Innovation in the tourism sector: results from a pilot study in the Balearic Islands

17

Tourism Economics, 2003, 9 (3), 279–295 Innovation in the tourism sector: results from a pilot study in the Balearic Islands M ARTA J ACOB IMEDEA (CSIC-UIB ), Institut Mediterrani d’Estudis Avançats, Miquèl Marqués 21, 07190 Esporles, Balearic Islands, Spain; and Departament d’Economia Applicada, Universitat de les Illes Balears, Carretera de Valldemossa, Km 7.5, 07071 Palma de Mallorca, Spain. E-mail: [email protected]. J OAQUÍN T INTORÉ IMEDEA (CSIC-UIB ) Institut Mediterrani d’Estudis Avançats, Miquèl Marqués 21, 07190 Esporles, Balearic Islands, Spain. E-mail: [email protected]. E UGENI A GUILÓ Departament d’Economia Applicada, Universitat de les Illes Balears, Carretera de Valldemossa, Km 7.5, 07071 Palma de Mallorca, Spain. E-mail: [email protected]. A LFONSO B RAVO Departamento de Economía e Historia Económica, Edificio FES, Campus Miguel de Unamuno, Fac Economía y Empresa, Universidad de Salamanca, 37007 Salamanca, Spain. E-mail: [email protected]. J UAN M ULET Fundación Cotec para la Innovación Tecnológica, Plaza del Marqués de Salamanca 11, 2º izda, 28006 Madrid, Spain. E-mail: [email protected]. This paper provides empirical evidence on innovation in various tourism firms in the Balearic Islands. The main results from this pilot study are as follows. Innovation is common in Balearic tourism firms, especially in the lodging and accommodation sector. Process, delivery and organizational changes are the most frequent forms of innovation. Non-technological innovation is common, especially in the lodging and accommodation sector. Technological innovation relates mainly to information and communication technologies. Firms The authors are grateful to Enric Tortosa, Vinceç Tur and Marco A. Robledo for comments and suggestions. Also, two anonymous referees significantly improved the manuscript. This article is the outcome of research activities carried out within the Fundación Cotec Project: ‘Innovación en el sector turístico balear. Análisis prospectivo de tecnologías’.

Transcript of Innovation in the tourism sector: results from a pilot study in the Balearic Islands

Tourism Economics, 2003, 9 (3 ), 279–295

Innovation in the tourism sector: resultsfrom a pilot study in the Balearic Islands

M ARTA J ACOB

IMEDEA (CSIC-UIB ), Institut Mediterrani d’Estudis Avançats, Miquèl Marqués 21,07190 Esporles, Balearic Islands, Spain; and Departament d’Economia Applicada,

Universitat de les Illes Balears, Carretera de Valldemossa, Km 7.5, 07071 Palma deMallorca, Spain. E-mail: [email protected].

J OAQUÍN T INTORÉ

IMEDEA (CSIC-UIB ) Institut Mediterrani d’Estudis Avançats, Miquèl Marqués 21,07190 Esporles, Balearic Islands, Spain. E-mail: [email protected].

E UGENI A GUILÓ

Departament d’Economia Applicada, Universitat de les Illes Balears, Carretera deValldemossa, Km 7.5, 07071 Palma de Mallorca, Spain. E-mail: [email protected].

A LFONSO B RAVO

Departamento de Economía e Historia Económica, Edificio FES, Campus Miguel deUnamuno, Fac Economía y Empresa, Universidad de Salamanca, 37007 Salamanca, Spain.

E-mail: [email protected].

J UAN M ULET

Fundación Cotec para la Innovación Tecnológica, Plaza del Marqués de Salamanca 11,2º izda, 28006 Madrid, Spain. E-mail: [email protected].

This paper provides empirical evidence on innovation in varioustourism firms in the Balearic Islands. The main results from thispilot study are as follows. Innovation is common in Balearic tourismfirms, especially in the lodging and accommodation sector. Process,delivery and organizational changes are the most frequent forms ofinnovation. Non-technological innovation is common, especially inthe lodging and accommodation sector. Technological innovationrelates mainly to information and communication technologies. Firms

The authors are grateful to Enric Tortosa, Vinceç Tur and Marco A. Robledo for comments andsuggestions. Also, two anonymous referees significantly improved the manuscript. This article is theoutcome of research activities carried out within the Fundación Cotec Project: ‘Innovación en elsector turístico balear. Análisis prospectivo de tecnologías’.

TOURISM ECONOMICS280

usually become involved in the design and development of thetechnologies needed to introduce an innovation. The major impactsof innovation are an improved company image, enhanced profitabilityand increased customer satisfaction. The most important objectivesin firms’ innovation strategies are satisfying customer needs, increasingand maintaining market share, gaining competitive edge and im-proving service quality. The lack of skilled personnel and a resistanceto change within the firm are the major obstacles to the introductionof innovations. After discussing these various findings, the authorsprovide methodological recommendations for the CommunityInnovation Survey (CIS) with regard to the tourism sector.

Keywords: innovation; tourism sector; pilot study; Balearic Islands

Tourism is an industry of great importance for social and economic develop-ment. In 1999 it accounted for 10.66% of the world’s gross domestic productand 8.06% of global employment (WTTC, 2001 ). Between 1995 and 1998,in most OECD member countries gross value added (VAB ) and employmentin the hotels and restaurants sector experienced higher growth than the globaleconomy and the service sector as a whole (OECD, 2000 ).

Given the economic contribution of tourism to employment and productionin OECD countries, we cannot ignore the role of innovation in the tourismsector when analysing the sources or drivers of economic growth. However, mostinnovation studies on the service sector have focused on the analysis of scale-intensive services or services that are dependent on information networks(financial, property or insurance services ) and knowledge-intensive businessservices (KIBS ), such as consultancy and design and software development. Theyhave not analysed the role of innovation in a third group of services, recentlyidentified as ‘non-knowledge or non-information-intensive services’ (Ducatel,2000 ). These include, among other service industries, the retail trade, distribution,cleaning and tourism. Certainly, given the economic contribution of tourismto employment and production in most OECD countries, the lack of innovationstudies in this sector represents a research gap.

