Investment in Machinery and Equipment is Essential to Canada's Future

26

Investment in Machinery and Equipment is Essential to Canada’s Future By Kevin Girdharry, Elena Simonova and Rock Lefebvre Issue in Focus

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Investment in Machinery and Equipment is Essential to Canada's Future

Investment in Machinery and Equipment is Essential to Canada’s Future

By Kevin Girdharry, Elena Simonova and Rock Lefebvre

Issue in Focus

2 Issue in Focus

About CGA-CanadaFounded in 1908, the Certified General Accountants Association of Canada (CGA-Canada) is a self-regulating, professional association of 75,000 students and Certified General Accountants — CGAs. CGA-Canada develops the CGA Program of Professional Studies, sets certification requirements and professional standards, contributes to national and international accounting standard setting, and serves as an advocate for accounting professional excellence. CGA-Canada has been actively involved in developing impartial and objective research on a range of topics related to major accounting, economic and social issues affecting Canadians and businesses. CGA-Canada is recognized for heightening public awareness, contributing to public policy dialogue, and advancing public interest.

For more information, contact can be made through:100 – 4200 North Fraser Way, Burnaby, BC, Canada, V5J 5K7Telephone: 604 669-3555 Fax: 604 689-5845

1201 – 350 Sparks Street, Ottawa, ON, Canada, K1R 7S8Telephone: 613 789-7771 Fax: 613 789-7772

Electronic access to this report can be obtained at www.cga.org/canada

ISSN 1925-1548

© By the Certified General Accountants Association of Canada, 2012.Reproduction in whole or in part without written permission is strictly prohibited.

3Investment in Machinery and Equipment is Essential to Canada’s Future

Investment in Machinery and Equipment is Essential to Canada’s Future

April 2012

Executive Summary ................................................................................................................... 4

Introduction ................................................................................................................................ 6

Machinery and Equipment – Why is it Important? .................................................................... 7

Machinery and Equipment in Detail – ICT and Non-ICT ......................................................... 10

ICT Investment and Being Competitive ..................................................................................... 15

ICT Investment and Research & Development .......................................................................... 16

ICT Investment, Firm Size and Small and Medium Enterprises (SMEs) .................................. 18

Government Taxation and Foreign Direct Investment ............................................................... 20

Closing Comments ..................................................................................................................... 22

References .................................................................................................................................. 24

4 Issue in Focus

Executive Summary

Machinery and equipment (M&E) is one of many imperative factors that influence Canada’s

future living standards. M&E investment and development is vital for long-term growth.

Despite Canada’s resilience to the global financial crisis, it is still vulnerable to weak future

growth due to lingering economic frailties such as rising consumer debt and continued low

productivity. Although not always apparent, there is a fundamental relationship between M&E

and productivity. M&E investments influence research and development (R&D) and labour.

These attributes, together with foreign direct investment (FDI) and taxation, stimulate a number

of variables, which can change the outcome of productivity and the standard of living.

As Canada’s future economic landscape changes, the above mentioned attributes must become

a priority for future prosperity. This continues to be a challenge for Canada in a number of

areas and as the following pages reveal:

Canadians need to become more aware of the importance of productivity drivers to

the future of Canada’s economy and well-being. A change in M&E investment directly

affects productivity; however its impact is usually not as immediate or visible to the public,

thus leaving the misconception that it is less important.

Canada trails in investment and adoption of information and communications technology

(ICT), a sub-group of M&E and the foundation for technological advancement in today’s

digital world, compared to a number of advanced economies including the U.S. It is important

for Canada to maintain investment levels similar to that of the U.S., its largest trading partner,

to retain a global competitive edge.

ICT acts as a vehicle that propagates R&D, which in turn advances innovation to its

highest potential. Canada is falling behind global R&D advancement; however there

is an opportunity to excel through collaboration between government, academic and

business communities.

Low investment in and adoption of ICT by small and medium enterprises (SMEs) is

another contributing factor to Canada’s productivity challenge. The effectiveness of

ICT in today’s business environment is still ambiguous among Canadian managers

as they may not be convinced that the reward is commensurate with the level of

financial investment.

5Investment in Machinery and Equipment is Essential to Canada’s Future

FDI is a highly effective way to rapidly increase ICT investment and adoption by allowing

qualified foreign companies to transfuse Canadian markets with their latest technologies.

Technology transfers represent the largest benefit from FDI and an opportunity exists for

Canada to adopt the latest technologies from around the world with minimal cost.

These issues provide insight of potential limitations to Canada’s economic future. Higher

importance needs to be placed on M&E as well as on the other productivity attributes with

support from public, private and academic resources. Canada’s economic landscape is bound

for change from unprecedented yet natural societal progression and M&E investment will be

instrumental in how these changes are adopted.

6 Issue in Focus

Introduction

Over the past decade, a number of significant events have changed the course of the global

economy, including the expansion of technology, and more recently, a recession. Changes in

technological machinery and equipment (M&E), which influences productivity, played an

instrumental role in both of these events. Although Canada adapted favourably to both events, it

continues to exhibit relatively low productivity growth. The last decade saw labour productivity on

average increase by only 0.7% per year. To ensure that sustainable living standards representative

of an advanced economy are attained in the future, Canada will need to improve its productivity

level by substantially investing in M&E.

M&E can be categorized into two groups; information and communications technology (ICT)

and non-ICT. In Canada, until the last 15 to 20 years, overall investment was predominately

in non-ICT M&E. Since then, the landscape has changed. In 2011, investment in ICT M&E

represented 48.9%1 of total M&E investment. As ICT M&E continues to shape Canada’s

economic forefront, a number of studies2 have identified that low overall investment in ICT is

a significant contributor to Canada’s continued lagging productivity. There are a number of

explanations for Canada’s low investment in ICT; those include underutilized potential of such

productivity factors as innovation and competition, and certain characteristics of the Canadian

business sector.

M&E is one of many critical drivers for productivity growth. CGA-Canada considers it timely

to examine investments in M&E and the potential long-term impact these investments may have

on Canada’s future. We begin our review by briefly discussing the relationship between M&E,

productivity and living standards. We then discuss the current situation and recent trends within

each M&E group. Finally, we assess how these issues converge and determine why the existing

relationships between M&E and research and development (R&D), Canadian firm sizes and

foreign direct investment (FDI) are underperforming in the economy. Furthermore, we identify

certain characteristics of the Canadian business sector which also impact M&E investment.

Investment in M&E is important to the future livelihood of Canadians and it is critical that it

is supported to ensure future progress.

1 Calculation based on CANSIM Table 031-0003 (in 2002 dollars).2 Previous studies include Sharpe, A. (2005). What Explains the Canada-US ICT Investment Gap? Centre for the Study of Living

Standards. International Productivity Monitor, No. 11, Rao, S. (2011). Cracking Canada’s Productivity Conundrum. Institute for Research on Public Policy Study No. 25, Rao, S. et all. (2006). What Explains the Canada-U.S. TFP Gap? Industry Canada, Working Paper 2006-08.

7Investment in Machinery and Equipment is Essential to Canada’s Future

Machinery and Equipment – Why is it Important?

M&E is a fundamental component to any growing economy. It includes all types of machines

and equipment except items acquired by households for final consumption. M&E is found in

all sectors of the economy. It plays an intricate role in the development of long-term social and

financial welfare through its impact on productivity growth. Advanced M&E has the ability

to stimulate a number of variables that directly contribute to productivity such as labour and

related skills, R&D, competition and innovation. M&E can influence labour by requiring higher

skilled workers for operation and development. It influences R&D by acting as an instrument for

exploration and discovery, and finally it indirectly stimulates competition and innovation through

reorganization and advancement of products and services. We turn our focus to some of these

attributes when discussing the specific groups of M&E in later sections. In order to understand the

importance of M&E investment to future economic welfare, we first briefly discuss the concepts

of productivity and the standard of living.

Productivity, Living Standards and Machinery and Equipment

Productivity can be defined as the measure of efficiency in producing goods and services using

economic resources; or output per unit of input. Simply put, productivity growth is critical for

long-term economic growth and improved living standards. Productivity influences a number of

socioeconomic variables in various economic sectors including real wages, consumption, social

status, employment, inventory, profitability, and tax revenues. The Centre for the Study of Living

Standards indicates that a 3% annual growth in productivity can lead to the doubling of living

standards over 24 years.3

A widely identified measure of productivity is labour productivity, which measures output per

hour worked or per worker. This indicator identifies changes to economic output from changes to

either employment or more efficient work from current employees. Major determinants of growth

in labour productivity include capital intensity, multifactor productivity (MFP) and human capital.

Capital intensity reflects changes in the amount of capital, such as M&E, per hour worked (or

capital-to-labour ratio);4 MFP reflects technological changes, organizational innovations and

economies of scale whereas investment in human capital identifies changes to the quality of

labour. In Canada, capital intensity was the dominant driver of the growth in labour productivity

in almost every province between 1997 and 2010.5

3 Sharpe, A. (2005). Six Policies to Improve Productivity Growth in Canada. Edited testimony to the Senate Standing Committee on Banking Trade and Commission. May 11, 2005, Ottawa, ON.

