L&T Annual Report 2019-20 - WIRC-ICAI.org

135

459 INDEPENDENT AUDITORS’ REPORT TO THE MEMBERS OF LARSEN & TOUBRO LIMITED Report on the Audit of the Consolidated Financial Statements Opinion We have audited the accompanying consolidated financial statements of Larsen & Toubro Limited (the “Parent”) and its subsidiaries, (the Parent and its subsidiaries together referred to as the “Group”) which includes 35 joint operations of the Group accounted on proportionate basis and the Group’s share of profit in its associates and joint ventures, which comprise the Consolidated Balance Sheet as at 31st March 2020, and the Consolidated Statement of Profit and Loss (including Other Comprehensive Income), the Consolidated Statement of Cash Flows and the Consolidated Statement of Changes in Equity for the year then ended, and a summary of significant accounting policies and other explanatory information. In our opinion and to the best of our information and according to the explanations given to us, and based on the consideration of reports of the other auditors on separate financial information of the joint operations, subsidiaries, associates and joint ventures referred to in the Other Matters section below, the aforesaid consolidated financial statements give the information required by the Companies Act, 2013 (the “Act”) in the manner so required and give a true and fair view in conformity with the Indian Accounting Standards prescribed under section 133 of the Act read with the Companies (Indian Accounting Standards) Rules, 2015, as amended (“Ind AS”), and other accounting principles generally accepted in India, of the consolidated state of affairs of the Group as at 31st March 2020, and their consolidated profit, their consolidated total comprehensive income, their consolidated cash flows and their consolidated changes in equity for the year ended on that date. Basis for Opinion We conducted our audit of the consolidated financial statements in accordance with the Standards on Auditing specified under section 143 (10) of the Act (“SA”s). Our responsibilities under those Standards are further described in the Auditor’s Responsibility for the Audit of the Consolidated Financial Statements section of our report. We are independent of the Group, its associates and joint ventures in accordance with the Code of Ethics issued by the Institute of Chartered Accountants of India (“ICAI”) together with the ethical requirements that are relevant to our audit of the consolidated financial statements under the provisions of the Act and the Rules made thereunder, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the ICAI’s Code of Ethics. We believe that the audit evidence obtained by us and the audit evidence obtained by the other auditors in terms of their reports referred to in the Other Matters section below, is sufficient and appropriate to provide a basis for our audit opinion on the consolidated financial statements. Emphasis of Matter We draw attention to Note [1](III) to the Consolidated Financial Statements in which the Group describes the uncertainties arising from the COVID-19 pandemic. Our report is not modified in respect of this matter. Key Audit Matters Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated financial statements of the current period. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. We have determined the matters described below to be the key audit matters to be communicated in our report. DELOITTE HASKINS & SELLS LLP Chartered Accountants Indiabulls Finance Centre, Tower 3 27th – 32nd Floor, Senapati Bapat Marg Elphinstone Road (West) Mumbai 400 013.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of L&T Annual Report 2019-20 - WIRC-ICAI.org

459

INDEPENDENT AUDITORS’ REPORTTO THE MEMBERS OF LARSEN & TOUBRO LIMITED

Report on the Audit of the Consolidated Financial StatementsOpinion

We have audited the accompanying consolidated financial statements of Larsen & Toubro Limited (the “Parent”) and its subsidiaries, (the Parent and its subsidiaries together referred to as the “Group”) which includes 35 joint operations of the Group accounted on proportionate basis and the Group’s share of profit in its associates and joint ventures, which comprise the Consolidated Balance Sheet as at 31st March 2020, and the Consolidated Statement of Profit and Loss (including Other Comprehensive Income), the Consolidated Statement of Cash Flows and the Consolidated Statement of Changes in Equity for the year then ended, and a summary of significant accounting policies and other explanatory information.

In our opinion and to the best of our information and according to the explanations given to us, and based on the consideration of reports of the other auditors on separate financial information of the joint operations, subsidiaries, associates and joint ventures referred to in the Other Matters section below, the aforesaid consolidated financial statements give the information required by the Companies Act, 2013 (the “Act”) in the manner so required and give a true and fair view in conformity with the Indian Accounting Standards prescribed under section 133 of the Act read with the Companies (Indian Accounting Standards) Rules, 2015, as amended (“Ind AS”), and other accounting principles generally accepted in India, of the consolidated state of affairs of the Group as at 31st March 2020, and their consolidated profit, their consolidated total comprehensive income, their consolidated cash flows and their consolidated changes in equity for the year ended on that date.

Basis for Opinion

We conducted our audit of the consolidated financial statements in accordance with the Standards on Auditing specified under section 143 (10) of the Act (“SA”s). Our responsibilities under those Standards are further described in the Auditor’s Responsibility for the Audit of the Consolidated Financial Statements section of our report. We are independent of the Group, its associates and joint ventures in accordance with the Code of Ethics issued by the Institute of Chartered Accountants of India (“ICAI”) together with the ethical requirements that are relevant to our audit of the consolidated financial statements under the provisions of the Act and the Rules made thereunder, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the ICAI’s Code of Ethics. We believe that the audit evidence obtained by us and the audit evidence obtained by the other auditors in terms of their reports referred to in the Other Matters section below, is sufficient and appropriate to provide a basis for our audit opinion on the consolidated financial statements.

Emphasis of Matter

We draw attention to Note [1](III) to the Consolidated Financial Statements in which the Group describes the uncertainties arising from the COVID-19 pandemic.

Our report is not modified in respect of this matter.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated financial statements of the current period. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. We have determined the matters described below to be the key audit matters to be communicated in our report.

DELOITTE HASKINS & SELLS LLPChartered AccountantsIndiabulls Finance Centre, Tower 327th – 32nd Floor, Senapati Bapat Marg Elphinstone Road (West)Mumbai 400 013.

460

AUDITORS’ REPORT ON CONSOLIDATED FINANCIAL STATEMENTS ANNUAL REPORT 2019-20

Revenue recognition – accounting for construction contracts

Key audit matter description

As described in Note No. [1](II)(i) of the Consolidated Financial Statements, the Group recognises revenue from contracts with customers when it satisfies its performance obligations.

Accounting for construction contracts is considered as a Key Audit Matter as there are significant accounting judgements in estimating revenue to be recognised on contracts with customers, including estimation of costs to complete and determining the timing of revenue recognition.

The Group recognises revenue and profit/loss based on stage of completion based on the proportion of contract costs incurred at balance sheet date, relative to the total estimated costs of the contract at completion. The recognition of revenue is thus dependent on estimates in relation to total estimated costs of each contract.

Cost contingencies are included in these estimates to take in to account specific uncertain risks, or disputed claims against the Group, arising within each contract. These contingencies are reviewed by the Management on a regular basis throughout the contract life and adjusted where appropriate.

The revenue on contracts may also include variable consideration (variations and claims). Variable consideration is recognised when the probability of reversal of such revenue is low.

Further, Refer to Note No. 47 for the disclosures made in the Consolidated Financial Statements as per Ind AS 115 ‘Revenue from Contracts with Customers’.

Principal Audit Procedures

The procedures performed included the following:

• obtained an understanding of the process followed by the Group in determination of the estimates and contract revenue;

• performed walkthrough procedures over the process of identification of performance obligation;

• tested the design and implementation of internal control over the quantification of the estimates used as well as the operating effectiveness of such control;

• tested segregation of duties while recording the contracts in the Group’s information system and recognising revenue from such contracts;

• tested the General IT Controls over the relevant information technology systems’ access and change management controls relating to contracts and related information used in recording and disclosing revenue in accordance with Ind AS 115 – Revenue from Contracts with Customers;

• tested sample of contracts for:

- appropriate identification of performance obligations;

- change orders and the impact on the estimated costs to complete;

- evaluation of reasonability of estimates of costs to complete; and

- tested the appropriateness of the timing of recognizing the revenue from the contracts;

• tested the appropriateness of the variable considerations recognised based on the low probability of reversal of such revenue; and

• tested appropriateness of the disclosures in the financial statements in respect of such construction contracts to ensure compliance with Ind AS 115.

Measurement of contract assets in respect of overdue milestones and receivables in respect of overdue invoices.

Key audit matter description

The Group, in its contract with customers, promises to transfer distinct services to its customers, which may be rendered in the form of engineering, procurement, and construction (EPC) services through design-build contracts, and other forms of construction contracts. The recognition of revenue is based on contractual terms, which could be based on agreed unit price or lump-sum revenue arrangements. At each reporting date, revenue is accrued for costs incurred against work performed that may not have been invoiced.

Identifying whether the Group’s performance has resulted in a service that would be billable and collectable where the works carried out have not been acknowledged by customers as of the reporting date, or in the case of certain defence contracts, where the evidence of work carried out and cost incurred are covered by confidentiality arrangements, involves a significant amount of judgment.

Assessing the recoverability of contract assets related to overdue milestones and amounts overdue against invoices raised which have remained unsettled for a significantly long period after the end of the contractual credit period also involves a significant amount of judgment. Refer to Note No. [1](II)(i) and [1](II)(r) of the Consolidated Financial Statements.

