HOT TOPICS IN LEASING by Nancy Connery, Esq. Schoeman ...

251

HOT TOPICS IN LEASING by Nancy Connery, Esq. Schoeman Updike Kaufman & Stern LLP New York, New York

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of HOT TOPICS IN LEASING by Nancy Connery, Esq. Schoeman ...

HOT TOPICS IN LEASING

by

Nancy Connery, Esq. Schoeman Updike Kaufman & Stern LLP

New York, New York

HOT TOPICS IN COMMERCIAL LEASING 2014

Copyright © 2014 Nancy Ann Connery All rights reserved.

Nancy A. Connery | Partner Schoeman Updike Kaufman & Stern LLP 551 Fifth Avenue, New York, NY 10176 (646) 723-1042 direct | (212) 661-5030 main (212) 687-2123 fax [email protected] | www.schoeman.com

HOT TOPICS IN COMMERCIAL LEASING 2014

SELECTED ISSUES IN LEASES INVOLVING NOT-FOR PROFITS

1. AMENDMENTS TO NOT-FOR-PROFIT LAW

a. Non-Profit Revitalization Act of 2013. The Non-Profit Revitalization Act of 2013

became effective July 1, 2014 (the “2013 Act”).

b. Internal Consent Process. The 2013 Act facilitates the process of obtaining required consents. For example:

i. Notices of meetings to members, member waivers of notices, member proxies, and member consents may be given by electronic mail.

ii. Unanimous director consents and waivers of notices may now be given by electronic mail or in writing.

iii. The provisions of the Not-For-Profit Corporation Law allowing directors to participate in meetings via conference telephone or similar communications equipment have been clarified and also expanded to add electronic video screen communication.

c. Related Party Transactions.

i. “Related party” transactions are now subject to strict scrutiny. Board members need to consider the “related party” rules if they are in any way involved in the transaction at issue.

ii. In addition, many not-for-profit corporations must adopt policies governing conflicts of interest and policies protecting whistleblowers.

d. Internal Approvals of Real Estate Transactions Involving the Sale, Lease, Exchange or Other Disposition of Real Property.

i. Transactions Involving Less Than All or Substantially All of the Not-for-Profit’s Assets. Board approval requirements for real estate transactions that do not involve the sale, lease, exchange or other disposition of all or substantially all of the corporation’s assets have been relaxed.

1. Under the 2013 Act, the purchase of real property need only be authorized by a majority of the Board of Directors (or a majority of a Board-authorized committee) unless the purchased property would, upon purchase, constitute all or substantially all of the assets of the corporation.

2. Under the 2013 Act, the sale, mortgage, lease, exchange or other disposition of the corporation’s real property need only be authorized by a majority of the Board of Directors (or a majority of a Board-authorized committee) unless the property constitutes all or substantially all of the corporation’s property.

ii. Transactions Involving All or Substantially All of the Not-for-Profit’s Assets. If the real property, if purchased, would constitute all or substantially all of the corporation’s assets, or if the real property being sold, mortgaged, leased, exchanged or otherwise disposed of constitutes all or substantially all of the corporation’s assets, the old rules apply (a two thirds vote of the Board is required unless the Board consists of more than 21 people, in which case a majority vote is sufficient).

e. Attorney General and Court Approval. If the transaction involves the sale, lease, exchange or other disposition of all, or substantially all, the assets of a charitable corporation, the corporation may now obtain the approval of either the Attorney General or the Supreme Court (formerly, court approval was required, with notice given to the Attorney General’s office) unless the corporation is insolvent or would become insolvent as a result of the transaction (in which event Supreme Court approval is required) or unless the Attorney General determines that a court should make the determination.

i. Note that the amendments to the Not-For-Profit Corporation Law with respect to Court approval did NOT modify the requirements of the Religious Corporation Law as to religious corporations.

f. Financial Reporting.

i. Financial thresholds for independent CPA audit reports and review reports have been raised.

ii. New requirements are imposed requiring the Board or an Audit Committee of any corporation required to file an annual audited financial report to, among other things, oversee financial reporting and review audit results.

2. SPECIAL CONSIDERATIONS: LEASES BY AND TO NOT-FOR-PROFITS

a. Negotiation Process 1. Decision making power is often exercised by a group.

b. Due Diligence

i. Internal Approval Process

1. Voting and decision making processes may be informal.

2. Charter documents may be old-fashioned, with voting requirements unclear or impossible to comply with.

3. If quorum requirement, as a practical matter, can’t be met because

of diminishing membership, the Supreme Court may be petitioned for a modification of the quorum requirement. N.Y. NPC Law § 608(e). If quorum requirements, as a practical matter, can’t be met because of the large size of the membership (in excess of 500 members), cost of mailing, and inability to send notice by e-mail, consider publication and posting. N.Y. NPC Law § 605(a).

ii. Consider whether amendments are needed to the Charter or By-laws.

iii. Approvals:

1. Not-for-Profit Lease of Property from Third Party.

a. No statutory requirement of a minimum Board vote or

membership vote. b. Review corporation’s certificate of incorporation and

by-laws.

2. Not-for-Profit Lease of its Real Property – Less Than All or Substantially All of the Corporation’s Assets.

a. Requires authorization by a majority of the Board of

Directors (or a majority of a Board-authorized committee). N.Y. NPC § 509.

b. Review corporation’s certificate of incorporation and by-laws.

3. Not-for-Profit Lease of its Real Property -- All or Substantially All of the Corporation’s Assets:

a. A two-thirds vote of the Board is required unless the Board consists of more than 21 people, in which case a majority vote is sufficient.

b. If members are entitled to vote on the transaction, the Board must adopt a resolution recommending the transaction and submit the transaction to the members for vote. By two-thirds vote, the members may approve the transaction according to the resolution or may authorize the Board to modify the terms of the transaction. If members are NOT entitled to vote on the transaction, then Board approval (see subpar. (a) above) will suffice.

c. Review certificate of incorporation and by-law

requirements.

d. Attorney General or court approval required, unless the corporation is insolvent or would become insolvent as a result of the transaction (in which event Supreme Court approval is required) or unless the Attorney General determines that a court should make the determination.

e. After authorization, the Board may, at its discretion,

abandon the transaction (subject to the rights of third parties to the transaction) without further action or approval.

f. See N.Y. NPC §§ 509, 510.

4. Religious Corporation/Disposition of Assets (including a Lease of

Church Property for a Term Exceeding 5 Years):

a. General.

i. Although the Not-For-Profit Corporation Law is generally applicable to religious corporations, not all of its provisions apply to religious corporations. RCL 2-b provides that the Not-For-Profit Corporation Law applies to every Religious Corporation, subject to specified exceptions. RCL 2-b further provides that if there is a conflict between the Not-For-Profit Corporation Law and the Religious Corporation Law, the Religious Corporation Law prevails.

ii. Notices of Member Meetings and Proxies. Sections

603 (notice of member meetings) and 609 of the Not-For-Profit Corporation Law (proxies) do not apply to religious corporations.

b. Court Approval/Notice to AG.

i. Lease of Real Property By a Religious Corporation from a Third Party. Court approval and Attorney General approval are not required for leases by religious corporations of property. N.Y. RCL Section 6 specifically permits religious corporations to acquire property for, among other things, chapels,

mission houses, school houses, housing for ministers, property for a home for the aged, and property for a day care center. Any disposition, however, must be effected in accordance with the N.Y. RCL §12.

ii. Approval Required. RCL § 12(1) requires every religious corporation to obtain court approval pursuant to NFC Law § 511 (with notice to be given to the Attorney General) for each of the following transactions:

1. Sale of any of the church’s real property

(except in connection with a foreclosure).

2. Mortgage of any of the church’s real property.

3. Lease of any of the church’s real

property for more than 5 years.

iii. Internal Approvals.

1. For certain hierarchical churches, designated bodies or parties must approve the lease.

2. Generally, for those churches whose trustees or governing body are elected by the congregation, approval of the members will be required.

c. Certain Churches. RCL Section 2-B (d-1) exempts certain

churches from the requirement that notice be given to the Attorney General, and RCL Section 12 (2) – (6) requires additional consents from the bishops, Presbyteries, etc. with respect to those churches. The churches include the Protestant Episcopal Church, Roman Catholic Church, Ruthenian Catholic Church, African Methodist Episcopal Zion Church, Incorporated Presbyterian Church, and the United Methodist Church.

iv. Real Property Due Diligence

1. Confirm that the not-for-profit actually owns the property it is leasing.

2. Are there any restrictions on the use of the real property?

v. For religious corporations, will approval of the church hierarchy be required or desirable?

c. Below Market Rents

i. It’s not unusual for a not-for-profit to grant a long term lease to a related not-for-profit whose activities support the activities of the owner of the real property.

1. Rent may be below-market. N.Y. RCL §12.

2. What if the tenant files for bankruptcy?

a. If the rent is deeply discounted, the lease may be very

valuable. Bankruptcy courts generally have the power to order an assignment of a tenant’s interest in a lease without the landlord’s consent to any entity, including a developer or for-profit entity. Generally, the not-for-profit landlord will be concerned about such a result.

b. Thoughts:

i. Set a fair market rent, with the tenant to receive a rent credit only for so long as the property continues to be leased by a not-for-profit tenant in accordance with the lease requirements.

ii. Draft the court order authorizing the lease transaction to clearly limit approval to the tenant named in the petition and to require court approval of any assignment of the lease or sublease of all or substantially all of the premises.

iii. Arguably an assignment of an approved lease with a term of more than 5 years constitutes a new lease of the religious corporation’s property requiring Supreme Court approval. Does the state law requirement trump the trustee’s right to assign?

d. Use Restrictions

i. It’s not unusual for a not-for-profit granting a long term lease to limit the uses to which the property can be put. This may be a function of the

proximity of the leased property to the church’s or not-for-profit corporation’s property or may constitute a quid pro quo for a reduction in the base rent.

ii. What if the tenant files for bankruptcy?

