IHS NETHERLANDS HOLDCO B.V. - IHS Towers

93

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED AND COMPANY FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of IHS NETHERLANDS HOLDCO B.V. - IHS Towers

IHS NETHERLANDS HOLDCO B.V.

CONSOLIDATED AND COMPANY FINANCIAL STATEMENTS FOR THE YEAR ENDED 31

DECEMBER 2019

IHS NETHERLANDS HOLDCO B.V. INDEX TO THE CONSOLIDATED AND COMPANY FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

2

CONTENTS

CORPORATE INFORMATION .................................................................................................................................................... 3 MANAGEMENT BOARD REPORT ............................................................................................................................................. 4 CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME ....................................... 12 CONSOLIDATED STATEMENT OF FINANCIAL POSITION ..................................................................................................... 13 CONSOLIDATED STATEMENT OF CHANGES IN EQUITY ..................................................................................................... 14 CONSOLIDATED STATEMENT OF CASH FLOWS ................................................................................................................. 15 NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS ............................................................................................... 16

1. General information ........................................................................................................................... 16 2. Summary of significant accounting policies .................................................................................... 16 3. Critical accounting estimates and judgements ............................................................................... 30 4. Financial risk management ............................................................................................................... 32 5. Revenue ............................................................................................................................................. 40 6. Cost of sales ...................................................................................................................................... 41 7. Administrative expenses ................................................................................................................... 41 8. Other income ..................................................................................................................................... 42 9. Finance income and costs ................................................................................................................ 42 10. Non-IFRS measures ........................................................................................................................... 43 11. Taxation .............................................................................................................................................. 43 12. Property, plant and equipment ......................................................................................................... 44 13. Intangible assets ................................................................................................................................ 45 14. Investments ........................................................................................................................................ 48 15. Derivative financial instruments ....................................................................................................... 48 16. Trade and other receivables ............................................................................................................. 49 17. Inventories ......................................................................................................................................... 49 18. Cash and cash equivalents ............................................................................................................... 50 19. Trade and other payables .................................................................................................................. 50 20. Borrowings ......................................................................................................................................... 50 21. Lease liabilities .................................................................................................................................. 53 22. Provisions for liabilities and other charges ..................................................................................... 53 23. Deferred taxation ............................................................................................................................... 54 24. Share capital ...................................................................................................................................... 55 25. Other reserves ................................................................................................................................... 55 26. Accumulated deficit ........................................................................................................................... 56 27. Cash generated from operations ...................................................................................................... 56 28. Business combinations ..................................................................................................................... 57 29. Related parties ................................................................................................................................... 57 30. Contingent liabilities and capital commitments............................................................................... 60 31. Events after the reporting period ...................................................................................................... 61

COMPANY STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME ................................................. 62 COMPANY STATEMENT OF FINANCIAL POSITION ............................................................................................................... 63 COMPANY STATEMENT OF CHANGES IN EQUITY ............................................................................................................... 64 COMPANY STATEMENT OF CASH FLOWS ........................................................................................................................... 65 NOTES TO THE COMPANY FINANCIAL STATEMENTS ......................................................................................................... 66 OTHER INFORMATION ............................................................................................................................................................ 79 INDEPENDENT AUDITOR’S REPORT ..................................................................................................................................... 80

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

3

CORPORATE INFORMATION

Commercial Register No. 66017912 Registered Office Haagsche Hof

Parkstraat 83, 2514 JG The Hague The Netherlands

Management Board Mr. DARWISH Mohamad Mr. VAN DIJK Bart (resigned 15 February 2019) Mr VAN SPALL Gerard Jan (appointed 15 February 2019) Mr. KLEIN Laurentius Ireneus Winfridus Mr. ORDMAN David Andrew

Independent Auditors PricewaterhouseCoopers Accountants N.V.

Bankers Citibank Europe Plc

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

4

MANAGEMENT BOARD REPORT

1. General Information

The Directors present the management board report on the affairs of IHS Netherlands Holdco B.V. (the "Company") and its subsidiaries (together hereafter referred to as the “Group”), for the year ended 31 December 2019. This report discloses the state of the Company and the Group. IHS Netherlands Holdco B.V. was incorporated in The Netherlands under Dutch Corporate Law as a private limited liability company.

The Company was incorporated on 12 May 2016 and is a fully owned subsidiary of IHS Netherlands (Interco) Coöperatief U.A. a Dutch Cooperative incorporated in The Netherlands. The ultimate parent is IHS Holding Limited, a company incorporated in Mauritius, the shares of which are held by several companies and individuals.

At 1 January 2019 the Group was comprised of the following: IHS Netherlands Holdco B.V. (Parent), IHS Netherlands NG1 B.V. (100% interest), IHS Netherlands NG2 B.V. (100% interest), IHS Nigeria Limited (100% interest1), IHS Towers NG Limited (100% interest1), Tower Infrastructure Company Limited (100% interest) and IHS Towers Netherlands FinCo NG B.V (100% interest).

On 18 September 2019 IHS Netherlands (Interco) Coöperatief U.A. transferred the shares it held (representing 100% ownership) in Nigeria Tower Interco B.V. to IHS Netherlands Holdco B.V., including its subsidiary, INT Towers Limited. INT Towers Limited is a fully owned subsidiary (100% interest1) of Nigeria Tower Interco B.V. This restructuring took place as part of a refinancing under which the $800m, 9.5% Senior Notes due 2021 (the “2021 Notes”) were fully redeemed and are no longer outstanding and IHS Netherlands Holdco B.V. issued $500 million 7.125% Senior Notes due 2025 (the “2025 Notes”) and $800 million 8.0% Senior Notes due 2027 (the “2027 Notes”) which are listed on The International Stock Exchange (TISE).

The significant subsidiaries, being IHS Nigeria Limited, IHS Towers NG Limited and, from 18 September 2019, INT Towers Limited are incorporated in Nigeria and are principally involved in providing shared telecommunications infrastructure services to Mobile Network Operators (MNOs) and other communications service providers, who in turn provide wireless voice and data services to their end users. These subsidiaries provide customers with opportunities to install active equipment on existing towers alongside current tenants, known as colocation, and provide opportunities for customers to commission the construction of new sites to their specifications. In certain strategic instances, they may also provide managed services, such as maintenance, security and power supply for towers owned by third parties. These subsidiaries provide all their services in Nigeria.

The Company is the “issuer” of the $500 million 7.125% Senior Notes due 2025 (the “2025 Notes”) and $800 million 8.0% Senior Notes due 2027 (the “2027 Notes”) (together “the Notes”) which are listed on The International Stock Exchange (TISE).

IHS Towers Netherlands FinCo NG B.V., a wholly owned subsidiary of the Company, is the “issuer” of the $250m 8.375%. Guaranteed Senior Notes due 2019 (the “FinCo Notes” and, together with the 2021 Notes, the “IHS Notes”), issued on 15 July 2014 and which have all been fully repaid at maturity on 15 July 2019 and are no longer outstanding.

The Company has no employees.

Performance

The summarized results for the year ended 31 December 2019 and the year ended 31 December 2018 are presented below:

Year ended 2019

Year ended 2018

Group $’000 Company $’000 Group $’000 Company $’000 Revenue 580,571 - 392,477 - Gross profit 226,034 - 161,528 - Total comprehensive (loss)/profit for the period (64,282) 91,378 (107,618) (87,333)

The Group had an operating profit of US$130.0 million for the year (2018: US$104.5 million). The total comprehensive loss results from net finance costs of US$207.0 million (2018: US$190.7 million) which includes unrealized foreign exchange losses of US$9.3 million (2018: US$26.9 million) primarily related to the translation of foreign currency loans. The directors do not recommend the payment of a dividend. The Group has total net liabilities of US$467.4 million (2018: US$592.7 million) and the Company has total net assets of US$1.8 billion (2018: US$18.7 million).

