The Bharat Microfinance Report 2013.pdf - Margdarshak

160

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of The Bharat Microfinance Report 2013.pdf - Margdarshak

FosteringClient-Centric Practices

through Compliance

The Bharat Microfinance Report 2013

12 & 13, Special Institutional Area2nd Floor, MPTCD Building, Shaheed Jeet Singh Marg

New Delhi - 110 067, IndiaTel. : +91-11-47174400 Fax : +91-11-47174405Email : [email protected], [email protected]

© Copyright reserved Sa-Dhan2013

Developed & Published by:Sa-Dhan

12 & 13, Special Institutional Area,2nd Floor, MPTCD Building, Shaheed Jeet Singh Marg,

New Delhi – 110 067, IndiaTel: +91-11-47174400 Fax: +91-11-47174405

E-mail: [email protected], [email protected]

Cover Design & Printed by:Anil

9810803375, 8860127811

Disclaimer:The views expressed in this publication do not necessarily reflect the opinions/views of any

supporters nor they be held responsible for the opinions/views in this report.

Preface

iii

Microfinance sector in India, after the Andhra Pradesh crisis, is inching back to normalcy, thanks to the regulatory comfort provided by RBI. The microfinance Bill, which is

before Parliament is expected to bring in further legitimacy to all forms of MFIs. The industry Code of Conduct implementation coupled with regulatory compliance by the sector would go a long way in infusing confidence among all the stakeholders.

In this context, I think there are three areas of our domain deserving our special attention. One is the need for articulating the fact that microfinance is a strategic part of financial inclusion agenda of the government and the central bank. The second is the criticality of re-demonstrating our collective intention to help the poor and the unbanked populace by way of right mission, social performance and client protection. The third area is projecting the fact that microfinance institutions are sustainable financial institutions and they continue to be the investable destination for the bankers and the investors.

In order to articulate these positions, we need empirical data. This report has been designed to provide new perspectives on the above three areas. Primary data received from 155 Sa-Dhan members and other MFIs, who represent around 95 percent of the client / the credit portfolio of MFIs in India, and analysis thereon are the basis for this report.

Sa-Dhan has been publishing The Bharat Microfinance Report for the past nine years. This year, in spite of MFIs preoccupation with their operational issues, 155 MFIs reported data, including 51 non-member of Sa-Dhan. We thank them for reposing confidence in us and valuing transparency through data reporting.

For the first time, we have included an elaborate account of SHGs and Cooperatives as microfinance intermediaries. The data and case studies provided by Self Help Group Promotion Institutions (SHPIs) and Cooperatives have been helpful in developing the chapter. NABARD Data sets have been analysed and lucidly presented to understand the SBLP trend.

A dedicated team at Sa-Dhan secretariat consisting of Dr. K.Natarajan and Mr. Ardhendu Nandi spearheaded the report work with active support of their colleagues Mr. P.M Kamalesh, Ms. Isha Gambhir and Ms. Neetu Lodhey. We appreciate them for their meticulous collection of data through repeated follow up with members, validation of the data analysis and compilation of the report. We appreciate the data collection support rendered by members of Sa-Dhan team, Mr. Krishna Reddy, Mr. Susanta K.Behera, Mr. Habib Shaik and Mr. T.Kumar from their respective regions of operation.

We are grateful to Mr. C.S.Ghosh, Mr. Suresh Krishna, Mr. Ravi Narasimham, Mr. V. S. Radha Krishnan, Mr. Royston Braganza, Mr.Parashuram Nayak, Mr.Vinod Jain,

The Bharat Microfinance Report 2013iv

Mr. V. Salimath, Mr. Rajesh Singhi, Ms. Kalpana Pant and Mr. Subrat Singh for their guid-ance and feedback on the framework and draft report.

Special thanks to Mr. Somesh Dayal, Mr. Alok Kumar Dubey and Mr. Chandan Kumar for providing technical inputs for the report work.

We are grateful to overall patronage from SIDBI, Ford Foundation, Citi Foundation, IFC, Hivos, NABARD, RBI and Government agencies for the work of Sa-Dhan.

We have attempted to provide some new insights in this report. We hope this would be useful to you. We look forward to receiving your comments and suggestions for improvement.

Mathew TitusExecutive Director

v

Contents

Preface i

List of Boxes viii

List of Figures ix

List of Tables xi

List of Abbreviations xii

Glossary xiv

Executive Summary xviii

Part 1: Microfinance And Financial Inclusion 1 1.1 Microfinance Complementing Banks 2 1.2 GOI and RBI stand on MicrofinanceRole and Financial Inclusion 3 1.3 Microfinance Outreach 4 1.4 Microcredit for Financial Inclusion 7 1.5 MFIs Reach to Special Segments of People 7 1.6 Non-Credit Financial services of MFIs 9 1.7 MFIs as Banking Correspondents (BCs) 10 1.8 Deepening Financial Inclusion through Finance + Development Services 12 1.9 Fruits of MFIs Inclusive Efforts -Impact on the Lives of Borrowers 15

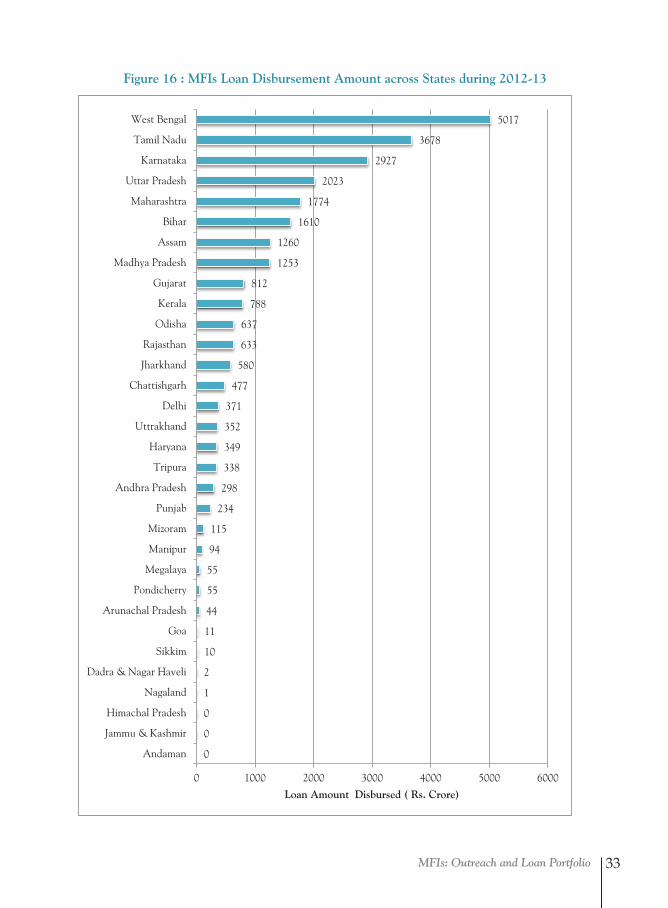

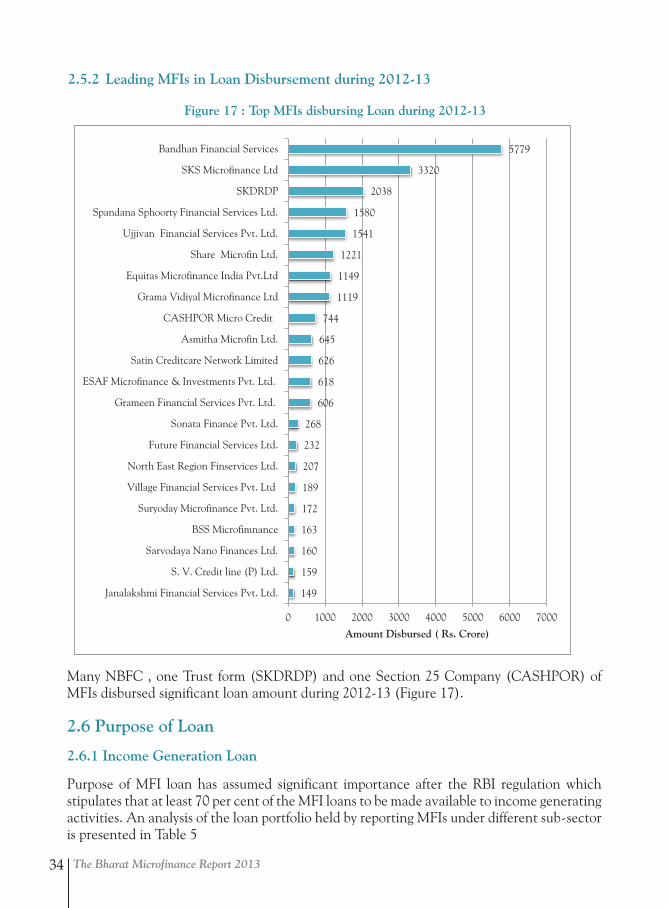

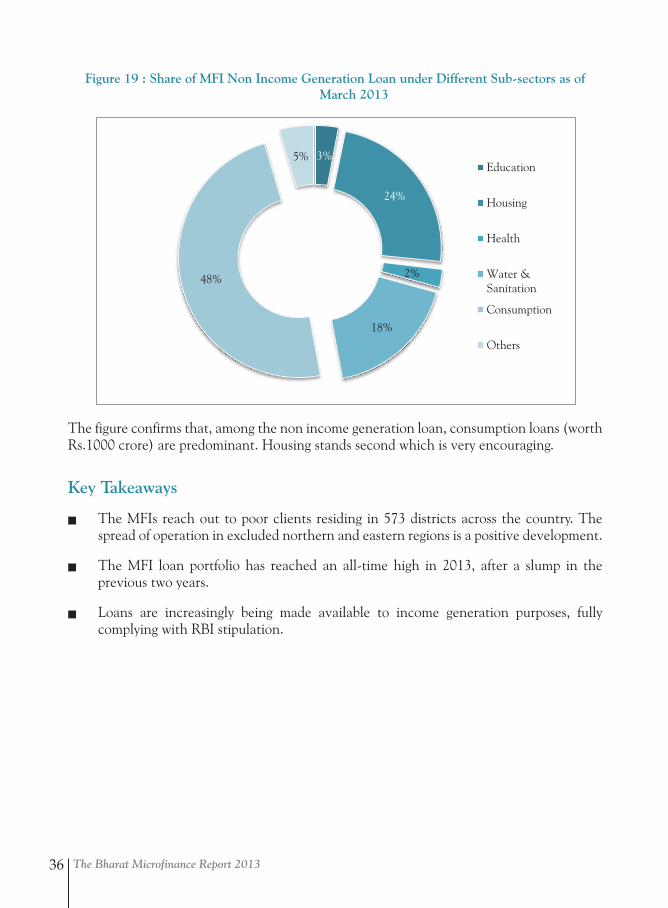

Part 2: MFIs: Outreach and Loan Portfolio 19 2.1 Geographical Spread 19 2.2 Client Outreach 20 2.2.1 The Regional Spread of MFI Clients 22 2.2.2 State-wise Client Outreach 22 2.2.3 Leading MFIs in Client Outreach 23 2.2.4 Types of Clients Reached 24 2.2.5 New Clients Acquired 24 2.3 Loan Portfolio of MFIs 25 2.3.1 Region-wise Loan Portfolio 27 2.3.2 Loan Portfolio across States 27 2.3.3 Managed Portfolio 28 2.3.4 Loan Amount Outstanding per Borrower 29 2.4 Growth Trend in MFI Borrowers and Loan Portfolio 30 2.5 Loan Disbursement 30 2.5.1 Loan Disbursement –Regional Variation 31 2.5.2 Leading MFIs in Loan Disbursement during 2012-13 34 2.6 Purpose of Loan 34 2.6.1 Income Generation Loan 34 2.6.2 Non-Income Generation Loans 35

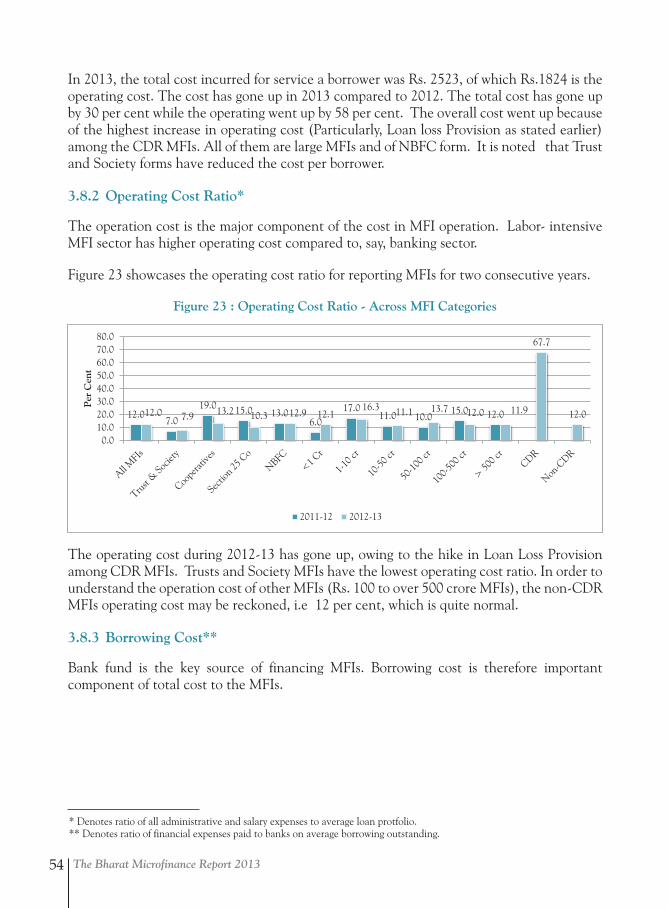

The Bharat Microfinance Report 2013vi

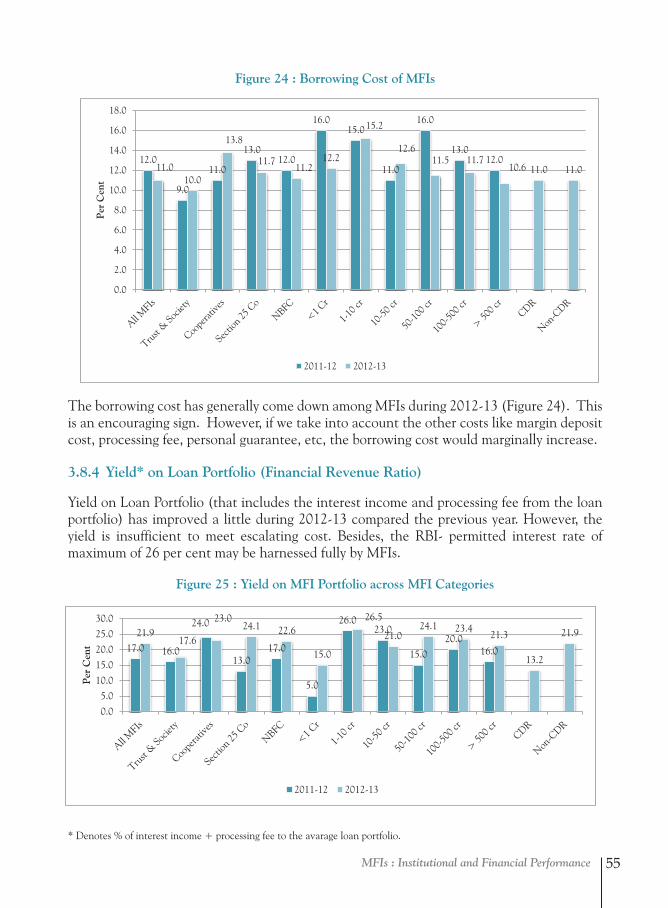

Part 3: MFIs – Institutional and Financial Performance 37 3.1 Branch Network 37 3.2 Workforce in MFIs 38 3.2.1 Active Borrowers per Credit Officer (ABCO) 40 3.3 Portfolio Quality 40 3.4 Assets and Liabilities of MFIs 42 3.4.1 MFI Assets 42 3.4.2 MFI Equity Outstanding 44 3.4.3 Fresh Equity Acquired 45 3.4.4 Leverage / Debt –Equity Ratio 47 3.4.5 Capital (Net owned Fund) to Total Assets Ratio 48 3.4.6 Gross Loan Portfolio to Total Assets 49 3.5 Income Analysis 50 3.5.1 Break-up of Income 50 3.6 Expenditure Analysis 51 3.7 Net surplus 52 3.8 Cost and Profitability Ratios 53 3.8.1 Cost Per Borrower 53 3.8.2 Operating Cost Ratio 54 3.8.3 Borrowing Cost 54 3.8.4 Yield on Loan Portfolio (Financial Revenue Ratio) 55 3.8.5 Operating Self Sufficiency 56 3.8.6 Margin Level 56 3.8.7 Profitability Ratios 57

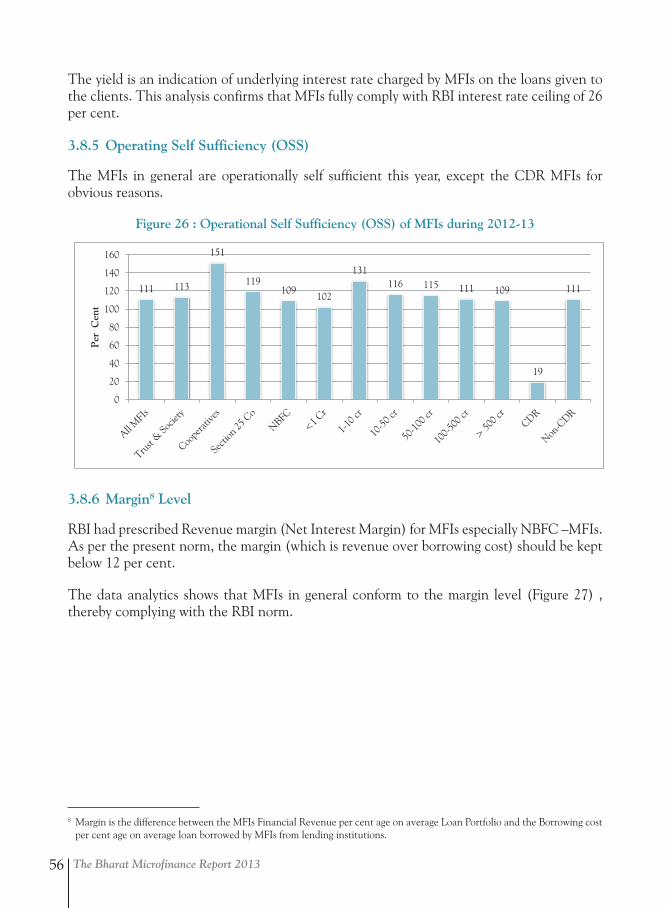

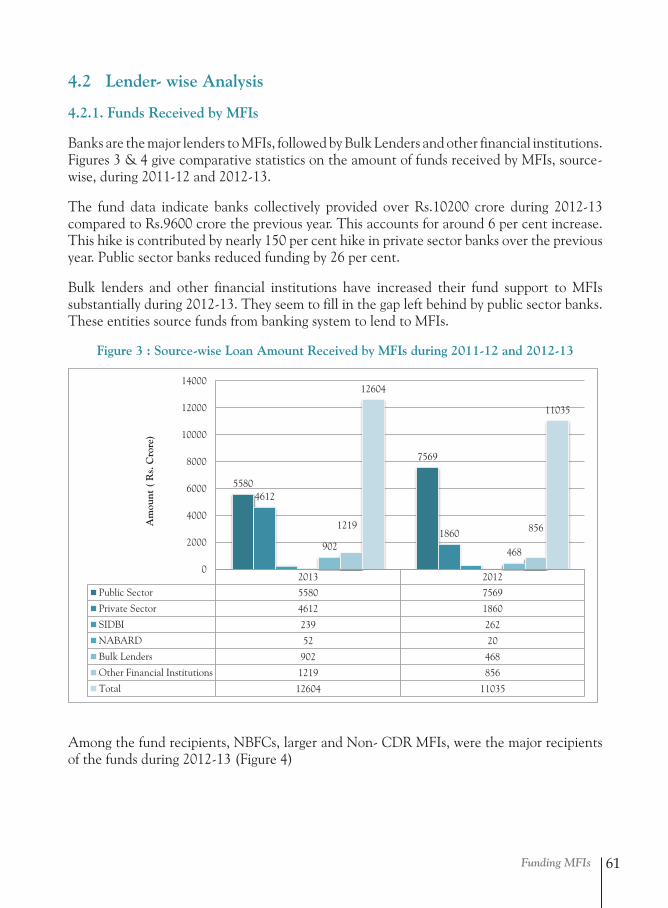

Part 4: Funding MFIs 59 4.1 Funding Instrument wise Analysis 59 4.1.1 MFIs Borrowing Instruments 59 4.2 Lender wise Analysis 61 4.2.1 Funds Received by MFIs 61 4.2.2 Target MFIs (Beneficiaries) for Funds lent during 2012-13 62 4.2.3 MFIs’ Outstanding Bank Loan Portfolio 63 4.2.4 Top Lenders to MFIs During 2012-13 65 4.3 Results of Bankers Survey on MFI lending 68 4.3.1 On MFIs being partners of Banks 68 4.3.2 On Performance of MFIs 68 4.3.3 On lending criteria to MFIs under priority sector lending 69 4.3.4 On Change of Risk Assessment under MFI lending 70 4.3.5 Banks views on Post-crisis Era being normal or ‘new normal’ 71

Part 5: Self Regulation 72 5.1 RBI Regulation 72 5.2 Microfinance Bill 72 5.3 RBI’s Say in Self Regulation 73 5.4 Sa-Dhan and Self Regulation 73 5.5 Lenders’ Forum – Reinforcing Self Regulation 75 5.6 Responsible Finance Forum – A Think Tank in Self Regulation 76 5.7 Sa-Dhan Members’ Self Regulation in response to the RBI Regulation 76

vii

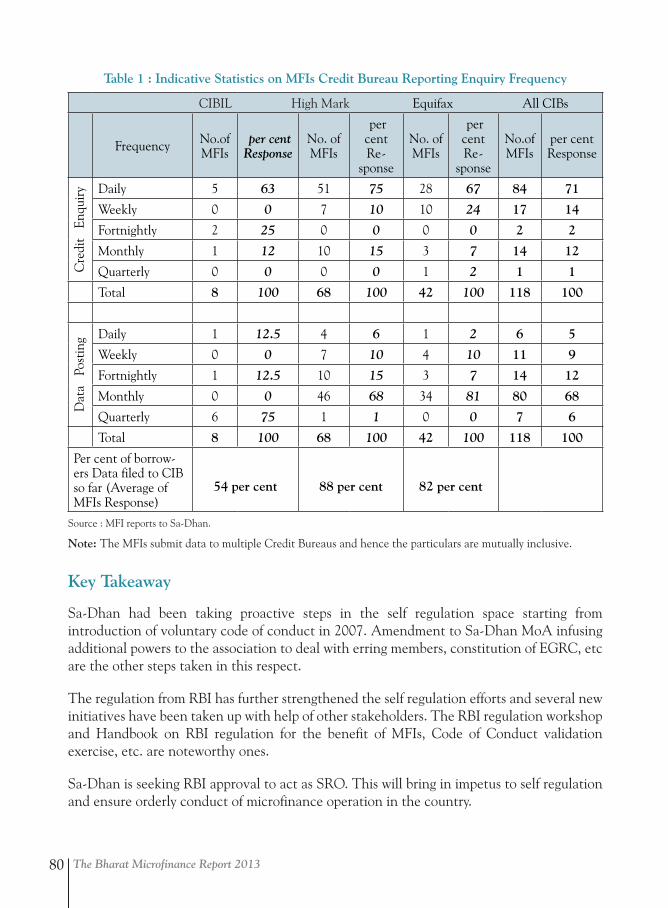

5.8 Self Regulation – State Level Efforts 78 5.9 Credit Bureau Checking as Self Regulation 79 Appendix - Perpective of a Credit Bureau-High Mark 81

