Internship Report An Organizational Study At CANARA BANK ...

82

Internship Report An Organizational Study At CANARA BANK Bangalore Submitted In Partial Fulfillment Of The Requirement Of The Bangalore University For The Award Of Degree In Master Of Business Administration Submitted By SHREYA SRIKANTH (11XQCMA133) Under The Guidance Of Prof. DEEPAK.R M. P. Birla Institute Of Management Associate Bhartiya Vidya Bhavan No. 43, Race Course Road, Bangalore-560001

-

Upload

khangminh22 -

Category

Documents

-

view

6 -

download

0

Transcript of Internship Report An Organizational Study At CANARA BANK ...

Internship Report

An Organizational Study

At

CANARA BANK

Bangalore

Submitted In Partial Fulfillment Of The Requirement Of The

Bangalore University For The Award Of Degree In

Master Of Business Administration

Submitted By

SHREYA SRIKANTH

(11XQCMA133)

Under The Guidance Of

Prof. DEEPAK.R

M. P. Birla Institute Of Management

Associate Bhartiya Vidya Bhavan

No. 43, Race Course Road,

Bangalore-560001

DECLARATION

I, SHREYA SRIKANTH (11XQCMA133) hereby declare that the internship report, an

organizational study conducted at CANARA BANK, Head office, Bangalore submitted in

partial fulfilment of the requirements of the Bangalore University for the award of degree in

Master of Business Administration is a bonafide work carried out by me under the guidance of

Prof. DEEPAK.R , Faculty, MPBIM, Bangalore.

This report has not been submitted earlier to any other university or institution for the

award of any degree/ diploma.

The contents of this report are based on the data collected by me at Canara Bank, Head

office under the guidance of Mr. N. Mohan Shankar, Senior Manager (HR&OD Section).

Place: Bangalore. Name of Student: SHREYA SRIKANTH

Date: 7th

September 2012 Reg. No: 11XQCMA133

ACKNOWLEDGEMENT

I would like to express my immense gratitude to N. Mohan Shankar, Senior Manager

(HR&OD Section) for having provided me the opportunity to do the internship training at

Canara Bank, Head office, Bangalore.

I also owe special thanks to all the other members of Canara Bank, HO.

I would also like to thank my internal guide Prof. Deepak R, faculty, M. P. Birla Institute of

Management for his constant guidance, assistance and the enormous confidence he put in me

during internship.

I would also like thank our Principal Dr. N S Malavalli, M. P. Birla Institute of Management

for giving us this opportunity. I would also like to thank all the teaching and non teaching staff of

our college.

Lastly I would like to thank my parents, my brothers and all my friends, without their support

this internship report would not have been possible.

CONTENTS

Chapter No TITLE Page No

1

Introduction 2

1.1 Background of the Study 3

1.2 Industry Profile 4

1.3 Company Profile 19

1.4 Vision, Mission and Objectives 41

2

Organization Structure 44

2.1 Corporate Organization Structure 45

2.2 Departmental Organization Structure 46

2.3 Authority and Responsibility Relationship 47

3

Functional Areas 51

3.1 Human Resources Wing 53

3.2 Financial Management and Subsidiaries Wing 61

3.3 Priority Credit and Financial Inclusion Wing 61

3.4 Customer Care and Business Planning Wing 63

3.5 Department Of Information Technology Wing 63

3.6 Marketing Department 64

4

SWOT Analysis 66

4.1 Strength and Weakness 67

4.2 Opportunities and Threats 68

5

Observations, Suggestions and Conclusion 69

5.1 Major Findings 70

5.2 Suggestions 70

5.3 Conclusion 71

Annexure 72

(Financials Statements) 73

Bibliography 75

Lists of tables and graphs

SL.no Title Page No:

Fig 1.3.1 Ownership Pattern In Canara Bank 29

Fig 1.3.2 Composition of Branch Network 30

Fig 1.3.3 Specialized Branches 30

Fig 1.3.4 Business performance 31

Fig 1.3.5 Operating and Net profit 31

Fig 1.3.6 EPS and Book Value 32

Fig 1.3.7 Income and Expenditure figures 32

Fig 1.3.8 Composition of Income 33

Fig 1.3.9 Composition of Expenditure 33

Fig 1.3.10 Key financial ratios 34

Fig 1.3.11 Total Income 34

Fig 1.3.12 Deposits Growth 34

Fig 1.3.13 Advances Growth 35

Fig 1.3.14 Productivity Ratios 35

Fig 2.1 Employees strength 50

Fig 2.2 Composition of SC/ST employees 50

2012

Organizational study, MPBIM Page 1

ORGANIZATIONAL STUDY

2012

Organizational study, MPBIM Page 2

CHAPTER - 1

INTRODUCTION

1.1 Background Of The Study

1.2 Industry Profile

1.3 Company Profile

1.4 Vision, Mission and Objectives

2012

Organizational study, MPBIM Page 3

1.1 BACKGROUND OF THE STUDY

A bank is a financial intermediary that accepts deposits, and channels those deposits into lending activities.

Banking is generally a highly regulated industry, and government restrictions on financial activities by banks

have varied over time and location. The current sets of global bank capital standards are called Basel II. The

oldest bank still in existence is Monte del Paschi di Siena, headquartered in Siena, Italy, which has been

operating continuously since 1472.

Finance is the life blood of trade, commerce and industry. Now a-days, bank money acts as the backbone of

modern business. Development of any country mainly depends upon the banking system. In the present

scenario, every banking concern follows the banking system concepts for its smooth operation but at the same

time the quality of system operations is equally important. It should be helpful and fit to both the customers as

well as the bank.

Objectives of the study

The main objectives of the study are as follows.

1. To study the profile of Banking Industry in India.

2. To study the detail profile of the Canara Bank.

3. To study history, performance, profitability of the Canara Bank.

4. To understand the organisational structure.

5. To study establishment, growth and progress of banking service

6. To understand the procedures and policies in Canara Bank.

7. To make a SWOT analysis.

8. To make observations and conclude with suggestions.

2012

Organizational study, MPBIM Page 4

1.2 INDUSTRY PROFILE

Introduction to Banking

The term bank is derived from the French word “Banco” which means a Bench or Money exchange table .A

bank is a financial institution and a financial intermediary that accepts deposits and channels those deposits into

lending activities, either directly or through capital markets. A bank connects customers that have capital

deficits to customers with capital surpluses. Oxford Dictionary defines a bank as "an establishment for custody

of money, which it pays out on customer's order."

Characteristics / Features of a Bank

Dealing in Money: Bank is a financial institution which deals with other people's money i.e. money

given by depositors.

Individual/Firm/Company: A bank may be a person, firm or a company. A banking company means a

company which is in the business of banking

Acceptance of Deposit: A bank accepts money from the people in the form of deposits which are

usually repayable on demand or after the expiry of a fixed period. It gives safety to the deposits of its

customers. It also acts as a custodian of funds of its customers.

Giving Advances: A bank lends out money in the form of loans to those who require it for different

purposes.

Payment and Withdrawal: A bank provides easy payment and withdrawal facility to its customers in the

form of cheques and drafts. It also brings bank money in circulation. This money is in the form of

cheques, drafts, etc.

Agency and Utility Services: A bank provides various banking facilities to its customers. They include

general utility services and agency services.

Profit and services Orientation: A bank is a profit seeking institution having service oriented approach.

Ever increasing Functions: Banking is an evolutionary concept. There is continuous expansion and

diversification as regards the functions, services and activities of a bank.

Connecting Link: A bank acts as a connecting link between borrowers and lenders of money. Banks

collect money from those who have surplus money and give the same to those who are in need of

money.

2012

Organizational study, MPBIM Page 5

Banking Business: A bank's main activity should be to do business of banking which should not be

subsidiary to any other business.

Name Identity: A bank should always add the word "bank" to its name to enable people to know that it

is a bank and that it is dealing in money.

History of Banking in India

Banking in India originated in the last decades of the 18th century.

The first banks were The General Bank of India, which started in 1786, and Bank of Hindustan, which

started in 1770, both are now defunct.

The oldest bank in existence in India is the State Bank of India, which originated in the Bank of Calcutta in

June 1806, which almost immediately became the Bank of Bengal. This was one of the three presidency

banks, the other two being the Bank of Bombay and the Bank of Madras, all three of which were

established under charters from the British East India Company. The three banks merged in 1921 to form

the Imperial Bank of India, which, upon India's independence, became the State Bank of India in 1955.

The Allahabad Bank, established in 1865 and still functioning today, is the oldest Joint Stock bank in India.

HSBC established itself in Bengal in 1869. Calcutta was the most active trading port in India, mainly due to

the trade of the British Empire, and so became a banking centre.

An entirely Indian joint stock bank was the Punjab National Bank, established in Lahore in 1895, which has

survived to the present and is now one of the largest banks in India.

Around the turn of the 20th Century, the Indian economy was passing through a relative period of

stability. Indians had established small banks, most of which served particular ethnic and religious

communities.

