harmony 2003 - Annual Report

159

THIS YEAR’S ANNUAL REPORT CONVEYS EXACTLY WHO WE ARE, WHAT WE HAVE DONE, WHAT WE ARE DOING AND WHERE WE ARE GOING. NO FUSS, NO FRILLS. HARMONY 2003

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of harmony 2003 - Annual Report

THIS YEAR’SANNUAL REPORTCONVEYS EXACTLYWHO WE ARE, WHATWE HAVE DONE,WHAT WE AREDOING AND WHEREWE ARE GOING.

NO FUSS, NO FRILLS.

HARMONY2003

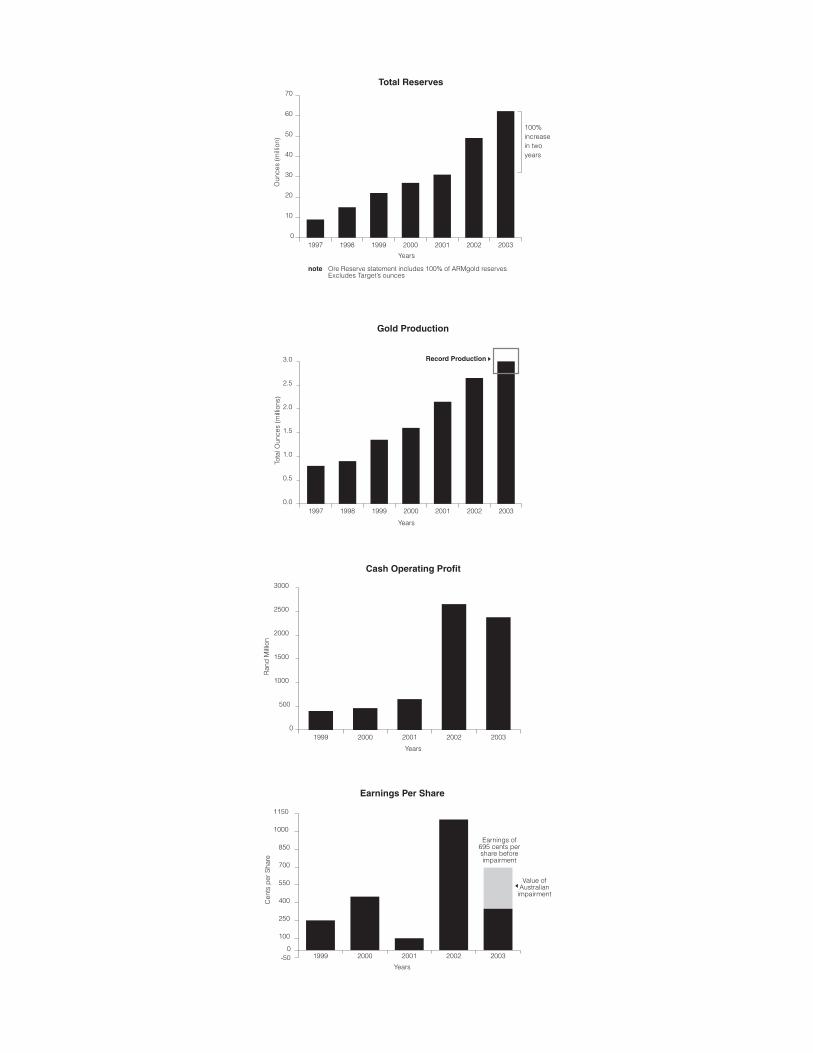

1997 1998 1999 2000 2001 2002 20030

10

20

30

40

50

60

70

Total Reserves

Oun

ces

(mill

ion)

100%increasein twoyears

note Ore Reserve statement includes 100% of ARMgold reservesExcludes Target’s ounces

Years

1997 1998 1999 2000 2001 2002 20030.0

0.5

1.0

1.5

2.0

2.5

3.0 Record Production

Tota

l Oun

ces

(mill

ions

)

Years

Gold Production

1999 2000 2001 2002 20030

500

1000

1500

2000

2500

3000

Cash Operating Profit

Ran

d M

illio

n

Years

1999 2000 2001 2002 2003-50

100

250

400

550

700

850

1000

1150

Earnings Per Share

Cen

ts p

er S

hare

Value ofAustralian

impairment

0

Earnings of695 cents pershare beforeimpairment

Years

Harmony Annual Report 2003 004

ANNUALHIGHLIGHTS� BECOMING SOUTH AFRICA'S LARGEST GOLD

PRODUCER FOLLOWING THE MERGER BETWEENHARMONY AND ARMGOLD

� BECOMING THE FIFTH LARGEST GOLD PRODUCERIN THE WORLD IN 2004

� ACHIEVING AN INCREASE OF 12% IN PRODUCTIONFROM 2.7 MILLION OUNCES TO A RECORD3.0 MILLION OUNCES

� RETURNING RECORD CASH OPERATING PROFIT OFUS$260 MILLION

� OWNING THE WORLD’S LARGEST GOLD RESOURCEOF 410 MILLION OUNCES OF WHICH 62 MILLIONOUNCES ARE IN THE RESERVE CATEGORY

� ENSURING THAT HARMONY WILL BE MINING INSOUTH AFRICA WELL INTO THE FUTURE WITH THEAPPROVAL OF ORGANIC GROWTH PROJECTS

� MAKING SIGNIFICANT PROGRESS INCORPORATINGTHE FREE GOLD AND HILL 50 ASSETS

� ACQUIRING A 34.5% STRATEGIC STAKE IN AVMINAND AN EFFECTIVE 26.1% STAKE IN AVGOLD

� MAKING HARMONY ONE OF THE MOST TRADEDGOLD STOCKS GLOBALLY, INCREASING LIQUIDITYFROM 410% TO 448%

� HAVING MORE THAN 50% OF HARMONY'S STOCKTRADED ON THE NEW YORK STOCK EXCHANGE

SECTION 1

CHAIRMAN’SOVERVIEW

Harmony Annual Report 2003 006

SECTION 1

CHAIRMAN’SOVERVIEWThrough the merger with ARMgold we created South Africa’s largest gold producer. We believe that the mergedcompany will be a role model in the SouthAfrican environment where transformationhas become a significant factor.

Over the past year, the benefits of a strongUS Dollar gold price were largely negatedby the strengthening South African Randand rising costs.

Although our short-term focus is onincreasing profit margins and containingcosts, we continue to invest in the long-term sustainability of Harmony.

IN OTHER WORDS

During 2002/03 Harmony established itselfas a major gold producer, both in SouthAfrica and internationally. This wasachieved during a time when ouroperational environment was significantlyinfluenced by a host of internal andexternal factors.

The most important event in thehistory of the company, both in terms ofsignificance and size, was the mergerbetween Harmony and ARMgold. Not onlydid the merger create South Africa’slargest gold producer, it also created aglobally competitive company which isrecognised as a role model in the SouthAfrican mining industry. We believe thatHarmony is now representative of the newSouth Africa and from a legal perspectivecomplies with the equity requirements ofthe Broad-Based Socio-EconomicEmpowerment Bill. We are committed tothose initiatives which are aimed atmaking South Africa a competitive andattractive destination for mining relatedinvestors.

Merging the two companies was animportant strategic step in the growthplans of both Harmony and ARMgold. Weshared one of the industry’s best goldassets in Free Gold and from a cultural,operational and strategic perspective, thefit seemed natural.

As the fifth-largest gold producer inthe world, the company is nowinternationally more competitive and willcontinue to look for value-addingopportunities in the major gold-producingregions of the world.

The most significant external factor thisyear was the continued strength of the USDollar price of gold. The current goldmarket, which has been in a bull trendsince 2000 continued to rise, with anactual average gold price of US$329/ozrealised for the year, compared to theUS$287/oz in the previous financial year.The main drivers of the increase in goldprice have undeniably been the continuedweakness of the US Dollar, the globaleconomic downturn and the political

uncertainty associated with the variousconflict situations in the world.

The gold price was also supported bythe dramatic reduction in hedging by goldproducers. During the 2002 calendar year,producer hedging decreased byapproximately 600 tonnes and this trend isexpected to continue until the end of 2003.During 2002, non-hedgers’ share pricesincreased some 154%, whilst hedgedproducers’ share prices increased by only63%. Even at a gold price of US$252/oz in1999 we remained unhedged. As astrategy it proved to be correct and ourshareholders saw the company’s shareprice increase by 158% during 2002. Thistrend was, however, reversed in the first halfof 2003, when South African gold stocksshowed weakness on the back of astrengthening Rand. Harmony will continueto be an unhedged gold producer, with thebulk of its production coming from SouthAfrica.