This paper examines the importance of innovation in the tourism sectorthrough the empirical evidence of a pilot study carried out in the BalearicIslands, one of the major European tourist destinations, where more than 80%of VAB in 1999 was generated by service activities, mainly in tourism, andmore than 70% of employment was located in the service sector (INE, 2000 ).

The paper thus contributes to our knowledge about innovation activities inthis important economic sector by providing empirical evidence gathered throughinnovation interviews with a number of tourism firms in the region. The resultsallow us to form an impression of firms’ innovation strategies and performancein the Balearic tourism sector and to detect possible tendencies in their innovationactivities. The analysis looks at the type of innovation introduced (product,process, delivery, organizational ), the importance of technological innovation,the objectives of innovation, obstacles to innovation, the information sourcesused in implementing innovations and the major impacts of innovation activities.

We begin with a short review of the literature concerning innovation in

281Innovation in the tourism sector

services, focusing on a typology of services innovation. We then describe themethodology used in this pilot study and discuss the results. The concludingsection of the paper summarizes the empirical findings, points out severaltendencies in innovation activities in the Balearic tourism sector and listsrecommendations for the Community Innovation Survey (CIS ) and other tour-ism-related innovation surveys.

Innovation in services: conceptual issues and typology

The study of innovation in services is complex, because innovation theory andmethodologies have been developed mainly for the analysis of technologicalinnovation in the manufacturing sector, and so the peculiarities of the servicesector have not been accounted for. Sirilli and Evangelista (1998 ) summarizethe main peculiarities of services commonly noted in the literature, which havedirect implications for the definition and analysis of innovation in the sector:

� the close interaction between production and consumption;� the intensive information, intangible content of products and processes;� the key role of human resources as a critical factor in competitiveness; and� the critical role of organizational factors in firms’ performance.

First, the close interaction between production and consumption makes it moredifficult to distinguish between product and process innovation and leads toa stronger orientation of innovation activities in the sector towards adaptationor customization to fulfil consumers’ needs. Second, the high informationcontent gives information technologies (IT ) a central role in the innovationactivities of service firms, and makes it difficult to protect innovations withtraditional methods such as patents. Third, the key role of the human factorin the organization and delivery of services requires a substantial investmentin people. Hipp, Tether and Miles (2000 ) point out that the knowledge andskills of the people involved in production and innovation activities arefundamental for the successful development of those activities. Finally, as Sirilliand Evangelista (1998 ) indicate, the importance of organizational factors in theservice sector requires a revision of the traditional concept of innovation to takeinto account organizational changes.

Besides these peculiarities, which require a modification of the concepts anddefinitions of innovation initially developed for the manufacturing sector (seefor example Evangelista and Sirilli, 1995; Eurostat, 1995 ), empirical evidenceon innovation activity in services suggests that non-technological innovationsare very common (see for example Gallouj, 1998; Sundbo and Gallouj, 1998;Miles, 1994 ). A study of financial services in Denmark (Sundbo, 1997 ) showedthat 54% of innovations introduced by the industry were non-technological,another 30% were essentially non-technological although dependent ontechnology, and only 16% could be considered technological in nature. Further-more, the results of an Australian innovation survey (Pattison, Ovington andFinlay, 1995 ) suggest that technological innovations are more common in themanufacturing than in the service sector (see Table 1 ). The survey found that13.9% of Australian service firms had introduced non-technological innovationsand 11.5% had introduced technological innovations. It seems therefore that

TOURISM ECONOMICS282

Table 1. Percentage of firms that have undertaken innovation activities in Australia.

Sector Technological innovations Non-technological innovations

Wholesale trade 18.0 25.9Retail trade 12.8 7.2Hotels and restaurants 10.6 15.9Transport 6.5 12.9Communication 20.9 18.2Finance and insurance 7.0 11.0Property and business services 11.4 14.6Education 17.0 23.1Health and community services 10.4 16.4Cultural and recreational services 19.9 17.6Personal services and other 9.2 15.4SERVICES 11.5 13.9MANUFACTURING 33.7 24.2

Source: Pattison, Ovington and Finlay, 1995, cited in Hauknes, 1996, p 100.

non-technological innovative efforts are more frequent in services than inmanufacturing.

The empirical evidence also suggests that service innovations are moreincremental than radical; they consist of small and incremental changes inprocesses and procedures so that they do not entail too much R&D. In fact,as Sundbo and Gallouj (1998 ) indicate, ‘few of the renewals that the servicefirms themselves consider as innovations are new to the market’.

Taking into account the peculiarities of services and the importance oforganizational innovations, Sundbo and Gallouj (1998 ) identify four types ofservice-sector innovation:

(1 ) Product innovations – the presentation of new or significantly improvedservices to customers. For example, in the last few years banks have offerednew financial accounts and products, and software firms regularly introducenew products and improvements in existing products.

(2 ) Process innovations – novelties or improvements in service production anddelivery processes. These may be innovations in production processes or indistribution and delivery (provision ) processes.

(3 ) Organizational innovations – new forms of firms’ organization or manage-ment.

(4 ) Market innovations – new market behaviours such as finding a new marketsegment or introducing the firm into a new industry and its market.

Organizational innovations contribute to productivity and quality improvementand facilitate better access to knowledge. Some types of organizational changecan stimulate innovations to respond to new challenges – for example, greatercompetition in telecommunications has led to the need to establish, access andmaintain directories of clients in new ways.

Keeping this classification in mind, innovation in services may be defined

283Innovation in the tourism sector

as the conversion of ideas into products, processes or services which are valuedby the market. These ideas can be technological, commercial or organizational.This definition has to be understood in a broad sense, because it covers all typesof firm activities that lead to a substantial change in the way of making things,including the services and products that firms offer, as well as in the way ofproducing, commercializing, distributing or organizing them. Therefore,‘technological innovations’ are new or improved services or processes due totechnology. ‘Non-technological innovations’ are changes in the organization ormanagement of firms or in a firm’s market behaviour.

Finally, innovation surveys (for example, Evangelista and Savona, 1998, onItaly; and Pattison, Ovington and Finlay, 1995, on Australia ) suggest that fewfirms undertake only one type of innovation, and that firms generally makeproduct, process and organizational innovations simultaneously. Frequently,service innovations are very dependent on software and require complementaryorganizational and technological changes. The problem is that organizationalinnovations are more difficult to measure than are technological ones, eventhough they are more frequent in the service sector (Miles, 1995; Marklund,1998 ).