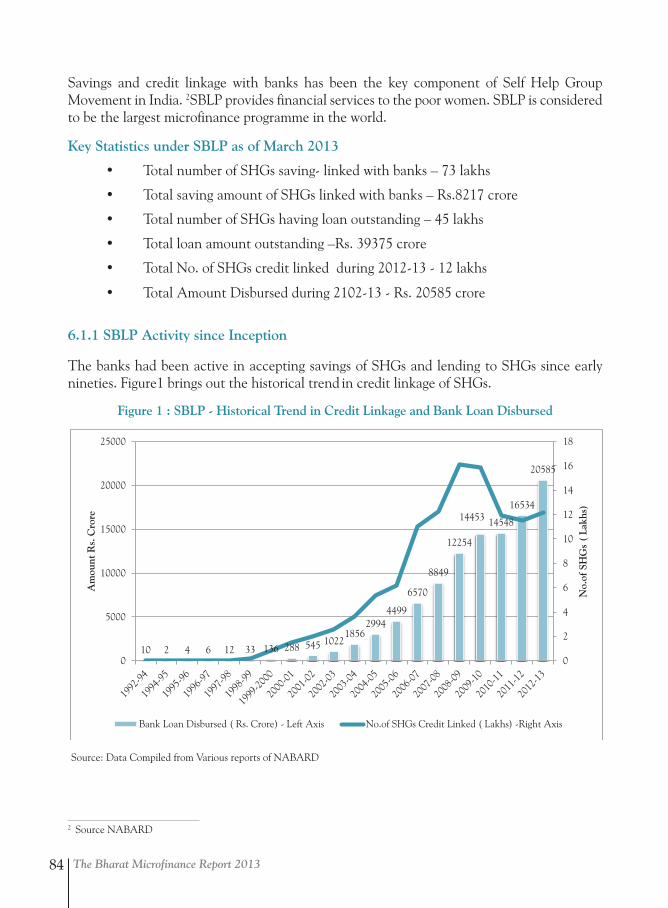

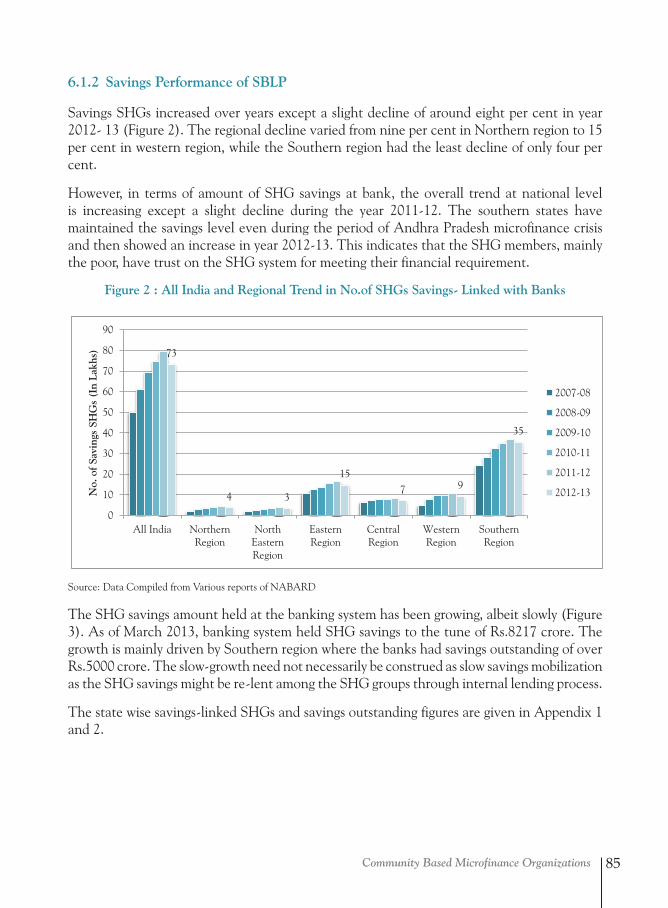

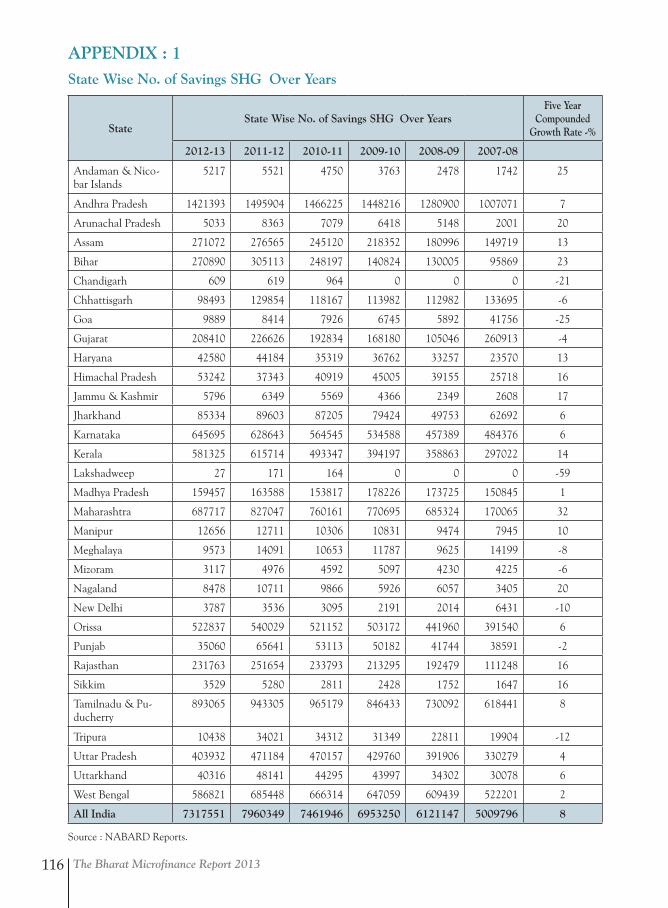

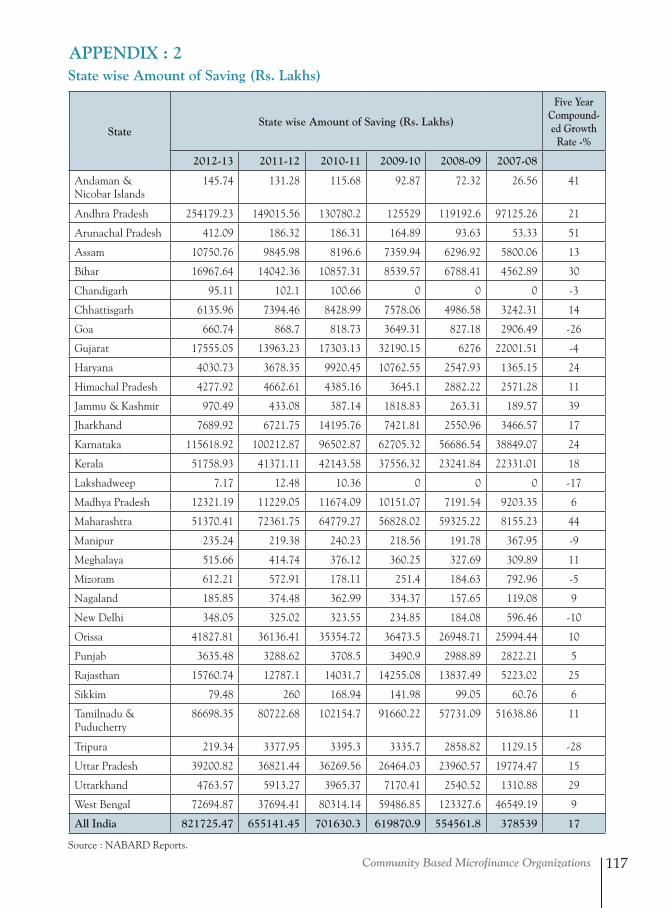

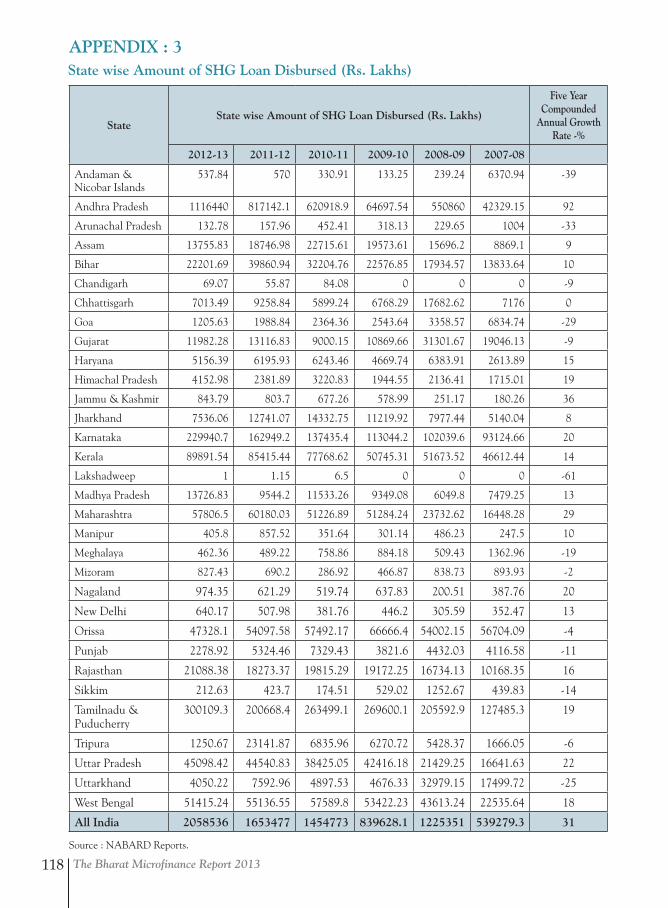

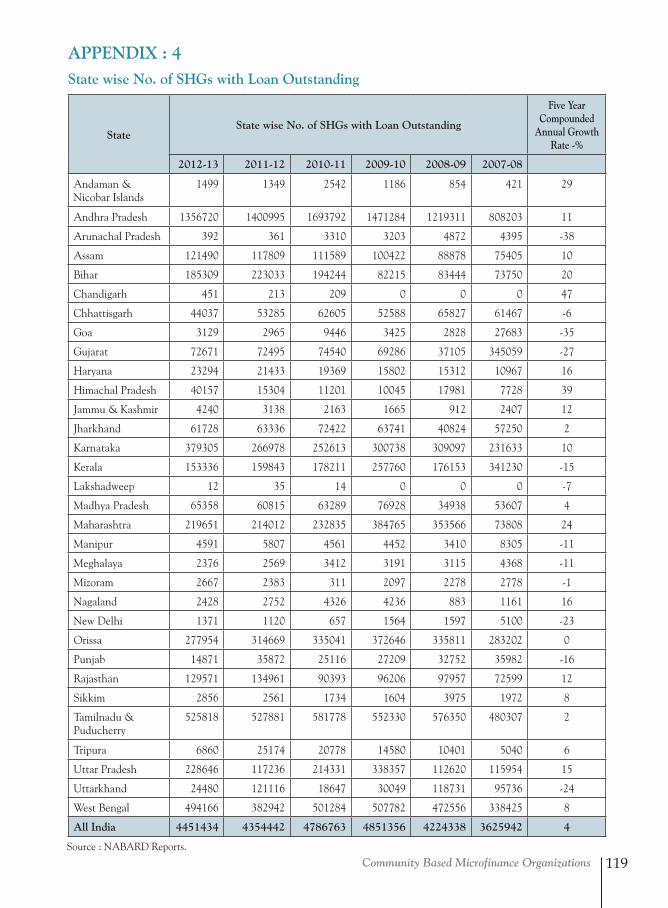

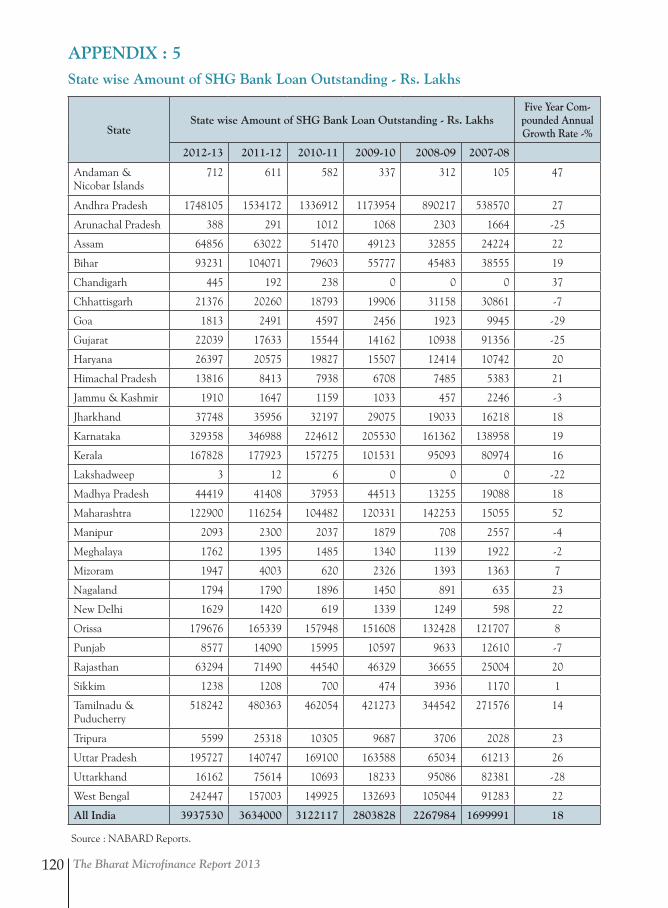

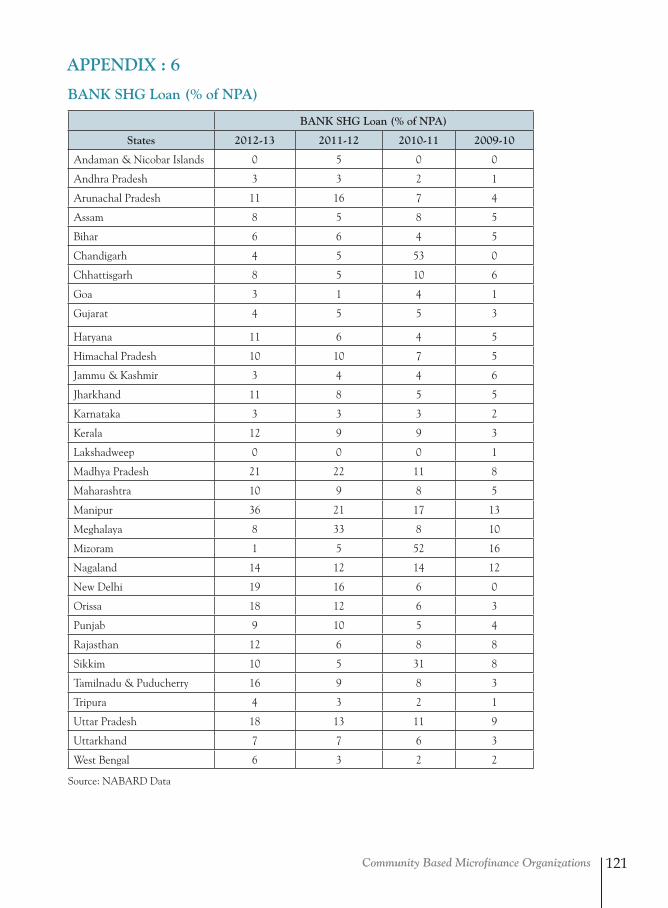

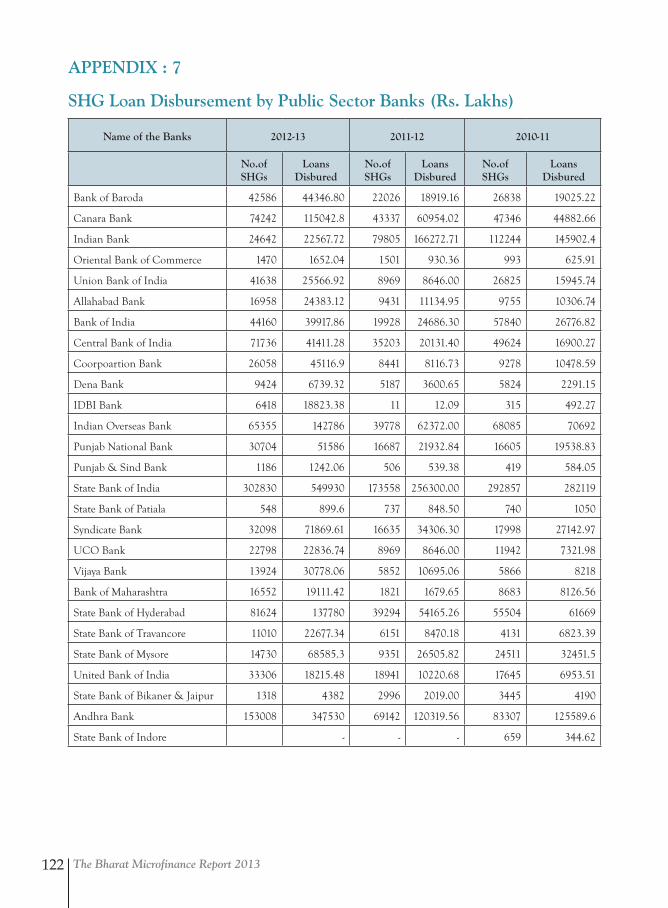

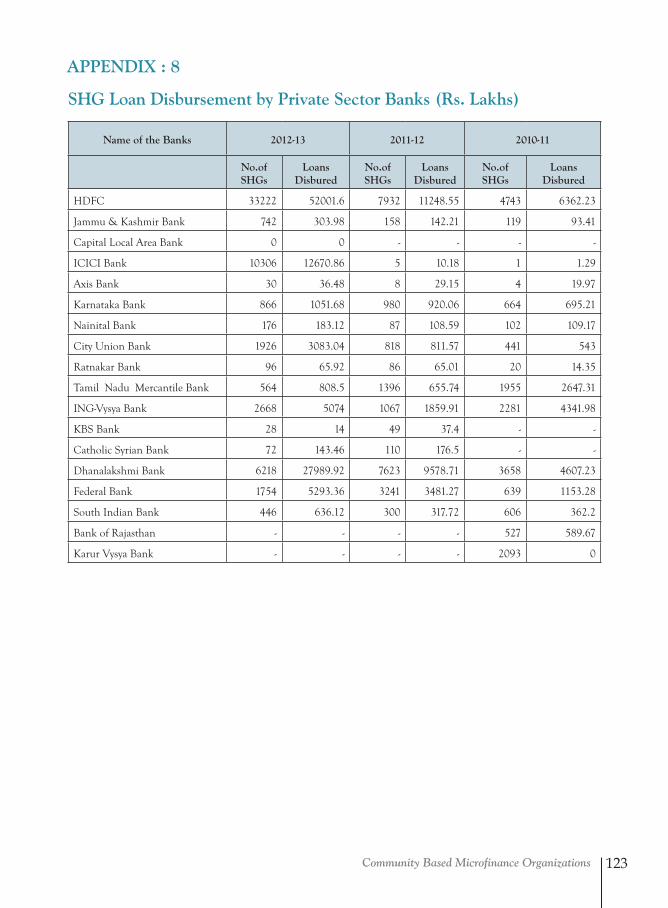

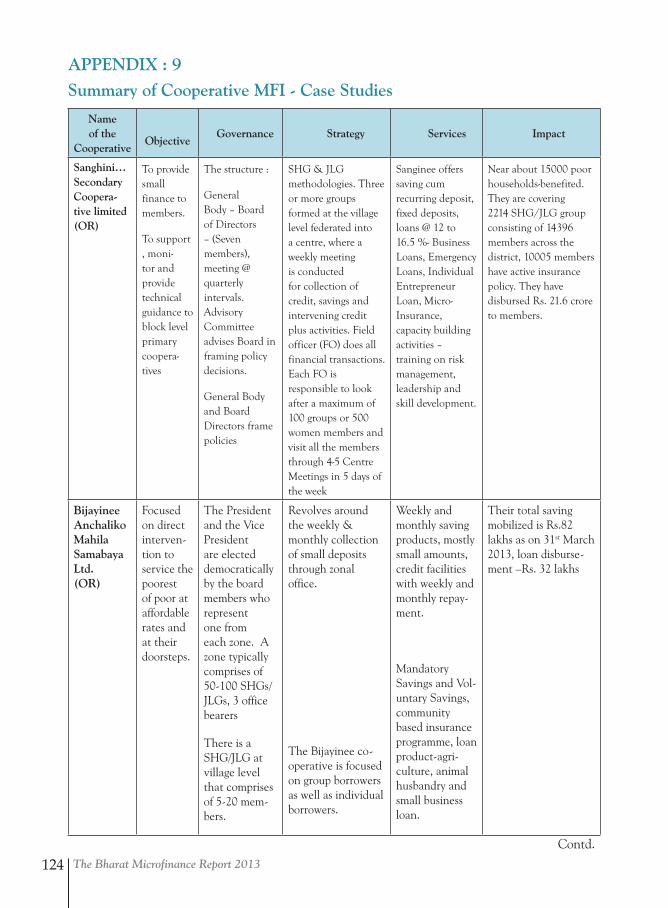

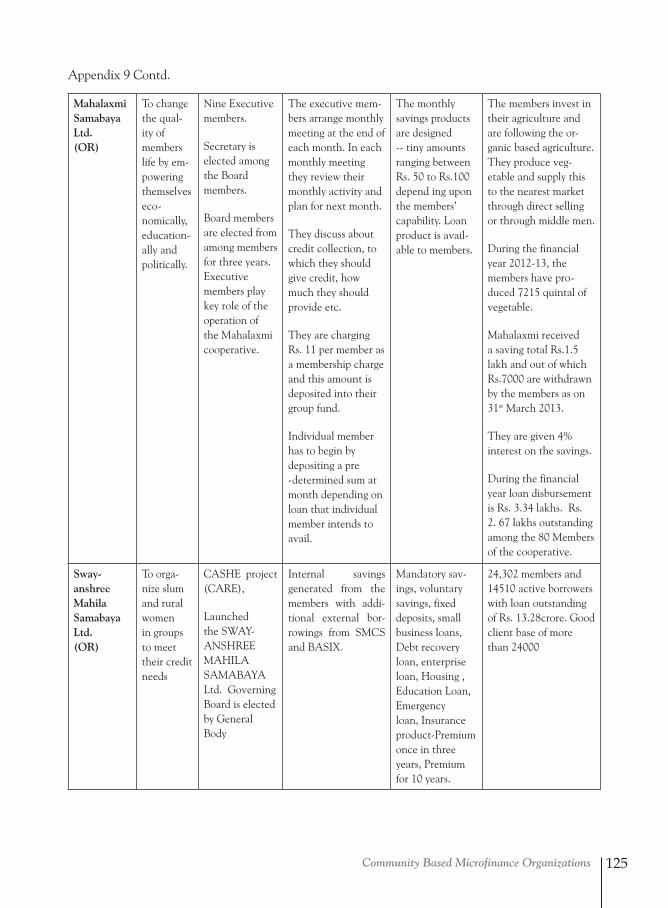

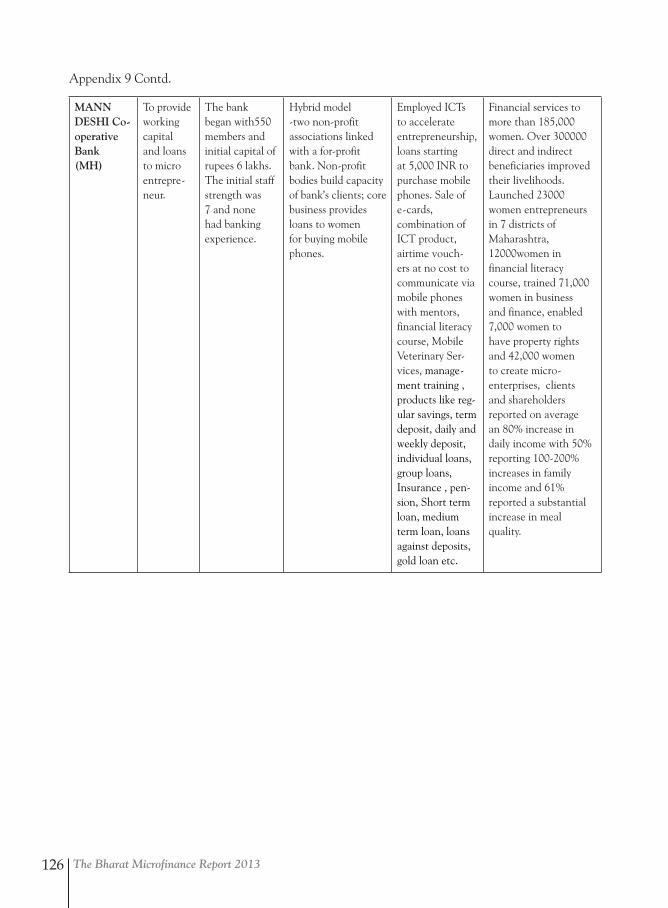

Part 6: Community Based Microfinance Organizations 6.1 Self Help Group Bank Linkage Programme (SBLP) 83 6.1.1 SBLP Activity since Inception 84 6.1.2 Savings Performance of SBLP 85 6.1.3 SHGs with Bank Loan 86 6.1.4 SHG Bank Loan –Portfolio Quality 91 6.2 SHGs and Their Federations-Some Observation 93 6.2.1 SHGs Quality 93 6.2.2 SHGs Federations 94 6.2.3 Good Practices in SHG Federation –A Typical Case 95 6.2.4 Strengthening SHGs and Federations – Some Suggestions for Future 97 6.3 Self Help Promoting Institutions (SHPIs) 98 6.3.1 The Key Findings from Eight SHPI Data-Source –Primary Data 98 6.3.2 SHPI survey -Salient Observation 100 6.3.3 Engagement of SHPIs by Ministry of Finance under Women Self Help 100 Groups (WSHGs) Scheme 6.4 Livelihoods Promotion through Self Help Groups 104 6.4.1 Summary of NGO Interventions 104 6.4.2 Value Chain Financing through SHGs (Care India)-A Typical Case of Livelihood 106 6.4.3 Aajeevika National Rural Livelihoods Mission – A Brief Intro 109 6.5 Microfinance through Cooperatives 110 6.5.1 Saving Facilitation by Cooperative MFIs 110 6.5.2 An Evoled Cooperative Microfinance Institution : SEWA Bank - A Case 111 6.5.2.1 Savings 112 6.5.2.2 Loan 113 6.5.2.3 Pension 114 6.5.2.4 Banksathis - SEWA’s Unique Banking Facilitator 114Appendix Appendix 1 : State wise No. of Saving SHG Over years 116 Appendix 2 : State wise Amount of Saving 117 Appendix 3 : State wise Amount of SHG Loan Disbursed 118 Appendix 4 : State wise No. of SHG with Loan Oustanding 119 Appendix 5 : State wise Amount of SHG Bank Loan Oustanding 120 Appendix 6 : Bank SHG Loan (% of NPA) 121 Appendix 7 : SHG Loan Disbursement by Public Sector Banks 122 Appendix 8 : SHG Loan Disbursement by Private Sector Banks 123 Appendix 9 : Summary of Cooperative MFI - Case Studies 124

AnnexruesDistribution of MFIs contributing data to Bharat Microfinance Report 2013 127Profile of MFIs Contributed Data for Bharat Microfinance Report 2013 129

List of Boxes

Part 1: Microfinance and Financial Inclusion

Box 1: Key Statistics in Banking Infrastructure in Village and Coverage 1

Box 2: Poorest States Inclusive Growth (PSIG) Programme 8

Box 3 MFIs Vis-a Vis Chit Funds 17

Part 3: MFIs – Institutional and Financial Performance

Box 1: Capital Inflow into the Indian Microfinance sector in 2012-13: Emergence of the ‘New Normal 46

Part 6: Community Based Microfinance Organizations

The Bharat Microfinance Report 2013viii

List of Figures

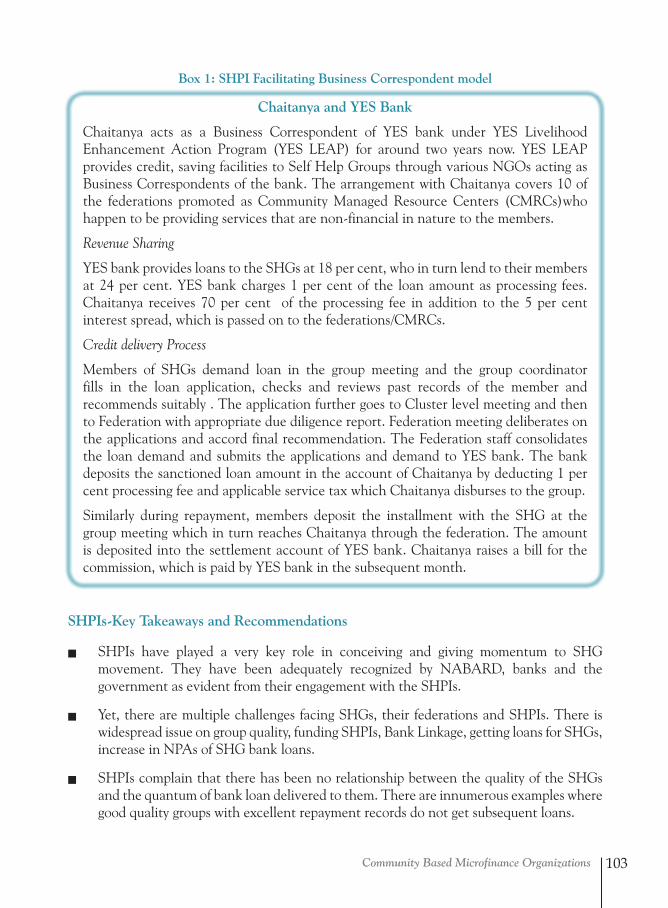

SHPI Facilitating Business Correspondent model 103

Part 1: Microfinance and Financial InclusionFigure 1 : Map Showing MFI Client Outreach ( CO) and Loan Portfolio ( LP) across States as on 31 March 2013 5Figure 2 : Map* Showing SHG Client Outreach (SCO) and SHG Loan Outstanding (SLO)Across Indian States as on 31 March 2013 6Figure 3 : Microcredit Outstanding through SHG Bank Linkage and MFI Programmes over the years 7Figure 4 : MFIs Outreach to the Unreached - SC/ST & Minority Clients over the years 9

