Islamic Banking Tergiversation or Solution.

39

FINAL-TERM PROJECT ISLAMIC ECONOMICS THEORY AND PRACTICE MS – IBF, BATCH 4 UNIVERSITY OF MANAGEMENT AND TECHNOLGY Islamic Subordinating Contracts and their Application in Contemporary Islamic Banking System By Reconciliatory View Point Group Final-Term Project Syndicate Research Report In Islamic Banking and Finance University of Management and Technology, Lahore, Pakistan Spring, 2014

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Islamic Banking Tergiversation or Solution.

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Islamic Subordinating Contracts and their Application in

Contemporary Islamic Banking System

By

Reconciliatory View Point Group

Final-Term Project

Syndicate Research Report

In

Islamic Banking and Finance

University of Management and Technology, Lahore, Pakistan

Spring, 2014

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

University of Management and Technology, Lahore, Pakistan.

Contemporary Islamic Banking

Tergiversation or Solution

A Syndicate Research Report presented to

University of Management and Technology, Lahore, Pakistan

As a Final-Term Project

in

MS Islamic Banking and Finance

By

Atta-UR-Rehman

Fahad Ahmed Qureshi

Hafiz Ahsan Israr

Huzaifa Khalil

Imran Ijaz

Noman Ali

Spring, 2014

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Contemporary Islamic Banking Practice

Tergiversation or Solution

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Table of Contents

ABSTRACT

CHAPTER 1.

INTRODUCTION 2

CONVENTIONAL BANKING INSTRUMENTS 3

CHAPTER 2.

CB CAN BE ISLAMIZE. 6

ISLAMIC BANKING INSTRUMENTS 10

CHAPTER 3.

ISLAMIC BANKING (SIMILARITIES & DIFFERENCE) 13

OPINIONS OF MODERN CONTEMPORARY JURISTS 24

CONCLUSION

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

ABSTRACT

The Conventional Banking system has spread its roots and branches to such

an extent that it does not allow any opposition. This resistance to anything

new is not only from the nature of its mechanisms but also from the people

and institutions, which are benefitting from the perpetuation of this

conventional banking system. Therefore, it very well known that in the past

the greatest opposition to an Islamic Banking system in Pakistan came from

the State Bank itself. This of course changed due to the tireless efforts of

Mufti Taqi Usmani and his team. The pinnacle of these efforts has been the

verdict given by the Supreme Court against riba. For now, not only

Pakistani scholars but many different scholars of west and Middle East also

take part in Islamization of contemporary banking system. The purpose of

these pages is to prove the argument that contemporary banking system

may be Islamize with the guidelines of Shari’ah.

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

INTRODUCTION

The Conventional Banking system has spread its roots and branches to such

an extent that it does not allow any opposition. This resistance to anything

new is not only from the nature of its mechanisms but also from the people

and institutions, which are benefitting from the perpetuation of this

conventional banking system. Therefore, it very well known that in the past

the greatest opposition to an Islamic Banking system in Pakistan came from

the State Bank itself. This of course changed due to the tireless efforts of

Mufti Taqi Usmani and his team. The pinnacle of these efforts has been the

verdict given by the Supreme Court against riba.

One point must realized that Mufti Taqi Usmani and his team maintain that

their effort to Islamize the banking system is not an attempt to patch up the

architecture. Rather what they have done is to introduce a parallel system,

which is in continuous opposition and friction with the Conventional

Banking system. This battle between the two systems will end once the

verdict of the Supreme Court is enforced and the conventional Interest

based system abolished and replaced with the Islamic Banking System.

Islamic financial institutions (IFIs) have experienced a steady growth

during the last decade thanks to strong economic development in their host

countries. The basic principles of IFIs have protected it from the global

financial crisis. Even if the sizes of IFIs relatively small compared to

international standards, it has to note that the prospects for growth and

expansion in non-Muslim countries are strong. Several papers analyzed the

performance of banking system across countries. The results from many of

the previous studies comparing performance of Islamic and conventional

banks are unsatisfactory for several reasons; in particular, the significance

of the differences in performance between the two types of banking is often

not tested. This paper takes a different stand by examining the performance

(on profitability, credit and asset growth, and external ratings) of the main

Islamic financial instruments during the recent financial crisis at two levels.

Using balance sheet data for 37 banks of the UAE and a compensating

differential framework, we assess the performance gap between the

conventional and Islamic banking systems. Unconditional and conditional

performance differences show that, unlike other GCC countries, the

conventional banking is performing better than the Islamic one.

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

TOOLS OF CONVENTIONAL BANKING

Deposits

Deposits collected from saver for reward irrespective a bank is operating

under Conventional system. There are mainly three type of deposits

1. Current deposit

2. Fixed deposit

3. Saving deposit

Current Deposit

These types of deposits accounts has established for the businessperson and

business firms to run their operations frequently by using the banking

channel. The Current Account is a transactional non-interest bearing

account wherein a deposit are placed with the Bank for an unspecified

period and the depositor can withdraw or transfer the funds whenever

required through different means. The current account allows the

accountholders to carry out business transactions in an efficient and hassle-

free manner.

Fixed deposit

A fixed deposit (FD) is a financial instruments provided by banks which

provides investors with a higher rate of intrest than a regular savings

account, until the given maturity date. It may or may not require the

creation of a separate account. It known as a term deposit or time

deposit in. They considered very safe investments. Term deposits used to

denote a larger class of investments with varying levels of liquidity. The

defining criteria for a fixed deposit is that the money cannot withdraw for

the FD as compared to a recurring deposit or a demand deposit before

maturity. Some banks may offer additional services to FD holders such as

loa.

Against FD certificates at competitive interest rates. It is important to note

that banks may offer lesser interest rates under uncertain economic

conditions. The interest rate varies between 4 and 11 percent. The tenure of

an FD can vary from seven, 15 or 45 days to 1.5 years and can be as high as

10 years.

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Saving Deposit

The saving account is generally open in banks by the salaried person and

the person who save the money and rise in the money. The rate of interest is

very low on this type of deposit. People can withdraw the money from the

account at any time. There is no restriction on the withdrawal.

Financing and Investments

The second phase in savings mobilization process is extension of credit

facility to business and industry for return. Conventional banks are

providing financing to productive channels for

Reward. Conventional banks are offering loan for a fixed reward (interest)

In conventional banking three types of loans issued to clients including

short-term loans, overdrafts and long-term loans

.

Overdrafts/Credit Cards etc.

Conventional banks offer the facility of overdrawing from account of the

customer on interest. One of its form is use of credit card whereby limit of

overdrawing for customer is set by the bank. Credit card provides dual

facility to customer including financing as well as facility of plastic money

whereby customer can meet his requirement without carrying cash. Under

conventional banking, a customer charged with interest once the facility

availed. Furthermore, in case of default customer charged with further

interest for the extra period under conventional system.

Short-term loans

Short term and medium term loans provided to customer to meet working

capital requirements of firm by conventional banks. Working capital

required by firms to invest in inventories and accounts receivables and meet

the expenses.

Medium to long-term loans

Medium to long-term loans are provided for purchase or building of fixed

assets by firms to expand or replace the existing assets۔

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Leasing

Leasing is relatively recent source of financing whereby usufruct of an

asset transferred to lessee for agreed amounts of rentals. Under leasing

ownership may or may not transferred.

Agricultural Loans

Agricultural loans include both types of loans short-term as well as long-

term. Short-term loans required by farmers for seeds, fertilizers, and long-

term loans are required to develop additional lands and purchase of

equipments. Normally farmers return these loans after selling the finished

crops. Conventional banks are providing credit facility by charging interest

House financing

Housing finance/Mortgages is the more secured form of financing for both

conventional banks and IFIs. Under conventional system loan provided for

interest

Investments

In order to maintain liquidity conventional banks have many avenues

including government securities, shorter-term loans and money at call and

short notices, leasing companies’ bonds, investment in shares etc.

Interestingly mandatory reserve maintenance by conventional banks with

central banks also rewarded in the form of interest. Conventional banks can

also create liquidity by issuing the bonds against their receivables.

Commercial banks also protected by central bank by providing liquidity in

rainy days for interest. Interbank deposits also rewarded in the form of

interest by commercial banks

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

THE CONTEMPORARY BANKING SYSTEM ISLAMIZED BY

MAKING POSITIVE CHANGES IN IT?

Over the last few decades, the Muslims have been trying to restructure their

lives based on Islamic principles. They strongly feel that the political and

economic dominance of the West, during past centuries, has deprived them

of the divine guidance, especially in the socio-economic fields. Therefore,

after acquiring political freedom, the masses are striving for the revival of

their Islamic identity to organize their collective life in accordance with the

Islamic teachings (Mufti Muhammad Taqi Usmani, 1998, p.12).

In the economic field, it was the biggest challenge for such Muslims to

reform their financial institutions to bring them in harmony with the

dictates of Shariah. In an environment where the entire financial system

based on interest, it was a formidable task to structure the financial

institutions on an interest free basis.

(Mufti Muhammad Taqi Usmani, 1998, p.12)

A criticism, which has put forward, is that the Islamic Banking system put

forward is not radically different from the system it is in conflict with

contemporary system. I believe this criticism is not strong enough if we

examine the details of the Islamic Banking System put forward by Mufti

Taqi Usmani.

Asset-backed Financing

One of the most important characteristics of Islamic financing is that it is an

asset-backed financing. The conventional / capitalist concept of financing is

that the banks and financial institutions deal in money and monetary papers

only. That is why they forbidden, in most countries, from trading in goods

and making inventories. Islam, on the other hand, does not recognize

money as a subject matter of trade, except in some special cases. Money

has no intrinsic utility; it is only a medium of exchange; each unit of money

is 100% equal to another unit of the same denomination.

Therefore, there is no room for making profit through the exchange of these

units inter se. Profit is generated when something having intrinsic utility is

sold for money or when different currencies are exchanged, one for another.

The profit earned through dealing in money (of the same currency) or the

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

papers representing them is interest, hence prohibited. Therefore, unlike

conventional financial institutions, financing in Islam always based on

illiquid assets, which create real assets, and inventories.

(Mufti Muhammad Taqi Usmani, 1998, p.12).

The real and ideal instruments of financing in Shariah are musharakah and

mudarabah. When a financier contributes money based on these two

instruments it is bound to convert into the assets having intrinsic utility.

