The Bharat Microfinance - Report 2016 - Moneymint

132

Supported by: NABARD TheBharatMicrofinance Report2016 TheBharatMicrofinance Report2016

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of The Bharat Microfinance - Report 2016 - Moneymint

Supported by:

NABARD

The�Bharat�Microfinance�Report�2016

The�Bharat�Microfinance�Report�2016

Mission of Sa-Dhan

“To build the field of community development finance in India, to help its members and associate institutions to better serve low income households, particularly women, in both rural and urban India, in their quest for establishing stable livelihoods and improving their quality of life”.

With best compliments from:

National Bank for Agriculture and Rural Development(Printing of this document is supported by NABARD)

Mission of NABARD

“Promotion of sustainable and equitable agriculture and rural develop-ment through effective credit support, related services, institution devel-opment and other innovative initiatives”.

A 1- 248, 3rd Floor, Safdarjung Enclave, New Delhi – 110029, India

Tel: + 91- 11-47174400, Fax: + 91-11-47174405E-mail: [email protected], [email protected]

The Bharat Microfinance Report 2016

© Copyright reserved Sa-Dhan2016

Developed & Published by:Sa-Dhan

A 1- 248, 3rd Floor, Safdarjung Enclave, New Delhi – 110029, India

Tel: + 91- 11-47174400, Fax: + 91-11-47174405E-mail: [email protected], [email protected]

Cover Design & Printed by:Anil

9810803375, 8860127811

Disclaimer:The views expressed in this publication do not necessarily reflect the opinions/views of any of the

insitutions referred to and they are not to be held responsible for the opinions/views in this report.

Preface

The Indian Microfinance Sector has witnessed a phenomenal growth over the past 17 years. The number of Institutions providing microfinance services has gone up from a few to several hundreds. The quantum

of credit made available to the poor and financially excluded clients has gone past `60,000 crore and number of clients benefitted is close to 40 million as of March 2016. The SHG bank linkage programme has equally grown to touch the lives of individuals through SHGs with an outstanding loan portfolio of `57,119 crores.

The Government of India and the Reserve Bank of India have created conducive policy and regulatory framework for Microfinance Institutions (MFIs) to operate in the country. This has provided necessary legitimacy and impetus to the sector. MFIs in general comply to the regulations, take care of client protection issues, adhere to the Industry Code of Conduct. These factors go a long way in infusing confidence among all the stakeholders.

In this context, there are three areas which continue to deserve special attention. One is the need for articulating the fact that microfinance is a strategic part of the financial inclusion agenda of the government and that of the central bank. The second is the criticality of re-demonstrating our collective intention to help the poor and the unbanked populace by way of having the right mission, social performance measures and client protection process. The third area is in projecting the fact that microfinance institutions are sustainable financial institutions and they continue to be the investible destination for bankers and investors.

In order to reemphasise these positions, the sector needs empirical data. This Bharat Microfinance Report has been designed to provide comprehensive information and newer perspectives on the above three areas. Primary data received from 166 MFIs who represent around 95 percent of the microfinance sector in India and analysis thereon form the basis for this report.

Sa-Dhan, as the leading association of community development finance institutions in India, has been publishing The Bharat Microfinance Report for the past thirteen years. This year 166 MFIs reported data, including 61 non-members of Sa-Dhan. We thank them for reposing confidence in us and valuing transparency through data reporting.

This year the substantial part of the work relating to the report has been shouldered by Mr. Ardhendu Nandi, right from data collection, consolidation, analysis to report writing in which he was ably supported by Ms. Shyamasree Nandan and Mr. P.M Kamalesh. Mr. Somesh Dayal provided a broad support to the report, especially in sourcing useful inputs.

Special thanks are due to Prime M2i Consulting Pvt. Ltd, CRIF Highmark, Bharat Financial Inclusion Limited, Grameen Financial Services Pvt. Ltd, Satin Creditcare Network Limited, ItzCash, MCID-NABARD and Greenlight Planet Inc, for inputs in bringing out this report.

We are grateful to overall patronage from NABARD for generously sponsoring the publication and dissemination of the report widely among all stakeholders. We are also thankful to SIDBI, World Bank Group (IFC), DFID, RBI and Government agencies for their support to the activities and initiatives of Sa-Dhan.

We hope this report would be extremely useful to you as a reference and data source. We welcome suggestions for further enhancing its coverage and utility.

P. SatishExecutive Director14 September, 2016

iii

The Bharat Microfinance Report 2016iv

Contents

Preface iii

List of Boxes vi

List of Figures vii

List of Tables ix

List of Abbreviations x

Glossary xiii

Executive Summary xv

Chapter 1: Inclusive Financial Sector: Progress with Continuity 1

1.1 Introduction 1

1.2 Priority Sector Lending Certificates (PSLCs) 2

1.3 Financial Inclusion Plan (FIP) 3

1.4 Committee on Medium-Term Path on Financial Inclusion 3

1.5 Roadmap for Banking Facilities 4

1.6 Financial Inclusion Advisory Committee (FIAC) 4

1.7 Mudra 4

1.8 Self Help Groups 4

1.9 Peer-to-Peer (P2P) Lending 5

1.10 MFIs as Channels for Govt. Programmes 5

Chapter 2: Outreach and Loan Portfolio 7

2.1 Geographical Spread of Microfinance 7

2.2 Branch Network 9

2.3 Client Outreach 14

2.3.1 Regional Outreach of MFIs 14

2.3.2 State-wise Client Outreach 15

2.3.3 Rural – Urban Share of MFIs Borrowers 16

2.3.4 Outreach to Special Segment of Borrowers (Women, SC/ST, and Minorities) 16

2.3.5 Leading MFIs in Client Outreach 17

2.4 Loan Portfolio of MFIs 18

2.4.1 Rural – Urban Share of Gross Loan Portfolio 20

2.4.2 Regional Spread of Loan Portfolio 20

2.4.3 Loan Portfolio Across States 21

2.4.4 Managed Portfolio 22

2.4.5 Business Correspondent (BC) Portfolio 23

2.4.6 Loan Outstanding per Borrower 24

2.4.7 Trends in Outreach and Outstanding Portfolio 24

2.5 Loan Disbursement 25

2.5.1 Loan Disbursement - States/UTs and Regional Pattern 26

2.5.2 Rural – Urban Share of No. of Loans Disbursed 27

2.5.3 Loan Amount Disbursed 28

2.5.4 Purpose of Loan 28

2.5.4.1 Income Generation Loans 29

2.5.4.2 Non- Income Generation Loans 29

v

Chapter 3: Operational and Financial Aspects 31

Section I: Workforce, Productivity and Portfolio Quality 31 3.1.1 Workforce in MFIs 31 3.1.2 Staff Productivity 32 3.1.3 Portfolio Quality 34

Section II: Cost & Revenue 35 3.2.1 Expenditure Analysis 35 3.2.2 Income Analysis 38 3.2.3 Margin 40 3.2.4 Yield, Cost and Margin: Performance Across MFI size 40

Section III: Surplus, Sufficiency and Profitability 41 3.3.1 Surplus 41 3.3.2 Operational Self-Sufficiency (OSS) 41 3.3.3 Profitability Ratios 42

Section IV: Balance Sheet Distribution and Capital Structure 44 3.4.1 MFI Assets 44 3.4.2 Pattern of Portfolio Financing 45 3.4.2.i Net Owned Fund (NOF) 45 3.4.2.ii Debt Financing 46 3.4.3 Capital (Net Owned Fund) to Total Asset Ratio 57 3.4.4 Leverage / Debt – Equity Ratio 58

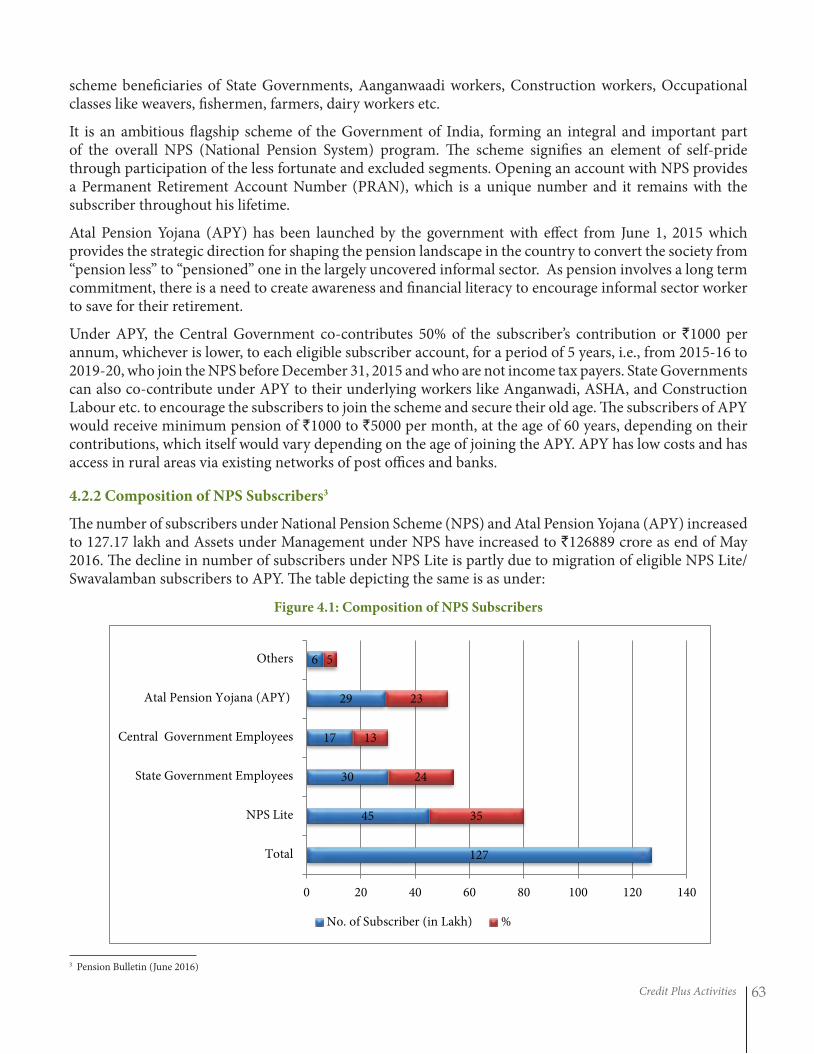

Chapter 4: Credit Plus Activities 59 4.1 Micro Insurance 59 4.1.1 MFIs Acting as Micro Insurance Agents 60 4.2 Micro Pension 62 4.2.1 NPS: Swavalamban 62 4.2.2 Composition of NPS Subscribers 63 4.2.3 Pradhan Mantri Bima Yojana 64 4.3 Other Development Services 65 4.4 Jagruti – An Initiative to Intensify client engagement and reduce client attrition. 70

