IMPACT OF CAPITAL STRUCTURE ON FINANCIAL PERFORMANCE OF CEMENT MANUFACTURING INDUSTRY IN NIGERIA:...

21

IMPACT OF CAPITAL STRUCTURE ON FINANCIAL PERFORMANCE OF CEMENT MANUFACTURING INDUSTRY IN NIGERIA: CASE STUDY OF ASHAKA AND DANGOTE CEMENT COMPANIES By NDULUE IFEYINWA THERESA Department Of Business Administration University Of Abuja +2348051746999 EKECHUKWU CHINONSO HENRY Department Of Business Administration University Of Abuja +2347038770909 [email protected] OPUSUNJU MICHAEL ISAAC +2347037242315 [email protected] This study empirically investigate the impact of capital structure on financial performance of cement manufacturing industry in Nigeria using Dangote and Ashaka cement as a case study. The annual financial statements of the companies were used for this study which covers a period of six (6) years from 2008-2013. Ordinary Least square regression analysis was applied on performance proxies (Return on Asset (ROA) and Return on Equity (ROE) as well as total debt (TD) and Total Equity (TE) as capital structure proxies. The results shows that, there is a positive significant relationship between ROE and Total equity and there is positive significant relationship with ROA and total debt, ROE and total Equity, ROA and total debt. The study recommends that, firms should not use equity as a source of finance since insignificant relationship exists between the capital structure and performance (total equity and ROE). They should try to finance their activities with retained earnings and debt and use equity as last option. Keywords: capital structure, financial performance, debt and equity. INTRODUCTION A firm funds its operation with capital raised from various sources like internal and external. A mix of these various sources is generally referred to as a firm capital structure. The internal source refers to the funds generated from within which are mostly retained earnings. It results from performance firm earn from its commercial activities. Funds sourced not from within the earnings of firm activities are called external financing. A firm capital structure affects the financial performance of the firm. It determines the success and failure of the firm. It is necessary

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of IMPACT OF CAPITAL STRUCTURE ON FINANCIAL PERFORMANCE OF CEMENT MANUFACTURING INDUSTRY IN NIGERIA:...

IMPACT OF CAPITAL STRUCTURE ON FINANCIAL PERFORMANCE OF CEMENTMANUFACTURING INDUSTRY IN NIGERIA: CASE STUDY OF ASHAKA AND DANGOTECEMENT COMPANIES

By NDULUE IFEYINWA THERESA

Department Of Business AdministrationUniversity Of Abuja

+2348051746999

EKECHUKWU CHINONSO HENRYDepartment Of Business Administration

University Of Abuja+2347038770909

OPUSUNJU MICHAEL ISAAC [email protected]

This study empirically investigate the impact of capital structure on financial performance ofcement manufacturing industry in Nigeria using Dangote and Ashaka cement as a case study. Theannual financial statements of the companies were used for this study which covers a period of six(6) years from 2008-2013. Ordinary Least square regression analysis was applied on performanceproxies (Return on Asset (ROA) and Return on Equity (ROE) as well as total debt (TD) and TotalEquity (TE) as capital structure proxies. The results shows that, there is a positive significantrelationship between ROE and Total equity and there is positive significant relationship with ROAand total debt, ROE and total Equity, ROA and total debt. The study recommends that, firms shouldnot use equity as a source of finance since insignificant relationship exists between the capitalstructure and performance (total equity and ROE). They should try to finance their activities withretained earnings and debt and use equity as last option.Keywords: capital structure, financial performance, debt and equity.

INTRODUCTION

A firm funds its operation with capital raised from various sources

like internal and external. A mix of these various sources is generally

referred to as a firm capital structure. The internal source refers to

the funds generated from within which are mostly retained earnings. It

results from performance firm earn from its commercial activities. Funds

sourced not from within the earnings of firm activities are called

external financing.

A firm capital structure affects the financial performance of the

firm. It determines the success and failure of the firm. It is necessary

to note that, when a firm has a good capital structure, such firm can

stand in the future against financial crises. Firm build up a good

capital structure (debt and equity) so it can generate return on

investment, return on asset, return on equity, net profit, gross profit,

return on earning etc.

This research attempts to fill the gap in this field by

investigating the impact of capital structure on financial performance of

cement manufacturing industry using different variables like return on

Asset (ROA), Return of Equity (ROE), and total debt both short and long

term (TD), Total Equity both common and preferred equity (TE) and a time

frame that is considered most recent when compared with the researches

reviewed in this work.

Despite firms using different sources of financing, some of them are

still stagnated and others are failing. This could be attributed to lack

of knowledge on the best sources of financing with majority of owners

having no ideas on how debts and equity influence their ROE and ROA.

Firms may also have a high mix of debt and equity because they are unable

to generate retained earnings. However, there is a little that has been

done on the impact of capital structure on financial performance of firms

especially in Nigeria. Therefore, this study analyzed impact of capital

structure on financial performance of cement manufacturing industry.

The significance of this study is that, it will help the investors

to create such a portfolio that yield them maximum profit. It will also

enable them to know the choice of capital structure and its effect on

financial performance of their company and also be of help for academic

research.

