Joint UNDP/World Bank Energy Sector Management ...

90

Joint UNDP/WorldBank Energy Sector ManagementAssistance Program Activity Completion Report No. 035/85 Country: THE GAMBIA Activity: PETROLEtM SUPPLY MANAGEMENT ASSISTANCE APRIL 1985 Report of the jointULNDP/Wold Bank Energy Sector Management Assistance Program This document hasa restricted distribution. Itscontents maynot be disclosed without authorization from the Govefinment, the UNDP or the WorlaBank. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Joint UNDP/World Bank Energy Sector Management ...

Joint UNDP/World BankEnergy Sector Management Assistance Program

Activity Completion Report

No. 035/85

Country: THE GAMBIA

Activity: PETROLEtM SUPPLY MANAGEMENT ASSISTANCE

APRIL 1985

Report of the joint ULNDP/Wold Bank Energy Sector Management Assistance ProgramThis document has a restricted distribution. Its contents may not be disclosed withoutauthorization from the Govefinment, the UNDP or the Worla Bank.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

THI GAMBIA

PETRLEUM SUPPLY MANAGEMENT ASSISTANCE

APRIL 1985

ABBnsVIATIuow

APRA Average Freight Rate AssessmentADO Auto Diesel8bls Barrel containing 42 US gallonsC.I.F or c.i.f Cost Insurance and FreightDCF Discounted Cash FlowDWT Dead Weigh. TonnageFIFO First-In First-OutFOB Free on BoardGal U.S. GallonGP General Purpose Class of ShipHDO Heavy Diesel OilK or k 1000km kilometer1 literL/C Letter of CreditLR-l 45-80 KDIT Class of ShipLIBOR London Interbank Offered RateLT Long Ton (2240 pounds)m2 millionm3 square meterm cubic meterMR 25-45 KDWT Class of ShipNT Metric Ton (1000 kilograms)NW megawattsq. square

BP British PetroleumCPA Communit6 Franciere AfricaineESNAP Energy Sector Management Assistance ProgramGOTC Government of The GambiaGPMB Gambia Produce Marketing BoardGPTC Gambia Public Transport CorporationGRTC Gambia River Transport CorporationGUC Gambia Utilities CorporationIMF International MQnetary FundISDB Islamic Development BankMEPID Ministry of Economic Planning and Industrial

DevelopmentMNT Ministry of Finance and TradeNEC National Energy CommissionmPC Nigerian National Petroleum CorporationOPEC Organization of Petroleum Exporting CountriesUNDP United Nations Development ProgramWs Worldsc&le

coavmsxou FACT0Rs

Currency 1/

Currency unit = Dalasi (D)1 = 100 bututsD S.00 = 1.00 UK Pound (t)US$1.32 = 1.00 UW Pound (£)D 3.79 * US$1.00

Energy

1 toe - 10.2 million kilocalories

Product million kcal/MT toe/MT liters/MT liters/too

LPG 10.8 1.059 1730 1634Gasoline 10.5 1.029 1357 1319Kero/Turbo 10.3 1.010 1229 1217Diesel 10.2 1.000 1187 1187Heavy Diesel 10.2 1.000 1165 1165Fuel Oil 10.0 0.980 1050 1071

I/ Exchange rates for November, 1984

This report is based on the findings of a mission comprising Messrs.A. Aruar (Mission Leader), K. Hornby (Consultant) and H. Williams (Con-sultant) which visited The Gambia in July 1984. The report was writtenby Messrs K. Hornby and S. Rivera, and discussed with the Covernmeat inNovember 1984 by a mission comprising Messrs. A. Ferroukbi (MissionLeader), K. Bornby and S. Rivera.

TAILU OF COUTUhM

EXECUTIVE SUMUARY ............,. . . . .i-xiii

I. OPTIMIZATION OF PETROLEUM PRODUCT IMPORTS.................* 1

Recet vie1ommt.....*.. ...... .....*.. *... ~.*e**.... 1Recent Dvlpet Findings and Rec ons . . . o. . 2Cost of Current Supply Arrangemenzs (Alternative A)... 3Review of the Landed Cost Compon ents*................. 3Importing Products at Spot Prices (Alternative B)..... 6Mechanism for Competitive Bidding on Product Imports.. 6Processing Nigerian Crude Through 8*1Refinery in Dakar (Alternative C) 7

Purchasing All Product Requirements ftomUNPC (Alternative D)... 8

Other Supply Arrangements.............................o 9

II. COMPULSORY STOCKS/EMERGENCY ALLOCATION PLAN............... 1

Findings and Recoumendationes............................ 11Present Terminal Operations........................... 11Compulsory Stocks ............. 12Emergenc7 Allocation Plan...................... . * 12

Optimum Use of Tankage at the Shell Storage Depot....... 12Other Product Tankage .............. , 13Determination of Working Inveztories.................... 13Compulsory Stocks.. .........................-...-... 14Emergency Allocation Plans. ...................... 16Implementing an Emergency Allocation Plan............. 18

III. PRICING OP PETROLEUM P2ODUCTS....................e...... 203v........................ r20

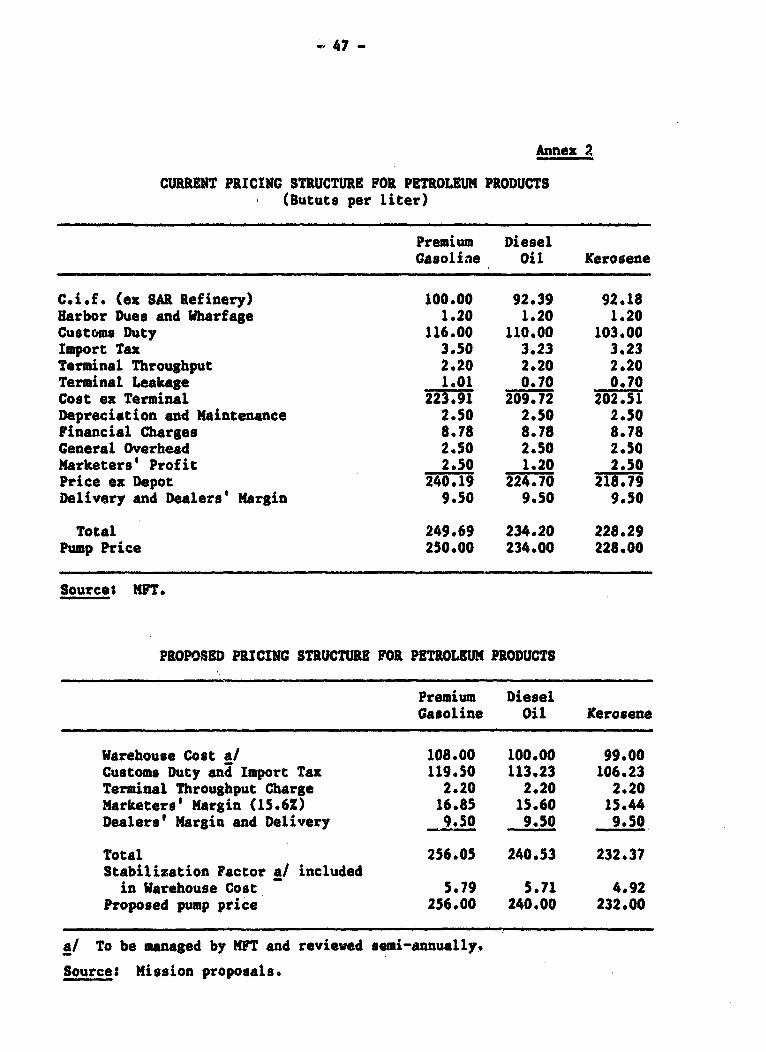

Findings and Recomendations..................... ... 20Current Pricing Structure* .........................*. 20Proposed Pricing Structure ................. 20

Current Situation................ 21lmport Cot-***.*-X************- 22Fitancial Charges................ . 24Depreciation and Maintenance Charges.................. 25Terminal Throughput Charges ......... 25Marketing Kargins.......................... ...... 26

Proposed Pricing Structure 27Warehouse Cs .......... ;27Cut'toms Duty and Import Tawes ......................... 28Terminal Throughput Charge............................ 28Marketers' Msrgin............................... 28Dealers' Retail Margin and Deliveryg................... 29

