Physical Activity And Cardiorespiratory Fitness: Does The 2:1 Concept Hold True?

Upload

khangminh22Category

view

0download

0

5 February 2018

Software & Services

Ctrip

Rating

Hold

Valuation & Risks

TechnologySoftware & Services

Price at 2 Feb 2018 (USD) 46.87

Price target - 12mth (USD) 50.00

52-week range (USD) 59.73 - 42.90

NASDAQ 100 6,760

Initiation of CoverageAsiaChina

Company

Ctrip

Reuters Bloomberg Exchange Ticker

CTRP.OQ CTRP US NSM CTRP

Date5 February 2018

Deutsche BankMarkets Research

A turbulent 2018; initiate with Hold

Dominant leader going through headwind; Initiate with HoldWe anticipate a turbulent 2018 for Ctrip, China's leading OTA player, and initiatewith a Hold rating. A series of mergers and strategic partnerships among leadingplayers is complicating the landscape again. Meituan-Dianping looks to be aformidable competitor in tier 3-5 cities while Alibaba-backed Fliggy is a unknownto competitive dynamics. Headwind to earnings, caused by the unbundling ofcross-sell products, should continue until 2H18E while coupon rates will likelyrise throughout 2018E to regain user trust. We believe the current 36x fwd P/E(vs. China internet avg. of 28x) fairly values the stock and our target price of US$50 yields minimal upside.

Consumption upgrade drives industry growth; Ctrip explores low-tier cityWe expect a booming 19% 2017-20E CAGR for the online travel market in China,benefiting directly from rising disposable income, flexible paid leaves, and easingvisa issuance. The clear consumption upgrade cycle in tier 3-5 cities createsopportunity for growth, but also brings intensifying competition. We expect thefragmented low-end hotel market to be a major battlefront in 2018. Ctrip andQunar have weak brand presence in lower-tier cities than its chief competitorMeituan-Dianping. We thus expect Ctrip to accelerate the marketing campaignfor Qunar and improve synergies with Bestone to facilitate market expansion.

A 1.0x PEG yields target price of US$50; Initiate HoldWe apply a 1.0x PEG ratio against FY18E EPS and FY18-20E EPS CAGR. Weassign 1.0x PEG due to Ctrip's dominant position in China's OTA industry. OurTP implies 39x FY18E P/E, vs. China internet avg. of 28x and Ctrip's five-yearhistorical average of 42x. Hold rated given the short-term unbundling pressureand uncertainty in intensity of market competition. Risks: industry growth, tier3-5 cities expansion, VAS product recovery, and couponing

Forecasts and ratios

Year End Dec 31 2015A 2016A 2017E 2018E 2019E

Sales (CNYm) 10,897.6 19,228.4 26,783.5 33,242.3 41,634.3

EBITDA (CNYm) 637.0 -1,107.1 3,401.4 4,296.8 6,687.9

Reported NPAT (CNYm) 2,507.7 -1,430.7 1,996.3 2,888.5 4,969.8

DB EPS FD(CNY) 9.19 4.30 6.57 8.16 12.08

DB EPS growth (%) 282.3 -53.2 52.6 24.2 48.1

PER (x) 23.9 67.0 44.8 36.0 24.3

EV/EBITDA (x) 88.1 – 46.9 36.6 22.9Source: Deutsche Bank estimates, company data

Eileen Deng

Research Analyst

+852-2203 6227

Han Joon Kim

Research Analyst

+852-2203 6157

Price/price relative

Ctrip NASDAQ 100 (Rebased)

Jul '16 Jan '17 Jul '17 Jan '18

40

60

20

80

Performance (%) 1m 3m 12m

Absolute 1.7 0.9 9.5

NASDAQ 100 3.8 8.4 31.3Source: Deutsche Bank

Key indicators (FY1)

ROE (%) 2.7

Net debt/equity (%) 5.0

Book value/share (CNY) 127.56

Price/book (x) 2.3

Net interest cover (x) 8.3

Operating profit margin (%) 10.5Source: Deutsche Bank

Deutsche Bank AG/Hong Kong

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should beaware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should considerthis report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONSARE LOCATED IN APPENDIX 1. MCI (P) 083/04/2017.

Distributed on: 05/02/2018 13:06:07 GMT

7T2se3r0Ot6kwoPa

5 February 2018

Software & Services

Ctrip

Investment thesisOutlook

We initiate on Ctrip with a Hold rating. We are positive on its dominant leadingposition in high tier cities, yet dark clouds on unbundling and the use of couponsmight continue to bring uncertainty to the company until 2019E. Our sensitivityanalysis on unbundling impact suggests a 30% deviation of 2018 net incomeif Ctrip sees a quick ramp-up of real demand upon consumption upgrade orfaces a strict ban of value-added product sales from CAAC. Ctrip, as an OTAleader, should benefit from China's overall consumption upgrade. China's OTAlandscape, however, has become sophisticated again. We believe Meituan-Dianping is a strong competitor in tier 3-5 cities given its wide user base andstrong local sales team. Fliggy has been quick in enriching its product offeringsalthough it is not a strategic focus for Alibaba. Ctrip is enhancing its one-stoptravel solution through deeper collaboration with travel partners. We expect Ctripto maintain its strengthen in high tier cities, while market share in the hotelsegment might see a slight dip due to the current weak branding in low tiermarkets. Our scenario analysis on low tier hotel expansion suggests that Ctrip'snet income CAGR in the next two years could accelerate to 46.5% or drop to35.5%, vs. our current estimate of 38.6%, in the case of accelerating growth andtotal loss of market share in low-end hotels. We believe Ctrip's current valuationhas already factored in the premium as an OTA leader.

Five reasons for our Hold rating on Ctrip:■ Consumption upgrade drives online travel growth, but Ctrip may not

benefit the most.

■ Solid supply and good service quality ensure a dominant leading positionin tier 1-2 cities; more efforts are needed to overcome the weak brandingin tier 3-5 cities.

■ Ctrip is facing competition from sophisticated players in low tier citiesand outbound travel market.

■ Headwind on unbundling of cross-sell products brings pressure to Ctripin 1H18E.

■ Uncertainty over the outlook in the outbound travel market despite someearly signs of recovery in a few key destinations.

Valuation and risks

We initiate on Ctrip with a Hold rating, mainly because of concerns overintensifying competition in new markets and its expensive valuation. We arepositive on its current dominant leading position in high tier cities. We adopt 1.0XPEG on FY18E EPS (DBe US$1.3) and FY18-20E CAGR (DBe 38.6%). We apply1.0X given its current industry dominant leading position. (We employ a PEGmethodology to be consistent with our China internet coverage which factors inthe net income growth of the next two years.) Our TP of US$50 implies 39x 2018EP/E, vs. China's internet peer average of 28x and the global OTA peer average of25x.

Page 2 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Upside risks include faster-than-expected industry growth/ recovery for outboundtravel, improved competitive position among OTAs and better integration amonginvestees' resources. Downside risks are macro economy slowdown, worse-than-expected competitive environment and unsuccessful investment integration andlower tier city penetration.

Deutsche Bank AG/Hong Kong Page 3

5 February 2018

Software & Services

Ctrip

Ctrip surviving in tripartitecompetitionConsumption upgrade drives online travel industry growth;Ctrip may not benefit the most

China's online travel should be a direct beneficiary of the China consumptionupgrade. Leisure travel should benefit from the country's rising disposableincome, more flexible paid leave and easing of visa issuance. Average disposableincome in the first nine months of 2017 increased 9% YoY, according to the NBS.The Chinese government is also encouraging corporates to grant more flexiblepaid annual leaves to employees. The average budget per trip per traveler in 2017rose 8%, according to xinhuanet.com. The demand seems to be stronger for high-end hotels, alternative accommodation, and diversified local services.

Ctrip, as a dominant one-stop online travel solution provider, should enjoy industrytailwind in tier 1-2 cities. We, however, envision a bigger opportunity for Ctrip intier 3-5 cities, where Meituan-Dianping has a much stronger branding than Ctrip.According to the NBS, per capita income in tier 3 cities has reached tier 2's levelsfrom five years ago. Ctrip intends to leverage Qunar to strengthen the coverageof tier 2-3 cities and utilize Bestone to penetrate into tier 3-5 cities.

