Microfinance and Rural Development in Cambodia

126

MICROFINANCE AND RURAL DEVELOPMENT IN CAMBODIA

Transcript of Microfinance and Rural Development in Cambodia

MICROFINANCEAND

RURAL DEVELOPMENT IN CAMBODIA

-------------About the Authors--------------------------------------------------------

Dr. Dy Davuth is currently holding the position of Vice RectorAcademic in Build Bright University, Phnom Penh, Cambodia. He hasbeen awarded Doctor of Philosophy in Business Administration fromRutherford University (USA) in 2005. His fields of Specialization areMicrofinance, Financial Management and Corporate Finance. He hasalso participated and contributed papers in various national andinternational conferences/seminars. Presently he is a member ofBoard of Directors and Chairman of Audit Committee ofHATTHA KAKSEKAR, a leading Microfinance Institution in Cambodia.Earlier he has worked as Administrative and Finance Manager withAMRET for nearly six years.

Dr. Tapas R. Dash is presently serving at Build Bright University,Phnom Penh, Cambodia as Professor and also holding the position ofDirector, Post-Graduate studies. Prior to joining this University, he hadserved in a National Institute (ICM, NCCT) in India funded by CentralGovernment and having more than 17 years of experience in teaching,training, research and consultancy. He has been awarded Doctor ofPhilosophy (Ph.D.) in Applied Economics from Utkal University (India)in 1994. His areas of interest include Rural Economics, ProjectManagement, Economics of Education, Managerial Economics andInternational Business. Dr. Dash has to his credit more than a dozenof articles/research papers published in national and internationaljournals. Also he has participated and contributed papers in variousnational and international conferences and seminars.

MICROFINANCEAND

RURAL DEVELOPMENT IN CAMBODIA

Dy DavuthTapas R. Dash

Build Bright University PublicationsPhnom Penh

Cambodia

No part of this book may be reproduced, stored in a retrieval system,or transmitted in any form or by any means, electronic, mechanicalphotocopying, recording or otherwise, without the prior writtenpermission from the authors.

Microfinance and Rural Development in CambodiaFirst Edition 2006© AuthorsAll rights reserved

ISBN 99950-846-0-0

Printed in Cambodia

Published by:Build Bright University Publications,Phnom Penh, Cambodia

Dedicated to our revered parentsfor their

Constant Inspiration, Guidance and Support

Preface

Microfinance as commonly known refers to the provision of financialservices, such as credit, saving and other assistances to supportself-employment of the poor. The delivery of microfinance has beenconsidered as an approach towards economic development ultimatelyto provide larger benefits to the people belonging to low-income group.As credit is considered as a vital input for the growth of any activity, theprovision of micro credit as a part of microfinance activity is a crucialmechanism for the overall development of the community. Thus,Microfinance Institutions (MFIs) have been playing a pivotal role in thesocio-economic upliftment of the Cambodians at large.

Microfinance sector has been developed since the early 1990s,driven by donors funding credit operations. Though someorganizations have successfully transformed and obtained licenses asspecialized banks or MFIs, to-day the process of transformation posesa major challenge for most non-government organizations (NGOs) interms of upgrading organizations, systems and human resources. Tomeet the present challenges, MFIs need to develop a consistentcorporate strategy as well as an effective business plan. Further, tomake the organizations more effective, the National Bank of Cambodia(NBC) has been issuing proper regulations from time to time in thelight of the changing environment. Thus to-day, to ensure a healthymicrofinance environment, the role played by the government, theNational Bank of Cambodia (NBC), Rural Development Bank (RDB)and other apex institutions are praiseworthy. Besides, the donorcommunity has been influential both in the design as well as the paceof development of microfinance sector.

The dependence on moneylenders for certain types of financialneeds has been reduced since the creation of Self-help Groups(SHGs) in certain provinces. Further, the availability of commercialmicrofinance through institutions significantly has marginalized themoneylenders power of credit supply to the low-income borrowers.Complete elimination of informal with institutional finance is expectedto improve the income levels of the poor in the near future.

To-day, microfinance operators are providing individual loans andgroup loans to people as well as small business enterprises in bothrural and urban areas. Over the years, they have modified their

operational methodology to make themselves more vibrant andeffective. However, sustainability is the key component formicrofinance operators in terms of their independence for subsidiesand sustainable returns on average assets. Though a lot of difficultiesare being faced by MFIs in their operations but as a matter ofsocio-economic commitment, their role is well recognized. Thus, as asocio-economic institution, the role played by MFIs in economicdevelopment of Cambodia is quite appreciated.

To seek answer to the issues like what extent the credit supplied byMFIs has helped to increase the standard of living of the beneficiaries,and to examine the role played by the MFIs in reducing poverty ingeneral and of beneficiaries in particular in Cambodian context thepresent study was undertaken.

It is our pleasure to express our appreciation to those who haveinfluenced this work. We are grateful to Dr. In Viracheat, Rector, BuildBright University, Cambodia for his continuous encouragement andsupport. We are also indebted to our other colleagues for their supportand, particularly, Dr. M.R. Behera, Professor, Build Bright University foroffering his valuable suggestions and comments for improving thedraft of the work. We are also thankful to Seang Sok Rotha for histechnical assistance in carrying out the present work.

During the research work, we have visited a number ofInstitutions/Organizations, such as the National Bank of Cambodia,Rural Development Bank, a large number of MFIs, etc. Weimmensely acknowledge the helps rendered by these organizations insupporting us with necessary information. Further, we wish to place onrecord the cooperations received from the respondents, whoresponded patiently with keen interest, for long hours, the tedious andintricate schedules.

Last but not the least, we are thankful to our family members whohave always been a source of inspiration and without theircooperation, the publication of this work would not have taken place.

Finally, we alone are responsible for any deficiency.

Dy DavuthTapas R. Dash

viii

Contents

Preface viiList of Tables xiList of Abbreviations xiii

1. Introduction 1-12

2 Institutionalization of Finance 13-28

3. Cambodian Banking System and Microfinance 29-49Operators

4 Microfinance and Beneficiaries 51-78

5. Summary and Conclusion 79-86

Appendix 87-109

References 101-118

List of Tables

2.1 Growth of MFIs During 1999-2005 193.1 Financial Highlights of ACLEDA During 2003-2004 353.2 Financial Highlights of AMRET During 2003-2004 383.3 Financial and Operational Highlights of AMK During

2003-2004 494.1 Distribution of Households on the basis of the Number

of Years of Business 524.2 Distribution of Households on the basis of type of

Business 544.3 Comparative Results of Investment in Equipment

between Beneficiariesand Non-Beneficiaries 614.4 Comparative Results of Expenditure on Improving

House between Beneficiaries and Non-Beneficiaries 634.5 Comparative Results of Educational Expenses between

Beneficiaries and Non-Beneficiaries 59 4.6 Comparative Results of Food Expenses between

Beneficiaries and Non-Beneficiaries 654.7 Comparative Results of Health Expenses between

Beneficiaries and Non-Beneficiaries 664.8 Comparative Results of Saving between Beneficiaries and

Non-Beneficiaries 674.9 Comparative Results of Expenses on Ceremony between

Beneficiaries and Non-Beneficiaries 684.10 Comparative Results of Daily Cash Flow between

Beneficiaries and Non-Beneficiaries 694.11 Comparative Results of Revenues between Beneficiaries

and Non-Beneficiaries 704.12 Comparative Results of Investment between Beneficiaries

and Non-Beneficiaries 714.13 Comparative Results of Investment in House Equipment

between Beneficiaries and Non-Beneficiaries 724.14 Distribution of Income of Beneficiaries Before and

