Mahindra & Mahindra - Google Groups

44

Please refer to the important disclosures and analyst certification on page 2 and the inside back cover of this document, or on our website www.macquarie.com.au/research/disclosures. INDIA MM IN Outperform Price 11 Jun 10 Rs606.70 12-month target Rs 740.00 Upside/Downside % 22.0 Valuation Rs 740.00 - Sum of Parts GICS sector Automobiles & Components Market cap Rsm 350,915 30-day avg turnover US$m 25.8 Market cap US$m 7,465 Number shares on issue m 578.4 Investment fundamentals Year end 31 Mar 2010A 2011E 2012E 2013E Total revenue bn 186.0 223.1 258.2 293.2 EBITDA bn 29.6 34.3 39.3 44.5 EBITDA growth % 170.7 16.0 14.6 13.3 EBIT bn 25.9 29.8 33.7 37.8 EBIT growth % 222.9 15.1 13.2 12.3 Reported profit bn 20.9 23.7 26.3 29.5 EPS rep Rs 36.92 41.81 46.53 52.12 EPS rep growth % 137.6 13.2 11.3 12.0 PER rep x 16.4 14.5 13.0 11.6 Total DPS Rs 6.23 11.00 11.75 12.50 Total div yield % 1.0 1.8 1.9 2.1 ROA % 17.1 17.2 17.1 17.0 ROE % 30.9 27.4 25.3 23.8 EV/EBITDA x 12.0 10.3 9.0 8.0 Net debt/equity % 14.4 21.7 17.0 10.4 P/BV x 4.4 3.6 3.0 2.6 Source: FactSet, Macquarie Research, June 2010 (all figures in INR unless noted) Key ratios excluding listed subsidiaries 2010A 2011E 2012E 2013E PER 12.1 10.3 9.3 8.3 EV/EBITDA 6.3 5.7 4.9 4.2 Price to Book 3.1 2.6 2.2 1.8 ROE 25% 24% 22% 21% ROA 18% 18% 17% 17% Source: Bloomberg, Macquarie Research, June 2010 Sanjay Doshi +91 22 6653 3061 [email protected] 14 June 2010 Mahindra & Mahindra Sowing seeds for next harvest Initiate with Outperform, TP of Rs740, upside of 22% We initiate coverage on Mahindra & Mahindra (M&M) with an Outperform rating and target price of Rs740, providing 22% upside from current levels. We rate M&M as a top pick in the Indian auto space. With leadership in the utility vehicle and tractor segments and a robust estimated 13% CAGR in earnings over the next three years, at 9.3x core auto FY12E PER, we think M&M remains one of the most attractively valued stocks in our coverage universe. Strong brands, new products to drive growth in auto space Strong products catering to all consumer segments, increasing urban demand backed by bank financing and benign competition, should help M&M’s utility vehicle segment to grow at a CAGR of 14% over next couple of years. In the light commercial vehicle (LCV) space, recently launched Gio and Maxximo have garnered good response and should help the segment grow by 40% in the FY11. Tractor segment to benefit from Punjab Tractor merger We expect the farm equipment segment (FES) to see 13-15% p.a. growth in the coming years, supported by rising rural income and increasing agricultural credit. M&M recently launched a new small tractor, targeting the small and marginal farmers. With tractor penetration of only 1%, the segment has strong growth prospects and could provide significant upside to volume assumptions. M&M’s dealer and vendor rationalisation programs post the merger of Punjab Tractor should also improve tractor business profitability in the medium term. New businesses to add value in the medium term M&M has entered into new auto segments — medium and heavy commercial vehicles (M&HCV) and two-wheelers — and has enhanced its presence in the defence space. Given strong growth prospects and a virtual duopoly in the M&HCV space, we believe that the segment could add significant value in the medium term. The company has also invested ~US$1bn in setting up a new plant, which should support its auto business expansion for the next 5 to 7 years. Solid earnings growth, attractive on valuation We forecast M&M’s earnings to grow at a CAGR of 13% over the next 3 years despite a minor decline in margins. Our estimates are 5-7% ahead of consensus, mainly on account of higher volume growth assumptions. The stock trades at a ~28% discount to peers on core auto business valuations. We ascribe a PER multiple of 14x, in-line with sector average, to core auto earnings, valuing it at Rs583 per share (78% of value). We value listed subsidiaries at a 20% discount to current market cap, in-line with our valuation methodology for other auto names. Key risks and catalysts Any material increase in diesel vehicle duties proposed by the Parikh oil sector reform committee will be a key risk for the stock. Other macro risks include a significant jump in raw material prices and a faster-than-expected hardening of interest rates. Stronger-than-expected response to recently launched products, positive response from the US market to the new pick-up planned in the current fiscal year and success in new business initiatives could be key catalysts.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Mahindra & Mahindra - Google Groups

Please refer to the important disclosures and analyst certification on page 2 and the inside back cover of this document, or on our website www.macquarie.com.au/research/disclosures.

INDIA

MM IN Outperform Price 11 Jun 10 Rs606.70 12-month target Rs 740.00 Upside/Downside % 22.0 Valuation Rs 740.00 - Sum of Parts GICS sector Automobiles & Components Market cap Rsm 350,915 30-day avg turnover US$m 25.8 Market cap US$m 7,465 Number shares on issue m 578.4

Investment fundamentals Year end 31 Mar 2010A 2011E 2012E 2013E Total revenue bn 186.0 223.1 258.2 293.2 EBITDA bn 29.6 34.3 39.3 44.5 EBITDA growth % 170.7 16.0 14.6 13.3 EBIT bn 25.9 29.8 33.7 37.8 EBIT growth % 222.9 15.1 13.2 12.3 Reported profit bn 20.9 23.7 26.3 29.5 EPS rep Rs 36.92 41.81 46.53 52.12 EPS rep growth % 137.6 13.2 11.3 12.0 PER rep x 16.4 14.5 13.0 11.6 Total DPS Rs 6.23 11.00 11.75 12.50 Total div yield % 1.0 1.8 1.9 2.1 ROA % 17.1 17.2 17.1 17.0 ROE % 30.9 27.4 25.3 23.8 EV/EBITDA x 12.0 10.3 9.0 8.0 Net debt/equity % 14.4 21.7 17.0 10.4 P/BV x 4.4 3.6 3.0 2.6 Source: FactSet, Macquarie Research, June 2010 (all figures in INR unless noted)

Key ratios excluding listed subsidiaries 2010A 2011E 2012E 2013E PER 12.1 10.3 9.3 8.3 EV/EBITDA 6.3 5.7 4.9 4.2 Price to Book 3.1 2.6 2.2 1.8 ROE 25% 24% 22% 21% ROA 18% 18% 17% 17% Source: Bloomberg, Macquarie Research, June 2010

Sanjay Doshi +91 22 6653 3061 [email protected]

14 June 2010

Mahindra & Mahindra Sowing seeds for next harvest Initiate with Outperform, TP of Rs740, upside of 22% We initiate coverage on Mahindra & Mahindra (M&M) with an Outperform rating and target price of Rs740, providing 22% upside from current levels. We rate M&M as a top pick in the Indian auto space. With leadership in the utility vehicle and tractor segments and a robust estimated 13% CAGR in earnings over the next three years, at 9.3x core auto FY12E PER, we think M&M remains one of the most attractively valued stocks in our coverage universe.

Strong brands, new products to drive growth in auto space Strong products catering to all consumer segments, increasing urban demand backed by bank financing and benign competition, should help M&M’s utility vehicle segment to grow at a CAGR of 14% over next couple of years. In the light commercial vehicle (LCV) space, recently launched Gio and Maxximo have garnered good response and should help the segment grow by 40% in the FY11.

Tractor segment to benefit from Punjab Tractor merger We expect the farm equipment segment (FES) to see 13-15% p.a. growth in the coming years, supported by rising rural income and increasing agricultural credit. M&M recently launched a new small tractor, targeting the small and marginal farmers. With tractor penetration of only 1%, the segment has strong growth prospects and could provide significant upside to volume assumptions. M&M’s dealer and vendor rationalisation programs post the merger of Punjab Tractor should also improve tractor business profitability in the medium term.

New businesses to add value in the medium term M&M has entered into new auto segments — medium and heavy commercial vehicles (M&HCV) and two-wheelers — and has enhanced its presence in the defence space. Given strong growth prospects and a virtual duopoly in the M&HCV space, we believe that the segment could add significant value in the medium term. The company has also invested ~US$1bn in setting up a new plant, which should support its auto business expansion for the next 5 to 7 years.

Solid earnings growth, attractive on valuation We forecast M&M’s earnings to grow at a CAGR of 13% over the next 3 years despite a minor decline in margins. Our estimates are 5-7% ahead of consensus, mainly on account of higher volume growth assumptions. The stock trades at a ~28% discount to peers on core auto business valuations. We ascribe a PER multiple of 14x, in-line with sector average, to core auto earnings, valuing it at Rs583 per share (78% of value). We value listed subsidiaries at a 20% discount to current market cap, in-line with our valuation methodology for other auto names.

Key risks and catalysts Any material increase in diesel vehicle duties proposed by the Parikh oil sector reform committee will be a key risk for the stock. Other macro risks include a significant jump in raw material prices and a faster-than-expected hardening of interest rates. Stronger-than-expected response to recently launched products, positive response from the US market to the new pick-up planned in the current fiscal year and success in new business initiatives could be key catalysts.

