KHAN WAHAB SHAFIQUE RAHMAN & CO. - WVB

180

A member of mg iworldwide j i ---1/ HEADOFFICE: _/ KHAN WAHAB SHAFIQUE RAHMAN & CO. CHARTERED ACCOUNTANTS RUPALI BIMA BHABAN 7, RAJUKAVENUE (5TH & 6TH FLOOR) MOTIJHEEl, DHAKA-1000 Tel :9565136,9551663,9551821 FAX: 880-2-9551821 E-mail: [email protected] Web : www.kwsrbd.com BRANCHOFFICE: FARUK CHAMBER (9TH FLOOR) 1403 SK. MUJIB ROAD AGRABAD CIA ,DOUBLE MOORING CHATTOGRAM,BANGLADESH Tel: 031-2520056 E-mail: [email protected] IndependentAuditors' Report To the Shareholders of Standard Bank Limited Report on the Audit of the Consolidated and Separate Financial Statements Opinion We have audited the consolidated financial statements of Standard Bank Limited and its subsidiaries (the "Group") as well as the separate financial statements of Standard Bank Limited (the "Bank"), which comprise the consolidated and separate balance sheets as at 31 December 2019 and the consolidated and separate profit and loss accounts, consolidated and separate statements of changes in equity and consolidated and separate cash flow statements for the year then ended, and notes to the consolidated and separate financial statements, including a summary of significant accounting policies and other explanatory information. In our opinion, the accompanying consolidated financial statements of the Group and separate financial statements of the Bank give a true and fair view of the consolidated balance sheet of the Group and the separate balance sheet of the Bank as at 31 December 2019, and of its consolidated and separate profit and loss accounts and its consolidated and separate cash flows for the yearthen ended in accordance with International Financial Reporting Standards (lFRSs) as explained in note 2. Basis for Opinion We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditors' Responsibilities for the Audit of the Consolidated and Separate Financial Statements section of our report. We are independent of the Group and the Bank in accordance with the International Ethics Standards Board for Accountants' Code of Ethics for Professional Accountants (IESBA Code), Bangladesh Securities and Exchange Commission (BSEC) and Bangladesh Bank, and we have fulfilled our other ethical responsibilities in accordance with the IESBA Code and the Institute of Chartered Accountants of Bangladesh (ICAB) Bye Laws. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Emphasis of Matter We draw attention to Note 2.1(xviii) of the notes to the financial statements where the management has described the possible effects ofIFRS 16 "Leases". Our report is not qualified in this regard. Key Audit Matters Key audit matters are those matters that, in our professionaljudgment, were of most significance in our audit of the consolidated and separate financial statements of the current year. These matters were addressed in the context of our audit of the consolidated and separate financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. In Practice since 1968

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of KHAN WAHAB SHAFIQUE RAHMAN & CO. - WVB

A member of

mg iworldwide ji---1/

HEADOFFICE: _/

KHAN WAHAB SHAFIQUE RAHMAN & CO.CHARTERED ACCOUNTANTS

RUPALI BIMA BHABAN7, RAJUKAVENUE (5TH & 6TH FLOOR)MOTIJHEEl, DHAKA-1000Tel :9565136,9551663,9551821FAX: 880-2-9551821E-mail: [email protected] : www.kwsrbd.com

BRANCHOFFICE:FARUK CHAMBER (9TH FLOOR)1403 SK. MUJIB ROADAGRABAD CIA ,DOUBLE MOORINGCHATTOGRAM,BANGLADESHTel: 031-2520056E-mail: [email protected]

IndependentAuditors' ReportTo the Shareholders of Standard Bank Limited

Report on the Audit of the Consolidated and Separate Financial Statements

OpinionWe have audited the consolidated financial statements of Standard Bank Limited and its subsidiaries (the"Group") as well as the separate financial statements of Standard Bank Limited (the "Bank"), which comprisethe consolidated and separate balance sheets as at 31 December 2019 and the consolidated and separate profitand loss accounts, consolidated and separate statements of changes in equity and consolidated and separate cashflow statements for the year then ended, and notes to the consolidated and separate financial statements,including a summary of significant accounting policies and other explanatory information.

In our opinion, the accompanying consolidated financial statements of the Group and separate financialstatements of the Bank give a true and fair view of the consolidated balance sheet of the Group and the separatebalance sheet of the Bank as at 31 December 2019, and of its consolidated and separate profit and loss accountsand its consolidated and separate cash flows for the year then ended in accordance with International FinancialReporting Standards (lFRSs) as explained in note 2.

Basis for OpinionWe conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilitiesunder those standards are further described in the Auditors' Responsibilities for the Audit of the Consolidatedand Separate Financial Statements section of our report. We are independent of the Group and the Bank inaccordance with the International Ethics Standards Board for Accountants' Code of Ethics for ProfessionalAccountants (IESBA Code), Bangladesh Securities and Exchange Commission (BSEC) and Bangladesh Bank,and we have fulfilled our other ethical responsibilities in accordance with the IESBA Code and the Institute ofChartered Accountants of Bangladesh (ICAB) Bye Laws.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for ouropinion.

Emphasis of MatterWe draw attention to Note 2.1(xviii) of the notes to the financial statements where the management hasdescribed the possible effects ofIFRS 16 "Leases". Our report is not qualified in this regard.

Key Audit MattersKey audit matters are those matters that, in our professional judgment, were of most significance in our audit ofthe consolidated and separate financial statements of the current year. These matters were addressed in thecontext of our audit of the consolidated and separate financial statements as a whole, and in forming our opinionthereon, and we do not provide a separate opinion on these matters.

In Practice since 1968

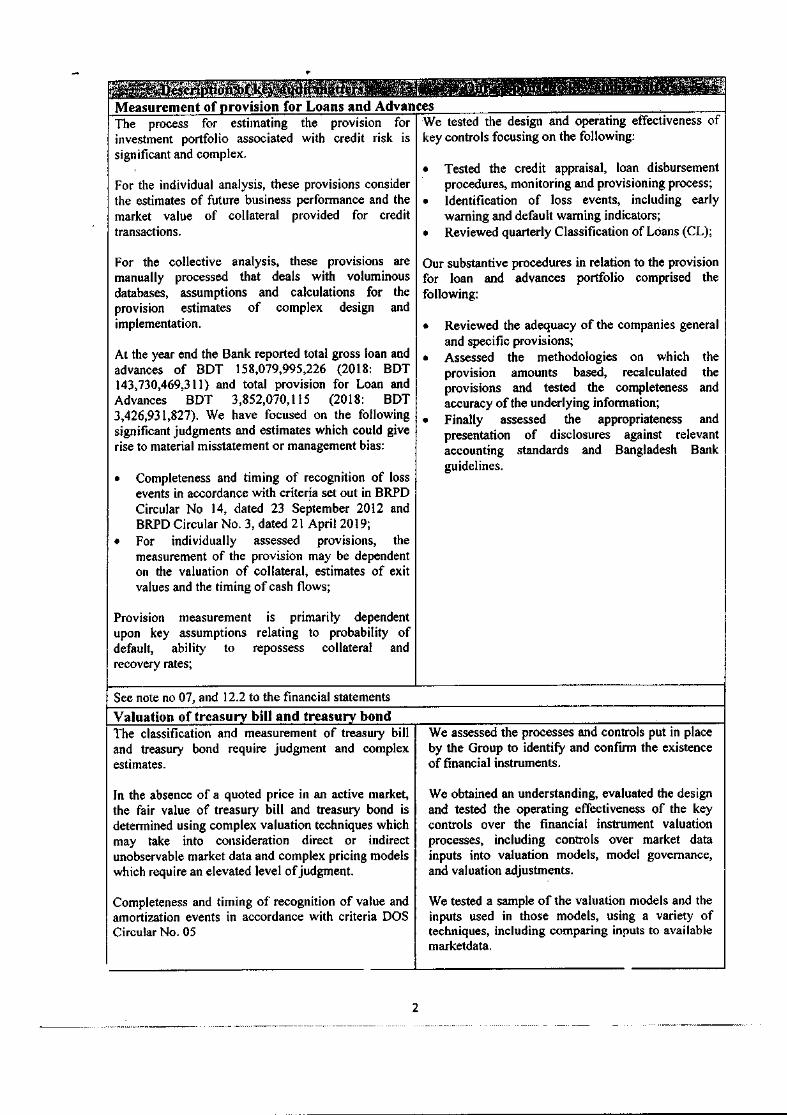

The process for estimatinginvestment portfolio associatedsignificant and complex.

We tested the design and operating effectiveness ofIS key controls focusing on the following:

For the individual analysis, these provisions considerthe estimates of future business performance and the •market value of collateral provided for credittransactions.

For the collective analysis, these provisions aremanually processed that deals with voluminousdatabases, assumptions and calculations for theprovision estimates of complex design andimplementation.

At the year end the Bank reported total gross loan and •advances of BOT 158,079,995,226 (2018: BOT143,730,469,311) and total provision for Loan andAdvances BOT 3,852,070,115 (2018: BOT3,426,931,827). We have focused on the following •significant judgments and estimates which could giverise to material misstatement or management bias:

• Completeness and timing of recognition of lossevents in accordance with criteria set out in BRPDCircular No 14, dated 23 September 2012 andBRPD Circular No.3, dated 21 April 2019;For individually assessed provisions, themeasurement of the provision may be dependenton the valuation of collateral, estimates of exitvalues and the timing of cash flows;

•

Provision measurement is primarily dependentupon key assumptions relating to probability ofdefault, ability to repossess collateral andrecovery rates;

See note no 07, and 12.2 to the financial statements

• Tested the credit appraisal, loan disbursementprocedures, monitoring and provisioning process;Identification of loss events, including earlywarning and default warning indicators;Reviewed quarterly Classification of Loans (CL);•

Our substantive procedures in relation to the provisionfor loan and advances portfolio comprised thefollowing:

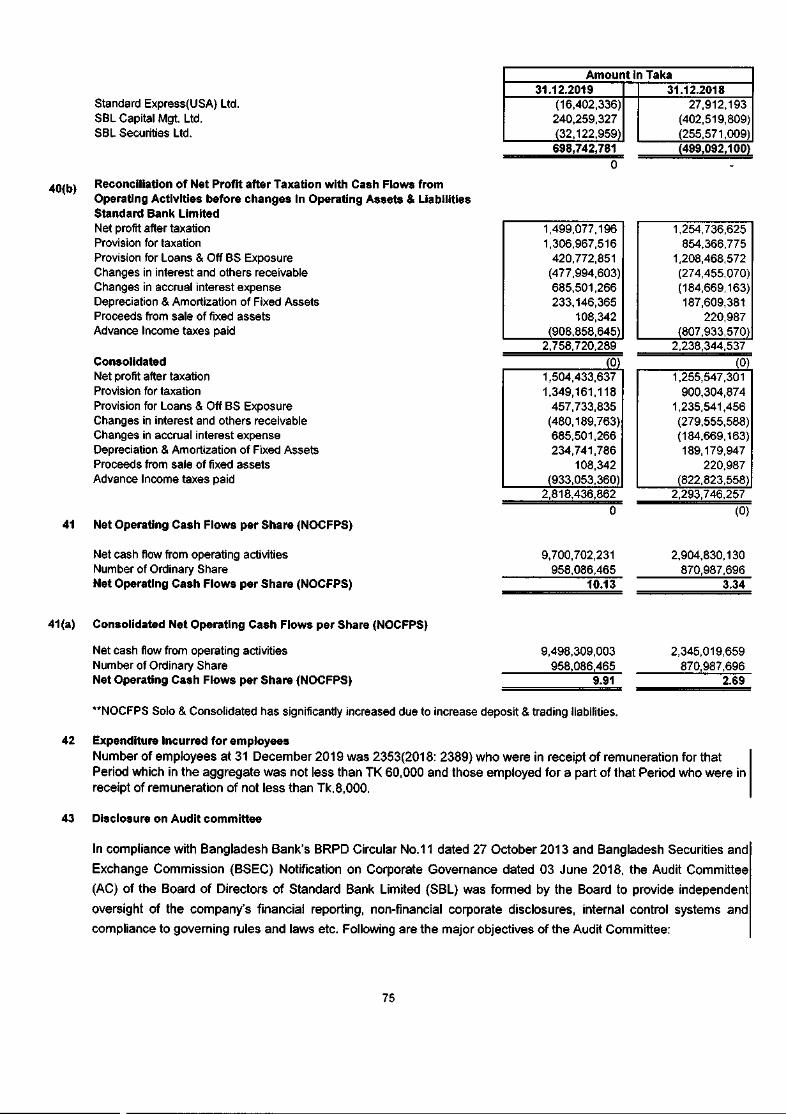

• Reviewed the adequacy of the companies generaland specific provisions;Assessed the methodologies on which theprovision amounts based, recalculated theprovisions and tested the completeness andaccuracy of the underlying information;Finally assessed the appropriateness andpresentation of disclosures against relevantaccounting standards and Bangladesh Bankguidelines.

The classification and measurement of treasury billand treasury bond require judgment and complexestimates.

In the absence of a quoted price in an active market,the fair value of treasury bill and treasury bond isdetermined using complex valuation techniques whichmay take into consideration direct or indirectunobservable market data and complex pricing modelswhich require an elevated level of judgment.

Completeness and timing of recognition of value andamortization events in accordance with criteria DOSCircular No. 05

We assessed the processes and controls put in placeby the Group to identify and confirm the existenceof financial instruments.

We obtained an understanding, evaluated the designand tested the operating effectiveness of the keycontrols over the financial instrument valuationprocesses, including controls over market datainputs into valuation models, model governance,and valuation adjustments.

We tested a sample of the valuation models and theinputs used in those models, using a variety oftechniques, including comparing inputs to availablemarketdata.

2

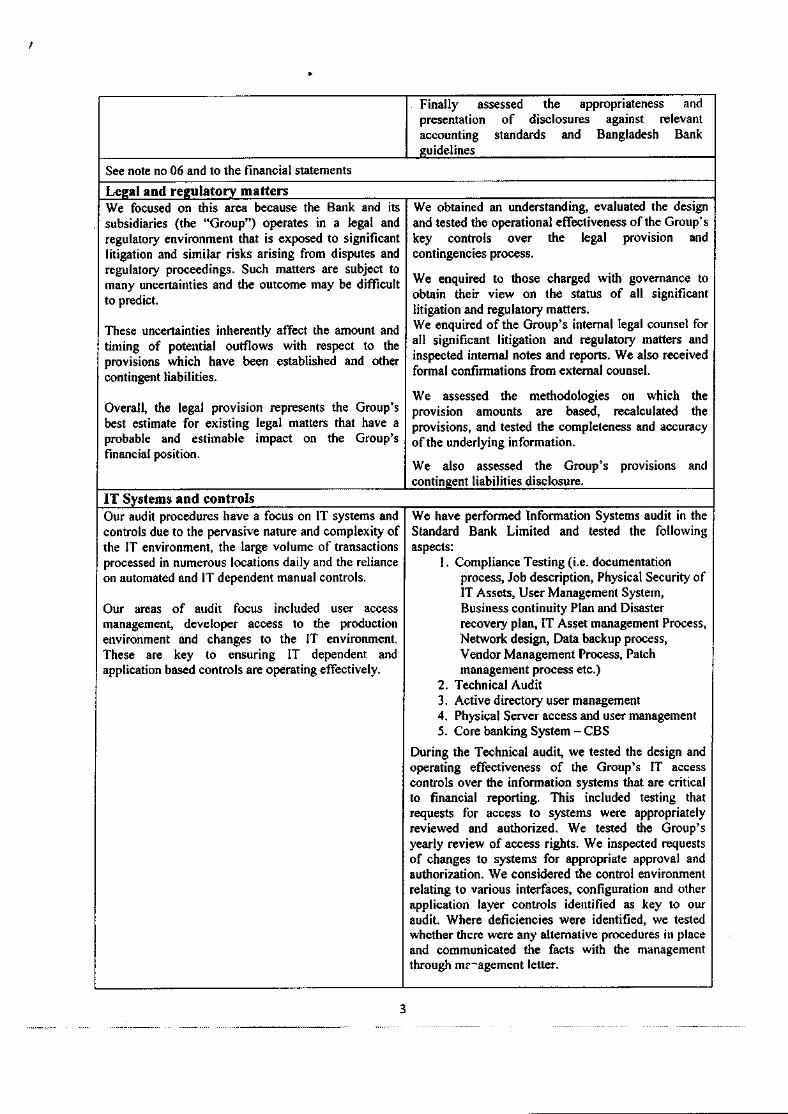

..Finally assessed the appropriateness andpresentation of disclosures against relevantaccounting standards and Bangladesh Bankguidelines

See note no 06 and to the financial statementsLegal and regulatory matters

We obtained an understanding, evaluated the designand tested the operational effectiveness of the Group'skey controls over the legal provision andcontingencies process.