After the Loan 734.15 Distribution of Expenditure of Beneficiaries Before and

After the Loan 744.16 Distribution of Asset Position of Beneficiaries Before

and After the Loan 754.17 Distribution of Daily Cash Flow of Beneficiaries

Before and After the Loan 76

List of Abbreviations

ACLEDA : Association of Cambodian Local Economic Development Agencies

ADB : Asian Development BankCCB : Cambodia Community BuildingCCRD : Credit Committee for Rural DevelopmentCDC : Cambodia Development CouncilCEB : Cambodian Entrepreneur BuildingCEDAC : Centre d’Etude et Development Agricole CambodgienCFD : Agent France DevelopmentCGAP : The Consultative Group to Assist the Poorest CRS : Catholic Relief ServicesDEG : Deutsche Investitions und Entwicklungsgesellscaft mbHEMT : Ennatien Moulethan TchonebatFMO : Netherlands Development Finance Company GRET : Group de Recherches et d’Echange TechnologiquesGTZ : German Development CooperationIFAD : International Fund for Agricultural DevelopmentIFC : The International Finance CorporationILO : International Labor OrganizationIRAM : Institute de Recherche et d’Application des Méthodes de

Dévelopment KWF : German Bank for ReconstructionMFI : Microfinance InstitutionNBC : National Bank of CambodiaNGO : Non Governmental OrganizationPCA : PRASAC Credit AssociationPRASAC : Support Programme for the Agricultural Sector in

Cambodia RDB : Rural Development BankRGC : Royal Government of CambodiaSHG : Self Help GroupsUNDP : United Nations Development ProgrammeUSAID : United States Agent for International DevelopmentVDC : Village Development Committees

I

Introduction

Agriculture is the foundation of our national economy. Being anagrarian economy, in the context of Cambodia, the importance ofmicrofinance needs no more explanation. Its role towardsstrengthening rural economy is enormous. Microfinance Institutions(MFIs) have been playing a pivotal role in the socio-economic uplift-ment of the poor Cambodians. Thus, they have been playing a majorrole in the economic development of Cambodia. To be broad-based,the MFIs need to gear up their activities by identifying the areas of theirstrengths and weaknesses.

Microfinance has been widely used in a development context in thethird-world nations and less developed countries to help the poor inimproving their standard of living. It has been playing a vital role ineconomic development, especially in rural areas. Cambodian Prakason Registration and Licensing of Microfinance Institution (2000), states“Micro-finance is the delivery of financial services, such as loans anddeposits to the poor and low-income households and micro-enterprises”. Its delivery has envolved as an economic developmentapproach intended to benefit low-income women and men. In addition,it also refers to small-scale financial services for both credits anddeposits, meant for people engaged in farming, fishing, operatingsmall or micro-enterprises, providing other services on wage basis,renting out a small amount of land, vehicles, animals or machinery andtools, in both rural and urban areas. Thus it gives access toentrepreneurs, to the financial services, such as credit and depositwith reasonable interest rate.

Micro-credit in terms of loan size varied from organization toorganization, hence it has no agreed definition. Micro financing hasbeen an effective tool to do with the persistence of rural poverty and

concomitant unemployment, which has been a major concern inalleviating poverty. Consultative Group to Assist the Poor (CGAP)stated that micro-finance is meant for providing poor individual andhouseholds with small loans (micro credit) that are repaid within ashort period of time in order to help them engage in productiveactivities or grow their tiny businesses. Capital is not the only factorthat allows the growth or creation of enterprises, but it is also vital, aswithout it, creativity, drive, and innovation cannot be transformed intomaterial actions.

Micro-finance refers to the provision of financial services, whichinclude credit, saving and other assistance to support self-employmentof the poor. Micro-finance is distinguished from micro credit in a sensethat micro-finance refers to the provision of full financial servicesincluded but not limited to the provision of micro credit.Micro-enterprises are enterprises performed by family members andsome hired laborers and income generated is used for familyconsumption and reinvestment.

Transformation lending is designed to bridge the gap betweeninformal sector and micro-enterprise lending programs and formalbanking sectors. Wholesale lending is defined as providing loans toinstitutions that lend or retail funds to end-borrowers. The corebusiness of the Rural Development Bank (RDB) is wholesale lendingby providing credit funds to program partners for significantlyincreasing outreach to target clientele and contribute to efforts ofnational government in alleviating poverty. Wholesale lending is theprocess of lending of RDB to MFIs that retail funds directly toend-borrowers or on-lends funds to other MFIs that retail fundsdirectly to end-borrowers. Micro-finance Institutions (MFIs) refer toinstitutions engaging in the delivery of micro-finance services. Theygenerally refer to the retailers of micro-credit or those directly dealingwith end borrowers. Moreover, micro-finance vision is a viable andsustainable private micro-financial market, with the governmentproviding a supportive and appropriate institutional framework to themarket.

2 Microfinance and Rural Development in Cambodia

Micro-finance: Cambodian Experience

Cambodia is one of the developing countries in the region, coveringa surface of 181,035 Km2 with a total population around 14 million,equivalent to 2,188,633 households. Eighty-five percent of thepopulation lives in rural areas where farming, fishing and traditionalcrafts are the daily business activities.

Cambodian economy has changed from a planned economy to afree market economy since 1989, when Vietnam withdrew its troopsfrom Cambodia. The micro-finance system in Cambodia was createdwith the help of micro credit promoters and international donors at thebeginning of the 1990s. The demand for micro credit in Cambodia islargely untapped and the government has strongly encouraged thedevelopment of the sector. After the general elections in 1993,Cambodia has become an internationally recognized government;additional foreign support has been available, and a number ofmicro-finance providers have emerged. The number of (national andinternational) organizations providing micro credit has increasedyearly ever since. The Royal Government of Cambodia (RGC) hasclearly recognized that providing small loans or savings (micro creditor saving) to poor citizens is a vital mechanism to the development ofrural areas (community development). In this connection, rural creditservices have been provided actively and directly to poor citizensthroughout the country. Although this is a new sector (industry)for Cambodia, the process is being improved and is growing quicklywith the active support of the Royal Government of Cambodia.

In 1990, the country was partially in peace. The demand for creditfrom that time has really been increased. People have become muchmore positive and hopeful in their future and consumer demands havegone up. For example, before 1990, sellers could sell only 5 chickensa day, but now they can sell more than 20 chickens a day. This showedthat people want large amount of loan to expand their businesses.Now, for the first time, they have really started planning for their futureand there is a positive outlook; such feelings of optimism breedsuccess and increase demands for our microfinance services. Many

Introduction 3

NGOs and international organizations operated in the 1990s, althoughthere was no legal framework for microfinance until 2000. This did nothamper the growth of such semi-formal microfinance. As a result, the1990s showed some key developments in terms of the legal andpolitical environment for microfinance. A major milestone for thedevelopment of the microfinance sector in Cambodia was planted inJanuary 2000 with the law (Prakas) on the establishment ofMicrofinance Institutions (MFIs). The new law allows formal MFIs to beestablished as private companies with a minimum capital of only US$65,000. The National Bank of Cambodia (NBC) for the first time in2000, issued regulations on the classification of MFIs into threecategories according to the level of their operations, and createdcriteria for licensing and registration. These regulations include criteriafor licensing and registration; minimum capital requirement; solvencyratio; liquidity ratio; uniform chart of accounts; reporting requirements;and interest calculation (NBC, 2006). These regulations are consistentwith the scope of work of the MFIs and support them in expanding theiractivities under an appropriate umbrella. Thus this has madeCambodia to the forefront of a progressive microfinance regulator inAsia.