Online travel penetration should continue to rise, in our view. We expect China'sonline travel market to register a 19% CAGR over 2017-2020E, vs. Ctrip's GMVCAGR of 20%. We envision Ctrip's air ticket growth to be largely in-line with thatof the industry, while hotels may see some challenges in penetrating into tier 3-5cities. The company is making solid progress in gaining market share in groundtransportation to enrich product offerings, such as train/coach tickets and carrental services. Ctrip's ground transportation has seen triple-digit revenue growthin the last several quarters, due to the wider coverage of destinations and productcategories. We estimate a 2017-2020E CAGR of 29% for ground transportationGMV. The wide product offerings should strengthen Ctrip's one-stop solutionpositioning.

Page 4 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Figure 1: Online travel penetration continues to rise driven by consumptionupgrade

Source: iResearch, DB estimates

We believe hotels should be the major battlefield for OTA players because of themarket is fragmented and has non-standardized products. The hotel segment is37% penetrated online, suggesting significant room for growth. We expect themarket size of online hotel booking to witness a 21% CAGR over 2017-2020E toreach RMB264bn in 2020E, vs. Ctrip's hotel GMV CAGR of 19%. We expect Ctripto have slower hotel GMV growth than the industry because it lacks a brandingadvantage in low tier markets.

Air ticket online penetration reached 81% in 2017 (DBe). We expect the air ticketmarket size to reach RMB586bn in 2020E, a 2017-2020E CAGR of 11%. We seeair ticket a commoditized segment considering the limited number of airlines andstandard products.

Figure 2: Online hotels have clear upside potential; DBe2017-20E CAGR of 21%

Figure 3: Online penetration of air tickets reached 81%in 2017E; DBe 2017-20E CAGR of 11%

Source: iResearch, DB estimates Source: iResearch, DB estimates

Deutsche Bank AG/Hong Kong Page 5

5 February 2018

Software & Services

Ctrip

Solid supply and service quality underpin success in hightier cities; more efforts needed to enhance branding in tier3-5 cities

Ctrip has built up its dominant leading position in the China OTA market viaa series of acquisitions and investment. Upon integration of resources, thecompany owns a large user base, ample travel product offerings, advancedtechnology and good customer services. We view the company as a one-stoponline travel solution provider with decent service quality. The express check-in and check-out service, for instance, skips the involvement of hotel staff andreduces customers' waiting time. Ctrip also leverages big data technology tofilter the appropriate recommendations per user preference. Qunar has helpedSkyscanner to convert the booking system into direct booking with a moresmooth booking experience. With a total of 8,000 engineers, the company aimsto expand investment in AI, Big data, and Cloud computing to provide better userexperience, especially in the international travel market.

However, we expect headwind in tier 3-5 cities because of Ctrip's weak brandingin these low tier cities. The company is utilizing Qunar to expand its tier 2-3 marketshare and is leveraging Bestone's network to cover tier 3-5 cities. There shouldmore branding activities to roll out throughout 2018E. We expect Ctrip to makemore efforts on integrated and localized services to cater to travel demand fromlow tier cities. Nonetheless, we are not worried about the hotel supply to Ctripand Qunar given the vast number of hotel vendors in the market.

Building up the investment basket to enhance one-stop solutionsCtrip has amplified its product offerings through investment and businesscooperation across China and international markets. The company has enhancedits hotel supply via investment in eLong and Tongcheng, and strengthened itsdominant position in the China OTA market upon the acquisition of Qunar in2015. The acquisition of Skyscanner locks product offerings in outbound travel.eLong and Tongcheng recently announced the intent to merger and integrateresources in transportation and hotels. Ctrip remains as a strategic investor in themerged company and continue to share the resources. We believe Ctrip shouldcontinue to take advantage of its one-stop solution and maintain a dominantleading position in high tier cities.

We illustrate Ctrip’s rich investment basket below. It has stakes of 92% inQunar, 100% in Skyscanner, 38% in E-long, ~50% in Tujia, 16% (DBe) in LY.com(Tongcheng), 4% in Tuniu, and 100% in Bestone.

Page 6 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Figure 4: Ctrip has a comprehensive investment basket across the travel industry

Source: company data, news flows

Competitive landscape becomes more sophisticated innew markets

Low tier city penetration and outbound travel have been Ctrip's two majorexpansion plans in the short and medium term. Strong competitors haveemerged in the two markets, i.e. Meituan-Dianping in low tier city penetrationand Fliggy in outbound travel. Meituan-Dianping is backed by Tencent, andreceived investment from Priceline in October 2017. Fliggy has been growingwell especially in outbound self-guided travel. It should be easy for Fliggy totake advantage of Alibaba's traffic, but travel seems not a core strategy of theAlibaba group at the moment, in our view. Besides, the domestic travel market haslarger room to grow than outbound due to international destination uncertainties.Consequently, we believe Meituan-Dianping may bring bigger pressure to Ctripthan Fliggy.

Rich investment basket and business cooperation have enabled Ctrip to carvea 59% market share in China's OTA market, including 59% in flights and 59%in hotels in 2017E. Ctrip app (61m MAU per Quest Mobile) has clear advantagein tier 1-2 cities, while Qunar app (41m MAU) has better presence in tier 2-3cities. We believe online hotel booking is the major battle ground for OTAs. Due tothe fast ramp-up of Meituan-Dianping, we expect Ctrip's market share in onlinehotel booking to dip slightly in the next few years. but its air ticket market shareshould largely be unchanged. The below charts represent market segmentationin China's online travel space, for flights and hotel.

Deutsche Bank AG/Hong Kong Page 7

5 February 2018

Software & Services

Ctrip

Figure 5: Online hotel market share in 2017E, based onGMV

Figure 6: Ctrip likely to see slight dip in online hotelbookings due to Meituan-Dianping fast ramp-up

Source: DB estimates Source: iResearch, Analysys,Travel Sky, DB estimates

Figure 7: Online air ticketing market share in 2017E,based on GMV

Figure 8: Ctrip+Qunar to maintain air ticket market sharein 2017-20E

Source: DB estimates Source: iResearch, Analysys,Travel Sky, DB estimates

Meituan-Dianping has ramped up its hotel supply and flights, although Ctripalso recorded decent growth in low tier hotels in 2Q17. In early 2017, Meituan-Dianping conducted its second company restructuring post the merger withDianping. It took only two quarters to ramp up its travel services. Total "connectedhotels" amounted to 320k as of July 2017. "Room nights" were also near Ctrip'sin 1H17, according to Meituan-Dianping. Our channel checks suggest hotelcoverage in tier 1-2 cities has also increased significantly, including five-starinternational hotels. Meituan-Dianping started cooperation with the IHG groupin December 2016 and received investment from Priceline (15% shareholding) inOctober 2017. We view Meituan-Dianping as a strong competitor in Ctrip’s low-tier-city-penetration strategy.

Fliggy ramped up its market share in flights and hotels to 7% and 15%(DBe), respectively, as of end-2017. Fliggy strategically focuses on outboundpackaged tours for the young generation. The platform is well connected with 100international airlines. We also note international five-star hotels, such as Hilton,IHG, and Marriott Group, have connected with Fliggy. Fliggy is working to utilizevarious value-added services to attract customers, i.e. visa application. We see

Page 8 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Fliggy a clear competitor in the outbound travel market, a segment that we believeits not a core strategy of the Alibaba group so far.

To seize the opportunity of rising income of low tier cities, Ctrip intends to leverageQunar to explore tier 2-3 cities, and to utilize the offline travel agency “Bestone”to penetrate into tier 4-6 cities. In our opinion, better marketing campaignand channel investment would be a more effective strategy than offline storeexpansion in tier 3-5 cities. Bestone was fully acquired by Ctrip in October 2016.Ctrip intends to penetrate into lower tier cities through franchised offline storesunder the Ctrip and Qunar brands, as well as 5,500 partnered franchised storesowned by Bestone. Under these three brands, the company targets to establishmore than 10k offline stores by end-2018, reaching product sales of RMB10bn,which is likely to contribute only ~1% of Ctrip's total GMV. There are 700 offlinestores established under the Ctrip brand in tier 1-2 cities, and we believe will likelyreach 1,500 stores by end-2018. Offline store strategy, therefore, would not movethe needle, in our view. We expect more marketing budget to be allocated to tier3-5 cities in 2018, with branding campaign and channel investment to improvethe brand names of Ctrip and Qunar.

