Lecture 2 Cost Behaviour: Analysis and Use

34

Lecture 2 Cost Behaviour: Analysis and Use 1

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Lecture 2 Cost Behaviour: Analysis and Use

Lecture 2Cost Behaviour:Analysis and Use

1

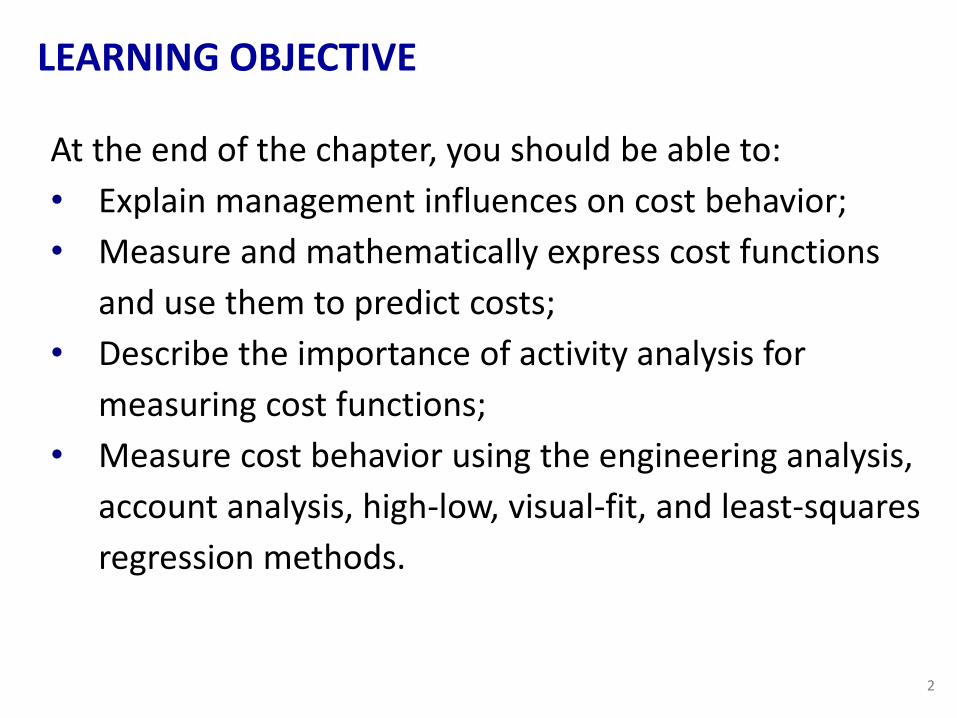

At the end of the chapter, you should be able to:

• Explain management influences on cost behavior;

• Measure and mathematically express cost functions

and use them to predict costs;

• Describe the importance of activity analysis for

measuring cost functions;

• Measure cost behavior using the engineering analysis,

account analysis, high-low, visual-fit, and least-squares

regression methods.

LEARNING OBJECTIVE

2

INTRODUCTION

3

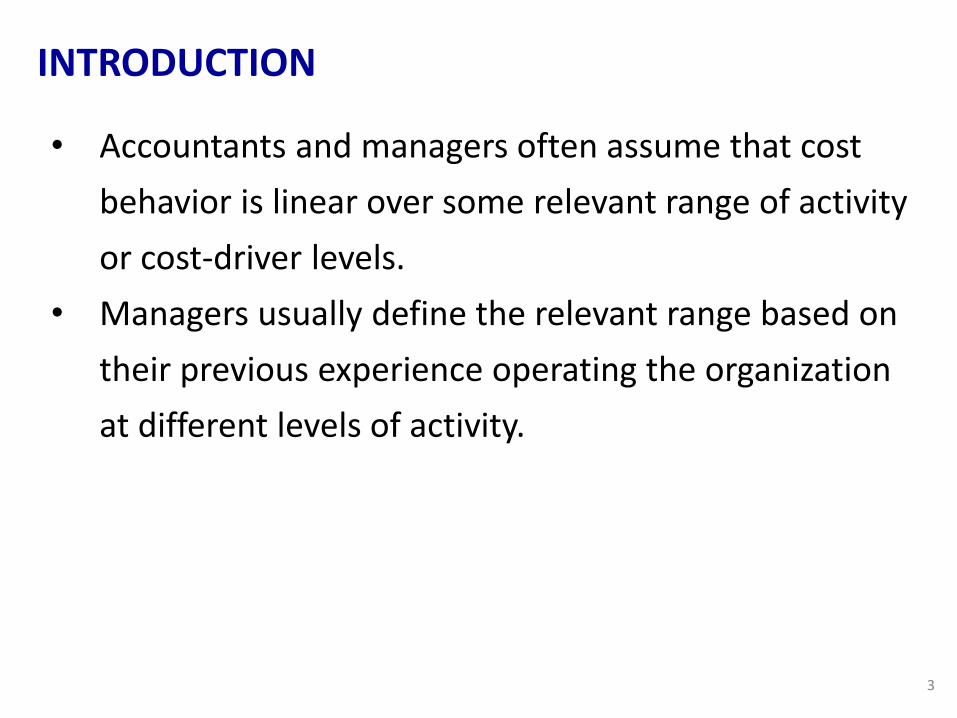

• Accountants and managers often assume that cost

behavior is linear over some relevant range of activity

or cost-driver levels.