461

Principal Audit Procedures

The procedures performed included the following:

• obtained an understanding of the Group’s processes in collating the evidence supporting execution of work for each disaggregated type of revenue;

• obtained an understanding of the Group’s processes in assessing the recoverability of amounts overdue and process over estimating the expected credit loss allowance;

• tested the design and operating effectiveness of the key controls over the completeness and accuracy of the key inputs and assumptions into the provisioning model;

• evaluated controls over authorisation and calculation of provisioning model;

• for defence contracts which are covered under statutory confidentiality arrangements, for sample of contracts, the auditors have compared the revenue recognised with amounts collected from customers to ensure that the gap between revenue recognised and collections is below the materiality threshold;

• evaluated the delivery and collection history of customers against whose contracts un-invoiced revenue is recognised;

• verified for the sample selected, receipts post balance sheet date upto the approval of the financial statements by the Board of Directors of the Parent Company;

• performed an overall assessment of the expected credit loss provision to determine if they were reasonable considering the Group’s portfolio, risk profile, credit risk management practices and the macroeconomic environment; and

• tested the appropriateness of the disclosures in the financial statements to ensure compliance with Ind AS 115.

Appropriateness of revenues and onerous obligations in respect of fixed price contracts involves critical estimates for services relating to Information Technology & Technology Services Segment

Key audit matter description

Estimated effort is a critical estimate to determine revenues and provision for onerous obligations on fixed price contracts. This estimate has a high inherent uncertainty as it requires consideration of progress of the contract, efforts/cost incurred till date, efforts/cost required to complete the remaining contract performance obligations.

Refer to Note No. [1](II)(i) of the Consolidated Financial Statements.

Principal Audit Procedures

The procedures performed by component auditors (being other firms of chartered accountants) included the following:

• evaluated the design and implementation of internal controls over recording of actual cost/efforts till date and the process of estimation of cost/efforts required to complete the performance obligations;

• tested the operating effectiveness of the said internal controls for a selected sample of contracts.

• selected a sample of new and existing contracts and performed following procedures;

o read, analysed and identified the distinct performance obligations in these contracts.

o compared such performance obligations with those identified and recorded by the Group.

o verified contract terms to determine the transaction price including any variable consideration and verified allocation of the transaction price to each performance obligation after adjusting the estimated variable consideration.

• in respect of a sample of fixed price contracts, progress towards satisfaction of performance obligation used to compute recorded revenue was verified with the efforts/cost recorded and estimated efforts/cost from the corresponding information systems;

• verified sample of contracts with unbilled revenues to identify possible delays in achieving milestones, which require change in estimated efforts to complete the remaining performance obligations.

462

AUDITORS’ REPORT ON CONSOLIDATED FINANCIAL STATEMENTS ANNUAL REPORT 2019-20

Provision for expected credit losses for financial services segment

Key audit matter description

Significant judgement is used in classifying loan assets measured at amortised cost and applying appropriate measurement principles. The allowance for expected credit losses (“ECL”) on such loan assets, measured at amortised cost, is a critical estimate involving greater level of management judgement.

As part of our risk assessment, we determined that the allowance for ECL on loan assets (including undisbursed commitments) has a high degree of estimation uncertainty, with a potential range of reasonable outcomes for the financial statements.

The elements in estimating ECL which involve increased level of audit focus are as follows:

• Qualitative and quantitative factors used in staging the loan assets measured at amortised cost;

• Basis used for estimating Probabilities of Default (“PD”);

• Basis used for estimating Loss Given Default (“LGD”);

• Judgements used in projecting economic scenarios and probability weights applied to reflect future economic conditions;

• Adjustments to model driven ECL results to address emerging trends.

Refer Note No. [1](II)(r)(i)(D) of the Consolidated Financial Statements

Principal Audit Procedures

We have examined the policies approved by the Board of Directors of the Company that articulate the objectives of managing each portfolio and their business models (including policies for sale out of amortised cost business model). We have also verified the methodology adopted for computation of ECL (“ECL Model”) that addresses policies approved by the Board of Directors, procedures and controls for assessing and measuring credit risk on all lending exposures measured at amortised cost.

Additionally, we have confirmed that adjustments to the output of the ECL Model is consistent with the documented rationale and basis for such adjustments and that the amount of adjustment has been approved by the Audit Committee of the Board of Directors.

Our audit procedures related to the allowance for ECL included the following, among others:

• Tested the design and effectiveness of internal controls over the:

– completeness and accuracy of the Exposure at Default (“EAD”) and the classification thereof into stages consistent with the definitions applied in accordance with the policy approved by the Board of Directors including the appropriateness of the qualitative factors to be applied;

– completeness and accuracy of information used in the estimation of the PD for the different stages depending on the nature of the portfolio; and

– computation of the ECL including methodology used to determine macro economic overlays and adjustments to the output of the ECL Model.

• Also, for a sample of ECL on loan assets:

– we tested the input data such as ratings and period of default and other related information used in estimating the PD;

– we evaluated reasonableness of LGD estimates by comparing actual recoveries post the loan asset becoming credit impaired with estimates of LGD;

– we evaluated the incorporation of the applicable assumptions into the ECL Model and tested the mathematical accuracy and computation of the allowances by using the same input data used by the Company.

• We also tested the adequacy of the adjustment after stressing the inputs used in determining the output as per the ECL Model and ensured that the adjustment was in conformity with the amount approved by the Audit Committee.

• We also assessed the disclosures made in relation to the ECL allowance to confirm compliance with the provisions of Ind AS 107.

463

Impairment of Toll Collection Rights of certain operating projects who have incurred continuous losses.

Key audit matter description

Toll collection rights obtained in consideration for rendering construction services, represent the right to collect toll revenue during the concession period in respect of Build-Operate-Transfer ("BOT") and Design-Build-Operate-Transfer (“DBOT”) projects. Toll collection rights are capitalised as intangible assets upon completion of the project at the cumulative construction costs plus the present value of obligation towards negative grants and additional concession fee payable to National Highways Authority of India ("NHAI")/State Authorities, if any.

The Group has carried out an evaluation for impairment of such toll collection rights where indicators of impairment were identified. Due to the multitude of factors and assumptions involved in determining the forecasted revenues/cash flows and discount rate in the projection period, significant judgments are required to estimate the recoverable values.

Management has estimated the future cash flows arising from achieving revenues and costs in line with the increase in traffic as well as refinancing/restructuring. As such estimations involve complex and subjective judgements by the Management, there is a risk that there may be an impairment that has not been recorded.

Refer Note No. [1](II)(o) of the Consolidated Financial Statements.

Principal Audit Procedures

The component auditors (being other firms of chartered accountants) have performed the following audit procedures:

• conducted discussions with Company personnel to identify factors, if any, that should be taken into account in the impairment analysis;

• evaluated the design and implementation of the relevant controls and the operating effectiveness of such internal controls in estimating the future projections including assumptions used in determining the value in use;

• compared the actual revenues and cash flows generated by the entities during the year as compared to the projections and estimates considered in the previous year and evaluated the basis of future projections with regard to the revenue and cash flows;

• evaluated the appropriateness of key assumptions in the valuations including discount rate, growth rate, and consulted internal specialists for such evaluation. The challenge was based on the auditors’ assessment of the historical accuracy of the Group’s estimates in the prior periods and an assessment of the consistency of assumptions across all the subsidiaries and comparison of the assumptions with public data wherever available;

• the component auditors have also performed a sensitivity analysis to assess the impact of possible different assumptions related to revenue and cost estimates including:

i. Increase/decrease in revenue growth rate; and

ii. Increase/decrease to cost forecasts.

Physical verification of inventory

Key audit matter description

The Company’s management conducts physical verification of inventories during the year at reasonable intervals, however, on account of the COVID-19 related lockdown restrictions, management was able to perform year end physical verification of inventories, only at certain locations. Management has carried out other procedures to validate the existence of its inventory as at the year end, such as carrying out consumption analysis, and performing roll-back procedures from the subsequent year end physical verification date to determine the quantities of the inventory at the balance sheet date.

Refer Note No. [1](II)(s) of the Consolidated Financial Statements.

The procedures performed included the following:

• Understood the process and tested the Management’s internal controls to establish the existence of inventory in relation to the process of periodic physical verification carried out by the management, the scope and coverage of the periodic verification programme, the results of such verification including analysis of discrepancies, if any;

464

AUDITORS’ REPORT ON CONSOLIDATED FINANCIAL STATEMENTS ANNUAL REPORT 2019-20

• At selected locations subsequent to year-end, where the management appointed third party independent chartered accountants to perform physical verification, sent instructions to the third party chartered accountants to carry out the physical verification and provided samples to be verified by them. We have received the report of the physical verification carried out by the third party independent chartered accountants. Obtained the roll back procedures performed by the management from the subsequent year-end physical verification date to arrive at the quantities as at the balance sheet date. Traced the samples physically verified by the third party independent chartered accountants roll back workings provided by the management.

• Inspected, for samples selected, supporting documentation relating to purchases and consumption, and such other third party evidences where applicable.

• Tested the analytical reviews performed by the Company such as consumption analysis.

Information Other than the Financial Statements and Auditor’s Report Thereon

i. The Parent’s Company’s Board of Directors is responsible for the other information. The other information comprises the information included in the Management Discussion and Analysis, Board’s Report including Annexures to Board’s Report, Business Responsibility Report, Corporate Governance and Shareholder’s Information, but does not include the consolidated financial statements, standalone financial statements and our auditor’s report thereon.

ii. Our opinion on the consolidated financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the consolidated financial statements, our responsibility is to read the other information, compare with the financial statements of the joint operations, subsidiaries, joint ventures and associates audited by the other auditors, to the extent it relates to these entities and, in doing so, place reliance on the work of the other auditors and consider whether the other information is materially inconsistent with the consolidated financial statements or our knowledge obtained during the course of our audit or otherwise appears to be materially misstated. Other information so far as it relates to the joint operations, subsidiaries, joint ventures and associates, is traced from their financial statements audited by the other auditors.

