Hebrew Translations of Lithuanian Literature in Interwar Lithuania

Upload

khangminh22Category

view

0download

0

1 ICT export strategy development for Lithuania – External analysis

Lithuanian ICT export strategy development

Germany, UK and the Netherlands

Authors:

Petri O. Roine

Frederik Willmes

Joel Thompson

Adomas Svirskas

Algimantas Nedzveckas

2 ICT export strategy development for Lithuania – External analysis

Table of contents

1. Management Summary ..................................................................................................................... 5

2. Introduction and Methodology ......................................................................................................... 8

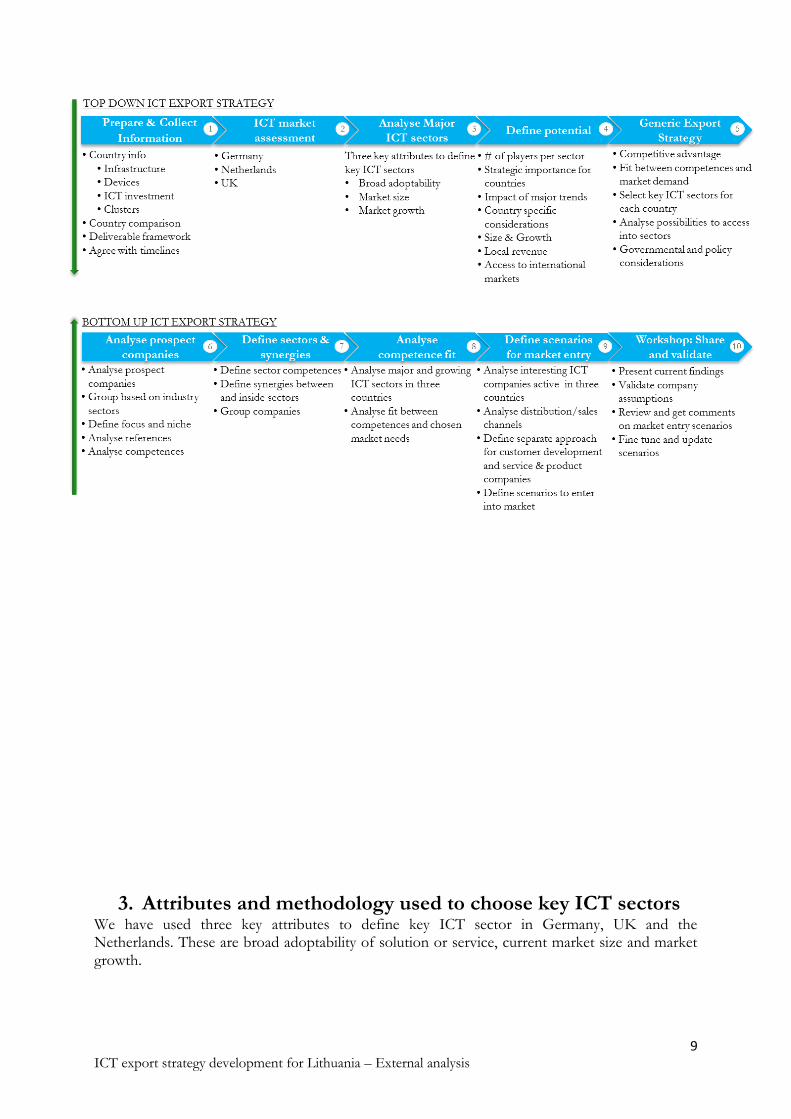

3. Attributes and methodology used to choose key ICT sectors ............................................................ 9

4. External analysis ............................................................................................................................. 11

A. Germany –country summary .......................................................................................................... 11

i. End consumer’s interest ................................................................................................................. 12

1. Market opportunity ..................................................................................................................... 12

2. Trends ........................................................................................................................................ 12

ii. Infrastructural landscape and trends ............................................................................................... 13

1. Infrastructure .............................................................................................................................. 13

2. Devices ....................................................................................................................................... 13

3. Bandwidth and Services .............................................................................................................. 14

iii. ICT employment and available workforce ....................................................................................... 16

1. Employment and education level ................................................................................................ 16

2. Available workforce and trend .................................................................................................... 17

iv. ICT investment............................................................................................................................... 18

v. Major clusters ................................................................................................................................. 18

vi. Governmental Policy and Regulations ............................................................................................ 18

i. Major ICT sectors ........................................................................................................................... 20

vii. Key ICT sector analysis .............................................................................................................. 23

1. The Telecom Sector .................................................................................................................... 23

2. Payment Services ........................................................................................................................ 26

3. E-Commerce .............................................................................................................................. 27

4. Cloud Computing ....................................................................................................................... 28

viii. Commonly used outsourcing destinations and practices .............................................................. 28

ix. Home market and ICT exports ....................................................................................................... 30

x. Commonly used partnership practices ............................................................................................ 30

1. Business culture and languages requirements .............................................................................. 30

2. Procurement practices and regulations ........................................................................................ 30

3 ICT export strategy development for Lithuania – External analysis

xi. IT associations, and other organization bodies ................................................................................ 30

B. UK – Country summary ................................................................................................................. 32

ii. End consumer’s interest ................................................................................................................. 32

1. Market opportunity ..................................................................................................................... 32

2. Trends ........................................................................................................................................ 33

iii. Infrastructural landscape and trends ............................................................................................... 34

1. Infrastructure .............................................................................................................................. 34

2. Devices ....................................................................................................................................... 35

3. Bandwidth and Services .............................................................................................................. 36

iv. ICT employment and available workforce ....................................................................................... 36

1. Employment and education level ................................................................................................ 36

2. Available workforce and trend .................................................................................................... 37

v. ICT investment............................................................................................................................... 37

vi. Major clusters ................................................................................................................................. 38

vii. Governmental Policy and regulations.......................................................................................... 40

i. Major ICT sectors ........................................................................................................................... 42

ii. Key ICT sector analysis .................................................................................................................. 45

1. Cloud computing ........................................................................................................................ 45

2. Business Solutions ...................................................................................................................... 46

3. E-Commerce .............................................................................................................................. 47

4. E-Health ..................................................................................................................................... 49

iii. Commonly used outsourcing destinations and practises .................................................................. 50

1. Local, near-shore, off-shore ............................................................................................................ 50

2. IT Personnel Costs....................................................................................................................... 52

iv. Home market and ICT exports ....................................................................................................... 54

v. Commonly used partnership practices ............................................................................................ 55

1. Business culture and languages requirements .............................................................................. 55

2. Practices and partnership schemes .............................................................................................. 56

3. Procurement practices and regulations ........................................................................................ 56

vi. IT associations, and other organization bodies ................................................................................ 56

vii. Specific industry related IT regulations and regulating institutions .............................................. 57

C. The Netherlands –country summary ............................................................................................... 58

i. End consumer’s interest ................................................................................................................. 58

1. Market opportunity ..................................................................................................................... 58

4 ICT export strategy development for Lithuania – External analysis

2. Trends ........................................................................................................................................ 58

ii. Infrastructural landscape and trends ............................................................................................... 59

1. Infrastructure .............................................................................................................................. 59

2. Devices ....................................................................................................................................... 59

3. Bandwidth and Services .............................................................................................................. 59

iii. ICT employment and available workforce ....................................................................................... 60

iv. ICT investment............................................................................................................................... 61

v. Major clusters ................................................................................................................................. 62

vi. Governmental Policy and Regulation .............................................................................................. 62

i. Major ICT sector analysis ............................................................................................................... 63

ii. Key ICT sector analysis .................................................................................................................. 67

1. Telecom ..................................................................................................................................... 67

2. Financial and payment services ................................................................................................... 72

3. Media and Entertainment ........................................................................................................... 74

4. E-Commerce .............................................................................................................................. 77

iii. Commonly used outsourcing destinations and practices .................................................................. 81

iv. Home market and ICT exports ....................................................................................................... 82

v. Commonly used partnership practices ............................................................................................ 82

vi. IT associations, and other organization bodies ................................................................................ 83

5. Internal analysis ................................................................................................................. 85

6. Conclusions ...................................................................................................................... 113

a. Business solution sector ................................................................................................................ 114

b. eHealth ......................................................................................................................................... 115

c. Finance and Payment services ....................................................................................................... 115

d. eCommerce&eSignature ............................................................................................................... 116

e. Custom ERP solutions ................................................................................................................. 117

f. Telecom, Finance & Payments ...................................................................................................... 118

5 ICT export strategy development for Lithuania – External analysis

1. Management Summary Germany

Cloud computing is considered the top trend by IT decision makers (66% of respondents), followed by mobile applications (53% of respondents), IT security (48% of respondents) and social media (35% of respondents).

