Islamic Microfinance in the Contemporary World: a Survey of Its Prospects and Challenges in...

109

1 ISLAMIC MICROFINANCE IN THE CONTEMPORARY WORLD: A SURVEY OF ITS PROSPECTS AND CHALLENGES IN IJEBU-ODE, OGUN STATE, NIGERIA BY SANNI, AHMAD ABIODUN MATRIC NUMBER: 20050306018 A RESEARCH PROJECT PRESENTED TO THE DEPARTMENT OF RELIGIOUS STUDIES (ISLAMIC STUDIES UNIT), COLLEGE OF HUMANITIES, TAI SOLARIN UNIVERSITY OF EDUCATION IJAGUN, IJEBU-ODE, OGUN STATE IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF B.A (Ed) IN ISLAMIC STUDIES NOVEMBER, 2009.

Transcript of Islamic Microfinance in the Contemporary World: a Survey of Its Prospects and Challenges in...

1

ISLAMIC MICROFINANCE IN THE CONTEMPORARY

WORLD: A SURVEY OF ITS PROSPECTS AND

CHALLENGES IN IJEBU-ODE, OGUN STATE, NIGERIA

BY

SANNI, AHMAD ABIODUN

MATRIC NUMBER: 20050306018

A RESEARCH PROJECT PRESENTED TO THE DEPARTMENT OF

RELIGIOUS STUDIES (ISLAMIC STUDIES UNIT), COLLEGE OF

HUMANITIES, TAI SOLARIN UNIVERSITY OF EDUCATION

IJAGUN, IJEBU-ODE, OGUN STATE

IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE

AWARD OF B.A (Ed) IN ISLAMIC STUDIES

NOVEMBER, 2009.

2

CERTIFICATION

This is to certify that this project was carried out by Mr Sanni, Ahmad Abiodun with

Matric Number 20050306018 in the department of Religious Studies (Islamic Studies

Unit), College of Humanities, Tai Solarin University of Education, Ijagun, Ijebu-Ode,

under my supervision.

………………………. ……………………

Mr Adepoju, R .I. Date

3

DEDICATION

This work is dedicated to:

Almighty Allah, who has made what seemed mirage to me, a reality;

The memory of my late beloved father, Alfa Sa`dullah Adekunle Sanni whom I lost to

death at my final year;

And

Finally, to my guardian, mentor and financier, who has solely financed my undergraduate

course, Sheikh Ahmad Olalekan Abdussalam (Khalifah Ipamuren).

4

ACKNOWLEDGEMENT

I wish to express my profound gratitude to all those who have contributed in any way to

the success of this project and my undergraduate course at large.

My heartfelt appreciation goes to my supervisor Mr. Rasaq Idowu Adepoju for his belief

in my ability as well as his meticulous guidance and excellent suggestions. His fatherly

role is highly acknowledged. Despite his tight schedules, he has found time to give all the

needed attention which gave me a sense of belonging at all stages of this study. May his

fountain of knowledge never dry.

To all others who have taught me in the Department of Religious Studies, Islamic Studies

Unit: Dr. I.A. Seriki, Mr. A.O. Azeez, Mr. M.A. Lawal, Dr. F.O. Jamiu, Alh. G.A.

Ahmed, Mrs. N.Y Raji, Mr. T.A. Salako, Mr. W.A.E Adeleke and Alh. F.O. Lawal – I

say a big thank you for your immeasurable contributions to my greatness in life. May

God Almighty bless you all.

To whom I have spent half of my life with, as at the time of this writing, as a student,

disciple and personal assistant, my sheikh, mentor, guardian and sole financier of this

project and my course as a whole, Sheikh Ahmad Olalekan Abdussalam (Khalifah

Ipamuren), I am greatly indebted. I pray to Almighty Allah to spare his life, so that he

can see the seed he planted turn to an oak. I must say that he is a rare breed in the circle

of Zumratul-Mumin in Nigeria because he loves investment in human capital

development.

5

I also wish to express my profound gratitude to my parents who trained me to be dogged

in whatever I pursue in life and taught me good morals like self-discipline, humility and

service to others right from my tender age. I will always admire and remember you for

good, whether living or dead. Also, I earnestly thank my “mother” Alhaja Baseerat

Adedayo Badmus (CEO, TITMUS Fashion Institute). “Mum” you have been highly

instrumental to my academic success. I will always love you.

My sincere appreciation goes to my darling spouse, Hajia Balqees Adenike Olesin

(Ummu Fawzaan). I have deprived her of her several marital rights in pursuance of my

academic success to which she never raised an eyebrow. Her supportive role and

encouragement contributed in no small measure to the successful completion of my

course. Her personal commitment to success of this project is worthy of appreciation. She

personally typed this project and for several days, we burnt the night candle together. I

also thank my two children, Fawzaan and Sa`daan for being nice all through the period of

this study; They did not give me any cause for anxiety. May Almighty Allah nurture them

to greatness.

I am very grateful to Mrs. Zainab Adeola Kassim of Zakas Ventures who gave me 75%

discount on my computer print-outs. Her husband, Mr. Hassan G. Kassim played a vital

role in the successful completion of this project. His unflinching support and persistent

urge to complete the project are duly appreciated.

6

To Ustadh Ishaq O. Abdussalam Al-Muthny, Ustadh Hakeem Yusuf Aduhawy and all

other colleagues at Qal`at Ath-Thaqafah Ipamuren, I say your sincerity to me as regards

our job – has filled the vacuum which my course had created at the Arabic school. Thank

you one, thank you all! Specifically, my sincere appreciation goes to my mentee and a

colleague at the Arabic school, Ustadh Ahmad Adesina AbdulHameed Al-Ibejuwiy for

the time expended and assistance rendered during the administration of the questionnaire.

I am not forgetting to appreciate the confidence reposed in me by my coordinator,

Oyekolade Sodiq Oyesanya, Ustadh Qausim O. Ishaq, Imam Bashir A. Oniwasi and all

other course colleagues in Islamic Studies Unit, Department of Religious Studies

throughout our course. We lived and interacted in an atmosphere filled with love and

understanding. I would have loved to mention all their names but space did not permit

me. To them all, I say they are winners!

Lest I forget, my thanks go to all micro-enterprise owners at Olabisi Onabanjo (New)

Market and Oba S.K. Adetona (Oke Aje) market, who cooperated in filling the

questionnaire. Also, worthy of appreciation are some members of executive councils of

Al-Hayat Relief Foundation, Assalam Development Foundation and Itun-Metala Iwade

Islamic Foundation for taking their time to fill the questionnaire.

Above all, my most humble appreciation goes to Almighty Allah for all His mercies on

me before and during my course at the university. Thee alone I shall worship and depend

on.

7

TABLE OF CONTENTS

Title Pages

Dedication i

8

Certification ii

Acknowledgement iii

Table of contents iv

Abstract ix

CHAPTER ONE: INTRODUCTION 1

1.1 Background to the study 1

1.2 Statement of the problem 3

1.3 Research Questions 4

1.4 Purpose of the study 4

1.5 Objectives of the study 5

1.6 Justification for study 5

1.7 Scope of the study 7

1.8 Limitation of the study 7

1.9 Operational definition of Terms 8

1.9.1 Microfinance defined 8

1.9.2 Islamic microfinance: A definition. 9

CHAPTER TWO: LITERATURE REVIEW 10

2.1 Theoretical framework 10

2.1.1 Concept and models of microfinance in conventional finance 10

9

2.1.2 Concept of Islamic microfinance 15

2.1.3 Conventional and Islamic microfinance compared 16

2.2 Origin & development of microfinance in the world. 21

2.3 Practice of Islamic microfinance in the contemporary world 24

2.3.1 Models of Islamic microfinance in the contemporary world 24

2.3.2 Modes of financing in Islamic microfinance 30

2.3.3 Islamic microfinance practice across the globe 33

2.3.4 Prospects of Islamic microfinance in the contemporary world 44

2.3.5 Current challenges facing Islamic microfinance in the world 46

CHAPTER THREE: RESEARCH METHODOLOGY 49

3.1 Research design 49

3.2 Area of Study 49

3.3 Population for the study 51

3.4 Sample and Sampling Technique(s) 51

3.5 Research Instrument 53

3.6 Validity of the research Instrument 53

3.7 Method of data collection and analysis 54

3.8 Limitation of data 55

CHAPTER FOUR: DATA ANALYSIS AND DISCUSSION 56

4.1 Data presentation and discussion of findings 56

10

CHAPTER FIVE: SUMMARY, CONCLUSION AND

RECOMMENDATIONS 81

5.1 Summary of the study 81

5.2 Conclusion 83

5.3 Recommendations 84

References 86

Appendices (Instruments used) 93

ABSTRACT

Recently, there has been clamour in the world for “diversified” micro financial services

to reach those that are excluded from such services on the basis of faith or any other

11

distinction. This research work is interested in surveying the prospects and challenges of

Islamic (interest-free) microfinance in Ijebu-Ode

Thus, the work employs two sets of questionnaires in gathering data; one for the

microenterprises managers, while the other is designed to elicit information from the

providers of Islamic (interest-free) microfinance in Ijebu-Ode.

