Mobile Enterprise Name Institution Date Running Head: MOBILE ENTERPRISE

Upload

independentCategory

view

3download

0

Presented to Asian Development Bank 6 ADB Avenue, Mandaluyong City 0401 Metro Manila The Philippines Team Members: Lord, Montague, Team Leader / PSD & SME Development Expert Ehmann, Markus, SME BDS Expert Slee, Laurence, SOE Privatization and Restructuring Expert Waheed, Mohamed, PSD and SME Development Expert Sattar, Shafeenaz, SME Financing Specialist Hussain, Hisaan, Legal Specialist

30 September 2007

M A L D I V E S

Preparing the Small and Medium Enterprise Development Project

TA 4745-MLD

TA 4745-MLD: SME Development Project – Draft Final Report

iv

TABLE OF CONTENTS

0. LOAN AND PROJECT SUMMARY viii I. THE SECTOR: PERFORMANCE , PROBLEMS, AND OPPORTUNITIES 1

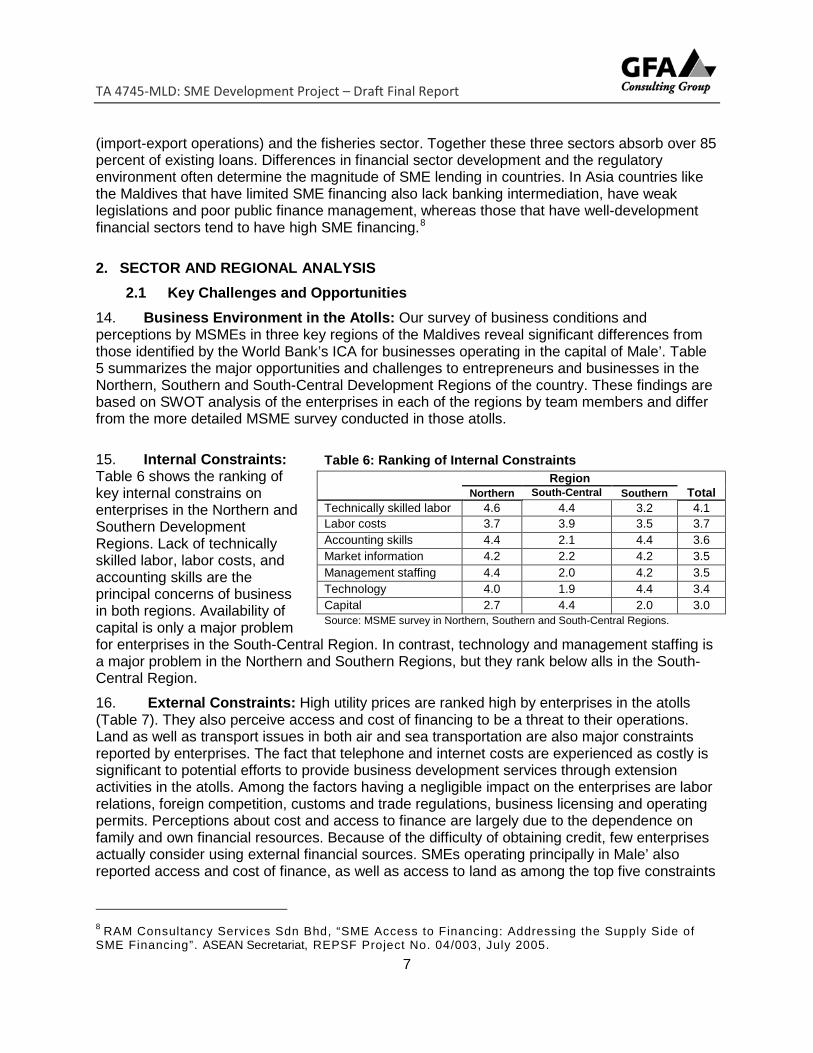

1. ECONOMIC AND REGULATORY CONTEXT 1 1.1 CHARACTERIZATION OF THE SMALL ISLAND ECONOMY 1 1.2 INTERNATIONAL COMPETITIVENESS 3 1.3 BUSINESSES REGULATOR ENVIRONMENT 4 2. SECTOR AND REGIONAL ANALYSIS 7 2.1 KEY CHALLENGES AND OPPORTUNITIES 7 2.2 GOVERNMENT STRATEGY FOR PRIVATE SECTOR DEVELOPMENT 11 2.3 EXTERNAL ASSISTANCE TO SECTOR IN THE ATOLLS 14

II. PROPOSED SECTOR DEVELOPMENT PROJECT 16 3. PROJECT COVERAGE AND IMPLEMENTATION PROCESS 16 3.1 OBJECTIVES, SCOPE AND STRATEGY 16 3.2 TARGETED SECTORS FOR SME DEVELOPMENT 18 3.3 TARGETED REGIONS FOR SME DEVELOPMENT 21 3.4 INSTITUTIONAL DELIVERY MECHANISM 22 3.5 POLICY AND REGULATORY FRAMEWORK 25 4. KEY FEATURE: BUSINESS DEVELOPMENT SERVICES 28 4.1 EXISTING SITUATION IN THE MALDIVES 28 4.2 CLUSTER DEVELOPMENT STRATEGY 28 4.3 ORGANIZATIONAL STRUCTURE 29 4.4 CAPACITY BUILDING 30 4.5 BDS CENTERS IN TARGET REGIONS 31 4.6 TECHNICAL ASSISTANCE AND PROJECT COSTING 33 5. KEY FEATURE: COST SHARING FACILITY 35 5.1 OBJECTIVE AND COVERAGE 35 5.2 OPERATIONAL FEATURES 38 6. KEY FEATURE: CREDIT GUARANTEE FACILITY 40 6.1 FINANCING APPROACH 40 6.2 OPERATIONAL FEATURES 42 6.3 ORGANIZATION 43 7. FINANCING PLAN AND IMPLEMENTATION ARRANGEMENTS 44 7.1 FINANCING PLAN 44 7.2 PROJECT PERFORMANCE MONITORING AND EVALUATION 45

III. TECHNICAL ASSISTANCE 48 IV. PROGRAM BENEFITS, IMPACT AND RISKS 49 V. SOE RESTRUCTURING AND PRIVATIZATION 49

8. OBJECTIVES AND SCOPE 49 9. PUBLIC ENTERPRISE ANALYSIS 52 10. PROPOSED STRATEGY 55

TA 4745-MLD: SME Development Project – Draft Final Report

v

ANNEX A: DESIGN AND MONITORING FRAMEWORK 57 ANNEX B: GOVERNMENT STRATEGY FOR PRIVATE SECTOR DEVELOPMENT 60 ANNEX C: MSME SURVEY OF THREE REGIONS 63 ANNEX D: CLASSIFICATION OF ENTERPRISES 72 ANNEX E: EXTERNAL ASSISTANCE 74 ANNEX F: CREDIT GUARANTEE FACILITY 83 ANNEX G: BUSINESS DEVELOPMENT AND COST SHARING FACILITY 89 ANNEX H: IMPLEMENTATION ARRANGEMENTS 93 ANNEX I: REFERENCES 100

TA 4745-MLD: SME Development Project – Draft Final Report

vi

CURRENCY EQUIVALENTS (as of June 2007)

Currency Unit MRf. 1.00 = US$ 0.0774

US$ 1.00 = MRf. 12.92

ABBREVIATIONS

6NDP Sixth National Development Plan 7NDP Seventh National Development Plan ACDBP Atolls Credit and Development Banking Project ADB Asian Development Bank ADFs Revolving Credit Funds ADSL Atoll Development Project for Sustainable Development BCMW Building Construction and Mechanical Works BDS Business Development Services BML Bank of Maldives CIP Commercially Important Passenger EA Executing Agency EDU Enterprise Development Unit ESTP Employment Skills Training Project gdp Gross Domestic Product HIES Household Income and Expenditure Survey IAS Island Aviation Services Limited IATA International Air Transport Association ICA Investment Climate Assessment IDA International Development Association IFAD International Fund for Agricultural Development IFC Finance Corporation IGAs Income Earning Opportunities IMF International Monetary Fund IPO Initial Public Offering IWDCs Island Women’s Development Committees LC Letter of Credit MACI Maldives Association of Construction Industry MCPI Ministry of Construction and Public Infrastructure MEDT Minister of Economic Development and Trade MEL Employment and Labor MFLC Maldives Finance Leasing Company MMA Maldives Monetary Authority MHREL Ministry of Human Resources, Employment and Labor MOAD Ministry of Atolls Development MoCPI Ministry of Construction and Public Infrastructure

TA 4745-MLD: SME Development Project – Draft Final Report

vii

MOFAMR Ministry of Fisheries Agriculture and Marine Resources MOFT Ministry of Finance and Treasury MPL Maldives Post Ltd MRf Maldivian Rufiyaa MTCC Maldives Transport and Contracting Company MWASS Ministry of Women Affairs and Social Security NDB National Development Bank PE Public Enterprise PEMEB Public Enterprise Monitoring and Evaluation Board PPTA Project Preparation Technical Assistance PSD Private Sector Development PWC Public Works Corporation RDMOS Regional Development and Management Offices SADP Southern Atolls Development Project SIE Small Island Economy SME Small and Medium-Sized Enterprise SME-DP Small and Medium-Sized Enterprise Development Project SOE State Owned Enterprise STO State Trading Organization Plc SWOT Strengths, Weaknesses, Opportunities, and Threats TA Technical Assistance ToR Terms of Reference UN United Nations UNDAF United Nations Development Framework UNFPA United Nations Population Fund UNICEF United Nations Children's Fund UNV United Nations Volunteers WHO World Health Organisation

TA 4745-MLD: SME Development Project – Draft Final Report

viii

LOAN AND PROGRAM SUMMARY

Borrower Republic of Maldives

Proposal The proposal consists of a loan of US$6.9 million for the development of ‘The Maldives Micro, Small and Medium Enterprises Development Project Loan’, preceded by US$1.7 million for activities related to capacity building.

