L3 Special Customers

56

Tyree, p66-77 SPECIAL CUSTOMERS

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of L3 Special Customers

Tyree, p66-77SPECIAL CUSTOMERS

1) Minors (incapacity)

2) Mentally unsound (incapacity)

3) Joint account holders

4) Executors & administrators

5) Trusts

6) Partnerships

7) Unincorporated associations

8) Companies/ corporations

SPECIAL CUSTOMERS

Identify the variety of customers that a bank may deal with

Understand the legal definition of such customers

Define the legal rules that impact the relationship between these customers and the banker

Explain what the banker must be aware of in dealing with these customers

LEARNING OUTCOMES

Incapacity issue/ lacking legal capacity

At common law, a person under 21 was considered as an infant and in need of special protection by law

Most contracts with infants voidable at the option of the infant and the contract cannot be enforced

The age of majority is now 18, s3 of Age of Majority Act 1977 (Vic) ie below 18, minor

1) MINORS P72

Minors can open accounts with a bank

Any charges can be debited to the account

A valid relationship

But, bankers need to be careful about advancing loans to minors

Such as allowing accounts to run into overdrafts

1) MINORS P72

S49 of the Supreme Court Act 1986 (Vic): contracts for the repayment of loan to minor are void

S50 of the Supreme Court Act 1986 (Vic): a contract entered into be a minor cannot be ratified after the minor turns 18

1) MINORS P72

What about his/ her guarantor? Will he/ she be liable?

Also not liable

Why?As the liability of a guarantor is dependent on valid liability of the principal debtor, which is the minor

Coutts & Co v Browne-Lecky [1947] 1 KB 104

1) MINORS P72

But note: Contract for necessariesThe bank will be able to recover only if he is able to prove that he loaned the money for the express purpose of enabling the minor to buy necessaries and that he in fact did so: Lewis v Alleyne (1888) 4 TLR 560

What are contract for necessaries?

1) MINORS P72

Necessaries are those things without which a person cannot reasonably exist and include food, clothing, lodging, education or training in a trade and essential services

The condition of life of the minor means his social status and his wealth. What is regarded as necessary for the minor residing in a stately home may be unnecessary for the resident of a council flat

Whatever the minor's status, the goods must be suitable to his actual requirements-if he already has enough fancy waistcoats, more cannot be necessary

1) MINORS P72

Nash v. Inman [1908] 2 KB 1, CA: N (tailor on Saville Row) supplied 11 fancy waistcoats to I who was adequately supplied with clothes

1) MINORS P72

The ancient rule of the common law was that a lunatic could not set up his own insanity so as to avoid an obligation which he had undertaken

But by 1847, Pollock C.B. was able to say, in delivering the judgment of the Court of Exchequer Chamber in Moulton v. Camroux, 2 Ex 487, that "the rule had in modern times been relaxed, and unsoundness of mind would now be a good defence to an action upon a contract, if it could be shown that the defendant was not of the capacity to contract 'and the plaintiff knew it."'

persons who are incompetent to contract by reason of mental incapacity as for minors

2) MENTALLY UNSOUND

Incapacity issue:

Common law: so long as a person understands the nature of a transaction they are entering into and they do so voluntarily, they will be likely to be seen as having contractual capacity

This needs to be assessed against the individual circumstances of each transaction

Gibbons v Wright (1954) 91 CLR 423

The banker must have due regard to the mental capacity of the customer before transacting banking business with them

2) MENTALLY UNSOUND

See also: Mental Health Act 1986 (Vic)

2) MENTALLY UNSOUND

Where the account is in the names of 2 or more persons

Joint property ownership

Banks need to be aware of the legal rules that affect joint property ownership and must ensure that directions given to the bank by the account holders are truly representative of all account holders and not just one of them

3) JOINT ACCOUNTS HOLDERS

Deposits in account: Debtor creditor relationship; the customer is the creditor and the bank is the debtor

Debt owed by the banker is owed to the parties jointly

Likewise, in an overdraft, the debt is owed to the bank jointly (or rather jointly and severally)