Chapter 5: SHG Movement and its Role in Financial Inclusion 765.1 Self Help Group Bank Linkage Programme (SBLP) 76

5.1.1 Savings Performance of SBLP 76

5.1.2 No of SHGs Availing Bank Loan during 2015-16 78

5.1.3 Loan Outstanding with SHGs 81

5.2 Aajeevika – National Rural Livelihoods Mission (NRLM) 84

Chapter 6: BC Model and Technology 866.1 Business Correspondent Model 866.2 Reaching doorsteps through Business Correspondents 866.3 Progress and Challenges 876.4 MFIs as Business Correspondents 896.5 Use of Technology 92

Annexures 95

State wise Presence of Different MFIs 95

District wise No. of MFIs in Operation. 98

Distribution of MFIs which Contributed data to this Report 104

Profile of MFIs which Contributed Data to this Report 106

The Bharat Microfinance Report 2016

List of Boxes

Chapter1 Inclusive Financial Sector: Progress with Continuity

Box 1.1 Core Values of Microfinance 6

Chapter 2 Outreach and Loan Portfolio

Box 2.1 Responsible Finance - an Essential Component of Microfinance Industry 11

Chapter 4 Credit Plus Activities

Box 4.1 Microfinance and Affordable Clean Energy Access: 72 A Path to achieve Sustainable Development Goals

Box 4.2 Pradhan Mantri Mudra Yojana 73

Box 4.3 Grievance Redressal Mechanism 74

Chapter 6 BC Model And Technology

Box 6.1 Peer-to-Peer Lending 88

Box 6.2 Cashless Project - Journey so far 93

vi

List of Figures

Chapter 2 Outreach and Loan Portfolio

Figure 2.1 Top 10 MFIs Operating in Number of Indian States/Union Territories 8

Figure 2.2 Top 10 MFIs Operating in Number of Indian Districts 8

Figure 2.3 MFI Branch Network – Yearly Trend and Category –wise Breakup 10

Figure 2.4 Top 10 MFIs in Terms of Branch Network 10

Figure 2.5 Outreach to Borrowers: Yearly Trend and Category – wise Breakup for 2015-16 14

Figure 2.6 Regional break up of Client Outreach 14

Figure 2.7 Trends in Rural – Urban Share of MFI Borrowers 17

Figure 2.8 List of Top 10 MFIs with Client Outreach as of March 2016 17

Figure 2.9 Gross Loan Portfolio – Yearly Trend and Category–wise Breakup for 2015-16 19

Figure 2.10 Percentage of Rural – Urban Share of Gross Loan Portfolio 20

Figure 2.11 Region wise Loan Portfolio 20

Figure 2.12 Managed Loan Portfolio – Yearly Trend and Category–wise Breakup for 2015-16 23

Figure 2.13 BC Loan Portfolio and Category–wise Breakup for 2015-16 23

Figure 2.14 Loan Outstanding per Borrower yearly trend and across regions for the FY 2015-16 24

Figure 2.15 Growth Fluctuations in Outreach and Loan Outstanding over the Years 24

Figure 2.16 Loan Disbursement over the years 25

Figure 2.17 Regional Pattern of Loan Disbursement 25

Figure 2.18 Top 10 MFIs in Loan Disbursement during 2015-16 27

Figure 2.19 Percentage of Rural – Urban Share of No. of Loans Disbursed 27

Figure 2.20 Share of income generation loans and non income generation loans 28

Figure 2.21 Share of MFIs Income Generation Loans under Different Sub-sectors as of March 2016 29

Figure 2.22 Share of MFIs Non-Income Generation Loans under Different Sub-sectors as of March 2016 29

Chapter 3.1 Workforce, Productivity And Portfolio Quality

Figure 3.1.1 No. of MFI Staff - Yearly Trend and MFI-Category-wise Break-up 31

Figure 3.1.2 MFI Field Staff vs Other Staff Distribution – 2015 & 2016 31

Figure 3.1.3 New Staff Recruited by the MFIs over the years 32

Figure 3.1.4 Distribution of MFIs based on clients served per Staff & per Credit Officer 33

Figure 3.1.5 ABCO Across MFIs 33

Figure 3.1.6 Distribution of MFIs Based on Loan Portfolio per Credit Officer 34

Figure 3.1.7 MFI Loan Portfolio at Risk (PAR) 34

Figure 3.1.8 Distribution of MFIs Based on PAR 34

Chapter 3.2 Cost and Revenue

Figure 3.2.1 Break up of Expenses by Indian MFIs 35

Figure 3.2.2 Break up of Expenses by Indian MFIs based on Portfolio size 36

Figure 3.2.3 Operating Expenditure Ratio across MFIs 36

Figure 3.2.4 Finance Cost Ratio Across MFI Categories 37

Figure 3.2.5 Trends of OER and FCR 38

Figure 3.2.6 Break-up of Income 38

Figure 3.2.7 Yield Trend of MFIs 39

Figure 3.2.8 Yield on Portfolio across MFIs 39

Figure 3.2.9 Yield, Cost and Margin of MFIs –size wise 40

vii

The Bharat Microfinance Report 2016

Chapter 3.3 Surplus, Sufficiency and Profitability

Figure 3.3.1 OSS Across MFIs 41

Figure 3.3.2 OSS based on average loan size 42

Figure 3.3.3 OSS based on yield category 42

Figure 3.3.4 OSS based on OER of MFIs 42

Figure 3.3.5 Return on Asset (ROA) and Return on Equity (ROE) across MFI types 43

Figure 3.3.6 Return on Asset (ROA) and Return on Equity (ROE) of MFI-Size wise 43

Chapter 3.4 Balance Sheet Distribution and Capital Structure

Figure 3.4.1 MFI Total Assets- Yearly Trend 44

Figure 3.4.2 Composition of Total Assets of MFIs 44

Figure 3.4.3 MFI Equity Outstanding - Yearly Trend and MFI- Category- wise Break-up of 2016 Figure 45

Figure 3.4.4 Fresh Equity Raised by MFIs and MFI-Category-wise Break-up 46

Figure 3.4.5 Top 10 MFIs in terms of Equity Raised 46

Figure 3.4.6 Sources of funding based on types of instruments 47

Figure 3.4.7 Sources of funding based on Institution types 47

Figure 3.4.8 Outstanding Borrowing – Yearly Trend and MFI-Category wise Break-up of 2016 Figure 48

Figure 3.4.9 Fund Received during the year – Yearly Trend and MFI-Category wise Break-up of 2016 Figure 48

Figure 3.4.10 Source wise Share of Loans lent among Different Legal Forms of MFIs during 2015-16 49

Figure 3.4.11 Capital to Total Asset Ratio 58

Figure 3.4.12 Debt - Equity Ratio Trend and Break–up of 2016 Figure Across MFI –Categories 58

Chapter 4 Credit Plus Activities

Figure 4.1 Composition of NPS Subscribers 63

Figure 4.2 Most Recalled Theme 70

Figure 4.3 Mode of Delivery 71

Chapter 5 SHG Movement and its Role in Financial Inclusion

Figure 5.1 Historical Trend in Credit Linkage and Bank Loan Disbursed 76

Figure 5.2 All India Trend in SHG Savings Amount Held in the Indian Banking System 77

Figure 5.3 All India Trend in Average per SHG Savings Held in the Banking System 77

Figure 5.4 Savings of SHGs with Banks as on 31 March 2016 78

Figure 5.5 No. of SHGs availed Bank Loan during 2015-16 from the Banking System 78

Figure 5.6 Top 10 Banks in terms of Savings 79

Figure 5.7 All India Trend in Bank Loan Amount Disbursed to SHGs 79

Figure 5.8 Agency-wise loan disbursement – No. of SHGs and Loan Amount disbursed 80

Figure 5.9 Top 10 Banks in terms of Disbursement 80

Figure 5.10 All India Trend in Average Bank Loan Amount Disbursed per SHG 81

Figure 5.11 All India Trend in SHG Loan Outstanding in the Books of Banking System 81

Figure 5.12 All India Trend in Average per SHG Loan Outstanding in the Banking System 82

Figure 5.13 Agency-wise Bank Loan outstanding against SHGs as on 31 March 2016 82

Figure 5.14 Non Performing Asset Per Cent of SHG Loans with Banks 83

Figure 5.15 NPAs of Banks against SHGs Loan Outstanding 83

viii

List of Tables

Chapter 2 Outreach and Loan Portfolio

Table 2.1 No. of MFIs in Indian States/UTs 7

Table 2.2 No. of MFIs in Indian States/UTs and No. of Districts with MFI Operations 9

