LED BY TRUST POWERED BY TECHNOLOGY

324

94 th Annual Report 2021-22 LED BY TRUST POWERED BY TECHNOLOGY

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of LED BY TRUST POWERED BY TECHNOLOGY

94th Annual Report 2021-22

LED BY TRUST POWERED BY TECHNOLOGY

TABLE OF CONTENTS

“Led by Trust Powered by Technology” depicts South Indian Bank’s two pillars of strength – Trust & Technology.

It articulates the Bank’s strong intent for growth, relying on our customers’ unflinching trust on the 93 years old rich legacy of delivering seamless, exemplary banking services, backed by a technology par excellence in the Banking Industry. SIB has TRUST ingrained in its founding legacy and renewed business model and technology for bettering the customer experience and accelerating growth.

Corporate Information 1About South Indian Bank 2Awards and Recognitions 3About South Indian Bank 4Key Performance Indicators 6Board of Directors 8Chairman’s Message 10MD and CEO’s Message 13Senior Management 17Human Resource Management 18Directors’ Report 21Business Responsibility Report 74Management Discussion and Analysis Report 82Report on Corporate Governance 91

LED BY TRUST POWERED BY TECHNOLOGY

Standalone Financial Statements

Independent Auditor’s Report 139Balance Sheet 148Profit and Loss Account 149

Cash Flow Statements 150Schedules to Balance Sheet 152Significant Accounting Policies 159Notes on Accounts 166

Consolidated Financial Statements

Independent Auditor’s Report 222Balance Sheet 232Profit and Loss Account 233Cash Flow Statements 234Schedules to Balance Sheet 236Significant Accounting Policies 244Notes on Accounts 253Disclosure Under Basel III Norms 268Nomination Form 304Cancellation or Variation of Nomination 306Form ISR – 1 308Form ISR – 2 312Form ISR - 3 313Form ISR - 4 314

Annual Report 2021-22

1

CORPORATE INFORMATION

Board of DirectorsMr.Salim GangadharanChairman

Mr. Murali RamakrishnanManaging Director & CEO

Mr. Parayil George John TharakanIndependent Director

Mr. V J KurianIndependent Director

Mr. M George Korah Independent Director

Mr. Pradeep M GodboleNon-Executive Director

Mr. Paul AntonyNon-Executive Director

Mr. R A Sankara NarayananIndependent Director

Mrs. Radha UnniIndependent Director

Mr. Benny P. ThomasNon-Executive Director

Joint Statutory AuditorsM/s Varma & Varma Chartered Accountants Sreeraghavam Kerala Varma Tower Building No.53/2600 B, C, D & E Off. Kunjanbava Road Vytilla P.O, Kochi – 682019

M/s CNK Associates LLPChartered Accountants5th Floor, Narain Chambers,Vile Parle - EastMumbai – 400 057

Chief Financial OfficerMs. Chithra H, FCA

Company SecretaryMr. Jimmy Mathew, A.C.S, A.C.M.A

Joint General Managers

Deputy General ManagersMr Shashidhar Y

Mr Joly Sebastian

Mr Peter A.D.

Mr John C.A.

Mr Pradeep V.N

Mr John C Lazar

Mr Jeevandas N.B.

Mr Bala Naga Anjaneyulu G.

Mr Ritesh Tulsidas Bhusari

Secretarial AuditorsSVJS & Associates Company Secretaries 65/2364A, Ponoth Road Kaloor, Kochi, Ernakulam – 682017 Contact : 0484 2950009 / 2950007 Email : [email protected], [email protected]

Top ManagementMr. Thomas Joseph K EVP & Group Business Head

Mr. Anto Geroge T Senior General Manager- Human Resources Department & Admin

Mr Sanchay Kumar Sinha Senior General Manager - Country Head-Liabilities and Branch Banking

Mr. Sony A General Manager-CIO

Ms. Minu Moonjely General Manager-Credit

Ms. Biji S S General Manager-Corporate Business Group

Mr. Nandakumar G General Manager-MSME

Ms. Chithra H General Manager-CFO

Mr. Thallam Sreekumar General Manager-Personal Loan Business Group

Mr Harikumar L General Manager-Retail Banking

Mr Abey Abraham General Manager-Housing Loan

Mr Senthil Kumar General Manager-Collections & Recovery

Mr. Sivaraman K General Manager-Banking Operations Group

Regd OfficeThe South Indian Bank Ltd. SIB House, T.B Road, Mission Quarters, Thrissur 680 001, Kerala, India Tel: +91-487 2420020 Fax: +91 487 2442021 www.southindianbank.com Email: [email protected]

ISIN: INE683A01023

CIN: L65191KL1929PLC001017

Stock Exchanges: BSE, NSE

Registrar and Share Transfer AgentsM/s. BTS Consultancy Services Pvt. Ltd M S Complex , 1st floor, No: 8 Sastry Nagar, Near 200 Feet Road/RTO Kolathur, Kolathur Chennai, Tamil Nadu – 600099 Tel: 044-25565121 Fax: 044-25565131 Email: [email protected]

Mr Sreekumar Chengath Mr Mohan T M Mr Joby M.C. Mr Shibu.K.thomas Mr Jimmy Mathew Mr Vijith S.

Ms Lakshmi Prabha T M Mr Jose Sebastian E. Mr Biju E Punnachalil Mr Vinod Francis Mr Jojo Antony Mr Vinod G

Mr Anand Subramaniam Ms Azmat Habibulla Mr Madhu MMr Krishna Kumar P.Ms Rekha V R

Mr Davis Jose Thettayil

Mr Baiju Karan

Mr Easwaran S.

Mr Rajesh I R

Mr Binoy R.K.

Mr Vivek Krishnan

Mr Venugopal C

Mr Gurmeet Singh

Mr Ramesh U.

Mr Biby Augustine

Mr Viji Yuvaraj C

Mr Rayner.H.Ephraim

Mr Ragesh Kumar R.S.

Mr Dhirendra Pratap Singh

Mr Sojan V.J.

Mr Jose K.A.

Mr Ram Mohan V

Experience Next Generation Banking

2

VISION

MISSION

To be the most preferred bank in the areas of customer service, stakeholder value and corporate governance.

To provide a secure, agile, dynamic and conducive banking environment to customers with commitment to values and unshaken confidence, deploying the best technology, standards, processes and procedures where customer convenience is of significant importance and to increase the stakeholders’ value.

Improving profitability by focusing on 6Cs

Capital

Beefing up the capital to strengthen financials, expand market share and to explore future growth opportunities.

Cost to Income

To bring down the Cost-to-Income ratio with focussed approach on increasing the net interest income as well as other income portfolio of the bank and by optimizing the cost across the organisation.

Customer Focus

Customer experience is critical for the success of any organization as the same is a competitive differentiator. Adoption of a “phygital” approach at branches with personalized services for legacy loyal customers and end to end digital experience for next-gen customers with a “Fair to customer, Fair to Bank” approach.

CASA

Improving CASA through focused drive on building a sustainable CASA book through our Pan India Presence.

Competency Building

Augmenting the talent of young resources and revamping the organizational structure to build a pool of senior talent to deliver continued excellence.

Compliance

Compliance continues to be the core for all strategies and will be the axis across all domains of banking activities by adopting the motto “compliance with conscience”.

Annual Report 2021-22

3

SIB won 6 awards at IBA’s 17th Annual Banking Technology Awards

AWARDS AND RECOGNITIONS

South Indian Bank’s Managing Director and CEO Mr. Murali Ramakrishnan and Executive Vice President and Group Business Head Mr. Thomas Joseph K launch the SIB – OneCard Co-Branded Credit Card.

Mr. Sony A, GM & CIO and Mr. Jose Sebastian E, JGM and Head IT Operations receiving the Finnoviti Awards 2022 from Banking Frontiers for South Indian Bank

Mr. Anto George T, SGM HR & Admin and Ms. Rekha V R, JGM and Head, RO Bangalore with the ‘South India Best Employer Brand Awards 2021’ for ‘Excellence in HR through Technology’, for the mHRMS Mobile App of South Indian Bank

Experience Next Generation Banking

4

ABOUT SOUTH INDIAN BANK

Customers

70,00,000+Digital Transactions

93.3%Total Business

` 1,50,958 Crore

Deposits

` 89,142 Crore

Advances

` 61,816 Crore

CASA

` 29,601 Crore

Established in 1929 at Thrissur in Kerala, South Indian Bank is one of the earliest banks in South India. The establishment of the Bank was in alignment with the Swadeshi movement. The core purpose of the Bank, as envisioned by its founders, was to provide an efficient and service oriented repository of savings and credit for the people and businesses at reasonable rates of interest.

Translating the vision of the founding fathers as its corporate mission, the Bank has during its long sojourn been able to project itself as a vibrant, fast growing, service oriented and trend setting financial intermediary. Over the last 10-years South Indian Bank has gone from strength-to-strength, growing by four to five times on parameters like Total Business, Advances, Deposits, NRI Deposits, and Operating Profits. The Bank has done well in Retail Banking, CASA, Mobile Banking and Digital.