Though a total of 100 questionnaires were used in this research, only 73% were collected

and analyzed. The outcome of the analysis, after using descriptive statistics, is that there

is huge demand for the service as well as good prospects. The research also identifies

some challenges facing its providers in Ijebu-Ode.

Thus, in the light of the findings, recommendations are made, which should be given

significant consideration.

CHAPTER ONE

INTRODUCTION

1.1 Background

12

It was discovered that over one billion of the world population had lived under

unacceptable condition of poverty and most of the people belong to the developing

nations, particularly the rural dwellers in Asia and the pacific Africa. Also, over 30,000

people in the world die every day because they were too poor to stay alive

(triumphnewspapers.com). The problem had attracted attention of all stakeholders in the

world.

To solve this problem, governments, international development organizations as well as

local NGOs have been actively involved in providing credit and saving services in recent

years to the poor (Khan, 2008). Bangladesh as a country has been in frontline when it

comes to provision of microfinance as a result of activities of Grameen bank of Professor

Muhammad Yusuf who won the Noble Peace Prize in 2006. The success of Grameen

bank model has been replicated in many countries worldwide. Thus, since 1970s, a fast

and unprecedented growth has been recorded in the sector across the globe. Today, over

25 million poor people with women being the majority, are served by over 7000 micro

lending organizations worldwide. (Muhammad et al, 2008).

Research has shown that microfinance is considered a very effective tool for

development. For this reason, year 2005 has been declared by the General Secretary of

United Nations “International Year of Microcredit”. Microfinance is also seen as a very

flexible tool that is adaptable to every environment, on the basis of local needs and

economic and financial situation (Segrado, 2005).

13

However, microfinance mostly involves conventional interest-based finance whereas

majority of poor Muslims would prefer to have interest-free finance in preservation of

their faith and in accordance to Shari’ah dictates. This has led to emergence of Islamic

microfinance today.

According to UNDP report, two-thirds of Nigeria population of about 150million and

GDP/capita of $641 (2006) - are poor. This makes Nigeria the third poorest country in the

world. Over 75million (54.7%) Nigerians live below the poverty line of $1 per day, in a

country where the life expectancy is 47. (BBC News, 17/04/2007).

It is on record that only 35% of the economically active population of Nigeria is served

by the formal and conventional banks, while the remaining 65% are excluded from

financial services. These 65% who are mainly poor people turn to the informal financial

sector, through NGO microfinance institutions, credit unions, money lenders,

etc.(Iganiga, 2008). Most of these poor people depend on micro and small scale farm and

off-farm enterprises to earn their living. This shows there is huge market for microfinance

in Nigeria. However, the CBN survey indicated that only 600,000 people were served by

the microfinance industry in 2001 and that they may not be above 1.5 million in 2003

(Anyanwu, 2004).

As at the time of this research, Nigeria has 898 licensed microfinance banks (MFBs)

operating in the financial sector (microfinance bank, 2008). For a country with a

population of 150 million or thereabout the number seems grossly inadequate. Even,

14

research recorded that the microfinance institutions in Nigeria charge high interest rate in

lending (up to 100%) and pay low interest rate for saving (as low as 5%). This aggravates

the poverty in the land (Muhammad et al, 2008).

In an attempt to solve the above pictured problem, CBN Governor, Sanusi Lamido

Sanusi, has emphasized the need for diversified and specialized financial services in the

country with particular reference to Islamic finance. It is against this development that

this study is conceived.

Considering the fact that, the majority of those who need microfinance in Nigeria are

Muslims, this study sets out to find out the viability of Islamic microfinance in Nigeria

with particular reference to Ijebu-Ode.

1.2 Statement of the problem

Recently, a lot of efforts are being made in the field of microfinance to provide interest-

free financial services in some Muslim countries while some are yet to join the train.

Nigeria as a Muslim country falls among the latter category, though there has been

consciousness and desire among the Nigerian Muslims to have access to shari`ah-

compliant microfinance (Muhammad et al, 2008). Noting Nigeria to be not fully a

Muslim nation, what are the likely problems to be faced with Islamic microfinance efforts

as well as likely prospects?

1.3 Research Questions

This research intends to answer the following questions:

15

i. Is there any demand for Islamic microfinance in Nigeria with particular reference

to Ijebu-Ode?

ii. Does Islamic microfinance have any prospects in Nigeria, particularly Ijebu-Ode?

iii. What are the challenges facing Islamic Microfinance providers in Ijebu-Ode?

1.4 Purpose of the study.

The purpose of this study is to examine the concept of Islamic Microfinance and x-ray its

practice in the contemporary world. The study also seeks to survey its prospects and

challenges in Nigeria, with a particular reference to Ijebu-Ode. Thus, the findings of this

work shall serve as source of information for existing and prospective providers of

Islamic microfinance in Nigeria with particular reference to Ijebu-Ode.

1.5 Objectives of the study

The major objective of this study is to survey the prospects and challenges of Islamic

(interest-free) microfinance in Ijebu-Ode, Ogun state.

1.5.1 Specific objectives

The specific objectives of the study are:

To identify and describe the socio-economic characteristics of the microenterprise

owners in the study area

To identify the sources of financing available to them.

To find out tendency and frequency rate of accessing interest-free loan, as well as

its likely sizes, if available to them.

16

To determine the level of preference for Islamic (interest-free) microfinance in the

study area.

To find out how long have Islamic (interest-free) microfinance providers been in

the study area as well as their nature.

To identify challenges facing Islamic (interest-free) microfinance providers in the

study area and suggest solutions to them.

1.6 Justification of the study

The Nigerian Microfinance sector has come a long way. As of 2001, there were 160

registered MFIs in Nigeria, according to a CBN study, with aggregate savings worth

N99.4 million and outstanding credit of N649.6 million (Anyanwu, 2004). However, the

existing microfinance in Nigeria serves less than 1million people out of 40million

potential people that need the service (CBN, 2005 cited in Muhammad et al, 2008). Also,

the total microcredit facilities in Nigeria, account for about 0.2 per cent of GDP and less

than 1 per cent of total credit to the economy.

Further, the commercial sectors are funded by most microfinance institutions to the

detriment of the agricultural and manufacturing sectors that sustain growth and

development. Statistically, only about 14.1 and 3.5 per cent of total microfinance funding

went to these latter sectors respectively, while the bulk, 78.4 per cent, was channeled to

commerce (Anyanwu, 2004). Islamic microfinance now has the potential of funding the

agricultural and manufacturing activities of majority of poor Nigerians and those who

17

have eschewed the conventional microfinance due to its incompatibility with their faith

(Muhammad et al, 2008.). Thus this kind of study that centers on Islamic microfinance is

justified considering the fact that only in Kano, Ilorin and Lagos could one find

microfinance institutions with Islamic window as at the time of this research.

It is hoped that this study will help the policy makers, researchers and practitioners on the

field appreciate the concept of Islamic Microfinance and see its huge market in Nigeria

and particularly Ijebu-Ode.

This study is thus important for all stakeholders in Microfinance industry and Muslim

NGOs that engage in Islamic Microfinance in Nigeria, particularly Ijebu-Ode.

1.7 Scope of the study

Though, this work intends to examine the practice of Islamic Microfinance in the

contemporary world, its scope shall be Nigeria, particularly Ijebu-Ode with focus on its

prospects and challenges. The concept of Islamic Microfinance is examined from Islamic

perspectives in the light of its practice in selected Muslim countries. Also covered is the

overview of Microfinance in Nigeria.

However, the survey of the prospects and challenges of Islamic Microfinance is restricted

to Ijebu-Ode, the second largest city in Ogun State, Nigeria, according to world-

gazetteer.com. It is therefore difficult to generalize findings to all other parts of the

country.

1.8 Limitation of the study

18

Work of this kind at this educational level cannot claim to be comprehensive. It is always

faced with problem of time because it is meant to be completed at a specific period. This

led to the restriction of the survey to Ijebu-Ode alone.

Another problem faced by the researcher is his inability to lay his hands on published

books on the subject matter. Thus, the work depends heavily on journal articles and

reports accessed on the internet. Other constraints to this research include the lack of co-

operation on the part of the respondents to give candid responses to the questions posed

to them, among others.

The study is also limited due to the fact that Islamic Microfinance is relatively new in the

academic and financial circles in Nigeria. As such, little works are available on the

subject and thus limiting the sources of information for this work.

1.9 Operational definition of terms

1.9.1 Microfinance

According to Microcredit Summit 1997 (cited in Abdul Rahman, 2007), microfinance

means extension of small loans to very poor people for self employment projects that

generate income in allowing them to take care of themselves and their families.