4 An increase in the capital-to-labour ratio is known as capital deepening. 5 Statistics Canada (2012). Factors in the Growth of Labour Productivity in the Provinces. The Daily, March 12, 2012.

8 Issue in Focus

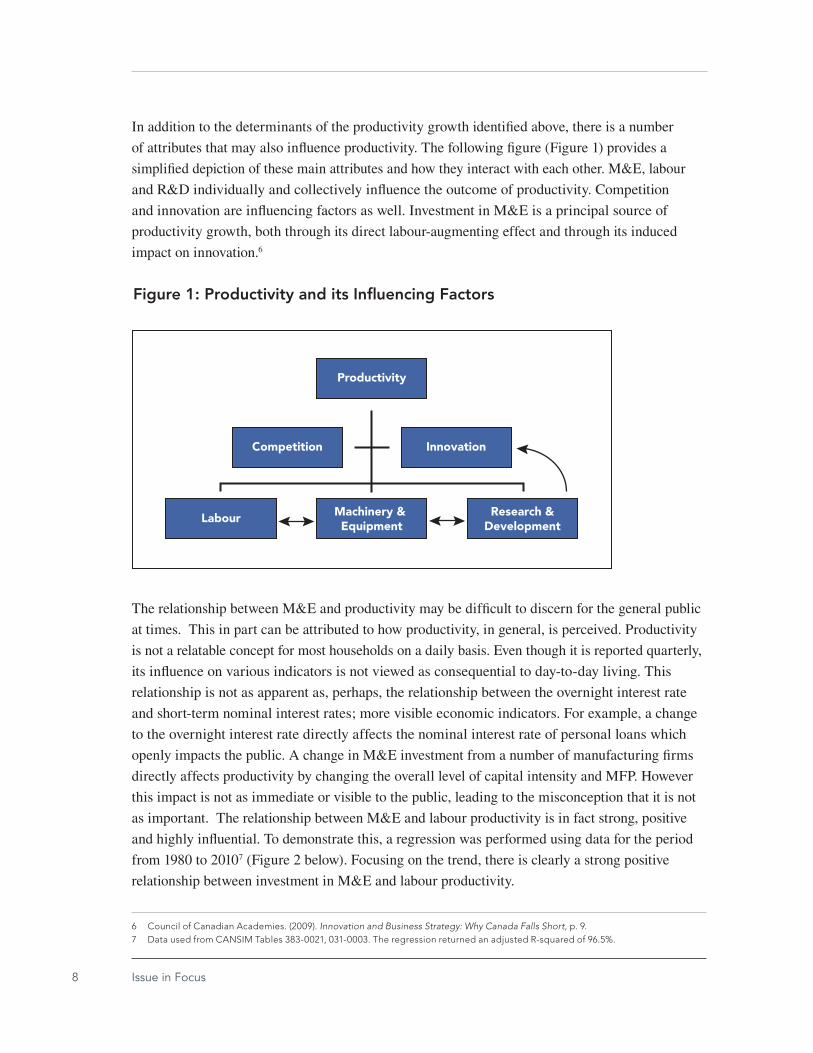

In addition to the determinants of the productivity growth identified above, there is a number

of attributes that may also influence productivity. The following figure (Figure 1) provides a

simplified depiction of these main attributes and how they interact with each other. M&E, labour

and R&D individually and collectively influence the outcome of productivity. Competition

and innovation are influencing factors as well. Investment in M&E is a principal source of

productivity growth, both through its direct labour-augmenting effect and through its induced

impact on innovation.6

The relationship between M&E and productivity may be difficult to discern for the general public

at times. This in part can be attributed to how productivity, in general, is perceived. Productivity

is not a relatable concept for most households on a daily basis. Even though it is reported quarterly,

its influence on various indicators is not viewed as consequential to day-to-day living. This

relationship is not as apparent as, perhaps, the relationship between the overnight interest rate

and short-term nominal interest rates; more visible economic indicators. For example, a change

to the overnight interest rate directly affects the nominal interest rate of personal loans which

openly impacts the public. A change in M&E investment from a number of manufacturing firms

directly affects productivity by changing the overall level of capital intensity and MFP. However

this impact is not as immediate or visible to the public, leading to the misconception that it is not

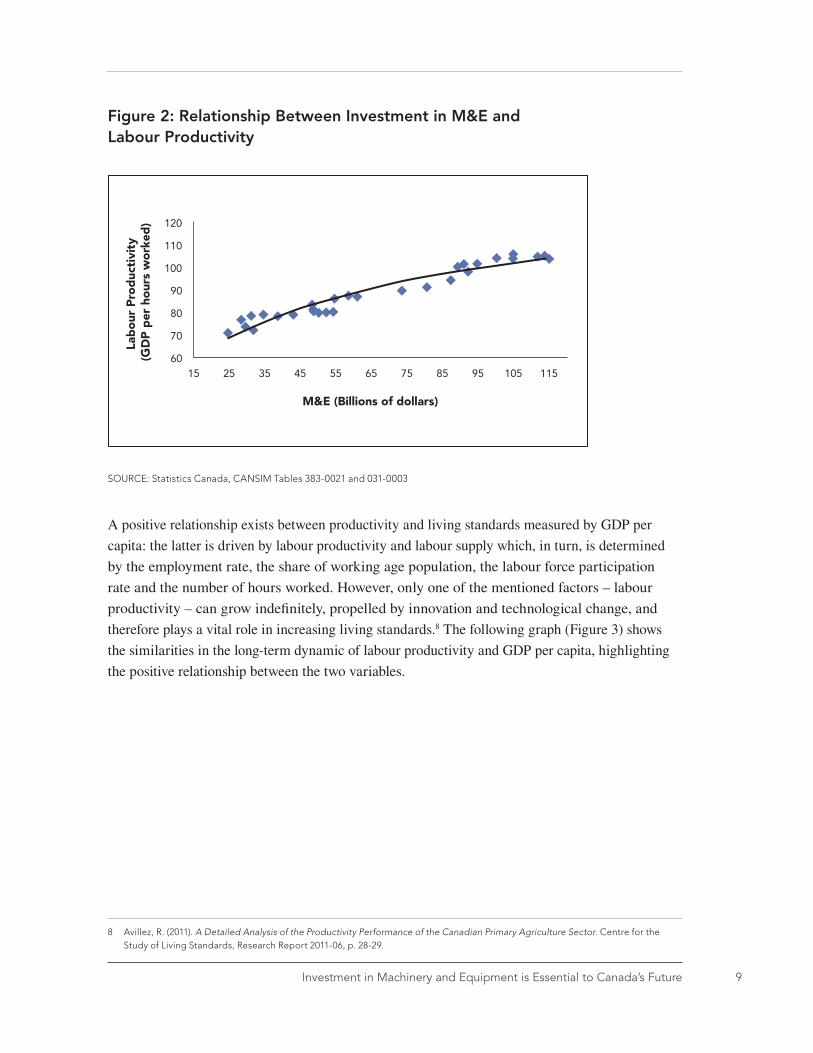

as important. The relationship between M&E and labour productivity is in fact strong, positive

and highly influential. To demonstrate this, a regression was performed using data for the period

from 1980 to 20107 (Figure 2 below). Focusing on the trend, there is clearly a strong positive

relationship between investment in M&E and labour productivity.

6 Council of Canadian Academies. (2009). Innovation and Business Strategy: Why Canada Falls Short, p. 9. 7 Data used from CANSIM Tables 383-0021, 031-0003. The regression returned an adjusted R-squared of 96.5%.

