Finding Yield - Merrill Edge

20

c58da9b710df662c >> Employed by a non-US affiliate of MLPF&S and is not registered/qualified as a research analyst under the FINRA rules. Refer to "Other Important Disclosures" for information on certain BofA Merrill Lynch entities that take responsibility for this report in particular jurisdictions. BofA Merrill Lynch does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Refer to important disclosures on page 17 to 20. Analyst Certification on Page 16. Price Objective Basis/Risk on page 10. Link to Definitions on page 16.11245282 Investment Strategy Finding yield The pursuit of yield Finding yield has been a big challenge for investors in recent years, and it’s not likely to get easier anytime soon. Money market rates are near zero and we think they will stay near zero until well into 2015. One of our high conviction themes for 2013 is the beginning of a “Great Rotation” from bonds to stocks. As global growth gradually recovers, we expect investors to gravitate towards stocks from bonds, causing a modest rise in bond yields. In our view, investors who reach for yield by extending into longer maturities face the prospect of seeing price declines on these bonds. Although we believe that some exposure to bonds remains an integral part of any diversified portfolio, we suggest that investors seeking income also look beyond the bond market to obtain yield. Doing so generally involves taking some credit risk, but we think that economic growth will be sufficient to justify that risk. We suggest some high-quality stocks with relatively high dividends, as well as some lower-quality stocks with higher dividends. We also suggest closed end funds, Master Limited Partnerships, and bonds whose returns have historically correlated well with the stock market. Idea #1 Dividend Paying Stocks Idea #2 Selected Leveraged CEFs Idea #3 Master Limited Partnerships Idea #4 Bonds that act like stocks Chart 1: The pursuit of yield 0 2 4 6 8 10 12 14 16 '53 '56 '60 '64 '68 '71 '75 '79 '83 '86 '90 '94 '98 '01 '05 '09 '13 10y r Treasury y ield S&P 500 div idend y ield Source: BofA M errill Lynch Global Research, GFD, Bloomberg United States 07 February 2013 Fixed Income Strategy Martin Mauro Fixed Income Strategist MLPF&S Evan Richardson Fixed Income Strategist MLPF&S Equity Strategy Cheryl Rowan Portfolio Strategist MLPF&S Elias Lanik CEF Analyst MLPF&S Kate Moore Global Equity Strategist MLPF&S Nigel Tupper Strategist Merrill Lynch (Hong Kong) Savita Subramanian Equity & Quant Strategist MLPF&S Equity Research Gabe Moreen Research Analyst MLPF&S Jeffrey Spector Research Analyst MLPF&S Kenneth Bruce Research Analyst MLPF&S

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Finding Yield - Merrill Edge

c58da9b710df662c

>> Employed by a non-US affiliate of MLPF&S and is not registered/qualified as a research analyst under the FINRA rules. Refer to "Other Important Disclosures" for information on certain BofA Merrill Lynch entities that take responsibility for this report in particular jurisdictions. BofA Merrill Lynch does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Refer to important disclosures on page 17 to 20. Analyst Certification on Page 16. Price Objective Basis/Risk on page 10. Link to Definitions on page 16.11245282