Profits generated through the sale of these real assets.

(Mufti Muhammad Taqi Usmani, 1998, p.12).

Financing on the basis of Salam and istisna’ also creates real assets. The

financier in the case of Salam receives real goods and can make profit by

selling them in the market. In the case of istisna, financing affected through

manufacturing some real assets, as a reward of which the financier earns

profit.

(Mufti Muhammad Taqi Usmani, 1998, p.12).

Financial leases and murabahah are not originally modes of financing. But,

in order to meet some needs they have been reshaped in a manner that they

can be used as modes of financing, subject to certain conditions, in those

sectors where musharakah, mudarabah, salam or istisna’ are not workable

for some reasons. The instruments of leasing and murabahah sometimes

criticized on the ground that their net result is often the same as the net

result of an interest-based borrowing. This criticism is justified to some

extent, and that is why the Shariah supervisory Boards are unanimous on

the point that they are not ideal modes of financing and they should use

only in cases of need with full observation of the conditions prescribed by

Shariah. Despite all this, the instruments of leasing and murabahah, too,

fully backed by assets and financing through these instruments is clearly

distinguishable from the interest-based financing on the following grounds

(Mufti Muhammad Taqi Usmani, 1998, p.13).

In conventional financing, the financier gives money to his client as an

interest-bearing loan, after which he has no concern as to how the money

used by the client. In the case of murabahah, on the contrary, no money

advanced by the financier. Instead, the financier himself purchases the

commodity required by the client. Since this transaction cannot completed

unless the client assures the financier that he wishes to purchase a

commodity, therefore, murabahah is not possible at all, unless the financier

creates inventory. In this manner, assets always back financing.

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

(Mufti Muhammad Taqi Usmani, 1998, p.13).

In the conventional financing system, loans may advanced for any

profitable purpose. A gambling casino can borrow money from a bank to

develop its gambling business. A pornographic magazine or a company

making nude films is as good customers of a conventional bank as a house-

builder. Thus, conventional financing not bound by any divine or religious

restrictions. However, the Islamic banks and financial institutions cannot

remain indifferent about the nature of the activity for which the facility is

required. They cannot affect murabahah for any purpose, which either is

prohibited in Shariah or is harmful to the moral health of the society.

(Mufti Muhammad Taqi Usmani, 1998, p.13).

It is one of the basic requirements for the validity of murabahah that the

commodity purchased by the financier, which means that he assumes the

risk of the commodity before selling it to the customer. The profit claimed

by the financier is the reward of the risk he assumes. No such risk assumed

in an interest-based loan.

(Mufti Muhammad Taqi Usmani, 1998, p.13).

In an interest-bearing loan, the amount to be repaid by the borrower keeps

on increasing with the passage of time. In murabahah, on the other hand, a

selling price once agreed becomes and remains fixed. As a result, even if

the purchaser (client of the Bank) does not pay on time, the seller (Bank)

cannot ask for a higher price, due to delay in settlement of dues. This is

because in Sharia, there is no concept of time due of money.

(Mufti Muhammad Taqi Usmani, 1998, p.13).

In leasing too, financing offered through providing an asset having

usufruct. The risk of the leased property is assumed by the lessor / financier

throughout the lease period in the sense that if the leased asset are totally

destroyed without any misuse or negligence on the part of the lessee, it is

the financier/lessor who will suffer the loss.

(Mufti Muhammad Taqi Usmani, 1998, p.14).

It is evident from the above discussion that every financing in an Islamic

system creates real assets. This is true even in the case of murabahah and

leasing, despite the fact that they are not believed to be ideal modes of

financing and are often criticized for their being close to the interest-based

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

financing in their net results. It is known, on the other hand, that interest-

based financing does not necessarily create real assets, therefore, the supply

of money through the loans advanced by the financial institutions does not

normally match with the real goods and services produced in the society,

because the loans create artificial money through which the amount of

money supply is increased, and sometimes multiplied without creating real

assets in the same quantity. This gap between the supply of money and

production of real assets creates or fuels inflation. Since financing in an

Islamic system is backed by assets, it is always matched with corresponding

goods and services.

(Mufti Muhammad Taqi Usmani, 1998, p.14).

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

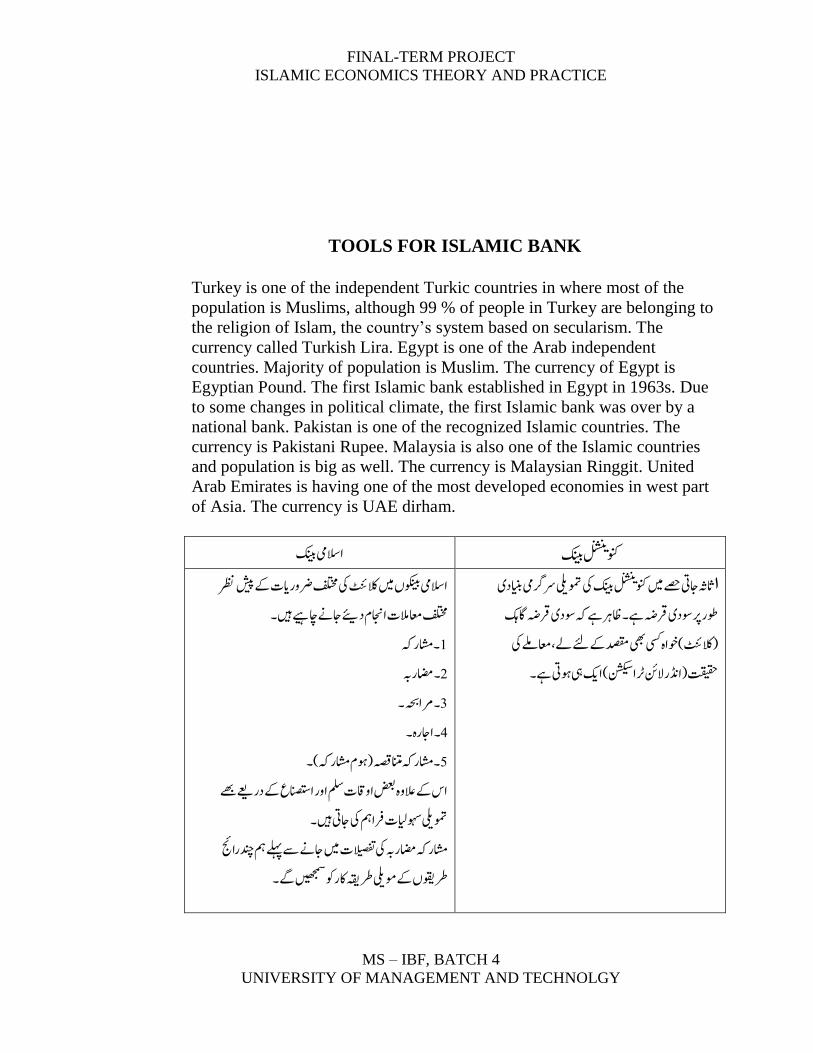

TOOLS FOR ISLAMIC BANK

Turkey is one of the independent Turkic countries in where most of the

population is Muslims, although 99 % of people in Turkey are belonging to

the religion of Islam, the country’s system based on secularism. The

currency called Turkish Lira. Egypt is one of the Arab independent

countries. Majority of population is Muslim. The currency of Egypt is

Egyptian Pound. The first Islamic bank established in Egypt in 1963s. Due

to some changes in political climate, the first Islamic bank was over by a

national bank. Pakistan is one of the recognized Islamic countries. The

currency is Pakistani Rupee. Malaysia is also one of the Islamic countries

and population is big as well. The currency is Malaysian Ringgit. United

Arab Emirates is having one of the most developed economies in west part

of Asia. The currency is UAE dirham.