The presidency banks dominated banking in India but there were also some exchange banks and a number

of Indian joint stock banks operating in different segments of the economy.

The exchange banks, mostly owned by Europeans, concentrated on financing foreign trade. Indian joint

stock banks were generally undercapitalized and lacked the experience and maturity to compete with the

presidency and exchange banks.

2012

Organizational study, MPBIM Page 6

The period between 1906 and 1911, saw the establishment of banks inspired by the Swadeshi movement.

Around this time, undivided Dakshina Kannada district was known as "Cradle of Indian Banking", as four

nationalised banks started in this district and also a leading private sector bank.

Period of world wars and pre-independence!

During the First World War (1914–1918) through the end of the Second World War (1939–1945), and two

years thereafter until the independence of India were challenging for Indian banking. The years of the First

World War were turbulent, and it took its toll with banks simply collapsing despite the Indian economy

gaining indirect boost due to war-related economic activities. At least 94 banks in India failed between 1913

and 1918.

Banking in India Post-independence!

The partition of India in 1947 adversely impacted the economies of Punjab and West Bengal, paralyzing

banking activities for months. India's independence marked the end of a regime of the Laissez-faire for the

Indian banking. The Government of India initiated measures to play an active role in the economic life of

the nation, and the Industrial Policy Resolution adopted by the government in 1948 envisaged a mixed

economy.

The Reserve Bank of India, India's central banking authority, was nationalized on January 1, 1949 under the

terms of the Reserve Bank of India (Transfer to Public Ownership) Act, 1948.

In 1949, the Banking Regulation Act was enacted which empowered the Reserve Bank of India (RBI) "to

regulate, control, and inspect the banks in India". It also provided that no new bank or branch of an existing

bank could be opened without a license from the RBI, and no two banks could have common directors.

Nationalisation

By the 1960s, the Indian banking industry had become an important tool to facilitate the development of the

Indian economy and it had emerged as a large employer, thus a debate had ensued about the nationalization

of the banking industry. The then Prime Minister of India, Indira Gandhi, brought The Government of India

to existence. In 1969, 14 largest commercial banks in India were nationalised. These banks contained 85

percent of bank deposits in the country.

2012

Organizational study, MPBIM Page 7

A second dose of nationalization of 7 more commercial banks followed in 1980. The stated reason for the

nationalization was to give the government more control of credit delivery. With this, the Government of

India controlled around 91% of the banking business of India.

1949: Enactment of Banking Regulation Act.

1955: Nationalization of State Bank of India.

1959: Nationalization of SBI subsidiaries.

1961: Insurance cover extended to deposits.

1969: Nationalization of 14 major banks.

1971: Creation of credit guarantee corporation.

1975: Creation of regional rural banks.

1980: Nationalization of seven banks with deposits over 200 crore.

Liberalization

In the early 1990s, the then Narasimha Rao government embarked on a policy of liberalization, licensing a

small number of private banks. These came to be known as New Generation tech-savvy banks, and included

Global Trust Bank (the first of such new generation banks to be set up), which later amalgamated with Oriental

Bank of Commerce, UTI Bank (since renamed Axis Bank), ICICI Bank and HDFC Bank. This move, along

with the rapid growth in the economy of India, revitalized the banking sector in India, which has seen rapid

growth with strong contribution from all the three sectors of banks, namely, government banks, private banks

and foreign banks.

The next stage for the Indian banking has been set up with the proposed relaxation in the norms for Foreign

Direct Investment, where all Foreign Investors in banks may be given voting rights with some restrictions.

The new policy shook the Banking sector in India completely. Bankers, till this time, were used to the 4-6-4

method (Borrow at 4%; Lend at 6%; Go home at 4) of functioning. The new wave ushered in a modern outlook

and tech-savvy methods of working for traditional banks. All this led to the retail boom in India.

The RBI in 1984 formed Committee on Mechanisation in the Banking Industry. The major recommendations of

this committee were introducing MICR Technology in all the banks in the metropolis in India. This provided

use of standardized cheque forms and encoders. Later, in 1988, focus shifted on computerisation of branches

2012

Organizational study, MPBIM Page 8

and increasing connectivity among branches through computers. Suggestions for implementing on-line banking

were also looked into.

The IT revolution had a great impact in the Indian banking system. The use of computers had led to

introduction of online banking in India. The use of the modern innovation and computerisation of the banking

sector of India has increased many folds after the economic liberalisation of 1991 as the country's banking

sector has been exposed to the world's market. The Indian banks were finding it difficult to compete with the

international banks in terms of the customer service without the use of the information technology and

computers.

In 1994, Committee on Technology Issues relating to Payments System, Cheque Clearing and Securities

Settlement in the Banking Industry was set up. It emphasized on Electronic Funds Transfer (EFT) system, with

the BANKNET communications network as its carrier. It also said that MICR clearing should be set up in all

branches of all banks with more than 100 branches. Also, the banks have been selling the third party products

like Mutual Funds, insurances to its clients.

In March 2006, the Reserve Bank of India allowed Warburg Pincus to increase its stake in Kotak Mahindra

Bank (a private sector bank) to 10%. This is the first time an investor has been allowed to hold more than 5% in

a private sector bank since the RBI announced norms in 2005 that any stake exceeding 5% in the private sector

banks would need to be vetted by them.

From around 2010, it is considered that banking in India is generally fairly mature in terms of supply, product

range and reach, even though reach in rural India still remains a challenge for the private sector and foreign

banks. In terms of quality of assets and capital adequacy, Indian banks are considered to have clean, strong and

transparent balance sheets relative to other banks in comparable economies in its region. The Reserve Bank of

India is an autonomous body, with minimal pressure from the government. The stated policy of the Bank on the

Indian Rupee is to manage volatility but without any fixed exchange rate-and this has mostly been true.

2012

Organizational study, MPBIM Page 9

BANKING STRUCTURE IN INDIA

Nationalized Banks NEW Private Sector Banks

OLD Private Sector Banks

Private Sector Banks Public Sector Banks

Regional Rural Banks Foreign Banks

Scheduled Commercial

Urban Co-operative State Co-operative

Scheduled co-operative

Scheduled Co-operative

RBI

Reserve Bank Of India

SBI and its Associates

2012

Organizational study, MPBIM Page 10

The Banking system in India is classified into three broad categories:

Reserve Bank of India (RBI)

The RBI is the central bank of the country having the authority and the responsibility to control the

banking system in the country. It keeps the reserves of all scheduled banks and hence known as Reserve

Bank.It was established in the year 1935 under the Reserve Bank of India Act 1934. The central board of

directors constituted of 20 members and they are responsible for the conduct of the main business of RBI. A

Governor will head the central board of directors.

The RBI manages the country's money supply and foreign exchange and also serves as a bank for the

government of India and for the country's commercial banks. In addition to central banking roles, they also

undertake developmental and promotional activities. It also performs many promotional and regulatory

functions like encouraging agricultural finance, industrial finance, export finance and controlling non

banking finance companies.

Commercial Banks

The main function of commercial banks in India is accepting deposits, granting loans and advances,

discounting of bills and promissory notes. Apart from these they also provide agency services and, general

utility services. The commercial Banks in India can be further classified into the following:

Public Sector Banks (PSBs): These are the banks which are owned by the central government directly

or through the Reserve bank of India. The PSBs are bank where a majority stake (i.e. more than 50%)

is held by a government. The shares of these banks are listed on stock exchanges. There are a total of

26 PSBs in India. Public Sector Banks includes all nationalized banks and State Bank of India with its

seven associate banks. It is the base of the Banking sector in India and accounts for more than 78 per

cent of the total banking industry assets. The State Bank of India (SBI) in the largest bank in the

country and along with its seven associate banks has an asset base of about Rs. 7,000 billion

(approximately US$150 billion). The other large public sector banks are Punjab National Bank,

Canara Bank, Bank of Baroda, Bank of India

Private Sector Banks: All those banks where greater parts of stake or equity are held by the private

shareholders and not by government are called as the private sector banks. These are the major players

in the banking sector as well as in expansion of the business activities India. The present private sector

banks equipped with all kinds of contemporary innovations, monetary tools and techniques to handle the

complexities are a result of the evolutionary process over two centuries. They have a highly developed

2012

Organizational study, MPBIM Page 11

organizational structure and are professionally managed. Thus they have grown faster and stronger since

past few years.

There are two categories of the private sector banks- “old” and “new”. The old private sector banks have

been operating since a long time and may be referred to those banks, which are in operation from before

1991.

The banks, which came in operation after 1991, with the introduction of economic reforms and financial

sector reforms are called as new private sector banks. Banking regulation act was then amended in 1993,

which permitted the entry of new private sector banks in the Indian banking sector. Yes Bank (2005) is

the latest entrant to the private sector banking industry . Some other main banks are ICICI Bank,

HDFC Bank and Axis Bank.