Germany has the highest number of mobile phones in the European Union and the second highest mobile penetration rate (130%) in Western Europe after Italy (147%). 94% of the overall population have at least one mobile phone. Smartphone penetration has also risen from 54% in 2012 to 61% in 2013.

ICT is the fastest growing sector: There are almost 1.4 million ICT professionals, which only represents 1.7% of the entire workforce. Rhine-Main-Neckar ICT cluster is currently one the world’s largest IT and high-tech clusters.

Interesting ICT sectors: Telecom, Finance and Payments, e-Commerce and Cloud computing

UK

The UK is Europe’s largest ICT market by revenue.

UK has fibre optic available in 50% of households and 74% of households already have a broadband connection. Mobile device penetration is 124% for all handsets and 51% for smart phones. UK is Europe’s leading couponing market, which is now transitioning to e- and m-commerce.

There is high demand for skilled IT professionals, due to a lack of higher education enrolment in computer science. The country’s major ICT cluster is located in London and is called Tech City - it is one of the fastest growing ICT developer hubs in Europe.

Interesting ICT sectors: Cloud computing, Business Solutions, e-Commerce and e-Health

The Netherlands

ICT is considered a focal point of innovation. It plays a critical role in 80% of large production innovations and 92% of process innovations. Strong, local online payment provider iDEAL has boosted online payments adoption and, as a result, consumers have gained trust in the technology. This has helped The Netherlands to achieve one of the highest numbers of e-shoppers in relative terms (9.8 million).

Dutch mobile penetration is 121% for all handsets and 60% for smart phones. In 2011, 83% of households had a broadband internet connection, while 94% had access to internet in 2012.

6 ICT export strategy development for Lithuania – External analysis

Dutch companies were also the original founders of the internet. 19% of all companies are selling goods and services via the web and 7% via EDI.

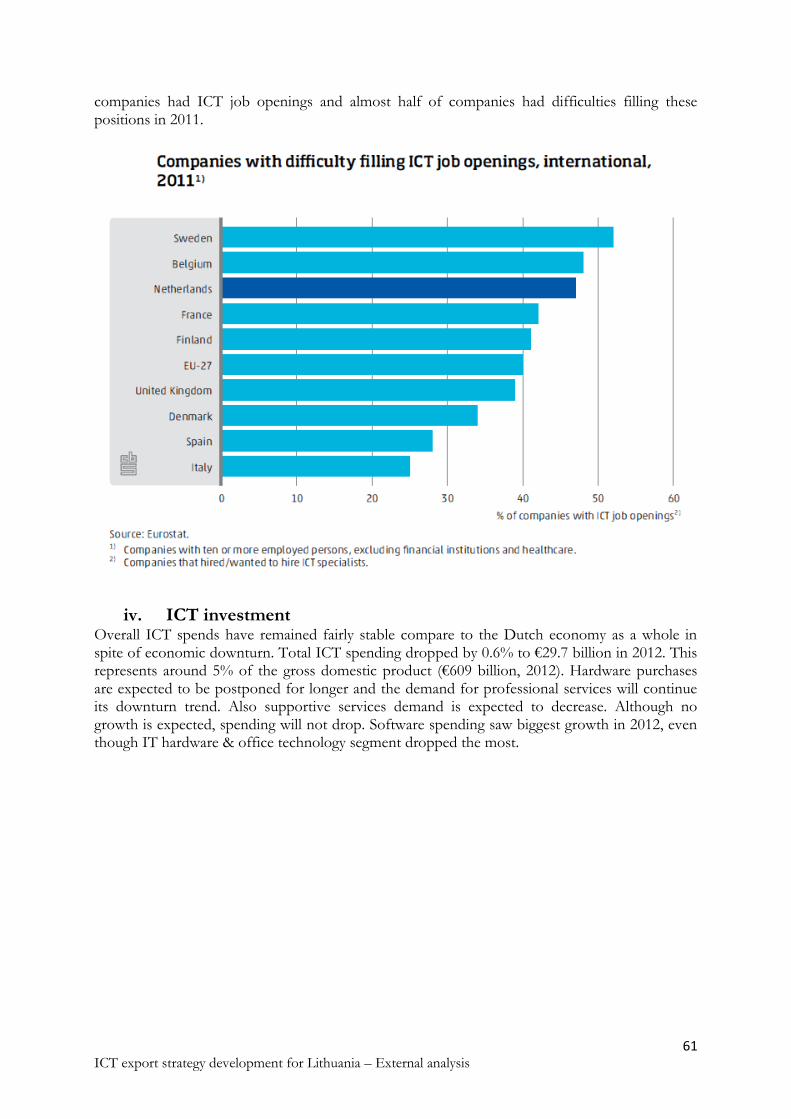

A recent study conducted by CBS (Dutch statistics office) discovered that almost half of companies in the ICT sector had job openings and more than half find it difficult to fulfil positions.

Interesting ICT sector: Telecom, Finance & payments, Media &Entertainment and e-Commerce

Country comparison

Key metrics of focus market countries Germany, UK and the Netherlands are compared below, providing a high level view of our external analysis findings.

There are two common ways to identify market attractiveness: size of addressable market and scalability. Online payments area good benchmark because they provide,first,insights about customers’ access to internet (addressable market) and, second, (influencing scalability)theoption to pay online. UK is the leader in Europe in terms of online purchases, whileboth Germany and Netherlands are in top 10. Nearly 60% of all EU internet users shop online.

Online Purchases by internet users in previous 12 months (2012)

1. UK 82% 9. Netherlands 69% 17. Poland 47%

2. Norway 80% 10. Malta 63% 18. Czech Rep. 43%

7 ICT export strategy development for Lithuania – External analysis

3. Denmark 79% 11. Austria 60% 19. Spain 43%

4. Sweden 79% 12. Ireland 57% 20. Latvia 37%

5. Germany 77% 13.Slovakia 56% 21. Greece 36%

6. Luxemburg 73% 14. Island 56% 22. Cyprus 35%

7. Finland 72% 15. Belgium 55% 23. Portugal 35%

8. France 69% 16 Slovenia 49% 24. Hungary 35%

Source: Eurostat 2013

Another benchmark providing insight on market size isthe percentage of value added to the country’s business sector by the ICT sector.

The ICT sector represent more than 9% of value added in UK, 9% in The Netherlands and 7% in Germany. All countries are part of the top 15 countries in OECD ranking (2009). UK is ranked number 6, just after other European countries Ireland, Finland, Sweden and Hungary. The Netherlands shares10th place with Japan. Due to the strong manufacturing percentage of value added, Germany is positioned in14th place in the OECD ranking (2009)

ICT usage in households

8 ICT export strategy development for Lithuania – External analysis

2. Introduction and Methodology Mobinance was requested to support development of ICT export strategic services for Lithuania. The objective of this research is to identify the fit between interesting and emerging ICT sectors in UK, Germany and the Netherlands (the “topdown approach”) and at a later phase evaluate thecompetence fit of 14 participating companies with emerging and interesting ICT sectors of the chosen countries (the “bottom-up approach”). These 15 participants will be used as a representative sample of Lithuanian ICT sector competencies in our study.

9 ICT export strategy development for Lithuania – External analysis

3. Attributes and methodology used to choose key ICT sectors We have used three key attributes to define key ICT sector in Germany, UK and the Netherlands. These are broad adoptability of solution or service, current market size and market growth.

10 ICT export strategy development for Lithuania – External analysis

Broad adoptability

Solution or service has broad audience o Addressable market is wide enough

Distribution channels are accessible

Technical solution available o Allows access to broad audience (addressable market) o Allows required independence from 3rd parties (Over-the-top possibility) o Tested, scalable and widely accepted

Infrastructure present

Access to suitable devices: Smartphones, Tablets and other devices o HTML5, Application o NFC &QR codes o SMS & USSD o Sonar and others

Current market size

Market already present

Market maturity level o Too early stage => Requires high investment and marketing o Early growth => Attractive stage, since market already present o Mature stage => Attractive for process and operational innovations

Total Revenue by sector o Current revenue o Ability leverage solution or service to other sectors or fields

Investments and R&D expenditures

Market growth

ICT sector is showing high growth potential

Ability to leverage horizontally and/or vertically between industries

Ability to serve new segments (e.g. Cloud computing – SME business solutions)

11 ICT export strategy development for Lithuania – External analysis

13 ICT sectors are evaluated in three countries and key sectors selected based on previously mentioned attributes Broad adoptability, Current market size and growth.

