Lilian Zephania FINAL Draft

71

STELLA MARIS MTWARA UNIVERSITY COLLEGE (A Constituent College of Saint Augustine University of Tanzania) FACULTY OF EDUCATION Assessment of the Contribution of Loan Services to Bank Development: A Case Study of CRDB Bank in Mtwara – Mikindani Municipality A Research Report Submitted to the Department of Economics in Partial Fulfillments of the requirements for the degree of Bachelor of Arts with Education at Stella Maris Mtwara University College (A Constituent College of Saint Augustine University of Tanzania)

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Lilian Zephania FINAL Draft

STELLA MARIS MTWARA UNIVERSITY COLLEGE (A Constituent College of Saint Augustine University of Tanzania)

FACULTY OF EDUCATION

Assessment of the Contribution of Loan Services to

Bank Development: A Case Study of CRDB Bank in Mtwara –

Mikindani Municipality

A Research Report Submitted to the Department of Economics

in Partial Fulfillments of the requirements for the degree

of Bachelor of Arts with Education

at Stella Maris Mtwara University College

(A Constituent College of Saint Augustine University of Tanzania)

By

ZEPHANIA, Lilian (BAED 15707)

APRIL, 2012DECLARATION

I, ZEPHANIA, Lilian hereby declare that this report is my

original work and that it has not been and will not be

presented to any other university for similar or any degree

award. No part of this work should be used without my

consult or Stella Maris Mtwara University College.

…………………………………………………

ii

Signature

……………………………………….……………

Date

ABSTRACT

The present study aimed at studying the contribution of

loans services to bank development at the CRDB bank in

Mtwara-Mikindani Municipality. The study specified the

development in customers’ services as loans services result

into higher profit than other services in banks. The

interview method was used for data collection from the bank

staffs at the loan department and the obtained data were

processed and analyzed using statistical programme viz

Microsoft Excel. The data showed that there is an

iii

improvement in customer services at bank consequent to the

profit obtained from customer loans. It can be concluded

that the loan service improves the customer services and as

the result leading to the development of the bank. The study

recommends that the bank officials and government team-up

and render a support to loans services provided by the CRDB

bank and other banks at every town and regions in the

country so as to achieve development in the bank services.

DEDICATION

This work is dedicated to

iv

my late father Zephania Mkama

and

my mother Imelda Mkama

whose guidance and support made me withstand today’s

pleasure in this busy and confused world.

v

ACKNOWLEDGEMENT

First and foremost I thank the almighty God for granting me

life and strength through out my study.

Special thanks go to Mr. Daniel Ngugi for supervising my work

to the successful level. I am indebted to Mr. Charles Buteta

Athuman who despite of his busy schedule trained me on

computer skills through the “Hands-on Computer Course” he

introduced and organized at STEMMUCO.

Moreover, I am very grateful to the administration and the

staffs of the CRDB bank in Mtwara for their assistance and

support during data collection.

Lastly, I wish to thank my colleagues in the class at

STEMMUCO and all friends for their material and moral

support.

vi

TABLE OF CONTENTS

Page

Declaration………………………………………..……………………………………….ii

Abstract…………………………………………………………………………………...iii

Dedication.….…………………………………………………………………...………..iv

Acknowledgement……………………….………………………………………………..v

Table of Contents…………………………………………………………………………vi

List of Tables……………………..………………………………………………………ix

List of Figures ………………………………………………………………….................x

List of Symbols and Abbreviations...…………………………………………………….xi

vii

CHAPTER ONE: GENERAL INTRODUCTION……………………….1

1.0

Introduction…...............................................

............................................................

.....1

1.1 Background of the Study………………...……………………………………………1

1.2 Statement of the Problem……………………………………………………………...2

1.3 Objectives of the Study……………...………………………………………………...2

1.4 Research Questions……………...…………………………………………………….2

1.5 Significance of the Study………………...……………………………………………3

1.6 Limitations and Delimitations of the Study……...

…………………………………....4

CHAPTER TWO: LITERATURE REVIEW……………………………5

2.0 Introduction……………………………………………………………………………5

2.1 Theoretical Framework………………………………………..…………...……….....5

2.2 Conceptual Framework……………………………………………………..…………5

2.3 Related Literature………...……………………………………………………………6

2.3.1 Banks………………………………………………………………………………...6

2.3.2 Commercial Banks…………………………………………………………………..7

viii

2.3.3 Operations of Commercial Banks…………………………………………………...8

2.3.4 Credit Creation by Commercial

Banks…………………………………………….10

2.3.5 The Role of Commercial Banks to the Community……………...

………………...13

2.3.6 Risks Faced by Commercial Banks………………………………………………..15

2.3.7 How Commercial Banks Prevent

Failure………………………………………….16

CHAPTER THREE: METHODOLOGY AND DESIGN……………...17

3.0 Introduction………………………………………………….………………………17

3.1 Research Design ……………………………………………………………………..17

3.2 Operational Design ………………………………………………………...………..17

3.3 Sampling and Sampling Procedures………………………………………...……….18

3.4 Sample Size…………………………………………………………………………..18

3.5 Scope of the Study……………………………………………………...……………18

3.6 Target Population…….………………………………………………………………18

3.7 Research Instruments………………...………………………………………...…….19

3.8 Data Collection Techniques………………………………………………………….19

3.9 Data Analysis Techniques…………………………………………...…………….…19

ix

CHAPTER FOUR: RESEARCH FINDINGS AND ANALYSIS……...20

4.0 Introduction…………………………………………………………………………..20

4.1 Amount of Money Provided as Loans……………………..……………...……...

….20

4.1.1 Personal Loans……………………………………...……………………………...20

4.1.2 SME’s Loans……………………………………………………………………….20

4.1.3 Cooperate Loans…………………………………………………………………...21

4.1.4 Microfinance Loans…………..…………………………………………………....21

4.2 Amount of Profit from Loans………………………………………………………..23

4.2.1 Application Fees…………………………………………………………………...24

4.2.2 Commitment Fee…………………………………………………………………...24

4.3 The Relationship between Loans and Profit at CRDB

Bank…………...……………26

4.4 The Relationship between Profit and Improvement in

Services to Customers……...28

CHAPTER FIVE: DISCUSSIONS, CONCLUSIONS AND

RECOMMENDATIONS………………………………………………....31

5.0 Introductions…………………………………………………………………………31

5.1 Discussions………..…………………………………………………………………31

x

5.2 Conclusions………...………………………………………………………………...34

5.3 Recommendations…………………………………………………………………....35

5.3.1 To Bank Customers………………………………………………………………...35

5.3.2 To Bank Officers…………………………………………………………………...35

5.3.3 To Government and other

Stakeholders…………………………………………...36

REFERENCES……………………………………………….…………………..……..37

APPENDIX: Interview Questions for Bank Officials…………..