Pilot study: methodology

Given the peculiarities of services in general, and the lack of innovation studiesin the tourism sector in particular, we must proceed with caution whenanalysing innovation in the sector. Therefore, it is wise to begin with exploratorystudies that will produce an adequate volume of quantitative and qualitativeempirical evidence, from which possible tendencies in innovation activities inthe sector can be detected. The research undertaken in this paper can bepositioned in this cautious line of work.

The information was obtained through personal interviews at firms’ head-quarters. Twenty-five firms were contacted, and 20 ultimately participated inthe exploratory study. These firms employ an average of 25.881 people1 andtheir average turnover in 2000 was 2,812,736,649. 2 Therefore, this smallsample of firms has great economic importance in the Balearic tourism sector.3

Personal interviews were carried out during May and June 2001. The inter-viewees, given their position and management responsibilities in the firm, wereable to supply detailed information on the changes and improvements that hadbeen introduced. The duration of the interviews varied, but each lasted at leastone hour.

The interviews followed a structured format in which firms were asked:

� to give basic information about the firm (trade name, commercial businessaddress, number of employees, turnover, year of foundation, etc );

� to list and describe any changes or improvements that had been introducedduring the last five years (1996–2000 ); and

� to characterize the firm’s innovation activity – the effects of innovation, itsobjectives, the information sources used, the obstacles encountered and thetechnological basis of the innovation.

TOURISM ECONOMICS284

Classification of firms

Firms were classified according to several characteristics, such as year offoundation; ownership (independent or belonging to a group ); size by numberof employees; sector of tourism activity; and scale or range of activities (inter-national, national, Balearic or insular ).

The criterion of a firm’s classification by sector of tourism activity requiresa brief comment. Traditionally, tourism activity comprises a set of differentactivities that can be grouped as follows (see, for example, Figuerola, 1995 ):

� travel organization – including travel agencies;� lodging and accommodation – firms involved in lodging activities such as

hotels, agritourism hotels, rural houses, etc;� restaurants – firms in the restaurant industry;� leisure and recreation – firms that offer leisure and recreation activities for

tourists, such as golf courses, aquatic parks, discothèques, etc;� transport – airlines, bus companies, etc; and� auxiliary – companies or organizations providing services to tourism firms,

such as private trade associations or catering companies serving airlines.

Classification criteria for innovations

When analysing innovations, we employ several classification variables, asfollows.

Innovation as object. (1 ) Product innovation: new or improved services. (2 )Process innovation: new or improved forms of producing an existing service.(3 ) Innovation in the commercialization and provision (delivery ) processes:changes or improvements in the distribution, delivery and commercializationof services. (4 ) Internal organizational innovation: changes and improvementsin the internal structure of the firm. (5 ) External organizational innovation:establishment of new relationships with other agents, such as strategic alliances,new types of interfaces, etc, or enlarging the business operations of firms toan international scale. (6 ) Market innovation: the entry of the firm into newmarkets.

This is based on the typology of Sundbo and Gallouj (1998 ) mentionedabove, with the difference that we have also distinguished between internal andexternal organizational innovations.

Innovation as activity. (1 ) Technological innovation. (2 ) Non-technologicalinnovation. This criterion considers that any innovation involves the carryingout of an activity by the firm itself or by another firm that provides theinnovation. We take into account only the fact that any innovation may or maynot require the use of technology. Technology may be developed by the firmitself or may be provided by another firm.

Technological innovation by technological area. (1 ) Information and communicationtechnologies (ICT ). (2 ) Other technological areas. Technological innovations canbe additionally classified by technological area, and we thus distinguish betweenICT and all other areas.

285Innovation in the tourism sector

Interview results

All the findings on innovation activities described in this section for firms thatare part of a corporation refer only to the activities of the Balearic segment ofthe corporation.4 For example, if a firm in the lodging and accommodationsector lists six innovations, it means that all those innovations have beenintroduced in most of the hotels in the Balearic Islands that belong to thecorporation.

In any case, these results should not be considered as indicative of generalinnovation behaviour in the tourism sector. They derive from an empiricalinvestigation of innovation activities in selected tourism firms in the Balearics,and may serve as a basis for future studies of innovation in the tourism sector.

Relevance of innovation in the tourism sector

The firms listed a total of 142 innovations, understood to be changes orimprovements introduced during the last five years. There were on average 7.10innovations – a high value, although variability was also high. Fifty-five percent of the firms can be considered highly or moderately innovative (five ormore innovations per firm), while the remaining 45% can be considered lessinnovative (fewer than five innovations per firm ).

The independent firms tended to be less innovative (5.73 innovations perfirm) than the firms belonging to a corporation (8.78 ). The firms that werefounded in the 1980s were the most innovative, with 10.8 innovations per firmagainst 5.5 for firms created before 1980 and 6.29 for firms created between1999 and 2001. Furthermore, the results suggest that firms tend to be moreinnovative as their range or scale of activities increases. In fact, the firmsoperating at the international level had an average of 7.83 innovations comparedto 7.11 in firms operating at a local level.

Innovation, firm size and sector of tourism activity

Firm size has commonly been related to levels of innovation in surveys ofmanufacturing firms. A recent study by Hipp, Tether and Miles (2000 ) analysedthis relationship in the service sector. According to empirical data on Germanservice firms, those authors found that the propensity to innovate increased withfirm size. But what happens in the tourism sector?

