Kenya Stabilization and Adjustment: Toward Accelerated Growth

185

Repoit No.9047-KE Kenya Stabilization and Adjustment: Toward Accelerated Growth October 17, 1990 Countrv Operations Division Eastern AfricaDepartment AfricaRegion FOR OFFICIAL USE ONLY Document of the World Bank Thisdocument has a restricted distribution andmaybe used by recipients only in the performance of their officialduties. Its contents may not otherwise bedisclosed withoutWorld Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Kenya Stabilization and Adjustment: Toward Accelerated Growth

Repoit No. 9047-KE

KenyaStabilization and Adjustment: TowardAccelerated GrowthOctober 17, 1990

Countrv Operations DivisionEastern Africa DepartmentAfrica Region

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Major Acronyis and Abbreviations

AFC Agriculture Finance CorporationASAL Arid and Semi-Arid LandsCBK Central Bank of KenyaCBS Central Bureau of StatisticsCLSMB Cotton Lint and Seed Marketing BoardCPI Consumer Price IndexDFI Development Finance InstitutionEEC European Economic CommunityEC Export CompensationEPZ Export Processing ZoneGATT General Agreement on Tariffs and TradeGDP Gross Domestic ProductGNFS Goods and Non-Factor ServicesHBS Household Budget SurveyICDC Industrial and Commercial Development BankICOR Incremental Capital Output RatioIDB Industrial Development BankIPC Investment Promotion CentreILO International Labour OfficeIMF International Monetary FundKAM Kenya Association of ManufacturersKGGCU Kenya Grain Growers Cooperative UnionKIE Kenya Industrial EstatesKMC Kenya Meat CommissionLPG Liquid Petroleum GasMUB Manufacturing-Under-BondNBFI Near-Bank Financial InstitutionNCPB National Cereals and Produce BoardNSE Nairobi Stock ExchangeNSSF National Social Security FundPOSB Post Office Savings BankPPI Producer Price IndexRER Real Exchange RateREER Real Effective Exchange RateRMPA Restrictive Trade Practices, Monopolies and Price Control ActSONY South Nyanza Sugar CompanyTSC Teachers' Services ComrnissionUBC Uplands Bacon CompanyULFS Urban Labour Force SurveyVAT Value Added TaxWPI Wholesale Price Index

NOTE: This report uses the convention of denoting fiscal years with an "FY" while periodaverages are shown as "-"; i.e., FY89 refers to fiscal year 1988/89 (July 1, 1988 toJune 30, 1989) and FY88-89 refers to the period 1987/88 to 1988/89. Academic andcrop years are also denoted with a "/"; e.g., crop year 1988/89. The notation ".."used in tables indicates that data are not available, and "-" indicates not applicable.

FOR OFFICIAL USE ONLY

Preface

The last comprehensive economic memorandum for Kenya, Recent Economic Developmentsand Selected Policy Issues (7411-KE), was issued in September 1988. This report, prepared as abackground document for the Kenya Consultative Group Meeting to be held in Paris on November19-20, 1990, updates recent economic develooments, focusing on stabilization and structuraladjustment issues and prospects for accelerated growth.

The first part of this report reviews Kenya's economic performance over recent years. Theevolution of major macroeconomic aggregates is briefly analyzed in Chapter 1. Recent fiscaldevelopments are reported only briefly, since both the last economic report as well as the 1989report, Kenya: Public Expenditure Issues (7508-KE), extensively covered fiscal and expenditureissurs. This chapter includes a discussion of recent inflationary trends in Kenya and somemeasurement problems. Chapter 2 attempts to evaluate implementation of sectoral adjustmentprograms in agriculture, industry and trade, and finance. The Chapter also provides a brief analysisof the types of reforms that would need to be considered to deepen adjustment in these sectors.Chapter 3 adopts a slightly different approach from that of past economic reports. Since Kenya hasexperienced a marked economic recovery in recent years, the analysis and projections attempt toanswer the quesdon: what would it take for Kenya to achieve faster economic growth?

This report is based on the findings of a mission which visited Kenya from June 25 to July20, 1990. The mission consisted of: Ian Bannon (mission leader, Eastern Africa Department), NishaAgrawal (Eastern Africa Department), Colin Bruce (Eastern Africa Department), Gerard Byam(Eastern Africa Department), and Kathleen Jordan (Eastern Africa Department). Also contributingto this report were: Richard Anson (Regiona' Mission in Eastern Africa), Roboid Covington (EasternAfrica Department), Sudhir Shetty (Eastern Africa Department), and David Ndii (Regional Missionin Eastern Africa).

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

TITLE: KENYA - STABILIZATION AND ADJUSTMENT: TOWARDACCELERATED GROWTH

COUNTRY: KENYA

REGION: EASTERN AFRICA

REPORT NO, TY CLASIFICATION MM/YY LANGUAGE9047-KE CEM Official Use 10/90 English

ABSTRACT: lIb report examines Kenya's recent growth and stabilization experience, progressin secol adjusment and th remaining medium-term agenda, and the need to adopt a bolder andm comprehensive reform effort in order to accelerate economic growth. Kenya has sustained a

marled ecoomic recovery over the past five years, averaging annual real growth of over S percent.The recovery, however, is somewhat fragile as it has relied excessively on foreign savings to financeimports and public expenditures. Over the past three years, the Government has made progress instabilzaon, reducing tde budget deficit and reliance on borrowing from the domestic baringsystem, but the level of government expenditures remains high and inflationary pressures haveresurfaced over the past two years. Implementation of the Government's sector adjustment programsin agricultre, industry and the financial sector, combined with a relatively improved macroeconomicfamework have cotibuted to the recovery in output and investment growth. Given Kenya's goodgrowth performance in recent years, the report examines the type of reform effort that would berequired to sstain and accelerate economic and social development. In addition to improvingmacrcnmi management, especially in fiscal policy, and deepening the reform process in keyproducdve sectrs, a fastr pace of development would require a major effort to reduce regulationsand controls on private sector activity, improve the quality and competence of the government itself,with particular emphasis on reform of parastatals and the civil service, as well as ensuring thateconomic growth is more equitable and environmentally sustainable.

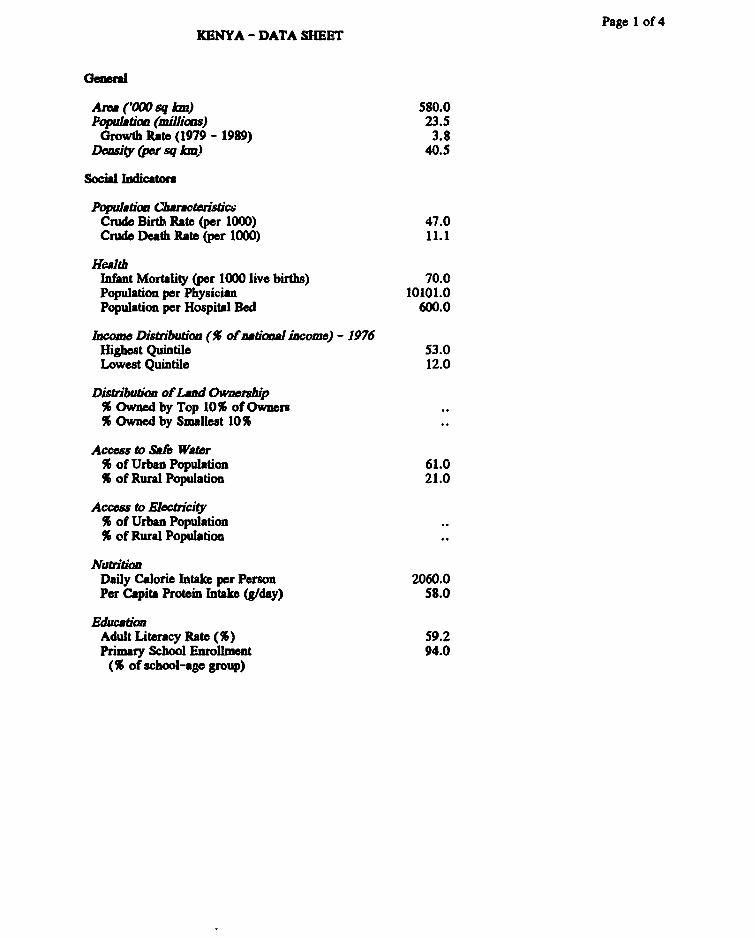

Page 1 of 4KENYA - DATA SHEET

Gema

Area ('000 sq Icn) 580.0Population (millions) 23.5

Growth Rate (1979 - 1989) 3.8Daity Ow sq ki) 40.5

Social dicatr

Poplation CaactedsticCrude Birth. Rate (per 1000) 47.0Crude Death Rate (per 1000) 11.1

HealdtInfant Mortality (per 1000 live births) 70.0Population per Physician 10101.0Population per Hospital Bed 600.0

lcome Distribution (X of awtioml income) - 1976Highest Quintile 53.0Lowest Quintile 12.0

Distrbution of Lnd Owrship% Owned by Top 10% of Owners% Owned by Smallest 10%

Access to Safe Water% of Urban Population 61.0% of Rural Population 21.0

Access to Electricity% of Urban Population% of Rural Population

NutriionDaily Calorie Intake per Person 2060.0Per Capita Protein Intale (glday) 58.0

EducationAdult Literacy Rate (%) 59.2Primary School Enrollment 94.0

(% of school-age group)

Gross National Product - 1989

TJ$ MII. 0fONP 9lS R4 1C 99

GNP at Market Prices 7894.6 100.0 5.5 4.1 5.5 4.7Gross Domestic Investment 2102.5 26.6 -0.1 3.4 9.3 6.6Gross National Savings 1373.4 17.4 -2.0 1.1 7.9 7.7Current Account Balance -584.2 -7.4 - - - -

Exports of Goods & NFS 1964.1 24.9 -0.0 3.8 4.6 10.1Imports of Goods & NFS 2593.3 32.8 -6.7 4.3 9.0 5.1GNP per capita 1/ 380.0

Output, Employment and Productivity - 1989

Agriculture 2198.0 31.0Industry 1415.2 19.9 ..

Manufacturing 827.8 11.7 ..

Services 3480.7 49.1 ..

Total 7093.9 100.0 10.9 100.0 652.1 100.0

Government Finance 2/(In fiscal years)

Current Receipts 1869.1 23.4 21.6Current Expenditure 1855.5 23.2 22.2

Current Surplus/Deficit 13.6 0.2 -0.6Capital Expenditures 574.3 7.2 6.9

I/ Calculated in accordance with Atlas methodology.2/ IMF estimates.

