Knowledge Transfer Program - Module 2 – Asset Allocation ...

140

Marketing Material For professional / Institutional clients only Knowledge Transfer Program Module 2 – Asset Allocation and Capital Market Expectations Global Sovereign Markets April 2021

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Knowledge Transfer Program - Module 2 – Asset Allocation ...

Marketing MaterialFor professional / Institutional clients only

Knowledge Transfer ProgramModule 2 – Asset Allocation and Capital Market ExpectationsGlobal Sovereign Markets

April 2021

1

UBS Asset Management: A centre of excellence for Sovereign institutions 35+ years' experience in partnering with Central Banks, SWFs, National Pension Funds, and other government agencies

Key strengths

Managing over USD 169bn AUM on behalf of public institutions

Global insight and expertise allows us to integrate our comprehensive range of investment capabilities in tailored solutions for you

A flexible range of advisory services to help you meet your long-term goals – including HF advisory experience

UBS AM is a member of the One Planet Sovereign Wealth Fund initiative

Knowledge partnerships and training with dedicated teams, tailored to sovereign clients

– Research papers and publications

– Financial Markets training courses

– Sovereign Trainee Programs

Dedicated Sovereign Client Solutions

Advisory services

Asset Management

Asset/Liability matching

Risk Management

Manager Selection

Knowledge Partnership

Training and development

Dedicated research team

Dedicated Global Sovereign Markets team

London

New York

Zurich

Singapore

Beijing

Taipei

Hong Kong

Dubai

Source: UBS Asset Management. Data as of 30 September 2020 unless otherwise stated.

2

UBS Knowledge transfer program UBS AM is an experienced long-term partner to sovereign clients

Key seminars offered to our Sovereign Clients:

Reserve Management Seminar, Switzerland: a forum for central bankers, multilateral organisations, finance ministries, frequent borrowers and representatives of SWFs to discuss and exchange ideas on best practices for managing reserves

Sovereign Investment Circle, Singapore: joint event between UBS AM and IMD, a leading business school, focusing long-term investing themes

Investment Training Seminar, Chicago: discussions on economic growth, fiscal and monetary policy and their impact on global markets

Greater China annual Conference, Shanghai: addressing latest investment trends/developments and providing access to China specialists

Topical research paper sand development opportunities that could be tailored to your needs

Greater ChinaConferenceChina

UBS AM Sovereign Investment Circle Singapore

Reserve Management SeminarSwitzerland

Investment Training SeminarUnited States

2x Reinvesting Bretton Woods SeminarUnited States

January June 28th-July 1st August 16th-18th October/November April & October

Client seminars: provide forum to discuss investment topics and an opportunity to meet peers

3

Knowledge transfer is one our key strengths Sharing industry know-how and investment expertise

The emphasis of an on-the-desk training program is to facilitate a knowledge-sharing environment whereby the participant is encouraged to openly engage with the investment professional and actively participate in the day-to-day activities of the team that they are seated with.

Ultimately, participants are equipped with the tools to learn and enhance practical skills for trading and investment and gain key industry insights into current developments across financial markets.

Examples of on-the-desk trainings:

Fixed Income Sovereign overview; Active global sovereign bond management; Introduction to passive fixed income Credit overview; Credit research with an analyst; Global credit investment process Foreign Exchange overview; Managing foreign exchange execution

Investment solutions

Strategic Asset Allocation Tactical Asset Allocation Currency exposure and hedging Scenario Analysis

Equities

Equity markets and the drivers Stocks and stock valuation, equity research Equity indices and passive investing Implementation of best execution

Risk Management Case studies demonstrating how to use the UBS AM's multi asset risk system in the context of the above scenarios

Table of contents

Asset allocation fundamentals – Michele Gambera Section 1 5

Capital Market Expectations, Portfolio optimization and risk management – Louis Finney Section 2 32

Integrating Alternatives and ESG into asset allocation frameworks – Michele Gambera, Louis Finney Section 3 57

Sample Portfolios, Capital Market Expectations and Advisory Services to Sovereign – Mohammad Ahmad, Massimiliano Castelli

Section 4 92

Biographies & important information Section 5 128

Asset allocation fundamentals –Michele Gambera

Section 1

Asset allocation basicsSection 1.1

7

Strategic asset allocationAn important workhorse of portfolio management

SAA generally based on long-term estimates of how asset classes are expected to behave

Asset allocation is important to determine the level of variability of a portfolio:

Brinson, Hood and Beebower (FAJ 1986) suggested over 90% of variability explained by AA

Xiong, Ibbotson, Idzorek, and Chen (FAJ 2010) suggest that it is more 50/50

Investors should establish risk and return guidelines for their portfolios.

This is important because of:

Suitability of the portfolio (risk capacity and risk tolerance)

Benchmarking and performance attribution

Choice of instruments, manager styles and asset classes

Liability driven investing

A strategic asset allocation (SAA) is a clear and intuitive way to express guidelines and quantify the 'ballpark' for managers

8

Assigning a strategic asset allocationEvolution of SAA approach

Prudent investors should have more prudent portfolios

Assessing personality is difficult, particularly when there are many people on a board

No relationship between goals, funding level and allocation

Risk aversion

Average return

Since risky asset classes have on average higher returns, investors that have low funding status should have riskier allocations

No relationship between horizon and allocation

This approach works about half the time!

Risk capacity

Quantify funding level and horizon and simulate future returns

Choose asset allocation that gives client highest probability of reaching goals

Use personal preferences as second-order variable

9

Advantages of the risk capacity approachThe more modern approach

Focus on probability and randomness of returns

Goals, funding status and time in the forefront

Help clients understand their funding status and whether their plan can be expected to succeed

Can be customized to take risk aversion and other preferences into account

10,000

100,000

1,000,000

10,000,000

0 5 10 15 20 25 30 35 40

Bala

nce

in a

ccou

nt

Years from today

10

Asset-Liability ManagementMaximizing the surplus instead of only assets

A portfolio of assets is geared towards a series of liabilities

The difference between assets and liabilities is the surplus (or deficit)

Liabilities are akin to a negative bond, with duration and all

We can use a portfolio of bonds among the assets to mimic duration, cash flows and credit quality so that changes in assets and in liabilities offset each other and keep the surplus stable

11

Core-Satellite approachThis may be implemented within an ALM framework

The core is the main part of the portfolio, close to the benchmark

Core often has low-cost, passive exposures

Satellite is the high-risk, high-return component

It has high tracking error and very active management with the objective of long-term growth

In an ALM framework, the core would offset the liabilities while the satellite would be geared toward growth to hopefully make the plan better funded over the long term

12

Risk parity approachEqual risk weights means high exposure to government bonds

Risk parity means that the decomposition of the portfolio variance yields the same contribution to risk for all asset classes

This asset allocation strategy is therefore based on risk only

No expected returns are involved

It worked particularly well during the great bull market in bonds from 1985 to 2020

It will have great difficulties if yields normalize

Risk weights

Gov. BondsStocks

CreditProperty

13

Investment Policy Statement (IPS)The clear agreement between portfolio managers and investor

Special situations

General investment objective

https://www.cfainstitute.org/-

/media/documents/article/position-

paper/investment-policy-statement-

institutional-investors.ashx

Risk objective, risk capacity

and risk aversion

Horizon

Return objective

Tax and legal constraints

Technical aspectsSection 1.2

15

Determining a strategic asset allocationThere are two main steps in determining an SAA

1. Quantify risk/return expectations for broad set of asset classes

Determine return, standard deviation, and covariance expectations for a broad set of asset classes based on relevant time horizon

Equilibrium: also known as Capital Market Expectations (CMEs); long-term (40+ year) expectations

Baseline: intermediate-term (5-10 years) expectations that consider current market conditions

2. Apply views to determine portfolio benchmark and SAA

Risk/Return expectations used in portfolio design depend upon the relevant time horizon.

In general:

– Utilize equilibrium assumptions for construction of portfolio benchmark

– Use baseline expectations to design target portfolio (Strategic Asset Allocation)

Client specific needs should also be considered:

liability hedging, liquidity constraints, risk preferences, income needs, etc.

US-I

16

It’s a matter of (time) perspectiveThree linked but different sets of asset class views: Equilibrium, Baseline and Tactical

Tactical views

Baseline expectations (the next 5–10 years)

Equilibrium expectations (an average over the next 40 or 50 years) Reflect our views for a

broad set of asset classes in a long-term, ideal equilibrium setting

Take equilibrium views and incorporate current market conditions with an intermediate time horizon

Set tactical asset allocation views in portfolios. Used to determine over- and under-weights around SAA.

US-I

17

Two different quantitative approachesBalancing both demand-side and supply-side approaches to modelling risk/return expectations lead to a more robust foundation for SAAs

Source: UBS Asset Management. For illustrative purpose only. A comparison of different supply- and demand-side approaches is summarized in Roger G. Ibbotson and Peng Chen (2003) "Long-Run Stock Returns: Participating in the Real Economy." Financial Analysts Journal, January/February. For ease of exposure, the analysis above excludes exchange rate adjustments as well as other adjustments we use in our methodology.

Demand-sideClassical approach

Investors demand ‘return premia’ for bearing risk

Determined by long-term historical risk premia, e.g. equity risk premium

Risk premia are time invariant but required returns influenced by starting values for interest rates and inflation

Supply-sideMore recent approach

Returns are supplied by the real economy & corporate earnings

Determined by forward-looking factors that drive asset class returns such as projected economic growth rates, current interest rates, etc.

