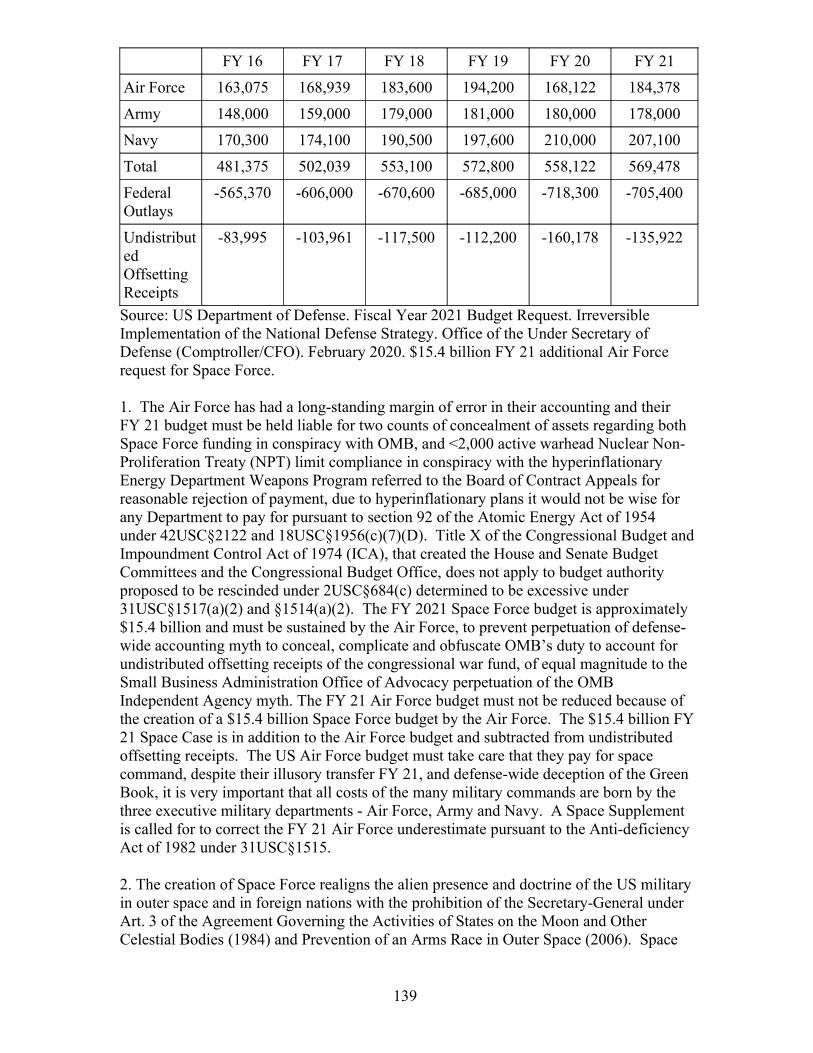

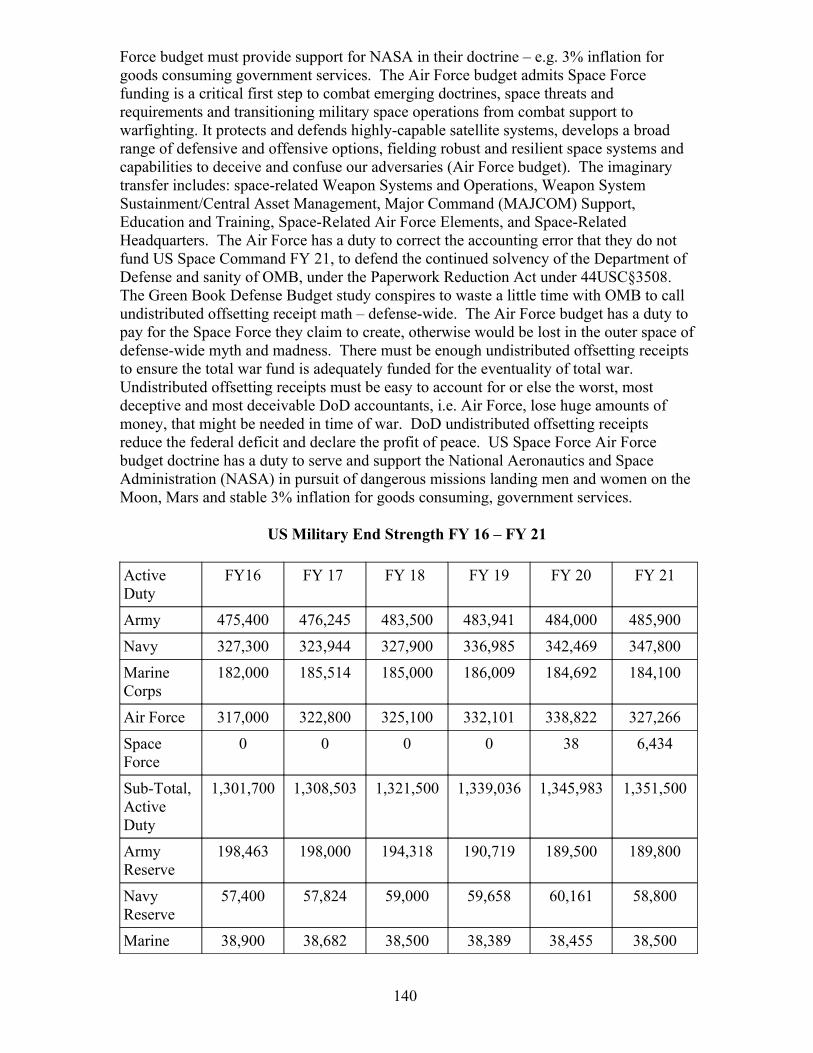

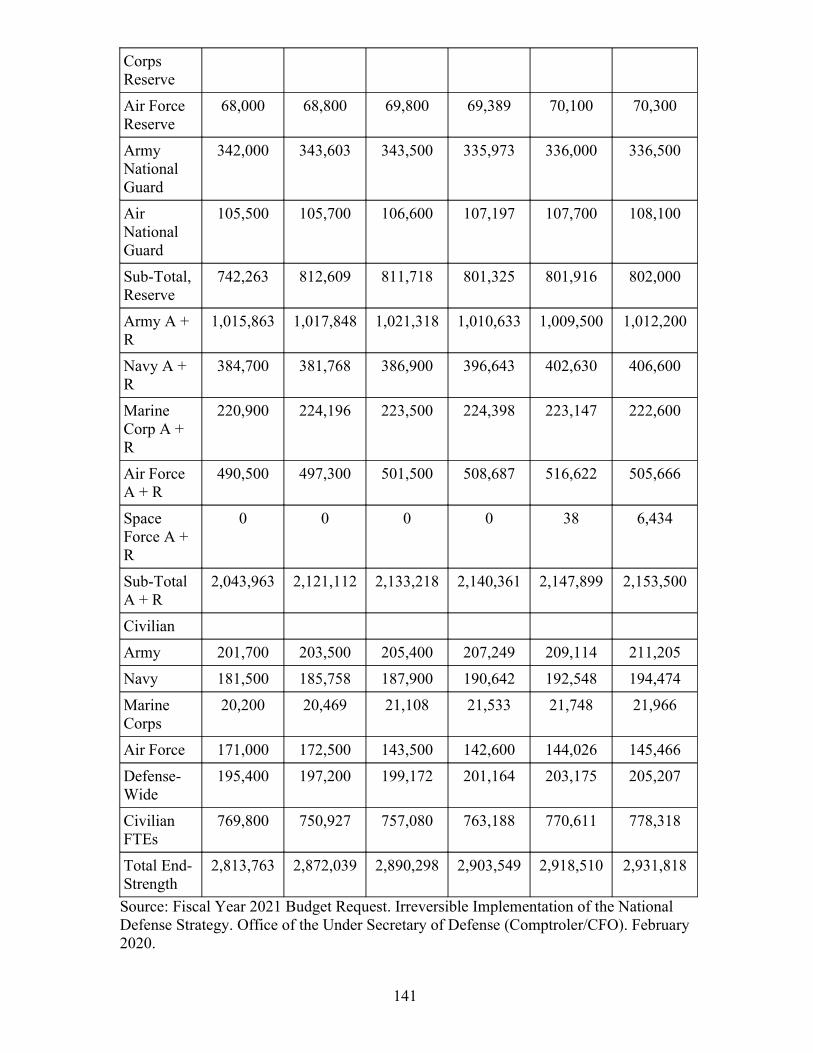

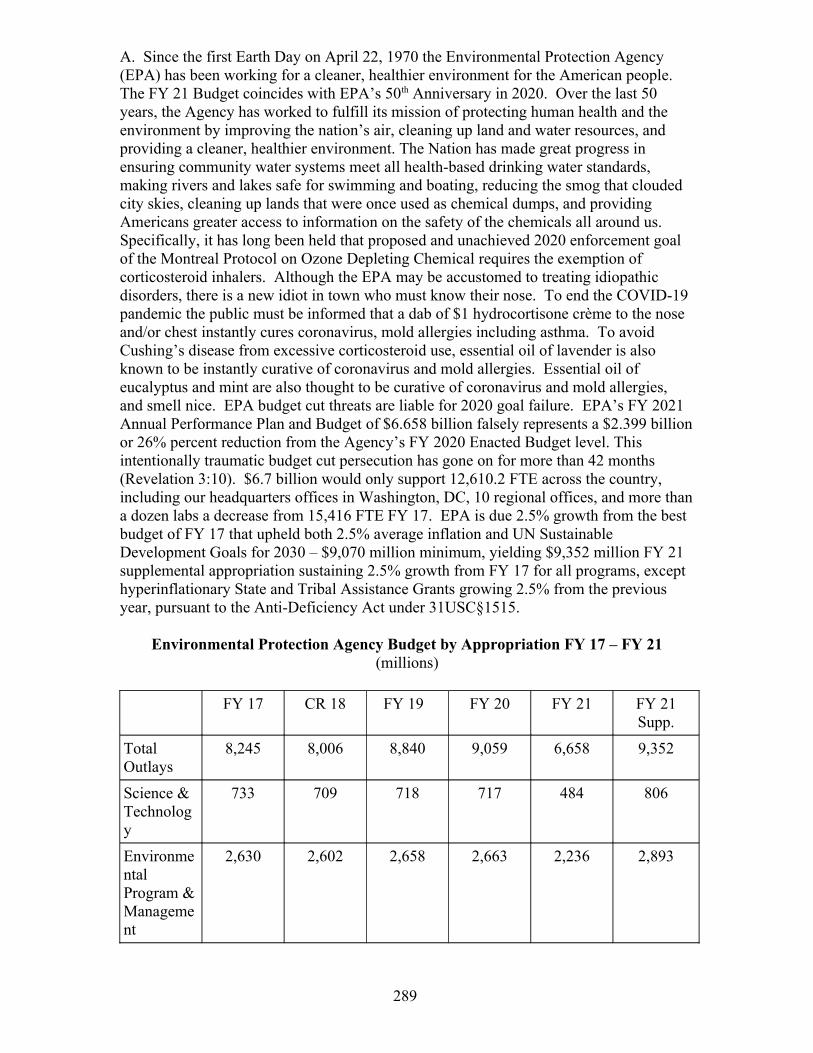

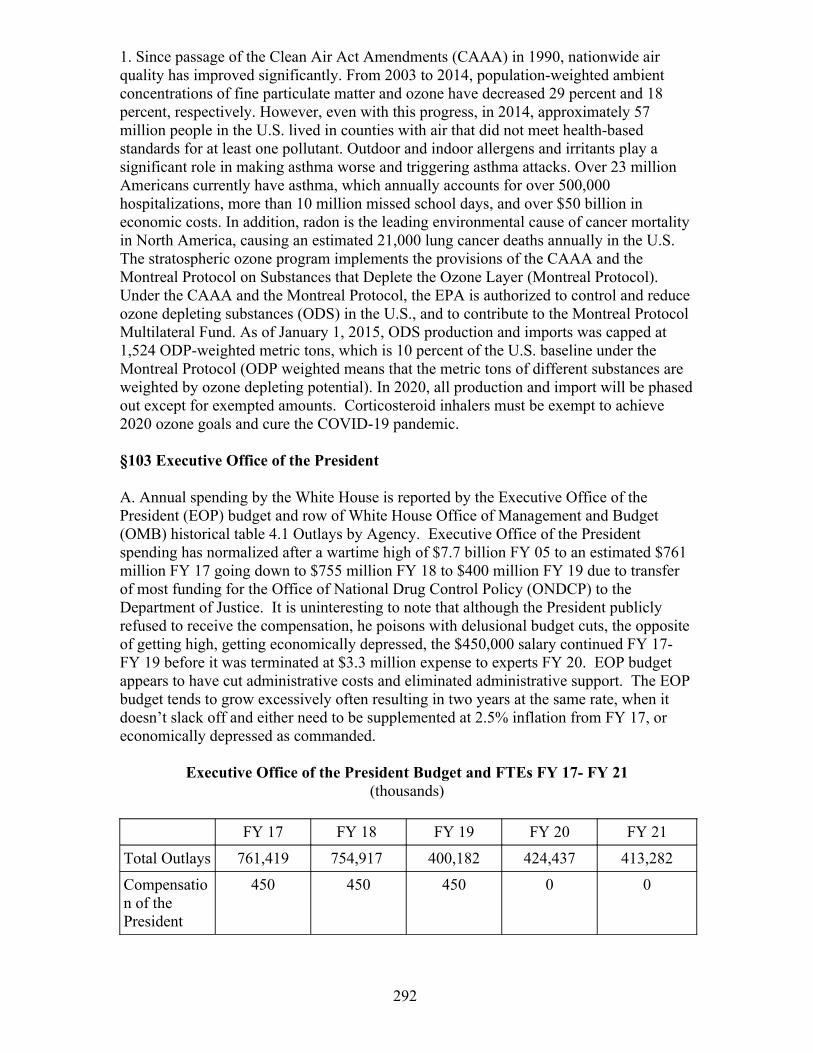

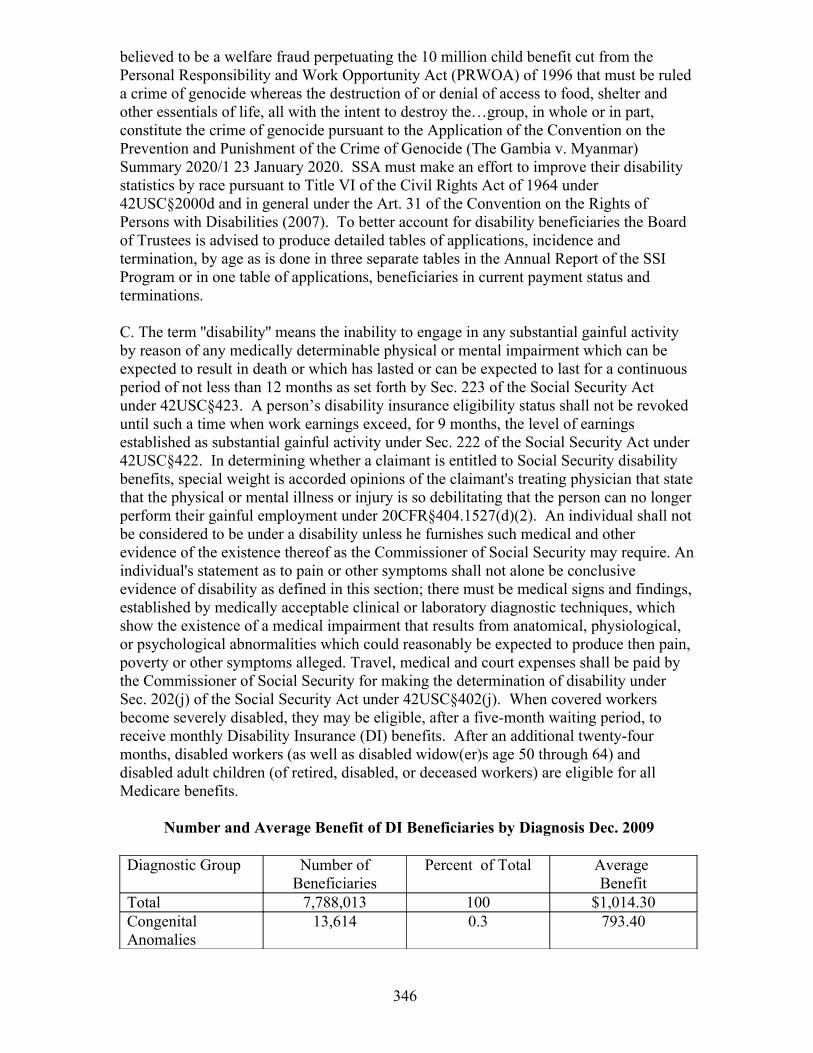

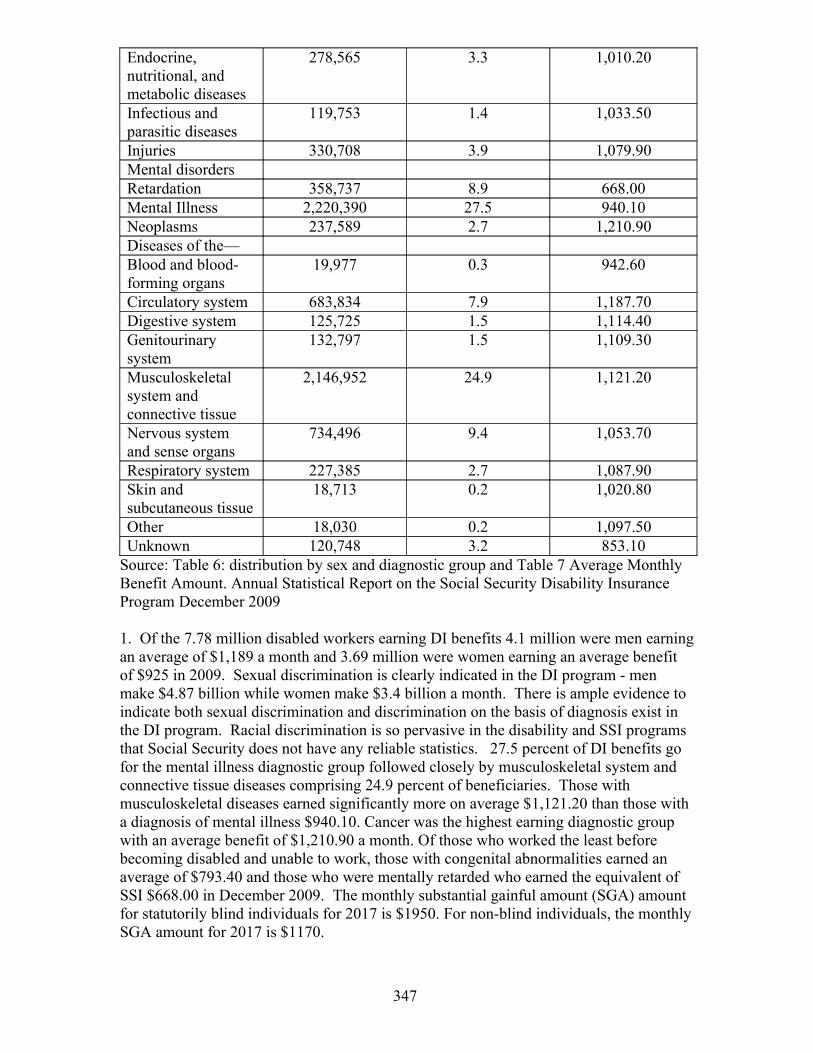

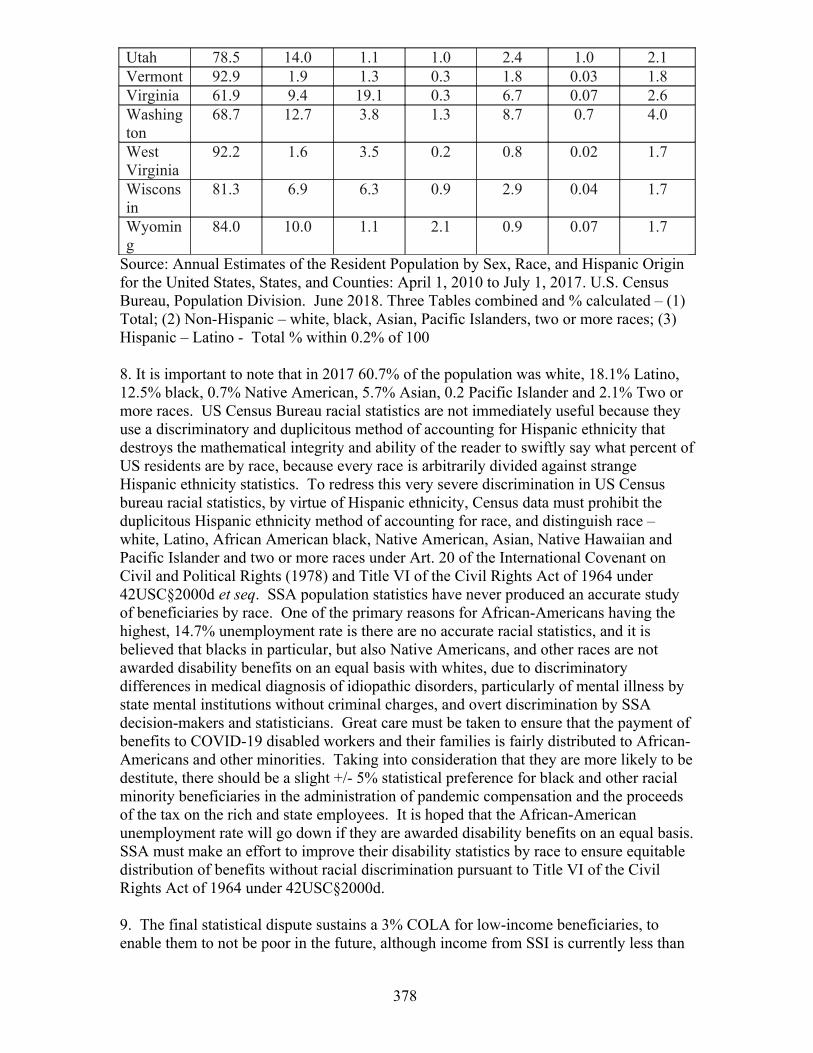

Statute of IIEST Shibpur under National Institute of Technology ...