(up from 89.8% in FY21) +6% YoY

+20% YoY+8% YoY

FY22 Highlights

Annual Report 2021-22

5

Experience Next Generation Banking

6

KEY PERFORMANCE INDICATORS*

(` in crore)

(` in crore)

(` in crore)

82,686

1,966

1,164.68*

92,279

2,020

1,098.75*

97,032

2,317

1,362.45*

94,149

2,407

1,661.60*

Total Assets

Net Interest Income

Operating Profit

FY20

FY20

FY20

FY19

FY19

FY19

FY18

FY18

FY18

FY21

FY21

FY21

FY22

FY22

FY22

(` in crore)

(` in crore)

(` in crore)

7,462.50*

585.98*

1,44,056

6,713.95*

521.14*

1,27,139

8,526.36*

762.56*

1,48,558

8,534.61*

1229.17*

1,42,129

7,620.64

1034.10

1,50,958

Total Income

Other Income

Total Gross Business

FY20

FY20

FY20

FY19

FY19

FY19

FY18

FY18

FY18

FY21

FY21

FY21

FY22

FY22

FY22

1,00,052

2,240

1,247.57

* Previous figures are regrouped as per RBI Guideline

* Previous figures are regrouped as per RBI Guideline

* Previous figures are regrouped as per RBI Guideline

Annual Report 2021-22

7

(%)

(` in crore)

(` in crore)

12.70

133.85

334.89

12.61

150.03

247.53

13.41

165.51

104.59

15.42

165.25

61.91

Capital Adequacy

Branch Productivity

Net Profit

FY20

FY20

FY20

FY19

FY19

FY19

FY18

FY18

FY18

FY21

FY21

FY21

FY22

FY22

FY22

(%)

(` in crore)

(Amount in `)

4.64

5,335

29.48

6.39

5,241

28.98

1.91

5,475

30.25

1.07

5,807

27.75

0.77

5,853

27.97

Return on Equity

Capital and Reserves

Book Value Per Share

FY20

FY20

FY20

FY19

FY19

FY19

FY18

FY18

FY18

FY21

FY21

FY21

FY22

FY22

FY22

15.86

154.77

44.98

* Previous year figures have been regrouped/reclassified wherever necessary to conform to current year’s classifications

Experience Next Generation Banking

8

BOARD OF DIRECTORS

Mr. Salim Gangadharan Chairman

Mr. Murali Ramakrishnan Managing Director & CEO

Mr. Pradeep M. Godbole Non-Executive Director

Mr. Paul Antony Non-Executive Director

Mr. R A Sankara Narayanan Independent Director

Mr. Parayil George John Tharakan Independent Director

AC AC

NRC NRCMC

MC MC MC

MC

NPARC NPARC

NPARC

RMC

RMC RMC PC

PC

CSC

CSCCSC

SRC

SRC

ITSC

ITSC

ITSC

ITSC

CSR

CSRCPIC CPIC

CPIC

SCBFSCBF SCBF

SCBF

C C

C

C

C

CC

Annual Report 2021-22

9

Ms. Radha Unni Independent Director

Mr. Benny P. Thomas Non-Executive Director

Mr. V. J. Kurian Independent Director

Mr. M. George Korah Independent Director

AC

AC

NRC NRC

MC NPARCNPARC

NPARC RMCRMC

PC

PC

CSC

SRC

SRC

ITSC

CSR

CSR

CPIC

CPIC

Audit Committee

Nomination & Remuneration Committee

Management Committee

NPA Review Committee

Risk Management Committee

Premises Committee

Customer Service Committee

Stakeholders Relationship Committee

IT Strategy Committee

Corporate Social Responsibility Committee

Capital Planning & Infusion Committee

Denotes Chair of the Committee

Special Committee for Monitoring and Follow Up of Frauds

Board Committee Indicators

AC

NRC

MC

NPARC

RMC

PC

CSC

SRC

ITSC

CSR

CPIC

SCBF

SCBFC

C

C

C

C C

Experience Next Generation Banking

10

CHAIRMAN’S MESSAGE

I am pleased to place before you, the highlights of the Bank’s performance during the financial year 2021-22. The details of the performance indicators and the initiatives undertaken by the Bank have been laid down in the enclosed Annual Report. After being ravaged by the Covid-19 pandemic for over two years, the global economy is currently grappling with adverse implications from geo-political conflicts and ensuing sanctions. The ramifications of the war, layered on top of a pandemic, have heightened the socio-economic humanitarian crisis, and has already triggered profound ripple effects on global trade and commerce. The war or the ‘special operation’, as Russia put it, resulted in significant supply chain bottlenecks, which led to multi-decadal spike in inflation and slowing growth across the globe. The heightened volatility in the global financial markets and growing stagflation worries have led to tightening of financial conditions and have posed a tangible threat to global growth and financial stability.

Most Central Banks have been weighing the difficult decision on how quickly to raise the rates to quench the inflationary spiral. The US Fed has reversed the track of the monetary policy stance, and has started raising the policy rates, along with normalizing the excessive liquidity in the system, as has been done by other Central Banks in major economies. At the national level, RBI resorted to off-cycle hikes in policy rates to contain inflation. The increases in policy rates had a cascading effect on interest rates on deposits and advances, and other financial instruments and currency. High interest rates in the US and other developed countries have led to flight to safety of capital from equities to bonds and from emerging economies to advanced economies. Every economic phenomenon would have the consequences of a tussle between debt and equity, and a clash between safety and growth. One of the two dominates with varying lengths of time. Now, debt is preferred for safety. How quickly equity and growth bounce

Dear Shareholders,

The Bank steps into its 94th year of successful corporate journey with significant contributions to the Indian banking industry and at the outset, I extend my sincere gratitude to each one of you for the continued support and guidance.

Salim GangadharanChairman

Annual Report 2021-22

11

Newly introduced Financial Inclusion Index and Digital Payments Index are expected to usher in greater improvement in the quality of banking services and deepening of digital payments. With operationalisation of UPI123 Pay, about forty crore feature phones would be digitally enabled. This would help making the economy ‘less cash’ more quickly.

The Bank has been successful in widening its network across India. On the business side, total deposits of the Bank grew by 8% from ` 82,710.55 Crore a year ago to ` 89,142.10 Crore as on 31.03.2022. During the year, gross advances increased by 4% from ` 59,418.40 Crore to ` 61,815.76 Crore. With the improvement in asset quality and focus on booking better rated customers, net non-performing assets of the Bank has declined by 35% from ` 2,734.52 Crore to ` 1,777.77 Crore. There has been a substantial improvement of 1,082 bps in Provision Coverage Ratio (PCR) from 58.73% to 69.55%. Capital Adequacy Ratio of the Bank as on 31.3.2022 stood at 15.86%, well above the minimum regulatory requirement of 11.50%, supporting the business strategy of higher loan growth.

back shall depend upon how soon the geo-political conflict would end and the lingering effects of Covid-19, supply chain bottlenecks and inflation would subside.

Keeping in view the current scenario, the International Monetary Fund (IMF) now expects the global economy to grow only by 3.6% in 2022 and 2023, down from its earlier estimate of 4.4% and 3.8%, respectively. It would be a steep decline compared to the 6.1%growth recorded in 2021.

On the domestic front, the inflation continues to be above the tolerance level of the RBI, posing a serious challenge to growth. The RBI also has trimmed India’s economic growth forecast for 2022-23 from 7.8% estimated earlier to 7.2%. Revised growth is significantly lower than the 8.7% growth achieved in 2021-22.Despite the lower estimate, India’s projected growth is still one of the highest in the world. India’s optimism is based on certain promising factors like the Production Linked Incentives Scheme (PLIS),expected normal monsoon, push for domestic defence supplies, digitisation, infrastructure push, fiscal stimulus, etc. The inflation risk continues to persist, which is triggered by elevated crude oil, commodity and food prices. Given the supply chain constraints, and external events, the RBI has since revised the projected inflation from 5.7% to 6.7% in 2022-23.

As mentioned by the RBI, the banking sector has been provided with sufficient liquidity to cushion against disruptions caused by the Covid-19 pandemic. Public and private sector banks have bolstered their capital through retention of earnings and mobilising capital from the market. Further, public sector banks were recapitalised by the Government. Gross non-performing assets (GNPA) ratio of all scheduled commercial banks has been moderated to its lowest level in six years. Throughout FY 2022, RBI undertook a slew of measures to deal with exceptional situations and improve liquidity, monetary transmission, and credit flow in the economy. Overall, the financial sector has remained fully functional and has anchored the process of recovery. The future performance of the banking system hinges quite clearly on the recovery of the economic performance in the years ahead.

Asset Quality Improvements in FY22

Net NPA

` 1,778Declined 35% year on year

PCR Ratio

69.55%From 58.73% in FY22

CAR

15.86%As son March 31, 2022

Experience Next Generation Banking

12

The Board gives utmost importance to corporate governance practices at the Bank, and we have been meticulously following RBI guidelines, SEBI guidelines, corporate laws issued by MCA, banking regulations and all applicable laws.

The Bank is quite confident of emerging from the current economic slowdown. We have made good progress on our journey of transforming the Bank to be among the best in class and expect to achieve our aspirations, led by consistent focus on execution. The focus on strengthening the balance sheet with higher capital adequacy ratio, quality loan book, better NIM, strong CASA growth, higher PCR, digitisation, and efficient recovery and collection have bolstered the financial profile of the Bank and cushioned the balance sheet from potential risks arising out of uncertainties.

As we enter FY 2023, the Bank is better positioned in the industry, given our strong liability profile, diversified and secured nature of our lending portfolio and strong credit underwriting and risk management practices. Over the past decade, the Bank has built a strong Retail franchise with customer centricity and superlative customer experience at the core of our diverse products and service offerings.

