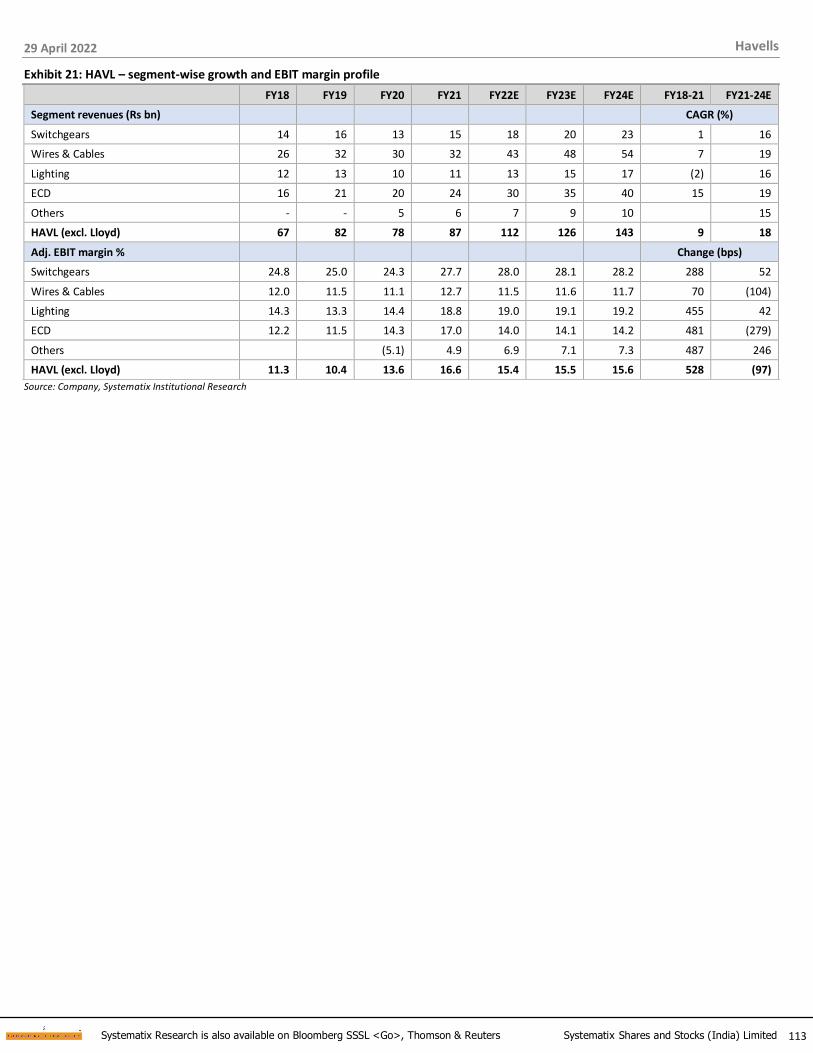

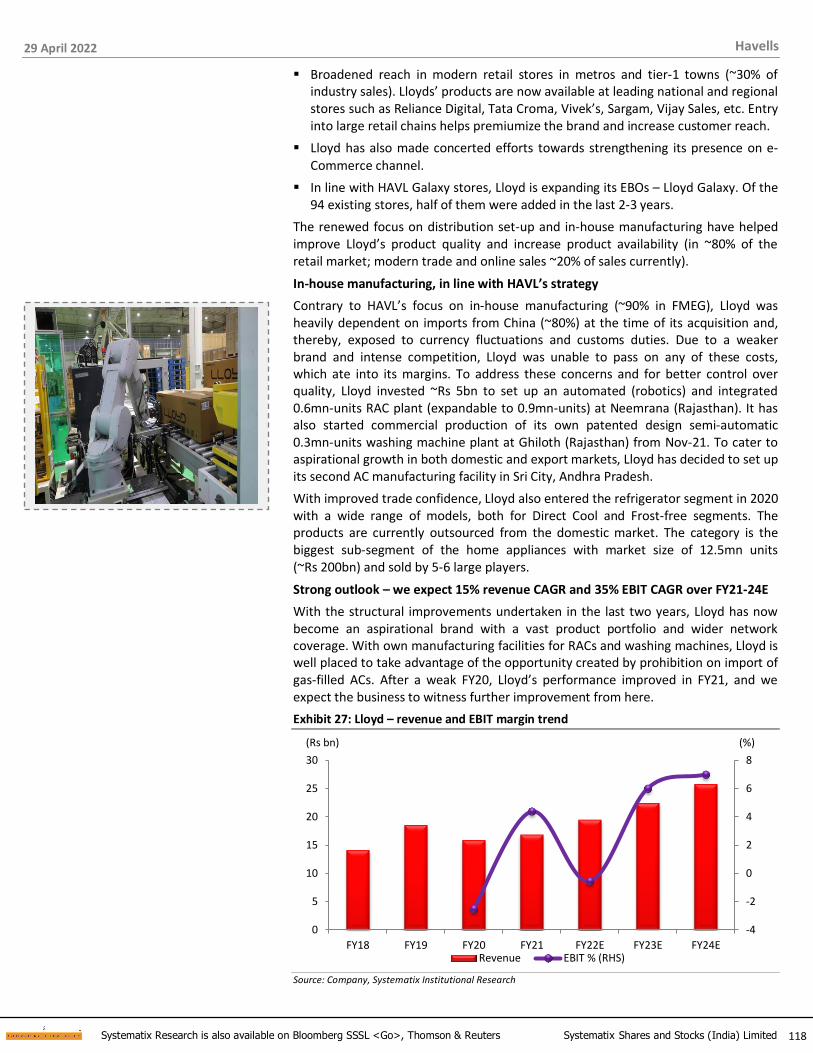

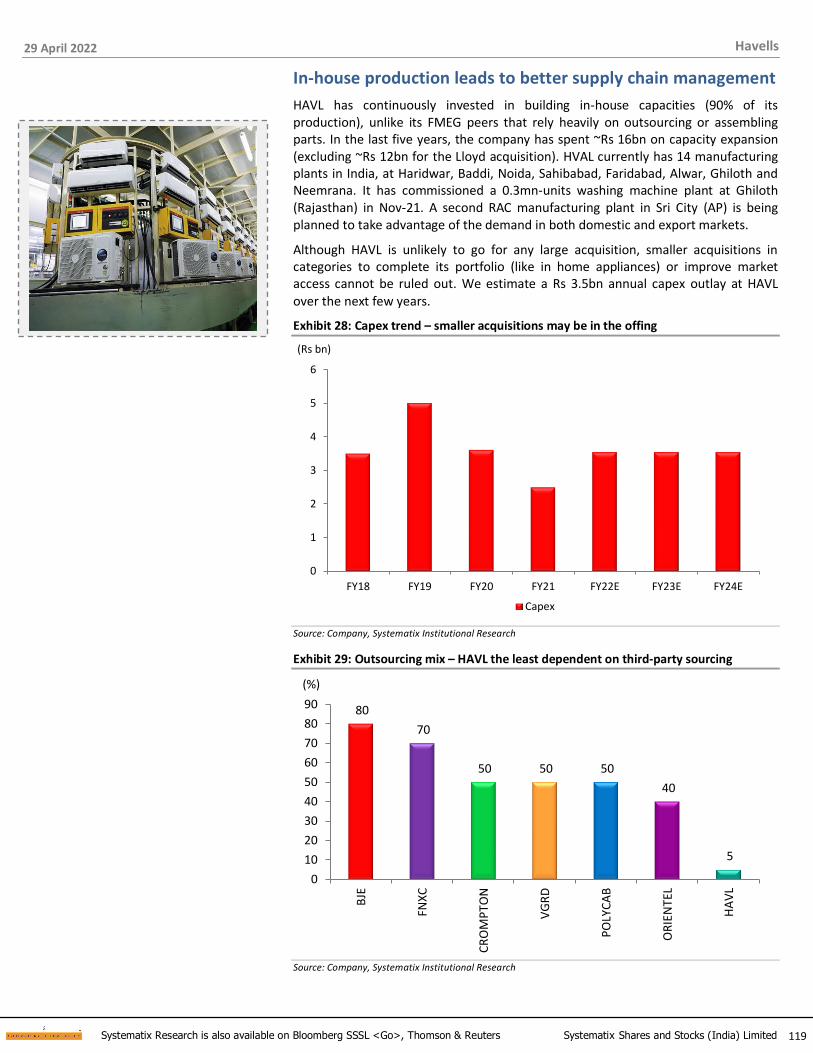

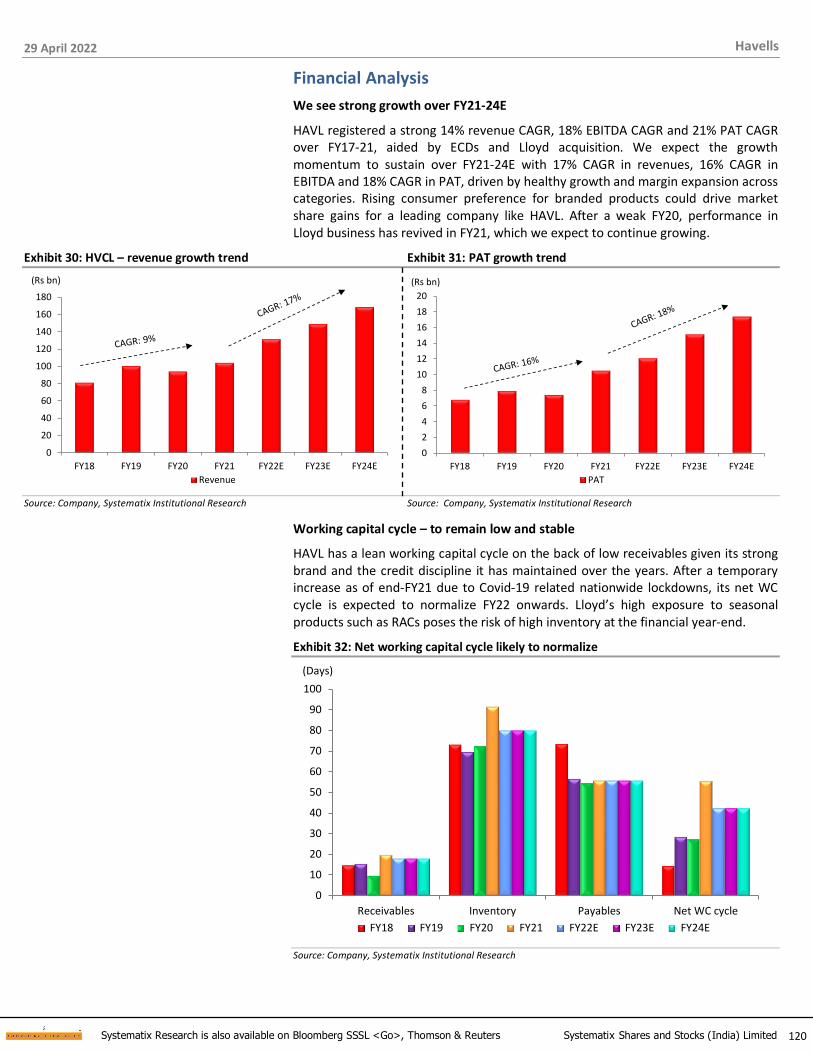

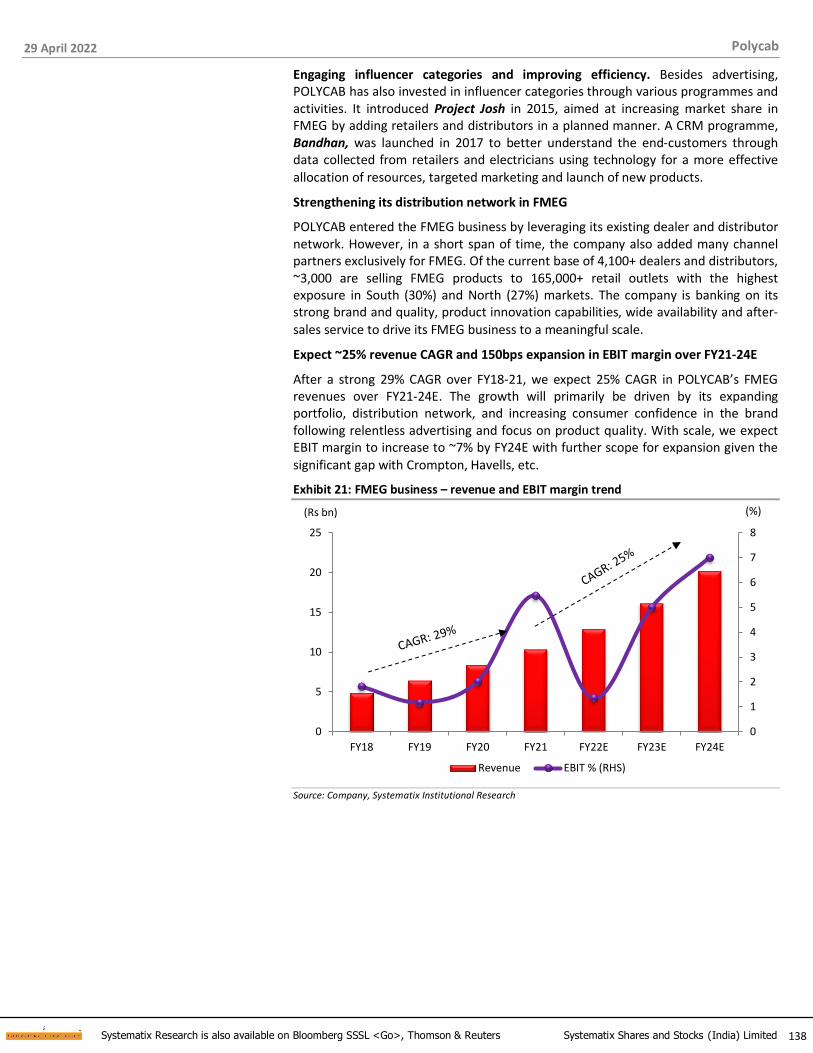

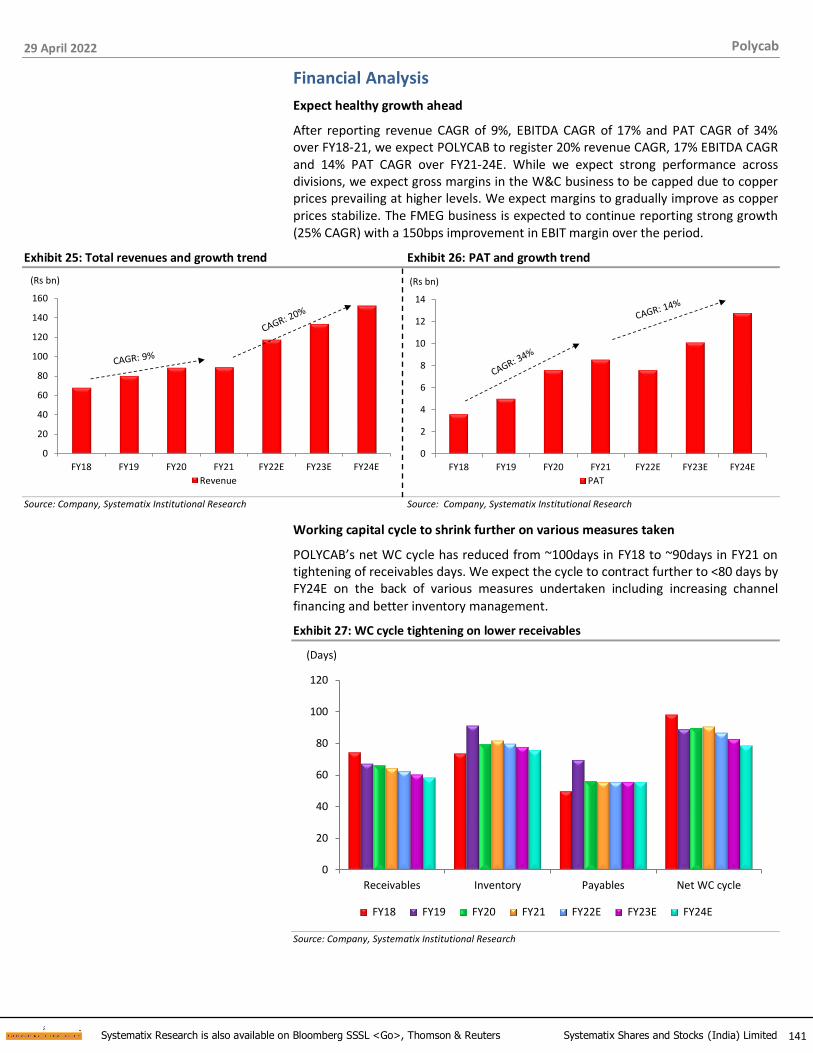

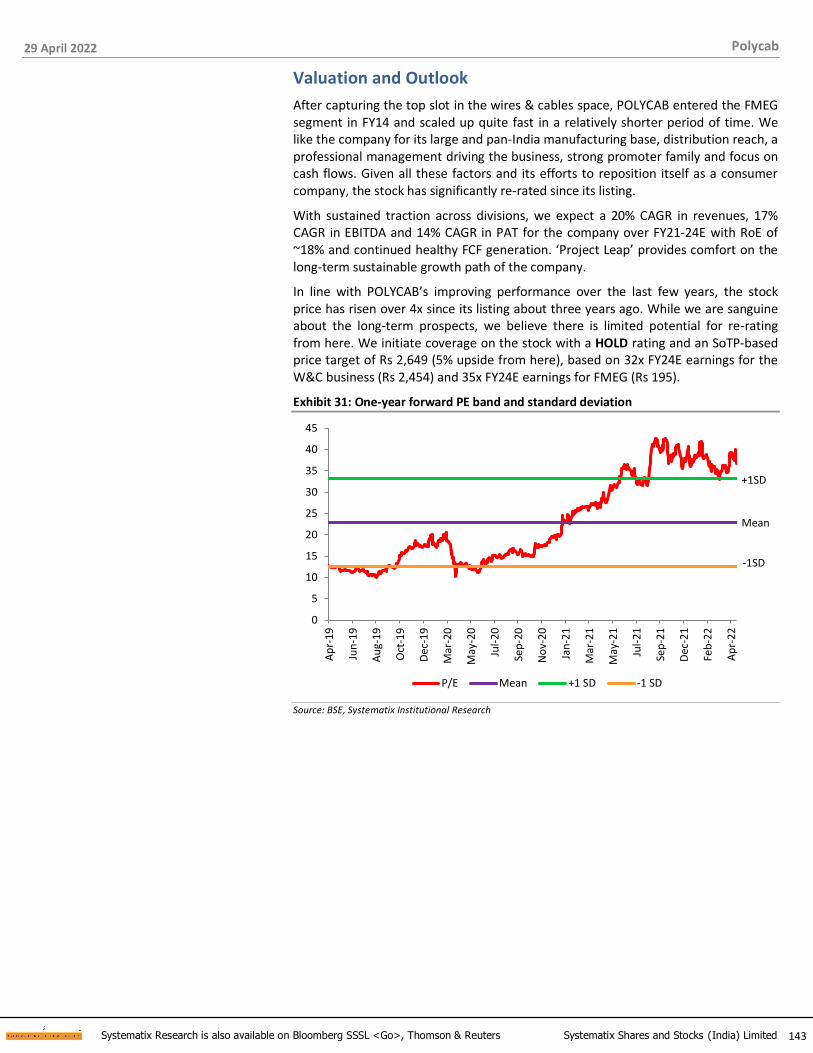

India Consumer Electricals - Systematix Group

185

Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited Investors are advised to refer disclosures made at the end of the research report. 1 India Consumer Electricals A sustainable growth story

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of India Consumer Electricals - Systematix Group

Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

Investors are advised to refer disclosures made at the end of the research report.

1

India Consumer Electricals A sustainable growth story

29 April 2022

2 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Contents

Story in charts – Industry segments and growth outlook ......................................................................................................... 4

Story in charts – Companies (peer comparison) ....................................................................................................................... 5

Executive Summary .................................................................................................................................................................. 7

Wires & Cables (W&C): Industry dynamics and outlook ..........................................................................................................13

Fans: Industry dynamics and outlook ......................................................................................................................................16

Lighting: Industry dynamics, outlook .......................................................................................................................................18

Switchgears: Industry dynamics and outlook ..........................................................................................................................19

Switches: Industry dynamics and outlook ...............................................................................................................................20

Water-heaters: Industry dynamics and outlook ......................................................................................................................21

Stock Views .............................................................................................................................................................................22

Companies section

Bajaj Electricals ........................................................................................................................................................................31

KEI Industries ..........................................................................................................................................................................49

Finolex Cables ..........................................................................................................................................................................68

Crompton Greaves Consumer ..................................................................................................................................................84

Havells ...................................................................................................................................................................................106

Polycab ..................................................................................................................................................................................130

V-Guard ................................................................................................................................................................................151