IV. ACCOUNTING SYSTEMS FOR PETROLEUM PRODUCTS................. 30Overview ..... , ,,, , ~~~~30

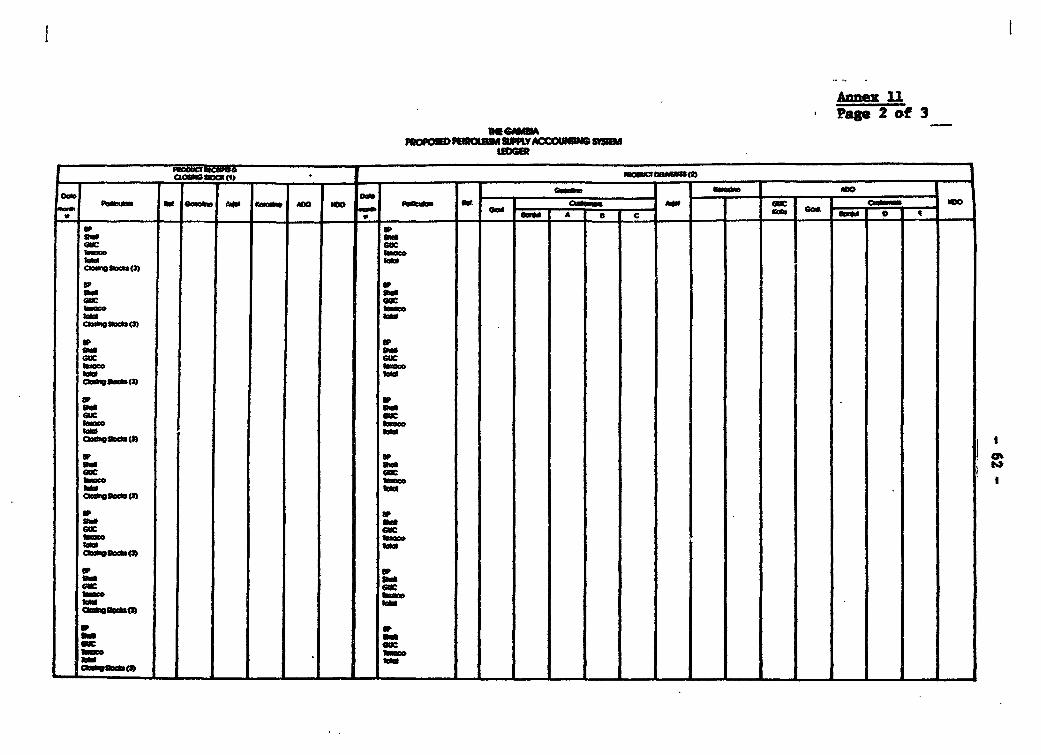

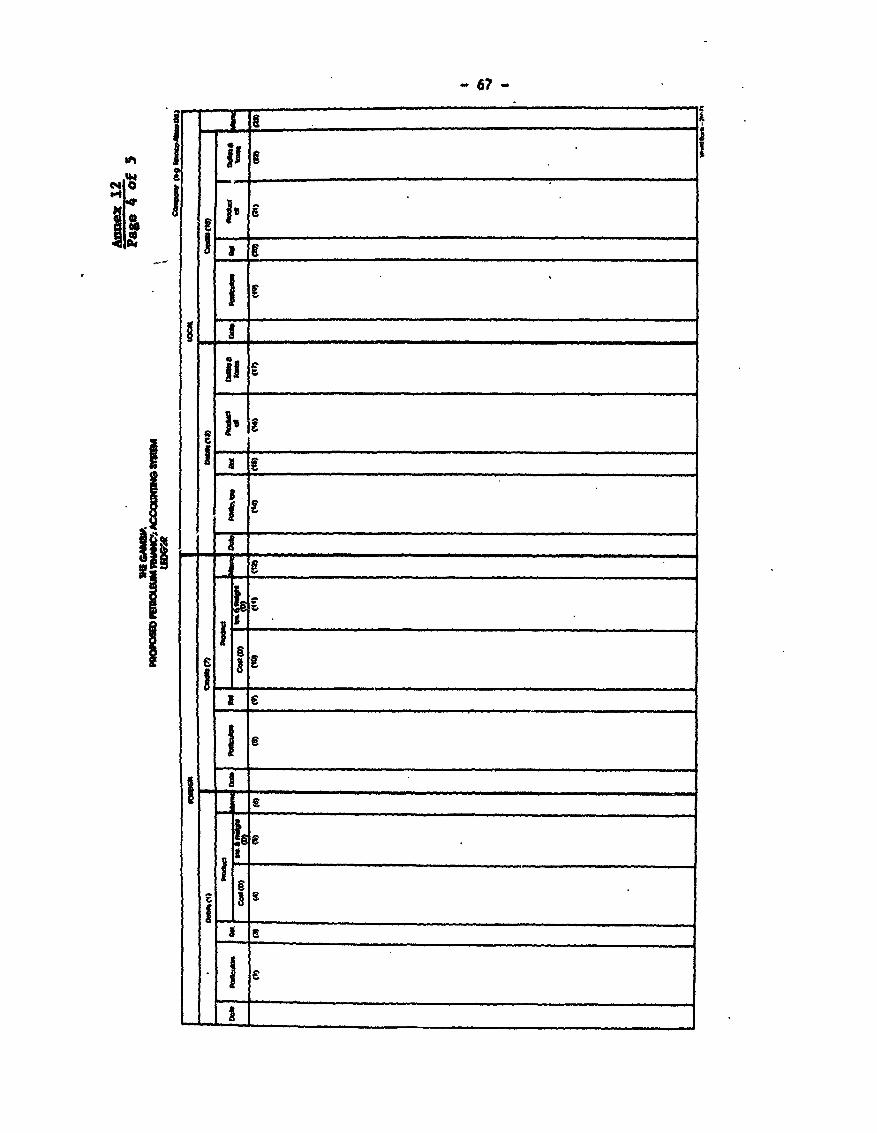

Current Situation ................................. 30Product Imports ....................................... 30Product Distribution .. 00 ... 0 e0.o..*****............... 31Payments for Imports.................................. 31

Proposed Accounting System for Petroleum Products....... 31Management of the 8ystem.............................. 32

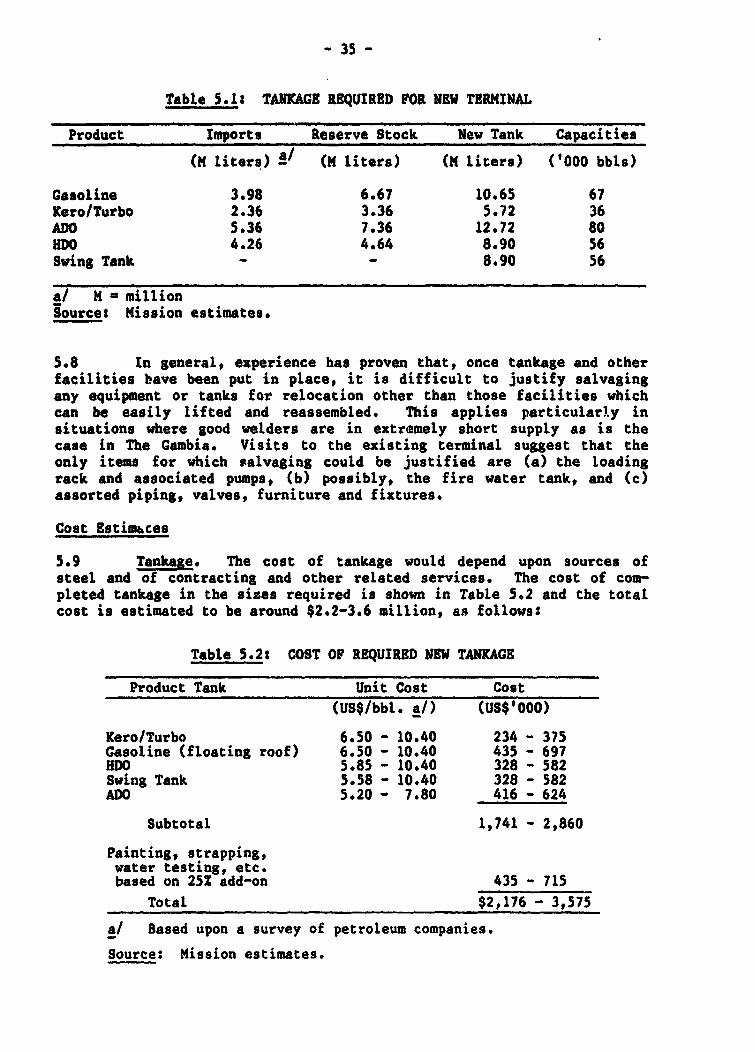

V. RELOCATION OF PETROLEUM STORAGE DEPOT..................... 33Overview ............. e0o0ooo ....oo. o...........o .....ooo 33Findings and Recommendationso........................... 33Current Situationo .***..00000.00....... . .000000000*00000 33New Facilities. ooo...O.o 00000000000 00.........*...*00.... 34Cost Esise ..........................*35Site Sizeeo.ooooo.............. 0000*oo 0*o 00 0oo0o 36Site Selectiono......................... 00040000oo0oo 37

Development of Bund Road Site...............0*.....00. 38Total Cost Estimate...................... *00000000000 39Alternative Considerationo..................... 0000000 39Other Considerationso........................o.o.o0o0o 39

VI. TECHNICAL ASSISTANCE AND TRAINING PROGRAMFOR ENERGY WNT. .......................... 41Overviewo.. o..oooooo...o..o..o.......................... 41Role of the National Energy Commission.................. 41Role of the Energy Unit .000 00.......................... 41Technical Assistance for the Energy Unit ................ 42Training o.oo..oooo.o.o.o..o.oooooo..o......o.....oo 42

ANNEXES

1 Principal Objectives of Assignmentt........................... 462 Petroleum Products P-icing Structure......................... 473 Proposed Petroleum Product Accounting System................. 484 Cost Summary of Relocation of Petroleum Storage Depot........ 495 Current Supply Arrangements Landed Cost Breakdown............ 506 Processing Nigerian Crude through BAR Refinery in Dakar ..... 527 Purchasing Products from Nigeria............................. 568 Other Product Tankage in the Cambiao.......................... 589 Development of Available Days Supply in Present Situation..... 5910 Communication Chart...0 0000.... oe*000*o0oo000o 00000*00040000* 6011 Petroleum Products Supply Accounting Systemo.... o.oo........ 6112 Petroleum Products Financial Accounting System............... 6413 Proposed Role of National Energy Commission................ 0. 6914 Energy Unit Terms of Reference..o.........o................ X 70

Introduetion

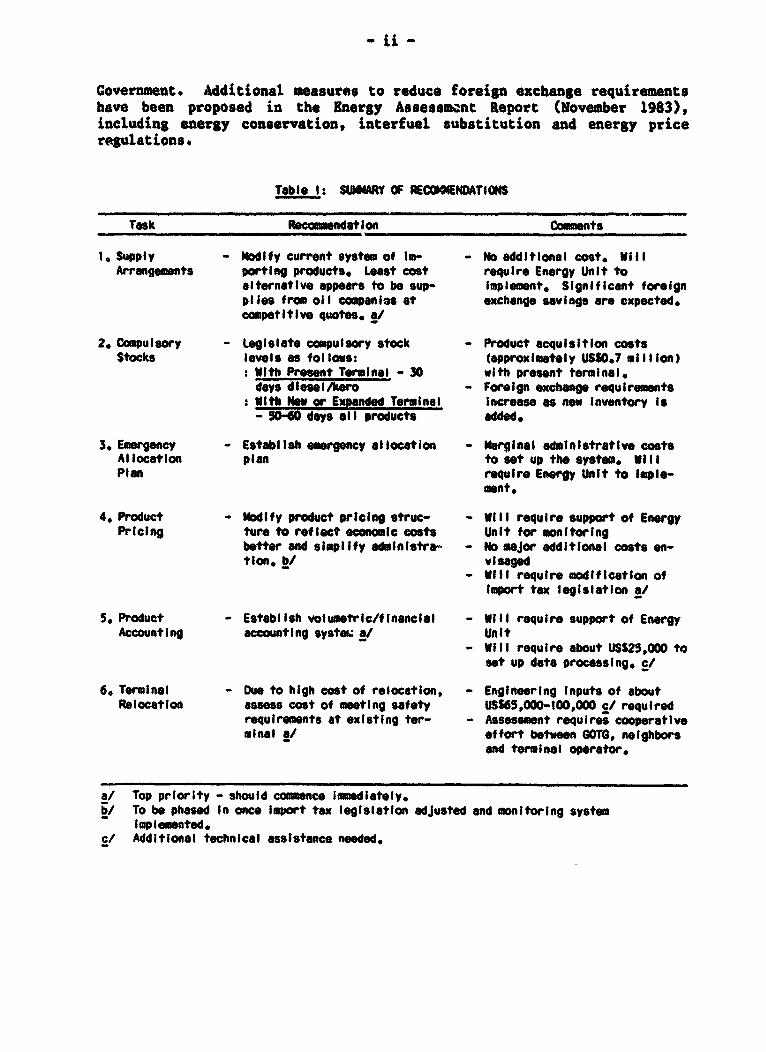

1. In April 1984, a World Bank mission visited The Gambia underthe auspices of the Energy Sector Management Assistance Program (ESMAP)to review the progress made since an earlier Energy Assessment took placein August 1983. I/ During this review mission, the Government of TheGambia (GOTM) requested technical assistance under ESMAP to improve themanagement of petroleum supplies in The Gambia. 2/ In response to thatrequest, a technical mission visited the field in July 1984 and madespecific recomiendations in regard to: (a) petroleum supply arrange-ments; (b) compulsory stocks; (c) an emergency allocation plan; (d) pro-duct pricing; (e) product accoun.ing; and (f) terminal relocation. Asummary of these recommendations is presented in Table 1.

Supply Arrangements

2. The Gambia is experiencing petroleum supply problems due mainlyto recurring foreign exchange shortages caused by depressed exportrevenues. Since 1981, the Government has resorted to a number of ad-hocsupply arrangements including an agreement with the Government of Senegalfor direct purchases from the SAR refinery in Dakar. This arrangementwas viewed by the Government as a necessary measu.e to arrest the worsen-ing situation and assure the continuity of supply. Concurrently, withthe above arrangement, the Government established a credit facility underthe Foreign Trade Financing Program of the Islamic Development Bank(IDB) to finance the procurement of diesel required by The CambiaUtility Corporation (GUC). In 1984, the IMF, as part -f a stand-byagreement, recommended that the Government investigate options to reducepetroleum import costs and improve the Government's capabilities tomonitor the petroleum sector.

3. To assist the Government of The Gambia to evaluate alternativearrangements to import petroleum products, the mission has identifiedleast cost petroleum supply options aimed at minimizing foreign exchangerequirements. However, it is important to stress that the proposedalternatives are workable only if the necessary foreign exchange for oilimports is made available regularly and on a timely basis by the

1/ The findings of this Energy Assessment mission are presented inReport No. 4743-GM: The Gambia: Issues & Options in the EnergySector, Nov. 1983.

2/ Terms of reference are presented in Annex 1.

- ii -

Government. Additional measures to reduce foreign exchange requirementshave been proposed in the 8nergy Assessmnt Report (November 1983),including energy conservation, interfuel substitution and energy priceregulations.

Table I: SW4ARY OF RECONOATIMS

Task Rei_nndation Comments

1. Supply - Modify current system of Im- - No additional cost. Wil lArrangements porting products. Least cost require Energy Unit to

alternative appears to be sup- lmple_ent. Significant foreignplies from oil companies at exchange savings are expected.competitive quotes. a/

2. Compulsory - Legislate compulsory stock - Product acqulsitlon costsStocks levels as follows: (approximately US$0.7 million)

: WIth Present Terminal - 30 with present terminal.days dlesel/kero - Foreign exchange requirements

: With New or Expanded Torminal increase as new inventory Is- 30-40 days all products added.

3, Emergency - Establish emergency allocation - Marginal administrative costsAllocatlon plan to set up the system. WillPlan require Energ Unit to lmple-

mnt.