The Bank has been focusing on building a quality loan book, especially to those having external credit rating of A and above. Gold loans is another promising area. Monthly disbursements in retail sector have been growing significantly, though we have adopted a cautious approach. We would be participating in funding some of the investments going into infrastructure sector. We have been investing in fintech to facilitate convenience in banking services. Further, our wholly owned subsidiary, SIB Operations and Services Ltd, is taking shape. Going forward, this non-financial subsidiary would enable us to streamline and optimize various operations and to improve the overall productivity, cost and efficiency of the Bank.

Keeping these factors in view, the Bank has targeted double digit growth in its loan book by the end of FY2023.This is one of the steps in our aspiration to become a big Bank in the years to come.

I would like to conclude by thanking all our customers, associates, partners, vendors, Auditors and other well-wishers for their continued support and trust. I wish to express my gratitude to RBI, SEBI, stock exchanges, and Central and State Governments for their guidance in statutory compliances. I also thank the employees at all levels, for their tireless effort and teamwork. Finally, I would like to thank all our shareholders and Board for their contribution in Bank’s growth over the years. I am confident that the Bank’s Retail franchise would continue to deliver stainable profitable growth without compromising on the quality and profitability.

By staying true to our values, we are upholding the trust extended by all and continually investing in building newer digital, financial, and intellectual capabilities to equip the Bank to fly high in future. Strong corporate governance, supported by sound risk management systems make us future ready. The Bank is positioned well to become the Bank of choice for all. The challenges as well as opportunities ahead are huge, and we are committed to invest in our people and capabilities to connect, insights to decisions and processes to outcomes. On behalf of the Board of Directors of the Bank, I thank you for your continued trust, confidence, and support. Stay healthy, stay safe!

Best Wishes

Salim GangadharanChairman

The Bank has targeted double digit growth in its loan book by the end of FY2023. This is one of the steps in our aspiration to become a big Bank in the

years to come.

Annual Report 2021-22

13

MD AND CEO’S MESSAGE

Murali RamakrishnanManaging Director & CEO

Dear Shareholders,

The Financial year 2022 was an eventful year in the banking industry wherein banks had to calibrate their strategies. SIB, with the efforts, we put in, for the organizational transformation and reengineering, had progressed positively on all our strategic objectives.

Though the external economic situations around us are cloudy, our suppleness, responsible business conduct and credence has facilitated us to navigate this volatile environment. Covid-19 pandemic could be the most serious challenge faced by the financial services industry in nearly a century. Going forward, I am sure the banking sector in India will continue to collaborate and assist various impacted sectors. However, the physical and financial well-being of all our stakeholders will continue to be dominant priority for the organization.

Stepping into FY23, the ongoing geopolitical discord between Russia and Ukraine is a matter of significant apprehension as the impacts are already being felt across the globe including India. Analysts conclude that the impact on Indian economy will be felt mostly through higher cost push inflation weighing in on all the economic agents-households, business and government. We are closely watching how various sectors are unfolding in order to diversify the risk through granular loan book. Quality growth will continue to be our priority to equip the bank to face any adverse external events.

Let me take you through the overview of our performance in FY22, initiatives and the way forward amidst the ongoing challenges. The key focus continues to be “profitability through quality credit growth’’ by continuing our ‘6C’ strategy.

The Bank could register growth in CASA and retail deposits on liability side and could on-board highly rated accounts in corporate segment, increase in gold loan and personal loan book on asset side. Currently, the Bank has a gross NPA of 5.90% and net NPA of about 2.97%. The Bank is aiming to bring down the net NPA to sub 2% level and gross NPA to sub 4% level by end of FY24. The Team under me is working hard to reach this milestone as envisaged in our Vision 2024.

Experience Next Generation Banking

14

To remain resilient, we adopted multiple strategies with respect to restructuring of our assets and liabilities, product & segment innovations and digitalization. During the year, the Bank followed the principle - “profitability through quality credit growth” and enforced higher standards of credit underwriting with enhanced credit administration standards. The Bank through an efficient recovery & collection team could recover ` 1,464 Crore. The Bank is effectively addressing the quality issues of the past portfolio while creating a healthy new loan book. The Bank’s advances aggregated to ` 61,815.76 Crore as at March 31, 2022, registering a sustainable growth of 4% from March 31, 2021. While the focus is on retail and SME businesses, we did a lot of churning in the corporate portfolio and added a lot of ‘A’ rated corporate(s) i. e almost 85%-90% of new additions were from ‘A’ rated and above corporate(s).

Realigning technology and business, the Bank has effectively harnessed the technology disruption to our advantage, ensuring better growth in the present competitive environment. A great deal of emphasis is being placed on offering a better customer experience, through technology and product features thereby increasing customer base, improving other Income, reducing Operation Cost and preparing the business for the future. Technology and digital innovation have improved productivity, efficiency and competiveness in the delivery of financial products and services. The Bank has made significant strides in digitalization

backed by robust Technology Infrastructure, Artificial Intelligence, Data Analytics and Innovation.

The Bank has been focusing on the innovation, improvement and implementation of projects on our digital platforms viz., ATM, Net Banking, Mobile Banking and other emerging technologies. During the financial year, there is a substantial increase in the volume of internet and mobile banking transactions. The Bank has successfully grown the share of digital transactions to 93.17% during March of FY 2021-22. We will continue to focus on quality lending while maximizing cross sell opportunities to the Bank’s existing customer base and leveraging the Bank’s wide geographical and digital infrastructure network for cost optimization. The Bank has introduced AI-driven chatbots, Video KYC for account opening, digital on-boarding and credit underwriting across all asset products. The Bank further accelerated its digital delivery with an array of new offerings to ensure uninterrupted services to the customers. During the year in association with OneCard, the Bank has launched the SIB – OneCard Credit Card by issuing 58,000+ Cards. The Bank is also exploring fintech association for gold and retail loans.

The Bank has been proactive in the ever-changing situation as it has strengthened the operational and technological infrastructure needed to ensure continuity of normal operations. In a dynamic world, where an individual defines the organization, Human resources are one of the most valuable assets. Achievement of an organization’s objectives depends on the individual and the collective efforts

The Bank’s advances aggregated to ` 61,815.76 Crore as at March 31, 2022,

registering a sustainable growth of 4% from March 31, 2021. While the

focus is on retail and SME businesses, we did a lot of churning in the

corporate portfolio and added a lot of ‘A’ rated corporate(s) i. e almost

85%-90% of new additions were from ‘A’ rated and above corporate(s).

During the financial year, there is a substantial increase in the volume of internet and mobile

banking transactions. The Bank has successfully grown the share of digital transactions to 93.17% during March

of FY 2021-22.

Annual Report 2021-22

15

of its workforce. Every employee is a vital factor for smooth functioning by bridging the gap between customer’s expectations and the organization’s delivery of the services. The Bank has a team of highly motivated, skilled, committed, vibrant and young staff members, who strive to meet customer aspirations and organizational goals. Learning & Development has assumed significant importance in the present banking scenario. The Bank’s Learning & Development division continues to work on the gaps

in the capabilities of the personnel and trains them for qualitative improvement. The development of employees is essential for the strength of our Bank. A strategic approach toward effective development and management of human resources is of paramount importance. To augment the workforce in tune with the Bank’s sustained growth and expanding network, major initiatives towards training, talent acquisition, motivation and retention have been continued in the FY 2021-22.

The year 2021-22 saw the Bank being honored with the following significant Institutional recognitions, awards and accolades:

• South India Best Employer Brand Awards 2021 – Excellence in HR through Technology for mHRMS mobile app

• UiPath Automation Excellence Award for Best Automation under Crisis for Business Continuity

• Six awards at IBA’s 17th Annual Banking Technology Awards:

– Winner - Best Technology Bank of the Year (Small Banks)

– Winner - Best IT Risk Management and Cyber Security Initiatives (Small Banks)

– Winner - Best Fintech Collaboration (Small Banks)

– Joint Winner - Best Use of AI/ML and Data Analytics (Small Banks)

– Runner Up - Best Cloud Adoption (Small Banks)

– Joint Runner Up - Best Payments Initiatives (among all Private Banks)

• The 11th Edition of UBS Forums’ Data Center Summit and Awards 2022 for the below categories:

– Winner – Physical Security (Security Design)

– Recognition – Risk Management (Availability)

– Recognition – Design Management (Infrastructure)

– Recognition – Innovation – New Initiatives (Infrastructure)

• Finnoviti Awards 2022 from Banking Frontiers

• Business Leader of the Year Award, 2022 from CMO Asia for ‘Workplace and People Development’.

• Most admirable BFSI Professional Award from World BFSI Congress to HR Team.

• Our Legal Team secured the Runners-Up position in the category - Best Banking & Finance Legal Team of the Year, at the 11th Annual Legal Era - Indian Legal Awards, 2022

Experience Next Generation Banking

16

The Bank could post all time high net profit of ` 272 Crore in Q4, 2022. In spite of the challenging environment, the Bank had achieved a total business of ` 1,50,958 Crore with the deposit base of ` 89,142 Crore and gross advances of ` 61,816 Crore as at March 31, 2022. During the financial year, the Bank has achieved an operating profit of ` 1,248 Crore.

• The Capital to Risk Weighted Assets Ratio (CRAR) of the Bank according to Basel III guidelines is 15.86 as at March 31, 2022 as against the statutory requirement of 11.50 and the Net Interest Margin (NIM) also improved from 2.61 to 2.80 as compared to the previous year.

• The net interest income and non-interest income for the year stood at ` 2,240 Crore and ` 1229 Crore respectively. However, high operating expenses and high provision & contingencies have resulted in a decline in net profit to ` 44.98 Crore from ` 61.91 Crore as compared to the previous year.

