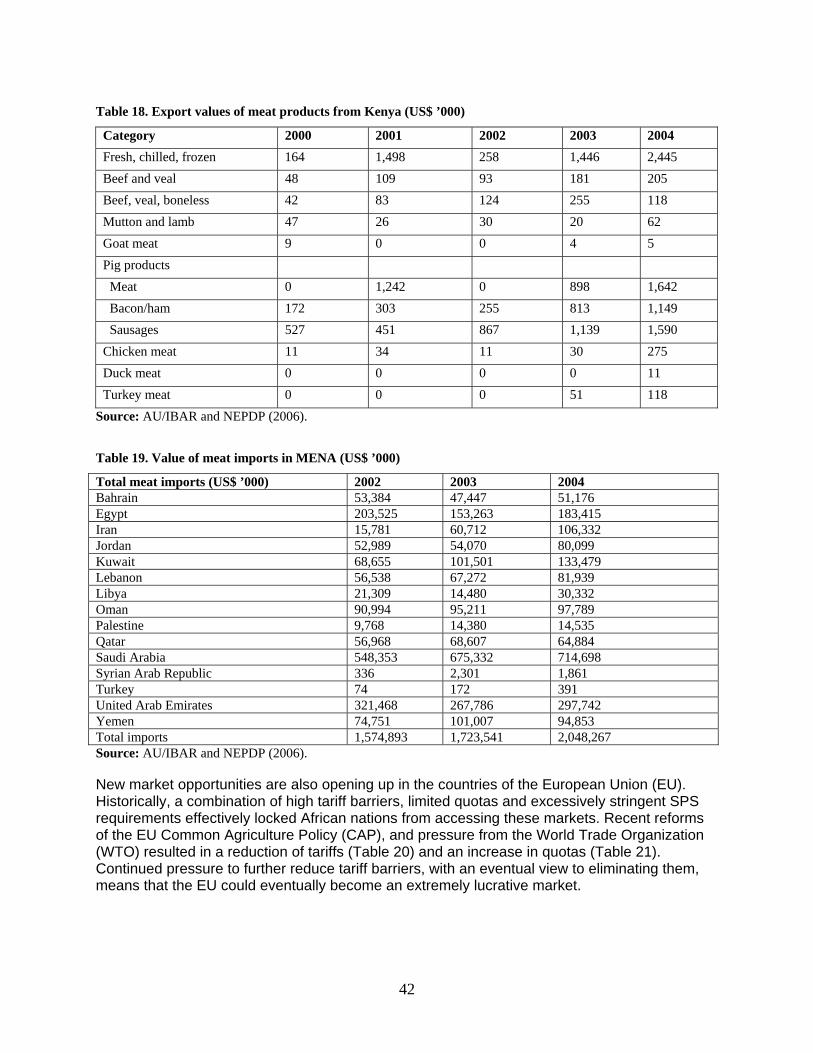

Investment Opportunities for Livestock in the North Eastern ...

72

ReSAKSS Working Paper No. 12 October 2008 Investment Opportunities for Livestock in the North Eastern Province of Kenya: A Synthesis of Existing Knowledge Manitra Rakotoarisoa Stella Massawe Andrew Mude Robert Ouma Ade Freeman Godfrey Bahiigwa Joseph Karugia

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Investment Opportunities for Livestock in the North Eastern ...

ReSAKSS Working Paper No. 12

October 2008

Investment Opportunities for Livestock in the North Eastern Province of Kenya: A

Synthesis of Existing Knowledge

Manitra Rakotoarisoa Stella Massawe Andrew Mude Robert Ouma Ade Freeman

Godfrey Bahiigwa Joseph Karugia

Regional Strategic Analysis and Knowledge Support System

(ReSAKSS)

ReSAKSS Working Paper No. 12

October 2008

Investment Opportunities for Livestock in the North Eastern Province of Kenya: A Synthesis of Existing Knowledge

Manitra Rakotoarisoa

Stella Massawe

Andrew Mude Robert Ouma Ade Freeman

Godfrey Bahiigwa Joseph Karugia

ii

About ReSAKSS The Regional Strategic Analysis and Knowledge Support System (ReSAKSS) is an Africa-wide network that provides analysis, data, and tools to promote evidence-based decisionmaking, improve awareness of the role of agriculture for development in Africa, fill knowledge gaps, promote dialogue and facilitate the benchmarking and review processes associated with the AU/NEPAD’s Comprehensive Africa Agriculture Development Program (CAADP) and other regional agricultural development initiatives in Africa. About the Working Paper series The goal of the ReSAKSS Working Paper series is to provide timely access to preliminary research and data analysis results that relate directly to strengthening ongoing discussions and critical commentaries on the future direction of African agriculture and rural development. The series undergoes a standard peer-review process involving at least one reviewer from within the ReSAKSS network of partners and at least one external reviewer. It is expected that most of the working papers eventually will be published in some other form and that their content may be revised further. For more information, contact: Coordinator Regional Strategic Analysis and Knowledge Support System, East and Central Africa (ReSAKSS-ECA) International Livestock Research Institute (ILRI) P.O. Box 30709 Nairobi, Kenya Telephone: +254 (20) 422 3000 Facsimile: +254 (20) 422 3001 Email: [email protected] Website: www.eca.resakss.org

iii

The authors Manitra Rakotoarisoa is a former researcher with the International Livestock Research Institute (ILRI) and currently working with the UN Food and Agricuture Orgnaization (FAO). Andrew Mude, Robert Ouma and Ade Freeman are researchers with ILRI. Stella Massawe and Joseph Karugia are researchers with ReSAKSS-ECA and Godfrey Bahingwa is the Director of the Plan for Modernisation of Agriculture (PMA), Uganda and a former Coordinator of ReSAKSS-ECA. Acknowledgements Funding for this work was provided by the United States Agency for International Development (USAID), the UK Department for International Development (DFID), and the Swedish International Development Cooperation Agency (SIDA) through their support to the Regional Strategic Analysis and Knowledge Support System (ReSAKSS). The International Livestock Research Institute (ILRI) also contributed towards funding this work. Manitra Rakotoarisoa, Stella Massawe, Andrew Mude, Robert Ouma, Ade Freeman, Godfrey Bahiigwa, and Joseph Karugia, October 2008. Investment Opportunities for Livestock in the North Eastern Province of Kenya: A Synthesis of Existing Knowledge. ReSAKSS Working Paper No. 12, IFPRI. Key words: Livestock investment options, North Eastern Province, Kenya, livelihoods, public and private sectors, and Kenya Vision 2030

Except where otherwise noted, this work is licensed under a Creative Commons Attribution 3.0 License.

iv

TABLE OF CONTENTS

1. INTRODUCTION ................................................................................................................................................ 1

2. THE NORTH EASTERN PROVINCE OF KENYA: DESCRIPTION AND CHALLENGES .................... 1

2.1 CONSTRAINTS TO LIVELIHOOD IN NORTH EASTERN PROVINCE ........................................................................ 2 2.2 THE LIVESTOCK PRODUCTION SYSTEM IN THE NEP .......................................................................................... 8 2.3 ONGOING AND RECENTLY COMPLETED PROJECTS/PLANS FOR THE NEP ........................................................... 9

3. CURRENT STATE OF THE LIVESTOCK SECTOR IN NORTH EASTERN PROVINCE .................... 11

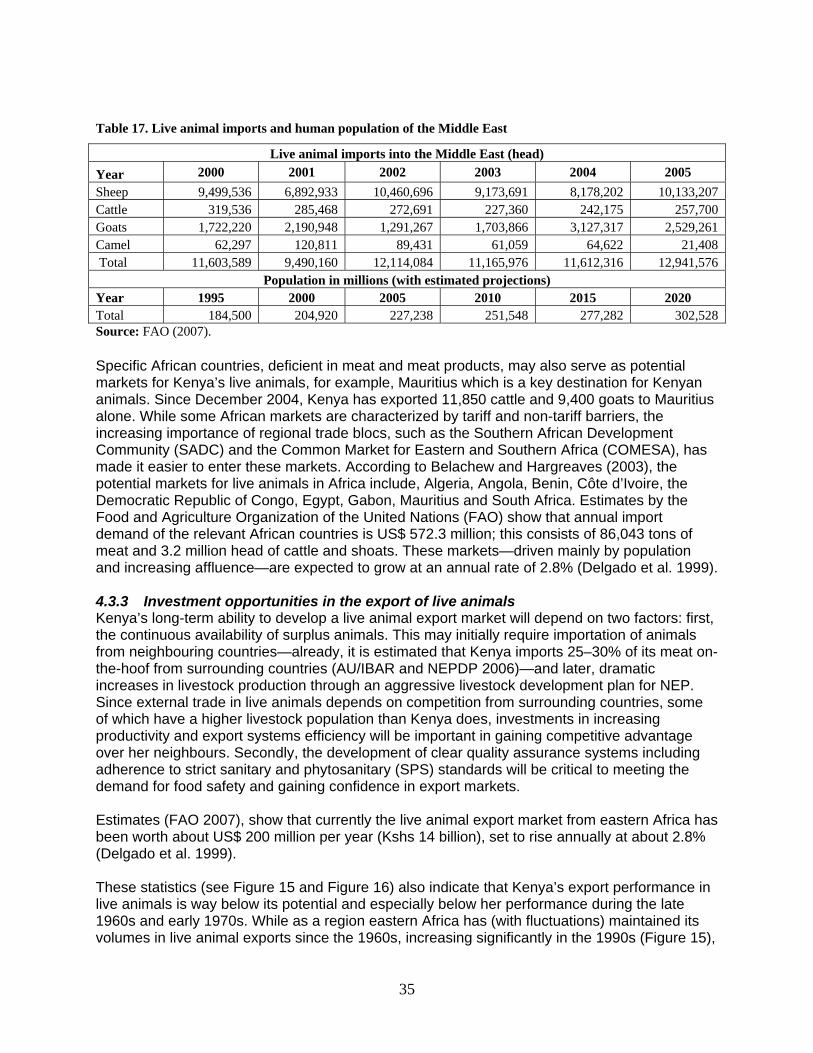

3.1 IMPORTANCE OF LIVESTOCK PRODUCTION TO NEP ....................................................................................... 12 3.2 TRENDS IN LIVESTOCK PRODUCTION .............................................................................................................. 14 3.3 LIVESTOCK AND LIVESTOCK PRODUCT SALE AND PRICES AND FARMERS’ EARNINGS ..................................... 14 3.4 EXTERNAL TRADE IN LIVESTOCK AND LIVESTOCK PRODUCTS ........................................................................ 17 3.5 SOME FIGURES ON THE LIVESTOCK VALUE-CHAIN FOR THE NEP ................................................................... 19

4 INVESTMENT AND GROWTH OPPORTUNITIES FOR THE NEP ........................................................ 21

4.1 FIRST SCENARIO: BUSINESS-AS-USUAL (STATUS QUO) .................................................................................. 21 4.1.1 Description of the status quo ..................................................................................................................... 21 4.1.2 Trends in livestock sector without any new investment ............................................................................. 21 4.1.3 Consequences of the status quo ................................................................................................................. 22

4.2 SECOND SCENARIO: PROCESSING TOWARDS DOMESTIC DEMAND-LED GROWTH (IMPORT SUBSTITUTION) ..... 23 4.2.1 Drivers: Domestic market opportunities .............................................................................................. 23 4.2.2 Proposed investment strategies for the domestic demand-led investment ........................................... 26 4.2.3 Consequences of the domestic demand led-investment ........................................................................ 28

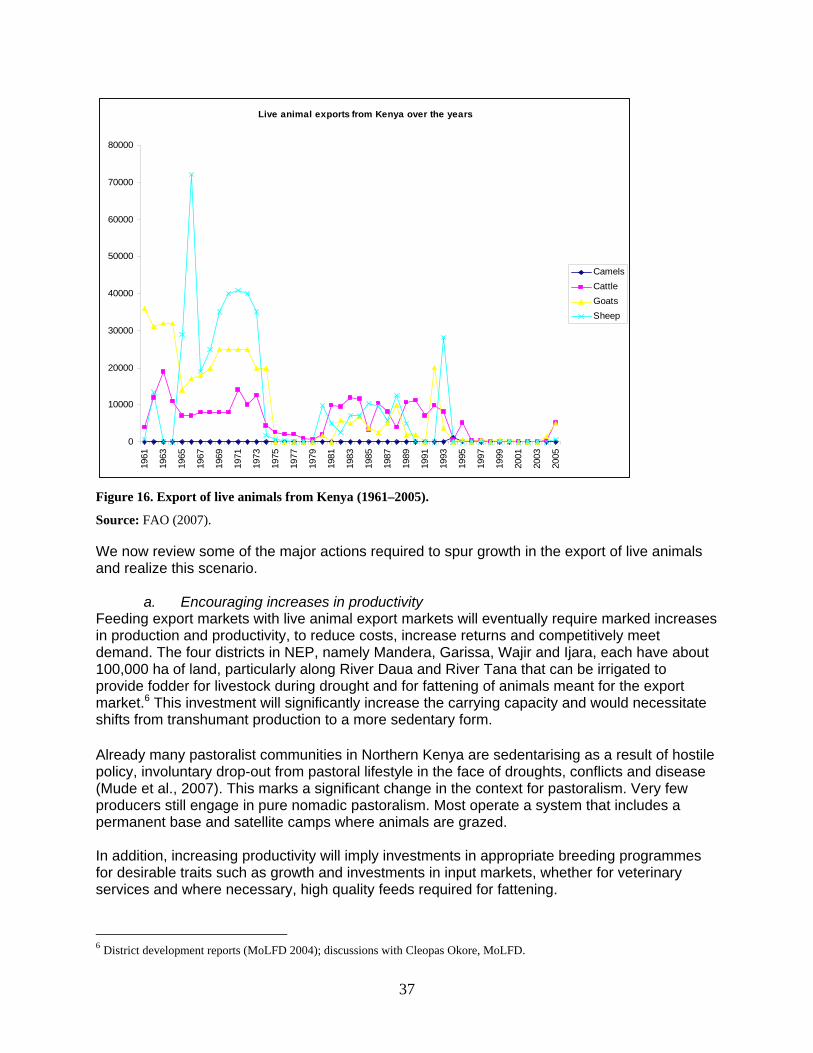

4.3 THIRD SCENARIO: IMPROVING THE EXPORT OF LIVE ANIMALS ....................................................................... 31 4.3.1 Introduction ......................................................................................................................................... 31 4.3.2 The drivers of demand in the live animals export market .................................................................... 32 4.3.3 Investment opportunities in the export of live animals ........................................................................ 35 4.3.4 Potential impacts of a resurgent live animals export market ............................................................... 39

4.4 FOURTH SCENARIO: EXPORT OF PROCESSED LIVESTOCK PRODUCTS ............................................................... 41 4.4.1 The drivers ........................................................................................................................................... 41 4.4.2 Requisite investments ........................................................................................................................... 44 4.4.3 Potential impact on the NEP economy ................................................................................................ 45

5 SOME IMPLICATIONS OF THE VISION ON THE ROLE OF THE PUBLIC AND PRIVATE SECTORS .................................................................................................................................................................. 47

