IJAR-BAE - CiteSeerX

14

Volume 02, 2013 Issue 01 SETScholars www.setsscholars.org International Journal of Applied Research in ISSN: 1839-8456 Perth, Australia www.setscholars.org/index.php/ijarbae Executive Editor-in-Chief Md. Al Mamun Chief, Editorial Board Md. Abdul Hannan Mia, PhD Editorial Board Members Shaokun Coral Yu, PhD Northern Illinois University, USA Dr. Iqbal Hossain, Post-Doc in Econometrics, Imperial College, UK M Kabir Hassan, PhD University of New Orleans, USA Md. Abdul Hannan Mia, PhD University of Dhaka, Bangladesh & University of Toronto, Canada. Md. Shariat Ullah University of Dhaka, Bangladesh & Ritsumaiken University, Japan. Saalem Sadeque University of Western Australia, Australia. Rami M. Ayoubi, PhD Damascus University, Syria Ondrej Zizlavsky PhD Brono University of Technology, Czech Republic Rarshid Mehrdoust, PhD University of Guilan, Iran Md. Moazzam Hossain Curtin University, Australia Jai Ganesh PhD Infosys Labs, Bangalore, India Md. Mohan Uddin, PhD University Utara Malaysia, Malaysia Mahfuja Malik University of Boston, USA Md. Anisur Rahman University of Dhaka, Bangladesh. Volume 02, 2013 Issue 01 The Relationship between Work Engagement and Job Resources: An Empirical Study. IJAR-BAE, 02 (2013) 02- 10. Zaynab Shukri Nadim Application of International Accounting Standards 37(IAS 37): A Study of Banking Sector in Bangladesh. IJAR-BAE, 02 (2013) 12–24. Mst. Joynab Siddiqua Consumer Perception of Country of Origin in the Bangladeshi Apparel Industry. IJAR-BAE, 02 (2013) 26–38. Md. Anamul Haque and Farhan Faruqui An Assessment of Fashionable Management Concepts’ Awareness Level amongst Bangladeshi Managers Move toward Knowledge Economy. IJAR-BAE, 02 (2013) 40–50. Laila Zaman, Farida Yasmeen, and Md. Al Mamun Risk Models and Assessment of Integrated Risk Impact. IJAR-BAE, 02 (2013) 52–60. Sharmin Chowdhury IJAR-BAE

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of IJAR-BAE - CiteSeerX

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 1

1

Volume 02, 2013

Issue 01

SETScholars

www.setsscholars.org

Inte

rnat

ion

al J

ou

rnal

of

Ap

pli

ed R

esea

rch

in

International Journal of Applied Research in

ISSN: 1839-8456 Perth, Australia

www.setscholars.org/index.php/ijarbae

Executive Editor-in-Chief Md. Al Mamun

Chief, Editorial Board Md. Abdul Hannan Mia, PhD

Editorial Board Members Shaokun Coral Yu, PhD Northern Illinois University, USA Dr. Iqbal Hossain, Post-Doc in Econometrics, Imperial College, UK M Kabir Hassan, PhD University of New Orleans, USA Md. Abdul Hannan Mia, PhD University of Dhaka, Bangladesh & University of Toronto, Canada. Md. Shariat Ullah University of Dhaka, Bangladesh & Ritsumaiken University, Japan. Saalem Sadeque University of Western Australia, Australia. Rami M. Ayoubi, PhD Damascus University, Syria Ondrej Zizlavsky PhD Brono University of Technology, Czech Republic Rarshid Mehrdoust, PhD University of Guilan, Iran Md. Moazzam Hossain Curtin University, Australia Jai Ganesh PhD Infosys Labs, Bangalore, India Md. Mohan Uddin, PhD University Utara Malaysia, Malaysia Mahfuja Malik University of Boston, USA Md. Anisur Rahman University of Dhaka, Bangladesh.

Volume 02, 2013

Issue 01 The Relationship between Work Engagement and Job

Resources: An Empirical Study.

IJAR-BAE, 02 (2013) 02- 10.

Zaynab Shukri Nadim

Application of International Accounting Standards

37(IAS 37): A Study of Banking Sector in

Bangladesh.

IJAR-BAE, 02 (2013) 12–24.

Mst. Joynab Siddiqua

Consumer Perception of Country of Origin in the

Bangladeshi Apparel Industry.

IJAR-BAE, 02 (2013) 26–38.

Md. Anamul Haque and Farhan Faruqui

An Assessment of Fashionable Management

Concepts’ Awareness Level amongst Bangladeshi

Managers Move toward Knowledge Economy.

IJAR-BAE, 02 (2013) 40–50.

Laila Zaman, Farida Yasmeen, and Md. Al Mamun

Risk Models and Assessment of Integrated Risk

Impact.

IJAR-BAE, 02 (2013) 52–60.

Sharmin Chowdhury

IJAR-BAE

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 1

2

Application of International Accounting Standards 37(IAS 37): A Study of Banking Sector in Bangladesh

Mst. Joynab Siddiqua 1* 1

Lecturer, Department of Business Administration, ASA University of Bangladesh, Dhaka, Bangladesh. * Corresponding author’s e-mail: [email protected]

Article History ABSTRACT

Received: 07-01-2013 Accepted: 24-01-2013 Available online: 08-02-2013

Keywords: Accounting Standards, BAS, Contingent Liabilities, IAS.

JEL Classification: G21, M410, M480.

This research paper attempts to find out about the application of BAS37 and how much is it complied according to the standard. BAS37 is related to the provisions, contingent liabilities and contingent assets. Provisions are the liability against uncertain timing or amount. Contingent liabilities are the apparent liabilities that may turn into actual liabilities in the future and contingent assets are the possible assets which may grow to be an actual asset from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity. To stumble on the application of this standard, 23 listed banking companies (out of 30 listed banking companies under Dhaka Stock Exchange) are selected on randomly and analyzed on the basis of compliance and non-compliance of BAS37. By analyzing the annual reports 2011 of the sample banking companies, it is found that all companies are complied and recognized provisions, contingent liabilities and contingent assets (BAS37) in the financial statements. Provisions are shown in the income statement, Contingent liabilities are in the off balance sheet and contingent assets in the notes of the financial statement. They also disclosed detailed information about reconciliation of provision among its beginning balance, current requirements and ending balance in the notes but there is no adequate disclosure about contingent assets.

Citation: Mst. Joynab Siddiqua (2013). Application of International Accounting Standards 37(IAS 37): A Study of Banking

Sector in Bangladesh. IJAR-BAE 2(1): 12 – 24.

