Initiation of coverage - Fuller Treacy Money

329

9 October 2017 Oil Services & Equipment Initiation of coverage Industrials Oil Services & Equipment Initiation of Coverage North America Canada United States Industry Initiation of coverage Date 9 October 2017 Deutsche Bank Markets Research Not Business as Usual We are initiating coverage of the Oilfield Service and Equipment sector, and in a break from our longstanding negative view, we have no Sell rated stocks and have nine Buy recommendations. Our top picks are PTEN, HAL and CJ . We are also initiating with Buy recommendations on SLB, CLB, RIG, WFT, SPN and SND. We are encouraged by the judicious selloff in the stocks year-to-date, and by what also appears to be a market that is acknowledging the obsolescence of the old cyclical playbook. Earnings revisions that had initially taken an impractical leap higher in 2H16 have been revised down considerably, providing a significantly better setup for the stocks. David Havens Research Analyst +1-212-250-3235 Jason Bandel Associate Analyst +1-212-250-1577 Chris Snyder Research Associate +1-212-250-0165 Matt Taylor Research Associate +1-212-250-1758 Deutsche Bank Securities Inc. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 083/04/2017. Distributed on: 09/10/2017 20:00:40 GMT 0bed7b6cf11c

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Initiation of coverage - Fuller Treacy Money

9 October 2017

Oil Services & Equipment

Initiation of coverage

IndustrialsOil Services & Equipment

Initiation of Coverage

North AmericaCanadaUnited States

Industry

Initiation ofcoverage

Date9 October 2017

Deutsche BankMarkets Research

Not Business as Usual

We are initiating coverage of the Oilfield Service and Equipment sector, and in abreak from our longstanding negative view, we have no Sell rated stocks and havenine Buy recommendations. Our top picks are PTEN, HAL and CJ . We are alsoinitiating with Buy recommendations on SLB, CLB, RIG, WFT, SPN and SND. Weare encouraged by the judicious selloff in the stocks year-to-date, and by whatalso appears to be a market that is acknowledging the obsolescence of the oldcyclical playbook. Earnings revisions that had initially taken an impractical leaphigher in 2H16 have been revised down considerably, providing a significantlybetter setup for the stocks.

David Havens

Research Analyst

+1-212-250-3235

Jason Bandel

Associate Analyst

+1-212-250-1577

Chris Snyder

Research Associate

+1-212-250-0165

Matt Taylor

Research Associate

+1-212-250-1758

Deutsche Bank Securities Inc.

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should beaware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should considerthis report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONSARE LOCATED IN APPENDIX 1. MCI (P) 083/04/2017.

Distributed on: 09/10/2017 20:00:40 GMT

0bed7b6cf11c

9 October 2017

Oil Services & Equipment

Initiation of coverage

IndustrialsOil Services & Equipment

Initiation of Coverage

North AmericaCanadaUnited States

Industry

Initiation ofcoverage

Date9 October 2017

Deutsche BankMarkets Research

Not Business as Usual

Initiation of coverageWe are initiating coverage of the Oilfield Service and Equipment sector, and in abreak from our longstanding negative view, we have no Sell rated stocks and havenine Buy and 15 Hold recommendations. Our top picks are Patterson-UTI (PTEN),Halliburton (HAL) and C&J Energy Services (CJ) . We are also initiating with Buyrecommendations on Schlumberger (SLB), Core Laboratories (CLB), Transocean(RIG), Weatherford (WFT), Superior Energy Services (SPN) and Smart Sand (SND).We are encouraged by the judicious selloff in the stocks year-to-date, and by whatalso appears to be a market that is acknowledging the obsolescence of the oldcyclical playbook. Earnings revisions that had initially taken an impractical leaphigher in 2H16 have been revised down considerably, providing a significantlybetter setup for the stocks.

Not business as usual for the oilfield services industryThis is an industry that is still in transition, and these are companies that still needto navigate this transition. The commercial development of tight oil reserves inthe US was disruptive and it derailed the normalization of the cycle. The businessmodels that worked last cycle will not necessarily work again this cycle. Webelieve in the long term, the oilfield service franchises that will be the winners willbe those that evolve with innovative business models, and those that acquire orinvest in niche technology leaders.

Pressure pumping demand poised to recover to 2014 highsThe biggest common denominator among our top picks is exposure to pressurepumping. As US producers tailor their drilling programs to focus increasingly ontheir core acreage and best wells, there will be a disproportionate mix of leadingedge, longer lateral wells with tighter stage spacing and higher sand loadings.This will drive the average completion intensity per well even higher, which shouldrestore the demand for horsepower to the 2014 highs despite a lower rig count.

Valuation and risksSee our Industry valuation and risks within the Executive Summary section ofthis report, and company specific valuation and risks within individual companypages.

David Havens

Research Analyst

+1-212-250-3235

Jason Bandel

Associate Analyst

+1-212-250-1577

Chris Snyder

Research Associate

+1-212-250-0165

Matt Taylor

Research Associate

+1-212-250-1758

Top picks

C&J Energy Services (CJ.N),USD29.66 Buy

Patterson-UTI (PTEN.OQ),USD20.76 Buy

Halliburton (HAL.N),USD44.93 BuySource: Deutsche Bank

Deutsche Bank Securities Inc.

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should beaware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should considerthis report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONSARE LOCATED IN APPENDIX 1. MCI (P) 083/04/2017.

9 October 2017

Oil Services & Equipment

Initiation of coverage

Executive Summary……………………..……..……….……..…....….....…..Page 3Baker Hughes, a GE company………..…..……..……….……...….....…..Page 58Basic Energy Services Inc………….…......……………..……..……….…..Page 70C&J Energy Services………….…......……………..……..……….…….…..Page 78Core Labs………….…......……………..……..……….……..….....………...Page 88Diamond Offshore Drilling………….…......……………..……..……….…..Page 98ENSCO International………….…......……………..……..……….…..…....Page 110Forum Energy Tech………….…......……………..……..……….……..…...Page 121Frank's International………….…......……………..……..……………..…..Page 131Halliburton………….…......……………..……..……….……..…....………..Page 139Helmerich & Payne………….…......……………..……..……….…….….....Page 153Nabors Industries………….…......……………..……..……….……..…......Page 165National Oilwell Varco………….…......……………..……..……….……….Page 177Noble Corp.………….…......……………..……..……….……..….....………Page 188Oceaneering Int'l.………….…......……………..……..……….……......…..Page 199Oil States………….…......……………..……..……….……..…................…Page 208Patterson-UTI………….…......……………..……..……….……….....……...Page 218Precision Drilling………….…......……………..……..……….……..….....…Page 229Rowan Companies………….…......……………..……..…………..…..........Page 239RPC Inc………….…......……………..……..……….……......…………….....Page 250Schlumberger………….…......……………..…….…….……..…..........…....Page 260Smart Sand………….…......……………..…….…….……..….....................Page 272Superior Energy Services……….….....………..……..……….……..….....Page 284Transocean………….…......…………….…..……….……..….....…………...Page 293Weatherford International…….…......……………..……..……….…….......Page 306