Orient Electric ........................................................................................................................................................................167

29 April 2022

3 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

India Consumer Electricals A sustainable growth story

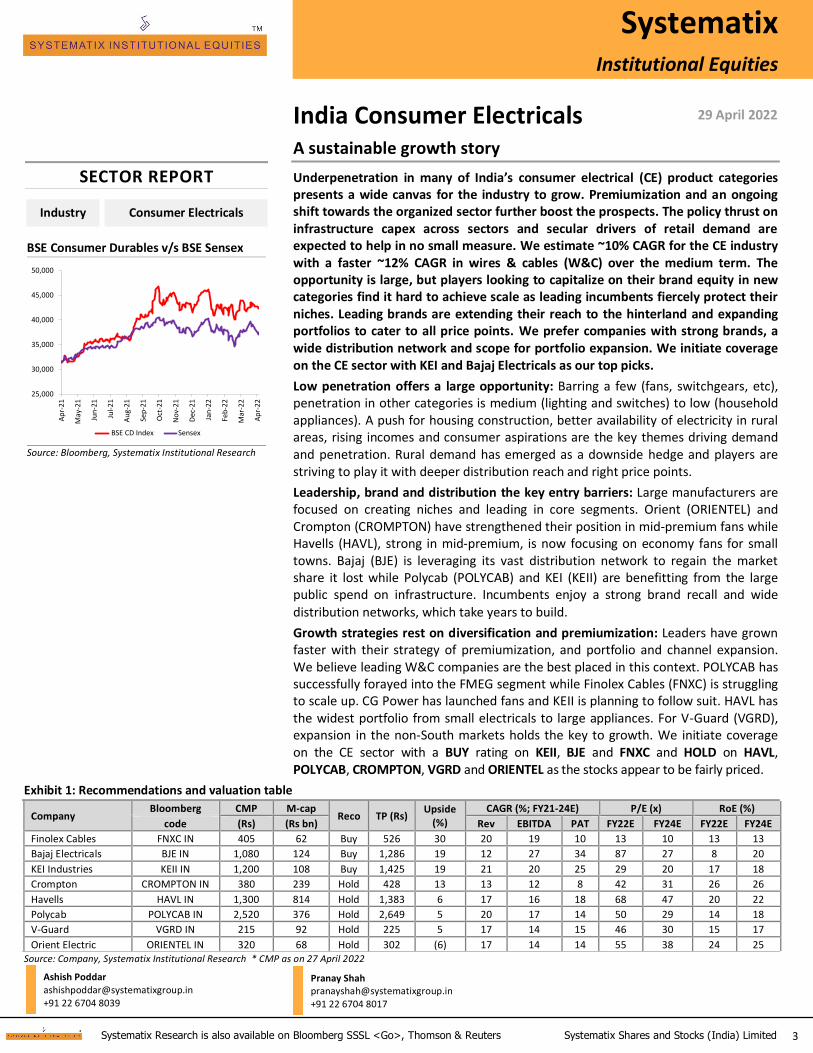

Underpenetration in many of India’s consumer electrical (CE) product categories presents a wide canvas for the industry to grow. Premiumization and an ongoing shift towards the organized sector further boost the prospects. The policy thrust on infrastructure capex across sectors and secular drivers of retail demand are expected to help in no small measure. We estimate ~10% CAGR for the CE industry with a faster ~12% CAGR in wires & cables (W&C) over the medium term. The opportunity is large, but players looking to capitalize on their brand equity in new categories find it hard to achieve scale as leading incumbents fiercely protect their niches. Leading brands are extending their reach to the hinterland and expanding portfolios to cater to all price points. We prefer companies with strong brands, a wide distribution network and scope for portfolio expansion. We initiate coverage on the CE sector with KEI and Bajaj Electricals as our top picks.

Low penetration offers a large opportunity: Barring a few (fans, switchgears, etc), penetration in other categories is medium (lighting and switches) to low (household appliances). A push for housing construction, better availability of electricity in rural areas, rising incomes and consumer aspirations are the key themes driving demand and penetration. Rural demand has emerged as a downside hedge and players are striving to play it with deeper distribution reach and right price points.

Leadership, brand and distribution the key entry barriers: Large manufacturers are focused on creating niches and leading in core segments. Orient (ORIENTEL) and Crompton (CROMPTON) have strengthened their position in mid-premium fans while Havells (HAVL), strong in mid-premium, is now focusing on economy fans for small towns. Bajaj (BJE) is leveraging its vast distribution network to regain the market share it lost while Polycab (POLYCAB) and KEI (KEII) are benefitting from the large public spend on infrastructure. Incumbents enjoy a strong brand recall and wide

distribution networks, which take years to build.

Growth strategies rest on diversification and premiumization: Leaders have grown faster with their strategy of premiumization, and portfolio and channel expansion. We believe leading W&C companies are the best placed in this context. POLYCAB has successfully forayed into the FMEG segment while Finolex Cables (FNXC) is struggling to scale up. CG Power has launched fans and KEII is planning to follow suit. HAVL has the widest portfolio from small electricals to large appliances. For V-Guard (VGRD), expansion in the non-South markets holds the key to growth. We initiate coverage on the CE sector with a BUY rating on KEII, BJE and FNXC and HOLD on HAVL, POLYCAB, CROMPTON, VGRD and ORIENTEL as the stocks appear to be fairly priced.

Exhibit 1: Recommendations and valuation table

Company Bloomberg CMP M-cap

Reco TP (Rs) Upside

(%)

CAGR (%; FY21-24E) P/E (x) RoE (%)

code (Rs) (Rs bn) Rev EBITDA PAT FY22E FY24E FY22E FY24E

Finolex Cables FNXC IN 405 62 Buy 526 30 20 19 10 13 10 13 13

Bajaj Electricals BJE IN 1,080 124 Buy 1,286 19 12 27 34 87 27 8 20

KEI Industries KEII IN 1,200 108 Buy 1,425 19 21 20 25 29 20 17 18

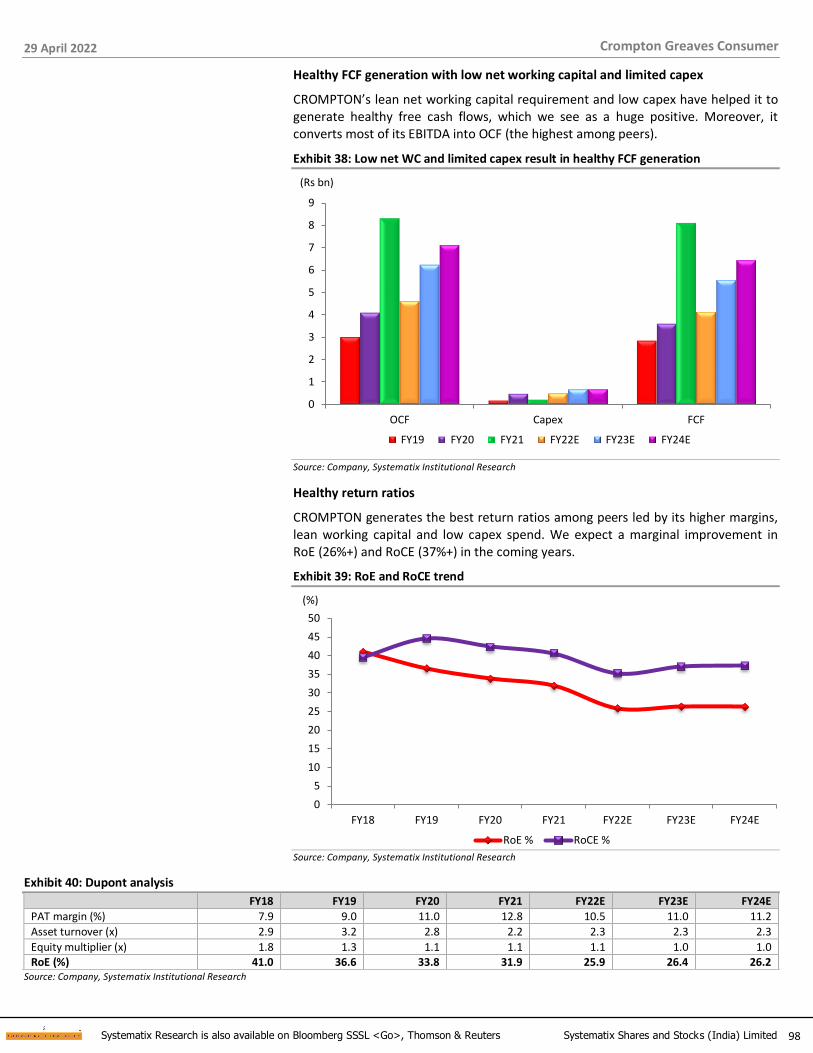

Crompton CROMPTON IN 380 239 Hold 428 13 13 12 8 42 31 26 26

Havells HAVL IN 1,300 814 Hold 1,383 6 17 16 18 68 47 20 22

Polycab POLYCAB IN 2,520 376 Hold 2,649 5 20 17 14 50 29 14 18

V-Guard VGRD IN 215 92 Hold 225 5 17 14 15 46 30 15 17

Orient Electric ORIENTEL IN 320 68 Hold 302 (6) 17 14 14 55 38 24 25 Source: Company, Systematix Institutional Research * CMP as on 27 April 2022