We enquired to those charged with governance toobtain their view on the status of all significantlitigation and regulatory matters.We enquired of the Group's internal legal counsel forall significant litigation and regulatory matters andinspected internal notes and reports. We also receivedformal confirmations from external counsel.

We focused on this area because the Bank and itssubsidiaries (the "Group") operates in a legal andregulatory environment that is exposed to significantlitigation and similar risks arising from disputes andregulatory proceedings. Such matters are subject tomany uncertainties and the outcome may be difficultto predict.

These uncertainties inherently affect the amount andtiming of potential outflows with respect to theprovisions which have been established and othercontingent liabilities.

Overall, the legal provision represents the Group'sbest estimate for existing legal matters that have aprobable and estimable impact on the Group'sfinancial position.

We assessed the methodologies on which theprovision amounts are based, recalculated theprovisions, and tested the completeness and accuracyof the underlying information.

We also assessed the Group's provisions andcontingent liabilities disclosure.

IT Systems and controlsWe have performed Information Systems audit in theStandard Bank Limited and tested the followingaspects:

1. Compliance Testing (i.e. documentationprocess, Job description, Physical Security ofIT Assets, User Management System,Business continuity Plan and Disasterrecovery plan, IT Asset management Process,Network design, Data backup process,Vendor Management Process, Patchmanagement process etc.)

2. Technical Audit3. Active directory user management4. Physical Server access and user management5. Core banking System - CBS

During the Technical audit, we tested the design andoperating effectiveness of the Group's IT accesscontrols over the information systems that are criticalto financial reporting. This included testing thatrequests for access to systems were appropriatelyreviewed and authorized. We tested the Group'syearly review of access rights. We inspected requestsof changes to systems for appropriate approval andauthorization. We considered the control environmentrelating to various interfaces, configuration and otherapplication layer controls identified as key to ouraudit. Where deficiencies were identified, we testedwhether there were any alternative procedures ill placeand communicated the facts with the managementthrough mer agernent letter.

Our audit procedures have a focus on IT systems andcontrols due to the pervasive nature and complexity ofthe IT environment, the large volume of transactionsprocessed in numerous locations daily and the relianceon automated and IT dependent manual controls.

Our areas of audit focus included user accessmanagement, developer access to the productionenvironment and changes to the IT environment.These are key to ensuring IT dependent andapplication based controls are operating effectively.

3

Other InformationManagement is responsible for the other information. The other information comprises all of the information inthe Annual Report other than the consolidated and separate financial statements and our auditors' reportthereon. The Annual Report is expected to be made available to us after the date of this auditor's report.

Our opinion on the consolidated and separate financial statements does not cover the other information and wedo not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other informationidentified above when it becomes available and, in doing so, consider whether the other information ismaterially inconsistent with the financial statements or our knowledge obtained in the audit or otherwiseappears to be materially misstated.

When we read the annual report if we conclude that there is a material misstatement therein, we are required tocommunicate the matter to those charged with governance.

Responsibilities of Management and Those Charged with Governance for the Consolidated andSeparate Financial Statements and Internal Controls

Management is responsible for the preparation and fair presentation of the consolidated financial statements ofthe Group and also separate financial statements of the Bank in accordance with IFRSs as explained in note 2,and for such internal control as management determines is necessary to enable the preparation of consolidatedand separate financial statements that are free from material misstatement, whether due to fraud or error. TIleBank Company Act, 1991 as amended in 2018 and the Bangladesh Bank Regulations require the Managementto ensure effective internal audit, internal control and risk management functions of the Bank. The Managementis also required to make a self-assessment on the effectiveness of anti-fraud internal controls and report toBangladesh Bank on instances of fraud and forgeries.

In preparing the consolidated and separate financial statements, management is responsible for assessing theGroup's and the Bank's ability to continue as a going concern, disclosing, as applicable, matters related togoing concern and using the going concern basis of accounting unless management either intends to liquidatethe Group and the Bank or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Group's and the Bank's financial reportingprocess.

Auditor's Responsibilities for the Audit of the Consolidated and Separate Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated and separate financialstatements as a whole are free from material misstatement, whether due to fraud or error, and to issue anauditor's report that includes our opinion. Reasonable assurance is a high level of assurance, but is not aguarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when itexists. Misstatements can arise from fraud or error and are considered material if, individually or in theaggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis ofthese consolidated and separate financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professionalskepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the consolidated and separate financial statements,whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtainaudit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detectinga material misstatement resulting from fraud is higher than for one resulting from error, as fraud mayinvolve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that areappropriate in the circumstances.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimatesand related disclosures made by management.

4

• Conclude on the appropriateness of management's use of the going concern basis of accounting and, basedon the audit evidence obtained, whether a material uncertainty exists related to events or conditions thatmay cast significant doubt on the Group's and the Bank's ability to continue as a going concern. If weconclude that a material uncertainty exists, we are required to draw attention in our auditor's report to therelated disclosures in the consolidated and separate financial statements or, if such disclosures areinadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the dateof our auditor's report. However, future events or conditions may cause the Group and the Bank to cease tocontinue as a going concern.

• Evaluate the overall presentation, structure and content of the consolidated and separate financialstatements, including the disclosures, and whether the consolidated and separate financial statementsrepresent the underlying transactions and events in a manner that achieves fair presentation.

• Obtain sufficient appropriate audit evidence regarding the financial information of the entities or businessactivities within the Group to express an opinion on the consolidated financial statements. We areresponsible for the direction, supervision and performance of the group audit. We remain solely responsiblefor our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope andtiming of the audit and significant audit findings, including any significant deficiencies in internal control thatwe identify during our audit.

We also provide those charged with governance with a statement that we have complied with relevant ethicalrequirements regarding independence, and to communicate with them all relationships and other matters thatmay reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were ofmost significance in the audit of the consolidated and separate financial statements of the current year and aretherefore the key audit matters. We describe these matters in our auditors' report unless law or regulationprecludes public disclosure about the matter or when, in extremely rare circumstances, we determine that amatter should not be communicated in our report because the adverse consequences of doing so wouldreasonably be expected to outweigh the public interest benefits of such communication.

Report on other Legal and Regulatory Requirements

In accordance with the Companies Act, 1994, the Securities and Exchange Rules 1987, the Bank Company Act,1991as amended in 2018 and the rules and regulations issued by Bangladesh Bank, we also report that:

(i) we have obtained all the information and explanations which to the best of our knowledge and belief werenecessary for the purpose of our audit and made due verification thereof;

(ii) to the extent noted during the course of our audit work performed on the basis stated under the Auditor'sResponsibility section in forming the above opinion on the consolidated financial statements of the Groupand the separate financial statements of the Bank and considering the reports of the Management toBangladesh Bank on antifraud internal controls and instances of fraud and forgeries as stated under theManagement's Responsibility for the financial statements and internal control:

a) internal audit, internal control and risk management arrangements of the Group as disclosed in thefinancial statements appeared to be materially adequate;

b) nothing has come to our attention regarding material instances of forgery or irregularity oradministrative error and exception or anything detrimental committed by employees of the Groupand its related entities {other than matters disclosed in these financial statements};

(iii) financial statements of Standard Bank Limited's subsidiaries namely, Standard Bank Securities Ltd., andStandard Bank Capital Management Ltd. have been audited by Khan Wahab Shafique Rahman & Co.,Chartered Accountants and have been properly reflected in the consolidated financial statements;

(iv) in our opinion, proper books of accounts as required by law have been kept by the Group and the Bank sofar as it appeared from our examination of those books;

(v) the record' and statements submitted by the branches hav been properly maintained and consolidated inthe financial statements;

5

(vi) the consolidated balance sheet and consolidated profit and loss account together with the annexed notesdealt with by the report are in agreement with the books of account and returns;

(vii) the expenditures incurred were for the purpose of the Bank's business for the year;(viii) the consolidated financial statements of the Group and the separate financial statements of the Bank have

been drawn up in conformity with prevailing rules, regulations and accounting standards as well asrelated guidance issued by Bangladesh Bank;

(ix) adequate provisions have been made for loans and advances, other assets, investment in share andgratuity as per Bangladesh Bank Letter No-DBI-l/ll112020-1447 dated: 23/03/2020.

(x) the information and explanations required by us have been received and found satisfactory;(xi) we have reviewed over 80% of the risk weighted assets of the Bank and spent over 4,191 person hours;

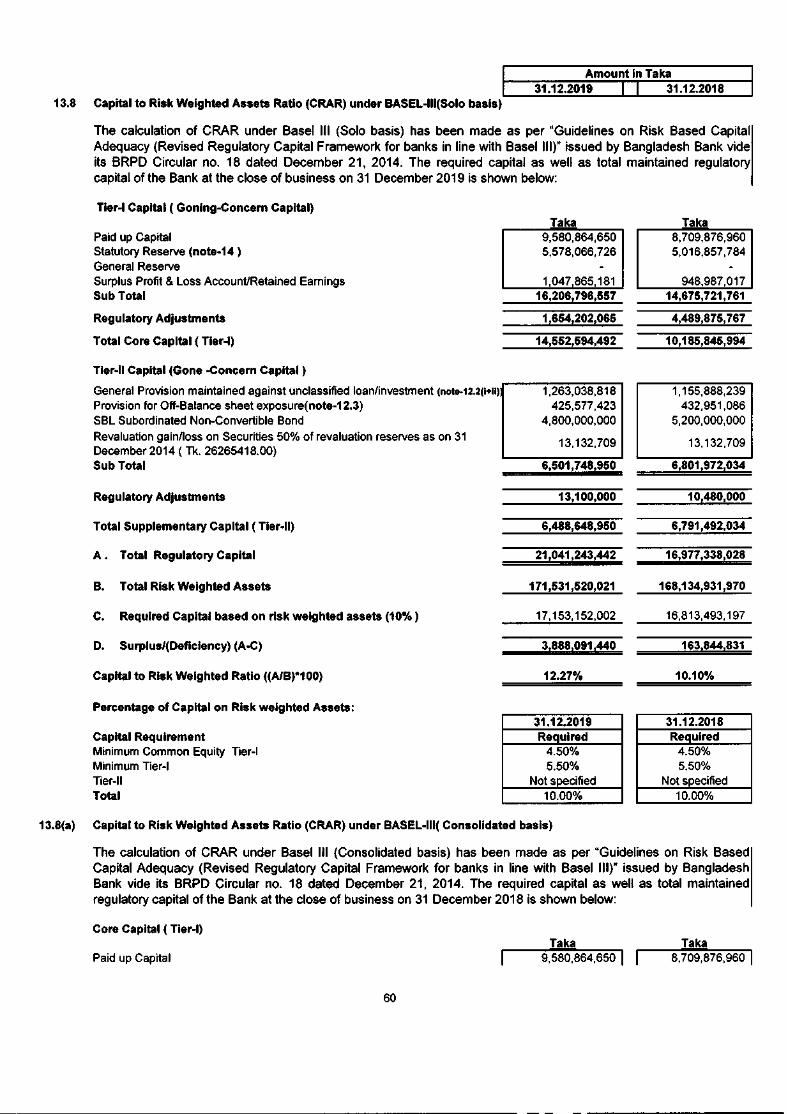

and(xii) Capital to Risk-weighted Asset Ratio (CRAR) as has been maintained shown at note no. 13.8 of notes to

the financial statements during the year.

Dated, Dhaka 24 March, 2020b..-~~&

Md. Anisur Rahman FCAKhan Wahab Shafique Rahman & Co.

Chartered Accountants

6

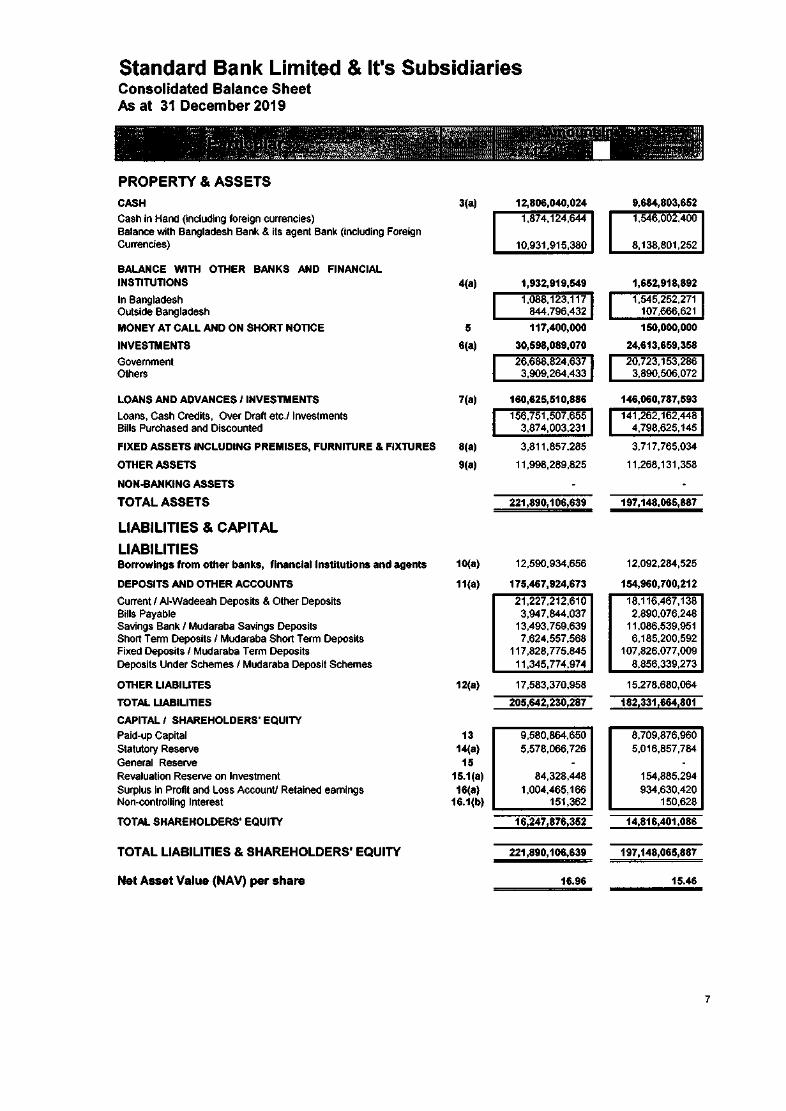

Standard Bank Limited & It's SubsidiariesConsolidated Balance SheetAs at 31 December 2019

PROPERTY& ASSETSCASH 3(a) 12,806,040,024 9,684,803,652

Cash in Hand (including foreign currencies) 1,874,124,644 1,546,002,400Balance with Bangladesh Bank & its agent Bank (including ForeignCurrencies) 10,931,915,380 8,138,801,252

BALANCE WITH OTHER BANKS AND FINANCIALINSTITUTIONS 4(a) 1,932,919,549 1,652,918,892

In Bangladesh 1,088,123,117 1,545,252,271Outside Bangladesh 844,796,432 107,666,621