Upload

khangminh22Category

view

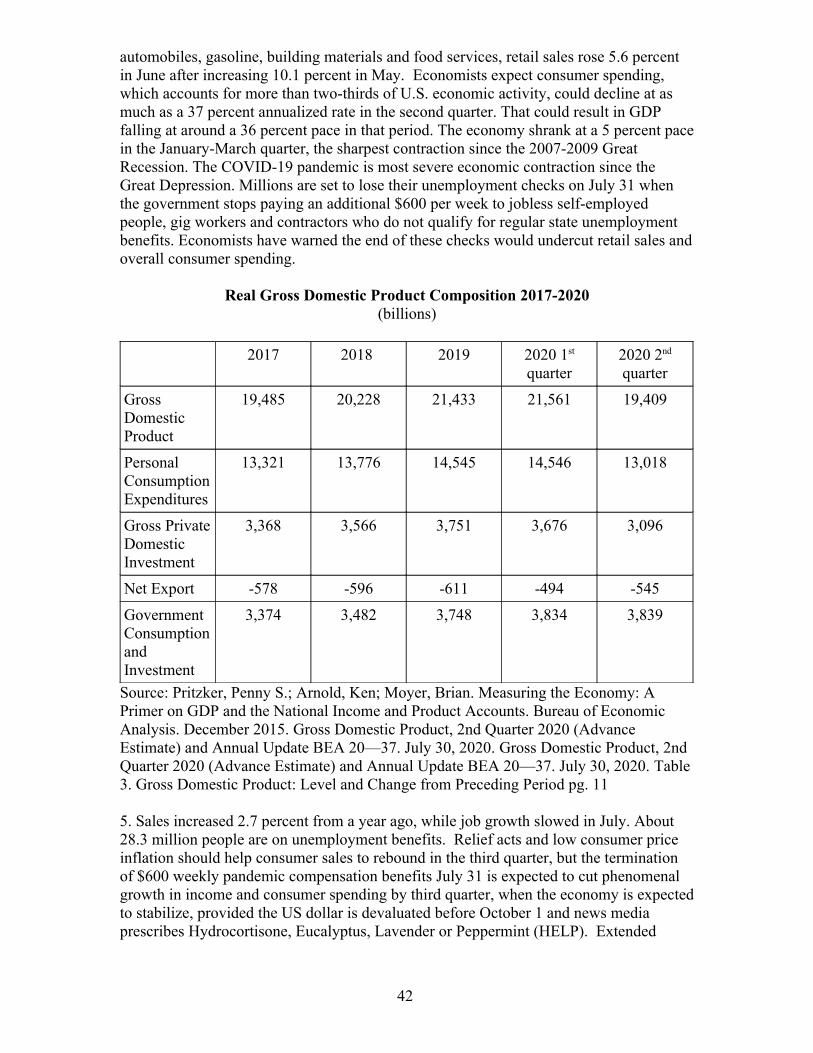

2download

0

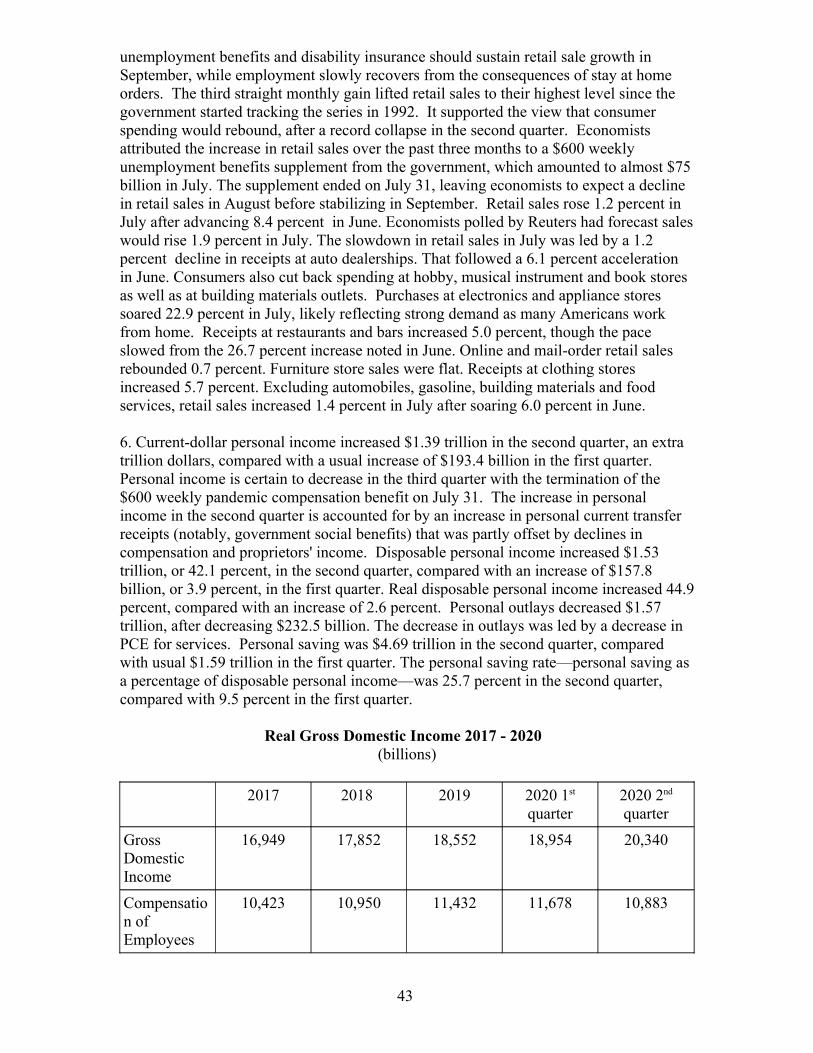

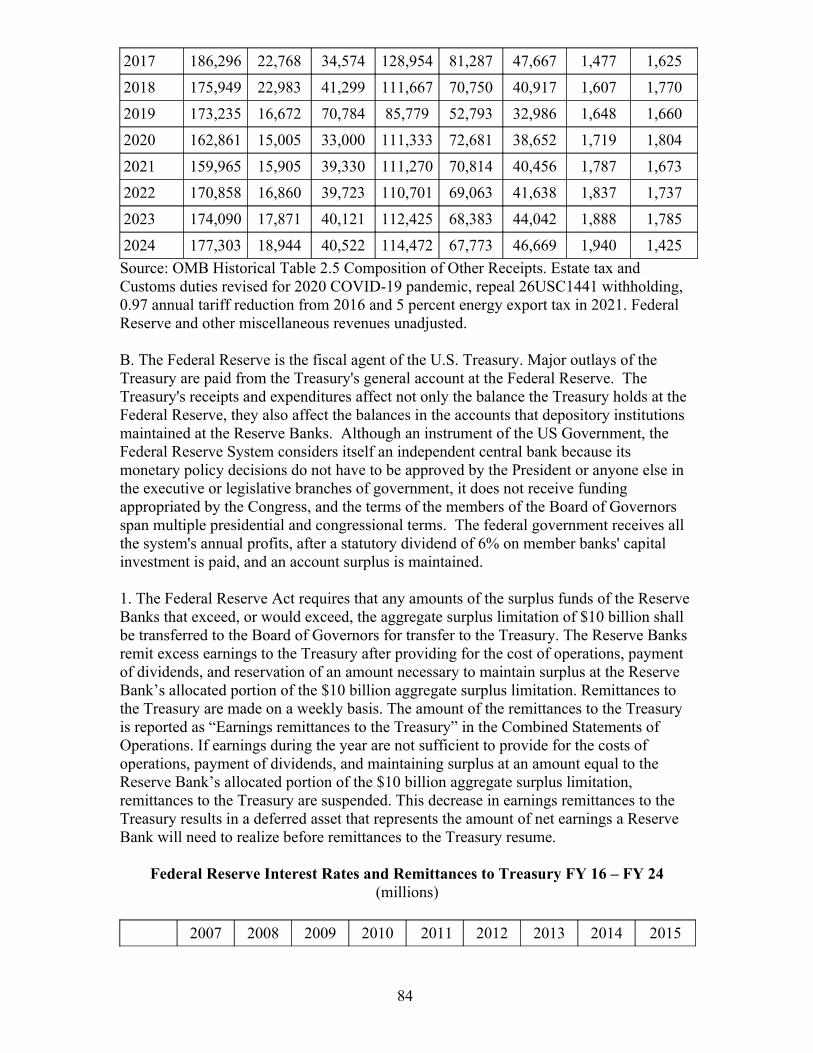

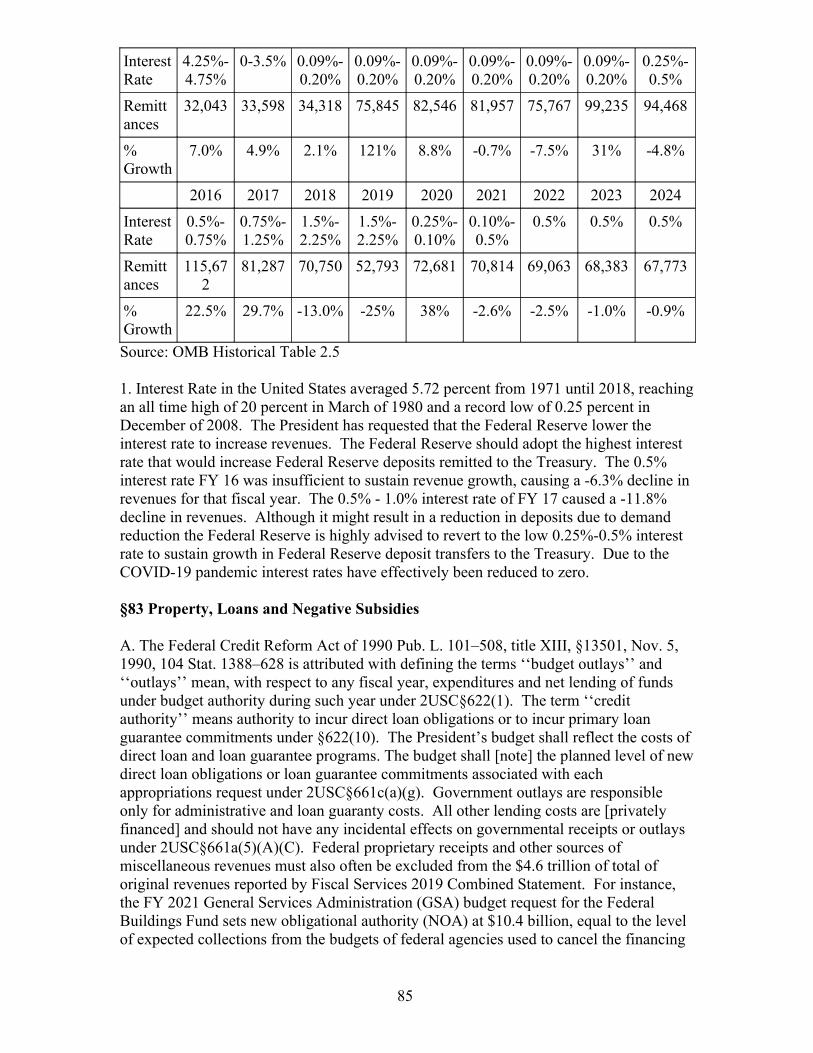

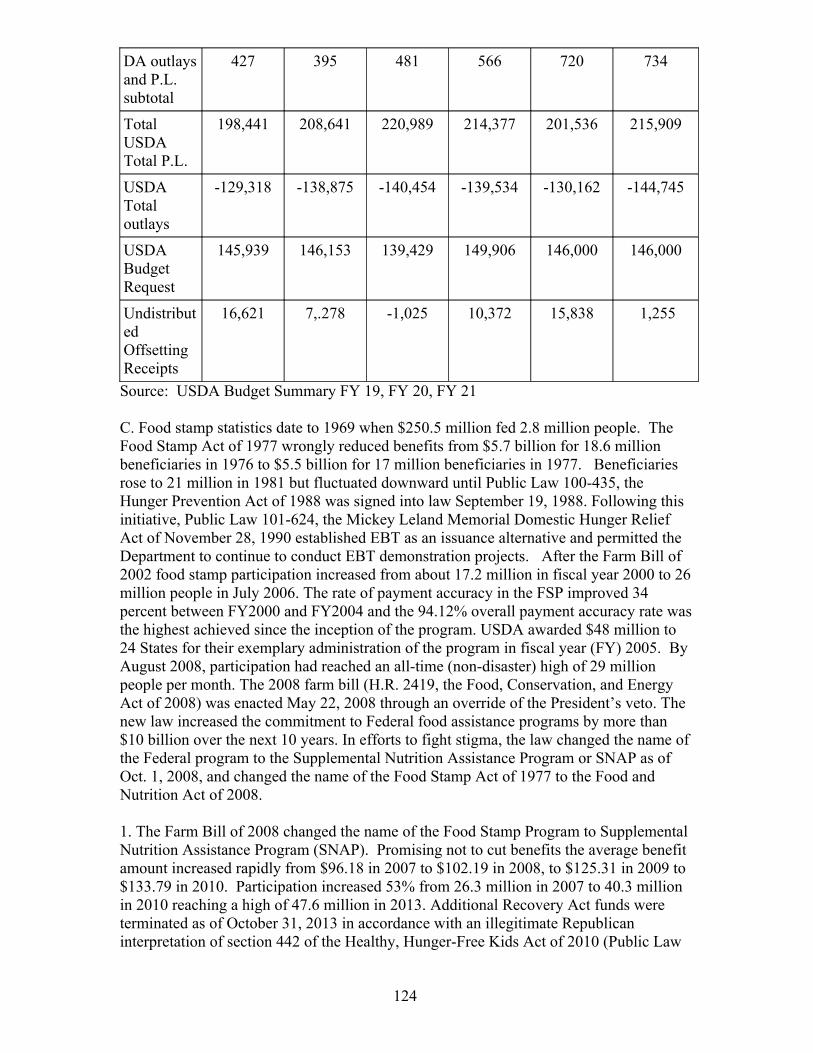

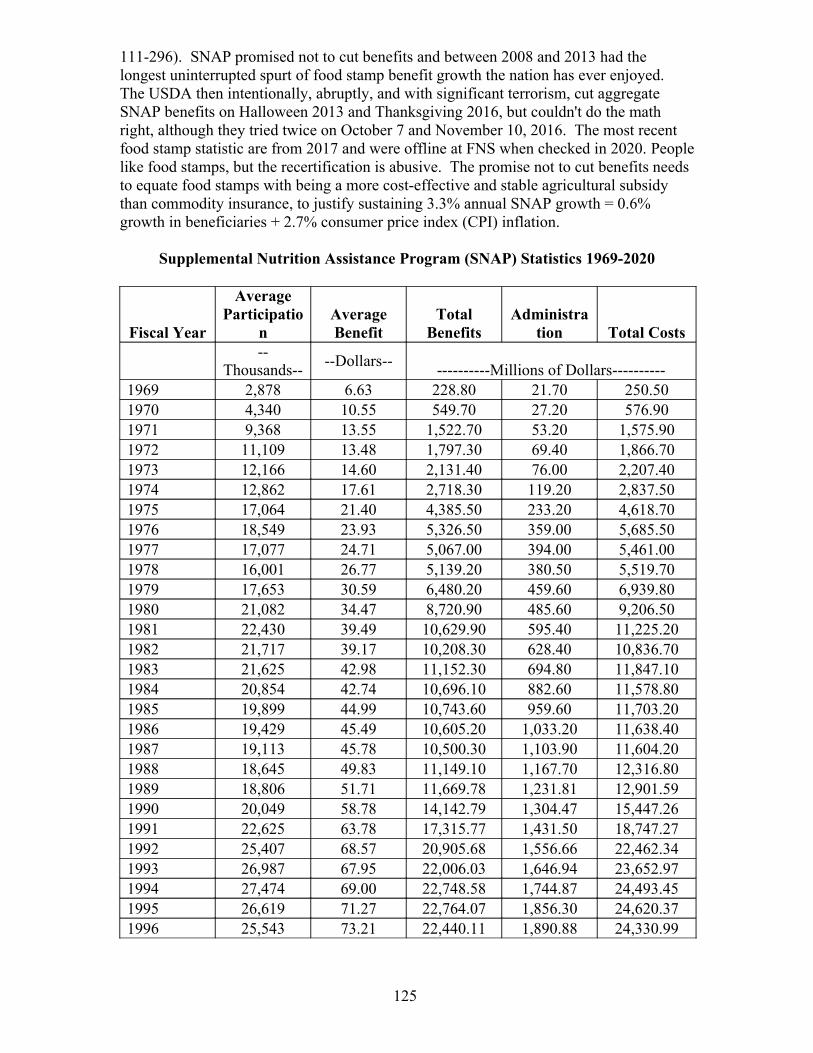

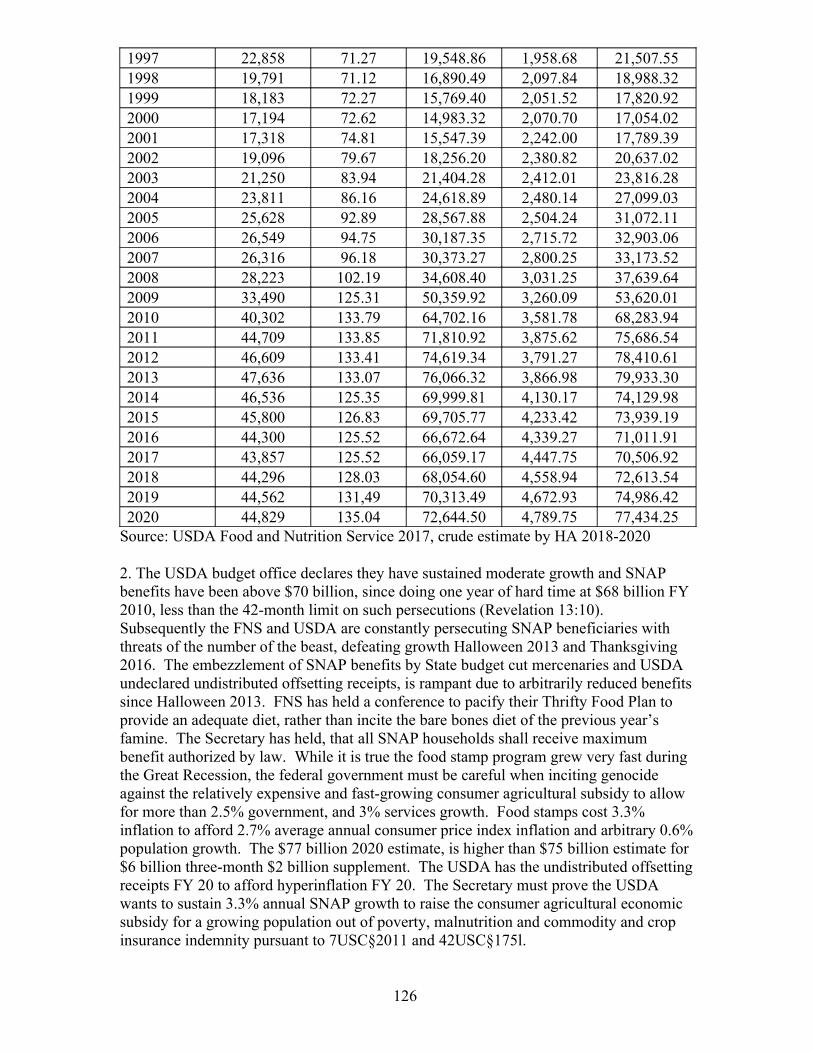

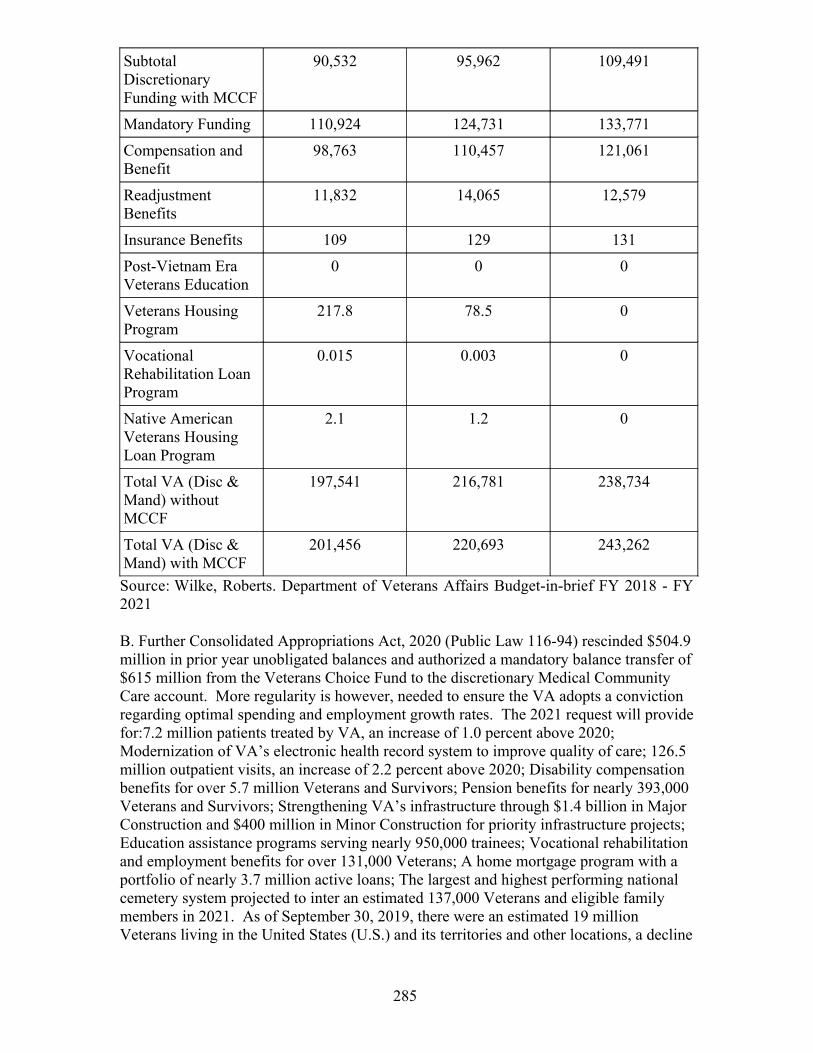

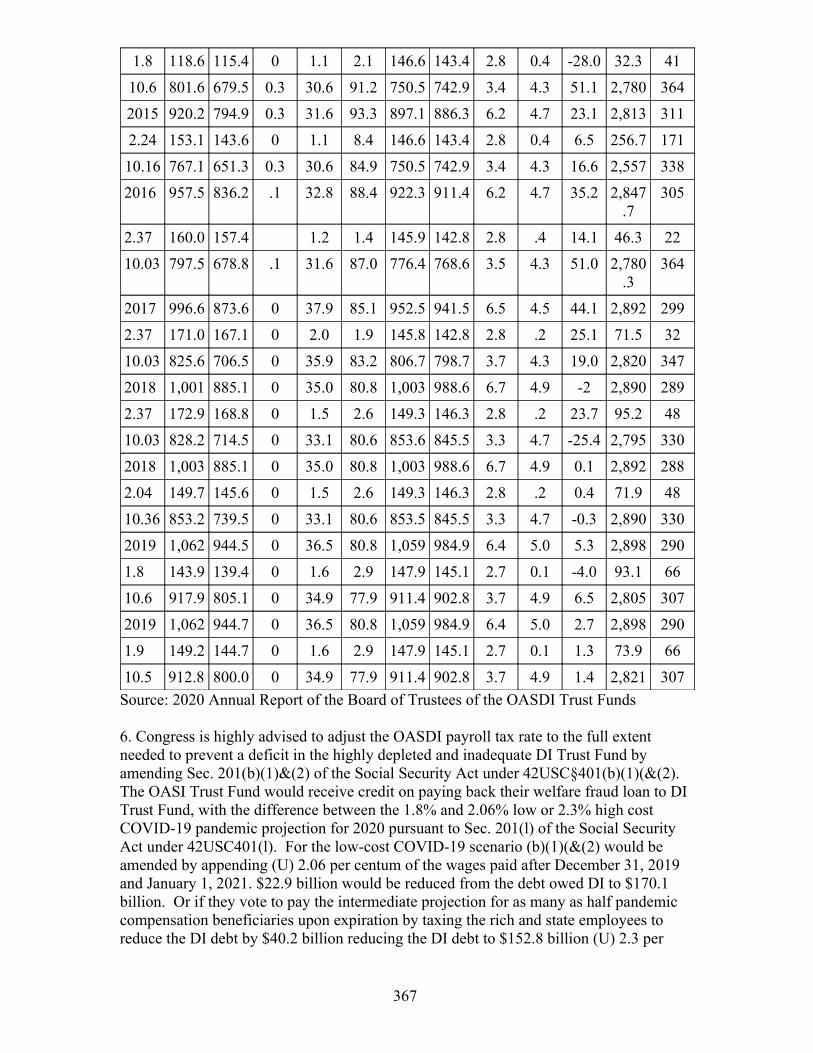

Hospitals & Asylums

Health and Welfare

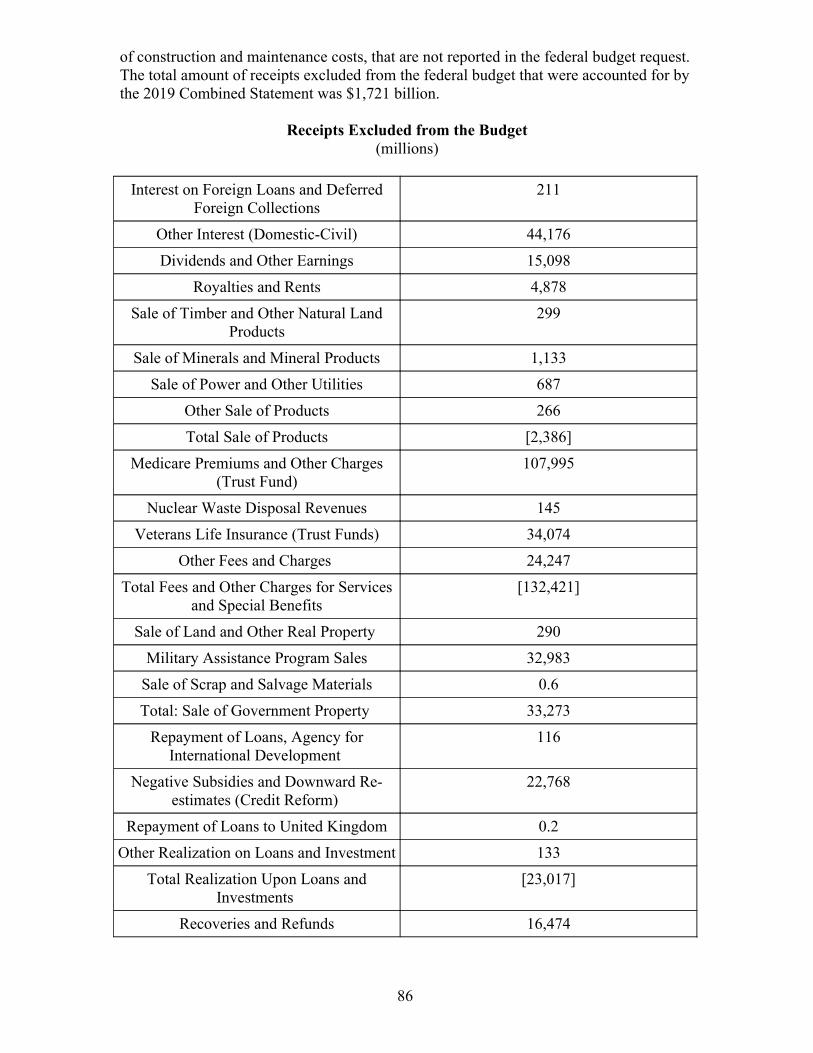

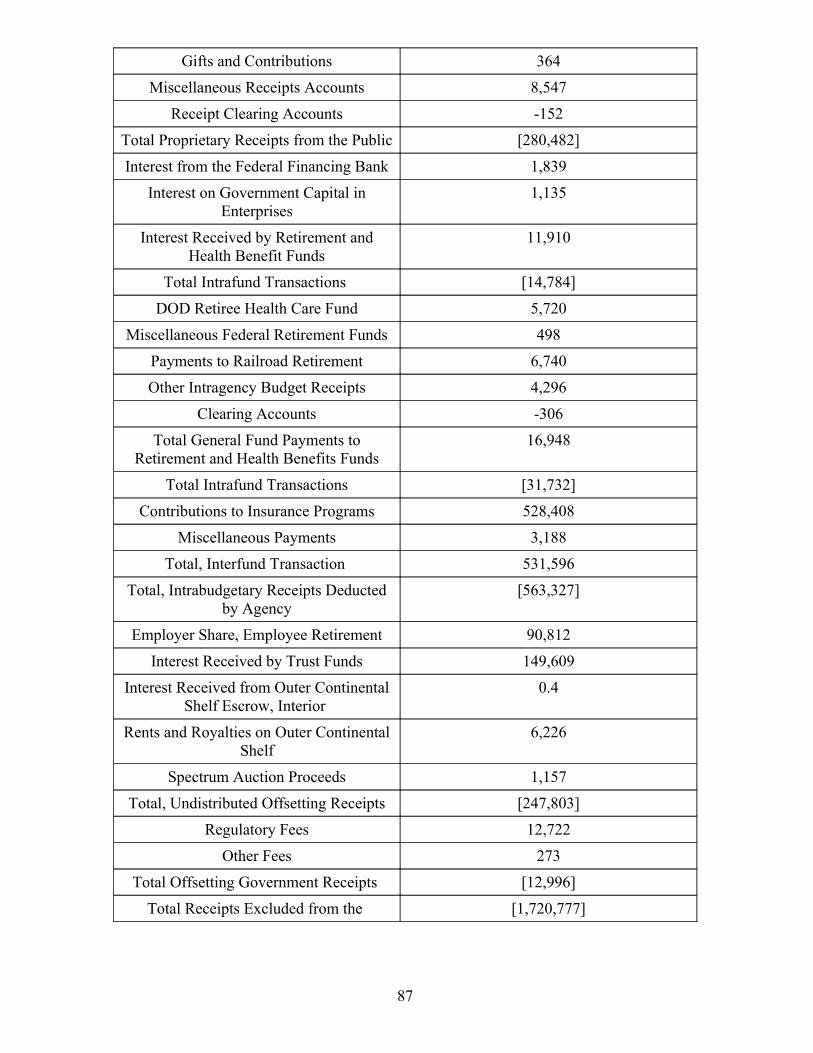

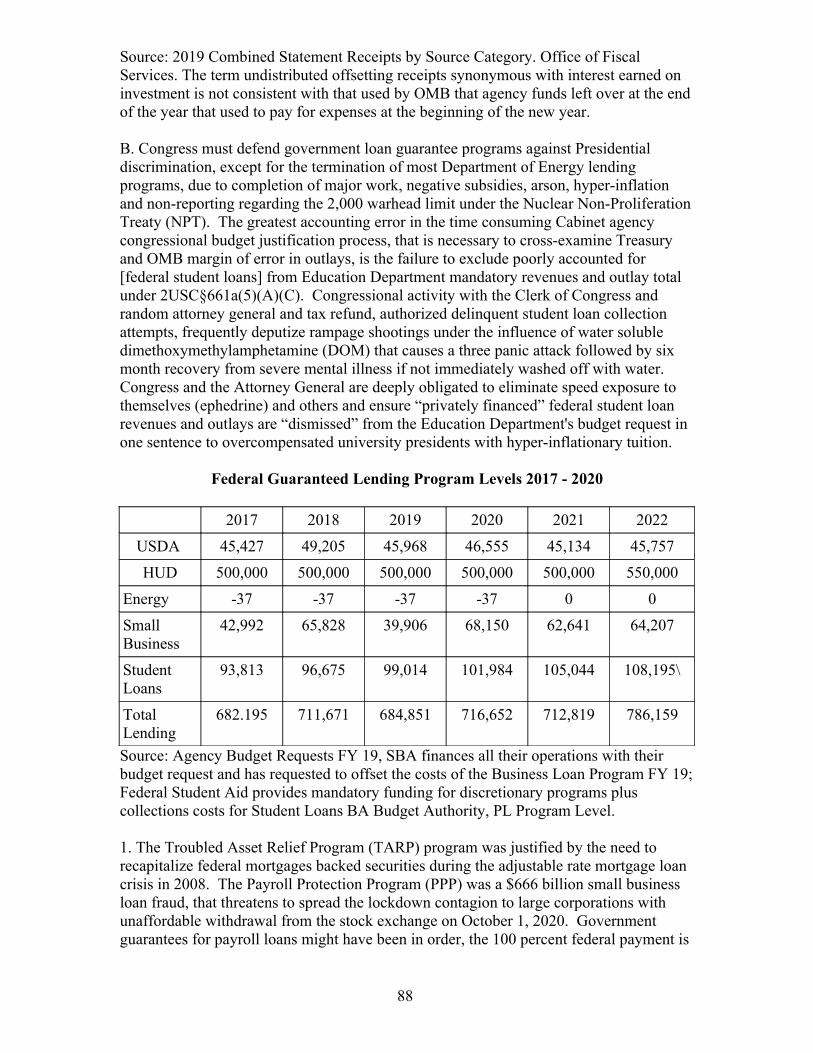

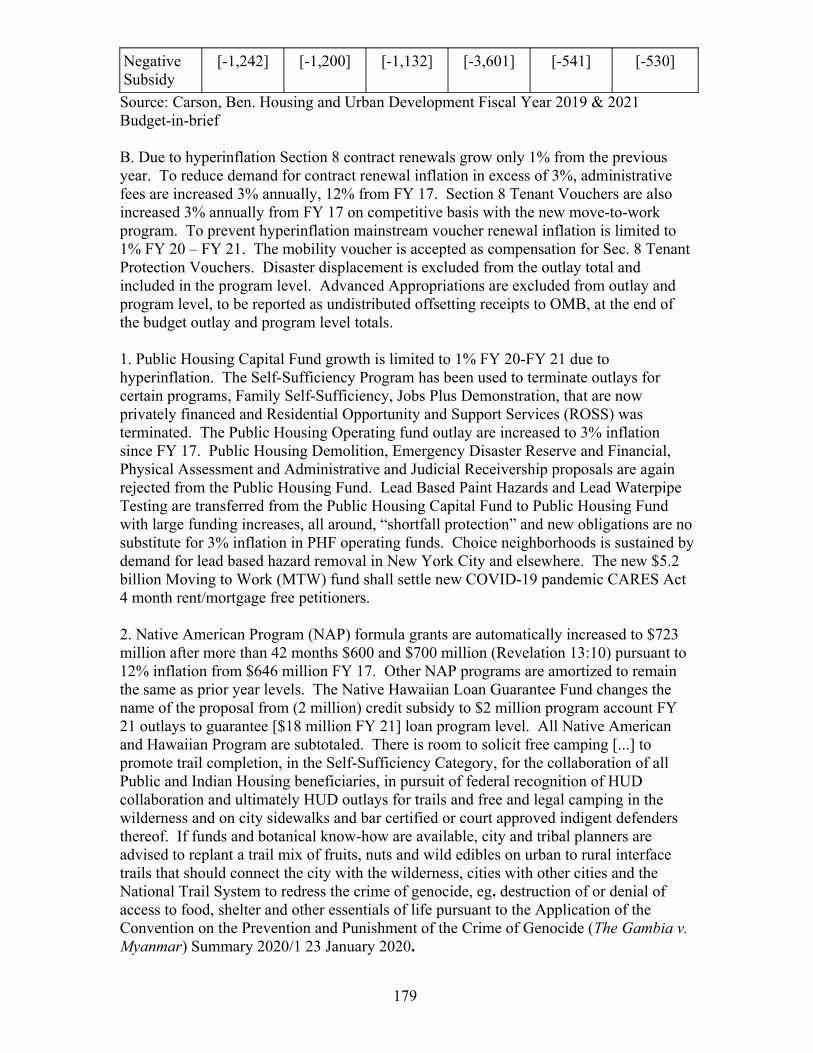

To supplement Chapter 3 National Home for Disabled Volunteer Soldiers §71-§154. To treat the COVID-19 pandemic by passing the included Hydrocortisone, Eucalyptus, Lavender, or Peppermint (HELP) Act before there are any more snot nose child deaths in the 2020-2021 school year. To devaluate the dollar by the $1.5 trillion amount of the Relief Acts, including forgiveness of the up to $10 billion postal service and $250 billion state unemployment compensation loans, plus whatever it takes to reduce the usual deficit to less than 3 percent of GDP, no more than -$596 billion FY 21, less +/- $133 billion foreign currency reserve, as a percent of recovering $19.9 trillion GDP, a $1.6 trillion, 8.2 percent devaluation if the tax measures are passed or $1.8 trillion, 9.0 percent devaluation without taxes FY 21 pursuant to the Marshall Lerner Condition under 19USC§4421 and 22USC§5301 et seq . To limit global -10 percent economic contractionto less than -2 percent, because instead of causing a reduction in prices, such as UN assessment of devaluating nations in 2019, devaluation of the US dollar should uniquely appreciate the size of the dollar backed global economy by the amount the dollar is devaluated, except for real US GDP pursuant to 2020 Revised estimates: effect of changes in rates of exchange and inflation Report of the Secretary-General A/74/585 of 11 December 2019. To continue to devaluate to maintain a deficit less than 3 percent of GDP until the TCJA expires in 2025, when the advantage of taxing is the deficit would certainly be less than 3 percent of GDP. To stop passing relief acts while addicted to speed (ephedrine). To close the loophole on energy export tax by amending 26USC§4612(b) to ‘In addition, there is imposed a flat 5% energy export tax (feet) by theUN Arrears and Certain Iranian Assets Bill of 2020.’ under 26USC§7201. To pay for a third of expiring pandemic compensation beneficiaries without depleting the neglected DItrust fund, it is necessary to close the OASDI tax loophole for the rich and state employees beginning as soon as October 1, 2020 and no later than January 1, 2021 to payfor COVID-19 disabled workers and create an SSI Trust Fund to end child poverty by 2024 and all poverty by 2030 by repealing the Adjustment to Contribution Base at Sec. 230 of the Social Security Act under 42USC§430. To improve the accounting of outlays,surplus or deficit and debt, the Combined Statement must exclude lending and interagency transfers from agency budget requests in a new and improved outlay overview table, for equal treatment with receipts by source category pursuant to 2USC§661a(5)(A)(C). To sustain 3 percent growth in federal education outlays, exclude privately financed student lending operations from the budget request total and make the education budget rows historically consistent to facilitate auditing FY 22. To sustain 3 percent growth in federal outlays for Housing and Urban Development it is necessary to adopt a method of accounting overview that distinguishes the revenues and outlays of federal and private programs. To sustain 2.5 percent growth in public land agencies and 3percent growth in Indian affairs outlays without trauma, it is necessary for the Interior Department to quantify and distribute their profit. To end the trade war it is necessary fortariffs to be reduced 0.97 annually from 2016 levels pursuant to the Swiss Formula for Unilateral Tariff Reduction (2007). To change the name of Homeland Security to Customs, make Federal Emergency Management Administration (FEMA) a historically accounted Cabinet agency, transfer the Secret Service to Treasury FY 21 and account for total Customs revenues in the Combined Statement and total outlays in the Budget-in-Brief. To reauthorize the Census Bureau Annual Statistical Abstract.

1

Be it enacted in the House and Senate Assembled

1st ed. 15 Sept. 2004, 2nd 1 June 2005, 3rd 18 June 2006, 4th 17 June 2007. 5th 12 June 2009,6th 31 July 2010, 7th 17 Aug. 2011, 8th 14 July 2012, 9th 26 July 2015, 10th 7 Sept. 2015,

11th 17 Sept. 2017, 12th 22 Sept. 2018, 13th 12 November 2018, 14th 27 August 2020

Art. 1 Fiscal Year 2020

§71 Balance§72 Revenues §73 Outlays§74 Debt§75 Gross Domestic Product

Art. 2 Revenues

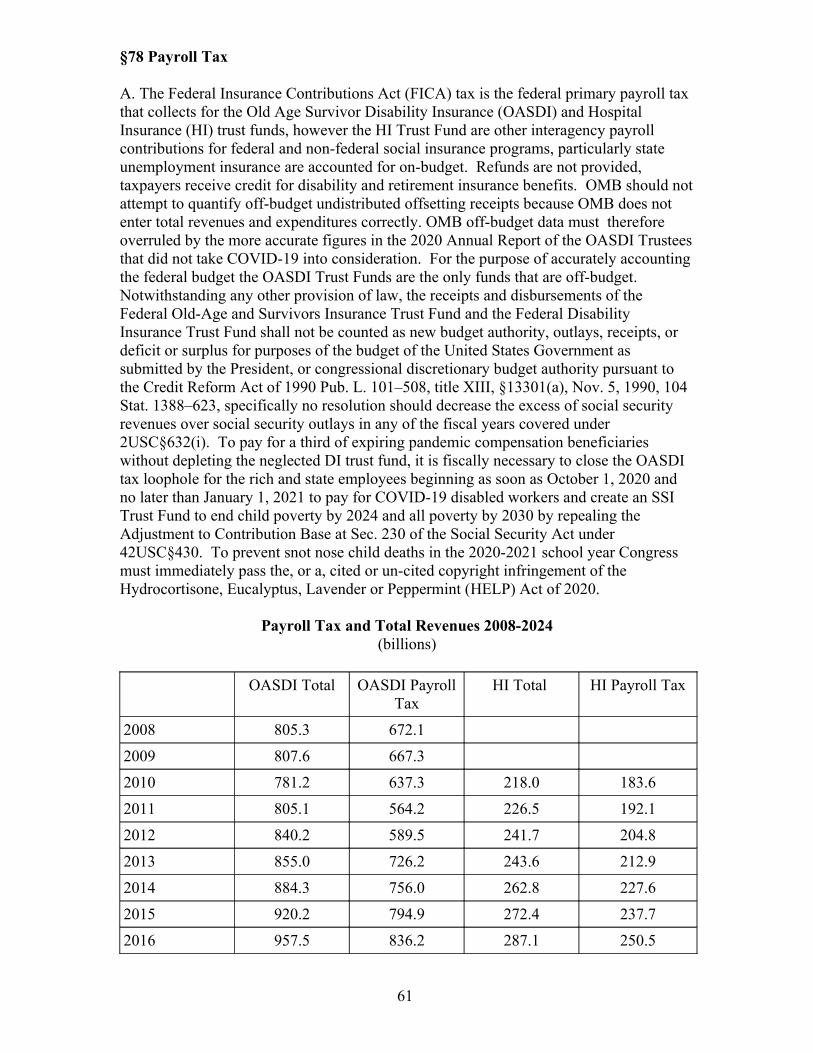

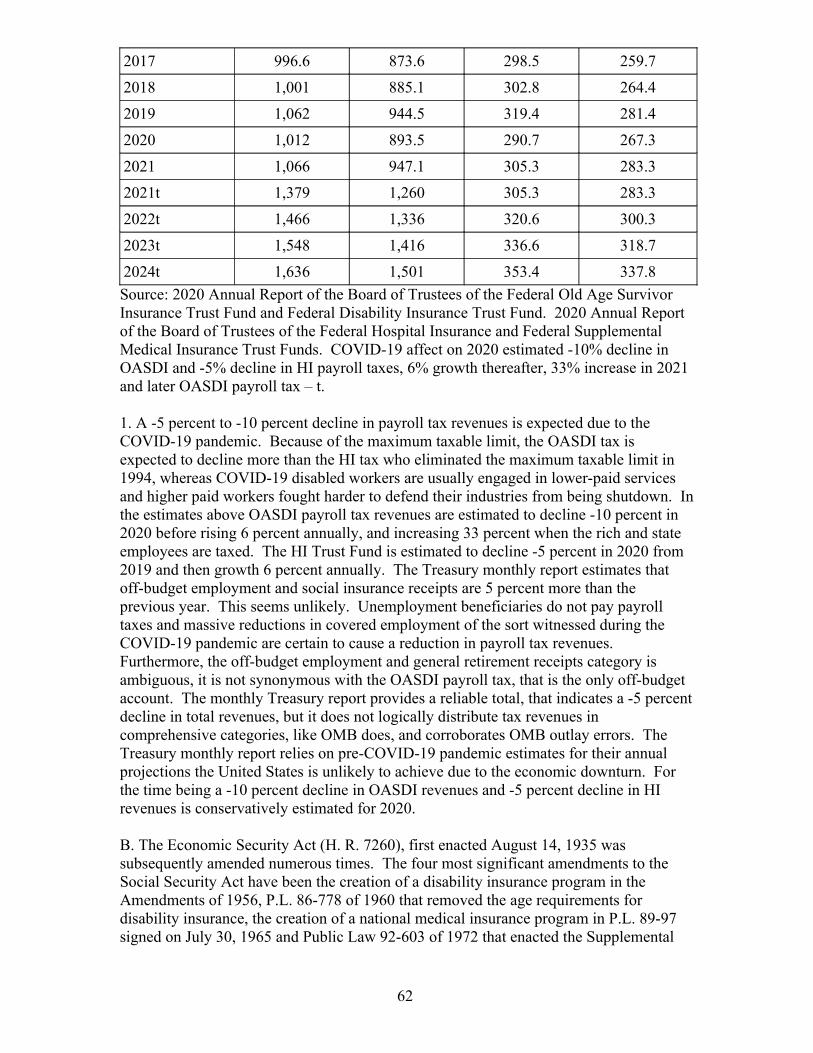

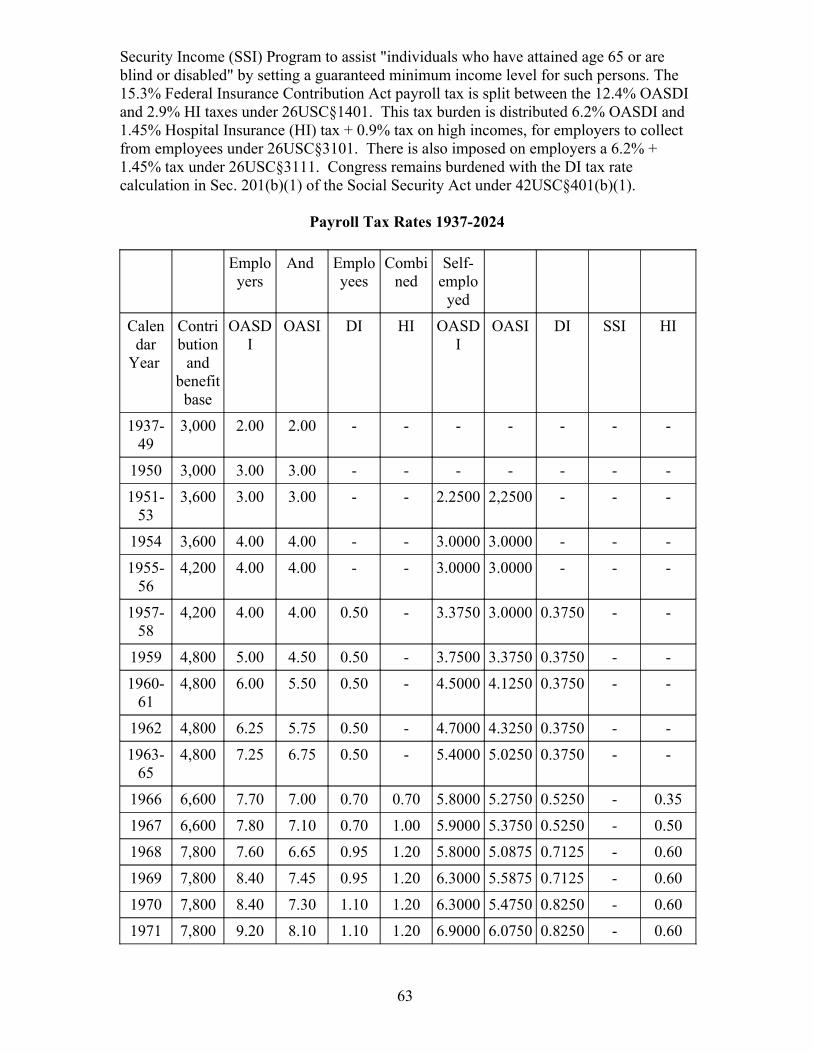

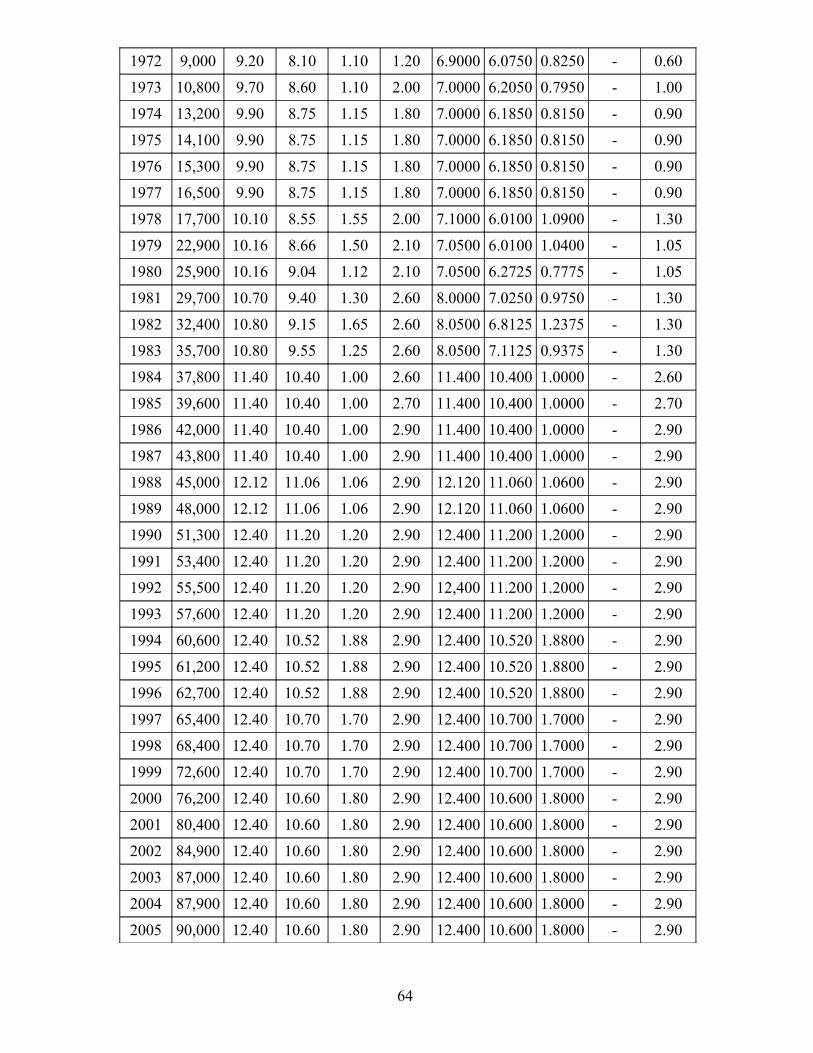

§76 Individual Income Tax §77 Corporation Income Tax §78 Payroll Tax §79 Excise Tax§80 Estate and Gift Tax§81 Customs Duties and Fees §82 Miscellaneous, Federal Reserve Deposits§83 Excluded Proprietary, Loan, and Negative Subsidy

Art. 3 Outlays by Agency

§84 Legislative Branch§85 Judicial Branch§86 Department of Agriculture§87 Department of Commerce§88 Department of Customs§89 Department of Defense – Military Programs§90 Department of Education§91 Department of Energy §92 Department of Health and Human Services§93 Department of Housing and Urban Development§94 Department of the Interior§95 Department of Justice§96 Department of Labor§97 Department of State and International Assistance§98 Department of Transportation§99 Department of the Treasury§100 Department of Veterans Affairs§101 Corp of Engineers – Civil Works§102 Environmental Protection Agency§103 Executive Office of the President§104 Federal Emergency Management Administration §105 General Services Administration and Office of Personnel Management

2

§106 National Aeronautics and Space Administration§107 National Science Foundation§108 Small Business Administration§109 Postal Service (private )

Art. 4 Social Security

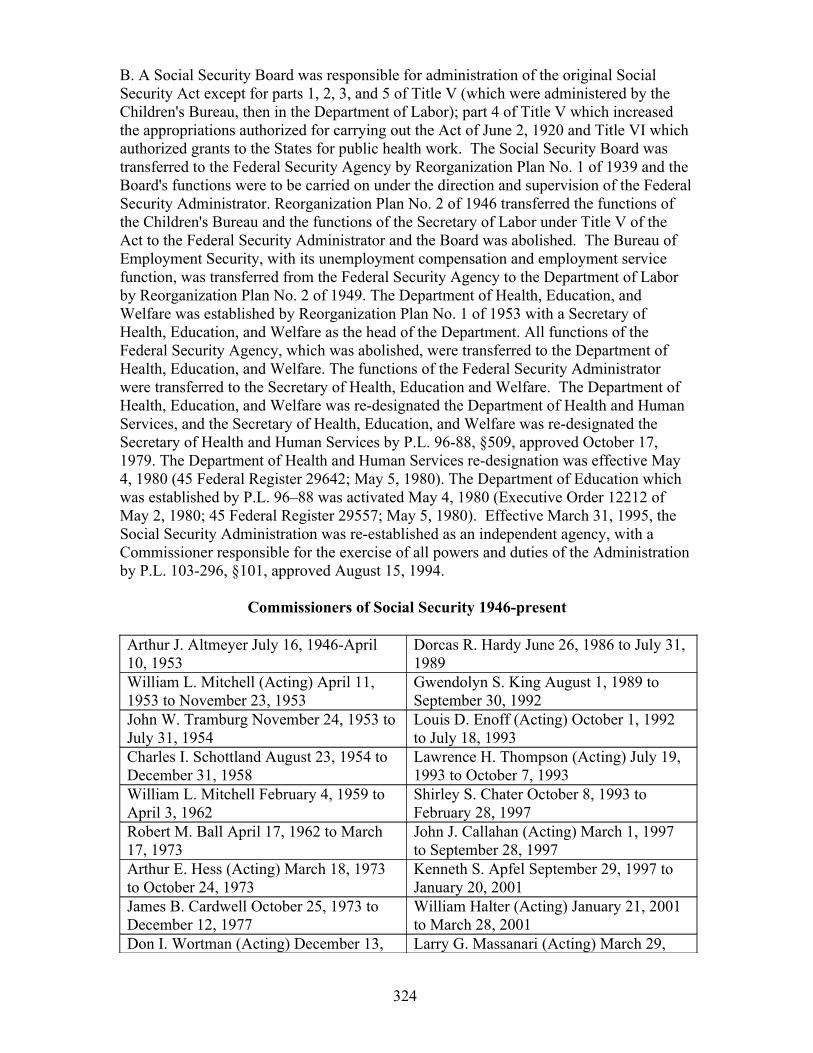

§110 Social Security Administration§111 Old Age and Survivor Insurance Trust Fund§112 Disability Insurance Trust Fund§113 Supplemental Security Income §114 Message of the Public Trustee

Art. 4A Hydrocortisone, Eucalyptus, Lavender or Peppermint (HELP) Act

§115 Preamble

Part. I Revenues

§116 Sec. 1 Devaluation§117 Sec. 2 Closure of tax loopholes for rich, state employees and energy exports

Part II Pandemic Social Security Benefits

§118 Sec. 3 Supplemental Security Income Trust Fund §119 Sec. 4 COVID-19 Disabled Workers§120 Sec. 5 Ticket to Work§121 Sec. 6 Tax Rate Adjustment Investigation Loan§122 Sec. 7 Insulin Rebate§123 Sec. 8 Orphan Benefit§124 Sec. 9 Three % Annual Increase in Cost-of-Living Adjustment and Minimum Wage§125 Sec. 10 Labor Insurance

Part III Federal Government

§126 Sec. 11 Speed Ticket§127 Sec. 12 President’s Budget§128 Sec. 13 Customs Impoundment§129 Sec. 14 Education, Housing and Interior Budget Credit Reform Accounting

Part IV Foreign Relations Equality Edition

§130 Sec. 15 Certain Iranian Assets §131 Sec. 16 United Nations Arrears

Part V Convention on Pandemic Treatment

§132 Sec. 17 Preamble§133 Sec. 18 Art. 1 Essential oils of eucalyptus, lavender and peppermint

3

§134 Sec. 19 Art. 2 Aromatherapy§135 Sec. 20 Art. 3 Soaps, cleansers and other medicinal herbs§136 Sec. 21 Art. 4 Hydrocortisone crème §137 Sec. 22 Art. 5 Corticosteroid inhaler exemption §138 Sec. 23 Art. 6 Prescription influenza drugs§139 Sec. 24 Art. 7 Ratification

§140-150 Repealed

Art. 5 Battle Mountain Sanitarium Reserve

§151 Battle Mountain Sanitarium Reserve§152 Name; control, rules and regulations§153 Perfecting bona fide claims to lands; exchange of private lands§154 Unlawful intrusion, or violation of rules and regulations