کنیب االسیم کنیب

شنش

ن

ونکی

رظن رویا تک پ شاالسیم وکنیبں ںیم الکٹنئ یک فلتخم

اجےن اچےیہ

ے

ںی۔فلتخم اعمالمک ااجنم دین

۔ اشماہک1

۔ اضماہب2

۔ رماہحب۔3

۔ ااجاہ۔4

۔ اشماہک انتمہصق )وہم اشماہک(۔5

ع پ دا ےع ےھاس پ العیہ ضعب ایاقک ملس ایا اانصتس

ومتیلی وہسایلک رفامہ یک اجیت ںی۔

ااجئ ے ےلہ مہ دناشماہک اضماہب یک الیصفتک ںیم اجےن

ے۔رطوقیں پ ومیلی رطہقی اکا وک ںیھجمس

کنیبا

شنش

ن

اینبدی یک ومتیلی رسرگیم اثہث اجیت ےصح ںیم ونکی

ہض اگکہ وطا رپ وسدی رقہض ےہ۔ اظرہ ےہ ہک وسدی رق

،ے اعم ےل یک )الکٹنئ( وخاہ یسک یھب دصقم پ ےئل

یت ےہ۔تقیقح )اڈناالنئ رٹانشکیس( اکی یہ وہ

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

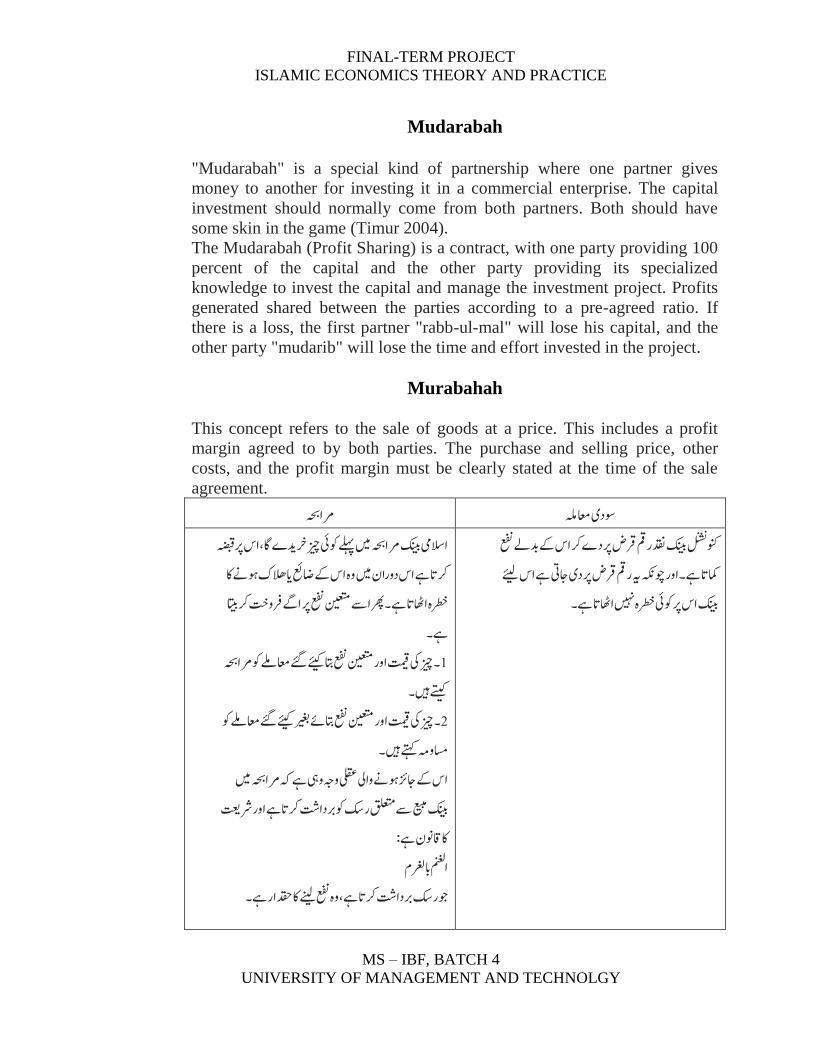

Mudarabah

"Mudarabah" is a special kind of partnership where one partner gives

money to another for investing it in a commercial enterprise. The capital

investment should normally come from both partners. Both should have

some skin in the game (Timur 2004).

The Mudarabah (Profit Sharing) is a contract, with one party providing 100

percent of the capital and the other party providing its specialized

knowledge to invest the capital and manage the investment project. Profits

generated shared between the parties according to a pre-agreed ratio. If

there is a loss, the first partner "rabb-ul-mal" will lose his capital, and the

other party "mudarib" will lose the time and effort invested in the project.

Murabahah

This concept refers to the sale of goods at a price. This includes a profit

margin agreed to by both parties. The purchase and selling price, other

costs, and the profit margin must be clearly stated at the time of the sale

agreement.

وسدی اعمہلم رماہحب

دی ےگ اگ اس رپ ہضاالسیم کنیب رماہحب ںیم ےلہ وکیئ زیچ

ہ ک وہےن اک رکات ےہ اس دیاان ںیم یہ اس پ اضعئ ت الھ

اے رفی ت رکاتینیعتم عفن رپرطخہ ااھٹات ےہ۔رھپ ا ے

ےہ۔

رماہحب عم اعم ےل وک۔ زیچ یک تمیق ایا نیعتم عفن اتب ےئیک1

ے ںی۔

ت کی

اعم ےل وک ےئیک عم ریغ۔ زیچ یک تمیق ایا نیعتم عفن اتبےئ2

ںی۔اسمیہم ےتہک

ںیم رماہحباس پ اجزئ وہےن یایل یلقع یہج ییہ ےہ ہک

اتش رکات ےہ ایا رشتعیوک ربد ے قلعت ا ک کنیب عیبم

اک اقونن ےہ:

امنغل ابرغلم

اک دقحاا ےہ۔ وج ا ک ربداتش رکات ےہ یہ عفن ےنیل

کنیب دقن امق رقض رپ دگ رک

شنش

اس پ لد،ے عفنونکن

یت ےہ اس ےئی امکات ےہ ۔ایا وچہکن ہی امق رقض رپ دی اج

۔کنیب اس رپ وکیئ رطخہ ںیہن ااھٹات ےہ

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

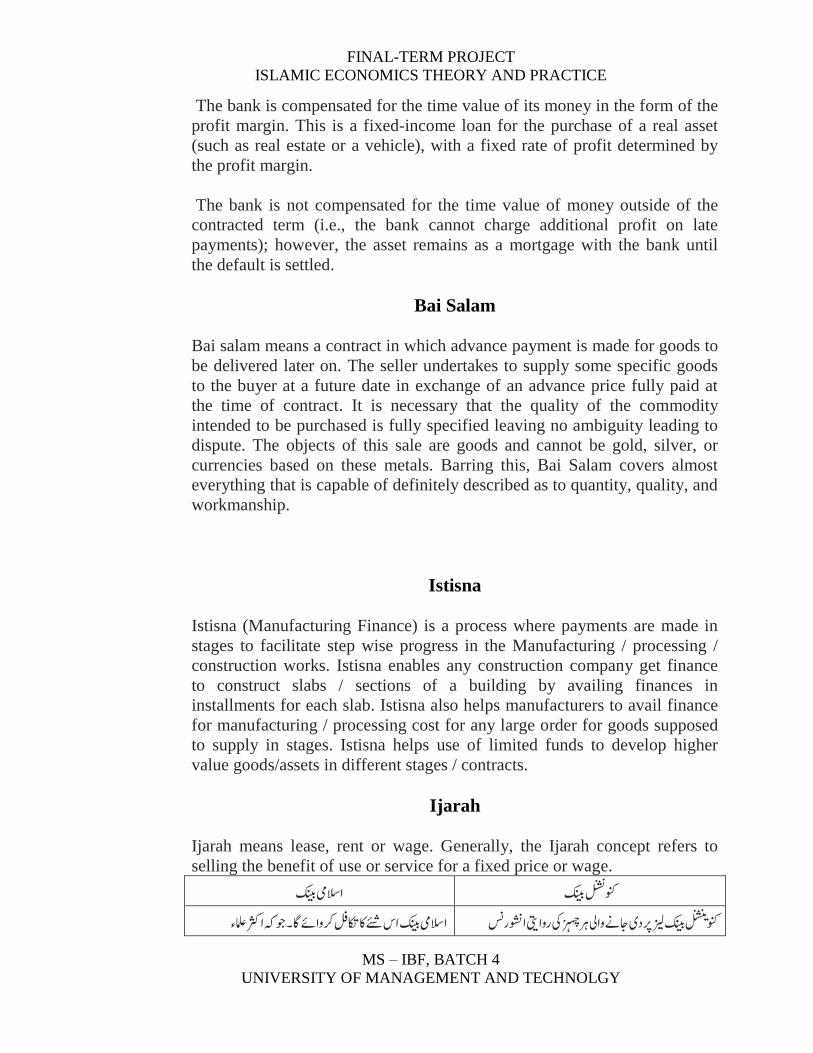

The bank is compensated for the time value of its money in the form of the

profit margin. This is a fixed-income loan for the purchase of a real asset

(such as real estate or a vehicle), with a fixed rate of profit determined by

the profit margin.

The bank is not compensated for the time value of money outside of the

contracted term (i.e., the bank cannot charge additional profit on late

payments); however, the asset remains as a mortgage with the bank until

the default is settled.

Bai Salam

Bai salam means a contract in which advance payment is made for goods to

be delivered later on. The seller undertakes to supply some specific goods

to the buyer at a future date in exchange of an advance price fully paid at

the time of contract. It is necessary that the quality of the commodity

intended to be purchased is fully specified leaving no ambiguity leading to

dispute. The objects of this sale are goods and cannot be gold, silver, or

currencies based on these metals. Barring this, Bai Salam covers almost

everything that is capable of definitely described as to quantity, quality, and

workmanship.

Istisna

Istisna (Manufacturing Finance) is a process where payments are made in

stages to facilitate step wise progress in the Manufacturing / processing /

construction works. Istisna enables any construction company get finance

to construct slabs / sections of a building by availing finances in

installments for each slab. Istisna also helps manufacturers to avail finance

for manufacturing / processing cost for any large order for goods supposed

to supply in stages. Istisna helps use of limited funds to develop higher

value goods/assets in different stages / contracts.

Ijarah

Ijarah means lease, rent or wage. Generally, the Ijarah concept refers to

selling the benefit of use or service for a fixed price or wage.

کنیب االسیم کنیب

شنش

ونکن

ء وج ہک ارثک املع اےئ اگ ۔االسیم کنیب اس ےئش اک اکتلف رکی کنیب زیل رپ دی اجےن یایل

شنش

ن

یک ایا یت اوشونکی

ش

زہ

اس رہ

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

ےہ۔زئرصع پ اہں اج

ااکس زا ا رکاگی ایا اتسمرج وکزادئ میلک وک کنیب اےنپ اہں ے وپا

امضتن وپاا یاسپ دےنی اک اپدنب وہاگ۔

رکیاات ےہ وج ہک رہب احل اناجزی ےہ۔

ہ لص ہدہ امق ے ڑاصقنن یک دقماا اوشاس ینپمک ے اح

ہک وپاا ای اجات ےہ وجاجےئ وت ااکس میلک الکٹنئ پ اہں ے

اناجزئ ےہ۔

Under this concept, the Bank makes available to the customer the use of

service of assets / equipment such as plant, office automation, motor

vehicle for a fixed period and price.

Ijarah Thumma Al Bai' (Hire Purchase)

Parties enter into contracts that come into effect serially, to form a complete

lease/ buyback transaction. The first contract is an Ijarah that outlines the

terms for leasing or renting over a fixed period, and the second contract is

a Bai that triggers a sale or purchase once the term of the Ijarah is complete.

For example, in a car financing facility, a customer enters into the first

contract and leases the car from the owner (bank) at an agreed amount over

a specific period. When the lease period expires, the second contract comes

into effect, which enables the customer to purchase the car at an agreed

price. The bank generates a profit by determining in advance the cost of the

item, its residual value at the end of the term and the time value or profit

margin for the money invested in purchasing the product to lease for the

intended term. The combining of these three figures becomes the basis for

the contract between the Bank and the client for the initial lease contract.

This type of transaction is similar to the contractum trinius, a legal

maneuver used by European bankers and merchants during the middle Ages

to sidestep the Church's prohibition on interest bearing loans. In a

contractum, two parties would enter into three concurrent and interrelated

legal contracts, the net effect being the paying of a fee for the use of money

for the term of the loan. The use of concurrent interrelated contracts

prohibited under Shariah Law.

Ijarah-Wal-Iqtina

A contract under which an Islamic bank provides equipment, building, or

other assets to the client against an agreed rental together with a unilateral

undertaking by the bank or the client that at the end of the lease period, the

ownership in the asset would transferred to the lessee. The undertaking or

the integral part of the lease contract to make it conditional. The rentals as

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

well as the purchase price fixed in such manner that the bank gets back its

principal sum along with profit over the period of lease.