Two different quantitative approaches provide more insight to consider when estimating returns

US-I

18

Example:Comparing supply and demand-side approach for US Equities

Source: UBS Asset Management. For illustrative purpose only. A comparison of different supply- and demand-side approaches is summarized in Roger G. Ibbotson and Peng Chen (2003) "Long-Run Stock Returns: Participating in the Real Economy." Financial Analysts Journal, January/February. For ease of exposure, the analysis above excludes exchange rate adjustments as well as other adjustments we use in our methodology.

US-I

Demand-sideBased on the investor’s required compensation for taking market risk

Supply-sideBased on the asset's capability to supply returns

Supply- and demand-side approaches to 5-year expected returns

Expected real cash 0.7%

+ Expected inflation 1.9%

+ Risk premium 3.8%

+ Δ Valuation -2.0%

TOTAL 4.4%

Current dividend yield 1.9%

+ Nominal earnings growth 4.8%

+ Δ Valuation -2.0%

TOTAL 4.7%

19

Low Real Rates

Low Real Rates

Low RealRates

Why have multiple sets of views? The result of an SAA optimization is only as good as its inputs

Static asset allocation based on equilibrium views works on average but only over long periods of time

Past performance is not necessarily indicative of future returns

Equilibrium views ignore current market conditions which can strongly influence intermediate return potential:

– Valuation at entry point

– Economic cycle

– Dramatic tail events may happen in the short term

– Changes in the structure of the economy or a market may affect expectations

– Ignores asymmetry of payoffs (tail risk, skewness)

Accordingly, we have baseline return expectations with an intermediate horizon (the next 5–10 years)

US-I

US Treasury Bill 1-Year Yield – US CPI All Urban Consumers

Source: UBS Asset Management views, Macrobond. Data as of December 2020.

-8

-6

-4

-2

0

2

4

6

8

10

1953 1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008 2013 2018

Fight against Inflation

Followed by “Great Moderation”

20

How do we think about multi asset investing?Valuation tells you direction but not timing

Market behavior analysis

Macroeconomic analysis

Cyclical and structural themes

Risk should only be taken where compensated

– Crucial to better understand sources of risk and return

Pric

e

Time

Overvalued

Undervalued

Valuation

Intrinsicvalue

US-I

21

Example: Valuation is useful (but a poor timing tool)Historically, Shiller P/E is a solid predictor of equity returns over 5–10 years

Source: Prof. Shiller, Standard & Poor’s and Bureau of Labor Statistics via Macrobond; UBS Asset Management.Note: Indexes are not directly investable. Data as of December 2020.

US-I

0

5

10

15

20

25

30

35

40

45

50-5%

0%

5%

10%

15%

20%

25%

1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014 2019

Shiller Cyclically A

djusted P/E Ratio (inverted axis)A

nnua

lized

Tot

al R

etur

n in

nex

t 10

Yea

rs o

ver

Infla

tion

S&P500 Real Total Returns next 10 Years Ann. Equity Indices, S&P, 500, Index (Shiller), Cyclically Adjusted P/E Ratio (CAPE)

22

Example: Macro cycles separate returns distributionsStock returns have had more losses and higher volatility in past recessions

Histograms of S&P 500 Index total returns minus CPI inflation

Source: Bureau of Labor Statistics, NBER and Standard & Poor’s via Haver; UBS Asset Management. Sample period: January 1970–March 2015. Indexes are not directly investable. Past performance is no guarantee of future results.

US-I

0%

5%

10%

15%

20%

25%

-24% -18% -12% -6% 0% 6% 12%

Freq

uenc

y

Monthly total return in excess of inflation

Recession Expansion

23

Caveat: Parameter stabilityWe cannot use estimates as if they were the “true” number

Estimated parameters such as returns or correlations have large error margins

Changes in market or economic structure create discontinuities

Serial correlation in returns biases estimates

The “true” number may not exist if data have random walk or regime switches

20-quarter correlation between S&P 500 and Ibbotson Associates Long-term Treasury Index

US-I

Source: Ibbotson Associates; UBS Asset Management. Sample: 1926–2020.

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1931 1941 1951 1961 1971 1981 1991 2001 2011

24

Caveat: Illiquid asset classesAppraised vs. economic volatility

Illiquid asset classes are appraised because they do not trade every day like listed asset classes

Appraisals are rather smooth (today's appraisal is equal to last quarter's appraisal plus any new information that the appraiser deems important)

This means that volatility is underestimated

There are statistical unsmoothing techniques, but they do more harm than good to the data

Based on recent academic research, our approach compares illiquid assets to comparable listed assets (e.g., venture capital and micro-cap stocks)

We have therefore an appraised volatility (from appraisal returns and IRR) and an economic volatility (from comparisons with equivalent listed assets)

25

How does an optimizer work?Examples among the most used portfolio optimizers

Mean-Variance optimizer

Inputs: vector of expected returns; covariance matrix; constraints

Good: simple to use

Bad: tends to produce concentrated portfolios; users introduce too many constraints to increase diversification; very sensitive to input changes; does not consider fat tails

Mean-CVaR optimizer

Inputs: vector of expected returns; covariance matrix; co-skewness and co-kurtosis tensors; or historical returns of a series of assets

Good: takes fat tails into consideration

Bad: many parameters make it unstable; complicated

26

Resampling and other robust approachesSolving the input sensitivity problem

Richard Michaud invented resampling: creating a series of expected return vectors etc. that are slightly different from the initial one (using random numbers) and computing the respective efficient frontiers. The average weights across all these efficient frontiers is the resampled frontier

Advances in cloud computing and data science have led to the invention of new optimizers, such as for example the IBM CPLEX. These optimizers find solutions that are already robust to changes in inputs, particularly in cases where one has hundreds of variables and constraints

For illustration purposes only. These charts are based on sample data.

27

Does ESG affect risk and returns?Four dimensions of sustainability in asset allocation

For illustration purposes only. The chart is not to scale and is intended to exaggerate the point for ease of exposition.

Long term: Modern ESG approaches are not detrimental to the investment process by reducing returns or increasing risk

Intermediate-term: Early adopters of ESG approaches may see improved risk-reward outcomes during the transition period to a low-carbon economy, with outsized alpha opportunity also available

Preferences: Strong exclusionary preferences are likely to have a negative effect on risk-return outcomes as the universe gets constrained too far

Spillovers to the economy: The ESG transition phase may elicit broader, more lasting ramifications for the economy and financial markets that must be monitored over time. In particular, engagement by investors and asset manager can accelerate this transition

28

Investment styles, indices and benchmarkingMaking sure that your funds give you the desired exposures

Fundamental (Portfolio-based) style analysis

Costly to set up database

Accurate as long as portfolio data are recent

Impossible if there is no transparency

More complicated for portfolios with derivatives

Statistical (Returns-based) style analysis

Simple as one only needs returns

Average exposure during time frame (36 or 60 months, typically)

Can be confused by spurious correlations

Constrained regression has analytical issues

29

Performance measurementTrying to interpret historical returns to understand skill

Historical measures based on returns

Sharpe ratio: excess return / standard deviation (no fat tails)

Sortino ratio: excess return / left semi-standard-deviation (no clear utility function)

Jensen's alpha and Fama-French (3, 4 or 5 factor) alpha: result of regression on factors (alpha is the excess return not captured by average factor exposures)

Morningstar Rating™: power average that takes fat tails into account

Historical measures based on portfolios

Active share: distance between weights in benchmark and weights in fund; normally, funds that deviate more from benchmark and survive have best returns

'Go fish' (Kacperczyk, Sialm and Zeng (2008): benchmarks portfolio against previous portfolio positions. Did the manager create value?

30

Performance attributionUnderstanding the alpha and beta mechanism

Attribution is the decomposition of returns in the following components:

Share of returns explained by the benchmark

Share explained by asset allocation

Share explained by security selection

Residual (unexplained part of the returns)

0%

1%

2%

3%

4%

5%

SAA: assetclasses

SAA:country/style

TAA SecuritySelection

Residual

31

Conclusion

Asset allocation is an important choice for a portfolio

It needs to be based more on risk capacity than risk aversion

There are several methods in addition to traditional mean-variance

Style and performance measurement are key in this framework

Risk management is the main objective

Capital Market Expectations, Portfolio optimization and risk management –Louis Finney

Section 2

Capital Market ExpectationsSection 2.1

34

Setting capital market assumptionsTwo sets of numbers: Risk and Return

Returns:

Time frame

Risk parameters

Standard deviation of returns

Correlation across asset classes

In theory, we could look at 'higher moments'

Skewness: whether returns have a higher tail to the upside or downside

– Negative skewness is similar to 'downside' risk

Kurtosis: how 'heavy' are the tails

This requires much advanced techniques and is very data intensive.

Covariance matrix

35

UBS calculates two sets of capital market returnsEquilibrium and Baseline

Equilibrium Returns:

Two interpretations:

– Pure equilibrium would imply pure fair value = market value for all asset classes

– Long run average: what the market will fluctuate around

Very useful in setting strategic asset allocations, doing very long run projections (20+ years)

– Important for modeling viability of pension and savings schemes

Baseline returns:

What we expect over the next 5 or 10 years

Dependent on current market pricing and how quickly markets revert to equilibrium values

UBS uses its market valuation tools (ValMod) to establish which markets look attractive on a forward looking basis

– Overlay with judgments about growth, inflation and path of convergence to equilibrium

36

It’s a matter of (time) perspectiveThree linked but different sets of asset class views: Equilibrium, Baseline and Tactical

Tactical views

Baseline expectations (the next 5–10 years)

Equilibrium expectations (an average over the next 40 or 50 years) Reflect our views for a

broad set of asset classes in a long-term, ideal equilibrium setting

Take equilibrium views and incorporate current market conditions with an intermediate time horizon

Set tactical asset allocation views in portfolios. Used to determine over- and under-weights around SAA.