MONEY AT CALL AND ON SHORT NOTICE 5 117,400,000 150,000,000

INVESTMENTS 6(a) 30,598,089,070 24,613,659,358

Government 26,688,824,637 20,723,153,286Others 3,909,264,433 3,890,506,072

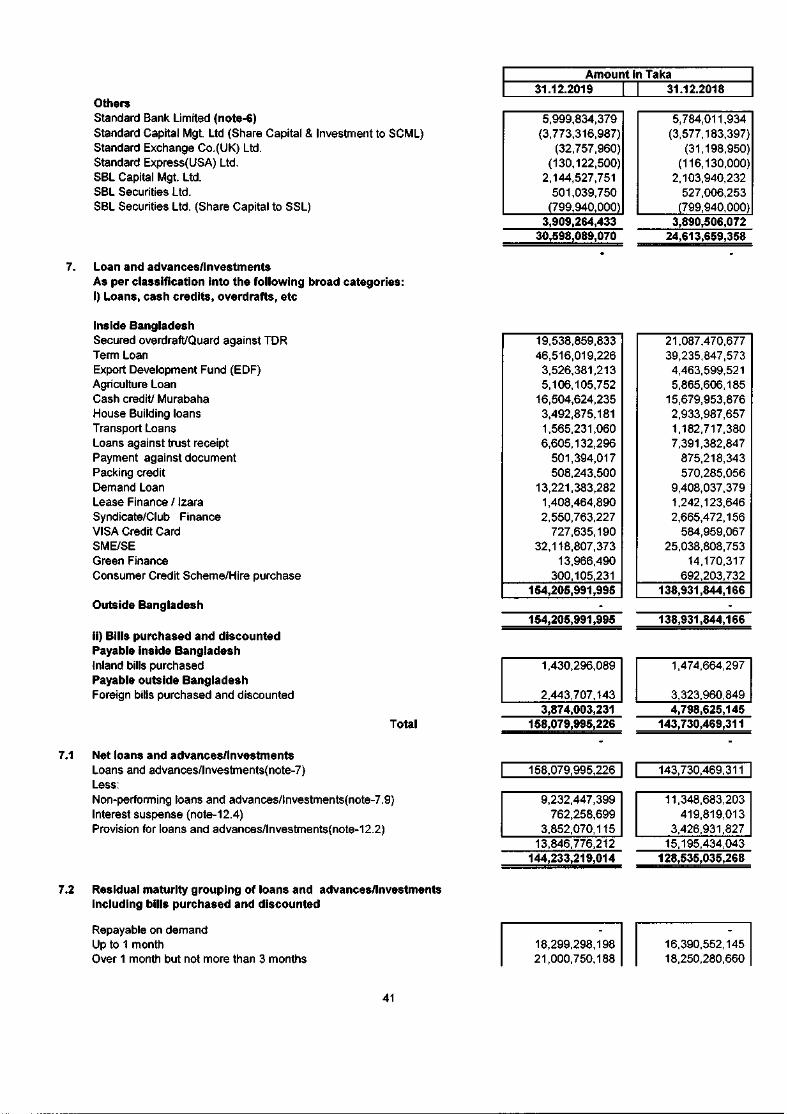

LOANS AND ADVANCES I INVESTMENTS 7(a) 160,625,510,886 146,060,787,593

Loans, Cash Credits, Over Draft etc.llnvestments 156,751,507,655 141,262,162,448Bills Purchased and Discounted 3,874,003,231 4,798,625,145

FIXED ASSETS INCLUDING PREMISES, FURNITURE & FIXTURES 8(a) 3,811,857,285 3,717,765,034

OTHER ASSETS 9(a) 11,998,289,825 11,268,131,358

NON-BANKING ASSETS

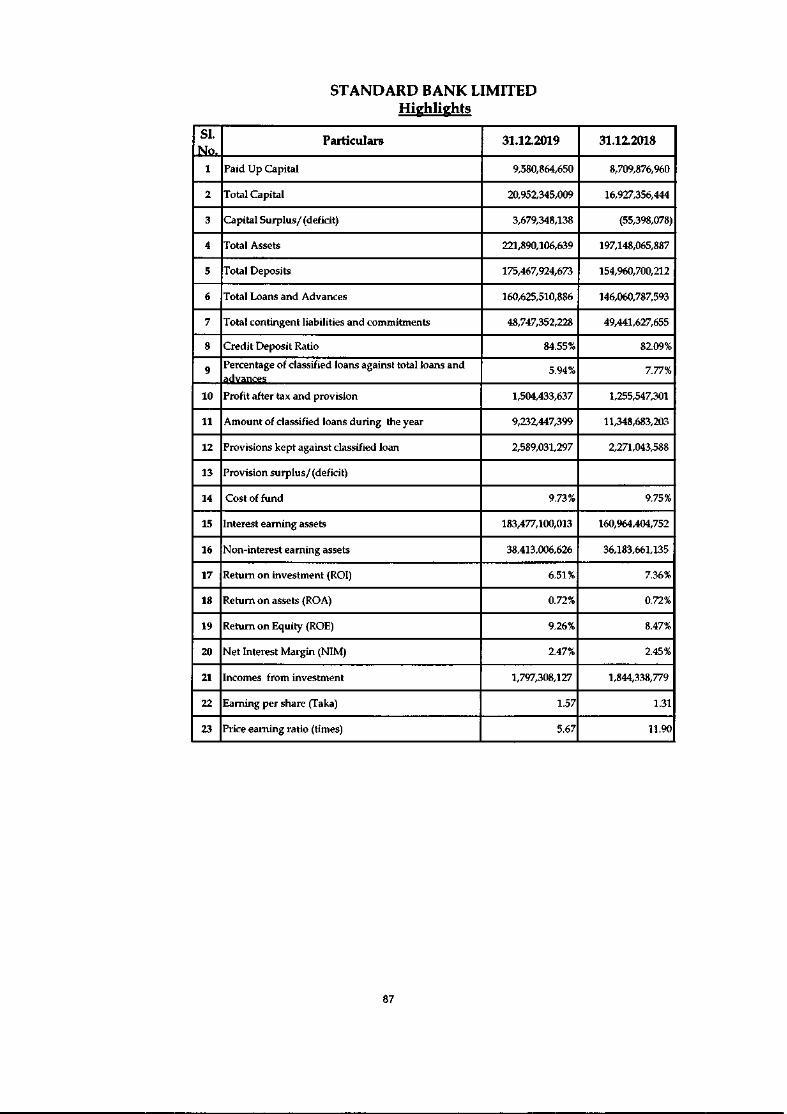

TOTAL ASSETS 221,890,106,639 197,148,065,887

LIABILITIES & CAPITALLIABILITIESBorrowings from other banks, financial Institutions and agents 10(a) 12,590,934,656 12,092,284,525

DEPOSITS AND OTHER ACCOUNTS 11(a) 175,467,924,673 154,960,700,212

Current I AI-Wadeeah Deposits & Other Deposits 21,227,212,610 18,116,467,138Bills Payable 3,947,844,037 2,890,076,248Savings Bank I Mudaraba Savings Deposits 13,493,759,639 11,086,539,951Short Term Deposits I Mudaraba Short Term Deposits 7,624,557,568 6,185,200,592Fixed Deposits I Mudaraba Term Deposits 117,828,775,845 107,826,077,009Deposits Under Schemes I Mudaraba Deposit Schemes 11,345,774,974 8,856,339,273

OTHER LlABILITES 12(a) 17,583,370,958 15,278,680,064

TOTAL LIABILITIES 205,642,230,287 182,331,664,801

CAPITAL I SHAREHOLDERS' EQUITYPaid-up Capital 13 9,580,864,650 8,709,876,960Statutory Reserve 14(a) 5,578,066,726 5,016,857,784General Reserve 15Revaluation Reserve on Investment 15.1(a) 84,328,448 154,885,294Surplus in Profit and Loss Account! Retained earnings 16(a) 1,004,465,166 934,630,420Non-controlling Interest 16.1(b) 151,362 150,628

TOTAL SHAREHOLDERS' EQUITY 16,247,876,352 14,816,401,086

TOTAL LIABILITIES & SHAREHOLDERS' EQUITY 221,890,106,639 197,148,065,887

Net Asset Value (NAV) per share 16.96 15.46

7

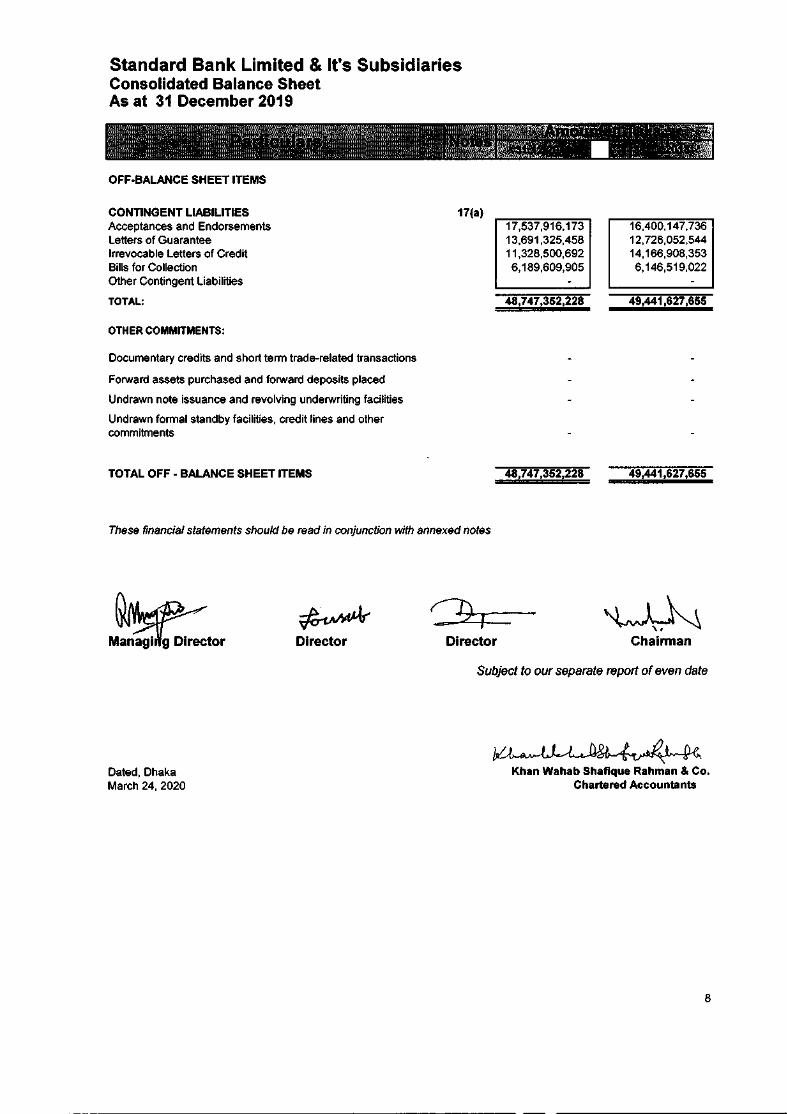

Standard Bank Limited & It's SubsidiariesConsolidated Balance SheetAs at 31 December 2019

OFF-BALANCE SHEET ITEMS

CONTINGENT LIABILITIESAcceptances and EndorsementsLetters of GuaranteeIrrevocable Letters of CreditBills for CollectionOther Contingent Liabilities

TOTAL:

17(a)

49,441,627,655

17,537,916,17313,691,325,45811,328,500,6926,189,609,905

16,400,147,73612,728,052,54414,166,908,3536,146,519,022

48,747,352,228

OTHER COMMITMENTS:

Documentary credits and short term trade-related transactions

Forward assets purchased and forward deposits placed

Undrawn note issuance and revolving underwriting facilities

Undrawn formal standby facilities, credit lines and othercommitments

TOTAL OFF - BALANCE SHEET ITEMS 48,747,352,228 49,441,627,655

These financial statements should be read in conjunction with annexed notes

Director Director Chairman

Subject to our separate report of even date

Dated, DhakaMarch 24, 2020

Khan Wahab Shafique Rahman & Co.Chartered Accountants

8

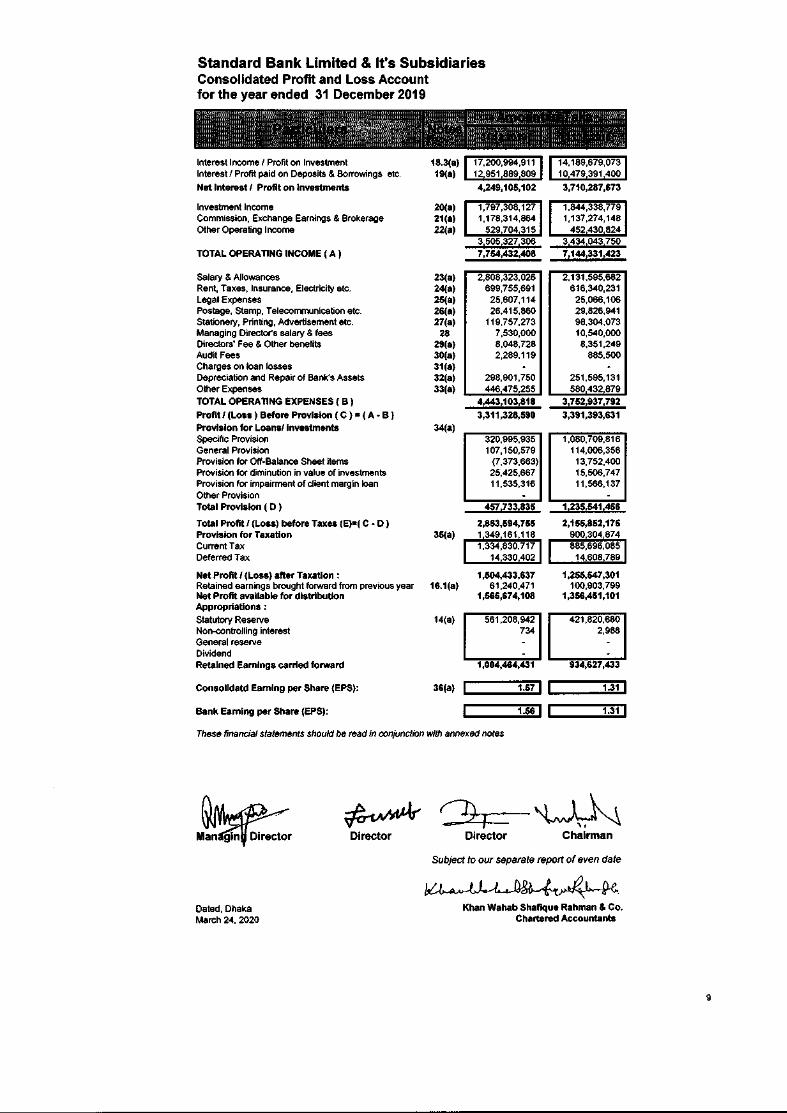

Standard Bank Limited & It's SubsidiariesConsolidated Profit and Loss Accountfor the year ended 31 December 2019

Interest Income I Profit on InvestmentInterest I Profit paid on Deposits& Borrowings etc.Net Interest I Profit on Investments

Investment IncomeCommission, ExchangeEarnings& BrokerageOther Operating Income

TOTAL OPERATING INCOME(A)

