Urban Tapestries: Wireless networking, public authoring and social knowledge

Upload

khangminh22Category

view

9download

0

Global Networking in WirelessTeletechnology Business

Lasse Baldauf, Michael Lovejoy, Jarmo Karesto, Laura Paija

Technology Review 114/2001

Global Networkingin Wireless Teletechnology Business

Lasse BaldaufJarmo Karesto

Michael LovejoyLaura Paija

Technology Review 114/2001Helsinki 2001

Tekes – your contact for Finnish technology

Tekes, the National Technology Agency of Finland, is the main financing or-ganisation for applied and industrial R&D in Finland. Funding is granted fromthe state budget.

Tekes’ primary objective is to promote the competitiveness of Finnish indus-try and the service sector by technological means. Activities aim to diversifyproduction structures, increase productivity and exports, and create a foun-dation for employment and social well-being. Tekes supports applied andindustrial R&D in Finland to the extent of some EUR 390 million, annually.The Tekes network in Finland and overseas offers excellent channels for co-operation with Finnish companies, universities and research institutes.

Technology programmes – part of the innovation chain

The technology programmes for developing innovative products and pro-cesses are an essential part of the Finnish innovation system. These pro-grammes have proved to be an effective form of cooperation and networkingfor companies and the research sector. Technology programmes promotedevelopment in specific sectors of technology or industry, and the results ofthe research work are passed on to business systematically. The programmesalso serve as excellent frameworks for international R&D cooperation. Cur-rently, a total of about 50 extensive national technology programmes are un-der way.

_ _ _

Finpro – Finnish business solutions worldwide

Finpro is an efficient expert and service organization. Finpro provides ser-vices, support and information to help Finnish companies enter the interna-tional market as swiftly, safely and efficiently as possible.

In addition to Finpro’s operations in Finland, Finpro has 48 Finland TradeCenters in 38 countries worldwide. Finpro´s global expertise areas focus onthe most important industry sectors of the Finnish economy. Finpro’s com-petence focuses on the industry sectors and market areas where Finnishcompanies have a special competitive advantage or that are interesting aspotential markets.

ISSN 1239-758XISBN 952-457-044-0

Cover: LM&COPage layout: DTPage Oy

Printers: Paino-Center Oy, 2001

Foreword

Networks, inter-firm alliances and cooperation between companies and the research communityare important elements of today’s business operations. Networking means not only vertical rela-tionships, i.e. buyer-supplier relationships, but also cooperation in manufacturing, marketing andin research and development. The depth of cooperation varies however, from subcontracting tostrategic partnerships.

The driving forces behind networking are access to new markets and, increasingly, a tendencyamong firms to focus on core competence of the firm, thus leading to outsourcing of non-criticalactivities. Companies are operating in an industrial ecosystem of mutually supporting, and interde-pendent companies and other partners. To a large extent, today’s competition means competitionbetween these networks.

For the National Technology Agency of Finland, Tekes networking is a strategic objective and acentral element of all R&D projects. The Agency has extensive experience and knowledge of net-working and cooperation trough national technology programmes, but its focus has been mainly onstrategic R&D partnerships between national players.

Although networking is an important element in private and public sector organizations, the impe-tus behind international networking as well as its mechanisms and benefits are not widely known.This report aims at helping companies initiate international cooperation in the field of mobile com-munications; it is designed as a networking aid providing vital information about networking envi-ronments in the most important mobile communications markets.

This report has been prepared by a Finpro working group supported by ETLA, the Research Insti-tute of the Finnish Economy, and other experts in the field of telecommunications. Tekes wishes toexpress its warm thanks to the project team for excellent work collecting benchmarking informa-tion on key players in the telecommunications industry and for analysing international networkingmechanisms. Special thanks are also given to the steering group, composed of companies, theFinpro team and the Tekes representative. Through benchmarking visits and highly productive dis-cussions this group contributed to gaining a deep understanding of the key elements of networking.

We hope you will find this report useful for your international business development.

Tekes, the National Technology Agency of Finland

Table of contents

Foreword

1 Executive summary · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 1

2 Introduction · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 3

3 The ICT cluster in the Finnish economy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 6Laura Paija, ETLA3.1 ICT cluster identification · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 6

3.1.1 What is a cluster? · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 63.1.2 The ICT cluster environment · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 6

3.2 The economic relevance of the ICT cluster · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 73.2.1 Domestic market position · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 73.2.2 Foreign trade and international market position · · · · · · · · · · · · · · · · · · · 8

3.3 The evolution of the ICT cluster· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 93.3.1 Network operation – a fragmented monopoly market· · · · · · · · · · · · · · · 93.3.2 The emergence of the telecommunications industry · · · · · · · · · · · · · · 11

3.4 The factors of the competitive advantage · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 133.4.1 Firm strategy, structure and rivalry · · · · · · · · · · · · · · · · · · · · · · · · · · · · 133.4.2 Factor conditions· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 133.4.3 Demand conditions · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 143.4.4 Supporting and related industries · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 143.4.5 Government· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 153.4.6 Coincidental factors· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 16

3.5 Dynamics in the ICT cluster · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 163.5.1 The government as an early catalyst of cluster development · · · · · · · · 163.5.2 Exceptional demand conditions have offered home-base advantage · 173.5.3 Intense firm interaction has induced upgrading · · · · · · · · · · · · · · · · · · 183.5.4 Deterioration in labor supply, improvement in capital supply · · · · · · · · 193.5.5 World-wide liberalization – pivotal and perfectly timed for Finland· · · · 19

3.6 Future opportunities and threats · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 203.6.1 Market positions at stake in the third generation competition · · · · · · · 203.6.2 Globalization behind most of the opportunities and threats · · · · · · · · · 213.6.3 Small firm size limits seizure of opportunities · · · · · · · · · · · · · · · · · · · · 213.6.4 Dynamic cluster relations support specialization and upgrading · · · · · 223.6.5 Electronic business will have implications on firm interaction · · · · · · · 223.6.6 How to guarantee sufficient supply of skilled labor? · · · · · · · · · · · · · · 233.6.7 Will content production grow into the third base of the ICT cluster? · · 23

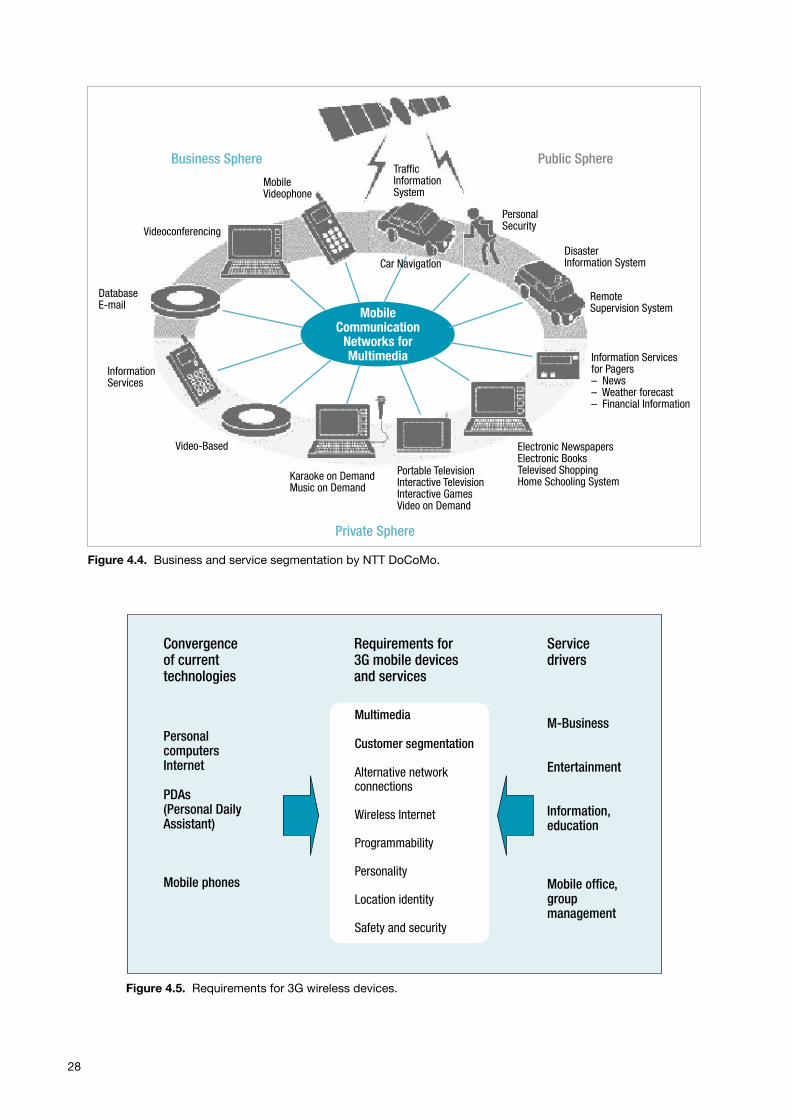

4 Trends in wireless services and products · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 25Jarmo Karesto, Finpro4.1 Drivers in wireless content· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 274.2 From mobile phones to wireless devices · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 274.3 Customer segmentation · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 294.4 Alternative network connections · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 294.5 Wireless Internet · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 294.6 Programmability· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 30

4.7 Personality · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 304.8 Location identity · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 304.9 Safety and security · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 31