Money, Credit and Prices

Money Supply 1313.4 1346.5 1784.3 1983.3 2140.9 2417.6Bank Credit to Public Sector 541.7 598.3 883.8 1144.7 1055.4 995.2Bank Credit to Private Sector 847.2 970.7 1134.2 1284.4 1535.8 1775.6

Money as % of GDP 29.4 26.7 30.4 30.4 28.7 28.4Nairobi Consumer PI (1980 = 100) 171.7 190.1 200.7 215.0 238.0 263.1Annual percentage changes in:

Nairobi Consumer Price Index 9.1 10.7 5.6 7.1 10.7 10.6Bank Credit to Public Sector 11.8 10.4 47.7 29.5 -7.8 -5.7Bank Credit to Private Sector 10.2 14.6 16.8 13.2 19.6 15.6

Balance of Payments

Exports of Goods & NFS 3/ 1551.6 1871.4 1698.2 1869.2 1933.3Imports of Goods & NFS 4/ 1616.8 1858.7 2104.1 2306.3 2528.1

(of which Petroleum) 5/ 461.4 300.4 348.4 289.8 343.9Resource Gap (deficit = -) -65.2 12.7 -405.8 -437.1 -594.8

Factor Service Payments (net) -223.0 -258.6 -301.7 -360.0 -351.3Net Private Transfers 81.5 58.2 71.9 88.7 101.1

Balance on Current Account -206.7 -187.7 -635.6 -708.4 -845.0excl. Net Official Transfers

Net Official Transfers 110.1 148.9 142.3 256.0 279.8Balance on Current Account -96.6 -38.8 -493.3 -452.4 -565.2

incl. Net Official Transfers

Capital Account -17.9 128.9 366.7 376.4 643.3Long-term (net) -51.3 105.2 316.5 312.7 607.0Short-term (net) 45.8 20.9 56.2 53.4 52.4Errors and Omissions -12.4 2.8 -6.0 10.3 -16.1

Overall Balance -114.5 90.1 -126.6 -76.0 78.1

Monetary Movements 114.6 -90.0 126.6 76.1 -78.0Change in Reserves -22.8 -24.6 151. i -59.5 -110.5IMF Transactions 128.0 -67.1 -62.3 123.0 20.2Other 9.4 1.7 37.8 12.6 12.3

3/ Goods,f.o.b excluding aircraft and ships' stores but including re-exports.4/ Goods,f.o.b including defence imports and exc,uding cinematographic films, newspapers,

periodicals and aircrft lease.5/ Crude and derivatives.

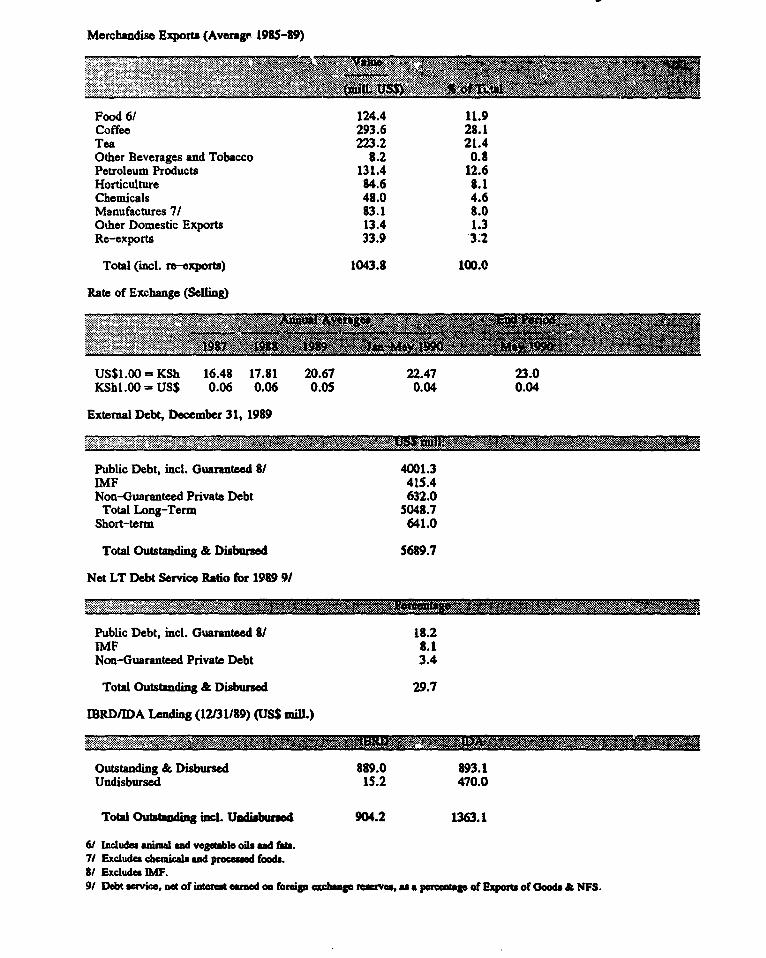

Merchandise Exports (Average 1985-89)

Food 6/ 124.4 11.9Coffee 293.6 28.1Tea 223.2 21.4Other Beverages and Tobacco 8.2 0.8Petroleum Products 131.4 12.6Horticulture 84.6 8.1Chemicals 48.0 4.6Manufactures 7/ 83.1 8.0Other Domestic Exports 13.4 1.3Re-exports 33.9 3.2

Total (incl. re-exports) 1043.8 100.0

Rate of Exchange (Selling)

US$1.00 = KSh 16.48 17.81 20.67 22.47 23.0KSh1.00 -USS 0.06 0.06 0.05 0.04 0.04

External Debt, December 31, 1989

Public Debt, incl. Guaranteed 8/ 4001.3IMF 415.4Non-Guaranteed Private Debt 632.0

Total Long-Term 5048.7Short-term 641.0

Total Outstanding & Disbursed 5689.7

Net LT Debt Service Ratio for 1989 9/

Public Debt, incl. Guaranteed 8/ 18.2IMF 8.1Non-Guaranteed Private Debt 3.4

Total Outstanding & Disbursed 29.7

IEBRD/IDA Leading (12131/89) (USS mill.)

Outstanding & Disbursed 889.0 893.1Undisbursed 15.2 470.0

Total Outanding incl. Undisbursed 904.2 1263.1

6/ Include aima nd vegeable oils nd fab.7/ Excludes chemicas and prcessd foods.8/ Excludes IMF.9/ Debt sevice, net of intereusaed om forei exchange rsrves.as a peratag of Expou of Goads A NFS.

TABLE OF CONTENTS

Sumnuary . .................................................. i

Chapter 1. Economic Growth and Stabilization ..........................

A. The Recent Economic Recovery ............. ................... 1Economic Growth, Investment and Employment ...................... 1

B. The Stabilization Path ....................................... 6Fiscal Policies ......................................... Monetary Policy ............. ............................ 11Inflation ......................................... 17The External Sector ....................................... 19Incentive Indicators ....................................... 23Short-Term Prospects ..................................... 4. 2

Annex 1.A: Measurement of Inflation in Kenya: Methodological Issues .... ..... 25Current MethodolGgy ...................................... 25Potential Biases and Inaccuracies ............ ................... 25Other Problems ........................................ 29

Chapter 2: Deepening Structural Adjustment ........................... 31

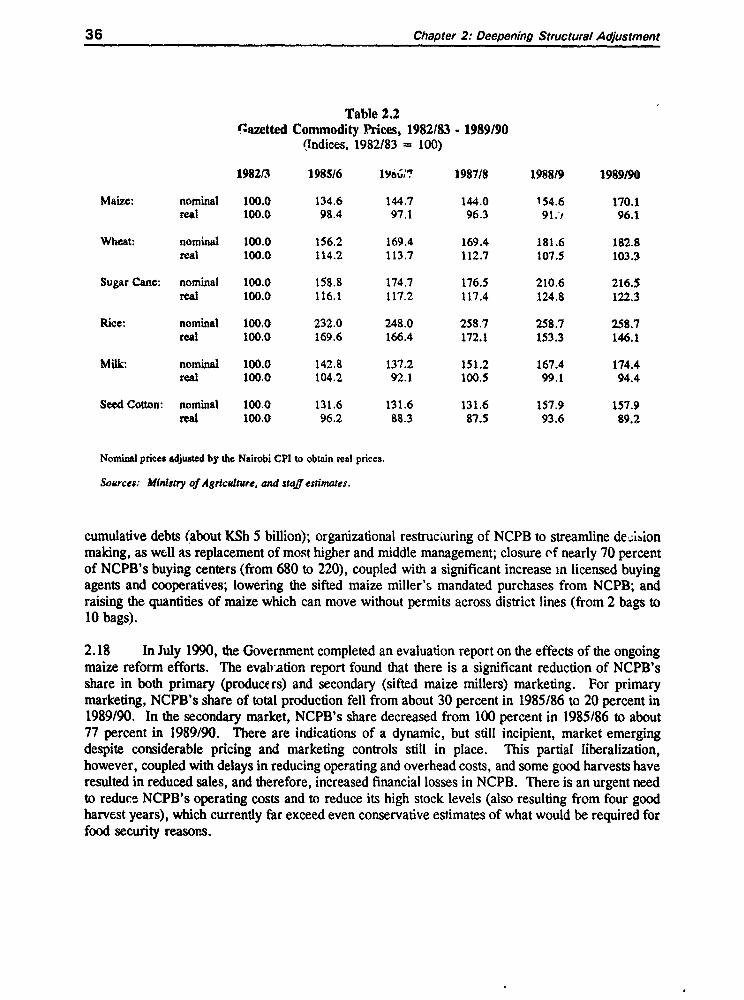

A. Reforming Agriculture ...................................... 31Structure and Reform Objecdves .......... ..................... 31Evaluation ............................................. 38The Medium-Term Agenda and Sources of Growth .................... 39

B. Adjustment in Industry and Trade .......... .................... 42Structure and Constraints . ................................... 42The Adjustment Program . ................................... 45Evaluation: The First Phase . ................................. 49The Medium-Term Agenda . .................................. 52

C. Strengthening the Financial System ......... .................... 55Structure and Constraints .................................... 55The Need for Adjustment .................................... 56Financial Sector Reforms .................................... 58The Medium-Term Agenda ................................... 60

Chapter 3: Growth Prospects . ................................... 63

A. Introduction .......................................... 63B. Toward Accderated Growth ............. .................... 63

C. Target Scenario ......................................... 67Growth Prospects ....................................... 69Consumption, Savings and Investment ............................ 70The Balance of Payments . ................................... 74Fiscal Performance ........................................ 76

D. Risks and Uncertainties . ..................................... 77Slippages in Policy Reform and Fiscal Discipline ..................... 77An Oil Shock ........................................... 80

Annex 3.A: Import Elasticities in Kenya: 1968-89 and Beyond .............. 85Approaches to the Specification of Import Elasticides ................... 85Econometric Results at a Glance ......... ...................... 86Unfinished Business ........................................ 89

Bibliographical Notes . ....................................... 93

Statistical Appendix .......................................... 99

Map

TEXT TABLES

Chapter 1

Table 1.1 Output Growth, 1980-89Table 1.2 Investment and Savings, 1985-89Table 1.3 Recordod Employment, 198549Table 1.4 Summary of Central Goveinent Finaces, FY86-90Table 1.5 Growth of Money and Credit in the Banldng System, 1985-89Table 1.6 Growth of Money and Credit in NBFIsTable 1.7 Actul Reserve Ratios, 1988-89Table 1.8 Summary of Balance of Payments, 1985-89Table 1.9 External Debt, 1985-89Table 1.10 Key Incentive Indicators, 198349

