Indonesia Development Prospects- and Policy Options

163

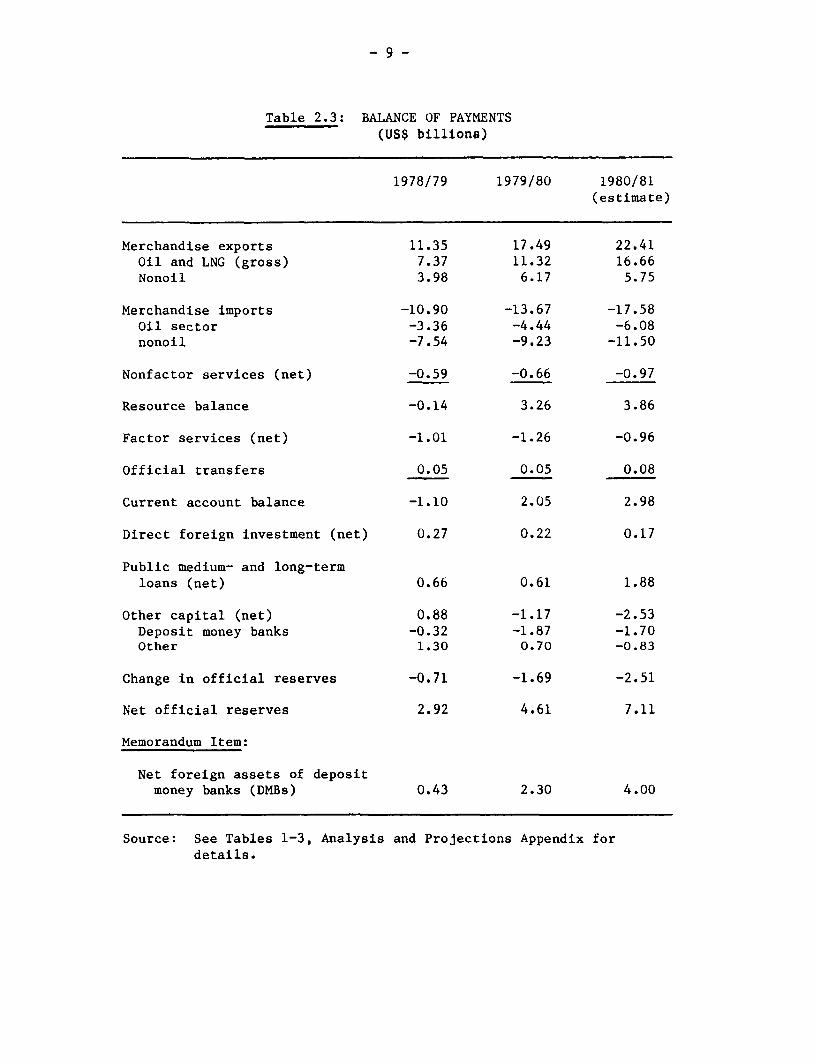

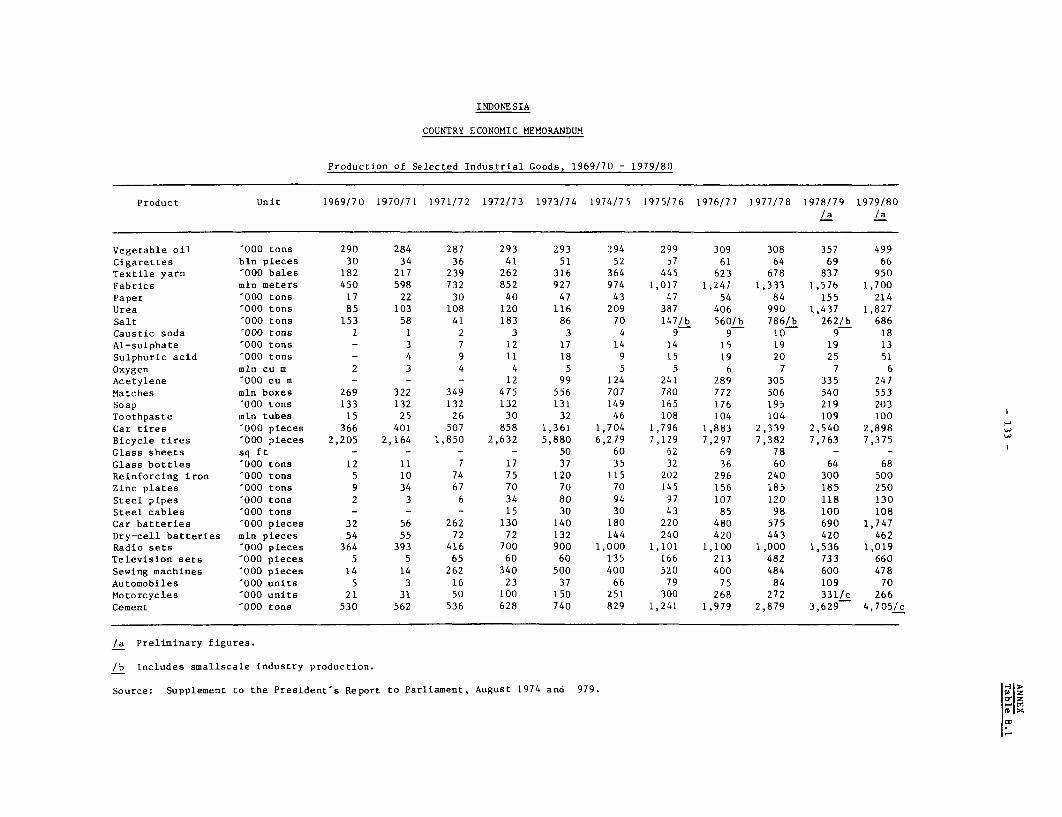

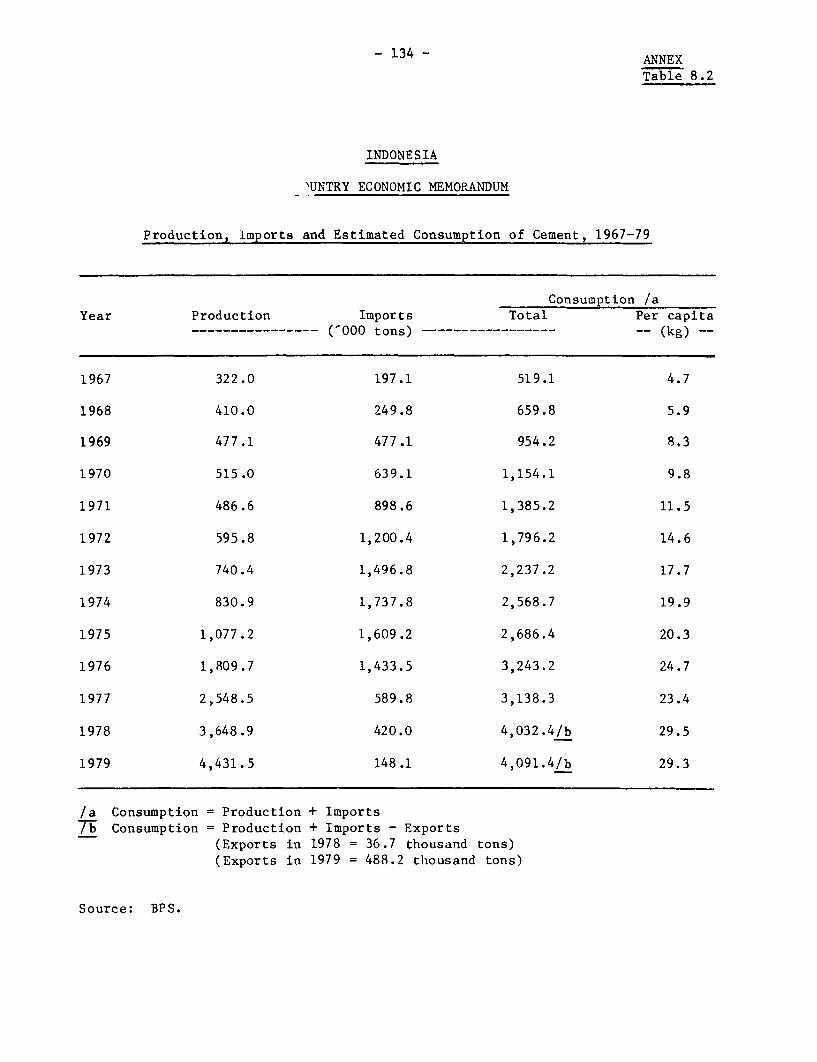

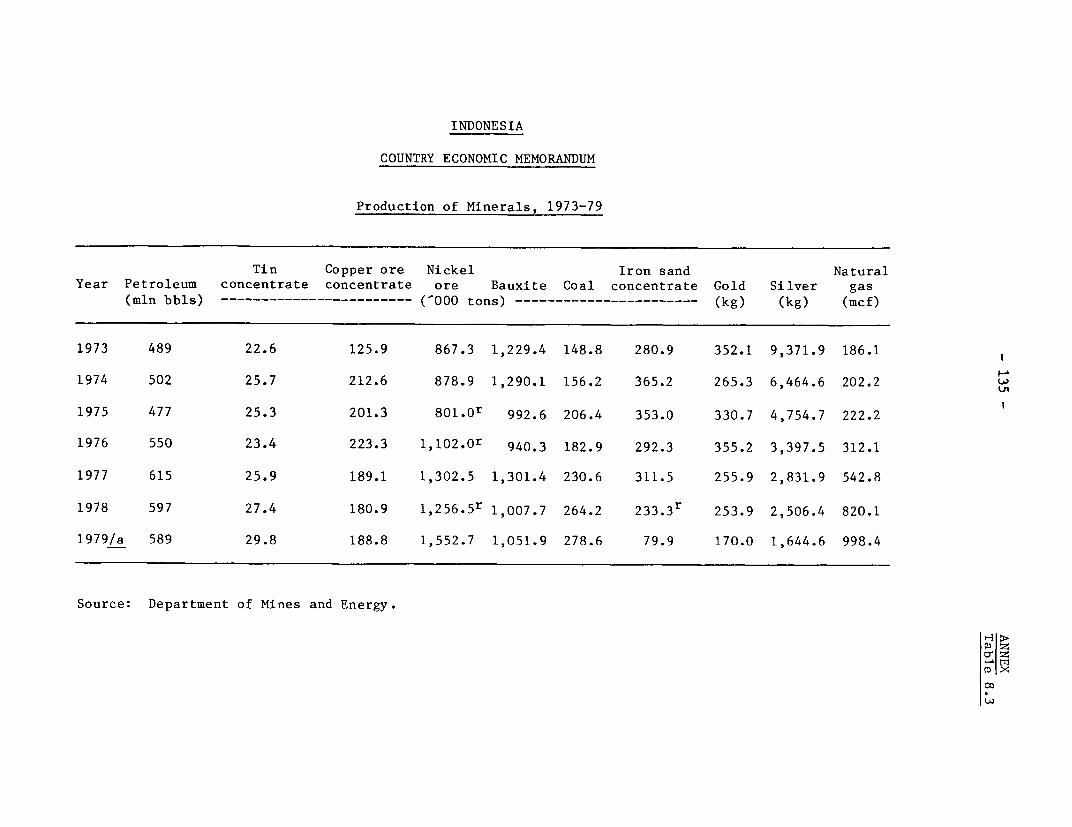

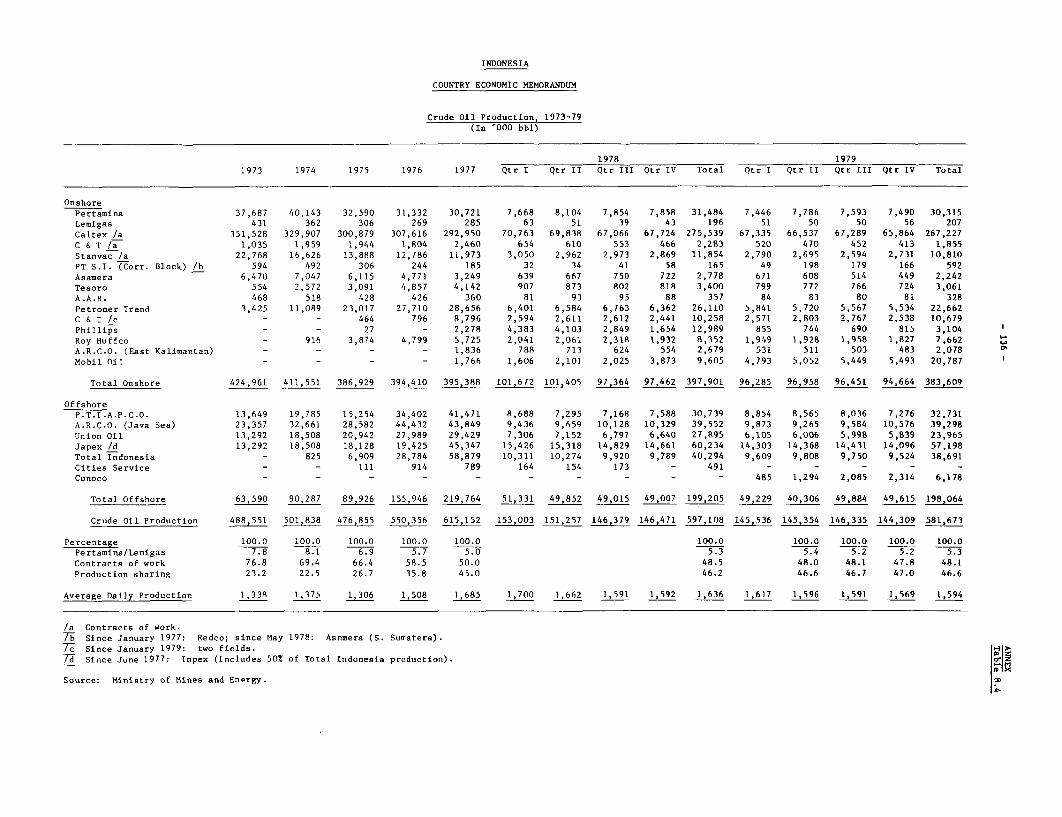

Report No. 3307-IND PILE COPY Indonesia Development Prospects- and Policy Options April 6, 1981 East Asia and Pacific Regional Office FOR OFFICIAL USE ONLY o Dm o z ~~m This document has a restricted distribution and may be used by recipients only in the performance of their official duties. its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Indonesia Development Prospects- and Policy Options

Report No. 3307-IND PILE COPYIndonesiaDevelopment Prospects- and Policy Options

April 6, 1981

East Asia and Pacific Regional Office

FOR OFFICIAL USE ONLY

oDm o

z ~~m

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

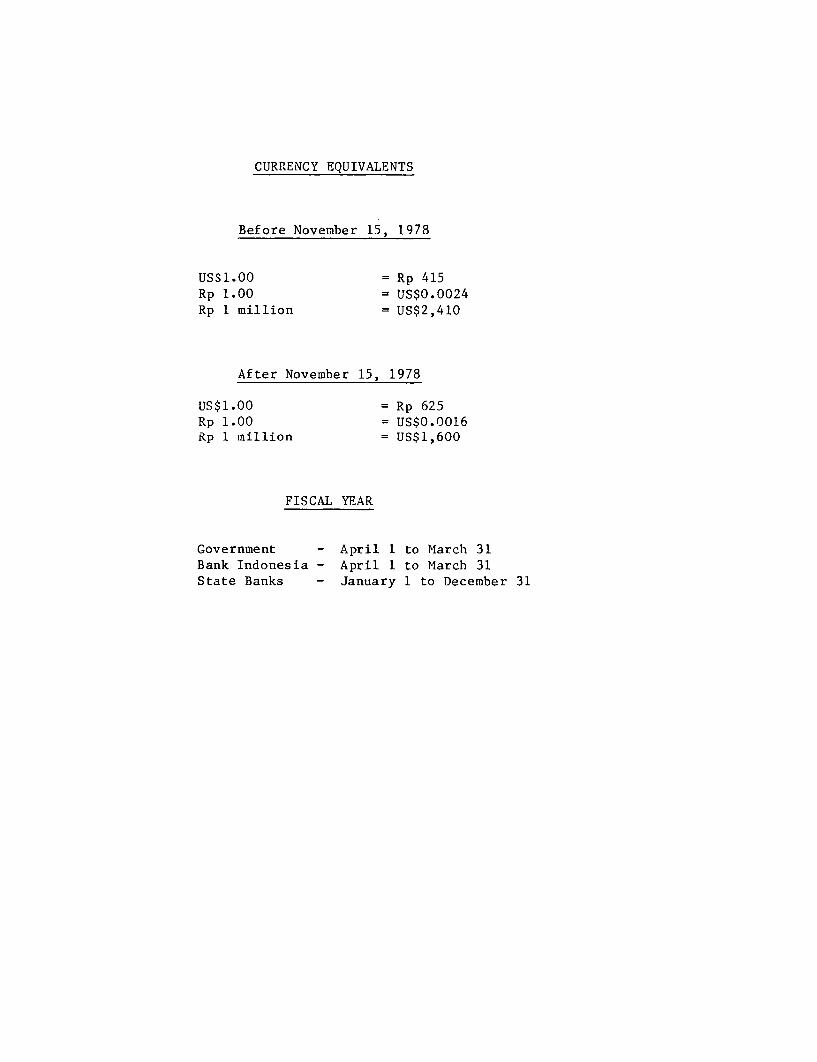

CURRENCY EQUIVALENTS

Before November 15, 1978

US$1.00 = Rp 415Rp 1.00 = US$0.0024Rp 1 million = US$2,410

After November 15, 1978

US$1.00 = Rp 625Rp 1.00 = US$0.0016Rp 1 million = US$1,600

FISCAL YEAR

Government - April 1 to March 31Bank Indonesia - April 1 to March 31State Banks - January 1 to December 31

FOR OFFICIAL USE ONLY

PREFACE

This report is based on findings of a mission comprising Nissim Ezekiel (IFC),Chandra Sharma (DPS), Lyn Squire, Andrew Steer, Michael Walton and SarathRajapatirana (Mission Leader), of the East Asia and Pacific Country ProgramsDepartment. The Mission visited Indonesia in October/November 1980. A draftof the report was discussed with the Government in March 1981.