Page 2 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

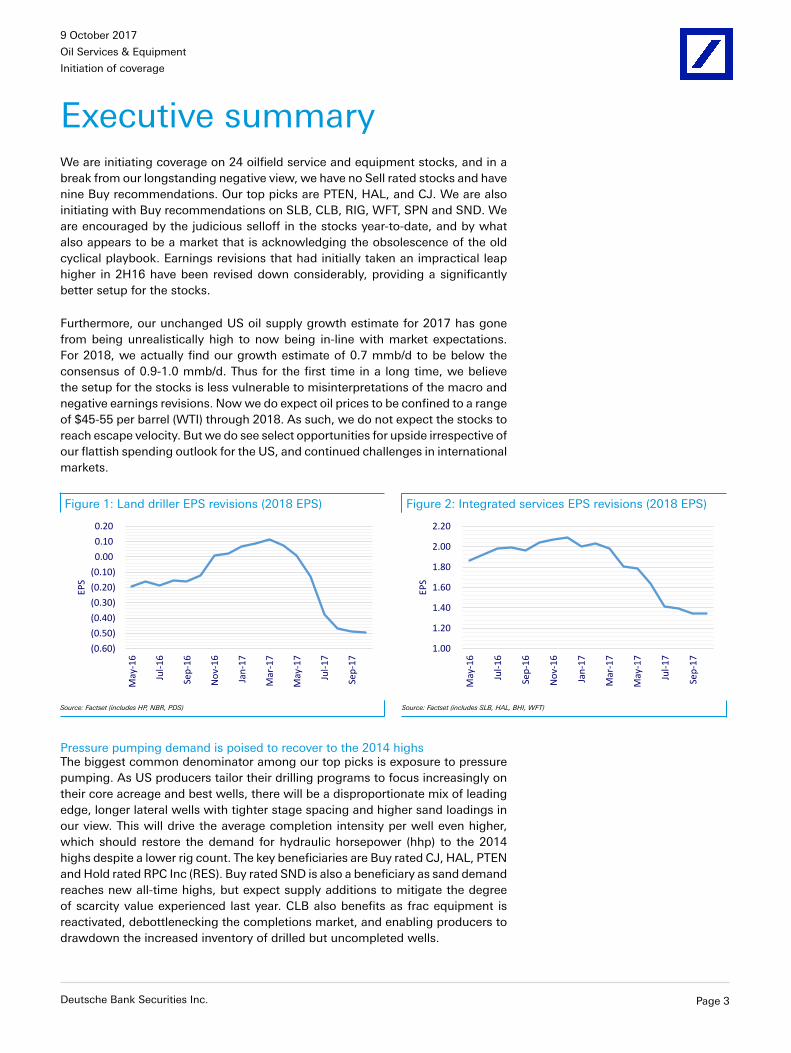

Executive summaryWe are initiating coverage on 24 oilfield service and equipment stocks, and in abreak from our longstanding negative view, we have no Sell rated stocks and havenine Buy recommendations. Our top picks are PTEN, HAL, and CJ. We are alsoinitiating with Buy recommendations on SLB, CLB, RIG, WFT, SPN and SND. Weare encouraged by the judicious selloff in the stocks year-to-date, and by whatalso appears to be a market that is acknowledging the obsolescence of the oldcyclical playbook. Earnings revisions that had initially taken an impractical leaphigher in 2H16 have been revised down considerably, providing a significantlybetter setup for the stocks.

Furthermore, our unchanged US oil supply growth estimate for 2017 has gonefrom being unrealistically high to now being in-line with market expectations.For 2018, we actually find our growth estimate of 0.7 mmb/d to be below theconsensus of 0.9-1.0 mmb/d. Thus for the first time in a long time, we believethe setup for the stocks is less vulnerable to misinterpretations of the macro andnegative earnings revisions. Now we do expect oil prices to be confined to a rangeof $45-55 per barrel (WTI) through 2018. As such, we do not expect the stocks toreach escape velocity. But we do see select opportunities for upside irrespective ofour flattish spending outlook for the US, and continued challenges in internationalmarkets.

Figure 1: Land driller EPS revisions (2018 EPS) Figure 2: Integrated services EPS revisions (2018 EPS)

(0.60)

(0.50)

(0.40)

(0.30)

(0.20)

(0.10)

0.00

0.10

0.20

May-16

Jul-16

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-17

Sep-17

EPS

1.00

1.20

1.40

1.60

1.80

2.00

2.20

May-16

Jul-16

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-17

Sep-17

EPS

Source: Factset (includes HP, NBR, PDS) Source: Factset (includes SLB, HAL, BHI, WFT)

Pressure pumping demand is poised to recover to the 2014 highsThe biggest common denominator among our top picks is exposure to pressurepumping. As US producers tailor their drilling programs to focus increasingly ontheir core acreage and best wells, there will be a disproportionate mix of leadingedge, longer lateral wells with tighter stage spacing and higher sand loadings inour view. This will drive the average completion intensity per well even higher,which should restore the demand for hydraulic horsepower (hhp) to the 2014highs despite a lower rig count. The key beneficiaries are Buy rated CJ, HAL, PTENand Hold rated RPC Inc (RES). Buy rated SND is also a beneficiary as sand demandreaches new all-time highs, but expect supply additions to mitigate the degreeof scarcity value experienced last year. CLB also benefits as frac equipment isreactivated, debottlenecking the completions market, and enabling producers todrawdown the increased inventory of drilled but uncompleted wells.

Deutsche Bank Securities Inc. Page 3

9 October 2017

Oil Services & Equipment

Initiation of coverageFi

gu

re 3

: V

alu

atio

n t

able

5-O

ct1

2-m

oM

kt c

ap

EP

S (

DB

e)

De

bt

Pri

ce/

Su

b-s

ect

or

(co

mp

an

y)S

ymb

ol

Ra

tin

gp

rice

targ

et

($m

)'1

7D

B'1

8D

B'1

9D

B'1

8'1

9'1

8D

B'1

9D

B'1

8D

B'1

9D

B'1

8'1

9'1

8D

B'1

9D

Btu

rns

bo

ok

INT

EG

RA

TE

D S

ER

VIC

ES

Sch

lum

be

rge

rS

LBB

uy

68

.87

78

94

,49

91

.47

2.3

8

3

.33

#N

/A#

N/A

28

.9

2

0.7

8,2

25

9

,74

0

8,5

68

10

,37

0

13

.1

1

1.0

2.3

2.4

Ha

llib

urt

on

HA

LB

uy

45

.09

54

38

,60

31

.14

2.2

2

2

.99

2.1

7

2

.96

20

.3

1

5.1

4,8

10

5

,62

9

4,7

61

5,7

74

9.9

8.5

2.3

4.3

Ba

ker

Hu

gh

es

BH

GE

Ho

ld3

6.4

83

51

5,6

74

0.1

2

1

.31

1.7

5

1

.27

1.9

7

2

7.9

20

.8

3

,08

3

3,7

02

3

,78

7

4

,87

3

4

.8

4

.0

1

.0

1

.3

We

ath

erf

ord

WF

TB

uy

4.2

76

4,1

40

(1.0

1)

(0

.28

)

0.0

2

(0

.45

)

(0.0

1)

n

m2

54

.0

90

5

1

,04

0

90

4

1,2

96

12

.5

1

0.9

8.5

2.8

SM

ID S

ER

VIC

ES

Co

re L

ab

ora

tori

es

CLB

Bu

y9

5.9

91

09

4,1

46

1.9

0

2

.92

3.6

7

2

.73

3.3

9

3

2.9

26

.1

1

88

22

8

1

80

2

18

2

3.4

19

.3

1

.2

2

8.1

Su

pe

rio

r E

ne

rgy

Serv

ice

sS

PN

Bu

y1

0.4

21

51

,53

2(1

.53

)

(0.8

5)

(0

.25

)

(0.6

9)

(0

.20

)

nm

nm

35

9

n

m3

92

4

67

7

.4

n

m3

.6

1

.3

Fra

nk'

s In

tern

ati

on

al

FI

Ho

ld7

.67

71

,65

9(0

.45

)

(0.2

6)

(0

.05

)

(0.2

5)

(0

.03

)

nm

nm

52

1

00

57

11

3

26

.9

1

3.8

0.0

1.3

Ba

sic

En

erg

y Se

rvic

es

BA

SH

old

19

.77

22

48

8(2

.05

)

(0.3

5)

0

.75

(0.2

5)

0

.98

nm

nm

13

4

n

m1

43

1

87

5

.3

n

m1

.9

1

.3

C&

J E

ne

rgy

Serv

ice

sC

JB

uy

29

.56

39

1,8

26

0.1

3

2

.16

3.6

8

2

.02

3.0

6

1

3.7

8.0

35

1

4

81

33

1

46

2

4.4

3.2

-

1

.6

RP

C,

Inc.