The Royal Government of Cambodia has given top priority to itssocial development programs for poverty alleviation in rural areas.This is further to develop the living standards of Cambodians.Realizing the fact, the government strongly encourages thedevelopment of microfinance sector as machinery towards achievingthe socio-economic objectives. At present, there are more than onehundred rural financial operators, including licensed MicrofinanceInstitutions, registered and non-registered Non-GovernmentalOrganizations in which most of them are in small size. By the end of2005, there were 16 licensed MFIs and 24 registered as rural creditoperators. Among those institutions, the majority of them weretransformed from NGOs, while others were local private companies.By September 2005, licensed MFIs accumulated a total loanoutstanding of KHR 190 billion (excluding loans of ACLEDA tomicrofinance sector) with 371,000 borrowers and has a total deposit ofKHR 9.4 billion, which equals to 5 percent of loan outstanding (NBC,

4 Microfinance and Rural Development in Cambodia

2006). Thus the microfinance operations (Non-GovernmentalOrganizations and Microfinance Institutions) are spreadingcountrywide across all the 24 provinces. The biggest Specialized Bankis ACLEDA, which has a total loan outstanding of USD 64.9 million atthe end of 2004 and presently operational in 21 provinces (ACLEDA,2004). The Rural Development Bank (RDB) being a national institutionwas established to promote microfinance in early 1998. It hasassigned the task of coordinating finance and refinancing to allMicrofinance Institutions, Specialized Banks and Commercial Banks,which have the intention to support rural economic activities. Parallelto this, the National Bank of Cambodia (NBC) has enacted a Law onBanking and Institutions, to govern and license MicrofinanceInstitutions. This law has been created to provide opportunities toNational and International Financial Organizations and Micro CreditProviders, to undertake microfinance activities as well as to linkmicrofinance activities to the formal banking system. Despite thissystematic and coordinated effort, the credit needs of the rural poorare not being met. There is a shortage of up to USD 120 million incredit available to this sector (Chandarot, 2002). The needs of the ruralpoor can only be addressed if either the present institutions are ableto access additional finance, or new institutions begin to provide microcredit. Ennatien Moulethan Tchonnebat (EMT), now the largestMicrofinance Institution in the country by the number of customers(105,283 by the end of 2004) and presently known as AMRET, wasestablished in 1991 as a GRET project in order to providemicro-credit to the poor rural people in Cambodia. In July 2000,Ennatien Moulethan Tchonnebat (EMT) was registered as a privatelimited company with a share capital of KHR 330 million and inNovember 2000, it (EMT) mad a request to the National Bank ofCambodia to obtain license of Microfinance Institution and obtainedthe same in 2001.

Thus so far the socio-economic development of Cambodia isconcerned, the Microfinance Institutions (MFIs) are playing a pivotalrole in the country. Against this backdrop, the present study hasfocused on the role of Microfinance Institutions in promoting ruraldevelopment in general and in strengthening the rural credit system in

Introduction 5

particular. Further, the study has examined the impact of creditsupplied by Microfinance Institutions on the standard of living of thepeople and thereby in reducing the rural poverty in general andbeneficiaries in particular.

Importance of the Study

In the present scenario, micro-finance plays a crucial role ineconomic development of Cambodia. The role played by MFIs instrengthening the rural economy through the provision ofmicro-finance services to the rural poor is noteworthy. To understandthe positive contribution made by the MFIs on the standard of living ofthe beneficiaries and thereby in reducing the poverty, the presentstudy has been undertaken. The results of the study certainly help theplanners, policy makers in the government as well as the NGOs andMFIs to design appropriate strategies for the development of thissector.

Objectives of the Study

Considering the crucial role played by the MFIs in the socio-economic development of the country, an attempt is made in thepresent study with the following objectives in mind.

(i) To assess the impact of credit supplied by MicrofinanceInstitutions on the standard of living of beneficiaries.

(ii) To examine the role of Microfinance Institutions in reducing ruralpoverty in general and beneficiaries in particular.

Hypotheses of the Study

With reference to the above objectives, the present study has takeninto account the following hypotheses for testing.

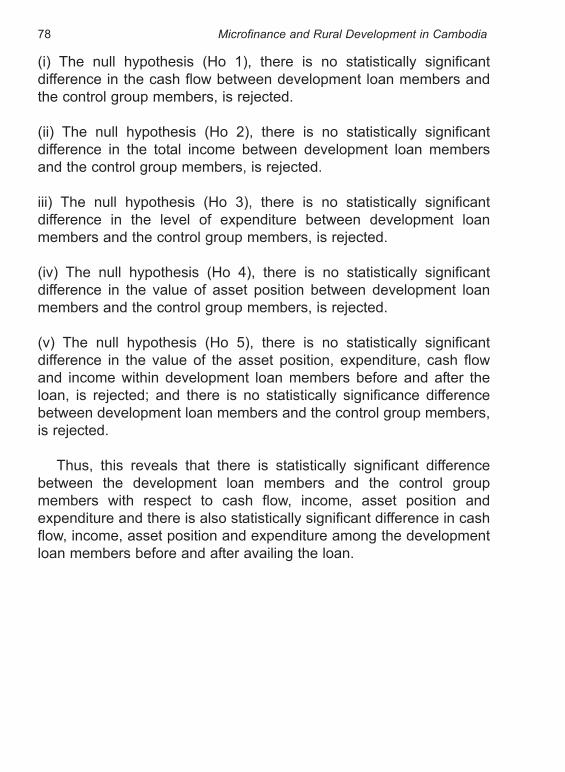

Ho 1: There is no statistically significant difference in the cash flowbetween the development loan members and the control group

6 Microfinance and Rural Development in Cambodia

members.

Ho 2: There is no statistically significant difference in the total incomebetween the development loan members and the control groupmembers.

Ho 3: There is no statistically significant difference in the levelof expenditure between the development loan members andthe control group members.

Ho 4: There is no statistically significant difference in the value of theasset position between the development loan members andthe control group members.

Ho 5: There is no statistically significant difference in the value of theasset position, expenditure, cash flow and income within thedevelopment loan members before and after the loan; and nostatistically significant difference between development loanmembers and the control group members.

Methodology

Sample Design

The study has been conducted in two provinces in Cambodia, i.e., Kompong Speu and Kompong Chhnang. The selection of these twoprovinces has been made out of 21 provinces of the country whereMFIs are operating on the basis of their levels of development. WhileKompong Speu is considered as a backward province, KompongChhnang is positioned as an average province. In Kompong Speu andKompong Chhnang provinces the number of loans to householdsduring the years 2000 to 2004 numbered 191 and 62 respectively. InKompong Speu alone, 83 households received one year loans,whereas in Kompong Chhnang, 51 households received one yearloans. All beneficiaries of these one year loans have been consideredas the treatment group selected for the purpose of the study. An equal

Introduction 7

number of control group members, who did not receive loans fromEnnatien Moulethan Tchonnebat (EMT) or any other Micro FinanceInstitutions (MFIs), have been selected from these two provinces forthe purpose of the study and the treatment group members(beneficiaries) have selected the control group members (non-bene ficiaries). After completion of the personal interview with thetreatment group member, that member has been asked to recommenda neighbor or friend, who is as close as possible to the treatmentmember in type and size of business, and family composition that didnot receive a loan. There after, this recommended control groupmember has been administered with the personal interview. In casethe selected control group member refused to supply information, theinterviewer has asked the original treatment member to provide thename of another person that is as close as possible to the treatmentmember in type and size of business, and family composition that didnot receive a loan to replace the first recommended control groupmember. Thus while the study has selected all beneficiaries of oneyear loans of EMT in the two provinces, the selection of non-beneficiaries have been done on the basis of purposive sampling.

Sources of Data and Collection Procedures

The study is based on both the secondary and primary data. Thesecondary data are collected from various sources, such as selectedMicrofinance Institutions (MFIs), National Bank of Cambodia (NBC),Rural Development Bank (RDB) and several Publications of AsianDevelopment Bank (ADB), etc.

For the purpose of collection of primary data a structurequestionnaire has been administered using personal interviews(Appendix A). However, before the finalization of the questionnaire thesame has been tested twice utilizing a pilot survey in Kandal Provincenear the capital city of Cambodia with ten treatment members(beneficiaries) and ten control group numbers (non-beneficiaries). Anyquestions or misunderstandings by the test subjects have beenrecorded in order to revise the final draft of the questionnaire beforebeing administered to the actual control and treatment members in the

8 Microfinance and Rural Development in Cambodia

study. The questionnaire consisted of questions on several personalcharacteristics of both the treatment and control group members. Thequestionnaire also included several questions relating to the income,asset position, the amount of expenditure made on education, food,health care, ceremony, purchase of gold or saving of the treatmentmembers before and after availing the loan from MicrofinanceInstitution and of control group members for a similar period of time.Further, it included questions on the amount of investment made onequipment for business, improvement of house, creation of householdassets, besides, questions relating to business cash flow, incomegenerated from business have been included.

Statistical Tools

After the collection of data, the same are computed and tabulatedkeeping the objectives of the study in mind. The interrelationshipamong the data has been formed as the basis for tabulation.

In order to measure the significance of the change on severalaspects, such as income, expenditure on various activities, assetpositions and cash flow, between the beneficiaries and non-beneficiaries, the ‘t’ test has been used.

