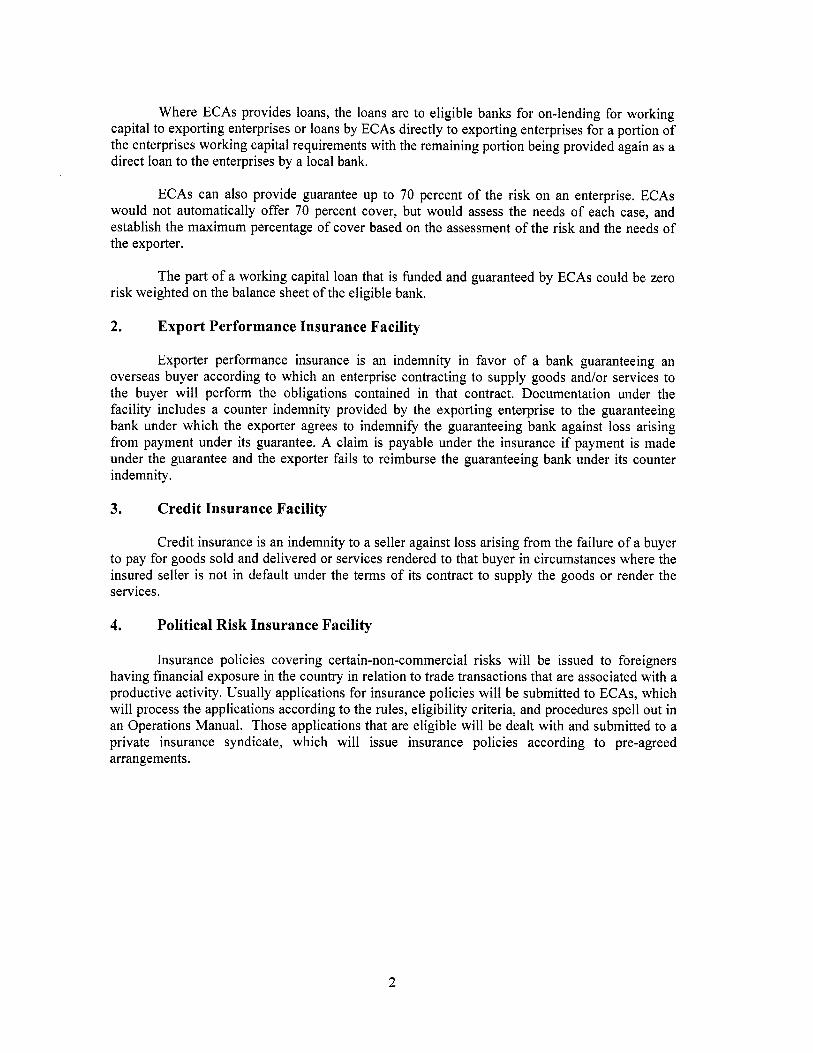

Georgia An Integrated Trade Development Strategy

170

November 5, 2003 Document of the World Bank Report No. 27264-GE Georgia An Integrated Trade Development Strategy Poverty Reduction and Economic Management Unit Europe and Central Asia Region Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