Note: ‘Joint and several liability’ means the account holders are both jointly and individually liable for the debt

3) JOINT ACCOUNTS HOLDERS

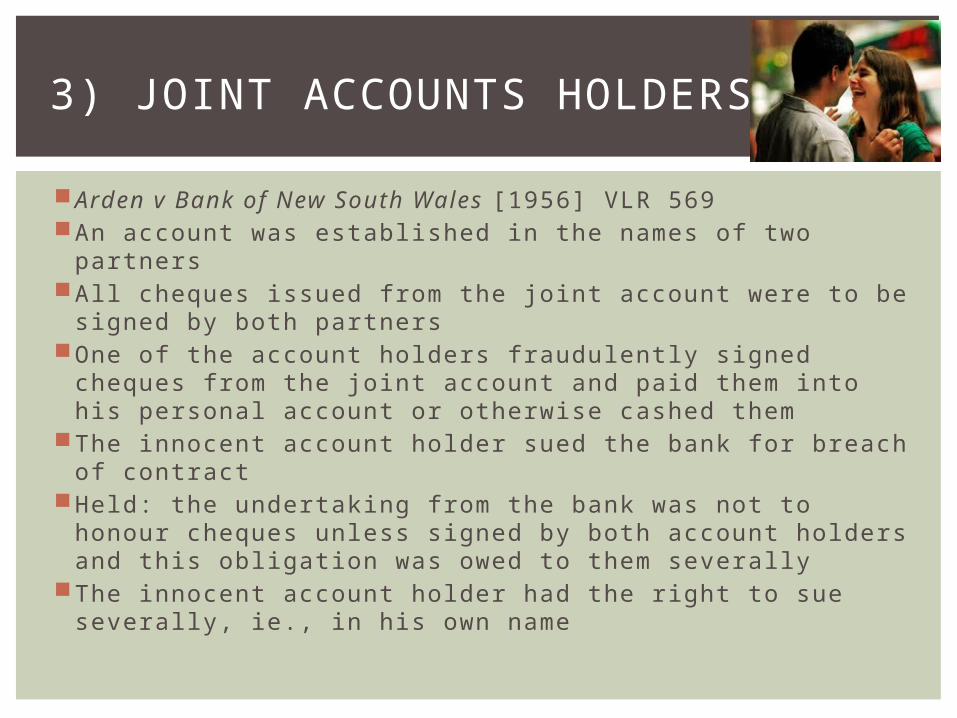

Arden v Bank of New South Wales [1956] VLR 569An account was established in the names of two partners

All cheques issued from the joint account were to be signed by both partners

One of the account holders fraudulently signed cheques from the joint account and paid them into his personal account or otherwise cashed them

The innocent account holder sued the bank for breach of contract

Held: the undertaking from the bank was not to honour cheques unless signed by both account holders and this obligation was owed to them severally

The innocent account holder had the right to sue severally, ie., in his own name

3) JOINT ACCOUNTS HOLDERS

Presumption of survivorshipIf one dies, the survivor remains possessed of the whole

There is a legal presumption the survivor is entitled to the full balance in the account

3) JOINT ACCOUNTS HOLDERS

But note: This is a presumption only and may be rebutted to the contrary if there is strong evidence to prove that the survivor is not entitled to the money

Eg 2 joint account holders with an account of $1,000. The will indicates that the money is to go to another person. This might rebut the presumption

Each situation must be considered on its facts

3) JOINT ACCOUNTS HOLDERS

Russell v Scott [1936] 55 CLR 440Joint account in the names of aunt and nephewEvidence the aunt intended the nephew to have the balance in the account on her death

Held: the presumption of survivorship applies and the nephew was entitled to the balance in the account because the aunt clearly intended the nephew to beneficially take the balance in the account

3) JOINT ACCOUNTS HOLDERS

When a person dies, burial must be arranged, outstanding debts must be paid and the property of the deceased be distributed either as dictated by his/ her will or by the law of intestacy where there is no will

