Lending Technologies in Italy: an Example of Hardening of Soft Information

27

1 Lending Technologies in Italy: an Example of Hardening of Soft Information? Pierluigi Murro * Abstract In questo articolo si studia il rapporto tra l’impresa e la sua banca principale in un ampio campione di imprese manifatturiere italiane. I risultati mostrano che le imprese ricevono credito attraverso differenti tecnologie di finanziamento. Questa complementarietà tra tecnologie sembra avere una base informativa, infatti la presenza della soft information risulta essenziale nella scelta di ciascuna tecnologia. Questo risultato conferma quel filone della letteratura che sottolinea la presenza di un processo di hardening of soft information, ossia la possibilità che anche le banche transazionali siano in grado di utilizzare l’informazione qualitativa, normalmente considerata una prerogativa delle banche relazionali, per concedere il credito alle imprese. We study the firm-main bank relationship in a large sample of Italy’s manufacturing enterprises. Our results show that the same firm tends to receive credit via different lending technologies. This complementarity across technologies may have an information basis, because the use of soft information is crucial for each lending technology. This supports the hardening-of-soft- information view, whereby also transactional lenders might somehow use difficult to codify qualitative information – traditionally believed a prerogative of relational banks – on borrowing enterprises. Key words: Lending technology, Transactional lending, Relationship lending and Small-and- medium sized enterprises JEL Classification: G21, L14, L22 * University of Bari (e-mail: [email protected] ).

Transcript of Lending Technologies in Italy: an Example of Hardening of Soft Information

1

Lending Technologies in Italy: an Example of Hardening of Soft Information?

Pierluigi Murro*

Abstract

In questo articolo si studia il rapporto tra l’impresa e la sua banca principale in un ampio

campione di imprese manifatturiere italiane. I risultati mostrano che le imprese ricevono credito

attraverso differenti tecnologie di finanziamento. Questa complementarietà tra tecnologie

sembra avere una base informativa, infatti la presenza della soft information risulta essenziale

nella scelta di ciascuna tecnologia. Questo risultato conferma quel filone della letteratura che

sottolinea la presenza di un processo di hardening of soft information, ossia la possibilità che

anche le banche transazionali siano in grado di utilizzare l’informazione qualitativa,

normalmente considerata una prerogativa delle banche relazionali, per concedere il credito alle

imprese.

We study the firm-main bank relationship in a large sample of Italy’s manufacturing enterprises.

Our results show that the same firm tends to receive credit via different lending technologies.

This complementarity across technologies may have an information basis, because the use of

soft information is crucial for each lending technology. This supports the hardening-of-soft-

information view, whereby also transactional lenders might somehow use difficult to codify

qualitative information – traditionally believed a prerogative of relational banks – on borrowing

enterprises.

Key words: Lending technology, Transactional lending, Relationship lending and Small-and-

medium sized enterprises

JEL Classification: G21, L14, L22

* University of Bari (e-mail: [email protected]).

2

Lending Technologies in Italy: an Example of Hardening of Soft Information?

Abstract

We study the firm-main bank rapport in a large sample of Italy’s manufacturing

enterprises. Our results show that the same firm tends to receive credit via different

lending technologies. This complementarity across technologies may have an

information basis, because the use of soft information is crucial for each lending

technology. This supports the hardening-of-soft-information view, whereby also

transactional lenders might somehow use difficult to codify qualitative information

– traditionally believed a prerogative of relational banks – on borrowing

enterprises.

1. Introduction

The choice of lending technology is a key component for the strategy of a small and

medium-sized enterprise (SME). Berger and Udell (2006) hold that lending

technologies play a key role as the conduit through which government policies and

national financial structures affect SME credit availability. These authors define a

lending technology as a unique combination of primary information source, screening

and underwriting policies/procedures, loan contract structure, and monitoring

strategies/mechanisms.

The mainstream literature generally distinguishes two ways in which SMEs are

financed by banks, depending on the type of information which is exchanged between

the firm and the bank. A transaction-based lending technology refers to a firm-bank

report in which the bank obtains from the borrowing firm “hard” type information, that

is quantitative in nature and, so, easily transferable. At the other extreme, a relationship

lending technology hinges on “soft” information, that is qualitative information that are

normally obtained via long-term informal/personal interaction and are, therefore, much

more difficult to transfer. Because of this, the academic literature views the “transaction

lending” technology as more desirable for relatively informationally transparent firms,

while judging the “relationship lending” technology to be more appropriate for

comparatively opaque firms (suffering more intense asymmetries of information).

Although this taxonomy is quite useful and interesting from a theoretical point of

view, its validity has been questioned on empirical grounds. In fact, this classification

derives from the idea that there are two types of production functions which use distinct

inputs: hard and soft information. However, the nature of information is not

exogenously fixed. The lenders practices of the latest years show us that it may be

possible to change the nature of information.

3

Berger and Udell (2006) underline that many banks lend to opaque SMEs by means

of transaction-based lending technologies, thereby dealing with informational

asymmetries by means of “hard” information. In fact, where no detailed and trustworthy

financial accounts are available, the large banks may often use other “hard” type

information to assess the probability that the enterprise will repay the loans it was

granted. This approach was tested by Uchida et al. (2006) investigating the choice of the

lending technologies on data for Japan. They found there is complementarity among

technologies. According to the authors, this result suggests that the banks, even though

possibly employing mainly some specific criteria to lend, might be using the various

lending technologies at the same time.

An alternative interpretation is that the “transactional” lending technologies have

become better substitutable to the “relational” ones, which could also explain the joint

adoption of different lending technologies at the same customers. For instance, Petersen

(2004) conjectures that transactional lenders might be able to “harden” soft information

to boost their local competitive behavior and allow them to compete more aggressively

outside core markets.

In the present paper, we utilize a novel component of survey micro-data allowing us

to learn the lending technology used by the firm’s main bank. The data refer to the end

of 2006 and come from the Tenth Survey of Italian Manufacturing Enterprises runs by

UniCredit Group. Based on these questions, we created four lending technology indices

which correspond to three transaction-based lending technologies and the one

relationship lending technology: (1) financial statement lending, (2) real estate lending,

(3) other fixed-asset lending; and (4) relationship lending. These indices represent the

extent to which a bank loan bears the characteristics of each of the four lending

technologies.

We first investigate (i) to what extent different lending technologies are used in terms

of the presence in the loan market, i.e., the level of usage of the four lending

technology. We then look into (ii) how complementary these technologies are. This

analysis focuses on the degree of correlation among the four indices. Finally, we

investigate by regression analysis (iii) what determines the choice of each technology.

Our dependent variables in these regressions are the four lending technologies as

measured by our indices. Our key independent variables of interest are the type of bank

lender and the availability of different kinds of information.

4

In line with the results obtained for Japan, we find indications of complementarity

among the various lending technologies, as the same firm obtains bank loans through

the various technologies. The existence of this complementarity makes it difficult to

identify the determinants of using a lending technology as an alternative to the others.

