Lone Star National Bancshares - Texas Inc. - Federal Reserve ...

101

AMENDED

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of Lone Star National Bancshares - Texas Inc. - Federal Reserve ...

AMENDED

Report Item

Lone Star National Bancshares-Texas, Inc.

McAllen, TexasIncorporated in Texas

100.00% 100.00%

Lone Star National BankPharr, Texas

Incorporated in Texas

Lone Star National Capital Trust IV

Wilmington, DelewareBusiness trust for

$10million trust preferred offering completed 6-21-07Incorporated in Delaware

100.00%

Lone Star Insurance Services, Inc.

McAllen, TexasIncorporated in Texas

100.00%

Lone Star Investment Sub-Nevada, Inc.Las Vegas, NV

Incorporated in Nevada

Form FR Y-6

Lone Star National Bancshares-Texas, Inc.

2b: Domestic branch verification listing enclosed.

Note: No entity in the organization has an LEI, including Lone Star National Bancshares-Texas, Inc.

McAllen, TexasFiscal Year Ending December 31, 2016

1: (a) The Bank Holding Company prepares an annual report for its shareholders and is not registered with the SEC. Enclosed is the unbound copy of the annual report, which includes all its major components. (b) Audited financial statements at year ended December 31, 2016 are included in the unbound copy of the annual report.

2a: Organizational Chart

AMENDED

Results: A list of branches for your holding company: LONE STAR NATIONAL BANCSHARES‐‐TEXAS, INC. (2325350) of MCALLEN, TX.The data are as of 12/31/2016. Data reflects information that was received and processed through 01/10/2017.

Reconciliation and Verification Steps1. In the Data Action column of each branch row, enter one or more of the actions specified below2. If required, enter the date in the Effective Date column

ActionsOK: If the branch information is correct, enter 'OK' in the Data Action column.Change: If the branch information is incorrect or incomplete, revise the data, enter 'Change' in the Data Action column and the date when this information first became valid in the Effective Date column.Close: If a branch listed was sold or closed, enter 'Close' in the Data Action column and the sale or closure date in the Effective Date column.Delete: If a branch listed was never owned by this depository institution, enter 'Delete' in the Data Action column.Add: If a reportable branch is missing, insert a row, add the branch data, and enter 'Add' in the Data Action column and the opening or acquisition date in the Effective Date column.

If printing this list, you may need to adjust your page setup in MS Excel. Try using landscape orientation, page scaling, and/or legal sized paper

Submission ProcedureWhen you are finished, send a saved copy to your FRB contact. See the detailed instructions on this site for more information.If you are e‐mailing this to your FRB contact, put your institution name, city and state in the subject line of the e‐mail

Note:To satisfy the FR Y‐10 reporting requirements, you must also submit FR Y‐10 Domestic Branch Schedules for each branch with a Data Action of Change, Close, Delete, or Add.The FR Y‐10 report may be submitted in a hardcopy format or via the FR Y‐10 Online application ‐ https://y10online.federalreserve.gov.

* FDIC UNINUM, Office Number, and ID_RSSD columns are for reference only. Verification of these values is not required.

Data Action Effective Date Branch Service Type Branch ID_RSSD* Popular Name Street Address City State Zip Code County Country FDIC UNINUM* Office Number* Head Office Head Office ID_RSSD* CommentsOK Full Service (Head Office) 842460 LONE STAR NATIONAL BANK 206 WEST FERGUSON PHARR TX 78577 HIDALGO UNITED STATES 16940 0 LONE STAR NATIONAL BANK 842460OK Full Service 3450325 BROWNSVILLE BOCA CHICA TOWER BRANCH 2100 BOCA CHICA BLVD BROWNSVILLE TX 78521 CAMERON UNITED STATES 442243 13 LONE STAR NATIONAL BANK 842460OK Full Service 3506053 BROWNSVILLE BRANCH 3300 NORTH EXPRESSWAY 83 BROWNSVILLE TX 78521 CAMERON UNITED STATES 360740 5 LONE STAR NATIONAL BANK 842460OK Full Service 3506204 EDINBURG BRANCH 117 SOUTH 10TH EDINBURG TX 78539 HIDALGO UNITED STATES 420393 6 LONE STAR NATIONAL BANK 842460OK Full Service 3506231 HARLINGEN BRANCH 1901 NORTH ED CAREY DRIVE HARLINGEN TX 78550 CAMERON UNITED STATES 420394 7 LONE STAR NATIONAL BANK 842460OK Limited Service 3506437 HARLINGEN MOTOR BANK BRANCH 918 WEST HARRISON AVE HARLINGEN TX 78550 CAMERON UNITED STATES Not Required Not Required LONE STAR NATIONAL BANK 842460OK Full Service 3252622 HIDALGO BRANCH 633 SOUTH INTERNATIONAL BLVD HIDALGO TX 78557‐2933 HIDALGO UNITED STATES 430051 11 LONE STAR NATIONAL BANK 842460OK Full Service 4054832 CORPORATE OFFICE BRANCH 520 EAST NOLANA AVENUE MCALLEN TX 78504 HIDALGO UNITED STATES 521882 25 LONE STAR NATIONAL BANK 842460OK Full Service 3922699 DHR MEDICAL BRANCH 5537 NORTH MCCOLL ROAD MCALLEN TX 78504 HIDALGO UNITED STATES 493425 21 LONE STAR NATIONAL BANK 842460OK Full Service 4351595 LA PLACITA BRANCH 2109 SOUTH 10TH STREET MCALLEN TX 78503 HIDALGO UNITED STATES 527033 30 LONE STAR NATIONAL BANK 842460OK Limited Service 4054823 MAIN STREET BRANCH 800 NORTH MAIN STREET, SUITE 600 MCALLEN TX 78501 HIDALGO UNITED STATES 495439 22 LONE STAR NATIONAL BANK 842460OK Full Service 3506240 MED‐POINT BRANCH 1300 EAST RIDGE ROAD MCALLEN TX 78503 HIDALGO UNITED STATES 430013 9 LONE STAR NATIONAL BANK 842460OK Full Service 3794690 NOLANA BRANCH 600 EAST NOLANA AVENUE MCALLEN TX 78504 HIDALGO UNITED STATES 479931 20 LONE STAR NATIONAL BANK 842460OK Full Service 2449911 NORTH MCALLEN BRANCH 5515 NORTH 10TH STREET MCALLEN TX 78504 HIDALGO UNITED STATES 257288 2 LONE STAR NATIONAL BANK 842460OK Full Service 2246718 SOUTH MCALLEN BRANCH 200 LINDBERG AVENUE MCALLEN TX 78501 HIDALGO UNITED STATES 257287 1 LONE STAR NATIONAL BANK 842460OK Full Service 2994774 MISSION BRANCH 2003 EAST GRIFFIN PARKWAY MISSION TX 78572 HIDALGO UNITED STATES 257289 3 LONE STAR NATIONAL BANK 842460OK Full Service 3365607 MISSION MEDICAL BRANCH 1100 SOUTH BRYAN ROAD MISSION TX 78572 HIDALGO UNITED STATES 442477 14 LONE STAR NATIONAL BANK 842460OK Full Service 3295311 PALMVIEW BRANCH 720 EAST VETERANS BOULEVARD PALMVIEW TX 78572‐7068 HIDALGO UNITED STATES 429616 8 LONE STAR NATIONAL BANK 842460OK Limited Service 3506398 PHARR MOTOR BANK 1201 SOUTH CAGE BLVD PHARR TX 78577 HIDALGO UNITED STATES Not Required Not Required LONE STAR NATIONAL BANK 842460OK Full Service 4195230 PHARR SOUTH CAGE BRANCH 118 SOUTH CAGE BOULEVARD PHARR TX 78577 HIDALGO UNITED STATES 521884 27 LONE STAR NATIONAL BANK 842460OK Limited Service 3450343 PORT ISABEL MOTOR BANK 202 EAST QUEEN ISABELLA BLVD PORT ISABEL TX 78578 CAMERON UNITED STATES Not Required Not Required LONE STAR NATIONAL BANK 842460OK Full Service 2994783 RIO GRANDE CITY BRANCH 2300 EAST HIGHWAY 83 RIO GRANDE CITY TX 78582 STARR UNITED STATES 357470 4 LONE STAR NATIONAL BANK 842460OK Full Service 4236188 RIO GRANDE CITY WEST BRANCH 201 NORTH TEXAS STREET RIO GRANDE CITY TX 78582 STARR UNITED STATES 519110 24 LONE STAR NATIONAL BANK 842460OK Full Service 3336689 ROMA BRANCH 305 EAST GRANT ROMA TX 78584 STARR UNITED STATES 438914 12 LONE STAR NATIONAL BANK 842460OK Full Service 4503741 HUEBNER BANKING CENTER 15236 HUEBNER ROAD SAN ANTONIO TX 78231 BEXAR UNITED STATES 538556 32 LONE STAR NATIONAL BANK 842460OK Full Service 4195221 SAN ANTONIO MEDICAL BRANCH 7954 FREDERICKSBURG ROAD SAN ANTONIO TX 78229 BEXAR UNITED STATES 521883 26 LONE STAR NATIONAL BANK 842460OK Full Service 4326593 SAN ANTONIO SAN PEDRO BRANCH 10000 SAN PEDRO AVENUE SAN ANTONIO TX 78216 BEXAR UNITED STATES 521885 28 LONE STAR NATIONAL BANK 842460OK Full Service 4540045 STONE OAK BANKING CENTER 381 NORTH LOOP 1604 W SAN ANTONIO TX 78232 BEXAR UNITED STATES Not Required Not Required LONE STAR NATIONAL BANK 842460OK Full Service 4366870 ZARZAMORA BRANCH 6986 SOUTH ZARZAMOR STREET SAN ANTONIO TX 78224 BEXAR UNITED STATES 532255 31 LONE STAR NATIONAL BANK 842460OK Full Service 3450334 SOUTH PADRE ISLAND BRANCH 601 PADRE BLVD SOUTH PADRE ISLAND TX 78597 CAMERON UNITED STATES 452213 16 LONE STAR NATIONAL BANK 842460OK Full Service 3302527 WESLACO BRANCH 214 SOUTH TEXAS BLVD WESLACO TX 78596 HIDALGO UNITED STATES 430050 10 LONE STAR NATIONAL BANK 842460OK Full Service 4351607 WESLACO NORTH BRANCH 620 WEST EXPRESSWAY 83 WESLACO TX 78596 HIDALGO UNITED STATES 526986 29 LONE STAR NATIONAL BANK 842460

gonzalezs

Typewritten Text

Branch Verification

Report Item 3: Shareholders(1)(a)(b)(c) and (2)(a)(b)(c)