……………...…….....39

LIST OF TABLES

Page

Table 2.1: Credit Creation in Commercial

Banks……………………………………….11

xi

Table 4.1: The Accumulated Money for Various Types of

Loans……………………...22

Table 4.2: Profit from Various Types of

Loans…………………………………………25

Table 4.3: The Percentage of Loans and Profit accumulated by

CRDB Bank………….27

Table 4.4: The Percentage of Profit from Various Departments

at CRDB Bank……….29

xii

LIST OF FIGURES

Page

Figure 2.1: Conceptual Framework………………………………………………………6

Figure 4.1: The percentage of various types of loans at CRDB

Bank…………………..23

Figure 4.2: The profit accumulated from various loans at

CRDB Bank in Mtwara…….26

Figure 4.3: The comparison trend between types of loans at

CRDB Bank……………..28

Figure 4.4: Percentage profit accumulated at various

departments……………………..30

xiii

LIST SYMBOLS AND ABBREVIATIONS

ATM Automatic Teller Machine

CRDB Commercial Rural Development Bank

GDP Gross Domestic Product

NBC National Bank of Commerce

NMB National Microfinance Bank

SME Small Medium Enterprise

xiv

CBCDL Commercial Bank’s Checkable Deposit

Liabilities

CBRR Commercial Bank Required Reserve

viz Namely

xv

CHAPTER ONE

GENERAL INTRODUCTION

1.0 Introduction

This chapter will present background of the study, statement

of the problem, objectives of the study, research questions,

significance of the study and limitations of the study.

1.1 Background of the Study

Mtwara - Mikindani Municipality like other Tanzanian towns

has different types of people with different tribes,

culture, behavior and experience. These people engage

themselves in different economic activities. Most of the

banks in the municipality are commercial banks, which accept

deposit and create loans. Examples of these commercial banks

are CRDB, NMB and NBC. During their operations, commercial

banks seek to improve their services to customers and

workers to win the competition available in the economy.

Since improvements or developments can be attained if the

revenue obtained exceeds the operating costs then there

1

should be enough profits for facilitating these

developments. (Frank and Bernmark, 2007) Commercial banks

creates money and earn profits from lending therefore loan

service can be important aspect in bank development because

it can help the bank to increase profit which can be used

in the developmental activities for the sustainability of

the banks create awareness to the bank workers concerning

the contribution of loans service to bank development.

1.2 Statement of the Problem

The CRDB bank in Mtwara – Mikindani Municipality offers loan

services to her clients which create profit to the bank

through interests which can be used to finance improvement

in service to customer, but still there is no visible bank

improvements in services provided to their customers. This

research aimed at finding out why CRDB bank fails to improve

their services to customers although they get significant

clients.

2

1.3 Objectives of the Study

The study aimed at assessing the contribution of the loan

service to the development of the CRDB bank in Mtwara -

Mikindani Municipality.

Specifically the study focused on;

(i) Finding out why there is invisible improvement in

services to customers.

(ii) Finding out the amount of money CRDB bank provide for

loans services.

(iii) Describing the profit obtained by CRDB bank from loans

service through interest.

(iv) Finding out the relationship between the amount of

loans given to clients and the amount of interest

received by bank.

(v) Describing how the CRDB bank use the profit obtained

from loan services especially in improving services to

customers.

1.4 Research Questions

3

The following questions shaded light on the research work;

(i) Why there is invisible improvement in services to

customers?

(ii) How much do the CRDB bank provide for loans service?

(iii) How much do the CRDB bank obtains as profit from loans

service?

(iv) What is the relationship between the amount of loans

provided to clients and the amount of interest to the

bank?

(v) What is the relationship between the profit and the

development in services to customers?

1.5 Significance of the Study

The present study intends to do the following to bank, bank

officials, bank customers, bank stakeholders, bank customers

and government as follows;

I. The study will provide baseline tool to CRDB bank on

how to make decisions towards loans services for

achieving bank development, this study will help the

4

bank to understand more on how loans services to

customers are important to bank development and

therefore this will emphasized them to be careful when

operating different works concerning loans services.

II. The will rescue the bank from losing the customers

because improvement in services will attract more

customers and thus reducing the advertisement costs.

III. The findings will create awareness amongst the bank

workers on how well to treat the customers.

IV. It will provide awareness to bank customers on how they

can get loans easily and hoe to use that money so as to

achieve personal development. The findings will create

awareness to the bank workers concerning the

contribution of loans service to bank development.

1.6 Limitations and Delimitations of the Study

During the study respondents were providing incomplete

information to be used in analysis and interpretations of

findings, also the bank officials were providing less

5

cooperation during data collection, which reduce the

confidence to conclude some ideas.

However, the few data obtained were taken and processed for

use though it could not suffice the plan of the study.

6

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

This chapter gives the theoretical and conceptual frameworks

along with the related literature to the present study.

2.1 Theoretical Framework

According to behaviorist theory, human being and other

organisms are shaped by environment (Rosenhan & Seligman,

1989). This implies that human being would be changed when

the environment is changed.

2.2 Conceptual Framework

Improvement in services to bank customers leads to increase

in number of bank customers (See Figure 2.1). This shows

that the improved the bank service the more the customers.