Table 2.3 Outreach (in lakh) of MFIs across States/UTs – 2015 & 2016 (decreasing order) 15

Table 2.4 Composition of Borrowers – Category wise 17

Table 2.5 List of Top MFIs with Loan Portfolio as of March 2016 19

Table 2.6 Loan Portfolio Outstanding across States/UTs – 2015 & 2016 (decreasing order) 21

Table 2.7 Loan Disbursement across States/UTs – 2015 & 2016 (decreasing order) 26

Table 2.8 Amount disbursed during the year 2015 and 2016 28

Chapter 3.1 Workforce, Productivity And Portfolio Quality

Table 3.1.1 Yearly trend of Total Staff vs Women Staff 32

Table 3.1.2 Staff Turn-over among MFIs during 2015-16 32

Chapter 3.4 Balance Sheet Distribution and Capital Structure

Table 3.4.1 List of lenders reported among Top 10 Lenders of the individual reporting MFIs 49

(in terms of Outstanding as of March 2016)

Table 3.4.2 MFI wise Loan Outstanding (based top 10 Lenders data) to Lenders 51

Table 3.4.3 Lender wise Loan Outstanding (based top 10 Lenders data) to MFIs 54

Chapter 4 Credit Plus Activities

Table 4.1 MFIs involved in Micro Insurance- Health 61

Table 4.2 MFIs involved in Micro Insurance - Non-health 62

Table 4.3 MFIs involved in Micro Pension 65

Table 4.4 Development Services of Reporting MFIs 65

Table 4.5 MFIs and Livelihoods Intervention 66

Table 4.6 MFIs and General Education Intervention 67

Table 4.7 MFIs and Preventive Healthcare Initiatives 68

Chapter 5 SHG Movement And Its Role In Financial Inclusion

Table 5.1 Present Status of NRLM 85

Chapter 6 BC Model And Technology

Table 6.1 Financial Inclusion Plan-Summary Progress of all Banks including RRBs 87

Table 6.2 MFIs as Banking Correspondents – No. of saving clients and amount saved 89

Table 6.3 MFIs as Banking Correspondents – No. of Loan clients, amount disbursed and amount outstanding 90

ix

The Bharat Microfinance Report 2016

List of Abbreviations

x

1 ABCO Active Borrowers per Credit Officer

2 APY Atal Pension Yojana

3 ATM Automated Teller Machine

4 AUM Assets Under Management

5 BC Business Correspondent

6 BCNM Business Correspondent Network Manager

7 BF Business Facilitator

8 BPL Below Poverty Line

9 BSBDA Basic Savings Bank Deposit Account

10 CAB College of Agricultural Banking

11 CAR Capital Adequacy Ratio

12 CBEO Community Based Economic Organization

13 CBS Core Banking Solution

14 CDR Corporate Debt Restructuring

15 CEO Chief Executive Officer

16 CGT Compulsory Group Training

17 CIB Credit Information Bureau

18 CIF Community Investment Fund

19 CmF Centre for Micro Finance

20 CO Credit Officer

21 CoC Code of Conduct

22 COCA Code of Conduct Assessment

23 CPPs Client Protection Principles

24 CRM Customer Relationship Management

25 CRR Cash Reserve Ratio

26 CSO Customer Service Officer

27 CSP Customer Service Point

28 DFS Department of Financial Services

29 DNBS Department of Non-Banking Supervision

30 DPD Days Past Due

31 DRDA District Rural Development Agency

32 DWCD Department of Women and Child Development

33 ECB External Commercial Borrowing

34 FCR Finance Cost Ratio

35 FDI Foreign Direct Investment

36 FER Finance Expense Ratio

37 FI Financial Institution

38 FIAC Financial Inclusion Advisory Committee

39 FIIs Foreign Institutional Investors

40 FIP Financial Inclusion Plan

41 FLCs Financial Literacy Centre

42 GCC General Credit Card

43 GIC General Insurance Corporation of India

xi

44 GLP Gross Loan Portfolio

45 GoI Government of India

46 GPRS General Packet Radio Service

47 GRT Group Recognition Test

48 HTTP Hyper Text Transfer Protocol

49 ICIB Inclusive Credit Information Bureau

50 ICT Information and Communication Technology

51 IMPS Immediate Payment Service

52 IPOs Initial Public Offerings

53 IRDA Insurance Regulatory Development Authority

54 IVR Interactive Voice Response

55 JLG Joint Liability Group

56 KCC Kisan Credit Card

57 KYC Know Your Customer

58 LAB Local Area Bank

59 MFDRC Micro Finance and Development Regulatory Council

60 MFIs Microfinance Institutions

61 MHL Mobile High-Definition Link

62 MIS Management Information System

63 MoA Memorandum of Association

64 MoF Ministry of Finance

65 MoRD Ministry of Rural Development

66 MoU Memorandum of Understanding

67 MSME Ministry of Micro Small & Medium Enterprises

68 MUDRA Micro Units Development & Refinance Agency

69 NABARD National Bank for Agriculture and Rural Development

70 NAMCABs National Mission for Capacity Building of Bankers

71 NBFC Non-Banking Finance Company

72 NBFC -SI -ND Systemically Important Non-Deposit taking NBFCs

73 NBFC-ND Non Deposit taking NBFCs

74 NCD Non-Convertible Debenture

75 NGO Non-Governmental Organization

76 NIM Net Interest Margin

77 NoF Net Owned Fund

78 NPA Non Performing Asset

79 NPCI National Payment Corporation of India

80 NPS National Pension System

81 NRLM National Rural Livelihood Mission

82 NULM National Urban Livelihood Mission

83 OD Overdraft

84 OER Operating Expense Ratio

85 OSS Operational Self Sufficiency

86 P2P Peer-to-Peer

87 PAR Portfolio at Risk

The Bharat Microfinance Report 2016

88 PFRDA Pension Fund Regulatory and Development Authority

89 PLF Primary Level Federation

90 PMDJY Pardhan Mantri Jan Dhan Yojana

91 PMMY Pradhan Mantri MUDRA Yojana

92 POS Point of Sale

93 PSIG Poorest State Inclusive Growth

94 PSL Priority Sector Lending

95 PSLCs Priority Sector Lending Certificates

96 PSU Public Sector Unit

97 RBI Reserve Bank of India

98 RF Revolving Fund

99 RFF Responsible Finance Forum

100 RFIP Rural Financial Institutions Programme

101 RIDF Rural Infrastructure Development Fund

102 RMK Rashtriya Mahila Kosh

103 RoA Return on Asset

104 RoE Return on Equity

105 RRBs Regional Rural Banks

106 RSETIs Rural Self Employment Training Institutes

107 SBLP Self-Help Group Bank Linkage Programme

108 SC/ST Scheduled Caste/Scheduled Tribe

109 SERP Society for Elimination of Rural Poverty

110 SFB Small Finance Bank

111 SHGs Self-Help Groups

112 SHPI Self Help Promoting Institute

113 SIDBI Small Industries Development Bank of India

114 SLBCs State Level Bankers’ Committees

115 SLR Statutory Liquidity Ratio

116 SMS Short Message Service

117 SPM Social Performance Management

118 SPOC Single Point Of Contact

119 SRO Self-Regulatory Organisation

120 TAT Turn Around Time

121 UCBs Urban Cooperative Banks

122 UT Union Territory

123 Y-O-Y Year On Year

xii

Glossary

ABCO

ABCO is an acronym for Average Borrower per Credit Officer, a measure of client-staff ratio. It is also known as Case Load

Average Loan Size

Average Loan size represents the client-per capita loan amount. It is calculated as: The Loan portfolio divided by the number of clients of an MFI.

Borrowing Cost

The total charge for taking on a debt obligation that can involve interest payments and other financing fees.

Capital Adequacy

Capital Adequacy is the means of measuring the solvency level of MFIs which is an important indicator of risk bearing ability of the entities. It is the proportion of the capital/own fund held by an MFI against its total asset

Capital to Total Assets

Ratio of net worth to total assets

Debt-Equity Ratio

Debt-Equity Ratio is the proportion of total debt borrowed to the total equity held at a given point of time.

Debt Funding

Debt Funding refers to the percentage of loan portfolio funded by outside borrowings

External Cost

External Cost here refers to Finance cost which is determined by the lending rate of banks and hence is beyond the control of MFIs

Finance Cost

Finance Cost here refers to the interest and other expenses incurred on average bank loan outstanding in the books of MFIs. This does not include notional cost of utilizing the equity fund.

Financial Inclusion

Financial Inclusion is the delivery of financial services at affordable costs to sections of disadvantaged and low income segments of society.

Margin

Margin refers to the difference between the finance cost on portfolio and the total yield on portfolio. This term is anal-ogous to the concept of Net Interest Margin (NIM) widely used in banking parlance. Margin Cap refers to the ceiling of Margin of 12 percent fixed by RBI.

Managed Loan Portfolio

Managed Loan Portfolio is the loan asset originated by MFIs and later sold to banks for getting liquidity. The MFIs continue to manage it i.e. collection of repayment on behalf of the banks which purchased the portfolio.

xiii

The Bharat Microfinance Report 2016

Non Performing Assets (NPA)

A debt obligation where the borrower has not paid any previously agreed upon interest and principal repayments to the designated lender for an extended period of time. The NPA is therefore not yielding any income to the lender in the form of principal and interest payments.

Operating Expense Ratio (OER)

Ratio of staff, travel, administration costs, other overheads and depreciation charges of the MFIs (non-financial costs) to the average loan portfolio during a year

Operating Self Sufficiency (OSS)

Operating Self Sufficiency (OSS) shows the sufficiency of income (operating income and investment income) earned by MFIs to cover the cost like operating cost, loan loss provision and finance cost, incurred for conducting the operations.