4. External analysis

A. Germany –country summary

12 ICT export strategy development for Lithuania – External analysis

i. End consumer’s interest

1. Market opportunity Germany is not an ICT leader in terms of value added in business sector in comparison to other EU countries but the country has been catching up from its laggard position since 2008 and has the strong ambition to further strengthen its ICT sectors in the future. This ambition is formulated at the federal government’s level with the Ministry of Transport and Digital Infrastructure’s ICT Strategy Digital Germany 2015. ICT growth in terms of products and services is therefore stimulated while the good ICT resources from helpdesk operators to programmers are scarce (www.make-it-in-germany.com). This shortage of resources leads to the conclusion that the planned growth will need to be facilitated through non-German labour sources.

Opportunities in terms of defined projects, support contracts, business process outsourcing and co-venturing can arise to companies that can export these to Germany or fulfil their services there. Some of the larger ICT driven companies have large operations in Germany such as SAP, Oracle and Microsoft. The shortage of qualified ICT professionals also applies to their operations and they have to increasingly rely on third party resources in the form of project based and general temporary labour.

Connecting the described labour shortage and growth in ICT driven industries to the business cultural demands of German companies, the market opportunities, for companies that want to export ICT skills to Germany, arise as a combination of:

offering mainly technologically grounded skills such as programming on an associate level, the manager level is well represented in Germany already,

in flexible labour structures (project, temporary on-site support, business process outsourcing) according to the specific need,

with a thorough cultural understanding of German business practices in terms of language and behaviour (respect for hierarchy, professional distance etc.).

2. Trends In highly developed countries the demand for flexibility is a common macro trend and while Germany is not seen as the most flexible country on the planet this trend has also gained ground here. More and more employment contracts offer flexibility in terms of hours and locations and other signs of flexibility (i.e. longer shopping hours, individualized education opportunities) are also very visible in Germany. Reflections of this trend in the ICT world are for example the growing cloud computing and mobile device markets.

Another macro trend is returning to stronger localization, people increasingly like to have things closer by than a decade ago. It is shown by an increased demand for “made in Germany” and the fact that people buy their food from increasingly local and organic sources. This trend is not reflected in ICT yet and offers first mover advantages to successful and demanded ICT interpretations both for reaching companies and individuals. Examples could include having on site representatives for outsourced processes or having project programmers work more at the client site. Translations or facilitations of this trend into ICT products or services could also be well received.

Currently Germans mainly use the internet for communication, information and e-commerce purposes. The scope of companies in terms of ICT utilizations is obviously broader, software

13 ICT export strategy development for Lithuania – External analysis

solutions track everything from incoming goods through production to sales and service. There is still development in these areas for companies to play an important role. For both groups a common trend is that utilizations of ICT infrastructures have become increasingly mobile through the rise of smart phones and tablet computers. Privacy is also strongly on the agendas of both though it is issue rather than a trend. Whereas 10 years ago ICT was a topic caught in desktop and notebook computers the hardware spectrum and flexibility demand has become much broader.

In a recent survey by European IT Observatory EITO, IT decision makers were asked to identify the major trends driving development of ICT industry in Germany in 2012. Cloud computing is still the top trend for the German ICT industry mentioned by 66% of respondents, followed by mobile applications (53% of respondents), IT security (48% of respondents) and social media (35% of respondents).

ii. Infrastructural landscape and trends

1. Infrastructure Germany’s infrastructure is of high quality with slight variations in rural areas. Generally a very internet-accommodating environment with high fibre and cable based bandwidths and even LTE connections; however a few rural areas are still behind in their development. 78.4% of the German population can be called internet-users and nearly 27,5% of the population has a broadband internet subscription. While fixed phone lines are decreasing the number of mobile phone subscriptions is stable at a very high level of 130% penetration (World Bank Communication Indicators)

Digital infrastructure has recently been recognized as a hot topic by the government; the former ministry of transport has been renamed and refocused into the ministry of transport and digital infrastructure after the 2013 election. One of this ministry’s core strategies is to strengthen Germany’s ICT sector in the coming years. This includes raising the number of ICT start-ups significantly as well as better enabling non-ICT businesses in the utilization of ICT technologies. (Ministry of Transport and Digital Infrastructure: ICT Strategy Digital Germany 2015)

2. Devices Germany has the largest amount of mobile phones in the European Union and the second highest mobile penetration rate (130%) in Western Europe after Italy (147%). 94% of the overall population have at least one mobile phone Smartphone penetration has also risen from 54% in 2012 to 61% in 2013 which means that 61% of German mobile phone owners can access the internet “on the go” and “from their pocket” (Nielsen, 2013).

The internet in general has a large penetration rate of 83% in Germany compared to 73% in the European Union; these connections are increasingly made through mobile devices. Tablet penetration has crossed the 25% mark in 2013 and is forecasted to reach more than 45% in 2017. Smartphones are more popular access devices growing above EU average while the growth of the tablet penetration rate is in line with the current EU average of 25%. Just like in many other countries, the mobile internet access rate is highest among teenagers (>75%) and lowest (<15%) in the 50+ age group. (TNS Infratest, 2013: “Ein Welt ohne Internet?”)

Desktop computers are the only shrinking product category when it comes to internet accessing devices which is in line with other Western European countries.

14 ICT export strategy development for Lithuania – External analysis

3. Bandwidth and Services Broadband access is available throughout Germany but in certain areas the band is broader than others. Downstream connections of at least 1Mbit/second are available throughout the country, the government’s goal is to make >50Mbit/second connections available to 75% of the German population by the end of 2014 (Ministry of Transport and Digital Infrastructure: ICT Strategy Digital Germany 2015).

On the demand side the trend for SME companies and households is to go for a significantly broader bandwidth by 2025, larger companies can be assumed to go for the best available bandwidth. By 2025 100% of SME companies and 90% of households will demand to be connected.

German Bandwidth Demand 2025:

Source: Wik Consult.

This demand profile is driven by several different services categories which consume the demanded bandwidth to different degrees.

DemandLevel Min.Down(Mbit/sec.) Min.Up(Mbit/sec.) NumberofHouseholds(k) NumberofCompanies(k)TopLevelPlus 350 320 6800 300

TopLevel 200 170 12300 0

MediumLevel 70 60 13300 2700

LowLevel 1 1 4300 590

NoBroadband 4300 0

15 ICT export strategy development for Lithuania – External analysis

Bandwidth Demand by Service Category:

Source: Wik Consult

Companies’ utilization of digital services shows an increase that is forecasted to continue further. Electronic Data Interchange (EDI) as well as ICT based e-procurement and e-sales systems have grown in utilization and their utilizations and penetration in business world are forecasted to grow further. In 2011 Germany ranks 2nd in e-procurement value and 6th in e-procurement take-up level in the EU27. From 2010 to 2011 the e-procured value grew by 28% and the growth curve is still in its initial stages. In 2011 € 38819m was e-procured which corresponds to just over 10% (take-up level). This figure in combination with the growth of 28% shows that e-procurement has been accepted widely enough to succeed and that the growth curve is still in its initial stage. On the e-sales side Germany is close to the European average, which shows that there is still ground to gain. When consumer e-commerce first became broadly known and available through the likes of E-Bay and Amazon, the main issue holding people back was trust in the systems. Being used to handing over money for a direct receipt of goods and the fact that Germans are quite resistant to change held e-commerce back for a long time but the recent and current developments show that this lack of trust has significantly decreased and that e-commerce has been on the rise for a while. While the penetration rate is already very high, further innovation challenges remain especially in the areas of payment systems and supply chain speed.