Annex l.A Measurement of Inflatn In Kenya: Methodological Issues

Table A. 1 Comparison of CPls Using Alternative WeightsTable A.2 Implicit Price Deflators, 1985-89

Chapter 2

Table 2.1 Fertlizer Availability and Usage, 1980181 - 1989/90Table 2.2 Gazetted Commodity prices, 1982/83 - 1989/90Table 2.3 Agriculture Ministries: Gross Expenditures, FY86-91Table 2.4 Personnel as Share of Total Recurrent Ministries of Agriculture

and Livestock, MY8O-90Table 2.5 Real Effective Exchange Rates (REER) and Anti-Export Bias,

1980489Table 215 Quantitative Restrictions and Average Tariffs, 1986/87-1990/91Table 2.7 Tariff Structure by End-Use, 1986/87 and 1988/89Table 2.8 Import Growth, 1988-89Table 2.9 Manufactured Exports, 1985-89

Chapter 3

Table 3.1 Aumptions Under the Target ScenarioTable 3.2 Selectd Indicators of Economic Growdt, 1985-2000Table 3.3 Seected Indicators of Economic Structure, 1985-2000Table 3.4 Aggregate Efficiency Indicators, 1986-89Table 3.5 Development Propects Without Further ReformsTable 3.6 Development Prospects After an Oil Shock

TEXI BOXES

Chapter 1

Box 1.1 Results of the 1986 Urbaa Labor Force SurveyBox 1.2 The Measurement of Inflation in KenyaBox 1.3 NBFIs and the Money Supply Target

Annex 3.A Measurement of Inflation In Kenya: Methodological L,ues

Box A. I Executive Cost of Living Indices

Chapter 3

Box 3.1 Kenya's Growth ImperativeBox 3.2 Smallholder Contribution to Agricultural Growth Prospects

Summary

Economic Growth and Stabilization. Kenya has enjoyed a marked economic recoveryover the past five years, reversing the relative stagnation of the first half of the 1980s. Followingrecovery from the severe drought in 1984, output and investment have responded to theGovernment's reform efforts and a relatively improved macroeconomic framework. Kenya'seconomic recovery is somewhat fragile, however, as it has relied on foreign savings, leaving theeconomy vulncrable to external shocks, and the remaining macroeconomic imbalances, unlesscorrected, threaten to undermine recent economic and stabilization gains. Since 1986-87, theGovernment has made progress toward stabilization, reducing the budget deficit and governmentborrowving from the domestic banking system, but the level of governrnent expenditures remains highand inflationary pressures have resurfaced over the past two years. To sustain Kenya's economicrecovery there is a need to both strengthen stabilization efforts and to deepen structural adjustment,especially toward greater export competitiveness. At the same time, however, Kenya faces a difficultexternal environment arising from the recent increase in world oil prices, which will place addedpressures on the balance of payments, the budget deficit and inflation.

ii. Economic growth slowed somewhat to 5 percent in 1989 compared to 5.2 percent in1988, largely due to lower agricultural growth. The more moderate growth in agriculture was aresult of the downturn in world coffee prices and inadequate rains in parts of the country.Manufacturing has continued to maintain annual growth rates close to 6 percent. The services sectorexpanded by 5.3 percent in 1989. Real fixed investment growth slowed considerably in 1989. Afteraveraging real aTnual growth of 6.5 percent over the period 1985-88, investment increased by only1.6 percent in 1989. Both public and private investment slowed, with public investment rising by1.5 percent and private investmnent by 1.7 percent. Although the gross investment rate at over 25percent of GDP over the past two years is high, Kenya has increasingly relied on foreign savings tofinance its capital formation. Sirce 1986, foreign savings have financed over one quarter of theeconomy's gross fixed investment. Domestic savings have maintained a downward trend since 1985as a result of both continued dissavings by the Central Governrnent and lower private savings. Therecently published 1986 Urban Labour Force Survey reveals a serious but largely static (since theprevious survey in 1977/78) urban unemployment problem in Kenya. The survey estimated an urbanunemployment rate of 16.2 percent, largely unchanged from 1977/78.

iii. Kenya's stabilization efforts have produced mixed results. While the budget deficithas been considerably reduced since 1987, the level of government spending remains high and theGovernment has found it difficult to restrain the growth of public sector employment and its attendantwage bill. After dropping sharply in 1988, money supply growth accelerated in 1989 and theeconomy appears to be overheating. Inflaton, fueled by a monetary overhang, international priceincreases, depreciation of the currency, price decontrol, and increases in agricultural producer prices,has remained above 10 percent. The Government's exchange rate policy has been appropriate butits external position has been affected by deteriorating terms of trade and the poor performance ofexports.

iv. The budget deficit (including grants), which peaked at 6.6 percent of GDP in FY87has been gradually reduced to 4.2 percent in FY90. Government spending, however, has remainedhigh at about 30 percent of GDP and the budget relies heavily on foreign financing. The budgetdeficit excluding grants has ranged between 6.5 and 7.1 percent of GDP over the past three years.

- ii -

The need to provide social services for a growing population, increased employment in the civilservice, transfers to parastatals, and increasing interest payments have all contributed to rising publicexpenditure levels.

v. As part of its stabilization program, the Government aims to contain monetaryexpansion and assign a greater role to market forces in credit allocation. Money supply growth (M2)has fluctuated over the past three years, falling from 11.2 percent in 1987, to 7.9 percent in 1988,and rising to 12.9 percent in 1989. This variability has been caused in large measure by fluctuationsin net foreign assets of the banking system. In recent years, the private sector has increased its shareof total credit from the banking system at the expense of the Central Government. The monetarypicture, however, changes considerably when near-bank financial institutions (NBFIs) are taken intoaccount. If NBFI deposits are included in a broader measure ot money supply (M3), the monetarystance in Kenya appears much more expansionary than indicated by trends in M2 alone. Theslowdown in money supply growth in 1988 as measured by M2 disappears when measured by M3,showing instead a steady acceleradon in monetary expansion since 1987--a pattern more in line withthe economy's recent inflation experience.

vi. The Government aims to adopt a market-determined interest rate structure in 1991.In recent years it has considerably raised interest rate ceilings and has removed controls on fees andcharges imposed by banks. As part of its interest rate policy, the Government has sought to widenthe spread between minimum and maximum rates to encourage commercial banks to enter the marketfor term lending, and has brought bank rates in line with those of NBFIs.

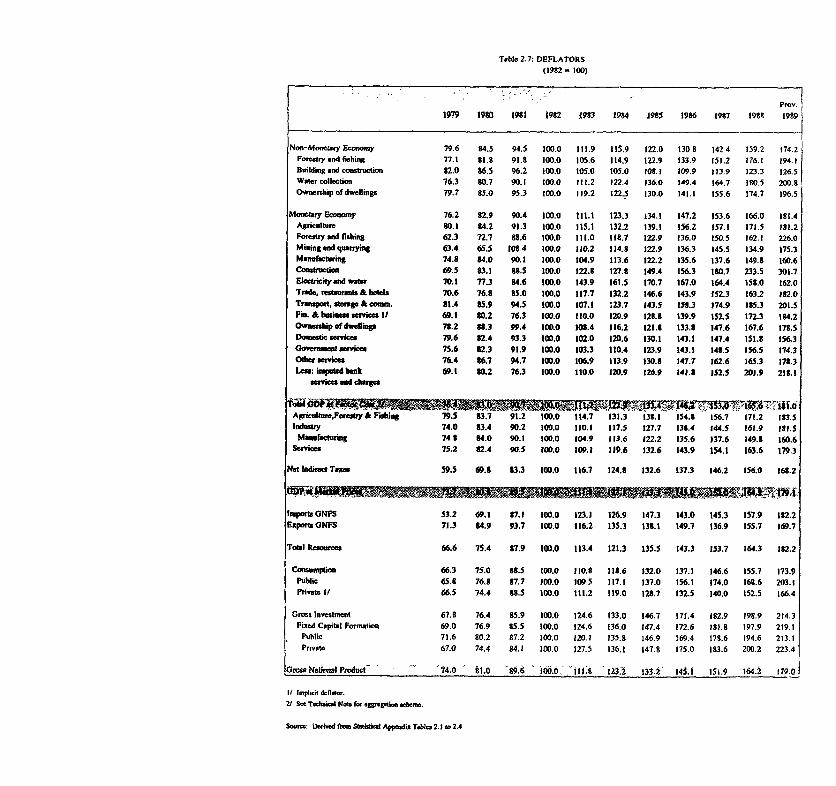

vii. The rise in inflation over the past two years has come at a time of growing concernover the accuracy of the index used to measure inflation in Kenya, the Nairobi Consumer Price Index(CPI). These concerns relate to the fact that the consumption weights and income brackets areoutdated, the inclusion of price controlled items, the treatment of housing costs, and the lack ofcoverage of price changes in rural and other urban areas. The Government is currently revising theCPI to correct some of these problems. In addition, there is a need to compute other indices suchas a Wholesale Price Index or a Producer Price Index.

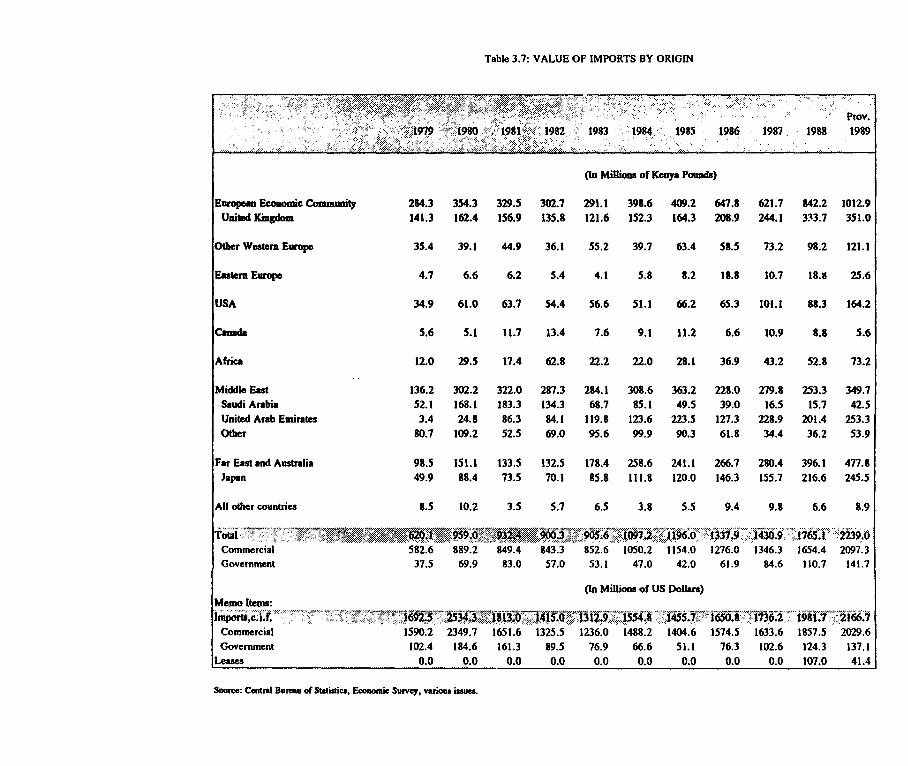

viii. Kenya's current account deficit (including grants) widened to 6.9 percent of GDP in1989, largely as a result of worsening terms of trade and the lack of growth in non-traditionalexports. Tourism continued to show strong growth, with foreign exchange earnings in 1989 of $418million, equivalent to more than 40 percent of total merchandise exports. In 1989, merchandiseimports increased by 8.9 percent in dollar terms and 5 percent in volume terms. Merchandiseexports fell by 9.1 percent in dollar terms compared with growth of 11.8 percent in 1988. Thehigher current account deficit in 1989 was financed largely through long-term borrowing by theGovernment and parastatals. Over the past three years, increased aid flows, especially quick-disbursing assistance to support the Government's adjustment program, have played a major role infinancing Kenya's current account deficit. Kenya's external debt at the end of 1989 stood at $5.7billion. As a result of debt forgiveness from a number of bilateral donors, Kenya's debt service hasfallen from $696 million in 1986 to $594 million in 1989. The total debt service has declined overthe past two years, from 38.7 percent of exports of goods and services to 29.6 percent in 1989.