5.1 CREATING AN ENVIRONMENT FAVOURABLE TO INVESTMENT: THE ROLE OF THE PUBLIC SECTOR ................. 48 5.2 THE ROLES OF PRIVATE FIRMS AND STAKEHOLDERS: MULTIPLIERS OF GROWTH ............................................ 49

5.2.1 Investment within the livestock sector .................................................................................................. 50 5.2.2 Investment outside but related to livestock sector ................................................................................ 50

6 CONCLUSIONS ................................................................................................................................................. 50

7 REFERENCES ................................................................................................................................................... 52

v

List of Figures Figure 1. Location of the North Eastern Province, Kenya. ............................................................. 2 Figure 2. Rural poverty in the North Eastern Province. ................................................................. 4 Figure 3. Proportion of people below standard food consumption level by Province. ................... 5 Figure 4. Primary and secondary school enrolment in Kenya. ....................................................... 5 Figure 5. Proportion of agricultural land in different categories by province. ............................... 6 Figure 6. Location of the North Eastern Province and agro-climatic zones of Kenya. .................. 6 Figure 7. Development domains (agricultural potential, market access and population density) in

the North Eastern Province. .................................................................................................... 7 Figure 8. Relative importance of livestock to NEP. ..................................................................... 13 Figure 9. Livestock trade routes from neighbouring countries. .................................................... 24 Figure 10. Number of animals slaughtered in Nairobi (1996–2000). ........................................... 25 Figure 11. Meat consumption estimates for Kenya up to 2030. ................................................... 25 Figure 12. Trends in beef deficit for Kenya (2004–2014). ........................................................... 26 Figure 13. Additional cattle required to meet beef demand in Nairobi and Mombasa each year. 30 Figure 14. Total meat consumption trends and meat deficit in the MENA region (1961–2002). 33 Figure 15. Export of live animals from eastern Africa (1961–2005). .......................................... 36 Figure 16. Export of live animals from Kenya (1961–2005). ....................................................... 37 List of Tables Table 1. North eastern Kenya in the Kenyan context 3 Table 2. Livestock populations in NEP 12 Table 3. Summary of economic activities in NEP 12 Table 4. Trends in livestock production for NEP 14 Table 5. Recorded sales of live animals (average prices and earnings to farmers), 2006 15 Table 6. National trends; value of sales of livestock and livestock products (in millions Kshs) 16 Table 7. Local livestock product sales and earnings to farmers in NEP, 2006 17 Table 8. Trade, values in million US$, and products 18 Table 9. Export/import dependency for livestock products 19 Table 10. Value addition from live animal marketing for the NEP (Kshs) 19 Table 11. Value addition from livestock product marketing for the NEP (Kshs) 20 Table 12. Livestock production and revenue in the NEP, 2003 22 Table 13. Livestock product balance sheet for the NEP 2003 23 Table 14. Sources of cattle, goats, and camels in Nairobi, Mombasa and Malindi 30 Table 15. Per capita income of major live animal importing countries 34 Table 16. Per capita meat consumption in some major meat importing countries in the MENA

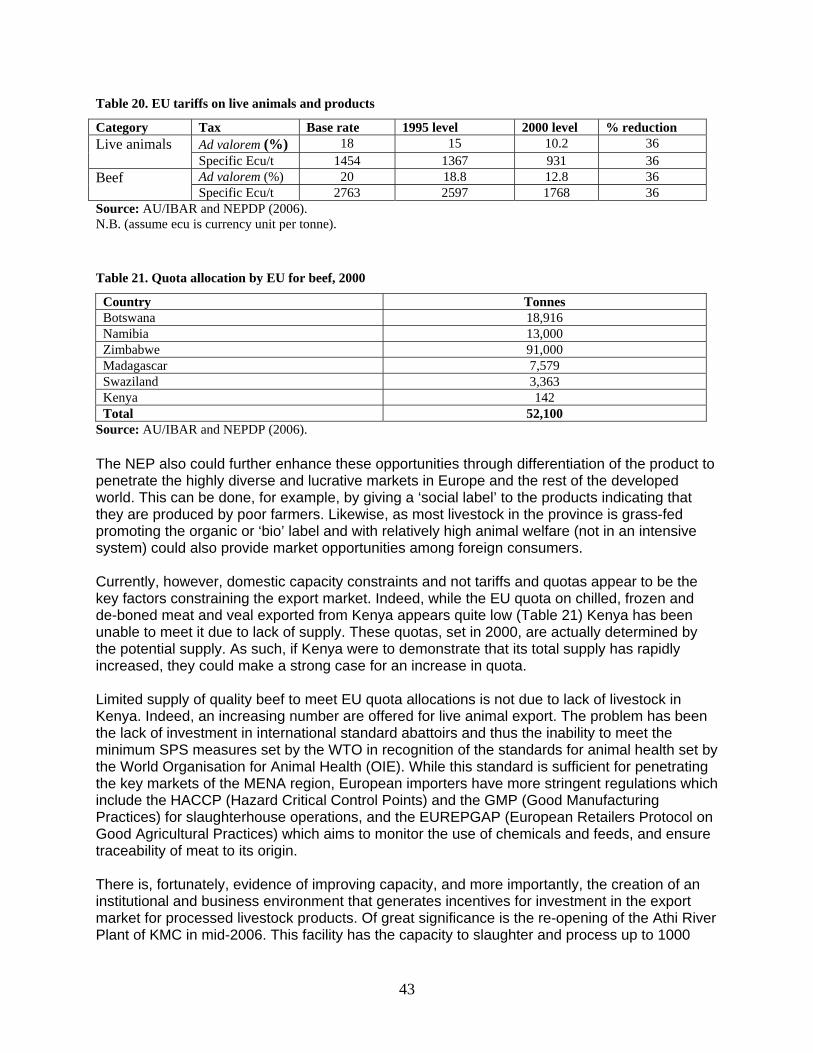

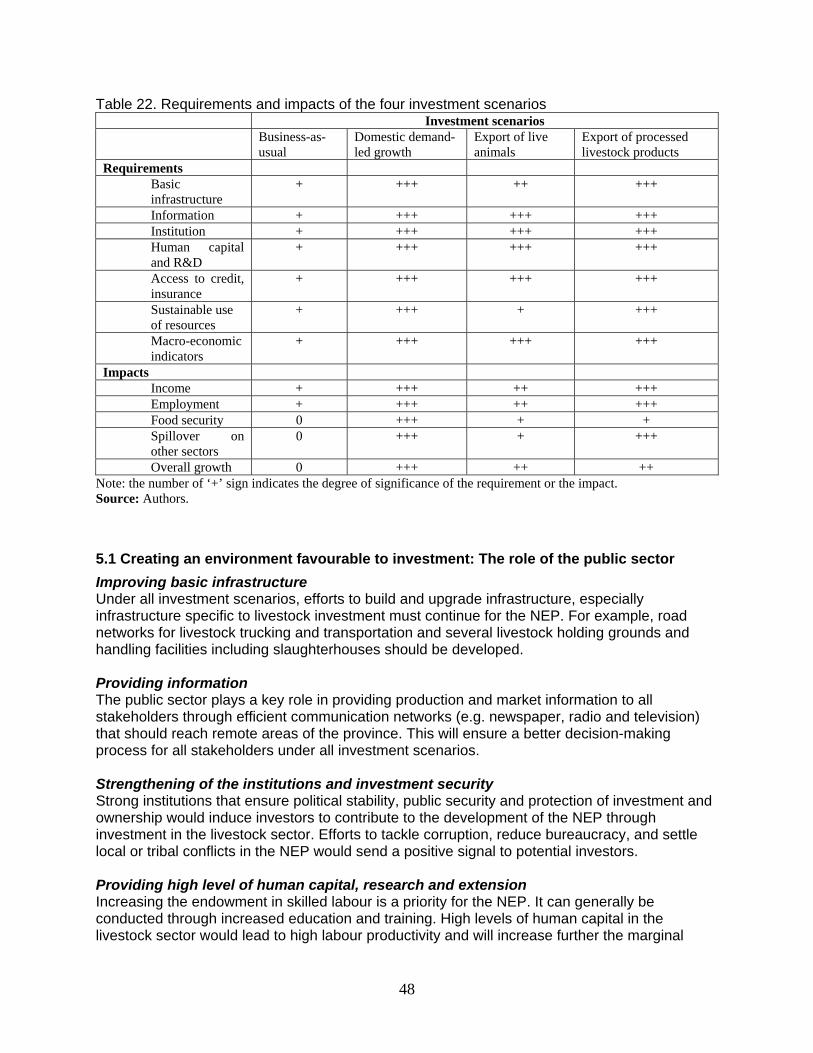

region 34 Table 17. Live animal imports and human population of the Middle East 35 Table 18. Export values of meat products from Kenya (US$ ’000) 42 Table 19. Value of meat imports in MENA (US$ ’000) 42 Table 20. EU tariffs on live animals and products 43 Table 21. Quota allocation by EU for beef, 2000 43 Table 22. Requirements and impacts of the four investment scenarios 48

vi

List of Boxes Box 1: Examples of the development initiatives operating in the North Eastern Province .......... 11 Box 2: Consequences on income, employment, and food security if the NEP can supply at least

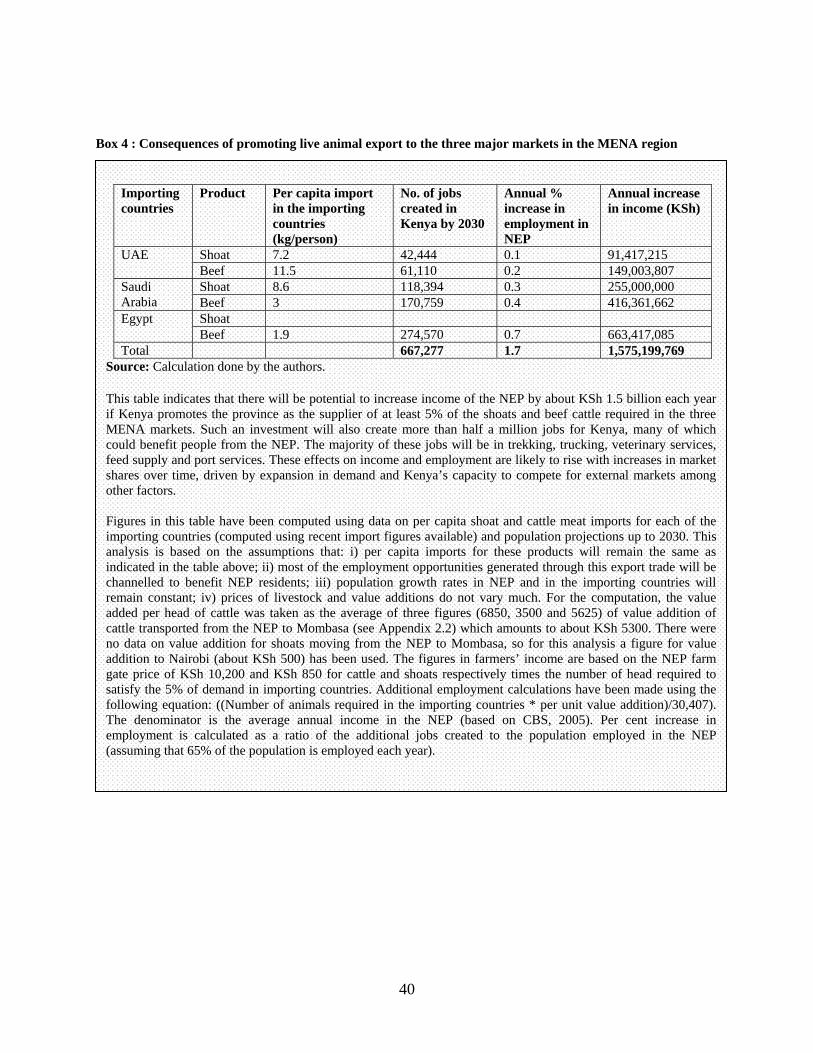

50% of the beef and mutton imported to Kenya ................................................................... 29 Box 3: Changes in been imports in Egypt and Saudi Arabia, 2001 and 2006 .............................. 33 Box 4 : Consequences of promoting live animal export to the three major markets in the MENA

region .................................................................................................................................... 40 Box 5: Consequences of promoting meat export to the three major markets in the MENA region

............................................................................................................................................... 46

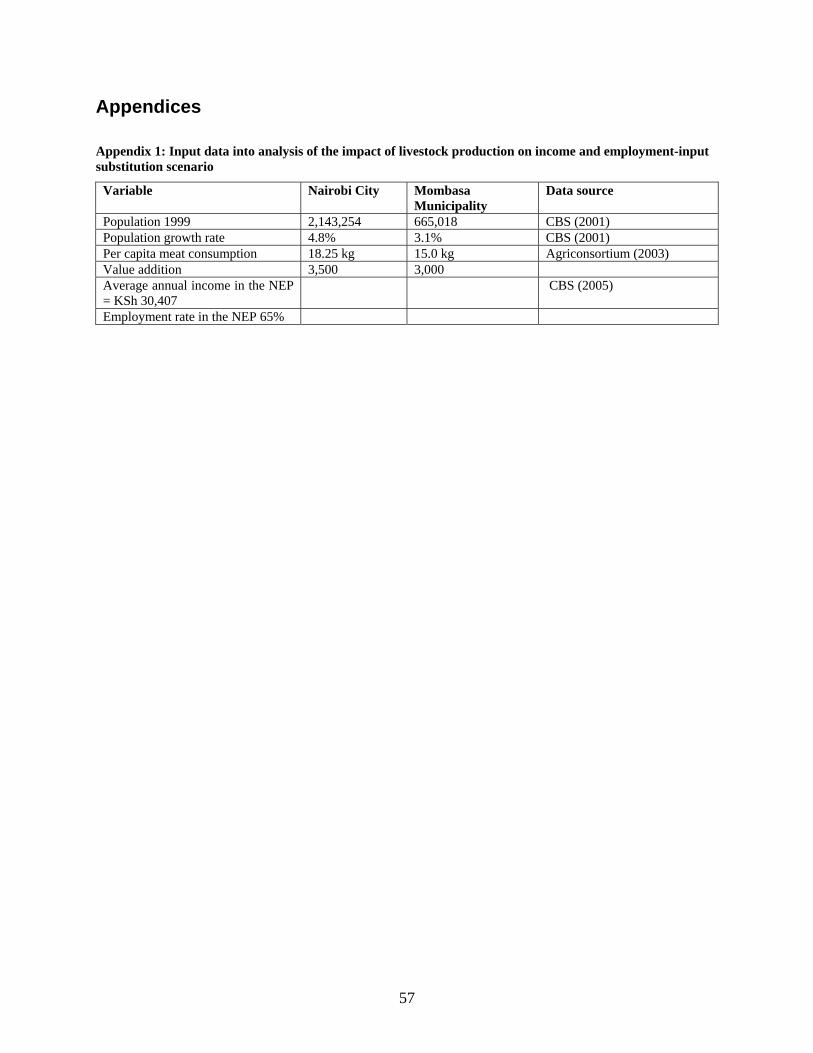

List of Appendices Appendix 1: Input data into analysis of the impact of livestock production on income and