1. The Bankruptcy Code voids any lease provision that gives the

landlord the right to terminate or modify the lease if the lease is assigned by the debtor/tenant or its trustee in bankruptcy. Bankruptcy Code §365(f)(3). This provision has been interpreted to invalidate any number of restrictions on assignment, including narrow use clauses. E.G., Robb v. Schindler, 142 B.R. 589 (D. Mass. 1992) (court refused to enforce profit recapture clause, citing cases invalidating various restrictions on transfer, including narrowly crafted use clauses that impeded assignment and clauses that increased rents to market rate upon assignment). There is the risk, therefore, that a bankruptcy court would invalidate an overly narrow use clause in order to facilitate an assignment of the lease in bankruptcy.

2. Thoughts:

a. Explicitly describe in the lease the nature of the special relationship, if any, between the tenant and landlord.

b. Draft the court order authorizing the lease transaction to clearly limit approval to the proposed use.

c. Arguably an assignment of an approved lease with a term of more than 5 years constitutes a new lease of the religious corporation’s property requiring Supreme Court approval. Does the state law requirement trump the trustee’s right to assign?

d. Limit the property’s use with a Declaration of Restrictions.

3. REAL ESTATE TAX EXEMPTION

a. Property Owned by Not-For-Profit. Real property owned by a corporation or association organized or conducted exclusively for charitable, educational, religious, hospital, or moral or mental improvement (an “exempt property owner”) that uses the property exclusively for such purposes is exempt from real estate taxes. N.Y. Real Property Tax Law § 420-a. Other exempt purposes are set out in N.Y. Real Property Tax Law § 420-b, 446, and 462.

i. If the exempt property owner leases a portion of the property to a commercial enterprise, its exemption will be lost as to the portion so leased.

1. To avoid transferring the exempt owner’s tax exemption to the commercial tenants, the lease will typically require each commercial enterprise to pay its share of increases in the building’s real estate taxes (or its share of such taxes as a direct pass-through), computed as if the property was not benefitted by the property owner’s tax exemption.

ii.If the exempt property owner leases a portion of the property to another

corporation or association organized or conducted exclusively for charitable, educational, religious, hospital, or moral or mental improvement for such tenant’s exempt purposes, the exempt property owner may retain its exemption as to the leased property but only if the rent payable by the tenant does not exceed normal carrying, maintenance, or depreciation charges with respect to the leased portion of the property.

b. Property Owned by a For-Profit Entity and Leased to a Charitable Corporation.

i. Generally, a For-Profit entity that leases real property to a Not-For-Profit

entity is not entitled to a real estate tax exemption with respect to the Not-For-Profit’s occupancy.

ii. Some Techniques For-Profit Landlords and Not-For-Profit Tenants Have

Used to Allow the Not-For-Profit Tenant to Obtain the Benefit of Its Exempt Status:

1. Symphony Space. a. Symphony Space Inc. v. Pergola Properties, Inc., 88

N.Y.2d 466 (1996) b. Property owner conveyed office building to a Not-For-

Profit for nominal consideration, was granted a lease at a nominal rent for the portion of the building not occupied by the Not-For-Profit, and was given an option to reacquire the entire building at the end of a specified period of time. The owner lost the building to the Not-for-Profit because of a Rule against Perpetuities issue that voided the purchase option.

i. Very risky. 2. Leasehold Condominium – Ground Lease.

a. For-Profit owner ground leases its property to a Not-For-Profit that constructs improvements.

b. The Not-For-Profit converts its leasehold estate to a leasehold condominium with fee ownership of the improvements.

c. Condominium units are separately assessed and taxed under NY Condominium Law § 339-y.

i. Note that there may be a lapse in time between the formation of the condo and creation of separate tax lots.

d. See NYC Dept. of Finance Letter Ruling dated February 13, 2009.

i. Lease was for 35 years with renewal options. ii. Tenant owed in fee the building.

iii. Leasehold condo unit tax exempt if §420-a criteria otherwise met.

e. What if Not-For-Profit Acquires Leasehold Estate Through a Non-501(c)(3) Entity Owned by a Not-For-Profit

i. If a leasehold estate is acquired for use by a Not-For-Profit for its exempt purposes, but the leasehold estate is held in the name of a single-member limited liability company owned by the Not-For-Profit (e.g., for financing or liability reasons), is the leasehold condominium unit still exempt from tax?

ii. There are a number of letter rulings from the New York City Department of Finance indicating that property owned in fee by a limited liability company (that is not a 501(c)(3) entity) owned solely by an exempt entity and used by the exempt entity for its exempt purposes, may be exempt from real estate taxes. Would the Department of Finance apply the same reasoning to a leasehold estate?

iii. Note that the letter rulings set out a number of criteria that must be met, including the following:

1. The sole member of the LLC must qualify for a 420-a exemption;

2. The limited liability company’s articles of organization and operating agreement must contain specific language relating to the company’s not-for-profit purposes.

3. There must be commonality between the LLC and its member.

4. The property must be managed and maintained by the single member or leased to another not-for-profit entity that would qualify for an exemption.

5. The rent can’t exceed carrying, maintenance and depreciation charges.

6. Upon termination of the LLC, the property must revert to its single member or another exempt entity. The LLC must continue to be owned by an exempt entity.

7. An annual affidavit must be filed with the Department of Finance.

HOT TOPICS IN COMMERCIAL LEASING 2014

Restaurant Leases

Copyright © 2014 Nancy Ann Connery All rights reserved.

Nancy A. Connery | Partner Schoeman Updike Kaufman & Stern LLP 551 Fifth Avenue, New York, NY 10176 (646) 723-1042 direct | (212) 661-5030 main (212) 687-2123 fax [email protected] | www.schoeman.com

HOT TOPICS IN COMMERCIAL LEASING 2014

RESTAURANT LEASES

1. DUE DILIGENCE A. LIQUOR LICENSE

i. Location may be an issue ii. Community Board approval

iii. Application to State Liquor Authority iv. Cooperation of landlord v. Possible termination right

B. HEALTH DEPT. i. Food Service Establishment Permit.

C. BUILDINGS DEPT./FIRE DEPT. i. Public assembly permit (if 75 or more persons indoors; or 200 or

more persons outdoors) (NYC) ii. Possible Landmarks approval (NYC)

iii. Zoning and Certificate of Occupancy 1. Certificate of Occupancy (or amendment) required? 2. Possible barriers to Certificate of Occupancy

A. Violations B. Open Buildings Dept. permits

iv. Consumer Affairs (NYC) 1. Cabaret license (if there’s music, dancing)

D. PHYSICAL DUE DILIGENCE i. Electric

1. Adequacy of electric 2. Direct meter

ii. Water 1. Submeter 2. Cost

iii. HVAC iv. Availability of Gas v. Availability of Steam vi. Drainage/sewer vii.Venting

E. ADA AND ACCESSIBILITY i. What if entrance is not accessible and can’t be made accessible ii. Indemnification

F. SIGNAGE RIGHTS AND STOREFRONT G. SIDEWALK CAFES/PATIOS/OUTDOOR AREAS

2. ASSIGNMENT AND SUBLET A. Investors will need ability to freely transfer interests. Landlord will want

the person who is the driving force behind the restaurant to retain a minimum equity interest and to retain operational control.

B. Concession and licensing rights. C. Franchising rights. D. Right to sell to a public company. E. No profit recapture. F. No space recapture. G. Death, incapacity, transfers to trusts f/b/o named person and family

members, so long as the principal retains control of operations H. Sale of business may be effected by assignment or subletting.

i. Subletting – non-disturbance agreement ii.Assignment – ability to come back in and cure

3. FINANCEABILITY OF LEASE

A. Financing agreements for equipment purchases B. Access agreement for lender. C. Right to collaterally assign lease to lender

i. Mortgage tax

4. USE A. Flexibility of use desirable

5. INSURANCE

A. Commercial General Liability: Serious coverage i. Mountain States Mut. Cas. Co. v. Roinestad, 296 P.3d 1020 (Colo. 2013). sewer explosion caused by buildup of sewer gas arising from buildup of grease not covered by commercial general liability insurance, which excluded damage arising from discharge of pollutants

B. Property Damage Insurance C. Business Interruption Insurance D. Plate Glass Insurance E. Liquor liability insurance F. Increases in fire insurance rates

6. CASUALTY

A. Tenant has obligation to rebuild restaurant. B. Who gets tenant’s insurance proceeds if tenant terminates the lease?

7. RENT

A. Possible percentage rent I. Restaurant located in a hotel or shopping center where significant

business is generated by building operations. B. Operating Expense Escalations/Pass-Throughs

C. Real Estate Taxes Escalations/Pass-Throughs

8. QUALITY OF LIFE ISSUES A. Use of balance of building B. Dealing with noise, odor, and vibration

i. Landlord ability to intervene ii.Immediate measures to ameliorate problems iii.Permanent solutions iv.Tenant indemnification of landlord against lawsuits

C. Pest control D. Garbage

i. Refrigeration of garbage ii.Regulation of garbage pickups iii.When garbage can be left on street (NYC)

9. OWNER REPAIRS AND SERVICES

A. Owner obligations probably limited. B. Tenant may be required to assume responsibility for sewer and water

connections to street if lines exclusively serve the leased premises.

