INTEGRATED THINKING - Next Step into Integrated Reporting

30

The next step in integrated reporting INTEGRATED THINKING

Transcript of INTEGRATED THINKING - Next Step into Integrated Reporting

The next step in integrated reporting

INTEGRATED THINKING

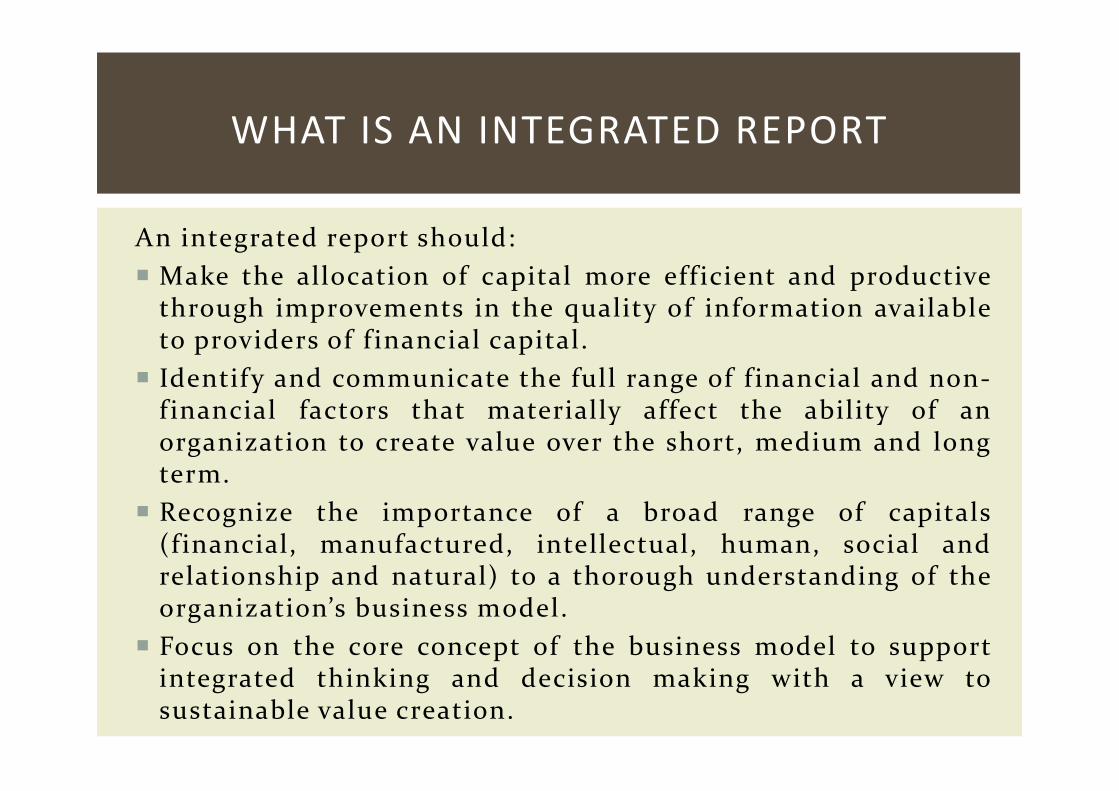

An integrated report should:

� Make the allocation of capital more eff icient and productivethrough improvements in the quality of information availableto providers of f inancial capital.

� Identify and communicate the full range of f inancial and non-f inancial factors that materially affect the ability of anorganization to create value over the short, medium and longterm.

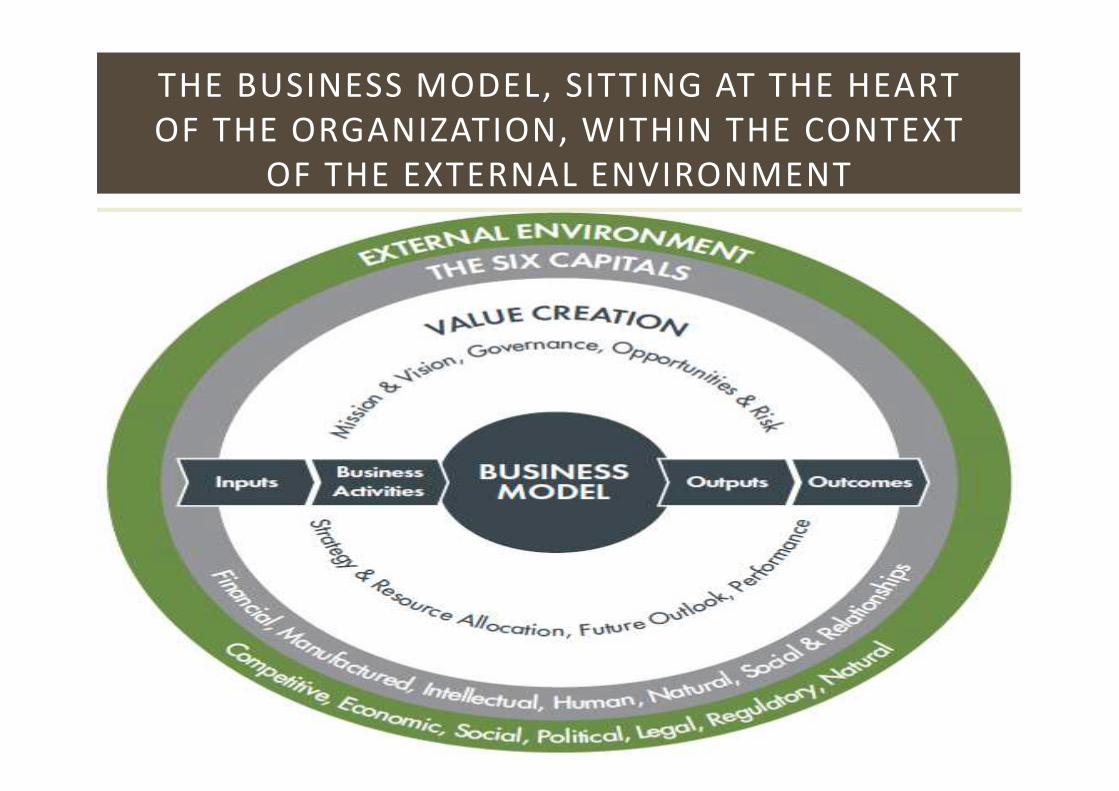

� Recognize the importance of a broad range of capitals(f inancial, manufactured, intellectual, human, social andrelationship and natural) to a thorough understanding of theorganization’s business model.

� Focus on the core concept of the business model to supportintegrated thinking and decision making with a view tosustainable value creation.