employment-input substitution scenario ............................................................................... 57 Appendix 2: Value addition from live animal marketing for the NEP domestic market ............. 58 Appendix 3: Occurrence of Droughts and Floods in Kenya ......................................................... 61 Appendix 4: Ruminant livestock populations and annual milk production in Kenya .................. 61 Appendix 5: Exchange rate (USD vs. Kshs) ................................................................................. 62

vii

List of Abbreviations and Acronyms ASAL: Arid and semi-arid land

AU/IBAR: African Union/Inter-African Bureau for Animal Resources

CAP: Common Agriculture Policy, EU

CIDA: Canadian International Development Agency

COMESA: Common Market for Eastern and Southern Africa

EMACK: Education for Marginalized Children in Kenya

EU: European Union

EUREPGAP: European Retailers Protocol on Good Agricultural Practices

FAO: Food and Agriculture Organization of the United Nations

FOB Free on Board

GMP: Good Manufacturing Practices

GoK: Government of Kenya

HACCP: Hazard Critical Control Points

KAPP: Kenya Agricultural Productivity Project

KMC: Kenya Meat Commission

LIME: Livestock Marketing Enterprise

NEP: North Eastern Province

NEPDP: North Eastern Province Pastoral Development Programme

NGO: Non-governmental organization

NOHA: Nomadic Heritage Aid

M&E: Monitoring and evaluation

MENA: Middle East and North Africa

OIE: World Organisation for Animal Health

PACE: Pan African Programme for the Control of Epizootics

PDO: Pastoralist Development Organization

PPC: Pastoralist production companies

PYGI: Pastoralist Young Girls’ Initiative

RSLTC: Red Sea Livestock Trade Commission

SADC: Southern African Development Community

SPS: Sanitary and Phytosanitary

SRA: Strategy for Revitalization of Agriculture

UAE: United Arab Emirates

USAID: United States Agency for International Development

WOKIKE: Womankind Kenya

WTO: World Trade Organization

viii

Abstract Pastoralism is the dominant livelihood activity in the North Eastern Province (NEP) of Kenya. It is supplemented only by a limited amount of agriculture along the rivers. The province faces various developmental challenges including chronic poverty and food insecurity, low human capital and poor health standards, high vulnerability to climate change, poor infrastructure, insecurity and low crop and livestock productivity. This study synthesises existing knowledge and provides recommendations on livestock investments to increase incomes, create employment and reduce food insecurity in the province. It examines investment opportunities in livestock and presents scenarios that meet the objectives of Kenya’s 2030 vision. Four scenarios are analysed. The first scenario consists of the business-as-usual case: a vision of the state of the livestock sector, and its contribution to NEP and national economy, if the current trajectory is maintained. The second scenario outlines a strategy that focuses on catering to domestic demand for livestock products. The third scenario focuses on feeding foreign demand for live animals, while the fourth scenario investigates the possibilities of a livestock sector driven by exports of processed livestock products. Also in these investment scenarios, the broad-based growth contribution to the economy is discussed. The analysis indicates that all three alternative scenarios have far better impacts on pastoralists’ income and employment than the ‘business-as-usual’ scenario. The second scenario is found to have the largest favourable impact. Besides creating jobs and income opportunities, it provides alternatives to meet the growing livestock product consumption spurred by population increase, rising incomes and urbanization in Kenya. However, there are several requirements for this scenario to work and yield the desired impact. The need for creating a favourable investment climate is discussed and specific roles of the public and private sectors are explained.

1

1. Introduction The North Eastern Province (NEP) is one of Kenya’s leading livestock production areas. Under the Strategy for Revitalization of Agriculture (SRA) set out by the Government of Kenya (GoK), the livestock sector, especially in the NEP, is expected to play a major role in promoting sectoral and economy-wide growth by the year 2030. This growth will benefit both local and national economies and especially the welfare of poor people living in the province. Such a vision, however, requires clear investment options that help design government policies and clarify decisionmaking. The objective of this report is to examine investment opportunities for livestock in the NEP of Kenya and present investment policy scenarios that meet the 2030 vision (i.e. to increase farmer’s income, create employment, and reduce malnutrition and food insecurity). The GoK and numerous non-governmental organizations (NGOs) have already initiated many projects aimed at stimulating the NEP economy by accelerating the development and productivity of the livestock sector. Several studies (Agriconsortium 2003; Perry et al. 2005; AU/IBAR and NEPDP 2006) on the comparative advantage of the region have resulted in various recommendations for creating an enabling environment best suited to optimizing the welfare effect of these projects. This report builds on these studies but places particular emphasis on clarifying tangible investment opportunities arising from the livestock sector. The report highlights those investment opportunities that are most likely to increase farmer’s income, create employment and reduce poverty and food insecurity in the province. The next section, describes the NEP and its challenges within the national context. Section 2 also describes the ongoing development projects and initiatives to address some of the main challenges facing the province. Section 3 explains the importance of the livestock sector in NEP and presents the current situation and trends in livestock production, marketing and trade. Section 4 presents and analyses four investment scenarios in NEP’s livestock sector and their likely impacts on farmers’ income, employment and food security. These scenarios are (i) business-as-usual; (ii) domestic demand-led growth; (iii) live animal export-led growth; and (iv) livestock product export-led growth. Section 5 explains the role of the public and private sectors in attracting investments and generating growth within and outside the livestock sector and Section 6 concludes the report.

2. The North Eastern Province of Kenya: Description and Challenges

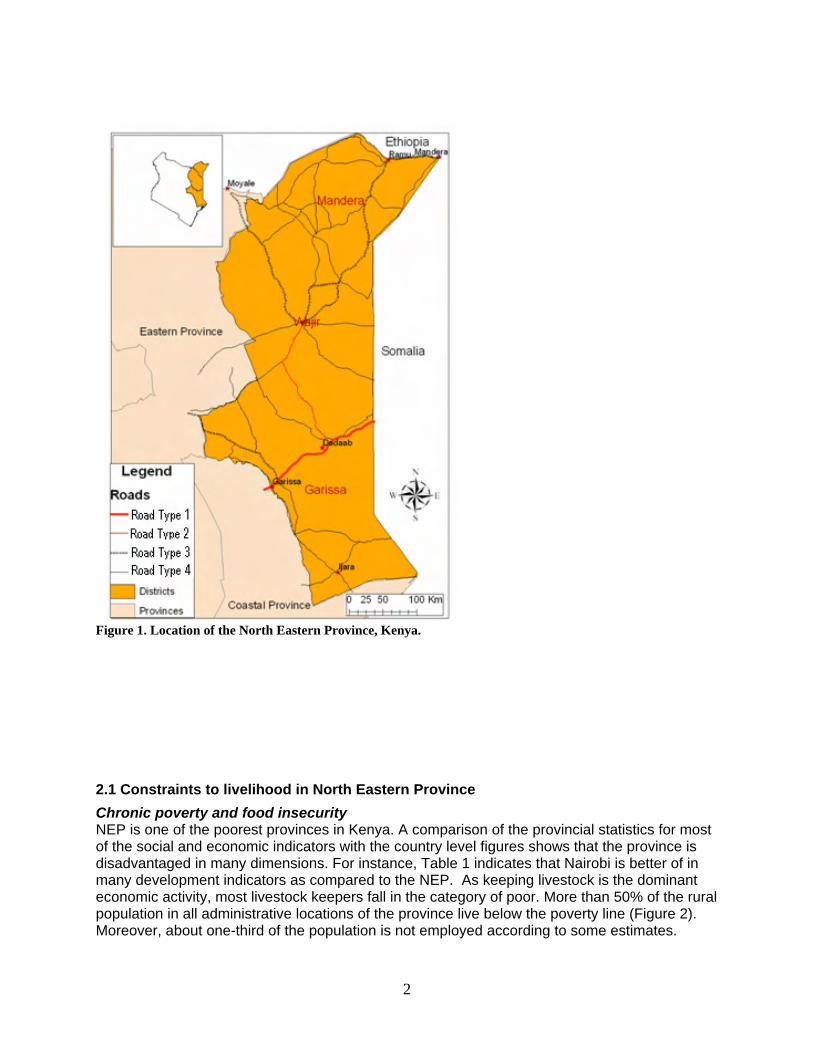

The North Eastern Province (NEP) is one of the eight administrative provinces of Kenya and is located in the arid communal rangeland of Kenya. The province has a total area of 126,902 km² and is divided into four administrative districts, namely: Garissa, Ijara, Wajir and Mandera. Garissa town is the provincial capital. The province is bordered by the Eastern Province to the west, Coast Province to the south, Ethiopia to the north and Somalia to the east (Figure 1). Pastoralism is the dominant livelihood activity in the province, supplemented by a limited amount of agriculture along the rivers. Most of the pastoralists are nomadic and shift with their livestock in search for water and pasture. Commonly reared types of livestock are cattle, goats, sheep, camels and chickens.

2

Figure 1. Location of the North Eastern Province, Kenya.

2.1 Constraints to livelihood in North Eastern Province

Chronic poverty and food insecurity NEP is one of the poorest provinces in Kenya. A comparison of the provincial statistics for most of the social and economic indicators with the country level figures shows that the province is disadvantaged in many dimensions. For instance, Table 1 indicates that Nairobi is better of in many development indicators as compared to the NEP. As keeping livestock is the dominant economic activity, most livestock keepers fall in the category of poor. More than 50% of the rural population in all administrative locations of the province live below the poverty line (Figure 2). Moreover, about one-third of the population is not employed according to some estimates.

3

Table 1. North eastern Kenya in the Kenyan context

Kenya Nairobi NEP Poverty and demography Human Development Index, 2001 (HDI value) 1 0.539 0.783 0.413 Poverty rate (% of individuals below poverty line) 2 53 44 64 Estimated population (1999 census) 28,686,607 2,143,254 962,143 Population density (persons per sq. km) (1999 census) 49 3,079 8 Health Life expectancy at birth (years) 54.7 61.6 52.4 People without access to health care (%)1 51 45 89 Number of hospitals in 20053 562 71 13 Number of health centres in 20053 691 61 14 Proportion delivered in health service (%)4 77.2 7.1 Education and other services Access to safe water (%)4 53.6 66 49 Total (male and female) literacy rates (2006)5 61.5 87.1 8.0 Male literacy rates (2006)5 64.2 87.1 12.3 Female literacy rates (2006)5 58.9 86.9 4.3 Total numeracy rates (2006)5 64.6 86.6 9.1 Male numeracy rates (2006)5 67.9 89.3 13.7 Female numeracy rates (2006)5 61.4 84.1 5.0

Food security Children underweight (%)1 26.4 16.3 35.8 Employment Wage employment in 20053 1,807,712 453,415 16,626 Earning from labour (Kshs million) in 20053 596875.1 181,360.3 5,462.6

1 Human Development Report 2001. 2 CBS (2005). 3 CBS (2006). 4 Kenya Demographic and Health Survey 2003. 5 Ministry of States for Planning, National Development and Vision 2030, 2008 (based on the Kenya National Adult Literacy Survey, 2006) and Kilele, 2007

4

Figure 2. Rural poverty in the North Eastern Province.

Source: Map made by ILRI based on data from CBS (2005). As of 2003, NEP was home to about 1.2 million people. It’s intercensal growth rate between 1989 and 1999 was the highest in the country at 9.5% as opposed to an average of 2.9% for Kenya (CBS, 2001). Agricultural, especially crop, production in the province is very limited due to the harsh climatic conditions (GoK 1997; GoK 2002a; GoK 2002b; GoK 2002c). This implies that the province is vulnerable to food insecurity as the growth in food supply lags behind the growth in food demand. The Kenya Integrated Household Budget Survey—2005/06 (KNBS 2007a) reported that the NEP has the highest ‘food poverty’ in the country with about 66% of the total population consuming less than the standard 2250 kilocalories per day (Figure 3). The same survey also indicated that about one-third of the food supply in the province comes from gifts including food relief (KNBS 2007a).

5

0

10

20

30

40

50

60

70

Na

iro

bi

Ce

ntr

al

Nya

nza

Rift

Va

lley

Ea

ste

rn

We

ste

rn

Co

ast

No

rth

Ea

ste

rn

Province

Pro

po

rtio

n o

f th

e p

eo

ple

wit

h

be

low

sta

nd

ard

fo

od

c

on

su

mp

tio

n l

ev

els

Figure 3. Proportion of people below standard food consumption level by Province.

Source: KNBS (2007b). Low human capital and poor health standards The NEP is also plagued with a critical shortage of human capital and extremely low investment in the education of upcoming generations. The literacy rate in the province is lower than the country average (Table 1). According to the findings of the 2006 Kenya National Adult Literacy Survey, the national average literacy level is at 61.5 while that of NEP is only 8.0 (Kilele, 2007) In addition, the province has the lowest primary and secondary school enrolment in the country (Figure 4).

0

20

40

60

80

100

Nai

robi

Cen

tral

Coa

st

Rift

Val

ley

Nya

nza

NE

Wes

tern

Eas

tern

Province

Per

cen

tag

e

Primary Secondary

Figure 4. Primary and secondary school enrolment in Kenya.

Source: CBS (2001).

6

The NEP also had the highest infant mortality rate (91 per 1000) and highest under-five infant mortality rate (163 per 1000) in 2003. The data presented in Table 1 indicate that all health indexes for the NEP are poor. High vulnerability to climate change and low agricultural potential All the land in NEP falls under the low agricultural potential category1 (Figure 5). The majority of the province falls under the arid agro-climactic zone (Figure 6), which is characterized by harsh climatic conditions, especially erratic rainfall patterns. The province frequently experiences floods and famines caused by droughts (Appendix 3). Moreover, recent studies show that NEP will be adversely affected by the impact of climate change: weather patterns will exhibit greater variability and more frequency of extreme weather events.

0.0

20.0

40.0

60.0

80.0

100.0

CE

NT

RA

L

CO

AS

T

EA

ST

ER

N

NA

IRO

BI

NE

NY

AN

ZA

RF

WE

ST

ER

N

Province

Per

cen

tag

e o

f th

e ag

ricu

ltu

ral

lan

d

high potential medium low

Figure 5. Proportion of agricultural land in different categories by province.

Figure 6. Location of the North Eastern Province and agro-climatic zones of Kenya.

1 Based on data from CBS (2006), these categories are defined as: high potential areas have annual rainfall of 857.5 mm (over 980 mm in the Coast Province); medium potential areas are those with annual rainfall of 735–857.5 mm (735–980 mm in Coast Province and 612.5–857.5 mm in Eastern Province); and low potential areas are those with annual rainfall of 612.5 mm or less.

7

Poor infrastructure Road networks and infrastructure in NEP are among the most underdeveloped in Kenya. The road network covers a very small fraction of the region; where roads exist, they are largely dry-weather roads that are mostly impassable during rainy seasons. Road types 1 and 2 (tarmac and murram/gravel road respectively) cover only the area around Garissa and Wajir while the rest of the province has poor quality roads (Figure 7). This dramatically increases transport and other transactions costs and is a major limitation to the marketing of agricultural products and other goods. The development domains for NEP, based on a combination of three criteria— agricultural potential, market access and population density—are presented in Figure 7. The classes in the development domain map portray these three criteria. For example, class LLL indicates that there is low agricultural potential, low market access (measured by the lack of quality roads) and low population density. Each of these domains is expected to have similar comparative advantages for different agricultural or rural development options. The LLL domain is the most dominant in the NEP indicating that the area is highly constrained as far as opportunities for rural development are concerned.