The South African Rand depreciateddramatically in November 2001. Since early

250

270

290

310

330

350

370

390

Share Price Premium to NAV - Senior Producers

NA Senior Average

South African Average

Australians Average

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Gold Price

May

01

Jun

01

Jul 0

1

Aug

01

Sep

01

Oct

01

Nov

01

Dec

01

Jan

02

Feb

02

Mar

02

Apr

02

May

02

Jun

02

Jul 0

2

Aug

02

Sep

02

Oct

02

Nov

02

Dec

02

Jan

03

Feb

03

Mar

03

Apr

03

May

03

Jun

03

source BMO Nesbitt Burns

Pre

miu

m

Gol

d pr

ice

(US

$/O

z)

graph 1

Major Gold Producers

Newmont

AngloGold

Barrick

Gold Fields

Harmony

Placer Dome

Kinross

Ashanti

0 1 2 3 4 5 6 7 8 9

source HSBC Senior Gold Book

Forecasted Annual Production Ounces (Millions)

graph 2

SECTION 1CHAIRMAN’S REVIEW

007

Harmony Annual Report 2003 008

2002 the Rand has reversed this trend andthe stronger Rand had a detrimental effecton the cash generating potential of thecompany.

The relatively higher cash operatingprofit margins which were achieved overthe past two years, resulted in SouthAfrican producers’ valuation, relative totheir Net Asset Value (NAV), increasingfrom a discount of approximately 26% toan average premium of 37%. NorthAmerican gold producers’ premium to NAVdecreased from a high of 60% to 44% overthe same period. Achieving such a re-rating, or reduction in the so-called SouthAfrican discount, during a period ofuncertainty with regards to the MiningCharter, bodes well for a South Africancompany like Harmony. see graph 1

The gold industry saw only marginalincreases in exploration expenditure and weexpect the need to find replacement ouncesto drive the continued consolidation of theindustry. Following our own as well as theproposed AngloGold/Ashanti merger, the goldproducers’ table is showing the second tier

gold producers more distinctly. see graph 2The consolidation of gold companies

into a few major producers could result infurther corporate activity. Harmony, as oneof the six major producers, is in a strongerposition than ever to fund our growthstrategies.

An increase in exploration expenditurewill result in future discoveries, however,we believe that the pipeline for major goldprojects has been all but depleted and it isunlikely that exploration expenditure willreturn to the levels achieved during the1990’s. see graph 3

Our company has built up significantexposure to some of the most exciting newprojects left in the world.

Gold producers have over the past twoyears been under increasing pressure toreport on the total costs of producing gold,compared to the emphasis on cash costsduring the time of lower US Dollar goldprices. The industry should now endeavourto deliver solid financial returns forshareholders, i.e. earnings, dividends andcapital growth on the shares, instead ofreporting on how they ensured survival

through low cash costs during the bearmarket.

The danger of exclusively focusing oncash costs, lies in the fact that producersare prone to overcapitalising orebodies andare tempted to high grade their reserves,instead of focusing on the optimalexploitation of their orebodies. This impactsadversely on both shareholder returns aswell as on the long-term viability of theirreserves. On average, during 2002, globalgold producers reported a 7% increase incash costs, from US$168/oz to US$177/oz.Included in the 7% increase is the effect ofthe strengthening of most currenciesagainst the Dollar. The South AfricanRand’s strength impacted adversely on theDollar cost of local producers.

On a total cost basis, the goldindustry’s costs increased from US$302/ozto US$335/oz in 2002. This illustrates thatthe industry requires a significantly highergold price than the US$329/oz achieved inorder to generate decent returns on newprojects. see graph 4

1996 1997 1998 1999 2000 2001 20020.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

200

220

240

260

280

300

320

340

360

380

400

Global Exploration Expenditure

US

Dol

lar

(Bill

ions

)

Global Exploration Expenditure

Gold Price (US$/Oz)

source BMO Nesbitt Burns

Years

Gol

d P

rice

(US

$/O

z)

graph 3

Rand/kg price

70000

75000

80000

85000

90000

95000

100000

105000

110000

115000

Rand/kg Gold price versus US Dollar Gold price/oz

250

270

290

310

330

350

370

390

Jul 02 Aug 02 Sep 02 Oct 02 Nov 02 Dec 02 Feb 03 Mar 03 Apr 03 May03 Jun 03

US$ gold price/oz source HSBC Senior Gold Book

Gol

d P

rice

(R/K

g)

Gol

d P

rice

(US

$/O

z)

graph 4

Despite the impact of the Mining Charter and theproposed Royalty Bill, weare comfortable with havingthe bulk of our operations in South Africa.

009

Presently the supply demand fundamentalsseem to be in a healthier position with worldproduction edging lower. In addition, thelarge-scale buy-back of hedging ounces byproducers has underpinned the currentstrength of the US Dollar price of gold. seetable 1

The South African mines probably havethe highest leveraged exposure to acombined depreciation of the South AfricanRand and a rising US Dollar gold price.However, increased production from SouthAfrican producers did not materialiseduring the past year and we don’t expectthis to happen in future. Our focus will beon increasing profitability in the short term,whilst making investments in the futuregrowth projects of the company.

Official Sector Sales continued atsteady levels. The Washington Accord,which limited central bank sales to 400tonnes per annum as from 1999, is due forrenewal by September 2004. We anticipatethat this agreement will be renewed for afurther period of five years, although thequantum of central bank sales could bedifferent. During periods of rising US Dollar

gold prices, bar hoarding and jewellerydemand decreases in line with the amountof disposable income available for thepurchasing of gold products. The past twoyears have seen lower levels of economicgrowth further impacting negatively onindividuals’ gold purchases.

Initiatives by the World Gold Council topresent investors with a gold productwhich will enable direct investment in goldbullion are currently under way. Theproduct is already listed on the AustralianStock Exchange, and similar products areplanned for the New York Stock Exchangeand JSE Securities Exchange. Harmonycurrently markets its physical goldinvestment products, manufactured indemarcations of 1/4 ounce, 1/2 ounce, one ounce and 10-tola bars to itsshareholder base and other investors.

The current economic, social andpolitical environment creates opportunitiesin which Harmony, as an unhedged goldcompany, will continue to delivershareholder value. The company isextremely excited about its future in anindustry which, from an investment

perspective, is healthier than ever before.Corporate Governance has been a

special focus area following the uncertaintycreated among investors by recentinternational corporate accountingscandals. The company has over the pastyear been exposed to changes in theregulations from the Securities andExchange Commission, the New York StockExchange and the JSE SecuritiesExchange in Johannesburg.

Our board is committed to the higheststandard of corporate governance, and ouractions support this. We recognise theimportance of an independent board, thatnot only focuses on maximisingshareholder value but, in doing so,recognises the needs and requirements ofall our stakeholders. Following the mergerof the two companies, the board nowconsists of competent non-executive andexecutive directors from both companies.

South Africa is in a phase oftransformation to a free-market economy ina sustainable democracy, serving all itspeople. These changes take time and arenot always well understood by the

Supply 2001 2002 2003*

Mine Supply 2 540 2 480 2 450

Official Sector Sales 677 560 530

Scrap Sales 720 845 880

Total Supply 3 937 3 885 3 860

Demand

Fabrication Jewellery 1 407 1 324 1 340

Investment Jewellery 1 875 1 475 1 600

Investment - Other 430 520 420

Net Producer Hedging 225 566 500

Implied Net Investment 211 361 370

Total Demand 4 148 4 246 4 230

Surplus Demand (211) (361) (370)

source Virtual Metals Research and Consulting *Annualised

GOLD SUPPLY AND DEMAND BALANCE (TONNES)

table 1

Harmony Annual Report 2003 010

investment community. We, as individualsand as a company, are committed to thefuture of our country and will activelyparticipate in this process of transformation,thereby ensuring a better future for all.

Although our safety statistics continueto compare favourably with the averages ofSouth African gold mining, I regret to informyou that a total of 26 employees andcontractors lost their lives at our operationsduring the year. I express my personal andthe company’s condolences with thefamilies, friends and colleagues affected.

Following the merger, I havesucceeded Adam Fleming as non-executive chairman. I want to thank himand the other retiring directors from bothboards for the contribution they made tothe success of the companies, especiallyduring a time when the challenges ofgrowth were real. Our best wishesaccompany all of them in their futurebusiness endeavours.

Patrice Motsepe

The industry focus will be on findingreplacement ounces. Our pipeline of organicgrowth projects willensure oursustainability andfuture growth.

SECTION 2

CHIEF EXECUTIVE’SOVERVIEW2.1 PAGES 13-14

OVERVIEW OF THE YEAR2.2 PAGE 15

THE WORLD IS NOTICING2.3 PAGES 16-20

ORGANIC GROWTH2.4 PAGES 21-22

OUR CHANGING ENVIRONMENT2.5 PAGES 23-26

STRATEGIC INVESTMENTS2.6 PAGES 27-36

OPERATIONAL REVIEW

CONTENT

Harmony Annual Report 2003 012

SECTION 2

CHIEF EXECUTIVE’SOVERVIEWOperationally, it was a tough year. The inclusion of a full year’s results fromFree Gold resulted in a steady overall performance.

We embarked on significant organicgrowth projects. We have formulated avery clear battle plan which includes theimplementation of continuous operations at some of our mines.

IN OTHER WORDS

The highlightof the year was theconclusion of an agreementto merge ARMgold andHarmony.