Tables

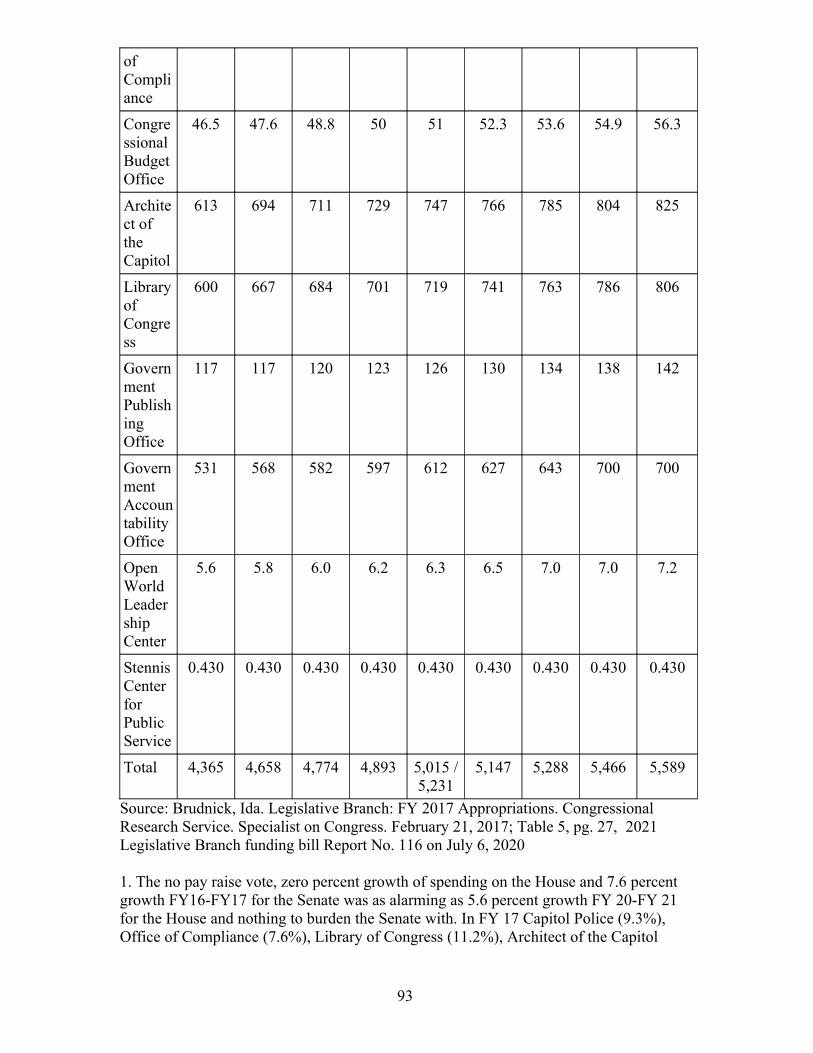

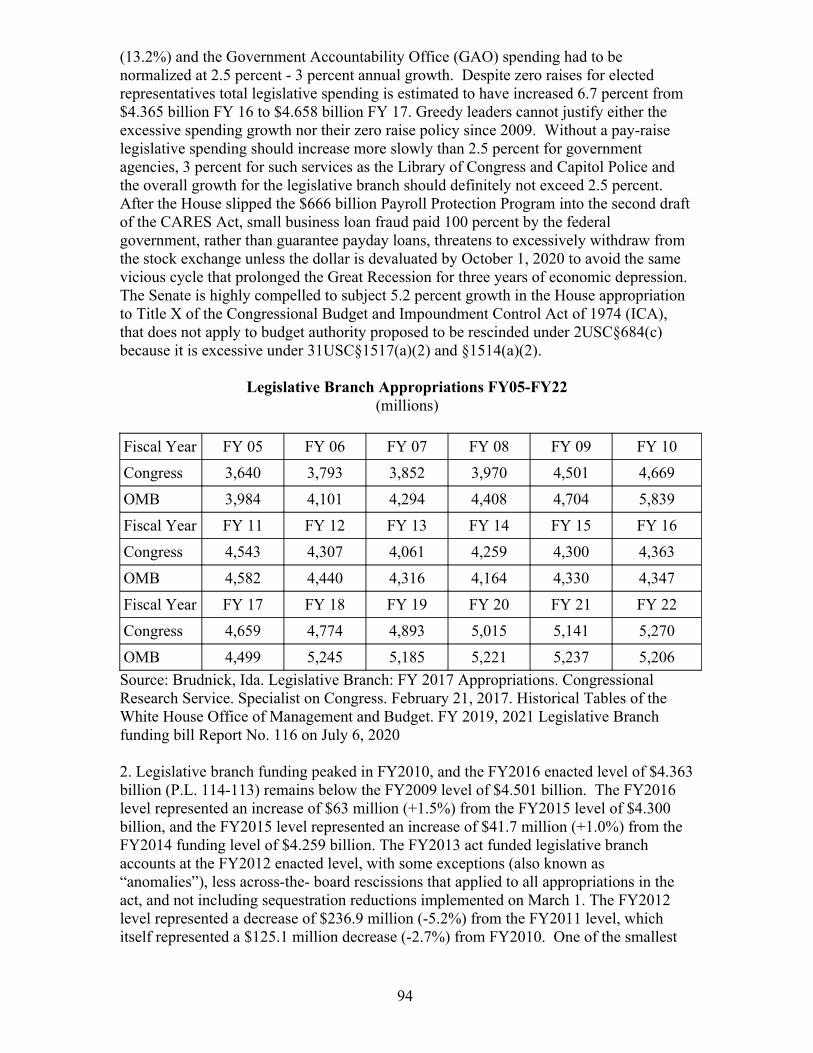

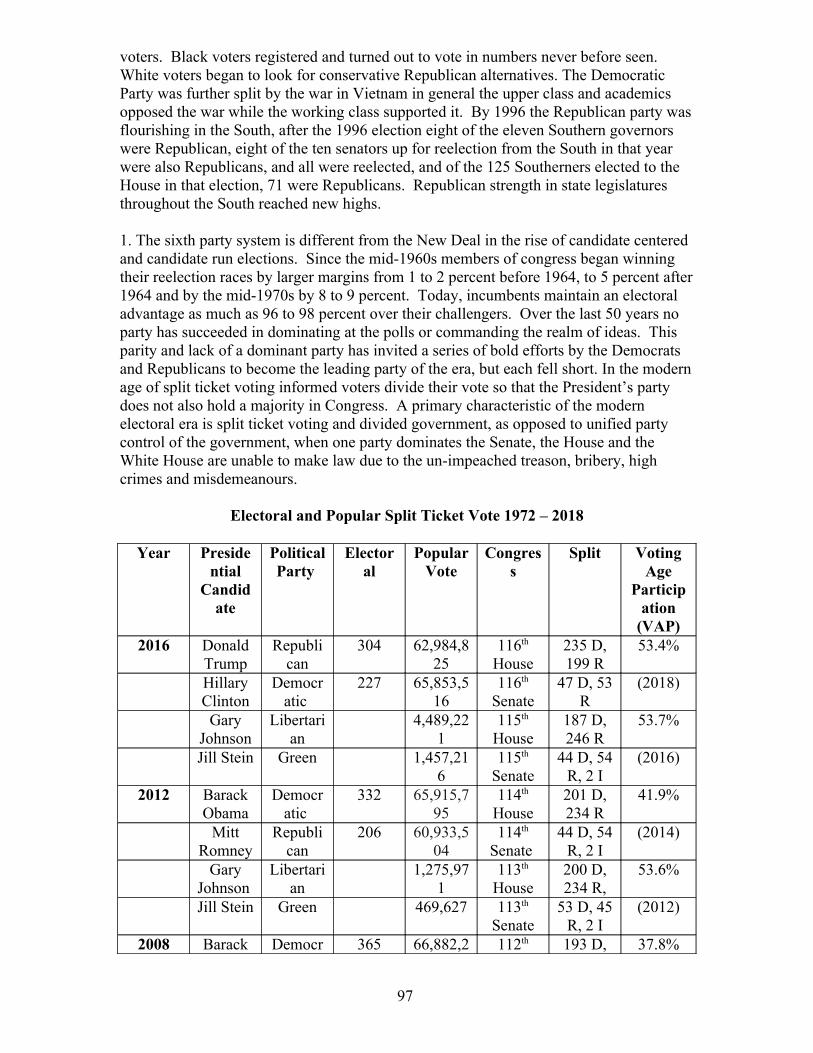

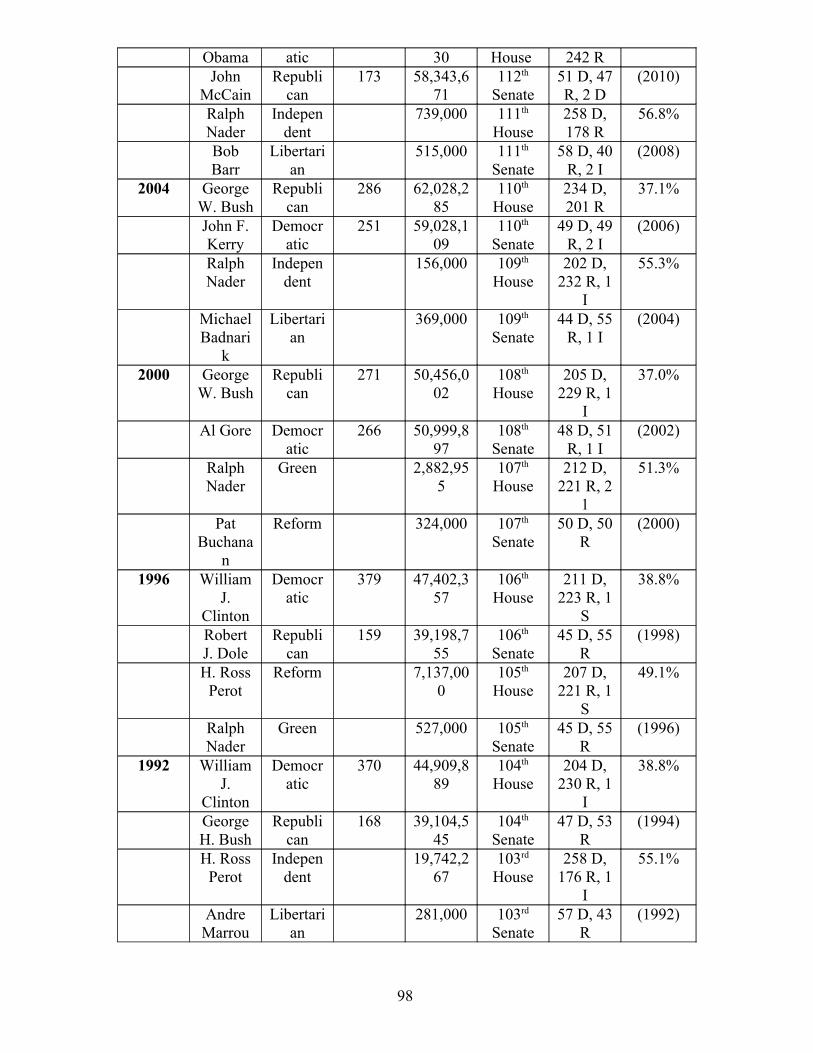

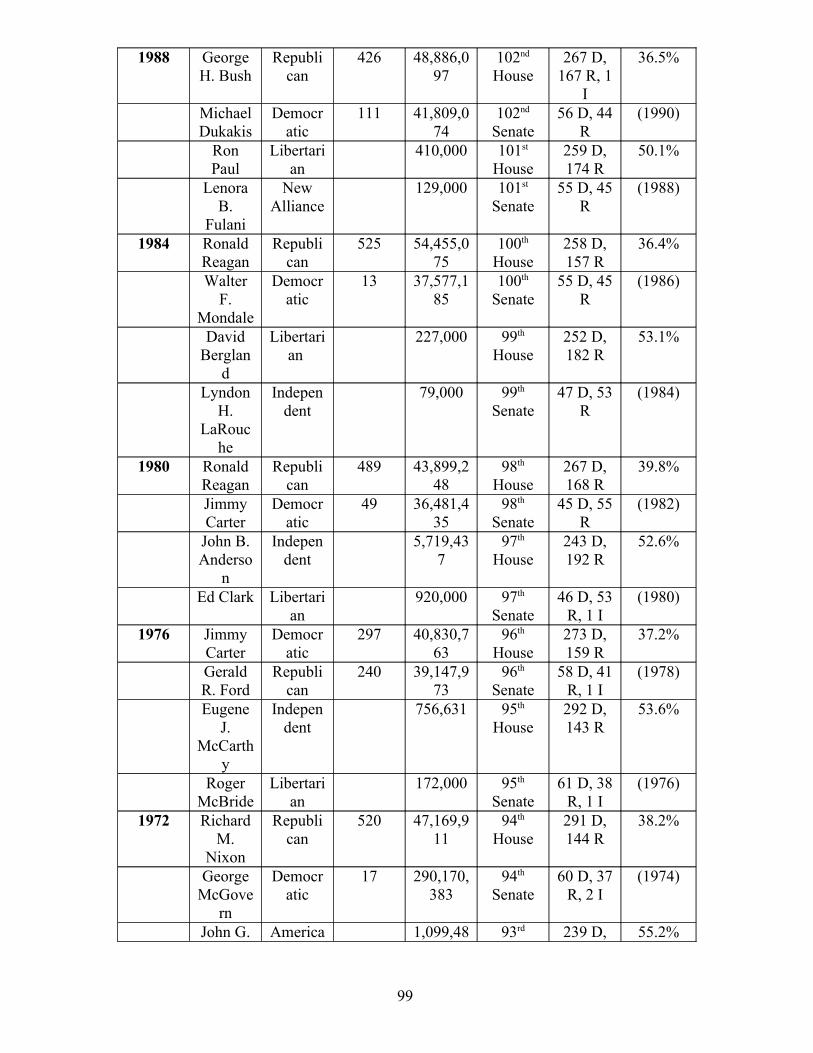

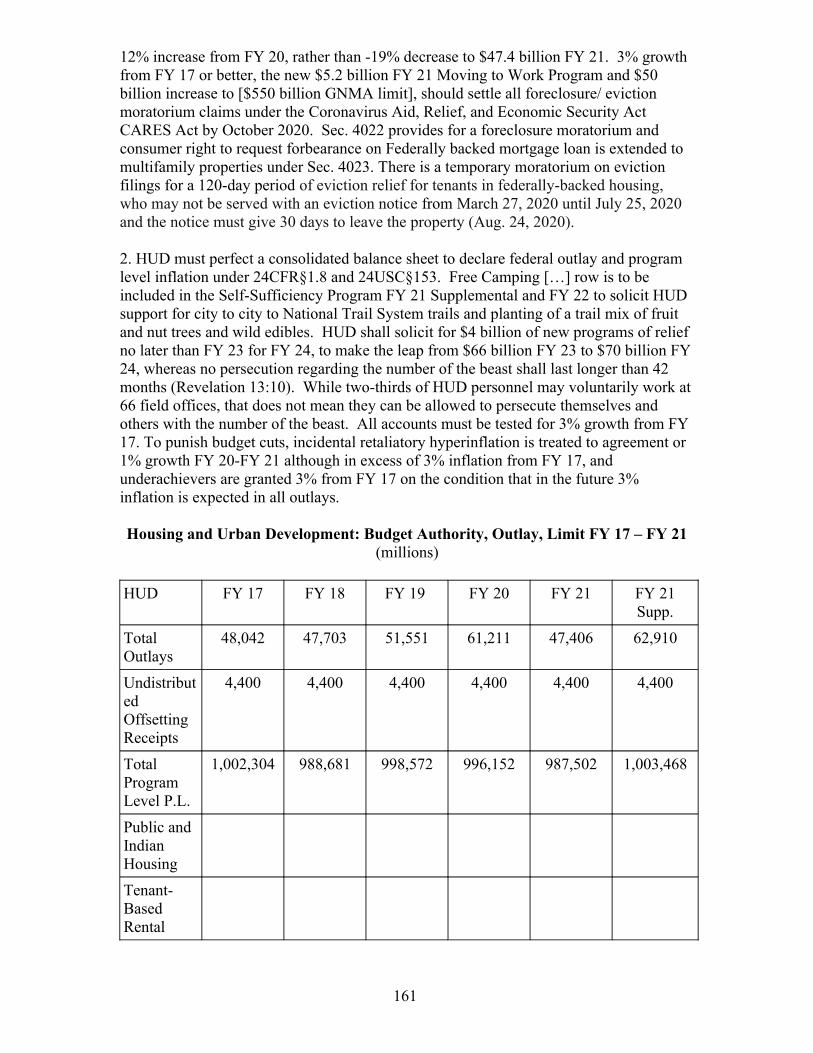

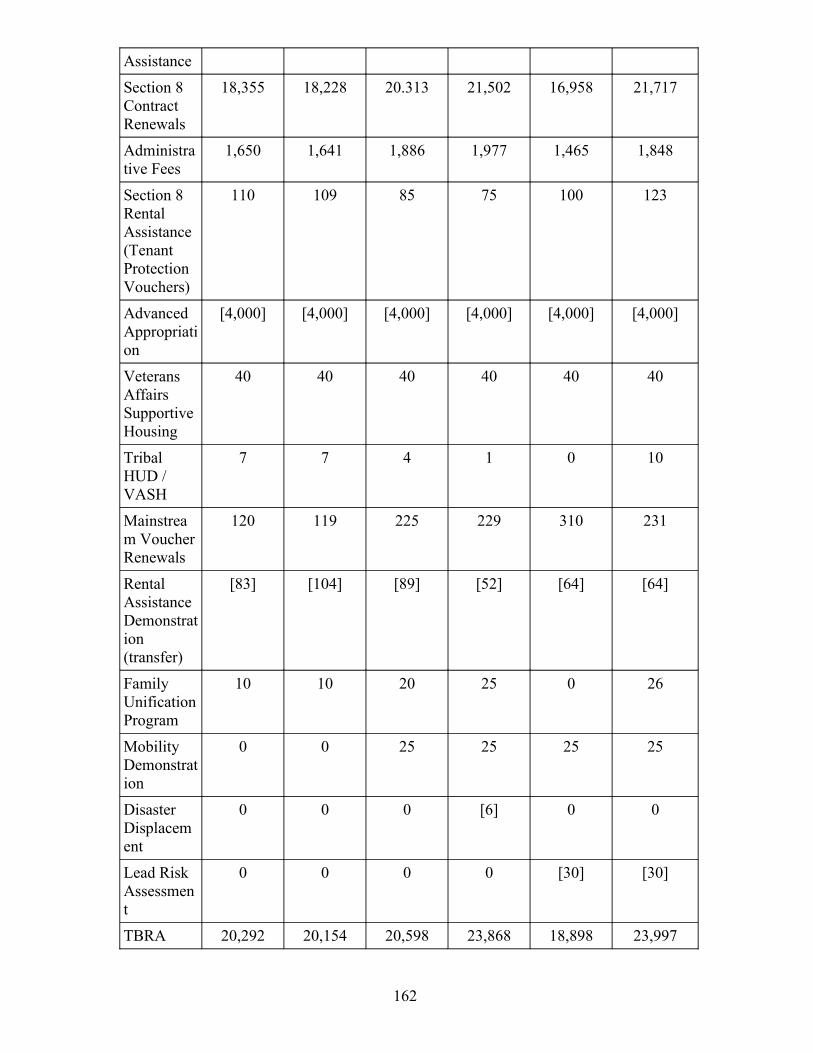

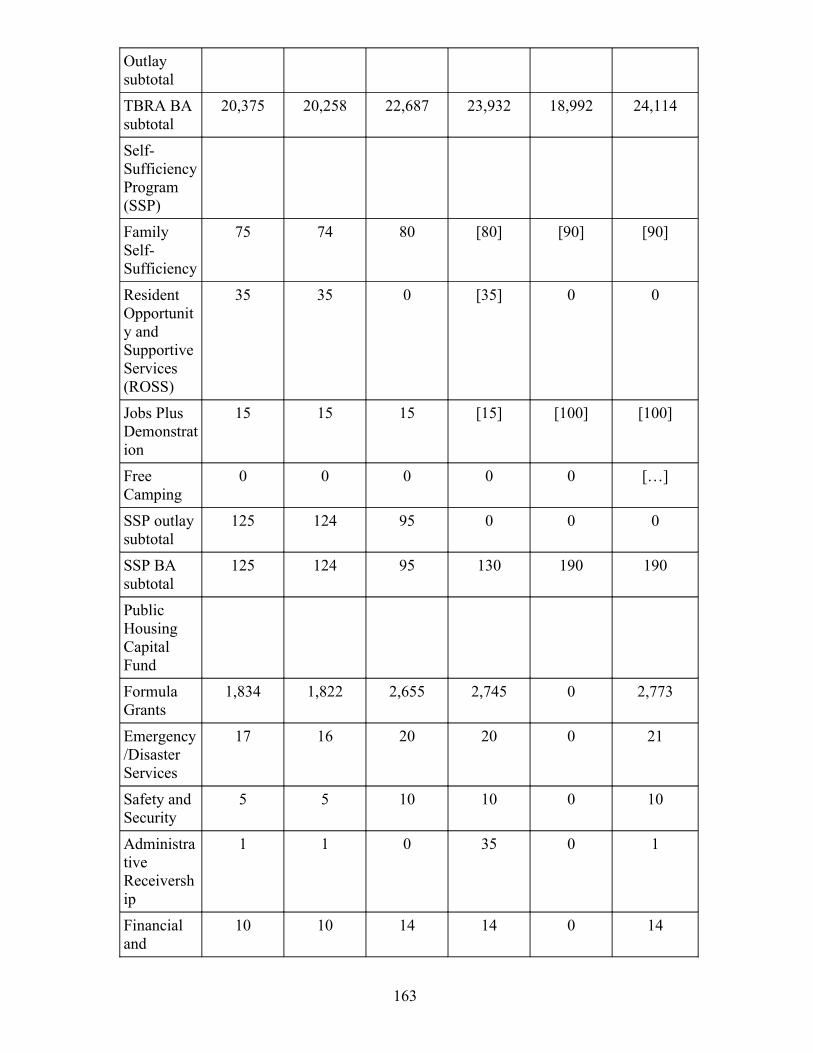

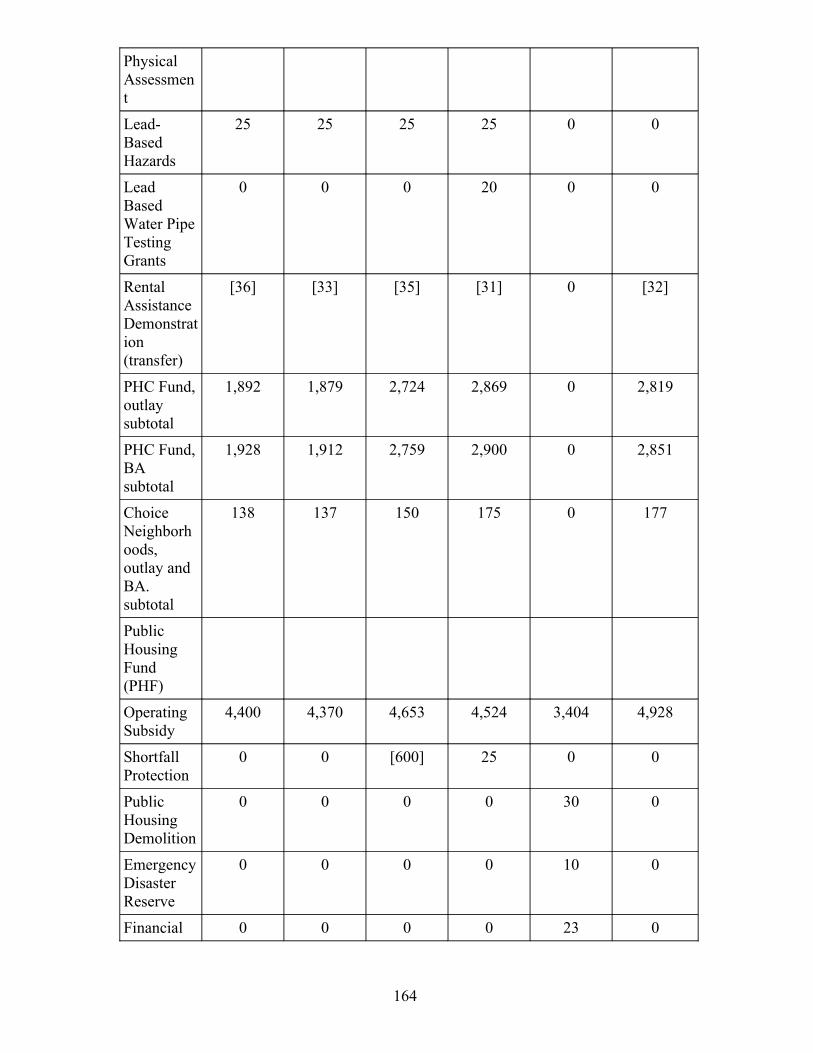

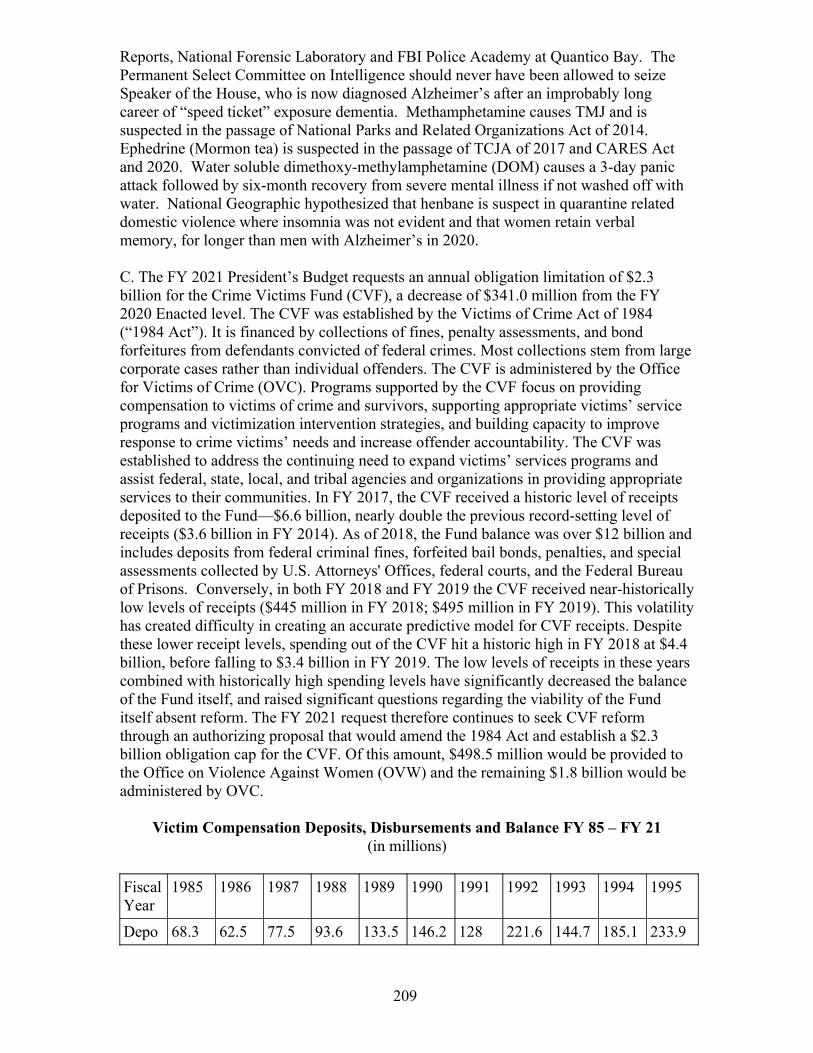

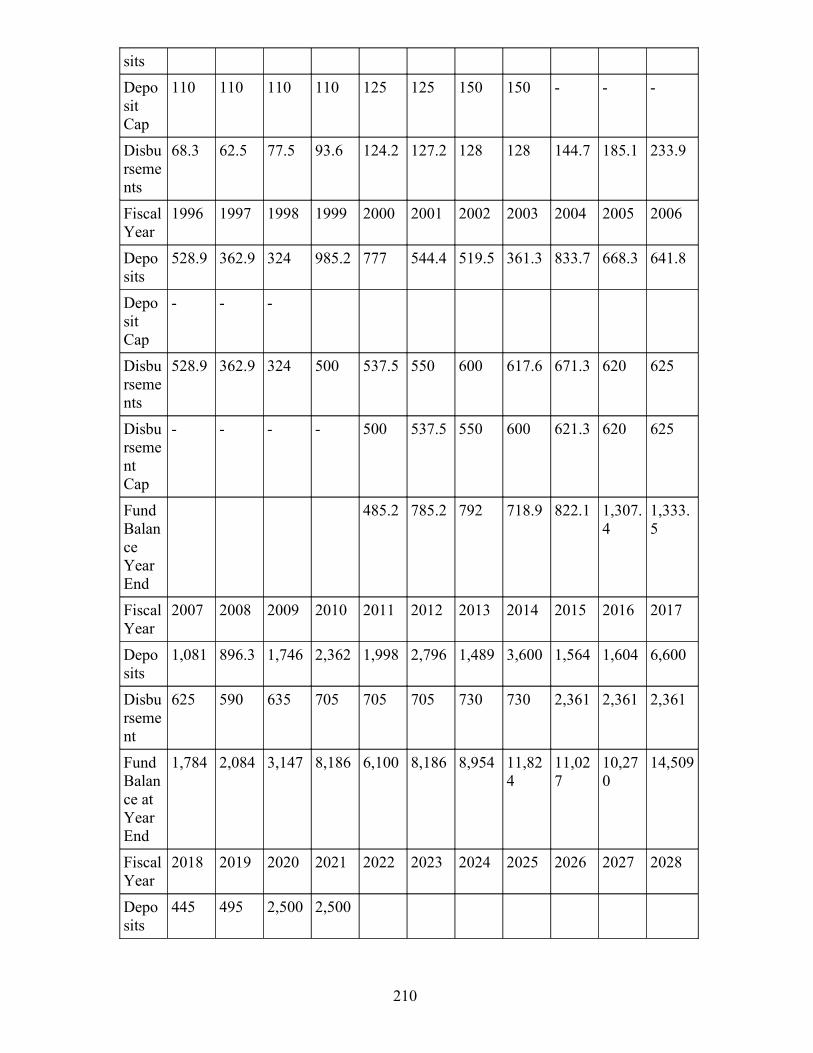

Table 1 United States Government Receipts, Outlays, Surplus or Deficit FY 16 – FY 24Table 2 Devaluation Equation FY 2021Table 3 Current Account Balance 2016-2020Table 4 Combined Statement Receipts by Source Categories 2019Table 5 Treasury Statement by Month October FY 19 – July FY 20Table 6 Preliminary Pandemic Revised Revenues FY 00 – FY 24 Table 7 Government Outlays by Agency Ledger FY 16 – FY 24Table 8 Undistributed Offsetting Receipts FY 16 – FY 21Table 9 Federal Government Financing and Debt 2019-2024Table 10 Estimates of US GDP 2004-2024Table 11 Real Gross Domestic Product Composition 2017-2020Table 12 Real Gross Domestic Income 2017 - 2020 Table 13 Individual Income Tax 2007 – 2024Table 14 Tax Rates Over the Last CenturyTable 15 Tax Brackets 2017-2018Table 16 Corporation Income Tax Revenues 2016 – 2024Table 17 State and Combined State and Federal Corporate Tax Rate 2018Table 18 Payroll Tax and Total Revenues 2008-2024Table 19 Payroll Tax Rates 1937-2024Table 20 Excise Taxes 2016 – 2024Table 21 Estate and Gift Tax Revenues 2007 – 2024Table 22 Customs Revenues 2007-2024Table 23 Customs Receipts by Source 2019Table 24 Composition of Other Receipts 2007-2024Table 25 Federal Reserve Interest Rates and Remittances to Treasury FY 16 – FY 24Table 26 Legislative Branch Appropriations by Agency FY 16 – FY 24Table 27 Legislative Branch Appropriations FY05 – FY 22Table 28 Electoral and Popular Split Ticket Vote 1972 – 2018Table 29 Judiciary Outlays and Budget Authority FY 17 – FY 21 Table 30 USDA Budget Overview FY 17 – FY 21Table 31 USDA Consolidated Balance Sheet FY 17 – FY 21

