l - Repository STIE YAI

23

b# E.- .i(9 (. eur rrr = Special lssue 2018 '] "iF l- trt: i-,8f' r'j:-1rl lt-tr..Jl ,: l t*: l} ".lJ * a rl.tii:i S MUK PUBLTcATToNS

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of l - Repository STIE YAI

b#E.-.i(9(.eurrrr

=

Special lssue 2018

'] "iF

l- trt:i-,8f' r'j:-1rl

lt-tr..Jl

,: l t*:

l} ".lJ

* a rl.tii:i

S MUK PUBLTcATToNS

AUIIII STOCHASTIC ANATYSIS

"ffir.h-0hiefYiri E Gliklikh

' ffirrdlffirematics Faculty

ffi * Uien$ty, Voronezh, Russia

EoFeranHsdldrcmaticalhns, Udvesily Meditenanea

dlbdr(*ilialbtytd-flrBemeEndMiedMathematicsffi tliuesfy, tuvdiv Bulgaria

HI IIJTHsrdldrematicsfryydthircsityEr{d&iar€s Sanlalia

ffieildMdrrnatbs,hff B.hafovlbd dDcpatnent of Geometry

&lsn Feerd Univensity

bro0o, Rtssb

Bo.tlkr3loilffisorof Deparhent olI#n#ard Statistics

ttirenlyof TunsoTmo,NuuayAlsi Kurhnerffissorof ltstitute of Control

&iemesRusiar Academy of Science,

llcry,RtssiaVahntin Y. LychaginPldessor of Departnent ofl,lattpmdics and Statisths

Univesig olTrcnsoTumo, Nomay

I. IuttahenDep{tner* d Mathematics

Al'qaft Mwlin Univemi$

Aligath202 002 , lndh

Juan J. ilietoln$ihte of Mdhematics

Univesity d Santiago de

CompctelaSantiago de Compctela, SPAIN

TeresaA, OliveiraDepartment of Sciences and

Technology, Open Univercity in

Lisbon, Put4allgor PavlovDon State Technical U niversity,

Russia

Sandra PinelasAcademia Militar

Departamento de Ci6nchs Exactas e

Naturais, Av. Conde Castro

GuimarSes, Portugal

R.K.Raina

Department of Mathematics (Basic

Sciences)

College of Techrrelogy and

Ergineering

M.P. Univ. of Agriculture and

Technology

Udaipur 313001, Rajasthan, INDIA

Yuri l. SapronovProfessor of Mathematics Faculty

Voonezh State UniversityVoronezh, Russia

Hassan SaoudDepartment of Mattpmatics

Lebanese UnivenityFaculty of Sciences ll, P.O. Box

90656, Fanar-Matn, Lebanon

Alerander l. ShnirelmanProfessor of Departnent ofMathematis and Statistics

Concodia UnivesityMontred, Canada

Vladimir SobolevSamara State UnivesitySamara, Russh

Tomasz ZashwniakProfessor of Departnent of

Mattpmatics,

Univenity of York, UK

m|ffi.m,HJE,u(ltlLlHrHffi,WdE--HHa-dffihr-h5h,IreLbH-h.sErlffitnlXinsityIE&s1.1659f,bhGfrcIffit-HWBstrrGs),ShttireGnry,ASedatsEreffisq, Depafir'entdre*t *e$lty,Atgeriit

MT]K PUBLICATIONSF.2562, PALAM VIHAR, GURUGRAM, HARYANA, INDIA

i

[r

ir.

ir

t,

I

rii

rIrll,

Irl

p

['F

IIF.

lr

h

!1t,

F!h)IF

Ip

hh

h

i,fihhp

IIrrh[1

I

tIfitH

IhFI

Lt

AND STOCHASTIC ANATYSIS

CONTENTS

C BAUCTION MPLEMENTATION IN INDONESIA ............I-I7IUE METHODE OF SUCCESS MODEL

*: f,rdilgono, Eapzi Ali,, Abdul Hamid, Hudalil Muttaqi,n

AND ECOTOURISM MANAGEMENT.............,. 19-32gf*i Gdfrt futourisn Destination, Gunung Kiilul,ru)f{i 8.f.r ud Hopzi Ak

QUAIION MODELING (SEM) : THE MODEL OF..............33-51r!P|IIONS OF EMPLOYEES.5 Sofud otrd Mthommail Nu*ji,rwan Harahap

ElnEssIoN ANALYSTS : DETERMINANT OF ...53-60OF PT PEGADAIAN (PERSERO)t'frrrfl, u, ffi Wio*sotto, Henny Ri,mawati,

th fi. Eqtnino.ond, Nurmala, Syahrud.di,n

lilt[tf EIUAIION MODELING : DETERMINANTS OF .................. 61-76(H]IEIXIAL COMIUITMENTS AND ITS IMPLICATIONTMIITE WORK PRODUCTIVITY OF MANAGERIAL LEVEL

h fuiwt, Anoesyirwon Moeins and,

|lrlrrd, Eooln Purnawon

AIIALYSE| : DETERMINANTS OF RETURN STOCK .....................77-97(UINIIIIY NBAL EifATE AND PROPERTY LOCATED INEltrm$r $TOCI( EKCTTANGE (rDX)

fuzic'Brcstomi onil Jerry Heikal

ffiHS AITALY$S : MODEL OF CORPORATE VALUE ....... 99-114Gan Nomwn Thomas; Nuzulul Hidayati. and Lely Ind,riaty

I tffi INALY$S : EFFECT OF QUALITY OF SERVICE .......LL5-127qUil,ITY PNODUGTS AND SALES PROMOTION OFcusillDdER SATISFACTI O N

Kosrw4 Udin Ahidi.n, Dadang Kumia, Juhaeri,Feri Lasnm

t EVIEWS ANALYSE : DETERMINANT OF BANK PROFITABILITY ........129-148TIID ITS IMPLICATION ON STOCK R.ETURN

@IPIRTAI, STUDY AT BANKING IN INDONESIAsfocr( ED(CHANGE 2010-2014 PERJOD)

Luqna,n Habirn ond Shatenti

m- SiTRUCTURAL EQUATION MODELING (SEM) : DETERMINANT ............ 149-162OF CTISTOMER LOYALTY IN BANKING INDUSTRY

Netty Mexliatg, Budi Rismayadi., Mumun Maemwtah and,

Sri lrulra Tlrigunarso

,:.

11,

EURNOUT AND SELF ESTEEM IN TANGERANG'S

JUNIOR HIGH SCHOOL TEACHERSRilla Souitriena. Febi Herilajani, Aziz Sud'armo and'

AnoesYirwan ltoeins

PATH ANALYSIS : SEGIvIENTAL ANALYSIS OF EMPLOYEES' """"""""' 179-186

PERFORMANCESri Inilra Tfi Gunarso and Anoesyirwan Moeins

MULTIPLEREGRESSIONANALYSIS:UNDERPRICI\9SToCK..........''.187-196LEVEL OF SHAREHOLD IN STOCK COMPANY DOING

INCOME SMOOTHING PROCEDURES AT THE PRICE OFFER OF

PRIME STOCK IN INDONESIA STOCK EXCHANGE

Theresia Siwi, Kartikawati, Elsa Sari Yukana'

Tashad,i Tarmi'zi, Bob Mustala and Oscar Rynand'i'

MULTIPLE R-EGRESSION ANALYSF : DETERMINANT OF 197-207

CUSTOMER SATISFACTION OF FRUIT LOOPY PRODUCT

H. MR. {Jlung Sembi'ring, Rosmaniar Sembiring'

H. Mali'kuddii Sembi'ring, H' Bachtiar Sembiring and'

HJ. Fatmai,ta Sembiring

STRUCTURALEQUATI0NMoDELING(SEM):DETERMINANT............209-218OF JOB SATISFACTION AND ORGANIZATION CITIZENSHIP

epHAVIOn (OCB) IN DKI JAKARTA HOSPITAL GOVERNMENT

Aler Zami, Fransisca Anri' Widyayani and Kasbuntoro

MULTIPLER,EGRESSIONANALYSIS:BUIDINGEMPLoYEE..................219-229PERFORMANCE

Deden Komar Pri'atna, Nanilang Diunaeily'

Wi,nna Roswi'nna, Mari'a Lusiana Yulianti anil

Anne Lasminingrat

STRUCTURAL EQUATION MODELING : GOING CONCERN """"""""""23t-243OPTBMTWENT OF COMPANIES,WITH FINANCIAL

PERFORMANCE AS INTERVENING VARIABLES

DennY Kurnia anil DeaiYantoro

MULTIPLE REGESSION ANALYS$ : DETERMINANTS OF "" " " " " " " " " "'245-255

nsiUNN ON ASSETS AND IMPLICATIONS ON STOCK

PRICE CHANGES LEVELEnd,ri' Endri, Yani Ri'gani, Kartawati Marili'ah'

Linila Suherma and Susan Ap'driana

EVIEWS ANALYSIS : UNDERPRICING bETERMINANTS AND """ """' "'257'275

IMPLICATIONS ON LONG-TERM UNDEhPERFORMANCE

iuenns Ipo oN INDoNESIA srocK ExexANGE (BEI)

Hamilah, Makmuri and Gusmiarhi'

EVIEWS ANALYSE : TAX AND NOT TAX ON CAPITAL """""""""""""'277-294STRUCTUR^E OF REAL ESTATE AND PROPERTY COMPANY

Enilri, Fauzi' Thali'b, Herd'i'yana' Ayi' Wahi'd

INDONESIA'S MEMBERSIIIP OF ASIA-PACIFIC SPACE """295-314

COOPERATION ORGANIZATION (APSCO) : ORGANIZATIONAL

PER"FORMANCE WITH STOCHASTIC ANALYS$Shinta Rahma Diana anil Maya Syafriana Effend'i'

t2.

