Implications of Trade Liberalisation on Indian Fisheries

122

POLICY RESEARCH:IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES ACASE STUDY FOR INDIA BY VENKATESH SALAGRAMA Project PR 26109 June 2004 Food and Agriculture Organization (FAO), Rome June 2004 ICM I I n n t t e e g g r r a a t t e e d d C C o o a a s s t t a a l l M M a a n n a a g g e e m m e e n n t t 64-16-3A, PRATAP NAGAR,KAKINADA 533 004 TELE: +91 884 236 4851 FAX: +91 884 235 4932 EMAIL: [email protected]; [email protected] Support unit for International Fisheries & Aquatic Research - SIFAR

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Implications of Trade Liberalisation on Indian Fisheries

POLICY RESEARCH: IMPLICATIONS OF LIBERALISATION OF FISHTRADE FOR DEVELOPING COUNTRIES

A CASE STUDY FOR INDIA

BY

VENKATESH SALAGRAMA

Project PR 26109

June 2004

Food and Agriculture Organization (FAO), Rome June 2004

ICM IIInnnttteeegggrrraaattteeeddd CCCoooaaassstttaaalll MMMaaannnaaagggeeemmmeeennnttt6644--1166--33AA,, PPRRAATTAAPP NNAAGGAARR,, KKAAKKIINNAADDAA 553333 000044 TTEELLEE:: ++9911 888844 223366 44885511 FFAAXX:: ++9911 888844 223355 44993322EEMMAAIILL:: iiccmm__kkkkdd@@ssaattyyaamm..nneett..iinn;; rrmmyy__ssuujjaattaa@@ssaanncchhaarrnneett..iinn

Support unit forInternationalFisheries &AquaticResearch -SIFAR

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India1

Contents

Acknowledgements..................................................................................................................... 2Abbreviations used in the Text ................................................................................................... 3

EXECUTIVE SUMMARY..................................................................................................................... 6INTRODUCTION .............................................................................................................................. 10

Rationale for the Study ............................................................................................................. 10Focus of the Study .................................................................................................................... 11Methodology ............................................................................................................................. 11Structure of the Report .............................................................................................................. 13

CHAPTER 1: BACKGROUND ............................................................................................................ 14General Context of India........................................................................................................... 14Fisheries Sector in India............................................................................................................ 16Main Stakeholders in Export Supply Chain in India ................................................................ 21The Poor within the Export Commodity Chain ........................................................................ 26

CHAPTER 2: ORIGINS AND DEVELOPMENT OF SHRIMP EXPORT SUPPLY CHAIN IN INDIA ............. 31Subsidies in the Pre-Independence Period................................................................................ 31Shrimp Export Chains and Modernisation................................................................................ 32Growth of Export Trade during 1961-2000 .............................................................................. 39Export Channels for the Important Varieties of Seafood in India ............................................ 43Benefits of Shrimp Production and Trade ................................................................................ 48Negative Impacts of Subsidy-Linked Technological Development ......................................... 49

CHAPTER 3: IMPACTS OF TRADE LIBERALISATION ON FISHERIES SUBSIDIES AND SEAFOODLEGISLATION IN INDIA ................................................................................................................... 56

Trade Liberalisation in India..................................................................................................... 56Impacts of Trade Liberalisation ................................................................................................ 57Subsidies and Seafood Legislation: the View from the Bottom ............................................... 71Changes in Subsidies and Impact on the Shrimp Export Industry in India .............................. 72Changes in Seafood Legislation and Impact on the Shrimp Export Industry in India ............. 81The Future Scenario .................................................................................................................. 84

CHAPTER 4: CONCLUSIONS AND RECOMMENDATIONS .................................................................. 91Conclusions............................................................................................................................... 91Recommendations..................................................................................................................... 93

REFERENCES .................................................................................................................................. 96APPENDICES................................................................................................................................. 102

A. Annexures .......................................................................................................................... 102B. Tables ................................................................................................................................. 107C. Figures................................................................................................................................ 113

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India2

ACKNOWLEDGEMENTS

A number of institutions and individuals helped this study in various ways. Our grateful thanksare due to: Mr V Vivekanandan and his team at SIFFS, Trivandrum; Prof (Dr) Mohan JosephModayil, Director, CMFRI, Kochi; Dr R Narayana Kumar, CMFRI-Kakinada; Mr Nero Shahin,MPEDA and Dr S S Gupta, CIFT, both at Visakhapatnam; many serving and past officers of theDepartments of Fisheries in Kerala, Andhra Pradesh and Orissa; and Mr B K Mishra at theFishcopfed (NCDC) at New Delhi.

The field interactions have been made possible with the kind assistance provided by MrMangaraj Panda and his colleagues at the United Artists’ Association, Ganjam; Mr Samson andhis colleagues at PENCODE, Puri; Mr M Srirama Murthy at FIRM; and Mr KHemasundareswara Rao at the United Fishermen’s Association; thanks are due to each one ofthem. Three studies done by ICM in recent times – one each for SIFAR/FAO, Oxfam (GB) andNRI – came particularly handy in preparing this document and we are grateful to Mr TimBostock, Ms Shaheen Nilofer and Dr Peter Greenhalgh who had commissioned the originalstudies.

A special word of thanks to Dr John Kurien at the Centre for Development Studies, Trivandrum.And a big thanks to Sebastian, Chandrika, Ramya and especially Venugopalan at the ICSF,Chennai, but for whose timely help and support with advice and reference material, this studywould have been much poorer.

Obviously, none of them is responsible for the abiding shortcomings and deficiencies, which aresolely mine.

Venkatesh Salagrama27 April 2004

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India3

ABBREVIATIONS USED IN THE TEXT

AAI Aquaculture Authority of IndiaAP Andhra PradeshAPEC Asia-Pacific Economic CooperationAPFC Andhra Pradesh Fisheries CorporationASCM (also SCM) (WTO) Agreement on Subsidies and Countervailing MeasuresBCV Palem Boddu Chinna Venkataya PalemBFDA Brackishwater Fisheries Development AgencyBIS Bureau of Indian StandardsBLC Beach landing craftBOBP Bay of Bengal ProgrammeDAHD Department of Animal Husbandry and Dairying (GOI)DFID Department for International Development (of the Government of United Kingdom)DOF Department of FisheriesDRDA District Rural Development AgencyEEZ Exclusive Economic ZoneEIA Export Inspection AgencyEIC Export Inspection CouncilEU European UnionFAO Food and Agriculture Organization of the United NationsFRP Fibre-reinforced plasticGDP Gross Domestic ProductGOAP Government of Andhra PradeshGOI Government of IndiaGOK Government of KeralaGOO Government of Orissaha HectareHACCP Hazard Analysis and Critical Control PointHDI Human Development IndexHPLC High Performance Liquid ChromatographyHSD High Speed DieselIBE Inboard engineICAR Indian Council for Agricultural ResearchICM Integrated Coastal ManagementICSF International Collective in Support of FishworkersIDP Inter-Departmental PanelIIM Indian Institute of ManagementIQF Individually quick frozenkm KilometreLPG Liquefied Petroleum GasMFB Madras Fisheries BureauMPEDA Marine Products Export Development AuthorityMT Metric TonneNABARD National Bank for Agriculture and Rural DevelopmentNCDC National Cooperatives Development CorporationNIPFP National Institute of Public Finance and PolicyNIRD National Institute of Rural DevelopmentOAL Overall LengthOBM Outboard motorOECD Organisation for Economic Cooperation and DevelopmentOGL Open General LicencePD Peeled and deveinedPDS Public Distribution Schemeppb Parts per billionppm Parts per millionPRA Participatory Rural AppraisalPUD Peeled and un-deveinedQR Quantitative RestrictionsRRA Rapid Rural Appraisal

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India4

SAT Supervisory Audit TeamSCICI Shipping Credit Investment Corporation of IndiaSEAI Seafood Exporters Association of IndiaSHG Self Help GroupsSIFAR Support Unit for Fisheries and Aquatic ResearchSIFFS South Indian Federation of Fishermen SocietiesSKO Kerosene OilSLA Sustainable Livelihoods ApproachSPS Sanitary and PhytosanitaryTCM Technical Cooperation MissionTED Turtle-excluder deviceUNDP United Nations Development ProgrammeUNEP United Nations Environment ProgrammeUSA (also US) United States of AmericaUSFDA United States Food and Drug AdministrationWTO World Trade Organisation

Conversion rates (Source: The Hindu, 27 April 2004; rounded off):1 US$ Indian Rupees (Rs.) 441 UK£ Rs. 781 € Rs. 52Denominations:1 Lakh 100 0001 Crore 10 000 000

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India5

MAP SHOWING THE THREESTATES COVERED BY THE STUDY

Kerala

Andhra Pradesh

Orissa

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India6

EXECUTIVE SUMMARY

Seafood export sector

1. The modernisation of Indian seafood industry began in 1950s and is inextricably linked to thegrowth of shrimp export trade. In turn, shrimp export trade is closely related to tradeliberalisation from the beginning. Shrimp continues to dominate the fisheries sector ingeneral and the seafood export sector in particular.

2. Subsidies and other assistance played a crucial catalytic role in the development of the exportsector, although the quantum of assistance declined subsequently as private sector took overthe activities. Promoting the sea as an open access resource has been an important subsidy inthe modernisation period and other direct subsidies encouraged entry of outsiders and privatecapital into the sector in a big way.

3. The key state-supported initiatives for increasing production have been the promotion ofmechanised trawling, aquaculture, deep-sea fishing and motorisation. Most of these systemshave come to depend on shrimp as the mainstay of their operations, increasingly so from1990s as the reduction in fish catches has been offset by the increase in value of shrimp.

4. Marine fish production in the country has grown significantly since 1950s. Shrimpproduction and exports from capture and culture sources grew rapidly through the period.

5. Exports have come to account for a quarter of the contribution of fisheries to the GDP.Culture shrimp contributes four-fifths of the total shrimp exports, which is mainly because ofthe decline in marine catches than from increased production from culture sources.

6. Japan, the EU and the US import a major proportion of India’s exports, and the main exportspecies is shrimp. This focus on a few developed countries on the one hand and on shrimp onthe other has implications on the profitability and sustainability of the export trade. There is agrowing trade in finfish exports to developing countries, characterised by large quantities andsmall margins.

7. The emphasis on production is not supplemented by developing adequate infrastructurefacilities to support them; the availability and quality of infrastructure remains insufficient.

8. The growth of shrimp trade brought a number of new intermediaries into the market chainalong with a complex range of trade relationships. It also necessitated entry of private capitaland informal credit into the fisheries sector in a big way and led to overcapitalisation offishing activities in due course.