Nevertheless, we can notice that the use of soft information is strongly associated with

the bank’s reliance on the relationship lending and financial statement lending, although

it seems to be important for all the lending technologies. These results help us interpret

the complementarity among the technologies that was already suggested previously. We

may label this “information complementarity”, since it turns out that SOFT is

significant for all the four technologies. This outcome seems consistent with the

possibility of hardening soft information.

In the rest of the paper section 2 briefly discusses the literature on the ways for the

SMEs to obtain external finance. Section 3 is devoted to present the dataset we use,

explaining also our methodology to construct the variables we employ. In section 4 we

run our econometric analysis and show our main results. Section 5 concludes the paper.

2. Survey of the Literature

Among the various lending technologies used to finance SMEs, the literature has

thus far focused on two classes: transaction-based lending technologies and

relationship lending technologies. These two classes can be primarily distinguished by

means of the type of information a bank uses in granting and monitoring the loan.

Transaction-based lending technologies are typically based (primarily) on “hard”

quantitative information (e.g. those derived from the borrowers’ balance sheets and/or

the collateral guarantees they offer), while instead relationship lending assigns a key

role to “soft” information (difficult to codify qualitative information obtained via

personal interaction/acquaintance).

Both the theoretical and the empirical literature have mainly focused on the

characteristics and the possible pros/cons of “relationship lending”. This is, in fact,

considered the most appropriate technology to lend to firms with significant

informational asymmetries, as a tighter firm-bank relationship helps overcome those

informational asymmetries, improving the efficiency of the bank’s allocation of loans.

Boot (2000) defines relationship lending as “the provision of financial services by a

financial intermediary that: i. invests in obtaining customer-specific information, often

proprietary in nature; and ii. evaluates the profitability of these investments through

5

multiple interactions with the same customer over time and/or across products”. The

definition hinges on two crucial aspects: eliciting the release of “proprietary”

information from the client to the bank and the presence of multiple interactions

between the two parties.

The empirical research tried to test the results derived from the theoretical models. In

particular, several papers have analyzed – in various countries – the impact

“relationship lending” has on the financing of the SMEs. For the US, Berger and Udell

(1995) show that a longer firm-bank relationship lowers the cost of credit and reduces

also the requirements of collateral guarantees. On data for Italy, Angelini et al. (1998)

find that the intensity of “relationship banking” reduces the probability that borrowing

firms will be rationed, even though the lending rates charged by the banks tend to

increase as the firm-bank relationship lengthens. For Belgian enterprises, Degryse and

Van Cayseele (2000) detect the impact relationship banking along two different

dimensions: borrowing rates increase as the firm-bank relationship lengthens, while

borrowing rates decrease when the scope of the firm-bank relationship – defined as the

purchase of additional information intensive services (other than the loan) – increases.

Recently, both the theoretical and the empirical strands of the literature analyze also

the transaction-based lending technologies. Often, the literature has used the transaction

lending label for any type of loan based on information that is easily verifiable by

anybody. Instead now some authors underline that transaction lending is not a single

homogeneous lending technology. There are a number of distinct transaction

technologies used by financial institutions. Berger and Udell (2006) suggest that into

transactions technologies are including financial statement lending, small business

credit scoring, asset-based lending, factoring, fixed-asset lending, and leasing. The

authors briefly define and describe each of the lending technologies, highlight its

distinguishing features, and show how the technology addresses the opacity problem.

Each technology is distinguished by a unique combination of the primary source of

information, screening and underwriting policies/procedures, structure of the loan

contracts, and monitoring strategies and mechanisms.

Also the empirical literature tries to explain the characteristics of the each

technology. There are a number of studies on each individual technology in isolation.

For example, Berger and Frame (2006) study credit scoring and Udell (2004) asset-

based lending. However, most of these studies focus only on one lending technology

without consideration of other technologies.

6

Differently from these studies, Uchida et al. (2006), utilizing survey micro-data on

Japanese SMEs, tested the importance of the various “lending technologies” proposed

by Berger and Udell (2006). Specifically, they consider four lending technologies:

financial statement lending, real estate lending, other fixed-asset lending, and

relationship lending. Using the responding firm’s answer to the question as to which

were – in the firm’s own view – the criteria followed by its main bank to grant its loans,

the authors created a distinct index for each of those four lending technologies.

Analyzing econometrically the determinants of each index, the authors find there is

complementarity among the indices of the four technologies. This result suggests that

the banks, even though possibly employing mainly some specific criteria to lend, tend to

use the various lending technologies at the same time.

Although the literature generally distinguishes the lending technologies on the basis

of the type of information which is exchanged between the firm and the bank, some

contributions have been exploring the ability of harden soft information. In the previous

literature, the idea has been that there are two types of production functions which use

distinct inputs: hard or soft information. However, Petersen (2004) highlights that the

nature of information is not exogenously fixed. This is a simplification. The lenders

practices of the latest years show us that it may be possible to change the nature of

information.

The development of credit scoring is a typical example of the lenders’ ability to

harden soft information. The results in Agarwal and Hauswald (2006) verify the

conjecture in Petersen and Rajan (2002) that technological progress in the form of credit

scoring allows banks to overcome distance-related limits to lending through the

hardening of soft information. Berger and Frame (2007), using a survey conducted by

the Federal Reserve Bank of Atlanta in 1998, show that banks tend to use the credit

scoring technology in very different ways to achieve quite different objectives. In some

cases, banks use “rules” to automatically accept/reject credit applicants and to set credit

terms based on purchased credit scores. Other institutions use more of their own

“discretion” by adding credit scores to information gathered through one or more of the

other lending technologies (i.e. relationship lending). The motives for these banks are

likely to reduce opacity problems and set the credit terms more accurately to reduce

future credit losses. Some contributions suggest that “discretion” banks are successful in

lowering the reported risk and lengthening the maturity of their small business credits.

Albareto et al. (2008), reporting the results of an Italian survey conducted by Bank of

7

Italy in 2007, illustrate that medium and large banks use soft information (like

qualitative information on the firm’s governance) in their credit scoring models.

Finally, are interesting the results in Bartoli et al. (2010), based on the same survey

that we use. The authors show that, although the same firm tends to receive credit via

different lending technologies, the soft information variable lowers (raises) the

probability of rationing if the firm’s main bank uses relationship (transactional) lending

technologies. Thus, it appears that the way the soft information becomes embodied in

the lending decision might still differ between relational vs. transactional

banks/technologies.

3. Data and Methodology

3.1 Presenting the Dataset and Some Descriptive Statistics

Our main data source is the Tenth Survey on Italian Manufacturing Firms (SIMF),

runs by the Unicredit banking group in 2007. Every three years this survey gathers data

on a sample of Italian manufacturing firms having more than 10 employees. The 2007

wave consists of 5,137 enterprises. All the firms with more than 500 employees are

included, while those having a number of employees in the range 11 to 500 are sampled

according to a stratified selection procedure based on their size, sector, and geographic

localization. The main strength of this database depends on the very detailed

information it collects on individual firms. In particular, the 2007 wave features

information regarding the firm’s: a) ownership structure; b) number and skill degree of

employees; c) attitude to invest in R&D and whether it has made innovations; d) extent

of internationalization and exports; e) quality of the financial management and

relationships with the banking system. This information is gathered through a survey on

the three years previous to the survey year (thus, for the wave we use data go from 2004

to 2006).

