduced by imposing a CO2 tax per unit ton of emissions. In this case

firms opt between undertaking in-house emission reductions, or paying the tax for their emissions, based on

their individual cost structures for pollution abatement. In both instruments the incentives for aggregate

cost minimization are the same. The only difference being that the emissions tax rate, or “price” per unit of

emissions, is imposed by the regulator; whereas in the cap and trade instrument the emission allowance

“price” is determined by the market and the regulator imposes only the cap, or overall “quantity” of

emissions allowed in a given period. Note that if the regulated community consists of homogeneous agents

facing identical cost structures for CO2 abatement (i.e. identical technology and processes), the rationale of

providing flexibility for aggregate cost-minimization through cap and trade, or emissions tax instruments,

disappears. If all regulated agents face identical cost structures, the flexibility afforded by these economic

or “market-based” environmental instruments is inconsequential, and the same result can be achieved

through direct regulation mandating all agents to abate the same “x” quantity of emissions across the board.

Pollution control is not the only environmental policy application of these types of instruments, they are

also applied to rationalize the use of natural resources and environmental services (water use charges,

environmental taxes on energy, forestry, mining etc.), or to create positive incentives for the conservation

and/or enlargement of forests and other stocks of natural capital providing spillovers in the form of

ecosystem services. Stavins’ categorization fails to include subsidies for investments or other activities with

positive environmental spillovers, however, we do not subscribe to that view. In Latin America and the

Caribbean countries reforestation subsidies have been used effectively and have a long standing tradition,

more recently many countries have also incorporated various forms of subsidization schemes for pollution

control and cleaner production investments into their policy packages. More widely, several countries such

as Germany and Spain have used feed-in tariffs successfully to begin incorporating renewable power

generation (i.e. wind, solar etc.) into national electric power markets. Chile has recently begun

experimenting with this instrument. On the other hand, agricultural and energy subsidies typically induce

9

negative environmental spillovers, and their modification must be considered within any comprehensive

initiative seeking to improve national policy coherence with declared environmental goals.

1.2 Motivation of Research Latin America offers an interesting opportunity for the empirical research of the application of

environmental policy instruments, as well as the policy dynamics driving instrument choice, instrument

implementation, and their final policy outcomes. The region is characterized by natural resource and

environmental endowments of global significance which continue to suffer well documented environmental

degradation that imposes high social costs on society at both the global, national and local levels9. During

the last two decades valuation studies of the social costs of environmental degradation have been

undertaken in several countries in the region (most notably on the public health costs of air and water

pollution)10. These studies have demonstrated that the social costs of environmental degradation are not

negligible and may increase under a business as usual scenario. Moreover the region’s comparative

advantage and its insertion in world trade is concentrated in agricultural, mining and oil exports, all of

which are natural resource based and highly environmentally sensitive industries. Given these regional

characteristics, it seems clear that Latin American countries’ policies to ensure sustainable development

and exploitation of their natural and energy resources are key to their long term economic performance and

development prospects.

During the 1990s Latin America underwent a decade of liberal economic policy reforms undertaken in

many countries to recover from the 1980s debt crisis with various degrees of success. The standard reform

package advocated by Washington-based institutions at the time, such as the International Monetary Fund,

World Bank, and U.S. Treasury Department, was codified by Williamson (1990) in ten major points and

termed the “Washington Consensus”11. Alongside fiscal discipline, open trade and capital account

9 United Nations Environment Program. “The State of the Environment. Latin America and the Caribbean”, in Global Environment Outlook 2000. (Nairobi: UNEP, 2000). 10 Larsen, Bjorn. “Cost of Environmental Damage: a socio-economic and environmental health risk assessment.” Prepared for Ministry of Environment, Housing and Land Development. ( Republic of Colombia: MAVDT, July 2004). 11 Williamson, John, ed., Latin American adjustment: how much has happened? (Washington, DC: Institute for International Economics, 1990). 29. Williamson, John, “What Should the World Bank Think about the Washington Consensus?” The World Bank Research Observer, 15(2), (World Bank, August 2000), 251-64. World Bank, Economic Growth in the 1990s: Learning from a Decade of Reform, Washington, DC, World Bank, 2005.