• The Bank has made a remarkable growth in CASA deposits and achieved a CASA ratio of 33.2 % with a total CASA value of ` 29, 601 Crore as at March 31, 2022.

• The Bank has been able to meet the targeted levels of recovery or upgrades which have helped in containing the NPA level despite higher slippages during the financial year on account of the weak economic scenario and the Covid-19 pandemic.

Hence, the Net NPA has decreased from 4.71% to 2.97% as at March 31, 2022.

• The Book value per share of the Bank has increased and stood at ` 27.97 (face value ` 1/-) as at March 31, 2022.

Over the last 93 years, the Bank has been a trustworthy and supportive financial partner for its customers and value creation has been our core purpose. During fiscal 2022, the Bank continued to strengthen its banking franchise.

We strongly believe that the Bank is agile as an organization and is alive to the challenges and opportunities in the environment. It is upon us to collectively take action to overcome the challenges and grab the opportunities. Our focus is on capitalizing on growth opportunities, while at the same time, taking fruitful steps to address challenges in the environment. Our strong customer support with staff’s enduring commitment is sure to improve the Bank’s performance during the current year.

With Technological capability combined with the young talented Human asset, the Bank is poised to use the mix of digital and traditional customer friendly products to build a strong, sustainable asset base in coming years. I want to thank and communicate to each one of you that our Bank is committed to enhance the value of each stakeholder. I strongly believe that the coming years will be the period for harvesting the value addition for the TRUST and support shown by all our stakeholders. I continue to seek your support in achieving the mission of our Bank to be the most preferred bank in the area of Customer service, Stakeholder value and Corporate governance.

Best Wishes

Murali RamakrishnanManaging Director & CEO

The Bank could post all time high net profit of ` 272 Crore in Q4, 2022. In

spite of the challenging environment, the Bank had achieved a total

business of ` 1,49,135 Crore with the deposit base of ` 89,142 Crore and

gross advances of ` 61,816 Crore as at March 31, 2022. During the financial

year, the Bank has achieved an operating profit of ` 1,248 Crore.

Annual Report 2021-22

17

TOP MANAGEMENT

Mr. Thomas Joseph K Executive Vice President

Mr. Anto Geroge T SGM-HR & Admin

Mr. Sanchary Kumar Sinha SGM & Country Head - Retail Banking

Mr. Sony A GM & CIO

Ms. Minu Moonjely GM - Credit

Ms. Biji S S GM & Head-Corporate Business

Mr. Nandakumar G GM & Head-MSME

Ms. Chithra H GM & CFO

Mr. Thallam Sreekumar GM - Personal Loan Group

Mr. Senthil Kumar GM - Collection and Recovery

Mr. Sivaraman K GM Banking Operations Group

Mr. Harikumar L GM - Retail Banking

Mr. Abey Abraham GM - Housing Loan

Experience Next Generation Banking

18

HUMAN RESOURCE MANAGEMENT

Personalised service and close knit relation with customers have always been the USP of South Indian Bank. Time and again, the employees at South Indian Bank have proved to be the factor driving its success. They have acted as the corner stone in tiding away with the adversities that came with the pandemic as well as managing the business transformation successfully.

Empowering the transformation process

As Part of the transformation process new exclusive asset verticals and specialised operational groups were formed. The human capital required for these areas were met by providing experts in the relevant field. This was achieved through redeployment of internal resource as well as lateral recruitment of experts from the industry. Moreover, fresh candidates were extensively hired through general and campus recruitments, with a view to staff branches and other operation centres, adequately.

Core values

Essence of SIB’s culture is the nine core values, ie Sensitivity, Resilience, Ownership, Digital, Integrity, Passion, Speed, Boundaryless and Quality, which constitutes the DNA and work culture at South Indian Bank.

Employees who excel in displaying attitudes and behaviours in alignment with the core values are given

a “Core Value Ambassador” title to encourage every member of the SIB family to fully align with these values.

In the revised performance management system, behavioural scoring of employees are arrived based on his or her alignment towards the core values of the Bank.

As a technology driven Bank, we have created “Exemplar portal”, a news feed portal which capture the extraordinary performance stories of employees and maps their performance aligned with the core values of the Bank.

All the executive level employees were subjected to first ever 360 degree feedback process. The feedback process was designed in tie up with a prominent service provider based on the Bank’s core values and common behaviour traits. The entire exercise gives feedback to executives from their superior, peers and subordinate employees.

Annual Report 2021-22

19

HR Service Delivery in the fingertip

The Bank has launched m-HRMS, an app based mobile HRMS solution for employees of the Bank. The application is made available in android and i OS platform and has empowered staff members to avail various services through their mobile 24*7. The App also bagged the prestigious “South India Best Employer Brand Awards 2021 for excellence in HR through Technology” by Employee Branding Institute.

Employee engagement for process excellence

The Bank has introduced ‘Suggestion Box’ wherein the suggestions given by employees relating to customer experience, employee friendliness, methods of cost reduction, process improvement, etc. are captured. Further, a dedicated committee with representatives from various departments periodically evaluated the suggestions received. Employees can track the status of his/her suggestions on a real time basis. This activity is aimed at generating more ideas, increase problem solving skills among employees and encourage seamless downward and upward communication in the organization.

Other engagement activities include ‘Synergy’ – an outreach program by Head of HR with field level staff members, Banks calendar 2022 showcasing employees artistic and photographic talents, SIB Pulse survey’s for feedback and process improvements.

New age learning

Bank’s new Learning management System (LMS) has enabled employees to adopt the new age learning methodologies. Learning & Development team has

created and acquired contents to cover most of the Functional and Behavioural (soft-skill) needs of the staff across grades for 100 + learning hours. New LMS system has the ability for competency building based on the roles undertaken by each staff member and gaps identified. Moreover, due weightage has been given to learning in the balance scorecard.

Specially curated long term leadership program based on individual assessment has been imparted to the top management. This program helps to increase the leadership dynamics as part of the transformation process in the Bank.

Performance Management system

The Bank has adopted new Balance scorecard based performance management system. This is done by identifying and finalising job roles in scientific way. Balanced score card framework has the ability to measure the performance using quantifiable parameters. The preparation of scorecard is done in a way that the bank’s strategic plans breaks down to quantifiable parameters and allotted to top to the bottom of the pyramid to have common direction across the Bank.

All the performance reviews are moved to the scorecard, with a view to have common focus area. Introduction of the half year appraisal with feedback mechanism enables the employees to identify gaps and improve the performance. The balance score card is also linked to the Performance Linked Inscentive Scheme, Promotions and Transfers to have a one parameter based transparent system in the Bank.

Number of employees

9,200+Average Age

32 years

HR Team

70+Learning Contents created

100+ hours

Number of Staff trained in FY21-22

6,065Number of experienced staff hired in FY21-22

400+Number of fresher recruitment FY21-22

1000+

Experience Next Generation Banking

20

Officers Clerks Peon PTS

3776

1085

20

2421843

2045

160

48

South India Best Employer Brand Awards 2021 for Excellence in HR through Technology by Employer Branding Institute: World HRD

Congress

Business Leader of the year award –workplace and people

development by CMO Asia

Most admired BFSI Professional award by World Leadership

Congress

Diversity and Inclusion

5151 Males4068 Female

Annual Report 2021-22

21

DIRECTORS’ REPORTTo the Members,

The Board of Directors is pleased to place before you, the 94th Annual Report on the business and operations of the South Indian Bank Ltd. (“the Bank”) along with the audited accounts for the Financial Year (FY) ended March 31, 2022.

PERFORMANCE OF THE BANK

The performance highlights of the Bank for the financial year ended March 31, 2022 are as follows:

Key Parameters ` in crore

2021-22 2020-21

Deposits 89,142.10 82,710.55

Gross Advances 61,815.76 59,418.40

Total Gross Business 1,50,957.86 1,42,128.95

Operating Profit 1,247.57 1,617.91

Net Profit 44.98 61.91

Capital & Reserves 5,853.13 5,807.16

Capital Adequacy (%) - Basel-III 15.86 15.42

Earnings Per Share (EPS)

(a) Basic EPS (in `) [face value ` 1/-]

0.21 0.34

(b) Diluted EPS (in `) [face value ` 1/-]

0.21 0.34

Book Value per Share (in `) [face value ` 1/-]

27.97 27.75

Gross NPA as % of Gross Advances

5.90 6.97

Net NPA as % of Net Advances 2.97 4.71

Return on Average Assets (%) 0.04 0.06

Previous year figures have been regrouped / reclassified, where ever necessary to conform to current year’s classification.

BUSINESS ACHIEVEMENTS

The Bank has achieved a Total Business of ` 1,50,957.86 crore, consisting of Deposits of ` 89,142.10 crore and Gross Advances of ` 61,815.76 crore as on March 31, 2022.

DEPOSITS

The Total Deposits of the Bank as on March 31, 2021 was ` 82,710.55 crore and reached to ` 89,142.10 crore as on 31.03.2022 registering a growth of 8%.

The break-up of the deposits as on March 31, 2022 is as under:

Amount (` in crore)

% to total Deposits

Current Deposits 4,861.52 5.45

Savings Deposits 24,739.85 27.75

Term Deposits 59,540.73 66.80

Total 89,142.10 100.00

The Bank during the year has focused on Retail advances and CASA.

CASA has grown from ` 24,589.80 crore as on March 31, 2021 to ` 29,601.37 crore as on March 31, 2022, with a growth of 20.38%. The Savings bank deposits grew by 22.06 % on a year on year basis.

The Bank has accorded priority to meaningful financial inclusion during the period under reporting while opening new banking relationships.