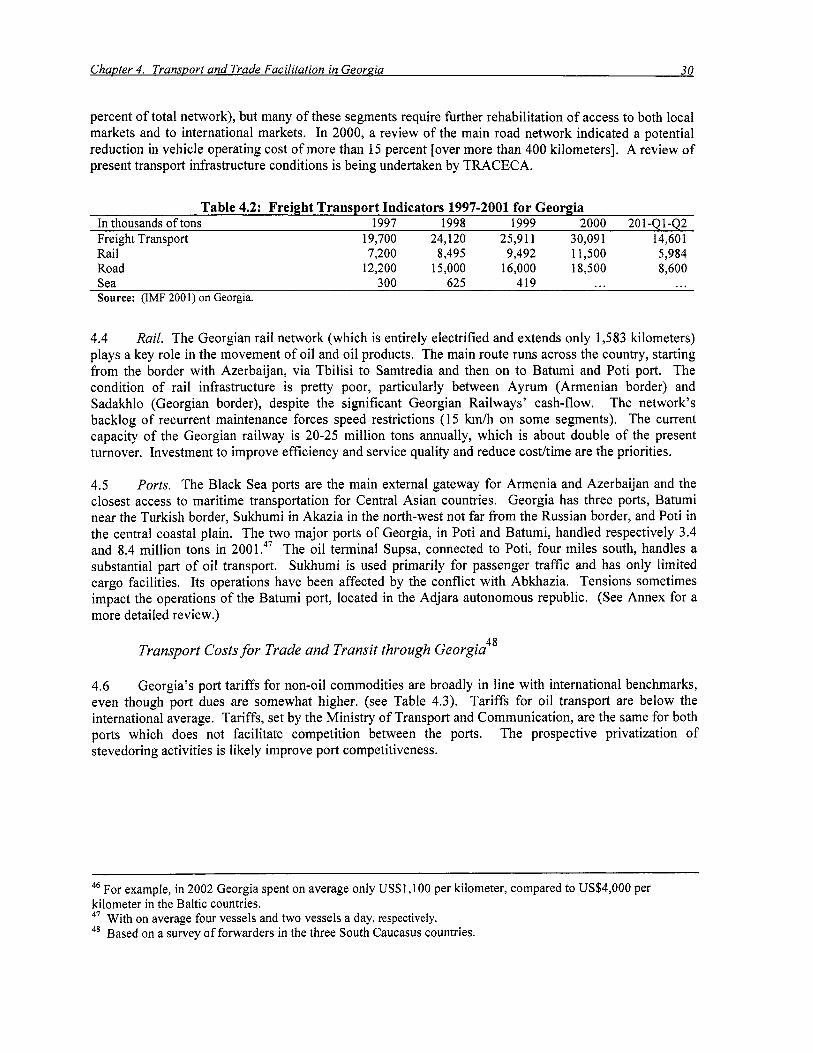

Upload

khangminh22 -

Category

Documents

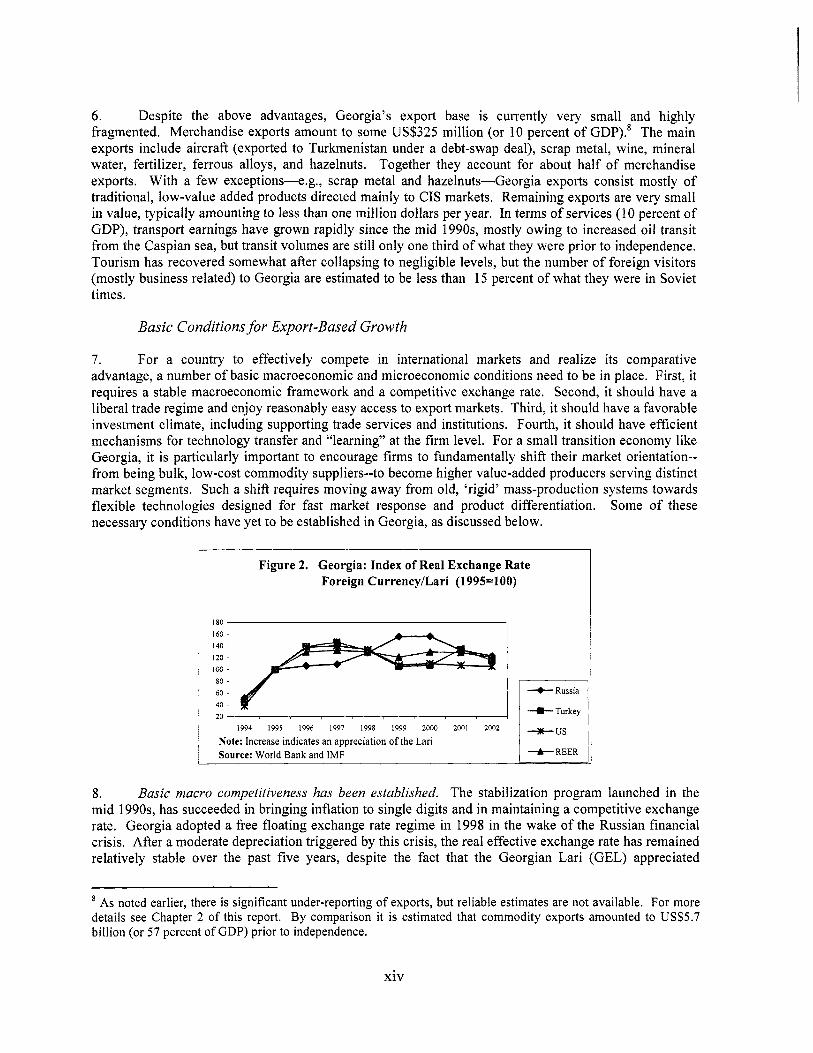

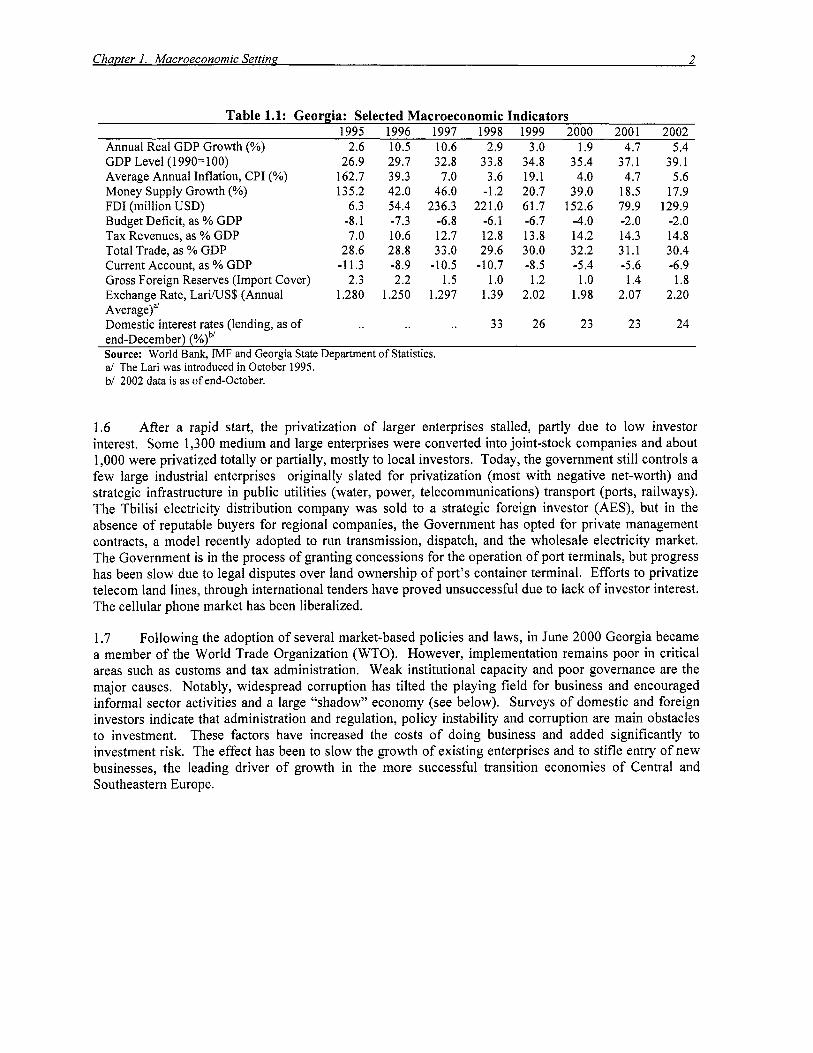

-

view

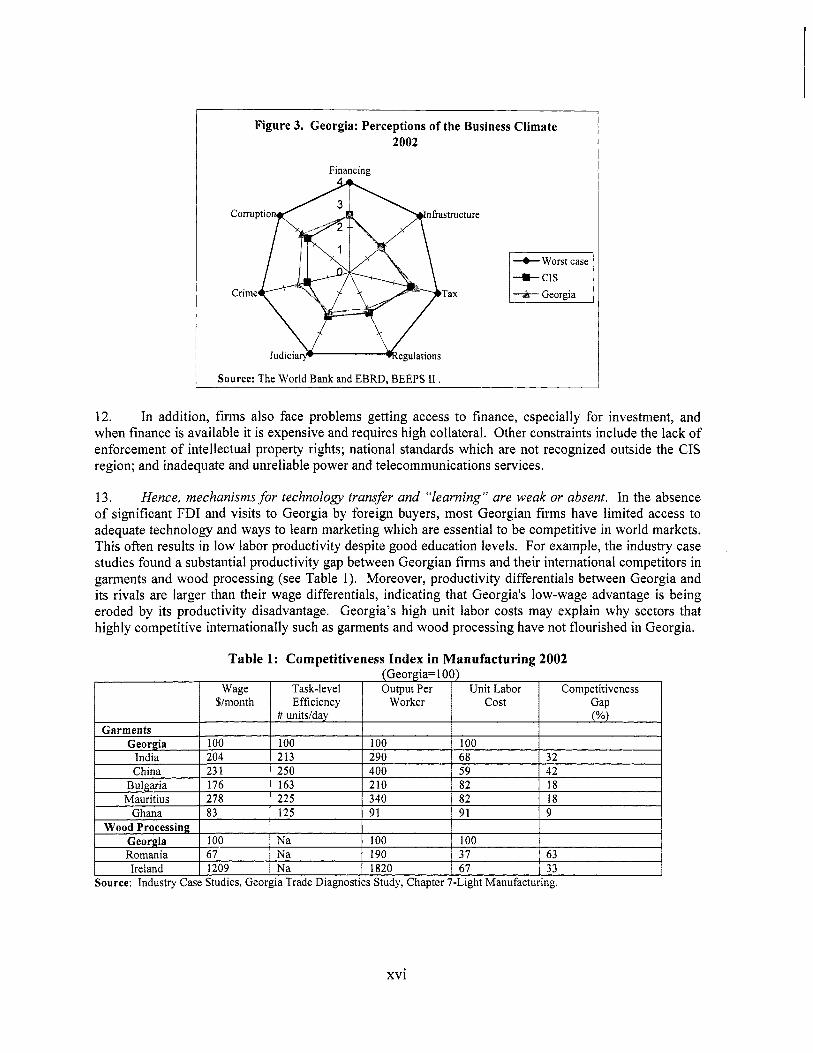

1 -

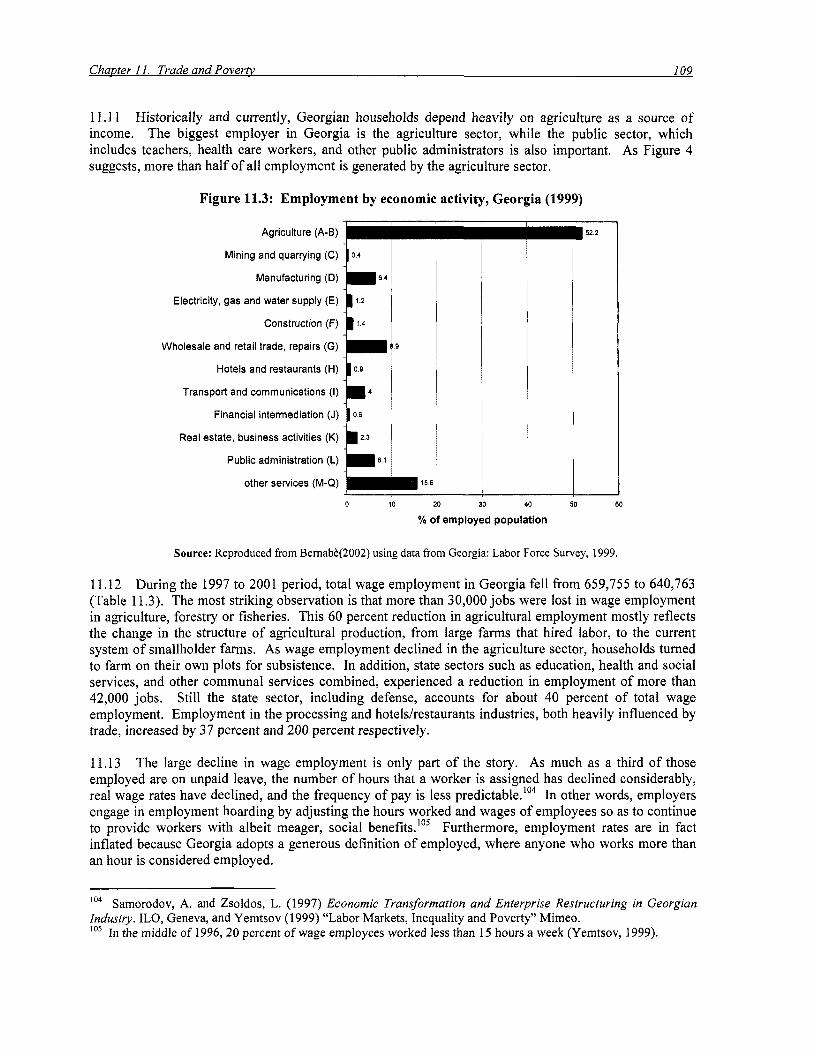

download

0

Transcript of Georgia An Integrated Trade Development Strategy

November 5, 2003

Document of the World BankR

eport No. 27264-G

EG

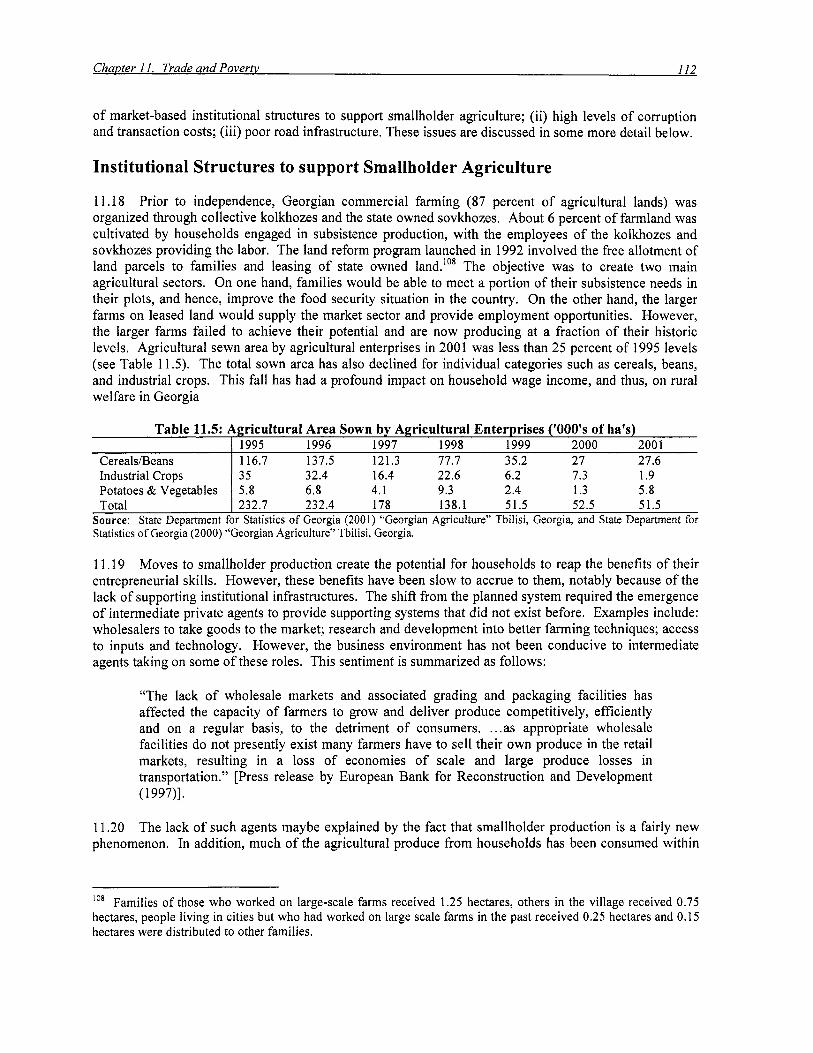

eorgiaA

n Integrated Trade Developm

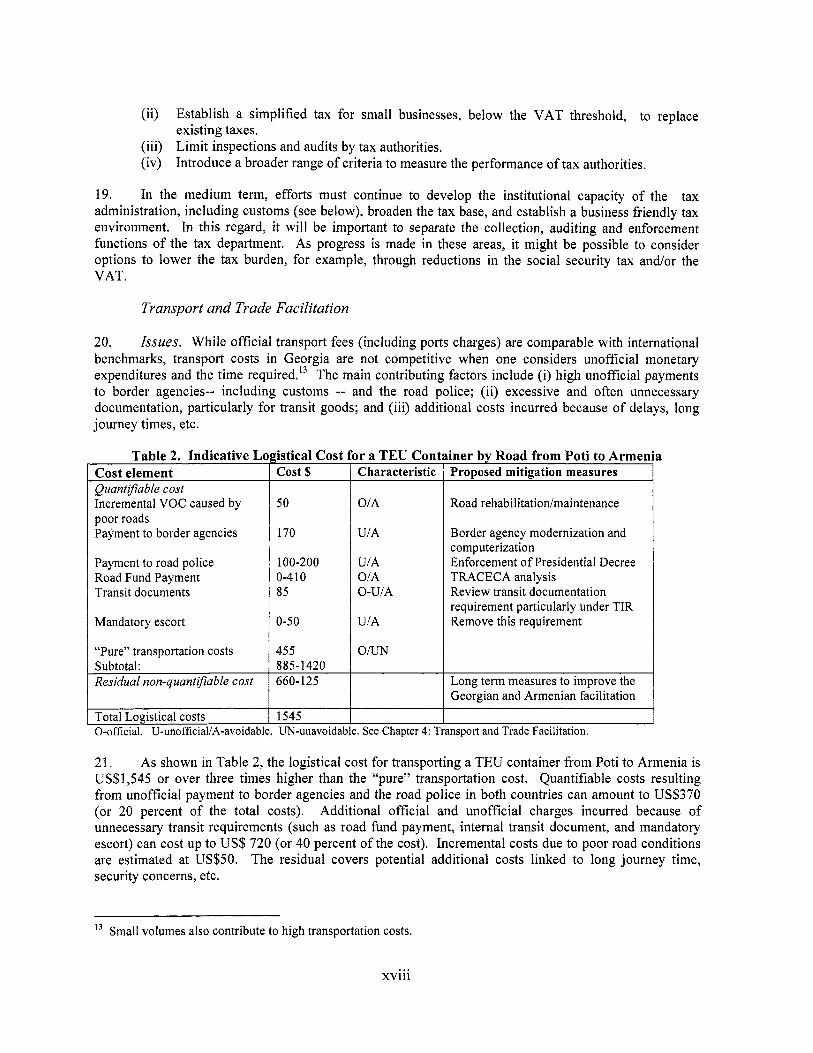

ent Strategy

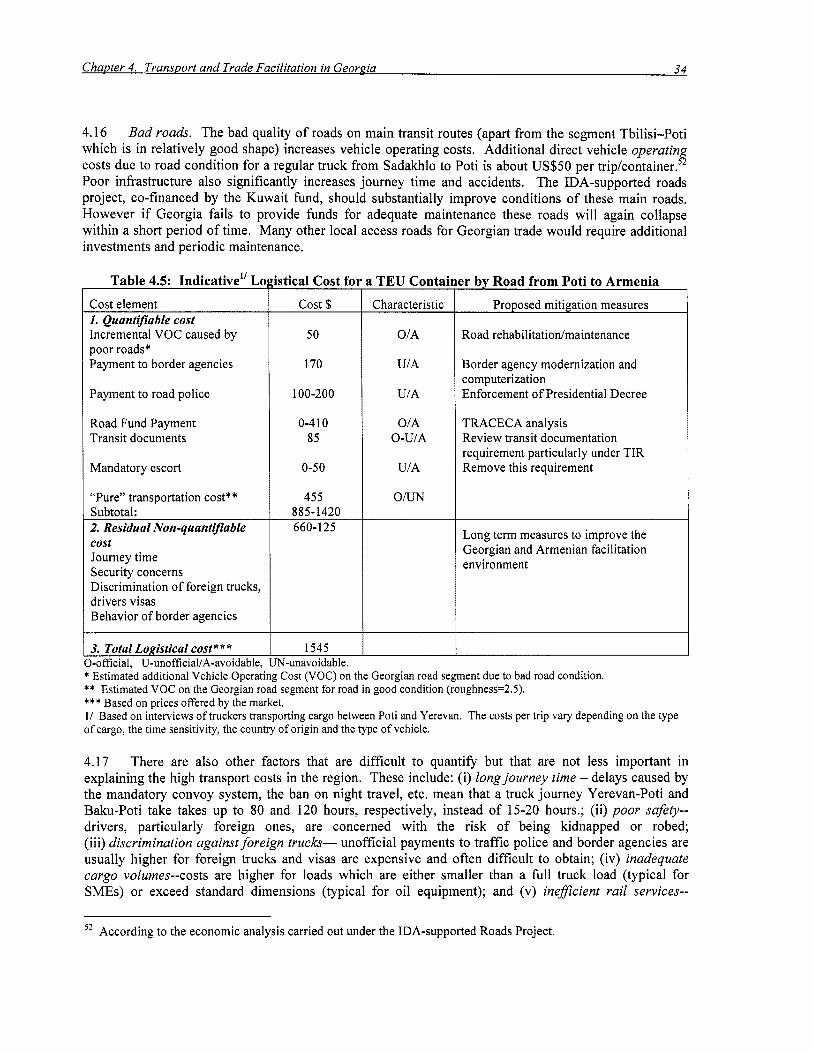

Report No. 27264-GE

GeorgiaAn Integrated Trade Development Strategy

Poverty Reduction and Economic Management UnitEurope and Central Asia Region

Pub

lic D

iscl

osur

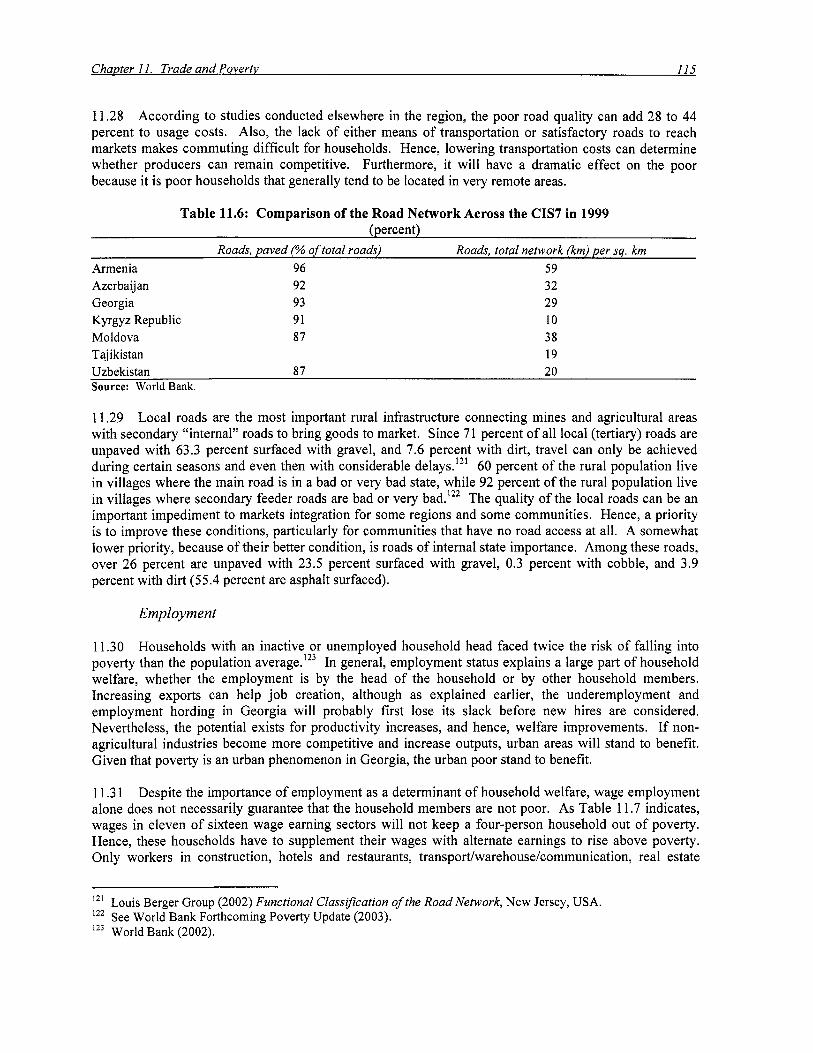

e A

utho

rized

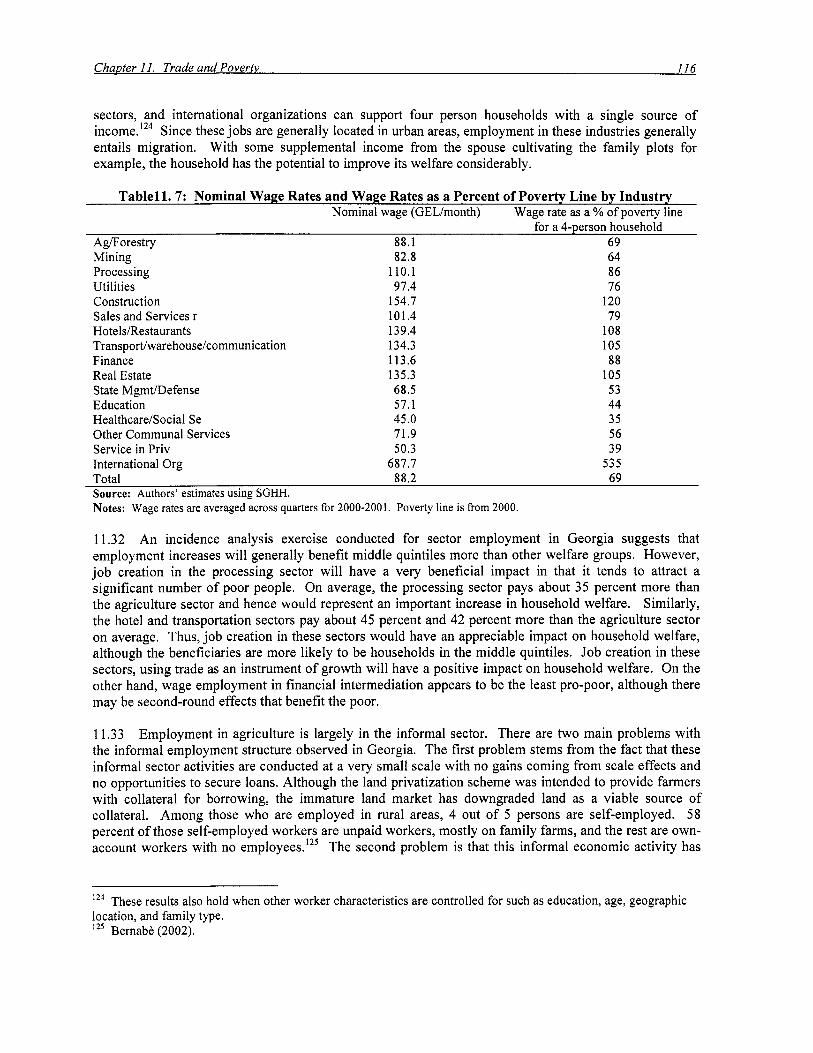

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

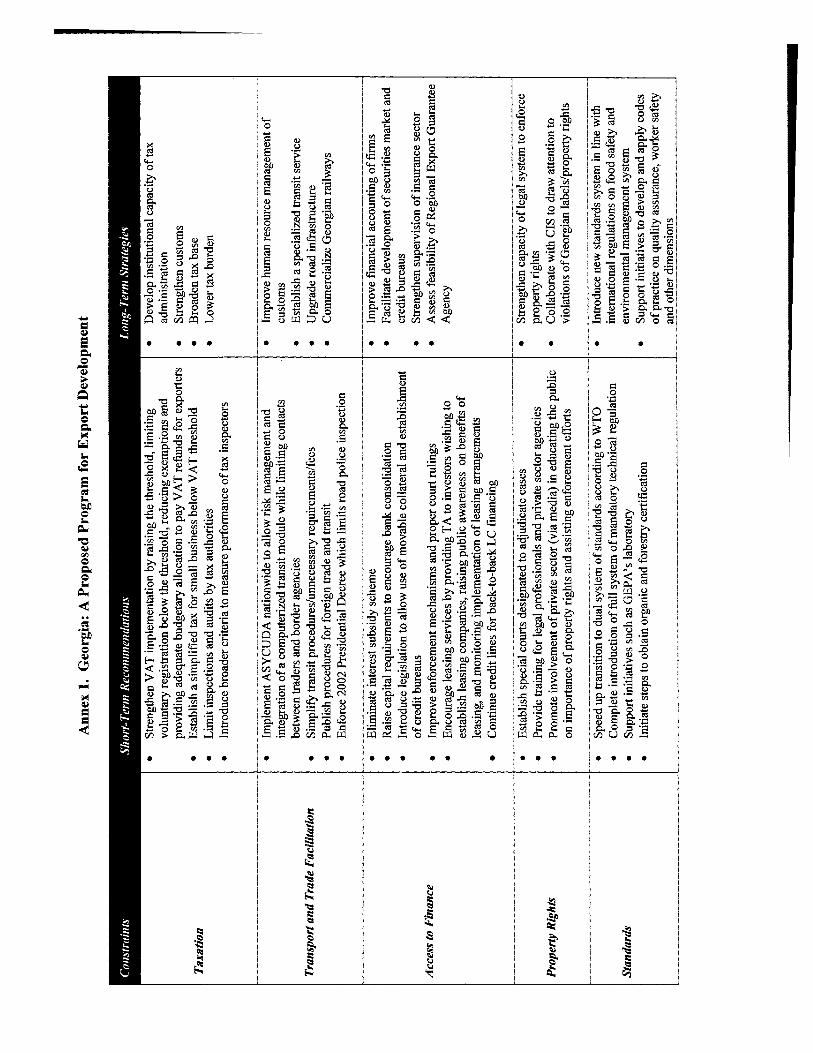

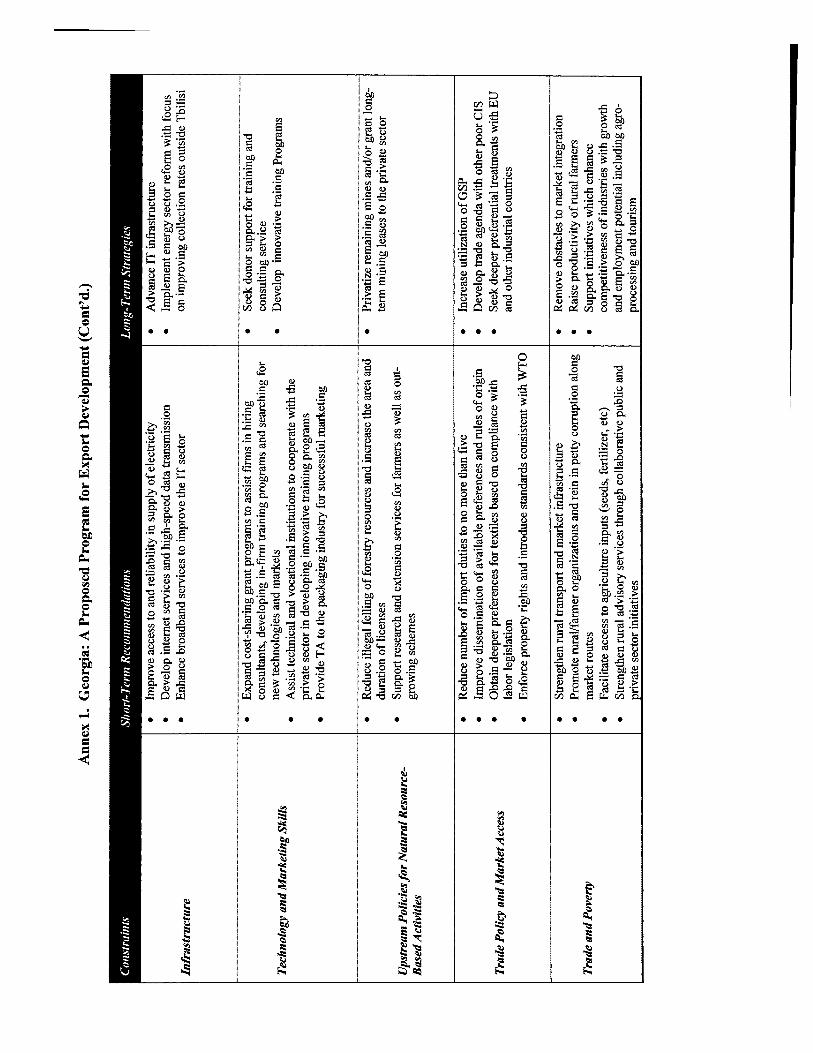

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ADR ADP AES AJC ASYCUDA BEEPS BTC CCOF CDB CEE CERMA CIF COMTRADE CIS CNC CMR CMT CODEX COMECON CPI DSA EBRD ECA ECAs ECMT EDPFU' EGA EU EUR FA0 FDA FDI FSC FIAS FOB FSU