If based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Management’s Responsibility for the Consolidated Financial Statements

The Parent’s Company’s Board of Directors is responsible for the matters stated in section 134(5) of the Act with respect to the preparation of these consolidated financial statements that give a true and fair view of the consolidated financial position, consolidated financial performance including other comprehensive income, consolidated cash flows and consolidated changes in equity of the Group including its associates and joint ventures in accordance with the Ind AS and other accounting principles generally accepted in India.

The respective Board of Directors of the companies included in the Group and of its associates and joint ventures are responsible for maintenance of adequate accounting records in accordance with the provisions of the Act for safeguarding the assets of the Group and its associates and its joint ventures and for preventing and detecting frauds and other irregularities; selection and application of appropriate accounting policies; making judgments and estimates that are reasonable and prudent; and design, implementation and maintenance of adequate internal financial controls, that were operating effectively for ensuring the accuracy and completeness of the accounting records, relevant to the preparation and presentation of the financial statements that give a true and fair view and are free from material misstatement, whether due to fraud or error, which have been used for the purpose of preparation of the consolidated financial statements by the Directors of the Parent Company, as aforesaid.

In preparing the consolidated financial statements, the respective Board of Directors of the companies included in the Group and of its associates and joint ventures are responsible for assessing the ability of the respective entities to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the respective Board of Directors either intends to liquidate their respective entities or to cease operations, or has no realistic alternative but to do so.

The respective Board of Directors of the companies included in the Group and of its associates and joint ventures are also responsible for overseeing the financial reporting process of the Group and of its associates and joint ventures.

Auditor’s Responsibility for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance but is not a guarantee that an audit conducted in accordance with SAs will always detect a material

465

misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements.

As part of an audit in accordance with SAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identifyandassesstherisksofmaterialmisstatementoftheconsolidatedfinancialstatements,whetherduetofraudorerror,design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtainanunderstandingofinternalfinancialcontrolrelevanttotheauditinordertodesignauditproceduresthatareappropriatein the circumstances. Under section 143(3)(i) of the Act, we are also responsible for expressing our opinion on whether the Parent Company has adequate internal financial controls system in place and the operating effectiveness of such controls.

• Evaluatetheappropriatenessofaccountingpoliciesusedandthereasonablenessofaccountingestimatesandrelateddisclosuresmade by the management.

• Concludeontheappropriatenessofmanagement’suseofthegoingconcernbasisofaccountingand,basedontheauditevidenceobtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the ability of the Group and its associates and joint ventures to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Group and its associates and joint ventures to cease to continue as a going concern.

• Evaluatetheoverallpresentation,structureandcontentoftheconsolidatedfinancialstatements,includingthedisclosures,andwhether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

• ObtainsufficientappropriateauditevidenceregardingthefinancialinformationoftheentitiesorbusinessactivitieswithintheGroup and its associates and joint ventures to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and performance of the audit of the financial statements of such entities or business activities included in the consolidated financial statements of which we are the independent auditors. For the other entities included in the consolidated financial statements, which have been audited by the other auditors, such other auditors remain responsible for the direction, supervision and performance of the audits carried out by them. We remain solely responsible for our audit opinion.

Materiality is the magnitude of misstatements in the consolidated financial statements that, individually or in aggregate, makes it probable that the economic decisions of a reasonably knowledgeable user of the consolidated financial statements may be influenced. We consider quantitative materiality and qualitative factors in (i) planning the scope of our audit work and in evaluating the results of our work; and (ii) to evaluate the effect of any identified misstatements in the consolidated financial statements.

We communicate with those charged with governance of the Parent Company and such other entities included in the consolidated financial statements of which we are the independent auditors regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide those charged with governance with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the consolidated financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

466

AUDITORS’ REPORT ON CONSOLIDATED FINANCIAL STATEMENTS ANNUAL REPORT 2019-20

Other Matters

• Wedidnotauditthefinancialinformationof28jointoperationsincludedinthestandalonefinancialstatementsofthecompaniesincluded in the Group whose financial information reflect total assets of R 3,728.86croreasat31stMarch,2020,totalrevenueof R 4,112.64crore,totalnetlossaftertaxofR 119.39 crore, total comprehensive loss of R 119.39 crore and net cash outflows amounting to R 115.90 crore for the year ended 31st March, 2020, as considered in the respective standalone financial statements of the companies included in the Group. The financial information of these joint operations have been audited by the other auditors whose reports have been furnished to us by the Management, and our opinion in so far as it relates to the amounts and disclosures included in respect of these joint operations and our report in terms of subsection (3) of Section 143 of the Act, in so far as it relates to the aforesaid joint operations, is based solely on the report of such other auditors.

• Wedidnotauditthefinancialinformationof68subsidiaries,whosefinancialinformationreflecttotalassetsofR 1,00,047.10 crore as at 31st March, 2020, total revenues of R 36,971.08crore,totalnetprofitaftertaxofR 3,965.32crore,totalcomprehensive income of R 3,236.04croreandnetcashinflowsamountingtoR 2,151.28crorefortheyearended31stMarch,2020, as considered in the consolidated financial statements. The consolidated financial statements also include the Group’s share of loss after tax of R 29.61crorefortheyearended31stMarch,2020andtotalcomprehensivelossofR 2.81crorefortheyearended31stMarch,2020,asconsideredintheconsolidatedfinancialstatements,inrespectof3associatesand8jointventures,whose financial information have not been audited by us. These financial information have been audited by other auditors whose reports have been furnished to us by the Management and our opinion on the consolidated financial statements, in so far as it relates to the amounts and disclosures included in respect of these subsidiaries, joint ventures and associates, and our report in terms of subsection (3) of Section 143 of the Act, in so far as it relates to the aforesaid subsidiaries, joint ventures and associates is based solely on the reports of the other auditors.

• Wedidnotauditthefinancialinformationof6jointoperationsincludedinthestandalonefinancialstatementsofthecompaniesincluded in the Group whose financial information reflect total assets of R 239.74 crore as at 31st March, 2020, total revenue of R 257.69crore,totalnetprofitaftertaxofR 15.40 crore, total comprehensive income of R 15.40 crore and net cash inflows amount to R 32.30 crore for the year ended 31st March, 2020, as considered in the respective standalone financial statements of the companies included in the Group. These financial information are unaudited and have been furnished to us by the Management and our opinion on the consolidated financial statements, in so far as it relates to the amounts and disclosures included in respect of these joint operations, is based solely on such unaudited financial information. In our opinion and according to the information and explanations given to us by the Management, these financial information are not material to the Group.

• Wedidnotauditthefinancialinformationof46subsidiaries,whosefinancialinformationreflecttotalassetsofR 1,019.63croreas at 31st March, 2020, total revenues of R 742.37 crore, total net loss after tax of R 6.01crore,totalcomprehensivelossofR 10.71 crore and net cash inflows amounting to R 36.85crorefortheyear31stMarch,2020,asconsideredintheconsolidatedfinancial statements. The consolidated financial statements also include the Group’s share of after tax of R 10.40 crore and total comprehensive loss of R 10.36crorefortheyearended31stMarch,2020,asconsideredintheconsolidatedfinancialstatements,inrespectof3associatesand6jointventures,financialinformationhavenotbeenauditedbyus.Thesefinancialinformationareunaudited and have been furnished to us by the Management and our opinion on the consolidated financial statements, in so far as it relates to the amounts and disclosures included in respect of these subsidiaries, joint ventures and associates, is based solely on such unaudited financial information. In our opinion and according to the information and explanations given to us by the Management, these financial information are not material to the Group.

Our opinion on the consolidated financial statements above and our report on Other Legal and Regulatory Requirements below, is not modified in respect of the above matters with respect to our reliance on the work done and the reports of the other auditors and the financial information certified by the Management.

Report on Other Legal and Regulatory Requirements

As required by Section 143(3) of the Act, based on our audit and on the consideration of the reports of the other auditors on the separate financial information of the joint operations, subsidiaries, associates and joint ventures referred to in the Other Matters section above we report, to the extent applicable that:

a) We have sought and obtained all the information and explanations which to the best of our knowledge and belief were necessary for the purposes of our audit of the aforesaid consolidated financial statements.

b) In our opinion, proper books of account as required by law relating to preparation of the aforesaid consolidated financial statements have been kept so far as it appears from our examination of those books and the reports of the other auditors.

467

c) The Consolidated Balance Sheet, the Consolidated Statement of Profit and Loss including Other Comprehensive Income, the Consolidated Statement of Cash Flows and the Consolidated Statement of Changes in Equity dealt with by this Report are in agreement with the relevant books of account maintained for the purpose of preparation of the consolidated financial statements.

d) In our opinion, the aforesaid consolidated financial statements comply with the Ind AS specified under Section 133 of the Act.

e) On the basis of the written representations received from the directors of the Parent Company as on 31st March, 2020 taken on record by the Board of Directors of the Company and the reports of the statutory auditors of its joint operation companies, subsidiary companies, associate companies and joint venture companies incorporated in India, none of the directors of the Group companies, its associate companies and joint venture companies incorporated in India is disqualified as on 31st March, 2020 from beingappointedasadirectorintermsofSection164(2)oftheAct.

f) With respect to the adequacy of the internal financial controls over financial reporting and the operating effectiveness of such controls, refer to our separate Report in “Annexure A” which is based on the auditors’ reports of the Parent company, subsidiary companies, associate companies and joint venture companies incorporated in India. Our report expresses an unmodified opinion on the adequacy and operating effectiveness of internal financial controls over financial reporting of those companies.

g) WithrespecttotheothermatterstobeincludedintheAuditor’sReportinaccordancewiththerequirementsofsection197(16)ofthe Act, as amended,

In our opinion and to the best of our information and according to the explanations given to us, the remuneration paid by the Parent Company to its directors during the year is in accordance with the provisions of section 197 of the Act.

h) With respect to the other matters to be included in the Auditor’s Report in accordance with Rule 11 of the Companies (Audit and Auditors) Rules, 2014, as amended in our opinion and to the best of our information and according to the explanations given to us:

i. The consolidated financial statements disclose the impact of pending litigations on the consolidated financial position of the Group, its associates and joint ventures;

ii. Provision has been made in the consolidated financial statements, as required under the applicable law or accounting standards, for material foreseeable losses, if any, on long-term contracts including derivative contracts; and

iii. There has been no delay in transferring amounts, required to be transferred, to the Investor Education and Protection Fund by the Parent Company and its subsidiary companies, associate companies and joint venture companies incorporated in India.

