JAN 2021.cdr - [email protected]

10

Circulated By Email Volume - XII | January 2021 Vadodara Branch of Western India Regional Council of The Institute of Chartered Accountants of India The Institute of Chartered Accountants of India (Setup by an Act of Parliament) Editorial Team CA. Krunal Brahmbhatt 78748 11551 Chairman CA. Vinod Pahilwani 98980 78176 Vice-Chairman CA. Manoj Sahu 90990 94500 Secretary CA. Rikin Patel 88667 09509 Treasurer CA. Vishal Doshi 98240 59901 Ex-officio CA. Hitesh Agrawal 99980 28737 IP - Chairman CA. Rahul Agrawal 97233 10418 Committee Member CA. Dhruvik Parikh 99795 39966 Committee Member CA. Krunal Brahmbhatt CA. Dhruvik Parikh CA. Nayan Kothari CA. Rahul Parikh CA. Hitesh Thakkar CA. Rachit Sheth CA. Chinmay Naik CA. Janki Gohil CA. Sakshi Somani CA. Neel Shah CA. Sahil Rao Managing Committee Contents Dear Members, Wishing you all a Very Happy New Year. I know year 2020 has been given not so positivity because of corona pandemic but here I am wishing you a great professional year with great positivity & Success. Friends, Optimism is a happiness magnet. If you stay positive good things of good people will be drawn to you. So be positive & spread positivity to make the world positive. Friends as we all know deadline of filling of the tax return is increased by CBDT & I am sure all our members are busy in strict compilation of contributions towards professional responsibility. As we all know deadline of CPE completion is also increased till end of 31st January. So, I request to each member to please complete required CPE Hour of a blocks & also complete CPE hours of Professional Ethics & Standard on Auditing which is mandatory. Wishing you all a great festival of Uttrayan & great professional year ahead. Regards, CA. Krunal Brahmbhatt Chairman Chairman Communication Direct Tax Updates Pg 02 Judicial Decisions on Indirect Taxes Pg 03 Financial Instruments Part-9 Pg 04 House Includes Furniture & Pg 06 Amenities!! Due Date Calendar Pg 09

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of JAN 2021.cdr - [email protected]

Circulated By EmailVolume - XII | January 2021

Vadodara Branch of Western India Regional Council ofThe Institute of Chartered Accountants of India

The Institute of Chartered Accountants of India(Setup by an Act of Parliament)

Editorial Team

CA. Krunal Brahmbhatt 78748 11551Chairman

CA. Vinod Pahilwani 98980 78176Vice-Chairman

CA. Manoj Sahu 90990 94500Secretary

CA. Rikin Patel 88667 09509Treasurer

CA. Vishal Doshi 98240 59901Ex-officio

CA. Hitesh Agrawal 99980 28737IP - Chairman

CA. Rahul Agrawal 97233 10418Committee Member

CA. Dhruvik Parikh 99795 39966Committee Member

CA. Krunal Brahmbhatt CA. Dhruvik Parikh

CA. Nayan Kothari CA. Rahul Parikh

CA. Hitesh Thakkar CA. Rachit Sheth

CA. Chinmay Naik CA. Janki Gohil

CA. Sakshi Somani CA. Neel Shah

CA. Sahil Rao

Managing Committee

Contents

Dear Members,

Wishing you all a Very Happy New Year. I know year 2020 has been givennot so positivity because of corona pandemic but here I am wishing youa great professional year with great positivity & Success.

Friends, Optimism is a happiness magnet. If you stay positive goodthings of good people will be drawn to you. So be positive & spreadpositivity to make the world positive.

Friends as we all know deadline of filling of the tax return is increased byCBDT & I am sure all our members are busy in strict compilation ofcontributions towards professional responsibility.

As we all know deadline of CPE completion is also increased till end of31st January. So, I request to each member to please complete requiredCPE Hour of a blocks & also complete CPE hours of Professional Ethics& Standard on Auditing which is mandatory.

Wishing you all a great festival of Uttrayan & great professional yearahead.

Regards,

CA. Krunal Brahmbhatt

Chairman

Chairman Communication Direct Tax Updates Pg 02

Judicial Decisions on Indirect Taxes Pg 03

Financial Instruments Part-9 Pg 04

House Includes Furniture & Pg 06Amenities!!

Due Date Calendar Pg 09

Vadodara Branch of WIRC of ICAI

Volume - XII January 2021

02

Contributed by : CA. Narendra Hindochacan be reached at [email protected]

Direct Tax Updatesdemand in case of the employer consideringCircular No.15 dated 8.5.1969 according to which,for the purpose of calculation of tax deductible atsource under section 192, self-certification on thepart of the employee was adequate

Additional arguments regarding uniform not evenbeing prescribed, on the basis of which issue wasdecided in favour of revenue in earlier year, wasignored on the ground that such issue was notra i s e d b e f o re t h e A s s e s s i n g O f f i c e r o rCommissioner (Appeals).

However, I would not recommend indiscriminateuse of the decision and such decision may bedifferent in case of a different assessee,represented by another Counsel.

3. Faceless Assessment

The SOPs about which I wrote last month gavehopes for better assessment process. However,the reality appears different at least for the timebeing.

What I understood and wrote last month was :

‘No calling for details in a wholesale manner forfishing enquiries. A focussed and issue specificquestionnaire to be issued. Seeking PAN/ TAN,correspondence address, e-mail/ e-filing addressand mobile number of the parties with whomtransactions have been done by the assessee onlyin such cases where the assessment proceedingsrequire such details for the purpose of verificationand enquiry.’