1 Less one share in each of IHS Nigeria Limited, IHS Towers NG Limited and INT Towers Limited which are held by a nominee shareholder, for local legal reasons.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

5

MANAGEMENT BOARD REPORT (CONTINUED)

2. Description of risks and uncertainties to which the Group is exposed

The Group is exposed to the following important risks:

A significant portion of our revenue is derived from a small number of Mobile Network Operators (MNOs). The Group derived over 90% of its revenue from three key customers in the period. These customers control the majority of the market share of the mobile network market in Nigeria and, in the absence of a more diverse mobile network market in Nigeria, if any of our major customers are unwilling or unable to perform their obligations under their tower lease agreements, our revenues, financial condition and or results of operations could be adversely affected. Conversely, as the major tower infrastructure provider in Nigeria, we have limited competition and strong barriers to entry.

The Group may experience volatility in terms of timing of invoice settlement or may be unable to collect amounts due. This is a risk which is present for most companies and is mitigated by the Group through active management of outstanding debtors and engagement with MNOs who pay late to understand the difficulties they are facing and implement payment plans. Management provides for debtors where there is a perceived increased risk of non-collectability.

The Group’s current and future markets involve additional risks compared to more developed markets. These risks relate specifically to the availability of infrastructure to facilitate growth and other microeconomic risks associated with a developing market like Nigeria.

The Group and our customers face foreign exchange risks, which may be material. This risk is described in more detail in section 6 below.

The Group relies on third-party contractors for various services, and any disruption in or non-performance of those services would hinder our ability to maintain our tower infrastructure effectively. Management actively monitors the performance of third-party contractors against the contracted levels of service in service level agreements. The risk is further mitigated through the selection of reliable vendors with a proven track record for providing management services.

Any increase in operating expenses, particularly increased costs for diesel or an inability to pass through increased diesel costs, could erode our operating margins. Diesel cost makes up just over 50% (2018: over 50%) of the cost of sales of the group (excluding depreciation, amortization and impairments) and diesel price fluctuations therefore have the biggest effect on operating results. To ensure that a portion of the increase in these costs is passed through to our customers, the Group’s contracts include clauses which increase a portion of the use fees annually, with the movement in the Nigeria CPI which is affected by the local diesel cost. Such resets do not however mitigate the short-term risk of price fluctuations.

Inability to renew and/or extend our ground leases or protect our rights to the land under our towers could lead to lost revenue and increased costs as towers would need to be taken down, customer equipment may need to be moved to new sites or larger rental costs may need to be paid to secure access to the site. Management mitigates these risks by entering into long-term lease agreements with landlords (usually 10-15 years) and renewing these leases with good time left before expiry, with the renewal process usually beginning three to nine months prior to expiry of the lease term.

The Group’s exposure to financial reporting risk is deemed to be medium given complexity in some transactions as noted in note 3. This is mitigated as the operational entities within the Group share common management and financial control staff and therefore apply consistently the same process and review procedures. All entities within the Group also apply the same accounting policies and there is therefore little risk of divergence in accounting treatment.

The potential impact of Coronavirus (COVID-19) on our business:

As explained in note 2.1.1 Going concern and note 31 Events after the reporting period, in the financial statements, the COVID-19 outbreak and resulting measures taken by the Nigerian federal and various state governments to contain the virus have required some changes in how we operate (for example travel restrictions, increased working from home, practicing social distancing, increased hygiene measures and enhanced risk and contingency planning). Thus far, however, we believe that the impact on our business is limited with no immediate adverse operational impacts on our business, particularly because the telecommunications industry has been designated an essential service by the Nigerian government.

However, in addition to the already known effects, the macroeconomic uncertainty causes disruption to economic activity and it is unknown what the longer term impact on our business may be. The scale and duration of this pandemic remain uncertain but are expected to further impact our business. We believe that the main risks arising from the current uncertain situation regarding COVID-19 are as discussed below.

Revenues and profitability – Our revenues, or more specifically, our ability to collect our revenues from our customers may be compromised should our customers and/or their end customers no longer be able to meet their obligations. However, the Group has long-term revenue contracts with its customers, who we are in regular and frequent dialogue with to see how we can provide support in the operation of their network. Keeping people connected is now even more important given the current circumstances, and the telecommunications industry has been designated an essential service by the Nigerian government. Thus far in 2020, we have continued to meet our customers’ expectations on service levels and our Network Operating Centre (NOC) has maintained normal service levels. We continue to review and develop our internal contingency plans should the need arise to manage the NOC remotely.

A significant reduction in profitability may lead to impairments in our intangible assets, PPE and receivables. See note 13 for further information on intangible impairment sensitivities and note 4(c) for details of our credit risk.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

6

MANAGEMENT BOARD REPORT (CONTINUED)

2. Description of risks and uncertainties to which the Group is exposed (continued)

The potential impact of Coronavirus (COVID-19) on our business: (continued)

Revenues and profitability (continued) – The Group is reviewing measures for cost savings whilst maintaining its ability to operate effectively. Capex investments are likely to be limited generally to necessary replacements of assets until greater certainty on timing of macroeconomic improvement is available.

Supply chain – our sites require supplies of diesel and regular maintenance to continue to operate and, while we maintain a level of inventory, there is a risk that supplies may not be able to be delivered to our sites or that supplies may not be available, particularly when inventories need to be replenished. The Group is working closely with its suppliers on their supply chain and the health and safety of their employees.

Internal controls – the need to have more staff working from home may impact the security of their internet connections which could increase the risk of fraud, data or security breaches, loss of data and the potential for other cyber-related attacks. Our IT team utilise security measures to mitigate such risks but certainty over security cannot be assured.

Financing and liquidity - Following the reduction in the oil price subsequent to the year end, as well as concerns over COVID-19, there has been pressure on foreign exchange reserves in Nigeria. The Nigerian government has taken measures to protect these reserves through devaluing the CBN rate, which has had a similar, but thus far more limited devaluation impact on the NAFEX rate. Such devaluation and reductions in US dollar liquidity in the Nigerian market may reduce our revenues until such time as our contract resets are applied (unless a divergence in the official CBN rate, as used in our contracts, and the NAFEX rate continues, which would continue to impact us) and impact our ability to make our interest payments on our US dollar denominated obligations, including debt facilities.

The Nigerian CBN and NAFEX Naira rates have both devalued against the US dollar since 31 December 2019 from a NAFEX rate of Naira365:US$1 to Naira387:US$1 at 31 March 2020 (CBN Naira307:US$1 to Naira361:US$1), as the Nigerian Government looks to stabilise the economy and also protect current foreign exchange reserves. While there has been a reduction in US dollar liquidity in the Nigerian market, we were still able to source US$ dollars locally to pay our semi-annual coupon in March 2020. Our current aggregate balance of cash and cash equivalents and margins for non-deliverable forward instruments, remains at a similar level to the 2019 year-end position, even after this coupon payment.

3. Expected business developments

The Group’s primary strategy is to expand our revenue-generating asset base and improve utilization on new and existing towers. We have multiple organic and inorganic paths to increase revenue, subject to continued compliance with the Group’s debt covenants. We aim to drive organic revenue through colocation, lease amendments, contractual lease fee escalations and new site construction. In addition, we believe strong operating leverage and initiatives, such as decommissioning and site consolidations, will help us drive margins and increase free cash flows.

We pursue investments in Nigeria and have a strong track record of value-enhancing incremental investments that have helped grow our asset base, secure our market leading position and provide the scale and market share necessary to sustain our growth. We see the potential for new and related services that will help enhance our value proposition to our customers, reduce their operating costs and help improve their quality of service.

While the Group does not plan to effect any substantial changes to the number of staff or to the current financing structure, the Group regularly reviews financing structures. Management have drafted and analyzed the Group business plan and noted that according to currently forecast expectations there is no need to obtain further financing for normal operations or for the implementation of growth strategies. The results of the forecast, in combination with group treasury forecasts, also indicates sufficient funds to meet debt service obligations.

As explained in note 2.1.1 Going concern and note 31 Events after the reporting period, in the financial statements, the COVID-19 outbreak and resulting measures taken by the Nigerian federal and various state governments to contain the virus have required some changes in how we operate our business in the first 3 months of 2020, but we believe that this has had no immediate adverse operational impacts on our business.