For DELOITTE HASKINS & SELLS LLP Chartered Accountants (Firm’sRegistrationNo.117366W/W-100018)

Sanjiv V. Pilgaonkar (Partner) (MembershipNo.039826) UDIN:20039826AAAADJ8143

Mumbai, June 5, 2020

468

AUDITORS’ REPORT ON CONSOLIDATED FINANCIAL STATEMENTS ANNUAL REPORT 2019-20

ANNEXURE “A” TO THE INDEPENDENT AUDITORS’ REPORT (Referred to in paragraph “(f)” under ‘Report on Other Legal and Regulatory Requirements’ section of our report of even date)

Report on the Internal Financial Controls Over Financial Reporting under Clause (i) of Sub-section 3 of Section 143 of the Companies Act, 2013 (the “Act”)

In conjunction with our audit of the consolidated financial statements of the Company as of and for the year ended March 31, 2020, we have audited the internal financial controls over financial reporting of LARSEN & TOUBRO LIMITED (hereinafter referred to as “Parent”) and its subsidiary companies which includes one of the Group’s 35 joint operations which is a company incorporated in India, its associate companies and joint ventures, which are companies incorporated in India, as of that date.

Management’s Responsibility for Internal Financial Controls

The respective Board of Directors of the Parent, its subsidiary companies, its joint operation, its associate companies and joint ventures, which are companies incorporated in India, are responsible for establishing and maintaining internal financial controls based on the internal control over financial reporting criteria established by the respective Companies considering the essential components of internal control stated in the Guidance Note on Audit of Internal Financial Controls Over Financial Reporting issued by the Institute of Chartered Accountants of India (“ICAI”). These responsibilities include the design, implementation and maintenance of adequate internal financial controls that were operating effectively for ensuring the orderly and efficient conduct of its business, including adherence to the respective company’s policies, the safeguarding of its assets, the prevention and detection of frauds and errors, the accuracy and completeness of the accounting records, and the timely preparation of reliable financial information, as required under the Companies Act, 2013.

Auditor’s Responsibility

Our responsibility is to express an opinion on the internal financial controls over financial reporting of the Parent, its subsidiary companies, its joint operation, its associate companies and its joint ventures, which are companies incorporated in India, based on our audit. We conducted our audit in accordance with the Guidance Note on Audit of Internal Financial Controls Over Financial Reporting (the “Guidance Note”) issued ICAI and the Standards on Auditing (“SA”), prescribed under Section 143(10) of the Companies Act, 2013, to the extent applicable to an audit of internal financial controls. Those Standards and the Guidance Note require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether adequate internal financial controls over financial reporting was established and maintained and if such controls operated effectively in all material respects.

Our audit involves performing procedures to obtain audit evidence about the adequacy of the internal financial controls system over financial reporting and their operating effectiveness. Our audit of internal financial controls over financial reporting included obtaining an understanding of internal financial controls over financial reporting, assessing the risk that a material weakness exists, and testing and evaluating the design and operating effectiveness of internal control based on the assessed risk. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error.

We believe that the audit evidence we have obtained and the audit evidence obtained by other auditors of the subsidiary companies, joint operation, associate companies and joint ventures, which are companies incorporated in India, in terms of their reports referred to in the Other Matters paragraph below, is sufficient and appropriate to provide a basis for our audit opinion on the internal financial controls system over financial reporting of the Parent, its subsidiary companies, its joint operation, its associate companies and its joint ventures, which are companies incorporated in India.

Meaning of Internal Financial Controls Over Financial Reporting

A company’s internal financial control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A Company’s internal financial control over financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorisations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detection of unauthorised acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Inherent Limitations of Internal Financial Controls Over Financial Reporting

Because of the inherent limitations of internal financial controls over financial reporting, including the possibility of collusion or improper management override of controls, material misstatements due to error or fraud may occur and not be detected. Also, projections of any evaluation of the internal financial controls over financial reporting to future periods are subject to the risk that

469

the internal financial control over financial reporting may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Opinion

In our opinion to the best of our information and according to the explanations given to us and based on the consideration of the reports of the other auditors referred to in the Other Matters paragraph below, the Parent, its subsidiary companies, its joint operation, its associate companies and joint ventures, which are companies incorporated in India, have, in all material respects, an adequate internal financial controls system over financial reporting and such internal financial controls over financial reporting were operating effectively as at March 31, 2020, based on the criteria for internal financial controls over financial reporting established by the respective companies considering the essential components of internal control stated in the Guidance Note.

Other Matters

Our aforesaid report under Section 143(3)(i) of the Act on the adequacy and operating effectiveness of the internal financial controls over financial reporting in so far as it relates to 31 subsidiary companies, 1 joint operation company, 3 associate companies and 7 joint ventures, which are companies incorporated in India, is based solely on the corresponding reports of the auditors of such companies incorporated in India.

Our aforesaid report under Section 143(3)(i) of the Act on the adequacy and operating effectiveness of the internal financial controls over financial reporting in so far as it relates to 12 subsidiary companies, 1 associate and 3 joint venture companies, which are companies incorporated in India, whose financial information is unaudited and whose efficacy of internal financial controls over financial reporting is based solely on the Management’s certification provided to us and our opinion on the adequacy and operating effectiveness of the internal financial controls over financial reporting of the Group is not affected as the financial information of such entities is not material to the Group.

Our opinion is not modified in respect of the above matters with respect to our reliance on the work done by and the reports of such other auditors and the financial information certified by the Management.

For DELOITTE HASKINS & SELLS LLP Chartered Accountants (Firm‘sRegistrationNo.117366W/W-100018)

Sanjiv V. Pilgaonkar Partner (MembershipNo.039826) UDIN:20039826AAAADJ8143

Mumbai, June 5, 2020

470

CONSOLIDATED BALANCE SHEET ANNUAL REPORT 2019-20

Consolidated Balance Sheet as at March 31, 2020As at 31-3-2020 As at 31-3-2019

Note v crore v crore v crore v croreASSETS:Non-current assets Property, plant and equipment 2 10103.79 10889.56 Capital work-in-progress 2 3224.91 2483.56 Investment property 3 3714.72 4254.56 Goodwill 4 8011.40 1826.91 Other intangible assets 5 19596.98 4222.91 Intangible assets under development 5 86.18 11435.93 Right-of-use assets 61(c)(iii) 2226.49 – Financial assets Investments in joint ventures and associates 43(e) 2851.01 2642.29 Other investments 6 4496.72 4318.64 Loans towards financing activities 7 58589.36 57788.88 Other loans 8 1522.33 1481.08 Other financial assets 9 638.15 1144.05

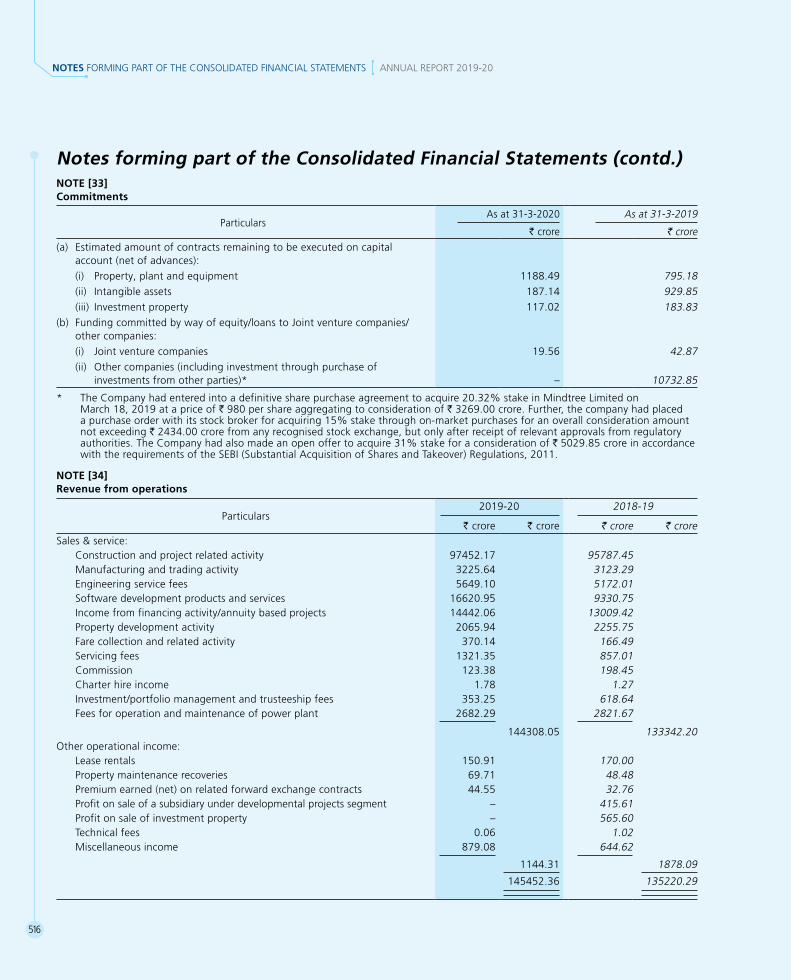

68097.57 67374.94 Deferred tax assets (net) 51(d) 3846.58 3418.93 Other non-current assets 10 6541.62 5648.62Current assets Inventories 11 5746.65 6413.93 Financial assets Investments 12 12699.75 13946.17 Trade receivables 13 40731.52 36845.87 Cash and cash equivalents 14 11324.57 6509.49 Other bank balances 15 3793.21 5216.75 Loans towards financing activities 16 41723.42 42530.82 Other loans 17 716.00 626.69 Other financial assets 18 2927.87 2551.25