In one of the Notices that I saw, I observed thefollowing:

- The questionnaire asked for details which arealready part of the return like email ID, contactnumber, details of holding and subsidiarycompany, method of accounting, details ofbank account

- The Questionnaire asked for details ofpersonal expenses in case of corporateassessee while I believe it is settled that acompany does not have personal expenses.

- The questionnaire asks for confirmation fromall the creditors. I would be surprised if anycompany actively in business can provideconfirmation from 50% of creditors in 15 days.

Now as part of enhanced Taxpayer services andto further streamline the Faceless Assessmentp r o c e s s , a d e d i c a t e d e m a i l I D [email protected] has beenmade functional by for taxpayers to registerfeedback pertaining to the FacelessAssessmentScheme

Income-tax

1. Extension of due dates

Several representations were made for extensionof due dates for furnishing Audit Reports andReturns of income by several institutions andindividuals and an extension of a couple of monthswas expected. However, I believe Governmenttakes into account Returns already filed and thesebeing substantial, short extensions are granted asunder:

a. Income Tax Returns for taxpayers (includingtheir partners) who are required to get theiraccounts audited or furnish report underTransfer Pricing regulations and companies -15th February. 2021.

b. Others -10th January, 2021.

c. A u d i t r e p o r t s r e p o r t i n r e s p e c t o finternational/specified domestic transaction:15th January, 2021.

c. Self-assessment tax for taxpayers whose self-assessment tax liability is up to Rs. 1 lakh-Respective due dates for Returns

2. Employer obligation regarding Tax Deductiblefrom salary

A number of allowances are taxfree if theemployee spends the relative amount for meetingspecified expenses. These include medicalexpenses reimbursements, leave travel expenses,uniform allowance, travelling etc. To what extentthe employer needs to go to verify genuineness ofsuch expenses is a question puzzling manydeductors.

In the case of Commissioner Of Income Tax (TDS)Versus Oil And Natural Gas Corporation Ltd, theclaim for exemption in respect of Uniformallowance was questioned by the AssessingOfficer on the ground that the employees had takenthis reimbursement on the basis of self-certification at the beginning of the year. and nofurther check had been observed by the deductoras to whether employees had actually incurredsuch expenditure or not by calling for bills andvouchers and examining genuineness. Even theamount of expenditure as well as its uniformity forall employees at Rs.52364/- was questioned.

The Hon’ble Gujarat High Court deleted the

Vadodara Branch of WIRC of ICAI

Volume - XII January 2021

03

Contributed by : CA Anirudh Sonpal.can be reached at [email protected]

Judicial Decisionson Indirect Taxes

I. ADJUDICATION - SHOW CAUSE NOTICE & ORDER

1.1 The Petitioner was issued summary of order dated18-9-20 for raising of demand for GST based onSCN dated 10-6-20 for the period September 2018to May 2019; however, the SCN was nevercommunicated to the petitioner. The revenueauthorities reiterated that the impugned SCN wascommunicated to the petitioner on his e-mailaddress and despite receiving the same, noresponse was filed by the petitioner.

The Honourable High Court accepted thepetitioner’s contention that Rule 142 of the CGSTRules, 2017 statutorily obliges the revenuedepartment to communicate show-causenotice/orders by uploading the same on thewebsite of revenue so that the aggrieved personcan have access to the same and be aware ofreasons behind the demand to enable theaggrieved person to avail alternative remedy beforethe higher forum under CGST Act. Observing that itis trite principle of law that when a particularprocedure is prescribed to perform a particular actthen all other procedures/modes except the oneprescribed are excluded, the Honourable HighCourt struck down the SCN & Order, with liberty tothe revenue authorities to proceed as per law.

[Akash Garg – MP High Court]

1.2 The Pet i t ioner, engaged in bus iness ofmanufacture of excisable goods, was availingcenvat credits on input and capital goods under theCenvat Credit Rules of different years. ThePetitioner was issued SCNs in 2006 alleging thatthe petitioner had availed excess cenvat credit; thepetitioner responded to the SCNs by submittingdetailed replies denying the allegations madeagainst it; and since there was no communicationand consequential decision taken, the petitionerwas under a boa fide belief that the revenueauthorities had accepted the submissions andhence the matter was concluded. However, afterabout 13 years, Petitioner was served with a letterissued from the office of Respondent authorityinforming the Petitioner that in connection with thetwo SCN, a personal hearing was fixed on August21, 2019. After the petitioner filed the petitionbefore the Honourable High Court, the orders were

also passed in November 2019.

The Honourable High Court held that such delayedadjudication after more than a decade, defeats thevery purpose of issuing SCN; When a SCN is issuedto a party, it is expected that the same would betaken to its logical consequence within areasonable period so that a finality is reached; aperiod of 13 years certainly cannot be construed tobe a reasonable period, and Petitioner cannot befaulted for taking the view that Respondents haddecided not to proceed with the SCN.

With reference to the Order-in Original being issuedafter the petition was filed, the Honourable HighCourt observed that when a matter is broughtbefore the Court or the Court is examining thematter, Respondents cannot initiate or proceedwith a parallel proceeding on its own to render theCourt scrutiny redundant; such an approach isneither acceptable nor permissible.

The Honourable High Court, observing that anaction which is unfair and in violation of theprinciples of natural justice cannot be sustained,held the adjudication proceedings to be invalid andalso set aside and quashed the order passed.

[Parle International Limited – Bombay HC]

II. RETURNS

The Honourable Supreme Court, upon petition filedby the UoI, has stayed Delhi High Court order bywhich the Honourable High Court had allowedForm GSTR-3B rectification.

