Islamic Banking in Bangladesh

45

Executive Summary "Islamic Banking is as old as the religion itself with its principles primarily derived from the Quran” - Mohammed Naveed (Revivalist) With an aim to explore the current Islamic banking scenario of Bangladesh, this study examines the key concepts of Islamic banking and its history in the world and in Bangladesh as well. This secondary data based research meets its objectives of reviewing relevant concepts, history and current performance of the Islamic banks of Bangladesh through both qualitative and quantitative approaches. From the establishment of first Islamic bank in 1983, this country has currently eight Islamic banks. Except one individual bank (ICBIBL), most of the Islamic banks show remarkable growth in their profitability in the last decade. One reason behind this consistent negative figure in profitability of this bank is the frequent change of ownership. But overall significant contribution of the Islamic banks in the banking industry is visible from the research. This paper provides up-to-date scenario of the Islamic banking in Bangladesh.

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Islamic Banking in Bangladesh

Executive Summary"Islamic Banking is as old as the religion itself with its principles primarily derived from the

Quran” - Mohammed Naveed (Revivalist)

With an aim to explore the current Islamic banking scenario of Bangladesh, this study examines the key concepts of Islamic banking and its history in the world and in Bangladesh as well. This secondary data based research meets its objectives of reviewing relevant concepts, history and current performance of the Islamic banks of Bangladesh through both qualitative and quantitative approaches. From the establishment of first Islamic bank in 1983, this country has currently eight Islamic banks. Except one individual bank (ICBIBL), most of the Islamic banks show remarkable growth in their profitability in the last decade. One reason behind this consistent negative figure in profitability of this bank is the frequent change of ownership. But overall significant contribution of the Islamic banks in the banking industry is visible from the research. This paper provides up-to-date scenario of the Islamic banking in Bangladesh.

Contents1.0 Introduction....................................................................................................................................4

1.1 Objectives............................................................................................................................................4

1.2 Methodology........................................................................................................................................5

2.1 Islamic Banking:..................................................................................................................................6

2.1 Concepts used Islamic Banking:..........................................................................................................7

2.2 Usury in Islam:.....................................................................................................................................7

2.3 Islamic Banking in Bangladesh:..........................................................................................................7

2.4 Principles in Islamic Banking:.............................................................................................................9

3.1 SOURCES OF FUNDS.....................................................................................................................11

3.1.1 Capital & Equity.............................................................................................................................11

3.1.2 Transaction Deposits.......................................................................................................................11

3.1.3 Investment Deposits........................................................................................................................11

3.2 UTILISATION OF FUNDS..............................................................................................................12

3.3 Difference between Balance Sheet of Conventional Banks and Islamic Banks................................13

4.1 Overview of Industrialization through Islamic Banking over the World:.........................................16

4.2 Evolution of Islamic Banking in Bangladesh:...................................................................................20

4.3 Profit Sharing:....................................................................................................................................21

4.3 Contribution in Industrialization:.......................................................................................................22

4.3.2 The operational success of Islamic banking in Bangladesh............................................................26

4.3.3 Achievement based on financial indicators....................................................................................28

4.3.4 Deposits...........................................................................................................................................28

4.3.5 Number of depositors......................................................................................................................29

4.3.6 Investment.......................................................................................................................................29

4.3.7 Classified Investment......................................................................................................................29

4.3.7 Remittance......................................................................................................................................30

4.3.8 Import..............................................................................................................................................31

4.3.9 Export..............................................................................................................................................31

4.3.10 Deposit-investment ratio...............................................................................................................31

4.4 Shari'ah Compliance..........................................................................................................................31

4.5 Human Resources Development Activities.......................................................................................32

5.0 Impact of Islamic Banking in Employment generation......................................................................34

5.1 Direct Job Creation:...........................................................................................................................34

5.2 Indirect Job Creation:.........................................................................................................................34

5.3 Job Creation through Industrialization, Infrastructure Development:...............................................35

5.4 Job Creation through Special Investment Scheme:...........................................................................35

5.5 Job Creation through SMEs and Agricultural Sector:.......................................................................35

5.6 Job Creation through Micro Financing:.............................................................................................36

5.7 Through poverty eliminatory schemes:.............................................................................................36

5.8 Through Entrepreneurship Development:..........................................................................................36

5.9 Through Encouraging Women:..........................................................................................................36

6.0 Distinct Advantages of Islamic Banking:...........................................................................................37

6.1 Encourages lending (to individuals without assets):..........................................................................37

6.2 Raises savings:...................................................................................................................................38

6.3 Enhances financial stability:..............................................................................................................38

6.4 Finances morally acceptable projects:...............................................................................................39

6.5 Lack of Economies of Scale:.............................................................................................................39

7.0 Challenges for Islamic Banking.........................................................................................................40

7.1 The Practice of Usury:.......................................................................................................................40

7.2 Shariah Risk:......................................................................................................................................40

7.3 Uncertainty in Laws:..........................................................................................................................41

7.4Absence of Codification:....................................................................................................................42

Conclusion...............................................................................................................................................43

1.0 IntroductionIslamic banking and finance is a creation of modern age. Capitalism argues, capital- one of the key factors of production, deserves fixed return whereas the entrepreneurs have to bear all the risks. The conflict of opinions with the Islamic values starts from this very basic point. As the conventional banking systems follow the philosophy of capitalism and interest which is forbidden according to Islamic Shariah, the Muslims made the first move toward the Islamic financial system was observed in the second half of 20th century when the Muslim world got liberation from colonial powers (Hanif, 2011). Conference of Foreign Ministers of Muslim countries (1973) can be marked as a landmark of the growth and popularity of Islamic Financial Institutions (IFIs). Soon after this conference, Bangladesh signed the Charter of Islamic Development Bank n August 1974. Analyzing the demand and feasibility of Islamic banking, Islami Bank Bangladesh Limited, the first Islamic bank of Bangladesh was established in March 19833 . Currently eight Shariah based Islamic banks are operating in Bangladesh with their significant contributions to the banking industry and to the financial system of the country as well.

1.1 ObjectivesThe key objectives of the study are:

To review the distinctive concepts of Islamic banking To analyze the history of Islamic banking To evaluate the current practice and performances of the Islamic banks of Bangladesh To evaluate contribution of the Islamic banks of Bangladesh in Industrialization To evaluate contribution of the Islamic banks of Bangladesh in Employment Generation

1.2 Methodology This is a secondary data based report. Information has been collected from various secondary sources like journal articles, annual reports of different banks, books and different websites. All the existing Islamic banks of Bangladesh are included in this study. The first two objectives of the research are subject to be achieved through the secondary data review and the qualitative discussion. Current Islamic banking practices and the performances of different Islamic banks are measured and analyzed from the financial statements of the banks and information from different relevant websites. Statistical analysis tool SPSS and MS Excel had been used for analysis and graphical presentations.

2.0 Overview of Islamic Banking Banking plays an important role in the economy of any country. Bangladesh is the third largest Muslim country in the world with around 150 million populations of which about 90 percent are Muslim. These people possess strong faith on Allah and they want to lead their lives as per the construction given in the holy Quran and the way shown by the prophet Hazrat Mohammad (Sm). But Islamic banking system was developed here up to 1983 was centered to interest, which strongly prohibited repeatedly in Islam. This interest based banking system had been in action right from the British colonial period and employment of the Muslims in banks was more or less restricted. During the period 1947-1971 when country was a part of Pakistan but the rulers did not take any practical attempt to establish economic system based on Islamic Principles.Since independence, Bangladesh saw a new trend in banking both at home and abroad. Islamic banking as a new paradigm started in Bangladesh in 1983 with the establishment of the first Islamic bank “Islami Bank Bangladesh Limited”. The innovation of interest-free banking systems, proved its worth in the country’s money market and many new banks have been established to operate in compliance with Shari’ah and many traditional banks have opened their Islamic banking branches.

2.1 Islamic Banking:Islamic banking is a banking system that is based on the principles of Islamic law (also known Shariah) and guided by Islamic economics. Two basic principles behind Islamic banking are the sharing of profit and loss and, significantly, the prohibition of the collection and payment of interest. Collecting interest is not permitted under Islamic law.Here's an example of how the Islamic banking system uses methods of profit/loss sharing to facilitate financial transactions: for some types of loans, the borrower only needs to pay back the amount owed to the lender, but the borrower can choose to pay the lender a small amount of money to serve as a gratuity. Since this system of banking is grounded in Islamic principles, all the undertakings of the banks follow Islamic morals. Therefore, it could be said that financial transactions within Islamic banking are a culturally distinct form of ethical investing (for example, investments involving alcohol, gambling, pork, etc. are prohibited). The Dubai Islamic Bank has the distinction of being the world's first full-fledged Islamic bank, formed in 1975.

2.1 Concepts used Islamic Banking:A number of economic concepts and techniques were applied in early Islamic banking, including bills of exchange, partnership (mufawada, including limited partnerships, or mudaraba), and forms of capital (al-mal), capital accumulation (nama al-mal), cheques, promissory notes, (Muslim traders are known to have used the cheque or ṣakk system since the time of Harun al-Rashid (9th century) of the Abbasid Caliphate, trusts (Waqf), transactional accounts, loaning, ledgers and assignments. Organizational enterprises independent from the state also existed in the medieval Islamic world, while the agency institution was also introduced during that time. Many of these early capitalist concepts were adopted and further advanced in medieval Europe from the 13th century onwards.

2.2 Usury in Islam: The word "riba" literally means “excess or addition”, and has been translated as interest, usury, excess, increase or addition. According to Shariah terminology, it implies any excess compensation without due consideration (consideration does not include time value of money).According to International Business Publications, the "common view of riba among classical jurists" of Islamic law and economics during the "Islamic Golden Age" was that it was unlawful to apply interest to gold and silver currencies, "but that it is not riba and is therefore acceptable to apply interest to fiat money -- currencies made up of other materials such as paper or base metals -- to an extent." Thus, when "currencies of base metal were first introduced in the Islamic world, no jurist ever thought that paying a debt in a higher number of units of this fiat money was riba" as they were concerned with "the real value of money."According to Islamic economists Choudhury and Malik by the time of Caliph Umar, the prohibition of interest was a well-established working principle integrated into the Islamic economic system.This interpretation of usury has not been universally accepted or applied in the Islamic world. A school of Islamic thought which emerged in the 19th century, led by Syed Ahmad Khan, argued for a differentiation between sinful "usury", which they saw as restricted to lending for consumption, and legitimate "interest", for lending for commercial investment.