Based on the actions taken to date by the Nigerian government and the nature of our long-term contracts we do not expect to see a material impact on our operational performance in 2020. However, the situation is changing rapidly and we will continue to review closely and take action if necessary. As a cash generative operation, with a substantial current cash balance and extended debt maturities we expect to meet our covenant obligations for the remainder of the year. Ultimately, whether this situation will continue to be maintained, in the remainder of 2020 and into 2021 is dependent on the period during which the regions in which we operate are exposed to COVID-19 and the extent to which government measures may be prolonged, expanded or scaled down and impact the economies we operate in.

The Group is reviewing measures for cost savings whilst maintaining its ability to operate effectively. Capex investments are likely to be limited generally to necessary replacements of assets until greater certainty on timing of macroeconomic improvement is available.

The current year performance, adjusted for the impact of INT Towers, is in line with the expectations of the prior year.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

7

MANAGEMENT BOARD REPORT (CONTINUED)

4. Research and development activities

The Group explores the potential for new products and services that will help enhance our value proposition to our customers, reduce their operating costs and help improve their quality of service. It is however not actively involved in the research and development of new technologies or products.

5. Subsequent events

Coronavirus (COVID-19)

The existence of novel coronavirus (COVID-19) was confirmed in early 2020 and has spread rapidly from mainland China across the globe, causing disruptions to businesses and economic activity. Many governments across the world have imposed travel restrictions, lock downs and social distancing with a view to reducing the spread of the virus and hopefully minimising the number of fatalities. The Group considers this outbreak to be a non-adjusting post balance sheet event.

Our main priority has been the health and safety of our employees and our dedicated supply chain. We have adhered to instructions issued by the Nigerian and/or state authorities, including travel restrictions and enforced working from home. Our secondary focus has been around business continuity planning and maintenance of the supply chain. The telecommunications industry has been designated by the Nigerian government as an essential service and, as the largest independent owner and maintainer of towers (towerco) in Nigeria, we have sought relevant permits to allow us to continue to access, fuel and maintain our tower portfolio. Consequently, we believe that the impact on our business is currently limited with no immediate material adverse operational impact. We intend to continue to follow the various national and/or state authorities’ policies and, in parallel, intend to do our utmost to continue our operations as the situation evolves.

Having refinanced our business in 2019, we have also extended our debt maturities, some of which extend well beyond 2021.

However, as the situation is fluid, rapidly evolving, and uncertainties remain, we do not consider it practicable to provide a quantitative estimate of the potential impact of this outbreak on the Group.

The impact of this outbreak on macroeconomic forecasts and our markets are expected to be incorporated into the Group’s estimates of expected credit loss provisions and other impairments assessments in 2020.

Please also see disclosures in note 2.1.1 Going Concern.

Devaluation in Naira to US dollar rate.

Following the reduction in the oil price subsequent to the year end, there has been pressure on foreign exchange reserves in Nigeria, which decreased from US$42 billion a year ago, to around US$35 billion presently. The Nigerian government has taken measures to protect these reserves through devaluing the CBN rate, which has had a similar, but thus far more limited devaluation impact on the NAFEX rate.

The Nigerian CBN and NAFEX Naira rates have both devalued against the US dollar since 31 December 2019 from a NAFEX rate of Naira365:US$1 to Naira387:US$1 at 31 March 2020 (CBN Naira307:US$1 to Naira361:US$1), as the Nigerian Government looks to stabilize the economy and also protect current foreign exchange reserves.

There are no other events after the reporting date that need to be disclosed in accordance with IAS 10 Events after the reporting period.

6. Exposure to and management of price risk, credit risk and liquidity and cash flow risk

The Group's activities expose it to a variety of financial risks including market risk (foreign exchange risk and interest rate risk), credit risk and liquidity risk. The Management Board has overall responsibility for the establishment and oversight of the Group’s risk management framework. The company has risk management oversight via the Executive Risk Management Committee at the level of the ultimate parent company (IHS Holding Limited), who is responsible for developing and monitoring the IHS Group’s risk management policies.

The Group’s risk management policies are established to identify and analyze the risks faced by the Group, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management policies and systems are reviewed regularly by the executive management to reflect changes in market conditions and the Group’s activities. The Group, through its training and management standards and procedures, aims to develop and maintain a disciplined and constructive control environment in which all employees understand their roles and obligations.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

8

MANAGEMENT BOARD REPORT (CONTINUED)

6. Exposure to and management of price risk, credit risk and liquidity and cash flow risk (continued)

The Board oversees how management monitors compliance with the Group’s risk management policies and procedures and reviews the adequacy of the risk management framework in relation to the risks faced by the Group. The Board is supported by various management functions that check and undertake both regular and ad hoc reviews of compliance with established controls and procedures.

It is the policy of the Group to develop controls and procedures to mitigate risks as far as possible within a reasonable cost/benefit range. Management accepts any low residual risks remaining after the implementation of appropriate mitigating controls.

Where appropriate we use derivative financial instruments solely for the purposes of hedging the currency risks arising from our operations and sources of financing. We do not enter into derivative financial instruments for speculative purposes. Foreign exchange risk The Group operates in Nigeria and is exposed to foreign exchange risk arising from exposures to currencies other than the Naira, in the books of the Nigerian subsidiaries, and to currencies other than the US Dollar upon consolidating the results and financial position of the Nigerian subsidiaries. Foreign exchange risk arises from future commercial transactions, recognized assets and liabilities and net investments in foreign operations.

The Group is exposed to risks resulting from fluctuations in foreign currency exchange rates. A material change in the value of any such foreign currency could result in a material adverse effect on the Group’s cash flow and future profits. The Group is exposed to exchange rate risk to the extent that balances and transactions are denominated in a currency other than the functional currency in which they are measured.

In managing foreign exchange risk, the Group aims to reduce the impact of short-term fluctuations on earnings. The Group has no export sales, but it has customers that are partly contracted using fees quoted in US Dollars, but with foreign exchange indexation. The Group’s significant exposure to currency risk relates to its loan facilities held by its subsidiaries that are mainly US Dollar denominated. The Group manages foreign exchange risk through the use of derivative financial instruments such as currency swaps and forward contracts. The Group monitors the movement in the currency rates on an ongoing basis.

Interest rate risk

The Group’s main interest rate risk arises from long term borrowings with variable rates, which expose the Group to cash flow interest rate risk. The Group’s borrowings at variable rate represent the senior facilities and are denominated in Naira and USD.

Most of the Group’s borrowings are at fixed rates of interest. The Group’s fixed rate borrowings and receivables are carried at amortized cost. They are therefore not subject to interest rate risk as defined in IFRS 7, since neither the carrying amount nor the future cash flows will fluctuate because of a change in market interest rates. The Group manages interest rate risk by issuing fixed rate debt.

Counterparty credit risk

Counterparty credit risk relates to the risk of loss resulting from non-performance or non-payment by counterparties pursuant to the terms of their contractual obligations. We utilize data and market knowledge to determine the concentration of risk by reference to independent and internal ratings of customers. Risks surrounding counterparty performance could ultimately impact the amount and timing of our cash flow and future profits. We seek to mitigate counterparty credit risk by having a diversified portfolio of counterparties. Counterparty credit risk is managed on a Group basis.

For banks and financial institutions, only independently rated parties with a minimum rating of “B” are accepted. The credit control department assesses the credit quality of a customer, taking into account its financial position, past experience and other factors. Individual risk limits are set based on internal or external ratings. The compliance with credit limits by customers is regularly monitored by management.

Liquidity and cash flow risk

Liquidity risk is the risk that the Group will encounter difficulty in meeting the obligations associated with its financial liabilities that are settled by delivering cash or another financial asset. The Group’s approach to managing liquidity is to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Group’s reputation.