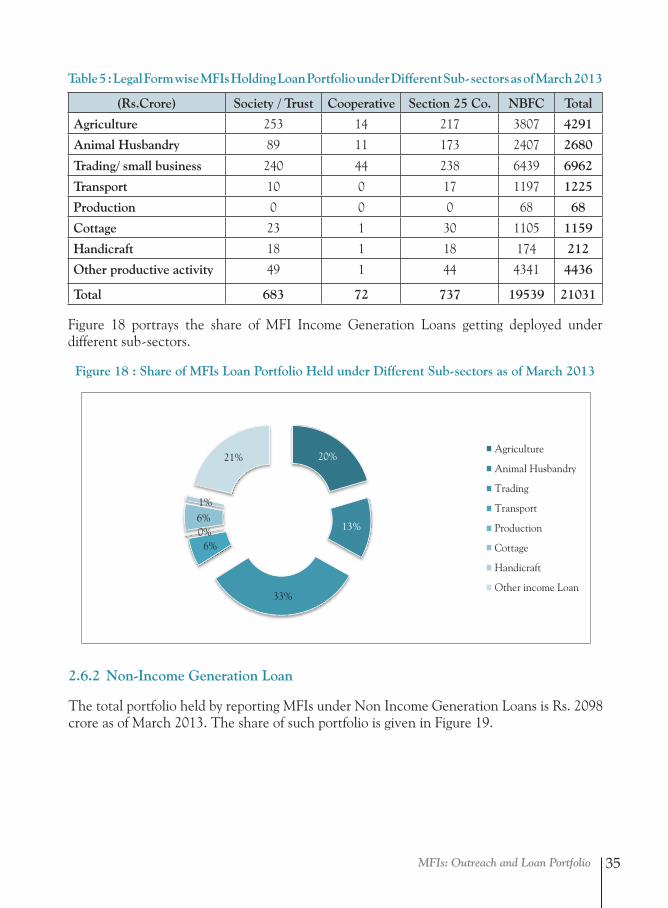

Part 2: MFIs: Outreach and Loan PortfolioFigure 1 : No.of MFIs in Indian States / UTs and No.of Districts with MFI Operation 19Figure 2 : List of MFIs Operating in Highest Number of Indian States / Union Territories 20Figure 3 : No. of MFI Borrowers Yearly Trend and MFI Category-wise Break-up of 2013 Figure 21Figure 4 : Rural-Urban Share of MFI Borrowers - 31 March 3013 21Figure 5 : MFI Borrowers - Region wise Trend over the years 22Figure 6 : MFI Borrowers - Numbers across State - 2012 & 2013 23Figure 7 : List of Top MFIs with Highest Client Outreach as of March 2013 24Figure 8 : MFI Borrowers Acquired - Yearly Trend and MFI- Category - wise Break-up of 2013 Figure 25Figure 9 : MFIs Gross Loan Portfolio Yearly Trend and MFI Category wise Break-up of 2013 Figure 26Figure 10 : MFIs Loan Portfolio – Region wise Trend over the years 27Figure 11 : MFIs Loan Portfolio Outstanding Amount across States - 2012 & 2013 28Figure 12: MFIs Managed Loan Portfolio - Yearly Trend and MFI Category wise Break-up of 2013 Figure 29Figure 13 : Growth Fluctuations in MFI Borrowers and Loan Outstanding over the Years 30Figure 14 : MFIs Loan Disbursement -Yearly Trend and MFI-Category-wise Break-up of 2013 Figure 31Figure 15 : MFIs Loan Disbursement during 2012-13 - Regional Variation 31Figure 16 : MFIs Loan Disbursement Amount across States during 2012-13 33Figure 17 : Top MFIs disbursing Loan during 2012-13 34Figure 18 : Share of MFIs Loan Portfolio Held under Different Sub -sector as of March 2013 35Figure 19 : Share of MFI Non Income Generation Loan under Different Sub-sectors as of March 2013 36

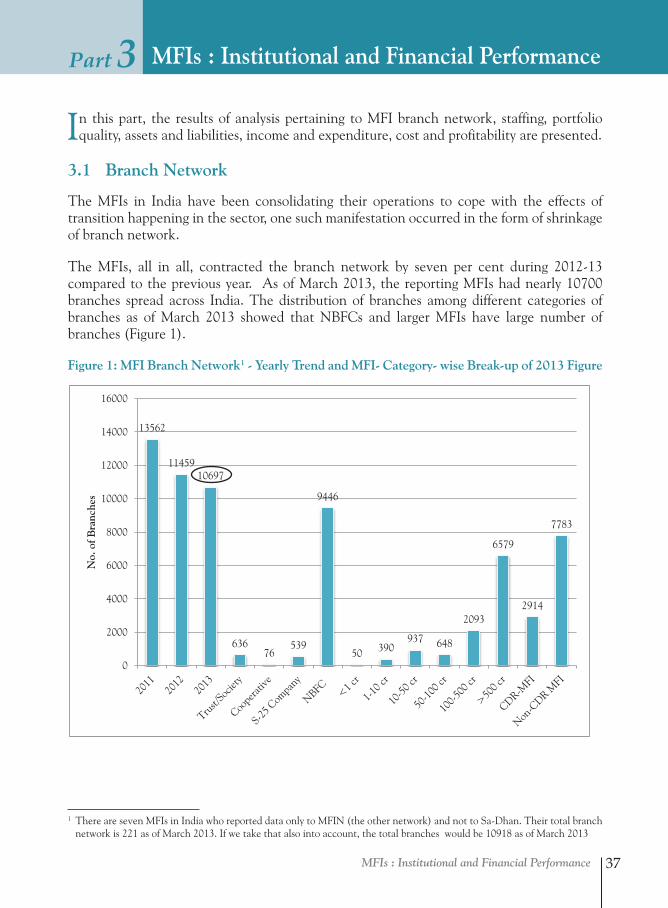

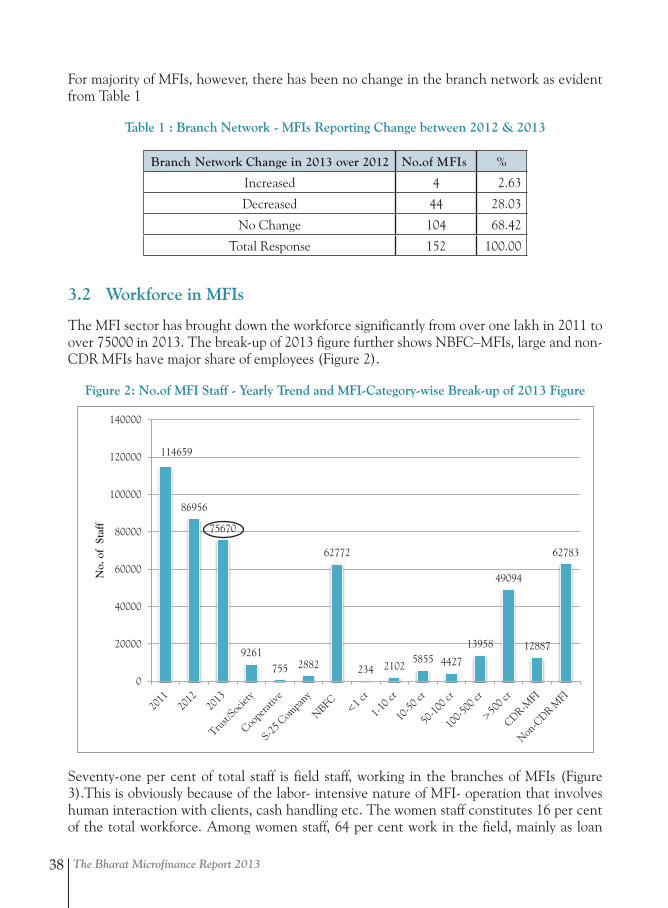

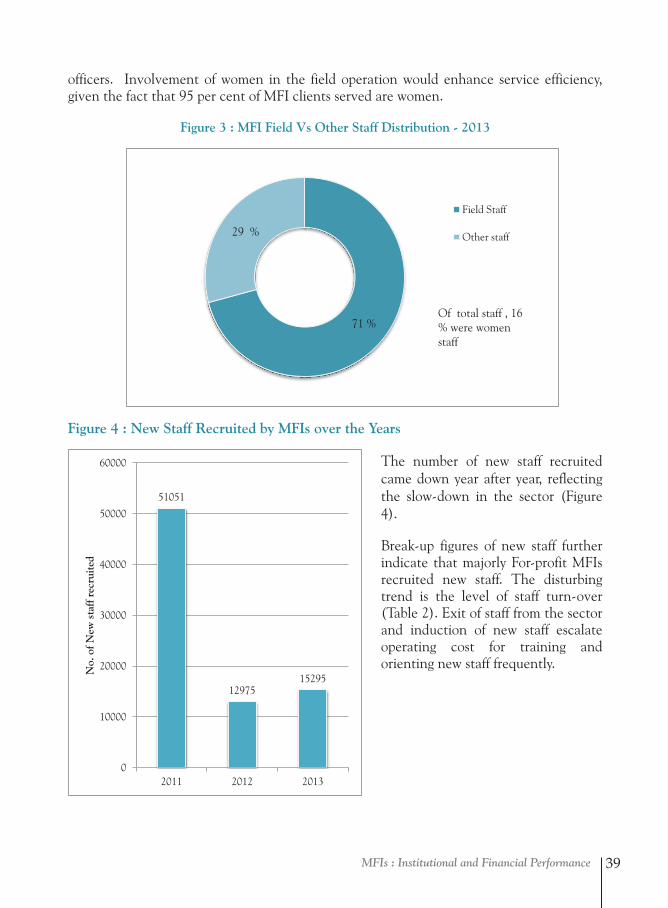

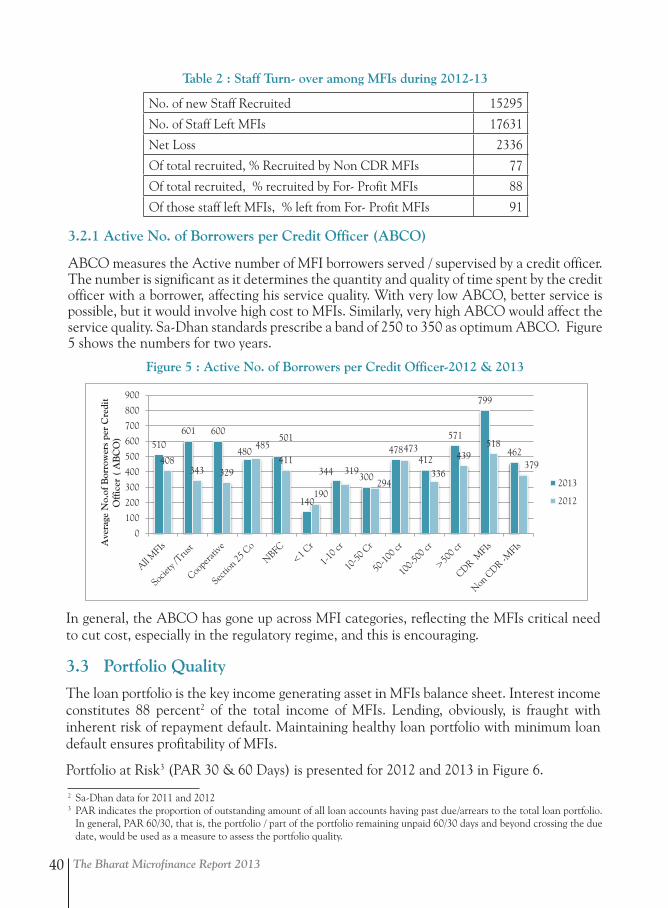

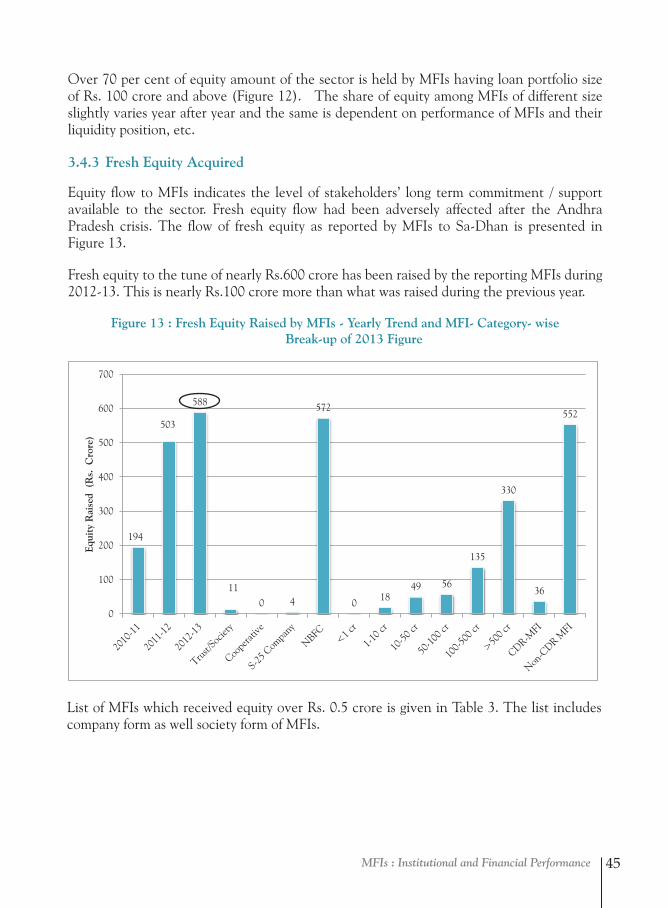

Part 3: MFIs – Institutional and Financial Performance Figure 1: MFI Branch Network - Yearly Trend and MFI- Category- wise Break-up of 2013 Figure 37Figure 2: No.of MFI Staff - Yearly Trend and MFI Category wise Break-up of 2013 Figure 38Figure 3 : MFI Field Vs Other Staff Distribution - 2013 39Figure 4 : New Staff Recruited by MFIs over the years 49Figure 5 : Active No. of Borrowers per Credit Officer -2012 & 2013 40Figure 6 : MFI Loan Portfolio at Risk (PAR) Ratio -Trend and MFI Category wise Break-up of 2013 Figure 41Figure 7 : Percentage Share of Overdue Installments (Over 180 days) among MFI Categories - 2013 41Figure 8 : Loan Write Off - Yearly Trend and MFI- Category- wise Break-up of 2013 Figure 42Figure 9 : MFI Total Asset - Yearly Trend and MFI- Category- wise Break -up of 2013 Figure 43Figure 10 : Major Components of MFI Total Asset 43Figure 11 : MFI Equity Outstanding - Yearly Trend and MFI- Category- wise Break-up of 2013 Figure 44Figure 12 : Percentage Distribution of Equity across Size of MFIs - 2012 and 2013 44Figure 13 : Fresh Equity Raised by MFIs - Yearly Trend and MFI- Category- wise Break-up of 2013 Figure 45

ix

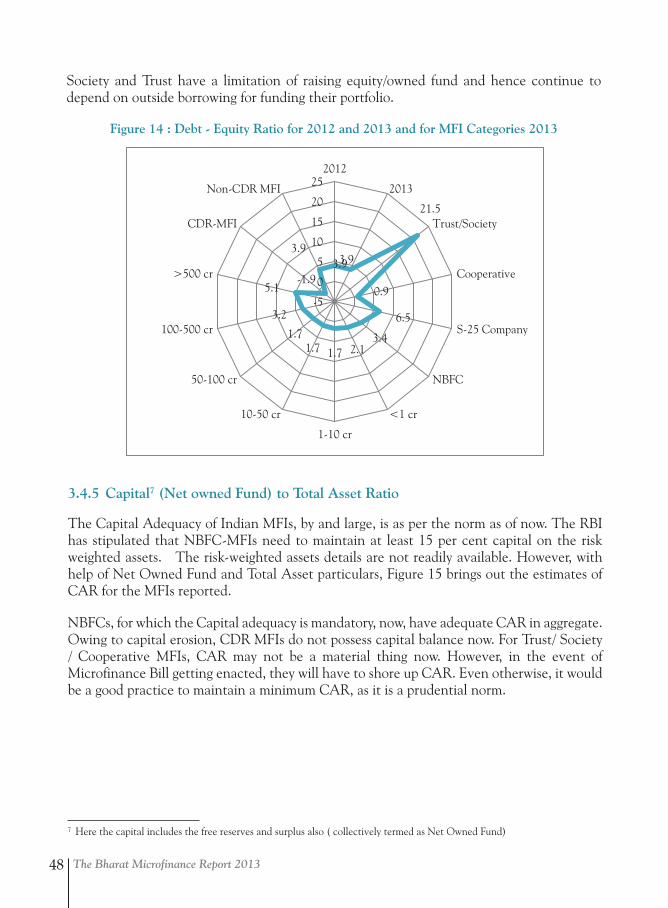

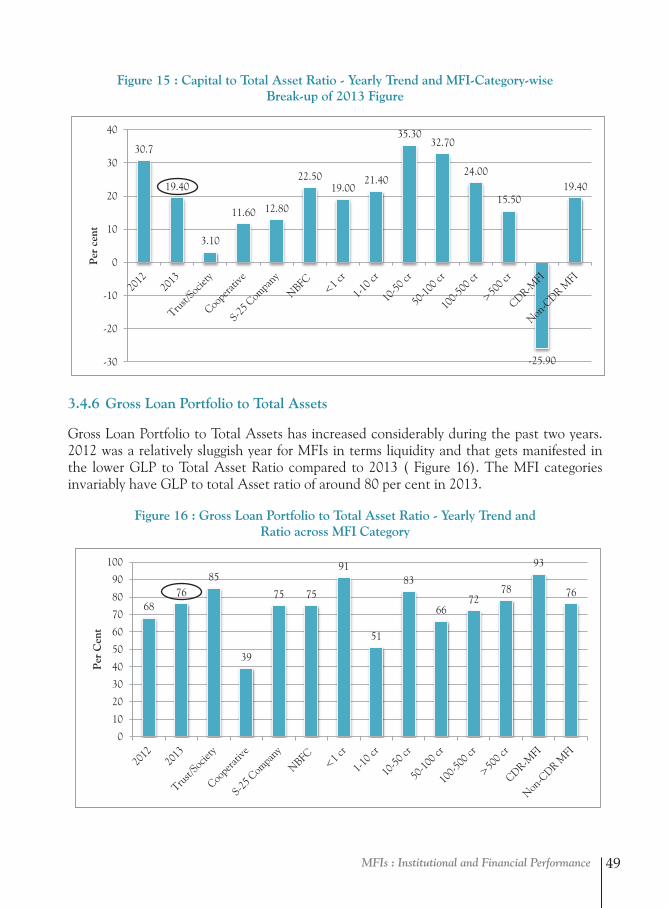

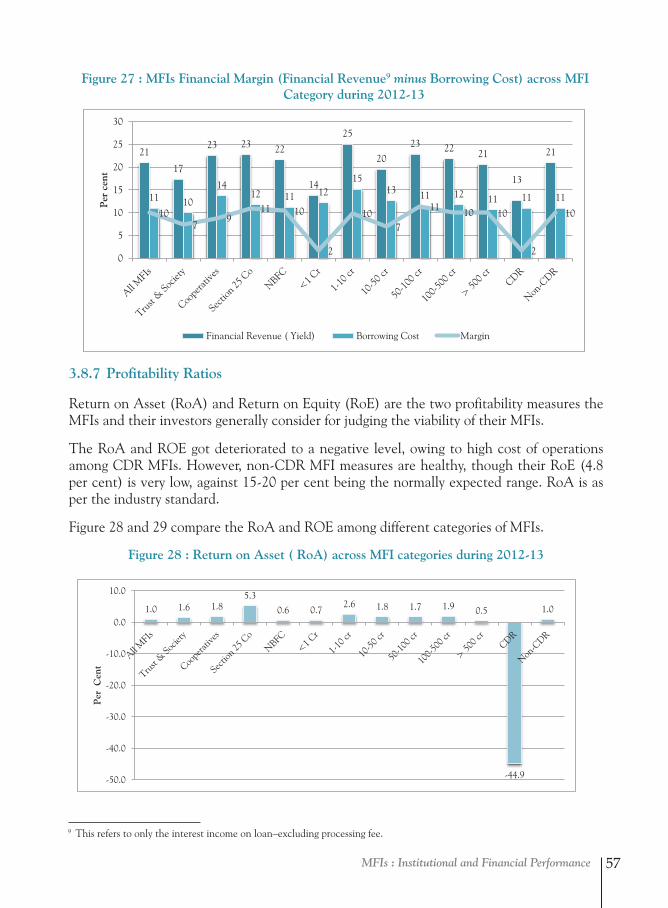

Figure 14 : Debt - Equity Ratio for 2012 and 2013 and for MFI Categories 2013 48Figure 15 : Capital to Total Asset Ratio - Yearly Trend and MFI-Category-wise Break-up of 2013 Figure 49Figure 16 : Gross Loan Portfolio to Total Asset Ratio - Yearly Trend and Ratio across MFI Category 49Figure 17 : Total income of Reporting MFIs - Yearly Trend and MFI- Category- wise Break-up of 2013 50Figure 18 : Composition of Total Income of MFIs-2012-13 50Figure 19 : Total Expenditure of Reporting MFIs - Yearly Trend and MFI-Category-wise Break-up of 2012-13 51Figure 20 : Financial and Operational Expenditure of MFIs for 2011-12 & 2012-13 51Figure 21 : Break-up of Operational Expenditure of MFIs 52Figure 22 : Net Surplus Income Realized by MFIs after All Expenditure and Tax-MFI-Category wise Break-up 52Figure 23 : Operating Cost Ratio - Across MFI Categories 54Figure 24 : Borrowing Cost of MFIs 55Figure 25 : Yield on MFI Portfolio across MFI Categories 55Figure 26 : Operational Self Sufficiency (OSS) of MFIs during 2012-13 56Figure 27 : MFIs Financial Margin (Financial Revenue minus Borrowing Cost) across MFI Category 57 during 2012-13Figure 28 : Return on Asset ( RoA) across MFI categories during 2012-13 57Figure 29 : Return on Equity (RoE) across MFI Categories during 2012-13 58