The objective of this study is to examine the impact of capital

structure on the financial performance of cement manufacturing industry

in Nigeria. Specifically, it is aimed at: establishing the extent

whether Total debt have any impact on Return on Asset and to ascertain

whether Total Cost of Equity have any negative impact on return on Equity

of a firm over the period 2008 – 2013 but, the limitation of this study

is the inability to considered other manufacturing industry away from

cement manufacturing industry.

In line with the above stated specify objectives of this study, the

following hypotheses are formulated in null form:

H01: There is no significant relationship between total debt and return

on Asset of a firm.

H02: There is no significant relationship between Total cost of Equity

and return on Equity of a firm.

Concept of Capital structure

Capital structure of a firm is not easy because it requires

selecting between debt and equity securities while taking into

consideration the different costs and benefits that are associated with

these securities (Osuji et al, 2012; Boopen et al, 2014).

Dare and Sola (2010) cited by Nwankwo (2014), capital structure is

the combination of equity and debt. Capital structure is defined as the

mix of debt and equity used to finance the operation of a firm (Coleman,

2006; Damodaran, 2001 cited by Suleiman, 2013). Sanghoon (2008) cited by

Nwankwo (2014), defined it as the ratio of different finance.

It is the combination of different sources of funds that firm uses

to finance its overall operations and growth (Fozia et al, 2009; Memon et

al, 2010; Memon et al, 2012), and is used to represent the proportionate

relationship between debt and equity where equity includes paid-up share

capital, share premium, reserve and surplus (retained earnings) (Pandey,

2010 cited by Leon (2013).

Nirajini et al (2013), it is a way in which a firm financed by

combining long term capital(ordinary shares and reserves, preference

shares, debentures, bank loans, convertible loan stock and so on) and

short term liabilities such as a bank overdraft and trade creditors. It

is the firm’s sources of long-term financing (Brealey, Myers& Marcus,

2001) cited by Babatunde et al (2014).

The combination of various financial sources of every company is

called capital structure (Ghalibafasl, 2005) cited by Pouraghajan et al,

(2012). It is a mix of debt and equity that will have the minimum cost of

capital and will maximize the value of the firm (Gupta et al, 2014) and

it is the mix of debt and equity maintained by a firm (Taiwo 2012;

Joshua, 2008; Athula et al 2011; and Damodaran, (2001) cited by

Suleiman, 2013). It relies upon the size of composition of debt or equity

(Muhammad et al, 2012; Tharmila et al, 2013). It is a blend of internal

and external sources of funds (Amara et al, 2014).

Mubeen et al (2014), capital structure is the different sources of

financing like Equity (Common and Preferred Equity) and Debt (Short-term

and Long-term) and can also includes short-term debt and working capital

requirements of the firm (Babatunde et al, 2014).

Fozia et al (2009); Naizuli (2011); Amara et al (2014), it is a mean

to finance company’s overall assets by selecting the appropriate mixture

of debt (long term and short term) and equity (common equity and

preferred equity) and the firm finances its assets through some

combination of equity, debt or hybrid securities (Peek and Rosengren,

2000 cited by Penvilia, 2013).

It is the total liabilities on the firm’s balance sheet (Brezeanu,

1986) cited by Mihaela (2012).And the ratio of short-term and long-term

financing (Toma et al, 1998) cited by Mihaela (2012). It is a

relationship between debt and equity (Depallens et al (1990) cited by

Mihaela (2012). It is the composition of secured capital, both according

to the sources and the duration of use of such capital (Giurgiu, 1992)

cited by Mihaela (2012).

Is the way firms finance its right hand side of the balance sheet

(Wajid et al, 2013; Heydar et al 2010). It indicates that, the firm value

concerns with and how the firm structures its capital in order to

determine its earning and create value for its assets and it is

independent of how the firm finance to invest, or to pay dividend to its

shareholders (DeAngelo et al, 2004) cited by (Wajid et al, 2013).

Puwanenthiren (2011), believed that, it is a means to finance

company’s overall assets by selecting the appropriate mixture of debt

(long term and short term) and equity (common equity and preferred

equity)

Concept of financial performance

The term performance is a controversial issue in finance largely

because of its multidimensional meanings (Prahalathan et al, 2011 cited

by Mihaela, 2012). It can be defined as outcome-based financial

indicators that are assumed to reflect the fulfilment of the economic

goals of the firm (Murphy et al., 1996) cited by Chepkemoi (2013).

It is the process of identifying the financial strengths and

weaknesses of the firm by` properly establishing relationship between the

items of the balance sheet and the profit and loss account (Leno, 2013),

and it relates to the motive of maximizing profit both to the

shareholders and on assets (Chakravarthy, 1986, cited by Ishaya et al

(2014), while the operational performance concerns with growth and

expansions in relations to sales and market value (Hofer & Sandberg,

1987) cited by Zeitun et al (2007.

A company’s performance can be measured based on the variables that

are involved in the productivity, returns, growth or even customer

satisfaction Mihaela (2012). Financial performance (reflected in profit

maximisation, maximising return on assets and maximising shareholders

return) is based on the firm’s efficiency (Chakravarthy, 1986) cited by

Mihaela (2012). But Barbosa (2005), financial performance is based on

the return on investment, residual income, earnings per share, dividend

yield, price/earnings ratio, growth in sales, market capitalisation, etc.