The Group has a clear focus on ensuring sufficient access to capital to finance growth and to refinance maturing debt obligations. As part of the liquidity management process, the Group has various credit arrangements with some banks which can be utilized to meet its liquidity requirements. Typically, the credit terms with customers are more favorable compared to payment terms to its vendors in order to help provide sufficient cash on demand to meet expected operational expenses, including the servicing of financial obligations. This excludes the potential impact of extreme circumstances that cannot reasonably be predicted, such as natural disasters.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

9

MANAGEMENT BOARD REPORT (CONTINUED)

7. Laws and regulations

Our business is subject to national, state and local regulations governing telecommunications, as well as the construction and operation of towers. In addition, the Group is required to comply with anti-bribery or anti-corruption laws and regulations such as the Foreign Corrupt Practices Act or similar international or local anti-bribery or anti-corruption laws, or Office of Foreign Assets Control requirements.

Environmental Regulation

Our operations are subject to various national, state and local environmental laws and regulations, including those relating to the management, use, storage, disposal, emission and remediation of, and exposure to, hazardous and non-hazardous substances, materials and wastes and the siting of our towers. We may be required to obtain permits, pay additional property taxes, comply with regulatory requirements and make certain informational filings related to hazardous substances or devices used to provide power such as batteries, generators and diesel at our sites. In Nigeria, environmental authorizations are required at two stages, the Federal Ministry of Environment requires an Environmental Impact Assessment to be issued prior to the construction of a site and every three years after a site is built an Environmental Audit Certificate needs to be issued or renewed by the National Environmental Standards and Regulations Enforcement Agency in respect of such site.

Local tax laws

The Group is required to comply with local tax laws in Nigeria and The Netherlands. Compliance is monitored by management, in some cases with the assistance of professional advisors.

8. Going concern

The directors have reasonable expectations that the Group has adequate resources to continue in operational existence for the foreseeable future. The results of management review of the Group’s market, operations and financials in the past year and a forecast for at least twelve months after the date of signing of the financial statements provides a sound basis for the appropriateness of using the going concern assumption in the preparation of the Group’s financial statements for the year ended 31 December 2019, though the existence of Coronavirus (COVID-19) means there is generally a level of uncertainty in the wider macro market.

Coronavirus

The existence of novel coronavirus (COVID-19) was confirmed in early 2020 and has spread rapidly from mainland China across the globe, causing disruptions to businesses and economic activity. Many governments across the world have imposed travel restrictions, lock downs and social distancing with a view to reducing the spread of the virus and hopefully minimising the number of fatalities. The Group considers this outbreak to be a non-adjusting post balance sheet event.

Our main priority has been the health and safety of our employees and our dedicated supply chain. We have adhered to instructions issued by the Nigerian and/or state authorities, including travel restrictions and enforced working from home. Our secondary focus has been around business continuity planning and maintenance of the supply chain. The telecommunications industry has been designated by the Nigerian government as an essential service and, as the largest independent owner and maintainer of towers (towerco) in Nigeria, we have sought relevant permits to allow us to continue to access, fuel and maintain our tower portfolio. Consequently, we believe that the impact on our business is currently limited with no immediate material adverse operational impact. We intend to continue to follow the various national and/or state authorities’ policies and, in parallel, intend to do our utmost to continue our operations as the situation evolves.

Revenues and profitability – The Group has long-term revenue contracts with its customers who we are in regular and frequent dialogue with to see how we can provide support in the operation of their network. Telecoms, and specifically telecoms infrastructure, is an important, stable and durable industry and keeping people connected is now even more important given the current circumstances, and the telecommunications industry has been designated an essential service by the Nigerian government. Thus far in 2020, we have continue to meet our customers’ expectations on service levels and our Network Operating Centre (NOC) has maintained normal service levels. We continue to review and develop our internal contingency plans should the need arise to manage the NOC remotely.

The Group is reviewing measures for cost savings whilst maintaining its ability to operate effectively. Capex investments are likely to be limited generally to necessary replacements of assets until greater certainty on timing of macroeconomic improvement is available.

Supply chain – our sites require supplies of diesel and regular maintenance to continue to operate. IHS presently has diesel inventory to hand and is continually looking to increase its supply and stock to avoid disruption. The Group is working closely with our suppliers on their supply chain in this regard.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

10

MANAGEMENT BOARD REPORT (CONTINUED)

8. Going Concern (continued)

Financing and liquidity - Following the reduction in the oil price subsequent to the year end, as well as concerns over COVID-19, there has been pressure on foreign exchange reserves in Nigeria. The Nigerian government has taken measures to protect these reserves through devaluing the CBN rate, which has had a similar, but thus far more limited devaluation impact on the NAFEX rate. Such devaluation and reductions in US dollar liquidity in the Nigerian market may reduce our revenues until such time as our contract resets are applied (unless a divergence in the official CBN rate, as used in our contracts, and the NAFEX rate continues, which would continue to impact us) and impact our ability to make our interest payments on our US dollar denominated obligations, including debt facilities.

The Nigerian CBN and NAFEX Naira rates have both devalued against the US dollar since 31 December 2019 from a NAFEX rate of Naira365:US$1 to Naira387:US$1 at 31 March 2020 (CBN Naira307:US$1 to Naira361:US$1), as the Nigerian Government looks to stabilise the economy and also protect current foreign exchange reserves. While there has been a reduction in US dollar liquidity in the Nigerian market, we were still able to source US$ dollars locally to pay our semi-annual coupon in March 2020. Our current aggregate balance of cash and cash equivalents and margins for non-deliverable forward instruments, remains at a similar level to the 2019 year-end position, even after this coupon payment.

Whilst inherently uncertain, and we expect some impact to our operations and performance, we currently do not believe that the the COVID-19 outbreak will directly have a material adverse effect on our financial condition or liquidity for the foreseeable future such that it is not appropriate to apply the going concern principal to these financial statements.

The following further forms the basis of management's use of going concern:

The market is growing, and the business has grown its share of the overall market.

The business has grown its revenues, gross profit margins, EBITDA margins and operating cash flows over the year, when compared to the prior period on an annualized basis.

The business has a strong cash and short-term deposits balance at 31 December 2019 of US$140.3 million (2018: US$183.5 million) of which US$20.8 million is held in US Dollars (2018: US$132.2 million).

The business maintains a high level of business ethics and regulatory compliance and there is no indication of any foreseeable material adverse change in the regulatory landscape.

The Group is in compliance with the debt covenants related to the listed bonds and the financial covenants related to the senior credit facilities as at 31 December 2019 and expects to remain compliant with these covenants over the duration of the forecast period (being for at least twelve months after the date of signing of the financial statements). Refer to note 20 for further details of the covenants.

The Group expects to have sufficient cash reserves and cash generated for the forecast period to meet its financing obligations, which during the current year saw a decrease in financing cost as a percentage of borrowings following the refinancing in September 2019 which resulted in lower interest rates being achieved on outstanding loans and bonds.

9. Donations and gifts

The Group made charitable donations of US$547,000 (2018: US$212,000) during the period and the Company did not make any donations or charitable gifts during the year. The charitable donations made by the Group were not to political institutions.

10. Management board

As at 31 December 2019 the management board was comprised of the following individuals:

Mr. DARWISH Mohamad Mr. VAN SPALL Gerard Jan (appointed on 15 February 2019) Mr. KLEIN Laurentius Ireneus Winfridus Mr. ORDMAN David Andrew Mr. VAN DIJK Bart resigned on 15 February 2019

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

11

MANAGEMENT BOARD REPORT (CONTINUED)

11. Uneven board seat allocation between men and women

On 1 January 2013, a new law on management on supervision (Wet Bestuur en Toezicht) came into effect in the Netherlands. The purpose of this law is to attain a balance (at least 30% of each gender) between men and women in the management board of large entities (as defined in the said law); the Group is not currently compliant with this regulation. After taking cognizance of the current nature and activities of the Group and the knowledge and expertise of the current management board members, the existing composition of the management board is considered to be appropriate. However, the new law will be taken into account while appointing the future members of the management board.