10

integration into world markets, increased deregulation and market competition, the dictum of “getting

prices right” pervaded new policy directions in both macroeconomic and sector level policies (i.e.

agriculture, energy etc.). At the sector level “Washington Consensus” reforms emphasized the removal of

existing price distortions, revision or dismantling of subsidies, simplification of tax structures, and the

general revision of public expenditure policy to reduce deficit spending and increase fiscal receipts.

The reform process also included substantial changes in the regulatory frameworks governing strategic

sectors like energy, electric power, water, mining and transport. Existing public monopolies and

infrastructure tasks were opened to increased competition and private investment. These changes included

dismantling of previous incentive structures driven by past regulatory choices and moving towards

“market-oriented” regulatory regimes designed to attract private investments into these sectors, as the

State’s role decreased. To what degree the revision of price distortions undertaken during the 1990s reform

period contributed to dismantle perverse incentives and to reduce market and policy failures behind

environmental degradation remains an open question.

The early ‘90s were also marked by the Earth Summit in Rio (UNCED 1992). The heavily publicized and

participatory multilateral process leading up to the United Nations Conference on Environment and

Development in Rio succeeded in engaging governments and civil society in a boom of environmental

policymaking inspired by the principles of Agenda 21. Following this, a majority of Latin American and

Caribbean countries enacted General Environmental Laws or Acts in the 1990s which included mandates to

internalize the social costs of environmental externalities in the price system through a variety of policy

instruments. These general environmental laws were modeled along the conceptual principles of Agenda

21, including the “polluter-pays-principle” and the mandates to address both “market failures”

(environmental externalities in this case) and “policy failures” (perverse incentives in current policies) in

order to achieve national environmental goals. The ongoing legislative activity throughout the nineties, also

established or significantly strengthened, the institutional standing of environmental agencies charged with

executing the new legal mandates at the national and state/provincial levels, elevating them in many cases

to the ministerial level.

11

During most of the 1990s and beyond, several international agencies such as the World Bank and UNDP,

openly advocated for greater use of economic instruments and “market-based” environmental policy in

developing countries12 extolling their theoretical advantages over direct regulation. This advocacy called

attention to the increased flexibility afforded by “market-based” instruments in contrast to more rigid

command and control regulation. In theory this increased flexibility would enable economic agents (i.e.

firms, consumers, etc.) to find the most cost-effective means to comply with environmental policy goals. It

would also encourage innovation to find cheaper and more efficient production/consumption alternatives as

firms and consumers seek to reduce the costs imposed by having to pay pollution charges/taxes from

continuing business-as-usual practices. Applying the “getting prices right” dictum to further environmental

policy goals, in the sense of harnessing price-signals and economic incentives to promote changes in the

behavior of economic agents towards improved environmental performance, made intuitive sense.

Another aspect of “getting prices right” related to the removal of existing economic distortions inherited

from previous price controls, subsidies, import tariffs and quotas, discriminatory tax structures etc. Energy,

water and agricultural subsidies in many cases contribute perverse incentives that tend to exacerbate

environmental degradation. For example the reduction of subsidies on dirtier fuels and fuel/electricity

prices in general would tend to encourage greater efficiency in energy use and substitution towards cleaner

fuel alternatives. It makes environmental sense to adjust marginal tax structures so that the final consumer

price of dirtier fuels at the pump, does not enjoy a cost advantage over cleaner alternatives. The same

12 World Bank. Five Years After Rio: Innovations in Environmental Policy. (Washington DC: World Bank, 1996). World Bank. Greening Industry: New Roles for Communities, Markets, and Governments. (New York: Oxford University Press, 2000). Theodore Panayotou. “Economic Instruments for Environmental Management and Sustainable Development.” Paper prepared for the UN Environment Program, Environmental Economics Series Paper no. 16 (1994).