ServiceCategories ServiceExamples BandwidthDemand

CloudComputing SaaS,IaaS,PaaS,... Veryhigh

MediaandEntertainment Video/Film,Web-TV,HD-TV,3D-TV,UltraHD-TV High

Communication Telephony,Chats,IM,Videotelephony Medium

HomeOffice VPN,Videoconferencing,E-Learning… Veryhigh

Gaming Online-Gaming,MMOG,virtualworlds,.. Medium

E-Health Monitoring,Remotediagnostics,AAL,... Low

E-Home/E-Facility SmartMeter,HomeNetworks,SmartGrid,Security,... Low

MobileServices Location-basedServices,MobileBusiness,Apps,WiFi-Offloading,... Low-Medium

BasicInternet Websurfing,News/Mail,Photo,Downloads,Videoclips,SocialNetworks,OnlineStorage,... Low

16 ICT export strategy development for Lithuania – External analysis

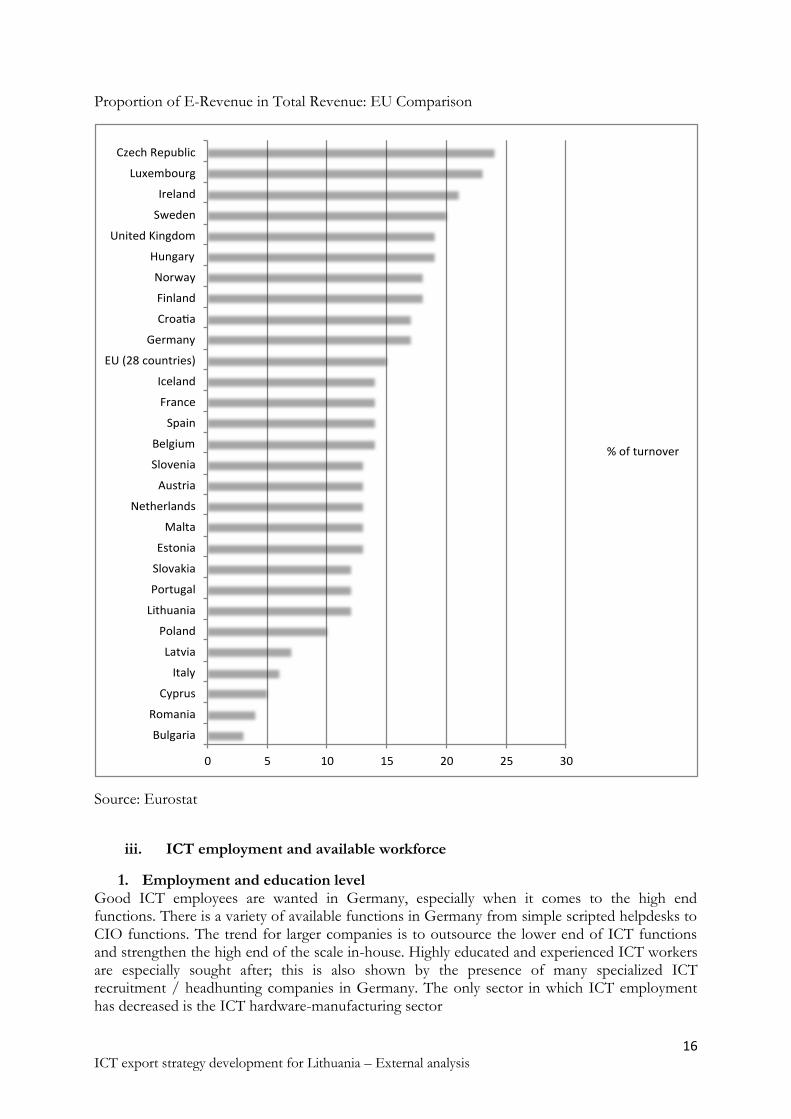

Proportion of E-Revenue in Total Revenue: EU Comparison

Source: Eurostat

iii. ICT employment and available workforce

1. Employment and education level Good ICT employees are wanted in Germany, especially when it comes to the high end functions. There is a variety of available functions in Germany from simple scripted helpdesks to CIO functions. The trend for larger companies is to outsource the lower end of ICT functions and strengthen the high end of the scale in-house. Highly educated and experienced ICT workers are especially sought after; this is also shown by the presence of many specialized ICT recruitment / headhunting companies in Germany. The only sector in which ICT employment has decreased is the ICT hardware-manufacturing sector

0 5 10 15 20 25 30

Bulgaria

Romania

Cyprus

Italy

Latvia

Poland

Lithuania

Portugal

Slovakia

Estonia

Malta

Netherlands

Austria

Slovenia

Belgium

Spain

France

Iceland

EU(28countries)

Germany

Croa a

Finland

Norway

Hungary

UnitedKingdom

Sweden

Ireland

Luxembourg

CzechRepublic

%ofturnover

17 ICT export strategy development for Lithuania – External analysis

Salaries for ICT workers vary largely by function and education level, the monthly average salary is € 3766 and the distribution by function is shown below:

Average Monthly Gross Salary (€) by ICT Function in Germany

Source: Salary Explorer. Note:Additional labor cost at 21% are paid on top of Labor costs (Gross Salary) Redline represent average salary (Gross salary), Blue line represents Average Salary (Net salary).

2. Available workforce and trend Germany has the second largest ICT workforce in Europe but it also has the largest population. In comparison with the other two countries in scope, Germany has the smallest percentage of ICT workers in its population. The percentage is actually in line with the EU average which shows the heritage of Germany’s former position as a European ICT laggard. Especially developers and expert level resources are in high demand. However the country is catching up and especially highly skilled university level ICT related educations are stimulated which is also driven by the Ministry of Transport and Digital Infrastructure’s ICT Strategy Digital Germany 2015.

Populations and ICT Workers:

Sources: Eurostat 2011, CIA World Factbook 2013.

The German government’s ICT expansion strategy clearly aims at increasing this workforce by creating more education opportunities and broader as well as more employment opportunities for ICT workers. One of the strategy’s central goals is to create 30000 new jobs for ICT workers in Germany by 2015. (Ministry of Transport and Digital Infrastructure: ICT Strategy Digital Germany 2015) In ICT, jobs usually create other jobs. One could think of taking over outsourced processes or providing project based programming services to the broadening industry.

2701,93

2954,82

3322,66

3667,51

3976,06

4226,53

4432,23

4952,53

5106,2

5236,88

5599,88

0 1000 2000 3000 4000 5000 6000

Web

Helpdesk and Support

Security

Other IT Jobs

Developers and Programmers

Database and Data

Administrators

Consultants

Networking

Analyst and Architects

Managers and Supervisors

Labor Cost

Average Salary

Country ICTWorkers Population InPercentofPopulationGermany 1373000 81147265 1,7%UK 1481000 63395574 2,3%Netherlands 339000 16805037 2,0%

18 ICT export strategy development for Lithuania – External analysis

iv. ICT investment ICT investments in Germany show moderate growth in spite of the European recession. Total spending amounted to €47 billion in 2012 and Germany’s GDP in the same year was €3401 billion meaning that ICT spending accounts for 1,4% of Germany’s GDP.

ICT Investments (billion €) per Category in 2011 & 2012

Source: Business Wire

Other sources quote similar numbers on hardware and software sales but differ when it comes to service sales, these differences are largely based on the definition of ICT service sales.

v. Major clusters Germany consists of sixteen federal states and companies that want to support the production industry with ICT solutions should focus on the federal states on NordrheinWestfalen, Bayern and Baden-Wurtenberg. These three combined are home to 60% of the German production industry (ING, 2011).Germany is also home to several ICT clusters with the most notable one in the Rhine-Main-Neckar area. Software development centres within this region are in the cities of Darmstadt, Karlsruhe, Kaiserslautern, Saarbrücken and Walldorf.

The IT-Cluster Rhine-Main-Neckar is a cluster of high-tech companies located in the Rhine-Main and the Rhine-Neckar metropolitan areas in Germany. It's currently one the world's largest IT and high-tech clusters. The region is home to companies such as SAP AG, Software AG, T-Systems or Crytek. The region has been referred to as the “Silicon Valley of Europe” and is seen as one of the major ICT clusters in the world.

Smaller, more service driven ICT clusters can be seen in any large German town with sufficient industry demand. The ICT clusters of Düsseldorf and Berlin should be mentioned as particularly well known. Especially Berlin is home to several, very innovative ICT companies.

In Germany, clusters are wanted and supported by the federal and local governments as Germany’s industry has always been grouped in certain cluster structures.

vi. Governmental Policy and Regulations It is Germany’s clear policy to strengthen the ICT industry and its sectors. After the 2013 election the former Ministry for Transport has been renamed into the Ministry for Transport and DigitalInfrastructure. The country has recognized its pre-2010 ICT laggard position in Europe and is willing to invest to become one of the ICT leaders. This is based on realizing that Germany has always been a country of ideas and innovations, a country where people like to create things. It is also based on the fact of having a good ICT infrastructure and successful ICT companies such as SAP present already.

Furthermore Germany has clearly realized the growing impact and influence of ICT in professional and individual lives and wants to move to the forefront of this trend. In 2010 government has developed its ICT Strategy Digital Germany 2015 aimed at growing and broadening the current ICT industry and its sectors, the defined goals are:

Category 2012 2011 Growth 2011 - 2012

Hardware Sales 12,6 12,4 1,2%

Software Sales 15,1 14,9 1,6%

Service Sales 19,3 19,1 1,2%

19 ICT export strategy development for Lithuania – External analysis

Strengthen competitiveness through the use of ICT in all segments of the economic process

Expand digital infrastructure and networks to meet future challenges

Safeguard the protected and personal rights of users in the future Internet and in the use of new media

Step up research and development in the ICT sec- tor and speed up the translation of R&D findings into marketable products and services

Strengthen basic, further and continuing education and training and competencies in handling new media

Make consistent use of ICT to cope with social problems, including sustainability and climate protection, health, mobility, administration and the improvement of the quality of life of citizens

These goals show the broad and deep impact of this strategy as ICT is reaching into all areas of life. Especially the commitment to health and climate protection shows that the strategically driven ICT investments of today will have far reaching impacts even beyond 2015.