SECTION 2CHIEF EXECUTIVE’S OVERVIEW

013

The past financial year was a watershedyear in Harmony’s history. Although nolarge acquisition was concluded in thefinancial reporting period, significantprogress was made when we incorporatedFree Gold and the Hill 50 assets. Post year-end, we concluded the merger withARMgold.

We have generated solid cashoperating profits (a record US$260 million)and invested these funds well in futuremining opportunities in South Africa,Russia, Australia and Papua New Guinea(PNG). In South Africa we approved arange of organic growth projects which willensure that Harmony will be mining inSouth Africa well into the future. We willbecome the largest producer of gold fromSouth Africa in 2003/04, producing some30% of the country’s gold. This is anexcellent achievement considering the factthat some eight years ago the companywas producing 580 000 marginal ouncesper annum or 3% from a single mine in theFree State province of South Africa.

As a responsible company operatingin South Africa, we have madeconsiderable progress in dealing with thecountry’s changing socio-politicalenvironment. The investments made in our

people and their communities and theparticipation of Black EconomicEmpowerment companies in past dealsconcluded, have positioned us well forfuture growth.

Probably the highlight of the year wasthe conclusion of an agreement to mergeARMgold and Harmony. Although thetransaction had been successfullyconcluded by the end of September 2003,the economic benefits will only be evidentin the last three quarters of the 2003/04financial year. This transaction positionsHarmony as the fifth-largest gold producerin the world, with the added benefit ofhaving the bulk of its production comingfrom South Africa. Together the companieshad acquired strategic stakes in bothAvmin and Avgold, before the conclusionof the merger agreement. The benefitsfrom these two investments will becomeevident as we participate in the next phaseof unlocking value in the South Africanmining industry.

Our management team has grown thecompany over the past eight years, from amarginal, lease-bound operation in theFree State to an international goldcompany which can claim to havedelivered value to all our stakeholders.

During this time we have relied on ouremployees to convert mature, loss-makingor marginal operations into profitable long-life mines. By remaining unhedged wenever tampered with shareholders’exposure to the volatility of the SouthAfrican Rand and the US Dollar price ofgold. This is a recipe which has served ourshareholders well and we will be looking totake advantage of further opportunities inthis respect.

Mainly due to the inclusion of a fullyear of production from our Free Gold JointVenture we achieved an increase of 12% inproduction, increasing from 2.7 millionounces to a record 3.0 million ounces. Thisalso was a period in which no additionalsignificant acquisitions were made andduring which continuous improvementssustained operational performance.

Continued economic and politicaluncertainty over the past year, as well as aweakening US Dollar, have seen a steadyrecovery in the US Dollar price of gold.

On average we realised a price ofUS$329/oz for the financial year, a 15%improvement over the US$287/oz reportedpreviously. The rising Dollar gold price isgreat news as it reflects interest frominvestors and speculators in gold as an

2.1 OVERVIEW OF THE YEARRecord cash operating profitfrom record production

3.03.54.04.55.05.56.06.57.07.58.08.59.09.5

10.010.511.011.512.012.5

3.03.54.04.55.05.56.06.57.07.58.08.59.09.510.010.511.011.512.012.5

Rand/US Dollar Exchange Rate1 January 1993 to September 2003

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

source I-Net Bridge; Deutsche Securities

Ran

d /

US

Dol

lar

exch

ang

e ra

te

Rand weakness allowed for stronggrowth in cash operating profits

Rand strength impacted oncash generating potential

Years

Harmony Annual Report 2003 014

graph 1

Year on Year Comparison

Production - kg 93 054 82 971 10 083 12

Production - oz 2 991 734 2 667 572 324 162 12

Revenue - R/kg 96 663 94 080 2 583 3

Revenue - US$/oz 329 287 42 15

Working costs - R/kg 71 146 62 848 (8 298) (13)

Working costs - US$/oz 242 192 (50) (26)

Cash operating

profit - R/m 2 374 2 591 (217) (8)

Cash operating

profit - US$/m 260 254 6 2

Earnings per share before

impairment (SA cents) 695 1 330 (635) (48)

Earnings per share after

impairment (SA cents) 359 1 094 (735) (67)

Average exchange

rate -R/US$ R9.13 R10.20 (R1.07) (10)

%VARIANCE

30 JUNE 2003

30 JUNE2002

ACTUAL VARIANCE

Our Five Year Scorecard

Gold produced - Kg 93 054 82 971 66 563 50 572 39 997

Gold produced - oz 2 991 734 2 667 572 2 140 043 1 625 925 1 285 931

Underground

recovery grade g/t 5.33 5.37 4.88 5.08 5.27

Cash operating profit

SA Rand - R’m 2 374 2 591 673 461 386

US$ - million 260 254 88 73 64

Cash operating cost

R/kg 71 146 62 848 57 416 50 121 46 759

Cash operating cost

R/tonne 234 227 224 213 240

Cash operating cost

US$/oz 242 192 234 246 240

JUN ‘03 JUN ‘02 JUN ‘01 JUN ‘00 JUN ‘99

table 1

table 2

alternative investment, hedging themselvesagainst the current uncertainty in worldmarkets. The price was also supported bythe current Dollar weakness, which hasalways been good for the gold price, andproducer de-hedging, which made someproducers net-consumers of gold. De-hedging is probably not sustainablebeyond the next few quarters. Thereafterthe main drivers of the price may be theUS Dollar and declining world production.

For Harmony the benefits from theincrease in the US Dollar gold price havebeen eroded by the strengthening of thevolatile South African Rand. During the2002 calender year it strengthened bysome 30% and was the strongest currencyin the world when measured against theDollar. see graph 1

The strong Rand adversely impactedon our working costs in US Dollar/ounceterms, which increased by 26% year onyear. However, our ability to control workingcosts is evident in Rand/tonne terms withcosts increasing by only 4% over theperiod. Although the Rand hasstrengthened to levels of R7.51 to theDollar by year-end, it is our expectationthat it will tend to depreciate towards theend of the new financial year.

Year on Year Comparisonsee table 1Whilst revenues increased by only 3% inR/kg terms, inflationary cost pressures andthe full incorporation of the higher costacquisitions of St Helena in South Africaand Hill 50 in Australia, eroded our margins.In Dollar terms we continued to generaterecord cash operating profits of US$260million compared to US$254 million for theprevious year. Higher interest paid andhigher amortisation charges resulted in lowerearnings before impairment at US$136million, compared to US$199 million for theprevious reporting period.

One of the main costs (±50%)associated with mining in South Africa islabour. During July 2003 we reached anagreement with our unions for a period of twoyears. For the first year a wage increase of10% was agreed to and for the second yearthe increase will be 2% above inflation (CPIX)with a guaranteed minimum of 7%.

The agreement also allows for a verynecessary re-grading of some of theemployee categories - e.g. operators whichcould result in additional cost increases. Theagreement has also removed some of thelast historically discriminatory practices withregards to leave and provision for retirement

benefits. The issue of housing foremployees, as provided for in the MiningCharter, was also captured in a bi-lateralagreement. The non-wage issues will add anadditional 2% to the wage bill of Harmony.

Our Five-Year Scorecard see table 2Harmony has over the past five yearscreated value through a strategy ofacquiring and subsequently turning aroundhigher-cost, lower-margin operations. Thebulk of these 23 acquisitions were madeduring a declining Dollar gold priceenvironment.

Despite these adverse conditions, ourshareholders have been rewarded with theappreciation of their investment, both interms of capital growth and cash dividends.

The difference made through theimplementation of the “Harmony Way” is asignificant and sustainable reduction in theworking cost structures of the acquiredmines. This typically results in an immediateincrease in profit margin and operatingprofits. Our challenge remains to keepworking cost increases lower than that of ourpeer group and below the South Africaninflation rate, thereby sustaining ourcompetitive advantage.

Shareholder Distribution by Country

36%

45%

8%

4%7%

36% South Africa and unknown

45% North America

8% United Kingdom

4% Switzerland

7% Rest of Europe

Year on year the liquidity of our stockincreased from 410% to 448%, making itone of the most traded gold stocks globally.The average issued share capital of thecompany increased from 153.5 millionshares to 178.0 million shares over thesame period.

The company’s presence in NorthAmerica continues to grow with more than51% of our stock trading on the New YorkStock Exchange.

Only 39% of the company’s stocktrades on the JSE Securities Exchange inSouth Africa, whilst the remainder is tradedon various exchanges in Europe. Moredetailed information on the company’sliquidity is available in the Investor Relationssection on page 150 of this report.

Inclusion in MSCI Emerging Markets IndexOn 30 May 2003, the MSCI announced thefirst annual review of its indices. TheEmerging Market Index includes 160companies from 27 countries.

Only 17 companies from South Africaare included, of which Harmony comprises0.4% of the index. We have been included in the fund on the basis of ourmarket capitalisation and in recognition ofour offshore liquidity, both of which make the stock attractive to tracker fundinvestors.

Harmony makes the top ten againand again and againHarmony was rated in 7th position in theFinancial Mail’s Top Companies Awards2003. We were the only company in SouthAfrica to be ranked amongst the Top TenCompanies over a one-year, five-year andten-year period in the annual Sunday TimesTop Companies ranking.