• Managers usually define the relevant range based on

their previous experience operating the organization

at different levels of activity.

4

MANAGEMENT INFLUENCE ON COST BEHAVIOUR

• In addition to measuring and evaluating current cost

behavior, managers can influence cost behavior

through decisions about such factors as product or

service attributes, capacity, technology, and policies

to create incentives to control costs.

5

• Product and Service Decisions and the Value Chain:

Throughout the value chain, managers influence

cost behavior.

This influence occurs through their choices of

process and product design, quality levels,

product features, distribution channels, and so on.

Each of these decisions contributes to the

organization’s performance, and managers should

consider the costs and benefits of each decision.

MANAGEMENT INFLUENCE ON COST BEHAVIOUR

6

• Capacity Decisions:

Strategic decisions about the scale and scope of

an organization’s activities generally result in fixed

levels of capacity costs.

Capacity costs are the fixed costs of being able to

achieve a desired level of production or service

while maintaining product or service attributes,

such as quality.

MANAGEMENT INFLUENCE ON COST BEHAVIOUR

7

• Committed Fixed Costs:

Even if a company has chosen to minimize fixed

capacity costs, every organization has some costs

to which it is committed, perhaps for quite a few

years.

A company’s committed fixed costs usually arise

from the possession of facilities, equipment, and a

basic organizational structure.

MANAGEMENT INFLUENCE ON COST BEHAVIOUR

8

• Discretionary Fixed Costs:

Some costs are fixed at certain levels only because

management decided to incur these levels of cost

to meet the organization’s goals.

These discretionary fixed costs have no obvious

relationship to levels of capacity or output activity.

MANAGEMENT INFLUENCE ON COST BEHAVIOUR

9

• Technology Decisions:

One of the most critical decisions that managers

make is choosing the type of technology the

organization will use to produce its products or

deliver its services.

Choice of technology positions the organization to

meet its current goals and to respond to changes

in the environment.

MANAGEMENT INFLUENCE ON COST BEHAVIOUR

10

• Cost-Control Incentives:

Finally, the incentives that management creates

for employees can affect future costs.

Managers use their knowledge of cost behavior to

set cost expectations, and employees may receive

compensation or other rewards that are tied to

meeting these expectations.

MANAGEMENT INFLUENCE ON COST BEHAVIOUR

11

• Cost behaviour is concerned with enabling managers

to make educated predictions of how costs will

respond to their decisions.

• Management and cost accounting is to support

managers’ decision making in their quest for the

most efficient and effective allocation of resources

with the aim to maximise the shareholders’ wealth.

• Therefore, decision making is concerned with

obtaining the highest sustainable spread between

revenues and costs.

COST CLASSIFICATIONS

12

• In order to analyse costs and predict useful patterns

it is necessary to categorise the cost.

• Once a manager is able to refer a cost to a specific

category, and the cost behaviour of that category is

known, then it will be easier to predict how that cost

will respond to decisions.

• Cost classification:

Variable cost vs. Fixed cost

Direct cost vs. Indirect cost

COST CLASSIFICATIONS

13

• Variable costs are those costs whose value changes in

proportion to changes in the volume of production. In

reality, very few costs behave exactly like this.

• The more a resource is used, the more efficient its use

may become as the workforce becomes more skillful,

the supervisors become more aware of how to reduce

wastages, managers are able to put in place more

effective control systems, consultants can apply past

experience to solve similar problems and so forth.

COST CLASSIFICATIONS – VARIABLE COSTS

14

• It is nevertheless true that if the variation in the

volume of output is within a limited range, then the

changes in the value of certain costs are not too far

from being proportional to the changes in production

volume.

• Hence, classifying such costs as variable costs is

justifiable due to their economic behaviour (within

that range of production volume), and this makes

them easier to analyse.

COST CLASSIFICATIONS – VARIABLE COSTS

15

• The opposite of variable costs are fixed costs, which

tend to be unaffected by fluctuations in the volume

of production.

• Fixed costs, similarly to variable costs, are not

necessarily completely fixed in economics terms.

• However, within sufficiently small ranges of

production these costs will be effectively represented

by straight, flat lines.