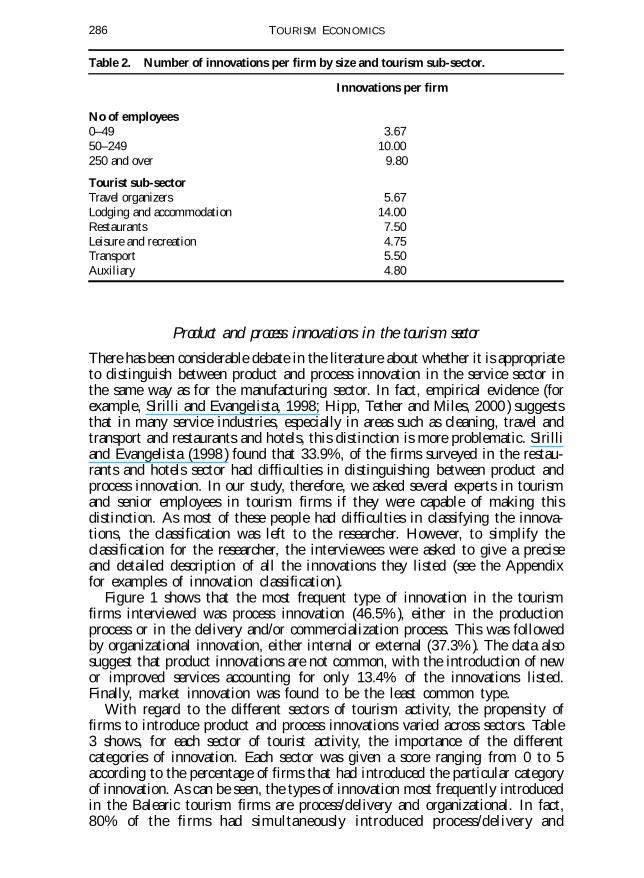

Table 2 shows the number of innovations per firm by size (number ofemployees ) and sub-sector of tourism activity. The figures suggest that smallfirms tend to innovate less than big companies; in fact the difference in thenumber of innovations per firm between small and medium to large companiesis striking (3.67 innovations per firm compared to 10 ). Hipp, Tether and Miles(2000 ) suggest that ‘this relationship is simply a reflection of the fact that largerfirms tend to have more lines of activity and therefore more areas in which toinnovate’.

With regard to tourism sub-sectors, empirical evidence indicates that thelodging and accommodation sector is by far the most innovative of the sample.Firms dedicated to leisure and recreation and to auxiliary services are the leastinnovative of the entire sample.

TOURISM ECONOMICS286

Table 2. Number of innovations per firm by size and tourism sub-sector.

Innovations per firm

No of employees0–49 3.6750–249 10.00250 and over 9.80

Tourist sub-sectorTravel organizers 5.67Lodging and accommodation 14.00Restaurants 7.50Leisure and recreation 4.75Transport 5.50Auxiliary 4.80

Product and process innovations in the tourism sector

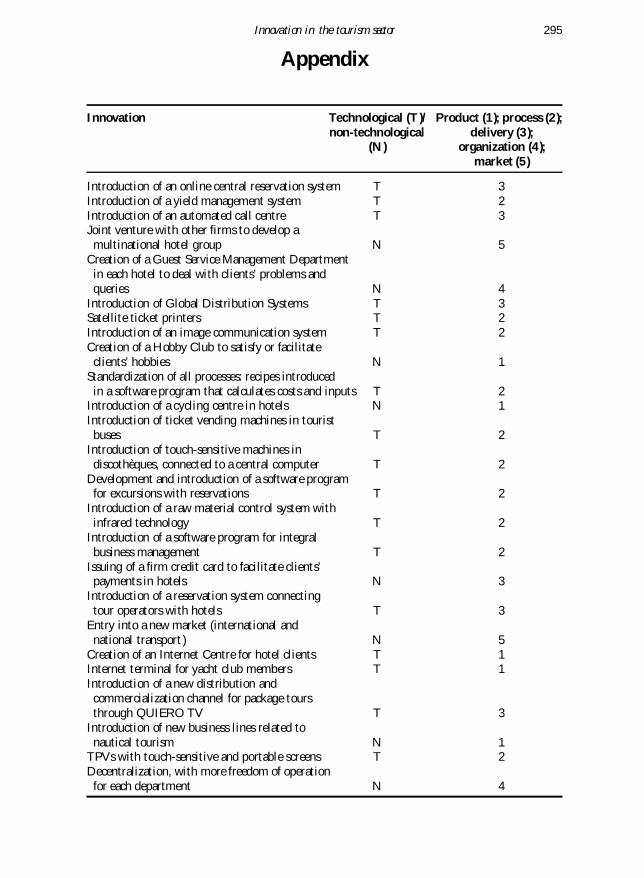

There has been considerable debate in the literature about whether it is appropriateto distinguish between product and process innovation in the service sector inthe same way as for the manufacturing sector. In fact, empirical evidence (forexample, Sirilli and Evangelista, 1998; Hipp, Tether and Miles, 2000 ) suggeststhat in many service industries, especially in areas such as cleaning, travel andtransport and restaurants and hotels, this distinction is more problematic. Sirilliand Evangelista (1998 ) found that 33.9%, of the firms surveyed in the restau-rants and hotels sector had difficulties in distinguishing between product andprocess innovation. In our study, therefore, we asked several experts in tourismand senior employees in tourism firms if they were capable of making thisdistinction. As most of these people had difficulties in classifying the innova-tions, the classification was left to the researcher. However, to simplify theclassification for the researcher, the interviewees were asked to give a preciseand detailed description of all the innovations they listed (see the Appendixfor examples of innovation classification ).

Figure 1 shows that the most frequent type of innovation in the tourismfirms interviewed was process innovation (46.5% ), either in the productionprocess or in the delivery and/or commercialization process. This was followedby organizational innovation, either internal or external (37.3% ). The data alsosuggest that product innovations are not common, with the introduction of newor improved services accounting for only 13.4% of the innovations listed.Finally, market innovation was found to be the least common type.

With regard to the different sectors of tourism activity, the propensity offirms to introduce product and process innovations varied across sectors. Table3 shows, for each sector of tourist activity, the importance of the differentcategories of innovation. Each sector was given a score ranging from 0 to 5according to the percentage of firms that had introduced the particular categoryof innovation. As can be seen, the types of innovation most frequently introducedin the Balearic tourism firms are process/delivery and organizational. In fact,80% of the firms had simultaneously introduced process/delivery and

287Innovation in the tourism sector

Figure 1. Classification by type of innovation.

organizational innovations during the period under consideration. Productinnovation is a less common occurrence in tourism firms, with only the lodgingand accommodation and leisure and recreation sectors showing scores of 4 or5. Market innovations are not common, although half of the firms (a score of3 ) in the lodging and accommodation sector and in the transport sector hadintroduced them during the last five years.