A deceased person (testator) leaves a will naming an executor

An executor is a person appointed by the testator under the terms of the will to carry out the directions contained in the will (for the benefit of the beneficiaries)

There can be more than one executor

4) EXECUTORS AND ADMINISTRATORS P70

When a person dies leaving a will, a grant of probate must be obtained by the executor (official evidence of the person’s title to act as executor)

This is approval by the Registrar of Probates of the Supreme Court of Victoria that the deceased’s will is in fact the last valid will in existence

It is upon the granting of probate that the executor can fully discharge his/ her duties under the will

Thus, it is important for the banker to confirm evidence of probate esp with withdrawals from the account

4) EXECUTORS AND ADMINISTRATORS P70

Where there is no will left by the deceased or if the named executor has predeceased the testator or refuses to carry out the duties, a person will be appointed by the court to be the administrator

The appointment is by means of a letter of administration issued by the court

A letter of administration must be obtained before the estate of the deceased may be distributed

The procedure is similar to that required for obtaining a grant of probate

4) EXECUTORS AND ADMINISTRATORS P70

Note: A grant of probate or letters of administration is required

because the assets of the estate may not otherwise be collected for the benefit of the beneficiaries of the will

For example, the deceased may have had a bank account and banks will only allow executors to have access to a deceased’s account if the executor concerned has received a grant of probate

4) EXECUTORS AND ADMINISTRATORS P70

The duties of an executor/ administrator include gathering in and accounting for the deceased’s assets and will include dealing with any liabilities of the deceased

He/ she will wind up the estate and any balance remaining will have to be held in trust by the executor for the survivors

The executor/ administrator is then transformed (perhaps unknowingly) into trustee who holds any remaining property in trust for the beneficiaries of the estate

4) EXECUTORS AND ADMINISTRATORS P70

The executor/ administrator may borrow on behalf of the estate

But the bank will only allow this upon proof of the grant of probate or letter of administration

Farhall v Farhall (1871) 7 Ch App 123: Held: if a bank grants a loan to the executor for purposed connected to his/ her duties as executor, the banker can only look to the executor for repayment of the loan and not the estate

The executor is then entitled to be reimbursed from the estate should they be called upon to repay the loan

4) EXECUTORS AND ADMINISTRATORS P70

We have heard of solicitor’s trust account (and other professionals and private individuals)

What is a trust?

5) TRUST ACCOUNTS

A trust is a legal relationship where one person or organisation, called the ‘trustee’ is responsible for safeguarding assets for another person or organisation, called the ‘beneficiary’

Generally, trusts are established by a deed that sets out the terms of the trust and specifies:

who can receive benefits from the trust (the beneficiaries)

when the beneficiaries can receive benefits from the trust

how the beneficiaries should receive the benefits

5) TRUST ACCOUNTS

The most common trust types are: Testamentary Trust: established by your will to manage your estate’s assets and income for your beneficiaries after you die

Minor’s Trust: designed to manage and protect assets for a child until they reach a specified age

Inter-Vivos Trust: set up during your lifetime to support beneficiaries, such as a family member with disabilities

5) TRUST ACCOUNTS

Injury and Compensation Trust: designed to protect and manage money paid in compensation for the beneficiary’s injury

Superannuation Minor’s Trust: established after you die to leave a share of your superannuation to a child

Special Disability Trust: set up to help immediate family members and guardians provide for the future of children with a disability

Charitable Trust: designed to provide on-going benefits to eligible charitable organisations or charitable purposes

5) TRUST ACCOUNTS

An obligation to deal with property (money) for the benefit of other parties

The trustee is bound at law to deal with the subject property for the benefit of the beneficiaries

5) TRUST ACCOUNTS

The trustee has the legal title to the property and the beneficiary has the equitable title

The legal title enables the trustee to act freely in dealing with the property for the beneficiaries’ benefit

This is the essential nature of the fiduciary obligations that trustees have to beneficiaries, being the requirement to deal with the property in the best interests of the beneficiaries