However, there are some terms often used interchangeably with microfinance. These

include microcredit and microenterprise credit. It must be noted that there are slight

19

distinctions between the three terms. Microcredit, according to Steger, et al (200), is to

provide credit services to people who do not have access to traditional banking services

because they lack expected collateral. The term Microenterprise credit refers to credit

invested in the Microenterprise and thus excludes use of cash for other purposes (Khan

2008).

From the foregoing, it is obvious that microfinance is a wider term that encompasses both

Microcredit and microenterprise credit.

1.9.2 Islamic microfinance

Islamic microfinance is the micro financial services based on and governed by Islamic

financial principles of prohibition of interest, profit and loss sharing and avoidance of

uncertainty and speculation (Gharar) (Al-Tamimi and company).

CHAPTER TWO

LITERATURE REVIEW

2.1 Theoretical framework

2.1.1 Concept and models of microfinance

The term microfinance has been adequately described and conceptualized by various

scholars. Different finance experts have given different meanings to the concept. To one

source, microfinance is the provision of financial services to low-income clients,

20

including consumers and the self-employed, who traditionally lack access to conventional

banking and related services (Wikipedia.org). Similarly, Wilson (2007) & Obaidullah and

Khan (2008), all posited that microfinance involves the provision of financial services for

those too poor to have access to conventional banks.

Ledgerwood (1997), cited in Dusuki (n.d.), expanded the above definition

when he wrote:

microfinance is the provision of financial services to low-income

clients including self-employed, low-income entrepreneurs in both

rural and urban areas. Thus, microfinance is seen as an economic

development approach intended to address the financial needs of

the deprived groups in the society and with ultimate goal of

making them self sufficient by means of saving, borrowing and

insurance.

Another definition puts microfinance as a type of banking services that is provided to

unemployed or low-income individuals or groups who would otherwise have no other

means of gaining financial services (microfinance, n.d.). Kimotha, 2005 (cited in Iganiga,

2008) defined microfinance simply as the provision of very small loans to the poor, to

help them engage in new productive business activities and/or to grow/expand existing

ones.

21

To Encyclopedia Britannica, microfinance is nothing but a means of extending credit,

usually in the form of small loans with no collateral, to nontraditional borrowers such as

the poor in rural or undeveloped areas. It is also the granting of financial services and

products such as very small loans to assist the exceptionally poor in establishing or

expanding their businesses (The American Heritage Dictionary of Business Terms,

2009). What is central to all the definitions given above is the description of microfinance

as banking for the “unbankable” poor.

Referencing Linari-Pierron and Flatter (2009), the concept of microfinance has to do with

the supply of loans, savings, insurance, transfer services and other financial products to

people who are traditionally excluded from the traditional banking system, mainly due to

their lack of guarantees which can protect a financial institution against a loss risk.

Though, not the most comprehensive definition of the concept, the definition given in this

paragraph points out some of the financial services usually rendered by microfinance,

which include microloans, micro-savings, micro-insurance, among others.

In addition to such financial services which include microcredit, savings and micro

insurance, microfinance entails provision of social intermediation services such as skill

trainings (Steger, et al 2007).

From the literature, microfinance is seen as a powerful tool for reaching the poor, raising

their living standards, creating jobs, boosting demand for other goods and services,

contributing to economic growth, and alleviating poverty (Sapcanin and Dhumale, n.d.).

22

However, microfinance is characterized, according to Fruman and Godberg (1997) (as

cited in Sapcanin and Dhumale, n.d.), by:

- Small, usually short-term loans and secure savings products.

- Streamlined, simplified borrower and investment appraisal.

- Alternative approaches to collateral.

- Quick disbursement of repeat loans after timely repayment.

- Above-market interest rates to cover high transaction costs inherent in micro.

- High repayment rates.

- Convenient location and timing of services.

All these characteristics that distinguish microfinance from other formal financial

products were summarized by Iganiga, (2008) as:

a. The smallness of the loans advanced or savings collected.

b. The absence of asset-based collateral and

c. Simplicity of operations.

Moreover, microfinance has a number of distinctive models, reflecting its evolvement in

different environments. However, leading microfinance models – according to

Obaidullah (2008) - include, but not limited to:

Grameen Bank model: is based on joint liability. Under this model, individuals come

together to form small groups of five each, while 10-15 groups form a center. Members

of groups are trained regarding the basic elements of the financing and the requirements

23

they will have to fulfill in order to continue to have access to funding. Financing of any

member of a group is subjected to the approval and guarantee of other members in the

group. This model is noted for shared responsibility where performance of any member

affects the whole group. Loan repayment schedule is usually weekly and for maximum of

50 weeks. In a nutshell, the key feature of this model is group-based and graduated

financing that substitutes collateral as a tool to mitigate default and delinquency risk.

However, this model has been replicated in many countries.

Village Bank model: involves implementing agency that established individual village

banks with 30-50 members and provides “external” capital for onward financing to

individual members. Individual loans are repaid weekly over a period of 4 months, at

which the village bank returns the principal with interest to the implementing agency.

Grant of subsequent loans are based on the full-repayment of earlier loan by village,

while the loan sizes are determined by the performance of village bank members in

savings accumulation. Like Grameen model, peer pressure is employed in maintaining

full loan repayment, assuring further injection of fund and encouraging savings.

Accumulated savings in a village bank is also put to financing. On accumulation of

sufficient capital internally, a village bank graduates to become an autonomous and self-

sustaining organization usually over a three-year period. This model is widely replicated

mainly in Latin America and Africa.

24

Credit Union model: The key feature of this model is concept of mutuality. It is owned

and controlled by its membership which based on common bond. Credit union mobilizes

savings, provides loans for productive and provident purposes. Such unions relate to an

apex body that promotes primary credit unions and provides training, while monitoring

their financial performance. Credit unions are quite common in Asia, notably Sir Lanka.

It is also practiced in Nigeria.

Self-Help Group model (SHG): This model originated from India. Each SHG comprises

about 10-15 members who are relatively on the same level of income. Members of SHG

pool savings together for the purpose of lending. SHGs also seek external funding to

supplement its internal resources. Depending on the democratic decisions of members,

the terms and conditions of loan differ among SHGs. Further, SHGs are promoted and

supported by NGOs with object of becoming self-sustaining. However, this model gives

room for combination of microfinance with other developmental activities.

Of all the models, both Grameen model and village bank are more structured than the rest

and have enhanced outreach. Indeed, Grameen model has become the typical model for

microfinance.

2.1.2 Concept of Islamic microfinance

Islamic finance and microfinance are the latest buzzwords in the world today (Frasca,

2008). Islamic microfinance represents the confluence of two rapidly growing industries:

microfinance and Islamic finance. It is seen as the combination of Islamic principle of

25

caring for the less fortunate with microfinance`s power to provide financial access to the

poor (Karim, Michael and xarier 2008). It is the micro financial services based on and

governed by Islamic financial principles of prohibition of interest, profit and loss sharing

and avoidance of uncertainty and speculation (Gharar) (Al-Tamimi & company; Allen &

Overy, 2008).

Islamic microfinance could be therefore defined as the provision of Shari`ah-compliant

financial services which include microcredit, micro-saving, etc to the poor and the

poorest who are denied access to such services in the conventional finance.

In other words, the ethical values of Islam combined with the social goals of

microfinance brought about a new tool for development, Islamic microfinance (Faussone,

2008). Similarly Ziauddin, 1991 (cited in Dhumale & Sapcanin, 2007) contented that

Islamic microfinance is an Islamic alternative to the conventional microfinance that is

based on riba (interest).

Furthermore, the ultimate goal of Islamic microfinance is the maximization of social

benefits as opposed to profit maximization, via creation of healthier financial services for

the grass roots (Segrado, 2005).

2.1.3 Conventional and Islamic microfinance compared

Most of the underpinning elements of the conventional microfinance are embedded in

Islamic microfinance. However, there are convergences and divergences between the

two.

26

Both focus on developmental and social goals and advocate financial inclusion,

entrepreneurship, partnership and participation by the poor (Obaidullah & Khain, 2008).

Other than being interest-free, Islamic microfinance differs from conventional

microfinance in several important ways. Despite being banking for the poor, the

conventional microfinance does not cater for the poorest of the poor who do not engage

in entrepreneurial activities. On the other hand, Islamic microfinance system identifies

being the poorest of the poor as the primary criterion of eligibility for receiving Zakah or

Sadaqah, which is part of its services.

The work of Ahmed (2002) has adequately compared and contrasted between the Islamic

microfinance and conventional microfinance. He used nine criteria to do this. These are

briefly encapsulated below:

1. Sources of Funds:

On the liability side, the sources of funds of conventional microfinance are

mainly from foreign donors, while Islamic microfinance, in addition, have access

to funds from religious institutions such as Zakat and Waqf .

2. Modes of Financing:

27

On the asset side of the balance sheet, the volumes of the assets of the

conventional microfinance are interest-bearing debt. On the other hand, the assets

of Islamic microfinance comprise of non-interest-bearing financial instruments.