4. Product - Modify product pricing struc- - Vill require support of EnergyPricing ture to reflect economic costs Unit for monitoring

better and simplify admlnistra- - No major additional costs en-tion. bl visaged

- Vill require modification ofImport tax legislation a/

5. Product - Establish volumetric/financial - Will require support of EnergyAccounting accounting syste. a/ Unit

- Will require about US$25,000 toset up data processing. c/

6. Terminal - Oue to high cost of relocation, - Engineering Inputs of aboutRelocation assess cost of meeting safety USS65,000-100,000 c/ required

requiremnts at existing ter- - Assessment requires cooperativeminal a/ effort between GOTG, neighbors

and terminal operator.

a/ Top priority - should commence imediately.b/ To be phased In once Import tax legislatlon adjusted and monitoring system

lmplemented.c/ Additional technical assistance needed.

- iii -

Continuing Current Supply Arranements (A)

4. The mission has reviewed four alternatives for the procurementof petrolem supplies to The Gambia. One option reviewed by the missionis the continuation of current supply arrangements wherebys (a) gasolineand diesel are supplied from the SAR Refinery in Dakar on small tankers;(b) Kero-turbo is supplied from the Curacao Refinery in the Caribbean onlarge tankers; and (c) GUC receives diesel as per its last import fromAlgeria.

Obtaining Competitive Quotes from Oil Companies :B)

5. Another option would be to solicit competitive c.i.f. quotesfrom the oil companies to supply the entire market. Under this arrange-ment, supplies would be priced at the bulk cargo quotations (spot mar-ket), and products would be transported in large oil company tankers ontheir sultiport discharge voyages to West Africa.

e Negotiations (C)

6. The Government of The Gambia might be able to negotiate anarranSement to purchase crude from a neighboring country, and it mightestablish a processing arrangement in a refinery at another location inthe region. For examplo, Nigerian Light Crude could be purchased andprocessed through the SAR Refinery in Dakar.

Negotiate Direct Purchase of Refined Product (D)

7. The Government of The Gambia might also consider negotiatingthe purchase of refined products directly from a neighboring country onfavorable terms. For example, products might be purchased in this wayfrom the Wigerian National Petroleum Corporation (NNPC).

8. These supply alternatives were evaluated in terms of theirindividual foreign exchange requirements based on current prices, tankerrates and an assessment of present credit arrangements:

Table 2: ANNUAL PETROLEUM IMPORT COSTS- (US$ million)

Supply AlternativeA B - C D

All Products 17.5 13.8 15.3 14.7

Source: Mission estimates based on 1982 product import requirements.

- iv -

9. The least cost supply option appears to be Alternative (B),whereby oil companies submit bids to supply products at bulk cargo quota-tions (spot market). If implemented as recommended this alternativecould save, under current oil market conditions about US$3.7 million p.a.to The Gambia. The mission recommends the supply alternative (B) asfirst choice.

10. CUC has obtained a credit facility from the ISDB which is beingused to import diesel oil from Algeria. Under this arrangement the totalc.i.f. cost is slightly lower than could be obtained from the spot mar-ket. lowever, GUC should always endeavor to negotiate better prices withpotential ruppliers and compare them with c.i.f. quotations using theproposed competitive bidding system.

11. The mission recommends that the Government hold exploratorytalks with the Nigerian Government to determine if supplies ut,Ier altern-ative (D) might be arranged at more favorable credit terms than wasassumed or if some of the payment could be made in local currency. Ifeither case was true, this alternative could become the least cost op-tion. Also, Government-to-Government discussions may lead to externalfinancing arrangements which otherwise might not be possible. The mis-sion examined the possibility of. obtaining refined products dieectly fromeither the Mauritania or the Abidjan refinery but found them to beuneconomical.

12. Institutional Framework. The need for security of oil suppliesand the ability to finance such supplies have become so important to TheGambian economy that the Government is considering the option of directstate participation in petroleum operations, including the possibleestablishment of a National Oil Company (NOC). This would not implydirect State participation in exploration, production, refining andtransportation. For the State to be directly involved in these opera-tions, The Gambia: (a) would need to mobilize important human andfinancial resources to undertske further petroleum exploration; and(b) would not justify the existence of a local refinery, given currentwor.dwide excess refining capacity and small local petroleum demand.These considerations make it imperative for The Gambia to rely, for theforeseeable future, on the services of the better endowed InternationalOil Companies (IOC).

13. Regarding the downstream operations (supply, storage, distribu-tion and marketing), the Mission believes that the Government's objec-tives, at this stage, should be to build up its capabilities for super-vising and monitoring the operations of the private oil companies in thecountry. The Energy Unit, which is being established as the "workingarm" of the National Energy Commission (Chapter VI), could undertake thisrole within the following framework:

(a) the Energy Unit would prepare a yearly petroleum productssupply program to meet domestic demand and, in collaboration

with the terminal operator, i.e., Shell, set up a deliveryschedule for the approval of the National Energy Commission;

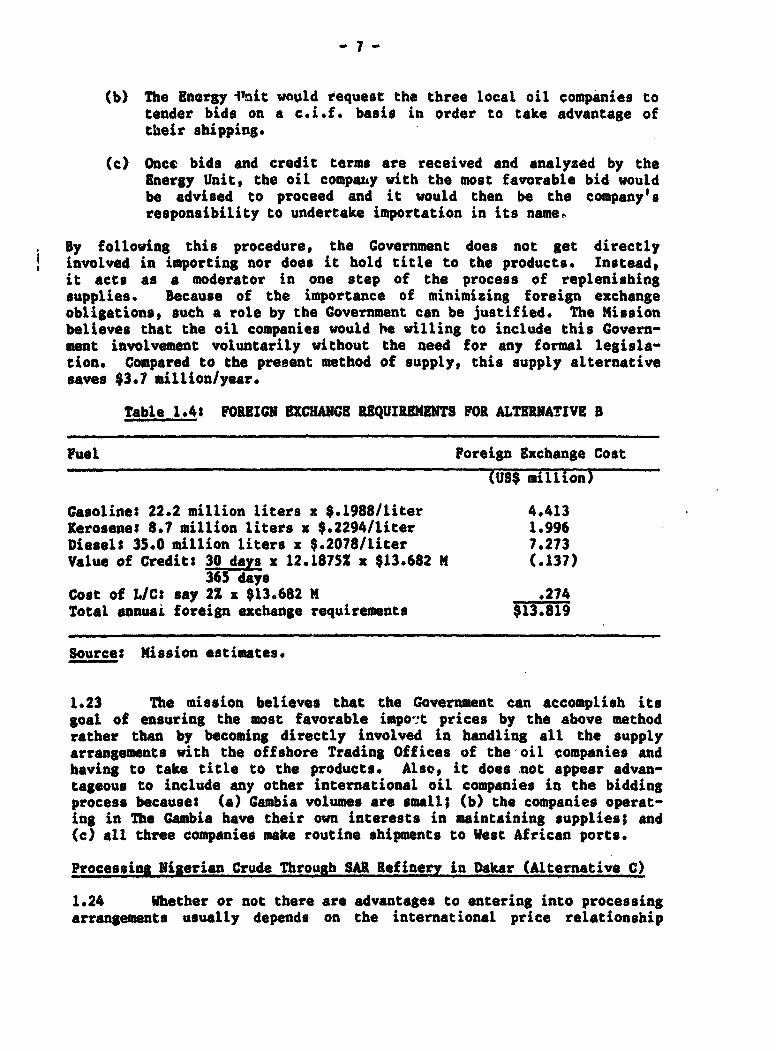

(b) the Energy Unit would request the three local oil companies tobid on a c.i.f. basis to supply the entire market; and

(c) once bids and credit terms are recorded and analyzed by theenergy unit, the oil company with the most favorable bid wouldbe advised to proceed and it would then be the company'sresponsibility to undertake importation in its name.

This framework, which is described in Chapter I (para. 1.22) should notexclude the possibility for Covernment-to-Government negotiations whichmight result in more favorable petroleum supply conditions and externalfinancing arrangements. In the case of direct negotations, the EnergyUnit, in cooperation with the local oil companies, would design the mostappropriate mechanism to take advantage of the areangemeLt.

Compulsory Stocks/Emergency Allocation Plan

Compulsory Stocks

14. Currently, The Gambia has no minimum compulsory stock require-ment. A minimum level of petroleum inventory is necessary, however, tominimize disruptions to the local economy caused by product shortageswhen supplies are interrupted. The level of these inventories, or com-pulsory stocks, is partially determined by the country's access to alter-nate supply sources and its ability to finance the additional volumesthat would be needed in the case of a supply interruption. For example,France requires 90 days supply based on forward consumption, whereas itsoverseas departments and former French colonies (some of The Gambia'sneighbors) normally have 72 days' supply on hand.

15. Another factor is the availability of storage capacity for anycompulsory stock. Table 3 shows the available tankage capacities at thepresent terminal in terms of the number of days supply at present averageconsumption rates. Kero/turbo has 40 days availabie tankage, and dieselhas 45 days' available for compulsory stocks at average consumptionrates.

16. Obviously, the compulsory stock inventory will be determinedlargely by the amount of foreign exchange required to pay the supplier.Recognizing The Gambia's current foreign exchange shortage, the missionrecommends that the Government consider legislation to gradually estab-lish a 30-day supply of compulsory stocks in both kero/turbo and dieselunder the following conditions: (a) the inventories would be built upgradually over a suitable time period as could be afforded; and (b) thekero/turbo compulsory stock would be allowed to decrease, as needed andwithout penalty, during the tourist season.

- vi -

Table 32 AVAILABLE TANM.-E CAPACITIES AT PRESENT TERMINAL(Days supply)

Tankage Available Gasoline Kero/Turbo Dieael

Total, Excluding Working Stocks 42 62 a?Optimum Replenishment 42 42 / 42Net Available for Compulsory Stocks 0 40 - 45

a/ Greater demand of kero/turbo during the tourist season would reducethis number considerably.

Source: Mission estimates.

1I. The foreign exchange required to purchase the recommended 30-day compulsory stock for both products would be about US$700,000. Theoil companies would have to carry this additional volume as part of theirnormal inventory, so an saount to cover the carrying cost of this higherinventory on all products should be considered as a component in theproduct price structure. At current prices this would translate into anadditional cost of about 0.8 bututs/liter.

18. In the medium-term, if a new terminal is constructed or thepresent terminal expanded, the mission recommends that a compulsory stockrequirement be incorporated in sizing new tankage for all products. Eachlevel of compulsory stock has different associated costs. Based on a1990 petroleum demand forecast, Table 4 shows the costs of increasedtankage and additional inventory at different levels of compulsory stockand the amount to be added to product prices to recoup the investment in10 years with a 201 return,

Table 4: REQUIRED INVESTMENT FOR LONS-TER CO#ULSORY STOCK

Required Investment. UWS miliIonCompulsory Increased Additlonal Investment RecoveryStocks Volume Tankoae inventory Total Component

(Days' Supply) (million (Bututs/l Iter)lIters)

30 9.4 0.35 1.97 2.32 1.960 16.8 0.70 3.94 4.64 3,890 28.2 1.05 5.91 6.96 5.7

Source: Mission estloetes.

19. If foreign exchange pressures subside somewhat in the future,the mission recommends a "middle-of-the-road" compulsory stock level of

- vii -

50-60 days supply be maintained in all products for the 1990s. A corres-ponding investment recovery component would be added to the product pricebuild-up.

Emergency Allocation Plan

20. The mission's analysis indicates that in spite of efforts tostreamline petroleum supply arrangements and to establish a minimum com-pulsory stock, the probability of occasional petroleum supply disruptionscannot be ruled out for The Cambia, thus the Government should establishas a national priority an Emergency Allocation Plan that would allocateavailable supplies in the event of product shortages. The NEC should beresponsible for establishing guidelines and, through its responsibleMinister, obtaining Cabinet approval (see Communication Chart). Theseguidelines would set forth the degree of rationing required according tothe severity of supply interruption and the number of days' supply ofeach product available as indicated by specific triggering elements.

