Alpha® Liner Patienteninformation - Wilhelm Julius Teufel ...

Upload

independentCategory

view

3download

0

BOARD OF DIRECTORS FUNCTIONS AND FINANCIAL

PERFORMANCE OF PRIVATE COFFEE COMPANIES

IN TANZANIA. A CASE OF KADERES PEASANTS

DEVELOPMENT COMPANY LIMITED IN

KAGERA, TANZANIA.

BY

JULIUS JASTINE KAMANA

2013/FEB/WKD/MAF/M1213

A RESEARCH DISSERTATION SUBMITTED TO NKUMBA UNIVERSITY

IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR

THE AWARD OF THE DEGREE OF MASTERS OF

SCIENCE IN ACCOUNTING AND FINANCE

i

OF NKUMBA UNIVERSITY

OCTOBER, 2014

DECLARATION

I, Julius Jastine Kamana, declare that this study is my original

work and has never been presented to any Institution or

University for both professional and academic purposes. Where the

work of others have been, due acknowledgements has been done.

Signed…………………………………….. Date……………………………….

JULIUS JASTINE KAMANA

ii

APPROVAL

I certify that, Mr. Julius Jastine Kamana has carried out

research on Board of Directors functions and Financial

Performance of Private Coffee Companies in Tanzania, using

Kaderes Peasants Development Company Limited in Kagera, Tanzania

as a case study under my supervision.

Signed……………………………...………. Date…………………….……….

Ms. IRENE NABUTSALE (SUPERVISOR)

iii

DEDICATION

This dissertation is dedicated to the memory of my beloved mother

and my father who has always shown me the way. You’re my heroes.

To my wife who has been by my side and has encouraged, and

advised me all along.

To my sisters, brothers and all lecturers of Nkumba University

who have had to sacrifice two years’ worth of weekends to allow

me study.

To the many, and lasting friends I have made among my classmates

during this endeavor.

iv

ACKNOWLEDGEMENT

I wish to thank my supervisor Mrs. Nabutsale Rachael for

generously giving me her time to avail me constructive ideas and

guidance throughout this dissertation.

I would also like to acknowledge and thank Kaderes Peasant

Development Company Limited in Kagera, Tanzania for the support

and important information they have provided me which has been

the foundation of this thesis.

I thank Nkumba University lecturers for sharing their knowledge

and insight with me during the 2 years study period of the

degree.

v

Thank you very much.

TABLE OF CONTENTDECLARATION...................................................iiAPPROVAL.....................................................iiiDEDICATION....................................................ivACKNOWLEDGEMENT................................................vTABLE OF CONTENT..............................................viLIST OF TABLES.................................................xLIST OF ABBREVIATIONS.........................................xiABSTRACT.....................................................xii

CHAPTER ONE:INTRODUCTION.......................................1Background of the study........................................1Statement of the Problem......................................6

vi

Purpose of Study...............................................8Objectives of the Study........................................8Research Questions of the Study................................8Research Hypotheses............................................8Scope of the Study.............................................9Setting of the Study..........................................10Significance of the study.....................................11Arrangement of the Report.....................................11

CHAPTER TWO:STUDY LITERATURE..................................13Introduction..................................................13Literature survey.............................................13Literature Review.............................................15

CHAPTER THREE:METHODOLOGY.....................................43Introduction..................................................43Research design...............................................43Demographic statistics of respondents.........................44Gender of respondents.........................................44Age of respondents............................................44Highest level of education attained...........................45Position of respondent........................................46Study population..............................................46Study population..............................................46Sampling procedure............................................47Census Sampling Technique.....................................47Data collection procedure.....................................48Data collection methods.......................................48The self administered questionnaires (SAQ):...................48Interview.....................................................49

vii

Review of related literature..................................49Data collection instruments...................................50The self administered questionnaire (SAQ).....................50Interview guide...............................................50Validity and Reliability of Instrument........................51Data processing...............................................52Data analysis.................................................52Measurement of variables......................................53Limitation of the study.......................................53

CHAPTER FOUR: HOW BOARD OF DIRECTORS HAVE ENSURED AVAILABILITY OFFINANCIAL RESOURCES IN KADERES PEASANTS DEVELOPMENT COMPANY LIMITED.......................................................55Introduction..................................................55The roles and duties of Board of Directors....................55Whether the Board size is adequate for the company............56Whether the Board of Directors act responsibly in the best interest of the company.......................................57Whether BODs apply corporate governance principles............58Whether the Board of Directors ensures that financial resources are available.................................................60Whether BODs effectively manage the organization's financial resources.....................................................61Table 4.6: Whether BODs effectively manage the organization's financial.....................................................61Whether the BODs exercise all the powers of the company to acquire funds.................................................62Table 4.7: Whether BODs exercise all the powers of the company to..............................................................62Whether financial resources are always available in the company..............................................................63Whether the financial resources are always adequate...........64

viii

Whether financial resources are always availed in time........65

CHAPTER FIVE: HOW BOARD OF DIRECTORS HAVE CARRIED OUT BUDGET FORMULATION, APPROVAL AND MONITORING IN KADERES PEASANTS DEVELOPMENT COMPANY LIMITED...................................66Introduction..................................................66Whether the annual budgets are properly formulated in KPDL. . . .66Whether Annual budgets formulated are based on the BODs overall goals or objectives...........................................67Whether departmental budgets are regularly prepared...........68Whether previous year annual budget performance reports are used for future planning...........................................70Whether the figures incorporated in the budgets are realistic. 71Whether Annual budgets are adequately approved by the Board. . .72Whether the board approves budgets within the timeframe set. . .73Whether the proper procedures of annual budget approval are followed......................................................74followed......................................................74Regular preparations of annual budget monitoring..............76

CHAPTER SIX: HOW BOARD OF DIRECTORS SELECT, SUPPORT, AND REVIEW THE PERFORMANCE OF THE COMPANY CEOS IN KADERES PEASANTS DEVELOPMENT COMPANY LIMITED...................................78Introduction..................................................78Whether there is proper selection of CEOs by the Board........78Whether CEOs are adequately qualified.........................79Whether CEOs are selected according to the set procedures.....80Whether there is proper appointment of CEO to the company.....82Whether the CEOs are adequately appointed.....................83Whether CEOs are appointed according to the set procedures. . . .84Whether there are regular reviews of CEOs.....................85

ix

Whether there is adequate review of CEO Performance by Board of Directors.....................................................86Review of CEO performance.....................................87Testing Hypothesis............................................88

CHAPTER SEVEN: WAYS AND MEANS OF IMPROVING THE ROLE OF BOARD OFDIRECTORS IN CORPORATE FINANCIAL PERFORMANCE................90Introduction..................................................90Availability of financial Resources...........................90Budget formulation, approval and monitoring...................91Selection, Appointment and Review of the Company’s CEO performance...................................................94Corporate Financial Performance...............................99