ADVANCES

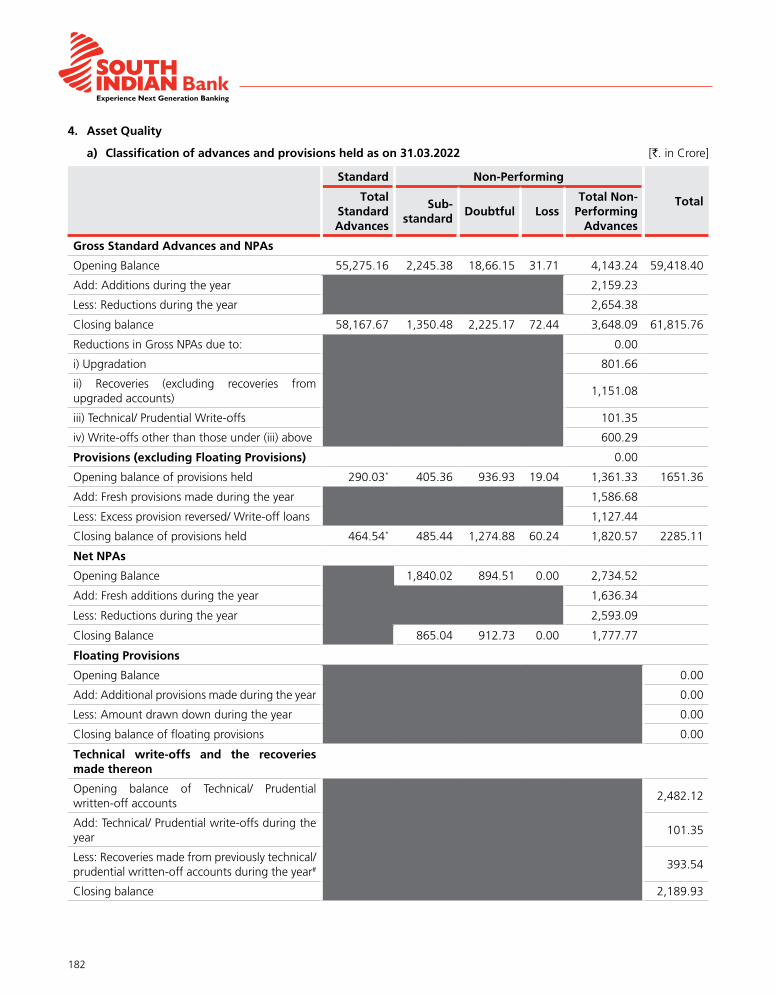

The Bank’s advances aggregated to ` 61,815.76 crore as on March 31, 2022, registering a growth of 4% from March 31, 2021. During the year, the Bank has followed the principle - “profitable credit growth through quality credit” and enforced higher standards for credit underwriting with enhanced administration standards. The Bank could also register a robust recovery and upgradation in GNPA amounting to ` 1307.00 crore, during the financial year 2021-22. The Gross and Net NPA levels of the Bank has improved to 5.90% and 2.97% respectively, as on March 31, 2022.

During this period of transformation and focus on quality loan book, the Bank could achieve a moderate growth in credit portfolio. However, certain portfolios viz. Personal Loan, Gold loan, low risk Large Corporate Advances etc. registered a substantial growth during the year. The Bank could achieve all the priority sector advance targets and also got an opportunity to generate additional source of revenue amounting to ` 118.27 crore during the year, through sale of PSLC.

% of Target% of

Achievement

Overall PSL 40.00% 42.45%

Agriculture 18.00% 20.26%

Small & Marginal Farmers 9.00% 10.84%

Non-Corporate Farmers 12.73% 14.44%

Micro Enterprises 7.50% 8.78%

Weaker Sections 11.00% 13.47%

Break-up of exposure under Priority Sector as on March 31, 2022 is furnished below:

Experience Next Generation Banking

22

Amount(` in crore)

(A) Agriculture & Allied activities (Net of PSLC) 10,820.66

(B) MSME (Net of PSLC) 18,143.67

(C) Other Priority Sector 2,503.02

(D) Total Priority Sector 31,467.35

(E) PSLC (General PS) 8,800.00

TOTAL PS (Net PSLC) = (D)-(E) 22,667.35

The Covid-19 pandemic and subsequent lockdowns adversely affected almost all the domestic demands. To ascertain the explicit market requirement and to offer specialised services & products that cater to and fulfill the necessities of that particular segment, the Bank reframed its business strategy in the year and different verticals were established namely Corporate business group, MSME business group, Jewel Loan business group, Agri business group, Housing Loan business group, Personal Loan business group etc. A separate unit has also been established to boost the portfolio under supply chain finance.

FINANCIAL PERFORMANCE

Profit

The Net Operating Income (Net Interest Income and other income) of the Bank decreased by ` 362.22 crore (9.96%)from ` 3636.08 crore to ` 3273.86 crore. The decrease in Non- Interest Income was ` 195.07 crore (15.87%) during the year, which was mainly on account of higher depreciation on investments charged during the FY 2021-2022. The Operating Profit for the year under review was ` 1247.57 crore (before taxes and provisions) as against ` 1,661.60 crore for the year 2020-21. The Net Profit for the year was ` 44.98 crore as compared to a net profit of ` 61.91 crore during the previous year and the profit available for appropriation are as per details given below:

(` in crore)

Profit before taxes and provisions 1247.57

Less: Provision for NPI (7.91)

Provisions for Non- Performing Assets 1161.40

Provision for FITL 69.67

Provision for Income Tax (136.97)

Provision for Standard Assets 175.57

Provision for Restructured Assets 1.22

Provision for Other Impaired Assets 3.41

Provision for Un-hedged Forex Exposure (1.06)

Provision for Non-Banking Asset Provision (62.74)

Net profit 44.98

Brought forward from previous year 4.63

Profit available for appropriation 49.61

Appropriations:

Transfer to Statutory Reserves 11.25

Transfer to Capital Reserves 76.22

Balance carried over to Balance Sheet (37.86)

Total 49.61

Dividend

The Bank has not recommended any dividend for the financial year ended March 31, 2022.

CAPITAL & RESERVES

The Bank’s issued and paid-up capital stood at ` 209.27 crore as on March 31, 2022. The Bank has not issued any securities during the financial year 2021-22.

The capital plus reserves of the Bank has moved up from ` 5,807.16 crore to ` 5,853.13 crore on account of plough back of profits during the current financial year

THE CAPITAL TO RISK WEIGHTED ASSETS RATIO (CRAR)- BASEL III

The Capital to Risk Weighted Assets Ratio (CRAR) of the Bank according to Basel III guidelines is 15.86 as on March 31, 2022 as against the statutory requirement of 11.50 (including Capital Conservation Buffer). Tier I CRAR constitutes 13.22 while Tier II CRAR works out to 2.64.

The Bank follows Standardized Approach, Standardized Duration Approach and Basic Indicator Approach for measurement of capital charges in respect of credit risk, market risk and operational risk, respectively.

LISTING AGREEMENT WITH STOCK EXCHANGES

The Bank’s shares continue to be listed on BSE Ltd. and The National Stock Exchange of India Ltd. The Tier I/II Bonds issued by the Bank is continue to be listed on BSE Ltd. The Bank confirms that it has paid the listing fees to all the Stock Exchanges for the year 2022-23. The securities of the Bank are actively traded on NSE (Shares only) and BSE (Shares and Bonds) and have not been suspended from trading.

EXPANSION PROGRAMME

The Bank has been successful in widening its network across India with 935 banking outlets (928 Branches (including 1 Banking outlet), 1 EC, 3 Satellite branches and 3 Ultra small branches) and 1,270 ATMs/CRMs as on March 31, 2022. The Bank has opened 7 new outlets and closed 3 Branches and 4 Extension Counters. Also opened 22 new ATMs, 11 CRMs across the country during the financial year 2021-22 and closed 75 ATMs and 3 CRMs. The branch network now covers 26 States and 4 Union Territories.

Annual Report 2021-22

23

The Bank plans to open 15 banking outlets (including 2 Digital Banking outlets) and 25 ATMs & 10 CRMs during the financial year 2022-23. Construction of currency chests at Kakkanad & Kannur are in progress and completion of its construction is expected within this FY 2022-23, as per the time line permitted.