2.3 Islamic Banking in Bangladesh:Banking sector is indispensable in a modern age and modern society.It always plays a vital role to the economic development of a country. In modern age of science and technology the banking sector all over the world has been undergoing a lot of changes due to deregulation, technological innovation and globalization. But Bangladeshi banking sector is lagging to keep pace with the other countries to adapt the changes. Basically bank take deposits from the customers against some interest payments and lend the money to the borrowers with a different interest rate and time period. To ensure safety of the depositors fund there are various types of credit facility. Also bank must hold adequate fund to meet the daily needs of the clients. The First Security Islami Bank Ltd (FSIBL) is a 3rd (Third) generation is doing its business with a view to serve the best to the customers and clients all over the country.

Kosmidou and Zopounidis (2008) evaluated and rated the performance and efficiency of the commercial and cooperative banks in Greece for the period 2003-2004. They found in this study that commercial banks are becoming more competitive and maximizing their profits by increasing their accounts, attracting more customers and improving their financial indices. But in case of the cooperative banks, it has been found that, some are enjoying considerably increased profits and market shares while financial indices have been found to be deteriorating for others.Moreover, the services of private commercial banks in this country are now better than before. As a result, the clients are rushing to the private banks. Consequently, the private commercial banks are constantly growing in different branches, creating employment opportunities, increasing deposit, loan disbursement, net income and earnings per share over a period of time. As competition is rising in the banking industry due to the emergence of new banks in the market, it has become important to evaluate the performance of every private commercial bank. (Chowdhury and Islam, 2007).Islamic banks are facing immense national and global challenges, when it is making financial transactions, trading or as a working partner. However, if appropriate laws and regulations persist in a society or at the global level, Islamic banks can manifest its performance appropriately. Two prolific writers of Islamic finance, Ahmad and Hassan remark that Islamic banks in Bangladesh came into existence with certain objectives, in line with the philosophy of Islamic economics that imply a direct and specific responsibility on their part to play an effective role in the socioeconomic development of the country. (Ahman, auf. and hassan, k.,2001)It has been found that these depositors and entrepreneurs have got the opportunity to practice Shariahbased banking and fulfil their religious obligation. Alam describes the reasons behind the success of IBBL and narrated that in addition of Shariahcompliance, senior officials of the bank also keep a regular contact with customers and bank managers frequently visit them in their places of business. Referring to the chief of the Investment Department of the IBBL, Alam commented that though this bank initially faced some challenges, the situation is getting better than before. (Alam, M.N., 2000)Referring to the existence of Islamic banking amid conventional banking system and economy, Sarkar expresses that Islamic banking system can provide efficient banking services if they are supported with appropriate banking laws, and regulations (Sarker, A.A.,1999)Hassan views that the successful launching and operation of Islamic banks in Bangladesh has established that banking without interest is feasible. He also observes that Islamic banks have brought together many new depositors and entrepreneurs under the banking system. (Hasan, K., 1999).Though there are a number of definitions exist, it is generally understood that economic development refers to the standard of living of the citizens improved through alleviating poverty and increased productivity. Also Kifle, Olukoshi, Wohlgemuth support this idea that there is a strong relationship between poverty alleviation and economic development. (Kifle, H., Olukoshi, A., Wohlgemuth, l., 1997)

Banks and financial institutions are contributing in the economic development of Bangladesh through exploring different lucrative economic segments in the form of investment and lending. Banks of our country play roles from conventional and Islamic perspective. Islamic Banks are operating based on Islamic sariah& principles that does not support interest based banking where as conventional banks are in favor of interest and conventional rules & regulation. So, it is necessary to determine how much extent of impact of Islamic Banking activities of a commercial bank on economic development in Bangladesh.

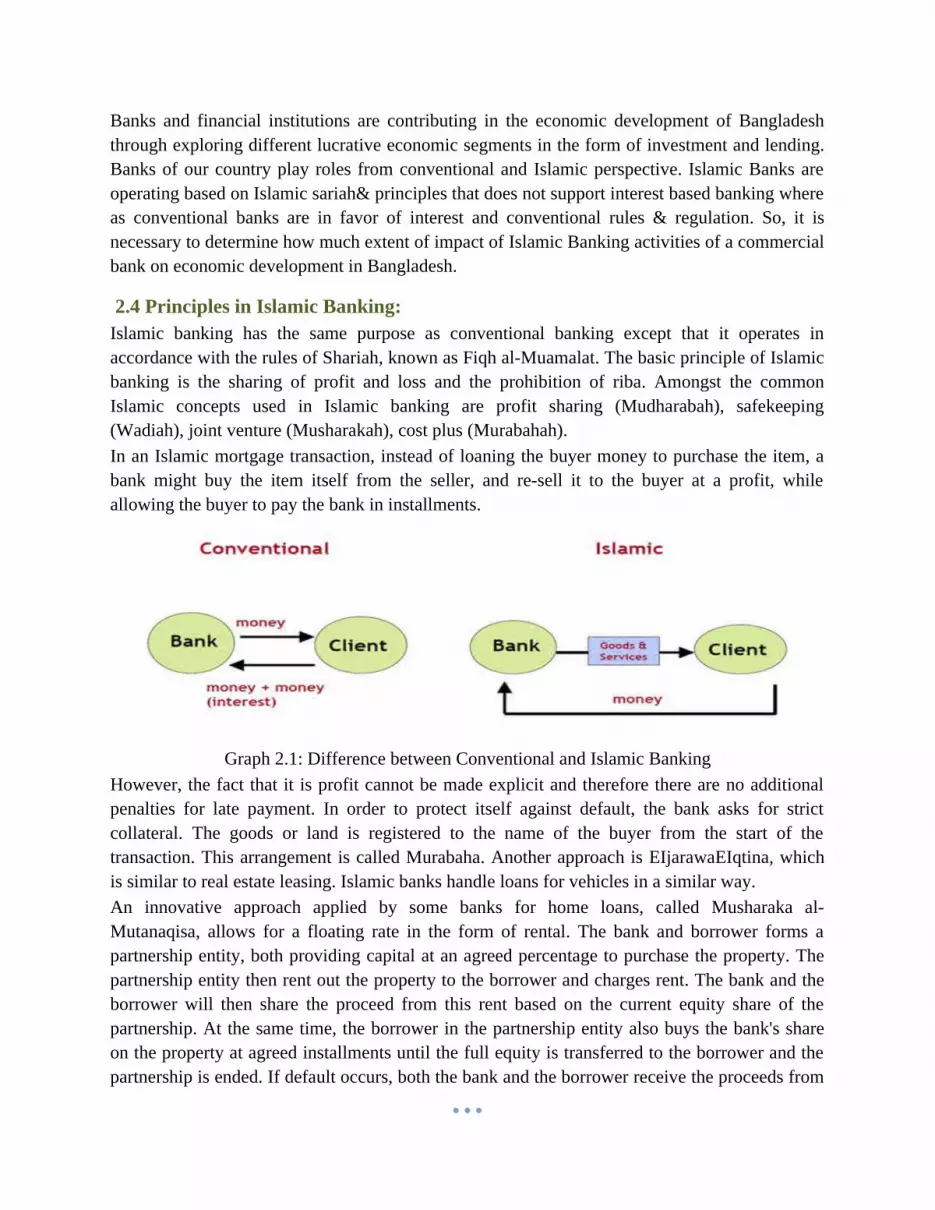

2.4 Principles in Islamic Banking:Islamic banking has the same purpose as conventional banking except that it operates in accordance with the rules of Shariah, known as Fiqh al-Muamalat. The basic principle of Islamic banking is the sharing of profit and loss and the prohibition of riba. Amongst the common Islamic concepts used in Islamic banking are profit sharing (Mudharabah), safekeeping (Wadiah), joint venture (Musharakah), cost plus (Murabahah).In an Islamic mortgage transaction, instead of loaning the buyer money to purchase the item, a bank might buy the item itself from the seller, and re-sell it to the buyer at a profit, while allowing the buyer to pay the bank in installments.

Graph 2.1: Difference between Conventional and Islamic BankingHowever, the fact that it is profit cannot be made explicit and therefore there are no additional penalties for late payment. In order to protect itself against default, the bank asks for strict collateral. The goods or land is registered to the name of the buyer from the start of the transaction. This arrangement is called Murabaha. Another approach is EIjarawaEIqtina, which is similar to real estate leasing. Islamic banks handle loans for vehicles in a similar way.An innovative approach applied by some banks for home loans, called Musharaka al-Mutanaqisa, allows for a floating rate in the form of rental. The bank and borrower forms a partnership entity, both providing capital at an agreed percentage to purchase the property. The partnership entity then rent out the property to the borrower and charges rent. The bank and the borrower will then share the proceed from this rent based on the current equity share of the partnership. At the same time, the borrower in the partnership entity also buys the bank's share on the property at agreed installments until the full equity is transferred to the borrower and the partnership is ended. If default occurs, both the bank and the borrower receive the proceeds from

an auction based on the current equity. This method allows for floating rates according to current market rate such as the BLR (base lending rate), especially in a dual-banking system like in Malaysia.There are several other approaches used in business deals. Islamic banks lend their money to companies by issuing floating rate interest loans.The floating rate of interest is pegged to the company's individual rate of return. Thus the bank's profit on the loan is equal to a certain percentage of the company's profits. Once the principal amount of the loan is repaid, the profit-sharing arrangement is concluded. This practice is called Musharaka. Further, Mudaraba is venture capital funding of an entrepreneur who provides labor while financing is provided by the bank so that both profit and risk are shared. Such participatory arrangements between capital and labor reflect the Islamic view that the borrower must not bear all the risk/cost of a failure, resulting in a balanced distribution of income and not allowing lender to monopolize the economy. And finally, Islamic banking is restricted to acceptable deals, which exclude those involving alcohol, pork, gambling, etc. Thus ethical investing is the only acceptable form of investment, and moral purchasing is encouraged. In theory, Islamic banking is an example of full-reserve banking, with banks achieving a 100% reserve ratio.However, in practice, this is not the case, and no examples of 100 per cent reserve banking are observed. Islamic banks have grown recently in the Muslim world but are a very small share of the global banking system. Micro-lending institutions founded by Muslims, notably Grameen Bank, use conventional lending practices and are popular in some Muslim nations, especially Bangladesh, but some do not consider them true Islamic banking. However, Muhammad Yunus, the founder of Grameen Bank and microfinance banking, and other supporters of microfinance, argue that the lack of collateral and lack of excessive interest in micro-lending is consistent with the Islamic prohibition of usury.