CURRENCY AND EQUIVALENT UNITS (Exchange Rate Effective as of November 5,2003)

Currency Unit = Lari US$1 .OO = GEL 2.10690000

WEIGHTS AND MEASURES Metric System

FISCAL YEAR January 1 to December 3 1

ACRONYMS AND ABBREVIATIONS

Accord Dangereux Routiers Agricultural Development Project The AES Corporation Apple Juice Concentrate Automated System for Customs Data Business Environment and Enterprise Performance Survey Baku-Tbilisi-Ceyhan California Certified Organic Farmers Cost of Doing Business Central and Eastern Europe Center for Enterprise Restructuring and Management Cost, Insurance and Freight United Nations Commodity Trade System Commonwealth of Independent States Computer Numerically Controlled Cargo Manifest Report Cut-Make-and-Trim Codex Alimentarious Commission Council for Mutual Economic Cooperation Consumer Price Index Debt Sustainability Analysis European Bank for Reconstruction and Development Europe and Central Asia Export Credit Agencies European Conference of Ministers of Transport Economic Development and Poverty Reduction Program Export Guarantee Agency European Union Euro Food and Agriculture Organization Food and Drug Administration Foreign Direct Investment Forestry Stewardship Council Foreign Investment Advisory Service Free on Board Former Soviet Union

.. 11

FTA GATT GBC GDP GEL GEOPRO GEPA GEPLAC GIC GHA GMP GNFS GOG GOST GSP HACCP IDA IFC IF1 IMF I S 0 IT ITB L/C LDCs LIBOR LPG MDF MEITT MFN MIGA MoF MOT NBG NTA OECD OPIC PCA PER REER SAMTREST SCD SDTR SDS SGHH SGMS SMEs TACIS TBT TEU TIR

Free Trade Agreement General Agreement o f Tariffs and Trade Georgian Business Confederation Gross Domestic Product Georgian Lari Georgian Pro-Committee for Trade and Transport Facilitation Georgian Export Promotion Agency Georgian-European Policy and Legal Advice Center Georgian Investment Council Georgia Hardwoods Association Good Manufacturing Practice Goods and Non-Factor Services Government of Georgia Gosudarstrennyi Standarty-ex-Soviet System of Standards Generalized System o f Preferences Hazard Analysis o f Critical Control Points International Development Association International Finance Corporation International Financial Institution International Monetary Fund International Standard Organization Information Technology Internationale Tourismus - Borse Letter o f Credit Less Developed Countries London Inter Bank Offering Rate Liquefied Petroleum Gas Medium Density Fiberboard Ministry o f Economy, Industry, Trade and Tourism Most-Favored Nation Multilateral Investment Guarantee Agency Ministry o f Finance Ministry o f Transport National Bank o f Georgia National Tourism Authority Organization for Economic Cooperation and Development Overseas Private Investment Corporation Partnership and Cooperation Agreement Public Expenditure Review Real Effective Exchange Rate State Industry Corporation for Viticulture and Winemaking State Customs Department State Department for Tourism and Resorts State Department o f Statistics Survey o f Georgian Household Agreement on International Railway Freight Communications Small and Medium Enterprises Technical Assistance to the Commonwealth o f Independent States Technical Barriers to Trade Twenty-foot Equivalent Unit Transport International Routier

... 111

TLE TRACECA TRIPS TS TTF UAE UNCTAD UNDP USAID VAT voc WTM WTO

Task Level Efficiency Transport Corridor Europe, Caucasus, Central Asia Trade-Related Intellectual Property Rights Transit Service Trade and Transport Facilitation United Arab Emirates United Nations Conference on Trade and Development United Nations Development Program United States Agency for International Development Value Added Tax Vehicle Operating Cost World Travel Market World Trade Organization

Country Director: Donna Dowsett-Coirolo Sector Director: Cheryl W. Gray Sector Manager: Samuel Otoo

i v

CONTENTS

.. EXECUTIVE SUMMARY .............................................................................................................. vi1

CHAPTER 1 . Macroeconomic Setting .............................................................................................. 1

Stabilization and Structural Reforms .............................................................. 1 The Economy ................................................................................................... 3 Poverty ............................................................................................................. 5

International Price Competitiveness ...................................................................... 6 The Business Climate ............................................................................................ 8

Recent Economic Developments ........................................................................... 1

CHAPTER 2 .

CHAPTER 3 .

CHAPTER 4 .

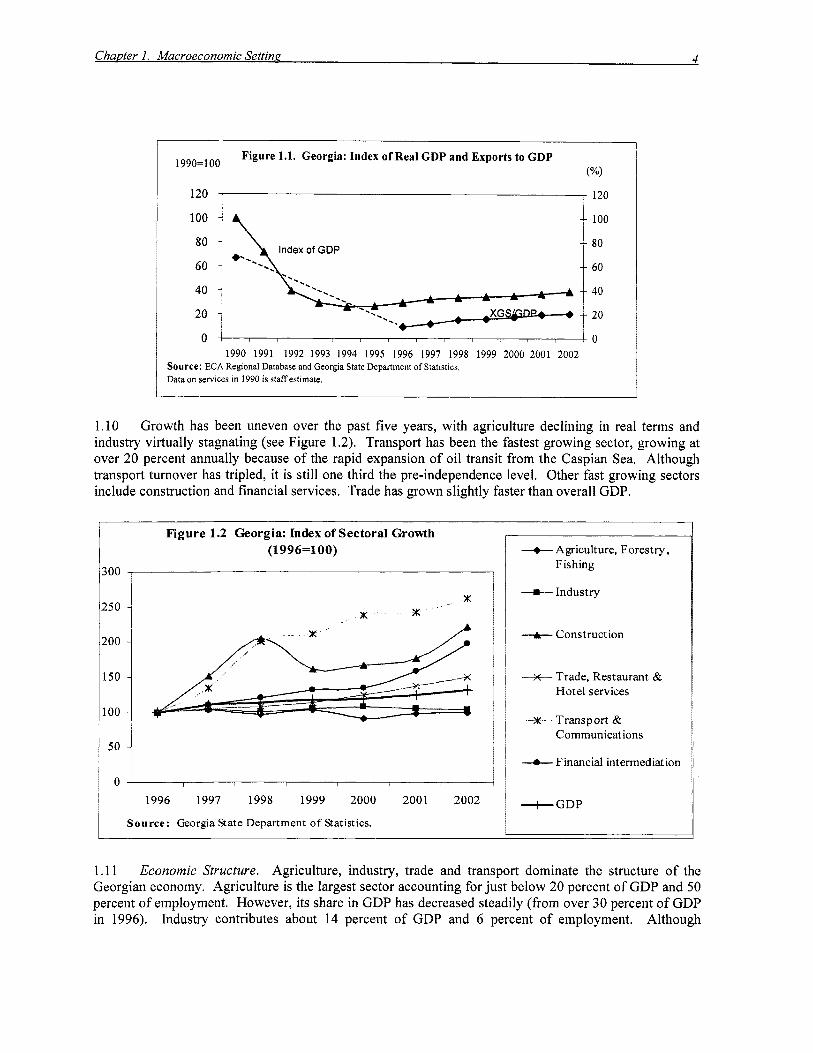

Trade and Investment Performance ....................................................................... 11 External Trade ..................................................................................................... 11

Merchandise Trade. ....................................................................................... 1 1 Trade in Services ..................................................................................

Private Income and Transfers ....................................................................... 16 Foreign Direct Investment (FDI) Flows ...............................

Trade Policy and Market Access ............................................................................ -18 The Trade Regime ................................................................................................ 18

Import Regime ................................ ......................................................... 18

The Investment Regime ................

Free Trade Agreements with CIS Countries .............................. Market Access to Non-CIS Countries. ...............

Georgia’s Accession to the WTO ................................................ Post-Accession Issues ...........................................................

Export Regime ...................................................

Terms of Market Access ....................................

.................... 23 Relations with the WTO ....................................

Trade and Investment Related Institutions ........................................................... 26 Conclusion ........................................................................................................... 28

Transport and Trade Facilitation in Georgia ........................................................ 29 International Transport Analysis .......................................................................... 29

Transport Sector ......... ............................................................................. 29

Explanatory Factorsfor Excess Transport Costs ......................

Current Transit .................................................................. The Future of Transit ......................................... West-East Transit ............................... ................................... 36 East- West Transit .................................................................. ........ 37 Potential Impact of Conflict Resolutions in the Region ........................... 37

Proposed Strategy and Recommendations ........................... ........................... 38 Institutional Development o f Border Agencies .................................................... 38

Transport Costs for Tr and Transit through Georgia ..........

Current and Potential Transit ............................................................................... 35 ...

..............

Implementation of Customs Reform ............. ........ ........... . 38 Upgrading Transport Infrastructure ..................................................................... 41

V

CHAPTER 5 . Finance Support Services ......................................................................................... 42 The Financial System ........................................................................................... 42

The Banking Sector ........................................................................................ 43 Export Finance ..................................................................................................... 47

Government’s Initiatives to Increase Access to Finance ............................... 48 Conclusion ........................................................................................................... 50

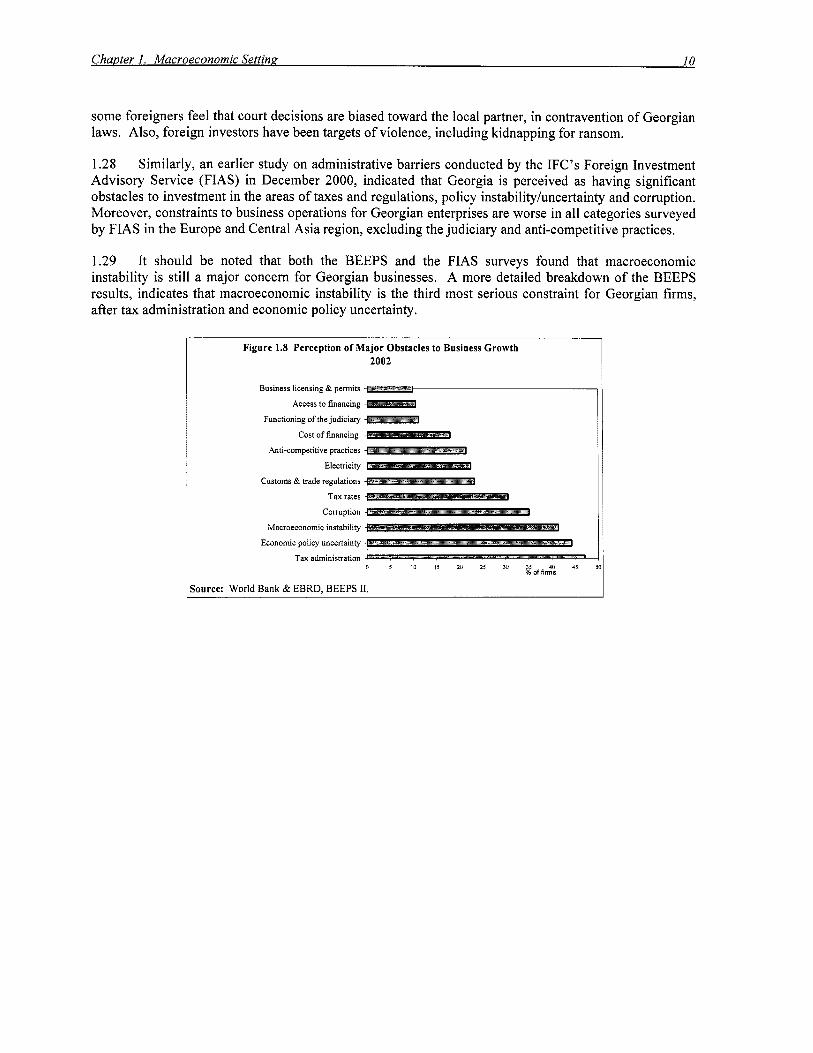

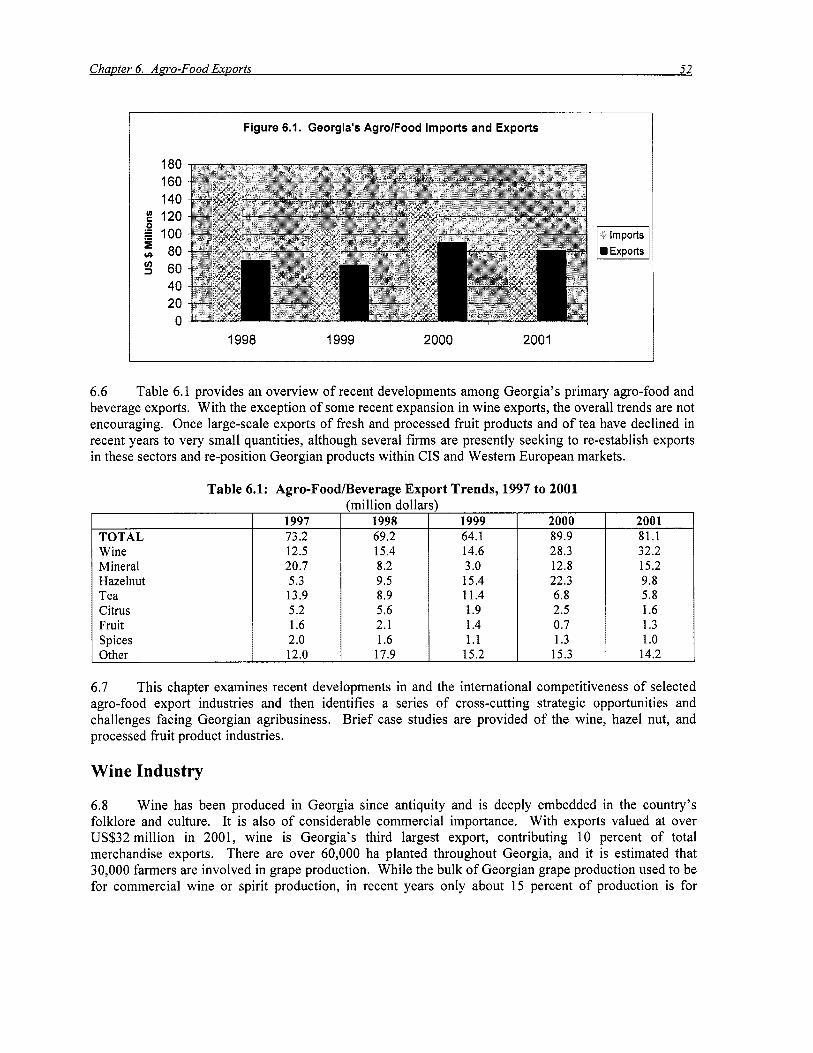

CHAPTER 6 . Agro-Food Exports ................................................................................................... 51 Introduction .......................................................................................................... 51 Wine Industry ....................................................................................................... 52

Grape Supply ...................................... ................................ 53 ............................................... 55

.............................. 56 ................................................................. 57

Hazelnut Sector .................................................................................................... 59

Number and Size of Vintners Industrial Efficiency .............

Production ...................................................................................

Markets .................................... .............................................. The Role of Government ..............................................

Industry Efficiency., ........................... ...........................

Processed Horticultural Products ......................................................................... 64 Crop Production ............................................................................................ 64 Industry Efficiency ....................................................................... Markets ........................................................................... ........................... 66 The Role of Government ................................................. ........................... 67

Strategic Orientation for Georgian Agribusiness ................................................. 68

Light Manufacturing ................................................................................................ 70 Garments Industry ................................................................................................ 70

CHAPTER 7 . Industry Characteristics ..................................................... Productivity .................................................

Wood Processing Industry ........................................ Other Constraints ...............................................

Industry Characteristics ............

Access to Inputs and Equipment .......... Productivity and Market Segment . A Strategy for the Wood Industry .. Government Policy: Access to Timber and Developing Strategic Marketing and Produ

Challenges in Realizing Opport ....................... 75

Raising Eficiency at the Firm Level ...........

CHAPTER 8 . Mining and Mineral-Based Exports ....................................................................... 84 Industrial Minerals ............................................................................................... 84

Export Opportunities and Proven Reserves .... ................................ 84 Upstream Government Policy ......................... ........................... 84 Downstream Constraints .................................