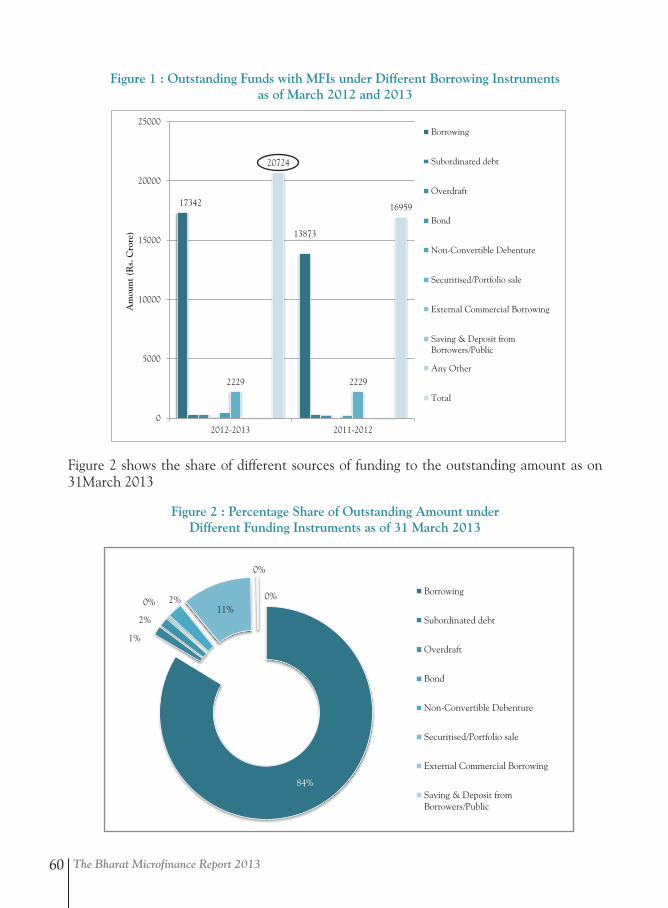

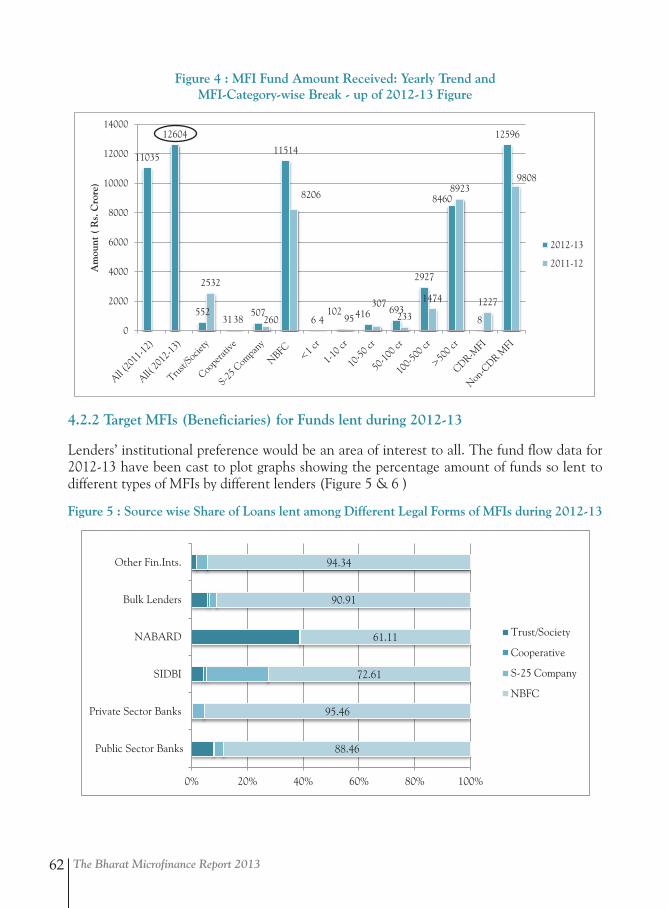

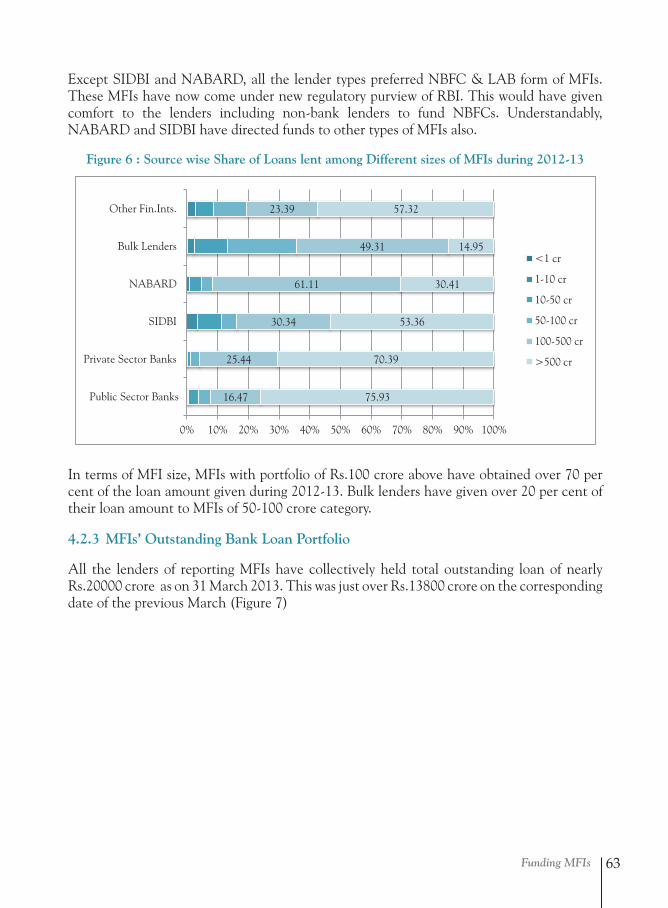

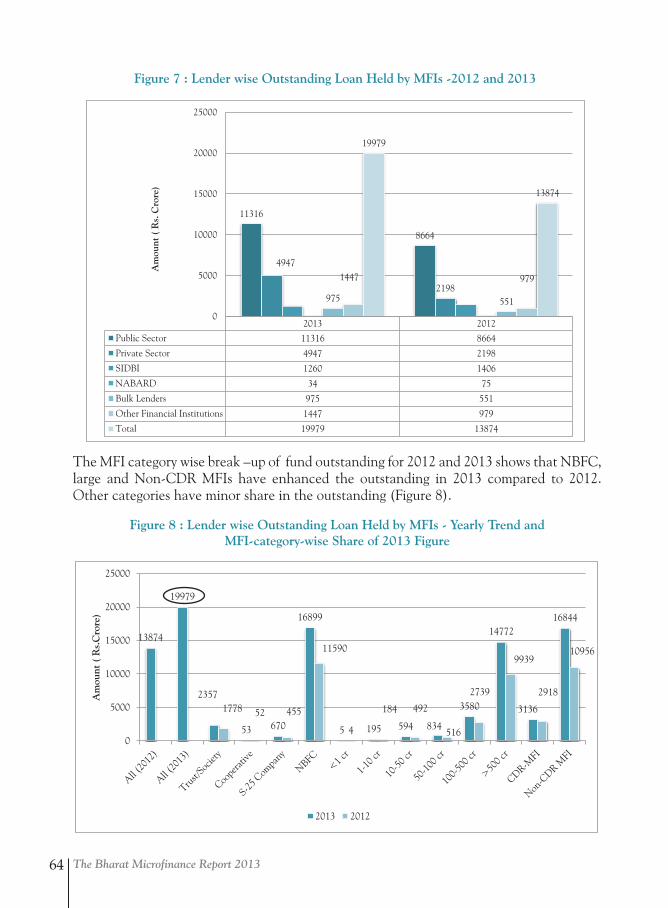

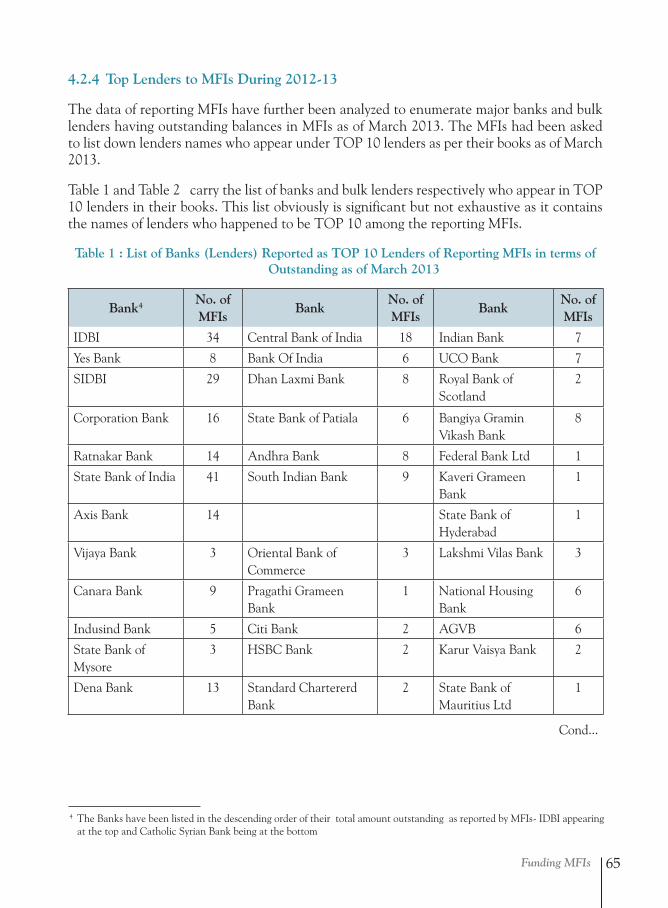

Part 4: Funding MFIsFigure 1 : Outstanding Funds with MFIs under Different Borrowing Instruments as of March 2012 & 2013 60Figure 2 : Percentage Share of Outstanding Amount under Different Funding Instruments as of 31 60 March 2013Figure 3 : Source wise Loan Amount Received by MFIs during 2011-12 and 2012-13 61Figure 4 : MFI Fund Amount Received: Yearly Trend and MFI-Category-wise Break - up of 2012-13 Figure 62Figure 5 : Source wise Share of Loans lent among Different Legal Forms of MFIs during 2012-13 62Figure 6 : Source wise Share of Loans lent among Different sizes of MFIs during 2012-13 63Figure 7 : Lender wise Outstanding Loan Held by MFIs -2012 and 2013 64Figure 8 : Lender wise Outstanding Loan Held by MFIs - Yearly Trend and MFI Category wise Share 64 of 2013 Figure

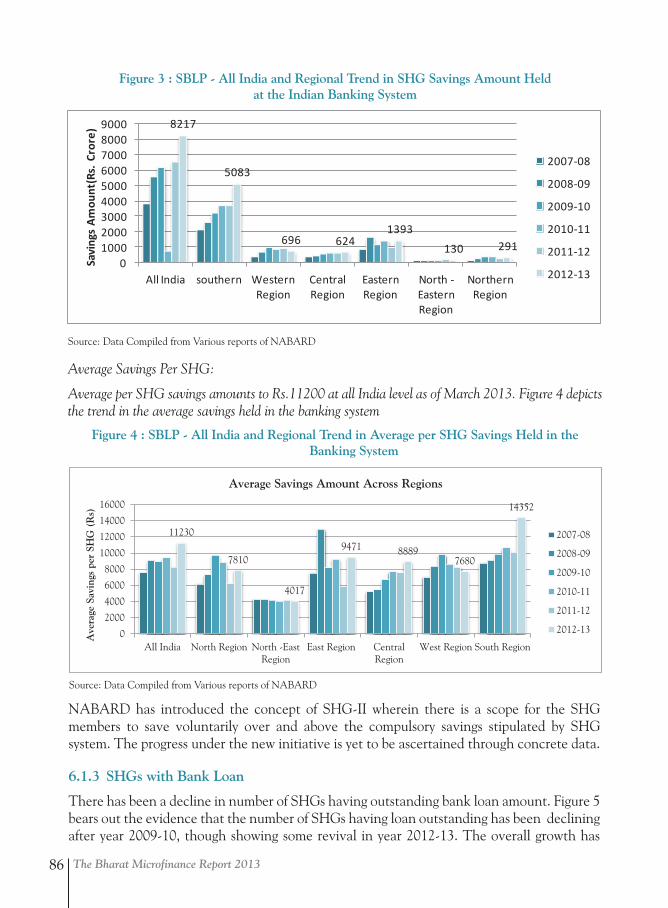

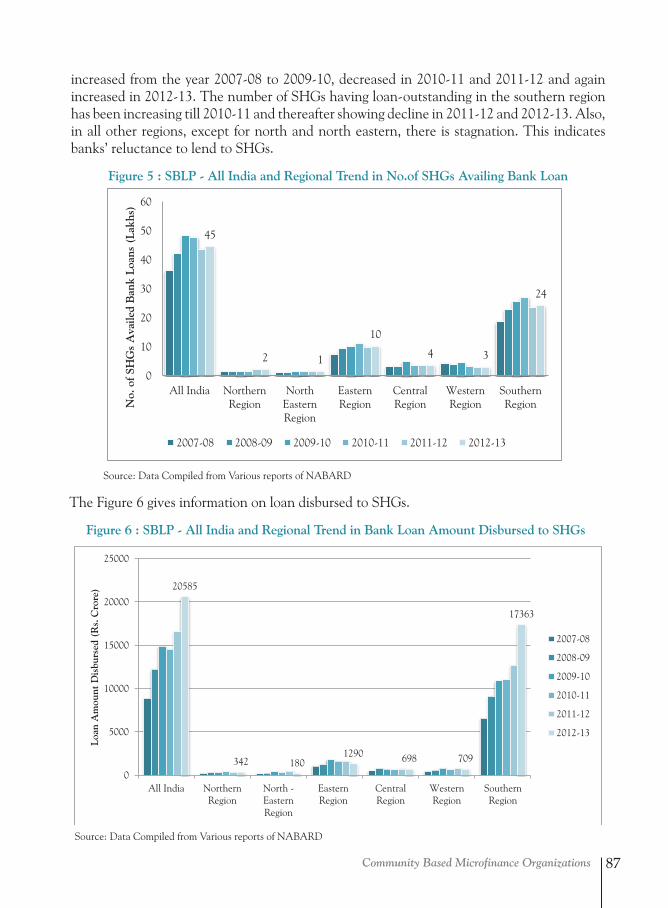

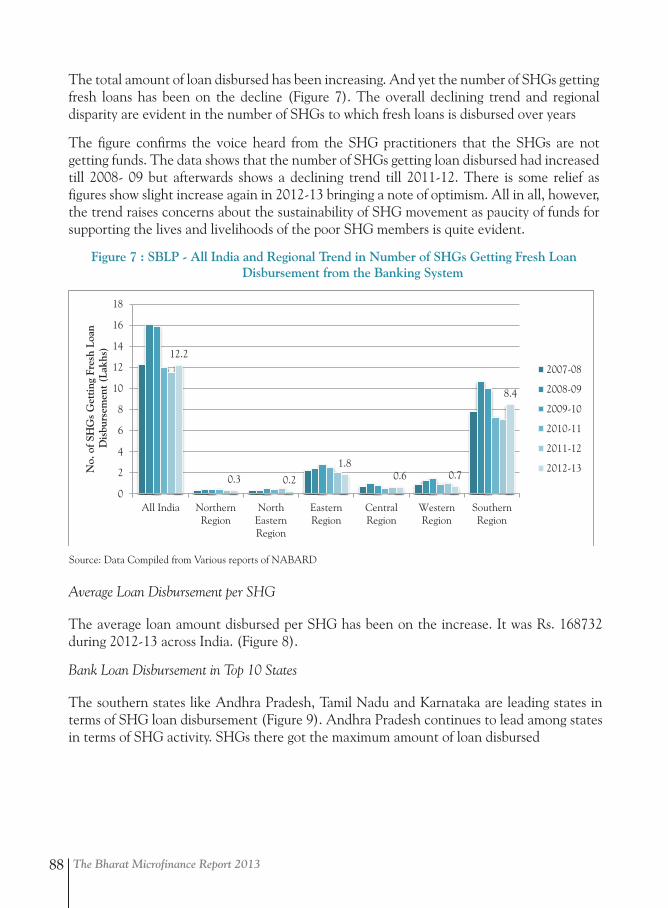

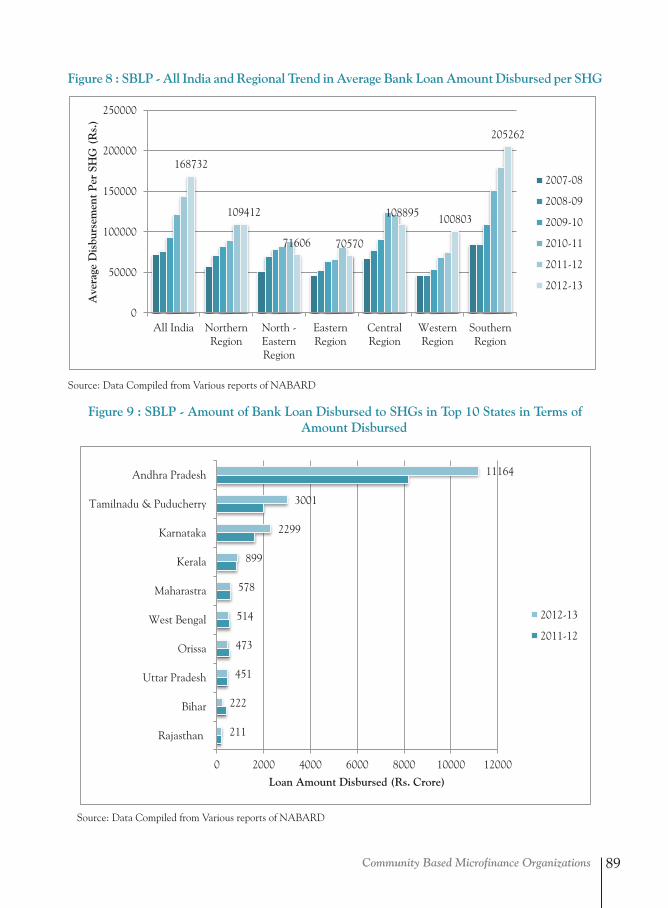

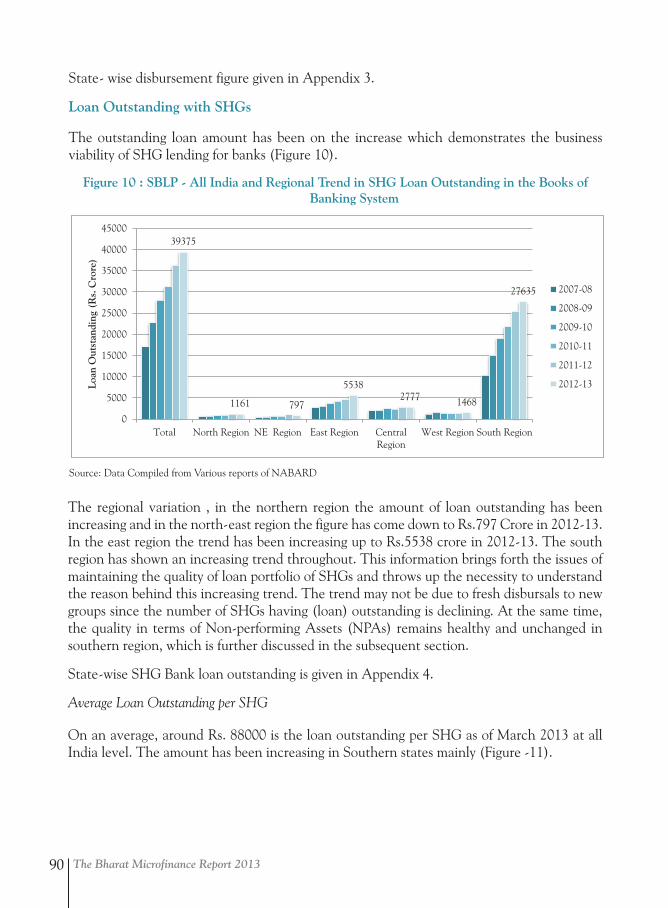

Part 6: Community Based Microfinance OrganizationsFigure 1 : SBLP - Historical Trend in Credit Linkage and Bank Loan Disbursed 84Figure 2 : All India and Regional Trend in No.of SHGs Savings Linked with Banks 85Figure 3 : SBLP - All India and Regional Trend in SHG Savings Amount Held at the Indian Banking System 86Figure 4 : SBLP - All India and Regional Trend in Average per SHG Savings Held in the Banking System 86Figure 5 : SBLP - All India and Regional Trend in No.of SHGs Availing Bank Loan 87Figure 6 : SBLP - All India and Regional Trend in Bank Loan Amount Disbursed to SHGs 87Figure 7 : SBLP - All India and Regional Trend in Number of SHGs Getting Fresh Loan Disbursement from the Banking System 88Figure 8 : SBLP - All India and Regional Trend in Average Bank Loan Amount Disbursed per SHG 89Figure 9 : SBLP - Amount of Bank Loan Disbursed to SHGs in Top 10 States in Terms of Amount Disbursed 89Figure 10 : SBLP - All India and Regional Trend in SHG Loan Outstanding in the Books of Banking System 90Figure 11 : SBLP -All India and Regional Trend in Average per SHG Loan Outstanding in the Banking System 91Figure 12 : SBLP - Non Performing Asset Percentage of SHG Loans with Banks 91Figure 13: SBLP – Non- Performing Asset of Bank SHG Loans With and Without SGSY Loans -

The Bharat Microfinance Report 2013x

List of Tables

a Comparison (March 2012) 92

Part 1: Microfinance and Financial InclusionTable 1 : Non - Credit Financial Services by Reporting MFIs 9Table 2 : MFIs as Banking Correspondents 10Table 3 : Key Learning from MFIs as Banking Correspondents 11Table 4 : Finance + Development Services of Reporting MFIs - Outreach Figures 12Table 5 : MFIs and Livelihoods Interventions 13Table 6 : MFIs and Women Empowerment Intervention 13Table 7 : MFIs and Education Intervention 14Table 8 : MFIs and Health Intervention 15

Part 2: MFIs: Outreach and Loan PortfolioTable 1 : MFIs and the No.of States of their Operation 20Table 2 : Loan Portfolio Outstanding - MFIs Reporting Change between 2012 & 2013 26Table 3 : MFIs Loan Outstanding per Borrower over the years 29Table 4 : Loan Disbursement – MFIs Reporting Change between 2013 and 2012 32Table 5 : Legal Form wise MFIs holding Loan Portfolio under Different Sub- sectors as of March 2013 35

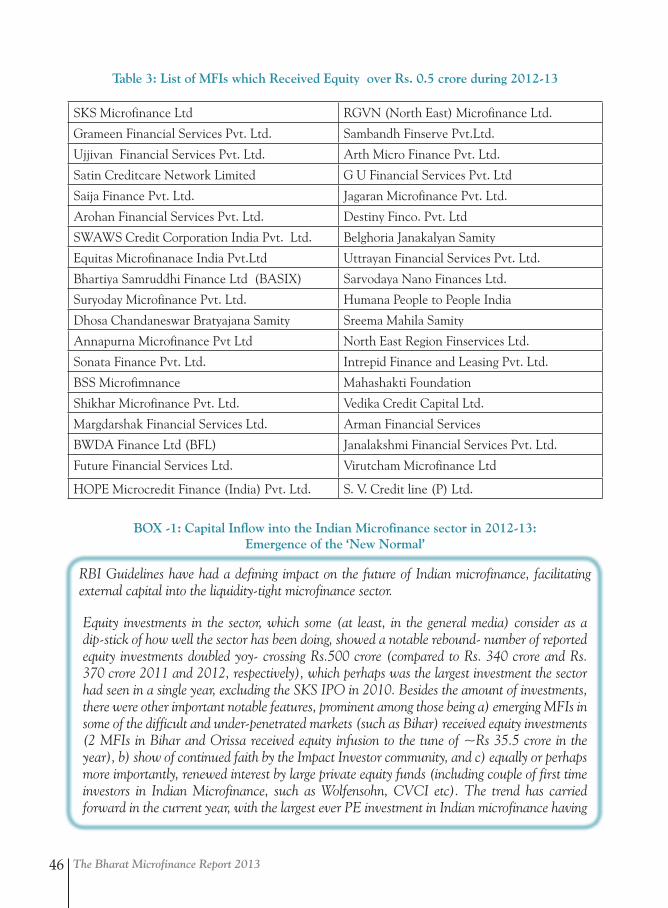

Part 3: MFIs – Institutional and Financial PerformanceTable 1 : Branch Network - MFIs Reporting Change between 2012 & 2013 38Table 2 : Staff Turn- over among MFIs during 2012-13 40Table 3: List of MFIs which Received Equity over Rs. 0.5 crore during 2012-13 46Table 4 : Cost per Borrower - across MFI Categories for 2012 and 2013 53

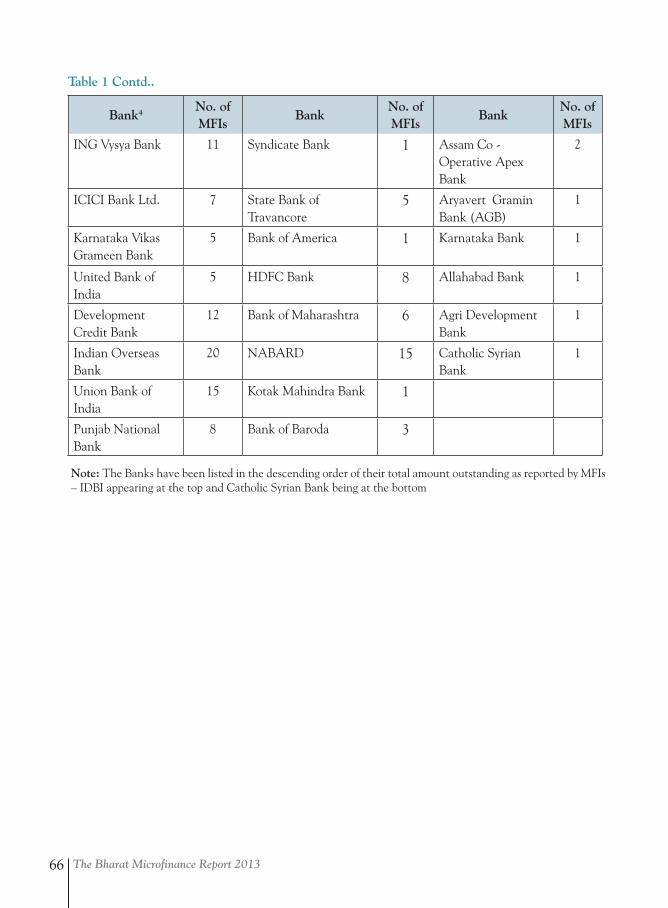

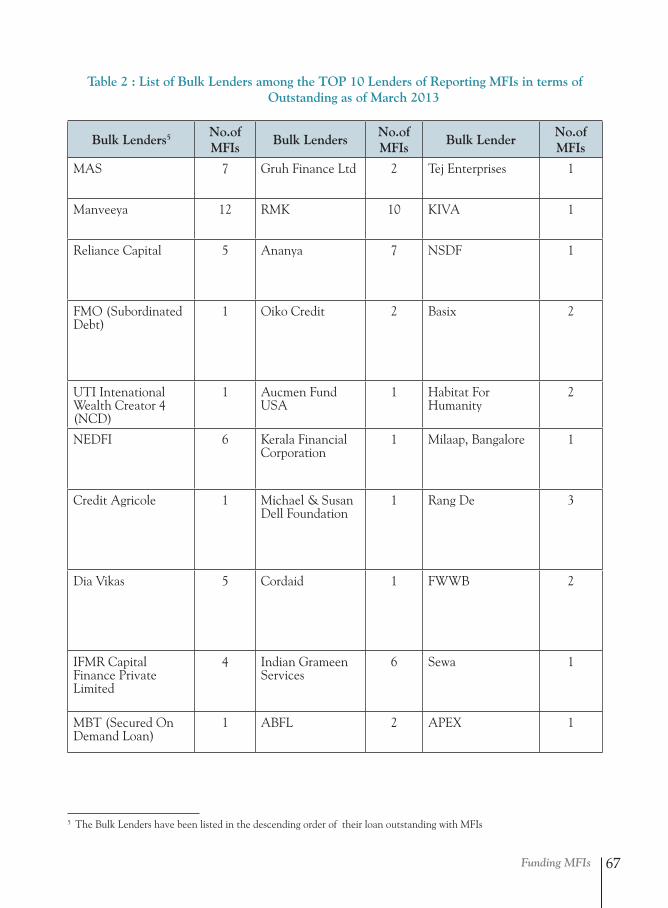

Part 4: Funding MFIsTable 1 : List of Banks (Lenders) Reported as TOP 10 Lenders of Reporting MFIs in terms of Outstanding as of March 2013 65Table 2 : List of Bulk Lenders among the TOP 10 Lenders of Reporting MFIs in terms of Outstanding as of March 2013 67

Part 5: Self Regulation Table 1 : Indicative Statistics on MFIs Credit Bureau Reporting Frequency 80