10. SNDA

11. GOING DARK/CONTINUOUS OPERATION

12. RESTORATION AT END OF LEASE

A. What has to be removed i. Trade fixtures ii.Other alterations and installations iii.Any required notice from landlord iv.Trademarked items

February 13, 2009 Re: Request for a Ruling Real Property Tax Law § 420-a Exemption FLR-08-4886 Dear Mr. : This is in response to your request dated February 21, 2008, on behalf of for a letter ruling regarding the application of § 420-a of the Real Property Tax Law (“RPTL”) to a leasehold condominium, created by on an underlying ground lease. On November 3, 2008, attorneys from the law firm of submitted a Memorandum of Law, setting forth additional information concerning the structure of this transaction. On December 31, 2008, pursuant to a request by the Department of Finance (“Finance”) you submitted to Finance, selected articles from the June 6, 2007 ground lease (the “Lease”) entered into between and . FACTS: The facts that we have relied upon for this letter ruling are based on the Memorandum of Lease dated June 6, 2007, selected articles from the June 6, 2007 Lease submitted to Finance, as well as representations made by in the above mentioned Memorandum of Law dated November 3, 2008. At the time of application for exemption, additional documentation may be requested to verify those actions yet to be taken by in support of the exemption request.

is a not-for profit corporation organized or conducted for educational purposes, and is exempt from federal income tax pursuant to section 501(c)(3) of the Internal Revenue Code. is currently a tenant pursuant to the Lease of premises located at . The Lease has a base period of thirty-five years and has the option to extend the Lease for six 10 year periods. Pursuant to the Lease, has a leasehold interest in the land (the “Land”) and has acquired title to the improvements (the “Improvements”). Section 5.1(b) of the Lease provides that “[t]he parties acknowledge that following completion of any New Improvements, Tenant shall hold title to the Improvements until the expiration of the Term.” is in the process of completing a reconstruction of the entire building located at Street (including the construction of additional floors). has advised Finance that expects to spend approximately 80 million dollars in order to convert the building from a parking garage into a first-class research laboratory. The Lease further provides that is solely responsible for all maintenance and property related expenses including paying all taxes assessed against the property.

Page 2, Real Property Tax FLR No: 08-4886

The Lease grants the right to use the property for any legally permitted uses other than residential and has indicated that intends to utilize the property for general office, medical research and education uses. The Lease further provides that may create a leasehold condominium and indicates that intends to create a leasehold condominium comprised of two (2) units, which units will be owned in fee for the term of the Lease. ISSUE: May a real property tax exemption pursuant to § 420-a of the RPTL be granted to property owned by that is in the form of a leasehold condominium, where the condominium declaration requires the unit owner to pay all taxes attributable to its units? CONCLUSION: Based upon applicable law regarding leasehold condominiums, real property owned by in the form of a leasehold condominium including the leasehold of the land will be eligible for an exemption pursuant to § 420-a of the RPTL. LAW: RPTL § 420-a provides a tax exemption for mandatory classes of nonprofit organizations in pertinent part as follows:

[r]eal property owned by a corporation or association organized or conducted exclusively for religious, charitable, hospital, educational, or moral or mental improvement of men, women or children purposes or for two or more such purposes, and used exclusively for carrying out thereupon one or more of such purposes either by the owning corporation or association as hereinafter provided shall be exempt from taxation as provided in this section.

Article 9B of the Real Property Law (“RPL”) the “Condominium Act” governs the creation, characteristics and management of condominiums. Specifically § 339-e, of the RPL provides the following relevant definitions:

Subdivision 2. “Common elements” unless otherwise provided in the declaration, mean and include: (a) the land on which the building is located …and (h) all other parts of the property necessary or convenient to the existence, maintenance and safety or normally in common use…

Subdivision 5. “Common interest” means the (i) proportionate, undivided interest in fee simple absolute, or (ii) proportionate undivided leasehold interest in the common elements appertaining to each unit, as expresses in the declaration…

Subdivision 11. “Property” means and includes the land, the buildings and all other improvements thereon, (i) owned in fee simple absolute, or (ii) in the case of a condominium devoted exclusively to non-residential purposes, held under a lease or sublease, or separate unit leases or subleases, the unexpired term of which on the date of the recording of the declaration shall not be less than thirty years…

Page 3, Real Property Tax FLR No: 08-4886

Subdivision 14. “Unit” means a part of the property intended for any type of use or uses, and with an exit to a public street or highway or to a common element or elements leading to a public street or highway… Subdivision 16. “Unit owner” means the person or person owning a unit in fee simple absolute or in the case either (i) of a condominium devoted exclusively to non-residential purposes or (ii) a qualified leasehold condominium owning a unit held under a lease or sublease.

In addition, RPL § 339-g provides that “each unit, together with its common interest, shall for all purposes constitute real property.” Finally, RPL § 339-y (1) (a) which governs taxation of condominiums, provides in pertinent part that:

With respect to all property submitted to the provision of this article…each unit and its common interest…shall be deemed to be a parcel and shall be subject to separate assessment and taxation by each assessing unit… except that the foregoing shall not apply to a unit held under lease or sublease unless the declaration requires that the unit owner to pay all taxes attributable to his unit.

ANALYSIS: is a not-for profit corporation, organized or conducted for educational purposes. The property in issue will be used by to carry out its educational and scientific exempt purposes. As the statute specifically requires ownership of real property by a corporation or association organized for exempt purposes, the sole issue is whether ownership of condominium units in the form of a leasehold condominium, constitutes ownership of real property for purposes of § 420-a of the RPTL. Under the Condominium Act, a condominium unit, which is devoted exclusively to a non-residential purpose, can be formed on property held by a condominium declarant either in fee or under leasehold with a remaining term of 30 years or more. has entered into a lease with for a minimum term of 35 years, whereby will own the building located at Street and have a leasehold interest in the land. During the term of the lease on the land, will utilize the property for general office, medical research and education use. As a result, each condominium unit will be condominium units devoted exclusively to non-residential purposes. Therefore, the land held under the leasehold will be deemed to be property for purposes of the RPTL. Once the contemplated declaration is filed, will own two units in fee simple for the term of the lease. Generally, the condominium form of ownership is manifested as a division of a single parcel of real property into individual units and common elements in which an owner holds title in fee to his individual unit as well as an undivided interest in the common elements of the parcel. See, Murphy v. State of New York 14 A.D. 3d 127, 787 N.Y.S. 2d 120 (2d Dept. 2004). The condominium ownership interest for units will include title to each unit and the unit’s respective common interest, including an undivided percentage interest in the common elements, which includes the underlying leasehold of the land. Consequently, since RPL § 339-g provides that each unit, together with its common interest, constitutes real property, it follows that the underlying leasehold of the land constitute real property for purposes of RPTL § 420-a. With regard to separate taxation, the Lease provides that is required to pay the taxes assessed on each of its units. Pursuant to RPL § 339-y (1) (a) each unit and its common interest is deemed to be a tax parcel. Accordingly, the tax parcel, which is subject to assessment, will consist of the unit and its common interest including the leasehold of the land. As a result, Finance will be required to assess each unit together

Page 4, Real Property Tax FLR No: 08-4886

with its common interest in the leasehold as a single tax parcel. Hence, as the owner of two units in the leasehold condominium will be assessed the full value of each unit, which will include the unit’s pro rata share of all of the common elements, one of which is the land.

RPTL § 420-a provides an exemption for real property owned by a corporation or association organized or conducted for an exempt purpose provided the property is used to carry out such exempt purpose. Consequently, a not for profit that does not own the property but is merely a lessee pursuant to a long term lease is not eligible for an exemption. However, we have determined that as the owner of two (2) condominium units created on an underlying ground lease with a term of 35 years or more is eligible for exemption from taxation pursuant to RPTL §420-a.

To receive its exemption will be required to file an application with the Exemption Unit. If the documents and facts presented at the time of the application are consistent with the representations made to Legal Affairs for the purposes of this letter ruling, the tax parcels consisting of the condominium units and their respective common interests should be granted an exemption pursuant to RPTL § 420-a.

Notwithstanding the analysis and conclusions discussed above, Finance reserves the right to review the information submitted.

Very truly yours,

Dara Jaffee Assistant Commissioner Legal Affairs Division

HGT:hgt

HOT TOPICS IN LEASING

by

Benjamin Weinstock, Esq. Ruskin Moscou Faltischek PC Uniondale, New

York

.&1r¡r¡¡ New York Stute Btr Associatiott

Real Property Ltw SectionNltst.J,A.

¡triffil&'

Þ{û? T$å}A{IS åN

å-åì,4SfiN{;Prcrcntcd bl

NANCY CONNERY, ESQ,Schoenran U¡rdike Kâufmâù & Steril LLP

BENJÀMIN WIIINSTOCK, ESQ.Ruskin Moscou Fåltischck PC

.&Èt¡{f I Netu York State Bar Associtttiott

Real Property Lnw Section'l\I:'fðIts-1À

Sublease RecognilionAgreemenls

Prcscntcd try

BENJAMIN WEINSTOCK, ESQ.Ruskin Moscoù Falfischck PC

Su b le qs e Reco gnìtìon Ag r e ements

A method to protect a sublessee ofproperty from the adverse consequencesof a termination or rejection of the primelease by the Landlord.

S u ble as e Rec o gnition Ap r eements

\ilhen negotiating the Prime Lease,

Tenant should require the Landlord toprovide protection to future Subtenants.

Normally, ground leases have very Iiberalassignment and subletting rights.Therefore, Landlords who agree simply tonon-disturb all subtenants may end upnon-disturbing a very weak orundesirable Subtenant.

t

S u b less e Reco p nitio n Ag r eements

Who will the Landlord "recognize"?

(a) Sublcase must be arm's length with a

subtenant that is not affiliatcd with thcTenant,

(b) Minimum Tangible Net Worth requirement,or rating agency approval.

(c) Minimum sublease rent is not less than the

[xxx7o multiplel rent ând âdditionâl rentpaid by the Tenant

S u b leas e Reco gnition Ag r eements

(d) Only one recognized subtenânt who occupiesthe entire site.