Macquarie Research Mahindra & Mahindra

14 June 2010 2

Inside

Sowing seeds for next harvest 3

Strong brands, new products to drive

growth in auto space 5

FES to benefit from Punjab Tractor merger10

New initiatives to add value in medium

term 16

Solid earnings growth for coming years 19

Valuation – trading attractively 23

Key risks and catalysts 26

Appendix I: Tech Mahindra 27

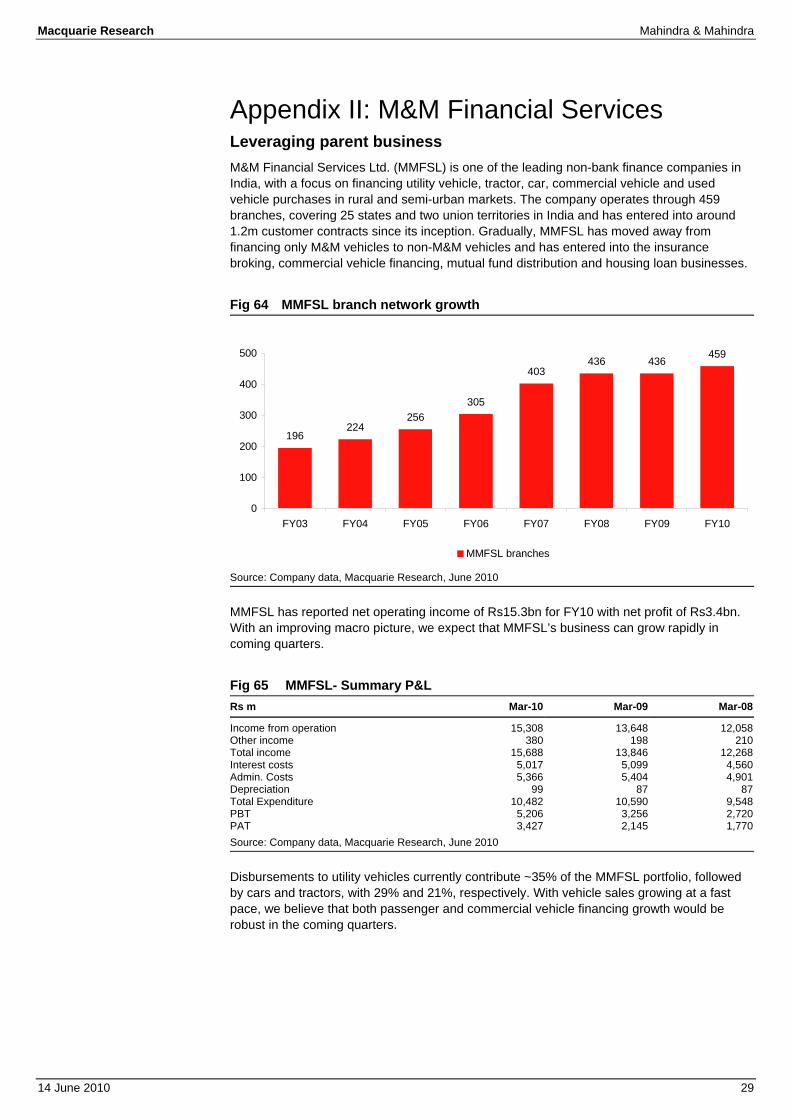

Appendix II: M&M Financial Services 29

Appendix III: M&M Systech 31

Appendix IV: Mahindra Holidays & Resorts33

Appendix V: Mahindra Lifespaces 34

Appendix VI: Utility vehicle segment 35

Appendix VII: Tractors 36

Appendix VIII: Light Commercial Vehicles38

Appendix IX: Medium & Heavy

Commercial Vehicles 39

Appendix X: Three-wheelers 40 MM IN rel BSE Sensex performance

Source: FactSet, Macquarie Research, June 2010

(all figures in INR unless noted)

Shareholding pattern

Source: BSE, Macquarie Research, June 2010

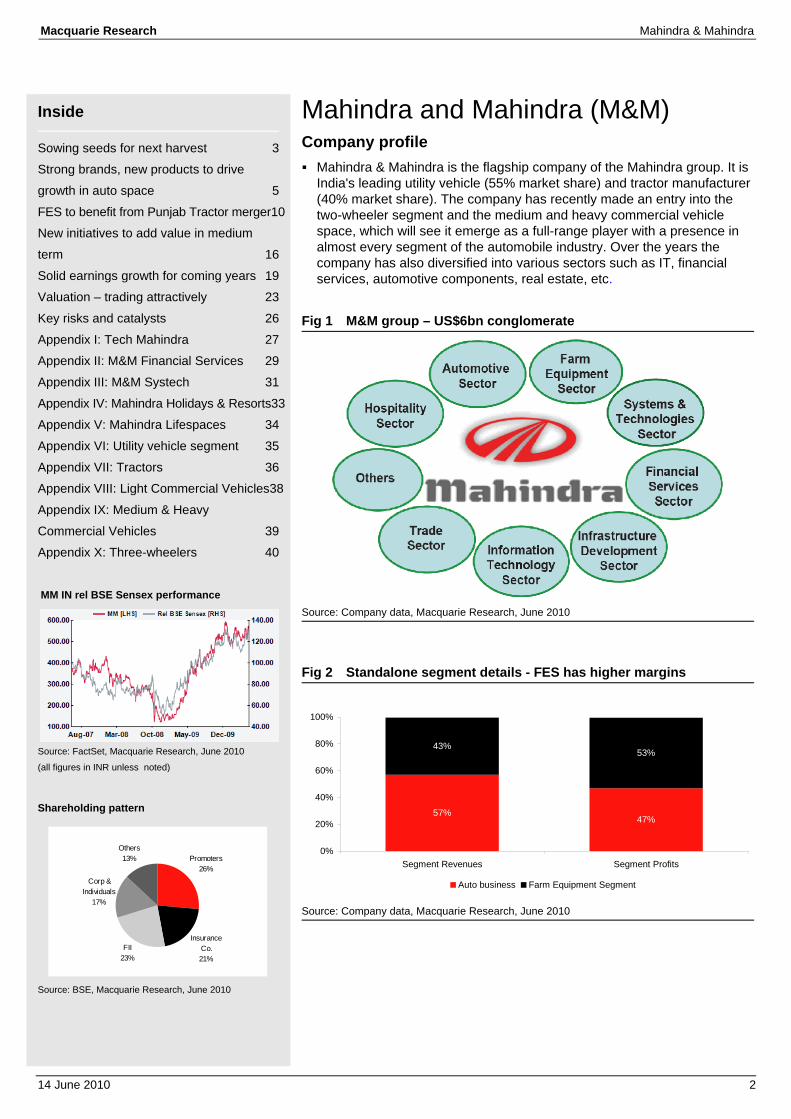

Mahindra and Mahindra (M&M) Company profile Mahindra & Mahindra is the flagship company of the Mahindra group. It is

India's leading utility vehicle (55% market share) and tractor manufacturer (40% market share). The company has recently made an entry into the two-wheeler segment and the medium and heavy commercial vehicle space, which will see it emerge as a full-range player with a presence in almost every segment of the automobile industry. Over the years the company has also diversified into various sectors such as IT, financial services, automotive components, real estate, etc.

Fig 1 M&M group – US$6bn conglomerate

Source: Company data, Macquarie Research, June 2010

Fig 2 Standalone segment details - FES has higher margins

Source: Company data, Macquarie Research, June 2010

Insurance Co.21%

FII23%

Others13%

Corp & Individuals

17%

Promoters26%

57%47%

43%53%

0%

20%

40%

60%

80%

100%

Segment Revenues Segment Profits

Auto business Farm Equipment Segment

Macquarie Research Mahindra & Mahindra

14 June 2010 3

Sowing seeds for next harvest Initiate with Outperform We initiate on Mahindra & Mahindra (M&M) with an Outperform rating and target price of Rs740, providing ~22% upside from current levels. The company has strong brands in the key bread-and-butter businesses, i.e., utility vehicles and tractors. With a robust 13% CAGR in earnings expected over the next three years, at 9.3x core auto FY12E PER, M&M strikes us as one of the most attractively valued stocks in our coverage universe.

Strong brands, new products to drive growth in auto space M&M has a significant presence in the utility vehicle and the light commercial vehicle segments through its auto division. We expect overall auto volumes to grow at a CAGR of 15.5% for next 3 years. The key factors supporting the growth are:

Strong brands in the utility vehicle space catering to all consumer segments. M&M is the only player with products spread across the spectrum, catering to both the rural populace and high-end urban segments.

Increasing urban demand for auto products, backed by higher bank financing

Key new products, Gio and Maxximo, launched in the LCV segment

Tractor segment to benefit from Punjab Tractor merger Mahindra’s Farm Equipment Sector is one of the world’s top tractor brands and has been the undisputed market leader in India for 25 years (FY10 market share of 41%). The company has consolidated its leadership position in the tractor space (53% of EBIT) with the acquisition of Punjab Tractors. We expect the tractor segment to witness 13-15% p.a. growth in the coming years, supported by the following key factors:

Increasing rural wealth due to rising minimum support prices and larger spending by government on rural development schemes and employment guarantee schemes

Expanding credit availability through private and public sector banks

Rising trend of tractors being used for commercial purposes like transportation of material over short distances, utilization for construction activities, to ferry water tankers etc

M&M has also recently launched a new small tractor, Yuvraj, targeting the bottom of the pyramid, i.e. small and marginal farmers. With tractor penetration of only 1%, the segment has strong growth prospects and can provide significant upside to volume assumptions. Further M&M’s dealer and vendor rationalisation programs post the merger of Punjab Tractor should improve tractor business profitability in the medium term

New businesses to add value in the medium term M&M has recently entered the US$7.5bn Indian M&HCV segment through a JV with US based Navistar Inc (NAV US, US$51, not rated) and has forayed into the two-wheeler space through acquisition of assets of Kinetic Motors (KNH IN, Rs20, not rated). Further it plans to enter the US light truck market with the Scorpio pick-up. Acceptance of the company’s products in these categories, we believe, will drive growth in the medium term. The company has also invested ~US$1bn in setting up a new plant, which should support company’s auto business expansion for the next 5 to 7 years.

Solid earnings growth in coming years We forecast the company’s earnings to grow at a CAGR of 13% over the next three years, backed by volume growth of 15%. The existing strong product portfolio in the tractor and utility vehicle spaces, along with key new product launches (Gio and Maxximo) in the LCV segment should drive this growth.