WHAT IS AN INTEGRATED REPORT

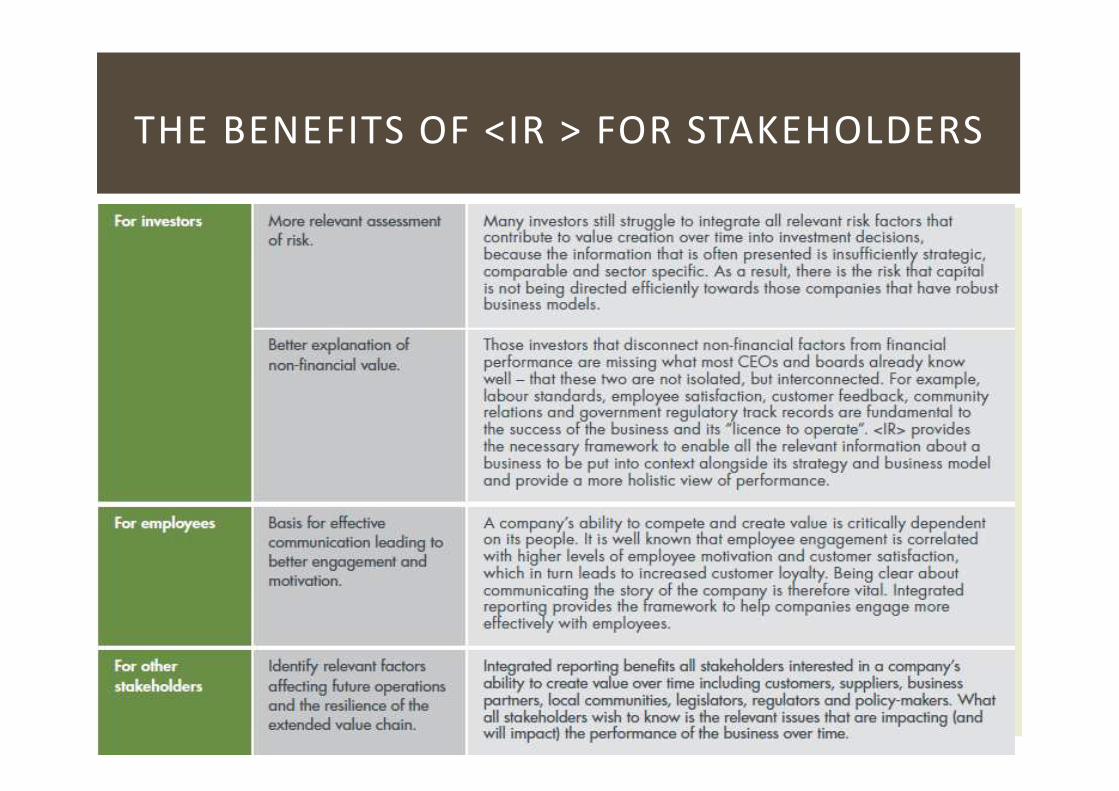

THE BENEFITS OF <IR > FOR STAKEHOLDERS

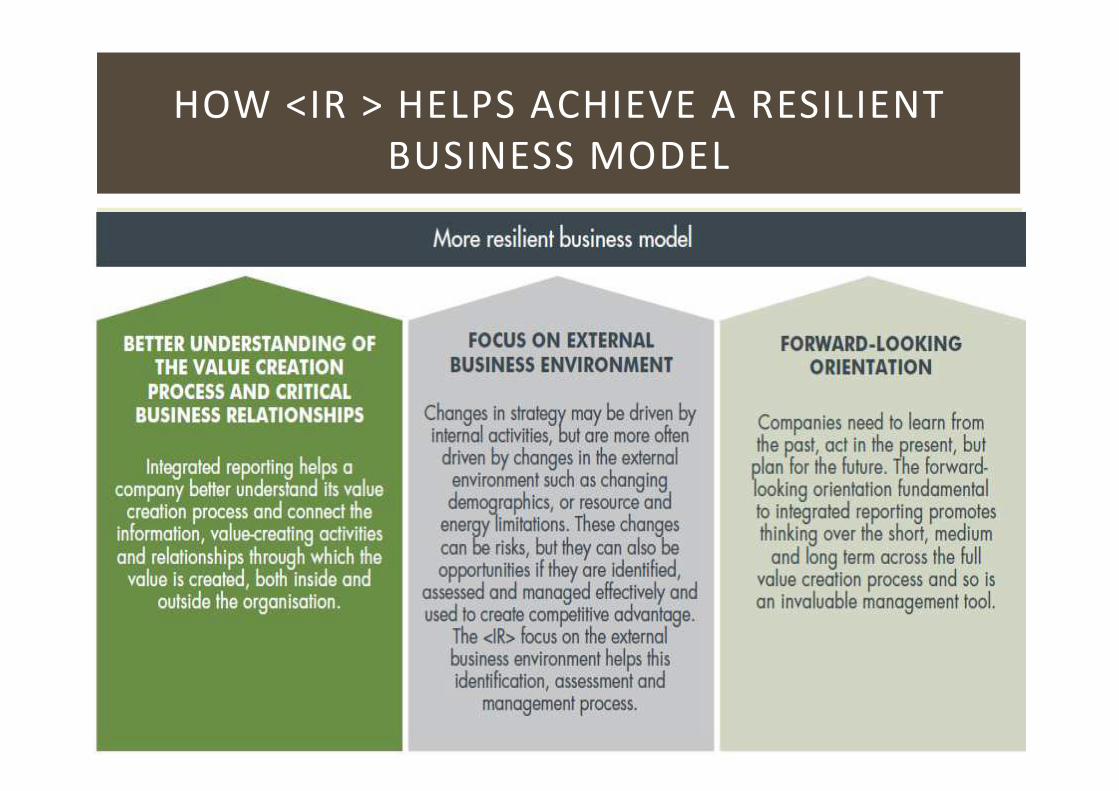

HOW <IR > HELPS ACHIEVE A RESILIENT

BUSINESS MODEL

THE BUSINESS MODEL, SITTING AT THE HEART

OF THE ORGANIZATION, WITHIN THE CONTEXT

OF THE EXTERNAL ENVIRONMENT

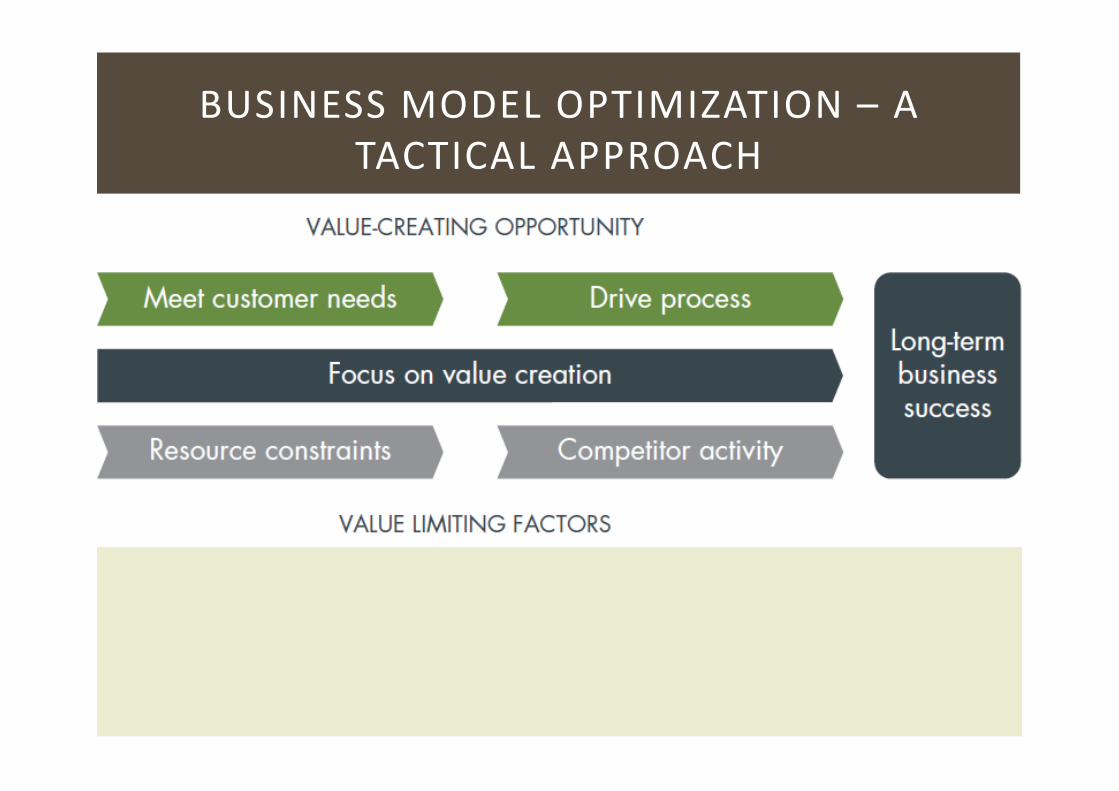

BUSINESS MODEL OPTIMIZATION – A

TACTICAL APPROACH

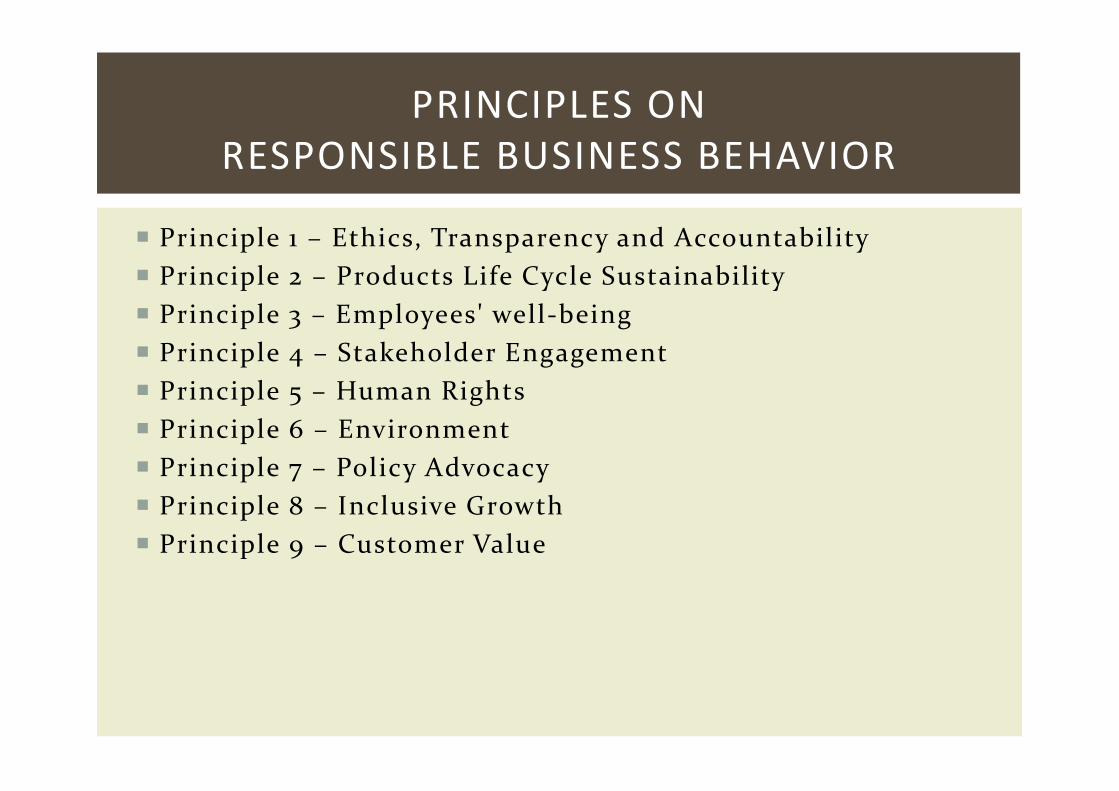

� Principle 1 – Ethics, Transparency and Accountability

� Principle 2 – Products Life Cycle Sustainability

� Principle 3 – Employees' well-being

� Principle 4 – Stakeholder Engagement

� Principle 5 – Human Rights

� Principle 6 – Environment

� Principle 7 – Policy Advocacy

� Principle 8 – Inclusive Growth