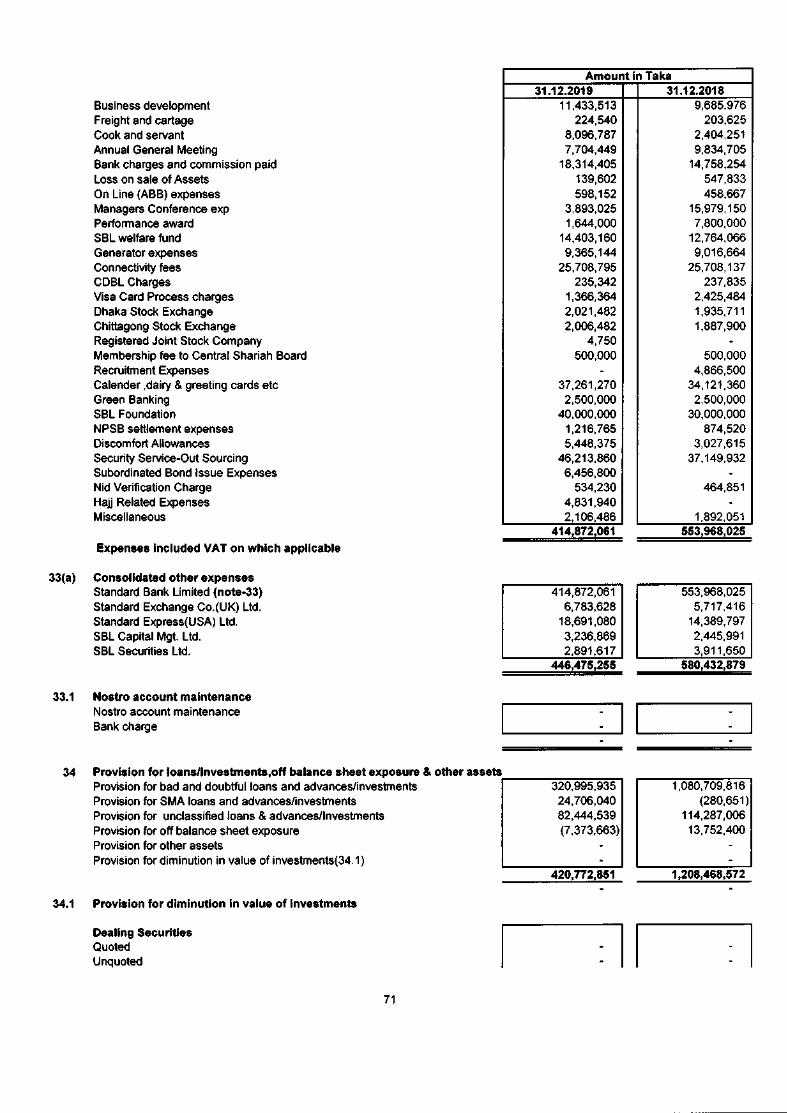

Salary & AllowancesRent, Taxes, Insurance, Electricityetc.Legal ExpensesPostage, Stamp,Telecommunicationetc.Stationery, Printing,Advertisement etc.Managing Director's salary & feesDirectors' Fee & Other benefitsAudit FeesCharges on loan lossesDepreciationand Repair of Bank'sAssetsOther ExpensesTOTAL OPERATINGEXPENSES(B)Profit I (Loss) Before Provision ( C ) = ( A • B )Provision for Loansl investmentsSpecific ProvisionGeneral ProvisionProvision for Off·BalanceSheet itemsProvision for diminution in value of investmentsProvision for impairmentof client margin loanOther ProvisionTotal Provision (D)

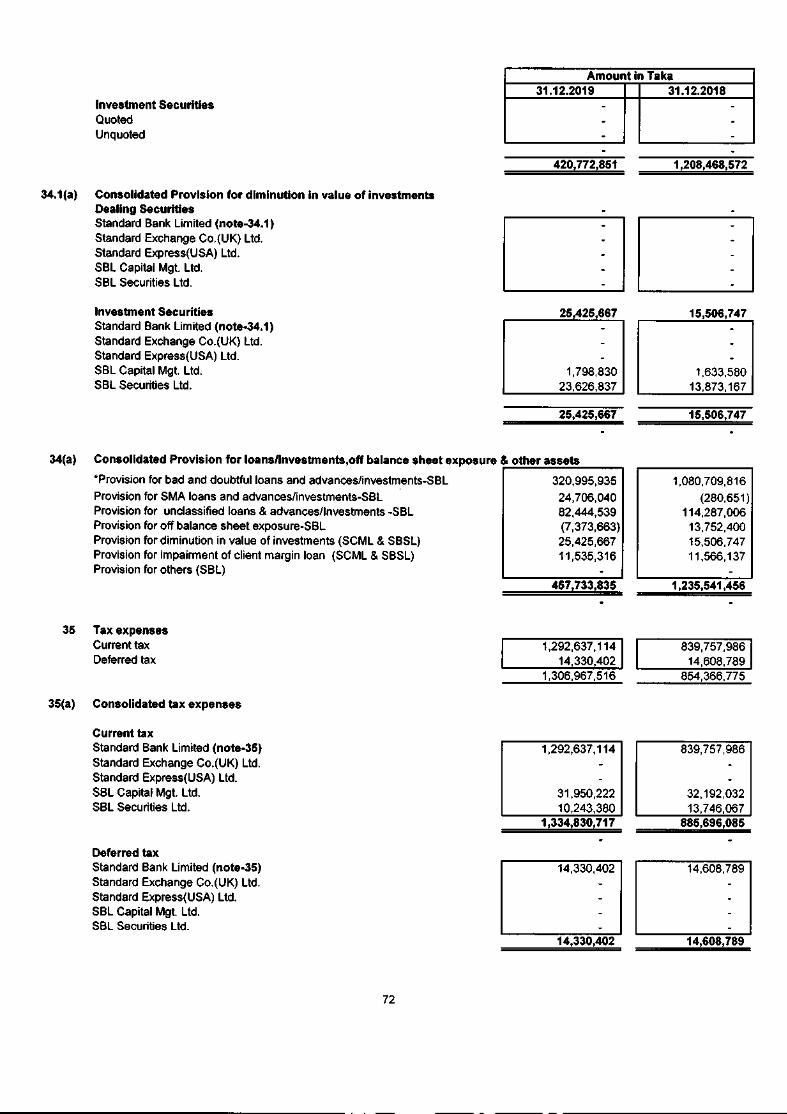

Total Profit I (Loss) before Taxes (E)=( C • 0 )Provision for Taxation 35(a)Current TaxDeferredTax

Net Profit I (Loss) after Taxation:Retainedearnings brought forward from previousyear 16.1(a)Net Profit available for distributionAppropriations:Statutory Reserve 14(a)Non-controlling interestGeneral reserveDividendRetained Earnings carried forward

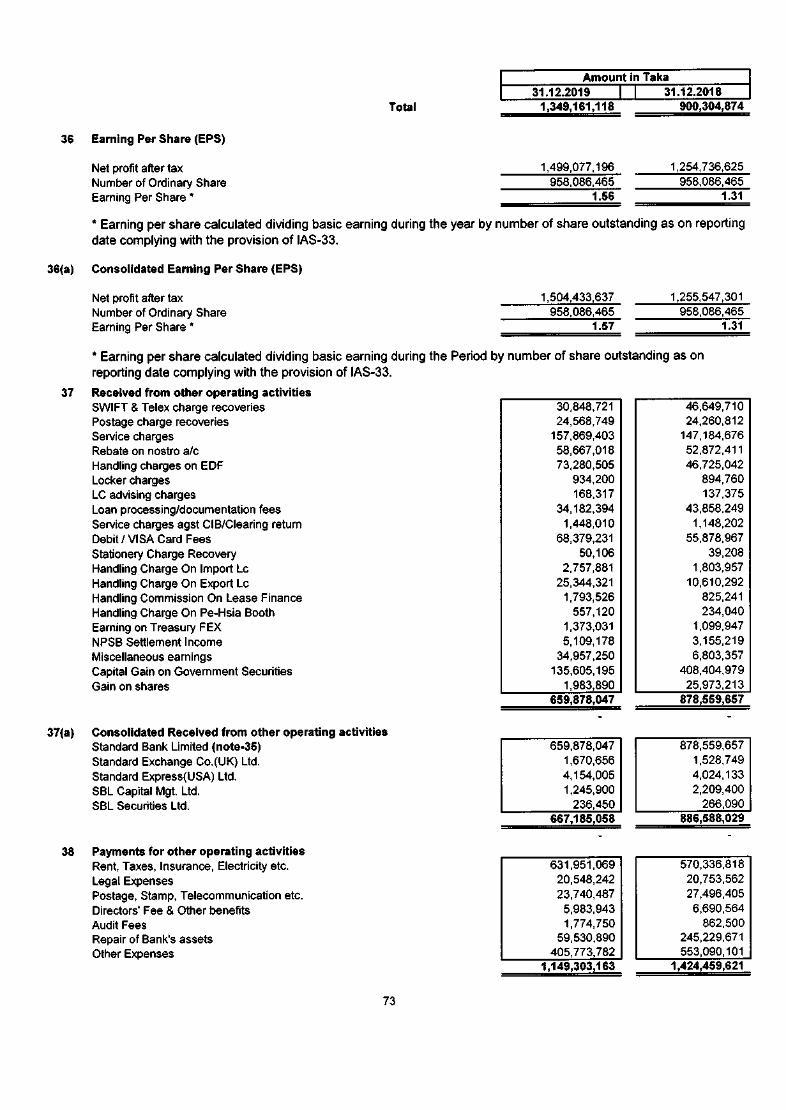

Consolidatd Earning per Share (EPS):

Bank Earning per Share (EPS):

20(a)21(a)22(a)

23(a)24(a)25(a)26(a)27(a)28

29(a)30(a)31(a)32(a)33(a)

34(a)

36(a)

4,249,105,102 3,710,287,673

1,797,308,127 1,844,338,7791,178,314,864 1,137,274,148529704315 452430824

3,505,327,306 3,434,O43?507,754,432,408 7,144,331,423

2,808,323,026 2,131,595,682699,755,691 616,340,23125,607,114 25,066,10626,415,860 29,826,941119,757,273 98,304,073

7,530,000 10,540,0008,048,728 8,351,2492,289,119 885,500

298,901,750 251,595,131446475255 580432,879

4,443,103,818 3,752,937,7923,311,328,590 3,391,393,631

320,995,935 1,080,709,816107,150,579 114,006,356(7,373,663) 13,752,40025,425,667 15,506,74711,535,316 11,566,137

457,733,835 1,235,541,456

2,853,594,755 2,155,852,1751349161118 9003048741,334,830,717 885,696,085

14330402 14608789

1,504,433,637 1,255,547,30161,240,471 100,903,799

1,565,674,108 1,356,451,101

561,208,942 421,820,680734 2,988- -- .

1,004,464,431 934,627,433

These financial statements should be read in conjunctionwith annexednotes

1.57! ",! ~1.:;;.31:..1!

1.56! ",! ~1.:;;.31:..1!

Director

Subject to our separate report of even date

Director Chairman

Dated, DhakaMarch 24, 2020

Khan Wahab Shafique Rahman & Co.Chartered Accountants

9

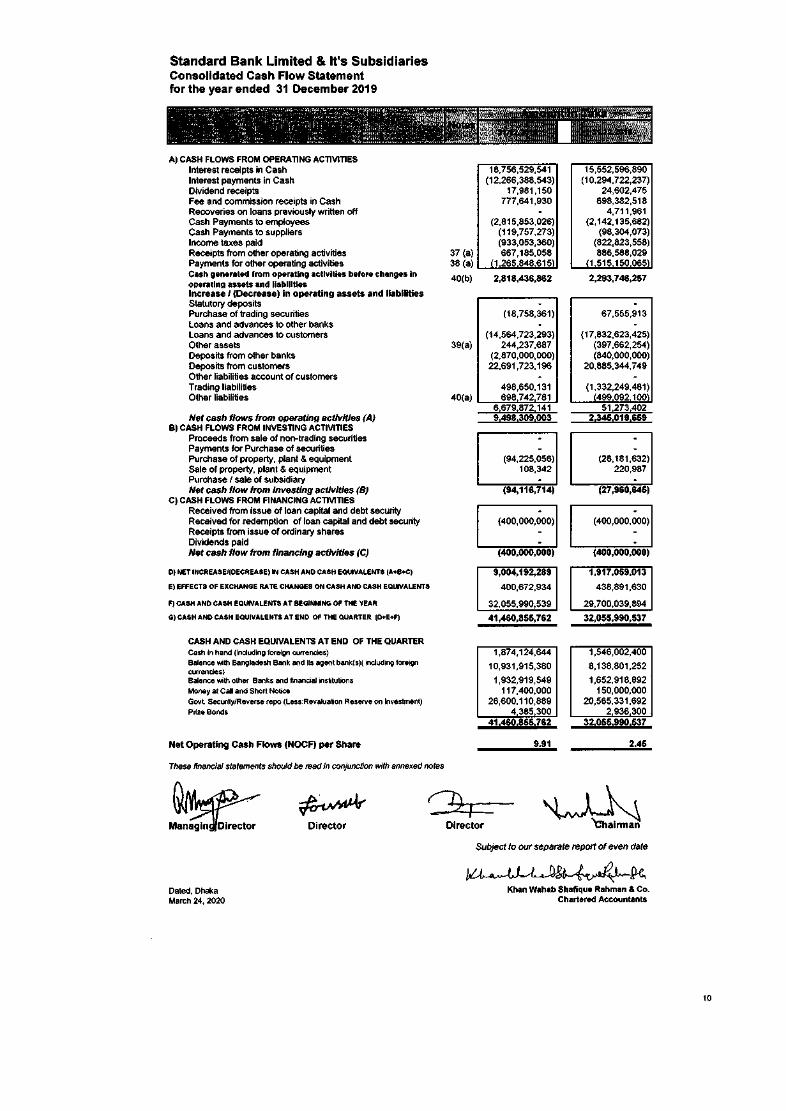

Standard Bank Limited & It's SubsidiariesConsolidated Cash Flow Statementfor the year ended 31 December 2019

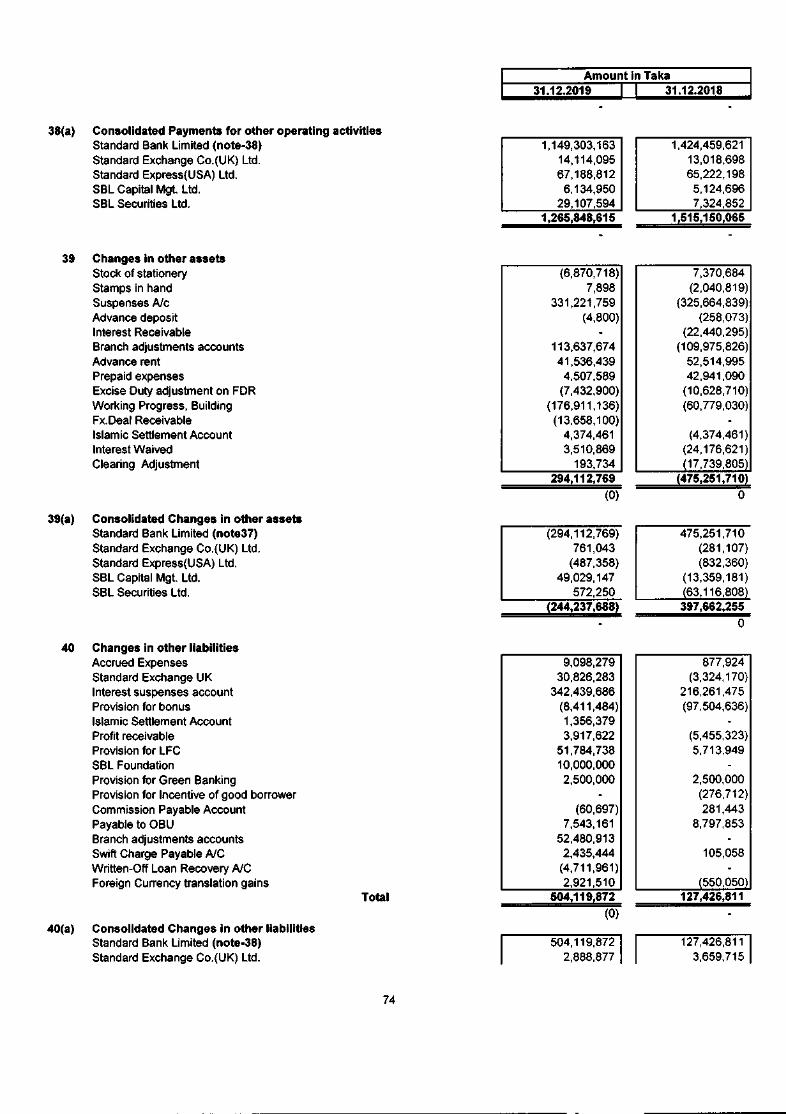

A) CASHFLOWSFROMOPERATINGACTIVITIESInterest receipts in CashInterest payments in CashDividend receiptsFee and commission receipts in CashRecoveries on loans previously written offCash Payments to employeesCash Payments to suppliersIncome taxes paidReceipts from other operating activitiesPayments for other operating activitiesCash generated from operating activities before changes inoperating assets and liabilitiesIncrease I (Decrease) in operating assets and liabilitiesStatutory depositsPurchase of trading securitiesLoans and advances to other banksLoans and advances to customersOther assets 39(a)Deposits from other banksDeposits from customersOther liabilities account of customersTrading liabilitiesOther liabilities 40(a)