20 ICT export strategy development for Lithuania – External analysis

i. Major ICT sectors

Sector Broad adaptability Current market

size

Market growth Score (/5

stars)

Telecoms Audience: direct end-

consumers, B2B and B2C

business

Technical solutions: available

but continued room for

innovations

Infrastructure level: good with

room to improve in

broadband width and other

areas

Device access: High mobile

phone penetration of 130%,

35 million internet subscribers

(estimated); 46 million 3G/4G

subscribers (2013)

€69272 million

(2010) for classic

(network mvn

operators)

telecom market

10,2 million

VOIP subscribers

in 2012

(PointTopic)

Fixed lines decline, mobile penetration is stagnant,

3G and broadband subscriptions are still strongly increasing. 3G has grown from 12,9 million subscriptions in 2009 with a compounded annual growth rate of 37%. Broadband subscriptions grow at more than 2% per year. Broadband bandwidth itself is also growing further stimulated by the government

VOIP subscribers yearly growth rate of 14% in 2012

****

Payment

Services

Audience: direct end-

consumers, B2B and B2C

business

Technical solutions: other than

credit cards, online banking

and direct debit mainly PayPal,

others have not broken

through

Infrastructure level: available

infrastructure for online

payments, not fully ready for

other mobile payment forms

Device access: high due to

broadband and mobile phone

penetration

10 million PayPal

accounts

Full population

has access to

bank based

methods (credit

and directdebit)

Number of non-cash transactions growing at 2,5% / year (CapGemini)

****

E-

commerce

Audience: Broad B2C and

B2B audiences

Technical solutions: mainly

website or web portal driven.

Most B2C solutions are

available on mobile devices

Infrastructure level: broadband

speed level is sufficient to

support website and portal

B2C: € 33,5

billion yearly

revenue, 41

billion yearly

buyers in B2C e-

commerce.

Amazon

dominant in the

B2C market

B2B:4,7% B2B e-

Current growth rate of 21,3% Market has more than doubled since 2009

****

21 ICT export strategy development for Lithuania – External analysis

traffic.

Device access: full access for

B2B world, almost full access

for B2C world

commerce

growth (2011) at

a market size of

€15,6 billion

22 ICT export strategy development for Lithuania – External analysis

Cloud

Computing

Audience: SME adoption

24%, trade industry adoption

29%, service industry 25%

Technical solutions: Available

/ Mature

Infrastructure level: Mature

Device access: High

Total B2B market

size:

€4.6 billion

Cloud services

(SaaS, PaaS,

IaaS): €2.3 billion

Cloud integration

and consulting:

€0.8 billion Cloud

technology:

€1.5 billion

Growth forecast for 2014 is at 50% Total B2B market is expected to reach €18.5 billion by 2017 Cloud services growing to reach €10.9 billion by 2017 Cloud integration & consulting reaching 2.6 by 2017

****

Big Data Audience: Largely driven by

internet, e-commerce and

advertising sectors, however

growth is expected in

optimized production,

logistics, and sales processes

services

Technical solutions: Data base

and analytics technology

expected to grow

Infrastructure level: Lack of

regulatory framework will

make the country’s companies

in disadvantage competitively

Device access: Medium/high

(ongoing transition to omni-

channel data dashboards

Total market size:

€651 million

Hardware

revenue:

€215 million

Software revenue:

€228 million

Service revenue:

€208 million

Total market is expected to grow to 1,687 million by 2016 Hardware revenue reaching €506 million by 2016 Software revenue reaching €523 million by 2016 Service revenue reaching €658 million by 2016 Based on data volume growth, following sectors to be addressed:

IT, Telco, Media

Mobility, logistics and health

Finance & Insurance

Professional services

***

Business

Solutions

Audience: Industry specific

solution audience and SMEs

Technical solutions: Mature

(ERP, CRM, ECM, BI,

product lifecycle management

and analytics) Infrastructure

level: Mature Device access:

High

Total market size

of ERP

technologies €2.5

billion

More than 70%

of all companies

expect social

applications

increase during

the next two

years

Fastest segment to recover are enterprise content management (ECM), Business intelligent (BI),

ERP expenditures is expected to remain relatively constant. The Best market opportunity exist for those providing more industry specific solutions paired with improved usability, business analytics capabilities for processing big data and integration with business processes and systems Smart social business platforms market growth potential is one of highest in the ICT sector in Germany

***

23 ICT export strategy development for Lithuania – External analysis

product life cycle management (PLM)

IT Security Audience: Technology based industries,IT companies (20%), data processing companies, electronic components, telecom, entertainment (12%) Technical solutions: Mature

Infrastructure level: Mature

Device access: High

IT security goods

and services

consumed in

2012: €6.6 billion

IT Security was

major trend

according to 48%

of IT decision

makers

Established solutions such as firewalls, encryption, virus scanners, and signature verification will not lose their relevance. Growth potential in the area of ICT and software almost inevitably means growth potential in the area of IT security.

***

vii. Key ICT sector analysis

1. The Telecom Sector The German telecom sector had a total value of €60600 million in 2009 the German telecom sector was already the biggest one in Europe and has grown further. (Eurostat).With the second highest mobile penetration rate of 130% in Western Europe and 94% of the population owning at least one mobile phone Germany is the largest national mobile phone market in Europe. There are four network operators and a clear market leader cannot be pointed out.

Mobile Phone Subscriptions to Network Operating Companies (2/3 of market)

Source: GSMA

The percentages above relate to 2/3 of the mobile phone market, 1/3 of the market are served by mobile virtual network operators (MVNO). There are 120 companies offering 186 mobile phone service brands in Germany, which means that 116 companies offer MVNO based brands. (prepaidmvno.com). These MVNOs use one of the four networks each in the following distribution. Many companies have gotten into providing MVNO services even supermarket giants Aldi and Lidl offer mobile phone services, other newcomers are purely dedicated Network Utilization by MVNOs in Germany.This makes MVNOs attractive partner or distribution channel to address specific target segments with new services. Looking at players

Deutsche Telekom

33%

Vodafone 29%

E-Plus (KPN) 21%

O2 (Telefónica)

17%

24 ICT export strategy development for Lithuania – External analysis

involved, MVNO sector can also provide cross-sectorial opportunities sectors for example in retail and media.

Mobile phone subscription to virtual network operators (1/3 of market)

Source: prepaidmvno.com

O2 and E-Plus have announced plans to merge in 2014, currently both EU and German market regulators are evaluating these plans critically. This merger further shows that the mobile phone subscription service market has reached such a penetration and saturation level that it is virtually only possible to gain market share by stealing it from a competitor. It can also be observed that an increasing amount of brands compete based on low prices which is another indicator for a mature market. Providing services or solutions that can facilitate in the consolidation phase is an opportunity for strong ICT companies. Specifically post-merger integration processes can offer opportunities. However, small and medium IT service market players are not well positioned to win such contracts.

Digital television is by now the standard in Germany, analogue satellite television has been discontinued at the end of 2012 and analogue terrestrial television reception has also been discontinued in most areas. The current standard followed is DVB-T. However there is still the basic decoding price / cost associated with television reception which does not include further costs for pay television or comparable services. Internet protocol (IP) based television is also on

E-Plus 38%

Vodafone 26%

T-Mobile 24%

O2 12%

25 ICT export strategy development for Lithuania – External analysis

the rise. IPTV market is largely dominated by few major players (Alice TV owned by Telefonica, Entertain owned by Deutche Telecom, and Vodafone), but new independent over-the-top players (including international) are expected to enter into market. While IPTV can currently only be received through internet connections it is highly likely that IP-television will also be accessible through cable or other means. Pay-tv services are also rising in popularity, it is estimated that the number of subscriptions will rise to 23 million by 2018 (digitalfernsehen.de). Providing services that help understanding and improving the current architecture in the phase of rising subscriptions and demands offers opportunities for ICT companies.

