James W. Brody, Esq. Chairman of Mortgage Banking Group ...

56

James W. Brody, Esq. Chairman of Mortgage Banking Group Johnston | Thomas, Attorneys at Law, P.C. T: 415/246-3995 E: [email protected] Thursday, May 10, 2018 10:30 a.m. PST/1:30 p.m. EST

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of James W. Brody, Esq. Chairman of Mortgage Banking Group ...

James W. Brody, Esq.Chairman of Mortgage Banking Group

Johnston | Thomas, Attorneys at Law, P.C.T: 415/246-3995

Thursday, May 10, 201810:30 a.m. PST/1:30 p.m. EST

Important Notice(s): Johnston Thomas, Attorneys at Law, P.C. (“JohnstonThomas”) makes available the information ("Information") in this presentation(“Presentation”) for general informational purposes only. The Information isnot intended to constitute, and does not constitute, legal advice or a solicitationfor the formation of an attorney-client relationship. No attorney-clientrelationship is created through your use of or your receipt of the Informationcontained within the Presentation. Johnston Thomas accepts clients only inaccordance with certain formal procedures, and renders legal advice only afterthe completion of those procedures, and/or completion and execution of anappropriate retainer agreement.

Any and all statements made by the moderator and the presenters, as part ofthis webinar program, reflect his or her own viewpoint and not necessarily thatof the program host, Johnston Thomas.

2

Johnston Thomas is a full suite boutique law firm, which amongst other practices such as real estate andcommercial litigation, has a nationally recognized Mortgage Banking Practice Group. With an experiencedteam of mortgage banking lawyers (including senior litigation attorneys, former in-house General Counseland in-house Compliance Counsel from a well-known bank and mortgage company, etc.), certified fraudexaminer(s) and forensic underwriter(s), and an extremely competent support staff, all of whom arededicated to aggressively and competently serving the needs of our valued clientele, Johnston Thomas’Mortgage Banking Practice Group is known all across the country for the experience and results that it bringsto the areas of regulatory compliance, mortgage banking litigation, and a broad range of mitigation services.

Amongst the many legal services Johnston Thomas offers the mortgage banking industry (e.g., brokers, lenders, servicers, vendors and more), such include, but are in no way limited to, as follows:

Mortgage Repurchase and Make-Whole Indemnification Litigation and Mitigation (e.g., Secondary Market Investors, Agencies, etc.)

Mortgage Industry Litigation (e.g., Servicer and Sub-Servicer Disputes, 3rd Party Fraud Recovery, CPL and Title Policy Actions, Appraiser E&O Claims, Loan Officer Actions, etc.

Mortgage Repurchase and Make-Whole Alternative Dispute Resolution (e.g., Arbitration, Mediation, etc.)

Regulatory Compliance, Administrative and Business Services (e.g., Mock Audits, LO Compensation, MSAs, Licensing, CA Dep’t of Business Oversight, HUD Review Board, etc.)

Transactional Matters (e.g., Drafting and Negotiating Broker and Correspondent Loan Purchase Agreements, Mergers & Acquisitions, etc.)

3

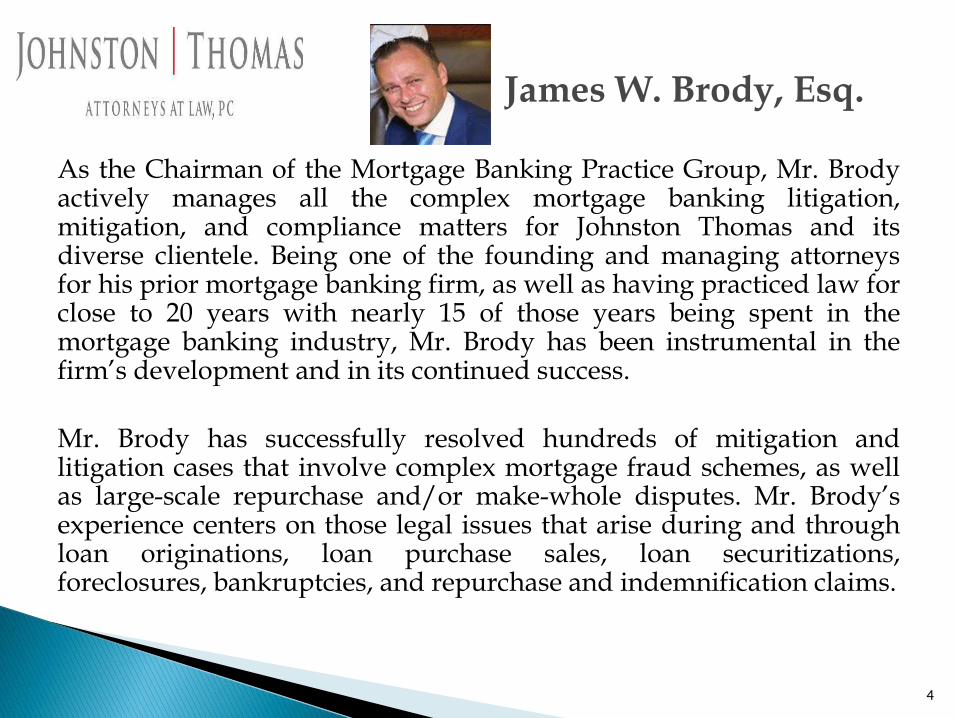

As the Chairman of the Mortgage Banking Practice Group, Mr. Brodyactively manages all the complex mortgage banking litigation,mitigation, and compliance matters for Johnston Thomas and itsdiverse clientele. Being one of the founding and managing attorneysfor his prior mortgage banking firm, as well as having practiced law forclose to 20 years with nearly 15 of those years being spent in themortgage banking industry, Mr. Brody has been instrumental in thefirm’s development and in its continued success.

Mr. Brody has successfully resolved hundreds of mitigation andlitigation cases that involve complex mortgage fraud schemes, as wellas large-scale repurchase and/or make-whole disputes. Mr. Brody’sexperience centers on those legal issues that arise during and throughloan originations, loan purchase sales, loan securitizations,foreclosures, bankruptcies, and repurchase and indemnification claims.

James W. Brody, Esq.

4

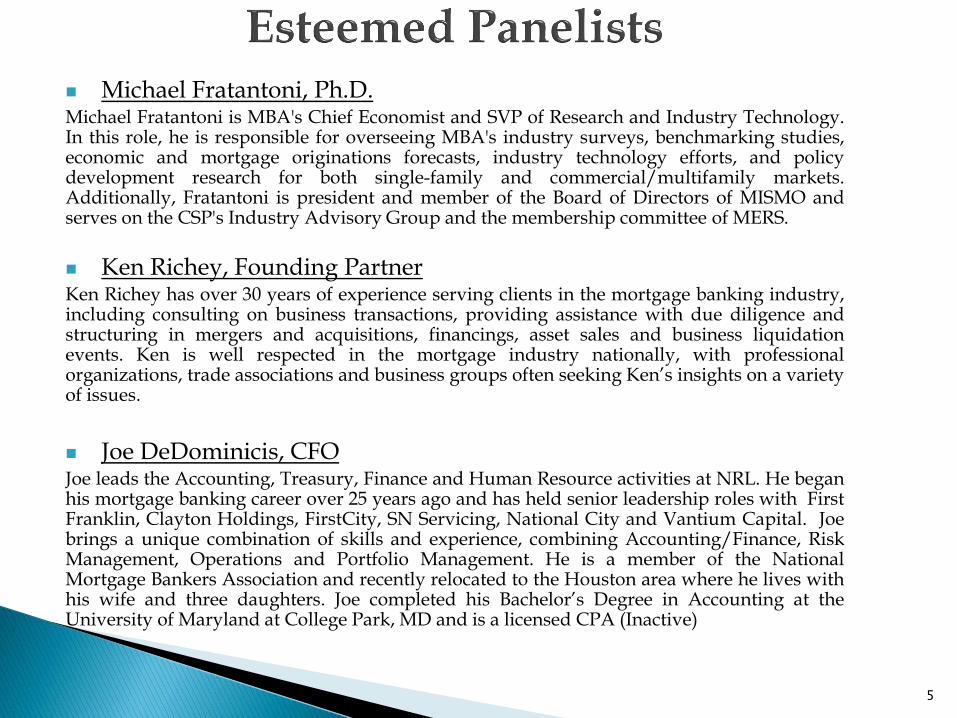

◼ Michael Fratantoni, Ph.D.Michael Fratantoni is MBA's Chief Economist and SVP of Research and Industry Technology.In this role, he is responsible for overseeing MBA's industry surveys, benchmarking studies,economic and mortgage originations forecasts, industry technology efforts, and policydevelopment research for both single-family and commercial/multifamily markets.Additionally, Fratantoni is president and member of the Board of Directors of MISMO andserves on the CSP's Industry Advisory Group and the membership committee of MERS.

◼ Ken Richey, Founding PartnerKen Richey has over 30 years of experience serving clients in the mortgage banking industry,including consulting on business transactions, providing assistance with due diligence andstructuring in mergers and acquisitions, financings, asset sales and business liquidationevents. Ken is well respected in the mortgage industry nationally, with professionalorganizations, trade associations and business groups often seeking Ken’s insights on a varietyof issues.