Classification Targeting classification: General intervention

Sector: Industry, agriculture, services and trade

Subsector: Small and medium enterprises (SMEs)

Themes: Sustainable economic growth, private sector development

Environmental Assessment

Category C

Social Sector Assessment

Category C: Involuntary resettlement

Category C: Impact on indigenous people

Program Rationale

The Maldives is a Small Island Economy (SIE) consisting of 26 natural atolls with a total land of less than 300 square kilometers spread over 900 kilometers. It has one of the fastest growing economies in the world, driven by its two leading sectors of tourism and fishing that has created linkages to other subsectors like local handicrafts, tourism-related activities and boatbuilding. Yet the benefits of economic growth have not been equitably distributed to the population at large. Decentralization of economic activity has been undermined by the lack of infrastructure, a poorly developed inter-island transportation system, financial system constraints to credit for businesses, and legal and regulatory barriers. Greater opportunities for people living in Male’ has produced a fourfold population expansion in the past 20 years, and it has given rise to a population density in Male’ that is among the highest in the world, a situation made all the more severe by the recent tsunami.

In an effort to ameliorate regional inequalities and reverse migration to the capital, the Government placed regional economic growth and diversification as a key objective of economic development in the Seventh National Development Plan (7NDP) for 2006-2010. As part of 7NDP, the Government is developing regional centers that are designed to have social and infrastructure facilities, and that will be complemented by focus islands on different atolls acting as atoll service hubs and growth centers. The focus islands identified under the 7NDP are to serve as growth centers, fostering employment and income generation opportunities by concentration of development efforts and provision of a higher level of infrastructure to achieve economies of scale. The Government expects that these efforts will reduce regional differentials and promote growth and employment opportunities outside of Male’.

Objective and Scope

The objective of the MSME Development Project Loan is to support the Government’s efforts to (i) develop the entrepreneurial climate and support services that will facilitate growth, (ii) provide the necessary conditions for converting existing entrepreneurial potential into innovative and successful business activities, (iii) attract entrepreneurial leadership from other regions of the country, and (iv) establish broader regional centers for SME activities that are

TA 4745-MLD: SME Development Project – Draft Final Report

ix

driven by growth nodes or networked clusters for supporting activities. To achieve the aforementioned objective, the project loan focuses on the following:

bolster human resource development by creating business development service centers that provide training programs in entrepreneurship, management, and technical skills for MSMEs and develop appropriate materials for such training, as well as help to identify commercial opportunities in specific sectors;

improve access to finance by developing innovative financing schemes using alternative financial instruments such as equity financing, while encouraging the development of cooperatives and associations;

promote a market-driven process through the public and private sector that in the short to medium-term will target specific types of activities in selected regions of the country; and

enhance the catalytic role of public sector for facilitating commercial activities in the atolls and strengthening MSME activities by improving the policy and regulatory environment.

The project framework is attached in Annex A.

Loan Amount and Terms

A loan of US$ 6.9 million with the guarantee of the Republic of Maldives from ADB’s ordinary capital resources will be provided under ADB’s London interbank offered rate (LIBOR)-based lending facility. Prior to the loan, US$ 1.7 million in assistance will support activities related to capacity building.

Counterpart Funds

The policy framework for the program includes specific components that bear distinct costs of structural adjustments and improvements in the regulatory environment. The Government will provided assurances that necessary funding will be made available to cover these costs.

Executing Agency Ministry of Economic Development and Trade (MEDT)

Risks and Assumptions

Risks include lack of Government capacity to implement program, and inadequate inter-ministerial coordination of private sector development initiatives.

Technical Assistance

The ADB will provide US$1,000,000 in 2008 to build the capacity for MSME development in the atolls. Under the loan and in 2009-2011 the Government will finance US$1.2 million of capacity building activities related to MSME development in the atolls. Support will be given for specific activities designed to (i) establish and sustain programs in the BDS centers, (ii) provide capacity building to the Enterprise Development Unit of the Ministry of Economic Development and Trade (MEDT) and business member organizations (BMOs), and (iii) ensure sustainable access to MSME financing.

TA 4745-MLD: SME Development Project – Draft Final Report

1

I. THE SECTOR: PERFORMANCE, PROBLEMS, AND OPPORTUNITIES

1. ECONOMIC AND REGULATORY FRAMEWORK

1.1. Characterization of the Small Island Economy

1. SIE Features: The Maldives is a Small Island Economy (SIE) consisting of 26 natural atolls with a total land of less than 300 square kilometers spread over 900 kilometers around the equator.1 There are 1,190 islands in the archipelago, of which 198 are inhabited by a population of 309,000.2 Only 28 islands have a land area greater than a square kilometer.3 Only four islands have a population greater than 5,000 people, and 70 percent of the inhabited islands have a population of less than 1,000 people. In addition to the inhabited islands, 87 islands have been designated and developed as tourist resorts, with an additional 11 islands currently being set aside for development. With a total land area of 2 square kilometers , the capital island of Male’ is home to a third of the population. It is the seat of the Government of the Maldives (Government) and the centre of commerce and business. Concentration of the population in the capital is growing, especially after the December 2004 tsunami destroyed the means of livelihood in many islands.

2. Special Challenges: The Maldives has a number of economic disadvantages similar to other SIEs that undermine the country’s international competitiveness. In small economies like the Maldives the percentage deviation of costs from a medium-size economy are over 70 percent for sea freight, nearly 50 percent for electricity and telephone service, more than 30 percent for both unskilled labor and fuel.4 In sectors like tourism, these high costs translate into a 60 percent overall increase in the cost of tourism, which can be passed onto the high-end consumer of tourism activities but are not readily transferable onto products like handicrafts, agro-industrial products and manufactured goods that compete in fairly homogeneous international product markets. From a policy perspective it does not suggest the need for protection against the rest of the world, but rather proactive policies that seek to overcome, or at least partially compensate for the economic disadvantages associated with the high production and trading costs.

3. Economic Growth: Despite its intrinsic competitive disadvantages, the Maldives has one of the fastest growing economies in Southeast Asia. Two sectors, tourism and fishing, have been the driving forces behind the expansion of Gross Domestic Product (GDP) and employment generation, and have created linkages to other subsectors like local handicrafts, tourism-related activities and boatbuilding. In 2006 the sharp rise in real GDP reflected a 1 For administrative purposes, these atolls are grouped in 20 atolls. 2 Based on 2002 census. 3 Most islands are part of large atolls that surround large lagoons, and all are low lying with none having an altitude higher than 1.8 meters above sea level. The surrounding barrier reefs act as natural protection for the islands from adverse weather conditions during the monsoon seasons. Although no official reference could be identified for the land-mass estimate, the 300 km2 figure is quoted in reports such as the UNEP State of the Environment Report and the FAO Agricultural (Horticultural) Crop Sector Report (FAO, 1994). More recent estimates based on satellite data estimate the area at 227.45 km2 (Naseer and Hatcher, 2004). 4 Based on a survey of SIE relative to other countries using the World Bank’s World Economic Indicators and Global Business Cost Survey, as well as the United Nations trade database (Comtrade), and reported in Winters (2003).

TA 4745-MLD: SME Development Project – Draft Final Report

2

resumption of growth following the devastation that occurred throughout the country as a result of the tsunami on 28 December 2004 (Table 1). The recovery has been largely driven by tourism sector and brings the country back to its steady-state growth path of around 6 percent a year. GDP per capita has expanded from US$ 2,094 in 2002 to an estimated US$ 2,757 in 2006, the highest in the South Asia region. The economy is largely driven by service industries, which account for about 79 percent of GDP. The main service industries, other than tourism, are real estate, wholesale and retail trade, transport and communications, government administration and financial services (Table 2).

Source: Ministry of Planning and National Development; Maldives Monetary Authority (MMA); and International Monetary Fund (IMF), World Economic Outlook database.

Table 2: Maldives Sectoral Contributions to GDP (percent), 2000 - 2005

2000 2001 2002 2003 2004 2005

Primary Sector 9.4 9.5 10.4 9.7 9.7 9.1 Agriculture 2.8 2.8 2.7 2.6 2.6 2.5 Fisheries 6.0 6.1 7.1 6.6 6.6 6.1 Coral and sand mining 0.6 0.6 0.6 0.6 0.6 0.6

Secondary Sector 14.4 15.1 15.6 15.6 15.6 16.1 Manufacturing 8.0 8.1 8.8 8.5 8.5 7.9

of which, fish preparation 2.1 2.3 3.0 3.0 2.7 2.5 Electricity and water supply 3.2 3.4 3.5 3.6 3.6 3.8

Construction 3.2 3.5 3.3 3.5 3.5 4.4 Tertiary Sector 80.1 79.3 77.9 78.6 78.6 78.8

Wholesale & Retail Trade 4.5 4.4 4.2 4.1 4.1 3.9 Tourism 33.0 31.9 30.9 32.7 32.7 32.3 Transport & communications 14.5 14.2 14.3 14.2 14.2 15.2 Financial services 3.4 3.4 3.4 3.3 3.3 3.2 Real estate 7.8 7.7 7.6 7.2 7.2 6.9 Business services 2.9 2.9 2.9 2.8 2.8 2.7 Government administration 11.8 12.7 12.6 12.4 12.4 12.8 Education, health and social services 2.2 2.1 2.0 1.9 1.9 1.8 Financial services, indirect measure (3.9) (3.9) (3.9) (4.0) (4.0) (4.0)

GDP total 100.0 100.0 100.0 100.0 100.0 100.0

Source: Ministry of Planning and National Development – Statistical Yearbook of Maldives 2006.