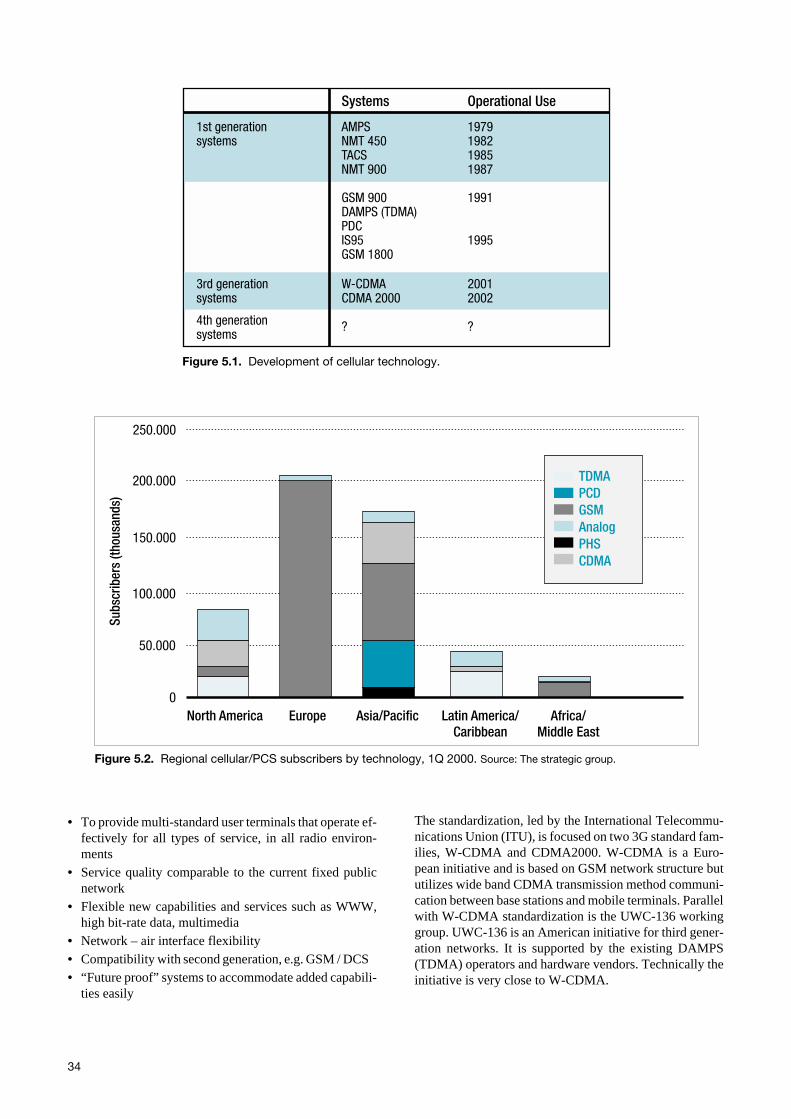

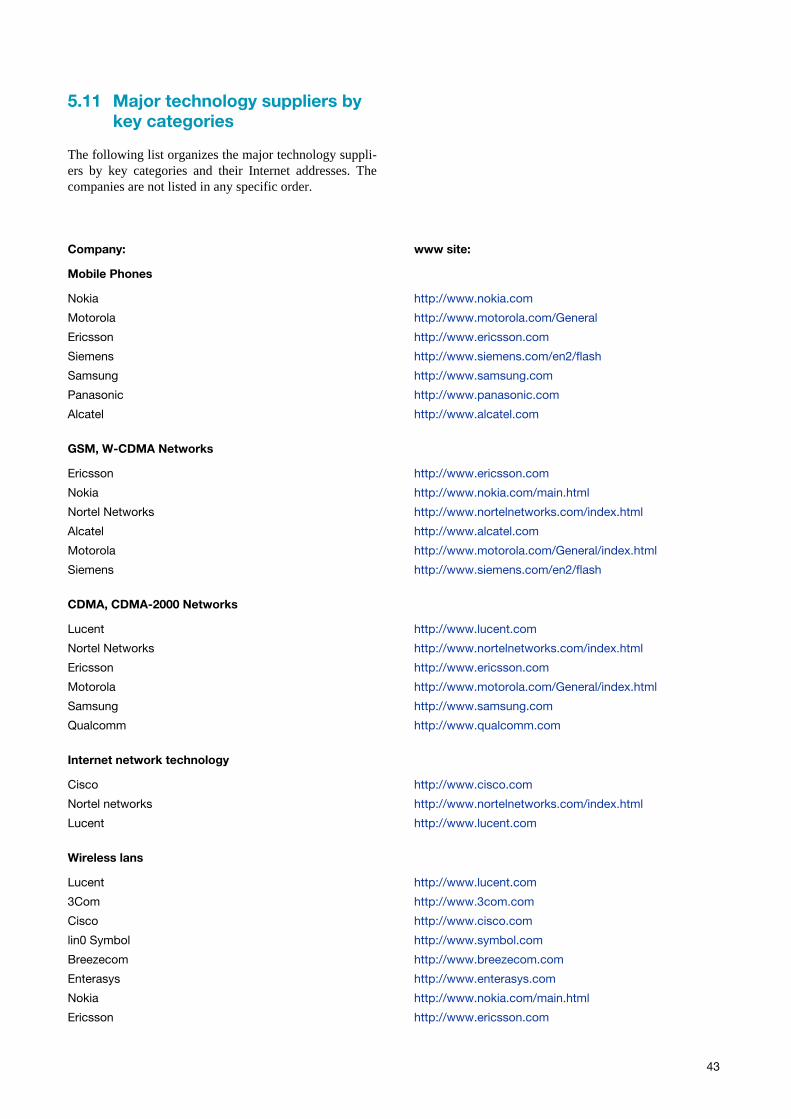

5 Promising standards and technology platforms· · · · · · · · · · · · · · · · · · · · · · · · · · · 33Jarmo Karesto, Finpro5.1 The evolution of third generation cellular networks· · · · · · · · · · · · · · · · · · · · · · 335.2 3G technology strategy plans by operators in major markets· · · · · · · · · · · · · · 365.3 CDMA terminology and definitions · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 385.4 W-CDMA · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 395.5 WAP · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 395.6 I-mode and other Japanese 3G approaches· · · · · · · · · · · · · · · · · · · · · · · · · · · 405.7 Bluetooth · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 415.8 Wireless local area networks · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 415.9 Operating systems in mobile devices, EPOC, Palm OS, and Windows CE · · · 415.10 Mobile Internet Protocol Version 6 · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 425.11 Major technology suppliers by key categories · · · · · · · · · · · · · · · · · · · · · · · · · 435.12 Useful links to get more free information: · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 44

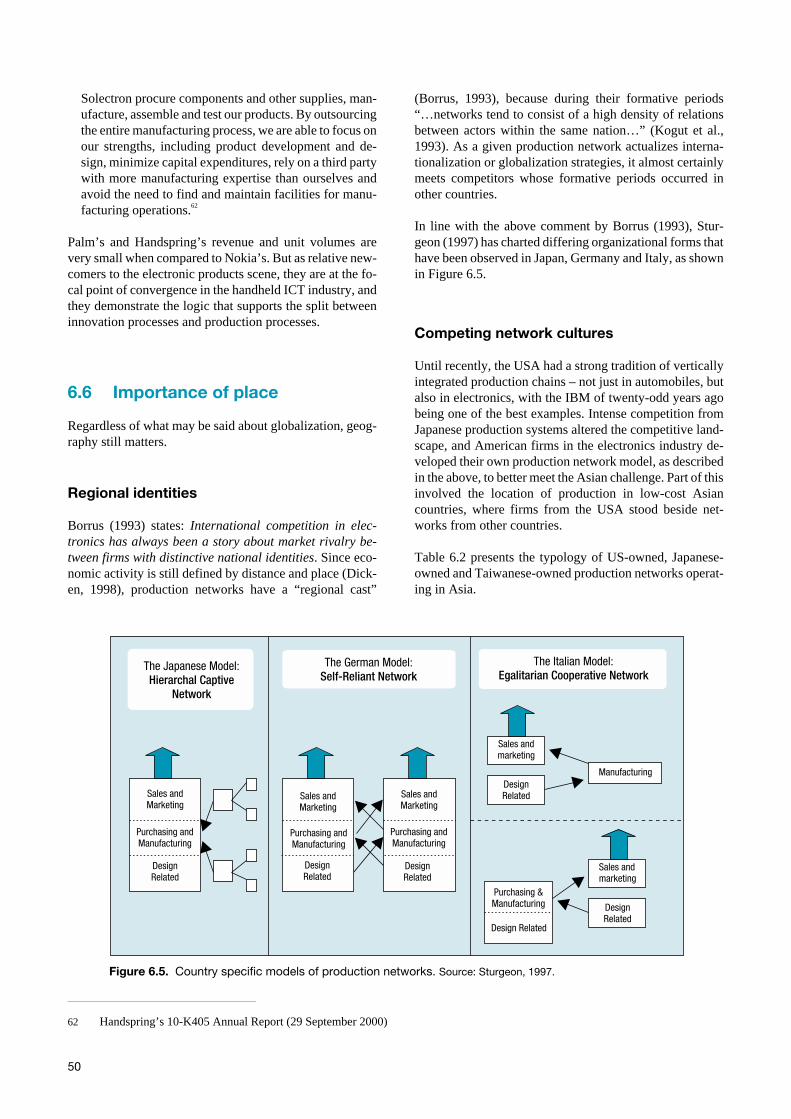

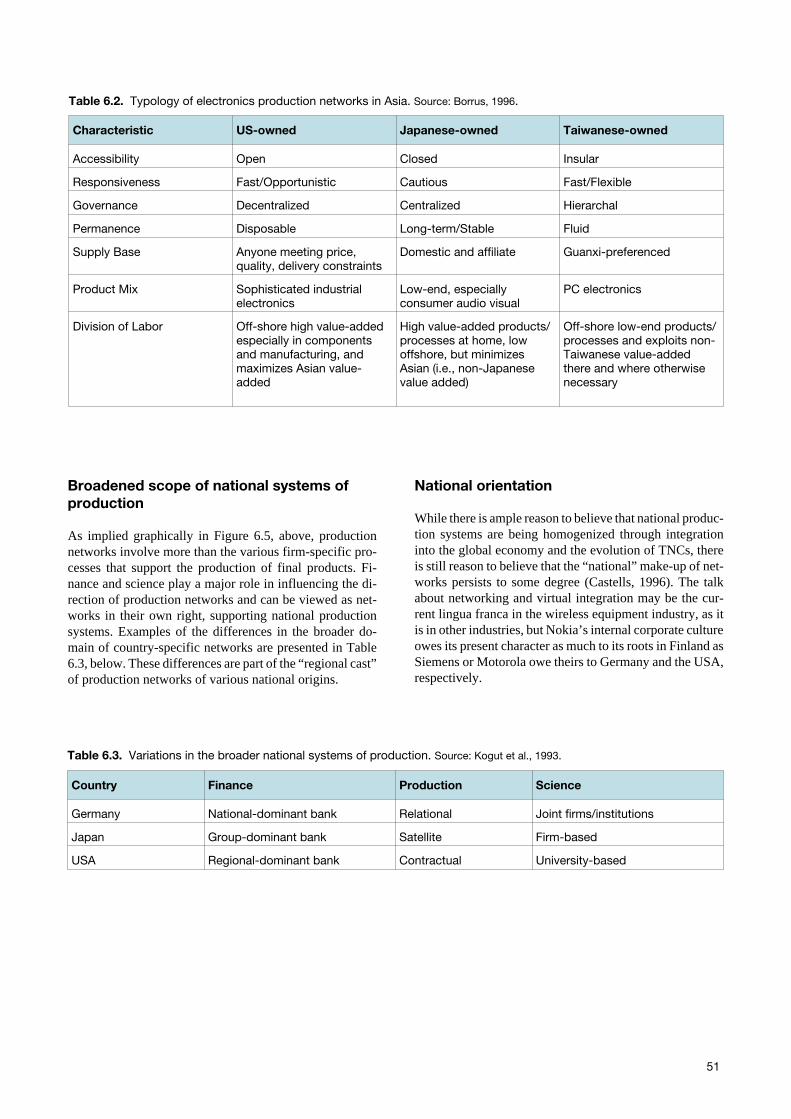

6 Trends in The Global business environment · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 45Michael Lovejoy, Finpro6.1 “Turbulent times” · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 456.2 Convergence · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 456.3 Globalization · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 466.4 Transnationalism · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 476.5 Virtual Integration· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 476.6 Importance of place· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 506.7 New model of production in the ICT industry · · · · · · · · · · · · · · · · · · · · · · · · · · 526.8 Globalization of the EMS model · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 536.9 Types of outsourcing services offered and utilized · · · · · · · · · · · · · · · · · · · · · · 556.10 Thoughts for the future · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 57

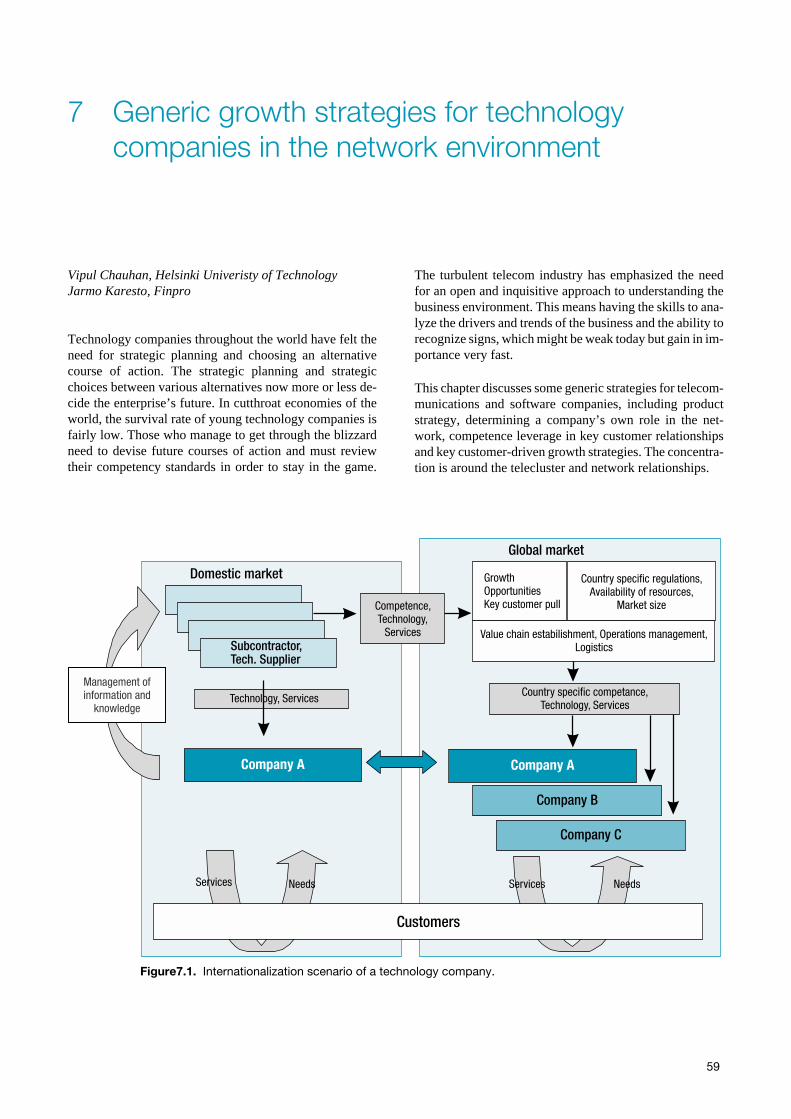

7 Generic growth strategies for technology companiesin the network environment · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 59Vipul Chauhan, Helsinki Univeristy of Technology,Jarmo Karesto, Finpro7.1 Product strategy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 607.2 Strategic roles of collaboration · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 617.3 Competence leverage in key customer relationship · · · · · · · · · · · · · · · · · · · · · 627.4 Key customer-driven growth strategies· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 637.5 Key customer risk · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 647.6 Managing Intellectual Property · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 64

7.6.1 IP Rights Protection: Strategic Aspect · · · · · · · · · · · · · · · · · · · · · · · · · 647.6.2 IP Rights in Relationships · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 64