The Honourable Delhi High Court had held thatfailure of the Government to operationalise thestatutory returns, GSTR 2, 2A and 3 prescribedunder the CGST Act, cannot prejudice theassessee. The GSTR 3B which was merely asummary return as an alternative did not have thestatutory features of the returns prescribed underthe Act. Therefore, if there were errors in capturingITC on account of which cash was paid fordischarging GST liability instead of utilising ITCwhich could not be captured correctly at that time,the return should be allowed to be rectified in thevery month in which the ITC was not recorded andthe cash paid should be available as refund. TheHigh Court read down para 4 of the impugnedCircular No. 26/26/2017-GST dated 29.12.2017which did not permit such rectification as beingcontrary to the scheme of the CGST Act.

[Bharti Airtel Ltd & Ors – Supreme Court]

Vadodara Branch of WIRC of ICAI

Volume - XII January 2021

04

Derecognition – Finer Concepts

We have started a journey to understand the keyconcepts of Ind AS related to Financial Instruments andthis is the 9th article in this series.

In the previous article, we have understood in detail thevarious nuances of derecognition of financial assetsand financial liabilities. Let us understand the finerconcepts of derecognition in this article through peculiarissues and case study.

Issues:

Continuing Involvement:

1. In case where the entity has not transferredsubstantially the whole of cash flows oftransferred financial asset, how the accountingshall be done?

If the entity has retained substantially all the risksand rewards of ownership of the transferred asset,the entity shall continue to recognise thetransferred asset in its entirety and shall recognisea financial liability for the consideration received. Insubsequent periods, the entity shall recognise anyincome on the transferred asset and any expenseincurred on the financial liability in Statement ofProfit or Loss.

2. Does the entity need to recognize any income orassociated expense in relation the Financial assetto the extent of continuing involvement?

Yes. The entity shall continue to recognise anyincome arising on the transferred asset to theextent of its continuing involvement in thetransferred asset and shall recognise any expenseincurred on the associated liability.

3. Does the entity need to apply derecognition testrequirement to Financial Asset as a whole?

Yes. The derecognition test needs to be applied tothe financial asset as whole, although thetransferor has not transferred all cash flows fromthe asset.

4. Does a transfer of an asset for part of its life qualifyas a separate asset for derecognition purposes?

Yes. The derecognition requirements can beapplied to the specifically identifiable cash flows oftransferred financial asset.

5. For subsequent measurement, does the entity hasan option to offset changes in the fair value of the

Contributed by : CA Ankur Maniar.can be reached at

Financial InstrumentsPart-9

transferred asset and the associated liability?

No. For subsequent measurement, the changes inthe fair value of the transferred asset and theassociated liability are accounted for consistentlywith each other in accordance with paragraph 5.7.1of Ind AS 109, and shall not be offset.

6. In case where the entity measures transferredasset at amortised cost, can the entity designatethe associated financial liability at Fair Valuethrough profit and loss?

No. If the transferred asset is measured atamortised cost, the option in this Standard todesignate a financial liability at fair value throughprofit or loss does not apply to the associatedliability.

Exchange/Modif icat ion of f inancial l iabi l i tyinstruments

Many a times, the entities re-negotiate terms of theirexisting debt with the lenders. In India, this is popularlyknown as “Strategic Debt Restructuring or SDR”. Inaccounting terms, such situations need to be evaluatedto determine whether the original debt is extinguished,and new debt has arisen.

As per paragraph 3.3.2 of Ind AS 109, an exchangebetween an existing borrower and lender of debtinstruments with substantially different terms shall beaccounted for as:

- an extinguishment of the original financial liability,and

- the recognition of a new financial liability.

Similarly, a substantial modification of the terms of anexisting financial liability or a part of it (whether or notattributable to the financial difficulty of the debtor) shallbe accounted as mentioned above.

As per application guidance in paragraph B3.3.6 of IndAS 109, the terms are substantially different if:

Accounting treatment:

If an exchange of debt instruments or modification ofterms is accounted for as an extinguishment, any costsor fees incurred are recognised as part of the gain or losson the extinguishment.

If the exchange or modification is not accounted for asan extinguishment, any costs or fees incurred are to beadjusted in the carrying amount of the liability and are

Vadodara Branch of WIRC of ICAI

Volume - XII January 2021

05

amortised over the remaining term of the modifiedliability.

In accordance with Ind-AS 109, the terms of exchangedor modified debt are regarded as ‘substantially different’,if the net present value of the cash flows under the newterms (including any fees paid net of any fees received)discounted at the original EIR is at least 10% differentfrom the discounted present value of the remainingcash-flows of the original debt instrument. In addition,there may be situations where the modification of thedebt is so fundamental that immediate derecognition isappropriate even though the ‘10% test’ is not satisfied.Given below are few examples of such changes:

• An entity had issued a ‘plain vanilla’ debtinstrument. It restructures the debt to include anembedded equity instrument.

• An entity has issued a 5% USD – denominated debtinstrument with current fair value of USD 500. Itrestructures the instrument to 14% INR –denominated debt instrument with the same fairvalue at time of the restructuring.

In both the above-mentioned instances, there is afundamental change in the risk exposure of theinstrument. Hence, it should be treated as ‘substantialmodification’ requiring derecognition of old liability andrecognition of new liability. This is despite the fact that10% test for substantial modification may not have beenmet.