18,756,529,541 15,552,596,890(12,266,388,543) (10,294,722,237)

17,981,150 24,602,475777,641,930 698,382,518

4,711,961(2,815,853,026) (2,142,135,682)(119,757,273) (98,304,073)(933,053,360) (822,823,558)

37 (a) 667,185,058 886,588,02938 (a) 11 265 848 615) 11 515150065)

40(b) 2,818,436,862 2,293,746,257

Net cash flows from operating activities (A)B) CASH FLOWSFROMINVESTINGACTlVITlES

Proceeds from sale of non-trading securitiesPayments for Purchase of securitiesPurchase of property, plant & equipmentSale of property, plant & equipmentPurchase I sale of subsidiaryNet cash flow from Investing activities (8)

C) CASHFLOWSFROMFINANCINGACTIVITIESReceived from issue of loan capital and debt securityReceived for redemption of loan capital and debt securityReceipts from issue of ordinary sharesDividends paidNet cash flow from financing activities (C)

D) NET INCREASElIDECREASE) IN CASH AND CASH EQUIVALENTS IA+B+C)

E) EFFECTS OF EXCHANGE RATE CHANGES ON CASH AND CASH EQUIVALENTS

F) CASH AND CASH EQUIVALENTS AT BEGINNING OF THE YEAR

G) CASH AND CASH EQUIVALENTS AT END OF THE QUARTER ID+E+F)

CASHAND CASH EQUIVALENTSAT END OFTHEQUARTERCash in hand (including foreign currencies)Balance wilh Bangladesh Bank and ils agenl bank(s)( including foreigncurrencies)Balance with other Banks and financial institutionsMoney at Call and Short NoticeGovt. Security/Reverse repo (Less:Revaluation Reserve on Investment)Prize Bonds

Net Operating Cash Flows (NOCF) per Share

These financial statements should be read in conjunction with annexed notes

Director

Dated, DhakaMarch 24, 2020

Director

(18,758,361) 67,555,913

(14,564,723,293) (17,832,623,425)244,237,687 (397,662,254)

(2,870,000,000) (840,000,000)22,691,723,196 20,885,344,749

498,650,131 (1,332,249,481 )698742781 i499 092 100i

6,679,872,141 51 2734029,498,309,003 2,345,019,659

(94,225,056) (28,181,632)108,342 220,987

(94,116,714) (27,960,645)

(400,000,000) (400,000,000)

(400,000,000) (400,000,000)

9,004,192,289 1,917,059,013

400,672,934 438,891,630

32,055,990,539 29,700,039,894

41,460,855,762 32,055,990,537

1,874,124,644 1,546,002,400

10,931,915,380 8,138,801,252

1,932,919,549 1,652,918,892117,400,000 150,000,000

26,600,110,889 20,565,331,6924385300 2936300

41146018551762 32105519901537

9.91 2.45

Subject to our separate report of even date

Khan Wahab Shafique Rahman & Co.Chartered Accountants

10

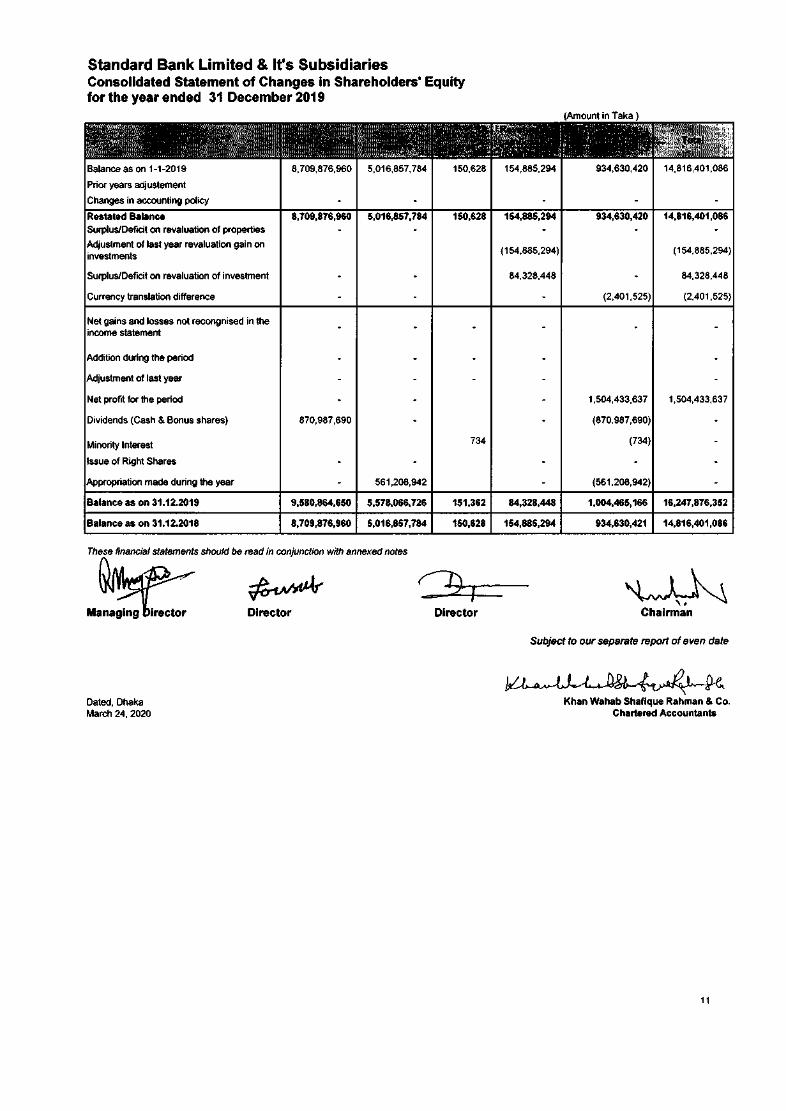

Standard Bank Limited & It's SubsidiariesConsolidated Statement of Changes in Shareholders' Equityfor the year ended 31 December 2019

Balance as on 1-1-2019 8,709,876,960 5,016,857,784 150,628 154,885,294 934,630,420 14,816,401,086

Prior years adjustementChanges in accounting policy

Restated Balance 8,709,876,960 5,016,857,784 150,628 154,885,294 934,630,420 14,816,401,086Surplus/Deficit on revaluation of propertiesAdjustment of last year revaluation gain on (154,885,294) (154,885,294)investments

Surplus/Deficit on revaluation of investment 84,328,448 84,328,448

Currency translation difference (2,401,525) (2,401,525)

Net gains and losses not recongnised in theincome statement

of last year

Net profit for the period 1,504,433,637 1,504,433,637

Dividends (Cash & Bonus shares) 870,987,690 (870,987,690)

Minority Interest 734 (734)

Issue of Right Shares

made during the year 561,208,942 (561,208,942)

Balance as on 31.12.2019 9,580,864,650 5,578,066,726 151,362 84,328,448 1,004,465,166 16,247,876,352

Balance as on 31.12.2018 8,709,876,960 5,016,857,784 150,628 154,885,294 934,630,421 14,816,401,086

These financial statements should be read in conjunction with annexed notes

M~~ ~,

~Director Director Chairman

Subject to our separate report of even date

Dated, DhakaMarch 24, 2020

Khan Wahab Shafique Rahman & Co.Chartered Accountants

11

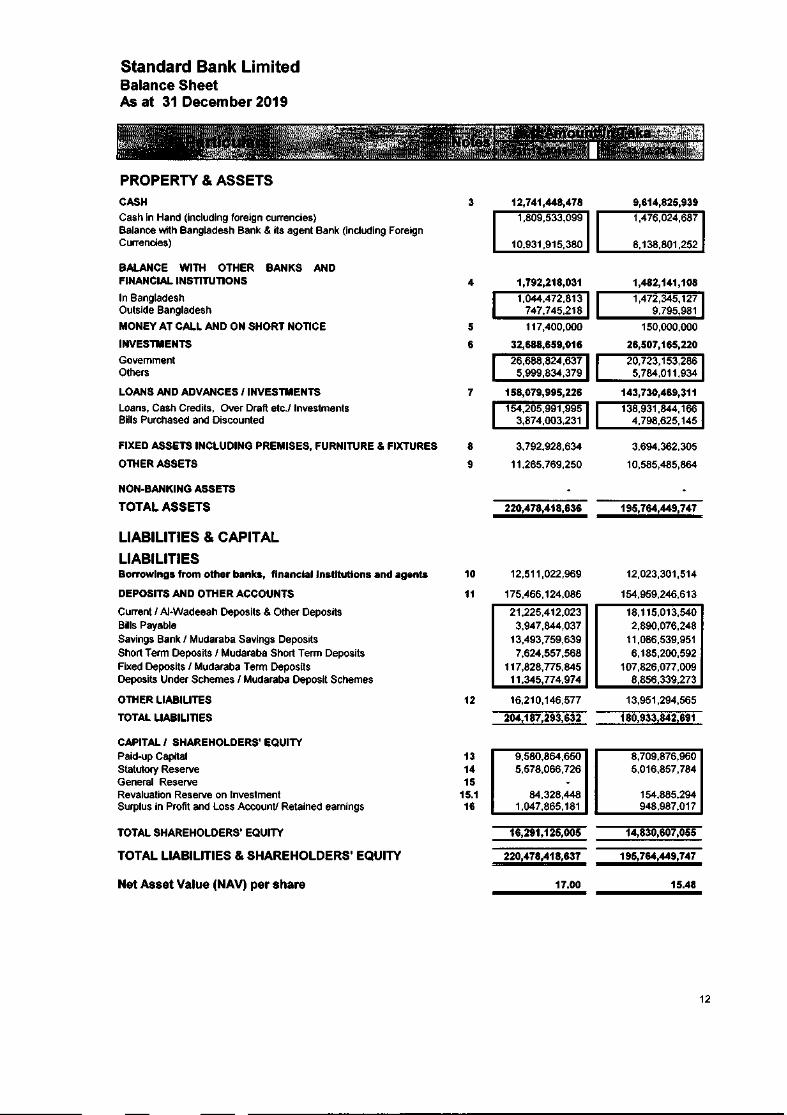

Standard Bank LimitedBalance SheetAs at 31 December 2019

PROPERTY& ASSETSCASHCash in Hand (including foreign currencies)Balance with Bangladesh Bank & its agent Bank (including ForeignCurrencies)

BALANCE WITH OTHER BANKS ANDFINANCIAL INSTITUTIONS

In BangladeshOutside Bangladesh

MONEY AT CALL AND ON SHORT NOTICE

INVESTMENTS

GovemmentOthers

LOANS AND ADVANCES 'INVESTMENTS

Loans, Cash Credits, Over Draft etc.llnvestmentsBills Purchased and Discounted

FIXED ASSETS INCLUDING PREMISES, FURNITURE & FIXTURES

OTHER ASSETS

NON-BANKING ASSETS

TOTAL ASSETS

LIABILITIES & CAPITALLIABILITIESBorrowings from other banks, financial Institutions and agents

DEPOSITS AND OTHER ACCOUNTS

Current' AJ-Wadeeah Deposits & Other DepositsBills PayableSavings Bank' Mudaraba Savings DepositsShort Term Deposits' Mudaraba Short Term DepositsFixed Deposits' Mudaraba Term DepositsDeposits Under Schemes' Mudaraba Deposit Schemes

OTHER LlABILlTES

TOTAL LIABILITIES

CAPITAL' SHAREHOLDERS' EQUITYPaid-up CapitalStatutory ReserveGeneral ReserveRevaluation Reserve on InvestmentSurplus in Profit and Loss AccounV Retained earnings

TOTAL SHAREHOLDERS' EQUITY

TOTAL LIABILITIES & SHAREHOLDERS' EQUITY

Net Asset Value (NAV) per share

3 12,741,448,4781,809,533,099

9,614,825,939

10,931,915,380

1,476,024,687

4 1,792,218,031

8,138,801,252

1,044,472,813747,745,218

5

6

117,400,000

32,688,659,01626,688,824,6375,999,834,379

1,482,141,1081,472,345,127

9,795,981150,000,000

26,507,165,22020,723,153,2865,784,011,934

143,730,469,311138,931,844,1664,798,625,145

3,694,362,305

10,585,485,864

195,764,449,747

12,023,301,514

154,959,246,613

7 158,079,995,226154,205,991,995

3,874,003,231

18,115,013,5402,890,076,24811,086,539,9516,185,200,592

107,826,077,0098,856,339,273

8

9

3,792,928,634

11,265,769,250

13,951,294,565

180,933,842,691

220,478,418,636

10

11

12,511,022,969

175,466,124,086

21,225,412,0233,947,844,03713,493,759,6397,624,557,568

117,828,775,84511,345,774,974

16,210,146,577

204,187,293,632

8,709,876,9605,016,857,784

12

13141515.116

154,885,294948,987,017

9,580,864,6505,578,066,726

84,328,4481,047,865,181

14,830,607,055

195,764,449,747

15.48

12

16,291,125,005

220,478,418,637

17.00

Standard Bank LimitedBalance SheetAs at 31 December 2019

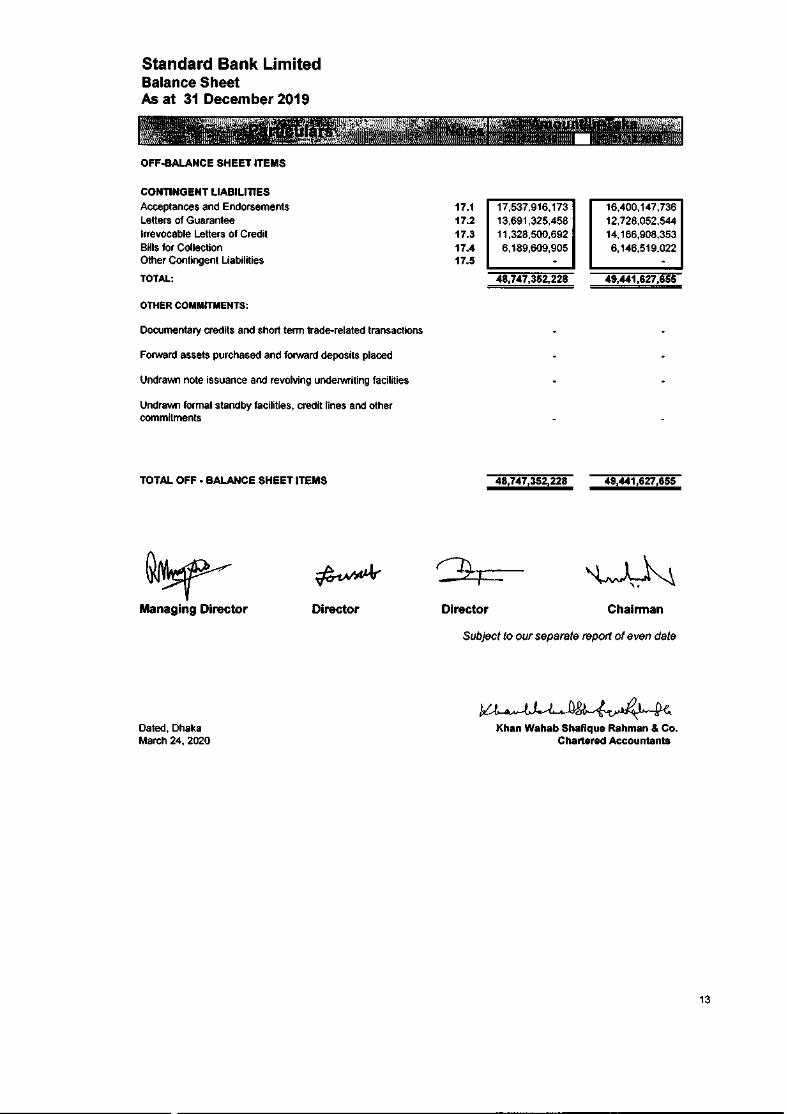

OFF-BALANCE SHEET ITEMS

CONTINGENT LIABILITIESAcceptances and EndorsementsLetters of GuaranteeIrrevocable Letters of CreditBills for CollectionOther Contingent Liabilities