We do not see Fliggy becoming a threat to Ctrip at the moment, although theycompete in the outbound travel market. Ctrip has been continuously building upits international travel partnership to enhance its product offerings. The deepercollaboration with Priceline (including Booking.com, Opentable) and Skyscannershould enable a better one-stop travel solution.

We illustrate our comparison of Ctrip, Meituan-Dianping, and Fliggy in the tablebelow.

Deutsche Bank AG/Hong Kong Page 9

5 February 2018

Software & Services

Ctrip

Figure 9: Key metrics comparison of Ctrip, Meituan-Dianping and Fliggy

Source: company data, news flows, and DB estimates

Scenario analysis on low tier city penetrationCompared to Meituan's 1000 cities/counties coverage, Ctrip and Qunar focus on150 cities with GDP per capita of above US$1000. We expect that a majorityof Ctrip's low-end hotel supply is through Qunar platform, which accountedfor 20-25% of total hotel GMV (16-20% of total hotel revenue) and 33% oftotal hotel coverage (DBe 190,000) in 2017. Meituan's hotel and package usersaccounted for 20% its total users base (i.e. 48m), similar to that of Qunar MAU. Weenvision a successful penetration into tier 3-5 cities, under the current competitivelandscape, will require a wider coverage of low-end hotels and expansion of lowtier cities. The effort in supply side will require a deeper integration of Bestone'snetwork and reallocation of sales resources, while MAU increase should largelyrely on branding and campaign. We illustrate our blue-sky scenario and bear casebelow.

■ Blue-sky scenario

Our blue-sky scenario assumes 3x growth of low-end hotel coverage by end-2018to catch up with that of Meituan-Dianping. We assume revenue to be 20%higher than that under our base case for 2018/19/20. We envision more sales andmarketing budget to be allocated to Qunar and Bestone, which may result in alower margin profile than that of high-end hotels. The likely growing market sharewould suggest long-term margin upside. We assume low-end hotels' non-GAAP

Page 10 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

operating margin of 5%/10%/15% for 2018/19/20. Our blue-sky scenario yields anincrease of net income of 6%/11%/15% in 2018/19/20, and a 2018-20 net incomeCAGR of 46.5% vs 38.6% under our base case.

Figure 10: Blue sky scenario - acceleration in low tier hotel coverage

Source: Deutsche Bank

■ Bear case

Our bear-case scenario assumes total loss of low-end hotel coverage amidcompetition with Meituan-Dianping, but assumes Ctrip maintains its dominantposition in high-end hotels. We assume bear-case revenue would decline by9%/12%/14% and non-GAAP net income would drop 3%/6%/11% in 2018/19/20,respectively. Our bear case yields a 2018-20 net income CAGR of 35.5% vs 38.6%in base case.

Figure 11: Bear case - loss of low tier hotel coverage

Source: Deutsche Bank estimates

Please note our current valuation on Ctrip is based on base case assumption.

Rising coupon rates likely to ease in 2019EWe select certain samples (2-5 star hotels in five tier 1-2 cities) from the platformsof Ctrip, Qunar, Fliggy, and Meituan-Dianping platforms, and check the hotelcoupon rate for month-end room rate per night. Our channel check suggestsMeituan-Dianping was the most aggressive player in granting coupons during2H17, but it dropped sharply by the end of the year. Qunar's coupon rates pickedup quickly in 2H17 especially for 4-5 star hotels. The rise of Qunar's coupon ratesis in-line with Ctrip's strategy of low tier city penetration. Ctrip's coupon ratesalso remained high throughout the year, but dipped sharply at year-end. Fliggy

Deutsche Bank AG/Hong Kong Page 11

5 February 2018

Software & Services

Ctrip

used to grant aggressive coupon for 5-star hotels, which eased sharply at year-end, similar to that of Ctrip.

According to Ctrip, coupon rates may rise in 2018 to attract customers and offsetthe adverse effect from the bundling issue. Giving out more coupons next year isunlikely, as neither Ctrip nor Meituan-Dianping has made aggressive statementsregarding subsidizing. According to Meituan-Dianping, it has no plan to burn cashto gain market share. Ctrip has also indicated the use of coupon is a short-termtactic. We therefore expect the coupon rate to ease in 2019.

Figure 12: Meituan-Dianping offered the highest couponrate for 5-star hotels among OTAs

Figure 13: Ctrip/Qunar remain low signal digit couponrate for 4-star hotels

Source: Company data, Deutsche Bank Source: Company data, Deutsche Bank

Figure 14: Coupon rate for 2/3-star hotels on Meituan-Dianping has increased

Source: Company data, Deutsche Bank

We notice the coupon system basically includes hotel coupons, price deductionand hotel/car services vouchers. Hotel coupons (mostly used by Ctrip) refer tocertain amount of cash credits offered to users upon check-out from hotels andsubmission of reviews, which is used to redeem in future bookings. For Ctrip, theestimated cost of coupon usage is counted in sales and marketing expenses. Anyprice deduction in air tickets and hotel bookings, for instance a RMB30 deductionper ticket/hotel booking for first-time users, could hit net revenue directly. OTAsalso provide vouchers for hotel and car services as a part of marketing expenses,i.e RMB38 hotel voucher which could be used to redeem RMB100 for the nexthotel booking. We believe the first two types of coupons, hotel coupons and price

Page 12 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

deduction, are more commonly used and we track these two coupons for thehotel business, as shown in the above charts. The street has revised up 2018 opexforecasts by 7% post 3Q17 earnings, to factor in the rising coupon. The companyalso guided for 1Q18 margin to be down QoQ due to coupon offerings.

Unbundling stress remains in 1H18

Ctrip share prices dropped in late August last year, after the Civil AviationAdministration of China (CAAC) reiterated the regulation of prohibiting air ticketsto be bundled with value-added products. These bundled products include travelinsurance, invoice delivery, car pick-up, airport VIP lounge, hotel coupon, etc. Allthese value-added products represent 10-15% of total net revenue (10% from opt-out, 5% from opt-in) and 20-30% of transportation ticketing revenue. Ctrip hasremoved most of its default setting and change "opt-out" to "opt-in" with clearlabel on its platform. There are still a small proportion of "opt-out" products forrepeated customers, who have ever proactively selected to purchase. We expectthese remaining "opt-out" products to change into "opt-in" as well when theCAAC's transportation regulation draft for comment is due on Feb 9. As a result,the company is be more conservative on 4Q17/1Q18 revenue growth and marginprofile forecasts. Our estimates is at the low end of the company guidance.

Ctrip has guided a conservative 2018 revenue growth to reflect the use of rebate/coupon to offset the short-term PR impact (e.g. bundled sales). The couponoffering is likely to cause short-term margin pressure. We therefore expect 1Q18non-GAAP operating margin to be lower than 4Q's. It may take time for Ctrip torid off the PR pressure; the company envisions a recovery in 2H18.

Sensitivity analysis on unbundling of cross-sell productsOur estimate has reflected the unbundling impact of 10% on 4Q17E and 1Q18Erevenue. Before the unbundling, 5% of Ctrip's revenue came from "opt-in"products. As such, we believe the real demand for these value-added products willresume gradually. Our estimates include 5% of opt-in products sales in 2018E, ashighlighted in the below table. Our sensitivity analysis suggests a 30% deviationon net income from our current estimate if opt-in product sale drops to 0% orincreases to 10% of 2018E revenue.

Our bear case assumes a complete removal of value-added products from Ctrip,which may materialize if the CAAC imposes a strict ban. Given that value-addedproducts gross margin is as high as 90%+, a complete removal will cause a 30%decline in 2018E net income. Our bull case assumes a quick ramp-up of realdemand along with consumption upgrade, and offset most of the unbundlingadverse effects. A 10% contribution from value-added products in our bull-casescenario will lead to a 30% increase in 2018E net income.

Deutsche Bank AG/Hong Kong Page 13

5 February 2018

Software & Services

Ctrip

Figure 15: Sensitivity analysis on unbundling products

Source: Deutsche Bank estimates

Outbound travel saw recovery signs in certain destinations;uncertainties still exist

International market expansion is one of the two key strategies for Ctrip. Ctrip’sline-up with Priceline and Skyscanner has secured international hotel and flightsupply. Ctrip also leveraged its technology to upgrade its overall booking services,e.g. changed Skyscanner meta search model to direct booking and enables aseamless booking experience.