US-I

37

Long run return and riskHistory

Over long time periods, we see a clear relationship between return and risk.

This relationship holds for US data going back 25 for more years.

The relationship is less tight outside the US. (Currency effects and the relative underperformance of non-US equities.)

Historic return and risk of US market from 1996 to 2020 (25 years)

FTSE

Russell Bloomberg-Barclays Indices 1-Mo Inflation

S&P 500 2500 US Cred US Treas US HY T-Bills CPI-U

Geometric Return 9.4 10.6 5.9 4.7 7.1 2.0 1.6

Arithmetic Return 10.2 11.9 5.9 4.7 7.3 2.0 2.0

Standard Deviation 15.3 18.9 5.2 4.3 8.8 0.6 1.3

Sharpe ratio 0.54 0.52 0.75 0.63 0.60 0.00

Source: Morningstar Direct. Analysis by UBS Asset Management

38

Two different quantitative approachesBalancing both demand-side and supply-side approaches to modelling risk/return expectations lead to a more robust foundation for SAAs

Demand-sideClassical approach

Investors demand ‘return premia’ for bearing risk

Determined by long-term historicalrisk premia, e.g. equity risk premium

Risk premia are time invariant but required returns influenced by starting values for interest rates and inflation

Supply-sideMore recent approach

Returns are supplied by the real economy

Determined by forward-looking factors that drive asset class returns such as projected economic growth rates, current interest rates, etc.

Equities explained by income, earnings growth and valuation changes.

Fixed income determined by starting conditions (yields, duration, etc and changes in yields.)

Two different approaches provide more insight to consider when estimating returns

US-I

Source: UBS Asset Management. For illustrative purpose only. A comparison of different supply- and demand-side approaches is summarized in Roger G. Ibbotson and Peng Chen (2003) "Long-Run Stock Returns: Participating in the Real Economy." Financial Analysts Journal, January/February. For ease of exposure, the analysis above excludes exchange rate adjustments as well as other adjustments we use in our methodology.

39

Example:Comparing supply and demand-side approach for US Equities

Source: UBS Asset Management. For illustrative purpose only. A comparison of different supply- and demand-side approaches is summarized in Roger G. Ibbotson and Peng Chen (2003) "Long-Run Stock Returns: Participating in the Real Economy." Financial Analysts Journal, January/February. For ease of exposure, the analysis above excludes exchange rate adjustments as well as other adjustments we use in our methodology.

US-I

Demand-sideBased on the investor’s required compensation for taking market risk

Supply-sideBased on the asset's capability to supply returns

Supply- and demand-side approaches to Equilibrium returns

Expected real cash 1.2%

+ Expected inflation 2.0%

+ Risk premium 4.2%

TOTAL 7.4%

Real earnings growth 2.3%

+ Expected inflation 2.0%

+ Dividend yield 1.9%

+ Buyback yield 1.0%

+ Δ Valuation 0.0%

+ Compound Effect 0.2%

TOTAL 7.4%

40

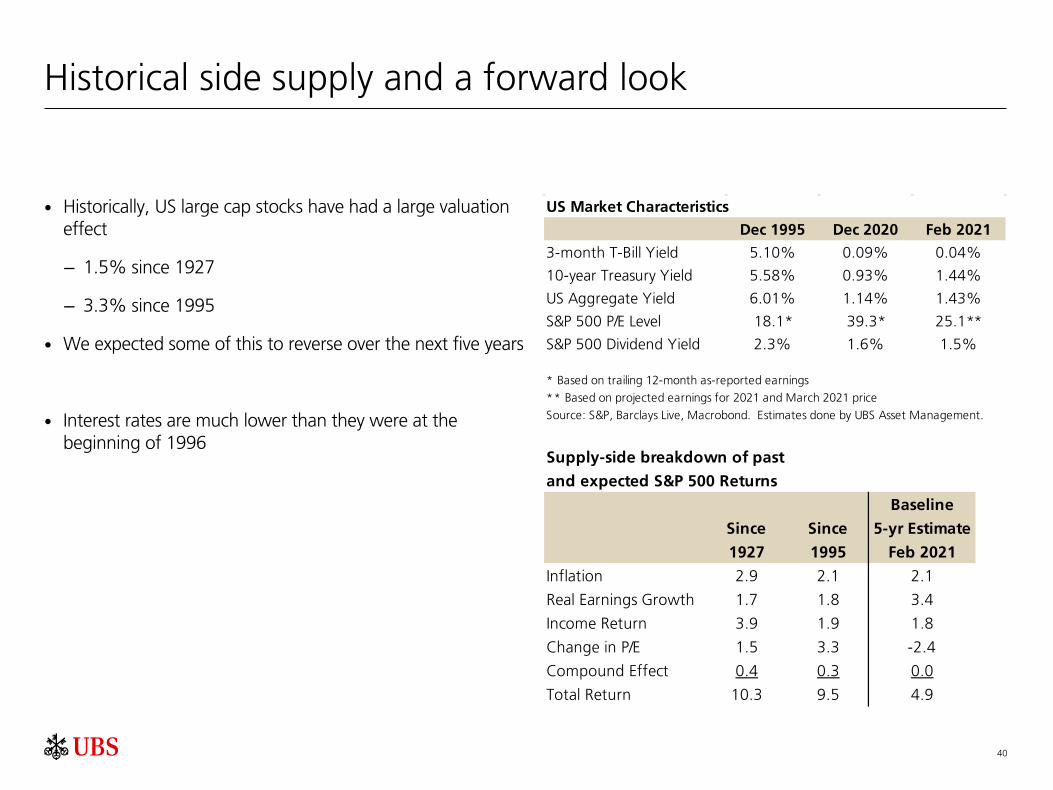

Historical side supply and a forward look

Historically, US large cap stocks have had a large valuation effect

– 1.5% since 1927

– 3.3% since 1995

We expected some of this to reverse over the next five years

Interest rates are much lower than they were at the beginning of 1996

US Market Characteristics

Dec 1995 Dec 2020 Feb 2021

3-month T-Bill Yield 5.10% 0.09% 0.04%

10-year Treasury Yield 5.58% 0.93% 1.44%

US Aggregate Yield 6.01% 1.14% 1.43%

S&P 500 P/E Level 18.1* 39.3* 25.1**

S&P 500 Dividend Yield 2.3% 1.6% 1.5%

* Based on trailing 12-month as-reported earnings

** Based on projected earnings for 2021 and March 2021 price

Source: S&P, Barclays Live, Macrobond. Estimates done by UBS Asset Management.

Supply-side breakdown of past

and expected S&P 500 Returns

Baseline

Since Since 5-yr Estimate

1927 1995 Feb 2021

Inflation 2.9 2.1 2.1

Real Earnings Growth 1.7 1.8 3.4

Income Return 3.9 1.9 1.8

Change in P/E 1.5 3.3 -2.4

Compound Effect 0.4 0.3 0.0

Total Return 10.3 9.5 4.9

41

Setting fixed income returnsStarting yields are good estimate

Adjust for:

Path of interest rates

– Use duration and convexity

Defaults effects

Inflation (for ILBs)

Income variability (prepayment, extension risk)

The closer the duration of the index is to the time horizon, the better the estimate:

For IG, you return very close to the starting yield over the duration horizon.

Expected Baseline Returns

February 2020

Yield-to-

Worst Duration 5-yr 10-yr

US Aggregate 1.4% 6.6 0.5% 1.3%

US 1-3 yr Treasury 0.2% 2.0 0.2% 0.5%

US 10+ yr Treasury 2.0% 18.9 -0.5% 0.8%

Source: Barclays Live. Analysis by UBS Asset Management

Expected Returns

42

Estimating risk from a top-down approach

Use a factor model to build consistent approach

Our group uses seven factors: growth, inflation, volatility, credit spreads, yield curve level, yield curve slope and illiquidity

Determine F1, the factor weighting matrix (also interpreted as a type of beta exposures) and set additional idiosyncratic risks 𝜎𝜎1𝑖𝑖 for each asset class

– Derive 𝐷𝐷1 the idiosyncratic covariance matrix from the 𝜎𝜎1𝑖𝑖's

Covariance matrix for these asset classes becomes:

Ω1 = 𝐹𝐹1′� Ω𝑓𝑓 � 𝐹𝐹1 + 𝐷𝐷1

The essential process can be repeated for additional levels of asset classes and complexity. From a relatively small set of assumptions, we can derive volatility and correlation for hundreds of asset classes.

Many practitioners just use historic data. (This means they are dependent on the historic regime.)

43

Demand side: applying the Black-Litterman process

Once the risk covariance for asset classes is formed, we can apply the Black-Litterman formula for determining equilibrium risk premium is:

𝑅𝑅𝑅𝑅 =𝑆𝑆𝑅𝑅𝑀𝑀𝜎𝜎𝑀𝑀

� Ω � 𝑊𝑊𝑀𝑀

where 𝑆𝑆𝑅𝑅𝑀𝑀 is the market Sharpe Ratio (a scalar), typically set between 0.25 and 0.5.