13.

ryrllil,,ilq ilmm_[rmu[]mmmmffntrn

m

4tn rln|rflnqElttr,rr

if,[{UffiS(mmmn"l!

ilr,mlltrmlErmfl-mlmil,t[rmrm&d

&t

f srilfqE[Iup,rrflrffifmflmltmlm'lmm

Tt

!i mmfflmeuEm||ImmU(ftfrd.H

&mm[,Int&ctrlt,otlGT rfl!,mwrft

flM[Wnil,smdWfrrOUmm[u,,mt@ llru

Lr.,r.!I|flT[m,r, ftrfr*m4FQg6A

rymD!,mmmBC

... -........ -. t63-t7 7

............209-218

- -................219-229

........... -.... 257 -27 5

.............277-294

295-3t4

TEGRESSTON ANALYSIS THE EFFECT OF ............................. 31 5_326Iil THE EXCHANGE RATE FOR IDR TO USMT INTEREST RATE CHANGES, CTTENCES U,Tr x[{Es rNDEx ro cHANGos cbnrposrrelltc8 INDEX (JCD rN TNDONESTA SrocxEA GEr)

Alet Joko Santosa, Oyan Suharyono, Iferni Suryoni,Uaryort| and, Rudi S Ahmadi

\L EQUATION MODEL : DETERMINANT OF .s27.34LSATISFACTION AND II'S IMPLICATIONS ONENGAGEMENT

$,I,/\WESI PROVINCE14 Suhrmo, Anoesyiwan Moe,ins, Muhammail Rid,wan,llie3c Rahoya ond, Meswantri.

ETUnAT EQUATTON MODELTNGFtcTrcN ASSESSMENT rN THEfilrc nrDusrRy

Jfu, Kurnir, Nonilan Limakt"isna, Aryantla and,Ddhi Sangotonr'r lrukYlsE : TrrE DETERMINANT oF sruDENT LEARNING ........ J67-g81illullfiS IN ACCOI]NTING INTROOUCTTON COURSESF* J W,c Eigher Educa,tion in J;;";;j

Ee*hiuati arut S oep ri.jadiT. M''IAAT EQUATION MODELING (SEM) : DETERTV,INANTS .........383-395C EpIOYEES PERT'ORMANCES OF COOPERATIVESf rrnJlWwG v--4urrrrLr

Solchudin anil Anoesyi.ttlan MoeinsI; ilOCf,ASTrc ANALYSTS : SHARTNG TrME LEARNTNG ............................3e2_40bEoGII) EACE AND ONLINE LEARIIING) [.{IAIDED I,EARNING

ywb Mulyoni Azis and, Rr. Wotie Rachmawati,L rrmrr^NA FESTryAL AS COMMUMCATION MEDIA........ .....................407-42rIFNTT @I'NTRY RELATIONS

hdong Caturwati

llx Tru}S TIIE PERFORJ\4ANCE OF DEPUTY OFIMOilSTRUCTION AND R,EHABU,METTON BOARD INUFB JAKAHTASetyo Riyanto

t|ncsyirlr,an Moeins, Agus Djoko Santosa,M Nwry Sulanayuda and, Mochamad iyarif Arbi

EQUATION MODELING (SEM) : ....................343_Bb1OF JOB SATISFACTION OF MIDWIVES

: EMPLOYEE ................................ BE3_866INDONESIAN

l,r:

d h.*adic Analysisfiou 5 r Spriel Issqe 2018

S }IUI\ PUBLICATI.N'

EflIESS ANALYSIS : {,NDERP RTCING DETERMINA NTs ANDTDTPLICATIONS ON IONG-TERM UNDERPERFORMANCEf,ll^Rr.S IpO ON INDONESIA STOCK EXCIIANGE 1nu)

IIAMILAII, IvIAKMURI AND GUSMIARNI

alb'd: Thb study aims to analyze factors that inlluence companies doingu*picing at the moment, companies conduct Ipos in the stock market and itsryr!:6bos on Long-Term Underperformance in proxy with JCI on IpO shares: DL A,"l,Eir of phenomena. By using sample data onto Ipo implementationh prs 2fi6 ,ntil Ipo 201_l with period of i year for every i-pr"-"rrtuiioo orlFtO. uhod done by using Sampling purposive Method.

lL fut eoalysis based on the data onto companies conducting initial publiceig GPO) in BEI during the period 2006 to i011, .nderpri"lrri *"rug"'tg,tclirrd- Tte average initial- return to companies underpricing i".iog i't

" irofu-g th period 2006 to 2011 average initial return to 81 percent, and thertL't h 2002 with Initial Return of 40 percent and the to*ot o""*."a], zriiri tri ptrcar.

Tb ryod ena\6is shows that the average of the age variable of company the..h dcrvitation, the voratility effect on tle lever of rinderpricing i" trre *-prrv-*r'qglnitial

Pubric offering (Ipo). while the company size iariabre, t t".""i

Fr F third analysis, the long-term performance of IHSG after firm IpO isi1{*U inlluenced by the

_Comparry," Age variables, Capitalization Value,

^bhtfity'_IEterest Rate, and Rupiah'E*chJnge Rate, while the variables inooq'"r size influence is not significant. This"study reinforces the asymmetrici&rstim theory of underpricing phenomena, due to information asy_metrytrt ea underwriters and fums. Difrerences in information ur"

"rppo.tua Uy "g;"yttay ud signal theory, whereby information published * .r, ui,o,-""*"oi *iir

Foride a sig.al to investors in making investment decisions.

fntroductionlL inphmentation of IPO in Indonesia has only started since the 1gg0s. Until thed d 1990 there werc Z4 companies listed in sttck exchangu. to tUe year Lggl upq_tb of 2011 there has been a very rapid growth of the implementationdlrisal Public offerin-g (Ipo) in the capital market,-which became 423 companiesrft,t r capitalization of Rp.2.860,82 trilion. However, the priraiiration process of**eaned enterprises is still very small. Of 141 state-owned enterprises consistingd lt mr sectors there are 18 companies that has done Ipo in the period 1gg1-8rr' rhich started with the company semen Gresik and the l*t ;;;;4ffi;Irlnoesia.

K egto o rl s : Underpricing, Long-Term Underperformance

TIAMILAH, IUAKMURI AND GUSMIARNI

The process of Initial Pubtic offering (IPO), Go PuLlic or. 3fte1

referred to as

the initial public offering is a stock offering activity conducted by the company to

i-rr" p"uri" ipublic). By o-fferi.g shares to the public, the company will be listed on

the stock to become a public / open company'

In the process of selling the first stock of a company to a general investor is

called an IpO. According f U* no.S of 1995 concerning capital market, public

offering is a security offerlng activity undertaken by issuers to sell securities to the

p,rUti""Uurud of tLe p,o"Jd""' set forth in the capital market law and its

i*pi"*"","tion regulations. C;ompanies that conduct public offering of shares, their

shares must be able to transacted on the stock so that investors can resell or buy if

It"y "u, not during the Ipo. The issued shares have a price known as a.n initial

O.,fi1f" .ff*rng (Ied) is an important factor of both the issuer and the underwriter

as it relates to the amount of iunds to be earned by the issuer and the risk that the

underwriter will bear. ihe amount of funds received by the issuer is a correlation

between the number of shares offered at the price per share, so the higher the price

per share then the funds received will be greater'

Initial Public offering (IPO) Initial Public offering (IPO) Initial Public offering

geOtf"itiuf public Ofiuri"g (feO; i* lower than the stock market price in the

secondary market on the firrt day,'there will be a low-price phenomenon in the

initial offer, called Underpricing. -on

the other hand, if the current price of Initial-p"ilii"

Offering (IPOI;ew higier than the stock price on the secondarv market on

the first day, then tt i, ptru"ori"non is called Overpricing (Hanafi, 2004)' Research

conducted Uy Aggra*al et al, (1993) concluded that underpricing phenomenon

occrrs to the ti*" or i.ritial public Offering (IPO). Another phenomenon is the

long-term negative return and the existence of cycles in terms of underpriciug and

volume of companie" "ona,r"ti"g

Initial Public offering (IPo), known as the three

urro*aly Initial Public Offering (IPO)' Underpricing has become a common

phenomenon in the initial pubhl offe.ing in various capital markets a,round the

world (Loungtrur, "J-o1.,

rdOa;, Underpricing is' after all' an indirect cost of an

Initial Public Offering (IPO)'

Accordingtoaeatty(1989),underpricingconditionshasdifferenteffectsofcompanies uod in