� Principle 9 – Customer Value

PRINCIPLES ON

RESPONSIBLE BUSINESS BEHAVIOR

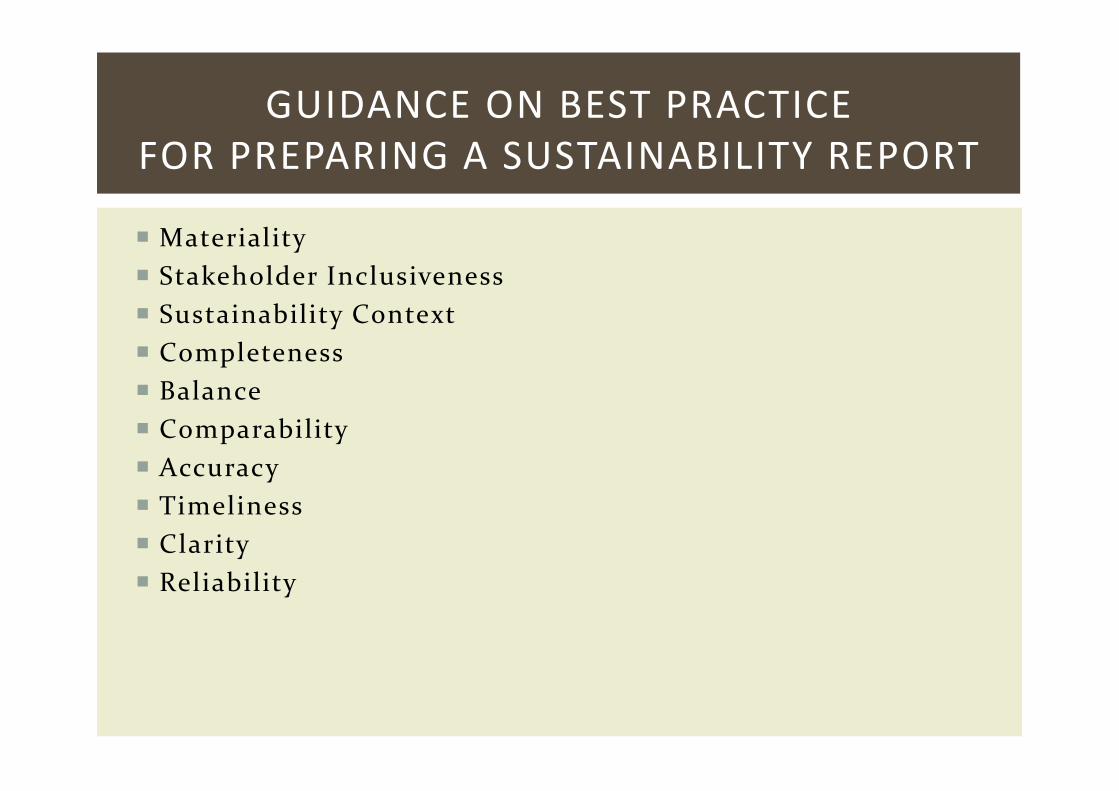

� Materiality

� Stakeholder Inclusiveness

� Sustainability Context

� Completeness

� Balance

� Comparability

� Accuracy

� Timeliness

� Clarity

� Reliability

GUIDANCE ON BEST PRACTICE

FOR PREPARING A SUSTAINABILITY REPORT

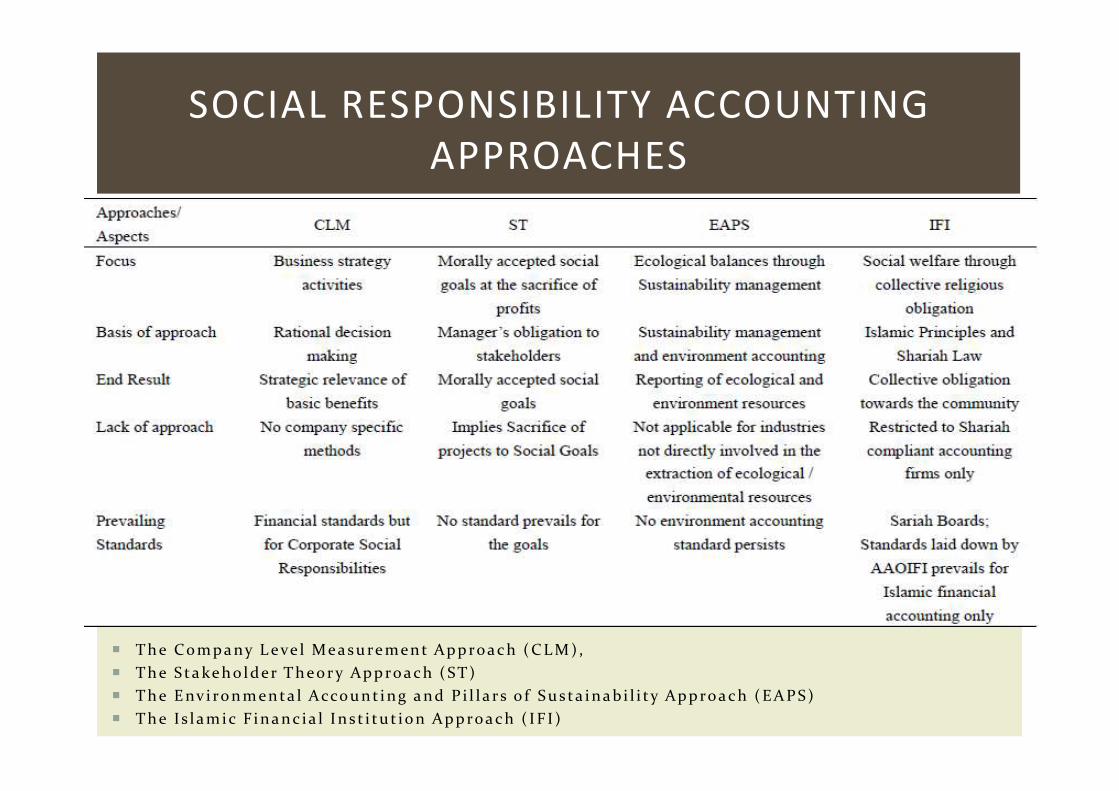

� T h e Co m p a ny L e ve l Me a su re men t Ap p ro a c h ( C L M ) ,

� T h e S t a ke h o l der T h e o r y Ap p ro a c h ( ST )

� T h e E nv i ro n m en t a l Acco u n t i n g a n d P i l l a r s o f S u s t a i n a b i l i t y Ap p ro a c h ( E A P S )

� T h e Is l a m i c F i n a n c i a l I n s t i t u t i o n Ap p ro a c h ( I F I )