CHAPTER EIGHT:SUMMARY, CONCLUSIONS AND RECOMMENDATIONS.......100Introduction.................................................100Summary of findings..........................................100Conclusion...................................................103Recommendations..............................................104REFERENCES...................................................106APPENDIX 1...................................................110SELF ADMINISTERED QUESTIONNAIRE (SAQ)........................110APPENDIX B: INTERVIEW GUIDE..................................116APPENDIX III: INFERENTIAL STATISTICS.........................118APPENDIX IV:FREQUENCY TABLES.................................122

x

LIST OF TABLESTable 3.1: Gender of respondentsTable 3.2: Age of respondentsTable 3.3: Highest level of education attainedTable 3.4: Position of respondentTable 4.1Roles and duties of Board of Directors………………………………Table 4.2: The Board size is adequate for the companyTable 4.3: Interest of the company and its shareholdersTable 4.4: Whether BODs apply corporate governance principlesTable 4.5: BODs ensure that financial resources are availableTable 4.8: Whether financial resources are always available in the company Table 4.9: Whether the financial resources are always adequateTable 4.10: Whether financial resources are always availed in timeTable 5.1: Whether annual budgets are properly formulated in KPDLTable 5.2: Whether annual budgets formulated are based on the BODs overall goals or objectives Table 6.3: Whether Departmental budgets are regularly preparedTable 5.4: Previous year’s annual budget performance reportsTable 5.5: Whether figures incorporated in the budgets are realisticTable 5.6: Whether annual budgets are adequately approved by the BoardTable 5.7: Whether the board approves budgets within the timeframe setTable 5.8: Whether proper procedures of annual budget approval are

xi

Table 5.9: Whether there is proper monitoring of annual budgets by theboard Table 5.10: Whether annual budget monitoring reports are regularly prepared Table 6.1: Whether proper selection of CEOs by the BoardTable 6.2: Whether CEOs are adequately qualifiedTable 6.3 Whether CEOs are selected according to the set proceduresTable 6.4: Whether there is proper appointment of CEO to the companyTable 6.5: Whether the CEOs are adequately appointedTable 6.6: Whether CEOs are appointed according to the set proceduresTable 6.7: Whether there are regular review of CEOsTable 6.8: Whether there is adequate review of CEO Performance by Board of Directors Table 6.9: Review of CEOs performanceTable 6.10: Coefficients

LIST OF ABBREVIATIONS

ACCA Association of Chartered Certified

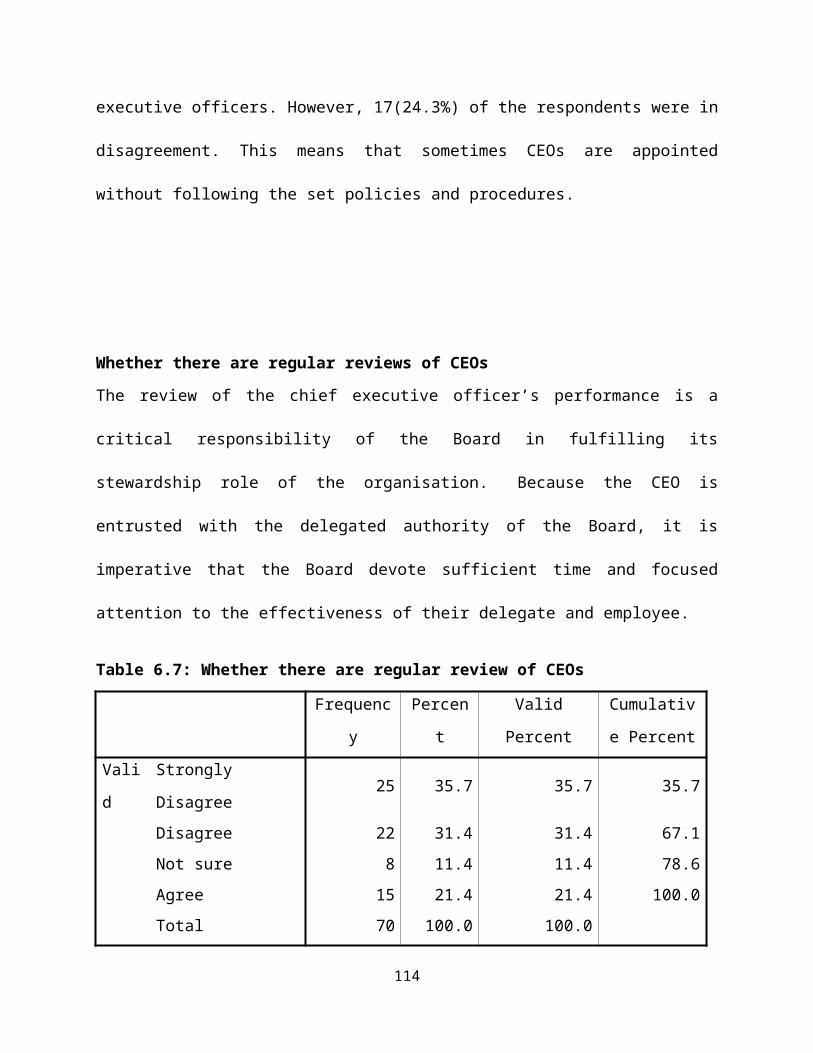

Accountants

BOD Board of Directors

CEOs Chief Executive Officers

KPDC Kaderes Peasants Development Company

Limited

SAQS Self Administered Questionnaire

SPSS Statistical Package for Social

Scientists

xii

TSHS Tanzania Shillings

PSCGT Private Sector Corporate Governance Trust

SHE Social, Health and Environmental

ABSTRACT

The study is about the Board of Director’s functions and

financial performance of private coffee companies in Tanzania. It

focused on Kaderes peasants Development Company Limited in

Kagera, Tanzania. The study was based on the following

xiii

objectives: (i) To examine how Board of Directors ensure

availability of financial resources in Kaderes Peasants

Development Company Limited (ii) To examine how Board of

Directors carry out formulation, approval and monitoring of

annual budgets in Kaderes Peasants Development Company Limited

and (iii) To establish how Board of Directors select, support,

and review the performance of the company CEOs in Kaderes

Peasants Development Company Limited.

The study used a total population of 70 respondents comprising of

Board of Directors and clients of Kaderes Peasants Company

Limited in Kagera, Tanzania. A sample size of 70 was selected

using census sampling technique. A cross sectional survey

research design was employed and both quantitative and

qualitative methods of data collection were used. Primary data

was analyzed in SPSS program version 18 and revealed a

significance between variables at P<0.001 for inferential

statistic .i.e. correlation and regression analysis.

The study findings revealed that Board of directors have not

satisfactorily ensured availability of financial resources,

formulation, approval and monitoring of annual budgets were not

properly carried out and the selection, support and review of the

CEO’s performance was not properly carried out.

The study recommends that the Board of Directors as major

stakeholders in the activities of the Company should ensure thatxiv

there are adequate financial resources for efficient and

effective operations of the company, proper formulation, approval

and monitoring of annual budgets, ensure proper selection,

support and review of CEO’s performance.

xv

CHAPTER ONE

INTRODUCTION

Background of the study

This study is about Board of Directors functions in financial

performance of private Coffee companies in Tanzania. It focuses

on Kaderes Peasants Development Company limited as a case study.

Coffee was introduced in Tanzania in the early 20th century as an

estate crop, but eventually became a smallholder crop. The area

planted with coffee expanded significantly during the 1970s and

the 1980s when prices were favorable. Approximately 70 percent of

coffee produced in Tanzania is Arabica, with most of this grown

in high altitude regions such as Mount Kilimanjaro. Robusta trees

are most commonly grown near Lake Victoria at a lower altitude.