4

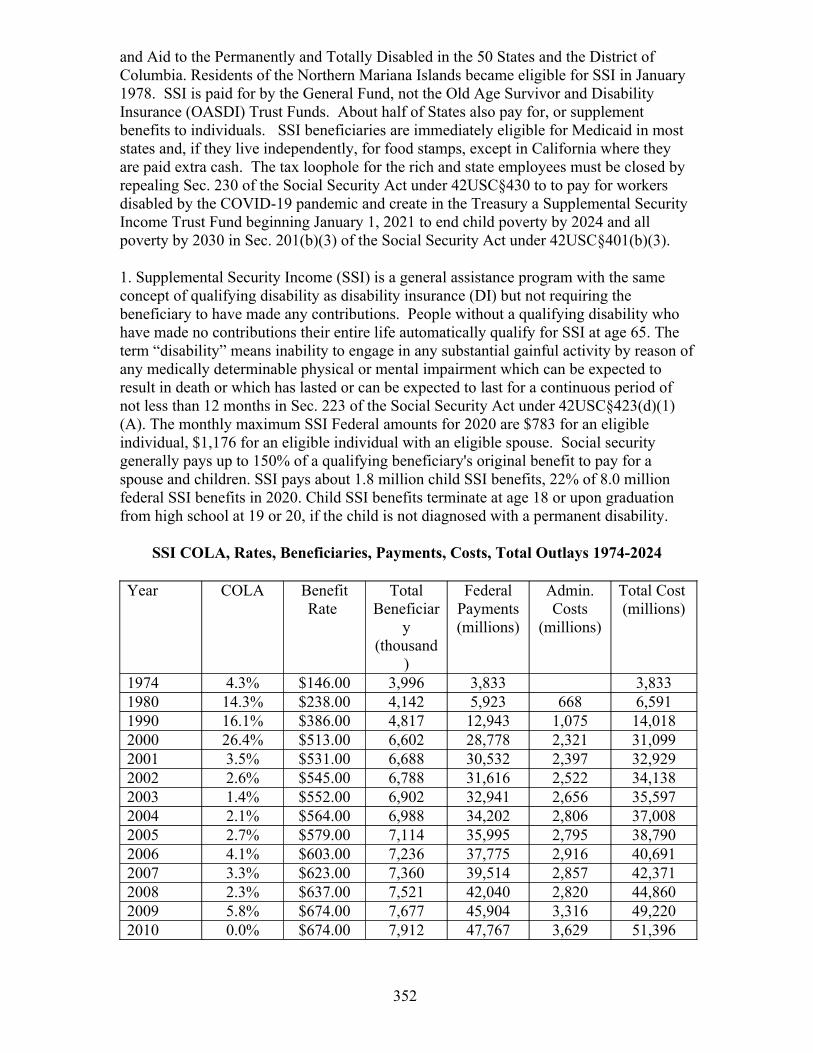

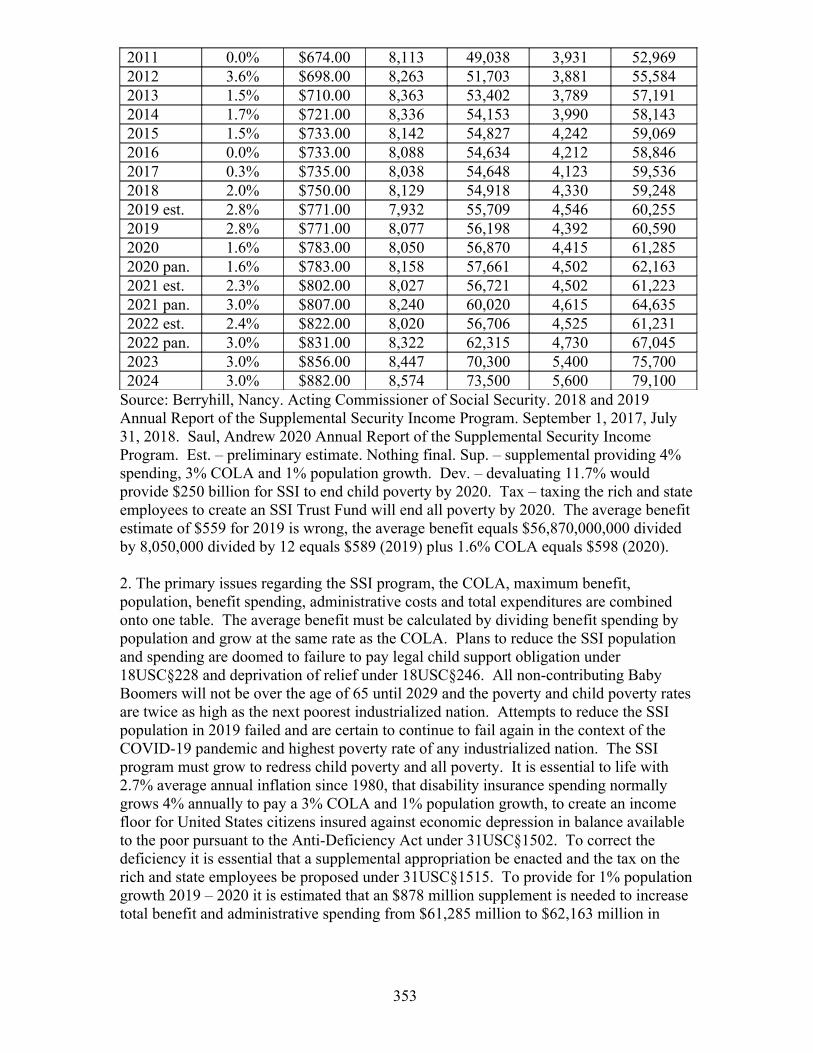

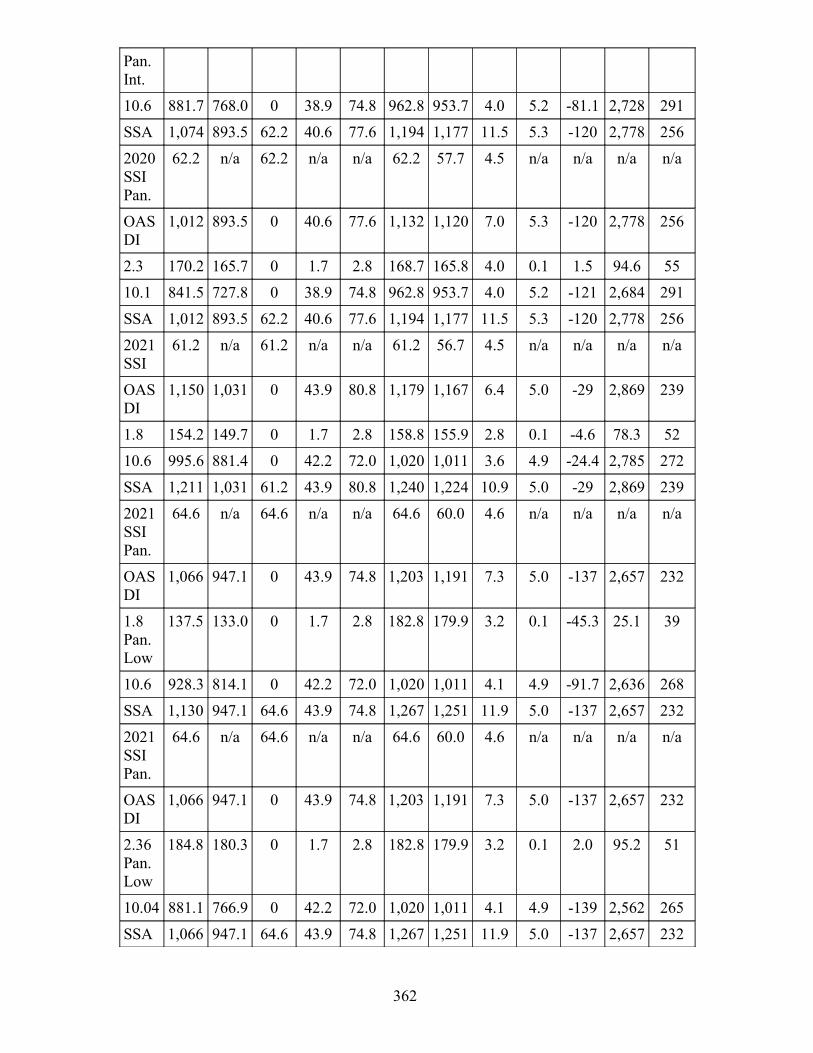

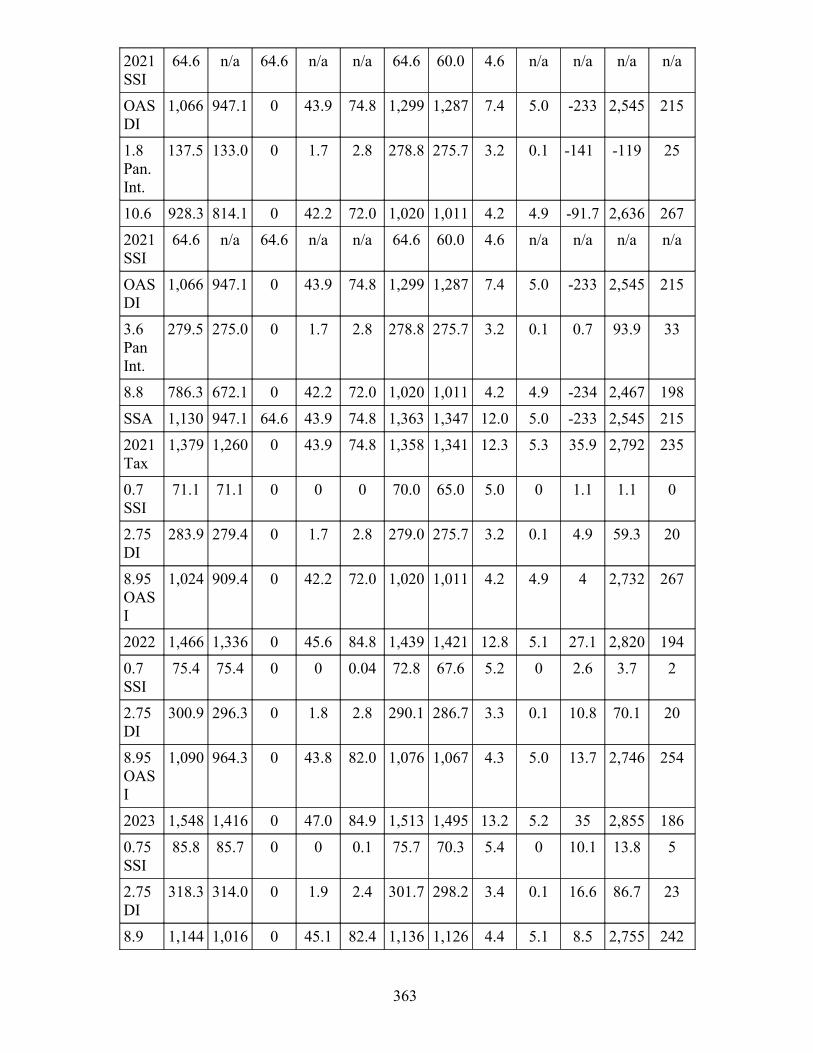

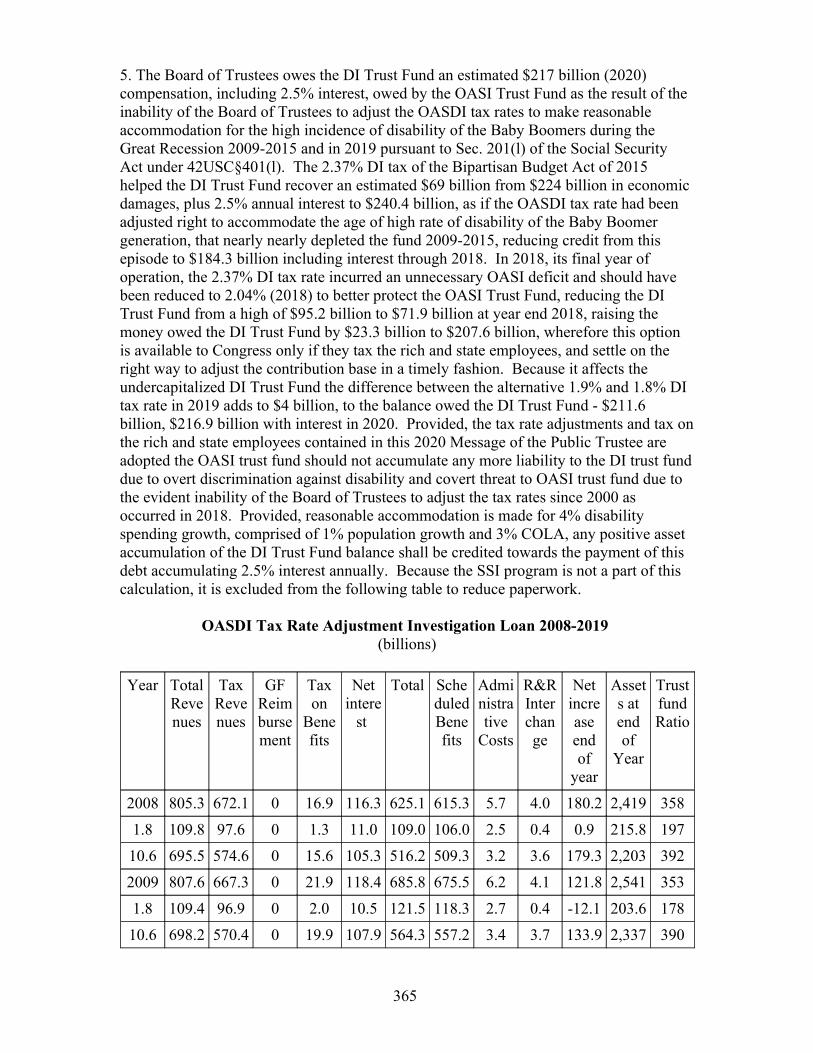

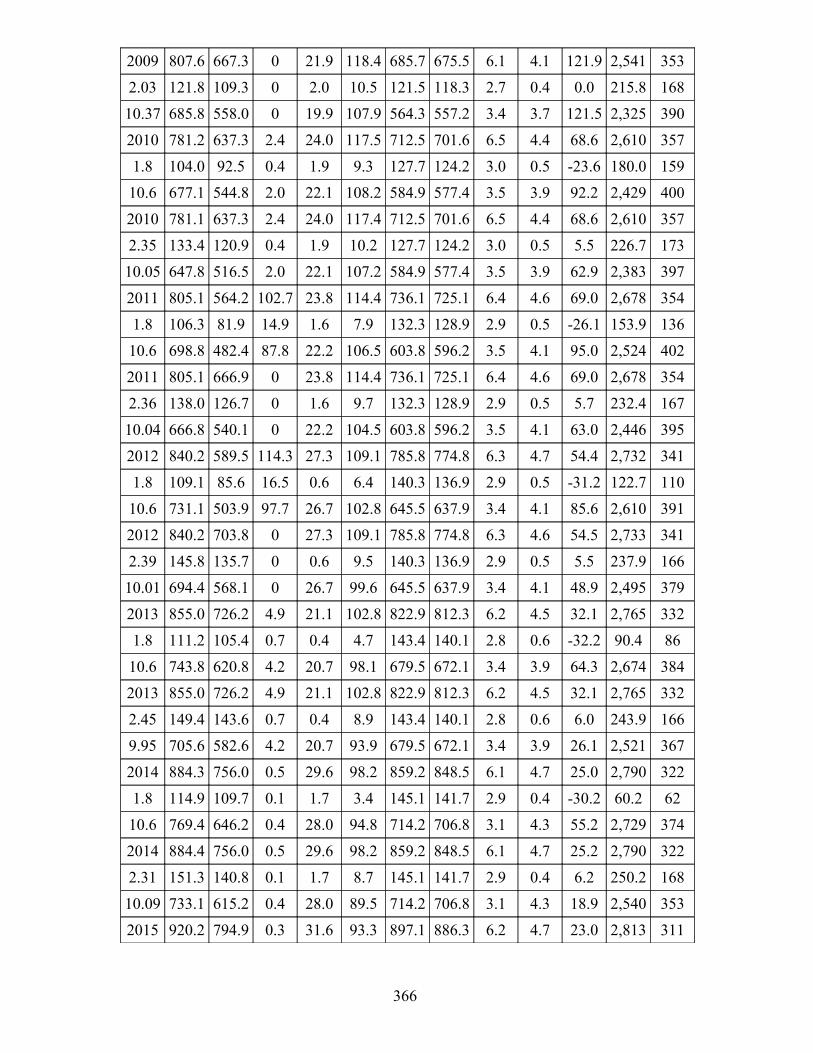

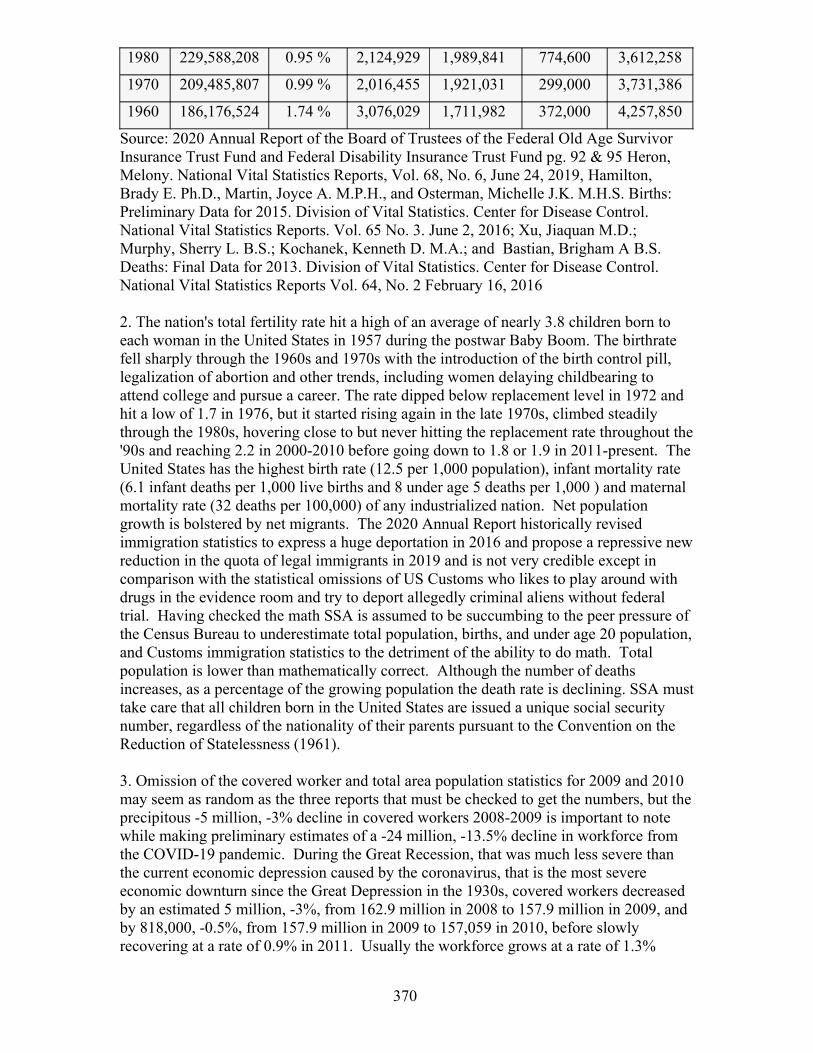

Table 32 Supplemental Nutrition Assistance Program (SNAP) Statistics 1969-2020Table 33 Commerce Department Budget FY 16 - FY 21Table 34 Commerce Department Full-Time Employment and Positions FY 17 – FY 21Table 35 Customs Budget FY17 - FY21Table 36 Military Programs Budget FY 16 – FY 21Table 37 US Military End Strength FY 16 – FY 21Table 38 Education Department, Total Outlays FY 17 – FY 21Table 39 Energy Department, Outlays FY17- FY21Table 40 Health and Human Services, Budget FY 17 – FY 21Table 41 Housing and Urban Development Budget Overview FY 17 – FY 21Table 42 HUD Budget Authority, Outlay, Limit FY 17 – FY 21Table 43 Interior Department Balance Available FY 17 – FY 21Table 44 Interior Total and Current Appropriations by Bureau FY17 - FY21Table 45 Justice Department, Budget Authority FY 16 – FY 21 Table 46 Victim Compensation Deposits, Disbursements and Balance FY 85 – FY 21Table 47 US Prison Population 1980 – 2014Table 48 Labor Department Budget FY 17 – FY 21Table 49 United Nations Regular and Peacekeeping Assessment FY 16 – FY 21Table 50 United States Contributions to International Programs FY 16 – FY 21 Table 51 State Department, Foreign Operations and Related Programs FY17 - FY21Table 52 Transportation Guaranteed Funding by Source FY 17 – FY 21Table 53 Treasury Budget Request FY 17 - FY 21Table 54 Treasury Discretionary Appropriations FY17 – FY21Table 55 Treasury Mandatory Funding FY 17 – FY 21Table 56 Veterans Affairs Budget FY17 – FY21Table 57 VA Appropriations, Collections and DoD Transfers FY 19- FY 21Table 58 Army Corp of Civil Engineers Budget FY17 – FY 21Table 59 Environmental Protection Agency Budget by Appropriation FY 17 – FY 21Table 60 Executive Office of the President Budget and FTEs FY 17- FY 21Table 61 Federal Emergency Management Administration Budget FY 17- FY 21Table 62 Combined GSA and OPM Budget FY 17 – FY 21Table 63 National Aeronautics and Space Administration Budget FY 17 – FY 21Table 64 National Science Foundation Budget FY 17 – FY 21Table 65 Small Business Administration Budget FY 17 – FY 21Table 66 SBA Credit Programs and Revolving Funds FY17 – FY 21Table 67 Postal Service Budget FY17 – FY18Table 68 Commissioners of Social Security 1946-presentTable 69 Social Security Administrative Costs 2016 – 2020Table 80 Old Age Survivor Insurance Trust Fund 2000-2024Table 81 OASI Beneficiaries with Benefits in Current-Payment Status 1945-2024Table 82 Fertility Rate and Deaths Per 100,000, by Age 1940-2020Table 83 Disability Insurance Trust Fund 2000-2024Table 84 DI Beneficiaries with Benefits in Current-Payment Status 1960-2024Table 85 Number and Average Benefit of DI Beneficiaries by Diagnosis Dec. 2009Table 86 SSI COLA, Rates, Beneficiaries, Payments, Costs, Total Outlays 1974-2024Table 87 Federally Administered SSI Population 1974-2020Table 88 Social Security Administration Six-Year Budget 2019-2024Table 89 OASDI Tax Rate Adjustment Investigation Loan 2008-2019Table 90 Population Growth 1960-2017

5

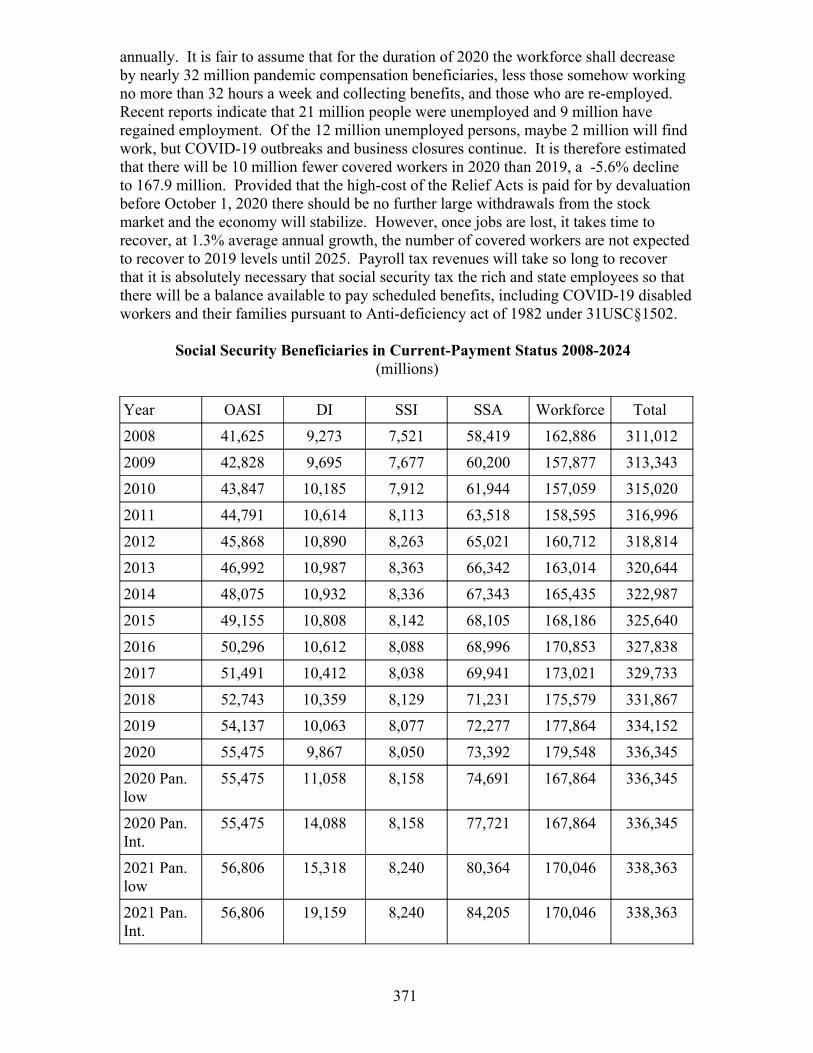

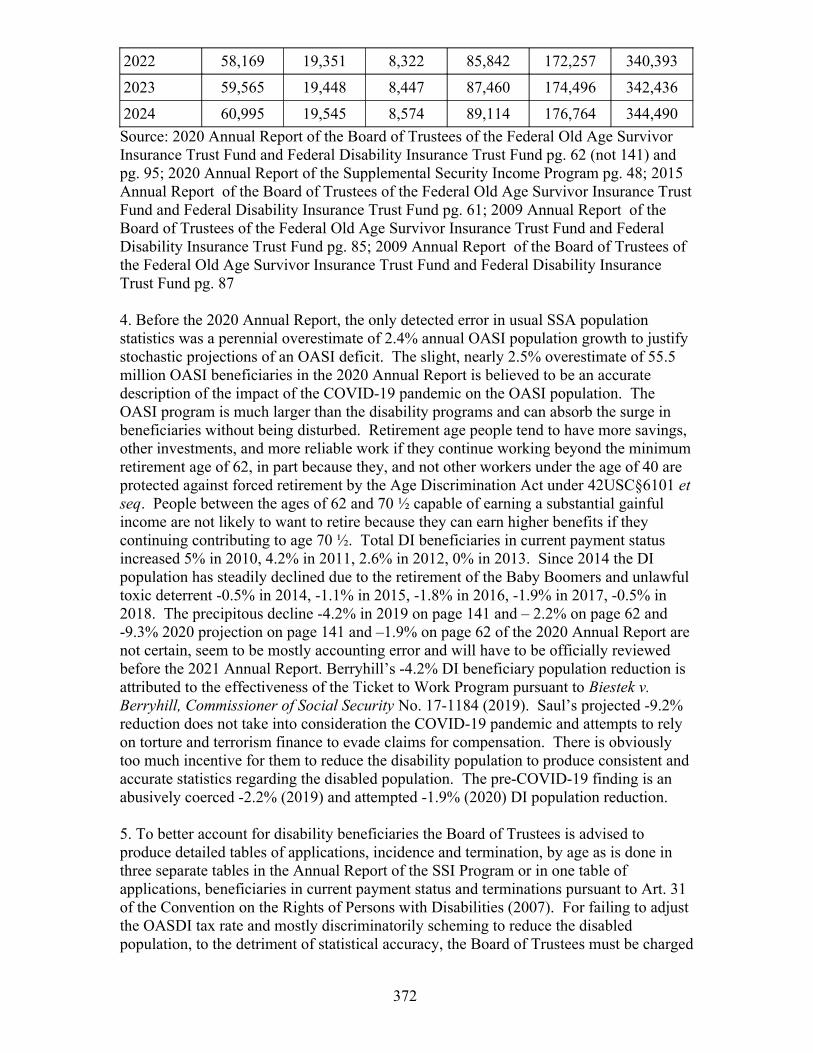

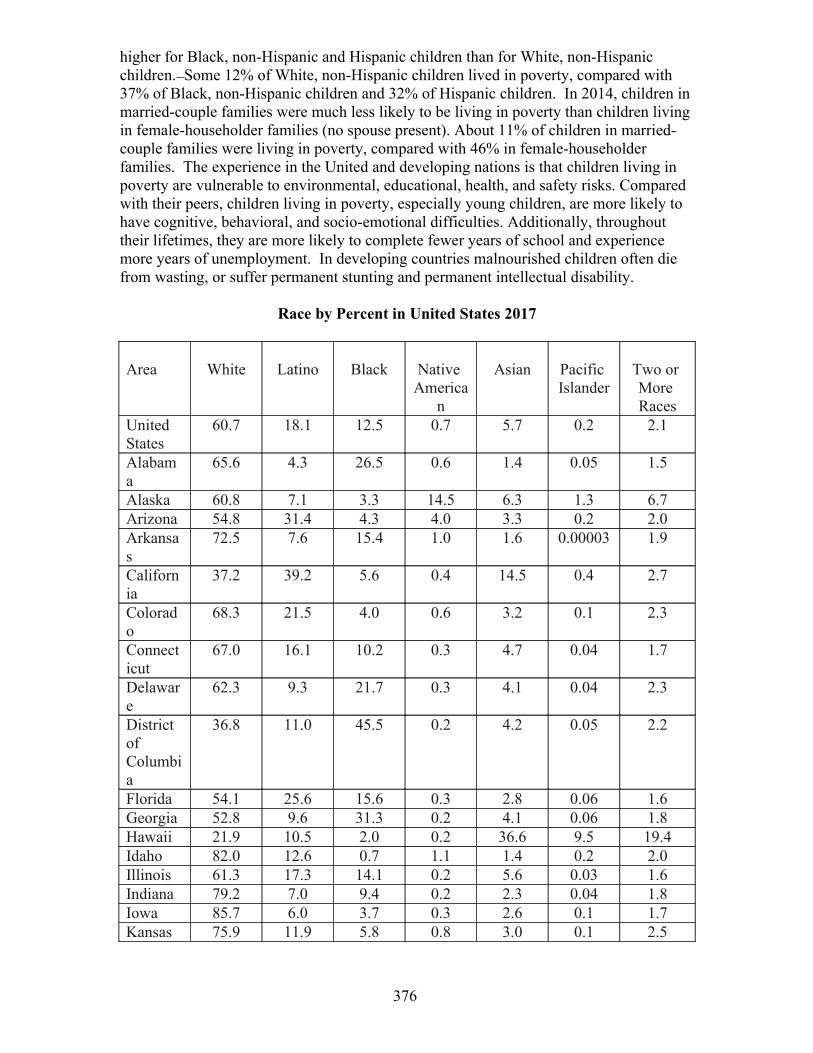

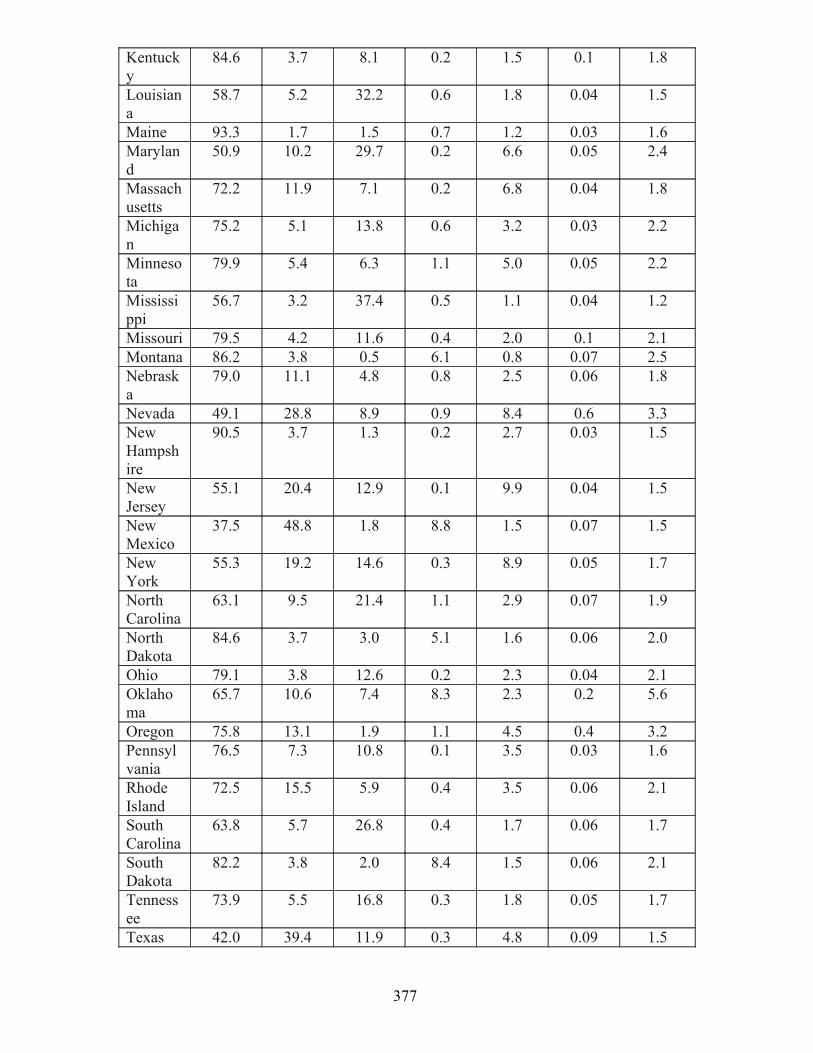

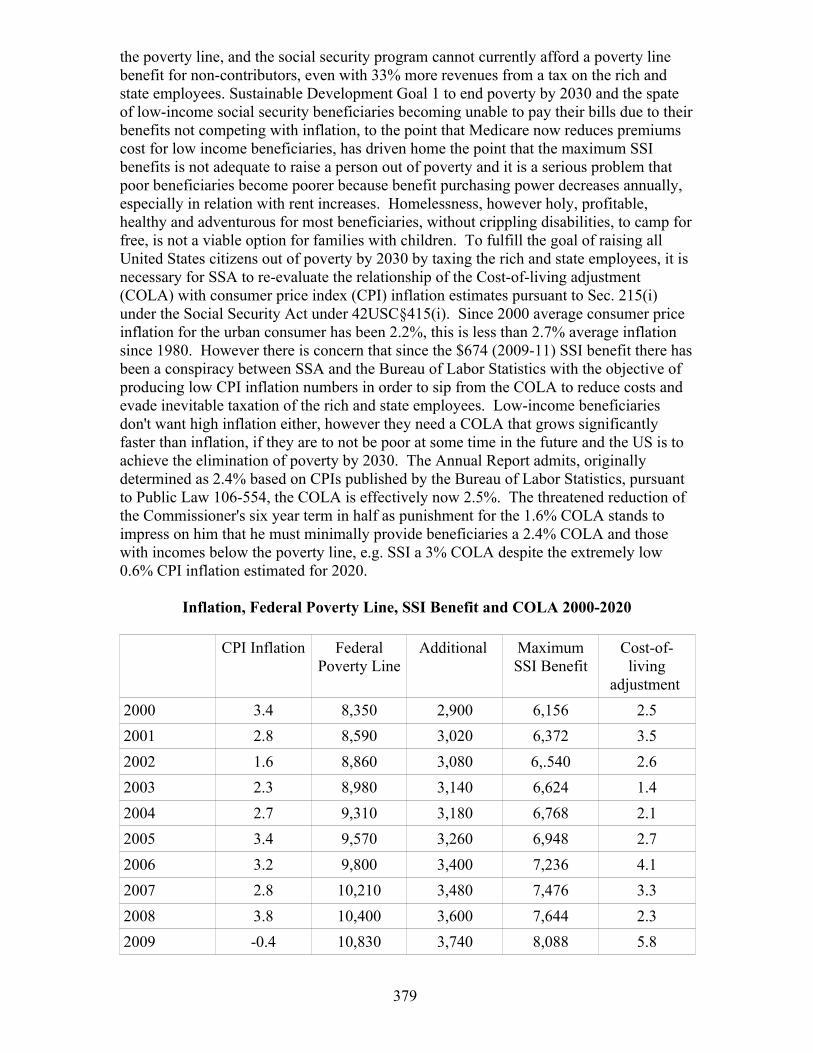

Table 91 Social Security Beneficiaries in Current-Payment Status 2008-2024Table 92 Poor Persons Residing in the United States 1973-2014Table 93 Race by Percent in United States 2017Table 94 Inflation, Federal Poverty Line, SSI Benefit and COLA 2000-2020

Bibliography

Article 1 Fiscal Year 2020

§71 Balance

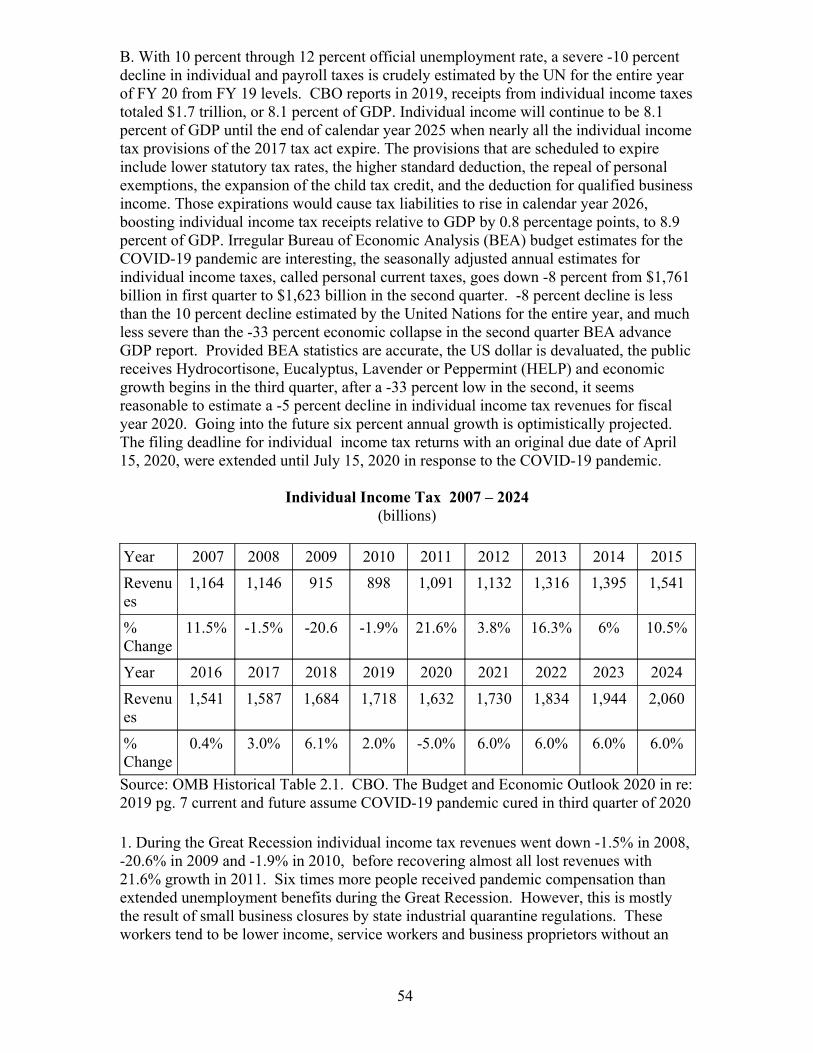

A. Title 24 US Code Chapter 3 National Home for Disabled Volunteer Soldiers, in preserved only in Subchapter V Battle Mountain Sanitarium Reserve under 24USC§151-154. Starting with Fiscal Year 2001, the Annual Report and Annual Report Appendix have been combined and renamed the Combined Statement of Receipts, Outlays, and Balances of the United States Government (Combined Statement). The Combined Statement is recognized as the official publication of receipts and outlays. All other federal government reports containing similar data must be in agreement with the Combined Statement. However, although budget receipt and total receipts are clearly distinguished, there is no attempt to comprehensively tabulate outlays and this compromises exact calculation of deficit / surplus. As the result of neglecting to methodically tabulate the outlay overview by category, the Combined Statement completely fails to distinguish between budget authority and excluded interagency and lending outlays and this perpetuates the myths sustaining a +/-12 percent margin of error in the annual estimate of outlays by agency in Table 4.1 of the Office of Management andBudget (OMB) Historical Tables that greatly exceeds the tendency to overestimate revenues by about 2 percent resulting in a larger deficit, t-bond sale and audit, further complicated by threatened budget cuts and arrears therefore, than is wanted.

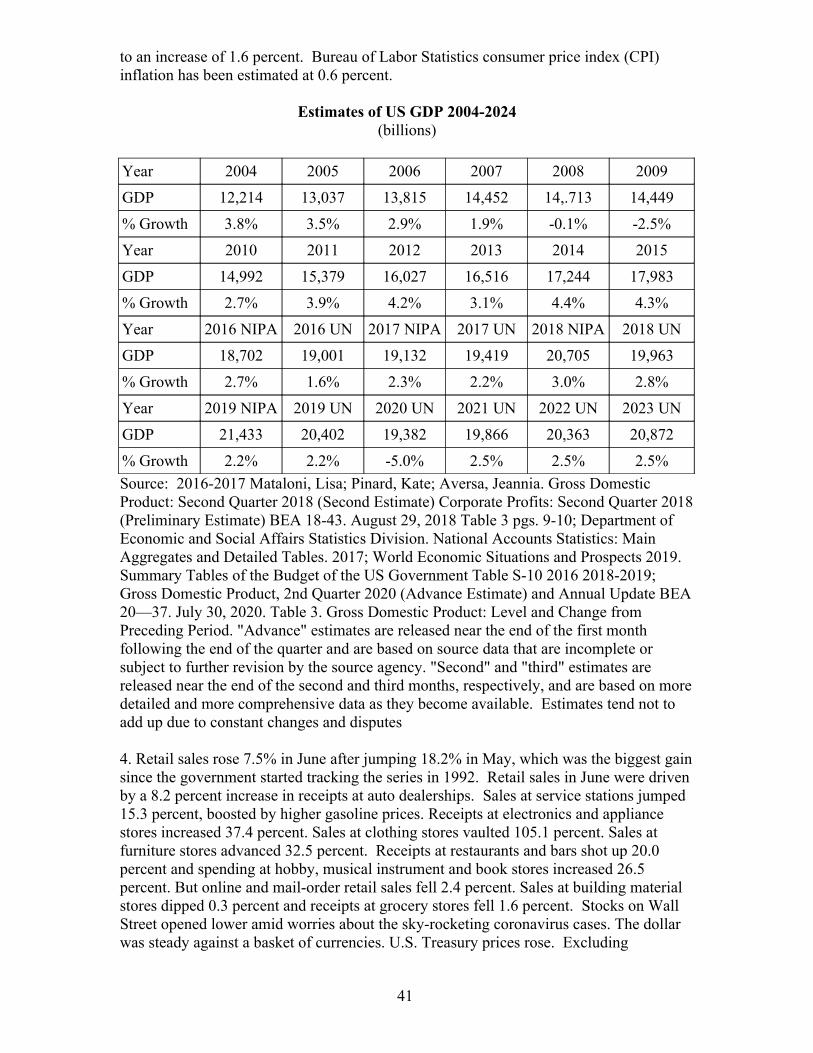

1. In the US and EU, the global COVID-19 pandemic caused a -33 percent economic decline in the second quarter, after a -5 percent decline in the first quarter. 2020 GDP is certain to be economically depressed from the previous year's dispute between real UN approved and nominal GDP. How long and severe the economic depression is going to be, in industrialized nations where “affluenza” is an aggravating factor, depends on two mitigating factors. First, how long does it take for public officials to stop restricting economic activity and prescribe Hydrocortisone, Eucalyptus, Lavender or Peppermint (HELP) to cure coronavirus and mold allergies. Second, whether the Treasurer decides to devaluate the dollar before October 1, 2020 to spare the stock market withdrawal from the ultra-expensive relief acts and deficit in excess of 3 percent of GDP. COVID-19 pandemic relief acts in the US cost four times as much as similar, more law-abiding, relief packages in the EU. The contagion of the $666 payroll protection program (PPP) loan fraud and other un-dismissed relief bills, including the Tax Cuts and Jobs Act (TCJA), believed to have been passed under the influence of speed (ephedrine), must be prevented from spreading from small businesses to C corporations, by devaluating the USdollar by October 1, 2020 pursuant to the Marshal Lerner Condition under 19USC§4421, 22USC§5301 et seq. and the Revised estimates: effect of changes in rates of exchange and inflation Report of the Secretary-General December 2019.

6

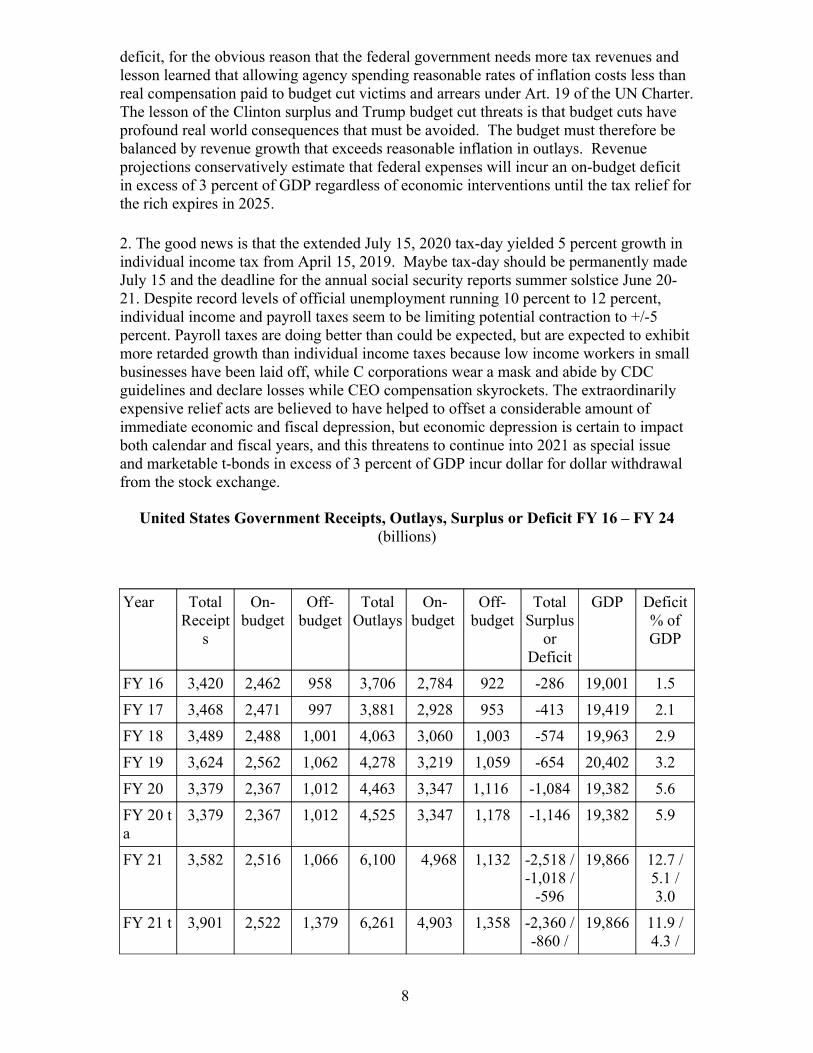

2. Economic depression is certain to have a negative impact on many sources of federal revenues and increase the real deficit preliminarily estimated at $1 trillion FY 20 by OMB, without taking into consideration revenues lost to the pandemic or deficit reduction from the annual HA audit. However the extended July 15, 2020 tax day yielded 5 percent growth in individual income tax from April 15, 2019. Maybe tax day should be permanently made July 15 and the deadline for the annual social security reports summer solstice June 20-21. Despite record levels of official unemployment running 10 percent to 12 percent, individual income and payroll taxes seem to be limitingpotential contraction to less than -10 percent. The extraordinarily expensive relief acts are believed to have helped to offset a considerable amount of immediate economic and fiscal depression, but economic depression is certain to impact both calendar and fiscal years, when the loan forgiveness expires at the end of the fiscal year and the deficit becomes debt to be sold as special issue and marketable t-bonds. To responsibly conclude the FY 20 overspending crisis, it is essential that the dollar is sufficiently devaluated by October 1, 2020, the first day of FY 21.