◼ Joe DeDominicis, CFOJoe leads the Accounting, Treasury, Finance and Human Resource activities at NRL. He beganhis mortgage banking career over 25 years ago and has held senior leadership roles with FirstFranklin, Clayton Holdings, FirstCity, SN Servicing, National City and Vantium Capital. Joebrings a unique combination of skills and experience, combining Accounting/Finance, RiskManagement, Operations and Portfolio Management. He is a member of the NationalMortgage Bankers Association and recently relocated to the Houston area where he lives withhis wife and three daughters. Joe completed his Bachelor’s Degree in Accounting at theUniversity of Maryland at College Park, MD and is a licensed CPA (Inactive)

5

8

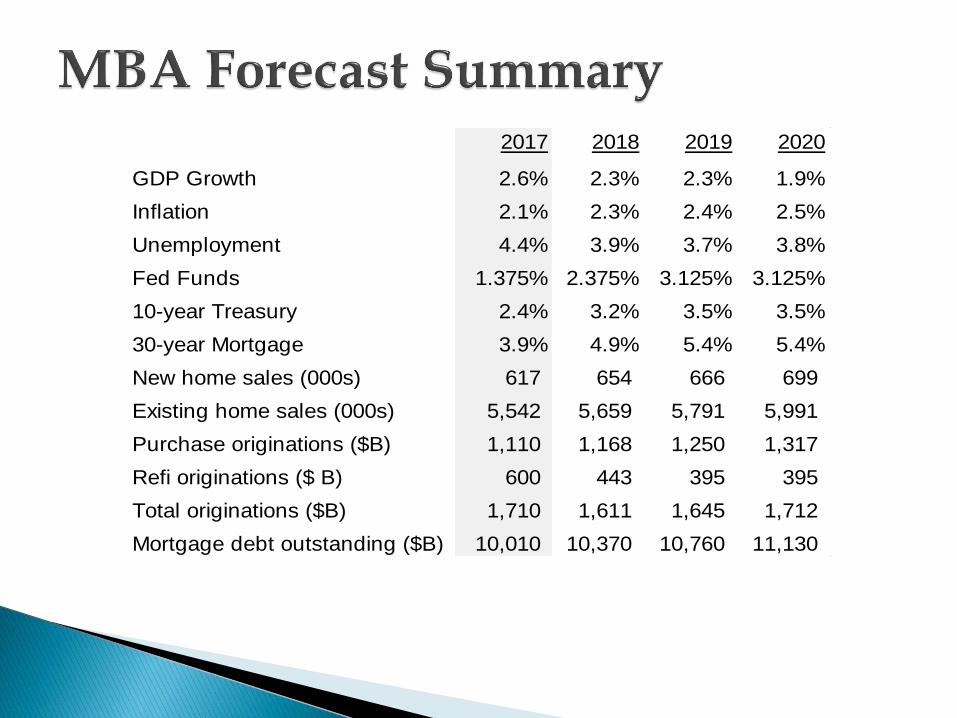

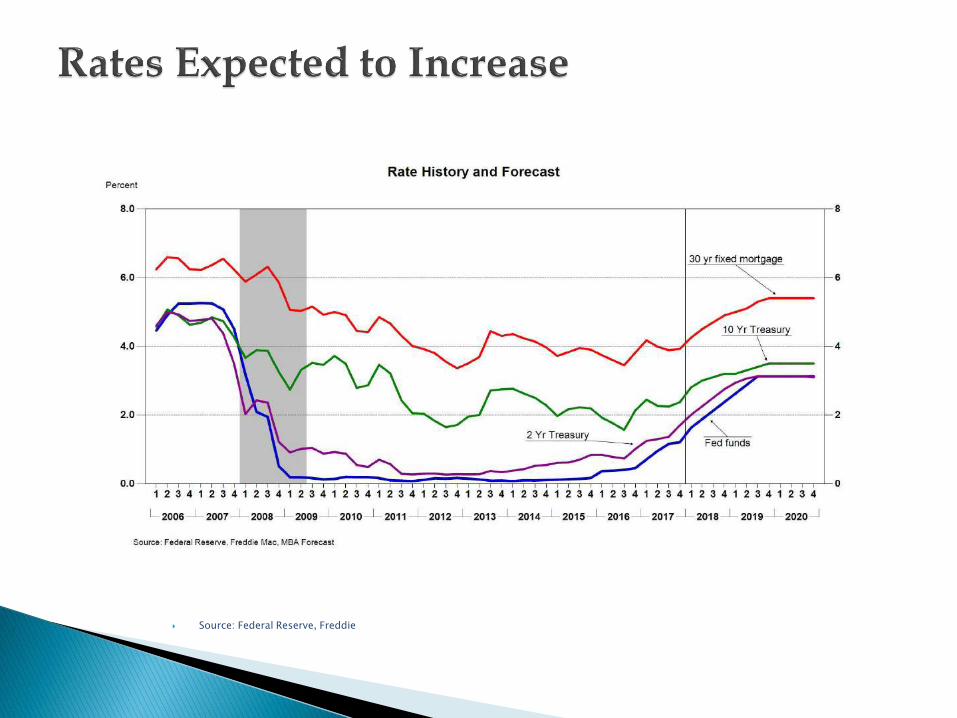

Source: MBA Forecast

2017 2018 2019 2020

GDP Growth 2.6% 2.3% 2.3% 1.9%

Inflation 2.1% 2.3% 2.4% 2.5%

Unemployment 4.4% 3.9% 3.7% 3.8%

Fed Funds 1.375% 2.375% 3.125% 3.125%

10-year Treasury 2.4% 3.2% 3.5% 3.5%

30-year Mortgage 3.9% 4.9% 5.4% 5.4%

New home sales (000s) 617 654 666 699

Existing home sales (000s) 5,542 5,659 5,791 5,991

Purchase originations ($B) 1,110 1,168 1,250 1,317

Refi originations ($ B) 600 443 395 395

Total originations ($B) 1,710 1,611 1,645 1,712

Mortgage debt outstanding ($B) 10,010 10,370 10,760 11,130

Source: MBA Weekly Applications Survey

8

0

50

100

150

200

250

300

350

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Week of the Year

Purchase Mortgage Applications Index(by week of the year, NSA)

2014 2015 2016 2017 2018

Source: MBA Weekly Applications Survey

9

0.00

1.00

2.00

3.00

4.00

5.00

6.00

0.0

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0Ja

n-1

3

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Jul-

16

Sep

-16

No

v-1

6

Jan

-17

Mar

-17

May

-17

Jul-

17

Sep

-17

No

v-1

7

Jan

-18

Mar

-18

Rat

e

Ind

ex

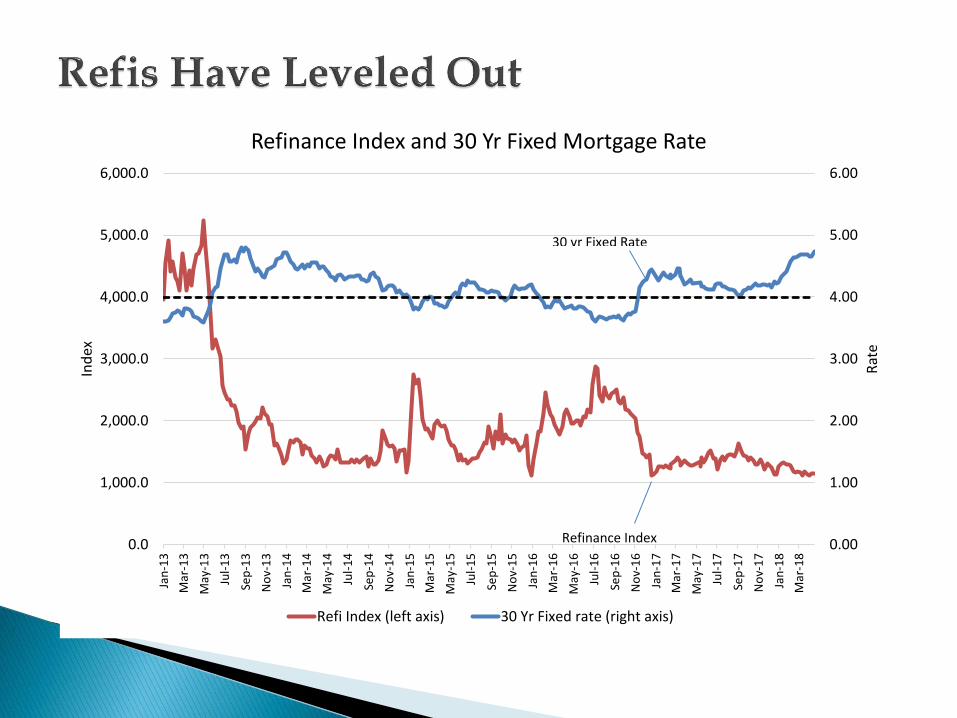

Refinance Index and 30 Yr Fixed Mortgage Rate

Refi Index (left axis) 30 Yr Fixed rate (right axis)