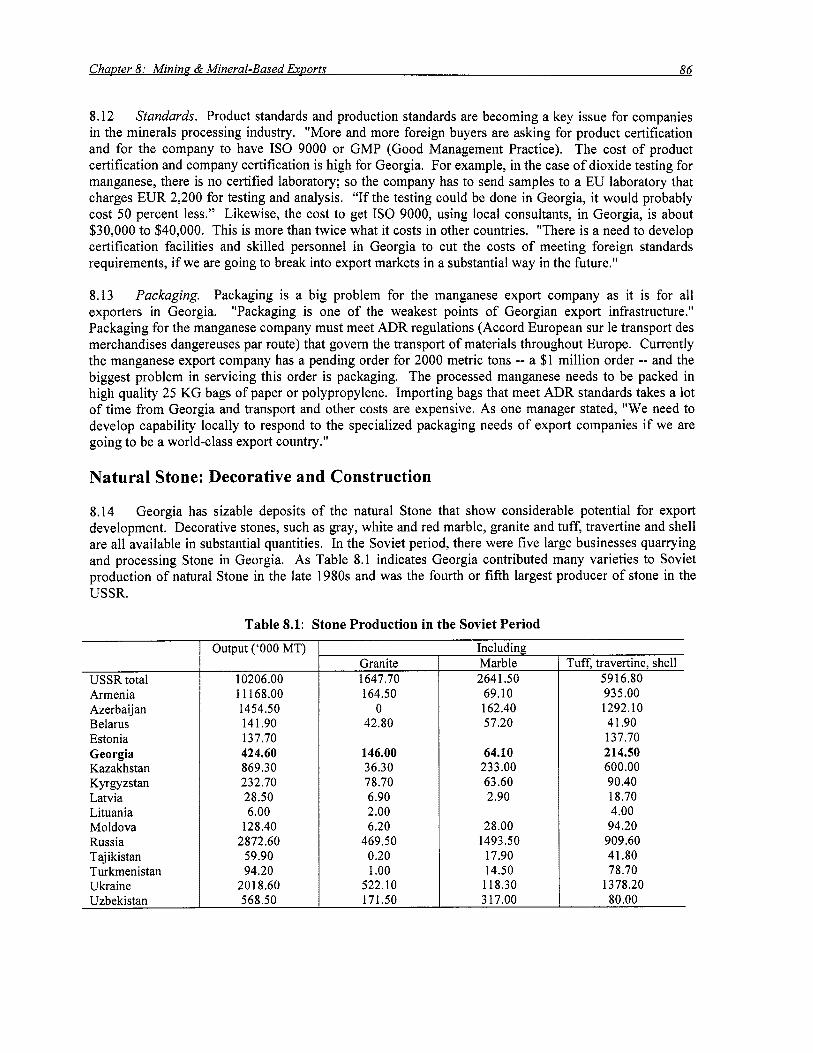

Natural Stone: Decorative and Construction ....................................................... 86 Access to Raw Material ................................................................................. 87 Technology ................................................................................. Marketing and Connections with Foreign Investors ................................ 88

vi

CHAPTER 9 . Services Exports .................................. . ............................ ....... ................................ 89 Information Technology ...................................................................................... 89

Labor .......................................................................................... Intellectual Property Rights .................................................

........................................ ...................................... 91 nd Administration .....................................

Engineering Services ........................................................................................... 92

Technology and Standards .. Corruption ........................... ..................................... ........................... 94 Tax Policy and Administration ...................................................................... 94

Labor ............................................................................................................. 93 ..................................................................... 93

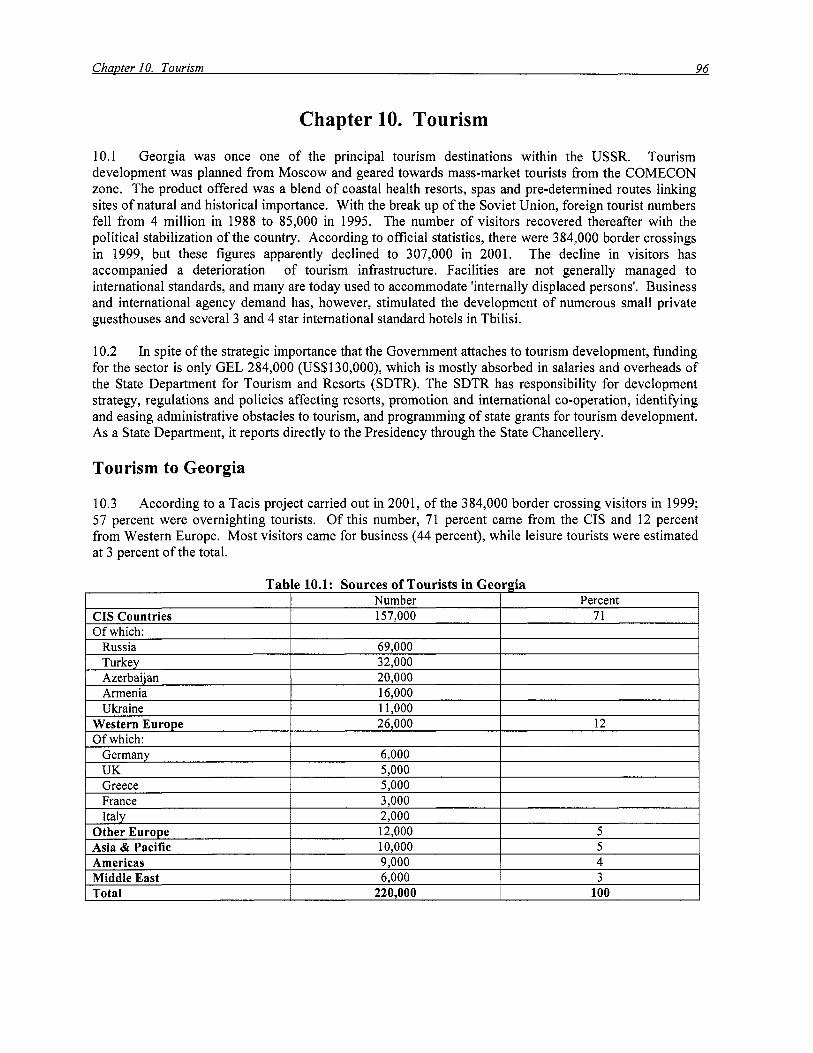

CHAPTER 10 . Tourism ................................................................................................................ 96 Tourism to Georgia .............................................................................................. 96 Opportunities for Tourism Growth ...................................................................... 97 Cross-cutting Barriers to Export Growth ............................................................. 97 Barriers Specific to the Tourism Industry ............................................................ 98 A Strategy for Tourism Development ................................................................ 102

Target Markets .............................. ..................................... 102 Entrepreneur Support ................................................................ National Tourism Marketing Authority .......................... Destination Marketing ................... Accommodation ............ .................................................. Attractions .......... ............................... ................... 104 Information .................................................................................................. 105 Quality ......................................................................................................... 105 Donor Co.ordination ..................................................... .................... 105

CHAPTER 11 . Trade and Poverty .................................................................................................. 106 Introduction ....................................................................................................... 106 Poverty in Georgia ............................................................................................. 106 Sources o f Household Income ........................................................................... 107

Labor Market ............................................................................................... 108 Internal Market Integration ................................................................................ 110 Institutional Structures to Support Smallholder Agriculture ............................. 112

Corruption ................................................................................................... 113 Rural Roads ................................................................................................. 114 Employment ................................................................................................. 115

Conclusion ......................................................................................................... 117

Map IBRD

vii

Tables

Table 1.1 Table 1.2 Table 1.3 Table 2.1 Table 2.2 Table 2.3 Table 2.4 Table 2.5 Table 2.6 Table 2.7 Table 3.1 Table 3.2 Table 4.1 Table 4.2 Table 4.3 Table 4.4

Table 4.5 Table 5.1 Table 5.2 Table 5.3 Table 5.4 Table 5.5 Table 6.1 Table 6.2 Table 6.3 Table 6.4 Table 6.5 Table 6.6 Table 6.7

Table 7.1 Table 7.2 Table 7.3 Table 7.4 Table 7.5 Table 7.6 Table 7.7 Table 7.8 Table 7.9 Table 7.10 Table 8.1 Table 10.1 Table 10.2 Table 11.1 Table 11.2 Table 11.3 Table 11.4 Table 11.5

Georgia: Selected Macroeconomic Indicators ............................................................. 2 Georgia: Share ofthe Shadow Economy ..................................................................... 5 Georgia: Key Non-tradable Costs, 1996-2002 ............................................................ 7 General Trade Statistics - Comparison of Data Sources ............................................ 11 Georgia: Trade Balance, 1994-2002 .......................................................................... 12 Georgia: Major Export Categories ............................................................................ 13 Georgia: Major Import Categories ............................................................................ 14 Georgia: Transport and Travel Services .................................................................... 15 Georgia: Foreign Direct Investment .......................................................................... 15 Georgia: Private Income and Transfers ..................................................................... 17 Georgia: 2003 Import Tariff Schedule ...................................................................... 19

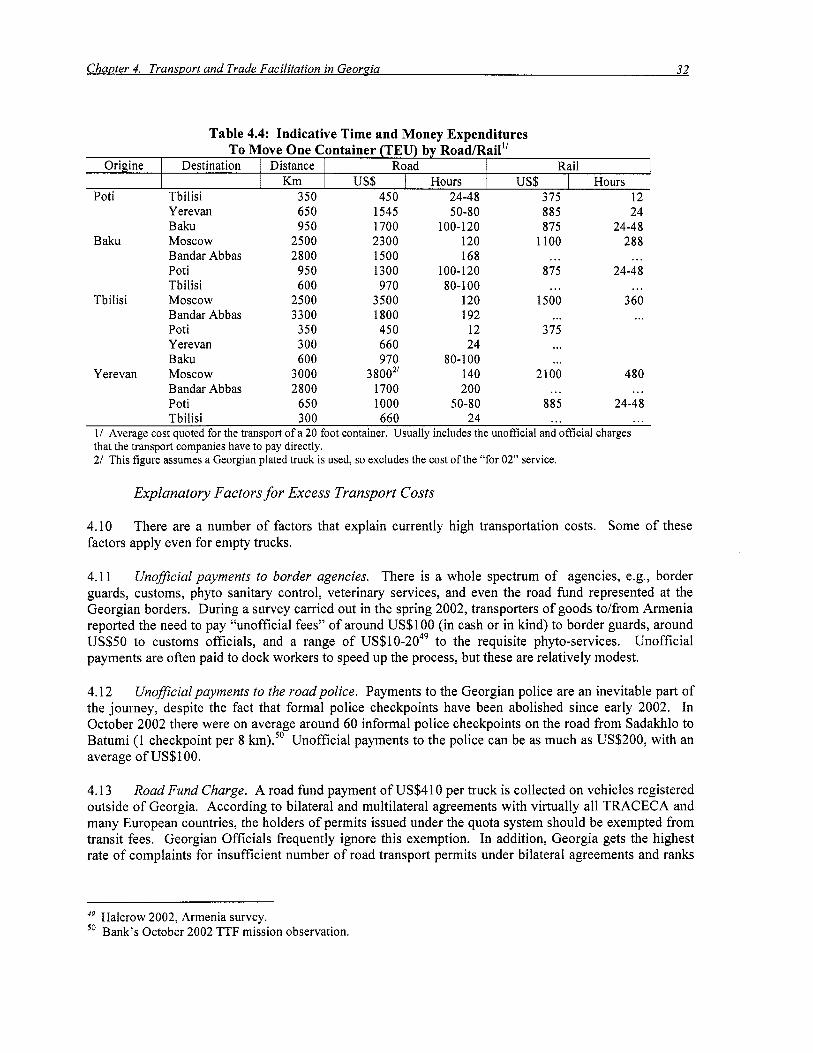

Transport Network in Georgia 1989-2000 ................................................................. 29 Freight Transport Indicators 1997-2001 for Georgia ................................................. 30 Port Tariffs on Dry Cargoes in Traceca and Other Countries .................................... 31 Indicative Time and Money Expenditures to Move One Container (TEU)

Indicative Logistical Cost for a TEU Container by Road from Poti to Armenia ....... 34 Georgia: Monetary Indicators .................................................................................... 44

Georgia: Taxation o f Imports, 1997-2001 ................................................................. 20

by RoadRail ............................................................................................................... 32

Georgia: Structure o f Lending by Sectors ................................................................. 45 Georgia: Average Interest Rates ................................................................................ 46 Georgia: Profit Margins of Commercial Banks ......................................................... 46 Georgia: Maturity o f Bank Loans .............................................................................. 47 Agro-Foodmeverage Export Trends, 1997 to 2001 ................................................... 52 Grape Yield Comparison ............................................................................................ 55 Comparative Efficiency in Georgian Wine Production .............................................. 55 Hazelnut Price History ............................................................................................... 61 Comparative Production Cash Costs o f Hazelnuts ..................................................... 61 Task Level Efficiency & Sales per Employee ............................................................ 61

Georgian Garments Exports 1999-2001 ..................................................................... 70

Apply Juice Concentrate Manufacturing Task Level Efficiency & Sales per Employee ................................................................................................ 65

Relative Competitiveness of Georgia’s Garments Industry ...................................... -72 Romania and Georgia’s Exports o f Wood Products ................................................... 74 Added Value for Wood Products’ Exports ................................................................. 74 Structure of the Wood Sector ..................................................................................... 75 Typical Cost o f Access to Timber .............................................................................. 76 Timber Exports from Georgia (FOB, 1999) ............................................................... 78 Productivity in International Furniture Making Firms ............................................... 78 Productivity in Georgian Firms .................................................................................. 78 Prices Obtained for Wooden Products ........................................................................ 79 Stone Production in the Soviet Period ........................................................................ 86 Sources of Tourists in Georgia ................................................................................... 96 Tourism Budgets and Staffing o f European Countries - 1999 ................................... 99 Change in Poverty between 1997 and 2000 ............................................................. 107 Percent of Individuals with Calorie intake below 1, 800 kcal/day ............................ 107 Georgia: Wage Employment ................................................................................... 110 Self-subsistence Rates in Rural Georgia .................................................................. 111 Agricultural Area Sown by Agricultural Enterprises (‘000 o f ha’s) ........................ 112

vii i

Table 11.6 Table 1 1.7

Figure 1.1 Figure 1.2 Figure 1.3 Figure 1.4 Figure 1.5 Figure 1.6 Figure 1.7 Figure 1.8 Figure 2.1 Figure 2.2 Figure 2.3 Figure 2.4 Figure 5.1

Figure 5.2 Figure 5.3 Figure 5.4 Figure 6.1 Figure 6.2 Figure 6.3 Figure 6.4 Figure 11.1 Figure 11.2 Figure 11.3 Figure 11.4

Box 1 . Box 4.1 Box 4.2 Box 4.3 Box 5.1 Box 7.1

Comparison ofthe Road Network Across the CIS7 in 1999 .................................... 115 Nominal Wage Rates and Wage Rates as a percent o f Poverty Line by Industry .... 1 16

Figures

Georgia: Index of Real GDP and Exports to GDP ...................................................... 4 Georgia: Index of Sectoral Growth ............................................................................. 4

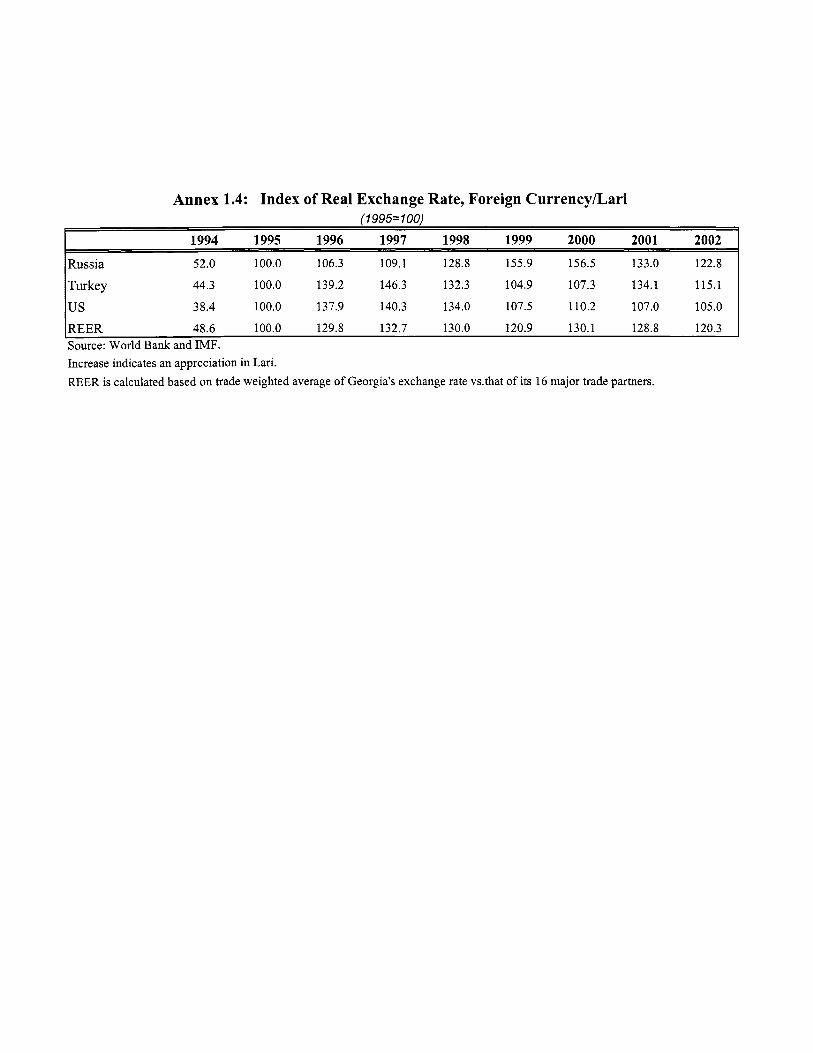

Georgia: Index of Real Exchange Rate ....................................................................... 7 Georgia: Perceptions of the Business Climate. 2002 ................................................... 9

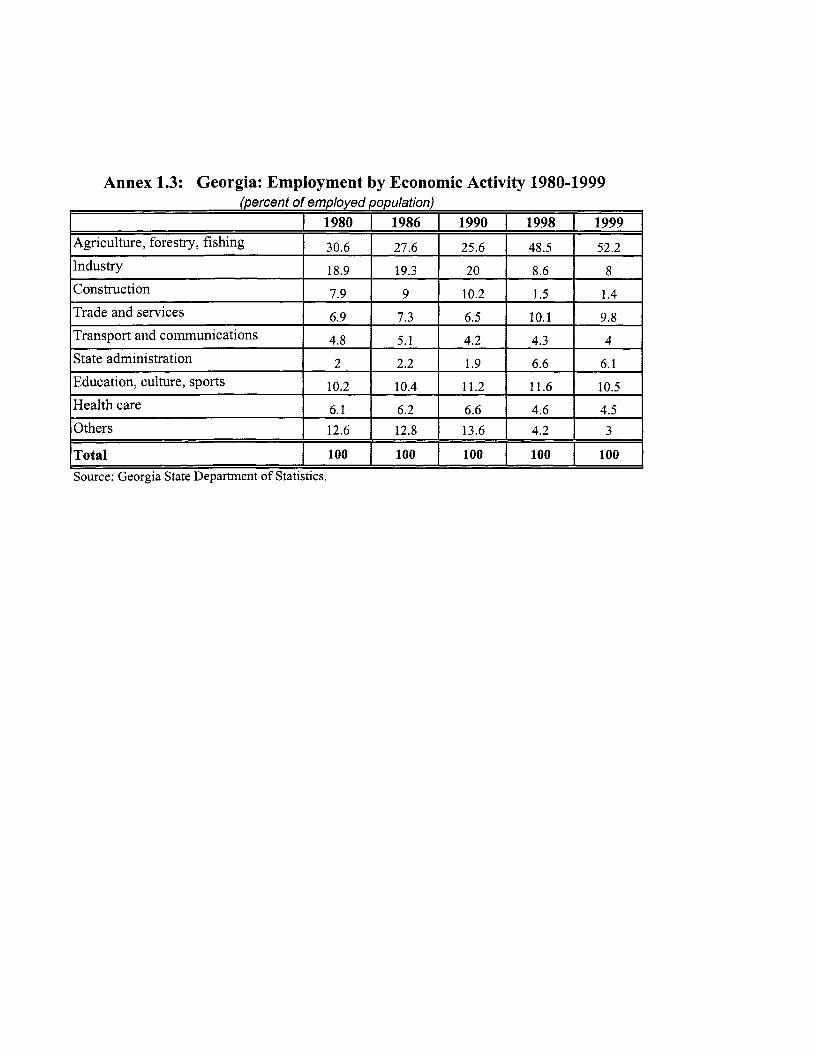

Georgia: Employment by Economic Activity (1 999) .................................................. 6