Initiate Outperform with target price of

Rs740 – implying 22% upside

Macquarie Research Mahindra & Mahindra

14 June 2010 4

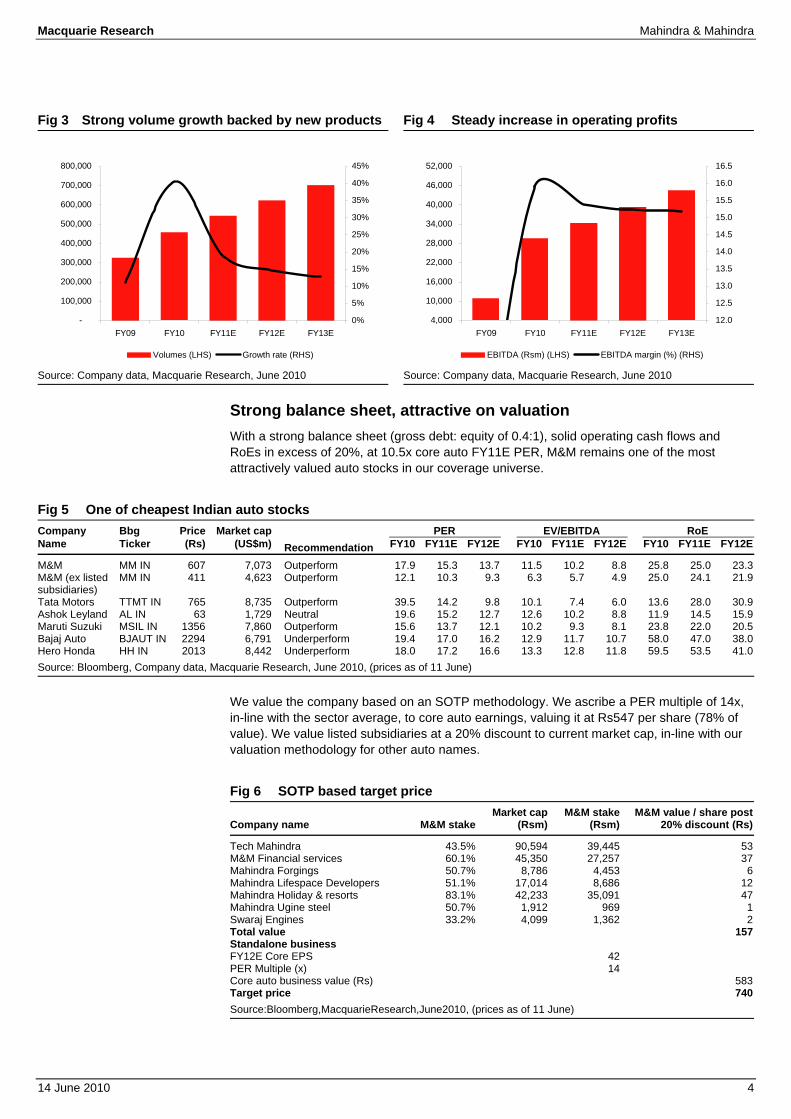

Fig 3 Strong volume growth backed by new products Fig 4 Steady increase in operating profits

Source: Company data, Macquarie Research, June 2010 Source: Company data, Macquarie Research, June 2010

Strong balance sheet, attractive on valuation With a strong balance sheet (gross debt: equity of 0.4:1), solid operating cash flows and RoEs in excess of 20%, at 10.5x core auto FY11E PER, M&M remains one of the most attractively valued auto stocks in our coverage universe.

Fig 5 One of cheapest Indian auto stocks Company Bbg Price Market cap PER EV/EBITDA RoE Name Ticker (Rs) (US$m) Recommendation FY10 FY11E FY12E FY10 FY11E FY12E FY10 FY11E FY12E

M&M MM IN 607 7,073 Outperform 17.9 15.3 13.7 11.5 10.2 8.8 25.8 25.0 23.3M&M (ex listed subsidiaries)

MM IN 411 4,623 Outperform 12.1 10.3 9.3 6.3 5.7 4.9 25.0 24.1 21.9

Tata Motors TTMT IN 765 8,735 Outperform 39.5 14.2 9.8 10.1 7.4 6.0 13.6 28.0 30.9Ashok Leyland AL IN 63 1,729 Neutral 19.6 15.2 12.7 12.6 10.2 8.8 11.9 14.5 15.9Maruti Suzuki MSIL IN 1356 7,860 Outperform 15.6 13.7 12.1 10.2 9.3 8.1 23.8 22.0 20.5Bajaj Auto BJAUT IN 2294 6,791 Underperform 19.4 17.0 16.2 12.9 11.7 10.7 58.0 47.0 38.0Hero Honda HH IN 2013 8,442 Underperform 18.0 17.2 16.6 13.3 12.8 11.8 59.5 53.5 41.0Source: Bloomberg, Company data, Macquarie Research, June 2010, (prices as of 11 June)

We value the company based on an SOTP methodology. We ascribe a PER multiple of 14x, in-line with the sector average, to core auto earnings, valuing it at Rs547 per share (78% of value). We value listed subsidiaries at a 20% discount to current market cap, in-line with our valuation methodology for other auto names.

Fig 6 SOTP based target price

Company name M&M stakeMarket cap

(Rsm)M&M stake

(Rsm) M&M value / share post

20% discount (Rs)

Tech Mahindra 43.5% 90,594 39,445 53 M&M Financial services 60.1% 45,350 27,257 37 Mahindra Forgings 50.7% 8,786 4,453 6 Mahindra Lifespace Developers 51.1% 17,014 8,686 12 Mahindra Holiday & resorts 83.1% 42,233 35,091 47 Mahindra Ugine steel 50.7% 1,912 969 1 Swaraj Engines 33.2% 4,099 1,362 2 Total value 157 Standalone business FY12E Core EPS 42 PER Multiple (x) 14 Core auto business value (Rs) 583Target price 740Source:Bloomberg,MacquarieResearch,June2010, (prices as of 11 June)

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

FY09 FY10 FY11E FY12E FY13E0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Volumes (LHS) Growth rate (RHS)

4,000

10,000

16,000

22,000

28,000

34,000

40,000

46,000

52,000

FY09 FY10 FY11E FY12E FY13E12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.5

16.0

16.5

EBITDA (Rsm) (LHS) EBITDA margin (%) (RHS)

Macquarie Research Mahindra & Mahindra

14 June 2010 5

Strong brands, new products to drive growth in auto space M&M’s automotive business (57% of revenues and 47% of EBIT) remains on a strong footing, with leading brands across segments. We expect overall auto volumes to grow at a CAGR of 15.5% for the next 3 years. Recently launched new products in the LCV space and robust demand in the utility vehicle segment, on the back of improving consumer sentiment and easy availability of bank finance, should drive this growth.

M&M has a significant presence in the utility vehicle and the light commercial vehicle segments through its auto division. The company has improved its position in the three-wheeler space through new model launches in the last year. M&M has also entered the two-wheeler space through acquisition of assets of Kinetic Motors, garnering ~6% market share in the scooter segment in the first year of operation. The company has a miniscule share in the car space, where it was present through a JV with Renault (RNO FP, €30.42, Neutral, TP: €41.00, Jens Schattner) until last month with a single product, an entry-level sedan–the Logan.

Fig 7 UV dominates auto business, new products to drive LCV

Product Segment Key brands

FY10 segment market

share (%)

Segment share in M&M total

automotive volume

Macquarie Comments

Utility Vehicles Bolero, Scorpio, Xylo

55.5% 41.3% Strong brands across all segments

Light Commercial Vehicles (LCV) Bolero Maxitruck, Bolero Pick-up, Maxximo, Gio

29.9% 25.3% Key new products in high growth LCV space

Three-wheelers Alpha, Champion 7.4% 12.3% Two-wheelers Rodeo, Duro,

Flyte 4.8% 19.4% Garnering 6%

market share in first year of operation

Cars Logan 0.3% 1.7% Source: SIAM, Company data, Macquarie Research, June 2010

Leader in utility vehicles for over a decade; to maintain market share M&M has been a leader in the Indian utility vehicle space (current ~270k units pa market) for over a decade. On the back of a strong product portfolio, the company has been able to increase its market share in FY10 to 55% from 47% in FY09. M&M is probably the only company which has reasonably successful products in the utility vehicle space for every consumer segment. Key brands in the M&M utility vehicle portfolio are:

Fig 8 Strong brands in utility vehicle portfolio catering to all segments Brand Engine capacity Ex-showroom price Delhi(Rs'000) Macquarie Comments

Bolero 2523cc 550-649 Low end multi purpose vehicle used largely in non-metro and rural areas

Xylo 2498cc 636-848 High end multi utility vehicle having strong acceptance in metros and large cities

Scorpio 2179cc 764-1083 High end sports utility vehicle Source: Company data, Macquarie Research, June 2010

Core automotive business on strong footing with leading

brands for all segments

Macquarie Research Mahindra & Mahindra

14 June 2010 6

Fig 9 Strong market share expected to be sustained Fig 10 Leader by far in utility vehicle space

Source: SIAM, Macquarie Research, June2010 Source: SIAM, Macquarie Research,June2010

Fig 11 Strong brands to cater to all segments in UV space

Brand/Car FY10 domestic

sales %change YoY Ex showroom price

Delhi(Rs.'000)

Mahindra & Mahindra Bolero 80,059 43% 550-649Scorpio 34,173 14% 764-1083Xylo 26,478 265% 636-848 Tata Motors Ltd Sumo 23,049 -6% 520-762Safari 10,482 -29% 782-1197 Toyota Kirloskar Motor Ltd Innova 47,294 24% 794-1166 Maruti Suzuki Ltd Gypsy 3,841 -47% 515-537 General Motors India Ltd Tavera 15,334 14% 622-935Source:CRISIL,MacquarieResearch,June2010

We expect the UV segment to grow by 13-15% over next couple of years. The key reasons why we believe demand will witness good growth in the UV space are as follows:

Revival in overall economic growth outlook and improving consumer sentiment, especially amongst the salaried class

Widening of income tax slabs (rates) should help to offset increase in overall cost of ownership due to a rise in excise duty, raw material prices, increased costs of meeting new emission norms, fuel prices and higher interest rates

Increasing financial penetration, which currently stands at ~70%, should help growth rates as both private and public banks remain focused on the four-wheeler space.

Demand for utility vehicles for commercial use should be supported by improved business confidence and higher profitability of companies. The recovery in the business environment for IT and BPO companies and growth in tourist arrivals should also be positive for UV demand.

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

E

FY12

E

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

Domestic UV sales (LHS) M&M market share % (RHS)

M&M55%

Tata Motors13%

Toyota20%

GM India6%

Others6%

Increasing bank financing and lack

of significant competition, key

positive in UV space

Macquarie Research Mahindra & Mahindra

14 June 2010 7

With no significant increase in competition expected for the key models of M&M, we expect the company to easily maintain its leading market share position in the UV space. Further the company is working on an all-new utility vehicle which is likely to hit markets in the next couple of years, and it will be introducing first diesel compact pick-up truck in the US market early next year. Success of these products should help the company to significantly grow its UV business in the medium term.