Mohamad Darwish David Ordman

Mr. Mohamad Darwish Mr. David Andrew Ordman

Gerard van Spall Laurentius Klein

Mr. Gerard Jan van Spall Mr. Laurentius Ireneus Winfridus Klein

6 April 2020

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

12

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

2019 2018

Note $'000 $'000

Revenue 5 580,571 392,477 Cost of sales 6 (354,537) (230,949) Gross profit

226,034 161,528

Administrative expenses 7 (89,164) (34,428) Loss allowance on trade receivables 4(c) (20,955) (35,868) Other income 8 11,299 13,259 Operating profit

127,214 104,491

Finance income 9.1 22,059 15,256 Finance costs 9.2 (229,105) (205,945) Loss before income tax

(79,832) (86,198)

Income tax benefit /(expense) 11 15,550 (28,338) Loss for the period

(64,282) (114,536)

Attributable to:

Owners of the Group 26 (64,282) (114,536) Loss for the period

(64,282) (114,536)

Other comprehensive income Items that may be reclassified to profit or loss: Fair value gain/(loss) through other comprehensive income 25 1 (2) Exchange differences on translation of foreign operations 25 644 6,920 Other comprehensive income for the period net of taxes

645 6,918

Attributable to:

Owners of the Group 25 645 6,918 Other comprehensive income for the period net of taxes

645 6,918

Attributable to:

Owners of the Group

(63,637) (107,618)

Total comprehensive loss for the period

(63,637) (107,618)

The accompanying notes are an integral part of these consolidated financial statements.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

13

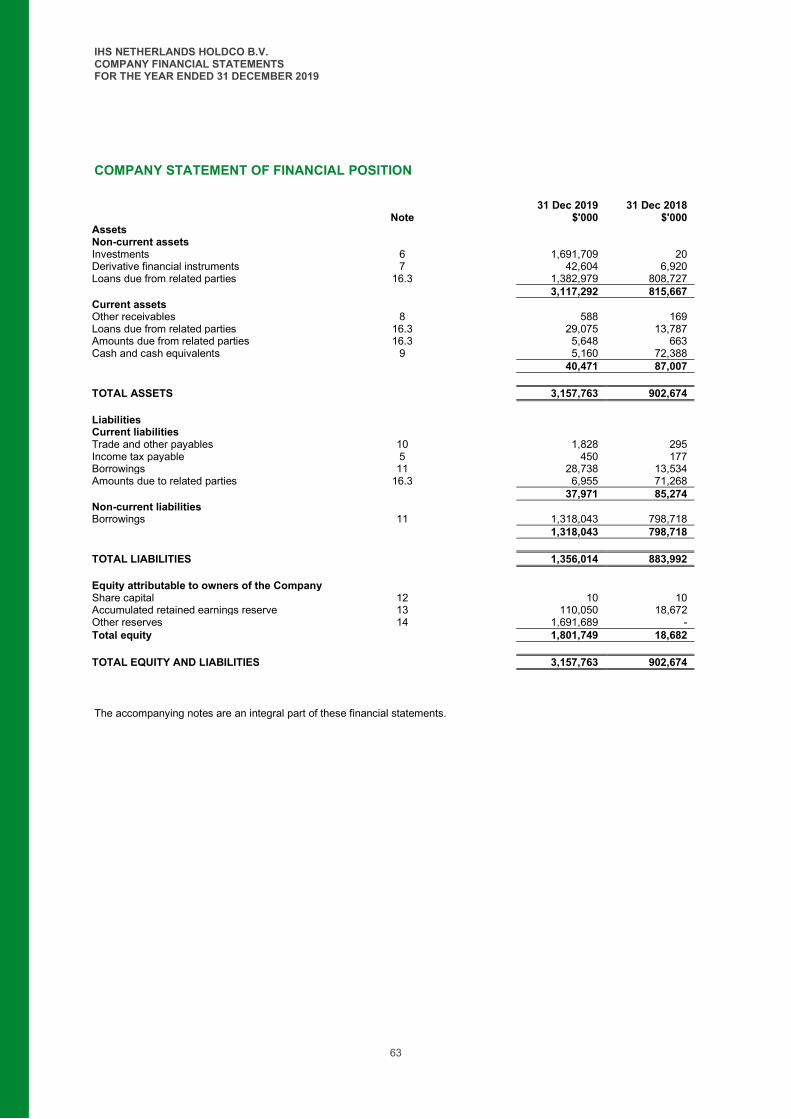

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

31 December

2019 31 December

2018 Note $'000 $'000

Assets Non-current assets Property, plant and equipment 12 1,054,220 473,059 Right of use assets 12 215,965 - Intangible assets 13 714,489 281,755 Investments 14 11 9 Derivative financial instruments 15 42,604 6,920 Trade and other receivables 16 12,992 89,918

2,040,281 851,661 Current assets Derivative financial instruments 15 53 - Inventories 17 43,317 4,585 Trade and other receivables 16 130,092 77,839 Amounts due from related parties 29 2,204 3,763 Cash and cash equivalents 18 140,250 183,513

315,916 269,700 TOTAL ASSETS 2,356,197 1,121,361

Liabilities Current liabilities Trade and other payables 19 280,888 106,866 Income tax payable 11 5,576 6,106 Borrowings 20 31,272 51,821 Lease liabilities 21 6,050 - Provisions for liabilities and other charges 22 3,768 3,334 Amounts due to related parties 29 4,194 6,942 Derivative financial instruments 15 - 310

331,748 175,379 Non-current liabilities Borrowings 20 1,770,989 844,349 Lease liabilities 21 27,172 - Amounts due to related parties 29 688,095 693,113 Provisions for liabilities and other charges 22 5,586 1,222

2,491,842 1,538,684 TOTAL LIABILITIES 2,823,590 1,714,063 Equity attributable to owners of the Group Share capital 24 10 10 Accumulated deficit 26 (96,926) (355,806) Other reserves 25 (370,477) (236,906) Total equity (467,393) (592,702) TOTAL EQUITY AND LIABILITIES 2,356,197 1,121,361

The accompanying notes are an integral part of these consolidated financial statements.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

14

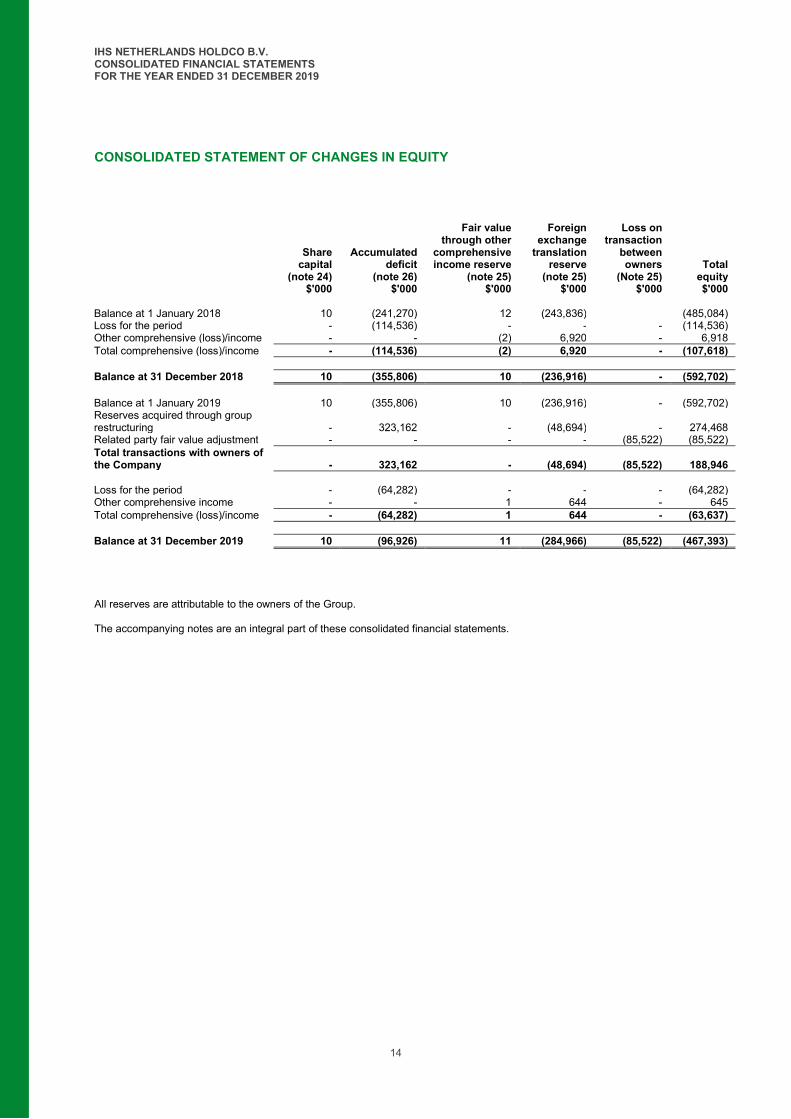

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

Share capital

(note 24)