"rior". Ct*pu"io will not benefit if there is underpricing, because

the funds obtained from go p,ruti" are not maximum. In the event of overpricing'

investors will lose *o""i becar"" they do not receive the initial return to the

shareholder's profit because of the difference in stock prices purchased in the initial

market at the IPO with the selling price in question on the first day on the seconda'ry

market. The phenomenon of underpricing and overpricing- occurs to the capital

markets of various co.rntrie". Amonl the ijnited States, Britain, Australia, South

nr,i"u,China,Malaysiaandludonesia.Underpricingisoneofthemostcommonphenomena in the firrpL*J",ion-of Initial Public Offering (IPO)' The second

anomaly are Long tei* uoa"rperformance, which is where in the long run, the

performance of IPO J;" has poor performance. This condition causes Cuurmulative

Abnormal Return tcenl or fro "L*", to form up and down pattern. This shows

that the price that f""*. to the beginning of the s"condary market is not the stock

pri"" ir, ^u""ordarrc"

with the varue of the company (fair price). In the long run'

ften referred to as

ry the company togr will be listed on

3eneral investor is

[I market, publicil securities to therket law and itsing ofshares, theircan resell or buy ifDo\rn as an initialrd the underwriterrd the risk that themr is a correlation[Lc higher the price

itial Public Offering

narket price in the

Fenomenon in thegeut price of Initialrcoudary market onfr,2004). Research

riring phenomenon,;fienomenon is the

of underpricing and

, Lnor,l'n as the three

become a commonnarkets arouud the

t indirect cost of an

r different effects of

nderpricing, because

nent of OverPricing,hitial return to the

lchased in the initialiday on the secondarY

Eurs to the caPital

:in, Australia, South

of the most common

[ (IPO). The second

l in the long run, the

lczruses Cummulative! pattern. This shows

mrket is not the stock

he). In the long run,

EI-IEI\-S ANALYSIS: UNDERPRICING DETERMINANTS..,

ffi6l retulls due to underpricing are eliminated because of long-term(Smtuel- 1996).

h Mmia rmderpricing phenomenon has also been done as shown in table 1

Table 1Underpricing phenomenon in Indonesia

llaiLFI Sample Underpricing (%)

brdlrnauihdilifuei*, $Hqlmro" S.mbel

ffifrl $tlrddiab,,'@mue. Ilr-

lkf,ll nrlmnho..faeMr'!0r3'ril5l:i rd l'rse (2013)

rydf,rrto (2013).

hb"itt {ils)frjurdSrrrpne (20t6)

131

90

92

96

300

28

44

67

98

169

7L

150

57

38,0

5,0

59,4

L2,l

2L,3

34,9

82,0

28,3

87,00

43,90

37,15

25,30

35,28

1994-2001

1994-2000

1999-2005

1993-1997

1990-2001

2000-2006

1998-21t03

2000-2006

2008-20L2

200G2011

2007-20L1

2007-20t2

2010-2013

Literature Review

ecrfutiDg underpricing theories so far none has dared to explicitly declare betterfo rflil*;ming underpricing phenomena. Most of the existing theories set out from& qimrnce of information inequality (information asymrn-etric) in the vicinity offfil Public Offering (IPO).

BGrttr (1989) erplains that underpricing or positive initial return in the primarydGt is due to the existence of information asymmetry (ex-ante Uncertainty)

is pice uncertainty in the future. Information asymmetry can occur if theilndr &es not have accurate information on information owned by the investor.Tbe strdy of the phenomenon of underpricing in the IPO was first performed

h & LS Securities and Exchange Commission (SEC) in 1g63. More than 10 yearsbc" Ibbotsou and Jaffe (1975) conducted the same study in the United Statesd obtaiml results that the initial average return obtained by investors whenhlffog sharcs through IPO mechanism is 16.88%

TLe occurence of under-pricing phenomena in stock trading the first daydlr tf,e IPo on the Indonesian stock exchange in the period lggg-1gg4 was

{ga$rcaused by: (i) government interference in stock eichanges, (ii) the statedtlc Irdonesian capital market experienced a boom in 19g9 uoa rggo with theder of bsuers as many as 67 companies that conduct initial publication. ThisL t{rd{rered consistent with the phenomena occurring in neighboring countriesrhe uuder-pricing phenomena in the 1990s were lower than those of the lateIlffi"

--

HAI{ILAH. \TAI(IUURI AND GUSMIARNI

Several factors are expected to affect underpricing and long-term under-

employment ie company Age, company size,. capitalization value, volatility,

mtlr"st Rate and Exchange R"ot" io Exchange Rate ($)'

The longer operating age of t[e company makes it possible to provide a wider

urrd *or" pr"fti" irrfor*Jiot' publication than the newly established company' The

iorg", ttre tife of the company, the rnore information the community can acquire

iri,iJiarr*i and Indriantoro, lggg) thereby reducing information asymmetry ard

minimizing uncertainty of the future' Rosyati and Sabeni (2.092) said that the

"o,opurry'r"uge had a nlgative and sigrrificant effect on underpricing while Ghozali

;;J'il;r", (zooz; aia n"ot show signihcant.influence. Similar research in Indonesia,

;; oth"rr, conducted by Tlisnawati (1ggg) who conducted research on the

Jakarta Stock Exchange by iaking data onto 1994 to 1995 successfully proves that

the age of the compu"i t * u porlti.,r" and significant effect on initial return.

company size can also be used as a measure of uncertainty, because large-scale

firmsaregenerallybetterknownsothattheinformationiscertainlymorethansmallfirms,ifthereismuchinformationkrrowntothepublicthenthelevelofuncertainty can be reduced so that the investment decision is right' It is estimated

that large_scul" "o*f.rries have low-er-levels of underpricing than small-scale

enterprises'ThisisinaccordancewiththeresearchofKimet.al.(1993)showingthe influenc" of .r"guiiu" and significant firm size of underpricing, which means the

irrg". tt "

size to tL" "o*pu.ry

fhe smaller the level of underpricingnya the smaller

the smaller the size of the company the greater the level of underpricing. Companies

;;ili;;;;,ir* taa to contain fewer Uncertainties, such companies will experience

alowerinitialreturn'ThegreatertheUncertaintyofthecompany'thegreatertheaverage initial return, larfe-scale companies tends not to be affected by market

conditions but rather'affeJt the market conditions (Retnowati' 2013)'

Volatility is the amount of distance between the fluctuation of the stock price

or the price of the stock or foreign currency. High volatility means the price rises

rapidlyandthen'"aa""rydrops"inrapidlyresultingina..huge'differencebetweenthe lowest and the highesi prices in time, ihe small volatility also changeable bias

there is clock hours *i"r" volatility slows volatility bias is aimed at the number of

certainpipsorabsolutenumbers.votutititymearrstheconditionalvariancebetweenan asset. Volatility analysis is useful iu portfolio formation' :i:I.T*"ry.i:lT1price formation, volatiliiy is also used in.predicting risk, volatility prediction has

an important influence "in

investment decision ma"king, Volatility modeling is

Autoregressive conditional Heteroskedatisitas (ARCH) permitted by Engte (1982)

and used in mea,surinf ii* fit u""ial risks and behavior of the mining sector' where

the result is that the volatility of mining stock returns has a reliance on time' And

ARCH can be a"t""t"aiittr" t*g" o,r*U* of samples and Generali'ed Autoregressive

conditional uut"rorrcJJicit;(GARcH) developed by Bollerslev in 1986 became

the method "o**orrty *"Ji.t hnancial analysis including stock return and volatility'

Thecapitalizationofsharesorothertermsofmarketcapitalizationisabusinessterm that points to the overall price of a company's stock that is a price to pay for

all shares of the ""-;;";. ihe magnitud" o.rd gro*th of a company's market

capitalizationisoftenanimportantmeasureoftlreSuccessorfailureofanopen

,,-,";i

Iii

li

i;

I

long-term under-Yalue, Volatility,

to provide a widercompany. Thety can acquire

asymmetry andsaid that the

ing while Ghozaliin Indonesia,

research on theproves that

initial return.

because large-scalenly more than

then the level of. It is estimated

than small-scaleal. (1993) showing

. which means the

the smallerCompanies

ies vrill experience

, the greater the

allected bY market

.2013).of the stock Price

rrr€ans the Price rises

dillerence between

also changeable bias

at the number of

variance between

risk management and

ility prediction has

atility modeling is

ted by Engle (1982)

, iring sector, where

reliance on time. And

bed Autoregressivetev in 1986 became

retun and volatilitY'

is a business

is a price to PaY for

a companY's market

or failure of an oPen

E\1E1\,S ANALYSIS: UNDERPRJCING DETERMINANTS...