Fig 12 No major product to be introduced in categories where M&M dominates Company/Model Launch date Price (in Rsm)

Skoda Yeti Jul-10 1.3 - 1.5Hyundai Santa Fe 1st half of 2010 2.3 - 2.6Nissan Murano 1st half of 2010 3.5 - 4.0BMWX1 Dec-10 2.5Volkswagen Tiguan Early 2011 2.5Tata Aria 2nd half of 2010 1.2Toyota Avanza Early 2011 0.7Source: Company data, Macquarie Research, June 2010

New products to drive growth in LCV space Around 95% of the M&M total LCV volumes is accounted for by the less-than-3.5ton category, one of the fastest growing segments in the Indian automobile space over the last five years (~30% CAGR). The segment has witnessed strong growth post the introduction of India’s first mini-truck with a sub one-ton payload, the Tata Ace, in May 2005. The product took away business from three-wheelers as it provided better economies to fleet operators for last mile transport. Further with development of road infrastructure, the hub-and-spoke model gained importance, leading to strong demand in the heavy truck segment on the one hand and for small LCVs for intra-city transport on the other. However, the success of the Ace also meant a decline in market share for M&M.

Fig 13 Sub 3.5T space gains market share in LCV Fig 14 M&M regaining lost market share

Source: Company data, Macquarie Research, June 2010 Source: Company data, Macquarie Research, June 2010

M&M has introduced many new products over the last couple of years to take on competition in the LCV space. The latest product launches, Gio and Maxximo, we believe should help the company increase its market share significantly from current levels and will be the key drivers of growth in the LCV space for M&M.

M&M created a new category, the compact truck segment, with the launch of the ‘Gio’ in October 2009. The product has a payload of 500kg, with maintenance and running costs similar to that of a three-wheeler and safety and comfort of a four-wheeler. The vehicle is also priced attractively at ~Rs170k. Further M&M launched the Maxximo, in direct competition to the segment leader Ace in February 2010. The product has a higher payload of 850kg and relatively better fuel economy at ~20kmpl, but at the same price as the market leader. Both these products have gotten good response and we expect the company’s LCV segment to see growth of 36% next year, driven largely by these new products.

-

30,000

60,000

90,000

120,000

150,000

180,000

210,000

240,000

FY04 FY05 FY06 FY07 FY08 FY09 FY1030%

40%

50%

60%

70%

80%

90%

Domestic volumes (< 3.5T) % in total LCV sales

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

FY04 FY05 FY06 FY07 FY08 FY09 FY1020%

22%

24%

26%

28%

30%

32%

34%

36%

38%

M&M domestic LCV volumes M&M market share

Gio and Maxximo to drive growth in LCV

space

Macquarie Research Mahindra & Mahindra

14 June 2010 8

Fig 15 Gio – First compact truck (0.5T) Fig 16 Maxximo – taking on the Ace

Source: Company data, Macquarie Research, June 2010 Source: Company data, Macquarie Research, June 2010

Three-wheelers to grow in line with industry The domestic three-wheeler market has grown at a 10% CAGR over the last six years, while M&M has been able to grow at over 20% in the same period. Thus the company has increased its market share by over 350bps in the three-wheeler market. Today M&M is the third-largest player in the domestic three-wheeler space, with market share of around 10%.

Fig 17 Driven by passenger three-wheelers Fig 18 M&M a distant third in three-wheeler space

Source: Company data, Macquarie Research, June 2010 Source: Company data, Macquarie Research, June 2010

Growth in the three-wheeler space is largely driven by the passenger segment, a CAGR of 16% over the last six years, as compared to decline of 2% in the goods segment. The decline in the goods segment was mainly due to increasing usage of low tonnage four-wheelers for last-mile transportation. Mahindra’s presence in three-wheeler space was largely in the goods segment till it launched the Alpha range of three-seater passenger vehicles in early 2008. Today around 60% of company’s three-wheeler volumes comes from the passenger space.

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

FY04 FY05 FY06 FY07 FY08 FY09 FY100.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Total domestic 3 wheeler M&M Market share

Bajaj Auto Ltd40%

Mahindra & Mahindra Ltd

10%

Piaggio Vehicles Pvt

Ltd41%

Others6%

Atul Auto Ltd3%

Macquarie Research Mahindra & Mahindra

14 June 2010 9

Fig 19 New products drive growth Fig 20 Affected by decline in overall industry

Source:SIAM,MacquarieResearch,June2010 Source:SIAM,MacquarieResearch,June2010

We expect M&M’s three-wheeler business to grow in line with industry for the next couple of years. Thus strong growth in the UV and LCV businesses should drive the company’s automotive business in the medium term.

Fig 21 Automotive volume growth – new products to drive LCV growth FY09 FY10 FY11E FY12E FY13E

Utility Vehicles 108,549 152,736 175,646 198,456 222,271 % change YoY 0.9% 40.7% 15.0% 13.0% 12.0% Three-Wheelers 44,806 45,433 48,408 51,843 55,673 % change YoY 31.5% 1.4% 6.5% 7.1% 7.4% LCV 52,640 83,326 116,527 143,441 167,728 % change YoY -0.9% 58.3% 39.8% 23.1% 16.9%Source: Company data, Macquarie Research, June 2010

100,000

150,000

200,000

250,000

300,000

350,000

400,000

FY04 FY05 FY06 FY07 FY08 FY09 FY100%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Domestic passenger 3W M&M market share

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

FY04 FY05 FY06 FY07 FY08 FY09 FY100%

5%

10%

15%

20%

25%

30%

Domestic goods 3W M&M market share

Macquarie Research Mahindra & Mahindra

14 June 2010 10

FES to benefit from Punjab Tractor merger M&M has consolidated its leadership position in the tractor space (53% of EBIT) with the acquisition of Punjab Tractors. We expect the tractor segment to witness 13-15% p.a. growth in the coming years, supported by rising rural income and increasing agricultural credit. M&M has recently launched a new small tractor, Yuvraj, targeting the small and marginal farmers. With tractor penetration of only 1%, the segment has strong growth prospects and can provide significant upside to volume assumptions.

Mahindra’s Farm Equipment Sector is one of the world’s top tractor brands, and has been the undisputed market leader in India for 25 years (FY10 market share of 41%). It is also the only tractor company to win the Deming Application Prize and the Japan Quality Medal, two of the highest quality accolades that can be won by any organization. Mahindra Tractors has two JVs in China which manufacture tractors for the growing Chinese market, as well as export tractors to the US and other western nations.

Tractor demand supported by rising rural incomes Total Tractor sales volume reached 440k units in FY10, with domestic volumes growing at a 14% CAGR since FY04 to over 402k units in FY10. While there were fears that tractor sales could be affected by severe drought last year, we believe that tractor growth was supported by increasing financial penetration, low growth in last few years and improved farm income supported by rising minimum support prices and higher crop output for the rabi season.

Fig 22 Tractor industry grows 14% over last 5 years

Source: CRISIL, MacquarieResearch,June2010

Some of the key factors that we believe are likely to benefit tractor sales in the medium term are as follows:

Increasing production + Rising MSP = Higher rural wealth: Key wheat and paddy production has seen a steady increase over the last few years, and the government-announced Minimum Support Prices (MSP) for key crops, like paddy, wheat, sugarcane, groundnut etc, have increased at a CAGR of 11-12% from 2003-04. This has significantly contributed to rural wealth. The increase in MSP alone has been more than the increase in tractor realisations, up by ~7-8%, thus making tractor usage more affordable.

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Domestic tractor sales (LHS) YoY growth rate (RHS)

Increasing rural wealth to support tractor demand in

medium term

Macquarie Research Mahindra & Mahindra

14 June 2010 11

Fig 23 Steady increase in production Fig 24 Strong increase in MSP

Source:Dept of Agriculture & Cooperation, Macquarie Research,June2010 Source:Dept of Agriculture & Cooperation, Macquarie Research,June2010

Government’s rural development initiatives: Increasingly, government policy decisions have been directed at having inclusive growth, and the rural population has been a major beneficiary of various schemes. Key among these initiatives have been:

⇒ NREGS: The National Rural Employment Guarantee Scheme (NREGS) assures a minimum 100 days employment in a year at a minimum wage of INR 100. Up to 2009-10, around 29m households have benefited from the scheme and over Rs920bn have been disbursed.

⇒ Farm loan waiver: The agriculture debt waiver announced by the government in 2008 has helped bring down Non Performing Assets (NPA) levels of banks and has also provided access to valuable credit to the farming sector. Loan waiver disbursements are pegged at Rs710bn.

⇒ Increasing rural development spending under various schemes like Pradhan Mantri Gram Sadak Yojana (PMGSY), Rajiv Gandhi Grameen Viduytikaran Yojana (RGGVY), Indira Awaas Yojana (IAY), etc also have an indirect positive impact on rural income.

Fig 25 Increased spending on rural development Fig 26 NREGS increasing spending

Source: Ministry of Rural Development, Macquarie Research, June 2010

Source: Mahatma Gandhi National Rural Employment Guarantee Act, Macquarie Research, June 2010

NREGS improving feasibility for tractors: The NREGS has indirectly lead to significant increase in wage rates, even for the farming sector, as people in rural areas have better employment opportunities, thus automatically making use of tractors more economical.

40

50

60

70

80

90

100

2004 2005 2006 2007 2008 2009

in m

n to

ns

Wheat production Rice production

400

500

600

700

800

900

1,000

1,100

1,200

FY04 FY05 FY06 FY07 FY08 FY09 FY10

Paddy (MSP per quintal) Wheat (MSP per quintal)

222 240275

315

627

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

FY06 FY07 FY08 FY09 FY10

in R

s. b

n

110143

120

160

391

0

50

100

150

200

250

300

350

400

FY06 FY07 FY08 FY09 FY10

Rs.

bn

NREGS spending (Rsbn)

Government’s rural schemes adding

significantly to rural employment and

income levels

Macquarie Research Mahindra & Mahindra

14 June 2010 12

Increased disbursals by banks for rural credit: Governments emphasis on increasing bank credit through priority-sector lending has played a crucial role in boosting tractor demand, as around 75-80% of tractors are financed. Disbursement to agriculture by banks has increased at a CAGR of over 20% since 2004 and is targeted to reach Rs3,250bn for 2010. Agriculture credit usage for farm mechanisation has been increasing steadily over the years thus improving farmer’s ability to buy tractors. While financing norms were made more stringent over the last few years due to increasing NPAs, norms have been relaxed and rates have been reduced by banks in early FY10.