During the year we received theBusiness Map Foundation EmpowermentAward and our Investor Relations teamreceived the Investment Analyst Society’stop award in the mining and resourcescategory.

015

Through theacquisition of34.5% of Avminand 11.5% ofAvgold, wehave increasedyour exposureto leveragedSA goldproduction.

2.2 THE WORLD IS NOTICINGThe world’s most liquid gold stock

chart 1

Harmony Annual Report 2003 016

Being anunhedgedproducer, wecannot influencethe price wereceive for ourgold. Thereforeour ability tomanage workingcost remains ourcompetitiveadvantage.

2.3 ORGANIC GROWTH

A range of capital projects was approvedand embarked upon during the year.Organic growth opportunities also existwithin our current operations which do notrequire any capital expenditure. Some ofthem are:� exploiting the potential of our greatest

asset, our employees. Harmony hasconsistently achieved productivity andefficiency improvements over the pastfew years. The process of empoweringour people has further potential toimpact positively on our performance.Through continued productivityimprovements, we can afford to givereal wage increases to our workforceand achieve a reduction in the unitcost of labour in real terms. In thisannual report we give you a feel forsome of the exciting transformationalissues we are dealing with through theeyes of ten of our employees.

We are doing pioneering work interms of communication with ourpeople. The objective of internal

communication within Harmony is tokeep all employees informed of thecompany’s direction, createunderstanding about where we’reheading strategically and show whereeach employee fits into the bigpicture. By providing information andcreating understanding, internalcommunication functions as a vehicleto improve motivation levels andultimately productivity. Everyemployee should understand how andwhere he could make a difference.

We segment our internal market ofemployees and develop appropriatemessages and media channels toappeal to each segment’s motivationaltriggers. We use a variety of differentchannels to reach different audiencesegments effectively.

The Harmony Way Manual (a cartoonhandbook which captures the essenceof the Harmony Way), which wassuccessfully targeted at our South

African supervisors and technicalmanagement last year, was followed upwith a route map of Harmony’s historyand the strategic direction goingforward. This route map is a cartoonvisual, which is debated and discussedin small groups throughout the technicalmanagement and supervisory levels.

Woza Nazo, our full-time communicationgroup drawn from within our workforce,has continued its successful trajectory.Research conducted among theworkforce has shown that 72% agreethat Woza Nazo helps them betterunderstand Harmony and provideinformation that helps them to do abetter job.

The internal roadshow whereby I meetwith all shaft and plant teams everyquarter has become, and will continueto be, a vital ingredient of thecommunication mix.

017

Looking ahead, we will take theconcept of internal marketing furtherthan ever before by appointing clientsegment champions. Each internalsegment (i.e. business managementlevel; technical management level;supervisory level and workforce) willhave a dedicated member or membersof the executive who will beresponsible for “marketing” thecompany to it – i.e. understanding theissues of that segment and integratingand making sense of companyinitiatives specific to that segment. An essential component of creating anenabling environment where all ourteams can perform at world-classlevels, is to develop a world-classservice culture – one which can servicethe teams at the face. This is what wecall “Service the Harmony Way”. Inorder to facilitate this we haveanalysed, simplified and reconstructedall pivotal service delivery mechanisms.We have separated service from controlfunctions and worked at creating aservice attitude and culture which iscloser to a retail model of serviceexcellence than the military style whichhas prevailed in the mining industry forthe past hundred years.

� “sweating our assets” includes allactivities related to optimising ourcurrent operations. ContinuousOperations (CONOPS) could see theproductivity of the capital assets onsome of the operations increasesignificantly. With CONOPS weincrease the number of productionshifts by as much as 25%. We hope toextend the agreements we reachedwith the unions at the Free Gold andARMgold shafts on CONOPS to ourother operations. Implementedcorrectly, CONOPS could result in anincrease in volume, a marginalreduction in cost, significant jobcreation and higher profits.

� remaining “cost obsessed”: throughinitiatives like the “Cost Marathon”, wewere able to restrict our costincreases, measured in R/kg terms, toonly 13% compared to the previousfinancial year. This occurred despitethe impact of a high inflationenvironment and the adverse effect ofacquiring and incorporating high-cost,low-margin operations in South Africaand Australia. Cost focus and costefficiency have always been ourstrengths. When measured inRand/tonne terms, working costs

increased by a mere 3% from R227per tonne to R234 per tonne.

� extending the application of theHarmony Value Creation Model, thebusiness model on which oursuccessful acquisition strategy hasbeen built, provides us withalternatives once the assets are fullyvalued. The investment environment inthe past year has allowed us toproceed with a range of organicgrowth projects which will add valueto our assets for years to come. see diagram 1

Whilst other producers in the industry facethe challenge of finding adequatereserves to replace the ounces mined, wehave, through a range of investments,ensured that we have sufficient high-quality replacement ounces, therebysecuring our long-term future.

Let us reflect on how successful ouracquisition and turnaround strategy hasbeen. see table 3

The progress on Free Gold onlyincludes the 50% attributable as at 30 June2003. Following the completion of themerger at the end of September 2003, itwas 100% owned by Harmony. Weanticipate complete payback of our

diagram 1

St Helena

Free Gold

Elandskraal

Masimong

Randfontein

Evander

Orkney

Free State

ValueCreationthroughmarginincreases

Win-windealmaking

Time in quarters

1 4 9

Restructurefor optimalreturn phase

Full valuephase –continuedimprovements

Restruct-uringphase

High impactinitial trans-formationphase

Harmony Value Creation Curve

InitialValue

PurchasePrice

Full value alternativesExpansionFurther operationalimprovementsOwn as an annuitySell and re-invest

Harmony Annual Report 2003 018

Return on Investments as at June 2003

Evander - June '98 R 415 R 1 274 10 quarters

Randfontein - Jan '00 R 750 R 1 735 8 quarters

Elandskraal - Apr '01 R 988 R 662 Building a

new mine

Free Gold (50%) - Dec '01 R 1 350 R 1 157 +/-8 quarters

PROJECT/OPERATION ACQUISITIONCOST (R'm)

CASH OPERATINGPROFIT TO DATE

(R'm)

PAYBACKACHIEVED

Our Assets

Harmony Evander Masimong Tshepong Morobe/Wafi

North

Joel Kalgold Elandskraal Phakisa Poplar

Rest of Free Gold Randfontein Tshepong Doornkop Rolspruit

St Helena Highland Bambanani Target Kalplats

Gold (31%) * (26%) *

Australian Operations Bendigo

(32%) *

Orkney Shafts 9.8% of

Aurion

(onsold)

* As with all our strategic investments our continued involvement with these projects will dependon our assessment of whether we can add additional value to such an investment

MARGINALOUNCES

QUALITYOUNCES

LONG LIFEQUALITYOUNCES

PROJECTGROWTHOUNCES

POTENTIALPROJECTS

table 4

table 3

investment in Free Gold by December2003, making it one of the most successfulacquisitions to date.

The progress of the company fromsurvival in 1995/96, the subsequentgrowth through acquisitions and currentfocus on long-life, quality, low-costproduction ounces in 2002/03 hasresulted in a spectacular portfolio ofassets. see table 4

Capital ProjectsDuring the past few quarters we approvedthe organic growth projects atRandfontein (Doornkop South ReefProject) and Free Gold (Tshepong NorthDecline Project and the development ofPhakisa Shaft). Questions have been putto us as to whether our growth strategy,which has so successfully built thecompany to the fifth largest in the worldtoday, has changed? Have we stoppedacquiring assets and are we now focusingon building mines?

The answer is that our strategy hasnever been an either/or approach. Webelieve that there will be furtherturnaround opportunities for acquisition inSouth Africa, which will deliver similarvalue upliftment to what we haveexperienced in the past. We do, however,

also own most of the next generation ofmines to be built in South Africa. We havethe skills and balance sheet to buildmines and we believe in the future of goldas a product and South Africa as aninvestment destination.

Included in the acquisition ofRandfontein in January 2000, Elandskraalin April 2001 and Free Gold in December2001, was a number of highly prospectiveprojects at zero cost. On acquisition ofthese assets our focus was to achieve anoperational turnaround as quickly aspossible. During the low gold pricescenario and with high working costs atthe time of acquisition, the project areas,although financially evaluated, providedinsufficient returns on the requiredinvestment.

After successfully restructuring theacquired operations for profitability andunder a current higher gold pricescenario, the projects were revisited.When compared to other availableacquisition opportunities or other growthprojects in the company, the approvedprojects delivered greater returns to allstakeholders and in each case a decisionwas taken to proceed.

The capital projects currently underway in Harmony are all brownfield projects.

This results in relatively low capitalrequirements which have been structuredtax-efficiently as part of the existingoperations. The geological and technicalrisks are also well understood.

All the projects depicted are discussedin detail under the relevant operations inthe operational overview section. seegraph 3

Ten years into the future Harmony willbe the owner and operator of many of thelarger mining projects still around in SouthAfrica. We do not anticipate relinquishing,in the near future, the position of beingSouth Africa’s largest gold producer, whichwe will became during the first half of the2004 financial year.