These sample results seem to accord with the little other empirical evidencethat is available. In fact, if we consider the lodging and accommodationtogether with the restaurants sector, the proportion of product innovation is19.72%, a result very similar to that obtained in the Netherlands (18.8% ) forthe same sector (Brouwer and Kleinknecht, 1995 ). In the other sectors, few orno product innovations had been introduced.

The organizational innovations listed by the firms were frequently changesin their internal structure or management, and were normally the consequenceof the introduction of technological innovations.

Finally, most of the firms (95% ) had introduced more than one type ofinnovation during the period. This result is consistent with recent literature

Table 3. Importance of innovations by type of innovation and sub-sector of tourismactivity.

Sub-sector Product Process and/or delivery Organization Market

Travel organizers 2 5 5 0Lodging and accommodation 5 5 5 3Restaurants 3 5 3 0Leisure and recreation 4 4 5 2Transport 0 5 5 3Auxiliary 0 4 4 0Total 3 4 4 1

Note: A score of 0 indicates that no firm has introduced that type of innovation; 1 = between 1% and20% have introduced that type of innovation; 2 = 21–40%; 3 = 41–60%; 4 = 61–80%; 5 = more than80%.

TOURISM ECONOMICS288

on innovation in services (for example, Evangelista and Savona, 1998; Pattison,Ovington and Finlay, 1995 ), which indicates that few firms undertake only onetype of innovation but rather implement product, process and organizationalinnovations at the same time. This is because a service innovation generallyrequires one or more complementary innovations. For example, the introductionof a complete new service will require the development of a new distributionsystem, and will cause changes in the organization of work and in the relation-ship between consumers and service providers.

Importance of technological innovation

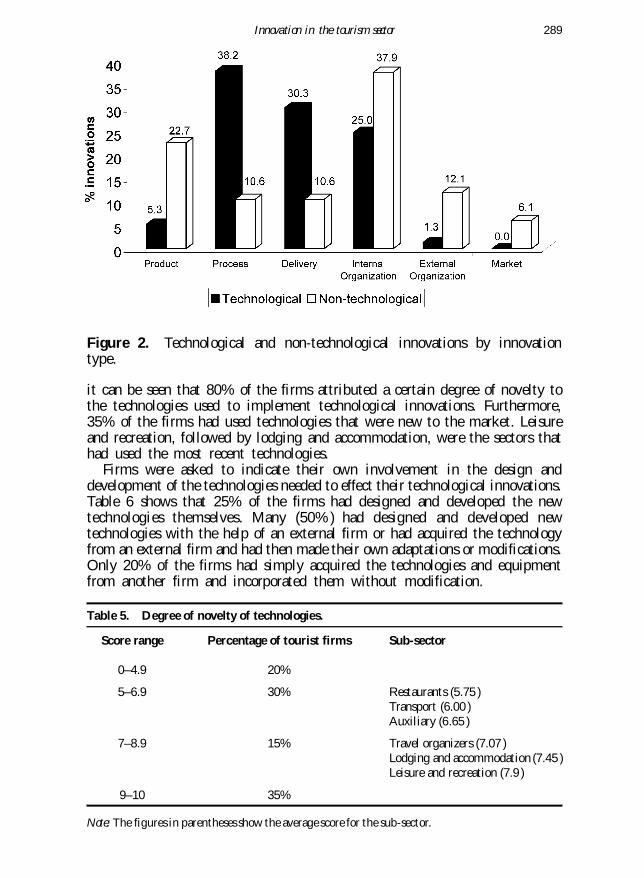

Empirical evidence suggests that non-technological innovations are very commonin services. However, there is little evidence about what happens in the tourismsector in particular. Results from the pilot study indicate that technologicalinnovations (53.5% ) are more frequent than non-technological innovations(46.5% ) in all sub-sectors of tourism except lodging and accommodation (seeTable 4 ). Most of these technological innovations (81.6% ) are ICT-related.Other technological innovations, such as those in cooking (10.5% ), environ-mental practices (5.3% ) or transport (2.6% ) play a less important role. However,environmental innovation seems likely to increase in the sector. Furthermore,as firm size increases the occurrence of technological innovation increases. Largefirms (71.4% ) reported a higher number of technological innovations than small(27.3% ) and medium-sized (53.3% ) firms.

It may be useful to identify the relative importance of technological innovationsacross the different categories of innovation. Figure 2 shows that the technologicalinnovations fell mainly into the process category (68.5% ), either in the production(38.2% ) or the delivery process (30.3 ), followed by innovations in the internalorganization of firms (25% ). Non-technological innovations related mainly tothe internal organization of firms (37.9% ) and to product innovations (22.7% ).

The degree of novelty in the market of technologies used to carry outtechnological innovation is an important factor. As noted earlier, the newtechnology may be developed by the firm itself or supplied by an external firm.To obtain detailed information on this aspect, firms were asked to attribute ascore from 0 (‘technology available a long time ago’ ) to 10 (‘totally new to themarket’ ) to the technologies they had used in introducing a technologicalinnovation. On average, the tourism firms interviewed awarded a 6.8 score,indicating a high degree of novelty. Table 5 summarizes that information, and

Table 4. Occurrence of technological/non-technological innovations by sub-sector oftourism activity.

Travel Lodging and Restaurants Leisure and Transport Auxiliaryorganizers accommodation recreation

Score 1 0 1 1 1 1

Note: 1 – more than 50% of innovations are technological; 0 – fewer than 50% of innovations aretechnological.

289Innovation in the tourism sector

Figure 2. Technological and non-technological innovations by innovationtype.

it can be seen that 80% of the firms attributed a certain degree of novelty tothe technologies used to implement technological innovations. Furthermore,35% of the firms had used technologies that were new to the market. Leisureand recreation, followed by lodging and accommodation, were the sectors thathad used the most recent technologies.