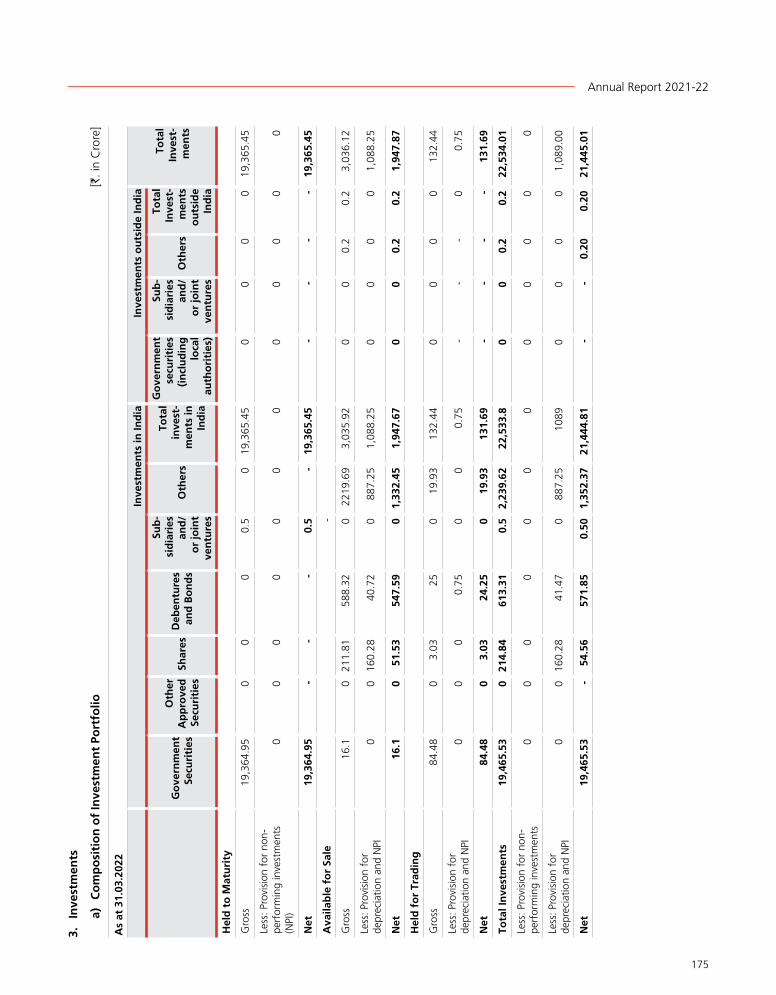

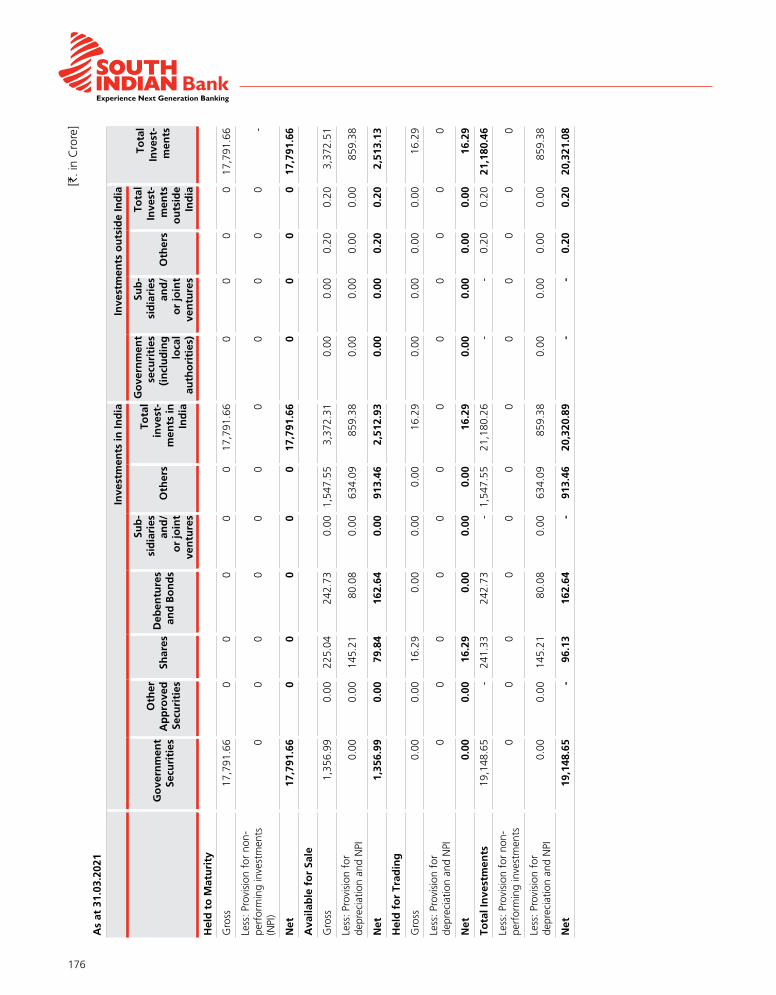

INVESTMENT

To curb the high inflation globally Central Banks, including RBI have started tightening the liquidity by hiking interest rates and normalising the balance sheet. Federal Reserve has hiked Fed fund rate by 75 bps and the central bank expects it to reach 2.8% by 2023. The RBI hiked repo rate by 90 bps to 4.9%, keeping the stance to “accommodative”. RBI hiked CRR by 50 bps to 4.5% (estimated around ` 870 bn of liquidity withdrawal from the Banking system), SDF rate was increased to 4.65% and MSF rate increased to 5.15%. The RBI is expected to do additional repo rate hikes of 75-100 bps, pushing repo rate to more than 5% in FY2023.

The Bank’s gross investment portfolio stood at ` 22,534.01 crore as on March 31, 2022 compared to ` 21,180.46 crore as on March 31, 2021, reported an increase of 6.39%. Investment Deposit ratio moved to 25.28 as on March 31, 2022 from 25.61 as on March 31, 2021. Profit on sale of investment for FY 2021-22 stood at ` 330.38 crore. Total interest income (Interest + Dividend) from investment for the year was ` 1,039.81 crore. Yield on investments (profit + interest earned to average investments) during FY 21-22 was 6.32%.

During the year, the fixed income instruments trading desk, the equity trading desk, and the forex trading desk in Treasury Department have all managed their portfolios well with data-backed analysis. The SLR trading desk also planned and executed the Bank’s participation in Government’s Securities Market. The desk has successfully managed the held-to-maturity (HTM) book. The equity trading desk took well thought out positions in the secondary market and participated actively in the various primary market offerings too. The forex trading desk too contributed actively to overall profits by taking gainful trading positions.

System liquidity remained in large surplus throughout the last year. The Fund Management and Money Markets Desks at Treasury Department successfully managed the liquidity risk by maintaining appropriate levels of surplus funds. The desk also ensured compliance with the regulatory requirements for cash reserve ratio (CRR) and statutory liquidity ratio (SLR).

Besides the above, the Forex Merchant Desk in Treasury Department offers to the Bank’s customers solutions for foreign exchange risk hedging and remittance-related services. A significant portion of the total Treasury profits for FY 2021-22 came from Forex Merchant activities. Going forward, Treasury Department intends to focus on Forex Merchant business and other similar offerings to customers for diversifying its revenue mix.

The Treasury Department was able to operate continuously and without interruptions during the year, even during the lockdown, which demonstrates the resilience of the risk management systems and processes in place.

NON-PERFORMING ASSETS (NPA)

During the FY 2021-22, as a result of focused and sustained efforts inspite of COVID 19 barriers and subsequent lockdowns enforced, through prompt and effective measures under the SARFAESI Act, follow up of recovery cases pending before DRTs and Civil Courts, one-time compromise settlements of accounts and Sale of Secured Assets, the Bank could recover as much as ` 1,464.04 crore in NPA accounts surpassing the annual recovery target of ` 1,200.00 crore. It may be further noted that the total recovery during FY 2021-22 including ARC Sale and restructuring is ` 2417.61 crore. Special thrust was given to selection and underwriting of credit, effective due diligence and improvement in credit administration to ensure improvement in the quality of assets. Due to the efforts put-in, during the financial year, the Gross NPA of the Bank has decreased from ` 4143.24 crore as on March 31, 2021’ to ‘` 3 648.09 crore as on March 31, 2022’ and Net NPA decreased from ‘` 2,734.52 crore as on March 31, 2021’ to ‘` 1,777.77 crore as on March 31, 2022’. In terms of percentages, the GNPA decreased from 6.97% as on March 31, 2021 to 5.90% as on March 31, 2022 and Net NPA has decreased from 4.71% as on March 31, 2021 to 2.97% as on March 31, 2022. As a result of Bank’s strong focus on recovery as well as the initiatives taken in underwriting credit and tracking early warning signals, the future NPA level is expected to be controlled.

PRODUCTS

During the FY 2021-22, the Bank has introduced new loan products to provide focused thrust on loans to Gold, MSME and Agricultural Sectors. The Bank entered into an agreement with M/s FPL Technologies for co-branded Credit Card and upto March, 2022 issued 58,000/- credit cards with outstanding book of ` 156 crore. The Bank proactively implemented all government schemes namely ECLGS, PM Svanidhi, Loan guarantee scheme to Covid affected sectors etc. to handhold the borrowers who were ailing because of the economic disruptions due to pandemic. In this financial year the Bank will introduce tailor made loan products to cater the requirements of various segments of the society.

DIGITAL AND INFORMATION TECHNOLOGY ENABLED SERVICES

The digital revolution of the past decade has disrupted all industries, with the Banking sector being no exception, changing the way the Bank do business. With the growing use of smart phones and emerging technologies like Artificial Intelligence (AI) and Machine Learning (ML), digitization has taken over the industry, resulting in new business paradigms and significantly fuelling the improvement of banking services.

Experience Next Generation Banking

24

With a plethora of digital tools at hand, market penetration, productivity and efficiency have soared. The Bank now has digital-only services unburdened by the brick-and-mortar method of providing banking services. Banks have now been redefined from a mere intermediary to a financial supermarket, providing an array of financial services under one roof.

Realigning technology and business, the Bank has effectively harnessed the technology disruption to our advantage, ensuring better growth in the present competitive environment. A great deal of emphasis is being placed on offering a better customer and staff experience, by increasing customer base, improving Other Income, reducing Operation Cost and preparing the business for the future. The Digital Banking Department has been focusing on the innovation, improvement and implementation of projects on our digital platforms viz., ATM, Net Banking, Mobile Banking, and other emerging technologies. The IT Operations Department ensures the highest level of service and integrity of our internal applications and infrastructural support to enable a seamless growth in the Bank’s business operations. Enhancing self-service capability across channels, empowering branches with technology solutions to nudge the customers to go digital and automating manual processes at branches & back offices to improve customer TAT using AI & RPA, form the three pillars of the Bank’s overall digital strategy. The Bank has successfully grown the share of our digital transactions to 93.17% during March of FY 2021-22.