4. Regional Growth Inequalities: Notwithstanding the country’s high economic growth rates in the past ten years, the benefits of that growth have not been equitably distributed to the population at large. Average household income in the atolls is 55 percent of that in Male’, according to the 2002-03 HIES by the Ministry of Planning (2004). Decentralization of economic activity has been undermined by the lack of infrastructure, a poorly developed

Table 1: Maldives General Economic Indicators, 2000 - 2006 2002 2003 2004 2005 2006 GDP at 1995 constant price (USD mn) 546.3 593.0 649.4 613.5 693.3 Real GDP Growth (%) 6.5 8.5 9.5 -5.5 13.0 Population (thousands) 306 315 325 335 345 GDP per capita (USD) 2,094 2,197 2,482 2,350 2,757 Consumer price inflation (avg %) 0.9 -2.8 6.3 3.3 7.0 Current account balance (USD mn) -35.7 -32.0 -129 -287 -358 Exchange rate (avg Rf/USD) 12.8 12.8 12.8 12.9 13.0

TA 4745-MLD: SME Development Project – Draft Final Report

3

inter-island transportation system, financial system constraints to credit for businesses, and legal and regulatory barriers. Greater opportunities for people living in Male’ has produced a fourfold population expansion in the past 20 years, and it has given rise to a population density in Male’ that is among the highest in the world, a situation made all the more severe by the recent tsunami.5 Lack of infrastructure in the atolls, underdeveloped inter-island transportation, a lack of financial services, and legal and regulatory barriers have all contributed to the wide disparity in average per capita income of Male’, resorts and industrial islands, on the one hand, and other islands in the outer atolls, on the other.

5. Regional Development Strategy: In an effort to ameliorate regional inequalities and reverse migration to the capital, the Government placed regional economic growth and diversification as a key objective of economic development in both the Sixth National Development Plan (6NDP) for 2001-2005 and the present Seventh National Development Plan (7NDP) for 2006-2010. As part of the 7NDP, the Government is developing regional centers that are designed to have airports, ports and other social and infrastructure facilities, and that will be complemented by focus islands on different atolls acting as atoll service hubs and growth centers. The focus islands identified under the 7NDP are to serve as growth centers, fostering employment and income generation opportunities by concentration of development efforts and provision of a higher level of infrastructure to achieve economies of scale. Islands that are of importance to the population consolidation program are likely to have the following characteristics: (a) sufficient land area to support greater numbers of population; (b) proximity to atoll capital; (c) substantial existing infrastructure; and (d) potential for growth because of land area, agricultural, fishery or other commercial activity. The Government expects that these efforts will reduce regional differentials and promote growth and employment opportunities outside of Male’. It also plans to address poverty among the most vulnerable groups, who may not be able to benefit from the growth strategy, by developing special targeted income support programs.

1.2. International Competitiveness 6. Effective Exchange Rate: The international competitiveness of the Maldives is reflected in the real effective exchange rate (RER), which takes into account both general price movements in the country relative to that of each of its trading partners, and the cross exchange rate between the Maldives and each of its trading partners.6 The Maldives has effectively pegged the rufiyaa against the U.S. dollar since 1994. Between 1995 and 2001 that policy 5 In 2006, 35% of the population was located in Male’ compared with 27% in 2000, according to the Ministry of Planning’s 2006 census (Ministry of Planning, 2006). 6 The real exchange rate is a measure of the relative price of non-tradables to tradables and, as such, it measures the cost of producing a good domestically. A relative price rise, for example, reflects an increase in the domestic cost of producing tradable goods, since it makes production of tradables less profitable and induces resources to move to the non-tradables sector. While the concept is straightforward, its empirical measurement is difficult for a country like the Maldives where price series for tradable and non-tradable products are not readily available. Two alternative measures of the real exchange rate can be constructed within the context of the country’s data limitations. The first uses partner-country and domestic price measured in terms of CPI data to construct a real exchange rate index that represents the ratio between non-tradable and tradable prices. Specifically, the real exchange rate is defined in this case as er

t = Pnt/Pf

t, where en is the nominal exchange rate, Pf is the foreign currency price of goods purchased abroad, and P is the domestic price level. The second uses purchasing power parity (PPP) definition to correct the nominal exchange rate by the relative price of domestic to foreign prices, as measured by CPI data. Using this approach, the real exchange rate is defined as er

t = (1/en)t Pnt/Pf

t , where en is the nominal exchange rate, Pf is the foreign currency price of goods purchased abroad, and P is the domestic price level.

TA 4745-MLD: SME Development Project – Draft Final Report

4

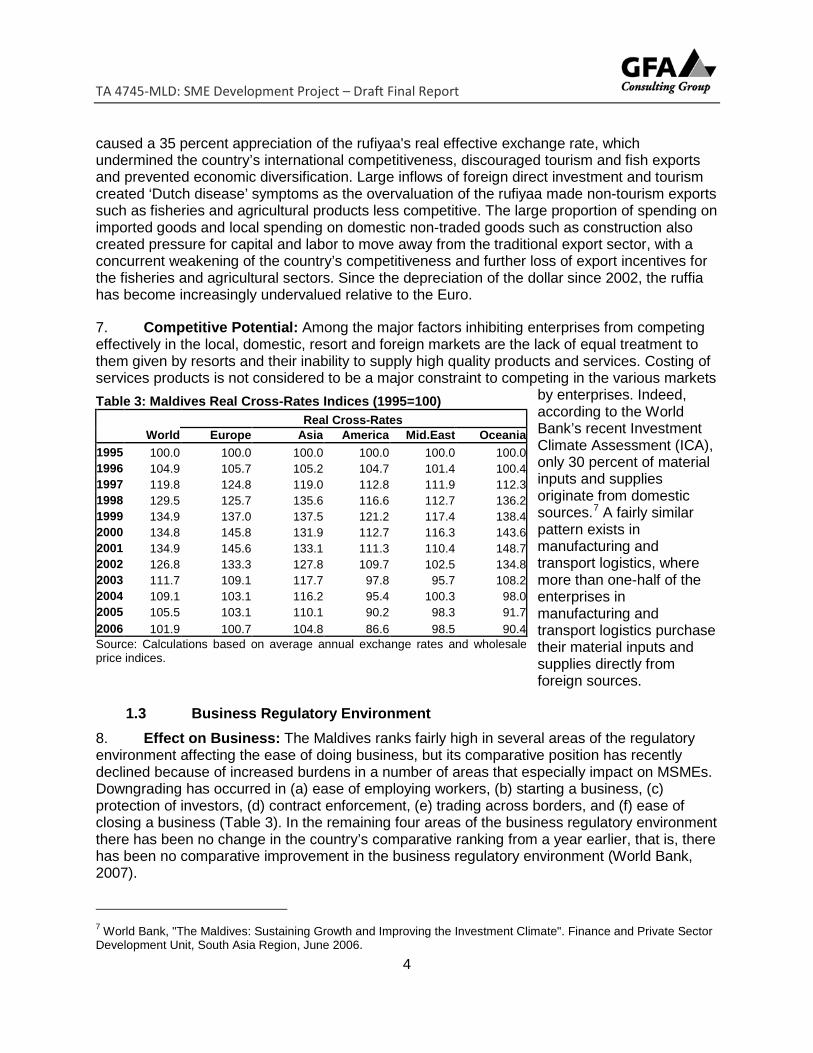

caused a 35 percent appreciation of the rufiyaa's real effective exchange rate, which undermined the country’s international competitiveness, discouraged tourism and fish exports and prevented economic diversification. Large inflows of foreign direct investment and tourism created ‘Dutch disease’ symptoms as the overvaluation of the rufiyaa made non-tourism exports such as fisheries and agricultural products less competitive. The large proportion of spending on imported goods and local spending on domestic non-traded goods such as construction also created pressure for capital and labor to move away from the traditional export sector, with a concurrent weakening of the country’s competitiveness and further loss of export incentives for the fisheries and agricultural sectors. Since the depreciation of the dollar since 2002, the ruffia has become increasingly undervalued relative to the Euro.

7. Competitive Potential: Among the major factors inhibiting enterprises from competing effectively in the local, domestic, resort and foreign markets are the lack of equal treatment to them given by resorts and their inability to supply high quality products and services. Costing of services products is not considered to be a major constraint to competing in the various markets

by enterprises. Indeed, according to the World Bank’s recent Investment Climate Assessment (ICA), only 30 percent of material inputs and supplies originate from domestic sources.7 A fairly similar pattern exists in manufacturing and transport logistics, where more than one-half of the enterprises in manufacturing and transport logistics purchase their material inputs and supplies directly from foreign sources.

1.3 Business Regulatory Environment 8. Effect on Business: The Maldives ranks fairly high in several areas of the regulatory environment affecting the ease of doing business, but its comparative position has recently declined because of increased burdens in a number of areas that especially impact on MSMEs. Downgrading has occurred in (a) ease of employing workers, (b) starting a business, (c) protection of investors, (d) contract enforcement, (e) trading across borders, and (f) ease of closing a business (Table 3). In the remaining four areas of the business regulatory environment there has been no change in the country’s comparative ranking from a year earlier, that is, there has been no comparative improvement in the business regulatory environment (World Bank, 2007).

7 World Bank, "The Maldives: Sustaining Growth and Improving the Investment Climate". Finance and Private Sector Development Unit, South Asia Region, June 2006.