The firms in the sample cover approximately 9% of the reference universe in terms

of employees and some 10% in terms of value added. Thanks to its stratification, the

sample is highly representative of the economic structure of Italian manufacturing.

Table 2 presents some descriptive statistics. At the mean, the surveyed firms have been

in business for 22 years; beyond 60% of them have fewer than 50 employees (below 4%

of the firms have more than 500 employees); 70% of them are localized in the North.

Only 1% are listed in the Stock Exchange, while 37% have their profit/loss and

8

financial statements certified by external auditors. As to sectoral specialization, almost

half of the enterprises belong to traditional sectors, according to the Pavitt classification,

while only 5% have their business in the high tech sectors.

Moving on their financial set up, the average length of the relationship with the main

bank is 17 years; 49% of the firms have a national bank as their main banking

counterpart, 10% entrust a banca popolare (larger-sized cooperative banks), 7% feature

a savings bank as their main bank, 5% entrust a banca di credito cooperativo (smaller-

sized cooperative mutual banks), while 28% of the firms have another type of bank as

their main bank. Finally, there is extensive multiple banking: on average firms have five

banks and the share of loans obtained from the main bank is 32% of the total banking

loans received.

Particularly relevant for our analysis, the 2007 wave of the survey features a

peculiarity with respect to the previous waves. Specifically, an entirely new set of

questions was introduced (partly inspired by an analogous detailed survey on SME

financing run in Japan, see Uchida et al. 2006; 2008), expressly tailored to investigate in

depth the relationship between the firm and its main bank. In this paper we will

particularly focus on two questions where the firm is asked to state which of the

characteristics – choosing from a given list – have been important in the firm’s selection

of its main bank, as well as stating which characteristics, in the firm’s view, best

describe the way its main bank grants credit. Unsurprisingly, given the fact that this

section of the survey required dedication, only one third of the total number of surveyed

enterprises (exactly 1,541 firms) answered these questions. Table 3 reports descriptive

statistics for this sub-sample of enterprises. We cannot rule out self-selection. In other

words, it is possible that the choice by a firm to answer this part of the questionnaire

was not random.

3.2 Construction of the Lending Technology Indices

We first characterize actual loans from a lending technology point of view. We

consider four indicators of lending technology similar to those in Uchida et al. (2006).

The indices are constructed to represent to what extent the relevant loans have

characteristics of different lending technologies. We capture these characteristics

inspecting the answers to the question “In your view, which criteria does your bank

follow in granting loans to you?”. In answering this question the firm was required to

give a weight (going, in descending order, from 1, very much, to 4, nil) to fifteen factors

9

(see the Appendix). Most of these factors are related to one of the lending technologies.

We then link the factors that we believe to be most closely associated with each lending

technology based on the Berger and Udell (2006) classification scheme. For reason of

comparability of our results with those in Uchida et al. (2006), we focus only on four

lending technologies from this classification.1

First, financial statement lending, is a transactions technology based primarily on the

strength of a borrower’s financial statements. Berger and Udell (2006) hypothesize that

banks underwrite commercial loans using the financial statement lending technology for

firms with a strong financial condition based on an assessment of verified (i.e., audited)

financial statements. From the list of fifteen criteria shown in the Appendix, we use the

initial four. These factors (financial solidity, profitability, growth of sales and ability of

the firm to repay its debt) represent qualities that are best assessed by an analysis of the

firms’ audited financial statements. From these four factors we created the financial

statement lending index, LT_FS, by calculating the average of the four dummy

variables which take a value of one if the firm answered 1 (very much) to the four

relevant lending factors, respectively. The virtue of using an average index is that it can

be directly compared with the other (averaged) indices, as we explain below, since all

the indices are constructed from dummy variables and thus take a value in the [0,1]

range.2

Next, we focus on fixed-asset lending. Fixed-asset lending technologies involve

lending against assets that are long-lived and are not sold in the normal course of

business (e.g., equipment, motor vehicles, or real estate). The factors that are related to

fixed-asset lending are items 5, 6 and 8. Keeping the distinction in Uchida et al. (2006),

we make a clear difference between real estate lending and other fixed-asset lending,

and so we construct two indices. The first, LT_RE, is a dummy variable that take the

value one if the firm answered 1 (very much) to lending factor no. 5. Second, LT_OF, is

an average of the two dummy variables which take a value of one if the firm answered

1 (very much) to lending factors no. 6 and 8, respectively.3

1 As mentioned above, Berger and Udell (2006) list six transaction-based lending technologies: (i)

financial statement lending, (ii) small business credit scoring, (iii) asset-based lending, (iv) factoring, (v)

fixed-asset lending, and (vi) leasing, together with relationship lending. 2 We also conducted preliminary analysis using the first principal component of the principal component

analysis over the dummy variables. Because the results were qualitatively the same, and because we

cannot easily compare these indices with each other, we only report results with the averaged indices. 3 Note that the basic technology used in real estate lending and other fixed-asset lending is the same, and

the distinction is solely based on the type of collateral.

10

Finally, we consider the relationship lending technology. Under relationship lending,

the financial institution relies primarily on soft information gathered through contact

over time with the SME, its owner and the local community to address the opacity

problem. We construct the relationship lending index, LT_RL, using the factors that

seem most related to soft information accumulation by banks through close

relationships. The index is an average of six dummy variables which take a value of one

if the firm answered 1 (very much) to lending factors, no. 9, 10, 11, 13, 14 and 15,

respectively.

These indices are not likely to be perfect proxies for the use of different lending

technologies, since they are based on the borrowers’ perception of the lending factors

used by the bank in underwriting its loans, and thus may not be precisely capturing the

banks’ screening process. However, this methodology of constructing the indices of

lending technologies has some advantages. We manage to perceive the actual features

of the bank (in the firm’s view) at the time the firm is asked. No such information was

available in the prior literature.

3.3 Methodology

In our analysis we will investigate the characteristics of the SME lending

technologies in Italy. Comparing across the various lending technology indices, we will

ascertain which one is more widespread. In addition, bearing in mind the results in

Uchida et al. (2006) referring to the Japanese market, we will analyze the degree of

complementarity among the various technologies, by looking at the correlation among

the indices as well as via a multivariate regressions of the indices. However, the most

important aspect pertaining to the study of the features of the SME lending technologies

regards identifying which factors affect the choice among these technologies.