We view the dark cloud in the outbound travel market has not yet fully passed.Some destinations, however, might start to see recovery, e.g. the end of Thailandmourning period. European has been be growing very fast (up 65% YoY in 1H17,according to Ctrip's industry report). According to chyxx.com, 2017 full yearoutbound traveller will likely see mild improvement to 6.6% YoY (vs. 4.3% YoY in2016). We expect the market to further recover to 7.6% in 2018E.

China outbound travel is further penetrated in lower tier cities. As of 1H17, eightout of the top 10 fastest growth outbound travel cities are from tier 2 cities.Some 50% of outbound travelers to Europe came from tier 2-3 cities, surpassingtier 1 cities (45%). Total number of personal passport holders increased to 120m(penetration less than 10%). We expect Qunar (41m MAU) to better leverage itsadvantage in tier 2-3 cities than Ctrip (61m MAU), yet Meituan-Dianping shouldremain as a strong competitor given its vast user base and line-up with Priceline.

Page 14 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Figure 16: Outbound travellers by key destinations in 2017E

Source: chyxx.com, DB estimates

Given the early signs of recovery in certain international destinations, we expectmodest recovery of outbound travel in the next few years. We are cautious aboutdestination uncertainties.

Figure 17: Outbound traveler number is likely to recover gradually from 2018

Source: CNTA, China Tourism Academy, DB estimates

Deutsche Bank AG/Hong Kong Page 15

5 February 2018

Software & Services

Ctrip

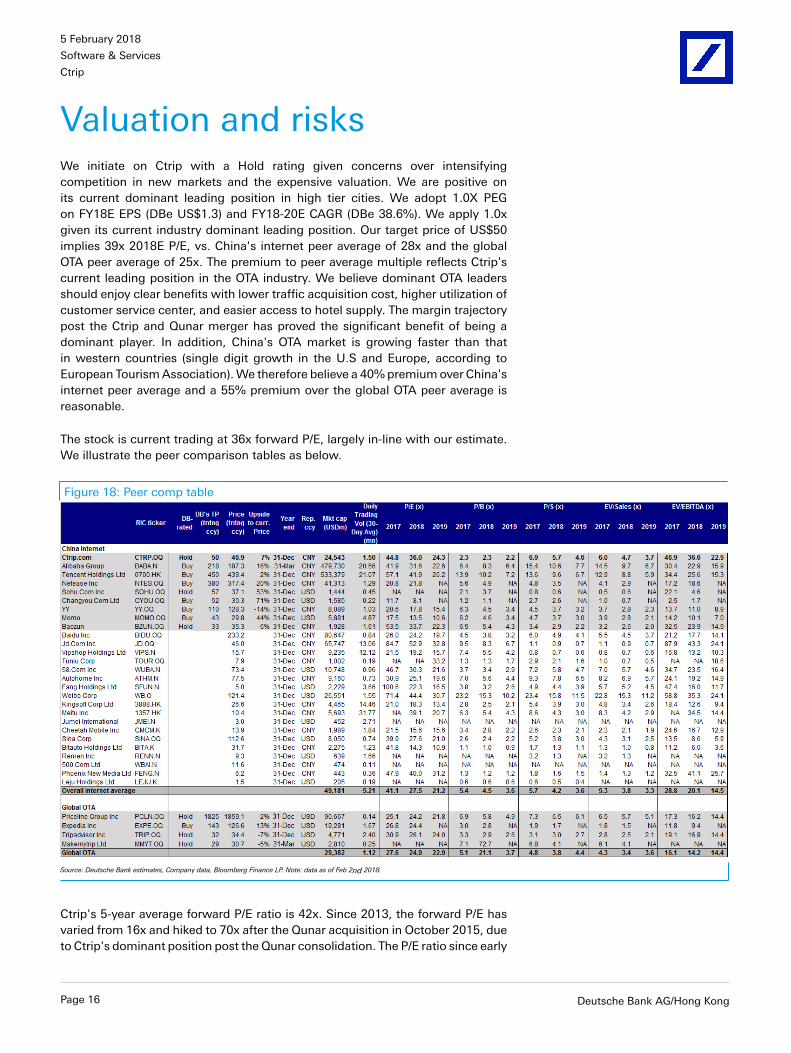

Valuation and risksWe initiate on Ctrip with a Hold rating given concerns over intensifyingcompetition in new markets and the expensive valuation. We are positive onits current dominant leading position in high tier cities. We adopt 1.0X PEGon FY18E EPS (DBe US$1.3) and FY18-20E CAGR (DBe 38.6%). We apply 1.0xgiven its current industry dominant leading position. Our target price of US$50implies 39x 2018E P/E, vs. China's internet peer average of 28x and the globalOTA peer average of 25x. The premium to peer average multiple reflects Ctrip'scurrent leading position in the OTA industry. We believe dominant OTA leadersshould enjoy clear benefits with lower traffic acquisition cost, higher utilization ofcustomer service center, and easier access to hotel supply. The margin trajectorypost the Ctrip and Qunar merger has proved the significant benefit of being adominant player. In addition, China's OTA market is growing faster than thatin western countries (single digit growth in the U.S and Europe, according toEuropean Tourism Association). We therefore believe a 40% premium over China'sinternet peer average and a 55% premium over the global OTA peer average isreasonable.

The stock is current trading at 36x forward P/E, largely in-line with our estimate.We illustrate the peer comparison tables as below.

Figure 18: Peer comp table

Source: Deutsche Bank estimates, Company data, Bloomberg Finance LP. Note: data as of Feb 2nd 2018.

Ctrip's 5-year average forward P/E ratio is 42x. Since 2013, the forward P/E hasvaried from 16x and hiked to 70x after the Qunar acquisition in October 2015, dueto Ctrip's dominant position post the Qunar consolidation. The P/E ratio since early

Page 16 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

2017 has been largely trending down due to competition with Meituan-Dianpingand it fluctuates further since the cross sales issue in last October.

The implied 39x forward P/E (compared to the average 45x forward P/E sincethe beginning of 2017) incorporates the competition with Meituan-Dianping andpressure from the short-term PR issue. We believe current competition is not asintense as that in 2013 - mid 2015 (before the Ctrip and Qunar merger) givenMeituan-Dianping's smaller travel business size . We therefore believe the implied39x is at a fair level and less likely to trend down.

Figure 19: Ctrip's 5-year historical P/E trend

Source: Deutsche Bank estimates, Company data, Bloomberg Finance LP.

Figure 20: Ctrip's 5-year forward PE band

Source: Deutsche Bank estimates, Company data, Bloomberg Finance LP.

Deutsche Bank AG/Hong Kong Page 17

5 February 2018

Software & Services

Ctrip

RisksUpside risks:

■ Faster penetration into low tier cities

■ Ease of low-end hotel competition

■ Faster ramp of real demand in VAS product

■ Better integration of investees/partners' resources

■ Faster recovery of outbound travel

Downside risks:

■ Slower penetration of low tier markets

■ Intensified low-end hotel competition with higher coupon rate

■ Stricter rules on selling VAS products

■ Failure of integration of investees/partners' resources

■ Further slow down of outbound travel.

Page 18 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Financial forecastsIncome statement

Long-term margin target to be back on track after short-term fluctuationsManagement recently reiterated the non-GAAP operating margin target of20-30% for the next two-three years. We envision 2018 as a tough year for thecompany given the unbundling impact and the increase in coupon rates. Ctriphas guided a conservative 2018 revenue and margin growth to reflect the impact.We believe both factors should ease from 2019, and operating leverage will likelystart to kick in. We expect non-GAAP operating margin/net margin to increasefrom 18%/15.7% in 2018 to 23.6%/20.5% in 2020.

Our margin forecast is slightly lower than Bloomberg consensus because ofour concern on intense competition, especially from the impact of rebates andcoupons. We illustrate our margin forecasts below.