Accumulated deficit

(note 26)

Fair value through other

comprehensive income reserve

(note 25)

Foreign exchange

translation reserve

(note 25)

Loss on transaction

between owners

(Note 25) Total

equity $'000 $'000 $'000 $'000 $'000 $'000

Balance at 1 January 2018 10 (241,270) 12 (243,836) (485,084) Loss for the period - (114,536) - - - (114,536) Other comprehensive (loss)/income - - (2) 6,920 - 6,918 Total comprehensive (loss)/income - (114,536) (2) 6,920 - (107,618) Balance at 31 December 2018 10 (355,806) 10 (236,916) - (592,702)

Balance at 1 January 2019 10 (355,806) 10 (236,916) - (592,702) Reserves acquired through group restructuring - 323,162 - (48,694) - 274,468 Related party fair value adjustment - - - - (85,522) (85,522) Total transactions with owners of the Company - 323,162 - (48,694) (85,522) 188,946 Loss for the period - (64,282) - - - (64,282) Other comprehensive income - - 1 644 - 645 Total comprehensive (loss)/income - (64,282) 1 644 - (63,637) Balance at 31 December 2019 10 (96,926) 11 (284,966) (85,522) (467,393) All reserves are attributable to the owners of the Group. The accompanying notes are an integral part of these consolidated financial statements.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

15

CONSOLIDATED STATEMENT OF CASH FLOWS

2019 2018 Note $'000 $'000

Cash flows from operating activities Cash generated from operations 27 336,920 238,618 Income taxes paid 11 (4,078) (4,783) Net cash from operating activities 332,842 233,835 Cash flows from investing activities Purchase of property, plant and equipment - capital work in progress 12 (ii)

(49,953) (29,128)

Purchase of property, plant and equipment - others 12 (ii) (8,393) (1,542) Payment in advance for property, plant and equipment (69,611) (75,955) Purchase of software 13 (970) (350) Proceeds from sale of property, plant and equipment 507 1,089 Payment for rent* 16.1 (4,376) (24,082) Insurance claim received 8 1,379 686 Interest income received 9.1 4,811 4,858 Cash acquired as part of business combination/restructuring 28 112,425 - Restricted cash transferred from other receivables - 34,618 Net cash used in investing activities (14,181) (89,806) Cash flows from financing activities Payment for the principal of lease liabilities (30,270) - Interest paid for lease liabilities (922) - Bonds issued 1,300,000 - Loans received from third parties 500,098 - Loans received from related parties 35,000 - Bank loans repaid 20.3 (1,534,687) (10,896) Principal repayment to related parties 20.3 (435,293) - Premium paid on early settlement of bonds 9.2 (22,153) - Fees on loans and financial derivatives in the period (48,088) (641) (Payment)/receipt of derivative (loss)/gain (1,763) 16,530 Net refund of NDF margins 931 4,738 Interest paid 20.3 (125,831) (95,589) Net cash used in financing activities (362,978) (85,858) Net (decrease)/increase in cash and cash equivalents (44,317) 58,171 Cash and cash equivalents at beginning of period 183,513 125,086 Effect of movements in exchange rates on cash 1,054 256 Cash and cash equivalents at end of period 18 140,250 183,513

* In 2019, following the implementation of IFRS 16, payment for rent represents amounts paid on short-term leases. In 2018, it represents rental paid on all leases.

The accompanying notes are an integral part of these consolidated financial statements.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

16

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

1. General information

This financial information is the consolidated financial statements of IHS Netherlands Holdco B.V. (the "Company") and its subsidiaries (together hereafter referred to as the “Group”). IHS Netherlands Holdco B.V. was incorporated in The Netherlands under Dutch Corporate Law as a private limited liability company having the commercial register number 66017912. The Company is domiciled in The Netherlands and the address of its registered office is:

Haagsche Hof Parkstraat 83, 2514 JG The Hague The Netherlands The Company was incorporated on 12 May 2016 and is a fully owned subsidiary of IHS Netherlands (Interco) Coöperatief U.A. a Dutch Cooperative incorporated in The Netherlands. The ultimate parent is IHS Holding Limited, a company incorporated in Mauritius, the shares of which are held by several companies and individuals.

At 1 January 2019 the Group is comprised of the following: IHS Netherlands Holdco B.V. (Parent), IHS Netherlands NG1 B.V. (100% interest), IHS Netherlands NG2 B.V. (100% interest), IHS Nigeria Limited (100% interest1), IHS Towers NG Limited (100% interest1), Tower Infrastructure Company Limited (100% interest) and IHS Towers Netherlands FinCo NG B.V (100% interest).

On 18 September 2019 IHS Netherlands (Interco) Coöperatief U.A. transferred the shares it held (representing 100% ownership) in Nigeria Tower Interco B.V. to IHS Netherlands Holdco B.V., including its subsidiary, INT Towers Limited. INT Towers Limited is a fully owned subsidiary (100% interest1) of Nigeria Tower Interco B.V. This restructuring took place as part of a refinancing under which the $800m, 9.5% Senior Notes due 2021 (the “2021 Notes”) were fully redeemed and are no longer outstanding and IHS Netherlands Holdco B.V. issued $500 million 7.125% Senior Notes due 2025 (the “2025 Notes”) and $800 million 8.0% Senior Notes due 2027 (the “2027 Notes”) which are listed on The International Stock Exchange (TISE).

The significant subsidiaries, being IHS Nigeria Limited, IHS Towers NG Limited and, from 18 September 2019, INT Towers Limited are incorporated in Nigeria and are principally involved in providing shared telecommunications infrastructure services to Mobile Network Operators (MNOs) and other communications service providers, who in turn provide wireless voice and data services to their end users. These subsidiaries provide customers with opportunities to install active equipment on existing towers alongside current tenants, known as colocation, and provide opportunities for customers to commission the construction of new sites to their specifications. In certain strategic instances, they may also provide managed services, such as maintenance, security and power supply for towers owned by third parties. These subsidiaries provide all their services in Nigeria.

The Company is the “issuer” of the $500 million 7.125% Senior Notes due 2025 (the “2025 Notes”) and $800 million 8.0% Senior Notes due 2027 (the “2027 Notes”)(Together ”the Notes”) which are listed on The International Stock Exchange (TISE).

IHS Towers Netherlands FinCo NG B.V., a wholly owned subsidiary of the Company, is the “issuer” of the $250m 8.375%. Guaranteed Senior Notes due 2019 (the “FinCo Notes” and, together with the 2021 Notes, the “IHS Notes”), issued on 15 July 2014 and which have all been fully repaid at maturity on 15 July 2019 and are no longer outstanding.

2. Summary of significant accounting policies

The principal accounting policies applied in the preparation of the financial statements are set out below.

2.1 Basis of preparation

The financial statements have been prepared in accordance with International Financial Reporting Standards as adopted by the European Union (“IFRS”), including interpretations issued by the IFRS Interpretations Committee (IFRS IC) applicable to companies reporting under IFRS and the statutory provisions of the Dutch Civil Code Book 2, Part 9. The consolidated statements have been prepared under the historical cost convention, as modified by the revaluation of financial assets and liabilities at fair value through other comprehensive income and other financial assets and liabilities (including derivative financial instruments) at fair value through profit or loss.