We run regressions in which the four lending technology indices introduced above

are used as dependent variables. We use the following equation:

Lending Technologyiz = + 1 Softi + 2 Auditi + 3 Locali + 4 Agei + 5 Age-squaredi + 6

Sizei + 7 Performance_DSi + 8 Performance_SDi + 9 Performance_DDi + 10 Centeri + 11

Southi + 12 HHi + 13 Branchi + 14 Leveragei + 15 ROAi + 16 GDPi + 17 Corporationi + 18

SITC5i + 19 SITC4i + 20 SITC3i +

14

1J

ijj Sector + ui (1)

11

where i = 1, …, N represents the firm, j = 1, …, 14 is the economic activity sector, and

z = financial statement, real estate, other fixed-asset and relationship lending.

The lending index for firm i depends on characteristics of the lender and of the

borrowing SME that affect the feasibility and efficacy of each individual lending

technology. Hence, the variables that we use are a proxy for the inputs of the

technologies. We may separate these variables among bank complexity, nature of

information, bank competition, and firm characteristics.

We first classify banks into two types: LARGE banks and LOCAL banks. LARGE is

a dummy variable that takes value one if the main bank is a national bank or a foreign

bank. In turn, LOCAL is also a dummy taking value one if the main bank is a banca di

credito cooperativo, banca popolare, a saving bank or “other type of bank”.

Next we control for the availability of hard and soft information. The variable that

we use for hard information is AUDIT, a dummy variable that takes value one if the

firm has its financial statements audited. Instead, for the soft information, we employ a

methodology used by Scott (2004) and Uchida et al. (2006), to construct SOFT. The

Scott index is a composite measure of soft information production based on the

borrowing firm’s ratings of bank performance characteristics obtained from the Credit,

Banks and Small Business survey conducted by the National Federation of Independent

Business in 2001 in the United States. Specifically, we use a question available in our

survey: “Which characteristics are key in selecting your main bank?”. In answering this

question the firm was required to give a weight (going, in descending order, from 1,

very much, to 4, nil) to fourteen factors (see the Appendix). Six of the fourteen

characteristics are related to soft information: characteristics no. 1 through 6. Using

these six characteristics and following a similar procedure to Scott (2004), we created

our measure of soft information production.4

We also use different variables to represent firm characteristics as controls. AGE is

the age of the firm (we consider also the age squared, AGE-squared), SIZE is the

logarithm of the number of employees, CORPORATION, a dummy variable that takes

value of one if the firm is a joint stock company, and the degree of financial leverage

(LEVERAGE), given by the ratio of total liabilities to the sum of the total liabilities and

the firm’s assets.

4 For each of the six characteristics related to soft information, we constructed a dummy variable, which

takes a value of one if the firm chose 1. SOFT is the first principal component of the principal component

analysis over the resulting six dummies.

12

We use four independent variables to represent the firm’s performance. Three of

them are based on the firm’s financial statements. PERFORMANCE_DS is a dummy

variable indicating that the firm first posted a deficit (D) and then a surplus (S) (i.e.,

unprofitable and then profitable) in the past two years. PERFORMANCE_SD and

PERFORMANCE_DD are created similarly (surplus followed next year by

deficit/deficit followed next year by another deficit). The base case reflects two

consecutive years of surplus. The fourth performance related explanatory variable is

ROA (Returns on Assets), to control for firm’s profitability. Another factor to consider

is the extent of diversification. Plausibly, the higher the number of sectors in which the

firm is active, the more diversified is the firm. We thus code dummy variables for

whether the firm is classified in a three-, four-, or five-digit SITC sector.

We control also for the firm’s geographic localization (CENTER and SOUTH

dummies), its sector according to two-digit SITC classification and the average rate of

growth of value added in the province (GDP). Finally, we insert some variables

describing the local bank competition: the mean of the province level Herfindahl-

Hirschman concentration index from 1990 to 2006 (HHI) and the average number of

branches in the province (BRANCH)5.

Due to possible complementarity among the lending technologies, it is possible that

endogeneity problems arise in our analysis. It is essentially for this reason that we

estimated our model also with a two-stage approach. Thus, we estimate the regressions

also using a 2SLS (two-stage least squares) method.6

4. Results

4.1 Complementarity Among the Lending Technologies

Let us consider first the relative importance of each lending technology individually,

by directly comparing the magnitude of the corresponding index together with the

5 The level of competition may not only affect the overall supply of credit from all types of lending

technologies but may have a different effect on relationship lending. Under high competition, banks may

use relationship lending as an instrument to differentiate themselves from other banks. Relationship

lending, however, may be a sunk cost that makes it extremely costly to rely on soft information. 6 We use three instrumental variables. The first one is a dummy variable (MEET) which takes a value of

one whether contact between the firm and the loan officer is typically direct rather than by telephone,

email or other indirect methods. The other two instruments are typical in the literature on bank- firm

relationship. They are: the number of saving banks – per thousand inhabitants – measured at the province

level, refer to 1936, when a long-lasting new banking law virtually froze Italy’s banking structure for

several decades; and the average number of net branches created by incumbents in the province in the

period 1991-1998. See Guiso et al. (2003, 2004) and Herrera and Minetti (2007) for a more detailed

justification of the use of these instruments.

13

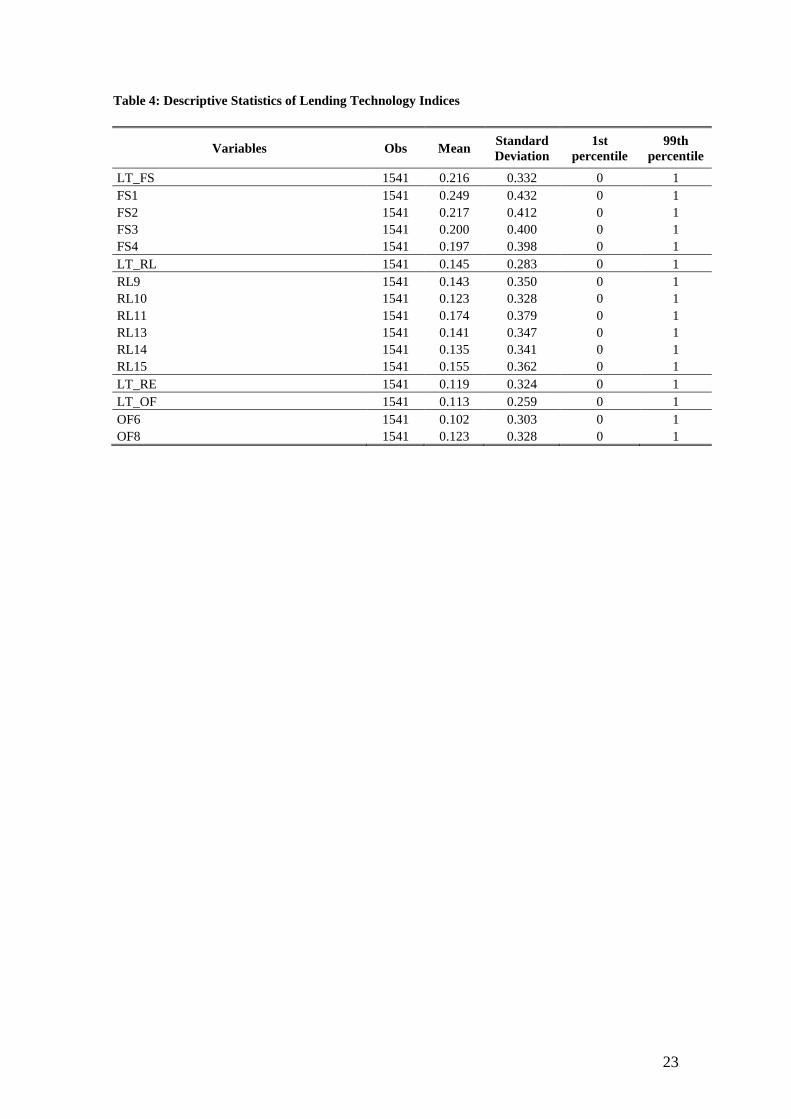

dummy variables constituting the index. Table 4 shows the summary statistics of these