(1) (a) (1) (b) (1)(c) (2) (a) (2) (b) (2) (c)Name & Address Country of Citizenship Number and Percentage Name & Address Country of Citizenship Number and Percentage(City, State & Country) or Incorporation of Each Class of (City, State & Country) or Incorporation of Each Class of

Voting Securities Voting SecuritiesAlonzo Cantu USA 1,069,248 - 17.49%McAllen, TX, USA Common Stock None

Victor Haddad USA 636,659 - 10.41%McAllen, TX, USA Common Stock

Cruz Cantu III USA 575,200 - 9.41%Pharr, TX, USA Common Stock

Elvia Saenz USA 592,132 - 9.69%McAllen, TX, USA Common Stock

S. David Deanda USA 531,382 - 8.69%Mission, TX, USA Common Stock

91,311 - 1.49%options on commonstock

Juan M. Pena USA 378,330 - 6.19%Pharr, TX, USA Common Stock

to vote during the fiscal year ending December 31, 2013.

Form FR Y-6Lone Star National Bancshares-Texas, Inc.

Fiscal Year Ending December 31, 2016

Current shareholders with ownership, control of holdings of 5% or more Shareholders not listed in (3)(1)(a) through (3)(1)(c) that with the power to vote as of fiscal year ending December 31, 2014. had ownership, control of holdings of 5% or more with power

AMENDED

(1) (2) (3)(a) (3)(b) (3)(c) (4)(a) (4)(b) (4)(c) Names & Address Principal Title & Position Title & Position Title & Position with Percentage of Voting Percentage of List names of(City, State,Country) Occupation if other with Bank Holding with Subsidiaries Other Businesses Shares in Bank Holding Voting Shares in other companies

than with Bank Company (include names (include names of Company Subsidiaries (includes partnerships)Holding Company of subsidiaries) other businesses) (include names if 25% or more of

of subsidiaries) voting securities areheld (List names of companies and percentage of votingsecurities held)

Alonzo Cantu Construction Director & Director & Chairman See Exhibit #1 17.49% None See Exhibit #1Pharr, TX / USA and Land Chairman of of the Board of

Development the Board each BHC subsidiary

Victor Haddad Physician Principal Securities N/A See Exhibit #2 10.41% None See Exhibit #2McAllen, TX / USA Holder

Cruz Cantu, III Investments, Director Director of each See Exhibit #3 9.41% None See Exhibit #3Pharr, TX / USA construction and BHC subsidiary

land development

Oscar R. Gonzalez Certified Director & Director of each See Exhibit #4 3.71% None See Exhibit #4Pharr, TX / USA Public Vice Chairman of BHC subsidiary

Accountant the Board

Abdala Kalifa Retail Apparel Director Director of each See Exhibit #5 2.44% None See Exhibit #5Pharr, TX / USA and Commercial BHC subsidiary

Development

S. David Deanda Banker Director & Director & President See Exhibit #6 10.18% None See Exhibit #6Pharr, TX / USA President for each BHC subsidiary

except Lone Star InsuranceServices, Inc.

Joe D. Zayas Dentist Director Director of each See Exhibit #7 0.53% None See Exhibit #7Brownsville, TX / USA BHC subsidiary

Form FR Y-6Lone Star National Bancshares-Texas, Inc.

Fiscal Year Ending December 31, 2016

Report Item 4: Insiders(1), (2), (3)(a)(b)(c) and (4)(a)(b)(c)

AMENDED

(1) (2) (3)(a) (3)(b) (3)(c) (4)(a) (4)(b) (4)(c) Names & Address Principal Title & Position Title & Position Title & Position with Percentage of Voting Percentage of List names of(City, State,Country) Occupation if other with Bank Holding with Subsidiaries Other Businesses Shares in Bank Holding Voting Shares in other companies

than with Bank Company (include names (include names of Company Subsidiaries (includes partnerships)Holding Company of subsidiaries) other businesses) (include names if 25% or more of

of subsidiaries) voting securities areheld (List names of companies and percentage of votingsecurities held)

Form FR Y-6Lone Star National Bancshares-Texas, Inc.

Fiscal Year Ending December 31, 2016

Report Item 4: Insiders(1), (2), (3)(a)(b)(c) and (4)(a)(b)(c)

Nolan E. Perez Physician Director Director of each See Exhibit #8 0.23% None See Exhibit #8Harlingen, TX / USA BHC subsidiary

George R. Carruthers, Jr. Banker EVP & Chief Secretary, Treasurer, See Exhibit #9 0.30% None See Exhibit #9Pharr, TX / USA Financial Officer EVP & CFO for Lone

Star Insurance Services, Inc.

Manny M. Vela Attorney Director Director of each See Exhibit #10 0.16% None See Exhibit #10Pharr, TX / USA BHC subsidiary

Ruben M. Torres Physician Director Director of each See Exhibit #11 0.11% None See Exhibit #11Harlingen, TX / USA BHC subsidiary

AMENDED

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #1

gonzalezs

Typewritten Text

EXHIBIT #2

gonzalezs

Typewritten Text

EXHIBIT #2

gonzalezs

Typewritten Text

EXHIBIT #2

gonzalezs

Typewritten Text

EXHIBIT #3

gonzalezs

Typewritten Text

EXHIBIT #4

gonzalezs

Typewritten Text

EXHIBIT #4

gonzalezs

Typewritten Text

EXHIBIT #5

gonzalezs

Typewritten Text

EXHIBIT #6

gonzalezs

Typewritten Text

EXHIBIT #7

gonzalezs

Typewritten Text

EXHIBIT #7

gonzalezs

Typewritten Text

EXHIBIT #8

gonzalezs

Typewritten Text

EXHIBIT #8

gonzalezs

Typewritten Text

EXHIBIT #9

gonzalezs

Typewritten Text

EXHIBIT #9

gonzalezs

Typewritten Text

EXHIBIT #10

gonzalezs

Typewritten Text

EXHIBIT #10

gonzalezs

Typewritten Text

EXHIBIT #11

gonzalezs

Typewritten Text

EXHIBIT #11

1

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL

CONDITION AND RESULTS OF OPERATIONS

The following discussion addresses information pertaining to the financial condition and results of operation of Lone Star National Bancshares-Texas, Inc. and subsidiaries (the “Company”) that may not be otherwise apparent from a review of the audited consolidated financial statements and related footnotes. It should be read in conjunction with those statements, as well as other information presented throughout the report. In addition to historical information, this discussion and other sections contained in this Annual Report include certain forward-looking statements regarding events and trends which may affect the Company’s future results. Such statements are subject to risk and uncertainties that could cause the Company’s actual results to differ materially. Such factors include, but are not limited to, those described in this discussion and analysis. The Company is a privately held bank holding company headquartered in McAllen, Texas, offering a broad array of financial services through its wholly-owned banking subsidiary, Lone Star National Bank (the “Bank”). The Bank operates from thirty-two banking locations: twenty-seven (27) banking locations in the Rio Grande Valley and five (5) banking locations in San Antonio, Texas. The Bank engages in a wide range of commercial and personal banking activities including the usual acceptance of deposits for checking, savings and time deposit accounts; extension of secured and unsecured loans to corporations, individuals and others; issuance of letters of credit; rental of safe deposit boxes; brokerage services and insurance services. The Bank’s lending services include commercial, industrial, real estate, installment and credit card loans and participation in loans with other banks. The members of the Bank’s management team have significant experience and contacts from their service at the Bank and their prior service with other successful community banks that have operated in the same market. The Bank seeks to provide its products and services through a high quality, experienced staff and local decision making. Year 2016 has proven to be a successful year for the Company reporting earnings of $13.814 million reflecting a net increase of $2.188 million over the prior year. At December 31, 2016, the Company had total assets of $2.184 billion, loans of $1.194 billion, deposits of $1.821 billion and shareholders’ equity of $251.962 million. The Company’s primary goal is to provide a higher quality service for its customers in the South Texas market by providing personal service, relationship banking and innovative technological solutions. In order to broaden the customer base, primarily through expanding the Company’s network of full-service banking offices, the Board of Directors is continuing its efforts to expand our banking organization in the Rio Grande Valley and San Antonio markets by selecting sites for future branches.

gonzalezs

Typewritten Text

Annual Report

2

The Company’s profitability is dependent on managing interest rate spreads, other operating income and expenses, and credit risk. Net interest income is the largest component of revenue for the Company. The Company manages interest rate risks through a funds management strategy which involves offering deposit and / or loan structures that tend to counter the natural rate risk profile of the Company. The Company addresses loan and deposit pricing, the asset and liability mix and interest rate sensitivity on a periodic basis. Yields on earning assets and rates paid on interest-bearing deposits within the Company declined during 2016. Through management’s efforts, the net interest margin of 3.38% for 2016 reflects a 5 basis points decline when compared to the net interest margin of 3.43% for 2015. The Company manages its credit risk by establishing underwriting guidelines, which address the characteristics of borrowers, industries, geographic locations and risk products. The credit process is controlled by continuous review and credit analysis. The Company evaluates its management of operating expenses through the efficiency ratio, which is approximately 79.6% for 2016. The efficiency ratio equates to the cost of recording one dollar’s worth of revenue. Analysis of Financial Condition Overview: Total assets of $2.184 billion at December 31, 2016 decreased by 0.9% or $19.0 million compared to $2.203 billion at December 31, 2015. Total deposits of $1.821 billion at December 31, 2016 decreased by 1.3% or $23.5 million compared to $1.845 billion at December 31, 2015. A more detailed description of changes to the balance sheet follows.