Fig 27 Increasing agriculture credit supports tractor demand

Source: Reserve Bank of India, Macquarie Research, June 2010

Increasing spend on irrigation: Indian agriculture is still dependant on the monsoon due to low irrigation facilities. Irrigation intensity is estimated to be below 50%. Availability of irrigation facilities is a key driver for tractor demand, as it ensures water supply for harvesting and thereby income. Through the various five-year plans, the government has tried to expand irrigation facilities, along with consolidating existing systems, for increasing the production of food grains. This in turn should lead to greater demand for tractors.

Fig 28 Cumulative irrigation potential utilised Fig 29 Increasing irrigation spending by state & centre

Source: Ministry of Water, Macquarie Research, June 2010 Source: CRISIL, Macquarie Research, June 2010

Use of tractors for commercial activities: In rural areas, tractors are increasingly being utilized in many activities other than farming, including the transport of materials and passengers over short distances, construction activities, to ferrying water tankers etc. Further, with labour costs rising, even farmers that traditionally hired labour rent tractors for a certain period of time. All these factors have helped to increase hourly tractor rentals by 20-25% in the past two years and the number of days a tractor can be employed during offseason periods has increased substantially, thus leading to higher tractor demand.

500

1000

1500

2000

2500

3000

3500

FY05 FY06 FY07 FY08 FY09 FY10 target

Total agriculture disbursements by banks (Rsbn)

58.8

68.6

77.280.1

83.6

99.6

40

50

60

70

80

90

100

110

VIth Plan(1980-85)

VIIth Plan VIIIth Plan IXth Plan Xth Plan XIthPlan(2007-

12)

m h

ecta

res

187

248255 251

275

359

150

200

250

300

350

FY04 FY05 FY06 FY07 FY08 FY09

Rs

bn

Increasing bank financing

supporting tractor growth in near term

Increasing irrigation a key positive for long term tractor

demand

Macquarie Research Mahindra & Mahindra

14 June 2010 13

Infrastructure investments & allied activities aiding rural income: Lastly, increasing investments being made by governments, companies and co-operative societies in improving rural infrastructure, storage etc have lead to better realisation and lowered overall wastage of agriculture produce. Rural wealth has also increased due to income from other occupations like horticulture, poultry, fish farming, floriculture etc.

We believe that all of the above factors will have a positive impact on farmers’ income in the medium to long term. Given the normal monsoon expected in the current year, the tractor industry should see strong growth of ~12-14% in the current fiscal.

New products to drive growth, targeting bottom of pyramid M&M has refurbished its entire range of tractors in the last year and has launched few key models in the domestic and international areas which should support growth in the tractor segment. Key amongst these are:

Yuvraj 215 – targeting farmers with small land holdings

Swaraj 843 – High HP tractors

Export market – compact tractors and high HP tractors

The Yuvraj 215, which has haulage capacity of 1.5tons, is specially designed for farmers with small land holdings. Through this product, M&M is looking to expand the tractor market at the bottom end of the pyramid. It is expected to cater to the demand from small and marginal farmers suffering from a lack of financing options and affordable products and looking to upgrade from power tillers and bullocks. According to a study by the NSSO, small (2.5-5 acres of land) and marginal farmers (<2.5 acres of land) account for 82% of the 82m farm households in India.

Fig 30 Yuvraj–targeting bottom of pyramid

Source: Company data, Macquarie Research, June 2010

M&M is currently test marketing the tractor in small numbers in Gujarat and then plans to sell it across the country in 16-18 months. We believe that this product could lead to strong volume growth in the medium term, as overall tractor penetration in this segment is only ~1%.

Competitive intensity declining, M&M to benefit from PTL acquisition The tractor industry has seen a couple of acquisitions in the last few years, reducing the competitive intensity. M&M has taken over Punjab Tractors (PTL), whilst TAFE has acquired Eicher Motors. Competition is unlikely to increase in the medium term as no major player is expected to enter the space. Also, the impact of foreign players has been fairly limited, as they lack strong products in the lower-horse-power segments that dominate India’s tractor market.

82 m farm households

Small Farmers 2.5-5 acres-19%

Marginal Farmers

<2.5 acres-63%

Large Farmers

>20 acres -1%

Medium Farmers

5-20 acres-17%

38%

18%

1%

Yuvraj – targeting bottom of pyramid,

huge growth option if successful

Macquarie Research Mahindra & Mahindra

14 June 2010 14

Fig 31 Market share in FY05 Fig 32 Lower competitive intensity in FY10

Source: CMIE, Macquarie Research, June 2010 Source: CMIE, Macquarie Research, June 2010

PTL acquisition benefits M&M significantly

M&M acquired Punjab Tractors (PTL) in 2007 by buying out 43% stake from the Actis group and the Burman family for around Rs10bn, later merging the company with its farm equipment division in August 2008. PTL sold its products under the Swaraj brand, which had good a reputation in market and M&M also added products in the 50HP+ category through this acquisition. M&M has improved its market share position post acquisition of Punjab Tractors and currently dominates the domestic tractors market, with ~41% market share. It commands over 50% market share in the South and East markets and enjoys a strong position in West and North India, with respective market shares of 42% and 36%. Further, the company also improved its position in the largest 31-40HP category.

Fig 33 Regional domestic tractor sales (FY10) Fig 34 M&M (incl PTL) regional market share

Source: Crisil, Company data, Macquarie Research, June 2010 Source: Crisil, Company data, Macquarie Research, June 2010

M&M26%

TAFE20%

Escorts13%

Punjab Tractors

12%

International Tractors

11%

Eicher Motors8%

Others10%

M&M & Punjab Tractors

41%

TAFE & Eicher22%

Escorts12%

International Tractors

9%

John Deere8%

Others8%

North43%

East14%

West25%

South18%

31%

41% 41%

48%

36%

51%

42%

51%

0%

10%

20%

30%

40%

50%

60%

North East West South

FY08 FY10

Relatively low competitive

intensity and PTL acquisition to

benefit Tractor division

Macquarie Research Mahindra & Mahindra

14 June 2010 15

Fig 35 Lower HP dominates domestic market (FY10) Fig 36 M&M (incl PTL) HP segment market share

Source: CMIE, Company data, Macquarie Research, June 2010 Source: CMIE, Company data, Macquarie Research, June 2010

Thus the PTL acquisition has strengthened M&M’s position in the key North Indian market, as well as in the lower HP market, where it was weak. The PTL manufacturing plants and foundry facility had lower utilisation, which should help M&M to improve its cost structure. M&M is also looking at dealer and vendor rationalisations, which should improve overall tractor business profitability in the medium term

Up to 30 HP17%

31 - 40 HP51%

41- 50 HP22%

51 HP and above10%

39% 41%

28%

58%

48%44%

28%

56%

0%

10%

20%

30%

40%

50%

60%

Up to 30 HP 31-40 HP 41-50 HP 51 HP & above

FY08 FY10

Macquarie Research Mahindra & Mahindra

14 June 2010 16

New initiatives to add value in medium term M&M has entered into new business areas like Medium and Heavy Commercial Vehicles (M&HCV), two-wheelers, aerospace, etc and has enhanced its presence in defence and auto ancillaries, all of which could add significant value in the medium term. The company has also recently inaugurated a new plant at Chakan which should take care of company’s expansion plans in the automotive business for the next 5 to 7 years.

M&HCV – strong growth prospects in medium term In 2005, M&M and International Truck and Engine Corporation — the operating company of Navistar Inc (NAV US; $53.15; not rated) — entered into a JV to manufacture light, medium and heavy commercial vehicles for India as well as export markets. The joint venture aims to be present in every segment of the commercial vehicle market, from 3.5 tonne Gross Vehicle Weight (GVW) to 49 tonne GVW, with variants of passenger transport, cargo and specialized load applications. These products will be manufactured at M&M’s new Chakan plant, which has initial annual production capacity of 50,000 medium and heavy commercial Vehicles. M&M has a 51% stake in two JV’s, Mahindra Navistar Automotives Ltd and Mahindra Navistar Engines Ltd.

Gradual roll out of product range

M&M Navistar has so far displayed different products in the 25T, 31T, 40T and 49T segments. The company plans to introduce its entire product range in the next couple of years as follows:

Commercial launch of 25T is expected by June 2010 followed by 31T.

40 & 49T products by end of the current fiscal year.

Lower tonnage vehicles will be launched in due course of time from FY12

Thus by FY13 the company plans to have all products in the market right from 9T to 49T in both the trucks and bus segments and to emerge as a full-range commercial vehicle player.

Building distribution network, increasing localisation

The company is setting up an alternative distribution network for the truck venture, after having added ~100 new dealers. It may also look at its existing dealerships in rural/semi-urban areas as points of servicing for its trucks. M&M is also ensuring that designing of the CV product range is done to fulfil the requirements specific to Indian business, with the technological support of Navistar. Further the company aims to have high localisation levels so as to ensure that pricing remains competitive.

Strong growth prospects in medium term

We believe that it will be challenging for M&M to make inroads into the Rs350bn Indian CV space which is currently a virtual duopoly. However with strong economic growth and government’s focus on road development, the space provides strong medium-to-long-term-growth opportunities for M&M. Having a strong technical partner, good understanding of local markets, wide distribution and service networks, and ensuring products meet local needs and aim for high levels of localisation should aid the company’s efforts to gain respectable market share in the CV space in the next 3-5 years.