Figure 1: Productivity and its In�uencing Factors

Productivity

Competition Innovation

Labour Machinery & Equipment

Research &Development

9Investment in Machinery and Equipment is Essential to Canada’s Future

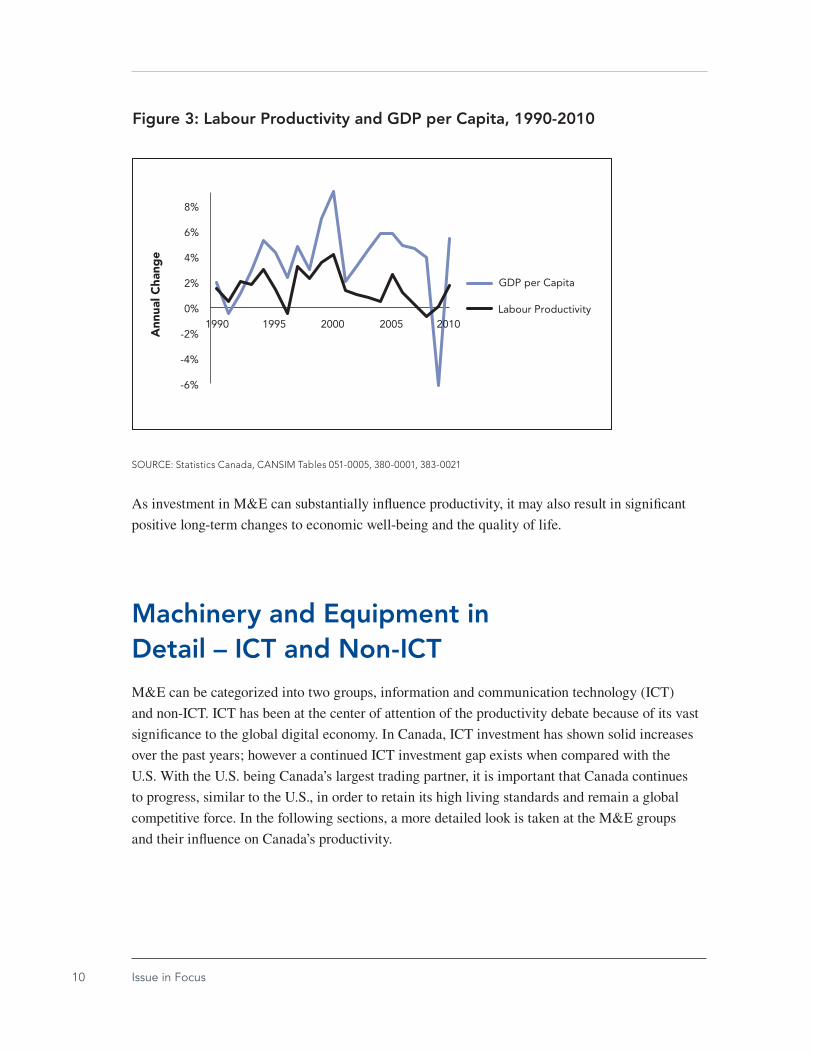

A positive relationship exists between productivity and living standards measured by GDP per

capita: the latter is driven by labour productivity and labour supply which, in turn, is determined

by the employment rate, the share of working age population, the labour force participation

rate and the number of hours worked. However, only one of the mentioned factors – labour

productivity – can grow indefinitely, propelled by innovation and technological change, and

therefore plays a vital role in increasing living standards.8 The following graph (Figure 3) shows

the similarities in the long-term dynamic of labour productivity and GDP per capita, highlighting

the positive relationship between the two variables.

8 Avillez, R. (2011). A Detailed Analysis of the Productivity Performance of the Canadian Primary Agriculture Sector. Centre for the Study of Living Standards, Research Report 2011-06, p. 28-29.

SOURCE: Statistics Canada, CANSIM Tables 383-0021 and 031-0003

60

70

80

90

100

110

120

15 25 35 45 55 65 75 85 95 105 115

Figure 2: Relationship Between Investment in M&E and Labour Productivity

M&E (Billions of dollars)

Lab

our

Pro

duc

tivi

ty

(GD

P p

er h

our

s w

ork

ed)

10 Issue in Focus

As investment in M&E can substantially influence productivity, it may also result in significant

positive long-term changes to economic well-being and the quality of life.

Machinery and Equipment in Detail – ICT and Non-ICT M&E can be categorized into two groups, information and communication technology (ICT)

and non-ICT. ICT has been at the center of attention of the productivity debate because of its vast

significance to the global digital economy. In Canada, ICT investment has shown solid increases

over the past years; however a continued ICT investment gap exists when compared with the

U.S. With the U.S. being Canada’s largest trading partner, it is important that Canada continues

to progress, similar to the U.S., in order to retain its high living standards and remain a global

competitive force. In the following sections, a more detailed look is taken at the M&E groups

and their influence on Canada’s productivity.

SOURCE: Statistics Canada, CANSIM Tables 051-0005, 380-0001, 383-0021

Figure 3: Labour Productivity and GDP per Capita, 1990-2010

-6%

-4%

-2%

0%

2%

4%

6%

8%

1990 1995 2000 2005

Ann

ual C

hang

e

GDP per Capita

Labour Productivity2010

11Investment in Machinery and Equipment is Essential to Canada’s Future

Non-ICT M&E Investment

Before the 1990s, investment in non-ICT was by far the dominant group in total M&E investment.

It comprised 92.8% of total M&E investment in 1980, and 84.4% in 1990.9 However, rapid

advancement of technology in the last two decades, specifically the global advancement of

semi-conductors, served to change the structure of M&E investment and development. The

proportion of non-ICT investment in total M&E investment decreased to 67.7% in 2000 and to

53.5% in 2010. As non-ICT investment continued to enjoy stable annual growth, intensifying

ICT growth became more dominant. ICT sector investment increased at 12.4% on average

between 1991 and 2000 and 8.6% between 2001 and 2010, where non-ICT grew at 2.4% and

2.3% respectively. The tech crash of 2000-2001 saw fluctuations in ICT investments; although

non-ICT investment experienced fluctuations as well, it grew at a more solid (though much

lower) rate on average.

Non-ICT M&E investment is significant to Canada’s infrastructure, and particularly to natural

resources industries which play an important role to Canada’s economy and overall well-being.

Canada is recognized as a country with abundant natural resources in oil and gas, forestry and

agriculture. In 2009, natural resources sectors accounted for 11.1% of Canada’s total GDP or

$133 billion. Additionally, exports from natural resource sectors comprised 46.7% or $166 billion

of Canada’s total export for the year. Non-ICT investments in natural resources sectors were

19.0% of total non-ICT investments in 2009 and 10.3% of total M&E investment.10

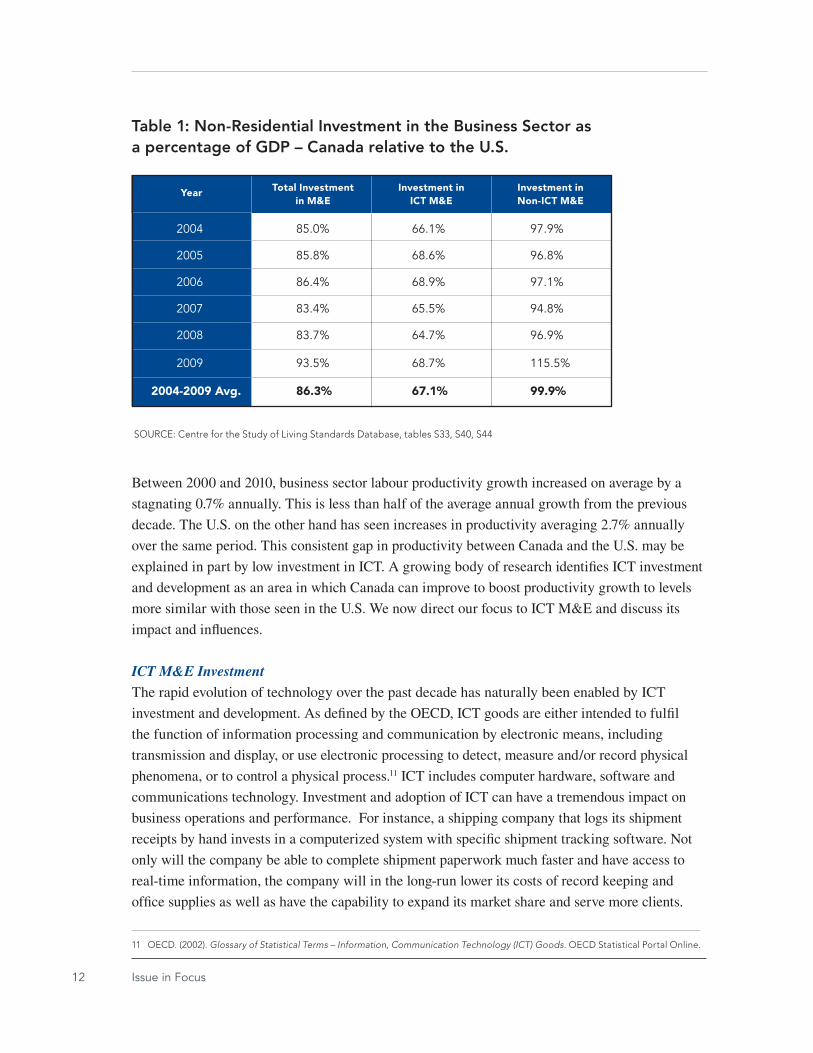

To gauge Canada’s performance in M&E investment, we compare investment levels to those in

the U.S. Given the difference in the size of the economies, investment measured as a percentage

of GDP is used to account for the scale factor. The following table (Table 1) shows Canada’s

investment in M&E (both ICT and non-ICT) in terms of U.S. investment. Between 2004 and

2009, the level of Canada’s non-ICT investment was very close to that of the U.S. on average as

a percentage of GDP. However, the table identifies a consistent gap between Canada and the U.S.

in ICT investment in the business sector.

9 Calculation based on CANSIM Table 031-0003 (in 2002 dollars).10 CANSIM Table 031-0003. Please note, this may not capture all non-ICT investments in natural resources as the percentages were

calculated by collecting the aggregate of NAICS sectors 11 (Agriculture, forestry, fishing and hunting) and 21 (Mining and oil and gas extraction).