9. There is little information on the role of different stakeholders – particularly the poor in theancillary category – in the export sector. Consequently, the impact of any changes on the lifeand livelihoods of the poor is often overlooked at the policy and implementation levels.

10. Since 1990s, three issues dominated Indian export scene: decline in overall catches,particularly shrimp; fluctuations in international markets depressing prices and profitability;and overcapitalisation of the production and marketing activities increasing risk.

Impacts of seafood export market chain

11. The benefits of the shrimp trade include increase in fish production and export earnings;fisheries – particularly shrimp trade – gaining social acceptance; increased affluence in thefishing villages (but skewed in terms of distribution), better housing, improved quality of life,

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India7

rising literacy and improved contacts with the wider world. The largely informal nature ofthe export chain allowed a large number of poor people to find work in support activities.

12. The negative impacts of shrimp exports include: increased social and economic inequality,environmental and resource degradation and unsustainable livelihoods. The gender balancein shrimp export industry is tilted in favour of men and many activities are not accessible tothe poor because of the need for high investment.

Trade liberalisation in India

13. India embarked upon a massive programme of liberalisation since 1990s and this has a far-reaching impact upon the economy and on the quality of life in general.

14. In spite of the strong emphasis on information and knowledge as fundamental features of thereform process, major knowledge gaps exist at the grassroots level on the process and thepotential impacts of trade liberalisation.

15. Liberalisation of Indian economy coincided with the establishment of the WTO, and thestructural adjustment policies had to contend with domestic fiscal reform and also make surethat the processes are in line with the global trade agreements.

16. The policy responses thus have been two-fold: at the domestic level, the focus is on fiscaldiscipline while at the international level, it is on arguing for exemptions for specialconditions that prevail in developing countries like India.

Subsidies in Indian fisheries

17. At the global level, the debates on subsidies in fisheries focus mainly on their impacts upontrade and environment, and largely bypass other dimensions like equity issues, livelihoodsand welfare. The debates take place at such a high level and in such abstruse language thatthe contribution of primary stakeholders to the evolving agreements has been extremely low.

18. Indian subsidies in fisheries, particularly those that are contingent upon exports, appear to beminiscule and are not likely to be affected in the context of a stricter disciplining of fisheriessubsidies. In fact, by focusing the discussion on subsidies to their trade related impacts alone,the international community might actually tempt countries like India to spend more onsubsidies of the ‘effort-and capacity-enhancing’ category.

19. In the general macro-economic context of India, subsidies are increasingly frowned upon atthe policy level and there is a proposal to cut the existing subsidies across different sectorsfrom the existing 10.7 percent of the GDP to 3 percent in five years. However, in practice,there is evidence that the total subsidies have actually grown in the late 1990s.

20. In terms of direct subsidies in fisheries, there does not appear to have been any cuts in thereform period, due perhaps to the fact that the total outlay of fisheries in the national plansworks out to a quarter of one percent and imposing fiscal discipline on such a minisculesector does not help the economy significantly. Subsidies in fisheries are also miniscule whencompared to other sectors like agriculture, prompting many people in the government itself todemand for more subsidies for fisheries, not less. Even if there is a cut in the direct subsidiesin the fisheries sector, the impact on many stakeholders may not be significant, except in caseof those providing some kind of social security.

21. The lifting of tariffs and quantitative restrictions in the fisheries sector during the 1990s isnot followed by any perceptible benefits or ill effects, but apprehensions about their possible

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India8

negative effect are widespread and generally justified. The possibility of fish importsswamping Indian markets and foreign deep sea fishing vessels allowed to operate in theIndian EEZ are two potential areas of concern for the producers.

22. In terms of exports, the new trade policies have not contributed much because of (i) declinein availability of shrimp and (ii) uncertainties in international markets. In fact, the Indianexport trade has stagnated since late 1990s and in many cases declined.

23. Although the negative environmental and livelihood implications of the modernisationprogramme are quite evident, there is continuing support at the policy level for moretechnological interventions in the capture sector. This aspect needs consideration and ablanket ban on the ‘effort-and capacity-enhancing’ subsidies – irrespective of their professedbenevolence – might be necessary.

24. Indirect subsidies in general category (i.e., not specific to fisheries) – such as petroleumproducts (HSD oil, Kerosene, LPG), electricity (affecting processing and ice making) andwelfare (health and food) – have been reduced with serious impacts on the stakeholders.

25. Changes to direct and indirect subsidies cover a range of areas and the primary stakeholdershave been finding it difficult to cope with the changes, not least because of unpreparednessand lack of alternatives. These changes have an impact upon the livelihood assets andstrategies of the poor, although in a context where change is occurring at different levels anddimensions simultaneously, the tangled skein of cause and effect is difficult to unravel.

26. The overwhelming impression among many informants is that the changes so far are only thetip of the iceberg, and that the real changes will become more significant in the coming years.

Seafood legislation issues

27. Many food exports from India – most notably, shrimp – have been affected adversely byselective application of sanitary and phytosanitary measures in the last decade. Shrimp facedrough weather over the issues of poor quality control, muddy smell and traces of antibioticsin farmed shrimp. The losses to the processing industry are quite high and affected theprofitability of operations significantly.

28. Intense and pro-active efforts by the government and the seafood industry have helped thelatter to survive the threats and actually emerge stronger after the ordeal, because the qualitystandards of the EU approved Indian plants are considered to be world class.

29. However the upgradation came with a big price tag: while some of the companies thatupgraded ended up with no working capital to organise operations, many companies simplyfolded up, unable to find the capital. This has meant a loss of livelihoods for a large numberof poor people, particularly women from single-headed households.

30. Besides high cost of adaptation, issues like irrelevance of foreign standards to localconditions, lack of timely and adequate information and consequent transaction costs,difficulties in understanding requirements as well as testing and monitoring them, perceivedlack of scientific data for specific threshold or limiting values and the uncertainty that arisesfrom rapidly changing requirements in overseas markets still persist and affect the industry.

31. The general feeling is that the Government of India’s quality inspection and monitoringsystem is very sensitive to the international food safety standards and is constantly evolvingto meet the SPS requirements. The government involves the industry in determining the bestcourse of action to meet the international demands and assisting it in various ways to cope

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India9

with the changes. In fact, it is felt that the government accommodates whatever demands theimporting countries might make, rather than take the issue up as an SPS measure.

32. At the international level, developing countries like India are constrained in theirparticipation and contribution to standard setting in the SPS process, and there is awidespread feeling that developed countries manage not only set the agenda but also changeit as they deem fit from time to time, adversely affecting the developing countries.

33. The exporting countries are also constrained because of poor domestic laws and qualitycontrol systems, lack or unaffordability of technology and infrastructure, poverty andunorganised nature of operations. These are exacerbated by the diversity in standards andverifying mechanisms prescribed by importing countries and the frequent changes tostandards and lack of clarity at various levels.

34. Within the country, the debate on standard setting is confined to a few organisations andindividuals, with the result that the country is not adequately prepared to offer effectivealternatives. Constituting multi-disciplinary taskforces at various levels and for differentsectors is an urgent necessity for a more comprehensive and forceful contribution to thestandard setting process and to meet the other requirements of the SPS Agreement.

35. Strict implementation of international seafood legislation (i.e., SPS measures) related to theissues of harmonisation, equivalence and transparency could lead to marginalisation of thesmall-scale operators from the export sector. Helping the small-scale producers to reachinternational markets through active state support might be considered an actionable, if notprohibited, subsidy although this may not happen immediately.

36. Stricter quality control would mean that, in the short term, there will be more serious lossesand many of the producers and exporters might not recover. In the medium term, this willlead to a reorganisation of the export sector, concentrating the ownership in fewer hands andmarginalising a number of poor stakeholders. In the long term, the international seafoodlegislation will begin to have an impact upon the domestic market chains as well and thequality requirements for domestic trade will begin to mount.

Future trends

37. Further changes in subsidies and seafood legislation are considered to have a positive impactupon the environment by reducing effort and making the users bear the cost of externalities.

38. In terms of trade, there is a likelihood of shrimp being replaced as prima donna of Indianexports by the entry of a number of other species and the international markets shifting fromdeveloped countries to developing countries and from export to domestic trade. From allaccounts, this is a healthy, sustainable, environment-friendly and equitable trend.

39. These positive impacts on the environment as well as trade will however be accompanied bydeclining access to the poor to the natural assets (fish) and the physical assets (productionand processing systems) on the one hand, and to the markets on the other. The reduction inaccess to livelihood assets is compounded by the state’s increasing withdrawal from itswelfare agenda and reduction in social subsidies, which means that for the poor in the exportsector, the worst may be yet to come, unless of course suitable safety nets are put in place.

40. Any new opportunities that liberalisation might offer are contingent upon certain basicrequirements at the individual level – assured access to resources, ability, skills andknowledge – and also at the macro level – a radical transformation in terms of infrastructureand other basic facilities – which necessarily constrain the poor from taking advantage.

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India10

POLICY RESEARCH: IMPLICATIONS OF LIBERALISATION OF FISHTRADE FOR DEVELOPING COUNTRIES – A CASE STUDY OF INDIA

INTRODUCTION

This case study is an output of the FAO-commissioned (SIFAR-coordinated) project“Implications of Fish Trade Liberalisation for Developing Countries” co-funded by DFID andGTZ. The main objectives of the India case study are to:

Review the key issues related to fish trade liberalisation in India focusing on, (a) changes insubsidies to the sector particularly during the period 1990 to 2004, and (b) internationalseafood legislation.

Analyse, from a macro-level perspective, the implications of trade liberalisation measures forlivelihoods issues based on secondary literature and primary data collected in field surveys inat least three locations of the country.

RATIONALE FOR THE STUDY

This is a particularly apt juncture to discuss the role of subsidies and international seafoodlegislation in the fisheries sector for three reasons.

Firstly, as the fisheries modernisation programme in the country completes a half-century, thereis a need to revisit some of the basic premises that underpinned the development of the sector –emphasis on exports, on increasing production, on subsidies and other incentives, on technicalimprovements – and assess their contribution to the process. It is essential to evaluate thecontinued validity of this framework. This becomes particularly important because the reformsprocess in the national economy, beginning from the 1990s, requires a further reinforcement ofsome of the fundamental features of modernisation, while demanding radical changes to others.

Secondly, the impact of some of the changes brought about by trade liberalisation is felt almostimmediately, but there are several others where a complete systemic overhaul is taking placebeneath the surface and their impacts are not visible yet. It is necessary to understand thechanges and their actual and potential impacts for designing and implementing more equitableand sustainable approaches and alternatives.