3.0 Sources & Application of Funds

3.1 SOURCES OF FUNDSIslamic banks rely on the following sources of funds:

1. Capital & Equity;2. Transaction deposits that are risk free and yield no return; and3. Investment deposits that carry the risks of capital loss for the promise of variable returns.

3.1.1 Capital & Equity Capital is the amount injected into the Islamic bank during the setting-up stages i.e. the

paid-up capital of the Islamic bank. Equity is usually the retained earning of the Islamic bank that accumulated during its

operational period.

3.1.2 Transaction Deposits Current accounts

Current accounts are based on the principle of Wadiah, whereby the depositors are guaranteed repayment of their funds. At the same time, the depositor does not receive remuneration for depositing funds in a current account, because the guaranteed funds will not be used for PLS ventures. Rather, the funds accumulating in these accounts can only be used to balance the liquidity needs of the bank and for short-term transactions on the bank’s responsibility.

Savings accountsSavings accounts also operate under the Wadiah principle. Savings accounts differ from current deposits in that they earn the depositors income: depending upon financial results, the Islamic bank may decide to pay a premium, hiba, at its discretion, to the holders of savings accounts.

3.1.3 Investment Deposits Investment accounts

An investment account operates under the Mudaraba al-mutlaqaprinciple, in which the Mudarib (active partner) must have absolute freedom in the management of the investment of the subscribed capital. The conditions of this account differ from those of the savings accounts by virtue of:1. A higher fixed minimum amount,2. A longer duration of deposits, and3. Most importantly, the depositor may lose some of or all his funds in the event of the bank making losses.

Special investment accountsSpecial investment accounts also operate under the Mudaraba principle, and usually are directed towards larger investors and institutions. The difference between these accounts and the investment account is that the special investment account is related to a specified project, and the investor has the choice to invest directly in a preferred project carried out by the bank.

3.2 UTILISATION OF FUNDSTo generate revenue, Islamic banks utilized the funds by giving out financing facilities. The financing facilities are done based on the Islamic concepts accepted by the Islamic bank Shariah Council / Committee.The concepts usually applied by the Islamic bank are as follows.

Murabaha (cost plus / mark up)This is the most commonly used mode of financing device. In aMurabaha transactions, the bank finances the purchase of a good or assets by buying it on behalf of its client and adding a mark-up before reselling it to the client on a cost-plus basis profit contract.

Bai’ muajjal (deferred payment)Islamic banks have also been resorting to purchase and resale of properties on a deferred payment basis. It is considered lawful in Fiqh (jurisprudence) to charge a higher price for a good if payments are to be made at a later date. According to Fiqh this does not amount to charging interest, since it is not a lending transaction but a trading one.

Bai’ salam (prepaid purchase)This method is really the opposite of the Murabaha. There the bank gives the commodity first, and receives the money later. Here the bank pays the money first and receives the commodity later, and is normally used to finance agricultural products.

Istisna’a (manufacturing)This is a contract to acquire goods on behalf of a third party where the price is paid to the manufacturer in advance and the goods produced and delivered at a later date.

Ijarah and Ijara Wa Iqtina (leasing)Under this mode, the banks buy the equipment or machinery and lease it out to their clients who may opt to buy the items eventually, in which case the monthly payments will consist of two components, i.e. rental for the use of the equipment and installment towards the purchase price.

Qard Hasan (benevolent loans/ Interest free loans)

This is the zero return type of loan that the Holy Quran urges Muslims to make available to those who need them. The borrower is obliged to repay only the principal amount of the loan, but is permitted to add a margin at his own discretion.

3.3 Difference between Balance Sheet of Conventional Banks and Islamic BanksIn general, the Balance Sheet of an Islamic Bank looks no different from a Conventional Bank. Conventionally, all deposits are managed internally and the Treasury team will use the funds as efficient as possible into the various instruments in the market. In this sense, all the deposits are used to fund mixed assets into a single pool, and its returns are a consolidation of all the returns derived from the assets.

Under the Islamic Banking regime, there is greater emphasis on matching the deposits against assets. While the management of the deposits into a single pool is not disallowed by Islamic Banking, it is the payment of returns that is most important under Sharia compliance where the fairness and justice to the customer is deemed to happen.

Graph 3.1 Balance Sheet of Conventional BanksAs such, to ensure that the returns to customer’s deposits (or investment) are fair, the level of transparency in the management of the deposits needs to be increased. Therefore, it is easier to

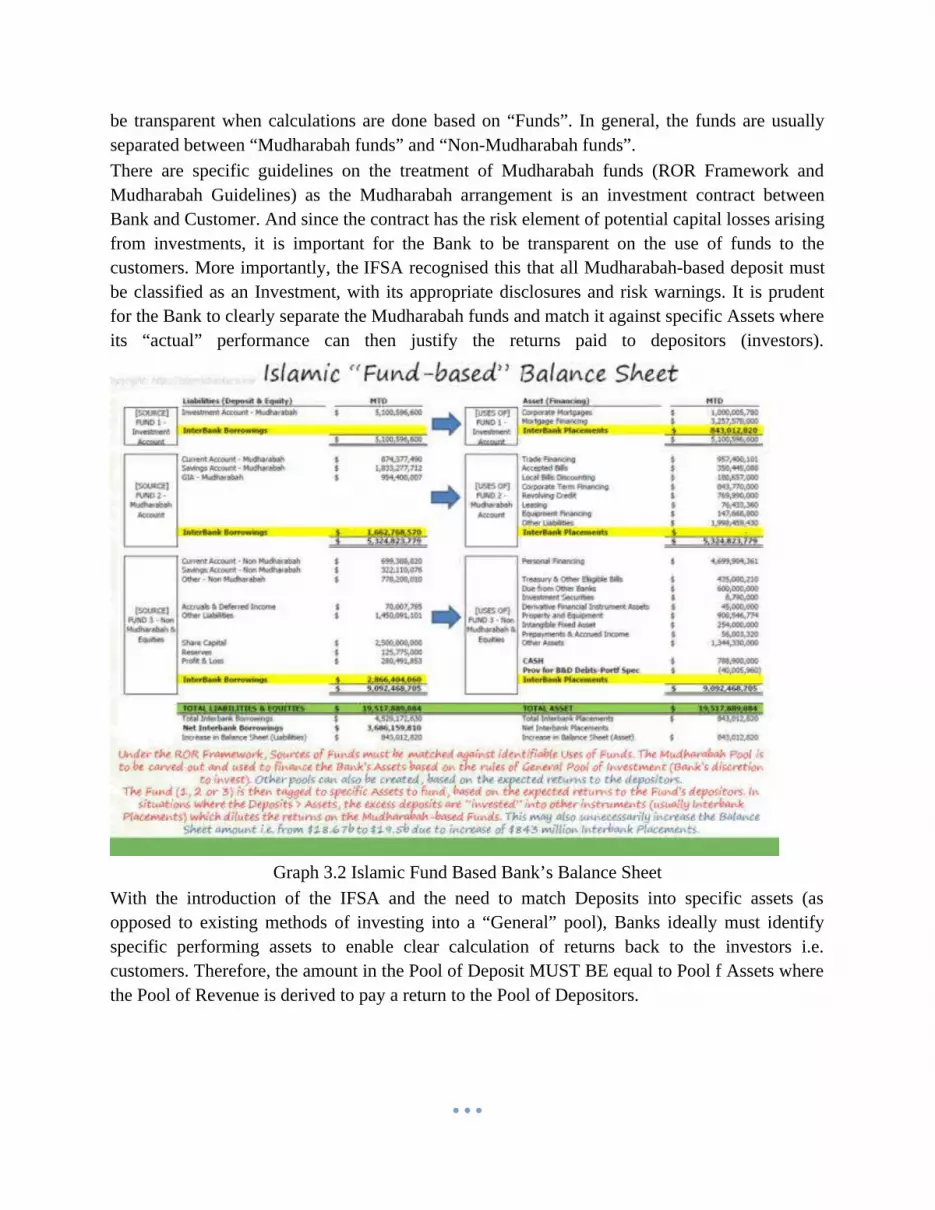

be transparent when calculations are done based on “Funds”. In general, the funds are usually separated between “Mudharabah funds” and “Non-Mudharabah funds”.There are specific guidelines on the treatment of Mudharabah funds (ROR Framework and Mudharabah Guidelines) as the Mudharabah arrangement is an investment contract between Bank and Customer. And since the contract has the risk element of potential capital losses arising from investments, it is important for the Bank to be transparent on the use of funds to the customers. More importantly, the IFSA recognised this that all Mudharabah-based deposit must be classified as an Investment, with its appropriate disclosures and risk warnings. It is prudent for the Bank to clearly separate the Mudharabah funds and match it against specific Assets where its “actual” performance can then justify the returns paid to depositors (investors).

Graph 3.2 Islamic Fund Based Bank’s Balance SheetWith the introduction of the IFSA and the need to match Deposits into specific assets (as opposed to existing methods of investing into a “General” pool), Banks ideally must identify specific performing assets to enable clear calculation of returns back to the investors i.e. customers. Therefore, the amount in the Pool of Deposit MUST BE equal to Pool f Assets where the Pool of Revenue is derived to pay a return to the Pool of Depositors.

4.0 Impact of Islamic Banking on Economic Development & Industrialization

Due to global economic recession, time is very much challenging and uncertain. Specially, this calamity become acute with eventual collapse of some major banking institution and massive dips in stock market indices across the globe. As a result, developing economy like Bangladesh economy deteriorated rapidly.

Bangladesh represents a underdeveloped financial system which leads a slow economic growth. According to the international monetary fund, Bangladesh ranked as the 48th largest economy in the world in 2009, with a GDP of US$256 billion. Although Bangladeshi economy is based on agriculture, more than half of the GDP is belongs to the service sector such as transport, financial institution, real estate education, public administration, health, social and personal service. From the financial institution, banking industry is the most essential.

The banking industry of Bangladesh is now highly competitive and challenging sector rather than previous period of time. Basically banking sector is involved with financial system. To have a healthy and vibrant economy it needs a financial system that moves funds from people who save people who have strong productive investment opportunities. And we know that, a country’s economic development means development the economy of a country which concern with trade, industry and wealth of the country.