RE

SH

old

23

.98

25

5,0

70

0.8

3

1

.42

1.5

0

1

.38

1.4

9

1

6.9

16

.0

6

28

66

0

6

32

6

92

7

.8

7

.4

-

6.0

SA

ND

SU

PP

LIE

RS

Sm

art

Sa

nd

SN

DB

uy

7.0

19

27

10

.33

0.8

6

0

.97

0.7

9

0

.98

8.1

7.2

68

7

7

64

72

3.1

2.7

0.0

1.6

LAN

D D

RIL

LER

S

He

lme

rich

& P

ayn

eH

PH

old

52

.17

45

5,5

84

(1.3

4)

(0

.79

)

(0.1

2)

(0

.66

)

(0.2

1)

n

mn

m4

50

55

1

4

61

5

39

1

2.1

9.9

1.1

1.3

Na

bo

rs I

nd

ust

rie

sN

BR

Ho

ld7

.99

92

,16

1(1

.47

)

(0.5

1)

0

.30

(0.6

1)

(0

.04

)

nm

27

.1

8

30

1,0

49

8

22

1

,02

3

6

.8

5

.4

4

.5

0

.7

Pa

tte

rso

n-U

TI

En

erg

yP

TE

NB

uy

21

.30

25

4,4

28

(0.9

1)

(0

.17

)

0.3

8

(0

.23

)

0.2

6

n

m5

5.7

78

7

9

69

77

1

92

3

6.2

5.0

0.9

1.2

Pre

cisi

on

Dri

llin

gP

D-C

AH

old

3.5

74

1,0

18

(0.3

5)

(0

.15

)

0.1

5

(0

.31

)

(0.0

4)

n

m2

4.4

39

2

5

22

38

1

49

3

7.1

5.3

4.7

0.5

OF

FS

HO

RE

DR

ILLE

RS

Dia

mo

nd

Off

sho

reD

OH

old

14

.88

15

2,0

20

0.9

5

0

.16

(0.3

2)

0

.16

(0.0

4)

9

3.7

nm

45

7

3

56

46

4

42

1

8.4

10

.8

4

.3

0

.5

En

sco

Plc

ES

VH

old

5.8

36

1,7

13

(0.5

7)

(1

.89

)

(1.1

3)

(0

.73

)

(0.7

5)

n

mn

m4

81

31

2

4

60

4

78

9

.6

1

4.7

9.9

0.2

No

ble

Co

rpo

rati

on

NE

Ho

ld4

.50

41

,01

7(1

.29

)

(1.3

9)

(1

.37

)

(1.3

9)

(1

.35

)

nm

nm

40

9

3

35

41

2

40

8

12

.6

1

5.4

9.9

0.2

Ro

wa

n C

om

pa

nie

sR

DC

Ho

ld1

3.0

21

51

,63

9(0

.61

)

(1.9

3)

(2

.23

)

(2.3

7)

(2

.52

)

nm

nm

23

1

1

50

20

8

15

6

13

.0

2

0.1

10

.9

0

.3

Tra

nso

cea

nR

IGB

uy

10

.54

13

4,0

04

0.0

3

(0

.94

)

(1.5

8)

(0

.94

)

(1.2

3)

n

mn

m8

88

62

9

9

09

8

21

9

.5

1

3.4

8.3

0.3

CA

PIT

AL

EQ

UIP

ME

NT

Na

tio

na

l Oilw

ell

Va

rco

NO

VH

old

36

.03

39

13

,35

6(0

.40

)

0.5

5

1

.32

0.4

3

1

.29

65

.6

2

7.3

1,0

07

1

,31

3

1,0

00

1,4

23

14

.9

1

1.4

3.2

1.0

Oil

Sta

tes

Inte

rna

tio

na

lO

ISH

old

25

.55

26

1,2

97

(0.9

9)

(0

.23

)

0.2

9

(0

.20

)

0.4

4

n

m8

8.9

10

6

1

46

10

0

14

4

11

.8

8

.6

0

.5

1

.1

Oce

an

ee

rin

g I

nte

rna

tio

na

lO

IIH

old

25

.47

28

2,4

80

0.0

3

0

.14

0.5

2

0

.09

0.5

2

1

84

.1

49

.1

2

39

28

5

2

52

3

13

1

1.7

9.8

3.3

1.7

Fo

rum

En

erg

y T

ech

no

log

ies

FE

TH

old

15

.50

17

1,6

21

(0.2

7)

0

.23

0.6

6

0

.21

0.6

1

6

7.3

23

.6

1

14

17

6

1

24

1

86

1

4.2

9.2

3.5

1.4

EP

S (

con

sen

sus)

PE

EB

ITD

A (

con

sen

sus)

EB

ITD

A (

DB

e)

EV

/EB

ITD

A

Sou

rce:

Deu

tsch

e B

ank,

Fac

tset

Page 4 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

Land drillers are looking to reestablish themselves in the value chainThere is a higher cadence of more productive wells being developed in the USthat is undermining the earnings power of the land drilling industry. The trendof drilling more with less threatens the marketability of the entire legacy land rigfleet as producers continue to demand technologies that enable improved drillingefficiencies and lower well costs. This has reserved pricing power for the preferredAC-electric and super-spec rigs, but even at above 90% utilization, pricing powerfor these rigs is struggling to breakout. Unlike the frac market, we do not expectrig counts to be restored to the 2014 highs by year-end 2018. But while thissub-sector was once an alpha short as earnings revision leaped to impracticallevels in 2016, revisions have since been sharply negative, leaving the stocks lessvulnerable in our view. We initiate with Hold ratings on Helmerich & Payne (HP),Nabors Industries (NBR) and Precision Drilling (PD). PTEN is Buy rated due to itsfrac exposure.

US service inflation will continue at a more modest paceInflation expectations got ahead of the market last year, but have since been ropedin. If oil prices stay within our $45-55 range, we expect inflation will stay below10% in 2018 with only pressure pumping stepping higher to about 15%. In alower oil price environment, moderate oil price inflation is not negative. Restoringvolumes at this stage of the cycle and absorbing fixed costs are the principaldrivers of margin expansion. If service inflation is allowed to breakout in a lowprice environment with increasingly louder calls for producers to exercise capitaldiscipline, we fear our flat rig count assumption for 2018 will have increaseddownside risk.

Rig count outlook domestically and abroad are flatteningThe US experienced a rapid drilling recovery once oil prices inflected, butinternational markets remained a lot more sluggish. We expect an ebb and flowof US upstream capital expenditures to keep pressure on oil prices and a lid on rigcounts both domestically and abroad. The one exception where we see continuedresilience is in Saudi Arabia. The standout exposures to Saudi Arabia are Buy ratedSchlumberger (SLB), and Hold rated NBR and Rowan Companies (RDC).

Figure 4: US onshore rig count Figure 5: International onshore rig count

0

500

1,000

1,500

2,000

2,500

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

0

200

400

600

800

1,000

1,200

01/12

05/12

09/12

01/13

05/13

09/13

01/14

05/14

09/14

01/15

05/15

09/15

01/16

05/16

09/16

01/17

05/17

Source: Baker Hughes, a GE Company Source: Baker Hughes, a GE Company

Deutsche Bank Securities Inc. Page 5

9 October 2017

Oil Services & Equipment

Initiation of coverage

Offshore markets bottoming, limited momentum, but some opportunityFor the offshore drillers, the negative sentiment remains firmly entrenched, butwe believe the alpha short is largely gone and the industry is bottoming. The issueis the recovery will lack momentum and earnings are still trending lower each yearthrough 2019. The competitive landscape will likely change significantly as moredeals are announced in an effort to reposition fleets. Attrition will likely continueonce deals are closed. We initiate with a Hold rating on DO, ESV, NE, and RDC,and Buy rating on RIG. RIG has delivered a strong positive free cash flow trackrecord and has preserved cash, and maintained a leading edge ultra-deepwaterfleet with above average marketability. We believe the company is well positionedto make opportunistic acquisitions in an otherwise financially stressed sub-sector.

Weatherford is one of the key idiosyncratic storiesCulture and process. The two things the new CEO needs to change at WFT. Notan easy fix, but if WFT can move up from being dead last on a 10-year averagecash conversion comparison (cash from operations/EBITDA) with 30 other oilfieldservice companies, we believe there is meaningful upside. Weatherford lost about$6 billion in free cash flow over the last ten years while SLB and NOV generatedapproximately $33 billion and $14 billion respectively. The new leadership hasidentified several operating and process related levers to pull, a key one beinginventory days that are approximately twice as high as SLB and HAL. Unrealisticto expect a similar level of working capital efficiency as these peers, but evenmeeting half way moves the needle. In the near-term, equity financing remains akey risk as its international land sales remain challenged.