Kaplan and Atkinson, (1998); Lau and Sholihin, (2005) cited by

Chepkemoi (2013), recognizes the inherent advantage of financial measures

and these measures include; accounting based measures calculated from

firm’s financial statements such as ROE, ROA, and GPM (e.g. Majumdar and

Chhibber, 1999; Abor, 2005) cited by Mohammad et al (2013), market based

measures such as stock returns and volatility (Welch, 2004) cited cited

by Mohammad et al (2013), Tobin’s Q measure which mixes market values

with accounting values (Zeitun and Tian, 2007) cited by Mohammad et al

(2013), Both accounting-based and Tobin’s Q measures (e.g. Abor, 2007)

cited by Mohammad et al (2013), and other measures such as profit

efficiency, i.e. frontier efficiency computed using a profit function

(Berger and Bonaccorsi di Patti, 2006) cited by Mohammad et al (2013).

The Tobin’s Q measures means the market value of equity plus book value

of debt divide by book value of assets.

It can also include financial ratios which is from balance sheet

and income statements ( Demsetz and Lehn 1985, Gorton and Rosen 1995,

Mehran 1995, Ang, Cole, and Lin 2000) cited by Allen et al, (2002), stock

market returns and their volatility (e.g., Saunders, Strock, and Travlos

1990, Cole and Mehran 1998) cited by Allen et al, (2002), and Tobin’s q,

which mixes market values with accounting values ( Morck, Shleifer, and

Vishny 1988, McConnell and Servaes 1990, 1995, Mehran 1995, Himmelberg,

Hubbard, and Palia 1999, Zhou 2001) cited by Allen et al, (2002).

ROA has been used by Abor (2007), Ehikioya (2007) and Ebaid (2009)

cited by Boopen et al (2014), to measure firm performance while ROE has

also been used by Abor (2005) cited by Boopen et al (2014).

Kaplan and Norton, (2001) and Otley, (2003) cited by Chepkemoi

(2013), suggests that, when monitoring firm performance, managers tend to

place less emphasis on traditional financial measures of performance such

as return on investment or net profit.

Guobing et al (2001) cited by Tianyu (2013), firm performance should

be evaluated by asset operating, finance benefit, the preservation and

increase of capital value in a certain period. Slywotzky et al (2001)

cited by Tianyu (2013), said operations situation, revenue growth and

customer relationships are the three important indexes to measure firm

performance.

Theories of capital structure

Modern theory of capital structure by Modigliani and Miller (1958)

cited by Athula et al, (2011), argued that capital structure is

irrelevant to the value of a firm under perfect capital market and provide

the base for theoretical directions for capital structure decisions.

Harris and Raviv (1991) cited by Athula et al, (2011), provide a neat

taxonomy of the capital structure theories that try to address some of

these imperfections namely; agency costs theory, asymmetric information

theory etc. To them, these theories suggest the proposition that, the

capital structure impacts firm performance.

Jensen and Meckling (1976) cited by Suleiman, (2013), developed

agency theory as the monitoring cost by the principal and a residual

loss. Jensen and Meckling (1976), agency problem exists due to a conflict

of interest between shareholders and managers (agency cost of equity) or

between shareholders and debt holders (agency cost of debt). Thus, the

use of debt capital will minimize the agency cost since the payment of

debt interest reduces the surplus cash.

Leland and Pyle (1977) cited by Coleman (2006), put forth a

“signaling” theory. They noted that, the problem of asymmetric or

incomplete information in small firms will make it difficult for lenders

to accurately assess the level of risk. Thus, an entrepreneur’s

willingness to invest in his own firm serves as a signal regarding the

quality of the firm’s assets and earnings prospects.

Myers (1984) and Myers and Majluf (1984) cited by Coleman (2006),

developed a “pecking order” theory of finance. To them, insiders have

information about the firm that outsiders do not necessarily have.

Because of this informational asymmetry, outside share purchasers will

tend to under-price a firm’s shares. This means that, it is more costly

to use external debt finance than using internal funds (Myers and Majluf,

1984) cited by Chepkemoi (2013) and they predicts that, firm will follow

the pecking order as an optimal financing strategy (Myers and Majluf,

1984 cited by Chowdhury et al 2010), and also firm follows a hierarchy in

financing projects (Myers and Majluf, (1984) cited by Shah (2011).

Berger and Udell (1998) cited by cited by Coleman (2006), put

forth a “life cycle” theory of financing which contends that firms used

different types of financing for different stages of growth and firm

obtaining external sources of financing and tend to be more reliant on

insider financing.

Kraus and Litzenberger (1973) cited by Anton (2010), suggest that,

capital structure reflects a trade-off between the tax benefits of debt

and expected costs of bankruptcy. The traditional (or static) trade off

theory (TOT), maintained that, firms select optimal capital structure by

comparing the tax benefits of the debt, the costs of bankruptcy and the

costs of agency of debt as well as funding (Modigliani and Miller, 1963;

Stiglitz, 1972; Jensen and Meckling, 1976; Myers, 1977; Titman 1984)

cited by Chepkemoi (2013).