Most Tanzanian coffee is grown by small farmers, with 95 percent

of the country's coffee farmers cultivating smaller than five

acres. Often the quality of this coffee is not high enough to be

sold on premium markets. Additionally, the yields of a typical

coffee tree in Tanzania are comparatively low. These factors

combine to make coffee a difficult business for Tanzanian

1

farmers. The highest grades of coffee are grown on Mount

Kilimanjaro and Mount Meru. These coffees are sold under the name

Arusha, Moshi, and Kilimanjaro (Kenneth David, 2001)

Tanzanian Arabica coffees are grown on the slopes of Mount

Kilimanjaro and Mount Meru in the Northern areas, under the shade

of banana trees, truly an exotic location for this east African

coffee, also in Southern Highlands of Mbeya and Ruvuma regions

where coffee is both intercropped with bananas and some areas are

pure stand. Arabica coffee makes up to 70% of total country

production. Robusta coffee is grown in the western areas along

Lake Victoria in Kagera region. This constitutes 30% of the total

coffee production in Tanzania.

The coffee industry of Tanzania is the 19th largest producer of

coffee in world. In 2006, Tanzania produced over fifty-five

million pounds of coffee Exports of coffee bring in over $60

million dollars each year to the Tanzanian economy. While coffee

has a long history in East Africa, it was not widely grown in the

territory comprising modern day Tanzania until the early 1900s.2

It is estimated that total area under coffee is 265,000 hectares

for both Arabica and Robusta. Average production is for the past

five years (2004/05 – 2008/09) is 51,777 tons of clean coffee.

98% of arabicas are wet processed and they dominate the Tanzanian

coffees exported to the specialty coffee market. Since the mid-

1990s, the country’s coffee industry has been in a state of

stagnation or decline. The reasons for this are diverse. Falling

world coffee prices, low productivity, high costs of production,

aging of coffee growers, among others.

This study is important because of the need to ensure proper

financial performance in the coffee industry by creating and

maintaining value through proper resource allocation and decision

making in order to improve on the peasants’ standard of living.

The sample study is significant because Kaderes peasants

developments company limited is one of the largest and the

leading indigenous coffee processing and exporter in Tanzania.

Kaderes Peasants Development (KPD) is a coffee co-operative local

company that was established in 2002 by peasants from where it

derived its name Kaderes Peasants and therefore fully registered

3

in 2005 as required by the Company Act of 2002 with its mission

being eradicating poverty of the peasants, and producing high

quality coffee. It is one of the largest and the leading

indigenous coffee processing and exporter in Tanzania. KPD is now

an independent company which does not only buy and export

farmers’ coffee, but also offer a service and training program to

improve the productivity and quality standards of the coffee.

The company is located in Karagwe District in Tanzania. Karagwe

is one of the 8 districts of Kagera region, that is, Karagwe,

Misenyi, Bukoba rural, Bukoba urban, Muleba, Biharamulo, Chato

and Ngara. The company is located in the North Western Corner of

Tanzania and borders with the Republic of Uganda in the North,

the Republic of Rwanda in the West, the districts of Ngara and

Biharamulo in the South and the districts of Bukoba and Muleba in

the East. It’s dedicated to facilitate the Peasants and Farmers

of Karagwe from four administrative divisions of Kituntu/Mabira,

Kaisho/Murongo and Bugene/Nyaishozi and Nyabiyonza.

4

Gavin et al (2004) define financial performance as financial

soundness of a company. It is a general measure of a firm's

overall financial health over a given period of time, and can be

used to compare similar firms across the same industry or to

compare industries or sectors in aggregation. Measures of

financial performance taken into consideration include: Reduced

operating costs, increased sales and customer loyalty, increased

productivity and quality, increased access to capital and

earnings. Cadburys (1992) states that financial performance is a

monetary measure of tasks against targets, the performance of

business organizations is affected by their strategies and

operations in market and non-market environments.

According to Krambia and Psaros (2006), good corporate financial

performance is as a result of good corporate financial

management. Corporate financial management is the application of

financial principles within a corporation to create and maintain

value through decision-making and proper resource management.

Corporate financial management is concerned with setting goals,

planning how to achieve them, and, perhaps most importantly,

5

deciding the best way to pay for them. It involves the process

through which the corporation creates value through its capital

allocation and acquisition decisions. Managers of any company are

expected to forecast financial needs and opportunities, assess

the value of these opportunities, and implement a strategy for

achieving the company's financial goals. Major corporate finance

decisions include capital budgeting decisions, valuation

analysis, financing decisions, risk management, and dividend

policy.

The Cadbury Committee (1992) states that BOD are top most elected

representative of shareholders engaged in directing the affairs

of the company on its behalf. They act in the best interest of

shareholders. Kosnik (1987) refers to BOD as agents, trustees or

managing partners. BODs are people responsible for laying down

matters of principle and of accounting, statistical and

management procedures. They are liable for negligence, breach of

trust and misfeasance in either of their capacities as agents or

trustees or as both.

6

Boards are critical members of an organization. At the

shareholders Annual General meeting dated December 1995, the

shareholders of appointed its first BOD especially to oversee the

company’s operations, guide behavior, policies formulations,

planning, budget approval, and monitor performance.

According to Kaderes Peasants Development Policy and Regulation

Manual (1995), the company’s BOD was set to achieve the following

objectives:

1. To ensure the availability of adequate financial resources

2. Ensuring selecting, appointing, supporting, policy

formulation and reviewing the performance of the Chief

Executive.

3. To ensure formulation, approval and monitoring of annual

budgets

4. Accounting to the stakeholders for the organization’s

performance

This study examines the extent to which the above first three

(3) objectives have been achieved by Kaderes Peasants

Development Company limited.

7

Statement of the Problem

In spite of the above well stated objectives of the Board of

directors, various reports reveal that the board is not doing

its work well. As a result, Kaderes Peasants Development

Company limited has continued to have problems in its corporate

financial performance.

According to Kaderes Peasants Development Company limited’s

financial report (2010/2011), Mkinga who was the manager at that

time complained about the deteriorating financial position of the

company. He attributed this to the failure of the key players who

are the members of the board of directors to solicit adequate

financial resources for the company. This has affected the smooth

running of the company’s operations.

Nkubana (2012) reports on non compliance of corporate governance

principles of the company by the board of directors. He blamed

the members of the board of directors for poor selection,

appointment, lack of support, poor policy formulation and lack of

adequate review on the performance of the Chief Executive of the

8

company. He further criticized the Board of Directors for

performing duties without clear policies and procedures or

guidelines. As a result, several resolutions made in various

meetings have not been implemented.

Rugaimukama audit report (2011/12) reports on poor formulation of

budgets which have made it difficult to compare actual

performance against budgeted as an effective tool for controlling

performance. This was attributed to non participation of other

members of staff in budget formulation. The report further

revealed that budget approval process is not followed by the

board of directors as there are no clear budget approval

procedures.

In a related development, Mudaki (2012) decried about lack of

strategic planning as there were no business plans and

operational budgets of the company. This had lead to poor

monitoring of annual budgets for example, the company lost Shs

500,000,000 during financial year 2011/2012 as this could not be

effectively monitored since there were no clear monitoring

guidelines.