Figure 6: Average 10-year cash conversions (cash from operations/EBITDA)

- 0.20 0.40 0.60 0.80 1.00 1.20 1.40

WFTNR

CRRRESBRSFTI

HALBHI

RDCOII

SLBCLB

HOSRIGDO

TDWPDS

DRQTS

ATWTTI

NBRESV

NOVSPN

NEUNTPESHP

OISPTEN

Cash from operations/EBITDA

Source: Factset, Deutsche Bank

Page 6 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

Not business as usual for the oilfield services industryThis is an industry that is still in transition, and these are companies that stillneed to navigate this transition. The commercial development of tight oil reservesin the US was a remarkable achievement, but it was disruptive, and it derailedthe normalization of the cycle. The business models that worked last cycle willnot necessarily work again this cycle. There is a louder call for capital disciplineamong producers, which are requiring increasingly more intellectual property,data analytics, Big Data and precision well placement capabilities to lower costsand improve returns. As such, we believe in the long-term, the oilfield servicefranchises that will be the winners will be those that evolve with innovativebusiness models, and those that acquire or invest in niche technology leaders.

Within this context, we believe the standouts are Buy rated SLB, HAL, PTEN, andCLB , and Hold rated NBR. These companies are evolving to maximize margin andreturns in an otherwise challenging market. SLB in particular has been addressingthe industry-wide sub-optimal asset turns and tool utilization in an effort to enableabove average margins in a market where its peers are fighting for market share.The company is also taking the most radical look at the future of the industry withits efforts in redefining the entire drilling process and industry workflows.

This cycle will not be like the prior two cyclesIn order for these stocks to sustain a rally, we need to see progress in therebalancing of the oil markets. While we do believe well productivity will continueto keep some pressure on oil prices, US production expectations got a bit ahead ofthemselves in our view. But we do not expect the same proliferation of spendingas last cycle, but instead a more measured outcome.

Figure 7: Global oil inventories showing some progress Figure 8: Higher cadence of more productive wells in US

900

950

1,000

1,050

1,100

1,150

1,200

1,250

1,300

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

mm

bb

ls

2010-2014 range 2016 2017 Avg

High: 248 mmbbls July: 207 mmbbls

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

01

/07

08

/07

03

/08

10

/08

05

/09

12

/09

07

/10

02

/11

09

/11

04

/12

11

/12

06

/13

01

/14

08

/14

03

/15

10

/15

05

/16

12

/16

mm

b/d

Conventional oil Tight oil

Source: EIA Source: EIA, Drilling Info

Industry valuation and risksOur price target methodology is based on either the five-year or ten-year multipleof each company's normalized earnings or EBITDA power. We then look astandard deviation above and below, and calculate the price target from aweighted average. The main investment risks include: 1) shifts in OPEC policyand the influence that would have on oil prices and ultimately US upstreamcapital expenditures, 2) negative revisions to global oil demand, 3) pricing tacticsgetting increasingly more aggressive for market share, and 4) another leg downin deepwater spending globally.

Deutsche Bank Securities Inc. Page 7

9 October 2017

Oil Services & Equipment

Initiation of coverage

The Ebb and Flow of US Capex Keeps Pressure on OilPrices

We are still mindful of the headwinds. US oil producers are developing a highercadence of more productive wells for less capital at lower breakeven prices. Theyhave built 10-20 year drilling inventories with 96% success rates and 3-6 monthcash conversions. They have capex budgets that can ebb and flow with oil pricesand they are standing ready to deploy capital once oil prices edge up above $50.

When all is said and done, the US is exerting more influence on global oil marketsthan it has in over 30 years. US producers collectively are undermining OPECand the oil rebalancing effort. We believe the ebb and flow of US capex and therehabilitation of US productivity will confine oil prices to a range of $45 – 55through 2018. This will restrain service inflation when oil prices are below $50,and it will be an obstacle to restoring earnings power.

The unintended consequences of higher density drilling and completionsThe rehabilitation of US well productivity is a direct result of longer laterals,tighter stage spacing, more frac clusters, and higher sand loadings. We expectthese trends to continue, and for the next 3+ years, US producers will enhancecompletion intensities in an effort to increase productivity. We also expect tosee increasingly more technology brought into the fold including precision wellplacement, data analytics, and real-time monitoring, all of which we believewill increase year-over-year estimated ultimate recoveries (EURs) and initialproduction (IP) rates.

But what merits close attention is the increasing trend toward close proximitydrilling. These 10-20 year drilling inventories are populated with a number of infilldrilling wells that present some risks including parent child well interference,which could drive actual EURs lower than expected. This is getting a lot of mindshare as producers return to existing pads to infill drill. While we have alwayshesitated to doubt future progress in well productivity, that was during the earlyinnings of tight oil development.

Figure 9: Average Permian horizontal lateral lengths Figure 10: Average Permian 30-day IPs per 1,000-ft

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2011 2012 2013 2014 2015 2016 2017 2018 2019

Feet

-

20

40

60

80

100

120

140

160

-

100

200

300

400

500

600

700

800

2011 2012 2013 2014 2015 2016 2017

Ytd

30

-da

y I

P p

er

1,0

00

-ft

of

late

ral

b/d

(o

il o

nly

)

Peak monthly production 30-day IP per 1,000-ft

Source: IHS Markit Source: Drilling Info, Deutsche Bank

Page 8 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

Figure 11: Permian type curves by vintage Figure 12: Eagle Ford type curves by vintage

2017

2016

2015

-

100

200

300

400

500

600

700

800

0 3 6 9 12 15 18 21 24 27 30 33 36

b/d

(o

il o

nly

)

Months

2017 Ytd

2016

2015

2014

2013

2012

2011

2017

2016

2015

-

100

200

300

400

500

600

700

800

900

0 3 6 9 12 15 18 21 24 27 30 33 36

b/d

(o

il o

nly

)

Months

2017

2016

2015

2014

2013

2012

2011

Source: Drilling Info, Deutsche Bank Source: Drilling Info, Deutsche Bank

Figure 13: Permian peak 30-day production averages Figure 14: Eagle Ford peak 30-day production averages

183

260 299

375

452

538

717

-

100

200

300

400

500

600

700

800

2011 2012 2013 2014 2015 2016 2017 Ytd

b/d

(o

il o

nly

) 24% CAGR (2011 - 2016)

405 415

471 502

572

635

808

-

100

200

300

400

500

600

700

800

900

2011 2012 2013 2014 2015 2016 2017

b/d

(o

il o

nly

)

9% CAGR (2011 - 2016)

Source: Drilling Info, Deutsche Bank Source: Drilling Info, Deutsche Bank

Developing a higher cadence of more productive wells in the USThe ebb and flow of US capex with oil prices is nothing new, but thedevelopment of US tight oil reserves has radically rehabilitated the cause-and-effect relationship between drilling and production. For over a decade, USoil production had remained relatively flat despite oscillations in oil-directedcapex. Tight oil has changed that and has encouraged significant investment inoptimizing completion designs that enhance reservoir contact and productivityper lateral foot. This has made the US a principal market for producers.

Since 2011, the average initial production (IP) rates and estimated ultimaterecoveries (EURs) for wells placed-on-production (POP) in the main tight oil basinshave been increasing. The peak 30-day production numbers for the Permian haveincreased at a CAGR of 24% while the Eagle Ford has increased at a CAGR of 9%.Most of the improvements were a direct result of longer laterals, more frac stages,and more sand. While we expect the positive trend to persist through 2018, wedo believe the rate of change will slow due to some interference from technicaland economic break points.