Systematix Institutional Equities

Systematix Institutional Equities

Systematix Institutional Equities

Systematix Institutional Equities

29 April 2022

xx December 2021

xx December 2021

xx December 2021

SECTOR REPORT

SECTOR REPORT

SECTOR REPORT

SECTOR REPORT

Industry

Industry

Industry

Industry

Consumer Electricals xxxxxx

xxxxxx

xxxxxx

Ashish Poddar [email protected] +91 22 6704 8039

Pranay Shah [email protected] +91 22 6704 8017

BSE Consumer Durables v/s BSE Sensex

25,000

30,000

35,000

40,000

45,000

50,000

Ap

r-2

1

May

-21

Jun

-21

Jul-

21

Au

g-2

1

Sep

-21

Oct

-21

No

v-2

1

Dec

-21

Jan

-22

Feb

-22

Mar

-22

Ap

r-2

2

BSE CD Index Sensex

Source: Bloomberg, Systematix Institutional Research

29 April 2022

4 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Story in charts – Industry segments and growth outlook

Exhibit 2: W&C is ~45% of the Rs 1.2trn CE industry… Exhibit 3: …with Polycab and Havells as the leaders

45%

19%

17%

8%

7%4%

C&W

Lighting

Switchgear

Fans

Others

Switches

86 81

48

36 33 24 20 19

0

10

20

30

4050

60

70

80

90100

PO

LYC

AB

HA

VL

CR

OM

PTO

N

KEI

BJE

FNX

C

OR

IEN

TEL

VG

RD

(Rs bn)Revenue (FY21)

Source: Polycab RHP, Systematix Institutional Research Source: Company, Systematix Institutional Research

Exhibit 4: W&C industry to continue growing the fastest Exhibit 5: Fans – industry growth and outlook

346

525 550

968

0

200

400

600

800

1,000

1,200

FY14 FY18 FY21 FY26P

(Rs bn)

63

80

99

131

0

20

40

60

80

100

120

140

FY14 FY18 FY21 FY26P

(Rs bn)

Source: Polycab annual report, Systematix Institutional Research Source: Polycab annual report, Systematix Institutional Research

Exhibit 6: Lighting – industry growth and outlook Exhibit 7: Switches and Switchgears – industry outlook

142

212227

365

0

50

100

150

200

250

300

350

400

FY14 FY18 FY21 FY26P

(Rs bn)

139

183210

337

0

50

100

150

200

250

300

350

400

FY14 FY18 FY21 FY26P

(Rs bn)

Source: Polycab annual report, Systematix Institutional Research Source: Polycab annual report, Systematix Institutional Research

29 April 2022

5 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Story in charts – Companies (peer comparison)

Exhibit 8: ECD – HAVL, CROMPTON and BJE are top-3 in sales Exhibit 9: ECD – Revenue CAGR (BJE to see strong revival)

49 48

33

20

10 8

1

0

10

20

30

40

50

60

HA

VL

CR

OM

PTO

N

BJE

OR

IEN

TEL

PO

LYC

AB

VG

RD

FNX

C

(Rs bn)Revenue (FY21)

43

74

8

18 16 16 18

36

25 24 17 17 16

13

0

10

20

30

40

50

60

70

80

FNX

C

PO

LYC

AB

BJE

VG

RD

OR

IEN

TEL

HA

VL

CR

OM

PTO

N

(%)

FY16-21 FY21-24E

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Exhibit 10: ECD – adj. EBIT margin trend Exhibit 11: ECD – outsourcing mix (%)

20

.5

18

.8

10

.3

8.9

5.5

3.7

5.5

20

.0

18

.0

10

.5

8.0

7.0

6.0

5.0

0

5

10

15

20

25

CR

OM

PTO

N

HA

VL

BJE

OR

IEN

TEL

PO

LYC

AB

FNX

C

VG

RD

(%)

FY21 FY24E

80

70

50 50 50

40

5

0

10

20

30

40

50

60

70

80

90

BJE

FNX

C

CR

OM

PTO

N

VG

RD

PO

LYC

AB

OR

IEN

TEL

HA

VL

(%)

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Exhibit 12: BJE has the largest network of retail touchpoints Exhibit 13: A&P spends (FY20) – 3-5% of B2C sales for leaders

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

BJE

CR

OM

PTO

N

HA

VL

PO

LYC

AB

OR

IEN

TEL

FNX

C

VG

RD

(No.)

3.4

3.6

2.3

2.2

1.2

2.4

0.9

4.5

4.0

3.8

3.1

3.1

3.0

1.3

0.00.51.01.52.02.53.03.54.04.55.0

HA

VL

OR

IEN

TEL

VG

RD

CR

OM

PTO

N

PO

LYC

AB

BJE

FNX

C

(%)

% Total sales % B2C sales (FMEG & wire)

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

29 April 2022

6 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Exhibit 14: W&C – POLYCAB, KEII and HAVL are top-3 in sales Exhibit 15: W&C – Revenue CAGRs (revival expected for FXNC)

76

36 32

23

8

0

10

20

30

40

50

60

70

80

POLYCAB KEII HAVL FNXC VGRD

(Rs bn) FY21

23

13 13

3

8

24

20 19 19

17

0

5

10

15

20

25

KEII POLYCAB HAVL FNXC VGRD

(%)

FY16-21 CAGR FY21-24E CAGR

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Exhibit 16: W&C – adj. EBIT % (FNXC has a higher wire mix) Exhibit 17: RoE trend – CROMPTON ranks as the best

13

.4

12

.7

12

.5

10

.0

8.8

12

.2

11

.7

11

.5

10

.5

8.7

0

2

4

6

8

10

12

14

16

FNXC HAVL POLYCAB KEII VGRD

(%)

FY21 FY24E

32

26

20

12

1815 17

14

2625

2220 18 18 17

13

0

5

10

15

20

25

30

35

CR

OM

PTO

N

OR

IEN

TEL

HA

VL

BJE

PO

LYC

AB

KEI

I

VG

RD

FNX

C

(%)

FY21 FY24E

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Exhibit 18: Net WC cycle – a sharp improvement for BJE and KEII Exhibit 19: FCF – HAVL, POLYCAB, CROMPTON and BJE to lead

11 20

55 73

155

90 100

120

19 30

42 50 55

79 90 90

0

20

40

60

80

100

120

140

160

180

CR

OM

PTO

N

OR

IEN

TEL

HA

VL

VG

RD

BJE

PO

LYC

AB

FNX

C

KEI

I

(Days)

FY21 FY24E

10.1

6.5 6.1 5.4

1.8 1.8 1.5 1.4

0

2

4

6

8

10

12

HA

VL

PO

LYC

AB

CR

OM

PTO

N

BJE

FNX

C

KEI

I

VG

RD

OR

IEN

TEL

(Rs bn)FY21-24E (average)

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

29 April 2022

7 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Executive Summary

The ~Rs 1.2trn Indian consumer electricals industry (including cables) has recovered smartly after the downturn induced by Covid-related disruptions for two years. Recovery was broad-based across the product categories and supported by pent-up demand initially. However, a strong revival in the housing market, consumer preference towards bigger and comfortable houses in a work-from-home (WFH) scenario, premiumization and underpenetration in many product categories have set the tone for a sustainable growth story for the industry. We initiate coverage on the Indian Consumer Electricals Sector with a positive outlook. Within the sector, we are more inclined towards Wires & Cables (W&C) companies owing to their robust growth prospects and scope for business diversification towards B2C wires and fast moving electrical goods (FMEG) segments, leading to a valuation re-rating. KEII and

BJE are our top picks in the space.

Exhibit 20: Consumer Electricals – Industry size, growth trends and key players

Product category FY21P FY14-21 FY21-24E Key players

Industry size (Rs bn)

CAGR (%) CAGR (%)

Wires & cables 550 7 12 Polycab, KEI, Havells, Finolex, V-Guard, RR Kabel, Apar Ind, Gupta Power

Lighting 227 7 10 Bajaj, Surya Roshni, Crompton, Havells, Orient, Philips, Syska, Wipro,

Polycab

Switchgear 210 6 10 ABB, Havells, Legrand, Schneider, Siemens, Polycab

Fans 99 7 6 Crompton, Bajaj, Havells, Orient, V-Guard, Polycab

Switches 50 8 10 Anchor, Cosmo Electro (Kolors brand), GM Modular, Havells, Philips,

Schneider, Polycab

Water Heater 23 10 6 AO Smith, Bajaj, Crompton, Havells, Racold, Venus, V-Guard, Polycab

Source: Company, Polycab RHP

Exhibit 21: Product portfolios of key manufacturers

Players Fans Lighting Switches Switchgears Water

Heaters Home

Appliances Kitchen

Appliances Wires & Cables

Bajaj Electricals ✓ ✓ ✓ ✓ ✓

CG Consumer ✓ ✓ ✓ ✓ ✓

Finolex Cables ✓ ✓ ✓ ✓ ✓ ✓

Havells ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

KEI ✓

Orient Electric ✓ ✓ ✓ ✓ ✓ ✓ ✓

Philips ✓ ✓ ✓

Polycab ✓ ✓ ✓ ✓ ✓ ✓

Schneider Electric ✓ ✓ ✓ ✓

Stove Kraft ✓ ✓ ✓ ✓

Surya Roshni ✓ ✓ ✓ ✓ ✓

TTK Prestige ✓ ✓

Usha International ✓ ✓ ✓ ✓

V-Guard Industries ✓ ✓ ✓ ✓ ✓ ✓ Source: Polycab RHP, Systematix Institutional Research

29 April 2022

8 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Structural demand drivers remain in place

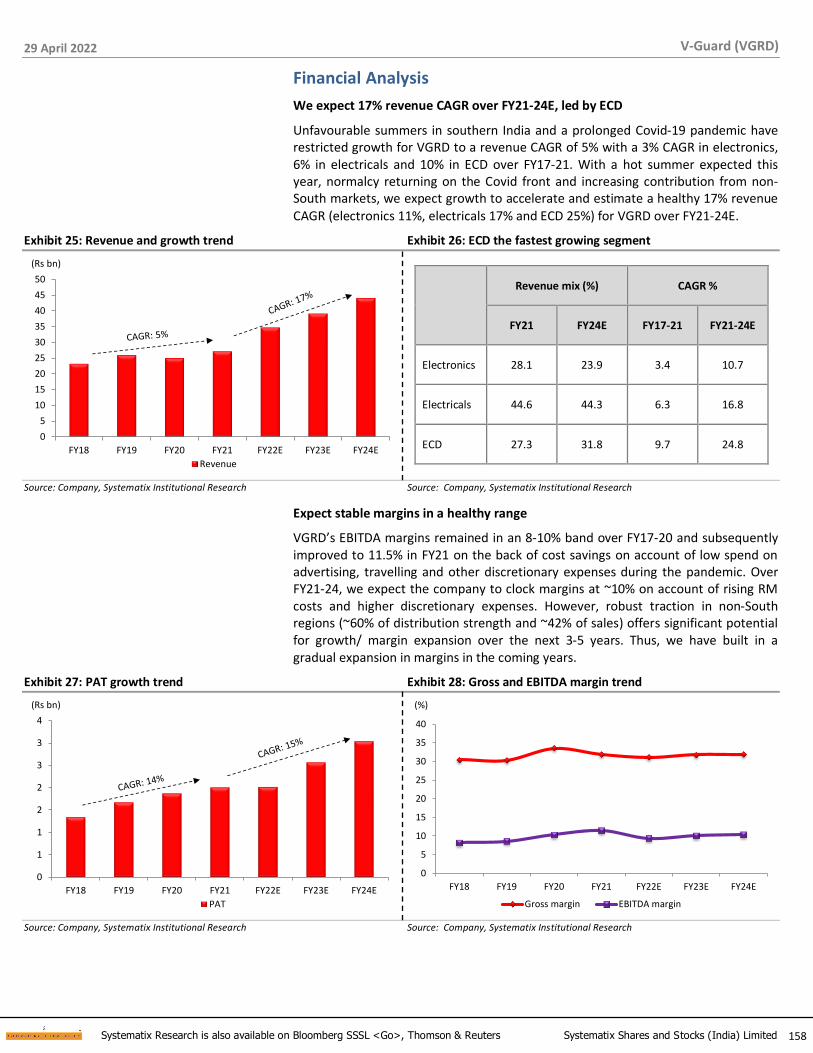

After significant demand destruction in the three months over March-May 2020 (the first phase of Covid-19 disruptions), the consumer electricals industry saw a swifter-than-expected recovery, with leading players at the forefront of the bounce-back. A subsequent resurgence in Covid-19 cases and the significant rise recorded in commodity costs did not deter consumers’ buying decisions, with sustained growth witnessed across retail categories. While the sharp rebound is partly attributable to pent-up demand in the aftermath of the pandemic, we believe the industry is on a secular growth trend. Demand is being stoked not only by the core drivers (a wide population base and increasing affordability), but also by industry trends like deeper penetration into rural areas, premiumization, government initiatives like electrification/ rural-urban infrastructure and the ‘Make in India’ push.