The formula for calculating the ‘t’ value has been given below:

Where,

X1 = mean of the first sample.

X2 = mean of the second sample.

n1 = number of observation in the first sample.

Introduction 9

n2 = number of observation in the second sample.

S = combined Standard Deviation

The value of S has been calculated as follows:

S =

When comparing between the beneficiaries and thenon-beneficiaries, the first sample was the beneficiaries (treatmentmembers) and the second was the non-beneficiaries (control mem-bers).

In order to measure the significance of change in the distribution ofincome, expenditure, asset position and cash flow of the beneficiariesbefore and after availing the loan, i.e. the development loan membersbefore and after 12 months of availing the loan, the chi-square test hasbeen used.

The formula for calculating of the Chi-square value (x2) has beengiven as follows:

Where:i = number of class in the distributionOi = observed frequencies in class iEi = expected frequencies in class iC = number of categories df = C - 1

Furthermore, in order to judge the statistical significance betweentwo groups, the research has worked out the Multiple DiscriminantAnalysis, which happened to be a generalized distance between

10 Microfinance and Rural Development in Cambodia

Introduction 11

beneficiary and non-beneficiary, where each group has beencharacterized by some set of equipment for business, improvinghouses, education expense, food expense, health expense, saving,revenue, ceremony expense, cash flow per day, investment and houseequipment variable, and where it has been assumed that discriminantcoefficient structure was identical for both groups. It has been workedout with the help or the following:

D = b1X1i + b2X2i + ….….. + bnXni

Where,Da = ith applicant’s discriminant scorebn = discriminant coefficient for the nth variableXni = applicant’s value on the nth independent variable

Limitations of the Study

The study has the following limitations:

(i) As already mentioned, the study has been undertaken in twoprovinces of Cambodia, i.e., in Kompong Speu and KompongChhnang out of a total of 21 provinces where MFIs are operating.Thus the geographical coverage of the study is quite limited.

(ii) To assess the impact of credit supplied by MFIs on the standard ofliving of the beneficiaries, only the beneficiaries of one MFI,namely EMT (AMRET) have been taken into account.

(iii)The study has selected the beneficiaries in both the provinces whohave availed one-year loan during the period 2000 to 2004.Thus the sample size of the study is also quite limited.

However, keeping the purpose, efforts, time, availability of data andseveral constraints in mind, the present study is a modest attempt inits desired direction.

12 Microfinance and Rural Development in Cambodia

Plan of the Study

The present study consists of five chapters. The first chapterintroduces the subject matter, examines the justification of the studyand discusses the objectives and methodology adopted in the study. Itthus serves as a prologue. The second chapter explains theimportance of institutionalization of finance in the context ofCambodian economy. Further, the role played by the Government andRural Development Bank are analyzed in this chapter. The thirdchapter highlights the cases of some major microfinance operators inthe country along with their achievements. In the fourth chapter, theimpact of micro credit on the standard of living of the beneficiaries isanalyzed. Further, this chapter makes a comparative analysis betweenbeneficiaries and non-beneficiaries to understand the impact of microcredit on their income, expenditure, cash flow, asset position, etc. Thelast chapter summarizes the main findings of the study policyrecommendations along with its conclusion. The study is appendedwith supplementary information sheets used for data analysis andpresentation.

II

Institutionalization of Finance

The basic function of credit, whether provided by formal or byinformal sources, is to enable individuals and business enterprises topurchase goods and services ahead of their ability to pay. Demand forcredit arises because of the time-consuming nature of the productiveand distributive process-consumers demand, credit to acquire goodsin advance for which payment can be done in future. Thus the gapbetween production, consumption and configurations give scope forthe wide use of credit. Savings accommodates demand for credit, butthe demand for credit for production purposes outstrips savings andthus, the necessity for additional funds crops up from financialinstitutions. Further, with the process of development of the economy,while the importance of informal sector has been reducing, the growthof formal sector takes place.

The credit for several purposes particularly, in rural sector inCambodia is provided by both organized and unorganized agencies.The organized agencies constitute of Institutions/organizationscommitted towards the development of the beneficiaries by supplyingtimely credit with a reasonable interest rate. The unorganizedagencies consist of professional money-lenders, traders, relatives andfriends and others. They freely supply credit for both productive andunproductive purposes, besides their methods of undertaking creditbusiness are simple and elastic but involved a lot of shortcomings.Normally, they charge very high interest rates and the detailedpractices on the basis of which they supply credit to the needyborrowers remain unclear to them. In fact, they commit manymalpractices, which are very well known. These unorganized agenciesnever care for the purpose for which the loans are used and hence,usually these borrowings go into unproductive channels. Therefore,these sources cannot be assigned any definite role for the socio-eco-nomic development of the economy in general and rural sectorin particular.

Informal Credit: Cambodian Experience

In the context of our economy, several moneylenders can be foundin both developed and open villages. Their interest rates normally varyfrom 1 to 10 percent per month and even up to 20 percent dependingon the situation. With limited access to financial services in rural areas,most people have relied on moneylenders for investment capital tofinance essential inputs for agricultural production and microenterprises. Thus, almost everyone uses this kind of credit to do theirbusinesses for a short time. Though villagers prefer to borrow moneyfrom moneylender sources because they can get it quickly, but indebtedness to moneylenders is the first cause of bankruptcy amonghouseholds.

Usually, it is seen that informal lending results in two different types:commercial (loans from moneylenders, traders, employers,commodity wholesalers, and landlords) and non-commercial (loansfrom friends, relatives, neighbors, and some forms of rotating savingand credit association). Non-commercial loans are common andusually carry no or low financial interest for small amount and shortterms for emergencies or for special occasions and specific purposes,such as purchase of land, weddings, house construction for youngcouple, etc. Informal commercial lenders, however, typically providecredit that can be used for both production and consumptionpurposes with a high interest rate.

As revealed from 1996 socio-economic survey in Cambodia, duringthe year 1994-95, approximately 704,000 rural households availedloans amounting to about USD 120 million. While 54,000 of themobtained loans from traders, the moneylenders provided support to114,000 people. The highest 400,000 availed services from therelatives and 114,000 from friends and neighbors. Of the remaining,only 71,000 got the support from NGOs and lowest 7,000 from banks(NBC, 2006).

Informal lenders are considered as a major cause of poverty in thecontext of our economy. Their interest rates charged are spectrums

14 Microfinance and Rural Development in Cambodia

ranging from zero interest to a very high rate of interest, such as 360percent per annum. Despite the prevalence of high interest rates,borrowers continue to demand for informal services due to severalreasons, such as ease of loans, flexibility in repayments, personalrelationship, and lack of alternatives to access to formal services. Thustheir elimination is considered necessary for the alleviation ofpoverty. In this situation, the replacement of informal finance with insti-tutional finance at lower cost is expected to improve income levels ofthe poor both in rural as well as in urban areas.

If the provision of credit is not available from either an NGO or oneof the alternative credit programs, farmers are forced to finance inputsby themselves. If they cannot afford the inputs by borrowing from othersources (friends/relatives, traders or moneylenders) often at arelatively high interest rates, the result is either a reduction in income– the considerable amount of interest that has to be paid on the loanor a reduction in self-sufficiency due to lower yields.

Reducing the role of moneylenders with credit scheme frommicrofinance operators is evenly spread throughout various categoriesof families and also pushes down the rate used by moneylenders. Itsimpact, therefore, lies in the saving generated when it takes the placeof the loan from a moneylender or supplier and, to a lesser extent, inthe lesser social dependency when it replaces a family loan. However,there may be reasons that people do not want to borrow money fromthe lender sources because they charge high interest rates, and theirstrict payment conditions make small businesses difficult to access theloan from those sources.

The creation of the Self-help Groups (SHGs) in a few provinces hasreduced the dependence on moneylenders for certain types offinancial needs. But through the number of loans from MFIs and NGOshas expanded considerably, loans from informal sources, such asmoneylenders, relatives and friends continue to be an importantsource of rural credit. People used to buy materials for their incomegenerating activities on credit from moneylenders, which they couldnot even bargain over the price. They generated less income, but after

Institutionalization of Finance 15

they received the credit they improve their income. The crucial point isthat lower-income borrowers who borrow from moneylendersgenerally pay much higher interest rates for credit, hence, it isnecessary if commercial microfinance is widely available throughinstitutions. This is of particular significance because the higher ratesof informal lenders tend to constrain the growth of micro-enterprises,and also the volume of informal commercial credit is very large.