12 Issue in Focus

Between 2000 and 2010, business sector labour productivity growth increased on average by a

stagnating 0.7% annually. This is less than half of the average annual growth from the previous

decade. The U.S. on the other hand has seen increases in productivity averaging 2.7% annually

over the same period. This consistent gap in productivity between Canada and the U.S. may be

explained in part by low investment in ICT. A growing body of research identifies ICT investment

and development as an area in which Canada can improve to boost productivity growth to levels

more similar with those seen in the U.S. We now direct our focus to ICT M&E and discuss its

impact and influences.

ICT M&E Investment

The rapid evolution of technology over the past decade has naturally been enabled by ICT

investment and development. As defined by the OECD, ICT goods are either intended to fulfil

the function of information processing and communication by electronic means, including

transmission and display, or use electronic processing to detect, measure and/or record physical

phenomena, or to control a physical process.11 ICT includes computer hardware, software and

communications technology. Investment and adoption of ICT can have a tremendous impact on

business operations and performance. For instance, a shipping company that logs its shipment

receipts by hand invests in a computerized system with specific shipment tracking software. Not

only will the company be able to complete shipment paperwork much faster and have access to

real-time information, the company will in the long-run lower its costs of record keeping and

office supplies as well as have the capability to expand its market share and serve more clients.

11 OECD. (2002). Glossary of Statistical Terms – Information, Communication Technology (ICT) Goods. OECD Statistical Portal Online.

Table 1: Non-Residential Investment in the Business Sector as a percentage of GDP – Canada relative to the U.S.

SOURCE: Centre for the Study of Living Standards Database, tables S33, S40, S44

Year Total Investment in M&E

Investment in ICT M&E

Investment in Non-ICT M&E

2004 85.0% 66.1% 97.9%

2005 85.8% 68.6% 96.8%

2006 86.4% 68.9% 97.1%

2007 83.4% 65.5% 94.8%

2008 83.7% 64.7% 96.9%

2009 93.5% 68.7% 115.5%

2004-2009 Avg. 86.3% 67.1% 99.9%

13Investment in Machinery and Equipment is Essential to Canada’s Future

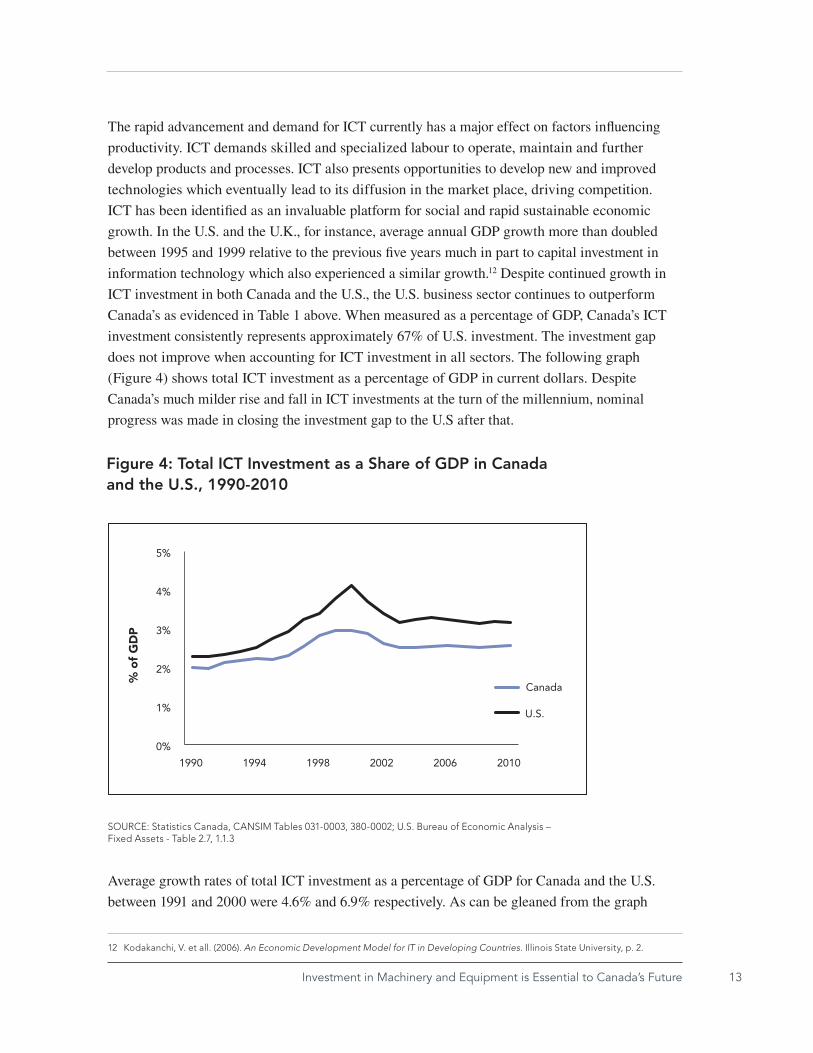

The rapid advancement and demand for ICT currently has a major effect on factors influencing

productivity. ICT demands skilled and specialized labour to operate, maintain and further

develop products and processes. ICT also presents opportunities to develop new and improved

technologies which eventually lead to its diffusion in the market place, driving competition.

ICT has been identified as an invaluable platform for social and rapid sustainable economic

growth. In the U.S. and the U.K., for instance, average annual GDP growth more than doubled

between 1995 and 1999 relative to the previous five years much in part to capital investment in

information technology which also experienced a similar growth.12 Despite continued growth in

ICT investment in both Canada and the U.S., the U.S. business sector continues to outperform

Canada’s as evidenced in Table 1 above. When measured as a percentage of GDP, Canada’s ICT

investment consistently represents approximately 67% of U.S. investment. The investment gap

does not improve when accounting for ICT investment in all sectors. The following graph

(Figure 4) shows total ICT investment as a percentage of GDP in current dollars. Despite

Canada’s much milder rise and fall in ICT investments at the turn of the millennium, nominal

progress was made in closing the investment gap to the U.S after that.

Average growth rates of total ICT investment as a percentage of GDP for Canada and the U.S.

between 1991 and 2000 were 4.6% and 6.9% respectively. As can be gleaned from the graph

SOURCE: Statistics Canada, CANSIM Tables 031-0003, 380-0002; U.S. Bureau of Economic Analysis – Fixed Assets - Table 2.7, 1.1.3

Figure 4: Total ICT Investment as a Share of GDP in Canada and the U.S., 1990-2010

% o

f G

DP

0%

1%

2%

3%

4%

5%

1990 1994 1998 2002 2006 2010

Canada

U.S.

12 Kodakanchi, V. et all. (2006). An Economic Development Model for IT in Developing Countries. Illinois State University, p. 2.

14 Issue in Focus

above, rates were similar through the next decade, where the average growth was approximately

a negative 1.5% in both countries.13 Slower growth in the latter decade might be the result of

the technology crash and financial recession as negative growth was observed in 2000-2001

(-2.2% in Canada and -9.9% in the U.S. on average) and 2007-2009 (-0.1% and -0.2% on

average respectively).

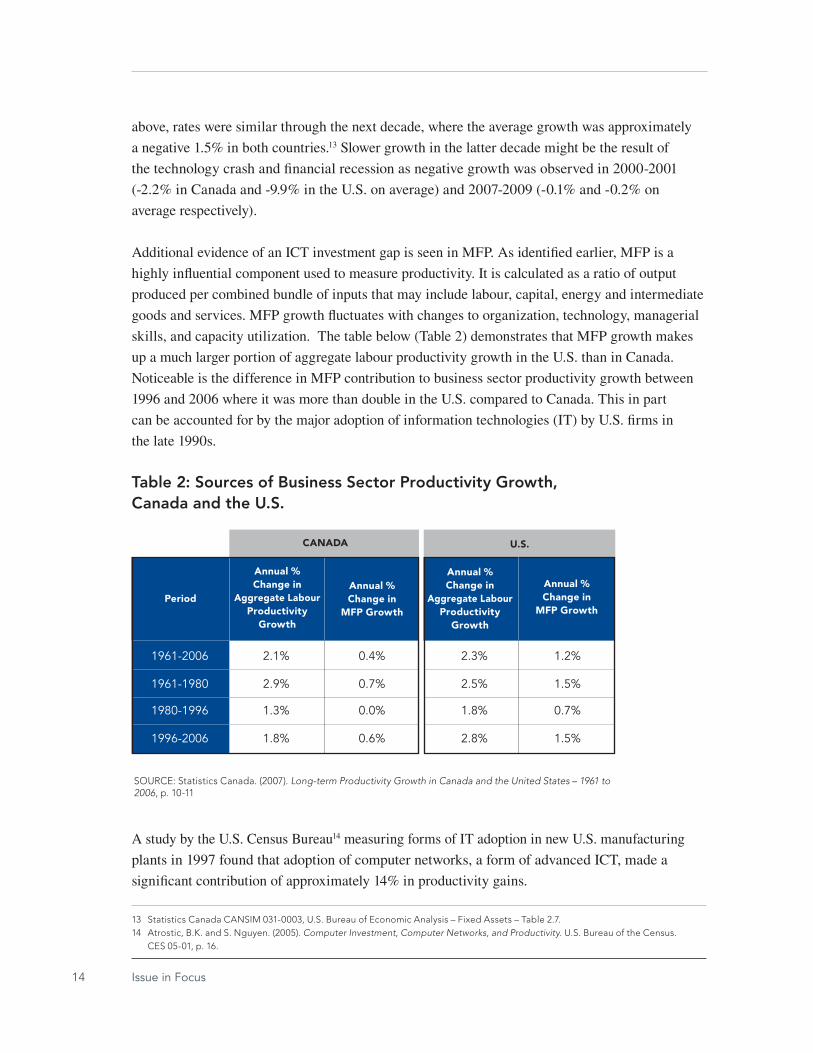

Additional evidence of an ICT investment gap is seen in MFP. As identified earlier, MFP is a

highly influential component used to measure productivity. It is calculated as a ratio of output

produced per combined bundle of inputs that may include labour, capital, energy and intermediate

goods and services. MFP growth fluctuates with changes to organization, technology, managerial

skills, and capacity utilization. The table below (Table 2) demonstrates that MFP growth makes

up a much larger portion of aggregate labour productivity growth in the U.S. than in Canada.