Figure 7. Development domains (agricultural potential, market access and population density) in the North Eastern Province.

8

Insecurity Socio-economic activities in the NEP are severely affected by insecurity. This situation, which has been endemic to the area, has its roots in a combination of factors including conflicts over natural resources (e.g. fighting for pasture, water and land); cattle rustling; and intertribal and clan clashes because of the fragile cohabitation of different groups living in the province that have often different family or tribal ties with people in the surrounding countries and others (Akiwumi 2002). The situation is exacerbated by instability in bordering countries (Ethiopia and Somalia). Low livestock productivity The NEP suffers from low livestock productivity due to limitations of feed resources and low access to technology. The livestock sector in the province is also constrained by several livestock diseases affecting animal health and livestock productivity. The major diseases include Rift Valley fever (outbreaks in 1997–98 and more recently in 2006–07); rinderpest that led to the closure of livestock markets in 2003; trypanosomosis due to the fact that the area is highly infested by tsetse flies; helminthiasis; Brucellosis; and camel diseases such as laaba and lahaw-gaal (camel fever).

2.2 The livestock production system in the NEP

The majority of the population of the NEP practice nomadic pastoralism. They maintain herds of camels, cattle, sheep and goats. Indigenous cattle breeds such as boran and the small East African Zebu are the main breeds kept in the province. Dairy (improved) breeds constitute less than 1% percent of the cattle population (Appendix 4). Indigenous breeds are resistant to most diseases e.g. tick borne diseases and others. Orma boran breed is resistant to Trypanosomosis. The indigenous breeds are also drought tolerant, able to walk long distance and are able to feed on rough pasture. However, their milk production capacity is very low hence they are mainly kept for sale as beef cattle while milk production is mainly for local consumption. Animals are fed through natural grazing using open grazing livestock management practice, supplementary feeding is uncommon in the province. The population practice seasonal migration to access pasture, settling near to water sources and good pasture for a few weeks before moving on. Distress migration is practised in times of hardship. Because of the prolonged drought many pastoralists have been forced to migrate long distances with herds in search of pasture (Rioba, Sheikh and Stevens, 2000). The most common livestock reproduction method is through natural breeding. In most cases management of diseases is by natural ways. Government/ public extension including veterinary service has for a long time been inadequate in the NEP as it is the case in many Arid and Semi Arid areas of Kenya. Reports indicate that despite the fact that more than 75% of Kenya’s livestock are in the ASAL areas, they are served by fewer than 10% of livestock service staff. This is mostly because the ASAL areas are considered a hardship post and few veterinary staff want to work there (Young, Kajume and Wanyama, 2003). Due to inadequate or lack of animal health services in ASAL/Pastoral areas, various private service delivery initiatives, including community-based animal health service delivery systems facilitated by various NGOs, have emerged as an alternative option (Okwiri, Kajume and Odondi, 2001; Riviere-Cinnamond and Eregae, 2003). Even with a combination of private and public extension providers, extension delivery in the pastoral areas is still challenging because of conditions such as insecurity, poor infrastructure, low cash economy, high cost of service delivery, vastness of the areas, and lack of veterinary personnel among others (Okwiri, Kajume and Odondi, 2001).

9

2.3 Ongoing and recently completed projects/plans for the NEP

Several projects aimed at tackling the major development challenges of the NEP and catalysing economic growth have been initiated over the years. The major projects that have large scope are discussed below. a) North Eastern Province Pastoral Development Programme The North Eastern Province Pastoral Development Programme (NEPDP) is a three-year programme funded by the United States Agency for International Development (USAID), and developed and executed by the African Union/Inter-African Bureau for Animal Resources (AU/IBAR) in collaboration with the GoK and private sector partners. The project is worth about US$ 2 million and aims to increase the incomes of pastoralists in Kenya’s NEP by focusing on constraints to livestock trade. The programme officially started in February 2005 and was scheduled to run until February 2008. The programme’s focus is to support development and strengthening of local and national level livestock trade commissions, provide animal health services that are required for domestic movement and international export of livestock, and provide limited support to infrastructural development (water points and their management) to enhance quality of livestock for trade. Trade associations will be strengthened in business services and trade capabilities. This programme will complement ongoing USAID support for increasing livestock trade in the Horn of Africa, funded and implemented by USAID/Kenya. More information on this project is available at http://tcbdb.wto.org/trta project.asp and http://www.usaidkenya.org/ke. b) The ASAL Based Livestock and Rural Livelihoods Support Project The project area consists of 22 districts covering the arid and semi-arid lands (ASALs). Garissa, Mandera and Wajir districts of NEP are part of this project. The overall objective is to contribute to poverty reduction at the national and household levels, consistent with the government’s policies of mainstreaming ASAL areas in the economic framework of the country. The specific objective of the project is to improve sustainable rural livelihoods and food security through improved livestock productivity, marketing and support for drought management and food security initiatives in the ASAL. The project is financed by the African Development Bank (some of the money being a loan and the rest a grant) and GoK, including contributions from the pastoralists in NE Kenya. Total project costs are estimated at US$ 38 million (KSh 2.8 billion). The project is being implemented over a six-year period beginning July 2004. For more information see http://www.livestock.go.ke. c) Livestock Marketing Enterprise The Livestock Marketing Enterprise (LIME) is a CIDA (Canadian International Development Agency)-funded project developed by CARE and the community, designed to address the challenges faced by pastoralists from the north-eastern part of Kenya through livestock marketing. LIME intervention emphasizes improved access to markets facilitated by improved credit provision. The project integrates pastoralists into the competitive livestock market through forward market contracts resulting in increased incomes. It has facilitated the establishment of pastoralist production companies (PPCs) around the watering holes it helped to rehabilitate across Garissa District. CARE has signed forward market contracts with Makram, one of the country’s largest livestock buyers. In coordination with the Ministry of Livestock and Fisheries Development, LIME ensures that cattle are screened, vaccinated, weighed, branded, and tagged, all on a fee-for-service basis. LIME then pays the farmers a fixed guaranteed price for

10

their cattle based on their weight, within 7 days. LIME hires local herdsmen to trek the cattle for 3 weeks down to the conditioning ranch at Galana in the Coast Province; this ranch is leased from the Agricultural Development Company. The price paid to LIME by Makram includes a premium that covers costs for trekking and ranch fees, and any profits generated are re-invested in more cattle for the next consignment. For further details on LIME visit http://www.care.ca/CEP/CEPportfolio e.shtm. d) The Kenya Agricultural Productivity Project The Kenya Agricultural Productivity Project (KAPP) is a GoK multi-sectoral and multi-institutional project funded by the World Bank. The total cost of the project is US$ 80.27 million and its operations started in June 2004; the project is scheduled to close in December 2008. It aims to support the agriculture research system, improve institutional and financial mechanisms that help farmers to access technology and to increase productivity. The project contributes to the SRA whose objective is ‘to provide a policy and institutional environment that is conducive to increasing agricultural productivity, promoting investments, encouraging private sector involvement in agricultural enterprises and agribusiness’ (MoA and MoLFD 2004). KAPP intends to contribute to the revitalization of agriculture through four project components: (i) policy and institutional reforms; (ii) extension system reform; (iii) research system reform; and (iv) farmer/client empowerment. KAAP pilot activities are ongoing with intervention in 20 districts across Kenya, out of which two (Wajir and Garissa) are in NEP. For more information visit http://web.worldbank.org and www.kari.org/KAPP/. e) Pan-African Programme for the Control of Epizootics The Pan-African Programme for the Control of Epizootics (PACE) is a project that conducts disease surveillance, and disease control and vaccination. The start date of PACE was 31st October 1999 and completion date was the 31st October, 2004.The main aim of PACE was surveillance of epizootic diseases in Africa to accurately determine their prevalence and impact on livestock production. The 5-year PACE programme covered 32 sub-Saharan countries. It is a € 72 million (Approximately $ 77 million) programme that is coordinated by AU/IBAR. The programme includes national operations planned and implemented in each country, and sub-regional and regional support and coordination components. The main activities of PACE in the NEP were on surveillance and control of rinderpest. The Community-based Animal Health and Participatory Epidemiology (CAPE) project – funded by DFID was an integral part of PACE. The MoU was signed in December 2000 between DFID and OAU-IBAR for a period of 4 years, till October 2004. The project was funded to the tune of £ 5.4 million (approximately $ 7 million).The unit promoted policy and institutional change to enable community-based animal health delivery systems, and promote the wider use of participatory approaches and methods in veterinary institutions. A range of awareness-raising, training and field experience activities were supported by the unit up to mid-2004. The unit was absorbed into the new Institutional and Policy Support Team in AU/IBAR in late 2004. In addition to these major projects, there are several other projects/initiatives carried out by various NGOs and local groups that aim to improve people’s socio-economic conditions in the province. Some examples of these projects and initiatives are provided in Box 1.

11

Box 1: Examples of the development initiatives operating in the North Eastern Province

These projects represent current attempts to improve socio-economic conditions of the NEP in an effort to overcome the development obstacles existing in the area. A number of projects are already focusing on boosting agricultural productivity in the region through investing in livestock production and marketing indicating an implicit recognition of the potential and capacity of this sector. Much can be learned from the successes and failures of these large-scale activities. Government efforts to assure that all such projects incorporate quality monitoring and evaluation (M&E) components from which powerful lessons to guide the optimal distribution of resources aimed at dramatically increasing the performance of the NEP livestock sector would yield high returns.

3. Current State of the Livestock Sector in North Eastern Province This section specifically describes the current state of the livestock sector in NEP. As returns to the livestock sector in the province, and indeed Kenya as a whole, are dependent on both domestic and international demands for livestock products, this section also summarizes the domestic, regional and international trends and examines obstacles to productivity and

i) WOMANKIND KENYA (WOKIKE) WOKIKE is an indigenous local NGO based in NEP with its head office in Garissa Municipality. WOKIKE was founded in 1989 as a welfare society by local Somali pastoral women who were committed to improving the living standards and the level of decisionmaking of their fellow pastoral women and the girl child in NEP. ii) Education for Marginalized Children in Kenya (EMACK) EMACK is an initiative that seeks to identify and address the unique educational needs of sedentary and nomadic pastoralist communities. Its objectives are to: 1.) increase community and parental participation in all aspects of school life; 2.) improve coordination and dialogue among service providers that contribute to and inform district, provincial and national education plans and maximize effective use of scarce resources; 3.) build human resource capacity and improve small-scale infrastructure to help meet educational needs identified at the provincial and district levels; 4.) identify and address the unique educational needs of pastoralist children by exploring viable approaches to providing them with relevant educational opportunities; and 5.) increase the chances for success in school of vulnerable children. iii) Nomadic Heritage Aid (NOHA) Established in 2003, NOHA works with ministries and local organizations that complement government efforts to provide basic social services to nomadic communities.

iv) Pastoralist Development Organization (PDO) Established in 2001 to help meet the needs of people living in Bura Division of Garissa District, PDO promotes poverty alleviation through education, women’s empowerment, rural development, community health and environmental conservation.

iv) Pastoralist Young Girls’ Initiative (PYGI) Established in 2001, PYGI works to improve living standards for pastoralist children, with a special focus on girls, using sensitization and awareness campaigns and larger community events.

v) Women Concern Kenya (WCK) WCK was established in 1998 to improve the socio-economic status of communities, especially women and girls, in Garissa and Tana River districts of Kenya by providing training and financial services, advocating on women and girls' behalf, and conducting community sensitization sessions on sending girls to school

12

production growth which would need to be addressed to optimize and fuel growth of the livestock sector.

3.1 Importance of livestock production to NEP

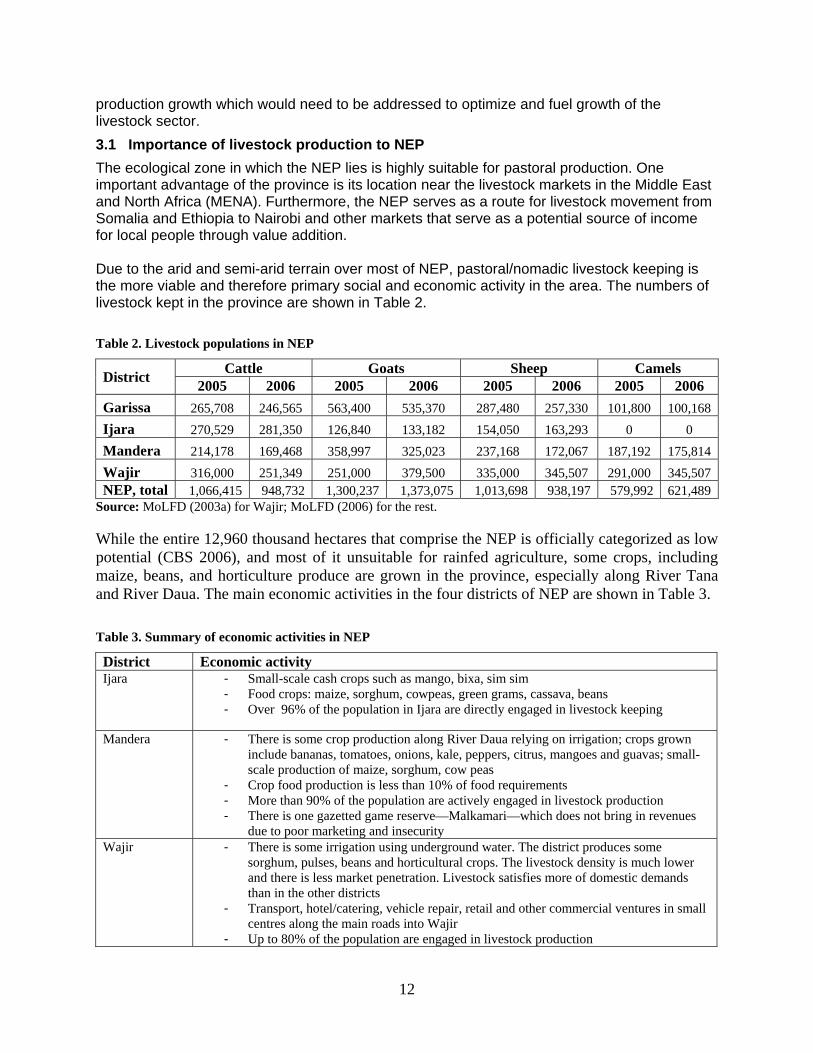

The ecological zone in which the NEP lies is highly suitable for pastoral production. One important advantage of the province is its location near the livestock markets in the Middle East and North Africa (MENA). Furthermore, the NEP serves as a route for livestock movement from Somalia and Ethiopia to Nairobi and other markets that serve as a potential source of income for local people through value addition. Due to the arid and semi-arid terrain over most of NEP, pastoral/nomadic livestock keeping is the more viable and therefore primary social and economic activity in the area. The numbers of livestock kept in the province are shown in Table 2.