Formal Credit: MFIs and Process of Transformation

Organized institutions have an intimate knowledge of people withwhom they have to deal with. The MFIs are specially meant for those(farmers and others) with small means. With the establishment ofRural Development Bank (RDB), the help and guidance to theseinstitutions have been enlarged and become more specialized. TheRural Development Bank plays a leading role to negotiate with donorcountries and international aid organizations to attract funding andassistance in order to finance and refinance rural lending operatorswith the sole intention of supporting and strengthening rural economicactivities.

The microfinance sector has developed since the early 1990s,driven by donors funding credit operations. In order to transform NGOsinto registered and licensed MFIs, the National Bank of Cambodia(NBC) in 2000 started to provide revised regulations and as a result,by the end of 2005, there were 16 licensed MFIs and 24 registered asrural credit operators. Certain organizations, such as ACLEDA, EMT(AMRET), Hattha Kaksekar, PRASAC, CEB, AMK, etc. have alreadysuccessfully transformed and obtained licenses as specialized banksor MFIs. The transformation process has posed a major challenge formost NGOs in terms of upgrading organizations, systems and humanresources. It required the MFIs to develop a consistent corporatestrategy and business plan. The transformation has also opened newopportunities, as transformed and licensed MFIs are permitted to offerdeposit facilities and mobilize public savings. An institution, i.e., astructure or form, through the operation of laws or regulations, hasofficially been given the institutionalization of a decentralized finance

16 Microfinance and Rural Development in Cambodia

scheme. The institutionalization is the assumption of responsibility forschemes by local nationals. In most cases, external support keepsthem in a situation of dependency. This requires official recognition,which starts with the adoption of legal constitution and continuesthrough accommodation under banking regulation by various relevantstate authorities. Furthermore, by the end of the project both thegovernment and donors decided on the final allocation of grant fundsto Microfinance Institutions.

Organizations have clearly recognized the untapped potentialinitiative and the desire of Cambodians having poor equipments andopportunities. The poor can and will improve their lives with convictionby the foundation of organization’s mission, which empowers the poorentrepreneurship to help themselves through financial services,including credit and savings program. Therefore, the goal of amicrofinance project is to create incomes and employment in poorcommunities through the development of local micro-enterprises and,in the process, to increase the financial well-being of borrowers, theirfamilies, and the community at large.

To reduce the costs in order to become sustainable and improve theoutreach, microfinance institutions should have to be innovative.However, the new development of finance postulates that the successof microfinance program is judged by their ability to reach theunbankable areas. The success in the outreach area is examined forthe breadth, depth, quality, length, cost and variety of products.Moreover, the quantitative dimension of outreach can be measured bythe number of clients, average loan size, percentage of loans toclientele below the poverty line, percentage of female clients, lengthand cost of the services. Quality of outreach can be assessed by therange of products offered to the poor, the level of transaction costslevied on them, and the extent of client satisfaction.

Policy makers need some evidence as to whether or not clients arereceiving direct measurable benefits from microfinance. In addition,considering the large number of dropouts reported by some MFIs,opportunities to redesign MFI products to better meet the demands of

Institutionalization of Finance 17

the clients and the issue of impact on clients is increasingly important.The law has made it clear on the process of transformation offinancial NGOs into formal and regulated financial institutions. Anorganization, ACLEDA, was the first to obtain the license in October,2000 as a Specialized Bank and is not under the MFI law. It is able toattract a group of foreign investors including the IFC, DEG ofGermany, FMO and Triodos-Doen along with Triodos Fair Share Fundof Netherlands to become shareholders. Hattha Kaksekar received thelicense as an MFI in October, 2001, second after EMT (presentlyknown as AMRET), and CCB (presently known as CEB) in 2003.

The Asian Development Bank in 1998 had attempted to determinethe existing and future demands for micro credit. It had estimated byundertaking studies of two operators – GRET and ACLEDA as well ason international norms. This exercise, however, was very hazardous,and the estimation varied from 91 to 162 million dollars and looking toto-day, the supply falls well short of demand. Thus there appears to bean impression that the demand for microfinance is higher than thesupply. A study by Uniconsult (June, 1998) estimated that the demandfor rural credit was in the range of USD 75-125 million, which left a gapof approximately USD 50-100 million between the demand and supplyof informal/semi-formal/formal sources. Thus to-day, the demand formicro credit is far from being met, and the expansion strategies ofmicrofinance operators should be more aggressive to meet thedemand for the market.

Credit demands have been separated into group-guaranteed microbusiness loans and individual small business loans. MicrofinanceInstitutions (MFIs) transformed from NGOs have continued of lendingin the form of solidarity groups where lending does not requirecollateral, whereas lending to individuals requires collateral, wherethere is no guarantor. By the end of September 2005, MFIs hadaround 371,000 borrowers with a total loan outstanding more than ofKHR 200 billion and a total deposit of KHR 9.4 billion. The growths ofMFIs with regard to total loans outstanding, number of borrowers, totaldeposits and number of depositors are presented in Table 2.1.

18 Microfinance and Rural Development in Cambodia

Table No. 2.1Growth of MFIs During 1999-2005

(In million Riel)Source: NBC, 2006.

The above table shows that since 2003, there have beenincreasing trends of total loan outstanding, number of borrowers andnumber of depositors. But, compared to 2004, up to September 2005,there has been a marginal increase in the total deposits of MFIs.

Support from Donor Community

For more than four decades, donors have employed creditprograms in low-income countries to stimulate production, investment,and use of modern inputs. Many of these efforts have involvedcooperatively supervised credit programs, private rural banks, andspecialized development banks. Donors have commonly supportedthese efforts by placing funds into the central bank being on-lentthrough a concessionary credit line.

In the early 1990s, as donors became increasingly interested inmicrofinance, many NGOs started microfinance projects in Cambodia.Following the signing of Paris Peace Agreements and theestablishment of UNTAC and then after the first coalition Government

Year Items

Total Loans Number of Borrowers Total Deposits Number of Depositors

1999 73,238.54 291,453 4,444.91 1,3.872

2000 113,439.04 370,631 5,357.85 165,995

2001 140,163.17 409,963 14,832.17 158,627

2002 201,483.46 328,295 27,859.68 107,150

2003 129,756.06 265,044 9,819.92 78,628

2004 164,488.01 322,056 8,074.72 122,984

2005 203,034.35 371,054 9,441.47 142,843

19

Institutionalization of Finance 19

in 1993, donor funds flowed into the country. Thus, MFIs only startedto emerge in the 1990s and the main factors that enabled theestablishment of MFIs or NGO microfinance projects (usually the firststep in establishing MFI) were the security considerations.

The vast majority of financial support to the credit sector has beennegotiated through official government channels, including fundingsources, such as UNDP, USAID, ILO, KWF, CFD, and GTZ. Thesignificant programs are planned, including the possibility of soft-dollarloan from partners. The donor community has been influential both inthe design and the pace of development of microfinance sector.Donor’s support has also reflected their own policy objectives. Onesignificant donor – ADB, has assisted the country government byproviding assistance through grants and soft loans which are on-lentto MFIs. It has placed greater emphasis on policy reforms andcapacity building. The shift stems from the institution’s recognition,enabling policy environment and strengthening MFIs for a viable andsustainable microfinance system, capable of reaching poorer clients.However, most microfinance programs have started and continued tobe managed by Non-Governmental Organizations. Their sources offunding have included grants and soft loans from donors, trusts,foundations, and occasionally from governments. As they grow andproliferate, however, these programs have begun to reach limit of suchresources.