SOCIAL RESPONSIBILITY ACCOUNTING

APPROACHES

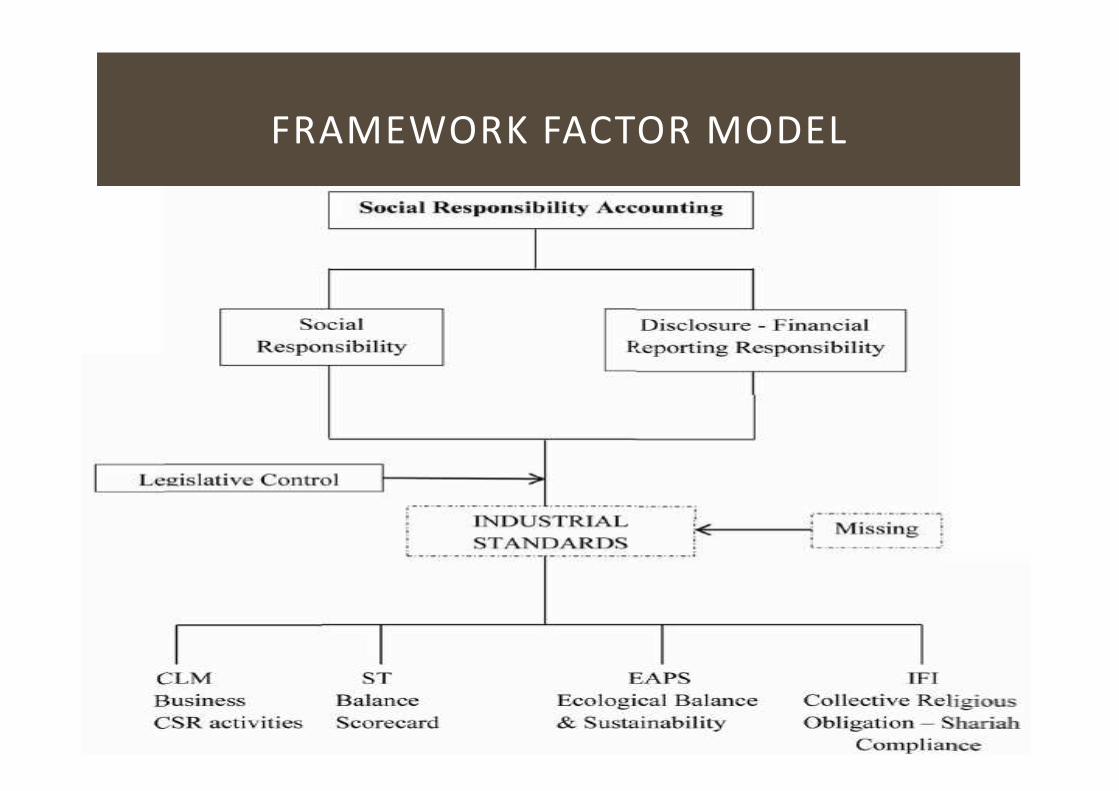

FRAMEWORK FACTOR MODEL

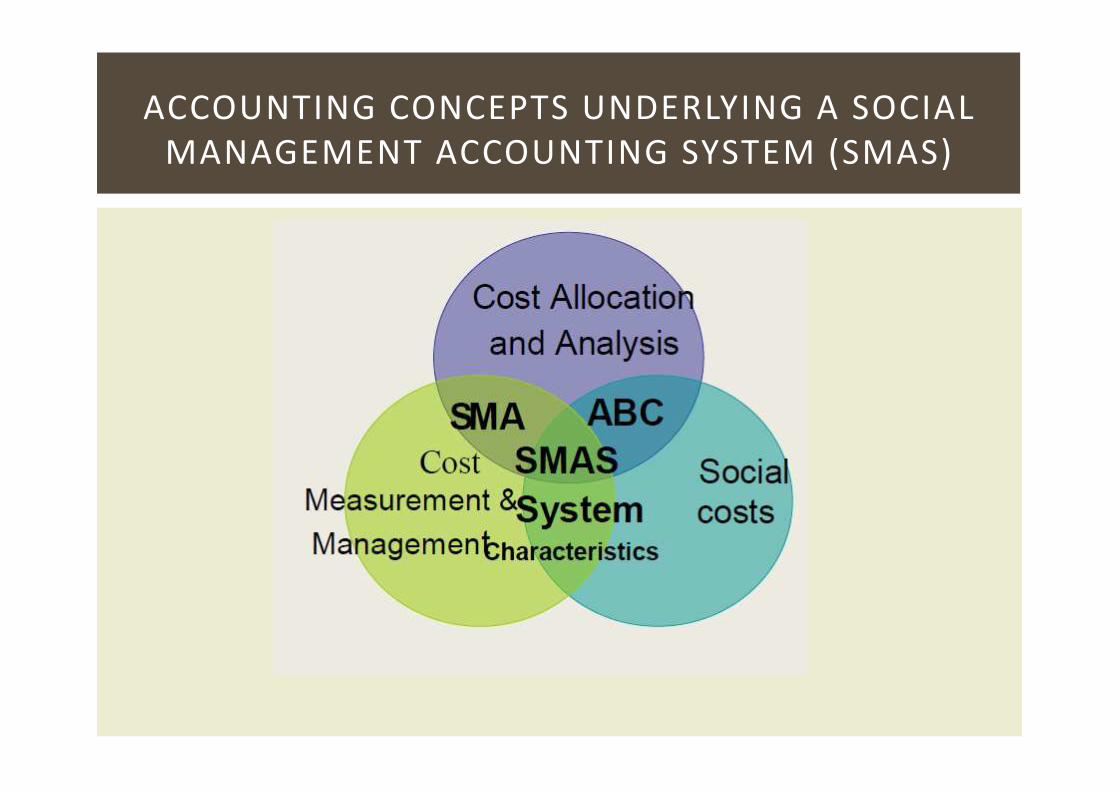

ACCOUNTING CONCEPTS UNDERLYING A SOCIAL

MANAGEMENT ACCOUNTING SYSTEM (SMAS)

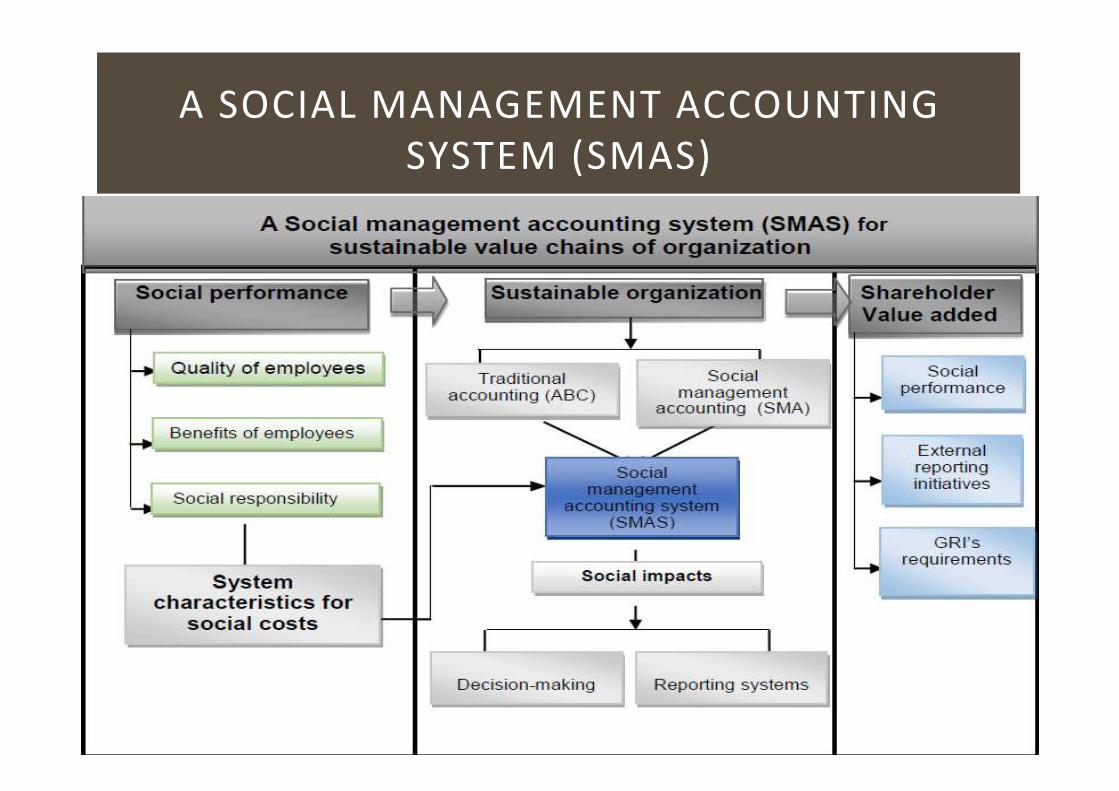

A SOCIAL MANAGEMENT ACCOUNTING

SYSTEM (SMAS)

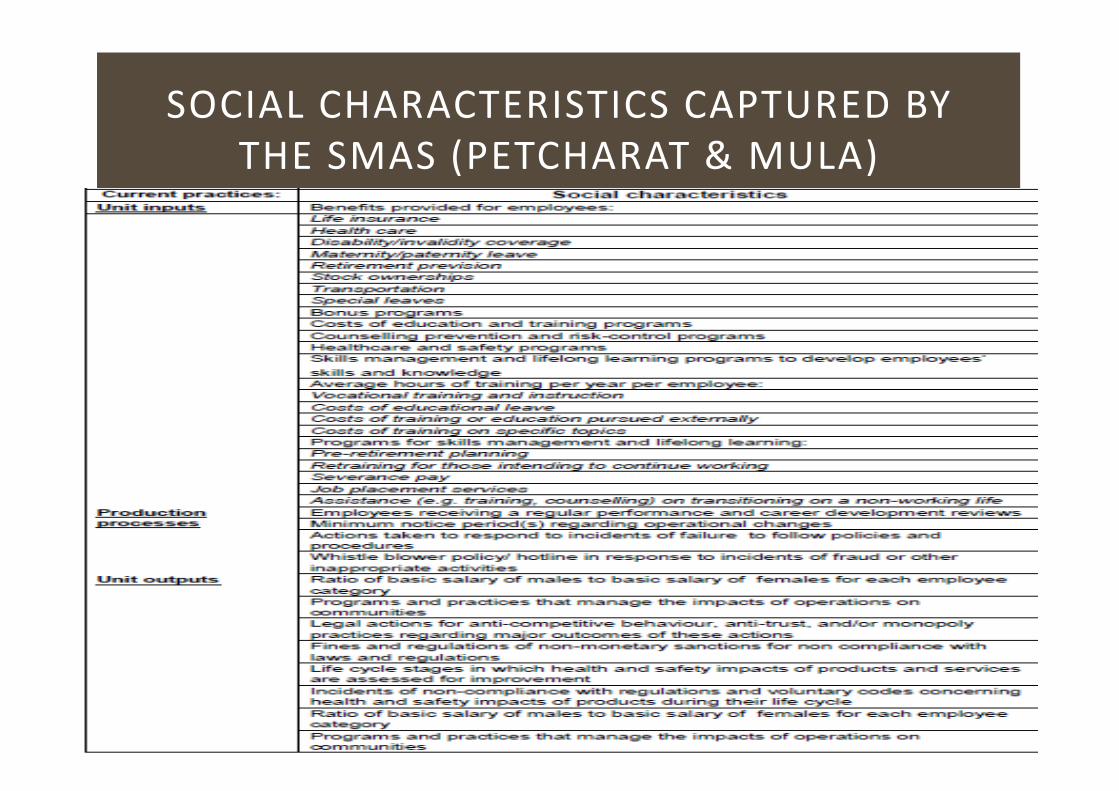

SOCIAL CHARACTERISTICS CAPTURED BY

THE SMAS (PETCHARAT & MULA)