Table 2. Livestock populations in NEP

District Cattle Goats Sheep Camels

2005 2006 2005 2006 2005 2006 2005 2006

Garissa 265,708 246,565 563,400 535,370 287,480 257,330 101,800 100,168

Ijara 270,529 281,350 126,840 133,182 154,050 163,293 0 0

Mandera 214,178 169,468 358,997 325,023 237,168 172,067 187,192 175,814

Wajir 316,000 251,349 251,000 379,500 335,000 345,507 291,000 345,507 NEP, total 1,066,415 948,732 1,300,237 1,373,075 1,013,698 938,197 579,992 621,489

Source: MoLFD (2003a) for Wajir; MoLFD (2006) for the rest. While the entire 12,960 thousand hectares that comprise the NEP is officially categorized as low potential (CBS 2006), and most of it unsuitable for rainfed agriculture, some crops, including maize, beans, and horticulture produce are grown in the province, especially along River Tana and River Daua. The main economic activities in the four districts of NEP are shown in Table 3.

Table 3. Summary of economic activities in NEP

District Economic activity Ijara - Small-scale cash crops such as mango, bixa, sim sim

- Food crops: maize, sorghum, cowpeas, green grams, cassava, beans - Over 96% of the population in Ijara are directly engaged in livestock keeping

Mandera - There is some crop production along River Daua relying on irrigation; crops grown include bananas, tomatoes, onions, kale, peppers, citrus, mangoes and guavas; small-scale production of maize, sorghum, cow peas

- Crop food production is less than 10% of food requirements - More than 90% of the population are actively engaged in livestock production - There is one gazetted game reserve—Malkamari—which does not bring in revenues

due to poor marketing and insecurity Wajir - There is some irrigation using underground water. The district produces some

sorghum, pulses, beans and horticultural crops. The livestock density is much lower and there is less market penetration. Livestock satisfies more of domestic demands than in the other districts

- Transport, hotel/catering, vehicle repair, retail and other commercial ventures in small centres along the main roads into Wajir

- Up to 80% of the population are engaged in livestock production

13

Garissa - Has greatest potential for crop production of the four districts (irrigation potential estimated at 28,000 ha compared to the current 1200 ha—main crops are bananas, tomatoes, oilseeds

- 385,000 ha of forest along River Tana (meets 98% of domestic wood fuel needs) - Sand harvesting—mainly for construction within Garissa - Some fishing on River Tana - Tannery in Garissa, and services industry (vehicle repair, retail and catering in the

town) - 75% of the population are engaged in livestock keeping

Source: GoK (1997). Despite this evidence of other important activities in the province, pastoral/nomadic livestock production of mainly goats, sheep, camels and cattle remains the mainstay of the local economy. While the livestock populations in NEP represent only a small fraction of the national livestock populations (Figure 8), the relative importance of this sector to the NEP economy is clearer when the livestock numbers are weighted against the population2 (Figure 8); for example, the per capita cattle kept in NEP is about 1 animal against a national per capita of 0.3. Arguably, productivity of livestock is much lower in NEP (pastoral systems) than in, say, the Rift Valley Province (ranching systems). However, because of its even lower potential in crop production relative to livestock production—it would benefit both NEP and the national economy if the province specialized in livestock production, where it has comparative advantages.

0

2

4

6

8

10

12

14

Othercattle

Goats Hair sheep Camels

NEP

Total national herd

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Catt le Goats Sheep Camel

Per capita livestock (NEP)

Per capita livestock(Nat ional)

Livestock numbers, NEP and national Per capita livestock (national and NEP)

Figure 8. Relative importance of livestock to NEP.

Source: MoLFD (2006).

2 NEP population is only 3.4% of the total Kenyan population.

14

3.2 Trends in livestock production

The livestock population in NEP has stagnated over the past 7 years, with significant variations during drought and flood years (Table 4)3. Drought is the most severe risk faced by pastoralists in Northern Kenya. Droughts have been occurring regularly since the 1970’s (Mude et al., 2007). In the year 2000 Kenya suffered its worst drought in 37 years. In 2006 there was another occurrence of drought and later floods in Garissa and Mandera districts (Appendix 3). Apart from affecting an increasingly larger number of people in the province, droughts have also had a clear effect on livestock production. This might explain why cattle and sheep numbers declined in these years. Floods that occurred in years 2001, 2005 and 2006 could explain the decline in production in subsequent years. Floods are usually associated with increased incidence of water-borne livestock diseases and increased mortalities.

Table 4. Trends in livestock production for NEP

Species 2000 2001 2002 2003 2004 2005 2006 Cattle 868,000 945,687 1,018,010 1,056,280 1,066,415 948,732 Sheep 1,268,250 1,233,994 557,743 596,662 1,013,698 938,197 Goats 782,888 882,931 1,300,237 1,373,075 Camels 501,500 502,929 520,116 546,232 579,992 621,489

Source: MoLFD (2006). There are two types of livestock movements that happen across the porous borders of northern Kenya. The first, involving movement of animals into Ethiopia and Somali in search of water and pasture intensifies during severe drought [MoLFD 2003b]. This type of migratory movement does not usually result in imports and is more correctly seen as a traditional coping mechanism. The second movement, estimated by AU/IBAR and NEPDP (2006) to represent 25–30% of the animals that are sold in Kenya, involves the trekking of animals destined for terminal markets in Kenya. These animals are subsequently trucked from livestock markets in Northern Kenya for slaughter. As observed by Knips (2004), livestock production data in a country like Kenya, that is a net importer, tend to be overrated. The inflows of livestock into Kenya are the result of stronger demand and higher prices in the country (AU/IBAR and NEPDP 2006). A survey by Agriconsortium (2003) found Nairobi prices for live animals and meat to be the highest in the Horn of Africa. In addition, the breakdown of the state in Somalia and the bad relations between Eritrea (which has a port) and Ethiopia has made Kenya a more attractive destination for re-export of live animals. With better infrastructure connecting Northern Kenya to the coastline, the country has potential to emerge as a re-export centre.

3.3 Livestock and livestock product sale and prices and farmers’ earnings

Based on recorded sales of live animals (Table 5), cattle provide most of the livestock income in NEP (over Kshs 1 billion); while shoats and camels generate Kshs 290 million and Kshs 260 million respectively. Nationally, approximately Kshs 13 billion and Kshs 2.5 billion was

3 These figures need to be interpreted with caution because no national livestock census has been carried out since the 1960s, and livestock population data are largely estimates, or single non-representative surveys from disparate sources whose findings often clash.

15

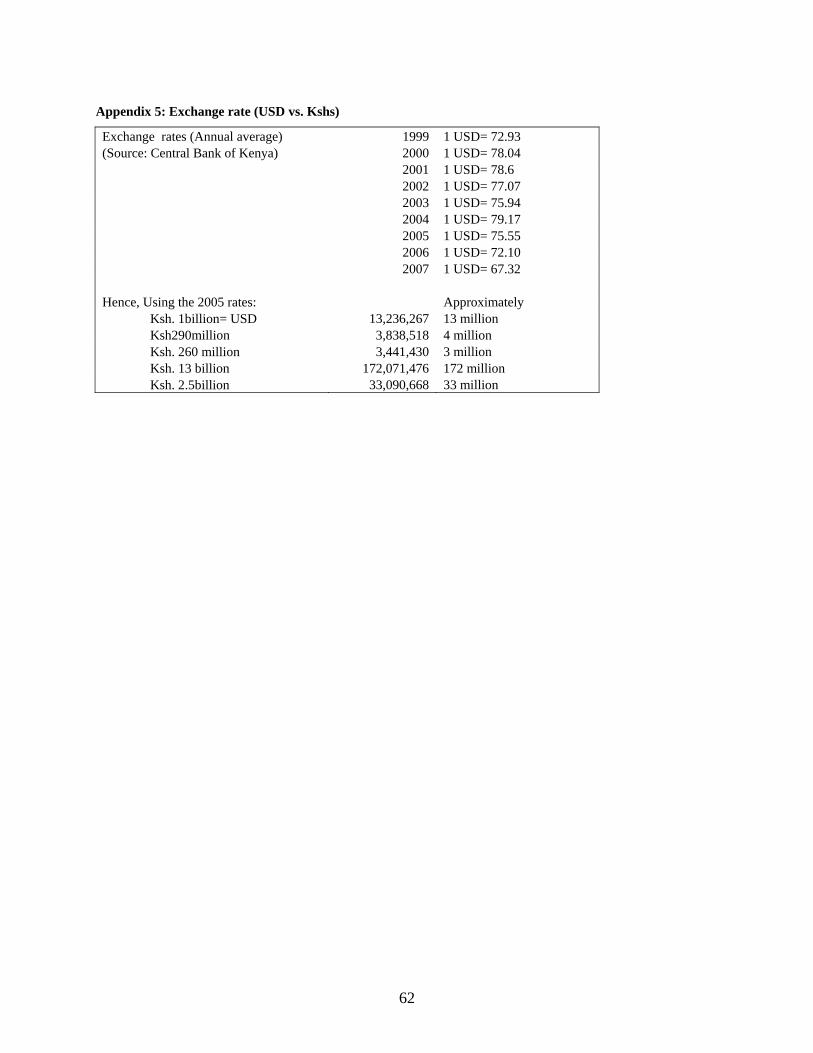

generated from sale of cattle and shoats, for slaughter in 2005 (Table 5). See Appendix 5 for dollar equivalents of these figures.

Table 5. Recorded sales of live animals (average prices and earnings to farmers), 2006

Species

Cattle Sheep & goats Camels

No.

Price (in

Kshs) Value

(in Kshs) No.

Price (in

Kshs) Value

(in Kshs) No.

Price (in

Kshs) Value

(in Kshs)

Garissa 51,323 7,850 402,885,550 36,883 1,460 53,849,180 139 12,560 1,745,840

Ijara 21,407 8,500 181,959,500 28,992 1,403 40,681,850 0 0 0

Wajir 29,598 7,950 235,304,100 66,169 1,342 88,765,714

15,783

8,187 129,210,1

60

Mandera 29,580 7,500 221,985,000 93,522 1,162 108,630,200

10,108

12,000 128,496,0

00 NEP, total

131,908

1,042,134,150 225,566 291,926,944

26,030

259,452,000

Source: MoLFD (2003a) for Wajir; MoLFD (2006) for the rest. The national trends in value of sales for cattle and shoats have been upward since 1999 (Table 6). This is largely due to increases in prices over the same period rather than improvements in productivity since the national slaughter went down over the same period. For example, the numbers of cattle and calves for slaughter went down from 2.5 million head in 1999 to 1.7 million head in 2003. Livestock is sold from NEP largely as live animals rather than slaughtered carcasses. These live animals are trekked from within the four districts (and some from neighbouring countries such as Somalia (see Agriconsortium 2003; AU/IBAR and NEPDP 2006) to local markets in northern Kenya. The main livestock markets that receive animals from NEP are at Garissa and Isiolo. However, there are many smaller livestock markets in the area. Middlemen buy livestock from these markets and transport them by either trekking or trucking to the terminal markets, mainly in Nairobi and Mombasa (Agriconsortium 2003; AU/IBAR and NEPDP 2006). Some animals are also transported to other towns. After years of such trade, elaborate trekking and trucking routes have been developed for live animals (AU/IBAR and NEPDP 2006). Significant proportions are kept in intermediate ranches, especially in the Rift Valley and at the Coast for fattening before sale or export.

16

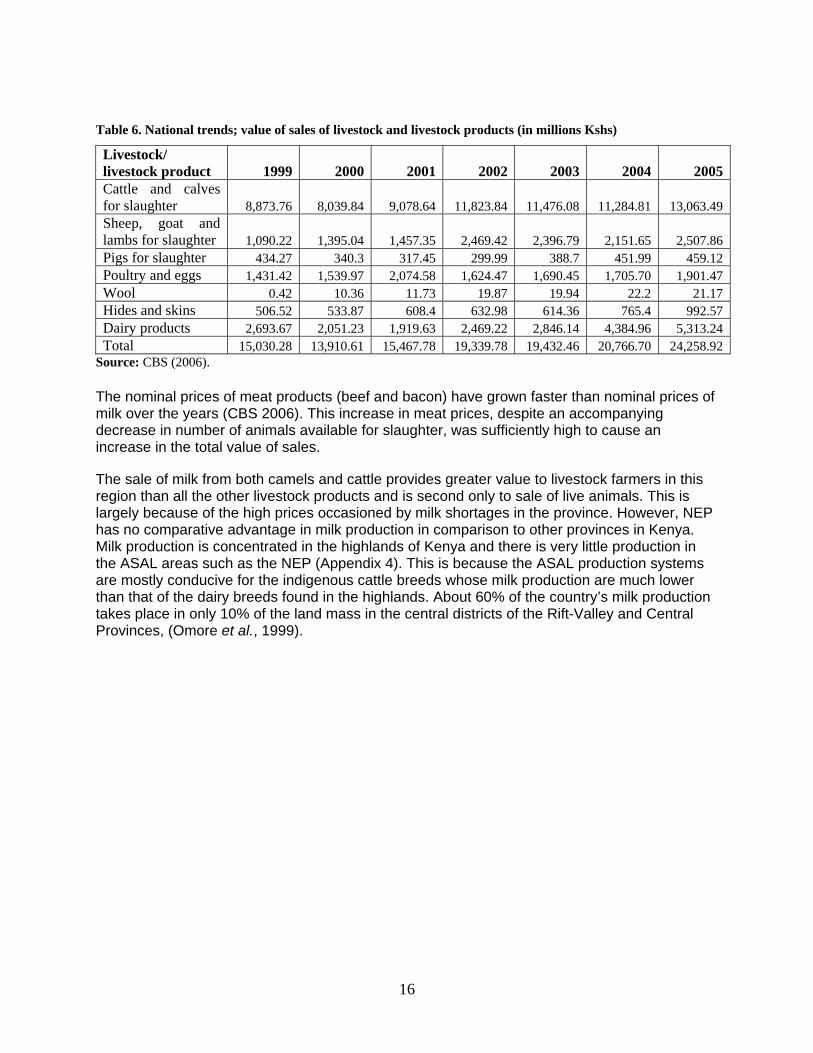

Table 6. National trends; value of sales of livestock and livestock products (in millions Kshs)

Livestock/ livestock product 1999 2000 2001 2002 2003 2004 2005Cattle and calves for slaughter 8,873.76 8,039.84 9,078.64 11,823.84 11,476.08 11,284.81 13,063.49 Sheep, goat and lambs for slaughter 1,090.22 1,395.04 1,457.35 2,469.42 2,396.79 2,151.65 2,507.86 Pigs for slaughter 434.27 340.3 317.45 299.99 388.7 451.99 459.12 Poultry and eggs 1,431.42 1,539.97 2,074.58 1,624.47 1,690.45 1,705.70 1,901.47 Wool 0.42 10.36 11.73 19.87 19.94 22.2 21.17 Hides and skins 506.52 533.87 608.4 632.98 614.36 765.4 992.57 Dairy products 2,693.67 2,051.23 1,919.63 2,469.22 2,846.14 4,384.96 5,313.24 Total 15,030.28 13,910.61 15,467.78 19,339.78 19,432.46 20,766.70 24,258.92

Source: CBS (2006). The nominal prices of meat products (beef and bacon) have grown faster than nominal prices of milk over the years (CBS 2006). This increase in meat prices, despite an accompanying decrease in number of animals available for slaughter, was sufficiently high to cause an increase in the total value of sales. The sale of milk from both camels and cattle provides greater value to livestock farmers in this region than all the other livestock products and is second only to sale of live animals. This is largely because of the high prices occasioned by milk shortages in the province. However, NEP has no comparative advantage in milk production in comparison to other provinces in Kenya. Milk production is concentrated in the highlands of Kenya and there is very little production in the ASAL areas such as the NEP (Appendix 4). This is because the ASAL production systems are mostly conducive for the indigenous cattle breeds whose milk production are much lower than that of the dairy breeds found in the highlands. About 60% of the country’s milk production takes place in only 10% of the land mass in the central districts of the Rift-Valley and Central Provinces, (Omore et al., 1999).