5) TRUST ACCOUNTS

The banker is not usually the trustee but merely the agent that facilitates the establishment of an account for the trustee

If bankers are involved either intentionally or negligently in a breach of trust, they may be held liable to the beneficiaries

The banker may be seen as having ‘trust like’ responsibilities

The bankers must take all effort to avoid being knowingly a party to a breach of trust

5) TRUST ACCOUNTS

May exist for sporting, charitable or other reasons that have no connection to any business or profit related activity (if they are with the view towards making profits, they are partnerships)

These are not separate legal entities capable of being sued or able to sue in their own name

Membership fluctuate

Members are not liable except to pay subscriptions

6) CLUBS AND UNINCORPORATED ASSOCIATIONS P66

The club may open an account eg current account with some members authorised to sign cheques

The banker should have regard to any constitution or some documentation which purports to grant authority to the members who wish to open the account

But the bank should refrain from loaning money/ overdraft as there may be a problem in recovering the money in the event of default

It was suggested that the authorised signatories might be answerable

6) CLUBS AND UNINCORPORATED ASSOCIATIONS P66

The banker should have regard to any constitution/ governing rules of the association

The constitution will determine its structure, who may act on its behalf and what are its objects or reasons for its existence

This will enable the bank to know which member(s) is/are responsible for the operation of such an account

Usually the executive of the association or the senior officer is responsible

6) CLUBS AND UNINCORPORATED ASSOCIATIONS P66

And where the security for the loan to come from

Any property of the club used as security may have an uncertain ownership

6) CLUBS AND UNINCORPORATED ASSOCIATIONS P66

Common business structure2 or more partnersEg lawyers, accountants, etc.Easy to establishNo formal legal documentation or filed with any government authority

The only requirement is to conform to the definition of partnership contained in the Partnership Act of each state

S5(1) of Partnership Act 1958 (Vic): “the relation which exists between persons carrying on business in common with a view to profit”

7) PARTNERSHIPS P68

A partnership is not a separate legal entity like a company

It cannot sue or be sued in its own name

If legal action was taken against the partnership, all names of the partners would be listed on the writ ie they are used as individuals and not collectively under the partnership name

So they cannot hide behind the corporate veil as directors of companies do

7) PARTNERSHIPS P68

Partners have the option to draw up a partnership agreement that will detail the key rules of internal management of the business

Useful for the banker to ask for it to view the agreement

Not mandatory and many partnerships do not have this agreement

7) PARTNERSHIPS P68

The concept of agency: someone authorised by another person (principal) to deal with 3rd parties on his/ her behalf

A ‘partner’ as an ‘agent’ for the other partners and the partnership/ a partner purporting to act on behalf of the partnership

Whether he/ she is properly acting on behalf of the partnership

The extent of the agent’s authority

7) PARTNERSHIPS P68

S9 of the Partnership Act 1958 (Vic): the capacity of the agent to bind other partners in situations where the partner is doing something connected to the partnership business

Also (implied), the partners will be bound only if the partner has acted within some kind of authority (either actual or ostensible authority)

7) PARTNERSHIPS P68

Most common circumstance: one of the partners misappropriates partnership funds

Fried v National Australia Bank [2001] FCA 907: 4 partners in the firm were authorised signatories

A partner, without explicit authority, drew on the account for purposes not connected with the business

Held: the withdrawals were in the absence of authority and the bank was required to reverse the debits to the account

7) PARTNERSHIPS P68

Incumbent on the bank manager to carefully consider the actions of a partner in opening an account in the partnership name and whether it is truly on behalf of the partnership

Prudent for the bank to ask for written authorisation from all partners that a particular partner can operate the account with his/ her signature

Eg application for a bank loan/ overdraft facilities from one partner on behalf of the partnership

Cheques payable to the partnership but placed into the private account of a partner: bank needs to enquire

7) PARTNERSHIPS P68

A company is an artificial person (not natural)

A company has a separate legal entity: it has the legal capacity to enter into contracts, own property, initiate legal action under its own name