When a financial liability (or part of a liability) isextinguished or transferred to another party, thestandard requires the difference between the carryingamount of the transferred financial liability (or part of aliability) and the consideration paid, including any non-cash assets transferred or liabilities assumed, to berecognised in statement of profit and loss. If an entityrepurchases only a part of a financial liability, itcalculates the carrying value of the part disposed of (andhence the gain or loss on disposal) by allocating theprevious carrying amount of the financial liabilitybetween the part that continues to be recognised andthe part that is derecognised based on the relative fairvalues of those parts on the date of the repurchase.

If the 10% test is passed, principle of “extinguishmentaccounting” are applied. It essentially involves following:

• De-recognition of existing liability;

• Recognition of the new liability at its fair value;

• Recognition of a gain or loss equal to the differencebetween the carrying value of the old liability andfair value of the new one;

• Recognising any incremental costs or feesincurred, and any consideration paid or received, inprofit or loss;

• Calculating a new effective interest rate for the newliability, which is then used in future periods.

Fair value of the new or modified liability is estimated,based on the expected future cash-flows of the modifiedliability, discounted using the interest rate at which theentity could raise debt with similar terms and conditionsin the market.

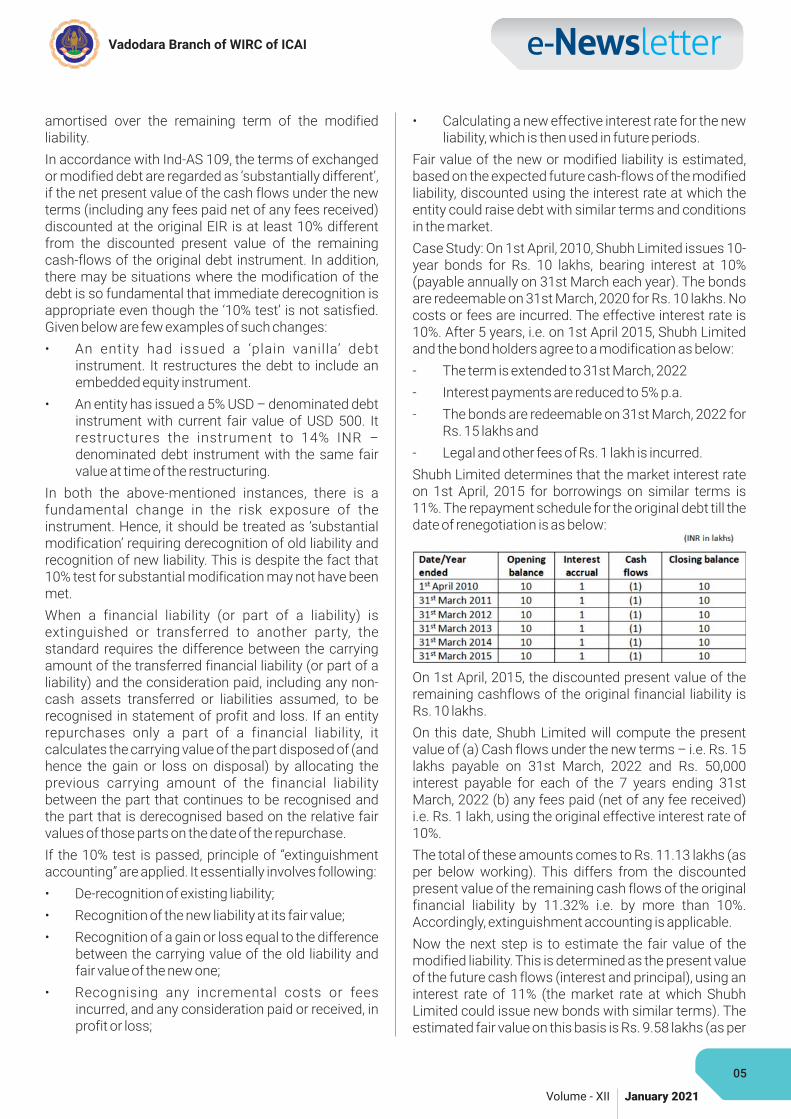

Case Study: On 1st April, 2010, Shubh Limited issues 10-year bonds for Rs. 10 lakhs, bearing interest at 10%(payable annually on 31st March each year). The bondsare redeemable on 31st March, 2020 for Rs. 10 lakhs. Nocosts or fees are incurred. The effective interest rate is10%. After 5 years, i.e. on 1st April 2015, Shubh Limitedand the bond holders agree to a modification as below:

- The term is extended to 31st March, 2022

- Interest payments are reduced to 5% p.a.

- The bonds are redeemable on 31st March, 2022 forRs. 15 lakhs and

- Legal and other fees of Rs. 1 lakh is incurred.

Shubh Limited determines that the market interest rateon 1st April, 2015 for borrowings on similar terms is11%. The repayment schedule for the original debt till thedate of renegotiation is as below:

On 1st April, 2015, the discounted present value of theremaining cashflows of the original financial liability isRs. 10 lakhs.

On this date, Shubh Limited will compute the presentvalue of (a) Cash flows under the new terms – i.e. Rs. 15lakhs payable on 31st March, 2022 and Rs. 50,000interest payable for each of the 7 years ending 31stMarch, 2022 (b) any fees paid (net of any fee received)i.e. Rs. 1 lakh, using the original effective interest rate of10%.

The total of these amounts comes to Rs. 11.13 lakhs (asper below working). This differs from the discountedpresent value of the remaining cash flows of the originalfinancial liability by 11.32% i.e. by more than 10%.Accordingly, extinguishment accounting is applicable.