Noticeable is the difference in MFP contribution to business sector productivity growth between

1996 and 2006 where it was more than double in the U.S. compared to Canada. This in part

can be accounted for by the major adoption of information technologies (IT) by U.S. firms in

the late 1990s.

A study by the U.S. Census Bureau14 measuring forms of IT adoption in new U.S. manufacturing

plants in 1997 found that adoption of computer networks, a form of advanced ICT, made a

significant contribution of approximately 14% in productivity gains.

13 Statistics Canada CANSIM 031-0003, U.S. Bureau of Economic Analysis – Fixed Assets – Table 2.7. 14 Atrostic, B.K. and S. Nguyen. (2005). Computer Investment, Computer Networks, and Productivity. U.S. Bureau of the Census.

CES 05-01, p. 16.

Table 2: Sources of Business Sector Productivity Growth, Canada and the U.S.

SOURCE: Statistics Canada. (2007). Long-term Productivity Growth in Canada and the United States – 1961 to 2006, p. 10-11

Period

Annual % Change in

Aggregate Labour Productivity

Growth

Annual % Change in

MFP Growth

Annual % Change in

Aggregate Labour Productivity

Growth

1961-2006 2.1% 0.4% 2.3% 1.2%

1961-1980 2.9% 0.7% 2.5% 1.5%

1980-1996 1.3% 0.0% 1.8% 0.7%

1996-2006 1.8% 0.6% 2.8% 1.5%

Annual % Change in

MFP Growth

CANADA U.S.

15Investment in Machinery and Equipment is Essential to Canada’s Future

Despite the great recession in 2008-2009, the U.S. continues to build productivity from higher

ICT investment than Canada. Continued investment in ICT combined with labour, higher

competition among companies, strong R&D support and favourable government policies are

reasons why the U.S. advantage prevails despite current economic conditions. In the following

section we take a closer look at some of these areas and identify where Canada falls short.

Furthermore, we take a look at Canada’s business sector where opportunity lies for significant

ICT advancement.

ICT Investment and Being Competitive

Competition and ICT investment are highly persuasive factors to productivity. Highly competitive

markets can drive companies to produce the best and highest quality goods and services that

appeal to customers and clients. The relationship between competition and ICT investment occurs

through innovative development. Continuous competition requires investment in ICT and vice

versa. For example, the development of the Apple iPhone was considered the most advanced piece

of wireless equipment when released to the public in 2008. The advanced touch screen technology

raised the bar in the wireless technology industry. The investment made to perfect this technology

which was adopted from previous apple products allowed Apple to introduce a product like no

other to the wireless market. Rival companies were then compelled to invest and create their

own products of similar calibre to stay competitive and retain market share.

Canada as a nation seems to be struggling to stay competitive, not only with the U.S., but against

other OECD nations. The World Economic Forum’s Global Competitive Index (GCI) ranks

countries based on their competitiveness, productivity and living standards using a number of

economic, social, business, environmental and government attributes.15 Canada ranked 3rd overall

in 2001, however has since experienced a decline in ranking, falling as far as 16th in 2006 and

ranking 12th in 2011.

Measuring actual competition between countries presents a number of difficulties tackling which

is beyond the scope of this paper; however an indirect method of comparing competition levels

between the two countries is by looking at corporate profits as a percentage of GDP.16 Lower

profits indicate higher competition since companies are consistently competing for market share.

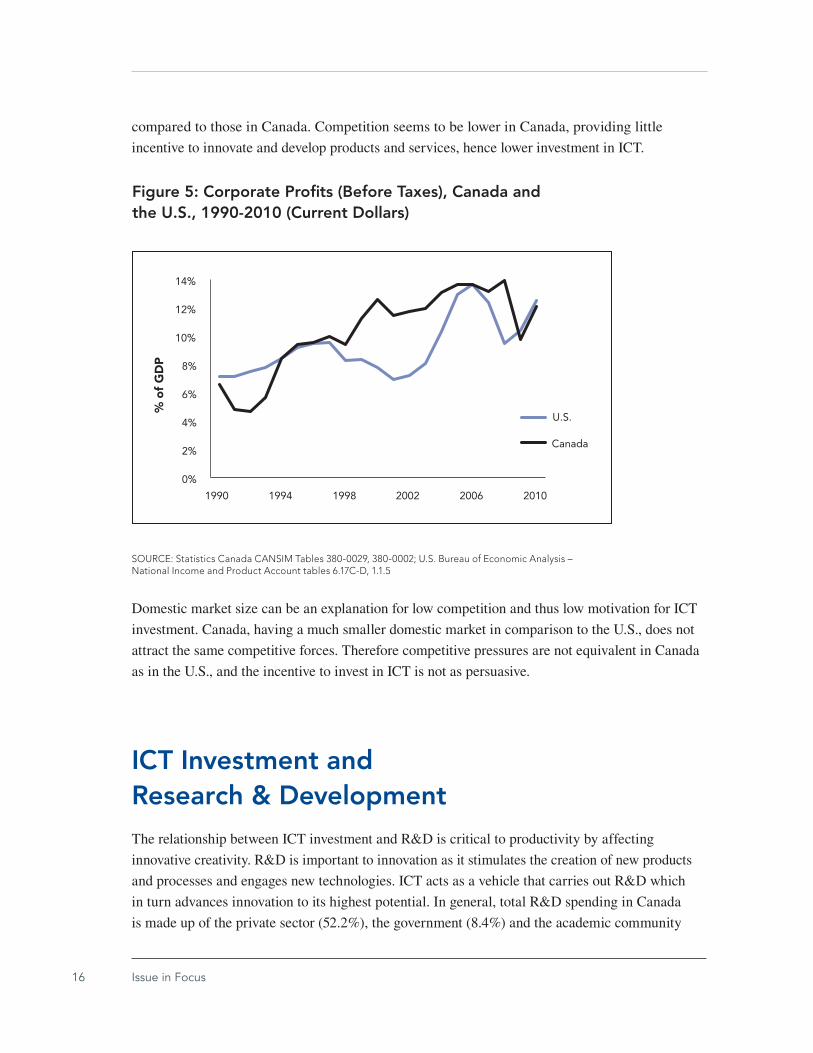

The following graph (Figure 5) shows that in general corporate profits in the U.S. are lower

15 The World Economic Forum’s GCI is an index that measures countries on their competitiveness by weighting 12 comprehensive pillars which are critical to driving productivity, innovation and competition. CGA-Canada’s report provides a brief description of the 2006 index. See CGA-Canada. (2007). Fading Productivity: Making Sense of Canada’s Productivity Challenge, for more details.

16 Council of Canadian Academies. (2009). Innovation and Business Strategy: Why Canada Falls Short. p. 14.

16 Issue in Focus

compared to those in Canada. Competition seems to be lower in Canada, providing little

incentive to innovate and develop products and services, hence lower investment in ICT.

Domestic market size can be an explanation for low competition and thus low motivation for ICT

investment. Canada, having a much smaller domestic market in comparison to the U.S., does not

attract the same competitive forces. Therefore competitive pressures are not equivalent in Canada

as in the U.S., and the incentive to invest in ICT is not as persuasive.

ICT Investment and Research & DevelopmentThe relationship between ICT investment and R&D is critical to productivity by affecting

innovative creativity. R&D is important to innovation as it stimulates the creation of new products

and processes and engages new technologies. ICT acts as a vehicle that carries out R&D which

in turn advances innovation to its highest potential. In general, total R&D spending in Canada

is made up of the private sector (52.2%), the government (8.4%) and the academic community

SOURCE: Statistics Canada CANSIM Tables 380-0029, 380-0002; U.S. Bureau of Economic Analysis – National Income and Product Account tables 6.17C-D, 1.1.5

Figure 5: Corporate Pro�ts (Before Taxes), Canada and the U.S., 1990-2010 (Current Dollars)

% o

f G

DP

U.S.