3. Financing the Poorest:

Extreme poverty causes diversion of funds from productive activities to

consumption and asset acquisition and results to lower rate of loan repayment.

Hence, conventional microfinance often leave out the poorest section of the

population. The Islamic microfinance, however, can employ the institutions of

Zakat and other forms of voluntary charity to finance the poorest people.

4. Amount of Funds Transferred to Beneficiaries:

Once a loan is authorized in conventional microfinance, part of the principal is

deducted for different funds (group and emergency funds) and the effective rate

of interest payable on the loan is increased, because the rate will be calculated on

the principal. Also, it is easy to divert funds. Rather, under Islamic microfinance,

no deduction is made and the probability of fund diversion is highly low because,

goods are mostly transferred.

5. Group Dynamics:

There will be some qualitative differences in the group dynamics of the

beneficiaries of Islamic microfinance compared to that of conventional one.

Group guarantee in repaying the funds back to the Islamic microfinance

28

institutions may take form of kafalah, making the group members guarantors for

repayment. They may provide qard-hasan (interest-free loans) to the person

facing the problem in repaying the installments.

6. Social Development Programme:

The social development programme of Conventional microfinance institutions is

secular and sometimes anti-Islamic. On the other hand, the Islamic microfinance

institutions’ social development programme is purely guided by Islamic

principles.

7. Objectives of Targeting Women:

The objective of targeting women in the conventional microfinance is to empower

them and increase their self-respect. However, this rationale has been refuted by

recent researches. Though the majority of beneficiaries of Islamic microfinance

institutions are women, their target group is family because both the woman and

the spouse sign the contract and are liable to repayment of the funds.

8. Work Incentive of Staff Members:

The employees of Islamic microfinance institutions, unlike their counterparts in

conventional microfinance, not only work to earn their living, but also see their

work as religious duty.

9. Dealing with Default:

29

Conventional microfinance institutions often result, if group pressure fails, to use

of threat and selling off assets of defaulters.

Items Conventional MFI Islamic MFI

Liabilities (Source of Fund) External Funds,

Saving of client

External Funds, Saving of clients,

Islamic Charitable Sources.

Asset

(Mode of Financing)

Interest-Based Islamic Financial Instrument

Financing the Poorest Poorest are left out Poorest can be included by

integrating with microfinance.

Funds Transfer Cash given Goods Transferred

Deduction at Inception of

Contract

Parts of the Funds

Deducted at Inception

No deduction at inception

Target group Women Family

Objective of Targeting

Women

Empowerment of

Women

Ease of Availability

Liability of the Loan (which

given to women)

Recipient Recipient and Spouse

Work incentive of

Employees

Monetary Monetary and Religious

Dealing with Default Group/Center Group/Center/Spouse Guarantee

30

pressure and threat and Islamic Ethic

Social Development

Program

Secular (non-Islamic)

behavioral, ethical,

and social

development)

Religious (includes behavior,

ethics and social

Source: Ahmed, H. (2002). Financing Microenterprises: An analytical Study of Islamic Microfinance Institutions.

2.2 Origin and development of microfinance in the world.

Seibel (2004) refutes the claim that microfinance was originated in Bangladesh in early

1970s. Indeed, microfinance has evolved and passed through many stages. Thus,

microfinance has a very long history of more than 3,000 years. In India, microfinance

was active more than 3 millennia while various rotating savings systems and credit

associations have been in existence for more than 5 centuries in Africa and South

America (Stager, U. et al, 2007).

The evolution of microfinance in Europe dates back to 18th century. In Germany, it began

some 150-200 years ago through self-help movement. The first thrift society was founded

in Hamburg in 1778, the first community bank in 1801 and the first urban and rural co-

operative credit associations in 1850 and 1864 respectively (Seibel, 2004).

Even, in Ireland, microfinance dates back to 1720s with the creation of the so-called Irish

loan funds. This fund initially provided interest-free loans to poor households using peer

monitoring as the key to enforce repayment (Steger, U et al, 2007). But, after a century of

31

slow growth, a special law was made in its favour in 1823, which turned the charities in

Ireland into financial intermediaries by allowing them to collect interest-bearing deposits

and to charge interest on loans. Meanwhile, the fierce competition with commercial

bankers and later legal restrictions led to gradual and final disappearance of the Irish

funds in the middle of the 19th century (Steger, U. et al, 2007).

In the rural regions of Latin America and south-east Asia, adaptations of the German and

Irish models surfaced in the early part of the 20th century. These institutions mostly

owned by government agencies or private banks became inefficient. The aim of these

institutions was to build up the agricultural sector by encouraging savings and providing

credit which resulted in increased investment. This system turned out to be neither

efficient nor sustainable (Steger. U. et al, 2007).

In Africa, the earliest evidence of financial institutions dates back to the 16th century.

Then, the institution known as esusu, a rotating savings and credit association was

practiced among the Yoruba. It was through the slave trade that this practice was

transported to the Caribbean islands and then to major cities of America. This institution

has also spread to Liberia, Congo and Zaire (Seibel, 2004).

The rise of the modern microfinance is traceable to the creation of Grameen Bank by

Professor Muhammad Yunus in 1976 in Bangladesh. This modern microfinance

movement in Bangladesh began as an experimental program, in which groups of poor

women with no collateral were given small loans at high, but not unfeasible interest rates

32

from a state funded NGO to invest in productive activities (Frasca, 2008). The success

recorded by the Grameen Bank and similar institution rekindled the international interest.

This led to massive support of such initiatives and many NGOs launched their own

microfinance programmes (Steger, et al, 2007).

In Nigeria, micro-financing is not new as evidenced by such cultural economic activities

as “Esusu”, “Adashi”, “Otataje”, etc. These have served as sources of funds for producers

in Nigerian rural communities (Iganiga, 2008).Virtually, every ethnic group has its own

institutions and most adults are members in one or several (Seibel, 2004).

With regards to Ijebu-Ode, microfinance has been and are still provided by various co-

operative societies, microfinance banks, money lenders, and NGOs. Prominent among the

NGO providers of conventional microfinance in Ijebu-Ode are Ijebu-Ode Development

Board on Poverty Reduction (IDBPR) and Justice, Development and Peace Commission

(JDPC).

2.3 Islamic Microfinance Practice in the Contemporary World

2.3.1 Models of Islamic microfinance in the contemporary world

There are three models of Islamic microfinance as postulated by Obaidullah (2008). They

are:

Mission (Charity)–Based Non-Profit Model.

Market-Based For-Profit Model, and

33

Composite (mixed) Model.

However, each of these models shall be briefly examined in the light of the work of

Obaidullah (2008).

2.3.1.1 Mission (Charity)-Based Non-Profit Model

The mission (charity) –based non-profit model of Islamic microfinance

involves several not-for-profit mechanisms such as, sadaqa, zakah, awqaf, and qard-

hassan. Sadaqa includes various forms of charity, such as tabarru`at (donations), heba

(gift), infaq (charitable spending).

Indeed, sadaqa connotes any act of kindness and charity. Sadaqa can be collected under

this model of Islamic microfinance and be given to the poorest of the poor without

expecting any return. Sadaqa can also be employed in settling the defaulted loans.

In addition, Zakah funds may be used in providing start-up capital for micro-enterprises

either as grants or interest free loan, or micro-equity without expectation of returns

depending upon their degree of their vulnerability. Hence, zakah fund will help the poor

to generate sustainable means of livelihood and get transformed from being zakah

recipient into the category of zakah payers. This could be through provision of revolving

credit via qard hasan loans out of pooled zakah proceeds.

However, management of zakah fund from an (Islamic) microfinance view point raises

two questions:

(1) Should the poor be granted loans or grants? and,

34

(2) Should the zakah funds be invested in mudarabah and other shari`ah compliant

investments.

It is noted, regarding the first issue, that there is inadequate and erratic flow of zakah fund

in contemporary Muslim societies. Also, worthy of mentioning is the fact that giving out

interest-free loan from pooled zakah funds is not meant for the poorest of the poor and

often leads to their further indebtedness if they take such loans at all. Indeed, this violates

the very essence of zakah – of pulling an individual out of indebtedness.

Regarding the second issue raised, Obaidullah (2008) concluded that if there is

undistributed surplus, which is highly not feasible in the current poverty-ridden Muslim

societies, such fund may be invested in short-term basis but not in high risk avenues.

Waqf, which is one of the not-for-profit mechanisms, is defined as an inalienable

endowment in Islam. Put in another words, it is the “holding of certain physical assets

and preserving it so that it benefits continuously flow to a specified group of beneficiaries

or community” (Obaidullah, 2008). Thus, it could be concluded that waqf is basically

characterized by perpetuity and specification of its use.

Moreover, waqf is categorized into three categories: religious waqf, which refers to

properties confined for generation of revenues for maintenance and settling of recurring

expenses of mosques; family waqf, which the children and descendants of the endower

have a first right to its benefits and revenues; and lastly philanthropic waqf, which target

is provision of benefits to the poor segments of the society (Obaidullah, 2008).