Now the next step is to estimate the fair value of themodified liability. This is determined as the present valueof the future cash flows (interest and principal), using aninterest rate of 11% (the market rate at which ShubhLimited could issue new bonds with similar terms). Theestimated fair value on this basis is Rs. 9.58 lakhs (as per

Vadodara Branch of WIRC of ICAI

Volume - XII January 2021

06

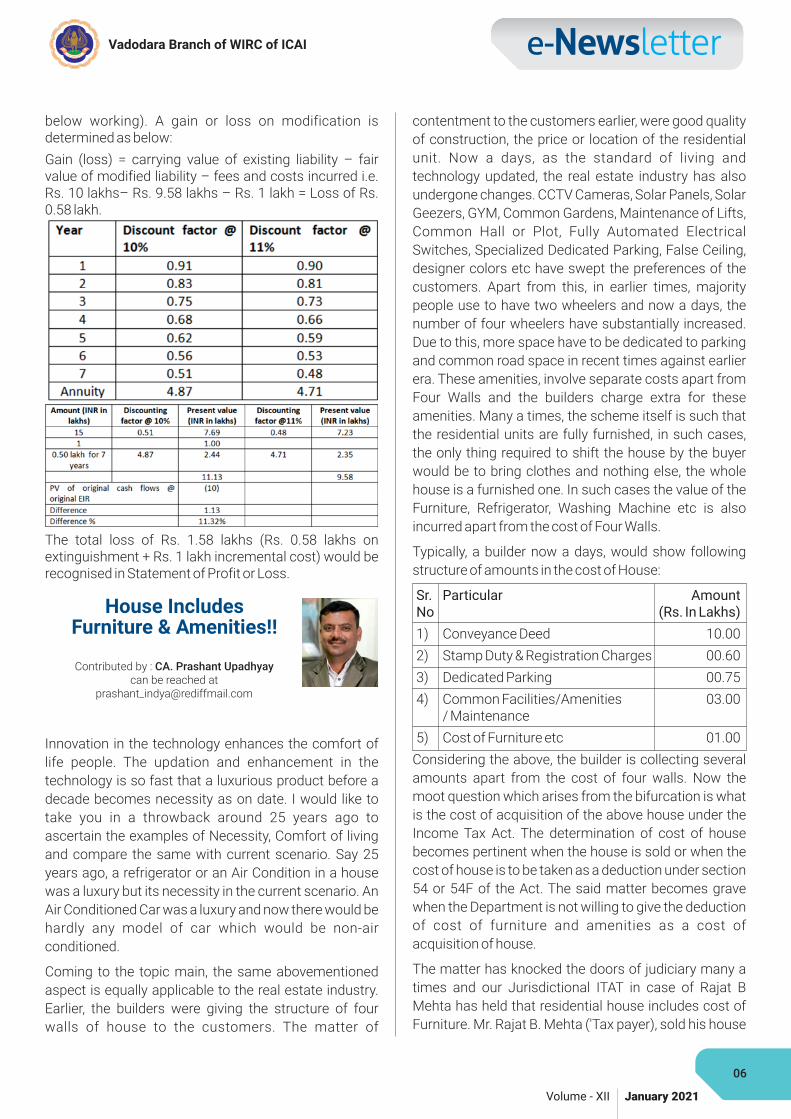

below working). A gain or loss on modification isdetermined as below:

Gain (loss) = carrying value of existing liability – fairvalue of modified liability – fees and costs incurred i.e.Rs. 10 lakhs– Rs. 9.58 lakhs – Rs. 1 lakh = Loss of Rs.0.58 lakh.

The total loss of Rs. 1.58 lakhs (Rs. 0.58 lakhs onextinguishment + Rs. 1 lakh incremental cost) would berecognised in Statement of Profit or Loss.

Contributed by : CA. Prashant Upadhyaycan be reached at

House IncludesFurniture & Amenities!!

Innovation in the technology enhances the comfort of

life people. The updation and enhancement in the

technology is so fast that a luxurious product before a

decade becomes necessity as on date. I would like to

take you in a throwback around 25 years ago to

ascertain the examples of Necessity, Comfort of living

and compare the same with current scenario. Say 25

years ago, a refrigerator or an Air Condition in a house

was a luxury but its necessity in the current scenario. An

Air Conditioned Car was a luxury and now there would be

hardly any model of car which would be non-air

conditioned.

Coming to the topic main, the same abovementioned

aspect is equally applicable to the real estate industry.

Earlier, the builders were giving the structure of four

walls of house to the customers. The matter of

contentment to the customers earlier, were good quality

of construction, the price or location of the residential

unit. Now a days, as the standard of living and

technology updated, the real estate industry has also

undergone changes. CCTV Cameras, Solar Panels, Solar

Geezers, GYM, Common Gardens, Maintenance of Lifts,

Common Hall or Plot, Fully Automated Electrical

Switches, Specialized Dedicated Parking, False Ceiling,

designer colors etc have swept the preferences of the

customers. Apart from this, in earlier times, majority

people use to have two wheelers and now a days, the

number of four wheelers have substantially increased.

Due to this, more space have to be dedicated to parking

and common road space in recent times against earlier

era. These amenities, involve separate costs apart from

Four Walls and the builders charge extra for these

amenities. Many a times, the scheme itself is such that

the residential units are fully furnished, in such cases,

the only thing required to shift the house by the buyer

would be to bring clothes and nothing else, the whole

house is a furnished one. In such cases the value of the

Furniture, Refrigerator, Washing Machine etc is also

incurred apart from the cost of Four Walls.