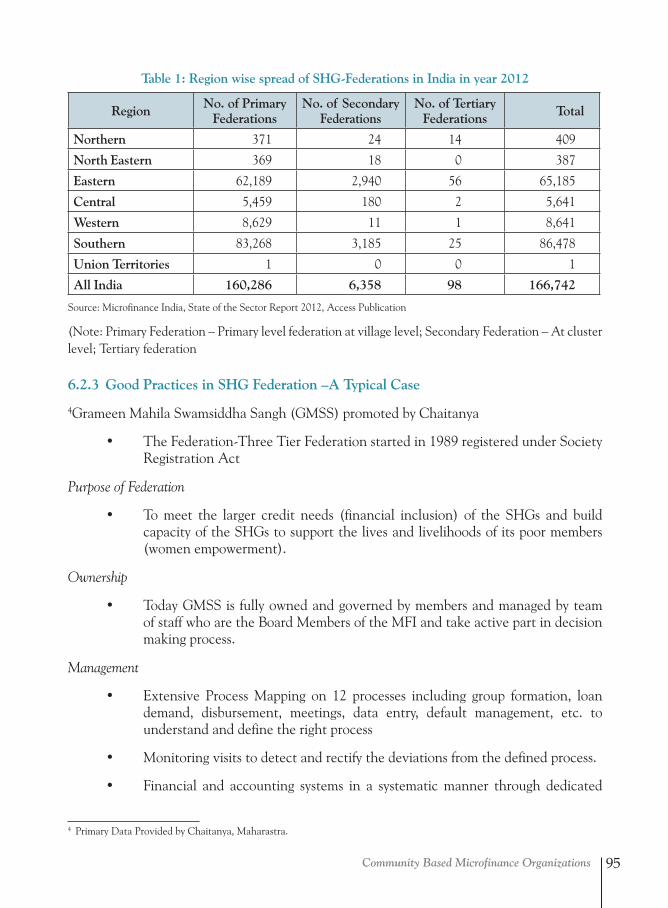

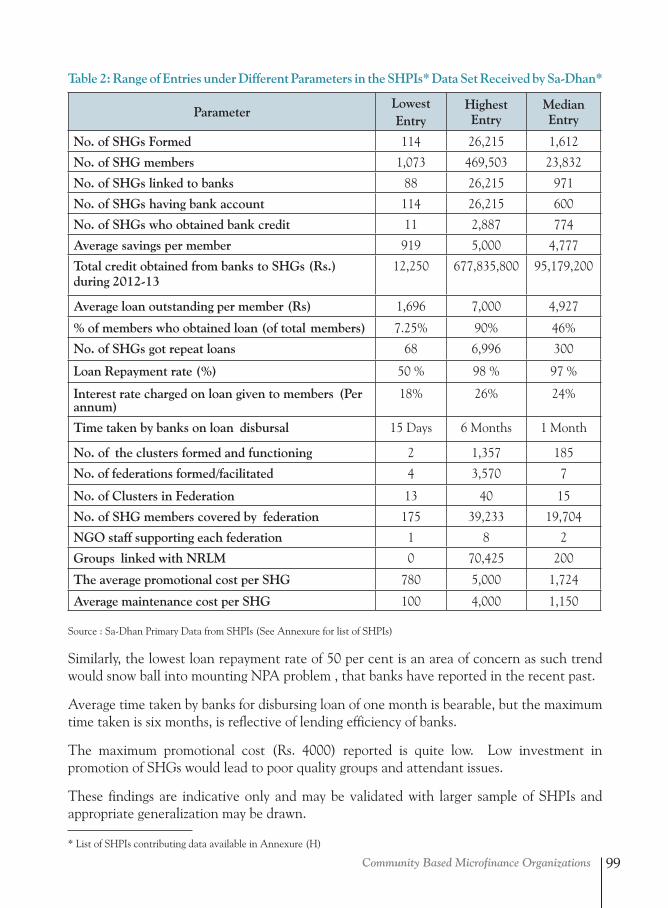

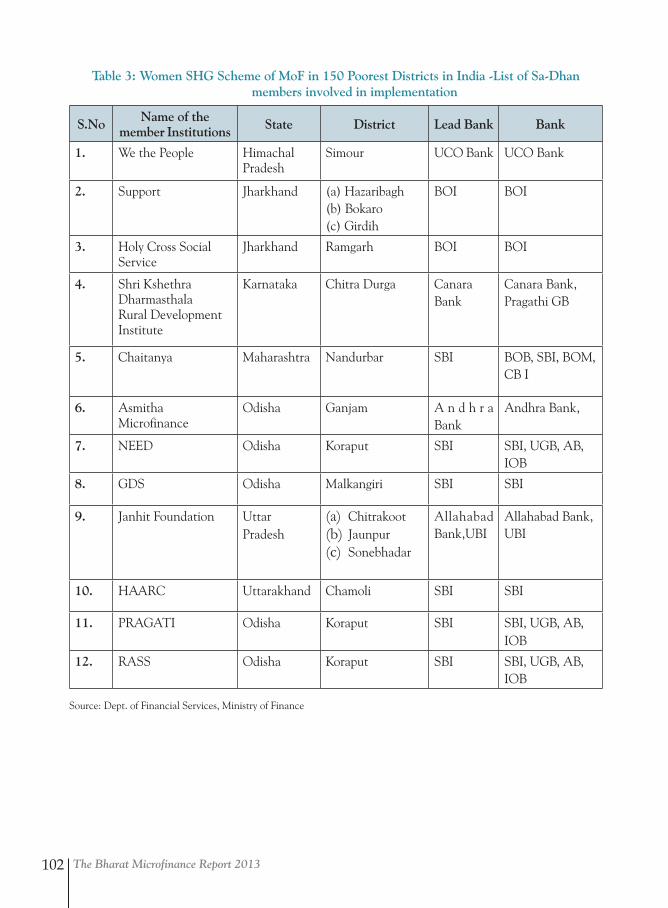

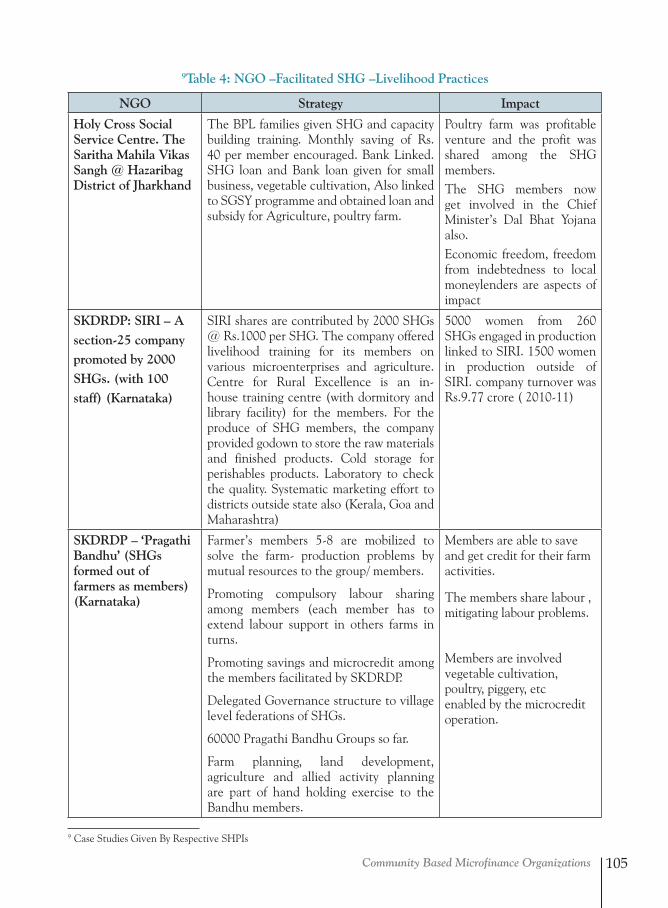

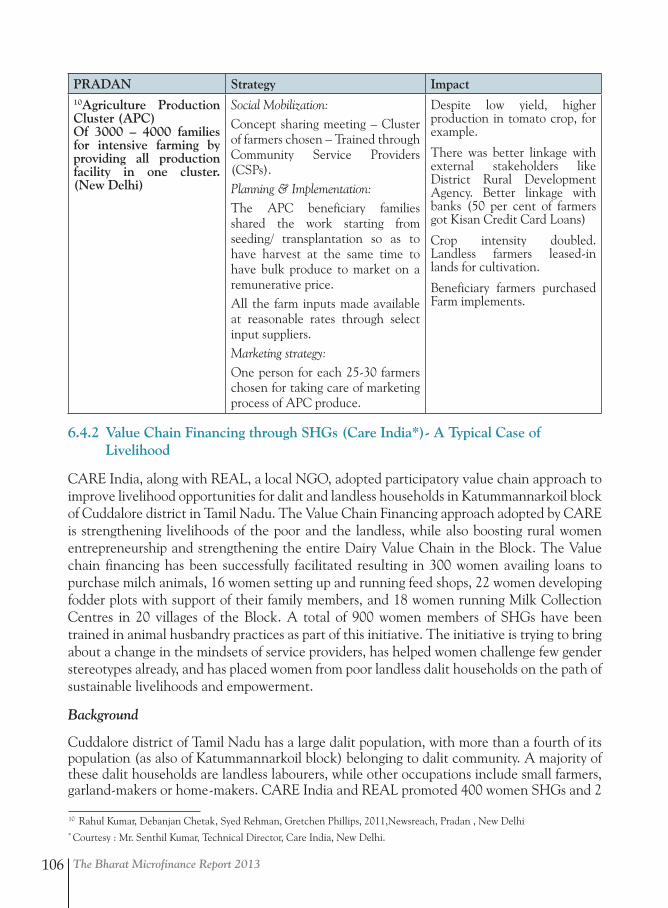

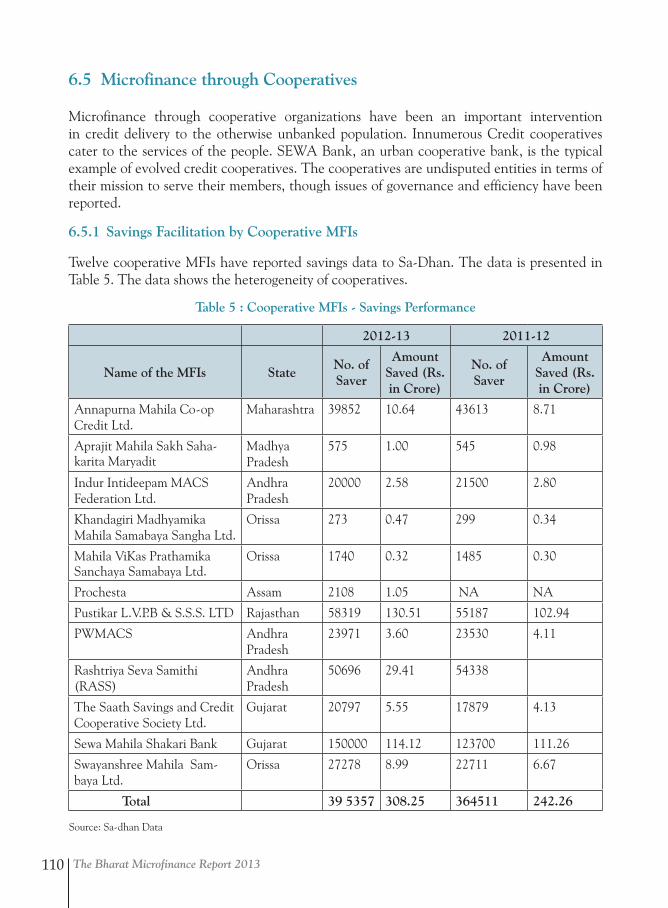

Part 6: Community Based Microfinance OrganizationsTable 1: Region wise spread of SHG-Federations in India in year 2012 95Table 2 : Range of Entries under Different Parameters in the SHPI Data Set Received by Sa-Dhan 99Table 3: Women SHG Scheme of MoF in 150 Poorest Districts in India -List of Sa-Dhan members 102 selected for implementation Table 4: NGO–Facilitated SHG–Livelihood Practices 105Table 5: Cooperative MFIs - Savings Performance 110

xi

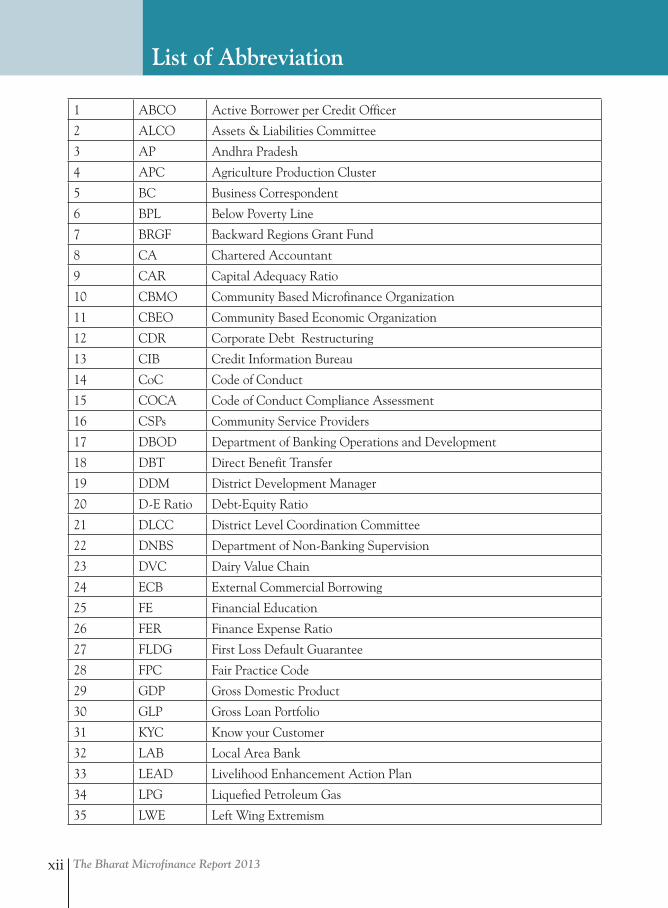

List of Abbreviation

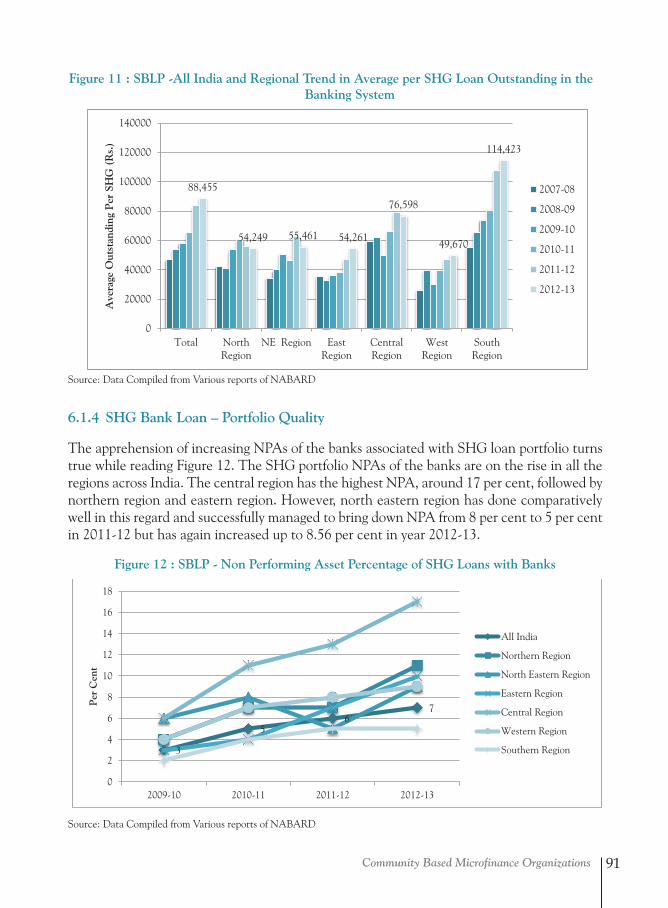

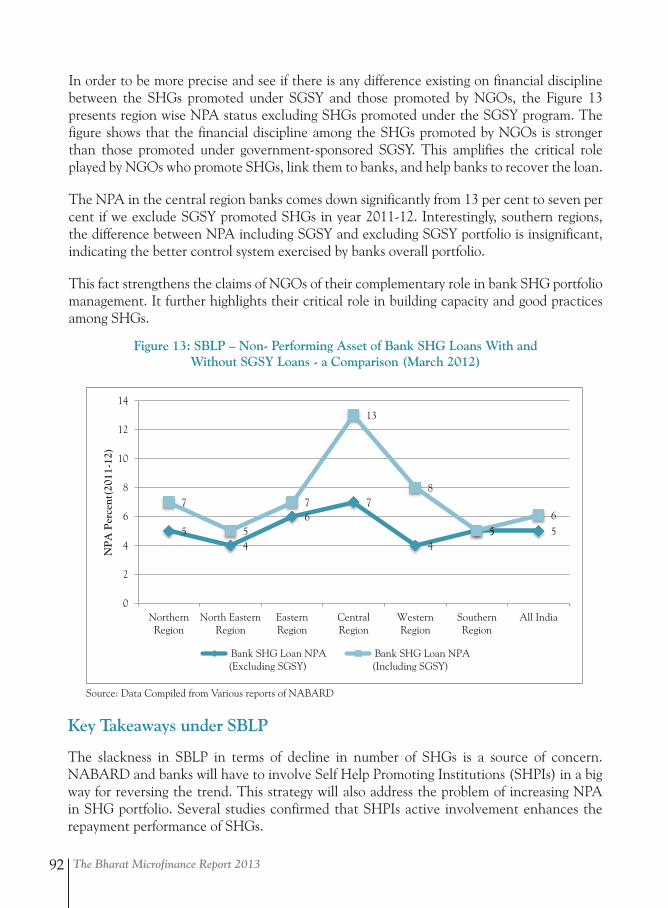

1 ABCO Active Borrower per Credit Officer

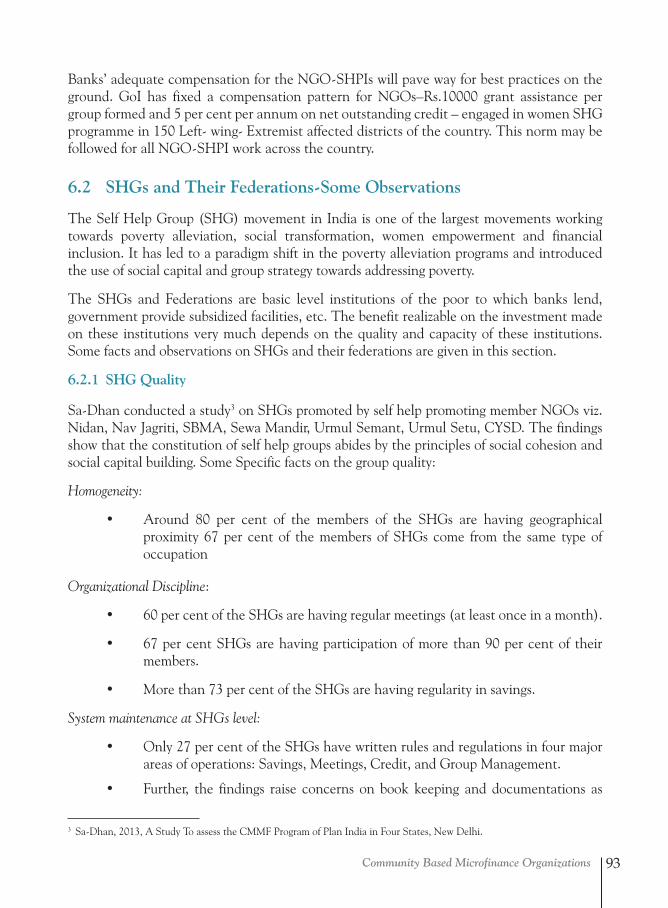

2 ALCO Assets & Liabilities Committee

3 AP Andhra Pradesh

4 APC Agriculture Production Cluster

5 BC Business Correspondent

6 BPL Below Poverty Line

7 BRGF Backward Regions Grant Fund

8 CA Chartered Accountant

9 CAR Capital Adequacy Ratio

10 CBMO Community Based Microfinance Organization

11 CBEO Community Based Economic Organization

12 CDR Corporate Debt Restructuring

13 CIB Credit Information Bureau

14 CoC Code of Conduct

15 COCA Code of Conduct Compliance Assessment

16 CSPs Community Service Providers

17 DBOD Department of Banking Operations and Development

18 DBT Direct Benefit Transfer

19 DDM District Development Manager

20 D-E Ratio Debt-Equity Ratio

21 DLCC District Level Coordination Committee

22 DNBS Department of Non-Banking Supervision

23 DVC Dairy Value Chain

24 ECB External Commercial Borrowing

25 FE Financial Education

26 FER Finance Expense Ratio

27 FLDG First Loss Default Guarantee

28 FPC Fair Practice Code

29 GDP Gross Domestic Product

30 GLP Gross Loan Portfolio

31 KYC Know your Customer

32 LAB Local Area Bank

33 LEAD Livelihood Enhancement Action Plan

34 LPG Liquefied Petroleum Gas

35 LWE Left Wing Extremism

The Bharat Microfinance Report 2013xii

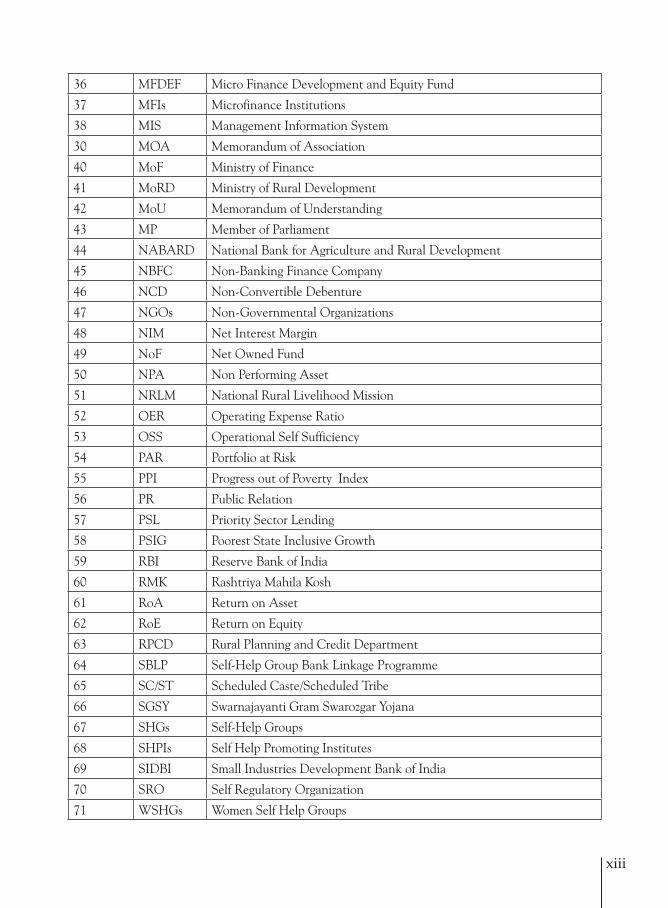

36 MFDEF Micro Finance Development and Equity Fund

37 MFIs Microfinance Institutions

38 MIS Management Information System

30 MOA Memorandum of Association

40 MoF Ministry of Finance

41 MoRD Ministry of Rural Development

42 MoU Memorandum of Understanding

43 MP Member of Parliament

44 NABARD National Bank for Agriculture and Rural Development

45 NBFC Non-Banking Finance Company

46 NCD Non-Convertible Debenture

47 NGOs Non-Governmental Organizations

48 NIM Net Interest Margin

49 NoF Net Owned Fund

50 NPA Non Performing Asset

51 NRLM National Rural Livelihood Mission

52 OER Operating Expense Ratio

53 OSS Operational Self Sufficiency

54 PAR Portfolio at Risk

55 PPI Progress out of Poverty Index

56 PR Public Relation

57 PSL Priority Sector Lending

58 PSIG Poorest State Inclusive Growth

59 RBI Reserve Bank of India

60 RMK Rashtriya Mahila Kosh

61 RoA Return on Asset

62 RoE Return on Equity

63 RPCD Rural Planning and Credit Department

64 SBLP Self-Help Group Bank Linkage Programme

65 SC/ST Scheduled Caste/Scheduled Tribe

66 SGSY Swarnajayanti Gram Swarozgar Yojana

67 SHGs Self-Help Groups

68 SHPIs Self Help Promoting Institutes

69 SIDBI Small Industries Development Bank of India

70 SRO Self Regulatory Organization

71 WSHGs Women Self Help Groups

xiii

Glossary*

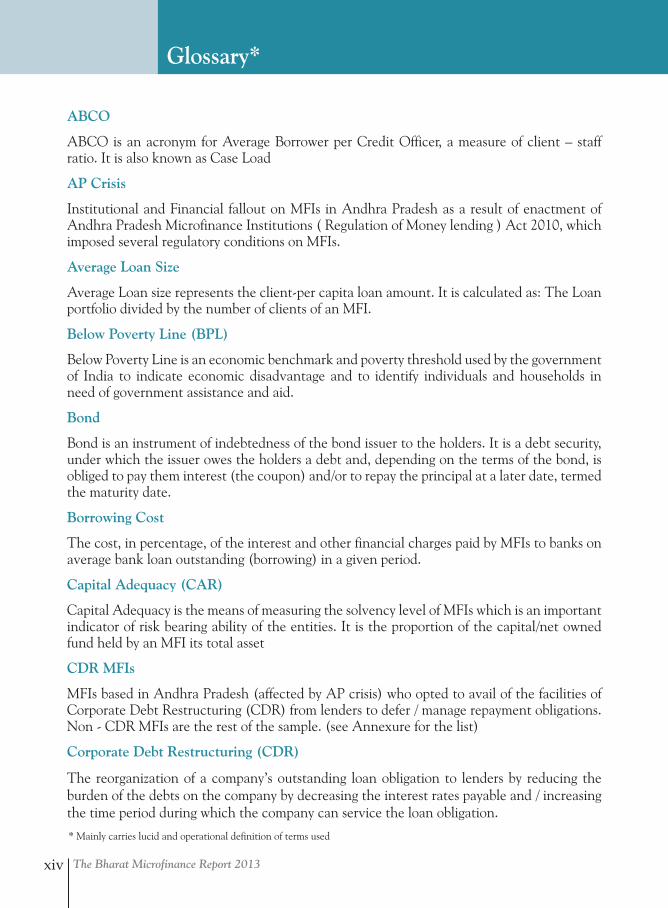

ABCO

ABCO is an acronym for Average Borrower per Credit Officer, a measure of client – staff ratio. It is also known as Case Load

AP Crisis

Institutional and Financial fallout on MFIs in Andhra Pradesh as a result of enactment of Andhra Pradesh Microfinance Institutions ( Regulation of Money lending ) Act 2010, which imposed several regulatory conditions on MFIs.

Average Loan Size

Average Loan size represents the client-per capita loan amount. It is calculated as: The Loan portfolio divided by the number of clients of an MFI.

Below Poverty Line (BPL)

Below Poverty Line is an economic benchmark and poverty threshold used by the government of India to indicate economic disadvantage and to identify individuals and households in need of government assistance and aid.

Bond

Bond is an instrument of indebtedness of the bond issuer to the holders. It is a debt security, under which the issuer owes the holders a debt and, depending on the terms of the bond, is obliged to pay them interest (the coupon) and/or to repay the principal at a later date, termed the maturity date.

Borrowing Cost

The cost, in percentage, of the interest and other financial charges paid by MFIs to banks on average bank loan outstanding (borrowing) in a given period.

Capital Adequacy (CAR)

Capital Adequacy is the means of measuring the solvency level of MFIs which is an important indicator of risk bearing ability of the entities. It is the proportion of the capital/net owned fund held by an MFI its total asset

CDR MFIs

MFIs based in Andhra Pradesh (affected by AP crisis) who opted to avail of the facilities of Corporate Debt Restructuring (CDR) from lenders to defer / manage repayment obligations. Non - CDR MFIs are the rest of the sample. (see Annexure for the list)

Corporate Debt Restructuring (CDR)

The reorganization of a company’s outstanding loan obligation to lenders by reducing the burden of the debts on the company by decreasing the interest rates payable and / increasing the time period during which the company can service the loan obligation.

The Bharat Microfinance Report 2013xiv

* Mainly carries lucid and operational definition of terms used

Capital to Total Assets

Ratio of net worth to total assets

Debt –Equity Ratio

Debt-Equity Ratio is the proportion of total debt borrowed to the total net owned fund held in a given point of time.

Debt Funding

Debt Funding refers to the percentage of loan portfolio funded by outside borrowings

External Commercial Borrowing

An external commercial borrowing (ECB) is an instrument used in India to facilitate the access to foreign money by Indian corporations

Finance Cost

Finance Cost here refers to the interest and other expenses incurred on average bank loan outstanding in the books of MFIs. This does not include notional cost of utilizing the equity fund.

Financial Inclusion

Financial Inclusion is the delivery of financial services at affordable costs to sections of disadvantaged and low income segments of society.

Income Generation Loan

Loan which Invested in the activities that create an income source to individual beneficiaries or beneficiary groups.

Legal Form of MFIs

MFIs referred to in this report are registered under any one of the following legal forms: Trust (under Trust Act), Society (Societies Act), Cooperatives (under Cooperative Societies Act), Section 25 company (under Section 25 of Indian Companies Act) and NBFC (under Indian companies Act and obtained license from RBI)

Margin

Margin refers to the difference between the Borrowing Cost and Financial Revenue of MFIs, expressed in percentage. This term is analogous to the concept of Net Interest Margin (NIM) widely used in banking parlance. Margin Cap refers to the ceiling of Margin of 12 percent fixed by RBI.

Managed Loan Portfolio

Managed Loan Portfolio is the loan asset originated by MFIs and later sold to banks for getting liquidity. The MFIs continue to manage it - collection of repayment on behalf of the banks which purchased the portfolio.

xv

MFI Size (used in MFI Category)

This refers to Loan Portfolio size of MFIs (Rupees in crore as of March 2013) contributing data to the report. In this report MFIs of different size : < 1 cr, 1-10 cr, 10-50 cr, 50-100 cr. 100-500 cr and >500 cr have been considered to analyze performance.

Non Convertible Debenture

The debentures cannot be converted into equity shares and will be redeemed at the end of the maturity period. During the life of the debenture, the investors receive semi0annual interest payment at a pre-specified rate.

Non Performing Assets (NPA)

A debt obligation where the borrower has not paid any previously agreed upon interest and principal repayments to the designated lender for an extended period of time. The NPA is therefore not yielding any income to the lender in the form of principal and interest payments.

Operating Cost/ Expense Ratio

Ratio of staff, travel, administration costs, other overheads and depreciation charges of the MFIs (non-financial costs) to the average loan portfolio during a year

Operating Model

Operating Model of an MFI in this report refers to the model under which majority of the clients are served by the MFI. The same MFI may serve a small portion of clients under other models also.

Operating Self Sufficiency (OSS)

Operating Self Sufficiency (OSS) shows the sufficiency of income (operating income and investment income) earned by MFIs to cover the cost like operating cost, loan loss provision and finance cost, incurred for conducting the operation.