Table 3: Maldives Real Cross-Rates Indices (1995=100)

World Real Cross-Rates

Europe Asia America Mid.East Oceania 1995 100.0 100.0 100.0 100.0 100.0 100.0 1996 104.9 105.7 105.2 104.7 101.4 100.4 1997 119.8 124.8 119.0 112.8 111.9 112.3 1998 129.5 125.7 135.6 116.6 112.7 136.2 1999 134.9 137.0 137.5 121.2 117.4 138.4 2000 134.8 145.8 131.9 112.7 116.3 143.6 2001 134.9 145.6 133.1 111.3 110.4 148.7 2002 126.8 133.3 127.8 109.7 102.5 134.8 2003 111.7 109.1 117.7 97.8 95.7 108.2 2004 109.1 103.1 116.2 95.4 100.3 98.0 2005 105.5 103.1 110.1 90.2 98.3 91.7 2006 101.9 100.7 104.8 86.6 98.5 90.4 Source: Calculations based on average annual exchange rates and wholesale price indices.

TA 4745-MLD: SME Development Project – Draft Final Report

5

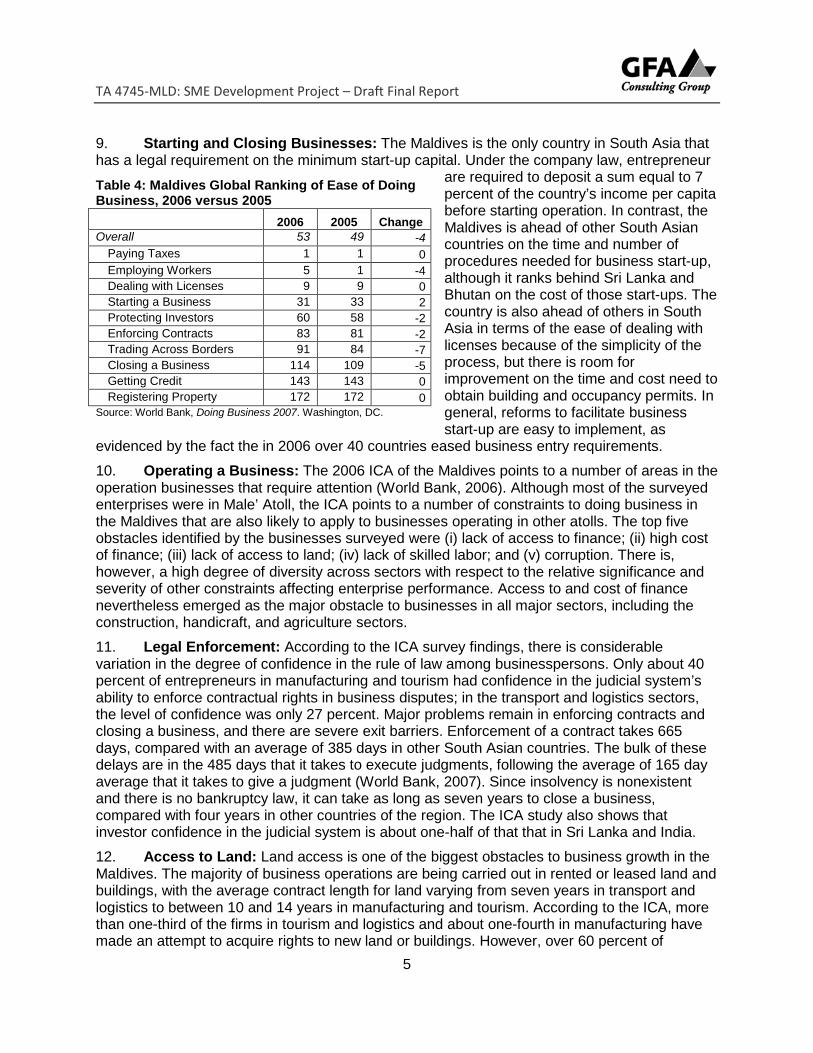

9. Starting and Closing Businesses: The Maldives is the only country in South Asia that has a legal requirement on the minimum start-up capital. Under the company law, entrepreneur

are required to deposit a sum equal to 7 percent of the country’s income per capita before starting operation. In contrast, the Maldives is ahead of other South Asian countries on the time and number of procedures needed for business start-up, although it ranks behind Sri Lanka and Bhutan on the cost of those start-ups. The country is also ahead of others in South Asia in terms of the ease of dealing with licenses because of the simplicity of the process, but there is room for improvement on the time and cost need to obtain building and occupancy permits. In general, reforms to facilitate business start-up are easy to implement, as

evidenced by the fact the in 2006 over 40 countries eased business entry requirements.

10. Operating a Business: The 2006 ICA of the Maldives points to a number of areas in the operation businesses that require attention (World Bank, 2006). Although most of the surveyed enterprises were in Male’ Atoll, the ICA points to a number of constraints to doing business in the Maldives that are also likely to apply to businesses operating in other atolls. The top five obstacles identified by the businesses surveyed were (i) lack of access to finance; (ii) high cost of finance; (iii) lack of access to land; (iv) lack of skilled labor; and (v) corruption. There is, however, a high degree of diversity across sectors with respect to the relative significance and severity of other constraints affecting enterprise performance. Access to and cost of finance nevertheless emerged as the major obstacle to businesses in all major sectors, including the construction, handicraft, and agriculture sectors.

11. Legal Enforcement: According to the ICA survey findings, there is considerable variation in the degree of confidence in the rule of law among businesspersons. Only about 40 percent of entrepreneurs in manufacturing and tourism had confidence in the judicial system’s ability to enforce contractual rights in business disputes; in the transport and logistics sectors, the level of confidence was only 27 percent. Major problems remain in enforcing contracts and closing a business, and there are severe exit barriers. Enforcement of a contract takes 665 days, compared with an average of 385 days in other South Asian countries. The bulk of these delays are in the 485 days that it takes to execute judgments, following the average of 165 day average that it takes to give a judgment (World Bank, 2007). Since insolvency is nonexistent and there is no bankruptcy law, it can take as long as seven years to close a business, compared with four years in other countries of the region. The ICA study also shows that investor confidence in the judicial system is about one-half of that that in Sri Lanka and India.

12. Access to Land: Land access is one of the biggest obstacles to business growth in the Maldives. The majority of business operations are being carried out in rented or leased land and buildings, with the average contract length for land varying from seven years in transport and logistics to between 10 and 14 years in manufacturing and tourism. According to the ICA, more than one-third of the firms in tourism and logistics and about one-fourth in manufacturing have made an attempt to acquire rights to new land or buildings. However, over 60 percent of

Table 4: Maldives Global Ranking of Ease of Doing Business, 2006 versus 2005

2006 2005 Change

Overall 53 49 -4 Paying Taxes 1 1 0 Employing Workers 5 1 -4 Dealing with Licenses 9 9 0 Starting a Business 31 33 2 Protecting Investors 60 58 -2 Enforcing Contracts 83 81 -2 Trading Across Borders 91 84 -7 Closing a Business 114 109 -5 Getting Credit 143 143 0 Registering Property 172 172 0

Source: World Bank, Doing Business 2007. Washington, DC.

TA 4745-MLD: SME Development Project – Draft Final Report

6

manufacturing respondents, around 45 percent of respondents in the tourism industry and transport-logistics have been unsuccessful in acquiring land. Moreover, a comprehensive and transparent regulatory framework for housing and urban management is lacking in the Maldives, and planning and building standards and regulations have been developed in an ad-hoc manner. Following the implementation of the 2002 Land Act, the Government is taking steps to create a market for land sales and is conducting a cadastral survey. Uncertainty nevertheless remains in a number of areas, including the ability of enterprises to transfer land.

Table 5: Strengths, Weaknesses, Opportunities, and Threats (SWOT) Analysis of MSME Development in Atolls Factors Internal External Positive S - Strengths O – Opportunities

Geographical location near tourist resorts Improvement of logistics through inter and intra-island transportations system

Artisan tradition and culture Communication system enhancements through mobile phones and internet

Regional development planning Possibilities to use existing facilities for BDS activities and services

Low cost skilled workers Political commitment to private sector development

Schools system for creating knowledge-base society

Development of entrepreneurial infrastructure for MSME services

Cultural, recreational and tourism capacities Existence of experienced entrepreneurs

Opportunities for agricultural commercialization, tourism related activities, handicrafts and small processing capacities

Location of growth modules in targeted regional developmental centers

Negative W - Weaknesses T - Threats Tradition of large enterprises Lack of entrepreneurial mindset

Narrow economic structure Few people oriented to modern working environment

Lack of entrepreneurial and managerial knowledge and skills Dependence on government for action

Lack of support for entrepreneurs Delays in privatization and restructuring of SOEs

Lack of finance for MSMEs Impact of government involvement on business decisions in enterprises

Fragmentation of the agricultural land; little experience with cooperatives Corruption and lack of good governance

Lack of financial resources

Lack of coordination of development activities, especially transportation and communication

13. Access to Financing: The lack of clarity on property rights is a major constraint to accessing finance, as lenders are unwilling to take land as collateral if they are unable to sell it freely upon the borrower’s default. Partly for this reason, access to credit is ranked as the number one impediment to doing business in the Maldives, according to both perceptions of entrepreneurs as reported in the ICA and actual financing conditions relative to those of other countries, as reported in the World Bank’s business survey (World Bank, 2007). The ICA reports that only one-third of businesses use bank loans for their activities. Instead, firms rely on internal funds for working capital. Domestic commercial banks contribute 11 percent to existing working capital and international commercial banks only 3 percent. Indeed, only 25 percent of respondents to the ICA questionnaire reporting making any efforts to apply for loans. Nearly 60 percent of the credit that has been extended is for the tourism sector, followed by commerce

TA 4745-MLD: SME Development Project – Draft Final Report

7

(import-export operations) and the fisheries sector. Together these three sectors absorb over 85 percent of existing loans. Differences in financial sector development and the regulatory environment often determine the magnitude of SME lending in countries. In Asia countries like the Maldives that have limited SME financing also lack banking intermediation, have weak legislations and poor public finance management, whereas those that have well-development financial sectors tend to have high SME financing.8

2. SECTOR AND REGIONAL ANALYSIS

2.1 Key Challenges and Opportunities

14. Business Environment in the Atolls: Our survey of business conditions and perceptions by MSMEs in three key regions of the Maldives reveal significant differences from those identified by the World Bank’s ICA for businesses operating in the capital of Male’. Table 5 summarizes the major opportunities and challenges to entrepreneurs and businesses in the Northern, Southern and South-Central Development Regions of the country. These findings are based on SWOT analysis of the enterprises in each of the regions by team members and differ from the more detailed MSME survey conducted in those atolls.