9

According to Manyama (2009) at a KPD PLC on business assessment

and strategies development, there were many problems identified

such as lack of common understanding and consensus building among

senior managers on business strategic development goal and

objectives. For example the difference in opinion about the

business profitability position and performance; that the

business was over geared as a result of overdrafts and bank loans

and that cost of products were not scientifically proven hence

cost of products and services were not based on actual cost. In

the same report, it was indicated that lack of strategic

planning, business planning and operational budgets had impeded

on achieving desirable financial performance.

Thus from the foregoing reports, it is apparent that corporate

financial performance deficiencies have persisted in Kaderes

peasants Development Company limited.

Purpose of Study

The purpose of the study is to examine the role of Board of

Directors in corporate financial performance of private limited

10

companies in the coffee industry focusing on Kaderes peasants

Development Company limited as a case study.

Objectives of the Study

The following are the objectives of the study are:

a) To examine how Board of Directors ensure availability of

financial resources in Kaderes Peasants Development Company

Limited.

b) To examine how Board of Directors carry out formulation,

approval and monitoring of annual budgets in Kaderes Peasants

Development Company Limited.

c) To establish how Board of Directors select, support, and

review the performance of the company CEOs in Kaderes

Peasants Development Company Limited.

Research Questions of the Study

The following are the research questions of the study:

a) How does Board of Directors ensure availability of financial

resources in Kaderes Peasants Development Company Limited?

11

b) How does Board of Directors carry out formulation, approval

and monitoring of annual budgets in Kaderes Peasants

Development Company Limited?

c) How does Board of Directors select, support, and review the

performance of the company CEOs in Kaderes Peasants

Development Company Limited.

Research Hypotheses

The study is set to test the following hypotheses:

H1o: There is no significant relationship between Board of

directors and corporate financial performance in KADERES Peasants

Development Company Limited.

H1A: There is significant relationship between Board of

directors and corporate financial performance in KADERES Peasants

Development Company Limited.

Scope of the Study

The study focused on board of directors and corporate financial

performance of private companies of coffee industry in Tanzania,

using Kaderes peasants Development Company limited as a case

study. The study specifically looked at availability of financial

12

resources; formulation, approval and monitoring of annual

budgets; and selection, support and review of performance of the

company CEOs. The study covered a period of three (3) years

running from financial year 2010/11 to 2012/2013.

Setting of the Study

Kaderes Peasants Development Company Limited (KPD) is located in

Karagwe District in Tanzania. Karagwe is one of the 8 districts

of Kagera region, that is, Karagwe, Misenyi, Bukoba rural, Bukoba

urban, Muleba, Biharamulo, Chato and Ngara. It is located in the

North Western Corner of Tanzania and borders with the Republic of

Uganda in the North, the Republic of Rwanda in the West, the

districts of Ngara and Biharamulo in the South and the districts

of Bukoba and Muleba in the East. It’s dedicated to facilitate

the Peasants and Farmers of Karagwe from four administrative

divisions of Kituntu/Mabira, Kaisho/Murongo and Bugene/Nyaishozi

and Nyabiyonza.

13

Kaderes Peasants Development Company Limited (KPDC) is a coffee

co-operative local company that was established in 2002 by

peasants from where it derived its name Kaderes peasants and

therefore fully registered in 2005 as required by the Company Act

of 2002 with its mission being eradicating poverty of the

peasants, and producing high quality coffee. It is one of the

largest and the leading indigenous coffee processing and exporter

in Tanzania. KPD is now an independent company which does not

only buy and export farmers’ coffee, but also offer a service and

training program to improve the productivity and quality

standards of the coffee.

Significance of the study

The study is significant to different stakeholders in the

following ways:

KPD Company Limited Management

14

The study findings and recommendations would guide the company

management to a new planning paradigm that would further change

strategies employed in improving corporate governance principles

and financial performance evaluation.

Government agencies

The Government agencies may make use of the study findings and

recommendations in establishing suitable policies and

interventions in the coffee industry.

Academicians and other researchers

The findings, conclusions and recommendations would be of

practical significance to academicians and researchers as it

would pave way for those who would be interested in this field

to learn from and expand upon the research. It would add on the

already existing literature in the coffee industry, about Board

of directors and corporate financial performance.

Arrangement of the Report

This study was arranged in eight chapters. Chapter one contains

an introduction to the study, background of study, problem

statement, study objectives, scope of the study, the setting of

the study, hypotheses, research questions, purpose of the study

and the significance of the study.

Chapter two the study literature, this contains two sections,

namely: literature survey and literature review.15

Chapter four present findings on how Board of Directors has

ensured availability of financial resources in Kaderes peasants

Development Company Limited.

Chapter five present findings on how Board of Directors have

carried out budget formulation, approval and monitoring in

Kaderes Peasants Development Company limited.

Chapter six present findings on how Board of Directors have

selected, supported and reviewed the performance of the company

CEOs in Kaderes Peasants Development Company limited.

Chapter seven presents the harmonization of the Board of

directors and corporate financial performance in Kaderes

Peasants Development Company limited.

Chapter eight presents the summary, conclusions and

recommendations of the study.

16

CHAPTER TWO

STUDY LITERATURE

Introduction

This chapter is made up of three sections, that is, literature

survey, literature review, and the conceptual framework. The

purpose of literature survey is to show what others have covered

about the problem, gaps left and how the current study intends to

fill these gaps. The chapter also reviews literature outside

Tanzania with the aim of establishing the models being applied

elsewhere.

Literature survey

A survey of literature on Board of directors and corporate

financial performance in the coffee industry reveals that many

studies have been carried in the coffee industry but none of them

has come up to explore the role of Board of Directors in

Corporate financial performance of private limited companies in

the coffee industry. For instance:

Kalimanzira (2009) studied about “Tanzania’s Coffee Sector:

Constraints and Challenges in a Global Environment”. The study findings

17

revealed that key constraints in the coffee sector are: an

complicated tax code with tax rates that are too high and in some

cases regressive; the excessive involvement of the state, which

discourages and weakens the private sector; the mandatory nature

of the coffee auction, which ought to be reconsidered; over

borrowing of funds; among others. The study recommended that: the

government with its people at heart could first, stop any

deductions (taxes) on the peasants’ earnings and declare borrowed

funds to the coffee industry as a start-up fund to facilitate

smooth running of the industry; allow private companies and

individuals buy coffee at a price competitive with that in

neighboring Burundi and Uganda; let the state completely pull out

of the coffee industry; among others. Kalimanzira in his study

was silent about formulation, approval, and monitoring of

budgets; and selecting, supporting, and reviewing the performance

of CEOs. The current study intends to fill this gap.

Ngaga (2010) carried out a study on “Improving efficiency and

performance in coffee producer organisations in Tanzania, using

co-operatives and self help groups as a case study”. The study

18

revealed that the efficiency and performance of producer

organisations have a major impact on farmers’ access to credit,

inputs and the level of returns. The cooperatives are faced with

such problems as poor governance, huge debts and structural

problems that have plagued the coffee co-operatives. The study

recommended that: there is need to address problems such as poor

governance, huge debts and structural problems that plague coffee

co-operatives by reviewing the co-operative Act to amend sections

that can improve the governance, transparency, and accountability

of co-operatives management. Co-operatives also need to be de-

politicised and be seen as economic entities. Debts should either

be written off or rescheduled. Furthermore, there is need for

training of society officials, carry out awareness campaigns to

sensitize members on their rights and obligations, policies and

strategies that encourage amalgamation of cooperatives to bigger

economical units are required. Ngaga in his study ignored

important aspects of budget formulation, approval, and

monitoring; and selecting, supporting, and reviewing the

performance of CEOs. The current study intends to fill this gap.