Overdraft

An overdraft occurs when money is withdrawn from a bank account and the available balance goes below zero. In this situation the account is said to be “overdrawn”. If there is a prior agreement with the account provider for an overdraft, and the amount overdrawn is within the authorized overdraft limit, then interest is normally charged at the agreed rate.

Portfolio Quality

It refers to the degree of risk of default in the loan portfolio. A high quality portfolio contains a lower amount of risk. Portfolio quality changes continually as loans are disbursed, payments are made, and payments become due.

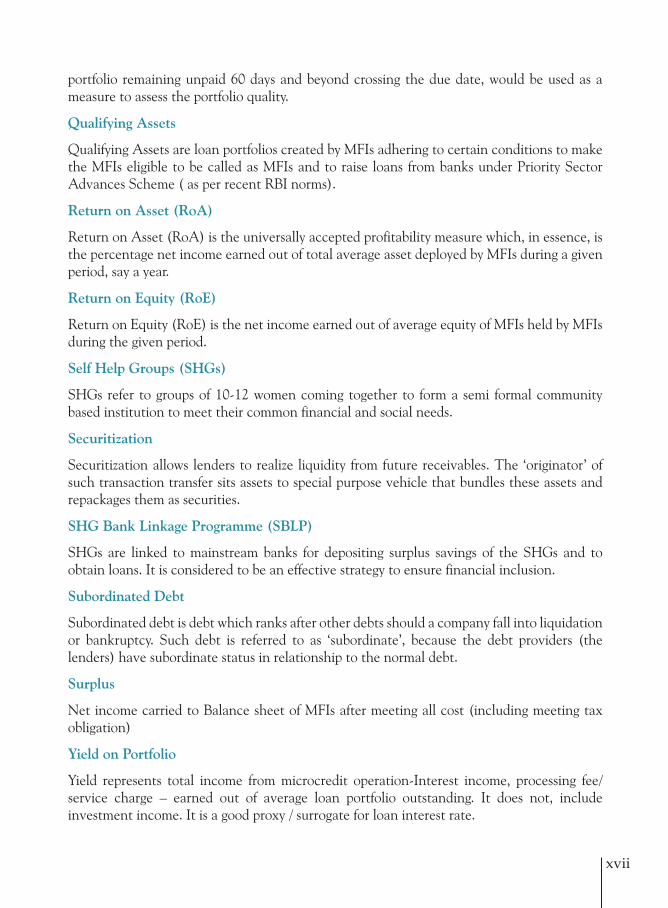

Portfolio at Risk (PAR)

PAR indicates the proportion of outstanding amounts of all loan accounts having past due/arrears to the total outstanding loan. In general, PAR 60, i.e., the portfolio / part of the

The Bharat Microfinance Report 2013xvi

portfolio remaining unpaid 60 days and beyond crossing the due date, would be used as a measure to assess the portfolio quality.

Qualifying Assets

Qualifying Assets are loan portfolios created by MFIs adhering to certain conditions to make the MFIs eligible to be called as MFIs and to raise loans from banks under Priority Sector Advances Scheme ( as per recent RBI norms).

Return on Asset (RoA)

Return on Asset (RoA) is the universally accepted profitability measure which, in essence, is the percentage net income earned out of total average asset deployed by MFIs during a given period, say a year.

Return on Equity (RoE)

Return on Equity (RoE) is the net income earned out of average equity of MFIs held by MFIs during the given period.

Self Help Groups (SHGs)

SHGs refer to groups of 10-12 women coming together to form a semi formal community based institution to meet their common financial and social needs.

Securitization

Securitization allows lenders to realize liquidity from future receivables. The ‘originator’ of such transaction transfer sits assets to special purpose vehicle that bundles these assets and repackages them as securities.

SHG Bank Linkage Programme (SBLP)

SHGs are linked to mainstream banks for depositing surplus savings of the SHGs and to obtain loans. It is considered to be an effective strategy to ensure financial inclusion.

Subordinated Debt

Subordinated debt is debt which ranks after other debts should a company fall into liquidation or bankruptcy. Such debt is referred to as ‘subordinate’, because the debt providers (the lenders) have subordinate status in relationship to the normal debt.

Surplus

Net income carried to Balance sheet of MFIs after meeting all cost (including meeting tax obligation)

Yield on Portfolio

Yield represents total income from microcredit operation-Interest income, processing fee/ service charge – earned out of average loan portfolio outstanding. It does not, include investment income. It is a good proxy / surrogate for loan interest rate.

xvii

Executive Summary

The Background and the Context

Microfinance has been recognized as one of the potent tools to address the issue of poverty. The positive outcomes of experiments in SEWA Bank in Gujarat and initiatives of

leading NGOs like MYRADA and PRADAN encouraged the Reserve Bank of India (RBI) and the National Bank for Agriculture and Rural Development (NABARAD) to nurture Self Help Groups ( SHGs) movement. This further led to Self Help Group Bank Linkage Programme (SBLP) commencing in the year 1992. Also, considering the fact that around 50 per cent of working population does not have access to banking services, the RBI recognized Microfinance Institutions (MFIs) as extended arms of banks to reach out to unbanked populace.

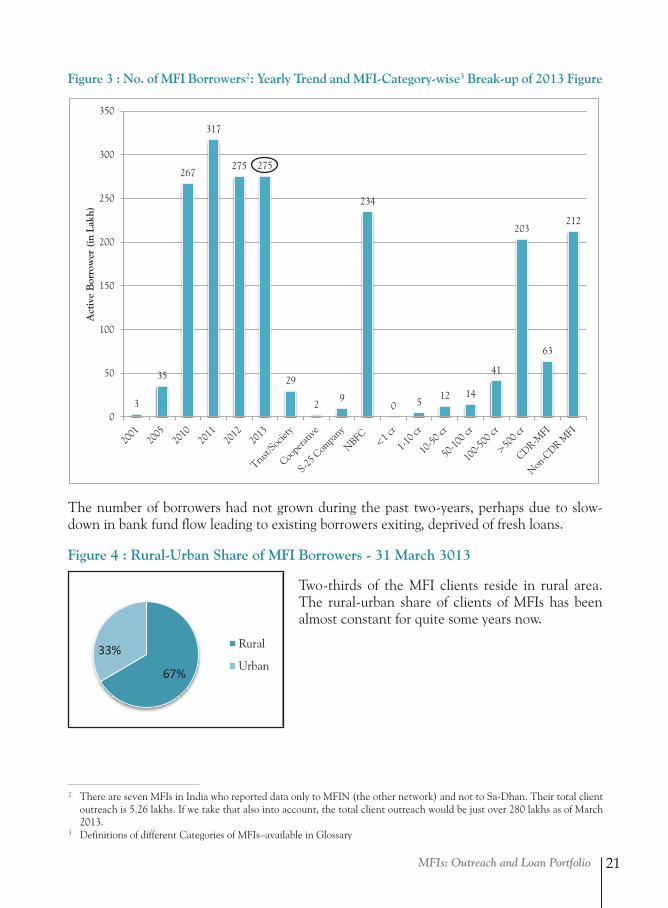

As per NABARAD data (2012-13), there are around 73 lakhs Self Help Groups operating in India. An estimated 500 MFIs, most of them operating in southern and eastern regions of the country, borrow funds from banks to on-lend to over 275 lakhs clients across the country.

The microfinance sector is undergoing a phase of transition now. In 2010 , MFIs in Andhra Pradesh state have been affected by Andhra Pradesh Microfinance Institutions (Regulation of Money lending) Act.2010. Consequently, the banks, whose funds constitute about 85 per cent of MFIs lending resources, have slowed down release of loans during the past two years. The growth in client outreach and loan outstanding has retarded during the past two years. This contagion has spread to Self Help Bank Linkage programme also affecting its loan repayment performance. This development is popularly known as Andhra Pradesh Crisis (AP Crisis) in the sector.

In response to the crisis, RBI studied the issues surrounding MFIs in the country through a special committee – Y.H. Malegam Committee and introduced regulatory framework through its circulars, 3 May, 2 December 2011 and 3 August 2012. Through these notifications, RBI has also created a separate category of NBFC-MFIs. Now all NBFC-MFIs are required to register themselves with RBI to continue their operation. Market report says over 30 NBFC-MFIs have received licenses from RBI so far.

The NBFC-MFIs directly and non-NBFC MFIs indirectly are required to comply with the RBI regulation and its Fair Practices code on the one hand and Code of Conduct prescribed by the sector associations on the other. Thus MFIs compliance to these norms is set to safeguard the interest of the poor clients being served by MFIs.

In the meantime Govt. of India introduced the draft Bill, Microfinance Institutions (Regulation and Development) Bill 2012 in Parliament with an intent to bring all the microfinance institutions, including Trust and Society forms under regulatory regime. The Bill is before the Standing Committee of Finance which has completed the public hearing on the provisions of the Bill. The committee is about to submit its report to Parliament/ Ministry.

The Bharat Microfinance Report 2013xviii

These two measures have instilled a sense of confidence among the stakeholders and banks particularly resumed their fund support to MFIs. Banks collectively have over Rs. 16000 crore exposure to the MFIs in the country.

The practitioners in the sector are looking forward to continued bank support for the funds and Microfinance Bill for the regulatory comfort. In the meantime, RBI has sought associations to apply for positions of Self Regulatory Organization (SRO) to facilitate the MFIs to better comply with regulation.

Target Audience for the Bharat Microfinance Report 2013

The report purports to provide a primary-data based analytical information to the government, policy makers, the RBI, banks, and MFIs enabling them to make informed intervention in the sector.

The Data behind the Report

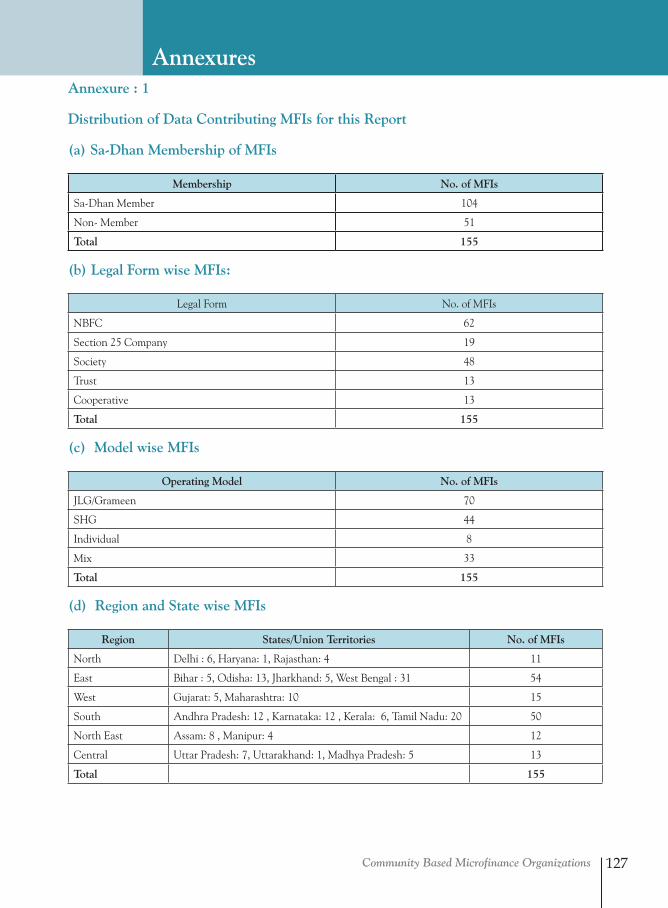

Sa-Dhan as an association collects data from their member organizations, mainly Microfinance institutions, Self Help Promoting Institutions (SHPIs) and Cooperatives. For this report, the data so received from 155 MFIs of all legal forms (Trust, Society, Cooperatives, Section -25 Company and NBFCs) have been collated, validated, analyzed and the results presented in Part 2, 3 and 4 of this report. The distribution of sample of MFIs which reported data is given in Annexure 1. The MFI category used were: Legal form, MFI Loan size ( as of March 2013) and CDR status.

Besides, NABARD data, data and case studies from SHPIs have benn used to carry out qualitative analysis and generate Part 1, 5 and 6 of the report. Secondary data, internal reports and insights have also been used to generate certain sections of the report.

The project team scrupulously scrutinized the self-reported data of the MFIs to improve the data quality through three rounds of validation- scrutiny of financial statements, calling the MFIs, wherever prima facie discrepancies are found, to confirm and sending the preliminary findings / ratios to contributing MFIs to validate / confirm the data. The team also reconciled NBFC data with that of MFIN data sets. The validity of the findings, however, is subject to the accuracy of the self –reported data, though the reconciliation techniques mentioned above would have minimized the data errors to the bare minimum.

The relevance of the findings has been improved to the extent possible through several rounds of consultation with the Advisory Group members who are industry leaders and practitioners.

The Report Coverage

Part 1 highlights the role of microfinance in financial inclusion. Part 2 covers MFI-outreach and loan portfolio. Part 3 discusses the Institutional and financial aspects of MFI operation. Part 4 deals with funding of MFIs and Part 5 introduces the Self Regulatory initiatives in the sector. For the first time in the report series, an elaborate account on Community based Microfinance organizations – like SHGs, Federations, Cooperatives and Self Help Promoting Institutions – is given in Part 6.

xix

Summary of the Report

On Microfinance and Financial inclusion

Microfinance has been the key intervention in the financial inclusion space, though its role is yet to be fully appreciated. Self Help Bank Linkage programme purveys bank credit to the mass that do not have any access to banking service. Similarly, the MFIs use bank funds to offer credit to the same kind of unreached people in the villages. They offer services to SC/ST and minority clients. They also offer variety of products- savings, insurance, pension, and livelihood, health and education services.

On MFI Outreach and Loan Portfolio

The MFIs reach out to poor clients residing in 573 districts across 33 states of the country. The spread of operation in excluded north and east is a positive development. The MFI loan portfolio has reached an all-time high in 2013 (Rs.22300 crore), after a slump in the previous two years. Loans are increasingly being made available to income generation purposes, fully complying with RBI stipulation.

On MFI Institutional and Financial aspects

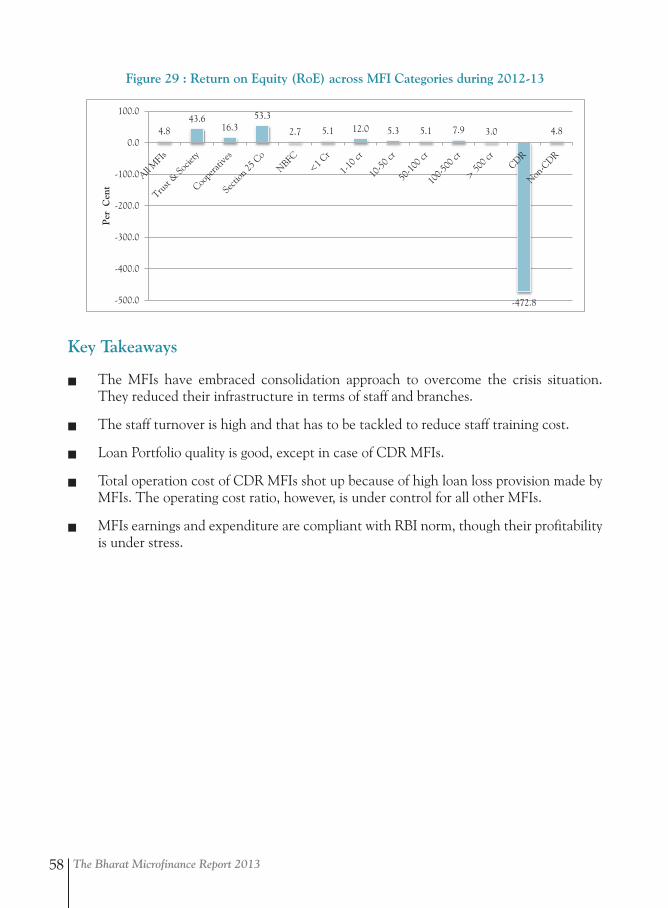

The MFIs have embraced consolidation approach to overcome the crisis situation. They reduced their infrastructure in terms of staff and branches. The staff turnover is high that has to be tackled to reduce staff training cost. Loan Portfolio quality is good, except in case of seen Corporate Debt Restructuring (CDR) MFIs who has the base in microfinance-beleaguered Andhra Pradesh. Total operation cost of MFIs shot up because of high loan loss provision made by MFIs especially among CDR MFIs. The operating cost ratio, however, is under control. MFIs earnings and expenditure are compliant with RBI norm, though their profitability is under stress.

On Funding MFIs

Bank borrowing is the sole resource for MFIs to fund their portfolio. Dwindling share of public sector bank lending to MFIs is an area of concern. Banks, in general, have positive notion on supporting MFIs and MFIs contribution to the priority sector lending. Their credit appraisal norms to fund MFIs have undergone significant change. The role of Bulk Lenders is very crucial for funding MFIs.

On Self Regulation

Sa-Dhan had been taking proactive steps in the self regulation starting from introduction of voluntary code of conduct in 2007. Amendment to Sa-Dhan Memorandum of Association (MoA) infusing additional powers to the association to deal with erring members, constitution of Ethics and Grievance Redressal Committee ( EGRC), etc are the other steps taken in this respect. The regulation from RBI has further strengthened the self-regulation efforts. The RBI regulation workshops, release of Handbook on RBI regulation for the benefit of MFIs, Code of Conduct validation exercise, etc. are the other Sa-Dhan efforts during the recent

The Bharat Microfinance Report 2013xx

past. Sa-Dhan is seeking RBI approval to act as SRO. This is expected to bring in further impetus to self regulation.

On Community Based Microfinance Organizations

The slackness in Self Help Group Bank Linkage Programme (SBLP) as evident from decline in number of SHGs, increase in Non Performing Assets (NPA) is a source of concern. NABARD and banks will have to involve Self Help Promoting Institutions (SHPIs) in a big way for reversing the trend.

SHPIs have played a very key role in conceiving and giving momentum to SHG movement. Yet, there are multiple challenges facing SHGs, their federations and SHPIs. There is widespread issue on group quality, funding SHPIs, Bank Linkage, getting loans for SHGs, etc. which warrant urgent attention.

Cooperatives are the only form of MFIs which offer savings service to the low income members. Through addressing issues like governance and managerial efficiency that often affect such institutions, cooperatives could be evolved as robust community based economic organizations.

xxi

Microfinance and Financial Inclusion 1

Microfinance and Financial InclusionPart 1

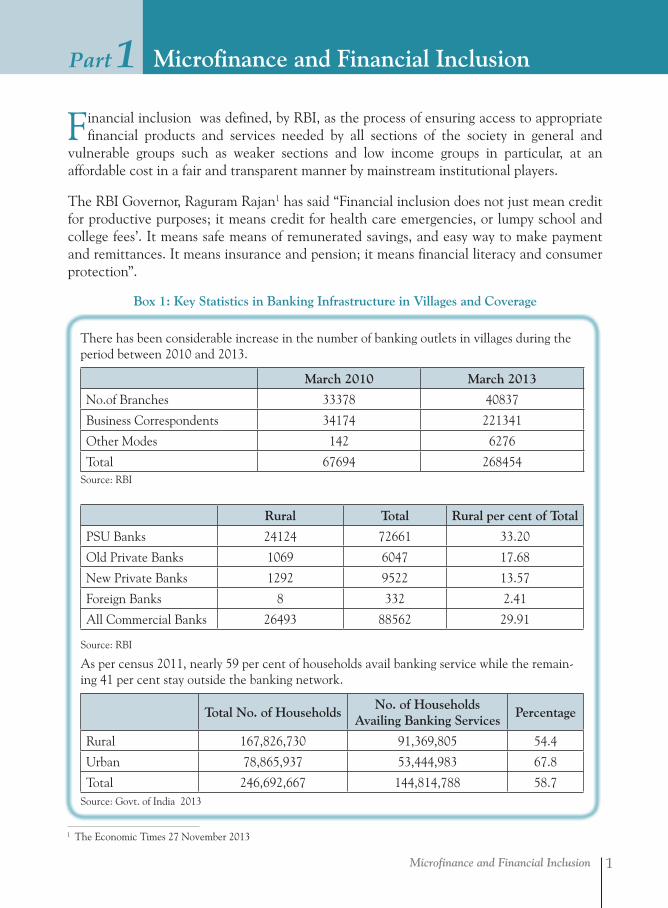

Financial inclusion was defined, by RBI, as the process of ensuring access to appropriate financial products and services needed by all sections of the society in general and

vulnerable groups such as weaker sections and low income groups in particular, at an affordable cost in a fair and transparent manner by mainstream institutional players.

The RBI Governor, Raguram Rajan1 has said “Financial inclusion does not just mean credit for productive purposes; it means credit for health care emergencies, or lumpy school and college fees’. It means safe means of remunerated savings, and easy way to make payment and remittances. It means insurance and pension; it means financial literacy and consumer protection”.

Box 1: Key Statistics in Banking Infrastructure in Villages and Coverage

There has been considerable increase in the number of banking outlets in villages during the period between 2010 and 2013.

March 2010 March 2013

No.of Branches 33378 40837

Business Correspondents 34174 221341

Other Modes 142 6276

Total 67694 268454Source: RBI

Rural Total Rural per cent of Total

PSU Banks 24124 72661 33.20

Old Private Banks 1069 6047 17.68

New Private Banks 1292 9522 13.57

Foreign Banks 8 332 2.41

All Commercial Banks 26493 88562 29.91

Source: RBI

As per census 2011, nearly 59 per cent of households avail banking service while the remain-ing 41 per cent stay outside the banking network.

Total No. of HouseholdsNo. of Households

Availing Banking Services Percentage

Rural 167,826,730 91,369,805 54.4

Urban 78,865,937 53,444,983 67.8

Total 246,692,667 144,814,788 58.7

1 The Economic Times 27 November 2013

Source: Govt. of India 2013

The Bharat Microfinance Report 20132

1.1 Microfinance Complementing Banks

The problem of banking access empirically shown in Box 1 is exacerbated when it comes to the poor people. The poor are always in a dilemma as far as financial services is concerned. Their problems for accessing formal banking services relate to collateral, distance from the bank branch, transportation expenses, potential wage loss during visiting / waiting period, cumbersome paper work, bankers approach, etc. Services from informal sources, on the other hand, are costly and exploitative.

Problem persists for the poor with respect to other financial products as well. According to the nation-wide survey carried out by IISS (India Incomes and Savings Survey, 2007), 97 per cent of all household do not have any health insurance and 61 per cent do not have any life insurance. According to NSSO surveys, roughly 25 per cent of households get into chronic indebtedness because of health related emergencies.

Since financial services are provided by market, both supply (financial inclusion) and demand (financial literacy) side consideration are important. There is need for institutions closer and approachable to the people and are reliable and non-exploitative.

Microfinance is an innovation in providing financial services to the excluded segment of the society. The microfinance practice, per se, addresses the lacunae associated with both formal and purely informal sources of financial services. The essential features of microcredit, for example, are:

i. The borrowers are low-income households.

ii. The loan size is small enough to suit the unbanked and poor borrowers.

iii. The loans are without collateral.

iv. The loans are generally taken for income-generating activities, although loans are also provided for consumption, housing and other purposes.

v. The tenure of the loans is short.

vi. The frequency of repayments is higher than, say weekly/fortnightly.

Microfinance and Financial Inclusion 3

1.2 GOI and RBI stand on Microfinance Role and Financial Inclusion

The then Finance Minister Sri. Pranab Mukherjee said the following in his budget speech 2011:

Microfinance Institutions (MFIs) have emerged as an important means of financial inclusion. Creation of dedicated fund for providing equity to smaller MFIs would help them maintain growth and achieve scale and efficiency in operations. I propose to create in the course of the year, ‘India Microfinance Equity Fund’ of Rs.100 crore with SIDBI . To empower women and promote their Self Help Group (SHGs), I propose to create a ‘women’s SHG’s Development Fund’ with corpus of Rs.500 crore. The committee set up by RBI to look into issues relating to microfinance sector in India has submitted its report. The Government is considering putting in place appropriate framework to protect the interest of small borrowers.

The Finance Minister recognized the crucial role played MFIs and SHGs as quoted above.Besides, the finance ministry has proposed The Microfinance Institutions (Development and Regulation) Microfinance Bill 2012 to regulate the MFI-sector. The Bill 2012 is a significant move in achieving the agenda of financial inclusion as it provides detailed regulatory framework for microfinance sector. The bill is before Parliament Standing Committee which has sought opinion of stakeholders including Sa-Dhan and the committee is about to submit its report.

Reserve Bank of India looks at core indicators which place a given population on the continuum of financial access, depending on its usage of formal, semi-formal, and informal financial services and those excluded from the use of financial services2. In particular the indicators are:

o the proportion of the population that uses a bank or bank like institution;

o the population which uses service from non-bank ‘other formal’ financial institutions, but does not use bank services;

o the population which only uses services from informal financial service providers

o the population which uses no financial services.

MFIs belong to non-bank ‘other formal’ financial institutions, providing services to people at the distal end of the access continuum.

Reserve Bank of India further clarifies that the degree of financial inclusion can be measured by looking into services offered. The services may be:

o Transactions or payment services

o savings (deposit) and investment services

o loan or credit services

o Risk transformation services such as insurance.

2 RBI (2009) Report on currency and Finance 2008

The Bharat Microfinance Report 20134

MFIs offer loan or credit services through small value, high volume transactions with unbanked population, facilitate savings among them by acting as Business Correspondents of banks, among Self Help Groups by linking them with banks, extend insurance services as agents of insurance service providers and offer money transfer services to migrant workers.

Reserve Bank of India patronizes MFIs, keeping the financial inclusion agenda of MFIs in view. RBI included bank lending to MFIs as priority sector credit which helped MFIs to source resources to on-lend to low end clients. Introduction of NBFC MFI category amplify further RBI commitment to the sector.

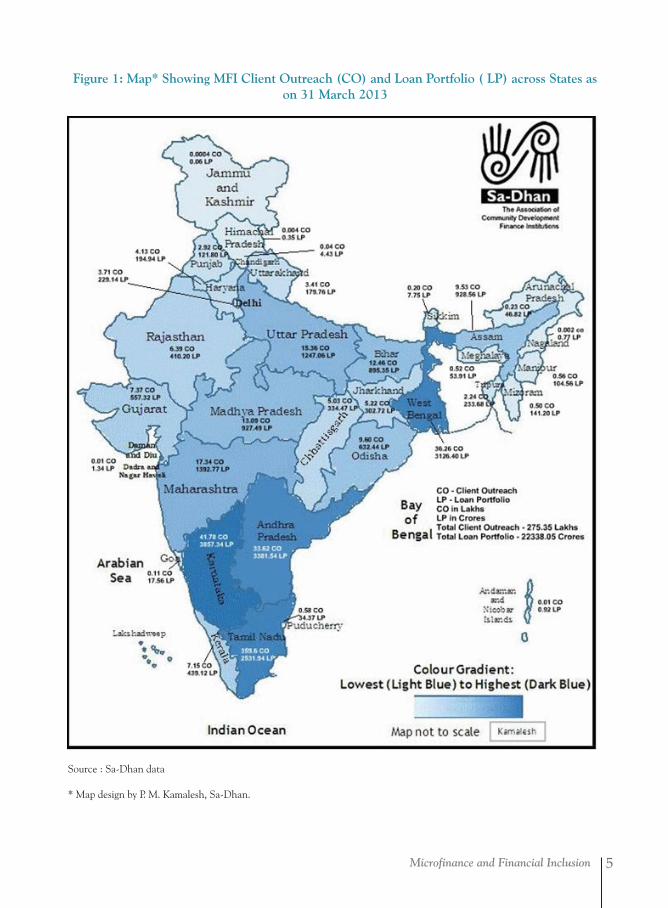

1.3 Microfinance Outreach

MFIs render their services in 28 States and five Union Territories of India. MFIs have a presence in 573 districts of the country and providing financial services. The MFI Map of India depicted in Figure-1 shows the numbers of MFI clients present (Client Outreach–CO) and loan portfolio (Loan Portfolio-LP) held in different states, with color gradients indicating the comparative concentration of state figures under the client outreach indicator.