Share of Annual Sales Reported for Tax Purposes. 2002 ............................................. 9 Share o f Annual Sales Paid in Bribes, 2002 ................................................................. 9 Perception of Major Obstacles to Business Growth, 2002 ......................................... 10 Georgia: Exports by Country Groups ......................................................................... 12 Georgia: Imports by Country Groups ........................................................................ 12 Average FDI Per Capita Over 1992 - 200 1 ............................................................... 16 Georgia: Private Income, Transfers, and FDI ............................................................ 16 Banking Sector Development: Cross Country Comparison in percentage o f GDP (2001) ...................................................................................... 42 Number o f Banks in Georgia, 1993-2002 .................................................................. 43 Level o f Bank Intermediation in Georgia, 1996-2002 ................................................ 43 The Spreads Charged by Georgian Commercial Banks ............................................. 46

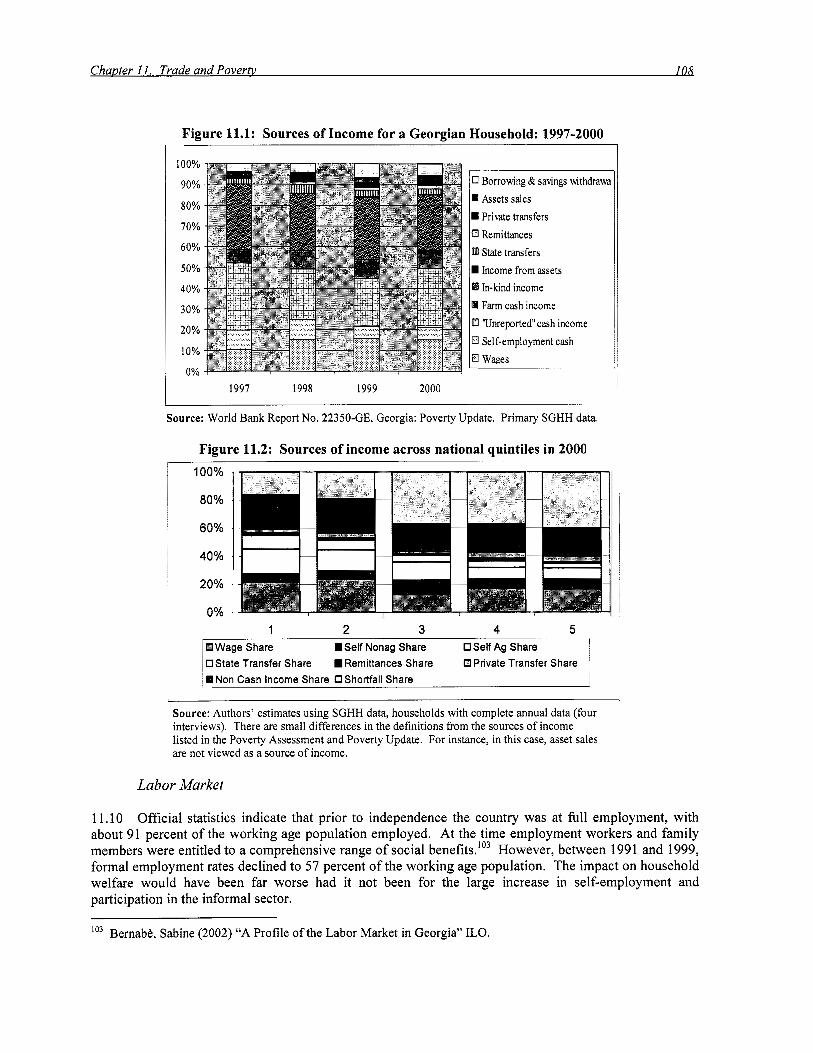

Grapes used in Wine & Spirits Production in Georgia, 1990 - 2002 ......................... 54 Russian Wine Import Trends ...................................................................................... 57 Hazelnut In-Shell Production Output in Georgia, 1998-2001 .................................... 60 Sources o f Income for a Georgian Household: 1997-2000 ..................................... 108 Sources o f Income Across National Quintiles in 2000 ............................................. 108 Employment by Economic Activity, Georgia (1 999) ............................................... 109 Poverty Among Rural Landowners and Poor Access to Markets by Regions ......... 111

Georgia’s Agro/Food Imports and Exports ................................................................ 52

Boxes

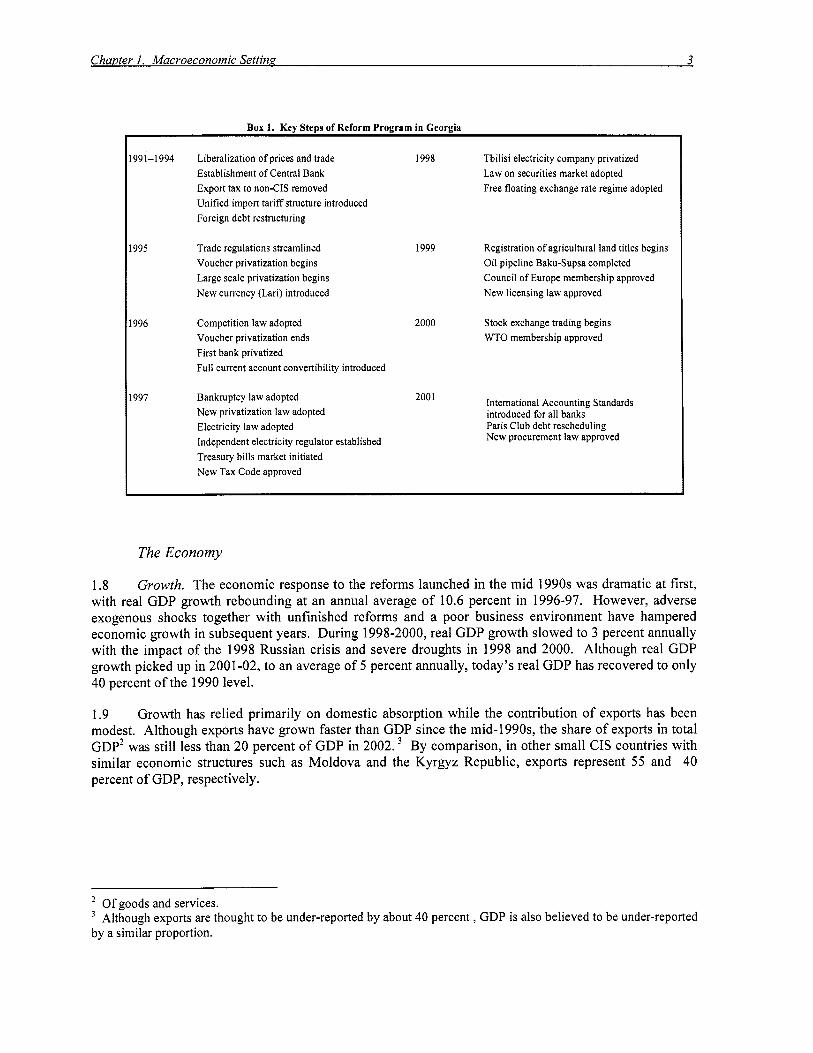

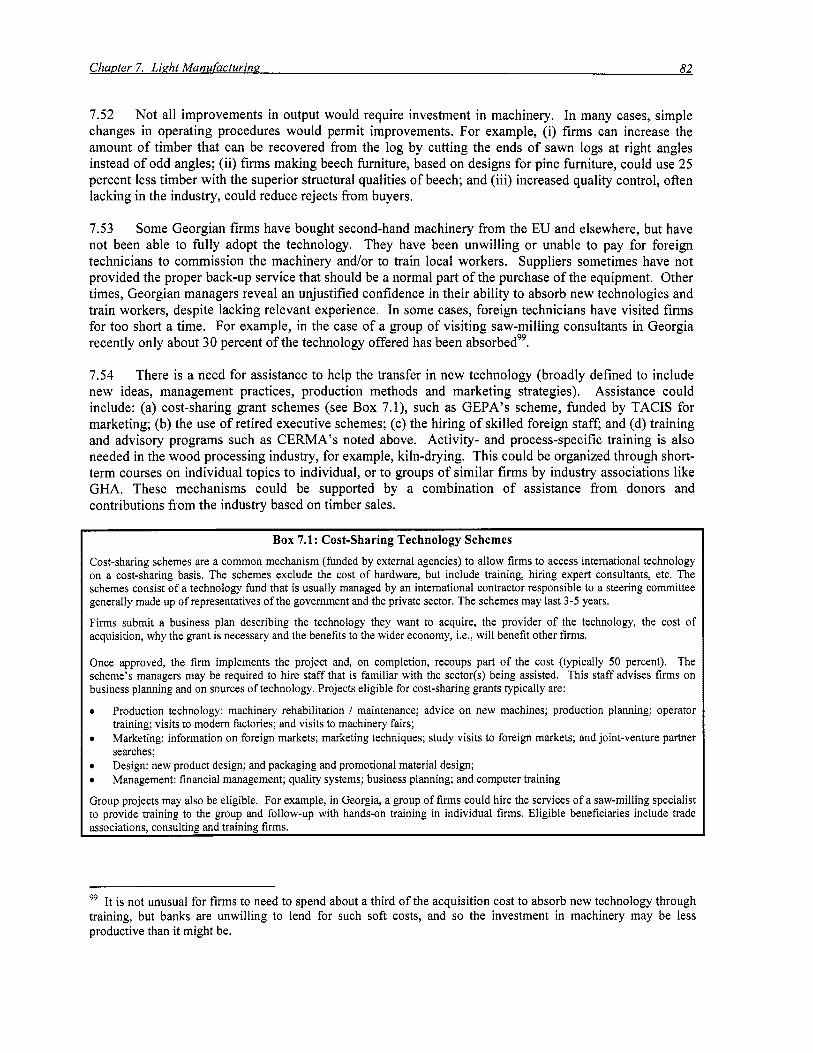

Key Steps o f Reform Program in Georgia .................................................................... 3 The Official and Unofficial Costs o f Importing to Georgia ....................................... 33 Trade and Transport Facilitation Program in Southeast Europe ................................ 39 Creation o f a Transit Service Unit: An Option for Discussion .................................. 40 Georgia: Trade Financing Facilities .......................................................................... 49 Cost-Sharing Technology Schemes ............................................................................ 82

ix

Annexes

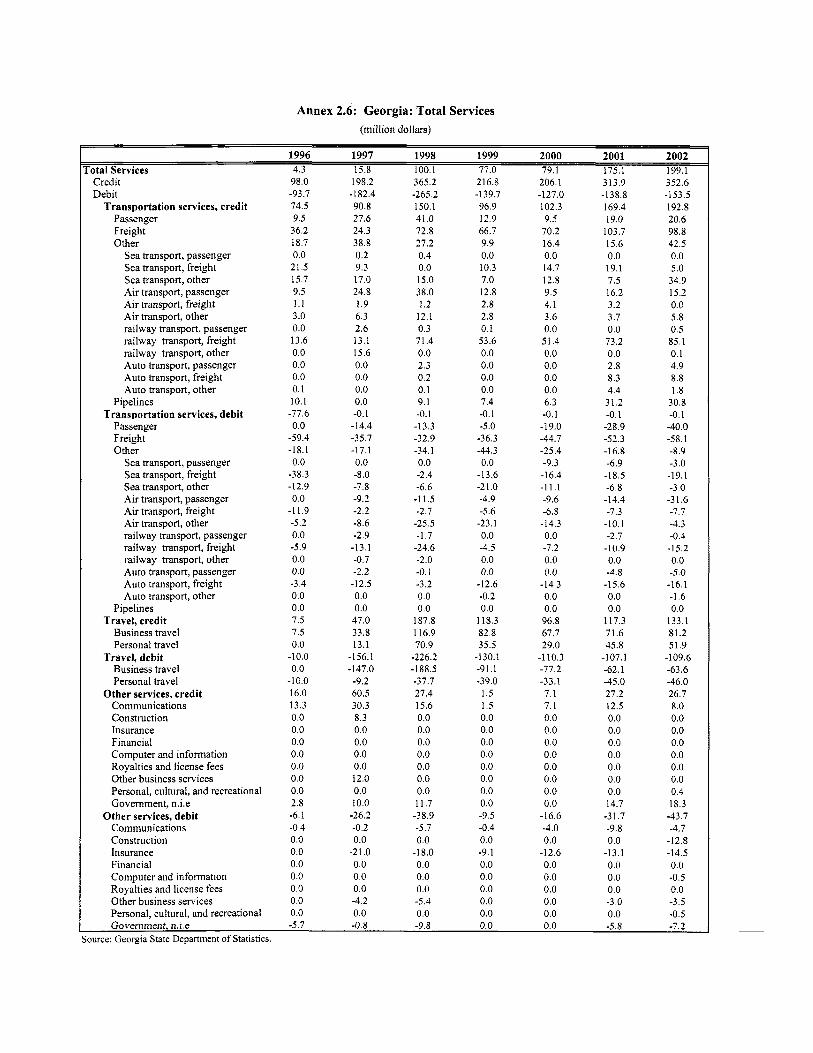

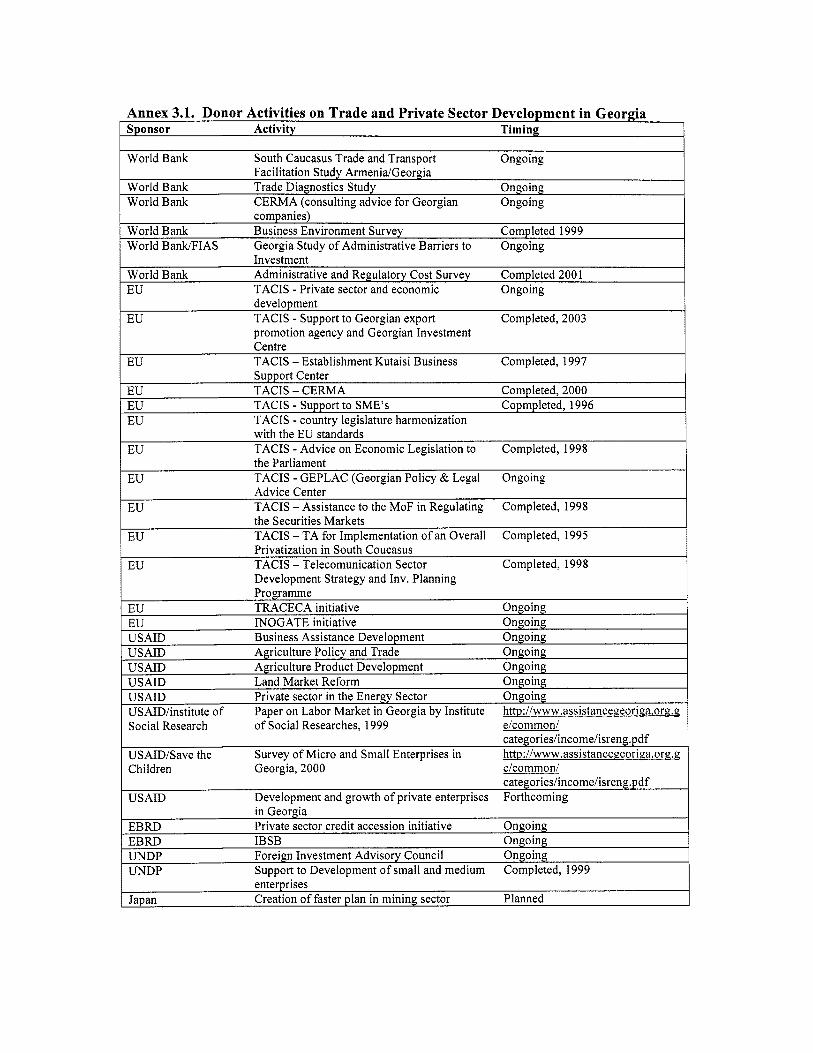

Annex 1.1 Annex 1.2 Annex 1.3 Annex 1.4 Annex 2.1 Annex 2.2 Annex 2.3 Annex 2.4 Annex 2.5 Annex 2.6 Annex 2.7 Annex 3.1 Annex 4