Due from Banks-interest bearing: Due from banks-interest bearing accounts of

$104.8 million at December 31, 2016 decreased $101.1 million or 49.1% compared to $205.8 million at December 31, 2015. These funds represent excess funds deposited with correspondent banks in interest bearing accounts, primarily the Federal Reserve Bank. These funds were reinvested in higher yielding earning assets.

Investment Securities: Total investment securities of $692.2 million at December 31, 2016 increased $700,000 or 0.1% compared to $691.5 million at December 31, 2015. Included in investment securities are municipal tax exempt bonds (“Tax Exempt Munis”). Tax Exempt Munis of $167.5 million at December 31, 2016 increased $17.2 million or 11.4% compared to $150.3 million at December 31, 2015. The strategy for investment securities during 2016 was to remain conservative on reinvesting of cash flows to avoid taking on additional interest rate / extension risk and to increase yield. Included in the Tax Exempt Munis are bonds primarily from school districts within the State of Texas that are guaranteed by the Texas Permanent School Fund and as such, well secured. The investment securities portfolio yield of 2.55% for 2016 increase 0.06% compared to 2.49% for 2015.

Loans: Loans held for sale and held for investment of $1.194 billion at December

31, 2016 increased $51.6 million or 4.5% compared to $1.142 billion at December 31, 2015. At December 31, 2016, the loan portfolio consisted primarily of $2.5 million of

gonzalezs

Typewritten Text

Annual Report

3

real estate loans held for sale, $112.4 million of commercial loans, $1.4 million of agriculture loans, $996.0 million of real estate loans and $81.8 million of consumer and other loans. These loans were primarily originated within our market area of the Rio Grande Valley and San Antonio, Texas and are generally secured by residential real estate, commercial real estate, business property or personal property. Despite the unprecedented contraction in the credit markets, we continued to lend to credit-worthy customers.

The Company manages credit risk by establishing and implementing strategies

and guidelines appropriate to the characteristics of borrowers, industries, geographic locations and products. Diversification of risk within each of these areas is a primary objective. Policies and procedures are developed to ensure that loan commitments conform to current strategies and guidelines. Management continues to refine the Company’s credit policies and procedures to address risks in the current and prospective environment and to reflect management’s current strategic focus. The credit process is controlled with continuous credit review and analysis, as well as reviewed by internal and external auditors and regulatory authorities. The Company’s loans are widely diversified by borrower and industry group.

The Company has lending policies in effect so that lending of all types is approached, to the extent possible, including low-to-moderate income neighborhoods and small business, on a basis consistent with safe and sound standards. Stress testing is utilized to take into consideration the potentially adverse economic conditions under which liquidation of the loan could occur. Generally, collateral accepted to secure the commercial loan portfolio is real estate, accounts receivable, inventory, marketable securities and equipment. However, for the consumer loan portfolio, autos, deeds of trust, life insurance and marketable securities are accepted as collateral.

The Company’s policy on maturity extensions and rollovers is based on

management’s assessment of individual loans. Approvals for the extension or renewal of loans without reduction of principal for more than one twelve-month period are generally avoided, unless the loans are fully secured and properly margined by cash or marketable securities, or are revolving lines subject to annual analysis and renewal.

Nonperforming Assets: The Company has procedures in place to assist in

maintaining the overall quality of its loan portfolio. Furthermore, the Company has established underwriting guidelines to be followed by its officers and monitors its delinquency levels for any negative or adverse trends, particularly with respect to credits which have total exposures of $10,000 or more.

Nonperforming assets consists of nonaccrual loans, loans for which the interest

rate has been renegotiated below originally contracted rates and real estate or other assets that have been acquired in partial or full satisfaction of loan obligations. At December 31, 2016, nonperforming assets totaled $76.1 million or 6.4% of loans plus repossessed assets. Nonperforming assets reflects a decrease of $6.2 million or 7.5% when compared to $82.3 million at December 31, 2015. Management has seasoned personnel to assist in

gonzalezs

Typewritten Text

Annual Report

4

turning nonperforming assets into performing assets or exiting the relationship. Management believes that it is unlikely that any material loss will be incurred on disposition of the collateral.

Management regularly reviews and monitors the loan portfolio to identify borrowers experiencing financial difficulties. Management believes that at December 31, 2016 all such loans have been identified and included in the nonaccrual, restructured or 90 days past due loan totals. Management continues to emphasize maintaining a low level of nonperforming assets and returning nonperforming assets to an earning status.

Allowance for Loan Losses: The allowance for loan losses at December 31, 2016

of $23.3 million decreased $2.1 million or 8.4% compared to $25.4 million at December 31, 2015. The allowance for loan losses at December 31, 2016 was 1.95% of loans held for investment.

Management analyzes the loan portfolio to determine the adequacy of the

allowance for loan losses and the appropriate provision required to maintain an adequate allowance. While management uses available information to recognize losses on loans, there can be no assurance that future additions to the allowance will not be necessary. Future adjustments could be necessary to the allowance for loan losses if circumstances or economic conditions differ substantially from the assumptions used in making the initial determinations. Additionally, as an internal part of the examination process, bank regulatory agencies periodically review our allowance for loan losses. The banking regulatory agencies could require the recognition of additions to our loan loss allowance based on their judgment of information available to them at the time of their examination.

Premises and Equipment: Premises and equipment of $55.8 million at December

31, 2016 decreased $0.5 million or 0.9% compared to $56.4 million at December 31, 2015. The net decrease in premises and equipment for 2016 is primarily attributable to depreciation expense.

Other Real Estate Owned: Other real estate owned (“OREO”) of $21.2 million at

December 31, 2016 increased $0.5 million or 2.3% compared to $20.7 million at December 31, 2015. OREO assets represent property acquired as the result of borrower defaults on loans. Management actively manages the OREO and records the value of each OREO at either the lower of the fair market value less estimated selling costs or at the cost of the asset. Write-downs occurring at foreclosure are charged against the allowance for possible loan losses. On an ongoing basis, OREO is appraised as required by market indications and applicable regulations. Any further write-downs as a result of subsequent declines in value are included in other noninterest expense along with other expenses related to maintaining the properties.

Bank Owned Life Insurance: Bank owned life insurance (“BOLI”) of $62.7 million at December 31, 2016 increased $13.6 million or 27.6% compared to $49.1 million at December 31, 2015. During 2016 an additional $12.0 million investment was made in BOLI. The investment in BOLI continues to provide strong earnings that provide

gonzalezs

Typewritten Text

Annual Report

5

financing for employee compensation and benefit plans. A split dollar benefit is provided for selected management and will be paid to the estate of the participant provided the participant is employed by the Company at date of death.

Deposits: Deposits at December 31, 2016 of $1.821 billion decreased $23.5

million or 1.3% compared to $1.845 billion at December 31, 2015. The decrease in deposits was attributable to a decrease in foreign, public funds and core deposits. Foreign deposits of $184.1 million decreased $9.0 million, public fund deposits of $627.3 million decreased $6.1 million and all other core deposit accounts of $1.010 billion decreased $8.4 million at December 31, 2016 compared to the prior year. Deposits are the Company’s primary source of funds. The Company offers a variety of products designed to attract and retain deposit customers, such as checking accounts, regular savings deposits, NOW accounts, money market accounts, select certificates of deposit savings, an interest-bearing club account and certificates of deposits. Deposits are obtained primarily from individuals, partnerships and corporations in our market areas. In addition, we obtain deposits from state and local public entities, commonly referred to as public fund deposits. The Company’s policies also permit the acceptance of brokered deposits. Generally, both brokered certificates of deposit and public funds are less expensive than retail deposits, and are easily managed.

The interest rates paid are competitively priced for each particular deposit product

and structured to meet our funding requirements. The Company’s management will continue to manage interest expense through deposit pricing. The Company’s management believes that additional funds, if needed, can be attracted and deposit growth can be accelerated through deposit pricing as the Company experiences increased loan demand or other liquidity needs. Capital Resources: Shareholders’ equity of $252.0 million at December 31, 2016 increased $4.7 million or 2.2% compared to $247.3 million at December 31, 2015. The increase was primarily attributable to: $13.8 million of earnings, partially reduced by $5.9 million decrease in accumulated other comprehensive income, and further reduced by $3.4 million of net Treasury Stock purchases. The Company has actively engaged in a buyback program of its stock during years 2012 to the present. During 2015, the Board of Directors retired $10.0 million of Treasury Stock. During 2016, the Board of Directors retired $10.4 million of Treasury Stock. Bank holding companies are required to maintain capital ratios in accordance with guidelines adopted by the Federal Reserve Board. The guidelines are commonly known as Risk-Based Capital Guidelines. The minimum Total Risk-Based Capital, Tier 1 Risk-Based Capital, Common Equity Tier 1 Capital, and Tier 1 Leverage Capital ratios which include an additional 2.5% Capital Conservation Buffer are 10.5%, 8.5%, 7.0% and 4.0%, respectively. At December 31, 2016, the Company’s Total Risk-Based Capital, Tier 1 Risk-Based Capital, Common Equity Tier 1 Capital, and Tier 1 Leverage Capital ratios were 18.7%, 17.4%, 17.4%, and 11.7%, respectively. Shareholders’ equity as a percentage of total year-end assets was 11.53% in 2016 and 11.23% in 2015.

gonzalezs

Typewritten Text

Annual Report

6

At December 31, 2016, the Company and the Bank met the criteria for classification as a “well-capitalized” institution under the prompt corrective action rules promulgated under the Federal Deposit Insurance Act. Designation as a well-capitalized institution under these regulations does not constitute a recommendation or endorsement of the Company or the Bank by federal bank regulators. Analysis of Results of Operations

Earnings Summary: Net income for 2016 was $13.814 million or $2.33 per fully diluted share, reflecting an increase of $2.188 million or $0.33 per fully diluted share, compared to the net income of $11.626 million or $1.94 per fully diluted share for the year 2015. A more detailed description of the results of operations is included in the material that follows.