Portfolio Quality

Amount of risk of default in the loan portfolio. A high quality portfolio contains a lower amount of risk. Portfolio quality changes continually as loans are disbursed, payments are made, and payments become due.

Portfolio at Risk (PAR)

PAR indicates the proportion of outstanding amounts of all loan accounts having past due/arrears to the total out-standing loan. In general, PAR 60, i.e., the portfolio / part of the portfolio remaining unpaid 60 days and beyond crossing the due date, would be used as a measure to assess the portfolio quality.

Qualifying Assets

Qualifying Assets are loan portfolios created by MFIs adhering to certain conditions to make the MFIs eligible to be called as MFIs and to raise loans from banks under Priority Sector Advances Scheme ( as per recent RBI norms).

Return on Asset (RoA)

Return on Asset (RoA) is the universally accepted profitability measure which, in essence, is the percentage net in-come earned out of total average asset deployed by MFIs during a given period, say a year.

Return on Equity (RoE)

Return on Equity (RoE) is the net income earned out of average equity of MFIs held by MFIs during the given period.

Self Help Groups (SHGs)

SHGs refer to groups of 10-20 women coming together to form a semi formal community based institution to meet their common financial and social needs.

SHG Bank Linkage Programme (SBLP)

SHGs are linked to mainstream banks for depositing surplus savings of the SHGs and to obtain loans. It is considered to be an effective strategy to ensure financial inclusion.

Surplus

Surplus is Yield minus Total cost

Yield on Portfolio

Yield represents total income from microcredit operation-Interest income, processing fee/ service charge – earned out of average loan portfolio outstanding. It does not, include investment income. It is a good proxy / surrogate for loan interest rate.

xiv

Executive Summary

Context

For the microfinance sector in India the year 2015 -16 was one of steady growth and stability, though

some islands of heavy growth should be a matter of concern. RBI’s continuing interest in the sector is

reflected in its engagement with both the SROs of the Microfinance sector-Sa-Dhan and MFIN, and coming

out with modifications and improvements in guidelines whenever required.

At the policy level, MUDRA’s progress reflects the depth of financing by the MFIs. The Pradhan Mantri Bima

Yojana (PMBY) and the Atal Pension Yojana provide additional financial instruments for MFIs to offer to

their clientele. Bandhan Bank which rose from the microfinance sector completed one year of its service,

Capital Small Finance Bank was the first SFB to start off its operations and other Small Finance Banks and

Payment Banks will be in place by the close of the financial year. Further, RBI is coming up with guidelines

for Peer To Peer lending. These are game changers for the banking and financial sector landscape of the

country in general and for financial inclusion scenario in particular.

Objective

This report is an attempt to collect primary data on MFI client outreach, their loan portfolio and other

financials of MFIs in India that includes both members as well as non-members of Sa-Dhan.

The report purports to provide primary data based analytical information to a wide range of stakeholders

such as the Government, policymakers, regulators, banks, investors, researchers, media, MFIs and others,

helping them to understand the current status and the underlying trends in the sector in order to take

appropriate decisions/actions that are critical for the development of the industry.

Methodology

The contributing MFIs have voluntarily provided their data and detailed information as sought through a

data acquisition sheet consisting of their financial outreach, geographic spread, credit plus and developmental

activities etc. For this report we have compiled data from MFIs representing all legal forms (Societies, Trusts,

Sec-8 Companies, NBFC-MFIs, Cooperatives) the data has been collated, validated, and analysed for peer

groups.

The project team rigorously scrutinized the self reported data, validated it from the MFI’s financial statements,

and reconciled from other secondary sources. The validity of the findings however, is subject to the accuracy

of the self-reported data, though reconciliation techniques used would have minimized such errors.

The analysis of the report was undertaken on the basis of a predesigned framework and the findings have

been improved to the extent possible though advisory inputs from microfinance experts and practitioners.

The chapters pertaining to SHGs and the BC model, while culled out from secondary sources, have been

further enhanced by inputs from the experts in the field.

The Report Coverage

The report is divided into two parts. Part one covers the MFI sector and is based on primary data, whereas

Part two covers the SHG sector and the BC model and is mainly culled out from secondary sources of

information.

xv

The Bharat Microfinance Report 2016

Part 1 is further divided into four chapters. Chapter 1 represents an overview of the microfinance sector

within the larger ambit of financial inclusion, Chapter 2 deals with growth and outreach of MFIs, Chapter

3 deals with operational and financial aspects of credit services, while Chapter 4 deals with credit plus

activities. Chapter 3 is further subdivided into 4 sections. Section 1 dwells upon the workforce, productivity

and portfolio quality. Section 2 represents the cost and revenue aspects of the MFIs. Section-3 represents

surplus, sufficiency and profitability of the MFIs, while Section 4 deals with capital structure and balance

sheet distribution.

In the Part 2 of the report, Chapter 5 deals with the SHG section of microfinance and Chapter 6 presents an

overview of the BC model and other technology led approaches of financial inclusion.

Highlights of the Report

Growth and Outreach

MFIs currently operate in 29 States, 4 Union Territories and 588 districts in India. The reported 166 MFIs

with a branch network of 12,221 employees have reached out to an all time high of 39 million clients with

an outstanding loan portfolio of `63,853 crore. This includes a managed portfolio of `16,914 crore. Out of

managed portfolio, BC portfolio accounts for `7,984 crore. The average loan outstanding per borrower

stood at `11,425 and 94% of loans were used for income generation purposes.

Outreach grew by 8% and loan outstanding grew by 31% over the previous year. The Southern region

continues to have the highest share of both outreach and loans outstanding, followed by East. However

growth rates are higher in the Northeastern and Central regions. Outreach proportion of urban clientele

has decreased marginally as against the rural population. The proportion of urban clientele which was 67%

in 2014-15 decreased to 62% in 2015-16. Women borrowers constitute 97% of the total clientele of MFIs,

SC/ST borrowers constitute 30% and minorities 27%.

Of the total, NBFC-MFIs contribute to 85% of clients outreach and 88% of outstanding portfolio, while NGO

MFIs contribute to the remaining. MFIs with portfolio size of more than `500 crore contribute significantly

to the total outreach (85%) and loan outstanding (88%) of the sector.

Operational and Financial Aspects

MFI sector employs 1,03,415 personnel, out of which 15% are women, and 62% are field staff. An active

borrower per credit officer (ABCO) is 440, which is higher than the previous year indicating higher focus

on client services without much of staff growth.

Financial expense is the major expense (53%) incurred by MFIs. Personnel expense and other administrative

expenses contribute 24% and 23% respectively. Median OER (Operating Expense Ratio) and FCR (Finance

Cost Ratio) remained at 10.2% and 13.83% respectively. It is seen that the OER comes down with scale of

operation. MFIs, with portfolio of more than `500 crore have a median OER of 7.5% and FCR of 13.9%.

The Yield of the sector for the year was 21%, which is the highest for the Section 8 Companies and

Cooperatives (24%) and lowest for the Society/Trust (20%). The Margin for different types of institutions

was in the range of 9 -12%. NBFC-MFIs maintained a median margin of 10%. Median OSS (Operational Self

Sufficiency) is 113%. Approximately 16% of MFIs have OSS less than 100%. This includes 4% of the NBFC-

MFIs on account of AP portfolio and 12% not for profit MFIs. Generally, the OSS improves with the average

loan size and yield of the institution.

xvi

Median ROA and ROE for the sector remained at 2.2% and 11.6% respectively. The returns are generally

higher for not for profit MFIs and very large sized MFIs.

The CAR (Capital Adequacy Ratio) for all types of MFIs remained above the desirable level of 15%. NBFC-

MFIs have CAR of 20.1%. Leveraging of the sector was 3.2. The sector received a sum of `39,331 crore,

which includes a portfolio sale of `8,834 crore. Total outstanding borrowing of MFIs stood at `44,822 crore,

with a substantial share of this derived by NBFC-MFIs (97%) especially from the very large MFIs (87%).

Self-Help Groups and the BC model

Number of SHGs linked to credit and bank loan amount to SHGs has witnessed an increasing trend after

2010-11. The number of saving linked SHGs has also n increased during the year.; till date, 103 million

families have been covered under the SBLP program with a total number of 79.03 lakh SHGs with a saving

amount of `13,691 crores. A total of 46 lakh SHGs have a gross loan outstanding of `57,119 crores.

The amount of savings and the average per SHG savings (`14,662) held in the banking system are both

increasing since 2011-12. Average loan disbursed per SHG for 2015-16 is reported at `203,526, whereas

average loan outstanding per SHG stood at `122,258

The aggregate NPA of SHG loans remain a concern though it has declined marginally by 0.59% from 7.4%

in 2014-15 to 6.4% in 2015-16. Quality of SHGs, their performance has emerged as one of the major issues

affecting the movement.

Also the fact that NRLM will push for improvement in the SHG bank linkage with better monitoring, lower

rates of interest and a sharper focus on livelihood generation, would give a greater fillip to the growth of

SHG programme.