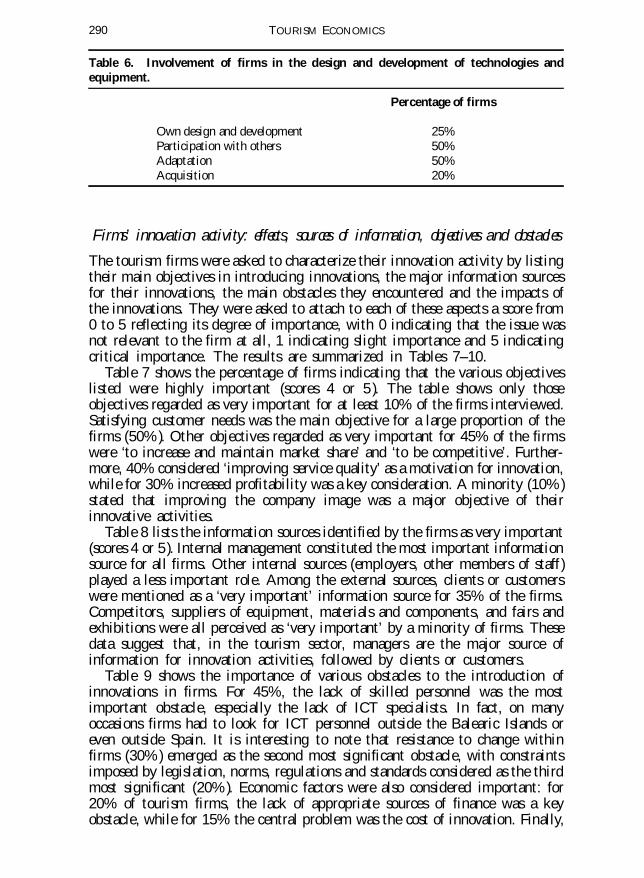

Firms were asked to indicate their own involvement in the design anddevelopment of the technologies needed to effect their technological innovations.Table 6 shows that 25% of the firms had designed and developed the newtechnologies themselves. Many (50% ) had designed and developed newtechnologies with the help of an external firm or had acquired the technologyfrom an external firm and had then made their own adaptations or modifications.Only 20% of the firms had simply acquired the technologies and equipmentfrom another firm and incorporated them without modification.

Table 5. Degree of novelty of technologies.

Score range Percentage of tourist firms Sub-sector

0–4.9 20%

5–6.9 30% Restaurants (5.75 )Transport (6.00 )Auxiliary (6.65 )

7–8.9 15% Travel organizers (7.07 )Lodging and accommodation (7.45 )Leisure and recreation (7.9 )

9–10 35%

Note: The figures in parentheses show the average score for the sub-sector.

TOURISM ECONOMICS290

Table 6. Involvement of firms in the design and development of technologies andequipment.

Percentage of firms

Own design and development 25%Participation with others 50%Adaptation 50%Acquisition 20%

Firms’ innovation activity: effects, sources of information, objectives and obstacles

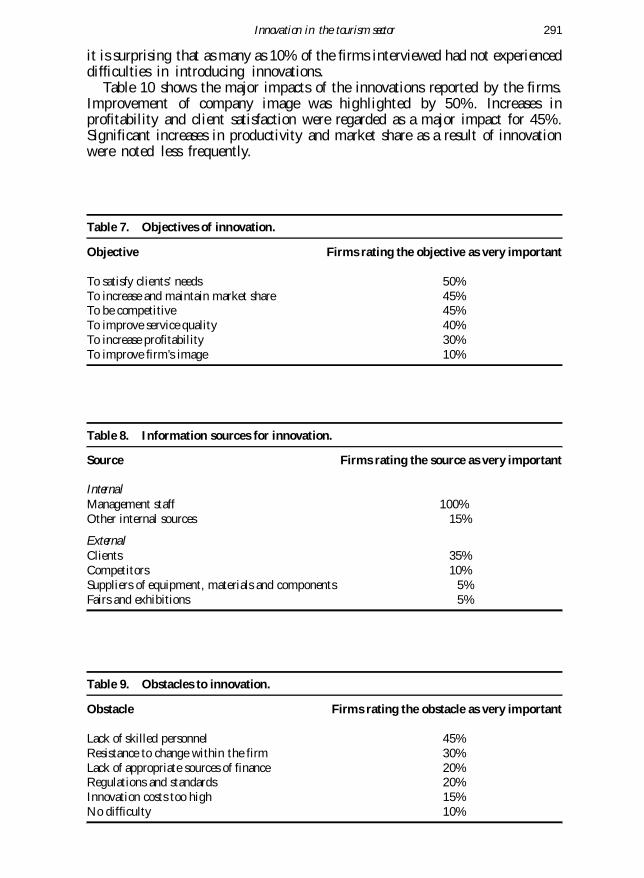

The tourism firms were asked to characterize their innovation activity by listingtheir main objectives in introducing innovations, the major information sourcesfor their innovations, the main obstacles they encountered and the impacts ofthe innovations. They were asked to attach to each of these aspects a score from0 to 5 reflecting its degree of importance, with 0 indicating that the issue wasnot relevant to the firm at all, 1 indicating slight importance and 5 indicatingcritical importance. The results are summarized in Tables 7–10.

Table 7 shows the percentage of firms indicating that the various objectiveslisted were highly important (scores 4 or 5 ). The table shows only thoseobjectives regarded as very important for at least 10% of the firms interviewed.Satisfying customer needs was the main objective for a large proportion of thefirms (50% ). Other objectives regarded as very important for 45% of the firmswere ‘to increase and maintain market share’ and ‘to be competitive’. Further-more, 40% considered ‘improving service quality’ as a motivation for innovation,while for 30% increased profitability was a key consideration. A minority (10% )stated that improving the company image was a major objective of theirinnovative activities.

Table 8 lists the information sources identified by the firms as very important(scores 4 or 5). Internal management constituted the most important informationsource for all firms. Other internal sources (employers, other members of staff )played a less important role. Among the external sources, clients or customerswere mentioned as a ‘very important’ information source for 35% of the firms.Competitors, suppliers of equipment, materials and components, and fairs andexhibitions were all perceived as ‘very important’ by a minority of firms. Thesedata suggest that, in the tourism sector, managers are the major source ofinformation for innovation activities, followed by clients or customers.