B. The ordinary expense of modern governments in time of peace is equal or nearly equalto their ordinary revenue according to Adam Smith's Inquiry into the Nature and Causes of the Wealth of Nations, (1776) Public Debts Book V Chapter III . Since 1980 several balanced budget amendments have been proposed however none were agreed to. Normally governments run on a deficit. According to the EU deficits should not exceed 3% of GDP. A federal budget surplus is an extremely elusive goal that has been achievedonly a few times in American history. Most famously the time President Andrew Jackson paid back the entire national debt in 1832 although Immanuel Kant had written earlier that this was theoretically impossible to do in Perpetual Peace (1795). Although the United States earned a $70 million surplus 1789-1849, the Civil War incurred a -$991million deficit 1850-1900. Between 1900 and 1920 the budget fluctuated tens of millionsdollars surplus or deficit, regardless of the war in Europe. From 1920 until after the stockmarket crash in 1931 there was a surplus. Since the end of World War II 1947 – 1948, the federal government has declared a surplus only in 1960 and 1999-2000. The surplus of 1999-2000 was doomed because it did not increase revenues. Emboldened the ease with which they were able to steal child welfare benefits 1996-2000, Clinton managed to generate a temporary budget surplus by cutting military and health spending, however this temporary surplus, was lost to the 9-11 suicide attacks and cost of international war.

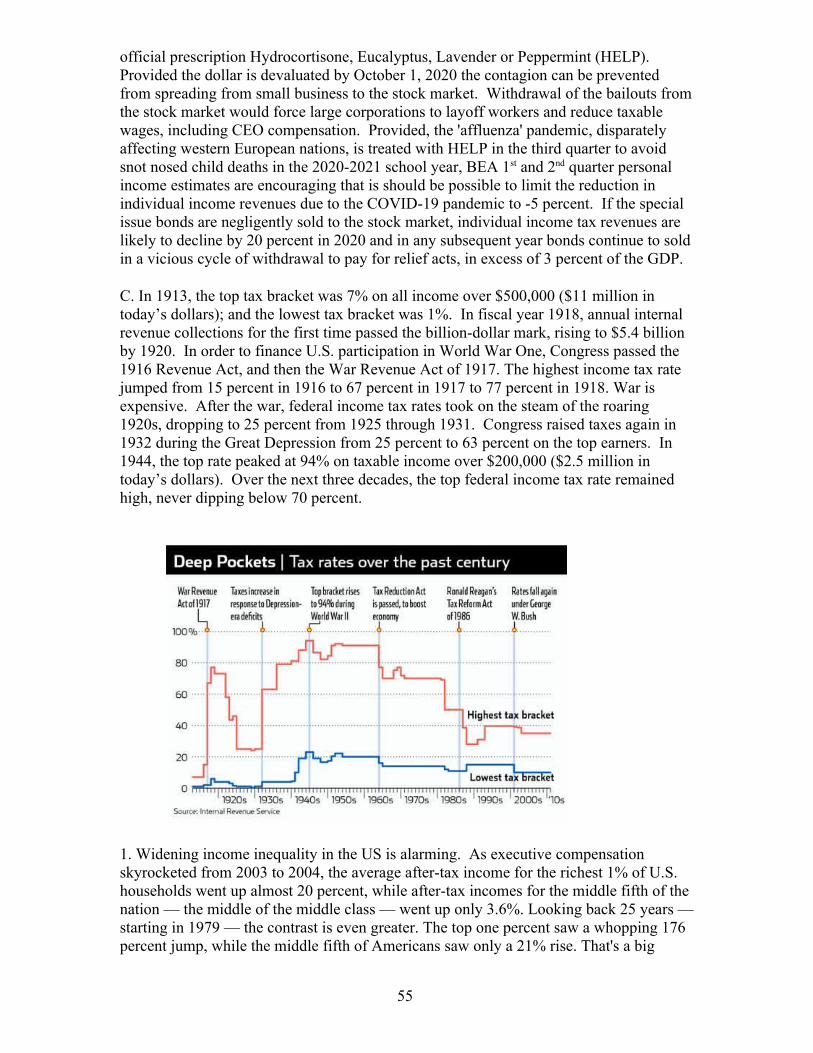

1. The Great Recession (2009-11) was in fact an economic depression lasting three years.Instead of devaluating the dollar to bailout financial institutions damaged by adjustable rate mortgage (ARM) loans, Congress and EU negligently got into debt, withdrawing the bailout funds from the stock market, causing economic depression and then engaging in avicious cycle of expensive Recovery Acts that served to prolong the economic depressionuntil a year after the relief acts stopped excessively withdrawing investment funds from the stock market. If revenue growth had not gone down due to xenophobia FY 16 - FY 17and temporary tax relief for the rich 2018-2025 not been passed, revenue growth in excess of outlay growth was predicted to generate a real budget surplus, after excluding fake outlay rows as soon as FY 17. However, xenophobia led to germaphobia and the ultra-expensive relief Act(s) have once again incurred the largest deficit in history. It remains to be seen if the United States devaluates the dollar to conclude the economic depression before withdrawal spreads from small to large business. Trump Administration tax and budget cut attempts have dramatically increased the projected

7

deficit, for the obvious reason that the federal government needs more tax revenues and lesson learned that allowing agency spending reasonable rates of inflation costs less than real compensation paid to budget cut victims and arrears under Art. 19 of the UN Charter.The lesson of the Clinton surplus and Trump budget cut threats is that budget cuts have profound real world consequences that must be avoided. The budget must therefore be balanced by revenue growth that exceeds reasonable inflation in outlays. Revenue projections conservatively estimate that federal expenses will incur an on-budget deficit in excess of 3 percent of GDP regardless of economic interventions until the tax relief forthe rich expires in 2025.

2. The good news is that the extended July 15, 2020 tax-day yielded 5 percent growth in individual income tax from April 15, 2019. Maybe tax-day should be permanently made July 15 and the deadline for the annual social security reports summer solstice June 20-21. Despite record levels of official unemployment running 10 percent to 12 percent, individual income and payroll taxes seem to be limiting potential contraction to +/-5 percent. Payroll taxes are doing better than could be expected, but are expected to exhibit more retarded growth than individual income taxes because low income workers in small businesses have been laid off, while C corporations wear a mask and abide by CDC guidelines and declare losses while CEO compensation skyrockets. The extraordinarily expensive relief acts are believed to have helped to offset a considerable amount of immediate economic and fiscal depression, but economic depression is certain to impact both calendar and fiscal years, and this threatens to continue into 2021 as special issue and marketable t-bonds in excess of 3 percent of GDP incur dollar for dollar withdrawal from the stock exchange.

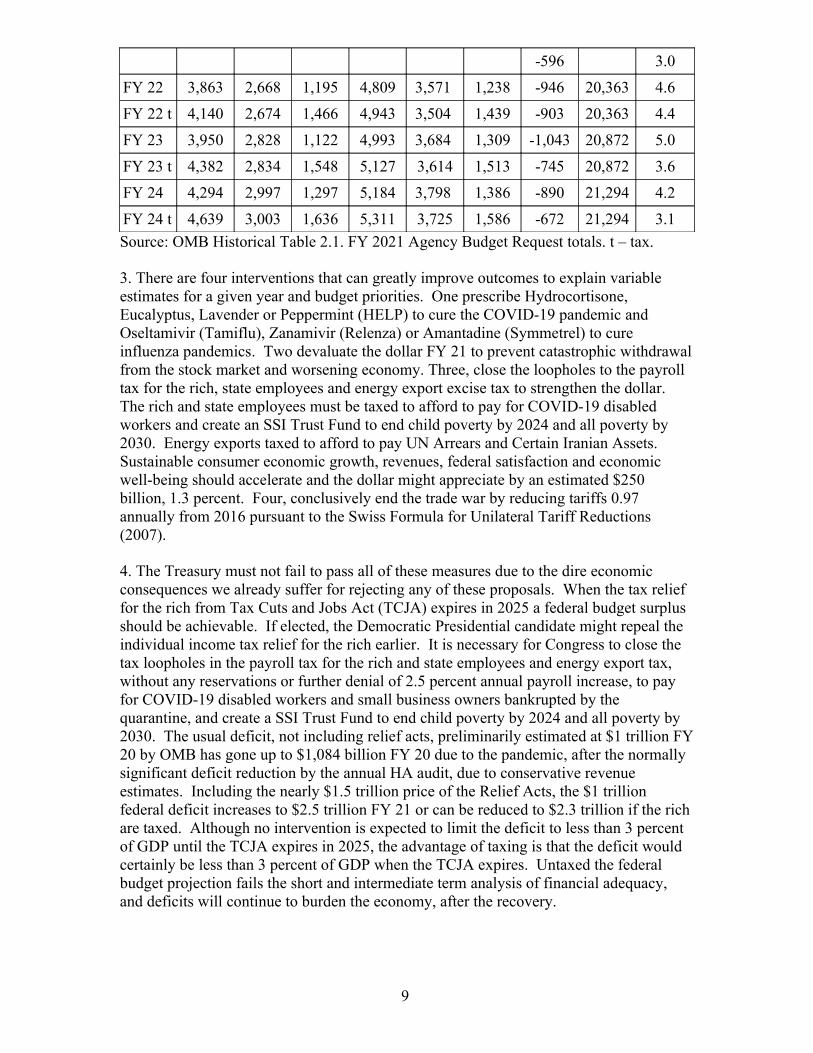

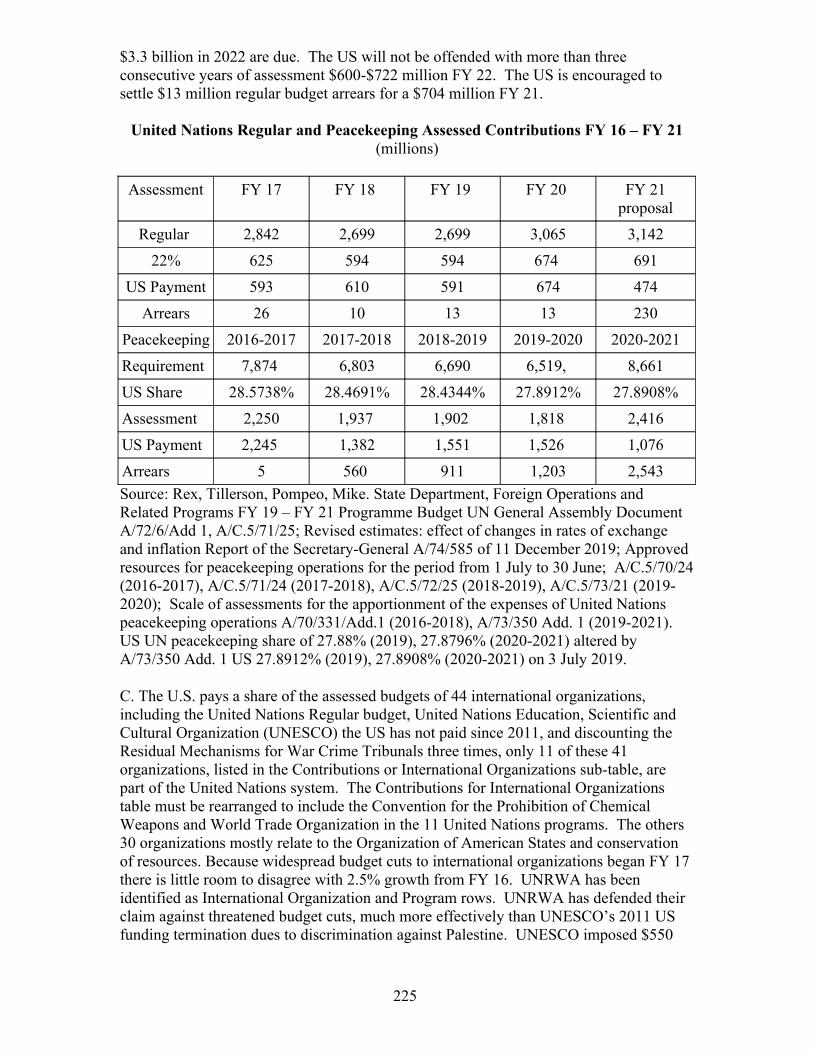

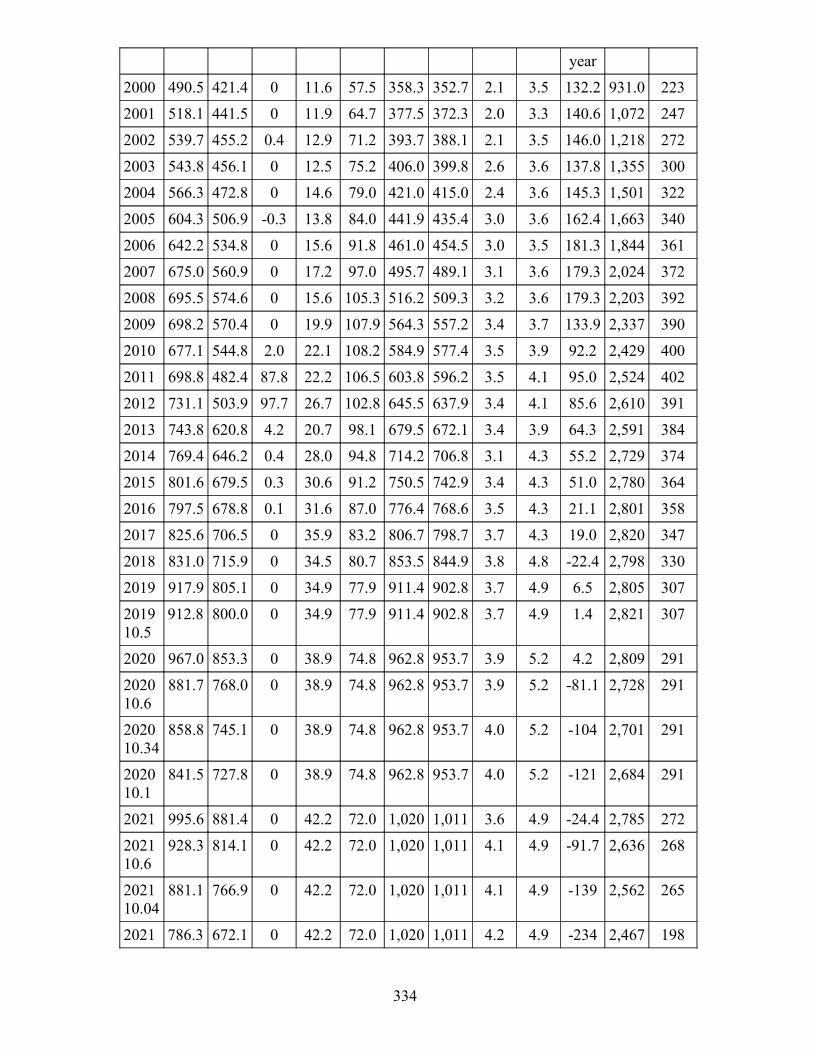

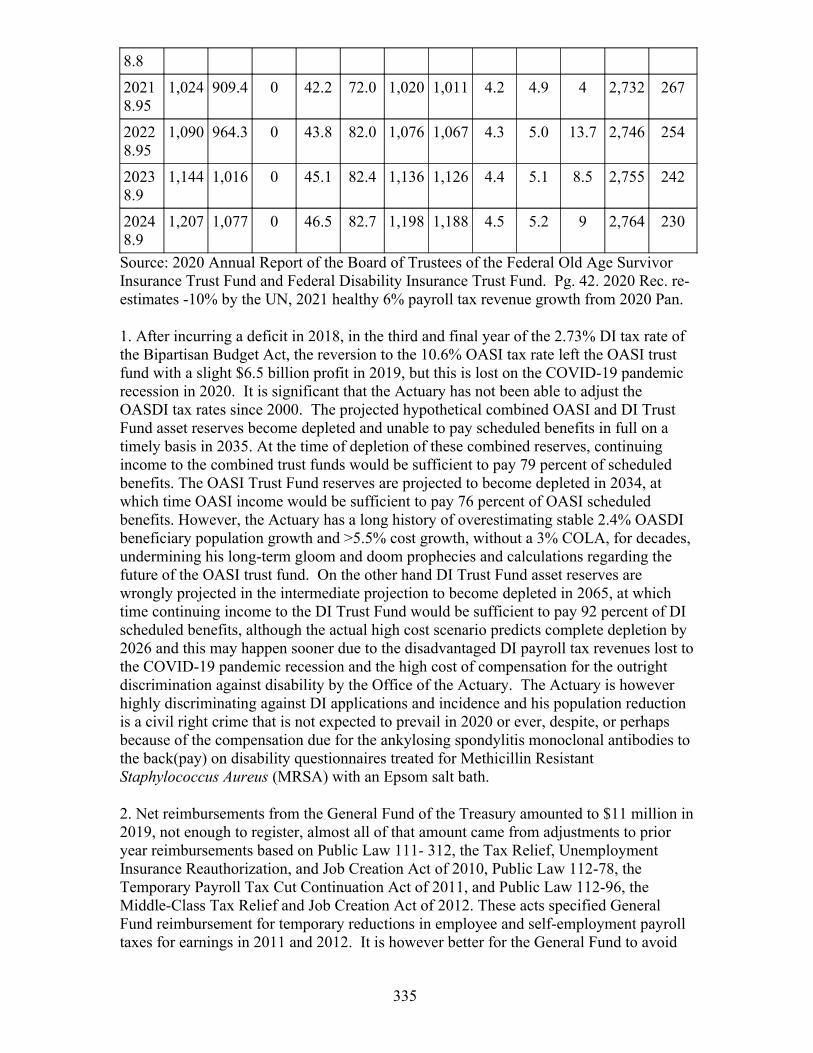

United States Government Receipts, Outlays, Surplus or Deficit FY 16 – FY 24(billions)

Year TotalReceipt

s

On-budget

Off-budget

TotalOutlays

On-budget

Off-budget

TotalSurplus

orDeficit

GDP Deficit% ofGDP

FY 16 3,420 2,462 958 3,706 2,784 922 -286 19,001 1.5

FY 17 3,468 2,471 997 3,881 2,928 953 -413 19,419 2.1

FY 18 3,489 2,488 1,001 4,063 3,060 1,003 -574 19,963 2.9

FY 19 3,624 2,562 1,062 4,278 3,219 1,059 -654 20,402 3.2

FY 20 3,379 2,367 1,012 4,463 3,347 1,116 -1,084 19,382 5.6

FY 20 ta

3,379 2,367 1,012 4,525 3,347 1,178 -1,146 19,382 5.9

FY 21 3,582 2,516 1,066 6,100 4,968 1,132 -2,518 /-1,018 /

-596

19,866 12.7 /5.1 /3.0

FY 21 t 3,901 2,522 1,379 6,261 4,903 1,358 -2,360 /-860 /

19,866 11.9 /4.3 /

8

-596 3.0

FY 22 3,863 2,668 1,195 4,809 3,571 1,238 -946 20,363 4.6

FY 22 t 4,140 2,674 1,466 4,943 3,504 1,439 -903 20,363 4.4

FY 23 3,950 2,828 1,122 4,993 3,684 1,309 -1,043 20,872 5.0

FY 23 t 4,382 2,834 1,548 5,127 3,614 1,513 -745 20,872 3.6

FY 24 4,294 2,997 1,297 5,184 3,798 1,386 -890 21,294 4.2

FY 24 t 4,639 3,003 1,636 5,311 3,725 1,586 -672 21,294 3.1

Source: OMB Historical Table 2.1. FY 2021 Agency Budget Request totals. t – tax.

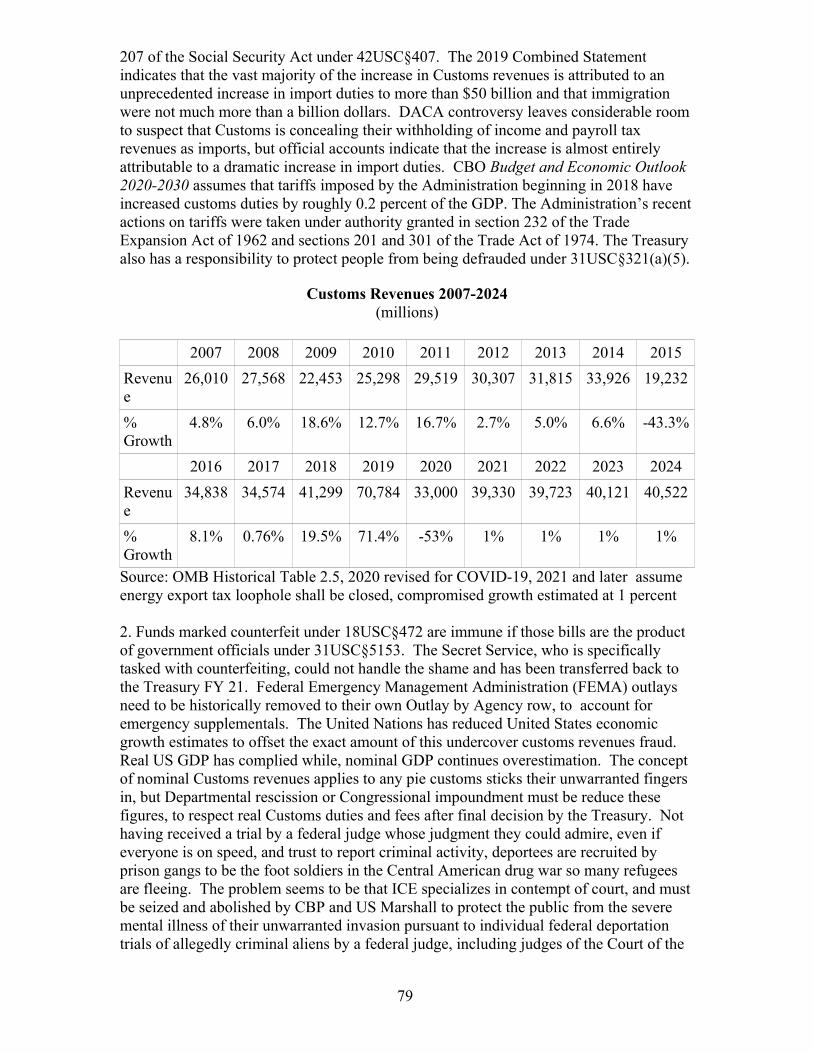

3. There are four interventions that can greatly improve outcomes to explain variable estimates for a given year and budget priorities. One prescribe Hydrocortisone, Eucalyptus, Lavender or Peppermint (HELP) to cure the COVID-19 pandemic and Oseltamivir (Tamiflu), Zanamivir (Relenza) or Amantadine (Symmetrel) to cure influenza pandemics. Two devaluate the dollar FY 21 to prevent catastrophic withdrawalfrom the stock market and worsening economy. Three, close the loopholes to the payroll tax for the rich, state employees and energy export excise tax to strengthen the dollar. The rich and state employees must be taxed to afford to pay for COVID-19 disabled workers and create an SSI Trust Fund to end child poverty by 2024 and all poverty by 2030. Energy exports taxed to afford to pay UN Arrears and Certain Iranian Assets. Sustainable consumer economic growth, revenues, federal satisfaction and economic well-being should accelerate and the dollar might appreciate by an estimated $250 billion, 1.3 percent. Four, conclusively end the trade war by reducing tariffs 0.97 annually from 2016 pursuant to the Swiss Formula for Unilateral Tariff Reductions (2007).

4. The Treasury must not fail to pass all of these measures due to the dire economic consequences we already suffer for rejecting any of these proposals. When the tax relief for the rich from Tax Cuts and Jobs Act (TCJA) expires in 2025 a federal budget surplus should be achievable. If elected, the Democratic Presidential candidate might repeal the individual income tax relief for the rich earlier. It is necessary for Congress to close the tax loopholes in the payroll tax for the rich and state employees and energy export tax, without any reservations or further denial of 2.5 percent annual payroll increase, to pay for COVID-19 disabled workers and small business owners bankrupted by the quarantine, and create a SSI Trust Fund to end child poverty by 2024 and all poverty by 2030. The usual deficit, not including relief acts, preliminarily estimated at $1 trillion FY20 by OMB has gone up to $1,084 billion FY 20 due to the pandemic, after the normally significant deficit reduction by the annual HA audit, due to conservative revenue estimates. Including the nearly $1.5 trillion price of the Relief Acts, the $1 trillion federal deficit increases to $2.5 trillion FY 21 or can be reduced to $2.3 trillion if the rich are taxed. Although no intervention is expected to limit the deficit to less than 3 percent of GDP until the TCJA expires in 2025, the advantage of taxing is that the deficit would certainly be less than 3 percent of GDP when the TCJA expires. Untaxed the federal budget projection fails the short and intermediate term analysis of financial adequacy, and deficits will continue to burden the economy, after the recovery.

9

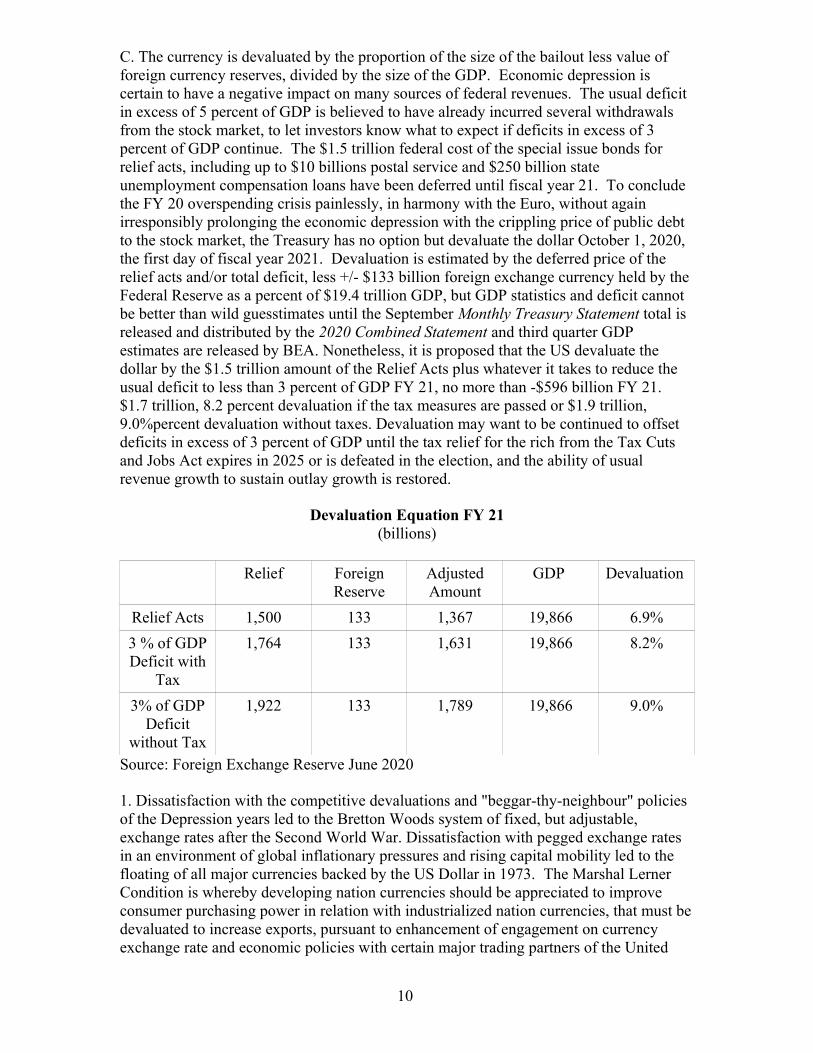

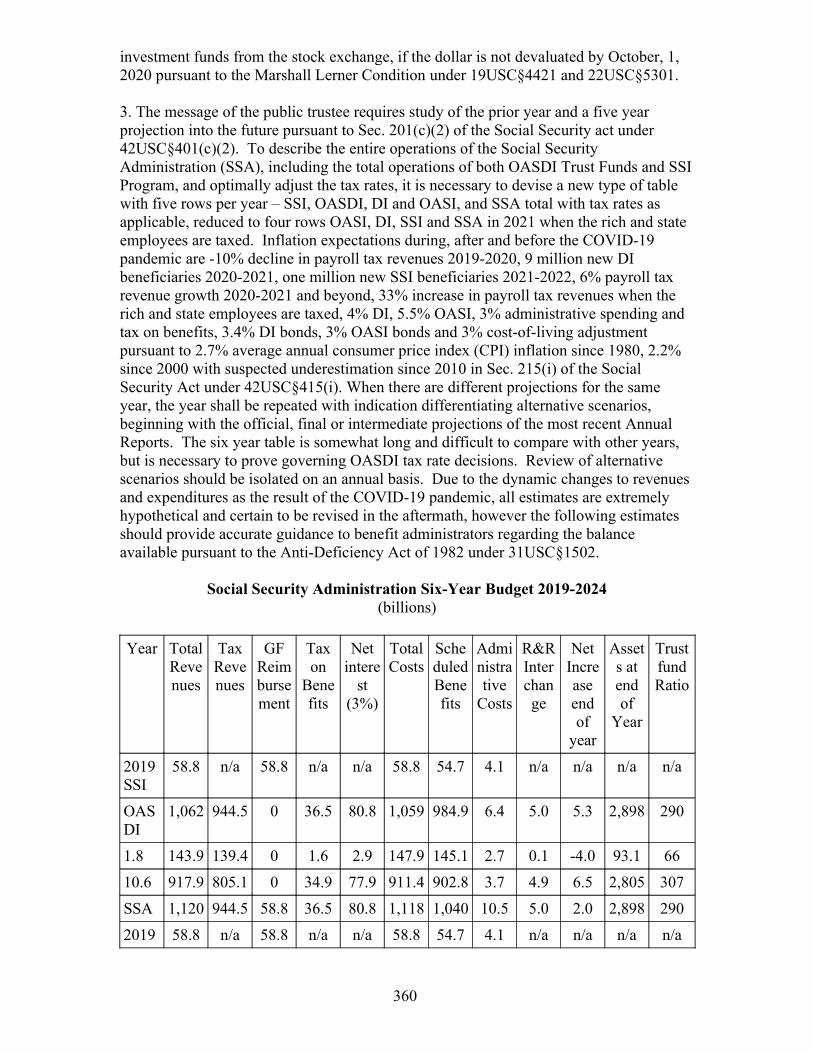

C. The currency is devaluated by the proportion of the size of the bailout less value of foreign currency reserves, divided by the size of the GDP. Economic depression is certain to have a negative impact on many sources of federal revenues. The usual deficit in excess of 5 percent of GDP is believed to have already incurred several withdrawals from the stock market, to let investors know what to expect if deficits in excess of 3 percent of GDP continue. The $1.5 trillion federal cost of the special issue bonds for relief acts, including up to $10 billions postal service and $250 billion state unemployment compensation loans have been deferred until fiscal year 21. To conclude the FY 20 overspending crisis painlessly, in harmony with the Euro, without again irresponsibly prolonging the economic depression with the crippling price of public debt to the stock market, the Treasury has no option but devaluate the dollar October 1, 2020, the first day of fiscal year 2021. Devaluation is estimated by the deferred price of the relief acts and/or total deficit, less +/- $133 billion foreign exchange currency held by the Federal Reserve as a percent of $19.4 trillion GDP, but GDP statistics and deficit cannot be better than wild guesstimates until the September Monthly Treasury Statement total is released and distributed by the 2020 Combined Statement and third quarter GDP estimates are released by BEA. Nonetheless, it is proposed that the US devaluate the dollar by the $1.5 trillion amount of the Relief Acts plus whatever it takes to reduce the usual deficit to less than 3 percent of GDP FY 21, no more than -$596 billion FY 21. $1.7 trillion, 8.2 percent devaluation if the tax measures are passed or $1.9 trillion, 9.0%percent devaluation without taxes. Devaluation may want to be continued to offset deficits in excess of 3 percent of GDP until the tax relief for the rich from the Tax Cuts and Jobs Act expires in 2025 or is defeated in the election, and the ability of usual revenue growth to sustain outlay growth is restored.

Devaluation Equation FY 21(billions)

Relief ForeignReserve

AdjustedAmount

GDP Devaluation

Relief Acts 1,500 133 1,367 19,866 6.9%

3 % of GDPDeficit with

Tax

1,764 133 1,631 19,866 8.2%

3% of GDPDeficit

without Tax

1,922 133 1,789 19,866 9.0%

Source: Foreign Exchange Reserve June 2020

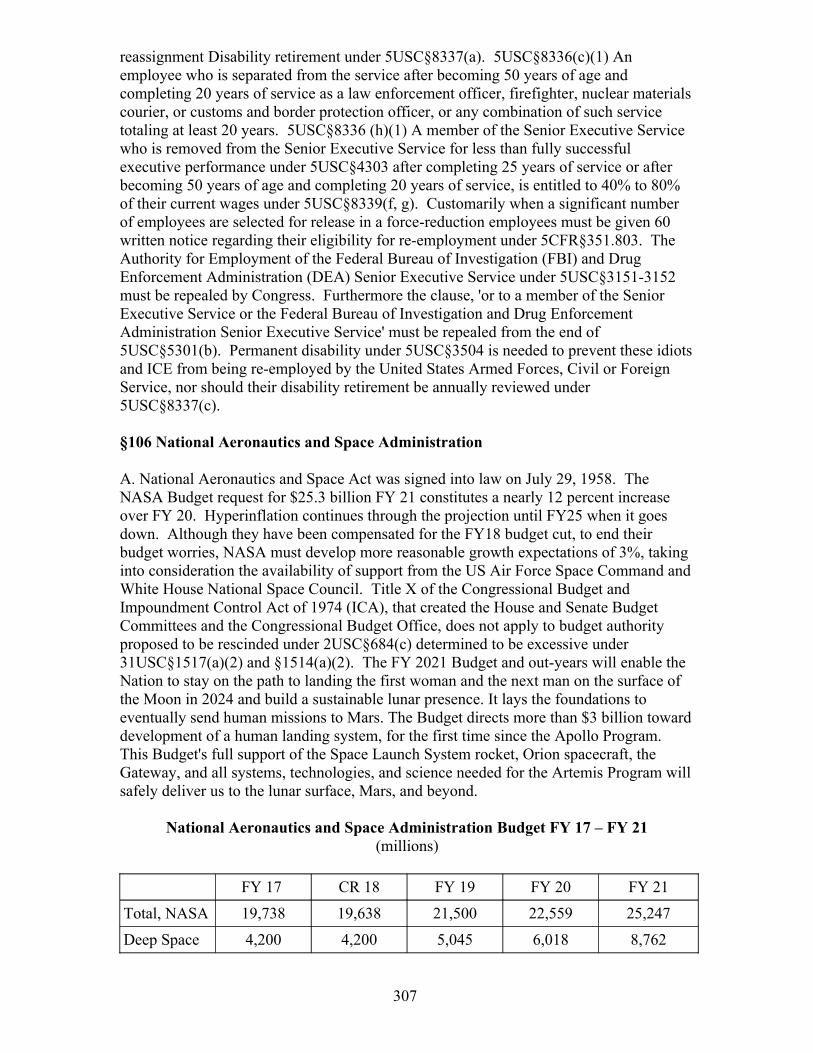

1. Dissatisfaction with the competitive devaluations and "beggar-thy-neighbour" policies of the Depression years led to the Bretton Woods system of fixed, but adjustable, exchange rates after the Second World War. Dissatisfaction with pegged exchange rates in an environment of global inflationary pressures and rising capital mobility led to the floating of all major currencies backed by the US Dollar in 1973. The Marshal Lerner Condition is whereby developing nation currencies should be appreciated to improve consumer purchasing power in relation with industrialized nation currencies, that must bedevaluated to increase exports, pursuant to enhancement of engagement on currency exchange rate and economic policies with certain major trading partners of the United