Figure 21: DBe non-GAAP operating margin to grow to23.6% in 2020E

Figure 22: DBe non-GAAP net margin should increase to20.5% in 2020E

Source: Company data, Deutsche Bank estimates Source: Company data, Deutsche Bank estimates

Quarterly financials previewCtrip has guided 25-30% YoY net revenue growth for 4Q17 and 15-20% YoY for1Q18. The relatively weak guidance reflects the impact from unbundled sales inair tickets (DBe 10-15% of total net revenue), as well as some other PR issue (i.e.kindergarten misconduct). The company plans to grant more coupons/rebatesto users to offset the negative impact. Revenue growth should normalize from2Q18E. We expect RMB6.4bn of net revenue for 4Q17 and RMB7.1bn for 1Q18.We expect non-GAAP operating margin of 13.4% and 12.3%, respectively, in4Q17 ad 1Q18. 1Q18 non-GAAP operating margin should be lower than 4Q17 dueto the increase of coupon/rebate usage.

Deutsche Bank AG/Hong Kong Page 19

5 February 2018

Software & Services

Ctrip

Figure 23: DB quarterly financials forecasts

Source: Deutsche Bank estimates

Annual income statement forecastsWe expect Ctrip to deliver 22-25% YoY revenue growth during 2018-20E, thanksto better Qunar integration and growing contribution from Skyscanner. The slowerrevenue growth rate in FY2018 reflects the ceased financial impact from the Qunarand Skyscanner consolidation. We expect impacts from the unbundling of cross-sell products to last until 2H18, and therefore forecast a relative conservative fullyear revenue growth. Margin improvement should be back on track from 2019E.We estimate non-GAAP operating margin will improve from 10.4% in 2016 to17.6%/18%/21.3%/23.6% in 2017-20E, respectively, on track to reach the long-term margin target of 20-30% as guided by management. We keep a cautiousview on potential coupon competition.

Page 20 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Figure 24: Income statement

Source: Company data, DB estimates

Comparison with consensus forecastsOur revenue forecasts for the next three years are 0%/1%/2% lower thanBloomberg consensus. Non-GAAP net income is 8%/3%/8% higher thanconsensus. Given that Ctrip has always beaten Bloomberg consensus' bottom

Deutsche Bank AG/Hong Kong Page 21

5 February 2018

Software & Services

Ctrip

line in the past two years, we believe consensus forecasts are usually overlyconservative.

Figure 25: DB forecasts vs consensus

Source: Deutsche Bank estimates, Bloomberg for consensus data. Consensus was last updated on Jan 30th 2018

Balance sheet

Ctrip had RMB18bn of cash balance as of end-2016, and we expect the companyto maintain the rich cash position driven by improved profitability. The companyis currently in a net debt position (DBe RMB3.6bn as at end-2017), inline withinternational players such as Priceline, Expedia, Makemytrip, etc. We expect itsnet debt to narrow down in 2018 and will likely turn into net cash from 2019,driven by business growth and improving margin profile.

Ctrip recorded a RMB56b goodwill in FY16, 77% of which reflected the goodwillfrom the acquisition of Qunar. Goodwill will be tested annually for impairment.No impairment was recorded in the past three years.

Page 22 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Figure 26: Balance sheet

Source: Company data, DB estimates

Cashflow statement

We expect operating cash flows to improve from RMB6.7bn in 2017E toRMB13.9bn in 2020E, driven by the gradual profitability improvement. We expectcapex to maintain at RMB600-800mn per year. Major capex is related to thepurchase of computers and website-related equipments. Ctrip invested in anoffice building in 2014, but we do not expect such scale of investment in fixedasset in the next few years. Long-term investment picked up in 2016 as Ctripinvested in Skyscanner, MakeMyTrip, Bestone, BTG Hotels and China EasternAirlines. Another noticeable amount of investment in 2017 was in Tujia's seriesE financing. Given that the company is continuing to strengthen its marketpositioning and enhance its one-stop travel solution, we expect continued long-term investments going forwards.

Ctrip issued convertible notes every year from 2012-2016. We envision similarfinancing tools in the next three years to enable strategic investment and businessline-up.

Deutsche Bank AG/Hong Kong Page 23

5 February 2018

Software & Services

Ctrip

Figure 27: Cashflow statement

Source: Company data, DB estimates

Page 24 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Appendix ABasic company introduction

Ctrip has been a dominant player in the OTA segment, fueled by its expandinginvestment basket including Qunar, eLong, Skyscanner, etc. Ctrip's business linesinclude transportation ticketing, accommodation, packaged tour, corporate traveland other travel-related services. The company was incepted in 1999 and listedin 2003, and completed a major merger with Qunar in late 2015.

Shareholding structureCtrip's major shareholders are Baidu (20.1% on the stock exchange in late 2015),Baillie Gifford & Co. (9.6%), and Priceline (8.9%) as of Feb 28, 2017. We illustratethe shareholder structure in the chart below.

Figure 28: Shareholding structure as of Feb 28th 2017

Source: Company data

Management profileCtrip was founded by James Liang, Min Fan, Neil Shen and Qi Ji, in 1999. JamesLiang served as Ctrip's CEO from 2000 to 2006, and 2013 to 2016. Jane Sunstepped up to be CEO in November 2016, after serving as CFO and COO of Ctrip.Maohua Sun has been COO since November 2016. Cindy Wang has served asCFO since November 2013. We summarize the management profile as below.

Deutsche Bank AG/Hong Kong Page 25

5 February 2018

Software & Services

Ctrip

Figure 29: Management profile

Source: Company data

Summary of China tier citiesBased on China Business Network (CBN), we show the detailed city list by tiers.There are four tier 1 cities – Beijing, Shanghai, Guangzhou and Shenzhen abd 15new tier 1 cities, such as Chengdu and Hangzhou. These cities have pick up interms of commercial attraction.

Page 26 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Figure 30: Details of China tier cities

Source: China Business Network

Deutsche Bank AG/Hong Kong Page 27

5 February 2018

Software & Services

Ctrip

Model updated: 05 February 2018

Running the numbersAsiaChinaSoftware & Services

CtripReuters: CTRP.OQ Bloomberg: CTRP US

HoldPrice (2 Feb 18) USD 46.87

Target Price USD 50.00

52 Week range USD 42.90 - 59.73

Market cap (m) USDm 24,790 EURm 19,916

Company ProfileCtrip.com International, Ltd. is a leading provider ofaccommodation reservation, transportation ticketing, packagetour and corporate travel management and other travel-relatedservices in China. It has gone through rapid growth since itsinception in 1999 and become Chinaâs largest travel company.The company currently employs over 30,000 people. With itsoperational headquarters in Shanghai, Ctrip has branches in other16 major cities in Mainland China.

Price Performance

Ctrip NASDAQ 100 (Rebased)

Jan '17 Jan '18Jul '16 Jul '1730

40

50

60

70

Margin Trends

EBITDA Margin EBIT Margin

14 15 16 17E 18E 19E-10

0

10

20

Growth & Profitibility

Sales growth (LHS) ROE (RHS)

14 15 16 17E 18E 19E0

100

25

50

75

-5

0

5

10

15

Solvency

Net debt/equity (LHS) Net interest cover (RHS)

14 15 16 17E 18E 19E-5

0

5

10

15

10

7.5

12.5

15

17.5

Eileen Deng+852 2203 6227 [email protected]

Fiscal year end 31-Dec 2014 2015 2016 2017E 2018E 2019E

Financial SummaryDB EPS (CNY) 2.40 9.19 4.30 6.57 8.16 12.08Reported EPS (CNY) 0.79 7.32 -2.89 3.38 4.52 7.62DPS (CNY) 0.00 0.00 0.00 0.00 0.00 0.00BVPS (CNY) 31.0 130.0 144.6 127.6 125.9 135.3Weighted average shares (m) 274 302 473 529 546 559Average market cap (CNYm) 45,636 66,415 136,507 155,520 155,520 155,520Enterprise value (CNYm) 40,100 56,148 145,534 159,638 157,199 153,398

Valuation MetricsP/E (DB) (x) 69.2 23.9 67.0 44.8 36.0 24.3P/E (Reported) (x) 210.8 30.1 nm 87.0 65.0 38.6P/BV (x) 4.52 2.24 1.84 2.31 2.34 2.17FCF Yield (%) nm 3.6 3.4 3.9 4.7 6.4Dividend Yield (%) 0.0 0.0 0.0 0.0 0.0 0.0EV/Sales (x) 5.5 5.2 7.6 6.0 4.7 3.7EV/EBITDA (x) nm 88.1 nm 46.9 36.6 22.9EV/EBIT (x) nm 147.4 nm 56.5 43.1 25.7