Copyright: @2013 Mst. Joynab Siddiqua. This is an open access article distributed according to the terms of the Creative Common Attribution (CCC) 3.0 License under PKW (Public Knowledge Work) of Simon Fraser University, Canada.

1.0 Introduction Application of accounting standards narrows drowns the difference and variety in accounting principles. Their application encourages improved accounting and establishing international harmony in accounting principles and practices. Use of standards ensure superior procedures, increase rationality and reduce conflicts. Application of accounting standards enhances comparability of accounting both nationally and internally. Their application standardizes accounting policies, principles and practices. Application of standards ensures best practices, and brings in greater uniformity. Application of accounting standards enable all, who are affected by or interested in accounting information, to better understand the purposes, contents, characteristics and limitations of information provided by accounting and reporting. The application of standards increases the usefulness of and confidence in financial statements. Standards attempt to bring about uniformity in accounting practices and facilitate comparison. Bangladesh/International Accounting Standards make financial statements more understandable, reliable, informative and uniform. International accounting standards are accounting standards issued by

IJAR-BAE Vol. 02. Issue 01. Article No. 02

Full length Original Research Paper

www.setscholars.org/index.php/ijarbae

IJAR-BAE ISSN: 1839-8456

International Journal of Applied Research in Business Administration and Economics 02 (2013) 12–24.

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 1

3

the International Accounting Standards Board (IASB) .and its predecessor, the International Accounting Standards Committee (IASC). Listed companies, and sometimes unlisted companies, are required to use the standards in their financial statements in those countries which have adopted them. International Accounting Standards (IAS) 37 deals with provisions, contingent liabilities & assets. Contingencies are potential gains and losses whose resolution depends on one or more future events. Loss contingencies are potential claims on a company’s resources and are known as contingent liabilities (Wild, Subramanyam & Halsey; 146). Contingent liabilities can arise from litigation, threat of expropriation, collectability of receivables, claims against from product warranties or defects, guarantees of performance, tax assessments, self-insured risks, and catastrophic losses of property. For recording, a loss contingency must meet two conditions. First, it must be probable that an asset will be impaired or a liability incurred. Second, the amount of loss must be reasonably estimable (Wild, Subramanyam & Halsey; 146). Generally banks are doing their business by other persons’ money so that accountability is very much needed. For that purpose, most of the banking companies are complied with International Accounting Standards (IAS) and they also disclosed in the notes in the financial statements. This paper emphasized on IAS 37, provisions, contingent liabilities & contingent assets and its application in banking sector of Bangladesh. Generally, provisions are shown in the income statement, contingent liabilities as the off balance sheet items and other disclosures are made in the notes to the financial statements.

2.0 Literature review Existing literature reveals very few studies that have been done on the topic. In the wake of record numbers of bank and thrift failures Kane (1989), Benston et al. (1986), Macey and Miller (1992) among others have advocated the reinstatement of contingent liability for bank. Benjamin C. Esty (1997) analyzed that contingent liability determined commercial bank risk taking. Lacy (2002) found in his survey research that most financial statement readers paid very little attention to contingent liabilities because these accounting items are highly uncertain, both in terms of the probability of occurrences and impact value. The importance of monitoring contingent liabilities was recognized in the Guidelines for Public Debt Management (IMF-World Bank, 2001). However, Sukchok et al (2002) found that creditors paid considerable attention to Contingent Liabilities and would prefer more disclosure on this item whereas investors were less critical and tended to request only standardized reports. In the study of Cayanan (2004) about the financial reporting practices of banks, annual reports of 16 banks were reviewed. He found that seven banks did not disclose the amounts of guarantees. Providing guarantees is one of the banks’ sources of revenues. Hence, as required by financial reporting rules, the extent of such guarantees has to be disclosed. The banks which were not compliant of this disclosure rule were: BPI, City state Savings Bank, PNB, Phil trust, PS Bank, Security Bank and Union Bank. Gapen et al (2004); Gapen et al (2005); Fisher and Gray (2006); Keller, Kunzel, Souto (2007); Gray and Malone (2008); Gray and Walsh (2008); Gray, Merton, Bodie (2008); and Gapen (2009) examined the ability of the contingent claims analysis to measure corporate risk like sovereign risk in banking sector. Asokan A. et al (2005) resulted that the existence of inefficiency in loan loss decisions and the causes of such inefficiency have far-reaching implications for regulators throughout Europe. There is a significant impact of contingent liabilities on tax (Derrick R. , 2006). Serkan A. and Yin Liao (2012) studied on the banking sector for 32 countries, including 18 advanced and 14 emerging market economies. From 32 countries, 245 banks are selected and analyzed. The study revealed that the following: 1. countries that had higher banking sector are, all else equal, more likely to have higher contingent liabilities; 2. countries, in which banks have a high “market leverage”, measured as market value of assets / market value of equity, tend to have higher contingent liabilities; 3. countries whose banks have more volatile business models, measured through their volatility of market assets, are exposed to higher contingent liabilities; and finally 4. Banking systems that are concentrated into a few banks will benefit less from the “diversification benefit” . Hence contingent liabilities may be much higher in these cases.

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 1

4

For smoothing income, Contingent liabilities are also important matter for banking sector. Collins, S., and Wahlen (1995); Liu and Ryan (1995); Kanagaretnam, Lobo, and Mathieu (2003); and Kanagaretnam, Lobo, and Yang (2004) among others have stated that banks should use provision for contingent liabilities like loan loss provision to smooth income. Then Heba A. El Sood (2012) strongly agreed with that statement. Contingent liability items when realized can have a great impact on the analysis of a firm’s financial position and the examination of a firm’s value without taking into account the risk from contingent liabilities can be misleading so that application of BAS37 may be the solution that sorts of crisis arising from banking companies. The approach of this study is to evaluate banking sector on the basis of compliance and noncompliance of Bangladesh Accounting Standard37.

2.01 Definition of contingencies and contingent liabilities

A contingency is defined in FASB Statement No. 5”As an existing condition or set of circumstances involving uncertainty as to possible gain (gain contingency) or loss (loss contingency) to an enterprise that will ultimately be resolved when one or more future events occur or fail to occur”. Loss contingencies are situations involving uncertainty as to possible loss. A liability incurred as a result of a loss contingency is a contingent liability.