The donating package includes financial start-up support for thenew branches and technical assistance for overall institutionaldevelopment crucial in the context of rural development. In addition,most rural microfinance sectors fund their lending activities with grantsfrom these donating packages in the form of NGOs and projects. Thusthe microfinance sector in Cambodia has been established since1990s by national and international NGOs. Though at the beginning,these organizations were activity involved in programs related to socialdevelopment but later on some NGOs played a role of microfinanceoperators with the financial support from various internationalorganizations. Through these services microfinance sector has beendeveloped since early 1990s. However, operators do not have the

20 Microfinance and Rural Development in Cambodia

same resources available to overcome the human resource constraint.The largest operator has received significant expatriate technicalassistance from donor’s fund. For example, in 1989 and 1990, withliberalization and due to the arrival of NGOs, solidarity credit schemewas provided and, millions of families became users with real ratesfrom 5 to 20 percent per month. For example, GRET began itsintervention on credit, in 1991 and initially experimental credit schemewas set up, using a solidarity credit system, without preliminarysavings, and with a monthly interest rate of 5 percent.

Many donors however, follow a policy of very limited intervention.As a matter of principle, there can be no doubt to argue that less inter-vention is preferred. However, in building a financial institution, the realissue is how much non-intervention is feasible if the objective of theproject is to be achieved. In reality, an institution-building projectrequires much higher degree of intervention and long-term commit-ment on the part of the donors than other types of projects.

Government Policies on Microfinance

Developing countries have promulgated certain laws to encourageinvestments in provincial and rural development. It has led to makingincentives available to encourage rural development. The Prakas hasclassified banks and microfinance into three different groups: (1)persons who own 5 percent or less are not required to register with orbe approved by the National Bank of Cambodia and have nopersonal liabilities; (2) persons holding 20 percent or more areautomatically presumed to have majority or effective shareholding andthus personal liabilities; (3) in the third group, in gray area between 5percent and 20 percent, in which a stockholder is not automaticallypresumed to be a majority or effective stockholder may be found to beone by the National Bank depending on other facts and circumstances.

Prime Minister Samdach Hun Sen, following the involvement of allministries and stakeholders, launched the National Poverty ReductionStrategy of Cambodia in March, 2003. The idea really is to get peoplethemselves to think about what poverty reduction means and what

Institutionalization of Finance 21

they can do towards getting out of poverty. With regard to this, goodgovernance is important when applied for formal microfinanceinstitutions, because the issues may result in potential transfer pricingand transparency. Both non-government and government shouldtransform themselves into commercial forms in order to enhancegovernance and ownership. In addition, Prime Minister Samdach HunSen (1998) stated (Prakas of RGC on implementing credit program ofADB on agriculture) that the Royal Government of Cambodia supportsthe expansion of rural credit and saving through cooperating with thelicensed microfinance institutions and commercial banks. He furtherindicated that improving Rural Development Bank is the key to providerefinancing to microfinance operators for providing long-term loans torural people with sustainability. For strengthening microfinance institutions, the government would create financial laws and regulationsthrough the National Bank. Furthermore, the government wouldmonitor and evaluate the credit activity of microfinance operators andencourage them to become microfinance institutions.

The government has actively participated and continued to ensureevery program related to food security and nutrition and to establish aneffective system of micro credit for providing credit to farmers with theobjective of alleviating poverty at rural level. The government hasestablished the Credit Committee for Rural Development for thepurpose of formulating strategies to improve the efficiency of ruralcredit and to support the institutional strengthening and promotingprivate sectors. The National Bank has the role to coordinate these bymaking a system for microfinance operators to transform them intomicrofinance institutions, recognized and licensed by the NationalBank of Cambodia. Therefore, fund can be preceded from the RuralDevelopment Bank, commercial banks, or local as well asinternational financial institutions.

The institutionalization is found to be necessary, because localcredit sources are important and not by depending on outside sourcesfor fund any more. The government has established RuralDevelopment Bank, under the supervision from the sponsoredpartners, such as ADB and with the active involvement of Ministry ofEconomy and Finance with the main purpose to improve thedevelopment of rural agro-economic activities.

22 Microfinance and Rural Development in Cambodia

In order to have a positive development of microfinance, thegovernment has tried to issue a number of policies through severalauthorities. Having a legal framework for sound supervision andregulation on microfinance and the role of Credit Committee for RuralDevelopment are important for development of microfinance. Withregard to this, loans from Asian Development Bank to the governmentconsisting of a subsidiary loan to Rural Development Bank forrefinancing licensed Micro Finance Institutions and are supervised bythe National Bank. The government has established a ProjectCoordination Committee whose members are from the Ministry ofEconomy and Finance, Ministry of Rural Development, Ministry ofAgriculture, Forest and Fisheries, National Bank, Rural DevelopmentBank, and Licensed Microfinance Institutions, in order to coordinatethe support for project activities, based on Loan number 1741-CAM(SF).

A new law on banking and financial institutions has beenpromulgated and the law provides a legal framework for organizationsand operations of all types of banking sector, including microfinanceinstitutions. The supervision of microfinance requires the samecommercial bank, such as their capital adequacy ratio and minimumreserve for microfinance institutions. With the advice from its partner,the National Bank has been issuing new regulations, circulations orannouncements to monitor and gain more control on the financialsector. All organizations giving credit must be registered with thegovernment and all organizations over a certain size must becomelicensed. Moreover, to promote microfinance institutions, the bank hasissued regulations on capital guarantee that shall be permanentlydeposited with certainty. For example, 10 percent is for a commercialbank and specialized bank and 5 percent for microfinance institutions.It has further indicated that the National Bank requires commercial,and specialized banks 8 percent, and microfinance institutions 5percent of their deposits received as a legal reserve. Thus in 2000, theNational Bank has classified MFIs into three categories according tothe level of their operations, and made provisions for licensing andregistration. Though the regulations are similar to commercial banks,the capital requirement is substantially less. The medium-sized MFIs

Institutionalization of Finance 23

registered by National Bank are exposed to lighter regulations,whereas the smallest MFIs can operate freely with no requirement tobe regulated and supervised due to high operating cost. As it isrealized, the NBC is strengthening the implementation of the uniformchart of accounts for MFIs and the disclosure requirements inaccordance with the international accounting standard with theultimate aim to strengthen the microfinance sector in the country.

Planet Finance concluded that having established a framework forsound supervision and regulation is crucial to address thedevelopment of human resources and mobilization of savings toenhance sustainability of microfinance businesses. Microfinancesector is one of the important tools of the government in promotingeconomic growth and alleviation of poverty in rural areas. With strongsupport from the government, its partners are now providing anopportunity to microfinance institutions licensed by the National Bank.The government has normally provided fund through an assignedMinistry; its partners have supported the amount of fund. As per themeeting of the Project Coordination Committee in 2001, the RuralDevelopment Bank is the source that borrowers can access to borrowa certain amount in US dollars. With respect to single borrowerexposure limit applied to Rural Bank, the National Bank considers thelong-term loans from the Government as subordinated debt. TheNational Bank has issued the PRAKAS requiring microfinanceoperators to obtain either a license or registration. The registration andlicensing are determined according to the level of loan portfoliooutstanding, saving mobilized, number of clients and geographiccoverage. A license allows a microfinance institution to conduct creditactivities and accept savings from the public. Thus, the National Bankhas tried to push microfinance by determining that licensing is acompulsory condition by limiting loan outstanding amount, number ofborrowers, saving amounts, and number of depositors. Moreover, theGovernment policy is to support the expansion of rural credit andsaving services by encouraging the entry of privately licensedmicrofinance institutions and commercial banks into the sector. Withregard to this, the Government has established the interbank marketto assist the National Bank in undertaking policy reforms. Additionally,

24 Microfinance and Rural Development in Cambodia

it has also established a Banking and Financial Service in order tosteer the restructuring process of the banking sector.

To speed up licensing to microfinance institutions, expandingoutreach and getting loan from Rural Development Bank are the tasksof the Project Coordination Committee that makes suggestion to theNational Bank of Cambodia. With regard to this, the National Bank hasprovided licenses to two microfinance institutions – Thaneakea Phumand CEB and issued regulations to three microfinance operators.These regulations focus on monitoring the microfinance institutions inorder to implement that can lead to sustainability.