17

The quantities, prices and values of relative livestock product sales in NEP, highlighting the importance to livelihoods in the region, are shown in Table 7. Pastoralists look at livestock as assets and not necessarily as sources of food.

Table 7. Local livestock product sales and earnings to farmers in NEP, 2006

Product Garissa Ijara Wajir Mandera Province (Total)

Milk (cattle) Litres 1,145,000 5,140,900 5,002,160 4,000,000 15,288,060 Price (Kshs) 50 30 35 40 Value 57,250,000 154,227,000 175,075,600 160,000,000 402,552,600 Milk (camel) Litres 4,680,000 Nil 20,758,000 9,000,000 34,438,000 Price 45 Nil 30 40 Value 210,600,000 Nil 622,740,000 360,000,000 119,340,000 Meats (beef) Kg 479,800 3,480 209,290 265,346 957,916 Price 150 120 120 120 Value 71,790,000 417,600 25,114,800 31,841,520 129,163,920 Sheep and goats Kg 345,440 279,252 300,240 359,000 1,283,932 Price 170 140 160 140 Value 58,724,800 39,095,280 48,038,400 50,260,000 196,118,480 Camel meat Kg 171,632 18,750 301,180 430,020 621,582 Price 150 180 140 120 Value 25,744,800 3,375,000 42,165,200 51,602,400 122,887,400 Poultry meat kg 171,632 653 7,232 8,500 188,017 Price 150 150 120 200 Value 25,744,800 97,950 867,840 1,700,000 28,410,590 Hides (cattle) Pieces 4472 241 1,674 2965 9,352 Price 60 50 52 50 Value 268,320 12,050 87,048 148,250 515,668 Camel (hides) Pieces 14,808 125 2,007 2150 19,090 Price 90 50 75 70 Value 1,332,720 11,440 150,525 150,500 1,645,185 Skins (shoats) Pieces 127,037 31921 30,024 5278 194,860 Price 52 46 40 40 Value 6,605,924 1,470,643 1,200,960 211,135 9,488,662

Source: MoLFD (2006).

3.4 External trade in livestock and livestock products

The livestock industry in NEP is very closely connected with that of Coast Province. Most of Kenya’s live animal exports are by sea through the coast. According to AU-IBAR and NEPDP (2006) a considerable proportion of cattle traded at the coast come from NEP, trekked or trucked from Garissa through Tana River District. These animals are either slaughtered or fattened at various ranches along the coast for export.

18

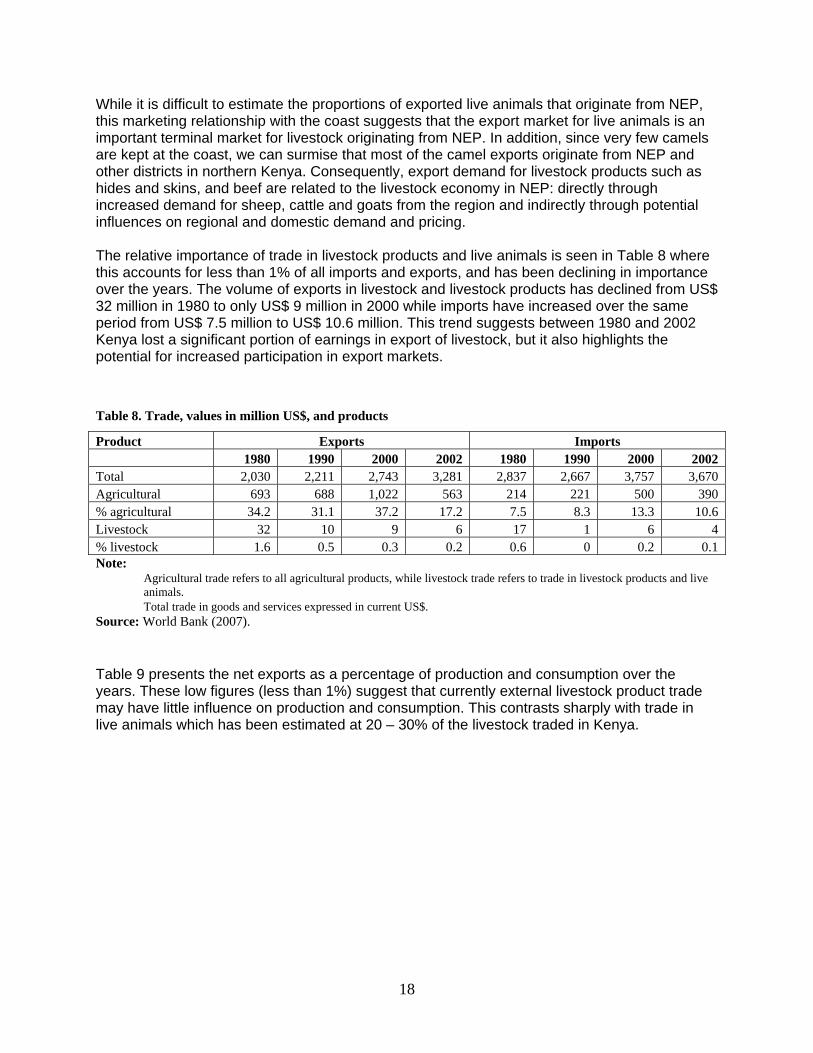

While it is difficult to estimate the proportions of exported live animals that originate from NEP, this marketing relationship with the coast suggests that the export market for live animals is an important terminal market for livestock originating from NEP. In addition, since very few camels are kept at the coast, we can surmise that most of the camel exports originate from NEP and other districts in northern Kenya. Consequently, export demand for livestock products such as hides and skins, and beef are related to the livestock economy in NEP: directly through increased demand for sheep, cattle and goats from the region and indirectly through potential influences on regional and domestic demand and pricing. The relative importance of trade in livestock products and live animals is seen in Table 8 where this accounts for less than 1% of all imports and exports, and has been declining in importance over the years. The volume of exports in livestock and livestock products has declined from US$ 32 million in 1980 to only US$ 9 million in 2000 while imports have increased over the same period from US$ 7.5 million to US$ 10.6 million. This trend suggests between 1980 and 2002 Kenya lost a significant portion of earnings in export of livestock, but it also highlights the potential for increased participation in export markets.

Table 8. Trade, values in million US$, and products

Product Exports Imports 1980 1990 2000 2002 1980 1990 2000 2002 Total 2,030 2,211 2,743 3,281 2,837 2,667 3,757 3,670 Agricultural 693 688 1,022 563 214 221 500 390 % agricultural 34.2 31.1 37.2 17.2 7.5 8.3 13.3 10.6 Livestock 32 10 9 6 17 1 6 4 % livestock 1.6 0.5 0.3 0.2 0.6 0 0.2 0.1 Note:

Agricultural trade refers to all agricultural products, while livestock trade refers to trade in livestock products and live animals.

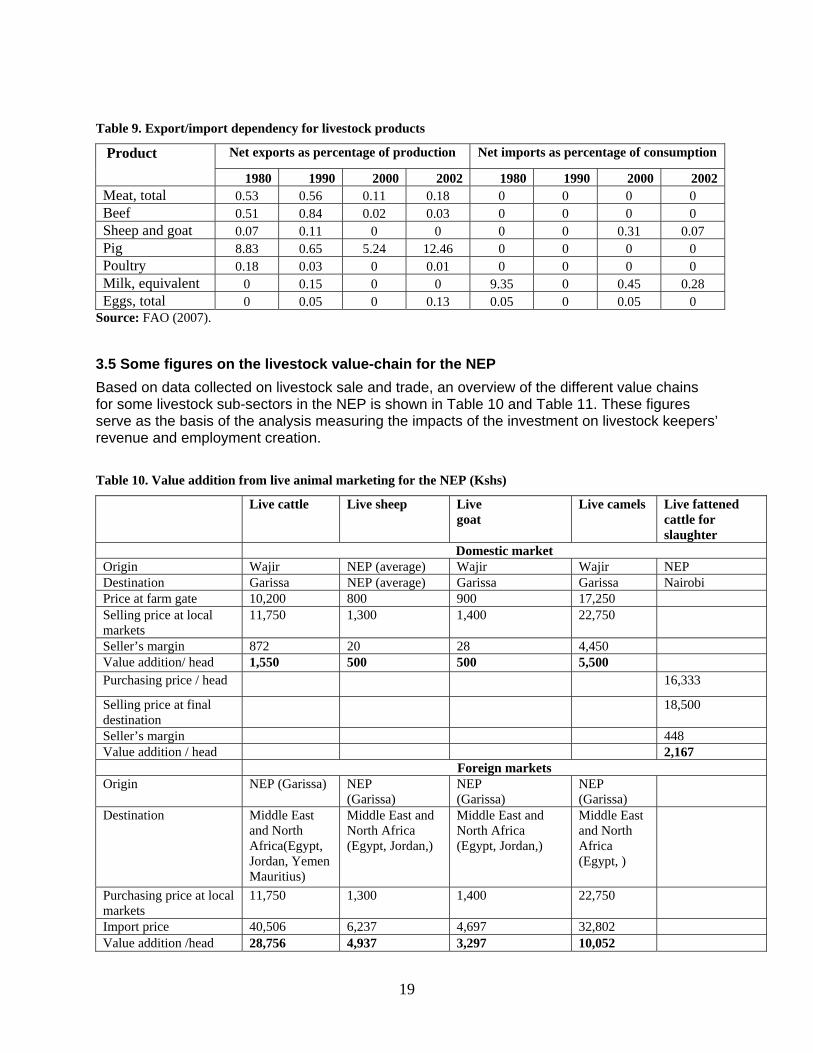

Total trade in goods and services expressed in current US$. Source: World Bank (2007). Table 9 presents the net exports as a percentage of production and consumption over the years. These low figures (less than 1%) suggest that currently external livestock product trade may have little influence on production and consumption. This contrasts sharply with trade in live animals which has been estimated at 20 – 30% of the livestock traded in Kenya.

19

Table 9. Export/import dependency for livestock products

Product Net exports as percentage of production Net imports as percentage of consumption

1980 1990 2000 2002 1980 1990 2000 2002 Meat, total 0.53 0.56 0.11 0.18 0 0 0 0 Beef 0.51 0.84 0.02 0.03 0 0 0 0 Sheep and goat 0.07 0.11 0 0 0 0 0.31 0.07 Pig 8.83 0.65 5.24 12.46 0 0 0 0 Poultry 0.18 0.03 0 0.01 0 0 0 0 Milk, equivalent 0 0.15 0 0 9.35 0 0.45 0.28 Eggs, total 0 0.05 0 0.13 0.05 0 0.05 0

Source: FAO (2007).

3.5 Some figures on the livestock value-chain for the NEP

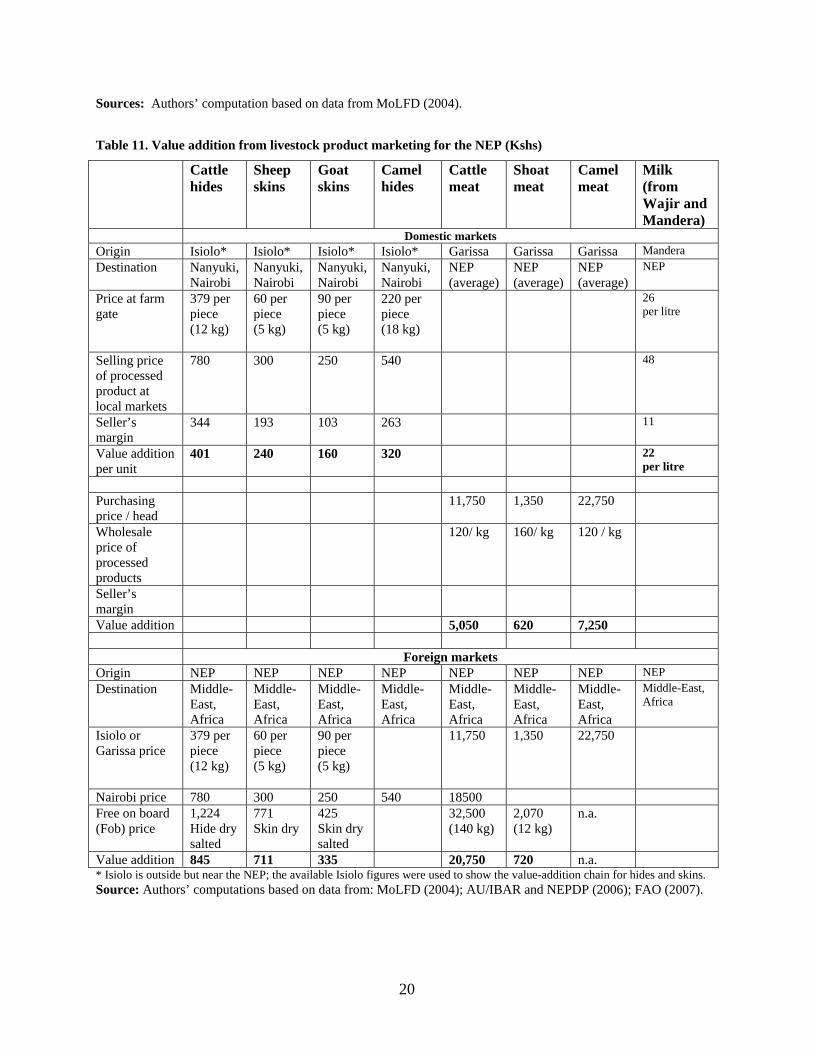

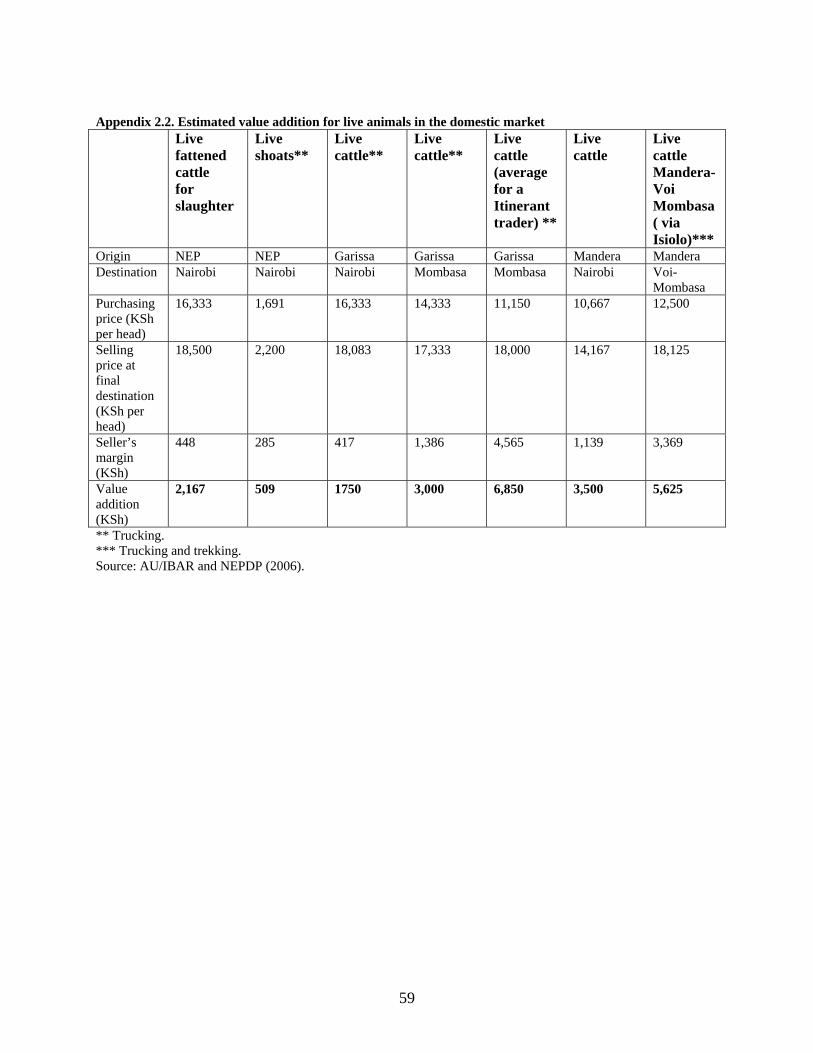

Based on data collected on livestock sale and trade, an overview of the different value chains for some livestock sub-sectors in the NEP is shown in Table 10 and Table 11. These figures serve as the basis of the analysis measuring the impacts of the investment on livestock keepers’ revenue and employment creation.