113916.34 108227.04 Other current assets 19 58659.69 52143.06Group(s) of assets classified as held for sale 45(d) 4367.21 7.41

TOTAL ASSETS 308140.13 278347.36

471

As at 31-3-2020 As at 31-3-2019Note v crore v crore v crore v crore

EQUITY AND LIABILITIES:Equity Equity share capital 20 280.78 280.55 Other equity 21 66442.44 62094.25

Equity attributable to owners of the Company 66723.22 62374.80 Non-controlling interests 9520.83 6826.11LiabilitiesNon-current liabilities Financial liabilities Borrowings 22 82331.33 74120.79 Lease liability 1741.60 – Other financial liabilities 23 901.14 354.83

84974.07 74475.62 Provisions 24 708.67 556.84 Deferred tax liabilities (net) 51(d) 1453.04 311.13 Other non-current liabilities 25 31.09 0.55 Current liabilities Financial liabilities Borrowings 26 35021.02 29223.84 Current maturities of long term borrowings 27 23654.77 22210.54 Lease liability 424.95 – Trade payables: Due to micro enterprises and small enterprises 479.51 261.12 Due to others 28 43164.42 42733.69 Other financial liabilities 29 4923.23 4622.78

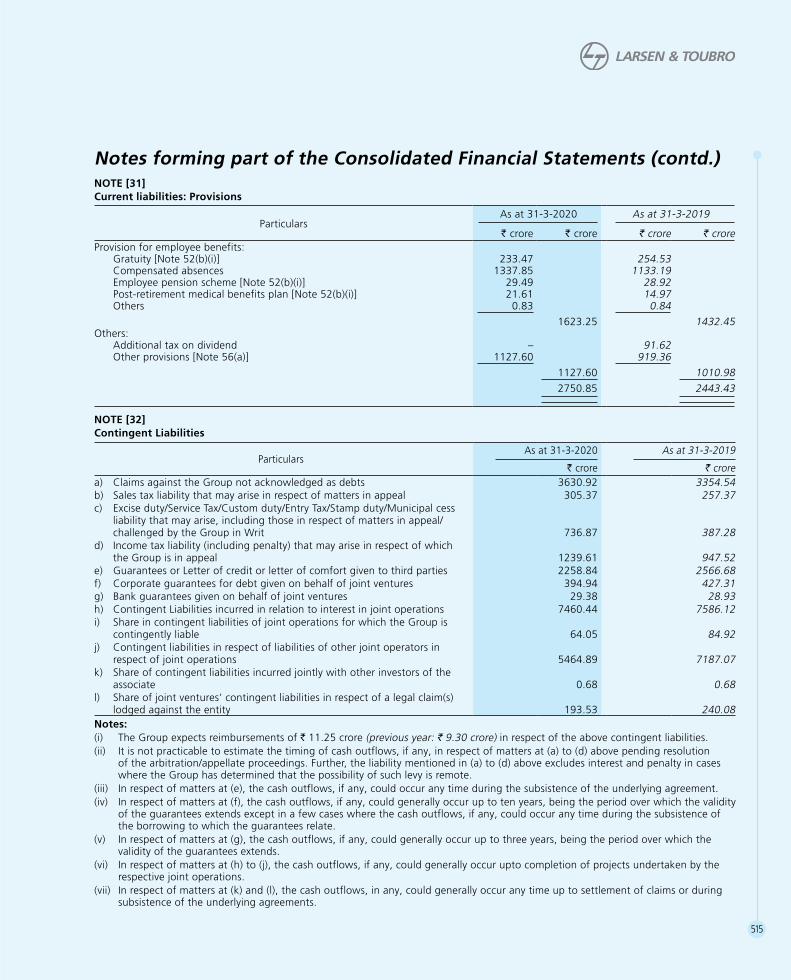

107667.90 99051.97 Other current liabilities 30 30816.67 31166.55 Provisions 31 2750.85 2443.43 Current tax liabilities (net) 1509.62 1137.16Liabilities associated with group(s) of assets classified as held for sale 45(d) 1984.17 3.20

TOTAL EQUITY AND LIABILITIES 308140.13 278347.36

CONTINGENT LIABILITIES 32 COMMITMENTS (capital and others) 33NOTES FORMING PART OF THE FINANCIAL STATEMENTS 1 to 64

Consolidated Balance Sheet as at March 31, 2020 (contd.)

In terms of our report attachedFor DELOITTE HASKINS & SELLS LLPChartered Accountants S.N.SUBRAHMANYAN

Chief Executive Officer & Managing Director (DIN02255382)

Chennai

Firm’sRegistrationNo.117366W/W-100018by the hand of

SANJIV V. PILGAONKAR Partner R.SHANKAR RAMAN M.M.CHITALE

Independent DirectorMembershipNo.39826 Whole-time Director & Chief Financial OfficerMumbai (DIN00019798) (DIN00101004)

Mumbai Mumbai

SIVARAM NAIR ACompany Secretary & Compliance OfficerM. No. FCS3939Mumbai

June 5, 2020

472

CONSOLIDATED STATEMENT OF PROFIT AND LOSS ANNUAL REPORT 2019-20

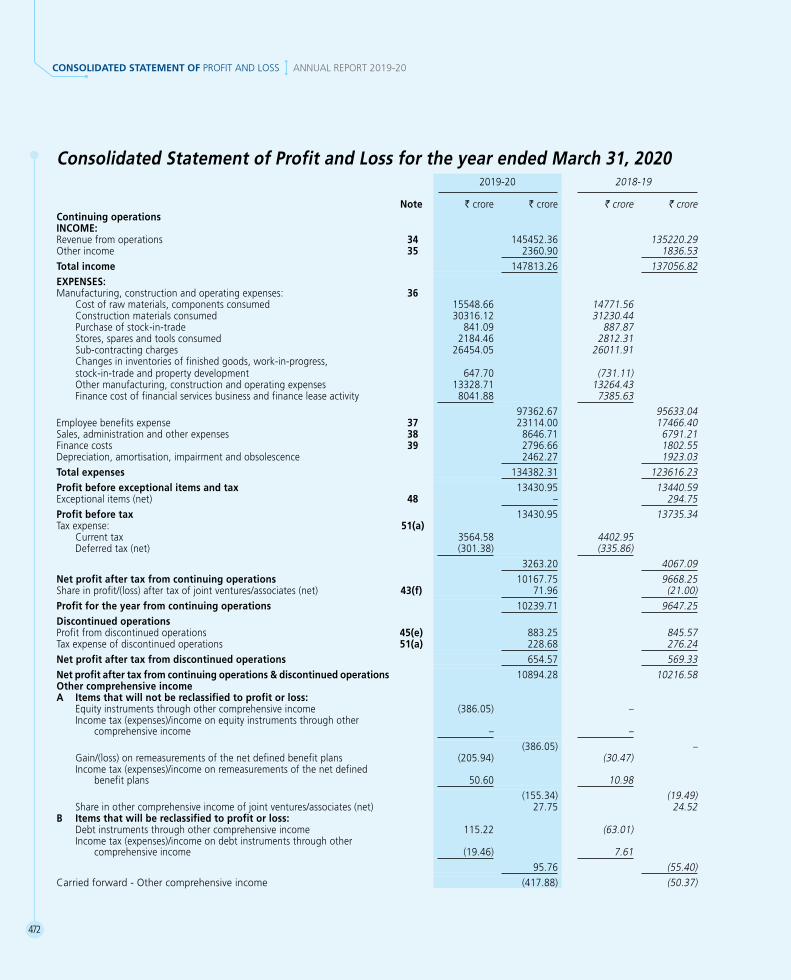

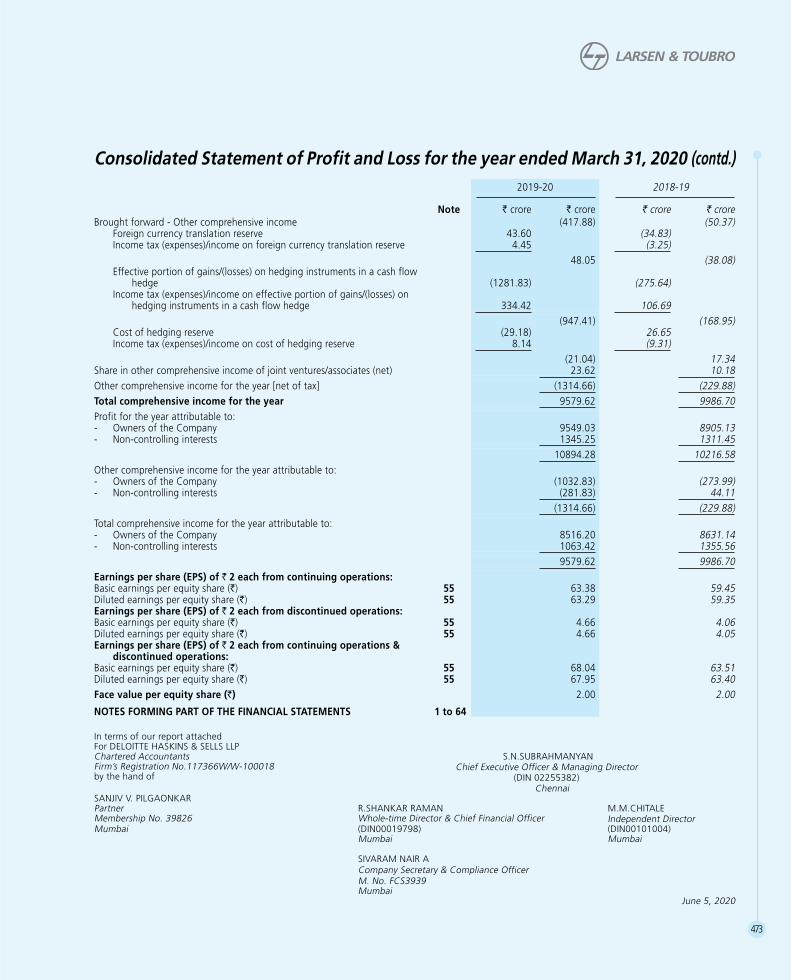

Consolidated Statement of Profit and Loss for the year ended March 31, 20202019-20 2018-19