The resource based theory, maintained that, firm’s competitive

advantage is based on the possession of tangible and intangible

resources, which are difficult or costly for other firms to obtain

(Barney, 1991; Peteraf, 1993) cited by Leno (2013).

Asymmetric information theory, developed on the basis of the needs

of public companies to disclose personal information and reduce the

effect of adverse selection (Harris and Raviv, 1991) cited by Aleksandr

(2014).

Baker and Wurgler (2002) cited Popescu et al (2004), market timing

theory of capital structure is the cumulative outcome of past attempts to

time the equity market. Equity market timing theory, posits that managers

issue equity when the market is overvalued, and issue debt when the

market is undervalued (Chinmoy, 2013).

The tax theory is the introduction of a tax element which brings

complexity to capital structure theory and assumption of no taxes was

relaxed to test the validity of Modigliani and Miller (1958) cited by

Rajib(2013). Mehrotra and Mikkelson (2005) cited by Rajib (2013),

observed that, other alternative tax shelters, like leasing, depreciation

and investment allowances could be made available to the firm which would

also make the tax shield redundant.

Bankruptcy cost theory is the assumption of Modigliani and Miller

(1958) cited by Rajib(2013), suggests that, all the assets of a firm can

be sold at their economic value without incurring any liquidating

expenses. But in reality, it is not so because of the direct and indirect

costs of bankruptcy (Barclay et al, (1999) cited by Rajib, 2013).

Free cash flow theory is the amount of cash that a company has left

over after it has paid all of its expenses, including investments. This

theory expresses that, mitigation of free cash flow by paying interest of

debt and dividends prevent a manager from abusing company’s income for

personal purposes (Jensen, 1986 cited by Samuel, 2013).

The Contemporary Capital Structure Theories advance the observation

that Corporate Finance Officers (CFOs) consider the most important factor

as maintaining financial flexibility, keeping debt low in order to be

ready for unforeseen opportunities (Graham and Harvey (2001) cited by

Samuel (2013).

EMPIRICAL STUDY

Modigliani and Miller (1958) cited by Drăniceanu et al (2013),

suggested that, capital structure and firm performance are unrelated;

many researchers provided evidence on their correlation, either positive

or negative.

Babatunde et al (2014), investigate the relationship between capital

structure and profitability of conglomerate, consumer goods, and

financial services firms quoted in Nigeria Stock Exchange. They Data

collected from the ten randomly selected firms among the three industries

were from 2000 to 2011 and sample size of 120. They used Return on Asset

(ROA) and Return on Equity (ROE) as performance proxies and debt equity

ratio (DER) and debt asset ratio (DAR) were used as capital structure

proxies and analysed using correlation coefficient and regression

techniques. They found that, the relationship between capital structure

(both DER and DAR) and return on asset (ROA) is not significant across

all firms except for 7up and Nestle. They also found that, there is an

insignificant relationship between return on equity (ROE) and DAR.

However, there was a significant relationship in almost all firms between

return on equity and debt to equity. To their findings, the nature of the

industry also determines the effect of capital structure on their

profitability. In the financial firms, there is a negative significant

relationship between return on equity and debt to assets ratio. In the

conglomerate firms, there is also a negative relationship between return

on assets (ROA) and debt to equity ratio however not significant.

Nirajini et al (2013), investigate the impact of capital structure

on financial performance of trading companies in Sri Lanka during 2006 to

2010 (05 years) financial year. Data was extracted from the annual

reports of sample companies. Correlation and multiple regression analysis

were used for analysis. The results revealed that, there is a positive

relationship between capital structure and financial performance. And

also, capital structure is significantly impact on financial performance

of the firm which shows that, debt asset ratio, debt equity ratio and

long term debt correlated with gross profit margin(GPM), net profit

margin(NPM), Return on Capital Employed(ROCE),Return on Asset (ROA) &

Return on Equity(ROE ).

Tharmila et al (2013), studied the impact of capital structure on

firm’s performance using a sample of thirty companies listed on the

Colombo Stock Exchange and a period of 5 five years from 2007 to 2011.

The study used Return on capital employed (ROCE), Return on Equity (ROE)

and Net Profit ratio as performance proxies and total debt (TD) and

Total Equity (TE) were used as capital structure proxies. The

relationship between independent variable capital structure and dependent

variable financial performance were tested by correlation analysis. The

results indicated that, there is a negative relationship between the

capital structure and financial performance.

Mohammad et al (2013), investigate the impact of capital structure

on firm performance using multiple regression with a pool panel data

procedure as well as four accounting-based measures of financial

performance (i.e. return on equity (ROE), return on assets (ROA), market

value of equity to the book value of equity (MBVR), Tobin’s Q ) and

capital structure measures (short-term debt to total assets (SDTA), long-

term debt to total assets (LDTT), total debt to total assets (TDTA) and

total debt to total equity (TDTQ)) and based on a sample of 85 firms

listed in Tehran Stock Exchange from 2006 to 2011. The results indicated

that, firm performance which is measured by (ROE,MBVR & Tobin’s Q) is

significantly and positively associated with capital structure, while

report a negative relation between capital structure and (ROA, EPS).