This document has a restricted distribution and may be used by recipients only in the performance of |their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

INDONESIA

DEVELOPMENT PROSPECTS AND POLICY OPTIONS

Table of Contents

Page No.SUMMARY AND CONCLUSIONS

1. INTRODUCTION .... . . . . . . . . . . . . . . . . . . . . . 1

2. RECENT TRENDS IN THE ECONOMY ... . . . . . . . . . . . . . . 4

Domestic Production and Expenditures . . . . . . . . . . . . 4The Balance of Payments. 8The Government Budget . . . . . . . . . . . . . . . . . . . 10Prices and Competitiveness .13Monetary Developments .15

3. OPTIONS FOR MACROECONOMIC POLICY . . . . . . . . . . . . . . . 17

Elements of the Policy Package Aimed at StructuralTransformation of the Economy . . . . . . . . . . . . . . 18

Foreign Trade Policies .18Investment, Efficiency and the Regulatory Enviroment . . . . 20Domestic Resource Mobilization and Financial

Intermediation 22Price Policy and the Role of Subsidies . . . . . . . 25Summary of the Two Policy Scenarios . . . . . . . . . . . . 29Implications for Incomes, Employment and Equity . . . . . . 31

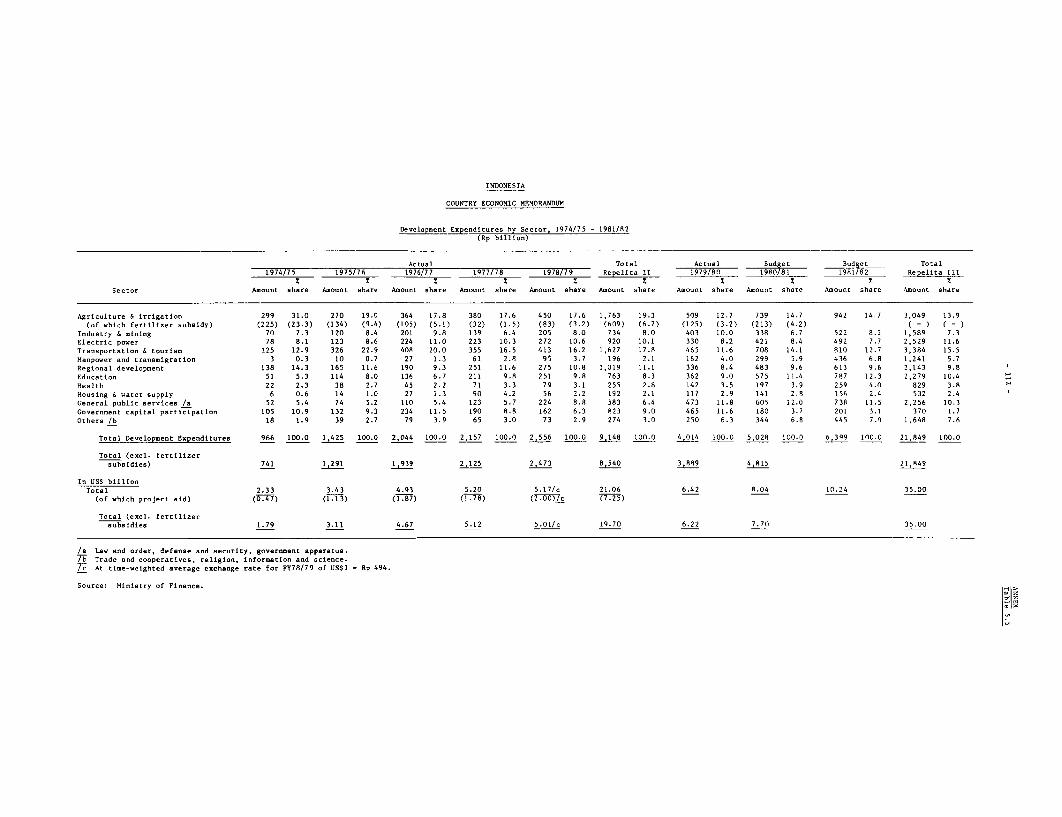

4. ISSUES IN PUBLIC EXPENDITURES ... . . . .... . . . . . . 34

Review of Sectoral Programs ... . . . . . . . ..... . 34Constraints to Implementation of Development Programs . . . 47

5. THE EMERGING RESOURCE POSITION ... . . . . . ....... . 50

Prospects for the Oil Sector . . . . . . . . . . . . . . . . 50Non-Oil Exports .54Import Policies and Projections . . . . . . . . . . . . . . 57The Budget .61

6. POLICY TOWARDS EXTERNAL CAPITAL INFLOWS AND DEBT MANAGEMENT . 64

Financing Requirements and Creditworthiness . . . . . . . . 64Capital Inflows from Official Sources . . . . . . . . . . . 65Policy Towards Private Capital Inflows . . . . . . . . . . . 68Foreign Exchange Reserves and Debt Management . . . . . . . 70

ANALYSIS AND PROJECTIONS APPENDIX .72STATISTICAL ANNEX .80M4AP .............................. .. . 146

Page No.

TABLES IN TEXT

2.1 Growth of Gross Domestic Product at 1973 Market Prices 52.2 Growth of Gross Domestic Expenditure at 1973 Market Prices 62.3 Balance of Payments - 1978/79-1980/81 92.4 Central Government Budget Summary 1977/78-1980/81 112.5 Selected Monetary Indicators 15

3.1 Effective Rates of Protection accorded to SelectedIndustries in 1975 19

3.2 Selected Public Enterprises Investment Programs 233.3 Alternative Scenarios for Domestic Oil Prices and

Subsidies 283.4 Summary of Two Growth Scenarios 303.5 Sector Employment Elasticities 32

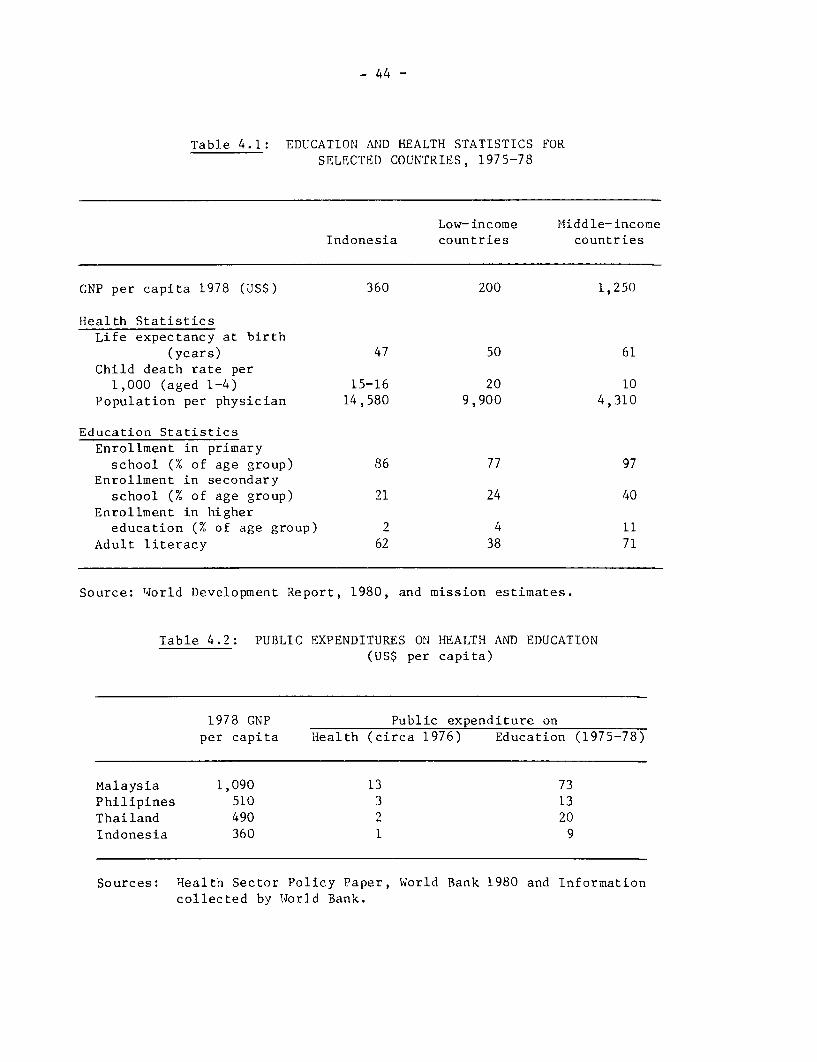

4.1 Education and Health Statistics for Selected Countries -1975/78 44

4.2 Public Expenditures on Health Education 444.3 Annual Additional Needs for Technical/Scientific/Managerial

Manpower 1980-90 and Output 1979 46

5.1 Indicators of Oil Exploration Activity 505.2 Key Oil Sector Projections - 1980/81-1990/91 515.3 Domestic Consumption of Oil Products 525.4 Net Oil Balance 535.5 Projected Exports under Alternative Cases 555.6 Projected Imports under Alternative Cases 585.7 Real Growth Rates of Exports and Imports under

Alternative Cases 595.8 Projected Resource Balances and Terms of Trade Development 605.9 Projected Government Revenue and Expenditure 1980/81-1985/86 62

6.1 Balance of Payments Projections Under High and Low Cases 656.2 New Commitments of External Public Debt by Source 1975-80 666.3 Projected New Commitments of Grants and Medium-

and Long-Term Loans: High Case 686.4 Disbursed Medium- and Long-Term Public Debt Outstanding 71

SIUMMARY AND CONCLUSIONS

i. The main theme of this report is that Indonesia will have aresource surplus during the first half of the 1980s, and that this comfort-able resource position provides Indonesia with a unique opportunity toundertake a series of policy reforms and an expanded program of investment inexport production, import replacement, and alternative energy supplies, thatin turn will ensure sustained development during the second half of thedecade and beyond. Implementing the policy changes and investment programsin support of these structural changes will pose many challenges for economicmanagement. They are nevertheless essential to address the vast and varieddevelopment needs of the country. Indeed, without such a program ofstructural adjustment, it will be difficult for the Government to continuemaking reasonable progress towards one of its major development goals - thealleviation of poverty - in the latter part of the decade when foreignexchange availabilities will again be limited.

Current Economic Trends

ii. The Indonesian economy was more buoyant in 1980 than 1979./1 Ahigher GDP growth rate, increasing income from a higher level of domesticeconomic activity and favorable terms of trade effects, a balance ofpayments surplus, and relative monetary stability characterized the 1980performance. Highlights of this performance include a record rice harvestof nearly 20 million metric tons, a current account surplus in the balance ofpayments of almost $3.0 billion, and a real GDP growth rate of over 7%. Thelatter compares with an increase of 4.9% in 1979 and an average annual realGDP growth rate of 6.6% in the 1973-79 period.

iii. The strong balance of payments was principally the result of oilsector related net export earnings which increased by $3.0 billion in1980/81. Although the volume of oil exports declined, an increase in theaverage price of oil by 46% to $33.00 per barrel, and an expansion in thevolume of LNG exports, produced the increase in oil sector earnings.Despite the rapid increase in liquidity stemming from the large inflow ofoil income, the rate of increase in consumer prices declined from 28% in1979 to 17% in 1980. While domestic prices continued to rise more rapidlythan international prices, half the gains in competitiveness secured throughthe November 1978 devaluation for manufactured exports and importsubstitutes were still retained by the end of 1980.

iv. The inescapable fact is that average per capita income in Indone-sia is still very low, the current resource surpluses notwithstanding. Each$1 billion earned in foreign exchange adds less than $7 to per capita

/1 The 1979 performance was analyzed in last year-s Bank report,"Indonesia: Long Run Development and Short Run Adjustment", Report rlo.

2788-IND, February 1980.

- ii -

income, which is provisionally estimated at $405 for 1980. The presentforeign exchange surplus tends to mask existing dimensions of poverty, whichinclude limited access to basic services and the urgent need for moreproductive utilization of Indonesia-s most important development resource -its large and rapidly growing labor force. Preliminary results of the 1980population census show total population to be 147 million. The futuregrowth of the labor force based on this estimate will be 3.2% p.a. comparedto the 2.3% estimate made in 1976. Some 2 million persons will thereforeenter the labor market each year in the first half of the 1980s. Thesefigures underscore the urgency of using the additional resources to expandproductive employment in agriculture, industry, public works and the servicesectors.

Growth Prospects and Policy Adjustments

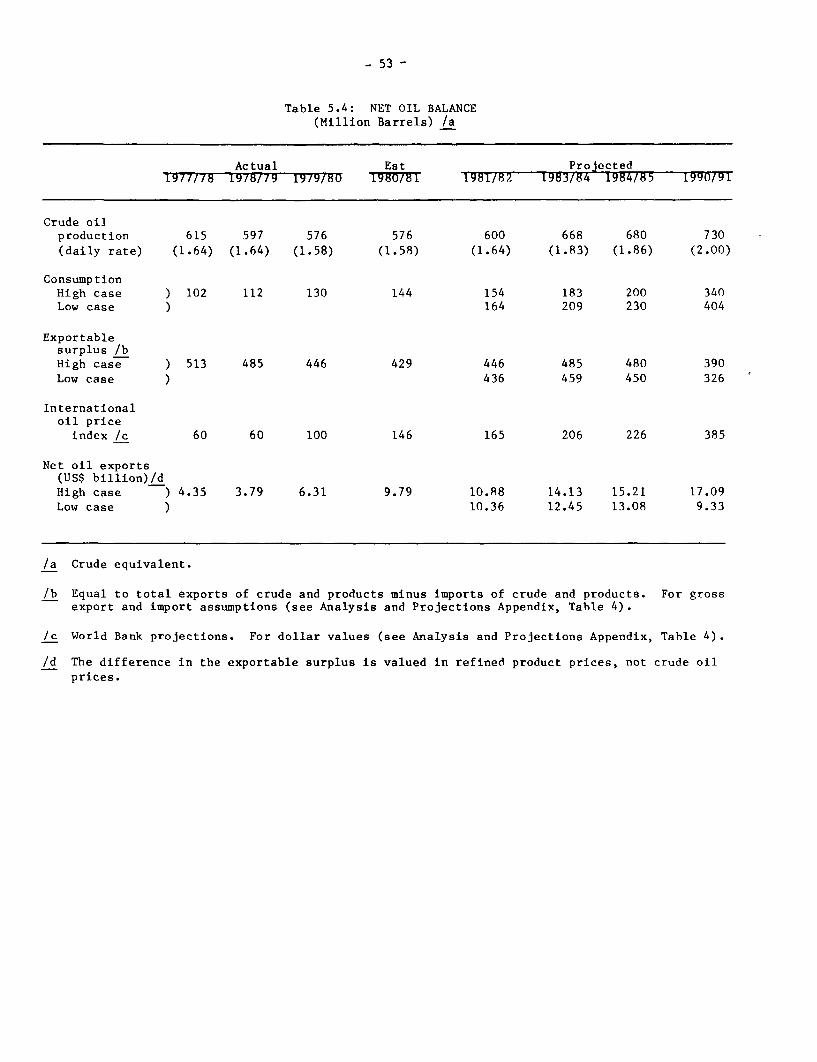

v. Higher oil prices have clearly improved the prospects for rapidgrowth in Indonesia. Foreign exchange surpluses are likely to continuethroughout the first half of the 1980s, during which time growth will beconstrained more by absorptive capacities of the economy and by the produc-tivity of domestic investment than by the availability of foreign exchange.In the second half of the 1980s, however, a secular decline in the volume ofoil available for export is probably inevitable, which, in the absence ofpolicy reforms aimed at a structural transformation of the economy, islikely to limit the growth of Indonesia's import capacity, thereby slowinggrowth in production, incomes, and employment.

vi. To help analyze the outlook, two sets of illustrative projectionshave been prepared: a "High" case, in which Indonesia adjusts successfullyin 1981-85, and thus ensures sustained rapid development after 1985; and a"Low" case in which it does not. In the former case, GDP continues to growin real terms at 7-8% a year throughout the decade. Per capita income wouldrise from an estimated $405 in 1980 to $710 by 1990 (at constant 1980prices), $70 higher than under the Low case. Even after a dramatic curtail-ment of import growth under the Low case, the balance of payments movesrapidly into a large and unsustainable deficit in the latter part of thedecade. Under the High case on the other hand, the transition from relativeforeign exchange surplus to shortage is altogether more gradual. By 1990,the current account deficit is projected to be stable and sustainable andequivalent to about 2.5% of GDP. It should be stressed that macroeconomicprojections for Indonesia are very sensitive to assumptions about oil and LNGprice changes. In this report all balance of payments projections assumethat the export price for oil and LNG will increase by 3% p.a. in realterms. The report's conclusions with regard to the overall superiority ofthe High case, however, remain valid regardless of the precise oil exportprice assumptions. Should the international oil price rise less fast thanprojected, the resource deficits would re-emerge sooner, which makes it moreurgent to adopt the High case policy scenario. The High case is achievable,depending on policies in key areas: the foreign trade regime, the regulatoryand investment climate, domestic resource mobilization and financialintermediation, and pricing and subsidies.

- iii -

vii. Foreign Trade Policy. To avoid the re-emergence of a seriousforeign exchange constraint in the latter part of the decade, substantiallyincreased investments will be required in export and import replacingindustries in which Indonsia has a comparative advantage. This will requireadjustments in the current trade regime which includes tariffs, subsidies,quantitative restrictions and excise duties. These adjustments must lead toa trade regime which approaches a degree of neutrality in the relativeprofitability of export and import competing activities. Towards this end,a number of elements will be required. These include a simplification ofthe system of protection so that import tariffs and excise taxes are thesole sources of protection for domestic industries; unification of thetariff structure and gradual reduction of the level and variance ofeffective rates of protection (to be achieved by reducing import tariffs andexport duties on final goods and raising tariffs in appropriate cases onintermediate goods). These changes would not only have the effect ofsetting Indonesia's non-oil export industries on a more competitive footing,but also of significantly reducing the current inflationary pressures withinthe country. The Government has already announced its intention to furtherreduce import tariffs, but further changes on the lines indicated above willbe needed.

viii. The Investment and Regulatory Environment. Indonesia's investmentrate with respect to GDP has risen from 17% in the early 1970s to about 23% in1980. By 1985 the investment rate would have to rise to about 27% of GDPand then level off close to 30% by the latter part of the 1980s. Both thevolume and the efficiency of new investment would be enhanced by asimplified regulatory environment. In combination with the reform of thetrade regime, such a simplification of the regulatory system will improvethe efficiency of investment by the ensuing changes in resource allocation.With few exceptions, the objectives of the regulatory system in Indonesiaare similar to those found in most countries. They include preservation ofnational control of particular activities, increasing domestic value addedand promotion of regional development. It is mostly in practice, applicationand in its complexity that Indonesia's system differs from other countries.Certain changes have already been undertaken, to reduce the complexity onthe system. But further reforms are an essential complement to changes intrade and financial policy. Simplification of the system is a long termgoal. Initial steps that could be taken in the short-run include:evaluation of applications on the basis of sound cost-benefit analysis (anattempt in this direction is already underway at BKPM); revision ofapplication forms to eliminate superfluous requirements; furthersimplification of the list of investment priorities; use of broadercategories of projects qualifying for special facilities.

ix. Domestic Resource Mtobilization and Financial Intermediation.Financial policies and institutions have a crucial role to play during andbeyond the restructuring process. Despite the present increase in national

- iv -

savings arising from oil revenues, medium and long term efforts will beneeded to raise domestic resource mobilization. This follows from theprospects of declining oil related revenues beyond the medium term and fromthe fact that an enhanced investment program has to be financed outside theGovernment's budget in the medium term. For example, investment programsplanned for industry, electricity and tree crop sectors will leave a gap inexcess of $6.0 billion even after accounting for retained earnings andtransfers from the Government budget. To fill this gap, it is important thatin the medium term policies are directed more towards mobilizing domesticresources, and in providing private and public enterprises with greateraccess to domestic and international capital markets. Efforts should alsobe made to raise non-oil revenues in the budget, through improved taxadministration, and to encourage deposit mobilization efforts through thebanks. In this latter respect, the Government is already exploring ways inwhich the expansion of credit by commercial banks could be also linked tosavings mobilization performance. In addition, consideration could be givento raising the costs of commercial banks access to Bank Indonesia'srediscount facilities thereby providing greater incentives for these banksto increase the level of their deposit liabilities. The present problem ofmaintaining price stability while raising public expenditures has to betackled through monetary surpluses in the implementation of the budget. Tothe extent that these surpluses are generated, bank credit can be extendedto the private sector and public enterprises.