MFIs are finding the BC model increasingly attractive to carry out their activities on the credit side and to

spread it to deposit taking activities 51MFIs had an exposure to a BC loan portfolio of ̀ 7,191 crores through

linkage to 25 banks. Apart from this 13 MFIs were undertaking deposit related activities for 13 banks. The

deposit portfolio of BCs amounted to `871 crores.

xvii

The Bharat Microfinance Report 2016

Indicators: MFI Model 2016 2015 Change

Client Outreach 399 lakh 371 lakh

Women Clients 97% 97% No Change

SC/ST Clients 30% 28%

Other Minorities 27% 18%

Rural Clients 38% 33%

Gross Outstanding Portfolio `63853 Cr. `48882 Cr

Own Portfolio `46939 Cr. `39028 Cr

Managed Portfolio `16914 Cr. `9854 Cr

Avg. Loan per Borrower `11425 `13162

Income Generation Loan 94% 80%

Female Staff in MFIs 15% 16%

ABCO 440 419

OER 10.22% 11.45%

FCR 13.3% 12.42%

Yield 21% 24%

Margin 10.00% 10.20%

OSS 113% 113% No Change

ROA 2.2% 1.73%

ROE 11.6% 8.19%

CAR 19.39% 19.10%

Leverage 3.2 2.9

Fund Flow (Outstanding) `44822 Cr. `40802 Cr

Equity Outstanding `4509 Cr. `4195 Cr

NPA 0.15% 0.21%

SHG Model

Total No of SHGs Linked 79.03 lakh 77.12 lakh

No. of Families Reached 103 million 101 million

Total Savings of SHGs `13691 Cr `11307 Cr

Total No. of SHGs Credit Linkage 18.32 lakh 16.26 lakh

Gross Loan Outstanding `57119 Cr `51721 Cr

Total Loan Disbursed `37286 Cr `30334 Cr

Avg. Loan Disbursed per SHG `203526 `186556

Avg. Loan Outstanding per SHG `122258 `115759

NPA 6.45% 7.40%

Performance Highlights: A Snapshot

xviii

Inclusive Financial Sector: Progress with Continuity 1

Inclusive Financial Sector: Progress with ContinuityChapter 1

1.1 Introduction

Developments in the year give us the confidence to claim that we are progressing well on the path to achieving universal financial inclusion. The government, regulators and financial markets have shown

immense faith in the model of financial inclusion which we have been pursuing. Provisional licenses provided to the Small Finance Banks and successful Initial Public Offerings (IPOs) of Ujjivan and Equitas are a testimony to that. The MFIs which had obtained provisional licenses are well on their course to establish Small Finance Banks and are expected to overcome their limitations of currently being able to offer only a limited set of products to their clients. Bandhan Bank which just celebrated the first anniversary of its establishment is already providing a gamut of services and experience to its customers, majority of whom are microfinance clients.

MFIs are beginning to enjoy benefits of scale and there is evidence that they are passing on this benefit to clients in terms of reduction in interest rates. In fact, the top 10 NBFC-MFIs contributing 80% of the sector’s Gross Loan Portfolio or over `40,000 crores have a weighted average interest rate of 23.13%, far below the 26% max cap under PSL guidelines. Sa-Dhan data shows that over 36 NBFC-MFI members have reduced rates significantly in the last financial year itself.

There are also efforts to reduce cash transactions to reduce risks and increase efficiency. Advances in the adoption of technology coupled with the banks accounts opened under the Prime Minister Jan Dhan Yojana (PMJDY) have certainly helped in doing this.

1.1.1 Credit History of Clients

Building a credit history for the microfinance clients goes a long way in achieving universal financial inclusion. Directions from the RBI and industry’s code of conduct require all the MFIs to share their data to the credit bureaus. Enhanced penetration of Aadhaar is helping increase accuracy of data obtained from Credit Bureaus and improving credit appraisal. Recent directions from the Reserve Bank of India (RBI) to share details of individuals borrowings from the SHGs to the Credit Bureaus is expected to further enhance their utility and effectiveness.

1.1.2 Revised Code of Conduct

This year the revised Code Conduct for sector which is forward looking was adopted despite some voices in favour of dilution of some of the provisions. MFIs have taken steps to implement this revised code of conduct in letter and spirit. Reports from our field visits suggest that MFIs are disclosing interest rates and other terms and conditions to the borrowers in clear terms. They have also set up effective grievance redressal mechanisms.

1.1.3 Risk Management Issues

Reports from Sa-Dhan’s field visits also point out to several risks which the MFIs and their clients may be facing. There is evidence of pockets with concentration of several MFIs in a limited geographical area which has the potential to lead to over-indebtedness and other undesirable practices. There is also evidence of some unauthorized agents acting on behalf of the MFIs and unscrupulous organisations posing as MFIs. In a rush to grow, the MFIs should not overlook the importance of having good internal controls and training their field staff.

The Bharat Microfinance Report 20162

1.1.4 Product Development

Product development is another area in which the MFIs need to invest more. Much of the portfolio growth so far has come from the standard income generation loans. MFIs need to be cognizant of the fact that clients need credit for various purposes including water and sanitation, housing and education. Limited experience of various MFIs in these needs to be documented and shared. There is also a greater need for MFIs to expand their portfolio to credit plus products like microinsurance and micropensions.

A large numbers of MFIs have been providing micro insurance products and micropensions. As per the self-reported data, 15 MFIs have reached to 3.66 lakh clients for health products, 39 MFIs have reached to 55.38 lakh clients for non-health products and 11 MFIs have been providing micropensions services to 18.59 lakhs clients.

1.2PrioritySectorLendingCertificates(PSLCs)In the meanwhile RBI has taken several steps to ease the process of financial inclusion. One of these is the introduction of Priority Sector Lending Certificates (PSLCs). This scheme of PSLCs was introduced in April 2016. The Reserve Bank provided a platform to enable trading in the certificates through its core banking solution (CBS) portal (e-Kuber). All scheduled commercial banks (including RRBs), urban co-operative banks, small finance banks (when they become operational) and local area banks are eligible to participate in trading. Some of the main features of the scheme are:

• Four kinds of PSLCs: Agriculture, Small and Marginal farmers (SF/MF), Micro enterprises and General can be bought and sold via the platform.

• The certificates will have a standard lot size of `2.5 million and its multiples.

• There will be no transfer of credit risk on underlying assets as there is no transfer of tangible assets or related cash flows.

• Banks will be permitted to issue PSLCs up to 50 per cent of the previous year’s priority sector lending achievement without having the underlying in their books. Banks should meet priority sector targets through direct lending and net PSLCs.

• Banks may be required to invest in the Rural Infrastructure Development Fund (RIDF)/other funds to the extent of the shortfall.

• A bank with a shortfall in achieving any sub-target (for example, SF/MF, micro enterprises) will have to buy specific PSLCs to achieve the target. However, if a bank has a shortfall only with respect to the overall target, it could buy any PSLC.

• PSLCs will not be valid beyond the reporting date (March 31), irrespective of the date of first sale.

• A bank’s priority sector lending achievement will be computed as the sum of outstanding priority sector loans and the net nominal value of the PSLCs issued and purchased. Such computation will be done separately where sub-targets are prescribed as on the reporting date

Further in a move to boost entrepreneurial sensitivity among banks’ field-level functionaries, the Reserve Bank in collaboration with the College of Agricultural Banking (CAB), Pune, launched the National Mission for Capacity Building of Bankers for financing the MSME sector (NAMCABS). Since its inception, NAMCABS has imparted training to about 3,000 bankers.

Inclusive Financial Sector: Progress with Continuity 3

1.3 FinancialInclusionPlan(FIP)

Financial Inclusion Plan (FIP) initiated by RBI saw a steady progress during the year. This plan (FIP) provides a structured and planned approach to financial inclusion with a commitment at the highest echelons within banks in terms of Board approval of the plans. Out of 2,259 rural bank branches opened during April 2015-March 2016, 1,670 branches were opened in unbanked rural centres under FIP. Around 71 million basic savings bank deposit accounts were added taking the total to 469 million by March 2016. The total number of small farm sector credits (Kisan Credit Cards) and small non-farm sector credits (General Credit Cards) stood at 47 million and 11 million, respectively. With the conclusion of FIP’s Phase II (2013-16) on March 31, 2016, all domestic scheduled commercial banks (including RRBs) were advised to set new Board approved FIP targets for the next three years (April 2016 to March 2019).

1.4 CommitteeonMedium-TermPathonFinancialInclusion

The Committee on Medium-Term Path on Financial Inclusion, Chaired by Mr Deepak Mohanty, ED, RBI, which was constituted to work out a medium-term (five year) measurable action plan for financial inclusion, submitted its report in December 2015. The Committee recognised that substantial progress had been made in terms of access to financial products and services especially after the launch of the Pradhan Mantri Jan Dhan Yojana (PMJDY). The Committee identified significant gaps in terms of usage, inadequate ‘last mile’ service delivery, exclusion of women and small and marginal farmers and a very low formal link for micro and small enterprises. Against this background, the committee set a much wider vision of financial inclusion as ‘convenient’ access to a basket of basic formal financial products and services that should include savings, remittances, credit, government-supported insurance and pension products to small and marginal farmers and low-income households at reasonable costs with adequate protection progressively supplemented by social cash transfers. The Committee also suggested increasing micro and small enterprises’ access to formal finance with a greater reliance on technology to cut costs and improve service delivery, such that by 2021 over 90 per cent of the hitherto underserved sections of society become active stakeholders in economic progress empowered by formal finance.

Some of the recommendations of the committee are:

1. Welfare scheme “Sukanya Shiksha” for the girl child with a view to linking education with banking habits.

2. A low-cost solution based on mobile technology for enhancing the effectiveness of last mile delivery as also to facilitate usage.

3. Phasing out of the interest subvention scheme and ploughing the amount into universal crop insurance.

4. An open specialised interest-free window with simple products like demand deposits, agency and participation securities, offering products based on cost-plus financing, deferred payment and deferred delivery contracts.

5. Exploring a system of professional credit intermediaries / advisors for MSMEs to help bridge the information gap and thereby help banks take better credit decisions.