𝜎𝜎𝑀𝑀 is the market standard deviation (a scalar)

Ω is the covariance matrix for the market (assume N asset classes, so this matrix is NxN

𝑊𝑊𝑀𝑀 is the vector of market weights (nx1 array).

UBS's 2018 Equilibrium Covariance Matrix consists of 94 market asset classes (equities, fixed income and alternatives), 15 currencies, 4 commodity categories, 11 hedge fund categories, and cash (total of 125 asset classes).

Market weights are collected from a variety of sources: index providers (MSCI, Citigroup, JP Morgan, Bloomberg, S&P), Prequin). To smooth the weights, we use trailing 5-year averages.

44

Correlation

Most risk assets have some correlation with each other

Correlation and volatility spike in stress events: diversification benefits appear low

Most alternatives have correlation with risk, too.

Stock-bond correlation is quite variable

Currently in a negative correlation regime, but this could change if inflation takes off

This has kept volatility low on a total portfolio basis for portfolios with significant bond allocations

It may be a reason interest rates are low: the covariance property requites a low-risk premium for stocks and bonds. This is priced into both markets

45

A brief note on currencies

We add both hedged and unhedged currency factors to asset classes.

Cash differentials determine hedging costs/gains

We use a purchasing power parity approach to determine currency mispricing and then overlay a reversion to fair value

– This path also adjusts for inflation differentials

Currency perspective is important. Currency correlations with asset classes can vary widely across the countries.

– From US and Euro perspective, asset class returns are in general uncorrelated with domestic and foreign returns. Thus, hedging will reduce risk.

– However, for some countries—typically small countries with commodity exposure—foreign returns are negative correlated with currency returns.

– Thus, hedging will increase risk! Optimal strategy is not to hedge.

– Examples: Australia, Thailand

OptimizationSection 2.2

47

Types of optimization

Basic approaches:

Mean-variance optimization: maximize expected return at different levels of risk

Semi-variance: maximize expected return, but at different levels of downside variance

Conditional value-at-risk (Cvar): maximize expected return at different levels of downside tail events

– If a normal distribution, Cvar estimation will provide the same portfolios as mean-variance optimization. No additional insight is provided.

– Ideally, we would combine variance with skewness and kurtosis. But this is very demanding in setting assumptions (i.e.- lots more of them).

Run multiple frontiers:

Resampled frontier

Robust optimization

Other SAA techniques.

Stochastic modeling

Deterministic scenario analysis

Historic returns

48

Mean-variance modelling and optimization

Strengths

Math is well-understood. Economic foundation is solid.

Excellent first-order estimate of risk and return.

Demonstrates the advantages of diversification

Can be extended in many ways:

– Currency and currency hedging can be accommodated.

– Leverage and shorting: return and risk implications are very accurate

– Alpha and tracking error: active management is overlay on existing asset classes.

– Asset-liability management: liabilities are a negative asset class.

Consistent covariance matrix can be constructed with simple factor models

Weaknesses

Optimization can be very sensitive to inputs

Returns are assumed to be normally or log-normally distributed

– Tail events occur far more often than predicted by these distributions

No accommodation of serial correlation. This is a problem for cash assets and some alternatives

Assumption of rebalancing for each period

– Not possible with illiquid assets

Stationarity of distribution

Does not apply to option based strategies. These incorporate huge skewness and kurtosis effects.

Does not explicitly include cash flows

Mean-variance optimization (MVO) was proposed in the 1950s.

It is still the workhorse of SAA modeling.

US-I

Source: UBS Asset Management. For illustrative purpose only. A comparison of different supply- and demand-side approaches is summarized in Roger G. Ibbotson and Peng Chen (2003) "Long-Run Stock Returns: Participating in the Real Economy." Financial Analysts Journal, January/February. For ease of exposure, the analysis above excludes exchange rate adjustments as well as other adjustments we use in our methodology.

49

Mean-variance efficient frontierNominal equilibrium terms

Maximize the expected arithmetic return at each level of risk (equivalent to minimize risk for a given level of arithmetic return.

In practice, constraints are common

– Liquidity, regulatory, risk preference

– Relative constraints: e.g., small cap stocks cannot be over-weighted relative to market by 10%

The current portfolios for this client look very close to efficient in long run terms. Also notice how 'balanced' the portfolio look across the efficient frontier. All the asset classes appear on the efficient frontier at some point.

50

Mean-variance efficient frontierReal 5-yr Baseline terms

Now, we adjust for inflation and use our 5-yr Baseline assumptions.

From this perspective, the portfolios don't look so efficient.

– Tilt heavily away from fixed income and into cash

– But bonds still play an important roll in downside protection, even under current conditions of low yields.

51

Geometric and arithmetic returns

The geometric return is the compound return over time. It can be thought of as the median return (50% above and 50% below).

The arithmetic return is the average return in any one time period.

Simple example. You start with $1. In year 1, it doubles to $2; the return is 100%. In year 2, it drops by half, so back down to $1; the return is -50%. In this case the geometric return over two years is (1/1)^(1/2)-1 = 0%. The arithmetic return is (100% + -50%)/2 = 25%

The approximation formula is:

𝑔𝑔 = 𝑎𝑎 − 𝜎𝜎2

2

The exact formula used is

𝑔𝑔 =1 + 𝑎𝑎

1 + 𝜎𝜎2(1 + 𝑎𝑎)2

− 1

– Note: the higher the standard deviation, the larger the 'drag' in converting from arithmetic to geometric terms.

– Example of simple formula: arithmetic return of 10%, standard deviation is 20%. The approximate geometric return is 0.10 – ((0.2)^2)/2 = 0.10 – 0.04/2 = 0.10 – 0.02 = 0.08 = 8.0%. The exact formula gives 8.23%.

The process is: analyze in arithmetic terms, use standard deviation to convert to geometric terms

52

Stochastic modelingAlso called Monte Carlo modeling

Can allow for more complicated analysis and richer analysis

– Regime switching (rotating between different economic scenarios)

– Conditional investment strategies (derisking and rerisking depending on market conditions and levels of wealth)

– Deals with serial correlation better

– Sophisticated models can include yields, inflation, credit spreads, wages as modeled variables

Very useful when cash flow are involved

– Projecting pension contribution over time

– Analyzing defined contribution plans with cash flow in during employment and cash flows out

Run thousands of trials (10,000 trial over 50 years for example)

Downsides:

– Very time-consuming

– Results are not as intuitive to interpret. Often we are looking a dispersion, so risk is defined as a 95th percentile result and return is a median wealth ratio, funded status or replacement ratio at a point in time

53

Deterministic economic scenarios

While stochastic modeling runs thousands of trial, just a few can demonstrate the range (especially in the over a one to five year time horizon).

We often use economic scenarios to better understand the up-side and down-side cases:

Typically we offer four scenarios. They all start with current conditions.

Baseline, using our models of valuation

Recession:

– Slumping equity markets

– Declining inflation and government bond yields

Stagflation

– Slumping equity markets

– Rising yields and rising inflation:

– Stock-bond correlation is positive

An upside scenario: Productivity Boost

– Moderate/low inflation with modest rise in yields

– Strong equity returns

54

Managing risk at the SAA level

SAA defines a benchmark for CIOs to implement and be monitored against. It is a top-down process.

Many dimensions to risk at the SAA level to consider:

Volatility, downside, liquidity

Direct factor exposures: currencies, duration, credit, equity beta

As important are:

Operational risk management

Bottom-up portfolio analysis: Model individual securities and aggregate to total portfolio

– Very valuable in assessing risk against a benchmark

– Typically done based on daily data over trailing periods (90 days to seven years)

– Thus, can be biased by recent experience

55

Summary

Historical data show clear trade-off in risk and return

However, the starting point is important. History does not necessary repeat in return and correlation.

– Low interest rates mean lower expected returns

– High equity valuations indicate lower expected returns

Modeling the risk parameters is more difficult

– Simple factor models can greatly ease computation burdens

– Volatility is relative stable: equity in mid-teens, bonds in mid-single digits, cash around 1.0%

– Extrapolate/interpolate as appropriate to other asset classes (via Black-Litterman process, mean-variance math of leverage and shorting, etc.)

Correlation is highly dependent on regime

– We are currently in a negative stock-bond regime, but from early 1960s to late 1990s (over 30 years) we had positive stock-bond correlation

56

Break

Integrating Alternatives and ESG into asset allocation frameworks – Michele Gambera, Louis Finney

Section 3

Integrating AlternativesSection 3.1

59

Size of the alternatives market

We estimate the size of the total investable capital markets to be USD 155 trillion.

Equities 43.1%

Fixed Income 42.6%

Alternatives 7.2%

Cash 7.1%

This doesn't count:

Gold

Hedge funds

Commodity funds

Dry powder in the private asset arena

60

Two broad categories of alternatives

Private assets/private capital

Private equity: buy-out, venture, growth funds

Private real estate

– Typically invested through open-end or closed end funds

– Use of leverage: core, value-added and opportunistic funds

Private credit

Infrastructure

Other: energy, timber, farmland

Liquid/semi-liquid strategies

Hedge funds

Commodity funds

Gold

Not considered here:

Systematic strategies: risk parity, smart beta, etc

Art

Crypto-currencies

61

Characteristics of the alternative markets

Most private assets: cash flow oriented as opposed to price/income oriented.