30 yr Fixed Rate

Refinance Index

Source: MBA Forecast

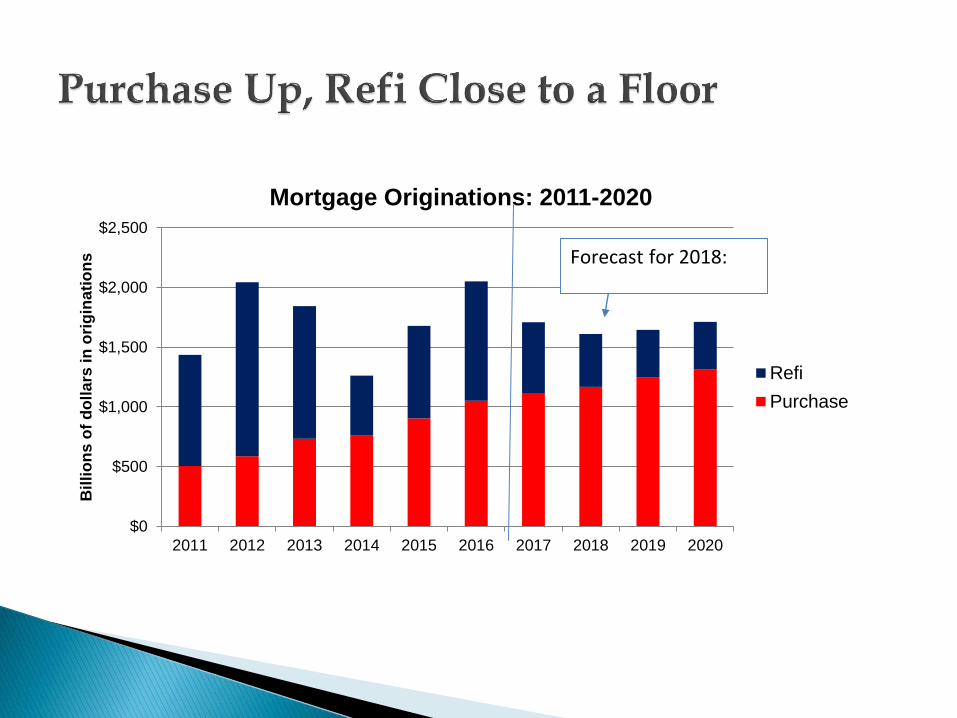

$0

$500

$1,000

$1,500

$2,000

$2,500

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Bil

lio

ns

of

do

lla

rs in

ori

gin

ati

on

s

Mortgage Originations: 2011-2020

Refi

Purchase

Forecast for 2018:

Source: Federal Reserve, Freddie Mac, MBA

11

Source: NAR, MBA

12

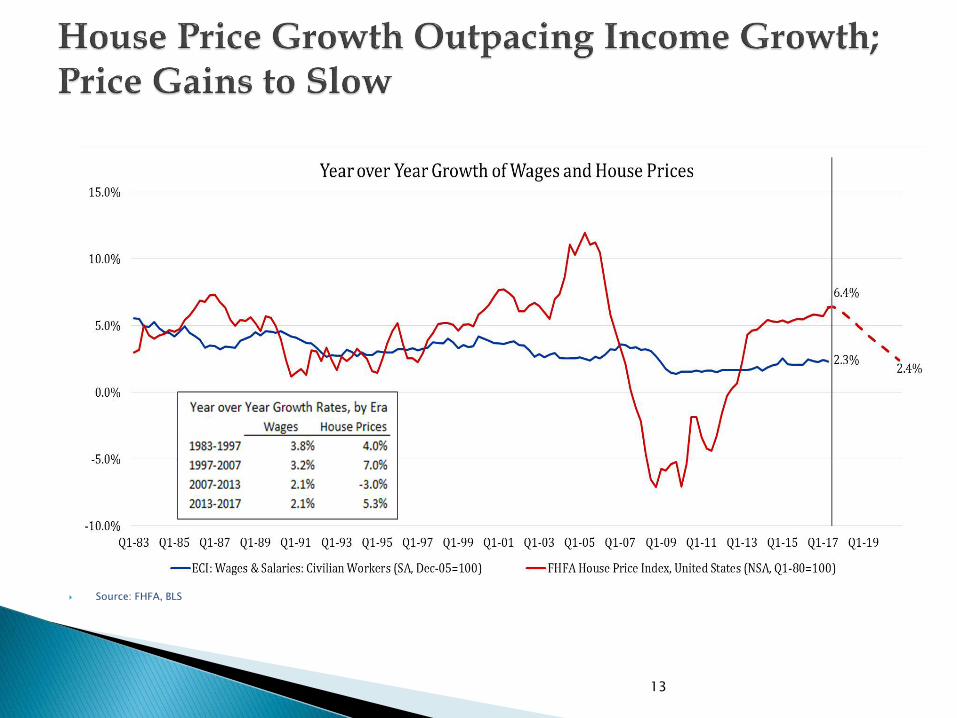

Source: FHFA, BLS

13

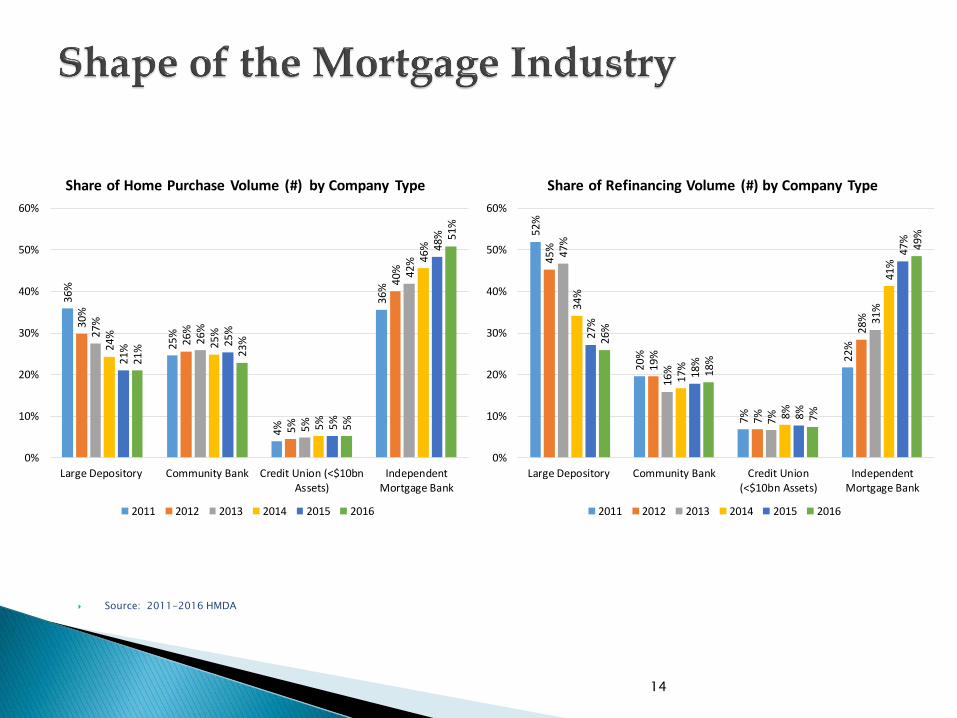

Source: 2011-2016 HMDA

14

36%

25

%

4%

36%

30%

26%

5%

40

%

27

%

26

%

5%

42%

24%

25

%

5%

46%

21

%

25

%

5%

48%

21% 23

%

5%

51

%0%

10%

20%

30%

40%

50%

60%

Large Depository Community Bank Credit Union (<$10bnAssets)

IndependentMortgage Bank

Share of Home Purchase Volume (#) by Company Type

2011 2012 2013 2014 2015 2016

52%

20

%

7%

22

%

45

%

19

%

7%

28

%

47

%

16%

7%

31

%34%

17%

8%

41%

27%

18%

8%

47%

26%

18%

7%

49

%

0%

10%

20%

30%

40%

50%

60%

Large Depository Community Bank Credit Union(<$10bn Assets)