The poverty reduction strategy primarily focuses on improving ruralroads, primary health care, sanitation, rural water supply, education,rural credit, community development, household family system,provisions of seeds, fertilizer, rice bank, micro-enterprises andinformation at the village level. With regard to this, some licensedmicrofinance institutions are now able to provide their credit servicesto the poor in a more effective manner. However, providing creditservices to the poor is still at risk. Generally, it is found thatNon-Governmental organizations take greater risk in trying to reachthe poor and other marginalized groups. The organizations thus, playa critical role in poverty reduction and the development of ruraleconomy. In addition, credit services also play an important role increating, supporting and expanding businesses as well as increasingproductivity that generates income and raising the standard of livingand thereby helps in reducing poverty.

Rural Development Bank is a source for providing credit to ruralfinancial sector. It has a clear mandate from the government to act asa wholesale bank. The new microfinance legislation passed in 2000requires that all credit providers must have to register with the NationalBank. It provides an opportunity for selected microfinance institutionsto obtain licenses as fledged MFIs with a minimum capital. Thegovernment also leaves the operators free to set their interest rates.Moreover, the policy of the National Bank of Cambodia has been asupport, in line with its concerns and responsibilities for preserving the

Institutionalization of Finance 25

integrity of the financial system, promoting public confidence in thefinancial system, protecting deposits, preventing fraud, andencouraging best management practices. Thus to ensure a healthymicrofinance environment, the government, along with the NBC hasset up a policy that urges all credit operators to register andsubsequently to obtain a license. However, the government inpromoting economic growth and financial stability, often providesvarious financial safety arrangements.

The indicator of success for immediate output has to be adopted bythe government policy enabling financial viable and sustainable creditand saving institutions to develop. The government has alsoundertaken financial sector reforms with the aim of developing a soundfinancial system, which is an important factor for stimulatingeconomic growth. It has adopted the rural credit policy to develop aneffective rural financial system, and has initiated the rural credit andsavings program and technical assistance for capacity building forrural financial services. In addition, NBC has continued to strengthenmicrofinance institutions with special emphasis on provision of ruralcredit. Its regulations have pushed some microfinance NGOs totransform themselves into licensed microfinance institutions. Themandate on a general guideline in the field of rural credit has beendeveloped by Credit Committee for Rural Development (CCRD) inorder to offer with legal frameworks (credit associations, articles ofassociation for the rural financial institutions), and to make sure thelaw is properly applied. During 1994 to 1996, the Decentralized RuralCredit Committee has facilitated to bring operators and the authoritiescloser and to allow the later to better understand the problems facedby decentralized financial systems. This jointly run organization,having ceased to exist the National Bank of Cambodia, assumed theresponsibility for supervising this sector through its Bureau for theSupervision of Decentralized Bank Systems. This Bureau was set upin 1997 within the Department of Banking Supervision and since 1998,this Bureau has been actively involved in providing help to introduceregulations specific to microfinance institutions.

26 Microfinance and Rural Development in Cambodia

The products of MFI are primarily loans, as non-registered MFIs arenot permitted to take deposits. Most MFIs have started with solidaritygroup loans, enabling them to reach people who would have nocollateral to access a loan. A more recent response to the demand aswell as the need to work towards sustainability due to donor andmicrofinance providers, such as Concern and Catholic Relief Services(CRS) have compulsory savings, which is kept in a village bank andre-loaned to community members as emergency loans. Thegovernment supports the expansion of rural credit services byencouraging the entry of private licensed microfinance institutions,specialized and commercial banks and by strengthening the role ofRDB as a wholesaler. RDB provides long term funding to encourageinstitutions to expand and to make long-term loans which arenecessary to finance the capital investments of the rural people.

The projects of ADB and IFAD have provided soft loans to the RuralDevelopment Bank through Royal Government of Cambodia in orderto implement rural microfinance component under its project toincrease food and income security for people in the area.

Role of Rural Development Bank

The RDB was established as a key mechanism to support andstrengthen microfinance services in rural areas includingdevelopment, promotion and financing of Small and MediumEnterprise (SME) activities. It is strongly believed that microfinanceand micro business development in the rural areas are crucial for thesocio economic development of rural Cambodia.

RDB is a public and autonomous financial institution. It is acting asa wholesale bank and executive agent of donor and other loanprograms and projects, providing financing and refinancing to licensedcommercial and specialized banks and microfinance institutions,which delivered credit and saving services to rural poor as well as toindividuals and small and medium enterprises.

The objective of the RDB is to promote rural, agricultural and

Institutionalization of Finance 27

economic development in order to participate in the poverty reductionand raise the living standards of the people. Also it is to providewholesale lending services to operators to on-lend to the people inrural areas in the Kingdom of Cambodia. The RDB is committed toprovide sustainable access to credit in support of agricultural and ruraldevelopment for selected commercial sectors (rural water supplyproject, family rubber plantations, rice and maize cultivations, etc.) aswell as for small and medium enterprise development (SME), basedon free market systems. Even though Cambodia is having a freemarket economy, the RDB has been trying hard to negotiate with itspartners so that the interest rate charged from the end-borrowersreduces step by step. Due to the efforts made by RDB, in the wholecountry, the interest rates have been reduced and in some places itdecreased from 5 percent to 2.5 percent per month. As a widercommitment, RDB and the credit operators have extended theiroperation, as a priority step, to the border and remote areas, which arefound to be economical potential areas for agriculture and agro-industry for the sole purpose of transforming them into agriculturaldevelopment areas.

From the above discussion, it is beyond doubt to justify that formalcredit has a positive role in developing the rural economy of Cambodiaand microfinance institutions has a further more definite role to playtowards the development of the economy as a whole. In building astrong financial base in the rural sector, the role played by the RoyalGovernment of Cambodia, the NBC and RDB are praiseworthy.Further, the committeemen to support the poor people by theinternational donors and local institutions is well recognized.

28 Microfinance and Rural Development in Cambodia

III

Cambodian Banking System and Microfinance Operators

Cambodian microfinance though is very young, has been recognizedinternationally as a fast developing sector. It is highly rated since itcommenced its path towards a sound regulatory, supervisory andmanagerial environment. Today it is seen as an emergingindustry in the country. It plays an important role to develop andexpand financial services in the rural areas and in the process,actively participate in alleviating poverty. The development ofmicrofinance institutions is to remove the restricted access, one of themain obstacles, to financial services in rural areas in order to improvethe living standard of the rural poor. The success of microfinanceinstitutions entirely depends on micro loan to the poor. The program offinancial and non-financial services for micro and small enterprisesaims at contributing to the country’s long-term economic development.This also has a direct impact on services provided to rural poorpeople, resulting in augmenting income and generating furtheremployment. It is an important mechanism for rural developmentwhose role is not only to create and diversify employment, but also toenhance productivity and generate income so that the standard ofliving of the people can be improved.

The Cambodian microfinance sector has been established since1990s by both the national and international non-governmentalorganizations. The National Bank of Cambodia (NBC) beganreforming the banking system in early 2000. It started to issue andrevise regulations in order to transform NGOs into registered andlicensed MFIs. Since 2002, some NGOs have been licensed andsome others have been registered. By the end of 2005, 16 licensedand newly established MFIs have been transformed from NGOs and24 registered as rural credit operators.

In spite of several constraints, there are some microfinanceoperators who are striving hard to bring success to their organizationson one hand and providing wider benefits in terms of income,employment, higher productivity, etc. to the target population on theother hand. Against this backdrop, the main purpose of the presentchapter is to highlight the Cambodian banking system along withcases of some of the major microfinance operators in the country.

Cambodian Banking System

The banking system in Cambodia was completely destroyed in theyear 1975 and in fact, there were absence of financial services from1975 to early 1979. A mono-banking system was established in 1979with NBC playing the role of both central and commercial bank througha network of provincial branches. Under the mono-banking system, theNBC financed state-owned enterprises as well as small loans to needyfarmers based on mutual guarantees, through twenty provincialbranches all over the country. With the privatization of the bankingsector in 1990 and the cessation of the NBC as a commercial bank,the needy borrowers/enterprises were deprived of accessing financialservices. However, in some areas in the country, the provision of smallfinancial assistance was taken over by non-licensed credit providers.After the adoption of the law on Banking and Financial Institutions atthe end of 1999, the NBC launched a banking system restructuringprogram by requiring all banks to apply for re-licensing. Further in2000, the NBC started to issue regulations on the classification ofMFIs into three categories according to the level of their operationsand revise regulations in order to transform NGOs into registered andlicensed MFIs as per their scope of operations. At the end of 2005, theCambodian banking system in composed of 15 commercial banks, ofwhich 12 are locally incorporated and 3 are foreign branch banks, 4specialized banks, of which one is state-owned and 3 are privateowned, 16 licensed MFIs and 24 registered micro operators operatingin the rural areas, which is presented below.