Typically, a builder now a days, would show following

structure of amounts in the cost of House:

Sr. Particular AmountNo (Rs. In Lakhs)

1) Conveyance Deed 10.00

2) Stamp Duty & Registration Charges 00.60

3) Dedicated Parking 00.75

4) Common Facilities/Amenities 03.00/ Maintenance

5) Cost of Furniture etc 01.00

Considering the above, the builder is collecting several

amounts apart from the cost of four walls. Now the

moot question which arises from the bifurcation is what

is the cost of acquisition of the above house under the

Income Tax Act. The determination of cost of house

becomes pertinent when the house is sold or when the

cost of house is to be taken as a deduction under section

54 or 54F of the Act. The said matter becomes grave

when the Department is not willing to give the deduction

of cost of furniture and amenities as a cost of

acquisition of house.

The matter has knocked the doors of judiciary many a

times and our Jurisdictional ITAT in case of Rajat B

Mehta has held that residential house includes cost of

Furniture. Mr. Rajat B. Mehta ('Tax payer), sold his house

Vadodara Branch of WIRC of ICAI

Volume - XII January 2021

07

earning LTCG and invested Rs. 78 Lakh in another

property for which he claimed deduction u/s 54. The Tax

payer had entered into two separate agreements, one for

purchase of house property for Rs 60,00,000 and

another for furniture for Rs 18,00,000 in the said

property. The Department was of the view that “the

assessee has executed the separate deed (for sale of

furniture and fixtures etc) to save stamp duty on it, (and)

now the assessee is trying to evade income tax”.

Department was of the opinion that expenses incurred

on buying furniture cannot be said to be expenses

incurred for making the house habitable. Considering

the same the Department did not allowed the deduction

u/s 54F to the extent of Rs. 18 Lakh paid under a

separate agreement for furniture and fixtures in the

residential property purchased by the Tax Payer. The

CIT(A) upheld the AO's order.

The Tax payer relying upon the co-ordinate bench

decision of Srinivas R Desai contended that the cost of

furniture & fixtures was incurred to make the house

habitable and it would qualify for deduction u/s 54. ITAT

observed that the Tax payer had entered into an

agreement to purchase the property for Rs. 78 Lakh on

January 19, 2011 and had made advance payments. In

furtherance of this agreement, he entered into 2

separate agreements on February 4, 2011 for purchase

of property for Rs. 60 Lakh and for purchase of furniture

for Rs. 18 Lakh. Therefore, ITAT observed that actual

consideration for purchase of property is Rs. 78 Lakh

and splitt ing of consideration is an ar tif icial

arrangement in substance. It further held that even if the

assessee was to buy the house, without the furniture, it

would have been Rs. 78 Lakh and such a splitting of

consideration had no bearing on de facto consideration

for purchase of house property. Therefore, ITAT held that

these two agreements cannot be considered in isolation

with each other on standalone basis and have to be

considered essentially as a composite contract-

particularly in the light of the undisputed contents of the

agreement to sell dated 19 January, 2011.

It was held that the cost of the residential house would

not remain confined to the cost of civil construction

alone but may include furniture and fixtures as its

integral part which would be included in the cost of

house. Accordingly, it was held that the cost of the new

asset has to be treated as Rs. 78 Lakh as the Tax Payer

did not have any choice about buying or not buying the

furniture at the assigned values, as irrespective of the

purchases of the furniture also, the assessee was under

an obligation to pay the same amount of Rs. 78 Lakh.

ITAT noted that the real beneficiary of splitting up the

arrangement was the seller of this property as the value

of Rs. 18 Lakhs was assigned to furniture which are

personal effects not covered within the definition of

capital asset u/s 2(14) and would therefore, not be

taxable as capital gains. ITAT remarked that “Only if the

Assessing Officer had read the agreement to sell

carefully and considered the same in the light of actual

sale deeds, he could have easily identified the manner in

which the revenue authorities were possibly taken for a

ride, and he could have initiated suitable remedial

action.”

In one of the another recent decision of Mrs. Rashmi

Dhanani by Mumbai ITAT, it is held that cost of

acquisition of House to include cost of amenities

covered by the contemporaneous agreements. The Tax

Payer had included cost of amenities like Garage Cost,

special water proofing in toilets/kitchen, special wood

for doors/windows etc. charges as cost of acquisition

for the purpose of indexation which AO held that they are

not in the nature of improvement cost.. The cost of

amenities amounted to Rs. 9.38 Lacs and the cost of

Furniture was allotted to Rs. 0.84 Lacs by the builder and

not covered in the conveyance deed. It was confirmed

that while purchasing the above flat it was regular

practice of the builder to divide purchase agreement into

2 parts i.e. purchase Agreement as well as Amenities

Agreement. It was held that that Tax Payer had paid

amenity charges which was reflected in the assessee's

balance sheet. It was observed that if amenities works

were actually been undertaken by the builder as per

amenities agreement, the same would certainly need to

be included in the cost of acquisition. The agreement of

amenities was made on plain paper and was not

registered. The ITAT held that only because the

agreement is in plain paper or not registered would not

deprive the assessee from getting the benefit of amount

paid towards amenities when she has actually paid such

amount.

ITAT, in the same case, had earlier directed Revenue to

investigate for flat owners who had entered into

amenities agreements with the builder to see if such an

arrangement was unusual or not. if at all other flat

owners have entered into similar agreement for

amenities and have made payment for such amenities, it

will definitely prove that there was an arrangement

between the builder to split the work into two different

agreement, for which the purchasers of flat cannot be

Vadodara Branch of WIRC of ICAI

Volume - XII January 2021

08

held responsible. Hence, no adverse view can be taken in

respect of the assessee and the amenities charges paid

by the assessee has to be treated as part of the cost of

acquisition for the purpose of indexation.