Increasing affordability with higher disposable incomes: Census 2011 put India’s population at ~1.2bn with ~246m households. After a 1.8% CAGR seen over 2001-2011, population is expected to touch 1.5bn by 2030 (1.2% CAGR) with India becoming the world’s most populous country. The proportion of the urban population (~35% of total) has been rising as people from rural areas move to cities for better job opportunities, education and a better life. India’s per capita income, a broad indicator of living standards, has been growing steadily over the years. According to media reports, the per capita net national income (NNI) at current prices and constant prices has recorded 10% and 6% CAGR respectively over FY12-18. These factors typically drive demand for housing and also accelerate expenditure on public infrastructure (railways, roads, malls, hospitals, educational institutes, etc) and purchase of discretionary items including consumer electricals.

Exhibit 22: India’s population growth Exhibit 23: Urbanization trend

0.4

0.60.7

0.91.0

1.21.3

1.5

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1961 1971 1981 1991 2001 2011 2017E 2030P

(Bn)

Population

295 382 460 484

758 849

893 899

1,053

1,231 1,353 1,383

0

200

400

600

800

1,000

1,200

1,400

1,600

2000 2010 2018E 2020E

Urban Rural

(Mn Households)

Source: GoI, Industry reports Source: GoI, Industry reports

Underpenetration in key categories, especially in lower tier and rural regions: Except fans and lights, penetration levels of organized retail in other product categories are medium-to-low. Increasing electrification in rural areas, improving electricity availability in small towns/ cities, rising aspirations with disposable incomes, availability of energy-efficient products and a shift in consumer preference towards reliable and branded products are the key factors driving penetration levels higher in the hinterland and supporting growth during spells of the economy slowing.

29 April 2022

9 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Exhibit 24: Category-wise penetration levels

Category Overall penetration Organized penetration

Cables - domestic/ industrial High/ High Low/ Medium

Fans High High

Lighting & fixtures High Medium

Other appliances Low Low

Switches High Medium

Switchgears (MCB) High High

Water heaters Low Low

Source: Polycab RHP, Systematix Institutional Research

Premiumization helps ensure modest value growth even with lower demand: Rising aspirations with higher disposable incomes and customers’ growing preference for technology-driven and aesthetically appealing products are stoking the premiumization trend in many categories (fans, switches, appliances, etc). Despite low volume growth, the industry has managed to capture modest value growth in a few categories in the recently turbulent times. We believe the trend is likely to sustain in the medium to long term.

Exhibit 25: Share of premium fans rising rapidly

43 40 34

5150

46

6 1020

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY18 FY23p

Economy Base Premium

CAGR ~4%

CAGR ~5%

CAGR ~21%

CAGR ~4%

CAGR ~5%

CAGR ~22%

Source: Polycab RHP, Systematix Institutional Research

29 April 2022

10 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Government initiatives providing additional growth impetus

Numerous government initiatives – including the National Infrastructure Pipeline (NIP), Production-Linked Incentives scheme, focus on indigenous manufacturing, higher budgetary allocations for capital expenditure, renewable energy, digital infrastructure push and Housing for All – have directly or indirectly benefitted the electrical goods industry in the B2B (cables, switchgears, lighting, etc) as well as B2C (all other FMEG products) segments. We expect the above initiatives to continue

supporting demand for electrical goods in the long term.

Government focus on improving electrification and rural/ urban infrastructure: Introduction of various schemes with specific objectives and targeted at different sections of the society has been a key catalyst for growth in the consumer electricals industry in the medium to long term. While a large base of houses in rural India is being electrified under the DDUGJY scheme, there exists immense scope till all rural areas get access to reliable electricity. Initiatives such as Saubhagya and DDUGJY could spur development of rural infrastructure as well as growth in household electrical products. The revival of DISCOMs through UDAY could support the government’s electrification initiatives. Schemes like the Domestic Efficient-Lighting Programme (DELP), Unnat Jyoti by Affordable LEDs for All (UJALA) and the Street Lighting National Program (SLNP), targeted at reducing costs and saving energy, are also envisaged to drive demand for LED bulbs.

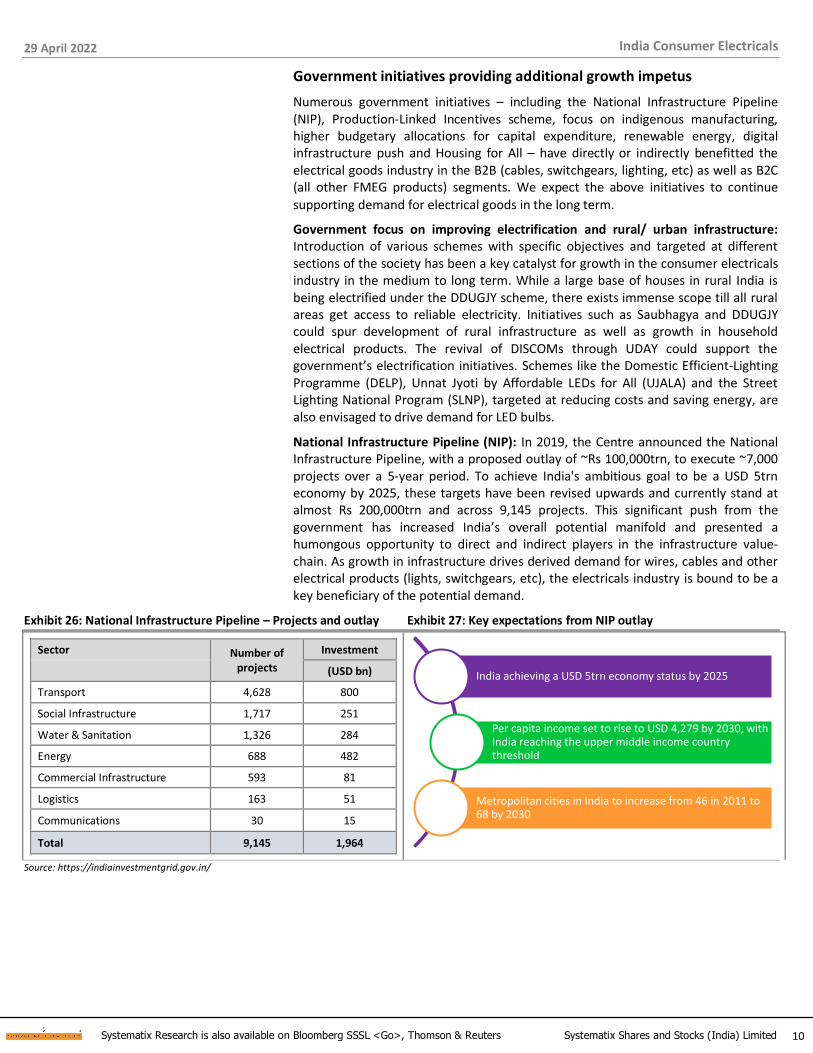

National Infrastructure Pipeline (NIP): In 2019, the Centre announced the National Infrastructure Pipeline, with a proposed outlay of ~Rs 100,000trn, to execute ~7,000 projects over a 5-year period. To achieve India's ambitious goal to be a USD 5trn economy by 2025, these targets have been revised upwards and currently stand at almost Rs 200,000trn and across 9,145 projects. This significant push from the government has increased India’s overall potential manifold and presented a humongous opportunity to direct and indirect players in the infrastructure value-chain. As growth in infrastructure drives derived demand for wires, cables and other electrical products (lights, switchgears, etc), the electricals industry is bound to be a key beneficiary of the potential demand.

Exhibit 26: National Infrastructure Pipeline – Projects and outlay Exhibit 27: Key expectations from NIP outlay

Sector Number of projects

Investment

(USD bn)

Transport 4,628 800

Social Infrastructure 1,717 251

Water & Sanitation 1,326 284

Energy 688 482

Commercial Infrastructure 593 81

Logistics 163 51

Communications 30 15

Total 9,145 1,964

India achieving a USD 5trn economy status by 2025

Per capita income set to rise to USD 4,279 by 2030, with India reaching the upper middle income country threshold

Metropolitan cities in India to increase from 46 in 2011 to 68 by 2030

Source: https://indiainvestmentgrid.gov.in/

29 April 2022

11 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Key trends shaping the consumer electricals industry

Incumbents enjoy a strong brand recall and wide distribution networks which take years to build. Rising consumer preference towards quality, innovative and branded products augurs well for the organized segment which has gained market share at the expense of the unorganized sector. In the last few years, leading players have grown ahead of the industry on the back of their portfolio and channel expansion initiatives as also focus on premiumization. We expect the trends to gain momentum in the coming period. Below we give a brief on the key trends prevailing in the consumer electricals industry:

Strong demand revival after the first Covid-19 wave: The first wave of Covid-19 had triggered widespread fears of demand destruction in the wake of job losses and a significant rise in commodity costs. However, the challenges were short-lived for the consumer electricals industry, especially leaders, across segments. Importantly, housing activity, one of the biggest drivers of demand for consumer electrical products, is witnessing some green shoots (after a prolonged lull) with reducing inventories. CE companies reported healthy EBITDA margins in FY21 as the impact of

lower demand was tackled by lower discretionary expenses including A&P spends.

Organized sector gaining market share via portfolio and distribution expansion: Large and organized players have gained significant market share in the last two years as smaller players were not resilient enough to survive the frequent lockdowns mandated during the Covid-19 pandemic. At the same time, larger players became aggressive on distribution expansion in untapped areas (including smaller towns) and innovative product launches to recover the sales lost during the lockdowns. Rural electrification and better quality of electricity supply in tier-3 and -4 cities and beyond are also helping generate demand for consumer durables and appliances. All key players are looking to strengthen their operations in the semi-urban and rural areas and gain market share through their less expensive portfolios under a different

brand targeted at these price-sensitive markets.

Emergence of alternate sales channels: Alternate channels (modern trade and e-Commerce) gained good traction (up to 35% share in sales in some kitchen appliance categories) owing to the ease of buying products at attractive discounts. We believe the traditional distribution channel will continue to dominate the overall sales in the longer term even as alternate channels will gradually gain market share.

Premiumization gaining good traction: Premiumization is another theme that has played out across categories in the last few years, and even accelerated during the pandemic as consumers spent more time at home and chose better quality and innovative products. The trend should continue given that buyer preference is

shifting towards technologically-advanced products offering innovative features.

Fast adoption of digitization to face unforeseen events like Covid-19: Technology helped leading companies manage their inventories and supply-chain issues better during the sudden challenge posed by Covid-19. We believe technology adoption at the back-end will further strengthen the market positioning of incumbents and be the differentiator vis-à-vis small regional players and the unorganized sector.

Exports limited to W&C; however, potential in other product categories too: India’s leading W&C companies (POLYCAB and KEII) have seen good traction in the global markets as they earn 10%+ of their total revenues from exports. Wide product portfolios and global certifications have helped these players to participate in prestigious global tenders and win orders as well. Given the government’s stated mission to make India a manufacturing hub for the world, we see a large opportunity in exports for other electrical goods categories as well.

29 April 2022

12 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Rising costs an overhang on growth and margins: While there are many structural drivers supporting demand for consumer electrical goods in the long term, the industry faces certain headwinds in the short to medium term. Currently, companies are facing margin pressure as most of the discretionary expenses have returned to normal levels and their limited ability to take adequate price hikes despite elevated raw material prices (copper, aluminium, ABS, etc) and other costs (freight among others). Leading companies have chosen to grow fast and gain market share at the cost of margins as they expect the margin pressure to be short lived and recoverable with adequate pricing action as also an eventual easing of commodity prices.

Exhibit 28: LME copper price trend Exhibit 29: LME aluminium price trend

0

2000

4000

6000

8000

10000

12000

Ap

r-1

2

Oct

-12

Ap

r-1

3

Oct

-13

Ap

r-1

4

Oct

-14

Ap

r-1

5

Oct

-15

Ap

r-1

6

Oct

-16

Ap

r-1

7

Oct

-17

Ap

r-1

8

Oct

-18

Ap

r-1

9

Oct

-19

Ap

r-2

0

Oct

-20

Ap

r-2

1

Oct

-21

Ap

r-2

2

(USD /t)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Ap

r-1

2

Oct

-12

Ap

r-1

3

Oct

-13

Ap

r-1

4

Oct

-14

Ap

r-1

5

Oct

-15

Ap

r-1

6

Oct

-16

Ap

r-1

7

Oct

-17

Ap

r-1

8

Oct

-18

Ap

r-1

9

Oct

-19

Ap

r-2

0

Oct

-20

Ap

r-2

1

Oct

-21

Ap

r-2

2

(USD /t)

Source: Bloomberg Source: Bloomberg

Positioning of leaders in various categories of the consumer electricals industry:

▪ HAVL continues to be a widely preferred brand among younger buyers owing to its mass-premium positioning, product design ability, quality of offerings and high advertisement and promotional spending. CROMPTON, on the other hand, is an older brand commanding loyalty from the older generation, while ORIENT is an emerging brand in premium fans.

▪ In fans, HAVL enjoys a 5-10% price premium to CROMPTON and a slightly higher premium to ORIENT and other brands. Likely introduction of energy ratings in

2022 will fuel a further market share shift towards the organized sector.

▪ CROMPTON and BJE are the preferred choice among builders owing to their competitive prices and wide product range

▪ For after-sales service, HAVL, CROMPTON and BJE are considered the best.

29 April 2022

13 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Wires & Cables (W&C): Industry dynamics and outlook

The W&C segment registered ~11% CAGR over FY14-18 (and a higher volume growth), followed by a flattish growth over FY18-21. At ~Rs 550bn, it comprises ~45% of the electrical equipment market in India (industry estimates). Upbeat construction activity in the housing sector and government initiatives in the power and infrastructure sectors has been the key factors driving growth. At 12% CAGR estimated over FY21-26, the W&C industry is expected to grow the fastest within the CE industry. POLYCAB, KEII, HAVL, FNXC, RR Kabel and VGRD are the key players in the category. Notably, W&Cs are manufactured fully in-house given customers’

technical requirement.