“A Contingent liability is a potential obligation that depends on a future event arising from a past transaction or event” (Wild, Larson & Chiappetta: 368). It is not a balance sheet item, it is an off balance sheet item. “Contingent liabilities are dependent-contingent-upon some future events. In a word, a Contingent liability is a potential liability that may become an actual liability in the future.” (Weygandt, Kimmel & Kieso, p. 491) How should companies report contingent liabilities? They use the following guidelines: 1. If the contingency is probable (if it is likely to occur) and the amount can be reasonably estimated,

the liability should be recorded in the accounts. 2. If the contingency is only reasonably possible (if it could happen), then it needs to be disclosed only

in the notes that accompany the financial statements. 3. If the contingency is remote (if it is unlikely to occur), it need not be recorded or disclosed.

(Weygandt, Kimmel &Kieso, p. 491).

2.02 Accounting for contingent liabilities Accounting for contingent liabilities depends on the likelihood that a future event will occur and the ability to estimate the future amount owed if this event occurs. Three different possibilities are identified in the following chart:

Table 02: Some examples and the general accounting treatment of Loss Contingencies

Loss related to ----------------------------------- Usually Accrued

Not Accrued

May Be Accrued

Collectability of receivables x Obligations related to product warranties and product defects

x

Premiums offered to customers x Risk of loss or damage of enterprise properly by fire, explosion, or other hazards

x

Table 01: Three different possibilities of contingent liabilities

Probable Reasonably possible Remote

Amount estimated Record contingent liability

Disclose liabilities in the notes

No action

Amount not estimated Disclose liability in the notes

Disclose liabilities in the notes

No action

Source: (Wild, Larson & Chiappetta, p.368)

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 1

5

General or unspecified business risk x Risk of loss from catastrophes assumed by property and casualty insurance companies, including reinsurance companies

x

Threat of expropriation of assets x Pending or threatened litigation X Actual or possible claims and assessments X Guarantees of indebtedness of others X Obligations of commercials banks under “Standby letters of credit”

X

Agreements to repurchase receivables (or the related party) that have been sold

X

Source: ( Kieso, Weygandt and Warfield, p.632)

2.03 Historical background of BAS37 In August 1997, Exposure Draft E59 “Provisions, Contingent Liabilities and Contingent Assets” was prepared for approval of the steering committee and the board. After reviewing by the board, it was first released September1998. This Exposure Draft E59 was amended subsequently in 2003, 2004, 2005, 2007 & 2008 that reflected the changes in a variety of standard. On the basis of IASB, the effective date of the standard was fiscal periods beginning on or after July1, 1999 and also on the basis of Canadian; it was effective from fiscal periods beginning on or after January1, 2011. ED after substantial revisions was released on June 30, 2005; no revised standard has yet been released the IASB has been unable to reach a final position regarding the measurement requirements and the removal of the probability recognition criterion in the ED.

3.0 Research objectives and methodology This study mainly tries to find out the application of IAS 37 (BAS 37) in the financial statements, the degree of compliance with the BAS 37, the points of deviation from the standards, the appropriate suggestions for improving the practice and the disclosure related to BAS 37 by the 23 sample banking companies of Bangladesh. For the research findings, two types of data were collected: Primary data and Secondary data. Primary data were obtained from the direct interviews of employees. Secondary data were collected from the annual reports of the banks, organization’s brochure, text books, websites etc. In this study, the annual reports of the banks (2011) were assessed in terms of their compliance with BAS 37. Assessment of the annual report will focus on: a. application of provisions, contingent liabilities and contingent assets, b. the recognition of provisions, contingent liabilities and contingent assets, c. Breakdown of total provisions into provisions before taxation and provisions for taxation, d. disclosure of provisions, contingent liabilities and contingent assets, and finally e. basis for valuation of liabilities and provisions, (f) The non-compliance of the standard is treated as the deviation of standard.

4.0 Summary of Bangladesh Accounting Standard (BAS) 37 4.01 Objectives of BAS37 The objectives of this standard is to ensure that appropriate recognition criteria and measurement bases are applied to provisions, contingent liabilities and contingent assets and that sufficient information is disclosed in the notes to the financial statements to enable users to understand their nature, timing and amount. All companies listed by Securities and Exchange Commission are to follow this standard. Some important Provisions of the standard are discussed below: A liability of uncertain timing or amount is called provision. Liability is a present obligation as a result of past events that is paid by an outflow of resources (Para-10). Contingent liability: Contingent liability is a possible obligation depending on whether some uncertain future event occurs or a present obligation but payment is not probable or the amount cannot be measured reliably. An

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 1

6

enterprise should not recognize and disclose a contingent liability unless the possibility of an outflow of resources embodying economic benefits is remote. (Paras-27 & 28) Contingent asset: Contingent asset is a possible asset that arises from past events, and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity. Contingent assets should not be recognized - but should be disclosed where an inflow of economic benefits is probable. When the realization of income is virtually certain, then the related asset is not a contingent asset and its recognition is appropriate. (Paras-31-35) Recognition of a provision: An entity must recognize a provision if, and only if: (i) a present obligation (legal or constructive) has arisen as a result of a past event (the obligating event), (ii) payment is probable ('more likely than not'), and (iii) the amount can be estimated reliably (Para-14).

A provision should be recognized for that present obligation if the other recognition criteria described above are met. If it is more likely than not that no present obligation exists, the entity should disclose a contingent liability, unless the possibility of an outflow of resources is remote (Para-15).

Table 03: Measurement of Provisions

IAS37, Para-36 Provision should be the best estimate of the expenditure required to settle the present obligation at the balance sheet date.

IAS37, Para-39 Provisions for large populations of events (warranties, customer refunds) are measured at a probability-weighted expected value.

IAS37, Para-40 Provisions for one-off events (restructuring, environmental clean-up, settlement of a lawsuit) are measured at the most likely amount.

IAS37, Para-45 & 47 Both measurements are at discounted present value using a pre-tax discount rate that reflects the current market assessments of the time value of money and the risks specific to the liability.