Note v crore v crore v crore v crore

Continuing operationsINCOME:Revenue from operations 34 145452.36 135220.29 Other income 35 2360.90 1836.53Total income 147813.26 137056.82EXPENSES:Manufacturing, construction and operating expenses: 36 Cost of raw materials, components consumed 15548.66 14771.56 Construction materials consumed 30316.12 31230.44 Purchase of stock-in-trade 841.09 887.87 Stores, spares and tools consumed 2184.46 2812.31 Sub-contracting charges 26454.05 26011.91 Changes in inventories of finished goods, work-in-progress, stock-in-trade and property development 647.70 (731.11) Other manufacturing, construction and operating expenses 13328.71 13264.43 Finance cost of financial services business and finance lease activity 8041.88 7385.63

97362.67 95633.04Employee benefits expense 37 23114.00 17466.40Sales, administration and other expenses 38 8646.71 6791.21Finance costs 39 2796.66 1802.55Depreciation, amortisation, impairment and obsolescence 2462.27 1923.03 Total expenses 134382.31 123616.23Profit before exceptional items and tax 13430.95 13440.59 Exceptional items (net) 48 – 294.75 Profit before tax 13430.95 13735.34 Tax expense: 51(a) Current tax 3564.58 4402.95 Deferred tax (net) (301.38) (335.86)

3263.20 4067.09Net profit after tax from continuing operations 10167.75 9668.25Share in profit/(loss) after tax of joint ventures/associates (net) 43(f) 71.96 (21.00)Profit for the year from continuing operations 10239.71 9647.25Discontinued operationsProfit from discontinued operations 45(e) 883.25 845.57Tax expense of discontinued operations 51(a) 228.68 276.24Net profit after tax from discontinued operations 654.57 569.33Net profit after tax from continuing operations & discontinued operations 10894.28 10216.58Other comprehensive incomeA Items that will not be reclassified to profit or loss: Equity instruments through other comprehensive income (386.05) – Income tax (expenses)/income on equity instruments through other comprehensive income – –

(386.05) – Gain/(loss) on remeasurements of the net defined benefit plans (205.94) (30.47) Income tax (expenses)/income on remeasurements of the net defined benefit plans 50.60 10.98

(155.34) (19.49) Share in other comprehensive income of joint ventures/associates (net) 27.75 24.52 B Items that will be reclassified to profit or loss: Debt instruments through other comprehensive income 115.22 (63.01) Income tax (expenses)/income on debt instruments through other comprehensive income (19.46) 7.61

95.76 (55.40)Carried forward - Other comprehensive income (417.88) (50.37)

473

2019-20 2018-19

Note v crore v crore v crore v croreBrought forward - Other comprehensive income (417.88) (50.37) Foreign currency translation reserve 43.60 (34.83) Income tax (expenses)/income on foreign currency translation reserve 4.45 (3.25)

48.05 (38.08) Effective portion of gains/(losses) on hedging instruments in a cash flow hedge (1281.83) (275.64) Income tax (expenses)/income on effective portion of gains/(losses) on hedging instruments in a cash flow hedge 334.42 106.69

(947.41) (168.95) Cost of hedging reserve (29.18) 26.65 Income tax (expenses)/income on cost of hedging reserve 8.14 (9.31)

(21.04) 17.34 Share in other comprehensive income of joint ventures/associates (net) 23.62 10.18Other comprehensive income for the year [net of tax] (1314.66) (229.88)Total comprehensive income for the year 9579.62 9986.70Profit for the year attributable to:- Owners of the Company 9549.03 8905.13- Non-controlling interests 1345.25 1311.45

10894.28 10216.58Other comprehensive income for the year attributable to:- Owners of the Company (1032.83) (273.99)- Non-controlling interests (281.83) 44.11

(1314.66) (229.88)Total comprehensive income for the year attributable to:- Owners of the Company 8516.20 8631.14- Non-controlling interests 1063.42 1355.56

9579.62 9986.70Earnings per share (EPS) of R 2 each from continuing operations:Basic earnings per equity share (R) 55 63.38 59.45 Diluted earnings per equity share (R) 55 63.29 59.35 Earnings per share (EPS) of R 2 each from discontinued operations:Basic earnings per equity share (R) 55 4.66 4.06Diluted earnings per equity share (R) 55 4.66 4.05 Earnings per share (EPS) of R 2 each from continuing operations & discontinued operations:Basic earnings per equity share (R) 55 68.04 63.51Diluted earnings per equity share (R) 55 67.95 63.40Face value per equity share (R) 2.00 2.00

NOTES FORMING PART OF THE FINANCIAL STATEMENTS 1 to 64

Consolidated Statement of Profit and Loss for the year ended March 31, 2020 (contd.)

In terms of our report attachedFor DELOITTE HASKINS & SELLS LLPChartered Accountants S.N.SUBRAHMANYAN

Chief Executive Officer & Managing Director (DIN02255382)

Chennai

Firm’sRegistrationNo.117366W/W-100018by the hand of

SANJIV V. PILGAONKAR Partner R.SHANKAR RAMAN M.M.CHITALE

Independent DirectorMembershipNo.39826 Whole-time Director & Chief Financial OfficerMumbai (DIN00019798) (DIN00101004)

Mumbai Mumbai

SIVARAM NAIR ACompany Secretary & Compliance OfficerM. No. FCS3939Mumbai

June 5, 2020

474

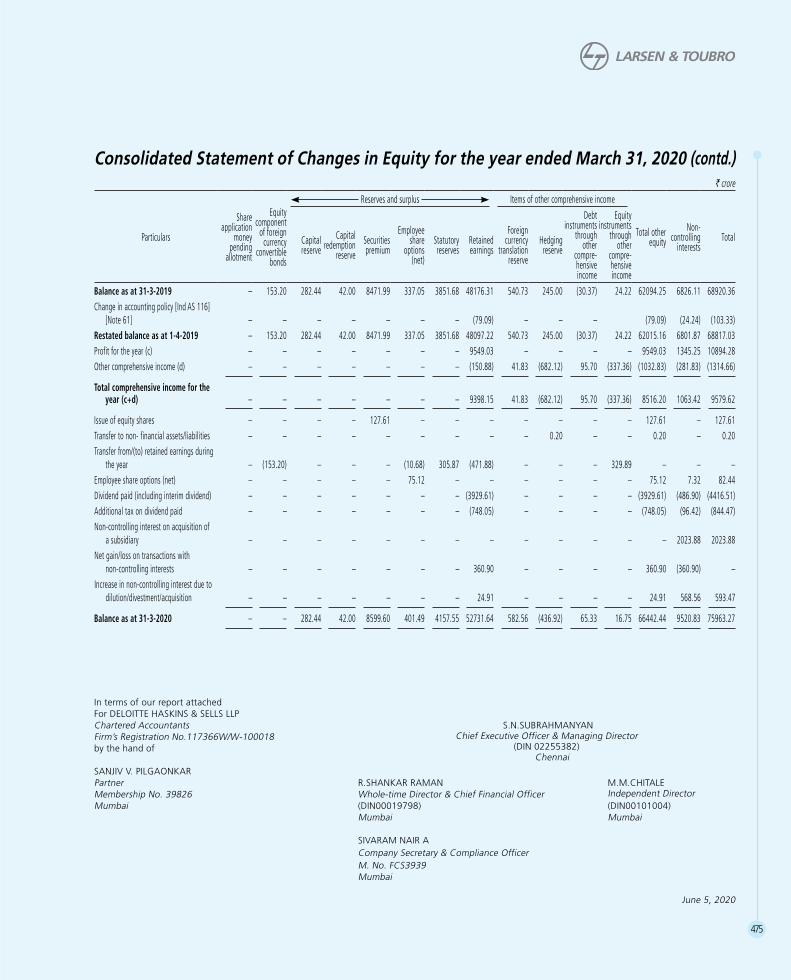

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY ANNUAL REPORT 2019-20

Consolidated Statement of Changes in Equity for the year ended March 31, 2020A. Equity share capital

Particulars

2019-20 2018-19

Number of shares

v crore Number of shares

v crore

Issued, subscribed and fully paid up equity shares outstanding at the beginning of the year 1,40,27,29,385 280.55 1,40,13,69,456 280.27Add: Shares issued on exercise of employee stock options during the year 7,83,249 0.16 13,59,929 0.28Add: Shares issued on conversion of foreign currency convertible bonds during the year 3,79,388 0.07 – –