Foreign Exchange Bank: These banks finance export and imports of the country. As such international

trade involves foreign exchange. These banks specialize in such trade apart from carrying on the usual

commercial banking activities. As many as 29 foreign banks originating from 19 countries are operating

in India through a network of 258 branches and about 900 ATMs. With total assets of more than

Rs2, 000 billion (about 44 billion US dollars) they are present in 40 centers across 19 Indian states and

Union Territories. Some of the leading international banks that are doing brisk business in India include

Standard Chartered Bank, HSBC Bank, Citibank N.A. and ABN-AMR0 Bank. In banks belonging to

14 countries were operating in India through their representative offices.

Regional Rural Banks: The Government of India set up five Regional Rural Banks (RRBs) on October

2, 1975. which were sponsored by Syndicate Bank, State Bank of India, Punjab National Bank, United

Commercial Bank and United Bank of India. Capital share being 50% by the central government, 15%

by the state government and 35% by the scheduled bank. They were established to grant loans and

advances to small and marginal farmers and agricultural laborers. Financial assistance is also provided to

co-operative societies, artisans and small entrepreneurs engaged in petty trade and home industry.

Though the RRB's have done tremendous job they are constantly aiming at duplicating the operations of

sponsoring banks. Many tremendous jobs they are constantly aiming at duplicating the operations of

sponsoring banks. Many of these banks are not doing well financially and the government is currently

engaged in restructuring and consolidating them. Local area banks were of recent origin and as on March

31, 2006 four such banks were operating in the country.

2012

Organizational study, MPBIM Page 12

Co-operative Banks

Co-operative bank is an autonomous association of persons united voluntarily to meet their member's financial

(loans, deposits, other services), economic, social, and cultural needs and aspirations through a democratically

controlled way. The co-operative banks are formed for the purpose of promoting the economic interests of a well

defined group of people. The co-operative banks have a three tier structure. At the primary level they may be

organized by members belonging to a particular caste, region, community or employees of an organization. At the

district level central co-operative bank function as federation of co-operative banks at the primary level. The

central co-operative banks accept deposits from the public and lend to the co-operative banks and primary co-

operative societies. At the state level apex co-operative banks functions as a federation of CCB's they provide

loans to CCB's and participate in clearing house activities for the cheques presented by CCB for collection.

Urban Cooperative Banks in India The term Urban Co-operative Banks (UCBs), though not formally

defined, refers to primary cooperative banks located in urban and semi-urban areas. These banks, till 1996,

were allowed to lend money only for non-agricultural purposes. They essentially lend to small borrowers

and businesses. Today, their scope of operations has widened considerably.

State co-operative banks The state co-operative bank is a federation of central co-operative bank and acts

as a watch dog of the co-operative banking structure in the state. Its funds are obtained from share capital,

deposits, loans and overdrafts from the Reserve Bank of India. The state co- operative banks lend money

to central co-operative banks and primary societies and not directly to the farmers.

Banking in India

Central bank

Reserve Bank of India

Nationalised banks

Allahabad Bank

Andhra Bank

Bank of Baroda

Bank of India

Bank of Maharashtra

Canara Bank

Central Bank of India

2012

Organizational study, MPBIM Page 13

Corporation Bank

Dena Bank

IDBI Bank

Indian Bank

Indian Overseas Bank

Oriental Bank of Commerce

Punjab & Sind Bank

Punjab National Bank

Syndicate Bank

UCO Bank

Union Bank of India

United Bank of India

Vijaya Bank

State Bank of India

State Bank of Bikaner & Jaipur

State Bank of Hyderabad

State Bank of Indore

State Bank of Mysore

State Bank of Patiala

State Bank of Travancore

State Bank of Saurashtra

Private Banks

Axis Bank

Catholic Syrian Bank

City Union Bank

Development Credit Bank

Dhanlaxmi Bank

Federal Bank

HDFC Bank

ICICI Bank

IndusInd Bank

ING Vysya Bank

2012

Organizational study, MPBIM Page 14

Jammu & Kashmir Bank

Karnataka Bank

Karur Vysya Bank

Kotak Mahindra Bank

Lakshmi Vilas Bank

Saraswat Bank

South Indian Bank

Tamilnad Mercantile Bank Limited

Yes Bank

Foreign banks

ABN AMRO

Abu Dhabi Commercial Bank

Antwerp Diamond Bank

Bank International Indonesia

Bank of America

Bank of Bahrain and Kuwait

Bank of Ceylon

Bank of Nova Scotia

The Bank of Tokyo-Mitsubishi UFJ

Barclays Bank

Citibank India

Credit Suisse

Deutsche Bank

HSBC

Royal Bank of Scotland

Standard Chartered

Regional Rural Banks

North Malabar Gramin Bank

South Malabar Gramin Bank

Vananchal Gramin Bank

2012

Organizational study, MPBIM Page 15

SCENARIO IN THE BANKING SECTOR

The Indian banking system has passed through three distinct phases from the time of inception.

The first was being the era of character banking, where you were recognized as a credible depositor

or borrower of the system. This era come to an end in the Sixties. The second phase was the social

banking. Nowhere in the democratic developed world, was banking or the service industry

nationalized. But this was practiced in India. Those were the days when bankers has no clue

whatsoever as to how to determine the scale of finance to industry.

The third era of banking which is in existence today is called the era of Prudential Banking. The main

focus of this phase is on prudential norms accepted internationally.

The banking sector supported by financial services industry has virtually become a revolution in the market for

financial services. This has been in demand by the need for liquid, readily transferable assets to effect

transactions, technological changes world-wide including electronic banking and electronic funds transfer

necessitating:

Over dressing of banks around the world with high risk portfolios, looking for ways to boost their

capital and incomes from fee-based business.

Better facilities and services for the customers, extending importance for innovative products and

prompt service at low cost because of stiff competition.

Erasing of linked costs and risks.

Mergers and alliances at home and across the borders are rising.

Banks world-wide are making the assets neat and tidy to act in accordance with risk-asset capital ratio

requirements because the financial environment has become competitive with focus on profitability and

efficiency, even though margins are narrowing.

Securitization provides banks the benefits of removing capital hungry assets from banks and trimming

balance sheets.

The use of updated technology and communication systems has become mandatory to keep in touch

with customers, top management, and branches and to provide better customer service.

As of 2011-12, growth in key monetary aggregates and money supply in this year reflected changing liquidity

conditions arising from domestic and global financial environment. The monetary policy stance during the year

was to contain inflation and actively manage liquidity to support growth.

2012

Organizational study, MPBIM Page 16

The banking sector in India remained healthy and resilient and performed reasonably well during 2011-12.

However the slowdown in macro economy has resulted in some deterioration in the asset quality. The year also

saw some key policy measures announced by the RBI.

CHALLENGES FACED BY THE BANKING INDUSTRY

To affirm and assert their global presence the Banks have to prepare for the competition and challenges at home

and abroad. Developing countries like India, still has a huge number of people who do not have access to

banking services due to scattered and fragmented locations. Also today, people’s expectations are rising as the

level of services is increasing due to the emergence of Information Technology, competition and entry of

foreign banks into the Indian market. Now, the existing situation has created various challenges for the Banks.

Risk Management: We have already witnessed the bankruptcy of some foreign banks. The changes in

bank capital today seem risk-based. The deregulated environment brings in its way risks along with,

profitable opportunities and technology which play a crucial role in managing these risks. In

addition to being exposed to credit risk, market risk and operational risk, the business of banks

would be susceptible to country risk, which will increase as controls on the movement of

capital are eased. In this context, banks are upgrading their credit assessment and risk

management skills and retraining staff, developing a cadre of specialists and introducing

technology driven management information systems.

Transparency and Disclosure: In pursuance of the Financial Sector Reforms introduced since 1991

and in order to bring about meaningful disclosure of the true financial position of banks to enable

the users of financial statements to study and have a meaningful comparison of their positions, a

series of measures were initiated. These norms as part of internationally accepted corporate

governance practices are assuming greater importance in the emerging environment. Banks are expected

to be more responsive and accountable to the investors. Banks have to disclose in their balance sheets a

plethora of information on the maturity profiles of assets and liabilities, lending to sensitive sectors,

movements in NPAs, capital, provisions, shareholdings of the government, value of investment in India

and abroad, operating and profitability indicators. In addition, banks should implement a process

for assessing the appropriateness of their disclosures, includ ing validation and frequency.

Global Banking and International Standards: It is practically and fundamentally impossible for any

nation to exclude itself from world economy. Therefore, for sustainable development, one has to adopt

2012

Organizational study, MPBIM Page 17

integration process in the form of liberalization and globalization. Introducing internationally

followed best practices and observing universally acceptable standards and codes is necessary

for strengthening the domestic financial architecture. This includes best practices in th e

area of corporate governance along with full transparency in disclosures. In today's

globalized world, focusing on the observance of standards will help smooth integration with

world financial markets.

Employee and Customer Retention: Today, diminishing employee morale results in decreased revenue.