The standard further states that If some or all of the expenditure required to settle a provision is expected to be reimbursed by another party, the reimbursement should be recognized as a separate asset, and not as a reduction of the required provision, when, and only when, it is virtually certain that reimbursement will be received if the entity settles the obligation. The amount recognized should not exceed the amount of the provision (para-53). In measuring a provision consider future events as follows: i. forecast reasonable changes in applying existing technology (para-49); ii. ignore possible gains on sale of assets (para-51); and iii. consider changes in legislation only if virtually certain to be enacted (para-50). Remeasurement of provisions: Under para-59, provisions should be reviewed and adjusted at each balance sheet date and if outflow no longer probable, reverse the provision to income. Restructuring is a sale or termination of a line of business, closure of business locations, changes in management structure, and fundamental reorganization of company (para-70). As per para-72, restructuring provisions should be accrued as follows: a. accrues provision only after a binding sale agreement (para-78). If the binding sale agreement is after balance sheet date, disclose but do not accrue; b. accrue only after a detailed formal plan is adopted and announced publicly. A board decision is not enough; c. provisions should not be recognized for future operating losses, even in a restructuring; d. accrue provision only if there is an obligation at acquisition date; and e. restructuring provisions should include only direct expenditures caused by the restructuring, not costs that associated with the ongoing activities of the entity (para-80). Regarding disclosures of provisions: An enterprise should disclose and reconcile the opening balance, additions, used (amounts charged against the provision), released (reversed), unwinding of the discount, closing balance for each class of business. Prior year reconciliation is not required (para-84). For each class of provision, a brief description of the nature, timing, uncertainties, and assumptions of outflow of economic benefits should be disclosed and also any amount is expected to reimbursement that has been recognized (para-85).

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 1

7

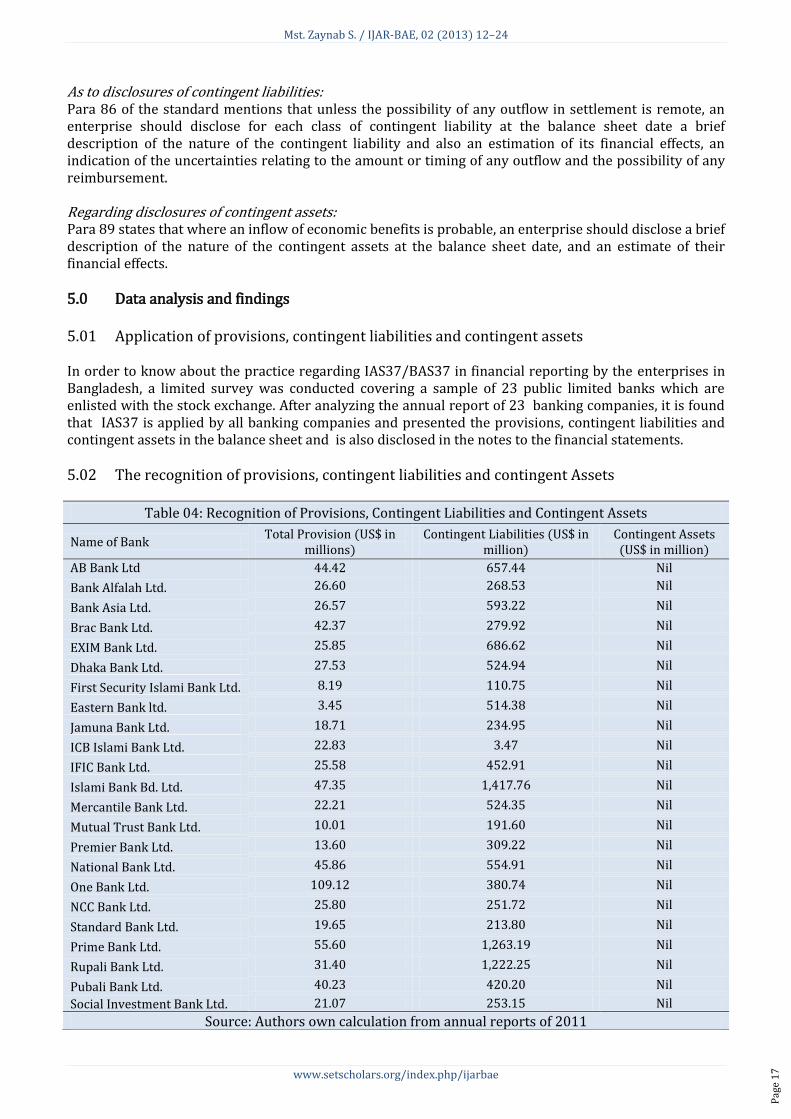

As to disclosures of contingent liabilities: Para 86 of the standard mentions that unless the possibility of any outflow in settlement is remote, an enterprise should disclose for each class of contingent liability at the balance sheet date a brief description of the nature of the contingent liability and also an estimation of its financial effects, an indication of the uncertainties relating to the amount or timing of any outflow and the possibility of any reimbursement. Regarding disclosures of contingent assets: Para 89 states that where an inflow of economic benefits is probable, an enterprise should disclose a brief description of the nature of the contingent assets at the balance sheet date, and an estimate of their financial effects.

5.0 Data analysis and findings 5.01 Application of provisions, contingent liabilities and contingent assets In order to know about the practice regarding IAS37/BAS37 in financial reporting by the enterprises in Bangladesh, a limited survey was conducted covering a sample of 23 public limited banks which are enlisted with the stock exchange. After analyzing the annual report of 23 banking companies, it is found that IAS37 is applied by all banking companies and presented the provisions, contingent liabilities and contingent assets in the balance sheet and is also disclosed in the notes to the financial statements.

5.02 The recognition of provisions, contingent liabilities and contingent Assets

Table 04: Recognition of Provisions, Contingent Liabilities and Contingent Assets

Name of Bank Total Provision (US$ in

millions) Contingent Liabilities (US$ in

million) Contingent Assets (US$ in million)

AB Bank Ltd 44.42 657.44 Nil

Bank Alfalah Ltd. 26.60 268.53 Nil

Bank Asia Ltd. 26.57 593.22 Nil

Brac Bank Ltd. 42.37 279.92 Nil

EXIM Bank Ltd. 25.85 686.62 Nil

Dhaka Bank Ltd. 27.53 524.94 Nil

First Security Islami Bank Ltd. 8.19 110.75 Nil

Eastern Bank ltd. 3.45 514.38 Nil

Jamuna Bank Ltd. 18.71 234.95 Nil

ICB Islami Bank Ltd. 22.83 3.47 Nil

IFIC Bank Ltd. 25.58 452.91 Nil

Islami Bank Bd. Ltd. 47.35 1,417.76 Nil

Mercantile Bank Ltd. 22.21 524.35 Nil

Mutual Trust Bank Ltd. 10.01 191.60 Nil

Premier Bank Ltd. 13.60 309.22 Nil

National Bank Ltd. 45.86 554.91 Nil

One Bank Ltd. 109.12 380.74 Nil

NCC Bank Ltd. 25.80 251.72 Nil

Standard Bank Ltd. 19.65 213.80 Nil

Prime Bank Ltd. 55.60 1,263.19 Nil

Rupali Bank Ltd. 31.40 1,222.25 Nil

Pubali Bank Ltd. 40.23 420.20 Nil

Social Investment Bank Ltd. 21.07 253.15 Nil

Source: Authors own calculation from annual reports of 2011

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 1

8

From Table 04, it is found that all banking companies are recognized the provisions, contingent liabilities in their financial statements and in the notes in accordance with the BAS37. The highest amount of contingent liabilities is shown by Islami Bank Bangladesh Ltd., Prime Bank Ltd. and Rupali Bank Ltd. respectively US$1,417.76, US$1,263.19 & US$1,222.25 and the lowest amount is shown by ICB Islami Bank Ltd. that is US$3.47. But they do not disclose about contingent assets.