ix. Kenya's economy faces difficult and uncertain short-term prospects, in large measurethe result of the recent oil crisis. Although the short-term outlook for world oil prices remainsuncertain, Kenya will face increased financing needs of at least $350 million over 1991-92 to meet

- iii -

its oil import bill. Higher oil prices are also likely to dampen economic growth and place addedpressures on government spending. Lower economic growth is likely to impact negatively ongovernment revenues, making it increasingly difficult for the Government to meet its deficit reductionobjectives unless additional revenue measures are adopted.

x. Deepening Structural Adjustment. The Government's structural adjustment effortshave focused on developing and implementing sector reform programs in agriculture, industry andtrade, and the financial sector. At the start of this process, the Government faced an extensive policyreform agenda, but assigned priority to renewing economic growth, while recognizing that reformswould need to be phased and deepened over the longer term to make growth sustainable. Althoughthe depth and coverage of reforms, as well as implementation experience, have varied in each sector,they have a number of common objectives: (i) enhancing the role of markets and the private sector;(ii) reforming incentives to encourage growth, investment and exports; (iii) rationalizing pubficexpenditures and restructuring selected parastatals; and (iv) reducing regulations and controls oneconomic activity.

xi. In early 1987, the Government adopted an agricultural reform program to increasegrowth in the sector and support fiscal stabilization. The program focused on three inter-relatedstrategies: (i) intensifying production through improved supplies of key inputs (especially fertilizers);(ii) enhancing producer incentives and market dereguladon; and (iii) improving the allocation andefficiency of public investments and expenditure in agriculture, including initial steps to formulateand implement reforms in a number of agricultural parastatals. Of the steps the Government plannedto take, actions involving fertilizers, maize marketing, and radonalization of public expenditures wereconsidered particularly important.

xii. Implementation of the agriculture reform program was rmixed. Good progress wasmade in: maintaining appropriate producer prices, and taking steps toward market deregulation(especially maize and beef); liberalizing ferdlizer prices; carrying out the financial and organizadonalrestructuring of two parastatals, NCPB and SONY; and improving cost recovery in the sector.Disappointing progress occurred in: removing supply constraints in fertilizer availability, andincreasing use; improving the efficiency of parastatals; and rationalizing the pattern of expendituresin the sector, especially by controlling the growth of employment in agriculture ministries.

xiii. In 1987, the Government began implementing an industrial sector reform program to:improve efficiency in the sector; stimulate growth and private investment; and increase exports. Thestrategy to achieve these objectives involves shifting incentives away from import substitution,exposing domesdc producers to greater competidon, and reducing controls and regulations. The firstphase of this reform program was implemented during 1988-89, with inidal actions taken in severalareas including import liberalizadon, export and investment incentives, and regulatory reform.During the second phase of the reform effort (to be implemented during 1990-92), the Governmentintends to accelerate the export supply response by sharpening the focus on export promotion,including measures to move the trade regime closer to neutrality and providing specdfic support tonon-traditional exporters, while continuing to reduce the level and variability of effective protecdon.

xiv. Although the Government implemented some policy reforms in 1986-88, acomprehensive financial sector adjustment program was launched in early 1989. This programincludes policy and institutional reforms intended to develop a more efficient and market-orientedfinancial system. Reforms aim to increase the efficiency of financial intermediadon, remove

- iv -

distortions in the mobilization and allocation of financial savings, and develop more flexible monetarypolicy instruments. Institutional reforms were designed to restore public confidence in the financialsystem, encourage development of capital markets, and to upgrade the skills required to superviseand regulate financial intermediaries. Over the past two years measures have been taken to relaxcontrols on interest rates, develop and utilize indirect monetary policy instruments, strengthen theregulatory and supervisory capacity of the Central Bank, restructure tU.lubled financial institutionsand provide incentives for capital market activity.

xv. Growth Prospects. Kenya's good economic performance in recent years has promptedmany observers to suggest that Kenyan policy makers should now set their sights beyond Sub-SaharanAfrica and seek to emulate the experience of rapidly-developing economies. This reporl argues thatimproved econonic nmanagement combined with a deepening and faster pace of adjustment, Kenyacould accelerate economic growth. The set of projections contained in Chapter 3 suggest that abolder and more determined effort would make higher economic growth possible.

xvi. Macroeconomic policies for stability and economic growth, especially focusing onfiscal policies, are necessary but far from sufficient for sustained development. They need to besupported by appropriate sectoral and regulatory policies that remove structural constraints, efficientinvestments in social and economic sectors, and improved quality and cornpetence of theGovernment. In addition, poverty alleviation and improved environmental management requirespecial attention--both in their own right and because on their influence on the sustainability ofdevelopment.

xvii. Kenya has made considerable progress in structural adjustment. As Kenya enters adeepening phase in its adjustrnent process, it faces a different and more difficult set of issues in eachsector. In a sense, during the first phase of adjustment the Government attempted to address themore immediate and, arguably, the relatively easier adjustment constraints. In agriculture, improvingproducer incentives has played a major role in stimulating agricultural growth. To sustain andaccelerate agricultural growth, however, the Government's reform effort will have to focus on themore difficult areas of liberalizing agricultural marketing and input supply, improving institutionalarrangements for research, extension and credit, and increasing the efficiency of public spending inthe sector. In the industrial sector, import liberalization of raw materials, intermediates and capitalgoods, and selected price decontrol have contributed to higher manufactnring growth. A deepeningof adjustment in the industrial sector, however, will now need to focus on lowering the level ofprotection, reducing the anti-export bias, loosening the regulatory environment, and reducinggovernment ownership in the sector. In the financial sector, the Government is taking steps toliberalize financial markets and interest rates, and to deepen capital markets. These measures willpose new challenges in terms of implementing monetary policy, regulating a freer financial system,and introducing the necessary legal and institutional changes that can deepen capital and moneymarkets. Although the Government has made substandal progress in implementing financial sectorreforms, the sustainability and impact of these measures will depend critically on the Government'sability to contain the growth in public expenditures and the budget deficit.

xviii. Although Kenya has a dynamic private sector, in recent years there has been a growingpercepdon that excessive government regulations and lack of transparency in their application areconstraining new private sector initiatives, both domestic and foreign. When coupled with the stilllarge public sector claim on the economy's resources, the regulatory environment constraints theability and willingness of the private sector to respond to improved policies and incentives. Although

- v -

the Government has made some progress in this direction, much can still be done to reduce the scopefor discretion and arbitrariness in economic decision making by simplifying and reducing controlson the private sector. The successful adoption of automatic import licensing shows that the scopefor reducing rent seeking and enhancing transparency can be greatly enhanced by removingdiscretionary powers.

xix. In creating an efficient enabling environment for development, there is a clear needto improve the quality and competence of the Government itself. Although by Sub-Saharan Africanstandards, Kenya has a competent and professional public service, a more ambidous pace of reformwould require improvements in four principal areas. First, there is a need to strengthen the coreagencies that formulate and implement economic and sectoral policies. The success of reformprograms will depend as much on Government commitment to adjustment, as on the public sector'sability to design, adopt and manage them efficiently and credibly. A critical element in this processwill be the Government's ability to mobilize the requisite support for reforms from the politicalestablishment and the public at large. Second, there is a need to rationalize and divest governmentownership of public enterprises. As discussed in this and previous Bank economic reports, the sizeand efficiency of the parastatal sector in Kenya, especially in commercially-oriented areas, is sharplyat odds with the Government's strategy of assigning the private sector a leading role in developmentand limiting government intervention to what it does best.

xx. Third, within the public sector itself there is an urgent need to improve the policiesand mechanisms for expenditure allocation, and financial management and control. Improving theway public expenditure priorities are established, reviewed and implemented is necessary tostrengthen the quality and impact of adjustment programs. Strengthening the Govermnent's budgetradonalization program and improving its public investment programing are critical priorities.Fourth, there is a need to gradually revamp personnel and incentive policies in the public sector.The problem lies not only in the large size of public sector employment in Kenya but also the qualityof personnel, which is largely linked to incentive policies. As a number of Bank reports havepointed out, continued expansion in recruitment has severely squeezed recurrent expenditureallocations to essential non-wage operations and maintenance. This constrains the flexibility of fiscalpolicy and reduces the efficiency of resource use in the public sector, especially in areas that arecritical to underpin rapid economic growth such as the provision of infrastructure and social services.In addition, the large and growing size of the civil service as well as the need to control spendingseverely hampers the Government's ability to recruit, retain and motivate qualified staff. At present,many civil service posts in the lower grades are overfilled, while middle and higher grades areunderfilled. Given that public sector salaries are not competitive with the private sector, it is notsurprising that professional and technical expertise is in short supply within the Government. Amajor civil service reform effort would need to focus on reducing recruitment at lower grades andudlizing these savings to substandally improve remunerations for skilled and professional staff.

xxi. In addition to deepening adjustment in producdve sectors and the public sector, overthe longer term Kenya faces the need ensure that economic growth is more equitable andenvironmentally sustainable. The Government's development strategy emphasizes rapid economicgrowth to reduce poverty. Although there are no reliable data on the incidence of poverty in Kenya,social indicators suggest that the process of economic development has helped to alleviate poverty,especially in light of the country's explosive populadon growth. It would be difficult to argue thata strategy that placed less emphasis on economic growth would have improved condidons for thepoor in Kenya. Poverty alleviation, however, should be a developme -t goal in itself. Many aspects

-vi -

of the Government's growth strategy are designed to benefit the poor directly, especially labor-intensive and smallholder-based growth. In addition, however, there s a need to improve theeffectiveness and targeting of public expenditure in the social sectors to ensure they directly benefitthe poor, as weHl as considering direct interventions that protect the poor from the effects of reformmeasures and assist those left behind by economic growth.

xxii. Environmental problems in Kenya stem largely from population pressures on limitedland resources. Depletion of woodlands is a major cause of land degradadon and soil erosion,contributing to lower productivity, decreased water holding capacity, a reduction of dry season wateravailability, and encroachment on wildlife and natural habitats. Environmental problems areparticularly severe in ASAL areas, which are more susceptible to ecological damage from populationpressures. The Government's immediate environmental priorities are to inprove policies andinstitutions in the forestry sector, arrest the deterioration in the wildlife sector, and begin formulatinga strategy for environmentally sustinable development in ASAL areas. While these priorities areappropriate, over the medium term there is a need to develop and implement a comprehensivenational environmental management and action program which can lay an appropriate foundation forsustainable development over the long term.