Bank services viz loan, deposit account, current account and

7

Bank’s Profit through

InterestsHigh Number of

Customers

Service Improvement

Development

Increase in Productivit

y

Increase in Income

fixed account will help customers to improve productivity

which increase the income of an individual. Level of income

will describe the level of development of an individual.

Increase in income of an individual will increase the bank

profit through interest payment and other fees. Increase in

bank profit describe the level of bank development and can

be used to improve customers’ services which attract more

customers, hence national development (Adam & Kamuzora,

2008).

8

Figure 2.1: Conceptual Framework (Author)

Key: Service Improvement = Independent variable, High Number of

Customers = Intervening variable, Development = Dependent variable

2.3 Related Literature

2.3.1 Bank

Bank is the financial institution in which the main product

offered for sale is money, as any business the incentives in

bank is to earn profits. Because banks hold bulk of

checkable deposits said (Gordon & Dawson, 1987). There are

four types of banks which are Central Banks, Commercial

Banks, Specialized Bank and Merchant Banks, where by Central

Bank is a financial institution whose aim is to control the

monetary system in the country that is each country has its

own central bank, it controls all financial institutions,

money supply and the general monetary policy, Specialized

Banks are banks that perform specialized functions example

the Tanzania Investment Bank in Tanzania was established to

9

promote long run project especially in manufacturing

industry, large scale agriculture, animal ranching and in

long term service sectors such as roads.

Brue (1990) further added that Federal Reserve Banks have

three major characteristics which are Central Banks, Quasi-

public Banks and Banker’s Banks. Where by central banks are

national bank and it is available in any country with the

aim of controlling the monetary values of the country

concerned. Quasi-public Banks are federal reserve banks;

they reflect an interesting blend of private ownership and

public control. They are owned by the member of banks in

their districts. Upon joining Federal Reserve System

commercial banks are required to purchase shares of stock in

Federal Reserve Bank. He also said the basic policies which

the Federal Reserve Bank pursues are set by the governmental

body- the board of governors.

2.3.2 Commercial Banks

10

Criffin and Ebert (1991) defined commercial banks as

companies that accept deposits and use the deposited money

to make loans and thus to earn profits which can be used to

facilitate bank development. The banks are chartered by an

individual state but not by the federal government, thus

making them part of Federal Reserve System. Commercial banks

help customers manage their money depending on the

individual’s situation; the bank office recommends different

investment opportunities to the customers.

According to Kindwell et al. (2000), commercial banks are

most diversified intermediaries based on range of assets and

liabilities issued. Although they earn profit from lending

activities, the commercial banks face a number of risks

during banking operations. These risks can be; credit risks,

which happen when the borrowers fail to pay the loan and

interests or delay to pay it, interest rate risks, liquidity

risks, foreign exchange risks and political risks. Again

Kindwell et al. (2000) suggested that for commercial banks to

overcome credit risks they should diversify their

portfolios, conduct careful credit analysis of the borrower

11

to measure default risk exposure and monitor the borrowers

over the life of the loan or investment to detect any

critical change in financial health. Financial

intermediaries such as banks, and other financial

institutions can save money for depositors and can provide

funds to borrowers through these funds given to borrowers

they earn profit which is used to pay interest to

depositors, operating costs and even fund bank development

activities (Mankiw, 2004).

2.3.3 Operations of the Commercial Banks

Commercial banks performs the following; check account where

by customers deposit his or her money in terms of check, and

saving account where by customers are allowed to keep and to

withdraw their money at any time they want, in this type of

account usually a minimum initial deposit is required to

open the account, although withdraws can be made at any time

but the interest paid to depositor is very little.

Commercial banks also provide current or demand account

where by no interest is earned by depositing money,

12

withdraws are made by use of cheques, overdraft is allowed

that is withdraw more than the balance, it also sell

certificate and make loans (McConnel & Brue, 2005). Through

making loans commercial banks can lend loans to borrowers

with interest and from that interest banks creates profit

which is used to pay the depositors interest, operating cost

and generally facilitate bank development. Therefore lending

is important in banking activities although there are some

other activities which increase the revenue of commercial

banks.

According to Nickels et al. (2001) commercial banks is a

profit making organizations, which receive deposits from

individuals and corporation in the form of checking and

saving accounts and then use some of these funds to make

loans. The bank has two types of customers who are

depositors and borrowers. The banks offer a variety of

services to individuals and corporations in need of loan.

Generally, loans are given based on the recipient’s

creditworthiness. They make profits, revenue generated by

13

loans exceed the interest posed to depositors plus all other

operating expenses. Banks want maximize the management their

funds effectively and are supposed to screen loan applicants

carefully to ensure that the loans plus interest will be

paid effectively and timely. Since the revenue obtained from

loans activities exceeds the interest posed to depositors

and all other operating costs then the remained revenues to

facilitate developmental activities of particular banks.

McEachem (2006) adds that, commercial banks attract deposits

from savers to lend to borrowers, earning a profit on the

difference between interest paid depositors and interest

charged borrowers.