21. The Energy Unit, as the working arm of the NEC, should workclosely with the oil industry, the bulk terminal operator, and all theessential-service consumers to assist them in developing individualemergency allocation plans. Each essential-service consumer, in colla-boration with its supplier, would formulate a plan of action. Each indi-vidual allocation plan would then be reviewed and jointly approved by theEnergy Unit and the NEC. The Energy Unit would monitor the progress ofeach plan in operation duriug emergencies. At the same time, the oilindustry and the bulk depot operator would play vital roles in providingnecessary and timely communications, product deliveries, and in control-ling all discretionary consumption. Some of the parastatals and theMinistry of Works and Communication already have systems in place forrationing. However, these must be refined and expanded to equate thenecessary level of rationing with the corresponding triggering element.

Pricing of Petroleum Products

22. The current price structure for petroLeum products is based ona formula proposed by the oil industry to the Government in July, 1973.The original proposal envisaged automatic adjustiuents in prices basedupon variations in the pricing components. However, the mechanism tomonitor these variations was never put in place. Therefore, pricechanges are negotiated periodically at the request of the industry.

23. Except for duties and taxes, the individual components of theproduct price structure bear little relation to the actual costs of therespective components. The financial risks, from delays in settlingforeign liabilities, have now made it very difficult to compute actualcharges for the individual components because of delays in settling

- viii -

foreign exchange liabilities. In recent years, the oil industry has beenspending about D 2 million a year to maintain fixed assets-a fact whichsupports the inclusion of the Depreciation and Maintenance component inthe pricing structure. Current price levels have proved sufficient tomaintain plants and equipment and achieve better-than-average profits inFY82 and FY83. However, continuing exchange rate fluctuations and short-ages of products could make it considerably more difficult for marketingcompanies to break even during 1984. Therefore, it is extremelyimportant that the Government monitor variations in cost and settleforeign liabilities as soon as they are incurred (or due). Annex 2 com-pares the existing and the proposed pricing structures.

24. Table 5 highlights some of the distortions in the currentpricing structure.

Table 5: EVALUATION OF CURENT PRICING STRUCTURE

Component Evaluation

c.l.f. prices The Government currently uses "standard" Instead of actual c.l.,fprices. Although simple to compute, this method distorts bothGovernment revenue and cost recovery systems. Actual c.l,f.

should be used as the basis for pricing.

Flnancial charges If the minimum 60-day stock originally envisaged was pertinent,the 8.78 bututs per liter charge would be too high. However, thevalidity of the figure Is difficult to assess because of thefinancial costs associated with delays In settling foreignliabilities, and the resulting Inability to maintain adequateminimum stock levels.

Depreciation and In 1982/83, actual costs were about 80% of the currently allowedMaintenance 2.50 bututs per liter.

Terminal Throughput The 2.20 bututs/liter charge allowed Is generally in lIne wIth theactual cost of this component.

Marketing Margins The current practice of fixed margins does not provide "normalcommercial profits" as originally envisaged when the structure wasdeveloped.

Retail Margins The validIty of these Is difficult to evaluate vithout access todealers' accounts. However, the margins appear low. This shouldbe Investigated further.

Source: Mission estimates.

COUICATIOC CMART OF EEtERGENCY ALLOCATION PIAN

CABINT

NEC

DEPOT OIL ALL ESSENTIAL-SERVICEOPEnAToR COMPANIES COISUMERS OR PURCUSING

6wml AGENTS:

RETAIL SPCIAL CUCDEALER CUSTOMERS CPN

I.e. Research GRTCInstitute, GPTC

IOpttl * ate. Ministry of VorksSPECIAL e & Comu.nication.ONSUERS . Ministry of Defense

isee, Truckers Ministry of InteriorHauling Cattle, etc. Ministry of Agriculture

25. Althousth the current pricing system is cumbersome, the missiondoes not recommend eliminating price controls because such a move wouldnot reduce the activities required to discharge GOTG's consumer protec-tion and demand management responsibilities. Some type of pricing mech-anism should be retained and rationalized to minimize the fluctuations inretail prices, and to simplify the structure for monitoring and makingroutine adjustments in prices.

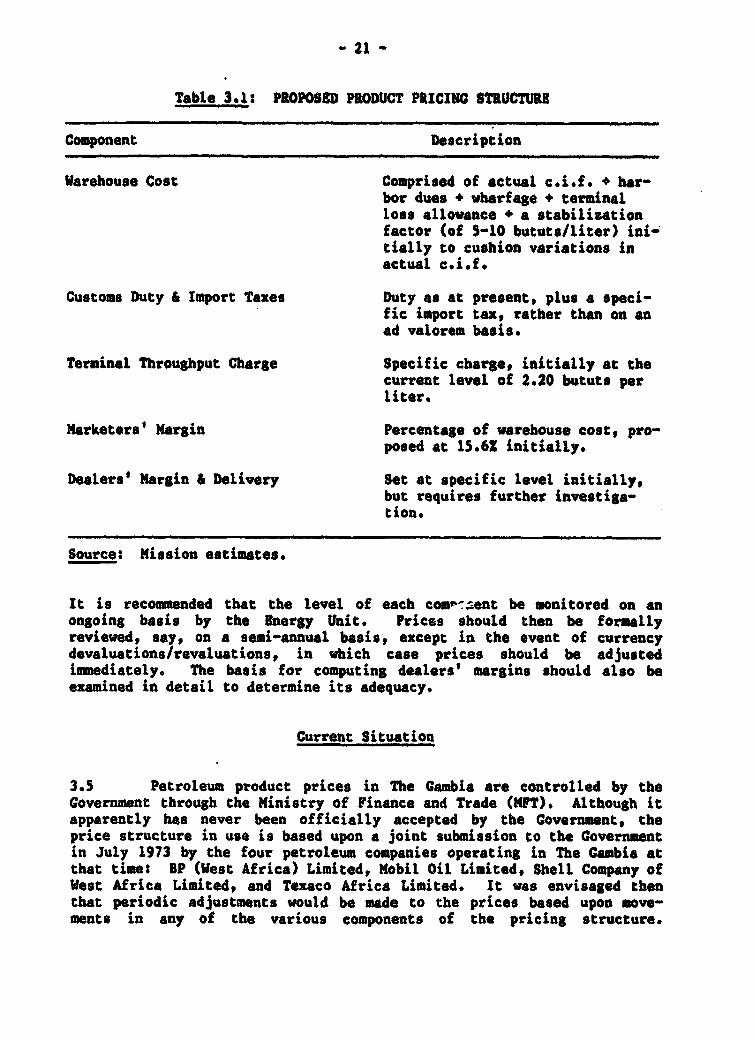

26. Table 6 outlines the pricing structure proposed by the mission,which consists of (a) warehouse cost, (b) customs duty and import taxes,(c) a terminal throughput charge, (d) marketers' margin, and (e) dealers'margin and delivery. The actual "Warehouse Cost" should include aStabilization Factor to absorb day-to-day changes resulting from c.i.f.prices and exchange rate fluctuations.

Table 6: PROPOSED PRICING STRUCUFRE

Cmponent Description Coments

1. Warehouse Cost Cost made up of actual c.l.f, + Stabilization factor to be usedharbor dues + wharfage + ter- to cushion variations in actualminal loss allowance + a stabi- c.l.f. and exchange fluctua-lization factor tions. Should be set at 5-10

bututs/liter itltially.

2. Customs Duty & All Government duties and taxes Set at averaie of currentImport Taxes on product Imports should be levels Initlaily. 6y

specific taxes.

3. Terminal throughput Specific charge, Initially at To be based on actual amount ofCharge the current level ol 2.20 last year plus 25% of charge to

bututs per liter, be adjusted upwards each yearby rate of Consumer Price IndexIncrease.

4. iMarketers' Margin Percentage of warehouse cost. Should be established at 1S.6%of warehouse cost,

5. Dealers' Margin & Continue at present level. Set at current level of 9.50Delivery bututs/iltar initially. May be

marginally low,. Will requirefurther investigation.

General: Actual costs should be monitored by the Energy Unit and prices reviewed semi-annually unless there is a currency devaluation; then prices shoid De changed Immedi-ately. The Energy Unit should provide technical support on product pricing to the Ministryof Finance and Trade who will continue to oversee price administration.

a/ GasolIne DIesel Kerosene

Duty 116.00 110.00 103.00Tax 3.50 3.23 3.23

Total (Bututs/liter) 119.50 113.23 106.23

- xi -

Accounting System for Petroleum Products

27. Most of the information needed to monitor finaneial and volu-metric transactions in the petroleum sector exists in one form or anotherbut it is not collated or analysed in any systematic way. These trans-actions shoult be monitored on a routine basis, preferably by the EnergyUnit, if COTG is to have effective control over the petroleum sector(Annex 3). The mission recommends two ledger systems for tracking theseactivities-one to monitor the volumetric, or supply and distributiontransactions, and one to monitor financial transactions. The lattercovers the import and distribution of products, and payments to offshoresuppliers.

Relocation of the Petroleum Storago Depot

28. All petroleum products are received and stored at the BulkTerminal located in lanjul. Over the years, residential dwellings, amosque, and a school have been built close to the terminal--some struc-tures right up to the terminal fence. Although the terminal operatorrecently has upgraded the fire protection facilities, many buildings aretoo close to the terminal to meat minimum safe distance standard.. TheGovernment ts concerned, and now wishes to relocate the terminal outsideof the Sanjul city limits.

29. The mission reviewed three possible locations for the terminals(a) along Bund Road, which would a'low continued use of the existing pro-duct reeoiving dock; (b) a site on the Atlantic Coasts and (c) a site onthe bank of the Gambia River near Kandinari Point. Constructing a newterminal along the Bund Road would cost US$4.4-8.3 millton dependingwhere along the Bund Road the terminal is actually sited (Annex 4). Thedepreciation charge that would be required to provide a 20S internal rateof return on the investment over 10 years would be at least 50S higherthen the current 2.50 bututs per liter.

30. The other two locations do not appear practical or economic.Both would require additional costs for offshore mooring facilities andconsiderable undersea pipeline amounting to US$8-10 million. These loca-tions would also suffer from adverse navigational, weather and ecologicalfactors.

31. Comparing the level of investment required to move the depotwith the present Public Sector Investment Program (PIP) and the country'sGDP, it is unlikely that the venture would ever be given a high priorityin the PiP. In addition, it is doubtful that the oil companies wouldagree to fund the venture because of the current uncertainty regardingforeign exchange and the increase in product pricing required to recoupthe investment.

- xii -

32. One alternative to relocating the present terminal would be torelocate the housing, school and mosque that have surrounded the ter-minal. In addition to this relocation cost, another US$1.3-2.0 millionwould be needed to cover the cost of building three new tanks at thepresent depot; one tank would replace the existing diesel tank which isleaking and beyond repair, and the others would be built to support 1990volume requirements. Space is available within the existing terdinsl forthese additional tanks. To evaluate the feasibility of the two alterna-tives, the Government should seek technical assist.nce from an engineer-ing firm to: (a) assess the cost of relocating housing and other facili-ties; and (b) evaluate in detail possible sites along the Band Road.

33. Whatever course is chosen, the Government may have to assumeall or part ownership of the new or the re-developed facilities. In sucha case the Government should attempt tot (a) minimize the risks andforeign exchange obligations incurred in any ownership venture; (b) be ina position to monitor the operation effectively; and (c) insure thatadequate compulsory stocks are available for emergencies.

34. Although the Government probably will end up being the largestshareholder, it should seek maximum participation in the terminal owner-ship from the oil industry. After deciding which course of action tofollow the Government should meet with and solicit equity participationfrom the oil industry.

35. Regardless of ownership, the mission recommends that the opera-tions of the bulk terminal continue to be managed by an cil company,which would have the following advantages: (a) knowledge and access toworldwide supply sources and shipping; (b) ability to use its knowledgeand contacts more easily in coordinating, planning and schedulingreplenishment of supplies; (c) expertise in handling product qualityproblem; (d) experience in terminal management; and (e) access to tech-nical and mechanical assistance when needed from affiliated offshorecompanies.

Energy Unit

36. In order to implement the report's recommendations, someinstitutional coordination in petroleum activities in the country isrequired. To this end, the Covernment has agreed to the establishment oftwo entities--a National Energy Commission (NEC), and an Energy Unitwithin the Ministry of Economic Planning and Industrial Development.