Rio Declaration on Environment and Development: Principle 16

'National authorities should endeavor to promote the internalization of environmental costs and the use of economic instruments, taking into account the approach that the polluter should, in principle, bear the cost of pollution, with due regard to the public interest and without distorting international trade and investment.'

Source: UN, UNCED 1993

12

applies for dirtier vs. cleaner13 power generation competing in electricity markets. The removal or

reduction of agrochemical subsidies and other agricultural policy incentives promoting continued

expansion of crop land use into forested areas, would also tend to have positive environmental effects. For

example in rationalizing fertilizer/pesticide use contributing to reduce surface water pollution from

agrichemical run off. Removal of subsidies and tax incentives for continuous expansion of crop land would

tend to encourage greater soil conservation efforts and reduced deforestation by readjusting incentives

towards agricultural intensification rather than crop land expansion.

Aside from these theoretical advantages for improving economic efficiency, the revenue collected from

greater use of ”market-based” environmental instruments could offer new sources of public revenue either

for general fiscal use or earmarked for public environmental investments, or partial self-financing of

national environmental management costs. It was also argued that increased reliance on “market-based”

instrument price-signals could save public resources by reducing the need for widespread compliance

monitoring and enforcement efforts, as required by widespread “command-and-control” environmental

regulations.

These are no doubt attractive features from the perspective of both fiscal and environmental authorities

facing chronic budget deficits. Although in hindsight the supposed administrative and enforcement cost

advantages of “market-based” environmental instruments over “command-and-control” regulation have

failed to materialize. In general the intensity of information, monitoring and enforcement resources

required for the effective operation of “market-based” environmental instruments has been shown to be as

demanding, if not more, than traditional “command-and-control” environmental regulation.

A key element of the “Washington Consensus” policy reform package had to do with ensuring fiscal

balances and expanding public revenue bases. In this context the theoretical argument for increased

taxation of “bads” such as environmental pollution seem to fit very well. International agencies’ advocacy

13 Dirtier vs. cleaner power refers here to electricity generation fueled by coal, fuel oil, diesel etc.(dirtier) vs. natural gas, hydro, other renewable energy sources such wind and solar, new clean coal technologies etc. which are relatively cleaner.

13

for introducing these types of instruments paralleled the overt “neo-liberal” bias in development policy

circles and the academic literature that characterized the nineties decade. It was only natural that the newly

emergent environmental policy-making were also permeated by this general optimism for market-based

policy advocacy, increased reliance on price-signals for resource allocation, scale-back of regulation, and a

reduced State role. The following developments through the 1990s lead one to expect that Latin American

countries would have moved to deploy “market-based” environmental policy instruments to internalize, at

least partially, the social costs of environmental degradation in the price system

Given that a decade has passed since these developments in Latin America, an empirical assessment of

policy outcomes constitutes a legitimate research goal. Clear legal mandates to do so have been in place

since the early 1990s, or earlier, in most countries; as evidenced by the incorporation of the “polluter-pays-

principle” in general environmental laws, and/or specific regulation mandating the application of economic

instruments by environmental authorities to internalize environmental costs.

a) Documentation of the social costs of environmental degradation and their economic impact has been

growing in the region during the same period and is widely available to political authorities.

b) During the 1990s most environmentally sensitive industry sectors (energy, agriculture, forestry,

mining, transport etc.) also underwent significant reforms in their regulatory framework oriented

towards deregulation, an increased role for private investment, greater international competition, and

alignment of domestic and international price signals.

The expectation to find evidence of actual application of policy instruments aligned with environmental

cost internalization14 is also well grounded in welfare economics, rational choice policy-making, and the

theory of environmental externalities. From a theoretical perspective polities of rational individuals

14 Environmental cost internalization through Pigouvian taxes, and/or optimum pollution charges, in the strict sense demanded by welfare economics theory, involves the economic valuation of environmental externalities. The informational requirements for the economic valuation of environmental externalities are enormous and presents severe analytical complications. In practice environmental charges on previously un-priced pollutant streams achieve partial cost internalization which can be adjusted through iterative adjustment process of charge levels as information is revealed.