6. Creating a registry for BCs, encouraging BC certification / training programmes.

7. Inter-operability for pre-paid instruments and mobile transactions.

8. Strengthening the financial literacy centre (FLC) network and grievance redressal mechanism and devising a scheme based on transparent criteria that incentivises banks to expeditiously address customer grievances.

The Bharat Microfinance Report 20164

1.5RoadmapforBankingFacilitiesIn its Roadmap for Banking Facilities in Unbanked Villages, RBI initially advised the banks to complete Phase II of the roadmap for covering all 490,298 unbanked villages with population less than 2,000 by March 31, 2016. The timeline was advanced to August 14, 2015 in view of the on-going implementation of the Pradhan Mantri Jan Dhan Yojana (PMJDY). At end-March 2016, as reported by the State Level Bankers’ Committees (SLBCs), 450,686 villages (91.9 per cent of the target) had been covered by 14,901 branches, 415,207 villages through BCs and 20,578 villages through other modes such as ATMs and mobile vans. Keeping in view the necessity of brick and mortar branches for promoting banking penetration and financial inclusion, a roadmap for establishing such branches in villages with population above 5,000 but without a bank branch of a scheduled commercial bank was rolled out in December 2015. SLBC convenor banks have been advised to ensure opening of bank branches under this roadmap by March 2017.

1.6 FinancialInclusionAdvisoryCommittee(FIAC)

The Reserve Bank set up an advisory body, the FIAC, in 2012 to review financial inclusion policies on an on-going basis and to provide expert advice to the Reserve Bank in this matter. Given the renewed focus on financial inclusion by the Government of India, the on-going implementation of the PMJDY and the need for convergence of the efforts of various stakeholders, FIAC was re-constituted in June 2015. Its revised terms of reference include: (i) preparing a national strategy for financial inclusion which aims at converging financial inclusion efforts of various stakeholders and PMJDY, apart from monitoring the progress; (ii) monitoring progress on FIP; and (iii) monitoring progress on financial literacy. Sa-Dhan is a member of this Committee.

1.7 MUDRA

Micro Units Development & Refinance Agency Limited (MUDRA) and Pradhan Mantri MUDRA Yojana (PMMY) were launched on 08 April 2015 by the Hon’ble Prime Minister, Shri Narendra Modi. The guidelines of PMMY issued by Department of Financial Services (DFS), GOI indicated that all banks are required to lend to microenterprises engaged in manufacturing, processing, trading and service sector activities for a loan upto `10 lakh. Further, it was also advised that the loan may be given in three categories, i.e. Loan upto `50,000 under Shishu; `50,000 to `5 lakh under Kishor; and `5 lakh to `10 lakh under Tarun. Also, it was envisaged that more focus will have to be given for the Shishu category. A target of `1,22,188 crore was set for F.Y. 2015-16.

As against the target of `122188 crore, the Banks and MFIs together have disbursed `132954.73 crore, thereby achieving 109%. The achievements by Public Sector Banks indicate a substantial credit growth in this segment. Based on the data collected from the PSBs, it was seen that the disbursement by these banks in this segment was around `33,000 crore during the 2014-15 which has recorded a growth of 70% during 2015-16.

The Union Cabinet has given its approval for the creation of a credit guarantee fund for Micro Units Development Refinance Agency (MUDRA) loans. The fund is expected to guarantee more than `1 lakh crore worth of loans to micro and small units.

1.8 SelfHelpGroups

Self Help Group Bank Linkage Programme (SBLP) is a step to bring the “unbanked” poor into the formal banking system and to inculcate thrift and credit habits. A natural corollary is for the group members to graduate into seeking better livelihood opportunities through access to credit from financial institutions.

Inclusive Financial Sector: Progress with Continuity 5

The year witnessed steady progress in the Programme with total number of SHGs saving-linked with banks reaching 79.03 lakh, with a total saving amount of `13691 crore. Likewise the total number of SHGs with loan outstanding stood at 46.72 lakh with a total loan amount outstanding of `57119 crore. During 2015-16 the total No. of SHGs credit linked stood at 18.32 lakh with a total amount disbursed being `37286 crore. Signifiactly the NPA level declined by 0.59% over previous year.

1.9 Peer-to-Peer(P2P)Lending

Another far sighted step taken by RBI is with regard to Peer-to-peer (P2P) lending. This is an innovative form of crowd-funding with financial returns. It involves the use of an online platform to bring lenders and borrowers together and help in mobilising unsecured finance. The borrower can either be an individual or a business requiring a loan. The platform enables a preliminary assessment of the borrower’s creditworthiness and collection of loan repayments. Accordingly, a fee is paid to the platform by both borrowers and lenders. Interest rates range from a flat interest rate fixed by the platform to dynamic interest rates as agreed upon by borrowers and lenders using a cost-plus model (operational costs plus margin for the platform and returns for lenders).

One of the main advantages of P2P lending for borrowers is that the rates are lower than those offered by money lenders/unorganised sector, while the lenders benefit from higher returns than those obtained from a savings account or from any other investment. In India, there are currently many online P2P lending platforms and the sector has been growing at a rapid pace. The Reserve Bank released a consultation paper on P2P lending in April 2016. The paper deliberated the advantages and disadvantages of regulating P2P platforms and underscored the need to develop a balanced regulatory approach that would protect lenders and borrowers without curbing the underlying innovations. Accordingly, P2P platforms are proposed to be regulated as a separate category of NBFCs. The feedback received on the paper from various stakeholders is being examined by RBI to finalise the regulatory framework.

1.10MFIsasChannelsforGovt.ProgrammesReserve Bank granted NBFC-MFIs general permission to act as channelising agents for distribution of loans under special schemes of central/state government agencies exempting such loans from the qualifying assets criteria. This would be a big boost to MFIs to take a rightful place in the implementation of credit-linked poverty alleviation programmes of central and state governments. At the same time it would give a fillip to the spread of implementation of these programmes to the difficult and remoter areas still unreached by banks.

The Bharat Microfinance Report 20166

e Core Values of Micro nance which Guide the Micro nanceInstitutions are as Follows:

A. INTEGRITYn To provide low-

income clients women, men, and their families, with access to nancial services that are client focused, designed to enhance their wellbeing, and delivered in a manner that is ethical, digni ed, transparent, equitable and cost effective.

E. PRIVACY OF CLIENT INFORMATION

n To safeguard personal information of clients, allowing disclosures and exchange of relevant information with authorized personnel only, and with the knowledge and informed consent of clients.

B. QUALITY OF SERVICE

n To ensure quality services to clients, appropriate to their needs, and delivered efficiently in a convenient and timely manner.

n To maintain high standards of professionalism based on honesty, non-discrimination and customer centricity.

F. INTEGRATING SOCIAL VALUES INTO OPERATIONS

n To ensure high standards of governance and management focused on not only nancial performance but also social impact of business.

n To monitor and report social as well as nancial data.

n To assess the social performance and social relevance of the institution from time to time.

C. TRANSPARENCYn To provide complete

and accurate information to clients regarding all products and services offered.

n To create awareness and enable clients and all other stakeholders to understand the information provided with respect to

nancial services offered and availed.

G. FEEDBACK & GRIEVANCE REDRESSAL MECHANISM

n To provide clients formal and informal channels for feedback and suggestions.

n To consistently assess the impact of services in order to enhance competencies and serve clients better.

n To provide a formal and easy to access grievance redress mechanism for clients.

D. FAIR PRACTICESn To ensure that clients

are protected against fraud and misrepresentation, deception or unethical practices.

n To ensure that all practices related to lending and recovery of loans are fair and maintain respect for client's dignity and with an understanding of client's vulnerable situation.

Source: Revised Code of Conduct

Box 1.1 Core Values of Microfinance

Outreach and Loan Portfolio 7

Outreach and Loan PortfolioChapter 2

Client outreach and loan portfolio are two key indicators of an MFI’s contribution to financial inclusion as well as the depth and breadth of financial deepening achieved by it. This chapter aims to provide

an overview of MFIs’ outreach in terms of client coverage and loan portfolio, based on the data received from 166 MFIs. This chapter is divided into two parts; the first part explains geographic distribution of microfinance institutions and their client outreach. The second discusses the issues of portfolio outstanding, loan disbursement, and purpose of loan.

2.1GeographicalSpreadofMicrofinance

MFIs currently operate in 29 States, 4 Union Territories and 588 districts in India. Table 2.2 shows the distribution of MFIs by state. In particular, it shows the number of MFIs operating in each state, their total number of branches in the state and the number of districts with microfinance operations. Annexure1 indicates the state wise presence of different MFIs.

Twenty five MFIs with a large outreach and portfolio have operations in more than five states, out of which five leading MFIs are operating in more than fifteen states. A total of 62 MFIs (38%) are operating in two to five states, while 79 MFIs (48%) have confined their operations to only one state. The details of States/ Union Territories wise operation of 165 MFIs are given in Table 2.1.

Table 2.1: No. of MFIs in Indian States/UTs

No. of States/UTs No. of MFI

1 79

2 to 5 62

6 to 10 16

11 to 15 4

> 15 5

Total 166

MFIs with a smaller scale or regional focus have concentrated their operations in 1-2 states only whereas other MFIs have spread across a higher number of states in order to increase their size, scale and simultaneously mitigate concentration risk. MFIs operating in multiple states, in general, are typically larger in size and follow the legal form of an NBFC-MFI. The geographical expansion of bigger MFIs is illustrated by the fact that while in 2013 -14 only 15 MFIs had operations in more than 5 states, that number increased to 25 in 2015 -16. List of top 10 MFIs operating in more number of states and more number of districts are presented in Figure 2.1 and 2.2 respectively.