Mahindra two-wheeler – entry through acquisition of Kinetic M&M entered the Indian two-wheeler market by acquiring the business assets of Kinetic Motor for Rs1.1bn in July 2008. M&M holds an 80% stake in the new company – Mahindra Kinetic Scooters and Motorcycles Ltd, with Kinetic accounting for the remaining 20%. The company has state-of-the-art manufacturing facility at Pithampur, Madhya Pradesh, with a capacity to assemble 500-600k units p.a. on a three-shift basis. Taiwan’s Sanyang Industry Company Limited (SYM) Sanyang Industry Co Ltd (2206 TT, Not Rated) is a technical partner in the alliance. M&M has also recently acquired Engines Engineering, Italy, specialised in designing two-wheelers.

Strong partner, local understanding

should help gain a footing in M&HCV

space

Turnaround in scooter business

post takeover, motorcycle next

target

Macquarie Research Mahindra & Mahindra

14 June 2010 17

Improved market share post new launches in last year

Fig 37 M&M - improving market share in scooter space

Source: SIAM, Macquarie Research, June 2010

Mahindra Two-Wheelers is currently present in scooters segment and has already launched three 125cc scooters since acquisition.

Mahindra Rodeo – specifically for males

Mahindra Duro – targeting the entire family

Mahindra Flyte – specifically for women commuters

Post acquisition and launch of new products, M&M has been able to steadily improve volumes for the scooter business. M&M’s total scooter sales for FY10 stood at over 70k units, more than double of what Kinetic was able to sell in FY08 prior to acquisition. The company’s market share now stands at ~6% in the domestic scooter segment.

Management expects strong growth in coming years

M&M targets double-digit growth for the two-wheeler business for the next couple of years. The company also plans to enter the motorcycle space in the current fiscal year. We expect M&M to take time to find its foothold in the two-wheeler space, especially faced with challenges from well-entrenched players like Hero Honda (HH IN, Rs2013, UP, TP: Rs1630) and Bajaj Auto (BJAUT IN, Rs2284, UP, TP:Rs1850). However, given M&M’s track record of new launches, good understanding of local market in particular rural markets and strong distribution and service networks, the returns on its small investments may be substantial over the medium term.

Renewed focus on defence Mahindra Defence Systems provides total solutions for the entire range of light combat / armoured vehicles and their derivatives for defence and security forces. It also addresses specific segments of the Government's import-substitution programmes like small arms and sea mines. Mahindra’s defence business is targeting revenue of Rs20bn in five years from Rs1 bn currently, which we believe is achievable given India’s huge defence spending. India’s total defence allocation currently standing at ~US$30bn and there is a separate allocation for Para-military and police forces thus providing a huge market. Further, the current offset clause, which mandates 30% of the overall expenditure in defence sector from a foreign company to be sourced from Indian companies, itself provides around US$10bn market over the next five years.

JV’s and new plant to support growth in defence

In March 2009, M&M inaugurated a defence-vehicle manufacturing plant in Haryana’s Prithla region. The Rs400m facility is expected to roll out 200 vehicles in a year’s time. In Nov 2009, M&M (74% stake) entered into a JV with BAE Systems (UK) (BAE LN; not rated; 321p) to focus on the manufacture of up-armoured light vehicles, specialist military vehicles, mine protected vehicles, artillery systems and other selected land system weapons and the upgrades. The JV is focusing on the India’s artillery system requirement which currently is ~US$4bn.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Apr-09 May-09

Jun-09 Jul-09 Aug-09

Sep-09

Oct-09 Nov-09

Dec-09

Jan-10 Feb-10

Mar-10

Apr-100.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

M&M domestic scooter sales (LHS) scooter market share (RHS)

Defence – a solid growth opportunity

in next 4-5 years

Macquarie Research Mahindra & Mahindra

14 June 2010 18

Entered aerospace, boat manufacturing and electric vehicle space Mahindra Odyssea

M&M entered the fibreglass power boat and catamaran industry through its product offering Mahindra Odyssea in 2009. In Feb 2009, Mahindra Odyssea unveiled its 22-foot and 33-foot fibreglass power boats at the Mumbai International Boat Show. Initially the company is targeting custom-designed fibreglass power boats ranging 20-40 feet and then expand into cabin cruisers and catamarans in the future. Mahindra Odyssea’s products are expected to attract the paramilitary and defence forces.

Mahindra Reva

M&M recently acquired a controlling stake in electric car manufacturer Reva and established Mahindra Reva Electric Vehicle Company. M&M will own 55.2% equity in Mahindra Reva by a combination of equity purchase from the promoters and a fresh equity infusion of over Rs450m into the company. Currently, Reva sells electric cars in 24 countries and has around 3500 vehicle on the road. A new manufacturing facility at Bangalore has expanded company’s production capacity from 6,000 to 30,000 vehicles.

Leveraging Reva’s technology for UV products in medium term

M&M will look to utilising REVA's technology for its products, including UVs, three-wheelers and mini-trucks. Further, M&M’s distribution network will be used to market REVA's products across the globe. This is a small investment from M&M’s overall perspective, but it gives the company a good start in the electric vehicle field, as REVA is a proven leader; in the medium term the company can benefit from leveraging REVA’s technology. The long -erm potential of electric vehicles can be big, and M&M expects the electric car market in India to grow to 80,000 cars by 2020, with Mahindra Reva accounting for at least 20,000.

Chakan to meet capacity needs for the medium term In March 2010, M&M inaugurated its new auto manufacturing plant in the industrial hub of Chakan in Maharashtra. Set up with a phased investment of over Rs40bn, the plant is spread across 700 acres. The plant’s initial capacity is slated at 300k vehicles p.a, 50k units of M&HCV and 250k for the rest of yhe automotive division, and it can be scaled up further to meet future growth. Thus Mahindra Chakan will manufacture Mahindra’s entire range of automotive products, from the 0.75-tonne Maxximo to the 49-tonne Mahindra Navistar truck. The company’s new SUV and Pik-Up range and product line for the US market will also be manufactured at this facility. These investments should help M&M meet all their automotive capacity needs for the next 5-6 years. Also such investments at one single location would provide flexibility to the company to manage production of its various new products and also provide benefits from economies of scale.

Huge investment in new capacities to

meet forecasted growth for next 3-5

years

Macquarie Research Mahindra & Mahindra

14 June 2010 19

Solid earnings growth for coming years We estimate the company’s earnings to grow at CAGR of 13% over the next three years, backed by volume growth of 15% but seeing a minor decline in margins. We are 5-7% ahead of consensus earnings estimates, mainly on account of higher volume assumptions.

Fig 38 Ahead of consensus driven by higher volume growth Net sales Net Profit FY11E FY12E FY11E FY12E

Macquarie 223,111 258,176 23,661 26,330 Consensus 215,433 247,573 22,051 24,977 Difference 3.6% 4.3% 7.3% 5.4%Source: Bloomberg, Macquarie Research, June 2010

Volume growth to be supported by new products We expect M&M volume to grow by 15% over the next three years. We estimate the utility and tractor segments to witness sales growth of ~11-15%, in-line with industry growth rates. The three-wheeler segment is expected to see lower growth as there is a shift to more robust lo- tonnage four-wheelers in the goods segment. With two key new product launches (Gio and Maxximo), we estimate the LCV segment will show solid growth of over 25%. Better-than-expected response to these products and acceptance of the Scorpio pick-up in the US market could be a big driver to our overall volume growth assumptions.

Fig 39 Volume growth across segments FY09 FY10 FY11E FY12E FY13E Macquarie comments

Utility Vehicles 108,549 152,736 175,646 198,456 222,271 In-line with industry % change YoY 0.9% 40.7% 15.0% 13.0% 12.0% Three-wheelers 44,806 45,433 48,408 51,843 55,673 Growth largely from passenger segment % change YoY 31.5% 1.4% 6.5% 7.1% 7.4% LCV 52,640 83,326 116,527 143,441 167,728 New products to drive growth % change YoY -0.9% 58.3% 39.8% 23.1% 16.9% Tractors 119,951 176,328 202,777 229,138 256,635 Growth largely in-line with industry % change YoY 21.3% 47.0% 15.0% 13.0% 12.0% Source: Company data, Macquarie Research, June 2010

Margins to decline due to rising RM costs, earnings growth robust We expect increasing prices of key raw materials like steel, aluminium and tyres to negatively impact margins in the coming fiscal year. However with strong growth in volumes, we expect some of the impact to be negated by the positive effect of operating leverage. Further, with a strong product portfolio in both the UV and tractor space and relatively subdued competition, we believe that some of the cost hikes will be passed on to consumers. Thus, overall we expect operating margins to go down by ~50-60bps in FY11. The impact could be larger if RBI becomes aggressive in tightening interest rates, as this may limit company’s capacity to increase prices. Further, taking into account the increased depreciation on account of the ramp-up of new Chakan plant, we expect overall earnings to grow by ~14% over the next three years.

Macquarie Research Mahindra & Mahindra

14 June 2010 20

Fig 40 Margin to decline incrementally Fig 41 Increasing depreciation, robust earnings

Source: Company data, Macquarie Research, June 2010 Source: Company data, Macquarie Research, June 2010

Robust balance sheet, comfortable cash flows despite huge capex M&M has planned huge capital expenditure of Rs70bn over the next three years (including investments in JVs and subsidiaries). Most of this will be on new plant at Chakan and new product developments. Despite this huge capex spending, we do not see any issue with the cash-flow situation, as the standalone business generates around Rs20-25bn of operating cash flows on annual basis and the company has over Rs17bn in cash and liquid investments. Further, the company’s total debt-to-equity ratio stands at very comfortable 0.4:1, and thus even if there is any significant decline in operating cash flows, the company can easily manage its investments through some additional debt.