IndependentMortgage Bank

Share of Refinancing Volume (#) by Company Type

2011 2012 2013 2014 2015 2016

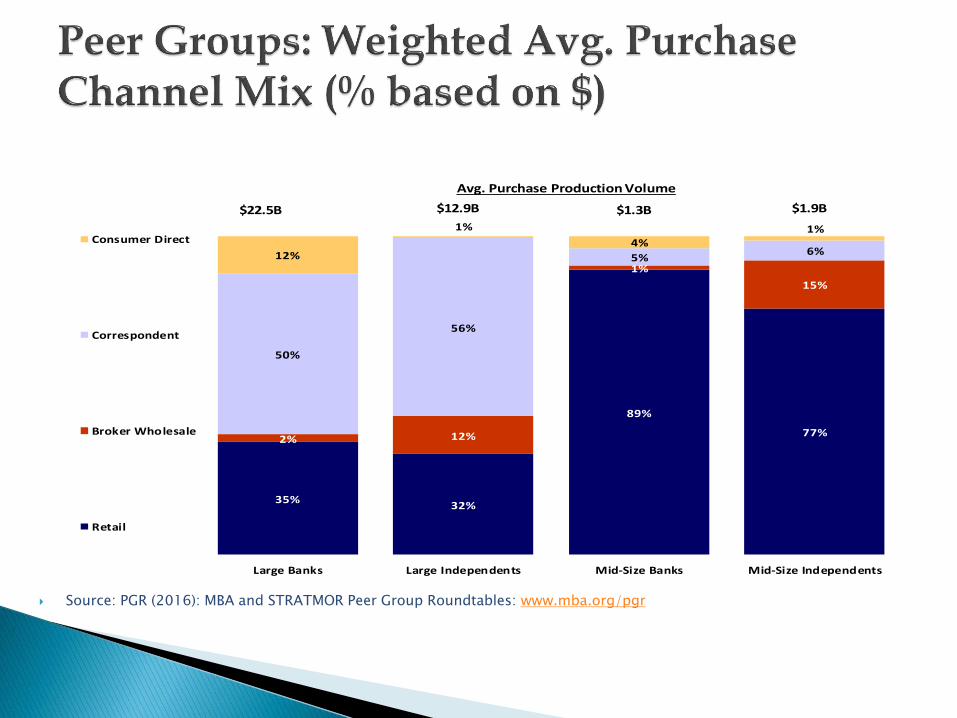

Source: PGR (2016): MBA and STRATMOR Peer Group Roundtables: www.mba.org/pgr 15

35%32%

89%

77%2% 12%

1%

15%

50%

56%

5%6%12%

1%

4%1%

Large Banks Large Independents Mid-Size Banks Mid-Size Independents

Consumer Direct

Correspondent

Broker Wholesale

Retail

Avg. Purchase Production Volume

$22.5B $12.9B $1.3B $1.9B

Source: PGR: MBA and STRATMOR Peer Group Roundtables: www.mba.org/pgr

15

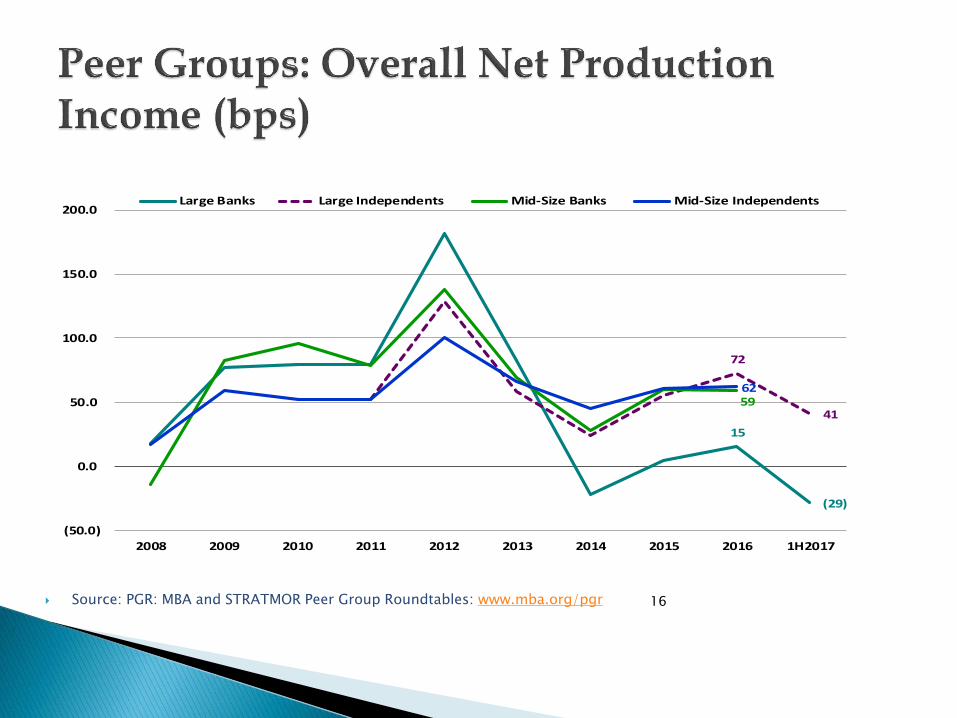

(29)

72

415962

(50.0)

0.0

50.0

100.0

150.0

200.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 1H2017

Large Banks Large Independents Mid-Size Banks Mid-Size Independents

16

17

107.4

86.5

74.6

38.2

8.7

(8.3)

45.7 42.1

32.1

60.4

67.3

55.3

21.6

33.2

72.6 73.7

24.0

10.4

45.7 40.5

9.3

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

Q115

Q215

Q315

Q415

Q116

Q216

Q316

Q416

Q117

Q217

Q317

Q417

Net Production Income (bps)

Avg. Production Volume ($M)

IMB Net Production Income (basis points)

Source: MBA’s Quarterly Mortgage Bankers Performance Report,

www.mba.org/performancereport

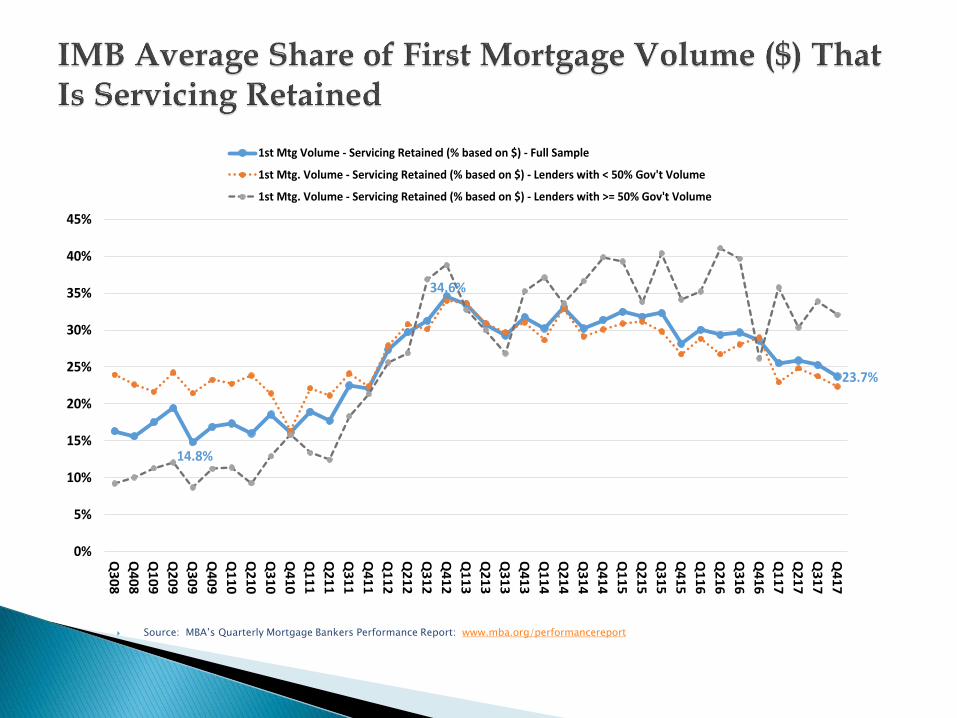

14.8%

34.6%

23.7%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Q3

08

Q4

08

Q1

09

Q2

09

Q3

09

Q4

09

Q1

10

Q2

10

Q3

10

Q4

10

Q1

11

Q2

11

Q3

11

Q4

11

Q1

12

Q2

12

Q3

12

Q4

12

Q1

13

Q2

13

Q3

13

Q4

13

Q1

14

Q2

14

Q3

14

Q4

14

Q1

15

Q2

15

Q3

15

Q4

15

Q1

16

Q2

16

Q3

16

Q4

16

Q1

17

Q2

17

Q3

17

Q4

17

1st Mtg Volume - Servicing Retained (% based on $) - Full Sample

1st Mtg. Volume - Servicing Retained (% based on $) - Lenders with < 50% Gov't Volume

1st Mtg. Volume - Servicing Retained (% based on $) - Lenders with >= 50% Gov't Volume

Source: MBA’s Quarterly Mortgage Bankers Performance Report: www.mba.org/performancereport

216

43 41

523

268 278

($250)

($150)

($50)

$50

$150

$250

$350

$450

$550

$650

Net Financial Income Net Operating Income

Source: MBA’s Servicing Operations Study and Forum (Prime Servicers): www.mba.org/sosf; PGR 1H2017

20

Tricia Migliazzo

Vice President, Member Engagement

https://www.mba.org/

202-557-2858

https://www.mba.org/members/member-resources/member-benefits

8

Ken RicheyFounding Partner

Business Advisory Partner, has over 30 years of experienceserving clients in the mortgage banking industry, includingconsulting on business transactions, providing assistance withdue diligence and structuring in mergers and acquisitions,financings, asset sales and business liquidation events. Ken iswell respected in the mortgage industry nationally, withprofessional organizations, trade associations and businessgroups often seeking Ken’s insights on a variety of issues.