Despite sluggish economic scenario, the FSIBL passed successfully with the help of their efficient and prudent workforce. Thus FSIBL has been able to close the balance sheet with an enormous pre-tax profit of Tk.750 million with an excellent growth rate of 300% while the whole financial sector faced a slowdown. Banking institution can create an impacton the economy through its general activities like deposit collection, giving loan, invest in different economic sector such as agriculture, garments, house building etc. export and remittance business.

There is a link between financial system and economy. Without financial sector an economic system can not draw its growth. Banks are the most financial intermediaries and FSIBL is not

different from them. General banking activities are like the flow of bloods of any bank which are practiced and operated to keep a bank alive.

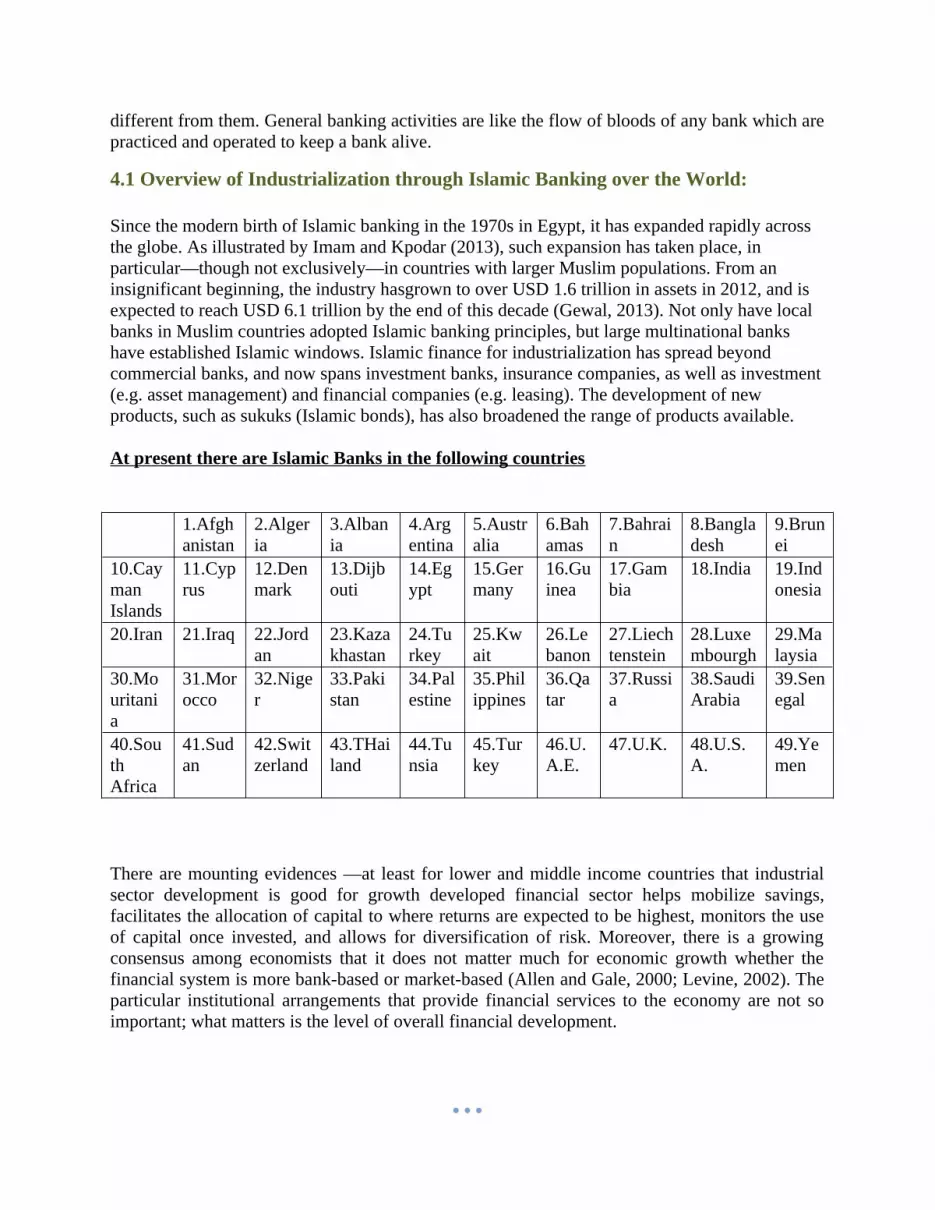

4.1 Overview of Industrialization through Islamic Banking over the World:

Since the modern birth of Islamic banking in the 1970s in Egypt, it has expanded rapidly across the globe. As illustrated by Imam and Kpodar (2013), such expansion has taken place, in particular—though not exclusively—in countries with larger Muslim populations. From an insignificant beginning, the industry hasgrown to over USD 1.6 trillion in assets in 2012, and is expected to reach USD 6.1 trillion by the end of this decade (Gewal, 2013). Not only have local banks in Muslim countries adopted Islamic banking principles, but large multinational banks have established Islamic windows. Islamic finance for industrialization has spread beyond commercial banks, and now spans investment banks, insurance companies, as well as investment (e.g. asset management) and financial companies (e.g. leasing). The development of new products, such as sukuks (Islamic bonds), has also broadened the range of products available.

At present there are Islamic Banks in the following countries

1.Afghanistan

2.Algeria

3.Albania

4.Argentina

5.Australia

6.Bahamas

7.Bahrain

8.Bangladesh

9.Brunei

10.Cayman Islands

11.Cyprus

12.Denmark

13.Dijbouti

14.Egypt

15.Germany

16.Guinea

17.Gambia

18.India 19.Indonesia

20.Iran 21.Iraq 22.Jordan

23.Kazakhastan

24.Turkey

25.Kwait

26.Lebanon

27.Liechtenstein

28.Luxembourgh

29.Malaysia

30.Mouritania

31.Morocco

32.Niger

33.Pakistan

34.Palestine

35.Philippines

36.Qatar

37.Russia

38.Saudi Arabia

39.Senegal

40.South Africa

41.Sudan

42.Switzerland

43.THailand

44.Tunsia

45.Turkey

46.U.A.E.

47.U.K. 48.U.S.A.

49.Yemen

There are mounting evidences —at least for lower and middle income countries that industrial sector development is good for growth developed financial sector helps mobilize savings, facilitates the allocation of capital to where returns are expected to be highest, monitors the use of capital once invested, and allows for diversification of risk. Moreover, there is a growing consensus among economists that it does not matter much for economic growth whether the financial system is more bank-based or market-based (Allen and Gale, 2000; Levine, 2002). The particular institutional arrangements that provide financial services to the economy are not so important; what matters is the level of overall financial development.

DZA

AGO

BGD

BWA

BFA

CMR

CHN

ZAR

COG

CIV

EGY

ETH

GAB

GMB

GHA

GIN

G N B

DNI

IDN

IRNJOR

KEN

LBN

LBR

LBY

GMD

MWI

MYS

MLI

MNG

MA R

MOZ

NAM

NER

AKP

P GN

PHL

SEN

ZAF

LKA

SDN

SYR

TZA

THA

TGO

TU N

TUR

UGA

MVNMYE

MBZWE

Log of average GDP per capita

mus

lim p

op s

hare

=75%

56

78

9

0 20 40 60 80 100Muslim population share

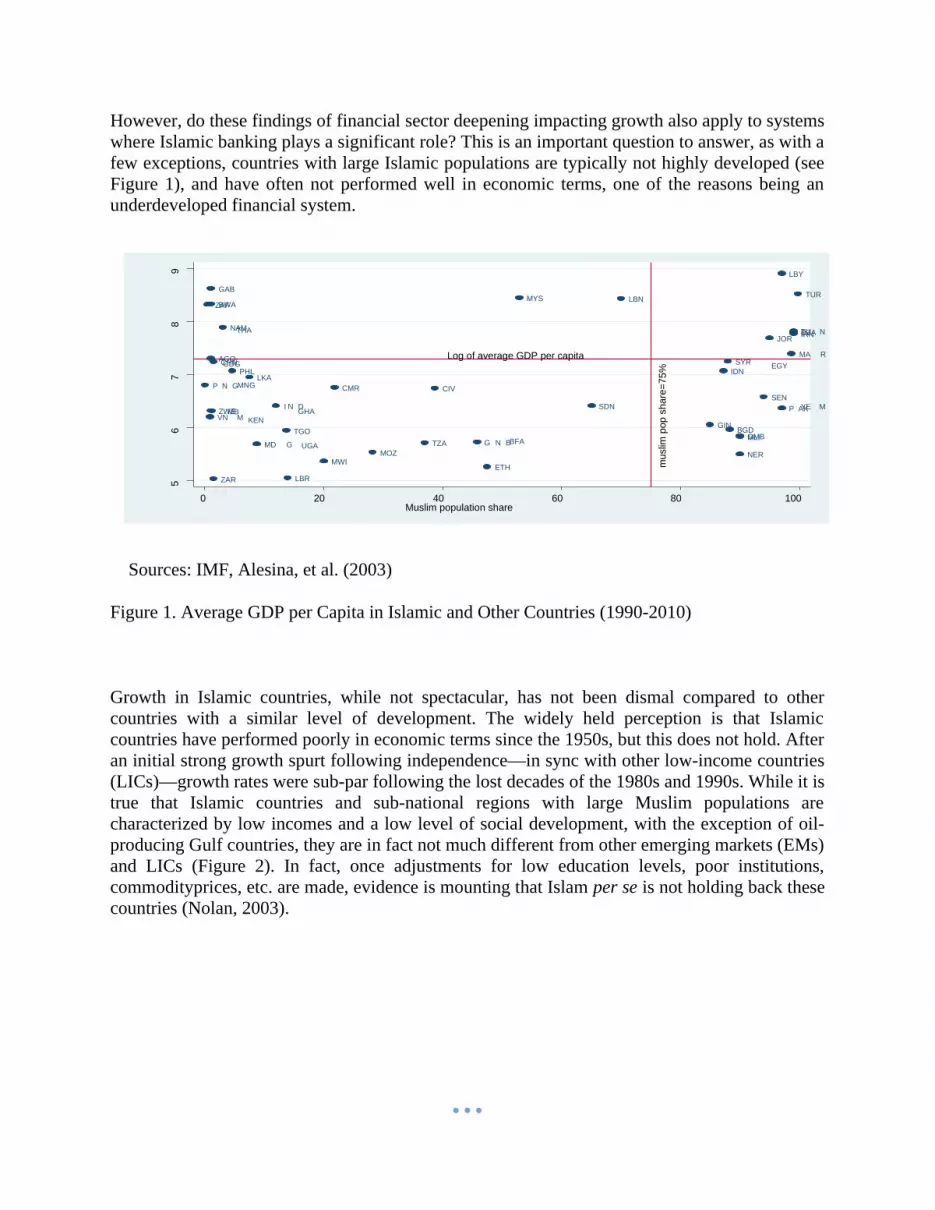

However, do these findings of financial sector deepening impacting growth also apply to systems where Islamic banking plays a significant role? This is an important question to answer, as with a few exceptions, countries with large Islamic populations are typically not highly developed (see Figure 1), and have often not performed well in economic terms, one of the reasons being an underdeveloped financial system.