Retail Customers:

The Bank offers the best in class technology services to cater the diverse requirements of retail clientele. The technology stack includes well designed customer touch points and robust back end systems providing 24/7 digital availability of the highest quality to our customers.

• Full Fledged enterprise level systems

• Internet Banking - Sibernet

• Mobile Banking – Mirror +

• All variants of VISA, Mastercard & Rupay Debit Cards are offered

• Credit Card – OneCard (in tieup with fintech)

• RuPay Prepaid Cards

• Student smart cards for Institutions- used for Identity cum financial transactions

• Debit card security controls on customer touch points - Mirror+, SiberNet, IVR and Branches

• ATM, Cash Recyclers (CRM) other Value added services

• Call Centre Solution catering to customers 24/7

• CRM solution providing 360 degree view of customers

• Business Process Management (BPM) to enable

centralization

• Technology backed Branch Infrastructure

• Latest version of Core Banking Solution (CBS) form Infosys, viz. Finacle 10

• Enterprise Risk Management Solution

• ATM network that spread across the country, which supports Mastercard, VISA and RuPay cards allowing customers quick access to money.

• Mobile Banking (with support for other bank money transfer through IMPS, P2A, P2M (issuer), USSD, UPI and Bharat QR.

• Missed call services for retrieving balance through SMS etc.

• Online investment in primary and secondary markets offered to customers through ASBA, e-trade and e-mutual fund modes.

• Portfolio Investment Scheme for NRIs, allowing them to invest in Indian equity market

• IMPS Facility to Exchange Houses for Foreign Remittance - For our international client exchange houses/banks the Bank has introduced IMPS based fund transfer on a 24*7 basis in addition to NEFT.

• Fraud Risk Management (FRM) Solution for channel transactions

• Acting as an issuer of FasTag for toll connection

• Kiosk based Financial Inclusion Solution to enable the Bank reach nook and corner of the country, even in remote villages using technology enabled tools.

• Payment Options such as Automated Clearing House (NACH) Payment Service, Cheque Truncation System (CTS), RTGS/ NEFT etc.

• Account Opening for NRI/MSME directly through Bank’s website.

• Instant QR code payments at merchant locations using Bharat QR, where Customers can use debit card (VISA/Mastercard/Rupay) as virtual card inside Mirror +

• Introduction of Interoperable Cash Deposit (ICD) Machines to facilitate remittance through our recyclers to other bank accounts and vice versa

• Enhancement in Security Operation Centre Operations

• ISO 9001:2015 Certified Bank owned Data Center (DC)

• ISO Certified Disaster Recovery and BCP Setup

• Zero Data Loss high availability setup with DC, DR and Near line DR Setup

Annual Report 2021-22

25

• Enhancements in DC, DR and NDR Setup

• Automation of procurement and payments

• Robotic Process Automation-30 processes has been automated in previous FY.

• Application Program Interface (API) banking-120 APIs has been made live on previous FY.

• Artificial Intelligence based banking services such as Chatbots like SAM and SONA.

• Central Plan Scheme Monitoring System (CPSMS), which links to the DBT (direct beneficiary transfer) for instant receipt of Govt. subsidies to the beneficiaries of various Govt. schemes.

• Tab based Aadhaar e-KYC instant account opening for individual Savings Accounts.

• Quick account opening facility at branch level through e-KYC acceptance with reduced paper involvement, processing time and interdepartmental dependency.

• Self on-boarding by opening SIB-Insta account through mobile devices using Aadhaar and PAN card.

• Housing Loan Interest Certificate made available through SIBerNeT and Mirror+.

• KYC Update and communication address modification through SIB Mirror Plus /SIBERNET.

• Pre Approved Car Loan through Channels.

• Instant Demat account opening through SIBERNET

Corporate Customers

• The Bank has Internet Banking facility, from Infosys which provides all the workflow capabilities required for each corporate. Moreover, it offers the security of Digital certificate integration thereby balancing convenience with security.

• The Bank also offers Host to Host Integration facility (“Hi- Hi Banking”) which will handle fund transfer in a seamless fashion by real time interface with ERP solutions of corporates. This facility is available for 365*24*7 and the clients can securely access the system from anywhere.

• Supply Chain Management Solution caters to the dealer/vendor financing requirement of corporates.

• The Bank is offering business debit cards to the business customers.

• On the business acquiring capabilities, the Bank has full suite of payment acquiring including POS terminals, Bharat QR, UPI QR, Payment Gateway etc. which gives the merchants a whole host of accepting payments instantly from their customers.

• Integration through APIs for full-fledged automation done with several corporate and Govt. agencies.

• Trade Finance Portal for Customers.

• SIB Merchant plus current account to cater the needs of business requiring POS as payment solution.

• Vayana Network for supply chain Finance

Digital/Technology initiatives/solutions embarked during the year

The services/solutions that the Bank has launched during the year inter-alia includes the following:

• Credit Card tie up with One Card.

• International Lounge Access facility for RuPay Debit cards.

• Tap & PIN for NFC transactions > INR 5,000

• Standardization of Electronic Journals in ATMs & CRMs

• Extending Voice Guidance facility in all ATMs

• Introduction of “Hyosung” ATMs and CRMs to Bank’s machine base

• ATM & CRMs – Replacing aged machines (75% of machine base) with new machines.

• TLS encryption for ATM to ATM Switch communication to thwart the risk of Man-in-The-Middle (MiTM) attacks.

• Ecommerce transaction tokenization for RuPay Debit cards.

• Issuance of Visa Student Smart Cards

• Incorporating Merchant Name and Amount of Txn in OTP SMS message for RuPay CNP transactions.

• Enablement of Cash @ POS facility in Bank’s POS devices

• Cash Tally Report using counter information available in EJs

• TDS/TCS certificate made available through SIBerNeT and Mirror +.

• Credit Card Against FD through Mirror+.

• Pre Approved Car Loan through Channels.

• Housing Loan Interest Certificate made available through SIBerNeT and Mirror +.

• Tie up with Delhi Jal Board for collection of payments against water/sewer bills.

• Trade Finance Portal for Customers.

• Inward/outward clearing cheque status is made available through Mirror+.

• Locker availability enquiry option is made available through SIBerNeT and Mirror+.

Experience Next Generation Banking

26

• Account Category Change can be done through SIBerNeT.

• Email ID update can be done through SIBerNeT and Mirror+.

• Automated customer upgrade to Priority Banking is made available through SIBerNeT and Mirror+.

• UPI POS Admin Dashboard and issuance charge.

• Brokers Tie-Ups with Our DEMAT- Motilal Oswal Financial Services.

• Salary Account opening made available through Video KYC.

• Instant Beneficiary approval is made available in SIBerNet.

• APY registration is made available through SIBerNet/Mirror Plus.

• Multilingual option (added Eight Indian Languages) is made in SIB Mirror+.

• UPI facility made available in NRE accounts.

• Tie-up arrangement with M/s Star Health & Allied Insurance Co Ltd as our third health insurance partner for soliciting Health Insurance business.

• Digital Documentation by Leegality-HL&PL

• Notional Rate Revaluation

• RuPay Classic White Plastic Certification - MCT

• Enabling VAN remittance through UPI

• SWIFT 20-20 validations

• Requirement of purchasing “Income Tax Analyzer”.

• Introduction of Other Bank ATM Decline Charges

• VAN Based remittance tie ups - Airtel Payments bank, Unimoni Financial Services Ltd.

• Requirement of creating a new product Loan guarantee scheme to MFIs

• Enabling Debit card in FCRA account.

• Bulk account opening, Video KYC and Co-branded card issuance for Christ University Students/Staffs account.

• New Gold Loan Variant -Special scheme for Onam

• New gold loan variant against specially Minted gold coins sold by banks

• To provide HiHi Banking for credits to loan account

• New Current Account Product - Merchant Plus Current Account.

• System level validations for Implementing Budgetary change-Sec 206 AB & Sec 206CCA.

• System level as part of extending the moratorium in KCC interest subvention accounts

• System level changes required for opening Top Up loan for HL borrower

• Housing loan Interest certificate and Provisional Certificate through Mobile Banking

• Snorkel registration RPA automation - Corporate

• Snorkel registration RPA automation -Retail

• Automation of address update in Internet Banking module

• Gold Loan takeover process -revision/modification

• Automated SIBerNet activation mailer to all retail NTB customers

• Snorkel self-registration and activation in SIBerNet

• UPI integration in Payment hub

• New Product “Agriculture Produce” under RLOSAGRI Module

• Instant Demat Account Opening through Branch, SIBerNet and Mirror Plus

• Enabling Form 60 generation through Internet Banking and Mirror Plus

• Introduction of new agri product ‘Agriculture Infrastructure Fund’

• Rollout of new product: SIB Institutional Account

• IT Service Management solution

• OTC Locks in ATMS- Phase FY 2020-21 (Phase I & II)

• LC/BG Automation: RPA

• HL -In principle sanction for Property Not Identified Cases

• Automation of calculation in CBS for gold ornaments and jewellery with a purity of 18 carat & above.

• TOP UP loan for HL Borrowers.

• Request for the approval to fund insurance product SIB - Super Suraksha with Personal Loan.

• Requirement for simplified renewal process for Working Capital facilities <=25 Lakhs-TBR Model.