The Bharat Microfinance Report 20168

Figure 2.1: Top 10 MFIs Operating in Number of Indian States/Union Territories

Figure 2.2: Top 10 MFIs Operating in Number of Indian Districts

10

11

12

13

15

16

17

18

24

0 5 10 15 20 25 30

Annapurna, Equitas, ESAF, NERFL, Utkarsh

NABARD Fin Services Ltd.

Spandana

AML

Basix

Satin Creditcare

SKS Microfinance Ltd

SML, Janalakshmi

Ujjivan

No. of States/UTs

102

118

130

148

174

183

199

207

305

0 50 100 150 200 250 300 350

Basix, Sonata, Utkarsh

SVCL

AML

Equitas

Satin Credit care

Spandana

Janalakshmi

SML, Ujjivan

SKS

No. of Districts

Outreach and Loan Portfolio 9

Table 2.2: No. of MFIs in Indian States/UTs and No. of Districts with MFI Operation

Name of the States/UTs

No. of MFIs operating in the

state (including those having

Head Quarters outside)

No. of districts of

the state where

MFIs operate

No. of Branches

Andhra Pradesh 9 13 213

Arunachal Pradesh 3 5 12

Assam 21 25 320

Andaman & Nicobar 2 1 2

Bihar 34 38 856

Chandigarh 2 1 6

Chhattisgarh 22 23 312

Delhi 12 7 49

Goa 3 1 7

Gujarat 22 33 458

Haryana 16 20 165

Himachal Pradesh 5 4 7

Jammu & Kashmir 1 1 1

Jharkhand 24 24 276

Karnataka 32 30 1373

Kerala 16 13 301

Madhya Pradesh 37 48 948

Maharashtra 42 36 1029

Manipur 6 9 38

Meghalaya 7 6 20

Mizoram 5 8 31

Nagaland 3 2 3

Odisha 26 31 692

Puducherry 12 4 20

Punjab 9 21 132

Rajasthan 21 31 279

Sikkim 3 2 8

Tamil Nadu 33 34 1519

Telangana 6 9 155

Tripura 9 8 28

Uttarakhand 16 9 92

Uttar Pradesh 25 71 1291

West Bengal 45 20 1001

Total 588 11644

2.2 BranchNetworkThe MFIs in India had been consolidating their operations to cope with the effects of transition taking place in the sector. While 2012 and 2013 witnessed a decline in the branch network, the trend was arrested in 2014. In 2014 -15, MFIs have expanded their branches, posting a marginal growth of 4.57 %. In 2015 -16, total branch network of the MFIs excluding Bandhan was 11644. In 2014 -15, Bandhan alone had 2022 branches out of total branch network of 12221. Number wise branch network in 2015-16 has declined to 11644 from 12221 but actually there is a growth of 14% (factoring in Bandhan’s exit as an MFI).

The Bharat Microfinance Report 201610

The distribution of branches among different categories of MFIs as of March 2016 showed that NBFC-MFIs had the lion’s share of 9775 branches.

Figure 2.3: MFI Branch Network – Yearly Trend and Category – wise Breakup

SKS is the MFI with largest number of branches at 1191. Names of Top 10 MFIs in terms of Branch Network are given in Figure 2.4.

Figure 2.4: Top 10 MFIs in Terms of Branch Network

13562

1145910697

1168712221

11644

90350

916

9775

0

2000

4000

6000

8000

10000

12000

14000

16000

341

380

397

431

469

494

523

697

1191

0 200 400 600 800 1000 1200 1400

Janalakshmi , Utkarsh

AML

Equitas

Satin Creditcare

Ujjivan

Cashpor

Spandana

SML

SKS

No. of Branches

Outreach and Loan Portfolio 11

Box 2.1: Responsible Finance - An Essential Component of Microfinance Industry

The idea of Responsible Finance pivots around transparency, inclusion and customer-centricity.

Though, these principles should make their way to the charter of every financial service they are

altogether more important in Microfinance industry given that the client base is the underserved

population. Prevailing higher interest rates for the Joint Liability Group (JLG) Loans which are

offered to perhaps the most needy and vulnerable (read financially-less-aware) borrowers tend to raise

eyebrows more often than rates in other loan categories. Concern of profit earning targets of private

capital overwhelming the social objectives primarily revolves around areas like over-indebtedness,

lack of customer interest, underserved geographies and customer education, among others.

Indebtedness

The gross loan portfolio of the Microfinance JLG industry increased more than five folds to nearly

`81000 crores in 2016 from about `15000 crores in 2011. The gross loan portfolio of top 100 districts

grew by 54% between March 2015 and March 2016, a good 20 percent points higher than the national

number. Few leading players have grown their gross loan portfolios by over 80% in the 12 months of

2015-16. Such steep growth in loan portfolios without proportionate growth in borrower base indicate

towards potential case of over-indebtedness and subsequent lack of client protection. Although the

portfolio at risk (30-day) has been under 0.3%, a close monitoring of the situation is needed in 16

districts of the top 200 districts where 7% of borrowers have loans with more than 2 lenders.

To promote Responsible Finance amongst microfinance lenders, the Reserve Bank of India and the

Self-Regulatory Organizations (Sa-Dhan & MFIN) had intervened by setting up a code of conduct -

capping interest rates, defining practices to control over-lending to an individual, and laying out other

best practices. RBI and SROs have been keeping a close watch on the happenings within the industry

to make sure code of conduct guidelines are adhered to.

Credit Bureaus such as CRIF High Mark have helped lenders to comply with these guidelines,

especially with the ones related to over indebtedness. However, the distribution of loan portfolios is

changing from NBFC-MFIs to other type of institutions. Bandhan which started as a microfinance

company in 2001 has become a private bank – Bandhan Bank, and other 8 erstwhile NBFC-MFIs are

transforming themselves into Small Finance Banks (SFBs). Other private players including banks and

NBFCs, and public sector banks are also building up significant JLG portfolios, directly as well as

through business correspondent channels. However, the guidelines still refer to NBFC-MFIs, whereas

currently 40% of portfolio is not with NBFC-MFIs. Once these 8 players become SFBs, the gross loan

portfolio with NBFC-MFIs will reduce further to just about 35-40%.

The assessment of indebtedness for a microfinance borrower is incomplete without the evaluation of

borrower’s exposure to individual and SHG loans. The Reserve Bank of India has advised all banks

to capture and share borrower level data for SHG loans, this data has just started flowing into the

credit bureau database. CRIF High Mark already provides information to lenders about indebtedness

of borrower on JLG loans and Individual loans. CRIF High Mark is working with many smaller

cooperative banks and NBFCs also to include their entire data into the bureau database; this will help

in getting a more accurate picture of the borrower’s indebtedness.

The Bharat Microfinance Report 201612

The code of conduct guidelines which now are required to be followed only by NBFC-MFIs, should

be reviewed with the changing legal structures of leading microfinance lenders to at least include all

lenders practicing JLG loans irrespective of their legal organization. Should the exposure limit of Rs 1

lakh also consider individual loans and SHG loans instead of just JLG loans? A revised guideline can

support lenders to avoid over burdening of the end-borrower.

Customer-Centricity

Microfinance lenders are significantly investing in improving process efficiencies, mostly through

technology-enabled solutions. Tablet based loan origination solutions have not only helped improve

productivity for the lender, but also improved service quality for the customer by lowering turnaround

time. The field executive is now able to check credit history of a customer real-time and take a lending

decision. Decision of whether to lend and how much to lend are being automated using high end

technology thus enforcing consistency in policies for the lender and minimizing reviewer’s subjectivity

for the consumer.

The personal identity of an individual may be misused by an intermediary for personal benefits if the

individual is not aware or present for the transaction with the lender. The consumer’s interest can be

protected against such misuse by improving upon authentication and avoidance of cash transactions

between end-beneficiary and the lender.

Aadhaar which is slated to address the authentication problems especially for such segment of

customers, is now the most available identifier in the country with coverage across nearly 79 crore

adults (as of August 2016). Barring few states such as Assam and Meghalaya, other states have 90%+

adult population is covered under Aadhaar. 55% of newly disbursed loans by MFIN members in last

15 months are seeded with Aadhaar (UID). Other lenders are also increasingly preferring Aadhaar as

the proof of identity. Lenders are now testing and exploring use of Aadhaar biometric-based eKYC

service, which once implemented across the system will help address the matter of “presence” in

addition to that of “identity”.

Under the Prime Minister’s Jan Dhan Yojana (PMJDY), 24 crore banking accounts have been opened

in last 2 years ensuring almost all households in India with banking access. This unforeseeable

penetration of banking accounts and growing availability of banking avenues even in rural areas can

enable electronic disbursements of microfinance loans only to banking account of the consumer,

thereby reducing dealing in cash through the intermediaries and thus, the possible misappropriation

of funds. The repayments of the loans could also be encouraged through digital means, to begin with

in urban areas.

MFIs (especially larger ones) have lowered interest rates over past few years. Well-performing MFIs

have been able to raise funds at lower cost. These MFIs have also been able to become more cost-

efficient over the years. These benefits seem to have been passed to the customer.

Outreach and Loan Portfolio 13

Inclusion of Deeper Geographies

It wouldn’t be totally incorrect to say that substantial part of country is now serviced by the Microfinance

industry. There are 200+ districts which have 20 or more lenders operating, 500+ districts which have

5 or more lenders operating and 40 more districts which now have more than two lenders active.

Despite such widening of coverage, 60% of JLG lending is concentrated in urban areas and 53 districts

(excluding districts of Andhra Pradesh and Telangana) are still not covered by microfinance lenders.

CRIF High Mark provides Pin Point reports generally at pin code level and occasionally at village

level to lenders to help them identify business opportunities in newer geographies, thus creating

possibilities for them to explore deeper geographies. Development Financial Institutions such as

SIDBI also use such reports to influence financing of the MFIs operating in under-penetrated areas.