Table 05: Breakdown of Total Provisions into Provisions before Taxation and Provisions for Taxation

Name of Bank Total Provisions before

Taxation (US$ in million) Provisions for Taxation

(US$ in million) Total Provisions (US$

in million) AB Bank Ltd 18.39 26.03 44.42 Bank Alfalah Ltd. 4.75 21.85 26.60 Bank Asia Ltd. 7.62 18.95 26.57 Brac Bank Ltd. 24.81 17.52 42.33 EXIM Bank Ltd. 6.85 19.00 25.85 Dhaka Bank Ltd. 8.47 19.06 27.53 First Security Islami Bank Ltd. 2.75 5.44 8.19 Eastern Bank ltd. 12.23 22.23 34.46 Jamuna Bank Ltd. 4.42 14.30 18.71 ICB Islami Bank Ltd. 22.77 0.06 22.83 IFIC Bank Ltd. 11.02 14.56 25.58 Islami Bank Bd. Ltd. 13.94 33.42 47.35 Mercantile Bank Ltd. 6.22 15.99 22.21 Mutual Trust Bank Ltd. 2.87 7.14 10.01 Premier Bank Ltd. 4.15 9.45 13.60 National Bank Ltd. 4.16 41.70 45.86 One Bank Ltd. 9.85 9.93 19.78 NCC Bank Ltd. 6.85 18.95 25.80 Standard Bank Ltd. 6.49 13.17 19.65 Prime Bank Ltd. 13.14 42.46 55.60 Rupali Bank Ltd. 13.81 1.84 15.65 Pubali Bank Ltd. 11.85 28.38 40.23 Social Investment Bank Ltd. 10.84 10.22 21.07

Source: Authors own calculation from annual reports of 2011 In Table 05 shows the breakdown of total provisions of sample banking companies’. Total provisions include provisions before taxation and provisions for taxation that is disclosed in the income statement and also disclosed in the notes. The all bank have specific provisions for classified loans, advances and other provisions for future.

Table 06: List of the Contingent Liabilities

Name of Bank Acceptance

& Endorsement

Letter of Guarantee

Irrevocable Letters of

Credit

Bills of Collection

Other Contingent Liabilities

Tax Liability

AB Bank Ltd 31.32% 20.55% 27.67% 20.46% 0.00% 0.00%

Bank Alfalah Ltd. 0.41% 0.08% 0.48% 0.04% 0.00% 0.00%

Bank Asia Ltd. 36.12% 14.51% 39.75% 9.62% 0.00% 0.00%

Brac Bank Ltd. 0.71% 20.26% 72.35% 2.80% 2.56% 0.52%

EXIM Bank Ltd. 0.00% 7.14% 27.74% 4.72% 60.40% 0.00%

Dhaka Bank Ltd. 34.78% 22.82% 21.98% 17.47% 2.94% 0.00%

First Security Bank Ltd. 45.65% 14.71% 37.83% 1.80% 0.00% 0.00%

Eastern Bank ltd. 51.47% 15.96% 27.67% 2.93% 1.97% 0.00%

Jamuna Bank Ltd. 8.77% 19.82% 61.85% 8.40% 1.16% 0.00%

ICB Islami Bank Ltd. 8.42% 69.18% 3.67% 18.74% 0.00% 0.00%

IFIC Bank Ltd. 35.74% 11.35% 32.03% 20.87% 0.00% 0.00%

Islami Bank Bd. Ltd. 6.44% 0.00% 76.62% 15.63% 1.31% 0.00%

Mercantile Bank Ltd. 41.95% 14.45% 39.54% 0.35% 3.71% 0.00%

Mutual Trust Bank Ltd. 0.00% 24.33% 25.34% 12.19% 38.14% 0.00%

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 1

9

Premier Bank Ltd. 30.19% 22.56% 43.58% 1.51% 2.16% 0.00%

National Bank Ltd. 42.92% 14.22% 26.73% 13.58% 2.54% 0.00%

One Bank Ltd. 45.13% 26.95% 27.78% 0.15% 0.00% 0.00%

NCC Bank Ltd. 43.32% 24.97% 30.74% 0.31% 0.66% 0.00%

Standard Bank Ltd. 37.96% 16.62% 42.20% 3.23% 0.00% 0.00%

Prime Bank Ltd. 28.66% 34.63% 29.40% 7.35% 0.00% 0.00%

Rupali Bank Ltd. 0.00% 2.21% 90.68% 7.11% 0.00% 0.00%

Pubali Bank Ltd. 0.00% 12.15% 83.36% 1.66% 2.83% 0.00%

Social Invest. Bank Ltd. 41.50% 16.19% 33.50% 8.81% 0.00% 0.00%

Source: Authors own calculation from annual reports of 2011 From analysis of the annual report of banking companies it is revealed that all companies made provision for contingent liabilities. These liabilities were for Acceptance and Endorsement, Letter of Credit, Irrecoverable Letters of Credit, Bills of Collection, Tax liability, other contingent Liabilities. In above Table-3, the percentage is on the basis of total contingent liabilities that are given in Appendix-B.