The Market

Highlights of IMB financial performance

Deal Structure

Company Valuation Concepts

What factors are driving the current M&A environment?

Is consolidation picking up or slowing down?

Is it still a seller’s market?

For how long?

Capital: requirements, access and costs are all rising simultaneously

Financial success is more elusive for many smaller lenders

Uncertainty of future interest rates and housing inventory

Risk sharing objectives (buyers with sellers) are emerging

Funding/Capital/Securitization – lower cost of capital (for sellers); better secondaryexecution

Customer Reach – new segments and geographics

Diversification – new distribution channels and products

Scale and Margin – realize operating efficiencies of scale

Better Technology, Marketing, Compliance, HR & Benefits Package

Deeper Talent Pool

Volume trending down but still reaching recordhighs for some

Secondary margins trending down

Profits trending down

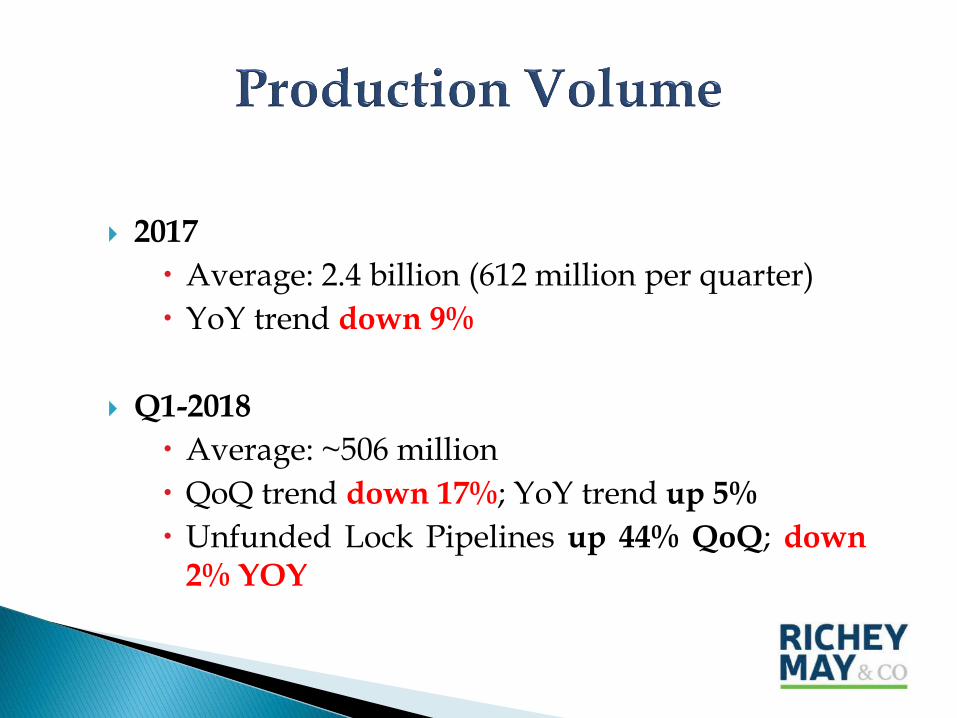

2017

Average: 2.4 billion (612 million per quarter)