Table 10. Value addition from live animal marketing for the NEP (Kshs)

Live cattle Live sheep Live goat

Live camels Live fattened cattle for slaughter

Domestic market Origin Wajir NEP (average) Wajir Wajir NEP Destination Garissa NEP (average) Garissa Garissa Nairobi Price at farm gate 10,200 800 900 17,250

Selling price at local markets

11,750 1,300 1,400 22,750

Seller’s margin 872 20 28 4,450

Value addition/ head 1,550 500 500 5,500

Purchasing price / head 16,333

Selling price at final destination

18,500

Seller’s margin 448 Value addition / head 2,167 Foreign markets Origin NEP (Garissa) NEP

(Garissa) NEP (Garissa)

NEP (Garissa)

Destination Middle East and North Africa(Egypt, Jordan, Yemen Mauritius)

Middle East and North Africa (Egypt, Jordan,)

Middle East and North Africa (Egypt, Jordan,)

Middle East and North Africa (Egypt, )

Purchasing price at local markets

11,750 1,300 1,400 22,750

Import price 40,506 6,237 4,697 32,802

Value addition /head 28,756 4,937 3,297 10,052

20

Sources: Authors’ computation based on data from MoLFD (2004).

Table 11. Value addition from livestock product marketing for the NEP (Kshs)

Cattle hides

Sheep skins

Goat skins

Camel hides

Cattle meat

Shoat meat

Camel meat

Milk (from Wajir and Mandera)

Domestic markets Origin Isiolo* Isiolo* Isiolo* Isiolo* Garissa Garissa Garissa Mandera

Destination Nanyuki, Nairobi

Nanyuki, Nairobi

Nanyuki, Nairobi

Nanyuki, Nairobi

NEP (average)

NEP (average)

NEP (average)

NEP

Price at farm gate

379 per piece (12 kg)

60 per piece (5 kg)

90 per piece (5 kg)

220 per piece (18 kg)

26 per litre

Selling price of processed product at local markets

780 300 250 540 48

Seller’s margin

344 193 103 263 11

Value addition per unit

401 240 160 320 22 per litre

Purchasing price / head

11,750 1,350 22,750

Wholesale price of processed products

120/ kg

160/ kg 120 / kg

Seller’s margin

Value addition 5,050 620 7,250

Foreign markets Origin NEP NEP NEP NEP NEP NEP NEP NEP

Destination Middle-East, Africa

Middle-East, Africa

Middle-East, Africa

Middle-East, Africa

Middle-East, Africa

Middle-East, Africa

Middle-East, Africa

Middle-East, Africa

Isiolo or Garissa price

379 per piece (12 kg)

60 per piece (5 kg)

90 per piece (5 kg)

11,750 1,350 22,750

Nairobi price 780 300 250 540 18500

Free on board (Fob) price

1,224 Hide dry salted

771 Skin dry

425 Skin dry salted

32,500 (140 kg)

2,070 (12 kg)

n.a.

Value addition 845 711 335 20,750 720 n.a. * Isiolo is outside but near the NEP; the available Isiolo figures were used to show the value-addition chain for hides and skins. Source: Authors’ computations based on data from: MoLFD (2004); AU/IBAR and NEPDP (2006); FAO (2007).

21

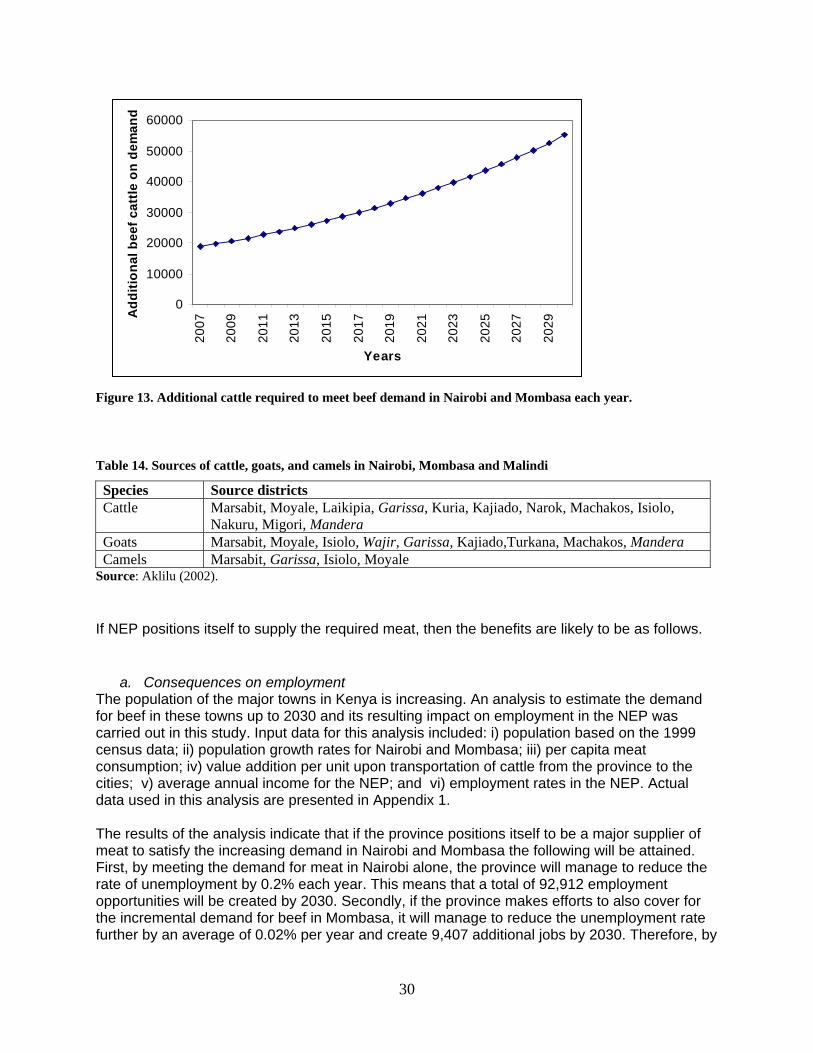

These tables show that in the domestic market for live animals, live camels yield the highest value added per head, followed by live cattle per head. However, cattle meat yields the highest value added per animal in the international markets.

4. Investment and Growth Opportunities for the NEP This section is motivated by the spirit of Vision 2030 of the GoK: projecting a clear image of a future in which Kenya has made optimal use of its resources and the opportunities presented by the national, regional and global economy to lift itself into a robust and vibrant middle-income economy with welfare benefits sufficiently distributed across the citizenry. While such a visioning exercise must by definition present an optimistic picture, it is only useful if one can chart a realistic path to arrive at the envisioned future. From the current situation in the livestock sector already laid out in Section 3, this report projects into the future, uncovering the opportunities and estimating the potential returns to different investment scenarios. The first scenario consists of the business-as-usual case: a vision of the state of the livestock sector, and its contribution to the NEP and national economy, if we maintain the current trajectory. The second scenario outlines a strategy that focuses on catering to domestic demand for livestock products especially for meet which leads to the demand of more live animals. The third scenario focuses on feeding foreign demand for live animals, while the fourth scenario investigates the possibilities of a livestock sector driven by exports of processed livestock products. Analysis in each scenario will assess the likely impact on three key indicators of success: increase in livestock income and production, employment generation, and state of food security. While not mutually exclusive, each investment scenario has a unique configuration of challenges and opportunities that demand a specific set of policies to generate optimal returns. For all scenarios, the focus in mainly on live animal and meat production where NEP has a comparative advantage.

4.1 First scenario: Business-as-usual (status quo)

4.1.1 Description of the status quo A visioning exercise presents one with a desired end which explicitly recognizes that its achievement is only possible if resources and efforts have been applied in a creative and proactive manner. In that sense, business-as-usual presents the counterfactual: a picture of the future if the necessary innovative steps to dramatically increase the productivity and profitability of the livestock sector are ignored. In this scenario, the main assumption is that, for the livestock sector, there is no vision to add new investment or to create and target new market opportunities. In other words, the livestock sector is left to grow at its current rate. 4.1.2 Trends in livestock sector without any new investment Currently the NEP produces and sells (i) live animals (mainly cattle, shoats and camel) for the domestic market (including Nairobi and Mombasa); (ii) hides and skins for the domestic and international markets; (iii) meat (beef, shoat and camel meat) for the local market; and (iv) milk for the local market. Live animals, mostly cattle and shoats, are shipped from the NEP to large markets such as Nairobi and Mombasa. It is, however, difficult to specify the actual number of livestock originating from and moved out of the province because the NEP is often used as an export route of live animals from neighbouring countries (Ethiopia and Somalia). Figures for livestock population and revenue from livestock production (Table 12) indicate that cattle production is

22

the largest revenue-generator in the NEP although it has the lowest growth rate (MoLFD 2004; AU/IBAR and NEPDP 2006). According to the same data sources, total revenue from livestock in the province amounted at least to about KSh 2 billion and the net value addition was about KSh 600 million. Such figures indicate the importance of livestock in the economy of NEP under current trends.

Table 12. Livestock production and revenue in the NEP, 2003

Livestock population (2003)

Growth rate of livestock population (%)2002–03

Number of animals sold in the local market

Meat produced for local market (kg)

Hides and skins (kg)

Average price per animal (KShs)

Revenue from livestock sales (Kshs)

Cattle 1,056,280 3.8 156,856 247,160 16,854 8,488 1,329,405,250

Sheep 596,662 7.0 86,639 274,716 (shoats) 232,506 1,303 100,540,139

Goats 882,931 12.8 121,168 n.a. 354,179 1,378 159,596,150 Camels 546,232 5.0 28,709 2,080,000 15,084 13,758 352,890,450 Chicken 137,782 8.2 0 n.a. 0 Donkeys 49,142 66.1 5,157 n.a. 4,667 20,557,500

Source: MoLFD (2004); AU/IBAR and NEPDP (2006).

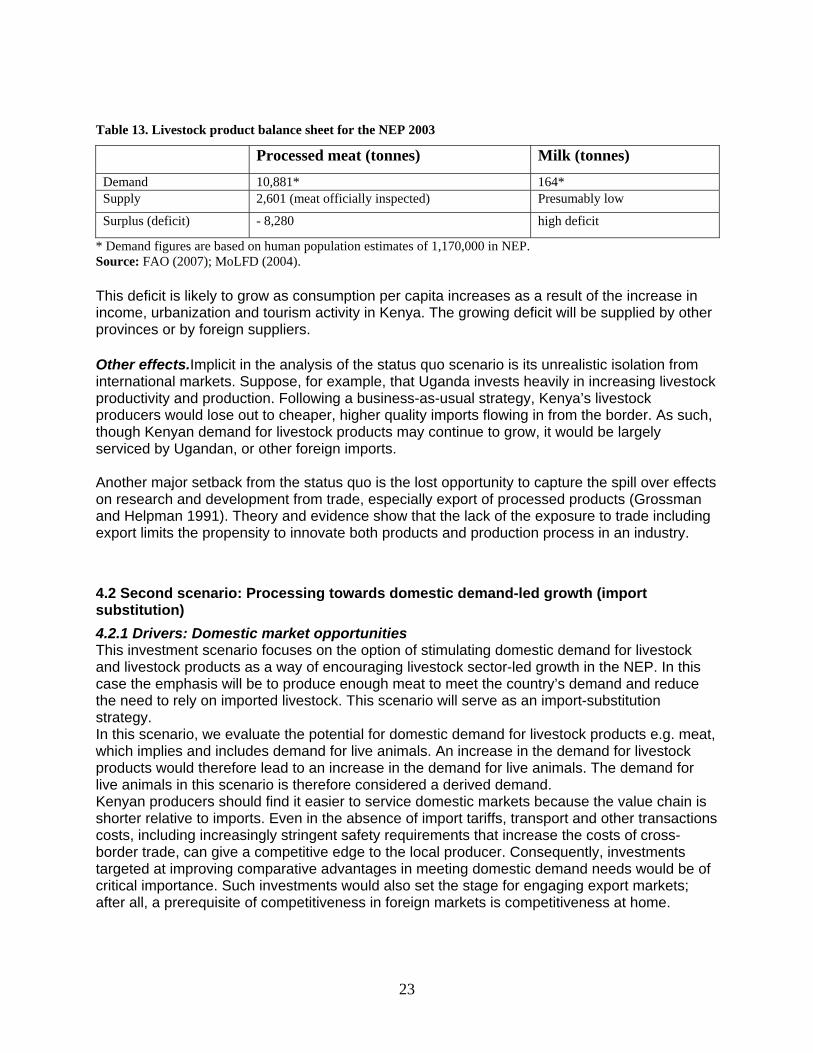

4.1.3 Consequences of the status quo Impact on livestock keepers’ income. The analysis focuses mainly on the domestic market where most NEP livestock are currently destined. With the annual increases in livestock population (Table 12), revenue for livestock keepers from total livestock sales would increase by about Kshs 115.5 million per year. This is under the assumption that average prices per head of animal remain constant. Such figures imply that livestock production and income may continue to grow even without new investment. But the concern is whether production under the status quo meets actual demands in both the domestic and international markets. Impact on employment creation. With the actual growth in livestock population shown in Table 12 and using the value addition per animal sold in the local market shown in Table 11, the increase in total value addition from livestock sale in the NEP will be about Kshs 29.1 million. The minimum wage in the agriculture sector is about Kshs 30,000 per year. Assuming that all the value addition goes to job creation, total value addition will create only about 1000 jobs per year. For instance, with a population of about 1.2 million, and an employment rate of about 65% in the NEP for 2003, the growth in the livestock sector could increase employment only by about 0.12% per year in the province which is only a tiny contribution towards reducing unemployment in Kenya. Impact on food security. The NEP has the highest population growth rate in the entire country. The latest census indicates that the population growth was about 9.5% between 1989 and 1999 compared with 3% for Kenya. Such a high growth rate is well above the growth rate of the livestock population (Table 13).