Sources: IMF, Alesina, et al. (2003)

Figure 1. Average GDP per Capita in Islamic and Other Countries (1990-2010)

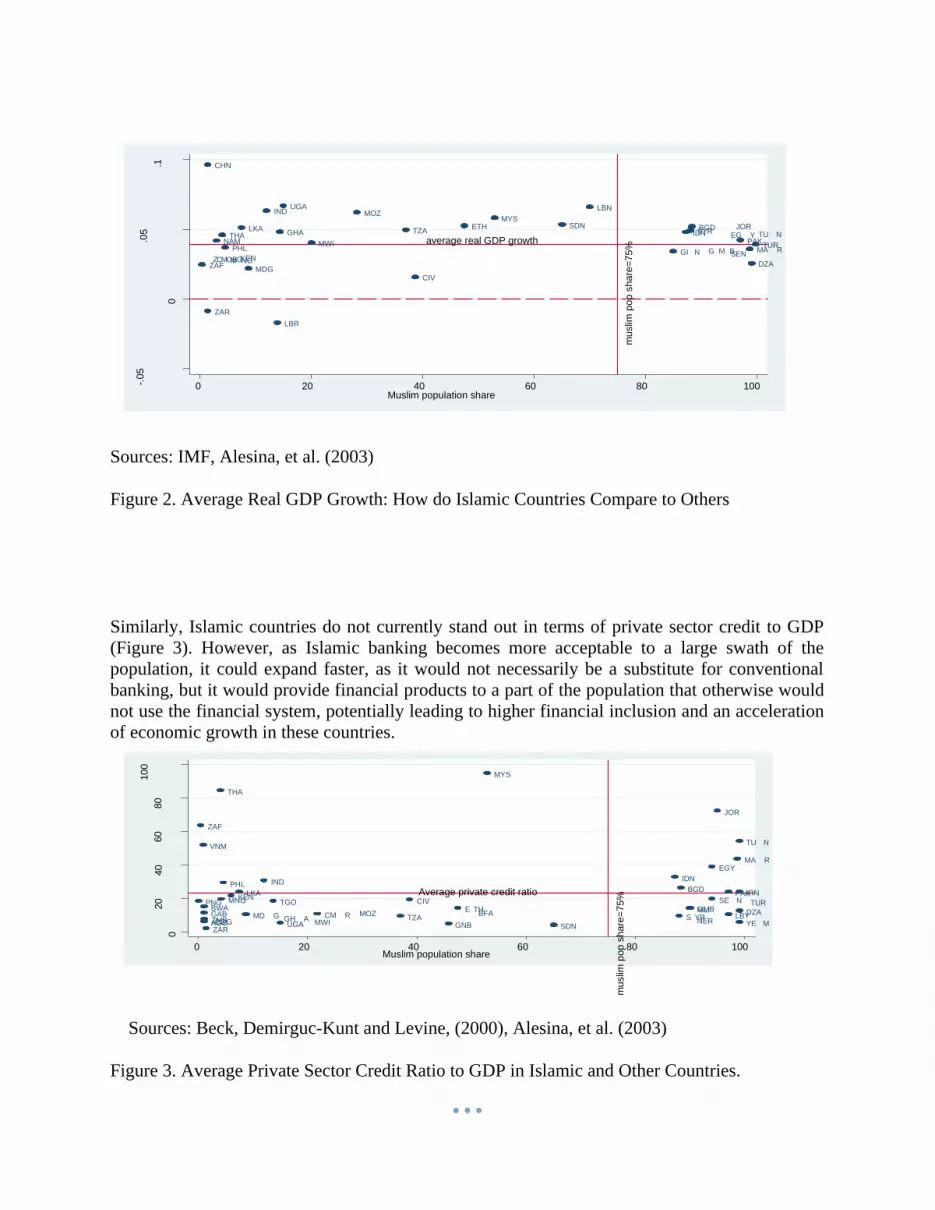

Growth in Islamic countries, while not spectacular, has not been dismal compared to other countries with a similar level of development. The widely held perception is that Islamic countries have performed poorly in economic terms since the 1950s, but this does not hold. After an initial strong growth spurt following independence—in sync with other low-income countries (LICs)—growth rates were sub-par following the lost decades of the 1980s and 1990s. While it is true that Islamic countries and sub-national regions with large Muslim populations are characterized by low incomes and a low level of social development, with the exception of oil-producing Gulf countries, they are in fact not much different from other emerging markets (EMs) and LICs (Figure 2). In fact, once adjustments for low education levels, poor institutions, commodityprices, etc. are made, evidence is mounting that Islam per se is not holding back these countries (Nolan, 2003).

DZA

BGD

CHN

ZAR

O GC

CIV

EG YETH

BMG

GHA

NGI

IND

IDNJOR

KEN

LBN

LBR

MDG

MWI

MYS

NGMMA R

MOZ

NAM PAKPHL

SENZAF

LKA SDNSYRTZATHA TU N

TUR

UGA

M BZ

average real GDP growth

mus

lim p

op s

hare

=75%

-.05

0

.05

.1

0 20 40 60 80 100Muslim population share

DZAAGO

BGD

BWABFARCM

ZARCOG

CIV

EGY

E THGAB GMBGH A

GNB

IND IDN

IRN

JOR

KEN

LBYGMDMWI

MYS

MLIMNG

MA R

MOZNER

PAKPNG

PHL

NSE

ZAF

LKA

SDNYRSTZA

THA

TGO

TU N

TUR

UGA

VNM

MYEZMB

Average private credit ratio

mus

lim p

op s

hare

=75%

020

4060

8010

0

0 20 40 60 80 100Muslim population share

Sources: IMF, Alesina, et al. (2003)

Figure 2. Average Real GDP Growth: How do Islamic Countries Compare to Others

Similarly, Islamic countries do not currently stand out in terms of private sector credit to GDP (Figure 3). However, as Islamic banking becomes more acceptable to a large swath of the population, it could expand faster, as it would not necessarily be a substitute for conventional banking, but it would provide financial products to a part of the population that otherwise would not use the financial system, potentially leading to higher financial inclusion and an acceleration of economic growth in these countries.

Sources: Beck, Demirguc-Kunt and Levine, (2000), Alesina, et al. (2003)

Figure 3. Average Private Sector Credit Ratio to GDP in Islamic and Other Countries.

Thus, the rapid diffusion of Islamic banking represents a growth opportunity for Islamic countries, as much of the empirical evidence suggests a strong link between financial sector development and growth (see Levine (2005) for a summary). However, the empirical literature has only looked at conventional banking, not Islamic banking. This paper aims to rectify this lacuna, by considering whether Islamic banking is also potent in raising growth. This paper aims to establish the positive relationship between Islamic banking and economic growth, and not to answer the question of whether the growth-enhancing effect of Islamic banking goes beyond that of conventional banking. Using a sample of low- and middle income countries with data over the period 1990-2010, we investigate the impact of Islamic banking on growth and discuss the policy implications. The results show that, notwithstanding its relatively small size compared to the economy or the overall size of the financial system, Islamic banking is positively associated with economic growth even after controlling for various determinants, including the level of financial depth. The results are robust across different measures of Islamic banking development, econometric estimators (pooling, fixed effects and System GMM), and to the sample composition and time periods.

The paper is structured as follows. Section II reviews the advantages, with a focus on how Islamic banking could help financial deepening, and ultimately growth. Section III presents the sample, the econometric model, and estimators, as well as the results. Section IV concludes with the policy implications.

Major Appraisal:

Although the finance–growth nexus continues to be heavily debated in the literature, the main thrust is that financial development has, by and large, a favourable impact on economic growth. Financial intermediaries carry out five basic functions that serve growth: they (i) Facilitate the trading, hedging, diversifying, and pooling of risk; (ii) Allocate resources; (iii) Monitor managers and exert corporate control; (iv) Mobilize savings; and (v) Facilitate the exchange of goods and services. In performing their functions, financial intermediaries mitigate the effects of information and transaction costs, and improve the allocation of resources, thus influencing saving rates, investment decisions, technical innovation, and ultimately long-run growth rates. In turn, economic activity can also influence financial development. It is worth noting that this whole literature implicitly refers to conventional banking. An interesting question is: does this also apply to Islamic banks?

While Islamic banks perform similar functions to conventional banks, they have distinct features. In fact, Islamic banking has many advantages, not only in Islamic countries, but also in low- and middle-income countries in general, that could explain why it is preferable in stimulating growth to conventional banking, under certain circumstances.

4.2 Evolution of Islamic Banking in Bangladesh:

Islamic banking system is a quiet new phenomenon in the money market of Bangladesh. At present there are 8 fully fledged Islamic banks, 7 banks have dual banking system and 6 other conventional banks have Islamic windows in Bangladesh. All the banks have their respective Shari’ah supervisory committees. Central Shari’ah Board for Islamic Banks of Bangladesh (CSBIBB) is an apex body of the Shari’ah committees of the Islamic banks and banks having Islamic branches or windows, established in the year 2002 with a view to oversee whether the Islamic banks are carrying out their operations in conformity with Islamic Shari’ah principles and give decisions on Shari’ah issues to the banks to run their business under uniform rules of Shari’ah.