37. The Energy Unit is intended to be the "working arm" of theNEC. To perform its monitoring responsibilities and provide thenecessary technical support to the NEC, the mission recommends that:

(a) the Energy Unit be manned as soon as possible with the approvedexpatriate expert and two full-time economists;

- xiii -

(b) the Energy Unit monitor product pricing and provide thenecessary analytical support for the Ministry of Finance andTrade (MFT) to adjust product prices regularly;

(c) locally available data processing facilities in the CentralStatistics Department be used to enhance the monitoring effortsof the Energy Unit;

(d) a training program (outlined in para. 6.10) be provided to thestaff of the Energy Unit and to the new Economics Graduate inMPT.

I. OPTMZATIO3 OF PIRLEU PRODUCT impoT

Overview

1.1 During the 1960s, petroleum supplies to The Gambia were handledjointly by several international oil companies under the West AfricanReplenishment irogram (WARP). Under WARP, each of the participatingcompanies alternatively delivered products into petroleum storage depotsat ports along the West African coast (including Banjul) every threemonths. The system functioned efficiently and substantially improved thelogistics of supply to the region because it provided the flexibility topurchase products in either Europe, the Mid-Rest, or the Caribbean,depending on prices and the availability of tankers. For countries suchas The Gambia, with market too small to warrant separate deliveries, WARPprovided sigpificant savings in the cost of petroleum imports. Theeffectiveness of WARP was greatly reduced in the mid-1960s however, whennational refineries were established in some of the West Africancountries. By the mid-1970s, the three oil companies decided to abandonWARP altogether and began to receive supplies individually on separatedeliveries.

1.2 The main source of supplies was company-owned refineries in theCaribbean and Europe, depending on available shipping which also suppliedother West African ports of that particular company. By the end of 1980-81, the oil companies operating in The Gambia had accumulated substantialdebts to their offshore suppliers because of the country's irregularremittances of foreign exchange to cover oil import payments. The supplysituation worsened when the oil companies could not arrange offshoresupplies without payment.

Recent Developments

1.3 In March 1983, the Covernment entered into a temporary arrange-ment with the Government of Senegal which permitted oil companies basedin The Cambia to purchase supplies directly from the SAR Refinery inDakar. The Cambia has better access to CPA Francs (through the WestAfrican Monetary Clearinghouse) than to the rapidly appreciating U.S.dollar for settling oil import billst including those costs incurredabroad by oil comanies for insurance and freight. This arrangement ledto significant increases ia the landed cost (c.i,f. Banjul) of productsbecause of the higher freight and ex-refinery prices at the SAR Refin-ery. Originally the arrangement covered only products for non-powerneeds in The Gambia but, since January 1984, also has been used to obtaindiesel oil for power generation by the Gambian Utilities Corporation(GUC). The Government is behind in meeting payments to the oil comr-panies' affiliates in Senegal who are supplying the products from the SARRefinery.

- 2 -

1.4 Concurrently with the above arrangement, the Government estab-lished a separate facility under the Foreign Trade Financing Program ofthe Islamic Development Bank (I8DB) to finance the procurement of dieseloil required by GUC. Under this arrangement, I8DB provided credit onfavorable terms to The Gambia to purchase three consignments of dieseloil from Algeria. Repayment to the ISDB for each consignment wasstretched over a nine-month period. The Government ran into arrears onthese repayments and I8DB suspended the credit facility in 1983. CUCtherefore resorted to direct purchases from the oil companies in Banjulbeginning in January 1984. The Government has settled its payments withI8DB and now has a new credit facility with I8DB under the same FTFP forUS$1.2 million to meet GUC's diesel requirements. The Government wasunable to negotiate similar credit for all of its petroleum needs.

Findings and Recommendations

1.5 With petroleum imports currently taking up more than 50X of TheCambia's export earnings, the Central Bank has been unable to providesufficient foreign exchange to pay overseas petroleum suppliers on time.Therefore, the immediate priority of the Government is to minimize petro-leum import costs and the need for foreign exchange. In considering areview of supply options as a basis for determining the least costarrangement for The Gambia, it is assumed that payments to overseassuppliers are made when due. The mission reviewed the following productimport alternatives in detail:

(a) continue present supply arrangements;

(b) obtain competitive c.i.f. quotes from the oil companies to sup-ply the entire market, price supplies at bulk cargo quotations(spot market), and transport products in large oil companytankers on their multiport discharge voyages to West Africa;

(c) through government-to-government deals, arrange to:

- purchase crude from a neighboring country, and- develop a processing arrangement in a refinery at another

location;

(d) government negotiates purchase of refined products direct fromneighboring country on favorable terms.

1.6 These supply alternatives have been evaluated in terms of theamount of annual foreign exchange required in each case (the associatedlocal costs are expected to be about the same for each alternative), andcurrent petroleum prices, tanker rates, and an assessment of presentcredit arrangements were used in this analysis.

-3-

1.7 The demand forecast for major petroleum products used in evalu-ating the various supply alternatives is shown in Table 1.1

Table 1. *1: D8MAND FORECAST FOR PETROLEUM PRODUCTS(million Liters)

Product 1982 1985

Turbo Fuel 8.2 10.8Kerosene 0.5 0.6Gasoline 22.2 22.2Auto Diesel, 24.8 28.4GUC Diesela/ 10.2 19.8 c

Total 5 "1I"

a/ Diesel for power generation in Banjul grid only.S/ Based on percent of total power generated (941).c/ Growth between 1982 and 1985 assumed to be totally at Kotu.

Assume heavy diesel can be used.Source: World Bank Report No. 4743-GM: The Gambia: Issues and

-ptions in the Energy Sector.

Cost of Current Supply Arrangements (Alternative A)

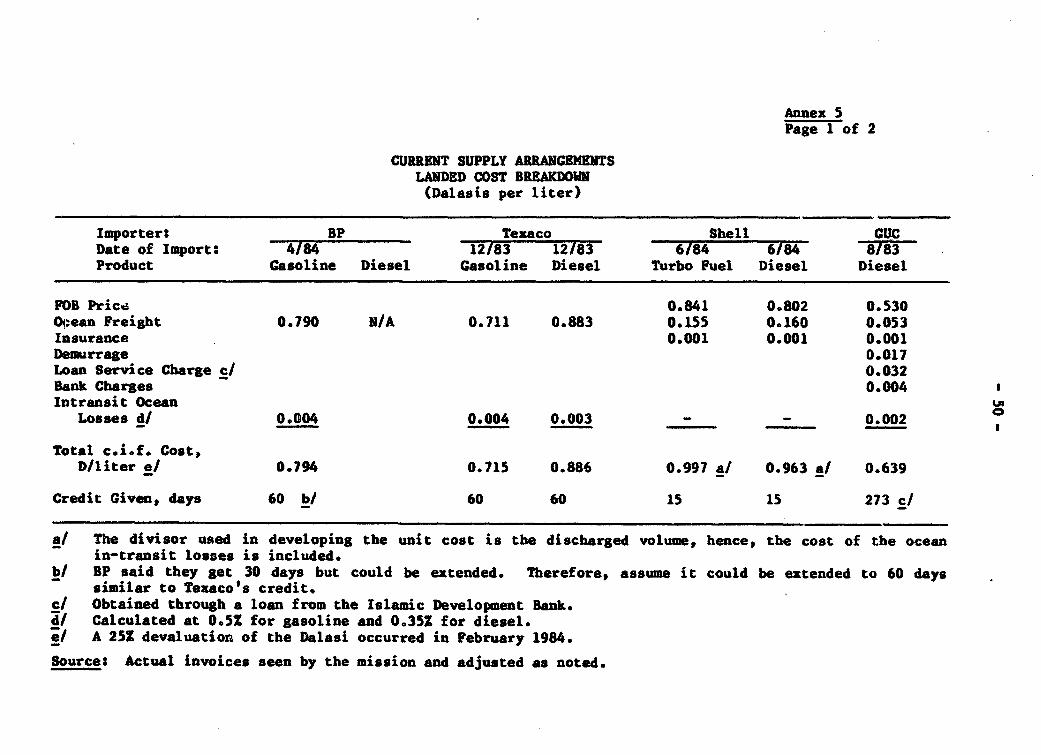

1.4 Using actual invoices to represent prices over the past year,the mission estimated the landed cost of importing products (Annex 5).The foreign exchange required to cover this annual volume of imports ifmade at the aforementioned prices would amount to US$17.5 million.Credit actually associated with the imports was taken into account andvalued at 12.1875Z. which represented six month LIBOR notes and wasassumed to be the value of foreign exchange deposits.

Review of the Landed Cost Components

1.9 For illustrative purposes, a breakdown of CUC's actual dieselimport costs last year is shown in Table 1.2.

1.10 The largest component of the landed cost price build-up is theFOB price, which usually makes up 80-85X of the total c.i.f. cost.Optimizing this component is where the greatest savings can be realized.For example, a 5X reduction in current FOB prices would be worth about$650,000 to The Gambia over one year. Product prices vary from officialGovernment Selling Prices (GSP's) to term prices (usually associated withcontractual arrangements) to bulk cargo or spot market quotations(reflecting current effects of supply/demand). There are several centersin the world that quote prices for bulk cargoes. All of the aforemen-tioned prices vary according to the supply/demand balance, with the bulkcargo quotes (spot market) reflecting current market conditions.

- 4 -

Table 1.2: BREAKOWnN O GUC DIEBEL IMPORT COSTS

Component Cost

(Dalasi/liter)

F.O.B. Price 0.530Ocean Freight 0.053Insurance 0.001Demurrage 0.017Loan Service Charge 0.032Bank Charges 0.004Intransit Ocean Losses 0.002

Total c.i.f. Cost D 0.639/liter

Credit Given m 273 days a/

a/ This I8DB credit is worth D 0.53/liter x 12.1875 z 273 * D0.048/liter. 365

Source: GUC.

1.11 Today, there is a surplus of crude and products, in theinternational petroleum market, and spot prices are the most favorable.In today's long supply situation, prices of both crude and products arebeing discounted from official GSP's. Both Arab Light and Nigerian Lightspot crude cargoes are selling at $1.60 per barrel below their GSP.Products are selling for $1-3 per barrel below their GSP's depending onthe product and its location in the world. A reduction of $1 per barrelin product prices is worth $415,000 to The Gambia over one-year.

1.12 The general outlook is for long supplies and relatively steadyprices, at today's levels, through 1985 and perhaps longer. Of course,there will always be seasonal adjustments to prices. The long supply/steady price outlook is based on the fact that (a) the industrial struc-ture of the major consuming countries is changing, with a larger rolebeing played by alternate energy sources such as coal, solar and nuclear,together with continued conservation efforts; (b) non-OPEC producingcountries will continue to increase their production. Between 1986 and1990, prices are expected to increase gradually in line with inflation,meaning that supplies are only expected to tighten slightly. 3/ Otherfactors that would change the present long supply outlook are the possi-bility of a global conflict or a major escalation of the Iran/Iraq War.

3/ World Bank "Primary Commodity Price Forecasts", July 13, 1984.

1.13 Direct government-to-government negotiations often result inmaking petroleum supplies available at prices below international levels.Many factors affect the success of such negotiations. In the case of TheGambia, membership in common confederations or organizations can be mosthelpful. 4/ Also, negotiations can involve barter arrangementst use ofsoft currencies for payment, and extended credit. Government-to-govern-ment discussions could lead to external financing arrangements whichotherwise might not be possible. It is recommended that the Governmentof The Gambia include a petroleum supply economist as its technicaladvisor in any governm"nt-to-government meetings where petroleum sup-plies, prices, shipping, credit, forms of payment, external financing,etc. are discussed.

1.14 The next largest component of the laaded cost price build-up isthe cost of freight. It is important to maximize the size of the ship-ment in order to minimixe the frequency of delivery. The storage depottherefore must be managed efficiently to insure that the largest ship-ments possible are being scheduled. The port of Banjul enjoys sufficientdraft (28 feet) and berthing facilities to handle tankers up to 35,000DWT (light loaded). Therefore, large ships should be used wheneverpossible. However, it is essential that dead freight costs be minimized;this can be accomplished by sharing the tanker with other West African.ports requiring replenishment at the same time. All the oil companieshave tankers making multiport discharges down the West African Coast.

1.15 The insurance charge is small, usually US$.07-.09 per $100value of cargo. Of course, this cost must be incurred to protect againstdamage and loss.