10

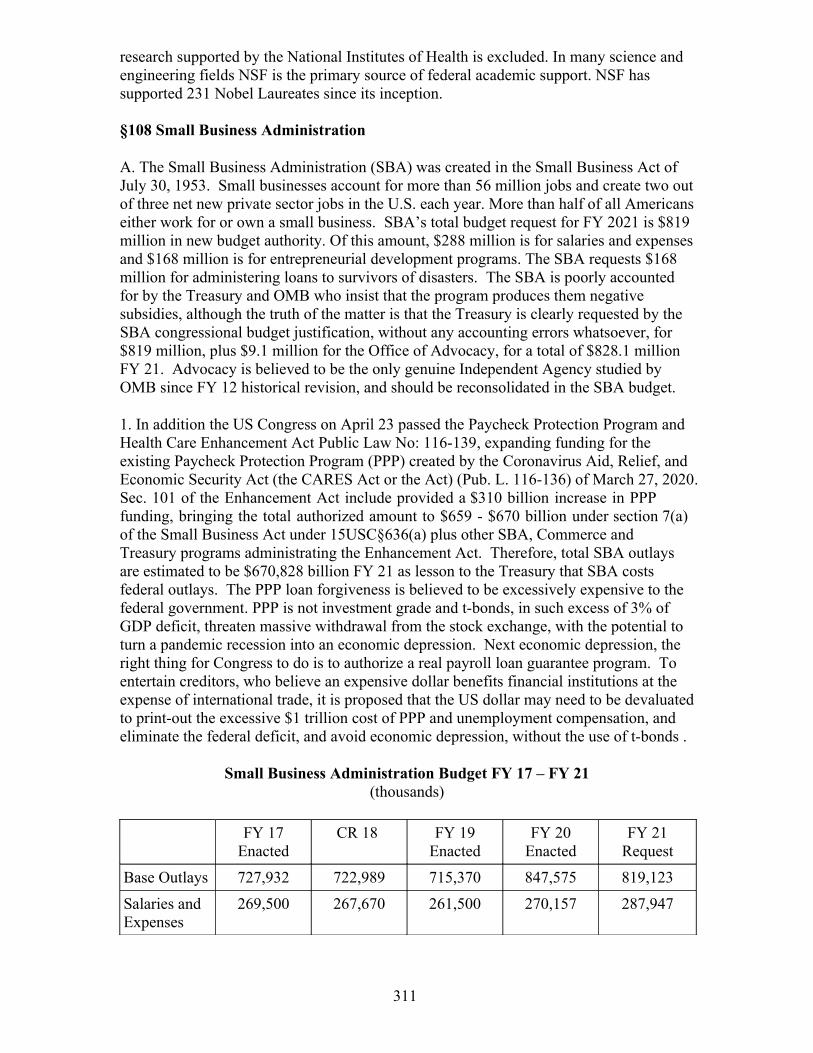

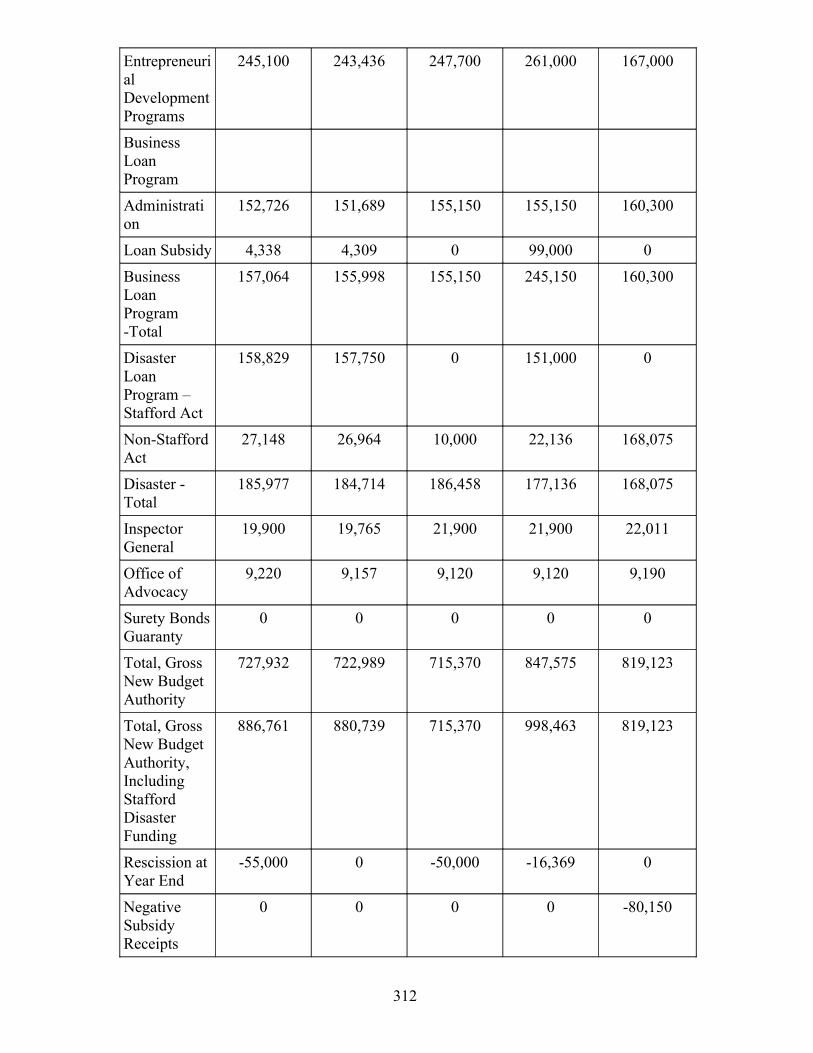

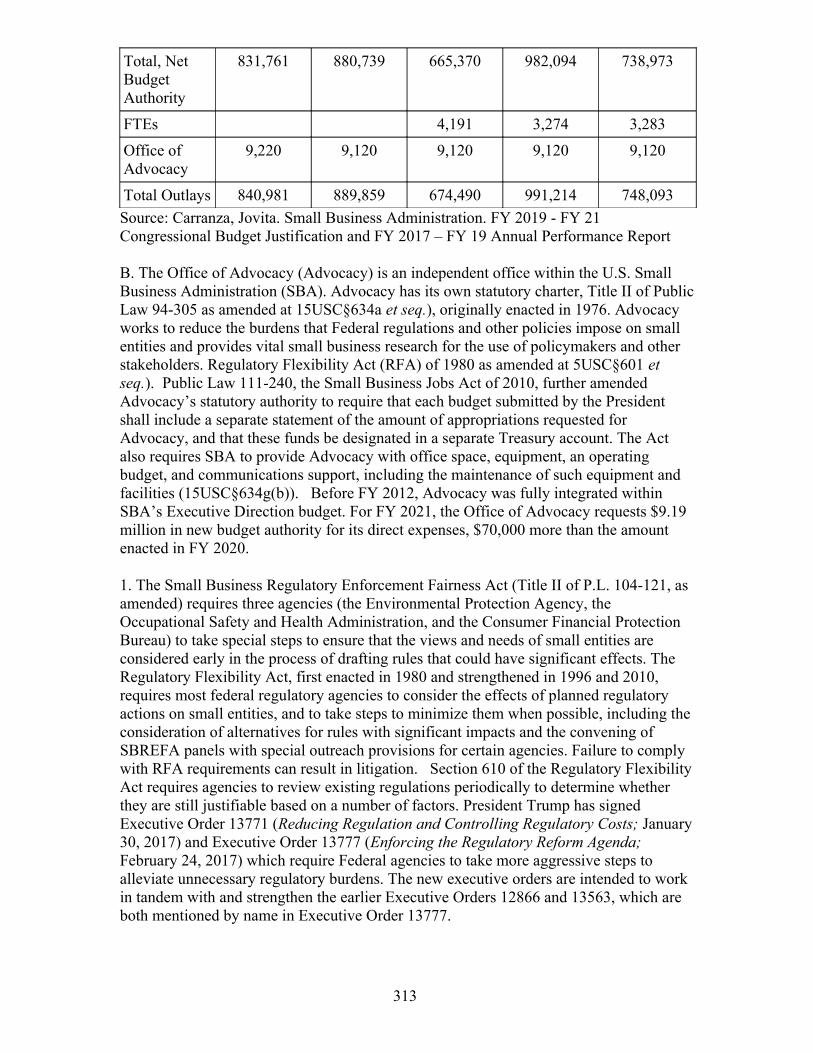

States under 19USC§4421 and 22USC§5301 et seq. It is the policy of the United States to encourage international economic negotiations to achieve macroeconomic policies and exchange rates consistent with appropriate and sustainable balances in trade and capital flows and to foster price stability in conjunction with economic growth. From time to time the United States shall, in close coordination with other major industrialized countries, adjust the international currency exchange rates of the United States and specified foreign nations to achieve macro-economic policy goals under 22USC§5303. Because the United Nations operates on a monetary system backed by, and quantified in the US dollar, instead of causing a reduction in prices, such 2019 UN assessments of devaluating nations, devaluation of the US dollar should uniquely increase the size of the global economy. The Gross World Product (GWP) total currencies worldwide become worth more in US dollar terms, depending on how much the US dollar is devaluated.

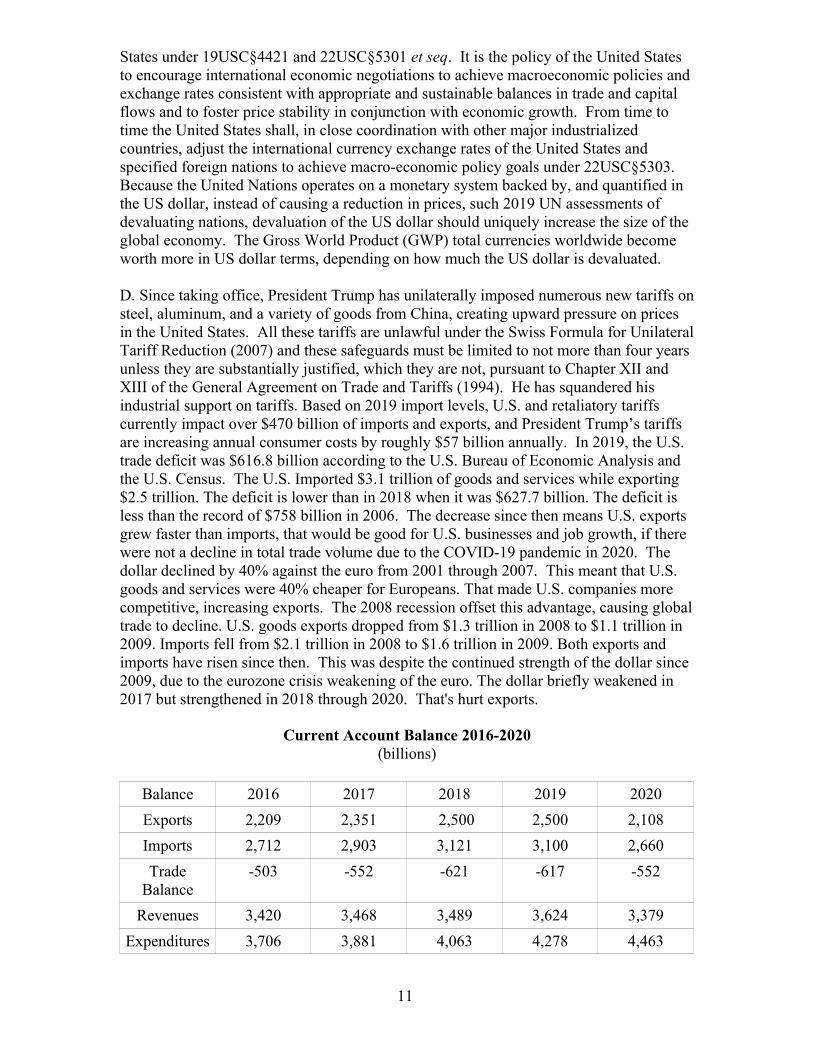

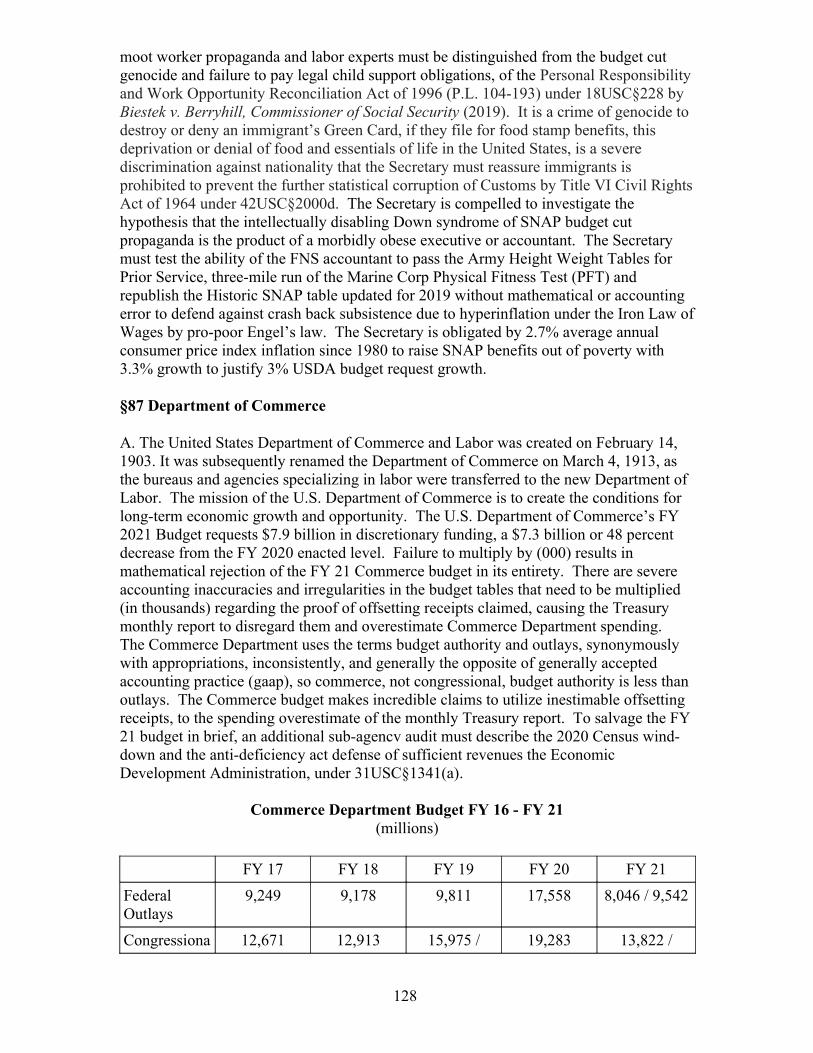

D. Since taking office, President Trump has unilaterally imposed numerous new tariffs onsteel, aluminum, and a variety of goods from China, creating upward pressure on prices in the United States. All these tariffs are unlawful under the Swiss Formula for UnilateralTariff Reduction (2007) and these safeguards must be limited to not more than four years unless they are substantially justified, which they are not, pursuant to Chapter XII and XIII of the General Agreement on Trade and Tariffs (1994). He has squandered his industrial support on tariffs. Based on 2019 import levels, U.S. and retaliatory tariffs currently impact over $470 billion of imports and exports, and President Trump’s tariffs are increasing annual consumer costs by roughly $57 billion annually. In 2019, the U.S. trade deficit was $616.8 billion according to the U.S. Bureau of Economic Analysis and the U.S. Census. The U.S. Imported $3.1 trillion of goods and services while exporting $2.5 trillion. The deficit is lower than in 2018 when it was $627.7 billion. The deficit is less than the record of $758 billion in 2006. The decrease since then means U.S. exports grew faster than imports, that would be good for U.S. businesses and job growth, if there were not a decline in total trade volume due to the COVID-19 pandemic in 2020. The dollar declined by 40% against the euro from 2001 through 2007. This meant that U.S. goods and services were 40% cheaper for Europeans. That made U.S. companies more competitive, increasing exports. The 2008 recession offset this advantage, causing globaltrade to decline. U.S. goods exports dropped from $1.3 trillion in 2008 to $1.1 trillion in 2009. Imports fell from $2.1 trillion in 2008 to $1.6 trillion in 2009. Both exports and imports have risen since then. This was despite the continued strength of the dollar since 2009, due to the eurozone crisis weakening of the euro. The dollar briefly weakened in 2017 but strengthened in 2018 through 2020. That's hurt exports.

Current Account Balance 2016-2020(billions)

Balance 2016 2017 2018 2019 2020

Exports 2,209 2,351 2,500 2,500 2,108

Imports 2,712 2,903 3,121 3,100 2,660

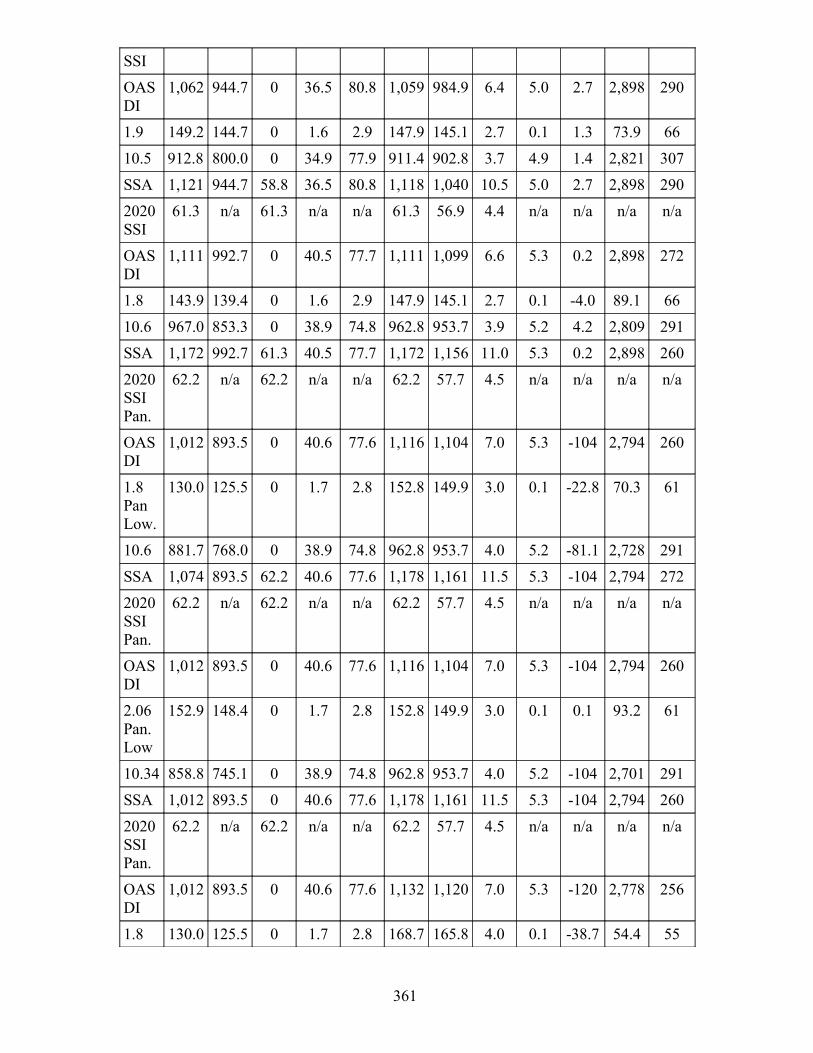

TradeBalance

-503 -552 -621 -617 -552

Revenues 3,420 3,468 3,489 3,624 3,379

Expenditures 3,706 3,881 4,063 4,278 4,463

11

Deficit -286 -413 -574 -654 -1,084

CurrentAccountBalance

-789 -965 -1,195 -1,271 -1,636

Source: Census Bureau, 2019. Monthly US International Trade in Goods and Services. June 2020 Year-to-date, the goods and services deficit decreased -7.8 percent, from the same period in 2019. Exports decreased -15.7 percent. Imports decreased -14.2 percent.

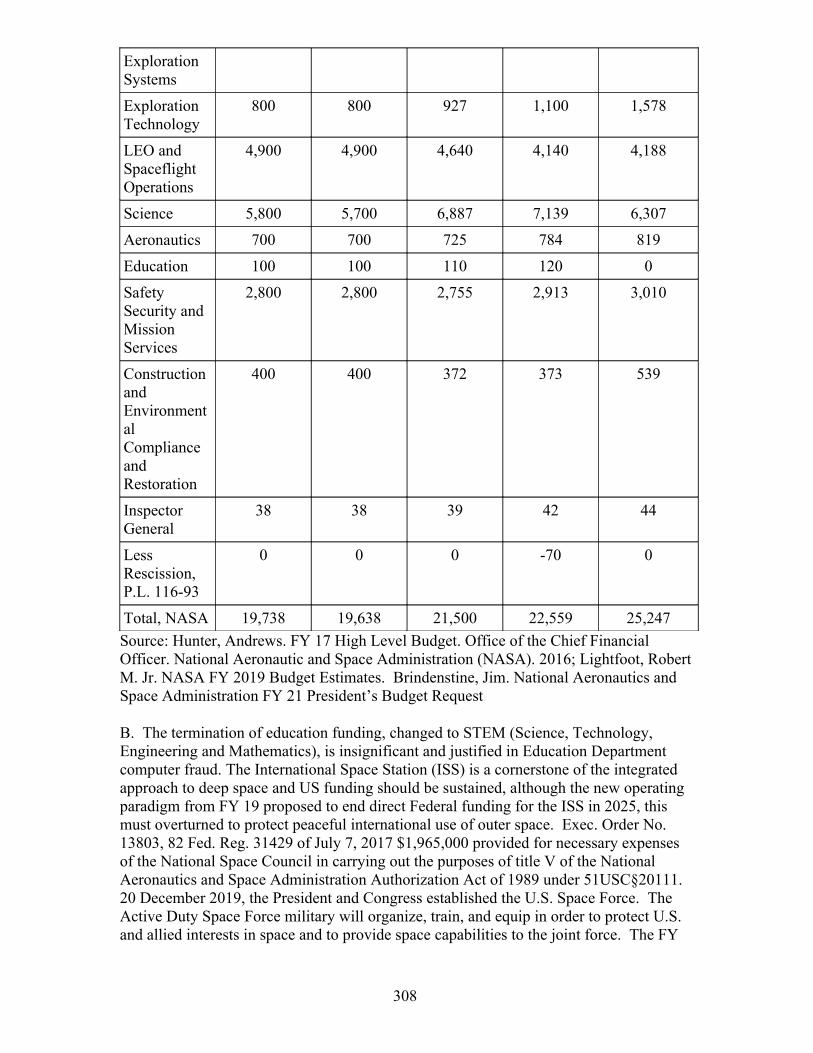

1. Although not as useful a statistic for determining solvency as the budget deficit or surplus, international trade deficit or surplus is widely respected as an indicator of credit-worthiness and is added to the budget deficit or surplus to produce the current account balance. CBO The Budget and Economic Outlook 2020-2030 released in January 2020, just before the COVID-19 pandemic reduced the total volume of international trade, admits increases in tariffs reduce U.S. economic activity in three ways. First, they make consumer goods and capital goods more expensive, thereby reducing the purchasing power of U.S. consumers and Some of those tariffs apply to imports from nearly all U.S. trading partners, including tariffs on washing machines, solar panels, U.S. imports in 2017. Second, they increase businesses’ uncertainty about future barriers to trade. Such uncertainty leads some U.S. businesses to delay or forgo new investments or make costly adjustments to their supply chains. Third, they prompt retaliatory tariffs by U.S. trading partners, which reduce U.S. exports by making them more expensive for foreign purchasers. All of those effects lower U.S. output. U.S. consumers and businesses replacecertain imported goods with goods produced in the United States, which offsets some of that decline. In addition, tariff revenues, by reducing the deficit, increase the resources available for private investment in later years. However, skyrocketing total Customs revenues are widely suspected to be fraudulent and are to be impounded aiming to eliminate language contrary to tariff reductions or total customs revenues.

E. The "power of the purse" provides "No money shall be drawn from the treasury, but inconsequence of appropriations made by law" under Article 1 Section 9, Clause 7 of the US Constitution. The text of a Balanced Budget Amendment whereby “Congress shall adopt a statement of receipts and outlays for that year in which total outlays are no greater than total receipts” was approved by the Senate (by a vote of 69 to 31) on 4 August 1982 but supported by an inadequate majority of the House of Representatives (with a vote of 236 to 187) on 1 October 1982. The Anti-deficiency Act (ADA) reauthorized September 12, 1982 (Pub.L. 97–258, 96 Stat. 923) is pre-eminent budget legislation enacted by the United States Congress to prevent the incurring of obligations or the making of expenditures (outlays) in excess of amounts available in appropriations or funds. The earliest version of the ADA legislation was enacted in 1870 (16 Stat. 251), after the Civil War, to end the executive branch's long history of creating coercive deficiencies. The act provided... that it shall not be lawful for any department of the government to expend in any one fiscal year any sum in excess of appropriations made by Congress for that fiscal year, or to involve the government in any contract for the future payment of money in excess of such appropriations. The Act was amended and expanded several times, most significantly in 1905 and 1906. It was further modified by an executive order in 1933 and significantly revamped in 1950 (64 Stat. 765).

12

1. The current version of the Anti-Deficiency Act was enacted on September 12, 1982 (96 Stat. 923). The balance of an appropriation or fund limited for obligation to a definiteperiod is available only for payment of expenses properly incurred during the period of availability or to complete contracts properly made within that period of availability and obligated under 31USC§1502(a). Obligations are apportioned on a basis that indicates the need for a deficiency or supplemental appropriation to the extent necessary to permit payment of such pay increases as may be granted pursuant to law under 31USC§1515(a).A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis.

2. The timetable with respect to the congressional budget process for any fiscal year is setforth under 2USC§631. The first Monday in February the President submits his budget under 31USC§1105. February 15 Congressional Budget Office submits report to Budget Committees. Not later than 6 weeks after President submits budget Committees submit views and estimates to Budget Committees. April 1 Senate Budget Committee reports concurrent resolution on the budget. On or before April 15 of each year, the Congress shall complete action on a concurrent resolution on the budget for the fiscal year beginning on October 1 of such year under 2USC§632(a). Concurrent resolution on the budget must be adopted before budget-related legislation is considered under 2USC§634. The Senate shall not vote on a concurrent resolution on the budget that is not mathematically correct under 2USC§636(d). May 15 Annual appropriation bills may be considered in the House. June 10 House Appropriations Committee reports last annual appropriation bill. June 15 Congress completes action on reconciliation legislation. June 30 House completes action on annual appropriation bills. Supplemental or additional budgeting changes and re-appraisements are submitted to Congress before July 16th of every year for the following fiscal year that begins October 1 under 31USC§1106.

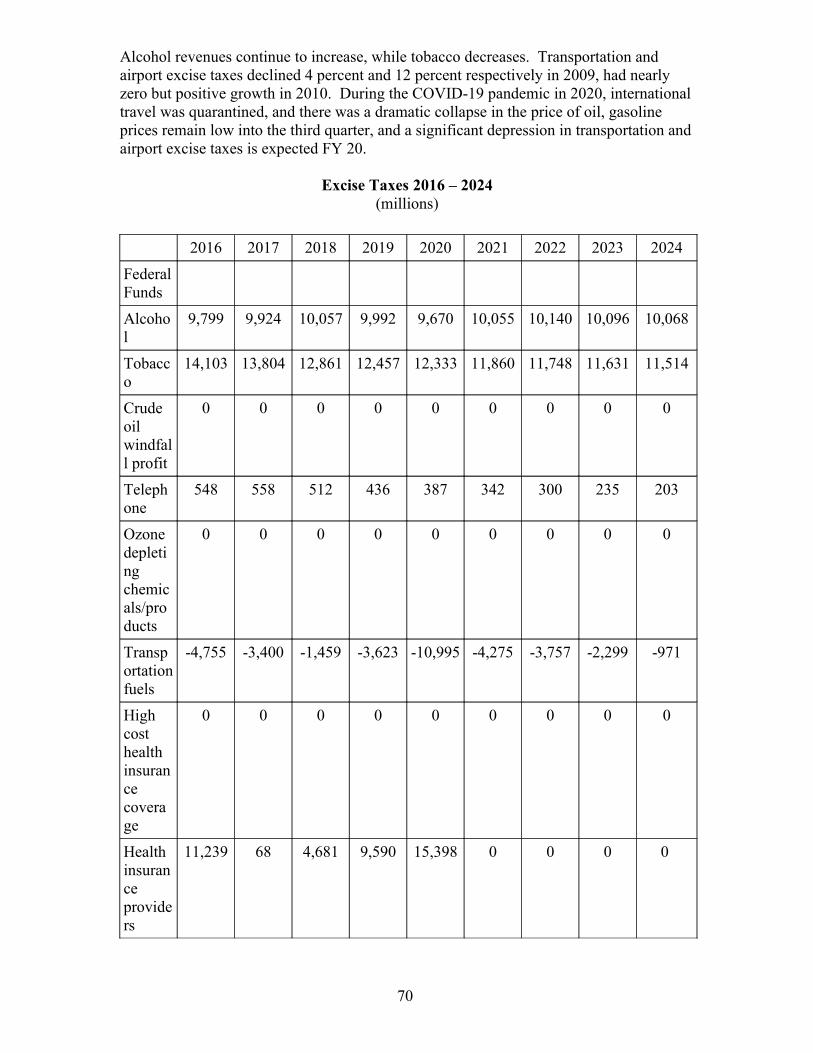

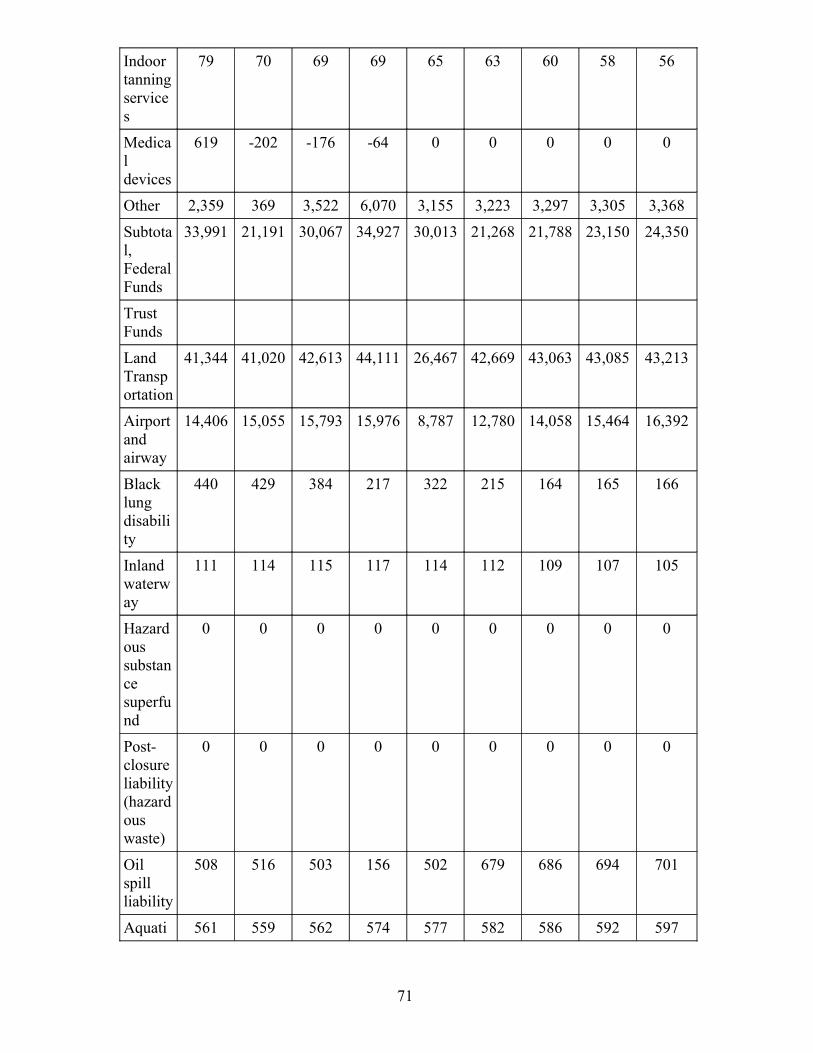

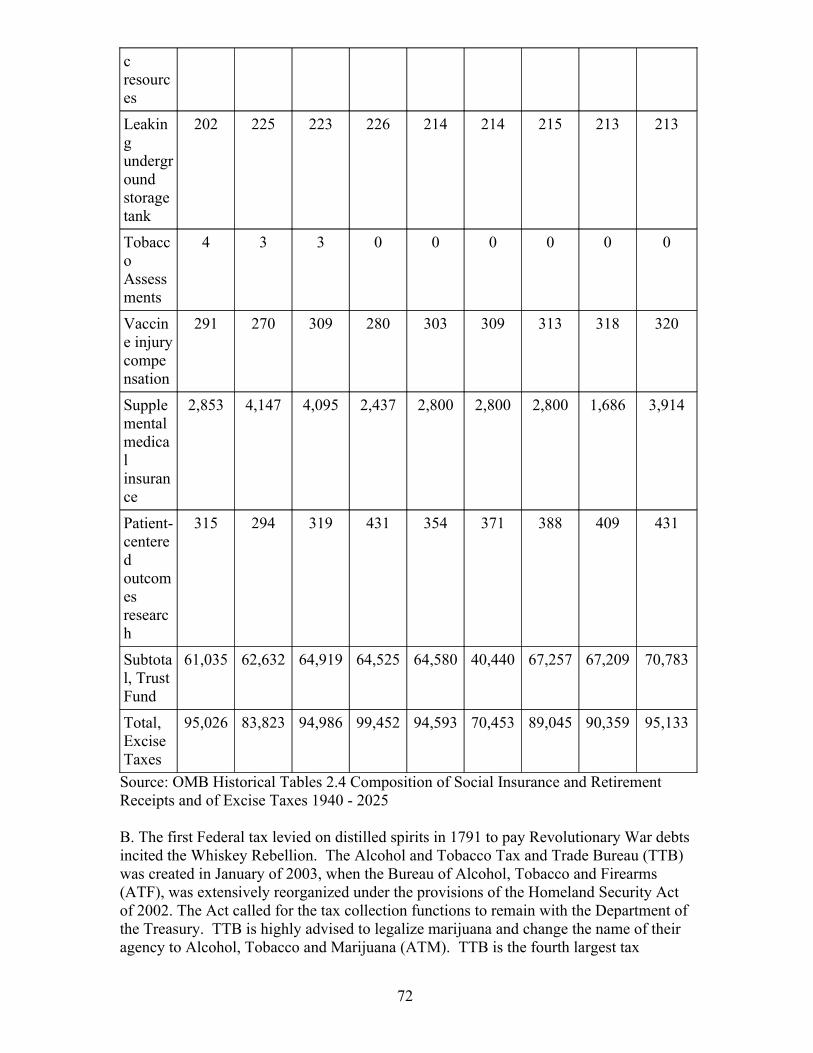

§72 Revenues

A. All Bills for raising Revenue shall originate in the House of Representatives; but the Senate may propose or concur with Amendments as on other Bills under Art. 2 Sec. 7 Clause 1 of the US Constitution. The Congress shall have Power to lay and collect Taxes, Duties, Imposts and Excises, to pay the Debts and provide for the common Defense and general Welfare of the United States; but all Duties, Imposts and Excises shall be uniform throughout the United States under Art. 1 Sec. 8 Clause 1. The nation was originally financed mostly with tariffs. The first Federal excise taxes levied on distilled spirits in 1791 by Alexander Hamilton paid off the Revolutionary War debts, at the cost of a Whiskey Rebellion. In the 20th century excise taxes, mostly on fuel, exploded on land, air and sea transportation. Energy exports remain to be taxed in the 21st century to potentially generate a customs surplus, or at least justify OMB reporting gross customs revenues and gross federal outlays. The Sixteenth Amendment to the United States Constitution passed by Congress on July 2, 1909 and ratified February 3, 1913 justifies the income tax, corporate income tax, estate and gift tax, and payroll tax that finance the vast majority of modern government and social safety net. The Consolidated Appropriations Act, 2020 (Public Law 116-93), and the Further

13

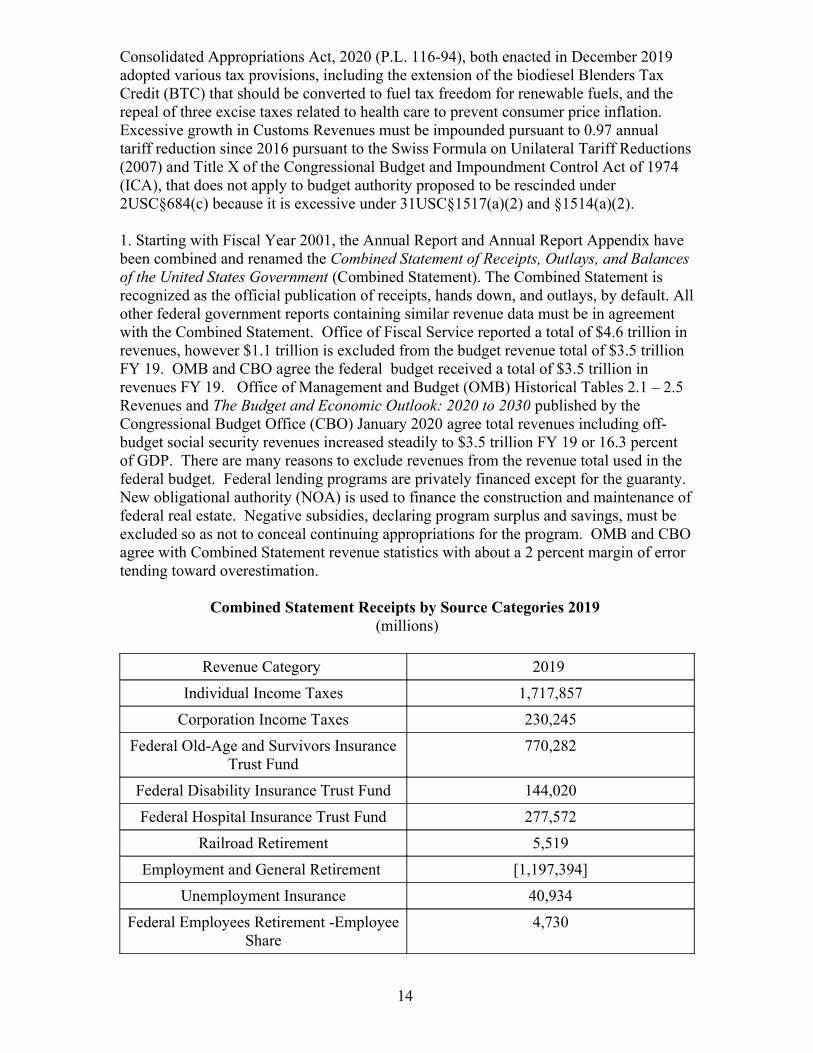

Consolidated Appropriations Act, 2020 (P.L. 116-94), both enacted in December 2019 adopted various tax provisions, including the extension of the biodiesel Blenders Tax Credit (BTC) that should be converted to fuel tax freedom for renewable fuels, and the repeal of three excise taxes related to health care to prevent consumer price inflation. Excessive growth in Customs Revenues must be impounded pursuant to 0.97 annual tariff reduction since 2016 pursuant to the Swiss Formula on Unilateral Tariff Reductions(2007) and Title X of the Congressional Budget and Impoundment Control Act of 1974 (ICA), that does not apply to budget authority proposed to be rescinded under 2USC§684(c) because it is excessive under 31USC§1517(a)(2) and §1514(a)(2).