The History of Islamic Banking system in Bangladesh and its growth has given below in a nutshell:

1974 - Bangladesh signed the charter of IDB;

1978 - Bangladesh government subscribed recommendation of Islamic Foreign Minister’s conference held in Senegal;

1979 - Mohammad Mohsin, Ambassador of Bangladesh in the UAE recommended establishment of an Islamic bank in Bangladesh;

1980 - Prof. ShamsulHuq, Foreign Minister, at Foreign Minister’s conference in Pakistan proposed for development of an Islamic international banking system;

1980 - Bangladesh Bank sent a representative to study the working of several Islamic banks of different countries. An international seminar on Islamic banking organized by Islamic Economics Research Bureau (IERF) held in Dhaka, inaugurated by the Governor of Bangladesh Bank;

1981 - President of the People’s Republic of Bangladesh (at 3rd Islamic Summit Conference in Makkah and Taif) suggested: ‘The Islamic countries should develop a separate banking system of their own in order to facilitate their trade and commerce’;

1982 - a delegation of IDB visited Bangladesh and showed keen interest to participate in establishing a joint venture Islamic Bank;

IERB was established in 1976 and BIBA (Bangladesh Islami Banker’s Association) established in 1980 made significant contributions towards introduction of Islamic banking in the country;

1983 - Islami Bank Bangladesh Limited was founded by 19 Bangladeshi nationals, 4 Bangladeshi institutions and 11 banks, financial institutions and government bodies of the Middle East and Europe including IDB and two eminent personalities of the Kingdom of Saudi Arabia;

1987 - Al Baraka Bank (The Oriental Bank) was established;

1995 - Al ArafahIslami Bank and Social Investment Bank was established;

1995 – Prime Bank started dual banking for the first time in Bangladesh. Prime Bank is the pioneer in such a kind of blending of conventional and Islamic banking in the country which is followed by other banks later.

1997 - Shamil Bank of Bahrain started its operation;

2001 - ShahjalalIslami Bank was established;

2004 - Exim Bank was converted to Islamic Banking;

2998- Bank Asia Limited started its Islamic Banking operation through opening of Islamic Windows at its Uttara Branch on 24 December 2008. Later another window at Shantinagar branch was opened on 21 January 2009. In 2010 the Bank opened three more windows and currently five windows are working in Dhaka, Chittagong and Sylhet with separate software, fund management and monitoring system.

2009 - The First Security Bank was converted to Islamic Banking;

2009 – Bangladesh Bank issued guidelines for Islamic banking;

2012 – Islamic Interbank Fund market (IIFM, Islamic money market) formally started its operation.

Islamic Banks Consultative Forum (IBCF) has been formed in the year 1995. It is comprised of all Chairmen and Managing Directors or CEOs of the Islamic Banks and Banks having Islamic Banking branches or windows and one representative of Bangladesh Bank. The forum is playing its role to pursue common interests of Islamic banks with Bangladesh Bank and other government agencies on different issues related to Islamic banking.

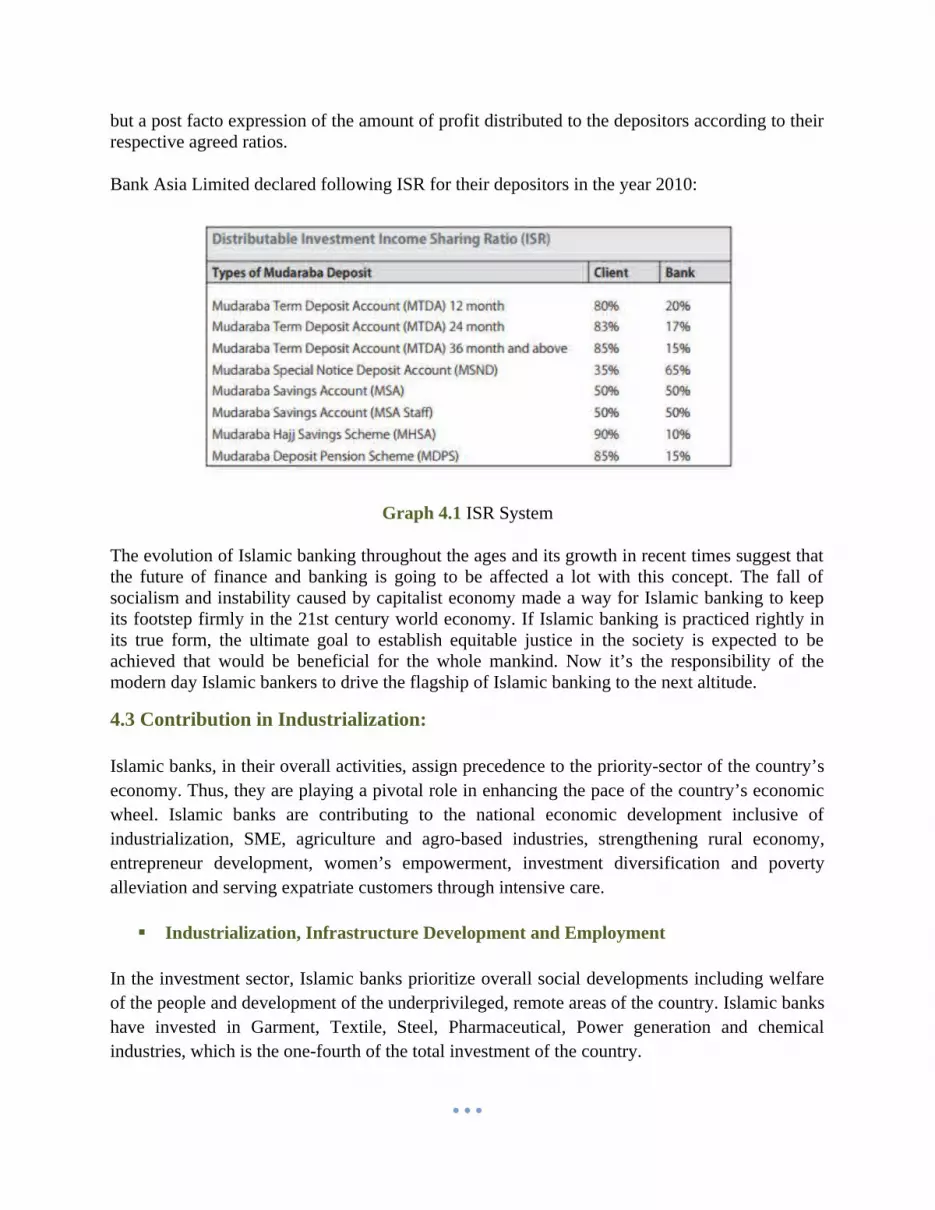

4.3 Profit Sharing:

For profit sharing there is weighted average system used by the Islamic Banks. Nevertheless there is a different type of sharing system in Bank Asia Islamic Banking operation. According to its Income Sharing Module, there will be pre-defined Investment Income Sharing Ratio (ISR) for each type of depositor and the Bank. ISR would determine the portion of distributable investment income to each type of depositor and the Bank. For example, the ISR of 70: 30 would mean that 70% of distributable income is to be shared by the concerned depositors and the rest 30% to be shared by the Bank as Management Fee and/or otherwise. Investment Income Sharing Ratios between each type of Mudaraba depositors and the Bank (Mudarib) to be duly disclosed at the time of Mudaraba contract (Account opening) or at the beginning of the concerned period. Profit rate would be emerged at actual, as derived from the income fetched from deployment of the concerned fund. In other words, rate of profit on deposit under Islamic Banking is nothing

but a post facto expression of the amount of profit distributed to the depositors according to their respective agreed ratios.

Bank Asia Limited declared following ISR for their depositors in the year 2010:

Graph 4.1 ISR System

The evolution of Islamic banking throughout the ages and its growth in recent times suggest that the future of finance and banking is going to be affected a lot with this concept. The fall of socialism and instability caused by capitalist economy made a way for Islamic banking to keep its footstep firmly in the 21st century world economy. If Islamic banking is practiced rightly in its true form, the ultimate goal to establish equitable justice in the society is expected to be achieved that would be beneficial for the whole mankind. Now it’s the responsibility of the modern day Islamic bankers to drive the flagship of Islamic banking to the next altitude.

4.3 Contribution in Industrialization:

Islamic banks, in their overall activities, assign precedence to the priority-sector of the country’s economy. Thus, they are playing a pivotal role in enhancing the pace of the country’s economic wheel. Islamic banks are contributing to the national economic development inclusive of industrialization, SME, agriculture and agro-based industries, strengthening rural economy, entrepreneur development, women’s empowerment, investment diversification and poverty alleviation and serving expatriate customers through intensive care.

Industrialization, Infrastructure Development and Employment

In the investment sector, Islamic banks prioritize overall social developments including welfare of the people and development of the underprivileged, remote areas of the country. Islamic banks have invested in Garment, Textile, Steel, Pharmaceutical, Power generation and chemical industries, which is the one-fourth of the total investment of the country.

Islamic banks give much importance to Import-substitute and export-oriented industries. These banks take up 23.11% of thier total investment in industrialization. Islamic banks are playing a vital role in infrastructural development, including private sector power generation.

Investing 45% of its resources in industrial sector, IBBL has been contributing in country’s industrialization process and has created employment for about 25 lakh people.

SMEs and the agricultural sector

The nature of investment of Islamic banks is more extensive than the size of their investment. These banks are investing in all priority sectors. They have invested 27.96% of their total investment in small and medium sector.

The Islami banks have made tangible contributions in sectors and sub-sectors of agricultural and rural investment programs. In 2013-14 fiscal year, Islamic banks have invested about Tk. 1700 crore on crops, fisheries, livestock, agricultural machinery, irrigation equipment and other poverty alleviation and income generation activities.

Islamic banks have been financing extensively in different types of small and medium industries, especially producing food, seed preservation, cold storage, hospitals and clinics, renewable energy, light engineering industry, plastics industry, jute and jute blended products, frozen food, leather and leather products, rice mill, a variety of small businesses, transport and communications etc.

4.3.1 Evolution of Islamic Banking as a Full Fledged Banking Sector:

People’s Initiative

In the early twentieth century, after the formation of East Bengal and Assam province, centering Dhaka as its capital, the socio-economic development of East Bengal was in a new spur. At that time an initiative was taken to set up and manage interest-free banks in different areas of Bangladesh including Jessore and Cox's Bazar. But those initiatives could not get solid foundation on the backdrop of then socio-economic and political circumstances. Although individual efforts and organizational initiatives continued, however, introduction of Shari’ah-based banking remained a dream for a long time.

State-level initiatives or interventions

After independence, a number of initiatives were taken up from different stages to establish an Islamic bank from the state level. The Bangladesh government signed the IDB Charter in 1974.