Table 9 shows the importance of various obstacles to the introduction ofinnovations in firms. For 45%, the lack of skilled personnel was the mostimportant obstacle, especially the lack of ICT specialists. In fact, on manyoccasions firms had to look for ICT personnel outside the Balearic Islands oreven outside Spain. It is interesting to note that resistance to change withinfirms (30% ) emerged as the second most significant obstacle, with constraintsimposed by legislation, norms, regulations and standards considered as the thirdmost significant (20% ). Economic factors were also considered important: for20% of tourism firms, the lack of appropriate sources of finance was a keyobstacle, while for 15% the central problem was the cost of innovation. Finally,

291Innovation in the tourism sector

it is surprising that as many as 10% of the firms interviewed had not experienceddifficulties in introducing innovations.

Table 10 shows the major impacts of the innovations reported by the firms.Improvement of company image was highlighted by 50%. Increases inprofitability and client satisfaction were regarded as a major impact for 45%.Significant increases in productivity and market share as a result of innovationwere noted less frequently.

Table 7. Objectives of innovation.

Objective Firms rating the objective as very important

To satisfy clients’ needs 50%To increase and maintain market share 45%To be competitive 45%To improve service quality 40%To increase profitability 30%To improve firm’s image 10%

Table 8. Information sources for innovation.

Source Firms rating the source as very important

InternalManagement staff 100%Other internal sources 15%

ExternalClients 35%Competitors 10%Suppliers of equipment, materials and components 5%Fairs and exhibitions 5%

Table 9. Obstacles to innovation.

Obstacle Firms rating the obstacle as very important

Lack of skilled personnel 45%Resistance to change within the firm 30%Lack of appropriate sources of finance 20%Regulations and standards 20%Innovation costs too high 15%No difficulty 10%

TOURISM ECONOMICS292

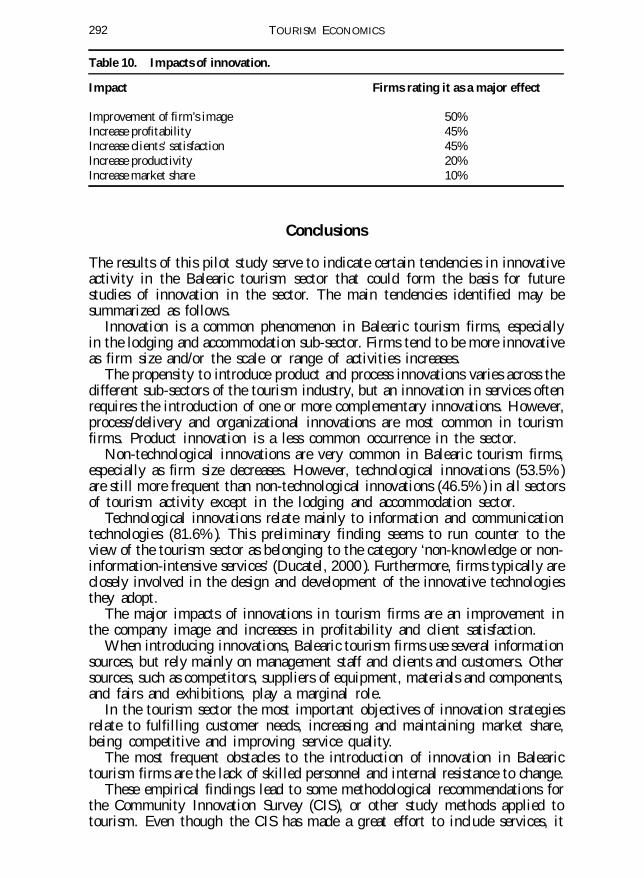

Table 10. Impacts of innovation.

Impact Firms rating it as a major effect

Improvement of firm’s image 50%Increase profitability 45%Increase clients’ satisfaction 45%Increase productivity 20%Increase market share 10%

Conclusions

The results of this pilot study serve to indicate certain tendencies in innovativeactivity in the Balearic tourism sector that could form the basis for futurestudies of innovation in the sector. The main tendencies identified may besummarized as follows.

Innovation is a common phenomenon in Balearic tourism firms, especiallyin the lodging and accommodation sub-sector. Firms tend to be more innovativeas firm size and/or the scale or range of activities increases.

The propensity to introduce product and process innovations varies across thedifferent sub-sectors of the tourism industry, but an innovation in services oftenrequires the introduction of one or more complementary innovations. However,process/delivery and organizational innovations are most common in tourismfirms. Product innovation is a less common occurrence in the sector.

Non-technological innovations are very common in Balearic tourism firms,especially as firm size decreases. However, technological innovations (53.5% )are still more frequent than non-technological innovations (46.5% ) in all sectorsof tourism activity except in the lodging and accommodation sector.

Technological innovations relate mainly to information and communicationtechnologies (81.6% ). This preliminary finding seems to run counter to theview of the tourism sector as belonging to the category ‘non-knowledge or non-information-intensive services’ (Ducatel, 2000 ). Furthermore, firms typically areclosely involved in the design and development of the innovative technologiesthey adopt.

The major impacts of innovations in tourism firms are an improvement inthe company image and increases in profitability and client satisfaction.

When introducing innovations, Balearic tourism firms use several informationsources, but rely mainly on management staff and clients and customers. Othersources, such as competitors, suppliers of equipment, materials and components,and fairs and exhibitions, play a marginal role.

In the tourism sector the most important objectives of innovation strategiesrelate to fulfilling customer needs, increasing and maintaining market share,being competitive and improving service quality.

The most frequent obstacles to the introduction of innovation in Balearictourism firms are the lack of skilled personnel and internal resistance to change.

These empirical findings lead to some methodological recommendations forthe Community Innovation Survey (CIS ), or other study methods applied totourism. Even though the CIS has made a great effort to include services, it

293Innovation in the tourism sector

still presents two serious limitations5 if the intention is to seek an understand-ing of the nature of innovation in service sectors. First, the coverage of servicesby the CIS (and other innovation surveys ) is still very limited, particularly asregards tourism. Basically, the lodging and accommodation, leisure and recreationand travel organizer sub-sectors are not included in the target population. Giventheir contribution to GDP and employment in many European Union countries,an additional effort should be made to cover these sub-sectors in service-sectorinnovation surveys such as CIS. Second, CIS only includes enterprises with tenor more employees in the service sector: this means that most tourism firmsare excluded – in the case of the Balearic tourism sector, almost 80% of alltourism firms are excluded because of this rule. Given both these limitations,the CIS results for services cannot be representative of innovation activities inthe service sector as a whole and, especially, in tourism.