We foresee underground recoverygrade to increase incrementally from 5.33 g/t for the 2002/03 financial year to inexcess of 6.0 g/t by 2009 under a givenset of gold price and currencyassumptions. Whilst there will be moreacquisition opportunities in South Africa,especially if the Rand remains strong, thelong-term future of Harmony in South Africahas been secured through thedevelopment of these long-life, qualityproduction ounces.

Harmony Project Production Profile

18001600140012001000800600400200

0

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Tshepong North Decline (-66 level)

Doornkop South Reef

Nyala

Masimong Expansion

Elandsrand

Phakisa Shaft

Recovery grade will incrementally increase from 5.3 g/t to above 6.0 g/t by 2009

Oun

ces

(mill

ions

)

Years

graph 3

019

Merging ARMgold and Harmony tocreate South Africa’s largest goldproducerOn 2 May 2003, the two companiesannounced details of a proposal to createa world-class unhedged gold producer,with the bulk of its production from SouthAfrica.

The merger creates the fifth largestgold producer in the world, producingapproximately 4.0 million ounces perannum. The transaction was effected bythe issue of two Harmony shares for everythree ARMgold shares held.Approximately 63.67 million Harmonyshares were issued after year-end, whichincreased the company’s outstandingshares to 257.8 million.

Post-merger, the aggregate number ofHarmony shares issued to ARMgoldrepresented 26% of the enlarged issuedshare capital of the merged company.African Rainbow Minerals and Exploration

Investments (Pty) Ltd (ARMI), representedby Patrice Motsepe, Harmony’s new non-executive chairman, became our largestshareholder, holding approximately 14% ofthe company at the time.

We are excited and look forward toincorporating the assets into the newHarmony. This transaction has as its focusnot only BEE compliance or short-termoperational synergies, but also creates along-term value proposition to ourshareholders.

Operational synergies at thecombined Free State operations, will addsome R10.0 million per month to thebottom line. see map 1

In addition, the growth projects atFree Gold, i.e. Tshepong North Declineand Phakisa Shaft, will optimise our futurecash-generating ability.

Our risk profile has diminishedsignificantly as the company now hasoperating mines in all the major gold-

producing regions in South Africa. Thishas the added benefit that we are wellpositioned to increase our production fromfurther acquisitions, as we have anestablished foothold in these gold-producing regions. see chart 2

Acquiring a 34.5% stake in AvminOn 2 May 2003, Harmony and ARMgoldannounced details of our 50/50 jointacquisition of a 34.5% stake in AnglovaalMining Limited (Avmin). Based on R43.50per share, the transaction was valued atR1 687 million and was paid for in cash.

Avmin, which has a marketcapitalisation of approximately R4.9 billion(at a share price of R43.50), holds sharesin and manages the following companies:� Gold - Avgold Limited - 42.7%� Manganese and Iron Ore - Assmang

Limited - 50.3% and Assore - 9.3%� Nickel - Nkomati Mine - 75.0%� Platinum - Two Rivers Project - 55%

map 1

New Harmony

Avgold (Harmony 26,1%)

President Steyn

Gold Fields

Various Mineral rights

The Free State Goldfields

South Africa

Target North

Unisel

Oryx

Beatrix

Joel

Harmony

Bambanani

St. Helena

Brand ShaftsPresident SteynMasimong

Welkom Operations

Matjhabeng

Tshepong

President Steyn

Jeanette

Target

Forecast Gold Production2003/2004

18%

30%

10%

12%

10%

9%

2%

9%

18% Free State

30% Free Gold

10% Evander

12% Randfontein

10% Elandskraal

9% Offshore

2% Kalgold

9% Orkney

Harmony Annual Report 2003 020

chart 2

table 5

Gold price per kg R93 000 R95 000 (2)

Total resources including project ounces (Moz) 410.2 295.9 39

Reserve base (Moz) 61.9 49.1 26

%VARIANCE

ORE RESERVESAS AT:

30 JUNE2003

30 JUNE2002

The rationale for the acquisition wasthat the merged Harmony would own aneffective strategic investment of 14.6% inAvgold which operates the new Target goldmine. Target holds 3.9 million ounces ofreserves and an extensive unexploited goldresource totalling some 75 million ounces inthe Northern Free State.

The acquisition of the stake in Avmingave us exposure to this resource andallowed us to participate in unlocking valuein both Avmin and Avgold.

On 15 July 2003, we announced thatwe had acquired an 11.5% stake in Avgold(at R7.91 per share) from Anglo South AfricaCapital (Pty) Ltd, thereby raising oureffective exposure to 26.1%. The companyissued 6 960 964 new ordinary shares,comprising 3.8% of the issued share capitalof Harmony, as consideration.

Target is different to typical labour-intensive mining companies in South Africaas it makes use of a high degree ofmechanisation in the exploitation of the

massive orebody. At full production, themine will produce approximately 350 000ounces of gold per annum at a cash cost ofbelow US$180 per ounce. The Target minehas a life of approximately 18 years.

Immediately adjacent to Target, Avgoldhas been busy with an extensive explorationprogramme on an area known as TargetNorth. This project is in pre-feasibility stageand current estimates show indicatedresources of 24.5 million ounces and anadditional inferred resource of 35.1 millionounces. The area has one of the world’slargest unmined deposits. It contains aseries of gold-enriched depositional fans atan average depth of 2 500m below surfaceand roughly 2 - 3km apart.

Harmony ore reserves increase by 26%Despite using a marginally lower gold priceof R93 000/kg, the company has seengrowth of 26% in its ore reserves followingthe merger. Total resources have increasedby 39% to 410.2 million ounces. For a year

on year comparison of reserves andresources see table 5.

The main difference is the inclusion ofthe other 50% of the Free Gold reserves andthe remainder of ARMgold’s reserves.Excluding ARMgold, our reserves haveincreased by 1 million ounces or 2%,indicating that we more than replaced the 3 million ounces mined in the past year. Thisis despite using a lower gold price in R/kgterms for this declaration. Although thecompany’s resource base in Australiaremains at 11 million ounces, reserves havedecreased from 2.34 million ounces to 1.5 million ounces, necessitating a write-down in the carry value of the assets byA$155 million to A$623 million.

The merged Harmony now owns thelargest gold resource base in the world,allowing it flexibility and even more leverageor optionality to the US Dollar gold price.

Includes 100% of ARMgold and Free Gold

021

The long awaited and much debated MiningCharter for the South African industry wasreleased on 9 October 2002. We believethat whilst the Charter prescribes some verydemanding conditions, the company is wellpositioned to meet them well ahead of thetargeted date in five years’ time.

The Charter has the following broadobjectives:� to expand opportunities for Historically

Disadvantaged South Africans (HDSAs)to enter the mining and mineralsindustry or benefit from the exploitationof the country’s mineral resources;

� to ensure that the relevant skills whichare required for entry into the miningsector by HDSAs, are transferred; and

� to ensure progress in employmentequity in the mining industry.

In addition, the Charter includes thefollowing specific objectives which will bemeasured using a scorecard system:� about 15% or R100 billion

(US$10 billion) worth of assets will beowned by Black companies within fiveyears, with an additional 11% beingachieved in the following five years;

� industry has undertaken to assist HDSAsin securing finance to fund participation,i.e. an amount of R100 billion within thefirst five years only;

� a baseline of 40% in respect ofemployment equity in junior and seniormanagement levels of the industry;

� companies undertake to offer everyemployee the opportunity to become

functionally literate and numerate by2005;

� stakeholders undertake to give HDSAspreferred supplier status;

� mining companies agree to identify theircurrent levels of beneficiation andindicate to what extent they intend togrow the baseline.

The measuring of success of ownershipwould be determined by:� attributable units of South African

production controlled by HDSA’s;� an allowance to be built in to allow for

credit offsets to allow for flexibility;� previous empowerment deals to be

included in calculating credits; and� government are considering special

incentives to encourage HDSA’s toretain newly acquired equity for areasonable period.

Companies undertake to report on anannual basis their progress towardsachieving their commitments through theirannual reports, to be verified by externalauditors.

We have dealt with our progress onsome of these issues in the SustainabilityReport, page 53-62.

Finalising the Charter through aprocess of negotiations which includedrepresentatives from the mining industry,government and the unions, has removedmost of the uncertainty which followed theleaking of a draft document in July 2002.

Harmony has demonstrated that the

ownership requirements of the Charter areachievable through our involvement in foursuccessful empowerment deals. In allinstances, the deals did not result in adilution of value to shareholders, but ratherfacilitated our continued growth during thattime.

Our most recent deal was theDoornkop South Reef Project atRandfontein. Effective 15 August 2003,Africa Vanguard Resources (AVR), a BlackEconomic Empowerment company,acquired 26% of the project for R250 million. In terms of the saleagreement, AVR acquired 26% of theDoornkop mineral rights, and paymentamounted to R140 million in cash andR110 million in call options on 290 000ounces of gold. (The 290 000 ounces ofgold being equal to 16% of gold producedat Doornkop during the first 10 years).

The project will be managed as a jointventure in which Randfontein will fund allthe project capital. The proceeds from theproject will be shared in a proportion of84% to Randfontein and 16% to AfricaVanguard Resources.