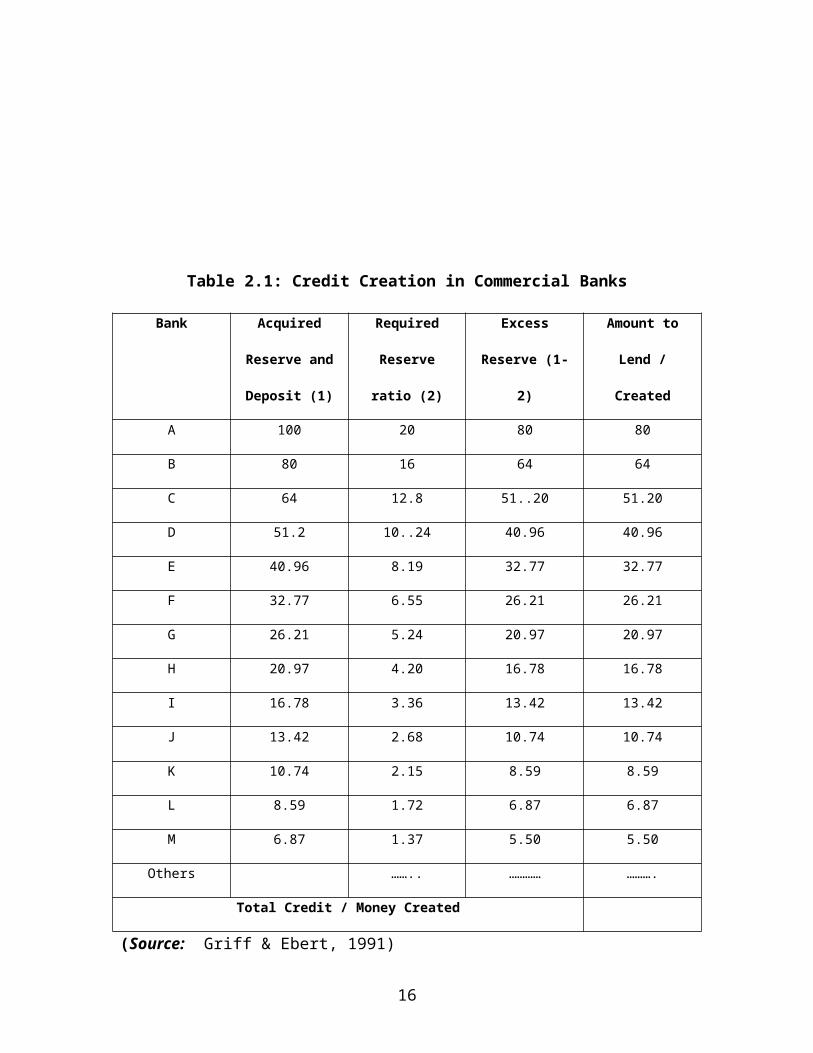

2.3.4 Credit Creation by Commercial Banks

Credit creation is the process where by commercial banks

using cheques facility to expand the volume of credit lent

out beyond the original credit that is commercial banks

increase the amount of money available to be lent. This is

done with the aim of increasing profit obtained from loans

14

department. Commercial banks can create money or credits

through lending where by the money or credits are created by

the interest obtained from different loans provided by

different types of commercial banks.

For instance, assuming that there are “n” commercial banks

in any economy and each provide loans to a certain

individual who deposit the loan provided to him or her to

another bank and also that bank lend such amount of money to

another customer and so on (Griff & Ebert, 1991).

Automatically the amount of money created in will be higher

than the previous amount. This process is shown below as

follows (Ibid, 1991).

If the reserve ratio = 20%

Initial deposit = 100/=

Total deposit will be obtained by summing up the amount to

be lent column which is obtained as shown in table 2.1

below;

15

Table 2.1: Credit Creation in Commercial Banks

Bank Acquired

Reserve and

Deposit (1)

Required

Reserve

ratio (2)

Excess

Reserve (1-

2)

Amount to

Lend /

Created

A 100 20 80 80

B 80 16 64 64

C 64 12.8 51..20 51.20

D 51.2 10..24 40.96 40.96

E 40.96 8.19 32.77 32.77

F 32.77 6.55 26.21 26.21

G 26.21 5.24 20.97 20.97

H 20.97 4.20 16.78 16.78

I 16.78 3.36 13.42 13.42

J 13.42 2.68 10.74 10.74

K 10.74 2.15 8.59 8.59

L 8.59 1.72 6.87 6.87

M 6.87 1.37 5.50 5.50

Others …….. ………… ……….

Total Credit / Money Created

(Source: Griff & Ebert, 1991)

16

Table 1.0 can be interpreted regarding the appropriate terms

as follows; Acquired Reserve is the amount of money acquired

by the bank system when some one deposit a certain amount of

money from the commercial bank, from the table above show

that the entire commercial bank system is able to lend 400

which is resulted from the accumulations of acquired

reserve.

Again the Reserve Ratio is a portion of total reserve

required to remain in bank deposits so as to meet day to day

cash requirements of their customers. Thus, it is the ratio

between banks required reserve and commercial bank’s

checkable deposit liabilities.

Then it can mathematically be quantified that;

Reserve Ratio = CBRRBCDL

Where;

CBRR = Commercial Bank Required Reserve

CBCDL = Commercial Bank’s Checkable Deposit Liabilities.

17

Credit Multiplier is the rate of change in total deposit

following an initial change in deposit.

Excess Reserve is the different between acquired reserve and

required reserve that is; it is the amount of deposits in

excess of loans to borrow;

Excess Reserve = Acquired Reserve - Required Reserve

Table 1.0 above therefore shows how much commercial bank

have the ability to create money or credits, it made up a

major part of our money supply in our economy.

From the table 1.0 the total deposit will be given by;

TD – Total Deposit

=

(80+64+51.2+40.96+32.77+26.21+20.97+16.78+13.42+10.74+8.59+6

.87+5.50+4.40)

= 100( r+r2+r3+r4+...+rn )

= G (11−r ), G is initial deposit,

Since r is given by taking G2G1 OR

GnG(n−1) , therefore r =

80100

=45

18

Thus TD =100(

1

1−45

)=100(115

)=500

, Thus TD = 500.

This value implies that the credit has been multiplied five

times and therefore the credit multiplier is 5.

2.3.5. The Role of Commercial Banks to Community

Banks play a particular important role as financial

institution (Tregarthen & Rittermberg 2000), explained the

following roles of commercial bank to any kind of community;

They accept depositors where by individuals or group of

people can keep their money in the commercial banks, through

their account open in that commercial bank. Commercial bank

keeps the money of their customer’s safety with some

interest to pay.

Commercial banks operate different accounts on behalf of

customers, they operate saving accounts, current accounts

and fixed account which help customers to choose the

appropriate account to own according to his or her or their

kind of activities they deal with.

19

They keep valuables and other crucial documents in safe

custody, for example commercial banks can keep title deeds,

jewels and certificates for customers.