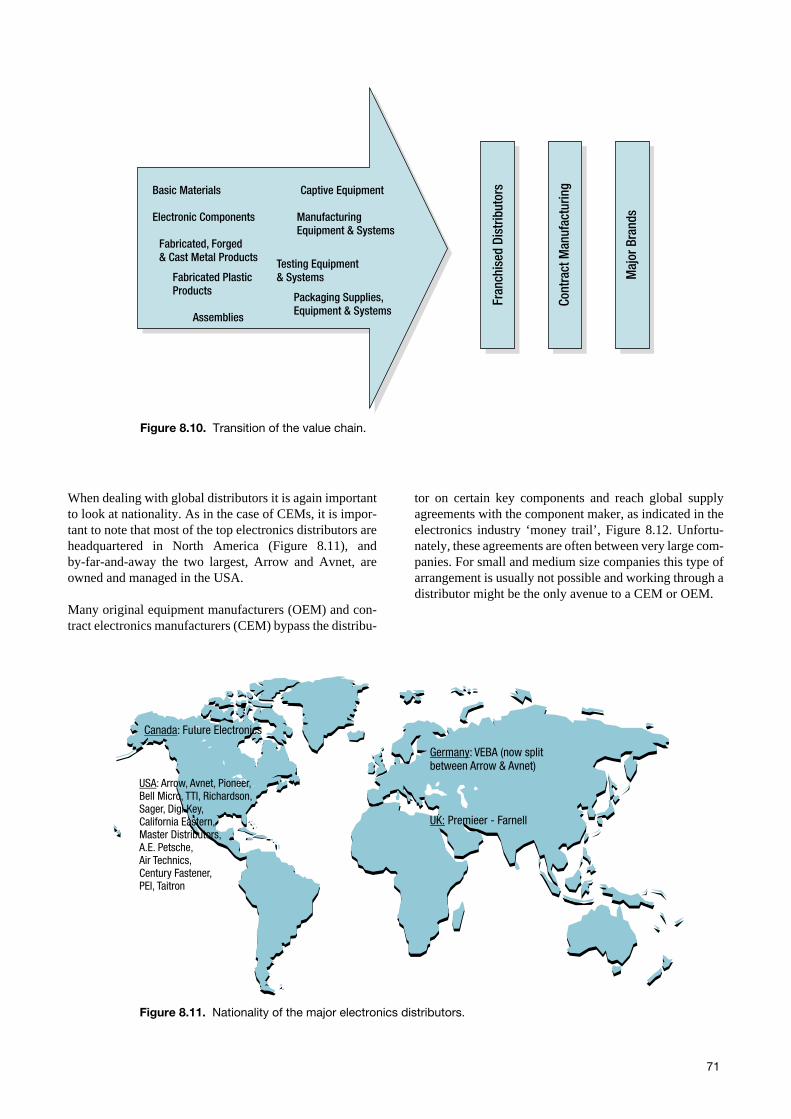

8 Getting global, road map for technology firms · · · · · · · · · · · · · · · · · · · · · · · · · · · · 65Lasse Baldauf, Finpro8.1 Which direction? · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 658.2 Needs and requirements for global business · · · · · · · · · · · · · · · · · · · · · · · · · · 658.3 The process for establishing a business abroad · · · · · · · · · · · · · · · · · · · · · · · · 688.4 Wireless telecommunications industry value chain · · · · · · · · · · · · · · · · · · · · · · 698.5 Connections to the business environment · · · · · · · · · · · · · · · · · · · · · · · · · · · · 728.6 Importance of the cluster for SME’s · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 738.7 Key Success Factors · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 73

9 Benchmarked companies · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 75Lasse Baldauf, Finpro9.1 General · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 759.2 Motorola· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 75

9.2.1 Key figures, major businesses· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 759.2.2 Global map · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 759.2.3 Business strategy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 769.2.4 Research and development· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 769.2.5 Distributors · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 769.2.6 Contract electronic manufacturers · · · · · · · · · · · · · · · · · · · · · · · · · · · · 76

9.3 Siemens · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 779.3.1 Key figures, major businesses· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 779.3.2 Global map · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 779.3.3 Business strategy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 779.3.4 Research and development· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 789.3.5 Distributors · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 789.3.6 Contract electronic manufacturers · · · · · · · · · · · · · · · · · · · · · · · · · · · · 78

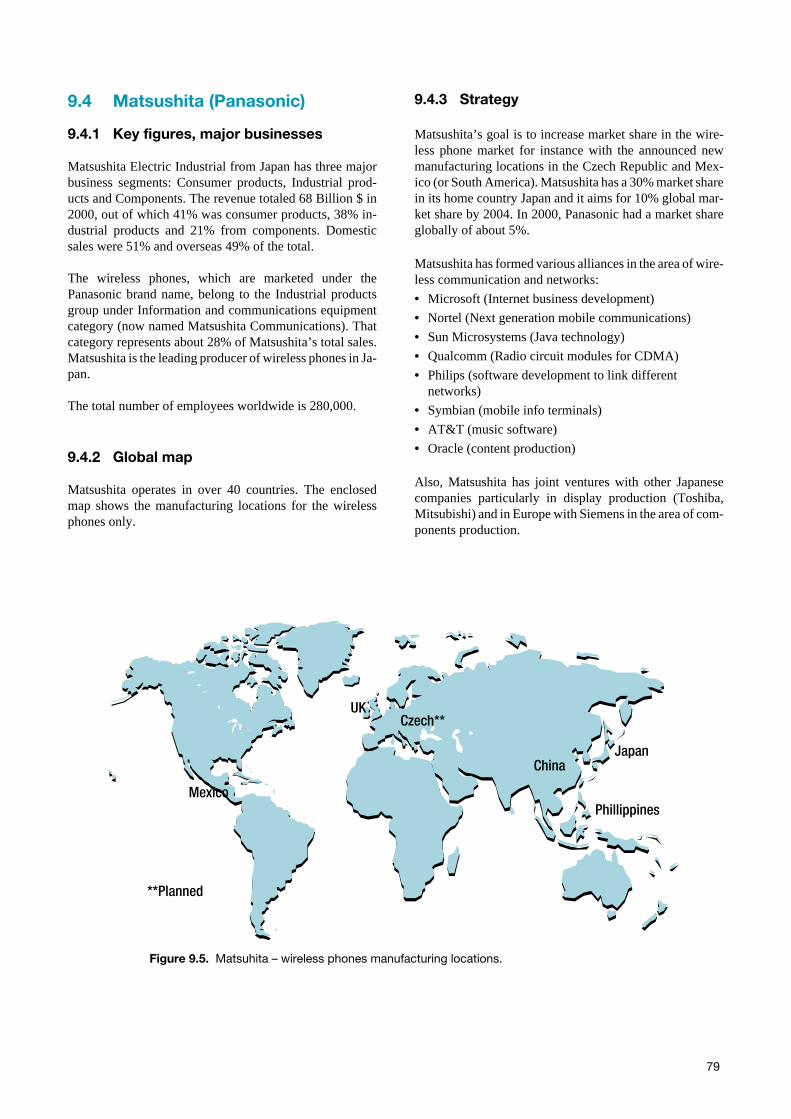

9.4 Matsushita (Panasonic) · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 799.4.1 Key figures, major businesses· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 799.4.2 Global map · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 799.4.3 Strategy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 799.4.4 Research and development· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 809.4.5 Contract manufacturers· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 80

9.5 Samsung · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 809.5.1 Key figures, major businesses· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 809.5.2 Global map · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 809.5.3 Strategy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 809.5.4 Research and development· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 809.5.5 Contract electronics manufacturers · · · · · · · · · · · · · · · · · · · · · · · · · · · 80

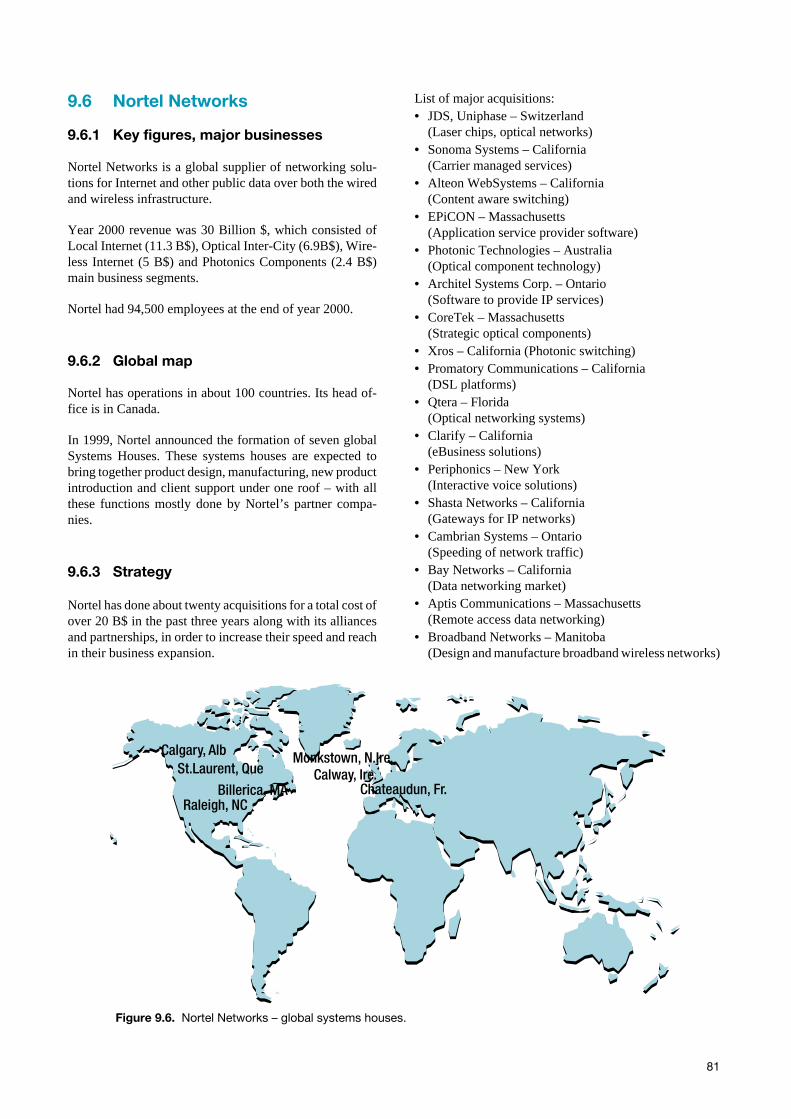

9.6 Nortel Networks · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 819.6.1 Key figures, major businesses· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 819.6.2 Global map · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 819.6.3 Strategy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 829.6.4 Research and development· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 829.6.5 Outsourcing, suppliers · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 82

9.7 Cisco Systems· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 829.7.1 Key figures, major businesses· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 829.7.2 Global map · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 829.7.3 Strategy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 829.7.4 Research and development· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 839.7.5 Distributors · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 839.7.6 Contract electronic manufacturers · · · · · · · · · · · · · · · · · · · · · · · · · · · · 83

9.8 Solectron · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 839.8.1 Key figures, major businesses· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 839.8.2 Global map · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 839.8.3 Strategy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 839.8.4 Research and development· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 849.8.5 Key customers· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 84

9.9 Celestica · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 849.9.1 Key figures, major businesses· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 849.9.2 Global map · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 859.9.3 Strategy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 859.9.4 Research and development· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 859.9.5 Key customers· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 85

9.10 Flextronics · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 859.10.1 Key figures, major businesses· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 859.10.2 Global map · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 859.10.3 Strategy · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 869.10.4 Research and development· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 869.10.5 Key customers· · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 86

10 Conclusion · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 87

Appendix 1 The NACE codes utilized in the calculation of economic indicatorsfor the ICT cluster · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 89

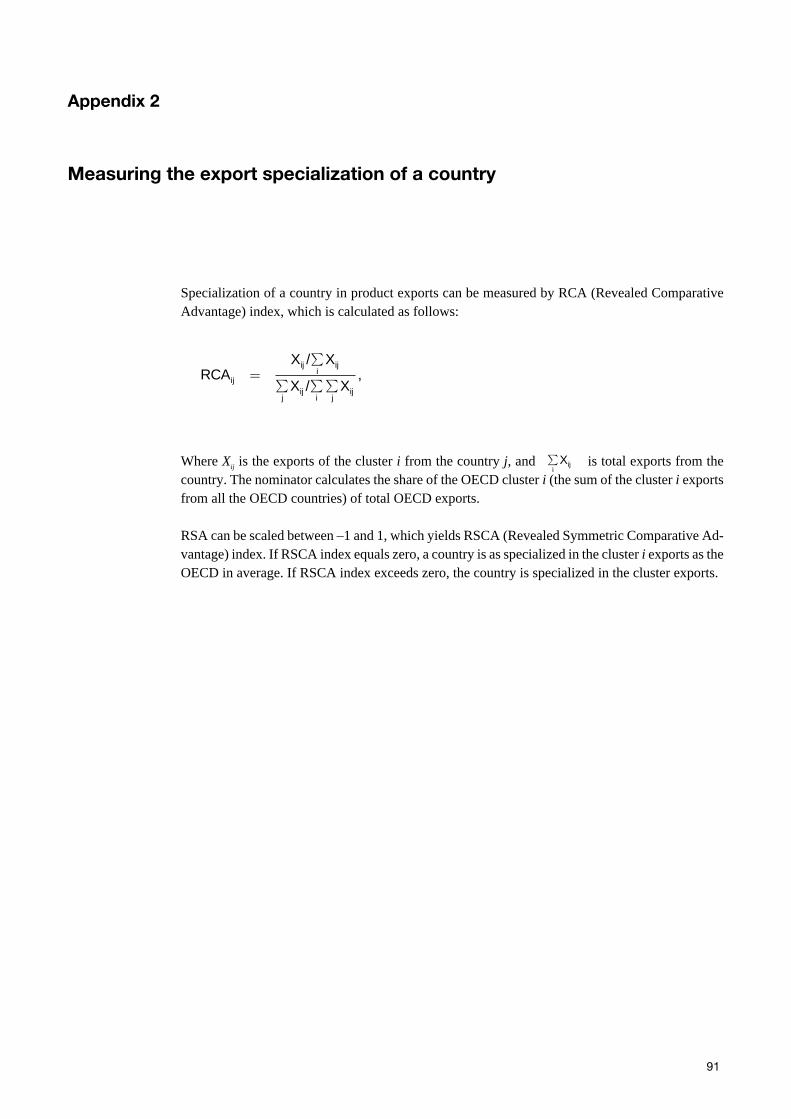

Appendix 2 Measuring the export specialization of a country · · · · · · · · · · · · · · · · · · · · · 91