19

Literature Review

The problem of board of directors and corporate financial

performance is not unique to Tanzania only. Others outside

Tanzania have researched on it.

To examine the problem, the researcher focused on the following

themes:

a) Board of directors roles

b) Business Financing

c) CEO selection, support and reviewing performance

d) Budget formulation, approval and monitoring.

Board of Directors Roles

Baxt (2002) states that BODs principle’s duties are to act

responsibly in the best interest of the company and its

shareholders, Flowing from this function is the obligation to

account to the shareholders for the performance of the company.

The performance of the company is a direct reflection and

attribution of the performance of BODs. Director’s responsibility

and accountability are the two sides of the same coin of BODs

duties.

20

Conger (1998) argues that the BOD has to obtain timeouts and

periodic information about all operating activity results for

review and assessment in relation to predetermined goals and

objectives. This is required to assess the effectiveness of

management, including the CEO and the board itself, and provides

the basis for formulating feedback to management and stakeholders

in three areas of sustainable development within the overall

performance. The board should present a balanced and

understandable assessment of the company’s position and

prospects. The directors should report that the business is going

concern, with supporting assumptions or qualifications as

necessary. They should explain in the annual report their

responsibility for preparing accounts and there should be a

statement by the auditors about director’s responsibility.

The board should install and review annually a sound system of

internal control to safeguard shareholders investment and the

company assets. The board should establish an audit committee of

at least three independent non executive directors (NEDs).At

least one member of the committee should have recent relevant

21

financial experience. The annual report should contain statement

of how the company applied corporate governance principles. The

accounts should explain their policies including any

circumstances justifying departure from the best practices

(Conger, 1998).

Gavin et al (2004) assert that Board effectiveness occurs via the

execution of roles set that is conceptualized by different

researchers in different ways. What is clear is that the roles of

the board have evolved over time. Defining a clear role set is

difficult as different disciplines concentrate on different areas

of interest. Pettigrew et al (1992) identified six themes of

academic research on the role of managerial elites such as

chairpersons, presidents, Chief executive Officers (CEOs) and

Directors. These include the study of interlocking directorates

and the study of institutional and societal power, the study of

boards and Directors, the composition and correlation of top

management teams, studies of strategic leadership, decision

making and change, CEO compensation and CEO selection and

22

succession. There are, however board roles that receive board

support as explained below.

Board size

When the board has adopted a clear view of its responsibilities

in governing the company, the directors can then move to discuss

and agree the most effective way of structuring the board.

Consideration could be given to the size of the board itself; is

the board too small or too large to adequately fulfill its

requirements, given the size and complexity of the organization?

The balance of the executive and non-executive directors and

whether independent directors are necessary is another structural

issue to consider. Likewise does the board have the optimal

skills mix to deliver effective governance considering the nature

of the company governed? Depending on the circumstances, the

board may benefit from having a member with industry experience,

legal expertise or perhaps a director representative of

stakeholder.

Board size defined as the total number of directors on a board

(Panasian and Bhara, 2003), has been regarded as an important

23

determination of effective corporate governance. The optimal

board size according to Goshi et al (2002) includes both the

executive directors and non executive directors.

Forbes and Daniel (1999) argued that although board size is not

truly a demographic attribute, it is unlikely to have effect on

board functioning. Despite the considerable amount of effort in

research on board size for more than a decade there is still

lack of consensus among researchers on its relevancy.

There has been considerable debate on whether large boards

perform better than smaller boards. Daily and Dalton (1992) argue

that greater number of directors might increase available

expertise and resource pool while Nicholson (2004) contends

expanding the size of the Board provides an increased pool of

expertise, information and advice quality not obtained from other

corporate staff. In contrast, the difficulty inherent in

coordinating the contributions of many members can be complex,

hindering them to use their knowledge and skills effectively.

From agency perspective, increase in board increases the Board’s

monitoring capacity but costs that accrue from large boards may

24

facilitate CEO dominance over board members. For instance large

boards have difficulty in building the interpersonal

relationships that further cohesiveness, or maintain high board

effort norms owing to social loafing that exists in large boards

(Forbes & Daniel, 1999). Studies such as Nicholson (2004) have

also supported previous authors and concluded that when the board

size is very large, the disadvantages such as lack of

cohesiveness, coordination difficulties and fractionalization are

most severe and they became less prevalent as board size

decreases. In contrast very small boards cannot enjoy the

advantages of the pool of expertise, information and advice of a

larger board and these benefits emerge when the board becomes

larger. To date there are still wide views on an optimal board

size. Goshi et al (2002) an 8-11 persons’ board may be considered

optimal. In a recent study by Nicholson (2004), a board of 9-13

members is typically right for most companies but too small for

large ones. Epstein et al (2002) considered an average of 16

directors (3 within and 13 outside directors) to be appropriate

for larger companies, though respondents in this study believed

that 12 is the most effective board size. The study by Connelly &

25

Limpaphayom (2003) revealed that the average board size of

insurance firms in Thailand was 10 but ranged from a low number

of 4 members to a high number of 16 members.

Policy and decision making

The final function that a board needs to consider is its duty

with respect to delegating authority. Given the complexity of the

business environment, it is impossible for the board to be the

sole decision making body in the company. Instead, each board

needs to work on developing an appropriate method and level of

delegation of authority. Obviously this will again vary with the

context facing the board but, in all circumstances, the board

needs to clearly articulate and document the delegations it makes

(Gavin et al, 2004).

Contingency, board roles and board effectiveness

While all boards are required to undertake activities within the

spectrum of this roles set, they contend that each organization

will need a different emphasis among these roles. Thus, there is

need to explicitly incorporate a contingency perspective, since a

particular board composition or behavior that is advantageous for

26

one corporation may prove “inappropriate or even detrimental in

another”. There is need to identify the control variables and

gaps in understanding how the board can impact on firm

performance (Heracleous, 2001).

The particular contingencies that will impact on board roles –

corporate performance would include organizational size,

management experience, industry turbulence, industry lifecycle,

and firm lifecycle. It is these contingencies that moderate the

relationship between board roles and board effectiveness. Thus

the current study includes external and internal contingencies to

moderate the relationship between board role execution and board

effectiveness (Dalton and Daily, 1992).

Board effectiveness

Herman et al (1997) states that individuals perceive

effectiveness partially or in different ways. The social

constructionist’s conception, for instance, holds that there only

judgments of effectiveness, thus effectiveness are judgmental.

Effectiveness is about doing the right things to achieve the

results. In terms of measurement, Kosnik (1990) suggests that the

27

current approaches measure elements associated with effectiveness

rather than effectiveness rather than effectiveness itself. Board

effectiveness can be conceptualized as a function of overall

contribution of the board to the organization performance,

standard of support provided by the organization, individual

contribution of directors to organization performance, board

dynamics, Board performance evaluation and review. Close

inspection of earlier literature revealed that board

effectiveness is almost based on individual experience. The

issue of measuring team outcomes is a difficult one and the

literature abounds with debates around team performance, which

mirror those surrounding organizational performance. However,

while there are various definitions of group effectiveness.