The map shows the MFIs have services in priority states viz., West Bengal, Odisha, Chhattisgarh, Madhya Pradesh, Assam, Uttar Pradesh, Bihar and Rajasthan, apart from pioneering southern states.

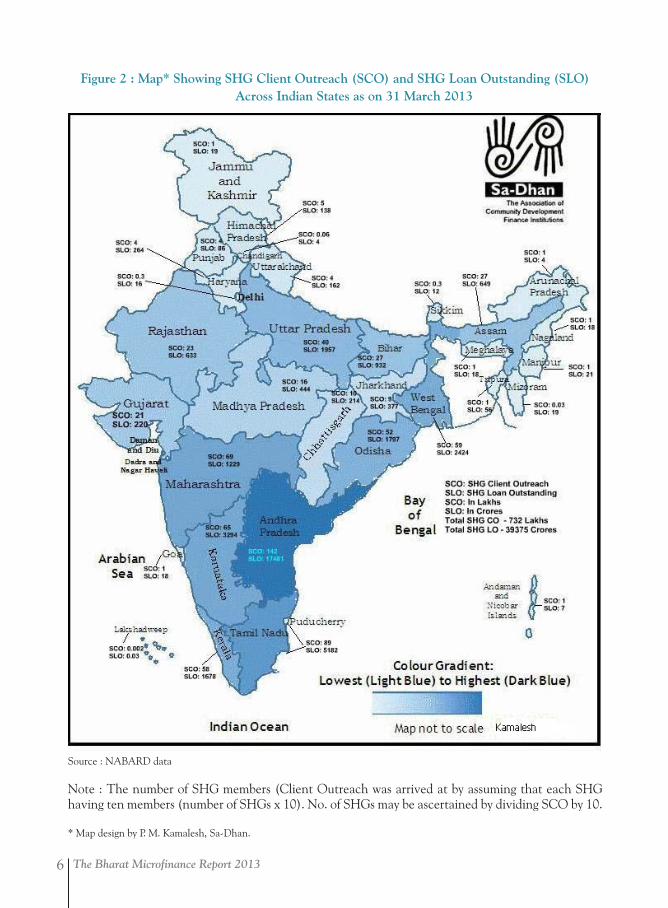

Figure-2, similarly, carries the image of Indian states with data on savings-linked SHG members and loan outstanding. The number of SHG members was arrived at by assuming that each SHG having ten members (number of SHG x 10). SHG concentration is high in southern states while it is relatively less in northern regions. The state wise statistics on SHG transactions is furnished in Part 6.

Microfinance and Financial Inclusion 5

Figure 1: Map* Showing MFI Client Outreach (CO) and Loan Portfolio ( LP) across States as on 31 March 2013

Source : Sa-Dhan data

* Map design by P. M. Kamalesh, Sa-Dhan.

The Bharat Microfinance Report 20136

Figure 2 : Map* Showing SHG Client Outreach (SCO) and SHG Loan Outstanding (SLO)Across Indian States as on 31 March 2013

Source : NABARD data

Note : The number of SHG members (Client Outreach was arrived at by assuming that each SHG having ten members (number of SHGs x 10). No. of SHGs may be ascertained by dividing SCO by 10.

* Map design by P. M. Kamalesh, Sa-Dhan.

Microfinance and Financial Inclusion 7

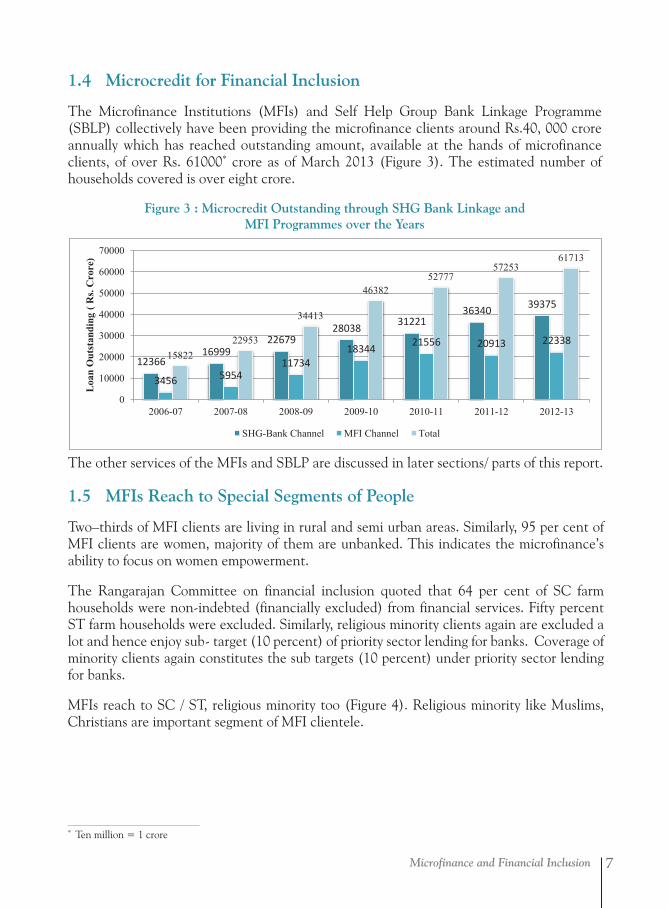

1.4 Microcredit for Financial Inclusion

The Microfinance Institutions (MFIs) and Self Help Group Bank Linkage Programme (SBLP) collectively have been providing the microfinance clients around Rs.40, 000 crore annually which has reached outstanding amount, available at the hands of microfinance clients, of over Rs. 61000* crore as of March 2013 (Figure 3). The estimated number of households covered is over eight crore.

Figure 3 : Microcredit Outstanding through SHG Bank Linkage andMFI Programmes over the Years

12366 16999

22679 28038 31221

36340 39375

3456 5954 11734

18344 21556 20913 22338 15822

22953

34413

46382 52777

57253 61713

0

10000

20000

30000

40000

50000

60000

70000

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Loa

n O

utst

andi

ng (

Rs.

Cro

re)

SHG-Bank Channel MFI Channel Total

The other services of the MFIs and SBLP are discussed in later sections/ parts of this report.

1.5 MFIs Reach to Special Segments of People

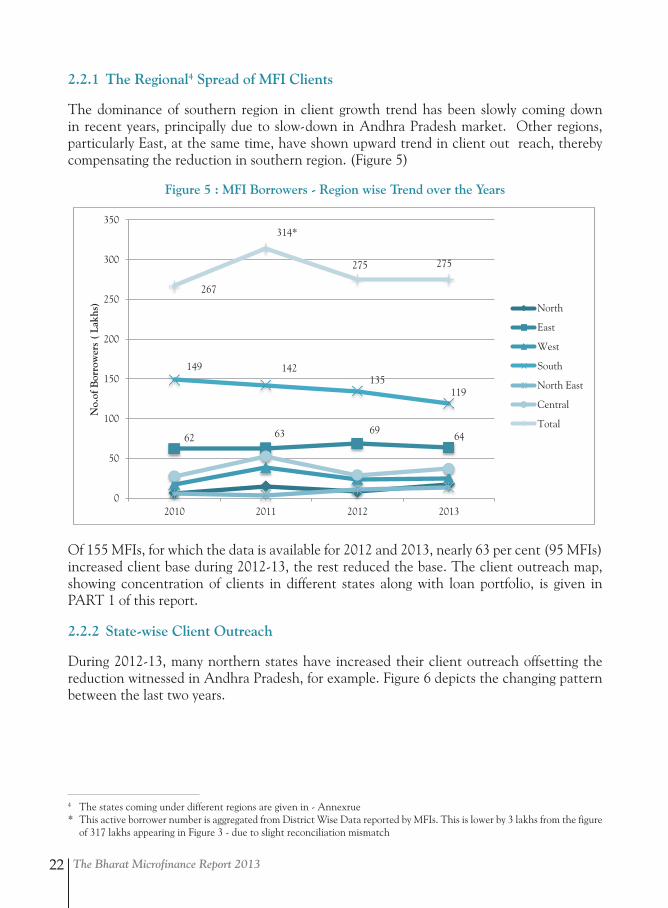

Two–thirds of MFI clients are living in rural and semi urban areas. Similarly, 95 per cent of MFI clients are women, majority of them are unbanked. This indicates the microfinance’s ability to focus on women empowerment.

The Rangarajan Committee on financial inclusion quoted that 64 per cent of SC farm households were non-indebted (financially excluded) from financial services. Fifty percent ST farm households were excluded. Similarly, religious minority clients again are excluded a lot and hence enjoy sub- target (10 percent) of priority sector lending for banks. Coverage of minority clients again constitutes the sub targets (10 percent) under priority sector lending for banks.

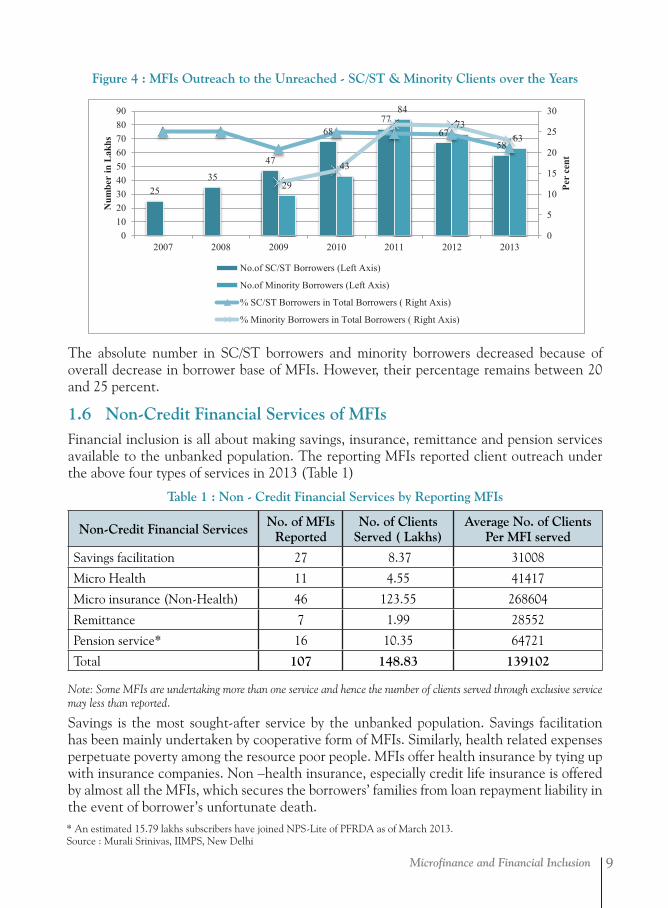

MFIs reach to SC / ST, religious minority too (Figure 4). Religious minority like Muslims, Christians are important segment of MFI clientele.

* Ten million = 1 crore

The Bharat Microfinance Report 20138

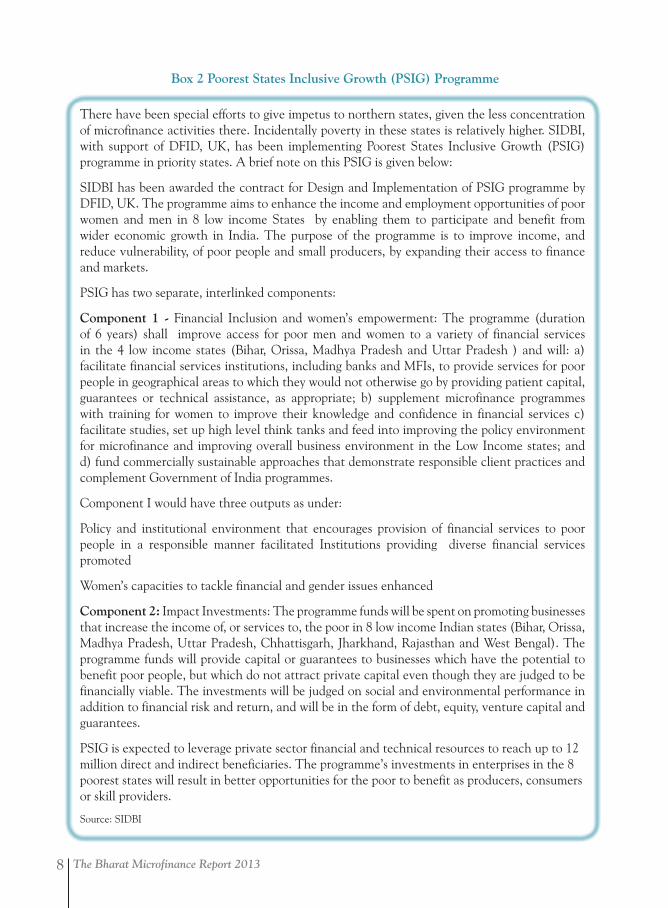

Box 2 Poorest States Inclusive Growth (PSIG) Programme

There have been special efforts to give impetus to northern states, given the less concentration of microfinance activities there. Incidentally poverty in these states is relatively higher. SIDBI, with support of DFID, UK, has been implementing Poorest States Inclusive Growth (PSIG) programme in priority states. A brief note on this PSIG is given below:

SIDBI has been awarded the contract for Design and Implementation of PSIG programme by DFID, UK. The programme aims to enhance the income and employment opportunities of poor women and men in 8 low income States by enabling them to participate and benefit from wider economic growth in India. The purpose of the programme is to improve income, and reduce vulnerability, of poor people and small producers, by expanding their access to finance and markets.

PSIG has two separate, interlinked components:

Component 1 - Financial Inclusion and women’s empowerment: The programme (duration of 6 years) shall improve access for poor men and women to a variety of financial services in the 4 low income states (Bihar, Orissa, Madhya Pradesh and Uttar Pradesh ) and will: a) facilitate financial services institutions, including banks and MFIs, to provide services for poor people in geographical areas to which they would not otherwise go by providing patient capital, guarantees or technical assistance, as appropriate; b) supplement microfinance programmes with training for women to improve their knowledge and confidence in financial services c) facilitate studies, set up high level think tanks and feed into improving the policy environment for microfinance and improving overall business environment in the Low Income states; and d) fund commercially sustainable approaches that demonstrate responsible client practices and complement Government of India programmes.

Component I would have three outputs as under:

Policy and institutional environment that encourages provision of financial services to poor people in a responsible manner facilitated Institutions providing diverse financial services promoted

Women’s capacities to tackle financial and gender issues enhanced

Component 2: Impact Investments: The programme funds will be spent on promoting businesses that increase the income of, or services to, the poor in 8 low income Indian states (Bihar, Orissa, Madhya Pradesh, Uttar Pradesh, Chhattisgarh, Jharkhand, Rajasthan and West Bengal). The programme funds will provide capital or guarantees to businesses which have the potential to benefit poor people, but which do not attract private capital even though they are judged to be financially viable. The investments will be judged on social and environmental performance in addition to financial risk and return, and will be in the form of debt, equity, venture capital and guarantees.

PSIG is expected to leverage private sector financial and technical resources to reach up to 12 million direct and indirect beneficiaries. The programme’s investments in enterprises in the 8 poorest states will result in better opportunities for the poor to benefit as producers, consumers or skill providers.

Source: SIDBI

Microfinance and Financial Inclusion 9

Figure 4 : MFIs Outreach to the Unreached - SC/ST & Minority Clients over the Years

The absolute number in SC/ST borrowers and minority borrowers decreased because of overall decrease in borrower base of MFIs. However, their percentage remains between 20 and 25 percent.

1.6 Non-Credit Financial Services of MFIs Financial inclusion is all about making savings, insurance, remittance and pension services available to the unbanked population. The reporting MFIs reported client outreach under the above four types of services in 2013 (Table 1)

Table 1 : Non - Credit Financial Services by Reporting MFIs

Non-Credit Financial Services No. of MFIs Reported

No. of Clients Served ( Lakhs)

Average No. of Clients Per MFI served

Savings facilitation 27 8.37 31008

Micro Health 11 4.55 41417

Micro insurance (Non-Health) 46 123.55 268604

Remittance 7 1.99 28552

Pension service* 16 10.35 64721

Total 107 148.83 139102

Note: Some MFIs are undertaking more than one service and hence the number of clients served through exclusive service may less than reported.

Savings is the most sought-after service by the unbanked population. Savings facilitation has been mainly undertaken by cooperative form of MFIs. Similarly, health related expenses perpetuate poverty among the resource poor people. MFIs offer health insurance by tying up with insurance companies. Non –health insurance, especially credit life insurance is offered by almost all the MFIs, which secures the borrowers’ families from loan repayment liability in the event of borrower’s unfortunate death.

25 35

47

68 77

67 58

29

43

84 73

63

0

5

10

15

20

25

30

0102030405060708090

2007 2008 2009 2010 2011 2012 2013

Per

cent

Num

ber

in L

akhs

No.of SC/ST Borrowers (Left Axis)

No.of Minority Borrowers (Left Axis)

% SC/ST Borrowers in Total Borrowers ( Right Axis)

% Minority Borrowers in Total Borrowers ( Right Axis)

* An estimated 15.79 lakhs subscribers have joined NPS-Lite of PFRDA as of March 2013. Source : Murali Srinivas, IIMPS, New Delhi

The Bharat Microfinance Report 201310

Money transfer/remittance service is critical for migrant workers to send money back home to their families. Access to banking services in urban areas is generally good; and yet most migrant workers do not have a bank account at the urban destination points where they are working. Many migrant workers do not have adequate information about formal financial services, and many of those who have accounts with banks do not use them effectively. MFIs provide remittance service through making suitable arrangements with banks.

All the workers of unorganized sector are deprived of pension as an old age security. MFIs have become aggregators of pension remittance to the Pension Schemes regulated by Pension and Regulatory and Development Authority (PFRDA).

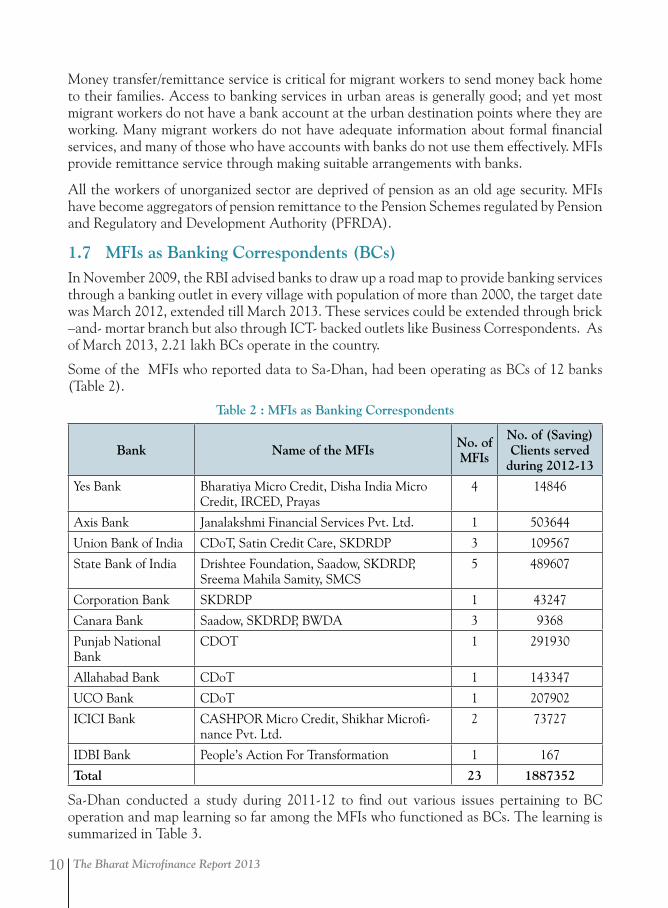

1.7 MFIs as Banking Correspondents (BCs)In November 2009, the RBI advised banks to draw up a road map to provide banking services through a banking outlet in every village with population of more than 2000, the target date was March 2012, extended till March 2013. These services could be extended through brick –and- mortar branch but also through ICT- backed outlets like Business Correspondents. As of March 2013, 2.21 lakh BCs operate in the country.

Some of the MFIs who reported data to Sa-Dhan, had been operating as BCs of 12 banks (Table 2).

Table 2 : MFIs as Banking Correspondents

Bank Name of the MFIs No. of MFIs

No. of (Saving) Clients served

during 2012-13

Yes Bank Bharatiya Micro Credit, Disha India Micro Credit, IRCED, Prayas

4 14846

Axis Bank Janalakshmi Financial Services Pvt. Ltd. 1 503644

Union Bank of India CDoT, Satin Credit Care, SKDRDP 3 109567

State Bank of India Drishtee Foundation, Saadow, SKDRDP, Sreema Mahila Samity, SMCS

5 489607

Corporation Bank SKDRDP 1 43247

Canara Bank Saadow, SKDRDP, BWDA 3 9368

Punjab National Bank

CDOT 1 291930

Allahabad Bank CDoT 1 143347

UCO Bank CDoT 1 207902

ICICI Bank CASHPOR Micro Credit, Shikhar Microfi-nance Pvt. Ltd.

2 73727

IDBI Bank People’s Action For Transformation 1 167

Total 23 1887352

Sa-Dhan conducted a study during 2011-12 to find out various issues pertaining to BC operation and map learning so far among the MFIs who functioned as BCs. The learning is summarized in Table 3.

Microfinance and Financial Inclusion 11

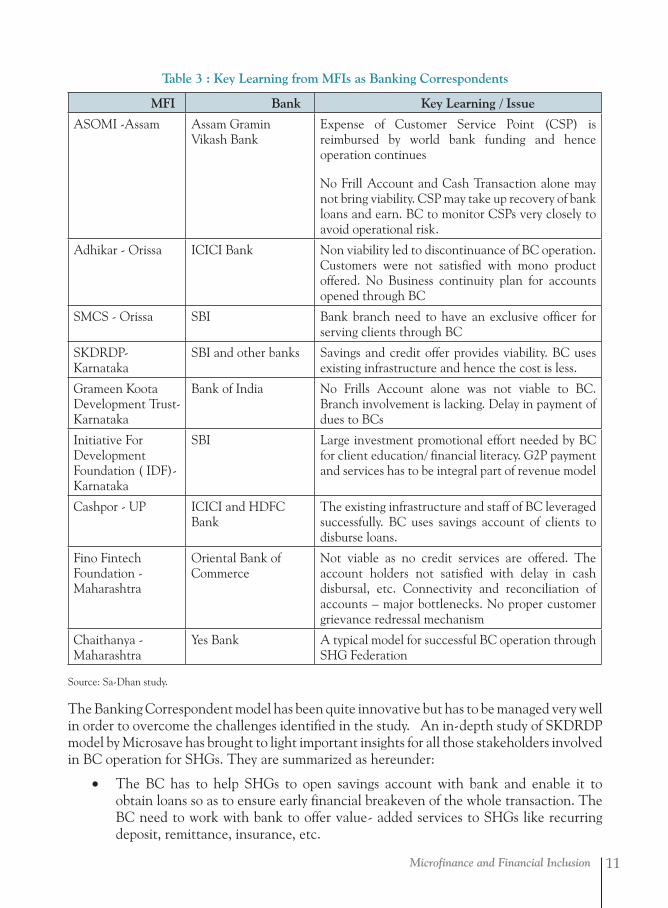

Table 3 : Key Learning from MFIs as Banking Correspondents

MFI Bank Key Learning / Issue

ASOMI -Assam Assam Gramin Vikash Bank

Expense of Customer Service Point (CSP) is reimbursed by world bank funding and hence operation continues

No Frill Account and Cash Transaction alone may not bring viability. CSP may take up recovery of bank loans and earn. BC to monitor CSPs very closely to avoid operational risk.

Adhikar - Orissa ICICI Bank Non viability led to discontinuance of BC operation. Customers were not satisfied with mono product offered. No Business continuity plan for accounts opened through BC

SMCS - Orissa SBI Bank branch need to have an exclusive officer for serving clients through BC

SKDRDP-Karnataka

SBI and other banks Savings and credit offer provides viability. BC uses existing infrastructure and hence the cost is less.

Grameen Koota Development Trust- Karnataka

Bank of India No Frills Account alone was not viable to BC. Branch involvement is lacking. Delay in payment of dues to BCs

Initiative For Development Foundation ( IDF)-Karnataka

SBI Large investment promotional effort needed by BC for client education/ financial literacy. G2P payment and services has to be integral part of revenue model

Cashpor - UP ICICI and HDFC Bank

The existing infrastructure and staff of BC leveraged successfully. BC uses savings account of clients to disburse loans.

Fino Fintech Foundation - Maharashtra

Oriental Bank of Commerce

Not viable as no credit services are offered. The account holders not satisfied with delay in cash disbursal, etc. Connectivity and reconciliation of accounts – major bottlenecks. No proper customer grievance redressal mechanism

Chaithanya - Maharashtra

Yes Bank A typical model for successful BC operation through SHG Federation

Source: Sa-Dhan study.

The Banking Correspondent model has been quite innovative but has to be managed very well in order to overcome the challenges identified in the study. An in-depth study of SKDRDP model by Microsave has brought to light important insights for all those stakeholders involved in BC operation for SHGs. They are summarized as hereunder:

• The BC has to help SHGs to open savings account with bank and enable it to obtain loans so as to ensure early financial breakeven of the whole transaction. The BC need to work with bank to offer value- added services to SHGs like recurring deposit, remittance, insurance, etc.

The Bharat Microfinance Report 201312

• SHPI- leadership is very critical to engage multiple stakeholders to take forward the BC operation.

• The BC need to prepare the bank in terms of understanding the grass root level challenges and transactions. The bank will have to devote committed branch team for taking care of the BC business.

• The BC need to obtain the due commission from the bank for various transactions and monitoring service rendered by it on time to make the BC operation sustainable.

• The field-focus is very vital for the successful BC operation. The feedback from clients and their satisfaction should drive continuous improvement of the product / process.

• Staff choice, training and motivation are equally important areas deserving the attention of BC. The BC staff quality and their relationship with bank staff may make or break BC system.