x. Improvements in the efficiency of financial intermediationprocesses will be a key element for transferring funds for increasedinvestments from surplus to deficit sectors. At present, the financialintermediation process must cope with the fact that the majority of foreignexchange resources accrues to the Government. Currently budget transfersand equity participation provide the primary mechanism for transferringthese funds to the nongovernment sector. With further major increases ininvestment in the private and public enterprise sectors, the financialsystem must become better equipped to deal with these transfers.

xi. Price Policy and Subsidies. Budgetary subsidies have risenrapidly in recent years to a level of Rp 2.1 trillion ($3.4 billion) in the1981/82 budget - equal to 15% of the total budget, or 4.0% of GDP. Thelargest subsidy is that on oil products which increased by 82% in the1981/82 budget to Rp 1.5 trillion ($2.4 billion). The economic subsidy (thedifference between international and domestic prices) on oil is muchlarger, and in 1980 amounted to more than $3 billion, equivalent to about 3.5%of GDP. Arguments in favor of maintaining low domestic oil prices are basedon poverty alleviation, inflation control, and environmental protectionconsiderations. The report describes why the subsidization of oil productsis an ineffective method of achieving those objectives, and recommends thatthe subsidy be gradually reduced, and eliminated by the latter part of the1980s. Such a policy would achieve annual foreign exchange savings of about$7 billion (at current prices) and annual budgetary savings of about

Rp 9 trillion (also in current prices), by the end of the decade, sufficientto virtually double the Government's investment program. In addition,realistic energy input pricing would improve resource allocation and thusprovide a more efficient foundation for sustained economic growth in thesecond part of the decade.

xii. The budgetary subsidy on oil products amounts annually to about $5for each person in the lowest 40% income group and about $13 for each personin the upper 60% income group. Despite the small absolute amount benefitingmembers of the poorest group, the abolition of the oil subsidy would howeverimpose a comparatively high burden upon them, and careful thought should begiven to the phasing of the price increases and to ways in which the budgetarysavings from reduced subsidies could be used to supplement the incomes ofthe poor. For example, the savings would over time be sufficient to financea large portion of the rural electrification program on Java, and could beused also to target subsidies toward the lower income groups for consumptionof other, more efficient, energy sources such as bottled LPG. In circum-stances of poverty, inflation and structural adjustment, movement of domesticprices to international and efficient levels has to be accomplished gradually,with due regard for its impact on income distribution. In some countriesthis can be accomplished through taxation policies and in others, where suchpolicies are not effective in redistributing income, targeted subsidies canbe used. The Government is aware of the long-term costs of continuingsubsidies as well as the short-run adjustment costs in raising domestic oilprices to international levels. The Government raised domestic oil pricesin May 1980 by 50% on average and in announcing the price increases reiter-ated its commitment to reduce the subsidy over time and stated inter aliathat such reductions will enable it to finance a larger development program.

xiii. Policy reform in the areas suggested above, would need to becomplemented by expanded public expenditure programs for supportingagricultural services and industrial production designed to raise income andemployment. In addition, expenditures on the social sectors are needed todirectly support poverty alleviation programs as well as raise labor produc-tivity through education, health and nutrition.

Sector Development Programs

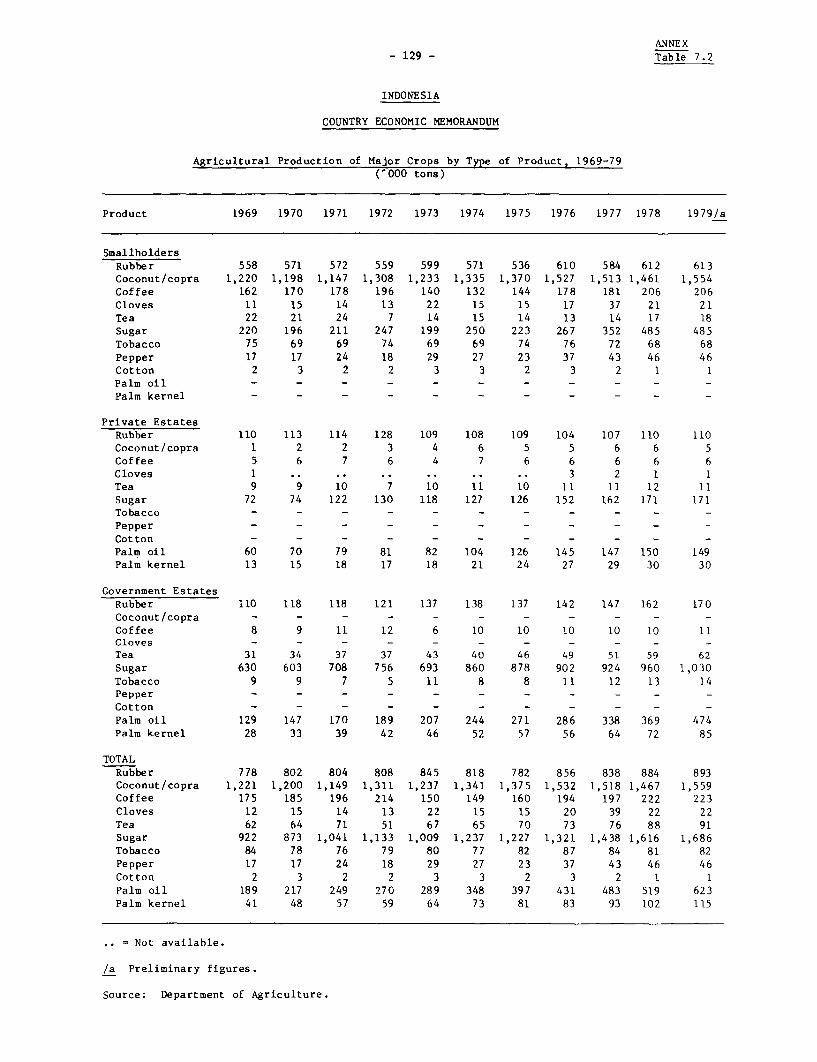

xiv. Agriculture. A continued good performance in this sector will becritical for improved food security, income generation, employment and thebalance of payments in the 1980s. Although agricultural institutions arepredominantly within the private sector, the Government plays a vital rolein provision of infrastructure and services. Large public investments willbe needed to maintain a 3.5% growth rate in the sector in the 1980s. Whileemphasis on rice production must continue, special attention to crops suchas sugar and soya, for which large gaps between production and consumptionhave emerged, will be needed. Key elements for expenditure expansion in thesector include continued intensification, specially further development ofirrigation systems in Java, extension of the cultivated area in the OuterIslands and the improvement of support services and better marketing andprocessing services. The future growth of the irrigation subsector will beincreasingly dependent on new irrigation development rather than rehabili-

- vi -

tation both in Java and the Outer Islands. With the additional resources,the Government is now in a position to develop large integrated dams whereeconomically justified. There is also an urgent need to expand tertiarycanal systems and to improve routine maintenance to reap greater productionbenefits from the existing systems, and to develop technical and managerialcapability to undertake new schemes.

xv. The tree crops subsector, which will be an important foreignexchange earner and in which there are millions of smallholders, will makean important contribution to the structural transformation. The Governmenthas a ten year development program for rubber, coconuts, oil palm, coffee,

and cocoa that aims at rehabilitation, replanting and expansion. Thesuccess of the program will depend on the alleviation of manpower,organizational and financial constraints. The latter constraint appliesespecially in regard to smallholders.

xvi. The transmigration program is seen by Government as an importantvehicle for easing population pressures in Java, and of providing low incomefamilies with greater access to opportunities to earn higher incomes.Performance of the program has improved considerably in relation to pastyears, but manpower shortages, weak interagency coordination, and shortagesof land appropriate for food production continue to hamper progress. Bettersite selection, improved reliability of agricultural inputs, cooperativedevelopment, and the provision of livestock are needed to improve incomes infood crop settlements.

xvii. Industry. A two-pronged approach to industrial development willbe needed in the 1980s. One element will be the development of a number ofcapital intensive projects designed to replace imports of intermediategoods or expand exports of raw materials where economical. The Governmenthas plans in hand for investments in petrochemicals (methanol, olefins,aromatics), fertilizers, cement, pulp and paper, basic metals and mining.A subsidiary objective of this part of the strategy is to deepen theindustrial structure. The other element of the strategy will be thepromotion of production from medium and small-scale industries using morelabor-intensive methods. The policy reforms suggested in the trade regimeand the investment licensing system will serve this element of theindustrial strategy. Increased profitability in manufactured exportindustries is essential for the successful development of the industrialstructure.

xviii. Energy. Domestic oil consumption is growing rapidly, and as aresult the volume of oil exports is expected to decline beyond the mid-1980s, even though production prospects have improved compared to earlierassessments. Development of alternative energy sources - especially coal,hydropower and geothermal - which currently account for less than 10% oftotal energy consumption has therefore become a priority. Successful

- vii -

development of nonoil energy sources will require heavy investment inexploration and development and a revision of the present pricing policy.For example, PLN plans to increase its installed generating capacity at anaverage of 16% a year from 2,700 MW at present to 11,700 MW in 1990. It isunlikely that a program of this size - with a total cost of $14 billion -can be financed without substantial local borrowing for the domestic currencycomponent, estimated at $4-5 billion. This underscores the need for thefurther development of the domestic capital market.

xix. Transport. Because of rapidly growing demand for transportfacilities arising both from income growth and from regional dispersion ofthis growth, an expanded expenditure program is warranted for the sector.Priorities for the 1980s will include increased budgetary allocations andimproved organization for road and bridge maintenance, rationalizing theexisting regulation framework to reduce costs, especially in inter-islandshipping, targeting of subsidies to specific routes and continuing emphasison expanding infrastructure to support development of new roads andsecondary ports in the Outer Islands.

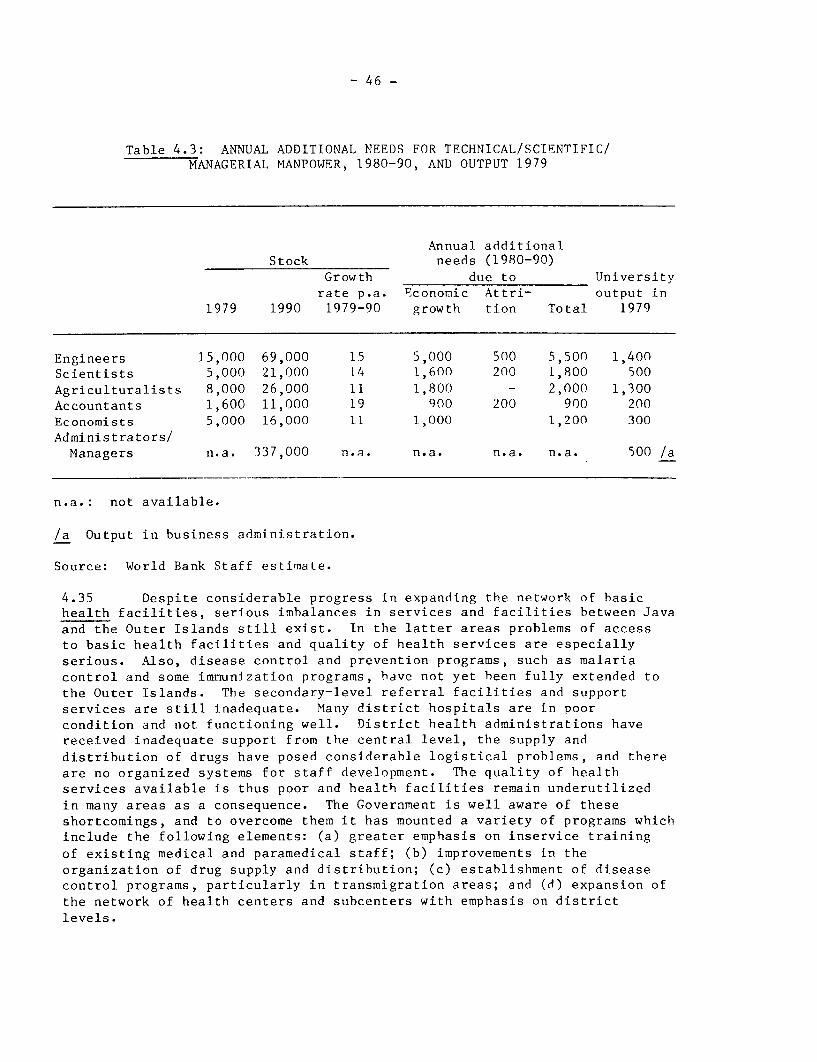

xx. Human Resource Development. Although much progress has been madein the provision of education, health and nutrition in the last decade, keysocial indicators for Indonesia suggest that the level of services avail-able remain relatively modest in comparison to many other countries.Increased emphasis on human resource development will thus be a majorchallenge for the 1980s. It will serve as a vehicle for raising laborproductivity as well as poverty alleviation. Although Indonesia has madegreat strides in expanding primary education, progress in secondary andtertiary levels has been much slower and participation rates at these levelsare lower than the averages for all low income countries. Given thatskilled manpower has emerged as the primary constraint to the use ofadditional resources, expanded expenditures on education and training shouldhave a high priority. Large, and in some areas growing gaps between supplyand demand for technical and professional manpower justify substantialinvestments in education beyond the secondary level. In the short andmedium-term the purchase of skills abroad, short-term training programs andon-the-job training facilities will help to bridge some of these gaps. Thesuccess of development programs in the 1980s will depend heavily on progressmade in alleviating the skilled manpower constraint.

xxi. In the field of health, physical achievements have been rapid inJava, but even here it is unclear whether the newly established infra-structure is effectively utilized. The secondary level referral facilitiesand support services are still inadequate. Many district hospitals are inpoor condition and not functioning well, while district health administrationshave received inadequate support from the central level. In the OuterIslands, both infrastructure and service facilities are needed. Extension ofdisease control and prevention programs such as malaria control andimmunization programs to the Outer Islands is a priority. The expenditure

- viii -

expansions must be accompanied by greater in-service training to raise thequality of health service, improved drug supply, and expansion of the networkof health centers and subcenters at district levels.

Balance of Payments and External Capital Inflows

xxii. The projected balance of payments surplus in the first half of the1980s clearly has significance for the Government-s external borrowingstrategy. Increased creditworthiness, as evidenced by attractive interestrates, maturities and grace periods on commercial debt incurred in 1980,ensures Indonesia's continued access to credit markets. But the questionshould be raised whether Indonesia should continue to borrow from externalsources while the current account surpluses persist. In examining thisquestion it is useful to distinguish between capital from official and fromcommercial sources.

xxiii. Since foreign exchange resources are not at present a bindingconstraint on development, continued capital aid to Indonesia has to bejustified more by technical assistance embodied in financial flows than byfinancial flows themselves. Foreign donors, and especially members of theIGGI, have been a major source of financial and technical assistance forIndonesia. Programs and projects developed with the capital and technicalassistance of donors are making an important contribution to the monumentaldevelopment tasks of overcoming poverty, disease, malnutrition, and the lackof basic services. Donors have developed a stock of knowledge in designingprojects and programs in specific sectors; they have a close associationwith the implementing agencies, and have a commitment to developmentassistance that goes well beyond financial transfers. There is therefore aclear case for continued capital assistance for programs and projects thatinclude technical assistance, training, and technology transfers. In thismanner donors can play an important role in assisting the Government in theprogram of structural adjustment.

xxiv. New commitments of loans from official bilateral and multilateralsources are projected to remain relatively stable at about $2.5 billionthroughout the 1980s. However, it is expected that the average terms forthis borrowing will harden. A declining share of loans at highly conces-sional rates is projected to be offset by increased use of official exportcredits.

xxv. With the prospect of continued resource surpluses for severalyears, Indonesia now has the option of using more of its own funds. For thisreason, the report suggests a reduced level of borrowing from private sourcesand especially from the Euro-dollar market in the first half of the 1980s.The level of public borrowing from private sources would, however, have torise again by the mid-1980s in anticipation of the projected balance of pay-ment deficits. New public and private borrowings from private markets are

- ix -

projected to reach about $6 billion annually by the end of the 1980s in theHigh case, a level that would be well within the limits of prudent borrowingfor Indonesia at that time.

xxvi. Direct private investment can also play an important role in thetransfer of managerial skills and technology and in employment creation inthe 1980s. If the policy reforms suggested under the High case were adopted,the decline in net real inflows of direct foreign investment that haspersisted since 1974, could be reversed. Under the High case net inflowsare therefore projected to rise by 5% a year in real terms from less than$200 million at present to $500 million a year by 1990. This rate isslightly above the rate at which direct investment in developing countriesgenerally is likely to grow in the future.

xxvii. Official reserves which at end of March 1981 stand at $7.1 billion(equivalent to 6.9 months of non-oil imports) are expected to rise under theHigh case to about $25 billion by the end of the decade (equivalent to 3.9months of imports). Under the Low case, balance of payments deficitstowards the end of the decade cause a rapid depletion of official reserves,which by 1990 are projected to amount to about $13 billion (equivalent toabout 2.9 months of imports).