variables. The lending factors related to financial statement technology are relatively

more frequently emphasized, so the index of financial statement technology is the

largest among the four indices. This shows that the financial statement technology is the

most frequently used lending technology. This result is robust also for each bank type.7

The relationship lending index is the second most important index. The real estate

lending index is the next largest, instead the other fixed-asset lending is the least

frequently used lending technology.

This finding does not allow for the possibility that these lending technologies may

not be strictly distinct from each other and, as a result, some complementarity might

exist among them.

For this reason we now proceed with the analysis of the interrelationship between the

four lending technologies. In fact, it is possible that different technologies complement

each other. In particular, it is possible that two technologies require screening and

monitoring processes that are similar in nature and in intensity, and so these may be

used in tandem.

The first analysis that we make is about the correlation among the four lending

technology indices. Table 5 shows their coefficients of correlation. Any combination of

indices appears significantly correlated, and the magnitude of the correlation is very

high among all the lending technologies. The correlation between LT_FS and LT_RL is

the biggest. An interpretation of this result is that the financial statement lending

technology and the relationship lending technology are highly complementary and their

technologies are used in tandem.

We obtain a similar result between LT_RE and LT_OF. This seems natural since

they are both based on an underwriting process that focuses on assessing the liquidation

value of a fixed-asset. Instead, the high correlation between LT_RL and LT_OF is

somewhat unexpected.

To confirm these results, we run a multivariate regression model among the four

indices. Furthermore, this analysis should contain information about which combination

of lending technologies is the most important when all the technologies are to some

7 The level of LT_FS was 0.192 for the firms for which the main bank is either a national bank, 0.214 for

those for which the main bank is a foreign bank, 0.166 for those of for which the main bank is a banca

popolare, 0.2 for those for which the main bank is saving bank, and 0.23 for those for which the main

bank is banca di credito cooperativo. The ranking among the four indices are the same even if we

compare by bank type, except for national bank, where the relationship lending index is the lower.

14

extent used at the same time. The results, shown in Table 6, are consistent with the

results in Table 5. Again, judging from the magnitudes of the coefficients, relationship

lending is closely tied with financial statement lending and other fixed-asset lending,

instead real estate lending is linked with other fixed-asset lending.

4.2 The Choice of the Lending Technology

Table 7 reports the results of the regressions on the four lending technologies we

considered. These results help us interpret the complementarity among the technologies

that was already suggested previously. We may label this as “information

complementarity”, since it turns out that SOFT is significant for all the four

technologies. In addition, for each one of the three transactional lending technologies

(financial statement, real estate and other fixed-assets), SOFT turns out more significant

than our proxy of hard information, that is the presence of external auditing. This

outcome might suggest that a process of “hardening of soft information” is under way8.

As to the other variables, in line with the results obtained by Uchida et al. (2006) for

the Japanese market, only few of the explanatory variables are significant. Starting with

the regression for the financial statement lending technology, we may notice that the

presence of external auditing is only marginally significant. This result is particularly

surprising, in as much as this technology is primarily based on the information retrieved

from the enterprise’s accounts. Thus, our a priori was that more trustworthy statements

would affect this lending technology to the largest extent.

An analogous result was obtained by Uchida et al. (2006). That paper shows that the

presence of external auditing significantly affects the use of this technology for the

smaller-sized firms. For this reason, we perform a similar procedure on Italy’s data.

Restricting the sample to those firms with fewer than 50 employees, our general result is

confirmed while AUDIT is barely significant. Beside SOFT, the other variables

increasing the likelihood of the choice of the financial statement lending technology are

a higher leverage and more diversification of the firm. The use of the financial

8 We have shown there is pervasive complementarity among lending technologies, and we have underline

the fundamental role of soft information. It would be interesting clarify how and if the increasing role of

soft information helps mitigate all the inefficiency stemming from information asymmetry. Bartoli et al.

(2010) try to do this. They show that, although the same firm tends to receive credit via different lending

technologies, the soft information variable lowers (raises) the probability of rationing if the firm’s main

bank uses relationship (transactional) lending technologies. Thus, it appears that the impact of soft

information still depend on lending technologies.

15

statement lending technology is instead less likely for higher ROA as well as having a

LOCAL bank as the firm’s main bank.

As to the real estate lending technology, both SOFT and AUDIT increase the

probability this technology will be chosen, while a high growth of provincial value

added lowers such probability. These results seem consistent with theory. Also using

the “fixed assets” lending technology is more likely when the firm has its statements

subject to external auditing and less likely when the firm exhibits low diversification.

As to the “relationship lending” technology, the only significant regressor in our

estimates is SOFT.

Table 8 reports the results of the regression performed using instrumental variables.

By and large these results confirm those obtained without instrumenting. Indeed, SOFT

is significant for all lending technologies excluding the real estate technology.

Furthermore, our tests to check for the endogeneity of SOFT find this situation is

confirmed only for “financial statement lending”.

5. Conclusions

In this paper we studied the extent of the recourse to the various technologies utilized

by the banks to lend to the SMEs in Italy. Employing the Tenth Survey on Italian

Manufacturing Firms, carried out by Unicredit at the end of 2006, we checked which

ones of the lending technologies are more widespread and which are the determinants

behind the choice of any of them. Specifically, we build on a recent strand of literature

stressing that banks lend to small and medium-sized enterprises via different lending

technologies. Accordingly, it is believed that, partly thanks to the enormous progress in

ICT, even transactional lenders – the banks once granting loans only based on “hard”

(e.g. balance sheet) information provided by the SMEs – may now be lending to SMEs

referring also to firm’s “soft” information (e.g. difficult to codify qualitative

information obtained via personal interaction/acquaintance). This process – labeled the

hardening-of-soft-information hypothesis – has three important implications. First, the

traditional distinction between relationship and transactional lenders becomes blurred.

Second, it is possible that different lending technologies – once believed alternatives –

are indeed complements. Third, in spite of the complementarity, the use of soft

information might have different implications depending on the lending technology. We

address these issues focusing particularly on the second one.