1.16 Demurrage is charged if the ship is delayed for any reasonoutside the ship's direct control in either the loading port or the dis-charge port. Normally, 72 hours are allowed for the complete load anddischarge. If the delay occurs at the loading port, the buyer usuallyhas recourse to claim against the seller. Good replenishment schedulingcan prevent the ship from arriving when the dock is busy with othershipping.

1.17 The credit given in this particular cargo was worth D 0.048/liter, as shown. Every 10 days of additional credit that can be obtainedby The Gambia from petroleum suppliers is worth D 175,000 over a periodof one year (using the 12.1875% interest rate).

1.18 Because the Government has been in arrears on remittances offoreign exchange to its offshore suppliers, ic is expected that allfuture suppliers will require a confirmed irrevocable Letter of Credit(LIC) before loading. The cost of an L/C varies but could amount to 2Z

4/ The Gambia is a member of West African Monetary Clearing House, theIslamic Development Bank, and other West African Confederations.

- 6 -

of the total value, which would cost The Gambia Ub$280,000/year. How-ever, once The Gambia reestablishes a good, reliable credit record, pay-ment terms could become more favorable and the L/C requirement bedropped.

Imoorting Products at Spot Prices (Alternative B)

1.19 As mentioned in Paragraph 1.11, purchases made on the spotmarket today are most favorable. If The Gambia received all its suppliesat a Mediterranean bulk FOB quote from the oil companies orJuly 20, 1984, the c.i.f. costs would be as shown in Table 1.3.

Table 1.3: C.I.FP PRICS BUILD-UP FROM SPOT MARKET QUOTE

Gasoline Kerosene Diesel(Dalasi/liter)

FOB Price, July 20 Med. bulk .694 .803 .720Freight and Associated Premium Chargeby oil companies .056 .062 .064

Intransit Loss .004 .004 .004

Total c.i.f. Cost .754 .869 .788

Source: Mission estimates.

1.20 The oil companies would have used their own tankers and replen-ishment would have been made in conjunction with other West Africanrequirements. The ability to be a part of the oil companies' voyage pat-terns ix a great benefit and usually will provide the most economicalfreight cost.

1.21 The total annual foreign exchange requirement associated withSupply Alternative B is shown in Table 1.4.

Mechanism for Competitive Bidding on Product Imports

1.22 As the PC) price is the largest component in the landed costand hence the item where the largest possible savings can be made, theGovernment should consider becoming more involved in deciding who shouldbe importing and at what price. The Government's involvement should takethe following form:

(a) The Energy Unit would prepare a yearly petroleum productssupply program to meet domestic demand and, in collaborationwith the terminal operator, set up a delivery schedule ortimetable for the approval of the N.E.C.

- 7 -

(b) The Energy i'nit would -'equest the three local oil companies totender bids on a c.i.f. basis in order to take advantage oftheir shipping.

(C) Once bids and credit terms are received and analysed by theEnergy Unit, the oil compazsy with the most favorable bid wouldbe advised to proceed and it would then be the company'sresponsibility to undertake importation in its name.

By following this procedure, the Government does not get directlyinvolved in importing nor does it hold title to the products. Instead,it acts as a moderator in one step of the process of replenishingsupplies. Because of the importance of minimizing foreign exchangeobligations, such a role by the Government can be justified. The Missionbelieves that the oil companies would he willing to include this Govern-ment involvement voluntarily without the need for any formal legisla-tion. Compared to the present method of supply, this supply alternativesaves $3.7 million/year.

Table 1.4: FOREIGN EXCHANGE REQUIREMENTS FOR ALTERNATIVE B

Fuel Foreign Exchange Cost

(US$ million)

Gasolines 22.2 million liters x $.1988/liter 4.413Kerosene: 8.7 million liters x $.2294/liter 1.996Diesels 35.0 million liters x $.2078/liter 7.273Value of Credit: 30 days x 12.18752 x $13.682 K (.137)

365 daysCost of L/Cs say 22 x $13.682 M .274Total 8nnuai foreign exchange requirements $13.819

Sources Mission estimates.

1.23 The mission believes that the Government can accomplish itsgoal of ensuring the most favorable impo- t prices by the above methodrather than by becoming directly involved in handling all the supplyarrangements with the offshore Trading Offices of the oil companies andhaving to take title to the products. Also, it does not appear advan-tageous to include any other international oil companies in the biddingprocess because: (a) Gambia volumes are small; (b) the companies operat-ing in The Cambia have their own interests in maintaining supplies; and(c) all three companies make routine shipments to West African ports.

Processing Niserian Crude Through SAR RefinerZ in Dakar (Alternative C)

1.24 Whether or not there are advantages to entering into processingarrangements usually depends on the international price relationship

-8-

between crude oil and finished products. An analysis for 1981-83 indi-cates that hydroskimming refineries in the main world centers have suf-fered a $2-3/bbl negative margin St based on official crude prices andspot product prices. Adding operating costs except for energy (at least$1/bbl), these refineries incurred operating losses on the order of $3-4/bbl. This situation is expected to continue as long as there is a sur-plus of crude and product supplies. Another factor that would make aprocessing arrangement somewhat more expensive for The Gambia is that itsdemand is made up entirely of clean products and, therefore, is notrepresentative of a normal yield from crude processing. However, pro-ducts usually can be interchanged on a value basis in a processingarrangement, but this tends to be expensive wken trading 1.5 bbls of fueloil for one barrel of gasoline.

1.25 In Supply Alternative C, it is assumed that a government-to-government agreement could be reached. for supplying Nigerian Light Crudeat the Official Government Selling Price with 90 days credit. Nigeriahas given 90 days credit to several purchasing governments (among themSenegal and Jamaica). Whether a price discount would be possible ispurely speculative; it, would have to be discussed in the negotiations.Also, it may be possible at least to obtain a partial payment in Dalasis,thereby reducing the foreign exchange requirement. Annex 6 presents theassumptions used in the supply alternative and the mechanics of this pro-cessing alternative.

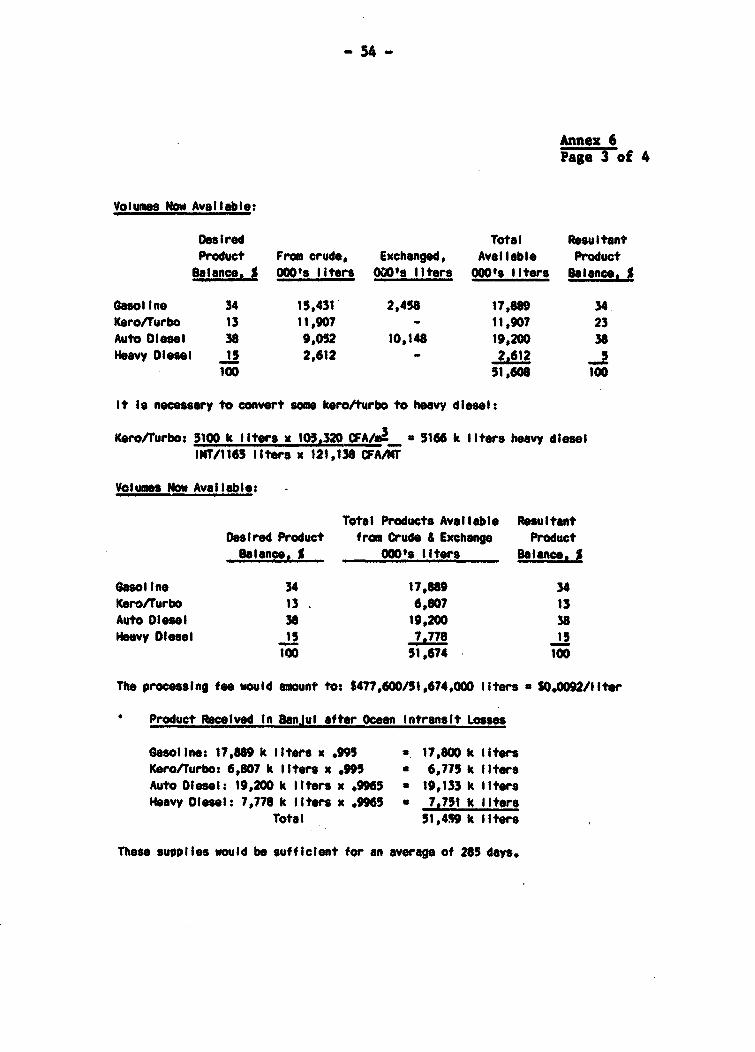

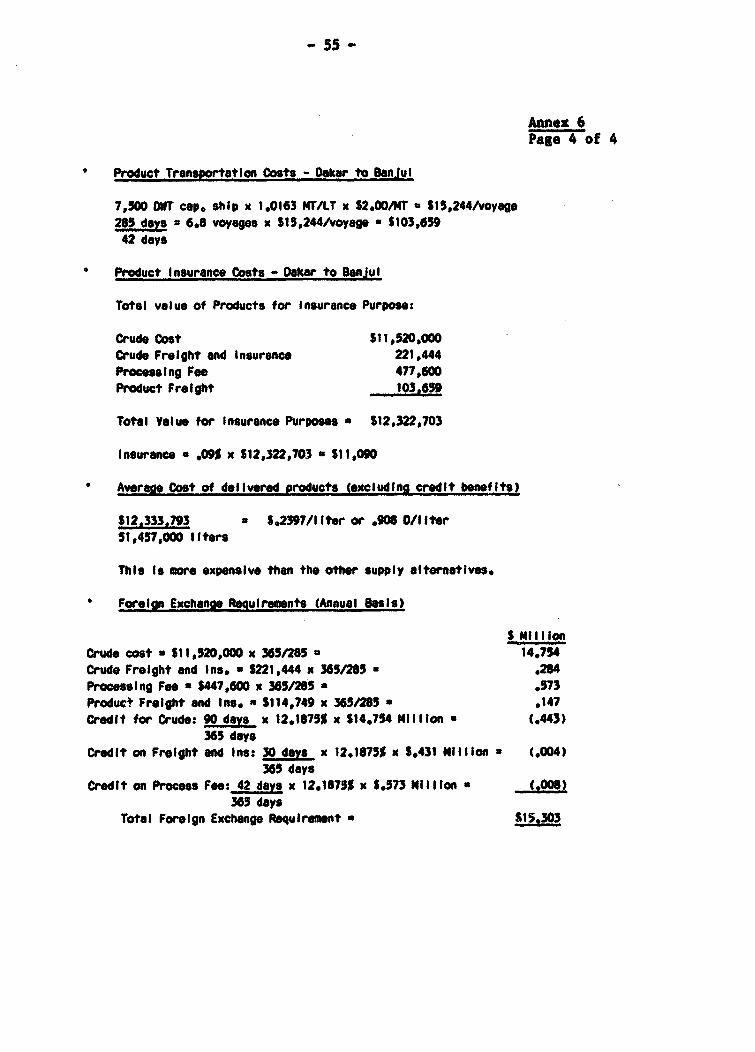

1.26 The average cost of products delivered into Banjul using thissupply alternative would be D 0.908/liter, which is more expensive thansome of the other methods studied. In fact, it is $4.73/Bbl more costlythan importing products at market prices. This confirms that, withtoday's crude/product price relationship, crude processing is not aneconomical alternative, as the ;otal foreign exchange requirements ofthis case amount to $15.303 million, which is also more costly.

Purchasing All Product Requirements from NNPC (Alternative D)

1.27 Nigeria is short of refining capacity and is importing some 20million barrels/year of refined products. These imports are produced forUNPC from Nigerian crude under offshore processing arrangements. The netcost of offshore processing for MNPC as of August 1983 was about$6.00/bbl. 6/ This cost depends on crude tanker rates, product tankerrate.e refinery processing costs, and revenues obtained from the sale ofsurplus products. In 1982, the price of crude oil transferred to NmPCfor processing was $13.80/bbl, which undoubtedly covered its total cost.

5/ This is the difference between the crude price and the compositeproduct realization price.

6/ World Bank Report No. 4440-UNI Nigeria: Issues and Options in theEner Sector, August 1983.