We are, in consultation with theNational Department of Minerals andEnergy, currently in the process of devel-oping a sophisticated approach to settingtargets and measure performance in BEEand transformation initiatives withinHarmony. We refer to this initiative as the“Harmony Transformation Scorecard” andwe shall describe the methodology in moredetail in the 2004 Annual Report.

2.4 OUR CHANGING ENVIRONMENTThe release of the Broad Based Socio-Economic Empowerment Charter for theSouth African Mining Industry

We have completedfour successfulempowermenttransactions to date. We believe that we are compliant with the equity ownershipcomponent of theMining Charter.

Harmony Annual Report 2003 022

In essence, it will provide clarity on the“measures” of empowerment and transfor-mation contained in the Mining Charter,but, at the same time, will enable Harmonyto set targets, plan initiatives and measureprogress on an integrated strategy fortransformation within the company over thenext ten years.

The “Harmony TransformationScorecard” will seek to address all transfor-mation initiatives (including initiatives suchas job creation and HIV/AIDS programsthat are not necessarily included in theCharter), and will seek to evaluateprogress on the three fundamental objec-tives underlying transformation:� developing people - skills develop-

ment, training and job opportunities;� stimulating economic participation –

job creation, equity ownership, jointventures, procurement opportunities,beneficiation opportunities; and

� positively impacting society and peo-ple’s welfare – living standards, ruraland community development, housing,migrant labour, environmental sustain-ability, health (including HIV), safety.

These three transformation objectivesare consistent with leading internationalthinking on development, and will applyboth to the way we address the “internal”or operational facets of the business (e.g.developing and empowering employees)and the manner in which we positively ben-efit our “external” environment (e.g. adja-cent communities).

The “Harmony Transformation

Scorecard” will enable key headline meas-ures of progress to be reported to share-holders and other stakeholders, while moredetailed internal targets and measures willbe used by management to ensure con-stant progress in transformation. It willensure consistency and compliance withthe scoring approach to be used byGovernment in assessing mineral rights’conversions in terms of the new Mineraland Petroleum Resources DevelopmentAct.

For example, we report progress onthe second key objective of transformation,namely “Stimulating EconomicParticipation”, on the basis of “equivalentempowered gold ounces of production”.Table 6 provides an illustrative calculationfor Harmony’s four past BEE transactions,indicating that transformation has alreadybeen achieved for 24% of production, thisbeing well in excess of the Charter’srequirement of 15% within five years. (Notethat table 6 excludes the positive impact ofprocurement, beneficiation, job creationand other related initiatives.)

It is in the understanding of the interde-pendence of these activities that we canidentify cost-effective opportunities toensure compliance. The successful trans-formation of the South African society andour mining industry will have significantlypositive benefits for Harmony.

In short, broader economic participa-tion will assist in normalising our society,increasing the country’s economic baseand, over time, reducing the country’s riskrating. Developing our people is already

paying spectacular dividends in higher pro-ductivity and the availability of adequateskills to sustain our growth.

Mineral and Petroleum Royalty BillOn 20 March 2003, the South AfricanGovernment released the draft Mineral andPetroleum Royalty Bill.

The Royalty Bill proposes to impose aquarterly royalty charge of 3% on revenue.The Bill’s underlying principle is that thecountry is entitled to a consideration/royaltyfor the extraction of its non-renewablemineral resources.

We are of the opinion that any royaltyimposed at revenue level will impactconsiderably on our financial results and thecost of mining in South Africa. By increasingour cost structure millions of tonnes of orewill be sterilised.

The Bill was submitted for publiccomment until 30 April 2003, whereafter itwas referred back to parliament. We madea submission to the treasury departmentand currently await government’s revisedposition.

The uncertainty caused by these andother regulatory changes highlights theneed for us to proactively engagegovernment on all legal, fiscal andenvironmental issues.

Harmony’s progress on Transformation: Empowered ounces ofproduction

Sale of 10% of Elandskraal to 36 000 10% of 360 000oz produced by

Khuma Bathong Elandskraal in 2003

Simane purchase of equity in 194 000 6.4% (original holding of Simane)

Harmony of Harmony’s total ounces of

production for 2003 )

Sale of 26% of mineral rights at 85 000 26% (AVR’s share) multiplied by

Doornkop to AVR the 330 000oz Doornkop is

expected to produce at full

production

Harmony/ARMgold merger 560 000 14% (shares in the merged

Harmony entity which will be held

by ARM Investments)

Total “equivalent empowered 875 000 Note that “equivalent empowered

gold ounces of production” ounces” reflects historical

transactions and not only current

BEE holdings

Total ounces of South African 3 600 000 Total South African production of

gold production of the merged Harmony for 2004

Harmony

Equivalent BEE Ounces as a % 24%

EQUIVALENTEMPOWERED

GOLD OUNCES OFPRODUCTION

CALCULATION NOTESBEE TRANSACTION

table 6

023

Abelle Limited – Exploration success On 26 February 2003 we made an offer tosubscribe for new shares as well as apublic offer for the ordinary shares andoptions in Abelle. The offer closed on 26 March 2003. We now own 87% of theshares and 68% of the listed options inAbelle. The total consideration payablewas A$151 million or US$98 million. On 30 June 2003, at a share price of A$1.10 pershare, our investment was valued at US$127million.

Through this and other investments overthe past few years, we have establishedaccess and exposure to world-classdeposits. Our bid values Morobe and Wafi,which are two of the largest undevelopedgold deposits in the world, at US$8.00 perresource ounce.

Identified Mineral Resources (IMR)estimates of the Morobe Project total 73.9million tonnes at 2.2 g/t gold and 30 g/t silverfor a combined 5.2 million ounces of goldand 71 million ounces of silver. The project isnow 100% owned by Abelle.

The Morobe ore is free milling and cashoperating costs were estimated at US$175per ounce. A feasibility study completed byLycopodium of Australia in October 2002,envisaged a single open pit mine containing2.8 million ounces of gold and 48 millionounces of silver.

Morobe is capable of producing 300 000 ounces of gold and 4.5 millionounces of silver per annum from a 5 milliontonne per annum processing plant for aperiod of approximately eight years.

A new feasibility study, which envisagesmining lower tonnage at higher grades withsubstantially reduced capital and operationalcosts, is currently being undertaken and willbe presented to the Abelle board byDecember 2003.

Abelle also owns the Wafi Projectsituated 60 km from Morobe. The project is inan advanced exploration stage, with a furtherphase of 5 000m of diamond drilling underway. Wafi consists of two large orebodies,approximately 1 km apart. One is asubstantial porphyry copper-gold deposit(“Golpu”) with a total identified IMR estimate

of 100 million tonnes at 1.3% copper and0.6 g/t gold. A pre-feasibility on the Golpuporphyry copper-gold project (inferredresources 2.3 million ounces gold; 1.27million tonnes copper) has commenced.

The other is a potentially world-classgold discovery which is known as the LinkZone orebody. The drilling programme atWafi which commenced in February 2003 isfocused on infill drilling (from 100m by 50mgrid down to 50m grid) and on extendingthe higher grade Link Zone orebody. For thefirst phase of the drilling programme 12holes have been planned of which fourholes have been completed.

The holes from which assay resultshave been received include the followingintersections:

Borehole No.WR177 159m @ 6.53 g/t from 275mWR178 71m @ 8.42 g/t from 316m

17m @ 5.25 g/t from 410m15m @ 9.34g/t from 454m

WR179 174m @ 4.03 g/t from 192m

Messrs Grobicki, Abbott and myselfhave been nominated to the board withmyself taking over the chairmanship.

The acquisition of Abelle Limited is inline with our strategy of creating asignificant gold business in Australasia. Inaddition to our current producing assets,we now have significant interests in threehigh-quality, prospective growth projects inBendigo, Morobe and Wafi.

Bendigo – decision timeThe 32% stake which Harmony acquiredon 14 December 2001, at a cost of A$50 million, was valued at A$55 million on30 June 2003.

The major activities during the 2002/03evaluation programme included thedevelopment of a production size declineto access several orebodies that hadpreviously been defined by drilling, and tomine and process approximately 60 000tonnes of ore. The objective was toestablish orebody shapes, grades andmining methods to determine metallurgical

processing parameters.In a briefing by the company earlier in

the year, it was indicated that the SwanDecline had reached a depth of 770mbelow surface, and had accessed the firstfour reefs in the 12.3 million ounce potentialresource. A further five reefs were evaluatedby August 2003. The current on-reefdevelopment and bulk sampling programmeis designed to convert the previouslyidentified Inferred Resources into Reserves.

Bendigo’s management is refining aconceptual plan which indicates a three-stage build-up to full production over four tofive years. Subject to the successfulestablishment of reserves during the bulksampling and evaluation programme, theplan envisages the following stages: � Stage 1 – 300 000 tonnes per annum to

produce approximately 100 000 ouncesper annum. Capital of A$50 to A$60million is estimated to be required tostart up the mine plan;

� Stage 2 – after a two to three-yearperiod, production is anticipated toincrease to 250 000 ounces for twoyears;

� Stage 3 – production increasing to over400 000 ounces per annum.