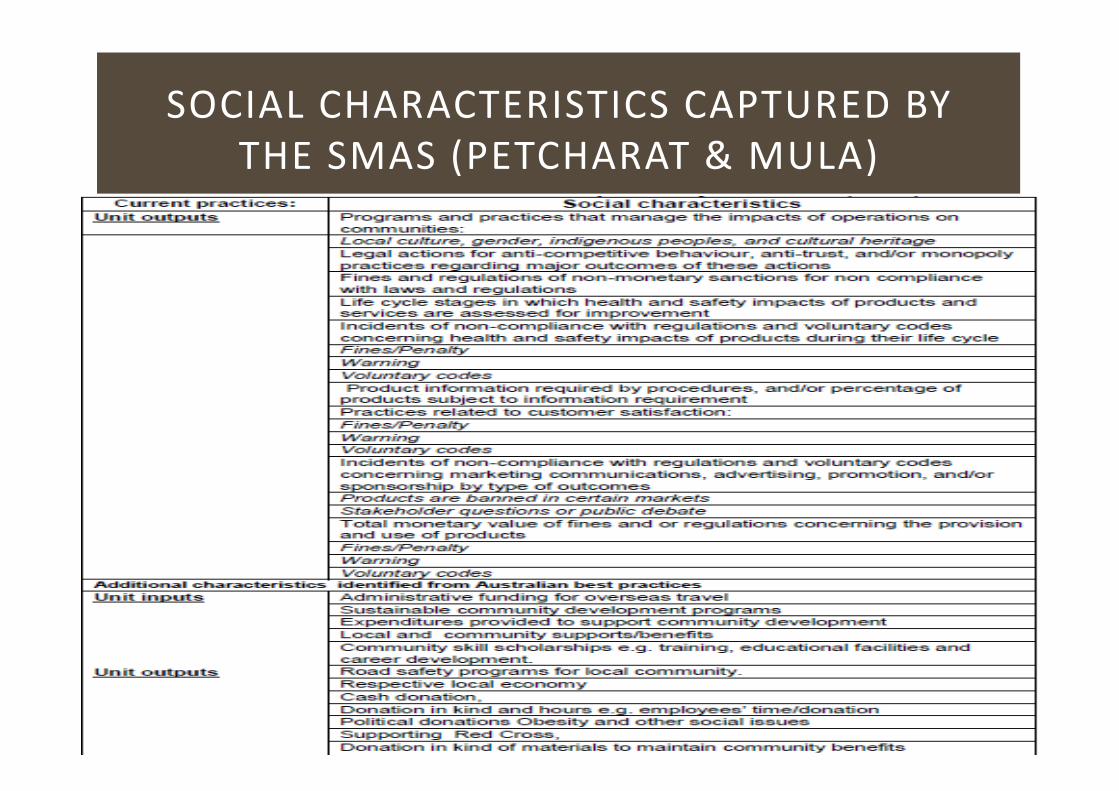

SOCIAL CHARACTERISTICS CAPTURED BY

THE SMAS (PETCHARAT & MULA)

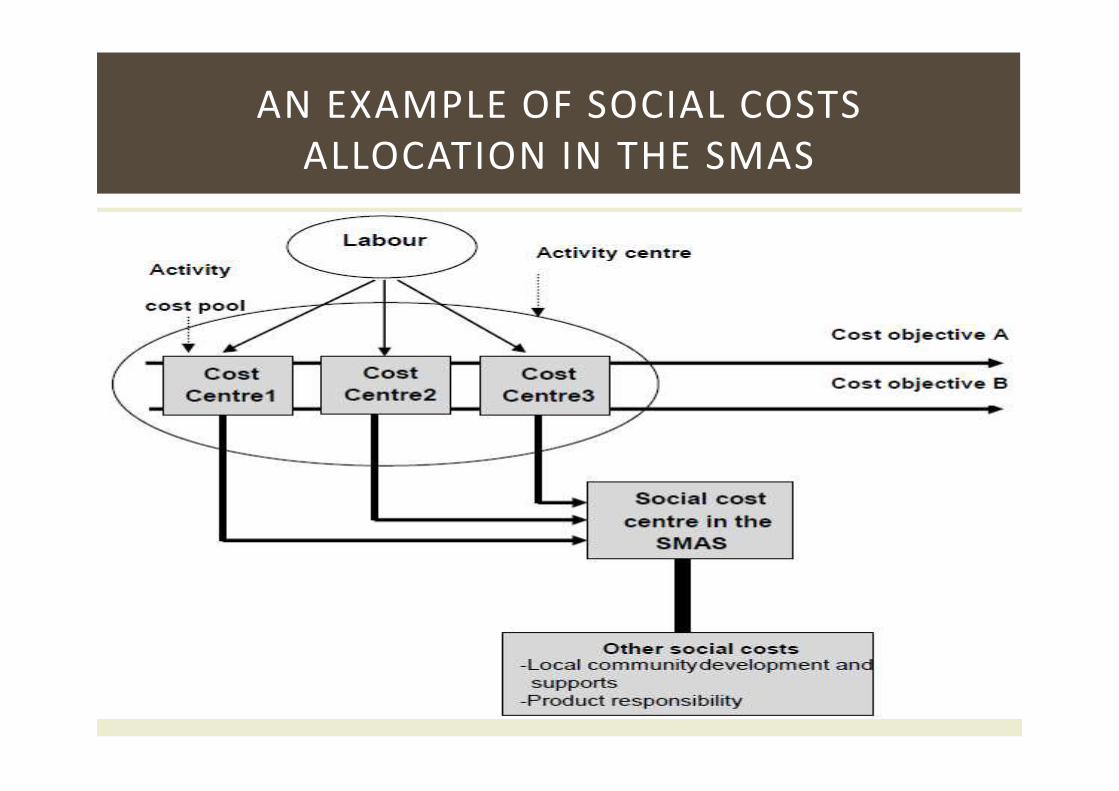

AN EXAMPLE OF SOCIAL COSTS

ALLOCATION IN THE SMAS

A

l

i

g

n

i

n

g

S

t

r

a

t

e

g

y

,

P

e

r

f

o

r

m

a

n

c

e

a

n

d

R

e

p

o

r

t

i

n

g

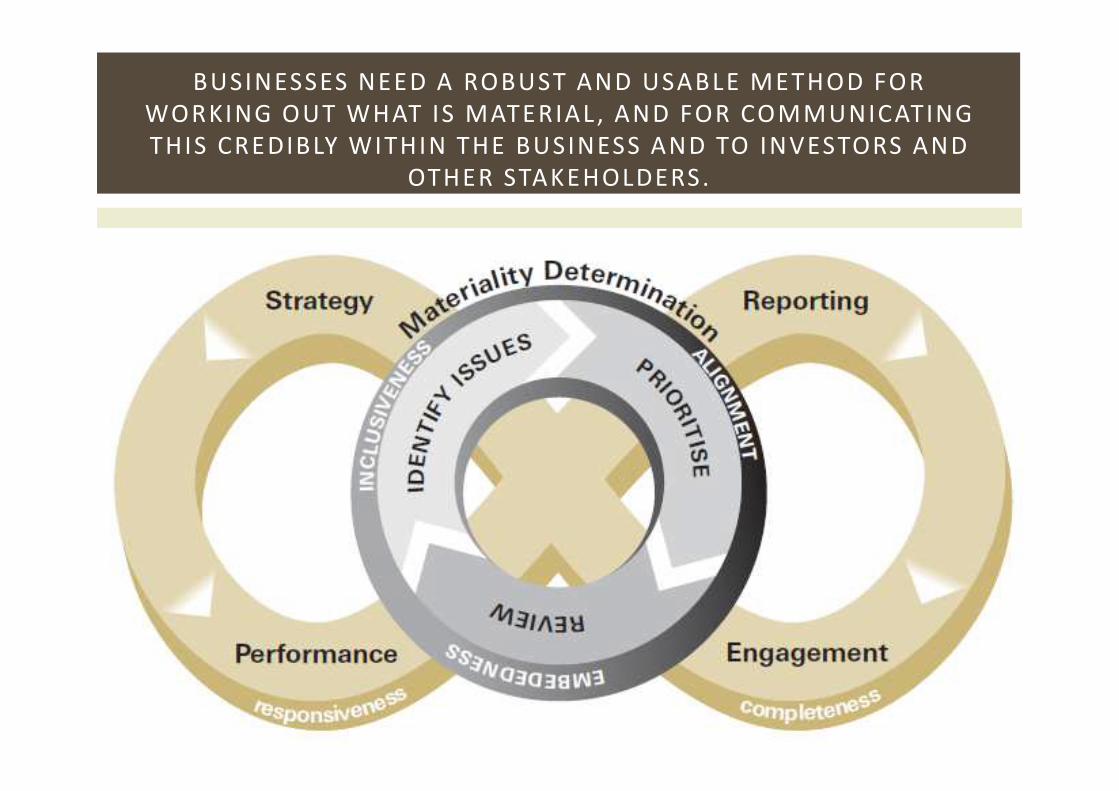

THE MATERIALITY REPORT

BUSINESSES NEED A ROBUST AND USABLE METHOD FOR

WORKING OUT WHAT IS MATERIAL , AND FOR COMMUNICATING

THIS CREDIBLY WITHIN THE BUSINESS AND TO INVESTORS AND

OTHER STAKEHOLDERS.