Due to the intrinsically close ties between staff and clients, losing those employees completely can mean

the loss of valuable customer relationships. The retail banking industry is concerned about employee

retention from all levels: from tellers to executives to customer service representatives because

competition is always moving in to hire them away. The competition to retain key employees is intense.

Top-level executives and HR departments are spending large amounts of time, effort, and money trying

to figure out how to keep their people from leaving. Determinants like service quality dimensions,

service features, service problems, service recovery and products have a major impact on customer

satisfaction and their intentions to switch. The strongest connection between retention and satisfaction

strategies turns out to be in terms of relationship and confidence. Also, banks will have to strive to

attract and retain customers by introducing innovative products, enhancing the quality of

customer service and marketing a variety of products through diverse channels targeted at

specific customer groups.

Banks on a regular basis face various other challenges like reinforcing and adopting latest technology to keep in

pace with the innovations and developments, recognizing and sharpening employee skills in specialized areas,

corporate governance, cost reduction, improving profitability and wealth maximization.

In particular, to sustain and battle the challenges of foreign banks at home and in their domicile Indian banks

have to:

Be alert and assertive to give directions to their operations.

Improve work culture and erase rigidities in labour practices that have hindered change.

Improve their service orientation and update skills to meet customer requirements.

Innovation of new products and services to meet customer requirements in the challenging market.

Computerize and update their techniques of operations.

Maintain high quality human resource to cope with and adapt to the new environment.

Develop a foresight in anticipating changing risk-return relationships.

2012

Organizational study, MPBIM Page 18

OUTLOOK FOR 2012-13

Global growth prospects are seen gradually strengthening but downside risks remain elevated. A global growth

at 3.5% for 2012 and a 4.1% for 2013 has been projected. However, there may emerge uncertainties in the form

of macroeconomic imbalances, disruption in currency markets etc. India’s GDP is expected to improve in 2012-

13 where services sector will be a major contributor.

Efforts to bring in more inclusive growth and focus on the rural economy would propel the economy further.

On the domestic front, the major challenges during the year relate to high fiscal and current account deficits,

low industrial growth, volatile foreign exchange markets, lower capital inflows and inflationary pressures.

Indian Banking Sector is expected to perform well during FY13. Major challenges before the banks remain on

improving the quality of advances.

2012

Organizational study, MPBIM Page 19

1.3 COMPANY PROFILE

CANARA BANK

HISTORY

Canara Bank was founded by late Shri Ammembal Subba Rao Pai, a philanthropist, as 'Canara Bank Hindu

Permanent Fund' in 1906 at Mangalore, which blossomed into a limited company as 'Canara Bank Ltd.' in 1910

and became Canara Bank in 1969 after nationalization.

FOUNDER

The Bank has gone through the various phases of its growth trajectory over hundred years of its existence.

Eighties was characterized by business diversification for the Bank.

In the year 1985 Canara bank opened its first overseas office in London and established a

subsidiary in Hong Kong, and opened its third foreign branch in Shanghai. It has established itself in

the areas of mutual funds, venture capital and factoring. It is the first maiden bank to start initial

Public offering (IP0). It has also launched internet and mobile banking services.

The growth story of Canara Bank in its first century was due, among others, to the continued patronage of its

valued customers, stakeholders, committed staff and uncanny leadership ability demonstrated by its leaders at

the helm of affairs. The bank strongly believes that the next century is going to be equally rewarding and

eventful not only in service of the nation but also in helping the Bank emerge as a "Global Bank with Best

Practices".

Sound founding principles, enlightened leadership, unique work culture and remarkable adaptability to

changing banking environment have enabled Canara Bank to be a frontline banking institution of global

standards.

“A good bank is not only the financial heart of the

community, but also one with an obligation of helping in

every possible manner to improve the economic conditions

of the common people"- A. Subba Rao Pai.

2012

Organizational study, MPBIM Page 20

Founding Principles

1. To remove Superstition and ignorance.

2. To spread education among all to sub-serve the first principle.

3. To inculcate the habit of thrift and savings.

4. To transform the financial institution not only as the financial heart of the community but the social

heart as well.

5. To assist the needy.

6. To work with sense of service and dedication.

7. To develop a concern for fellow human being and sensitivity to the surroundings with a view to make

changes/remove hardships and sufferings.

Canara Bank occupies a premier position in the comity of Indian banks. With an unbroken record of profits

since its inception, Canara Bank has several firsts to its credit. These include:

Launching of Inter-City ATM Network

Obtaining ISO Certification for a Branch

Articulation of ‘Good Banking’ – Bank’s Citizen Charter

Commissioning of Exclusive Mahila Banking Branch

Launching of Exclusive Subsidiary for IT Consultancy

Issuing credit card for farmers

Providing Agricultural Consultancy Services

Over the years, the Bank has been scaling up its market position to emerge as a major 'Financial Conglomerate'

with as many as nine subsidiaries/sponsored institutions/joint ventures in India and abroad.

As at March 2012, the Bank has further expanded its domestic presence, with 3595 branches spread across all

geographical segments. Keeping customer convenience at the forefront, the Bank provides a wide array of

alternative delivery channels that include 2858 ATMs, covering 1139 centres.

In June 2006, the Bank completed a century of operation in the Indian banking industry. The eventful journey

of the Bank has been characterized by several memorable milestones.

2012

Organizational study, MPBIM Page 21

SIGNIFICANT MILESTONES

Year

1st July

1906

Canara Hindu Permanent Fund Ltd. formally registered with a capital of 2000 shares of 50/- each,

with 4 employees.

1910 Canara Hindu Permanent Fund renamed as Canara Bank Limited

1969 14 major banks in the country, including Canara Bank, nationalized on July 19

1976 1000th branch inaugurated

1983 Overseas branch at London inaugurated

Cancard (the Bank’s credit card) launched

1984 Merger with the Laksmi Commercial Bank Limited

1985 Commissioning of Indo Hong Kong International Finance Limited

1987 Canbank Mutual Fund & Canfin Homes launched

1989 Canbank Venture Capital Fund started

1989-

90

Canbank Factors Limited, the factoring subsidiary launched

1992-

93

Became the first Bank to articulate and adopt the directive principles of “Good Banking”.

1995-

96

Became the first Bank to be conferred with ISO 9002 certification for one of its branches in Bangalore

2001-

02

Opened a 'Mahila Banking Branch', first of its kind at Bangalore, for catering exclusively to the

financial requirements of women clientele.

2002-

03

Maiden IPO of the Bank

2012

Organizational study, MPBIM Page 22

2003-

04

Launched Internet Banking Services

2004-

05

100% Branch computerization

2005-

06

Entered 100th Year in Banking Service. Launched Core Banking Solution in select branches. Number

One Position in Aggregate Business among Nationalized Banks.

2006-

07

Retained Number One Position in Aggregate Business among Nationalized Banks. Signed MoUs for

Commissioning Two JVs in Insurance and Asset Management with international majors’ viz., HSBC

(Asia Pacific) Holding and Robeco Groep N.V respectively.

2007-

08

Launching of New Brand Identity. Incorporation of Insurance and Asset Management JVs. Launching

of 'Online Trading' portal. Launching of a ‘Call Centre’. Switchover to Basel II New Capital

Adequacy Framework.

2008-

09

The Bank crossed the coveted 3 lakh crore in aggregate business. The Bank’s 3rd foreign branch at

Shanghai commissioned.

2009-

10

The Bank’s aggregate business crossed 4 lakh crore mark.

Net profit of the Bank crossed 3000 crore. The Bank’s branch network crossed the 3000 mark.

2010-

11

The Bank’s aggregate business crossed 5 lakh crore mark. Net profit of the Bank crossed 4000

crore. 100% coverage under Core Banking Solution. The Bank’s 4th foreign branch at Leicester and a

Representative office at Sharjah, UAE, opened. The Bank raised 1993 crore under QIP. Govt.

holding reduced to 67.72% post QIP.

2011-

12

Total number of branches reached 3600. The Bank’s 5th

foreign branch at Manama, Bahrain opened.

As at March 2012, the total business of the Bank stood at 559544 crore.

2012

Organizational study, MPBIM Page 23

NATURE OF BUSINESS

Canara Bank is a public sector company undertaking administered by the government of India. It was

nationalized in the year 1969.This commercial bank has a total share capital of 443 crore out of which 300

crore is held by the Central Government. Global business of the Bank rose to a level of 559544 crore as at

March 2012, recording a y-o-y growth of 10.9%. Canara Bank offers to the industries, NRI's and all the

classes of people such as personal banking, corporate Banking , NRI banking Priority credit and other services

which includes Saving and deposits, Loan product, technology products, Mutual Funds, insurance business,

international services, Card services, .consultancy services, Depositary services, Ancillary services, Accounts

and banking, cash management services, Loans and services, syndication services, IPO, Merchants banking,

TUF schemes, deposit services, loans and advances, remittance facilities, consultancy services.