If thc Landlord is willing to non-disturb multiplesubtenânts, then considcr:

i, The maximum number of subtenânts

ii. Minimum size and shapc of the space

iii. Minimum rent payable by each subtenant

iv, Sixe of Sublesase - contigues floors

2

S u b less e Recog nition Ag r eements

A"Recognized Subtenønf'shall be a retail subtenant

who bas entered into an arms-length sublease withTenant, provided that,

(i) the subtenant is uot an affiliate or subsidiary ofTenant, and not controlled by Tenant,

(ii) the configuration ofthe subleased space is

comrnercially reasonable and would not unreasonably

interfere with or l¡aterially and adversely impair the

utility and rnarket value of any part or parts of the

Leased Prernises not then sublet,

(iii) Subtenant's (or its guarantor's) creditrvorthinessis cornmercially reasonable under the circumstances,

Su b leøs e Reco gnition Ag r eements

(iv) any "free rent" or rent abatement periods are

commercially reasonable,

(v) payrnents offixed or base subrerrt shall notdecrease during the tenn ofsuch sublease,

(vi) Tlre Subtenant is subject to in peßonamjurisdiction in the courts ofthe State ofNew York,and not subject to any immunity from suit unless allsuclr immunity is waived for the benefit of Landlordand Terrant and each present and future LeaseholdMortgagee and Fee Mortgagee,

S u ble øs e Re cog nitio n Ag r ee me nts

(vii) the sublease allows the subtenant to use and occupy its

premises for lawful purposes consistent with the certificate ofoccupancy of the Building,

(viìi) all other terms and conditions of the sublease are

commercially ¡easonable,

(ix) ifthere is a Leasehold Mortgage, the Leasehold Mortgageehas entered (or simultaneously enters or has agreed in writing toenter) ìnto a subordination, non-disturbance, and AttornmentAgreement with the Subtenant, and Tenant has given Landlordwritten evidence thereof, and

(x) the term (including option and renewal terms) ofthe Sublease

shall not extend beyond the Expiration ofthe Te¡m ofthe Lease.

aJ

S u b leas e Re co gniÍio n Ag r eements

Tenant's Deliverables

L Copy of the Sublease and Guaranties

2. Identifrcation of Subtenaut's and Guarantor(s) principals

3. Fìnancial inlormatiou for Subtenant and Guarantor(s)

4. Landlord's review fee (ifany)

5. Plan showing area to be subletif less thanthe entirepremises

6. Leasehold Mortgagee's SNDA

7. Recognition Agreernent with an attornlnelìt clause signed by

the Tenant, Subtenant and Guarantor(s)

S u b le as e Rec oenition A g r eements

Threshold Issues

Do I put the recognition clause in the Lease

draft I send the Tenant?

Do I agree to give "recognition" on

"çommercially reasonable" terms?

Do I negotiate the terms of the RecognitionAgreement in advance of knowing who I ambeing asked 1o " r ecognize"?

S u b less e Re co p nitio n Ag r eeme nts

Landlord, Tenant and Subtenant executea "simple" Recognition Agreement.

It provides, that if the prime lease is

terminated, Landlord will recognize thesublease, which will become a directlease between the Subtenant and

Landlord.

4

S u b le as e Re c ognition Ag r eements

Ground Lease

20 yr. initial term

15 successive 5 year renewals : 75 years

Total = 95 years

S u b le øs e Recog nìtio n Ag r eements

Bis Box Sublease

25 yr. initial term

2 successive 10 year renewals = 20 years

Total : 45 years

S u b leas e Reco gnilion Ag r e ements

Ground Lease B¡g Box Sublease

lnitial Term 20 Years 25 Years

Renewâl Opl¡ons 15 x 5 Years 2 x 10 Years

Tolal Term 95 Years 45 Years

Bese Rent $30,000Payable Semiannually;

$60,000 per annum

$15,000 PayabìeMonthly;

$180,000 perannum

Expenses Triple Ne{ Prorala share of taxesand CAI\4; Subtenant

Pays all ut¡lities

Slructural repairs byLandlord, all other repairs

by Tenant

I\¡arnlenance andRepairs

Triple Net

5

Su b leas e Recopnition Ag r eements

Mission accomplished!

If the Prirne Lease is terrninated, the

Subtenant attorns to the Landlord and

becomes the direct Tenant ofthe Landlord

S u b less e Rec o gniÍion Ag r eements

Non-l)isturbance. So long as the Sublease is in full force and

effect,Subtenant's usc. Dossession. or cniovment of the SublcasePremises be interfered rvith, nor shall the subleaseholdestate granted by the Sublease be affected in any manner, nor

shall any ofthe rights of Subtenant granted under the

Sublease be affected in any manner, by a termination orsur¡ender ofthe Lease, in any action or proceeding instituted

to evict Tenant by reason of ÍI&!3!l!51þbg!!-s!frcL.l!¡9Lease. (ii) Tenant's surrender of the Lease. or (iii) anvtermination of the Lease due to foreclosure, casualtv.condemnation or anv other cause.

S u b le as e Re cog nilio n Ag r eements

Subtenant shall be bound to the Sublease under all of the

terms, covenants and conditions of the Sublease for the

l¡alance ofthe term ofthe Sublease, including any

extension terms (to the extent that Subtenant shall elect or

has elected to exercise any or all ofits options to extend

the Sublease), with the same force and effect as ifLandlord were the sublesso¡ under theSublease... .Landlord shall have all rishts andobligations of Tenant as the sublessor undcr theSublease as thoueh Landlord had originallv executedthc Sublease in place of Tenant. and Landlord shall be

bound by all ofthe terms, covenants and condìtìons oftheSublease, except as otherwise set forth in this Agreement,

6

S u b le as e Rec ognition Ag r eements

The Recognition Agreement convefts thepassive Ground Lease Landlord to an activeoperating Landlord.

Landlord may not be equipped to be an

operator, or, even ifthe Landlord is capable

of active management, the Landlord does notwant to do this.

S u b leas e Reco g nition Ap r eements

Let's make the Ground Lease the operativelease between the Landlord and the

Subtenant, except for the rent clause, whichwill be the rent clause in the Sublease (withsignificantly higher rents).

S u bleas e Recognition AR r eements

. . . and Landlord shall be bound by all of the

terms, covenants and conditions oftheSublease, except as otherwise set forth inthis Agreement.

7

Su ble as e Re co g ttitio n Ag r e ements

except that Landlord shall not be:

i. liable for any representation orwarranty of Tenant, any act or omission of ordefault by Tenant under the Sublease (but the

foregoing shall not relieve Landlord from any

liability to remedy a curable default that iscontinuing which Landlord (as sublessor under

the Sublease) is obligated to remedy pursuant

to the Sublease);

Sublease Recognition Asreements

except that Landlord shall not be:

ii. subjectto any credits, claims, setoffs

or defenses which Subtenant might have

against Tenant as a result of any acts oromissions of Tenant;

S u b le as e Recog nitio n Agr ee ments

except that Landlord shall not be:

iii. bound by rent, additional rent orother amounts which Subtenant may have paidto Tenant more than one (l) month in advance

of the month to which such payments relate,

and all such prepaid sums shall remain due and

owing to Landlord without regard to such

prepayment except as may have actually been

received by Landlord for any period beyond themonth in which the Lease was terminated;

8

S u b le ss e Reco p n it ion Ag r e ements

except that Landlord shall not be:

iv. responsible for repairs in or to the

Building in the case of damage or destructionof the Building or any part thereof due to f,rreor other casualty or by reason ofacondemnation, [unless Landlord (as sublessor

under the Sublease) shall be obligated under

the Sublease to make such repairs]; or

Su b le as e Rec o p nition Ag r eemenls

except that Landlord shall not be:

v. liable under any indemnity provisionofwhatever nature contained in the Sublease,

including, but not limited to, any

environmental indemnification, except to the

extent the hazardous environmental conditionwas caused by Landlord subsequentto the date

that the Sublease becomes a direct Lease

between Landlord an Subtenant;

S u b leas e Recognìtion Ag r eements

Landlord's Exculpation :

The liability ofLandlord under the Sublease fordamages or otherwise shall be limited to Landlord'sínterest in the Prernises (as defined in the Lease)

including rents, net sale proceeds, net insuranceproceeds and net condemnation proceeds therefrom.

Neither Landlord nor any directors, officers,shareholders, members, managers, partners,

principals, agents, servants or employees ofLandlordshall have any personal liability to Tenant,

9

S u bleas e Re c o g nit io n Ag r eements

Landlord's Exculpation:

ii. No other property or assets oflandlord or any

property of the directors, offi cers, shareholders,

rnembers, managers, partners, principals, agents orservants or ernployees ofLandlord shall be subject to

Ievy, execution or other enforcement procedure forthe satisfactior-r ofSubtenant's retnedies hereunder orunder the Sublease.

S ub le as e Re cog nition Ag r e ements

Exclusive Use Provisions:

1. Restrict the excusive use clause to this Property ifit is a multi-tenant proporty.

2. Carve out violations by existing uses on the

Property,

3, Carve out violations that occur as a result ofapermitted change in use under existing leases.

4. Carve out violations that exist on after acquired

properties that are in the restricted territory.

S u b le øs e Rec og nition A g r eements

Fire and Casualty:

l. Is the obligation to rebuild governed by the

Ground Lease or Sublease?

2. IfSubtenant is permitted to use insuranceproceeds to rebuild, is there a mechanism in place

to release the insurance proceeds in the same

mauner as a building loan?

3. Do the Ground Lease or Sublease conflict withthe fee or leasehold mortgages?

10

S ub leas e Re cog nition Ag r eements

Condemnation:

A Ground Lease generally penlits the Tenatìt to

recover the value ofthe unexpired temt ofthe Lease.

An Operating Lease will be t.uore restrictive,allowing the Tenant to recover only the value ofTenant's fixtures takeu. Tenant nay not seek

damages for the value of the unexpired term.