Net Interest Income: Net interest income represents the largest source of income

for the Company. Net interest income is the difference between interest earned on assets and interest expense incurred for the funds supporting those assets. The largest category of earning assets consists of loans. The second largest category of earning assets is investments, followed by due from banks-interest bearing deposits.

Earning assets are funded by consumer and commercial deposits and short-term

borrowings. In addition to these interest-bearing funds, assets are also supported by interest-free funds, primarily demand deposits and shareholder’s equity. Variations in the volume and mix of assets and liabilities and their relative sensitivity to interest rate movements determine changes in net interest income.

Net interest income (see table below) of $65.6 million for 2016, reflects a

decrease of $1.8 million or 2.6% compared to the prior year of $67.4 million. The decrease in net interest income was attributable primarily to a decrease in loan volume and partially due to a decline in interest earned. The decline in loan volume is primarily attributable to sluggish economic growth, low interest rates and intense competitive pressures. Management’s efforts to control the cost of funds by reducing the rate paid on deposits helped offset the decline in noninterest income. The net yield on total interest-earning assets (see table below), also referred to as net interest margin, represents net interest income, on a tax equivalent basis, divided by average interest-earning assets. Since a significant portion of the Company’s funding is derived from interest-free sources, primarily demand deposits and shareholders’ equity, the effective rate paid for all funds is lower than the rate paid on interest-bearing liabilities alone. The net interest margin of 3.38% for 2016 decreased 5 basis points compared to 3.43% for the prior year. The Company continued to experience intense market competition for both loans and deposits during 2016. The yield on interest-earning assets of 3.96% for 2016 decreased 10 basis points compared to 4.06% for the

gonzalezs

Typewritten Text

Annual Report

7

prior year. The rates paid on interest-bearing liabilities of 0.80% for 2016 decreased 6 basis points compared to 0.86% for the prior year. The following table presents for the last three calendar years the total dollar amount of interest income from average interest-earning assets and the resultant yields, reported on a tax-equivalent basis, as well as the average interest-bearing liabilities, expressed both in dollars and rates. Average balances are derived from average daily balances and the yields and costs are established by dividing income or expense by the average balance of the asset or liability. Income and yield on interest-earning assets include amounts to convert tax-exempt income to a taxable-equivalent basis, assuming a 35% effective tax rate for 2016, 2015 and 2014. NOTE: INSERT NEW EXCEL WORKSHEET FOR NET INTEREST MARGIN

Provision for Loan Losses: The amount of provision for loan losses is based on periodic (not less than quarterly) evaluations of the loan portfolio, especially nonperforming and other potential problem loans. During these evaluations, management considers various factors. For additional information concerning the factors in these evaluations, see the “Allowance for Loan Losses” section of this Report.

The provision for loan losses is charged to earnings to bring the allowance for

loan losses to a level deemed appropriate by management based on factors such as historical experience, the volume and type of lending conducted by the Company, the amount of nonperforming assets, regulatory policies, generally accepted accounting principles, general economic conditions, particularly as they relate to the Company’s lending area, and other factors related to the collectibility of the Company’s loan portfolio. The provision for loan losses for the year 2016 and 2015 was zero. A zero provision for loan losses for year 2016 and 2015 was partially due the allowance for loan losses being at a level deemed appropriate by management based on various factors discussed in the “Allowance for Loan Loss” section of this Report.

Noninterest Income: Noninterest income for 2016 of $25.2 million increased $1.8

million or 7.7% compared to $23.4 million for prior year. The net increase in noninterest income for 2016 compared to the prior year was primarily attributable to increases in Other service charges and fee income; Gain on securities, Bank Owned Life Insurance cash value, and Other noninterest income partially offset by decreases in Service charges on deposit accounts.

Service charges on deposit accounts for 2016 of $6.6 million decreased $512,000

or 7.2% compared to $7.1 million for the prior year. Non-sufficient check income more commonly referred to as net overdraft charges for 2016 of $5.0 million decreased $229,000 or 4.4% compared to $5.2 million for the prior year. Account analysis charges for 2016 of $377,000 decreased $209,000 or 35.7% compared to $585,000 for the prior year and was primarily attributable to an increase in earnings credit for said accounts.

gonzalezs

Typewritten Text

(attached)

gonzalezs

Typewritten Text

Annual Report

8

Other service charge and fee income for 2016 of $8.2 million increased $511,000 or 6.6% as compared to $7.7 million for the prior year. The net increase in other service charge and fee income for 2016 was primarily attributable to increases in: Debit card interchange fee income, Merchant services fees and ATM surcharge fees, partially offset by a net decrease in Foreign currency fees. Debit card interchange fee income of $4.9 million for 2016 increased $304,000 or 6.7% compared to $4.6 million for the prior year. The increase in debit card fee income is attributable to volume of activity and production bonuses. Merchant services income of $818,000 for 2016 increased $119,000 or 17.1% compared to $699,000 for the prior year and was attributable to an increased volume of business conducted by Bank customer merchants. ATM surcharge fees of $941,000 for 2016 increased $210,000 or 28.8% compared to $731,000 for the prior year and was attributable to an increased volume of business. Foreign currency fees for 2016 of $256,000 decreased $70,000 or 21.3% as compared to $326,000 for the prior year. The decline in Foreign currency fees was due to a decline in currency exchange activity.

Gain on securities for 2016 of $1.8 million increased $51,000 or 2.8% compared

to $1.8 million for the prior year. Securities were sold out of the Available for Sale portfolio to accomplish investment portfolio objectives aimed at maximizing the total return of the investment portfolio and to manage the Bank’s liquidity.

Bank Owned Life Insurance (BOLI) for 2016 of $1.6 million increased $200,000

or 14.7% compared to $1.4 million for the prior year. The investment in BOLI continues to provide strong earnings that provide financing for employee compensation and benefit plans.

Other noninterest income for 2016 of $6.9 million increased $1.6 million or

29.2% compared to $5.4 million for the prior year. The net increase in Other noninterest income for 2016 was primarily attributable to increases in: Gains on sale of loans held for sale of $348,000; Insurance services commission income of $232,000; Lawsuit settlement of $1.9 million; partially offset by a net decrease in brokerage services – commission income of $886,000.

Noninterest Expense: Noninterest expense for 2016 of $72.3 million decreased $2.7 million or 3.6% compared to $75.0 million for prior year. The decrease in noninterest expense was primarily attributable to a decrease in four subcategories: Legal and professional fees; FDIC insurance; Advertising expense; and Other real estate, net. The decrease in noninterest expense was partially offset by an increase in employee compensation and employee benefit expense and telephone expense. The largest category of noninterest expense is personnel expense of $41.8 million, which is comprised of employee compensation of $35.0 million and employee benefits of $6.9 million, for 2016 these categories increased $1.5 million or 3.7% compared to $40.3 million for the prior year. Personnel expense increase was primarily a result of increases for merit, promotions, taxes and medical benefit expenses. The Company group medical benefits are primarily provided through a self-funded plan which is supplemented by employee premiums. The funding for the self-funded is adjusted each year for

gonzalezs

Typewritten Text

Annual Report

9

anticipated claims. Net employee group insurance expense of $3.1 million for 2016 increased $30,000 or 1.0% compared to $3.0 million for the prior year. As of year-end 2016, the self-funded group medical plan had excess reserves of $501,000 for future medical claims. Legal and professional expense of $4.8 million for 2016 decreased $1.0 million or 16.8% compared to $5.8 million for the prior year. The decrease is primarily due to a decrease in consulting fees incurred to review and enhance compliance with the Bank Secrecy Act.

FDIC insurance expense of $2.0 million for 2016 decreased $832,000 or 29.3% compared to $2.8 million for the prior year. The FDIC Insurance Fund has reached a reserve ratio of 1.15% with a result that future premiums from all banks would be reduced. The net decrease is primarily attributable to the FDIC changing the methodology for the computation of the premium for the insurance.

Advertising expense of $1.7 million for 2016 decreased $171,000 or 9.0%

compared to $1.9 million for the prior year. The net decrease is primarily attributable to television and radio production / broadcast (down $97,000) and sports marketing (down $159,000) with all other categories reflecting a net increase in expense. The marketing focus is to continue to promote the bank in the communities that we serve and to promote product awareness.

The other real estate owned net expense of $198,000 for 2016 decreased $2.2

million or 91.9% compared to $2.4 million for the prior year. This category includes direct expenses for foreclosed real estate including property taxes, maintenance costs, write-downs, less rent income and net gains on the sale of properties. Net gains of $982,000 from the sale of OREO for years 2016 increased $1.6 million or 259.7% when compared to a net loss of $615,000 for the prior year. OREO expenses of $1.2 million for 2016 decreased $642,000 or 35.0% compared to $1.8 million for the prior year. The decline in expenses is also reflective of the decline in OREO holdings for 2016. Management is aggressively working to reduce total OREO holdings to return the investment in said properties to earning assets.