Canara Bank has been recognized as a Systemically Important Financial Institution in India catering to the

needs of more than 4.2 corer customers. The bank continues to invest in information technology, customer

service, staff knowledge and new products/ service process to strengthen its position in the market. During the

year, the bank opened 343 branches and 642 ATM’s. It has come to the forefront of the commercial and

financial services and established a leadership in the financial services. The Bank has also carved a Distinctive

mark, in various corporate social responsibilities, namely, serving national priorities, promoting rural

development, enhancing rural self employment through several training institution and spearheading financial

inclusion objectives.

PRODUCTS OF CANARA BANK

Cards:

Cancard master Card

Cancard Visa International Gold Card

Credit Cards

Cancard Visa Credit Card

Others:

CHOICe – Canara HSBC OBC Life Insurance Company Ltd

Tax assistance

Estate and Consultancy services

2012

Organizational study, MPBIM Page 24

Trustee Services

Commercial Banking:

Deposits:

Saving Bank Deposits

Canara Super savings salary A/c

Current Account

Saving Bank Gold A/c

Fixed deposits

Kamadhenu Deposits

Recurring Deposits

Credit Services:

Cash credit for working capital

Bill Discounting

Bank Guarantee

Loan for SME’s

Finance to SSI’s

Agriculture loan

Other Services:

Merchant Banking

Industrial and Agricultural advisory services

Taxation and Debenture trustee services

NRI Services:

Deposits:

NRE(Non-resident external rupee) Account

NRO(Non-resident ordinary) Account

FCNR(Foreign currency Non-resident) Account

RFC Deposits

Loans:

Home Loans

Can cash (shares)

Canaramobile (Vehicles)

2012

Organizational study, MPBIM Page 25

Swarna Gold Loan

Can rent

Can mortgage

Loan Against Securities

Other Services:

Safe Deposits Lockers and vaults

Nominal Facility

Remittance

Priority Credit:

SME Business

SME Marketing

PRD Division

Agri Marketing

Rural Development

CED for Women

Recent developments in other services:

The bank has a tie up arrangements in both life and non – life insurance segments under its

‘Bancanssurance’ arm.

The bank has invented e-payment of customs in one or three location as per the direction of Central

Board of Excise and Customs, New Delhi.

Executor, Trustee and taxation services outfit of the bank provides services like Debentures/Security

Trusteeship, Personal Tax Assistance and Power of Attorney services.

The Bank has introduced e-stamping project in five branches in Bangalore.

The bank is authorised as one of the accredited bankers for Unique Identification Authority of India

(UIDAI). The bank branches at eight centres have been designated for handling the UIDAI accounts.

Corporate Cash Management Services (CCMS) network of the bank, covering 60 operating centres,

provides services related to local and upcountry cheque collection facilities.

They have also an agricultural consultancy services (ACS).

2012

Organizational study, MPBIM Page 26

Subsidiaries

1. CANARA ROBECO ASSET MANAGEMENT COMPANY LIMITED

2. CANBANK FINANCIAL SERVICES LIMITED

3. CANARA BANK SECURITIES LIMITED

4. CANBANK COMPUTER SERVICES LIMITED

5. CAN FIN HOMES LIMITED

6. CANBANK FACTORS LIMITED

7. CANBANK VENTURE CAPITAL FUND LIMITED

Corporate Social Responsibilities (CSR)

Following the century old tradition, the bank is engaged in varied CSR Activities like training unemployed

rural youth, providing primary health care, drinking water, community development, empowerment of women

and other activities.

They achieve their rural activities through their Canara Bank Centenary Rural Development Trust (CBCRDT)

and have established 30 exclusive training institutes where they have trained 24,072 candidates during 2011-12.

The bank has also supported the setting up of Entrepreneurship Development Training Institute in Jammu and

Kashmir.

Canara Bank’s Rural Clinic Service Scheme provides incentives to doctors for providing basic health care

services in remote areas lacking basic facilities. Total number of clinic as at March 2012 is 565.

The bank donated in HI-Tech, Custom built, solar power “Mobile Sales Van” to assists women Entrepreneurs,

SHGs and artisans to market their products.

During the year, the bank’s Social Action Cell organized blood donation camps, health camps and assisted

people affected by natural calamities and challenged section of the society.

2012

Organizational study, MPBIM Page 27

CANARA BANK LOGO

CANARA BANK “TOGETHER WE CAN”

Canara bank changed its logo from flower and petals to a set of two interlinked triangles to suit the new high

tech and innovative generation of today. It was released by Union Minister P.Chidambaram in the last week of

December 2007.

The interlinked triangles symbolize the idea of a bond which is a representation of the close ties between the

Bank and its shareholders, customers, employees, investors, related institutions and the society at large. The

Bank has a very rich heritage of banking expertise and is also well known for its dedicated customer service

and corporate social responsibility that it has carried through the years to help its stakeholders achieve their

goals. Canara Bank being a powerful enabler, with its new brand identity captures the essence of the

partnership they intend to share. The rich blue represents stability, scale and depth. This contrasts with accents

of bright yellow that evoke optimism, warmth and energy.

2012

Organizational study, MPBIM Page 28

BOARD OF DIRECTORS 2012-13

1. Mr. S RAMAN Chairman and Managing Director

2. Smt. ARCHANA S BHARGAVA Executive Director

3. Mr. ASHOK KUMAR GUPTA Executive Director

4. Dr. THOMAS MATHEW Director representing Government Of

India

5. Smt. MEENA HEMCHANDRA Director representing Reserve Bank Of

India

6. Mr. G V SAMBASIVA RAO Workmen Employee Director

7. Mr. G V MANIMARAN Officer Employee Director

8. Mr. KHALID LUQMAN BILGRAMI Part-time Non-official Director under

Chartered Accountant Category

9. Mr. SUTANU SINHA Part-time Non-official Director

10. Mr. P V MAIYA Shareholder Director

11. Mr. SUNIL GUPTA Shareholder Director

2012

Organizational study, MPBIM Page 29

OWNERSHIP PATTERN

Fig 1.3.1: Showing Ownership pattern of Canara Bank

AREAS OF OPERATION

Over the years, Canara bank has built a lot of reputation, as a premier commercial bank in India. It has a distinct

track record in the service industry for over 106 years. The bank has a network of more than 3500 branches

spread over the nation, administered through Head Office in Bangalore and 34 Circle Offices. The bank has an

overseas presence at London, Hong Kong, Shanghai, Manama, Leicester, joint venture with SBI in Moscow, an

exchange establishment in Qatar. They have further identified 21 overseas centres for opening branches/offices

in the near future. The bank has a Rupee drawing arrangement with 29 Exchange House and 17 Overseas

Branches in the Middle East for remittance of expatriates. Also Electronic Fund Transfer (EFT) was introduced

with 11 Exchange Company/Banks for crediting remittance.

BRANCH NETWORK

Continuing its major branch expansion drive, the Bank added 342 domestic branches during the year. This

includes 106 branches and 106 ATMs opened across the country on 19th

Nov 2011 to commemorate its

Founder's Day and 106th

year of service to the nation. The bank opened an overseas branch at Manama,

Bahrain and a representative office at Sharjah during the year.

As at March 2012, Canara Bank boasts of having 3600 branches, including 5 overseas branches.

Business per Branch improved to 155.43 crore as at March 2012.

67.7

13.6

7.5

4.5 1.0 5.8

Govt of India FIIs Insurance Companies Resident Individuals Banks Others

2012

Organizational study, MPBIM Page 30

Fig 1.3.2: Composition of Branch Network

CATEGORY

NUMBER OF BRANCHES

March 2011 March 2012

Metropolitan 758 777

Urban 762 792

Semi-urban 922 1019

Rural 811 1007

Oversees 4 5

TOTAL BRANCHES 3257 3600

The Bank has 145 specialized branches, catering to the specific clientele segment.

Fig 1.3.3: Specialized Branches

Categories Of Specialized Branches 31.03.2012

1. SMEs 53

2. Oversees 16

3. Agri-Finance 10

4. Micro Finance Branches 19

5. Savings 6

6. NRIs 7

7. Asset Recovery Management 8

8. Prime Corporate 10

9. Industrial Finance 4

10. Stock Exchange 3

11. Capital Market 3

12. Mahila Banking 2

13. Consumer Finance 1

14. Housing Finance 1

15. Branch for Physically Challenged 1

16. Specialized Govt. Business Branch 1

17. TOTAL 145

2012

Organizational study, MPBIM Page 31

BUSINESS PERFORMANCE FOR THE YEAR 2011-12 and FINANCIAL RATIOS

Global business of the Bank rose to a level of 559544 crore as at March 2012, recording a y-o-y growth of

10.9%.

During the year, along with slackened business growth

and increase in stressed assets at the industry level, the

Bank has taken a conscious decision to consolidate its

business position and rebalance assets and liabilities so

as to improve profitability.

The Bank added record 342 domestic branches and one

overseas branch at Manama, Bahrain, taking the total

tally under the branch network to 3600.