Income Statement (CNYm)Sales revenue 7,347 10,898 19,228 26,783 33,242 41,634Gross profit 5,246 7,854 14,499 21,814 26,084 32,972EBITDA 23 637 -1,107 3,401 4,297 6,688Depreciation 174 256 461 578 646 728Amortisation 0 0 0 0 0 0EBIT -151 381 -1,568 2,823 3,651 5,960Net interest income(expense) 142 143 -165 -341 -236 194Associates/affiliates 87 -136 602 65 129 129Exceptionals/extraordinaries 0 0 0 0 0 0Other pre-tax income/(expense) 144 2,481 -27 642 400 400Profit before tax 135 3,005 -1,760 3,124 3,815 6,554Income tax expense 131 470 478 1,105 916 1,573Minorities -151 -108 -206 88 140 140Other post-tax income/(expense) 0 0 0 0 0 0Net profit 243 2,508 -1,431 1,996 2,889 4,970DB adjustments (including dilution) 497 643 3,560 1,883 2,325 2,907DB Net profit 739 3,150 2,129 3,879 5,213 7,877

Cash Flow (CNYm)Cash flow from operations 1,959 3,049 5,273 6,692 8,311 11,232Net Capex -4,789 -638 -683 -696 -731 -791Free cash flow -2,830 2,411 4,590 5,996 7,579 10,441Equity raised/(bought back) -260 -147 0 0 0 0Dividends paid 0 0 0 0 0 0Net inc/(dec) in borrowings 5,579 15,433 11,287 1,733 1,819 1,910Other investing/financing cash flows -4,475 -3,841 -18,139 -6,935 -10,935 -12,435Net cash flow -1,986 13,856 -2,263 794 -1,536 -83Change in working capital 1,431 1,697 3,420 1,826 2,055 2,237

Balance Sheet (CNYm)Cash and other liquid assets 11,740 27,451 32,548 39,276 43,675 49,526Tangible fixed assets 5,221 5,556 5,592 5,324 5,023 4,707Goodwill/intangible assets 2,561 56,698 69,940 69,940 69,940 69,940Associates/investments 5,423 13,973 20,632 21,632 26,632 33,132Other assets 6,347 15,164 15,702 19,740 23,516 27,281Total assets 31,291 118,843 144,414 155,913 168,787 184,587Interest bearing debt 11,626 31,157 41,538 43,271 45,090 47,000Other liabilities 9,287 24,001 27,355 33,220 39,050 45,053Total liabilities 20,913 55,158 68,893 76,490 84,140 92,052Shareholders' equity 9,529 44,551 71,537 75,351 80,434 88,182Minorities 849 19,134 3,984 4,072 4,212 4,353Total shareholders' equity 10,378 63,685 75,521 79,423 84,647 92,534Net debt -113 3,705 8,990 3,994 1,415 -2,526

Key Company MetricsSales growth (%) 36.4 48.3 76.4 39.3 24.1 25.2DB EPS growth (%) -49.6 282.3 -53.2 52.6 24.2 48.1EBITDA Margin (%) 0.3 5.8 -5.8 12.7 12.9 16.1EBIT Margin (%) -2.1 3.5 -8.2 10.5 11.0 14.3Payout ratio (%) 0.0 0.0 nm 0.0 0.0 0.0ROE (%) 2.7 9.3 -2.5 2.7 3.7 5.9Capex/sales (%) 65.2 5.9 3.6 2.6 2.2 1.9Capex/depreciation (x) 26.3 2.0 0.9 0.7 0.7 0.7Net debt/equity (%) -1.1 5.8 11.9 5.0 1.7 -2.7Net interest cover (x) nm nm nm 8.3 15.5 nm

Source: Company data, Deutsche Securities estimates

Page 28 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Appendix 1

Important Disclosures

*Other information available upon request

Disclosure checklistCompany Ticker Recent price* Disclosure

Ctrip CTRP.OQ 46.87 (USD) 2 Feb 2018 2, 6, 9*Prices are current as of the end of the previous trading session unless otherwise indicated and are sourced from local exchanges via Reuters, Bloomberg and other vendors . Otherinformation is sourced from Deutsche Bank, subject companies, and other sources. For disclosures pertaining to recommendations or estimates made on securities other than theprimary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr. Aside from within this report, important conflict disclosures can also be found at https://gm.db.com/equities under the "Disclosures Lookup" and "Legal"tabs. Investors are strongly encouraged to review this information before investing.

Important Disclosures Required by U.S. RegulatorsDisclosures marked with an asterisk may also be required by at least one jurisdiction in addition to the United States.SeeImportant Disclosures Required by Non-US Regulators and Explanatory Notes.

2. Deutsche Bank and/or its affiliate(s) makes a market in equity securities issued by this company.

6. Deutsche Bank and/or its affiliate(s) owns one percent or more of a class of common equity securities of thiscompany calculated under computational methods required by US law.

Important Disclosures Required by Non-U.S. RegulatorsDisclosures marked with an asterisk may also be required by at least one jurisdiction in addition to the United States.SeeImportant Disclosures Required by Non-US Regulators and Explanatory Notes.

2. Deutsche Bank and/or its affiliate(s) makes a market in equity securities issued by this company.

6. Deutsche Bank and/or its affiliate(s) owns one percent or more of a class of common equity securities of thiscompany calculated under computational methods required by US law.

9. Deutsche Bank and/or its affiliate(s) owns one percent or more of any class of common equity securities of thiscompany calculated under computational methods required by India law.

For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of thisresearch, please see the most recently published company report or visit our global disclosure look-up page on our websiteat http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr

Analyst Certification

The views expressed in this report accurately reflect the personal views of the undersigned lead analyst(s) about thesubject issuer and the securities of the issuer. In addition, the undersigned lead analyst(s) has not and will not receive anycompensation for providing a specific recommendation or view in this report. Eileen Deng

Deutsche Bank AG/Hong Kong Page 29

5 February 2018

Software & Services

Ctrip

Historical recommendations and target price. Ctrip (CTRP.OQ)(as of 02/02/2018)

Current RecommendationsBuyHoldSellNot RatedSuspended Rating

** Analyst is no longer atDeutsche Bank

Date

Secu

rity

pric

e

1 23

4

5

6

May '16 Sep '16 Jan '17 May '17 Sep '17 Jan '180.00

20.00

40.00

60.00

80.00

1. 03/18/2016 Buy, Target Price Change USD 50,00 Alvin Jiang** 4. 11/24/2016 Buy, Target Price Change USD 58,00 Alvin Jiang**2. 05/19/2016 Buy, Target Price Change USD 60,00 Alvin Jiang** 5. 02/23/2017 Buy, Target Price Change USD 60,00 Alvin Jiang**3. 09/06/2016 Buy, Target Price Change USD 57,00 Alvin Jiang** 6. 05/11/2017 Buy, Target Price Change USD 62,00 Alvin Jiang**§§§§$$$$$§§§§§

Equity Rating Key Equity rating dispersion and banking relationships

Buy: Based on a current 12- month view of total share-holderreturn (TSR = percentage change in share price from currentprice to projected target price plus pro-jected dividend yield ) ,we recommend that investors buy the stock.Sell: Based on a current 12-month view of total share-holderreturn, we recommend that investors sell the stock.Hold: We take a neutral view on the stock 12-months out and,based on this time horizon, do not recommend either a Buyor Sell.

Newly issued research recommendations and target pricessupersede previously published research.