Gordon & Dawson (1987) said; bank primarily is not a place

to deposit valuables particularly money, for protection

against the hazards of theft and fire although each of these

serves a particular purpose they all have activity in common

which is collecting money from a source that does not need

it immediately and channeling it to the others that do need

it immediately. Thus these various financial institutions

are intermediaries in the flow of money throughout the

economy, in addition to this general activity, banks and

other financial institutions carry on specialized functions.

Commercial banks exchange currency for customers this help

business man to continue with their business activities

without any problems, also it facilitate easy and quick

payments of debts by the use of cheques and standing orders

20

which is the form from the customer authorizing his bank to

make regular payments to creditors.

Commercial banks also facilitate international trade by

giving travelers cheques to traders moving from country to

country, they also give financial advice to customers on

business and money also they create deposit money through

credit creation. The banks give loans and overdraft

customers for project financing, they lend loans to

borrowers with the interest, they earn on their loans are

able to pay interest to their depositors cover their

operating costs and earn profit. Any company achieve

development by using the profit obtained in the business

also commercial banks can use the profit obtained to pay

interest to their depositors, cost of operating and the

remaining can be used in enhancing bank’s development like

opening more branches and increase the number of ATMs

stations.

21

According to Wild et al. (2007) banks play important role as

financial institution they accept both demand deposit where

by money is available on the demand of the owner or

depositor and time deposit where by the money is available

only at the end the certificate of maturity. They also lend

money to borrowers who repay them with interest. These

interests and repayments create money and earn profits,

which facilitate various activities in the bank development.

Commercial banks creates money by making loans when proceeds

of those loans are spent the person receiving the money will

deposit much of it in a bank deposit which is new money

(Spencer, 1990).

2.3.6 Risks Faced by Commercial Banks

Commercial banks also bear risks found within their

organizations so as to achieve gains like other different

organizations; Kindwell et al (2000) outlined the risks faced

by commercial banks during their operations:

a)Diversity their portfolios.

22

b)Conduct careful credit analysis of the borrower to

measure default risk exposure.

c)Monitor the borrower over the life of the loan or

investment to detect any critical change in financial

health.

d)Other risks are interest rate risks, liquidity risks,

foreign exchange risks and political risks.

2.3.7 How Commercial Bank Prevent Failure

According to Tregarthen & Libby (2000), commercial banks

like other organizations faces some risks when operating

their daily work but to prevent them they:- Borrow from

other financial organizations so as to ensure the

availability of money needed by customers are there although

they lend them to other customers who borrow from them.

Commercial banks maintain a minimum level of worth as a

fraction of total assets. Apart from that they also perform

auditing to ensure that there is no any amount of money lost

23

or stolen from the bank so that they can meet day to day

demand of the bank.

CHAPTER THREE

METHODOLOGY AND DESIGN

3.0 Introduction

This chapter entails the research design, the sampling

technique and procedures, target population and the

24

validation of research instruments along with the data

analysis techniques.

3.1 Research Design

Research design is conceptual structure which is conducted.

It is a logical sequence in which the study is to be carried

out and constitute the blue print for the collection and

measuring and analysis of data (Kothari, 1990.) The research

was conducted under case study design on CRDB bank in Mtwara

– Mikindani Municipality which aimed at assessing the

contribution of loan services to bank development in

services to customers.

3.2 Operational Design

The research was testing the altitude of the respondents on

why there is no visible improvement in services to customers

while the bank offers loan services which provide a lot of

profit than other department which can be used to create

credits and therefore bank development.

25

3.3 Sampling and Sampling Procedures

The samples were obtained using snowball sampling due to the

fact that a researcher had no sure of the real participants

in the bank. However, few participants were consulted for

clarification of who was to be involved in giving the

desired information for this work.

3.4 Sample Size

The research interviewed 01 Loan Officer at the CRDB bank

because he was the only personnel at the loans department

along with the bank manager. Information on the amount of

money used in loans department by the bank, the profit

obtained from it, the relationship between profit obtained

and money used and the relationship between profit and

development in services to customers were collected

appropriately.

26

3.5 Scope of the Study

The study area were including the contribution of loan

service to bank development; specifically the study will

focus on why there is no visible improvement in bank

services while the bank offers loan services to clients in

order to achieve economic welfare.

3.6 Target Population

This study was conducted in Mtwara – Mikindani Municipality

with a view to CRDB bank. This is because the Municipality

currently experiences lack of improved bank services to

customers. The target population for this study was 05 CRDB

bank workers in the loans service department and the bank

manager due to the fact that CRDB bank in Mtwara – Mikindani

Municipality is a just a branch and not the main bank.

3.7 Research Instruments

Research instrument can be referred as a tool for collecting

data. The study used two types of data collection viz face to

face interview and documentation. This process took place in

CRDB Bank office where by the records of the responses were

27

being recorded on the notebook for further analyses. Various

documents concerning loan services at the respective bank

were collected from the participants.

3.8 Data Collection Techniques

The study used both quantitative and qualitative techniques

in collection of data. These techniques need descriptive

information, facts and figures in collecting and analyzing

data. Quantitative data were obtained from documentaries

technique while qualitative data were obtained through

interview schedule.

3.9 Data Analysis Techniques

The collected data were analyzed using statistical packages

following Bluman (2009), Gupta (2006), Francis (2004) and

Healey (2002). The data were further processed on Microsoft

Excel to obtain charts and graphs for easy interpretation.

28

CHAPTER FOUR

RESEARCH FINDINGS AND ANALYSIS

4.0 Introduction

This chapter explains the finding from the study as

conducted at the CRDB bank in Mtwara- Mikindani

Municipality.

4.1 Amount of Money Provided as Loans

The study found that the bank provide a lot of money as

loans to her customers according to the type of customers

demand that loan, from this there are four types of loans

given to customers according to their category as stipulated

below.

4.1.1 Personal Loans

29

These are loans given to individual person who is employed

in a certain organization, the customer should provide his

or her salary slip to the Bank and his or her employer

should accept to be his or her sponsor.