Investment Strategy

Finding yield

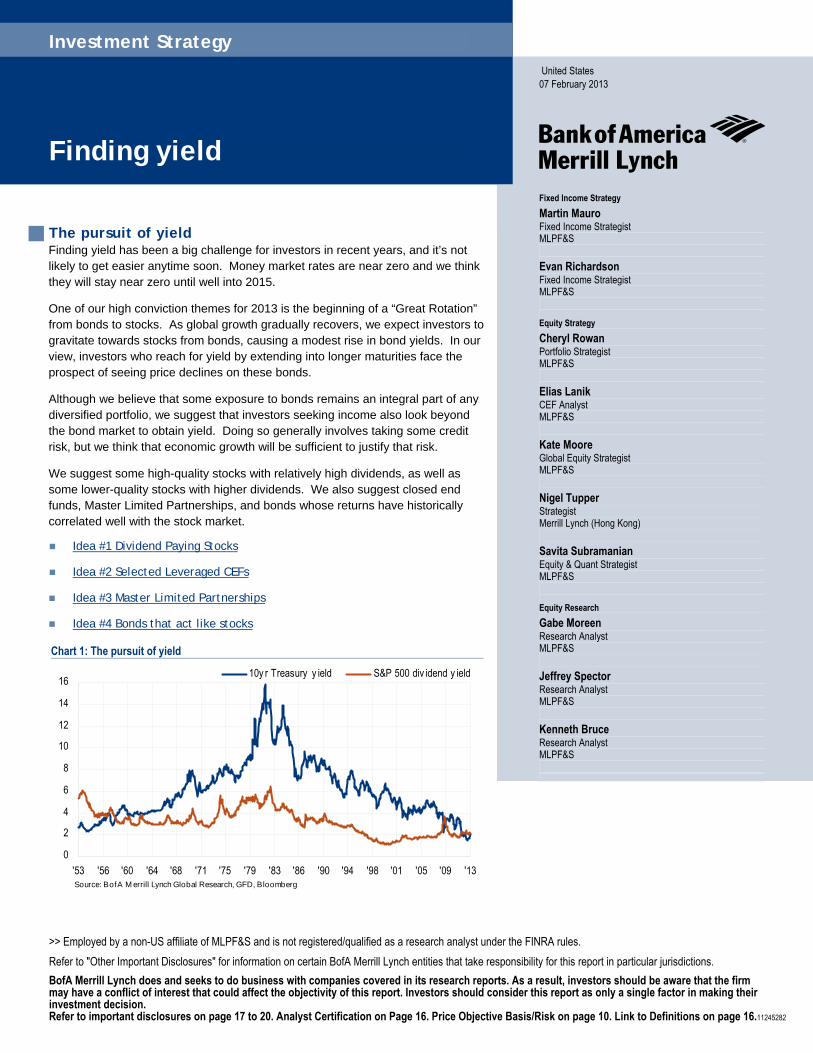

The pursuit of yield Finding yield has been a big challenge for investors in recent years, and it’s not likely to get easier anytime soon. Money market rates are near zero and we think they will stay near zero until well into 2015.

One of our high conviction themes for 2013 is the beginning of a “Great Rotation” from bonds to stocks. As global growth gradually recovers, we expect investors to gravitate towards stocks from bonds, causing a modest rise in bond yields. In our view, investors who reach for yield by extending into longer maturities face the prospect of seeing price declines on these bonds.

Although we believe that some exposure to bonds remains an integral part of any diversified portfolio, we suggest that investors seeking income also look beyond the bond market to obtain yield. Doing so generally involves taking some credit risk, but we think that economic growth will be sufficient to justify that risk.

We suggest some high-quality stocks with relatively high dividends, as well as some lower-quality stocks with higher dividends. We also suggest closed end funds, Master Limited Partnerships, and bonds whose returns have historically correlated well with the stock market.

Idea #1 Dividend Paying Stocks

Idea #2 Selected Leveraged CEFs

Idea #3 Master Limited Partnerships Idea #4 Bonds that act like stocks

Chart 1: The pursuit of yield

0

2

4

6

8

10

12

14

16

'53 '56 '60 '64 '68 '71 '75 '79 '83 '86 '90 '94 '98 '01 '05 '09 '13

10y r Treasury y ield S&P 500 div idend y ield

Source: BofA M errill Lynch Global Research, GFD, Bloomberg

United States 07 February 2013

Fixed Income Strategy Martin Mauro Fixed Income Strategist MLPF&S Evan Richardson Fixed Income Strategist MLPF&S

Equity Strategy Cheryl Rowan Portfolio Strategist MLPF&S Elias Lanik CEF Analyst MLPF&S Kate Moore Global Equity Strategist MLPF&S Nigel Tupper Strategist Merrill Lynch (Hong Kong) Savita Subramanian Equity & Quant Strategist MLPF&S

Equity Research Gabe Moreen Research Analyst MLPF&S Jeffrey Spector Research Analyst MLPF&S Kenneth Bruce Research Analyst MLPF&S

Inves tment S t ra tegy 07 February 2013

2

Finding yield Finding yield has been a big challenge for investors in recent years, and it’s not likely to get easier anytime soon. Yields on almost all types of bonds are close to all-time lows. Money market rates are near zero and we think they will stay near zero until well into 2015.