Member countries, through the signing of the charter, were committed to reconstructing their banking system in consonance with the Islamic principles.

The definition of Islamic banks was approved in the Dakar conference of OIC member countries in Senegal in 1978. Member Countries of the OIC also approved a set of recommendations for gradual transformation of their banking system into Islamic. Bangladesh actively participated in the conference and qualified to become a partner in implementing the recommendations.

Bangladesh Bank’s supportive role

From the very inception, the Bangladesh Bank has been playing a highly active and positive role in implementing the principles and procedures of Islamic banks in the country.

On 4 April 1981, Ministry of Finance issued a letter to Bangladesh Bank, directing all state-owned banks of the country, on the experimental basis, to open separate Islamic banking counter in all of their branches in towns and villages and to keep separate ledgers for them.

In November 1980, A. S. M. Fakhrul Ahsan, the research director of Bangladesh Bank, was deputed to the Middle Eastern countries to see for himself the activities of Islamic banks and Islamic financial institutions operating there. In January 1981, he submitted a comprehensive report with a set of recommendations to initiate the process of setting up Islamic banks in Bangladesh.

Later, on 18-19 March 1981, on the initiative of BIBM a two-day seminar on Islamic banking was organized in Dhaka. The then first deputy Governor of Bangladesh Bank M. Khalid Khan inaugurated the seminar as chief guest, where recommendations were taken up to set up Islamic banks in both public and private sectors.

On June 9-11, 1981, a senior official of the Bangladesh Bank took part in an international seminar held in Geneva, Switzerland on Islamic Banking and Insurance.

On 16 October, 1982, at the 4th Bankers’ meeting of the Bangladesh Bank, chaired by the then-governor Nurul Islam, decision was taken to introduce Islamic banking in all branches of six state-owned commercial and two specialized banks at metropolitan and district headquarters level as soon as possible.

In the light of the decision of Bangladesh Bank and for creation of suitable manpower for Islamic Banking, a one-month long full-time residential course was held on 6 October 1981 at Sonali Bank Staff College. A total of 37 officers from Bangladesh Bank, all state-owned banks, BIBM and then-proposed 'Dhaka International Islamic Bank Limited (now, the Islami Bank Bangladesh Limited) took part in the course.

The then Principal of Sonali Bank Staff College M. Azizul Haq played a vital role in the successful implementation of the course. The opening ceremony was presided over by M. Khaled, the then Chairman and Managing Director of Pubali Bank.

While the training course was underway, M. Khaled was appointed second deputy governor of Bangladesh Bank. He was the special guest at the closing ceremony of the training program as the Deputy Governor of Bangladesh Bank.

Other Initiatives

From 1979 to 1982, a number of public and private institutions in the country took part in the preparatory work for the establishment of Islamic banks. At the time, a `Working Group for the Islamic banking in Bangladesh’ was constituted under the leadership of M. Khaled. He also led the reorganizing process of the group and subsequently it came to be known as ‘Bangladesh Islamic Bankers Association (BIBA).

At that time, several national and international seminars and training courses on Islamic banking were organized by Bangladesh Institute of Bank Management (BIBM), Islamic Economics Research Bureau, Bai’tus Sar’f Islamic Research Institute, Chittagong where, senior bankers, economists and professionals of the country took part. In the mean time, more than 300 bank officials were trained on Islamic banking.

Emergence of a real entity

A number of local individuals as well as Islamic Development Bank (IDB) and various financial institutions began to extend their cooperation to establish Islamic banks in the country. With the commendable initiative of Islamic Development Bank (IDB) Kuwait Finance House, Dubai Islamic Bank, Bahrain Islamic Bank, Islamic Investment and Exchange Corporation of Luxemburg, Al-Razi Company for Currency Exchange and Commerce of Saudi Arabia and three Ministry of Kuwait provided 70% capital for the establishment of an Islamic bank for the first time in Bangladesh.

The remaining capital came from local entrepreneurs, where Bangladesh Government’s share was five percent. On 13 March 1983, Islami Bank Bangladesh Limited was registered as the first shari’ah-based Bank in South-East Asia and began operation on 30 March of the year.

Along the path of success of the country’s first Islamic bank, several Islamic banks were established in later years. In 1987 Al Baraka Bank, in 1995 Al-Arafah Islami Bank and Social Investment Bank and in 2001 Shahjalal Islami Bank were established.

On 1 July 2004, Exim Bank and 1 January 2009 First Security Bank have transformed their activities to Islamic banking style. Shari’ah-based 'Union Bank' was established in 2013.

4.3.2 The operational success of Islamic banking in Bangladesh

On August 1, 1983, on the occasion of launching of the first Islamic bank in Bangladesh, special supplements were brought out in different national dailies. Dr. MN Huda, a senior professor of economics, Dhaka University noted in his writing, "Islamic banking has won theoretical level. Now, this method will have to be won in operational areas….”

After three decades of Islamic banking operations in Bangladesh since its inception, one can see how successful this system is in fulfilling the expectations of the common people.

Objective Achievement

Islamic banks assign precedence to universal welfare, inclusive growth and equitable distribution of resources in their entire activities. One should therefore gauge the success of this system applying objective criteria instead of traditional financial indicators. To assess the contribution of Islamic banking and its position, asset or profit considerations that are used conventionally will provide us only a partial picture.

In this regard, it can be mentioned here a significant comment by noted Islamic banking personality Dr. Saleh Kamel. In the 35th annual conference of the Islamic Development Bank in Baku, the capital of Azerbaijan in 2012, Dr. Saleh Kamel, the then Chairman of `General Council for Islamic Banks and Financial institutions’ (CIBAFI), an international organization comprising Islamic banks and financial institutions, drawing attention of concerned all and said:

"... Over the past decades, academic researchers and professional Islamic banking practitioners and Shari’ah specialists have emphasized more on the procedural side of Islamic Banking. We have gained some success in following Interest-free transactions and legal procedures. But the underlying strength of the Islamic Banking and the 'Maka’sida' or the purposes of this system like justice in wealth distribution, public welfare and emancipation from economic slavery, were not received due importance and priority in the works of Bankers and Shari’ah experts’ as much as it was needed.”

Islamic banking is based on the principles of serving as the masses in the light of Islamic economy or its 'Maqa’sid' or purpose. The savings policy in Islamic Banks is to bring deposits—

big or small--- within the Banking framework and to utilize those in national growth and development.

The first Islamic bank of the country has been opening deposit accounts only for Tk. 100 since its inception and farmer accounts for Tk. 10 since 1994, even long before when the central bank have passed a directive in this regard.

In the mid of the last century, development was considered as `strength of the national economy’ to the economists. Average per capita income of the rich and the poor was the basis of this concept of development. Now, in view of modern economists, `how wealth is produced is not the main question. Instead, to ensure fair distribution of the wealth is the prerequisite for development.’

Explaining reasons for poverty and famine, Nobel laureate economist Amartya Sen stated: "It is not the limitation of resources; rather lack of rights of people on resources is the causes of famine.”

Decentralization and the social distribution of resources is one of the core principles of Islamic economy. Thus, determining the shape and nature of the investment and diversification of economic activities and geographical location is a moral obligation and an essential strategy for Islamic banks.

Shari’ah-based banks have obligations to devote their accumulated resources to people-oriented welfare works, complying with Islamic legal principles of `halal-haram’. Islamic banks can not invest in any inauspicious sector even it is financially advantageous. To comply with the policy of financing to those sectors beneficial for the society and the state, the IBBL has not invested a single penny in tobacco sector during last three decades.

In terms of financial cost, micro-credit programs may seem a cumbersome and non-profitable venture to many people. Nevertheless, considering the social return, Islamic banks are playing an important role in this sector. Islami Bank Bangladesh Limited has deployed 4 percent of its total investment to the micro-credit sector and approximately 20 % of its workforce is engaged in managing this area. It mirrors a clear institutional mindset of Islamic banking.

Islamic banks finance activities that gear towards poverty alleviation. In addition to financing they generate resources to distribute them among the people through various mandatory and optional transfer payments including Zakat, Osarah, Sada’qah, Atonement and Waq’f. 'Kalyanamukhi (welfare-oriented) Banking'. 'Building a Compassionate Society', 'Better Service' --- these slogans of the Islamic Banks manifest its broader outlook.

4.3.3 Achievement based on financial indicators

Now, a total of 23 public and private commercial banks are operating full-fledged or partially Islamic banking operations in Bangladesh. Among them, 8 full-fledged Islamic banks are operating with 843 branches, 8 conventional commercial banks with 19 Islamic banking branches and 7commercial banks with 25 Islamic banking windows in the country. A total of 26,135 employees are working in 887 Islamic banking branches and windows.

The average growth of deposit in the banking sector in last five years (2009-2013) was 19% which was 20% for Islamic banks.

During this period the average investment growth of country’s banking sector was 18%, which was 20% for Islamic banks. For the same period, the total assets in banking sector increased by 19%. In contrast, Islamic banks have achieved 21% growth.

In the last five years, mentioned above, the average growth of equities in Islamic banks was 24%, which was 27% for the total banking sector of the country. A number of public banks have increased their capital in 2013, which has contributed to raise the equity index.

Graph 4.2: Comparison of Average Growth between Conventional & Islamic Banks

4.3.4 Deposits

Total deposit of the Islamic banks stood at Tk. 1,13,360 crore in December 2013, which was 18.00% of total deposits of the country and 29% deposits of the private commercial banks. Total deposits of the Islamic banks stood at Tk. 1,33,561 crore in June 2014.

Deposit Investment Asset Equity

20 2021

24

19 1819

27

Average Growth (2009-'13)

Islamic Banks Banking Industry

4.3.5 Number of depositors

In March 2014, the customer deposits of Islamic banks in the country were 1 crore and 17 lakh, which was 17.92% of the total customer deposits. Until this period, country's total customer deposits for all private commercial banks were 2 crore and 78 lakh, of them 42.12% was in the Islamic banks.

4.3.6 Investment

Total investment of the Islamic banks was Tk. 97,530 crore on December 2013, which was 21% of total investments in the country's banking sector and 30% investment of the private commercial banks. Islamic banks’ investment stood at Tk. 113,796 crore on June 2014.