4.1.2 SME’s Loans

These are loans given to people owning small business, he or

she should provide securities, Bank statement, Business

registration and number of business team to the bank so that

the bank will see how his business doing and decide how much

he or she will be given as loan and decide how she is going

to pay it that is if the business is doing well the bank

will assign large amount of loan as they know that they can

not he will gain more profit.

4.1.3 Cooperate Loans

These are loans given to people who own a large business;

usually their loans are larger than of that in small medium

enterprise loans. They also provide similar documents as the

small business man provide, and then the bank is the one

30

which decide the amount of loan to be given to that kind of

customers.

4.1.4 Microfinance Loans

These are loans given to different organizations like

Sacco’s and other association formed by different people in

the society, this is done so as to help people who wants to

borrow from the bank but they do not have securities to

allow them to borrow therefore this organization may borrow

from the bank and then they can use that loan to help heir

members to borrow from their own organization. In this type

of loan service the microfinance organization does not

provide any security to the bank for them to be allowed to

borrow.

The results from the study show also that the amount of

loans allocated to different types of loans differs

according to the types of loans (See table 4.1).

31

Table 4.1: The Accumulated Money from Various Types of Loans

Type of Loans Amount (Billions)

Percentage

(%)

Personal Loans 8 23

SME's Loans 16 46

Cooperate Loans 5 14

Microfinance

Loans 6 17

TOTAL 35 100

(Source: Field data, 2011)

However the data shows that, SME’s type of loan take higher

percentage of money at the CRDB bank as shown in figure 4.1.

The cooperate type of loan at the respective bank take lower

amount of money (See also Fig. 4.1).

32

0

5

10

15

20

25

30

35

40

45

50

Personal Loans SM E's Coperate Loans M icrofinance LoansTypes of Loans

Percentage

Figure 4.1: The percentage of various types of loans at CRDB

Bank

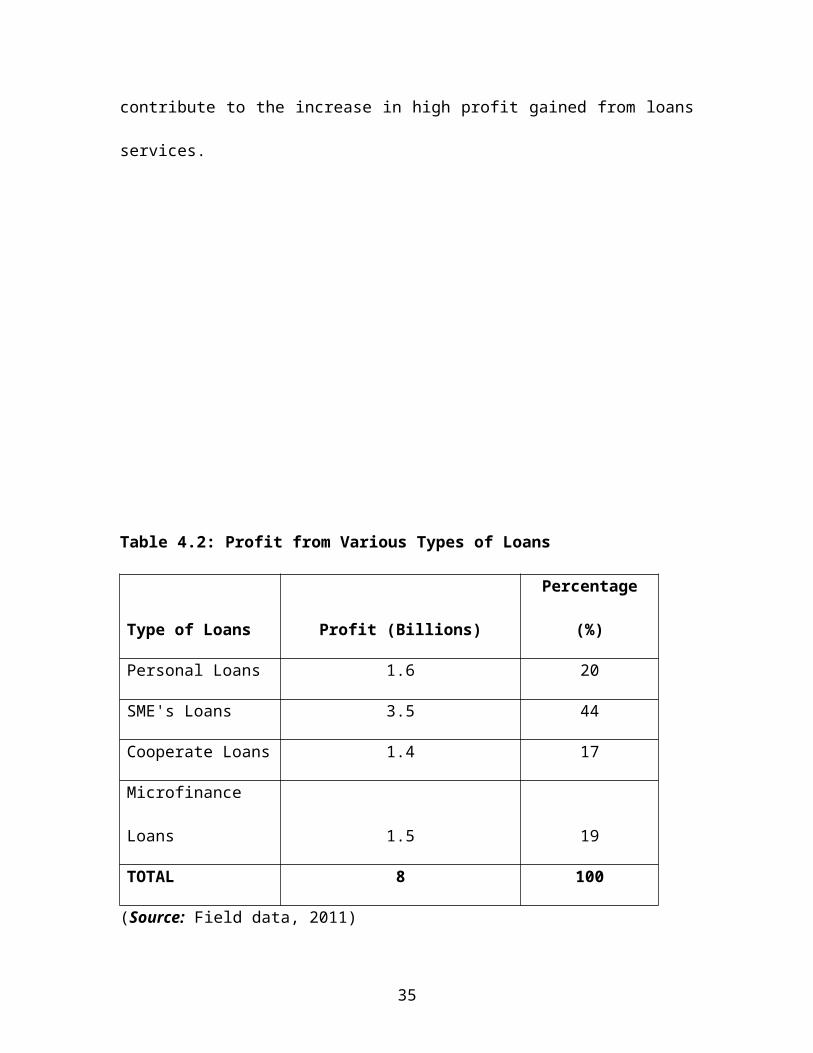

4.2 Amount of Profit from Loans

The study found that the profit obtained from loans services

is high compared to any other services provided to the

33

customers. The bank never get loss in loans services because

even if the customer delay or refuse to pay it at the end

the loan will be paid through different ways like selling

his or her securities or force his sponsor to pay it. The

profit is high because the customers have to pay interests

and various charges as explained underneath;

4.2.1 Application Fee

This is the fee paid by every customer who wants to borrow

from a certain bank; usually it is 1.5% of the whole loan.

That is from the whole loans give to customers its 1.5% is

the application fees

4.2.2 Commitment Fee

This is the fee for accepting the loan given to the

customers. It is usually 0.5% of the whole loans.

Other fees like documentation fees, loan facility fees,

grantee and indemnity fee, and debaucher fees all together

34

contribute to the increase in high profit gained from loans

services.

Table 4.2: Profit from Various Types of Loans

Type of Loans Profit (Billions)

Percentage

(%)

Personal Loans 1.6 20

SME's Loans 3.5 44

Cooperate Loans 1.4 17

Microfinance

Loans 1.5 19

TOTAL 8 100

(Source: Field data, 2011)

35

The data show that, the amount of profit obtained from

various types of loans differs accordingly with higher

profit accumulated from SME’s loans (See Table 4.2 and

Figure 4.2).