Thirdly, both fisheries subsidies and the sanitary and phytosanitary (SPS) measures are issues ofglobal importance. The issue of fisheries subsidies will be discussed at the next round of WTOnegotiations in 2005. It is necessary to develop a clear stand on the issue at the national level byreviewing the existing subsidies and developing appropriate policy responses to change and,where appropriate and necessary, to argue for the retention of subsidies. Similarly, India hasrepeatedly faced problems with sanitary and phytosanitary measures (SPS) in recent times, andmeasures are also needed to address this problem at the global and at the national level.

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India11

FOCUS OF THE STUDY

The issue of subsidies and seafood legislation are complex and are constantly evolving.Considering the importance and the sensitive nature of the issues at the national and internationallevels, they need a much broader, more informed and comprehensive treatment than is possiblewithin the time and resources (particularly of the cerebral kind) available to this study. In India,the issues have only recently begun to be discussed in any depth, which means that even theterms and contours of the discussion are not clear yet. Under the circumstances, the objectives ofthe study are necessarily modest, but (hopefully) significant in providing a new dimension to thedebate. Besides providing a brief overview of the dimensions of the liberalisation process, itfocuses on the issue from the perspective of primary stakeholders and their livelihoods.Secondary literature will be used extensively to provide a broad picture of the changes and theirimpacts, which is necessitated by the diversity that characterises Indian fisheries sector.

For convenience, the study focuses largely – but not exclusively – on shrimp export marketingchain. The choice of shrimp is apt for two reasons: firstly, it is the development of shrimp exportchain that has set the process of modernisation in Indian fisheries sector in motion and dictatedthe pattern of development of other market chains in the country. Secondly, shrimp has alsocome to dominate many fishing operations and changes in its production or prices have thewidest – and the most acute – repercussions on the sector. It is the shrimp export chains that havebeen the most affected by the changes in international seafood standards from mid-1990s.

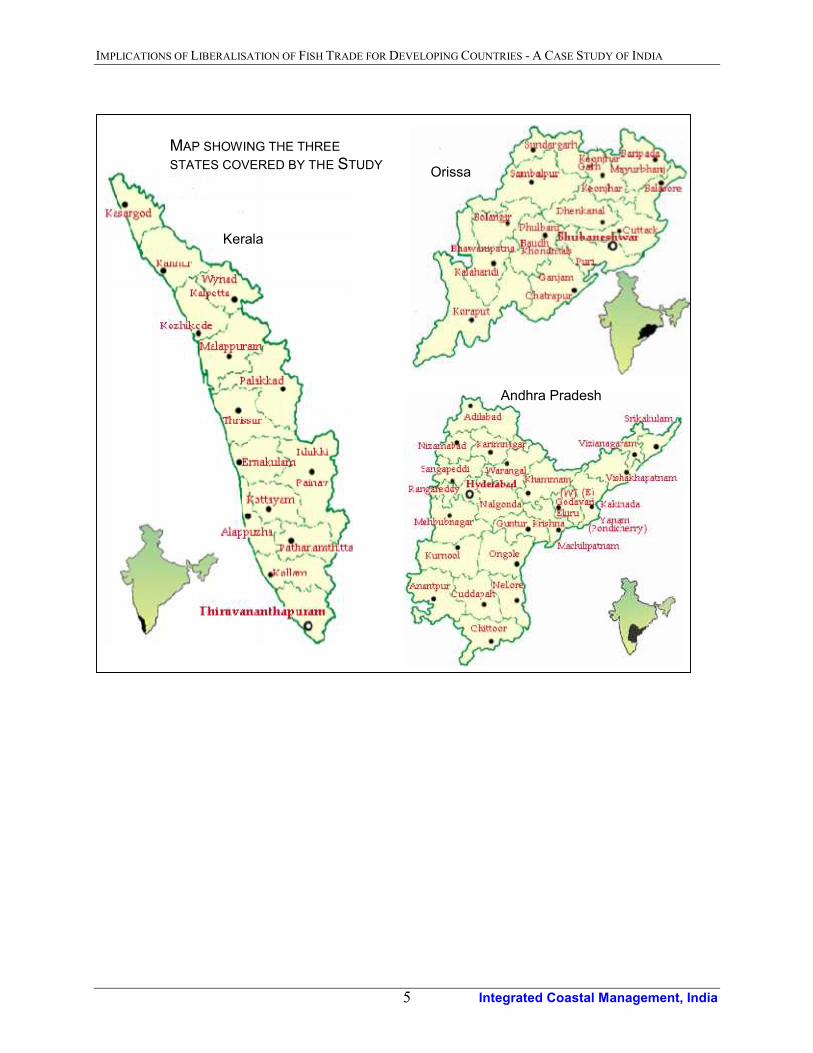

The study is located in three coastal states of India – Andhra Pradesh and Orissa on the east coastand Kerala on the west coast – and the data collection was done during March-April 2004.Logistical limitations and prior existence of good secondary data on Kerala meant that the studyconcentrated Andhra Pradesh and Orissa for the fieldwork, where 3 major mechanised landingcentres (Paradeep, Vizag and Kakinada); two large motorised landing centres (Puri and Uppada);three medium-sized landing centres (BCV Palem, Chinaganjam and Arjipalli); and three majoraquaculture centres (Nellore, Narsapuram in West Godavari and Tallarevu in East Godvari) havebeen covered (see Map).

METHODOLOGY

The field studies had two main objectives: one, to determine the different stakeholders in theexport processing chain and to assess their relative poverty; and two, to assess the impact ofchanges in subsidies and seafood legislation on different categories of stakeholders.

Participatory poverty assessment

Using a two-fold process of assessing poverty, food insecurity and vulnerability among thecoastal fishing communities developed by ICM for FAO/SIFAR during 2002-3 (ICM 2003),participatory poverty appraisals were undertaken in selected locations. In the first stage, a tieredprocess of interactions, beginning at the village level, followed by the export stakeholder level,which led to the household level, provided a number of features at the general, exportstakeholder and household levels. At the household level, a checklist of 16 indicators was used todevelop an aggregate score. The indicators are based upon the three critical dimensions of well-

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India12

being, as defined by the Human Development Report (UNDP 2001:3): (i) longevity — theability to live long and healthy life; (ii) education — the ability to read, write and acquireknowledge; and (iii) command over resources — the ability to enjoy a decent standard of livingand have a socially meaningful life. The score thus obtained was used to assign the households ina particular stakeholder category – and, by common agreement, the export stakeholder group towhich they belonged in the village – with a rank from 1 (destitute) to 8 (affluent). The simplearithmetic mean of the ranks received by a particular stakeholder group in different villages isconsolidated and the different stakeholders are classified into four categories: well off, moderate,poor, very poor and the characteristics of poverty/wellbeing in each category are summarised andrevalidated in selected locations.

Obviously, this categorisation must come with a number of caveats, which is inevitableconsidering the complexity that characterises poverty in different locations, among differentstakeholder groups within and between areas. Differences in terms of caste, religion, gender,occupation, and age will play a role in deciding whether a family is sustainably employed or not.Many of the categories are not specific to export chain, not only because the producers targetother varieties of fish as well, but also because the livelihood profile of a fishing household is notexclusively confined to fisheries. However, as an indicative measure of poverty among thedifferent export stakeholder groups, this has been found to be a useful and workable proposition.

Changes in subsidies and seafood legislation and impact on different stakeholders

It is evident that many of the changes related to subsidies and seafood legislation are stillunfolding and are only beginning to make an impact upon the industry in general and on thelivelihoods of the different stakeholders in particular. Thus, it has been found necessary, whendiscussing impacts with the stakeholders, not to confine the interactions to what the actualchanges and impacts have been, but also to explore (i) what is likely to happen if the existingsubsidies are further reduced or withdrawn or the seafood legislation made more stringent, usingthe conclusions of the global and national debates on the two issues as the basis to formulate thefuture scenarios and (ii) the capacity of the individuals and institutions in the country to adapt tothe challenges posed by these changes. The methodology used at the group/village level wasinformal discussions using checklists, while at the household level a number of informal tools –developed by ICM based upon the sustainable livelihoods (SL) framework and used extensivelyduring the study mentioned above – were applied.

The changes from the community’s perspective were brought out through:

Trend analyses, where the key trends affecting the life and livelihoods of the keystakeholder groups were identified. The factors contributing to these changes were exploredat the household level or at the village-level or in discussion with institutional stakeholders.

Open-ended discussions on the potential impact of changes in direct subsidies in fisherieson different stakeholders yielded the relevance of the existing subsidies on their livelihoodsand their impressions of the impact in case of withdrawal of the subsidies.

Key strands of the debate on subsidies at the international and national levels – for instance,the different ‘modalities’ of subsidies as discussed by the APEC study (APEC, 2000) – werediscussed in terms of their implications to the export stakeholder groups.

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India13

STRUCTURE OF THE REPORT

This report has four sections. The first section briefly describes the general context of India,followed by a general description of the fisheries sector. The section also provides theinstitutional context and the key stakeholders involved in the export supply chains in the country.The section concludes with a description of the poor stakeholders in the export supply chains.The second section describes the origins and development of the shrimp export supply chain inthe country, the role played by subsidies in its development, followed by an overview of thecurrent status of seafood export industry in the country. The third section discusses the impact oftrade liberalisation in terms of changes in subsidies and seafood legislation at two levels – themacro level, including the global and national context; and the grassroots level, providing theperceptions of the primary stakeholder groups. The last section summarises the key changes andimpacts from a livelihoods perspective using the SL framework, and suggests a fewrecommendations.

LIMITATIONS

This is one of the few studies where there was an information surplus on some of the macro-levelissues, which was almost as big a problem as not having sufficient data (which normally is thecase when doing a study of this kind). The literature is growing almost daily on the issues ofsubsidies and SPS issues (not to speak of trade liberalisation), and having access to the internethas not made things any easier. This surfeit of information threw up three concerns: one, theproblem of sifting through vast documentation to take out bits and pieces that are relevant to thestudy (and even more difficult, to reject large chunks of it); two, ensuring that the study resultsboth fit into, and fill a gap, in the existing literature; and three, that the information does notoverwhelm the study process to an extent that the researchers are no longer in the ‘driving seat’.Conscious attempts were made to keep the study in line with the overall frameworks of debate,while retaining some sort of independence over the field research.

Secondly, establishing the links between the macro-level changes and their impacts at thegrassroots level is not a straightforward process at all. Change is taking place on a number ofplanes simultaneously, and ascribing the changing livelihoods or living conditions of astakeholder group to particular changes is fraught with difficulties. As the study will show, mostchanges taking place in the sector are indirect, and have their sources outside the fisheries sector,and it will require more time, effort and expertise to explore the changes in a more integratedmanner.

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India14

CHAPTER 1: BACKGROUND

GENERAL CONTEXT OF INDIA

With a land area of 3.3 million km², India is the seventh largest country in the world and isreferred to as a sub-continent in its own right. Stretching from the snowy Himalayas in the northto the tropical rain forests of the south, from the desert plains of Rajasthan on the west to thewooded hill ranges of the east, the country encompasses a wide range of ecosystems and is hometo a large variety of flora and fauna.