Page 30 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Additional Information

The information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively"Deutsche Bank"). Though the information herein is believed to be reliable and has been obtained from public sourcesbelieved to be reliable, Deutsche Bank makes no representation as to its accuracy or completeness. Hyperlinks to third-party websites in this report are provided for reader convenience only. Deutsche Bank neither endorses the content noris responsible for the accuracy or security controls of those websites.??If you use the services of Deutsche Bank in connection with a purchase or sale of a security that is discussed in this report,or is included or discussed in another communication (oral or written) from a Deutsche Bank analyst, Deutsche Bank mayact as principal for its own account or as agent for another person.??Deutsche Bank may consider this report in deciding to trade as principal. It may also engage in transactions, for itsown account or with customers, in a manner inconsistent with the views taken in this research report. Others withinDeutsche Bank, including strategists, sales staff and other analysts, may take views that are inconsistent with those takenin this research report. Deutsche Bank issues a variety of research products, including fundamental analysis, equity-linkedanalysis, quantitative analysis and trade ideas. Recommendations contained in one type of communication may differfrom recommendations contained in others, whether as a result of differing time horizons, methodologies, perspectivesor otherwise. Deutsche Bank and/or its affiliates may also be holding debt or equity securities of the issuers it writeson. Analysts are paid in part based on the profitability of Deutsche Bank AG and its affiliates, which includes investmentbanking, trading and principal trading revenues.??Opinions, estimates and projections constitute the current judgment of the author as of the date of this report. They donot necessarily reflect the opinions of Deutsche Bank and are subject to change without notice. Deutsche Bank providesliquidity for buyers and sellers of securities issued by the companies it covers. Deutsche Bank research analysts sometimeshave shorter-term trade ideas that may be inconsistent with Deutsche Bank's existing longer-term ratings. Trade ideasfor equities can be found at the SOLAR link at http://gm.db.com. A SOLAR idea represents a high-conviction belief by ananalyst that a stock will outperform or underperform the market and/or a specified sector over a time frame of no less thantwo weeks and no more than six months. In addition to SOLAR ideas, analysts may occasionally discuss with our clients,and with Deutsche Bank salespersons and traders, trading strategies or ideas that reference catalysts or events that mayhave a near-term or medium-term impact on the market price of the securities discussed in this report, which impactmay be directionally counter to the analysts' current 12-month view of total return or investment return as describedherein. Deutsche Bank has no obligation to update, modify or amend this report or to otherwise notify a recipient thereofif an opinion, forecast or estimate changes or becomes inaccurate. Coverage and the frequency of changes in marketconditions and in both general and company-specific economic prospects make it difficult to update research at definedintervals. Updates are at the sole discretion of the coverage analyst or of the Research Department Management, and themajority of reports are published at irregular intervals. This report is provided for informational purposes only and doesnot take into account the particular investment objectives, financial situations, or needs of individual clients. It is not anoffer or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy.Target prices are inherently imprecise and a product of the analyst ’ s judgment. The financial instruments discussedin this report may not be suitable for all investors, and investors must make their own informed investment decisions.Prices and availability of financial instruments are subject to change without notice, and investment transactions can leadto losses as a result of price fluctuations and other factors. If a financial instrument is denominated in a currency otherthan an investor's currency, a change in exchange rates may adversely affect the investment. Past performance is notnecessarily indicative of future results. Performance calculations exclude transaction costs, unless otherwise indicated.Unless otherwise indicated, prices are current as of the end of the previous trading session and are sourced from localexchanges via Reuters, Bloomberg and other vendors. Data is also sourced from Deutsche Bank, subject companies, andother parties.??The Deutsche Bank Research Department is independent of other business divisions of the Bank. Details regardingorganizational arrangements and information barriers we have established to prevent and avoid conflicts of interest withrespect to our research are available on our website under Disclaimer, found on the Legal tab.??

Deutsche Bank AG/Hong Kong Page 31

5 February 2018

Software & Services

Ctrip

Macroeconomic fluctuations often account for most of the risks associated with exposures to instruments that promiseto pay fixed or variable interest rates. For an investor who is long fixed-rate instruments (thus receiving these cashflows), increases in interest rates naturally lift the discount factors applied to the expected cash flows and thuscause a loss. The longer the maturity of a certain cash flow and the higher the move in the discount factor, thehigher will be the loss. Upside surprises in inflation, fiscal funding needs, and FX depreciation rates are among themost common adverse macroeconomic shocks to receivers. But counterparty exposure, issuer creditworthiness, clientsegmentation, regulation (including changes in assets holding limits for different types of investors), changes in taxpolicies, currency convertibility (which may constrain currency conversion, repatriation of profits and/or liquidation ofpositions), and settlement issues related to local clearing houses are also important risk factors. The sensitivity of fixed-income instruments to macroeconomic shocks may be mitigated by indexing the contracted cash flows to inflation, toFX depreciation, or to specified interest rates – these are common in emerging markets. The index fixings may – byconstruction – lag or mis-measure the actual move in the underlying variables they are intended to track. The choice ofthe proper fixing (or metric) is particularly important in swaps markets, where floating coupon rates (i.e., coupons indexedto a typically short-dated interest rate reference index) are exchanged for fixed coupons. Funding in a currency that differsfrom the currency in which coupons are denominated carries FX risk. Options on swaps (swaptions) the risks typical tooptions in addition to the risks related to rates movements.??Derivative transactions involve numerous risks including market, counterparty default and illiquidity risk. Theappropriateness of these products for use by investors depends on the investors' own circumstances, including theirtax position, their regulatory environment and the nature of their other assets and liabilities; as such, investors shouldtake expert legal and financial advice before entering into any transaction similar to or inspired by the contents of thispublication. The risk of loss in futures trading and options, foreign or domestic, can be substantial. As a result of thehigh degree of leverage obtainable in futures and options trading, losses may be incurred that are greater than theamount of funds initially deposited – up to theoretically unlimited losses. Trading in options involves risk and is notsuitable for all investors. Prior to buying or selling an option, investors must review the "Characteristics and Risks ofStandardized Options”, at http://www.optionsclearing.com/about/publications/character-risks.jsp. If you are unable toaccess the website, please contact your Deutsche Bank representative for a copy of this important document.??Participants in foreign exchange transactions may incur risks arising from several factors, including: (i) exchange rates canbe volatile and are subject to large fluctuations; (ii) the value of currencies may be affected by numerous market factors,including world and national economic, political and regulatory events, events in equity and debt markets and changes ininterest rates; and (iii) currencies may be subject to devaluation or government-imposed exchange controls, which couldaffect the value of the currency. Investors in securities such as ADRs, whose values are affected by the currency of anunderlying security, effectively assume currency risk.??Deutsche Bank is not acting as a financial adviser, consultant or fiduciary to you or any of your agents with respect toany information provided in this report. Deutsche Bank does not provide investment, legal, tax or accounting advice, andis not acting as an impartial adviser. Information contained herein is being provided on the basis that the recipient willmake an independent assessment of the merits of any investment decision, and is not meant for retirement accounts orfor any specific person or account type. The information we provide is directed only to persons we believe to be financiallysophisticated, who are capable of evaluating investment risks independently, both in general and with regard to particulartransactions and investment strategies, and who understand that Deutsche Bank has financial interests in the offering ofits products and services. If this is not the case, or if you or your agent are an IRA or other retail investor receiving thisdirectly from us, we ask that you inform us immediately.

Unless governing law provides otherwise, all transactions should be executed through the Deutsche Bank entity in theinvestor's home jurisdiction. Aside from within this report, important risk and conflict disclosures can also be found athttps://gm.db.com on each company ’ s research page and under the "Disclosures Lookup" and "Legal" tabs. Investorsare strongly encouraged to review this information before investing.

United States: Approved and/or distributed by Deutsche Bank Securities Incorporated, a member of FINRA, NFA and SIPC.Analysts located outside of the United States are employed by non-US affiliates that are not subject to FINRA regulations,including those regarding contacts with issuer companies.??