35

Further reference to Obaidullah (2008) reveals that to achieve the object of Islamic

microfinance, i.e. poverty alleviation, the philanthropic waqf has a major role to play.

Under this mission (charity)–based not-for-profit model, another mechanism is qard

hasan. Literarily, qard hasan means a beautiful loan. It is a loan granted by the lender

without expectation of any return on the principal. From the standpoint of a microfinance

institution, a qard hasan may be seen as an instrument of savings mobilization and

financing. As a financing mechanism by a microfinance institution, qard hasan gives the

advantage of placing cash in the hands of the borrower for consumption or productive

use. However, it must be noted that provider of qard hasan is allowed to recover the cost

of operations from the borrower. Such charge should not be linked with the time or

quantum of the loan (Obaidullah, 2008).

However, a typical model of non-profit Islamic microfinance which combines all the

above-explained three mechanisms is succinctly described in terms of eleven (11)

activities as follows:

1. Islamic Microfinance Institution creates a zakah fund with contribution from

muzakki, zakah payers;

2. Programme facilitates Waqf of physical assets as well as monetary assets. The

physical assets are used to facilitate education and skills training. The monetary

assets may be in the form of a cash waqf, or simply as ordinary sadaqa;

36

3. Program carefully identifies the poorest of the poor and the destitute who are

economically inactive and directs a part of zakah towards meeting their basic

necessities as grant, seeks to provide a safety net;

4. Program provides skills training to economically inactive, utilizing community-

held physical assets under waqf;

5. Beneficiaries graduate with improved skills and managerial acumen;

6. Beneficiaries are formed into groups with mutual guarantee under the concept of

kafala;

7. Financing is provided on the basis of qard hasan to the group; also to individuals

backed by guarantee under the concept of kafala;

8. Group members pay back and in turn, are provided higher levels of financing;

9. Additional guarantee against default by the group is provided by the zakah Fund

and actual defaulting accounts are paid off with zakah funds; this is indeed the

distinct feature of this model;

10. Group members are encouraged to save under appropriate micro-savings

schemes;

11. Group members are encouraged to form a takaful fund to provide micro-insurance

against unforeseen risks and uncertainties resulting in loss of livelihood, sickness

and so on (Obaidullah, 2008).

37

This model is distinguished by the use of kafala (mutual guarantee) as a guarantee

mechanism at the group or individual level.

2.3.1.2 Market–Based For–Profit Model.

Microfinance in Islam need not be restricted to not- for-profit model only, because unlike

this model which caters majorly for the poorest of the poor, the economically active poor

people are financed under the for-profit model to generate wealth for themselves, Islamic

microfinance and the larger society. Thus, for-profit model provides financial

sustainability for Islamic microfinance institution. According to Obaidullah (2008),

among services to be provided by for-profit model are: wadia – microsavings, micro

credit, micro Leasing, micro – Equity, etc.

All these models of financing in Islamic microfinance shall be reviewed under the sub-

title of modes of financing in Islamic microfinance.

2.3.1.3 Composite (Mixed) Model

This is the combination of the both mission (charity) –based and market – based into a

composite. This model is presented by Obaidullah (2008) as follows:

1. Islamic microfinance Institution creates a zakah;

2. Program facilitates waqf of physical assets as well as monetary assets. The

physical assets are used to facilitate education and skills training. The monetary

assets may be in the form of a cash waqf, or simply as ordinary sadaqa;

38

3. Program carefully identifies the poorest of the poor and the destitute who are

economically inactive and direct a part of zakah founds towards their basic

necessities as grant, seeks to provide a safety net;

4. Program provides skill training to economically inactive, utilizing community-

held physical assets under waqf;

5. Beneficiaries graduate with improved skills and managerial acumen;

6. Beneficiaries are formed into groups with mutual guarantee under the concept of

kafala;

7. Financing is provided using a combination of for-profit debt-based modes, such

as, bai`-muajjal, ijara, salam,istisna or isijrar or equity-based modes, such as,

mudarabah or musharaka or declining musharaka;

8. Group members pay their debt, and perform and meet the expectation of the

equity providers and, in turn, are provided higher level of financing;

9. Guarantee against default by the group provided by the Zakah Fund and actual

defaulting accounts are paid off with zakah funds;

10. Group members are encourage to save under appropriate micro-savings schemes;

11. Group members are encourage to form a takaful fund to provide micro-insurance

against unforeseen risks and uncertainties resulting in loss of livelihood, sickness

and so on.

39

2.3.2 Modes of financing in Islamic MicrofinanceA review of a work by Obaidullah

& Khan (2008) indicates that all modes of financing under Islamic microfinance can be

broadly categorized into four categories, namely:

Participatory profit-loss-sharing (PLS) modes such as mudarabah and

musharakah.

Sale – based modes, such as murabarah,

Lease – based modes, such as ijarah, and

Benevolent loans or qard hasan with service charge.

Meanwhile, a technical note by Dhumale, R and Sapcanin, A (n.d.) classified all the financing

schemes under Islamic microfinance into just two categories vi-a-viz profit and loss-sharing.

Here, all the last three categories in Obaidullah and Khan (2008) are grouped under the profit and

loss-sharing and non-profit and loss-sharing schemes. However, all the financing modes will be

briefly reviewed.

2.3.2.1 Profit and Loss-sharing schemes

Under a mudarabah scheme, both the microfinance institution and the microenterprise

are partners with the former investing money and the latter investing labour (Segrado,

2005).

40

However, the profits from the project are shared on pre-agreed ratio between the

institution and the entrepreneur. Financial losses are assumed by the institution only

while the liability of entrepreneurs is limited to his/her time and effort.

Another form of Mudarabah is Muzar`ah which is trustee financing in farming. In this

context, the institution provides land or funds in return for a share of the harvest (Khan,

2008.).

Musharakah, in this context, is an equity participation contract between the Islamic

microfinance institution and the microenterprise. Under this arrangement, both parties

contribute both the capital and the expertise to the investment. Both profit and losses are

shared according to the amounts of capital invested. Also, musaqat is another specific

type of musharah employed in financing orchards. Under this scheme, the harvest is

shared among all the equity partners according to their contributions (Abdul Rahman,

2007).

2.3.2.2 Non-Profit and Loss-sharing schemes

Qard Hasan involves loans with zero return. However, it must be noted that Islamic

microfinance institution can charge a service fee to cover the administrative and

transactions costs, provided such charges are not linked with the maturity or quantum of

the loan (Sapcanin & Khan, n. d.).

Another scheme here is bay` mu’ajjal. It is a spot sale in which the Islamic microfinance

selling a product accepts deferred payments in installments or in a lump sum. The price is

41

agreed on between the buyer and the Islamic microfinance at the time of sale and under

no circumstance can the Islamic microfinance add any charge for deferring payment.

(Abdul Rahman, 2007.)

Similarly to bay’ mu’ajjal is murabahah. This is commonly used for short-term

financing. This scheme is very close to the conventional concept of purchase finance. In

other words, it is cost plus mark-up sale. The Islamic microfinance reports the actual cost

of acquiring or producing a good to the micro-enterprise and thus, a profit margin is

negotiated between the two parties. Payment is usually in installments (Khan, 2008).

Another non-profit and loss-sharing scheme is bay’ salam and bay’ salaf. Both entail

payment of the fully negotiated price of a product by a micro-enterprise which the

Islamic microfinance promises to deliver at a future date. However, the quantity and

quality of the product involved must be explicitly specified at the time of the contract

(Sapcanin & Khan, n.d.).

Ijarah wa`iqtina involves pure leasing (ijarah) or lease purchase (ijarah wa’iqtina’)

transactions. Under the ijarah Islamic microfinance institution leases a specific product

for a specific sum of money for a specified period of time. In Ijarah wa’iqtina’ (lease

purchase), a portion of each payment is applied to the final purchase of the product at

which time ownership is transferred to the leasee. (Khan, 2008; Abdul Rahman, 2007.)

Finally, Jo`alah are service charges. Islamic microfinance institution charges users of its

services like skill-training a specified fee. (Sapcanin & Khan, n.d.)

42

However, it must be noted that the major difference between profit-loss-sharing schemes

and non-profit-loss-sharing schemes is that returns for the former may be calculated at

the final stage as a fixed percentage of the total investment.

2.3.3. Islamic microfinance practice across the globe

Presently, Islamic microfinance is concentrated in a few countries and accounts for just

about 0.5% of the global microfinance despite a global Muslim population of about 1.2

billion which accounts for about 20% of the current world population (CGPA, 2008).

However, the table 1 below shows the outreach of Islamic microfinance by country:

43

Source: CGPA Survey Report, 2008.

However, for proper review of the practice of Islamic microfinance across the globe, the

world shall be straddled into major five regions viz-a-viz:

44

Middle East North Africa (MENA),

South Asia,

South East Asia,

Central Asia, and

Sub-Saharan Africa.