Many investments are closed-end funds.

Different set of metrics: IRR, DPI, Capitalization Rate, etc.

Risk very difficult to assess

– Volatility based off of appraised values is biased downward. Valuations are sometimes months late.

High degree of active management. Constant spending/staff to maintain exposure.

Turnover of managers.

Distributions from closed-end funds need to be constantly recycled. There is a cycle of commitments, capital calls and distributions to manage.

Many transactions are negotiated

Requires a quick decision-making structure:

– A major complaint within large funds is the ability to make decisions on deals within days. Boards must design a structure that allows billions of USD to invested each year.

It's not buy-and-hold, but buy-and-continuously recycle.

62

Historic returnsAlternatives

Private Equity:

Historic data show a 1.8% to 4.1% premium over public equities

This would indicate a return in the high single digits, not low teens as seen over last two decades

Private credit:

Historically, private credit IRRs by vintage year are about 70 bps about the high yield yield-to-worst

Probably coming down closer to high yield

63

Historic returnsAlternatives

Real estate

For unlevered property, returns are between stocks and bonds

As leveraged is increased, returns become equity like in terms of return and risk

Hedge funds

Like real estate, performance is between stocks and bonds

Portfolios of hedge funds can range from highly aggressive (with equity-like features) to highly risk controlled with low volatility and low correlation to equities.

64

Setting returnsAlternatives

Private Equity: Historic data show a 2.0% to 3.0% premium over public equities This would indicate a premium in the high single digits, not low teens as seen over last two decades

Private credit: Historically, private credit IRRs by vintage year are about 70 bps about the high yield yield-to-worst Probably coming down closer to high yield

Real estate: On unlevered basis, treated between stocks and bonds Leverage increases returns, but increases risks as well Highly levered funds (Opportunistic, Value-added) approach equity like returns and risk

Infrastructure Difficult asset class to get a handle on Very long duration in cash flows: 10+ years

Hedge funds Typically modeled versus cash, but with an equity beta added (about 0.25 beta historically) Can vary widely, but well-constructed portfolios can achieve bond-like returns and bond-volatility but with low

correlation to other asset classes

65

Economic Risk and Appraised Volatiilty

Most alternatives have NAVs for funds, but few to no market transactions.

The appraised volatility underestimates actual risk.

Various methods can infer some higher volatilities.

For private equity, we use basic economic theory to determine the return and risks.

Private equity overall has a beta of 1.7

Summary Statistics: 1Q 1994-1Q2020

Private Real Hedge 10-yr S&P

Equity Estate Funds Commod T-Bills Treas 500

Estimates based on quarterly returns

Geometric Return 13.7 9.2 4.3 1.2 2.3 5.4 8.9

Arithmetic Return 13.6 8.9 4.5 2.7 2.3 5.6 9.9

Standard Deviation 10.1 4.1 7.0 16.7 1.0 8.2 16.1

Quarterly Serial Correlation 0.35 0.85 0.19 0.16 0.98 -0.01 0.01

Equity correlation 0.77 0.20 0.72 0.30 0.03 -0.48 1.00

Equity beta 0.48 0.05 0.31 0.31 0.00 -0.24 1.00

Skew -0.6 -2.9 -0.7 -0.9 0.3 0.7 -0.7

Kurtosis 2.4 11.8 3.2 2.0 -1.5 0.7 0.7

Estimates based on annual returns

Standard Deviation 14.8 7.5 8.3 18.0 2.0 7.2 17.3

Annual Serial Correlation 0.20 0.35 -0.12 -0.01 0.85 -0.21 0.20

Equity Correlation 0.80 0.28 0.65 0.29 0.10 -0.34 1.00

Equity Beta 0.68 0.13 0.31 0.29 0.01 -0.14 1.00

Skew -0.7 -2.4 -0.1 -0.4 0.3 0.0 -0.7

Data Private Equity Cambridge Associates US Private Equity

Real Estate NCREIF Property

Hedge Funds HFRI Fund of Funds Composite USD

Commod Bloomberg Commodity TR USD

T-Bills FTSE Treasury Bill 1 Mon USD

10-yr Treasury BBgBarc US Trsy Bellwethers 10Y TR USD

S&P 500 S&P 500 TR USD

66

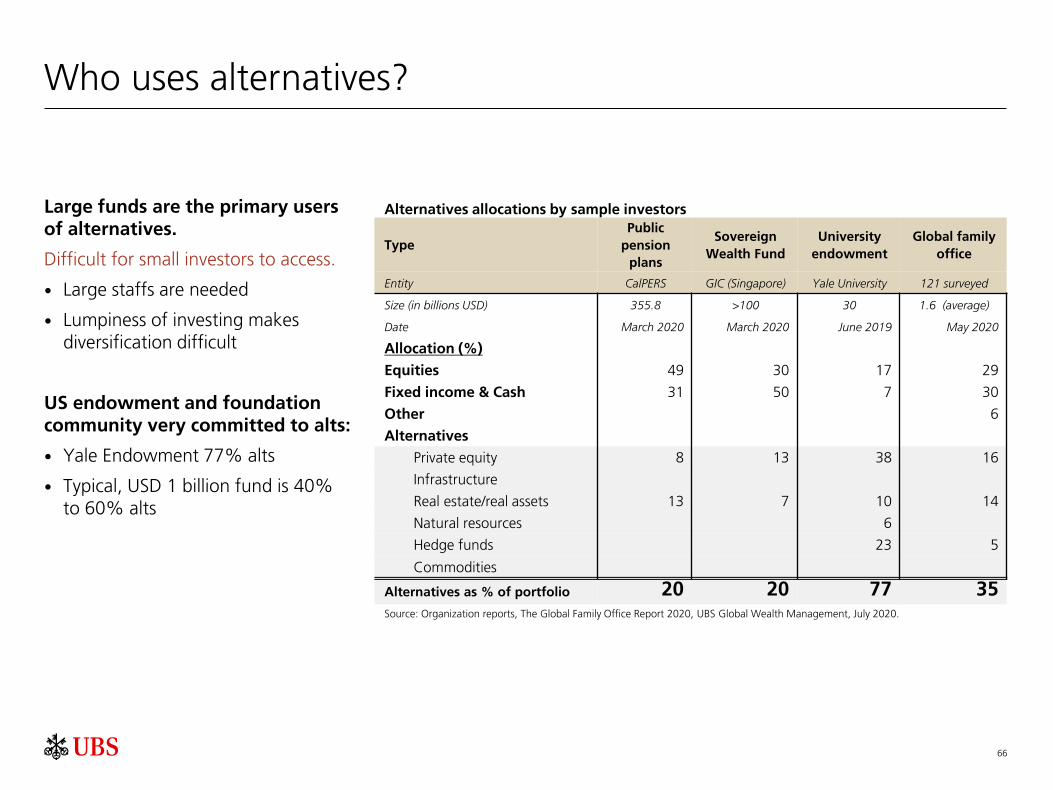

Who uses alternatives?

Large funds are the primary users of alternatives.

Difficult for small investors to access.

Large staffs are needed

Lumpiness of investing makes diversification difficult

US endowment and foundation community very committed to alts:

Yale Endowment 77% alts

Typical, USD 1 billion fund is 40% to 60% alts

Alternatives allocations by sample investors

TypePublic

pension plans

Sovereign Wealth Fund

University endowment

Global family office

Entity CalPERS GIC (Singapore) Yale University 121 surveyed

Size (in billions USD) 355.8 >100 30 1.6 (average)

Date March 2020 March 2020 June 2019 May 2020

Allocation (%)

Equities 49 30 17 29

Fixed income & Cash 31 50 7 30

Other 6

Alternatives

Private equity 8 13 38 16

Infrastructure

Real estate/real assets 13 7 10 14

Natural resources 6

Hedge funds 23 5

Commodities

Alternatives as % of portfolio 20 20 77 35Source: Organization reports, The Global Family Office Report 2020, UBS Global Wealth Management, July 2020.

67

Return and Risks of Portfolios

Alternatives can improve the return of portfolio, but offer more in diversification.

Note the higher Sharpe ratios for these portfolios over the 60/40 portfolio.

Appraised volatility makes these appear even more attractive, but this is misleading.

Endowments and foundations have run into liquidity crunches.

– Harvard in the GFC

– Several foundations procured loans in 2020 to avoid liquidity issues

Prospective 5-year Performance in USD Terms

September 2020

Public Sovereign Global

Pension Wealth University Family Standard

Plan Fund Endowment Office 60/40

5-yr Expected Geometric Return 5.3% 4.7% 7.2% 5.3% 4.5%

Economic Risk 11.3% 10.0% 14.1% 10.3% 10.5%

Sharpe Ratio 0.50 0.49 0.56 0.54 0.46

Appraised Volatility 10.0% 8.6% 9.9% 8.3% 10.5%

68

Summary

We see more and more acceptance of alternatives.

– Large efforts to figure out ways to bring them to the retail level

– The do offer substantial diversification benefits

Tremendous innovation in the field.

Returns should be lower, but returns are lower in the public markets, too.