0

5

10

15

20

25

30

35

40

45

50

Personal Loans SM E's Cooperate Loans M icrofinance LoansTypes of Loans

Percentage

Figure 4.2: The profit accumulated from various loans at

CRDB Bank in Mtwara

4.3 The Relationship between Loans and Profit at CRDB Bank

36

The study found that in loans services usually the profit

increase with the increase in loans provided because all the

loans given to customers are paid even if it delays but at

the end it is paid and proper returns on loans provided to

borrowers (Table 4.3). Although sometimes bank officials in

loan department are forced to travel so as to know what

happens to their customers who failed or delay to pay back

the loan but still the amount of money used for that purpose

does not affect the profit obtained that is profit increase

with the increase in amount of money provided as loan.

Table 4.3: The Percentages of Loans and Profit accumulated

by CRDB Bank

Type of Loans Percentage Loan (%) Percentage Profit (%)

Personal Loan 23 20

SME's Loan 46 44

Cooperate Loan 14 17

Microfinance

Loan 17 19

TOTAL 100 100

(Source: Field data, 2011)

37

The data also from the present study show a positive trend

amongst the types of loans with higher percentage amount of

profit accumulated from SME’s loans (Figure 4.3).

0

5

10

15

20

25

30

35

40

45

50

Personal Loans SM E's Coperate Loans M icrofinance LoansTypes of Loans

Percentag

e

Figure 4.3: The comparison trend between types of loans at

CRDB Bank

38

4.4 The Relationship between Profit and Improvement in

Services to Customers

The study found that the CRDB bank distribute the profit

obtained from all bank operations to the department, in

these department the department of research and marketing

deal with finding out how to develop more and market more

their services to their customers by improving their

services as the way out to win the competitions. The

research found that the higher amount of bank profit comes

from the loans department therefore the profit obtained from

loans department and profits from other departments are

added together and used in different activities in bank (See

Table 4.4).

CRDB bank used to facilitate daily bank operations like

buying raw materials like computers, printers and other

resources used in banking operations. The bank also uses

profit obtained in paying salaries to their workers like

accountants, tellers and other different managers, who

always help customers to know different services to be

39

provided to them and thus their daily operations can lead to

development.

Again the bank use the profit in different management to

ensure that their work continue appropriately, CRDB bank

achieve this by employing external auditor so that he can

check the performance of the bank this reduce theft and

corruption. CRDB bank also increase salaries to their

workers so that they can work without any problem, where by

all these management activities motivate bank workers to

work hard and develop customers services they also help

their customers to achieve personal development.

The study found that CRDB bank provides a certain percentage

to research and marketing department for conducting research

so as to increase efficiency.

Table 4.4: The Percentage of Profit from Various Departments

at CRDB Bank

Department Percentage Profit (%)

Research and Marketing Department 20

40

Loans Department 25

Other Department 55

TOTAL 100

(Source: Field Data, 2011)

However, the data depicts higher trend of profit from other

departments (55%) but the loans department alone accumulate

a total profit of 25% which is very high profit compared any

other department at CRDB Bank in Mtwara-Mikindani

Municipality (Figure 4.4).

41

0

10

20

30

40

50

60

Research & marketing Loan Department Other DepartmentsDepartments

Percentage

Figure 4.4: Percentage profit accumulated by various

departments

CHAPTER FIVE

42

DISCUSSIONS, CONCLUSIONS AND RECOMMENDATIONS

5.0 Introduction

This chapter details the implications of the research

results and the conclusions drawn along with the

recommendations for future work.

5.1 Discussions

The study found that the CRDB bank plays great roles to the

community at Mtwara – Mikindani Municipality like other

commercial banks, they give loans to customers and advice

for business and money for project financing, it facilitate

foreign exchange to their customers and also operate

different accounts that is saving account, current account

and fixed account. This implies that the CRDB bank can gain

profit from these activities which can be used to finance

development in services to customers.

From the data obtained by this study shows that the CRDB

bank provide a lot of money to finance the loans

services to their customers they give personal loans to

43

individual customers with appropriate qualifications, Small

Medium Enterprise loans to small business man found in

Mtwara – Mikindani Municiplity and in other Mtwara Rural

areas like Tandahimba, Newala and other areas. This implies

that the bank gains more from loans department thus why a

large amount of money is located to it.

The present study found that CRDB bank gains profit from

loans service to customers, since profit is obtained from

the following formula; TP=TR−TC

Where;

TP= Total Profit

TR = Total Revenue

TC= Total Costs

The above equation shows that CRDB bank’s total revenue in

loans department is higher than the cost used to give out

loans this is the result of appropriate returns on loans

lent to borrowers. These indicate that CRDB bank can use the

profit to develop services to customers and even to the

44

whole bank departments since they can achieve them without

affecting their daily activities.

The data also show that in CRDB bank there is strong

positive relationship between the amount of loans they

provide to customers and the profit they gain from loans

services that is the profit from loans department increase

with the increase this is because the CRDB bank receive

appropriate interest and charges from loans they lend to

borrower that is they receive a lot from application fees,

commitment fees, guarantee fees, and interests on the loans

given to different kind of their customers. This implies

that the bank can develop the services to customers without

any problems because they gain a lot only from loans

department.

The result also show that there is relationship between the

profit obtained and the development in services to customers

because through the profit obtained by the whole bank which

includes all the profit obtained from loans department the

45

CRDB bank have developed customer services like they have

increased the amount of loans to customers which help these

customers to borrow more than before this can increase their

customers income which also result into personal development

and national development in whole, also CRDB bank introduced

SIM banking and mobile banks which help customers to operate

different services found in bank area without going at the

bank buildings, this reduce time to be spent in going at the

bank area and therefore customers can use such time to do

other works which can facilitate development of the whole

country.

Again CRDB bank provided different social services to the

society they provide different helps in term of money to

orphans, they help different primary school to construct

school buildings and also they sponsor sports and games.

Therefore CRDB bank support development in services to their

customers.