2.3.3.1 Islamic microfinance practice in Middle East North Africa (MENA)

According to Obaidullah & Khan (2008), three successful experiments have been taken

recently in this region. They include:

1. the Jabal Al-hoss “Sanadiq” (village banks) in Syria. This experiment has the

following features:

musharakah – type structure owned and managed by the poor;

financing based on the concept of murabahah – high profit rates with net profits

shared among members;

good governance through committees with sound election and voting procedures;

project management team responsible for creating awareness of microfinance

practices, training of committee members;

financial management of the funds via promulgation of by-laws and statutes for

each of the village funds resulting in “fair” credit decisions and low transaction

costs;

financially viable operations with repayment rates close to hundred per cent;

45

equal access to both males and females as owners and users;

sanadiq aoex fund for liquidity exchange and refinancing; and

support from UNDP in the form of matching grant equal to minimum share

capital of village fund.

2. The Mu`assasat Bait Al-mal. This is based in Lebanon and an affiliate of a

political party, the Hezbollah. It has two sub-institutions, namely: Hasan Loan

Institute (Al-Qard Al-Hasan) and Al-Yusor for finance and investment (Yusor lil

Istismar wal Tamweel). The former engages in qard al-hasan financing, while the

latter provides financing on profit-loss-sharing mode. This program is unique and

characterized by its emphasis on voluntarism. It enjoys close relationship with the

people and complete confidence from its network of donors due to its credibility.

Under this program, financing is backed with collateral in the form of capital

assets, land, gold, guarantor and bank guarantee (Obaidullah & Khan, 2008).

3. The Hodeidah microfinance program in Yemen. This program is tailored after

group and graduated financing methodology pioneered by Grameen bank. But,

unlike Grameen bank, it uses a murabahah mode for financing. (Obaidullah &

Khan, 2008).

2.3.3.2 Islamic Microfinance in South Asia.

In South Asian region, Bangladesh, Pakistan and India lead the field in Islamic

microfinance. Bangladesh leads the group of organizations like Islamic Bank Bangladesh,

46

Social and Investmant Bank Bangladesh, Al-Fallah and Rescue. India, in the first place,

has recorded some experiments largely outside its formal financial system, such as, Bait-

un-Nasr and AICMEU (Obaidullah & Khan, 2008).

Being one of the first countries to adopt microfinance, Bangladesh was also one of the

first to introduce Islamic microfinance, which currently accounts for about 1 per cent of

the country`s microfinance, and currently has the highest outreach level globally (Allen

& Overy, 2009).

The Islamic microfinance institutions in Bangladesh majorly base their financing on

murabahah and bay` mu`ajjal (deferred payment) modes. They also compete with

conventional microfinance institutions such as Grameen Bank and BRAC. Though these

conventional giants have a far greater outreach than Islamic microfinance institutions, the

latter have displayed better financial performance than the former (Obaidullah & Khan,

2008).

Islamic microfinance in Bangladesh largely depends on its members` savings and funds

from Palli Karma–Sahayak Foundation (PKSF) (Allen & Overy, 2009).

In Pakistan, the most prominent provider of Islamic microfinance is Akhuwat. This

program dispenses small interest-free charitable loans (qard hasan) with an administration

fee of 5 per cent in a spirit of Islamic brotherhood (Obaidullah & Khan, 2008).

The programme enjoys no funding from international donors or financial institutions. All

its activities are mosque-centered and involve close relationship with the community.

47

There are no independent officers and loans are disbursed and recovered in the mosque.

This attaches a religious sanctity to the oath of returning it on time (Allien & Overy,

2009).

Further, Islamic Relief is another player in the field of Islamic microfinance in Pakistan.

This programme engages in murabahah – based financing to individuals, based on a

combination of personal guarantors, group savings accounts, co-signers and community

recommendations to ensure repayment. Murabahah financings are typically delivered to

borrowers` business premises. Thus, this programme records repayment rate range of 95-

99 percent. In addition, HSBC Amanah (an Islamic Bank in Pakistan) assists in

development of shari`ah structure for financing models and contracts, and provision of

Islamic finance training to Islamic Relief staff. Islamic Relief will, in turn, manage

microfinance projects, identify and screen beneficiaries, set out eligibility criteria and

provide financial and social reports to HSBC Amanah (Allen & Overy, 2009).

2.3.3.3 Islamic Microfinance in South East Asia

Though cases of Islamic microfinance projects have been recorded in Thailand, Brunei

and Philippines, Malaysia leads the field, while Indonesia follows (Obaidullah & Khan,

2008).

Malaysia, with its rather developed Islamic banking system and capital markets, has

established several organizations under the aegis of government agencies to provide

microfinance to small and medium–sized enterprises using a wide range of Islamic

48

financial products. Efforts were also made in diversifying sources of loans for micro-

enterprises and the poor, which includes Amanah Ikhtiar Malaysia (AIM) and Islamic

pawn–broking (Ar-Rahnu). Established in 1987 with the objective of helping hardcore

poor households, AIM`s Islamic microfinance schemes have been patterned after

Grameen Bank model, except that no interest is charged. Nonetheless, borrowers are

charged service charge which is usually below the prevailing market rates. It is on record

that AIM has disbursed over RM 2.3 billion in loans to its clients, since its inception

(Allien & Overy, 2009).

On the other hand, establishment of Ar-Rahnu took place in 1993 as a result of the

inclusion of Shari`ah regulation in the banking system in 1983. Ar-Rahnu offers short-

term interest-free loans that require collateral which is valued at current prevailing prices.

During the lending period, the lender will charge a fee for safekeeping the collateral. At

the end of the period, financing must be repaid and the collateral reclaimed. Unless

extensions are granted, the lender reserves the right to seize and auction the collateral to

recover its financing costs with any remaining balance returned to the borrower, if the

loan is not repaid within the agreed duration (Allien & Overy, 2009).

In Indonesia, Islamic microfinance institutions may be categorized into three categories:

I. The microfinance divisions of Islamic banks;

II. The Islamic rural banks (BPRS) a subcategory of the rural banks (BPR); and

49

III. The Islamic financial co-operatives that are not part of formal financial sector.

These are generally referred to as Baitul Maal wal Tamwil (BMT). (Obaidullah &

Khan, 2008).

The Baitul maal wal Tamwil (BMTs) are a large network of over two thousand

institutions serving millions of poor Indonesians Muslims at the grassroots level. These

BMTs are linked to various organizations and backed, at times by Islamic organizations.

Also integrated to BMTs are Zakah funds. Above all, Islamic microfinance institutions in

Indonesia have diversified products–based on various Islamic financing mechanisms like

mudarabah, musharakah, murabahah, ijarah and qard hasan (Obaidullah, 2008).

According to Obaidullah & Khan (2008), Islamic microfinance institutions in Indonesia

have demonstrated their sustainability and robustness during grave financial crises even

when the mainstream banks had to depend on governmental assistance for bail-out

(Obaidullah & Khan, 2008).

2.3.3.4 Islamic microfinance in Central Asia.

In central Asia, only Afghanistan and Azerbaijan witnessed experiments in Islamic

microfinance. The leading Islamic microfinance program in Afghanistan is run by

FINCA (Foundation for International Community Assistance). This program involves

qard hasan with service charge which is not related to amount of financing as a

percentage and that is charged upfront as a fee. FINCA`s village Banking methodology

targets the working poor with its “solidarity” group guaranteed loans (Obaidullah &

50

Khan, 2008). FINCA`s operations date back to 2004. In addition to provision of qard

hasan, FINCA offers a revamped murabahah product which incorporates the element of

risk sharing. Thus, FINCA Afghanistan`s operational sustainability rose from 15 to 54%,

while the number of active clients also rose from 14,000 to over 44,000 and the total

portfolio increased from US $1.7million to nearly $10million in 2007 (ABAC Malaysia,

2008).

Moreover, worthy of mentioning as another provider of Islamic microfinance in

Afghanistan is WOCCU (World Council Credit Union) – Islamic financial co-operative.

Twenty Investment Finance Centers (IFCs) in some provinces of Afghanistan have been

developed by WOCCU through ARIES (Agriculture, Rural Investment and Enterprise

Strengthening established by USAID) program. The goal is to enable the clients join a

financial institution that is owned, controlled and operated by its members. This model is

based on both the cooperative principles and the Islamic value of risk and reward sharing

with members owing investment accounts, rather than traditional interest bearing share

account. This program – as at the end of 2007 – has attracted about 6,671 clients with a

portfolio outstanding of US$926,251 and total deposit of US$182,107 (ABAC Malaysia,

2008).

2.3.3.5 Islamic microfinance in sub-Saharan Africa

Obaidullah & Khan (2008) claimed that the only Islamic microfinance program that has

been documented well operates in Northern Mali. This program was established with the

51

cooperation from both German Technical Cooperation (GTZ) and German financial

cooperation (KFW) in the former civil war areas of Mali (ABAC Malaysia, 2008). The

object of this program, among others, was to provide financial services to all the tribes of

the area; It was felt only Islamic bank could be acceptable to all previous civil war

opponents. Consequently, Azaouad Finance plc was established.