4.3.7 Classified Investment

On December 2013, 8.90% investment of the country's banking sector was in classified, which was 4.2% for Islamic banks. At the same time, the amount of classified investments in Islamic banks, compared to equity was 39.9%, which was 20% lower than the country's banking sector.

Assets

Islamic Banks (8)

17%

Conventional Banks (48)

83%

Asset Share in Banking Industry'13

Islamic Banks (8)

27%

Conventional Banks (31)

73%

Asset Share among PCBs'13

Classified to Total Inv. Classified to Equity0.00

10.0020.0030.0040.0050.0060.00

4.20

39.90

8.90

59.80Classified Investment'13

Islamic Banks Banking Industry

On December 2013, the size of Islamic banks assets stood at Tk. 135,900 crore, which was 17 % of country’s banking assets and 27.40% of the total assets of private commercial banks. Total amount of assets of Islamic banks was Tk. 147,604 crore on June 2014.

Equity

Islamic Banks (8)

15%

Conventional Banks (48)

85%

Equity Share in Banking Industry'13Islamic Banks

(8)23%

Conventional Banks (31)

77%

Equity Share among PCBs'13

By following the principles of capital adequacy rules set by the central bank, Islamic banks’ share in total equity was in a satisfactory level in the past years. Total equity of Islamic banks was Tk. 10,280 crore on December 2013. It is 15 percent equity of the country's banking sector and 23 percent equity share of private commercial banks. Total equity of the country’s Islamic banks stood at Tk. 11,382 crore in June 2014.

4.3.7 Remittance

Islamic Banks (8)

28%

Conventional Banks (48)

72%

Remittance Share in Banking Industry(Jan-Jun'14)

Hard-earned remittance by Bangladeshi expatriates is one of the main pillars of country’s overall economy. Islamic banks play a significant role in transferring it to beneficiaries. Bangladesh received a total of Tk. 57,044 crore in first 6 months (January-June) of 2014. Of the amount, Tk. 15,952 crore has come through the Islamic banks, which was 28% of the total remittance inflow in the country and 43% of PCB’s.

Islamic Banks (8)43%Conventional

Banks (31)57%

Remittance Share among PCBs)(Jan-Jun'14)

4.3.8 Import

The amount of total imports in Bangladesh, during January-June of 2014, was Tk. 167,014 crore. Islamic banks imported over Tk. 34,952 crore; which was 21% of the total imports. The Islamic banks were at the forefront in importing various raw materials and essential goods including fertilizers, cotton, rice, wheat, etc.

4.3.9 Export

Total exports of the country, during January-June 2014 period, stood at Tk. 110,096 crore. The amount of Tk. 26,787 crore has been exported through the Islamic banks, which was 4% of total national exports. Islamic banks have been playing a leading role in drawing of foreign exchange through the export of various products including ready-made garments.

4.3.10 Deposit-investment ratio

The Central bank has set the deposit-investment ratio at 90%, in contrast, the deposit-investment ratio of Islamic banks was 85.10% in December 2013. This ratio was 71.18% in the country's overall banking sector.

4.4 Shari'ah Compliance

Under the condition that banking activities should be operated in consonance with the provisions of Shari'ah, Islami banks have secured approval from Bangladesh Bank. These banks are under the surveillance of Bangladesh Bank for ensuring the terms of this agreement. In 2009, Bangladesh Bank issued some guiding principles for the Islamic Banks in regards to Shari’ah compliance. The Islamic Banks are following these guidelines.

Besides, to ensure the upholding of Shari’ah, each bank has a independent Shari’ah supervising committee, which stay free of the control of the banks’ Board of Directors. Famous Aleems, Fika’h experts, economists and lawyers constitute the committee. They conduct their supervisory

Conven-tional Banks

(48) 79%

Islamic Banks (8)

21%

Import Share in Banking Industry (January-June'14)

Conventional

Banks (48)76%

Islamic Banks (8) 24%

Export Share in Banking Industry (January-June'14)

works independently. Other than administrative activities of the Shari’ah secretariat, it supervises all policy-related and critical macro level issues of these banks.

‘Central Shari’ah Board for Islamic Banks of Bangladesh’ (CSBIB), a body formed by combining the Shari’ah committees of all the Islamic banks of the country, provides instructions or guidance regarding Shari’ah from time to time.

The internal audit teams of the Islamic Banks work vigorously to ensure internal control and compliance. The central bank supervise, monitor and audit through off-site and on-site basis. Leading audit firms of the country also conduct audit and reports the activities of each bank.

Moreover, Shari’ah Muraqibs of the Islamic banks serve to audit Shari’ah compliance of the banks under their own Shari’ah supervisory committee. The Shari’ah supervisory committee prepares assessment and evaluation report on the basis of audit report from Muraqibs. Report of the statutory auditor of the bank as well as the certificate given by Shari’ah supervisory committee is included in the annual report of the Islamic banks.

Islamic banks follow the guidelines of different International organizations regarding their management, quality assessment, administration and for setting accounting policies and management rules and procedures. These organizations include `the International Financial Services Board '(IFSB); `Accounting and Auditing Organization for Islamic Financial Institute '(AAOIFI); and `the Islamic International credit rating agency’ (IICRA).

4.5 Human Resources Development Activities

Currently, more than 26,000 employees are working in Islamic banking sector in the country. They were recruited from different academic disciplines through rigorous competitive examinations. The banks encourage their workforces to achieve professional degrees at higher level. Meanwhile, 14 officers of IBBL have earned Ph.D. on various subjects like economy, Islamic banking, Islami Shari’ah, human resources development etc., from different universities of home and abroad. Among the 306 officers, having the ‘Certified Documentary Credit Specialist’ (CDCS) certificate, 171 are working in different Islamic banks. Of them, 136 are working exclusively in the Islami Bank Bangladesh Limited (IBBL). Moreover, the officials of the Islamic banks regularly take part in the banking diploma examinations under the ‘Institute of Bankers Bangladesh’ (IBB). For this, the banks concerned encourage their employees to obtain diplomas to develop professionalism in their respective fields.

Along with practice of the banking rules and regulations, Islamic banks also train regularly their officials on the subject of Shari’ah. Almost all Islamic banks have their HRD/training centres. Islamic Bank Training and Research Academy (IBTRA) along with training their own staff,

provides Islamic banking foundation training for the new recruits. It also organizes seminars and workshops for the employees of both private and public banns including Agrani Bank, First Security Islami Bank and Shahjalal Islami Bank. Moreover, IBBL has arranged training programs for high officials of the Jaiz Bank International of Nigeria and the bank of Ceylone of Sri Lanka on Islamic banking in Dhaka.

To make the Islamic bank workforce competent, ‘Islamic bank Training and Research Academy’ (IBTRA) introduced ‘Islami Banking Diploma’ (DIB) in 1997. So far, the first and the second part of the diploma have been completed by 3739 and 1696 officers respectively, of different banks.

5.0 Impact of Islamic Banking in Employment generation

Islamic banks, in their overall activities, assign precedence to the priority-sector of the country’s economy. Thus, they are playing a vital role in enhancing the pace of the country’s economic wheel as well as the pace of employment generation. Islamic banks are contributing to the national economic development inclusive of industrialization, SME, agriculture and agro-based industries, strengthening rural economy, entrepreneur development, women’s empowerment, investment diversification and poverty alleviation and serving expatriate customers through intensive care. All these activities directly or indirectly increase the employment vacant.

5.1 Direct Job Creation:According to Resume of Banks and Financial Institutions 2009-2010 published by the government of Bangladesh, ministry of finance, there are 7 Islamic banks and 23 conventional banks in Bangladesh. All of those are local private banks. Data shows that the conventional banks employed 23,358 and 47,187 employees in the year 2009 and 2010 respectively demonstrating a growth of 9 per cent. On the other hand, Islamic banks employed 16,296 and 17,249 employees during the same period showing 6 per cent growth. Both conventional and Islamic banks generated employment for 64,433 persons in the year 2010 in which the share of Islamic banks is 37 per cent. This share reduces to 13 per cent if compared with all banks including state owned and foreign banks.

5.2 Indirect Job Creation:In case of indirect job creation, data collected from Investment Administration Division of Islami Bank Bangladesh Limited shows that till the end of January 2012, four hundred thousand jobs were created in Rural Development Scheme (RDS). Similarly, one hundred thousand in Micro

Enterprise Investment Scheme, six hundred thousand in small and medium enterprises, 2,810 in spinning, 780 in weaving, dyeing and finishing , 2,132 in composite knit, 3,400 in ready made garments.

5.3 Job Creation through Industrialization, Infrastructure Development:In the investment sector, Islamic banks prioritize overall social developments including welfare of the people and development of the underprivileged, remote areas of the country. Islamic banks have invested in Garment, Textile, Steel, Pharmaceutical, Power generation and chemical industries, which is the one-fourth of the total investment of the country.Islamic banks give much importance to Import-substitute and export-oriented industries. These banks take up 23.11% of their total investment in industrialization. Islamic banks are playing a vital role in infrastructural development, including private sector power generation. Investing 45% of its resources in industrial sector, IBBL has been contributing in country’s industrialization process and has created employment for about 25 lakh people.

5.4 Job Creation through Special Investment Scheme:Islamic banks have embarked upon different kinds of welfare-oriented investment programs. With the objective of improving the life style of low-income and lower middle class, they have made investments in ‘Housing Investment scheme,' Rural Housing Investment scheme, 'Home Appliances scheme,' Women Entrepreneurship Development scheme, Small Business Investment scheme, 'Doctor Investment scheme, etc. Through these schemes, these Banks have been increasing the job opportunity and investing to meet the mundane needs of the people.

5.5 Job Creation through SMEs and Agricultural Sector:The nature of investment of Islamic banks is more extensive than the size of their investment. These banks are investing in all priority sectors. They have invested 27.96% of their total investment in small and medium sector. The Islamic banks have made tangible contributions in sectors and sub-sectors of agricultural and rural investment programs. In 2013-14 fiscal year, Islamic banks have invested about Tk. 1700 crore on crops, fisheries, livestock, agricultural machinery, irrigation equipment and other poverty alleviation and income generation activities.Islamic banks have been financing extensively in different types of small and medium industries, especially producing food, seed preservation, cold storage, hospitals and clinics, renewable energy, light engineering industry, plastics industry, jute and jute blended products, frozen food, leather and leather products, rice mill, a variety of small businesses, transport and communications etc. These industries create a lot of job opportunities. And Islamic banks are indirectly responsible for these job creation.