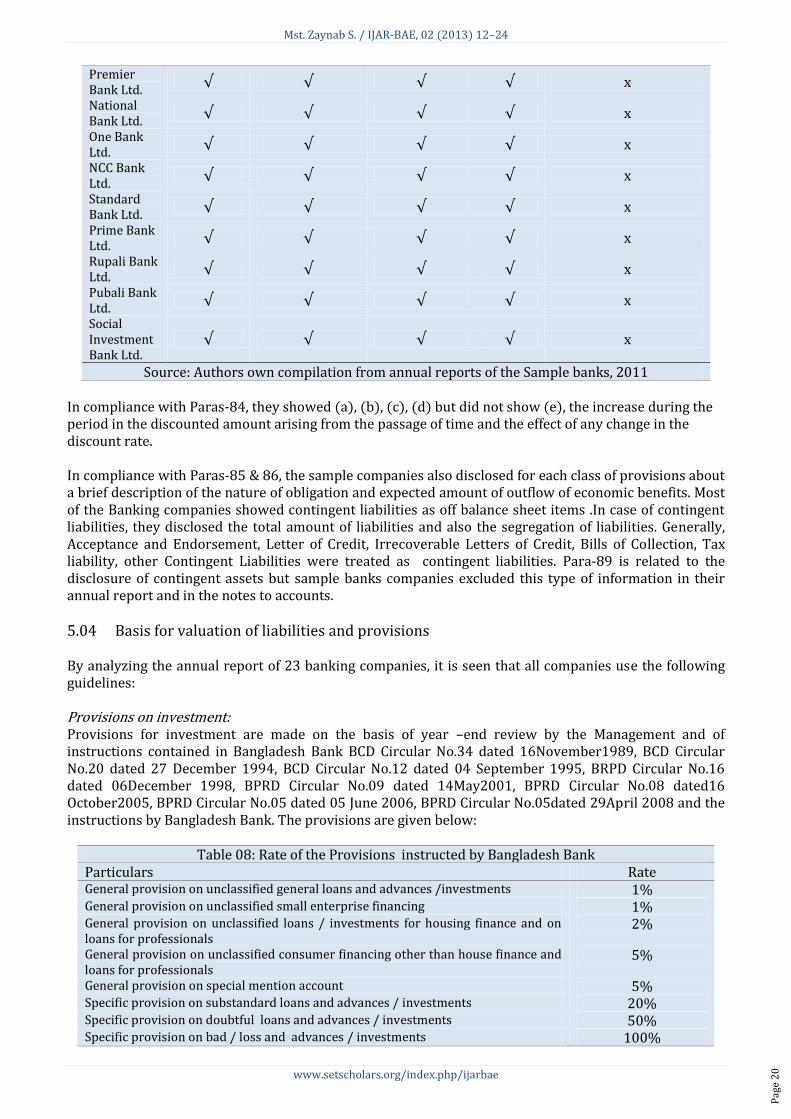

5.03 Disclosure of provisions, contingent liabilities and contingent assets: According to Para-84, for each class of provision, an enterprise shall disclose the following information presented in the table 07:

Table 07: Disclosure requirements according to Para 84 Name of the company

The carrying amount at the beginning and end of the period

Additional provisions made in the period, including in increases to existing provisions.

Amounts used (incurred and charged against the provision ) during the period

Unused amounts reversed during the period

The increase during the period in the discounted amount arising from the passage of time and the effect of any change in the discount rate

AB Bank Ltd √ √ √ √ x Bank Al Arafah Ltd

√ √ √ √ x

Bank Asia Ltd.

√ √ √ √ x

Brac Bank Ltd

√ √ √ √ x

EXIM Bank Ltd.

√ √ √ √ x

Dhaka Bank Ltd.

√ √ √ √ x

First Security Islami Bank Ltd.

√ √ √ √ x

Eastern Bank ltd.

√ √ √ √ x

Jamuna Bank Ltd.

√ √ √ √ x

ICB Islami Bank Ltd.

√ √ √ √ x

IFIC Bank Ltd.

√ √ √ √ x

Islami Bank Bd. Ltd.

√ √ √ √ x

Mercantile Bank Ltd.

√ √ √ √ x

MutualTrust Bank Ltd.

√ √ √ √ x

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 2

0

Premier Bank Ltd.

√ √ √ √ x

National Bank Ltd.

√ √ √ √ x

One Bank Ltd.

√ √ √ √ x

NCC Bank Ltd.

√ √ √ √ x

Standard Bank Ltd.

√ √ √ √ x

Prime Bank Ltd.

√ √ √ √ x

Rupali Bank Ltd.

√ √ √ √ x

Pubali Bank Ltd.

√ √ √ √ x

Social Investment Bank Ltd.

√ √ √ √ x

Source: Authors own compilation from annual reports of the Sample banks, 2011 In compliance with Paras-84, they showed (a), (b), (c), (d) but did not show (e), the increase during the period in the discounted amount arising from the passage of time and the effect of any change in the discount rate. In compliance with Paras-85 & 86, the sample companies also disclosed for each class of provisions about a brief description of the nature of obligation and expected amount of outflow of economic benefits. Most of the Banking companies showed contingent liabilities as off balance sheet items .In case of contingent liabilities, they disclosed the total amount of liabilities and also the segregation of liabilities. Generally, Acceptance and Endorsement, Letter of Credit, Irrecoverable Letters of Credit, Bills of Collection, Tax liability, other Contingent Liabilities were treated as contingent liabilities. Para-89 is related to the disclosure of contingent assets but sample banks companies excluded this type of information in their annual report and in the notes to accounts. 5.04 Basis for valuation of liabilities and provisions By analyzing the annual report of 23 banking companies, it is seen that all companies use the following guidelines: Provisions on investment: Provisions for investment are made on the basis of year –end review by the Management and of instructions contained in Bangladesh Bank BCD Circular No.34 dated 16November1989, BCD Circular No.20 dated 27 December 1994, BCD Circular No.12 dated 04 September 1995, BRPD Circular No.16 dated 06December 1998, BPRD Circular No.09 dated 14May2001, BPRD Circular No.08 dated16 October2005, BPRD Circular No.05 dated 05 June 2006, BPRD Circular No.05dated 29April 2008 and the instructions by Bangladesh Bank. The provisions are given below:

Table 08: Rate of the Provisions instructed by Bangladesh Bank Particulars Rate General provision on unclassified general loans and advances /investments 1% General provision on unclassified small enterprise financing 1% General provision on unclassified loans / investments for housing finance and on loans for professionals

2%

General provision on unclassified consumer financing other than house finance and loans for professionals

5%

General provision on special mention account 5% Specific provision on substandard loans and advances / investments 20% Specific provision on doubtful loans and advances / investments 50% Specific provision on bad / loss and advances / investments 100%

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 2

1

Provisions for off balance sheet item exposure /contingent liabilities: BRPD Circular No. 10 ( 18 September 2007) requires a general provision for off balance sheet exposure to be calculated at 1% (2007:0.50%) on all balance sheet exposures as defined in BPRD Circular No.10 (24November 2002). Accordingly, they recognized a provision of 1% on the following off balance sheet items: (a) Letter of Guarantee, (b) Letter of Credit, (c) Bills for Collection, (d) Acceptance and endorsements and (e) Other contingent liabilities. Provisions for other assets: BPRD Circular No.14 (25 June 2001) requires a provision of 100% on the assets which outstanding for one year and above. Provisions for taxation:

Current tax: Provision for Current income tax has been made @42.5% as prescribed in the Finance Act 2010 of the profit made by the considering taxable add-back of income and disallowance of expenditure in compliance with BAS-12 “Income Taxes ”. Tax return for the income year 2010 (assessment year 2011-2012) has been filed but assessment is to be done by the tax authority.