Primarily, the bank`s operation is based on PLS basis and linked with the SWIFT

international payments system, thus giving a filling to local trade and commerce in a big

way (Obaidullah, 2008).

Islamic microfinance as an institution is relatively new in Nigeria. As at the time of this

study at formal level, no specialized Islamic microfinance institution exists in the

country. However, some conventional microfinance institutions are offering Islamic

compliant services. According to Islamicfinance.de, it is reported in Daily Trust/All

africa on 28 January 2009 that the Kwara Commercial Microfinance Bank which would

offer Islamic compliant services along with conventional micro banking services –was

officially commissioned in Ilorin on 27 January, 2009.

Earlier, Integrated Microfinance Bank (IMFB) in Lagos has introduced Islamic –

compliant banking products such as ijarah, musharakah Marana and musharakah Nasat.

In each of these products, customers contribute funds and both the bank and the customer

share in the profits (and losses) from the product. The introduction of Islamic–compliant

banking products by IMFB dates back to mid – 2008 (microcapital.org).

52

Recently, the InNyx Center for Microfinance Development (ICMD), a UK non-profit

making organization with main interest in the promotion and development of

microfinance banks in sub-Saharan Africa has recently concluded scoping study for the

establishment of a Greenfield microfinance “Shari`ah compliant banking institution”

(www.1888pressrelease.com).

Moreover, in March 2009, as reported on the 234 Next portal on 13 June 2009, a

framework for non-interest banking was released by the CBN. All these posit that full-

fledge Islamic microfinance institutions are yet to be founded in Nigeria.

However, Islamic microfinance has been provided at the non-formal level by some self-

help-Muslim organizations in Nigeria. In Ijebu-Ode, for instance, activities of these self-

help groups are well pronounced because not less than four of such Islamic registered

NGOs engage in provision of Islamic microfinance, with two of them having not less

than a decade experience such. These organizations are Al-Hayat Relief Foundation

(established 1997), Assalam Development (founded 1999), Itunmetala Iwade Islamic

Foundation (January 2009) and Al-Amanah Islamic Foundation (June 2009) [Field

Survey, 2009].

2.3.4 Prospects of Islamic Microfinance in the contemporary world

Nothing best confirms the fact that there is prospect for Islamic microfinance in

the world today than the CGAP`s 2008 Focus Note on Islamic microfinance which states:

53

… just as there are many mainstream banking clients who demand

Islamic financial products, there are also many poor people who insist on

these products … Shari`ah compliance in some societies may be less a

religious principle than cultural one and even the less religiously

observant prefer Shari`ah compliant products.

Segrado (2005) identified four reasons why Islamic microfinance enjoys high demand in

the world. They are:

Microfinance could be tailored on the local socio-economic and cultural

characteristics;

In countries where Muslims form majority or significant minority of the

population, the potential demand for tailored microfinance services still remains

largely unmet;

Some surveys have proved that there is high demand for Islamic banking services

(microfinance inclusive) especially in low and middle income predominantly

Muslim societies; and

Commercial banks could show interest in Islamic microfinance in order to reach

interesting market riches, create loyalty in their clients and ensure their

satisfaction.

What is apparent from all this is that Islamic microfinance has a lot potential across the

globe.

54

Considering the fact that the Nigerian microfinance market is the next biggest

microfinance market after China and India and the size of Muslim population in Nigeria

which hovers around 55-70% of the country`s population, one cannot but admit that there

is huge potential market for Islamic microfinance in the country.

This is further corroborated by its potentiality of funding agricultural and manufacturing

activities of many poor Nigerians (Mohammed & Hasan, 2008).

Moreover, another factor showing the demand for Islamic microfinance in Nigeria is the

discountenance of some Muslims to conventional microfinance in defense of their faith.

This was the finding of Gusau and Bawa (1993) cited in Mohammed & Hasan, (2008).

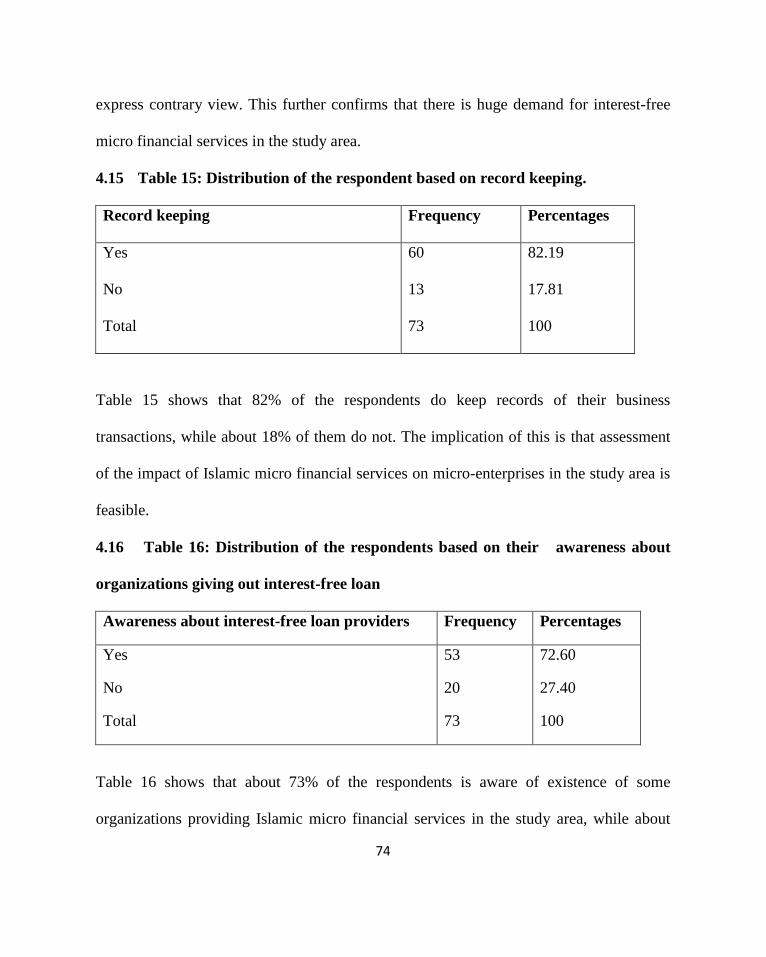

In our field survey, 82% of the respondents expressed their preference for Islamic

(interest-free) microfinancial services over the conventional ones. This indicates huge

prospects for Islamic microfinance in the area.

2.3.5 Current challenges facing Islamic Microfinance in the world

A review of the works like Obaidullah & Khan, (2008) and CGAP`s 2008 focus note

reveals the following challenges facing Islamic microfinance:

Diverse Organizational Structures: The majority of microfinance institutions in

the world are set up as NGO`s. Thus, their status hinders their operation of for-

profit model which pays dividends to its shareholders.

Shari`ah compliance: none of the Islamic microfinance institutions has instituted

Shari`ah supervisory board (SSB). Whereas, to ensure eligibility of their products

55

and strict Shari’ah compliance, Islamic microfinance institutions could set-up

joint SSB (Dahila, El-Hawary & Grais,2005).

Divergent views among scholars: Islamic scholars hold differing views on some

financing modes like murabahah and ijarah. Hence, some Islamic microfinance

institutions feel uncomfortable with such modes and view them as interest-bearing

schemes.

Divergent clients` perceptions: This entails some clients` perception of qard

hasan as free money not to be repaid or be paid whenever they feel like; and

murabahah as non-Shari`ah compliant; because to them, the mark-up is interest.

Lack of Product Diversification: Many Islamic microfinance institutions are

highly murabahah–centric despite the availability of other modes and richness of

fiqh literature.

Operational efficiency: This is a key to affordable financial services to the poor.

Though managing small transactions is expensive, Islamic microfinance must

innovatively reduce the transaction cost.

Risk management: To be sustainable, Islamic microfinance institutions need to

effectively and efficiently manage credit risk. Hence, pressure from the religious

community and appeal to sense of religious duty should be employed in addition

to peer pressure.

56

Capacity building: To achieve the full potential of Islamic microfinance, capacity

building must be accorded the needed attention. Thus, Islamic microfinance

institution managers and staff must be adequately trained.

Another challenge that faces Islamic microfinance, as argued by Obaidullah (2008), is

possibility of willful default on loan repayment. Since Islamic microfinance cannot take

any interest, talkless of additional interest, Islamic scholars generally permit these

Institutions to impose a penalty on the defaulting client to serve as deterrent against

willful default. However, such penalty should be given in charity so that it would not

tantamount to riba.

57

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Research Design

The researcher finds it more convenient to use descriptive sample survey research in

approaching this work. This is because survey is oriented towards the determination of

the status of a given phenomenon, which is prospects and challenges of Islamic

microfinance in this context.