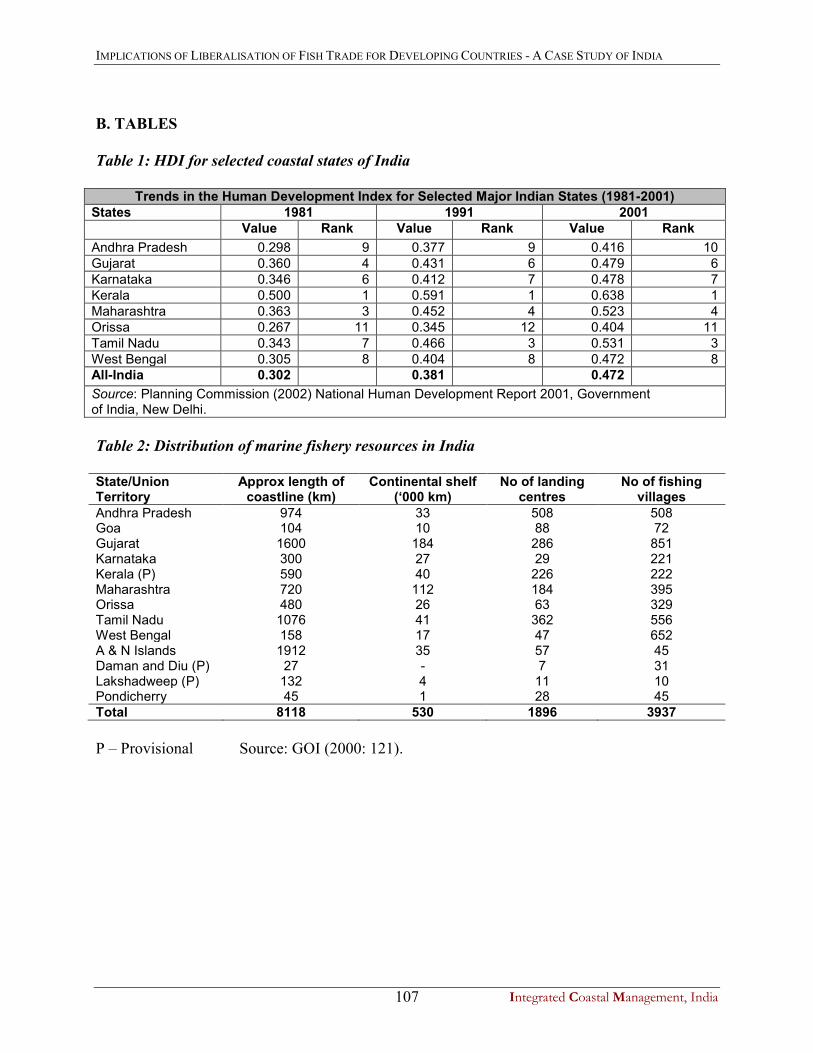

India has the distinction of being the second most populous country (after China) with a totalpopulation of 1,027 million (16.7 percent of the world population), which works out to apopulation density of 324 per sq km (GOI, 2003: 6-7). Some 742 million people or 72.25 percentof the population reside in rural areas (NIRD 2003: 4). 360 million people live in coastal areas(Hosch & Flewweling, 2004). The sex ratio (number of females per one thousand males) showeda consistently declining trend from 972 in 1901 to 927 in 1991, and has showed a slightimprovement to 933 in 2001 (GOI 2003: 11).

Agriculture is the lifeblood of Indian economy, contributing 25 percent of Gross DomesticProduct. About 70 percent of the population is dependent on agriculture for a livelihood (GOI,2003: 395). However, the land-ownership pattern continues to be skewed; in 1991, nine percentof the households owned half the farm land in the country (NIRD, 2000: 35). Right from 1951,when the First Five-Year Plan was launched, successive plans have given prominence to thesector both to ensure food sufficiency as well as to support livelihoods, particularly in the ruralareas. The survival of agriculture is dependent upon a number of subsidies – direct (for inputsand working capital) and indirect (income tax exemptions, minimum support price support) –and any changes to the subsidies in agriculture could prove catastrophic for the national economyas a whole. The structure of the economy has changed over the last 20 years, with the agriculturecontribution to GDP (including fisheries) falling from over one third in 1982 to only one quarterin 2002, and the service sector growing from 37.2% in 1982, to 49.2% in 2002 (Hosche &Flewweling, 2004).

Poverty & quality of life indicators

In terms of Human Development Index (HDI), India stands 115th among the world community(http://www.undp.org/hdr2001/indicator/cty_f_IND.html). The incidence of poverty in thecountry has declined by nearly half from 54.88 percent in 1973-74 to 26.10 in 1999-2000, which– when expressed in numbers – still means over 260 million people being poor in the country,down by only 60 million from the 1973-73 estimate (NIRD 2003: 85). In case of urban poverty,the percentage decline from 49 to 23.6 during the period is actually accompanied by an increasein the total number of poor by 7 million people! Incidence of hunger in rural areas in 1999-2000is as follows (Source: NIRD 2003: 98)

Members of households (percentage) getting two square meals a dayThroughout the year Only some months of the year Not even some

monthsNot reported

All India 96.2 2.60 0.70 0.50

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India15

This indicates that over twenty-six million people in the rural areas have access to two squaremeals a day only during some months of the year, while another seven million do not have twosquare meals even in some months! Average monthly expenditure on food per person in thecountry amounts to nearly 60 percent (NIRD, 2003: 81). Seasonal and long-term migration – intourban areas and non-traditional occupations – has been rising steadily and is a cause for concern.

Deprivation also stems from, or is exacerbated by, social inequality arising from systemicprocesses like caste, religion, gender and geographic origin, which determine the access to, andavailability of, resources to a household.

In 1991, access to the three basic facilities - safe drinking water, electricity and toilets – wasconfined to less than 4 percent of the rural households in the country. The following tableindicates the reach of other services in the rural areas of India (NIRD 2003: 333-4):

Availability of different facilities by percentage in villages of India (1995-96)Bus stand Bank Post office Fair price shop Vet centre PHC Primary school31.40 9.15 28.89 46.60 12.03 21.45 81.00Adult EducationCentre

All weather roads Police station Weekly market Supply depot(agricultural)

Coop society

48.25 65.25 4.54 14.40 10.87 22.10

Within the country, wide variations exist between states in terms of their human developmentachievements. Table 1 gives the HDI for selected coastal states of India, which shows Keralatopping the list with the highest HDI (0.638), while Orissa (at 0.404) comes last. Kerala ranksfirst in quality of life indicators like literacy, life expectancy and health. It has a sex ratio infavour of females and lowest infant mortality rate and birth rate when compared to Indianaverage (SIFFS, 2001). On the other hand, as an analysis done by Sundaram & Tendulkar(2003:1385-1393) shows, Orissa is one of the three states where the poverty situation (in termsof depth and severity) worsened over the period from 1993-94 to 1999-2000. Such differencesbetween states make it difficult to generalise the conclusions any study – including the presentone – across the country.

Social support programmes relevant to coastal fishing communities in India

The annual outlay for centrally sponsored anti-poverty programmes constitutes between 5 and 8percent of the total Government of India (GOI) expenditure, and about 1 percent of the GDP(NIRD, 2000: 102). Right from the launching of the First 5-Year Plan, the governments havegiven priority to livelihood generation and provision of basic services like housing, drinkingwater, sanitation, roads, cyclone shelters, health and education. Food security is sought to beachieved through the Public Distribution Systems (PDS) schemes, which provide subsidised foodto the people below the poverty line. For the weaker sections of the society – characterised byoccupation, caste, gender, age or physical ability – positive discrimination policies have beenenacted and reservations made at various levels. Some packages of insurance – for old people,widows and for helping the poor to tide over lean seasons – have been put in place. Althoughmuch criticism is levelled against the focus, content, scope and implementation of theseprogrammes, they undoubtedly address some basic needs of the poor. National drinking watermissions, public healthcare, rural sanitation, universal literacy campaigns, housing and public

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India16

distribution system are some of the public services relevant to the fishing communities of India(NIRD, 1999; ICM 2003).

FISHERIES SECTOR IN INDIA

People involved in fisheries sector

The coastal fishing communities in the country are among the poorest sections of the society (seeICM, 2003; Kurien, 1995; Tietze 1986; Vivekanandan et al, 1996). Traditionally marginalisedfrom the mainstream by the nature of their occupation, the fishers’ access to basic services is lowand a number of changes related to their livelihoods have made their condition more precarious.

According to livestock census of 1992 (cited in GOI, 2000), the total number of fishers in thecountry is 6.7 million, of whom men numbered 2.4 million, women 2 million and children 2.3million. Lacking disaggregated data from the 2001 Census, it has not been possible to ascertainthe current figures. Just over one third of full-time fishermen are located on India’s east coast,and 70% of the marine fish production originates from the west coast (Vivekanandan, 2002). Animportant feature of the fisheries sector is the gender-based division of labour and the active roleplayed by the women in the production and market-related activities in several states, particularlyon the east coast. Shrimp aquaculture provides livelihood to one million people, about a third ofthem employed directly in culture operations and the rest in ancillary activities (Mathew 2003).

Fisheries resources

India has a coastline of 8 041 kilometres spread along nine coastal states and four unionterritories. The exclusive economic zone (EEZ) stretches over 2.02 million km2, and thecontinental shelf covers 0.5 million km2. Table 2 provides the state wise details of coastline andcontinental shelf. The potential resources available from the Indian waters are 3.9 million tonnes,(2.2 million t in the inshore and the rest in the offshore waters) (GOI, 1996). India also hasinland water sources covering over 190 000 km and open water bodies with a water-spread areaof over 66 lakh hectares (GOI 2000: 122). Brackishwater area available for aquaculture purposesin the country is 1.2 million ha, of which 165 thousand ha is developed.