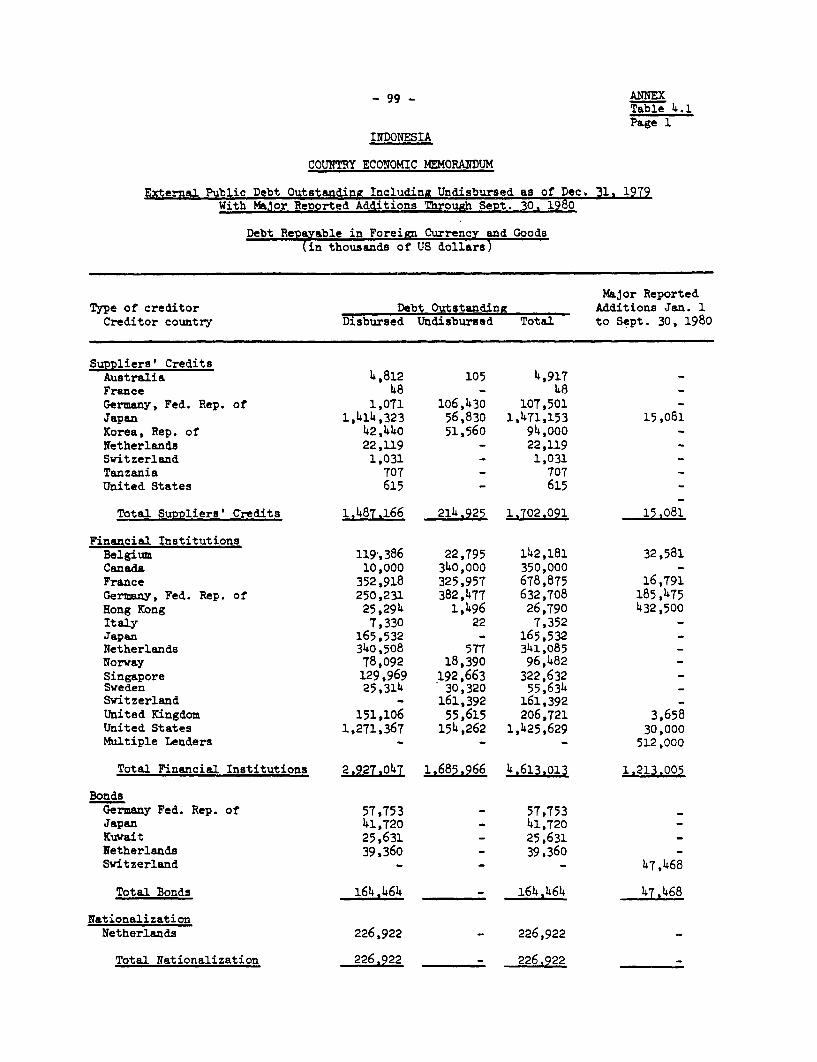

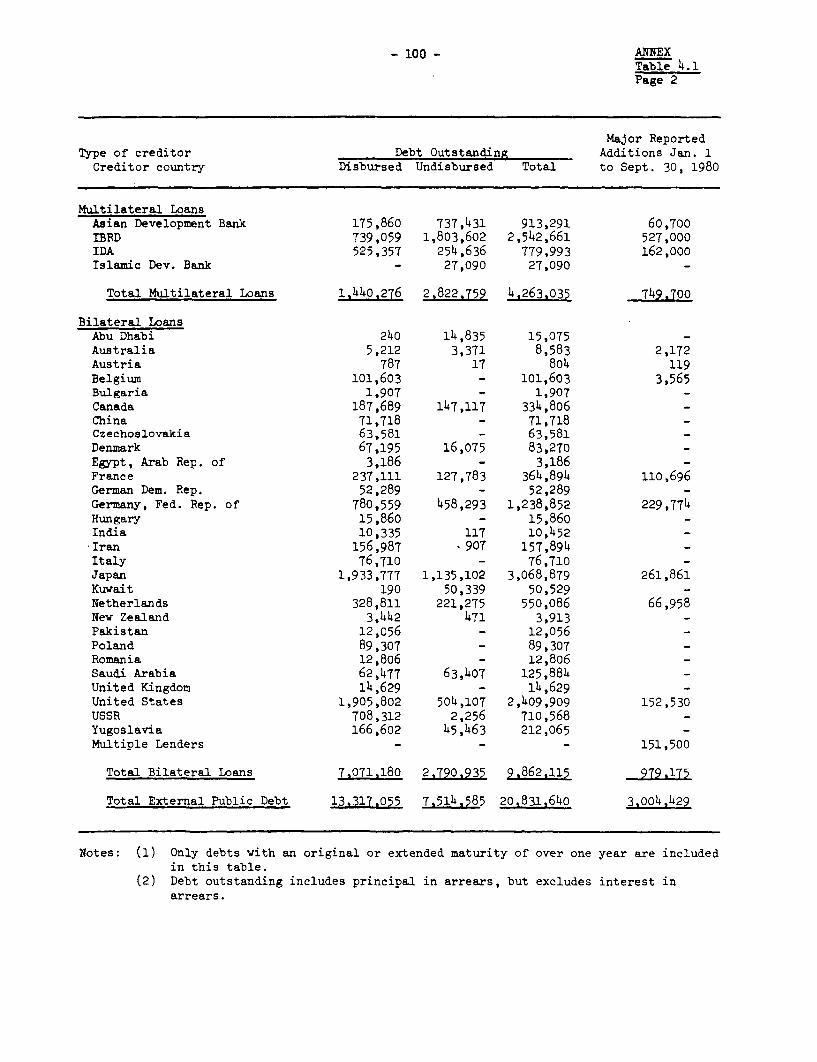

xxviii. Disbursed and outstanding external public debt is estimated to be$15.2 billion at the end of March 1981 and is projected under the High caseto grow by about 9% annually to about $34 billion by 1990. The ratio ofinterest and amortization payments (on public and private debt) to exportreceipts which declined sharply in 1980/81 is expected to remain stable atabout 12% during the first half of the 1980s. Under the High case it wouldrise only slightly to 13% by 1990. Under these circumstances Indonesiashould have no difficulty in maintaining a manageable external financialposition.

1. INTRODUCTION

1.01 There were two central themes in last year-s economic report onIndonesia,/1 namely: (a) how to contain in the near future the inflationarypressures associated with the windfall revenues from oil; and (b) how touse the windfall revenues to lay the foundations for sustained economicgrowth and greater equity in the longer-term. These are retained in thepresent report. But there is more emphasis this time on policy changes andinvestment programs needed for long-term structural reform and less onshort-term monetary and fiscal management issues. The special features ofoil-associated resource surpluses - and especially their external origin -will pose many challenges for the economic management of Indonesia in the1980s. The main theme of this report is that a program of structural reformis needed in the first half of the 1980s to ensure rapid growth and improveddistribution during the second half of the decade and beyond.

1.02 Indonesia's medium-term economic prospects appear brighter than ayear ago. Higher oil and LNG prices and improved production prospects, atleast for the next few years, are likely to increase Indonesia-s foreignexchange resource surpluses in the medium-term. This gives the opportunityto maintain GDP growth at 7-8% p.a. in real terms during the 1981-84 period,exceeding the 6.5% p.a. visualized at the time of preparation of Repelita III.Nevertheless, the longer-term prospects for growth, employment, and equitywill depend crucially on policy changes made between now and the mid-1980s.Mainly as a result of rapid domestic consumption growth, oil exports areexpected to decline from the mid-1980s.

1.03 Foreign exchange surpluses have, for the time being, overcome thefinancial constraint which plagued Indonesia for the most of the past twodecades. However, other constraints to development remain and have now cometo the fore. These include skilled manpower, administrative capacity and thecapacity of the construction sector. Because the resource surpluses werenot anticipated when Repelita III was drawn up, strategies to break thenonfinancial constraints have to be articulated, expenditure programsidentified, and the implementation machinery improved. The Government isnow gearing up to these new tasks as there is growing awareness

/1 "Indonesia: Long run Development and Short Run Adjustment," World Bankreport No. 2788-IND, February 1980.

- 2 -

of the unique opportunity afforded by the oil revenues to address the manyand varied development needs of the country.

1.04 By all standards Indonesia remains a poor country despite thecurrent resource surpluses. Each $1 billion earned in foreign revenues addsless than $7 to per capita income, which is provisionally estimated at $405for 1980. Although this level is much higher than that of most low incomecountries, it masks existing dimensions of poverty, limited access to basicservices and the need for more productive utilization of Indonesia-s mostimportant development resource: its large and rapidly growing labor force.From the data on distribution of households by levels of per capitaconsumption, it is estimated that in 1976, the latest year for which data isavailable, some 40% of the total population were subsisting on less than $90per year.

1.05 In the areas of health, education, water supply and other basicservices, there is both the need and the scope for a substantial effort inthe 1980s. Provisional 1980 population census results suggest that lifeexpectancy in Indonesia has increased from less than 50 years in early 1970 toaround 55 years in 1980. But this is still less than that in the majority ofmiddle income countries. The challenges in education are formidable in viewof the shortages of skilled manpower. While primary school enrollment ishigher than for most other low income countries, secondary and high schoolenrollment at 21% and 2% are below the averages of 24% and 4% respectively forlow income countries, and only about one-half and one-fifth respectively ofthe middle income country averages.

1.06 Preliminary results of the 1980 population census put the totalpopulation at 147 million, about 2 million more than had been generallyexpected on the basis of earlier projections. This has important implicationsfor the provision of basic services and for policies aimed at increasing therate of labor absorbtion in the economy. Recent estimates for the futuregrowth of the labor force at 3.2% p.a. compare with the 2.3% p.a. estimatemade in 1976. The revised growth rate for the labor force raises the numberof new entrants to the labor market from 1.5 million p.a. to 2.0 million p.a.during the 1981-84 period. This underscores the urgency of using resourcesnow available to expand productive employment in agriculture, industry, publicworks and service sectors.

1.07 The duration of foreign exchange surpluses cannot be predicted withaccuracy. Even though oil production prospects have improved, the analysisof this report suggests that, if present domestic oil consumption ratescontinue, net exports of oil will begin to decline in the mid-1980s. In theabsence of policy changes and investment programs to stimulate alternativesources of export and income growth, significant resource deficits areprojected to re-emerge during the second-half of the 1980s. But even if oilproduction prospects were to improve beyond current expectations, the case

-3 -

for structural transformation would remain valid. Production in the oilsector is highly capital and skill-intensive and therefore input requirementsdiffer from domestic factor supplies. Hence, domestic consumption and pro-duction linkages are very limited and it will be very difficult to achieveemployment and equity goals within the present structure of the economy.

1.08 The plan of the report is as follows: Chapter Two reviews recenteconomic trends. Chapter Three considers broad macroeconomic options formanaging the resource surplus in the medium-term and policy changes requiredfor longer-term growth. Chapter Four focuses on sectoral development issuesand investment programs and identifies a number of constraints that cut acrossmany sectors. Chapter Five presents balance of payments and budget pro-jections for the 1980s under the alternative scenarios. Finally, Chapter Sixreviews policies towards external assistance and borrowing, in the light ofthe prevailing foreign exchange surplus.

- 4 -

2. RECENT TRENDS IN THE ECONOMlY

2.01 Key economic indicators confirm that the Indonesian economyrecovered fully in 1980 from the 1979 slump. A higher GDP growth rate,improved terms of trade, a balance of payments surplus, and relative monetarystability characterized the 1980 performance. Private consumptionexpenditures also rose sharply, as reflected for example in a 50% increase inmotor vehicle purchases and larger-than-ever numbers of Indonesian pilgrimsto Mecca.

2.02 Underlying these recent developments were three dominant factors:continuing adjustments to the November 1978 devaluation resulting, inter-alia,in the recovery of domestic production; a bumper rice harvest and strongagricultural growth generally; and increases in foreign exchange earningsbrought about by increases in the international price of oil. This chaptertraces the impact of these factors on domestic production and expenditures,the balance of payments, the Government's budget and the domestic price leveland monetary policy.

Domestic Production and Expenditures

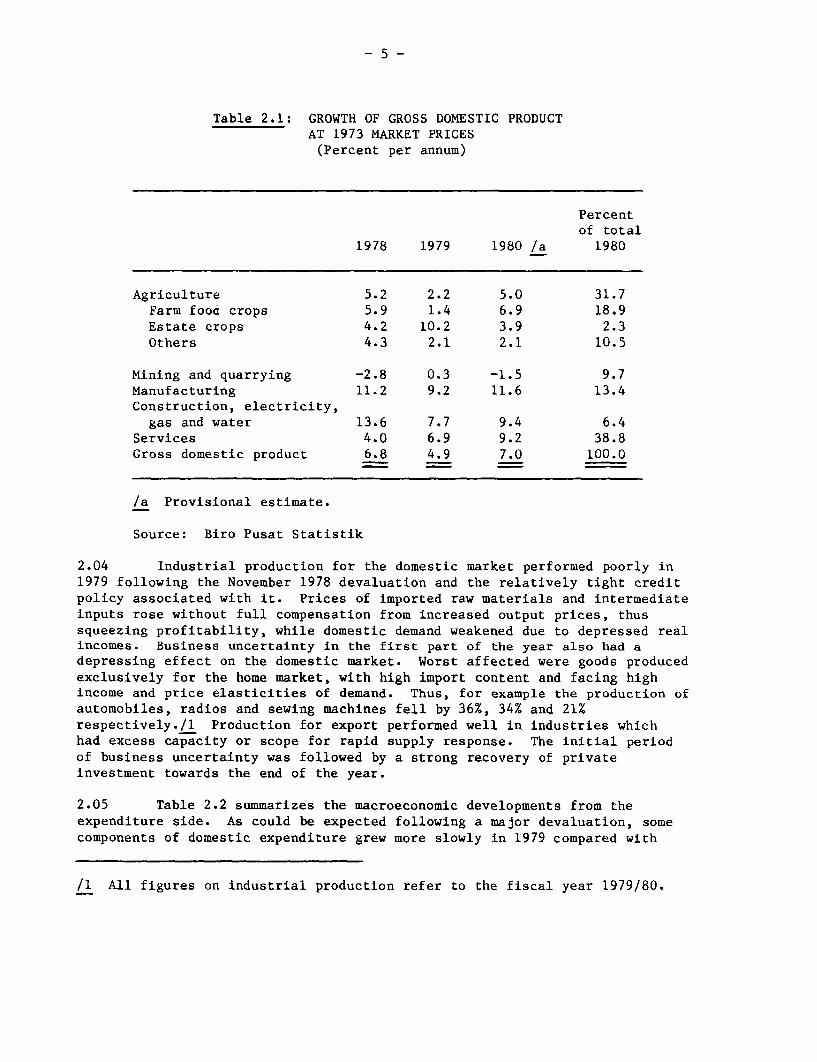

2.03 Economic growth in 1979 was well below that of the previous fewyears. In constant 1973 prices GDP grew by 4.9%, compared with an annualgrowth rate of 6.9% in the period 1973-78 (Table 2.1). The rice harvest,which jumped by a remarkable 10.4% to 17.5 million tons in 1978, increasedonly 2.2% to 17.9 million tons in 1979; while the production of corn, sweetpotatoes and ground nuts was lower than in 1978. The production of logsalso fell despite favorable world market prices. Estate crop production onceagain showed the strongest growth in the agriculture sector due to earliergovernment investments in the public estates, particularly in oil palm andtea, production of which grew by 20% and 39% respectively.

- 5 -

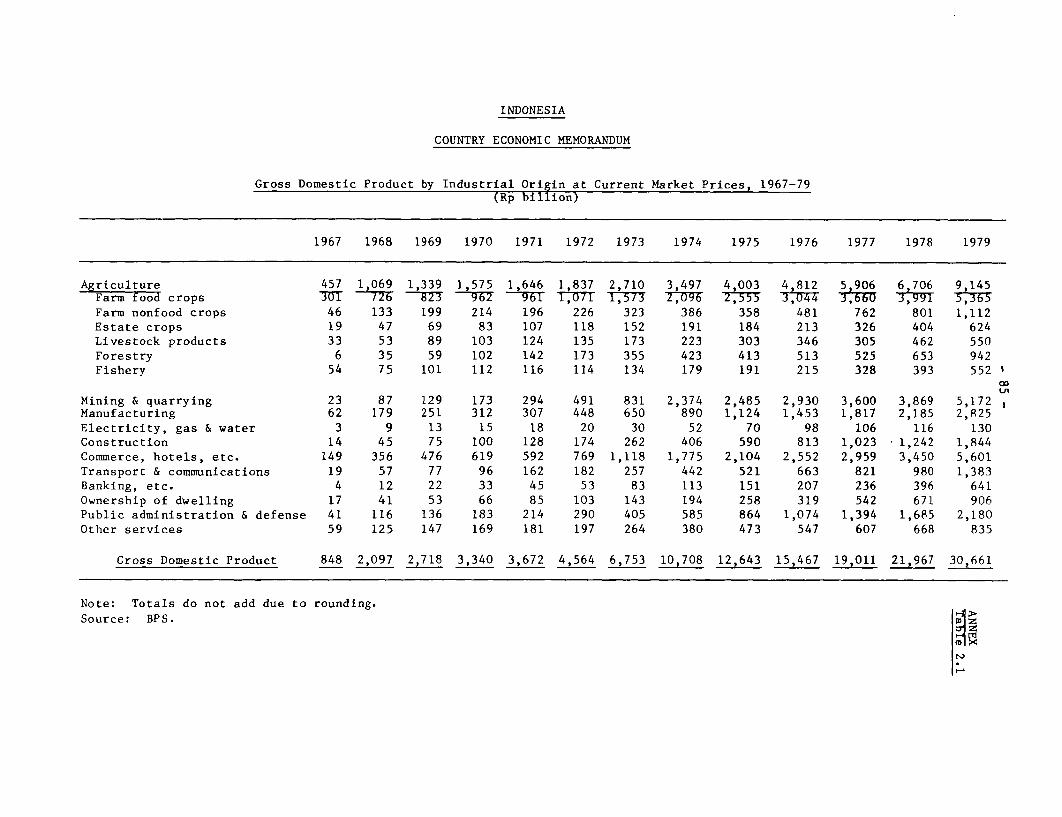

Table 2.1: GROWTH OF GROSS DOMESTIC PRODUCTAT 1973 MARKET PRICES(Percent per annum)

Percentof total

1978 1979 1980 /a 1980

Agriculture 5.2 2.2 5.0 31.7Farm food crops 5.9 1.4 6.9 18.9Estate crops 4.2 10.2 3.9 2.3Others 4.3 2.1 2.1 10.5

Mining and quarrying -2.8 0.3 -1.5 9.7Manufacturing 11.2 9.2 11.6 13.4Construction, electricity,

gas and water 13.6 7.7 9.4 6.4Services 4.0 6.9 9.2 38.8Gross domestic product 6.8 4.9 7.0 100.0

/a Provisional estimate.

Source: Biro Pusat Statistik

2.04 Industrial production for the domestic market performed poorly in1979 following the November 1978 devaluation and the relatively tight creditpolicy associated with it. Prices of imported raw materials and intermediateinputs rose without full compensation from increased output prices, thussqueezing profitability, while domestic demand weakened due to depressed realincomes. Business uncertainty in the first part of the year also had adepressing effect on the domestic market. Worst affected were goods producedexclusively for the home market, with high import content and facing highincome and price elasticities of demand. Thus, for example the production ofautomobiles, radios and sewing machines fell by 36%, 34% and 21%respectively./l Production for export performed well in industries whichhad excess capacity or scope for rapid supply response. The initial periodof business uncertainty was followed by a strong recovery of privateinvestment towards the end of the year.

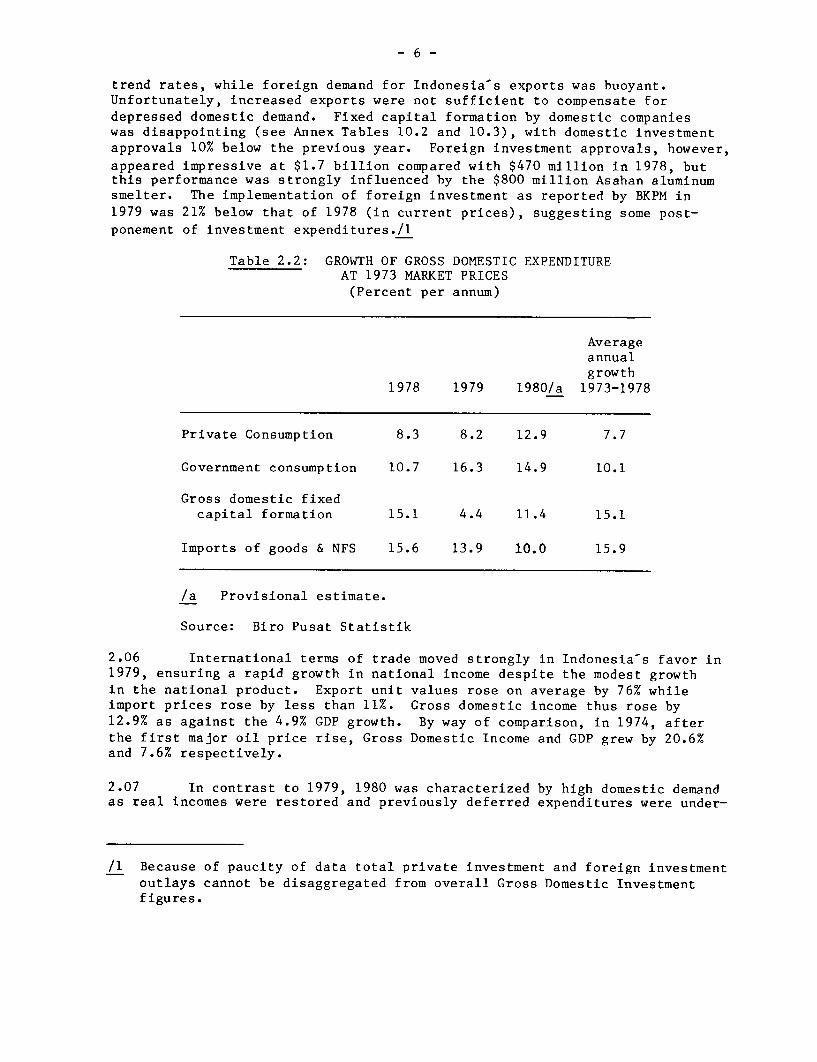

2.05 Table 2.2 summarizes the macroeconomic developments from theexpenditure side. As could be expected following a major devaluation, somecomponents of domestic expenditure grew more slowly in 1979 compared with

/1 All figures on industrial production refer to the fiscal year 1979/80.