Fig 42 Huge capex spending over next three years Fig 43 Strong cash flow despite huge capex

Source: Company data, Macquarie Research, June 2010 Source: Company data, Macquarie Research, June 2010

4,000

10,000

16,000

22,000

28,000

34,000

40,000

46,000

52,000

FY09 FY10 FY11E FY12E FY13E12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.5

16.0

16.5

EBITDA (Rsm) (LHS) EBITDA margin (%) (RHS)

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

FY09 FY10 FY11E FY12E FY13E1,000

2,000

3,000

4,000

5,000

6,000

7,000

PAT Rsm (LHS) Depreciation Rsm (RHS)

-

5,000

10,000

15,000

20,000

25,000

FY09 FY10 FY11E FY12E FY13E

Capex and investments in JV's (Rsm)

(6,000)

(4,000)

(2,000)

-

2,000

4,000

6,000

8,000

10,000

12,000

FY09 FY10 FY11E FY12E FY13E(0.40)

(0.20)

-

0.20

0.40

0.60

0.80

1.00

FCF (Rsm) (LHS) Net Debt:Equity (RHS)

Macquarie Research Mahindra & Mahindra

14 June 2010 21

Condensed Financial statements

Fig 44 Condensed Profit and loss account (Rs m) Yearto31March FY09 FY10 FY11E FY12E FY13E Macquarie comments

Net sales 131,260 186,041 223,111 258,176 293,208 Supported by strong volume growth and minor increase in realisation

% change YoY 13.9% 41.7% 19.9% 15.7% 13.6% Raw Material expenses 92,742 123,360 150,448 175,308 199,699 Rising prices of steel, aluminium and tyres % of net sales 70.7% 66.3% 67.4% 67.9% 68.1% Manufacturing & other expenses 17,773 21,818 25,381 28,812 32,370 To benefit from higher volumes % of net sales 13.5% 11.7% 11.4% 11.2% 11.0% Total operating costs 120,334 156,466 188,795 218,862 248,665 % of net sales 91.7% 84.1% 84.6% 84.8% 84.8% EBITDA 10,926 29,575 34,316 39,314 44,543 Margins to decline by 60-80bps mainly

on account of rising RM prices Less: Interest 1,341 1,542 1,375 1,350 1,350 Add: Other Income 3,592 3,249 3,578 3,241 3,360 Less: Depreciation 2,915 3,706 4,544 5,623 6,695 Depreciation to increase with ramp up at

new Chakan plant Add: Exceptional Items 410 908 - - - Pre tax profit 10,672 28,484 31,975 35,581 39,858 Less: Tax 1,997 7,591 8,313 9,251 10,363 Net Profit 8,342 20,227 23,661 26,330 29,495 Earnings to grow by ~13% over next 3

years EPS (Rs.) 29.88 35.74 41.81 46.53 52.12 Source: Company data, Macquarie Research, June 2010

Fig 45 Condensed Balance Sheet (Rs m) Yearto31March FY09 FY10 FY11E FY12E FY13E Macquarie comments

Shareholders’ Equity 52,621 78,262 94,626 113,161 134,363 Secured & Unsecured Loans 40,528 28,802 28,802 28,802 28,802 Comfortable debt:Equity of 0.4:1, to decline

further Deferred Tax Liability - 2,403 2,403 2,403 2,403 Accounts Payable 33,368 32,879 38,794 44,972 47,689 Provisions 12,776 17,965 18,960 19,458 19,955 Total Current Liabilities 47,978 51,992 59,017 65,819 69,173 Total Liabilities 93,148 109,467 125,831 144,366 165,568 Net Fixed Assets 32,143 36,937 49,393 58,770 65,075 Chakan project to add significantly in

coming years Investments 57,864 63,980 72,480 80,980 88,980 Significant liquid investments Inventories 10,607 11,838 17,691 20,263 22,806 Strong control on inventories Accounts Receivables 10,437 12,433 16,493 19,110 21,712 Cash & Bank Balances 15,744 17,525 8,243 9,616 14,818 Solid cash balance despite Rs70bn of

capex and investment in JV over next 3 years

Total Current Assets 50,810 60,318 62,750 70,210 80,462 Total Assets 93,148 109,467 125,831 144,366 165,568 Source: Company data, Macquarie Research, June 2010

Macquarie Research Mahindra & Mahindra

14 June 2010 22

Fig 46 Condensed Cash Flow (Rs m) Yearto31March FY09 FY10 FY11E FY12E FY13E Macquarie comments

Cash Flow from Operating Activities Net Profit before Tax 10,262 28,484 31,975 35,581 39,858 Solid auto and tractor business Depreciation 2,915 3,706 4,544 5,623 6,695 Total Working Capital changes 5,918 (8,215) (5,800) 90 (2,332) Good working capital management Direct taxes paid 1,003 6,644 8,313 9,251 10,363 Net cash from operating activities 16,313 19,025 21,027 31,210 32,961 Strong operating cash flows Cash Flow from Investing Activities Purchase of Fixed Assets (Capex) (9,297) (8,500) (17,000) (15,000) (13,000) Huge capex on new capacities and

product development Purchase of Investments (171,186) (6,116) (8,500) (8,500) (8,000) Investments mainly in new JV’s/

business like M&HCV, two-wheeler etcSale of Investments 161,957 - - - - Net cash used in investing activities (19,410) (11,904) (22,632) (21,190) (18,615) 4,408 (4,473) 7,710 11,961 Cash Flow from Financing Activities Dividends paid (3,203) (3,121) (6,302) (7,297) (7,795) Rewarding shareholders through

increased dividends Interest paid (952) (1,542) (1,375) (1,350) (1,350) Net cash used in financing activities 6,969 (5,339) (7,677) (8,647) (9,145) Cash and Cash Equivalents at Beginning of the year

11,746 15,744 17,525 8,243 9,616

Net Increase/(Decrease) in Cash 3,872 1,781 (9,282) 1,373 5,201 Cash and Cash Equivalents at End of the year

15,744 17,525 8,243 9,616 14,818 Pretty comfortable on cash flow situation despite high capex

Source: Company data, Macquarie Research, June 2010

Fig 47 Key Ratios (%) FY09 FY10 FY11E FY12E FY13E Macquarie comments

Growth Revenue 13.9 41.7 19.9 15.7 13.6 Strong growth supported by new productsEBITDA (20.0) 170.7 16.0 14.6 13.3 Margins to decline mainly on account of

rising raw material prices PBT (23.9) 166.9 12.3 11.3 12.0 Net income (13.5) 142.5 17.0 11.3 12.0 Margins EBITDA Margin 8.3 15.9 15.4 15.2 15.2 Operating margins to decline on account of

rising raw material prices EBIT Margin (incl. other income) 8.8 15.7 14.9 14.3 14.1 Pre-tax Margin 8.1 15.3 14.3 13.8 13.6 Tax rate 18.7 26.7 26.0 26.0 26.0 No major change in effective tax rate Net Margin 6.4 10.9 10.6 10.2 10.1 Return Ratios RoNW 15.9 25.8 25.0 23.3 22.0 Solid returns to shareholders from core

business RoCE 12.5 27.2 27.0 26.0 25.3 Source: Company data, Macquarie Research, June 2010

Macquarie Research Mahindra & Mahindra

14 June 2010 23

Valuation – trading attractively Ex-subsidiaries, stock at attractive valuation Excluding valuation of listed subsidiaries (at 20% discount) M&M currently trades at 11.3x FY11E and 10.2x FY12E core EPS. This is at significant ~28% discount to other auto names and one of the least expensive stocks in the Indian auto space coverage universe. This sharp discount in valuation we believe is not justifiable.

Fig 48 Trading cheap ex-listed subsidiaries

Company name Market cap (Rs m) M&M stake (Rs m)

M&M value / share post 20% discount

(Rs)

Tech Mahindra 90,594 39,445 53 M&M Financial services 45,350 27,257 37 Mahindra Forgings 8,786 4,453 6 Mahindra Lifespace Developers 17,014 8,686 12 Mahindra Holiday & resorts 42,233 35,091 47 Mahindra Ugine steel 1,912 969 1 Swaraj Engines 4,099 1,362 2 Total value 157 M&M share price (Rs) 607 Contribution of subsidiaries 26% Net value for standalone auto business 450 Core standalone EPS FY11E 39.7 11.3 Core standalone EPS FY12E 44.2 10.2 Core standalone EPS FY13E 49.5 9.1 Source: Bloomberg, Company data, Macquarie Research, June 2010, (prices as of 11 June)

There are no directly comparable companies with a presence in both the auto and tractor segments; thus, we have taken the entire group of large-cap Indian auto names and also regional players in UV, M&HCV and tractor spaces for comparison. We see that M&M appears very attractively valued not only with respect to Indian auto companies, but also compared to auto companies from China, Korea and Japan,.

Fig 49 One of cheapest Indian auto stock, attractive on regional basis also Market cap PER EV/EBITDA RoE Company Name (US$m) Year ending FY10 FY11E FY12E FY10 FY11E FY12E FY10 FY11E FY12E

M&M 7,073 March 17.9 15.3 13.7 11.5 10.2 8.8 25.8 25.0 23.3 M&M (ex listed subsidiaries)

4623 March 12.1 10.3 9.3 6.3 5.7 4.9 25.0 24.1 21.9

Tata Motors 8,735 March 39.5 14.2 9.8 10.1 7.4 6.0 13.6 28.0 30.9 Ashok Leyland 1,729 March 19.6 15.2 12.7 12.6 10.2 8.8 11.9 14.5 15.9 Maruti Suzuki 7,860 March 15.6 13.7 12.1 10.2 9.3 8.1 23.8 22.0 20.5 Bajaj Auto 6,791 March 19.4 17.0 16.2 12.9 11.7 10.7 58.0 47.0 38.0 Hero Honda 8,442 March 18.0 17.2 16.6 13.3 12.8 11.8 59.5 53.5 41.0 Mazda Motor 4,360 March NA 24.3 10.8 8.6 6.6 5.6 - 1.0 3.3 6.5 Isuzu Motors 5,468 March 62.3 18.3 12.5 15.2 8.2 7.0 2.7 9.2 12.2 Nissan Motors 31,828 March 39.2 13.0 9.2 8.2 7.5 6.6 2.6 6.9 9.2 SAIC 15,463 December 11.1 9.6 8.2 11.0 9.8 7.0 19.9 20.4 20.1 Dongfeng 9,541 December 8.9 7.9 7.3 4.6 4.0 3.6 23.2 21.6 19.3 FAW Car 3,973 December 12.7 10.7 9.1 7.2 6.4 5.6 23.1 23.6 22.9 Jiangling Motors 2,051 December 12.0 10.3 8.6 5.5 5.0 4.3 22.9 22.6 22.3 Hyundai Motor 25,800 December 10.4 9.6 8.9 6.3 6.0 5.7 16.2 15.1 14.0 KIA Motors 10,027 December 8.0 7.4 6.8 7.2 6.8 6.6 20.1 18.7 17.0 Source: Bloomberg, Macquarie Research, June 2010 (prices as of 11 June)

The company also appears to trade very favourably on one-year forward PER basis, given robust growth in earnings and its very sound balance sheet and cash flow.