Requires dedicated efforts to build portfolios:

– Either pay up in building staff expertise or in higher management fees

69

Assumptions

Return and risk assumptions: USD Terms

September 2020

5-yr

Expected Economic Appraised

Asset Class Return Risk Volatility

USD Cash 0.3% 1.3%

Intermediate Global IG Fixed Income 0.4% 2.6%

Global Investment Grade Fixed Income 0.0% 5.5%

Global Equities Unhedged 7.2% 16.0%

Global High Yield Hedged 3.0% 10.5%

Global Private Equity Unhedged 9.5% 24.5% 15.0%

Global Infrastructure (Equity) Unhedged 6.2% 14.0% 8.0%

Global Core Real Estate Unhedged 6.2% 12.6% 7.2%

Hedge Funds (Hedged) 4.0% 4.3%

Note: Expected returns are geometrc. We develop 5-year expected returns in the capital markets

based on current market markets and our expectations of inflation, growth and the path of interest

rates. We then overlay our assessment of fair value and the reversion and how quickly the market will

react. From here we extrapolate to the different sectors of the capital markets.

Global Equity, Private Equity, Infrastructure, and Core Real Estate are assumed to be unhedged. Cash,

fixed income and hedge funds are assumed to be hedged.

Integrating ESGSection 3.2

71

The Evolution of SustainabilityTraditional approach: Value-based Investing

From plain exclusion to overweighting good actors

Limited negative screening

Positive screening with multiple dimensions

– Environment

– Social issues

– Governance

Typical client: anyone

Modern approach: ESG

Negative screening (exclusion)

Focus on excluding "sin stocks"

– Tobacco

– Gambling

– Alcohol

Typical client: religious groups

72

The definition of ESG

Environment Pollution, global warming and use of sustainable practices

Social Responsibility

Diversity in the workforce, human rights and attention to work conditions including subcontractors

Governance Structure of the company and compensation levels, rights of shareholders and transparency

Together, these concepts incorporate the sustainability approach to investing

73

Engagement

Engagement is a special feature of ESG investing

Asset management firms are more active in encouraging firms to adhere to higher ESG standards and increase disclosure

This is unusual as traditionally asset management firms have been either voting with management or following consultant advice

UBS is part of the United Nations PRI initiative that helps investors and asset managers collaborate in engagements with firms

74

Impact Investing

Impact investing is a type of ESG investing

Objective is to help firms that are making a difference by doing business with underserved people or improving the environment

The function is not to maximize profits

Profits are not excluded but are a secondary objective

Impact investing is beyond the scope of this presentation

75

Is there a trade-off when using an ESG approach?

ProFocus on ESG may reduce negative skewness due to environmental damages or accounting scandals

ConNegative screening may reduce diversification and exclude profitable companies in fields such as tobacco or oil

PuzzleIf everyone prefers ESG, will I be able to buy sin stocks for a P/E of 1?

76

Is there an ESG factor, such as value or small cap?

No evidence of a priced ESG factor similar to, say, the Fama-French factors

Some evidence that top ESG grades are earned by mega-caps, quality firms. So there might be size and quality factor exposures while more firms disclose ESG variables

The most widely-used ESG indexes however are factor-neutral with respect to the equivalent traditional indexes

77

Academic findings

Most sustainable investors think only of E not S or G

Companies producing more carbon emissions have higher cost of capital

Stock prices outperform for firms that recently had a successful ESG engagement“ “ “

Hartzmark and Sussman2018

Bolton and Kacperczyk2019

Dimson, Karakas and Li2016

78

More academic findings

Philip Morris outpaced the S&P 500 by almost 9% a year in 1957—2003 (Sears, too, outperformed!)

[exclusion] ESG funds lag their traditional counterparts

ESG decreases value with simple exclusion, but increases it with positive ESG screening“ “ “

Siegel and Schwartz 2006

Renneboog, Ter Horst and Zhang 2008

Barnett and Salomon 2006

79

Is governance new?

Board of directors' quality is not a novel measure of corporate value

Many investment books, starting from Berle and Means (1932) and Graham and Dodd (1933), see management incentives as a key part of security analysis

Think of theory of the firm (e.g. Coase, Williamson, Marris) that started in the 1960’s, spelling out conflicts of interest between managers and shareholders

80

Does ESG Work?Sustainability and the client's interests

In theory

Pedersen, Fitzgibbons and Pomorski (2019): in a model with three types of investors (low/medium/high ESG enthusiasm), an abundance of ESG enthusiasts will lead “sin stocks” to outperform in the long run

Pastor, Stambaugh and Taylor (2020): a preference for sustainability will increase the ESG impact on firms because it will motivate firms to be better sustainability actors

In practice

Dunn, Fitzgibbons and Pomorski (2018): bottom ranked stocks (for ESG scores) have materially higher volatility during the 8 years examined

Auer and Schuhmacher (2016): in ESG ratings from Sustainalytics (2004–2012), companies with high ESG ratings provided superior risk-adjusted performance

81

Simple exclusion example (1/2)

Using world indexes, we see that both tobacco and oil & gas have similar risk and return to the aggregate

Individual companies may have huge runs, as seen in the US example above

Whole sample (1973–2020) S&P 500 Exxon Mobil AltriaArithmetic average 11.8% 12.8% 20.0%Geometric average 10.3% 10.9% 15.9%Standard deviation 16.7% 18.7% 27.3%Skewness -0.57 -0.81 0.14Kurtosis 0.94 3.05 1.31Min -25.2% -44.8% -33.6%Quartile 1 -1.5% -2.6% -4.2%Median 3.3% 3.4% 5.2%Quartile 3 8.0% 9.4% 13.3%Max 23.0% 26.9% 53.9%Observation # 190 190 190

Source: UBS AM. For illustrative purposes only.

82

Simple exclusion example (2/2)

The more we try to neutralize factor exposure, the more even the effect of negative screening fades

More modern positive screening approaches give about the same returns for traditional and ESG

Source: UBS AM. For illustrative purposes only.

2011-2020 S&P 500 S&P 500 ESGSimple

ExclusionFactor-Neutral

ExclusionArithmetic average 15.1% 15.3% 15.7% 15.6%Geometric average 13.9% 14.1% 14.5% 14.4%Standard deviation 16.7% 16.4% 16.5% 16.6%Skewness -0.98 -0.87 -0.96 -0.99Kurtosis 2.40 2.26 2.34 2.43Min -19.6% -18.60% -18.90% -19.1%Quartile 1 1.0% 1.1% 1.1% 1.1%Median 4.1% 4.3% 4.3% 4.4%Quartile 3 7.5% 7.5% 7.7% 7.7%Max 20.50% 21.2% 20.5% 20.5%Observation # 40 40 40 40Sharpe Ratio 0.87 0.89 0.91 0.90

83

Performance in Moments of Stress

March-April 2020

Conservative portfolio (30% global equity, 70% bonds), no rebalance

Traditional and ESG portfolio have the same returns

Same for 60/40 portfolio

$8,700.00

$8,900.00

$9,100.00

$9,300.00

$9,500.00

$9,700.00

$9,900.00

$10,100.00

18-Feb-20 03-Mar-20 17-Mar-20 31-Mar-20 14-Apr-20

30/70 esg no reb 30/70 trad no reb

84

Is there a trade-off in long-term risk-adjusted performance?Long-term expectations

A modern, multi-dimensional approach to sustainability (that is, not simply based on bare-bones exclusion) has no negative effects on investment performance

Therefore, as far as we can see, there is no trade off over the long term

Traditional and ESG portfolio can use the same capital market expectations

We saw in the previous page that performance is close even during times of stress

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0% 5% 10% 15% 20% 25% 30%

Exce

ss R

etur

n

Standard Deviation

Base Case Conventional ESG Long Term

85

A trade-off in medium-term risk-adjusted performance?A possible reward for early adopters

The interest in ESG among retail and institutional investors has been growing steadily

It is possible that over the next 5–10 years, as more interest arises, highly-rated ESG names may be bid up due to scarcity

In this case, early ESG adopter will gain

Over the long term, more firms will adopt sound ESG practices and improve disclosure, so this outperformance will not last forever

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0% 5% 10% 15% 20% 25% 30%

Exce

ss R

etur

n

Standard Deviation

Base Case Conventional ESG Short Term

86

A trade-off in the preference levelConventional vs. high ESG preferences

Conventional ESG benchmarks are geared towards delivering high ESG ratings with low tracking error from traditional benchmarks

However, an investor with very strong ESG preferences may exclude a large amount of names and incur high risk, underperformance

Think for example of excluding all firms that are not carbon-neutral

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0% 5% 10% 15% 20% 25% 30%

Exce

ss R

etur

n

Standard Deviation

Base Case Very Strong ESG

87

Special case: Loss-averse clients

We could use mean-CVaR optimization for clients that cannot bear losses

It is possible that firms with high ESG rating, by having good governance and low risk of environmental or social liabilities, may have a better "left tail" in the return distribution

If ESG portfolios have better left-tail characteristics, approaches like Rockafellar and Uryasev (2001) would prefer them

That approach uses historical returns for higher moments and VaR estimation

88

Security Selection

Intuitive suggestion: portfolio managers can provide better security selection if they know more about the likelihood of future legal and reputational liabilities from ESG violations

Possibility of rating arbitrage adding to alpha

We do not have enough data to support this finding, but it seems reasonable

89

Conclusion

ESG does not appear to affect risk-adjusted portfolio performance over the medium and long term

Asset allocations for traditional and ESG portfolios can be computed using the same capital market expectations

It is reasonable to expect highly-rated ESG firms to outperform as the world evolves towards sustainability

It is possible that ESG disclosures help active portfolio managers in security selection

We don't have enough data and will have a clearer view in the future

For illustration purposes only.The chart is not to scale and is intended to exaggerate the point for ease of exposition.