Deutsche Bank Securities Inc. Page 9

9 October 2017

Oil Services & Equipment

Initiation of coverage

Figure 15: The impact of adding 100 rigs has increased significantly

457

656

873

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800Ja

n-1

8

Au

g-1

8

Ma

r-1

9

Oct

-19

Ma

y-2

0

De

c-2

0

Jul-

21

Fe

b-2

2

Se

p-2

2

Ap

r-2

3

No

v-2

3

Jun

-24

Jan

-25

Au

g-2

5

Ma

r-2

6

Oct

-26

Ma

y-2

7

De

c-2

7

kb

/d

Months

2014 avg IP 2016 avg IP 2017 Ytd avg IP

Source: Drilling Info, Deutsche Bank

Tight oil has rehabilitated the influence of the US rig countA producer working a single rig on a multi-well pad in the Permian can drill a wellin 20 days and can have a three-well pad placed on production in 130 days orless. It can spud 18 wells per year with a completed well cost normalized for a7,500-ft lateral of $5.5 – 6.0 million. Total annual drilling and completion (D&C)expenditures for this single rig would be $100 – 110 million.

Scale this up to a development program with 100 rigs and $10 – 11 billion ofannual D&C expenditures, and within 12-months of spudding the first wells,this program can produce 0.4 mmb/d of oil. By the end of year-three, output isupwards of 0.9 mmb/d. This is almost double what the industry was doing in2014. This is what seduces US producers and brings capital into the US.

Figure 16: Permian year-end flow rate contributions when adding 100 rigs

224

368 457

527 584

321

528

656

755 838

427

704

873

1,006

1,116

0

200

400

600

800

1,000

1,200

2018 2019 2020 2021 2022

kb

/d

2014 avg IP (EOP) 2016 avg IP (EOP) 2017 Ytd avg IP

Source: Drilling Info, Deutsche Bank

Page 10 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

Capex Recovery is rapidly Reviving US Oil Production

We believe the upstream capex recovery that began in June 2016 has put the USon track to realize 9.5 mmb/d of oil production by year-end 2017. This would be a1.0 mmb/d revival since the September 2016 lows, of which 0.55 mmb/d has beenrestored as of June 2017. While the drawdown of drilled but uncompleted wells(DUCs) has contributed about 0.24 mmb/d of the restored oil so far, we expectthe 450 oil-directed rigs that have returned to work since June 2016 to contributeabout 0.85 mmb/d of oil production by year-end 2017.

We believe this rapid revival of US production is exerting pressure on global oilprices and is likely to flatten 2018 capex budgets and US rig count growth. Wedo not expect it will once again drive oil prices down into the $30s.

Figure 17: US upstream capex bottomed in 3Q16 andhas risen 65% through 2Q17 with oil prices averaging$47

Figure 18: The Permian has absorbed 54% of theland rigs returning to the field since the May 2016 riginflection

$0

$20

$40

$60

$80

$100

$120

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

Oil

pri

ces

$ in

mill

ion

s

US capex Crude oil prices ($/bbl)

0

50

100

150

200

250

300

350

400

450

500

Ma

y-1

6

Jun

-16

Jul-

16

Au

g-1

6

Se

p-1

6

Oct

-16

No

v-1

6

De

c-1

6

Jan

-17

Fe

b-1

7

Ma

r-1

7

Ap

r-1

7

Ma

y-1

7

Jun

-17

Jul-

17

Au

g-1

7

Rig

s

Permian Eagle Ford Cana Bakken Other

Source: Company reports from the top 30 active US producers Source: Baker Hughes, a GE Company

Figure 19: DUCs responded quickly and at the peak arecontributing about 0.24 mmb/d

Figure 20: Newly drilled wells contributingapproximately 0.85 mmb/d by year-end 2017

0

50

100

150

200

250

300

04

/16

06

/16

08

/16

10

/16

12

/16

02

/17

04

/17

06

/17

08

/17

10

/17

12

/17

02

/18

04

/18

06

/18

08

/18

10

/18

12

/18

kb

/d

Permian Eagle Ford Bakken Niobrara Other

0

200

400

600

800

1,000

1,200

1,400

1,600

04

/16

06

/16

08

/16

10

/16

12

/16

02

/17

04

/17

06

/17

08

/17

10

/17

12

/17

02

/18

04

/18

06

/18

08

/18

10

/18

12

/18

kb

/d

Permian Eagle Ford Bakken SCOOP/STACK

Source: Wood Mackenzie, Drilling Info, Deutsche Bank Source: Wood Mackenzie, Drilling Info, Deutsche Bank

Deutsche Bank Securities Inc. Page 11

9 October 2017

Oil Services & Equipment

Initiation of coverage

Figure 21: Permian production by well vintage

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

01

/10

06

/10

11

/10

04

/11

09

/11

02

/12

07

/12

12

/12

05

/13

10

/13

03

/14

08

/14

01

/15

06

/15

11

/15

04

/16

09

/16

02

/17

b/d

< 2010 2010 2011 2012 2013 2014 2015 2016 2017

Source: Drilling Info, Deutsche Bank

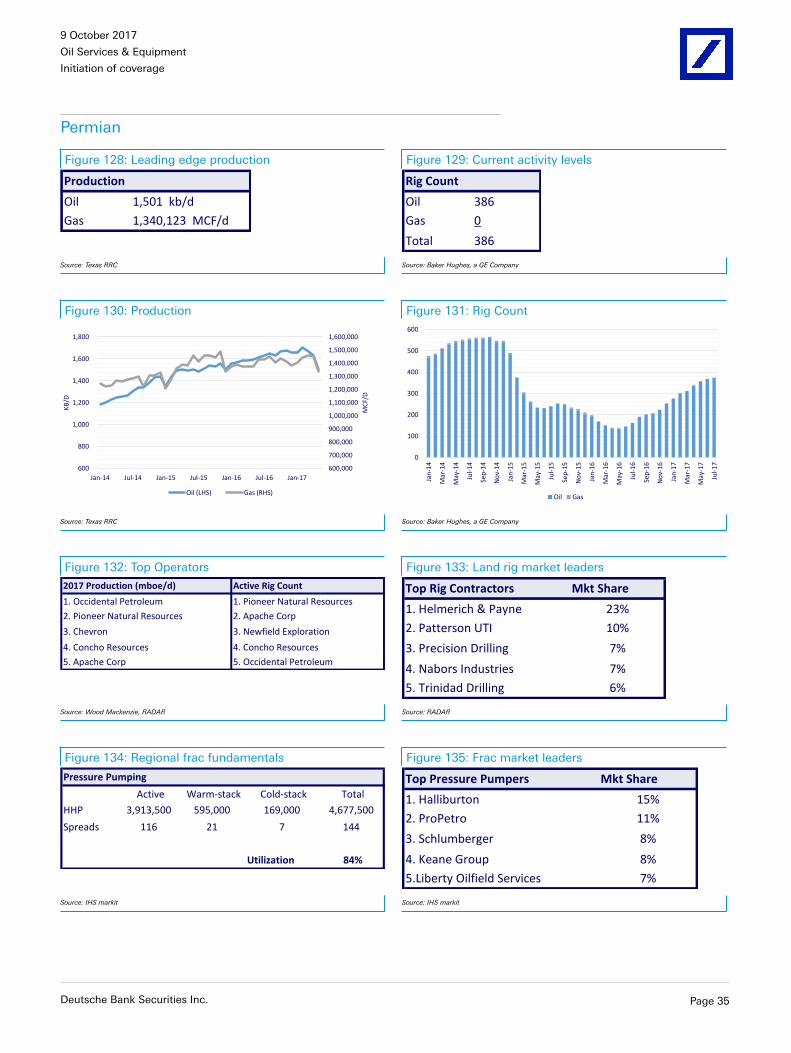

The Permian is the principal driver of activity and oil production growthThe rapid revival of production is happening largely in the Permian. Over 50% ofthe rigs that have returned to work since the June 2016 inflection have gone tothe Permian. We expect these rigs will contribute approximately 0.55 mmb/d ofproduction by year-end 2017.

But even before the inflection in drilling activity, the Permian has experiencedsignificant production growth with over 65% of the total output coming fromwells placed on production since 2015. To put that into context, wells placed onproduction in the Eagle Ford since 2015 are only contributing about 30% of thetotal output.

The Permian has become the epicenter of US drilling activity and is one of thefew regions where there is differentiated service pricing.