The consolidated financial statements comprise the consolidated statement of profit or loss and other comprehensive income for the year ended 31 December 2019 (comparative: year ended 31 December 2018), the consolidated statement of financial position as at 31 December 2019 (comparative: 31 December 2018), the consolidated statement of changes in equity for the year ended 31 December 2019 (comparative: year ended 31 December 2018), the consolidated statement of cash flows for the year ended 31 December 2019 (comparative: year ended 31 December 2018), and the notes, comprising a summary of significant accounting policies and other explanatory notes.

The financial information is presented in the functional currency of the parent, US Dollars (US$), rounded to the nearest thousand.

1 Less one share in each of IHS Nigeria Limited, IHS Towers NG Limited and INT Towers Limited which are held by a nominee shareholder, for local legal reasons.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

17

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

2. Summary of significant accounting policies (continued)

2.1 Basis of preparation (continued)

The financial statements were approved on 6 April 2020 by the Management Board.

The preparation of these financial statements requires the use of certain critical accounting estimates. It also requires the Directors to exercise judgement in the process of applying the Group’s accounting policies. Changes in assumptions may have a significant impact on the financial information in the period the assumptions changed. The Directors believe that the underlying assumptions are appropriate and that the Group’s financial information therefore present the financial position and results fairly. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the financial information, are disclosed in note 3.

2.1.1 Going concern

The directors have reasonable expectations that the Group has adequate resources to continue in operational existence for the foreseeable future. The results of management review of the Group’s market, operations and financials in the past year and a forecast for at least twelve months after the date of signing of the financial statements provides a sound basis for the appropriateness of using the going concern assumption in the preparation of the Group’s financial statements for the year ended 31 December 2019, though the existence of Coronavirus (COVID-19) means there is generally a level of uncertainty in the wider macro market.

Coronavirus

The existence of novel coronavirus (COVID-19) was confirmed in early 2020 and has spread rapidly from mainland China across the globe, causing disruptions to businesses and economic activity. Many governments across the world have imposed travel restrictions, lock downs and social distancing with a view to reducing the spread of the virus and hopefully minimising the number of fatalities. The Group considers this outbreak to be a non-adjusting post balance sheet event.

Our main priority has been the health and safety of our employees and our dedicated supply chain. We have adhered to instructions issued by the Nigerian and/or state authorities, including travel restrictions and enforced working from home. Our secondary focus has been around business continuity planning and maintenance of the supply chain. The telecommunications industry has been designated by the Nigerian government as an essential service and, as the largest independent owner and maintainer of towers (towerco) in Nigeria, we have sought relevant permits to allow us to continue to access, fuel and maintain our tower portfolio. Consequently, we believe that the impact on our business is currently limited with no immediate material adverse operational impact. We intend to continue to follow the various national and/or state authorities’ policies and, in parallel, intend to do our utmost to continue our operations as the situation evolves.

Revenues and profitability – The Group has long-term revenue contracts with its customers who we are in regular and frequent dialogue with to see how we can provide support in the operation of their network. Telecoms, and specifically telecoms infrastructure, is an important, stable and durable industry and keeping people connected is now even more important given the current circumstances, and the telecommunications industry has been designated an essential service by the Nigerian government. Thus far in 2020, we have continue to meet our customers’ expectations on service levels and our Network Operating Centre (NOC) has maintained normal service levels. We continue to review and develop our internal contingency plans should the need arise to manage the NOC remotely.

The Group is reviewing measures for cost savings whilst maintaining its ability to operate effectively. Capex investments are likely to be limited generally to necessary replacements of assets until greater certainty on timing of macroeconomic improvement is available.

Supply chain – our sites require supplies of diesel and regular maintenance to continue to operate. IHS presently has diesel inventory to hand and is continually looking to increase its supply and stock to avoid disruption. The Group is working closely with our suppliers on their supply chain in this regard.

Financing and liquidity - Following the reduction in the oil price subsequent to the year end, as well as concerns over COVID-19, there has been pressure on foreign exchange reserves in Nigeria. The Nigerian government has taken measures to protect these reserves through devaluing the CBN rate, which has had a similar, but thus far more limited devaluation impact on the NAFEX rate. Such devaluation and reductions in US dollar liquidity in the Nigerian market may reduce our revenues until such time as our contract resets are applied (unless a divergence in the official CBN rate, as used in our contracts, and the NAFEX rate continues, which would continue to impact us) and impact our ability to make our interest payments on our US dollar denominated obligations, including debt facilities.

The Nigerian CBN and NAFEX Naira rates have both devalued against the US dollar since 31 December 2019 from a NAFEX rate of Naira365:US$1 to Naira387:US$1 at 31 March 2020 (CBN Naira307:US$1 to Naira361:US$1), as the Nigerian Government looks to stabilise the economy and also protect current foreign exchange reserves. While there has been a reduction in US dollar liquidity in the Nigerian market, we were still able to source US$ dollars locally to pay our semi-annual coupon in March 2020. Our current aggregate balance of cash and cash equivalents and margins for non-deliverable forward instruments, remains at a similar level to the 2019 year-end position, even after this coupon payment.

Whilst inherently uncertain, and we expect some impact to our operations and performance, we currently do not believe that the the COVID-19 outbreak will directly have a material adverse effect on our financial condition or liquidity for the foreseeable future such that it is not appropriate to apply the going concern principal to these financial statements.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

18

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

2. Summary of significant accounting policies (continued)

2.1 Basis of preparation (continued)

2.1.1 Going Concern (continued)

The following further forms the basis of management's use of going concern:

The market is growing, and the business has grown its share of the overall market.

The business has grown its revenues, gross profit margins, EBITDA margins and operating cash flows over the year, when compared to the prior period on an annualized basis.

The business has a strong cash and short-term deposits balance at 31 December 2019 of US$140.3 million (2018: US$183.5 million) of which US$20.8 million is held in US Dollars (2018: US$132.2 million).

The business maintains a high level of business ethics and regulatory compliance and there is no indication of any foreseeable material adverse change in the regulatory landscape.

The Group is in compliance with the covenants related to the listed bonds and senior credit facilities as at 31 December 2019 and expects to remain compliant with these covenants over the duration of the forecast period (being for at least twelve months after the date of signing of the financial statements). Refer to note 20 for further details of the covenants.

The Group expects to have sufficient cash reserves and cash generated for the forecast period to meet its financing obligations, which during the current year saw a decrease in financing cost as a percentage of borrowings following the refinancing in September 2019 which resulted in lower interest rates being achieved on outstanding loans and bonds.

2.1.2 Changes in accounting policies and disclosures

(a) New standards, amendments and interpretations adopted by the Group

The Group has applied the following standards and amendments for the first time for its annual reporting period commencing January 1, 2019:

IFRS 16 “Leases” refer to further information below. IFRIC 23 “Uncertainty over Income Tax Treatments” refer to further information below.

IFRS 16 “Leases”

IFRS 16 was issued in January 2016 and it replaces IAS 17 Leases, IFRIC 4 Determining whether an Arrangement contains a Lease, SIC-15 Operating Leases-Incentives and SIC-27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease. Under IFRS 16, lessors continue to classify leases as operating or finance, with IFRS 16’s approach to lessor accounting substantially unchanged from IAS 17. For lessees however, the standard provides a single lessee accounting model requiring lessees to recognise assets and liabilities for all leases which will result in a ‘right of use’ asset for the leased item and a financial liability to pay related rentals. The only allowable exceptions are short-term and low-value leases. As a lessor, the Group has revenue contracts with customers that contain an operating lease component for colocation revenues. Given that lessor accounting under IFRS 16 is largely unchanged, the Group did not have any accounting impact on its revenue from contracts with customers on implementing IFRS 16. The revenue recognition policy for such colocation revenue is described in note 2.4. As a lessee, the Group’s leases primarily comprise real estate leases. The significant majority of these are site land leases for our tower sites but the Group also holds a small number of office space leases and warehouse leases. These leases were classified as operating leases under IAS 17. The Group adopted IFRS 16 from 1 January 2019 using the modified retrospective approach which requires the recognition of the cumulative effect of initially applying IFRS 16, as of 1 January 2019, to the accumulated deficit and not to restate prior years. The Group applied the practical expedient to grandfather the definition of a lease on transition. This means that it will apply IFRS 16 to all contracts entered into before 1 January 2019 and identified as leases in accordance with IAS 17 and IFRIC 4. In applying IFRS 16, the group has used the following practical expedients permitted by the standard:

The Group has elected not to recognize right-of-use assets and lease liabilities for short-term leases (i.e. < 12 months) and leases of low-value assets (i.e. < US$5,000).