14

incurring negative spillovers from private production and consumption decisions, would mobilize to correct

these market failures through the various institutionalized means at their disposal.15

1.3 Statement of research objectives This dissertation attempts to:

1) Assess the extent of implementation of “market-based” environmental policy instruments in Latin

America since 1990;

2) Identify plausible independent variables or factors associated with the observed instrument

implementation outcomes (dependent variable); and

3) Discuss Latin American findings in contrast with relevant literature on the application of “market-

based” environmental policy in general to derive possible policy implications.

15 For a survey of literature on the economic valuation of environmental externalities, and its application to cost/benefit analysis in public policy decision-making please refer to: Maureen Cropper and Wallace Oates. “Environmental Economics: A Survey”. Journal of Economic Literature, Vol. XXX (June 1992), pp. 675-740.

15

1.4 Research questions The following research questions were prepared as means to attain the above research objectives:

1) To what extent have “market-based” environmental policy instruments been implemented in Latin

America? What instrument choices have countries made to address environmental externalities16 in the

region? What implementation outcomes were obtained from attempts to introduce “market-based”

instruments into the environmental policy mix? (method: national surveys were undertaken on the

extent of implementation and outcomes).

2) What variables or factors can be identified with plausible explanatory power to account for the

observed implementation outcomes? What characterized the implementation process of “market-

based” environmental instruments? What barriers and political/institutional context did environmental

authorities face? (method: process tracing of instrument design and implementation processes for each

case).

3) Are the implementation outcomes and associated variables observed in Latin American and Caribbean

countries, any different from those reported in the literature on “market-based” environmental

instruments at the international level? This literature has tended to emphasize weak institutional

capacity and poor enforcement as major factors associated with poor environmental policy outcomes.

Are there any (method: case studies analysis and comparison with literature)

1.5 Overview of dissertation contents and main results The first part of the dissertation assesses the extent of implementation of “market-based” policy instruments

that has taken place in Latin America since the 1990s, the decade when a majority of countries in the region

embarked in widespread economic policy reforms. This task was accomplished through national surveys

that documented 81 cases of “market-based” instruments in thirteen countries17. The national surveys

16 Externalities are spillovers or side-effects of production/consumption activities that impact the welfare of third parties that are not part of the transaction, or society in general. These external costs/benefits imposed on third parties, or society in general, are not reflected in the price signals that drive individual market transactions and private production/consumption decisions. 17 These surveys and case studies were made possible by virtue of their being incorporated as part of two U.N ECLAC policy research and capacity building projects which the author developed and held main responsibility for during 2000-2004. Survey reports and case study data were prepared in each country by national consultants selected jointly between U.N ECLAC and the national environmental authority acting as counterpart for the purposes of the project. The writing of national survey reports and case studies was supervised by the author and edited for publication by U.N ECLAC as project outputs. Each case study was published separately under the national consultant name as a U.N ECLAC project publication, the detailed references are included in the bibliography.

16

focused on documenting the implementation process of all cases of “market-based” instruments (i.e. taxes,

charges, subsidies, tradable quotas, etc.) applied towards environmental policy goals in each country for

which information was available.

Chapter 2 surveys relevant literature for the dissertation research objectives. The literature review is

organized in three parts. The first part explains in detail the various types of policy instruments which

comprise the broad categorization of “market-based” environmental instruments. The second part covers

the normative theory relevant to “market-based” instrument design and instrument choice as applied in

environmental policy. The last part covers relevant literature on both OECD and developing countries’

experience with the application of “market-based” instruments, and international trends regarding their use

in environmental policy. This section also covers selected topics from the literature on the political

economy of “market-based” environmental regulation, fiscal-environmental federalism literature, and

policy instrument mixes in second best settings; which are relevant to understand the complex institutional

and political context in which Latin American environmental authorities attempt to implement “market-

based” instruments.