Fishing fleet

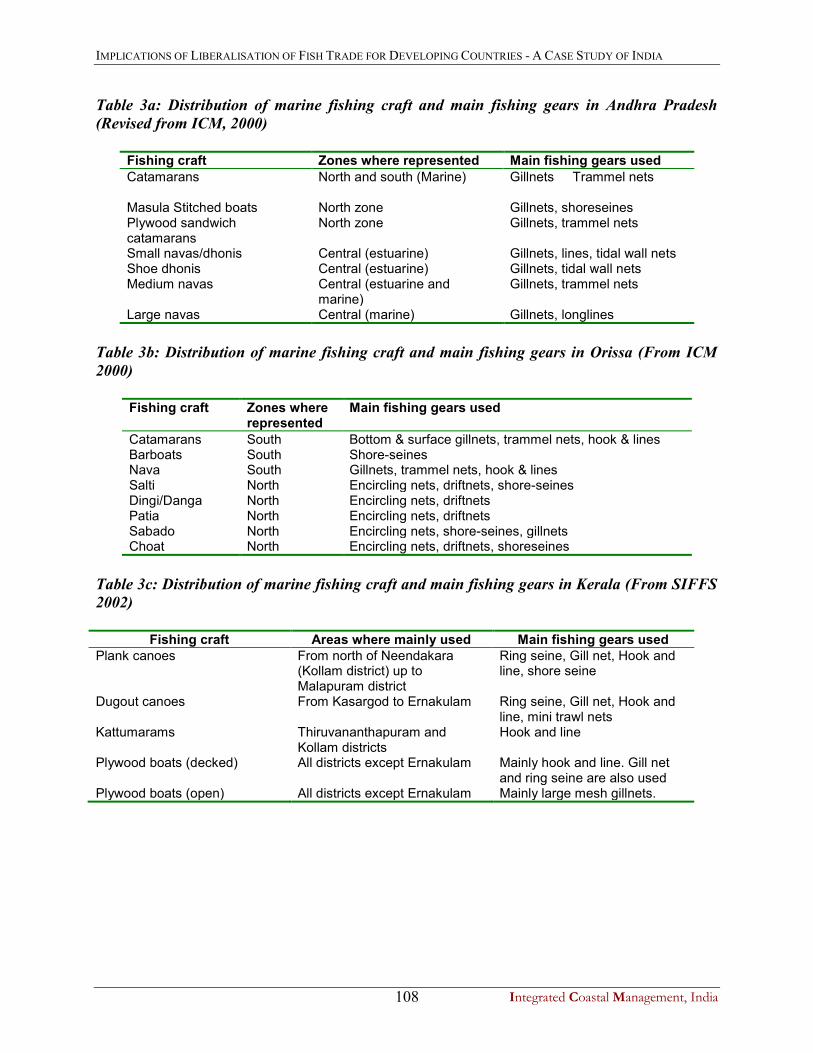

The methods of exploitation of marine fisheries resources vary from simple traps to largetrawlers and from simple hand-lines to sophisticated purseseiners (Vivekanandan, 2002). Thefishing crafts can be classified into two types: artisanal crafts with or without engine and themechanised boats. There are a total of 181 284 artisanal (i.e., non-motorised), 44 578 motorisedand 53 684 mechanised fishing crafts in the country making a total of 280 491 boats in all (GOI,2000: 128). The main fishing gears used can be classified as (i) encircling, (ii) drifting, (iii)dragging, (iv) seining and (v) lining types. Stationary gears include (i) set nets and (ii) fixed nets.The mechanised sector is largely dependent upon trawling, although gill-netting, purse-seiningand long-lining are also prevalent, particularly along the west coast of India. The design, size,construction, operations and economics of the fishing crafts – particularly the artisanal ones – arelocation-specific. Details of different artisanal fishing boats and the important nets used in

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India17

Andhra Pradesh, Orissa and Kerala are provided in Table 3 (a, b, c). New boat designs, FRP andplywood boat building, motorisation, synthetic nets are recent developments in artisanal sector.

Current level of exploitation

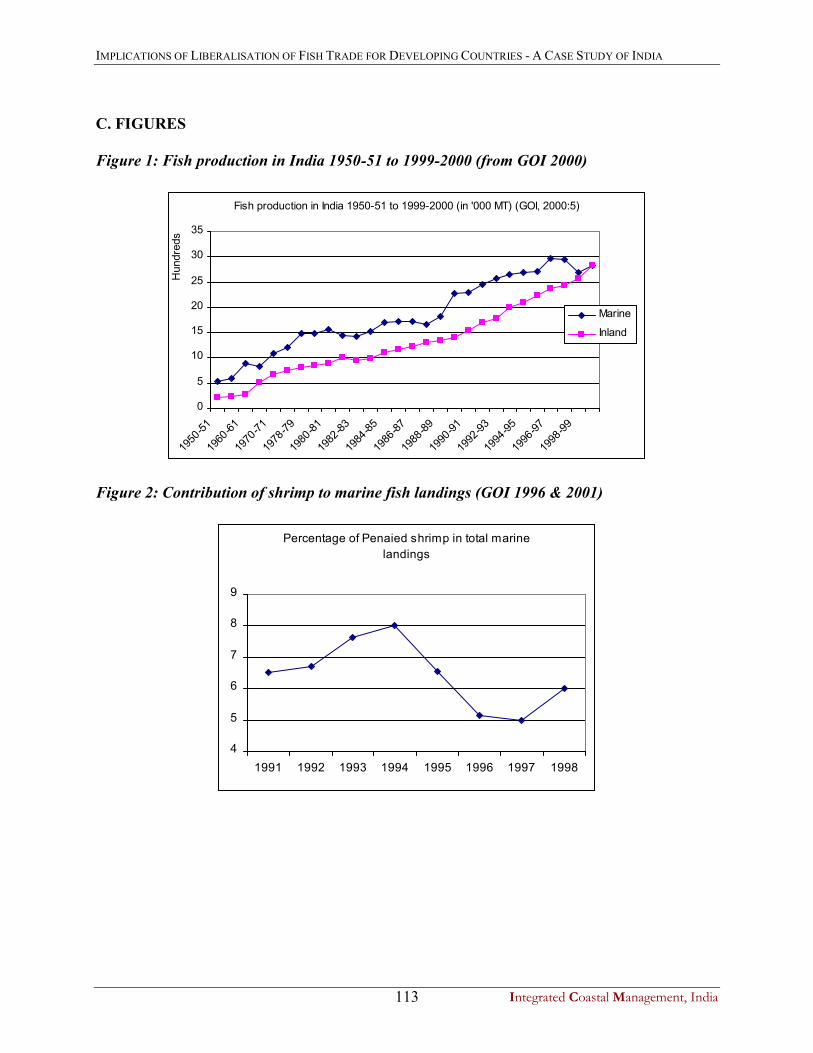

In 1950-51, the total fish production in the country was 0.75 million MT, of which marine fish(0.5 million MT) accounted for 71 percent. By 1999-2000, the total production has grown to 5.6million MT, but contribution of marine catches came down to 50 percent at 2.8 million MT, thedecline being due to increased production in inland and culture sectors. Marine production hasalso remained static since 1993-94 (GOI, 2000) (Figure 1). The catches from inshore waters arereported to have reached their full potential (Vivekanandan, 2002) and there is potential forincreasing the catches of only the cheaper varieties (small pelagics), supporting the contentionthat fishing effort in recent years has concentrated on specific high-value varieties (Salagrama,2004). The production from offshore can add 1.2 million tonnes to overall landings.

The annual average landings by the trawlers increased from 300 thousand t in 1980-1981 to 1.3million t in 1999-2000, increasing their share in marine production from 29.4% to 48.8%(Vivekanandan, 2002). The annual per capita production of active fishermen in the artisanalsector declined from 2 590 kg in 1980 to 420 kg in 1996-97, while it increased from 5 260 to8 130 kg in the mechanised sector (Sathiadhas, 1998: 466).

The composition of the Penaied shrimp in the total marine fish catches ranged between 5 and 8percent during 1991-98 (GOI, 1996 & 2000) (Figure 2), but there has been a decline in theoverall landings of marine shrimp since 1994. The culture production of shrimp rose from 28thousand MT in 1988-89 to 86 thousand MT in 1999-2000 making up for the shortfall in marinesupplies (MPEDA, 2001). East coast, particularly Andhra Pradesh, West Bengal and TamilNadu, dominates culture shrimp production, with Andhra Pradesh producing more than half thetotal production in the country (GOI 2000: 128). The average production per hectare, which grewto 820 kg per ha during 1994-95, fell back to 550 kg by 1999-2000. Andhra Pradesh, whichreached the one tonne per ha mark in 1994-95 slid down to 665 kg by 1998-99 (MPEDA 2001).Besides penaeids, scampi (Macrobrachium rosenbergii) is being cultivated in over 12 thousandhectares in the country with an estimated production of 7 140 MT during 1999-2000.

Contribution of fisheries to national economy

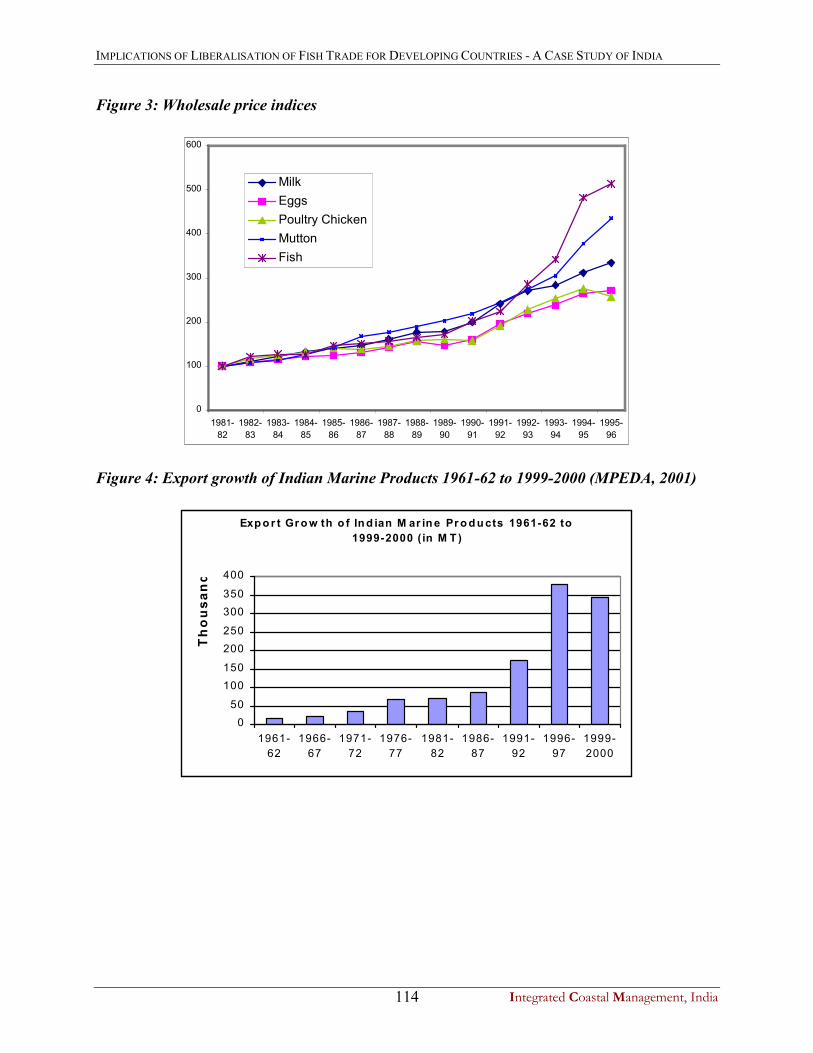

The gross investment on fishing component is estimated as Rs 8 000 crores (Vivekanandan,2002), much of it is in the private sector. Fisheries contributes Rs. 19 555 crore to the GrossDomestic Product (GDP), which works out to 1.3 percent of the total GDP or 4.6 percent of theGDP from agriculture sector. The contribution of fisheries to the GDP has shown a consistentincrease from 1970-71 when it was 0.62 percent of the total GDP and 1.46 percent of the GDPfrom Agriculture (GOI, 2000: 130). India’s contribution to world fish production has gone upmarginally from 3.7 percent in 1950 to 4.18 in 1997, but the contribution of marine sectordeclined from 2.97 to 2.86 percent during the period. Figure 3 provides the wholesale price indexfor different sources of protein in India indicating that the increase in real value of fish is muchfaster than that of the other food items (GOI, 1996: 117; GOI, 1997:121).