Deferred tax:

The bank also recognized deferred tax in accordance with the provision of BAS-12. Deferred tax arises due to temporary difference deductible or taxable for the events or transaction recognized in the income statement. A temporary difference is the difference between the tax bases of assets or liability and its carrying amount/reported amount in the financial statement. Deferred tax assets or liability is the amount of income tax payable or recoverable in future period(s) recognized in the current period. The deferred tax assets/expenses do not create a legal Liability/recoverability to and from the income tax authority. The bank recognizes deferred tax on 100% specific provision investment which will be written off as per Bangladesh Bank Circulars. 6.0 Conclusion and recommendations The occurrence of contingent liabilities is uncertain and may not be wholly within the control of a company. The disclosure of a possible contingency, a loss contingency in this case, is recorded in the notes to the financial statements. Accounting standards make the financial reporting process a way to provide investors needed statistics of not only the current firm’s performance but also the forward-looking information. The disclosure of contingent liabilities in the notes to financial statement, though being required by regulation, no specific detail has been described as to how to disclose these contingencies. The variation of disclosure format makes it difficult for analysts and investors to analyze the impact. However, the significant findings in the majority of analyses in this study confirm the need to take contingency items into equity security analysis and subsequent firm’s valuation. The survey revealed that the financial statements disclosure by sample companies fully compiled with BAS37. Banking companies take money from others and give loans to others so that there is a possibility of default in loans and advances. So, they should maintain different provisions and disclose contingent liabilities. In addition to that, this type of companies should be more conscious about it.

References Anandarajan, Asokan., Hasan, Iftekhar,, & Lozano-Vivas, Ana. (2005).Loan loss provision decisions: an

empirical analysis of Spanish depository institutions, Journal of International Accounting, Auditing and Taxation14, 55–77.

Arslanalp, Serkan., & Liao, Yin. (2012). Contingent Liabilities and Sovereign Risk: Evidence from Banking Sectors. Centre for Applied Macroeconomic Analysis (CAMA), Australian National University, Australia.

Benston, G.J., Eisenbeis, R.A., Horvitz, P.M., Kane, E.J., Kaufman, G.G., (1986). Perspectives on Safe & Sound Banking: Past, Present, and Future. The MIT Press, Cambridge, MA.

Bushman, Robert M., & Williams, Christopher D. (2012). Accounting discretion, loan loss provisioning, of Banks’ risk-taking. Journal of Accounting and Economics54, 1–18.

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 2

2

Cayanan, Arthur S. (2004). An assessment of the financial reporting practices of listed Philippine banks in 2003. Philippine Management Review, Vol. 11, 1-11.

Collins, J., Shackelford, D., & Wahlen, J. (1995). Bank differences in the coordination of regulatory capital, earnings, and taxes. Journal of Accounting Research, 33(2), 263–291.

Coopers & Lybrand. (1993). Accounting for Contingencies, Accounting Standards Board (ASB), (1980), SSAP No. 18.

Dermine,J.,& Carvalho, C. Neto de.(2008). Bank loan-loss provisioning, central bank rules vs. estimation: The case of Portugal. Journal of Financial Stability4, 1–22.

Esty, Benjamin C. (1998). The impact of contingent liability on commercial bank risk taking. Journal of Financial Economics 47,189-218.

FASB. (1975). Accounting for Contingencies, Statement of Financial Accounting Standards no.5, par.1. Financial Accounting Standards Board.(1975). FAS No. 5, Accounting for Contingencies, Norwalk, Connecticut.

Fisher, Matthew, Gray, Dale. (2006). Measuring Sovereign and Banking Sector Risk in Indonesia: An Application of the Contingent Claims Approach, IMF Country Report No. 06/318.

Gapen, M. T. (2009). Evaluating the Implicit Guarantee to Fannie Mae and Freddie Mac Using Contingent Claims, Working Paper, Board of Governors of the Federal Reserve System.

Gapen, Michael T., Gray, Dale F., Xiao, Yingbin, Lim, Cheng Hoon .(2004). The Contingent Claims Approach to Corporate Vulnerability Analysis: Estimating Default Risk and Economy-wide Risk Transfer. IMF Working Paper 04/121 (Washington: International Monetary Fund).

Gapen, Michael T., Gray, Dale F., Xiao, Yingbin, Lim, Cheng Hoon .(2005). Measuring and Analyzing Sovereign Risk with Contingent Claims. IMF Working Paper 05/155 (Washington: International Monetary Fund).

Gray, D. and J. Walsh .(2008). “Factor Model for Stress-testing with a Contingent Claims Model of the Chilean Banking System.” IMF Working Paper 08/89. (Washington: International Monetary Fund).