Telephone expense of $1.6 million for 2016 increased $201,000 or 14.2%

compared to $1.4 million for the prior year. The net increase is primarily attributable to data communication expenses (up $339,000), mobile phone / device expenses (down $60,000), and all other expenses (down $78,000). The increase in data communication expenses were a result of restructuring bandwidth and number of data lines to all locations.

Federal and State Income Taxes: Federal and state income taxes of $4.7 million for the year 2016 increased $600,000 compared to $4.1 million for the prior year. The increase in federal and state income taxes is attributable to an increased level of pretax income during 2016. The increased level of pretax income was partially achieved by the increase in noninterest income and the decrease in noninterest expenses.

gonzalezs

Typewritten Text

Annual Report

10

Net Income: Net income for 2016 was $13.8 million or $2.33 per fully diluted share, reflecting an increase of $2.2 million or $0.39 per fully diluted share, compared to the net income of $11.6 million or $1.94 per fully diluted share for the prior year.

gonzalezs

Typewritten Text

Annual Report

Taxable-Equivalent Basis Average Yield/ Average Yield/ Average Yield/(Dollars in Thousands) Balance Interest Rate Balance Interest Rate Balance Interest RateAssetsInterest-Earning Assets Loans Held for Sale* 1,316$ 50$ 3.79% 1,000$ 42$ 4.20% 6,862$ 270$ 3.94% Loans Held for Investment Commercial 164,320 7,767 4.73% 191,383 9,193 4.80% 236,375 11,516 4.87% Real Estate 949,649 50,450 5.31% 967,860 54,001 5.58% 979,037 56,961 5.82% Consumer 28,974 1,337 4.62% 28,519 1,242 4.36% 30,101 1,269 4.21% Total Loans Held for Investment 1,142,943 59,554 5.21% 1,187,762 64,437 5.43% 1,245,512 69,746 5.60% Securities Taxable 565,167 12,950 2.29% 525,059 11,798 2.25% 567,077 12,887 2.27% Tax-Exempt 165,948 5,686 3.43% 125,821 4,433 3.52% 65,434 2,570 3.93% Total Securities 731,114 18,635 2.55% 650,880 16,231 2.49% 632,511 15,457 2.44% Due from Banks-interest bearing 118,848 614 0.52% 164,038 430 0.26% 148,090 372 0.25% Total Interest- Earning Assets 1,994,221 78,853 3.95% 2,003,680 81,139 4.05% 2,032,975 85,845 4.22%Cash and Due from Banks 36,270 34,378 33,212 Premises and Equipment, Net 57,088 58,334 62,212 Other Real Estate Owned 19,766 26,539 37,282 Bank Owned Life Insurance 54,960 48,390 36,450 Other Assets 21,880 20,261 21,782 Allowance for Loan Losses (24,968) (26,957) (29,467) Total Assets 2,159,217$ 2,164,624$ 2,194,446$ LiabilitiesInterest-Bearing Liabilities Saving Accounts & Select CDs 135,533$ 328$ 0.24% 126,029$ 298$ 0.24% 150,037$ 393$ 0.26% NOW & Money Market Checking 588,193 1,772 0.30% 557,764 2,052 0.37% 556,135 2,725 0.49% Time Deposits 606,875 6,012 0.99% 676,547 6,661 0.98% 713,613 7,666 1.07% Total Savings and Time Deposits 1,330,601 8,112 0.61% 1,360,340 9,011 0.66% 1,419,784 10,784 0.76% Federal Funds Purchased and Securities Sold Under Repurchase Agreements 2,643 22 0.84% 2,328 22 0.95% 8,082 58 0.72% FHLB Borrowings 88,333 2,851 3.23% 75,137 2,744 3.65% 85,562 3,190 3.73% Notes Payable- Trust Debentures 21,237 611 2.88% 27,837 755 2.71% 27,837 740 2.66% Total Interest-Bearing Liabilities 1,442,814 11,596 0.80% 1,465,642 12,532 0.86% 1,541,265 14,773 0.96%Demand Deposits 445,930 440,933 411,327 Other Liabilities 11,973 12,815 10,751 Shareholders' Equity 258,500 245,234 231,103 Total Liabilities and Shareholders' Equity 2,159,217$ 2,164,624$ 2,194,446$ Net Interest Income 67,257$ 68,607$ 71,072$ Net Yield on Total Interest- Earning Assets 3.37% 3.42% 3.50%

*Interest on loans held for sale exclude fees in effort to represent more accurate yields. Fees include: origination fees, late charges, processing fees, underwriting fees, document handling fee and lender credit fees.

For analytical purposes, income from tax-exempt assets, primarily securities issued by state and local governments orauthorities, is adjusted by an increment which equates tax-exempt income to interest from taxable assets (assuming a35% effective federal income tax rate for 2016, 2015 and 2014).

2015 20142016

gonzalezs

Typewritten Text

Net Interest Margin

gonzalezs

Typewritten Text

Annual Report

Consolidated Financial Statements

and Independent Auditor’s Report

Years Ended December 31, 2016 and 2015

gonzalezs

Typewritten Text

Annual Report

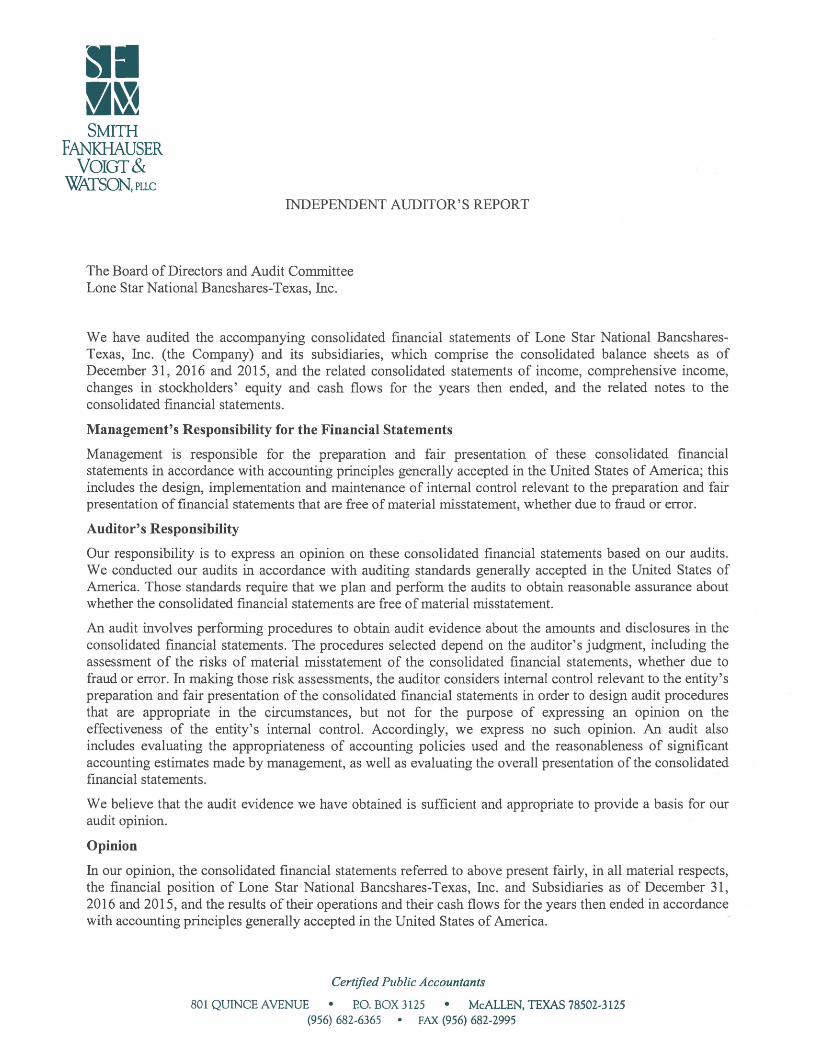

Ill ~~ SMITH

FANKHAUSER VOIGT&

WATSON, PLLC

INDEPENDENT AUDITOR'S REPORT

The Board of Directors and Audit Committee Lone Star National Bancshares-Texas, Inc.

We have audited the accompanying consolidated financial statements of Lone Star National BancsharesTexas, Inc. (the Company) and its subsidiaries, which comprise the consolidated balance sheets as of December 31, 2016 and 2015, and the related consolidated statements of income, comprehensive income, changes in stockholders' equity and cash flows for the years then ended, and the related notes to the consolidated fmancial statements.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free of material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the consolidated fmancial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated fmancial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Lone Star National Bancshares-Texas, Inc. and Subsidiaries as of December 31, 2016 and 2015, and the results of their operations and their cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

Certified Public Accountants

801 QUINCE AVENUE • P.O. BOX 3125 • McALLEN, TEXAS 78502~3125 (956) 682~6365 FAX {956) 682~2995

gonzalezs

Typewritten Text

Annual Report

Report on Other Legal and Regulatory Requirements

We have also examined, in accordance with attestation standards established by the American Institute of Certified Public Accountants, management's assertion that Lone Star National Bancshares-Texas, Inc. maintained effective internal control over financial reporting, including internal control over the preparation of regulatory financial statements, in accordance with the instructions for the Call Report, as of December 31, 2016, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission ("2013 framework") and our report dated March 30, 201 7 expressed an unqualified opinion thereon.