- 6 -

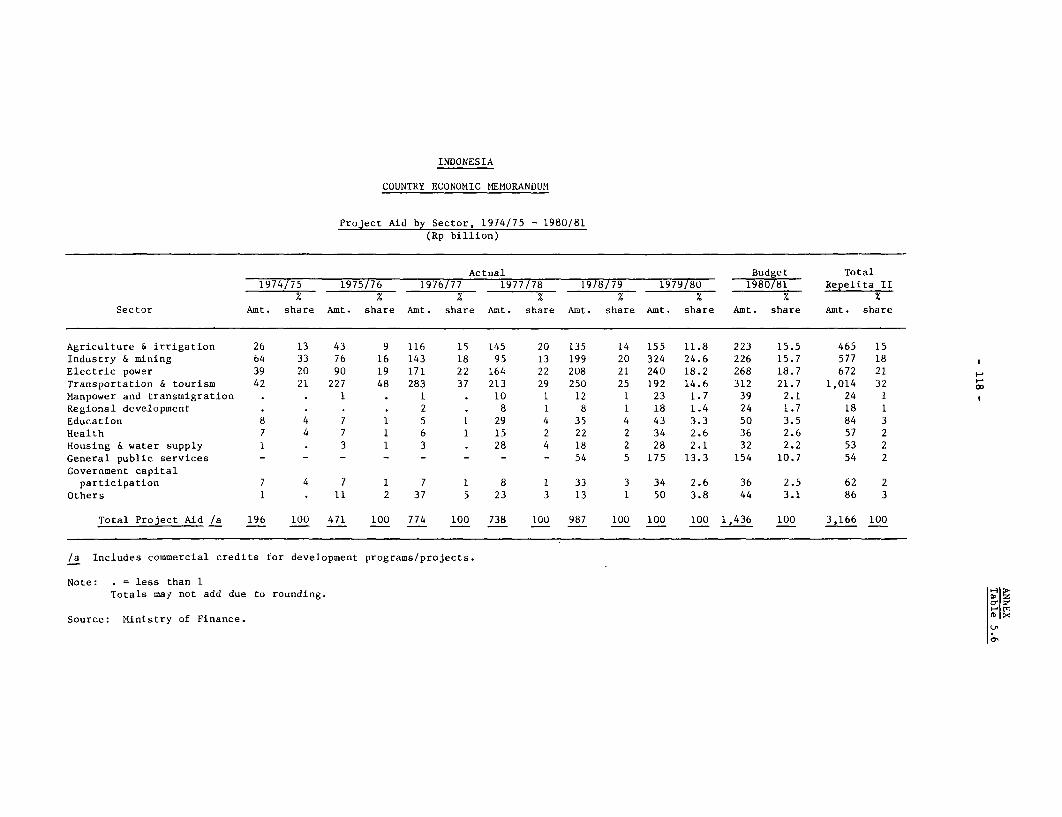

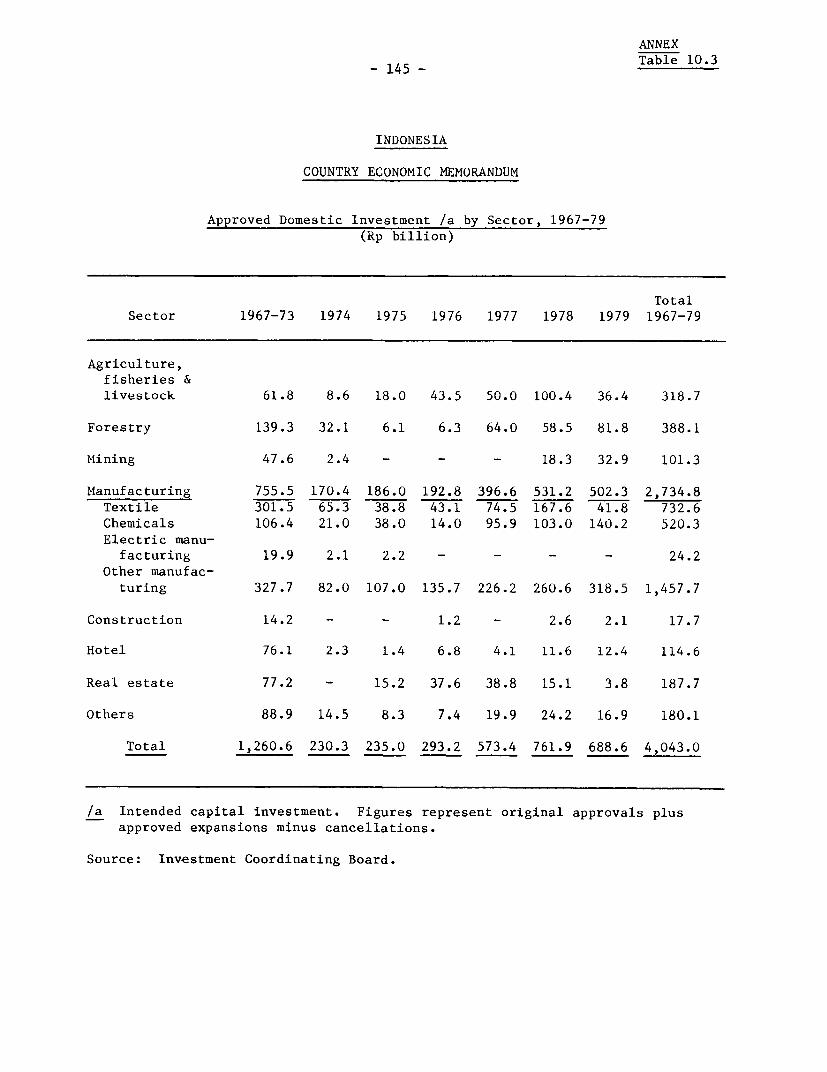

trend rates, while foreign demand for Indonesia's exports was buoyant.Unfortunately, increased exports were not sufficient to compensate fordepressed domestic demand. Fixed capital formation by domestic companieswas disappointing (see Annex Tables 10.2 and 10.3), with domestic investmentapprovals 10% below the previous year. Foreign investment approvals, however,appeared impressive at $1.7 billion compared with $470 million in 1978, butthis performance was strongly influenced by the $800 million Asahan aluminumsmelter. The implementation of foreign investment as reported by BKPM in1979 was 21% below that of 1978 (in current prices), suggesting some post-ponement of investment expenditures./I

Table 2.2: GROWTH OF GROSS DOMESTIC EXPENDITUREAT 1973 MARKET PRICES(Percent per annum)

Averageannualgrowth

1978 1979 1980/a 1973-1978

Private Consumption 8.3 8.2 12.9 7.7

Government consumption 10.7 16.3 14.9 10.1

Gross domestic fixedcapital formation 15.1 4.4 11.4 15.1

Imports of goods & NFS 15.6 13.9 10.0 15.9

/a Provisional estimate.

Source: Biro Pusat Statistik

2.06 International terms of trade moved strongly in Indonesia-s favor in1979, ensuring a rapid growth in national income despite the modest growthin the national product. Export unit values rose on average by 76% whileimport prices rose by less than 11%. Gross domestic income thus rose by12.9% as against the 4.9% GDP growth. By way of comparison, in 1974, afterthe first major oil price rise, Gross Domestic Income and GDP grew by 20.6%and 7.6% respectively.

2.07 In contrast to 1979, 1980 was characterized by high domestic demandas real incomes were restored and previously deferred expenditures were under-

/1 Because of paucity of data total private investment and foreign investmentoutlays cannot be disaggregated from overall Gross Domestic Investmentfigures.

- 7 -

taken. Consumer and investor confidence returned as the cost-inducedinflationary pressures of the post-devaluation period were gradually broughtunder control. Real GDP growth is estimated by the Government at 7.1% in1980 - higher than the average Repelita III target of 6.5%. With furtherimprovements in Indonesia's terms of trade, national income growth exceeded10% in 1980.

2.08 Domestic investment approvals amounted to Rp 1.5 trillion in 1980compared with Rp 689 billion in 1979, indicating the beginning of a newprivate investment boom. In real terms /1 approvals of domestic investmentin 1980 were higher than for any previous year. Applications for investmentlicenses in 1980 were particularly high in the chemical, wood processing andforestry industries, the latter two reflecting the recent government emphasison domestic processing of timber (see para. 2.16).

2.09 Foreign investment approvals amounted to $776 million in 1980,down from $1,765 million in 1979 (which was dominated by the $800 millionAsahan aluminum smelter), but about equal in real terms to the annualaverage of the past five years. However, many of the new approvals relatedto expansion of existing facilities and to revisions in cost estimatesrather than to new investments. The general decline in new foreigninvestment in the nonoil sectors that has prevailed since the mid-1970sappears to be continuing.

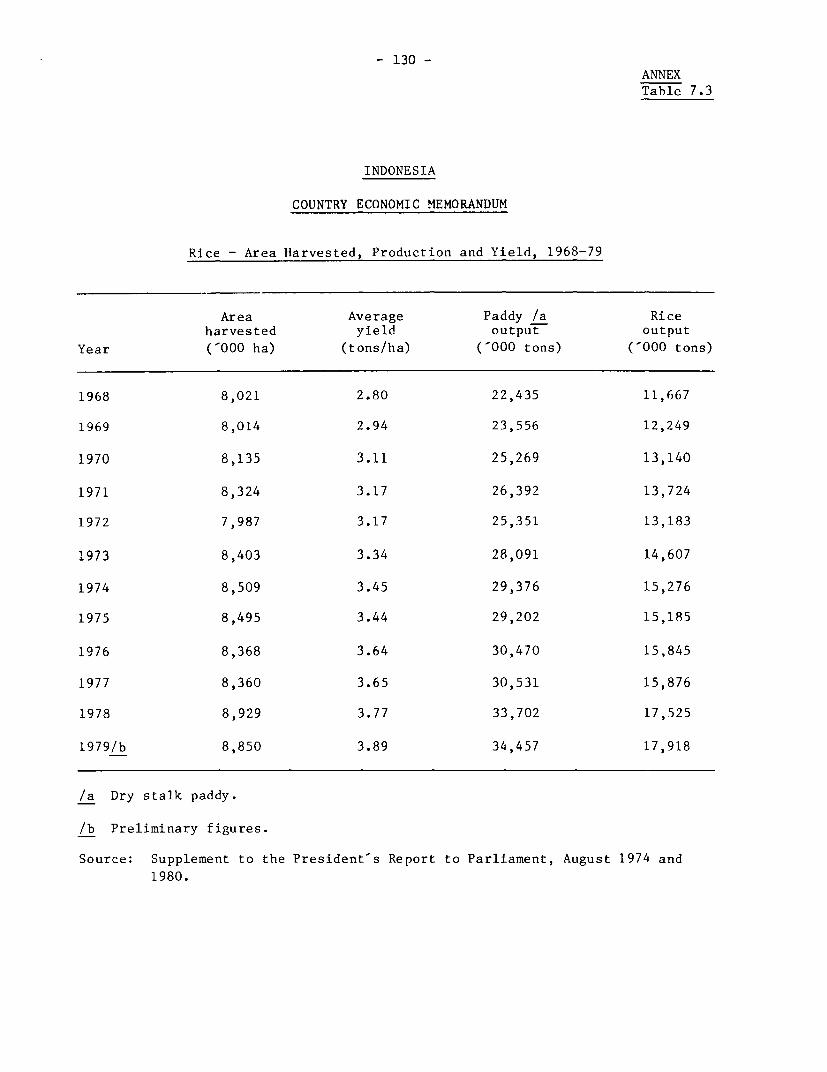

2.10 The agricultural sector provided a strong impetus to the economyin 1980, growing by about 5%. The excellent rice crop of almost 20 milliontons, up 11% from last year, was due to relative absence of pests, expandeduse of fertilizer and favorable weather. It has resulted in strongconsumer demand in rural areas (particularly East Java) and stable grainprices. Aggregate output of secondary food crops was relatively stable in1980, with increases in some crops such as cassava, peanuts and soybeans beingoffset by lower corn production. The area under corn, which fell by 15% in1979, declined again in 1980. The main reasons were the increased intensityof rice cultivation, which precludes intercropping with corn, and substitutionof cassava for corn due to high export demand for staples. Reflecting stronggrowth in demand and the slow rate of increase in production, imports of sugarand soyabean grew rapidly in 1980, as did imports of wheat.

2.11 The construction sector showed particularly impressive growth in1980, but was still unable to meet the demand for construction services.The excess capacity which characterized the building industry in 1979 hasbeen superceded by shortages of construction materials and skilled labor.In the first ten months of 1980, construction costs rose at a rate doublethat of the overall wholesale price index./2 Cement consumption, which in

/1 Wholesale price index used as deflator.

/2 Between December 1979 and October 1980, the wholesale price index forconstruction materials rose by 20.3% while the overall non-export WPIrose by 10.2%.

- 8 -

1979 rose by only 1.4% increased by over 20% in 1980, resulting in severe

shortages. Cement imports were at their highest levels since 1976 andexceeded exports.

Balance of Payments

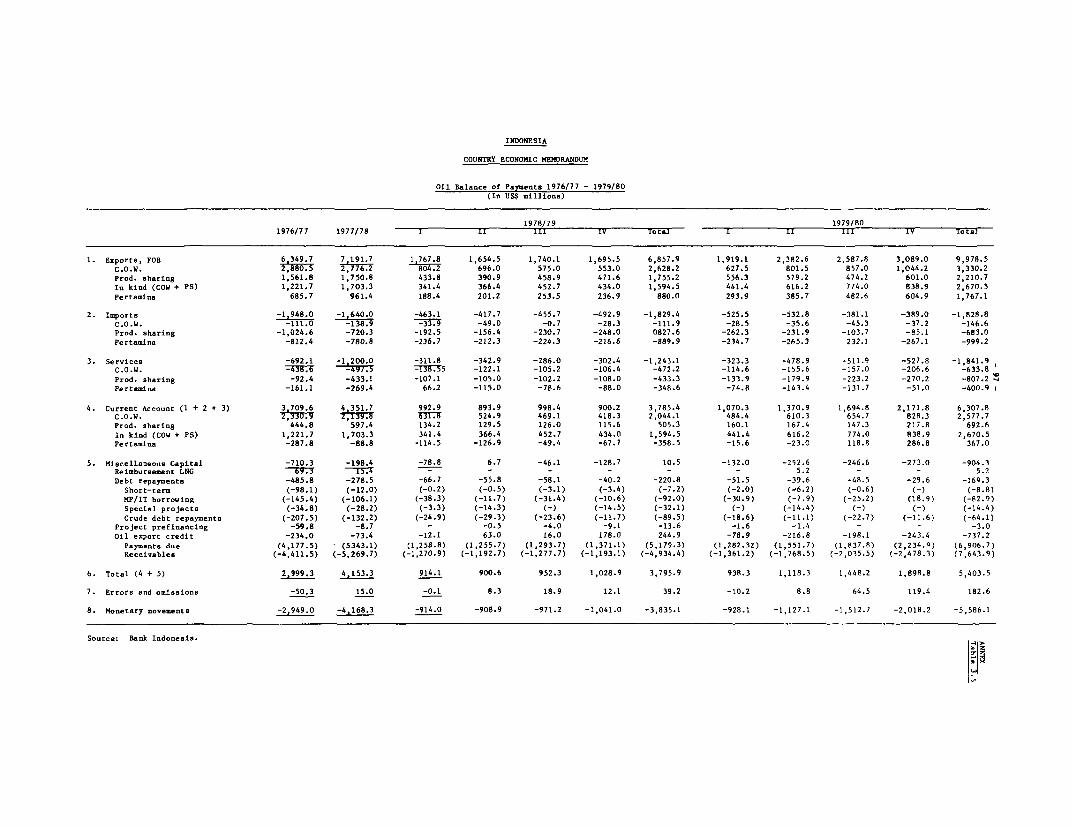

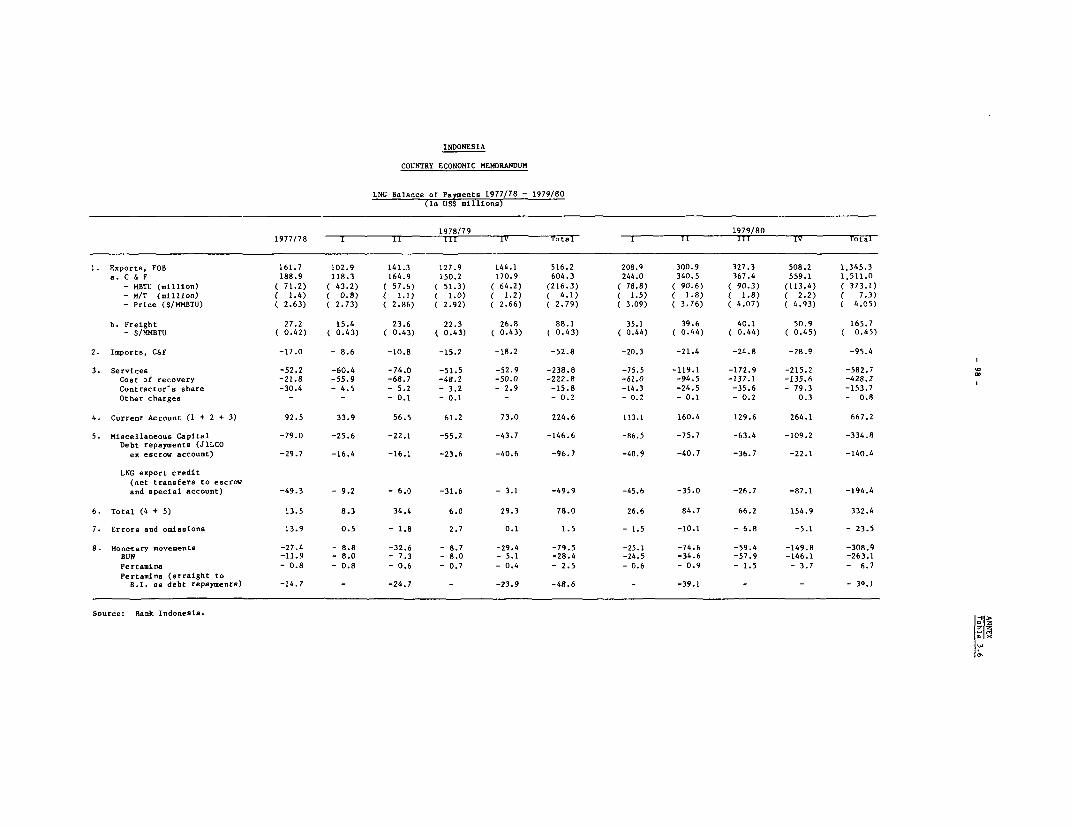

2.12 In 1979/80 Indonesia enjoyed a current account surplus in more thantwo decades. The $2.0 billion surplus was a $3.1 billion improvement over theprevious year and matched the increase in net earnings from oil and LNGexports. Although the volume of oil exports declined by 7% in 1979/80, theincrease in the average export price from $13.50 per barrel in 1978/79 to$22.50 in 1979/80, and the 78% increase in the volume of LNG exports from alow base, accounted for the increase in net oil and LNG export earnings.