Sample Portfolios, Capital Market Expectations and Advisory Services to Sovereign –Mohammad Ahmad, Massimiliano Castelli

Section 4

91

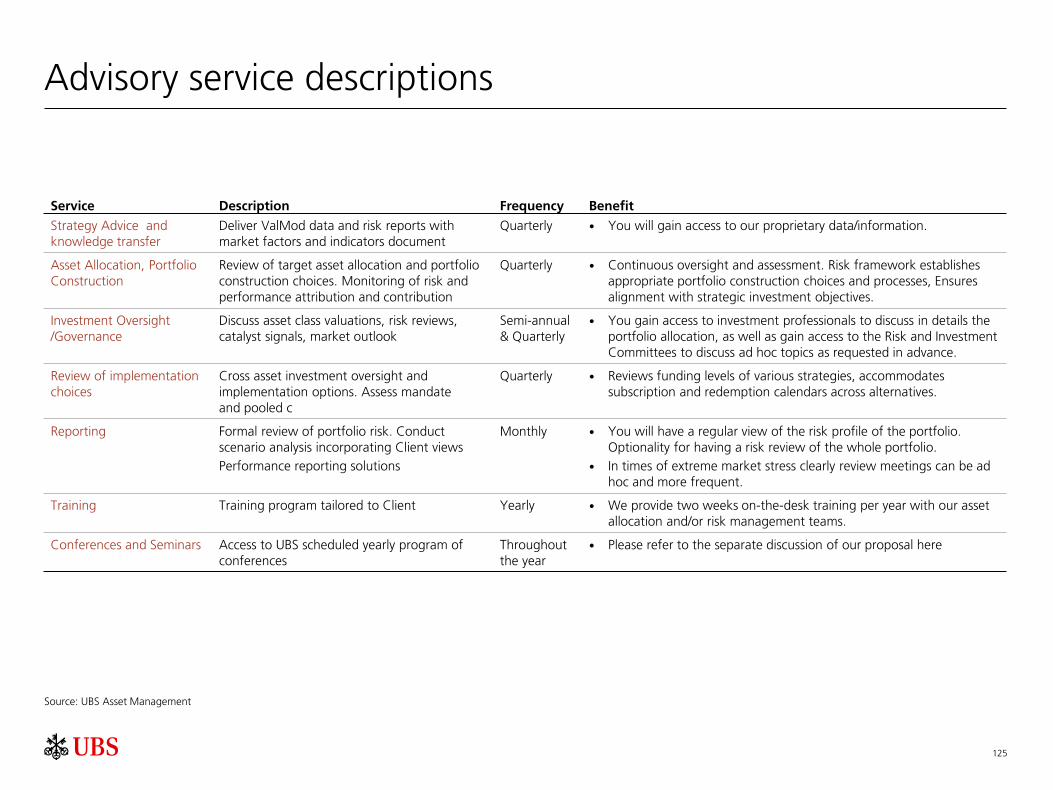

Advisory service descriptions

Service Description Frequency Benefit

Strategy Advice and knowledge transfer

Deliver ValMod data and risk reports with market factors and indicators document

Quarterly You will gain access to our proprietary data/information.

Asset Allocation, Portfolio Construction

Review of target asset allocation and portfolio construction choices. Monitoring of risk and performance attribution and contribution

Quarterly Continuous oversight and assessment. Risk framework establishes appropriate portfolio construction choices and processes, Ensures alignment with strategic investment objectives.

Investment Oversight /Governance

Discuss asset class valuations, risk reviews, catalyst signals, market outlook

Semi-annual & Quarterly

You gain access to investment professionals to discuss in details the portfolio allocation, as well as gain access to the Risk and Investment Committees to discuss ad hoc topics as requested in advance.

Review of implementation choices

Cross asset investment oversight and implementation options. Assess mandate and pooled c

Quarterly Reviews funding levels of various strategies, accommodates subscription and redemption calendars across alternatives.

Reporting Formal review of portfolio risk. Conduct scenario analysis incorporating Client viewsPerformance reporting solutions

Monthly You will have a regular view of the risk profile of the portfolio. Optionality for having a risk review of the whole portfolio.

In times of extreme market stress clearly review meetings can be ad hoc and more frequent.

Training Training program tailored to Client Yearly We provide two weeks on-the-desk training per year with our asset allocation and/or risk management teams.

Conferences and Seminars Access to UBS scheduled yearly program of conferences

Throughout the year

Please refer to the separate discussion of our proposal here

Source: UBS Asset Management

Sovereign Sample Portfolios, Capital Market Expectations and Performance Monitoring

Section 4.1

93

Different setups for different objectivesWhen selecting the most suitable setup, the efficient frontiers differ based on constraints of each type of portfolio.

Risk vs. SDR cash basket1

Source IMF. Note: For illustrative purposes only. Current SDR mix is USD 41.73%, EUR 30.93%, CNY 10.92%, JPY 8.33%, GBP 8.09%1 SDR: Special Drawing Right currency basket is used as a proxy for the central bank risk free asset. This differs for each central bank

Risk

Pre

miu

m

Efficient frontiers

Stabilization PF

Savings PF

Reserve PF

94

Sovereign Portfolios: Different portfolios with different goalsLiquidity and investment tranche separation

Source: UBS AM. For illustrative purposes only.

CB Working CapitalObjective

• Liquidity management for market operations

Key considerations

• Preservation of capital and liquidity

• Currency mix/reference

• Import Coverage (3-6 months)

• Short term external debt coverage (100%)

Stabilization portfolioObjective

• Offset oil price movements to fill gap in revenues to fund public expenditure

Key considerations

• Preservation of capital and liquidity

• Precaution/buffer during national emergencies

• Explicit/implicit liabilities

• Diversify natural/structural endowment

Savings portfolioObjective

• Accumulate wealth for future generations

• Managing inflation impact

Key considerations

• Maximise (risk-adjusted) returns over longer time horizons

• Exploit illiquidity premium

• Return above relevant inflation target (reflecting import structure)

Liquidity Tranche Investment Tranche

95

Sample Portfolios (1) – Liquid Portfolios Sample portfolios have different levels of risk tolerance and diversification

Source: UBS AM. For illustrative purposes only.

Liquidity Fixed Income DiversificationEquity

DiversificationEquity and more

EMDMost liquid – CB working

capital managementDiversification across fixed income to improve risk-adjusted returns

Liquid equity to boost risk-adjusted returns

Equity and EMD to boostrisk-adjusted returns

CB1 CB2 CB3 CB4 CB5

Liquidity Cash 50 10 10 10 10

GGB 1 – 3 50 50 30 30 25

Division GGB 10 10 10 10

Spread Supranationals 10 10 8 5

Corporates 10 10 8 5

Securitised 10 10 8 5

Inflation hedge TIPS 10 8 5

Risk premium EMD 10 3 15

Equities 15 20

10

30

1088

8

8

81010

30

101010

10

1010

50

1010

10

1010

5050

10

25

10555

5

15

20

96

Sample Portfolios (2) – Stabilization FundsMajority of assets invested into liquid and high-grade government bonds but longer duration to boost returns and also investing in equity and real estate

Liquidity + Equity + Equity and RE50% in liquid GGB 1 – 3;

GGB/Corporates to boost returnsEquity to boost risk –

adjusted returnsEquity + RE to boost risk –

adjusted returns

Stab1 Stab2 Stab3

Liquidity GCB 1 – 3 50 45 40 Investment grade

Division GGB 40 35 35

Spread Corporates 10 10 10

Risk premium Equities 10 10

Real Estate 5

40

35

10

105

45

35

1010

5040

10 0

Source: UBS AM. For illustrative purposes only.

97

Sample Portfolios (3) – Saving FundsHigh risk tolerance but implementation can differ in terms of allocation to illiquid asset classes

Listed liquid Assets + AlternativesLarge allocation to illiquid assets

Norwegian model majority of assets in liquid public markets

Equity to boost risk –adjusted returns

Endowment modelLarge allocation to alternatives

Sav1 Sav2 Sav3

Duration GGB 22.5 22.5 15 Investment grade

Spread Corporates 10 10

Risk premium EMD 2.5 2.5

Equities 60 40 35

Real Estate 5 12 10

Private Equity 13 20

Hedge Funds 10

Infrastructure 5

Commodity 5

15

35

10

20

105 5

22.5

102.5

40

12

1322.5

102.560

5

Source: UBS AM. For illustrative purposes only.

98

Asset classes: high returns in fixed incomeIn risk-adjusted terms, fixed income assets performed strongly

Historical Returns and Standard Deviation, 2002 – 2021YTD

Source: UBS AM. Please note that past performance is not a guide to the future. Data as of end of February 2021.Note: Data for Private Equity and Real Estate for 2003 – 3Q 2020.

Sharpe Ratios, 2002 – 2021YTD

1.1

1.0

0.8

0.7

0.7

0.7

0.6

0.6

0.5

0.5

0.3

0.3

0.3

0.2

0.0

-0.1

-0.5 0.0 0.5 1.0 1.5

Securitised

Supra

EMD

Corp

GGB

GGB 1 3

TIPS

Hedge Funds

Real Estate

Private Equity

EMD Local

Global Equity

Infrastructure

EM Equity

Cash

Commodity

Cash

HF

GGBTIPSSupra

Securitized

EMD

EMDlocal

Global EQ

EM EQ

RE

Corporates

Infra

Commodities

PE

GGB 1-3

-2%

0%

2%

4%

6%

8%

10%

12%

14%

0% 5% 10% 15% 20% 25%

99

Diversification to improve returns (1)Diversification across fixed income and equity provided a substantial increase in returns while keeping risk/return relationships relatively stable

Historical Returns and Standard Deviation, 2002 – 2021YTD

Source: UBS AM. Please note that past performance is not a guide to the future. Data as of end of February 2021.