16

Our analysis on the factors affecting the choice of one technology over the others

showed that the use of soft information is crucial for each one of the technologies. This

suggests the complementarity across technologies may have an information basis. In

other words, the various lending technologies may be used at the same time exactly

because they employ a common information support. This evidence is partly at odds

with the theoretical prediction that the transactional technologies should rely almost

exclusively on hard information. The role played by soft information in accounting for

the use of transactional lending technologies seems to confirm the existence of a process

of “hardening of soft information”. Recently, the theoretical literature on SME

financing – and especially that addressing credit scoring – has, in fact, underscored the

trend by which the banks tend to include qualitative information within transactional

lending technologies.

Our analyses suggest deeper studies are needed to understand all the underpinnings

of how soft information affects SME lending. In fact, if, on the one hand, the use of

qualitative information seems fundamental to explain the choice of each lending

technology, on the other hand, it is possible that such use have rather different impacts

on the bank’s decisions depending on the prevailing lending technology of the bank.

Particular attention should be devoted to studying the determinants affecting the choice

of each lending technology. In carrying out this study, it could prove most useful to

explicitly consider the complementarity among technologies, which makes it more

difficult identifying the key elements behind the bank’s decisions.

17

References

Albareto, G., Benvenuti, M., Mocetti, S., Pagnini, M., Rossi., P., 2008.

L’organizzazione dell’attività creditizia e l’utilizzo di tecniche di scoring nel

sistema bancario italiano: risultati di un’indagine campionaria. Questioni di

Economia e Finanza 12, Bank of Italy.

Agarwal, S., Hauswald, R., 2006. Distance and Private Information in Lending, mimeo,

FRB of Chicago and American University.

Angelini, P., Di Salvo, R., Ferri, G., 1998. Availability and cost of credit for small

businesses: customer relationships and credit cooperatives. Journal of Banking and

Finance 22 (6-8), 925-54.

Bartoli, F., Ferri, G., Murro, P., Rotondi, Z., 2010. What’s Special About Banking in

Italy? Lending Technologies, Complementarity, and Impact of Soft Information,

in G. Bracchi and D. Masciandaro (Eds), The XV Report on Financial System:

“Le banche italiane sono speciali? Nuovi equilibri tra finanza, imprese e Stato”,

Italian Banking Association.

Berger, A.N., Frame W.S., 2006. Small business credit scoring and credit availability.

Journal of Small Business Management 46.

Berger, A.N., G.F. Udell 1995. Relationship lending and lines of credit in small firm

finance. Journal of Business 68, 351-81.

Berger, A. N., Udell, G.F., 2006. A more complete conceptual framework for SME

finance. Journal of Banking and Finance 30, 2945–2966.

Boot, A.W.A., 2000. Relationship banking: what do we know?. Journal of Financial

Intermediation 9 (1), 7–25.

Degryse, H., Van Cayseele, P.J.G., 2000. Relationship lending within a bank-based

system: evidence from European small business data. Journal of Financial

Intermediation 9 (1), 90-109.

Jappelli, T., 1990. Who is credit constrained in the US economy?. Quarterly Journal of

Economics 105, 219-234.

Levenson, A.R., Willard, K.L., 2000. Do Firms Get the Financing They Want?

Measuring Credit Rationing Experienced by Small Businesses in the U.S. Small

Business Economics 14, 83-94.

Petersen, M., 2004. Information: Hard and Soft, mimeo, Northwestern University.

18

Petersen, M. and Rajan, R., 2002. Does Distance Still Matter? The Information

Revolution in Small Business Lending. Journal of Finance 57, 2533-2570.

Scott, J.A., 2004. Small business and the value of community financial institutions.

Journal of Financial Services Research 25, 207-230.

Stein, J. C., 2002. Information production and capital allocation: Decentralized vs.

hierarchical firms. Journal of Finance 57, 1891-1921.

Uchida, H., Udell, G. F., Yamori, N., 2006. SME financing and the choice of lending

technology. RIETI Discussion Paper Series 06-E-025.

Uchida, H., Udell, G. F., Watanabe, W., 2008. Bank size and Lending relationship in

Japan. Journal of the Japanese and International Economies 22 (2), 242-267.

Udell, G.F., 2004. Asset-Based Finance. The Commercial Finance Association, New

York.

19

Appendix

Table 1. Variables definition

Variable Definition

LT_FS

Index for financial statement lending technology. We use a question

available in the Survey: “In your view, which criteria does your bank follow

in granting loans to you?”. In answering this question the firm was required

to give a weight (going, in descending order, from 1, very much, to 4, nil) to

fifteen factors. From the list of fifteen criteria shown in the Appendix, we

use the initial four. For each of the four characteristics we constructed a

dummy variable, which takes a value of one if the firm chose 1. LT_FS is

the average of these four dummy variables.

LT_RE

Index for real-estate lending technology. We use a question available in the

Survey: “In your view, which criteria does your bank follow in granting

loans to you?”. In answering this question the firm was required to give a

weight (going, in descending order, from 1, very much, to 4, nil) to fifteen

factors. LT_RE, is a dummy variable that take the value one if the firm

answered 1 (very much) to lending factor no. 5.

LT_OF

Index for other fixed-asset lending technology. We use a question available

in the Survey: “In your view, which criteria does your bank follow in

granting loans to you?”. In answering this question the firm was required to

give a weight (going, in descending order, from 1, very much, to 4, nil) to

fifteen factors. LT_OF, is an average of the two dummy variables which

take a value of one if the firm answered 1 (very much) to lending factors no.

6 and 8, respectively.

LT_RL

Index for relationship lending technology. We use a question available in

the Survey: “In your view, which criteria does your bank follow in granting

loans to you?”. In answering this question the firm was required to give a

weight (going, in descending order, from 1, very much, to 4, nil) to fifteen

factors. LT_RL, is an average of six dummy variables which take a value of

one if the firm answered 1 (very much) to lending factors, no. 9, 10, 11, 13,

14 and 15, respectively.

LT_TRANS

Index for the transactional lending technology. To construct this index, we

aggregate the three transactional lending technologies (LT_FS, LT_RE and

LT_OF) in a single index.

AUDIT

Dummy taking value one if firm has its statements externally certified; 0

otherwise.

AGE Log of the age of firm since foundation, in years.

AGE-squared Square of the age of firm since foundation, in years.

ROA

Average value of the ratio of firm’s EBIT to firm’s total assets during 2004-

2006 period.

LEVERAGE

Ratio of firm’s total loans to the sum of firm’s total loans and firm's equity

as of the end of December 2006.

CORPORATION

Dummy variable taking value one if firm is a join stock company; 0

otherwise.

BANKS Total number of firm’s reference banks

LARGE

Dummy variable taking value one if the main bank is either a national bank

or a foreign bank; 0 otherwise.

LOCAL

Dummy variable taking value one if the main bank is a smaller-sized

cooperative mutual banks, a larger-sized Volksbank type cooperative banks,

a saving bank or “other type of bank”; 0 otherwise.

SITC5

Dummy taking value one if firm has a 5 digit SITC classification; 0

otherwise.