Technology Reviews from Tekes · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · · 93

1 Executive summary

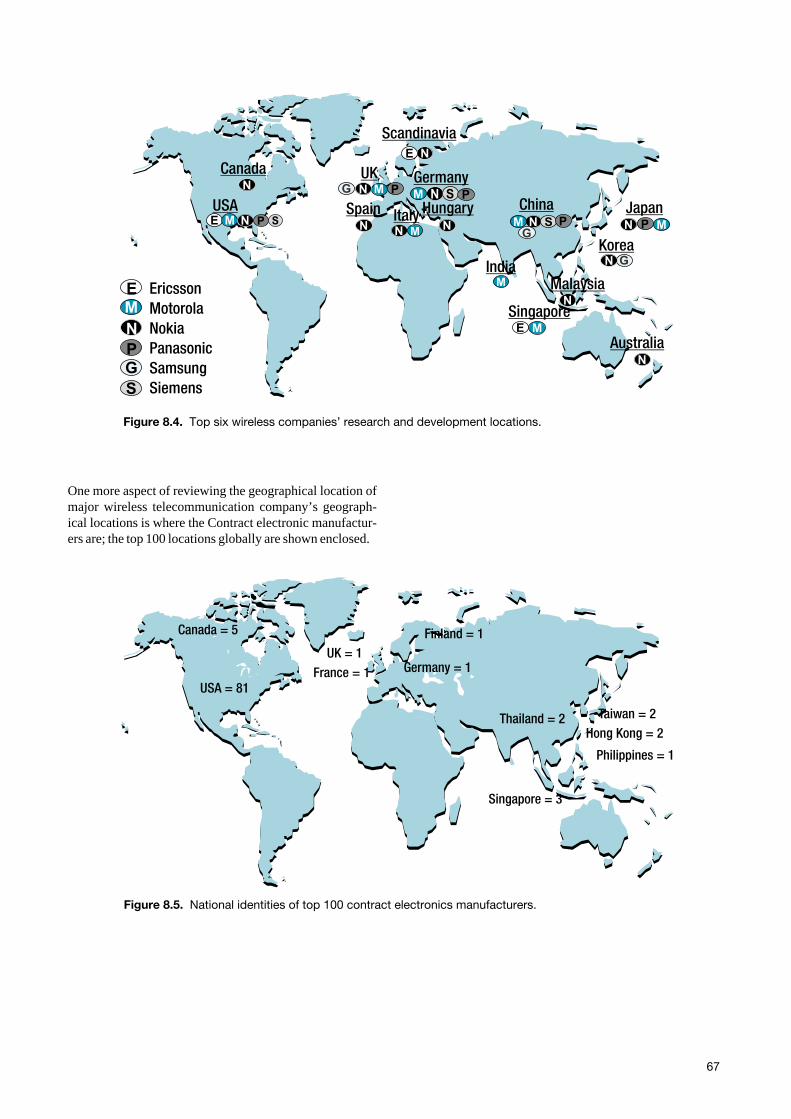

Production of Telecommunications equipment in Finlandincreased from about 5 Billion Fim in 1990 to nearby 80Billion Fim in 2000. The production incorporates directlyseveral hundred companies in electronics, metal, plasticand software industries and employs approximately 40–50.000 people. Major part of the production was exported.This miraculous development is a sum of many factors,which have successfully supported each other. Liberaliza-tion of telecom services in early stage, building NMT net-work jointly with the other Nordic countries, great successof mobile phones worldwide, opening of telecom servicesfor competition globally and growth of Nokia are all fac-tors which have contributed to the success and created avery strong telecommunication industry in Finland. As aresult the Finnish telecom technology know-how today isworld class.

However this blessed situation is extremely fragile andcontinuous growth is not at all granted. Nokia’s role as a lo-comotive of the whole cluster in Finland will probably notcontinue forever. Nokia is growing fast outside Finland.More and more decision makers in Nokia’s organizationare representing other nationalities than Finns and we allknow how important personal relationships are in business.At this moment the most critical issue is the international-ization of the cluster. If the smaller technology and servicecompanies in the cluster can expand their business to newcustomers globally, it reduces their operational risk and theimpact on the whole Finnish economy.

The companies in telecom business face new type of chal-lenges. Technology is developing fast and the future is notat all predictable. The business is much more innovationdriven than capital driven. Merge of Internet, mobilephones and computers may create totally new needs forservices and products, which are not identified yet. Thebusiness environment is moving fast. Earlier several lo-cally operating companies in each business were sharingthe market but the trend is to smaller number but globallyoperating key players. This is a result of globalization.R&D and production are organized globally according tothe rules of the business not by following artificial bordersand barriers. This new world map shows how R&D and

production are concentrating in few locations. In the “R&Dmap” Finland and Sweden are centrally located besideUSA and Japan. Manufacturing sites are locating nearmain markets. The other trend is networking. Companiesare outsourcing non-critical activities and enhancing col-laboration with partners and even competitors. Nokia is agood example of this. Totally new actors, like global pro-viders of contract manufacturing services, have emerged inthe business rebuilding the value chain. Speed has becomea crucial competitive edge. Cisco System’s famous slogan“Innovations by acquisitions” describes well the phenome-non. Companies are no longer doing everything by them-selves anymore as it was still few years ago.

Globalization and networking open totally new possibili-ties for smaller technology companies but the old strategiesdo not work any more. Global approach, focus on cus-tomer, concentration on core competencies, understandingvalue networks and the progress in business environment,networking with others, speed and capability to finance thefast growth are raw materials in building a successful strat-egy in telecom technology business. A key customer rela-tionship can be a springboard to new customers and even tonew businesses as many of the Nokia’s smaller partnershave recognized. Innovations, work processes, references,social competencies among many others are gaining im-portance beside technical competencies in new businessenvironment.

What should then be done to ensure that success continues?As mentioned earlier the most critical issue is the interna-tionalization of the cluster. It is important to capitalize onthe success with Nokia when entering new markets. Thiscan translate to a speedier access to new customers andability to manage the business through international net-working. The focus of the national system of innovationshould be more on innovativeness, global customer needsand ability to help the smaller companies in organizingtheir operations in international market environment. Thekey issue for public supporting organizations involved is tounderstand the new logic of the global telecom businessand develop their services and mutual cooperation accord-ingly.

1

2 Introduction

This report is an outcome of the Global Networking in Mo-bile Teletech business project conducted by the leadingtechnology companies in mobile business in Finland (CCCGroup, Elektrobit Oy, Fortel Invest Oy, JOT AutomationOy, Orbis Oy and Nokia Mobile Phones) Tekes (the Na-tional Technology Agency) and Technopolis Oyj. Finprohas been in charge of managing the project and producingthis report.

The goal of the project was to support the strategy processof each participant in the fast transforming business envi-ronment. The major focus was on mobile technology busi-ness, global business environment, corporate strategies,networking and small and medium-sized enterprise ap-proach. Mobile services and applications were just brieflydiscussed when they had some relevance with technologybusiness (but otherwise they were left out of this study).

The project was carried out between fall 2000 and summer2001. The working methods were workshops, study toursto USA, Germany and Japan and the company bench-marking studies. ETLA (the Research Institute of FinnishEconomy) and Helsinki University of Technology werehelping by carrying out part of the research work.

The chapter ICT Cluster in Finnish Economy is a brief butan important review of the emergence and development ofthe telecom industry in Finland. The formation of the clus-ter and the growth of Nokia have mainly taken place in1990’s but their roots are much deeper in the history. Spe-cial focus is put on cluster analysis to help the reader to un-derstand the importance of various elements in the businessenvironment which are discussed in later chapters. TheICT Cluster in Finnish Economy chapter was written byLaura Paija from ETLA.

The Chapter Trends in Wireless Services and Productssummarizes the various thoughts and views about theemerging customer needs defining the direction for thewhole business. The chapter is not a comprehensive studyof the subject but rather a summary of the those issues onwhich the leading people in the industry believe today.Customer needs concerning services and physical productsare driving the business but hardware products and soft-ware applications make the services possible.

The chapter Emerging Standards and Technology Plat-forms is worked out similar way as the previous chapter.The focus in this chapter has been on identifying thosetechnological standards, either official or de facto, andplatforms that are supposed to play important role in theforeseeable future. Standards and platforms create a solidbase for fast changing, short time living products and ser-vices aimed at end users. They can also be important cornerstones in strategies of small technology companies.

The chapter Trends in Global Business environment dis-cuss the forces and development trends, which are redraw-ing the business environment making the old strategies ob-solete. Liberalization of global trade and investmentsmakes it possible for businesses to reorganize globallytheir activities following the laws of business, not accord-ing to artificial regulations and boundaries. Fast develop-ing information and communication technologies and lo-gistical services greatly support this trend. Global businessnetworks are emerging. Firms focus on their core compe-tencies and grow their added value through alliances andcooperation. Old value chains are redrawn. Nokia, Elcoteq,JOT Automation and Elektrobit are good examples of com-panies, which have understood the ongoing change andhave been able to quickly utilize the emerging opportuni-ties in their businesses.

The chapter Generic Growth Strategies for TechnologyCompanies in Network Environment focuses on corporatestrategies. This chapter is an introduction to the followingchapter Getting global, Road Map for Technology Firms.The chapter introduces and offers generic strategy alterna-tives for small and medium-sized technology enterprises innetwork environment. This part was created together withthe Institute of Strategy and International Business ofHelsinki University of Technology. In the chapter Gettingglobal, Road Map for Technology Firms the focus isturned to mobile telecom business in global market envi-ronment. The chapter introduces business cases and mod-els and is created by studying various Finnish and interna-tional companies in Europe, USA and Asia.

3

The chapter Benchmarked Companies introduces severalleading technology companies, their strategies and activi-ties in mobile business. The companies were selectedbased on their importance for Finnish industry or based ontheir interesting business models. The benchmarked com-panies were thoroughly studied and interviewed. Summaryof strategies, business models and other key findings arepresented in this chapter.

The last chapter Conclusions outlines the key findings ofthis project and gives recommendations to governmentaland public business development organizations workingclosely with the ITC-cluster.