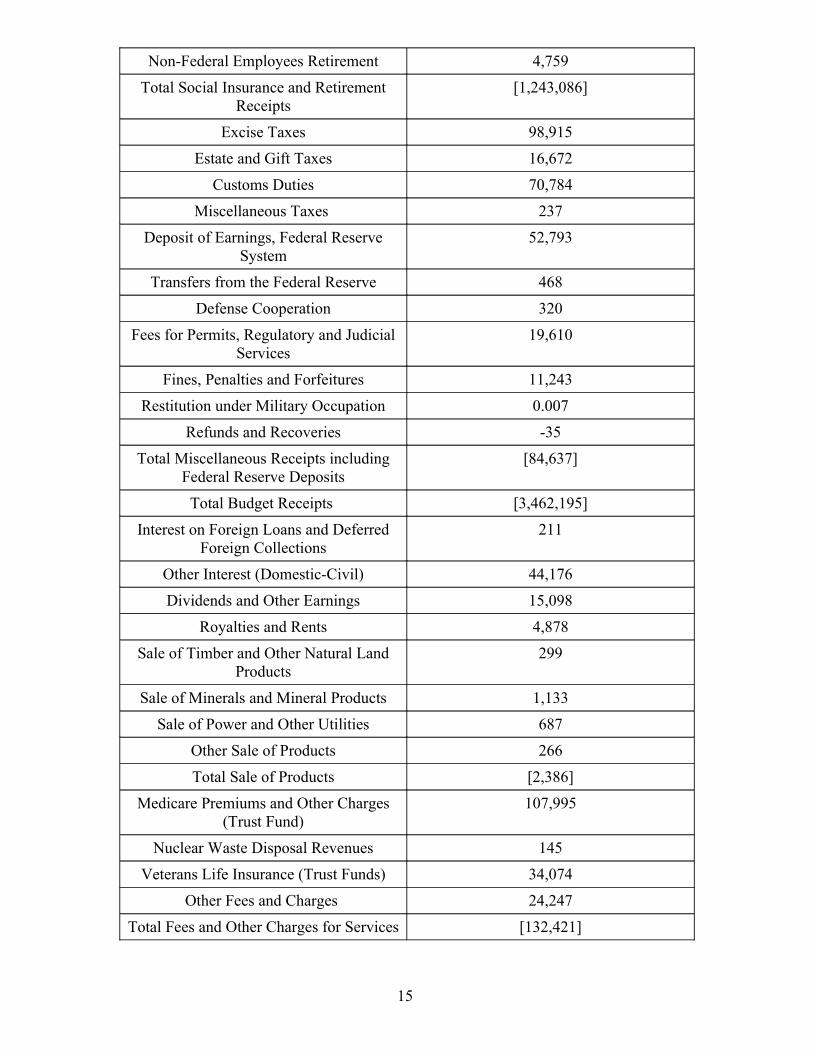

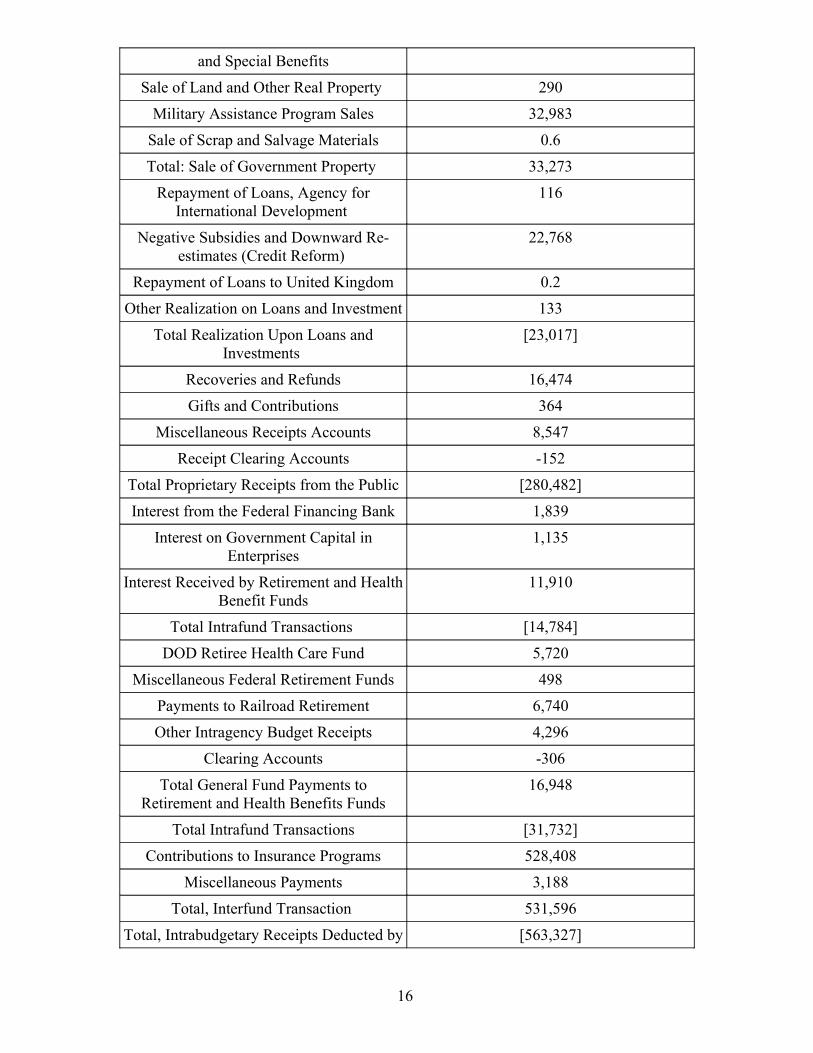

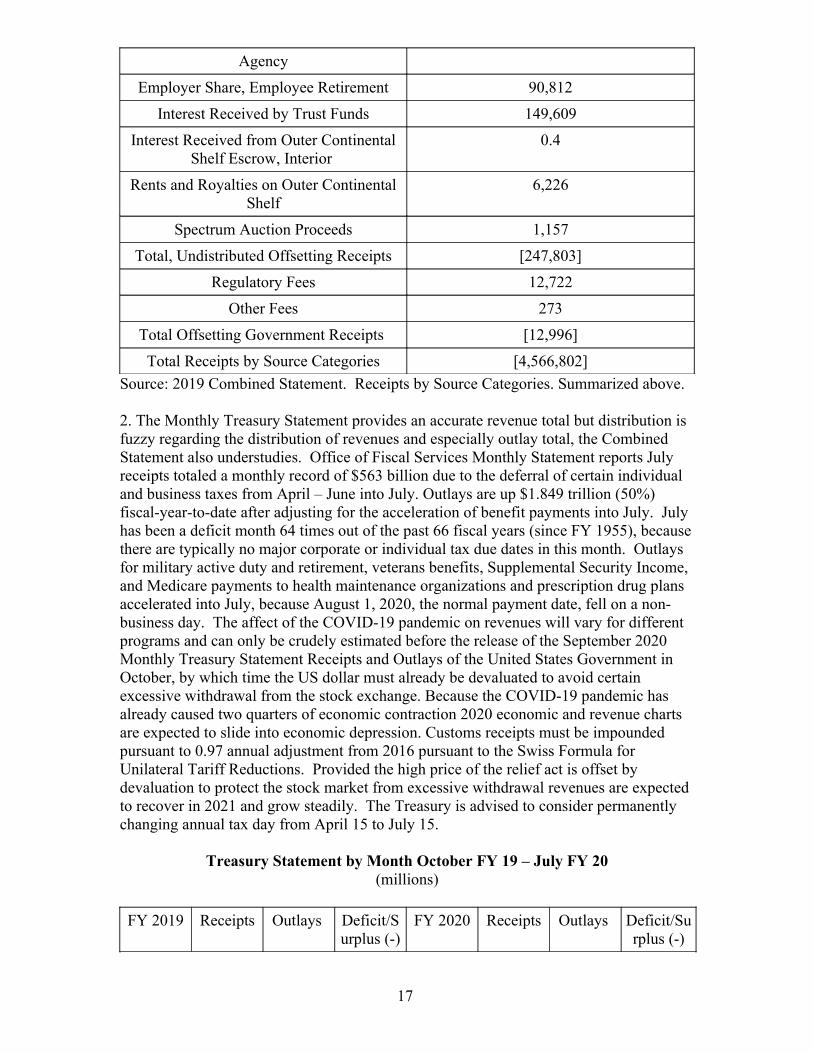

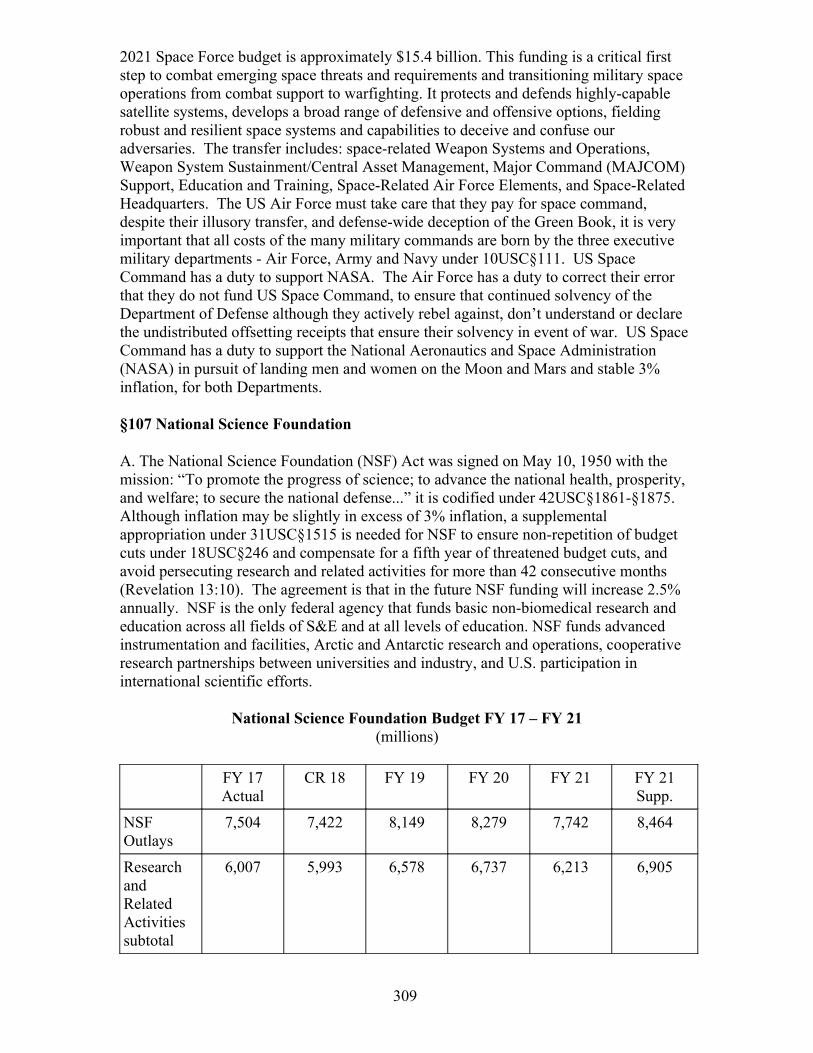

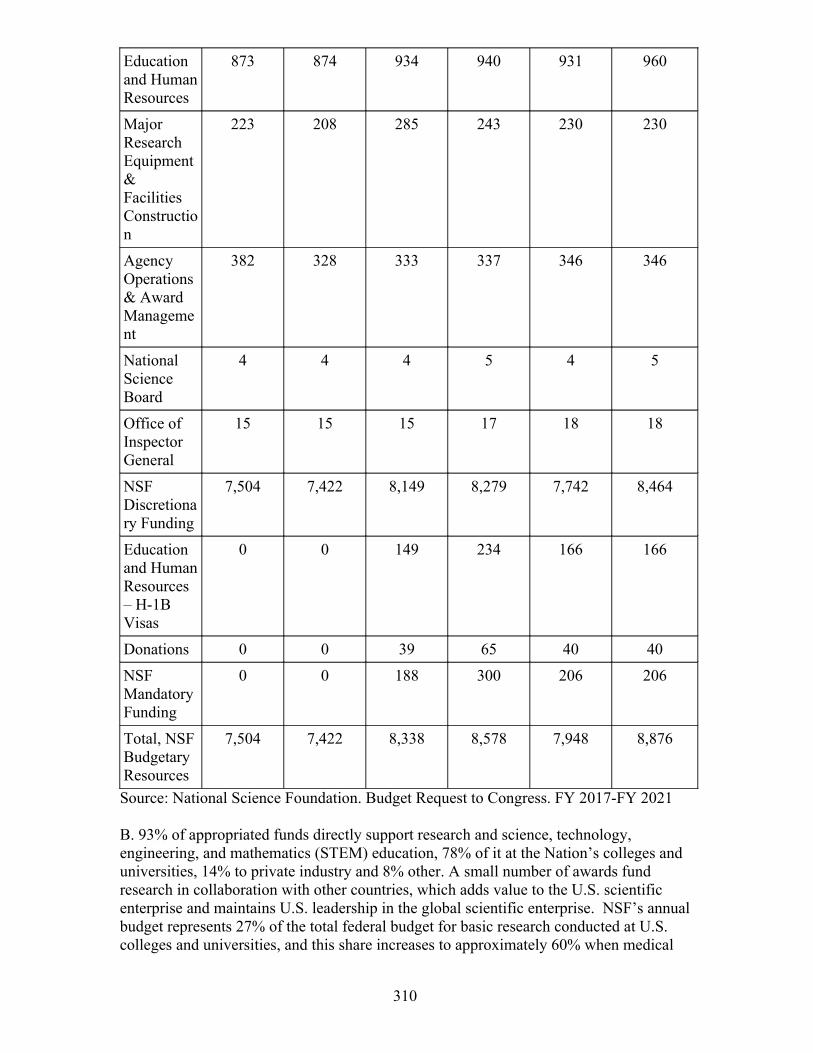

1. Starting with Fiscal Year 2001, the Annual Report and Annual Report Appendix have been combined and renamed the Combined Statement of Receipts, Outlays, and Balancesof the United States Government (Combined Statement). The Combined Statement is recognized as the official publication of receipts, hands down, and outlays, by default. Allother federal government reports containing similar revenue data must be in agreement with the Combined Statement. Office of Fiscal Service reported a total of $4.6 trillion in revenues, however $1.1 trillion is excluded from the budget revenue total of $3.5 trillion FY 19. OMB and CBO agree the federal budget received a total of $3.5 trillion in revenues FY 19. Office of Management and Budget (OMB) Historical Tables 2.1 – 2.5 Revenues and The Budget and Economic Outlook: 2020 to 2030 published by the Congressional Budget Office (CBO) January 2020 agree total revenues including off-budget social security revenues increased steadily to $3.5 trillion FY 19 or 16.3 percent of GDP. There are many reasons to exclude revenues from the revenue total used in the federal budget. Federal lending programs are privately financed except for the guaranty. New obligational authority (NOA) is used to finance the construction and maintenance offederal real estate. Negative subsidies, declaring program surplus and savings, must be excluded so as not to conceal continuing appropriations for the program. OMB and CBOagree with Combined Statement revenue statistics with about a 2 percent margin of error tending toward overestimation.

Combined Statement Receipts by Source Categories 2019 (millions)

Revenue Category 2019

Individual Income Taxes 1,717,857

Corporation Income Taxes 230,245

Federal Old-Age and Survivors InsuranceTrust Fund

770,282

Federal Disability Insurance Trust Fund 144,020

Federal Hospital Insurance Trust Fund 277,572

Railroad Retirement 5,519

Employment and General Retirement [1,197,394]

Unemployment Insurance 40,934

Federal Employees Retirement -EmployeeShare

4,730

14

Non-Federal Employees Retirement 4,759

Total Social Insurance and RetirementReceipts

[1,243,086]

Excise Taxes 98,915

Estate and Gift Taxes 16,672

Customs Duties 70,784

Miscellaneous Taxes 237

Deposit of Earnings, Federal ReserveSystem

52,793

Transfers from the Federal Reserve 468

Defense Cooperation 320

Fees for Permits, Regulatory and JudicialServices

19,610

Fines, Penalties and Forfeitures 11,243

Restitution under Military Occupation 0.007

Refunds and Recoveries -35

Total Miscellaneous Receipts includingFederal Reserve Deposits

[84,637]

Total Budget Receipts [3,462,195]

Interest on Foreign Loans and DeferredForeign Collections

211

Other Interest (Domestic-Civil) 44,176

Dividends and Other Earnings 15,098

Royalties and Rents 4,878

Sale of Timber and Other Natural LandProducts

299

Sale of Minerals and Mineral Products 1,133

Sale of Power and Other Utilities 687

Other Sale of Products 266

Total Sale of Products [2,386]

Medicare Premiums and Other Charges(Trust Fund)

107,995

Nuclear Waste Disposal Revenues 145

Veterans Life Insurance (Trust Funds) 34,074

Other Fees and Charges 24,247

Total Fees and Other Charges for Services [132,421]

15

and Special Benefits

Sale of Land and Other Real Property 290

Military Assistance Program Sales 32,983

Sale of Scrap and Salvage Materials 0.6

Total: Sale of Government Property 33,273

Repayment of Loans, Agency forInternational Development

116

Negative Subsidies and Downward Re-estimates (Credit Reform)

22,768

Repayment of Loans to United Kingdom 0.2

Other Realization on Loans and Investment 133

Total Realization Upon Loans andInvestments

[23,017]

Recoveries and Refunds 16,474

Gifts and Contributions 364

Miscellaneous Receipts Accounts 8,547

Receipt Clearing Accounts -152

Total Proprietary Receipts from the Public [280,482]

Interest from the Federal Financing Bank 1,839

Interest on Government Capital inEnterprises

1,135

Interest Received by Retirement and HealthBenefit Funds

11,910

Total Intrafund Transactions [14,784]

DOD Retiree Health Care Fund 5,720

Miscellaneous Federal Retirement Funds 498

Payments to Railroad Retirement 6,740

Other Intragency Budget Receipts 4,296

Clearing Accounts -306

Total General Fund Payments toRetirement and Health Benefits Funds

16,948

Total Intrafund Transactions [31,732]

Contributions to Insurance Programs 528,408

Miscellaneous Payments 3,188

Total, Interfund Transaction 531,596

Total, Intrabudgetary Receipts Deducted by [563,327]

16

Agency

Employer Share, Employee Retirement 90,812

Interest Received by Trust Funds 149,609

Interest Received from Outer ContinentalShelf Escrow, Interior

0.4

Rents and Royalties on Outer ContinentalShelf

6,226

Spectrum Auction Proceeds 1,157

Total, Undistributed Offsetting Receipts [247,803]

Regulatory Fees 12,722

Other Fees 273

Total Offsetting Government Receipts [12,996]

Total Receipts by Source Categories [4,566,802]

Source: 2019 Combined Statement. Receipts by Source Categories. Summarized above.

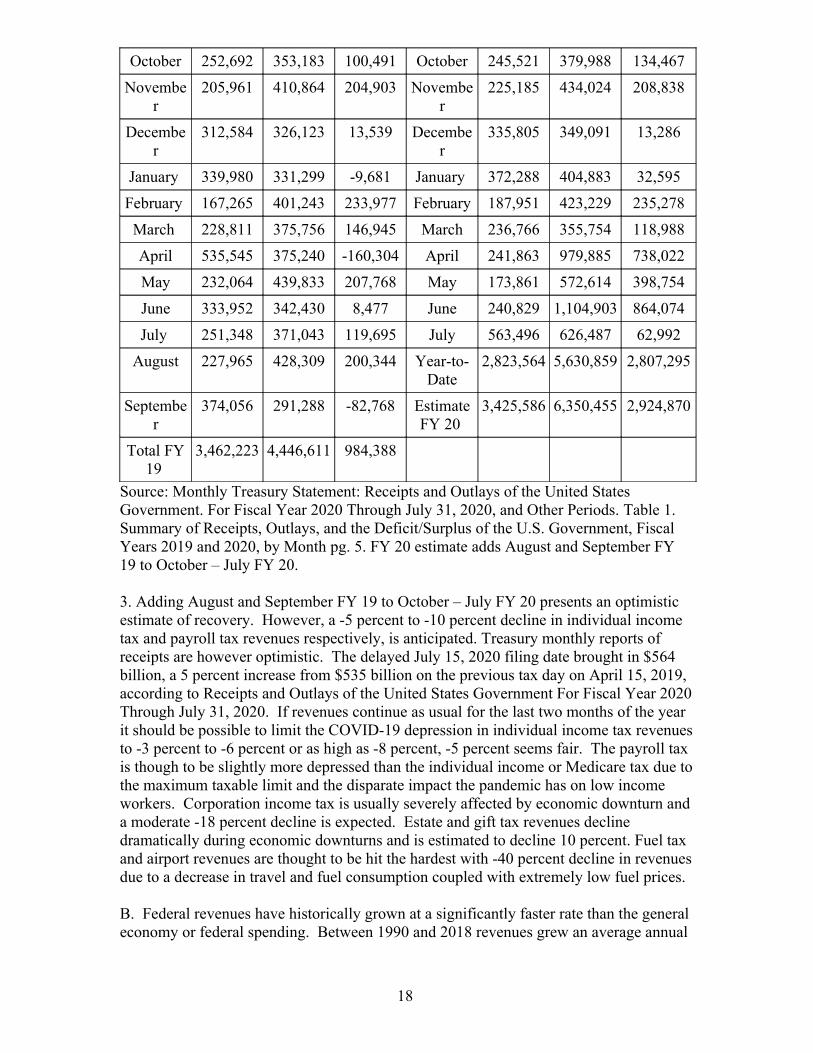

2. The Monthly Treasury Statement provides an accurate revenue total but distribution is fuzzy regarding the distribution of revenues and especially outlay total, the Combined Statement also understudies. Office of Fiscal Services Monthly Statement reports July receipts totaled a monthly record of $563 billion due to the deferral of certain individual and business taxes from April – June into July. Outlays are up $1.849 trillion (50%) fiscal-year-to-date after adjusting for the acceleration of benefit payments into July. July has been a deficit month 64 times out of the past 66 fiscal years (since FY 1955), becausethere are typically no major corporate or individual tax due dates in this month. Outlays for military active duty and retirement, veterans benefits, Supplemental Security Income, and Medicare payments to health maintenance organizations and prescription drug plans accelerated into July, because August 1, 2020, the normal payment date, fell on a non-business day. The affect of the COVID-19 pandemic on revenues will vary for different programs and can only be crudely estimated before the release of the September 2020 Monthly Treasury Statement Receipts and Outlays of the United States Government in October, by which time the US dollar must already be devaluated to avoid certain excessive withdrawal from the stock exchange. Because the COVID-19 pandemic has already caused two quarters of economic contraction 2020 economic and revenue charts are expected to slide into economic depression. Customs receipts must be impounded pursuant to 0.97 annual adjustment from 2016 pursuant to the Swiss Formula for Unilateral Tariff Reductions. Provided the high price of the relief act is offset by devaluation to protect the stock market from excessive withdrawal revenues are expected to recover in 2021 and grow steadily. The Treasury is advised to consider permanently changing annual tax day from April 15 to July 15.

Treasury Statement by Month October FY 19 – July FY 20(millions)

FY 2019 Receipts Outlays Deficit/Surplus (-)

FY 2020 Receipts Outlays Deficit/Surplus (-)

17

October 252,692 353,183 100,491 October 245,521 379,988 134,467

November

205,961 410,864 204,903 November

225,185 434,024 208,838

December

312,584 326,123 13,539 December

335,805 349,091 13,286

January 339,980 331,299 -9,681 January 372,288 404,883 32,595

February 167,265 401,243 233,977 February 187,951 423,229 235,278

March 228,811 375,756 146,945 March 236,766 355,754 118,988

April 535,545 375,240 -160,304 April 241,863 979,885 738,022

May 232,064 439,833 207,768 May 173,861 572,614 398,754

June 333,952 342,430 8,477 June 240,829 1,104,903 864,074

July 251,348 371,043 119,695 July 563,496 626,487 62,992

August 227,965 428,309 200,344 Year-to-Date

2,823,564 5,630,859 2,807,295

September

374,056 291,288 -82,768 EstimateFY 20

3,425,586 6,350,455 2,924,870

Total FY19

3,462,223 4,446,611 984,388

Source: Monthly Treasury Statement: Receipts and Outlays of the United States Government. For Fiscal Year 2020 Through July 31, 2020, and Other Periods. Table 1. Summary of Receipts, Outlays, and the Deficit/Surplus of the U.S. Government, Fiscal Years 2019 and 2020, by Month pg. 5. FY 20 estimate adds August and September FY 19 to October – July FY 20.

3. Adding August and September FY 19 to October – July FY 20 presents an optimistic estimate of recovery. However, a -5 percent to -10 percent decline in individual income tax and payroll tax revenues respectively, is anticipated. Treasury monthly reports of receipts are however optimistic. The delayed July 15, 2020 filing date brought in $564 billion, a 5 percent increase from $535 billion on the previous tax day on April 15, 2019, according to Receipts and Outlays of the United States Government For Fiscal Year 2020Through July 31, 2020. If revenues continue as usual for the last two months of the year it should be possible to limit the COVID-19 depression in individual income tax revenuesto -3 percent to -6 percent or as high as -8 percent, -5 percent seems fair. The payroll tax is though to be slightly more depressed than the individual income or Medicare tax due tothe maximum taxable limit and the disparate impact the pandemic has on low income workers. Corporation income tax is usually severely affected by economic downturn and a moderate -18 percent decline is expected. Estate and gift tax revenues decline dramatically during economic downturns and is estimated to decline 10 percent. Fuel tax and airport revenues are thought to be hit the hardest with -40 percent decline in revenuesdue to a decrease in travel and fuel consumption coupled with extremely low fuel prices.

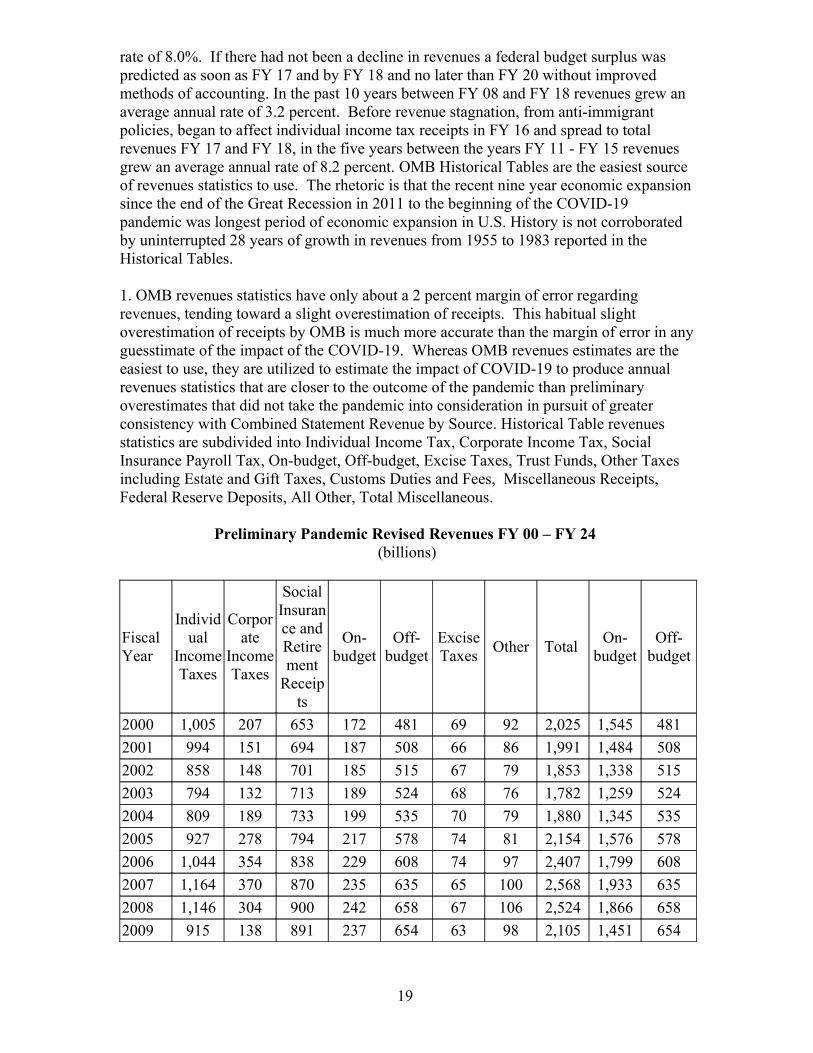

B. Federal revenues have historically grown at a significantly faster rate than the general economy or federal spending. Between 1990 and 2018 revenues grew an average annual

18

rate of 8.0%. If there had not been a decline in revenues a federal budget surplus was predicted as soon as FY 17 and by FY 18 and no later than FY 20 without improved methods of accounting. In the past 10 years between FY 08 and FY 18 revenues grew an average annual rate of 3.2 percent. Before revenue stagnation, from anti-immigrant policies, began to affect individual income tax receipts in FY 16 and spread to total revenues FY 17 and FY 18, in the five years between the years FY 11 - FY 15 revenues grew an average annual rate of 8.2 percent. OMB Historical Tables are the easiest source of revenues statistics to use. The rhetoric is that the recent nine year economic expansionsince the end of the Great Recession in 2011 to the beginning of the COVID-19 pandemic was longest period of economic expansion in U.S. History is not corroborated by uninterrupted 28 years of growth in revenues from 1955 to 1983 reported in the Historical Tables.

1. OMB revenues statistics have only about a 2 percent margin of error regarding revenues, tending toward a slight overestimation of receipts. This habitual slight overestimation of receipts by OMB is much more accurate than the margin of error in anyguesstimate of the impact of the COVID-19. Whereas OMB revenues estimates are the easiest to use, they are utilized to estimate the impact of COVID-19 to produce annual revenues statistics that are closer to the outcome of the pandemic than preliminary overestimates that did not take the pandemic into consideration in pursuit of greater consistency with Combined Statement Revenue by Source. Historical Table revenues statistics are subdivided into Individual Income Tax, Corporate Income Tax, Social Insurance Payroll Tax, On-budget, Off-budget, Excise Taxes, Trust Funds, Other Taxes including Estate and Gift Taxes, Customs Duties and Fees, Miscellaneous Receipts, Federal Reserve Deposits, All Other, Total Miscellaneous.

Preliminary Pandemic Revised Revenues FY 00 – FY 24 (billions)

Fiscal Year

Individual

IncomeTaxes

Corporate

IncomeTaxes

SocialInsurance andRetirement

Receipts

On-budget

Off-budget

ExciseTaxes

Other Total On-

budgetOff-

budget

2000 1,005 207 653 172 481 69 92 2,025 1,545 481

2001 994 151 694 187 508 66 86 1,991 1,484 508

2002 858 148 701 185 515 67 79 1,853 1,338 515

2003 794 132 713 189 524 68 76 1,782 1,259 524

2004 809 189 733 199 535 70 79 1,880 1,345 535

2005 927 278 794 217 578 74 81 2,154 1,576 578

2006 1,044 354 838 229 608 74 97 2,407 1,799 608

2007 1,164 370 870 235 635 65 100 2,568 1,933 635

2008 1,146 304 900 242 658 67 106 2,524 1,866 658

2009 915 138 891 237 654 63 98 2,105 1,451 654

19

2010 899 191 865 233 632 67 141 2,163 1,531 632

2011 1,092 181 819 253 566 72 140 2,304 1,738 566

2012 1,132 242 845 276 570 79 151 2,450 1,881 570

2013 1,316 274 948 275 673 84 153 2,775 2,102 673

2014 1,395 321 1,024 288 736 93 189 3,022 2,286 736

2015 1,541 344 1,065 295 770 98 202 3,250 2,480 770

2016 1,546 300 1,147 312 835 95 212 3,297 2,462 835

2017 1,587 297 1,191 317 874 84 186 3,345 2,471 874

2018 1,684 205 1,209 326 883 108 185 3,391 2,508 883

2019 1,718 230 1,284 343 941 108 163 3,503 2,562 941

2020 1,632 202 1,201 326 875 54 153 3,242 2,367 875

2021 1,730 214 1,274 346 928 64 162 3,444 2,516 928

2021t 1,730 214 1,580 346 1,234 64 168 3,756 2,522 1,234

2022 1,834 227 1,351 367 984 68 172 3,652 2,668 984

2022t 1,834 227 1,675 367 1,308 68 178 3,982 2,674 1,308

2023 1,944 241 1,432 389 1,043 72 182 3,871 2,828 1,043

2023t 1,944 241 1,776 389 1,387 72 188 4,221 2,834 1,387

2024 2,061 255 1,517 412 1,105 76 193 4,102 2,997 1,105

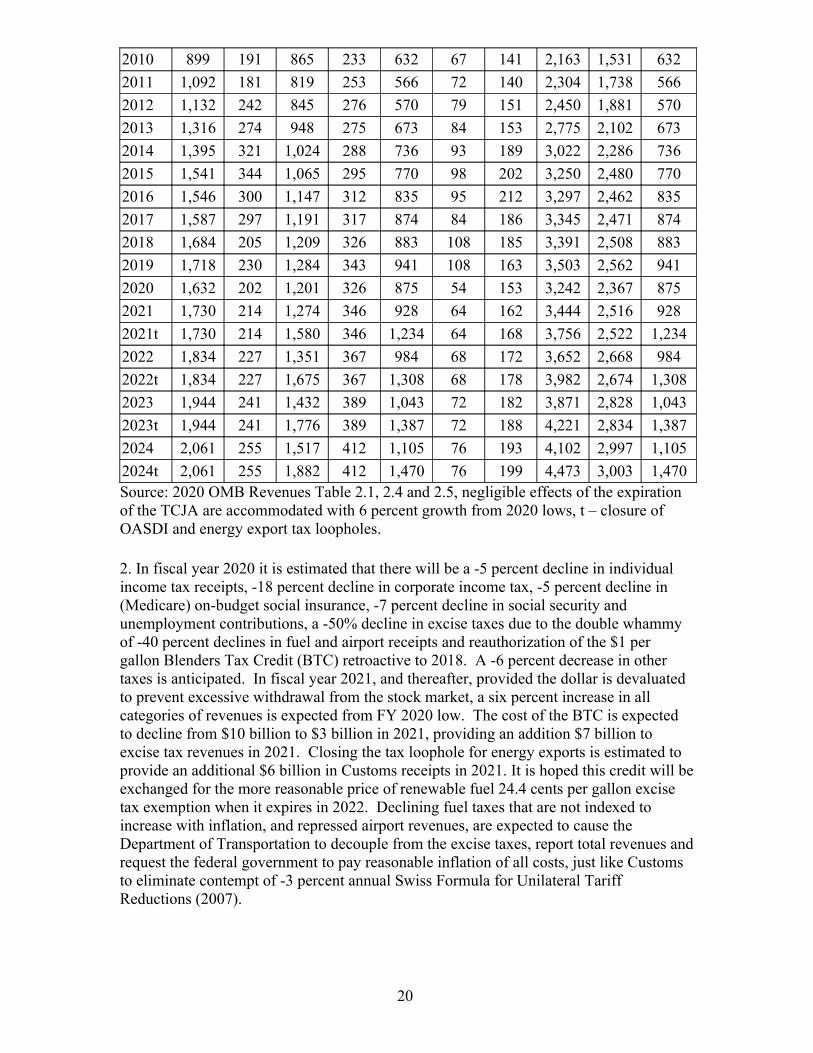

2024t 2,061 255 1,882 412 1,470 76 199 4,473 3,003 1,470Source: 2020 OMB Revenues Table 2.1, 2.4 and 2.5, negligible effects of the expiration of the TCJA are accommodated with 6 percent growth from 2020 lows, t – closure of OASDI and energy export tax loopholes.

2. In fiscal year 2020 it is estimated that there will be a -5 percent decline in individual income tax receipts, -18 percent decline in corporate income tax, -5 percent decline in (Medicare) on-budget social insurance, -7 percent decline in social security and unemployment contributions, a -50% decline in excise taxes due to the double whammy of -40 percent declines in fuel and airport receipts and reauthorization of the $1 per gallon Blenders Tax Credit (BTC) retroactive to 2018. A -6 percent decrease in other taxes is anticipated. In fiscal year 2021, and thereafter, provided the dollar is devaluated to prevent excessive withdrawal from the stock market, a six percent increase in all categories of revenues is expected from FY 2020 low. The cost of the BTC is expected to decline from $10 billion to $3 billion in 2021, providing an addition $7 billion to excise tax revenues in 2021. Closing the tax loophole for energy exports is estimated to provide an additional $6 billion in Customs receipts in 2021. It is hoped this credit will beexchanged for the more reasonable price of renewable fuel 24.4 cents per gallon excise tax exemption when it expires in 2022. Declining fuel taxes that are not indexed to increase with inflation, and repressed airport revenues, are expected to cause the Department of Transportation to decouple from the excise taxes, report total revenues andrequest the federal government to pay reasonable inflation of all costs, just like Customs to eliminate contempt of -3 percent annual Swiss Formula for Unilateral Tariff Reductions (2007).

20

C. The Congressional Budget and Impoundment Control Act of 1974 requires the federal budget to list tax expenditures, and every year the staff of the Joint Committee on Taxation (JCT) and the Treasury’s Office of Tax Analysis each publish estimates of individual and corporate income tax expenditures. Sec. 3(3) of the Congressional Budgetand Impoundment Control Act of 1974 under 2 U.S.C. §622(3) (2006) defines tax expenditures as “those revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability.”

1. To create sustainable customs revenue growth and respond to demand from National Geographic and the United Nations, the United States must close the loophole on energy export tax by replacing 26USC§4612(b) – ‘In addition, there is imposed a flat 5% energy export tax (feet) by the UN Arrears and Certain Iranian Assets Bill of 2020.’ under 26USC§7201. To pay for a third of expiring pandemic compensation beneficiaries without depleting the neglected DI trust fund, it is fiscally necessary to close the OASDI tax loophole for the rich and state employees beginning as soon as October 1, 2020 and no later than January 1, 2021 to pay for COVID-19 disabled workers and create an SSI Trust Fund to end child poverty by 2024 and all poverty by 2030 by repealing the Adjustment to Contribution Base at Sec. 230 of the Social Security Act under 42USC§430.

§73 Outlays

A. The Combined Statement overview of outlays is inadequate and the laborious understudy must be consistent with annual Cabinet agency congressional budget justifications, as is this one, and be summarized. As the result of neglecting to methodically tabulate outlays, the Office of Fiscal Services totally fails to enable OMB todistinguish between budget authority and interagency transfers that must be excluded from the President's budget and perpetuates the myths sustaining a 12 percent margin of error in the annual over-estimate of outlays by agency in Table 4.1 of the Office of Management and Budget (OMB) Historical Tables that greatly exceeds the tendency to overestimate revenue by about 2 percent. The Federal Credit Reform Act of 1990 Pub. L.101–508, title XIII, §13501, Nov. 5, 1990, 104 Stat. 1388–628 defined the terms ‘‘budgetoutlays’’ and ‘‘outlays’’ to mean, with respect to any fiscal year, expenditures and net lending of funds under budget authority during such year under 2USC§622(1). Government outlays are responsible only for administrative and loan guaranty costs. All other [interagency transfers] and lending costs are [privately financed] and should not have any incidental effects on the tabulation of governmental receipts or outlays under 2USC§661a(5)(A)(C). The new Combined Statement outlay and undistributed offsetting receipt overview table must outlaw fictitious, interagency transfer, lending, etc. unoriginal outlays from the budget request as they do for the revenue by source category, for the edification of OMB Historical Table 4.1 Outlays by Agency. The Combined Statement must agree to the definition of undistributed offsetting receipts often called advanced appropriations – unspent funds remaining at the end of year that are used to reduce the deficit and pay the first obligations of the new year – and rename the undistributed offsetting receipt revenue category “earnings on investments”. CBO must cross-examine the outlays by agency and undistributed offsetting receipts table.

21

1. Before it is possible for the Combined Statement to begin adding Outlays by Agency pursuant to the regulation of Table 4.1 of the Historical Tables: Other Defense – Civil Programs, Other Independent Agencies (On-budget and Off-budget), Allowances, Off-budget Undistributed Offsetting Receipts, and new Infrastructure Initiative row, need to be excluded from the budget request or deleted. Department of State and International Assistance rows need to be added together by the State Department, whereas that is how they are reported, and International Assistance Programs row deleted. These outlay row falsely represent transfers of funds from agency to a sub-agency or another agency, if they exist at all. These rows must be deleted by OMB and excluded from the budget request by the Combined Statement. Overall Table 4.1 is historically about 12 percent overestimated and it is hoped to report the reduction in the margin of error in regards to overestimating outlays to 3 percent in order to ensure enough revenues collected and t-bonds sold to guarantee agencies balance available to pay inflation adjusted costs pursuant to the Anti-Deficiency Act of 1982 under 31USC§1502.

2. The HELP Act provides, The terms ‘‘budget outlays’’ and ‘‘outlays’’ mean, with respect to any fiscal year, expenditures and net lending of funds under budget authority during such year under 2USC§622(1), to this should be appended:

(A) The term ‘‘on-budget outlays’’ means, with respect to any fiscal year, the President's budget, all the expenditures of the United States Government, except those for the Federal Old Age Survivor Disability Insurance Trust Funds, “referred to as off-budget outlays”, and the repayment of debt principal or negative subsidy revenues, excluded.

(B) The new Office of Fiscal Services Combined Statement outlay and undistributed offsetting receipt overview table must outlaw fictitious, interagency transfer, lending, etc.unoriginal outlays from the budget request as they do for the revenue by source category, for the edification of OMB Historical Table 4.1 Outlays by Agency. The Combined Statement must agree to the definition of undistributed offsetting receipts often called advanced appropriations – unspent funds remaining at the end of year that are used to reduce the deficit and pay the first obligations of the new year – and rename the undistributed offsetting receipt revenue category “earnings on investments”. CBO will then cross-examine the outlays by agency and undistributed offsetting receipts table under these new rules.