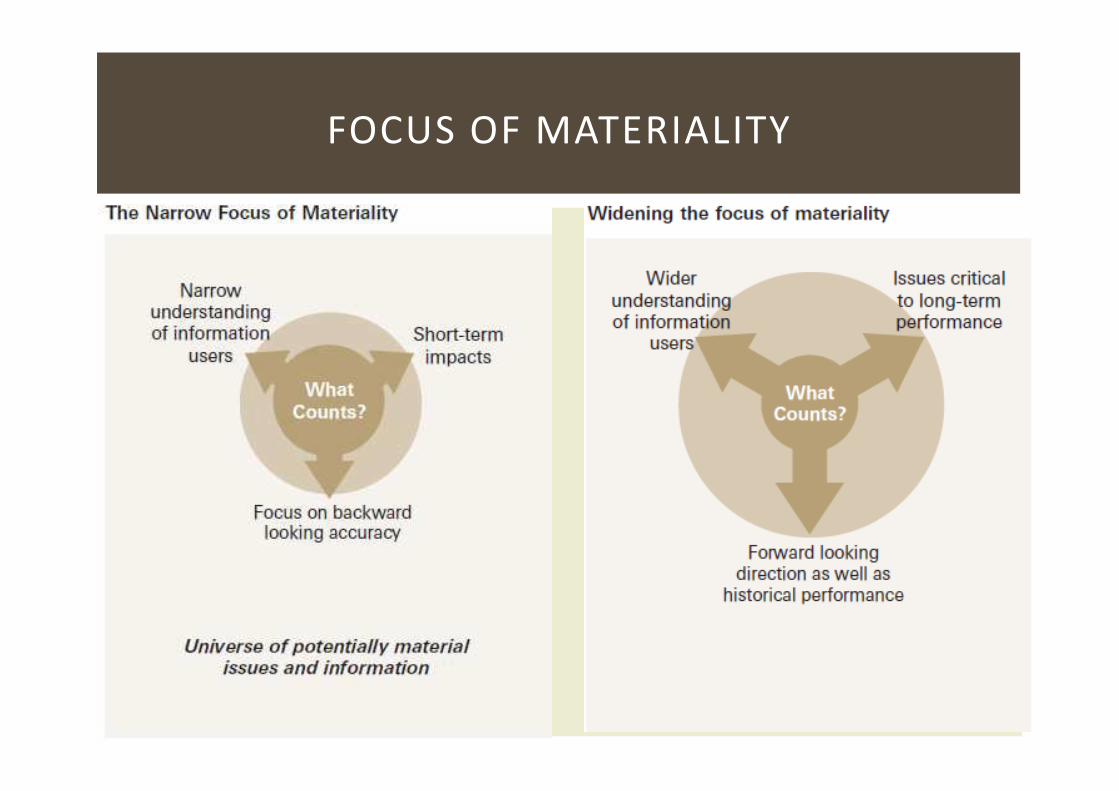

FOCUS OF MATERIALITY

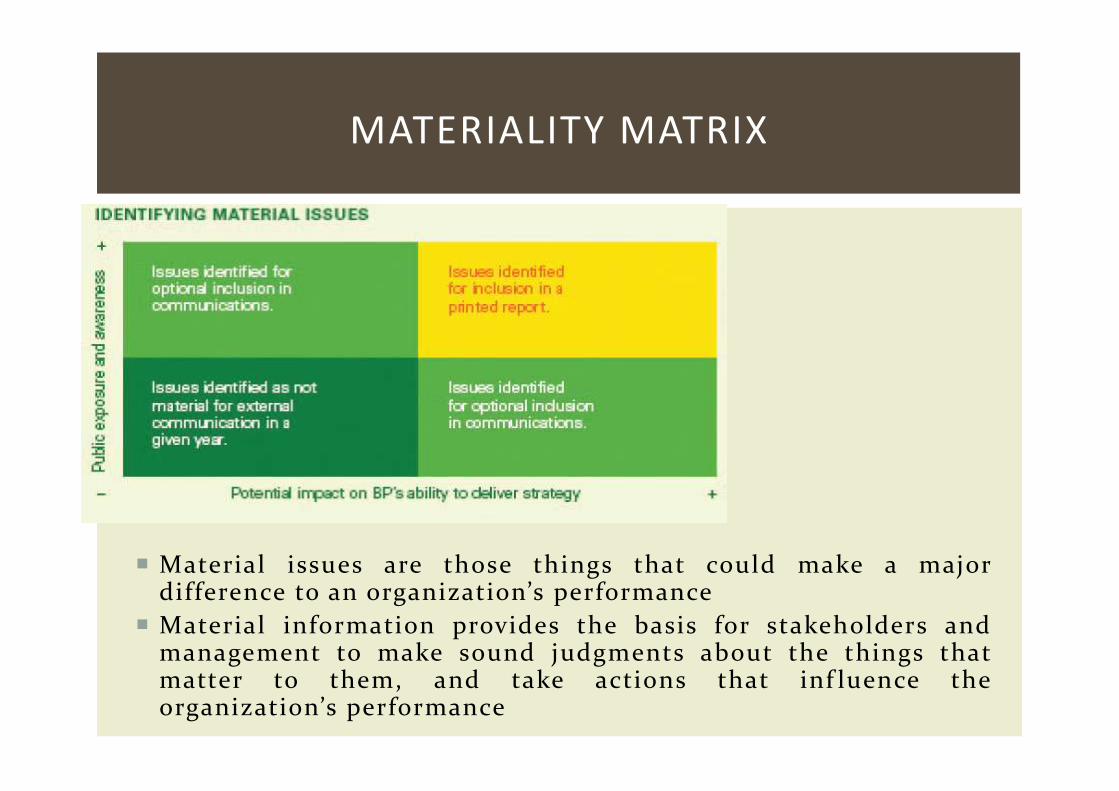

� Material issues are those things that could make a majordifference to an organization’s performance

� Material information provides the basis for stakeholders andmanagement to make sound judgments about the things thatmatter to them, and take actions that inf luence theorganization’s performance