• Video-CIP – On board customers remotely by establishing the customer’s identity.

• SIB Namaste-Virtual Booking system.

• Virtual Data Room (VDR) Setup for sharing documents securely

• SaaS model Cloud Adoption

• Cloud Adoption Strategy Framework

Annual Report 2021-22

27

Major initiatives/solutions embarked during the year

Fintech tie-ups:

• Launch of Bank’s Credit Card SIB-ONE CARD tie up with M/S FPL Technologies PVT LTD.

• Digital Signing of Legal documents.

• Tie up with Vayana Network for supply chain Finance

Other initiatives:

• SIB TF ONLINE Trade Finance Portal for corporate Customers in SIBERNET.

• BPM Platform migration to IBPS version.

• Pre -Approved Car Loan through Channels.

• Instant Demat account opening through SIBERNET

• Introduction of transaction decline charges in other Bank ATMs due to insufficient funds.

• SIB Thejas Loan against sovereign Gold loans.

• KYC Update and communication address modification through SIB Mirror Plus SIBERNET.

• Launch of Multilingual functionality in SIB Mirror+

• Implementation of new CRM Application CRM-NXT

• LC/BG Automation: RPA

• Launch of RuPay Platinum explorer NCMC Contactless debit cards.

• IT Service Management solution

• OTC Locks in ATMS- Phase FY 2020-21

• Introduction of “Hyosung” ATMs and CRMs to Bank’s machine base

• ATM & CRMs – Replacing aged machines (75% of machine base) with new machines.

• Compliance related to ATM – TLS, network concealing, Cassette swapping and Windows 10.

• Voice Guidance Enabling in NCR ATMs

• Notional Rate Revaluation

• SWIFT Version migration

• ICDMS Software revamping / Upgrade

Awards and Certifications received on Technology Front

The Bank has won various awards and accolades in the Financial Year 2021-22 also. These awards are a testimony of the Bank’s strategy, commitment and execution of various digital / IT initiatives and has brought in an acclaim from both customers and stakeholders.

• The 17th edition of the IBA Banking Technology Awards, 2022, for the below categories.

a) Winner - Best Technology Bank of the Year (Small Banks)

b) Winner - Best IT Risk Management and Cyber Security Initiatives (Small Banks)

c) Winner - Best Fintech Collaboration (Small Banks)

d) Joint Winner - Best Use of AI/ML and Data Analytics (Small Banks)

e) Runner Up - Best Cloud Adoption (Small Banks)

f) Joint Runner Up - Best Payments Initiatives (among all Private Banks)

• The UiPath Automation Excellence Awards, 2021, for Best Automation under Crisis for Business Continuity.

• The 11th edition of UBS Forums’ Data Center Summit and Awards, 2022, for the below categories.

a) Winner – Physical Security (Security Design)

b) Recognition – Risk Management (Availability)

c) Recognition – Design Management (Infrastructure)

d) Recognition – Innovation - New Initiatives (Infrastructure)

IT Training

During the year, many training programmes had been attended by the Bank’s officers in premier institutions such as IDRBT, NIBM, IBA, UIDAI to keep themselves abreast with the advancements in IT, Information Security, CRM, Databases, Operating Systems, Virtualization, Network, Mobile banking, ITIL (IT Infrastructure Library) Foundation Training etc. The Bank has also tied-up with leading online technology training platforms to offer all year-free technology training and certification programmes for its technology team.

Business Continuity planning

As per BCP Policy, the Bank has already setup a full-fledged BCP location and DR site at Bangalore which is ISO 27001:2003 certified. Also Bank has set up necessary infrastructure at Kalamaserry, Ernakulam as a secondary BCP site. Planned BCP drills are conducted on regular basis from both the locations to ensure connectivity and functionality test of critical applications. The necessary infrastructure and technology are adequate and people are trained enough to respond and act quickly to a BCP or disaster recovery situation. BCP location is manned with adequate staff members who can handle the IT operations during disasters, with the support of the primary IT team. Considering the pandemic situation arising due to Covid-19, various measures were implemented including usage of laptops and arranging WFH for critical personnel with necessary security policies. Meetings and conferences

Experience Next Generation Banking

28

were changed to online mode. Thus, ensuring uninterrupted customer services round the clock. As per recommendations from BCP committee, zero data loss replication methods are used for primary to DR synchronization. The Bank has implemented 3 way replication also for most critical applications, to achieve zero RPO and better RTO. A testimony of Bank’s robust BCP program and preparation is that, during the forecasted flood situation in 2020, the BCP operations were invoked, and all critical systems were switched to DR in a time bound manner without any hindrance to customers. Systems of the Bank worked at full potential capability without any disturbance to the customers during the period. The BCP policy for information systems is also periodically reviewed and updated with latest industry standards.

Information Security and Risk Management

As banks adopt sophisticated technology to roll-out the most effective banking solutions to customers, they are increasingly exposed to technology risks. It is therefore imperative for each Bank to work out appropriate IT risk management strategies to secure its most vital information assets and to ensure that related risk management systems and processes are strengthened for smooth and continuous banking operations.

• IT Departments including Data Centre, DR Site & BCP site and CISO Office are ISO 27001 certified for the implementation of Information Security Management System (ISMS). As a part of ISMS implementation, the Bank has prepared IS Security Policy and related IT risk management procedures.

• The Bank also ensures that all cyber security requirements as per statutory/regulatory guidelines and best industrial practices are implemented on priority basis.

• Bank has a separate full time CISO Office for surveillance of the security architecture/infrastructure and for coordinating security incident-response activities. The Bank has formulated Cyber Security Policy and Cyber Crisis Management Plan to provide guidance in addressing various cyber threat scenarios. The Bank has also identified various types of IT risks and the required preventive, detective and corrective cyber security controls are being implemented/updated.

• The Bank has also ensured that Security Operation Centre (SOC) does 24*7 surveillance and keeps itself regularly updated on the latest nature of cyber threats. The Bank is using Security Information and Event Management (SIEM) monitoring tool, for identifying, monitoring, recording and analysing security events or incidents within the real-time IT environment.

• The Bank has put in place a number of security solutions to manage cyber-attacks. As part of advanced security solutions, the Bank has implemented Anti-Advanced Persistent Threat (APT) Solution, Server Protection

Solution, Network Protection Solution, other advanced security solution/services etc. to handle a variety of threats and malicious attacks.

• Employees are updated with the latest security threats and the best security practices. In order to ensure continuous awareness on best cyber security practices and cyber security risks, a dedicated internal web portal to disseminate relevant security information has been set up and it is accessible to all employees.

• The Bank provides cyber security awareness to its customers on a continuous basis through various channels like SMS/ Email/Website/Social media, etc.

• Bank is also committed to Data Privacy of customers, employees, stakeholders, etc and is undertaking initiatives to further enhance and improve its Data Privacy posture.

Gopalakrishna Committee recommendations, management philosophy & measures for the effective implementation of Cyber Security Framework

• Effective measures have been taken to address the identified gaps in each area such as IT Governance, Information Security, IT Service outsourcing, IS Audit, IT Operations, Cyber Frauds, Business Continuity Plan (BCP), Customer Education and Legal issues. Information Security policy is revamped incorporating various guidelines and stipulations mentioned in regulatory framework/guidelines/other best practices. In addition, other IT Policies such as IT Operation Policy and IT Governance Policy are also enforced.

• IT Strategy Committee of the Board, IT Steering Committee and Information Security Committee are in place. Cyber security preparedness of the Bank is reviewed by Information Security Committee, IT Strategy Committee of Board and Board of Directors on a quarterly basis.

BUSINESS OPERATIONS GROUP (BOG)

Business Operations Group (BOG) has been set up to centralize and to streamline various operations which were happening at branches/sales/product, making them free from those operational activities. This helps to empower the sales teams/branches to focus and garner more business improving the top line as well as bottom line of the Bank. BOG undertakes the following functional operations in a centralized environment with a view to bring standardization of processes and procedures, scalability in line with business expansion, compliance with regulatory and statutory requirements, enforcement of internal controls, besides expeditious service to the customers. To ensure business continuity, BOG is operational from different locations, Ernakulam-Kerala, Kottayam-Kerala, Chennai-Tamilnadu, Coimbatore-Tamilnadu, Hyderabad- Telangana & Bangalore-Karnataka. The operational activity is a hybrid of in house and outsource; and multiple vendors are employed for outsourced operations

Annual Report 2021-22

29

to avoid single point of failure, wherever applicable.

The operations are governed by underlining SLA and TAT through vivid dissemination of Job role and Job description for operating/supervising staff. Productivity and FTR (First Time Right) are the metrics used to measure the efficacy of daily operations. Training is given on continuous manner for improvement in the operation in tandem with changed management, both in resources and processes.

A) ASSET OPERATIONS

This broadly covers:

1) Loan Login Acceptance

2) Neo Score (Rating Model for Retail) Checking

3) Data Entry (Retail)

4) Pre Sanction Mandatory Checking of all specified conditions (Retail)

5) Post Sanction Document Verification (Retail)

6) Post Sanction Compliance (Retail)

7) Loan Opening (All loans)

8) Loan Disbursement (All loans)

9) Post Disbursement Compliance (Retail)

10) Document/Record Preservation (Retail Loans)

Bank has already commenced centralized storage of physical loan documents Pan India with partnership with a service provider. Bank is in the process of launching a new retail platform for onboarding and underwriting which has enhanced features including quite a lot of APIs for seamless flow of processes thereby reducing the TAT and increasing the efficiency, besides enabling digital onboarding.