Exhibit 30: W&C segment – expect ~12% CAGR Exhibit 31: National Infrastructure Pipeline – Projects and outlay

346

525 550

968

0

200

400

600

800

1,000

1,200

FY14 FY18 FY21 FY26P

(Rs bn)

Source: Polycab annual report, Systematix Institutional Research Source: https://indiainvestmentgrid.gov.in/

Exhibit 32: Category-wise growth factors and key players

Category Apar Finolex Cables

Gupta Power

Havells KEC KEI Polycab R R Kabel V-Guard

Power Cables (LT/ HT) ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

Growth drivers: (a) investments in power transmission and distribution (b) capacity addition in solar and wind energy, and (c) Smart Cities mission

Building Wires ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

Growth drivers: (a) affordable Housing scheme (b) growing nuclearization of families, and (c) investments in commercial and residential infra

Flexible Cables/ Wires ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

Growth drivers: (a) growing demand for household appliances and automobiles on revival in per capita income (b) increasing investments in railways for electrification, and (c) increased construction activity supported by growing infrastructure projects

EHV Cables ✓ ✓

✓ ✓ ✓

Growth drivers: (a) investments in power transmission and distribution, and (b) Smart Cities mission

Control/ Instrumentation Cables ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

Growth drivers: (a) industrial capex rising across industries such as auto, steel, oil and gas, and power (b) Investment expenditure by Indian Railways and in other mass transit systems (c) Increased focus on automation in manufacturing and processing to monitor and control quality Source: Polycab RHP, Systematix Institutional Research

Number of

projects

Investment

USD bn

Transport 4,628 800

Social Infrastructure 1,717 251

Water & Sanitation 1,326 284

Energy 688 482

Commercial Infrastructure 593 81

Logistics 163 51

Communication 30 15

Total 9,145 1,964

29 April 2022

14 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Exhibit 33: Wires & Cables – trends, demand drivers and outlook

Market size Segment’s share in CE

industry (FY21) CAGR (FY14-21) CAGR (FY21-26E)

EBITDA margin range for key listed players

~Rs 550bn ~45% 7% 12%+ 10-15% (ECD division)

Trends

• Government focus on power, infrastructure and housing construction have been the key growth drivers

• The formal sector (comprising all-India brand-named manufacturers) capturing market share from the non-regulated sector (smaller regional manufacturers). Industry estimates put the share of organized at ~75% currently, and much higher in high voltage (HV) and extra-high voltage (EHV) products

• To protect margins, companies typically pass on any meaningful changes in raw material prices (mainly copper and aluminium) to the end-consumer within 15-30 days

• W&C manufactured fully in-house due to technical requirement of customers

Demand drivers

• Numerous government initiatives such as NIP, PLI scheme, focus on indigenous manufacturing, higher budgetary allocation for capital expenditure, renewable energy and digital infrastructure push, Housing for All

• Electrification of rural villages and households (schemes such as Power for All, Saubhagya, etc)

• Investments in modernizing transmission & distribution systems and for improving efficiency

• Increased demand from renewable power generation, particularly solar and wind energy

• Infrastructure development such as Smart Cities mission and mass-transit systems

• Commercial establishments and public utilities (metro-rail, airports, hospitals, educational institutions, etc)

• Industrial sectors (auto and FMEG) to drive demand for flexible cables & wires and control cables

Outlook The W&C industry expected to register ~12% CAGR by value over 2021-2026. Leading players likely to grow faster as they gain market share due to operational challenges faced by small regional players

Risks and challenges

• Realizations and profitability in W&C industry dependent on RM prices (mainly copper and aluminium). Companies usually pass on any meaningful changes in raw material prices to end-consumer within 15-30 days to protect margins. However, high volatility in RM prices may impact growth or margins, depending on the overall demand situation and economic outlook

• As a large part of key raw materials is imported by players given economies of cost and the quality required, margins are exposed to exchange rate fluctuations. To mitigate the risk, companies enter into a price escalation clause for long-term contracts and hedge their future purchases

Key players Polycab, KEI, Havells, Finolex Cables, RR Kabel and V-Guard

Source: Industry reports, Systematix Institutional Research

29 April 2022

15 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

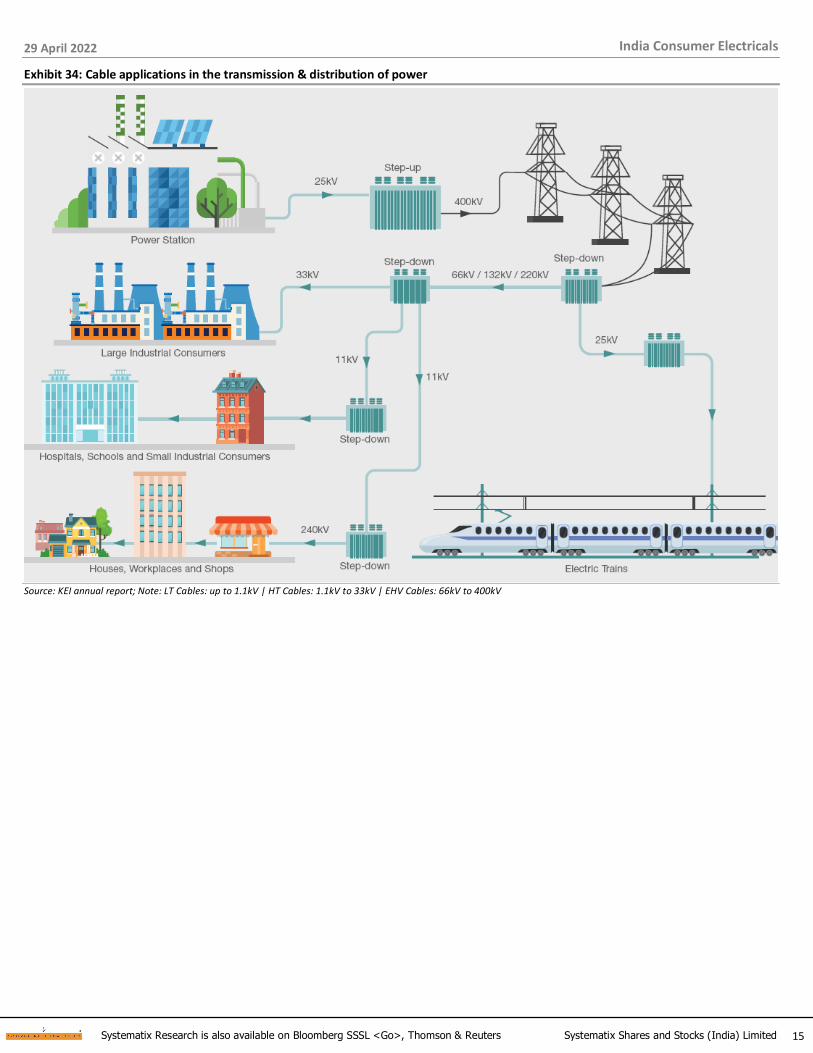

Exhibit 34: Cable applications in the transmission & distribution of power

Source: KEI annual report; Note: LT Cables: up to 1.1kV | HT Cables: 1.1kV to 33kV | EHV Cables: 66kV to 400kV

29 April 2022

16 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Fans: Industry dynamics and outlook

The ~Rs 100bn electric fans market in India is dominated by ceiling fans (~70% share by value). Domestic demand for fans is largely met locally. The trend of premiumization has been catching pace, driven by product innovation (decorative, anti-dust, tech-enabled fans, etc) – mainly in replacement demand which accounts for ~65% of the total demand. Therefore, the category’s dependency on new construction is relatively lower. The share of regulated players in the category is quite high at an estimated ~80%. CROMPTON (the market leader with ~25% share), ORIENTEL, Usha, HAVL, BJE and POLYCAB are the key players in the fans space. After

a 7% CAGR over FY14-21, the category is expected to report 6% CAGR over FY21-26.

Exhibit 35: Fans – growth trend

63

80

99

131

0

20

40

60

80

100

120

140

FY14 FY18 FY21 FY26P

(Rs bn)

Source: Polycab annual report, Systematix Institutional Research

Exhibit 36: Category-wise break-up of the fans segment Exhibit 37: Share of premium fans rising rapidly

71%

19%

5%5%

Ceiling

TPW

Exhaust

Industrial

43 40 34

5150

46

6 1020

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY18 FY23p

Economy Base Premium

CAGR ~4%

CAGR ~5%

CAGR ~21%

CAGR ~4%

CAGR ~5%

CAGR ~22%

Source: Polycab RHP, Systematix Institutional Research Source: Polycab RHP, Systematix Institutional Research

29 April 2022

17 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Exhibit 38: Fans – trends, demand drivers and outlook

Market size Segment’s share in CE

industry (FY21) CAGR (FY14-21) CAGR (FY21-26E)

EBITDA margin range for key listed players

~Rs 100bn ~8% 7% 6% 10-15% (ECD division)

Trends

• While volume growth in ceiling fans (~70% of the fans sector) has been hit by the slowdown in real estate sector in the past few years, value growth has been driven primarily by increasing buyer preference for premium products (2-4x higher realizations), including decorative, energy-efficient and customized fans

• Various government initiatives towards facilitating electricity availability in rural areas have been driving demand for table, pedestal, and wall (TPW) fans

• The regulated (or formal) segment, at ~80%, has consistently gained market share with the rising preference for branded, aesthetically pleasing and quality products. Likely energy rating introduction in FY22 will further fuel the shift

• As the technology to manufacture fans is fairly standardized (mainly economy/ base segments), outsourcing production to smaller players is prevalent. The industry estimates that, given the cost-benefits from outsourcing production, the trend is expected to continue in the medium to long term

Demand drivers

• The economy and base fan sub-segments have seen a low ~5% CAGR, while the premium segment has registered >20% CAGR with its share in ceiling fans rising to 10%+

• Premium fans are likely to continue witnessing strong growth with rising preference for brand-named, aesthetic and quality products

• 2-4x higher realizations for premium fans would support value growth in the fans sector

• Demand for technology-driven higher-priced products (silent, dust-free and bladeless, with temperature or proximity sensors and those controlled by wi-fi or mobile apps) gaining traction

• Rising disposable incomes and changing preferences of the urban population are shortening home-improvement cycles and boosting replacement demand of fans.

• Also, improving electricity availability in rural areas resulting in deepening rural penetration and rising demand for economy ceiling, table, pedestal and wall-mounted (TPW) fans

• The focus on energy-efficient fans under the EESL-financed procurement and incentivization programmes would also drive demand for electric fans in the medium to long term

Outlook The fan category is expected to clock 6% CAGR over FY21-26 to Rs 131bn, driven by premium ceiling fans

Risks and challenges

• As penetration of fans is already quite high in urban areas, revival in housing activity is necessary to support volume growth, which already has a high base

• Air-coolers and air-conditioners are substitutes for fans. Demand for these is growing, especially in housing and offices in urban areas. Alternative products becoming more affordable may restrict growth in the fan industry

Key players Crompton, Bajaj Electricals, Havells, Orient Electric, Usha, Polycab, V-Guard, etc

Source: Industry reports, Systematix Institutional Research

29 April 2022

18 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Lighting: Industry dynamics, outlook

The lighting industry registered a 7% CAGR over FY14-21 to Rs 227bn, driven mainly by huge demand for LEDs from EESL (a government agency). We expect a 10% CAGR in the segment over FY21-26, driven by retail demand for LEDs after a significant price drop and better aesthetics vis-à-vis CFLs. BJE, CROMPTON, HAVL, ORIENTEL, Philips, Syska, Wipro and POLYCAB are the key players in the category and follow a mixed strategy of in-house manufacturing and outsourcing.

Exhibit 39: Lighting – growth trend

142

212227

365

0

50

100

150

200

250

300

350

400

FY14 FY18 FY21 FY26P

(Rs bn)

Source: Polycab annual report, Systematix Institutional Research

Exhibit 40: Lighting – trends, demand drivers and outlook

Market size Segment’s share in CE

industry (FY21) CAGR (FY14-21) CAGR (FY21-26E)

EBITDA margin range for key listed players

Rs 227bn ~19% 7% 10% 10-15% (ECD division)

Trends

• Rapid adoption of higher priced light-emitting diodes (LEDs), aided by government measures and a shift away from conventional lighting products including GLS, FTL and CFLs

• The initially high prices of LEDs had restricted growth to the institutional category (large organizations and government agencies like EESL) only. Street and flood lights are the key products targeted at institutions

• With technological advancement, LED chip prices have fallen significantly in the last few years. This, along with growing awareness about their energy efficiency, has resulted in increasing sales in B2C segment

• The formal sector, at ~65%, has significantly gained market share on the introduction of LEDs, which required investment in technology and were priced much higher than conventional lighting

• A large part of LED components is outsourced by the majors in this segment and the trend is expected to continue

Demand drivers

• Segment growth driven by LED sales over the last five years, largely to institutions due to high prices. From 2015 to 2017, EESL procured ~300m LED lamps out of the industry demand for 500m+

• Industry growth in the next five years to be mainly decided by growth of LEDs in retail after significant reduction in prices and enhanced aesthetics than CFLs

• Demand for conventional lighting to be limited to rural areas and low-income groups

Outlook The lighting industry expected to clock a 10% CAGR over FY21-26 to reach Rs 365bn, driven by LEDs in retail

Risks and challenges The longer life span of LEDs would restrict volume growth in the medium to long term

Key players Bajaj Electricals, Crompton, Havells, Orient Electric, Philips Lighting, Syska, Wipro Consumer, Polycab, etc

Source: Industry reports, Systematix Institutional Research

29 April 2022

19 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Switchgears: Industry dynamics and outlook

After a 6% CAGR over FY14-21 to Rs 210bn, we estimate ~10% CAGR in the switchgears segment over FY21-26 to Rs 337bn. Growth will be driven primarily by the low voltage (LV) segment (~70% of domestic switchgears). Revival in the real estate sector and industrial capex augur well for demand of these products. ABB, HAVL, Legrand, Schneider, Siemens and POLYCAB are the leading players having in-house manufacturing due to significant technology and certification requirements.