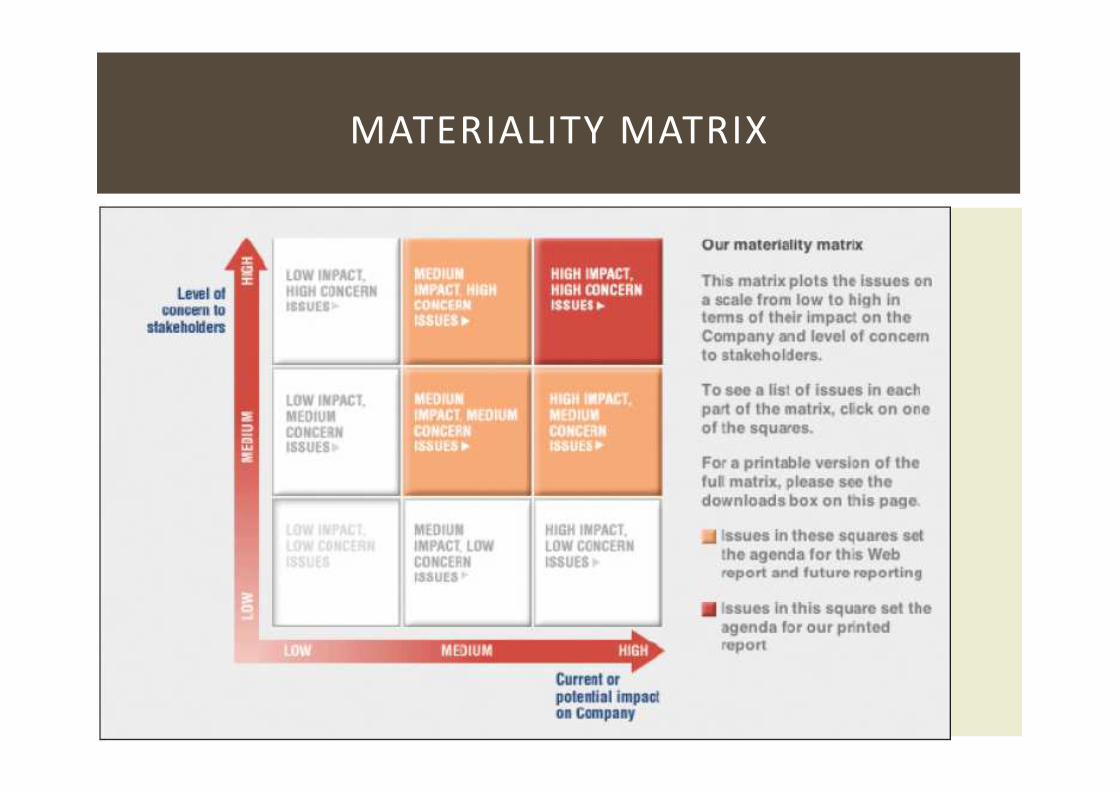

MATERIALITY MATRIX

MATERIALITY MATRIX

SUMMARY ASSESSMENT OF LEADING EDGE

SUSTAINABLE MATERIALITY PRACTICE

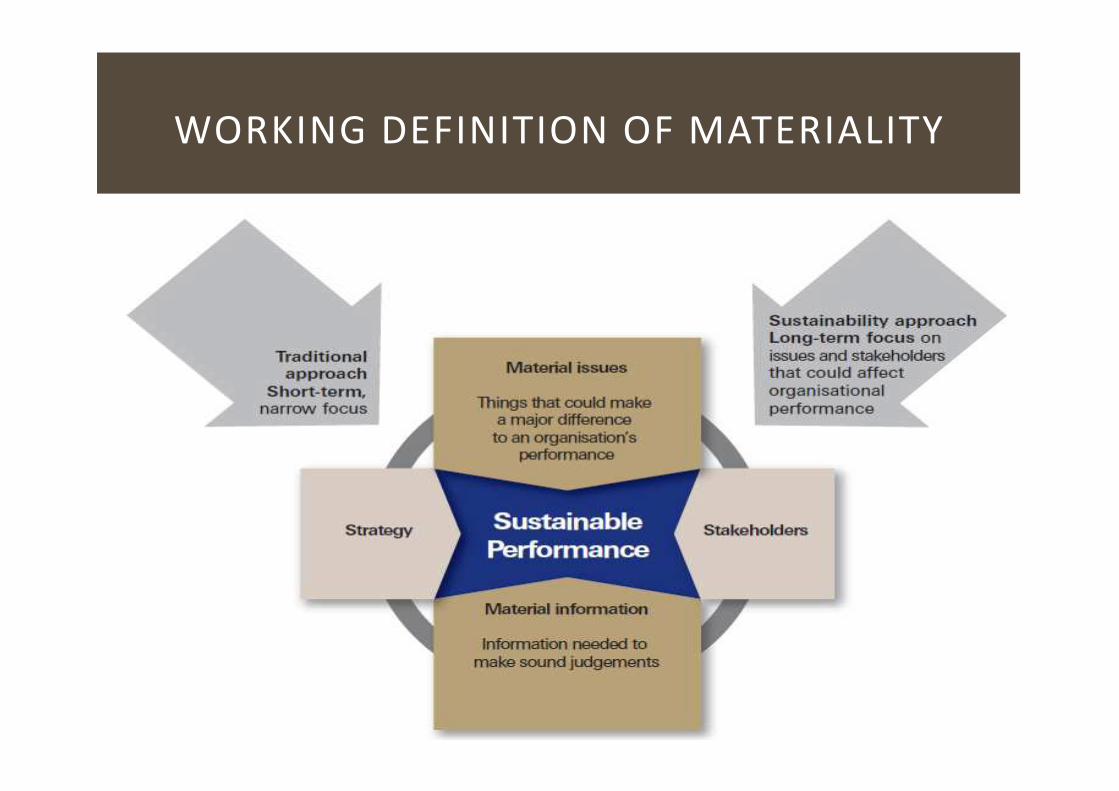

WORKING DEFINITION OF MATERIALITY

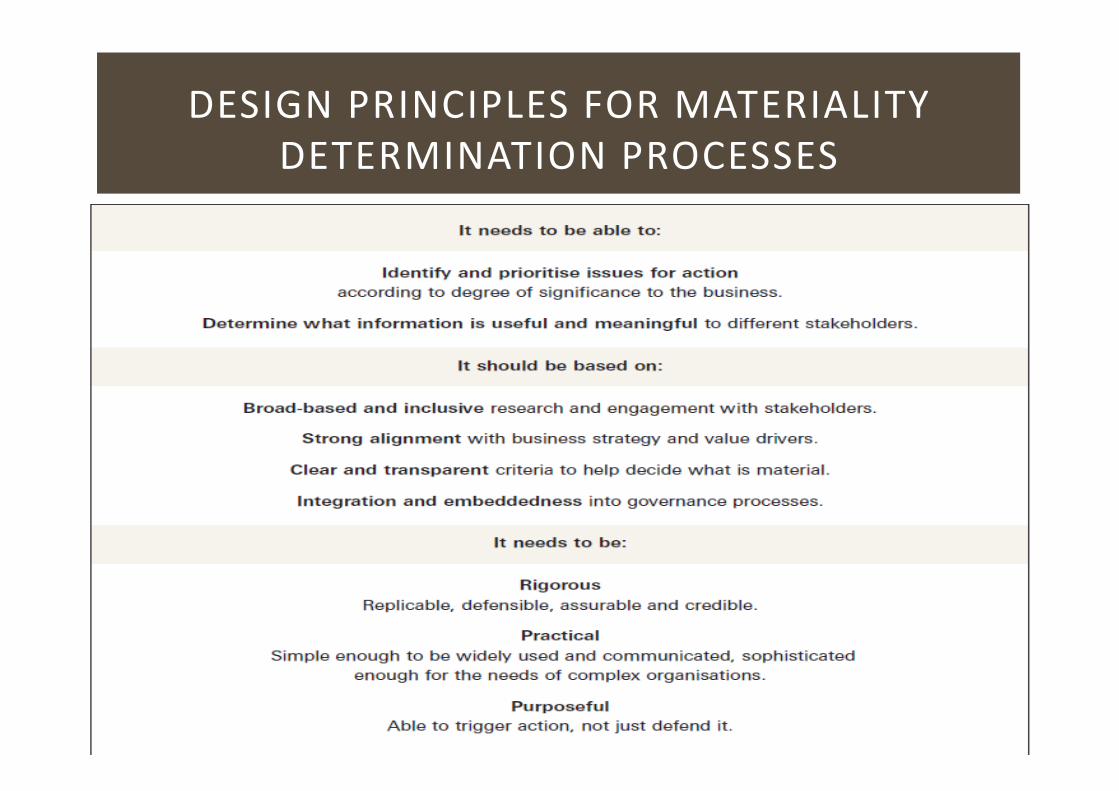

DESIGN PRINCIPLES FOR MATERIALITY

DETERMINATION PROCESSES

IMPLEMENTATION QUESTIONS

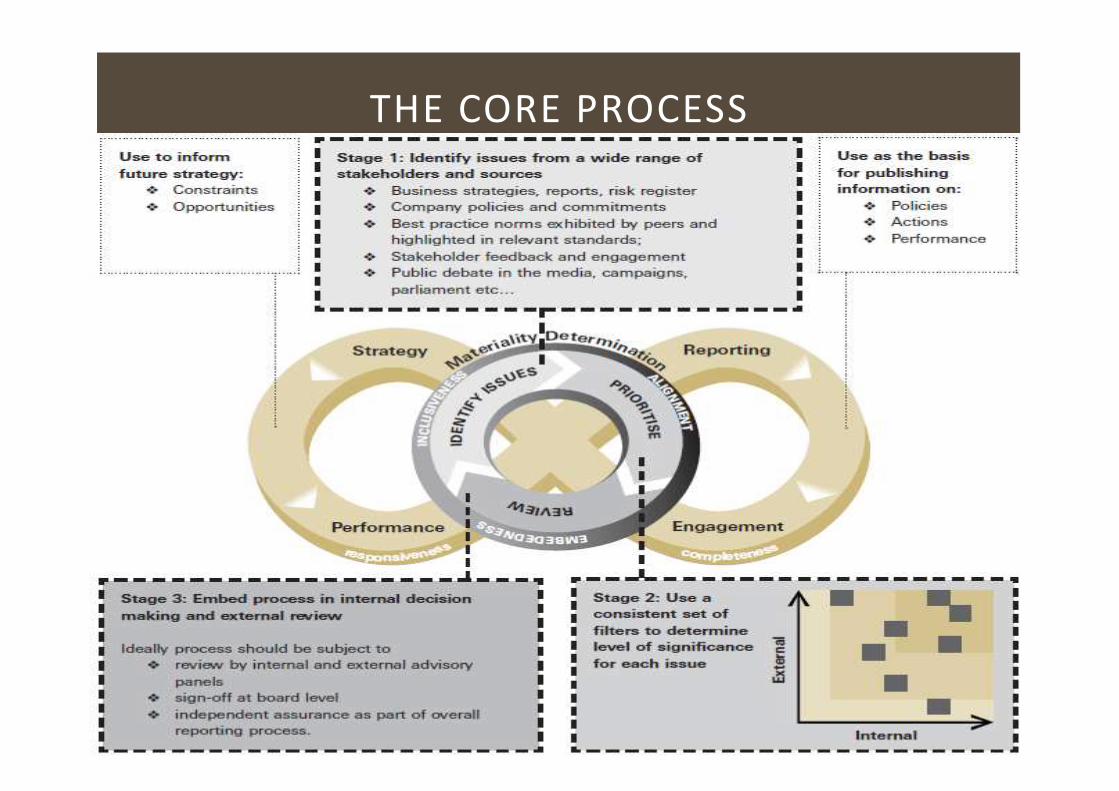

THE CORE PROCESS

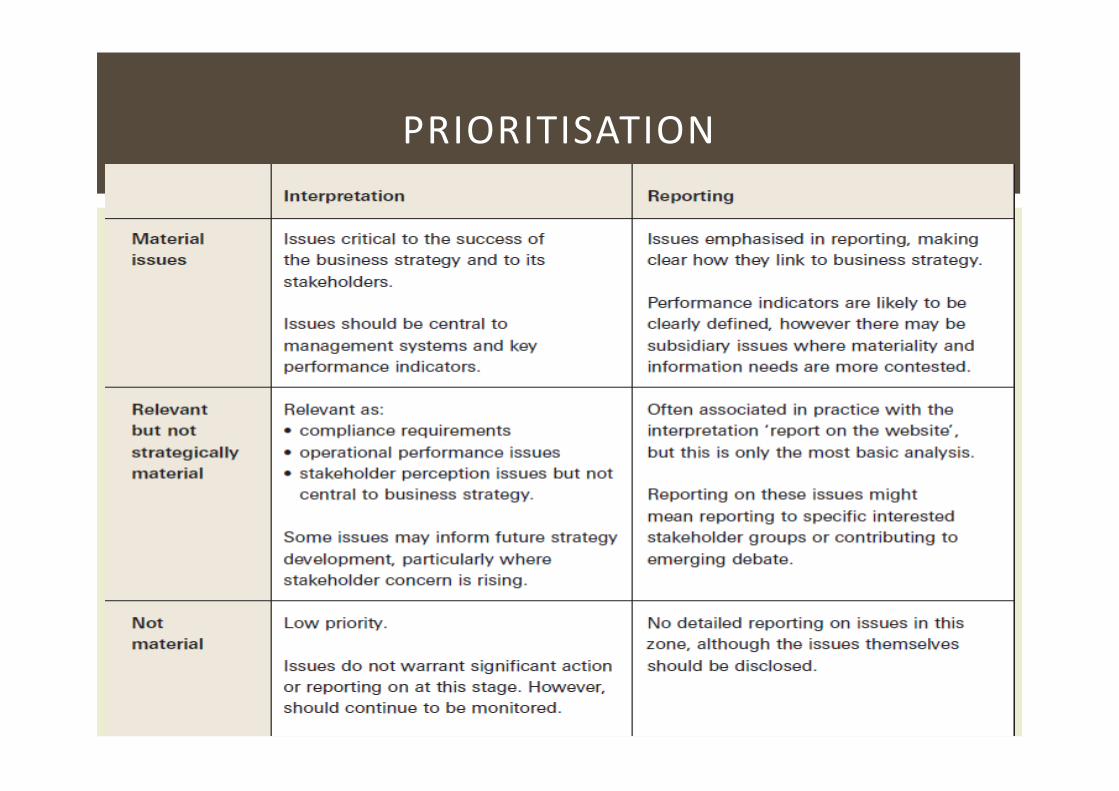

PRIORITISATION

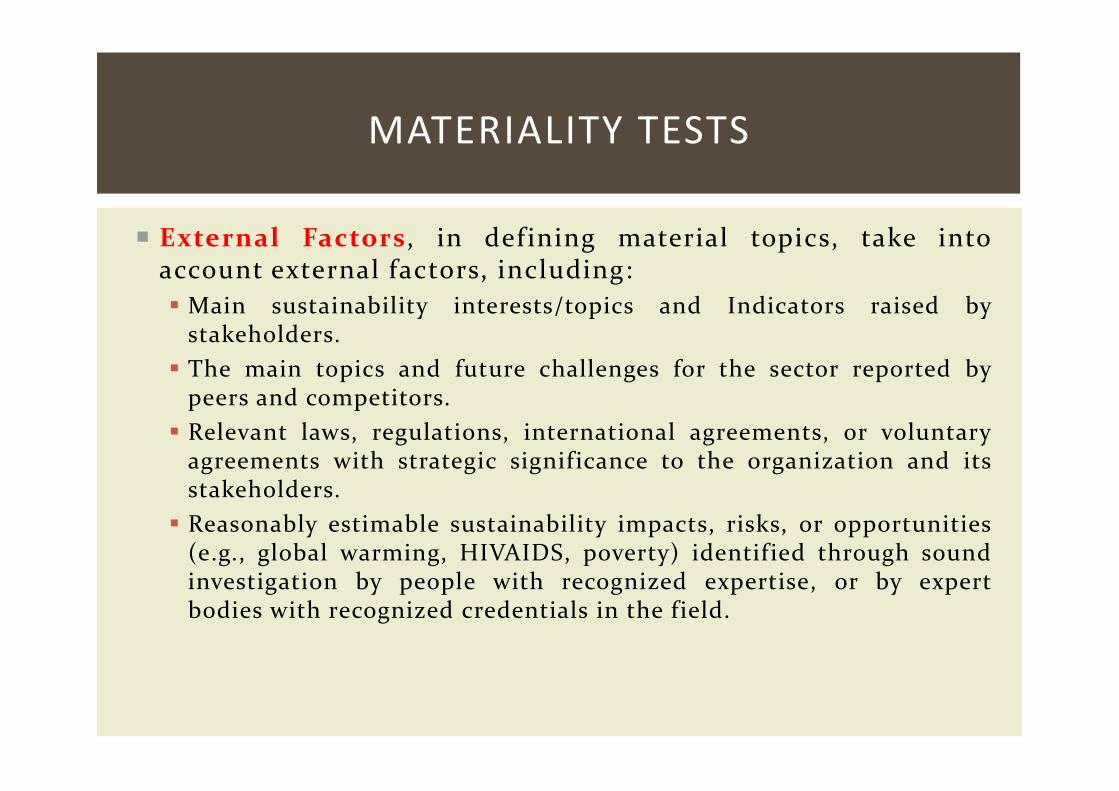

� External Factors, in defining material topics, take intoaccount external factors, including:

� Main sustainability interests/topics and Indicators raised bystakeholders.

� The main topics and future challenges for the sector reported bypeers and competitors.

� Relevant laws, regulations, international agreements, or voluntaryagreements with strategic significance to the organization and itsstakeholders.

� Reasonably estimable sustainability impacts, risks, or opportunities(e.g., global warming, HIVAIDS, poverty) identified through soundinvestigation by people with recognized expertise, or by expertbodies with recognized credentials in the field.

MATERIALITY TESTS

� External Factors, in defining material topics, take intoaccount internal factors, including:

� Key organizational values, policies, strategies, operationalmanagement systems, goals, and targets.