15. Internal Constraints: Table 6 shows the ranking of key internal constrains on enterprises in the Northern and Southern Development Regions. Lack of technically skilled labor, labor costs, and accounting skills are the principal concerns of business in both regions. Availability of capital is only a major problem for enterprises in the South-Central Region. In contrast, technology and management staffing is a major problem in the Northern and Southern Regions, but they rank below alls in the South-Central Region.

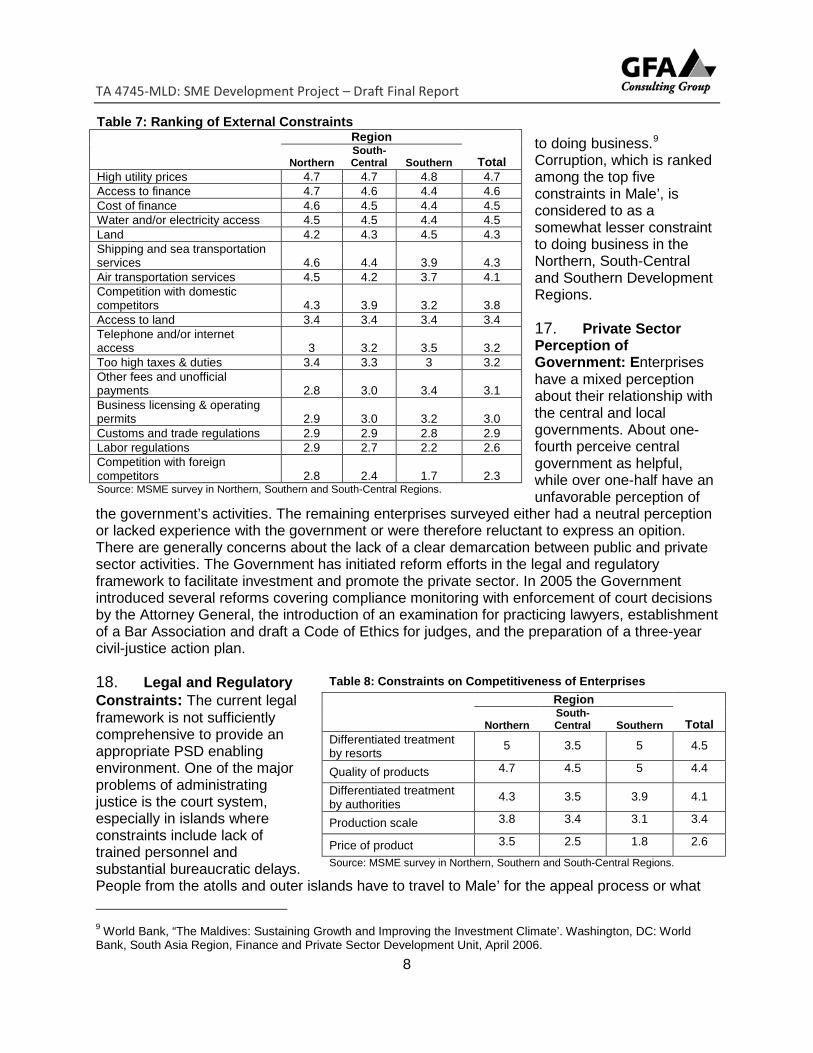

16. External Constraints: High utility prices are ranked high by enterprises in the atolls (Table 7). They also perceive access and cost of financing to be a threat to their operations. Land as well as transport issues in both air and sea transportation are also major constraints reported by enterprises. The fact that telephone and internet costs are experienced as costly is significant to potential efforts to provide business development services through extension activities in the atolls. Among the factors having a negligible impact on the enterprises are labor relations, foreign competition, customs and trade regulations, business licensing and operating permits. Perceptions about cost and access to finance are largely due to the dependence on family and own financial resources. Because of the difficulty of obtaining credit, few enterprises actually consider using external financial sources. SMEs operating principally in Male’ also reported access and cost of finance, as well as access to land as among the top five constraints

8 RAM Consultancy Services Sdn Bhd, “SME Access to Financing: Addressing the Supply Side of SME Financing”. ASEAN Secretariat, REPSF Project No. 04/003, July 2005.

Table 6: Ranking of Internal Constraints

Region

Total Northern South-Central Southern Technically skilled labor 4.6 4.4 3.2 4.1 Labor costs 3.7 3.9 3.5 3.7 Accounting skills 4.4 2.1 4.4 3.6 Market information 4.2 2.2 4.2 3.5 Management staffing 4.4 2.0 4.2 3.5 Technology 4.0 1.9 4.4 3.4 Capital 2.7 4.4 2.0 3.0 Source: MSME survey in Northern, Southern and South-Central Regions.

TA 4745-MLD: SME Development Project – Draft Final Report

8

to doing business.9 Corruption, which is ranked among the top five constraints in Male’, is considered to as a somewhat lesser constraint to doing business in the Northern, South-Central and Southern Development Regions.

17. Private Sector Perception of Government: Enterprises have a mixed perception about their relationship with the central and local governments. About one-fourth perceive central government as helpful, while over one-half have an unfavorable perception of

the government’s activities. The remaining enterprises surveyed either had a neutral perception or lacked experience with the government or were therefore reluctant to express an opition. There are generally concerns about the lack of a clear demarcation between public and private sector activities. The Government has initiated reform efforts in the legal and regulatory framework to facilitate investment and promote the private sector. In 2005 the Government introduced several reforms covering compliance monitoring with enforcement of court decisions by the Attorney General, the introduction of an examination for practicing lawyers, establishment of a Bar Association and draft a Code of Ethics for judges, and the preparation of a three-year civil-justice action plan.

18. Legal and Regulatory Constraints: The current legal framework is not sufficiently comprehensive to provide an appropriate PSD enabling environment. One of the major problems of administrating justice is the court system, especially in islands where constraints include lack of trained personnel and substantial bureaucratic delays. People from the atolls and outer islands have to travel to Male’ for the appeal process or what 9 World Bank, “The Maldives: Sustaining Growth and Improving the Investment Climate’. Washington, DC: World Bank, South Asia Region, Finance and Private Sector Development Unit, April 2006.

Table 7: Ranking of External Constraints

Region

Total Northern South-Central Southern

High utility prices 4.7 4.7 4.8 4.7 Access to finance 4.7 4.6 4.4 4.6 Cost of finance 4.6 4.5 4.4 4.5 Water and/or electricity access 4.5 4.5 4.4 4.5 Land 4.2 4.3 4.5 4.3 Shipping and sea transportation services 4.6 4.4 3.9 4.3 Air transportation services 4.5 4.2 3.7 4.1 Competition with domestic competitors 4.3 3.9 3.2 3.8 Access to land 3.4 3.4 3.4 3.4 Telephone and/or internet access 3 3.2 3.5 3.2 Too high taxes & duties 3.4 3.3 3 3.2 Other fees and unofficial payments 2.8 3.0 3.4 3.1 Business licensing & operating permits 2.9 3.0 3.2 3.0 Customs and trade regulations 2.9 2.9 2.8 2.9 Labor regulations 2.9 2.7 2.2 2.6 Competition with foreign competitors 2.8 2.4 1.7 2.3 Source: MSME survey in Northern, Southern and South-Central Regions.

Table 8: Constraints on Competitiveness of Enterprises

Region

Total Northern South-Central Southern

Differentiated treatment by resorts 5 3.5 5 4.5

Quality of products 4.7 4.5 5 4.4

Differentiated treatment by authorities 4.3 3.5 3.9 4.1

Production scale 3.8 3.4 3.1 3.4

Price of product 3.5 2.5 1.8 2.6

Source: MSME survey in Northern, Southern and South-Central Regions.