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India18

Institutional context of fisheries

Under the Constitution of India, fisheries is a state subject, i.e., individual states within theIndian Union can frame and implement fisheries policies of their own. The maritime states ofIndia have control of the seas up to a distance of 22 kilometres from the shore, while the CentralGovernment has control over the EEZ (Exclusive Economic Zone) beyond 22 km, stretching upto 200 km limit. In general, as Anjani Kumar et al (2003:15) have noted, the national policies inIndia have been export oriented, supporting relatively large-scale fisheries for shrimp, while formany states the primary concern was the welfare of local small-scale fishermen. A wide range offisheries development programmes have been administered by a large number of central andstate government agencies in the country. The nature, quantum, focus and impact of theprogrammes have been subject to changes from time to time and from state to state. Thefollowing section will provide an overview of the institutions working in the sector along withthe nature of support they extend to the seafood export industry.

Central Government organisations

At the central level, fisheries is under the purview of the Department of Animal Husbandry &Dairying (DAHD) which is part of the Ministry of Agriculture, Government of India. TheFisheries Development Commissioner in the DAHD heads the fisheries wing. The divisionimplements and monitors the central sector schemes and centrally sponsored schemes1

implemented through the state governments. It also undertakes pilot projects and acts as aconduit for externally funded development projects in several states (GOI, 2000). The followingis a summary of different fisheries development programmes funded by DAHD.

Subsidy for motorisation of traditional craft and for purchase of fishing gear Reimbursement of Excise Duty on HSD oil (currently Rs. 0.35 per litre) to mechanised

fishing vessels below 20 Metres. It does not cover motorised boats2. Fishing harbour facilities at major and minor ports. Subsidy ranging from 100% (for

fishing harbours at major ports) to 50% (for minor harbours and fish landing centres); inthe Ninth Plan, assistance for improving hygienic conditions to meet internationalstandards was made available.

Integrated coastal aquaculture through Brackishwater Fisheries Development Agency:

Subsidy for renovation/construction of fish farm including cost of inputs for the first year. Subsidy for establishment of shrimp seed hatchery of 2-5 million capacity

Welfare programmes

Development of Fishing Villages (DFV) programme provides basic civic amenities suchas housing, drinking water and community halls.

Savings-cum-relief (SCR) provides assistance to the fishermen during the lean period. Accident insurance. Premium subsidised to cover fishermen of age 18-65 years.

1 The latter have a component of contribution by the state governments2 In Kerala, motorized boats receive subsidized kerosene, but this is not available in other states

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India19

The Ministry of Food Processing Industries extends support for:

Setting up of infrastructure facilities for preservation and processing of fish Assistance (through MPEDA) for deep sea fishing and processing venture Assistance for diversified fishing Interest subsidy on loans for acquisition of deep sea fishing vessels Communication facilities for Coast Guard Grant-in-aid for setting up research & development and quality improvement in fish

processing technology

Other central ministries, such as the Ministry of Commerce (through MPEDA and EIA),Ministry of Environment and Forests (conservation and management), the Ministry of Shipping(fishing ports), the Ministry of Rural Development, Ministry of Ocean Development, and theMinistry of Defence (Coast Guard) play a determining role in the fisheries sector. The NationalCooperative Development Corporation (NCDC) provides assistance to fishermen cooperativeson liberal terms, implements the following schemes to enable the fisheries cooperatives to takeup activities related to production, processing, storage and marketing:

Purchase of operational inputs such as fishing boats, nets and engines Creation of infrastructure facilities for marketing (transport, cold-storages, retail outlets) Establishment of processing units including ice plants and cold storages

The Marine Products Export Development Authority (MPEDA) functions under the Ministryof Commerce, Government of India and acts as a coordinating agency with different Central andState Government establishments engaged in fisheries sector. The role envisaged for theMPEDA is comprehensive – covering fisheries of all kinds, increasing exports, specifyingstandards, processing, marketing, extension and training in various aspects of the industry. TheMPEDA has the mandate to develop the local seafood industry by providing technical assistance(through extension services and contact programmes), financial assistance (in the form ofsubsidies and loans) and promoting its products abroad. The MPEDA’s subsidy assistanceschemes cover marine capture fisheries, culture fisheries, processing industries and exportpromotion and, in terms of seafood export, the most significant and substantial support receivedby different stakeholders.

The Export Inspection Council (EIC) was set up in 1963 under the control of the Ministry ofCommerce in order to ensure sound development of export trade of India through quality controland inspection. The EIC is the apex authority under the Government of India, which isresponsible for monitoring of quality standards and issuing of licences. The EIC works throughthe regional Export Inspection Agencies, which are the implementing arms of the council andissue certification of quality to exporters of fish and fish products.

State government organisations

The State Department of Fisheries (DOF) is the nodal agency responsible for formulation ofpolicy, development and management programmes and their implementation. The DOF providesdirect support for increasing supply from both capture and culture fisheries. It monitors and

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India20

promotes improved management of the resources, and actively promotes the involvement ofsmall-scale and poorer participants in the sector. Its main activities include construction offishing harbours and setting up marketing and processing infrastructure, technical support,training and extension, subsidies and credit assistance to fishermen for acquiring fishingequipment, support to fishermen cooperatives, compiling fisheries statistics, and implementingvarious welfare measures and activities for the fishers (DOF-AP, 1998).

Many states like Kerala have programmes for social insurance, fishermen’s relief funds,rehabilitation programmes, special transport services, schools and scholarships, assistance forrepair of houses, and even for diversification of occupation (GOI, 1983: 14-19). Village accessroads, transport facilities and provision of infrastructure for drying were some of the programmesthat most state governments have taken up. Since 1990, budgetary constraints have forced thestates to confine themselves to implementing the central programmes. Many state departments offisheries have set up apex cooperative bodies to source funds from the NCDC. Some statedepartments started corporations to undertake input and output marketing with poor results.

The Department of Rural Development (through the District Rural Development Agency –DRDA), Department of Forests, Shore Area Development Authority (SADA), Department ofPorts and various bodies set up for development of weaker sections, such as the BackwardClasses (BC), Scheduled Castes (SC) and women and child welfare, have a role to play at thestate level in the fisheries sector. The main activities of DRDA are to promote enterprisedevelopment and employment generation among the rural youth and women, extending trainingand financial support, setting up infrastructure facilities like fish drying platforms, net-mendingand fish storage rooms, community halls, etc.

Research organisations

Fisheries research is undertaken by both the central government and the individual stategovernments. The central government research institutions generally fall under the control of theIndian Council of Agricultural Research (ICAR). Fisheries research in the states is done byagricultural universities and their colleges of fisheries. The following are the fisheries relatedinstitutions under the control of the ICAR.

Central Inland Capture Fisheries Research Institute (CICFRI), Barrackpore, W Bengal,conducts research on open inland water systems and undertakes extension and training.

Central Institute of Brackish water Aquaculture (CIBA), Chennai, Tamil Nadu conductsresearch for development of finfish and shellfish culture in brackish water.

Central Institute of Freshwater Aquaculture (CIFA), Bhubaneswar, Orissa conductsresearch on production and productivity issues in freshwater aquaculture.

Central Institute of Fisheries Education, Mumbai (CIFE), Mumbai, Maharashtra is theonly fisheries university in India undertaking education and research in fisheries.

Central Marine Fisheries Research Institute (CMFRI), Kochi, Kerala carries out work onmarine fisheries resources and their exploitation; and training and extension programmes.

Central Institute of Fisheries Technology (CIFT), Kochi, Kerala undertakes research infishing technology, craft and gear, processing and preservation; it also helps in qualitycontrol certification for export of seafood.

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India21

Two other fisheries research organisations – National Research Centre on Coldwater Fisheries(NRCCWF), Bhimtal and National Bureau of Fish Genetic Resources (NBFGR), Lucknow arealso affiliated to ICAR.

Financial institutions

The National Bank for Agriculture and Rural Development (NABARD) has a specialcomponent for preferential lending to the fisheries sector at subsidised rates of interest.NABARD’s support to fishing sector included refinancing mechanised and other boats andaquaculture (Upare, 2004:66). In the X-5 Year Plan period, NABARD plans to refinance loansworth over 6 thousand crores (GOI, 2001a: 41). Mechanised trawling was financed by thecommercial banks until 1980s (see next chapter), and the brackishwater boom in the early 1990salso encouraged financial institutions like Industrial Finance Corporation of India (IFCI),Industrial Development Bank of India (IDBI), Shipping Credit and Investment Company of India(SCICI), State Finance Corporations (SFC) and NCDC to lend credit, but much of this supportdried up by mid-1990s for a number of reasons (Anjani Kumar et al 2003: 13-14).

Trade associations

The Seafood Exporters Association of India (SEAI) is the representative body of seafoodexporters. It takes an active part, in conjunction with the MPEDA, in conducting theInternational Seafood Fairs in India, besides participating in the various international fairs andexhibitions. It brings out the Seafood Exporters Journal.

MAIN STAKEHOLDERS IN EXPORT SUPPLY CHAIN IN INDIA3

The seafood export industry comprises of four distinct entities. They are: (i) producers (ii)intermediaries (iii) processing/export industry and (iv) ancillary workers. The last groupconstitutes numerically the largest grouping in the sector and includes a wide range of poorpeople involved in miscellaneous wage earning activities. Frequently, the people in this grouphave no direct stake in the economics of operation and any changes in the sector affect themsecondarily, although no less drastically.

1. Producers

Capture operations are largely carried out by people from traditional fishing castes, while manyoutsiders are also involved in aquaculture. Processing and export industries are owned by non-fishing entrepreneurs.