Economic Growth and Stabilization

1.01 Kenya has enjoyed a notable economic recovery over the past five years, reversing therelative stagnation of the first half of the 1980s. Following recovery from the severe 1984 drought,output and investment have responded to the Government's reform efforts and a relatively improvedmacroeconomic framework. Kenya's recovery, however, is somewhat fragile as it has relied onforeign savings, leaving the economy vulnerable to external shocks, and the remaining domesticmacroeconomic imbalances, unless corrected, threaten to undermine recent economic and stabilizadongains. Since 1986-87, the Government has made progress toward stabilization, reducing the budgetdeficit and government borrowing from the domestic banking system, but the level of governmentexpenditures remains high and inflationary pressures have resurfaced over the past two years. Tosustain Kenya's economic recovery there is a need to both strengthen stabilization efforts and todeepen structural adjustment, especially toward greater export competitiveness.

1.02 The remainder of this chapter briefly reviews recent economic performance, focusingon major output, investment and employment trends over the 1985-89 period, the evolvingmacroeconomic framework, Kenya's external position, and key incentive indicators. Progress instructural adjustment and the need to deepen the process in agrculture, industry and trade, and thefinancial sector are discussed in Chapter 2.

A. The Recent Economic Recovery

Economic Growth, Investment and Employment

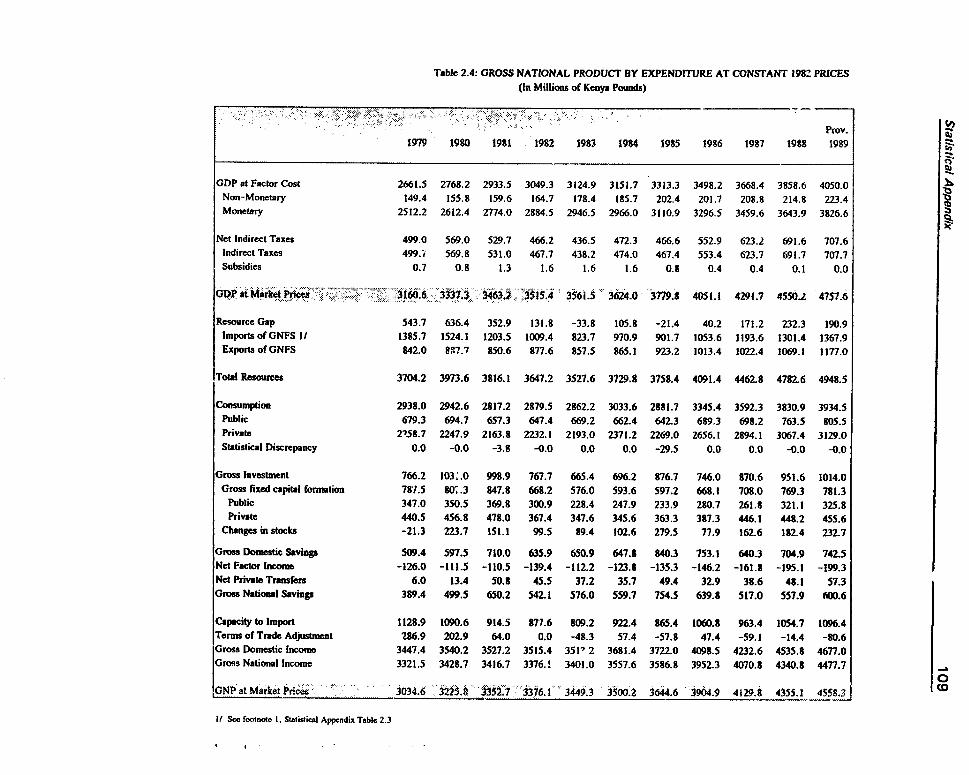

1.03 Economic Growth. Kenya's economy has sustained a marked economic recovery sincethe 1984 drought. Over the past five years, real GDP (at factor cost) has averaged annual growthof 5. 1 percent (Table 1.1). This is in sharp contrast with the relative stagnation that characterizedthe first half of the 1980s, with average annual GDP growth of only 3.3 percent (1980-84). As aresult of Kenya's good growth performance, output per capita has increased by 6 percent between1985 and 1989. Adjusted for the effects of changes in Kenya's extemal terms of trade, however,GDP per capita has remained approximately constant over the period.

2 Chapter 1: Economic Growth and Stabilization

Table 1.1Output Growth, 1980-89

(Kenya Pounds at Constant 1982 Prices, and Percentages)

19804 1985 1986 1987 1988 1989 19849

Growth rates (%):GDP market prices 2.1 4.3 7.2 5.9 6.0 4.6 5.6GDP factor cost 3.3 5.1 5.6 4.9 5.2 5.0 5.1Agriculture 2.8 1.0 4.9 4.2 4.7 4.0 4.4Manufacturing 3.7 4.5 5.8 5.7 6.0 5.9 5.6Services 4.1 5.6 6.7 5.1 5.4 5.3 5.6

GDP per capita (KE) 162 165 168 170 172 175 170Adjusted GDP ' 162 162 169 160 165 160 163

Real per capita GDP at factor coat adjusted for changes in Kenya's external terms of trade.

Sources: Satistical Appendix. Tables 2.2, 2.4 and 2.6; and Econoomic Survey, various years.

1.04 Economic growth slowed somewhat to 5.0 percent in 1989 compared to 5.2 percent in1988, largely due to lower growth in the agricultural sector. The more moderate 1989 growth inagriculture was a result of the downturn in world coffee prices, which fell by 23 percent in 1989,and inadequate rains in parts of the country. The manufacturing sector, which is greatly influencedby performance in agriculture, has continued to maintain annual growth rates close to 6 percent. Theservices sector, which accounts for about 42 percent of GDP expanded by 5.3 percent in 1989.Subsectors experiencing rapid real growth in 1989 included: electricity and water (8.4 percent); thefinancial system (7.5 percent); ownership of dwellings (6.8 percent); tourism; and governmentservices (5.5 percent). The rapid increase in government services was driven by salary increases forthe armed forces and continuing pressures on education spending, especially at the university level,to accommodate the new 8-4-4 education system. The tourism sector continued to play a major rolein Kenya's economy. Foreign exchange receipts increased by 6.7 percent to reach $418 million in1989 and arrivals increased by 5 percent.

1.05 Agriculture, Kenya's leading economic sector, has averaged growth of 4.4 percent overthe past five years. The growth in agricultural value added dropped somewhat to 4.0 percent in1989, following the good performance of the previous year, largely due to a 9 percent fall in coffeeoutput. Tea output, on the other hand, continued to rise. Over the past five years tea output hasaveraged growth of over 9 percent annually. Favorable weather conditions in tea growing regions,improved prices and government efforts to encourage expansion in area planted and processingcapacity, have been responsible for the steady increase in tea production. Maize producdon declinedin 1989 due to a reduction in area planted and somewhat unfavorable weather in parts of the countryduring the long rains, while wheat production increased by 3.8 percent due to higher prices, goodrains and improved yields. Cotton output increased for the first time in 1989 after several years ofstagnadon, with cotton sales to the Cotton Lint and Seed Marketing Board increasing by 27 percent,but the level remains about one thired that attained in 1985. Sugarcane output as reflected in factory

Chapter 1: Economic Growth and Stabilization 3

intake increased by 11 percent, due to expansion programs and improved cane crushing efficiency.The livestock sector, benefiting from the decontrol of prices in 1987, has continued to grow strongly.

1.06 Real manufacturing value added increased by 5.9 percent in 1989, slightly below the 6.0percent achieved in 1988. Employment in manufacturing industries increased by 2.8 percent in 1989,reaching an estimated 182,300 persons, implying a 3 percent improvement in average laborproductivity. Manufacturing's good growth performance has been influenced by the recovery inagriculture, ensuring adequate supplies of raw materials for agro-based industries, strong domesticdemand, government measures to encourage manufacturing growth (e.g., price decontrol, reductionsin corporate taxes), and the import liberalization program which, combined with increased foreigncapital flows, helped sustain the availability and timeliness of imported inputs for the sector. As inprevious years, most manufacturing subsectors recorded positive growth. The exceptions weregrainmill products (-21.9 percent), bakery products (-0.1 percent) and non-electrical machinery(4.3 percent). Subsectors recording strong growth in 1989 included metallic products (16.2 percent),petroleum and other chemicals (15.5 percent), and clay and glass products (10.3 percent).

1.07 Value added in the building and construction sector recorded real growth of 5.4 percentin 1989. Employment in the sector increased by 7.8 percent in 1989, to reach 67,400 persons.Cement consumption, usually a good indicator of construction activity, exceeded one million tons in1989, an increase of 7.7 percent over #he previous year. The continued growth in the sector'sactivities was a result of increases in commercial bank credit to the private construction sector andpublic sector projects. Credit extended by commercial banks for building and construction increasedby 34 percent in 1989. The public sector contributed to the growth in building and constructionthrough increased expenditure in road development, housing and the expansion of educationalfacilities for implementation of the 8-4-4 system.