Annex 5

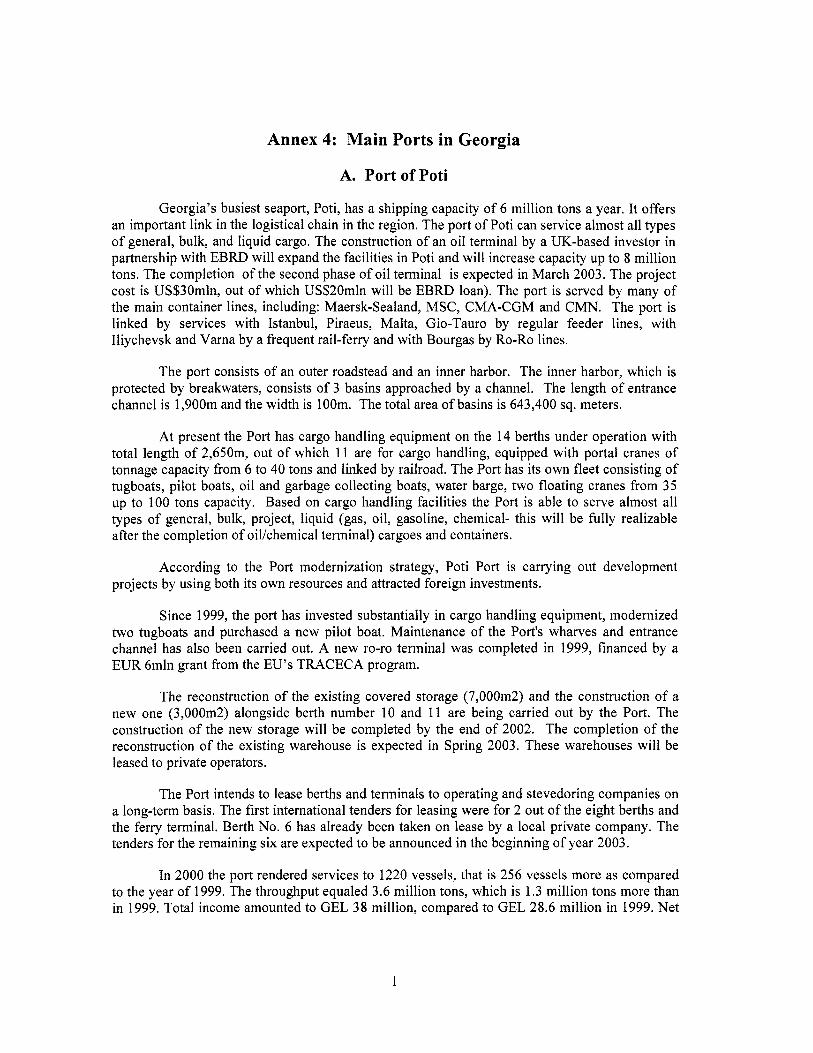

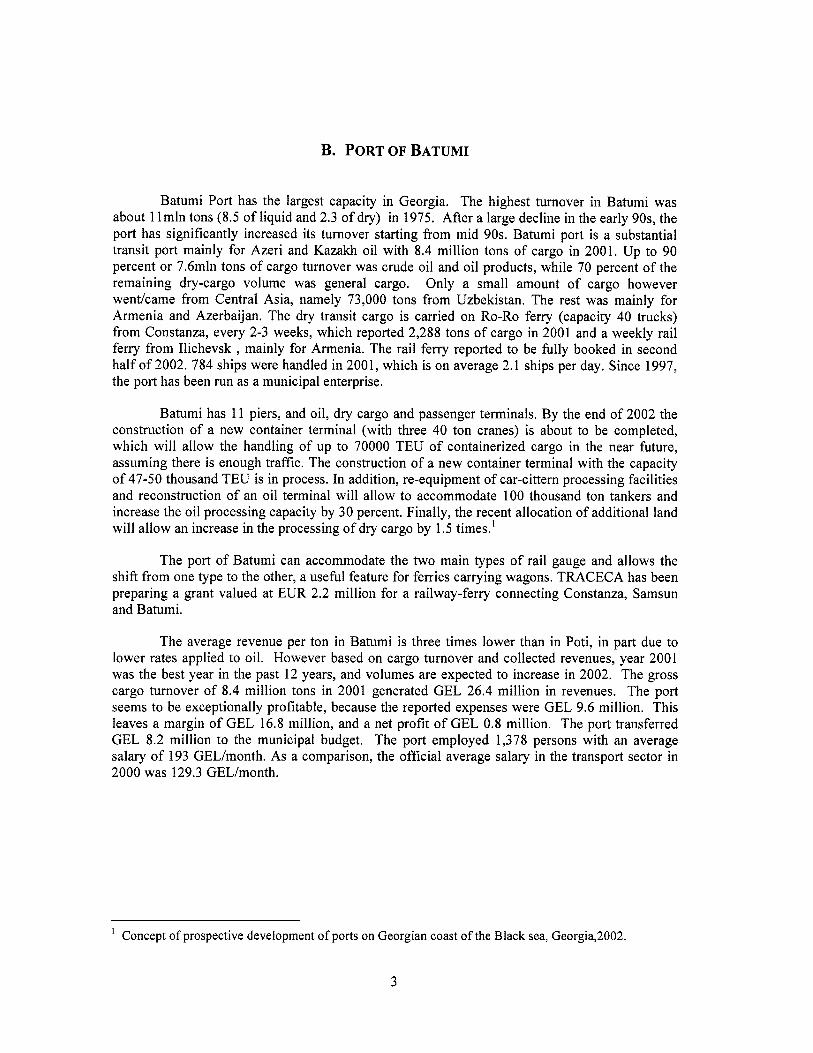

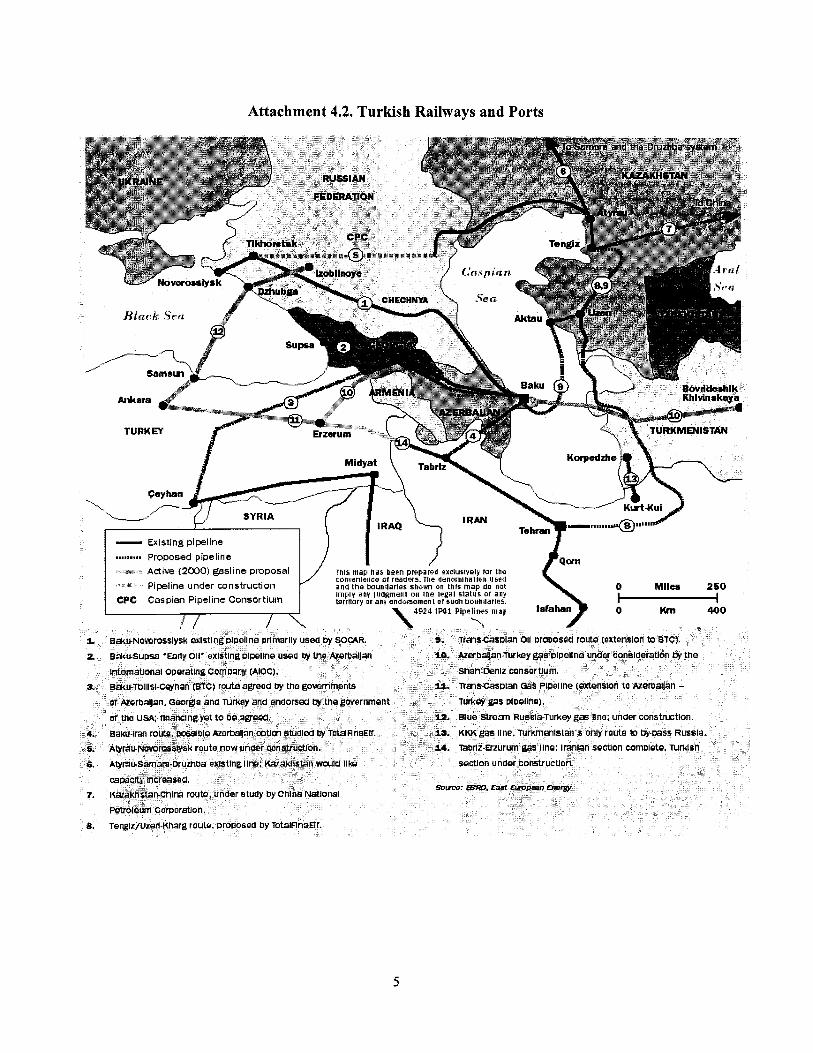

Georgia: Gross Domestic Product Structure Georgia: Index o f Gross Domestic Product, in constant prices Georgia: Employment by Economic Activity 1980-1999 Index o f Real Exchange Rate, Foreign CurrencyILari Georgia: Major Export Categories Georgia: Major Import Categories Georgia: Geographic Distribution o f Exports Georgia: Geographic Distribution o f Imports Georgia: Exports and Imports by Country Group Georgia: Total Services Georgia: Income and Transfers Donor Activities on Trade and Private Sector Development in Georgia Main Ports in Georgia A. PortofPoti Table 4A. 1 : Statistical Data for the Port o f Poti in 1999-200 1 Table 4A.2: Turnover o f Poti Port 1999-2002 Table 4A.3: Poti Port Transit Distribution B. Port o f Batumi Attachment 4.1. Map of Existing and Proposed Pipelines Attachment 4.2. Turkish Railways and Ports Export Credit Agencies 1. Working Capital Facility 2. Export Performance Insurance Facility 3. Credit Insurance Facility 4. Political Risk Insurance Facility

X

Acknowledgements

This report was prepared by Rocio Castro (Task Team Leader) based on the findings of a World Bank mission which took place in November 2002. The mission interviewed 65 Georgian firms. The report reflects the contributions of Tyler Biggs (coordinator o f firm-level interviews), Gerald Tyler, David Neubert, Sean Browne (Consultants), who elaborated the industry case studies presented in Chapters 6- 10. Contributions were also received from Afsaneh Sedghi (Macro and Trade, Investment Flows), Sergo Vashakmadze (Privatization), Evgeny Polyakov (Trade Policy and Market Access), Ramin Shojai (Financial Support Services), Gerald Ollivier and Gevorg Sargsyan (Trade and Transport Facilitation); Ihsan Ajwad, Stephen Miller (Trade and Poverty), and Steve Jaffee (Agro-business and Standards). The Peer Reviewer was Jeffrey D. Lewis. Dolly Teju and Zakia Nekaien-Nowrouz assisted in the production of the report and Richard Carroll provided editorial support.

The team wishes to thank CERMA and the Georgian Exporters’ Association for their assistance in conducting the firm-level interviews, as well as N ia Sharashidze who helped coordinate the mission’s work and compile relevant statistics.

The report was disseminated and discussed at a workshop held in Tbilisi, Georgia, on September 29, 2003 with the participation of government officials, the private sector, and NGOs. The team would like to thank the staff o f the World Bank Country Office in Georgia for their assistance in organizing the workshop.

x i

Executive Summary

Introduction

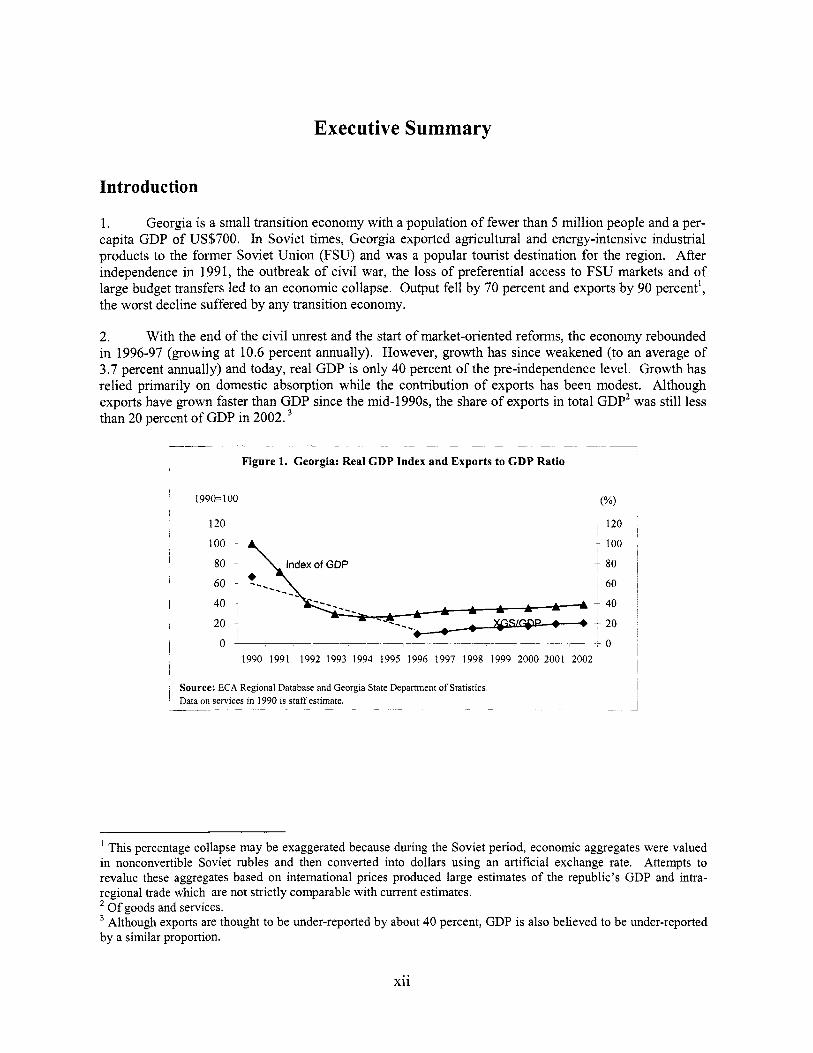

1. Georgia i s a small transition economy with a population o f fewer than 5 mil l ion people and a per- capita GDP o f US$700. In Soviet times, Georgia exported agncultural and energy-intensive industrial products to the former Soviet Union (FSU) and was a popular tourist destination for the region. After independence in 1991, the outbreak of civi l war, the loss o f preferential access to FSU markets and o f large budget transfers led to an economic collapse. Output fe l l by 70 percent and exports by 90 percent', the worst decline suffered by any transition economy.

2. With the end o f the civi l unrest and the start o f market-oriented reforms, the economy rebounded in 1996-97 (growing at 10.6 percent annually). However, growth has since weakened (to an average o f 3.7 percent annually) and today, real GDP i s only 40 percent o f the pre-independence level. Growth has rel ied primarily on domestic absorption while the contribution o f exports has been modest. Although exports have grown faster than GDP since the mid-l990s, the share o f exports in total GDP2 was st i l l less than 20 percent o f GDP in 2002.

Figure 1. Georgia: Real GDP Index and Exports to GDP Ratio I I

1990= 100 ("/.I

80 80

r 60

I - 40

I 20 7

I

40 -I

I 7 0 -~ ________.- 0 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Source: ECA Regional Database and Georgia State Department o f Statistics ' Data on services in 1990 i s staff estimate.

' This percentage collapse may b e exaggerated because during the Soviet period, economic aggregates were valued in nonconvertible Soviet rubles and then converted into dollars using an art i f ic ial exchange rate. Attempts to revalue these aggregates based o n international prices produced large estimates o f the republic's GDP and intra- regional trade which are not strictly comparable with current estimates.

O f goods and services. Although exports are thought to b e under-reported by about 40 percent, GDP i s also believed to be under-reported

by a similar proportion.

x i i

3. The initial fal l in output and the recent modest economic growth have led to a severe decline in welfare. In particular, agriculture and industry: both traditional mainstays o f export activity and important sources o f employment have virtually stagnated following their post-independence collapse. Georgia’s annual income per-capita i s 56 percent below the pre-independence level, unemployment rates are high (16 percent in 2001) and many Georgians are underemployed. The incidence o f poverty has increased from 14 percent o f the population in 1997 to 23 percent in 2001 .’ Moreover, inequality has also increased over the period. Georgia needs to achieve higher economic growth rates to reduce poverty and improve the welfare o f i t s population. Given the small size o f the domestic market, sustained high growth rates w i l l only be achieved through a stronger expansion in export activities, especially o f those in which Georgia has a comparative advantage and have the potential to generate new job opportunities, such as agro-processing.6

4. This report examines the opportunities for and constraints to achieving export-based economic growth in Georgia. It analyzes key aspects o f both the internal and external environment, including macroeconomic risks, business environment issues, market access, transport and trade facilitation. An important consideration in the analysis, i s the scope for enhancing the participation o f the rural and lower income segments o f the population in both domestic and external trade. Based on this comprehensive analysis a medium term program o f actions i s developed and presented for Government consideration. An important methodological innovation i s the use o f qualitative and quantitative information obtained from interviews with 65 f i rms. These firms were selected from sectors where Georgia appears to have a comparative such as agro-processing (hazelnuts, horticulture and wine); light manufacturing (garments and wood processing); industrial minerals and stone processing; information technology and engineering; and tourism. The firm level interviews were used to gather qualitative information on the constraints faced by firms and, to the extent possible, quantitative data (e.g., cost structures) for the purpose o f comparing firm performance with international competitors.

Opportunities and Constraints to Export Development

5. Georgia i s well endowed with natural resources such as forests, minerals, fert i le agricultural lands, scenic beauty, good climatic conditions. Unlike other low-income countries outside the region, Georgia has a well educated and relatively low-cost labor force which could allow it to be competitive in producing high value goods and services.’ In addition, while much o f the country‘s physical capital base has depreciated, there are s t i l l equipment and facilities that can be used in export activities. Georgia also has significant transportation infrastructure facilities and i s located close to important regional and high- income European markets. Moreover, being the most direct link between the Black Sea and the Caspian Sea and the Central Asian countries, Georgia has the potential to become a regional transit hub, particularly for rapidly growing o i l producing countries such as Azerbaijan and Kazakhstan.

In the Soviet period, mining activities contributed about 10 percent o f output and for some towns was the major source o f income and employment.

While the incidence of poverty i s relatively low, it i s estimated that 60 percent o f the population i s at risk o f falling into poverty at least once during the year.

There i s some, yet limited potential for import substitution in a number o f industries (Le., food processing) which could provide a platform for competitive exports. ’ Georgia’s enrollment rates in basic education are almost universal, and while enrollment rates in secondary and tertiary education are declining they are s t i l l relatively high. In addition, the average wage for a semi-killed /skilled worker i s about US$55 per month, which is low by international standards.