Furthermore, organizational innovations seem to be important in the tourismsector, and these are often a consequence of previous technological innovations.At the same time, market innovation seems to be common in some tourismsub-sectors. Additional questions should therefore be incorporated into the CISquestionnaire to obtain more information about organizational and marketinnovations in tourism. These questions should focus on (a ) changes in theinternal structure of firms that may be considered as organizational innovations;(b ) changes in the management of firms that represent an innovation with apositive effect; (c ) the relationship between the introduction of organizationalinnovations and previous technological innovations; and (d ) new marketbehaviours.

Endnotes

1. Based on the information available from 19 of the firms.2. Information available for 16 firms; eight of them provided the data for the group of firms to

which they belonged, instead of data for the individual firm.3. For example, some of the firms operating in the lodging and accommodation sector had more

than 100 hotels throughout the world with a turnover in 2001 of more than 300 million.4. For example, four of the firms interviewed are in the lodging and accommodation sector. Three

of them are large corporations (Barceló, Marina Balear and Iberostar) with many hotels operatingthroughout the world. Another three belong to the ‘travel organizers’ sector and they are alsolarge international corporations (Ultramar Express, Astral and Sol-Melia Viajes ).

5. Other innovation surveys for services carried out in other countries (for example, Canada) presentthe same limitations.

References

Brouwer, E., and Kleinknecht, A. H. (1995), ‘An innovation survey in services: the experience withthe CIS questionnaire in the Netherlands’, STI (Science Technology Industry) Review, Vol 16, pp 141–148.

Ducatel, K. (2000), ‘Information technologies in non-knowledge services: innovations on the margin?’in Metcalfe, J. S., and Miles, I., eds, Innovation Systems in the Service Economy: Measurement and CaseStudy Analysis, Economics of Science, Technology and Innovation, Vol 18, Kluwer, Boston, MA,pp 221–245.

Eurostat (1995), Report of the Eurostat Pilot Project to Investigate the Possibilities to Measure Innovationin the Service Sectors, Eurostat, Luxembourg.

Evangelista, R., and Savona, M. (1998), ‘Patterns of innovation in services: the results of the ItalianInnovation Survey’, paper presented to the 7th Annual RESER Conference, Berlin.

TOURISM ECONOMICS294

Evangelista, R., and Sirilli, G. (1995), ‘Measuring innovation in services’, Research Evaluation, Vol 5,No 3, pp 207–215.

Figuerola, M. (1995), Economía para la Gestión de Empresas Turísticas: Producción y Comercialización,CEURA, Madrid.

Gallouj, F. (1998), Innovation in Reverse Services and the Reverse Product Cycle, SI4S Topical Paper No 5,STEP Group, Lille.

Hauknes, J. (1996), Innovation in the Service Economy. STEP Report 7, Oslo.Hipp, C., Tether, B. S., and Miles, I. (2000), ‘The incidence and effects of innovation in services:

evidence from Germany’, International Journal of Innovation Management, Vol 4, No 4, pp 417–453.

INE (2000), Contabilidad Regional de España, Base 1995, Series 1995–2000, Instituto Nacional deEstadística, Madrid.

Marklund, G. (1998), Need for New Measures of Innovation in Services, SI4S Topical Paper No 9, STEPGroup, Stockholm.

Miles, I. (1994), ‘Innovation in services. Part 2: Sectoral and industrial studies of innovation’, inDodgson, M., and Rothwell, R., eds, The Handbook of Industrial Innovation, Edward Elgar,Cheltenham, pp 243–256.

Miles, I. (1995), Services Innovation, Statistical and Conceptual Issues, Working Group on Innovationand Technology Policy, Doc DSTI/EAS/STP/NESTI (95 )12, OECD Paris.

OECD (2000), Services: Statistics on Value Added and Employment, OECD, Paris.Pattison, W., Ovington, J., and Finlay, E. (1995), ‘Innovation in selected Australian industries’, paper

presented to the 10th meeting of the Voorburg Group on Service Statistics, Australian Bureauof Statistics, Canberra.

Sirilli, G., and Evangelista, R. (1998), ‘Technological innovation in services and manufacturing:results from Italian surveys’, Research Policy, Vol 27, No 9, pp 881–899.

Sundbo, J. (1997), Innovation in Services in Denmark: Service Development, Internationalisation andCompetences, Working Paper No 2, SI4S WP3-4, Roskilde University, Roskilde.

Sundbo, J., and Gallouj, F. (1998), Innovation in Services, SI14S Project Synthesis, WP 3-4, Roskilde.WTTC (2001), Year 2001: Tourism Satellite Accounting Research, World, World Travel and Tourism

Council, London.

295Innovation in the tourism sector

Appendix

Innovation Technological (T)/ Product (1 ); process (2 );non-technological delivery (3 );

(N ) organization (4 );market (5 )

Introduction of an online central reservation system T 3Introduction of a yield management system T 2Introduction of an automated call centre T 3Joint venture with other firms to develop a

multinational hotel group N 5Creation of a Guest Service Management Department

in each hotel to deal with clients’ problems andqueries N 4

Introduction of Global Distribution Systems T 3Satellite ticket printers T 2Introduction of an image communication system T 2Creation of a Hobby Club to satisfy or facilitate

clients’ hobbies N 1Standardization of all processes: recipes introduced

in a software program that calculates costs and inputs T 2Introduction of a cycling centre in hotels N 1Introduction of ticket vending machines in tourist

buses T 2Introduction of touch-sensitive machines in

discothèques, connected to a central computer T 2Development and introduction of a software program

for excursions with reservations T 2Introduction of a raw material control system with

infrared technology T 2Introduction of a software program for integral

business management T 2Issuing of a firm credit card to facilitate clients’

payments in hotels N 3Introduction of a reservation system connecting

tour operators with hotels T 3Entry into a new market (international and

national transport ) N 5Creation of an Internet Centre for hotel clients T 1Internet terminal for yacht club members T 1Introduction of a new distribution and

commercialization channel for package toursthrough QUIERO TV T 3

Introduction of new business lines related tonautical tourism N 1

TPVs with touch-sensitive and portable screens T 2Decentralization, with more freedom of operation

for each department N 4