4

3 The ICT cluster in the Finnish economy

Laura Paija, ETLA

3.1 ICT cluster identification

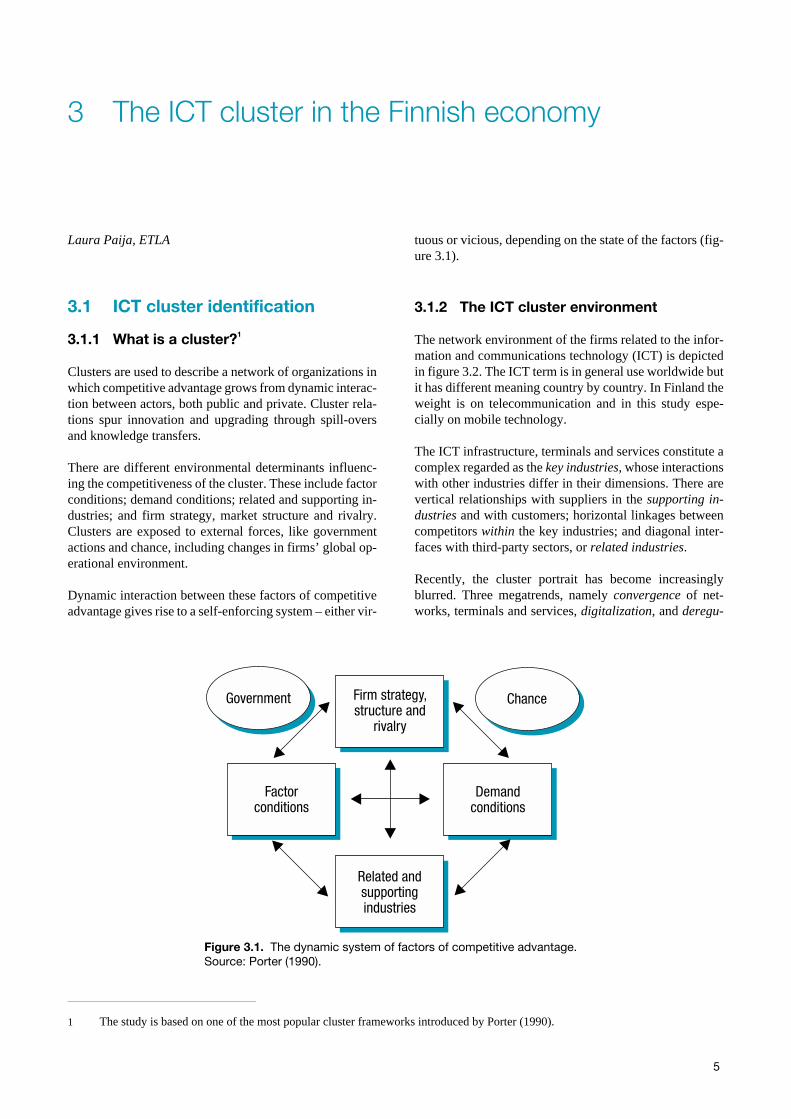

3.1.1 What is a cluster?1

Clusters are used to describe a network of organizations inwhich competitive advantage grows from dynamic interac-tion between actors, both public and private. Cluster rela-tions spur innovation and upgrading through spill-oversand knowledge transfers.

There are different environmental determinants influenc-ing the competitiveness of the cluster. These include factorconditions; demand conditions; related and supporting in-dustries; and firm strategy, market structure and rivalry.Clusters are exposed to external forces, like governmentactions and chance, including changes in firms’ global op-erational environment.

Dynamic interaction between these factors of competitiveadvantage gives rise to a self-enforcing system – either vir-

tuous or vicious, depending on the state of the factors (fig-ure 3.1).

3.1.2 The ICT cluster environment

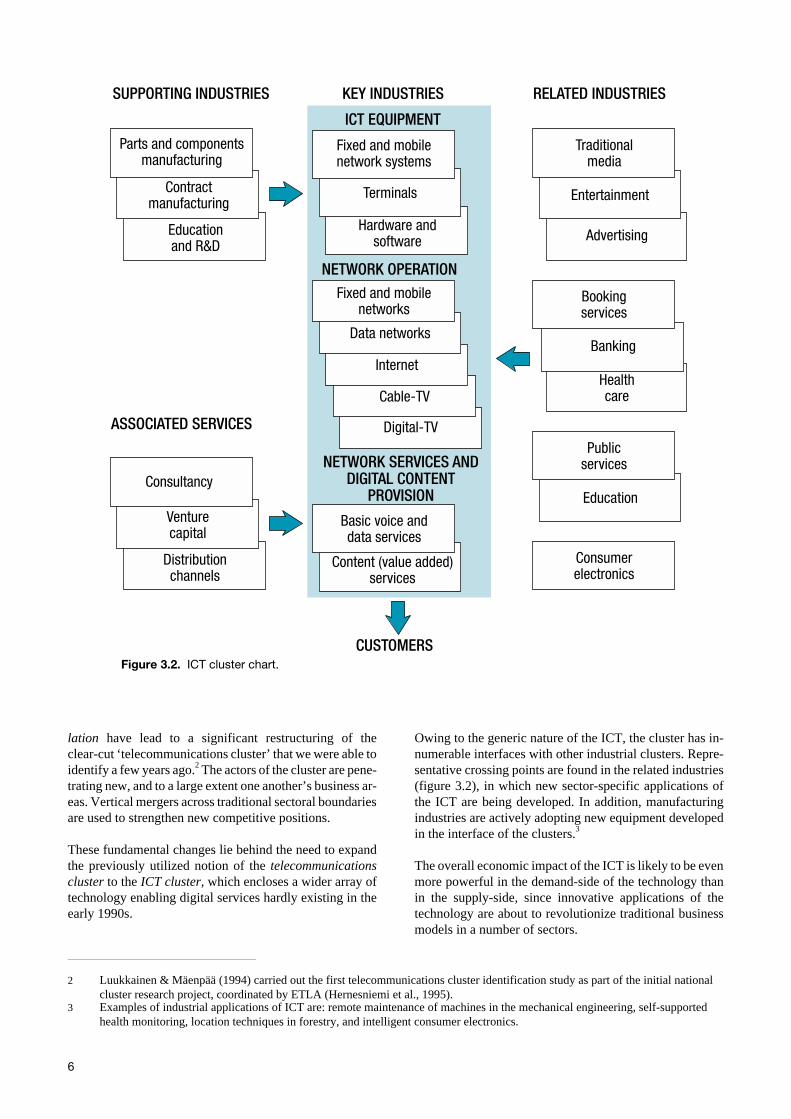

The network environment of the firms related to the infor-mation and communications technology (ICT) is depictedin figure 3.2. The ICT term is in general use worldwide butit has different meaning country by country. In Finland theweight is on telecommunication and in this study espe-cially on mobile technology.

The ICT infrastructure, terminals and services constitute acomplex regarded as the key industries, whose interactionswith other industries differ in their dimensions. There arevertical relationships with suppliers in the supporting in-dustries and with customers; horizontal linkages betweencompetitors within the key industries; and diagonal inter-faces with third-party sectors, or related industries.

Recently, the cluster portrait has become increasinglyblurred. Three megatrends, namely convergence of net-works, terminals and services, digitalization, and deregu-

5

Firm strategy,structure and

rivalry

Demandconditions

Related andsupportingindustries

Factorconditions

Government Chance

Figure 3.1. The dynamic system of factors of competitive advantage.Source: Porter (1990).

1 The study is based on one of the most popular cluster frameworks introduced by Porter (1990).

lation have lead to a significant restructuring of theclear-cut ‘telecommunications cluster’ that we were able toidentify a few years ago.2 The actors of the cluster are pene-trating new, and to a large extent one another’s business ar-eas. Vertical mergers across traditional sectoral boundariesare used to strengthen new competitive positions.

These fundamental changes lie behind the need to expandthe previously utilized notion of the telecommunicationscluster to the ICT cluster, which encloses a wider array oftechnology enabling digital services hardly existing in theearly 1990s.

Owing to the generic nature of the ICT, the cluster has in-numerable interfaces with other industrial clusters. Repre-sentative crossing points are found in the related industries(figure 3.2), in which new sector-specific applications ofthe ICT are being developed. In addition, manufacturingindustries are actively adopting new equipment developedin the interface of the clusters.3

The overall economic impact of the ICT is likely to be evenmore powerful in the demand-side of the technology thanin the supply-side, since innovative applications of thetechnology are about to revolutionize traditional businessmodels in a number of sectors.

6

KEY INDUSTRIES

NETWORK OPERATION

NETWORK SERVICES ANDDIGITAL CONTENT

PROVISION

ICT EQUIPMENT

Hardware andsoftware

Terminals

Fixed and mobilenetwork systems

Digital-TV

Cable-TV

Internet

Data networks

Fixed and mobilenetworks

Content (value added)services

Basic voice anddata services

SUPPORTING INDUSTRIES

Educationand R&D

Contractmanufacturing

Parts and componentsmanufacturing

RELATED INDUSTRIES

Advertising

Entertainment

Traditionalmedia

Healthcare

Banking

Bookingservices

Education

Publicservices

Consumerelectronics

ASSOCIATED SERVICES

CUSTOMERS

Distributionchannels

Venturecapital

Consultancy

Figure 3.2. ICT cluster chart.

2 Luukkainen & Mäenpää (1994) carried out the first telecommunications cluster identification study as part of the initial nationalcluster research project, coordinated by ETLA (Hernesniemi et al., 1995).

3 Examples of industrial applications of ICT are: remote maintenance of machines in the mechanical engineering, self-supportedhealth monitoring, location techniques in forestry, and intelligent consumer electronics.

3.2 The economic relevance ofthe ICT cluster

3.2.1 Domestic market position

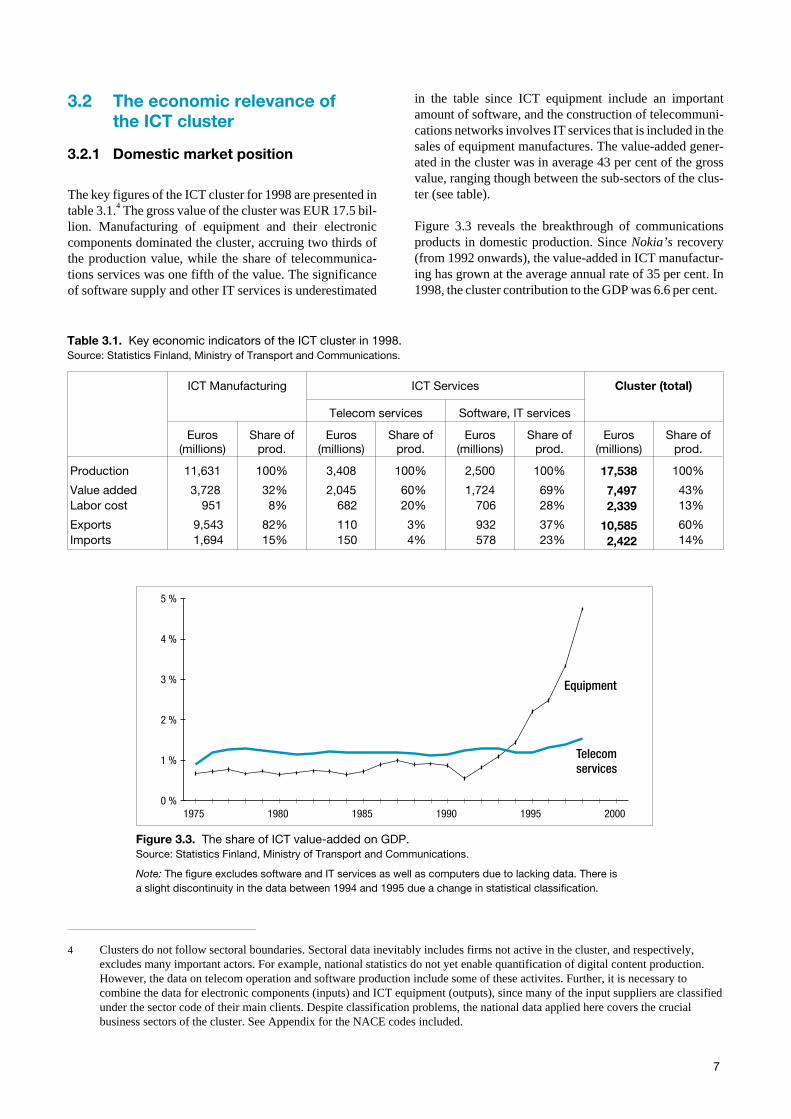

The key figures of the ICT cluster for 1998 are presented intable 3.1.4 The gross value of the cluster was EUR 17.5 bil-lion. Manufacturing of equipment and their electroniccomponents dominated the cluster, accruing two thirds ofthe production value, while the share of telecommunica-tions services was one fifth of the value. The significanceof software supply and other IT services is underestimated

in the table since ICT equipment include an importantamount of software, and the construction of telecommuni-cations networks involves IT services that is included in thesales of equipment manufactures. The value-added gener-ated in the cluster was in average 43 per cent of the grossvalue, ranging though between the sub-sectors of the clus-ter (see table).

Figure 3.3 reveals the breakthrough of communicationsproducts in domestic production. Since Nokia’s recovery(from 1992 onwards), the value-added in ICT manufactur-ing has grown at the average annual rate of 35 per cent. In1998, the cluster contribution to the GDP was 6.6 per cent.

7

ICT Manufacturing ICT Services Cluster (total)

Telecom services Software, IT services

Euros(millions)

Share ofprod.

Euros(millions)

Share ofprod.

Euros(millions)

Share ofprod.

Euros(millions)

Share ofprod.

Production

Value addedLabor cost

ExportsImports

11,631

3,728951

9,5431,694

100%

32%8%

82%15%

3,408

2,045682

110150

100%

60%20%

3%4%

2,500

1,724706

932578

100%

69%28%

37%23%

17,538

7,4972,339

10,5852,422

100%

43%13%

60%14%

Table 3.1. Key economic indicators of the ICT cluster in 1998.Source: Statistics Finland, Ministry of Transport and Communications.

1975 1980 1985 1990 1995 20000 %

1 %

2 %

3 %

4 %

5 %

Equipment

Telecomservices

Figure 3.3. The share of ICT value-added on GDP.Source: Statistics Finland, Ministry of Transport and Communications.

Note: The figure excludes software and IT services as well as computers due to lacking data. There isa slight discontinuity in the data between 1994 and 1995 due a change in statistical classification.