Musharakah (Joint Venture)

Musharakah is a relationship between two parties or more that contribute

capital to a business and divide the net profit and loss pro rata. This used in

investment projects, letters of credit, and the purchase or real estate or

property. In the case of real estate or property, the bank assess an imputed

rent and will share it as agreed in advance. All providers of capital are

entitled to participate in management, but not necessarily required to do so.

The profit distributed among the partners in pre-agreed ratios, while the

loss is borne by each partner strictly in proportion to respective capital

contributions. This concept is distinct from fixed-income investing (i.e.

issuance of loans).

Qard hassan/ Qardul hassan (good loan/benevolent loan)

Qard hassan is a loan extended on a goodwill basis, with the debtor only

required to repay the amount borrowed. However, the debtor may, at his

discretion, pay an extra amount beyond the principal amount of the loan

(without promising it) as a token of appreciation to the creditor. In the case

that the debtor does not pay an extra amount to the creditor, this transaction

is a true interest-free loan. Some Muslims consider this be the only type of

loan that does not violate the prohibition on 'riba, for it alone is a loan that

truly does not compensate the creditor for the time value of money.

Sukuk (Islamic bonds)

Sukuk, plural of صكSakk, is the Arabic name for financial certificates that

are the Islamic equivalent of bonds. However, fixed-income, interest-

bearing bonds are not permissible in Islam. Hence, Sukuk are securities that

comply with the Islamic law (Shariah) and its investment principles, which

prohibit the charging or paying of interest. Financial assets that comply

with the Islamic law can classified in accordance with their tradability and

non-tradability in the secondary markets.

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

یم کنیبوموجدہ االس وجمزہ االسیم کنیب

ےہ ںیہن ںی۔ ذموکاہ رطےقی ارگہچ اجزی ںی نکیل دنسپ

ز تدہ انفس رکےن یک اضماہب ی اشماہک یک اینبد رپ ز تدہ ے

وکشش رکان اچےیہ ےہ۔

وج صخ الز ا وموجد وہاگرہ رہ رباچن ںیم مک از مک وکیئ اکی ااسی

اٹسف پ اسھت رتہب وطا رپ ولعم اک ااتھک وہ ایا دیرسگ

اینپ ولعم اک رئیش رکگ۔

اک اک اپس یھب حیحص ولعم اٹسف پ اسھت اسھت الکسٹنئ پ

وہان رویای ےہ۔

ین اچےیہ ابلس ایا یعض ی عطق رشتیع پ اطمقب وہ

الکسٹنئ یھب۔وخانیت اک اب رپدہ وہان رویای ےہ اےسییہ

ااجاہ یریغہ ےسیج وموجدہ االسیم اکنیبای اظنم ںیم رماہحب

م د ت اج ااہ ےہوک رشیع ااکح اک پ اطمقب ااجناعمالمک

ں ے رشیع اوصل ی وکنیبں ںیم وموجد المزنیم فلتخم اداای

ےت ا ےت ںی۔وضاطب یک رتتیب یاتق وقفات اح لص رک

اد اک ابلس ایا یعض یاالسیم وکنیبں ںیم اکم رکےن یا،ے ارف

شنش

م وکنیبں ںیم اکعطق یھب اس رطح وہیت ےہ ےسیج ونکن

یا،ے ارفاد یک وہیت ےہ۔ رکےن

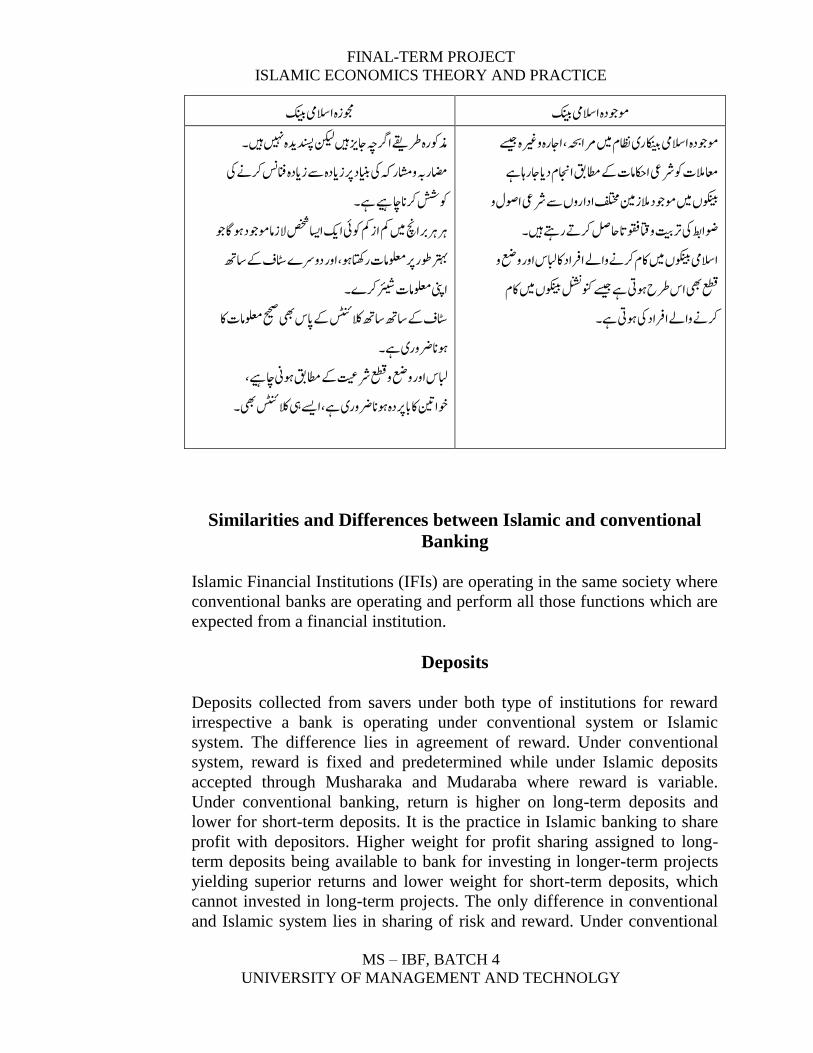

Similarities and Differences between Islamic and conventional

Banking

Islamic Financial Institutions (IFIs) are operating in the same society where

conventional banks are operating and perform all those functions which are

expected from a financial institution.

Deposits

Deposits collected from savers under both type of institutions for reward

irrespective a bank is operating under conventional system or Islamic

system. The difference lies in agreement of reward. Under conventional

system, reward is fixed and predetermined while under Islamic deposits

accepted through Musharaka and Mudaraba where reward is variable.

Under conventional banking, return is higher on long-term deposits and

lower for short-term deposits. It is the practice in Islamic banking to share

profit with depositors. Higher weight for profit sharing assigned to long-

term deposits being available to bank for investing in longer-term projects

yielding superior returns and lower weight for short-term deposits, which

cannot invested in long-term projects. The only difference in conventional

and Islamic system lies in sharing of risk and reward. Under conventional

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

system, total risk is born by the bank and total reward belongs to it after

servicing the depositors at fixed rate while under Islamic system risk and

reward both shared with depositors. Reward of depositors linked with

outcomes of investments made by IFIs. Under Islamic financial system,

only those IFIs will be able to collect deposits who can establish trust in the

eyes of masses hence leading to optimal performance by financial industry.

Financing and Investments

The second phase in savings mobilization process is extension of credit

facility to business and industry for return. Both types of institutions

(Islamic and Conventional) are providing financing to productive channels

for reward. The difference lies in financing agreement. Conventional banks

are offering loan for a fixed reward while IFIs cannot do that because they

cannot charge interest. IFIs can charge profit on investments but not interest

on loans. In conventional banking, three types of loans issued to clients

including short-term loans, overdrafts and long-term loans. Islamic banks

cannot issue loans except interest free loans (Qarz e Hasna) for any

requirement however; they can do business by providing the required asset

to client.

Overdrafts/Credit Cards

Conventional banks offer the facility of overdrawing from account of the

customer on interest. One of its form is use of credit card whereby limit of

overdrawing for customer is set by the bank. Credit card provides dual

facility to customer including financing as well as facility of plastic money

whereby customer can meet his requirement without carrying cash. As for

facility of financing is concerned that is not offered by Islamic banks except

in the form of Murabaha (which means IFI shall deliver the desired

commodity and not the cash) however facility to Shop/meet requirement

provided through debit card whereby a customer can use his card if his

account carries credit balance. Under conventional banking, a customer

charged with interest once the facility availed however under Murabaha

only profit is due when the commodity delivered to the customer.

Furthermore, in case of default customer charged with further interest for

the extra period under conventional system however extra charging not

allowed under Murabaha.

Third under conventional system customer can, avail the opportunity of

rescheduling by entering into a new agreement to pay interest for extended

period which is not the case under Murabaha. IFIs can claim only the

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

original receivable amount agreed in initial contract. Another practical issue

under Murabaha is how to deal with intentional defaulters. Different

options are lying with IFIs including to blacklist the defaulter for any

further financing facility, to stipulate in the contract that in case of default

all installments will be due at once, to stipulate in the contract a penalty

Shall be imposed but the same shall not form income of IFIs rather it will

go in charity

Short-term loans

Short term and medium term loans provided to customer to meet working

capital requirements of firm by conventional banks. Working capital

required by firms to invest in inventories and accounts receivables and meet

the expenses. As for inventory, investment is concerned that provided by

Islamic banks through Murabaha.

As for meeting of day-to-day expenses of business is concerned financing

provided through participation, term certificates where by profit of a certain

period (e.g. quarter, six month, one year) is shared by IFIs on prorate basis.

However financing through participation term certificates is not as easy as a

short-term loan from conventional bank due to risk involved for IFIs in the

transaction. Firm seeking short-term facility from IFIs has to prove the

viability of the project/business to the satisfaction of investor. For meeting

the working capital requirements of nonprofit organizations to date there is

no arrangement under Islamic financial system

Personal consumption loans are not issued by IFIs however, any individual

of sound financial position can acquire anything for his personal use under

Murabaha financing whereby a certain percentage of profit is added on cost

by IFIs.