&Iitstization is sometimes used as a synonym for market capitalization& be market capitalization and long-term debt. The stock market is a

gwal trading and related financial instruments (including stock options,

-l stork index estimates). According to (Robert, 1997) in Boeli (2008)mrbt price multiplied by the number of shares in circulation will be in

vahre or so.called Market Capitalization.

thfolcerst rate (BI Rate) based on the explanation given by Bank IndonesiaigD-id), the BI rate is the policy rate reflecting the stauce or stance of

policy stipulated by Bank Indonesia and announced to the public, BIruced by the Board of Governors of Bank Indonesia, and implemented

qerations conducted by Bank Indonesia through the management ofiB the money market to achieve the operational targets of monetary

lh qeational objectives of moneta,ry policy are reflected on the developmentrrxxrey market interest rates. While inflation according to Samuelson

tlrt infla.tion as a condition where there is an increase in general prices,

3mds, services and factors of production. This definition indicates thelr3 of purchasing power followed by the declining real value of a country's

e a"hange rate is the price of a currency of a state that is measured orin rdher crurerrcy. Exchange rate plays an important role in spending

{itrrn barce rate allows us to translate prices from different countrieslaaguage. If all other conditions remain, the depreciation of a country's

Gf rGrinst all other currencies (the increase in foreign exchange prices fort omy oocerned) causes its exports to be cheaper and its imports more

rytre. While appreciation (decline in foreign exchange prices in the country

-rpd) rnilres its exports more expensive and imports cheaper.

mr*rnge rate is very important to the foreign exchange market (foreignfree mr*et). Although foreign exchange trading takes place in various financialffi ryead acrorxi the globe, modern telecom technology has linked them into afihDrfu ehrin that operates 24 hours daily. One important category of foreign

trE trading is forwa.rd trading, in which some parties agree to exchangein the future of the basis of the exchange rate they have agreed upon.

o*,ber categories, ie spot trading (spot trading) directly execute the exchange

Pih mally for urgent or practical purposes).

!gr.ethe exchange rate is the relative price ofthe two.sets, then the exchangerhfo cmsidered to be the asset price itself. the basic principle of asset pricing ish fbsrrent asset value is determined by its estimated future purchasing power.hGnbeting assets, investors always display the asset's estimated value of return,r L r& of increase in the value of investments embedded in the asset at later'll" The returns to deposits traded with the foreigu exchange market arehaed by interest rate and estimated exchange rate changes.

Mbr by the Journal of Indonesian Applied Economics vol 2 no.2 october-lL Stitt€n by Imam Mukhlis, the development of the current liberalism andrft5r&ation of the world has caused its own concerns for each State. To addressfr {yuanics that occlus every State formulates a framework of multi sector

U.f,IIII,I.H. TTAKMURI AND GUSMIARNI

ili: ?fi ffi ;i# ;frr**;,r' in maintaini ng t he ru ndame nr'al s o r this. econoqy

can have an impact ,"'-*-"*L*ic stability. One of l,he macroeconotnic indicatom

that are tentative to external economic turmoil is the exchange rate of :lrr:trcy

(currency exchange ,*i. -r"

rni' case the exchange ral,e reflects the strength of the

economy as a result oi"tnu p""*ration Td "ttu:T.":::::iii:111"i3fl{;I}i::::X|lil|", i'nJ""ilffi;;;J;;""f -i'v''-"^*Il-"I-:,*"":i'-t':t""":#renciesorothercountries,themoreitst.o*,"thefundamentalstrengthofthecountry,seconomy.[4otherwords,thegovernmeut(monetaryauthority)isabletoconductmonetary;ii;r';;d fro* in-*ohangL rate of crrrrency that can encourage economic

competitiveness ot " ".i"i*Tn"

rise of the currency exchange rate in the money

market (appreciatio"";;;p;iatiod shows the magnitude of the volatilitv that

occurs to the "rrr"rr#Ttl!** *rtil the currency of another country (cho',

2000).rncreasing*"1t,iii'o,y'""'"::."?L:::::T:-i"::Xi,f."#L}"T'fl|:

cooperation. On the other hand. it cau aLso be explained that the exist"i'" liberalisn

andgrobarizationu.ingllffi e:'*"ltP,:::i:f1".::11*:i:1':"'-i;f*":::y,

zuuu)' rncreas,"B ""'';;;ir;;i"-*r"o"y;. This gives an overvalued overview and(appreciation / DePre

undervalued "*"t'uog"'uie against other.currencies of the State' When the exchange

rate is experiencing *i."*"Lfatility, then the economy will experience instability

both from the macro and micro'

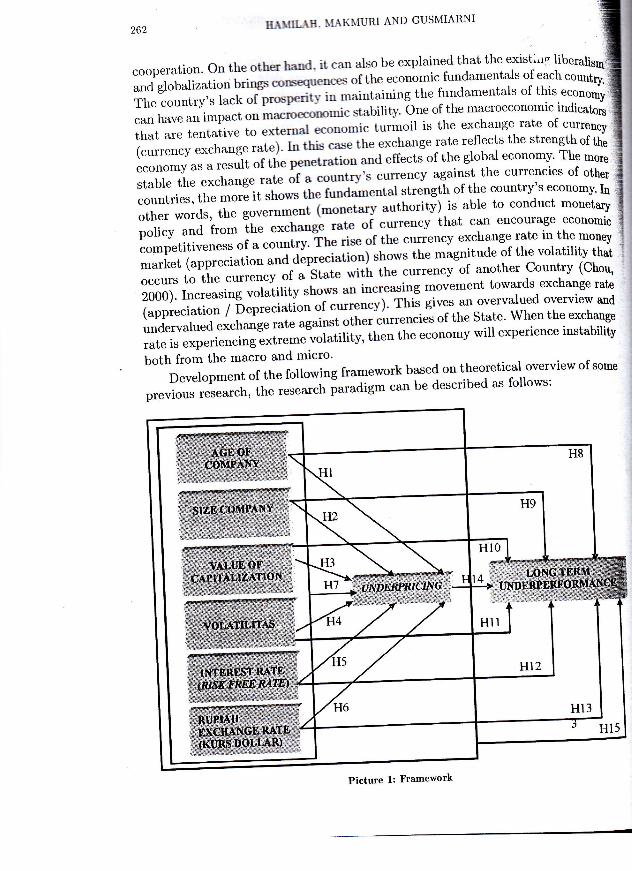

Development or ti" totto*ing framework ba;sed on theoretical overview of some

previous research, tf'" '"s"u'"t'

faradigm can be described as follows:

Picture 1; Framework

.j.,:i'"....l.".--...^.#

-ri6!lir* jilla.r*--*-.".

Le existi,r. liberalisq,atals of each s6untry.

ntals of this econoqy

troeconornic indicators

tage rate of cunencypts the strength of thej economy. The more

fe currencies of other,country's economy. Itr,to conduct monetary

i cncourage economic

Ege rate in the money :

le of the volatility thatpther Country (Chou,

,tos'ards exchange rate

Frr-alued overview and

gc- When the exchange

ll experience instability

lntical overview of some

Jm follows:

{qrnq,}

1E"ifq)&)

frDohfu iH-)

ilmlnlrntu (EJ

qlln{Nt*d,q iHJqmetu{EJ

fuietu(Eu)q6gll'*t.qrtr {Err)esorllsftr (EJ

&odhic (EJ

erpnbcsto (EJ

E\IEIVS ANALYSIS: UNDERPRICING DETERMINANTS...

The Effect of the Company's Age on Underpricing of IPOShares

The Influence of Company Size on Underpricing Shares IPOThere is a positive effect of Capitalization Value on IPO StockUnderpricingThe Effect of Volatility on IPO Stock UnderpricingThere is an effect of Interest Rate on IPO Stock UnderpricingThe effect of the Rupiah Exchange Rate on Undelpricing ofIPO Shares

Tnflusass of company age, company size, capitalization value,volatility, interest rate and exchange rate of Rupiah tounderpricing IPO sharesThe Effect of the Company's Age on Long-TermUnderperformance

Effect of Company Size on Long-Term I-Inderperformance

The Effect of Stock Capitalization Value on Long-TermUnderperformance.EfIect of Volatility on Long-Term UnderperformanceEflect of Interest Rate on Long-Term UnderperformanceEffect of Rupiah Exchange Rate on Long-TermUnderperformancethe InJluence of Underpricing of IPO Sha.res to Long-TermUnderperformanceInlluence of company age, company size, capitalization value,volatility, interest rate and exchange rate of Rupiah tounderpricing IPO sha.res and its application to Long-TermUnderperform&nce.

Research Methods

h t4#E dissertation is used a combination of descriptive and inferential methodsdq Listorical data onto a long period of time. Selection of a long period of timeb rryccted to provide a more accurate picture of the phenomenon of underpricingd h&t€rm underperformance in the stock market of Indonesia.

Frytrlation of this research is Company which does go public since 2006 untilm"I d ladonesia stock exchange (BEI).

s-.fle in detail is the Company of companies that have been doing IPO since'm dil the end of 2011 and up to now still listed in the Indonesian stock foamqm}" Companies that are still listed on the Stock Exchange but not available past&r le not included in the unit resea.rch.

Th data and information used is from Boomberg & Real Time InformationliMfTf information service providers,Indonesia Stock Exchange (BEI) website, OJK

264 EAIIII"IIf, - f,LAKIIIIIRI AND GUSMIARNI

website, website of publicly listed companies, Bank Indonesia website (BI), Ministrvof Finance website, TICMI rehite (The Indonesia Capital Market Institute).