Trading very attractively in

comparison to domestic auto

companies as well as regional players

Trading very attractively in

comparison to domestic auto

companies as well as regional players

Macquarie Research Mahindra & Mahindra

14 June 2010 24

Fig 50 M&M stands out on earnings growth and relative valuation

Source: Bloomberg, Macquarie Research, June 2010

Fig 51 Trading around historical average – rolling forward PER

Source: Bloomberg, Macquarie Research, June 2010

Value on SOTP basis – 22%potential upside We value M&M based on Sum of the parts (SOTP) methodology and arrive at target price of Rs740, implying 22% upside from current levels. We ascribe a PER multiple of 14x to standalone core earnings (excluding dividend from subsidiaries), in-line with the sector average and valuing the core auto business at Rs583 per share. We value the listed subsidiaries at a 20% discount to existing market cap, in-line with our methodology for other auto names.

Maruti Suzuki

Bajaj AutoHero Honda

M&M

Dongfeng

FAW

Hyundai KIA

SAIC

Tata MotorsJiangling

4%

6%

8%

10%

12%

14%

16%

18%

20%

6 8 10 12 14 16 18 20 22

One year forward PER (x)

FY11

E EP

S gr

owth

-4.0

1.0x

6.0x

11.0x

16.0x

21.0x

26.0x

Apr-0

5

Aug

-05

Dec

-05

Apr-0

6

Aug

-06

Dec

-06

Apr-0

7

Aug

-07

Dec

-07

Apr-0

8

Aug

-08

Dec

-08

Apr-0

9

Aug

-09

Dec

-09

Apr-1

0M&M share price Average PER

SOTP based target price of Rs740 –

implying 22% upside

Macquarie Research Mahindra & Mahindra

14 June 2010 25

Fig 52 SOTP based target price

Company name M&M stakeMarket cap

(Rsm) M&M stake

(Rsm)

M&M value / share post 20%

discount (Rs)

Tech Mahindra 43.5% 90,594 39,445 53 M&M Financial services 60.1% 45,350 27,257 37 Mahindra Forgings 50.7% 8,786 4,453 6 Mahindra Lifespace Developers 51.1% 17,014 8,686 12 Mahindra Holiday & resorts 83.1% 42,233 35,091 47 Mahindra Ugine steel 50.7% 1,912 969 1 Swaraj Engines 33.2% 4,099 1,362 2 Total value 157 Standalone business FY12E Core EPS 42PER Multiple (x) 14Core auto business value (Rs) 583 Target price 740Source: Bloomberg, Macquarie Research, June 2010, (prices as of 11 June)

We also calculate standalone business value through DCF basis and we arrive at a value of Rs551 per share based on 3.5% terminal growth rate and a WACC of 12.4%.

Fig 53 Assumptions for DCF Effective tax rate (Te) 27% CAPM cost of equity (Ke) 14.3%Pre tax cost of debt (r*) 9.0% Debt/(debt+equity) proportion (D/EV) 25.0%Market risk premium (Em) 6.0% Equity/(debt + equity) proportion (E/EV) 75.0%Risk-free rate (Rf) 8.0% Terminal growth rate (g) 3.5%Beta 1.05 WACC (r) = 12.4%Source: Company data, Macquarie Research, June 2010

Fig 54 DCF value Particulars RsmNPVFCF 123,663.6

PV OF TV 184,234.1 PV of (FCF+ TV) 307,897.7 Net Debt (12,775.7)Total Value 320,673.4 Shares Outstanding 582.0 Per share price 550.99 Source: Company data, Macquarie Research, June 2010

Sensitivity analysis

Fig 55 Sensitivity to holding company discount and standalone business multiple Standalone business multiple

13.0 13.5 14.0 14.5 15.0

Hol

ding

co

mpa

ny

disc

ount

(%

)

30% 679 700 721 742 763 25% 689 710 731 752 773 20% 698 719 740 761 782 15% 708 729 750 771 792 10% 717 738 759 780 801

Source: Company data, Macquarie Research, June 2010

Macquarie Research Mahindra & Mahindra

14 June 2010 26

Key risks and catalysts Key risks Increase in taxes on diesel vehicles: The Kirit Parikh committee report on oil sector

reforms has suggested an excise duty of Rs 80,000 on diesel vehicles. If implemented, the recommendation is expected to adversely affect M&M as it would lead to higher costs of diesel-based products and hence impact demand for same. However, the probability of the committee recommendation being carried out in its current form is low, with the industry players opposing it and putting their suggestions through the industry forum to the government for consideration.

Significant jump in raw material prices: An increase in the prices of key raw materials like steel and aluminium would lead to decline in margins and profitability. However with a leadership position in key segments and a strong product portfolio, M&M should be able to pass on most of the rise in prices on to customers and thus reduce the impact on margins.

Faster than expected hardening of interest rates: An increase in interest rates would negatively impact M&M’s sales, since around 70-80% of the tractor and UV sales by the company are purchased via the financing option. Further, this can also limit the company’s ability to increase prices to offset rising raw material prices. However, our economists expect a gradual increase in interest rates, which can be absorbed.

Lower demand due to less than normal monsoon: M&M tractor sales and also sales of key products like Bolero in the automotive division can be affected if the monsoon is less than normal or its distribution affects rural income. While the Indian meteorological department has forecasted a normal monsoon, two continuous years of drought can severely impact rural spending.

Managing diverse business: M&M is well-diversified and is entering new businesses and markets, like M&HCV, two-wheelers and the US. This clearly adds to the complexity of the business and requires strong systems and management band-width. Though the company has so far been able to manage its operations well, a stretch in management band-width remains a risk.

Key catalysts Stronger-than-expected sales in the domestic market: A widening in the direct tax

slabs in India would lead to an increase in disposable income for consumers and might result in higher UV sales. Similarly, a bumper crop or acceptance of the new tractor targeted at the bottom of the pyramid can lead to stronger-than-expected growth in the tractor space.

New LCV products garnering significant market share: With the launch of Gio and Maxximo, M&M has entry into the fast-growing low-tonnage LCV segment. If the company manages to take away around 15-20% market share from the lone player in the segment, it can meaningfully add to overall volumes for the company.

Positive response from the US market: M&M is looking to launch the Scorpio pick up in the US by the end of 2010. The company has already tied up with a US distributor having alliances with around 300 dealers. A positive response from the 4.5m US light truck market will pave the way for an increase in revenue from international operations.

.

Macquarie Research Mahindra & Mahindra

14 June 2010 27

Appendix I: Tech Mahindra Crown gems Tech Mahindra, the ~44% owned IT services subsidiary of M&M, is one of the leading IT services outsourcing firms in India (amongst top 10 IT companies by market cap). It provides Telecom IT Services and Solutions to global communications industry, with a presence across the telecom value chain and operates through 16 regional offices and 11 delivery centres. The company, with a talent pool of ~30,000, has a long history of serving major global telecom service providers, with BT Group (BT/A LN, £1.32, Underperform, TP: £1.10, Guy Peddy) as the key customer. Although dependence on BT for business has reduced over the years (from 64.1% in FY07 to 48.2% in FY10), top ten clients still contribute ~82.3% of the revenue in FY10. We believe that, with continued focus on diversification, the share of non-BT revenue would continue to rise in the coming years.

Fig 56 Tech Mahindra –robust revenue & PAT growth Fig 57 Sales diversification –Non-BT growing faster

Source: Company data, Macquarie Research, June 2010 Source: Company data, Macquarie Research, June 2010

Fig 58 Impressive client ramp-up Fig 59 BT skews geographical sales mix to Europe

Source: Company data, Macquarie Research, June 2010 Source: Company data, Macquarie Research, June 2010

As growing competition impacts profitability, telcos are more inclined towards reduction in time to market and shifting focus from managing services to offering value-added services. This, in turn, is encouraging outsourcing of telecom services and is likely to benefit Tech Mahindra over the medium and long term due to their long-term growth strategy and unique delivery capabilities.

280

648

935985 977

53136

192 224152

0

200

400

600

800

1000

1200

FY06 FY07 FY08 FY09 FY10

US$ mn

Revenue PAT

415596 575

470

339 410506

233

0

200

400

600

800

1000

1200

FY07 FY08 FY09 FY10

US$ mn

BT Non-BT

Non-BT Sales CAGR -30%

2944 44 47 47 49 48

8

13 1315 17 18 18

6

6 88 9 9 11

0

10

20

30

40

50

60

70

80

FY07 FY08 FY09 1Q'10 2Q'10 3Q'10 4Q'11

>=US$ 1mn >=US$ 5mn >=US$ 10mn

Europe56%

North America30%

ROW14%

Macquarie Research Mahindra & Mahindra

14 June 2010 28

Fig 60 Tech Mahindra strategy Fig 61 Tech Mahindra –unique delivery model

Source: Company data, Macquarie Research, June 2010 Source: Company data, Macquarie Research, June 2010

Tech Mahindra has added ~6,000 employees over the last seven quarters with peak utilization rate of ~75% in 2Q’10. With traction of the business ramp-up improving due to a better macro outlook, we believe utilization rates will remain high in the medium term.

Fig 62 Employee growth robust Fig 63 Employee utilization at highest level

Source: Company data, Macquarie Research, June 2010 Source: Company data, Macquarie Research, June 2010

With an eye to diversifying its presence across verticals and expanding client base, the company has acquired 42.7% stake in scandal-ridden Satyam Computers (renamed Mahindra Satyam) in CY09 to gain foothold in the BFSI, manufacturing, healthcare and retail/travel/logistics verticals apart from its traditional stronghold of telecom. Since Satyam was poorly governed, Tech Mahindra is focusing on improving the operating matrix and cost rationalization in order to optimize the full potential of Satyam. As the customer stability and financial restatement concludes, Satyam could be a feather in Tech Mahindra’s cap, given its strong and diverse customer base, coupled with various fast-growing vertical capabilities.

24.4 25.1 25.4 25.0 25.5 26.5

30.433.5

15% 21% 19% 18% 17% 19% 21% 26%

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10

'000

0%

5%

10%

15%

20%

25%

30%

Headcount Attrition

69%68%

70%71%

75%

73% 73%

64%