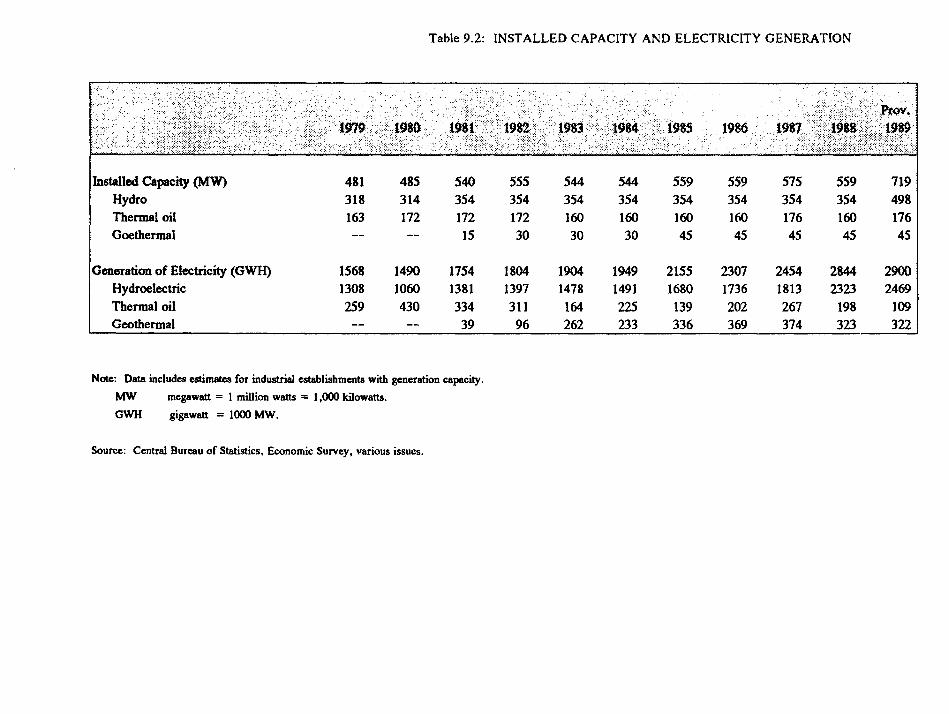

1.08 Installed electricity capacity increased by 160 MW to 719 MW in 1989, largely as aresult of the coming on stream of the Kiambere project. Electricity generation increased marginallyby 56 GWH to 2,900 GWH in 1989. While hydro-based electricity increased by over 6 percent,thermal-based generation dropped by 50 percent in 1989. With the expected commissioning of theTurkwell project in 1990, hydro is expected to rise significantly.

1.09 Investment and Savings. Real fixed investment growth slowed considerably in 1989.After averaging real annual growth of 6.5 percent over the period 1985-88, investment increased byonly 1.6 percent in 1989 (Table 1.2). Both public and private investment slowed in 1989, withpublic investment risii ; by 1.5 percent and private investment by 1.7. In recent years, the patternof investinent growth has been greatly affected by bulky public sector investmnents such as theconstruction of silos for the National Cereals and Produce Board (NCPB) and large hydroelectricprojects, particularly in 1986 and 1988, when public investment recorded real growth of over 20percent. Private investmnent has also behaved erratically. After recovering in the mid 1980s and asurge in 1987, private fixed investment has averaged growth of only 1.1 percent over the past twoyears. While fixed investment has remained approximately constant since 1986, the past three yearshave seen a considerable build up in stocks. Large reserves of coffee and maize during 1988 and1989 largely explain the increase in stocks.

1.10 Although the gross investment rate at over 25 percent of GDP over the past two yearsis high and compares well with that for low- and middle-income economies, over the past three years

4 Chapter 1: Economic Growth and Stabilization

Table 1.2Investment and Savings, 1985-89

(As Percentages of GDP)

1985 1986 1987 1988 1989

Gross Investment 25.5 21.8 24 4 25.3 25.5Fixed Investment 17.5 19.6 19.7 20.4 20.1

Public 6.8 8.1 7.2 8.4 8.2Private 10.7 11.5 12.5 12.0 11.9

Change in Stocks 8.0 2.2 4.7 4.9 5.4

Financed by:Foreign Savings 1.1 -0.1 5.1 5.2 5.8

Grants' 1.9 2.1 1.8 3.1 3.4Net Borrowing -0.8 -2.2 3.3 2.1 2.4

Domestic Savings 24.4 21.9 19.3 20.1 19.7Central Government -1.2 -1.5 -1.9 -0.8 -1.2Private2 25.6 23.4 21.2 20.9 20.9

Memo Items:Real Growth inFixed Investment 0.6 11.9 6.0 8.7 1.6

Public 5.7 20.1 -6.7 22.7 1.5Private 5.1 5.8 16.9 -0.2 1.7

The contribution of grants is somewhat overstated since it is not possible to disaggregate capitaland current grant.

a Private savings is a rcsidual which includes all non-Central Governnent savings.

Source: Srdsucat Appendix, Tables 2.3 and S. 1.

Kenya has increasingly relied on foreign savings to finance its capital formation.' Since 1986,foreign savings have financed over one quarter of the economy's gross fixed investrnent. Domesticsavings have maintained a downward trend since 1985 as a result of both continued dissaving by theCentral Government and lower private savings. Domestic savings, which financed all grossinvestment in 1986, contributed only 77 percent in 1989. It is difficult to find an explanation forthe decline in the private savings rate. Interest rates have remained largely positive in recent yearsand while real wages have not recovered to the levels achieved in 1980, they have been rising since1985 (Table 1.10).

The gross domestic investment rate in 1988 was 18 percent for other low-income economies (low-income excluding Chinaand India), 25 percent for middle-income economies, and 23 percent for lower-middle-income economies (World Bank,1990b).

Chapter 1: Economic Growth and Stabilization 5

1.11 Employment trends. Official data only covers wage and salary employment in themodern sector, and in urban and rural small-scale enterprises (previously referred to as informalsector), which combined are esdmated to account for less than 20 percent of Kenya's total laborforce. In 1989, excluding small-scale agriculture, Kenya's economy generated 76,600 new jobs,represending a growth rate of 4.5 percent (Table 1.3). Job creation in the modern wage sectorincreased by 2.4 percent in 1989, significantly lower than the 4.1 percent achieved in 1988. In linewith the Government's strategy of encouraging the expansion of small-scale enterprises, the sectorhas been the most dynamic source of employment growth in recent years. Over the period 1985-89, employment growth in the small-scale sector averaged 10.8 percent annually, or an average of27,000 new jobs every year. Although employment growth in the Central Government moderatedsomewhat in 1989 (increasing by 3.8 percent), employment by the Teachers' Services Commission(TSC) and in parastatals has continued to grow rapidly. Over the past five years, employment inTSC has averaged annual growth of 5.3 percent, well above the growth in the total labor forcewhich is estimated to be expanding by about 4 percent annually.

Table 1.3Recorded Employment, 1985-89(In Thousands, and Percentages)

AverageGrowth

1985 1986 1987 1988 1989 1985-89

Wage Employment 1174 1227 1274 1327 1359 4.0

Private 600 621 647 671 678 3.3Agiculture 186 193 199 .97 194 1.4Manufacturing 124 130 136 142 143 3.6Other 290 298 312 332 341 4.2

Public 575 606 627 655 681 4.7Cental Govemment 252 260 274 271 281 4.0TSC 151 164 173 185 195 8.1Pamastatals 90 ICO 97 104 108 2.5Other publc 82 82 83 95 97 3.2

Smal-Scale Entetpris 255 281 312 346 390 10.8

Self-Employed 33 35 38 44 44 6.5

TOTAL 1462 1543 1624 1717 1793 5.3

Sommev Siddcat Append., TabIes 1.3 ad 5.8.

1.12 The recendy published 1986 Urban Labour Force Survey (ULFS), which updatesinformation since the last survey in 1977/78, reveals a serious but largely static urban unemploymentproblem in Kenya (Box 1.1). Although definidonal differences regarding labor force activity andunemployment in sample and questionnaire design do not permit a simple comparison between thetwo surveys, work carried out in the Long Range Planning Unit of the Ministry of Planning and

6 Chapter 1: Economic Growth and Stabilization

National Development indicates that although unemployment increased slightly, the differencebetween the two unemployment rates was statistically insignificant, implying that there has been littlechange in Kenya's urban unemployment problem between 1978 and 1986 (Republic of Kenya, 1988).The 1977/78 ULFS estimated an urban unemployment rate of 6.1 percent but it utilized a single dayas reference period. The 1986 ULFS, which relied on a one week reference period, found an urbanopen unemployment rate of 16.2 percent. When the unemployment rates for 1986 were adjusted forthe single day reference period, the corresponding rate became 6.9 percent. The overallunemployment rate for males declined slightly but that for women increased significantly, probablyrelated to inczeases in participation rates for women in urban areas. The ULFS also providesinformation on the extent of underemployment. The Long Range Planning Unit estimates thatunderemployment adds only one percent to the rate of open unzmployment.

B. The Stabilization Path

1.13 In 1987 there was a significant deterioration in Kenya's terms of trade following the endof the mini coffee boom in 1986. The current account deficit widened and the overall balance ofpayments reverted to a deficit. There was a major drain of foreign exchange reser'es and the importregime was tightened to control imports. The budget deficit increased and credit expansion remainedhigh. Inflation began to rise, fueled by large increases in the money supply during 1986. Partly dueto a slowdown in agriculture, GDP growth (at factor cost) fell below 5 percent. In view of thedeterioration in financial and economic conditions, and in line with the objectives set out in the 1986Sessional Paper, the Government in late 1987 adopted a major stabilization and structural adjustmentprogram. The program was supported by an 18-month Stand-by arrangement from the IMF and athree-year arrangement under the IMF's Structural Adjustment Facility, both of which becameeffective in February 1988. In early 1989, the Government requested support under a three-yearEnhanced Structural Adjustment Facility, currently in its second year of implementation. Theprogram was also supported by IDA sectoral adjustment lending for the agricultural, industrial, andfinancial sectors, with significant cofinancing by a number of donors.

1.14 The Govtriment's stabilization program aims to: (i) reduce the budget deficit to a moresustainable level that can be financed by foreign and non-inflationary domestic sources, and that doesnot crowd out the private sector; (ii) control monetary expansion and reduce the rate of inflation torates more in line with Kenya's major trading partners; (iii) maintain an appropriate exchange ratepolicy that supports the Government's import liberalization program and corrects for differentials indomestic and international infladon; (iv) limit the use of new nonconcessional foreign borrowing togradually reduce Kenya's debt service ratio; and (v) reduce the current account deficit and build upforeign exchange reserve levels.

1.15 Kenya's efforts to stabilize the economy have produced mixed results. While the budgetdeficit has been considerably reduced since 1987, the level of government expenditures remains highand the Government has found it difficult to restrain the growth of public sector employment and itsattendant wage and salary bill. After dropping sharply in 198, money supply growth acceleratedin 1989 and the economy appears to be overheating. Inflation, fueled by a monetary overhang,internadonal price increases, depreciation of the shilling, price decontrol, and increases in agriculturalproducer prices, has remained above 10 percent for the past two years. The Government's exchangerate policy has been appropriate but its external position has been adversely affected by deterioratingterms of trade and the poor performance of a number of its major exports. To provide the imports

Chapter 1: Economic Growth and Stabilization 7

Box 1.1Results of the 1986 Urban Labour Force Survey

Just over 70 percent of the working age population (15-64 years) are economically active.Of those employed, almost 80 percent have one job activity as a paid employee, about 20 percentare self-employed, and a small proportion have at least one activity of each type. Since 1977178,there appear to be increasing numbers of females joining the labor force. Participation rates forfemales, however, remain about one third lower than for males in all age groups between 20-64.