Chapter 3 covers the methodology and data acquisition procedures that resulted in the data set of 81

instrument cases, was well as the methods used in the analysis of this data set in light of the three research

objectives of the dissertation. The methods chapter also explains the procedures devised for coding both

dependent variables (instrument implementation outcomes) and plausible independent explanatory

variables in the data set. As well as how these coded variables were interpreted and analyzed, within and

across cases, to arrive at conclusions. The case selection rationale for further in-depth analysis in the last

part of the dissertation is also presented.

Chapter 4 is the core analytical chapter of the dissertation. The analysis of the n=81 data set is organized in

three sections. The first two sections focus on determining the extent of implementation of “market-based”

instruments in the region, and describing the outcomes and instrument choices observed in the data set

(research objective 1). The third section of the chapter focuses on the identification of plausible

17

independent variables or factors associated with the observed implementation outcomes (research objective

2). Contrary to 1990s expectations that the introduction of “market-based” instruments could achieve rapid

improvements in environmental policy outcomes, their actual implementation in Latin America seems to

have been hindered by a variety of factors exogenous to environmental authorities themselves. Nearly half

of the cases documented for this dissertation make reference to lack of cooperation by fiscal authorities and

between levels of government within the State structure (i.e. national, state, municipal) as playing an

important role in explaining poor implementation outcomes. The main findings and patterns identified in

the data set are summarized and interpreted.

Chapter 5 is a case study on the implementation of a national level water pollution charge in Colombia.

This case illustrates in detail the institutional and political context in which the implementation of “market-

based” environmental instruments operate in the region. This experience illustrates the complex

interactions with fiscal authorities, public finance, and municipal infrastructure constrains, that

environmental authorities confront in their attempts to introduce “market-based” instruments into the

existing regulatory structures.

Chapters 6 discusses findings and draws conclusions and general policy implications. Findings indicate that

environmental authorities operate in Latin American countries in complex political and institutional

contexts, where “market-based” instrument implementation outcomes depend on the orchestration of a

wide range of incentives across multiple bureaucracies and public agencies (horizontal coordination), and

between the national/state/and municipal levels of government (vertical coordination). The data shows that

Latin American countries have not shied away from experimenting with “market-based” environmental

instruments, but the implementation outcomes obtained have been conditioned by policy interactions

largely exogenous to environmental authorities. The main findings are compared with relevant literature

(research objective 3).

18

CHAPTER 2. Literature Review

It should be a sobering fact to economists that their policy recommendations are so seldom adopted. Incentive policies, such as taxes and subsidies are the typical prescriptions of economists for the problem of environmental degradation. These policies are designed to bring private and social costs more in line with corresponding benefits via the price system. Economists are seldom makers of public policy; equally seldom do we find that the gainers compensate the losers. We find numerous alternatives proposed in an attempt to eliminate pollution and environmental deterioration. These politically motivated solutions are quite different from those suggested by the economist….. ….….The reason is quite straightforward. The efficiency criteria of the economist play little of no part in political decision making. Any lawmaker who did decide public policy by such criteria would not survive long in office.

Douglass C. North , “Political Economy and Environmental Policies” Environmental Law Journal 7, (1976-1977): 449-462,

The literature review has been organized in three sections centered around the following points: a) What are

“market-based” environmental instruments, and how are these instruments applied to support

environmental policy objectives?; b) What is the normative theory that informs their design and

application?; and c) What political economy implications have been identified in the literature on

environmental regulation and instrument choice in developing countries?. The first section describes in

more detail the various types of “market-based” instruments applied in environmental policy according to

their definition in OECD Environment Directorate publications. It is useful to review these definitions since

the OECD maintains the largest international cross-country databases on the use of environmentally related

policy instruments and these are categorized according to the organizations criteria. The second section

covers topics in normative theory related to the design of environmental taxes and charges. The third

sections covers relevant points from the political economy literature of environmental regulation, and

international organizations publications (i.e. OECD, World Bank, Inter-American Development Bank etc.)

regarding policy trends in the application of “market-based” instruments in OECD countries and in Latin

American and Caribbean region..