SITC4

Dummy taking value one if firm has a 4 digit SITC classification; 0

otherwise.

SITC3

Dummy taking value one if firm has a 3 digit SITC classification; 0

otherwise.

20

CENTER

Dummy variable taking value 1 if the bank branch where the credit

relationship with the firm takes place is located in Central Italy; 0 otherwise.

SOUTH

Dummy variable taking value 1 if the bank branch where the credit

relationship with the firm takes place is located in Southern Italy; 0

otherwise.

HHI

Average value of the Herfindhal Hirschman index of concentration on bank

loans in the province during 1991-2004 period.

BRANCH

Average number of branches per thousands inhabitants in the province

during 1991-2004 period.

GDP

Average rate of growth of value added in the province in the 1989–1998

period.

PERFORMANCE_DS

Dummy variable indicating that the firm first posted a deficit (D) and then a

surplus (S) in the past two years.

PERFORMANCE_DD

Dummy variable indicating that the firm posted two deficit (D) in the past

two years.

PERFORMANCE_SD

Dummy variable indicating that the firm first posted a surplus (S) and then a

deficit (D) in the past two years.

PERFORMANCE_SS

Dummy variable indicating that the firm posted two surplus (S) in the past

two years.

SOFT

We use a question available in our survey: “Which characteristics are key in

selecting your main bank?”. In answering this question the firm was

required to give a weight (going, in descending order, from 1, very much, to

4, nil) to fourteen factors. Six of the fourteen characteristics are related to

soft information. For each of the six characteristics related to soft

information, we constructed a dummy variable, which takes a value of one if

the firm chose 1. SOFT is the first principal component of the principal

component analysis over the resulting six dummies.

SIZE Log of the firm’s number of employees as of the end of December 2006.

MEET

Dummy variable which takes a value of one whether contact between the

firm and the loan officer is typically direct rather than by telephone, email or

other indirect methods.

SAVINGBANKS_1936

Saving banks, per thousand inhabitants, measured at the province level, refer

to 1936.

NBRANCHES_INC

Average of the annual number of branches created minus those closed by

incumbent banks per inhabitants in the province in the 1991–1998 period.

21

Table 2. Summary statistics: Full Sample

Variables Mean Standard

Deviation Min Max

AUDIT 0.376 0.485 0 1

LISTED 0.013 0.113 0 1

AGE 22.663 14.388 1 134

ROA 0.025 2.097 -0.100 0.836

LEVERAGE 0.899 0.113 0.092 0.997

CORPORATION 0.331 0.471 0 1

BANKS 4.973 3.959 1 100

LARGE 0.497 0.500 0 1

LOCAL 0.503 0.500 0 1

PERFORMANCE_DS 0.100 0.301 0 1

PERFORMANCE_DD 0.109 0.342 0 1

PERFORMANCE_SD 0.135 0.312 0 1

PERFORMANCE_SS 0.655 0.475 0 1

SITC 5 0.281 0.450 0 1

SITC 4 0.416 0.493 0 1

SITC 3 0.282 0.450 0 1

CENTER 0.162 0.369 0 1

SOUTH 0.118 0.323 0 1

HHI 0.111 0.048 0.048 0.369

BRANCH 0.467 0.113 0.183 0.938

GDP 0.072 0.045 -0.131 0.236

SOFT -0.001 1.743 -1.065 5.823

SIZE 3.553 1.118 0 9.093

22

Table 3. Summary statistics: Sub-Sample

Variables Mean Standard

Deviation Min. Max.

AUDIT 0.345 0.476 0 1

LISTED 0.018 0.134 0 1

AGE 24.499 15.634 2 116

ROA 0.053 0.069 -0.339 0.836

LEVERAGE 0.890 0.113 0.092 1

CORPORATION 0.409 0.492 0 1

BANKS 5.690 4.286 1 50

LARGE 0.500 0.500 0 1

LOCAL 0.500 0.500 0 1

PERFORMANCE_DS 0.101 0.301 0 1

PERFORMANCE_DD 0.160 0.366 0 1

PERFORMANCE_SD 0.099 0.298 0 1

PERFORMANCE_SS 0.641 0.480 0 1

SITC 5 0.295 0.456 0 1

SITC 4 0.402 0.490 0 1

SITC 3 0.282 0.450 0 1

CENTER 0.170 0.376 0 1

SOUTH 0.097 0.296 0 1

HHI 0.110 0.048 0.048 0.332

BRANCH 0.474 0.107 0.188 0.938

GDP 0.072 0.043 -0.131 0.236

SOFT -0.001 1.743 -1.065 5.823

SIZE 3.826 1.304 0 9.093

23

Table 4: Descriptive Statistics of Lending Technology Indices

Variables Obs Mean Standard

Deviation

1st

percentile

99th

percentile

LT_FS 1541 0.216 0.332 0 1

FS1 1541 0.249 0.432 0 1

FS2 1541 0.217 0.412 0 1

FS3 1541 0.200 0.400 0 1

FS4 1541 0.197 0.398 0 1

LT_RL 1541 0.145 0.283 0 1

RL9 1541 0.143 0.350 0 1

RL10 1541 0.123 0.328 0 1

RL11 1541 0.174 0.379 0 1

RL13 1541 0.141 0.347 0 1

RL14 1541 0.135 0.341 0 1

RL15 1541 0.155 0.362 0 1

LT_RE 1541 0.119 0.324 0 1

LT_OF 1541 0.113 0.259 0 1

OF6 1541 0.102 0.303 0 1

OF8 1541 0.123 0.328 0 1

24

Table 5: Correlation Among Lending Technology Indices

Variables LT_FS LT_RE LT_OF LT_RL

LT_FS 1.000

LT_RE 0.560 1.000

(0.000)

LT_OF 0.607 0.635 1.000

(0.000) (0.000)

LT_RL 0.714 0.556 0.682 1.000

(0.000) (0.000) (0.000)

The table reports the correlation coefficients among lending technology

indices and p-value (between parentheses).

Table 6: Multivariate Regression Among Lending Technology Indices

Variables Intercept LT_FS LT_RL LT_OF LT_RE

LT_FS 0.085 0.606*** 0.175*** 0.189***

(0.000) (0.000) (0.000) (0.000)

LT_RL 0.009* 0.389*** 0.392*** 0.064***

(0.086) (0.000) (0.000) (0.001)

LT_OF 0.005 0.104*** 0.363*** 0.271***

(0.306) (0.000) (0.000) (0.000)

LT_RE -0.006 0.222*** 0.118*** 0.534***

(0.406) (0.000) (0.001) (0.000)

The table reports regressions coefficients and associated standard errors (between

parentheses). The dependent variables are the four lending technologies. The

regressions are estimated by OLS. (*): coefficient significant at 10% confidence

level; (**): coefficient significant at 5% confidence level; (***): coefficient

significant at less than 1% confidence level.