Mechanised trawling fleet

In 1997, the mechanised fishing fleet in the country numbered over 47 000 boats and employed200 000 people (Sathiadhas, 1998:466), of whom 150 000 were employed in trawling. However,considering that at least a quarter of the boats are idling at any given time, the actual numbers of

3 Drawn from ICM (2002) and SIFFS (2002) and revised and updated.

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India22

people employed may be less. The organisation of mechanised trawling is different fromartisanal fishing in at least three respects: (i) the crew are generally from the fishing castes andemployed on wage basis, although they do receive a small share in the catches of the bycatch; (ii)the owners are seldom active fishers themselves and (iii) their operations are focused on shrimp.

Artisanal fishing fleet

According to GOI (2000:128), there are over 225 000 motorised and non-motorised boats in thecountry, so approximately 900 000 people are possibly employed in sea and estuarine fishing.Sharing systems vary across the regions, but it is commonly understood that the crews earn ashare in the catches and not a regular wage. Sizeable quantities of shrimp are caught usingtrammel nets and small gillnets in the artisanal/motorised sector. Many fishing operations arefocused on shrimp through the 1990s because its high value helped the fishers to overcome thereduction in overall catches, but the current study shows that the fishers are shifting back tofinfish again. In Andhra Pradesh and Orissa, a motorised, open-sea based fishing boat targetsshrimp for about 3 months spread over two peak fishing periods in a year. The income fromshrimp might account for 60 percent of the annual income of a fisherman, and in some years, thiscould be much higher, although it has come down to 40 -50 percent in the last couple of years. Innon-motorised estuarine fishing, shrimp contributes up to 90% of income.

Among the crew, the fishers working in non-motorised boats are the poorest and those workingon mechanised trawlers are relatively better off, although recent trends indicate that working onmechanised boats is not considered a profitable proposition anymore. Mechanised boat ownersform the most prosperous category in the capture sector and have strong associations, whichlobby for their interests at various levels. The other stakeholders are not so well organised. Insocial and economic terms, the motorised boat owners fall in between the non-motorised and themechanised boat owners. The levels of indebtedness amongst the mechanised and motorised boatowners are the highest among all categories of fishworkers. The non-motorised sector is stressednot so much in economic terms as in terms of reduced access to fishing grounds (SIFFS, 1991).

Culture sector

The participants in export commodity chains from the culture sector are: (i) small-scaleaquaculturists, who own farms of about 1 – 2 ha size and for whom aquaculture is a largelysubsistence activity; and (ii) large-scale aquaculturists, who could be individual/family operatorsor the corporate operators. At present, there are only a few large corporate farms continuing withshrimp farming. The individual/family operations are as lucrative as they are risky. Onecharacteristic feature of this category is generally the ownership lies in the hands of people withnon-fishing backgrounds. Small-scale farmers, who constitute over 90 percent of the farmers inall states, generally obtained their landholdings under development programmes or by sharingthe village commons among themselves. A majority of the coastal farmers are from the fishingcommunities, many of them active fishers themselves, and even now, they frequently shuttlebetween the two occupations depending on whichever looked less risky or more lucrative. Ineconomic terms, the status of the small farmers is little different from that of the marine fishersand, in economic terms, more risky.

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India23

2. The intermediaries

Commission agents and independent traders

The commission agent and the middlemen-trader are relatively new phenomena, who arrived onthe scene only after the shrimp export markets began to grow in the 1980s and 1990s. There isvery little information available on the various categories of the trade intermediaries in fisheries.Considering the debate that the ‘exploitative practices’ of ‘middlemen’ have generated, it israther surprising that they have not received more scholarly attention. In rural areas, theygenerally come from the fishing community or a neighbouring agrarian community, frequentlyfrom the elite or affluent sections while outsiders are also observed in this trade in urban areas.They play an important social and economic function and – in the absence of institutional safetynets – bear most of the risk that a highly risky trade like shrimp export carries.

The numbers of commission agents and traders varies from place to place and from time to time.Each commission agent has an arrangement with a particular company, which provides a softloan in cash or kind to him in return for procuring shrimp from individual fishers/farmers on itsbehalf. The commission agent in turn lends the money to the fishers and the farmers in return forthe right to sell their products on commission basis. The independent traders do not borrow fromprocessing/exporting firms and use their own funds in business, hence they obtain a better priceby selling to whichever company or peeling shed is willing to pay them well. The owners ofpeelings sheds form an important category of independent traders in Kerala.

Investments in trade by the individual traders could range between Rs. 25 000 to Rs. 1 500 000or more. Both independent traders and the commission agents obtain shrimp from the boats towhich they have advanced money and also from others. They frequently form cartels to controlthe prices and resort to various malpractices in rural areas. The larger traders increasingly act ascollection points for shrimp brought by a number of smaller traders, and the interrelationshipsbetween the various categories of traders are amazingly complex, and a simple cost-benefitanalysis to assess the profitability of this trade is almost impossible.

Company agents

Company agents are employed by processing plants to purchase raw material conforming to theprice and quality specifications given to them by the company. They receive monthly wages (inAndhra Pradesh) or commission on a per kg basis (in Kerala). They ensure that the raw materialprocured is iced adequately and hygienically at the harbour and transferred to the company byinsulated vans. Their influence is on the rise as processing plants are taking a greater control onthe supply chain as a response to the EU legislation (SIFFS 2002).

3. Processors & Exporters

The pre-processing and processing activities are the only areas in shrimp export chain wherewomen take a lead role, albeit as wage labourers.

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India24

Pre-processing and peeling centres

These pre-processing centres are individually owned. The owners have arrangements with theprocessing plants for supplying shrimp. Until recently, pre-processing activities generallyinvolved beheading and peeling, but increasingly peeling is being done at the processing plantitself. The number of people employed in a pre-processing centre varies depending on the placeand season, as workers are employed on a daily wage basis depending on availability of shrimp.Decreasing work (due to declining supplies and the insistence of the factories on buying wholeshrimp) and increasing competition have caused many women to move out of this activity.

The peeling shed industry is an important source of employment in Kerala. There are regular(registered) and seasonal peeling sheds, employing between 25 and 100 women each – generallyfrom the local fishing community – and pays a fixed rate based on the quantity peeled. Manywomen also collect raw material from the large peeling sheds for peeling at home, and are paid afixed, but lesser, rate than those who peel in the shed.

Processing industry

Processing for the export sector is different from the other activities in the fishing industry in thatit is in the organised sector (even though the product it processes comes from the informalsector). A large share of the processing and export markets is held by a relatively few companiesin Andhra Pradesh and Kerala. SIFFS 2002 notes that 87 percent of the seafood processed inKochi belt in Kerala during 1999-2000 was done by eight processors out of a total 69 processingplants in the area. Nearly 70-80 percent of the seafood in Andhra Pradesh is reportedly processedby four or five large companies. Some of the large processors also own factory vessels to have abetter control over the quality of the catches and the operations. There are different categories ofprocessors/ exporters in the country. Not all the players are involved in both activities.

Processors who also export

Most major exporters own their own processing plant(s). They secure orders from clients abroad,procure raw material, process and pack it at their processing plant and export it. Some of the bigexporters have their own brands and sell their products in semi cooked or ready-to-eat form tosuper market chains in foreign countries.

Processors who do not export directly

This category mostly comprises of people who invested heavily in plant and machinery in theaftermath of the EU ban and currently have no working capital or are facing supply problems.They lease their idle plants on a fixed (per kg) commission basis to other processors/ exporters orto exporters who do not have processing plants of their own.

Exporters who do not have a processing facility

Not having one’s own production facility places definite limitations on the degree of control anexporter can have on the quality of the final output. However, a few people who have the export

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India25

license and the required working capital continue to take processing infrastructure on lease. Thiscategory is likely to vanish as seafood legislation becomes more stringent.

Workers in shrimp processing activities

The seafood processing plants employ women for pre-processing, grading, sorting and packing.MPEDA (2002) notes that nearly 80 percent of the workers in seafood processing plants arewomen from economically weaker coastal communities. The number of women employed in aprocessing plant ranges between 100 and 250, and considering there are about 400 registeredprocessing plants in the country, the total number of women employed in these plants couldrange between 40 000 and 100 000. The income from processing activities is significant for thefamilies of these women.

The fact that a large percentage of the processing workers are generally poor migrant girls fromKerala leading cloistered lives inside the factory premises under poor living and sanitaryconditions makes them vulnerable to exploitation (Beena, 1992). Processing workers receive lowwages (Rs. 1 200 to Rs. 1 500, going up to Rs. 2 000 per month) and work long and irregularhours (12 hours or more at a stretch). The hard and tedious work leads to frequent ill health andmany girls suffer from anaemia due to malnutrition. The plight of the migrant workers isworsened by competition from the local women, which reduces their bargaining powerconsiderably. Many processing plants keep the girls in the ‘temporary labourer’ category,effectively blocking their chances for a fair deal through legal mechanisms. The Factory Act andthe Inter-State Migrant Workers (Regulation of Employment and Conditions of Service) Act of1979 are largely bypassed. The EU regulations impose certain basic standards on the status ofemployment as well as the quality of life of the processing workers, which reportedly have apositive impact on the conditions of the processing women.

4. Other participants

Hatchery owners, operators and workers

There are 260 shrimp hatcheries in the country, with more than half of them – 133 – located inAndhra Pradesh and another 72 in Tamil Nadu (AAI, 2001: 15). Little information is availableon the working conditions inside hatcheries, but it is believed that, being a sophisticatedtechnological activity run along professional industrial lines, the working conditions here aremuch superior to the rest of the fisheries sector.

Feed mill owners, operators and workers

There are 33 feed mills in the country, with Andhra Pradesh and Tamil Nadu accounting for 27of them (AAI, 2001:15). The feed mills are generally set up with active foreign collaboration, orare the Indian subsidiaries of international companies and often form part of an integrated systemof supply and procurement, which makes it difficult to assess their performance individually. Asin the case of hatcheries, the working conditions are reportedly better in the feed mills.