March 30, 2017

gonzalezs

Typewritten Text

Annual Report

2016 2015Assets

Cash and due from banks 38,917$ 30,420$ Due from banks-interest bearing 104,755 205,815

Total cash and cash equivalents 143,672 236,235 Securities available for sale 692,199 691,499 Loans held for sale 2,728 1,174 Loans, less allowance for loan losses

of $23,272 and $25,405, respectively 1,168,010 1,115,860 Properties and equipment, net 55,827 56,351 Net deferred tax asset 13,684 10,454 Overpayment of federal income tax 586 235 Accrued interest receivable 7,940 7,356 Other real estate 21,213 20,727 Bank owned life insurance 62,674 49,112 Other assets 15,883 13,993

Total assets 2,184,416$ 2,202,996$

LiabilitiesDeposits

Demand 482,845$ 490,226$ NOW accounts 558,814 583,462 Savings and money market deposit accounts 176,411 161,205 Time $250 and over 352,202 339,829 Other time 250,868 269,942

Total deposits 1,821,140 1,844,664 Accrued interest payable 920 952 Allowance for off-balance-sheet losses 685 885 Other liabilities 5,649 5,113 Federal funds purchased and securities sold

under repurchase agreements 3,750 1,250 Guaranteed preferred beneficial interest in Company's

subordinated debentures 10,310 27,837 Other borrowed money 90,000 75,000

Total liabilities 1,932,454 1,955,701

Stockholders' equityCommon stock, par value $5; authorized 50,000,000

shares; 5,863,634 and 6,107,833 shares issued and 5,863,634 and 5,941,654 shares outstanding 29,318 30,539

Paid-in capital 54,976 57,221 Retained earnings 166,900 159,947 Accumulated other comprehensive income 768 6,668 Treasury Stock 0 and 166,179 shares - (7,080)

Total stockholders' equity 251,962 247,295 Total liabilities and stockholders' equity 2,184,416$ 2,202,996$

LONE STAR NATIONAL BANCSHARES-TEXAS, INC. AND SUBSIDIARIESConsolidated Balance Sheets

(Dollars in Thousands, Except Share Data)

December 31,

The accompanying notes are an integral part of the consolidated financial statements.- 3 -

gonzalezs

Typewritten Text

Annual Report

2016 2015Interest income

Loans, including fees 59,696$ 64,605$ Securities available for sale 16,743 14,748 Due from banks and other earning assets 800 583

77,239 79,936 Interest expense

Deposits 8,112 9,011 Federal funds purchased and repurchase agreements 22 21 Subordinated debentures 611 755 Other borrowed money 2,851 2,745

11,596 12,532 Net interest income 65,643 67,404

Provision for loan losses - - Net interest income after provision for loan losses 65,643 67,404

Noninterest incomeService charges on deposit accounts 6,634 7,146 Other service charge and fee income 8,248 7,737 Gain on securities 1,849 1,798 Bank owned life insurance 1,562 1,362 Other noninterest income 6,914 5,352

25,207 23,395 Noninterest expense

Employee compensation 34,973 33,526 Employee benefits 6,856 6,788

41,829 40,314 Net occupancy and equipment expense 9,073 9,213 Data processing expense 5,580 5,610 Legal and professional 4,796 5,763 FDIC insurance 2,009 2,841 Advertising expense 1,733 1,904 Telephone expense 1,617 1,416 Supplies 517 533 Business development 410 353 Other real estate, net 198 2,431 Other noninterest expense 4,551 4,657

72,313 75,035 Income before income tax expense 18,537 15,764 Income tax expense 4,723 4,138 Net income 13,814$ 11,626$

LONE STAR NATIONAL BANCSHARES-TEXAS, INC. AND SUBSIDIARIESConsolidated Statements of Income

(Dollars in Thousands)

Year Ended December 31,

The accompanying notes are an integral part of the consolidated financial statements.- 4 -

gonzalezs

Typewritten Text

Annual Report

2016 2015

Net income 13,814$ 11,626$

Other comprehensive income, before federal income tax

Securities available for sale

Unrealized holding losses arising during year (6,580) (1,724)

Reclassification adjustment for gains included in net income (1,849) (1,798)

(8,429) (3,522)

Federal income tax benefit related to other comprehensive income 2,529 1,709

Other comprehensive loss, net of federal income tax (5,900) (1,813)

Comprehensive income 7,914$ 9,813$

Year Ended December 31,

LONE STAR NATIONAL BANCSHARES-TEXAS, INC. AND SUBSIDIARIESConsolidated Statements of Comprehensive Income

(Dollars in Thousands)

The accompanying notes are an integral part of the consolidated financial statements.- 5 -

gonzalezs

Typewritten Text

Annual Report

Common Paid-in Retainedstock capital earnings

Balance at December 31, 2014 31,828$ 59,579$ 154,668$

Comprehensive incomeNet income - - 11,626 Other comprehensive loss, net of tax - - -

Purchase of treasury stock, 113,561 shares - - - Sale of treasury stock, 44,802 shares - - (20) Retirement of treasury stock, 257,685 shares (1,289) (2,412) (6,299) Share-based compensation - 45 - Tax benefit from stock options exercised - 9 (28)

Balance at December 31, 2015 30,539 57,221 159,947

Comprehensive incomeNet income - - 13,814 Other comprehensive loss, net of tax - - -

Purchase of treasury stock, 125,880 shares - - - Sale of treasury stock, 47,860 shares - - (87) Retirement of treasury stock, 244,199 shares (1,221) (2,448) (6,774) Share-based compensation - 170 - Tax benefit from stock options exercised - 33 -

Balance at December 31, 2016 29,318$ 54,976$ 166,900$

LONE STAR NATIONAL BANCSHARES-TEXAS, INC. AND SUBSIDIARIESConsolidated Statements of Changes in Stockholders' Equity

(Dollars in Thousands)

The accompanying notes are an integral part of the consolidated financial statements.- 6 -

gonzalezs

Typewritten Text

Annual Report

Accumulatedother Total

comprehensive Treasury stockholders'income (loss) stock equity

8,481$ (14,213)$ 240,343$

- - 11,626 (1,813) - (1,813)

- (4,797) (4,797) - 1,930 1,910 - 10,000 - - - 45 - - (19)

6,668 (7,080) 247,295

- - 13,814 (5,900) - (5,900)

- (5,406) (5,406) - 2,043 1,956 - 10,443 - - - 170 - - 33

768$ -$ 251,962$

- 7 -

gonzalezs

Typewritten Text

Annual Report

2016 2015Operating activities

Net income 13,814$ 11,626$ Adjustments to reconcile net income to net

cash provided by operating activitiesDepreciation and amortization 3,717 4,141 Amortization/accretion of investment

security premiums and discounts, net 5,040 4,516 Share-based compensation 1,066 26 Loss (gain) on sale of other real estate 318 (970) Gain on sale of investment securities (1,847) (1,798) Gain on foreclosure of real estate (1,758) (244) Loss on retired property and equipment 20 18 Donation of real estate 80 - Dividend from Federal Reserve Bank (49) - Income from bank owned life insurance (1,562) (1,363) Addition to other real estate owned valuation reserve 226 78 Writedown of other real estate owned 320 1,641 Provision for off-balance-sheet losses (200) (81) (Increase) decrease in overpayment of federal income tax (351) 143 Increase in deferred income tax benefit (700) (2,484) Increase in accrued interest receivable (584) (154) Increase in loans held for sale (1,554) (103) Decrease (increase) in other assets 282 (80) Decrease in accrued interest payable (32) (81) Decrease in other liabilities (327) (2,587)

Net cash provided by operating activities 15,919 12,244

Year Ended December 31,

LONE STAR NATIONAL BANCSHARES-TEXAS, INC. AND SUBSIDIARIESConsolidated Statements of Cash Flows

(Dollars in Thousands)

The accompanying notes are an integral part of the consolidated financial statements.- 8 -

gonzalezs

Typewritten Text

Annual Report

2016 2015

Investing activitiesSecurities available for sale

Purchases (431,570) (750,305) Maturities, calls and principal repayments 51,568 565,237 Proceeds from sale 367,679 110,027

Proceeds from sale of properties and equipment 25 5 Purchase of bank owned life insurance (12,000) - Purchase of FHLB stock (2,300) (15) Purchase of FRB stock (1) - Purchase of properties and equipment (3,060) (835) Net (increase) decrease in loans (58,366) 78,723 Net proceeds from sale of other real estate 6,544 12,060

Net cash (used) provided by investing activities (81,481) 14,897

Financing activitiesNet (decrease) increase in demand deposits,

NOW accounts, savings and money market accounts (16,823) 112,313 Proceeds from sale of treasury stock 1,956 1,910 Proceeds of other borrowed money 110,000 - Repayment of other borrowed money (95,000) - Repayment of guaranteed preferred beneficial interest

in Company's subordinate debentures (17,527) - Net increase (decrease) in federal funds purchased and

securities sold under repurchase agreements 2,500 (6,400) Net decrease in time deposits (6,701) (78,381) Purchase of treasury stock (5,406) (4,797)

Net cash (used) provided by financing activities (27,001) 24,645

(Decrease) increase in cash and cash equivalents (92,563) 51,786 Cash and cash equivalents at beginning of year 236,235 184,449 Cash and cash equivalents at end of year 143,672$ 236,235$

LONE STAR NATIONAL BANCSHARES-TEXAS, INC. AND SUBSIDIARIESConsolidated Statements of Cash Flows (Continued)

(Dollars in Thousands)

Year Ended December 31,

The accompanying notes are an integral part of the consolidated financial statements.- 9 -

gonzalezs

Typewritten Text

Annual Report

LONE STAR NATIONAL BANCSHARES-TEXAS, INC. AND SUBSIDIARIES Notes to Consolidated Financial Statements