2.1 Taxonomy of “market-based” instruments in environmental policy

There is no standardized definition for “market-based” instruments. Earlier treatments of the role of

economic instruments in environmental policy emphasized the alignment of private costs with social costs

to reduce externalities. In theory, economic instruments can be used as a complement or substitute for other

environmental policy instruments, such as direct regulation through mandatory compliance with

19

environmental standards, fines for non-compliance, licensing of industrial operations based on specific

parameters of environmental performance, strict liability for environmental damages (i.e. tort law). In

practice, the use of economic instruments in environmental management has not reduced the need for

standards, controls, sanctions and other forms of direct governmental intervention. In industrialized

countries this type of instrument is being increasingly used to complement the traditional regulatory

framework. The rationale for their introduction is to introduce flexibility into the regulatory mix to enable

efficiency gains, provided that : (a) the regulated agents are able to minimize their individual cost of

complying with environmental standards or mandatory targets, and (b) that national environmental and

pollution reduction objectives have successfully been reoriented to encompass cost-efficiency criteria,

which requires flexible allocation of the burden of attaining environmental quality goals flexibly across

economic agents to minimize the overall cost to society.

The use of economic instruments in environmental management has had a slow but continuous evolution

since the early 1970s, when the most industrialized countries began to develop their environmental policies.

Since then the tendency has been towards increasing the variety of instruments used in environmental

policy. Whereas charges for the use of natural resources (user charges) were already common in the 1970s,

other types of environmental charges for the control of air, water, soil, solid waste and noise pollution have

seen increasing application since the early 1990s in several OECD18 member countries.19

Apart from charges and taxes for the use of natural resources, or per unit volume of pollution released into

the water or air, other types of have also appeared, such as deposit-reimbursement schemes to promote

emergence of recycling markets, environmental performance labeling and certification. Environmental

performance certification and labeling has been gaining importance in several European countries and the

U.S. International certification schemes on the sustainable production of tradable commodities such as

tropical timber, and agricultural exports, are also increasingly influencing consumer preferences and the

market access of environmentally sensitive commodities exported to OECD markets. As industrialized

18 OECD stands for Organization for Economic Cooperation and Development, which encompasses the more industrialized economies and a number of developing countries (European Union member countries, USA, Japan, Korea, Australia, New Zealand, Mexico, among others). 19 Jean Philippe Barde, The use of economic instruments for environmental protection in OECD countries, Organization for Economic Cooperation and Development (Paris: OECD, 1992).

20

countries adopt stricter environmental and energy/fuel efficiency standards, and international certification

and labeling schemes of environmentally sustainable production proliferate; they are also becoming key

drivers of environmental investments and cleaner technology adoption in the export sectors of developing

countries increasingly preoccupied with maintaining access to discriminating OECD markets.

The following sections provide a brief description of the different types of instruments used within the

context of environmental management following the definitions developed in the OECD Environment

Directorate publications.

2.1.1 Environmental taxes

The 1990s saw the increasing use of taxes linked to environmental parameters. This environmental tax

reform has proceeded along three complimentary lines: (a) the introduction of new taxes, generally applied

on products with harmful environmental externalities (e.g., pesticides, fertilizers, automotive vehicles,

hazardous waste, etc.); (b) the restructuring of certain existing taxes on relevant environmental sectors (e.g.,

transportation and power) to incorporate an environmental element, as occurred in the case of the so-called

carbon tax that is applied to different types of fossil fuels; and (c) the modification or elimination of

subsidies and tax exemptions on activities that are potentially damaging to the environment (e.g.,

agricultural subsidies, tax exemptions for the transportation sector, etc.). Some industrialized countries are

in the process of studying the feasibility of even more ambitious “green” fiscal reforms. These would

mainly entail displacing part of the fiscal charge that currently falls on capital and labor factors (for

example, through the reduction or elimination of taxes on profits, capital goods, labor contributions, etc.)

and compensating for the lost revenues through the introduction of new taxes on environmentally harmful

activities, while being careful not to raise the total tax burden of the productive sector.