... XI11

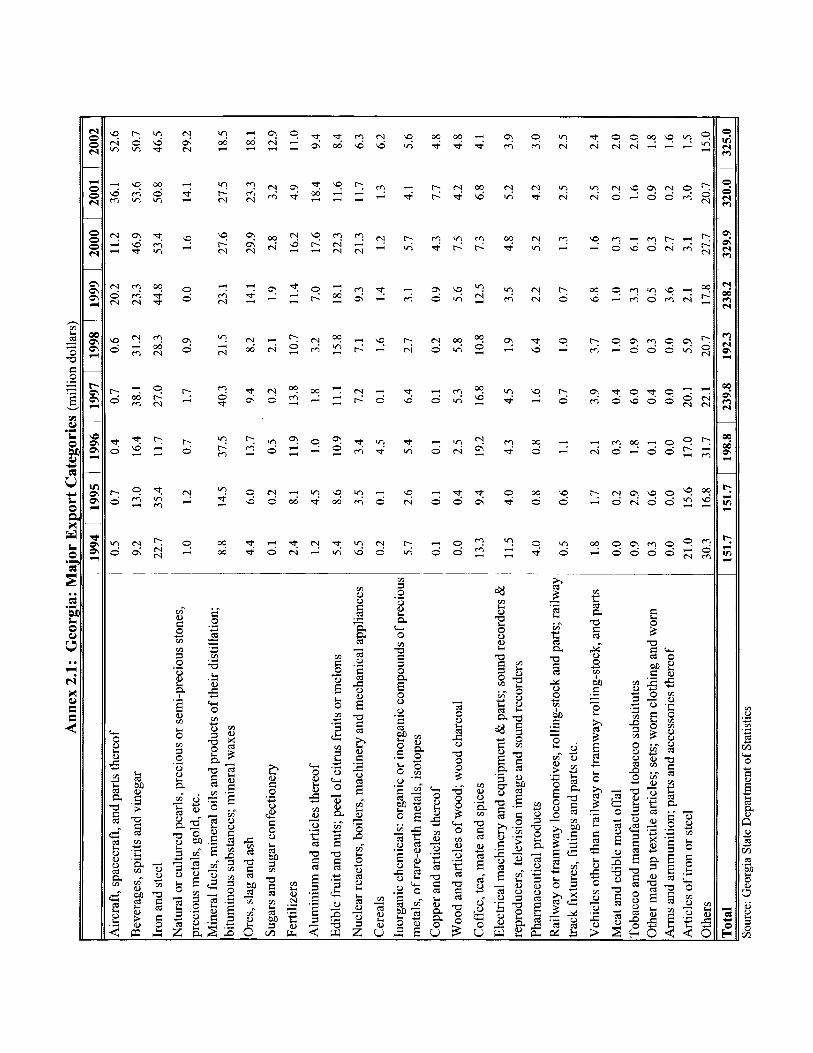

6. Despite the above advantages, Georgia’s export base i s currently very small and highly fragmented. Merchandise exports amount to some US$325 million (or 10 percent o f GDP).’ The main exports include aircraft (exported to Turkmenistan under a debt-swap deal), scrap metal, wine, mineral water, fertilizer, ferrous alloys, and hazelnuts. Together they account for about half o f merchandise exports. With a few exceptions-e.g., scrap metal and hazelnuts-Georgia exports consist mostly o f traditional, low-value added products directed mainly to CIS markets. Remaining exports are very small in value, typically amounting to less than one million dollars per year. In terms o f services (1 0 percent o f GDP), transport earnings have grown rapidly since the mid 1990s, mostly owing to increased oil transit from the Caspian sea, but transit volumes are st i l l only one third of what they were prior to independence. Tourism has recovered somewhat after collapsing to negligible levels, but the number of foreign visitors (mostly business related) to Georgia are estimated to be less than 15 percent o f what they were in Soviet times.

Basic Conditions for Export-Based Growth

7. For a country to effectively compete in international markets and realize i t s comparative advantage, a number of basic macroeconomic and microeconomic conditions need to be in place. First, it requires a stable macroeconomic framework and a competitive exchange rate. Second, it should have a liberal trade regime and enjoy reasonably easy access to export markets. Third, it should have a favorable investment climate, including supporting trade services and institutions. Fourth, i t should have eff icient mechanisms for technology transfer and “learning” at the firm level. For a small transition economy like Georgia, it i s particularly important to encourage f i r m s to fundamentally shift their market orientation-- from being bulk, low-cost commodity suppliers--to become higher value-added producers serving distinct market segments. Such a shift requires moving away from old, ‘rigid’ mass-production systems towards flexible technologies designed for fast market response and product differentiation. Some o f these necessary conditions have yet to be established in Georgia, as discussed below,

Figure 2. Georgia: Index of Real Exchange Rate Foreign Currencyhari (1995=100)

180 , I60

120 I aa

:: 40 20 i

Note: Increase indicates an appreciation o f the Lari Source: World Bank and IMF

1994 1995 1996 1997 1998 1999 2000 2001 2002

+Russia

-W- Turkey

+ REER

8. Basic macro competitiveness has been established. The stabilization program launched in the mid 1990s, has succeeded in bringing inflation to single digits and in maintaining a competitive exchange rate. Georgia adopted a free floating exchange rate regime in 1998 in the wake o f the Russian financial crisis, After a moderate depreciation triggered by this crisis, the real effective exchange rate has remained relatively stable over the past five years, despite the fact that the Georgian Lari (GEL) appreciated

~~ ~

As noted earlier, there i s significant under-reporting o f exports, but reliable estimates are not available. For more details see Chapter 2 of this report. By comparison it i s estimated that commodity exports amounted to USS5.7 billion (or 57 percent o f GDP) prior to independence.

xiv

substantially against the Russian Ruble in the years immediately after the crisis. In general, real exchange rate movements have reflected market conditions both internally and in major partner countries. However, with gross international reserves at less than two months o f imports, Georgia i s vulnerable to external shocks, especially given i t s high external debt burden. (see Chapter 1). This macroeconomic vulnerability i s likely reflected in the substantial risk premium observed in Georgia.

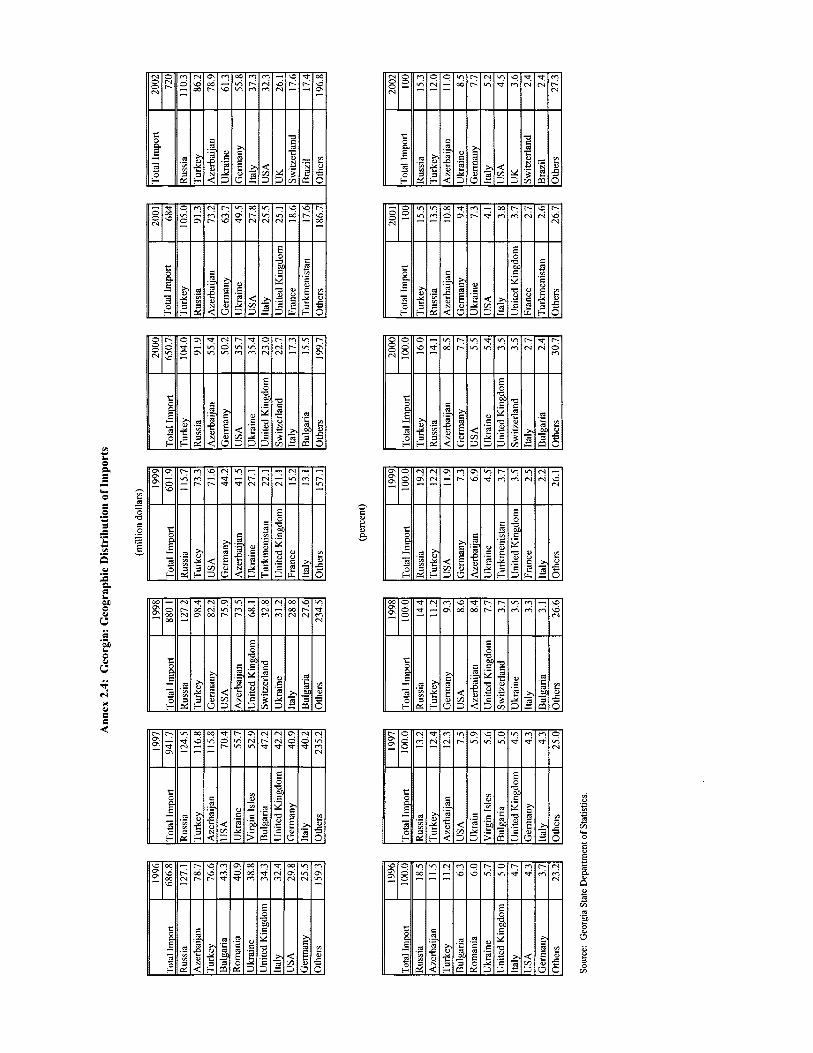

9. Georgia has a liberal ‘statutory’ trade regime and faces no significant trade barriers in world markets. Georgia became a member of WTO in June 2000. It has low import tariffs and no quantitative restrictions. The VAT (20 percent) and excise taxes are equally applied to imports and domestic output. However, the implementation o f trade policies i s undermined by corruption and poor customs and tax administration. Moreover, a new tariff schedule adopted in January 2003 increased the number o f tariffs from four to 22! and the top duty rate from 12 to 30 percent. Although the weighted average tariff w i l l go up only by a fraction of a percent and the new tariffs are in line with the upper bounds agreed with the WTO upon accession, such a schedule i s a step back f iom the previous, simpler schedule. Georgia faces no significant trade barriers in world markets and main export destinations include the CIS region (45 percent)-e.g., Russia, Azerbaijan, Ukraine, and Armenia- where Georgia enjoys duty-free access, followed by Turkey (20 percent), and the EU (1 8 percent)-mainly Germany.

10. However, Georgia’s unfavorable business climate undermines the competitiveness offrms. Like most CIS countries, the cost o f doing business in Georgia is high and adds significant investment risk. Not surprisingly, outside o f two large energy project^,^ foreign direct investment (FDI) in Georgia has been insignificant. According to the 2002 Business Environment and Enterprise Performance Survey (BEEPS)” conducted in Georgia, taxation and corruption are the main obstacles to doing business. Along with crime, these problems are somewhat worse in Georgia than i t s regional counterparts. Issues relating to regulations, the judiciary, infrastructure, and access to finance while s t i l l problematic appear more or less the same across the CIS region.

11. More specifically, the industry case studies conducted for this study identified several institutional constraints which significantly undermine the export competitiveness o f Georgian firms and create barriers to entry, a critical issue for a transition economy. Notably, exporters do not have assured access to inputs at world prices, particularly o f those procured in the domestic market, because o f the lack of a functioning VAT refund mechanism. Moreover, the tax code i s subject to frequent changes and i ts administration i s unpredictable and highly corrupt. Transportation costs are high primarily due to considerable unofficial payments to border agencies and the road police. At the same time, widespread smuggling reflecting corruption and weak customs administration, means that formal firms are undercut from the domestic market which limits their possibilities to achieve economies o f scale.” This environment encourages the proliferation o f informal and small-scale activities, creates a bias against formal domestic tradable activities, and does not allow the already small domestic market to become a platform for export growth.

Related to the construction o f the Baku-Supsa pipeline and the privatization o f the Tbilisi electricity company to AES . Io Survey conducted jointly by the World Bank and the European Bank o f Reconstruction and Development (EBRD), covering 6,000 firms in 27 transition countries. ‘I With respect to food products, the problem i s not simply competition from unrecorded imports but that a significant proportion o f these imports are of adulterated or mis-labeled products, further eroding the confidence o f the Georgian consumer in packaged foods.

xv

Figure 3. Georgia: Perceptions o f the Business Climate 2002

Financing

+Worst case

1 Source: The World Bank and EBRD. BEEPS I1

12. In addition, firms also face problems getting access to finance, especially for investment, and when finance i s available it i s expensive and requires high collateral. Other constraints include the lack of enforcement o f intellectual property rights; national standards which are not recognized outside the CIS region; and inadequate and unreliable power and telecommunications services.

13. Hence, mechanisms for technology transfer and “learning” are weak or absent. In the absence of significant FDI and visits to Georgia by foreign buyers, most Georgian firms have limited access to adequate technology and ways to learn marketing which are essential to be competitive in world markets. This often results in low labor productivity despite good education levels. For example, the industry case studies found a substantial productivity gap between Georgian firms and their international competitors in garments and wood processing (see Table 1). Moreover, productivity differentials between Georgia and i t s rivals are larger than their wage differentials, indicating that Georgia’s low-wage advantage i s being eroded by i t s productivity disadvantage. Georgia’s high unit labor costs may explain why sectors that highly competitive internationally such as garments and wood processing have not flourished in Georgia.

Table 1: Competitiveness Index in Manufacturing 2002 (Georgia=lOO)

Task-level I Output Per I UnitLabor I Competitiveness I

Source: Industry Case Studies, Georgia Trade Diagnostics Study, Chapter 7-Light Manufacturing.

xvi

A Proposed Program for Export Development

14. Interviews with approximately 65 exporting firms conducted for this study, show that firms are beginning to move into import substitution and many export activities. But, the situation i s fragile, many firms are newly formed- most as a result of privatization-- and there are significant challenges ahead. The sections below summarizes the main constraints to export development identified by this study and propose recommendation to address them.

Taxation and VAT Refunds

15. Issues: Most firms complain that tax administration i s arbitrary and unpredictable. The tax code i s complex, changes frequently, and i s difficult to interpret. These difficulties give tax authorities too much discretion and opportunities to extract bribes. Also, firms say that tax collectors are not accountable and the appeals mechanism i s weak. For example, under the law companies should be audited once a year, but some are audited as much as once a month, especially smaller firms. Generally, tax authorities target firms that can pay, or firms that lack political protection, rather than non-payers, in order to meet their tax collection monthly target or extract a bribe. In response, firms become informal operators, under-report revenue, or forego entering certain businesses that might be more visible to tax officials--like manufacturing-- and/or buy political support.

16. VAT administration i s another major problem for exporters. Exporters are supposed to get a refund on VAT paid on inputs, or they can put up a bank guarantee at the time inputs are imported and pay nothing, as long as the final product i s exported within six months. Firms able to do the latter, generally have no problems. But for those that pay VAT, either at the border or to the local supplier, it i s almost impossible to get it refunded, unless they have “political connections”. In addition, since many inputs are smuggled into the country, it i s difficult to obtain VAT invoices from local sellers. Tax collectors often ask firms to pay VAT for inputs that do not have proper invoices. To get around such problems an industry has grown up in Georgia to provide fake invoices which cost 8-10 percent o f the value of purchases, but, o f course, these costs cannot be deducted when goods are exported.

17. Recently, the Ministry o f Finance presented a tax package to Parliament which aims at raising the VAT threshold and simplifying taxes. In addition, it plans to allocate funds (about 5 percent of revenue) to pay VAT refunds in the 2003 budget. While the proposed allocation may be short of what is needed, it would be a step in the right direction, if actually implemented.

18. Recommendations. As documented by this report and others12, there i s an urgent need to make the tax system more predictable and to ensure that exporters get their inputs at world prices. USAID has been providing technical assistance to the tax department for several years, but much i s yet to be done to address current distortions. This will require striking a better balance between fiscal objectives and the need to promote private sector development, especially o f the export sector. More importantly, it will require a great deal o f political commitment to enforce proper implementation o f tax regulations and remove incentives for corrupt practices by tax inspectors. Immediate priorities are to stabilize revenues, improve the tax environment for exporters and small businesses, and facilitate tax administration. Some o f the proposed measures are included in the above mentioned tax package prepared by the MoF.

(i) Strengthen VAT implementation, by raising the threshold and limiting voluntary registration below the threshold, reducing exemptions, and providing adequate budgetary allocations to pay VAT refunds for exporters.

l2 See Georgia: Public Expenditure Review (PER), World Bank, November 25,2002.

xvii

(ii) Establish a simplified tax for small businesses, below the VAT threshold, to replace existing taxes.

(iii) Limit inspections and audits by tax authorities. (iv) Introduce a broader range o f criteria to measure the performance o f tax authorities.

~ ~~ ~

Total Logistical costs

19. In the medium term, efforts must continue to develop the institutional capacity o f the tax administration, including customs (see below), broaden the tax base, and establish a business friendly tax environment. In this regard, it w i l l be important to separate the collection, auditing and enforcement functions o f the tax department. As progress i s made in these areas, it might be possible to consider options to lower the tax burden, for example, through reductions in the social security tax and/or the VAT.

1545

Transport and Trade Facilitation

20. Issues. While official transport fees (including ports charges) are comparable with international benchmarks, transport costs in Georgia are not competitive when one considers unofficial monetary expenditures and the time req~ired.’~ The main contributing factors include (i) high unofficial payments to border agencies-- including customs -- and the road police; (ii) excessive and often unnecessary documentation, particularly for transit goods; and (iii) additional costs incurred because o f delays, long journey times, etc.

Table 2. Indicative LI Cost element QuantlJiable cost Incremental VOC caused by poor roads Payment to border agencies

Payment to road police Road Fund Payment Transit documents

Mandatory escort

“Pure” transportation costs Subtotal: Residual non-quant$able cost

istical Cost for a TEU Con1 cost $ 1 Characteristic

50

170

100-200 0-4 10 85

0-50

455 885-1 420 660- 125

OIA

U/A

UIA OIA 0-UIA

UIA

O/UN

h e r by Road from Poti to Armen ProDosed mitieation measures

Road rehabilitatiodmaintenance

Border agency modernization and computerization Enforcement o f Presidential Decree TRACECA analysis Review transit documentation requirement particularly under TIR Remove this requirement

Long term measures to improve the Georgian and Armenian facilitation

nsport and Trade Facilitation.

a

21. As shown in Table 2, the logistical cost for transporting a TEU container from Poti to Armenia i s US$l,545 or over three times higher than the “pure” transportation cost. Quantifiable costs resulting from unofficial payment to border agencies and the road police in both countries can amount to US$370 (or 20 percent o f the total costs). Additional official and unofficial charges incurred because o f unnecessary transit requirements (such as road fund payment, internal transit document, and mandatory escort) can cost up to U S $ 720 (or 40 percent o f the cost). Incremental costs due to poor road conditions are estimated at US$50. The residual covers potential additional costs linked to long journey time, security concerns, etc.

l3 Small volumes also contribute to high transportation costs.

xviii

22. Some of these incremental costs apply only to goods in transit, but the costs o f importing goods i s also expensive, due to bribes to customs officials and the road police. For example, in moving a generic container from Northern Europe to Tbilisi, the Georgian leg accounts for 46 percent o f the cost, despite representing a small portion of the distance. Unofficial payments account for 7-40 percent of the cost, mostly to border agencies and the road police.

23. Given widespread smuggling in Georgia and the need to improve fiscal revenues, a trade and transport facilitation strategy needs to target both reductions in logistical costs as well as in illegal trade. Trade facilitation and revenue enhancing objectives need not be in conflict, as shown by the experience in South Eastern Europe where increased fiscal revenues were achieved along with lower processing time o f transit goods. Meeting these objectives will require significant improvements in customs administration and other government agencies dealing with foreign trade and transit, including the road police. In addition, well targeted interventions will be needed to upgrade the transport infrastructure. In both cases, the improvement o f road transit conditions seems to be the most urgent priority.