The biggest uncertainty remaining iswhether the planned tonnages could beachieved and then scaled up withoutsignificantly reducing the recovery grades.

The development, drilling andevaluation programme to access the 17previously identified orebodies in theSheepshead and Deborah reefs progressedwell during the June 2003 quarter.

The study to determine costs toconstruct the mine, mill and associatedinfrastructure is well advanced.

The combination of sampling andmining studies have to date provided aresource of 130 000 ounces and have atarget to prove in excess of 200 000ounces of reserves by the December 2003quarter. It is envisaged that the Bendigoboard will soon consider its options withregard to the construction of a mine.

2.5 STRATEGIC INVESTMENTS

Harmony Annual Report 2003 024

High River Gold –exposure to RussiaWe own approximately 17% of High RiverGold (TSA:HRG), a Toronto-basedcompany with gold interests in Russia,Canada and West Africa.

The total purchase considerationamounted to R141 million (US$14.5million) which represented a 16% discounton the weighted average share price forthe 30-day trading period prior to theexecution of the agreement. Following asignificant rise in the High River shareprice, our investment was valued atapproximately US$22 million on 30 June2003.

The principle assets of High RiverGold are:� a 56% equity interest in OJSC

Buryatzoloto, the fifth-largest goldproducer in Russia, with twooperating mines producingapproximately 150 000 ounces peryear;

� a 100% interest in the BerezitovoyeProject which is a deposit amenableto low-cost open-pit mining;

� a 50% interest and joint operatorshipof the New Britannia gold minesituated in Manitoba Canada,producing approximately 110 000ounces per year; and

� an 80% interest in the Taparko goldproject in Burkino Faso which has agold resource of approximately 1 million ounces.

Highland Gold Limited –production ounces from RussiaOn 18 December 2002, Highland GoldLimited successfully listed on AIM(“Alternative Investment Market of LondonStock Exchange plc”).

Highland Gold is the owner ofMnogovershinoe (“MNV”), Russia’s fourth-largest producing gold mine in 2001, aswell as two development projects –Darasun and Novoshirokinskoye – whichtogether comprise four gold deposits.

In 2002 MNV had proven andprobable reserves of 2.3 million ounces.

Measured, indicated and inferredresources total 3.0 million ounces of gold.Of the above 31.7% is for our account.

Highland Gold believes that theabundance of natural resources and therecent positive developments in theRussian gold industry will provide anopportunity for the company to establish aportfolio of Russian gold projects.

The acquisition of a 32.5% stake atUS$18.9m in Highland Gold on 31 May 2002 and a subsequentinvestment of US$7.5 million, allowed for apromising entry point for Harmony into there-emerging Russian gold sector. Our totalinvestment of US$26.6 million was valuedat approximately US$128 million on 30 June 2003.

For the 2002 calendar year, HighlandGold produced 178 000 ounces at cashand total costs of US$145/oz andUS$179/oz respectively. For the next sixmonths ending June 2003, the companyproduced 90 133 ounces at cash andtotal costs of US$174/oz and US$221/ozrespectively.

Unless we can increase our exposureat asset, company or board level to that ofsignificant influence or control, in both thecases of High River Gold and HighlandGold Limited, we may be required by theSouth African exchange control rules todispose of this stake during the comingyear.

Kalplats – our platinum discovery Work on our platinum discovery continuedwith some R45 million so far being spenton exploration, the excavation of theKalplats box-cut, bulk sample collectionand pilot plant flotation tests. The box-cutinvolved excavating 1.5 million tonnes ofwaste rock. A 500 tonne ore sample wascollected at a depth of approximately 45mbelow surface with sampling of the variousreefs under different weathering conditionsas the pit advanced.

Using a US$450/oz basket for PGM’sand R8.00 to the US Dollar, and using atwo-stage mill with float concentrator, weanticipate the following results:

Tonnes milled 150 000 tonnesCapex R260 millionPlant costs R45/tonneRecovery 75%Recovered value R215/tonne

Recoveries of 73% – 75% andconcentrate grade above 100 g/t PGMwere achieved with a two-stage floatconcentrator. Laboratory scale testwork atMintek on the recovered core samplescontinues. Based on the outcome of thesetests we will take a decision on the miningof the orebody and whether any furtheractivities will be undertaken to enhance ourunderstanding and valuation of the fivedemarcated orebodies.

Expenditure is focused on thecompletion of the drilling programme toupdate ore resource calculations andorebody models on the Crater and Orionorebodies. Work on preliminary minedesigns and on pit optimisation continues.It is anticipated that the work will becompleted by the end of September 2003.Phase 2, which will culminate in thecompletion of a full feasibility study, isexpected to be completed six monthsthereafter.

Making good money out of a strategic investmentThe company’s acquisition during February2000 of a 21% stake in Goldfields Limitedof Australia at a cost of R165 million, is agood example of making excellent returnsfrom strategic investments. South Africanexchange rate constraints at the timeresulted in the cost and funding ofacquiring 100% of Goldfields Limited ofAustralia being beyond Harmony’s reach.The additional R60 million investment byHarmony, and subsequent merger ofGoldfields with Delta and its acquisition byPlacer Dome, saw the value of our initialR225 million investment increase toR855 million. During the year the companyannounced that it had disposed of thisasset, realising approximately US$85million.

When I think of where we came from andwhere we’re heading to, the change hasbeen remarkable.”

“

Is the lid important on an automatic kettle? It can’t make the kettleboil – the element will. But take the lid off and the kettle will boil out.Engineering is the lid – it’s a service. I was involved in redesigningthe bridge of change – to create ownership. Now I’m running theengineering side of the changes.

Providing quality service means separating service and control.But the old mining culture of control means it’s difficult to make thatchange. People have to understand that the ultimate client on themine is the team at the face. But that doesn’t mean your role is notas important.

Gold mining is all about people. Attitude plays a bigger role thanskill and knowledge itself. I’ve seen people who I thought wouldnever change. Then they tasted it. And now there’s no stopping them.Change touches the comfort zones – but change brings opportunities.

Some ask when it will stop. They still see change as an event. It’snot. It’s like the baton in a relay: the race doesn’t stop when you handit over. If we take a step back people see it as failure. It’s not. It’s aprocess – and sometimes it’s necessary to realign, put systems inplace – and move forward.

When I think of where we came from and where we’re heading to,the change has been remarkable. We’re doing all the right things,but still not doing all things right. My day would be empty if therewasn’t a challenge. I’d like to stay part of the change.

NameJohan HennopTime at Harmony25 yearsWorks atFree StateStarted asElectricalApprenticePosition todayEngineer,Coordinator ETHW(Engineering TheHarmony Way)

TEN PEOPLE. ONE STORTEN PEOPLE. ONE STORYY..

027

SafetyOn behalf of the board, we would like toextend our sincere condolences to thefamilies, friends and colleagues of the 26employees who lost their lives at ouroperations during the past year.

The lost time injury frequency rate(LTIFR) showed a regression of 3.5% and thefatal injury frequency rate (FIFR) per millionman-hours worked improved by 19%. Ourtarget for LTIFR for the financial year ending30 June 2003 was 20 and for FIFR a rate ofzero. We continue to aim for these targets inthe coming year. see table 1

Total Injury / Accident

Frequent Rate (TIAFR) - 54.72 59.29 7.71

Lost Time Injury

Frequency Rate* (LTIFR) 20.00 24.61 23.78 (3.49)

Shifts Lost Frequency

Rate* (SLFR) 340 421.33 430 2.09

Fall of Ground Incident

Frequency Rate* (FOGIFR) 6.00 7.79 8.86 12.08

Fatality Injury Frequency

Rate* (FIFR) 0.00 0.30 0.37 18.92

* Measured in per million man-hours worked

%CHANGE

OBJECTIVE 2002 /2003

2001 /2002

INDICATOR

Operations June 2003 June 2002 Variance

Free State 364 478 (114)

Evander 272 468 (196)

Randfontein 525 615 (90)

Elandskraal 186 415 (229)

Kalgold 74 49 25

Australian Operations 284 79 205

Sub-total 1 705 2 104 (399)

Free Gold (50%) 669 487 182

Total 2 374 2 591 (217)

TOTAL CASH OPERATING PROFIT (R’MILLION)

table 1

The main areas of incident severityremain fall of ground (50%) and trucks andtramways (15%). Since safetytransformation has been introduced therehas been an improvement in fall of groundsafety awareness. Increased training andcommunication have also improved theidentification and assessment of risk. Webelieve that our rates compare favourablywith the rest of the underground miningindustry.

We produced 22% of South Africa’sgold and incurred 14.5% of the fatalaccidents in the gold mining industry.