Figure 22: Permian oil production by the year in whichthe wells were placed on production

Figure 23: Permian monthly change in oil production bythe year in which the wells were placed on production

< 2010

6%2010

5% 2011

3%

2012

4%

2013

4%

2014

11%

2015

14%

2016

25%

2017

28%

(60,000)

(40,000)

(20,000)

-

20,000

40,000

60,000

80,000

< 2010 2010 2011 2012 2013 2014 2015 2016 2017

b/d

Source: Drilling Info, Deutsche Bank Source: Drilling Info, Deutsche Bank

Page 12 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

Does this make the Permian the only game in town?The US is a bigger threat if there is a broader contribution of oil supplies. Thusfar the Permian has contributed the lion’s share of the restored oil productionwith the Eagle Ford only now showing signs of recovery. With two-thirds of thePermian output coming from wells that were placed on production within the lastthree-years, the revival of US oil production since the lows is somewhat vulnerableto the hyper-decline phases these wells are in. We estimate the Permian needsto replace about 110 kb/d (and growing) from wells brought online before 2017.Wells placed on production in 2017 are contributing in excess of 300 kb/d, whichis clearly sufficient and still enough to cover the losses thus far from the EagleFord and the Bakken.

We expect the 40+ rigs added to the Eagle Ford since June 2016 will add about200 kb/d of oil production by year-end 2017. Wells placed on production prior to2017 are currently declining by about 55 kb/d and growing. We expect the EagleFord data which comes at a lag to show a positive pivot in August. The Bakkenis not keeping up in terms of activity. While the drawdown of DUCs contributedmore than 100 kb/d, less than 30 rigs returned to work in the Bakken, which setsit up for small declines through year-end.

Figure 24: Eagle Ford oil production by well vintage Figure 25: Bakken oil production by well vintage

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

01

/10

06

/10

11

/10

04

/11

09

/11

02

/12

07

/12

12

/12

05

/13

10

/13

03

/14

08

/14

01

/15

06

/15

11

/15

04

/16

09

/16

02

/17

b/d

< 2010 2010 2011 2012 2013 2014 2015 2016 2017

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

01

/10

06

/10

11

/10

04

/11

09

/11

02

/12

07

/12

12

/12

05

/13

10

/13

03

/14

08

/14

01

/15

06

/15

11

/15

04

/16

09

/16

02

/17

b/d

< 2010 2011 2012 2013 2014 2015 2016 2017

Source: Drilling Info, Deutsche Bank Source: Drilling Info, Deutsche Bank

Figure 26: Eagle Ford monthly change in oil productionby year in which wells were placed in production

Figure 27: Bakken monthly change in oil production byyear in which wells were placed in production

(15,000)

(10,000)

(5,000)

-

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013 2014 2015 2016 2017

b/d

(30,000)

(20,000)

(10,000)

-

10,000

20,000

30,000

2010 2011 2012 2013 2014 2015 2016 2017

b/d

Source: Drilling Info, Deutsche Bank Source: Drilling Info, Deutsche Bank

Deutsche Bank Securities Inc. Page 13

9 October 2017

Oil Services & Equipment

Initiation of coverage

Figure 28: US upstream capex guidance for 2017

120,790

82,772

43,568

61,205

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2014 2015 2016 2017

$ in

millio

ns

Source: Company reports from some of the top 36 most active producers

The 100+ rig count decline is not in our forecast through year-endThere has been a great deal of speculation that the US rig count was going tolose 100+ rigs into year-end. We expect US producers will have small 2H17 capexrevisions, but nothing that triggers a significant slide in activity. Any declineswe see are also likely to be more gradual, especially now that oil prices haverebounded.

Currently US budget plans take annual capex up 40% in 2017 versus 2016. Thisimplies a 14% increase in 2H17 versus 1H17.

Figure 29: Small downside risk to 2H17 implied guidance

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1H14 2H14 1H15 2H15 1H16 2H16 1H17 2H17

$ in

mil

lio

ns

Source: Company reports from some of the top 36 most active US producers

Page 14 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

2018 Rig Count Outlook Weighed Down by Oil Prices

Figure 30: Rig count forecast (DBe)(e) (e) (e) (e)

Rig count forecast 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 2016 2017 2018

United States

Oil-directed rigs 427 315 374 449 573 699 746 735 391 688 744

Gas-directed rigs 108 82 85 117 148 174 182 170 98 168 167

Total U.S. land rigs 535 397 459 565 721 873 928 904 489 856 911

Sequential chg -26% -26% 16% 23% 27% 21% 6% -3% -48% 75% 6%

Gulf of Mexico 26 23 18 22 20 21 21 21 22 21 21

Canada 166 48 121 181 295 117 206 300 129 230 241

North America 727 468 598 769 1,036 1,011 1,155 1,225 641 1,107 1,173

Source: Baker Hughes, a GE Company, Deutsche Bank

The US rig count will likely be obstructed by low oil prices in 2018We expect the ebb and flow of US upstream capex and the rehabilitation of USproductivity to confine oil prices to a range of $45 – 55 through 2018. With the USalready on track to realize 9.5 mmb/d of production by year-end 2017, the setupfor 2018 is challenging. Our rig count forecast has oil-directed rigs climbing 6%in 2018 versus the 75% increase in 2017. We expect this will keep a lid on serviceinflation with the exception of hydraulic fracturing, which is poised to return to2014 demand levels.

In terms of oil production, we expect the US to grow by 0.7 mmb/d to 10.2 mmb/d by year-end 2018. There will likely be some slower growth periods in 2018because of a build-up in DUCs. Producers are already waiting for frac equipmentthat is in the process of being reactivated. Nonetheless, 2018 is setup to be amilestone for the industry as production surpasses the all-time high of 10.0 mmb/d set back in November 1971.

Figure 31: US oil output still rises with slowing rig count Figure 32: US oil production outcome using DB rig count

5,000

6,000

7,000

8,000

9,000

10,000

11,000

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

Jan-14

Jul-14

Jan-15

Jul-15

Jan-16

Jul-16

Jan-17

Jul-17

Jan-18

Jul-18

kb/d

Months

7,0

83

7,9

18

9,4

65

9,2

29

8,7

71

9,4

67

10

,18

3

0

2,000

4,000

6,000

8,000

10,000

12,000

2012 2013 2014 2015 2016 2017 2018

(a) (a) (a) (a) (a) (e) (e)

kb

/d

US production US production (EOP)

Source: Baker Hughes, a GE Company, Deutsche Bank Source: EIA, Deutsche Bank

A 100 rig decline versus our base case would trim 2% off 2018 oil outputWe ran a sensitivity analysis of our rig forecast versus our production outcomeand found that a 100 rig decline through year-end 2017 would trim 2% from ourbase case by year-end 2018. The addition of 100 rigs would add 4%. In large scaletight oil developments, rig additions tend to add more upside than subtractionsdo downside, assuming gradual increases in productivity.

Deutsche Bank Securities Inc. Page 15

9 October 2017

Oil Services & Equipment

Initiation of coverage

Figure 33: US oil production outcomes using +/- 100 rigs versus DB basecase

+4%

-2%

8,000

8,500

9,000

9,500

10,000

10,500

11,000Ja

n-1

6

Ma

r-1

6

Ma

y-1

6

Jul-

16

Se

p-1

6

No

v-1

6

Jan

-17

Ma

r-1

7

Ma

y-1

7

Jul-

17

Se

p-1

7

No

v-1

7

Jan

-18

Ma

r-1

8

Ma

y-1

8

Jul-

18

Se

p-1

8

No

v-1

8

kb

/d

+100 rigs -100 rigs Base case

Source: Deutsche Bank, EIA

Can well productivity and service intensity continue to improve?Enhancements in drilling efficiency and completion design have been driving ahigher cadence of more productive wells for seven consecutive years now. Whilethere are some technical and economic break points that are interfering, and alot of the heavy lifting has already been done, we believe the underlying trendsdriving increased reservoir contact will continue to push IPs and EURs higher, butat a slower pace.

In 2017, there was a jump in 30-day IPs in both the Permian and Eagle Ford.The reason for this was producer mix, not a step change in productivity. Whilethe underlying trends are positive, the lower range in oil prices has curbed thenumber of producers placing lower quality wells on production. So far, there are14% fewer producers placing wells on production in the Permian in 2017 versus2016, and 22% fewer than in 2014. Oil prices above $55 would likely bring someback and lead to more development of lower quality acreage, which would thencreate a drag on average productivity metrics.