-9-

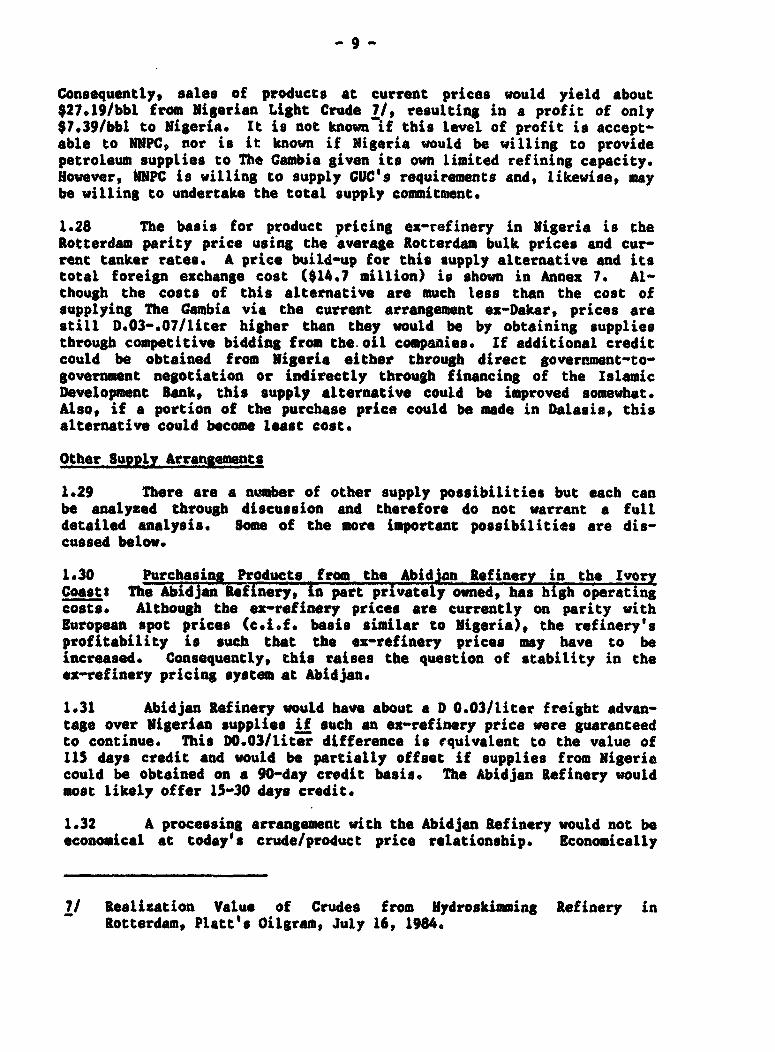

Consequently, sales of products at current prices would yield about$27.19/bbl from Nigerian Light Crude 7/, resulting in a profit of only$7.39/bbl to Nigeria. It is not known if this level of profit is accept-able to NNPC, nor is it known if Nigeria would be willing to providepetroleum supplies to The Gambia given its own limited refining capacity.However, NNPC is willing to supply CUC's requirements and, likewise, maybe willing to undertake the total supply commitment.

1.28 The basis for product pricing ex-refinery in Nigeria is theRotterdam parity price using the average Rotterdam bulk prices and cur-rent tanker rates. A price build-up for this supply alternative and itstotal foreign exchange cost ($14.7 million) is shown in Annex 7. Al-though the costs of this alternative are much less than the cost ofsupplying The Gambia via the current arrangement ex-Dakar, prices arestill D.03-.07/liter higher than they would be by obtaining suppliesthrough competitive bidditg from the oil companies. If additional creditcould be obtained from Nigeria either through direct government-to-government negotiation or indirectly through financing of the IslamicDevelopment Bank, this supply alternative could be improved somewhat.Also, if a portion of the purchase price could be made in Dalasis, thisalternative could become least cost.

Other Supply Arrangements

1.29 There are a number of other supply possibilities but each canbe analyzed through discussion and therefore do not warrant a fulldetailed analysis. Some of the more important possibilities are dis-cussed below.

1.30 Purchasins Products from the Abidjan Refinery in the IvoryCoast The Abidjan Refinery, In part privately owned, has high operatingcosts. Altbough the ox-refinery prices are currently on parity withEuropean spot prices (c.i.f. basis similar to Nigeria), the refinery'sprofitability is such that the es-refinery prices may have to beincreased. Consequently, this raises the question of stability in thees-refinery pricing system at Abidjan.

1.31 Abidjan Refinery would have about a D 0.03/liter freight advan-tage over Nigerian supplies if such an ex-refinery price were guaranteedto continue. This D0.03/liter difference is rquivalent to the value of115 days credit and would be partially offset if supplies from Nigeriacould be obtained on a 90-day credit basis. The Abidjan Refinery wouldmost likely offer 15-30 days credit.

1.32 A processing arrangement with the Abidjan Refinery would not beeconomical at today's crude/product price relationship. Economically

I/ Realization Value of Crudes from fydroskiming Refinery inRotterdam, Platt's Oilgram, July 16, 1984.

- 10 -

priced surplus products might be available from time to time. It wouldbe worthwhile to establish communications with Abidjan to be advised whenand if such products might become available. Other considerations suchas extended credit or favorable payment arrangements are not likely to begiven due to the terms of refinery ownership.

1.33 Purchasing Products from the Mauritania Refinery: Currently,the Mauritania refinery is not operating. BesidAs, this refinery'sminimum operable throughput far exceeds Mauritania's domestic consumptionneede. Adding The Gambia's relatively small demand still would not allowthe refinery to achieve its minimum turndown throughput rate. Nor wouldit be practical to rely on export market sales to increase throughputgiven the worldwide refining over-capacity that exists today. Efficientrefineries operate at negative margins under today's depressed productprices. Under present pricing conditions, it is about $11.00/bbl cheaperto import products into Mauritania than to produce them from processedcrude. Therefore, this is not a viable supply alternative.

1.34 Processing Arab Light or Nigerian crude in Caribbean Refin-e.des: Processing agreements for The Gambia cannot be considered viabletoday due to: (a) the unfavorable crude/product pricing relationship(para. 1.27); and (b) the cost of holding large crude/product inventoriesfor so long because of The Gambia's relatively small demand. The proces-sing alternative discussed in paragraph 1.26 shows that the deliveredproduct costs into Banjul are higher by an average of D .0225/liter($4.73/bbl) than competitive bidding or using the spot price supplyalternative. Using the Caribbean refineries for processing would requiremanaging large inventories because shipping from either Nigeria or SaudiArabia to these refineries normally is done in super tankers of 300,000DWT which would be equivalent to four years of The Cambia's totalrequiremants (based on 1985 forecast volumes). If 50,000 DVT tankerswere used for crude transportation as in Alternative C, the longer haulto the Caribbean plus the longer backhaul of product on more expensiveclean shipping would add about $1.85/bbl to the cost of processing in theCaribbean over the SAR Refinery in Dakar. Therefore, this supplyalternative is not economically feasible.

- 11 -

II. CmPULsmRY SToCrB/EnERnEICY ALLoCC21O PLAN

Overview

2.1 The Gambia currently has no minimum compulsory stock require-ment, and there is no active plan for managing supplies in an emer-gency. However, the mission learned that the National Economic AdvisoryCommittee has put forth some recommendations on the rationing of productssuch as service station closings, etc.

2.2 When inventories get down to about 30 days' supply, the oilcompanies advise the Ministry of Finance and Trade (their regulatory min-istry) of the impending shortage and request guidance. Without specificadvice from the Ministry, which is usually the case, the oil companiesarbitrarily begin to restrict supplies and the major or essential serviceconsumers do not become aware of a shortage until they are given reducedvolumes or are denied replenishment altogether. This lack of notifica-tion to essential service consumers prevents them from implementing theirown controls at an early stage. For example, The Gambia Public TransportCorporation (GPTC) has a three-step contingency plan that it could imple-ment if it were given advanced notice.

2.3 The severe foreign exchange shortages and the Central Bank'sarrears in remitting obligations of the oil companies to their offshoresuppliers have created a situation in which only small parcels of pro-ducts are being imported to The Gambia. Consequently, not enoughproducts are available to consumers over extended periods to allow themto build normal inventories.

Findings and Recommendations

Present Terminal Operations

2.4 The present method of importing products is inefficient in thateach marketer imports into the tankage space assigned to him. It isrecommended that total tankage in the terminal be used for each import tominimize freight costs.

2.5 There is an extra tank in the terminal that is used as a swingtank when repairs are made to the other tanks. It is recommended thatthis tank be used to hold heavy diesel for the Gambia UtilitiesCorporation (CUC) to allow it to take advantage of the small savings inproduct price.

- 12 -

Compulsory Stocks

2.6 Working inventories were determined for each product and asuggested allowance for unforeseen shipping and scheduling deviations wascalculated. It is recommended that a 23-day supply (see 3,18) of safetystock be considered when arranging imports.

2.7 The limited tankage at the Shell Terminal would only accomodatecompulsory stocks in kero/turbo and diesel. Therefore, it is recommendedthat a 30-day compulsory stock gradually be established for diesel andkero/turbo.

2.8 When additional tankage is constructed at the existing terminalor a new terminal is provided, the new tank sizes should take intoaccount the need for compulsory stock volume. Based on practices inother countries and The Gambia's own particular situation and location,it is recommended that a "middle-of-the-road" compulsory stock level of50-60 days be consid3red.

Emergency Allocation Plan

2.9 The Energy Unit should develop guidelines for an EmergencyAllocation Plan and, through the National Energy Commission (NEC),present it to Cabinet for approval as part of the Government's nationalpolicy.

2.10 The parastatals, Ministries of Works & Comnunication, Defense,Agriculture, and Interior, the oil companies, and all other essentialservice consumers must prepare their own detailed Emergency AllocationPlans with assistance from the Energy Unit. If developed according tothe appropriate guidelines, these Plans would help to determine thedegree of rationing required at various levels of available inventory.

Optimum Use of Tankass at the Shell Storage Depot

2.11 The current method of mnaging inventories and storage space atthe Shell Terminal is too inefficient to use as a basis for rationingavailable supplies. A portion of each tank is allocated to each marketer(CUC should also be assigned some space for diesel) -- a practice whichcontributes to higher freight rates because replenishment parcels aresmall (to fit into allocated space) since total tank capacities are notutilized. The total unused tank space (ullage) must be utilized indetermining the size of each product import.

2.12 The present storage depot has an extra tank that could be usedfor storing a heavier diesel for GUC during those periods when the extratank is not needed to cover for tanks being serviced. HRevy diesel couldbe used by GUC without any investment in either tankage or heating equip-ment. This product could be combined with normal diesel stocks at Kotu.

- 13 -

The savings would only amount to about $5/HT ($60,000/year) but theycould be obtained at no cost by simply employing proper ordering andscheduling practices. Depending on the spot market, the savings could betwice this amount during certain times of the year.

2.13 Based on the high investment cost of installing a segregatedblack product system plus the heating facilities that would be requiredif GUC converted to fuel oil, such a conversion at this time would not beappropriate. 8/ There are constraints to raising the necessary financ-ing, and the conversion would fit better into GUC's plans after the baseload on the Banjul system exceeded 10-12 MW.