Osuji et al (2012), examines the impact of capital structure on

financial performance of Nigerian firms using a sample of thirty non-

financial firms listed on the Nigerian Stock Exchange during the seven

year period, 2004 – 2010 with a Panel data for the selected firms and

analyzed using ordinary least squares (OLS). They found that, a firm’s

capital structure surrogated by Debt Ratio, DR has a significantly

negative impact on the firm’s financial measures (Return on Asset, ROA,

and Return on Equity, ROE).

Khalaf (2013), investigate the relationship between capital

structure and firm performance across different industries using a sample

of Jordanian manufacturing firms in Jordan. The annual financial

statements of 45 manufacturing companies listed on the Amman Stock

Exchange were used for the study which covers a period of five (5) years

from 2005-2009. Multiple regression analysis was applied on performance

indicators such as Return on Asset (ROA) and Profit Margin (PM) as well

as Short-term debt to Total assets (STDTA), Long term debt to Total

assets (LTDTA) and Total debt to Equity (TDE) as capital structure

variables. The results indicated that, there is a negative and

insignificant relationship between STDTA and LTDTA, and ROA and PM; while

TDE is positively related with ROA and negatively related with PM. STDTA

is significant using ROA while LTDTA is significant using PM.

Forough et al (2014), examine the relationship between capital

structure and firm performance based on the competitive advantage in the

firms listed on the Tehran Stock Exchange. They used lagged leverage,

square of lagged leverage, relative leverage, square of lagged relative

leverage, as the independent variables and Herfindahl-Hirschman as the

mediator variable and sample composed of 202 firms selected among 13

different industries over a period from 2006 to 2011. They found that,

there is a positive significant relationship between leverage and the

financial performance and also found that, there is an inverse

significant relationship between square leverage and firm performance.

Gupta et al (2014), examines the capital structure of selected

construction companies listed in the Bombay Stock Exchange in India

between the periods 2009 to 2013 using data from the secondary sources

i.e. from the annual reports of the selected sample companies. Multiple

Regression and correlation were used to analyze the data. The variables

used for the study were Debt Equity Ratio, Long term debt and Debt Asset

Ratio as the independent variable and Gross Profit Margin (GPM), Net

Profit Margin (NPM), Return on Capital Employed (ROCE), Return on Assets

(ROA) and Return on Equity (ROE) as the dependent variables. The result

revealed that, there is a positive relationship between the capital

structure and financial performance of the selected firms.

Muhammad et al (2012), examines the impact of capital structure on

firms’ financial performance in Pakistan of top 100 consecutive companies

in Karachi Stock Exchange for a period of four years from 2006 to 2009.

Exponential generalized least square regression were use to test the

relationship between capital structure and firms’ financial performance.

The results showed that, all the three variables of capital structure,

Current Liabilities to Total Asset, Long Term Liabilities to Total Asset,

Total Liabilities to Total Assets, negatively impacts the Earning before

Interest and Taxes, Return on Assets, Earning per Share and Net Profit

Margin whereas Price Earning ratio shown negative relationship with

Current Liabilities to Total Asset and positive relationship were found

with Long Term Liabilities to Total Asset where the relationship is

insignificant with Total Liabilities to Total Assets. The results also

indicated that, Return on Equity has an insignificant impact on Current

Liabilities to Total Asset and Total Liabilities to Total Assets but a

positive relationship exists with Long Term liabilities to Total Asset.

Methodology The research used historical research design and ordinary Least

square regression to analysed data. Data for this study was gathered from

the financial statements as published by cement manufacturing companies.

The sample interval is for five-year period from 2009 to 2013. The

population of the study is made up of the 10 cement manufacturing

companies in Nigerian and two sample size was chosen as a sample studied

( Danagote and Ashaka Cement company).

Return on asset (ROA) and return on equity (ROE) were used as

proxies for firms performance while the proxies used for capital

structure include total debt (TD) and total equity (TE). Using the SPSS

view (e-view) software and data obtained from these companies were

tabulated and analyzed using simple regression models.

ROA is calculated by dividing net income plus interest expenses with

total assets (Net income/shareholder fund), return on equity (ROE) is

defined by dividing net income by equity (earnings before tax/total

asset).

Total debt is adding Short-term and Long-term debt while total

equity is adding Common and Preferred Equity and the simply regression

model is stated below:

ROA = AI+ ßISTD+ß2LTD+ +E

ROE = AI+ ßICE+ß2PE+ E

Data analysisTable 1

Hypothesis 1: Dangote cement Plc (2008-2013)