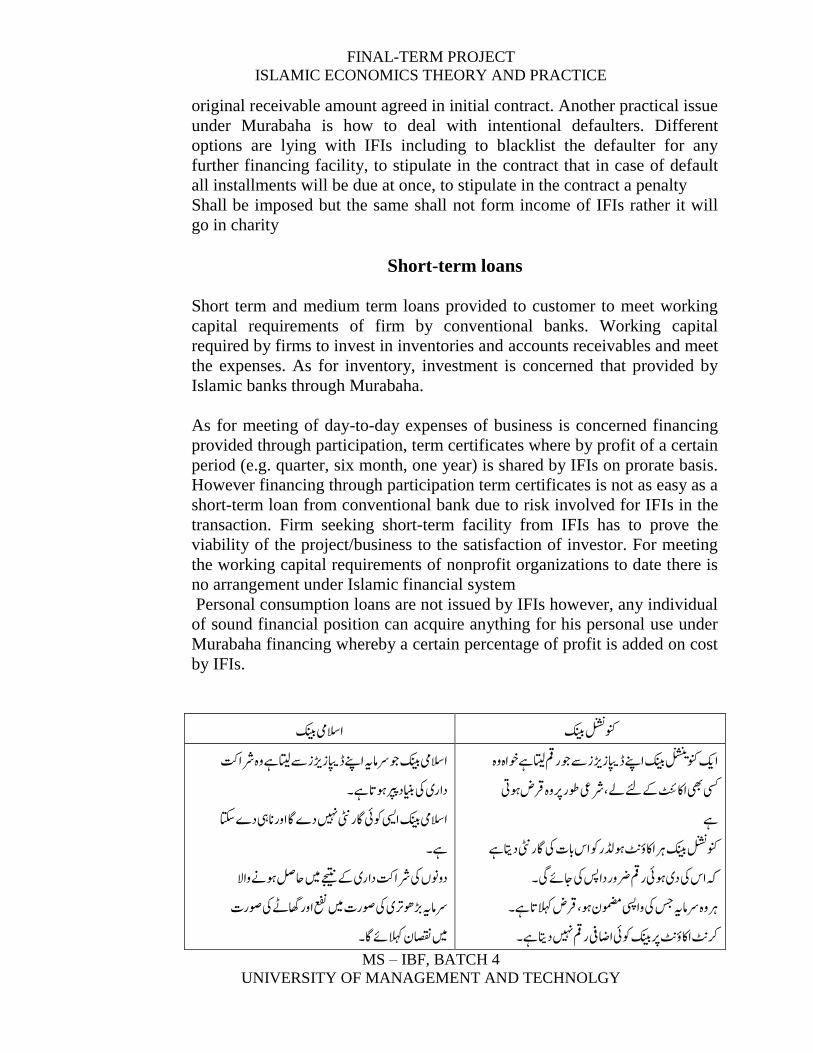

کنیب االسیم کنیب

شنش

ونکن

ے اتیل ےہ یہ رشاتک االسیم کنیب وج رس اہی اےنپ ڈاپیزڑیز

وہات ےہ۔ داای یک اینبد پ

دگ اگ ایا ان یہ دگ اتکاالسیم کنیب ایسی وکیئ اگایٹن ںیہن

ےہ۔

اح لص وہےن یاال دیونں یک رشاتک داای پ ےجیتن ںیم

ک ےٹ یک وصاک عفن ایا اھگرس اہی ڑوھرتی یک وصاک ںیم

ںیم اصقنن الہکےئ اگ۔

کنیب اےنپ ڈاپیزڑی

شنش

ن

اہ یہ ز ے وج امق اتیل ےہوخاکی ونکی

وطا رپ یہ رقض وہیت رشیع یسک یھب ااکٹنئ پ ےئل ،ے

ےہ

کنیب رہ ااکؤٹن وہڈلا وک اس اب

شنش

ےہ ک یک اگایٹن داتونکن

ی۔ہک اس یک دی وہیئ امق رویا داسپ یک اجےئ

ات ےہ۔رہ یہ رس اہی سج یک یایسپ ومضمن وہ رقض الہک

مق ںیہن دات ےہ۔رکٹن ااکؤٹن رپ کنیب وکیئ ااضیف ا

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

دگ اگ۔االسیم کنیب یھب وکیئ ااضیف امق ںیہن

و ف ی و فڈاپیزڑیز ے اح لص ہدہ امق وک االسیم کنیب

اجزی دماک ںیم اگلےن اک اپدنب وہ اگ۔

اجزئ رہ رطح یک اجزی ایا انڈاپیزرٹی ے اح لص ہدہ امق وک‘

دماک ںیم دیچ رکات ےہ۔

Murabaha financing is very useful for short to medium term financial

requirements of business/nonprofit organizations and individuals.

Murabaha financing is asset based financing and anyone can request to an

IFI for provision of an asset generally used for Halal (lawful) purposes. By

default under Islamic financial system IFIs cannot lend cash for interest

(only exception is Qarz e Hasna—Charity loan). One of the features of

Murabaha is in case of delay in payment by customer IFI cannot ask for

extra amount as time value of money like conventional banks. However,

penalty imposed on defaulter if stipulated in original contract of Murabaha

duly signed by the customer but it cannot be included in the income of IFI.

This penalty must spent for charitable purposes Under Murabaha scheme of

financing facility is linked with assets, which leads to economic stability

and creates linkage between real and financial sector.

Although Murabaha is being used by IFIs successfully and have succeeded

in meeting short to medium term requirements of firms by providing a

successful replacement of conventional loans yet certain differences exist in

both type of financing. First is one cannot get cash under Murabaha.

Second asset is purchased by IFI initially then transferred to customer

hence IFI participate in risk. Third refinancing facility is not available

under Murabaha. Fourth, in case of default price of the commodity cannot

be enhanced however, penalty may imposed if stipulated in original

contract of Murabaha however; it cannot be included in income of IFI.

Fifth, only those assets can supplied by IFIs under Murabaha whose general

and/or intended use is not against the injunctions of Sharia (e.g. supply of a

machine to produce liquor).

Medium to long-term loans

Medium to long-term loans are provided for purchase or building of fixed

assets by firms to expand or replace the existing assets. Under Islamic

financial system requirement of firms and individuals fulfilled through

Murabaha, Bai Muajjal and Istasna (discussed in appendix B). Another

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

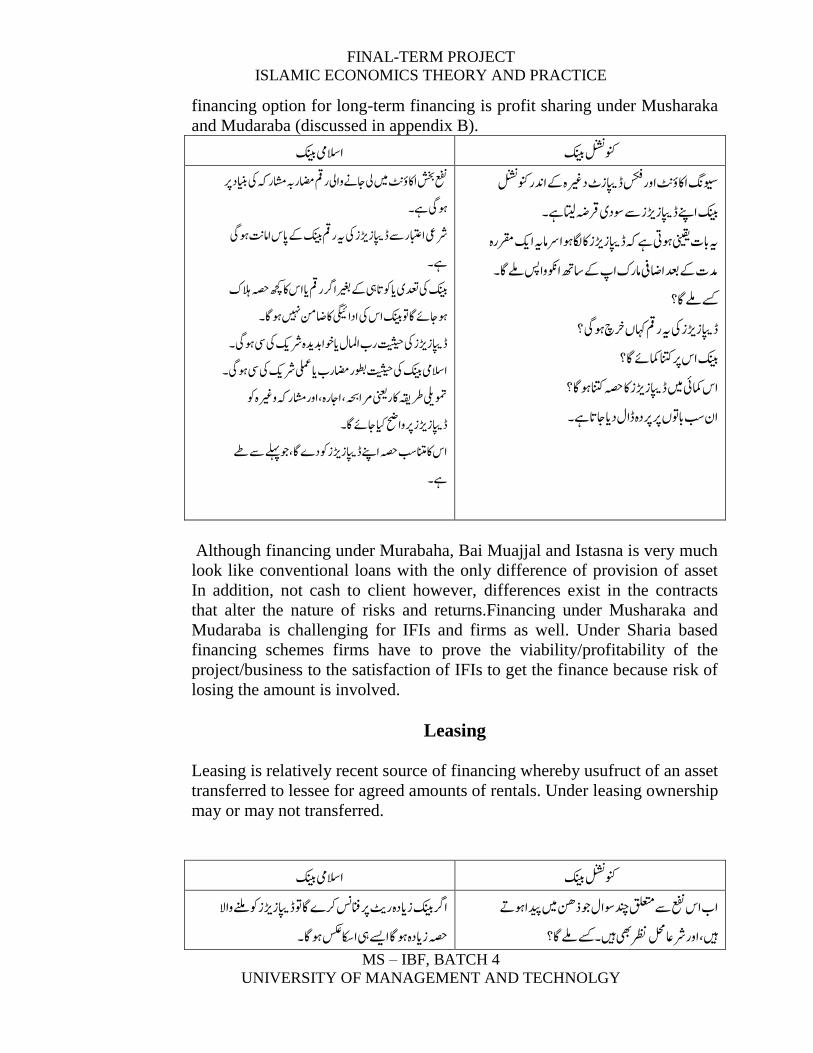

financing option for long-term financing is profit sharing under Musharaka

and Mudaraba (discussed in appendix B).