Canada

0%

2%

4%

6%

8%

10%

12%

14%

1990 1994 1998 2002 2006 2010

17Investment in Machinery and Equipment is Essential to Canada’s Future

(38.8%).17 Private enterprises constitute Canada’s largest R&D spender, where ICT-sector R&D

spending comprised 38.5% of total private R&D spending in 2009. However, in comparison

to other OECD countries, Canada ranked 20th in business expenditures on R&D (BERD) as

a percentage of GDP, well below the OECD average; the U.S., in turn, ranked 7th. ICT R&D

spending in communications equipment and services, Canada’s largest ICT investment area,

played a factor for low BERD in Canada where it accounted for 26.9% (equivalent to $1.6 billion)

of total ICT private R&D spending and 10.4% of total private R&D spending. At the industry

level, between 2002 and 2005 communications equipment R&D spending decreased by an

average of 11.6% and only rebounded to an average increase of 4.3% between 2006 and 2009.18

Domestic market size also plays a factor for low BERD in Canada. Canada’s relatively small

domestic market makes it challenging for substantial R&D to progress. Canadian ICT firms

are finding that there are greater opportunities, lower risks and easier growth transition to sell

or merge with giant foreign firms than to take the “next step” on their own. Although certain

companies do move forward, such as the CGI Group and CAE, a number of companies instead

choose to merge or outright sell their existing patents and ideas resulting in displacement from the

Canadian landscape. Examples include the Canadian firm Cognos, which was acquired by IBM

and later absorbed into IBM Infosphere as well as Newbridge Networks, a company recognized

for its ATM products which was bought and absorbed by the French firm Alcatel in 2000.

Although the business sector is Canada’s largest source of R&D spending, its share has been

declining over the last years bringing the spotlight to Canada’s higher education R&D (HERD).

As a percentage of GDP, HERD was ranked 6th among OECD countries (first among

G7 nations). Businesses also seem to be taking more interest in university performed R&D,

where business-financed R&D was at 6.3% of total funding in 2008; the highest in over a decade.

Business-sponsored R&D performed by academics is a source that has the potential to provide

significant breakthroughs, driving R&D further. As such, an opportunity exists to advance R&D

by strengthening the relationship between Canadian businesses and the academic community.

Budget 2012 measures such as refocusing the work of the National Research Council on business

needs and transforming the Business-Led Networks of Centres of Excellence initiative into a

permanent program represent a step in the right direction. Further support in this area may help

Canada achieve higher returns on R&D investment efforts and boost productivity in a number

of industries.

17 Based on 2011 intentions. The Daily – January 13, 2012 – Spending on R&D. Statistics Canada. 18 Industry Canada. (2009). ICT Sector Intramural R&D Expenditures.

18 Issue in Focus

ICT Investment, Firm Size and Small and Medium Enterprises (SMEs)

Firm size can be a substantial factor in ICT investment and adoption in Canada. Overall, the

Canadian business sector is heavily comprised of SMEs.19 They account for some 1.14 million

business entities or 99.7%20 of all businesses with employees located in Canada. SMEs employed

48% of total labour in the private sector and produce 54.2% of Canada’s business-sector GDP.21

SMEs are an important component to Canada’s economy and it is important that they continue

to progress.

The progress of ICT products and services over the last decade has changed the way companies

conduct business. Information is more readily available, barriers to international markets are

lower and communication is in real time. In order for companies to stay competitive, they must

adapt to the changing environment and therefore make the investment in ICT. A 2006 OECD

study found that company productivity increased by 1.3% for every 10% increase in employees

using computer technology.22 However, a 2006 survey performed by the Information Technology

Association of Canada found that 43% of SMEs23 that already had low investment in ICT did

not see the quantifiable benefits to ICT adoption. Moreover, a recent 2011 study24 by the Centre

francophone d’informatisation des organisations (CEFRIO) found that the biggest obstacle

SMEs face in investing in ICT was inadequate funding with 23.2% of respondents reporting this

as a reason. Inadequate or lack of competent staff was ranked second and reported by 18.7% of

surveyed. The effectiveness of ICT in today’s business environment is still questioned by some

businesses where management is not convinced that investment in ICT is worth the reward.

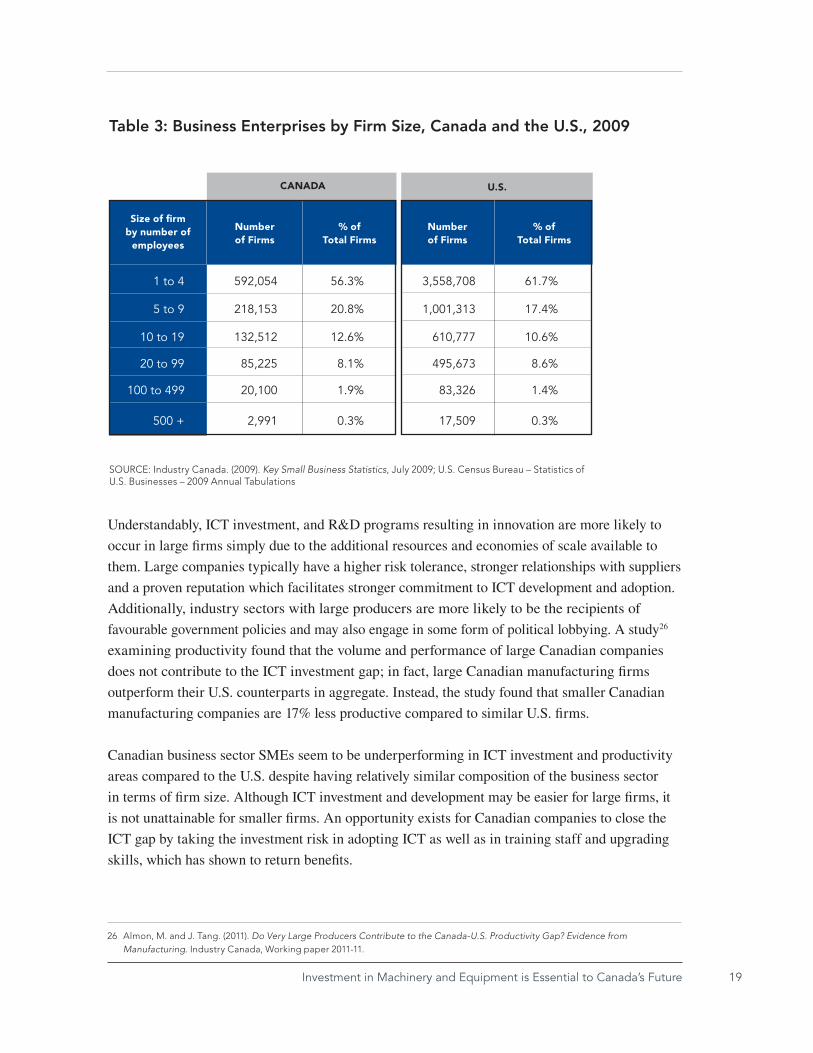

The U.S. in fact does have similar traits in terms of SME demographics. Similar to Canada,

SMEs in the U.S. employ 49.4% of all workers. SMEs comprised 99.6% of total businesses in

2009. A comparison of specific size groups of SMEs presented in Table 3 further confirms these

similarities. However, despite the similarity in the importance of SMEs to the business sector,

Canada’s ICT investment as a percentage of GDP is only two thirds (68.7%)25 of that in the U.S.

It appears that U.S. SMEs are investing and adopting more ICT and a greater potential for

Canadian SMEs to engage in ICT investment may exist.

19 SMEs are defined as companies with fewer than 500 employees.20 Based on Industry Canada (2011). Key Small Business Statistics, p. 7.21 Leung, D. and L. Rispoli. (2011). The Contribution of Small and Medium-sized Businesses to Gross Domestic Product: A Canada-

United States Comparison. Statistics Canada, Catalogue no. 11F0027M – No. 070.22 Hagén, H-O and J. Zeed. (2006). Does ICT use matter for firm productivity? Science and Technology Sector. OECD 23 In this study, the term “SMEs” refers to “small and medium businesses” as opposed to a more commonly used “small and medium

enterprises”.24 Le Centre francophone d’informatisation des organisations. (2011). NetPME 2011 – Use of ICT in Canadian SMEs. October 2011. 25 Calculated as a ratio of Canada ICT investment expressed as a share of GDP to U.S. ICT investment expressed as a share of GDP.

Source: the Centre for the Study of Living Standards Database – Table S9.

19Investment in Machinery and Equipment is Essential to Canada’s Future

Understandably, ICT investment, and R&D programs resulting in innovation are more likely to

occur in large firms simply due to the additional resources and economies of scale available to

them. Large companies typically have a higher risk tolerance, stronger relationships with suppliers

and a proven reputation which facilitates stronger commitment to ICT development and adoption.

Additionally, industry sectors with large producers are more likely to be the recipients of

favourable government policies and may also engage in some form of political lobbying. A study26

examining productivity found that the volume and performance of large Canadian companies

does not contribute to the ICT investment gap; in fact, large Canadian manufacturing firms

outperform their U.S. counterparts in aggregate. Instead, the study found that smaller Canadian

manufacturing companies are 17% less productive compared to similar U.S. firms.