In common parlance, the amenities in nature of

electrification, balcony fixtures, windows, sanitary

wares etc are not construed as the cost of civil

construction of the house but these amenities are

embedded in the house. Hence, the total cost of house

cannot be separated from these costs and amenities.

Relevance of Stamp Value: Section 50C for seller or

Section 56 for purchaser, prescribes the bare minimum

value of the house to be declared by the seller or buyer in

the conveyance deed for payment of Stamp Duty and

Income Tax levy. The same is nothing but the stamp

value or Jantri value of the house determined in

accordance with valuation prescribed by the State

Government and norms thereof. The intention to

substitute the stamp value is to check evasion in taxes

by hiding the actual consideration passed through black

money. Merely, the said Stamp Value, can neither be

construed nor be substituted with the purchase cost of

house allowed as a deduction, whether for indexation or

for claiming exemption.

Financial Assistance Scheme forCA Students of Vadodara

The Vadodara Branch of WIRC of ICAI has a strong tradition of providing the best tools

and support to CA students of Vadodara, for achieving their goal of becoming

Chartered Accountants. Finance should not be a constraint for deserving Students

who want to be a CA. Since past few years, with the contribution of the big hearted

members, the Vadodara Branch of WIRC of ICAI has been taking responsibility to

sponsor a part of the total educational cost of the needy CA students.

Financial Assistance is given to students of Intermediate & Final after systematically

evaluating their eligibility (i.e.) screening their applications, interviewing them, cross-

verifying the credential and so on. Students will get the reimbursement of Institute

Fees..!!

The following are current registration fees of our Institute for a CA student:

For any further details on the same please contact

Vadodara Branch of WIRC of ICAI

on

02652680593/2681115/8511077115

Form:-https://drive.google.com/file/d/18axKPdQMd5Ua4vMnfc3NKh25B3U7IVDI/view?usp=sharing

Intermediate : Rs. 17,000/-

Final : Rs. 22,000/-

Vadodara Branch of WIRC of ICAI

Volume - XII January 2021

09

DueDates

07-Jan-21

07-Jan-21

07-Jan-21

11-Jan-21

13-Jan-21

15-Jan-21

15-Jan-21

15-Jan-21

15-Jan-21

18-Jan-21

20-Jan-21

20-Jan-21

22-Jan-21

24-Jan-21

28-Jan-21

30-Jan-21

30-Jan-21

31-Jan-21

31-Jan-21

31-Jan-21

ReportingPeriod

Dec-20

Dec-20

Dec-20

Dec-20

Dec-20

Nov-20

Nov-20

Dec-20

Dec-20

Oct-20to

Dec-20

Dec-20

Dec-20

Dec-20

Dec-20

Dec-20

Dec-20

Dec-20

AY 2020-21

Oct-20 toDec-20

Oct-20 toDec-20

Compliance Details

Deposit of Tax Deducted/TaxColected (TDS/TCS) Under ITAct, 1961

GSTR 7

GSTR 8

GSTR 1

GSTR 6

TDS Certificate under section194-IA and 194-IB - Form 16Band Form 16C

TDS Certificate for taxdeducted under section 194M

Deposit of Provident FundConstribution

Deposit of ESIC Contribution

GST CMP-08

GSTR 3B

GSTR 5

GSTR 3B

GSTR 3B

GSTR 11

Due date for furnishing ofchallan-cum-statement inrespect of tax deducted undersection 194-IA & IB

Due date for furnishing ofchallan-cum-statement inrespect of tax deducted undersection 194-M

Income Tax Return

GSTR 1

TDS Return Filling

Applicability

All Non Governemnt Deductors/Collectors

Government Authorities and Government Companies

E-Commerce Operators

GST Registered Taxpayers with Annual Turnover morethan 1.5 crores.

Input Service Distributors (ISD)

As Applicable

As Applicable

Any Person registered with PF Authorities

Any Person registered with ESIC Authorities

Comosite Dealers registered under GST

Any Person Registered Under GST having turnovermore than 5 Cr in Previous Year

Non-Resident Foreign Taxable person & OIDAR

Any Person Registered Under GST having turnover lessthan 5 Cr in Previous Year and registered under Gujarat

All Registered GST Taxpayers (taxpayers having anaggregate turnover of less than Rs. 5 Crores in theprevious financial year) For Some of the States

A taxpayer claiming Refund and having UIN

As Applicable

As Applicable

Assesee's who's accounts are required to get auditedand partners thereof Partnerhip Firm

GST Registered Taxpayers with Annual Turnover lessthan 1.5 crores and opted for Quarterly Return

As Applicable

Details to be Furnished

Details relating to transaction of Tax Deducted/TaxColected (TDS/TCS).

Tax Deducted at source under GST u/s 51 of the Act(TDS)

Tax Collected at source Under GST u/s 52 of the Act(TCS)

Details relating to Outward Supplies made during themonth.

Return for details of ITC received and distribution

Deduction of tax at source from payment on renting ofImmovable property

TDS on payment to resident contractors andprofessionals (Individuals and HUFs)

Employer and Employees Contribution to PFAuthorities along with Admin Charges

Employer and Employees Contribution to ESICAuthorities along with Admin Charges

Statement-cum-challan to declare the details orsummary of his/her self-assessed tax payable for agiven quarter under GST Act

Summary of Supplies Made, RCM Discharged, ITCClaimed and Tax Payment

Summary Return of Outward taxable supplies and taxpayable

Summary of Supplies Made, RCM Discharged, ITCClaimed and Tax Payment

Summary Return of Outward & Inward Supplies andRCM Liability along with Tax Payment

Details regarding goods and services purchased inIndia.