Issued, subscribed and fully paid up equity shares outstanding at the end of the year 1,40,38,92,022 280.78 1,40,27,29,385 280.55

B. Other equityv crore

Particulars

Share application

money pending

allotment

Equity component

of foreign currency

convertible bonds

Reserves and surplus Items of other comprehensive income

Total other equity

Non-controlling

interestsTotalCapital

reserveCapital

redemption reserve

Securities premium

Employee share

options (net)

Statutory reserves

Retained earnings

Foreign currency

translation reserve

Hedging reserve

Debt instruments

through other

compre-hensive income

Equity instruments

through other

compre-hensive income

Balance as at 31-3-2018 3.56 153.20 282.44 42.00 8363.02 313.56 3352.91 41077.32 572.67 437.77 24.78 – 54623.23 5201.43 59824.66 Change in accounting policy [Ind AS 115] – – – – – – – (1237.65) – – – – (1237.65) (2.73) (1240.38)Restated balance as at 1-4-2018 3.56 153.20 282.44 42.00 8363.02 313.56 3352.91 39839.67 572.67 437.77 24.78 – 53385.58 5198.70 58584.28 Profit for the year (a) – – – – – – – 8905.13 – – – – 8905.13 1311.45 10216.58 Other comprehensive income (b) – – – – – – – (18.72) (31.94) (192.40) (55.15) 24.22 (273.99) 44.11 (229.88)

Total comprehensive income for the year (a+b) – – – – – – – 8886.41 (31.94) (192.40) (55.15) 24.22 8631.14 1355.56 9986.70

Issue of equity shares (3.56) – – – 108.97 – – – – – – – 105.41 6.50 111.91 Transfer to non- financial assets/liabilities – – – – – – – – – (0.37) – – (0.37) – (0.37)Transfer from/(to) retained earnings during

the year – – – – – (12.19) 498.77 (486.58) – – – – – – – Employee share options (net) – – – – – 35.68 – – – – – – 35.68 117.43 153.11 Dividend paid for previous year – – – – – – – (2243.18) – – – – (2243.18) (199.53) (2442.71)Additional tax on dividend paid for the

previous year – – – – – – – (427.02) – – – – (427.02) (50.01) (477.03)Net gain/loss on transactions with

non-controlling interests – – – – – – – 2634.66 – – – – 2634.66 (2634.66) – Increase in non-controlling interest due to

dilution/divestment/acquisition – – – – – – – (27.65) – – – – (27.65) 3032.12 3004.47

Balance as at 31-3-2019 – 153.20 282.44 42.00 8471.99 337.05 3851.68 48176.31 540.73 245.00 (30.37) 24.22 62094.25 6826.11 68920.36

475

Consolidated Statement of Changes in Equity for the year ended March 31, 2020 (contd.)v crore

Particulars

Share application

money pending

allotment

Equity component

of foreign currency

convertible bonds

Reserves and surplus Items of other comprehensive income

Total other equity

Non-controlling

interestsTotalCapital

reserveCapital

redemption reserve

Securities premium

Employee share

options (net)

Statutory reserves

Retained earnings

Foreign currency

translation reserve

Hedging reserve

Debt instruments

through other

compre-hensive income

Equity instruments

through other

compre-hensive income

Balance as at 31-3-2019 – 153.20 282.44 42.00 8471.99 337.05 3851.68 48176.31 540.73 245.00 (30.37) 24.22 62094.25 6826.11 68920.36 Change in accounting policy [Ind AS 116]

[Note 61] – – – – – – – (79.09) – – – (79.09) (24.24) (103.33)Restated balance as at 1-4-2019 – 153.20 282.44 42.00 8471.99 337.05 3851.68 48097.22 540.73 245.00 (30.37) 24.22 62015.16 6801.87 68817.03 Profit for the year (c) – – – – – – – 9549.03 – – – – 9549.03 1345.25 10894.28 Other comprehensive income (d) – – – – – – – (150.88) 41.83 (682.12) 95.70 (337.36) (1032.83) (281.83) (1314.66)

Total comprehensive income for the year (c+d) – – – – – – – 9398.15 41.83 (682.12) 95.70 (337.36) 8516.20 1063.42 9579.62

Issue of equity shares – – – – 127.61 – – – – – – – 127.61 – 127.61 Transfer to non- financial assets/liabilities – – – – – – – – – 0.20 – – 0.20 – 0.20 Transfer from/(to) retained earnings during

the year – (153.20) – – – (10.68) 305.87 (471.88) – – – 329.89 – – – Employee share options (net) – – – – – 75.12 – – – – – – 75.12 7.32 82.44 Dividend paid (including interim dividend) – – – – – – – (3929.61) – – – – (3929.61) (486.90) (4416.51)Additional tax on dividend paid – – – – – – – (748.05) – – – – (748.05) (96.42) (844.47)Non-controlling interest on acquisition of

a subsidiary – – – – – – – – – – – – – 2023.88 2023.88 Net gain/loss on transactions with

non-controlling interests – – – – – – – 360.90 – – – – 360.90 (360.90) – Increase in non-controlling interest due to

dilution/divestment/acquisition – – – – – – – 24.91 – – – – 24.91 568.56 593.47

Balance as at 31-3-2020 – – 282.44 42.00 8599.60 401.49 4157.55 52731.64 582.56 (436.92) 65.33 16.75 66442.44 9520.83 75963.27

In terms of our report attachedFor DELOITTE HASKINS & SELLS LLPChartered Accountants S.N.SUBRAHMANYAN

Chief Executive Officer & Managing Director (DIN02255382)

Chennai

Firm’sRegistrationNo.117366W/W-100018by the hand of

SANJIV V. PILGAONKAR Partner R.SHANKAR RAMAN M.M.CHITALE

Independent DirectorMembershipNo.39826 Whole-time Director & Chief Financial OfficerMumbai (DIN00019798) (DIN00101004)

Mumbai Mumbai

SIVARAM NAIR ACompany Secretary & Compliance OfficerM. No. FCS3939Mumbai

June 5, 2020

476

CONSOLIDATED STATEMENT OF CASH FLOWS ANNUAL REPORT 2019-20

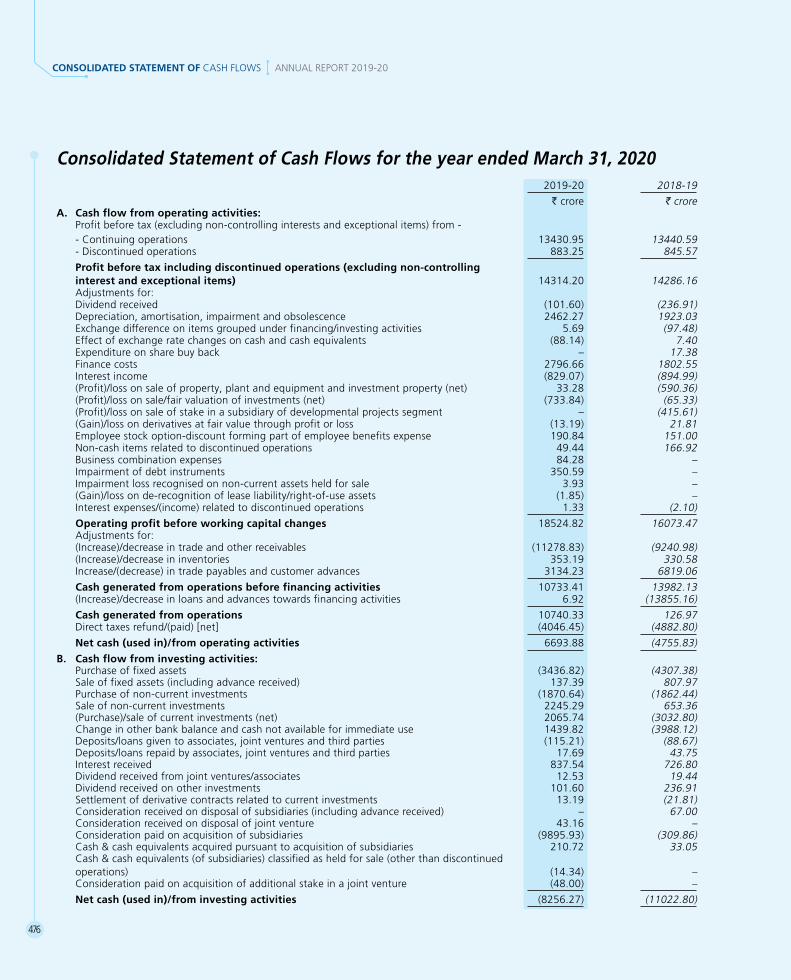

Consolidated Statement of Cash Flows for the year ended March 31, 20202019-20 2018-19

v crore v croreA. Cash flow from operating activities:

Profit before tax (excluding non-controlling interests and exceptional items) from -- Continuing operations 13430.95 13440.59 - Discontinued operations 883.25 845.57

Profit before tax including discontinued operations (excluding non-controlling interest and exceptional items) 14314.20 14286.16Adjustments for:Dividend received (101.60) (236.91)Depreciation, amortisation, impairment and obsolescence 2462.27 1923.03 Exchange difference on items grouped under financing/investing activities 5.69 (97.48)Effect of exchange rate changes on cash and cash equivalents (88.14) 7.40 Expenditure on share buy back – 17.38Finance costs 2796.66 1802.55Interest income (829.07) (894.99)(Profit)/loss on sale of property, plant and equipment and investment property (net) 33.28 (590.36)(Profit)/loss on sale/fair valuation of investments (net) (733.84) (65.33)(Profit)/loss on sale of stake in a subsidiary of developmental projects segment – (415.61)(Gain)/loss on derivatives at fair value through profit or loss (13.19) 21.81Employee stock option-discount forming part of employee benefits expense 190.84 151.00 Non-cash items related to discontinued operations 49.44 166.92Business combination expenses 84.28 –Impairment of debt instruments 350.59 –Impairment loss recognised on non-current assets held for sale 3.93 –(Gain)/loss on de-recognition of lease liability/right-of-use assets (1.85) –Interest expenses/(income) related to discontinued operations 1.33 (2.10)