Canadian business sector SMEs seem to be underperforming in ICT investment and productivity

areas compared to the U.S. despite having relatively similar composition of the business sector

in terms of firm size. Although ICT investment and development may be easier for large firms, it

is not unattainable for smaller firms. An opportunity exists for Canadian companies to close the

ICT gap by taking the investment risk in adopting ICT as well as in training staff and upgrading

skills, which has shown to return benefits.

Table 3: Business Enterprises by Firm Size, Canada and the U.S., 2009

SOURCE: Industry Canada. (2009). Key Small Business Statistics, July 2009; U.S. Census Bureau – Statistics of U.S. Businesses – 2009 Annual Tabulations

Size of firm by number of

employees

Number of Firms

% of Total Firms

Number of Firms

1 to 4 592,054 56.3% 3,558,708 61.7%

5 to 9 218,153 20.8% 1,001,313 17.4%

10 to 19 132,512 12.6% 610,777 10.6%

20 to 99 85,225 8.1% 495,673 8.6%

100 to 499 20,100 1.9% 83,326 1.4%

500 + 2,991 0.3% 17,509 0.3%

% of Total Firms

CANADA U.S.

26 Almon, M. and J. Tang. (2011). Do Very Large Producers Contribute to the Canada-U.S. Productivity Gap? Evidence from Manufacturing. Industry Canada, Working paper 2011-11.

20 Issue in Focus

Government Taxation and Foreign Direct Investment

Government taxation in regards to ICT investment and development has been a topic of great

debate over recent years. Corporate taxation in Canada has transformed over the past decade;

becoming less of a burden on company revenues in order to promote productivity growth.

In 2007, Canada had one of the highest marginal corporate income tax rates among OECD

countries, however rates have been lowered annually since 2009 to a much more competitive level

– effective 2012, the federal corporate income tax rate is 15%. This reduction provides companies

with the opportunity to allocate funds toward ICT investment and/or R&D that would otherwise

be remitted to the government.

A well-recognized incentive program provided by the federal government is the Scientific

Research and Experimental Development (SR&ED) tax credit. Being a tax-credit program in

existence since 1944, this incentive currently encourages all Canadian companies to conduct

R&D that can lead to new and improved technological advancements. The program provides a

35% refundable tax credit to all Canadian companies for up to the first $3 million in qualified

expenditures.27 Amounts exceeding this limit qualify for a 20% credit thereafter. Recognized as

one of the most generous R&D incentives among OECD countries, it is the single largest support

program for R&D. As of 2006, the program has served over 18,000 claimants and provided over

$3 billion in tax credits where almost 75% have been received by SMEs.28

Although the intent of these incentives is to encourage corporate investment and raise productivity,

some observers suggest that these programs and initiatives are not as effective as prospected. A

study29 by the Canadian Centre for Policy Alternatives estimates that the reduction in corporate

taxes will result in a $6 billion annual loss in tax revenues with only $600 million generated

in new business investment. The study finds that corporate tax cuts have no direct impact on

business investment while the indirect impact is small and continues to be weak. It may also be

that the SR&ED tax credit provides little benefit where companies end up paying high consulting

fees for preparation of the tax credit application.

The measures announced in Budget 2012 may further diminish the incentives for

commercialization of innovation intended by the SR&ED program. For instance, the budget

proposed to reduce the investment tax credit rate from 20% to 15% and to exclude capital

expenditures from the list of eligible SR&ED expenditures. It is important to ensure that the

27 Foreign companies are eligible for a non-refundable credit. 28 Canada Revenue Agency. Overview of Scientific Research and Experimental Development Tax Incentive Program, p. 4. 29 Stanford, J. (2011). Having Their Cake and Eating it Too – Business Profits, Taxes, and Investment In Canada: 1961 Through 2010.

Canadian Centre for Policy Alternatives.

21Investment in Machinery and Equipment is Essential to Canada’s Future

shift in the approach to funding innovation does not adversely affect the promotion of business

growth and innovation.

Foreign Direct Investment

FDI is an area in which both liberalization and restriction exists in regards to increasing ICT

investment and adoption. In broad terms, there are two forms of FDI, inbound and outbound.

The benefits of inbound FDI on an economy are in the technology transfers which stimulate

ICT investments and introduce globally competitive wages. Multinational companies located in

Canada have access to technology from their foreign headquarters which can eventually transfer

to the domestic market. Employees of foreign firms tend to be paid competitively to international

standards, including bonuses and other compensations. Outbound benefits include international

market expansion and possible higher exports of domestically produced goods. Canadian

companies investing abroad create an international presence and reputation which can contribute

to higher revenues.

Canadian companies actually do more business abroad than foreign nationals do in Canada. The

trade liberalization agreements Canada has with other countries, such as the North American Free

Trade Agreement (NAFTA), allow Canadian companies to do business in other countries without

having to pay high tariffs. Companies are able to invest in markets without paying high taxes that

would otherwise be the case if they directly exported to those markets.

A 2010 study30 found that the benefits of FDI far outweigh any drawbacks for Canada. Empirical

evidence showed that the presence of multinational firms in Canada have positive influences on the

economy through the diffusion of new technology, stimulating innovation, as well as job growth.

Domestic R&D and inbound FDI were found to be complements rather than substitutes to one another

indicating that domestic R&D still requires domestic support but is enhanced with inbound FDI.

Indeed not all inbound FDI is beneficial: in some cases foreign firms, both private and state-

owned may pose threats to the Canadian economy and its welfare. The government provides

protection to unwarranted foreign investment threats through rules, regulations and additional

requirements; however these restrictions sometimes bode poorly for Canada’s reputation to

attract capital. For instance the attempted takeover of the Canadian company Potash Corp. by

an Australian firm was presented with an additional hurdle by the federal government, making it

nearly impossible for the takeover to occur. The benefits of stopping such a takeover are subject

to further considerations; however there is no question that foreign nationals may be hesitant

to do business with Canada in the future. It is important for Canada to maintain a reputation of

welcoming foreign investment considering low domestic investment in ICT.

30 Hejazi, W. (2010). Dispelling Canadian Myths about Foreign Direct Investment. Institute for Research on Public Policy, No. 1, January 2010.

22 Issue in Focus

Some studies31 suggested that foreign companies may be contributing to slower labour

productivity growth, however it was also found that economic conditions (e.g. exchange rates) as

well as the type of firms (e.g. export oriented) were significant influencing factors. With economic

conditions improving and technology advancing faster than ever, suitable foreign multinationals

can help drive productivity as the economy recovers.

Closing Comments

Support for M&E investment is imperative to the livelihood of Canada’s future. Increased

M&E investment has the ability to stimulate a number of socioeconomic attributes that drive

productivity and enrich living standards. Although Canada survived the great recession of 2008

better than most other countries, continued underperforming productivity can place Canada

in a vulnerable declining state in the long run if not addressed immediately. The relationship

between M&E and productivity is not as attractive as other economic indicators and is potentially

overlooked. However, as seen from consistent declines in rankings and continued disparities to

other countries, inadequate investment in M&E results in less innovation and low productivity,

all of which affect overall economic well-being. It is clear that strong investment in ICT, a

sub-group of M&E, is vital for productivity growth in today’s digital world.

Canada is falling behind in R&D advancement. Low productivity growth and a continued

ICT investment gap with the U.S. serve as evidence of this. Canada can excel in R&D through

collaborative opportunities. An increase in the number of joint projects, studies and contracts

between the academic community, private sector and the government can increase the likelihood

of the production of new and innovative goods and services. A higher allocation of funds,

support and capital can be dedicated to research areas of high interest. This includes support

for investment and adoption of ICT.

SMEs are a valuable component to the landscape of Canadian business. With over one million

SMEs currently doing business in Canada, it is essential that ICT investment and adoption play

a significant role. The benefits of ICT in everyday business clearly outweigh the investment risk

associated with it. Companies that adopt ICT have a clear advantage over their competitors and

provide themselves with a greater opportunity to survive and expand. Although adequate funding

is a substantial obstacle to ICT adoption, it should not prevent advancement. Further support from

the government in addition to tax credits can help SMEs enhance their presence and impact on

31 Studies include Baldwin, J., W.Gu and B. Yan. (2011). Export Growth, Capacity Utilization and Productivity Growth: Evidence from the Canadian Manufacturing Plants. Statistics Canada Catalogue No. 11F0027M- No. 075, Baldwin, J. and W. Gu. (2009). Productivity Performance in Canada, 1961 to 2008: An Update on Long-term Trends. Statistics Canada, Catalogue no. 15-206-X – No. 025.

23Investment in Machinery and Equipment is Essential to Canada’s Future

the Canadian economy. Support in the form of tax simplification, additional refundable tax

credits and direct government contributions for ICT equipment and services will support SMEs

and pay high future dividends.