Payment of tax at source from payment on renting ofImmovable property/Buyer of Immovable Property

TDS on payment to resident contractors andprofessionals (Individuals and HUFs)

Details relating to Income

Details relating to Outward Supplies made during themonth.

Quarterly statement of TDS deposited for the quarterending December 31, 2020

Due Date CalendarContributed by : CA. Himesh D. Gajjarcan be reached at [email protected]

1. Due Date tabulated below is as notified till December 28, 2020

Vadodara Branch of WIRC of ICAI

DISCLAIMER : The ICAI and the Vadodara Branch of WIRC of ICAI is not in any way responsible for the result of any action taken on the basis of the advertisement published in theNewsletter. The members, however, may bear in mind the provisions of the Code of Ethics while responding to the advertisements. The views and opinion expressed or implied inthe Newsletter are those of the authors / contributors and do not necessarily reflect those of Vadodara Branch. Unsolicited matters are sent at the owner's risk and the publisheraccepts no liability for loss or damage. Material in this publication may not be reproduced, whether in part or in whole, without the consent of Vadodara Branch. Members arerequested to kindly send material of professional interest to The same may be published in the newsletter subject to availability [email protected]/[email protected] & editorial editing.

Vadodara Branch of WIRC ofThe Institute of Chartered Accountants of India

www.baroda-icai.org WIRC : www.wirc-icai.org ICAI: www.icai.orgl l

Half Page (1 Color) 5,500

ADVERTISEMENTS : The tariff for advertising given below are duly approved by the Managing Committee of the Vadodara Branch. Advertisements are received directly by theBranch and no advertising agency has been appointed for this purpose. This Newsletter is circulated without any charges to its members and otherSUBSCRIPTION RATES :important categories of recipients as per ICAI Advisory on Newsletters. Subscription rate is Rs. 20/- per issue for others. : on behalf ofPUBLISHED BY CA. Krunal BrahmbhattVadodara Branch of WIRC of ICAI “ICAI Bhawan”, Kalali-Tandalja Road, Atladra, Vadodara - 390 012PUBLISHED AT

Designed by Multiprints, 30/B, Gandhi Oil Mill Compound, Near BIDC, Gorwa, Vadodara - 390 016. Ph.: 0265-228 5592

“ICAI Bhawan”, Kalali-Tandalja Road, Atladra,Vadodara - 390 012. +91 265 268 0593Telefax :M: 85110 77115 / 0265 268 1115 (DCO)

8,500

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIAICAI Bhawan, Post Box No. 7100, Indraprastha Marg,New Delhi - 110 002.

+91 (11) 3989 3989 | [email protected].: E-mail:www.icai.orgWeb:

WESTERN INDIA REGIONAL COUNCILICAI Tower, Plot no C-40, G Block, Opp MCA Ground,Bandra Kurla Complex, Bandra (E), Mumbai - 400 051

+022 - 3367 1400 / 3367 1500 | [email protected].: Email:www.wirc-icai.orgWeb:

Back Cover (4 color) 16,500 Inside Front/Back Cover (4 color) Full Page (1 Color)

* Discount - 3 to 6 issue of 10%, 7 to 12 issue 15% * Circulated to more than Chartered Accountants2200ADVERTISEMENT RATE :

11,000

Volume - XII January 2021

� ABOUT US:

is the wholly owned subsidiary of Norfolk Technology Services LimitedVSE Stock Services Ltd. (VSSL)incorporated under the Companies Act, 1956 and having its registered office situated at 3rd Floor Fortune TowerSayajigunj-390020, Vadodara, Gujarat, INDIA, We are registered with SEBI as a Stock Broker and DepositoryParticipant of CDSL, We are member of BSE, NSE and MCX.

We are inviting for the post of CAs.Latest CV/Resume (via e-mail only, as under)

� HOW TO APPLY?

As per below table, suitable candidates can apply via e-mail to us. E-Mail mark to with CC mark [email protected]@vselindia.com with APPLY FOR WITH YOUR FULL NAMEsubject line “Designation”

VACANCY NOTICE[TOTAL 3 (THREE) VACANCIES OF CHARTERED ACCOUNTANTS IN OUR ORGANIZATION]

Sr. Particulars of Requirements/Education/ knowledge Designation Number ofNo. Vacancy

1. At least 4 to 5 years post qualification experienced required for the MANAGER 1 (One)-ACCOUNTS“Accounts Department”

Educational qualification:

Qualified Chartered Accountant (CA) from ICAI andany other commerce degree.

Expected working knowledge/skill:

Good knowledge of accounting practice, Finance products, Good commandover English Language, Preparation of MIS and reports.

2. At least 2 to 3 years experienced required for the DEPUTY MANAGER 2 (Two)“Accounts Department”

Educational qualification: -ACCOUNTS

Qualified Chartered Accountant (CA) from ICAI andany other commerce degree

Expected working knowledge/skill:

Knowledge of accounting practice, Finance products, Good command overEnglish Language, Preparation of MIS and reports.

• Vadodara, Gujarat • Stock Broking and Depository ParticipantsJob location : Industry :

� SELECTION PROCESS AND NOTE:-

• Based on the suitable candidates, we will shortlist and have a VC interview.

• The Company has reserved all right on above posts at all time.Note:

10