TA 4745-MLD: SME Development Project – Draft Final Report

9

are often complex commercial issues. The courts lack trained judicial persons throughout all magistrate courts. Nor does the court system have an effective summons procedure or a comprehensive judgment enforcement process. The Government needs to formulate legislations on taxation, bankruptcy, banking and taxation. It also needs to introduce accounting and auditing standards for the private sector. Minimum wage levels need to be introduced as well. Finally, it is essential that impact assessments be carried out a part of the formulation of major pieces of legislations to measure their impact on PSD and MSMEs in particular. Based on a review of relevant commercial and investment laws and regulations, including accounting standards, land tenure and property rights, the focus of support to MSME activity in the atolls should be based on realistic and sustainable approaches for strengthening the MSME policy, legal, regulatory, and accounting framework, and one that contains a detailed strategy and time-bound action plan for MSME development. 19. Transportation: At present the transport of cargo between Male’ and the outer islands relies on the traditional cargo and passenger vessels operating on a fairly unscheduled basis, while the transport of passengers relies on these same vessels and, where possible, on the use of air transport services. There is a fairly significant network of transport operations within islands in the same atoll and between islands of adjacent atolls. While Male’ remains the centre of the transport system, there are growing numbers of hubs. Two regional ports are opening in Kulhudhufushi and S. Hithadhoo, while State Trading Organization Plc (STO) imports cargo directly into S. Gan, and Fari Maldives Pvt. Ltd imports cargo directly into Theefaridhoo.10 The domestic aviation network is largely dependent on seaplanes for the tourist market and wheeled aircraft for the local population. Plans exist to increase the number of domestic airports from four to eleven. Limited ferry routes exist, but regular services tend to be unscheduled and subject to weather conditions. From time to time, foreign companies have established regular ferry services, but these have been short-lived.

20. Skills Deficiencies: According to the 7NDP, the Maldives has one of the lowest labor force participation rates in South Asia (47.7 percent). Youth unemployment is also substantial and has been increasing in recent years, with the result that 40 percent of young women and over 20 percent of young men are currently unemployed. One of the problems is the lack of appropriate skills needed for existing employment opportunities in the Maldives. Educational and vocational institutions have not inculcated enterprise as a career option or provided appropriate business orientation and support skills. According to the ICA survey, most schools only offer commerce subjects and the average pass rate is 25 percent, while the pass rate for English is only 6 percent. In contrast, the pass rate for chemistry, physics, commerce, fisheries, and science ranges from 25 to 45 percent. Difficulty in access to gainful employment has increased the incidence of drug use and delinquency. Despite some improvements, lack of local skilled labor continues to be a major problem in Maldives. Moreover, unskilled worker from a foreign country collects an average monthly pay of MRf 2,000, while a local person needs to be paid at least MRf 2,500 per month. This situation has creates reliance on migrant labor from neighboring countries. In 2004 there were 38,413 expatriates employed in the Maldives, compared with 33,765 in 2003 because of the growth and expansion of business activities.

21. Getting credit: Historically, most of the credit in the Maldives has been channeled to larger corporations, and the upper end of the medium size market. Particularly small enterprises as well as low and middle-income households still lack access to adequate financial services, in

10 ADB, “Domestic Maritime Transport Project”. Draft Final Report. TA 4395-MLD, August 2005.

TA 4745-MLD: SME Development Project – Draft Final Report

10

particular long-term finance either for capital investment or permanent working capital needs. The lack of suitable collateral, viable qualitative information, financial statements and accounts usually places the MSMEs in the high-risk category and they are therefore considered non-bankable. In general, the Maldives ranks 143rd worldwide on the comparative ease of getting credit, which is well below most other South Asian countries. The poor ranking is largely due to the complete absence of a public or private credit registry to facilitate the exchange of credit information amongst lenders. The legal rights of borrowers and lenders are also deficient in most respects because the law requires a specific description of the assets in the security agreement. As a result, it is impractical to use a changing pool of assets (such as in an inventory or accounts receivable) as security for a loan. The secured lender has no priority right to the collateral either in or outside bankruptcy, reducing the chances of loan recovery. If a borrower defaults, creditors are required to go through a lengthy court enforcement process. The lack of a bankruptcy law further reduces the chances of loan recovery in the event a borrower becomes insolvent. All this makes security agreements for MSMEs highly risky, costly and difficult to enforce. The situation could improve if the authorities carry through on plans to set up a credit information bureau with the assistance of the World Bank’s International Finance Corporation (IFC). The Bank of Maldives is also planning to introduce mobile phone banking, which will improve outreach in the atolls. 22. Financial Sector: The financial sector of the Maldives is narrow. There is one locally owned commercial bank, Bank of Maldives (BML), branches of three South Asian state-owned commercial banks, and a branch of HSBC international bank. The BML is jointly owned by the Government (51 percent), island communities (25 percent), and other government agencies (24 percent). The BML has 18 branches that include five mobile branches (dhonis). All these banks follow normal international banking practices and offer letter of credit (LC) facilities and other financing. Banking is regulated by Maldives Monetary Authority (MMA), which acts as the central bank. Banks seldom extend loans with maturities of more than three to five years and the spreads remain high. Lending rates vary from 8 to 13 percent for domestic currency and 7.75 to 13 percent for foreign currency; similar rates apply to the Government. This situation, gives rise to serious impediments to sustained growth of the private sector in the Maldives because of the lack of available information and mechanisms to collect information that makes lenders unable to identify enough profitable projects in a risky environment. The provision of financial services is consequently restricted to low-risk clients or based on excessive collateral requirements instead of a credit analysis relying on financial statements and business plans. Experience from other countries shows that a more flexible and dynamic credit information system will improve the accuracy and cost-effectiveness of credit risk decisions made by financial institutions that, in turn, results in improved access to financial services, in particular for small businesses and individual borrowers.

23. Non-Banking Financial Sector: The non-bank financial sector consists of a government provident fund, a finance leasing company, a housing bank, two insurance companies registered in the country, and some agents for overseas insurance companies. The Maldives Finance Leasing Company (MFLC) provides medium and long-term capital equipment financing. The company was established with assistance from International Finance Corporation (IFC), with technical assistance provided by the National Development Bank (NDB) of Sri Lanka. To date, it has provided lease financing for capital equipment mainly to the tourism sector (nearly 80 percent of the total) for such items as speedboats, live-aboard safari and fishing vessels, dhonis, computers, and excavators. There are limited capital market operations securities trading. Three SOEs are quoted on the stock exchange (BML, State Trading

TA 4745-MLD: SME Development Project – Draft Final Report

11

Organization (STO), and the Maldivian Transport and Construction Company). The Government plans to list more enterprises on the stock exchange.

24. Lack of Capacities of Domestic BDS Providers. An effective method to build captioned capacities within the MSMEs is to incorporate external business development services. However, the MSME sector in the Maldives is characterized by an almost complete lack of use of these external services, mainkly because of the limited market for BDS that is almost wholey concentrated in Male‘. Government spending on BDS is limited, which in turn effectively constrains the size and development scope of commercial BDS markets. Opening these markets to commercial operators would effectively optimize the allocation of government funds by increasing employment opportunities for the skilled work force in innovative markets, ensuring a more market-oriented BDS with immediate benefits to clients and reduced cost per trainee by allowing for competition.

25. Weak business linkages. Though The Maldives’s tourism sector is booming, impact on the development of rural enterprises and in particular rural manufacturing industries is low due to weak or missing links in value chains e.g. agriculture, agro-industries and tourism. Although the Government has adopted a clusters approach in its 7NDP, it is neither effectively and systematically supporting the development of those clusters nor strengthening of value chains through well-targeted BDS support programs in close cooperation with private sector stakeholders and private BDS providers, which could otherwise build the capacity to sustain and disseminate such programs.

26. Limited Instruments and Capacities to Coordinated MSME Development Policies, Programs and Projects. One of the greatest risks to MSME in the Maldives is the possibility of a continued lack of Government capacity to implement the MSME development program due to inadequate inter-ministerial coordination of private sector development initiatives. At present, the development of a common MSME development and implementation strategy suffers from a profound fragmentation of strategy formulation and decision making, weak communication and weak coordination among government ministries and agencies. These weaknesses have prevented the formulation and implementation of a common MSME development strategy, as well as programs and projects that complement and build on one another. At present, the inter-ministerial MSME Policy Committee is chaired by the Ministry of Economic Development and Trade and consists of representatives from the ministries of finance and treasury, economic development and trade, atolls development, planning and national development, agriculture and fisheries, transport and communications, youth and sports, and higher education and employment. The Committee needs to be strengthened to ensure involvement of senior officials from the ministries and it should meet on a recurrent basis to monitor and maintain quality control of the technical assistance, as well as ensure full participation by key ministries and coordination of existing strategies, programs and projects.

2.2 Government Strategy for Private Sector Development 27. Government Strategy: There are a number of principles underlying the strategy of the Seventh National Development Plan (7NDP) that point to the leading role of MSMEs in private sector development, especially those in the atolls and outer islands, as well as the supportive role of the public sector in creating an enabling environment for the private sector. The Government’s strategy as it relates to the private sector in the regions outside the capital of Male’ aims to improve economic growth by increasing the number and coverage of MSMEs activities and reducing or restructuring state owned enterprises (SOEs).

TA 4745-MLD: SME Development Project – Draft Final Report

12

28. Sectoral Strategies by Line Ministries: At the sectoral level several development strategies aim to enhance the capabilities of the private sector, specifically microenterprises in the atolls. In the past, many of these took the form of financial arrangements targeting microenterprises, but these have mostly been eliminated.11 These schemes include loans to boat purchase and repairs and to fish processing by the Ministry of Fisheries Agriculture and Marine resources (MOFAMR), micro-credit to disadvantaged women by the Ministry of Women Affairs and Social Security (MWASS), the Atolls Credit and Development Banking Project (ACDBP) and the Southern Atolls Development Project (SADP) by the Development-Banking Cell (DBC) of the Bank of Maldives, and the Atoll Development Project and Atoll Development Funds of the Government, UNDP and International Fund for Agricultural Development (IFAD). The Atolls Credit and Development Banking project is part of a long-term program for the BML to operate as a development finance institution and support its financial service operations in outer atolls.12 The project has been costed at $6 million with IFAD contributing $3 million, the Government of Maldives $2.5 million and UNDP $0.5 million. The project covers 15 out of 19 outer atolls in the Northern and South-Central regions, specifically Haa Alifu, Haa Dhaalu, Shaviyani, Noonu, Raa, Baa and Lhaviyani, in the Northern atolls; and Vaavu, Meemu, Faafu, Dhaalu, Thaa, Laamu, Gaafu Alifu and Gaafu Dhaalu in the South-Central atolls. It targets 3,250 atoll households directly from credit access and to benefit 6,000 indirectly through improved earning opportunities. The target population comprises households with a per capita income below MRf 2,000 per annum, equivalent to MRf1,000 per month for a family of six persons. The objective is to develop a credit delivery system for the outer atolls, thereby reducing income disparities between the outer atolls and Male’ by increasing the employment opportunities and income levels.