YoY trend down 9%

Q1-2018

Average: ~506 million

QoQ trend down 17%; YoY trend up 5%

Unfunded Lock Pipelines up 44% QoQ; down2% YOY

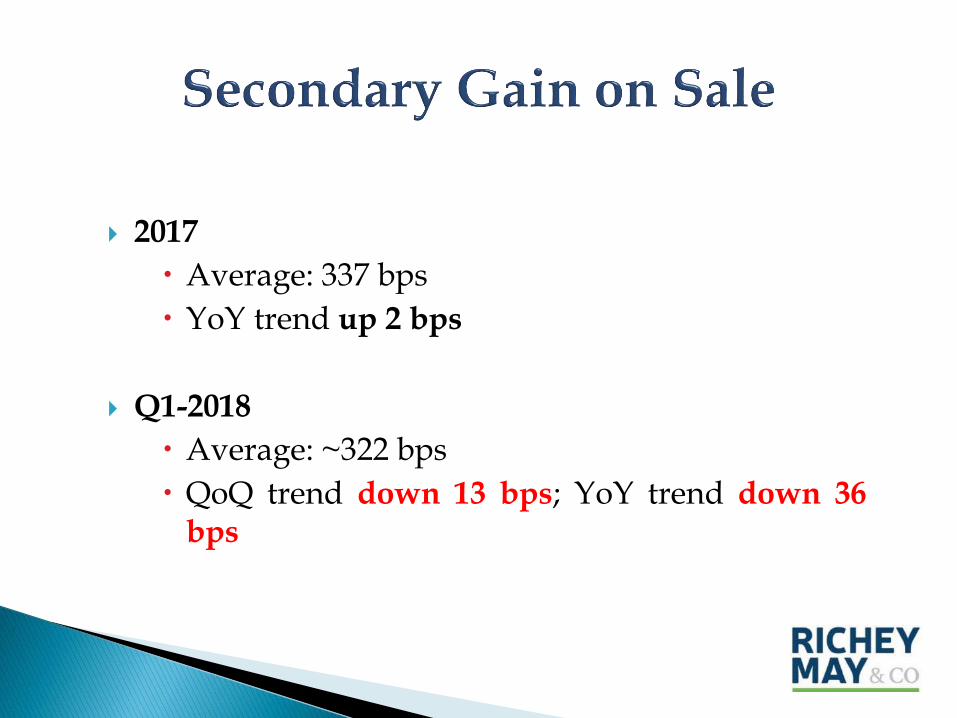

2017

Average: 337 bps

YoY trend up 2 bps

Q1-2018

Average: ~322 bps

QoQ trend down 13 bps; YoY trend down 36bps

2017

Average: $8,214 per loan

YoY trend up $728 per loan

Q1-2018

Average: ~$8,993 per loan

QoQ trend up $695; YoY trend up $172

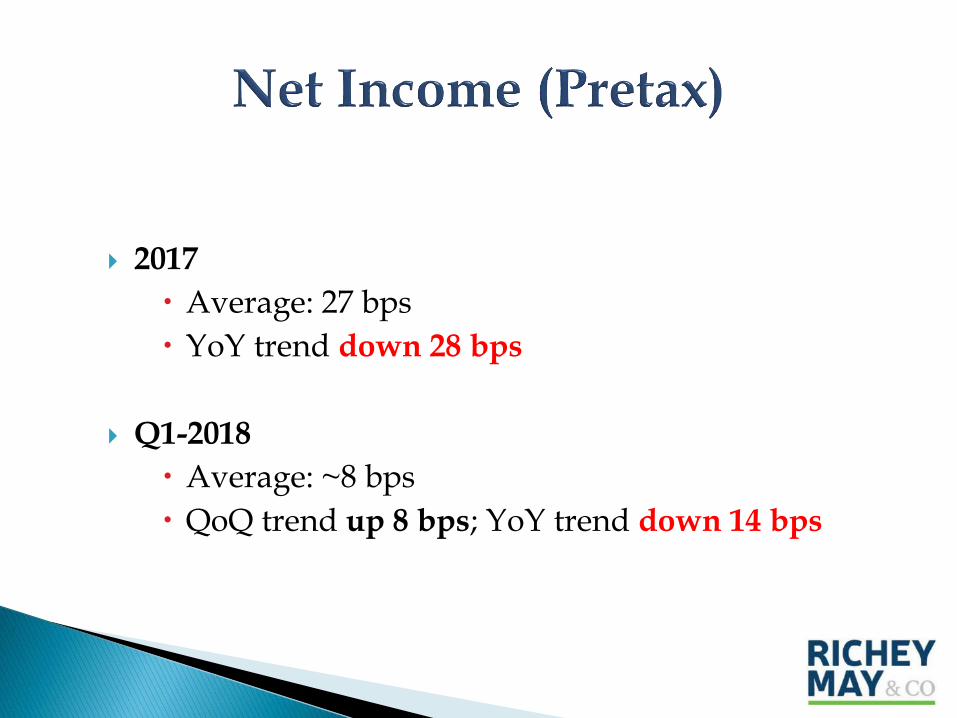

2017

Average: 27 bps

YoY trend down 28 bps

Q1-2018

Average: ~8 bps

QoQ trend up 8 bps; YoY trend down 14 bps

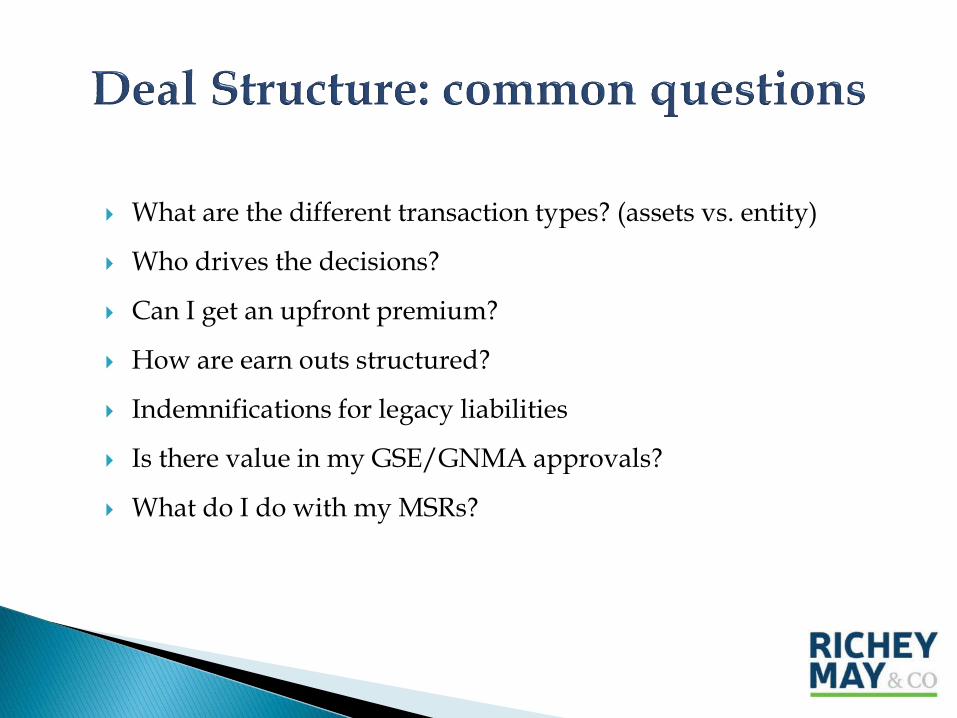

What are the different transaction types? (assets vs. entity)

Who drives the decisions?

Can I get an upfront premium?

How are earn outs structured?

Indemnifications for legacy liabilities

Is there value in my GSE/GNMA approvals?

What do I do with my MSRs?

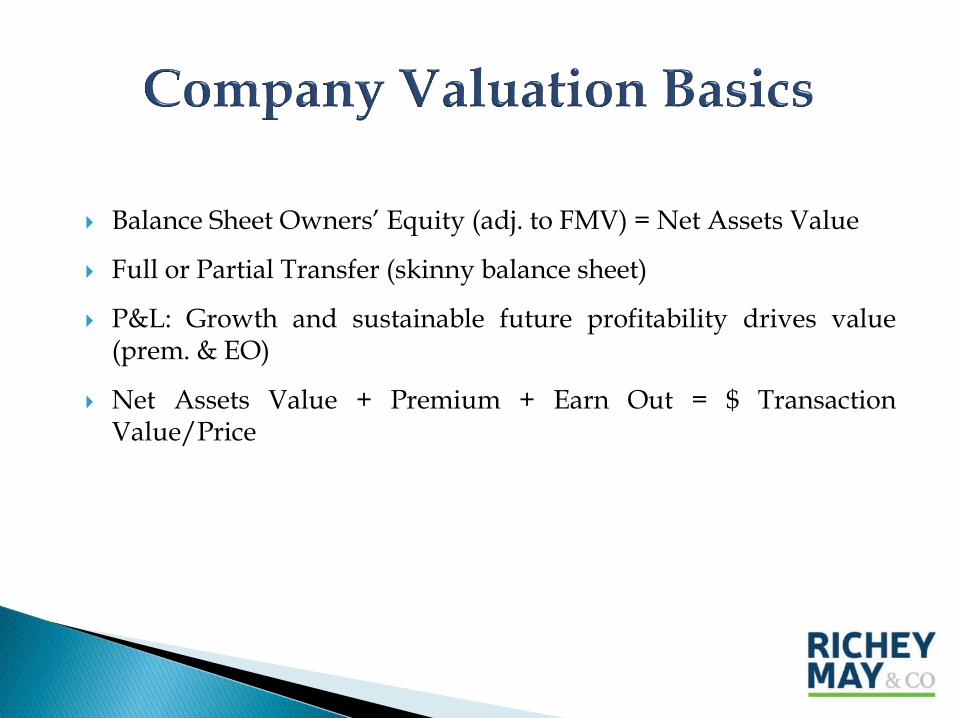

Balance Sheet Owners’ Equity (adj. to FMV) = Net Assets Value

Full or Partial Transfer (skinny balance sheet)

P&L: Growth and sustainable future profitability drives value(prem. & EO)

Net Assets Value + Premium + Earn Out = $ TransactionValue/Price

• Valuation is based on after tax cash flows

◦ – Investors consider corporate and personal taxes

◦ – TCJA lowers taxes

◦ – Valuations, generally, are expected to increase

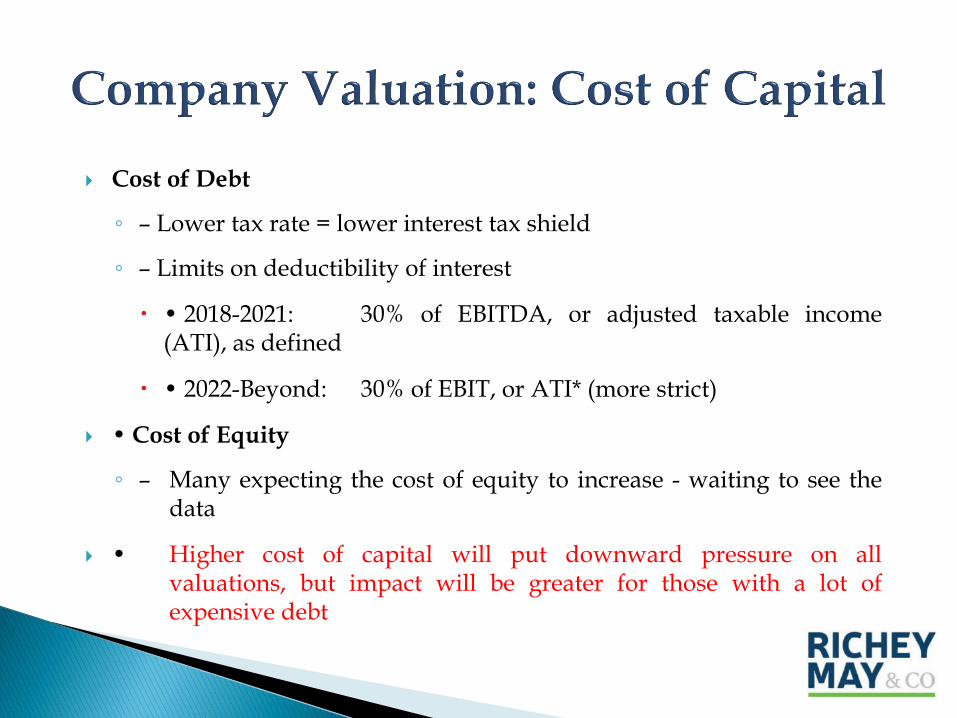

Cost of Debt

◦ – Lower tax rate = lower interest tax shield

◦ – Limits on deductibility of interest

• 2018-2021: 30% of EBITDA, or adjusted taxable income(ATI), as defined

• 2022-Beyond: 30% of EBIT, or ATI* (more strict)

• Cost of Equity

◦ – Many expecting the cost of equity to increase - waiting to see thedata

• Higher cost of capital will put downward pressure on allvaluations, but impact will be greater for those with a lot ofexpensive debt

First-time, or less experienced buyers with strong equity and liquidity

Mature, repeat buyers are getting more astute and skilled at transaction execution and integration

Very anxious to buy retail, purchase production especially where significant synergies & profitability enhancement opportunities exist

Wider discrepancies in buyers’ financial performance compared to peers potentially yielding greater discrepancies between buyers’ bid prices and terms

Some buyers willing to pay bps x production as portion of earn out (less seller risk)

Earn outs based on forward pretax income under new platform is most common (1 to 3x+)

Slightly longer earn out periods

Some very aggressive closing premiums where appropriate attributes & value is present