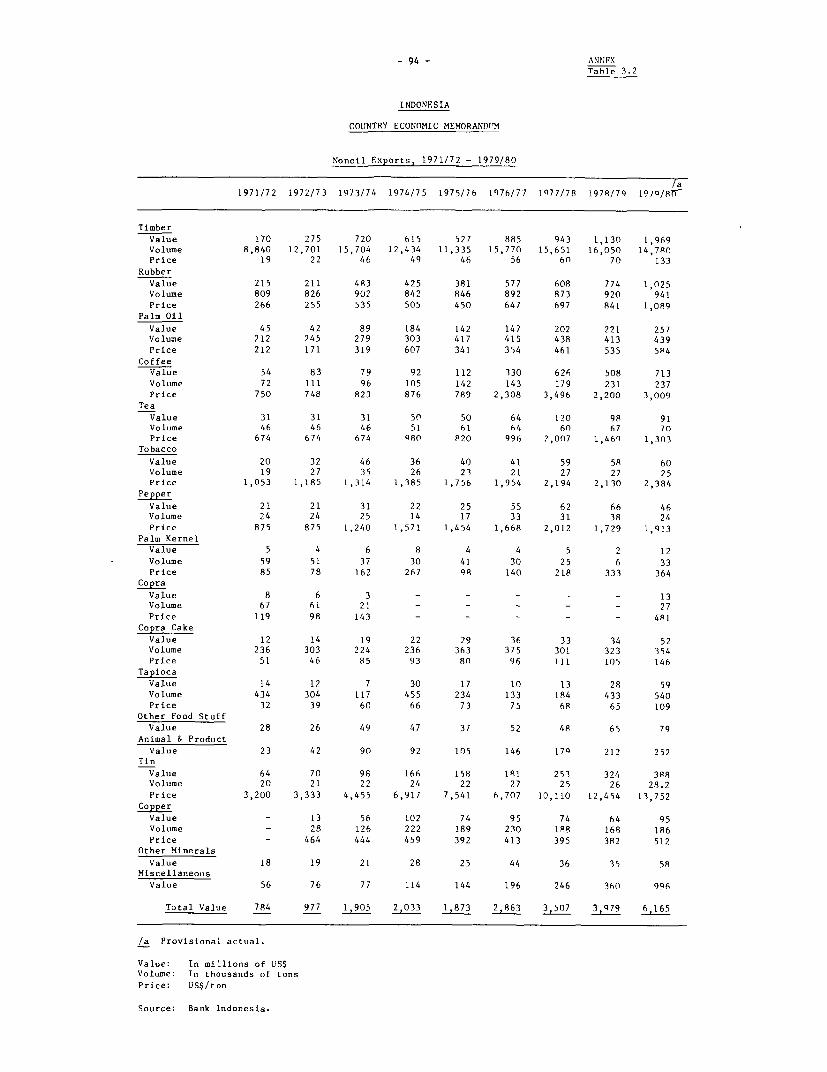

2.13 Nonoil merchandise exports, which account for 35% of total earnings,increased by 55% in 1979/80, largely due to higher prices. Volume increaseswere confined to palm oil, coffee, tin, copper and miscellaneous manufactures.The most dramatic volume increase for any one category was in manufacturedexports including garments, textiles, and electronic parts. These items grewby 140% to $1.0 billion under the impetus of the devaluation and the exportcertificate scheme. The increased volume of exports of manufactures primarilystemmed from a reallocation of existing production capacity from the weakdomestic market to the more profitable overseas market rather than fromcreation of new production capacity just for the export market.

2.14 In 1979/80 total nonoil imports grew by 23% to $9.2 billion (orabout 8.7% in real terms). Although similar in the aggregate to the averagegrowth of 8.4% a year in real terms between 1973 and 1978, the composition ofthe import growth in 1979/80 was markedly different from the past. Riceimports rose to $744 million, an increase in volume of 140%. Imports ofintermediate goods increased by 16% reversing a downward trend. The largestgains here were in chemical inputs and textiles, reflecting the strongdemand from manufacturing plants for export-oriented production. Thereduction of tariffs on these imports was also a factor which contributed totheir rapid growth. Capital goods imports, however, remained at a relativelymodest level in 1979/80, reflecting the previously-mentioned weak investmentclimate. Imports of nonrice consumption goods fell by 7.5% in real terms,due to the devaluation-induced relative price shifts and the low level ofconsumer spending.

2.15 In the capital account, disbursements of public medium- and long-term loans declined in nominal terms; net transfers (disbursements lessamortization plus interest payments) were already negative. This was largelydue to the prepayment of over $400 million of debt. The net foreign assets(NFA) of Indonesian commercial banks rose by $1.9 billion, and officialreserves by $1.7 billion. Official reserves rose to $4.6 billion, the equiva-lent of 5.6 months of nonoil imports and net nonfactor services. In additionthe state-owned commercial banks were holding NFA amounting to $2.3 billion.

- 9 -

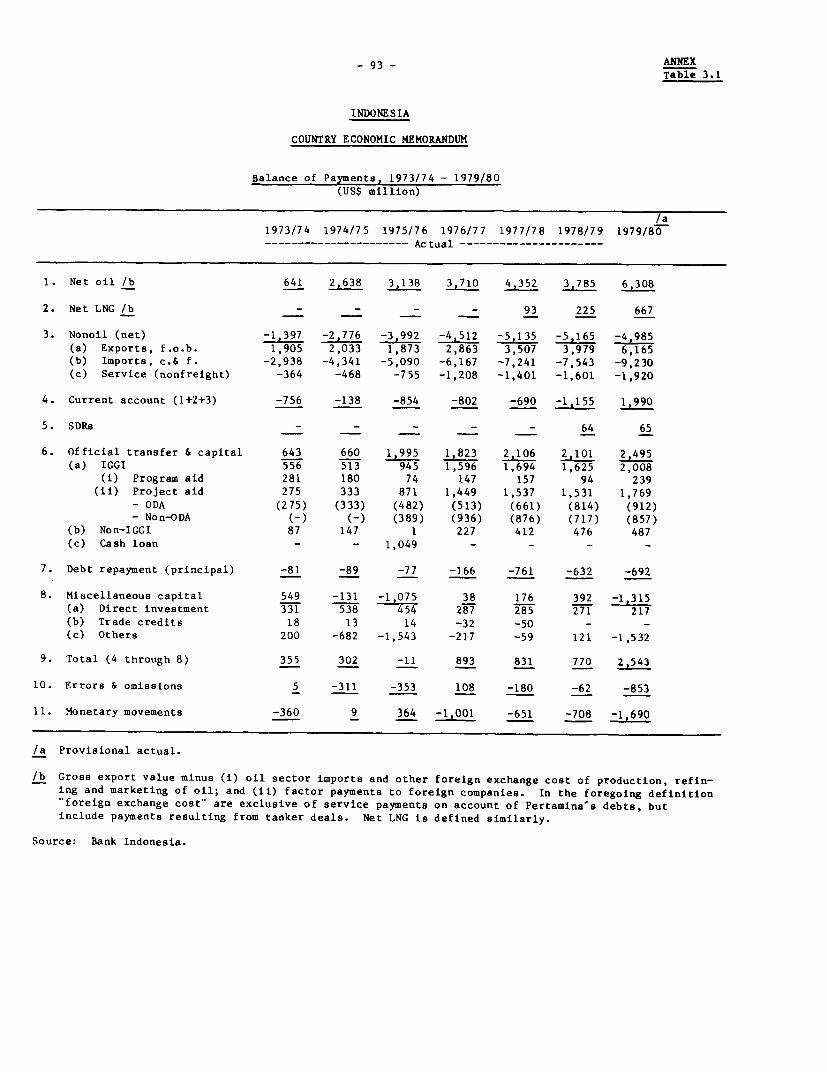

Table 2.3: BALANCE OF PAYMENTS(US$ billions)

1978/79 1979/80 1980/81(estimate)

Merchandise exports 11.35 17.49 22.41Oil and LNG (gross) 7.37 11.32 16.66Nonoil 3.98 6.17 5.75

Merchandise imports -10.90 -13.67 -17.58Oil sector -3.36 -4.44 -6.08nonoil -7.54 -9.23 -11.50

Nonfactor services (net) -0.59 -0.66 -0.97

Resource balance -0.14 3.26 3.86

Factor services (net) -1.01 -1.26 -0.96

Official transfers 0.05 0.05 0.08

Current account balance -1.10 2.05 2.98

Direct foreign investment (net) 0.27 0.22 0.17

Public medium- and long-termloans (net) 0.66 0.61 1.88

Other capital (net) 0.88 -1.17 -2.53Deposit money banks -0.32 -1.87 -1.70Other 1.30 0.70 -0.83

Change in official reserves -0.71 -1.69 -2.51

Net official reserves 2.92 4.61 7.11

Memorandum Item:

Net foreign assets of depositmoney banks (DMBs) 0.43 2.30 4.00

Source: See Tables 1-3, Analysis and Projections Appendix fordetails.

- 10 -

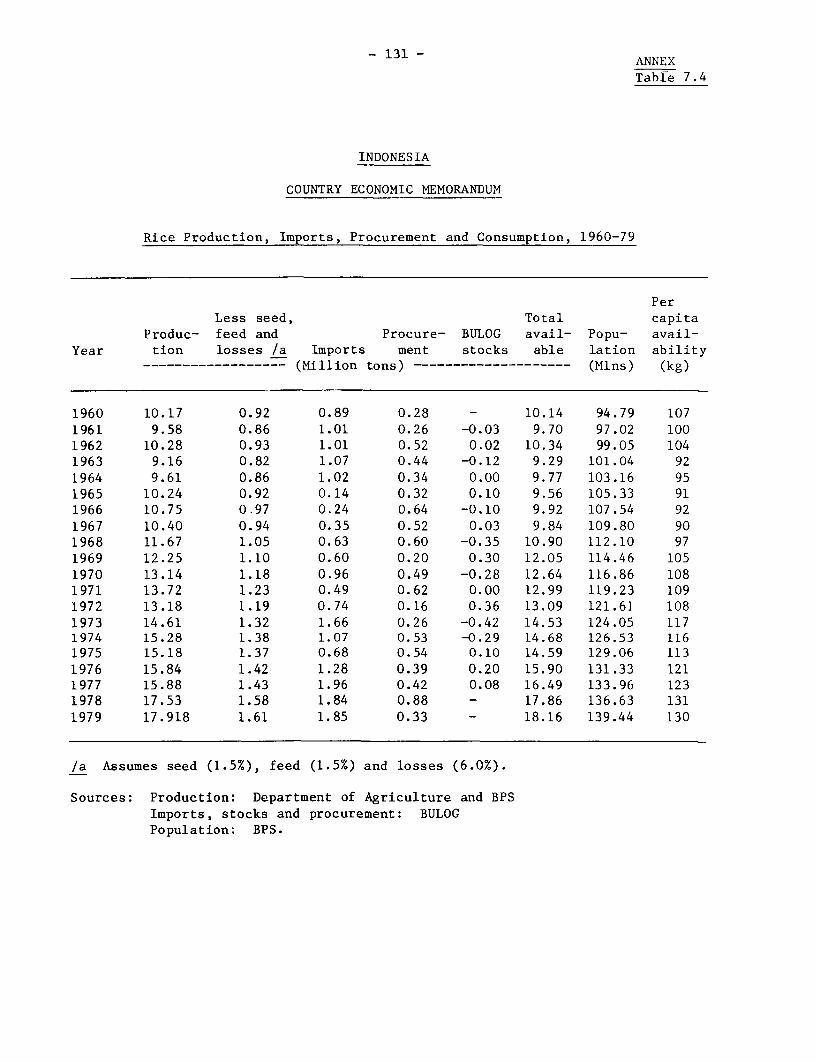

2.16 For 1980/81 total gross receipts from oil and gas exports areexpected to be about $16.9 billion, an increase of 50% over the previous year.Nonoil exports on the other hand are expected to decline slightly in 1980/81.This is mainly due to an expected decline in timber exports, a modest increasein the value of perennial crop exports (palm oil exports are expected tofall), lower coffee and rubber prices, and a much weaker performance inmanufactured exports. Timber exports, which account for one-third of totalnonoil exports, are expected to fall in volume by about 30% in 1980/81, due tothe introduction of the "Three Minister-s Decree" in May 1980 which requiresthat a certain proportion (currently 66%) of domestic logs be processed withinIndonesia. The poor performance of manufactured exports is mainly due to therecovery of domestic demand, including in particular fertilizer and cement.

2.17 Nonoil imports are expected to increase by about 10% in real termsin 1980/81. Increased capital imports, reflecting an improved investmentclimate as well as the sharp rise in public sector development spending, andlarge imports of cement and fertilizer to meet domestic shortages, account forthe higher rate of import growth. Rice imports on the other hand areprojected to decline given the 1980 bumper harvest which enabled BULOG toprocure a record 1.6 million tons of rice domestically. With the increasedrate of economic activity, other consumer goods imports are expected to growby about 10% in real terms for the year.

2.18 The current account is expected to record a surplus of almost $3billion in 1980/81, to which must be added net inflows of medium- andlong-term loans of about $1.9 billion and direct private investment inflowsof about $170 million. An outflow of $2.5 billion on the "other capital"account is expected, mainly as a result of a large increase (about $1.7billion) in the foreign assets held by the commercial banks and to tradefinancing (about $700 million) provided by Indonesia in connection with itsoil exports. Official reserves are expected to rise by about $2.5 billion to$7.1 billion, equivalent to nearly seven months of nonoil imports.

The Government Budget

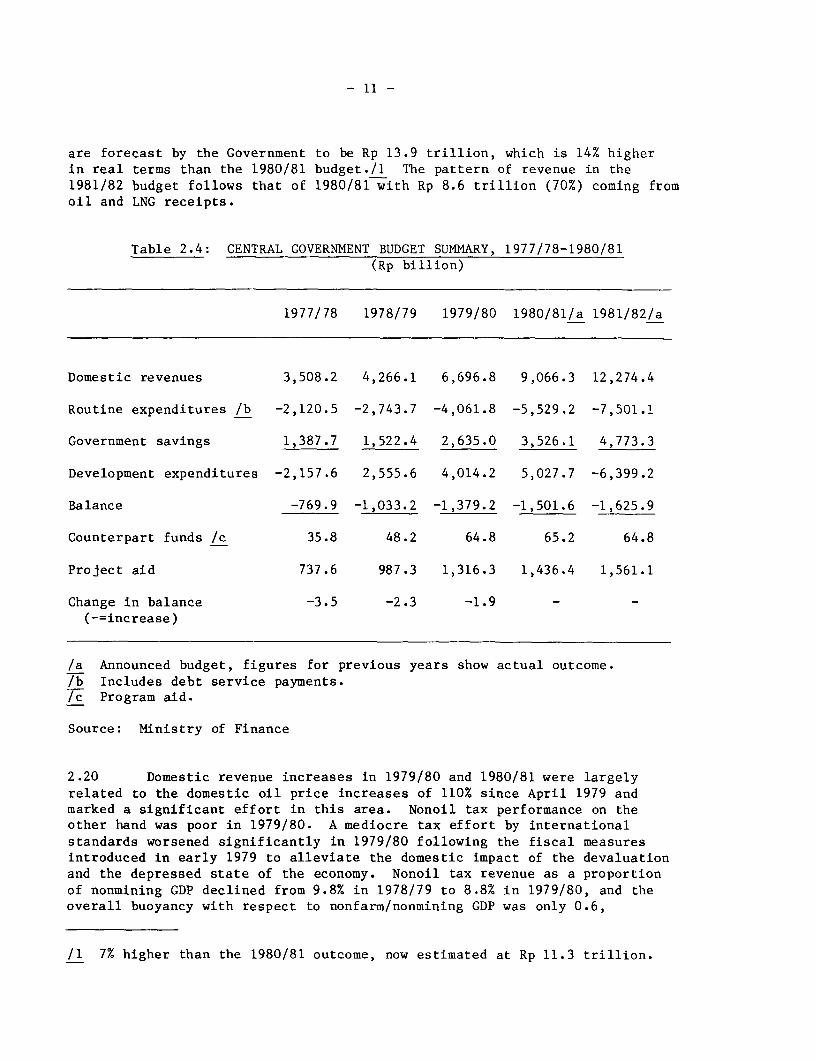

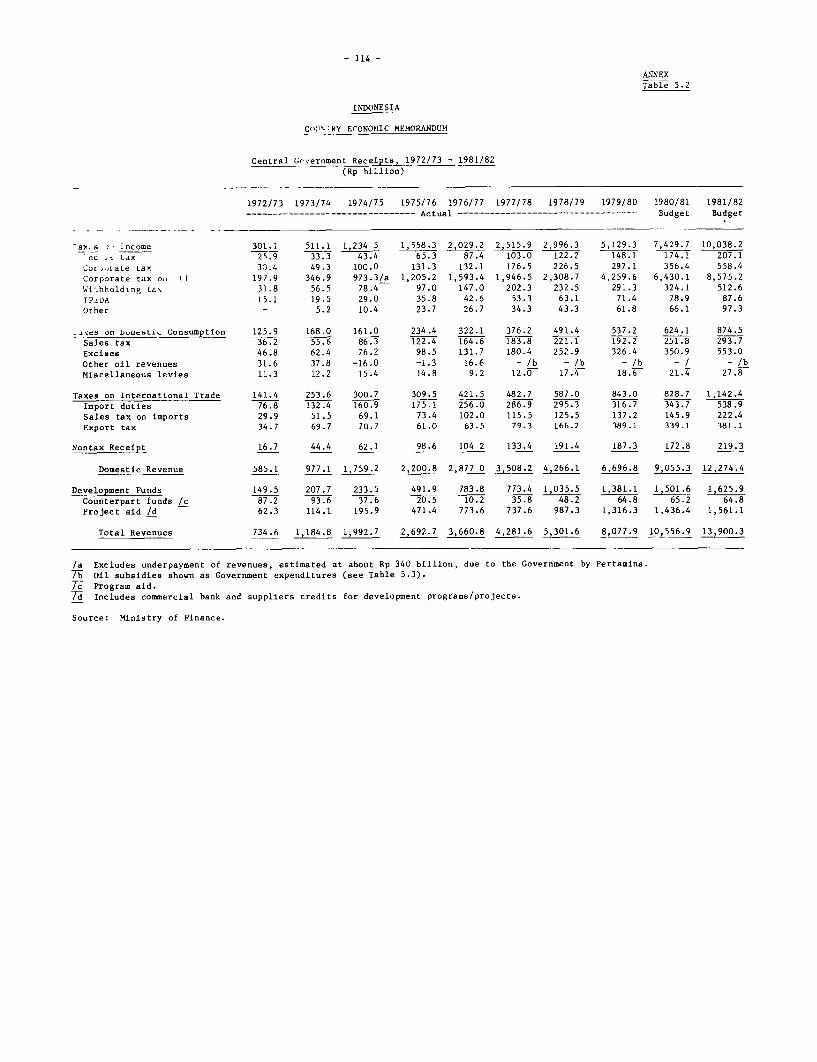

2.19 Revenues. Government revenue continues to grow rapidly. The1979/80 domestic revenue of Rp 6.7 trillion was equivalent to an 18% increasein real terms over 1978/79, and the expected receipts of about Rp 10 trillionfor 1980/81 is equivalent to a further 25% real increase./l These gains arealmost entirely due to higher oil revenues which in 1980/81 account for 70% oftotal domestic revenue. The 1981/82 budget revenues (including foreign aid)

/1 The estimated receipts for 1980/81 include a revised estimate of oilrevenue and an upward revaluation of nonoil tax revenue to take accountof high first semester returns and a higher inflation estimate.