Exhibit 41: Switchgears – growth trend

139

183210

337

0

50

100

150

200

250

300

350

400

FY14 FY18 FY21 FY26P

(Rs bn)

Source: Polycab annual report, Systematix Institutional Research

Exhibit 42: Switchgears – trends, demand drivers and outlook

Market size Segment’s share in CE

industry (FY21) CAGR (FY14-21) CAGR (FY21-26E)

EBITDA margin range for key listed players

Rs 210bn ~17% 6% 10% 15-20%

Trends

• Sluggish activity in the real estate sector and industrial capex have kept demand subdued

• Low-voltage switchgears account for ~70% of the domestic switchgears industry. Demand of key products (MCBs, DBs, RCCBs, etc) primarily arises from residences and industries

• The MV/ HV segment products are used mainly in power distribution stations and sub-stations requiring high voltage. The segment experienced muted growth given the challenges in the power distribution sector

• At ~90% market share, LV and MV/ HV switchgears are regulated due to significant technology requirements

• The technology-intensive nature of the product driving most players to opt for in-house manufacturing

Demand drivers

• After modest growth in the last five years, LV switchgears expected to accelerate backed largely by the government's push for infrastructure development (affordable housing, Railways, metro-rail, etc)

• Higher use of power in residences and industries due to more electrification would drive demand for switchgears in the medium to long term

• GoI initiatives such as DDUGJY and Saubhagya schemes and the expected revival of DISCOMs under UDAY would aid growth of the MV/ HV category

Outlook Led by LV category, the switchgears segment is expected to clock a 10% CAGR over FY21-26 to Rs 337bn on account of consumption demand and electrification

Risks and challenges Any slowdown in real estate and industrial capex will restrict growth of switchgears

Key players ABB, Havells, Legrand, Schneider, Siemens, Polycab, etc

Source: Industry reports, Systematix Institutional Research

29 April 2022

20 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

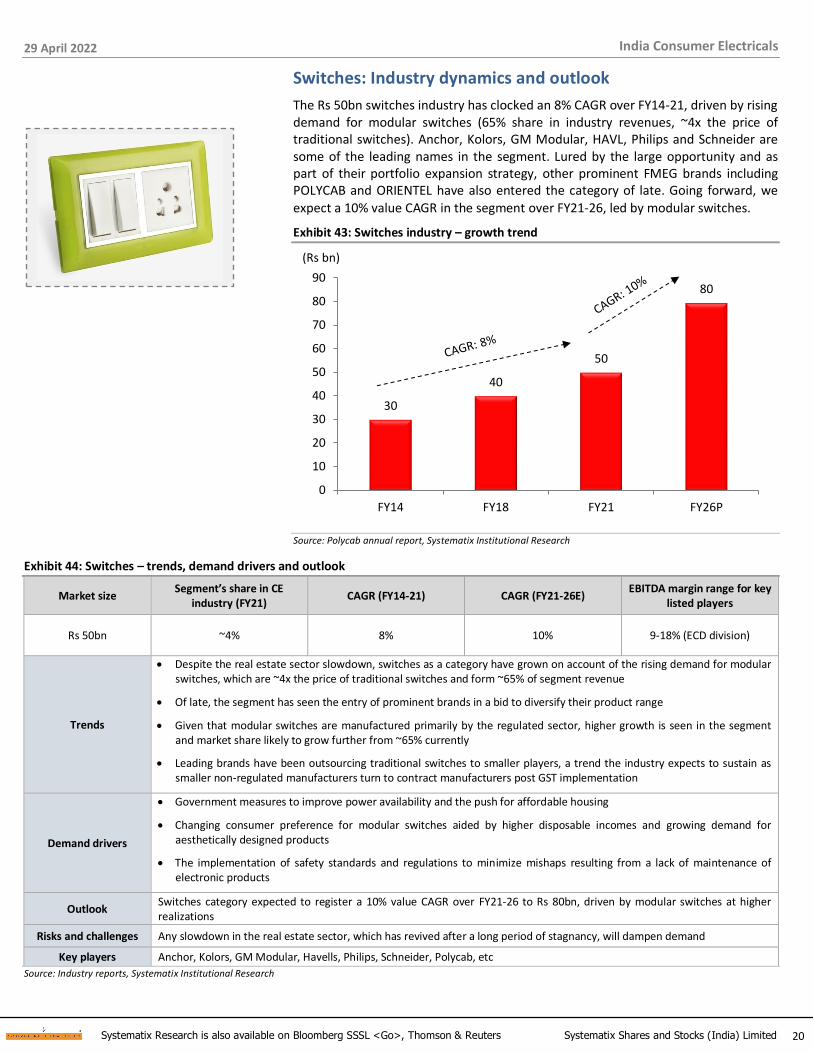

Switches: Industry dynamics and outlook

The Rs 50bn switches industry has clocked an 8% CAGR over FY14-21, driven by rising demand for modular switches (65% share in industry revenues, ~4x the price of traditional switches). Anchor, Kolors, GM Modular, HAVL, Philips and Schneider are some of the leading names in the segment. Lured by the large opportunity and as part of their portfolio expansion strategy, other prominent FMEG brands including POLYCAB and ORIENTEL have also entered the category of late. Going forward, we

expect a 10% value CAGR in the segment over FY21-26, led by modular switches.

Exhibit 43: Switches industry – growth trend

30

40

50

80

0

10

20

30

40

50

60

70

80

90

FY14 FY18 FY21 FY26P

(Rs bn)

Source: Polycab annual report, Systematix Institutional Research

Exhibit 44: Switches – trends, demand drivers and outlook

Market size Segment’s share in CE

industry (FY21) CAGR (FY14-21) CAGR (FY21-26E)

EBITDA margin range for key listed players

Rs 50bn ~4% 8% 10% 9-18% (ECD division)

Trends

• Despite the real estate sector slowdown, switches as a category have grown on account of the rising demand for modular switches, which are ~4x the price of traditional switches and form ~65% of segment revenue

• Of late, the segment has seen the entry of prominent brands in a bid to diversify their product range

• Given that modular switches are manufactured primarily by the regulated sector, higher growth is seen in the segment and market share likely to grow further from ~65% currently

• Leading brands have been outsourcing traditional switches to smaller players, a trend the industry expects to sustain as smaller non-regulated manufacturers turn to contract manufacturers post GST implementation

Demand drivers

• Government measures to improve power availability and the push for affordable housing

• Changing consumer preference for modular switches aided by higher disposable incomes and growing demand for aesthetically designed products

• The implementation of safety standards and regulations to minimize mishaps resulting from a lack of maintenance of electronic products

Outlook Switches category expected to register a 10% value CAGR over FY21-26 to Rs 80bn, driven by modular switches at higher realizations

Risks and challenges Any slowdown in the real estate sector, which has revived after a long period of stagnancy, will dampen demand

Key players Anchor, Kolors, GM Modular, Havells, Philips, Schneider, Polycab, etc

Source: Industry reports, Systematix Institutional Research

29 April 2022

21 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Water-heaters: Industry dynamics and outlook

The Rs 23bn water heater industry has registered a 10% CAGR over FY14-21. Introduction of energy-efficient products and rising consumer aspirations have accelerated the penetration level, which otherwise was slow due to seasonal nature of the product. Low volumes have led to companies (AO Smith, BJE, CROMPTON, HAVL, Racold, Venus, VGRD, etc.) outsourcing production to smaller players. We expect the outsourcing trend to prevail over the medium term.

Exhibit 45: Water heaters – growth trend

12

18

23

30

0

5

10

15

20

25

30

35

FY14 FY18 FY21 FY26P

(Rs bn)

Source: Polycab annual report, Systematix Institutional Research

Exhibit 46: Water heaters – trends, demand drivers and outlook

Market size Segment’s share in CE

industry (FY21) CAGR (FY14-21) CAGR (FY21-26E)

EBITDA margin range for key listed players

Rs 23bn ~2% 10% 6% 9-18% (ECD division)

Trends

• Largely seasonal demand for water heaters has translated into low penetration. Also, high operational cost (energy charges) deters adoption

• The formal segment’s share has increased to ~65% over the years with rising preference for branded and energy-efficient products, new brands’ extension into the category, rising compliance to meet energy-efficiency parameters and a growing network of service centers; the momentum likely to be sustained

• Low volumes have led to leading brands outsourcing production to smaller players. Given the cost benefits, the trend is likely to continue over the medium term

Demand drivers

• Rising disposable incomes and demand for energy-efficient products

• Better availability of electricity in smaller towns and rural areas

• New features (wi-fi-enabled, better coatings, auto temperature adjustments and leak detection) differentiate electric water heaters from solar and gas-operated ones

• Stricter compliance affecting non-regulated manufacturers

Outlook Low penetration, rising disposable incomes and energy-efficient products to drive an estimated 6% CAGR over FY21-26 in water heaters to ~Rs 30bn

Risks and challenges Solar water heaters rapidly gaining ground as a substitute. Operating on renewable energy, solar water heaters are more energy-efficient than the electric ones

Key players AO Smith, Bajaj, Crompton, Havells, Racold, Venus and V-Guard

Source: Industry reports, Systematix Institutional Research

29 April 2022

22 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Stock Views

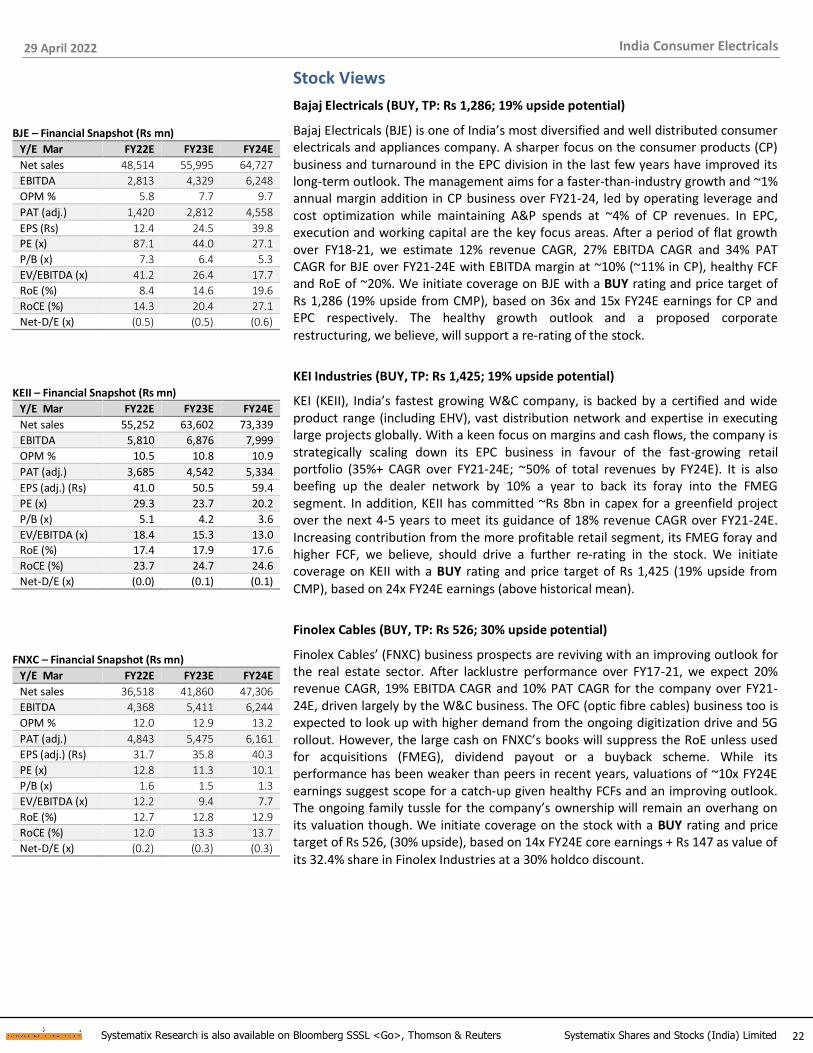

Bajaj Electricals (BUY, TP: Rs 1,286; 19% upside potential)

Bajaj Electricals (BJE) is one of India’s most diversified and well distributed consumer electricals and appliances company. A sharper focus on the consumer products (CP) business and turnaround in the EPC division in the last few years have improved its long-term outlook. The management aims for a faster-than-industry growth and ~1% annual margin addition in CP business over FY21-24, led by operating leverage and cost optimization while maintaining A&P spends at ~4% of CP revenues. In EPC, execution and working capital are the key focus areas. After a period of flat growth over FY18-21, we estimate 12% revenue CAGR, 27% EBITDA CAGR and 34% PAT CAGR for BJE over FY21-24E with EBITDA margin at ~10% (~11% in CP), healthy FCF and RoE of ~20%. We initiate coverage on BJE with a BUY rating and price target of Rs 1,286 (19% upside from CMP), based on 36x and 15x FY24E earnings for CP and EPC respectively. The healthy growth outlook and a proposed corporate

restructuring, we believe, will support a re-rating of the stock.

KEI Industries (BUY, TP: Rs 1,425; 19% upside potential)

KEI (KEII), India’s fastest growing W&C company, is backed by a certified and wide product range (including EHV), vast distribution network and expertise in executing large projects globally. With a keen focus on margins and cash flows, the company is strategically scaling down its EPC business in favour of the fast-growing retail portfolio (35%+ CAGR over FY21-24E; ~50% of total revenues by FY24E). It is also beefing up the dealer network by 10% a year to back its foray into the FMEG segment. In addition, KEII has committed ~Rs 8bn in capex for a greenfield project over the next 4-5 years to meet its guidance of 18% revenue CAGR over FY21-24E. Increasing contribution from the more profitable retail segment, its FMEG foray and higher FCF, we believe, should drive a further re-rating in the stock. We initiate coverage on KEII with a BUY rating and price target of Rs 1,425 (19% upside from

CMP), based on 24x FY24E earnings (above historical mean).