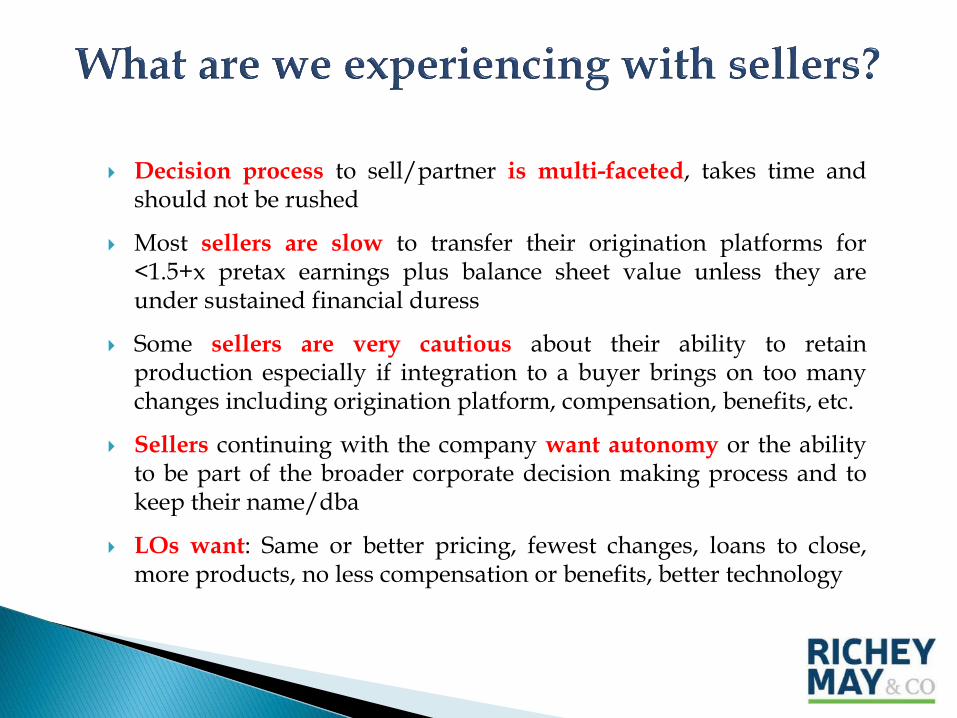

Decision process to sell/partner is multi-faceted, takes time andshould not be rushed

Most sellers are slow to transfer their origination platforms for<1.5+x pretax earnings plus balance sheet value unless they areunder sustained financial duress

Some sellers are very cautious about their ability to retainproduction especially if integration to a buyer brings on too manychanges including origination platform, compensation, benefits, etc.

Sellers continuing with the company want autonomy or the abilityto be part of the broader corporate decision making process and tokeep their name/dba

LOs want: Same or better pricing, fewest changes, loans to close,more products, no less compensation or benefits, better technology

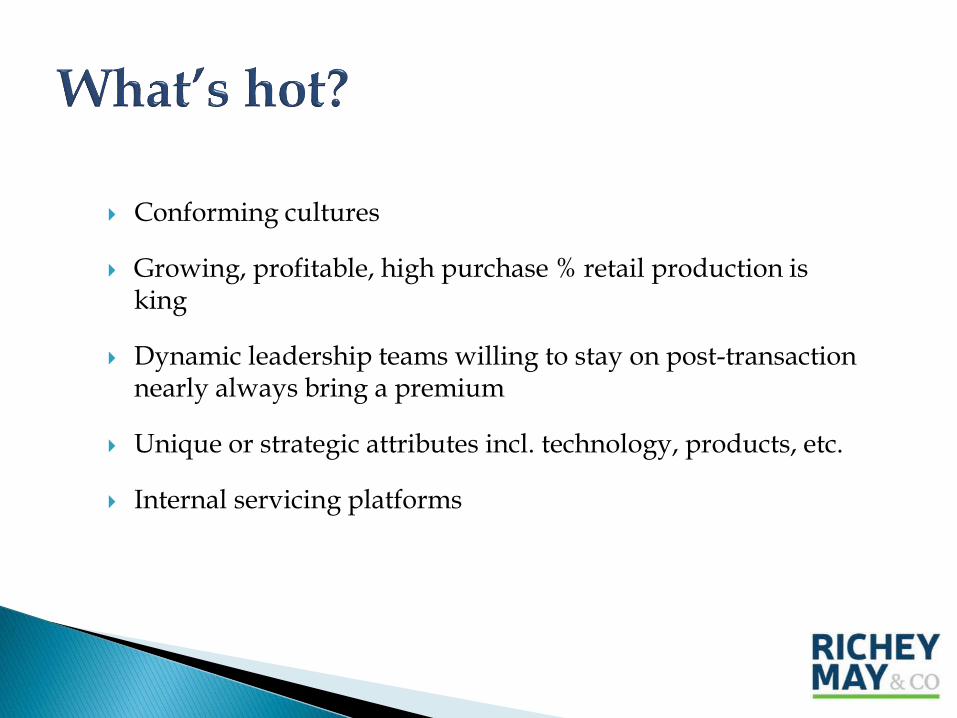

Conforming cultures

Growing, profitable, high purchase % retail production is king

Dynamic leadership teams willing to stay on post-transaction nearly always bring a premium

Unique or strategic attributes incl. technology, products, etc.

Internal servicing platforms

High historic refinance volume

Wholesale, except for higher volume, higher profitabilityplatforms

Consumer direct channel

High jumbo volume percentage

Reverse mortgage

Strong leadership team with clear vision

Cultures are close

Business models reasonably match up

Financially qualified to buy (buy side diligence)

Superior financial performance

Experience with previous successful transactions

Do not fall in love with the first opportunity

Highest bidder may not be the best buyer

Prior to Sale

◦ Some buyers are seeking distressed situations or “walk-overs” and likely not to paymarket value

◦ Other buyers understand the market and are willing to pay competitively

◦ PE buyers often expect more than production including leadership, sustainableprofitability or other unique or strategic attributes (e.g. technology, etc.)

◦ Selling/partnering or capital raising is a very demanding, time consuming andexhausting process

Post Sale

◦ The key: a smooth and effective integration/transition plan well executed with veryminimal immediate operational changes

◦ Expect employee turnover

◦ Use retention compensation to prevent loss of key executives and high producingLOs

WWW.SLIDEFOREST.COM

43

NRL MORTGAGENRLMORTGAGE.COM

Presented By: Joe DeDominicis

WWW.SLIDEFOREST.COM

44

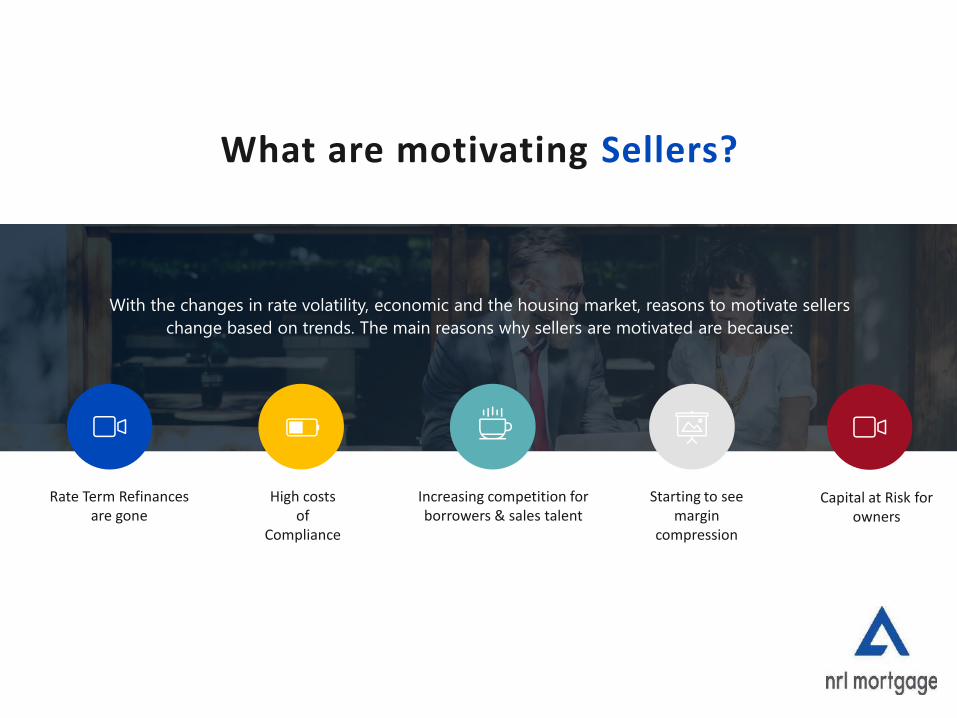

Starting to see margin

compression

Rate Term Refinances are gone

High costs of

Compliance

Increasing competition for borrowers & sales talent

With the changes in rate volatility, economic and the housing market, reasons to motivate sellers

change based on trends. The main reasons why sellers are motivated are because:

What are motivating Sellers?

Capital at Risk for owners

WWW.SLIDEFOREST.COM

45

Opportunity to

deploy substantial

amounts of capital

Opportunity to

tap into customer

database for cross sell

Potential

Returns

Growth opportunities

on both origination

& servicing

What are motivating Buyers?

Faster to buy

than build organically

WWW.SLIDEFOREST.COM

46

Small to Medium Sized Banks

PE Firms

Medium to Large IMB’s

Who are the Buyers?