کنیب االسیم کنیب

شنش

ونکن

د رپ اہب اشماہک یک اینباضمعفن شخب ااکؤٹن ںیم یل اجےن یایل امق

وہی ےہ۔

پ اپس ا اتن وہیرشیع اابتعا ے ڈاپیزڑیز یک ہی امق کنیب

ےہ۔

ہ ک امق ت اس اک ھچک ہصح الہ کنیب یک دعتی ت وکاتیہ پ ریغ ارگ

نم ںیہن وہاگ۔وہاجےئ اگ وت کنیب اس یک ادایگیئ اک اض

وہی۔کی یک یڈاپیزڑیز یک تیثیح اب ااملل ت وخالد ےہ رش

۔ رشکی یک ی وہیاالسیم کنیب یک تیثیح وطبا اضماب ت یلمع

اہک یریغہ وک ومتیلی رطہقی اکا ینعی رماہحب ااجاہ ایا اشم

ڈاپیزڑیز رپ یاحض ای اجےئ اگ۔

اگ وج ےلہ ے ےط اس اک انتمبس ہصح اےنپ ڈاپیزڑیز وک دگ

ےہ۔

اردا ویسگن ااکؤٹن ایا سکف ڈاپیزٹ دریغہ پ

شنش

ونکن

ےہ۔کنیب اےنپ ڈاپیزڑیز ے وسدی رقہض اتیل

اہ وہا رس اہی اکی رہی ابک ینیقی وہیت ےہ ہک ڈاپیزڑیز اک اگل

۔اوکن یاسپ ےل اگ دمک پ دعب ااضیف ااہ ک اپ پ اسھت

ےسک ےل اگ؟

ڈاپیزڑیز یک ہی امق اہک ں دیچ وہی ؟

کنیب اس رپ انتک امکےئ اگ؟

اگ؟اک ہصح انتک وہ اس امکیئ ںیم ڈاپیزڑیز

ان بس ابوتں رپ رپدہ ڈال د ت اجات ےہ۔

Although financing under Murabaha, Bai Muajjal and Istasna is very much

look like conventional loans with the only difference of provision of asset

In addition, not cash to client however, differences exist in the contracts

that alter the nature of risks and returns.Financing under Musharaka and

Mudaraba is challenging for IFIs and firms as well. Under Sharia based

financing schemes firms have to prove the viability/profitability of the

project/business to the satisfaction of IFIs to get the finance because risk of

losing the amount is involved.

Leasing

Leasing is relatively recent source of financing whereby usufruct of an asset

transferred to lessee for agreed amounts of rentals. Under leasing ownership

may or may not transferred.

کنیب االسیم کنیب

شنش

ونکن

یاال وت ڈاپیزڑیز وک ےنلارگ کنیب ز ت دہ اٹی رپ انفس رکگ اگ

ہصح ز ت دہ وہاگ اےسی یہ ااکس سکع وہاگ۔

ںیم دیپا وہ ےت اب اس عفن ے قلعت دن وسال وج ذنھ

اگ؟ںی ایا رشاع لحم رظن یھب ںی۔ےسک ےل

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

ی ت ا ے رہ احل ںیماالسیم کنیب ڈاپیزڑیز ے رس اہی ےتیل

ےہ۔ یایسپ یک اگایٹن ںیہن دگ اتک

رکگ ںیہن رک اتک ےہ ان یمتح عفن ت اصقنن یک رشح یھب ےط

اگ۔

ڈاپیزڑیز یک ہی امق اہک ں دیچ وہی ؟

کنیب اس رپ انتک امکےئ اگ؟

اگ؟وہاس امکیئ ںیم ڈاپیزڑیز اک ہصح انتک

ان بس ابوتں رپ رپدہ ڈال د ت اجات ےہ۔

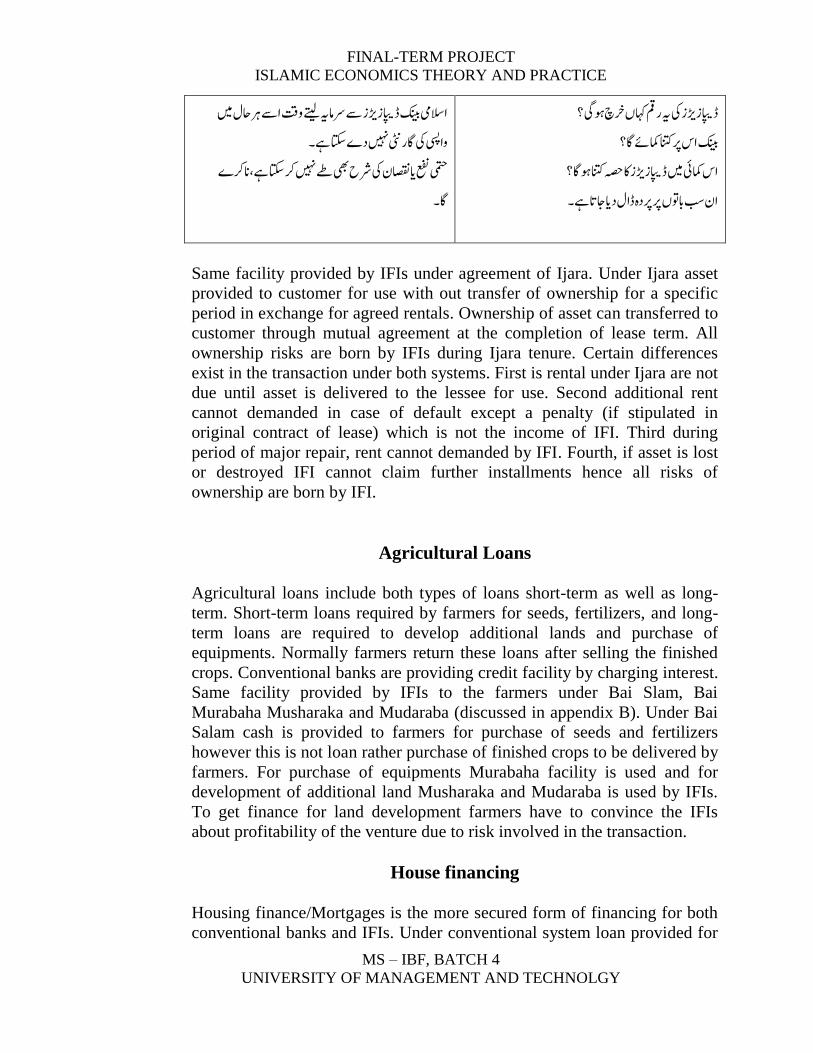

Same facility provided by IFIs under agreement of Ijara. Under Ijara asset

provided to customer for use with out transfer of ownership for a specific

period in exchange for agreed rentals. Ownership of asset can transferred to

customer through mutual agreement at the completion of lease term. All

ownership risks are born by IFIs during Ijara tenure. Certain differences

exist in the transaction under both systems. First is rental under Ijara are not

due until asset is delivered to the lessee for use. Second additional rent

cannot demanded in case of default except a penalty (if stipulated in

original contract of lease) which is not the income of IFI. Third during

period of major repair, rent cannot demanded by IFI. Fourth, if asset is lost

or destroyed IFI cannot claim further installments hence all risks of

ownership are born by IFI.

Agricultural Loans

Agricultural loans include both types of loans short-term as well as long-

term. Short-term loans required by farmers for seeds, fertilizers, and long-

term loans are required to develop additional lands and purchase of

equipments. Normally farmers return these loans after selling the finished

crops. Conventional banks are providing credit facility by charging interest.

Same facility provided by IFIs to the farmers under Bai Slam, Bai

Murabaha Musharaka and Mudaraba (discussed in appendix B). Under Bai

Salam cash is provided to farmers for purchase of seeds and fertilizers

however this is not loan rather purchase of finished crops to be delivered by

farmers. For purchase of equipments Murabaha facility is used and for

development of additional land Musharaka and Mudaraba is used by IFIs.

To get finance for land development farmers have to convince the IFIs

about profitability of the venture due to risk involved in the transaction.

House financing

Housing finance/Mortgages is the more secured form of financing for both

conventional banks and IFIs. Under conventional system loan provided for

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

interest while under Islamic financial system facility provided through

diminishing Musharaka. Under diminishing Musharaka house purchased

jointly by IFI and customer. IFI rents out its share in property to customer

for an agreed amount of rent. Share of financier divided in units of small

denomination. Customer pays the installments to IFI consist of rentals and

purchase price of a unit. Stake of customer in property is increasing while

of IFI is decreasing with payment of every installment. Finally, with the

payment of last installment stake of IFI reaches to zero and property

transferred in the name of customer. Diminishing Musharaka model can

help out in avoiding the real estate crisis (like of 2008) because when

market value of property decreases both IFI and customer suffers according

to their share in property and whole burden is not shifted on customer

alone. Hijazi, & Hanif (2010) have raised certain questions about the

existing practice of IFIs working in Pakistan and needs to be addressed by

policymakers, Sharia boards and management of IFIs

Investments

In order to maintain liquidity conventional banks have many avenues

including government securities, shorter-term loans and money at call and

short notices, leasing companies’ bonds, investment in shares etc.

Interestingly mandatory reserve maintenance by conventional banks with

central banks rewarded in the form of interest. Conventional banks can also

create liquidity by issuing the bonds against their receivables. Commercial

banks protected by central bank by providing liquidity in rainy days for

interest. Interbank deposits rewarded in the form of interest by commercial

banks. For IFIs, avenues are very limited to create required liquidity at the

same time to earn some revenue by investing in short term and liquid

securities. IFIs cannot invest in government securities, short-term loans,

bonds and money at call and short notices because of interest based

transactions.

Mandatory reserve with central bank maintained by IFIs but they are not

rewarded like conventional banks. Looking towards central bank in rainy

days to maintain liquidity is also not as straightforward due to interest

demand of central bank. IFIs cannot demand interest on interbank deposits.

As for investment in market able securities are concerned again, IFIs are

not free to invest in any equity security due to two reasons. First Halal

business of the underlying firm is required. Second financial operations of

underlying firm should be interest free. Keeping in view the dominance of

conventional banking and existing business practices one can conclude

safely that a very negligible number of firms meet both conditions. The

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

much appreciable job has been done by Almeezan investment management

limited (AIML) a subsidiary of leading Islamic bank in Pakistan (Meezan

bank) in this regard. A list of Sharia compliant securities maintained and

updated every six monthly out of which 30 companies selected for Kse

Meezan Index (KMI). KMI established in June 2008.IFIs can invest only in

those securities, which declared Sharia compliant securities through

filtering of Sharia compliance criteria. Listing here the major conditions to

qualify a security as Sharia compliant is worth mentioning as follow.

Meeting of following tests is required to declare a security as Sharia

compliant (KMI-2008).

First, the core business of the company should be Halal (not prohibited by

Islamic Law such as liquor, pork etc). Second illiquid assets should be

equal to 20% of total assets of the company. Shares of a company merely

dealing in liquid assets are not Sharia compliant. Hence, IFIs cannot invest.

Third ratio of all interest based debts including preferred stock should be

less than 40% of total assets of the company. Fourth ratio of non-Sharia

compliant investments to total assets of the company should be less than

33%. Fifth revenue from non-compliant investments should be less than 5%

of total revenue of the company and even then, IFIs are required to purify

their earnings by spending this non-compliant revenue as charity. Finally,

market price per share should be greater than the net liquid assets per share.