December 31, 2016 and 2015

- 10 -

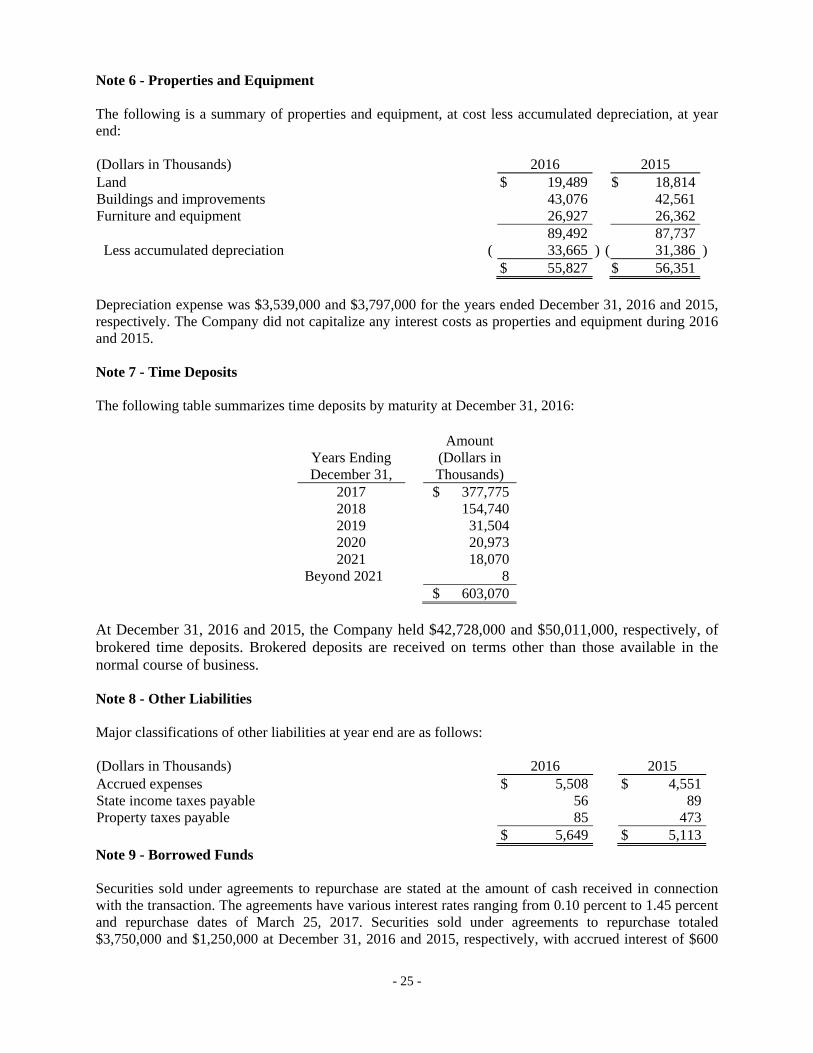

Note 1 - Summary of Significant Accounting Policies Lone Star National Bancshares-Texas, Inc. (the “Parent” or “Company”), its primary subsidiary, Lone Star National Bank (the “Bank”) and its other subsidiaries (collectively the “Company”) are headquartered in McAllen, Texas. The Company provides a broad array of customary banking services and operates 32 regulatory banking locations throughout the Rio Grande Valley of Texas and San Antonio, Texas. The accounting principles and reporting policies conform to accounting principles generally accepted in the United States of America and to general practices within the banking industry. A summary of the more significant accounting policies follows:

Basis of Presentation. The consolidated financial statements include the accounts of Lone Star National Bancshares-Texas, Inc. and its wholly-owned subsidiaries. The Company eliminates all significant intercompany transactions and balances in consolidation. The accounting and financial reporting policies the Company follows conform, in all material respects, to accounting principles generally accepted in the United States of America. The Company determines whether it has a controlling financial interest in an entity by first evaluating whether the entity is a voting interest entity or a variable interest entity under accounting principles generally accepted in the United States of America. Voting interest entities are entities in which the total equity investment at risk is sufficient to enable the entity to finance itself independently and provides the equity holders with the obligation to absorb losses, the right to receive residual returns and the right to make decisions about the entity’s activities. The Company consolidates voting interest entities in which it has all, or at least a majority of, the voting interest. As defined in applicable accounting standards, variable interest entities (“VIE”) are entities that lack one or more of the characteristics of a voting interest entity. A controlling financial interest in an entity is present when an enterprise has a variable interest, or a combination of variable interests, that will absorb a majority of the entity’s expected losses, receive a majority of the entity’s expected residual returns, or both. The enterprise with a controlling financial interest, known as the primary beneficiary, consolidates the VIE. The Company’s wholly-owned subsidiary, Star National Capital Trust IV is a VIE for which the Company is not the primary beneficiary. Accordingly, the accounts of this entity are not included in the Company’s consolidated financial statements.

Use of Estimates. The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from these estimates. The allowance for possible loan losses, the fair value of financial instruments and the status of contingencies are particularly subject to change.

Cash and Cash Equivalents. For the purpose of reporting cash flows, the Company considers cash on hand, amounts due from banks, deposits with other financial institutions that have an initial maturity less than 90 days when acquired by the Company and federal funds sold to be cash and cash equivalents. Generally, federal funds sold are purchased and sold for one-day periods. The Company has maintained balances in various operating and money market accounts in excess of federally insured limits.

Repurchase/Resell Agreements. The Company purchases certain securities under agreements to resell.

The amounts advanced under these agreements represent short-term loans and are reflected as assets in the accompanying consolidated balance sheets. The securities underlying these agreements are book entry securities. The Company also sells certain securities under agreements to repurchase. The agreements are

gonzalezs

Typewritten Text

Annual Report

- 11 -

treated as collateralized financing transactions and the obligations to repurchase securities sold are reflected as a liability in the accompanying consolidated balance sheets. The dollar amount of the securities underlying the agreements remain in the asset accounts.

Investments in Securities. Securities that management has both the positive intent and ability to hold to

maturity are classified as securities held to maturity and are carried at cost, adjusted for amortization of premium or accretion of discount, using the level-yield method. Amortization and accretion on mortgage-backed securities are adjusted for prepayments. Securities that may be sold prior to maturity for asset/liability management purposes, or that may be sold in response to changes in interest rates, to changes in prepayment risk, to increase regulatory capital or other similar factors, are classified as securities available for sale and carried at fair value with any adjustments to fair value reported in stockholders’ equity as a component of accumulated other comprehensive income (loss), net of tax. Declines in the fair value of individual held to maturity and available for sale securities below their cost that are other than temporary result in write-downs of the individual securities to their fair value. The related write-downs are included in net income as realized losses. Securities purchased for trading purposes are held in the trading portfolio at fair value, with changes in fair value included in noninterest income. Interest and dividends on securities, including the amortization of premiums and the accretion of discounts, are reported in interest income on securities using the level-yield method. Gains and losses on the sale of securities are recorded on the settlement date and are calculated using the specific identification method.

Loans. Loans that management has the intent and ability to hold for the foreseeable future or until maturity or pay-off generally are reported at their outstanding unpaid principal balances adjusted for charge-offs, the allowance for loan losses, any deferred fees or costs on originated loans and unamortized premiums or discounts on purchased loans. Interest accruals are generally discontinued when management has determined that the borrower may be unable to meet contractual obligations and/or when loans are 90 days or more in arrears, unless management believes that collateral held by the Company is clearly sufficient and full satisfaction of both principal and interest is highly probable, or the loan is accounted for as a purchased credit-impaired loan. When a loan is placed on nonaccrual, all interest previously accrued but not collected is reversed against current period income and amortization of deferred loan fees is discontinued. Interest received on nonaccrual loans is either applied against principal or reported as income according to management’s judgment as to the collectability of principal. Nonaccrual loans may be returned to an accrual status when principal and interest payments are no longer delinquent, and the risk characteristics of the loan have improved to the extent that there no longer exists a concern as to the collectability of principal. Loans are considered past due based upon their contractual terms. Loans are considered impaired when, based on current information and events, it is probable the Company will be unable to collect all amounts due in accordance with the original contractual terms of the loan agreement, including scheduled principal and interest payments. Impairment is evaluated on an individual loan basis. If a loan is impaired, a specific valuation allowance is allocated, if necessary, so that the loan is reported net, at the present value of estimated future cash flows using the loan's existing rate or at the fair value of collateral if repayment is expected solely from the collateral. Interest payments on impaired loans are typically applied to principal unless collectability of the principal amount is reasonably assured, in which case interest is recognized on a cash basis. Impaired loans, or portions thereof, are charged off when deemed uncollectible.

Allowance for Possible Loan Losses. The allowance for possible loan losses is a reserve established

through a provision for possible loan losses charged to expense, which represents management’s best estimate of probable losses that have been incurred within the existing portfolio of loans. The allowance,

gonzalezs

Typewritten Text

Annual Report

- 12 -

in the judgment of management, is necessary to reserve for estimated loan losses inherent in the loan portfolio. The allowance for possible loan losses includes allowance allocations calculated in accordance with Accounting Standards Codification (“ASC”) Topic 310, Receivables and allowance allocations calculated in accordance with ASC Topic 450, Contingencies.

Loans Held for Sale. The Company originates mortgage loans primarily for sale in the secondary

market. These loans are generally sold on a non-recourse basis and are carried at the lower of cost or market on an aggregate basis.

Properties and Equipment. Land is carried at cost. Other premises and equipment are carried at cost, net of accumulated depreciation. Depreciation is computed using the straight-line method over the estimated useful lives of the assets. Depreciation for tax purposes is computed by using the Accelerated Cost Recovery System and the Modified Accelerated Cost Recovery System required by the Internal Revenue Code.

Impairment of Long-Lived Assets. Long-lived assets and certain identifiable intangibles are reviewed by the Company for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable.