Fig 1.3.4: Showing Business performance

The Operating Profit and Net Profit

The bank earned a net profit of 3283 crore compared to 4026 crore last year. Operating profit stood at

5943 crore compared to 6091 crore last year. This is due to general slowdown in economy world-wide and

Increase in stress in a number of industries like textiles, steel, mining, infrastructure etc.

Fig 1.3.5: Showing Operating and Net Profit for FY12

0

1000

2000

3000

4000

5000

6000

7000

2009-10 2010-11 2011-12

Operating Profit

Net Profit

3 Yr CAGR at 18%

2012

Organizational study, MPBIM Page 32

ENHANCING SHAREHOLDER VALUE!

THE BOARD HAS PROPOSED A DIVIDEND OF 110% FOR FY12.

This is quite an increase from the dividend declared in FY07 which was 70% then.

While the Book Value increased to 431.26 as at March 2012 as compared to 359.25 for the previous

financial, EPS stood at 74.10 as at March 2012 compared to 97.83 year ago.

YEAR

2007-08 2008-09 2009-10 2010-11 2011-12

BOOK

VALUE ( )

202 245 306 359 431

EPS

( )

38.17 50.55 73.69 97.83 74.10

Fig 1.3.6: Showing EPS and Book Values

INCOME EXPENDITURE ANALYSIS

FY11 FY12

Interest Income 22940 30851

Interest Expenditure 15241 23161

Net Interest Income 7699 7689

Non-Interest Income 2811 2928

Total Income 25752 33778

Total Expenditure 19660 27835

Operating Expenses 4419 4674

Employee Cost 2955 2973

Operating Profit 6091 5943

Net Profit 4026 3283

2012

Organizational study, MPBIM Page 33

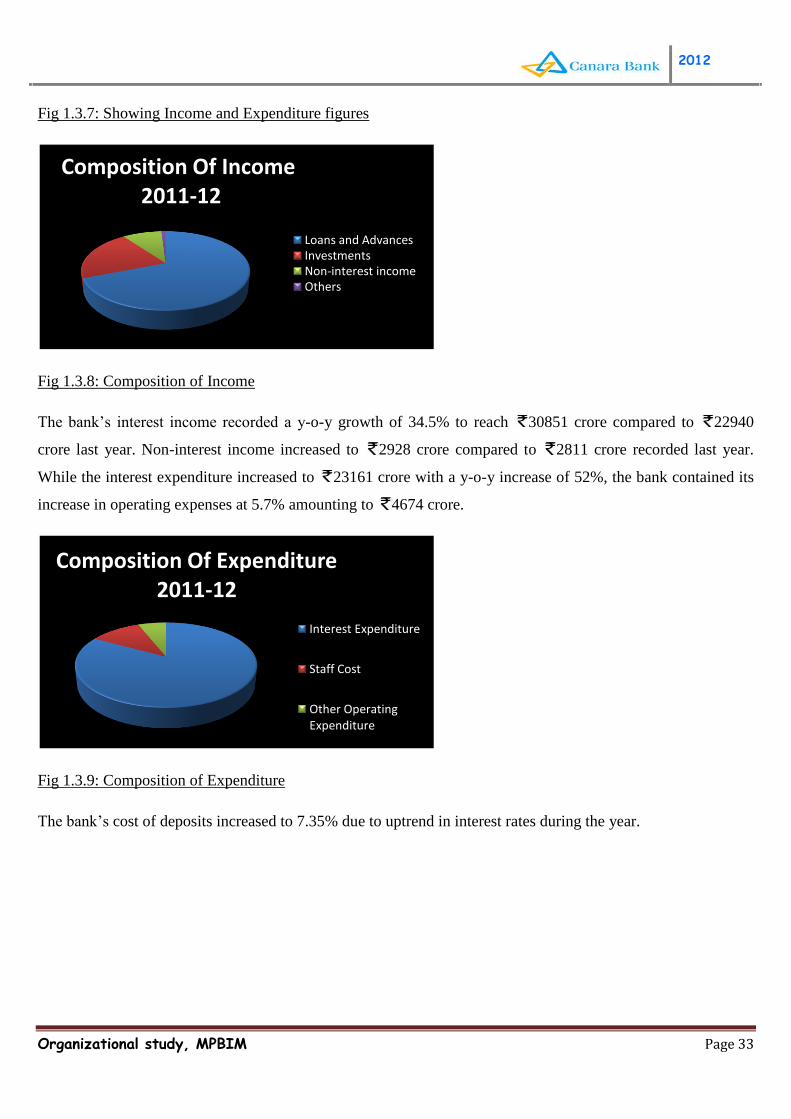

Fig 1.3.7: Showing Income and Expenditure figures

Fig 1.3.8: Composition of Income

The bank’s interest income recorded a y-o-y growth of 34.5% to reach 30851 crore compared to 22940

crore last year. Non-interest income increased to 2928 crore compared to 2811 crore recorded last year.

While the interest expenditure increased to 23161 crore with a y-o-y increase of 52%, the bank contained its

increase in operating expenses at 5.7% amounting to 4674 crore.

Fig 1.3.9: Composition of Expenditure

The bank’s cost of deposits increased to 7.35% due to uptrend in interest rates during the year.

Composition Of Income 2011-12

Loans and Advances Investments Non-interest income Others

Composition Of Expenditure 2011-12

Interest Expenditure

Staff Cost

Other Operating Expenditure

2012

Organizational study, MPBIM Page 34

KEY FINANCIAL RATIOS MARCH 2011 MARCH 2012

Cost of Funds 5.37 6.72

Yield on Funds 8.13 8.95

Cost of Deposits 5.80 7.35

Yield on Advances 9.73 10.93

Yield on Investments 7.72 7.96

Return on Avg. Assets (ROAA) 1.42 0.95

Return on Equity (ROE) 29.47 18.75

Net Interest Margin (NIM) 3.12 2.50

Fig 1.3.10: Showing Financial ratios for FY12

GROWTH RATIOS

Total Income

YEAR

2009-10 2010-11 2011-12

Total Income (in crores) 21610 25767 33778

Growth (%) 11.21 15.2 31.0

Fig 1.3.11: Total Income

The total income over the years has been increasing. The growth in income is 31% as at March 2012, much

greater than 15.2% in the previous year. Income from loans/advances grew by 37.5% to 23443 crore. The

Bank's non-interest income during the year rose to 2928 crore.

Deposits Growth

YEAR

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

Total Deposit (in crores) 142381 154072 186893 234651 293973 327054

Growth (%) 21.90 8.21 21.30 25.55 25.7 11.5

Fig 1.3.12: Deposits Growth

2012

Organizational study, MPBIM Page 35

Total deposits of the Bank registered a growth of 11.5% to reach 327054 crore as at March 2012 compared to

293437 crore a year ago. Savings deposits rose by 10.5% to 64792 crore as at March 2012. During FY12,

the Bank launched nationwide campaign to mobilize SB deposits in two phases. During this, the Bank has

brought in about 24 lakh fresh SB clientele and about 3000 crore SB deposits in the new accounts.

Advances Growth

Fig 1.3.13: Advances Growth

During 2011-12 the Bank’s net advances witnessed a growth of 10%to reach 232490 crore compared to

211268 crore a year ago. The Bank’s diversified credit portfolio include all productive segments of the

economy like agriculture, MSME, exposure to corporate and infrastructure segments.

Credit-Deposit ratio shows the ratio of total advance to total deposits.

Credit to deposit ratio stood at 71.09% in financial year 2011-12 compared to 72.23% in 2009-10.

PRODUCTIVITY RATIOS

(in crore) MARCH ‘11 MARCH’12

Business per

Employee

11.96 13.74

Business per Branch 154.96 155.43

Fig 1.3.14: Showing Productivity ratios

Global business of the Bank rose to a level of 559544 crore as at March 2012, recording a y-o-y growth of

10.9%. The Bank’s domestic business constituted about 96% of the total business. Productivity as measured by

Business per Employee increased to further 13.74 crore, Business per Branch improved to 155.43 crore as

at March 2012.

YEAR

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

Total Advances (in crores) 98506 107238 138219 169335 173794 232490

Growth (%) 24.02 8.86 28.89 22.51 23.7 10.0

2012

Organizational study, MPBIM Page 36

AWARDS AND ACCOLADES

Received during 2011-12

In recognition of the varied initiatives, the Bank was conferred with the following awards –

National Award - 2011 for excellence in the field of Khadi and Village Industries – Best Bank, South Zone

for PMEGP.

Corporate Social Responsibility Award for the year 2010-11 conferred by Institute of Public Enterprises and

Subir Raha Centre for Corporate Governance, Hyderabad.

The prestigious 'SKOCH Award' for outstanding progress under financial inclusion on 5.01.2012 at New

Delhi. A certificate of merit was handed over to General Manager Financial Inclusion Wing for Canara

Banks role in providing Access to Banking and Financial Services.

NABARD’s Best Performance Award, 2010-11, for SHG credit linkage and Best Performing Farmers’ Club

Award of NABARD, 2010-11, in Karnataka.