Research Result

Data analysis of the company coducting initial public offering in 2011.

Description of StatisticsI$le f

Data llescriptfor Lilirl Pdlic Olfering of 2011

AGE ESHM IHSG KAPT

Meau

Maxirnum

Minirnunt

Std. Dev.

C)bservations

t4.23077

26.O

3.0

7.OL7321

65

793,8077

3750.mO

50.m000

855.2656

65

4494.673

5491.340

3679.829

514.1398

65

5372.014

12642.93

2198.465

1832.762

65

Source: Data is processed usirrg eviews 9.0

Table 1 shows that the data of 13 firms over the period 2011 to 2015

a) of the 65 company Age data (AGE), a minimum of 3 years and a maximum

value of 26 years. With an average of. 14.23077 yeam and a standard deviation

from 7.017321 years.

b) of 65 data share prices (HSHM), minimum value of Rp 50.00 and maximum

value of Rp 3750,00. With an average of Rp 793.8077 and a standard deviation

from Rp 855.2656.

c) Of the 65 Composite Stock Price Index (IHSG), the minimum value of 3679,829

and the maximum value of 5491.340. With an average of 4494,673 and a standard

deviation from 514. 1398.

d) Of the 65-capitalization data (KAPT), the minimum value of 2198,465 billion

Rp and the maximum value of 12642.93 billion Rp. With an average of.5372.0L4

billion Rp and a standard deviation from 1832'762 billion Rp'

Table I (continued)

Data Description: Initial Public Offering of 2011

KURS NATE SIZE VOLA

s.293417

13.85237

2.t28004

2.076263

65

Sou,rce:DaLa is processed u.sing eviews 9'0

Table 1 (continued) shows thtttto 2015

the data of 17 cornpanies over the period 2011

Mearr

MaximurnIllirrimutnStd. Dev.

Observatiom

10492.85

12500.00

8523.000

r.354.623

65

0.063423

0.075000

0.006000

0.018270

65

13.03349

26.01083

5.626433

4.512825

65

(BI), Ministrylnstitute).

2011.

KAPT

5372.014

12642.93

2198.465

1832.762

b5

to 2015

and a maximumdeviation

and maximumdeviation

rralue of 3679,829

T3 and a standard

of 2198,465 billion8\;'erage of 5372.0L4

Rp.

VOLA

5.293417

13.85237

2.128004

2.076263

65

the period 2011

EVIEWS ANALYSIS: UNDERPRICING DETERMINANTS...

ril Of the 65 Exchange Ra,te data (KURS), a rr,rinimum value of Rp 8523.00. rr-l a ma:cimum value of Rp 12500.00. With an average of Rp 10492.85

and a standard deviation from Rp 1354.623

W Of the 65 Interest Rate (RATE) data, the minimum value is 0.0060 andthe maximum value are 0.0750. With an average of 0.059618 and a standarddeviation from 0. 063423.

G! Of the 65 Company Size (SIZE) data, a minimum value of 5.626433 and aEaxirnum value of 26,01083. With an average of 13.03349 and a standard&viation from 4.512825.

{l Of tbc 65 Volatilization data (VOLA), a minimum value of 2.128004 billionRp and a maximum value of 13.85237 billion Rp. With an average of5293417 billion Rp and standard deviation of.2.076263 billion Rp.

L3Accuacy Tesc

L. hm Eftct vs Fixed Effecttb cho*test t€st is used to determine which model will be selected in ther.I data regression model estimation, whether the common effect or fixedr&cf model. This test is done by using statistical test of F or chi-square withLypothesis as follows:

Ec Common effect model is better than fixed effect

trr Eired effect model is better than common effect

f tbe value of F arithmetic (F-test) and chi-squa,re test is smaller than a :0.IE (5%), thea Ho is rejected and Hi is accepted. This shows that the effectDd€{ lsmains better than the common effect model in estimating panel datangrcssiorx- Conversely, if Ho is accepted and H! rejected, which mearui that theaonrnoneffect models is better than the fixed effect model in estimating panel&rregession.

L lhdEfiect vx Random EffectTLechoice of which model is used between the fixed effect model or the randomcfiect model, the Hausman test is performed. (Hausman test). The hypothesisir tb Hau.sman test is as follows:

Eo : Random effect model is better than fixed effect

f tte probability value (Prob) Chi-Square Hausman Test is smaller than a :OIE (5%), then Ho is rejected and Hi is accepted.

G honEffect vs RandomEffectIlcrprmination of use of which model is used in panel data regression, whether[!Drr effect model or random effect model through Lagrange MultiplierF,U-tcst) Breusch-Pagan test. The hypothesis in this test is as follows:

f,o : the common effects model is better than the random effect

lE : Ihe random effect model is better than the common eflectf Lil{ test> chi-squa,res with Alpha: a : 0.05 and df : 3, then Ho is rejectedd Hi is accepted. Based on the calculation of Breusch-Pagan LM test (BP)

EAIII.TE trAKTfl'RI AND GUSMIARNI

chi-squares table with l: O(}$" or the probability value of LM-test Breusch-

Puguo 0.0000 is smaller then a - 0-61 it can be concluded that the random

effJct model is better rather than the common effect model in eliminating the

influence of internrl and extrnal factors of underpricing and its implicationg

on the long-term underperhrmance of IPOs in Indonesia' Hypothesis tests

results as follows:

tU.2Hypothrak atd Brrrb Slructurel Data 2011

Iafoanc oa HSHM

Corlffraiatt Prcb

DecisionHgpothesis Varioble

H1

H2

H3

H4

H5

H6

H7

R_Square

Source: Data is processed using eviews 9'0

Information:S : significant;

TS : no significant

Model AccuracY Test

a. Common Effect vs Fixed Effect

The chow-test test is used to determine which model will be selected in the

paneldataregressionmodelestimation,whetherthecommoneffectorfixedeffect model. This test is done by using statistical test F or chi-square with

hypothesis as follows:

Ho : Common effect model is better than fixed effect

Hi : The fixed effect model is better than commot etfect

If the value of F arithmetic (F-test) and chi-square test is smaller than a =

0.0b (5%), then Ho is rejected and iti is accepted. This shows that the fixed

effect model is better than the common effect model in estimating panel data

reglession. Conversely, if Ho is accepted and Hi is rejected, which means that

the common effect model is better than the fixed effect model in estimating

panel data regression.

b. Fixed Effect vs Random Effect

The choice of which model is used between the fixed effect model or the random

effect model, tt "

ir,rr*an test is performed. (Hausman test). The hypothesis

in the Hausman test is as follows:

Ho : Random effect model is better than fixed effect

FIi : The fixed effect model is better than random etfect

AGE

ROA

KAPTVOLARAIEKUR,S

Together

0.291944

-38,17,185

-23,48465

0,fix295-r4,rl42l-r468806-0,066122

F= 3,985729

0.2238

0.0884

o.8442

o.5276

0.9549

0.1761

0.002088

p>0,05;TSp>0,05;TSp>0,05;TSp > 0,05 ;TSp>0,05;TSp>0,05;TSp<0,05;S

h

[-test Breusch-at the randomliminating thets implicationsypothesis tests

Decisron

p>0.05;TSp>0.05;TSp>0,05;TSp>0.05;TSp>0,05;TSp>0.05;TSp<0.05;S

be selected in the

no effect or fixed

n chi-square with

r sEaller than a =ms that the fixed

hating Panel data

,rhich means thatpdel in estimating

I

pdel or the raudom

S). The hYPothesis

E\.IEWS ANALYSIS: UNDERPRICING DETERMINANTS... 267

fom p*i*bility value (Prob7 Chi-Square Hausman Test is smaller than a:t0lt{flS, ,5% t. theu Ho is rejected and Hi is accepted.

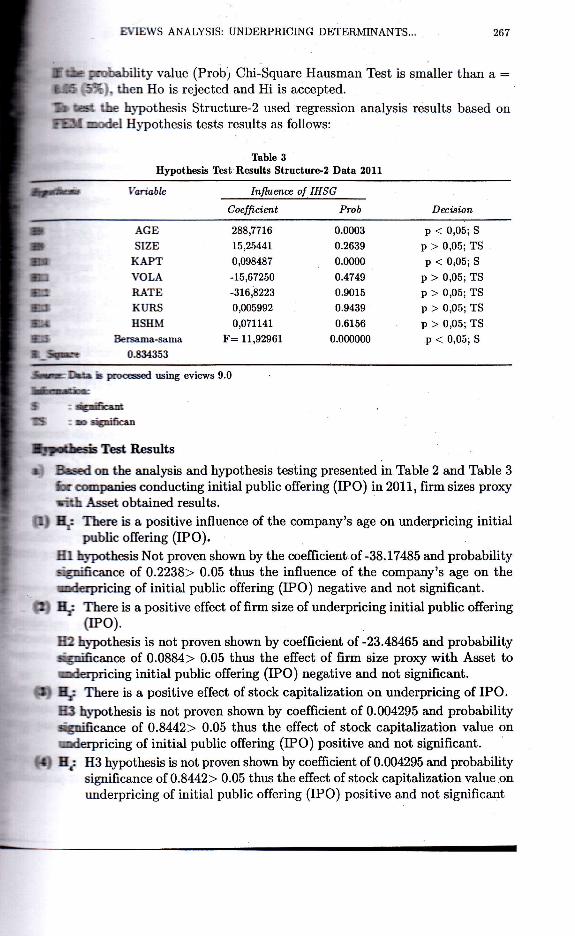

Eo mm the hlpothesis Structure-2 used regressioil analysis results based ontrf,h,t Epdel Hlpothesis tests results as follows:

Table 3

Eypothesis Test Results Structure-2 Data 2011

frrd!!, l'oriable Influence of IHSG

Coefticient Prob Decision

I

DDmnfllffilrmm

m{mffiD-Xtft

AGESIZE

KAPTVOLARATEKURS

HSHMBersama-sama

0.tj:14353

288,7716

15,2544t

0,098487

-15,67250

-316r8223

0,005992

0,071141

F: 11,92961

0.0003

0.2639

0.0000

0.4749

0.9015

0.9439

0.6156

0.000000

p < 0,05; S

p > 0,05; TSp < 0;05; S

p > 0,05; TS

p > 0,05; TSp > 0,05; TS

p > 0,05; TS

p < 0,05; S

Xrill: Drt L procssed 6ing eviews 9.0

*rrrroI

-ri6amlli 6 rtnificen

lp;tothds Test R€sults

L,i{ Beed on the Analysis and hypothesis testing presented in Table 2 and Table 3h companies conducting initial public offering (IPO) in 2011, firm sizes proxyTith Asset obtained results.

{lI} E : There is a positive influence of the company's age on urderpricing initialpublic offering (IPO).

El h1'pothesis Not proven shown by the coefficient,of -38.17485 and probabilityqignificAnce of 0.2238> 0.05 thus the influence of the company's age on theunderpricing of initial public offering (IPO) negative and not significanl.

P| ry There is a positive effect of firm size of underpricing initial public offering(rPo).

B2 h1'pothesis is not proven shown by coefficient of -23.48465 and probabilitysignificance of 0.0884> 0.05 thus the effect of firm size proxy with Asset towr&rpricing initial public offeriug (IPO) negative and not significant.

{81 Ej There is a positive effect of stock capitalization on underpricing of IPO.83 h1'pothesis is not proven shown by coefficient of 0.004295 and probabilitysiEnificance of.0.8442> 0.05 thus the effect of stock capitalization value onmnderpricing of initial public offering (IPO) positive and not significant.

fi) Ej H3 hypothesis is not proven shown by coefficient of 0.004295 and probabilitysignificance of.0.8442> 0.05 thus the effect of stock capitalization value onunderpricing of initial public offering (IPO) positive and not significant

HAIITLTE, XAKT{URI AND GUSMIARNI

(5)

(6)

(7)

H4hypottre.isisnotprwenshmnbycoefhcientof'-l4.ll42landprobability,is;i"fi"*rr"" of 0.52?6> 0-o5 thu.s the effcct of volatilization on underpricing

i"ilirf pubtic offering (IPO) resptive and not significant'

H-:Thereisanegativeetfectoftheinterestrateontheunderpricingofinitial" public offering (PO))'H5hypotlresisnotprovenshowlbycoefficienteqrralsto-46'g806andprobability;i;ih;"""" equat to oBsaD 0,6-hence influence of interest rate to underpricing

i"ilirf public offering.(IPO) negative and not significant'

II^: There is a positive influer':e of the rupiah exchange rate against underpricingo

of initial Public offering (PO)'

H6 hypothesis is not proven "!9Y" by coefficient of^-0'066122 and

,r.UiUfilt, signifi"onc" of 0'1761> 0'05 thus the effect of rupiah

exchange rate on ,rrraurp.i"i"g of initial public offering (IPo) negative and

not significant. r !r ,! ,lH-: There is influence of compauy age' company size' stock capitalization"n ;;;;", *r"rii*"ii"n, iot"'""t ttt9, *a rupiah exchange rate together with

.roJ", pri"irrg of initial pubtic offering (IPO)'

The H7 hypothesis proved to be shown by probability significance of 0'002088

<0.05thusfirmage,n'*'i'",stockcapitalizationvalues'volatilization'interestrate, and rupiah ";[""g"

rate together with under pricing of IPO' If there is

an increase i* "t.;;1;;; the value of stock price will increase positively by

-0,002088.

(g\ Ir-: There is a positive influence of firm age on long-term underperformance'

Hg hypothesis proved shown by the coefficient of 288'7716 and the probability

significanceoro.ooos.o.os-tt'.,'theinfluenceoffirmageonlong-termunderperfor*u.r"u"f,"o"rtti"" *a significant. If an increase in the age of the

"o*purry will increase the JCI value of 288'7716'

(9) Hr: There is a positive effect of firm size of long-term underperformance'

Hglrypothesisisnotprovenshownbycoefficien|ofls.2S44landprobabilitysignificance "r

oldgg, 0.05 thus the effect of firm size to long-term

,rid".p"rformance positive and not significant'

(10)Hro: There is a positive effect of stock capitalization on long-term

underPerformalrce'

HlOhypothesisprovedshownbycoefficientof0.0g848Tandtheprobabilitysignificance or ohooo <0.05 thus the effect of stock capitalization values to

long-termunderperformancepositiveandsignificant.Meaningthata,rryincreasein Lpitalization value will increa'se the JCI of 0'098487'

(11)H,':Thereisanegativeeffectofvolatilizationonlong-termunderperformance.H11 hypothesis iJnot proven shown by coefficient of -15.67250 and probability

significance * i.qlii, 0.05 thus the effect of volatilization on long-term

,id"rp".formance is negative and not significant'

(12)H.,:Thereisanegativeeffectofinterestrateonlong-termunderperformance.I{l2hypothesisnotprovenshownbycoefficientequalto8T,0T803probability

underpricing

aud probabilityto underpricing

-0.066122 and

ililization, interest

of IPO. If there is

probability

ing of initial

t of rupiah

) negative and

capitalizationtogether with

of 0.002088

positivelY bY

formance.

the probabilitYtge on long-termin the age of the

I and ProbabilitYeize to long-term

on long-term

end the ProbabilitYvalues to

that anY increase

underPerformance'

and probabilitYon long-term

underPerformance'

8I.07803 ProbabilitY

AGE

SIZE

trAPT

VOLA

RATE

KI'RS

simultaneous Significant 0.45254L

0,239348 0.061839

Signilicant T

Significant 0.539926 Significant

0.865513 0.060963 0.291944

B'IE\YS ANALYSIS: UNDERPRICING DETERMINANTS... 269

sqnal [s 09015> 0,05 hence influence of interest rate to long-termpositive and not significant.

*flere is a negative influence of the rupiah against long-term' ^rformance.

tfpothesis not proven shown by coefficient of 0,005992 and probability

;!flclre equal to 0,9439> 0,05 hence influence of rupiah exchange rate tormderperformance positive and not signifi cant.

the b an underpricing effect on long-term underperforrlance.

mf tlrpothesis not proven shown by coefficidnt of 0.071141 and probability

tfrre of 0.6156> 0.05 thus the influence of underpricing to long-term*pcrhrmance positive and not significant.

lhrc b influence of company age, firm size, stock capitalization value,detility, interest rate, rupiah exchange rate and underpricing together.Erirxt long-term underperformance.

D fU'p*hesis H15 is shown by the probabilii;y significance of 0.0000 <0.05blbin0uence of firm age, firm size, stock capitalization values, volatilization,Grafe, rupiah exchange rate and underpricing jointly against significantlX*crn underperformaace.

Discu.ssion

o the data *',alysis of the company conducting iuitial public offering in7 to 2Xlll aod testing the hypothmis that has been done, Iirst Regression of

to prove the influence of company age, Company size where company

Fry uith Ln (Asset) denoted by SIZE, Capitalization of shares (KAPT),(VOLA),Interest Rate (RATE) and Rupiah Exchange Rate (KURS)

HEFidng Share Price (IISHM).hnsry of hypothesis testing results

Ihble 4Hypothesis Test Rcsults Structure-l

lh*ir Voniloble Strttcture-I: Intluene on HSHM

2010 201 InDL

nnL

Significant

Significant

Significant

LltFr0.699775

0.057235

270 f,,ilBdtr- MAKIIruru AND GUSMIARNI

TaHe 5SrGl-t f,YPPrlni5 Test Results-2

Str.rlcture-2:

2010 2011

AGE

SIZE

KAPTVOLARATE

KUN,S

HSHM

sirnultaneous Significant Significant Significarrt Sigrrificattt Significant Significant

0.860242 0.838245 0.934422 0.953878 0.087028 0.834353

Hgpothesis

H8

H9

H10

H11

H12

Hl3H14

Sigdfrcaut Significant Significarrt

Significant Sie'niftaut Siguificant

Significant Significant

Signifrcant

Signi6cant Sigrificaut Significant Significant

Significant

Significant

Significant

Significant

Significant

H15

R_Square

Conclusions and Recommendations

Conciusion

Based on the empirical findings and in accordance with the formulation of the

problem, the conclusions of this study are as follows:

1. The company's age had a negative and significant effect on 2006 ou

Underpricing, while in 2007 until 2011 it wers not significant. The empirical

findings in the research hypothesis stating that the age of the company has

a positire effect on underpricing on initial public offering (IPO) in Indonesia

Stock Exchange.