30 Microfinance and Rural Development in Cambodia

Cam

bodi

an B

anki

ng S

yste

m20

05

Man

ey C

hang

ers

Reg

iste

red

2,1

58- P

hnom

Pen

h 2

63- P

rovi

ncia

l 1

,895

2

Rep

rese

ntat

ive

Offi

ces

- Sta

ndar

d Ch

arte

red

- Vie

tnam

Ban

k fo

r Agr

icul

ture

and

Rur

al D

evel

opm

ent

Firs

t Com

mer

cial

Ban

kKr

ung

Thai

Ban

kM

ay B

ank

3 Fo

reig

n Br

anch

Ban

ks

Fore

ign

Trad

eBa

nkof

Cam

bodi

aAd

vanc

ed B

ank

ofAs

iaC

ambo

dia

Asia

Ban

kC

anad

ia B

ank

Ltd.

(2)

Cam

bodi

an C

omm

erci

al B

ank

(1)

(Sia

m C

omm

erci

alBa

nk)

Cam

bodi

a M

ekon

g Ba

nk(3

)C

ambo

dian

Pub

lic B

ank

(6)

(Pub

lic B

erha

rdBa

nk)

Sing

apor

e Ba

nkin

g Co

rpor

atio

nU

nion

Com

mer

cial

Bank

(4)

Vatta

nac

Bank

(8)

ACLE

DA B

ank

Plc

(5)

ANZ

Roy

al B

ank

Cam

bodi

a (9

)

12 L

ocal

lyIn

corp

orat

ed

15 C

omm

erci

al B

anks

Rur

al D

evel

opm

entB

ank

1 St

ate

Own

Peng

Hen

gS.

M.E

Lim

ited

Cam

bodi

a Ag

ricul

ture

Indu

stria

lSp

ecia

lized

Ban

kFi

rst I

nves

tmen

t Spe

cial

ized

Ban

k

3 Pr

ivat

e O

wn

4 Sp

ecia

lized

Bank

s

AMR

ET C

o Lt

d.H

atth

a Ka

ksek

arTo

ng F

ang

Mic

rofin

ance

Than

eake

a Ph

umC

ambo

dia

Cam

bodi

aEn

trepr

eneu

r Bui

ldin

g Lt

d.Se

ilani

thih

Angk

or M

ikro

hera

nhva

tho

(Kam

puch

ea)

Visi

on F

und

(Cam

bodi

a) L

td.

CR

EDIT

Co.

Ltd.

PRAS

AC M

icro

finan

ceIn

stitu

tion

Farm

er U

nion

Dev

elop

men

tFun

dC

ambo

dia

Busi

ness

Inte

grat

ed in

Rur

al D

evel

opm

ent

Max

ima

Mik

rohe

rahv

atho

Inte

an P

oalro

ath

Rong

roeu

rng

CH

C Li

mite

d

16 L

icen

sed

23 R

egis

tere

d

Unr

egis

tere

dar

ound

60

NGO

s

NG

Os

Mic

ro-fi

nanc

e In

stitu

tions

Kam

pong

Cha

m (A

pr25

, 200

0)Si

hano

ukVi

lle(M

ay 3

, 200

0)Si

em R

eap

(Jun

e11

,200

0)Ba

ttam

bang

(Feb

17,

2003

)Sv

ay R

ieng

(Feb

24,2

003)

Kand

alPr

ey V

eng

Kam

pong

Tho

mTa

keo

Purs

atKa

mpo

ng C

hnan

gKa

mpo

ng S

peu

Kam

pot

Koh

Kong

Prea

h Vi

hear

Krat

ieR

atan

akiri

Mon

dolki

riSt

ung

Tren

gBa

ntea

y M

eanc

hey

20N

BC P

rovi

ncia

l Bra

nche

s

NAT

ION

AL B

ANK

OF

CAM

BOD

IA(C

ENTR

AL B

ANK)

Cambodian Banking System and Microfinance Operators 31

Registered NGOs

1. Agriculture and Tourism Development Association2. Aid Farmers Association3. Association for Business Initiative4. Association for Development of Diversified Khmer Nation5. Buddhism for Development Association and Supporting

Environment6. Cambodia Community Saving Federal7. Cambodia Credit to Abolish Poverty Organization8. Cambodia Rural Economic Development Organization9. Cambodia Women's Development Agency10. CICM Cambodia11. Crop Supporting National Association12. Islamic Local Development Organization13. Khmer Rural Development Association14. Kratie Women Welfare Association15. Lutheran World Federation Organization16. Ministry of Rural Development Credit Scheme17. Northwest Development Association18. Rural Development Association19. Rural Economic Development20. Rural Family Development21. Social Development in Rural22. Ta Ong Soybean Development Association23. Women's Saving and Development Cooperative

Microfinance Operators

It has been widely recognized that even if the Cambodian bank-ing sector grows quickly, the country needs to promote themicrofinance sector as it provides credit to the needy borrowers inrural areas with reasonable interest rates to fund their investments. Abrief elaboration of some selected microfinance institutions ispresented below:

32 Microfinance and Rural Development in Cambodia

ACLEDA Bank Plc.

In January 1993, the Association of Cambodian Local EconomicDevelopment Agencies (ACLEDA) was established as an independentCambodian NGO with the sole purpose of developing small and microenterprises. It was aiming at raising the standards of living of the poorby promoting economic activities ranging from self-employment andsmall to medium size business. The Ministry of Commerce issuedACLEDA a Certificate of Incorporation as a Public Limited LiabilityCompany in August 2000. ACLEDA completed the transformation fromNGO to a bank and the National Bank of Cambodia granted ACLEDAa license on 7th October, 2000. Thus, following the transformation intoa licensed specialized bank, ACLEDA Bank was established inOctober 2000, and the original ACLEDA was officially renamed theACLEDA NGO. Under the process, the existing NGO transferred theassets and on-lent its liabilities (long term loans from donors) to thenew ACLEDA Bank. On 1st December 2003, the National Bank ofCambodia issued a license for the bank to become a privatecommercial bank for a period of three years commencing from 1stDecember, 2003. Thus, the most momentous event of 2003 was theconversion of ACLEDA from a specialized bank to a full commercialbank and this had entailed an increase of its paid-up capital from USD4 million to USD 13 million. Further, with the granting of a commercialbanking license, it has laid to build the bank into a leading micro, retailand commercial bank in the country. In 2004, it expanded more thanat any time in its history and now ranks among the top threecommercial banks in the country. In ACLEDA Bank, 51 percent ofequity is owned by Cambodian interests, including its staff while theremaining 49 percent has been taken up by foreign investors in equalparts, such as International Finance Corporation (a division of theWorld Bank), DEG (Germany), FMO (Netherlands) and Triodos-Doenalong with Triodos Fair Share Fund (Netherlands). To sum up, todayout of the 15 commercial banks in the country, only ACLEDA hastransformed from an NGO operating microfinance into a specializedbank and finally to a commercial bank.

33

Cambodian Banking System and Microfinance Operators 33

In 2004, one of the significant developments on the part ofACLEDA Bank Plc. was of obtaining a rating from an InternationalCredit Rating Agency, i.e. Moody’s Investors Service. This was the firsttime that an international credit rating has been done to a Cambodianfinancial institution. It has assigned in awarding a Bank FinancialStrength Rating (BFSR) of ‘D’ with rating outlook of ‘stable’. Moody’scommented that this reflected ACLEDA’s rapidly building franchisestrength and its strong profitability, capitalization and asset quality(Annual Report 2004).

Today ACLEDA has claimed of having the largest bank network inthe country, i.e., the net work expanded by 23 percent to 119branches and offices and, with the addition of Kratie and Koh Kong,now it covers 21 out of 24 provinces (Annual Report 2004). This isshown with the help of the map given below.