Under the implementation of Rajbhasha, the bank received the Indira Gandhi Rajbhasha Purskar Yojna-

2009-10 –Encouragement Prize.

The Bank was conferred 5 Awards by the Public Relations Council of India (PRCI), in the following

categories

o Silver Award for Corporate Advertisement - Single Language

o Bronze Award for Annual Report

o Bronze Award for Corporate Brochure on CSR activities

o Bronze Award for Corporate Single Advertisement - English

o Bronze Award for Shreyas In-house Magazine - English

Received during 2010-11

Canara Utsav & SLBC Kerala-Declaration of total banking coverage

The Bank has been conferred with the Second Best Bank Award under National Awards for Excellence

in lending to Micro Enterprises for the year 2009-10, by the Ministry of MSME and Outstanding

2012

Organizational study, MPBIM Page 37

Performer at National level for implementation of Interest Subsidy Eligibility Scheme (ISEC) of KVIC

in the country for 2009-10.

The Bank was conferred 4 awards by the Public Relations Council of India (PRCI), in the following

categories

Silver Award for Corporate Film ( TV Commercial ) – English

Bronze Award for House Journal/Magazine – Languages

Bronze Award for Table Calendar

Bronze Award for Corporate Advertisement – Single - English

2012

Organizational study, MPBIM Page 38

COMPETITORS INFORMATION

State Bank of India (SBI) is the largest banking and financial services company in India by revenue, assets

and market capitalisation. It is a state-owned corporation with its headquarters in Mumbai, Maharashtra,

founded on 1 July 1955. Today, SBI has about 27,000+ ATM and has 99345 offices in India and about 292,215

employees. As of 31 March 2012, the bank had 173 overseas offices spread over 34 countries in places like

Colombo, Dhaka, Frankfurt, Hong Kong, Tehran, Johannesburg, London, Los Angeles etc..

SBI has five associate banks: State Bank of Bikaner & Jaipur, State Bank of Hyderabad, State Bank of Mysore,

State Bank of Patiala, State Bank of Travancore.

Products offered are: Credit cards, Consumer banking, corporate banking, finance and insurance, investment

banking, mortgage loans, private banking, wealth management.

The State Bank of India is the 29th most reputed company in the world according to Forbes. Also, SBI is the

only bank featured in the coveted "top 10 brands of India" list in an annual survey conducted by Brand Finance

and The Economic Times in 2010.

ICICI Bank Limited is an Indian diversified financial services company founded in 195 headquartered in

Mumbai, Maharashtra. It is the second largest bank in India by assets and third largest by market capitalization.

The Bank has a network of 2,763 branches and 9,363 ATM's in India, and has a presence in 19 countries,

including India, United Kingdom, Russia, and Canada and many more. The employee strength is about 79,978.

The bank has subsidiaries branches in United States, Singapore, Bahrain, Hong Kong, Sri Lanka, Qatar and

Dubai International Finance Centre; and representative offices in United Arab Emirates, China, South Africa,

Bangladesh, Thailand, Malaysia and Indonesia.

Products offered are: Credit cards, Consumer banking, corporate banking, finance and insurance, investment

banking, mortgage loans, private banking, wealth management.

2012

Organizational study, MPBIM Page 39

ICICI Bank’s Green initiative ranges from Green offerings/incentives, Green engagement to Green

communication with their customers.

In 2012, ICICI Bank won the "Best Bond House (India) 2011", by IFR Asia, Best Bank (India) by Global

Finance, "Century International Quality Era Award" at Geneva, "Best Foreign Exchange Bank (India)" by

Finance Asia Country Awards.

HDFC Bank Limited is an Indian financial services company that was incorporated in August 1994. HDFC

Bank is the fifth or sixth largest bank in India by assets and the second largest bank by market capitalization.

HDFC Bank has 1,986 branches and over 5,471 ATMs, in 996 cities in India. Employee strength is 66,076.

HDFC Bank deals with three key business segments. - Wholesale Banking Services, Retail Banking Services,

Treasury.

HDFC offers Credit cards, consumer banking, corporate banking, finance and insurance, investment banking,

mortgage loans, private banking, private equity, wealth management.

INDIAN BANK is an Indian state-owned financial services company headquartered in Chennai, India. It has

22,000 employees, 1923 branches and is one of the big public sector banks of India. It has overseas branches in

Colombo, Jaffna, Sri Lanka, Singapore, and 229 correspondent banks in 69 countries. The bank celebrated its

centenary in 2007. It is the only Indian Bank other than State Bank of India to feature in the List of Fortune 500

Companies in the World.

It has 3 Subsidiary companies: Indbank Merchant Banking Services Ltd., IndBank Housing Ltd., and IndFund

Management Ltd.

The Revenue of the bank is 211,988 crore (2012) and its Net income is 13,463 crore.

2012

Organizational study, MPBIM Page 40

Bank of Baroda (BoB) is the highest profit-making public sector undertaking (PSU) bank in India and the

second largest PSU bank in terms of number of total business in India. It is the country's first largest public

sector lender in terms of annual profit. BoB is ranked 715 on Forbes Global 2000 list. BoB has total assets in

excess of Rs. 3.58 lakh crores, a network of 4007 branches (out of which 3914 branches are in India) and

offices, and over 2000 ATMs. It plans to open 400 new branches in the coming year. It offers a wide range of

banking products and financial services to corporate and retail customers through its delivery channels and

through its specialized subsidiaries and affiliates in the areas of investment banking, credit cards and asset

management. Its total global business was Rs. 6,722.48 billion as of 31 March 2012. Its headquarters is in

Baroda.

It also has 2 representative offices in Thailand and Australia. The Bank of Baroda has a joint venture in Zambia

with 16 branches.

2012

Organizational study, MPBIM Page 41

1.4 VISION, MISSION AND OBJECTIVES OF CANARA BANK

VISION STATEMENT

To emerge as a ‘Best Practices Bank’ by pursuing global benchmarks in profitability, operational efficiency,

asset quality, risk management and expanding the global reach.

MISSION STATEMENT

To provide quality banking services with enhanced customer orientation, higher value creation for stakeholders

and to continue as a responsive corporate social citizen by effectively blending commercial pursuits with social

banking.

Main Objectives of Bank:

The main objectives of the bank, as memorandum of association are as follows:

To establish and carry on the business of the bank where of the head office or place of

business shall be with such branches or agencies as may from time to time be determined upon.

To carry on the business of the banking in all its branches and departme nt

including the borrowing or raising or taking up of money, the discounting, buying and

selling of and dealing in government securities, bills of exchanges, promissory notes and

other negotiable and transferable instrument and securities, the granting and issuing of

letter of credit and circular notes, buying and selling of and dealing in bullion such as

gold, silver etc, the negotiation of loans and advances, the receiving of money and

valuable on deposits, or for safe custody or otherwise the lending or advancing of

money of promoters, on the security of jewels , government securities, port trust

bonds, municipal debenture, share or debenture of any other companies , insurance

policies or other valuable securit ies, or merchandise or any other movable

property and also on the security on immovable property, by deposits of tiles deeds or

otherwise the collecting and transmitting of money and securities and the transaction of

all agency business, commonly transacted by bankers.

To take or acquire the whole or any part of any business similar to that of this bank or

ally business which this is authorized to carry on such other business which is capable

of being conducted to the benefit directly or indirectly of this bank.

2012

Organizational study, MPBIM Page 42

To purchase or otherwise acquire any sites with or without building thereon, erect or

constructed buildings and repair and improved them for the purpose of

investment or otherwise as may be determined upon.

Generally to purchase, take on lease or in exchange, higher or otherwise acquire any

immovable or movable property and may rights or privileges which the bank may think

necessary or convenient with reference to any of the objects for which the bank is

established or acquisition of which may seem calculated to facilitate to the realization

of any securities held by the bank or to prevent or diminish any apprehended loss or

liability.

To take shares or otherwise acquire shares in banking companies or in the j oint stock

business companies at the discretion of the directors.

To encourage, assist and finance any and every description of financial ,

commercial mercantile, industrial manufacturing and directors.

To take or concur ill the taking up of all such steps and proceedings as may see best

calculated to uphold and support the credit of the bank.

To establish and support or aid in the establishment and support of associations,

institutions, funds, trust and conveniences calculated to benefit employees or ex

employees of the bank, or the dependents the connections of such persons, to grant

pensions and allowances and to make payment towards insurance and set apart and

appropriate from the annual net profits, towards the general, mental, moral and physical

advancement of the members of the Dravida Brahmin Community, such sums as

may be deemed fit.

To sell and dispose of the entire undertaking of the bank but not part of it only for such

considerations as the bank may think fit either for cash or shares, debentures or

securities of any other company having objects altogether or in part similar to those of this

bank.

To sell, manage develop exchange lease mortgage, dispose off, turn to account, or

otherwise deal with all or any part of the property and rights of the bank.