S u b le as e Re co gnitio n Ag r eements

Ownership of Leasehold Improvements and

Buildinss:

A Ground Lease frequently separates ownershipofthe land from ownership ofthe buildings and other

improvements.

Will the Tenant's claim to ownership of the

buildirg and improvements allow Tenant to recover

their value in a taking?

S u bleas e Reco g nitio n A$ eeluqÛlt

OÞportunitv to Fix Mistakes:

The Recognition Agreement may be a

convenient way to corrects matters that wereoverlooked in the original Ground Lease.

For example, the failure to have the Ground Lessee

waive claims to development rights. See MacMilløn,Inc. v. CF Lex Associates,425 NYS2d 377 (1982)

11

Suhlease Asrccm.enls

Overlandlord's Bankruplçy

Will the Overlandlord's rejection of the Overlease

cause the sublease to temrinate?

Bankruptcy Code Section 3 65(h)( I )(A)(ii) permits'fenant to remain in possession attd grants the Tenaut

the right ofoffset for the cost ofproviding Landlord's

services under the rejected Overlease.

S u b le as e Re co g nÍtion Ag r eements

The End Run

The Subtenant may avoid the Recognition Agreement

cornpletely and get the benefits ofthe Ground Lease (cheaper

rent and fewer restrictions on assignment, subletting,alteration and financing) by taking a conditional assignment

ofthe Ground Lease froln the Tenant.

The Ground Lease should prohibit any conditionalassignment of the Ground Lease to a Subtenant or to any

eniity or person that is controlled by or an affiliate oftheSubtenant, ìncluding the Guarantor

Define assignment to include entity transfers.

T2

Æed¡AA&I

New York StlÍe Bar Assocítttiott

Renl Property Law Sectìott.l\r YStì^

Green BuildingLeases

Prcscntcd bl

BENJÂMIN WEINSTOCK, ESQ.Ruskfu Moscou F¡ltischek PC

llhnl is n Green Buìldine?

USGBC

The United States Green Building Council

1

USGBC

The United States Green Building Council

LEED Certification

USGBC

The United States Green Building Council

ffiffi''"d'ii,;1ïÈìLEED Cerlification

Green Buìlding ønd Leed Certilication

Why do landlords and Tenants want LEEDCertifrcation?

l. Healthier and happier work spaces.

2. Reduction of irnpact on the environlnent.

3. Reduced operating costs and greater profitabiliry

4. Higher rents, Iiigher occupancy rates

5, Higher sales prices.

6. Cornpliance increases project costs only 2o/o.

2

Green Buildittg ttnd Leed Certìfìcatiott

Why do landlords and Tenants rvant LEEDCertification?

7. Energy lndependence and Security Act of2007requires at least an Energy Star rating for US

Covenìnlcnt Âgency leases.

L Local laws are being adopted with increasingmonrentunl, NYC Local Law 86 adopted effective

January 1,2007

9. Non Green Buildings are at risk of becorning

obsolete and relegated to a lower tier of"contps"

Green Leasìng Issues

Term

Longer telm leases generate mole LEED"points" because they |educe waste fromnew buildouts fot'new tenants, with a

col'l'espondil-rg decrease in transpol'tation and

manufactuling of the building materials

Green Leasing Issues

Permitted Use

Even in a straight office use clause or retail

use clause, add:

"...provided such use does not violate the

certification of the building by the U.S.

Green Building Council LEED rating system

or Landlord's Environrnental Managernent

Plan"

3

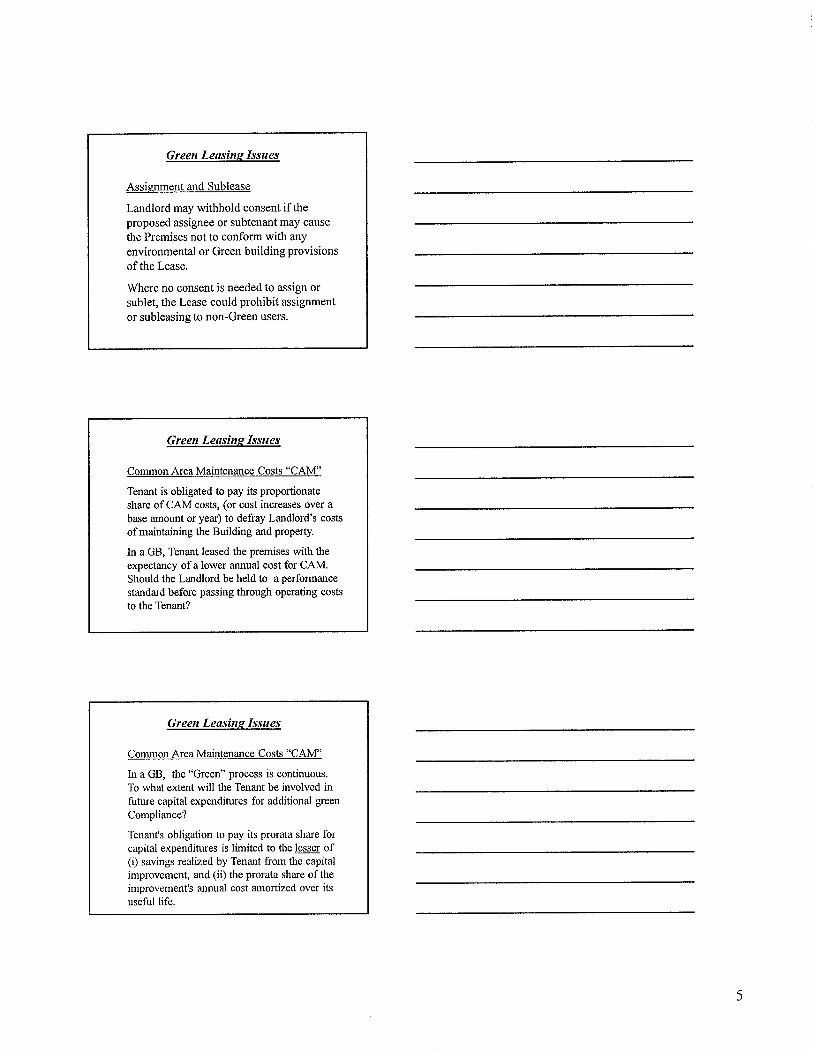

Green Leasing Issues

Assignment and Sublease

Landlord may withhold consent if theproposed assignee or subtenant rnay cause

the Premises not to conform with any

envilonrnental or Green buildiug pt'ovisionsofthe Lease.

Whele no conscnt is needed to assign ot'

sublet, the Lease should prohibit assigntnent

to non-Green users.

Green Le0sitts Issues

Common Area Cnsts "CAM"

'lþnant is obligated to pay its proportionatc

sharc of CAM costs. (or cost rncreases ovcr a

base amount or year) to defray Landlord's costs

of rnaintaining the Buildiug and property.

In a GB, Tennat leased the premises with thegxpectancy of a lower annual cost for CAM.Should the Landlord be held to a perlormauce

standard before passing through operatillg costs

to the Teuant?

Green Leasinp Issues

Common Area Maintenance Costs "CAM"

lrr a Cì8, lhe "Creen" proccss is continuous.

To what extent will the Tenant be involved infuture capital expenditures for additional green

Compliance?

'I'enant's obligation to pay its prorata share forcapital expenditures is limited to the lesser of(r) savings realiz,ed by Tenant lrorn tlie capitalimprovement, and (ii) the prorata share of the

improvement's annual cost atnortized over itsuseful life.

4

Green Leasittg Issues

Utilities (Gas. Electric and Water')

Utility charges should be sepalately rnetered

ol sub metel'ed to a gloen tenant to

incentivize energy savir.rgs throughconservation.

Tenant should requile that the environrnerttalsystems (thermostats and other controls for'

heating and air conditioning, humidistats,water conservation and frltration) should be

undel' Tenant's coutlol.

Green Leasing Issue;

Opelating Covenants

Tenants in Gl'een Buildings need to be aware

that Landlords may lequire thern to complywith operating rules, r'egulations and

scl.redules that may be inconsistent with the

Tenant's business ueeds.

Green Leasing Issues

Operatiuq Covenants - Rules and Requlations

Counsel should play close attention to the

ubiquitous rules and regulations schedule oftheLease.

Avoid this:

"Subject to the applicable provisions ofthe Lcase,

Tcnant shall comply with all rules, regulations and

nleasures adopted by Landlord froln time to timein connection with any green/l-EED prograrn(s)

undertaken or maintained by Lartdlord from timeto time."

5

Greett Leosins Issues

Audit Rishts

A'l'enar-rt in a Green Building may be paying a

higher base rent but is attracted to the property

because ofthe lorver operating costs protnised

or predicted,

Tenant should have the right to audit the

operating costs ifthey exceed Tenant's

expectation,

Green Leasing Issues

Work Letter

Tlie Tenant's and Landlord's work letters should

identify the sustainability standard that the pârties

have agreed to achieve, i.e.,

Energy Staq or I.,EED - Certified, silver, gold or

platinurn

Landlord nray require Tonant to hire an accredited

LEED Professional to mattage the sustainabilíty

aspects ofTenant's buildout. Tenant may have a

reciprocal requiretnent for Landlord.

Green Leasing Issues

Work Letter

Landlord marketed the premises clairningspecific green attributes. Tenant will require

Landlord 10 meot the promised conditions.

It costs more to build and tear-out consistent

with Green standards. Therefore, Tenant

should negotiate for a higher work allowance,

6

Green Leosins Issues

Parking

Extra LEED points arc ar.varded to a property that

does not have excess parking (more than tlre

minirnurn required by the local zoning code).

Solid Wastc Managetnent

LEED points are affected by solid waste

lìranagement. Tlie property needs a SWM protocolwitlr easily accessible locatiorrs for recycling,

Green Leasing Issues

S ignage

Signage will affèct the building's I-EED score fbr"Light Pollutiorì Reductìon" and energy

consumption.