3.2 Area of Study

According to Wikipedia, Ijebu-Ode is a city in south-western Nigeria. Situated some 60

km northwest of Lagos along Shagamu/Benin high way and with an estimated population

of 381,966, it is the second largest city in Ogun State after Abeokuta (The World

Gazetteer, 2009). Ijebu-Ode is the largest city inhabited by the Ijebus, a sub-group of the

Yoruba ethnic group who speak Ijebu dialect of Yoruba; It is historically and culturally

the headquarters of Ijebu land (wikipeadia).

Due to limited employment opportunities in the city, the economically active adults can

hardly be greater than 25–30% of the total population. The establishment of the city is

claimed to have been in A.D. 900. There was already reference to it by Pereira in the 16th

century, while John Barbot noted it as a place “where good fine cloths are made and sold

by the natives to foreigners, who have a good vent for them at the Gold

Coast…”(Mabogunje, 2004).

58

Modern Ijebu-Ode is a major collecting point for kolanuts, cocoa and palm oil and

kernels. Its industry includes printing and publishing, while its artisans are known for

their handiwork in iron. Local trade is primarily in yams, cassava, maize, palm produce

and rubber. Both rubber and timber have become important commercial products of the

city (Ijebu-Ode, 2009). Further, manufactured in Ijebu-Ode are textiles, metal and clay

products, processed timber and plywood, canned fruit and juice, and milled rice (Ijebu-

Ode, 2008).

The city has dual administrative systems: traditional and modern. Under the traditional

administrative system, Ijebu-Ode is organized into three major wards, namely Iwade,

Ijasi and Porogun. Each ward comprises quarters or neighbourhoods known as “Ituns”

which are directly under the auspices of Olorituns, the heads of neighbourhoods. At

present, there are 36 ituns and 15 suburban districts as a result of modern expansion. The

chief head of this traditional administrative system is the Awujale of Ijebuland, the

Ogbagba II, Oba Sikiru Kayode Adetona. However, the modern administration of the city

is undertaken by Ijebu-Ode local council. The council has 11 electoral wards. Each ward

is represented by a councilor, while the executive head is the Chairman. Meanwhile, the

modern local government system straddles the city between the local governments: Ijebu-

Ode, Odogbolu and Atan (Mabogunje and Robert, 2004).

According to Odugbemi & Oyesiku (1998), less than 20% of people living in Ijebu-Ode

were wage-earners; over 60% were petty traders; 8% were subsistence farmers, while the

59

remaining were in informal sector as self-employed artisans and providers of various

services. The study further revealed that 90% of people in the city lived below

international extreme poverty line of $1.00 per day.

To sum up, Ijebu-Ode is noted for its commercial activities, socio-cultural and religious

richness and extreme poverty.

3.3 Population for the study

The population of this study comprises micro enterprises owners in the two major

markets in Ijebu-Ode, namely Oba S. K. Adetona market (popularly known as ‘OkeAje’

market) and Olabisi Onabanjo Market (popularly known as ‘Ita-Osu’/New market) as

well as organizations that provide Islamic (interest-free) microfinance in the study area.

The rationale for the selection of those markets and organizations as the population for

this study is to enable the researcher has a well-defined population from which the

sample can be easily drawn.

3.4 Sample and Sampling Technique(s)

A total of one hundred micro enterprises owners, fifty from each market are used as

sample for this research. The sampling technique adopted here is disproportionate

stratified random sample. For this purpose, each market is divided into five broad

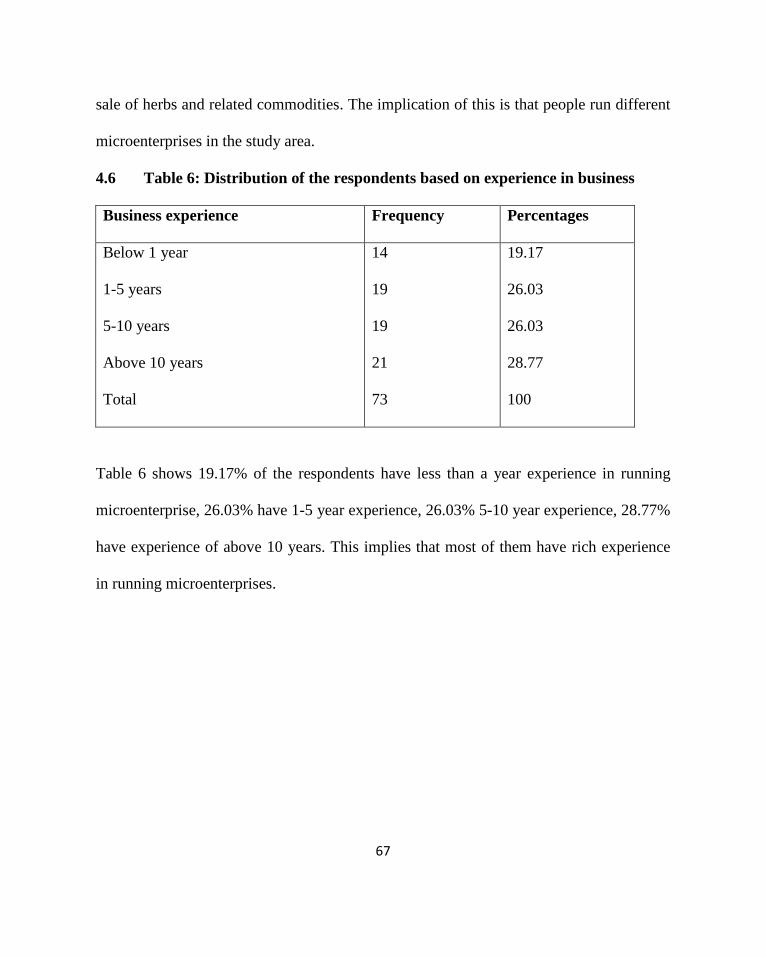

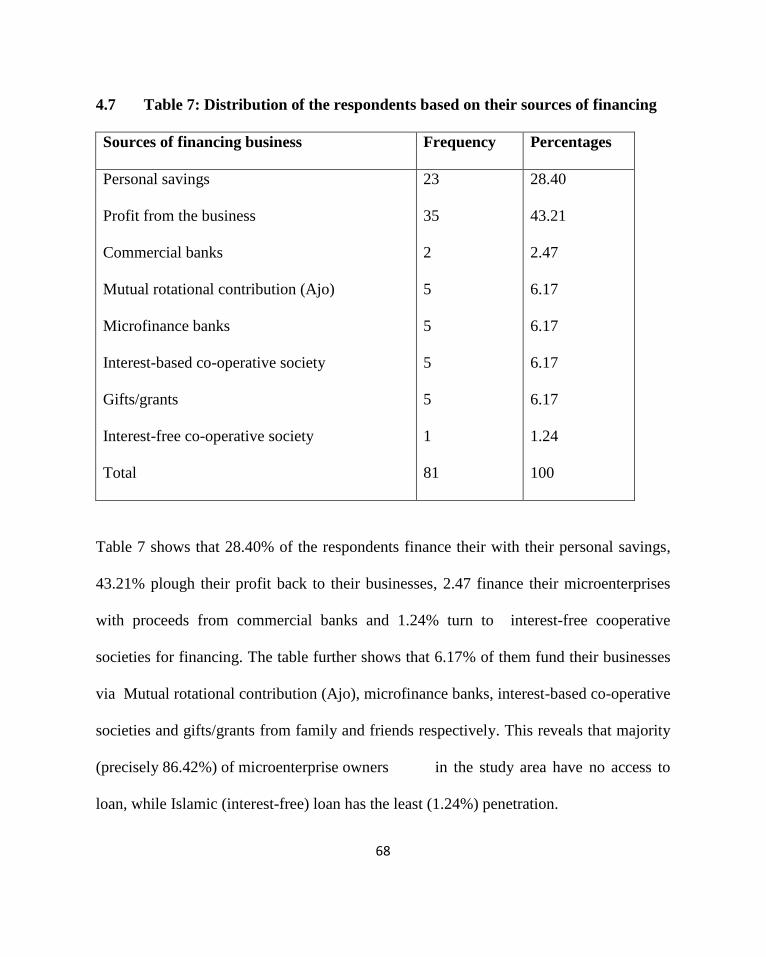

categories based on the nature of their business as shown in the table below:

60

MARKET

CATEGORY OF MICRO

ENTERPRISE

NO. OF SAMPLES

Olabisi Onabanjo

Market (popularly

known as ‘Ita-

Osu’/New market)

Foodstuff 10

Home utensils 10

Clothing materials 10

Provisions 10

Herbs and related commodities 10

Oba S. K. Adetona

market (popularly

known as ‘OkeAje’

market)

Foodstuff 10

Home utensils 10

Clothing materials 10

Provisions 10

Herbs and related commodities 10

TOTAL 100

Also, a member from each executive council of the three organizations that provide