TOTAL: 49,441,627,655

17.117.217.317.417.5

17,537,916,17313,691,325,45811,328,500.6926.189,609.905

16,400.147.73612,728.052.54414,166.908,3536,146.519.022

48,747,352,228

OTHER COMMITMENTS:

Documentary credits and short term trade-related transactions

Forward assets purchased and forward deposits placed

Undrawn note issuance and revolving underwriting facilities

Undrawn formal standby facilities. credit lines and othercommitments

TOTAL OFF - BALANCE SHEET ITEMS 48,747,352,228 49,441,627,655

Managing Director Director Director Chairman

Subject to our separate report of even date

Dated, DhakaMarch 24, 2020

Khan Wahab Shaflque Rahman & Co.Chartered Accountants

13

Standard Bank LimitedProfit and Loss Accountfor the year ended 31 December 2019

Interest Income I Profit on InvestmentInterest I Profit paid on Deposits & Borrowings etc.Net Interest I Net Profit on Investments

Investment IncomeCommission, Exchange Earnings & BrokerageOther Operating Income

TOTAL OPERATING INCOME (A)

Salary & AllowancesRent, Taxes, Insurance, Electricity etc.Legal ExpensesPostage, Stamp, Telecommunication etc.Stationery, Printing, Advertisement etc.Managing Director's salary & feesDirectors' Fee & Other benefitsAudit FeesCharges on loan lossesDepreciation and Repair of Bank's AssetsOther ExpensesTOTAL OPERATING EXPENSES (B)Profit I (Loss) Before Provision ( C ) = ( A • B )Provision for Loans I Investments 34Specific ProvisionGeneral ProvisionProvision for Off-Balance Sheet itemsProvision for diminution in value of investmentsOther ProvisionTotal Provision ( D )

Total Profit I (Loss) before Taxes (E)=( C • D )Provision for Taxation 35Current TaxDeferred Tax

Net Profit I (Loss) after Taxation:Retained earnings brought forwardNet Profit available for distributionAppropriations:Statutory ReserveGeneral reserveDividendRetained Earnings carried forward

Earning Per Share (EPS):

1819

4,234,717,588

202122

1,738,046,891999,881,423444402452

1,705,963,5331,022,613,963522397305

3,182,330,7666,905,855,413

3,250,974,8017,485,692,389

2324252627282930313233

2,743,218,639 2,059,315,460631,951,069 570,336,81820,548,242 20,753,56223,740,487 27,496,405116,578,379 93,090,436

7,530,000 10,540,0005,983,943 6,690,5641,774,750 862,500

. .292,677,255 245,229,671414872 061 553968025

4,258,874,8253,226,817,563

3,588,283,4413,317,571,972

320,995,935 1,080,709,816107,150,579 114,006,356(7,373,663) 13,752,400

. .- -

16.1

420,772,851 1,208,468,572

2,806,044,712 2,109,103,4001 306967516 854 366 7751,292,637,114 839,757,986

14330402 14608789

1,499,077,196 1,254,736,625109,996,927 116,071,072

1,609,074,123 1,370,807,697

561,208,942 421,820,680

1,047,865,181 948,987,017

1.5611 1.31136

These financial statements should be read in conjunction with annexed notes

Director Director Chairman

Subject to our separate report of even date

Dated, DhakaMarch 24, 2020

Khan Wahab Shafique Rahman & Co.Chartered Accountants

14

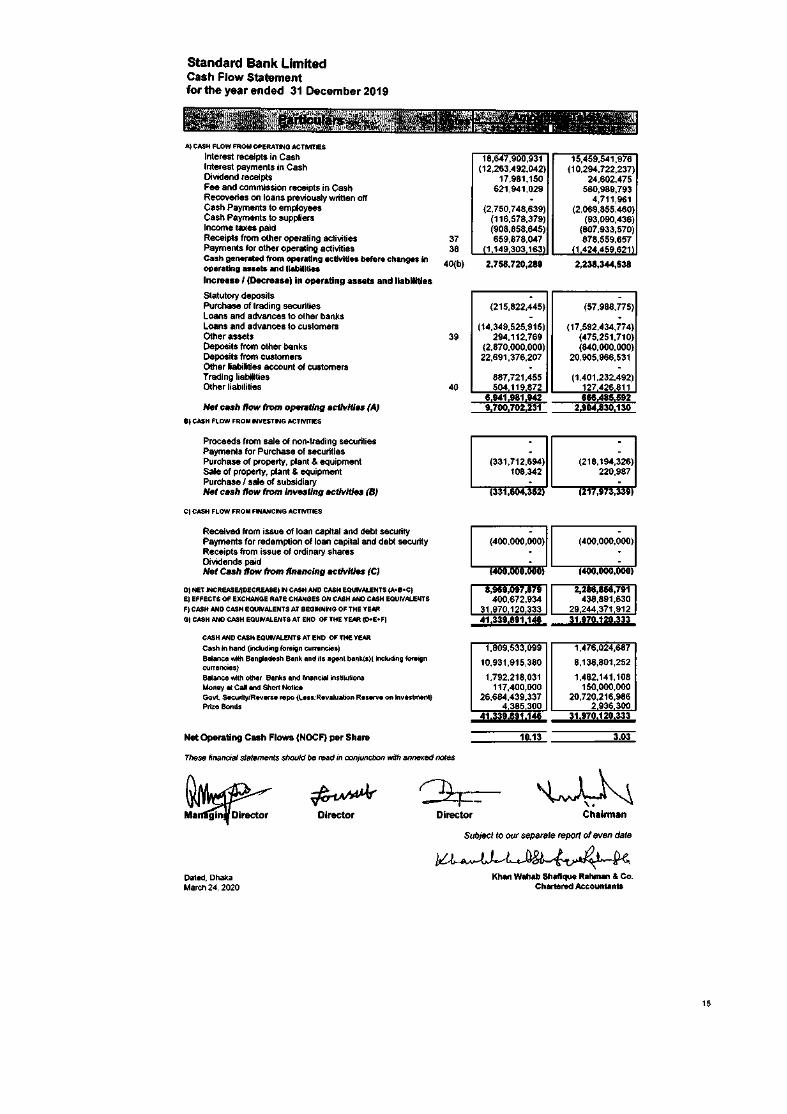

Standard Bank LimitedCash Flow Statementfor the year ended 31 December 2019

A) CASHFLOWFROMOPERATINGACTIVITIESInterest receipts in CashInterest payments in CashDividend receiptsFee and commission receipts in CashRecoveries on loans previously written offCash Payments to employeesCash Payments to suppliersIncome taxes paidReceipts from other operating activitiesPayments for other operating activitiesCash generated from operating activities before changes Inoperating assets and liabilitiesIncrease I (Decrease) In operating assets and liabilities

Statutory depositsPurchase of trading securitiesLoans and advances to other banksLoans and advances to customersOther assetsDeposits from other banksDeposits from customersOther liabilities account of customersTrading liabilitiesOther liabilities

Net cash flow from operating activities (A)B) CASHFLOWFROMINVESTINGACTIVITIES

Proceeds from sale of non-trading securitiesPayments for Purchase of securitiesPurchase of property, plant & equipmentSale of property, plant & equipmentPurchase I sale of subsidiaryNet cash flow from investing activities (B)

C) CASHFLOWFROMFINANCINGAcrrvmEs

Received from issue of loan capital and debt securityPayments for redemption of loan capital and debt securityReceipts from issue of ordinary sharesDividends paidNet Cash flow from financing activities (C)

D) NETINCREASEI(DECREASE)IN CASHANDCASHEQUIVALENTS(A_B_C)E) EFFECTSOFEXCHANGERATECHANGESONCASHANDCASHEQUIVALENTSF) CASHANDCASHEQUIVALENTSAT BEGINNINGOFTHEYEARG)CASHANDCASHEQUIVALENTSAT END OF THEYEAR (D-E-F)

CASHANDCASHEQUIVALENTSAT END OF THEYEARCash in hand (including foreign currencies)Balance with Bangladesh Bank and its agent bank(s)( including foreigncurrencies)Balance with other Banks and financial institutionsMoney at Call and Short NoticeGovt. Security/Reverse repo (Less: Revaluation Reserve on Investment)Prize Bonds

Net Operating Cash Flows (NOCF) per Share

These financial statements should be read in conjunction with annexed notes

3738

40(b)

18,647,900,931 15,459,541,976(12,263,492,042) (10,294,722,237)

17,981,150 24,602,475621,941,029 560,989,793- 4,711,961

(2,750,748,639) (2,069,855,460)(116,578,379) (93,090,436)(908,858,645) (807,933,570)659,878,047 878,559,657

(1 149303163 (1424459621)2,758,720,289 2,238,344,538

39

- -(215,822,445) (57,988,n5)- -

(14,349,525,915) (17,592,434,774)294,112,769 (475,251,710)

(2,870,000,000) (840,000,000)22,691,376,207 20,905,966,531- -

887,721,455 (1,401,232,492)504119872 12742681140

6,941,98119429,700,702,231

6661485,5922,904,830,130

- -- -(331,712,694) (218,194,326)

108,342 220,987- -(331,604,352) (217,973,339)

- -(400,000,000) (400,000,000)

- -- -(400,000,000) (400,000,000)

2,286,856,791438,891,630

29244371 912

8,969,097,879400,672,934

31 970 120 33341,339189U48 311970,120,333

1,809,533,099 1,476,024,68710,931,915,380 8,138,801,2521,792,218,031 1,482,141,108117,400,000 150,000,000

26,684,439,337 20,720,216,9864385300 2936300

41,339,891,148

10,13

311970,120,333

3,03

Director ChairmanDirector

Dated, DhakaMarch 24, 2020

Subject to our separate report of even date

Khan Wahab Shafique Rahman & Co.Chartered Accountants

15

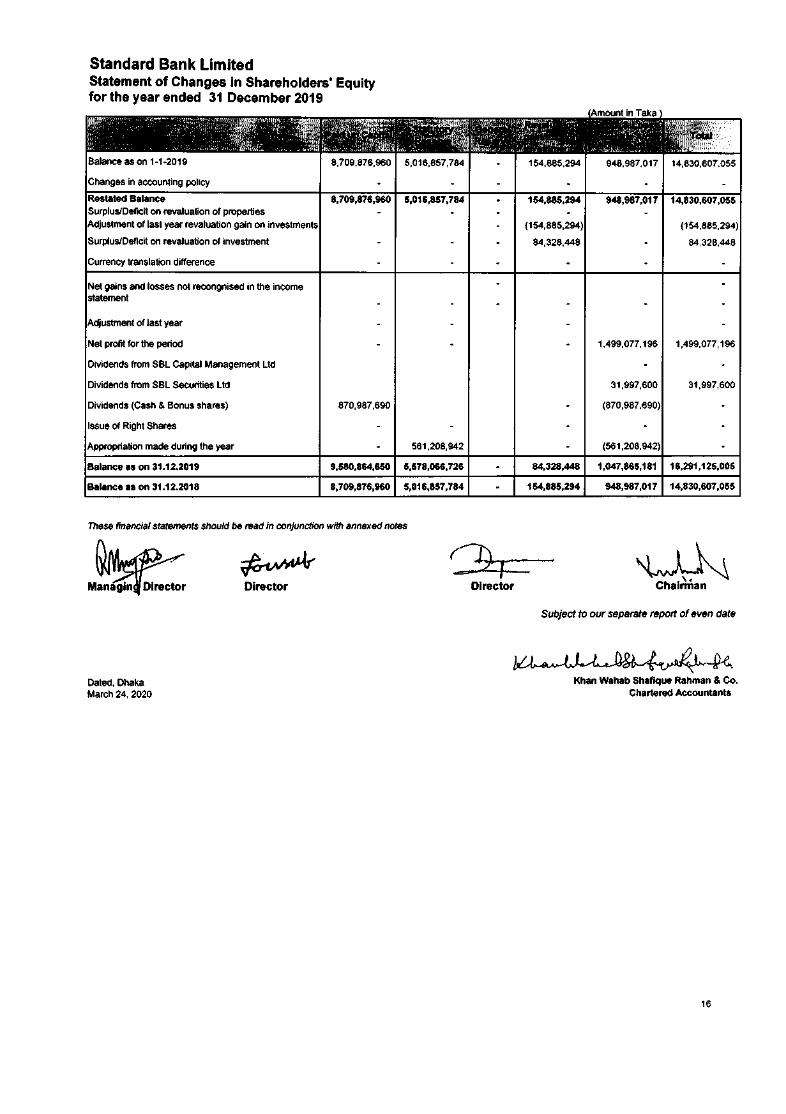

Standard Bank LimitedStatement of Changes in Shareholders' Equityfor the year ended 31 December 2019

870,987,690

1"~IJU5;tmlemoflast year revaluation gain on investments

Surplus/Deficit on revaluation of investment

Currency translation difference

31,997,600

154,885,294 948,987,017

(154,885,294)

84,328,448 84,328,448

Net gains and losses not recongnised in the incomestatement

Net profit for the period

Dividends from SBl Capital Management Ltd

Dividends from SBl Securities Ltd

Dividends (Cash & Bonus shares)

Issue of Right Shares

1,499,077,196 1,499,077,196

31,997,600

(870,987,690)

as on 31.12.2019

as on 31.12.2018

These financial statements should be read in conjunction with annexed notes ~,DirectorDirector

Dated, DhakaMarch 24, 2020

~ Chairman

Subject to our separate report of even date

Khan Wahab Shafique Rahman & Co,Chartered Accountants

16

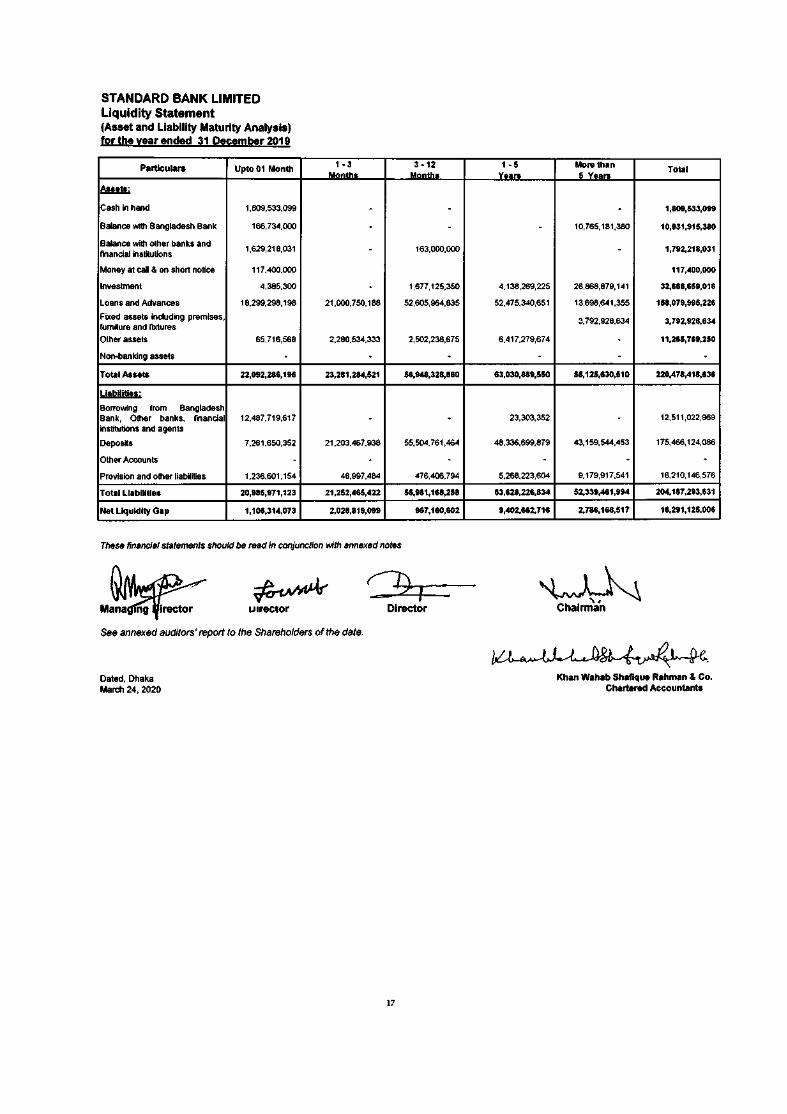

STANDARD BANK LIMITEDLiquidity Statement(Asset and Liability Maturity Analysis)for the year ended 31 December 2019

Particulars Upto 01 Month 1·3 3·12 1 ·5 More than TotalMonth. Month. V..a", ~ V..ant

~Cash in hand 1,809,533,099 · · · 1,809,533,099

Balance with Bangladesh Bank 166,734,000 · · . 10,765,181,380 10,931,915,380

Balance with other banks and 1,629,218,031 163,000,000financial institutions · · 1,792,218,031

Money at caD & on short notice 117,400,000 117,400,000

Investment 4,385,300 · 1,677,125,350 4,138,269,225 26,868,879,141 32,688,659,016

Loans and Advances 18,299,298,198 21,000,750,188 52,605,964,835 52,475,340,651 13,698,641,355 158,079,995,226

Fixed assets including premises, 3,792,928,634 3,792,928,634fumiture and fixturesOther assets 65,716,568 2,280,534,333 2,502,238,675 6,417,279,674 · 11,265,769,250

Non-banking assets . · · . ·Total Asseta 22,092,285,196 23,281,284,521 56,848,328,860 63,030,889,550 55,125,630,510 220,478,418,636

liabilities:

Borrowing from BangladeshBank, Other banks, financial 12,487,719,617 · · 23,303,352 · 12,511,022,969institutions and agents

Depos~s 7,261,650,352 21,203,487,938 55,504,761,464 48,338,699,879 43,159,544,453 175,466,124,086

Other Accounts . · · . . .