COST CLASSIFICATIONS – FIXED COSTS

16

• In Figure, it can be seen that within the range of

production between level A and level B the cost is

fixed, but it is not between level B and level C.

COST CLASSIFICATIONS – FIXED COSTS

17

• However, many costs will comprise two components:

one that can be represented as a fixed cost and the

other that can be represented as a variable cost.

• For example, the cost of utilities may incur a fixed fee

that must be paid regardless of the amount of utility

consumed and also a variable fee that depends on

the amount of the utility consumed.

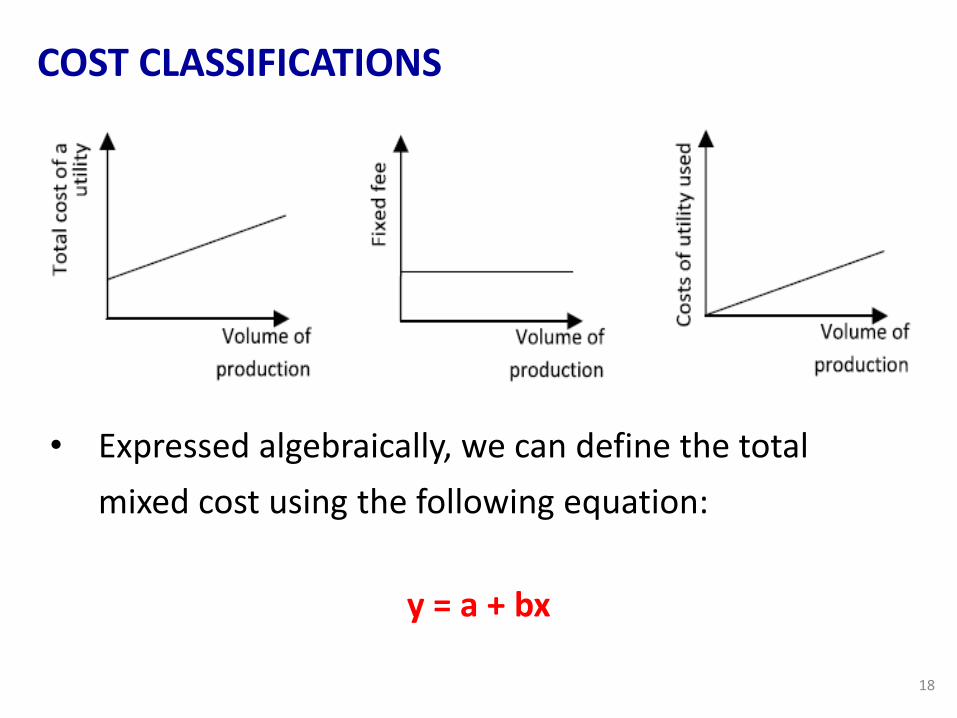

COST CLASSIFICATIONS

18

• Expressed algebraically, we can define the total

mixed cost using the following equation:

y = a + bx

COST CLASSIFICATIONS

19

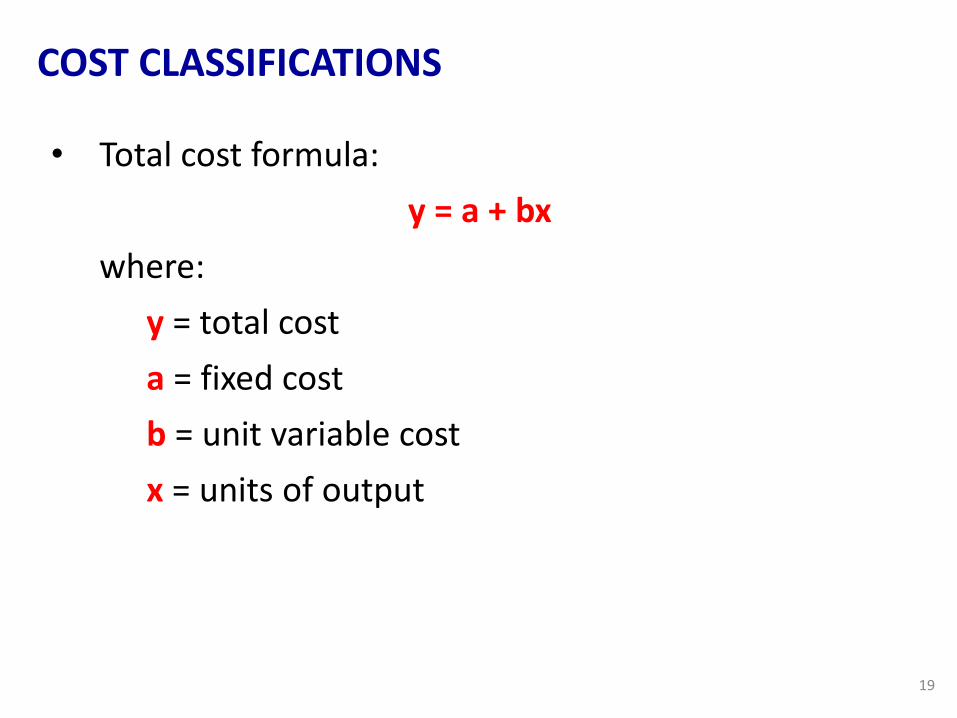

• Total cost formula:

y = a + bx

where:

y = total cost

a = fixed cost

b = unit variable cost

x = units of output

COST CLASSIFICATIONS

20

• Direct costs are those that can be related directly to

the cost object as, for example, the cost of raw

materials used in manufacturing a product or

providing a service, labour costs that can be

identified as the work needed in manufacturing a

product or providing a service, and any other

expense that is directly related to a product or

service.

• Direct costs are also known as prime costs.

COST CLASSIFICATIONS – DIRECT COSTS

21

• All the other costs, i.e. those that are needed for the

production of more than one type of product or

service. Indirect costs are also known as ‘overheads’.

• Overheads are often divided into the following

categories:

Production Overheads

Administration Overheads

Selling Overheads

Distribution Overheads

COST CLASSIFICATIONS – INDIRECT COSTS

22

• Production Overheads

supervisors’ costs, cost of the energy that powers

the machines, cost of depreciation of machines,

costs of internal logistics.

• Administration Overheads

cost of administrative staff, cost of the middle and

top management.

COST CLASSIFICATIONS – INDIRECT COSTS

23

• Selling Overheads

costs of marketing.

• Distribution Overheads

costs of packaging, transporting, delivering

finished product or transporting staff who deliver

services.

COST CLASSIFICATIONS – INDIRECT COSTS

24

• As a manager, cost functions will be used often as a

planning and control tool.

• The reasons why cost functions are important:

1) Planning and controlling the activities of an

organization require useful and accurate

estimates of future fixed and variable costs.

2) Understanding relationships between costs and

their cost drivers allows managers in all types of

organizations to make better operating,

marketing, and production decisions.

COST FUNCTIONS

25

• Form of Cost Functions:

Y = F + VX

Where:

Y = Total Cost

F = Fixed Cost

V = Variable Cost per unit

X = number of output

COST FUNCTIONS

26

• Choice of Cost Drivers: Activity Analysis

Managers use activity analysis to identify

appropriate cost drivers and their effects on the

costs of making a product or providing a service.

The final product or service may have several cost

drivers because production may involve many

separate activities.

The greatest benefit of activity analysis is that it

helps management accountants identify the

appropriate cost drivers for each cost.

METHODS OF MEASURING COST FUNCTIONS

27

• After determining the most plausible drivers behind

different costs, managers can choose from a broad

selection of methods for approximating cost

functions.

• These methods include:

(1) engineering analysis

(2) account analysis

(3) high-low analysis

(4) visual-fit analysis

(5) least-squares regression analysis

METHODS OF MEASURING COST FUNCTIONS

28

(1) Engineering Analysis:

Engineering analysis measures cost behavior

according to what costs should be in an on-going

process.

It entails a systematic review of materials,

supplies, labor, support services, and facilities

needed for products and services.

METHODS OF MEASURING COST FUNCTIONS

29

(2) Account Analysis

In contrast to engineering analysis, users of

account analysis look to the accounting system

for information about cost behavior.

The simplest method of account analysis

classifies each account as a variable or fixed cost

with respect to a selected cost driver.

METHODS OF MEASURING COST FUNCTIONS

30

(3) High-Low Method

A simple method for measuring a linear-cost

function from past cost data, focusing on the

highest-activity and lowest-activity points, and

fitting a line through these two points.

METHODS OF MEASURING COST FUNCTIONS

31

(4) Visual-Fit Method

A method in which the cost analyst visually fits a

straight line through a plot of all the available

data.

(5) Lease-Squares Regression

Measuring a cost function objectively by using

statistics to fi t a cost function to all the data.

METHODS OF MEASURING COST FUNCTIONS

• Accountants classify costs as variable or fixed

depending on whether the cost changes with respect

to a particular cost driver.

• Variable cost

A cost that changes in direct proportion to changes

in the cost-driver level.

• Fixed cost

A cost that is not affected by changes in the cost-

driver level.

COST BEHAVIOUR

32

• Step cost

A cost that changes abruptly at different intervals

of activity because the resources and their costs

come in indivisible chunks.

• Mixed cost

A cost that contains elements of both fixed- and

variable-cost behavior.

COST BEHAVIOUR

33

THE END

34