Z. The size of the firm is not significant against underpricing in companies

that conduct an IPO. The empirical findings in the resetrrch hypothesis

stating that firm size have a positive effect on underpricing on initial public

offering (IPO) in Indonesia Stock Exchange'

B. The value of capitalization significantly affected the underpricing in 2006'

2010 aud 2011 wtrile not significaut in 2007 until 2009. While the empirical

findings in the research hypothesis which sttr,tes there is tr positive effect of

stock capitalization value on underpricing IPOs in Indonesia Stock Exchange'

Volatility had a significant neg&tive effect of 2006 while 2007 to 2011 was

not significant. Enipirical findings ip the hypothesis of the study there is a

positiie effect of voiatilization on urrdetpricirrg initial public offering (IPO)

in Indonesia Stock Exchange.

Non-significant interest rates in 2007, 2008, 2010 and 2011 were negative

while 2b06 and 2009 were positive fgr urrderpricing. Tle empirical findingB

in the research hypothesis have negative influence tlf interest rate ou

underpricing of IPO in Indonesia Stock Exchange'

The exchange rate of the Rupi&lr (Excha,nge rate $) 2006 to 2010 is negatirrely

insignifica,ul, while in 2011 the positivcs tue iruignificant. The cmpirical findins

ip t[e hypothesis colttrined a positivc irtfluelce of the rttpiah exchange ra'te

against the underpriciug of IPos on the Indoncsia Stock Exchtr,nge.

4.

5.

6.

)

2010

Significant

Significant

Signi6caut

Significant

$gnificant Significant

0.987028 0.834353

formulation of the

effect on 2006 ou

. The empiricalof the company has

(IPO) in Indonesia

in companies

re..jearch hypothesison initial public

underpricing in 2006,

\4'hile the empiricalis a positive effect of

Stock Exchange.

2007 to 2011 was

ofthe study there is a

public offering (IPO)

2011 were negative

empirical findings

o[ interest rate on

to 2010 is negativelY

The cmpirical findings

ruPiah excllange ra'te

Exchange.

EVIEWS ANALYSIS: UNDERPRICING DETERMINANTS... 271

Hlcnce along with company age, firm sizel stock capitalization value,nlrtilization, interest rate, and rupiah exchange rate against underpricingLrln6, 2007, 2008, 2010 were positivery insignificant-while in 200g and-lll qignifi.ant. The empirical findings are consistent.with the hypothesis-' t there is influence of company age, firm size, stock capitalization[,lrcs, volatilization, interest raie, and rupiah exchange ratefftaaeously to underpricing initiar public offering (Ipo) in Indonesiat* F;vshar*..

L xno corporare age was negativery insignificant while 2007 to 2011n pcitively significant in accordance with the empirical finding of theurh hypothesis that there was a positive influence of firm age on rong-k nnderperformance in Indonesia Stock Exchange.p dze of firm positive is not significant to long-term underperformanceLmrdance with em-pirical findings hypothesis research there is a positive*ct o1 firm size of long-term underperformance in Indonesia stockH.-L-nge in Bursa Efek Indonesia.

n *ilcast positive capitalization in 2006, 2007,200g,2010, 201r except intPbare negative effect is not significant in accordance wiih the empiiicalL&Us hypothesis research there is a positive effect of stock capitalization& rgo;r,st long-term underperformance in Indonesia stock hxchange.

ut tt5titysignilicantly negatively influenced in 2006, 2oor,2}ogand 2009hr a significant non-significant positive effect in zbro and 2011 have nolFficsat negative effect in accordance with the empirical findingsrgpotheais research there is a positive effect of volatilization to long-termUrpcrformance in Indonesia Stock Exchange.

E bcrcst rat€s itr 2006 and 2010 were significanily negative, 2007, 200g andltl neg8tively insignificant, in 2009 positive not siglnficart io *"ordro"urrl the empirical findings of the research hypothJsis there is a negative.frct of interest rate on long-term underperibrmance in Indonesia stockErfurnge.

l8- tt'c-nhange rate of Rupiah (Exchange Rate $) in 2006 to 200g has aiuricaat negative effect, in 2010 the negative effect is not significant and- ilu have a significant positive effect in accordance with empilcJft"il;pelch hypothesis there is a negative effect of rupiah exchange rrt" ,g"i;tlq+etm underperformance in Stock Exchange Indonesia.

"l*- rha:rpricins in 2006, 2007,2008,2010 has significant negative effect, 200gd Xllr have no significant positive effect in accordanc" iuitn the empiricalLfus of the research hypothesis there is innuence of underpricing toh*erm underperformance in Indonesia Stock Exchange.lf Hrece together is significant in accordance with the empirical findingsd tLe research hypothesis there is influence of compaoy'ug", Ii.* ,ir",rb& e-pitalization value, volatilization, interest ruiu, ,opiun exchangeilc and underpricing jointly against long-term underperformance in

hdmesia Stock Exchange.

272 HAMIIJTE, MAKMURI AND GUSMIARNI

References

1. Aggarwal, R.eerra trld Pietra Rivoli, 1990, "Fads irr The ltial Public Offering lr{arket?" ' Fi'nanciol

Managenrent 19 (1990)' 45-57.

R.. Leal and L. Herrrautlez, 1993, " The Afterrnnrket Perfonnatrce of htitiol Public Otfaing

irr Latirr America " Financial rn'on'agenr'ent 22 (1993)' 42-53'

2. Allerr. F. autl Faulhaber, G.R.., 1989, "signalingby un,derpric.irr.gin the IPO Market "' Jountal

OJ Finan,cial Ecottomics23 (1989)' 303-323'

Managerial Implications

Theoretical Implic ations

Based on empirical research findings, underpricing phenomena that occur t0Indonesia can be explained by the age of the company, the value of capitalization.

volatility, and the dollar exchange rate. While for long term underperformance

after Ipd is explained by variable age of company, value of capitalization, volatilitv,

interest rate and exchange rate. The results of this study strengthen the theory oi

a,symmetric information (Asssimetric Information Theory) will occur underpricing

pi"oo*"rroo is also supported by agency theory (Agency Theory) and Signal theor|

(Signaling Theory), it also reinforces the theory of efficient market hypothesis that

u*p1uir,r tLat an efficient market is a market where the price of all traded securities

ref:lects all available information. Where investors should seek information about a

personnel or corporate approach to seek information that is not contained in the

analysis of fi nancial statements fundamentally'

Suggestion

1. Based on the results of research IPO success is much greater by underwriter, itis recommended that underwriters in determining stock prices prime can pay

more attention to information that is non-accounting so that all parties concernd

with the IPO process can have enough information so that is not based only on

data is fundamental so I suggest that not all cheap stoc]rs or underpricing are

good for the long term.

2. For independent audits or public accounting firms that will issue an opinion for

u "o*purry

for the phases of the IPo process should be able to preseut

transparently in accordance with a predetermined code ofpublic accountants.

3.

4.

5.

6.

Ariefiarrto, Moch. Docldy. 2012, Ecouornics of Essettce atnl Applicutiolrs by Usirrg eViews' 'Iakarta,

PT. Gelortr Aksara Prata.tna

Ari{iu, Zreurl. 2005. "Firrarrcial Thexrry zrud Capitrrl Nlttrket". Yogyaktrrtn' UII'

Arikuuto. 2002. Research l\{ethodology A Proposal Approach, .Itrkarta, PT. Rirreka cipta'

Arrders<rrr, s,c. Be.rr{,T.L., & Bonr.T.A. (1995), Initr:ol Pubtic oJlerhr'gs .Fil1li'1g and Tltonu '

Br.rston: I(luwer Acndetnic.

7. Bentty, R..P. arrrl .I.R.. R.itter, 1986, "hrvr:strnerrt Baukirrg, Reprtt&tiotr, atrl underpricing-of

Initial public olferirrg" . Jorunol of Fit}ottciol econ'ontics 15 (Jonuaty/Pebruary 1956)'213-32

Briglrarn, Bugeue F, I\{ichael c.Elrrhardt, 20o5, Fittottcial Managenr.ett, Tlrcory anil Pmctice'

Irrternatir-,nal Edition, 1 1'r' Eclitiolr, SOUm-WESTBRN CDNCACE Learnitg

Ba.ron,D.P.aucl [Itrnstroug (1980)."The lttvestrttettt Bllrrkirrg cotttract for New Issues under

Asyrnrrretric Irrf<rrrn.tiotr:Delegrtion :rnd The Iucetrtive Problettr," ,Iotu,nal oJ Firt'ttrr.ce ,35(5),1115-

1 138.

9.

t

31. Hwang C.Y. and NEvidence" Workirtg

EArtll.f,f," XAKMUru AND GUSMIARNI

Jalreremr *Long-term Performance of IPOs and Non.,IPO"s'^;IaPanese

p"p*, f-fl' Kru Graduate School Of Business, University of Pittsburg\

(1ee2).