Education and Support

The borrowers need to be educated on how to manage debt better. MFIs as part of their initial training

module help borrowers understand importance of better debt management. The World Bank has also

taken initiatives to create educational material for more awareness amongst borrowers. MFIs also

support customers in taking their concerns to credit bureaus in case of any potential dispute on the

credit report. We at CRIF High Mark have been investing resources to provide adequate support to

address such queries.

Collectively, MFIs, other lenders, developmental institutions, industry associations and regulators can

help make micro-lending more responsible by continuing initiatives on more inclusion, customer-

centric solutions and customer education. We as CRIF High Mark Credit Bureau are geared up to

provide the required support to keep the underserved customer at the centre and include them in the

mainstream.

Courtesy: CRIF High Mark

The Bharat Microfinance Report 201614

Client Outreach grew by 8% 2016 relative to 2015 without Bandhan which indicates a sound growth of MFIs in 2015-16. This rise in the number of borrowers is positively correlated with an increase in fund flow from banks, MUDRA and financial institutions to MFIs.

2.3.1 Regional Outreach of MFIs

1 Clients of MFIs are essentially Loan Borrowers. ‘Clients’ and ‘Borrowers’ have been interchangeably used in this report.

2.3 Client1 OutreachThe total number of clients served by MFIs stood at 399 lakh as on 31 March, 2016. Client outreach of MFIs had grown substantially from 2005 to 2011, reaching a level of 317 lakh. This trend slowed down during 2012 and 2013 and the number of clients slumped to 275 lakh. The trend reversed in 2014 with a growth and reached a level of 330 lakhs. This trend continues in 2016 with a huge rise in clients/borrowers to an all time high of 399 lakh. Majority of these clients are being served by NBFC-MFIs (84.94%), primarily the larger ones. MFIs with outstanding portfolio above `500 crore are responsible for reaching out to 85.41% of the clients in the industry.

Figure 2.5: Outreach to Borrowers: Yearly Trend and Category–wise Breakup for 2016

335

267

317

275 275

330

371399

46

1 13

339

0.1 3 8 840

341

0

50

100

150

200

250

300

350

400

450

No

. o

f B

orr

ow

er (

in l

akh

)

Out of the total client base of 399 lakh, Southern region alone contributes to 39% followed by 20% each in East and Central region whereas West and North have 13% and 6% of total outreach respectively. Northeast has the least client outreach numbers with 3%. Share in outreach has expanded only in case of Central, West and North regions from 15 to 20 %, 11 to 13% and 4 to 6 % respectively.

Figure 2.6: Regional break up of Client Outreach

39%

20%

20%

13%

6%

2%

South East Central West North Northeast

Outreach and Loan Portfolio 15

This year, a positive growth trend in client outreach is observed across all regions except East and Northeast. North region has grown at 62%, followed by Central and West regions at 42% and 25% respectively. The South region has maintained a moderate growth rate of 8% whereas Northeast and Eastern regions have declined by 55% and 15% respectively.

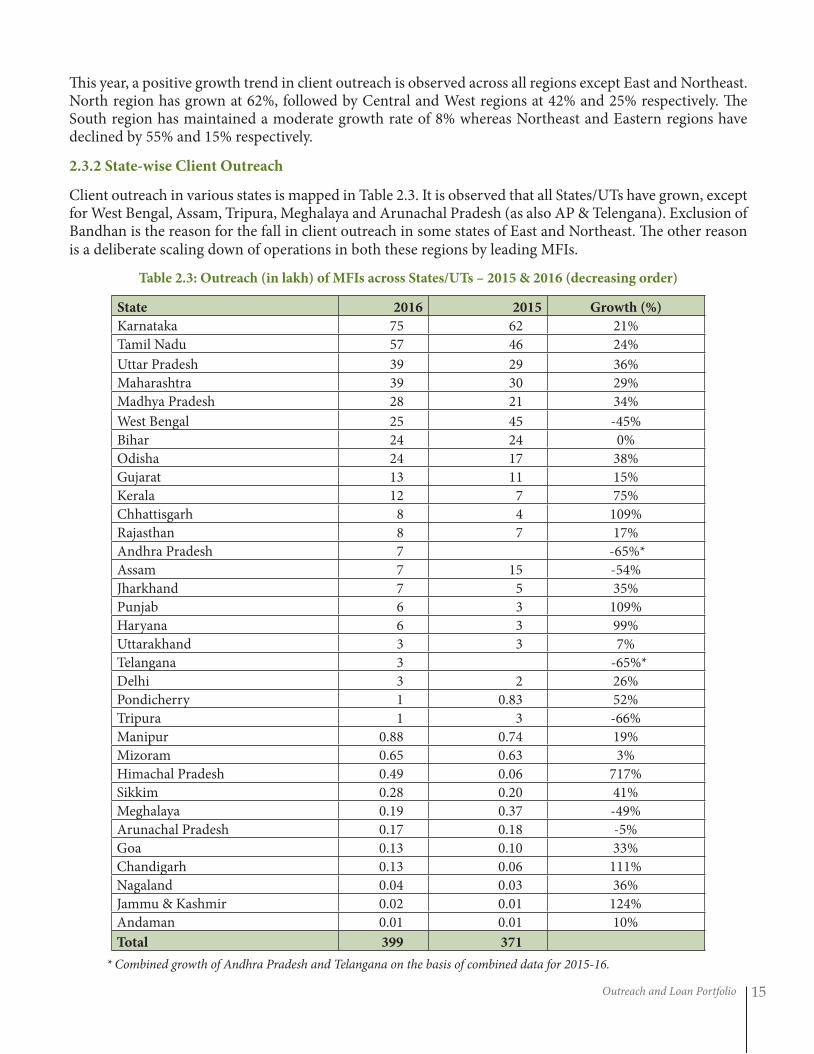

2.3.2 State-wise Client Outreach

Client outreach in various states is mapped in Table 2.3. It is observed that all States/UTs have grown, except for West Bengal, Assam, Tripura, Meghalaya and Arunachal Pradesh (as also AP & Telengana). Exclusion of Bandhan is the reason for the fall in client outreach in some states of East and Northeast. The other reason is a deliberate scaling down of operations in both these regions by leading MFIs.

Table 2.3: Outreach (in lakh) of MFIs across States/UTs – 2015 & 2016 (decreasing order)

State 2016 2015 Growth (%)

Karnataka 75 62 21%

Tamil Nadu 57 46 24%

Uttar Pradesh 39 29 36%

Maharashtra 39 30 29%

Madhya Pradesh 28 21 34%

West Bengal 25 45 -45%

Bihar 24 24 0%

Odisha 24 17 38%

Gujarat 13 11 15%

Kerala 12 7 75%

Chhattisgarh 8 4 109%

Rajasthan 8 7 17%

Andhra Pradesh 7 -65%*

Assam 7 15 -54%

Jharkhand 7 5 35%

Punjab 6 3 109%

Haryana 6 3 99%

Uttarakhand 3 3 7%

Telangana 3 -65%*

Delhi 3 2 26%

Pondicherry 1 0.83 52%

Tripura 1 3 -66%

Manipur 0.88 0.74 19%

Mizoram 0.65 0.63 3%

Himachal Pradesh 0.49 0.06 717%

Sikkim 0.28 0.20 41%

Meghalaya 0.19 0.37 -49%

Arunachal Pradesh 0.17 0.18 -5%

Goa 0.13 0.10 33%

Chandigarh 0.13 0.06 111%

Nagaland 0.04 0.03 36%

Jammu & Kashmir 0.02 0.01 124%

Andaman 0.01 0.01 10%

Total 399 371

* Combined growth of Andhra Pradesh and Telangana on the basis of combined data for 2015-16.

The Bharat Microfinance Report 201616

2.3.3 Rural – Urban Share of MFIs Borrowers

2014-15 can described as watershed year as far as the rural-urban divide in Indian microfinance is concerned. Hitherto Indian microfinance was touted as basically a rural phenomenon as compared to microfinance in Latin America as also in large parts of Africa and Asia. But that statement is no longer valid. A very interesting trend is seen in the rural-urban focus of MFIs. The share of rural clientele which was 69 % in 2012 decreased to 56 % in 2014 and has drastically come down to 33 %. The proportion of rural to urban clients for the year 2014-15 is 33% to 67%. In the year 2015-16, there is a slight improvement in the share of rural clientele which increased to 38% because of exclusion of Bandhan. One of the key findings from our research shows that the business models of MFIs are becoming urban centric in order to minimize operational expenses and maximize their operational efficiency so that regulation on margin cap is complied and a reasonable profitability is maintained.

Figure 2.7: Trends in Rural - Urban Share of MFI Borrowers

2.3.4 Outreach to Special Segment of Borrowers (Women, SC/ST, and Minorities)

Worldover the focus of microfinance has always been on serving women. In India as an alternate vehicle of credit, microfinance serves a large segment of people from Scheduled Castes, Scheduled Tribes and Minorities. Women clients constitute 97% of the total clients of MFIs. Similarly, SC/ST borrowers also constitute a substantial chunk (27%) of the clients. A trend analysis of women borrowers, SC/ST borrowers and minority borrowers is shown in numbers using a table. From the Table 2.4 below, it is observed that women borrowers, SC/ST borrowers and Minority borrowers have been consistently increasing for last four years.

For the first time, in 2014 -15, data for differently abled borrowers and borrowers having Aadhaar Cards has been collected. Coverage of MFIs in these two parameters is not satisfactory. Differently abled borrowers and borrowers with Aadhaar constitute only 0.05% and 10% of the total respectively. The reason for a low coverage under these heads is the non-collection of such data at MFI level.