Recommendations.

24. Implementation of customs reform i s critical to reduce transportation costs as well as illegal imports. While the Government has already articulated a sound reform strategy, it has achieved l i t t le in terms o f implementation. Immediate actions need to be taken to set the basic conditions for improved customs controls and trade facilitation:

Accelerate the implementation of ASYCUDA nationwide, to allow risk management and the integration o f a transit module, while limiting physical contact between traders and border agencies. (On-going with support of U S Customs). Simplify transit procedures by establishing a single window and removing unnecessary requirements for transporters with TIR carnets; e.g., the VVT, transit insurance, transit road charge, and mandatory escort for non-excise goods in transit.

(iii) Publish procedures for foreign trade and transit in a user-friendly format. (iv) Enforce the 2002 Presidential Decree which limits road police inspections.

(i)

(ii)

25. In the medium-term, efforts should focus on establishing a professional customs administration. In this regard, particular attention needs to be given to improving human resource management, through training, testing, and establishment o f performance-based incentives and sanctions. In order to attract additional transit, particularly o f products going to Azerbaijan, the Government may wish to consider a more focused institutional approach to transit. This would involve the delegation of powers o f all border agencies to a single transit administration which would have overall responsibility for facilitating transit with oversight by an independent monitoring body. In addition, building on the transit strategy developed by the Ministry o f Transport and Communications, complementary measures are needed to upgrade the road infrastructure, according to economic priorities, and to harmonize rail tariffs. It i s also important that steps are taken to commercialize the operations o f Georgian railways.

Access to Finance

26. Almost al l firms interviewed for this study indicated that access to finance i s a considerable impediment to business development, including exports. Main concerns include high interest rates (about 20 percent) and high collateral requirements (often twice the value of the loan). Firms also complain about the short maturity o f loans, mostly less than a year, which make investment financing through credit very difficult. As it is often the case, well established firms are able to access credit at more favorable terms, while smaller firms are at a disadvantage.

Issues.

xix

27. Interviews with exporters in Georgia revealed that most are not used (or keen) to utilizing any export financing instruments such as letters o f credit (L/C) and export guarantees. Some of this reluctance i s due to the cost charged by banks for such facilities. Most importantly, the majority o f buyers of Georgian exports in the CIS region (which account for about half o f total exports) prefer to deal with direct payments (20-30 percent prepayments and/or payments after delivery) instead of using financial instruments. l4

28. In order to facilitate access to finance for exporters, the Government has recently introduced an interest subsidy scheme (up to percent o f 70 percent o f lending rates), targeted mostly to exporters. While provisions have been made to ensure that the subsidy i s paid only to compliant beneficiaries, the impact o f such scheme i s bound to be ad-hoc and limited (funds were only US$0.5 million in 2002). The Government also plans to establish an Export Guarantee Agency (EGA), to provide insurance and guarantee facilities to exporters, but this could be premature given Georgia’s small export base and low demand for this type of services.

29. Recommendations. The development o f the financial sector and the real side o f the economy are linked. Therefore, given Georgia’s nascent private sector and adverse investment climate, it wi l l take some time for the costs and risks o f financial transactions to come down. Interest rates have been declining and are comparable to most CIS countries. Interest rate subsidies or credit lines with government taking all or part o f the credit risk, can be ineffective and unsustainable. Besides, interest rates subsidies provided exclusively to exporters constitute a violation of the GATT of the WTO. Instead, the government should concentrate efforts on improving the business environment and take specific measures to support the development o f the financial sector. Short term priorities include:

(i) Eliminate interest subsidy scheme (ii) Raise capital requirements to encourage further bank consolidation (iii) Establish legislation to allow the use o f movable collateral and the establishment credit

bureaus. (iv) Improve enforcement mechanisms and proper court rulings (v) Encourage leasing services by providing technical assistance to investors wishing to

establish leasing companies, raising public awareness o f the benefits o f leasing, and monitoring implementation o f leasing arrangements. Continue credit lines for back-to-back L/C financing. (vi)

30. While establishing an EGA may be premature at this time, the Government could start considering options for implementation at a later stage. To ensure the financial sustainability o f such an agency, an option could be to establish a regional agency for the Caucasus, for example. Over time, improved financial accounting by companies should facilitate the development o f the securities market and o f credit bureaus. Efforts should also continue to strengthen the supervision o f the rapidly growing insurance sector.

Property Rights

31. The lack of protection o f property rights i s a serious problem for some export activities such as wine, mineral water, and information technology (IT). Despite having a sound framework of related legislation, administrative procedures and a National Intellectual Property Center, responsible for matters involving industrial intellectual property, actual enforcement o f intellectual and industrial property rights i s extremely weak in Georgia, and more generally within the CIS region. For example, in order to deal with counterfeiting, Georgia’s mineral water company has been forced to change i ts bottling structures

l4 Reportedly, CIS buyers prefer to under-report their activities to avoid taxes.

xx

(including lids) several times and has been actively involved with other private companies in the Russian market to raise consumer awareness of mislabeled products. Although relatively successful, these initiatives create additional costs. In the IT industry, weak enforcement o f property rights also raises costs and product prices for local companies, particularly software producers and hinders the development o f IT services exports. Foreign software companies are reluctant to buy programming services from Georgian companies when they lack confidence that their source codes will be protected. They are also less than enthusiastic about joint ventures and direct investments where property rights are not enforced.

32. Recommendations. Improved property rights protection w i l l be critical to promote more foreign investment and to increase technology transfer to Georgia in IT and other sectors. Efforts wi l l be needed to further strengthen the capacity of the legal system to enforce property rights in Georgia. Recommended endeavors might be:

(i) Establish special courts designated to adjudicate cases. (ii) Provide training for legal professionals and private sector agencies on property rights

issues. (iii) Foster private sector organizations to become more involved in assisting enforcement

efforts and in educating business and consumers about the importance o f property rights protection (e.g., through media advertisements). Collaborate with CIS countries, through Georgian embassies/commercial attaches in those countries, to draw attention to violations o f Georgian 1abeMproperty rights.

(iv)

Standards

33. Lack o f adequate standards in Georgia, i s an impediment to access non-CIS markets, especially for food and agro-processed products. Georgia has yet to adopt internationally recognized standards (Le,, CODEX) or harmonize its standards with that o f potential trading partners (i.e., the EU). The country has numerous testing laboratories, but none are internationally accredited. It has a multiplicity o f inspection and control agencies-cutting across different ministries-however official certifications (of safety, authenticity, etc.) are generally not recognized as valid. The result has been duplicative product testing (adding to costs), quality-related price discounts paid on Georgian products (reducing revenues), and missed market opportunities (ie., for products certified as organic).

34. Georgian legislation i s in line with the GATT 1994 Agreement on Technical Barriers to Trade and the Agreement on the Application o f Sanitary and Phytosanitary Measures. Under the WTO agreement, Georgia must adopt by end-2003 a dual system comprising voluntary standards and mandatory international technical regulations, thus replacing the current GOST system.15 Despite the deadline approaching, the progress in the elaboration o f technical regulations has been very slow. The stalling o f the standards reform stems from powerful political pressures to retain the status quo, including pressures from the national standards agency, and to protect opportunities for rent-seeking.

3 5. Recommendations. The introduction o f an internationally recognized system o f product certification i s necessary for Georgia to access new, higher-value markets, particularly outside the CIS region. Given the imminent accession to the WTO o f large CIS trading partings such as Russia and the Ukraine, it i s important that Georgia accelerates the process o f reform in this area. The main recommendations include:

Is Technical regulations include not only the characteristics o f the products but also the characteristics o f technological processes involved, and the methods o f testing.

xxi

Accelerate the transition to the dual (voluntary/mandatory) system of standards in accordance with Georgia’s obligations with the WTO. Complete the introductions of the full system o f mandatory technical regulations as soon as possible. Increase awareness with and move to adopt internationally recognized standards (Le,, CODEX, ISO) Support initiatives such as the establishment o f a laboratory for food testing sponsored by the Georgian Export Promotion Agency (GEPA). Initiate steps to obtain organic certification and forestry certification, through the private sector. Strengthen the awareness and capacities o f private f i r m s to adopt internationally recognized food safety (i.e., HACCP) and environmental (i.e., I S 0 14000) management systems. Support industry-based initiatives to develop and apply ‘codes of practice’ to cover quality assurance, worker safety and/or other dimensions.

Infrastructure

36. Firms report that unreliable power supply i s the biggest infrastructure problem affecting their operations’6. Frequent power outages stop production and reduce productivity, increase wastage of raw material, and increase operating costs. Most companies use generators to deal with this problem and note that, while s t i l l problematic in some areas, the electricity situation i s beginning to improve.

37. In the IT sector, Internet services and high-speed data transmission are reported to be underdeveloped and quite expensive relative to competitor countries at similar levels of income. Also, enhanced services l ike broadband are costly and difficult to obtain. These I T infrastructure deficiencies are hampering the efficiency of I T companies and constraining their ability to develop services exports.

3 8. Recommendations. The continued unreliability o f power supply, reflects modest progress in restructuring the sector. Despite adjustments in tariff rates, collections are low, because o f theft and corruption. The problem i s particularly serious outside Tbilisi where the distribution companies are s t i l l in state-owned hands.

(i) Implement energy sector reform program, focusing on improving collection rates,

(ii) particularly outside Tbilisi. Develop broad-band systems to improve conditions for the information technology sector.

Technology and Marketing Skills

39. A number of factors may contribute to low productivity at the firm level: (i) low-value added market segments (e.g., “cut-make-trim” garments, juice concentrate, timber, etc.), which means that earnings per factor o f production are low; (ii) inadequate technologies, often old Soviet machinery designed for mass production and cheap energy, which cannot be adapted to flexible production runs; (iii) weak management ski l ls and training; (iv) lack o f specialization as firms tend to produce too many products for too many market segments, partly as a means o f diversifying risk; (v) lack of economies of scale, linked to the lack of specialization and to small size of the domestic economy; (vi) overstaffing and workers’ attitudes, inherited from the Soviet times and have not adapted to market real i t ie~.’~

l6 According to the BEEPS for Georgia, there are 60 days o f with power cuts in the year. l7 For example, some Georgian firms retain older workers as a form o f social safety net.

xxii

40. To a large extent, low productivity at the firm level reflects weak technical and marketing capabilities. Part o f the reason i s that most of the learning mechanisms firms usually rely on are weak or missing. There is very l i t t le FDI, buyers and suppliers are not visiting Georgia in large numbers, and companies often do not have the resources or do not understand how to go about visiting buyers in other countries. In fact, the majority o f firms interviewed for this study do not make an effort to visit foreign buyers in person, unless it i s through occasional trade fairs.

4 1. Recommendations. Strengthening learning mechanisms for both technology and marketing skills will depend largely, but not exclusively on the quality o f the investment climate. Direct foreign investment and the number of buyers and suppliers traveling to Georgia will not increase much without significant improvements in the political climate, personal security and the administration o f public institutions. However, a sound investment climate alone will not generate higher productivity. Enterprise learning i s also required. When firms cannot meet their learning needs through their own efforts, there i s a strong case for the Government to intervene by supporting existing efforts to strengthen learning mechanisms. Main areas o f focus include:

Expand cost-sharing grant programs such as the marketing scheme currently run by the GEPA, to assist firms in hiring industry consultants, developing in-firm training, and searching for new technologies and markets.

(ii) Continue training and consulting services by organizations such as the IDA-funded CERMA project.

(iii) Assist technical and vocational institutions (public and private) to cooperate with the private sector in developing innovative training programs.

(iv) Provide technical assistance to the packaging industry, which i s essential for successful marketing.

(i)

Upstream Policies for Resource-Based Activities

42. Issues. Some resource-based export activities are also constrained by inappropriate upstream policies which affect the firms’ access to raw materials and the efficiency o f downstream production. In the case of wood processing,, the pervasiveness of illegal felling of trees leads to the wastage o f forestry resources. In addition, the small area and short duration o f felling licenses are inadequate to ensure predictability of supplies over the long term and prevent firms to plan investments. In the case of industrial mineral processing, the state continues to own most of Georgia’s mines and mineral reserves, for example for manganese and natural stone. State-owned mines are managed inefficiently and do not permit integration between mining and processing. These mines have not been privatized, partly because o f lack o f foreign investor interest and their large outstanding debts. Finally, in amo-processing there are concerns about the sustainability o f supplies due to aging perennial crops (e.g., apples) and vineyards. These problems reflect to some extent the lack o f basic agricultural support services for farmers, e.g., research and extension services and access to fertilizer and improved seeds, due to weak integration with agro-processors and other marketing intermediaries. In fact, agro-processors are increasingly relying on their own land plots to source their inputs, which has adverse consequences on the welfare of rural households.

43, Recommendations. The development of downstream production depends importantly on the sustainability and predictability of natural resource inputs. Unless these issues are properly addressed, Georgia will not be able to realize i t s comparative advantage in these sectors.

(i) (ii) (iii)

Reduce illegal felling and increase the size and duration of licenses; Privatize remaining mines and/or grant long-term mining leases to the private sector; Support research and extension services for farmers as well as out-growing schemes.

xxiii

Trade Policy and Market Access Issues

44. Tariff Regime. As mentioned earlier, the new tariff schedule recently adopted by Georgia i s a step back from the previous, simpler schedule. Clearly the rationale for setting this schedule has been to serve the interest o f groups lobbying for increased protection. In an environment characterized by poor customs administration, the new schedule will only increase the opportunities for corruption and rent seeking activities as well as worsen economic distortions.

45. CIS Markets. Free trade agreements (FTAs) with a number o f CIS countries provide duty-free market access to important regional markets, such as Russia and the Ukraine." Georgia can compete in these markets, despite current institutional weaknesses, because these problems are also common to the region. In addition, Georgia enjoys protection from international competitors which face import duties in the CIS markets. For example, Georgian exporters of frozen vegetables are able to compete with Polish suppliers in Russia because the latter face duties of 18 percent. However, dealing with CIS markets does not currently provide incentives for integration with global markets (e.g., old Soviet GOST standards which are recognized in the CIS region are not recognized in the rest o f the world; CIS countries do not rely on L/C financing for exports and other financial instruments). I n addition, FTAs incorporate product exemptions and are subject to unilateral action by the parties involved and there i s no settlement mechanism in case o f dispute.

46. As a member of the WTO, Georgia enjoys most favored nation (MFN) treatment. In addition Georgia i s beneficiary of the Generalized System o f Preferences (GSP) of the EU, US, Canada, Switzerland, Japan, Turkey, Poland and Estonia. But, despite being a low-income country, the preferences that Georgia receives under the GSP are not as deep as those granted to least developed countries (LDCs). Tariffs for Georgia in the EU are relatively high for sensitive products, such as agricultural products and textiles. Moreover, available preferences under the EU GSP are not fully utilized owing to lack o f information and difficulty in complying with complex rules o f origin. Georgia could obtain deeper preferential treatment on textiles on account o f i t s sound labor legislation, but it has not made an application in this respect. In addition, as stated earlier, Georgia i s constrained in trading outside the CIS by i t s weak systems o f quality assurance and standards and by weaknesses in enforcing trade and intellectual property rights (TRIPS).

Non-CIS Markets.

47. Recommendations. The FTAs provide a favorable framework to foster regional trade and have the potential for helping member countries to integrate into the world trading system (e.g., in the case of harmonized standards), if large trading partners such as Russia and Ukraine become members of WTO in the near future, as it i s anticipated. This underscores the need for Georgia to decisively address current institutional weaknesses and to position i tse l f to compete in a more demanding regional environment which, at the same time, wil l help to achieve greater integration with world markets.

(i) Reduce the number o f import duties to no more than five and lower the maximum rate. (ii) Increase utilization o f GSP by better dissemination of available schemes, including

information about rules o f origin. (iii) Seek deeper preferential treatment through bilateral agreements with EU and other

industrialized countries, and obtain deeper preferences for textiles based on compliance with labor legislation.

(iv) Enforce property rights and introduce standards consistent with WTO as discussed in earlier sections.

Georgia has fi-ee trade agreements with Armenia, Azerbaijan, Kazakhstan, Russia, Turkmenistan, and Ukraine.

xxiv

48. At the same time, it i s important that as a poor country, Georgia obtains preferences comparable to those granted to LDCs. Otherwise, other things being equal, foreign investors wil l decide to locate in LDCs where such preferences are available.

Trade and Poverty

49. As discussed in earlier sections, several 'behind the border' constraints prevent the Georgian economy from successfully integrating internally and into the world trading system. The lack of internal integration affects the productivity o f the smallholder agricultural sector in rural areas and indirectly affects industry in urban areas. This has serious poverty implications, since agriculture accounts for half of employment and given industry's potential for generating wage employment.

Internal Market Integration

50. Market integration i s an important determinant o f poverty. Recent analysis shows that there i s a close correlation between the poverty rates of Georgian rural households and the extent to which they are linked to markets (expressed as percentage of households with land not recording a single transaction selling agricultural products during the whole year of ob~ervation).'~ However, on average almost two thirds o f rural household agricultural production i s for self-subsistence. Many Georgians, especially in rural areas, are effectively isolated from the national economy. In fact, it i s estimated that about a fifth o f all rural households do not trade at all. There would appear to be incentives for rural households to rely on self-subsistence and limit their interactions with markets. In such an environment, there i s a risk that households wil l tend to produce many products and not benefit from returns to specialization and scale. In addition, households that rely on subsistence generally have lower yields, mostly due to low use o f improved seeds, fertilizer and other inputs.

51. In addition to having an adverse impact on welfare levels, the prevalence of corruption in Georgia affects the ability o f rural households to integrate with domestic and external markets . At the household level, about 3 percent o f household income i s allocated to bribes. Almost 40 percent o f rural households report paying bribes, while less than 20 percent o f urban households report paying bribes. Much o f these bribes are paid during interactions between farmers and the traffic police, who extract payments when farmers travel to markets to sel l their produce.20 More indirectly, corruption affects the ability o f the poor to engage in trading activities in other ways. First, the poor are generally less efficient producers and are unable to compete with illegal imports. Second, small and medium scale enterprises, which are more likely to provide employment opportunities for poor people, face a higher incidence o f bribery on a day-to-day basis and are more vulnerable to competition from smuggled goods than are larger firms. Third, high transactions costs discourage the development o f marketing channels, such as wholesalers.

Corruption.