Gray, D. F., Merton, R. C., and Bodie, Z. (2008). A Contingent Claims Analysis of the Subprime Credit Crisis of 2007-2008, Paper for CREDIT 2008 Conference on Liquidity and Credit Risk Venice, 22-23 September 2008

Gray, Dale, and Samuel Malone. (2008). Macrofinancial Risk Analysis. Wiley. Hong Kong Society of Accountants (HKSA), (1984), SAP No. 8, Accounting for Contingencies, Hong Kong,

March. IMF and World Bank (2001), Guidelines for Public Debt Management, Washington: International

Monetary Fund. International Accounting Standards Committee (IASC), 1974 (reformatted 1994), IASC No. 10,

Contingencies and events occurring after the balance sheet date. Kane, E.J. (1989). The S&L Insurance Mess: How Did it Happen? The Urban Institute Press, Washington,

DC. Kanagaretnam, K., Lobo, G., & Mathieu, R. (2003). Managerial incentives for income smoothing through

bank loan loss provisions. Review of Quantitative Finance and Accounting, 20(1), 63–80. Kanagaretnam, K., Lobo, G., & Yang, D. (2004). Joint tests of signaling and income smoothing through

bank loan loss provisions. Contemporary Accounting Research, 21(4), 843–844. Kieso, Donald E., Weygandt, Jerry J., & Warfield, Terry D. (1984).Intermediate Accounting .Current

Liabilities and Contingences, pp.630-639(11th Edition). Lacy, J. Y. (2002). Probability Expressions and Ambiguity: An Experimental Study of Disclosure

Perceptions for Contingent Liabilities. George Washington University, Washington D.C., USA. Liu, C., & Ryan, S. (1995). The effect of bank loan portfolio composition on the market reaction to and

anticipation of loan loss provisions. Journal of Accounting Research, 33(1), 77–93. Miller, G., (1997). Accounting Practices for Contingent Liabilities, working paper. Macey, J.R., Miller, G.P.(1992). Double liability of bank shareholders: history and implications. Wake

Forest Law Review 27, 31Ð62. Reagle, Derrick. (2006). Back on the balance sheet: The tax effects of contingent claims in commercial

banking. Review of Financial Economics15, 19–27. Sarma, Dr. Binoy Krishna and Ahmed., Dr. Sultan (1995), Application of International Accounting

Standards: A Study of Some Selected Jute Mills in Chittagong, Chittagong University Studies (Commerce), Vol.XI.1995 (p.177-193).

Sukchoksuwan, D., Chayawadhanangkur, A., & Sorakraikitikul, P. (2002). The perceptions of the users of Financial Statements on Off-Balance Sheet Disclosure. Thammasat University, Bangkok, Thailand.

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 2

3

Taylor and Associates. (1995). Full Disclosures 1994: An International Study of Disclosure Practices,London.

The Institute of Charterd Accountants of Bangladesh (2008) Bangladesh Financial Reporting Standards(Volume-3)

Weygandt, Jerry J., Kieso, Donald E., & Kimmel, Paul D. (2008) Accounting Principles. (9th Edition). Wild,John J., Larson, Kermit D., & Chiappetta, Barbara, Financial & Managerial Accounting-Information for

Decision,Volume-1.

Appendix: (Percentage is calculated on the basis of total contingent liabilities)

List of the Contingent Liabilities

Name of Bank Acceptance & Endorsement

(US$ in million)

Letter of Guarantee

(US$ in million)

Irrevocable letters of

Credit (US$ in million)

Bills of Collection

(US$ in million)

Other Contingent Liabilities

(US$ in million)

Tax Liability (US$ in million)

AB Bank Ltd 205.88 135.13 181.94 134.49 - -

31.32% 20.55% 27.67% 20.46% 0.00% 0.00%

Bank Alfalah Ltd. 108.70 22.65 127.89 11.88 - -

0.41% 0.08% 0.48% 0.04% 0.00% 0.00%

Bank Asia Ltd. 214.28 86.10 235.78 57.06 - -

36.12% 14.51% 39.75% 9.62% 0.00% 0.00%

Brac Bank Ltd. 2.00 56.72 202.51 7.83 7.16 1.44

0.71% 20.26% 72.35% 2.80% 2.56% 0.52%

EXIM Bank Ltd. - 49.05 190.50 32.38 414.70 -

0.00% 7.14% 27.74% 4.72% 60.40% 0.00%

Dhaka Bank Ltd. 182.59 119.81 115.37 91.72 15.45 -

34.78% 22.82% 21.98% 17.47% 2.94% 0.00%

First Security Islami Bank Ltd. 50.56 16.29 41.90 1.99 - -

45.65% 14.71% 37.83% 1.80% 0.00% 0.00%

Eastern Bank ltd. 264.74 82.11 142.32 15.06 10.16 -

51.47% 15.96% 27.67% 2.93% 1.97% 0.00%

Jamuna Bank Ltd. 20.62 46.57 145.31 19.74 2.72 -

8.77% 19.82% 61.85% 8.40% 1.16% 0.00%

ICB Islami Bank Ltd. 0.29 2.40 .13 0.65 - -

8.42% 69.18% 3.67% 18.74% 0.00% 0.00%

IFIC Bank Ltd. 161.87 51.41 145.08 94.54 - -

35.74% 11.35% 32.03% 20.87% 0.00% 0.00%

Islami Bank Bd. Ltd. 91.28 - 1,086.27 221.59 18.62 -

6.44% 0.00% 76.62% 15.63% 1.31% 0.00%

Mercantile Bank Ltd. 220 76 207 2 19 -

41.95% 14.45% 39.54% 0.35% 3.71% 0.00%

Mutual Trust Bank Ltd. - 46.61 48.56 23.35 73.08 -

0.00% 24.33% 25.34% 12.19% 38.14% 0.00%

Premier Bank Ltd. 93.36 69.76 134.75 4.66 6.69 -

30.19% 22.56% 43.58% 1.51% 2.16% 0.00%

National Bank Ltd. 238.17 78.91 148.33 75.38 14.12 -

42.92% 14.22% 26.73% 13.58% 2.54% 0.00%

One Bank Ltd. 171.82 102.59 105.75 0.58 - -

45.13% 26.95% 27.78% 0.15% 0.00% 0.00%

NCC Bank Ltd. 109.04 62.86 77.38 0.78 1.67 -

43.32% 24.97% 30.74% 0.31% 0.66% 0.00%

Standard Bank Ltd. 81.15 35.53 90.22 6.90 - -

Mst. Zaynab S. / IJAR-BAE, 02 (2013) 12–24

www.setscholars.org/index.php/ijarbae

Pag

e 2

4

37.96% 16.62% 42.20% 3.23% 0.00% 0.00%

Prime Bank Ltd. 362.04 437.44 371.33 92.87 - -

28.66% 34.63% 29.40% 7.35% 0.00% 0.00%

Rupali Bank Ltd. - 27.02 1,108.34 86.87 0.02 -

0.00% 2.21% 90.68% 7.11% 0.00% 0.00%

Pubali Bank Ltd. - 51.06 350.26 7.00 11.89 -

0.00% 12.15% 83.36% 1.66% 2.83% 0.00%

Social Investment Bank Ltd. 105.06 40.97 84.80 22.31 - -

41.50% 16.19% 33.50% 8.81% 0.00% 0.00%

Source: Authors own calculation from annual reports of 2011