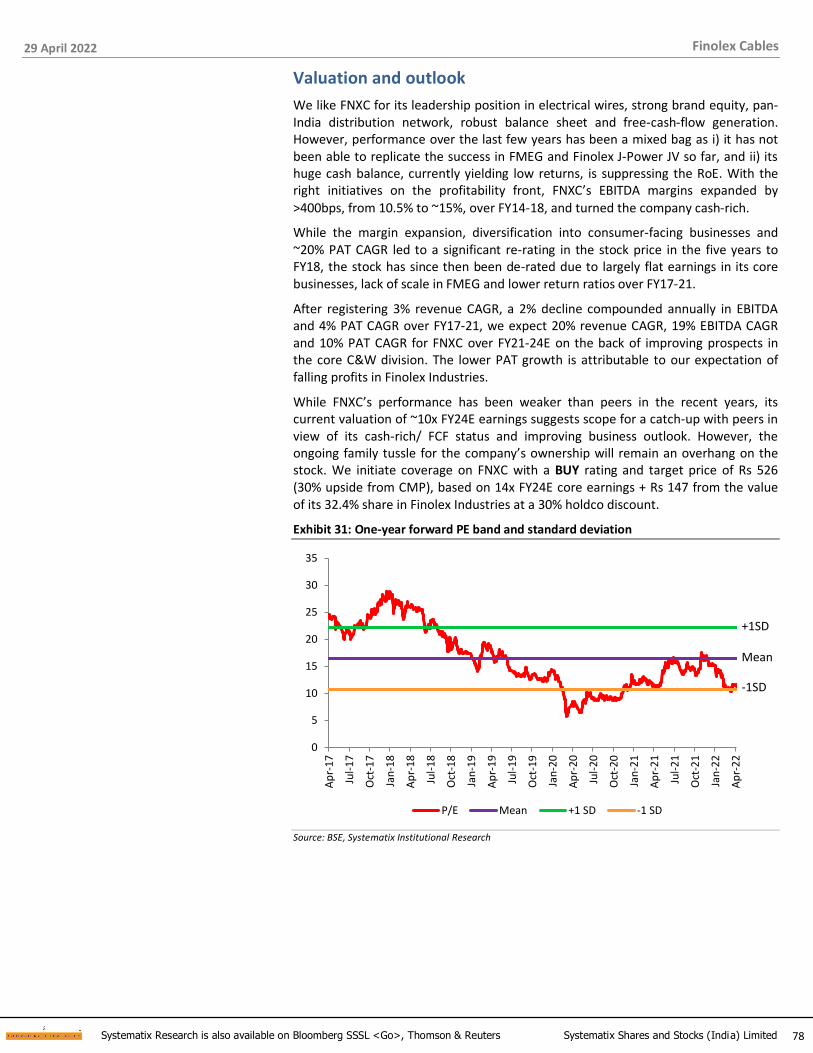

Finolex Cables (BUY, TP: Rs 526; 30% upside potential)

Finolex Cables’ (FNXC) business prospects are reviving with an improving outlook for the real estate sector. After lacklustre performance over FY17-21, we expect 20% revenue CAGR, 19% EBITDA CAGR and 10% PAT CAGR for the company over FY21-24E, driven largely by the W&C business. The OFC (optic fibre cables) business too is expected to look up with higher demand from the ongoing digitization drive and 5G rollout. However, the large cash on FNXC’s books will suppress the RoE unless used for acquisitions (FMEG), dividend payout or a buyback scheme. While its performance has been weaker than peers in recent years, valuations of ~10x FY24E earnings suggest scope for a catch-up given healthy FCFs and an improving outlook. The ongoing family tussle for the company’s ownership will remain an overhang on its valuation though. We initiate coverage on the stock with a BUY rating and price target of Rs 526, (30% upside), based on 14x FY24E core earnings + Rs 147 as value of

its 32.4% share in Finolex Industries at a 30% holdco discount.

BJE – Financial Snapshot (Rs mn)

Y/E Mar FY22E FY23E FY24E

Net sales 48,514 55,995 64,727

EBITDA 2,813 4,329 6,248

OPM % 5.8 7.7 9.7

PAT (adj.) 1,420 2,812 4,558

EPS (Rs) 12.4 24.5 39.8

PE (x) 87.1 44.0 27.1

P/B (x) 7.3 6.4 5.3

EV/EBITDA (x) 41.2 26.4 17.7

RoE (%) 8.4 14.6 19.6

RoCE (%) 14.3 20.4 27.1

Net-D/E (x) (0.5) (0.5) (0.6)

KEII – Financial Snapshot (Rs mn)

Y/E Mar FY22E FY23E FY24E

Net sales 55,252 63,602 73,339

EBITDA 5,810 6,876 7,999

OPM % 10.5 10.8 10.9

PAT (adj.) 3,685 4,542 5,334

EPS (adj.) (Rs) 41.0 50.5 59.4

PE (x) 29.3 23.7 20.2

P/B (x) 5.1 4.2 3.6

EV/EBITDA (x) 18.4 15.3 13.0

RoE (%) 17.4 17.9 17.6

RoCE (%) 23.7 24.7 24.6

Net-D/E (x) (0.0) (0.1) (0.1)

FNXC – Financial Snapshot (Rs mn)

Y/E Mar FY22E FY23E FY24E

Net sales 36,518 41,860 47,306

EBITDA 4,368 5,411 6,244

OPM % 12.0 12.9 13.2

PAT (adj.) 4,843 5,475 6,161

EPS (adj.) (Rs) 31.7 35.8 40.3

PE (x) 12.8 11.3 10.1

P/B (x) 1.6 1.5 1.3

EV/EBITDA (x) 12.2 9.4 7.7

RoE (%) 12.7 12.8 12.9

RoCE (%) 12.0 13.3 13.7

Net-D/E (x) (0.2) (0.3) (0.3)

29 April 2022

23 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Crompton Greaves Consumer (HOLD, TP: Rs 428; 13% upside potential)

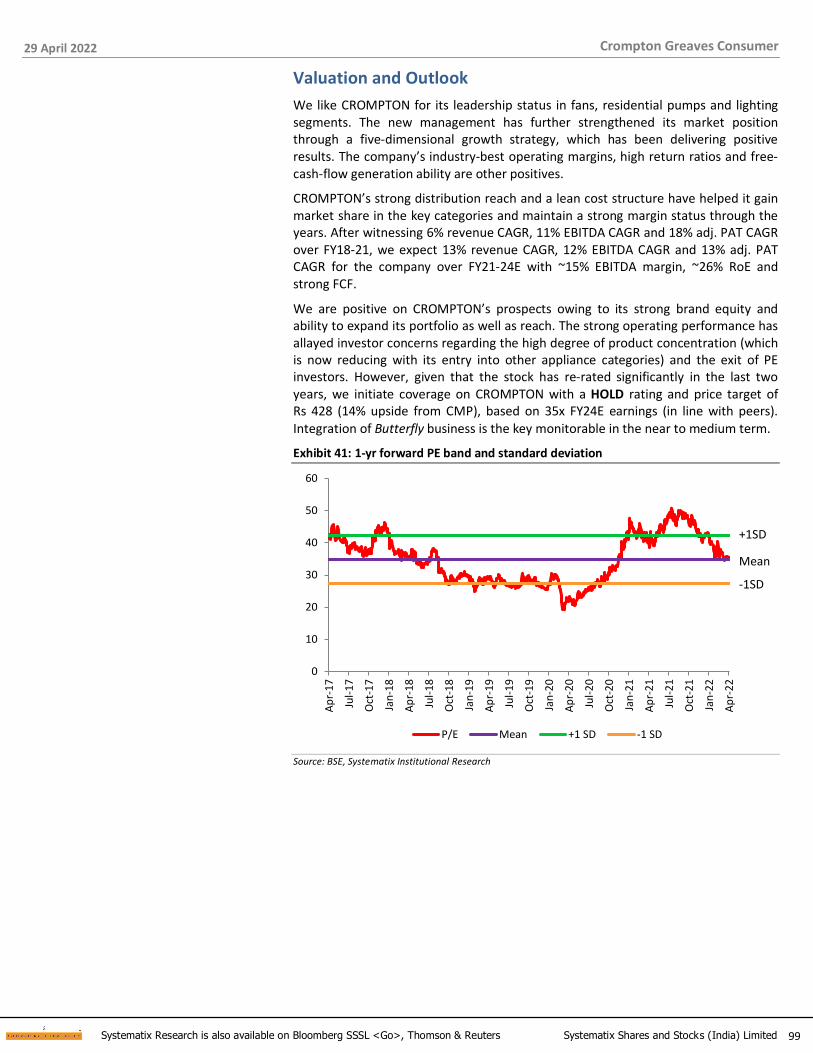

Crompton Greaves Consumer (CROMPTON), leader in the fans and residential pumps segments, maintains a keen focus on innovation, brand-building and reach. While this helps the company further consolidate its position in core segments, product portfolio expansion enables it to capture market share in newer categories (geysers a case in point, where it has become the third largest player in 4-5 years). While the recently acquired Butterfly business will bring scale in kitchen appliances, it may not be earnings-accretive for the next two years. We are positive on CROMPTON’s prospects given its strong brand equity, product innovation skills and ample scope for portfolio/ network expansion. Its entry in other appliance categories should also allay investor concerns on product concentration. Excluding Butterfly business, we expect 13% CAGR each in revenue and PAT over FY21-24E with ~26% RoE by FY24E. Given the significant re-rating in the last two years, we initiate coverage on CROMPTON with a HOLD rating and price target of Rs 428 (13% upside from CMP), based on 35x FY24E earnings (in line with peers). Integration of Butterfly business is the key monitorable in the near to medium term.

Havells (HOLD, TP: Rs 1,383; 6% upside potential)

Havells (HAVL), one of India’s leading consumer durables companies, is among the top-3 in many of its product categories on the strength of its brand pull, vast distribution network and robust processes. The Lloyd acquisition gave it an entry into the large home appliances segment, wherein the long-term outlook is as strong as in FMEG. Several corrective measures (brand repositioning, sales channel re-structuring and in-house manufacturing) taken at Lloyd have placed the brand/ portfolio on the path of sustainable growth. Also, rising consumer preference for quality branded products augurs well for HAVL. We expect a 17% revenue CAGR and 18% PAT CAGR for the company over FY21-24E with RoE of ~22% by FY24E and healthy FCF. However, its rich valuations (47x FY24E earnings at CMP) compel us to initiate coverage on the stock with a HOLD rating and price target of Rs 1,383 (6% upside from here), based on 50x FY24E earnings. Strong growth/ FCF and a higher RoE are

key to the company sustaining such high valuations.

Polycab (HOLD, TP: Rs 2,649; 5% upside potential)

The leader in the Indian wires and cables (W&C) industry, Polycab’s (POLYCAB) entry in FMEG has been successful with the company emerging as a prominent B2C brand. A vast and backward-integrated manufacturing base, wide distribution network and enthusiastic promoters supported by a professional management team have helped it grow faster than the industry. Going forward, rising infra spends, export opportunities and expansion to adjacent categories would drive its B2B portfolio. In FMEG, we estimate 25%+ revenue CAGR as also margin expansion for POLYCAB. Project Leap (to achieve Rs 200bn+ in revenues by FY26E), we believe, sets the stage for holistic growth for the company. However, the stock price has run up significantly (4x since its listing in 2019) and we see limited room for further re-rating in the near term. We initiate coverage on POLYCAB with a HOLD rating and an SOTP-based price target of Rs 2,649 (5% upside from CMP), based on 32x P/E for W&C (Rs 2,454) and 35x P/E for FMEG (Rs 195) on FY24E earnings.

CROMPTON – Financial Snapshot (Rs mn)

Y/E Mar FY22E FY23E FY24E

Net sales 54,584 61,120 68,442

EBITDA 7,728 8,742 9,991

OPM % 14.2 14.3 14.6

PAT (adj.) 5,725 6,713 7,682

EPS (Rs) 9.1 10.7 12.2

PE (x) 41.7 35.5 31.0

P/B (x) 10.8 9.4 8.1

EV/EBITDA (x) 29.3 25.6 22.0

RoE (%) 25.9 26.4 26.2

RoCE (%) 35.3 37.0 37.3

Net-D/E (x) (0.6) (0.6) (0.6)

HAVL – Financial Snapshot (Rs mn)

Y/E Mar FY22E FY23E FY24E

Net sales 131,778 149,335 168,968

EBITDA 17,469 21,630 24,565

OPM % 13.3 14.5 14.5

PAT (adj.) 12,014 15,068 17,310

EPS (adj.) (Rs) 19.2 24.1 27.7

PE (x) 67.7 54.0 47.0

P/B (x) 13.8 11.8 10.1

EV/EBITDA (x) 45.5 36.4 31.7

RoE (%) 20.3 21.9 21.6

RoCE (%) 26.4 29.1 29.1

Net-D/E (x) (0.3) (0.4) (0.4)

POLYCAB – Financial Snapshot (Rs mn)

Y/E Mar FY22E FY23E FY24E

Net sales 117,302 133,513 152,164

EBITDA 11,477 14,559 18,114

OPM % 9.8 10.9 11.9

PAT (adj.) 7,585 10,104 12,792

EPS (adj.) (Rs) 50.9 67.8 85.8

PE (x) 49.5 37.2 29.4

P/B (x) 7.1 6.3 5.4

EV/EBITDA (x) 32.0 24.9 19.7

RoE (%) 14.3 16.8 18.3

RoCE (%) 19.8 23.5 25.8

Net-D/E (x) (0.2) (0.2) (0.3)

29 April 2022

24 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

V-Guard (HOLD, TP: Rs 225; 5% upside potential)

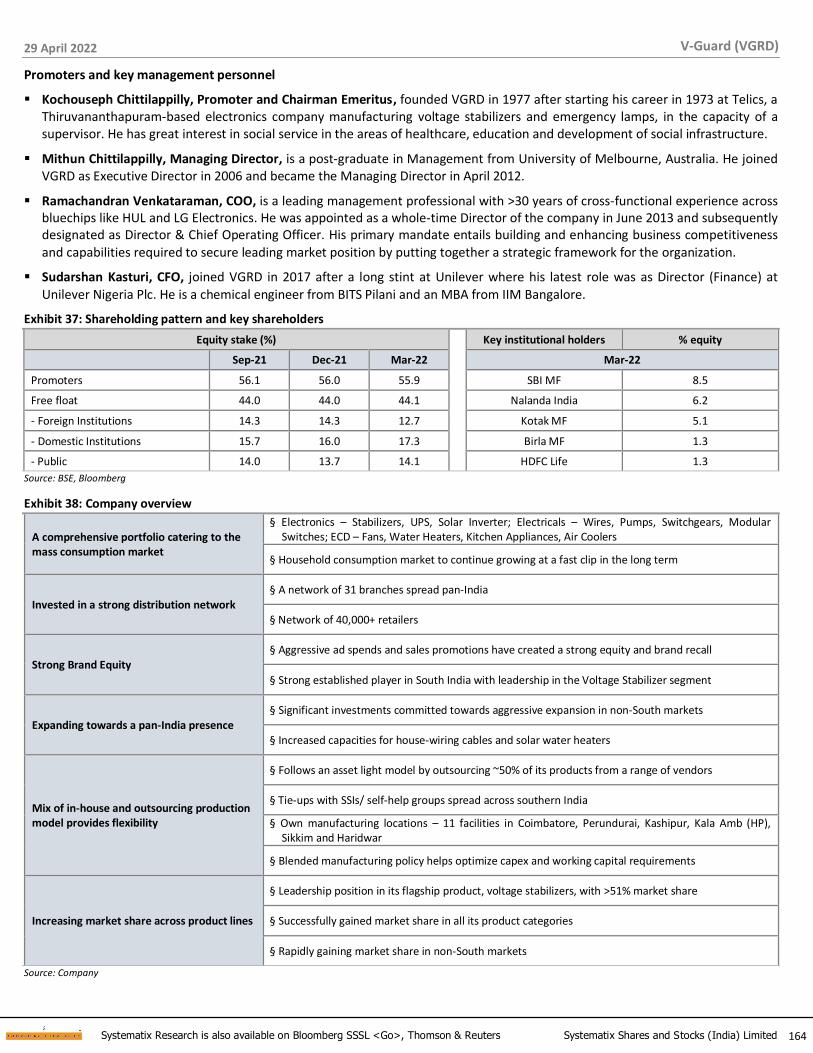

V-Guard (VGRD), initially into voltage stabilizers, has diversified its portfolio to a wide range of light electrical products over the last decade. Already a leader in South India, it is now fortifying its pan-India footprint. While growth has remained muted in the last few years, robust traction in the non-South regions (~42% of revenues and ~60% of distribution reach) offers significant potential for growth. We estimate 17% revenue CAGR, 14% EBITDA CAGR and 15% PAT CAGR for VGRD over FY21-24E, led by growth across product categories and stable margins as RM cost pressure gets offset by operating leverage benefits. While we like the company for its pan-India aspiration, cash-rich status and healthy FCF, we believe the stock trades close to its fair valuations at ~30x FY24E earnings. We initiate coverage on VGRD with a HOLD rating and price target of Rs 225 (5% upside from CMP), based on 32x FY24E earnings (~10% discount to comparable peers due to a relatively weaker brand in markets outside the South and operating parameters).