4 Clusters do not follow sectoral boundaries. Sectoral data inevitably includes firms not active in the cluster, and respectively,excludes many important actors. For example, national statistics do not yet enable quantification of digital content production.However, the data on telecom operation and software production include some of these activites. Further, it is necessary tocombine the data for electronic components (inputs) and ICT equipment (outputs), since many of the input suppliers are classifiedunder the sector code of their main clients. Despite classification problems, the national data applied here covers the crucialbusiness sectors of the cluster. See Appendix for the NACE codes included.

With its 75,000 employees, the ICT cluster accounted for 3per cent of the total national employment in 1998. Nokiaalone employed 21,000 persons in Finland and thus ac-counted directly for almost 30 per cent of the cluster employ-ment. According to estimations Nokia employed indirectlyan additional 14,000 persons through its first-tier subcon-tractor firms.5 As production networks go further to sequen-tial tiers, the employment effect of the major firm is signifi-cant, but cannot be readily quantified. However, without thechronic shortage of skilled labor the employment potentialof the cluster would allow much higher recruitment.

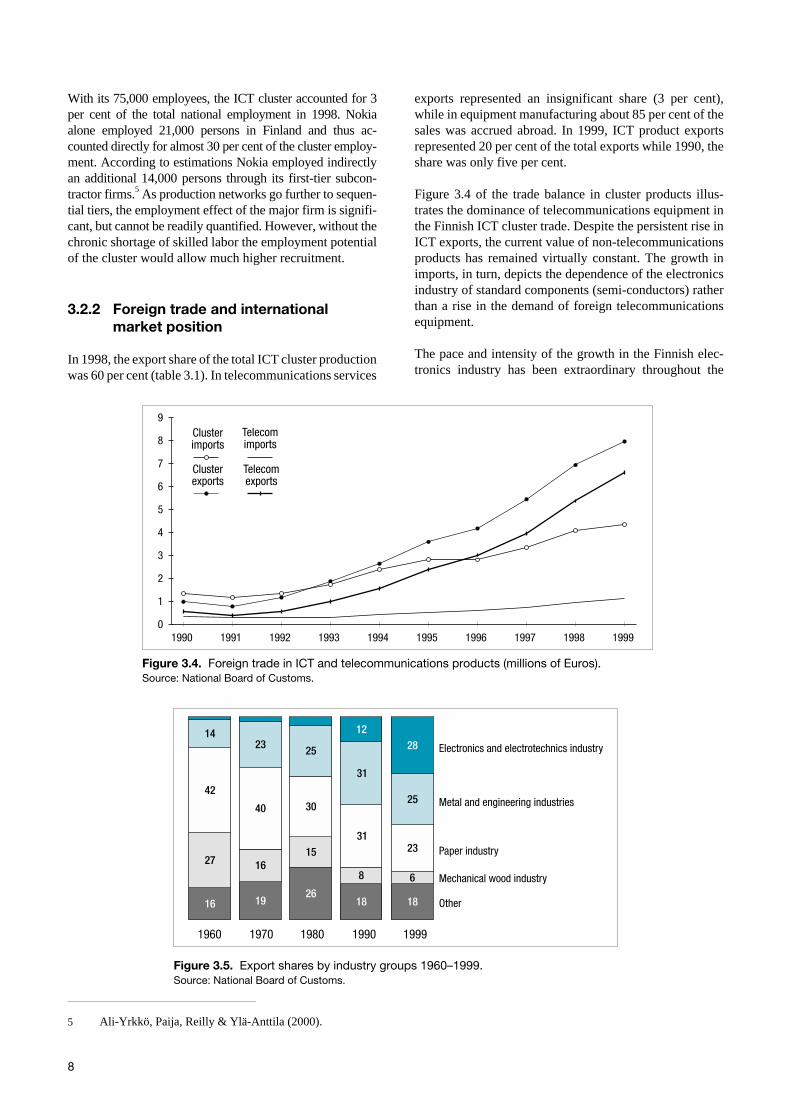

3.2.2 Foreign trade and internationalmarket position

In 1998, the export share of the total ICT cluster productionwas 60 per cent (table 3.1). In telecommunications services

exports represented an insignificant share (3 per cent),while in equipment manufacturing about 85 per cent of thesales was accrued abroad. In 1999, ICT product exportsrepresented 20 per cent of the total exports while 1990, theshare was only five per cent.

Figure 3.4 of the trade balance in cluster products illus-trates the dominance of telecommunications equipment inthe Finnish ICT cluster trade. Despite the persistent rise inICT exports, the current value of non-telecommunicationsproducts has remained virtually constant. The growth inimports, in turn, depicts the dependence of the electronicsindustry of standard components (semi-conductors) ratherthan a rise in the demand of foreign telecommunicationsequipment.

The pace and intensity of the growth in the Finnish elec-tronics industry has been extraordinary throughout the

8

1990 1991 1992 1993 1994 1995 1996 1997 1998 19990

1

2

3

4

5

6

7

8

9Clusterimports

Clusterexports

Telecomimports

Telecomexports

Figure 3.4. Foreign trade in ICT and telecommunications products (millions of Euros).Source: National Board of Customs.

1228

1423 25

31

2542

40 30

3123

27 1615

8 6

16 1926

18 18

Electronics and electrotechnics industry

Metal and engineering industries

Paper industry

Mechanical wood industry

Other

1990198019701960 1999

Figure 3.5. Export shares by industry groups 1960–1999.Source: National Board of Customs.

5 Ali-Yrkkö, Paija, Reilly & Ylä-Anttila (2000).

1990s. It has lead to an industrial restructuring in the for-mer forest and metal based economy, in which knowledgehas replaced capital, raw materials and energy as the domi-nant factors of production. During the past decade, Finlandbecame the world leader in high-tech trade surplus (high-tech exports/imports ratio) among indigenous high- techproducers. The share of electronics and electrotechnics ex-ports has almost tripled at the expense of pulp and paperand metals, representing close to 30 per cent of the totalmanufacturing exports in 1999 (figure 3.5).

In OECD comparison, Finland ranked the second in ICTexports specialization after Japan in 1997 (figure 3.6 left;see Appendix 2 for the definition). Limiting the compari-son to telecommunications equipment6 reveals that Finlandhad become the most telecommunications-oriented coun-try in its exports in 1998 (figure 3.6 right). During the1990s, Japan has lost its lead to the two Nordic countries,which have been racing for the leading position. In abso-lute terms, Finland accounted for 4.4 per cent of totalOECD telecommunications equipment exports, being inthe seventh position in cross-country comparison in 1997.7

3.3 The evolution ofthe ICT cluster

3.3.1 Network operation – a fragmentedmonopoly market

Despite the prominent role the telecommunications manu-facturing sector has played in the recent industrial struc-tural change in Finland, a glance at the history reveals thatit was the advanced network operation – rather than equip-ment manufacturing – that formed the ground for the indus-try to develop.

Since its early days, the Finnish telecommunications mar-ket has had a tendency of early adoption of the latest tech-nology – both in the manufacturing and operator sector.The first indication of this feature was the introduction ofthe telephone in Finland only a year after its invention in1876. The first telephone companies were established in1882, and by the end of the century, all the cities of Finlandhad a telephone company.

9

Finland

Sweden

UK

Japan

USA19971990

ICT equipment

Finland

Sweden

UK

Japan

USA

1998

-0.2 0.20 0.4 0.6 0.8 -0.2 0.20 0.4 0.6 0.8

19971990

Telecom equipment

Figure 3.6. Export specialization in 1997 (RSCA index). Source: OECD.

Note: The 1998 data was not yet available for all countries. See Appendix 2 for the definition of the RSCA index.

6 SITC rev3 class 764 (Telecommunications equipment n.e.s & parts n.e.s).7 Shares of OECD telecommunications exports in 1997 (totalling USD 104 billion):

1. USA 20.52. Japan 14.53. UK 9.74. Sweden 9.55. Germany 8.66. France 6.17. Finland 4.48. Korea 4.49. Canada 4.2

10. Mexico 4.2

Unlike in most of the European countries, the telephonenetwork ownership was not monopolized by the state. Be-side the national public telecommunications operator(PTO) there was a growing number of private local tele-phone companies that operated in their exclusive conces-sion areas. In the 1930s, their number was no less than 815(yet it decreased drastically between 1950–65 due to struc-tural regulations). Thus, the market could be characterizedas a fragmented monopoly market.

Initially the fragmented market structure was a politicaloutcome. In the turn of the 20th century, when Finland wassetting the ground for its telecommunications, it was a Rus-sian Grand Duchy. The Tsar authorized the Finnish Senateto grant licenses in telephony operation. However, therewas a threat of seizure of the national telephony by theTsar, which provoked the Senate to decentralize the net-work ownership to discourage confiscation.

In 1921, the private companies founded the Association ofTelephone Companies aiming at administrative coopera-tion and joining forces in face of the PTO, who acted as theregulatory body authorized to redeem poorly performingoperators. Indeed, the threat of nationalization worked asan effective means of technical upgrading. Over the years,the Association grew a powerful opponent to the PTO, giv-ing rise to a duopolistic market structure.

There were several intentions throughout the decades tonationalize the private operation, but there was nor enoughpolitical coherence neither financial means to realize suchendeavours. State redemption of the long distance opera-tion in 1934 was one exception to the rule.8

In 1971, the Nordic Telecom Conference, consisting of na-tional Post and Telegraph Administrations, initiated a re-search project on an automatic Nordic mobile telephone(NMT) network, which was going to set the foundation forthe consumer-oriented mobile communications. The Con-ference agreed upon the rules on the cross-border roaming,billing and, perhaps most notably, the openness of the tech-nical specifications. Based on their experience, the Confer-ence played an active role in initiating the Groupe SpecialMobile (GSM) in 1982, and in designing the pan-Europeandigital mobile network.

The introduction of the NMT in 1981–82 made the Nordiccountries the largest mobile market. The number of sub-scribers expanded at an unanticipated rate, exceeding theinitial capacity in a short time in all member countries. Themobile market started to attract also private operators,whose license applications were however rejected by the

regulator-PTO that pleaded to the natural monopoly natureof the market.

In fact, the dispute over the PTO’s monopoly rights had itsroots in the 1960s. The operative Imperial Telephone De-cree of 1886 could not provide an unambiguous interpreta-tion of the statutory rights to provide novel network ser-vices, such as data transfer, telefax and teletex. As a re-sponse to the intensifying dispute the new Telecommuni-cations Services Act was enacted in 1987, reflecting thestart of a new era in the telecommunications regulation.

For example, it separated the administrative and opera-tional functions of the PTO, transferring the regulatory au-thority to the Telecommunications Administration Centre,which was established under the Ministry. It also madepossible the license of Datatie, a joint venture of privateoperators and their main corporate clients, in 1988, repre-senting the first major chunk of the public monopolizedmarket allocated to the private sector.

The first amendment to the hundred years old TelephoneDecree was followed by a gradual but full liberalization ofthe telecommunications competition, finalized in 1994.

Having been repeatedly denied a license to operate anNMT network, private operators established with theirmain corporate customers a joint venture, Radiolinja. Itwas to operate a GSM network that was constructed andleased by local operators. This was made possible by thenew Act that authorized full telecom service provisionwithin concession areas. However, in order to provide na-tion-wide services Radiolinja needed a license.

The license application necessitated fundamental changesin the telecommunications regulation provoking a funda-mental political dispute – primarily ideological of nature.In 1991, Radiolinja, as the winner of the regulatory battle,was the first operator in the world to launch commercialGSM services.

The liberalization meant fundamental organizational andregulatory changes for the PTO. In order to be able to re-spond to the competition it was changed into a public cor-poration with no budget obligations to the government. Itlaunched GSM service soon after Radiolinja – thus, amongthe very first in Europe.

In 1994, the PTO was demerged, and Telecom Finland be-came a limited company with the State as the major share-holder. In 1998, the name of the company was changed toSonera to pinpoint the change in the strategic focus redi-rected to mobile services and technologies.9 The company

10

8 There were also occasional acquisitions of operators by the state, motivated by national defence and technical concerns.9 In 1999, the digital mobile services represented 60 per cent of the turnover.

underwent a quick metamorphosis from a national tele-phony operator to a global pioneer in Internet and mobileapplications.10 The Government has reduced its ownershipand indicated further privatization in due course.

3.3.2 The emergence of thetelecommunications industry

Unlike in many other countries, in Finland the equipmentmarket has always been open to competition. Up until the1980s, the market was dominated by leading foreign manu-facturers, like Siemens, Ericsson, and ITT. Attracted by themulti-operator market, they had set up production facilitiesin Finland. The established, capital-intensive foreign com-panies put a pressure on the emerging domestic industry.To illustrate, in 1970 the turnover of the Siemens Groupwas EUR 2 billion – almost equaling the total Finnish Statebudget of EUR 2.5 billion.11

The seeds of the Finnish radiophone industry were plantedin three companies, Salora, Suomen Kaapelitehdas, andValtion Sähköpaja in the 1920s. New radio technology wastypically developed in the sideline of main activities by fer-vent engineers, often under suspicion and opposition ofconservative colleagues. During a complex organizationalevolution process, finalized in 1987, the three companiesmerged under Nokia’s roof.