Figure 34: Permian lateral lengths vs. productivity Figure 35: Eagle Ford lateral lengths vs. productivity

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

-

100

200

300

400

500

600

700

800

2011 2012 2013 2014 2015 2016 2017

Ytd

Fe

et

b/d

(o

il o

nly

)

Peak monthly production Lateral length

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

-

200

400

600

800

1,000

2011 2012 2013 2014 2015 2016 2017

Fe

et

b/d

(o

il o

nly

)

Peak monthly production Lateral length

Source: IHS Markit, Drilling Info, Deutsche Bank Source: IHS Markit, Drilling Info, Deutsche Bank

Page 16 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

Longer laterals to drive further productivity gains despite some interferenceWhile we are seeing gains in the average 30-day IP per 1,000-ft of lateral slowafter years of substantial increases, producers are still extending the overalllateral lengths, which is positive for the services industry. For years we haveall questioned the industry on the technical and economic limits of horizontallaterals. Since 2011, the average lateral length has increased by 40% to 6,000-ft. The leading edge is up to 12,000-ft with some experimenting with 20,000+feet. So far the limitations have been related to limits on friction reducing agents,availability of continuous acreage capable of accommodating longer laterals, andrisk. Risk because laterals are drilled open-hole, not cased hole. When lateralsextend out to 12,000-ft, costs escalate as does the risk of well integrity. Somesmaller, less sophisticated producers are unwilling to take on that risk. But wefound that over the last three years, about 50% of the wells placed on productionin the Permian and Eagle Ford were drilled by one of the top 30 most activeproducers, the vast majority of which are pressing ahead with longer laterals.

Figure 36: Average Permian horizontal lateral lengths Figure 37: Average Permian 30-day IPs per 1,000-ft

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2011 2012 2013 2014 2015 2016 2017 2018 2019

Feet

-

20

40

60

80

100

120

140

160

-

100

200

300

400

500

600

700

800

2011 2012 2013 2014 2015 2016 2017

Ytd 30

-da

y I

P p

er

1,0

00

-ft

of

late

ral

b/d

(o

il o

nly

)

Peak monthly production 30-day IP per 1,000-ft

Source: IHS Markit Source: IHS Markit, Drilling Info, Deutsche Bank

Figure 38: Permian frac stages per well Figure 39: Permian sand volumes per lateral foot

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015 2016 2017 2018 2019

Fra

c st

ag

es

pe

r w

ell

100

600

1,100

1,600

2,100

2,600

2011 2012 2013 2014 2015 2016 2017 2018 (e) 2019 (e)

Lbs.

pe

r la

tera

l ft

Source: IHS Markit Source: IHS Markit

Deutsche Bank Securities Inc. Page 17

9 October 2017

Oil Services & Equipment

Initiation of coverage

Land Drilling Darwinism

Improved drilling efficiencies and enhanced completions have enabled USproducers to drill a higher cadence of more productive wells using fewer rigs.Not only are producers drilling more with less, but now the US is exerting moreinfluence on global oil markets than it has in over 30 years. We believe thiswill confine oil prices to a range of $45-55 through 2018 and will deflate someof the operating leverage that is customary in the land drilling industry. This isundermining the earnings power of the land drillers, and is forcing key players todevise strategies that will reestablish them in the value chain.

Figure 40: Wells spud per year per rig is up 50% Figure 41: DB rig count forecast

12.0

13.2

15.6 16.0 15.8

17.3 18.0

6

8

10

12

14

16

18

20

2011 2012 2013 2014 2015 2016 2017

We

lls

spu

d p

er

rig

0

500

1,000

1,500

2,000

2,500

Jan-12

May-12

Sep-12

Jan-13

May-13

Sep-13

Jan-14

May-14

Sep-14

Jan-15

May-15

Sep-15

Jan-16

May-16

Sep-16

Jan-17

May-17

Sep-17

Jan-18

May-18

Sep-18

Forecast Actual

Source: IHS Markit Source: Baker Hughes, a GE Company, Deutsche Bank

Since the US recovery began in June 2016, the industry has returned about 450oil-directed rigs to work. It was a quick snap back driven by lower breakevenprices and an inventory of wells with 96% success rates and 3-6 month cashconversions. But we do expect activity to flatten through year-end 2018.

Figure 42: US upstream capex vs. oil-directed rig count Figure 43: We expect recovery to flatten out

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

Rig

s

$ in

mill

ion

s

US capex US oil-directed rigs

'02-'08

'09-'14

'16+

'01-'02

'08-'09 '14-'160

50

100

150

200

250

300

350

0 26 52 78 104 130 156 182 208 234 260 286 312

Ind

exe

d t

o 1

00

Weeks

Source: Company reports from the top 36 active US producers, Baker Hughes, a GE Company Source: Baker Hughes, a GE Company

Page 18 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

Figure 44: Permian is key destination for returning rigs Figure 45: Regional distribution of total US rig count

0

50

100

150

200

250

300

Permian Eagle Ford Cana Bakken Other

Rig

s

Barnett

1%

Cana Woodford

7%DJ-Niobrara

3%

Eagle Ford

7%

Haynesville

5%

Marcellus

5%

Permian

42%

Utica

3%

Williston

5%

Other

19%

Source: Baker Hughes, a GE Company Source: Baker Hughes, a GE Company

A large-scale, industrialized development of tight oil resourcesThe industry is in the midst of a large-scale, industrialized development of tight oilresources, which creates a high demand for technologies that enable improveddrilling efficiencies and lower wells costs. The Permian has become the epicenterof it all, attracting over half of the rigs that have returned to the market sincethe US recovery began. This has created a bifurcated market where drilling daysand pricing are reserved for the preferred 1,500hp AC-electric and super-spec rigsthat have leading edge functionality, performance and mobility. HP is the leadingprovider of super-spec rigs.

On the other side of the fence are the legacy mechanical and SCR (silicon-controlled rectifier) rig fleets that have endured large scale retirements, but a smallpopulation has survived and are still competing for horizontal work.

Figure 46: Producers prefer the 1,500hp AC-electric rigs Figure 47: Utilization restored for premium rigs

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

1Q16

3Q16

1Q17

Rigs

AC SCR Mechanical

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan

-11

Ma

y-1

1

Se

p-1

1

Jan

-12

Ma

y-1

2

Se

p-1

2

Jan

-13

Ma

y-1

3

Se

p-1

3

Jan

-14

Ma

y-1

4

Se

p-1

4

Jan

-15

Ma

y-1

5

Se

p-1

5

Jan

-16

Ma

y-1

6

Se

p-1

6

Jan

-17

Ma

y-1

7

Uti

liza

tio

n

1,500-1,999 HP 1,000-1,499 HP 500-999 HP

Source: Company reports, IHS Markit, Land Rig Newsletter Source: Land Rig Newsletter

Deutsche Bank Securities Inc. Page 19

9 October 2017

Oil Services & Equipment

Initiation of coverage

Figure 48: Average dayrates across asset classes Figure 49: Average realized dayrate assumptions

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

$22,000

$24,000

Jan

-11

Ma

y-1

1

Sep

-11

Jan

-12

Ma

y-1

2

Sep

-12

Jan

-13

Ma

y-1

3

Sep

-13

Jan

-14

Ma

y-1

4

Sep

-14

Jan

-15

Ma

y-1

5

Sep

-15

Jan

-16

Ma

y-1

6

Sep

-16

Jan

-17

Ma

y-1

7

Da

yra

te

1,500+ HP 1,000-1,500 HP < 1,000 HP

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

$22,000

$24,000

$26,000

$28,000

$30,000

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

1Q16

3Q16

1Q17

3Q17

1Q18

3Q18

Forecast Actual

Source: Land Rig Newsletter Source: Deutsche Bank, includes HP, PTEN, NBR and PDS

The pricing leverage customary in land drilling will be deflated in 2018While we have seen a bounce in the average pricing for 1,500hp AC-electric rigsfrom $16 kpd to $18 kpd, with leading edge at $20-22 kpd, pricing traction isslowing. Utilization for 1,500hp AC-electric rigs is above 90% and producers aresaying there is a very limited selection of high-specification rigs left, but we expectthe subdued level of activity in 2018 will keep prices from breaking out to andabove the $25 kpd level.