S124 of Corporations Act 2001: From the date of incorporation, a company has full legal capacity

Case law: Salomon v Salomon and Co Ltd [1897] AC 22

Lee v Lee’s Air Farming Ltd [1961] AC 12

8) COMPANIES/ CORPORATIONS P72

The bank will need to confirm the date of its incorporation signifying when it becomes a separate legal entity

S119 of Corporations Act: the company comes into existence at the start of the day of registration with the ASIC

Process of company formation and registration includes advising the names of directors and shareholders to ASIC

Issued with a number called Australian Company Number (ACN)

8) COMPANIES/ CORPORATIONS P72

In opening an account, the bank will require incorporation details and confirmation about who my operate the company account

Reference to minutes of directors’ meetings or some other written verification

8) COMPANIES/ CORPORATIONS P72

The old ultra vires rule was that the banker had to be certain that the transaction was within the powers of the company

A transaction that exceeded those powers (ultra vires) was void

Catastrophic! A loan made to a company which had no power to borrow was irrecoverable by the lender

Unfair

Now abolished under ss128-130

8) COMPANIES/ CORPORATIONS P72

The indoor management rule illustrated in:Royal British Bank v Turquand (1856): A bank sued the company to recover an unpaid loan signed by 2 directors of the company

The company argued that the action of the directors had not bound the company since there had been no resolution passed by the company’s board of directors

Held: the bank was assumed that the necessary resolution had been passed. It is not necessary for a person dealing with the company to ensure that all of the indoor requirements of the company have been complied with

8) COMPANIES/ CORPORATIONS P72

Freeman & Lockyer Buckhurst Part Properties Ltd [1964] 2 QB480

A company held out an officer of the company as a managing director even though he was not expressly appointed to the position

It sought to avoid the contract on the basis he had no authority to bind the company

Held: the company was bound under the doctrine of ostensible authority

8) COMPANIES/ CORPORATIONS P72

Under the Corporations Act, there are ‘replaceable rules’ that may be used by a company for its internal management

These will apply unless the company directors decide to use their own company constitution

The actions of a company will not be invalid simply because they are outside the stated objects noted in its constitution

The banker needs to consider the rules that operate for the particular company

8) COMPANIES/ CORPORATIONS P72

Also the bank needs to confirm the company signatories

And that the actions of the company through its agents (directors or senior employees) are carried out under the authority granted to them by the company

8) COMPANIES/ CORPORATIONS P72

The actions of a company will not be invalid simply because they are outside the stated objects noted in its constitution: s125(1) of Corporations Act

Outside 3rd party dealing with the company; no way of knowing what is going on behind closed boardroom doors

8) COMPANIES/ CORPORATIONS P72

A company must act through its agents (directors or senior managers)

The company is the principal

Consider the position of the company as principal that can be bound by the actions of its agents provided they acted under some kind of authority granted to them by the principal

8) COMPANIES/ CORPORATIONS P72

Express or implied actual authority

Ostensible authority (the authority the agent appears to have to 3rd parties based on the way the principal has allowed the agent to appear)

Eg the company has allowed a senior employee to appear to others as the managing director (MD) even though the employee has never been appointed to that position formally

The 3rd party believes him to be the MD and any action will bind the company

8) COMPANIES/ CORPORATIONS P72

And to make certain statutory assumptions under s129:

That the company’s constitution have been complied with

A person appearing on the public record as a director or company secretary has been properly appointed and has the authority to exercise the powers and perform the duties

Anyone held out as an officer or agent of the company has been properly appointed and has the authority to exercise the powers and perform the duties

Etc.

However, the assumptions cannot be relied on if he/ she knows or suspects that the assumption is incorrect s128(4)

8) COMPANIES/ CORPORATIONS P72

The bank should sight various documents eg:Certificate of incorporationThe company’s constitution A list of directorsThe location of the company’s registered office

The names and details of other officers in the company eg the company secretary

Information as to who may sign on the company’s accounts

Other documentations considered relevant

8) COMPANIES/ CORPORATIONS P72