Recently IFIs have created an avenue to meet their liquidity requirement in

the form of Skuks (Islamic Bonds) whereby servicing is fixed like

conventional bonds however such types of Skuks can be issued against

Ijara receivables. Under Ijara Skuks initially asset is given on rent to the

customer for an agreed period and rentals while ownership remains with

IFI. To meet liquidity requirements IFI issues Skuks (bonds) to the

investors equal to the value of asset, hence ownership of the asset

transferred to Skukholders.

While it known the rentals of the asset, so the return on investment is

predetermined and known with certainty to the investors. Skuks of

Murabaha cannot sold except at par being sale of loans. Other types of

Skuks (Musharaka etc) are not carrying fixed return although tradable in

secondary security market. Underlying principle in issue of Skuks is that

illiquid assets should dominate in the portfolio against which Skuks issued.

Under Islamic financial system, Skuks are ownership certificates and not

mere debt securities hence all risks and rewards shared by Skuk-holders.

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Opinions of the Modern Jurists of our time about contemporary

Islamic Banking.

Many modern jurists of our time, which is of the same view that Moalan

Taqi Usmani hold. They also gave valuable feedbacks in precious books, so

it shows that the proposed Islamic banking concept of Hazrat Mufti

Mohammad Taqi Usmani he is not all alone, but many contemporaries also

bear the image of the proposed system.

A few expert contemporaries mentioned their views as:

DR. Ahmad Mustafa Zarqa’s views.

ایل ذا رجعنا قد منا اول ھذا الفصل ان الفقہ السالمی ود اقر الشخصیۃ احلمکیہ ای الاعتباریۃ و رتب علیھا احاکما، و ا

خصیۃ الاعتباریۃ بنظر النصوص و املصادر الاصلیۃ یف الرشعیۃ وجدان فیھا احاکما نشعر ابنھا امنا ینبت رشعا عیل فکرۃ الش

مقوماتہ و خصاصصہ یف اجامیل یس تلزم اجیاب احلمک و وجدان ایضا احاکما اخری تمتثل فیھا صورۃ الشخص الاعتباری سوای بلک

النظر القانوین احلدیث۔

احلدیث النبوی: ففی

املسلمون تتاکفا دماوھم و یسعی بذمتھم ادانھم و ھم ید عیل من سواھم۔

مان من ذمۃ و یممنی سارای فالفقرۃ الثانیۃ منہ قد اعترب بھا النیب صیل ہللا علیہ وسمل ما یعطیہ احد املسلمنی للمحارب طامل الا

عیل جامعتھم و ملزما لھم کام لو صدر منھم مجیعا۔

(۲۲أ ۶۵۲۳ل الفقہیی العام للزرقا، ج)املدخ

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Famous Jurist Ali Al-Khafif’s view

ویۃ یف کتابہ: احلق و اذلمۃ اطلعت یف العام املایض و اان مبرص عیل حبث لالس تاذ اجللیل الفقیہ عیل اخلفیف عن اخشصیۃ املعن

تقر علیہ حبیث ھنا من ا فاذا بہ یس تقر عیل مثل ما اس اذلی بدا ابخراج جانب منہ منذ ثالثۃ اعوام یف الوقت الاویل من کتابہ ھذ

ھذا الامس الوقانوین ان فکرۃ الشخصیۃ احلمکیہ قد ایمان بھا الفقہ الاسالمی قدمیا و بین علیھا احاکما ھامۃ قبل ان تسمی ب

احلدیث۔

مث قال الاس تاذ اخلفیف حفظہ ہللا ما خالصتہ :

کومات و املنشاٹ، و املصاحل و ابلفقہ یف ھذہ الاایم ان احلنفیۃ ال یقولون اب لشخصیۃ احلو بنا عیل ما تقدم قال بعض املش تغلنی

الرشاکت۔

ان لھا حقوقا جتاہ غریھا یبطلھا ولکننا نری یف مولفاتھم الفقھیۃ و الاصولیۃ انھم کثریا ما تقررون ملثل ھذہ الھجات احاکما تقتیض

اانھا یف ذل واجبات مالیۃ یطلبھا اراببہا ممن لہ الوالیۃ ویل ھذہ اجلہات الییت من یقوم علیہا من ویل او انظر، و ان علیہا

اان الصیب غری املمزی و من یف حمکہ۔

( ۶۵۲۳۳ج ملدخل الفقہیی العام)ا

Shaikh-Ul-Islam Moalana Mufti Taqi Usmani’s view.

ملضاربۃ و حقوقھا ترحج ایل فاذا تقرر ان املضارب ھو املوسسۃ او البن او الرشکۃ بصفہ کونہا خشصا معنوای، فان مجیع الزتامات ا

نفقات ھوال ھذا الشخص املعیوی، و مبا ان الشخص املعنوی ال یس تطیع ان یعمل فانہ یعمل من خالل موظفیۃ و عاملہ ق

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

تامثر، امارواتب املوظفنی نوی و لیست عیل مال املضاربۃ ان مل نفقات الیت ختص معلیات الاس املوظفنی العامل عیل الشخص املع

و خیانۃ املاکتب و یم ثیثھا و نفقات الکھرابصے و ما الیھا فلکھا عیل الشخص املعنوی۔

(۲۵۱۳۳)حبوث یف قضاای فقھیہ معارصہ ج

DR. Wahba Zuhayli’s view for Islamic Banking

املساھمۃ:رشکۃ

ھم غری قابل للتجزصۃ ھی اھم انواع الرشاکت الاموال و ھی الیت یقسم فیھا راس املال ایل اجزا صغریۃ متساویۃ یطلق عیل لک س

ۃ و عاملھا اجر عند و یکون قابال للتداول و تتحد مس ئوولیۃ املساھم بقدر القمیۃ الامسیۃ ال سھمیۃ و یعترب مدیر الرشک

املساھمنی۔۔ اخل۔

(۶۳۳۳أ ۵۶۳۳۵لفقہ الاسالمی و ادلتہ ج)ا

Consult the pages mentioned below from fifth volume:

(۳۳۔۳۔۳۶۔۳۱۔۳۳۔۳۲۔۔۶۳۔۲۱۔۱۳۔۱۳۔۶۵۱)

From sixth volume:

(۲۔۲۱۔۵۱۳۳)

From seventh volume:

اما الاسھم: فھیی حصص الرشاک یف الرشاکت املساھمۃ۔۔۔۔۔۔۔۔

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

(۳۶۳۔۳۶۳)

From ninth Volume:

عامالت املصارف )البنوک( مقابل اخلدمات او الضامانت۔۔۔۔۔

(۳۔۳۵۔۳۶۔۳۳)

جتاھات او اجملاالت الثالثۃ ان انواع عوصد الاستامثر یف البنوک الاسالمیۃ کثریۃ و متنوعۃ فالبن الاسالمی یقوم ابلعمل یف الا

االتیۃ۔۔۔۔

۔(۳۳۳۔۳۳۳۔۳۳۳۔۳۳۵۔۳۳۶۔۳۳۱)

( بشان اس تفسارات البن الااسالمی للتمنیۃ۔۲ار رمق )قر

(۳۲۲۔۳۲۳)

حمک التعامل مع املصارف الاسالمیۃ۔۔۔

(۳۳۔۳۳۔۳۵۔۳۶۔۳۳۔۳۲۳)

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Shaikh Ibn-e-Baaz’s (Grand Mufti Saudi Arabia) view about Islamic

Banking

فتوی سامحۃ الش یخ ابن ابز

الارااد ابململکۃ بن ابز الرصیس العام الدارات البحوث العلمیۃ و الافتا و ادلعوی وصدرت فتوی سامحۃ الش یخ عبد العزیز

م۔ ۱۳۲۲ابریل س نۃ ۱۳املوافق ۱۵۳۲جامدی االخرۃ ۱۳العربیۃ السعودیۃ حیث وجہ الیہ السوال التایل بتارخی

و اجاب الش یخ عبد العزیز بن ابز مبا ییل:

ی و حازہ الیہ من مل حرج یف املعاملۃ املذکورہ اذا اس تقر املبیع یف مل البن الاسالماذا اکن الواقع ما ذکر یف السوال فال

ابصعہ، لعموم الادلۃ الرشعیۃ وفق ہللا امجلیع ملا یرضیہ۔

(۱۱)بیع املراحبۃ لالمر ابلرشا للقرضاوی ص

Dr Yousaf Qarzawi’s View

Dr yousaf Qarzawi is of the same view mufti Taqi usmani, that contemporary

system can be Islamize by making positive changes in it with respect to Sharia.

He stated his view in his famous book mentioned below:

)بیع املراحبۃ لالمر ابلرشا کام جتریہ املصارف الاسالمیہ دکتور یوسف القرضاوی(

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Dr Shabaan Muhammad Islam Barwari’s View Point.

اوال: معین حصص التاسیس:

حصۃ من ارابح الرشکۃ حصص التاسیس: صکوک من دون قمیۃ امسیۃ قابلۃ للتداول، تصدرھا الرشاکت املساھمۃ متنع احلق یف

لبعض الااخاص او الھیئات مقابل ما قدموہ من براۃ اخرتاع او الزتام حصل علیہ خشص اعتباری عام۔

(۱۳۳)ورصۃ الاوراق املالیۃ من منظور اسالمی ص

(۱۳۳کذا یف معجم املصطلحات املرصفیۃ للباز )ص

(۱۵۱رشاکت املساھمۃ یف الترشیع املرصی و القطاع العام، رضوان ابو زید )ص

(۶۳۲رشکۃ السامھمۃ یف النظام السعودی للبقمی )ص

(۲۵۶۳۳الرشاکت التجاریۃ للقیلیویب )ج

Dr. Muhammad Tofeeq Ramzan Boti’s View Point

صا اعتبارای( اہ۔اعین ابحلقوق الاعتباریۃ تل احلقوق املعنویۃ او الادبیۃ الیت ختص انساان معینا اور ھجۃ معینۃ )خش

محمد توفیق رمضان ابرشاف الاس تاذ ادلکتور وھبہ الزحییل( ۲۳۳)البیوع الشاصعۃ ص

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Dr. Yasir Ajeel Al-Nashami’s View Point

تعریف رشکۃ املساھمۃ:

رشی فیھا موس ئوال رشکۃ املساھمۃ ھی ارشکۃ الیت یکون داس مالھا مقسام ایل امسھم متساویۃ قابلۃ للتداول، و ال یکون لک

اک و س ئولیۃ الرش الا مبقدار حصتہ یف راس املال، و ھی من رشاکت الاموال، و لھا احاکم رشکۃ العنان الا ما یتعلق بتحدید م

امتناع الفسخ من احد الرشاک۔

(۵۵۱،۲۵۱،۱۵۵،۳۵۲)البندین

ر مبین یممل معھا ، و یرتتب عیل رشکۃ املساھمۃ تثبت لھا الشخصیۃ الاعتباریۃ من خالل الااھار القانوین لھا حبیث ینتفی التغری

دود الیت تتطلبھا ت الاھلیۃ لھا ابحلذال اس تقالل ذمتھا املالیۃ عن ذمم الرشاک املسامھنی )احصاب حقوق املالکیۃ( و ثبو

احلاجۃ۔۔۔ اخل۔

دکتور ایرس جعیل النشمی( ۲۲۲)الاحرتاق یف املعامالت املرصفیۃ، ص

، لدلکتور ایرس جعیل النشمی تقدمی جعیل جامس النشمی(۳،۱۳،۶)الفروق ص

Dr. Abdul Azeem Abu Zaid’s View Point.