Model R

RSquare

AdjustedR Square

Std.Error of

theEstimate

Change Statistics

R SquareChange

FChange df1 df2

Sig. FChange

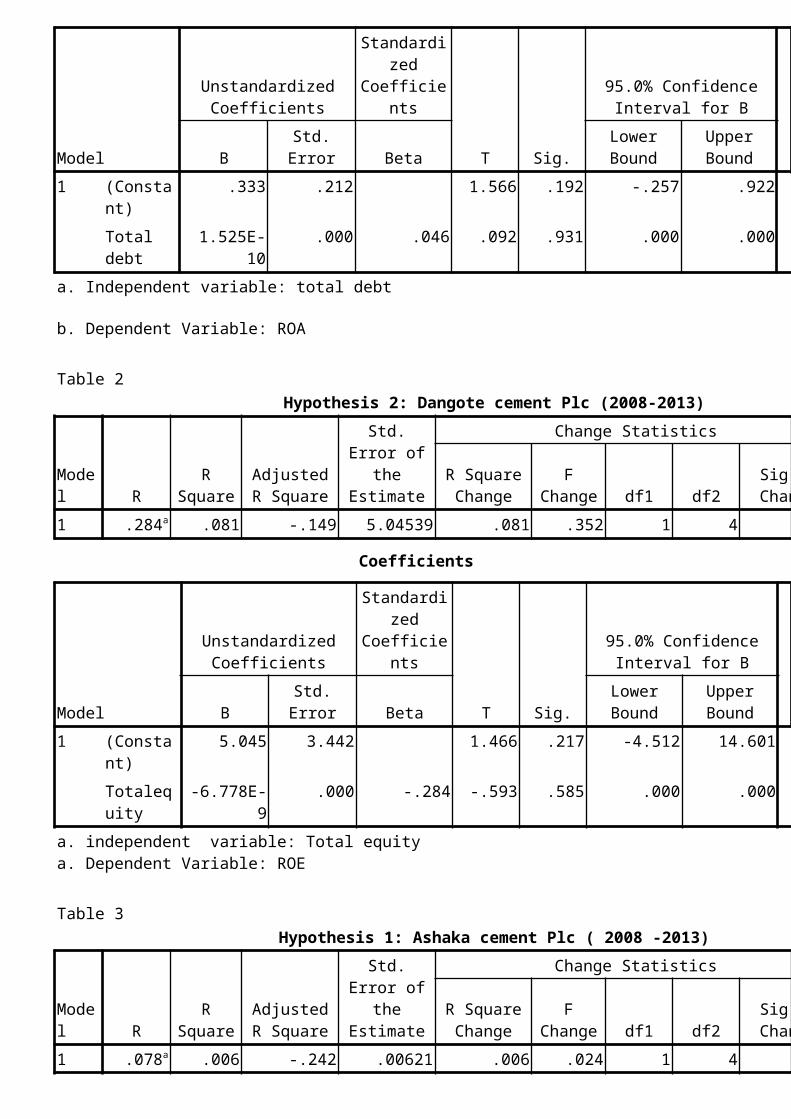

1 .046a .002 -.247 .18939 .002 .008 1 4

Coefficients

Model

UnstandardizedCoefficients

Standardized

Coefficients

T Sig.

95.0% ConfidenceInterval for B

BStd.Error Beta

LowerBound

UpperBound

1 (Constant)

.333 .212 1.566 .192 -.257 .922

Total debt

1.525E-10

.000 .046 .092 .931 .000 .000

a. Independent variable: total debt

b. Dependent Variable: ROA

Table 2Hypothesis 2: Dangote cement Plc (2008-2013)

Model R

RSquare

AdjustedR Square

Std.Error of

theEstimate

Change Statistics

R SquareChange

FChange df1 df2

Sig. FChange

1 .284a .081 -.149 5.04539 .081 .352 1 4

Coefficients

Model

UnstandardizedCoefficients

Standardized

Coefficients

T Sig.

95.0% ConfidenceInterval for B

BStd.Error Beta

LowerBound

UpperBound

1 (Constant)

5.045 3.442 1.466 .217 -4.512 14.601

Totalequity

-6.778E-9

.000 -.284 -.593 .585 .000 .000

a. independent variable: Total equitya. Dependent Variable: ROE

Table 3Hypothesis 1: Ashaka cement Plc ( 2008 -2013)

Model R

RSquare

AdjustedR Square

Std.Error of

theEstimate

Change Statistics

R SquareChange

FChange df1 df2

Sig. FChange

1 .078a .006 -.242 .00621 .006 .024 1 4

Coefficients

Model

UnstandardizedCoefficients

Standardized

Coefficients

T Sig.

95.0% ConfidenceInterval for B

BStd.Error Beta

LowerBound

UpperBound

1 (Constant)

.060 .030 1.964 .121 -.025 .144

Totaldebt

2.461E-10

.000 .078 .156 .884 .000 .000

a. independent variable: Total debta. Dependent Variable: ROA

Hypothesis 2: Ashaka cement Plc (2008 -2013)

Model R

RSquare

AdjustedR Square

Std.Errorof theEstimat

e

Change Statistics

Durbin-Watson

RSquareChange

FChange df1 df2

Sig. FChange

1 .184a

.034 -.208 .01829 .034 .141 1 4 .727 2.348

Coefficients

Model

UnstandardizedCoefficients

StandardizedCoefficients

T Sig.

95.0% Confidence Intervalfor B

B Std. Error Beta Lower Bound Upper Bound

1 (Constant) .072 .014 4.993 .008 .032 .112

totalequity

-1.363E-10 .000 -.184 -.375 .727 .000 .000

a. Independence variable: Total equity a. Dependent Variable: ROE

Discussion on finding Table 1: Based on the result from the analysis examined, the t-value

is 1.566 and the result showed that, the t-tabulated was less than thecalculated value of t-falls in the rejection area at 95% level ofsignificance than the Null hypothesis that, there is no significantrelationship between total debt and return on Asset of Dangote cement Plcis rejected. Hence, H1 is accepted, which states that, there is asignificant relationship between return on Asset as a result of totaldebt. The result of 0.46 confirmed that there is positive and significant

relationship between ROA and total debt of Dangote Cement Plc. The resultfrom R-square showed that, ROA in the company is explained by about 0.6%of total debt.