Provision and other liabilities 1,238,601,154 48,997,484 476,406,794 5,268,223,604 9,179,917,541 16,210,146,576

Total Liabilities 20,985,971,123 21,252,465,422 55,981,168,258 53,628,226,834 52,339,461,994 204,187,293,631

Net liquidity Gap 1,106,314,073 2,028,819,099 967,160,602 9,402,662,716 2,786,168,517 16,291,125,006

These financial statements should be read in conjunction with annexed notes

uirector Director~

ChairmanCJ),

See annexed auditors' report to the Shareholders of the date.

Dated, DhakaMarch 24, 2020

Khan Wahab Shafique Rahman & Co.Chartered Accountanta

17

Standard Bank LimitedNotes to the Financial Statementsfor the year ended 31 December 2019

1. LEGAL STATUSANDNATUREOF THE COMPANYStandard Bank Limited was incorporated in Bangladesh as a Public Limited Company with limited liability underthe Companies Act, 1994 on II th May, 1999 and commenced commercial operation on 3rd June, 1999. The Bankwent for the public issue of shares in 2003 and its shares are listed with Dhaka Stock Exchange Ltd and ChittagongStock Exchange Ltd. Now it has 138 Branches allover Bangladesh.The commercial banking activities of the Bank encompass a wide range of services including accepting deposits,making loans, discounting bills, conducting money transfer and foreign exchange transactions and performing otherrelated services such as safe keeping, collections, issuing guarantees, acceptances and letters of credit.

a) Conventional Banking:The principal activities of the bank are to provide all kinds of commercial banking services to its respectedcustomers through its branches, SME branches, ATM outlets, Agent Banking outlets and foreign currency Booths.

b) Islamic Banking:The Bank operates Islamic banking in two branches designated for this purpose in complying with the rules ofislamic shariah. A separate balance sheet, income statement are presented as recommended by the Central ShariahBoard for Islamic Banking in Bangladesh.

c) Off-Shore Banking Unit (OBU) :The Bank obtained OtT-shore Banking Unit Permission vide Letter No. BRPD (P-3)744(110)/2010-839 datedMarch 11,2010 and commenced operation on March 23, 2015. The OtT-shore Banking Unit is governed under therules and guidelines of Bangladesh Bank. The principal activities of the Unit are to provide all kinds of commercialbanking services to its customers in foreign currencies approved by the Bangladesh Bank.

d) Mobile Financial Services 'Spot Cash' & Digi banking:With the view to bring the unbanked people to the banking facilities SBL started Mobile Banking Services underthe title of 'Spot Cash' in 2014. The bank obtained the license from Bangladesh Bank for mobile banking businessvide letter no. PSD/37(Q)/2013-1035 dated 3rdSeptember, 2013.

SBL DigiBaning is an app based solution which connects customers to bank's core banking system securely so thatcustomer can carry out the transaction 2417 from anywhere.This documents clearly describes the day to dayoperational process ofSBL DigiBanking System.

1.1 Subsidiary Companies1.1(a) SBL Capital Management Ltd (SCML):

The Bank obtained permission to embark upon Merchant banking from the Bangladesh Securities and ExchangeCommission(BSEC) vide its certificate no. SECIReglMB/SUBII3/2010/529 dated January 05, 2011 Under theSecurities and Exchange Commission Act,1993. The main objectives of the Company are to carry out the businessof full fledged merchant banking activities like issue management, portfolio management, underwriting, corporateadvisory services etc.

1.1(b) Standard Exchange Company (UK)Limited:Bangladesh Bank vide their letter No.BRPD(M) 204/15/2009-18 Dated 15th February 2009 has accorded approvalto the bank for opening a fully owned subsidiary company in the name and style of Standard Exchange Company(UK) Limited. The company was incorporated 19th March, 2009 under the Companies Act 2006 of UK with theregistration number 06851946 as private company limited by shares. The registered office is located at 101whitechapel Road, London. The main activities of the exchange house are to carry on the remittance business andto undertake and participate in transactions, activities and operation commonly carried on or undertaken byremittance and exchange houses.

1.I(c) Standard Co (USA)Inc.DBA : Standard Express:Bangladesh Bank vide their letter No. BRPD(M) 204115/2009-116 Dated 27th October ,2009 has accordedapproval to the bank for opening a fully owned subsidiary company in the name and style of Standard Co (USA)Inc.DBA: Standard Express, in short we presented "Standard Express (USA) Ltd". The company was incorporatedon 151 February, 2010 with the registration number 27-2118554 as private company limited by shares. Theregistered office is located at 37-22 73'd street #28 Jackson heights, New York. The main activities of the exchangehouse are to carry on the remittance business and to undertake and participate in transactions, activities andoperation commonly carried on or undertaken by remittance and exchange houses.

18

1.1(d) Standard Bank Securities LimitedStandard Bank Securities Limited was incorporated on November 22,2012 as a public limited company under theCompanies Act ,1994 vide certificate of incorporation no. C-I05725/12. Standard Bank Securities Limited becomemember of Dhaka Stock Exchange Limited for brokerage transaction. Standard Bank Securities Limitedcommenced its operation from 21 June, 2013. The main objectives of the company is to carry on the business ofstock broker Istock dealer and other related business in connection with the dealing of listed securities . Otherobectives of the company are to buy,sell, hold or otherwise acquire or invest the capital of the company inshares, stocks and fixed income securities etc.

2. SIGNIFICANT ACCOUNTING POLICIES2.1 Statement of compliance

The financial statements of the Bank have been prepared in accordance with "First Schedule" (section 38) of theBank Companies Act, 1991 (amendment upto 2018) ,International Financial Reporting Standards (IFRSs) and therequirements of the Banking Companies Act, 1991 (amendment upto 2018), the rules and regulations issued byBangladesh Bank, the Companies Act ,1994. In case any requirement of the Banking Companies Act 1991 asamended, and provisions and circulars issued by Bangladesh Bank differ with those of IFRSs, the requirements ofthe Banking Companies Act 1991 as amended, and provisions and circulars issued by Bangladesh Bank shallprevail. Material departures from the requirements oflFRSs are as follows:

i) Basis of Preparation for Financial Statements

IFRSs: As per lAS I Financial Statements shall comprise statement of financial position, comprehensive incomestatement, changes in equity, cash flows statement, adequate notes comprising summary of accounting policies andother explanatory information. As per para 60 ofiAS I, the entity shall also present current and non-current assetsand current and non-current liabilities as separate classifications in its statement of financial position.

Bangladesh Bank: The presentation of the financial statements in prescribed format (i.e. balance sheet, profit andloss account, cash flows statement, changes in equity, liquidity statement) and certain disclosures therein are guidedby the "First Schedule" (section 38) of the Bank Companies Act, 1991 (amendment upto 2013) and BRPD Circularno. 14 dated 25 June, 2003 and subsequent guidelines ofBB. In the prescribed format there is no option to presentassets and liabilities under current and non-current classifications.

Bank's Methodology: The Financial statements of the Bank are made upto 31st December 2019 and are preparedunder the historical cost convention and in accordance with the "First Schedule (Sec-38) of the Bank CompaniesAct, 1991, BRPD Circular # 14 dated 25 June 2003, other Bangladesh Bank Circulars, International AccountingStandards and International Financial Reporting Standards adopted by the Institute of Chartered Accountants ofBangladesh, Companies Act, 1994, the Securities and Exchange Rules 1987, Dhaka & Chittagong Stock ExchangeListing Regulations and other laws and rules applicable in Bangladesh. In case of the requirement of BangladeshBank differs with those ofiASIIFRS ,the requirement of Bangladesh Bank have been applied" .

ii) Investments in shares and SecuritiesIFRS: As per requirements of IFRS 9 investment in shares and securities generally falls either under "at fair valuethrough profit and loss account" or under "available for sale" where any change in the fair value (as measured inaccordance with IFRS 13) at the year-end is taken to profit and loss account or revaluation reserve respectively.

Bangladesh Bank: As per BRPD circular no. 14 dated 25 June ,2003 investments in quoted shares and unquotedshares are revalued at the year end at market price and as per book value oflast audited balance sheet respectively.Provision should be made for any loss arising from diminution in value of investment; otherwise investments arerecognised at cost.

iii) Revaluation gains/losses on Government securitiesIFRS: As per requirement of IFRS 9 where securities will fall under the category of Held for Trading (HFT), anychange in the fair value of held for trading assets is recognised through profit and loss account. Securitiesdesignated as Held to Maturity (HTM) are measured at amortised cost method and interest income is recognisedthrough the profit and loss account.

Bangladesh Bank: HFT securities are revalued on the basis of mark to market and at year end any gains onrevaluation of securities which have not matured as at the balance sheet date are recognised in other reserves as apart of equity and any losses on revaluation of securities which have not matured as at the balance sheet date arecharged in the profit and loss account. Interest on HFT securities including amortisation of discount are recognisedin the profit and loss account. HTM securities which have not matured as at the balance sheet date are amortised atthe year end and gains or losses on amortisation are recognised in other reserve as a part of equity.

iv) Provision on Loans and AdvanceslInvestments

19

IFRS: As per IFRS 9 an entity should start the impairment assessment by considering whether objective evidenceof impairment exists for financial assets that are individually significant. For financial assets that are notindividually significant, the assessment can be performed on an individual or collective (portfolio) basis.

Bangladesh Bank: As per BRPD Circular no. 03,Dated 21 April,2019, 14 dated 23 September 2012, and BRPDCircular no. 16 dated 18 November 2014, a general provision @ 0.25% to 5% under different categories ofunclassified loans (Standard/SMA loans) should be maintained regardless of objective evidence of impairment.And specific provision for sub-standard/doubtful/bad-Ioss loans should be made at 20%, 50% and 100%respectively on loans net off eligible securities (if any). Also, a general provision @ 1% should be provided forcertain off-balance sheet exposures except bills for collections. Such provision policies are not specifically in linewith those prescribed by IFRS 9.

v) Recognition of interest in suspenseIFRS: Loans and advances to customers are generally classified as 'loans and receivables' as per IFRS 9 andinterest income is recognised through effective interest rate method over the term of the loan. Once a loan isimpaired, interest income is recognised in profit and loss account on the same basis based on revised carryingamount.

Bangladesh Bank: As per BRPD circular no. 14 dated 23 September 2012, once a loan is classified (other thanbad loss), interest on such loans are not allowed to be recognised as income, rather the corresponding amount needsto be credited to an interest in suspense account, which is presented as liability in the balance sheet.

vi) Other comprehensive incomeIFRS: As per lAS I Other Comprehensive Income (OCI) is a component of financial statements or the elements ofOCI are to be included in a single Other Comprehensive Income statement.

Bangladesh Bank: Bangladesh Bank has issued templates for financial statements which will strictly be followedby all banks. The templates of financial statements issued by Bangladesh Bank do not include OtherComprehensive Income nor are the elements of Other Comprehensive Income allowed to be included in a singleOther Comprehensive Income (OCI) Statement. As such the Bank does not prepare the other comprehensive incomestatement. However, elements of OCI, if any, are shown in the statements of changes in equity.

vii) Financial instruments - presentation and disclosureIn several cases Bangladesh Bank guidelines categories, recognise, measure and present financial instrumentsdifferently from those prescribed in IFRS 9. As such full disclosure and presentation requirements ofiFRS 7 andlAS 32 cannot be made in the financial statements.

viii) Financial guaranteesIFRS: As per IFRS 9, financial guarantees are contracts that require an entity to make specified payments toreimburse the holder for a loss it incurs because a specified debtor fails to make payment when due in accordancewith the terms of a debt instrument. Financial guarantee liabilities are recognised initially at their fair value, and theinitial fair value is amortised over the life of the financial guarantee. The financial guarantee liability issubsequently carried at the higher of this amortised amount and the present value of any expected payment when apayment under the guarantee has become probable. Financial guarantees are included within other liabilities.

Bangladesh Bank: As per BRPD 14 dated 25June,2003, fmancial guarantees such as letter of credit, letter ofguarantee will be treated as off-balance sheet items. No liability is recognised for the guarantee except the cashmargin.

ix) Repo transactionsIFRS: When an entity sells a financial asset and simultaneously enters into an agreement to repurchase the same (ora similar asset) at a fixed price on a future date (REPO or stock lending), the arrangement is accounted for as acollateralized borrowing and the underlying asset continues to be recognized in the financial statements. Thistransaction will be treated as borrowing and the difference between selling price and repurchase price will betreated as interest expense.Bangladesh Bank: As per BB circulars/guidelines, when a bank sells a financial asset and simultaneously entersinto an agreement to repurchase the same (or a similar asset) at a fixed price on a future date (REPO or stocklending), the arrangement is accounted for as a normal sale transaction and the financial assets should bederecognized in the sellers book and recognized in the buyer's book.

x) Cash and cash equivalentIFRS: Cash and cash equivalent items should be reported as cash item as per lAS 7.Bangladesh Bank: Some cash and cash equivalent items such as 'money at call and on short notice', treasury bills,Bangladesh Bank bills and prize bond are not shown as cash and cash equivalents. Money at call and on shortnotice presented on the face of the balance sheet, and treasury bills, prize bonds are shown in investments.

20

xi) Non-banking assetIFRS: No indication of Non-banking asset is found in any IFRS.Bangladesh Bank: As per BRPD 14, dated 25 June ,2003, there must exist a face item named Non-banking asset.

xii) Cash flow statementIFRS: The Cash flow statement can be prepared using either the direct method or the indirect method. Thepresentation is selected to present these cash flows in a manner that is most appropriate for the business or industry.The method selected is applied consistently.

Bangladesh Bank: As per BRPD 14,dated 25 June ,2003, cash flow is the combination of direct and indirectmethods.

Bank's Methodology: Cash Flow Statement is prepared in accordance with IAS-7 "Cash Flow Statement" underdirect method and indirect method as recommended in BRPD circular no. 14 dated 25 June ,2003 issued byBangladesh Bank.

xiii) Balance with Bangladesh Bank: (Cash Reserve Requirement)IFRS: Balance with Bangladesh Bank should be treated as other asset as it is not available for use in day to dayoperations as per lAS 7.Bangladesh Bank: Balance with Bangladesh Bank is treated as cash and cash equivalents.

xiv) Off-balance sheet itemsIFRS: There is no concept of off-balance sheet items in any IFRS; hence there is no requirement for disclosure ofoff-balance sheet items on the face of the balance sheet.

Bangladesh Bank: As per BRPD 14, dated 25 June ,2003 ,off balance sheet items (e.g. Letter of credit, Letter ofguarantee etc) must be disclosed separately on the face of the balance sheet.