� The interests/expectations of stakeholders specifically invested inthe success of the organization (e.g., employees, shareholders, andsuppliers).

� Significant risks to the organization.

� Critical factors for enabling organizational success.

� The core competencies of the organization and the manner in whichthey can or could contribute to sustainable development.

� Prioritising

� The report prioritises material topics and Indicators.

MATERIALITY TESTS

� Different levels of assurance may require different levels ofevidence.1. Is there a process in place to determine what is material?

2. Does the process include an evaluation of relevance?

3. Does the process include an evaluation of importance?

4. Does the process fairly represent the views and importance ofstakeholders?

5. Are the criteria for evaluation clear and understandable?

6. Is there a process for resolving conf licts or dilemmas betweendifferent expectations regarding materiality?

7. Have the processes been systematically applied?

8. Is the determination of materiality consistent with stakeholderviews?

9. In your professional judgement, are there any material omissions ormisrepresentations?

AA1000 MATERIALITY GUIDANCE NOTE

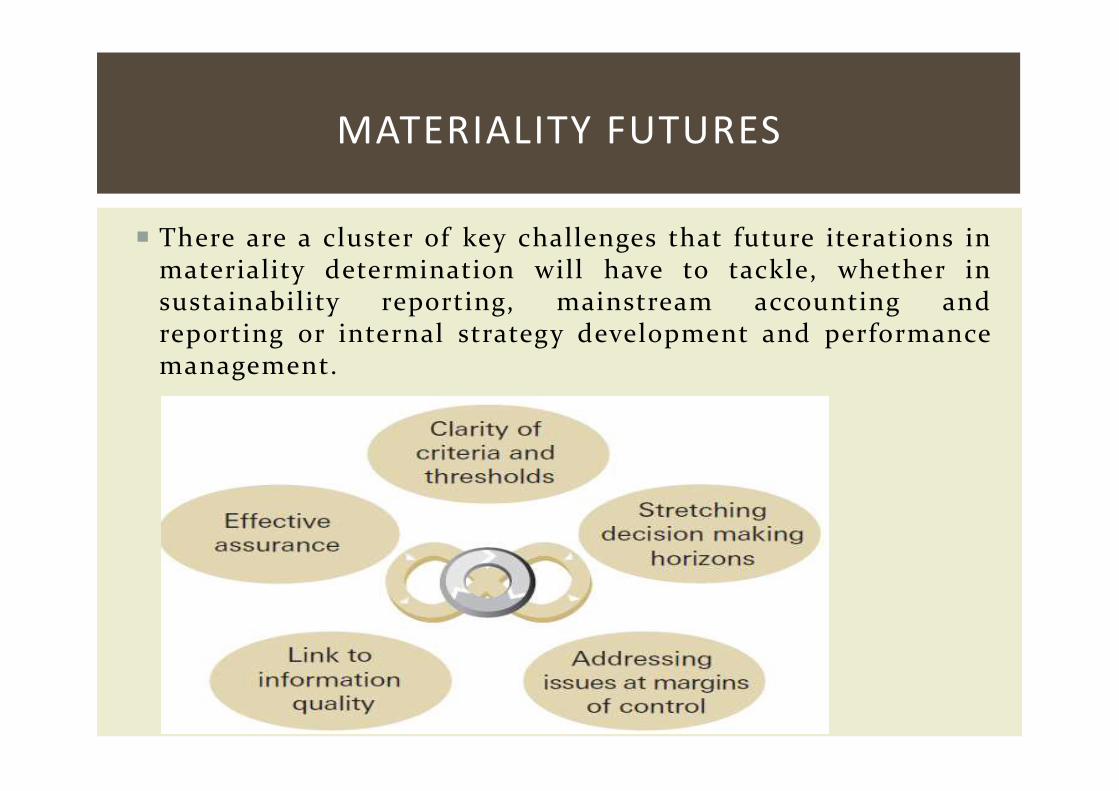

� There are a cluster of key challenges that future iterations inmateriality determination will have to tackle, whether insustainability reporting, mainstream accounting andreporting or internal strategy development and performancemanagement.

MATERIALITY FUTURES