Most contractors do not intend to fund newbuilds in this environmentIn the late 1990s, HP began rolling out its proprietary FlexRig designs, which wereleading edge land rigs with enhanced mobility and faster rates of penetration.The company delivered over 390 of these rigs, mainly in the US, and was ableto exploit a significant competitive edge for almost a decade. In the mid-2000s,the peers developed their own proprietary rigs and started their own newbuildprograms with some deliveries still in the pipeline.

Figure 50: AC-electric fleet growth Figure 51: Additions of AC-electric rigs

0

200

400

600

800

1,000

1,200

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

1Q16

3Q16

1Q17

HP NBR PTEN PD Other

0

10

20

30

40

50

60

70

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

Source: Company reports Source: Company reports

Page 20 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

But since the collapse in oil prices, the playbook has changed. While the industrycontinues to demand technology that increases drilling efficiencies and reducescosts, the imbalance in the land rig market is not supporting the $25 kpddayrate threshold many contractors say is needed to justify newbuilds. With spotrates in the high-teens, the industry is focused on upgrading rigs to super-speccapabilities, which are earning leading edge rates of $20-22 kpd.

The alternative to funding newbuilds is funding upgrades to super-specSuper-spec rigs are 1,500hp AC-electric rigs that are pad capable, have a thirdmud pump, a 7,500 psi mud system, a 750k lb. hook load, a fourth engine anda 25,000-ft pipe racking capacity. In essence it is a rig with superior mobilitycharacteristics that enables a producer to drill longer, better quality laterals at afaster rate of penetration, and then move quickly to the next well on the pad.There is high demand for these rigs and producers are paying a $2 kpd premiumon 12-24 month contracts to secure access. Utilization of super-spec rigs is nowabove 90%, but pricing is not acting like utilization is that high.

Figure 52: Super-spec rig market share Figure 53: Inventory of potential upgrades to super-spec

HP

32%

PTEN

23%

NBR

16%

PD

13%

Other

16%

0

20

40

60

80

100

120

140

HP PTEN NBR PD

Rigs

Source: Company reports Source: Company reports

There are varying opinions of how many super-spec rigs there really are, butPatterson-UTI has guided to a fleet of 465 as of 2Q17, which is up from 375 in4Q16. Helmerich & Payne has the largest market share and the largest inventoryof rigs it can upgrade, with 122 candidates that would cost $2-3 million each.Patterson-UTI is currently upgrading seven of its APEX 1000 rigs from theAppalachia region for about $8 million apiece and moving them to west Texas.Nabors has about 23 left as of 2Q17, and intends to complete all of them by early2018.

Overall, there is the potential to add another 200 super-spec rigs through 2018,which probably has something to do with the less than customary leverage inpricing. But the $2 kpd premium is attracting the upgrade capital, so the questionbecomes opportunity set. As of August 2017, 26% of the horizontal or directionalwells being drilled were done so using mechanical or SCR rigs. Assuming a flatrigs count in 2018, replacing these rigs for performance reasons seems to be themain opportunity.

Deutsche Bank Securities Inc. Page 21

9 October 2017

Oil Services & Equipment

Initiation of coverage

Encouraging that the consensus acknowledged the EPS vulnerabilityThe rapid snap back in the US rig count prompted swift positive EPS revisionsbecause that was the customary course of action. That was discouraging and itstretched out our long-standing negative outlook on the group because in ourview the old cyclical playbook was obsolete. The development of tight oil involveda series of disruptive technologies that had derailed the normalization of thecycle. While it created new, more service intense markets (hydraulic fracturingand sand), it also created challenges for markets including land drilling. So it is atleast encouraging that expectations have been reset lower. The standout is PTEN,which because of its shift in revenue mix toward frac, the company rightfully ismaintained a strong earnings growth outlook.

Figure 54: HP 2018 EPS revisions Figure 55: PTEN 2018 EPS revisions

(0.70)

(0.60)

(0.50)

(0.40)

(0.30)

(0.20)

(0.10)

0.00

0.10

0.20

0.30

0.40

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

EPS

(1.20)

(1.00)

(0.80)

(0.60)

(0.40)

(0.20)

0.00

0.20

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

EPS

Source: Factset Source: Factset

Figure 56: NBR 2018 EPS revisions Figure 57: PDS 2018 EPS revisions

(0.70)

(0.60)

(0.50)

(0.40)

(0.30)

(0.20)

(0.10)

0.00

0.10

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

EPS

(0.25)

(0.20)

(0.15)

(0.10)

(0.05)

0.00

0.05

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

EPS

Source: Factset Source: Factset

Earnings power has been in a longer-term down trendWith the exception of HP, the top North American land drillers have beenexperiencing a long-term erosion in earnings power. We expect this cycle to takeit another leg down for the group in terms of peak earnings achieved, with themost resilient being PTEN because of its increased exposure to the frac market.

Page 22 Deutsche Bank Securities Inc.

9 October 2017

Oil Services & Equipment

Initiation of coverage

Figure 58: HP annual EPS Figure 59: PTEN annual EPS

4.15

6.20

(2.00)

(1.00)

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

(a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (e) (e)

EP

S

4.03

2.08

(3.00)

(2.00)

(1.00)

0.00

1.00

2.00

3.00

4.00

5.00

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

(a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (e) (e)

EP

S

Source: Company reports, Deutsche Bank Source: Company reports, Deutsche Bank

Figure 60: NBR annual EPS Figure 61: PDS annual EPS3.60

1.72

(2.00)

(1.00)

0.00

1.00

2.00

3.00

4.00

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

(a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (a) (e) (e)

EP

S

0.66

(0.80)

(0.60)

(0.40)

(0.20)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

(a) (a) (a) (a) (a) (a) (a) (a) (e) (e)

EP

S

Source: Company reports, Deutsche Bank Source: Company reports, Deutsche Bank

PTEN’s leverage to frac market embeds more operating leverage to cycleWhile HP had remarkable growth through 2014, this cycle is likely to deflate itsleverage more so than its peers. All four are devising strategies to rejuvenateearnings, and HP is so far focusing on market share while the others, especiallyNabors, are adding service content to extract more value per rig.

Figure 62: Top 4 land drillers EBITDA combined Figure 63: PTEN has retained most EBITDA leverage

-

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

(e) (e)

$ in

mill

ion

s

-

50

100

150

200

250

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

(e) (e)

Ind

exe

d t

o 2

00

7

HP PTEN NBR PD

Source: Company reports, Deutsche Bank Source: Company reports, Deutsche Bank

Deutsche Bank Securities Inc. Page 23

9 October 2017

Oil Services & Equipment

Initiation of coverage

Figure 64: Total US land drilling market share Figure 65: AC rig market share

HP

21%

PTEN

16%

NBR

11%PD

7%

Other

45%

EN

16%

HP

29%

PTEN

20%NBR

16%

PD

8%

Other

27%

Source: Company reports, Deutsche Bank Source: Company reports, Deutsche Bank

Emerging trendsProducers are focused on lowering well costs, drilling wells faster, and increasingreservoir contact. They are tailoring drilling programs to harvest core acreage tofast track cash flow. Ultimately producers are striving for increasingly higher IPsand EURs per F&D dollar invested as the call for capital discipline gets louder.That means there is high demand for technologies that improve rig functionalityand performance for:

■ Mobility (pad drilling)

■ Rates-of-penetration (ROP)

■ Tripping performance

■ Precision well placement

Drilling contractors are focused on competitive positioning. They are achievingthis through improving rig functionality, performance and mobility. The keyenablers for industrialized resource development are efficiency, reduced costs,technology and scale. Every step is measurable, benchmarked, and improved. Assuch, contractors are emphasizing their technology and applications that enabledrilling automation and machine learning. They are increasing service content toextract more value from their installed base of rigs. Some of the core disciplinesin focus are:

■ Tubular running services (TRS)