To do-all or any of the above things as principles, agents, contractors trustees or

otherwise and by or through trustees, agents or otherwise.

2012

Organizational study, MPBIM Page 43

To do all such other things as are incidental or conducive to the attainment of the above

objects.

To engage in all or any one or more of the forms of business enumerated in section 6(1)

of the Banking Regulations Act, 1949.

To open establish maintain and operate currency chests and small coins depots on such

terms and conditions as may be required by the reser ve bank of India established

under the Reserve Bank of India Act 1934,and enter into all administrative or

other arrangements for undertakings with the Reserve Bank of India.

GOALS FOR FY13

Aiming at a Total Business of 6.50 lakh crore, comprising total deposits of ` 3.75 lakh crore and

advances of ` 2.75 lakh crore.

Thrust on Retail Business, especially retail deposits and retail advances.

Expanding the delivery channels, the Bank plans to open 325 branches and take ATM strength to 4000.

Thrust on technology and business process reengineering to enhance business.

The Project on Enterprise-wide Data Warehousing and Business Analytics has been initiated.

Expanding global footprints, the Bank plans to open branches/ offices in Johannesburg, Qatar,

Frankfurt, New York and Tokyo.

2012

Organizational study, MPBIM Page 44

CHAPTER - 2

ORGANIZATION STRUCTURE

2.1 CORPORATE ORGANIZATION STRUCTURE

2.2 DEPARTMENTAL ORGANIZATION STRUCTURE

2.3 AUTHORITY AND RESPONSIBILITY RELATIONSHIP

2012

Organizational study, MPBIM Page 45

CORPORATE ORGANISATION STRUCTURE

BOARD OF DIRECTORS

CHAIRMAN AND MANAGING DIRECTOR

EXECUTIVE DIRECTOR

CHIEF VIGILIANCE OFFICER

SEVERAL WINGS HEADED BY

RESPECTIVE GENERAL

MANAGERS

2012

Organizational study, MPBIM Page 46

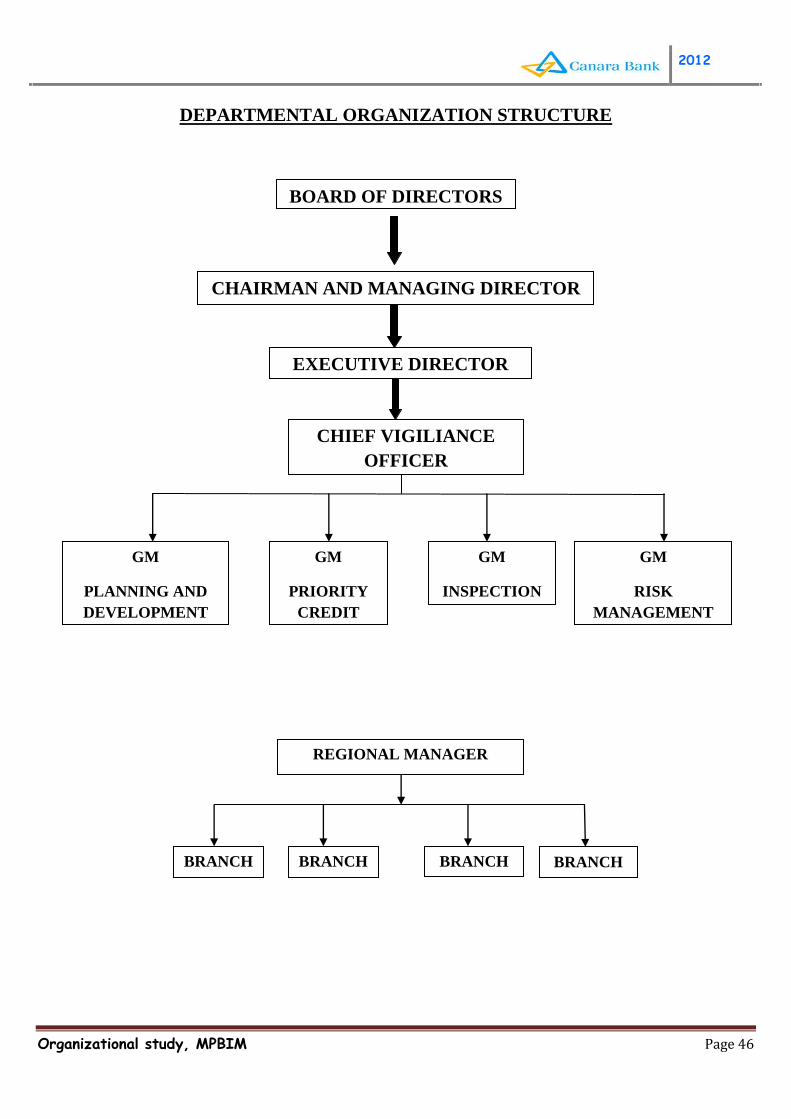

DEPARTMENTAL ORGANIZATION STRUCTURE

BOARD OF DIRECTORS

CHAIRMAN AND MANAGING DIRECTOR

EXECUTIVE DIRECTOR

CHIEF VIGILIANCE

OFFICER

GM

PLANNING AND

DEVELOPMENT

GM

PRIORITY

CREDIT

GM

RISK

MANAGEMENT

GM

INSPECTION

REGIONAL MANAGER

BRANCH BRANCH BRANCH BRANCH

2012

Organizational study, MPBIM Page 47

AUTHORITY AND RESPONSIBILITY RELATIONSHIP

MANAGING DIRECTOR

CHIEF GENERAL MANAGER

GENERAL MANAGER

PLANNING AND

DEVELOPMENT

DGM

SOUTH

ZONE

DGM

NORTH

ZONE

DGM

EAST

ZONE

DGM

WEST

ZONE

AGM AGM AGM AGM

REGIONAL

MANAGER

REGIONAL

MANAGER

REGIONAL

MANAGER

REGIONAL

MANAGER

BRANCH

MANAGER

BRANCH

MANAGER

BRANCH

MANAGER

BRANCH

MANAGER

BRANCH

MANAGER

BRANCH

MANAGER

GENERAL

MANAGER

FINANCE

GENERAL

MANAGER

OPERATIONS

2012

Organizational study, MPBIM Page 48

ORGANISATION OF CANARA BANK AT BRANCH LEVEL

BRANCH MANAGER

SUB STAFF

AWARD STAFF

OFFICER

DEPUTY MANAGER

ASSISTANT MANAGER

2012

Organizational study, MPBIM Page 49

HIERARCHICAL POSITIONS

Chairman and Managing Director

Executive Director

General Manager

Deputy Manager

Assistant General Manager

Divisional/Chief Manager

Senior Manager

Manager

Officer

Special Assistants

Clerks

Sub Staffs

Part Time Employees

GRADE DESIGNATION SCALE

Chief Executive Grades

Top Executive Grades

Senior Management Grades

Middle Management Grade

Junior Management Grade

Workmen

SCALE 7

SCALE 6

SCALE 5

SCALE 4

SCALE 3

SCALE 2

SCALE 1

2012

Organizational study, MPBIM Page 50

MANPOWER PROFILE

As at March 2012, the Bank had 42272 employees on its rolls.

Fig 2.1: Showing employees strength

MARCH 2011 MARCH 2012

Total No of Employees 43397 42272

Officers 17649 17419

Clerks 16178 15802

Sub staff* 9570 9051

*includes Part time employees (PTEs)

The Bank's staff comprised 41.2% Officers, 37.4% Clerks and 21.4% Sub -Staff. Women

employees comprising 10256 constituted over 24.3% of the Bank's total staff. The Bank recruited

517 women employees and promoted 186 women employees under various cadres during the year.

During the year, the Bank recruited1188 persons in various cadr es, out of which 269

belonged to Scheduled Castes (SCs) and54 to Scheduled Tribes (STs) categories. The total number

of ex-servicemen staff as at the end of March 2012 stood at 1703. Out of which 151 were recruited

in various cadres during the year. There were 886 Physically Challenged Employees on the rolls of the

Bank.

Reservation Policies in respect of SCs and STs

As at March 2012, the number of Scheduled Castes and Scheduled Tribes together constituted

26% of total staff strength of the Bank.

Fig 2.2: Composition of SC/ST employees

Cadre SC ST

Officers 3162 1139

Clerks 2817 910

Sub Staff+ PTEs 2542 404

Total 8521 2453

The Bank has been strictly adhering to the Reservation Policy in respect of SC and ST as per the Government

of India guidelines.

2012

Organizational study, MPBIM Page 51

CHAPTER - 3

FUNCTIONAL AREAS

3.1 HUMAN RESOURCES WING

3.2 FINANCIAL MANAGEMENT AND SUBSIDIARIES WING

3.3 PRIORITY CREDIT AND FINANCIAL INCLUSION WING

3.4 CUSTOMER CARE AND BUSINESS PLANNING WING

3.5 DEPARTMENT OF INFORMATION TECHNOLOGY WING

3.6 MARKETING DEPARTMENT

2012