Orient Electric (HOLD, TP: Rs 302; 6% downside potential)

Orient Electric (ORIENTEL), the leader in fans, is growing rapidly in new categories (lighting, appliances and switchgears) as well. A renewed focus on innovative new launches and portfolio premiumization have helped the company reposition itself as a vibrant and new-age brand. Higher A&P spends at ~4% of sales have enhanced brand visibility while its wide distribution network has supported entry in new categories. The company aspires to expand margins despite the RM cost headwind, aided by operating leverage and premiumization. We expect 17% revenue CAGR, 14% EBITDA CAGR and 14% PAT CAGR for ORIENTEL over FY21-24E with growth across categories and stable margins. We expect RoE to sustain at ~25% and healthy FCF generation to continue. While we like ORIENTEL’s business, current valuations at 38x FY24E earnings adequately capture the growth prospects. We initiate coverage on the stock with a HOLD rating and price target of Rs 302 (6% downside from CMP), based on 36x FY24E earnings (in line with peers vs its 42x 5-year mean). Increasing competitive intensity is a key risk to our earnings estimates.

VGRD – Financial Snapshot (Rs mn)

Y/E Mar FY22E FY23E FY24E

Net sales 34,769 39,157 44,102

EBITDA 3,270 3,946 4,579

OPM % 9.4 10.1 10.4

PAT (adj.) 2,017 2,569 3,042

EPS (adj.) (Rs) 4.7 6.0 7.1

PE (x) 45.9 36.0 30.4

P/B (x) 6.8 6.0 5.2

EV/EBITDA (x) 27.3 22.4 19.1

RoE (%) 14.9 16.7 17.2

RoCE (%) 21.4 24.0 25.0

Net-D/E (x) (0.2) (0.3) (0.3)

ORIENTEL – Financial Snapshot (Rs mn)

Y/E Mar FY22E FY23E FY24E

Net sales 25,681 28,762 32,214

EBITDA 2,291 2,738 3,228

OPM % 8.9 9.5 10.0

PAT (adj.) 1,244 1,511 1,781

EPS (adj.) (Rs) 5.9 7.1 8.4

PE (x) 54.6 44.9 38.1

P/B (x) 12.9 11.1 9.5

EV/EBITDA (x) 28.9 24.2 20.4

RoE (%) 23.6 24.6 24.8

RoCE (%) 35.0 33.4 32.3

Net-D/E (x) (0.3) (0.3) (0.3)

29 April 2022

25 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Exhibit 47: Peer comparison valuations

Company

Bloomberg

code

CMP M Cap Reco.

Target Price (Rs)

Upside (%)

Target P/E (x)

5-year P/E (x) P/E (x) RoE (%)

(Rs) (Rs bn) FY24E Mean +1 SD -1 SD FY22E FY24E FY22E FY24E

Finolex Cables FNXC IN 405 62 Buy 526 30 13 16 22 11 13 10 13 13

Bajaj Electricals BJE IN 1,080 124 Buy 1,286 19 32 46 63 29 87 27 8 20

KEI Industries KEII IN 1,200 108 Buy 1,425 19 24 16 20 12 29 20 17 18

Crompton CROMPTON

IN 380 239 Hold 428 13 35 35 42 27 42 31 26 26

Havells HAVL IN 1,300 814 Hold 1,383 6 50 48 58 39 68 47 20 22

Polycab POLYCAB IN 2,520 376 Hold 2,649 5 31 23 33 13 50 29 14 18

V-Guard VGRD IN 215 92 Hold 225 5 32 48 56 40 46 30 15 17

Orient Electric ORIENTEL IN 320 68 Hold 302 (6) 36 42 49 34 55 38 24 25

Source: Company, Systematix Institutional Research

Exhibit 48: Peer comparison

Company EPS (Rs) CAGR (%; FY16-21) CAGR (%; FY21-24E) RoIC (%) RoCE (%)

FY22E FY23E FY24E Rev EBITDA PAT Rev EBITDA PAT FY22E FY24E FY22E FY24E

Finolex Cables 31.7 35.8 40.3 3 1 7 20 19 10 15 17 12 14

Bajaj Electricals 12.4 24.5 39.8 (0) 3 12 12 27 34 11 41 14 27

KEI Industries 41.0 50.5 59.4 12 13 34 21 20 25 19 21 24 25

Crompton 9.1 10.7 12.2 6 11 24 13 12 8 66 74 35 37

Havells 19.2 24.1 27.7 7 16 (4) 17 16 18 28 37 26 29

Polycab 50.9 67.8 85.8 11 18 36 20 17 14 18 26 20 26

V-Guard 4.7 6.0 7.1 8 11 12 17 14 15 20 25 21 25

Orient Electric 5.9 7.1 8.4 8 17 23 17 14 14 43 37 35 32

Source: Company, Systematix Institutional Research

29 April 2022

26 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

Exhibit 49: PE band and standard deviation (one-year forward)

FNXC BJE

0

5

10

15

20

25

30

35

Apr

-17

Jul-1

7

Oct

-17

Jan-

18

Apr

-18

Jul-1

8

Oct

-18

Jan-

19

Apr

-19

Jul-1

9

Oct

-19

Jan-

20

Apr

-20

Jul-2

0

Oct

-20

Jan-

21

Apr

-21

Jul-2

1

Oct

-21

Jan-

22

Apr

-22

P/E Mean +1 SD -1 SD

-1SD

+1SD

Mean

0

10

20

30

40

50

60

70

80

90

100

Apr

-17

Jul-1

7

Oct

-17

Jan-

18

Apr

-18

Jul-1

8

Oct

-18

Jan-

19

Apr

-19

Jul-1

9

Oct

-19

Jan-

20

Apr

-20

Jul-2

0

Oct

-20

Jan-

21

Apr

-21

Jul-2

1

Oct

-21

Jan-

22

Apr

-22

P/E Mean +1 SD -1 SD

-1SD

+1SD

Mean

Data points of this period is ignored due to distored PE band coming out of negative EPS in FY20.

KEII CROMPTON

0

5

10

15

20

25

30

Apr

-17

Jul-

17

Oct

-17

Jan-

18

Apr

-18

Jul-

18

Oct

-18

Jan-

19

Apr

-19

Jul-

19

Oct

-19

Jan-

20

Apr

-20

Jul-

20

Oct

-20

Jan-

21

Apr

-21

Jul-

21

Oct

-21

Jan-

22

Apr

-22

P/E Mean +1 SD -1 SD

-1SD

+1SD

Mean

0

10

20

30

40

50

60

Apr

-17

Jul-1

7

Oct

-17

Jan-

18

Apr

-18

Jul-1

8

Oct

-18

Jan-

19

Apr

-19

Jul-1

9

Oct

-19

Jan-

20

Apr

-20

Jul-2

0

Oct

-20

Jan-

21

Apr

-21

Jul-2

1

Oct

-21

Jan-

22

Apr

-22

P/E Mean +1 SD -1 SD

-1SD

+1SD

Mean

HAVL POLYCAB

0

10

20

30

40

50

60

70

80

Ap

r-17

Jul-

17

Oct

-17

Jan-

18

Ap

r-18

Jul-

18

Oct

-18

Jan-

19

Ap

r-19

Jul-

19

Oct

-19

Jan-

20

Ap

r-20

Jul-

20

Oct

-20

Jan-

21

Ap

r-21

Jul-

21

Oct

-21

Jan-

22

Ap

r-22

P/E Mean +1 SD -1 SD

-1SD

+1SD

Mean

0

5

10

15

20

25

30

35

40

45

Apr

-19

Jun-

19

Aug

-19

Oct

-19

Dec

-19

Mar

-20

May

-20

Jul-

20

Sep-

20

Nov

-20

Jan-

21

Mar

-21

May

-21

Jul-

21

Sep-

21

Dec

-21

Feb-

22

Apr

-22

P/E Mean +1 SD -1 SD

-1SD

+1SD

Mean

VGRD ORIENTEL

20

25

30

35

40

45

50

55

60

65

70

Apr

-17

Jul-

17

Oct

-17

Jan-

18

Apr

-18

Jul-

18

Oct

-18

Jan-

19

Apr

-19

Jul-

19

Oct

-19

Jan-

20

Apr

-20

Jul-

20

Oct

-20

Jan-

21

Apr

-21

Jul-

21

Oct

-21

Jan-

22

Apr

-22

P/E Mean +1 SD -1 SD

-1SD

+1SD

Mean

20

25

30

35

40

45

50

55

60

65

May

-18

Aug

-18

Nov

-18

Feb-

19

May

-19

Aug

-19

Oct

-19

Jan-

20

Apr

-20

Jul-

20

Oct

-20

Jan-

21

Apr

-21

Jul-

21

Oct

-21

Jan-

22

Apr

-22

P/E Mean +1 SD -1 SD

-1SD

+1SD

Mean

Source: BSE, Company, Systematix Institutional Research

29 April 2022

27 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares and Stocks (India) Limited

India Consumer Electricals

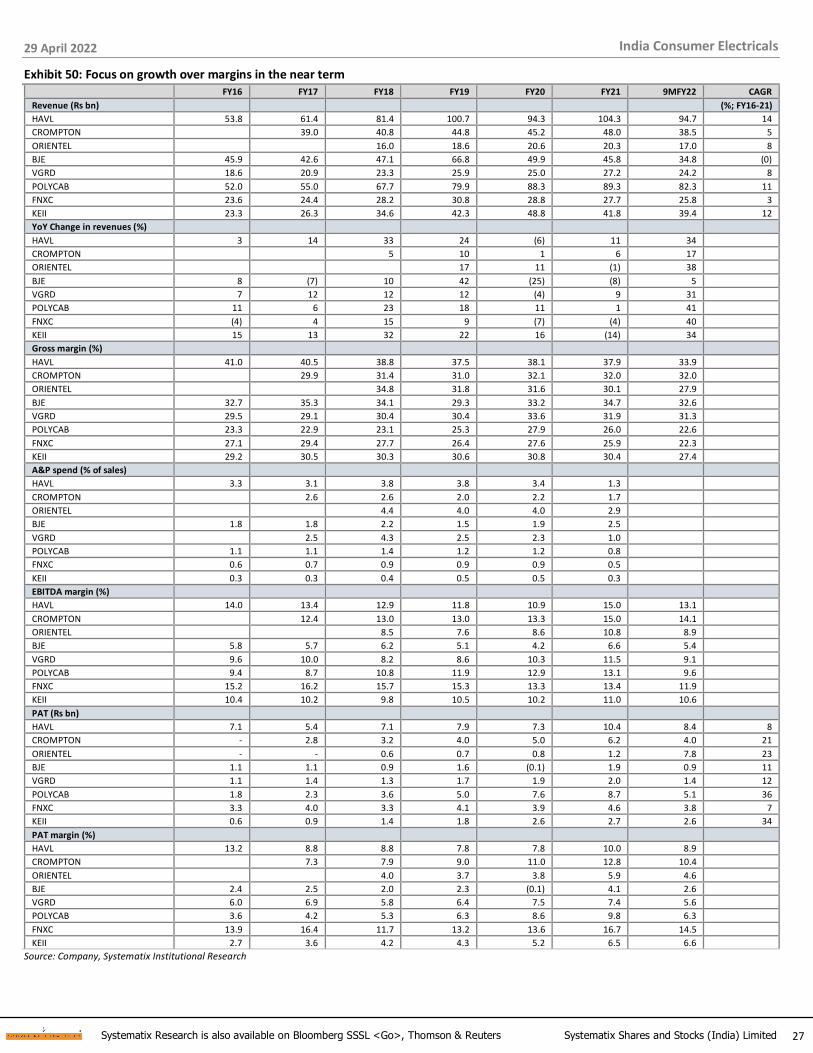

Exhibit 50: Focus on growth over margins in the near term

FY16 FY17 FY18 FY19 FY20 FY21 9MFY22 CAGR

Revenue (Rs bn) (%; FY16-21)

HAVL 53.8 61.4 81.4 100.7 94.3 104.3 94.7 14

CROMPTON 39.0 40.8 44.8 45.2 48.0 38.5 5

ORIENTEL 16.0 18.6 20.6 20.3 17.0 8

BJE 45.9 42.6 47.1 66.8 49.9 45.8 34.8 (0)

VGRD 18.6 20.9 23.3 25.9 25.0 27.2 24.2 8

POLYCAB 52.0 55.0 67.7 79.9 88.3 89.3 82.3 11

FNXC 23.6 24.4 28.2 30.8 28.8 27.7 25.8 3

KEII 23.3 26.3 34.6 42.3 48.8 41.8 39.4 12