Table 2: As showed from the analysis examined, the t-value is 1.964and the result showed that, the t-tabulated was less than the calculatedvalue of t-falls in the rejection area at 95% level of significance thanthe Null hypothesis that, there is no significant relationship betweentotal equity and return Equity of Dangote cement Plc is rejected. Hence,H1 is accepted, which states that, there is a significant relationshipbetween return on equity as a result of total equity. The result of .284confirmed that there is positive and significant relationship between ROEand total equity of Dangote Cement Plc. The result from R-square showedthat, ROA in the company is explained by about 69.1% of total equity.

Table 3: In line with the result from the analysis examined, the t-value is 1.964 and the result showed that, the t-tabulated was less thanthe calculated value of t-falls in the rejection area at 95% level ofsignificance than the Null hypothesis that, there is no significantrelationship between total debt and return Asset of Ashaka cement Plc isrejected. Hence, H1 is accepted, which states that, there is a significantrelationship between return on Asset as a result of total debt. Theresult of .078 confirmed that there is positive and significantrelationship between ROA and total debt of Ashaka Cement Plc. The resultfrom R-square showed that, ROA in the company is explained by about 0.6%of total debt.

Table 4: as indicated from the analysis, the t-value is 4.993 and theresult showed that the t-tabulated was less than the calculated value oft- falls in the rejection area at 95% level of significance than the Nullhypothesis that, there is no significant relationship between total debtand return Asset of Ashaka cement Plc is rejected. Hence, H1 is accepted,which states that, there is a significant relationship between return onEquity as a result of total equity. The result of .184 confirmed thatthere is positive and significant relationship between ROE and total debtof Ashaka Cement Plc. The result from R-square showed that, ROE in thecompany is explained by about (2.08%) of total equity.

Conclusion

This study examines the impact of capital structure on firm performance.

Based on the selected sample size of two and capital structure proxies

like TD, TE as well as ROA and ROE as performance proxies, there is a

positive and insignificant relationship between capital structure and

firm performance. The study concludes that statistically, capital

structure represented by Total debt (TD) and Total Equity (TE) is the

major determination of firm performance. Although, the study also found

statistically that, there is significant relationship between capital

structure and firm performance in Ashaka cement Plc and this study was

consistency with the study of Muhammad et al (2012), Nirajini et al

(2013), Gupta et al (2014) and Forough et al (2014).

Recommendation

The study recommends that firms should use debt and equity as a source of

finance since positive significant relationship exists between the

capital structure and performance (total equity and ROE) and Total debt

and ROA used in this work. They should try to finance their activities

with retained earnings, debt and equity.

References

Anup Chowdhury, Suman Paul Chowdhury (2010), impact of capital structure on firm’s value:

evidence from Bangladesh , Peer-reviewed and Open access journal, Vol 3, Issue 3Amara and Bilal Aziz (2014), impact of Capital Structure on Firm Performance: Analysis of Food Sector Listed on Karachi Stock Exchange,International Journal of Multidisciplinary Consortium, vol . 1, Issue 1Abbasali Pouraghajan and Esfandiar Malekian (2012), the Relationship between Capital Structure and Firm Performance Evaluation Measures: Evidence from the Tehran Stock Exchange, International Journal of Business and Commerce, Vol. 1, No. 9 Aleksandr Klimenok ( 2014), The influence of capital structure on the value of the firm.:A study of European firms, Bodo graduate school of business journalAthula Manawaduge, Anura De Zoysa, Khorshed Chowdhury and Anil Chandarakumara (2011), capital structure and firm performance in emerging economies: an empirical analysis of sri lankan firms,

corporate ownership & control, Volume 8, Issue 4Allen N. Berger and Wharton (2012), capital structure and firm performance: a new approach to testing agency theory and an application to the banking industry, Italy Anton Miglo (2010), the pecking order, trade-off, signaling and market-timing theories of Capital Structure: a Review, University of Bridgeport, School of Business, BridgeportBabatunde Yusuf, Akinwunmi Onafalujo, Khadijah Idowu and Yusuf Soyebo (2014), capital structure and profitability of quoted firms: the nigerian perspective (2000-2011), Vienna 10th International AcademicConference, Lagos state University, Ojo, NigeriaBoopen Seetanah, Keshav Seetah, Kevin Appadu and Padachi K (2014), capitalstructure and firm performance: evidence from an emerging economy, the business & management review, Vol. 4, No 4Coleman Susan (2006), capital structure in small manufacturing firms: evidence from the data, journal of entrepreneurial finance, vol. 11,iss.3Chinmoy Ghosh, Milena Petrova and Adam Wang (2013), Determinants of Capital Structure: A Long Term Perspective, London Drăniceanu Simona Maria (2013), capital structure and firm value. Empirical evidence from Romanian listed companies, USA Fozia Memon , Niaz Ahmed Bhutto and Ghulam Abbas (2010), capital structure and firm performance: A case of textile sector of Pakistan, Asian Journal of Business and Management Sciences ,Vol. 1 No. 9