29. Institutional and Infrastructural Goals: Line ministries have increasingly shifted their goals to the enhancement of private sector development through institutional and infrastructural enhancements as a means of facilitating growth and development of MSMEs in the atolls. The Ministry of Human Resources Employment and Labor has established two important programs for matching vocational training and higher education with employment opportunities and needs in the country. The first is the program to expand and improve the quality of vocational and technical education, and the second is the program to expand post-secondary education opportunities. The former includes increased youth skills training opportunities focusing on employable skills for youth, and the latter includes increased numbers of private training providers offering career oriented vocational and technical training. The Ministry of Transport and Civil Aviation has recently focused its efforts on identifying strategies for the development of domestic maritime transport, largely because of the recognition that private sector development has been hindered by the undeveloped status of the country’s transport network. In an effort to ensure adequate access among all inhabited islands, the Ministry is working to implement greater access to all inhabited islands, as well as to establish a sustainable harbor maintenance program. At the same time, the Ministry of Fisheries Agriculture and Marine Resources is making efforts to enhance the role of the private sector and facilitate investment in some areas and activities that will benefit small scale industries in the atolls. Current programs are supporting the establishment and development of a mariculture industry, and implementing fisheries community development programs that provide extension, and other services and 11 H. Abdullah and Z. Ismail, “An Overview of Micro credit and SME financing activities in the Maldives”. Country Paper for SAARC Finance Seminar on Micro Credit Operations, Dhaka, Bangladesh, 21 Dec 2002. 12 EFAD, “Atolls Credit and Development Banking Project Republic of Maldives: Atolls Credit and Development Banking Project: Completion Evaluation Executive Summary. (Undated).

TA 4745-MLD: SME Development Project – Draft Final Report

13

support to communities. It is also formulating schemes to improve access to knowledge, technology and finance. In agriculture the Ministry is promoting commercial agriculture and poultry farming with the introduction of new crop varieties and animal breeds require comprehensive planning for the sustainable utilization of the nation’s limited land and water resources. A study on agricultural commercialization was conducted to promote MSME development based on a cluster approach to development of the sector in the atolls.

30. Employment Targets: The 2006 Census revealed that 8.3 percent of the adult population is unable to find suitable employment or lacks employment opportunities, thereby being officially unemployed.13 Of the total adult population, 22 percent are economically inactive in the sense of not actively seeking work. The Government has not elaborated any specific targets in its 7NDP to increase the number of economically active population, but is has provided specific guidelines on its strategies to increase employment opportunities for Maldivians. These strategies include (a) the preparation of a human resource needs assessment and design, develop and deliver programs in the key sectors of tourism, fisheries and agriculture, transport and the social sectors; (b) development and implement a national apprenticeship scheme to train school leavers to meet the national skills demand; (c) institute an Employment Act which would include provisions on unfair dismissal, equal pay, sexual harassment and discrimination including an awareness campaign to make the public and institutions and agencies with employment responsibilities familiar with the new provisions; (d) Undertake a joint study with the Human Rights Commission and private sector organizations to improve working conditions in accordance with national and international human rights standards: (e) Establish Employment Services Centre in Male’ and job centers in Baa, Dhaal, Lhaviani and Laamu atolls to provide employment advice to job seekers and employment exchange services for employers and employees and establish job information kiosks; (f) Set up a labor market information system in the Ministry of Higher Education, Employment and Social Security to collect and analyze labor market data for policy development purposes; and (g) promote youth interest in employment.

31. Goals of 7NDP: The overall goal for economic and social development, as set out in the 7NDP and Vision 2020, is the eliminate poverty and improvement in the well-being of the greatest number of Maldivians. The link between achieving this overarching goal and the private sector development in the Maldives is formally recognized in the 7NDP. It explicitly targets private sector participation as one of the key strategies to be pursued in 2006-2010, recognizing that private sector development is critical to achieving the levels of sustainable economic growth required by the country. It recognizes need for partnership between the Government and private sector, a situation that in the past has not always existed and that will require a radical shift in perceptions, attitudes and approaches during the 7NDP period.

32. Private Sector Development Channels: The 7NDP sets out the following key mechanisms needed for developing the private sector: (a) formalizing the economy; (b) improving corporate governance and transparency; (c) promoting responsible business 13 Ministry of Planning and National Development, Maldives Population and Housing Census conducted during 21-28 March 2006. Census 2006 was carried out in all the 196 administrative islands, 88 resort islands and 34 industrial and other islands of the country. Data relating to the size, geographical distribution and socio-economic characteristics of the population such as sex, age, educational attainment, marital status and employment were collected and are presented in these tables. Four questionnaires were administered for census data collection, namely: Household Listing Form, Person's Listing Form, Household Form (includes household and persons information) and Establishment Form.

TA 4745-MLD: SME Development Project – Draft Final Report

14

practices; (d) maximizing the potential of public-private partnerships, with a view to increasing; (e) private investment in the national economy and to providing opportunities for SMEs and small-scale entrepreneurs to participate in a more competitive environment; and (f) developing linkages within the domestic and international private sectors to share knowledge, expertise, resources, and technology. Within the various sub-goals of the 7NDP, those that apply to the development of the private sector and SMEs are the following ones: (a) a diversified economy (goal 3); (b) improved access and expanded opportunities (goal 4); (c) the elimination of poverty, increased equity, and gender equality (goal 5); and (f) support for the rapid recovery of sub-sectors damaged by the tsunami (goal 1).

33. Measurable Indicators: Realization of these goals is recognized as too broad for developing an action plan with policies, projects, programs and institutional mechanisms. In an effort to operationalize the goals, the 7NDP establishes a set of measurable objectives to increase private sector development, including SME and micro-enterprise development. Volume II of the 7NDP lays out a set of roadmaps within 34 themes covering the 2006-2010 goals. Annex B presents the specific benchmarks associated with actions to be taken in the area of private sector development and related activities in the regulatory environment, skills development and SOE restructuring and privatization.

2.3 External Assistance in the Atolls

34. Asian Development Bank Strategy: The ADB’s operational strategy for 2006-2008 encompasses (i) fiscal management, (ii) regional development, and (iii) the environment.14 Fiscal management supports prudent control that is needed to support a stable and balanced growth, currently projected at 5 to 6 percent a year. The longer-term concern, however, is regional development. The ADB’s support for regional development currently comprises technical assistance for regional planning studies and assistance to prepare future social infrastructural investment projects in specific regional growth centers. It is also assisting in human resource development plans for education, health and population to increase the countrywide availability of these services. Apart from the Tsunami Emergency Assistance Program, it has the Outer Island Development Project ($12 million), the Outer Island Electrification Project ($8 million), the Regional Development Project ($20 million), the Post-Secondary Education Development ($21 million), Information Technology Development Project ($11 million), Domestic Maritime Transport Development Project ($8 million), and the Strengthening Public Accounts and Governance ($5 million).

35. ADB Lending Activity: Up to now the ADB has provided six loans to the Government totally $33.9 million and primarily directed to the power and ports subsectors. The first loan under the Inter-Island Transport Project was unsuccessful because it underestimated fuel costs for two vessels purchased under the loan.15 The second loan for an included five subprojects for atoll harbors, power, and meteorological development.16 The subsequent four loans mainly benefited Male’ and had little direct benefit to the outer atolls.17 Indeed, the ADB’s 2006-2008

14 ADB, “Country Operational Strategy Study: The Republic of Maldives”. STS MLD 95017. October 2005. 15 ADB, “Loan No. 513-MLD(SF): Inter-Island Transport for $1.0 million”. Approved 18 June 1981. For a review of the loan, see ADB, “Interislands Transport Operations Review”. TA No. 679-MLD. 25 April 1985. 16 ADB, “Loan No. 681-MLD(SF): Multiproject, for $2.38 million”. Approved 29 March 1984. 17 ADB, “Loan No. 848-MLD(SF): Power System Development, for $6.1 million”. Approved 28 October 1987; ADB, “Loan No. 911-MLD(SF): Male Port Development, for $6.4 million”. Approved 20 October 1988; ADB, “Loan No.

TA 4745-MLD: SME Development Project – Draft Final Report

15

country operations strategy notes that, “the Bank’s exclusive focus on Male’ has contributed to the income disparities between those who live in Male’ and the surrounding areas, and those who live in the atolls and more remote regions.”18 The ADB has also provided sixteen advisory TAs totaling $4.75 million, a TA for the preparation of an environmental management strategy, and six TAs for the preparation of loan projects for $0.87 million. These have supported, among others, the preparation of the National Development Plans, including those supporting regional development.

36. United Nations: Five United Nations (UN) organizations maintain residences in the Maldives, namely, United Nations Development Program (UNDP), United Nations Children's Fund (UNICEF), United Nations Population Fund (UNFPA), World Health Organisation (WHO), and United Nations Volunteers (UNV). Their activities are coordinated under the United Nations Development Framework (UNDAF) for Maldives.19 Of these, UNDP provides considerable support to private sector development, and specifically microenterprises and SMEs. In recent years it has provided assistance for agriculture development and credit schemes on the outer atoll groups and for health, women in development, and population planning. Its projects include Atoll Development and Local Governance, Social Mobilization, and a micro-credit fund for schools, jetties and other activities amounting to $400,000.