Huat and David (2001) argue that board performance has been

measured along the dimension of the board’s ability to perform

its functions. Indeed, an earlier study by Forbes & Daniel (1999)

defined board effectiveness as the board’s ability to perform its

control and service tasks effectively. From empirical

perspective, Brown (2004) found that overall judgments by

28

respondents of board effectiveness were strongly related to how

effectively the boards were judged to perform various functions.

Basing on the above literature, it fairly holds that board

performance has been largely defined in terms of roles played by

the BODs. These roles have been identified from various

perspectives including; agency, service, resource dependency,

legal and strategic theories. However, some of these perspectives

are interrelated, for instance resource dependency, service and

strategy, agency and legal. Using these perspectives, the

following roles have been identified;

Skills and knowledge

Presence and use of skills and knowledge has been identified as

another important dimension of board effectiveness. Board members

must have the right mix of skills and knowledge. For instance,

they should possess both functional knowledge in traditional

areas of business such as accounting, finance, legal or marketing

as well as industry specific knowledge that will enable members

to truly understand specific company issues and challenges. In

addition, board members must have enough general knowledge to

29

provide good input on all topics of discussion, ask questions of

all special interest until they are comfortable enough to cast

votes Espstein et al, (2002). Thus, for boards to work

effectively, Hay et al (1987) emphasize that board members must

possess necessary knowledge and skills, given the unique nature

of their tasks. Similarly, for a board to effectively perform the

supervisory role, it should be composed in a manner that enhances

the presence of skills and knowledge.

Committees

According to Gavin and Geoffrey (2004), significant research

effort has focused on the impact of committees most notably the

audit committee, remuneration committee, and nominating committee

with findings that there is a link between the presence of board

committees and board effectiveness. A committee is a group of

members to whom some specific role has been delegated by a full

board. Committees can be used to gather, review and summarize

information and report back to the full board for decision or can

be delegated specific decision making powers.

30

Delegation

The final function that a board needs to consider is its duty

with respect to delegation authority. Given the complexity of the

business environment, it is impossible for the board to be the

sole decision- making body in the company. Instead, each board

needs to work on developing an appropriate method and level of

delegation of authority. Obviously this will again vary with the

context facing the board but, in all circumstances, the board

needs to clearly articulate and document the delegations it makes

(Gavin and Geoffrey, 2004).

Risk management

Risk management includes the identification of all significant

risks faced by the company and ensuring that appropriate policies

are in place to moderate the impact of these risks Klein, (2004).

This study will focus on committees like budget and pricing board

committee, procurement committee, advertising committee and the

roles delegated by board to the committees. Appropriate policies

put in place to moderate the impact of risks in the industry will

be considered.

31

Financial Performance

Measuring firm performance using accounting ratios is common in

the Corporate Governance literature Demaetz and Lehn, (1985), in

particular, return on capital employed, return on assets, and

return on equity. Similarly, economic value added can be as an

alternative to purely accounting- based methods to determine

shareholder value by evaluating the profitability of a firm after

the total cost of capital, both debt and equity are taken into

account Zahra and Pearce (1989) Other measures of financial

performance in manufacturing firms are Market share and Sales

growth.

Measuring the company’s profitability

Pandey (1999) states that most growing businesses ultimately

target increased profits, so it's important to know how to

measure profitability. The key standard measures are:

Gross profit margin - how much money is made after direct

costs of sales have been taken into account or the

contribution as it is also known.

32

Operating margin - this lies between the gross and net

measures of profitability. Overheads are taken into account,

but interest and tax payments are not. For this reason, it is

also known as the EBIT (earnings before interest and taxes)

margin.

Net profit margin - this is a much narrower measure of

profits, as it takes all costs into account, not just direct

ones. All overheads, as well as interest and tax payments, are

included in the profit calculation.

Return on capital employed - this calculates net profit as a

percentage of the total capital employed in a business. This

allows you to see how well the money invested in your business

is performing compared with other investments you could make

with it, like putting it in the bank.

Corporate Governance

Soldan (2001) defines governance as the existence of key actors

inside the chain which are responsible for the division of labour

between the firms, and for the capacities of individual

participants to upgrade their operations or functions.

33

The Organisation of Economic Co-operation and Development (OECD)

(2004) provide the most authoritative functional definition of

Corporate Governance: “Corporate governance is a system by which

business corporations are directed and controlled. The corporate

governance structure specifies the distribution of rights and

responsibilities among different participants in the corporation,

such as the board, managers, shareholders and other stakeholders

and spells out the rules and procedures for making decisions on

corporate affairs. By doing this, it also provides the structure

through which the company objectives are set and the means of

attaining those objectives and monitoring performance.”

Corporate governance is referred to as the manner in which the

power of an organization is exercised in the stewardship of the

Corporation’s total portfolio of assets and resources with the

objective of maintaining and increasing shareholders value with

the satisfaction of other stakeholders in the context of its

corporate mission (Private Sector Corporate Governance trust,

(1999). The committee on the financial aspects of corporate

governance (the Cadbury Committee), defines corporate governance

34

as the system by which companies are directed and controlled.

Corporate Governance is both about ensuring accountability of

management in order to minimize downside risks to shareholders

and about enabling management to exercise enterprise in order to

enable shareholders to benefit from upside potential of firms

(Keasey and Wright, 1993).

Corporate governance is important because it promotes good

leadership within the corporate sector. Corporate governance has

the following attributes; leadership for accountability and

transparency, leadership for efficiency, leadership for integrity

and leadership that respect the rights of all stakeholders,

Institute of Corporate Governance of Uganda, (2000). Lack of

sound corporate governance has enabled bribery, acquaintance and

corruption to flourish and has suppressed sound and sustainable

economic decisions.

All companies whatever their size or nature of business, need

access to outside resources if their businesses are to succeed.

These resources vary enormously from company to company, but fall

into main categories, as information and physical resources.

35

Developing business networks and working to promote the

reputation of the firm are two other important ways that a board

can add value to the company. By acting in an open, professional

and ethical manner in their dealings with people outside the

organization, board members also raise the profile of the firm

and enhance its reputation (Garvin and Geoffrey, 2004).

Ensuring Availability of Financial Resources

Garvin and Geoffrey (2004) argue that all companies regardless of

their size or nature of the business need access to outside

resources if their businesses are to succeed. These resources

vary enormously from company to company, but fall into main

categories, as information and physical resources. Developing

business networks and working to promote the reputation of the

firm are two other important ways that a board can add value to

the company. By acting in an open, professional and ethical

manner in their dealings with people outside the organization,

36

board’s members also raise the profile of the firm and enhance

its reputation.

The acquisition (or rising) of financial resources and effective

allocation of these financial resources within a firm in order to

enable it achieve its predetermined objectives remains key board

role to an organization. According to Hinrichs and Tay (1996),

the task of raising finances rests with the board, through

delegated to head of finance (Finance manager).Once the board has

raised the required funds, they have to ensure that the funds are

committed into long term and short requirements of the firm.

Today’s business environment is characterized by external forces

of stiff corporate competition, technological changes, volatility

in inflation and interest rates and global economic uncertainty

all of which have an increasing impact on the business

performance and survival. The board must have the flexibility to

adapt to the changing external business environment, and

effectively and efficiently invest in those assets that in

enhance success and ultimately the overall success of the economy

in which the business operates. Therefore, through efficiently

37

acquiring, financing and managing assets, financial management

contributes to the economy as a whole.