The lease liability is initially measured at the present value of the lease payments that are not paid at the adoption date, discounted using a relevant incremental borrowing rate (based on the related risks of each country and the lease term) at the adoption date. The weighted average incremental borrowing rate across all leases was 14.55%.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

19

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

2. Summary of significant accounting policies (continued)

2.1.2 Changes in accounting policies and disclosures (continued)

(a) New standards, amendments and interpretations adopted by the Group (continued)

IFRS 16 “Leases” (continued)

In addition:

Options (extension/termination) on lease contracts were considered on a case by case basis in order to determine the term of the lease for accounting purposes. Past experience was used as a practical expedient for leases in place at 1 January 2019.

In determining the economic incentives to renew, or not to terminate a lease, the Group considers any termination costs under terms of the lease, and the remaining useful life of tower structure located on the leased land. Where the Group has the right to terminate or renew a lease and the tower structure has remaining estimated useful life, it is assumed that such lease will not be terminated or will be renewed as there is an economic incentive to continue operating that site.

Refer to note 2.6 for the accounting policy applicable to leases.

Impact of adopting IFRS 16: Impact on Consolidated Statement of Financial Position line items at the date of adoption, 1January 2019

As reported 31 December 2018

Impact of IFRS 16

At adoption 1 January 2019

Note $’000 $’000 $’000 Non-current assets Right of use assets (i) - 82,965 82,965 Prepaid land rent (ii) 43,572 (43,572) - Current assets Prepaid land rent (ii) 8,626 (6,177) 2,449 Current liabilities Lease liabilities (iii) - (9,326) (9,326) Non-current liabilities Lease liabilities (iii) - (23,890) (23,890)

i. Right of use assets: Non-current assets have increased due to recognition of right-of-use assets on 1 January 2019. The right-of-use assets are initially measured at cost, which comprises the initial amount of the lease liability adjusted for any prepaid lease payments made at or before the adoption date (refer to prepaid land rent below) less any lease incentive received at or before the adoption date.

ii. Prepaid land rent: The balance of prepaid land rent at 31 December 2018 is capitalized to the right of use asset insofar as it relates to leases accounted under IFRS 16. The prepaid land rent in respect of short term or low value leases, which are exempt from being capitalized for under IFRS 16, continues to be accounted for as short-term prepayments.

iii. Lease liabilities: Financial liabilities have increased due to the recognition of lease liabilities. This liability is initially measured at the present value of the lease payments that are not paid at the adoption date, discounted using the relevant incremental borrowing rate. The lease liabilities have been classified between current and non-current.

iv. Discount rate: When measuring lease liabilities for leases that were classified as operating leases, the Group discounted lease payments using its incremental borrowing rate at 1 January 2019. The weighted-average rate applied is 14.55%.

There are no related deferred tax assets and there is no net asset impact. Net current assets are US$15.5 million lower due to the presentation of a portion of the liability as a current liability and the capitalization of the short-term portion of prepaid rent against the right of use asset. Right of use assets exceed the value of lease liabilities by US$49.7 million due to the inclusion of prepaid lease rentals. There is no impact on retained earnings.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

20

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

2. Summary of significant accounting policies (continued)

2.1.2 Changes in accounting policies and disclosures (continued)

(a) New standards, amendments and interpretations adopted by the Group (continued)

IFRS 16 “Leases” (continued)

Reconciliation of the 31 December 2018 operating lease commitments to the IFRS 16 lease liability recognised on adoption:

At 31 December 2018, the Group had non-cancellable operating lease commitments of US$24.6 million, see note 30.2. Under IFRS 16, at 1 January 2019, the Group has recognised lease liabilities which differ from this commitment due to differences in the assessment of the lease term, and the impact of discounting.

2019 $'000

Operating lease commitments as 31 December 2018 as disclosed under IAS 17 24,561 Additional payment cycles* 50,844 Discounted using the incremental borrowing rate at 1 January 2019 (42,599) Other differences 410 Lease liabilities as at 1 January 2019 33,216

* These are payment cycles which were not considered under IAS 17 as they were not contractually committed. Under IFRS 16, the Group considers whether we are more likely than not to exercise renewals as opposed to whether the renewals are automatic and compulsory. This increases the future expected payments for lease renewals where previously not assumed.

IFRIC 23 “Uncertainty over Income Tax Treatments”

IFRIC 23 (effective 1 January 2019) provides guidance on the accounting for current and deferred tax liabilities and assets in circumstances in which there is uncertainty that affect the application of IAS 12 Income Taxes. The Interpretation requires:

The Group to contemplate whether uncertain tax treatments should be considered separately, or together as a group, based on which approach provides better predictions of the resolution;

The Group to determine if it is probable that the tax authorities will accept the uncertain tax treatment; and If it is not probable that the uncertain tax treatment will be accepted, measure the tax uncertainty based on the most likely

amount or expected value, depending on whichever method better predicts the resolution of the uncertainty.

The Group has applied IFRIC 23 Uncertainty over Income Tax Treatment as 1 January 2019 and elected to apply it retrospectively with any cumulative effect recorded in retained earnings as at the date of initial application.

The adoption of IFRIC 23 has no impact on the Group’s financial statements.

(b) New standards, amendments and interpretations not yet adopted by the Group

Certain new accounting standards, interpretations and amendments have been published that are not effective for 31 December 2019 reporting period and have not been early adopted by the Group. They are:

Definition of a Business (Amendments to IFRS 3) Definition of Material (Amendments to IAS 1 and IAS 8) Interest Rate Benchmark Reform (Amendments to IFRS 9, IAS 39 and IFRS 7)

The above amendments to standards are not expected to have a material effect on the Group’s financial statements.

2.2 Consolidation

(a) Subsidiaries

The consolidated financial statements include the financial information and results of the Company and those entities in which it has a controlling interest. The Group controls an entity when the Group is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. Subsidiaries are all entities (including structured entities) over which the Group has control. Subsidiaries are fully consolidated from the date on which control is transferred to the Group. They are deconsolidated from the date the control ceases. All intercompany balances and transactions have been eliminated.

IHS NETHERLANDS HOLDCO B.V. CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2019

21

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (CONTINUED)

2. Summary of significant accounting policies (continued)

2.2 Consolidation (continued)

(b) Business combinations

The consideration transferred for the acquisition comprises the fair value of the assets transferred, liabilities incurred, equity interests issued by the Group and any contingent consideration. Where settlement of any part of cash consideration is deferred, the amounts payable in the future are discounted to their present value as at the date of exchange. The discount rate used is the entity’s incremental borrowing rate, being the rate at which a similar borrowing could be obtained from an independent financier under comparable terms and conditions.

The Group has elected to use predecessor accounting for transfers of interest in subsidiaries between entities under common control (from the holding company to another subsidiary or between commonly controlled subsidiaries). The assets and liabilities of the transferred entities are incorporated into the consolidated financial statements at their carrying values on the date of the transfer, being the date that control was obtained. The Group will continue to apply this elected accounting policy for all future transfers of interest in subsidiaries between entities under common control. These financial statements only include the results of IHS Nigeria Limited, IHS Towers NG Limited and INT Towers Limited from their respective restructuring dates (15 September 2016, 15 September 2016 and 18 September 2019 respectively).

If the Group gains control in a business combination achieved in stages, the acquisition date carrying value of the acquirer’s previously held equity interest in the acquiree is remeasured to fair value at the acquisition date; any gains or losses arising from such remeasurement are recognized in the consolidated statement of profit or loss and other comprehensive income.

The Group has considered whether any of its business combinations represent a sale and leaseback transaction from a lessor perspective and determined that since towers are able to be leased to multiple tenants without restriction, that no such arrangement exists.