- 11 -

are forecast by the Government to be Rp 13.9 trillion, which is 14% higherin real terms than the 1980/81 budget./1 The pattern of revenue in the1981/82 budget follows that of 1980/81 with Rp 8.6 trillion (70%) coming fromoil and LNG receipts.

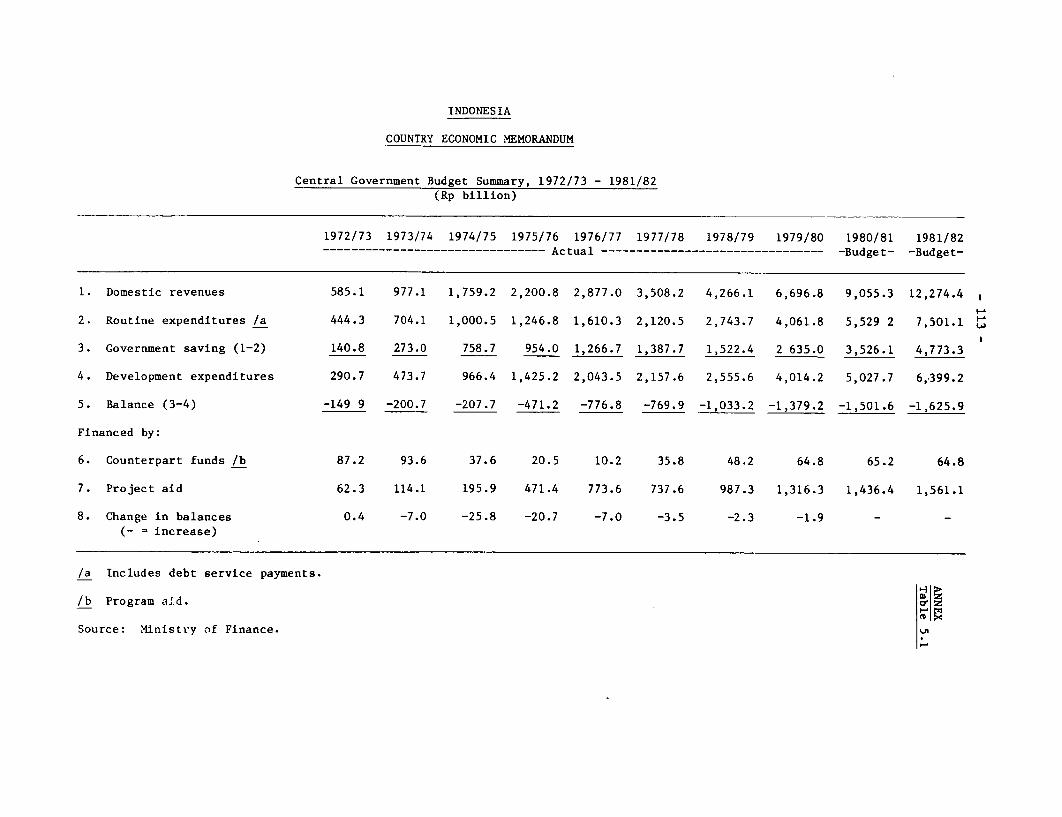

Table 2.4: CENTRAL GOVERNMENT BUDGET SUMMARY, 1977/78-1980/81(Rp billion)

1977/78 1978/79 1979/80 1980/81/a 1981/82/a

Domestic revenues 3,508.2 4,266.1 6,696.8 9,066.3 12,274.4

Routine expenditures /b -2,120.5 -2,743.7 -4,061.8 -5,529.2 -7,501.1

Government savings 1,387.7 1,522.4 2,635.0 3,526.1 4,773.3

Development expenditures -2,157.6 2,555.6 4,014.2 5,027.7 -6,399.2

Balance -769.9 -1,033.2 -1,379.2 -1,501.6 -1,625.9

Counterpart funds /c 35.8 48.2 64.8 65.2 64.8

Project aid 737.6 987.3 1,316.3 1,436.4 1,561.1

Change in balance -3.5 -2.3 -1.9 - -(-=increase)

/a Announced budget, figures for previous years show actual outcome./b Includes debt service payments./c Program aid.

Source: Ministry of Finance

2.20 Domestic revenue increases in 1979/80 and 1980/81 were largelyrelated to the domestic oil price increases of 110% since April 1979 andmarked a significant effort in this area. Nonoil tax performance on theother hand was poor in 1979/80. A mediocre tax effort by internationalstandards worsened significantly in 1979/80 following the fiscal measuresintroduced in early 1979 to alleviate the domestic impact of the devaluationand the depressed state of the economy. Nonoil tax revenue as a proportionof nonmining GDP declined from 9.8% in 1978/79 to 8.8% in 1979/80, and theoverall buoyancy with respect to nonfarm/nonmining GDP was only 0.6,

/1 7% higher than the 1980/81 outcome, now estimated at Rp 11.3 trillion.

- 12 -

compared with a historical experience of slightly over 1.0./I In the 1981/82budget, nonoil revenues are estimated at Rp 3.7 trillion, indicating aslightly improved tax effort, despite selected rate reductions. Personalincome taxes, domestic sales taxes, customs duties and sales taxes on inputsall declined significantly in real terms, and only export taxes increased.Some improvement in the buoyancy is likely in 1980/81. Good first semesterreceipts suggest a buoyancy of about 0.9, which implies a further slightdecline in tax effort. No major new measures to raise revenues from nonoilrevenues were introduced during 1979/80 or 1980/81 mainly because oil revenueshave been adequate for Government needs. This continues to be true for the1981/82 budget.

2.21 External assistance passing through the budget has been steadilydeclining in relative importance. In 1979/80 this source of funds stagnatedin real terms, and the budgeted value of Rp 1.5 trillion in 1980/81 impliesa decline of at least 5% in real terms. In 1980/81 external assistance fundsaccount for less than 15% of domestic revenues, compared with 20% in 1978/79.This trend is likely to continue. The 1981/82 budget estimates foreign aidreceipts at Rp 1.6 trillion, implying a further 6% real decline over the1980/81 budget. These external assistance funds were used to financedevelopment expenditures and in 1978/79 they accounted for 41% of totaloutlays. Since then, these funds have financed a steadily declining share ofdevelopment expenditures and in the 1981/82 budget they are projected to meetonly 25% of these outlays.

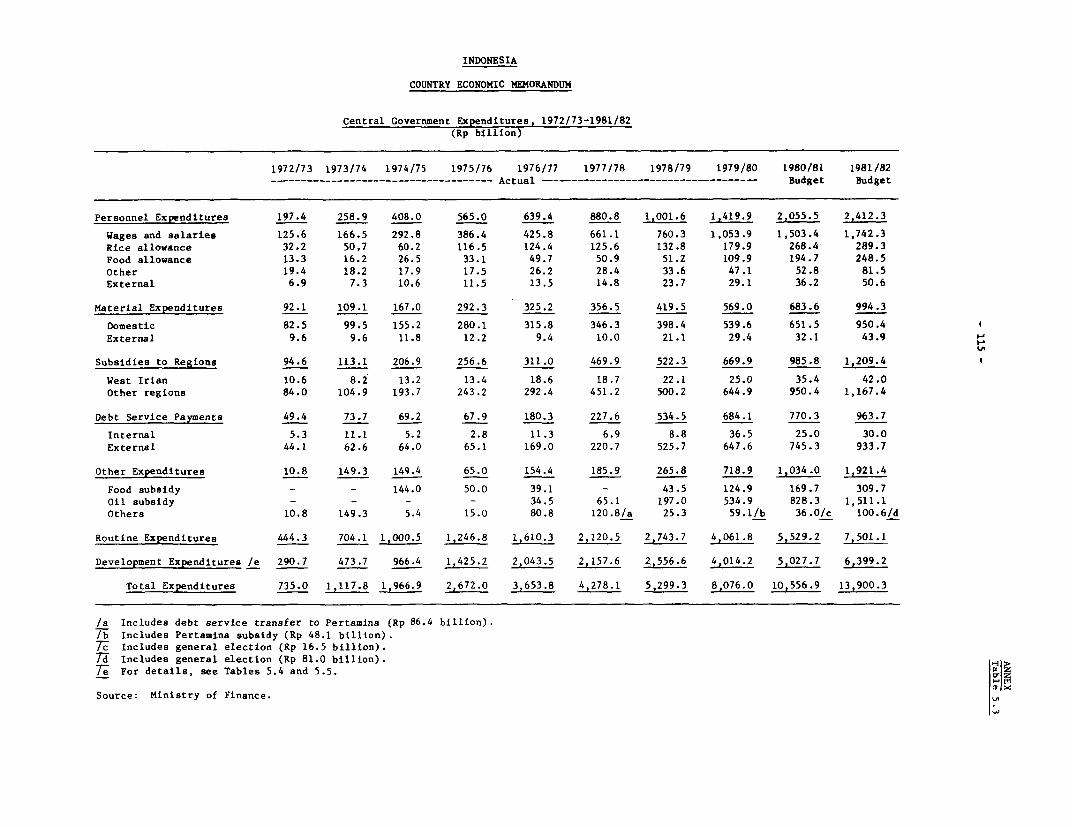

2.22 Expenditures. The routine budget accounted for 50% of totalexpenditures in 1979/80. Its share in total expenditures is expected torise to 52% in 1980/81, owing to further large increases (about 47% innominal terms) in subsidies, personnel expenditure and transfers to theregions. For the last two items a 50% increase in salaries to publicservants and military personnel is the main cause of the increase inroutine expenditures. In the 1981/82 budget, there is a further shifttowards routine expenditures which account for 54% of the total outlays.This shift is largely due to the increased subsidies.

2.23 Producer and consumer subsidies have risen from Rp 97 billion in1977/78, or 2% of routine and development expenditures, to an estimatedRp 1,450 billion in 1980/81, nearly 13% of expenditure. The 1981/82 budgetallocated Rp 2.1 trillion or 15% of total budgeted expenditures to subsidies.Of this amount, Rp 1.5 trillion is on account of the oil subsidy. Since

/1 The buoyancy is the proportionate change in tax divided by the propor-tionate change in the tax base. A buoyancy greater than unity indicatesa rising tax effort. Nonmining GDP is used in calculating the taxeffort to abstract from the impact of the oil sector, but retain afigure comparable with other countries. Nonfarm nonmining GDP is usedfor the buoyancy as the best aggregate proxy for the various tax bases.

- 13 -

1977/78, about a quarter of the Government's incremental revenue has been usedto increase subsidies. The most dramatic increase has been in the oilsubsidy (Table 3.3). The food subsidy has risen to an estimated Rp 170billion and the fertilizer subsidy to Rp 213 billion in 1980/81. The foodsubsidy, covering rice, wheat and sugar has been rising owing a higher foodimports, increased prices, and the decision to hold domestic prices down forequity and social stability reasons. Fertilizer prices have been decliningin real terms to improve producer incentives. This rapid increase insubsidies has been a major vehicle for distributing the windfall incomefrom higher oil prices among the population. One consequence, however, hasbeen a steady decline in the share of development outlays in totalexpenditures. In 1977/78 these accounted for 50% of the total; by 1981/82they are expected to be about 46% of total expenditures. An emerging issuefor policy is whether subsidies can and should be maintained at their currenthigh levels. The report takes up this question in Chapter Three.

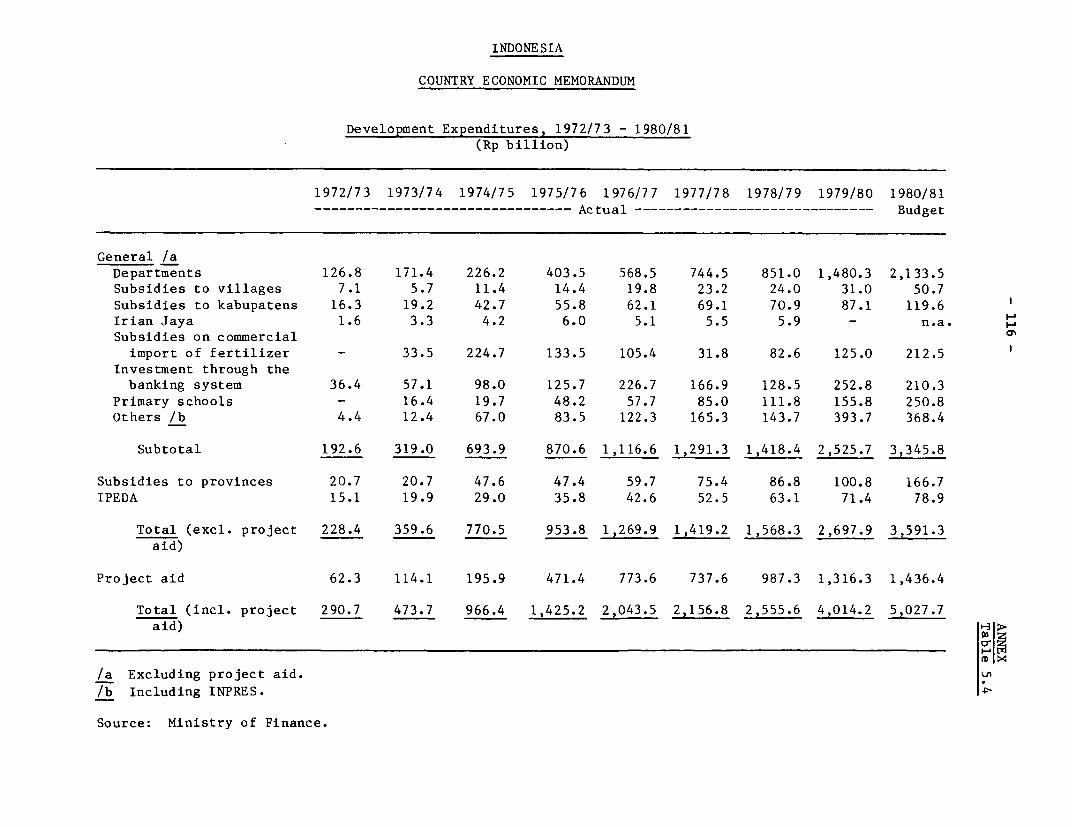

2.24 For the last two years, the composition of incremental expenditurein the development budget has been markedly different from the historicalpattern. In 1979/80, 17% was allocated to Government capital participationand 14% to general public services (comprising law, defence and security,and government apparatus). The social sectors - health, education and housingand water supply also experienced significant increases in expenditurewhereas allocations to the main productive sectors other than industry andmining grew little or declined. Overall, basic development expenditure,excluding the fertilizer subsidy, Government capital participation and generalpublic services, grew at a steady 6-8% p.a. in real terms for the three yearsto 1979/80. The 1980/81 development budget showed a real growth rate ofnearly 20%, with the main beneficiaries of incremental resources beingtransportation, education, agriculture and regional development (mainlyINPRES). In the 1981/82 budget the largest beneficiaries of incrementaldevelopment expenditures are education, industry and mining, and manpower andtransmigration.

Prices and Competitiveness

2.25 Indonesia's inflationary experience over the last two years has beendominated by the influence of the November 1978 devaluation, the rising priceof oil exports, and the monetary and fiscal policy consequent upon thoseevents. In the period October 1978-November 1980 the consumer priceindex for Indonesia rose by 55%, while world consumer prices rose on averageby 30%. Internal prices inevitably rise following a major devaluation dueto increased prices for tradable goods, but the extent to which domesticinflation may exceed the internatonal rate without eroding competitivenessis open to question and depends on the foreign exchange or "traded" componentof domestic expenditure. An "appropriate" consumer price rise may be definedas that which would maintain the gain in competitiveness secured from the

- 14 -

devaluation. Calculations based on import requirements derived from input-output tables for Indonesia suggest that domestic prices could "appropriately"adjust by about 15% above world prices. Thereafter, any excess of Indonesianinflation over world rates would result in a gradual reduction in competi-

tiveness. The extent to which gains in competitiveness are being eroded bydomestic cost inflation differs according to sector and no single measure cancapture trends in competitiveness in all export and import substitutionindustries. Separate indices have been constructed for traditional exports,manufactured exports and import substitutes./l The competitiveness oftraditional nonoil exports, which rose by 65% between October 1978 and October1979, has remained virturally unchanged since than, as international commodityprices have continued to rise at about the same rate as domestic prices. Formanufactured exports and import substitutes almost half the gains in competi-

tiveness have been retained two years after the devaluation despite domesticprice inflation. In mid-1980, the indices for manufactured goods and importsubstitutes, which had both risen by 50% in November 1978 were respectively19% and 25% above their predevaluation levels.

2.26 On a year-over-year basis the rate of increase of the consumer priceindex (CPI) rose from 7.3% in September 1978 to 31% in October 1979 and thenfell steadily /2 for the next eleven months to reach a low of 15% in

/1 Traditional Exports: since producers are "price-takers" in internationalmarkets, domestic profitability is a better measure of competitivenesthan international price differences. The ratio of the nonoil exportcomponent of Indonesia's wholesale price index (WPI) to the price indexfor Essential Commodities in rural Java and Madura is employed here tomeasure supply incentives.

Manufactured Exports: since Indonesian exports compete primarily againstmanufactured exports from other Asian countries, the ratio of exchangerate-adjusted average price indices of eight Asian countries (Malaysia,Thailand, Singapore, Philippines, Taiwan, Korea, Sri Lanka and India) tothe manufactured goods component in Indonesia-s WPI, is used here tomeasure changes in competitiveness.

Import Substitutes: ratio of trade-weighted export unit values (adjustedfor exchange rate changes) of seven industrial countries to Indonesia'sConsumer Price Index (Trade weights are Japan 45%, USA 21%, Germany 11%,

Singapore 9%, Netherlands 5% and Australia 4%).

/2 With the exception of May 1980, when domestic prices for oil and oilproducts were increased an average of 50%.