For the year 2003/04 our emphasis willremain on safe production. Safety is afocus during the planning phase and at sitemeetings. There is self-regulation throughthe Harmony Risk Management System,regular audits of compliance and constantcommunication. We are convinced that thisteam effort will enhance safety at all ouroperations.� Kalgold achieved 750 000 fatality free

shifts on 19 July 2002

� Evander 8 Shaft achieved 500 000fatality free shifts on 9 October 2002

� Merriespruit 1 achieved 750 000fatality-free shifts on 6 January 2003

� Masimong mine achieved 500 000fatality-free shifts on 5 June 2003

� Mt Magnet Gold Mill, Admin andGeology departments achieved over1 100 days LTI free during the quarter

� Merriespruit 3 Shaft ended the Junequarter on 1.3 million fatality-freeshifts. This mine has been fatality-freefor five years

� Brand 3 achieved 500 000 fatality-freeshifts on 28 June 2003

� St Helena and Evander 8 Shaft bothachieved a million fatality-free shiftsstatus subsequent to year-end

� Free Gold had a fatality-free quarterfor the first time in its history

OperationsA year on year analysis of the cashoperating profit for the various operationsfollows. see table 2

Safety. Better, but not yet good enough.

2.6 OPERATIONAL REVIEW

table 2

Harmony Annual Report 2003 028

Excellentorganic growthopportunities.

Free Gold In line with similar previous acquisitions,these operations were restructured andaligned to the best practices in bothARMgold and Harmony. This involvesmining the orebody to its optimum grade,thereby eliminating high grading whilstfocusing on recapitalising the orebody toallow for more mining flexibility in future.

Underground tonnage was higher at 2 348 000 tonnes. At a 10% lower recoverygrade of 7.07 g/t compared to the 7.82g/tfor the previous reporting period,attributable gold production was up 115%to 16 587 kg. This year’s results includetwelve months whereas the previous year’sresults included only six months.

Underground working costs whenmeasured in R/kg increased by 16% andfrom R50 867/kg to R58 809/kg and inR/tonne terms by only 5% fromR398/tonne to R416/tonne.

Tonnes milled (000's) tonnes 2 348 988 138

Recovery grade g/t 7.07 7.82 (10)

Gold produced Kg 16 587 7 731 115

Oz 533 282 248 556 115

Working cost R/t 416 398 (5)

R/Kg 58 809 50 867 (16)

Capital Expenditure

(000's) ZAR 125 434 19 500 (543)

UNDERGROUND 2003 2002* VARIANCE %

* Results for six months only

Tonnes milled (000's) tonnes 2 333 1 198 95

Recovery grade g/t 0.59 0.79 (25)

Gold produced Kg 1 382 950 45

Oz 44 432 30 545 45

Working cost R/t 37 32 (16)

R/Kg 63 117 40 382 (56)

Capital Expenditure

(000's) ZAR 6 668 12 223 45

SURFACE 2003 2002* VARIANCE %

* Results for six months only

Capital expenditure of R82.5 millionwas incurred as part of therecapitalisation phase to increase theoperational flexibility at these operations.Capital expenditure, including new projectcapital, totalled R132.1 million.

Tonnages from surface were similar involume but at a lower recovery grade. Atotal of 2 333 000 tonnes at a recoverygrade of 0.59 g/t were treated, resulting ina gold recovery of 1 382kg.

The Free Gold operations will remainan important contributor to our company’sbottom line. The re-establishment offlexibility and the implementation ofcontinuous operations (CONOPS), willassist in achieving payback quicker thanany of our other spectacular acquisitions.

Whilst Joel continues to deliverimproved operational performance,encouraging development results arebeing achieved in the North Shaft area.

This bodes well for the shaft’s futureproduction programme as an increase inore reserves could result in either anextension of mining operations orincreased production in the medium term.

St Helena, whose assets wereacquired from Gold Fields Limited on29 October 2002, is marginal and has notyet contributed to the Free GoldOperations. Although profitable by June2003, a higher gold price is required tofully exploit the potential of this orereserve.

The Free Gold operations are nowwell balanced in terms of operationalefficiency and optimisation of theorebody. The successes achieved at FreeGold by first lowering the working coststructure and then by mining to theoptimum grade of the orebody, havepositioned these operations for furtherproduction growth. A number of projectshave been announced and are currentlyunder way.

029

Phakisa Shaft Project

Project DescriptionPhakisa Shaft, a surface shaft, was sunk toaccess the ore reserve to a depth of 2 421m below surface. It is estimated thatthe area will yield 18 million tonnes,recovering 136 tonnes of gold over aproject life of 20 years. Project completionrequires sinking (178m), equipping andcommissioning of the shaft with accessdevelopment and stoping to maximumproduction build-up at a capital cost ofR550 million. The project will, at fullproduction in 2010, achieve rates of 280000 ounces per annum. Based on a long-term gold price of R93 000/kg and a realdiscount rate of 8%, the project returns aNPV of R900 million and an IRR of 32%.

General GeologyThe ore is mined from the higher gradeBasal Reef.

Reserves/Resourcessee table 3

Project StatusSite establishment has taken place andtender documents have been issued forshaft sinking and related activities.

Nyala Shaft Project

Project DescriptionThe project, which involves the extractionof a shaft pillar and mining of previouslyabandoned areas, recently commenced ata capital cost of R67.4 million.It is planned to mine the shaft pillarconcurrently with the remaining reserveblocks. Mill tonnage is placed at51 600 tonnes at a recovered grade ofapproximately 5.0g/t per month. A total of15 950kg (513 000 ounces) will berecovered over a seven-year period.

General GeologyThe economically viable reefs are theBasal, Leader and A Reefs.

Project StatusThe project commenced in March 2003and we expect production tonnage toreport to the plant during the September2003 quarter. Approximately 1 570 jobs willbe created.

Reserves 18.6 7.68 142.7 4.6

Resources 72.4 9.83 712.2 22.9

RESOURCES TONNES GRADE GOLD OUNCES(mil) (g/t) (tonnes) (million)

Phakisa Shaft Project Reserves/Resources

Reserves 6.5 9.00 58.5 1.9

Resources 8.3 11.20 93.4 3.0

Tshepong North Decline Project Reserves

RESOURCES TONNES GRADE GOLD OUNCES(mil) (g/t) (tonnes) (million)

table 3

table 4

Tshepong North Decline Project

Project DescriptionThe Sub 66 Level Decline Project extendsbelow the lowest current working level ofTshepong North Shaft. The Project willconvert the high-grade resource toreserves and increase production fromTshepong North Shaft.

General Geology The planned Sub 66 Level Decline willaccess the UF1 and UF2 reefs.

Reserves/Resourcesee table 4

Project StatusThe project, which was approved duringthe December 2002 quarter, involves thesinking of a decline at a cost of R280 million. The area will be mined at arate of 49 000 tonnes per month and, at agrade of 8.77 g/t per tonne, will add 167 000 ounces per annum to the FreeGold production profile. The project isexpected to reach full production by July2007.

Opportunities� Extension of the known payshoot� Low risk geology structure� Potential for expansion� Earlier gold from Phakisa Shaft

resource

Harmony Annual Report 2003 030

ElandskraalThe Elandskraal operations experienced adifficult year due to a lack of miningflexibility and problems associated with theinfrastructure at the old Elandsrand mine.The development and construction ofinfrastructure for the new mine receivedpriority and progressed well. The newfinancial year will see tonnage from the newhigher grade mine starting to report to theplant.

Underground tonnage was 15% lowerat 1 874 000 compared to 2 194 000 tonnesreported previously. As indicated before,flexibility at the old Elandsrand mine willremain tight until more stopes becomeavailable in the new mine, accessing thehigher grade payshoot.

Underground recovery grades were 8%lower at 5.76 g/t, whilst gold produced was22% lower at 10 802 kg compared to the 13 770 kg for the previous financial year.

The lower tonnage, recovery grade andinflationary cost pressures impactedadversely on working costs in both R/kgand R/tonne terms. When measured in R/kgterms, working costs increased by 24%from R65 507/kg to R81 095/kg. Whenmeasured in R/tonne terms, working costsincreased by 14% from R411 per tonne toR467 per tonne.

Elandskraal incurred R136.8 million incapital expenditure of which R106.1 millionwas spent on the New Mine Project which ison track and within budget.

The principal reason for theunderperformance at Elandskraal can beattributed to problems experienced with theorepass system at Elandsrand. The oldshaft orepass system comprises two reeforepasses and one waste orepass from 73to 98 levels. These orepasses werepreviously never lined but, as a result of thedepth, they have scaled considerably withtime.

The reef orepasses started to hang upregularly in mid-2000 due to scaling andthis was temporarily rectified. SinceOctober 2002 more serious delays startedto manifest themselves and a decision wastaken to rehabilitate one of the orepasses.For the duration of the process only onereef orepass was available. Therehabilitation of the orepass was completedduring August 2003. During this periodElandsrand experienced severe dilution ofgrade as waste tonnages were unavoidablymixed with reef tonnages. Although the oldElandsrand mine suffers from a lack offlexibility it can continue to produceprofitably at 6 g/t until the new mine kicks inover the next three years.

Deelkraal, which has been sufferingfrom the lack of face availability during thelatter half of the year, has holed two raisesin the March quarter, and has two moreplanned for the September 2003 quarter.The increased flexibility will improvetonnages and grade from this operation.

Tonnes milled (000's) tonnes 1 874 2 194 (15)