The BODs may exercise all the powers of the company to borrow

money and to mortgage or bind its undertaking and property or

may part thereof, and to issue other securities for any debt,

liability or obligation of the company or any third party,

provided that the amount for the time being remaining un

discharged in respect of moneys borrowed or secured by the

directors as aforesaid (apart from temporary loans obtained from

the company’s bankers in the ordinary course of business) shall

not at any time, without the prior sanction of the company in

annual general meeting, exceed one-half of the amount of the

issued share capital plus the amount of the share premium account

(if any) or of the stated capital (Leblanc, 2003).

Budget Formulation, approval and Monitoring

Budgeting is a process involving planning, in financial terms, of

a comprehensive a coordinated framework for guiding the

periodical, spending and control of funds in order to achieve the

desired performance efficiency, effectiveness and equity

38

(Pandey,1999). Saleemi (2008) defines a budget “As a plan of

action expressed in quantitative terms, financial and/or

quantitative statement prepared and approved prior to a defined

period of time. It may include income, expenditure and employment

of capital”.

Aduka (2006) describes budgeting as a process of preparing, in

financial terms, a meaningful time-based course of action for

achieving management expectation. He adds that budgeting is

recognized and has received reputation as one of approaches that

fundamentally and comprehensively assist management in stating

and communicating its goals. That is provides a frame work for

implementing a planned course of action using the available

resources and therefore provides means of controlling the

performance of individuals, units within an enterprise, and of

the enterprise, and of the enterprise as a whole, so that desired

results are achieved.

Sharp and Slinger (1970) note that the budget provides a yard

stick onto which financial performance of an organization is

measured, it helps in identifying the variance between the

39

planned and actual activities and charting ways of dealing with

them. The budget is a vehicle of bringing the action of different

parts of the organization together in a reconciled plan. The

various managers have to make coordinated decisions so as to

reduce costs, avoid duplication of efforts and wastage of

resources, and above all minimize organizational conflict.

Budgets serve as useful tools for motivating in any organization.

The objectives of the firm set out what is to be achieved and the

budget specifies the costs of these activities. Managers and

employees, if have participated in preparing the budget, they

would feel strong obligation to achieve its specification.

Welsch (2001) claims that a budget provides an important tool

for the control and evaluation of sources and the uses of

resources. Using the accounting system to enact the will of the

governing body, administrators are able to execute and control

activities that have been authorized by the budget and to

evaluate financial performance on the basis of comparisons

between budgeted and actual operations. Thus, the budget is

implicitly linked to financial accountability and relates

40

directly to the financial reporting objectives established by

the organization.

Pandey (1999) added that budgeting focuses on the determination

of what should be done, how the goals may be reached, and what

individuals and units are to assume responsibility and be held

accountable. These observations are also implied in a number of

works by others such as Philip G. Young (2003) and Johnston

(1982). Indeed, according to World Bank (1992), budgeting is

potentially capable of leading to any level of performance, which

may be effective, beyond expected effectiveness, or even in

effective. Johnston (1982) notes that as having observed that

budgeting can be conducted in such a way that the stated targets

are too unrealistic, or too high to attain using the available

resources, be the human, material or financial. He argued that

high and unattainable targets put pressure on employees.

Employees view such targets as impossible to achieve and this may

cause a depressing effect on their morale.

According to Hyder and Miller (1986), once employees know that

the targets are unrealistic and unattainable, they tend not to

41

put serious efforts to achieve them, thereby registering in

effective performance. Budgets are important because: it compels

planning. It sets clear guidelines on how financial, material and

human resources can be utilized and achieve specific targets; the

budget help to improve communication and coordination among the

management and employees; they are also used to evaluate the

performance of business enterprise; and finally, a helps to

clarify authority and responsibilities of the departmental;

managers and employees.

Hilton (2000) added that the set budgetary targets may also be

too unrealistically low to provide any meaningful challenge to

employees. He noted that the achievement of such targets does not

require any normal or even special effort and therefore employees

do not feel motivated to perform as expected. In the end, the

desired performance is not achieved. Greg Harrison (2003) have

for long time observed that budget may also come up with targets

which are so unclear and ambiguous that they confuse the

implementation process. Unclear targets will make budgeting lead

to ineffectiveness performance because implementation will not be

42

systematic. In absence clear targets, employees lack a proper

direction and something to aim at. This leads to confusion of

what should be done. Employees can not clearly tell what they are

expected to do and achieve. They finally fail to achieve desired

performance as effectively as projected.

Shapiro (1989) views budgeting as a tool that tends to reflect

what top management expects to achieve. In so doing, budgeting

wins management support, confidence, acceptance and support,

which all combine to make budgeting an important vessel for

pushing for desired performance. This observation implies that

budgeting produces a program of action that must represent the

expectations of management if it is gainful management support

and lead to effective performance. This is because management

will facilitate it and ensure that subordinates carry out their

assigned tasks to attain desired performance.

Budget may be prepared for the business as a whole for

departments, for functions such as sales and production or for

financial and resource items such as cash, capital expenditure,

manpower, purchases et cetera. BODs are entrusted with budget

43

management and control. This refers to the whole process right

from budgeting or budget planning, implementation and control

(Hinrichs and Tay, 1996).

A budget planning also identifies grounds for approving and

justifying allocations made. It also specifies who is responsible

for authorizing spending (Aucoin, 1990). In effect, as all these

are being put into effect, budget implementation takes place.

However, although none of the for-cited authors mentions it, as

budget implementation gets underway, it impacts on achievement of

desired performance. As such, the manner in which the budget is

planned and implemented determines the extent to which desired

performance is achieved. Organizations where funds are spent

without regard to budgets, the likelihood of failing to achieve

the desired performance is high.

Supervision involves ongoing checks on expenditures to ensure

funds are spent on the every programs and activities for which

they are realized. As such, effective supervision minimizes waste

and unnecessary spending. It also guards against spending outside

44

the budget. It therefore facilitates the achievement of desired

performance, be it in the form of effectiveness, efficiency and

equity.

The board reviews strategic issues on a regular basis and

exercises control over the performance of each operating business

within the group by agreeing budgetary targets and monitoring

performance against targets. Certain matters are specifically

reserved for approval by the board and the board has overall

responsibility for the group system of internal control and risk

management.

These matters include strategic plans, annual budgets, review of

operating and financial performance, individual appraisal of

significant new projects, safety and governance compliance. All

business units and functions are required to develop formal

succession plans which are reviewed annually by the board. This

evaluation process includes the board as well as the various

committees which they have formed. Each year the directors

complete a comprehensive survey and the results are collated and

assessed against previous results. Following a review of results,

45

a prioritized action plan is drawn up to implement improvements.

The performance of individual directors also evaluated taking

into account factors such as attendance, objectivity in decision

making, experience and ability to contribute effectively to board

meeting. Formal evaluations of a company’s CEO by its board of

directors are becoming increasingly common place. The process

should involve three stages: establishing evaluation targets at

the start of the fiscal year, reviewing performance at midyear,

and assessing results at the end of the year.