IMPLICATIONS OF LIBERALISATION OF FISH TRADE FOR DEVELOPING COUNTRIES - A CASE STUDY OF INDIA

Integrated Coastal Management, India26

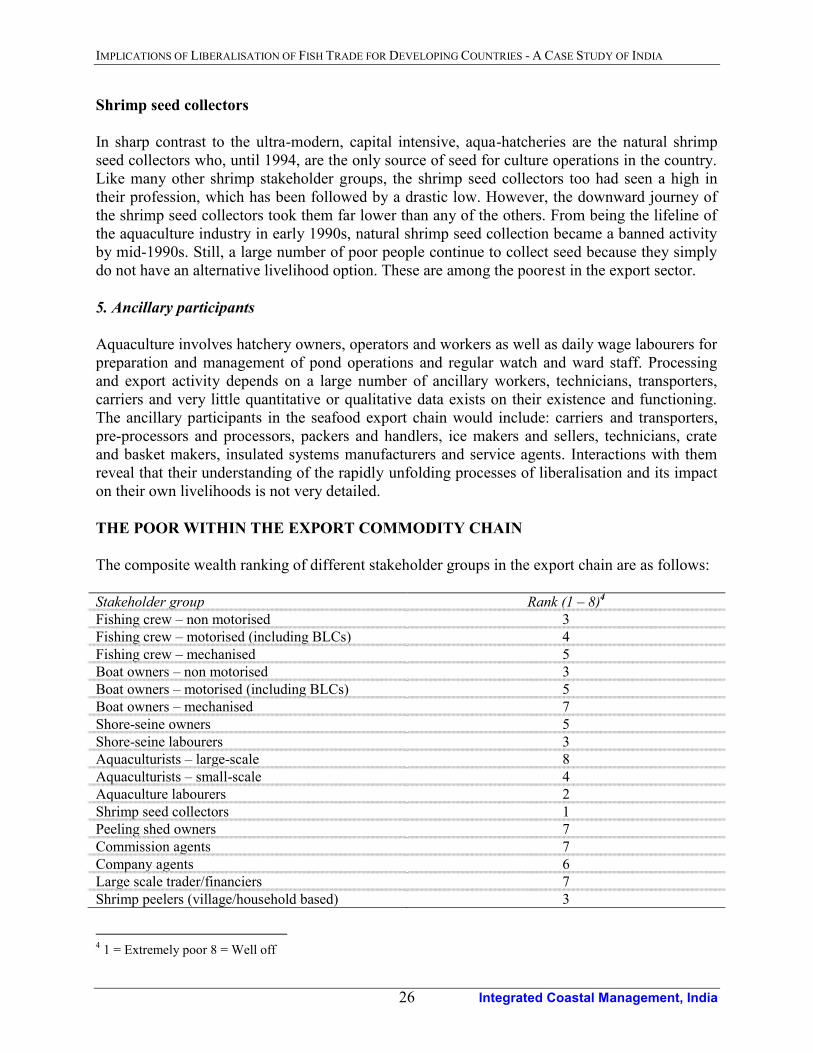

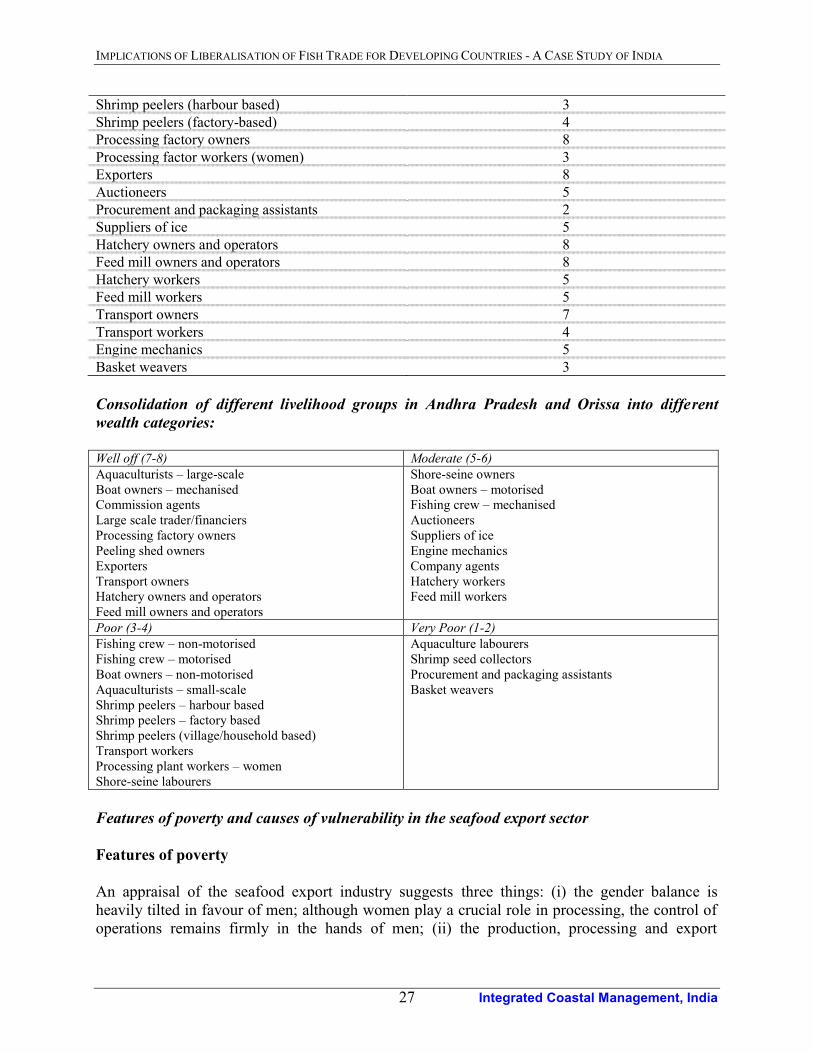

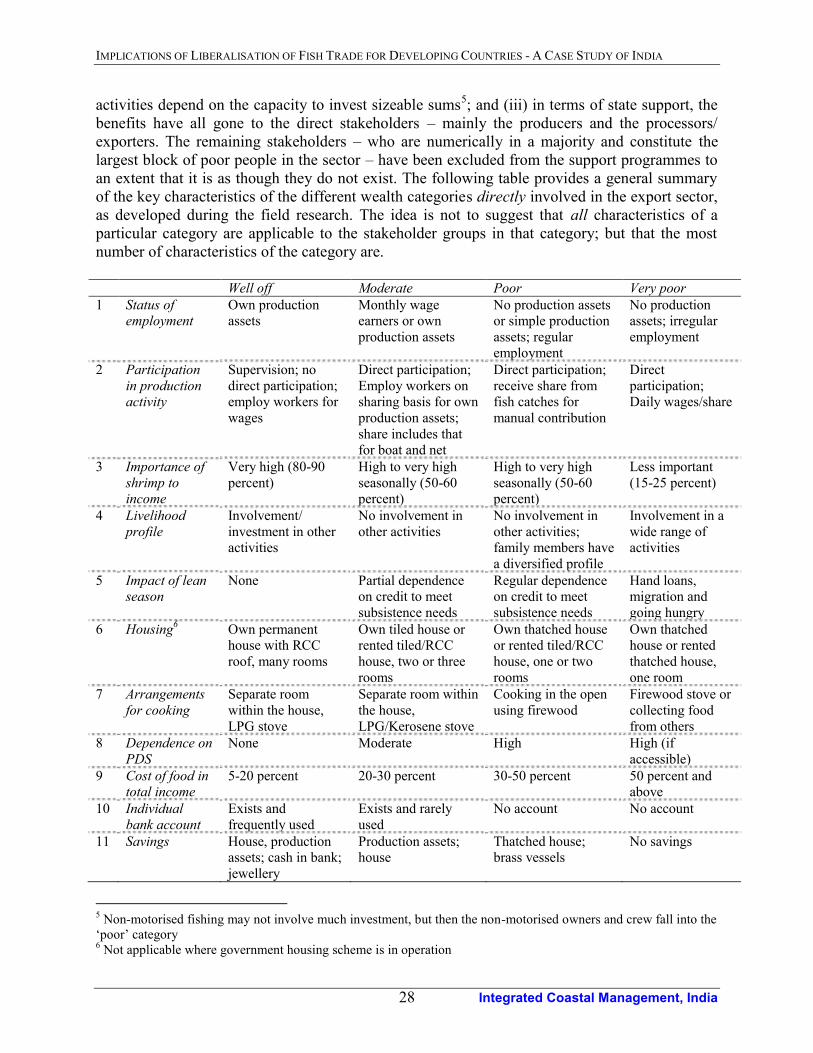

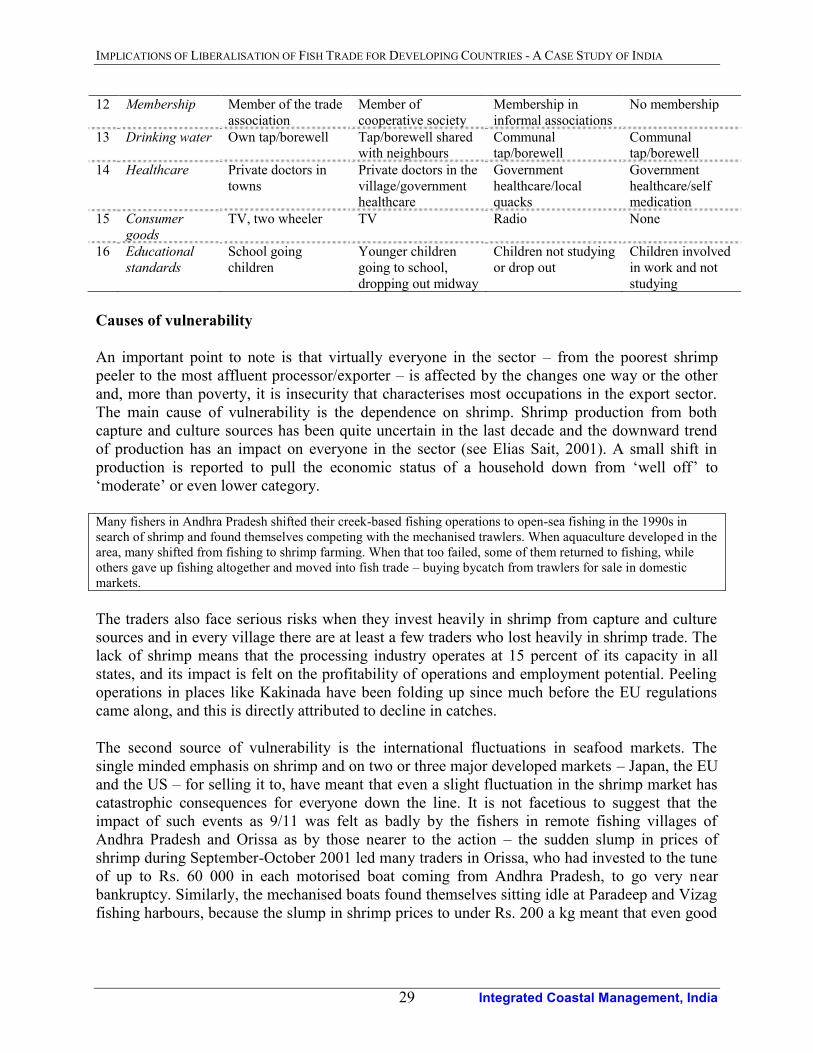

Shrimp seed collectors