Forough Heirany, Shahnaz Nayebzadeh and Hossein Esmailkhani (2014), the effect of capital structure on the performance of the firms listed on the Tehran stock exchange based on the competitive advantage,

interdisciplinary journal of contemporary research in business, vol.5, no 9Gupta, Naresh Kumar and Gupta, Himani (2014), impact of capital structure on financial performance in Indian construction companies, International Journal of Economics, Commerce and Management, United Kingdom Vol. II, Issue 5Heydar Mohammadzadeh Salteh1, Elham Ghanavati, Vahid Taghizadeh Khanqah and Mohsen Akbari Khosroshahi (2010 ), capital structure and firm performance: evidence from Tehran Stock Exchange, Islamic Azad University press, Marand, IranIshaya Luka Chechet and Abduljeleel Badmus Olayiwola (2014), capital structure and profitability of Nigerian Quoted Firms: The Agency CostTheory Perspective, American International Journal of Social Science Vol. 3 No. 1Ishaya Luka Chechet, Sannomo Larai Garba andAbu Senni Odudu (2013), determinants of capital structure in the Nigerian chemical and paints sector, International Journal of Humanities and Social Science Vol. 3 No. 15;Jude Leon S. A., (2013), the impact of Capital Structure on Financial Performance of the listed manufacturing firms in Sri Lanka, global journal of commerce and management perspective, vol 2(5)Khalaf Al-Taani (2013), the relationship between capital structure and firm performance: evidence from Jordan, journal of Finance and Accounting 1(3)Mohammad Reza Ebrati, Farzad Emadi, Reza Saadati Balasang, Ghorban Safari(2013), the Impact of Capital Structure onFirm Performance: Evidence from Tehran Stock Exchange, Australian Journal of Basic and Applied Sciences,7(4)Mihaela Brînduşa Tudose (2012), capital Structure and Firm Performance, Economy Transdisciplinarity Cognition, Vol. 15, Issue 2Muhammad Umar, Zaighum Tanveer, Saeed Aslam and Muhammad Sajid (2012), impact of capital structure on firms’ financial performance: evidence from Pakistan, Research Journal of Finance and Accounting, vol 3, No 9Mubeen Mujahid and Kalsoom Akhtar (2014), impact of capital structure onfirms financial performance and shareholders wealth: textile sector ofPakistan, International Journal of Learning & Development, Vol. 4, No. 2Naizuli Ruth Wakida (2013), capital structure and financial performance: A case of selected medium sized enterprises in Kampala, Makerere University Press.Nwankwo Odi (2014), effect of capital structure of Nigeria firms on economic growth, Mediterranean Journal of Social Sciences, Vol. 5 No 1Nirajini,A and Priya, K. B (2013), impact of capital structure on financial performance of the Listed Trading Companies in Sri Lanka, International Journal of Scientific and Research Publications, Volume 3,

Issue 5

Osuji C. Chinaemerem and Odita Anthony (2012), impact of capital structure on the financial performance of Nigerian firms, Arabian Journal of Business and Management Review, Vol. 1, No.12Penvilia Chepkemoi (2013), an analysis of the effects of capital structure of small and medium enterprises on their financial performance: a case of Nakuru town, Kabarak University press, Kabarak Puwanenthiren Pratheepkanth (2011), capital structure and financial performance: evidence from selected business companies in colombo stock exchange sri lanka, International Refereed Research Journal,

Vol. II, Issue 2,Rajib Datta, Tasnim Chowdhury and Haradhan Mohajan (2013), Reassess of capital structure theories, International Journal Of Research In Computer Application & Management, vol. 3, issue no. 10Suleiman Alawwad (2013), capital structure effect on firms’ performance: Evidence from Saudi listed Companies, Saint Mary’s University press, Saudi Shah Khalid (2011), financial reforms and dynamics of capital structure choice: a case of publically Listed firms of Pakistan, Journal of Management Research, vol. 3(1)Samuel Kipkorir Koech (2013), the effect of capital structure on profitability of financial firms listed at Nairobi stock exchange, Kenyatta University Press. Tianyu He (2013), the comparison of impact from capital structure to corporate performance between Chinese and European listed firms, International Financial Analysis, USATharmila K. and Arulvel K. K., (2013), The impact of the capital structure and financial performance: A study of the listed companiestraded in Colombo stock exchange, Merit Research Journal of Accounting,

Auditing, Economics and Finance Vol. 1(5)Taiwo Adewale Muritala (2012), an empirical analysis of capital structureon Firms’ performance in Nigeria, international Journal of Advances in Management and Economics, vol.1, issue 5 Wajid Khan, Arab Naz, Madiha Khan, Waseem Kh, Qaiser Khan and Shabeer Ahmad (2013), the Impact of Capital structure and financial performanceon stock returns: a case of Pakistan textile industry, Middle-East Journal of Scientific Research 16 (2)Zeitun R., and Tian G. G.,( 2007), capital structure and corporate performance: evidence from Jordan,

Australasian Accounting, Business and Finance Journal, vol. 1, Issue4