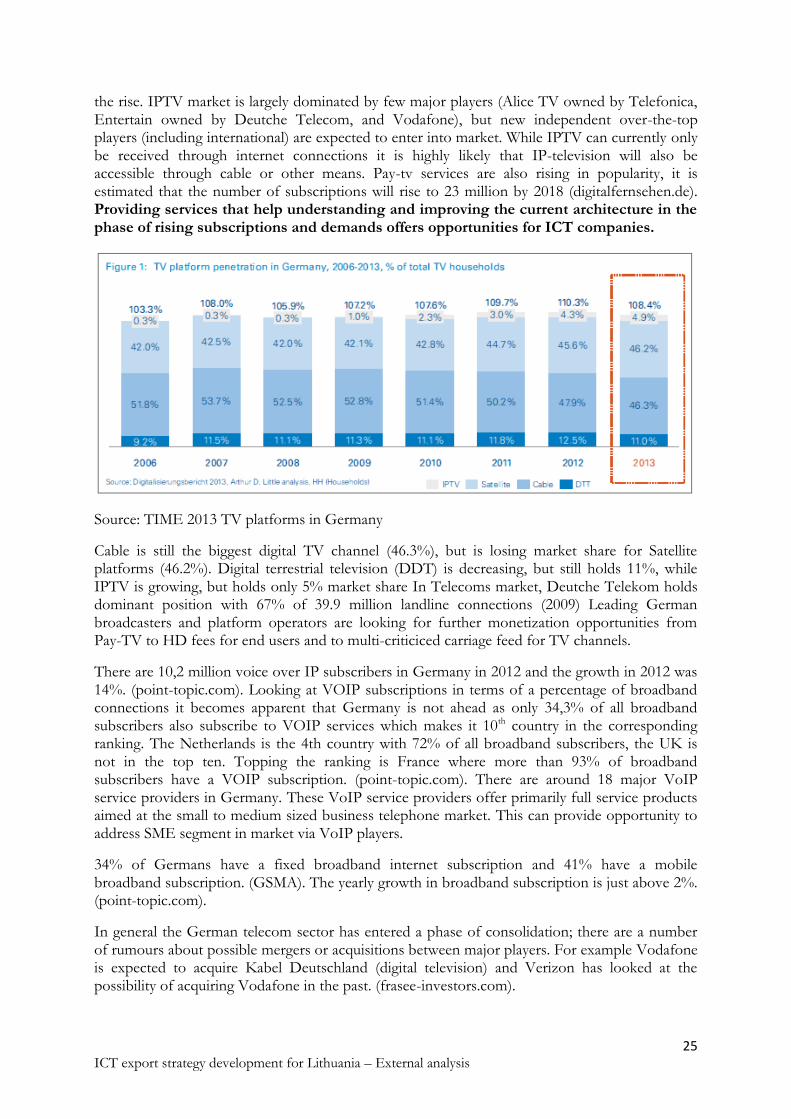

Source: TIME 2013 TV platforms in Germany

Cable is still the biggest digital TV channel (46.3%), but is losing market share for Satellite platforms (46.2%). Digital terrestrial television (DDT) is decreasing, but still holds 11%, while IPTV is growing, but holds only 5% market share In Telecoms market, Deutche Telekom holds dominant position with 67% of 39.9 million landline connections (2009) Leading German broadcasters and platform operators are looking for further monetization opportunities from Pay-TV to HD fees for end users and to multi-criticiced carriage feed for TV channels.

There are 10,2 million voice over IP subscribers in Germany in 2012 and the growth in 2012 was 14%. (point-topic.com). Looking at VOIP subscriptions in terms of a percentage of broadband connections it becomes apparent that Germany is not ahead as only 34,3% of all broadband subscribers also subscribe to VOIP services which makes it 10th country in the corresponding ranking. The Netherlands is the 4th country with 72% of all broadband subscribers, the UK is not in the top ten. Topping the ranking is France where more than 93% of broadband subscribers have a VOIP subscription. (point-topic.com). There are around 18 major VoIP service providers in Germany. These VoIP service providers offer primarily full service products aimed at the small to medium sized business telephone market. This can provide opportunity to address SME segment in market via VoIP players.

34% of Germans have a fixed broadband internet subscription and 41% have a mobile broadband subscription. (GSMA). The yearly growth in broadband subscription is just above 2%. (point-topic.com).

In general the German telecom sector has entered a phase of consolidation; there are a number of rumours about possible mergers or acquisitions between major players. For example Vodafone is expected to acquire Kabel Deutschland (digital television) and Verizon has looked at the possibility of acquiring Vodafone in the past. (frasee-investors.com).

26 ICT export strategy development for Lithuania – External analysis

Given the governmental digital growth strategy our expectation is a current and future high level of IT and R&D expenditures in the telecom sector. Public investments and incentive usually drive investments in the private sector by subsidising them in various ways. Within these R&D expenditures we expect the big four network operators to invest mainly into their network, also in order to fulfil the bandwidth demands of the future. Other companies will invest in a broader way and can be closer to the end-user.

2. Payment Services Finance and payment service is a sector where Germany still has room for innovation. This is mainly a cultural issue as Germans need full trust into a payment method before adopting it. Germans are generally very concerned about their privacy and guard their valuables well which is the cultural aspect driving this adoption issue. Therefore Germans are also very careful when it comes to surrendering their bank or credit card details.

PayPal has managed to bridge this trust gap to a large extent and is the second most preferred e-commerce payment method in Germany. It is even more preferred than bank authorisations (automatic deductions) and credit card utilization. When it comes to e-commerce, the graph below shows which payment methods Germans prefer in e-commerce payments.

Payment Methods in E-Commerce

Source: BITKOM 2013

Because Germans are conservative in adopting payment methods it is important to create trust through reliability and privacy. If this can be done successfully then a lot of consumer whitespace is available to successful incumbents.

Near field communication (NFC) through RFID or other means is an interesting field that many parties are looking into for developing new payment systems. These solutions are an interesting alternative to carrying cash and if developed well they can speak to the safety and privacy concerns. Both, banks, mobile phone network operators and other parties are spending resources on creating potential NFC solutions for consumers. Currently the mobile network operators are ahead in introducing workable solutions, all four of them have pilot projects running and Vodafone has recently introduced a market ready solution called NFC mobile wallet which is currently in its starting phase. Banks are active because they have seen through the rise

0% 10% 20% 30% 40% 50%

ClickandBuy

Cash on delivery

Direct transfer

Advance payment / bank transfer

Credit card

Direct debit

Paypal

Purchase on account

27 ICT export strategy development for Lithuania – External analysis

of PayPal that they need to be closer to the forefront of developments in order not to lose control of financial transactions.

3. E-Commerce E-commerce had a difficult start in Germany but has grown throughout the last years and is expected to grow further. It is one of the biggest B2C e-commerce sectors in the world and had total revenue of € 33.5 billion and 41 million buyers in 2013. (Germany Trade & Invest: The E-Commerce Market in Germany). Its growth rate of 21,3% is also impressive, the sector has more than doubled in revenue since 2009. (Germany Trade & Invest: The E-Commerce Market in Germany). The B2B market amounts to € 870 billion and has seen impressive yearly growth throughout the last years. The B2C market is clearly dominated by Amazon and the Otto GmbH as the table of the top ten B2C sellers’ shows.

Top 10 B2C E-Commerce Retail Companies in Germany 2011

With mobile phones sales revenue of € 8,8 billion (on & offline), mobile devices such as tablets and phones account for a large part of the B2C revenue but only 2%-10% of the retail goods are bought with a mobile device. (BITKOM). This shows large room for growth as people increasingly use their mobile devices to access the internet. This is further amplified by the fact that 25% of smartphone users use their phones for e-commerce purposes. The current challenge for companies active in e-commerce is to redefine the “e” from electronic to everywhere for all users.

Next to secure payment systems, one of the German growth drivers has been the excellent service provided by B2C e-commerce retailers. Examples of this include fast delivery, free returns and efficient handling of order and return processes. Concepts like same day delivery have created flexibility and speed on the customer side and challenges on the retailer side. Especially the return stream has become larger than in the pre-e-commerce mail-order world, 40% of all German e-shoppers already take potential returns into account. Better solutions are needed in the future to handle the increasing supply chain challenges.

Method of payment is one of the most important success factors in e-commerce. A study conducted by the E-Commerce-Center confirms that over 80% of people making online purchases consider the availability of their preferred payment procedure to be very or absolutely important. Purchase on account, followed by PayPal and direct debit remains the preferred payment options in Germany. Payment methods are a direct factor when it comes to acquiring new customers as they evaluate potential retailers also by the availability of their preferred payment method.

A rather new development is the combination of online and offline services, customers demand a multi-channel experience as they want to access the retailers through their momentarily preferred method which can differ by location and personal situation throughout a single shopping process.