35. Isnurhadi et. al "The Analysis of Short-Rur and- Long-Run Performance.of Privatization Initiol

Public OfJeringio f"f.f.ySi; Wo"firy Paper' Sriwijava Urriversity (2008)

--, J. sindelar aud J. Rittrr'Ioitial Public offerings." Jout"nal of applied corporate Finance

(lees).

36' Jog, V.M' arr<l A' L. Riding "ItrrdaTtir;ittgin Canadian |Pos', Financial Analysis Journal (198,t,

48-5537. Keloharju,M' "Winner's cur*, legal liability' and the l""S !*lT^tT' gerliormance ol Initial Public" " 'Oii"rmi

in Finland." i'""i ifaoatcial eotomics 31' (1993)'2b1-277'

38. Li.M., Zheng, S'X',&Melancon' M'V'(2ff)5)'"-Uailetpricing' Share Retention' and the IPO

Aftermarket l,iquiOt,, i"to" iA^a tirr-i ol Manogeilal Finance, Vol.l'No.2, pp.76-94.

39' Levis, M. .The Long-run Performance of Initiat Public offerings: The UK Experience 1980.88.,

' Financiol Management 22 (1993)' 2e11'

40. Loughran, T and J. R Ritter " The Timing and Subsequent Performance of IPos: Implications

for the cost or "qritv ".iiioi."

UrrpoUri"nJ Uuiversity of lllionis worki,g paper(1993)'

-------and-----'tt. New Issues Puzzle' " Tlrc Journal of finance 50 (1995)'23-51'

It. Loughran, T ., nitter, J' R and Rydqvyst '-K ",Initial Public Offerings: International lnsights"'--

Porill"-Dosin Finance Journol 2 (qdotetl 2010)' 165-199'

12,Lowry,M.,oflicer,M.SandSchwert,G.W."TheVariabilityofIPoInitialR,eturrrs:International'-' fn"ighir", Pasific-Basi,n Finone Jountol 2 (qdated' 2010)' 165-199'

lS.Lucas,DandR.McDonald..EquitylssuesarrdStockPriceDynarnics,,JoumolofFinanceSS(1 990),101 9- 1013.

MakhiSa, A., Bhandari, A', Gramrnatikos' T'' and Papaioanrrou' G

;;;ial";il" " Jountal o! Financial Research 12 (1989)' 90-102'

McDonakl, J and A K Fisher " New Issue Stock Price Behavior"

1972),97-102.

16. Milter, R and F Reily' u An Examination

Public Offerings." Finoncial Manogernent

17. Manurung, Adler Haymarts (2{113)'Initiol

.Iakarta: PT Adler Manurung Press'

18. Muscarella, Crish .L"a rt'riai"f V:9.'I:1" i*t:f.t* test Baron's Model of IPO Unilerpricin!'

'lou*ot o! Financial Econornits 24 (1989)' 125-135'

and " T\e l)ntlerpncing of Seconcl Initial Public Offerings " Joumal oJ

fiioniil n"t"ora, lc 0sag), 183-192'

,r. ;ffi;;;;,;;;; "'i* (t'1,,1 A, sl'dJ-:r -uI !.::::f:,:!J1,'i1,.Ti*"?:$.ly':i

And Impact o, p".fo.rnarr#.iii,o'it."t" i"l"ai.r Firrancial Markets, social sciertce Research

Network.

Plram,P.,Kalev,V&Steen,A'(2003)'"IJnd4ricing'StockAllocatiol'OwnershipStructureand post Listirrg Liquidfrr'.i'il-*ir'f,isted Firms,"liournol o! DanLing an'il Finance'Vol'27,

44.

45.

" Risk And Return on Newly

Jownal oJ Filtance 27 (March

. of Mispricing, retur-ns, and I|ncertainty for Initial

16 (1987). 33-38.

Public OlJering (IPO) KonseP' don Prcses

50.

No.5,pp.919 - 924 .

,, ffi#;:;-nlil c,u*,*,Fco,.IR,&Aquirue,R's'(2006)' ,"P:::.^!*n'1^"#f: otlerins Have

i:,}ili:,ffi ". iiti,ol#'i,i 'i"'ai's Activitv'"Finone onit Accountins' pp'84-e8'

KO Rrrdoni,Ahrna<ldarrHerrriAli,20to,Mo.leruFirrarrcialManagernent,Issrreone,MitraWacanaMedia.

5S. Ross, steplrerr.A, "The Arbitrage Theory of Capital Asset Tlicirt'g"'Jotnnal ol Economic Theorg'

December 1976.

54.Ritter,.IayR.,andIvowelch,2002,,AReviewofIPoActivity,Pricing,andAllocations''Joum,al ol Financt ST, 1795-1828'

55. Ritter, .Iay.,(2012)' "Ecorrotnies of scope and IPO activity irt

soll / papers. cftrt'/ ab strttct'id= 2 I 69 96 6

Enrope, " lttt1t: / /papers.ssm' com /

,.H

on IPOs: ,opunou 't*

mirl- of piusburgh

ffiPrir.atizationInitiol

€CorVorate Finanu $

'I

Joumal (1987, .

ol Initial Public

ion, aud the IpOo.2, pp.76-94.

Experience 1980-88.'

of IPOs: lmplication:spaper(1993).

s0 (1995),23-51.

Ideroational Insights',

Returns: International

' Jorrlnal oJ Finonrc 38

.And Return on Newly

o! Finance 27 (Match

Linarrtoin|g for Initial

Teori, don Proses ,

offn.O underPricin!'

Olferings " Journal ot

Public Offers (IPO)

S ociol S cien ce Re s earch

OwnershiP Structure

aul Finance,Vol'27,

PfiEc OJfering Have

pp.84-98.

tsrre One, Mitra Wacana

ol Economic Theorg'

Itticing, and Allocations"'

' hltp : / /PaPet s. s sr:r"' coflr /

EVIEWS ANALYSIS: UNDERPRJCING DETERMINANTS..

!!olJrl t " The Long-run performance of Initial public offerings,,, Journar oJ linane j6@ 1991),3-27.

Hy'F.K. Brown, K.c, edisi terbaru, Inuestment Analysis ar,"d, portforio Managemml brhedition,L llrt den Press, Chicago.

t1 *?!en A, Randolph w.westerfield, Jeffrey F. Jaffe,(2005), corporate Finane,, seventhfryn' McGraw - Hill International Edition.D.h K- "why New Issues a.re underpriced", Joumar o! Financiar Economics li (January/fllry 1986). 187-212

EIUD' J " UndentriterPrice Support and the IPO ItnderpricingPtzzle.,, Joumol o! Financial@a&s 31 (1993), tSS-151.

sdes, Anthony. The [tnderpricing of Initiar public olferings (Ipod in singapore; publi,clh lllltes oful Possible solutions. Singapore : Institute oi Souin*"t Ariuo StuA"" tiSsOifuul R- Ajija, Dyah w. sa.r_i, xahmat H. setianto, and Martha R. primanti. 2011. smart way5 !i*er EViews. Publisher Salemba Empat.

____iDd Joseph Lim, " Underpricing and the New Isuue proses in Singapore,,, Joumol o!bEag otd Finone. 1l (Agustus 1990), eg1-509.$!t' RL- and P Bornstein.' why New Issues are Lousy Investments." Forbes 136 (December p,t,'s) ,52-90.

F rrr swee. ' Ilnderpricing of Ipos in gingapore,' Asian posijic Joumal of Monaganent g(Odib 1991) 175-184.

Dgrrt, R, cdisi terbaru, Quontitatiae Analysis for Inaesment Management, prentice Hall.T-"- th" M " Anatomy of Initial public offerings of common sr,ock.: Jounat o! finanex JS(Sqtanlrr 198s) 1s|-sZzrrh& s. ad. B h"-""^ ",_ISgrmation euarity and the Valuation of new issues,, Joumar o!

oltd eotomics I (19 6); 159-17ell+Ecae, J-, edisi terbaru, Financiol Market Rates and Frouts, prentice HallHct" Ito " Seasoned Offerings, Immitation Cost and the Und,erpricingof Initial public Offerirg*,,.|olllul of Fiaance ll Qune 1gS9), lLt-149.

-------, N. Jegadeesh, and M Weinstein " An Empirical Investigation of IpO Returns andrt*sed Fqnitv offerings " Joannar ol Financior Einomics sa lisssl.tii-ils.*Gb' RE "The Market for Initial Public Olfering; An Analysis of the Amsterdam Stockrtange-" In A B,apprais-ar of the elficiency of finonciar marrrets, R Guimaraes, et or (ds),tuEq Springer-Verhg (t 989 ).filg Wahru Winarno. 2009. Anolytiu,l Econometrics ond Stotisti.cs with EVi.ews, Second, Ed,itiol"UPP College of Management Sciences yKpN.

Irrlg : UmvsRsrrAs Prnseol lroorBsn. y.A.I. J*erre. Irooresn

k-rnr, Gusur.lR'r : SnKou,c,H Tr*ccr ft,uu Er<onorr,rr yAI, Jeurm. Iroouesu

275

I!

Jj

3

!

*ET&aat

I.

TL