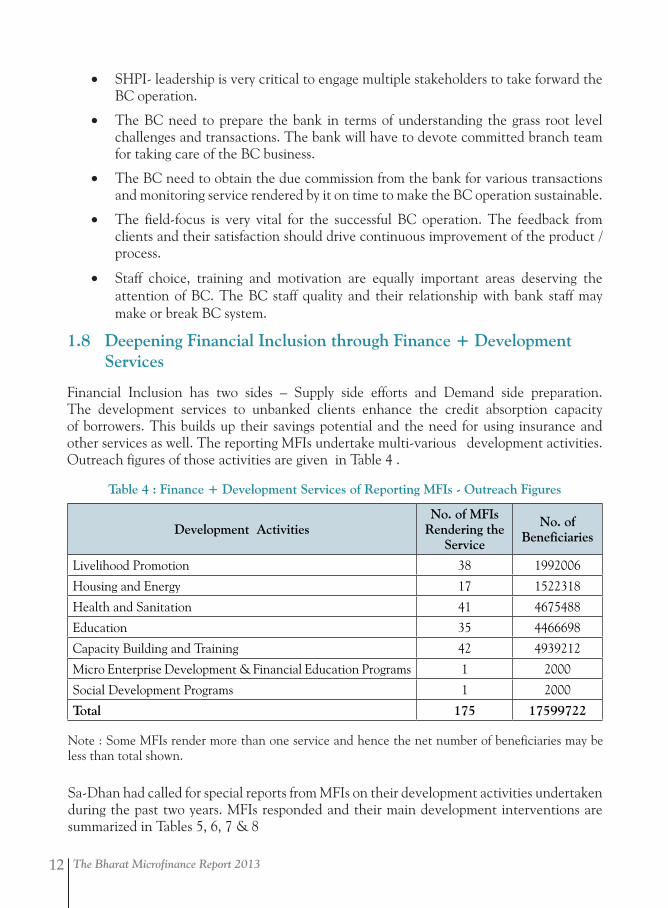

1.8 Deepening Financial Inclusion through Finance + Development Services

Financial Inclusion has two sides – Supply side efforts and Demand side preparation. The development services to unbanked clients enhance the credit absorption capacity of borrowers. This builds up their savings potential and the need for using insurance and other services as well. The reporting MFIs undertake multi-various development activities. Outreach figures of those activities are given in Table 4 .

Table 4 : Finance + Development Services of Reporting MFIs - Outreach Figures

Development ActivitiesNo. of MFIs

Rendering the Service

No. of Beneficiaries

Livelihood Promotion 38 1992006

Housing and Energy 17 1522318

Health and Sanitation 41 4675488

Education 35 4466698

Capacity Building and Training 42 4939212

Micro Enterprise Development & Financial Education Programs 1 2000

Social Development Programs 1 2000

Total 175 17599722

Note : Some MFIs render more than one service and hence the net number of beneficiaries may be less than total shown.

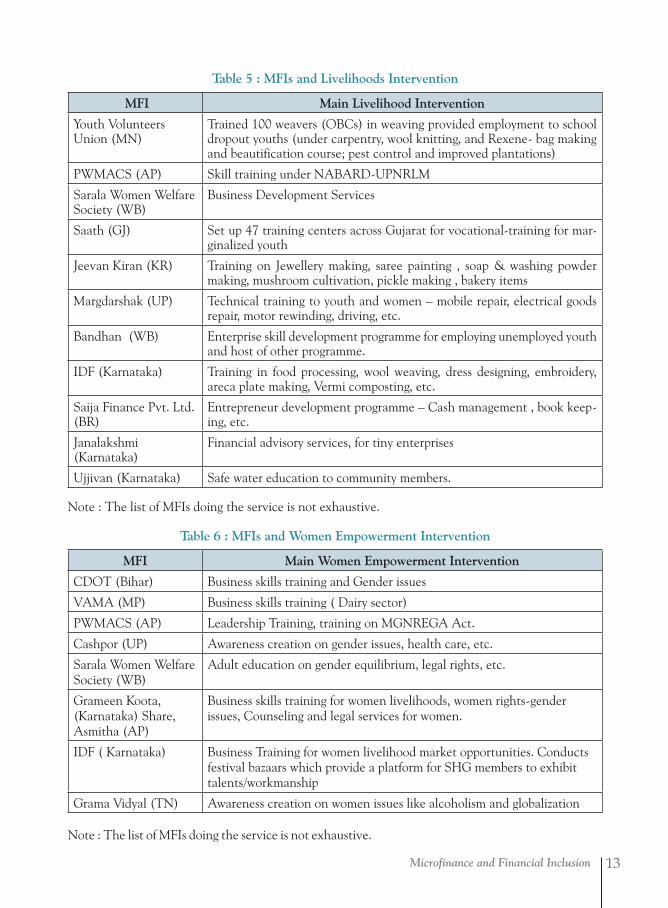

Sa-Dhan had called for special reports from MFIs on their development activities undertaken during the past two years. MFIs responded and their main development interventions are summarized in Tables 5, 6, 7 & 8

Microfinance and Financial Inclusion 13

Table 5 : MFIs and Livelihoods Intervention

MFI Main Livelihood Intervention

Youth Volunteers Union (MN)

Trained 100 weavers (OBCs) in weaving provided employment to school dropout youths (under carpentry, wool knitting, and Rexene- bag making and beautification course; pest control and improved plantations)

PWMACS (AP) Skill training under NABARD-UPNRLM

Sarala Women Welfare Society (WB)

Business Development Services

Saath (GJ) Set up 47 training centers across Gujarat for vocational-training for mar-ginalized youth

Jeevan Kiran (KR) Training on Jewellery making, saree painting , soap & washing powder making, mushroom cultivation, pickle making , bakery items

Margdarshak (UP) Technical training to youth and women – mobile repair, electrical goods repair, motor rewinding, driving, etc.

Bandhan (WB) Enterprise skill development programme for employing unemployed youth and host of other programme.

IDF (Karnataka) Training in food processing, wool weaving, dress designing, embroidery, areca plate making, Vermi composting, etc.

Saija Finance Pvt. Ltd. (BR)

Entrepreneur development programme – Cash management , book keep-ing, etc.

Janalakshmi (Karnataka)

Financial advisory services, for tiny enterprises

Ujjivan (Karnataka) Safe water education to community members.

Note : The list of MFIs doing the service is not exhaustive.

Table 6 : MFIs and Women Empowerment Intervention

MFI Main Women Empowerment Intervention

CDOT (Bihar) Business skills training and Gender issues

VAMA (MP) Business skills training ( Dairy sector)

PWMACS (AP) Leadership Training, training on MGNREGA Act.

Cashpor (UP) Awareness creation on gender issues, health care, etc.

Sarala Women Welfare Society (WB)

Adult education on gender equilibrium, legal rights, etc.

Grameen Koota, (Karnataka) Share, Asmitha (AP)

Business skills training for women livelihoods, women rights-gender issues, Counseling and legal services for women.

IDF ( Karnataka) Business Training for women livelihood market opportunities. Conducts festival bazaars which provide a platform for SHG members to exhibit talents/workmanship

Grama Vidyal (TN) Awareness creation on women issues like alcoholism and globalization

Note : The list of MFIs doing the service is not exhaustive.

The Bharat Microfinance Report 201314

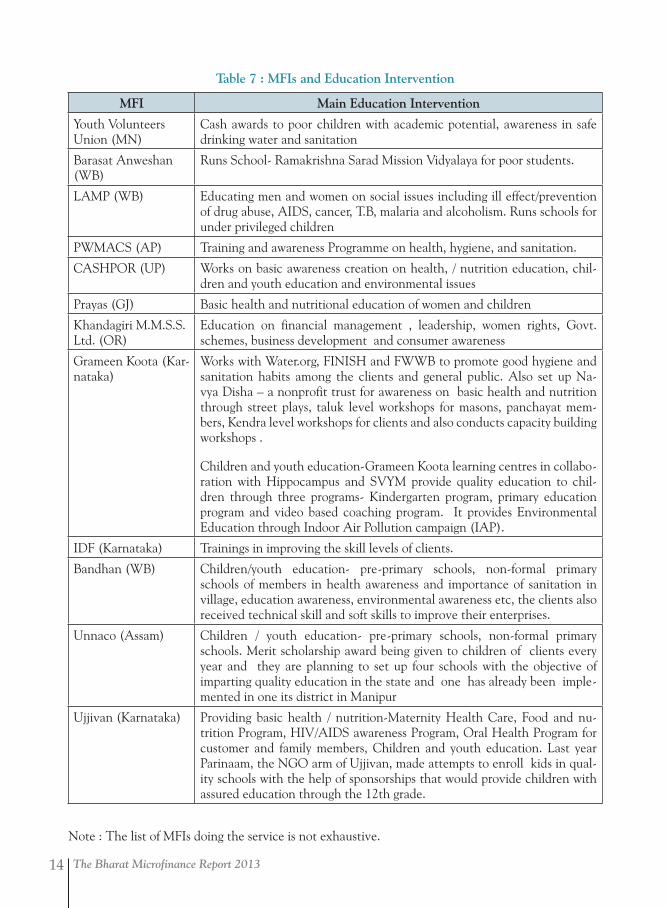

Table 7 : MFIs and Education Intervention

MFI Main Education Intervention

Youth Volunteers Union (MN)

Cash awards to poor children with academic potential, awareness in safe drinking water and sanitation

Barasat Anweshan (WB)

Runs School- Ramakrishna Sarad Mission Vidyalaya for poor students.

LAMP (WB) Educating men and women on social issues including ill effect/prevention of drug abuse, AIDS, cancer, T.B, malaria and alcoholism. Runs schools for under privileged children

PWMACS (AP) Training and awareness Programme on health, hygiene, and sanitation.

CASHPOR (UP) Works on basic awareness creation on health, / nutrition education, chil-dren and youth education and environmental issues

Prayas (GJ) Basic health and nutritional education of women and children

Khandagiri M.M.S.S. Ltd. (OR)

Education on financial management , leadership, women rights, Govt. schemes, business development and consumer awareness

Grameen Koota (Kar-nataka)

Works with Water.org, FINISH and FWWB to promote good hygiene and sanitation habits among the clients and general public. Also set up Na-vya Disha – a nonprofit trust for awareness on basic health and nutrition through street plays, taluk level workshops for masons, panchayat mem-bers, Kendra level workshops for clients and also conducts capacity building workshops .

Children and youth education-Grameen Koota learning centres in collabo-ration with Hippocampus and SVYM provide quality education to chil-dren through three programs- Kindergarten program, primary education program and video based coaching program. It provides Environmental Education through Indoor Air Pollution campaign (IAP).

IDF (Karnataka) Trainings in improving the skill levels of clients.

Bandhan (WB) Children/youth education- pre-primary schools, non-formal primary schools of members in health awareness and importance of sanitation in village, education awareness, environmental awareness etc, the clients also received technical skill and soft skills to improve their enterprises.

Unnaco (Assam) Children / youth education- pre-primary schools, non-formal primary schools. Merit scholarship award being given to children of clients every year and they are planning to set up four schools with the objective of imparting quality education in the state and one has already been imple-mented in one its district in Manipur

Ujjivan (Karnataka) Providing basic health / nutrition-Maternity Health Care, Food and nu-trition Program, HIV/AIDS awareness Program, Oral Health Program for customer and family members, Children and youth education. Last year Parinaam, the NGO arm of Ujjivan, made attempts to enroll kids in qual-ity schools with the help of sponsorships that would provide children with assured education through the 12th grade.

Note : The list of MFIs doing the service is not exhaustive.

Microfinance and Financial Inclusion 15

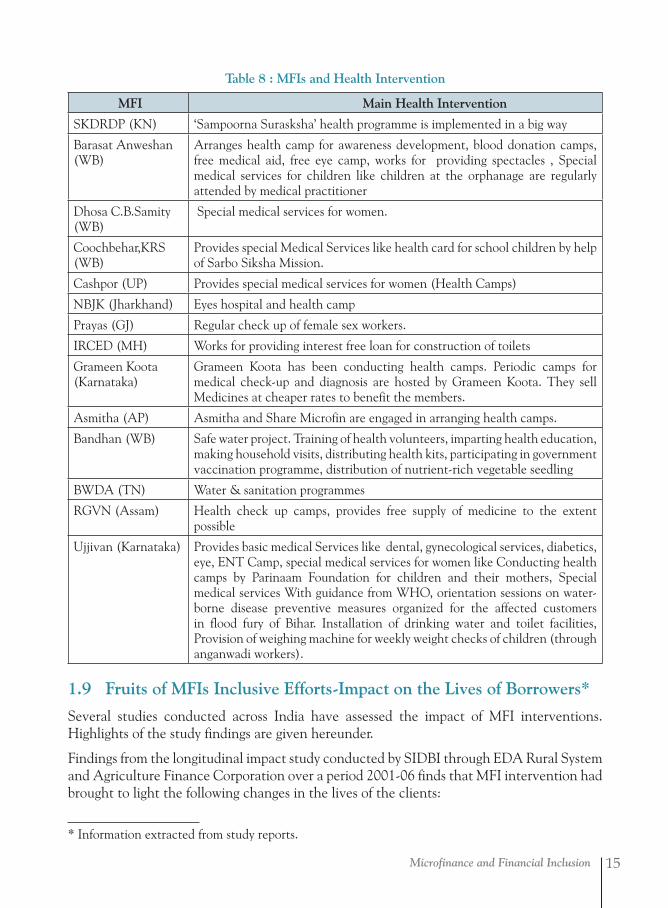

Table 8 : MFIs and Health Intervention

MFI Main Health Intervention

SKDRDP (KN) ‘Sampoorna Surasksha’ health programme is implemented in a big way

Barasat Anweshan (WB)

Arranges health camp for awareness development, blood donation camps, free medical aid, free eye camp, works for providing spectacles , Special medical services for children like children at the orphanage are regularly attended by medical practitioner

Dhosa C.B.Samity (WB)

Special medical services for women.

Coochbehar,KRS (WB)

Provides special Medical Services like health card for school children by help of Sarbo Siksha Mission.

Cashpor (UP) Provides special medical services for women (Health Camps)

NBJK (Jharkhand) Eyes hospital and health camp

Prayas (GJ) Regular check up of female sex workers.

IRCED (MH) Works for providing interest free loan for construction of toilets

Grameen Koota (Karnataka)

Grameen Koota has been conducting health camps. Periodic camps for medical check-up and diagnosis are hosted by Grameen Koota. They sell Medicines at cheaper rates to benefit the members.

Asmitha (AP) Asmitha and Share Microfin are engaged in arranging health camps.

Bandhan (WB) Safe water project. Training of health volunteers, imparting health education, making household visits, distributing health kits, participating in government vaccination programme, distribution of nutrient-rich vegetable seedling

BWDA (TN) Water & sanitation programmes

RGVN (Assam) Health check up camps, provides free supply of medicine to the extent possible

Ujjivan (Karnataka) Provides basic medical Services like dental, gynecological services, diabetics, eye, ENT Camp, special medical services for women like Conducting health camps by Parinaam Foundation for children and their mothers, Special medical services With guidance from WHO, orientation sessions on water-borne disease preventive measures organized for the affected customers in flood fury of Bihar. Installation of drinking water and toilet facilities, Provision of weighing machine for weekly weight checks of children (through anganwadi workers).

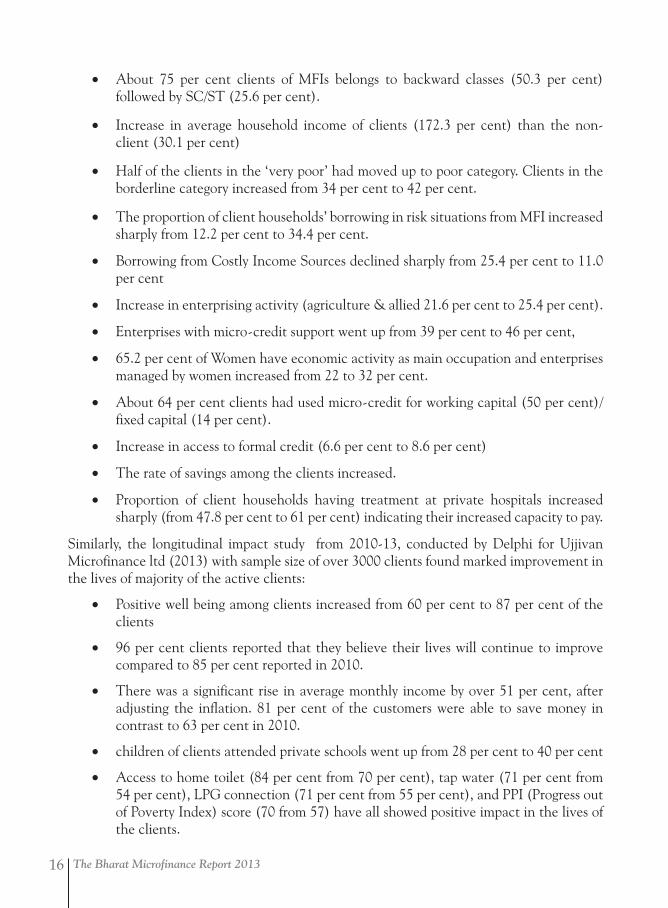

1.9 Fruits of MFIs Inclusive Efforts-Impact on the Lives of Borrowers*

Several studies conducted across India have assessed the impact of MFI interventions. Highlights of the study findings are given hereunder.

Findings from the longitudinal impact study conducted by SIDBI through EDA Rural System and Agriculture Finance Corporation over a period 2001-06 finds that MFI intervention had brought to light the following changes in the lives of the clients:

* Information extracted from study reports.

The Bharat Microfinance Report 201316

• About 75 per cent clients of MFIs belongs to backward classes (50.3 per cent) followed by SC/ST (25.6 per cent).

• Increase in average household income of clients (172.3 per cent) than the non-client (30.1 per cent)

• Half of the clients in the ‘very poor’ had moved up to poor category. Clients in the borderline category increased from 34 per cent to 42 per cent.

• The proportion of client households’ borrowing in risk situations from MFI increased sharply from 12.2 per cent to 34.4 per cent.

• Borrowing from Costly Income Sources declined sharply from 25.4 per cent to 11.0 per cent

• Increase in enterprising activity (agriculture & allied 21.6 per cent to 25.4 per cent).

• Enterprises with micro-credit support went up from 39 per cent to 46 per cent,

• 65.2 per cent of Women have economic activity as main occupation and enterprises managed by women increased from 22 to 32 per cent.

• About 64 per cent clients had used micro-credit for working capital (50 per cent)/fixed capital (14 per cent).

• Increase in access to formal credit (6.6 per cent to 8.6 per cent)

• The rate of savings among the clients increased.

• Proportion of client households having treatment at private hospitals increased sharply (from 47.8 per cent to 61 per cent) indicating their increased capacity to pay.

Similarly, the longitudinal impact study from 2010-13, conducted by Delphi for Ujjivan Microfinance ltd (2013) with sample size of over 3000 clients found marked improvement in the lives of majority of the active clients:

• Positive well being among clients increased from 60 per cent to 87 per cent of the clients

• 96 per cent clients reported that they believe their lives will continue to improve compared to 85 per cent reported in 2010.

• There was a significant rise in average monthly income by over 51 per cent, after adjusting the inflation. 81 per cent of the customers were able to save money in contrast to 63 per cent in 2010.

• children of clients attended private schools went up from 28 per cent to 40 per cent

• Access to home toilet (84 per cent from 70 per cent), tap water (71 per cent from 54 per cent), LPG connection (71 per cent from 55 per cent), and PPI (Progress out of Poverty Index) score (70 from 57) have all showed positive impact in the lives of the clients.

Microfinance and Financial Inclusion 17

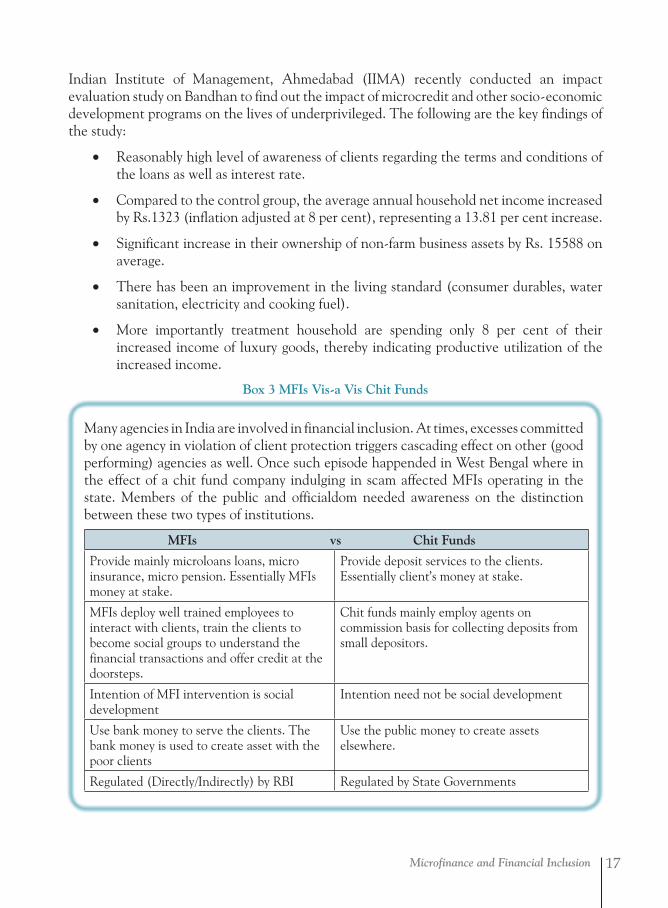

Indian Institute of Management, Ahmedabad (IIMA) recently conducted an impact evaluation study on Bandhan to find out the impact of microcredit and other socio-economic development programs on the lives of underprivileged. The following are the key findings of the study:

• Reasonably high level of awareness of clients regarding the terms and conditions of the loans as well as interest rate.

• Compared to the control group, the average annual household net income increased by Rs.1323 (inflation adjusted at 8 per cent), representing a 13.81 per cent increase.

• Significant increase in their ownership of non-farm business assets by Rs. 15588 on average.

• There has been an improvement in the living standard (consumer durables, water sanitation, electricity and cooking fuel).

• More importantly treatment household are spending only 8 per cent of their increased income of luxury goods, thereby indicating productive utilization of the increased income.

Box 3 MFIs Vis-a Vis Chit Funds

MFIs vs Chit Funds

Provide mainly microloans loans, micro insurance, micro pension. Essentially MFIs money at stake.

Provide deposit services to the clients. Essentially client’s money at stake.

MFIs deploy well trained employees to interact with clients, train the clients to become social groups to understand the financial transactions and offer credit at the doorsteps.

Chit funds mainly employ agents on commission basis for collecting deposits from small depositors.

Intention of MFI intervention is social development

Intention need not be social development

Use bank money to serve the clients. The bank money is used to create asset with the poor clients

Use the public money to create assets elsewhere.

Regulated (Directly/Indirectly) by RBI Regulated by State Governments

Many agencies in India are involved in financial inclusion. At times, excesses committed by one agency in violation of client protection triggers cascading effect on other (good performing) agencies as well. Once such episode happended in West Bengal where in the effect of a chit fund company indulging in scam affected MFIs operating in the state. Members of the public and officialdom needed awareness on the distinction between these two types of institutions.

The Bharat Microfinance Report 201318

Key Takeaways

Q Microfinance has been the key intervention in the financial inclusion space, though its role is yet to be fully appreciated. Self Help Bank Linkage programme purveys bank credit to the mass that do not have any access to banking service. Similarly, the MFIs use bank funds to offer credit to the same kind of unreached people in remote villages.

Q Ultimate objective of financial inclusion would be to make the bank funds/ services accessible to the mass. Addressing both supply side and demand side issues will pave for financial inclusion. SBLP and MFIs intervene in both the sides of financial inclusion continuum appropriately.

Q SBLP and MFIs will continue to perform this critical role till a sound alternative is evolved for financial inclusion unexplored thus far.

MFIs: Outreach and Loan Portfolio 19

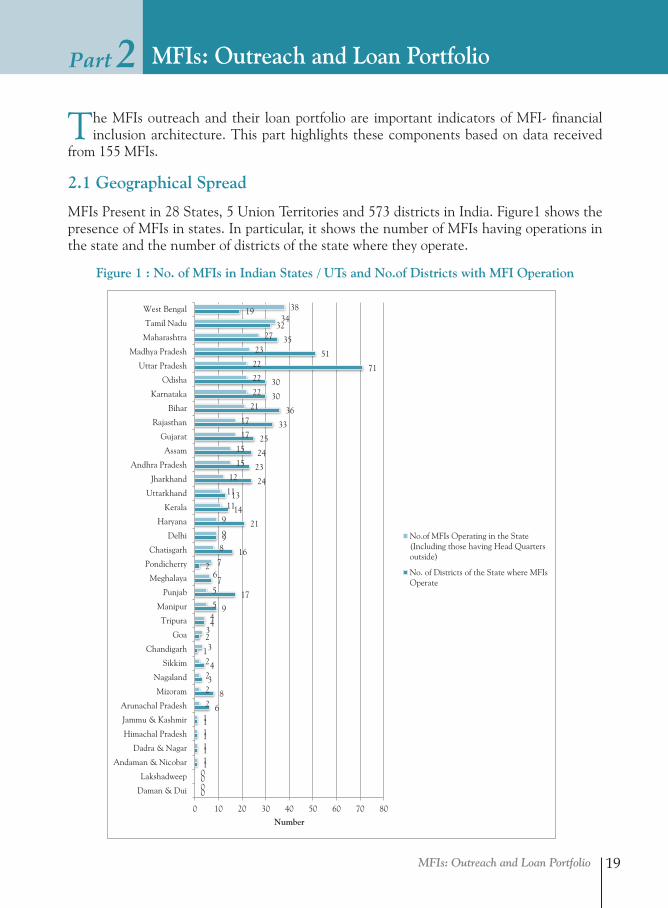

MFIs: Outreach and Loan PortfolioPart 2

The MFIs outreach and their loan portfolio are important indicators of MFI- financial inclusion architecture. This part highlights these components based on data received

from 155 MFIs.

2.1 Geographical Spread

MFIs Present in 28 States, 5 Union Territories and 573 districts in India. Figure1 shows the presence of MFIs in states. In particular, it shows the number of MFIs having operations in the state and the number of districts of the state where they operate.

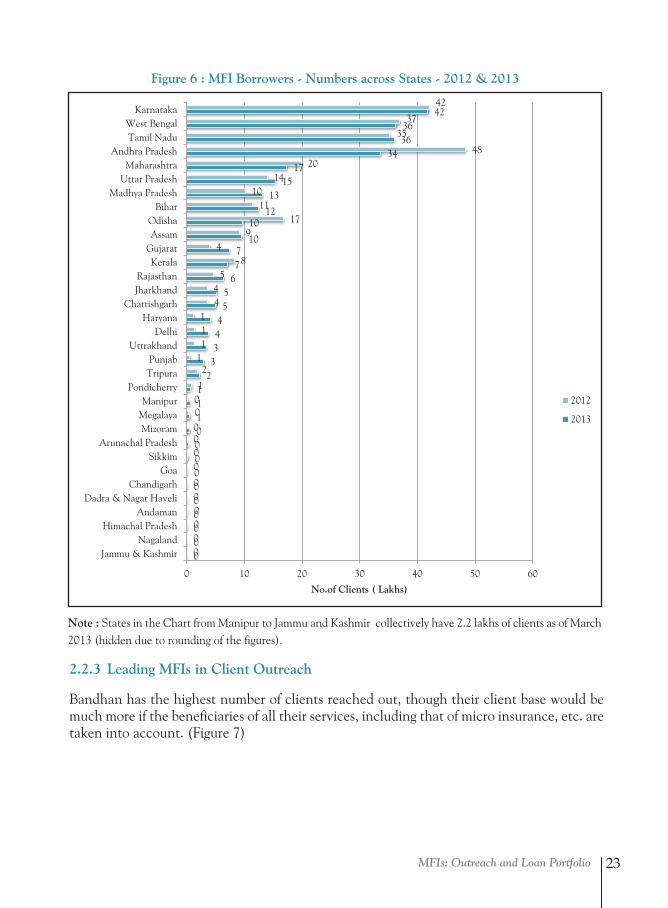

Figure 1 : No. of MFIs in Indian States / UTs and No.of Districts with MFI Operation

0

0

1

1

1

1

6

8

3

4

1

2

4

9

17

7

2

16

9

21

14