According to Hilton (2000), assessing CEO is one of the board’s

primary governance responsibilities and is critical to the

success of the chief executive and to the organization as a

whole. Three stages encompasses assessment of the chief

executive’s responsibilities, job expectations and annual goals;

captures the board’s perception of the executive strengths,

limitations and overall performance, and foster growth and

development of the chief executive and the organization. The CEO

is responsible to the board for the overall management and

performance of the company. The CEO should manage the company in

46

accordance with strategy, plans and policies approved by the

board to achieve the agreed goals. The board has to obtain

timeouts and periodic information about all operational activity

results for review and assessment in relation to predetermined

goals and objectives. This is required to assess the CEOs

effectiveness and provides a basis of reporting back to

shareholders and other stakeholders in the three areas of

sustainable development-the economic are, social/health area and

environmental area-within the overall business environment.

CEOs Selection, Support and Review of Performance

The selection of the CEO has profound impact on the success of

the enterprise and is the exclusive responsibility of the board

of directors. When seeking a new CEO, the board must fully

understand the prevailing dynamics of the company’s situation and

objectively assess how well personal attributes of each CEO

candidate meet the requirements of the role. Because corporations

evolve as their competitive environments change, the leading

candidate for the CEO position at one stage in the life cycle of

the enterprise may well be ill-suited at another stage. If the

47

board fails to grasp how these changes affect the role

requirements, it makes a seemingly obvious selection that in fact

fails to serve the requirements of the position.

The level of objectivity with which the board approaches

selection of a new CEO often suffers because of a long

association with presumptive their apparent. The selection of CEO

therefore should constitute stand-alone, discrete process. Except

for the initial selection of the CEO for a start-up company, CEO

selection is always in the context of choosing a successor. For

going concerns that have reached steady-state operations,

succession planning should contribute the first step in the

process of CEO selection.

The question invariably arises as to whether the board should

focus on so –called internal candidates; usually loyal and

diligent long-term employees who naturally might feel that they

should be considered for the top job. Undoubtedly, these

executives will have demonstrated an ability to work effectively

as a member of the team of the outgoing CEO. An inside candidate

has the following advantages: being well known to decision

48

making; having probably managed his or her career path with the

top spot in mind; being generally predict table behavior and

attitude towards others; and possessing substantial knowledge of

the inner workings of the enterprise. Nonetheless, in insider is

also saddled with certain disadvantages, including; having his or

her weakness likewise well known to the selection; the inevitable

presence of adversaries within the organization who may work

subtly to tarnish the performance of new CEO.

Outside candidates likewise bring their own set of advantages and

disadvantages such as: a reputation and perhaps mystique built

entirely independently the enterprise; and standards of

performance that are discrete and inevitably differ from though

not necessarily in conflict with, those of the prospective

employer, yielding the possibility of fresh standard for success.

Conversely, the outside candidate is burdened as well with

inherent disadvantages such as: initial board skepticism of the

candidate’s ability to lead the enterprise as a result of the new

CEO’s lack of understanding and appreciation of the subtleties of

its history and culture; and in many cases the absence of strong

49

relationships with both major vendors and customers and perhaps a

narrow window within which to build them.

Board of Directors must weigh carefully all the nuances that

surrounds the insider versus outsider succession issue. CEO’s

evaluation is one of the very important duties of the board.

Evaluation, as a process, should be used to identify how the CEO

is currently performing, so that planning for the future

including corrective actions can occur. The purpose of evaluation

is more like introspection and neither to be critical nor to act

in a policing role. Performance evaluation is a flexible and

dynamic process that includes the act of setting goals and

standards for performance. These goals need to be measurable and

achievable. Regular evaluation will help ensure accountability

and effectiveness of the CEO.

According to Cadburys (1992), the following guidelines could be

used for CEO evaluation: establish task standards for example

through financial ratios; establish functional standards such as

communication skills, financial management, and organization

50

climate; conduct an evaluation through an open, frank and

positive discussion.

Formal evaluations of a company’s CEO by its board of directors

are becoming increasingly common place. The process should

involve three stages: establishing evaluation targets at the

start of the fiscal year, reviewing performance at midyear, and

assessing results at the end of the year. Just before the start

of the company’s fiscal year. The CEO and his or her direct

reports should work with the board to develop annual strategic

plan establishing the company’s long-term and short term

objectives. Finding the right objectives is a critical part of

the process. This should include financial and non-financial

objectives. These can further be defined clearly in three levels

of performance for each objectives-poor, acceptable and

outstanding. Once the objectives are defined, the CEO must

translate them into a set of personal performance targets and

specify how his or her progress will be measured against each.

The CEO then shares these targets and metrics with a committee of

the board-normally, compensation or board governance committee

51

that ideally consists solely of outside directors. This committee

makes recommendation to the full board, resolving any differences

between the perceptions of the CEO and the outside directors

regarding objectives. This committee also establishes financial

rewards that will result from meeting the targets. Committee

members must collaborate with the CEO to ensure that targets are

realistic but challenging. When the CEO and committee members

agree on objectives and measures, the committee presents them to

the full board for discussion and final approval. The mid-year

review-which is like any mid-year employee review, is a chance

for the board to assess whether the CEO is on a course to meet or

exceed objectives and, if no to determine where the problem lies.

The midyear review encourages directors to act before minor

problems become major ones and ensures that the objectives as

originally framed are still relevant. Such reviews may need to

occur more frequently than once a year in industries where

products and market conditions change rapidly.

52

The final stage of the CEO’s evaluation should take place at the

end of the fiscal year, when the board’s compensation committee

compares the executive’s actual performance against targets and

determines the compensation it will recommend to the full

complement of outside directors. Typically, this stage starts

with the CEO completing a written self-evaluation that gauges his

or her performance over the year. Individual outside board

members should also complete a short questionnaire assessing the

CEO’s performance.

The committee should also collect and consider pertinent outside

information, such as perceptions of the CEO by the investment

community and by its most valued customers. Using all this

material as background, the committee should then prepare its

recommendation, and outside directors should meet to discuss and

approve a final compensation package. The board should give the

CEO a written evaluation, as committing thoughts to paper force

deeper reflection and greater clarity. It also gives CEO’s

something concrete that they can review at their leisure after

meeting. Written proposals also ensure that every director is

heard-not merely those who are the most vocal.

53

Corporate Governance and Financial Performance

Two broadly defined theories co- exist in the corporate

governance literature. One stresses the discipline of the market,

claiming that threat of hostile takeovers and leveraged buyouts

in firms was sufficient to ensure full efficiency. Where managers

neglect to invest in those projects that add value to the firm

and its shareholders but divert recourses to their own benefit,

the financial markets act to restore good governance. A number of

mechanisms have been suggested, such as removing senior managers

in poorly performing firms (Krambia et al. 2006); demanding cash

flow payments in the form of debt service; and linking executive

compensation to performance, including equity and options.

Managers and owners of companies showing efforts and intention to

implement good corporate governance will increase market

credibility. Subsequently, they will collect funds at lower cost

and lower risk. It can be argued that better corporate governance

will lead to higher performance. Some empirical evidences support

this argument, Cadburys, (1992) investigated the relationship

between corporate performance and good corporate governance in

54

Korea. They find positive relationship between corporate

performance and corporate governance.

Keasey and Wright (1993) studied firm’s performance from 27

developed countries. They find evidence that there is higher

valuation of firms in countries with better protection of

minority shareholders. Parallel with this study, Heracleous,