Page 32 Deutsche Bank AG/Hong Kong

5 February 2018

Software & Services

Ctrip

Germany: Approved and/or distributed by Deutsche Bank AG, a joint stock corporation with limited liability incorporatedin the Federal Republic of Germany with its principal office in Frankfurt am Main. Deutsche Bank AG is authorized underGerman Banking Law and is subject to supervision by the European Central Bank and by BaFin, Germany ’ s FederalFinancial Supervisory Authority.??United Kingdom: Approved and/or distributed by Deutsche Bank AG acting through its London Branch at WinchesterHouse, 1 Great Winchester Street, London EC2N 2DB. Deutsche Bank AG in the United Kingdom is authorised by thePrudential Regulation Authority and is subject to limited regulation by the Prudential Regulation Authority and FinancialConduct Authority. Details about the extent of our authorisation and regulation are available on request.??Hong Kong: Distributed by Deutsche Bank AG, Hong Kong Branch or Deutsche Securities Asia Limited (save that anyresearch relating to futures contracts within the meaning of the Hong Kong Securities and Futures Ordinance Cap. 571shall be distributed solely by Deutsche Securities Asia Limited). The provisions set out above in the "Additional Information"section shall apply to the fullest extent permissible by local laws and regulations, including without limitation the Code ofConduct for Persons Licensed or Registered with the Securities and Futures Commission. .??India: Prepared by Deutsche Equities India Private Limited (DEIPL) having CIN: U65990MH2002PTC137431 and registeredoffice at 14th Floor, The Capital, C-70, G Block, Bandra Kurla Complex Mumbai (India) 400051. Tel: + 91 22 71804444. It is registered by the Securities and Exchange Board of India (SEBI) as a Stock broker bearing registrationnos.: NSE (Capital Market Segment) - INB231196834, NSE (F&O Segment) INF231196834, NSE (Currency DerivativesSegment) INE231196834, BSE (Capital Market Segment) INB011196830; Merchant Banker bearing SEBI Registrationno.: INM000010833 and Research Analyst bearing SEBI Registration no.: INH000001741. DEIPL may have receivedadministrative warnings from the SEBI for breaches of Indian regulations. The transmission of research through DEIPLis Deutsche Bank's determination and will not make a recipient a client of DEIPL. Deutsche Bank and/or its affiliate(s)may have debt holdings or positions in the subject company. With regard to information on associates, please refer to the“Shareholdings” section in the Annual Report at: https://www.db.com/ir/en/annual-reports.htm.??Japan: Approved and/or distributed by Deutsche Securities Inc.(DSI). Registration number - Registered as a financialinstruments dealer by the Head of the Kanto Local Finance Bureau (Kinsho) No. 117. Member of associations: JSDA, TypeII Financial Instruments Firms Association and The Financial Futures Association of Japan. Commissions and risks involvedin stock transactions - for stock transactions, we charge stock commissions and consumption tax by multiplying thetransaction amount by the commission rate agreed with each customer. Stock transactions can lead to losses as a resultof share price fluctuations and other factors. Transactions in foreign stocks can lead to additional losses stemming fromforeign exchange fluctuations. We may also charge commissions and fees for certain categories of investment advice,products and services. Recommended investment strategies, products and services carry the risk of losses to principaland other losses as a result of changes in market and/or economic trends, and/or fluctuations in market value. Beforedeciding on the purchase of financial products and/or services, customers should carefully read the relevant disclosures,prospectuses and other documentation. "Moody's", "Standard & Poor's", and "Fitch" mentioned in this report are notregistered credit rating agencies in Japan unless Japan or "Nippon" is specifically designated in the name of the entity.Reports on Japanese listed companies not written by analysts of DSI are written by Deutsche Bank Group's analysts withthe coverage companies specified by DSI. Some of the foreign securities stated on this report are not disclosed accordingto the Financial Instruments and Exchange Law of Japan. Target prices set by Deutsche Bank's equity analysts are basedon a 12-month forecast period..??Korea: Distributed by Deutsche Securities Korea Co.??South Africa: Deutsche Bank AG Johannesburg is incorporated in the Federal Republic of Germany (Branch RegisterNumber in South Africa: 1998/003298/10).??Singapore: This report is issued by Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, SingaporeBranch (One Raffles Quay #18-00 South Tower Singapore 048583, +65 6423 8001), which may be contacted in respectof any matters arising from, or in connection with, this report. Where this report is issued or promulgated by DeutscheBank in Singapore to a person who is not an accredited investor, expert investor or institutional investor (as defined in theapplicable Singapore laws and regulations), they accept legal responsibility to such person for its contents.??

Deutsche Bank AG/Hong Kong Page 33

5 February 2018

Software & Services

Ctrip

Taiwan: Information on securities/investments that trade in Taiwan is for your reference only. Readers shouldindependently evaluate investment risks and are solely responsible for their investment decisions. Deutsche Bank researchmay not be distributed to the Taiwan public media or quoted or used by the Taiwan public media without written consent.Information on securities/instruments that do not trade in Taiwan is for informational purposes only and is not to beconstrued as a recommendation to trade in such securities/instruments. Deutsche Securities Asia Limited, Taipei Branchmay not execute transactions for clients in these securities/instruments.??Qatar: Deutsche Bank AG in the Qatar Financial Centre (registered no. 00032) is regulated by the Qatar Financial CentreRegulatory Authority. Deutsche Bank AG - QFC Branch may undertake only the financial services activities that fall withinthe scope of its existing QFCRA license. Its principal place of business in the QFC: Qatar Financial Centre, Tower, WestBay, Level 5, PO Box 14928, Doha, Qatar. This information has been distributed by Deutsche Bank AG. Related financialproducts or services are only available only to Business Customers, as defined by the Qatar Financial Centre RegulatoryAuthority.??Russia: The information, interpretation and opinions submitted herein are not in the context of, and do not constitute, anyappraisal or evaluation activity requiring a license in the Russian Federation.

Kingdom of Saudi Arabia: Deutsche Securities Saudi Arabia LLC Company (registered no. 07073-37) is regulated by theCapital Market Authority. Deutsche Securities Saudi Arabia may undertake only the financial services activities that fallwithin the scope of its existing CMA license. Its principal place of business in Saudi Arabia: King Fahad Road, Al OlayaDistrict, P.O. Box 301809, Faisaliah Tower - 17th Floor, 11372 Riyadh, Saudi Arabia.??United Arab Emirates: Deutsche Bank AG in the Dubai International Financial Centre (registered no. 00045) is regulatedby the Dubai Financial Services Authority. Deutsche Bank AG - DIFC Branch may undertake only the financial servicesactivities that fall within the scope of its existing DFSA license. Its principal place of business in the DIFC: DubaiInternational Financial Centre, The Gate Village, Building 5, PO Box 504902, Dubai, U.A.E. This information has beendistributed by Deutsche Bank AG. Related financial products or services are available only to Professional Clients, asdefined by the Dubai Financial Services Authority.??Australia and New Zealand: This research is intended only for "wholesale clients" within the meaning of theAustralian Corporations Act and New Zealand Financial Advisors Act, respectively. Please refer to Australia-specificresearch disclosures and related information at https://australia.db.com/australia/content/research-information.htmlWhere research refers to any particular financial product recipients of the research should consider any product disclosurestatement, prospectus or other applicable disclosure document before making any decision about whether to acquirethe product.??Additional information relative to securities, other financial products or issuers discussed in this report is available uponrequest. This report may not be reproduced, distributed or published without Deutsche Bank's prior written consent.Copyright © 2018 Deutsche Bank AG

Page 34 Deutsche Bank AG/Hong Kong

David Folkerts-LandauGroup Chief Economist and Global Head of Research

Raj HindochaGlobal Chief Operating Officer

Research

Michael SpencerHead of APAC Research

Global Head of Economics

Steve PollardHead of Americas Research

Global Head of Equity Research

Anthony KlarmanGlobal Head ofDebt Research

Paul ReynoldsHead of EMEA

Equity Research

Dave ClarkHead of APAC

Equity Research

Pam FinelliGlobal Head of

Equity Derivatives Research

Andreas NeubauerHead of Research - Germany

Spyros MesomerisGlobal Head of Quantitative

and QIS Research

International Production Locations

Deutsche Bank AGDeutsche Bank PlaceLevel 16Corner of Hunter & Phillip StreetsSydney, NSW 2000AustraliaTel: (61) 2 8258 1234

Deutsche Bank AGMainzer Landstrasse 11-1760329 Frankfurt am MainGermanyTel: (49) 69 910 00

Deutsche Bank AGFiliale HongkongInternational Commerce Centre,1 Austin Road West,Kowloon,Hong KongTel: (852) 2203 8888

Deutsche Securities Inc.2-11-1 NagatachoSanno Park TowerChiyoda-ku, Tokyo 100-6171JapanTel: (81) 3 5156 6770

Deutsche Bank AG London1 Great Winchester StreetLondon EC2N 2EQUnited KingdomTel: (44) 20 7545 8000

Deutsche Bank Securities Inc.60 Wall StreetNew York, NY 10005United States of AmericaTel: (1) 212 250 2500

Copyright © 2022 FDOKUMEN