WWW.SLIDEFOREST.COM

47

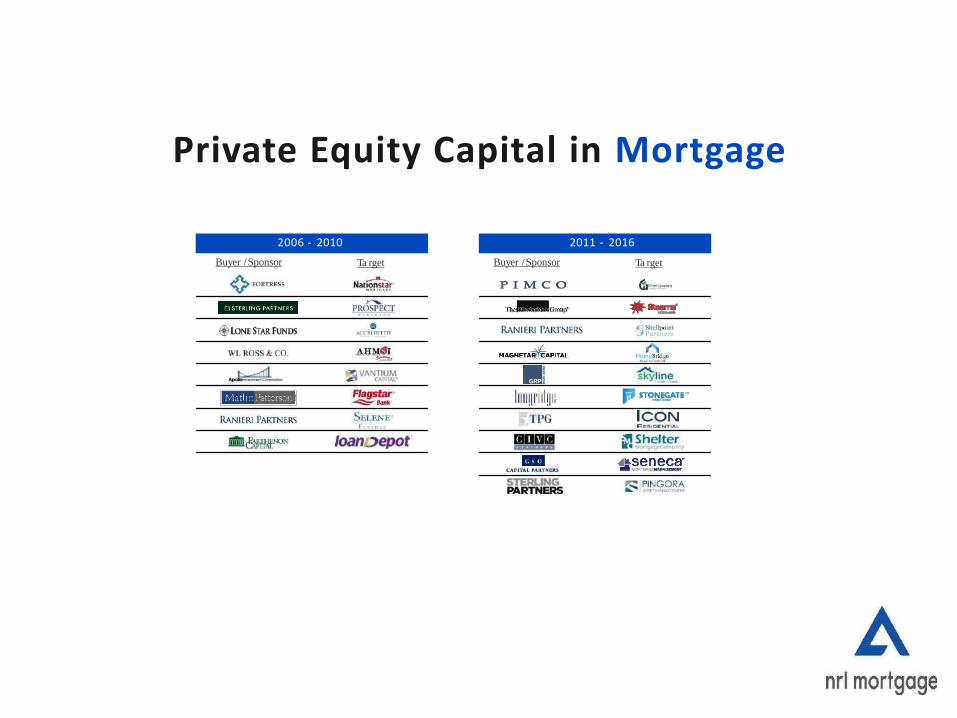

Buyer /Sponsor Buyer /SponsorTa rget Ta rget

6

2011 - 20162006 - 2010

Private Equity Capital in Mortgage

WWW.SLIDEFOREST.COM

48

• Regional and Community Banks looking to enter or expand their mortgage presence

• Opportunities to expand their bank footprint• Ability to tap into larger customer base to cross sell

Bank Buyers

• IMB’s seeking to grow their production, typically in areas where they do not have a presence or a significant presence

• Potentially to expand into different origination channels (Broker, Correspondent, etc…)

• Adding production volume to grow servicing portfolio

Strategic Buyers

Different Types of Buyers?

WWW.SLIDEFOREST.COM

49

Seller Perspective

• Cultural Fit

• Maximize Return on Sale

• Opportunity to earn premium to purchase

valuation through earn out

• Exit strategy that enhances or preserves

existing company values and employees

Buyers Perspective

• Increase production scale (geographic,

channel mix, product mix)

• Increase operational efficiency and overall

profitability

• Retain salespeople and key management

• Replace servicing run-off

Success Goals of a Transaction

WWW.SLIDEFOREST.COM

50

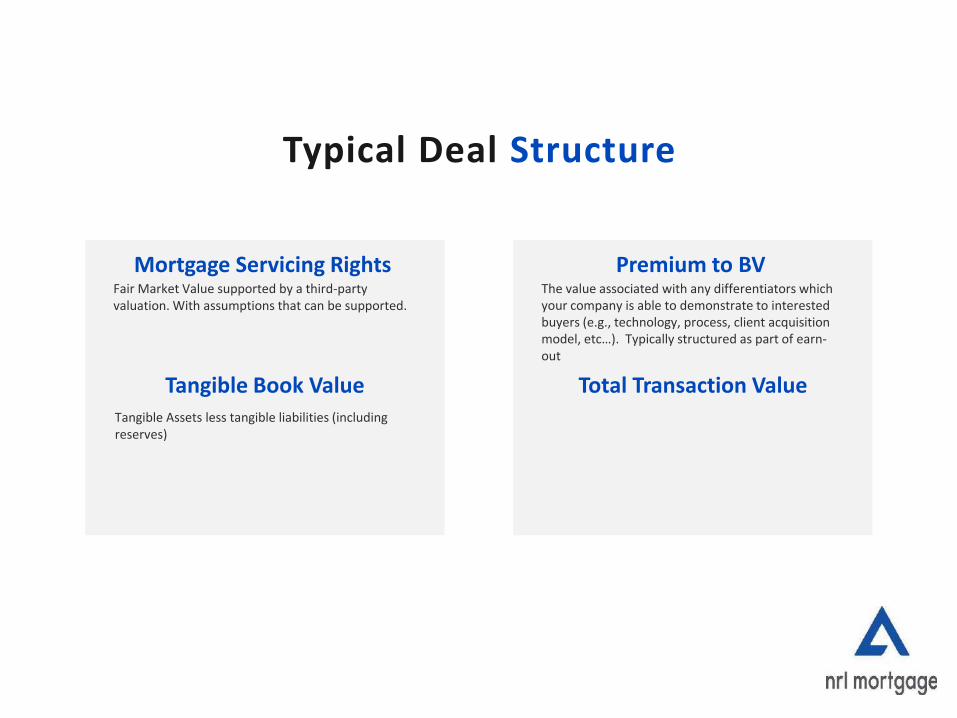

Mortgage Servicing RightsFair Market Value supported by a third-party valuation. With assumptions that can be supported.

Typical Deal Structure

Tangible Book ValueTangible Assets less tangible liabilities (including reserves)

Premium to BVThe value associated with any differentiators which your company is able to demonstrate to interested buyers (e.g., technology, process, client acquisition model, etc…). Typically structured as part of earn-out

Total Transaction Value

WWW.SLIDEFOREST.COM

51

Transaction Payout• All proceeds paid at closing

• Payment of BV with an earnout

• Combination of some payment and some stock

• Payment with holdback to fund contingent

liabilities

WWW.SLIDEFOREST.COM

52

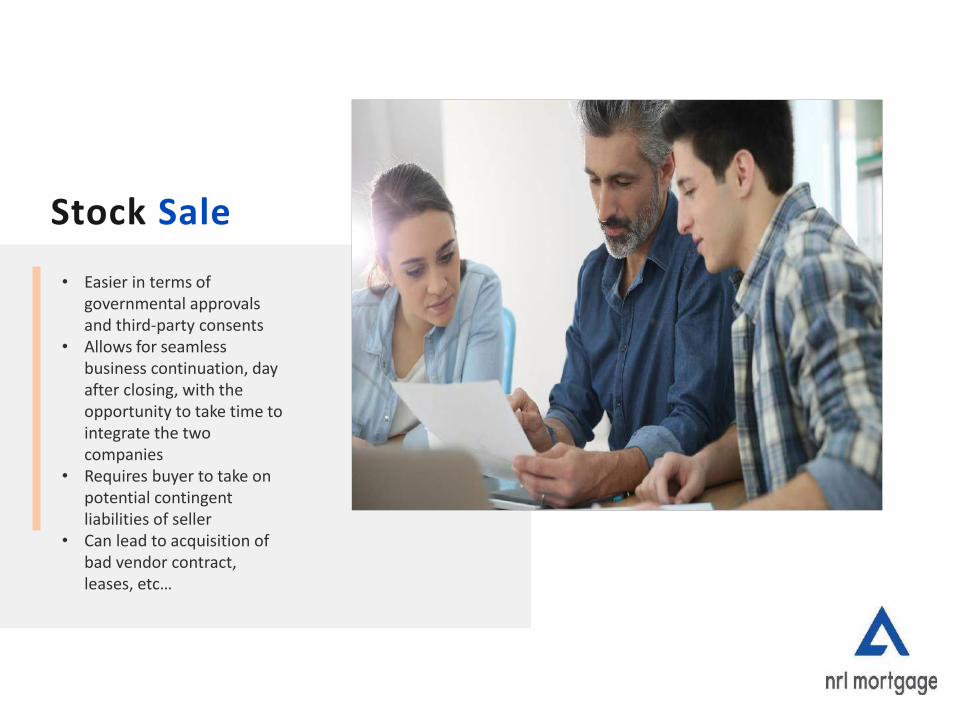

• Easier in terms of governmental approvals and third-party consents

• Allows for seamless business continuation, day after closing, with the opportunity to take time to integrate the two companies

• Requires buyer to take on potential contingent liabilities of seller

• Can lead to acquisition of bad vendor contract, leases, etc…

Stock Sale

WWW.SLIDEFOREST.COM

53

Purchaser can be more selective in the assets, liabilities and operations it wishes to assume

Generally allows for purchaser to avoid legacy liabilities from prior company

Can lead to delays in part or all of the acquisition due to state and MLO licensing

Can lead to parts of company not being acquired

Asset Sale

WWW.SLIDEFOREST.COM

54

• Agreement on true FMV of key assets (i.e., MSR’s)• Conversion of key branches and/or LO’s• Quantification of contingent liabilities• Audit and/or compliance issues• Underwriting quality

DEAL HURDLES

WWW.SLIDEFOREST.COM

55

KEYS TO A SUCCESSFUL DUE DILLIGENCE

Provide believable revenue and net income forecasts

Emphasize key differentiators & be able to tell the story

Assist in conversion of key branches and loan officers

Make sure everything is organized& be realistic with expectations

THANK YOU!

56