To make matters more difficult, we think that yields on many intermediate and long-term bonds will rise in 2013, albeit gradually. One of our themes for 2013 is a Great Rotation from bonds to stocks. We think that investors will gravitate towards stocks from bonds, and that bond yields will rise as a result. In our view, investors who reach for yield by extending into longer maturities face the prospect of seeing price declines on these bonds.

Although we believe that some exposure to bonds remains an integral part of any diversified portfolio, we suggest that investors seeking income also look beyond the bond market to obtain yield. Doing so generally involves taking some credit risk, but we think that economic growth will be sufficient to justify that risk. In the following pages we suggest some high-quality stocks with relatively high dividends, as well as lower-quality stocks with high dividends. We also suggest certain closed end funds, Master Limited Partnerships, and bonds whose returns typically correlate well with the stock market.

Seeking equity yield Our central thesis is that investors should consider the stock market as a source of yield. Before moving to some specific recommendations, we’ll make some general comments.

Chart 2: Stocks yielding more than Treasuries

0%

2%

4%

6%

8%

10%

12%

14%

16%

'53 '57 '61 '65 '69 '73 '77 '81 '85 '89 '93 '97 '01 '05 '09 '13

10y r Treasury y ieldS&P 500 div idend y ield

Source: Federal Reserve, S&P, BofA Merrill Lynch Global Research

The three decade long rally in the bond market has altered the relationship between bond yields and the dividend yield on stocks. Chart 1 traces the course of the dividend yield on the S&P 500 and the yield on the 10-year Treasury. Both are down from their peaks, but in recent years, dividend yields have held roughly steady, while Treasury yields have declined. Dividend yields on S&P 500 stocks are now a bit higher than the 10-year Treasury yield, something that has not happened on a sustained basis since the 1950s.

Money market rates may stay near zero for another couple of years.

Dividend yields on S&P 500 stocks now exceed the yield on the 10-year Treasury.

Inves tment S t ra tegy 07 February 2013

3

Favorable tax treatment of dividends remains Some, but not all, of the securities that we highlight in the next few pages pay Qualified Dividend Income (QDI).

The tax package that Congress passed at the turn of the year maintained the preferential treatment for long-term capital gains and QDI over interest income. For taxable incomes above $400k/$450k (single/joint filers), Congress raised the top rate on QDI to 20% and the top rate on interest income to 39.6%. The tax rates for long-term capital gains and QDI in lower income levels were left unchanged, at a maximum rate of 15%. The 3.8% medicare surtax that applies at income levels above $200k/$250k covers capital gains, dividends and taxable non-municipal interest income equally.