Salora (originally Nordell & Korhonen Ltd, established in1928) was a manufacturer of TV and radio sets, whosebrand grew strong beyond national borders. The develop-ment and production of radiophones initiated in 1964 wasbased on pioneering experiments conducted aside core ac-tivities. Salora’s accumulated experience in serial produc-tion and marketing proved valuable in the later mobilephone business development.

Suomen Kaapelitehdas (lit. Finnish Cable Works, foundedin 1917), in turn, was a producer of telecommunications ca-bles. The trade with the Soviet Union, originated during thedeliveries of war indemnities, was decisive to the develop-ment of the company’s technical skills. As a demandingbut patient customer, the Soviet Ministry of Communica-tions spurred elaboration of modern digital technology.

The radio laboratory of the Ministry of Defence (estab-lished in 1925) initiated public development and produc-tion of radio equipment. The wars against the Soviet Unionrevealed the strategic need for national development of ra-dio technology. After the wars, the activities were industri-alized by founding Valtion Sähköpaja (lit. State Electric

Works), and in 1948, merged with the R&D unit of thePTO. The company was renamed Televa, and in 1976, itbecame a state-owned limited company serving mostlypublic establishments for which it was the prime, but notexclusive provider.

In 1963, the Army gave a decisive stimulus to the domesticindustry by putting out an invitation for tenders for a radio-phone. This was the first in a series of impulses by whichthe Government provoked companies to exceed their ca-pacity to meet demanding technology requirements. Forthe first time the firms were given an economic motive todevelop a radiophone, generally regarded as a toy for amarginal group of users. In fact, rather than a business op-portunity, firms regarded the order as a chance to give aphysical form to the know-how accumulated in the “backstage” of core operations.

Virtually, the Army did not have the funds to redeem thephone, but for the bidding firms12 the prototypes served indeveloping new portable phones, which soon found theirway to export markets.

In 1966, Suomen Kaapelitehdas was merged with SuomenGummitehdas (lit. Finnish Rubber Works) and Nokia, a100 year-old wood grinding mill that gave its name to thenew corporation. The merger of Suomen Kaapelitehdaswith the companies in stable industries secured sustainedR&D investments in telecommunications, which was nowregarded as one of the strategic business areas of the com-pany.

In the 1970s, it became apparent that the market was toosmall and resources too scarce for parallel development ofdigital exchanges in both Televa and Nokia. Consequently,in 1977, the companies combined their R&D and market-ing efforts on digital transfer technology in a joint venture,Telefenno.

Lengthy and laborious R&D in digital technology led fi-nally, in 1982, to the introduction of the first domestic digi-tal exchange – shortly after the leading resource-intensivemanufacturers Ericsson, AlcateI, ITT and Siemens. It wasthe first fully digital exchange installed in the whole Eu-rope, and thus, served in convincing the market of the do-mestic competence vis-à-vis the foreign manufacturers.For years the exchange was the most successful export arti-cle of Nokia.

In 1979, Nokia and Salora, in turn, joined their comple-mentary resources. The fifty-fifty owned Mobira was setup to market and develop radio technology and especiallythe NMT terminal that was under design in the Nordic

11

10 For example, in December 2000, Sonera was awarded as the best mobile operator in the World Communication Awards 2000.Sonera was granted the award in recognition of its high-quality service and technological innovations. The company was alsoregarded as a European forerunner in developing new mobile communications services.

11 Mäkinen (1995).12 Televa, Suomen Kaapelitehdas, Salora, Vaisala and Swedish Sonab.

Telecom Conference. Mobira was the first to launch a ter-minal approved to the NMT network.

The design phase of the NMT standard in the 1970sbrought the Nordic telecommunications administrators andcompanies in close cooperation. While active in terminaldevelopment, the Finnish industry was not yet able to con-tribute to network specifications. Fierce pressure from thePTO’s side to engage the industry in cellular exchange de-velopment materialized finally, in 1981, in the base stationsupplied by Mobira. In the retrospect, it turned out to becrucial in maintaining the company’s position in theemerging market.

The introduction of the NMT in 1981–82 marked the startof a fast-expanding new industry. The specifications werekept open to pursue the objective of the Conference to pro-mote competition in equipment provision. No less than tenmanufacturers entered the Nordic market.

Following its vision of global mobile communications,Mobira took substantial risks in investing in large develop-ment projects and pioneering production techniques and inentering markets all over the world.13 By 1985, it had ob-

tained a leading position in a number of markets. Between1982–87, the average annual growth rate of sales was 50per cent, owing to both general market expansion and to anincreased market share.14

In order to intensify foreign market penetration, Mobira al-lied with established local actors.15 International coopera-tion taught the company, among other things, the impor-tance of the brand – which was later going to distinguish aNokia from other mobile phones in the challenging con-sumer market.

Mobira became famous for its “crazy” organizational spiritthat referred to the passionate, pioneering and risk-takingstyle with which is it pursued its ambitious targets.16 Thesame kind of stamina and general enthusiastic – if not fa-natic – attitude towards new radio technology has beenseen behind much of the technological progress in theFinnish telecommunications industry.

Virtually in 1986–87, the Finnish telecommunicationsknow-how was organized under one management whenNokia got full ownership of Mobira and the State’s share ofTelefenno.

12

0

10

20

30

40

50

60

70

80

90

100

1967 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99

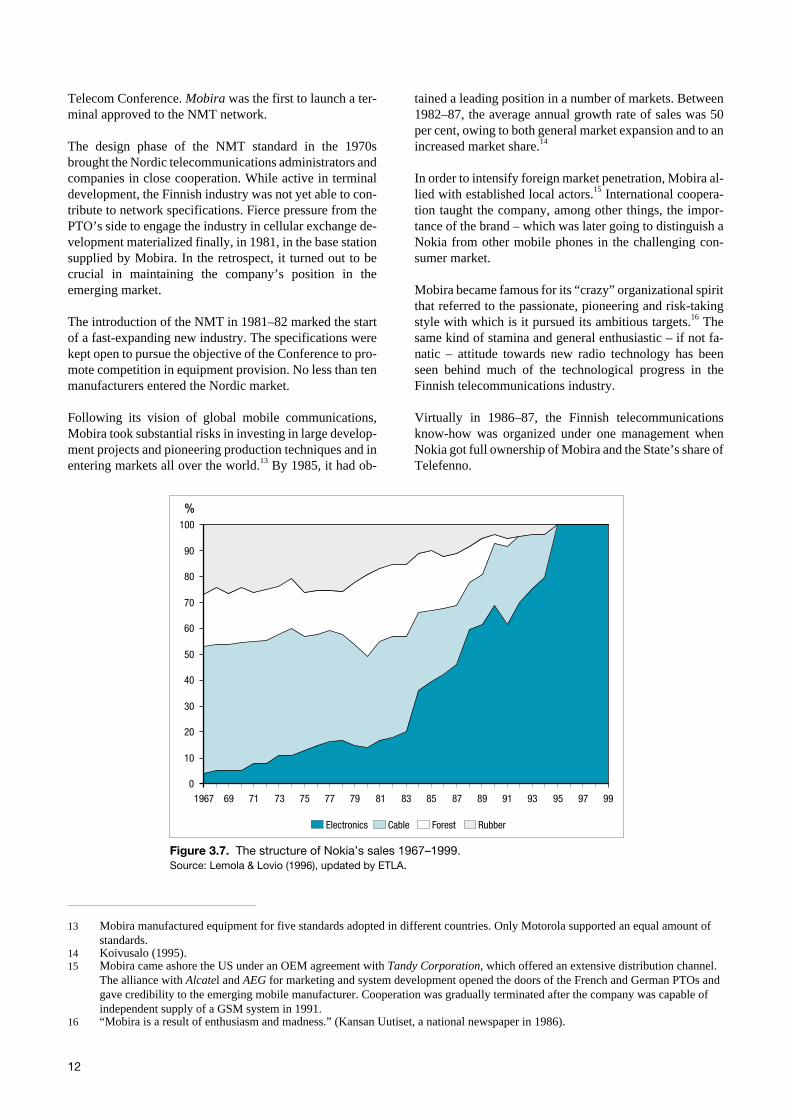

Electronics Cable Forest Rubber

%

Figure 3.7. The structure of Nokia’s sales 1967–1999.Source: Lemola & Lovio (1996), updated by ETLA.

13 Mobira manufactured equipment for five standards adopted in different countries. Only Motorola supported an equal amount ofstandards.

14 Koivusalo (1995).15 Mobira came ashore the US under an OEM agreement with Tandy Corporation, which offered an extensive distribution channel.

The alliance with Alcatel and AEG for marketing and system development opened the doors of the French and German PTOs andgave credibility to the emerging mobile manufacturer. Cooperation was gradually terminated after the company was capable ofindependent supply of a GSM system in 1991.

16 “Mobira is a result of enthusiasm and madness.” (Kansan Uutiset, a national newspaper in 1986).

In the search of rapid growth and global market presence,Nokia ran into serious production and financial difficultiesthat almost destroyed the company. Towards the end of thedecade, it started loosing positions in the export markets.The downturn was aggravated by the severe externalchocks, the collapse of the Russian bilateral trade and theabrupt economic recession, which put the future of Nokiaat stake.

The crisis gave a stimulus to a drastic dismantling of busi-ness sectors – varying from tissue paper and rubber bootsto cable machines and consumer electronics – preservingexclusively the telecommunications activities. The struc-tural changes were coupled with an important redesign ofthe company governance.

At the same time, however, the world witnessed a wave oftelecommunications liberalization. The boost in global de-mand for digital mobile equipment with Nokia’s global po-sition built in the 1980s saved the company from a dive thatwould probably have destroyed the company.

Owing to the recession hitting hard on consumer demand,it was crucial to dismantle the luxurious image of the porta-ble phone. With the softer aesthetic design and the user-friendlier customer interface Nokia was the first manufac-turer to invent the key to the consumer markets. Since thefirst consumer-targeted model in 1994, Nokia has high-lighted the life-style feature of communications in brandbuilding – a strategy that explains an important share of itsbreakthrough in the consumer market. In 2000, Nokia wasthe fifth most valuable global brand.17

In 1999, Nokia accounted for about a third of the world mo-bile phone market, and the phones represented almost 70per cent of the turnover. In network systems, the companyholds a market stake of close to 20 per cent.

3.4 The factors of the competitiveadvantage

In order to provide an analysis of the competitive advan-tage of the ICT cluster as suggested in chapter 3.1.1, thefactors involved will be briefly described below.

3.4.1 Firm strategy, structure and rivalry

Nokia dominates the ICT cluster by size and effect. Thecompany accounted for almost 50 per cent of the clustersales and 66 per cent of the cluster exports in 1998. How-ever, there is a number of other ICT companies that have

also established their positions in international markets.Moreover, many companies with their roots deep in theFinnish cluster have attracted foreign acquisitions (e.g.LK-Products, Martis, NK Cables, Solitra).

In the wake of the ICT boom there has been an intensiveemergence of start-ups finding narrow but lucrative nichesin the wireless and Internet applications sectors. Importantconquests have been made notably in the data security do-main. At the other end of the spectrum, there are estab-lished companies with accumulated world-class compe-tence particularly in network technology.

Despite the global business environment the core activitiesof companies, namely the headquarters and R&D, are stillpredominantly located in Finland.18 Established tradition incooperation in the local innovation system and advancedR&D activities anchor companies to their home base. Thefertile environment has attracted a number of leading for-eign companies to base their R&D centres in Finland, too(e.g. ICL, IBM, Siemens, Hewlett Packard, Ericsson).

Today, domestic competition has little effect on firm strat-egy. Competitors, regardless of their origins, operate glob-ally determining the scope and perspective of companystrategies. Unlike in a host of monopolized markets, theFinnish equipment industry has evolved under competitivepressure from the outset.

In network operation, the fragmented, yet monopolisticmarket structure has had implications on the market,non-existent in monopoly markets. For example, the pre-conditions for duopolistic competition were in place at theopening of the market, spurring price efficiency and ser-vice improvements that made the Finnish telecommunica-tions very competitive in international comparison.

The liberalization has affected the strategic relationshipswithin the private sector, as well. In the Finnet Group (thenewly named Association of Telephone Companies), therehave emerged regional alliances to form competing camps,while there are still joint ventures in nation-wide serviceprovision.

3.4.2 Factor conditions

Liberalization of the capital market in Finland at around theturn of the 1990s has revolutionized the institutional envi-ronment of corporate funding. Established structures ofpower concentrations and cross-ownership were disman-tled, providing firms an access to abundant internationalresources at market price.

13

17 Interbrand.18 Nokia, as an example, spends approximately 60 per cent of its R&D input in Finland (Ali-Yrkkö et al., 2000).

Between 1994–1999, the value of private capital invest-ments grew tenfold, to EUR 286 million.19 Perhaps mostnotably, the weight in risk ownership has been shiftingfrom the public to the private sector. The role of the state isbeen refocused on carrying the technology risk, while ven-ture capitalists have come to bear the commercial risk of anew company.