No. Name Type CountryofOrigin Revenue(EURMillion)

1 AmazonEUS.a.r.l. Allround USA 34332 OttoGmbH Allround Germany 15523 Neckermann(OttoGmbH) Allround Germany 6914 Notebooksbilliger.deAG Computer,phonesconsumerelectronics Germany 4555 ConradElectronicSE Allroud Germany 4086 VerlagsgruppeWeltbildGmbH Allround Germany 3717 BonprixHandelsgesellschaftmbH Allround Germany 3568 EspritRetailB.V.&Co.KG Apparel,textiles,shoes USA 2979 CyberportGmbH Computer,phonesconsumerelectronics Germany 28410 AppleInc. Computer,phonesconsumerelectronics USA 273

28 ICT export strategy development for Lithuania – External analysis

E-commerce has become an essential channel for every retailer and will gain further in importance. Looking at extensive growth figures, it is safe to say that R&D investments will remain high and challenges are plentiful. Companies that can provide solutions in the areas of payments, supply chain and customer service can succeed in partnering with German based e-commerce retailers.

4. Cloud Computing Following a joint study by BITKOM and KPMG, the attitude of German companies towards cloud computing has improved significantly between 2012 and 2013. More than one third of all German enterprises already use cloud computing solutions; with a growth rate of 32% in one year flagging up the significant growth potential for the coming years. In 2014 growth in cloud services could even reach 50%, which makes it the hardest growing ICT sector in Germany (Germany Trade & Invest).

Currently, cloud computing accounts for 5% of corporate German ICT expenditures with a total size of € 4,6 billion. Due to the current rapid growth the sector is expected to account for € 18 billion by 2017. (Germany Trade & Invest). In terms of the sector’s revenue breakdown 50% of the current cloud sector revenue is incurred through cloud services, 30%-35% comes from cloud technology and 15%-20% comes from cloud integration and consulting. (Experton Group 2013).

Germany has comprehensive cybercrime legislation and good intellectual property protection in place, the combination of both provides a sufficiently good legal basis for enabling the cloud sector. (cloudscorecard.bsa.org) Also the ICT Strategy Digital Germany 2015 is geared at adding bandwidth to Germany’s broadband network drives the positive development of cloud computing.

As the fastest growing German ICT sector, cloud computing offers opportunities both for new cloud companies and service providers to the sector.

viii. Commonly used outsourcing destinations and practices Growth in ICT opportunities and investments have driven outsourcing of inputs since the 1990s, Germany is no exception to this practice. About half of all German companies outsource part of their corporate IT function, half of the outsourcing companies’ contract with multiple sources and destinations. (European IT Outsourcing Intelligence Report: Germany, 2012).

Outsourced projects mainly fall into four different areas. Outsourcing companies were surveyed to understand the preferred outsourcing project areas; multiple answers per respondent were possible.

Outsourcing Project Areas in Germany

29 ICT export strategy development for Lithuania – External analysis

Source: European IT Outsourcing Intelligence Report: Germany, 2012.

The main reasons for companies to outsource ICT areas are in line with other countries where outsourcing is high on the agenda:

1. reducing operating costs, 2. freeing up key resources, 3. focuson core competence.

When it comes to choosing outsourcing destinations geographical proximity is a surprisingly important factor for German companies, the two and equally most important factors are the availability of talent and cultural proximity. Language skills (German) and positive references from other German companies are also of high importance. (European IT Outsourcing Intelligence Report: Germany, 2012).

When it comes to choosing an outsourcing partner experience and references dominate the list of factors. Low cost and successful completions of pilot projects are also important when it comes to choosing the right partner (European IT Outsourcing Intelligence Report: Germany, 2012).

Combining all of these results and factors it becomes clear that Germans prefer near-shoring and need trust, cultural proximity, cost advantages and good references to make an outsourcing decision.

00% 10% 20% 30% 40% 50% 60% 70%

Web

Mobile

Enterprise

Cloud

30 ICT export strategy development for Lithuania – External analysis

ix. Home market and ICT exports

There are more than 72000 ICT companies in Germany, employing 876000 people. More than 90% of IT companies are active in IT and software development. However, today’s market for ICT services in Germany suffers from a shortage of IT professionals. The skills shortage predicted for 2012 indicates that more than 32000 additional IT professionals are needed in Germany (ciklum.com).

There are still ICT exports but Germany continues to be a net importer of ICT services and goods. This is particularly in the understanding that Germany is a net exporter in most categories of goods. On the other side there is a strong yearly growth in ICT service exports in Germany of almost 10% on a yearly basis since 2009(data.worldbank.org/indicator/BX.GSR.CCIS.ZS).

x. Commonly used partnership practices

1. Business culture and languages requirements Germany’s business culture is characterized by exactness and predictability. It is important to deliver exactly what has been promised and for when it has been promised, Germans do not like surprises when it comes to business. It is also important to be able to communicate in German to achieve a successful business relationship. Not all German companies are international and in international companies not every employee has international contact points. Generally speaking Germans are not as good at English as for example Scandinavians or people from the BeNeLux. Therefore it is important to speak the language and offer predictability to succeed in partnering with a German company.

2. Procurement practices and regulations Companies and institutions follow professional procurement processes when it comes to ICT, which is due to the generally high total cost and mid-long term orientation in the ICT category. Bidding ICT providers must expect to go through a request for information (RFI) and request for proposal (RFP) process where they will be asked to submit extensive company information and cost breakdowns. This is usually followed by several rounds competitive negotiations. Governments and institutional customers usually have to follow a public RFP process, which is less flexible than corporate RFP processes and usually takes more time to complete. It is worth informing about the specific bid process and its requirements before bidding for a larger project.

Bid ranges tend to vary significantly according to project size, ranging between €70,000 and several hundred million Euros. Larger contracts, as in the Netherlands and UK, tend to be broken down into smaller sub-contracts by the successful bidder. Where sub-contracting involves body shopping, local consultants are remunerated at a rate of around €60-120 per hour.

xi. IT associations, and other organization bodies The most significant organizational body is the government’s ministry of transport and digital infrastructure. This is the top down strategist of all activities. Another important political body Is the Federal Network Agency which regulates the detailed policies The Fraunhofer Institute is an important and the biggest ICT research institution in the sector. BITKOM is the most important ICT industry association in Germany. Contacts to all three can facilitate a desired market entrance further as well as linking up with Germany Trade & Invest, a foreign trade and investment association in Germany.

31 ICT export strategy development for Lithuania – External analysis

eHealth:ghec.de, BVMed Association

Business solutions:cebit.de, crm-expo.com, entscheiderforum.net, germantop500.de, systems.de

Bundesnetzagentur: Information about regulations and consumer rights in the German telecommunications market. http://www.bundesnetzagentur.de/cln_1911/EN/Home/home_node.html;jsessionid=97B27AC21800F20CF5A0621678313AE6

BundesverbandInformationswirtschaft, Telekommunikation und neueMediene.V.: Association of more than 1,700 businesses in the IT, Telecom and New Media industries in Germany.

http://www.bitkom.org/en/Default.aspx

Association of Telecommunications and Value-Added Service Providers: Represents 90 active telecom companies in the German market and works with government agencies to promote business interests in the telecom sector.

http://www.vatm.de/128.html

32 ICT export strategy development for Lithuania – External analysis

B. UK – Country summary

ii. End consumer’s interest

1. Market opportunity Despite on-going economic struggles in 2013, the UK economy has benefited from a small boom in manufacturing and strong inward investment in the ICT sector in recent years. According to the European Information Technology Observatory (EITO), the UK ICT market is the largest in Europe by revenue (see bar chart, “Europe’s top ICT Markets by Revenue”, below) and growth areas include cloud computing, e-commerce, e-health and business solutions.

The ICT sector contributes 8% of GVA to the UK economy (Gross Value Added: contribution a sector makes to GDP before taxes and subsidies are applied) and more than two million are employed in the sector. London has Europe’s largest end-user market: 392,000 registered businesses and a population of nearly 8m. Within the ICT market, telecoms and info tech services dominate, as illustrated below:

Source: London & Partners, Ltd.

Within info tech, the software industry is estimated to be worth £9.2bn – the second most valuable market in the EU and accounting for 5% of the worldwide market. The IT service industry is estimated to be worth £25.2bn – accounting for 21% of the EU market and 7.2% of the worldwide market.

The key ICT sectors identified and analysed for the UK are cloud computing, e-commerce, e-health and business solutions. While each of these sectors has its own unique context and opportunities, the cross-sector opportunities in the UK are particularly strong among these sectors because of the combination of the following:

Advanced, integrated infrastructure.