- 15 -

September 1980. By December 1980 the rate had again risen to 17.1%. Inthe past year the smallest increase has come from the food component ofthe CPI (12.0% October 1979-October 1980) due in part to ample rice supplies.BULOG purchased a record /1 1.6 million tons of domestically produced riceto support the price paid to farmers. The highest price rise (18.4%) wasin the "housing" component due in part to the 50% increase in the price ofkerosene in May and to rapidly rising construction costs.

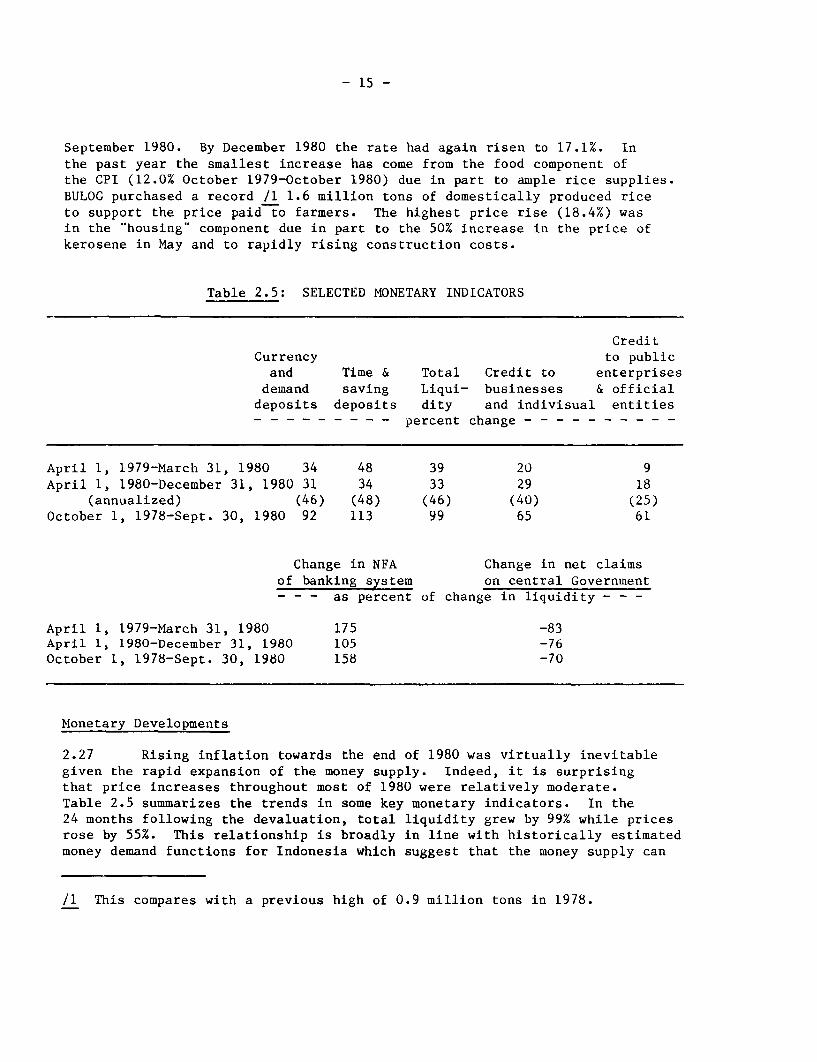

Table 2.5: SELECTED MONETARY INDICATORS

CreditCurrency to publicand Time & Total Credit to enterprises

demand saving Liqui- businesses & officialdeposits deposits dity and indivisual entities- - - - - - - - - percent change - - - - - - - - - -

April 1, 1979-March 31, 1980 34 48 39 20 9April 1, 1980-December 31, 1980 31 34 33 29 18

(annualized) (46) (48) (46) (40) (25)October 1, 1978-Sept. 30, 1980 92 113 99 65 61

Change in NFA Change in net claimsof banking system on central Government- - - as percent of change in liquidity - - -

April 1, 1979-March 31, 1980 175 -83April 1, 1980-December 31, 1980 105 -76October 1, 1978-Sept. 30, 1980 158 -70

Monetary Developments

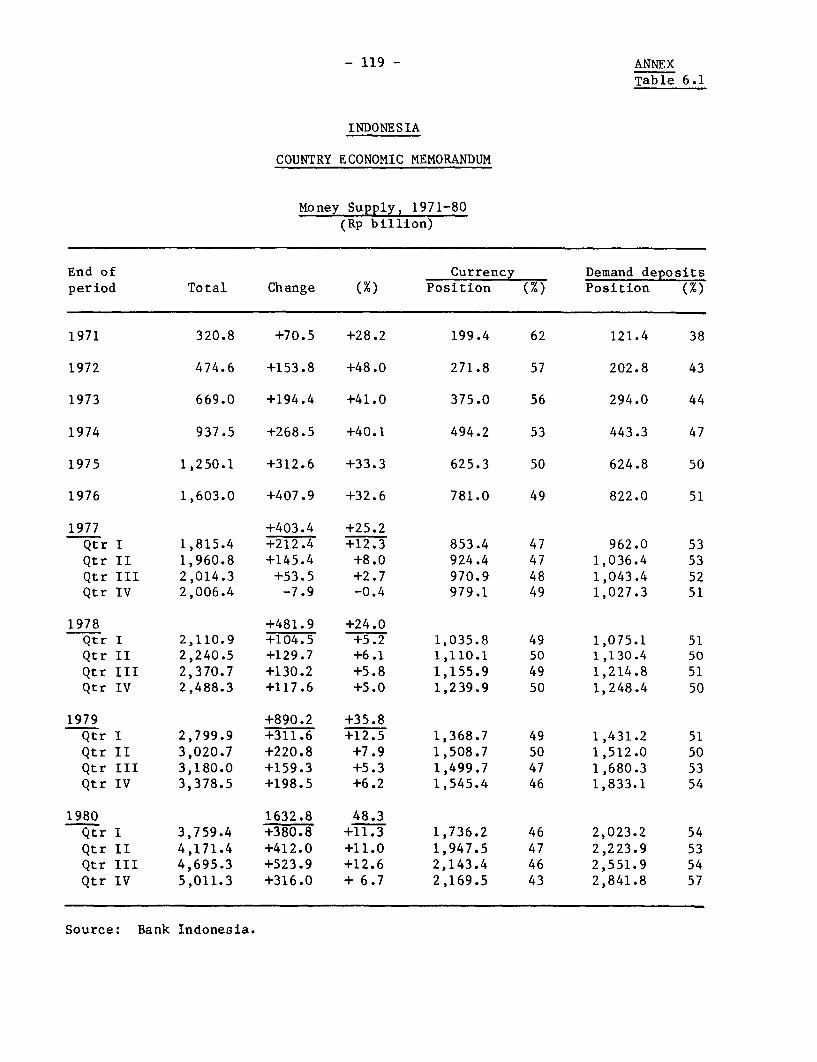

2.27 Rising inflation towards the end of 1980 was virtually inevitablegiven the rapid expansion of the money supply. Indeed, it is surprisingthat price increases throughout most of 1980 were relatively moderate.Table 2.5 summarizes the trends in some key monetary indicators. In the24 months following the devaluation, total liquidity grew by 99% while pricesrose by 55%. This relationship is broadly in line with historically estimatedmoney demand functions for Indonesia which suggest that the money supply can

/1 This compares with a previous high of 0.9 million tons in 1978.

- 16 -

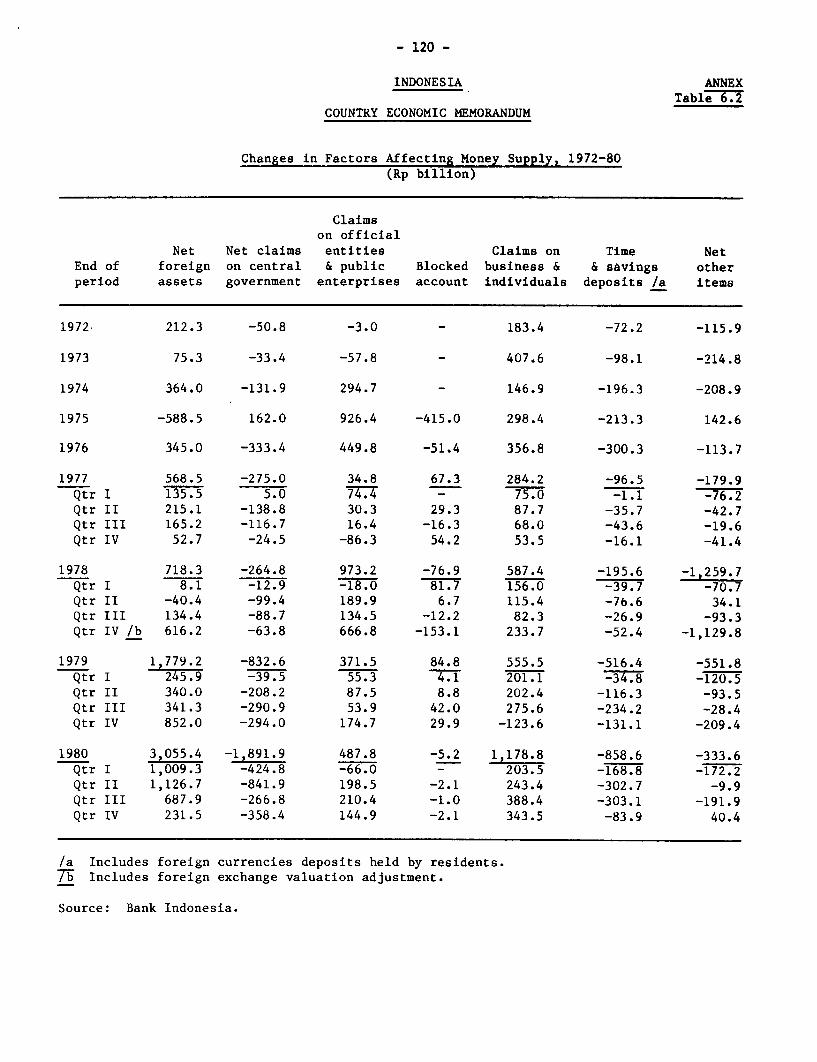

expand at about 12% a year before creating inflationary pressures./l Realmoney balances were run down during 1979 due to a high and uncertain inflationrate, but appear to have been fully rebuilt during 1980. It is, therefore,very unlikely that the money supply could continue to expand at its currentpace (about 46% for the 1980/81 fiscal year) without causing a substantialincrease in inflation. From Table 2.4 and Annex Table 6.1 it is evident thatthe primary reason for such rapid monetary expansion is the high proportion ofthe foreign exchange accruing to the Government being changed into rupiah andspent domestically through the budget./2 On the other hand, credit to theprivate sector has increased in real terms over the last two years by only6.5%.

/1 This is derived from an estimated income elasticity of money demand of1.5.

/2 The Government presents a balanced budget and balanced accounts everyyear and, as a result, budgetary outlays rise with revenues. However,some expenditures are not disbursed during the same year. The monetarysurplus (change in net claims of the banking system on the CentralGovernment) thus generated - Rp 1.2 trillion in 1979/80 - was not suffi-cient to sterilize the balance of payments surplus (change in net foreignassets of the banking system).

- 1 7 -

3. OPTIONS FOR MACROECONOMIC POLICY

3.01 Indonesia-s short- and medium-term resource outlook is dominatedby developments in the energy sector. The two key features of the currentsituation are:

(a) Indonesia's current account surplus in the balance of paymentsis likely to continue until the mid-1980½s; but

(b) In the absence of policy changes aimed at a structural transfor-mation of the economy, large resource deficits are likely tore-emerge in the second half of the decade.

3.02 Higher oil prices have clearly improved the prospects for rapidgrowth in Indonesia, at least in the first half of the 1980s. In this reportit has been assumed that the real export price for oil and LNG will rise at3% p.a. throughout the decade of the 1980s. In this period, growth will beconstrained more by absorptive capacity than by the availability of foreignexchange. A secular decline in the volume of oil available for export beyond1983/84 is probably inevitable, and this will lead to the re-emergence of aforeign exchange constraint. Since earnings from oil exports would stillaccount for some 55% of total export receipts in the mid-1980s, the overallgrowth of exports may decline sharply, thereby limiting the growth inIndonesia's import capacity and slowing the growth in incomes, production andemployment.

3.03 Thus, Indonesia faces a major challenge over the next few years -to adjust to the declining volumes of oil exports and the consequentpotentially severe constraints imposed on import capacities. The adjustmentprocess has two stages. In the first half of the 1980s, when the balance ofpayments position is likely to be strong, it will be possible to undertake aseries of major policy reforms and an expanded program of investment in exportpromotion, import replacement and alternative energy sources. Such a programof structural adjustment would lay the foundations for sustained economicdevelopment in the latter part of the decade. In this latter period, currentaccount deficits would emerge again, but with adjustment along the linesproposed, these would be moderate both in relation to Indonesia's GDP and itscapacity for foreign borrowing. Sustained growth at 7-8% a year in real termswould be possible while maintaining a manageable internal and externalfinancial position.

3.04 Without a program of structural adjustment along the lines proposedin this chapter, Indonesia would face the prospect of foreign exchangeconstraints that would lead to a sharp slowdown in the growth of incomes andemployment. In these circumstances, it would be difficult indeed for theGovernment to make much progress towards one of its major developmentobjectives - the alleviation of poverty.

- 18 -

3.05 To help analyze the outlook with and without significant policy

changes, two sets of illustrative projections have been prepared. They are

designated "High" and "Low" cases, and they are based on alternative policy

responses to the current situation. The Low case shows an unsuccessful

adjustment in 1980-85; the foundations for a manageable balance of payments

position and sustained growth in the latter part of the decade are notestablished. The High case represents a much more successful adjustment,

with growth being maintained throughout the 1980s at 7-8% a year. The High

case is achievable, depending on policy actions in key areas: policiestowards external trade and export promotion; regulation and productivity of

investment; domestic resource mobilization and financial intermediation;

and changing the pattern of energy production and consumption. A successful

outcome will require carefully designed programs in each of these areas.

Elements of a Policy Package Aimed at Structural Transformation of the

Economy

3.06 The proposed package comprises measures in four policy areas: theforeign trade regime, the efficiency and regulation of investment, financial

policies, and subsidies. The proposed measures are inter-related and should

be conceived as a package because, in combination with each other, they are

likely to be more effective than if taken in isolation. For example, a

simplification of the investment licensing system and certain financial

reforms are important complements to the liberalization of the trade regime,

since without them, entrepreneurs would find it more difficult to respond to

the changed market signals brought about by the new trade regime. Similarly,

a reduction of the oil subsidy is an essential complement to the continuedhigh investment program advocated in this chapter. Without it, the

investment program would have to be severely reduced in the second half of

the 1980s owing to re-emerging foreign exchange and budgetary constraints.

3.07 Foreign Trade Policies./l Indonesia depends heavily on exports of

oil and gas (75% of total earnings) and on agricultural products and

minerals (21% of earnings) for its foreign exchange. Manufactures other

than processed agricultural products account for less than 5% of total

earnings. The projected rapid increase in earnings from LNG exports will be

largely offset by the decline in the volume of oil exports from the middle

of the decade. Export receipts may not keep pace with the growth in demand

for foreign exchange which will be associated with economic growth of 7-8% a

year./2

/1 A more detailed analysis of the foreign trade regime and the regulatory

environment and the policies needed to develop a more dynamic foreign

trade sector and investment environment is found in "Indonesia: Selected

Issues of Industrial Development and Trade Strategy" (World Bank draft

report 1980).

/2 Details of export projections are set out in Chapter 5.

- 19 -

3.08 If, over the longer-term, Indonesia is to avoid the constraint ongrowth that would be imposed by a lack of foreign exchange, a substantiallybetter performance in the growth of exports and further progress in importsubstitution based on a liberalized import regime, will be needed in the1980s. Increased investments will have to be made in the export sector andin import-replacing industries. This, in turn, will require improved profit-ability, especially in a number of export industries, and a continuation ofrecent efforts to reform the trade regime in Indonesia. The devaluation ofthe Rupiah in November 1978, together with associated policy measures,represented the first significant attempt in recent years to reduce theinward-looking bias of the trade regime by encouraging exports andliberalizing imports. The Government has already announced its intention tofurther reduce import tariffs. There is therefore already movement in theright direction, but further changes will be needed.

3.09 The trade regime in Indonesia is characterized by the use ofnumerous policy instruments, including tariffs, subsidies, differentiatedcredit and interest rates, tax and MPO rates, import prepayments,quantitative restrictions and government directives. International tradealso tends to be restricted by port and customs procedures that cause delaysand raise costs. Though the average level of effective protection inIndonesia is relatively moderate (about 30%),/l the range of rates isextremely wide, as is illustrated in Table 3.1 below.

Table 3.1: EFFECTIVE RATES OF PROTECTION ACCORDEDTO SELECTED INDUSTRIES IN 1975

Batik industries - 35%Sugar refining - 9%Palm oil - 5%Rice milling 1%Cigarettes 5%Industrial electrical machinery and apparatus 10%Spinning industries 56%Wearing industries 192%Made-up textile goods (excl. wearing apparel) 298%Electrical appliances and housewares 341%Motor vehicles 718%

3.10 The present trade regime not only has the effect of discouraginginternational trade, but it also fosters a misallocation of resources byprotecting high cost domestic market-oriented industries at much higherrates than labor-intensive production for export. A further result of theprotective policies followed in the later half of the 1970s has been the

/1 Source: "Indonesia: Selected Issues of Industrial Development and TradeStrategy"; (World Bank draft report 1980).

- 20 -

creation of excess capacity in many industries such as cable, furniture, carassembly, pharmaceuticals, corrugated boxes and canvas fabrics.

3.11 The main objective of the reform of the trade regime is torestructure the economy along more competitive lines to promote exports. Atthe same time expansion of some major new import substitution activities canbe justified on comparative cost grounds. Some of these activities includeindustries that are capital intensive and would not contribute toemployment, although they would have a significant impact on the balance ofpayments and value added. The basic elements of a reform of the traderegime would include: (a) simplification of the system of protection.Import tariffs combined with appropriate excise taxes should, as a rule, bethe sole source of protection for domestic industries; (b) unification ofthe tariff structure and reduction in average tariff levels over time. TheGovernment appears to be committed to move towards lower tariffs generally,but the desirability of movement towards unification at the same time maynot be fully recognized; and (c) simplification and standardization of theexport certificate scheme. A broader range of manufactured goods could beincluded in the scheme, whether or not they are currently exported, andcertificate levels could be set according to more broadly defined commoditygroups than at present.

3.12 Some of these policy changes will not be easy to bring about andwill have to be undertaken gradually. For example, a program to rationalizeand lower the tariff structure may have to be phased over a period ofseveral years and even then special facilities to assist potentiallyefficient industries in adjusting to the new rates may be needed. Theadoption of these general principles for tariff reform does not precludecontinued protection of certain industrial activities when justified oninfant industry or strategic considerations.

3.13 The recommended trade policy reform would also have the effect ofreducing inflationary pressures in the economy which is an extra advantageunder the current economic circumstances in Indonesia. Any expenditure onimported, rather than on domestically produced goods results in a lowergrowth of the domestic money supply and consequently tends to hold down therate of inflation. Therefore, for any given monetary target, a liberaliza-tion of imports will allow a significantly higher domestic investmentprogram.