Bank's Methodology:Off-Balance Sheet items have been disclosed under contingent liabilities and other commitments as per BangladeshBank's guidelines. BRPD circular NO.7 dated 21 June, 2018 requires a general provision for Off Balance Sheetexposures except bills for collections to be calculated @ I%which has been followed by the bank properly on thefollowing Off Balance Sheet Items:a. Acceptance and endorsementsb. Irrevocable letter of creditc. Letter of guarantee

xv) Presentation of intangible assetIFRS: An intangible asset must be identified and recognised, and the disclosure must be given as per lAS 38.Bangladesh Bank: There is no regulation for intangible assets in BRPD 14 dated 25 June ,2003 hence,it is shownin fixed assets.

xvi) Loans and advanceslInvestments net of provisionIFRS: Loans and advanceslInvestments should be presented net of provision.Bangladesh Bank: As per BRPD 14, dated 25 June ,2003 provision on loans and advances/investments arepresented separately as liability and can not be netted off against loans and advances.Bank's Methodology: Loans and advances have been shown at gross amounts at 31 December 2019.

xvii) Disclosure of appropriation of profitIFRS: There is no requirement to show appropriation of profit in the face of statement of comprehensive income.

Bangladesh Bank: As per BRPD 14, dated 25 June 2003, an appropriation of profit should be disclosed on theface of Profit & Loss Account.

xviii) Implication ofIFRS 16 "Leases"The Bank currently has lease agreements at 131 (One hundred thirty one) of its branch offices and has incurred Tk.37,76,83, 552.00 as expenses on the lease payments. The leases are short term leases with different tenure.Resultantly the leases are not treated as right-of-use assets. As such the effect of IFRS 16 is very immaterialcompared to the volume of whole financial statements.

2.2 Basis of Consolidation:The consolidated financial statements include the financial statements of Standard Bank Limited, Islamic BankingWindow, Offshore Banking Units (OBU) and its subsidiaries SBL Capital Management Ltd, Standard BankSecurities Ltd, Standard Exchange Company (UK) Ltd and Standard Co (USA) Inc.DBA : Standard Express madeup to the end of the financial year. A Banking software system "Stelar" consolidated all transactions of branches aswell as head office and produces consolidated Balance Sheet and Profit & Loss Account . These consolidatedrecords are maintained at the Head office of the Bank based on which these financial statements have beenprepared.The consolidated financial statements have been prepared in accordance with International Financial ReportingStandard 10: consolidated financial statements & lAS 27 Separate Financial Statements. The consolidated financialstatements have been prepared to a common reporting period ending in 31 December,2019.

21

Subsidiaries:Subsidiaries are that enterprise which are controlled by the Bank. Control exists when the Bank has thepower,directly or indirectly , to govern the financial and operating policies of an enterprise from the date thatcontrol commences until the date that control ceases. The financial statements of subsidiary are included in theconsolidated fmancial statements from the date that control effectively commences until the date that the controleffectively ceases. Subsidiary Companies are consolidated using the cost method of accounting.

Transactions eliminated on Consolidation:All intra-Company balances & transactions, and any unrealised income & expenses (Except for foreign currencytranslation gain/losses) arising from intra-company transactions are eliminated in preparing consolidated financialstatement. Unrealised losses are eliminated in the same way as unrealised gains but only to the extent that there isno evidence of impairment. The investments in shares of subsidiaries held by the bank in the separate FinancialStatements are eliminated against the corresponding shares capital of subsidiaries in the consolidated financialstatements.

2.3 Statement of Cash flowsStatement of cash flows is prepared by using the 'Direct Method' in accordance with lAS 7 "Statement of CashFlows" and under the guidance of Bangladesh Bank BRPD Circular No. 14 dated 25.06.2003 & BRPD CircularNo. 15 dated 09.11.2009 whereby gross cash receipts and gross cash payments on Operating Activities, InvestingActivities and Financing Activities have been recognized. Cash and Cash Equivalents comprise short term, highlyliquid investments that are readily convertible and are subject to an insignificant risk to changes in value.

2.4 Reporting PeriodThese financial statements cover one calendar year from January 01 to December 31, 2019.

2.5 Statement of Changes in EquityStatement of changes in Equity has been prepared in accordance with lAS I "Presentation of Financial Statements"and under the guidance of Bangladesh Bank BRPD Circular No. 14 dated 25.06.2003 & BRPD Circular No. 15dated 09.11.2009

2.6 Statement of LiquidityThe liquidity statement of assets and liabilities as on reporting date has been prepared on residual maturity term asper following basis:a. Balance with other banks and financial institutions ,money at call etc are on the basis of their maturity term.b. Investments are on the basis of their residual maturity.c. Loans and advances are on the basis of their repayment/maturity schedule.d. Fixed assets are on the basis of their useful lives.e. Other assets are on the basis of their realization lamortization.f. Borrowing from other banks, financial institutions and agents as per their maturity Irepayment terms.g. Deposits and others accounts are on the basis of their maturity term and behavioral past trend.h. Others loan term liabilities are on the basis of their maturity term .i. Provisions and other liabilities are on the basis of their settlement.

2.7 Significant Judgement and Estimates

The preparation of Financial Statements in conformity with Accounting Standards and Statutory requirement whichrequires the use of critical accounting estimates. It also requires management to exercise its judgment in the processof applying accounting policies. The areas involving a higher degree of judgment or complexity or major areaswhere assumptions and estimates are significant to the Financial Statements are described in the following:

I Income Taxes2 Deferred Taxation3 Depreciation4 Provisions for investment & other

2.8 Goin~ ConcernThe accompanying financial statements have been prepared on a going concern basis,which contemplates therealization of assets and the satisfaction of liabilities in the normal course of busines.The accompanying financialstatements do not include any adjustments should the Bank be unable to continue as a going concern.

2.9 FOREIGN CURRENCY TRANSACTION

a) Fereign Currencies Transactioni) Transaction in foreign currencies are converted into taka at the foreign exchange rates ruling on the

transaction date.ii) Monetary assets and liabilities in foreign currency are expressed in taka terms at the rates of exchange

ruling on the balance sheet date.

22

iii) Forward foreign exchange contracts and foreign bills purchased are valued at forward rates applicable totheir respective maturities.

b) CommitmentsCommitments for outstanding forward foreign exchange contracts disclosed in these financial statements aretranslated at contracted rates. Contingent liabilities/commitments for letters of credit and letters of guaranteedenominated in foreign currencies are expressed in taka terms at the rates of exchange ruling on the balancesheet date.

c) Translation gains and lossesThe resulting exchange transaction gains and losses are included in the profit and loss account, except thosearising on the translation of net investment in foreign branches, subsidiaries and associates.

2.10 Loans write-offLoans are normally written off, when there is no realistic prospect of recovery of these amounts and in accordancewith BRPD Circular No.1 (6th February, 2019). A separate Credit Recovery Division (CRD) has been set up at theBanks Head Office which monitors loans written off and legal action taken through the Arth Rin Adalat. Thesewrite -offs do not undermine or affect the amount claimed against the borrower by the bank.

The CRD maintains a separate ledger for all individual cases written offby each branch. The CRD follow up on therecovery efforts of these written off loans and reports to management on periodic basis. Written off loans andadvances are reported to the Credit Information Bureau (CIB) of Bangladesh Bank.

2.11 Earning Per ShareThe company calculates Earning Per Share (EPS) in accordance with International Accounting Standards (lAS)-33"Earning Per Share" which has been shown on the face of profit and loss account. This has been calculated bydividing the Basic earnings by the weighted average number of ordinary shares outstanding during the year.

2.12 Retirement benefits to the employeesProvident FundProvident Fund benefits are given to the employees of the bank in accordance with the locally registered ProvidentFund Rules. Separate Board of Trustee of the Bank operates it.GratuityThe Bank operates an Employees Gratuity Fund Trust by a Board of Trustees consisting of seven members. Allconfirmed employees who have been in the service of the Bank should eligible to have the benefit under the gratuityschemes. The Gratuity trust rule got recognised from the National Board of Revenue(NBR). The bank has startedmaking provision against gratuity from the year 2006. Provision for the year ended 31 December 2019 for thescheme has been made and the entire amount of the gratuity fund are transferred to a savings account under thecontrol of the Board of trustee.

Welfare FundStandard Bank Limited Employees' Welfare Fund is subscribed by monthly contribution of the employees. TheBank also contributes to the fund from time to time. The fund is established to cover the accidental coverage in theevent of death or permanent disabilities, retirement benefit and stipend to the employees' children.Workers Profit Participation Fund (WPPF)Consistent with the industry practice and in accordance with The Bank Company Act. 1991, no provision has beenmade for WPPF.

2.13 SBL FoundationThe Bank, as part of corporate social responsibility , has established SBL Foundation for the benefit of thecommunity in which it operates and as part of its said responsibility it commits itself to human development,poverty alleviation and overall national economic development. The Bank contributes to the fund from the annualprofit of the bank on requirement basis. The fund is governed and administered by the Board of Trustees consistingof seven members.

2.14 Significant accounting policiesThe accounting policies set out below have been applied consistently to all periods presented in these financialstatements, and have been applied consistently by group entities except otherwise instructed by the Central Bank asprime regulator. Certain comparative amounts in the financial statements have been reclassified and rearranged toconform to the current year's presentation.Accounting policies of subsidiariesThe financial statements of subsidiaries which are included in the Consolidated Financial Statements of the Grouphave been prepared using uniform accounting policies of the Bank (Parent) for transactions and other events insimilar nature. The financial statements of subsidiaries have been prepared using the year ended 31 December 2019which is also same for the Bank. There is no significant restriction on the ability of subsidiaries to transfer funds tothe parent in the form of cash dividends or to repay loans and advances.

23

A. Assets and basis of their valuationCash and cash equivalentsCash and cash equivalents include notes and coins in hand and at ATM, unrestricted balances held withBangladesh Bank and its agent bank, balance with other banks and financial institutions, money at call and on shortnotice and prize bond which are not ordinarily susceptible to change in value.

ii) Investments

i)

All investments (other than government treasury securities) are initially recognized at cost, including acquisitioncharges associated with the investment. Accounting treatment of government treasury securities (categorized asHFTorHTM) is made following Bangladesh Bank DOS Circular no. 05 dated 26 May, 2008 and subsequentclarifications on 28 January, 2009.

Held to Maturity (HTM)Investments which are intended to be held till maturity are classified as "Held to Maturity". These are measured atamortized cost at each year end by taking into account any discount or premium on acquisition. Premiums areamortized and discount are accredited, using the effective or historical yield method. Any increase or decrease invalue of such investments is booked to equity.

Held for Trading (HFT)These are investments primarily held for selling or trading. After initial recognition, investments are marked tomarket weekly and any decrease in the present value is recognized in the Profit and Loss Account and any increaseis booked to Revaluation Reserve Account through Profit and Loss Account as per Bangladesh Bank DOS Circularno. 05 dated 28 January, 2009.

REPO and Reverse REPOSince I September 20 10 transactions of REPO and Reverse REPO are recorded based on DOS Circular no. 06,dated 15 July, 2010 of Bangladesh Bank. In case ofREPO of both coupon and non-coupon bearing (Treasury bill)securities, the Bank adjusts the Revaluation Reserve Account for HFT securities and stops the weekly revaluation(if the revaluation date falls within the REPO period) of the same security. For interest bearing security, the Bankdoes not accrue interest during REPO period.Investments -Initial recognition and subsequent measurement at a glanceValue of investments has been shown as under'

Items ADDlicable Accountinl! ValueGovernment Treasurv Bills and Bonds (HFn At nresent value (usinz markinz to market concept)Government Treasury Bills and Bonds (HTM) At present value (using amortization concept)Bangladesh Government Islamic Bond At costPrize Bond At costShares & Debentures At costInvestment in SubsidiariesInvestment in subsidiaries are accounted for under the cost method of accounting in the Bank's financial statementsin accordance with lAS 27 "Separate Financial Statements and IFRS 10 Consolidated Financial Statements" andIFRS 3 "Business Combination". Impairment of investment in subsidiaries is made as per the provision of lAS 36"Impairment of Assets".

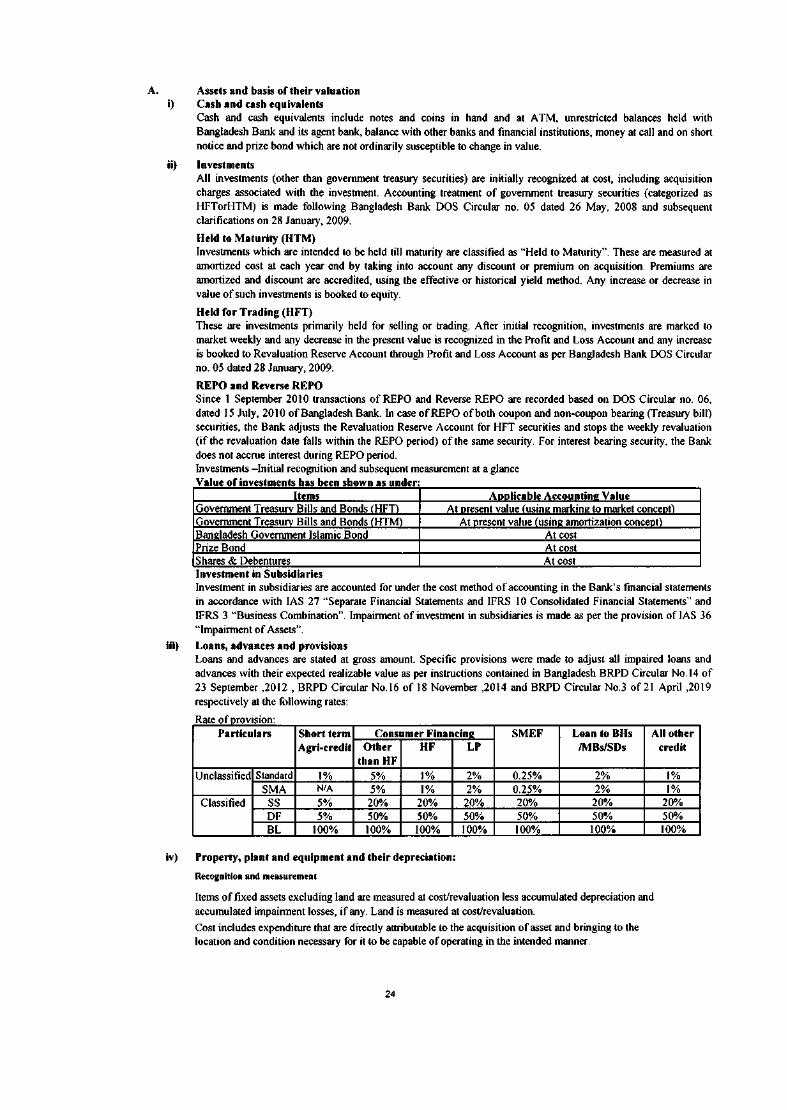

iii) Loans, advances and provisionsLoans and advances are stated at gross amount. Specific provisions were made to adjust all impaired loans andadvances with their expected realizable value as per instructions contained in Bangladesh BRPD Circular No.14 of23 September ,2012, BRPD Circular No.16 of 18 November ,2014 and BRPD Circular No.3 of21 April ,2019respectively at the following rates:

fRate 0 .prOVISIOn:Particulars Short term Consumer Financing SMEF Loan to BHs All other

Agri-credit Other HF LP IMBs/SDs creditthan HF

Unclassified Standard 1% 5% 1% 2% 0.25% 2% 1%SMA N/A 5% 1% 2% 0.25% 2% 1%

Classified SS 5% 20% 20% 20% 20% 20% 20%DF 5% 50% 50% 50% 50% 50% 50%BL 100% 100% 100% 100% 100% 100% 100%

iv) Property, plant and equipment and their depreciation:

Recognition and measurement

Items of fixed assets excluding land are measured at cost/revaluation less accumulated depreciation andaccumulated impairment losses, ifany. Land is measured at cost/revaluation.Cost includes expenditure that are directly attributable to the acquisition of asset and bringing to thelocation and condition necessary for it to be capable of operating in the intended manner.

24