Government regulations and restrictions can stimulate innovation in some sectors; however it

does not seem to always be the case for FDI. Canada has various regulations for inbound FDI

which suppresses technological transfers in the form of ICT and non-ICT M&E development,

job growth, and managerial talent, among other benefits to the Canadian market. There is a

concern that inbound FDI from foreign state-owned companies can in fact be damaging the

country’s economic and social welfare through, for example, poor financial performance,

tax evasion or even infringement on national sovereignty. Certainly, the government has a

responsibility to protect Canadian markets from such interests, particularly in the case of foreign

takeovers that threaten national security.

However, policies should be in place to rapidly and thoroughly identify qualified firms with

purely commercial interests and allow them to easily enter the market, establish themselves as

quickly as possible and compete with Canadian counterparts. A 2011 report32 ranks Canada

20th in filing for international patents and 28th in exporting of high-tech goods. Canada offers a

weaker encouragement compared to the U.S. to harness new technologies or produce or export

innovative tech products to international markets. The welcoming of qualified foreign firms will

stimulate the development and innovation of technologies. The federal government is encouraged

to continue to work with other nations to establish trade liberalizations that are rewarding for

both countries and improve its reputation, as trade agreements are a corner stone for international

business of which many benefits follow.

Investment and development of M&E play significant roles in Canada’s future through its

prominent influence on productivity and living standards. It is imperative that the government,

the business sector, and the academic community increase the investment to all inputs of

productivity, not just M&E, in order for Canada to remain a long-term competitive force in

the global arena.

32 Dutta, S. and I. Mia. (2011). Global and Information Technology Report 2010-2011. World Economic Forum. p. 17.

24 Issue in Focus

References

1. Abdi, Tahir. (2004). Machinery and Equipment and Growth: Evidence from the Canadian

Manufacturing Sector. Department of Finance. Working paper 2004-04.

2. Almon, Michael and Jianmin Tang. (2011). Do Very Large Producers Contribute to the

Canada-US Productivity Gap? Evidence from Manufacturing. Industry Canada. Working

Paper 2011-11.

3. Atrostic, B.K. and Sang Nguyen. (2005). Computer Investment, Computer Networks, and

Productivity. U.S. Bureau of the Census. CES 05-01.

4. Avillez, R. (2011). A Detailed Analysis of the Productivity Performance of the Canadian Primary

Agriculture Sector, Centre for the Study of Living Standards, Research Report 2011-06.

5. Baldwin, J., W.Gu and B. Yan. (2011). Export Growth, Capacity Utilization and Productivity

Growth: Evidence from the Canadian Manufacturing Plants. Statistics Canada, Catalogue

No. 11F0027M – No. 075.

6. Baldwin, John and Wulong Gu. (2009). Productivity Performance in Canada, 1961 to 2008:

An Update on Long-term Trends. Statistics Canada. Catalogue no. 15-206-X – No. 025.

7. Brox, James A. and Jeremy Leonard. (2009, May). Shoring Up the Competitive Posture of

Canadian Manufacturers – What are the Policy Levers? Institute for Research on Public

Policy. IRPP Choices Vol. 15 no. 4.

8. Le Centre francophone d’informatisation des organisations. (2011). NetPME 2011 – Use of

ICT in Canadian SMEs. October 2011.

9. Conference Board of Canada (2008). Securing Our Future: Components of a Comprehensive

IT Workforce Development Strategy. Presentation to Bell Canada on January 16, 2008.

10. Conference Board of Canada. (2011). Labour Productivity. Economy Online. Retrieved

January 12, 2012 from http://www.conferenceboard.ca/hcp/Details/Economy/measuring-

productivity-canada.aspx.

11. Conference Board of Canada. (2011). Why is M&E Investment Important to Labour Productivity.

Hot Topic: Investment and Productivity Online. Retrieved December 20, 2011 from

http://www.conferenceboard.ca/hcp/hot-topics/investProd.aspx.

12. Council of Canadian Academies. (2009, April). Innovation and Business Strategy:

Why Canada Falls Short. Report in Focus.

13. Dion, Richard. (2007). Interpreting Canada’s Productivity Performance in the Past Decade:

Lessons from Recent Research. Bank of Canada Review. Summer 2007.

14. Dutta, Soumitra and Irene Mia. (2011). Global and Information Technology Report

2010-2011. World Economic Forum.

15. Hagén, H-O and J. Zeed. (2006). Does ICT use Matter for Firm Productivity? Science and

Technology Sector. OECD

16. Hejazi, Walid. (2010, January). Dispelling Canadian Myths about Foreign Direct Investment.

Institute for Research on Public Policy. No. 1, January 2010.

25Investment in Machinery and Equipment is Essential to Canada’s Future

17. Industry Canada. (2010). ICT Sector Intramural R&D Expenditures. Ottawa ON:

Industry Canada.

18. Information and Communications Technology Council. (2010). Trends in the ICT Labour

Market. Outlook for Human Resources in the ICT Labour Market, 2011-2016 Online.

Retrieved on February 1, 2012 from http://www.ictc-ctic.ca/Outlook_2011/trends_en.html.

19. Khondaker, Joseph. (2005). Key Trends in Canada’s International Trade in Machinery and

Transport Equipment, 1980 to 2003. Statistics Canada Catalogue no. 65-507-MIE – No. 002.

20. Kodakanchi, V. et all. (2006). An Economic Development Model for IT in Developing

Countries. Illinois State University.

21. Krzepkowski, Matt and Jack Mintz. (2010, October). Canada’s Foreign Direct Investment

Challenge: Reducing barriers and Ensuring a Level Playing Field in the Face of Sovereign

Wealth Funds and State-Owned Enterprises. The School of Public Policy, University of Calgary.

22. Macklem, Tiff. (2003). Future Productivity Growth in Canada: Comparing to the United

States. Bank of Canada, International Productivity Monitor No. 7, Fall 2003.

23. Martin, Roger L. and James B. Milway. (2007). Enhancing the Productivity of Small

and Medium Enterprises through Greater Adoption of Information and Communication

Technology. Information and Communications Technology Council.

24. McFetridge, Donald G. (2008, April). Innovation and the Productivity Problem. Institute for

Research on Public Policy. IRPP Choices Vol. 14, No. 3.

25. Milway, James. (2011, October 13). Trade, Competitiveness & Innovation - Why Management

Matters to Canada’s Prosperity. Presentation at the Insights from Survey of Innovation &

Business Strategy. Toronto, ON.

26. Natural Resources Canada. (2012). Important Facts on Canada’s Natural Resources Online.

Retrieved on January 4, 2012 from http://www.nrcan.gc.ca/statistics-facts/home/887.

27. Nicholson, Peter. (2009). Innovation and Business Strategy: Why Canada Falls Short.

Council of Canadian Academies. International Productivity Monitor No. 18, Spring 2009.

28. OECD Statistics. Glossary of Statistical Terms online. Retrieved on January 5, 2012 from

http://stats.oecd.org/glossary/detail.asp?ID=6274.

29. Rao, Someshwar et. all. (2002). The Importance of Skills for Innovation and Productivity.

Industry Canada, International Productivity Monitor No. 4, Spring 2002.

30. Rao, Someshwar et. all. (2006). What Explains the Canada-US TFP Gap? Industry Canada.

Working Paper 2006-08.

31. Rao, Someshwar. (2011, November). Cracking Canada’s Productivity Conundrum. Institute

for Research on Public Policy, No. 25.

32. Review of Federal Support to Research and Development (2011). Innovation Canada: A Call

to Action. Industry Canada.

33. Sala-I-Martin, Xavier et all. (2011). The Global Competitiveness Index 2011-2012: Setting the

Foundations for Strong Productivity. World Economic Forum.

34. Science, Technology and Innovation Council. (2011). Imagination to Innovation – State of

the Nation 2010. Government of Canada.

26 Issue in Focus

35. Sharpe, Andrew and Dylan Moeller. (2011, June). Overview of Development in ICT

Investment in Canada, 2010: Rebounding From the Recession. Centre for the Study of

Living Standards.

36. Sharpe, Andrew. (2005). What Explains the Canada-US ICT Investment Gap? Abridged

version. Centre for the Study of Living Standards. International Productivity Monitor.

No. 11, Fall 2005.

37. Shaw, Daniel. (2009). Productivity: Its Increasing Influence over Canadians’ Standard of

Living and Quality of Life. Government of Canada: Industry, Infrastructure and Resources

Division. Retrieved from http://www.parl.gc.ca/Content/LOP/ResearchPublications/

prb0315-e.htm.

38. Statistics Canada. (2007). Long-term Productivity Growth in Canada and the United States

1961-2006. Statistics Canada. Catalogue no. 15-206-XIE – No. 013.

39. Statistics Canada (2012). Factors in the Growth of Labour Productivity in the Provinces.

The Daily, March 12, 2012.

40. TD Economics. (2005, October). Canada’s Productivity Challenge. TD Bank Financial Group.

41. The Canadian Chamber of Commerce. (2011). Regaining Competitiveness: Canada’s

Biggest Challenge. The Canadian Chamber of Commerce June 2011.

42. Wolfe, David A. and Allison Bramwell. (2008). Growing the ICT Industry in Canada:

A Knowledge Synthesis Paper. University of Toronto. Social Sciences and Humanities

Research Council.