عۃ او بضاعۃ معینۃ او ما اعتباری او حقیقی ایل املرصف الاسالمی راغبا یرشأء سلتمتثل صورۃ ھذاالبیع یف ان یلحا خشص

حمدودۃ بصفات أہ۔

ادلکتور عبد العظمی ابو ذید( 32)بیع املراحبۃ۔تطبیفاتہ املعارصۃ یف املعارف الاسالمیہ ص

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Dr. Nazia Ham’mad’s View Point.

ئالۃ ارایض بیت املال النشاط الاقتصادی( یف الفقہ الاسالمی یلزمنا التعریض ملس احملاولۃ تلمس دور ادلولۃ الستامثر )یف

والاموال الفاءضۃ عن مصارفھا فیہ کنقطۃ انطالق یف تناول املوضوع بلبحث العلمی املوصل۔۔اخل

Dr. Usama Mohammad Al-Fouli & Dr. Zainab Awoz-Ullah.

امات من قبل ااخاص او ا بہ نقدیۃ او نقدیۃ من نوع مغا یر متثل مجیعھا الزت الاول۔ویمتثل یف احلصول عیل اصول حقیقۃ

اقتصادیۃ معینۃ۔۔اخل

(382)اقتصادایت النقود والمتویل۔ص

Dr. Muhammad Ali Muhayudin Al-Qur’ra Dag’gi’s View Point

لتامنی الاسالمی احلایل ھو یۃ التبادلیۃ،ویف اواملومن ھو یف التامنی التحاری الرشکۃ ویف التامنی التعاوین التبادیل ھی امجلع

ھی وکیلۃ عن ذال حساب التامنی، او صندوق التامنی او ھیئۃ املشرتکنی واانلرشکۃ املساھمۃ املرخصۃ ابلتامنی الاسالمی

احلساب ، واما املومن لہ او املس تامن فھو الشخص الطبیی او الاعتباری۔۔

(23انصیلیۃ ص )التامنی الاسالمی دراسۃ فقھیۃ

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Dr. Ahmad Zaki Badawi & Dr. Sadiqa Yousaf Mahmood’s View Point

م ما ینشا عن ھذا رشکۃ اتفاق خشصنی او اکرثابن یساھم لک منھم یف مرشوع ما یل بتقدمی حصہ من راس مال القسا

ون اہ۔۔ املرشوع من رحب او خسارہ وللرشکۃ خشصیۃ اعتباریۃ تمتتع بھا عن طریق اھرھا طبقا الحاکم القان

دکتور امحد زیک بدوی، صدیقہ یوسف محمود( 43،47،83رصفیۃ، ص )معجم املصطلحات التجاریۃ التجاریۃ و املالیۃ و امل

Dr. Younus Al-Misri’s View Point

الرایض (وسوأء بیت املال یعین بیوت اموال ادلولۃ سوأء اکنت ھذہ الامواملنقولۃ ) اکلنقود والعروض ( او غری منقولہ )اک

ب ان ال یفھم من بیت املال ا نہ حمرد۔۔۔اخلاکنت ھذہ الاموال جامدات او حیواانت اذلل حی

( 78 ص)اصول الاقتصادی الاسالمی ۔

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

CONCLUSION

The preceding discussion makes it ample clear that the Islamic Banking

System put forward by Mufti Taqi Usmani is radically different from the

Conventional system. It is due to these differences that they are in constant

friction and clash with each other. Having said this there is another

important dimension to the reality.

Islam, being a practical way of life, has two sets of rules; one is based on

the ideal objectives of Shariah which is applicable in normal conditions,

and the second is based on some relaxations given in abnormal situations.

The real Islamic order is based on the former set of principles, while the

latter is a concession which can be availed at times of need, but it does not

reflect the true picture of the real Islamic order.

Mufti Taqi Usmani has dealt with both types of Islamic rules. Living under

constraints, the Islamic banks are mostly relying on the second set of rules.

The Banking system put forward by Mufti Taqi Usmani is based on the best

possible concessions that may be availed of in the transitory period where

the Islamic Institutions are working under pressure of the existing legal and

fiscal system.

Even with these concessions, the system that has been put forward is in a

collision course with the conventional Banking system and in the future one

of them will have to totally move out of the picture. The two systems are

working in parallel and there is friction between them. This system put

forward by Mufti Taqi Usmani is not a patch up effort. This Islamic

Banking system has an identity of its own.

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

References (Ph.D), Abdulqadir Ibrahim Abikan. 2012. "Contract of Kafalah (Guarantee): A Veritable

Product of Islamic Financing?" ISRA 18.

Ahmad, Ashfaq. 2010. "Islamic Banking Experience of Pakistan: Comparison between."

International Journal of Business Management 7.

Al-Jazari. 1943 A.D. Al-Fiqh ala Madahib Al-Arba'ah. Beruit: Dar Lhya Al-urath Al-

Arabi.

Aman, Sunjun. 2012. Difference between Islamic banking and Conventional banking

system: EXIM Bank limited. BBA program Requirment, Canada: BRAC

University.

ANNUAR, HAIRUL AZLAN BIN. 2001. "Al- Wakalah: Impact on the Performance of

Takaful Operators." IIUM 24.

Ayub, Muhammad. 2007. Understanding Islamic Finance. England: John wiley & Sons,

LTD.

BADER, MOHAMMED KHALED. 2008. "COST, REVENUE, AND PROFIT

EFFICIENCY OF ISLAMIC BANKS." Islamic Economics 54.

BAKAR, MUDZAFFAR ABU. 2011. "BROAD DISTINCTION BETWEEN ISLAMIC

AND CONVENTIONAL BANKING." MALYSIAN PRESS INSTITUTE 18.

Clement M. Henry, Rodney Wilso. 2004. The Politics of Islamic Finance. Edinburgh:

Edinburgh University Press.

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

Eisenberg, David. 2012. Islamic Finance: Law and Practice. UK: Oxford University

Press.

El-Gamal, Mahmoud A. 2006. Islamic Finance: Law, Economics, and Practice. New

York,NY: Cambridge University Press.

Faizulayev, Alimshan. 2006-2009. "Comparative Analysis between Islamic Banking and

Conventional Banking Firms in terms of Profitability,." Institute of Graduate

Studies and Research 65.

Frank E. Vogel, Samuel L. Hayes. 1998. Islamic Law and Finance: Religion, Risk, and

Return. Netherland: Kluwer Law International.

Furqani, Dr. Hafsa. 2013. "Fatwa in Islamic Finance." ISRA 6.

Gohou, Hela Miniaoui and Gaston. 2011. "Did The Islamic Banking Perform Better

During Crisis." International Conference on Management, Economics and Social

Sciences2011 6.

Hanif, Muhammad. 2011. "Differences and Similarities in Islamic and Conventional

Banking." International Journal of Business and Social Science 10.

Haseeb Shahid, Ramiz ur Rehman,Ghulam Shabbir Khan Niazi,Awais Raoof. 2010.

"Efficiencies Comparison of Islamic and Conventional Banking." International

Research Journal of Finance and Economics 19.

Hassan, Abdullah Alwi Haji. 2007. Sales and Contracts in Early Islamic Commercial

Law. Islamabad: Islamic Research Institute.

FINAL-TERM PROJECT

ISLAMIC ECONOMICS THEORY AND PRACTICE

MS – IBF, BATCH 4

UNIVERSITY OF MANAGEMENT AND TECHNOLGY

IRAF. 2011. "Shariah Issues in Relation to the Operations of Supporting Institutions in

Islamic Finance." IRAF 22.

Usmani, Mufti Muhammad Taqi. 1998. An Introduction to Islamic Finance. Faisalabad:

Maktaba Al-Arafi.

.دار الندوا :بحرین .مذکرہ البیوع الشرعیۃ .۵۸۹۱ .دکتور عصام ,العنزی

.ساقی کتب :لبنان .لمعامالت العالیۃ المعاصرۃ فی ضو الفقہ و الشرعیۃ .۴۰۰۲ .دکتور محمد رواس قلعۃ ,جی

.الصیرفۃ االسالمیۃ :اردن .النظام المصر فی االسالم .۴۰۵۰ .دکتور محمد ,سراج

الفکردار :مصر .المعامالت العالیۃ المعاصرۃ .۴۰۰۲ .دکتور محمد عثمان ,شبیر .

.المکتبہ االسکندریۃ :مصر .دراستہ فقیہۃ .۴۰۵۵ .شیخ االزھر محمد سید ,طنطاوی

.دار الدعوی :استمنبول .عقود الشرکات .۴۰۰۲ .دکتور محمد عبید ہللا ,عتیقی

.دار اللھیہ و الفراک :بیروت .مذکرۃ الوکاالت االستثمار و التورق و التوریق .۴۰۰۵ .دکتور عبدالباری ,مشعل

.دار الفکر :بیروت .دراسۃ شرعیۃ الھم العقود المالیۃ المستحدث .۴۰۰۸ .دکتور محمد ,مصطفی

.لحیہ السنت النبویۃ :مصر .احکام االسواق العالیۃ .۴۰۵۴ .دکتور محمد صبری ,ھارون