The overall rate of open urban unemployment is approximately 16 percent of theeconomically active population, 12 percent for males and 24 percent for femnales. Importantdeterminants of unemployment include age, sex, education, and location. One of the more importantand unambiguous changes since 1977/78 is the increase in the number of unemployed women.Whereas in 1977/78 unemployed men outnumbered women by a factor of three to one, in 1986 theunemployed included a majority of women. Rates are highest for the younger members of the laborforce (63 percent for males in the 15 to 19 age group and 45 percent for females in the 20 to 24 agegroup) and remain high for all males under 30 and femnales under 40. Unemployment rates are muchlower for those with an education beyond secondary school, and are highest for those who havecompleted between Form I and IV. The highest unemployment rates were in Nairobi (20 percent)and urban areas in Western (18 percent) and Rift Valley (18 peiwent) Provinces. Underemploymentin the 1986 UTLFS is estimated to increase the rate of unemployment by only one percent. Theunderemployed tend to be predominantly males in the 20-35 age bracket.

The labor force as a whole is becoming increasingly educated. The proportion of the laborforce reporting no formal education has dropped significantly, and the proportion with universitytraining has almost doubled since the previous ULFS. In general, males are still more educated thanfemales, but the gap seems to be narrowing. Skill development through various training programsis not as widespread as might have been anticipated since the majority of respondents cited no formaltraining for the jobs they hold. On the job training by employers, either while at work or in specialcourses, is important for paid employees. For the self-employed, acquisidion of job skills throughinformal methods such as friends and relatives is the dominant form of training.

T'he methods of job search are more varied in 1986 than in 1977/78. The percentage ofdirect approaches to employers among all job-seeking activities declined from over 60 percent in1977J78 to less than 20 percent in 1986. There appears to be a marked increase in the use offriends or relatives to secure work, by either providing information on available work or otherwisegaining advantages over other job seekers. Most Kenyans in urban areas experience an extendedperiod of job search. Sixty percent of job seekers have been looking for work for more than oneyear, and over 35 percent have been looking for over two years. Nevertheless, the period wasshorter than in 1977/78 when fewer searched for less than one year. Increases in the cost of livingand job search may play a role in this trend.

Source. RepubRc of Kenya, ]988.

8 Chapter 1: Economic Growth and Stabilization

needed to sustain economic growth, the Governrment has had to increase its reliance on external aid,leaving the economy vulnerable to further external shocks and uncertain aid flows.

Fiscal Policies

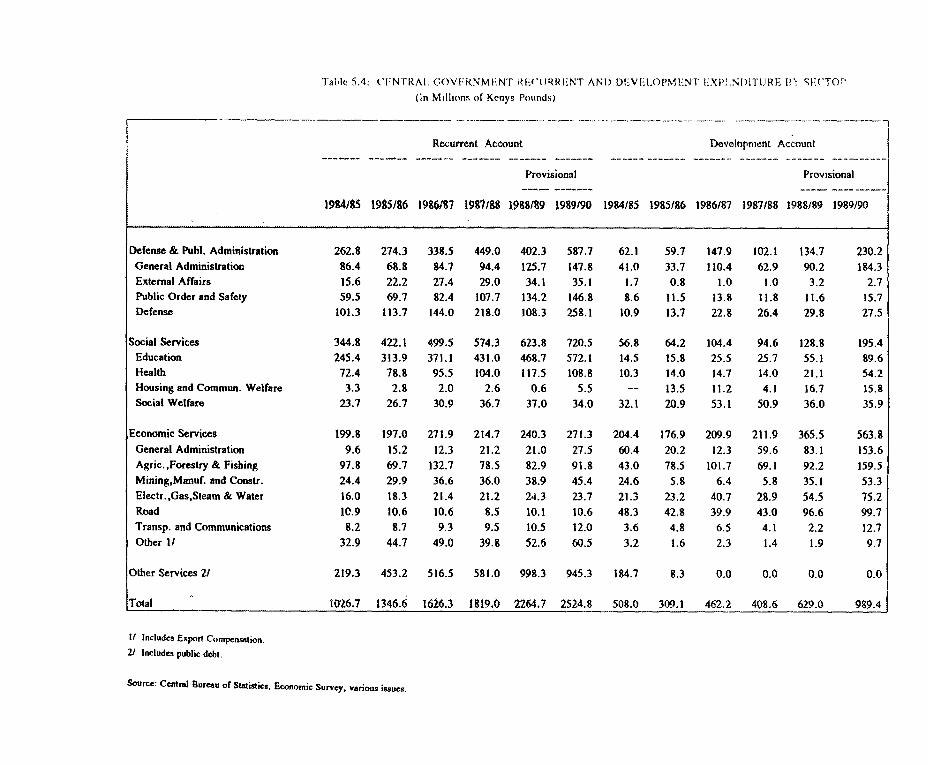

1.16 Containing Expenditures. As discussed in the last Kenya Country EconomicMemorandum (World Bank, 1988), the Government's ability to control the budget defiLut played akey role in Kenya's efforts to stabilize the economy and reduce inflation during the first half of the1980s. By FY84, the cash deficit (including grants) had been reduced to a manageable 3.9 percentof GDP and government spending absorbed 27 percent of GDP. Kenya's fiscal situation suffereda gradual deterioration during FY84-87. The overall cash deficit (including grants) increased from3.9 percent of GDP in FY84 to 5.0 percent in FY85 and 5.3 percent in FY86 (Table 1.4). Thebudget deficit continued to rise in FY87, peaking at 6.6 percent of GDP. The worsening fiscalstance in FY87 was the result of higher expenditure and lending levels which increased by 17 percentin nominal terms. Following adoption of the Government's stabilization program in 1987, the deficitwas substantially reduced, ranging between 4.2 and 4.7 percent of GDP during the past three years,but the Government has found it difficult to push the deficit below 4 percent of GDP. Moreover,governmnent spending has remained high at around 30 percent of GDP and reliance on external grantsalso remains high. The budget deficit excluding grants has ranged between 6.5 and 7.1 percent ofGDP over the past three years.

1.17 A number of factors account for the Government's difficulties in controlling the growthof expenditures.2 First, Kenya's high population growth rate and the Government's commitment tomeet demand for social services places enormous pressures on social expenditures. Spending oneducation in particular has been rising rapidly as a result of the demographic momentum, the highdemand for education, and the adoption of the 844 system, which added one year to primaryeducation and is placing increasing pressures on university enrollments. Second, public sectoremploym-ent, in the civil service and TSC, is the ma;> driving force behind the rapid increase inrecurrent spending. Third, interest payments on domestic debt are rising rapidly, as the Governmenthas shifted some deficit financing to nonbank sources through Treasury Bills and Bonds, and asdomestic interest rates have risen. Fourth, much of the fiscal adjustment during the mid-1980sfocused on reducing development expenditures rather than recurrent spending. Although this allowedthe Government to rationalize somewhat its public investment program, especially by cancelling anumber of marginal projects, there is a limit to how much development spending can be squeezedin a country such as Kenya without endangering essential infrastructure and human capitalinvestments. Moreover, as development spending is compressed this runs the risk of affectingproject-aid levels and, to the extent that the Government reduces its own contributions to t-ireign-assisted projects, threatening the viability of projects. Fifth, although accurate estimates are notavailable, transfers to parastatals are large and the Government is increasingly being called upon tohonor external debt of parastatals.'

2 Fiscl policy and public expenditure issues were extensively analyzed in the last Country Economic Memorandum (WorldBank, 1988a), and the recent Public Expenditure Rev;cw (World Bank, 1989a), respectively.

In this year's budget speech, the Vice-President and Minister for Finance expressed great concern over the widespread lackof financial control and discipline among parastatals. He noted that Treasury is increasingly forced to divert funds frombudgeted purposes to meet debt obligations which parastatals are unable to service.

Chapter 1: Economic Growth and Stabilization 9

Table 1.4Summary of CentraJ Govermnent Finances, FY86-90

(In Millions of Kenya Pounds)

Revised Prelini. Budget EstimateFY86 FY87 FY88 FY89 FY90 FY90

Revenue and grants 1269 1461 1796 2056 2590 2413Revenue 1215 1398 1637 1869 2204 2204Grants 55 63 159 187 386 209

Exnenditures 1597 1872 1991 2430 3016 2805Recurrent 1222 1378 1532 1856 2094 2145Development andNet Lending 375 494 459 54 922 660

Defic.t -328 411 -195 -374 -427 -392

Adjustment 37 3 -103 -5 - --

Cash Deficit -291 -408 -297 -379 -427 -392

Financing:Foreign (net) -48 2 72 200 355 316Domestic 339 406 226 179 72 75Bank 97 251 -6 103 39 45Nonbank 243 155 232 77 33 30

Memo Items (% of GDP):Expenditures 29.3 30.2 28.5 30.4 -- 30.1Deficit:Including grants 5.3 6.6 4.3 4.7 4.2 4.2Excluding grants 6.3 7.6 6.5 7.1 6.5 6.5

Nominal GDPmp 5456 6199 6997 7996 - 9333

The cash deficit for FY89 was increased by Kg 91.3 maillion to reflect the increase in the stock ofunpresenred checks at the er4 of June 30, 1989. which were largely liquidated through bank financingin early July 1989. ITc figure for domestic bank financing was adjusted accordingly. Nominal GDPon a fiScl basis is an averege of calendar years

Source: I eslimtes, and st 4gesdmares.

10 Chapter 1: Economic Growth and Stabilization

1.18 Preliminary data for FY89 show that the budget deficit reached 4.7 percent of GDP,slightly higher than the program target of 4.i percent. Excluding grants, the budget deficit increasedto 7.1 percent of GDP. Both revenue and expenditures were lower than anticipated. Revenueshortfalls were largely the result of lower grants and lower-than-programmed import duty collections,the latter reflecting lower than expected import levels. Total expenditures increased by 22 percentin nominal terms. Interest payments also increased by 22 percent, largely as a result of a 33 percentincrease in foreign interest payments. Foreign financing of the deficit was equivalent to 1.3 percentof GDP. When adjusted for the increase in the level of unpresented checks, which were largelyliquidated in early July 1989, domestic financing amounted to 2.3 percent of GDP. Foreignfinancing of the cash deficit amounted to K£ 200 million (2.5 percent of GDP), slightly higher thanthe programmed level. Bank financing, when adjusted for unpresented checks, reached 1.3 percentof GDP.

1.19 Preliminary estimates for FY90 suggest that the budget deficit was contained to 4.2percent of GDP (6.5 percent excluding grants), somewhat lower than the budgeted 4.6 percent. Newrevenue measures were introduced to raise an additional K£ 58 million, of which abou; K£ 25 millionwere generated by a sales tax increase and about K£ 10 million from customs duties. On January1, 1990 the manufacturing sales tax was replaced by a value added tax (VAT) which retained theoriginal 17 percent sales tax rate. In line with the Government's policy of placing greater relianceon cost recovery, user charges were introduced for health and education, and tariffs were raised forroad use and some agricultural services. These changes are expected to increase user chargecollecdons from about 0.6 percent of GDP in FY89 to 1.3 percent in FY90. To contain the deficit,the Government reduced development spending in line with a fall in foreign grants from the levelsprojected in the original FY90 budget. Interest payments increased by 13 percent, as a result ofhigher interest rates on domestic debt, which were partially offset by debt forgiveness from a numberof bilateral donors (Canada, France, Germany, Netherlands, United Kingdom, and United States).