46

The study found also that the percentage given to the

department which can deal with the improvement in customer

services is granted the lowest percentage of profit. This is

consequence of absence of visible improvement in customer

services. The percentage given to the respective department

is also not enough to attain visible improvement. However,

the research and marketing department as well is given the

lowest percentage of the profit but still there is some

improvement generated interms of services to customers.

5.2 Conclusions

The study concludes that there is a significant improvement

in services to customers in CRDB bank in Mtwara - Mikindani

Municipality. This is consequent to loan service granted by

bank to the customers. The data show also that the profit

obtained from loans service at CRDB bank is higher than the

47

profit obtained from other services and thus promoting

sustainable development of bank.

The study conclude that there is a contribution of loans

service to bank development that is there is some

improvements in services to customers especially in the bank

studied CRDB bank in Mtwara - Mikindani Municipality

although the department with the mandate for improving the

customer service is given the lowest percentage of profit.

Therefore, it can be concluded that there is a significant

contribution of loans service to the bank development as it

improves services to customers which attracts more

customers. The customers in turn increase the bank profit

through interests and other charges hence fostering bank

development.

48

5.3 Recommendations

From the course of this study the following interventions

are recommendable for sustainable development of services to

customers at CRDB bank in Mtwara-Mikindani Municipality.

5.3.1 To Bank Customers

The study suggests that the bank customers especially in

loans services should make sure that they pay back their

loan on time to reduce some cost the bank incurs in

collecting these loans from them. That is customers should

provide true and valid information about themselves which

can be used when some problems occurs also they should

inform the bank if there is a problem which may lead to the

delay of paying back the loans given to them on time.

5.3.2 To Bank Officers

49

Bank officers especially for these who are concerned with

loans department they should provide training or seminars to

their customers so that they will know kind of loans

provided by the bank and how to use and allocate the loan s

given to them before he or she receive the loan, this will

help reduce the problems of customers failing to pay back

the loans just because they failed to plan for that loan.

Also bank officers should plan to develop services to

customers more than what they have done because the

customers are the one who help them to run their business

appropriately, thus if their services is improved

automatically the bank’s profit will increase.

5.3.3 To Government and other Stakeholders

The government should put policies and laws which will

sustainably support the acquisitions of loans by most of the

citizens regardless of the level and type of activities.

This intervention shall help customers and other

stakeholders to increase their income, employ themselves

which eventually result into increased GDP.

50

Also government should help their citizens to get education

on different services provided by different commercial banks

in the country as it is not possible for a bank to reach all

citizens at all. Thus government should try even to allow

seminars and training to be given to their citizens by

advising them to attend in those seminars and invite the

bank officers to provide training about their activities and

how they can be helped through those activities.

Also government should allow and support other individuals

who want to open other commercial banks; they should reduce

unnecessary requirements for some one to be allowed to open

the bank business. This will help citizens to get the bank

services at appropriate time since the available banks can

not afford to provide bank services to all citizens

appropriately.

51

REFERENCES

Adam, T. & Kamuzora, F. (2008) Research Method for Business

and Social Studies.

Mzumbe Book Project, Mzumbe,

Tanzania

Bluman, A.G. (2009) Elementary Statistics: A Step by Step

Approach, 7th Edition,

McGraw-Hill, New York.

Brue, S. L. (1990) Macro –Economics: Principles, Problems

and Policies, McGraw-Hill

New York.

Francis A. (2008) Business Mathematics and Statistics, 6th

Edition, C & C Offset, China.

Gordon, S. D. & Dawson, G. G. (1987) Introductory Economics,

6th Edition, D.C and

Health Company, Canada.

Griffin, R. W. & Ebert, R. J. (1991) Business, 2nd Edition.

Prentice Hall, Englewood

52

Cliffs, New Jersey.

Gupta, .S. P. (2006) Statistical Methods, 34th Edition,

Sultan Chand & Sons, New Delhi.

Kindwell, D. S, Peterson, R. L. & Blackwell, D. W. (2000)

Financial Institutions,

Markets and Money, 7 th edition,

Harcourt College publisher.

Mankwi, N. G. (2004) Essential of Economics, 3rd edition,

Thomson South –Western.

USA.

McConnel, R. C. & Brue, I. Stanley (2005) Economics:

Principles, problems and

Policies, 6 th Edition, McGraw-

Hill Irwin, New York.

McEachem, W. A. (2006) Economics: A Contemporary

Introduction, Thomson south -

Western, New York.

Nickels, W. G., McHugh, J.M. & McHugh, S.M. (1996)

Understanding Business, 5th

53

Edition, McGraw- Hill Irwin,

New York.

Spencer, D.E. (1990) Study Guide Parking Economics, Addis –

Wesley, New York.

Rosenhan, D. & Seligman, M. E. P. (1989) Abnormal

Psychology, 2nd Edition, Library of

Congress Cataloging, New

York.

Tregarthen, T. & Rittermberg, L. (2000) Economics, 2nd

Edition, Worth Publishers,

New York.

Wild, J. J., Subrarnyan, K. R. and Halsey, R. F. (2007)

Financial Statement Analysis,

McGraw- Hill Irwin, New York

54

APPENDIX

Interview Questions for Bank Officials

I am a student from Stella Maris Mtwara University College

conducting a research at your organization for partial

fulfillment of my degree Bachelor of Arts with Education. I

kindly request your assistance and support in answering

these questions.

.

1)How much do you provide for loans service?

55

…………………………………………………………………………………………………………………………………………………

…………………………..

2)How much do you obtain from loans service as profit?

…………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………..

3)What is the relationship between the amount you provide

as loans and the amount of money you obtain as profit

from loans service?

…………………………………………………………………………………………………………………………………………………

……………………………………………………………………………………………………………………

4)What is the relationship between the profit obtained

and the development on services to customers?

…………………………………………………………………………………………………………………………………………………

……………………………………………………………………………………………………………………

56

![Tulkintoja olennaisesti kiistellyistä käsitteistä [Final draft]](https://static.fdokumen.com/doc/165x107/632058f518429976e4062a20/tulkintoja-olennaisesti-kiistellyistae-kaesitteistae-final-draft.jpg)