Foreclosed Assets. Assets acquired through or instead of loan foreclosure are held for sale and are

initially recorded at fair value less estimated selling costs when acquired, establishing a new cost basis. Costs after acquisition are generally expensed. If the fair value of the asset declines, a write-down is recorded through expense. The valuation of foreclosed assets is subjective in nature and may be adjusted in the future because of changes in economic conditions. Foreclosed assets are included in the accompanying consolidated balance sheets as other real estate and include foreclosed residential real estate properties where physical possession has been obtained totaling $4,336,000 and $4,432,000 at December 31, 2016 and 2015, respectively. The recorded investment in consumer mortgage loans secured by residential real estate properties where formal procedures are in process total $369,000 and $332,000 at December 31, 2016 and 2015, respectively.

Earnings per Share of Common Stock. Basic earnings per share are computed by dividing earnings

available to common stockholders by the weighted average number of common shares outstanding during the period. Diluted earnings per share reflect per share amounts that would have resulted if dilutive potential common stock had been converted to common stock.

Loan Origination Fees and Costs. Loan origination fees and costs are deferred and recognized over

the life of the loan as an adjustment of yield using the interest method.

Interest Income on Loans. Interest income on loans is accrued and credited to income based on the principal amount outstanding. The accrual of interest on loans is discontinued when, in the opinion of management, there is an indication that the borrower may be unable to meet payments as they become due. Upon such discontinuance, all unpaid accrued interest is reversed. Subsequent interest payments received on loans in which accrual of interest has been discontinued are either applied against principal or reported as income, depending upon management’s assessment of the ultimate collectability of principal.

Advertising. Advertising costs are expensed as they are incurred.

Income Tax Expense. Income tax expense is the total of the current year income tax due or refundable and the change in deferred tax assets and liabilities (excluding deferred tax assets and liabilities related to components of other comprehensive income). Deferred tax assets and liabilities are the expected future tax amounts for the temporary differences between carrying amounts and tax bases of assets and liabilities, computed using enacted tax rates. A valuation allowance, if needed, reduces deferred tax assets to the expected amount most likely to be realized. Realization of deferred tax assets is dependent upon the

gonzalezs

Typewritten Text

Annual Report

- 13 -

generation of a sufficient level of future taxable income and recoverable taxes paid in prior years. Although realization is not assured, management believes it is more likely than not that all of the deferred tax assets will be realized.

Off-Balance-Sheet Instruments. In the ordinary course of business, the Company has entered into off-balance-sheet financial instruments consisting of commitments to extend credit, commitments under credit card arrangements, commercial letters of credit and standby letters of credit. Such financial instruments are recorded in the financial statements when they are funded or related fees are incurred or received.

Derivative Financial Instruments. FASB ASC Topic 815 Derivatives and Hedging requires companies

to recognize all derivatives as either assets or liabilities in the statement of financial position and measure those instruments at fair value. Changes in fair value of a derivative must be recognized currently in earnings unless specific hedge accounting criteria are met. The Company’s risk management activities do not presently include entering into derivative contracts to manage interest rate risk.

Share-Based Payments. The Company accounts for all stock-based compensation transactions in accordance with ASC Topic 718, Compensation — Stock Compensation, which requires that stock compensation transactions be recognized as compensation expense in the statement of operations based on their fair values on the measurement date, which is the date of the grant. Cost of the unvested portion of options issued is recognized using the Black-Scholes-Merton option pricing model.

Subsequent Events. The Company has evaluated subsequent events for potential recognition and/or

disclosure through March 30, 2017, the date which these consolidated financial statements were available to be issued.

Reclassifications. Certain amounts in the prior year’s presentation have been reclassified to conform

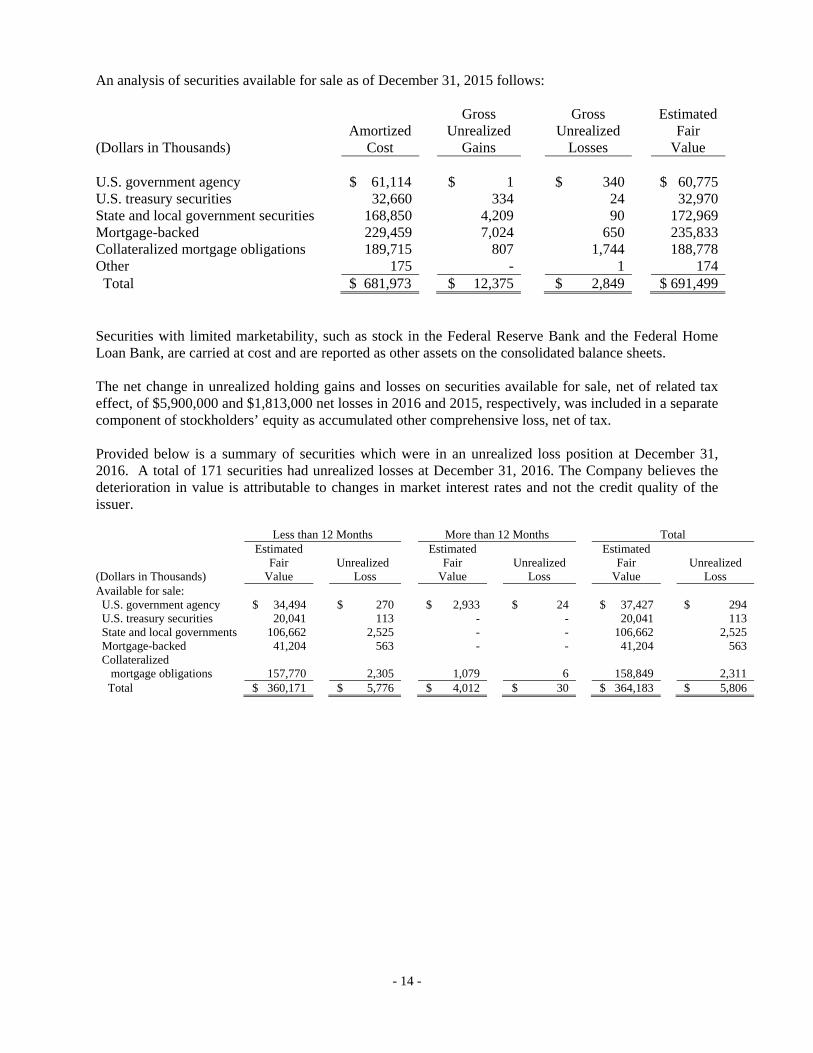

to the current year’s presentation. These reclassifications have no effect on previously reported net income. Note 2 - Restriction on Cash and Due From Banks The Company is required to maintain reserve funds in cash or on deposit with the Federal Reserve Bank. The required reserve balance at December 31, 2016 and 2015 was $16,637,000 and $16,345,000, respectively. Note 3 - Investment Securities An analysis of securities available for sale as of December 31, 2016 follows: Gross Gross Estimated Amortized Unrealized Unrealized Fair (Dollars in Thousands) Cost Gains Losses Value U.S. government agency $ 45,740 $ 21 $ 294 $ 45,467U.S. treasury 47,702 314 113 47,903State and local government securities 189,891 1,166 2,525 188,532Mortgage-backed 143,725 4,223 563 147,385 Collateralized mortgage obligations 263,869 1,179 2,311 262,737Other 175 - - 175 Total $ 691,102 $ 6,903 $ 5,806 $ 692,199

gonzalezs

Typewritten Text

Annual Report

- 14 -

An analysis of securities available for sale as of December 31, 2015 follows: Gross Gross Estimated Amortized Unrealized Unrealized Fair (Dollars in Thousands) Cost Gains Losses Value U.S. government agency $ 61,114 $ 1 $ 340 $ 60,775U.S. treasury securities 32,660 334 24 32,970State and local government securities 168,850 4,209 90 172,969Mortgage-backed 229,459 7,024 650 235,833Collateralized mortgage obligations 189,715 807 1,744 188,778Other 175 - 1 174 Total $ 681,973 $ 12,375 $ 2,849 $ 691,499 Securities with limited marketability, such as stock in the Federal Reserve Bank and the Federal Home Loan Bank, are carried at cost and are reported as other assets on the consolidated balance sheets. The net change in unrealized holding gains and losses on securities available for sale, net of related tax effect, of $5,900,000 and $1,813,000 net losses in 2016 and 2015, respectively, was included in a separate component of stockholders’ equity as accumulated other comprehensive loss, net of tax. Provided below is a summary of securities which were in an unrealized loss position at December 31, 2016. A total of 171 securities had unrealized losses at December 31, 2016. The Company believes the deterioration in value is attributable to changes in market interest rates and not the credit quality of the issuer. Less than 12 Months More than 12 Months Total Estimated Estimated Estimated Fair Unrealized Fair Unrealized Fair Unrealized (Dollars in Thousands) Value Loss Value Loss Value Loss Available for sale: U.S. government agency $ 34,494 $ 270 $ 2,933 $ 24 $ 37,427 $ 294 U.S. treasury securities 20,041 113 - - 20,041 113 State and local governments 106,662 2,525 - - 106,662 2,525 Mortgage-backed 41,204 563 - - 41,204 563 Collateralized mortgage obligations 157,770 2,305 1,079 6 158,849 2,311 Total $ 360,171 $ 5,776 $ 4,012 $ 30 $ 364,183 $ 5,806

gonzalezs

Typewritten Text

Annual Report

- 15 -

The amortized cost and estimated market value of securities available for sale at December 31, 2016, by contractual maturity, is shown below. Expected maturities will differ from contractual maturities because borrowers may have the right to call or prepay obligations with or without call or prepayment penalties.

Securities Available for Sale Estimated Amortized Fair