Unequalled opportunities for innovative start-ups haveopened up in the form of “intelligent” venture capital,which has actually become their most common source ofcapital. The share of the ICT sector was 30 per cent of thetotal private capital investments in 1999.20

The level of R&D investments on ICT has been in inten-sive growth. In OECD comparison, the share of privateICT-related R&D of total manufacturing R&D was thehighest in Finland in 1998. During the period 1991–97,Finland turned from a below-average investor into theworld leader. In the public sector there was an outspokenobjective in 1996 to increase systematically the share ofR&D expenditure of the GDP. Today it amounts to over 3per cent being the second highest share in the world afterSweden.

Thus, the critical factor in the development of the cluster isnot scarcity in capital but rather in human resources that isvirtually impeding full-scale exploitation of the availablefunds. There is a structural mismatch in available skills notonly on the macro level, but also within the cluster, notablyin the software industry owing to the fast pace of techno-logical development. Owing to the lengthy lead-time in ed-ucation, the increased intake in the education system hasnot yet alleviated the shortage of skills. Worse yet, the lackof employees draws both students and personnel fromhigher education institutions to the industry, eroding se-verely future resources.

3.4.3 Demand conditions

Since 1996, Finland has been the world leader in mobilepenetration. All in all, households have adopted mobilephones as consumer products: in 1999, they held morewireless terminals (78.5%) than wired (75.8%). 60 per centof households have both terminals, while no less than 20per cent rely solely on mobile communications.21 Also inInternet host penetration rate Finland ranked the second af-ter the US, by 121 per thousand inhabitants in 1999.22

Since the full liberalization in 1994, the telecommunica-tions price level has declined by about 25 per cent in realterms. The sharpest reductions have been witnessed in dig-ital mobile and data services making Finland the leader inlow-cost telecommunications services in the OECD in1998.23 Reasonable pricing together with the cheaper andconsumer-oriented handportables, introduced in the early1990s, boosted swift expansion of the market. Digitalvalue-added services were soon adopted by consumers andhave established their role in every-day communications.

The national attraction towards technology together withthe high level of basic education has been seen behindmuch of the communications boom in Finland. All thesame, the small home market has served as a test laboratoryfor the development of new products and services – despitethe fact that its importance to Finnish firms is decreasing inmonetary terms.

3.4.4 Supporting and related industries

In the recent years, the domestic supporting sector hasevolved very specialized for the needs of the originalequipment manufacturers (OEM). Customers’ growing re-quirements in production volume and product sophistica-tion have generated a number of new companies, and in-duced redirection of activities in the existing ones.

The strength of the domestic supporting sector is in highlycustomized inputs. Special competence resides in the pro-duction of ASIC, rf-filters, hybrid circuits, silicon wafers,printed circuit boards and their surface mounting technol-ogy, as well as in electronic manufacturing services, auto-mation, and precision mouldings. Standard components, inturn, requiring large scale and effective global distributionchannels, are practically fully imported.24

In the wake of Nokia, many of the suppliers have learnedfast the requirements of global operation and grasped theopportunity of rapid growth.25 Domestic partnerships havebeen stretched to foreign markets to benefit from estab-lished operative processes and trust-based relations. Globalextensions of domestic partnerships have involved suppli-ers’ green-field investments as well as acquisitions of thecustomer’s foreign production facilities.

The versatile and world-class supporting sector has greatlyenhanced manufacturers’ possibilities to contract out non-core activities. This has been imperative in the sector inwhich time-based competition and risks involved in con-

14

19 Holtron Ltd.20 Ibid.21 Ministry of Transport and Communications.22 EITO 2000.23 OECD (1999).24 92% of the electronic component market value is composed of imports (Hienonen, 2000).25 Eight suppliers, with Nokia as a prime customer, had gone public by the end of 2000.

tinuous technology race call for disintegration of the pro-duction process.

There is a trend towards growing responsibility of suppli-ers in independent product development by which manu-facturers seek to take advantage of specialized externalknowledge. Suppliers are being increasingly engaged inearly-phase product and production process design to pro-duce more effective and innovative solutions. Indeed, thescope of outsourcing has widened from mere standardoutsourcing to R&D activities.

The relative size of Finnish suppliers in global perspectiveis small. Global operations of customers, most particularlyNokia, put tremendous pressure on suppliers’ capabilitiesand resources. Any firm aspiring to be connected to the net-work will have to be able to grow in pace with the cus-tomer, which has direct bearing on the firm’s risk leverageand management skills required.

As a general rule, the presence of a competitive industrycontributes to the development of related industries. 26 As aprovider of infrastructure technology, the ICT cluster haslinkages to a number of industries providing service prod-ucts, or content, complementing basic network services.27

The digital content industry is still in its early phase in Fin-land, yet there are numerous signs of emerging activities.The notion of digital content embraces a whole array of ser-vice concepts, from transaction and information services toeducation and entertainment. Yet the borders of the ‘con-tent industry’ are difficult to draw, they can be regarded toinclude the ‘digitized products’ of a number of traditionalsectors (see figure 3.2). Non-fixed definitions severelycomplicate quantitative valuation of the industry.

In 1999, there was a group of some fifty firms in the gamesand entertainment software production that generated EUR10-12 million. Despite advanced technological skills, thisgroup still operates in the fringe of the software sector,lacking sectoral concentration and volume. In addition, thesub-sector tends to have difficulty in attracting profes-sional business skills as it suffers from low credibility ascompared with more “serious” software sectors.28 How-ever, technology leadership and new business models en-abled by the Internet (digital mass distribution) providegreat opportunities for the Finnish digital entertainment in-dustry.

All in all, it is clear that the most value-adding applicationsof the Internet and mobile services are still to come. Al-though entertainment will draw the largest demand vol-

umes, applications in, say, education and health care willbe likely among those enhancing the efficiency andwell-fare of the economy.

3.4.5 Government

The appropriate role of the government with regard to clus-ters is to create a context that encourages upgrading, andestablishes a stable economic and political environment.29

Even though all government actions matter for the nationalcompetitiveness, competition, technology and educationare the domains with most direct effects on the ICT clustercompetitiveness.

Competition policy. The competitive conditions in theFinnish telecommunications market – both in manufactur-ing and operation – have differed somewhat from the inter-national tradition. Not only have both the markets beenfragmented in ownership, but also there has not been an ex-clusive symbiosis between the PTO and a national cham-pion in equipment provisioning.

Through the Association of Telephone Companies the pri-vate sector grew a counterweight to the national monopoly,non-existent in most markets prior to the worldwide waveof liberalization in the 1990s. Deregulation and the marketopening were initiated among the first countries, soon afterthe UK and the US in the early 1980s. Thereafter, the regula-tory approach has based on pro-competitive, light-handedregulation and technology neutrality. The market is subjectto general competition and consumer protection legisla-tion.

The approach is still less interventionist than in many otherOECD countries; some mandatory EU requirements havebeen regarded as regressive to the liberal market function-ing of the Finnish market.30 Following the fortifying trendin national telecommunications policies, the Finnish gov-ernment is also looking for an opportunity to withdrawfrom telecommunications activities.

Technology policy. The purposeful orientation in technol-ogy policy has a twenty-year history, materializing in e.g.continuous growth in the R&D share of the GDP. Between1985 and 1999, the share doubled reaching EUR 3.75 bil-lion at the end of the period, of which 30 per cent was pub-lic investments. By the 3.1 per cent GDP share Finland po-sitioned the second in the world in R&D intensity afterSweden.

15

26 Porter (1990).27 A distinction is made between the industries exploiting the network in digital distribution of service products, and those

rationalising their business procedures (electronic business) with the ICT. ‘Related industries’ refer here to the former case.28 Autere, Lamberg & Tarjanne (1999).29 Porter (1998) as in Rouvinen & Ylä-Anttila (1999).30 Ministry of Transport and Communications (2000).

In the 1990s, amidst the general cutback objectives in publicexpenditure, the government decided, in 1996, to system-atize the increase in public R&D funding to sustain the posi-tive development of the electronics sector discernible by thetime. Part of the proceeds from privatization was earmarkedfor public funding of technology development. The objec-tive for the period 2001–2004 is to connect the increase inpublic funding to the general growth rate of the economy.

Digitized content and enabling software applications, askey factors in the ICT cluster’s future success, have beenappointed high status on the national agenda. Concur-rently, there has been a need to redirect the focus in publicfunding. From traditional technology-oriented product andprocess development there has been an extension in focus,towards service products and market-orientation to facili-tate the emergence of export-oriented service products.The shift in policy direction has been manifested in a seriesof digital media technology programs since the mid-1990s.

In addition, there has been a need to re-evaluate the role ofthe public sector in risk funding altogether. The emergenceof abundant private venture capital enables a more focusedpublic strategy in technology risk funding, and a clearerrole differentiation with the private sector financiers. In ad-dition, through technology programs, the public sector hasbeen active in practicing the role of a facilitator betweenfirms and venture capitalists.

Education policy. The threat of exhausted labor resourceshas been attacked by increasing openings in higher educa-tion institutions. Between 1993–98, the total intake in uni-versities grew nearly twofold and in polytechnics nearlythreefold. However, established institutional structures aswell as resources lagging behind increased utilization ofeducational capacity seem to frustrate efficient achieve-ment of policy objectives.

The dialogue between the industry and the government oneducational issues has been active since the upsurge of theindustry. In the early 1998, the government adopted a pro-gram for increasing education in the information industryfields between 1998–2002. The industry has committed it-self to its implementation by providing internships, butavoiding recruitment of under-graduates, and encouraginggraduation of employed students. Moreover, companies aimat increased participation in training and education, and do-nation of equipment for education and research purposes.

3.4.6 Coincidental factors

The turn of the 1990s entailed several external incidentswith momentous implications on the Finnish ICT cluster,without which, it is fair to say, the average 30 per cent an-

nual growth rate of the electronics industry would not havematerialized.

Following the agreements within the EU and the WTO, thetraditionally monopolized telecommunications equipmentand service markets were gradually liberalized, startingwith terminal equipment in 1988 in Europe. The opening ofthe East European market gave an additional boost to mo-bile equipment demand.

The effects of liberalization were momentous. Between1990–98, the value of OECD exports of telecommunica-tions equipment grew almost 2.5-fold, reaching USD 110billion at the end of the period.31 Correspondingly, 96 percent of the OECD market, as measured by telecommunica-tions revenue, was open to competition by the beginning of1999.32

In contrast, the collapse of the Soviet Union together withthe severe recession in Finland hit hard on the ICT clusterdemand in the early 1990s. Without the counterbalancingeffects of market liberalization, the Finnish economywould have taken a somewhat different and slower path inits revival process.

3.5 Dynamics in the ICT cluster

The ICT cluster has been evolving for a hundred years. Thecluster as we see it today looks like a product of a masterplan: a vigorous industrial innovation system with high na-tional competitive advantage. However, it is an outcome ofa dynamic self-reinforcing process in which coincidentalfactors do not play the least consequential role.

In order to get a grasp on the factors behind the ICT clusterdevelopment, the most influential dynamic linkages be-tween the factors of competitive advantage will be ana-lyzed within the framework suggested in chapter 3.1.1. It isobvious that the causes and the effects of interactive factorsbecome blurred and ambiguous, but the framework helpsin providing some systematic in the analysis.

3.5.1 The government as an early catalystof cluster development

The earliest and perhaps most influential factors on clusterdevelopment relate to those government policies that havepromoted competitive market structure.

The foundation of the developed telephony infrastructurewas laid already in the 19th century, under the Tsar’s reign.

16

31 OECD (1999) and OECD trade statistics.32 ITU (1999). The remaining six countries are committed to liberalisation in coming years.

By dividing the network ownership between public andprivate companies, and allowing for a fragmented marketstructure, the Finnish Senate, yet motivated by foreign-pol-icy objectives, contributed more or less unintentionally tothe industry development in a crucial way. The decentral-ized market catalyzed several dynamic implications.

To begin with, the decentralized ownership contributed tothe technical improvement of the infrastructure. First, thecontinuous threat of nationalization of incompetent opera-tors spurred technological upgrading in the private net-work. There were several intentions, throughout the de-cades to nationalize the whole private sector in view of im-proving the technical level of the heterogeneous infrastruc-ture. These proposals were however dismissed due to thelack of political consensus and financial means.33 Second,as cooperative societies, the telephone companies pursuedthe interests of their owners through technical improve-ments and cost-based pricing. Third, as important commu-nal status symbols, telephone companies pursued latesttechnology to promote community authority.

Furthermore, the multi-operator market structure, coupledwith another local peculiarity, free equipment supply, hadfar-reaching dynamic repercussions. The competitive mar-ket regarded as a test laboratory attracted contemporaryleading manufacturers. Not only did their presence stimulatelocal economy through local production facilities andknow-how spillovers to the emerging industry, above all, itspurred operators’ skills in interface technology, required inrendering the competing vendors’ equipment compatible.