(C) Fictitious rows: off-budget offsetting receipts, Other Defense-Civil Programs, Allowances, On and Off Budget Independent Agencies, Off-budget Undistributed Offsetting Receipts, International Assistance Programs [added to State], and novel Infrastructure Improvement rows shall be deleted from OMB Table 4.1 and Bureau of Fiscal Services. To ensure there is a balance available for federal outlays, t-bond sales shall allow for up to a three percent margin of error more than scheduled expenditures pursuant to the Anti-deficiency Act of 1982 under 31USC§1502.

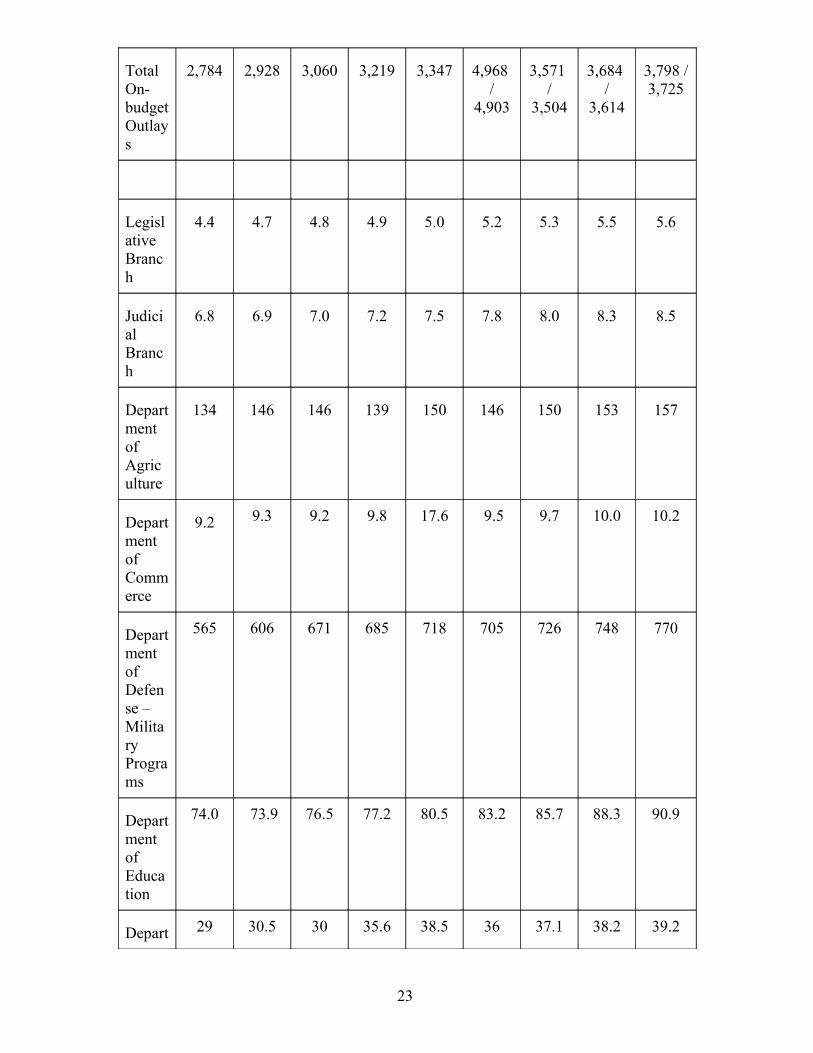

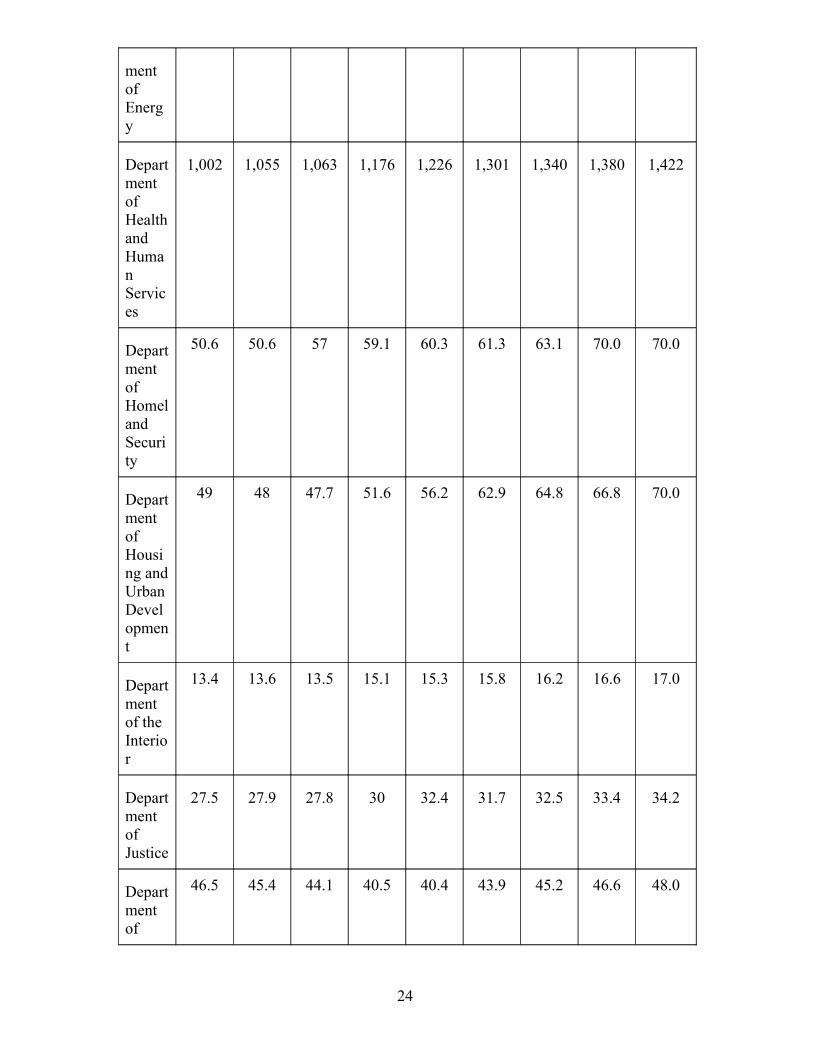

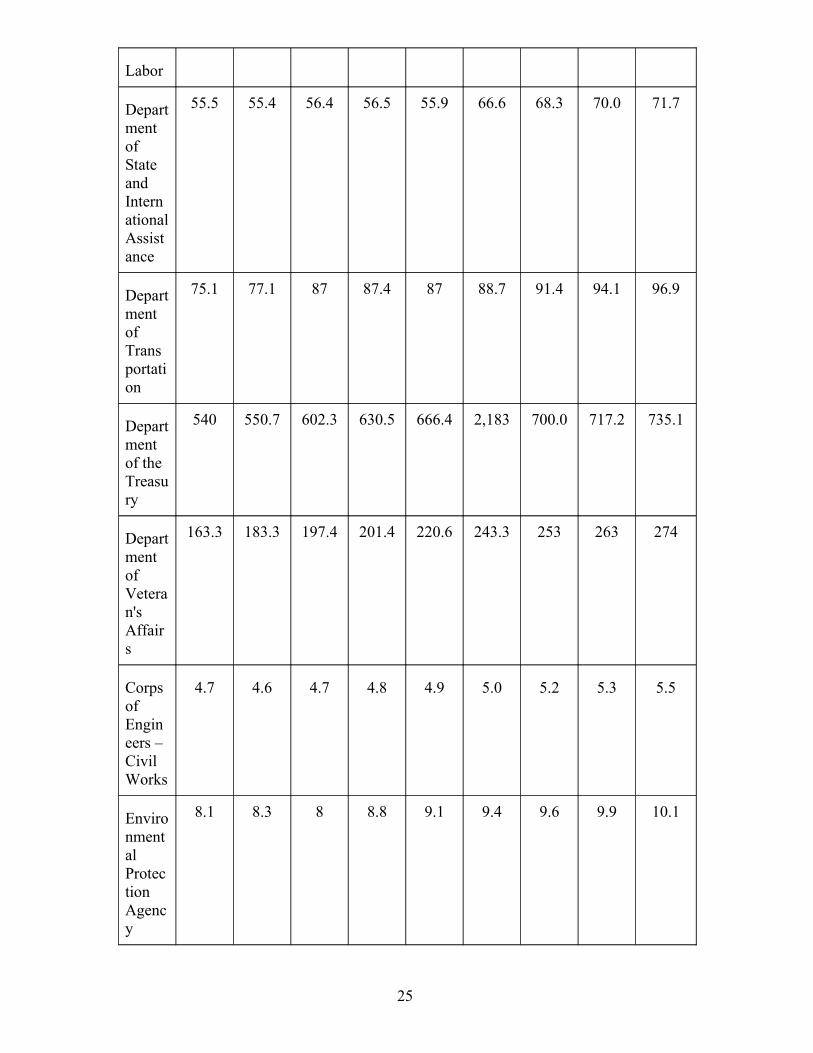

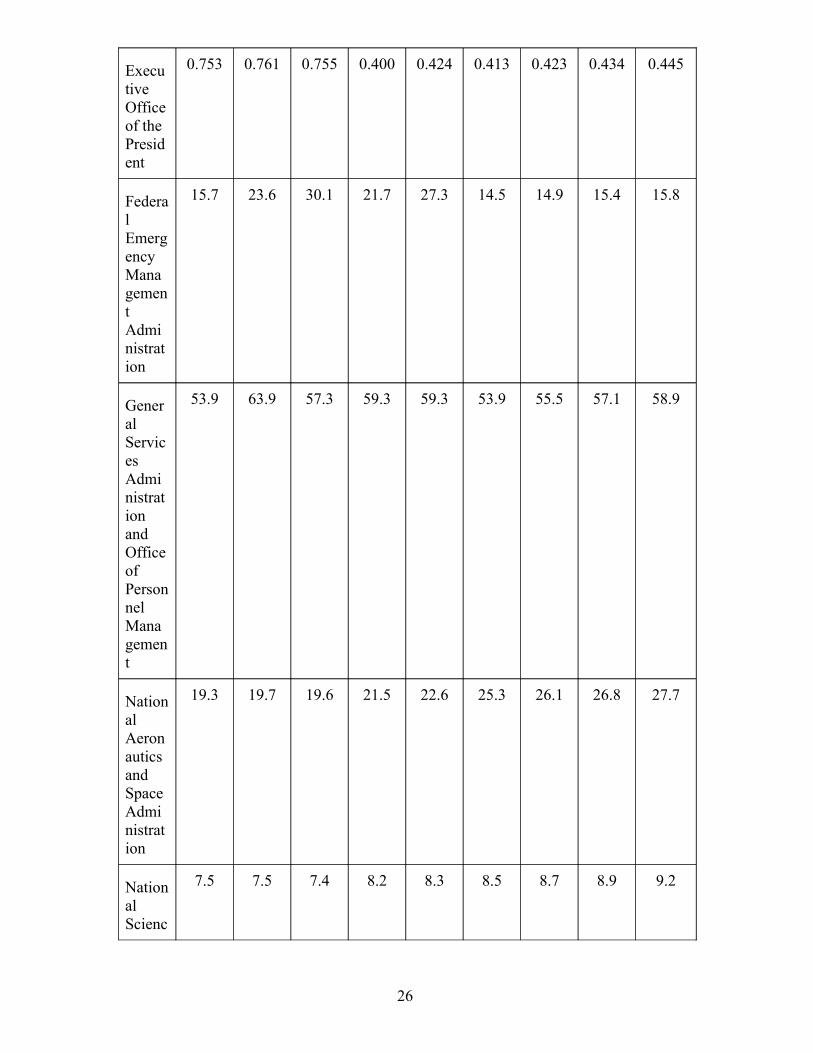

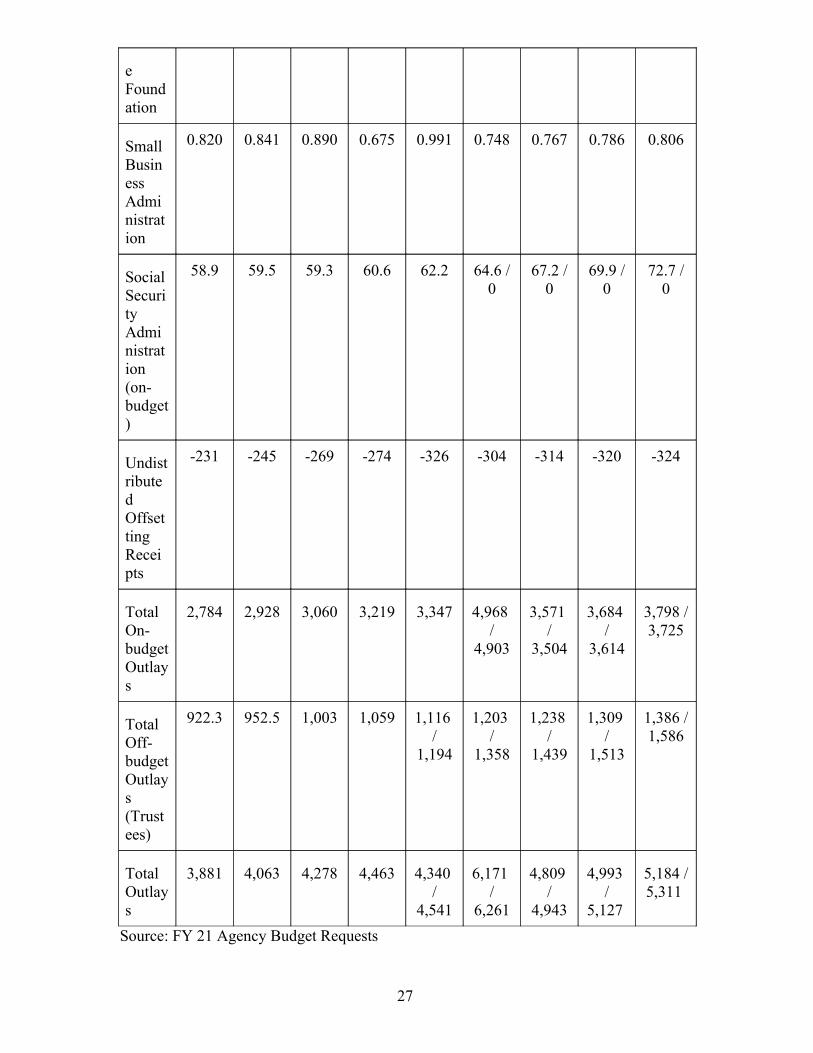

Government Outlays by Agency Ledger FY 16 – FY 24(billions)

FY 16 FY 17 FY 18 FY 19 FY 20 FY 21 FY 22 FY 23 FY 24

22

Total On-budgetOutlays

2,784 2,928 3,060 3,219 3,347 4,968 /

4,903

3,571 /

3,504

3,684 /

3,614

3,798 /3,725

Legislative Branch

4.4 4.7 4.8 4.9 5.0 5.2 5.3 5.5 5.6

Judicial Branch

6.8 6.9 7.0 7.2 7.5 7.8 8.0 8.3 8.5

Department of Agriculture

134 146 146 139 150 146 150 153 157

Department of Commerce

9.2 9.3 9.2 9.8 17.6 9.5 9.7 10.0 10.2

Department of Defense – Military Programs

565 606 671 685 718 705 726 748 770

Department of Education

74.0 73.9 76.5 77.2 80.5 83.2 85.7 88.3 90.9

Depart 29 30.5 30 35.6 38.5 36 37.1 38.2 39.2

23

ment of Energy

Department of Healthand Human Services

1,002 1,055 1,063 1,176 1,226 1,301 1,340 1,380 1,422

Department of Homeland Security

50.6 50.6 57 59.1 60.3 61.3 63.1 70.0 70.0

Department of Housing andUrban Development

49 48 47.7 51.6 56.2 62.9 64.8 66.8 70.0

Department of the Interior

13.4 13.6 13.5 15.1 15.3 15.8 16.2 16.6 17.0

Department of Justice

27.5 27.9 27.8 30 32.4 31.7 32.5 33.4 34.2

Department of

46.5 45.4 44.1 40.5 40.4 43.9 45.2 46.6 48.0

24

Labor

Department of State and InternationalAssistance

55.5 55.4 56.4 56.5 55.9 66.6 68.3 70.0 71.7

Department of Transportation

75.1 77.1 87 87.4 87 88.7 91.4 94.1 96.9

Department of the Treasury

540 550.7 602.3 630.5 666.4 2,183 700.0 717.2 735.1

Department of Veteran's Affairs

163.3 183.3 197.4 201.4 220.6 243.3 253 263 274

Corps of Engineers – Civil Works

4.7 4.6 4.7 4.8 4.9 5.0 5.2 5.3 5.5

Environmental Protection Agency

8.1 8.3 8 8.8 9.1 9.4 9.6 9.9 10.1

25

Executive Officeof the President

0.753 0.761 0.755 0.400 0.424 0.413 0.423 0.434 0.445

Federal Emergency Management Administration

15.7 23.6 30.1 21.7 27.3 14.5 14.9 15.4 15.8

General Services Administration and Officeof Personnel Management

53.9 63.9 57.3 59.3 59.3 53.9 55.5 57.1 58.9

National Aeronautics and Space Administration

19.3 19.7 19.6 21.5 22.6 25.3 26.1 26.8 27.7

National Scienc

7.5 7.5 7.4 8.2 8.3 8.5 8.7 8.9 9.2

26

e Foundation

Small Business Administration

0.820 0.841 0.890 0.675 0.991 0.748 0.767 0.786 0.806

Social Security Administration (on-budget)

58.9 59.5 59.3 60.6 62.2 64.6 /0

67.2 /0

69.9 /0

72.7 /0

Undistributed Offsetting Receipts

-231 -245 -269 -274 -326 -304 -314 -320 -324

Total On-budgetOutlays

2,784 2,928 3,060 3,219 3,347 4,968 /

4,903

3,571 /

3,504

3,684 /

3,614

3,798 /3,725

Total Off-budgetOutlays (Trustees)

922.3 952.5 1,003 1,059 1,116 /

1,194

1,203 /

1,358

1,238 /

1,439

1,309 /

1,513

1,386 /1,586

Total Outlays

3,881 4,063 4,278 4,463 4,340 /

4,541

6,171 /

6,261

4,809 /

4,943

4,993 /

5,127

5,184 /5,311

Source: FY 21 Agency Budget Requests

27

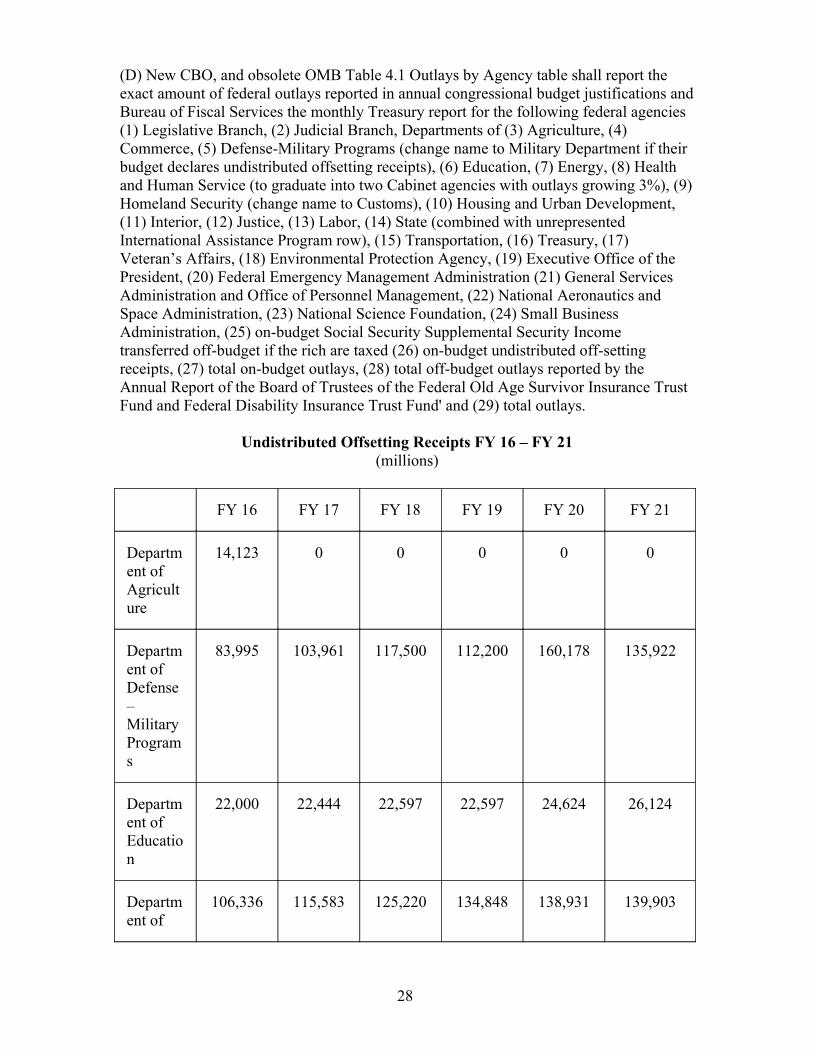

(D) New CBO, and obsolete OMB Table 4.1 Outlays by Agency table shall report the exact amount of federal outlays reported in annual congressional budget justifications andBureau of Fiscal Services the monthly Treasury report for the following federal agencies (1) Legislative Branch, (2) Judicial Branch, Departments of (3) Agriculture, (4) Commerce, (5) Defense-Military Programs (change name to Military Department if their budget declares undistributed offsetting receipts), (6) Education, (7) Energy, (8) Health and Human Service (to graduate into two Cabinet agencies with outlays growing 3%), (9)Homeland Security (change name to Customs), (10) Housing and Urban Development, (11) Interior, (12) Justice, (13) Labor, (14) State (combined with unrepresented International Assistance Program row), (15) Transportation, (16) Treasury, (17) Veteran’s Affairs, (18) Environmental Protection Agency, (19) Executive Office of the President, (20) Federal Emergency Management Administration (21) General Services Administration and Office of Personnel Management, (22) National Aeronautics and Space Administration, (23) National Science Foundation, (24) Small Business Administration, (25) on-budget Social Security Supplemental Security Income transferred off-budget if the rich are taxed (26) on-budget undistributed off-setting receipts, (27) total on-budget outlays, (28) total off-budget outlays reported by the Annual Report of the Board of Trustees of the Federal Old Age Survivor Insurance Trust Fund and Federal Disability Insurance Trust Fund' and (29) total outlays.

Undistributed Offsetting Receipts FY 16 – FY 21(millions)

FY 16 FY 17 FY 18 FY 19 FY 20 FY 21

Department of Agriculture

14,123 0 0 0 0 0

Department of Defense – Military Programs

83,995 103,961 117,500 112,200 160,178 135,922

Department of Education

22,000 22,444 22,597 22,597 24,624 26,124

Department of

106,336 115,583 125,220 134,848 138,931 139,903

28

Health and Human Services

Department of the Interior

3,200 2,033 2,772 2,949 1,694 1,012

Corps ofEngineers – CivilWorks

1,000 1,000 1,000 1,000 1,000 1,000

Total 230,654 245,021 269,089 273,594 326,427 303,961

Source: USDA FY 18 – FY 21; DOD FY 18 – FY 21; Education FY 18 -FY 21 Interior FY 18 – FY 21; Centers for Medicare Medicaid Services FY 18 – FY 21; Army Corp of Engineers FY 18.

(E) Undistributed offsetting receipts are agency revenues remaining from the previous year, often called advanced appropriations, that are used to pay for the following year budget, to reduce outlays by the General Fund. Only five agency budget justifications produce reliable undistributed offsetting receipts, the Departments of Defense, Education,Health and Human Services, Interior and Corp of Engineers – Civil Programs. The annual tabulation of undistributed offsetting receipts is mathematically necessary to calculate total federal outlays and surplus / deficit. The Department of Agriculture has been saving money stolen from food stamps cuts in the Commodity Credit Corporation and does not produce undistributed offsetting receipts, nor make any additional “trade war” compensation payments, for that matter of concealing the proceeds of domestic program robbery. Elementary and Secondary Education and Medicaid declare Advance Appropriations in their budget tables, with explanation that these savings are used to pay for the difference between the school year and the fiscal year and to pay for the beginningof the next year medical claims. The Corp of Engineers – Civil Programs budget vacillates between the sound financial strategy of openly declaring precisely $1 billion in undistributed offsetting receipts and total incompetence, but having once made the declaration, predictably produces $1 billion undistributed offsetting receipts annually as the cornerstone of their federal outlay total. The Departments of Defense and Interior budgets are impaired by the failure to openly declare undistributed offsetting receipts in their budget overview. The Defense Department shall declare undistributed offsetting receipts with the difference between the congressional budget request and the total outlays of the three military departments – Air Force, Army and Navy. The Department of Interior turns a tidy profit in undistributed offsetting receipts, that must be declared to ensure payment of 2.5 percent growth for public land agencies and 3 percent for Indian Affairs programs.

29

(F) Usual federal spending inflation is estimated to grow 2.5 percent for government, 3 percent for services, education, minimum wage, cost-of-living adjustment, 3.3 percent forfood stamps, 4 percent for disability and child welfare and 5.5 percent for retirement annually. Any shortfall is due compensation for deprivation of relief under 18USC§246 pursuant to the Application of the Convention on the Prevention and Punishment of the Crime of Genocide (The Gambia v. Myanmar) Summary 2020/1 23 January 2020 and Art. 14 of the Convention against Torture and Other Cruel, Inhuman or Degrading Treatment or Punishment (CAT)(1987).

B. A fundamental principle of the FY 21 budget is that persecutions regarding the number of the beast, should not last more than 42 months (Revelation 13:10). Department of Defense spending has been rapidly increasing 4.6 percent annually from $606 billion FY 17 to $718 billion FY 20 before declining to $705 billion FY 21 after which time normal three percent growth is anticipated. The prophecy underlying the COVID-19 pandemic economic depression is mostly that Treasury spending grew slowlyfrom $602 billion FY 18 to $666 FY 20. Having concealed the number of the beast in theaddition of discretionary and mandatory funding, they do not perform although the total is what is reported by OMB, Treasury spending was not projected to grow fast enough without justifying a $1.5 trillion Relief Act FY 21 driving up Treasury spending to an estimated $2,183 billion FY 21 with a will to achieve $700 billion in outlays FY 22. There are dozens of number of the beast settlements accelerating growth to make the leapfrom 6 to 7 in less 42 months, 3 ½ years. The cost is negligible in comparison with the happiness it brings to do this curse justice. The UN is burdened by an obese Secretary-General who has accursed the Peacekeeping with budget cuts from $7.8 billion 2016-2017 to $6.5 billion 2019-2020 and not published a budget for 2020-2021 in time for the June 30 fiscal year. Paying arrears bring State Department spending from $55.9 FY 20 to$66.6 billion FY 21 and with this head start and normal 2.5 percent growth is expected to reach $70 billion FY 23. Appropriation of hyper-inflationary Immigration and Customs Enforcement (ICE) responsibilities to justify growth in excess of 3 percent annually by the US Marshal and Customs and Border Protection (CBP) is expressed as a $6 billion budget for ICE aiming to abolish unwarranted deportation agency within 42 months.

1. It is necessary to abolish the unwarranted criminal agencies defending themselves by wastefully attempting to sanction the innocent pursuant to Art. 54 of the Fourth Geneva Convention Relative to the Protection of Civilians in Times of War (1949). To outlaw outlays right, it is necessary to redress the highest concentration of detainees in the world and unjust war by a reduction in force that seeks to terminate terrorism financing for unwarranted secret police forces, not indiscriminately impair 3 percent annual national defense spending growth. Police defunding is popular in many localities, force reduction must require police officers have at least a Bachelor degree to prevent recidivism 100 percent of court orders. 400 prominent economists and intellectuals petitioned the White House to legalize marijuana by repealing marijuana from Schedule I(c)(17) of the CSA under 21USC§812(c) and abolish drug enforcement. To abolish slavery while improvingsecurity despite the post-traumatic stress disorder (PTSD) from the Civil War, the US Marshall shall justify their increases in excess of 3 percent annually based upon the usurpation by the federal court of any legitimate responsibilities of the FBI (protecting only Uniform Crime Reports, National Forensic Laboratory and Police Academy), DEA (destroying the DEA stockpile and all drugs seized by the police, and terminating DEA Diversion Control if the Department of Health and Human Services does not want to

30

charge the biannual fee), ICE (shared with CBP), Interagency Drug and Crime Enforcement. To prevent terrorism it is necessary that federal criminal action, such as deportation, is warranted on an individual basis by a federal judge under Rule 4 Fed. Crim. P. The Authorization for employment of FBI and DEA Senior Executive Service under 5USC§3151-§3152 must be repealed. To stop corruption of the Attorney General, whereas the White House refuses to receive anymore Office of National Drug Control Policy (ONDCP) financing from the Centers for Medicare and Medicaid Services (CMS),all such ONDCP financing by CMS shall be terminated. The FBI, with lethal norovirus coffee prior from 2016, and Department of Justice Health Care Fraud Enforcement is suspected of being the only agency who tortures with live coronavirus, during the course of their routine unwarranted breaking and entering (B&E) of Attorney General petitioners. The White House Office of National Drug Control Policy and judiciary Sentencing Commission also need to be abolished. The CIA (protecting the World Factbook), international military finance, international military education, international narcotic control and law enforcement and non-UN peacekeeping are to be completely abolished by the State Department. These monies from abolition can be used to reduce the deficit, however, they have not been abolished and the total savings do not need to be quantified until they have been terminated.

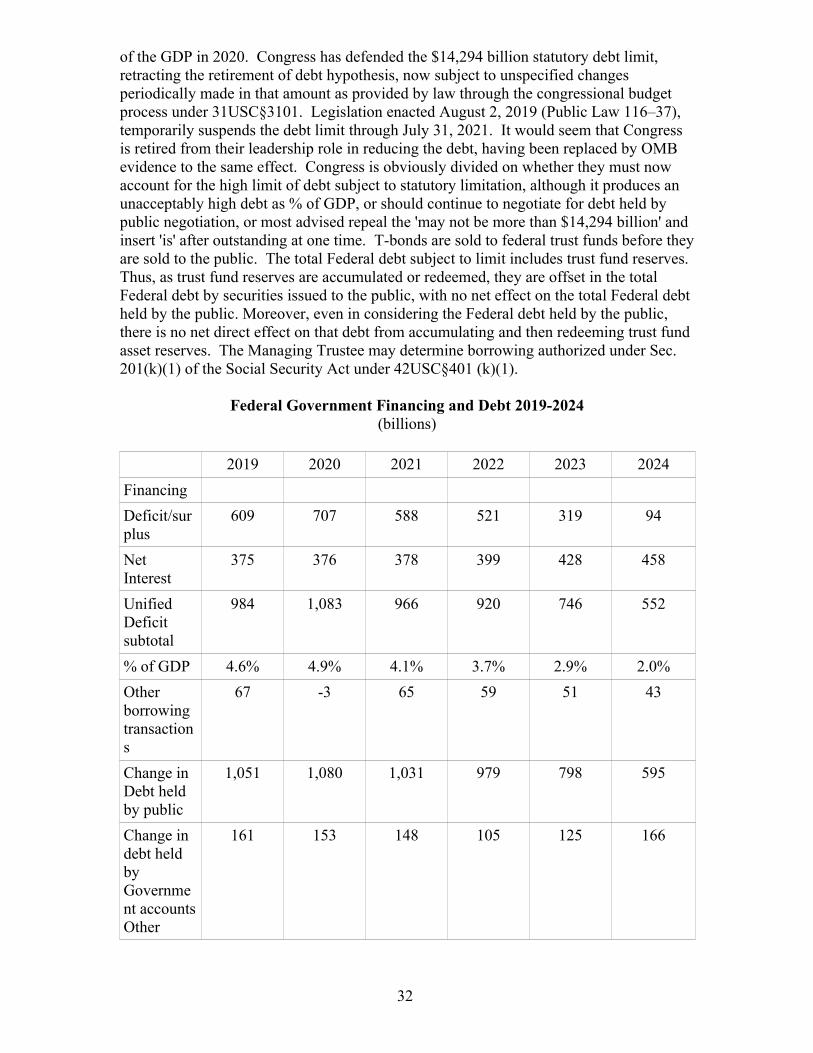

§74 Debt

A. When the federal government spends more than it takes in, the United States has to borrow money to cover that annual deficit. Each year’s deficit adds to the growing national debt. The federal government usually runs on a deficit, with some famous exceptions, such as when Andrew Jackson paid off the federal debt in 1835 and more recently when Bill Clinton turned a federal budget surplus in 1998-2000. The power of Congress to borrow money on the credit of the United States is conferred by the Constitution at Art. 1 Sec. 8 Cl. 2 and Sec. 4 of the 14th Amendment to the US Constitution. The Articles of Confederation and Perpetual Union had granted to the Continental Congress the power to borrow money, or emit bills on the credit of the United States, transmitting every half-year to the respective States an account of the sumsof money so borrowed or emitted. Article I, Section 8, Clause 2 of the Constitution grantsto the United States Congress the power to borrow money on the credit of the United States. At the time that the Constitution came into effect, the United States had a significant debt, primarily associated with the Revolutionary War. The issue of the federal debt was next addressed by the Constitution within Section 4 of the Fourteenth Amendment (proposed on 13 June 1866 and ratified on 9 July 1868): whereby the validity of the public debt of the United States, authorized by law, including debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellion, shall not be questioned. To eliminate Jim Crow it has been proposed to repeal all but Equal Protection Section One of the Fourteenth Amendment, without impairing Native American tax-exemptions or lawful public debt.

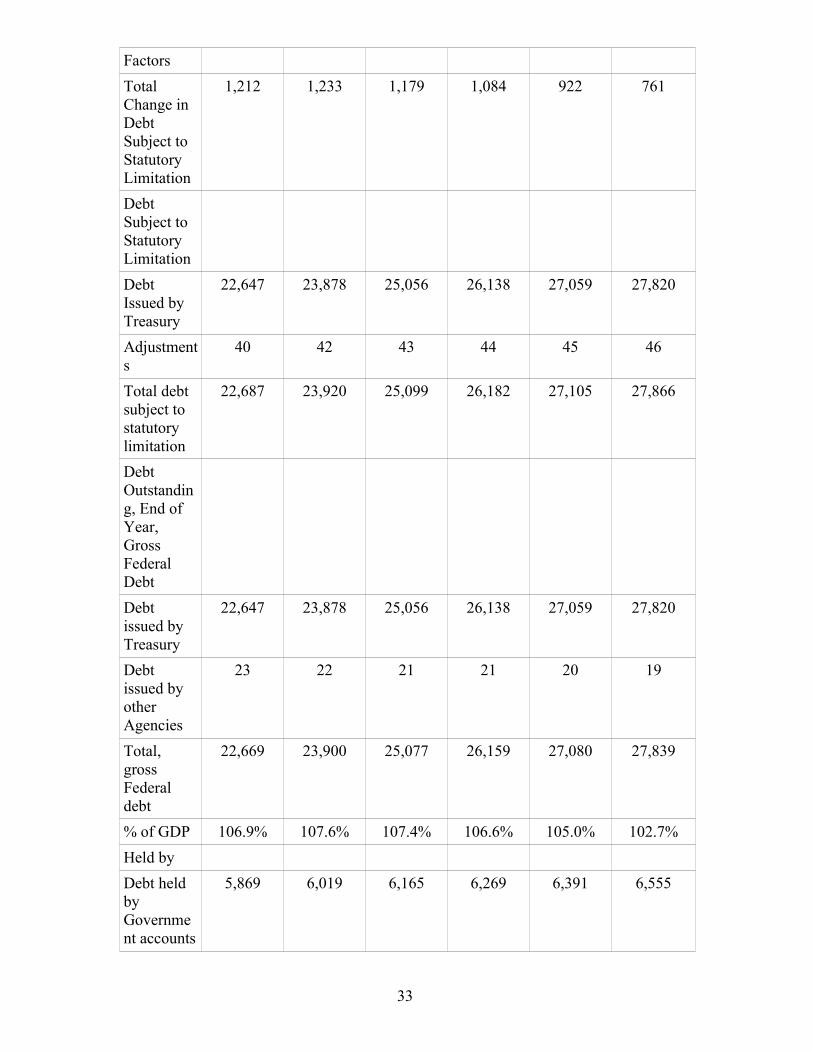

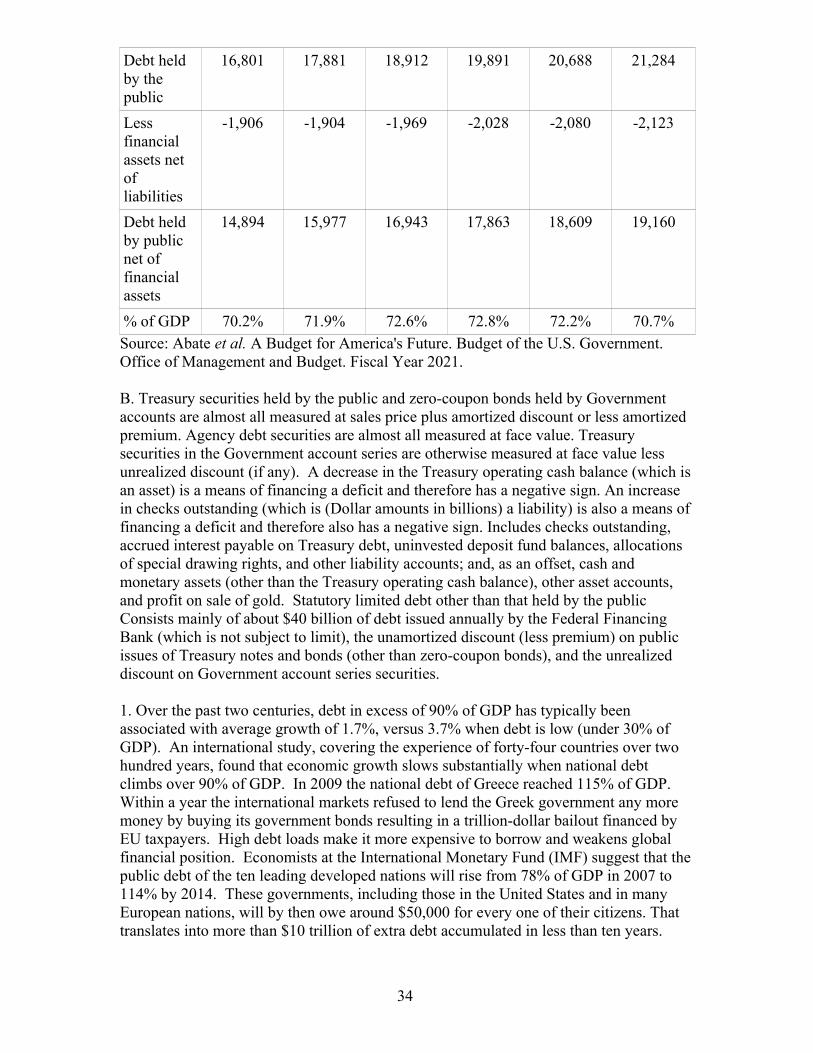

1. At the end of 2019, the Federal Reserve Banks held $2,113.3 billion of Federal securities and the rest of the public held $14,687.4 billion. Although the Fiscal Year 2021Budget does not declare any revenues whatsoever, the Office of Management and Budget(OMB) did an excellent job defending debt held by the public against overestimation, reducing the $23.9 trillion debt subject to statutory limitation outstanding at end of year 107.6% of GDP, to $16.0 trillion Debt Held by the Public Net of Financial Assets 71.9%

31