Solid Waste Manageme nt

I-EED points are af'fècted by solid waste

mar'ìagelneut. The property needs a SWM protocolu'ith easily accessible locations for recycling.

Green Leasinp Issues

End ofTenr Rernoval

The award ofl I-EED poilìts takes into cousideration

how tlre Tenant will ret¡ove its FF&E.

'lenant's should avoid tlte lollowing:

"Tenant's removal of leasehold improvernents, trade

fixtures or personal property frorn the prernises shall

be perforrned by'lènartt in an environtnentallysustainable manner, including reuse and recycling,all of which must be reported to the Landlord in the

forrnat requested by the L,andlord."

7

Green Leasing Issues

Insurance - "lf vou had a sreen buildinq before the

fire, vou wrll have a sreen buildins after the fire"

Landlord and Tenant have a vested ìnterest in knowingthat their policies cover the increased tinle and cost ol'resloring a Green Building. Increnrental costs include:

L The cost ofLEED ceíified professionals2. AII LEED lees

3. Recycling debris rather than durnping in a landllll4. Purchase ofgrid porver until alternate energy

source is back online5, I.oss ofutility credits while the butlding is under

repair

Green Leasinp Issues

Property Taxes

Ifthere are tax incentives, rebates or reductions

tied to the LEED Certification, deterrnine in the

Lease rvhether tl-rey benefit the Tenant, the

Landlord or both.

Green Leøsing Issue;

Renewal

Even if the building is not Green now, it rnay

become Green in the fiture. When renewing

expired leases, collsider whether a Green Ridershould be attached for luture Green

conversions.

8

Green Leasins Issues

Remedies

Light Green Leases - the green

requirements are aspilational only.

Dark Green Leases - Traditionalbreach lemedies.

9

.&dl!¡Il New York State Bør Association

Real Property Law SectiottNì¿SI3.l\

Subleøse RecognìtionAgreements

Prcscnlcd by

BENJAMTN WEINSTOCK, ESQ.Ruskin Moscou Fâltischek PC

S u b I e øs e Re co g nition A gr e ements

AKA Sublease NonDisturbancc Agreements,

A method to protect a

sublessee of propertyfrom the adverseconscquences of a

termination or rejectionof the prime lease.

S u bleas e Rec o g nitio n A g r e eme nts

When negotiating the Prime Lease,Master Lease or Ground Lease, (or anyothc¡' leusc lvhere sublettiug is

contcrnplafetl) the Tenant shouldrequire the Landlord to provideprotection to future Subtenants.

Su bleas e Recopnitìon Agr eements

Inability to protcct a subtenant from eviction as

a result of the prinrary tenant's default mayadversely rffect the primary tenant's rbility tosublet.

S u b le as e Re c o g nitio n A g r eeme nts

Normally, ground leases (master leases)have very liberal âssignment ândsubletting rights. Therefore, Landlordsrvho agree simply to "non-disturb allsubtenants" may end up non-disturbing a

very weâl( or undesirable Subtenant.

I

S u bleas e Recop nilion Ag r eemenls

Who rvill the Landlord írecognize"?

(a) Sublease must be arm's length rvith a

subtenant that is not affiliated with theTcnant,

(b) Minimum Tangiblc Ne t Worth requirement,or rating agency approval.

(c) Minimum sublease rent is not less than the

[150%] rent and additional rent pnid by theTenan t,

2

S u b le øs e Re co g nitio n A g r eements

(d) Only one recognized subtcnânt rvho occupiesthe entire site,

If thc Landlord is rvilling to non-disturb multiplesubtcnants, then consider:

i, The maximum number of subtenants

ii. Minimum sizeand shape of thc spâce

iii. Minimum rcnt payable by each subtenant

iv. Size of Sublease Prernises - contiguousfloors, larvfully demised spnces thît âremarketable and codc compliânt

Subleas e Recog nitio n A gr eements

(iv) any "free rent" or rent abatement periods are

commercially reasonable,

(v) payments offixed or base subrent shall notdecrease during the term ofthe sublease,

(vi) The Subtenant is subject to in personantjurisdìction in the courts of the State of _, and

not subject to any immunity from suit unless all such

immunity is waived for the benefít of Landlord and

Tenanl and each present and future Leasehold

Mortgagee and Fee Mortgagee,

S u b le øs e Rec o p nìtion Ag r eeme nts

A"Recognized Subtenanf'shall be a ¡etail subteuant

who has entered into an arms-length sublease withTenant, provided that,

(i) the subtenant is not an Afüliate or subsidiary ofTenant, and not controlled by Tenant,

(ii) the configuration ofthe subleased space is

commercially reasonable and would not unreasonably

interfere with or materially and adversely impair theutility and market value ofany other part or parts ofthe Leased Premises not then sublet,

(iii) Subtenant's (or its guarantor's) credihvorthinessis commercially reasonable under the circumstances,

J

S u ble as e Re c o g nition A g r e eme nts

(vií) the sublease aìlows the subtenant to use and occupy its

premises for lawful purposes consistent with the certificate ofoccupancy of the Building,

(viii) Landlord shall not be required to contribute to any tenant

work,

(ix) if there is a Leasehold Mortgage, the Leasehold Mortgageehas entered (or simultaneously enters or has agreed in writing toenter) into a subordination, non-disturbance, and AttornmentAgreement with the Subtenant, and Tenant has given Landlordwritten evidence thereof, and

(x) the term (including option and renewal terms) ofthe Sublease

shall not extend beyond the Expiralion of the Term of the Lease.

S u bl eas e Rec o g nitio n A p r e ements

Tenant's Deliverables

I . Copy of the Sublease and Guaranties

2. Identification of Subtenant's and Guarantor(s) principals

3. Financial information for Subtenant and Guarantor(s)

4. Landlord's review fee (ifany)

5. Plan showingarea to be sublet if less than the entirepremises

6. Leasehold Mortgagee's SNDA

7. Recognition Agreement with an attornment clause signed bythe Tenant, Subtenant and Guarantor(s)

Su bleøs e Recopnition Ag reements

(xi) The subrent shall not be less than the MinimumRecognized Rent.

The term "Minimum Recognized Renf'shall mean twohundred percent (200%) of the Annual Fixed Rent payable

under this Lease for the portion of the Leased Premises

occupied by a subtenant allocated ratably on a square

footage basis, calculated separately fo¡ retail space and fornon-retail space, with retail space being valued hvice the

value of non-retail space

4

Su bleas e Recog nilion AgreemenÍs

Landlord, Tenant and Subtenant execute

a "basiÇ" Recognition Agreement.

It provides, that if the prime lease is

terminated, Landlord will recognize the

sublease, which will become a directlease between the Subtenant and

Landlord.

S u b le as e Reco Ê nition Ag r e ements

Non-Disturbance. So long as the Sublease is in full force and

effect, the Sublease shall not be terminâted. nor shallSubtenânt's use. Dossession, or eniovment of the SubleasePremises be interfered with, no¡ shall the sub-leasehold

estate granted by the Sublease be affected in any manner, nor

shall any of the rights of Subtenant granted under the

Sublease be affected in any manner, by a tennination orsurrender of the Lease, in any action or proceeding institutedto evict Tenant by reason of (i) Tenant's default under theLease. (ii) Tenant's surrcnder of the Lease, or (iii) anvtermination of the Leasc due to foreclosure. câsuâltv.condemnâtion. bankruptcy or ânv other câuse.

S u b leas e Reco p nition A p r eements

Mission Accomplished!

If the Prime Lease is terminated, the

Subtenant attorns to the Landlord andbecomes the direct Tenant ofthe Landlord

5

Sublease RecosnìtÍon Agreements

Ground Lease

20 yr. initial term

15 successive 5 year renewals = 75 years

Total = 95 years

Annual Rent = $60,000 NNN

S u b le us e Rec o g niti o n A g r eeme nts

Bis Box Sublease

25 yr. initial term

2 successive l0 year renewals = 20 years

Total : 45 years

Annual Rent = $180,000 + CAM andTaxes

S u b le as e Re co g nitio n A gr e e me nts

Subtenant shall be bound to the Sublease under all oftheterms, covenants and conditions of the Sublease for the

balance of the term of the Sublease, including any

extension terms (to the extent that Subtenant shall elect orhas elected to exe¡cise any or all ofits options to extendthe Sublease), with the same fo¡ce and effect as ifLandlord were the sublessor under theSublease....Landlord shall have all rishts andobliqations ofTenant as the sr¡blessor under theSublease as thoush Landlord hnd orisinallv executedthe Sublease in place of Tenant, and Landlord shall bebound by all of the terms, covenants and condìtions oftheSublease, except as otherwise se1 forth in this Agreement.

6

S u b le øs e Re c o g nitio n Agr e emerytt

Ground Lease Big Box Sublease

lnil¡ãl Term 20 Years 25 Years

Renewal Options 15 x 5 Years 2 x 10 Years

Tolâl Tem 95 Years 45 Years

Base Rent $30,000Payable Semiannuallyì

S60,000 perannum

$15,ooo Payable¡ronthly:

$180,000 per annum

Expenses Triple Net Prorala share of taxesand CAI\¡; Súblenant

pays aìl ulil¡ties

I\¡aintenance andRepairs

Triple Nel StructuralLandlord, all

repairs byolher rêpa¡rs

by Tenant

Sublease R Aørc,cmp,nls

The Recognition Agreement converts thepassive Ground Lease Landlord into an

active operating Landlord.

Landlord may not be equipped to be an

operator, or, even ifthe Landlord is capable

of active management, the Landlord does notwant to do this.

Su b le as e Re co gnitìo n A g r e ements

Let's make the Ground Lease the operativelease between the Landlord and the

Subtenant, except for the rent clause, whichwill be the rent clause in the Sublease (withsignificantly higher rents).