Return/Risk, 2002 – 2021YTD

3.0

1.7

1.5

1.5

0.0 1.0 2.0 3.0 4.0

CB1

CB2

CB3

CB4

CB1

CB2

CB3

CB4

0%

1%

2%

3%

4%

5%

6%

0% 1% 2% 3% 4% 5%

Retu

rns

Standard deviation

Worst 12 months, 2002 – 2021YTD

Higher returns

Less risk

0.2%

-1.1%

-1.9%

-7.5%

-10.0% -5.0% 0.0% 5.0%

CB1

CB2

CB3

CB4

15% EQ

100

Diversification to improve returns (2)Based on historical analysis, diversified portfolios provided higher returns; diversification into alternatives boosted returns in saving portfolios

Source: UBS AM. Please note that past performance is not a guide to the future. Data as of end of February 2021.

Historical Returns and Standard Deviation, 2002 – 2021YTD

GGB

Stab1

Stab2

Stab3

40/60

Sav1

Sav2

Sav3

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0% 2% 4% 6% 8% 10% 12% 14%

Retu

rns

Standard deviation

Returns, 2002 – 2021YTD

9.1%

8.8%

7.8%

5.8%

4.4%

4.0%

3.5%

4.4%

0.0% 5.0% 10.0%

Sav3

Sav2

Sav1

40/60 portfolio

Stab3

Stab2

Stab1

GGB

50% Alt

25% Alt

5% Alt

101

Central Bank portfolios: Recent market performance

Sample central bank portfolios tracking model output

Source: UBS AM model based on publicly available information, using broad indices and funds to replicate CBs and SWF portfolios.For illustrative purposes only. Please see appendix for more information on portfolios. Please note that past performance is not a guide to the future.

CB1 CB2 CB3 CB42021 January 0.01% -0.13% -0.33% -0.38%2021 February -0.05% -0.62% -1.09% -0.41%

Performance 2021 YTD -0.04% -0.75% -1.42% -0.79%Performance 2020 1.52% 4.28% 5.14% 6.81%

Performance 2019 2.76% 5.56% 7.10% 9.33%

Performance 2018 2.00% 1.04% 0.46% -0.47%

Performance 2017 0.90% 2.00% 3.07% 5.22%

Performance 2016 0.91% 2.29% 3.34% 3.50%

Performance 2015 0.51% 0.31% 0.39% 0.29%

Performance 2014 0.46% 2.84% 4.13% 3.89%

Performance 2013 0.29% -1.06% -1.86% 2.38%

Performance 2012 0.52% 3.10% 4.96% 5.63%

Performance 2011 0.95% 4.08% 5.41% 3.52%

Performance 2010 1.23% 3.60% 4.94% 5.61%

Performance 2009 1.19% 4.76% 7.04% 8.80%

Performance 2008 4.91% 4.19% 2.95% -3.70%

Performance 2007 6.03% 6.67% 6.70% 7.12%

Performance 2006 4.58% 3.80% 4.26% 6.23%

While portfolios that included spread products or equities suffered during the Coronavirus crisis, they more than offset these losses in the dramatic rally in risk assets that started in April 2020.

CB sample portfolio performance (indexed, 31.12.2015 = 100)

102

Post-COVID 19 Economic ScenariosUncertainties over the way out of the Coronavirus crisis and the fate of the global economy remain high

Source: UBS AM as of 3Q 2020. This does not constitute a guarantee by UBS AG, Asset Management.

Growth & Productivity upside (10%)Economic growth and productivity picks up significantly; secular P/E ratio rise to reflect lower risk premium

Inflation (US) at constant 1.8%

US T-Bills reaching 3.0% in five years

US 10-year yields rising to 3.8% in five years

Equities (S&P 500) with average P/E ratio of 22.0

Return to moderate growth (45%)Moderate rise in global rates and equity prices

Inflation (US) at 2% in 5 years

US T-Bills settling at 2.3% in 5 years

US 10-year yields rising only moderately to reach 3.2% in five years

Equities (S&P 500) with average P/E ratio of 17.4

Stagflation (20%)Recession followed by low growth and inflation; positive correlation for stocks & bonds

Inflation (US) ultimately reaching 4.0% in five years

US T-Bills reaching 3.8% in five years

US 10-year yields rising to 5.0% in five years

Equities (S&P 500) with average P/E ratio of 15.8

Long-lasting recession (25%)Long recession followed by low growth

Inflation (US) declining, reaching 1.5% in five years

US T-Bills declining, reaching 0.5% over five years

US 10-year yields settling at 2.3% over five years

Equities (S&P 500) with average P/E ratio of 15.8

Higher growth

Lower growth

Low

er r

ates

Hig

her

rate

s

• Quick and surprising breakthrough in the fight against the virus (e.g., discovery of antivirals)

• Return to higher productivity levels similar to the 1996-2004 period

• Inflation rates would be kept in check by productivity achievements

• Central banks would raise rates again

• Slow recovery from the virus marked by additional waves and setbacks, additional multi-trillion stimulus efforts globally

• Additional tariffs and trade wars, supply chain disruptions and shortages of food and medicine boost inflation

• Stock-bond correlation turns positive

• Global growth recovers over the next year with no major setbacks but enough uncertainty to keep rates at ultra-low levels

• Only gradual end of QE over the next 5 years

• Equity better than fixed income

• Setbacks in the fight against the virus, amplified by global tensions and trade wars

• High volatility for risky assets

• L-T yields approaching zero-bound. Negative stock-bond correlation protects diversified portfolios

103

Scenario A (Return to moderate growth)

Source: UBS AM. See Appendix for details about sources and details of asset class returns and calculations. Data as of end of December 2020. Past performance of investments is not necessarily an indicator of future results.

0.92

0.65

0.49

0.45

0.40

0.33

0.32

0.26

0.19

0.15

0.13

0.10

0.04

0.04

-0.04

-0.17

-0.5 0.0 0.5 1.0

Hedge Funds

Real Estate

EMD Hard Currency

Global Equity

Private Equity

Infrastructure

EMD Local Currency

Global Government…

Cash

Securitized

Supranational

Corporates

Gold

Commodity

Global Government…

TIPS

Return/Risk profileExpected Returns 5 years and Standard Deviation, %

Cash

GCB 1-3GGB

Corporates

TIPS

SecuritizedSupranational

EMD Hard Currency

EMD Local Currency

Global Equity

Real Estate

Private Equity

Hedge Funds

Infrastructure

Gold

Commodity

-2%

0%

2%

4%

6%

8%

10%

12%

0% 5% 10% 15% 20% 25% 30%

Retu

rns,

5ye

ars

Standard deviation

Fixed income with low real returns; equity/alternatives outperform

104

Scenario B (Recession)Equity underperform; fixed income assets and certain alternatives preserve capital

Expected Returns 5 years and Standard Deviation, % Return/Risk profile

CashGGB 1-3

GGB

Corporates

TIPS

SecuritizedSupranational

EMD Hard Currency

EMD Local Currency

Global Equity

Real Estate

Private Equity

Hedge Funds

Infrastructure

Gold

Commodity

-1%

0%

1%

2%

3%

4%

5%

6%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Retu

rns,

5ye

ars

Standard deviation

0.61

0.40

0.25

0.25

0.24

0.20

0.17

0.14

0.13

0.12

0.06

0.05

0.04

0.03

0.01

-0.03

-0.2 0.0 0.2 0.4 0.6 0.8

EMD Hard Currency

Corporates

EMD Local Currency

Supranational

Hedge Funds

Securitized

Real Estate

Global Government…

Infrastructure

Gold

TIPS

Global Equity

Global Government…

Commodity

Private Equity

Cash

Source: UBS AM. See Appendix for details about sources and details of asset class returns and calculations. Data as of end of December 2020. Past performance of investments is not necessarily an indicator of future results.

105

Scenario C (Stagflation)Real assets perform well, but most asset classes show negative real returns

Expected Returns 5 years and Standard Deviation, % Return/Risk profile

Cash

GCB 1-3

GCB

Corporates

TIPS

Securitized

Supranational

EMD Hard Currency

EMD Local CurrencyGlobal Equity

Real Estate Private EquityHedge Funds

Infrastructure

Gold

Commodity

-4%

-2%

0%

2%

4%

6%

8%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Retu

rns,

5ye

ars

Standard deviation

0.46

0.40

0.35

0.26

0.24

0.18

0.17

0.16

0.08

0.06

0.00

-0.04

-0.10

-0.28

-0.35

-0.65

-1.0 -0.5 0.0 0.5 1.0

EMD HC

Hedge Funds

Commodity

TIPS

Real Estate

Gold

Infrastructure

EMD Local

Global Equity

Private Equity

Cash

Securitized

Corporates

Supranational

GGB 1-3

GGB

Source: UBS AM. See Appendix for details about sources and details of asset class returns and calculations. Data as of end of December 2020. Past performance of investments is not necessarily an indicator of future results.

106

Scenario D (Growth and Productivity upside scenario)Risk assets do well, while government bonds perform poorly