Other Product Tankage

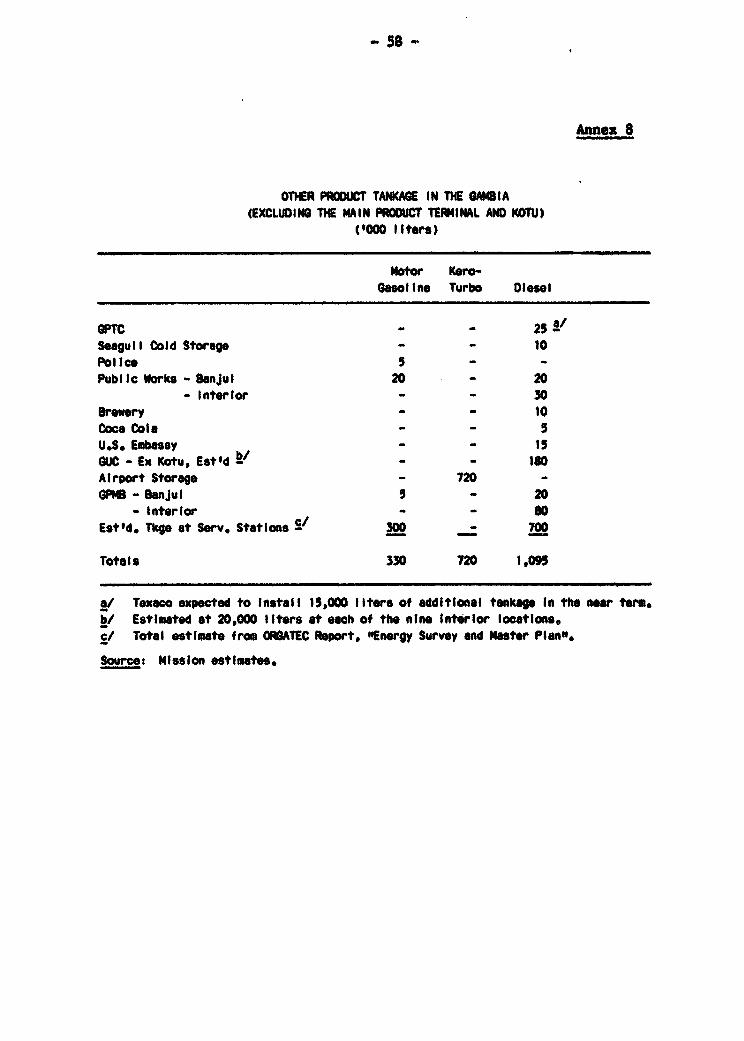

2.14 The total available tankage in the country must be identifiedto ascertain how much capacity can be set aside for compulsory stocks.In addition to the main storage depot, other tankage that will be takeninto account in determining available inventories in the country is shownin Annex 8. GUC also has two tanks each with a capacity of 750,000liters located at its Rotu plant. When calculating the capacityavailable in these miscellaneous tanks it was assumed that only 50%ullage would be available.

Determination of Working Inventories

2.15 Working inventories can be defined as the tankage space notnormally utilized (i.e., non-pumpable tank bottoms, unusable areas in thetop of tanks and a safety stock allowed to handle normal replenishmentscheduling and shipping deviations). Horizontal tanks or tanks with conebottoms have pumpable bottoms. However, horizontal tanks do not haveunusable areas in their tops. Consequently, only tankage in the Shellstorage depot and the CUC tanks at Kotu will be considered as having non-pumpable or unusable space. As a rule-of-thumb, this space usuallyamounts to about 101 of the rated capacity of the tank.

2.16 Scheduling and shipping deviations are normally calculated innumber of days supply; hence, the total Gambia demand must be determinedin terms of average daily consumption. This will vary somewhat duringthe year according to the seasonality of demand for each product. Inscheduling replenishment cargoes, the supplier usually is given a loadingrange to satisfy the routine variation experienced in ship scheduling andoperation plus possible congestion at the loading berth. This loading

8/ World Bank Report No. 4743-CM: The Gambia: Issues and Options inthe Energy Sector, p.20.

- 14 -

range is commonly designated as 10 days "in the 'industry unless certaincircumstances and/or experience will allow less time. Even the mostroutine voyages where shipping is readily available and full cs-oes aresent out, five-day loading ranges are still required. In the case of TheGambia, where the most economical supply alternative involves thesupplier scheduling other parcels for other destinations on the sameship, a 15-day loading range should be considered. This means that theship could be expected to arrive up to 15 days later than its earliestcalculated arrival date.

2.17 In addition to scheduling deviations, the ship, once loaded,can be expected to experience delays due to weather, congestion in dis-charge ports prior to Banjul, and the possibility that another ship willbe in its berth on arrival in Banjul. Such ship delays commonly take upto five days. In the case of The Gambia where the most economical supplyalternative involves a multiport discharge voyage, five days should beallowed for a possible late arrival.

2.18 The supplier is normally required to meet a volume tolerance ofplus or minus 5X. If cargoes are scheduled about every 42 days, thisvolume tolerance would amount to 3 days' supply. This factor onlyaffects working inventories if the ship arrives early with additionalproduct. Therefore, the total number of days to be considered in deter-mining safety stock for scheduling and shipping deviations can be sum-marized as follows:

Days' Supply

Scheduling Deviation 15Ship Delays 5Volume Tolerance 3

Total Days' Supply 23

Compulsory Stocks

2.19 Many countries have legislated that a certain level of inven-tory be maintained to minimize product shortages caused by supply inter-ruptions. Two criteria used to set the compulsory stock level areremoteness from alternate supply sources and the ability to finance theadditional volumes in the case of a supply interruption. Such an inven-tory, or "compulsory stock", does not exist in The Gambia.

2.20 The development of available days supply for optimum replenish-ment scheduling is shown in Annex 9 using 1982 demand. According tothis, replenishment should be scheduled every 42 days to take advantageof importing parcels of at least 6000 MT. However, accepting shipmentsof this size would allow no additional tankage capacity for compulsorystocks of gasoline. Nevertheless, on an average basis, there are 40, 31and 78 additional days supply available for kero/turbo, light diesel and

- 1S -

heavy diesel, respectively. During the peak tourist season, the addi-tional days supply of kero-turbo would be reduced considerably. If heavydiesel cannot be imported for GUC regularly, then Tank No. 3 could be putinto light diesel service, making 45 days' supply of capacity availablefor compulsory stock of light diesel at average consumption rates. Thisis shown in Table 2.1.

Table 2.1 AVAILABLE TANKAGE CAPACITIES AT PRESENT TERMINAL(Days' Supply)

Total, Excl. Optimum Net Available forWorking Stocks Replenishment Compulsory Stock

Gasoline 42 42 0Kero/Turbo 82 42 40 a/Light Diesel 87 42 45

a/ Heavy demand for kero/turbo during the tourist season would reducethis availability considerably.

Source: Mission estimates.

2.21 Since foreign exchange availability will dictate the level ofcompulsory stock, the mission recommends that the Government considerlegislation to gradually establish a 30 days' supply of compulsory stocksin both kero/turbo and diesel under the following conditions:

- The inventories would be built up gradually over a suitabletime period as can be afforded; and

- The kero/turbo compulsory stock level be allowed to decrease,as needed and without penalty, during the tourist season.

About $700,000 would be needed in foreign exchange to purchase the entirerecomended 30 days' compulsory stock. The oil companies would have tocarry this additional volume as part of their normal inventories. How-ever, an amount to cover the carrying cost of this higher inventoryshould be considered as a component in the product price structure (about0.8 bututs/liter).

2.22 In the near term, if the present terminal is expanded or a newterminal is constructed, the mission recommends that a compulsory stockrequirement in all products be incorporated in the sizing of new tank-age. Using the 1990 demand forecast, Table 2.2 shows the costs ofincreased tankage and additional inventory at different levels of compul-sory stock and the amount which should be added to product prices torecoup the investment in 10 years and allow a 20X return. The cost oftankage construction used in Table 2 was assumed to be $6/bbl, which is

- 16 -

the current estimate for 40,000-70,000 bbl tanks. Also, the value of theadditional inventory was based on a cost of $0.21/liter c.i.f. which isrepresentative of today's spot market. Af foreign exchange pressuresease up in the long run, the mission recommends maintaining a "middle-of-the-road" compulsory stock level of 50-60 days in all products for the1990 period. A corresponding investment recovery component would beadded to the product price build-up.

Table 2.2: REQUIRED INVESTMENT FOR LONG TEFiN COOULSORY STOCK

Compulsory Volume, Required Investment, S m i lIon InvestmentStocks, million Increased Additional Recovery Components

Days Supply liters Tankage Inventory Total Bututs/LIter

30 9.4 0.35 1.97 2.32 1.960 18.8 0.70 3.94 4.64 3.890 28.2 1.05 5.91 6.96 5.7

Source: Mission estimates,

Emergency Allocation Plans

2.23 The various ministries of the Government and each of the para-statals (except GUC) receive their petroleum supplies through competitivebidding from the oil companies. Government fuel purchases are made bythe Ministry of Interior (fuel for fire & police), Ministry of Works andCommunication, Ministry of Defense, Ministry of Agriculture, and Ministryof Information (Radio Gambia). A priority program must be developed forthe Ministries of Defense, Agriculture and Information to identify theiressential service consumers.

2.24 Besides purchasing for its own ministry needs, the Ministry ofWorks and Communication, also purchases for the following departments/ministries: the President's Office (includes security), Legislature,Office of the Auditor General, Ministry of Information and Tourism,Ministry of External Affairs, Ministry of Justice, Ministry of Financeand Trade, Ministry of Locat Government and Lands, Ministry of WaterResources and the Environment, Ministry of Economic Planning and Indus-trial Development, Ministry of Education, Youth Sports and Culture, andMinistry of Health, Labor, Social Welfare. The Supplies Officer of theMinistry of Works and Communications has a priority list of essentialservices that includes but is not limited to: the President and Secur-ity; Ambulances/Hospital; Civil Aviation (airport) - excluding fuel foraircraft; and Postal Services.

2.25 The CPTC consumes 3,000 liters/day of diesel in transportingsome 20,000 passengers. This is an essential service. The demand is

- 17 -

expected to increase to 4,000-4,500 liters/day later this year after thearrival of 22 new buses which will extend the bus service. There is a101 variation in demand between the summer months and the peak demandperiod associated with the tourist season. The CPTC already has anemergency plan and is prepared to cut back on consumption by variousdegraes of rationing, as follows:

Level I: All the old buses would be taken off the line, leaving justthe mote efficient, newer ones;

Level II: Operation would be restricted to peak hours (between 7-10am and 3-6 pm); and

Level III: Diesel would be imported by tank-wagon from Dakar Refinery.However, this is an expensive alternative and would only beenvisioned as a last resort.

2.26 Fuel purchased by The Gambia Product Marketing Board (GPMB) isused for the transportation of produce (mostly groundnuts). What littlefuel is required by farmers for planting and harvesting is purchaseddirectly from retail service stations. The transportation of groundnutsfrom eight field storage depots to either the oil processing mill or todockside for export takes place between December and July/August. Theoil mill maintains self-sufficiency in fuel through the burning ofgroundnut shells. The transportation of groundnuts is an essentialservice and, if an emergency allocation program was implemented, the CPMBhas stated that it would be able to limit consumption to meet onlyscheduled shipping and production requirements. If it is assumed thatthe GPMB fuel storage tanks (100,000 liters of diesel) are half full onaverage, there would always be about 12 days' supply available at normalconsumption rates during the transportation season.

2.27 The fuel requirements of the Cambia River Transport Corporation(CRTC) are handled by and stored in tanks owned by CPMB. The CPMB couldalso control GRTC's consumption during critical supply periods. Continu-ation of fery operation is an essential service.

2.28 Another essential-service is the road transportation of cattleto market for slaughter (35/day) or export. The cattle is transported bythe Livestock Marketing Board and fuel is provided from retail servicestations.

2.29 Except for the past eight months, CUC has purchased its dieselrequirements independently from offshore sources through special arrange-ments. GUC has the ability to control its output and supply power to itslist of essential consumers, which includes: hospitals, coimunications,continuation of water supplies, Seagull cold storage, and bakeries.

- 18 -

2.30 The oil companies supply fuel directly to several essential-service consumers such as a local research institute, and certain commu-nications installations. The oil companies can control overall distribu-tion (excluding GUC) and are in a position to implement any approvedallocation program.

Implementing an Emergency Allocation Plan

2.31 Any Emergency Allocation Plan that is developed for The Gambiamust be formally outlined and established as Government policy. TheNational Energy Commission (NEC) should be responsible for establishingthe proposed guidelines and, through its responsible Minister, obtainingCabinet approval. The guidelines would set forth the degree of rationingrequired depending upon the severity of shortage and the number of dayssupply of each product on hand as determined by specific triggering ele-ments. The Inergy Unit, as the working arm of the NEC, should workclosely with the oil companies, the bulk terminal operator and all theessential-service consumers to assist them in developing individualEmergency Allocation Plans. Each individual allocation plan should bereviewed and jointly approved by the Energy Unit and the NEC. The essen-tial-service consumers, in collaboration with their suppliers, will beresponsible for formulating their individual plans of action settingforth the controls needed to meet any reduced level of consumption. TheEnergy Unit will be responsible for monitoring the progress of theoverall Emergency Allocation Plan in operation during emergencies andinsuring that all responsible parties are adhering to the requiredconsumption levels. The Energy Unit will keep the NEC informed throughregular reports. (See the Communication Chart in Annex 10).