7

Su bleas e Recog n ition A gree ments

. . . and Landlord shall be bound by all of theterms, covenants and conditions oftheSublease, except as otherwise set forth inthis Aqreement.

S u bleqs e Recognition Agr eements

except that Landlord shall not be:

(i) liable for any representation orwarranty of Tenant, any act or omission of ordefault by Tenant under the Sublease (but theforegoing shall not relieve Landlord tiom anyliability to remedy a curable default that iscontinuing which Landlord (as Sublessor underthe Sublease) is obligated to remedy pursuantto the Sublease);

Sublease RecosnÍlion Agreements

except that Landlord shall not be:

(ii) subject to any credits, claims, setoffsor defenses which Subtenant might haveagainst Tenant as a result ofany acts oromissions of Tenant;

8

S u h le as e Reco pnilio n Ag r e e ments

except that Landlord shall not be:

(iii) bound by rent, additional rent orother amounts which Subtenant may have paid

to Tenant more than one (1) rnonth in advance

of the month to which such payments relate,

and all such prepaid sums shall remain due and

owing to Landlord without regard to such

prepayrnent except as may have actually been

received by Landlord for any period beyond the

month in which the Lease was terminated;

S u b leas e Re cog nition Agr e ements

except that Landlord shall not be:

(iv) responsible for repairs in or to theBuilding in the case of damage or destructionof the Building or any part thereof due to fireor other casualty or by reason ofacondemnation; or

S ub le as e Re c o p nitio n A g r e ente nts

Fire and Casualtv:

1. Is the obligation to rebuild govemed by the

Ground Lease or Sublease?

2. If Subtenant is pcrmitted to use insurance

proceeds to rebuild, is there a mechanism in place

to release the insurance proceeds in the same

manne¡ as a building loan?

3. Do the Ground Lease or Sublease conflict withthe fee or leasehold mortgages?

9

Sublease Recosnition Agreements

Condemnation:

A Ground Lease generally permits the Tenant torecover the value ofthe unexpired term ofthe Lease.

An Operating Lease will be more restrictive,allowing the Tenant to recover only the value ofTenant's fixtures taken. Tenant may not seek

damages for the value of the unexpired term.

Sublease Recopnition Agreements

Ownership of Leasehold Improvements andBuildings:

A Ground Lease frequently separates ownershipofthe land from ownership ofthe buildings and otherimprovements.

Will the Tenant's claim to ownership of thebuilding and improvements a'llow Tenant to recove¡their value in a taking?

S u bleas e Recognitio n Agreemenls

except that Landlord shall not be:

(v) liable under any indemnity provisionofwhatever nature contained in the Sublease,including, but not limited to, anyenvironmental indemnification, except to theextent the hazardous environmental conditionwas caused by Landlord subsequent to the datethat the Sublease becomes a direct Leasebetween Landlord and Subtenant;

10

S u b I e as e Re cog nitio n Ag r e eme nts

Landlord's Exculpation :

(i) The liability ofLandlord under the Sublease fordamages or otherwise shall be limited to Landlord'sinterest in the Premiscs (as defìned in the Lease)

including rents, net sale proceeds, net insuranceproceeds and net condernnation proceeds therefrom,

Neither Landlord nor any directors, officers,shareholders, members, managers, partners,

principals, agents, servants or employees ofLandlordshall have ary personal liabilitv to Tenant.

S u b le as e Re c o g nitio n A g r e eme nts

Landlord's Exculpation:

(iÐ No other propertv or assets ofLandlord orany property ofthe directors, officers, shareholders,

members, managers, partners, principals, agents orservants or employees ofLandlord shall be subject tolevy, execution o¡ other enforcement procedure forthe satisfaction ofSubtenant's remedies hereunder orunder the Sublease.

S u b le as e Re c o p nition A g r e e ments

Exclusive Use Provisions:

1. Restrict the exclusive use clause to this Property ifit is a multi-tenant property.

2. Carve out violations by existing users on the

Property. Landlord did not create the violation.

3. Carve out violations that occur as a resuìt ofapermitted change in use under existing leases.

4. Carve out violations that exist on after acquiredproperties that are in the restricted territory.

11

S u b le øs e Re c o g n it io n A g r e ements

Opportunity to Fix Mistakes:

The Recognition Agreement may be a

convenient way to conect matters that were

overlooked in the original Ground Lease.

For example, the failure to have the GroundLessee waive claims to development rights. See

MacMillan, Inc. v. CF Lex Associates,425 NYS2d3'17 (1982)

S u b le as e Re co g nition A p r e eme nts

Overlandlord's Bankruptcy

Will the Overlandlord's rejection of the Overleasecause the sublease to terminate?

Under applicable NY Law, the termination of thePrime Lease automatically terminates the sublease,

which is an interest derivative of the Prime Lease.23 I Centre Street Assocs. v. Post Bros. ServiceStations, Inc., 675 NYS 2d 92 (lstDept. 1998).

S u b le as e Rec o g nitÍo n Ag r e ements

Overlandlord's Bankruptcy

Ifthe Sublandlord rejects both the Prime Lease and the

Sublease, the outcome lor the Subtenant is uncertain.

Bankruptcy Code Section 365(hXtXAXiD permits the

Subtenant 1o remain in possession and grants the

Subtenant the right ofoffset for the cost ofprovidingSublaudlord's services under the rejected Overlease.

Flowever, the Sublandlord's rejection ofthe Prime Lease

will result in the termination of lhe Subtenant'spossessory right under state law, leaving the Subtenant's

fate uncertain.

12

Final Agreement Reldined Against Landlord's First Draft

WH-ËNlìl+Ç,8ItÐHÐMlLJe

SUBLEASE NON-DISTURBANCE AGREEMENT

THIS SUBLEASE NON-DISTURBANCE AGREEMENT (this "Agreement") made as

of the _ day of 20-by and among: (i)(hereinaftercalled''Landlord'')havinganofficeat;(ii).

having an office at

_(" Tenant") ; û**+(iiÐhaving an office at

( " S ubtenant " ).iêDdl-iy)

^. havins an of'lìce

a

WITNESSETH:

WHEREAS, Landlord is the owner of that certain parcel of land located in theState of City of and County of "Land") moreparticularly described on Schedule A annexed hereto and the lessor of the Land to Tenantpursuanttothatcertainlease(the''LeaSe'')datedaSof;and

WHEREAS, SubtenanLÇgar;¡l¡qo*I and Tenant have entered into a sublease datedas of . æ (the "Sublease") demising

to Subtenant (the "SubleasePremises"); and

WHEREAS, Landlord, Tenant, anêSubtenant ¿urd Guaranlordesire toenter into this Agreement with respect to the Sublease and related matters.

NOW, THEREFORE, in consideration of the premises and the executionof this Agreement by the parties, Landlord, Tenant-an<{. Subtenant:rnd GualeLntor herebyagree as follows:

l---1---Subordination. Landlord hereby acknowledges receipt of the Sublease.

The Sublease and Subtenant's interest in the Sublease Premises thereunder is now and atall times shall continue to be su$ceurr+e1-subordinate i,n-eaeh-a+:r¿l-e*;et\-re$fleÊt*û-Ll*epro+-isio ns-oÊtl¿cJ=e"ase,

S¡*blease,*h¿ll-nst+ e.-poss1.{;sìt+n^ er.-cx1it¡¡men+<rf

Me-i*r+er*eæ,ilut+Iease-bc-affeetee{ìn-ar4'm¿+nnepno¡,s'h*llarlv-olthr*,rigJ+ts-s'l-Sul+tenaulgranteelurNlet+heáublease-be-+fae+ffx*lh-proee'edin5i*sti{ute&+o-€+iie++€$ffnt bt' rc+se,n elf TeLeíìsii;

+en¿ìÐËs- €lcÊ¿+lt*thr;'retrndE¡r-orby.+€ytsoì+-o{.-Ëen¿ntþ-JìJlrer*c1er*t+f*+he-l--eas*ranel-ifS++)tenen+-sh

'A.--$.ub{cn¿ml-slr*ll-åe-bær+d-ts-+he-S+rblease-+ne1er-a}l-eÈthe4o'r*ns.e$r,eníì+Ìt e-

ineluéling aìry' extensi et-eu=-þa¡'¡elee+e++o

exerreise-ar+y-t+rå11-€ÌÊit'j-epÈions-te>exten++åe€'ühl€@ee-anåeffbel¿tsiS-tandl es4ercb'¡ar+orn-+etanrllold; *r; its ,landlord. srrid atton*rnent to be efTeetive and seli{ìoperati+e-++i,,#et*-{he

exeeutio+r+F*ny+u eeding*e-+he-inferesfi#-jlena*tB*reler tlre Subþase, Lalldlord slmll-have all rights of Tenant as the su.lrlessor-u+rder tlrest¿+ndl<+r*-sha ll-beåotrn@ever+¿l+ts-m#eenditiens-+rÈ+he-Suhle¿scle*ee

lJ--S+ùten¿rnt-*lr.alþbe-beu+r#t+åandkxd-+rndel-,-anel-++ha+l-per.{br{+1-+t}t+trt]H. teilnrr çoven,ent e+R+rmed+y-Subtena*t,hereunde+ forthe .reffietindeï of the $u,blease {erffi. i*el$dir+g aft} extensisn perilods; (t€}

tlx>e,çte*rt{haçSnbteÐarrt-shal}-e}e€+-or-hås-eleete€l--tt+-s.xereis o{:i+s-optit+ns-te

eN+ell4+he-{enar-t#+he{}lnst

tr,anc{lcrx{*-e*thc+-bneae reÈ+he-St#}ease-thaÊ$+bto'r+ant-+n+ght-h+ve-hadtmdePth{rer-r