Vibrant investment environment.

A dynamic market attracting international talent and businesses.

Clusters across the country supported by the government, incubating start-ups – many on which have grown to be highly successful.

London: A hub of innovation and global finance, London has been described as the “gateway to Europe” because it is home to the European headquarters of global

33 ICT export strategy development for Lithuania – External analysis

companies and offers access to these companies, which are keen on optimising their ICT spends.

The UK’s unique position in regard to the above presents broad opportunities to a wide range of ICT sectors and, as such, is certainly not limited to the four key sectors mentioned (cloud computing, e-commerce, e-health and business solutions). For example:

The UK is home to global defence companies and a thriving space industry offering potential for companies specialising in satellite technology.

Concerns over data security is driving growth among consultancies and professional services companies in the cyber security and data protection industries, fuelled by growing demand from large retailers, banks and mobile network operators.

The 3D CAD sector is well-established in the UK with small and larger companies tapping the VARS (Value added resellers) and bundled add-ons market for industry-leading products such as AutoCAD.

VARS opportunities are also present in the business platform sector, with a market for Microsoft Dynamic bundles and opportunities being tapped by both small and larger players.

The UK is home to a large financial services sector offering various opportunities to payment companies, including international transfer services, app-based m-commerce, Omni channel technology and cross-sector opportunities in banking, retail and telecoms.

2. Trends The UK is a competitive mobile market for 4G providers. For example:

O2, Vodafone and Three joined the 4G market in 2013, upsetting EE’s (Everything Everywhere) monopoly.

4Gis drivingsmart phone adoption (the UK already has the highest smartphone penetration in the EU5).

Financial services are increasingly being accessed via mobile banking apps, with most commercial banks offering a mobile app to customers (the UK mobile banking market grew by an estimated 47% in 2013).

E-commerce is also expected to benefit from this trend. For example:

Advances in mobile data access have helped drive a 47% increase in total e-commerce sales in the UK from 2008-2012.

o This is because mobile device adoption has driven adoption of e-commerce o Tablet e-commerce in particular is expected to outpace smartphone e-commerce

in the UK and contribute 25% of e-commerce sales by 2017

A major driver of e-commerce and m-commerce in particular has been the digitization of coupons and discount vouchers. The UK hasthe highest paper coupon usage in Europe with an estimated combined redemption value in 2013 of £2bnandhas been described as having an “extreme” coupon culture.

This coupon culture is now transitioning to e- and m-commerce, with cashbackwebsiteQuidco dominating the market. Quidco has:

3.5m users,

4,000 member/participating retailers and retail chains, and

90,000 new members joining each month.

34 ICT export strategy development for Lithuania – External analysis

There is also a strong, exponential trend among UK companies to better target their services for e-commerce and m-commerce users by harvesting big data to determine consumer trends and sentiment.

Finally, MVNOs (Mobile Virtual Network Operators) are allowing more players to come into the UK market and provide services independent of bandwidth operators. For example, supermarket retailer Tesco has used its capacity as an MVNO tolaunch 4G plans to all customers in October 2013and to grow its customer base to more than 3m in FY 2011/2012

Tesco is an example of leveraging MVNO capability to attract a wider customer base through the marketing, special offers or e-commerce that MVNO data allows. It therefore can offer an advantage over traditional non-MVNO services such as SMS or selling minutes, and allows the new data services to be bundled into packages. Partly as a result, bundles have proliferated in the UK, including bundles offered by:

Tesco,

Virgin Mobile – the world’s first MVNO,

Sky: considering becoming an MVNO to offer data to customers and support its popular Sky Go “TV Anywhere” package (as of 2013),

BT: announced in October 2013 that it will return to the mobile market after a 10-year absence, partnering with EE to provide MVNO services.

Cloud computinghas a role in facilitating both e-commerce and MVNO services (for example through cloud company SpatialBuzz) by offering simplified customer experiences – cloud computing is therefore also a key sector in the UK market.

iii. Infrastructural landscape and trends

1. Infrastructure UK ICT trends are being facilitated by infrastructure investment. For example, investment in superfast broadband (SFBB) is expected to provide a downlink of 24 Mb/sec to 90% of local authority areas by 2015. The government and private sector have also worked together to increase public wifi access; for example, through Virgin Media’s partnership with Transport for London, or through BT’s “open zones”. The government has also sought to increase bandwidth efficiency by auctioning off spectrum in 2013 as part of its LTE and digital strategy. The principal targets of the government’s strategy for ICT infrastructure are featured in the timeline below:

The principal targets of the government’s strategy for ICT infrastructure

Broadband Rural Broadband “Creating the best broadband in Europe by 2015” 2015

Adequate BB to all Adequate broadband access and capacity for all 2020

Fiber to UK

Cabinet

BT fiber reaches two-thirds of UK population 2019

IPv6 Migration from IP4 to IPv6 Core + ISP’s service offering 2017

Government Capacity “Internet of Things” 2030

PSN Installation and migration of services to PSN 2016

Mobile 4G/LTE 0.8/2.6GHz public spectrum auction 2013; LTE services 2013; 2024

35 ICT export strategy development for Lithuania – External analysis

evolve

Femto/mesh

technology

Femto/Mesh networks established 2019

Source: adapted from Engineering for the Future

Key infrastructure facts and figures:

Telecoms o Fiber optic penetration: 50% of households. o Average range of fiber broadband speeds: 22-35Mbps (download), 6.7-8.8

(upload). o Mobile penetration: 124%. o Fixed broadband take-up: increased from 3% in 2002 to 74% in 2010. o Average broadband speed: 6.8 Mb/sec (2011). o £830m allocated by UK government to assist in improving the UK broadband

network, including achieving 90% superfast broadband coverage in each local authority area by 2015.

Government investment in IT and data processing o In 2003, the government had 100 major IT projects valued at £10bn. o In 2009, annual government expenditure on IT projects was £16bn. o One of the largest projects in recent times was the National Health Service

(NHS) IT Project, worth £12bn. o Cloud computing provides greater business efficiency and lower start-up costs - in

line with government objectives. o The government’s private cloud computing program, G-Cloud, is expected to

enable £3.2bn in government savings.

2. Devices Mobile device penetration in the UK is 124% for all handsets (2011) and 51% for smart phones in Q4 2012 – up from 30% in Q1 2011. The UK has the highest smart phone penetration of the EU5 (UK, Spain, Germany, Italy and France) with 41.9m smart phone users forecast by 2016 (65% of population). Tablet penetration is currently 29% (Nov 2013). This compares favorably to both Germany and the Netherlands, as indicated in the table below:

Tablet penetration

Country 2013 penetration 2017 forecast

UK 27% 50% (regular user of tablet)

Germany 25% 45% (penetration)

Netherlands 23% -

The high rate of tablet adoption in the UK is driven by the availability of low-cost Android tablets. For example, Tesco launched Hudl in September 2013, a low-cost alternative to Apple’s iPad, which currently still has the largest market share. Tablet adoption by businesses is

36 ICT export strategy development for Lithuania – External analysis

also expected to fuel growth as the global forecast for the market share of enterprise devices is expected to rise to 20% of all tablet devices by 2017.

3. Bandwidth and Services UK fixed-line residential broadband speeds have been steadily increasing from an average speed of 3.6Mb/sec in November 2008 to 14.7Mb/sec in May 2013. Moreover, by May 2013, 19% of residential connections were “superfast” (30Mb/second or more), more than doubling on the previous year. Higher speeds have been made possible, in part, by Virgin Media’s network upgrade to double its customers’ broadband speeds, resulting in average speeds on the network of nearly 35Mb/sec.

Bandwidth is expected to increase further due to the spread of fibre optic cable, which currently covers only 50% of UK households. The median household is expected to require 19Mb/sec of bandwidth by 2023 and the top 1% of households by usage are expected to require 35-39 Mb/sec. The government is also moving to reduce the bandwidth required for signals in a bid to tackle a pending “spectrum crisis”. The UK regulator, Ofcom, has sought to enhance LTE by exploiting the spectrum made available by the digital switch over and auctioned spectrum in 2013.

There are strong service trends in e-commerce (including digital coupons) and also in mobile media penetration:

56% of mobile users use mobile media

34% use location based services

63% use social media

66% use web browsing

56% use applications

26% use Mobile shopping/m-commerce

E-commerce: a. 19% of all UK sales revenue came from e-commerce in 2011 b. 95% of e-commerce sales were B2B in 2011, 5% were B2C c. In 2012, online food sales grew 27%, online department store items grew 25%

and clothes sales rose 15%.

iv. ICT employment and available workforce