37. World Bank: The World Bank’s involvement in the Maldives has been somewhat limited. Since 1979 it has financed six projects and produced five formal economic reports. Two educational projects contributed to manpower development and upgrading of the airport in Male’ supported the growth of tourism. Three projects helped modernize the fishing fleet and strengthen public sector capacity in collecting, processing, and exporting fish. Apart from its Post-Tsunami Emergency Relief and Reconstruction Project and Second Post Tsunami Emergency Recovery Credit, the World Bank has a $16 million International Development Association (IDA) funded Integrated Human Development Project. Its four components aim to strengthening delivery of (a) education services; (b) health services; (c) employment services; and (d) community services. The fourth component on strengthening community services will improve service delivery by strengthening community services. The project will strengthen and improve community groups by providing: (a) leadership and management skills training to community based organizations; (b) financial support to community groups, through a community development fund and cooperatives offering community-wide services; (c) support to the development of multi-purpose buildings to consolidate the provision of services; and (d) the development of broad networks on each focus island.

38. International Finance Corporation: The IFC has a portfolio in Maldives that consists of three investments, made up of $1.2 million of equity and $25.5 million of loans outstanding. Its activities have supported private investment in tourism, logistics and the financial sector. Specific projects that is has undertaken since 1995 are as follows: (a) Wataniya Telecom Maldives Pvt. Ltd (August 2005; information sector); (b) Universal Maldiv (March 2005; accommodation and tourism services); Taj Maldives Private Limited (April 2003) Maldives Villa

1121-MLD(SF): Second Power System Development, for $9.2 million. Approved 19 November 1991; ADB, “Loan No. 1226-MLD(SF): Second Male Port, for $8.8 million. Approved 1 April 1993. 18 ADB, “Country Operational Strategy Study: The Republic of Maldives”. STS MLD 95017. October 2005. 19 United Nations, “Development Assistance Framework for Republic of Maldives 2003-2007”. Malé. 26 July 2002.

TA 4745-MLD: SME Development Project – Draft Final Report

16

Shipping (February 2002; accommodation and tourism services); Maldives Leasing Company (December 2000; finance and insurance); and Villa Shipping & Trading Co. Ltd (May 1995).

II. PROPOSED SECTOR DEVELOPMENT PROJECT

3. PROJECT COVERAGE AND IMPLEMENTATION PROCESS 3.1 Objectives, Scope and Strategy

39. Vision: The present project has been designed within the context of an overall SME development vision in the atolls, and one that is driven by strategic and operational goals that, in turn, define the programs to achieve those goals and projects to be implemented (Figure 1). The SME development vision consists of the creation of conditions necessary for achieving dynamic growth of SME activities for particular sectors and industries in targeted regions of the country by 2010. These conditions will be realized by (i) developing the entrepreneurial climate and support services that will facilitate growth; (ii) providing the necessary conditions for converting existing entrepreneurial potential into innovative and successful business activities; (iii) attracting entrepreneurial leadership from other regions of the country; and (iv) establishing broader regional centers for SME activities that are driven by growth nodes or networked clusters for supporting activities.

40. Strategic Goals: The overall strategy and operational goals for SME development support the creation and strengthening of institutional mechanisms that provide entrepreneurs with business development services and financing on a sustainable basis. A clusters approach integrates production, marketing and distribution activities for targeted sectors and geographic areas, and policies and institutional support facilitate the public sector’s involvement in enabling MSME business activities in the atolls.

41. Programs: Four broad-based programs aim to compensate for the unfavorable competitive position that businesses in the atolls face relative to foreign goods and services by lowering the transactions cost of doing business and ensuring the delivery of business services and information where the market fails to provide them. These programs give special attention to those activities that provide differentiated products and services to markets, those that target niche markets, and those that contain high value added. The following key programs form part of the operational strategy for achieving the goals set out for MSME development in the atolls, and aim to translate the vision and operational strategy into reality:

A program to bolster human resource development by creating business development service centers that provide training programs in entrepreneurship, management, and technical skills for MSMEs and develop appropriate materials for such training, as well as helping to identify commercial opportunities in specific sectors;

A program to improve access to finance by developing innovative financing schemes using alternative financial instruments such as schemes such as equity financing, while encouraging the development of cooperatives and associations;

A program to promote a market-driven process through the public and private sector that in the short to medium-term will target specific types of activities in selected regions of the country; and

TA 4745-MLD: SME Development Project – Draft Final Report

17

A program to enhance the catalytic role of public sector for facilitating commercial activities in the atolls and strengthening MSME activities by improving the policy and regulatory environment.

VisionCreate

conditions necessary for

achieving dynamic SME growth for particular

sectors and industries in targeted regions of the country by 2010.

Figure 1 SME Development Strategy for the Maldives

Strategic Goal 1Develop Regional

Support of Business Services

Strategic Goal 3Strengthen

Institutional Support at National Level

Strategic Goal 2Enhance Financial System for MSMEs

in Atolls

Strategic Goal 4Improve

Environment for Doing Business

Programs to Achieve GoalsBusiness Development Services in AtollsNew Funding Sources MSMEs in Atolls

Institutional Capacity Building of Public and Private Sectors

Projects to be ImplementedBDS Centers in Target Regions

Credit Guarantee Program for MSMEsCost Sharing Facility

Media Campaign and SME PortalCapacity Building of Economic Development Unit (EDU) in MEDT

Support for National Chamber of Commerce and Industries

Strategic Goal 5Cluster Approach to

Integrate Target Activities in Atolls

42. Projects: Operational activities focus on a set of projects designed within clusters framework that ensure the mutual support of each activity. The projects are grouped into two types of activities. The first is the set of activities that deliver business development services both in the selected regions of the country and through public and private institutions at the national level. They encompass the BDS regional centers, capacity building of the Enterprise Development Unit of MEDT, support to the national chamber of commerce and industry, and the media campaign and SME portal. The second is the set of financing mechanisms aimed at expanding available funds for MSMEs in the atolls. These include the credit guarantee program, cost-sharing facility and risk capital fund, as well as training and other support needed to ensure their delivery. In several of the proposed pilot projects there exist one or more prerequisites that

TA 4745-MLD: SME Development Project – Draft Final Report

18

could be immediately addressed as a means of providing the appropriate facilitating environment for the commercialization activities. Effective implementation of these projects depends upon one or more prerequisites that can be addressed within a short timeframe in order to provide an appropriate facilitating environment for the project activities. These prerequisites are in the form of policies to facilitate the use of productive and financial resources, programs to support production, distribution and marketing of products, new or enhanced institutional capacities, modifications in the legal and regulatory environment, and infrastructural services and support, including transportation and communications.

3.2 Targeted Sectors for MSME Development 43. Rationale for Prioritizing Sectors: Measurable results of MSME development in the atolls will be gauged by the ability of the project to generate successful outcomes that produce high-profile outcomes in a relatively short period of time. To achieve these outcomes, specific sectors are given priority in terms of project support from BDS and financing from preferential sources such as the cost-sharing facility and risk capital fund. Selection of the priority activities has been based on wide-ranging interviews with private sector individuals, especially those located in the atolls, as well as public sector officials in both the atolls and capital. Consideration has also been given to the country’s strategic goals and objectives in the 7th National Development Plan, as well as the broad directions established by Vision 2020, and the Strategic Economic Plan (SEP) and the Integrated Framework (IF).20

44. Competitiveness and Development Impact of Prioritizing Sectors: The sectors that have been selected as having high profiles with potentially large demonstrable effects on the country share several common characteristics such as their strong competitiveness in domestic as well as international markets in terms of high value added products having strong niche market potential, as well as their potentially strong impact on economic development in the atolls and large job creation opportunities. In agriculture, for example, several fruits and vegetables have been identified as having a high commercial market potential, and their selection criteria has been based on the degree of year-round availability, technology needs, transportation and storage requirements, production costs, potential in the domestic, resort and export markets, and value adding capabilities. Indeed, among the vegetable products having commercial potential, medicinal plants score the highest because of their year-round production capability, low storage and transportation requirements, large market potential for resorts and export, and considerable value adding capabilities. In handicrafts, the local industry has suffered from cheap substitute products from Indonesia, Malaysia and Thailand, but the potential for high value-added handicrafts with authenticated product labeling is enormous. Skills development in this sector would provide the basis for establishing supplies to both the booming tourism industry and foreign niche markets in Europe and the United States. Tourism-related activities, like handicrafts, have huge employment generating capabilities. They involve wide ranging activities in the atolls related to housing, water sports, as well as handicraft activities in woodworking and ‘Kunaa’ (‘Thundukunaa’) mats that are authentic to the Maldives. Similarly, fish processing activities rank high in terms of their actual and potential contribution to atoll development and employment generation, and they have a large market potential in the domestic, resort and foreign sectors that have yet to be exploited. The prioritized sectors should 20 See Ministry of Planning and National Development (2005a), “Strategic Economic Plan”. Maldives: Republic of Maldives; and Integrated Framework (2005), “Integrated Framework Diagnostic Trade Integration Study for the Maldives. Draft Report”. Geneva, November 2005.

TA 4745-MLD: SME Development Project – Draft Final Report

19

ultimately lead to (a) diversification and growth in activities in which the country has a competitive advantage relative to other supply sources, (b) the generation of employment opportunities in rural atolls and island communities, and (c) an equitable improvement of livelihoods across the main regions of the country.