+ UaUle for enl'represefttåtior-+n+issi de+*@åore ge*ng-shalt.nsçrcfieve+andk¡rtlf +on+- aqv-liab i'li+y+o+'entetþ*eu+

lgâte#**¡--*en+e+y-pursu.tnr-+s-t¡eSublcv*s<l);

,{iubtenanf-mþl+t---har.e-againslrle-nar+l-*s-a-lcostilt-+>Èa*}-aetri-oroneis¡;ir*¡+s-sf lFenar*tr

2

$iubtc,nant-n+ayltwe-p*i*L+<#lìu+ant-n+ore-dralreme-(-1-)-:nor+th-in*d¡'mee of tne urcnt to wprepft iMe--anel-e+ving-te-I'arìÉ+:l€{d--+vi+h€{"t+rcgaxl-to-suc{r-prepayment-exeept-as-ma1'-ha+e-aett+ai-l-+-been

eri od*be-r'or*4+}rc-n*olt+h-ilrr+hiel+M

int+hexetr{:eftie {<+--**s*er-stl+er--easuttlt-*- or--t¡,-¡s¿son-of-aeonden+na+iont-unle@e+--undeþtjce+ut¡+ea*eis

v, li¿'

eonenvilonme*ta{-indenmi{ìe¿*io*-{t*--4ry.-le6{'iabili{y, e'kri*r-<*

n+-ee{ìùired-i+""

interes+i*+heBtri tái-ng¡

G-=lil=S+rglease-.,b++<sas@

i, lltie liaUltitv of Em e-fer_+affiag€#-o1-

i*es"(atù

e{efinerl-.in-+he--teaseþnelr*ef ing-'ents;--aet-+*le-pro eeeds--netrceeeds--thecetieæ.'

Ne m--employees-sha.rehsleler*i.ì+at{ru¡rs,-pì+r+eip*ls;-agent*-or-+er*-ants-<vf=tandlstetr

@?, =*:"N=e=x Lp=ssç, Il=-tlrç=j*pgç h f,srsdn=4,-Lsd=þr;lçaçe-s=qf==l"ç+a$llÞ. ç[=eJ=+glf

thereundeL, or bv ï su.fpLr-Clqf=qf-thgl=e¿se--4rc-rciççtiarroflhe lcase-ln

wi¡hiu-tbirtrl3-()) ¿avs foll owins of th

-l_ç,ase. the "Neil'Lease poses as of the date of fuI"p"minafioq.@

A. The Tenn of the Nerv shall exnire on I lr

lh-e- $rú l,e¡s,c" ttÌç_!.t$i ne a l l

3

þç,le,si,snçl= LJuf

Ç,,,, ,, - $.i.+;=ul1iÌp=çpuÞ--lx:yith=!=hg,çxs-c'slipn=çt,1tL-%N.ç==)=v:=I'p=sq=e=,=$==uþlç$+plsnatt rrav tne neUn

p,.rp.:-viçiççt=l'+ndle¿çl hß,ç, si*yç¡],"wittçn nstiç'ç,,1=o:$uþJ=-e=,n4t=,4, fthg li.Qe=linss-e'=$p-v=

Notice"l of sucn

no-t Latcr than s-ixt-v ffi_0-) days-al,ter-thc--da"tç"s'rchBayne¡.t "was*-d,u"ç"ancl n-o-x Baid, Acopv of anv notice of default fì'om Landlor<l to 'I'enant that is sent to SubtcnantsnaU ne ¿eeme¿ to U

Tçn"ant,[o I"and.lor-d-, or sf]r-e-r-wi.sç Le-c"o-yelçd by"l*a-ndlo-rd"-p-rior.-to--thelçlni¡atisn"llvent shall be cxcluilecl lì'orn the Delinqueff Amount.

ii, |lo other prepertj' or a.¡*ets of Landlerd or an)' proper+v-€fi.1..- l:.-,.^+,--- ^.f-'lì^,--^ ^.,*,.1^.,,.^. .-L^,'^1.^1Ä^-. n¡*i-a¡c

n. Extti¡it n toP-e-rni t-tsd E"xç"çn"ti"çn s",

g. _ Section Z t.0l of t"applic,ablç- ancl sh"all hç" d-e-lçtçct, from -thç N"e-\-v- Lcase-.

e. ilfo amendment, molNloclificalisn)" irr thc S"u"blçasç s-halJ be bind-ins on Landlerd u,nlç-s-s s-Lrch

M==o:çUfJçalisnhíN,hççnítp=prç"yeç1''þv:-L-a¡1çll-oJd,'ldiscretion.

I

thc Sub.lea-se"

4

M$,]rlkineJhisAel;ççmspl,g-L,i$,çsì+ilp=çlipnxilh,'lnvMoclificæion Le _bv feuant-$ubtenarrt oL Çuarantor, sh ferullor S-r"rh"tcna¡t and sha]l he de"çmscl "te be Acl-ditiona-l Rent -utìdçr -th"c l"qas"e. thç-

Sub!,:ase .a[cljbe-N ew Lease-

H, G""uar"alitor shall rsma.in habl,"ç f-o-L ali "o-b[ga'ti.c,"ns gf-T,ç.na"nl""and

tcasgiufuliqNe\ñ Lease, and shal

,liorm annçx-e-cl1o, t]rç l*casç "as- Exhihil D* l-her-e-t"o-,

:. tnterirn Non-nis inninf¡ on the date o

s+r.þl thp",$uþ=lsaçç þçv'pnç1.g,,-lll=æpliçaþl -shdfl.lotlr--qtc.l$r@gü-q!ì¡=sl,l4lt$-_eg4rËltts-q.-ræsse@=sqqtqrrxenrcIÉs=S-Lbtçslsl1¡çpri":ruJrçjr¡.çrlÞ¡s4-r.,:irl¡b:I"andlord'hçïsip:shr¡ll O=prç=rl..ç=¡li Lrt04lsliç1=fiprnpslm¡$=ç=pçisg sll= E+l=Ép,lni+e.anv ,?çIis$.srprocceditl{instituted to e reason of Tenant

qçf 'fu i-:!,h. ¡,p,, l,

uaintainfue any action or proceed

in ttris agLeernent (iiil Lequire ltbcJçnaulsobli.qa-tions as- l"ancll-cixl uncler the S.ublease.

+. fte guildins. Lan

t¡q=]¿=uilsling.,tne Su¡tease. PreProperl)."). In conside¡atio-n of'tlrc Subtçnaft's exec,ution of -the Ngu'Le-ase"

the LanclloLd's Lig SuhrcruLjulbe-sænrarner th,e Çonyçyscl ProBç.rty ,was cqnye::ed -fi,o""m Tçnant tg I"andiord in çp"mtçc1icn

wim,'t¡s==lp ltne ¡lew fease, as t

mamrer as tlle Con Èoperl adS-ubicnail aç:kn-o- w:ledee and -agre-e IhaX ;-Ìoi]r-ing hçrcin, in -the Lças--e- -p-r in 'thç SLrblease

exnlesslv set forth above.

5= 4-*--Covenants of Subtenam

5

,A-, ,Ç-subtenant agrees for the benefit of Landlord that Subtenant

will not pay any rent more than oneQne (1) month in advance of the month forwhich such rents accrue except as may be per .

B, Il--If any act or omission of Landlord or Tenant would give

Subtenant the right, immediately or after notice or lapse of a period of time orboth, to cancel or terminate the Sublease or to claim a partial or total eviction orconstructive eviction, Subtenant shall not exercise such right and no notice ofcancellation;g termination-t¡rabate+l+shall be effective, unless and until:

L i. Subtenant has given written notice of such act oromission to Landlord o[ -an-v: sric,p-çssor to l",andl.o-rd"o-JÌ-w]ic].r S-r-rb"tenanl".has

; and

ii, ü=Lancllgr"d or su-c. andlord shall have notcured the same within the time l-imi+sfpdods set forth in the Sublease'

NetwìthstanelinÊ the feregoing;if streh ele'f.ault is noleElab],*of etne

ì#i+hin:e-60_dayf€riotJ; theft previded th+t Landlo,rd Llas eemrneneed suelr

euru.'withi+the-60-daype+i,oÇthersu allbe-elxtende#so-kxrg

@ef+

Aureemenf .

tunde.l' tlæ Suhlease or rm)' eilreums+anee \ùhielr wêuld entitþ Subtenalí$-to eaßÊel or

teff{+inat$-+1.1e*--Sr}blease-or-.-aba+e-{he-+ents, ae{ditional-+enlv-or-ether-*un+.--p¿yaUlethE e+i*lea¿iem-is-d

ob,l+gæionl+o-eu¡*-sttelrdef-a*l+¡arxtr-$r+btenan+shall-not-tenfthmte-the-Sr*hle¿rse-ol-¿batet-he-rer

l'etr thirtï (30) days a,i+er Landlerd'+ reeei,q*rFsueþ*otieets-eure-st+eh-defäutrt-antl-æ'n*asor+¿r6|srpcriod-o1ìjme-ie-ad€liti€i1-+hereto4}++-+neeì,rÊHrnstanees-aïe

€Ð+"y*er;e+ eh*we;^-or'6Ðtinringnd--a*Te,r-anl-litìgat-i+en-aetio'r,r-ineiucling-a-tìxeck>surq-ba*rkruPtey-ptlssessol-h¿d{on-+r-æes*ila@ei*ea[y*gre Ar¿

f,mdtr+rd{++@6-

of and shallors and As This Agreement shall inure to the benefit

be binding upon Tenant, Landlord-and* Subtenant-an-d Guara¡1or, and their

respective successors and assigns.

7. @. This Agreement shall be governed by and

construed in accordance with the laws of the State of

6

without giving effect to any

principles of conflict of laws which would result in the selection or application of the law

of any other jurisdiction.

[email protected] parties to this Agreement in any number of separate countetparts, and all of said