1.20 The Government's stabilization program for FY91 aims to further reduce the budgetdeficit to 3.8 percent of GDP. This will be difficult to achieve, as considerable expenditure pressureswill remain throughout the coming fiscal year, especially from the rising intake in public universidesand the planned increase of civil service wages. Under these circumstances, it is likely that non-wage operations and maintenance expenditures will be further squeezed. Moreover, as liberalizadonof the financial system proceeds there will be increasing pressure on interest rates on domestic debtas the Government attempts to shift its financing needs toward nonbank sources. The Government'sstabilization efforts will need to focus increasingly on containing the growth of the public sector wagebill and on reducing transfers to parastatals.

1.21 Strengthening the Revenue Base. As part of its stabilization and adjustment efforts, theGovernment is attempting to increase the yield and efficiency of the tax system. Kenya's taxrevenues, which amounted to 21 percent of GDP in FY89, compare favorably with those of low- andmiddle-income countries. Kenya also has a relatively broad-based tax system, with taxes oninternational trade acccunting for only 16 percent of total revenues in FY90, and taxes on incomesand consumption of goods and services accounting for 29 percent and 58 percent, respectively.Kenya's tax structure, however, has had relatively low elasticity with respect to GDP (estimated at0.8 percent) which has required the continuous adoption of discretionary tax measures to maintaintax buoyancy. Moreover, personal and corporate tax rates have been high.

Chapter 1: Economic Growth and Stabilization 11

1.22 In recent years the Government has been attempting to address these problems. In 1990,the Government began implementing a Tax Modernization Program designed to improve taxcollection and admiristration. The program includes measures to computerize the tax system,improve coordination among the various departments responsible for tax collection, enhance training,and strengthen the institutional capacity for tax policy analysis. As part of its effort to increase theelasticity and economic efficiency of the tax system, on January 1, 1990 the Government replacedthe sales tax with a VAT that also includes all services. It was originally set at 17 percent, the sameas the sales tax, but was raised to 18 percent in June 1990.

1.23 To rationalize the tax structure and improve incentives, in 1988 investment allowanceswere increased and in 1989 the individual income tax rate was lowered from 50 percent to 45percent. The revenue loss from these measures was partly offset by the introduction in 1989 of apresumptive tax of 5 percent on the value of gross sales of agricultural produce, and by theintroduction of the VAT. The FY91 budget announced a further lowering of the corporate tax ratefrom 42.5 percent to 40 percent (following a reduction from 45 percent in the preceding year), andthe deductibility of contributions to registered pension plans and provident funds from taxable income(both personal and corporate). In order to promote foreign investment in the newly-created ExportProcessing Zones (EPZ), tax exemptions were provided for the first 10 years of operations in theEPZs, while a rate of 25 percent on income earned would be applied during the following ten years.Also, payments from an EPZ enterprise to non-residents will be exempt from withholding taxes forthe first 10 years. In order to stimulate Kenya's embryonic capital market, the Government alsoeliminated the double taxation of dividends, abolished the stamp duty for share transactions quotedin the stock exchange, and allowed the deductibility of legal fees and other costs associated with thepublic issue of shares, debentures and bonds.

1.24 As part of its industrial sector reform program, in addition to replacing a number ofquantitative restrictions with tariffs, the Government has begun to move away from reliance onimport duties to mobilize revenues. Under the trade liberalization program, import tariffs will beused primarily for protective purposes, increasingly relying on the VAT to raise revenues. Theprocess of lowering tariffs was initiated in the 1989 Budget. In June 1990, the Governmentannounced a duty reduction of about 5 percentage points on imported raw materials, intermediategoods and spare parts on all import schedules except 3C. To compensate for revenue losses, VATrates were increased. The import liberalization program is analyzed in greater detail in Chapter 2.

Monetary Policy

1.25 As part of its stabilization program, the Government aims to contain monetary expansionand assign a greater role to market forces in credit allocation. Money supply growth (M2) hasfluctuated over the past three years, falling from 11.2 percent in 1987, to 7.9 percent in 1988, andrising to 12.9 percent in 1989 (Table 1.5). This variability has been caused in large measure byfluctuations in net foreign assets (NFAs) of the banking system, which in turn reflected monetarymovements in Kenya's balance of payments. The composition of total credit shows a sharpcontraction in the growth of domestic credit from 28.6 percent and 20.4 percent in 1986 and 1987,respectively, to growth of 6.7 percent in 1988 and 6.9 percent in 1989.

12 Chapter 1: Economic Growth and Stabilization

Table 1.5Growth of Money and Credit in the Banking System, 1985-89

(Percentages at Year End)

1985 1986 1987 1988 1989

LIABILITIES 6 S 35.1 16.7 1.4 11.9Broad Money M2 (MI QM) 2.5 32.5 11.2 7.9 12.9Money (MI) -3.6 32.6 9.7 5.9 8.6Quasi-Money (QM) 12.6 32.4 13.3 10.8 18.6

Other Items (net) 61.2 57.2 57.4 -32.8 3.4

ASSETS (domestic) 13.0 28.6 20.4 6.7 6.9Credit to:

Central Government 9.8 55.6 30.0 -8.7 -3.0Other public sector 13.4 16.3 26.8 -2.8 -19.8Private sector 14.6 16.8 13.2 19.6 15.6

Memo Item:Private sector as %of total credit 61.9 56.2 52.9 59.3 64.1

M2/GDP 0.27 0.30 0.30 0.29 0.28

Source: Stadstca Appendix, Table 6. 1.

1.26 In recent years, the private sector has increased its share of total credit from the bankingsystem at the expense of the Central Government and public enterprises. After large increases in1986 and 1987, credit to the Central Government fell by 8.7 percent and 3.0 percent in the twosubsequent years. There was a simnilar trend for parastatals. Credit to the private sector, in contrast,grew by 19.6 percent in 1988 and a further 15.6 percent in 1989. As a result, the share of theprivate sector in total credit from the banking system rose from 53 percent in 1987 to 59 percent in1988 and 64 percent in 1989.

1.27 The monetary picture changes considerably when near-bank financial institutions (NBFIs)are taken into account. As discussed in Chapter 2, the rapid growth of NBFIs in Kenya is a recentphenomenon. Many of them were created during the 1980s to get around the tighter regulations thenexercised by the Central Bank of Kenya (CBK) on commercial banks. On paper, the NBFIs appearto be constituted as merchant or investment banks, which would normally undertake much of thewholesale end of the banking business and provide longer-term finance. In practice, however, NBFIsoperate as much at the short end of the market as commercial banks, taking retail deposits andmaking short-term loans. Moreover, NBFIs play an important role in Kenya's financial system.Deposits in NBFIs are substantial and averaged 14 percent of GDP during 1985-89, while the total

Chapter ?: Economic Growth and Stabilization 13

savings and time deposits of the banking system (i.e., the stock of quasi-money) averaged only 12percent. The growing importance of NBFIs suggests that they should be included in the analysis ofmonetary developments in Kenya.

1.28 Following a crisis of confidence in NBFIs during 1986, caused by the failure of anumber of these institutions, the growth rate of NBFI deposits fell from 14.8 percent in 1986 to 5.7percent in 1987. Following Government efforts to restore confidence, however, NBFI depositsincreased by 21.8 percent in 1988 and 22.8 percent in 1989. If NBFI deposits are included in somebroader measure of money supply (say, M3), the monetary stance appears much more expansionarythan indicated by trends in M2 alone. As shown in Table 1.6, the slowdown in money supplygrowth in 1988 as measured by M2 disappears when measured by M3, showing instead a steadyacceleration in money supply growth since 1987. As discussed below, this pattern is more in linewith Kenya's recent inflation experience.

1.29 The differences in the growth rates of liabilities of the two types of institutions are alsoreflected on the asset side. As compared with the domesdc credit of the banking system, which grewby modest amounts in 1988 (6.7 percent) and 1989 (6.9 percent), loans and advances from the NBFIsincreased by 15.9 percent in 1988 and 17.7 percent in 1989. Additionally, while credit to theCentral Government from the banking system fell by 3.0 percent in 1989, loans and advances to itfrom NBFIs increased by 28.3 percent. Thus, while the Government reduced its borrowing fromcommercial banks, it replaced some of this credit by sharply increasing its borrowing from NBFIs.

Table 1.6Growth of Money and Credit in NBFIs, 1985-89

(Percentages at Year End)

1985 1986 1987 1988 1989

Deposits in NBFIs 15.5 14.8 5.7 21.8 22.8

Credit to:Central Government 46.2 17.6 -0.3 -15.6 28.3Other public sector 2.9 113.9 23.4 158.9 -60.6Private sector 19.0 4.6 15.5 20.9 18.2

Total Credit 23.1 7.5 12.4 15.9 17.7

Mcmo Item:M3 (M2 + NBFIs) 6.6 26.5 9.5 12.1 16.1M3/GDP 0.41 0.44 0.43 0.43 0.43

Source: radsucat Appendix, Tables 6.1 and 6.3.

14 Chapter 1: Economic Growth and Stabilization

1.30 Monetary Policy Instruments. CBK currently has three main monetary policyinstruments: minimum reserve rados (cash and liquid asset ratios), rediscount and advance facilities,and credit ceilings. Of these, CBK has relied most heavily on quantitative credit ceilings toimplement its monetary and credit policies. These instruments, however, have not been entirelyeffective.

1.31 Since December 1986, all commercial banks have been required to maintain dailyminimum non-interest bearing cash balances with CBK, equivalent to 6 percent of their deposits.In addition, both commercial banks and NBFIs are required to maintain a minimum holding of liquidassets, primarily in Treasury bills (about 50 percent), cash and inter-bank balances. Since early1983, the minimum ratio of liquid assets to total deposit liabilities has been 20 percent for thecommercial banks and 24 percent for NBFIs. These reserve requirement ratios, however, have notbeen an effective monetary policy tool because the minimum reserve levels have been set below thosethat most of these institutions voluntarily hold for prudential and business reasons. This is reflectedin the fact that, on average, the actual cash and liquidity rados have been greater than legalminimums at the end of each quarter throughout 1988 and 1989 (Table 1.7). Because the financialinstitutions generally hold more reserves than legally required, and because these excess reserves arevariable and unpredictable, the reserve ratios have not been effective in controlling liquidity.

Table 1.7Actual Reserve Ratios, 1988-89

(Percentages)

i--- 1988 - 1989

Ql QZ Q3 Q4 QI Q2 Q3 Q4

Cash ratio 6.4 6.5 7.2 6.3 8.4 6.3 7.2 6.1

Liquid assets ratio:Banks 27.0 26.0 26.0 24.0 27.0 25.0 27.0 26.0NBFIs 28.4 24,8 27.1 28.0 26.6 30.0 29.0 29.0

Source: CentralBank of Kenya.