Operating profit before working capital changes 18524.82 16073.47Adjustments for:(Increase)/decrease in trade and other receivables (11278.83) (9240.98)(Increase)/decrease in inventories 353.19 330.58Increase/(decrease) in trade payables and customer advances 3134.23 6819.06

Cash generated from operations before financing activities 10733.41 13982.13(Increase)/decrease in loans and advances towards financing activities 6.92 (13855.16)

Cash generated from operations 10740.33 126.97Direct taxes refund/(paid) [net] (4046.45) (4882.80)

Net cash (used in)/from operating activities 6693.88 (4755.83)

B. Cash flow from investing activities:Purchase of fixed assets (3436.82) (4307.38)Sale of fixed assets (including advance received) 137.39 807.97Purchase of non-current investments (1870.64) (1862.44)Sale of non-current investments 2245.29 653.36(Purchase)/sale of current investments (net) 2065.74 (3032.80)Change in other bank balance and cash not available for immediate use 1439.82 (3988.12)Deposits/loans given to associates, joint ventures and third parties (115.21) (88.67)Deposits/loans repaid by associates, joint ventures and third parties 17.69 43.75 Interest received 837.54 726.80Dividend received from joint ventures/associates 12.53 19.44 Dividend received on other investments 101.60 236.91Settlement of derivative contracts related to current investments 13.19 (21.81)Consideration received on disposal of subsidiaries (including advance received) – 67.00Consideration received on disposal of joint venture 43.16 –Consideration paid on acquisition of subsidiaries (9895.93) (309.86)Cash & cash equivalents acquired pursuant to acquisition of subsidiaries 210.72 33.05 Cash & cash equivalents (of subsidiaries) classified as held for sale (other than discontinued operations) (14.34) –Consideration paid on acquisition of additional stake in a joint venture (48.00) –

Net cash (used in)/from investing activities (8256.27) (11022.80)

477

Consolidated Statement of Cash Flows for the year ended March 31, 2020 (contd.)2019-20 2018-19

v crore v croreC. Cash flow from financing activities:

Proceeds from issue of share capital (including share application money) 17.56 11.31 Proceeds from non-current borrowings [Note 50] 42587.43 24181.62Repayment of non-current borrowings [Note 50] (33685.03) (14081.42)Proceeds from other borrowings (net) [Note 50] 4915.20 7765.14Payment (to)/from non-controlling interest (net)- including sale proceeds on divestment of part stake in subsidiary companies (60.05) 2884.85Settlement of derivative contracts related to borrowings 308.29 308.95Dividends paid (3929.61) (2243.18)Additional tax on dividend (621.72) (403.93)Repayment of lease liability [Note 50] (258.03) –Interest paid on lease liability (162.79) –Interest paid (including cash flows on account of interest rate swaps) (2739.70) (2983.17)Net cash (used in)/from financing activities 6371.55 15440.17 Net (decrease)/increase in cash and cash equivalents (A + B + C) 4809.16 (338.46)Cash and cash equivalents at beginning of the year 6460.23 6798.69Cash and cash equivalents for discontinued operations (classified as held for sale) (151.44) –Cash and cash equivalents at end of the year 11117.95 6460.23

Notes:1. Statement of Cash Flows has been prepared under the indirect method as set out in the Indian Accounting Standard (Ind AS) 7

“Statement of Cash Flows” as specified in the Companies (Indian Accounting Standards) Rules, 2015.2. Purchase & Sale of fixed assets represents additions & deletions to property, plant and equipment, investment property and

intangible assets adjusted for movement of (a) capital work-in-progress for property, plant and equipment and investment property and (b) Intangible assets under development during the year.

3. Cash and cash equivalents included in the Statement of Cash Flows comprise the following:

2019-20 2018-19

v crore v crore(a) Cash and cash equivalents disclosed under current assets [Note 14] 11324.57 6509.49(b) Other bank balances disclosed under current assets [Note 15] 3793.21 5216.75(c) Cash and bank balances disclosed under non-current assets [Note 9] 273.82 290.07

Total cash and cash equivalents as per Balance Sheet 15391.60 12016.31

Add: (i) Unrealised exchange (gain)/loss on cash and cash equivalents (reflected in Statement of Profit and loss) (116.39) (28.25)

Add: (ii) Unrealised exchange (gain)/loss on cash and cash equivalents (reflected in Other Comprehensive Income) (90.23) (21.01)

Less: (iii) Other bank balances disclosed under current assets [Note 15] 3793.21 5216.75Less: (iv) Cash and bank balances disclosed under non-current assets [Note 9] 273.82 290.07

Total cash and cash equivalents as per Statement of Cash Flows 11117.95 6460.23

4. Previous year’s figures have been regrouped/reclassified wherever applicable.

In terms of our report attachedFor DELOITTE HASKINS & SELLS LLPChartered Accountants S.N.SUBRAHMANYAN

Chief Executive Officer & Managing Director (DIN02255382)

Chennai

Firm’sRegistrationNo.117366W/W-100018by the hand of

SANJIV V. PILGAONKAR Partner R.SHANKAR RAMAN M.M.CHITALE

Independent DirectorMembershipNo.39826 Whole-time Director & Chief Financial OfficerMumbai (DIN00019798) (DIN00101004)

Mumbai Mumbai

SIVARAM NAIR ACompany Secretary & Compliance OfficerM. No. FCS3939Mumbai

June 5, 2020

478

NOTES FORMING PART OF THE CONSOLIDATED FINANCIAL STATEMENTS ANNUAL REPORT 2019-20

NOTE [1](I)

Corporate Information

The Consolidated Financial Statements comprise financial statements of “Larsen & Toubro Limited” (“L&T”, the “Parent Company”) and its subsidiaries (collectively referred to as “the Group”) for the year ended March 31, 2020.

The principal activities of the Group, its Joint Ventures and associates consist of providing Engineering and Construction solutions in key sectors such as Infrastructure, Hydrocarbon, Power, Process Industries and Defence, Information Technology and Financial Services. FurtherdetailsofthebusinessoperationsoftheGrouparementionedinNote[46]SegmentInformation.

NOTE [1](II)

Significant Accounting Policies

(a) Statement of compliance

The Group’s financial statements have been prepared in accordance with the provisions of the Companies Act, 2013 and the Indian Accounting Standards (Ind AS) notified under the Companies (Indian Accounting Standards) Rules, 2015 and amendments thereof issued by the Ministry of Corporate Affairs in exercise of the powers conferred by section 133 of the Companies Act, 2013. In addition, the guidance notes/announcements issued by the Institute of Chartered Accountants of India (ICAI) are also applied except where compliance with other statutory promulgations require a different treatment. These financials statements have been approved for issue by the Board of Directors at their meeting held on June 5, 2020.

(b) Basis of accounting

The Group maintains its accounts on accrual basis following historical cost convention, except for certain assets and liabilities that are measured at fair value in accordance with Ind AS.

Fair value measurements are categorised as below based on the degree to which the inputs to the fair value measurements are observable and the significance of the inputs to the fair value measurement in its entirety:

(i) Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that the Group can access at measurement date

(ii) Level 2 inputs are inputs, other than quoted prices included in level 1, that are observable for the asset or liability, either directly or indirectly; and

(iii) Level 3 inputs are unobservable inputs for the valuation of assets or liabilities

Above levels of fair value hierarchy are applied consistently and generally, there are no transfers between the levels of the fair value hierarchy unless the circumstances change warranting such transfer.

(c) Presentation of financial statements

The Balance Sheet, Statement of Profit and Loss and Statement of Changes in Equity are prepared and presented in the format prescribed in the Schedule III to the Companies Act, 2013 (“the Act”). The Statement of Cash Flows has been prepared and presented as per the requirements of Ind AS 7 “Statement of Cash Flows”. The disclosure requirements with respect to items in the Balance Sheet and Statement of Profit and Loss, as prescribed in the Schedule III to the Act, are presented by way of notes forming part of the financial statements along with the other notes required to be disclosed under the notified Accounting Standards and the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 as amended.

Amounts in the financial statements are presented in Indian Rupees in crore [1 crore = 10 million] rounded off to two decimal places as permitted by Schedule III to the Companies Act, 2013. Per share data are presented in Indian Rupees to two decimal places.

(d) Basis of consolidation

(i) The consolidated financial statements incorporate the financial statements of the Parent Company and its subsidiaries. For this purpose, an entity which is, directly or indirectly, controlled by the Parent Company is treated as subsidiary. The Parent Company together with its subsidiaries constitute the Group. Control exists when the Parent Company, directly or indirectly, has power over the investee, is exposed to variable returns from its involvement with the investee and has the ability to use its power to affect its investor’s returns.

Notes forming part of the Consolidated Financial Statements

479

(ii) Consolidation of a subsidiary begins when the Parent Company, directly or indirectly, obtains control over the subsidiary and ceases when the Parent Company, directly or indirectly, loses control of the subsidiary. Income and expenses of a subsidiary acquired or disposed of during the year are included in the consolidated Statement of Profit and Loss from the date the Parent Company, directly or indirectly, gains control until the date when the Parent Company, directly or indirectly, ceases to control the subsidiary.