2.1.2 Charges

Charges are defined as payment for the use of environmental resources, infrastructure and/or services.

Three main types of charges are used in environmental management: emissions charges, user charges and

impact charges. Each category can be further subdivided as follows.

21

Emissions charges

Emissions charges are levied based on either the flows of pollutants or waste produced in the course of

certain activities and released into different media (e.g., air, waterways or land) or the amount of solid

waste. Examples include:

• emissions charges for atmospheric pollution;

• hazardous waste charges;

• other waste disposal charges; and

• charges on effluents discharged in waterways.

User charges

Examples of user charges include the following:

• sewage and water use charges;

• charges for the use of municipal waste collection and treatment services;

• charges for the use of electricity and/or power in critical areas; and

• charges for access to parks, beaches and protected areas.

Impact charges

Impact charges seek to internalize the external costs to the environment and/or scenery that are associated

with certain types of private investment, such as construction, tourism, industrial development, etc.

Examples:

• noise pollution charges for take-off and landing cycles (airplanes); and

• charges per square meter of construction or development in critical areas.

2.1.3 Tradable permit systems Tradable permit systems have mostly been applied in the United States, where they have been used

primarily to control atmospheric pollutants, particularly SO2 and, regionally, CO2 emissions.20 Such

systems establish an aggregate level of emissions allowed for each air quality control zone. The total

emissions cap is then distributed among the different sources either by auction or allocated in accordance

20 This type of system is also used to rationalize exploitation in designated fishing areas, whereby the fishermen receive tradable permits granting them the right to limited annual quotas. The aggregate total quota should not surpass the level of exploitation that the fishing grounds can sustain, which is determined by the schools’ annual capacity for regeneration.

22

with their volume of production or current volume of emissions. Because the total quota is set below the

current level of emissions, the permits acquire a positive value, and the different polluting agents can trade

them on the market. The different agents trade their permits with the objective of minimizing their

individual cost of reducing emissions at the same time that they comply with the goal imposed by the total

quota. If the marginal cost of reducing pollution is lower than the market price of the permits, the firm has

an incentive to reduce emissions and sell surplus permits. If, on the other hand, the marginal cost of

lowering pollution is greater than the price of the permits, the polluters will be forced to purchase additional

permits to continue operating at the same level of production.

2.1.4 Deposit-reimbursement schemes Deposit-reimbursement schemes have traditionally been used in relation to bottles for beverages. In recent

decades they have also been used for products such as car batteries, pesticide containers, household goods,

lubricants and other products that could represent eco-toxicological or public health risks if they were not

disposed of properly.

2.1.5 Fines for non-compliance with standards Provisions for levying fines on the basis of infringement of environmental standards are common in both

industrialized and developing countries. The application of fines rarely makes any real difference in the

budget estimates of regulated companies, however. In order to generate an effective economic incentive,

the amount of the fine should be significant or at least greater than the economic savings implied by

postponing the investments necessary to comply with the standard.

OECD member countries employ different systems of fines for noncompliance with environmental

standards. Some examples are shown in table 1, which outlines the different areas of application, methods

for calculating the fine, applied rates and the number of times the fine is imposed. There are basically two

methods for calculating the fine. One method consists in calculating the amount of environmental damage

caused by the regulated agent’s noncompliance with the standard. The second method is based on the

magnitude by which the legal limit of pollution has been exceeded.

23

2.1.6 Environmental performance bonds Systems based on environmental performance bonds seek to shift the responsibility for controlling,

monitoring and enforcing compliance with standards onto the individual producers and consumers by

charging them in advance for potential damages21. If the productive activity or product is completed

without causing damages, then the regulatory body returns the amount deposited as a performance bond.

Environmental performance bonds can guarantee the following, for example: that companies which extract

resources and which are potential sources of pollution take appropriate measures to minimize the