25

Table 7. Lending Technologies Regressions

Variables LT_FS LT_RL LT_RE LT_OF

Soft 0.083*** 0.074*** 0.056*** 0.054***

0.009 0.008 0.011 0.009

Local -0.050** 0.007 -0.011 -0.013

0.020 0.012 0.017 0.015

Audit 0.042* -0.003 0.043** 0.044***

0.022 0.013 0.020 0.017

Age -0.001 -0.001 0.001 -0.001

0.001 0.001 0.001 0.001

Age-squared -0.000 0.000 -0.000 0.000

0.000 0.000 0.000 0.000

Size -0.014 0.005 -0.004 0.002

0.009 0.005 0.008 0.007

Performance_DS 0.008 0.020 -0.008 -0.005

0.038 0.024 0.031 0.024

Performance_SD -0.071** 0.008 -0.015 0.044

0.029 0.020 0.028 0.029

Performance_DD -0.065** -0.021 -0.035 -0.032

0.028 0.017 0.026 0.020

Center -0.007 0.016 -0.023 -0.009

0.025 0.016 0.024 0.020

South -0.009 0.024 -0.036 -0.052*

0.038 0.024 0.039 0.031

HHI 0.005 -0.058 -0.034 0.018

0.239 0.128 0.176 0.146

Branch 0.054 0.084 -0.080 -0.048

0.108 0.069 0.101 0.088

Leverage 0.152** 0.061 0.093 0.049

0.076 0.045 0.080 0.067

ROA -0.408*** -0.109 -0.175 -0.082

0.135 0.088 0.123 0.118

GDP -0.215 0.117 -0.328* -0.225

0.248 0.108 0.192 0.161

Corporation 0.023 -0.009 0.016 0.006

0.023 0.015 0.023 0.017

SITC 5 0.076*** -0.031 0.024 -0.100

0.025 0.031 0.018 0.048

SITC 4 0.108*** -0.020 0.037* -0.057

0.026 0.031 0.020 0.049

SITC 3 0.058** -0.016 0.010 -0.058

0.025 0.032 0.019 0.049

Constant 0.059 0.016 0.062 0.142

0.098 0.064 0.091 0.094

Observations 778 778 778 778

R squared 0.2525 0.3559 0.1471 0.2097

The table reports regressions coefficients. The endogenous variables are the four transactional lending technologies.

For the definition of the explanatory variables see Table 1. The regressions are estimated by OLS. The regressions

include sector dummies. Robust standard errors are reported below coefficients. (*): coefficient significant at 10%

confidence level; (**): coefficient significant at 5% confidence level; (***): coefficient significant at less than 1%

confidence level. The table also reports, as goodness-of-fit tests, the R-squared.

26

Table 8. Complementarity among lending technologies (instrumented)

Variables LT_FS LT_RL LT_RE LT_OF

Soft 0.180*** 0.061** 0.028 0.054*

0.051 0.025 0.042 0.029

Local 0.010 0.001 -0.038 -0.010

0.038 0.019 0.029 0.021

Audit 0.014 0.001 0.019 0.028

0.031 0.016 0.025 0.020

Age -0.000 -0.002 0.000 -0.001

0.002 0.001 0.002 0.001

Age-squared -0.000 0.000 0.000 0.000

0.000 0.000 0.000 0.000

Size -0.023* 0.004 0.003 0.008

0.012 0.006 0.010 0.008

Performance_DS -0.022 0.001 -0.005 -0.004

0.052 0.024 0.037 0.024

Performance_SD -0.112** 0.015 -0.000 0.065**

0.044 0.024 0.037 0.032

Performance_DD -0.080* -0.016 -0.017 -0.022

0.042 0.019 0.032 0.023

Center -0.013 0.023 -0.013 0.013

0.033 0.018 0.032 0.026

South -0.050 0.016 -0.061 -0.081**

0.058 0.029 0.051 0.039

HHI 0.192 -0.002 0.088 0.086

0.339 0.141 0.204 0.184

Branch -0.062 0.092 -0.175 -0.092

0.161 0.085 0.120 0.106

Leverage 0.106 0.039 0.073 0.005

0.109 0.047 0.093 0.073

ROA -0.536** -0.119 -0.130 -0.067

0.224 0.106 0.159 0.148

GDP -0.005 0.110 -0.168 -0.131

0.325 0.136 0.232 0.204

Corporation 0.027 -0.012 0.012 -0.006

0.033 0.015 0.026 0.017

SITC 5 0.027 -0.025 0.042 -0.105*

0.043 0.029 0.027 0.056

SITC 4 0.087* -0.013 0.058* -0.059

0.046 0.030 0.029 0.058

SITC 3 0.007 -0.005 0.014 -0.062

0.046 0.031 0.029 0.058

Constant 0.229 0.037 0.082 0.181

0.153 0.072 0.112 0.112

Observations 572 572 572 572

Test of excluded instruments, F-

statistic 5.225 5.225 5.225 5.225 Endogeneity test of instrumented

regressor 5.053** 0.272 0.694 0.022

Overidentification test,

Sargan 2-statistic 3.246 2.002 5.347 0.997

The table reports regressions coefficients. The endogenous variables are the four lending technologies. For the definition of the explanatory variables

see Table 1. The regressions are estimated by 2SLS. The regressions include sector dummies. Robust standard errors are reported below coefficients.

(*): coefficient significant at 10% confidence level; (**): coefficient significant at 5% confidence level; (***): coefficient significant at less than 1%

confidence level. The table also reports the F-test and the Sargan score as test of validity of the instruments, the Wooldridge test as a test of

endogeneity of SOFT.

27

Survey questions

Which of these characteristics are key in selecting your main bank?

1. The bank knows you and your business.

2. The bank knows a member of your Board of directors or the owners of the firm.

3. The bank knows your sector.

4. The bank knows your local economy.

5. The bank knows your relevant market.

6. Frequent contacts with the credit officer at the bank.

7. The bank takes quick decisions.

8. The bank offers a large variety of services.

9. The bank offers an extensive international network.

10. The bank offers efficient internet-based services.

11. The bank offers stable funding.

12. The bank offers funding and services at low cost.

13. The bank’s criteria to grant credit are clear.

14. The bank is conveniently located.

In your view, which criteria does your bank follow in granting loans to you?

1. Ability of the firm to repay its debt (e.g. years needed to repay its debt).

2. Financial solidity of the firm (capital/asset ratio).

3. Firm’s profitability (current profits/sales ratio).

4. Firm’s growth (growth of sales).

5. Ability of the firm to post (not personal) real estate collateral.

6. Ability of the firm to post tangible non-real estate collateral.

7. Support by a guarantee association (e.g. loan, export, R&D, etc.).

8. Personal guarantees by the firm’s manager or owner.

9. Managerial ability on the part of those running the firm’s business.

10. Strength of the firm in its market (number of customers, commercial network).

11. Intrinsic strength of the firm (e.g. ability to innovate).

12. Firm’s external evaluation or its evaluation by third parties.

13. Length of the lending relationship with the firm.

14. Loans are granted when the bank is the firm’s main bank.

15. Fiduciary bond between the firm and the credit officer at your bank.