23

Table 13. Livestock product balance sheet for the NEP 2003

Processed meat (tonnes) Milk (tonnes)

Demand 10,881* 164* Supply 2,601 (meat officially inspected) Presumably low

Surplus (deficit) - 8,280 high deficit

* Demand figures are based on human population estimates of 1,170,000 in NEP. Source: FAO (2007); MoLFD (2004). This deficit is likely to grow as consumption per capita increases as a result of the increase in income, urbanization and tourism activity in Kenya. The growing deficit will be supplied by other provinces or by foreign suppliers. Other effects.Implicit in the analysis of the status quo scenario is its unrealistic isolation from international markets. Suppose, for example, that Uganda invests heavily in increasing livestock productivity and production. Following a business-as-usual strategy, Kenya’s livestock producers would lose out to cheaper, higher quality imports flowing in from the border. As such, though Kenyan demand for livestock products may continue to grow, it would be largely serviced by Ugandan, or other foreign imports. Another major setback from the status quo is the lost opportunity to capture the spill over effects on research and development from trade, especially export of processed products (Grossman and Helpman 1991). Theory and evidence show that the lack of the exposure to trade including export limits the propensity to innovate both products and production process in an industry.

4.2 Second scenario: Processing towards domestic demand-led growth (import substitution)

4.2.1 Drivers: Domestic market opportunities This investment scenario focuses on the option of stimulating domestic demand for livestock and livestock products as a way of encouraging livestock sector-led growth in the NEP. In this case the emphasis will be to produce enough meat to meet the country’s demand and reduce the need to rely on imported livestock. This scenario will serve as an import-substitution strategy. In this scenario, we evaluate the potential for domestic demand for livestock products e.g. meat, which implies and includes demand for live animals. An increase in the demand for livestock products would therefore lead to an increase in the demand for live animals. The demand for live animals in this scenario is therefore considered a derived demand. Kenyan producers should find it easier to service domestic markets because the value chain is shorter relative to imports. Even in the absence of import tariffs, transport and other transactions costs, including increasingly stringent safety requirements that increase the costs of cross-border trade, can give a competitive edge to the local producer. Consequently, investments targeted at improving comparative advantages in meeting domestic demand needs would be of critical importance. Such investments would also set the stage for engaging export markets; after all, a prerequisite of competitiveness in foreign markets is competitiveness at home.

24

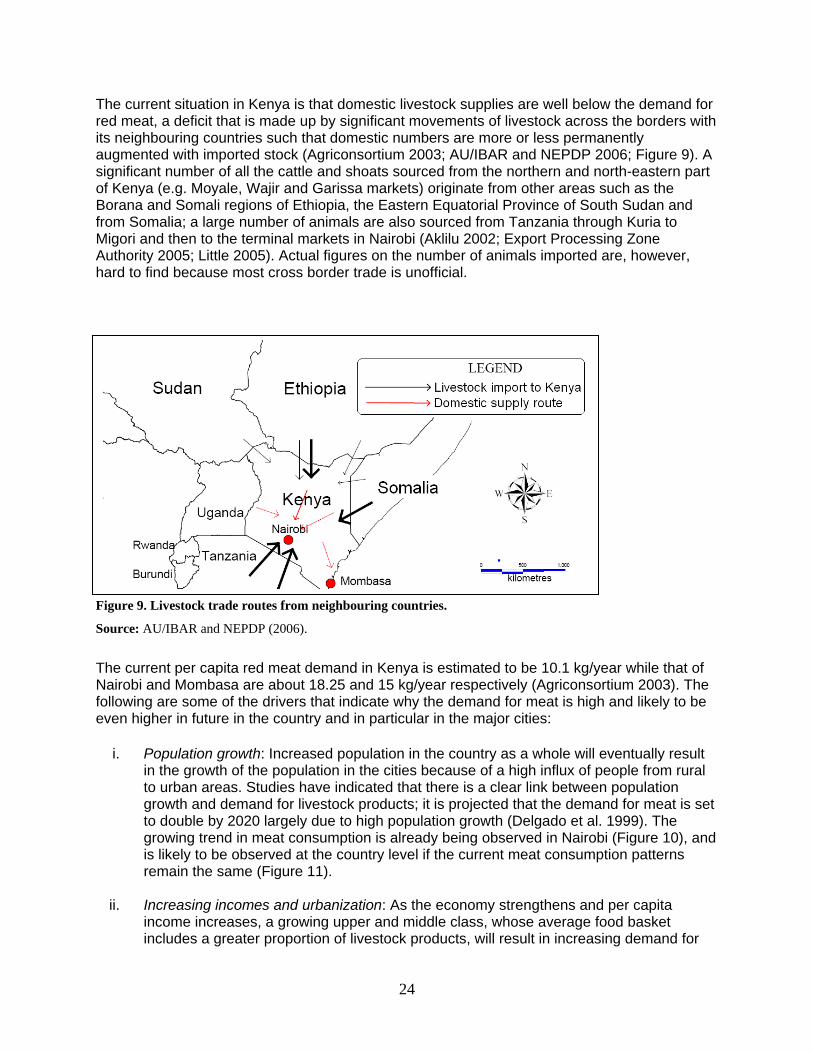

The current situation in Kenya is that domestic livestock supplies are well below the demand for red meat, a deficit that is made up by significant movements of livestock across the borders with its neighbouring countries such that domestic numbers are more or less permanently augmented with imported stock (Agriconsortium 2003; AU/IBAR and NEPDP 2006; Figure 9). A significant number of all the cattle and shoats sourced from the northern and north-eastern part of Kenya (e.g. Moyale, Wajir and Garissa markets) originate from other areas such as the Borana and Somali regions of Ethiopia, the Eastern Equatorial Province of South Sudan and from Somalia; a large number of animals are also sourced from Tanzania through Kuria to Migori and then to the terminal markets in Nairobi (Aklilu 2002; Export Processing Zone Authority 2005; Little 2005). Actual figures on the number of animals imported are, however, hard to find because most cross border trade is unofficial.

Figure 9. Livestock trade routes from neighbouring countries.

Source: AU/IBAR and NEPDP (2006).

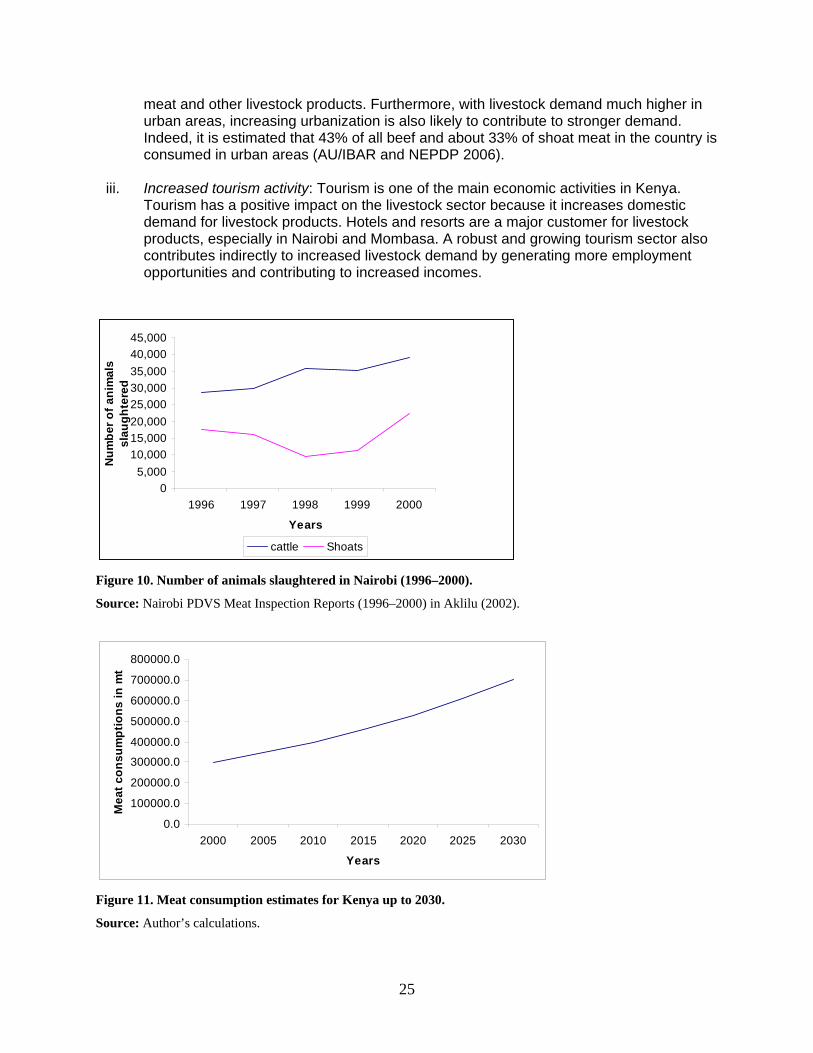

The current per capita red meat demand in Kenya is estimated to be 10.1 kg/year while that of Nairobi and Mombasa are about 18.25 and 15 kg/year respectively (Agriconsortium 2003). The following are some of the drivers that indicate why the demand for meat is high and likely to be even higher in future in the country and in particular in the major cities:

i. Population growth: Increased population in the country as a whole will eventually result in the growth of the population in the cities because of a high influx of people from rural to urban areas. Studies have indicated that there is a clear link between population growth and demand for livestock products; it is projected that the demand for meat is set to double by 2020 largely due to high population growth (Delgado et al. 1999). The growing trend in meat consumption is already being observed in Nairobi (Figure 10), and is likely to be observed at the country level if the current meat consumption patterns remain the same (Figure 11).

ii. Increasing incomes and urbanization: As the economy strengthens and per capita

income increases, a growing upper and middle class, whose average food basket includes a greater proportion of livestock products, will result in increasing demand for

25

meat and other livestock products. Furthermore, with livestock demand much higher in urban areas, increasing urbanization is also likely to contribute to stronger demand. Indeed, it is estimated that 43% of all beef and about 33% of shoat meat in the country is consumed in urban areas (AU/IBAR and NEPDP 2006).

iii. Increased tourism activity: Tourism is one of the main economic activities in Kenya.

Tourism has a positive impact on the livestock sector because it increases domestic demand for livestock products. Hotels and resorts are a major customer for livestock products, especially in Nairobi and Mombasa. A robust and growing tourism sector also contributes indirectly to increased livestock demand by generating more employment opportunities and contributing to increased incomes.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1996 1997 1998 1999 2000

Years

Nu

mb

er

of

an

ima

ls

sla

ug

hte

red

cattle Shoats

Figure 10. Number of animals slaughtered in Nairobi (1996–2000).

Source: Nairobi PDVS Meat Inspection Reports (1996–2000) in Aklilu (2002).

0.0

100000.0

200000.0

300000.0

400000.0

500000.0

600000.0

700000.0

800000.0

2000 2005 2010 2015 2020 2025 2030

Years

Me

at

co

ns

um

pti

on

s i

n m

t

Figure 11. Meat consumption estimates for Kenya up to 2030.

Source: Author’s calculations.

26

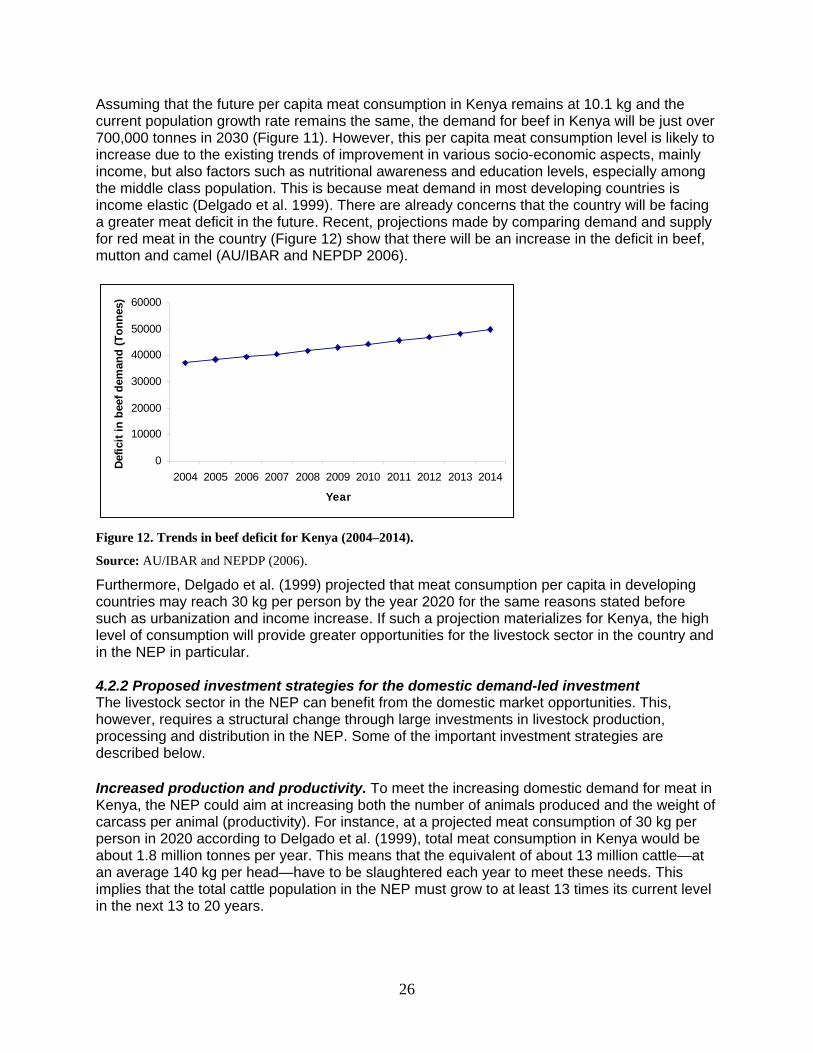

Assuming that the future per capita meat consumption in Kenya remains at 10.1 kg and the current population growth rate remains the same, the demand for beef in Kenya will be just over 700,000 tonnes in 2030 (Figure 11). However, this per capita meat consumption level is likely to increase due to the existing trends of improvement in various socio-economic aspects, mainly income, but also factors such as nutritional awareness and education levels, especially among the middle class population. This is because meat demand in most developing countries is income elastic (Delgado et al. 1999). There are already concerns that the country will be facing a greater meat deficit in the future. Recent, projections made by comparing demand and supply for red meat in the country (Figure 12) show that there will be an increase in the deficit in beef, mutton and camel (AU/IBAR and NEPDP 2006).

0

10000

20000