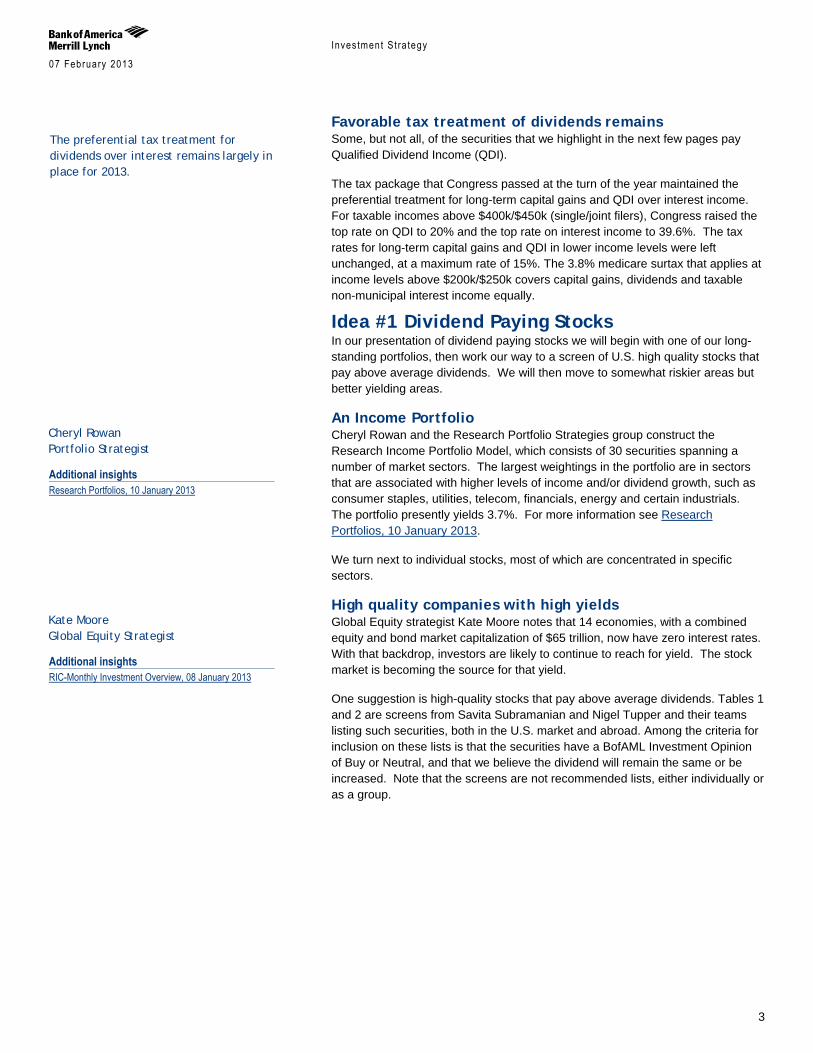

Idea #1 Dividend Paying Stocks In our presentation of dividend paying stocks we will begin with one of our long-standing portfolios, then work our way to a screen of U.S. high quality stocks that pay above average dividends. We will then move to somewhat riskier areas but better yielding areas.

An Income Portfolio Cheryl Rowan and the Research Portfolio Strategies group construct the Research Income Portfolio Model, which consists of 30 securities spanning a number of market sectors. The largest weightings in the portfolio are in sectors that are associated with higher levels of income and/or dividend growth, such as consumer staples, utilities, telecom, financials, energy and certain industrials. The portfolio presently yields 3.7%. For more information see Research Portfolios, 10 January 2013.

We turn next to individual stocks, most of which are concentrated in specific sectors.

High quality companies with high yields Global Equity strategist Kate Moore notes that 14 economies, with a combined equity and bond market capitalization of $65 trillion, now have zero interest rates. With that backdrop, investors are likely to continue to reach for yield. The stock market is becoming the source for that yield.

One suggestion is high-quality stocks that pay above average dividends. Tables 1 and 2 are screens from Savita Subramanian and Nigel Tupper and their teams listing such securities, both in the U.S. market and abroad. Among the criteria for inclusion on these lists is that the securities have a BofAML Investment Opinion of Buy or Neutral, and that we believe the dividend will remain the same or be increased. Note that the screens are not recommended lists, either individually or as a group.

The preferential tax treatment for dividends over interest remains largely in place for 2013.

Cheryl Rowan Portfolio Strategist

Additional insights Research Portfolios, 10 January 2013

Kate Moore Global Equity Strategist

Additional insights RIC-Monthly Investment Overview, 08 January 2013

Inves tment S t ra tegy 07 February 2013

4

US High Quality & Dividend Yield Screen (Methodology on page 9) Table 1: High Quality & Dividend Yield Screen (February 2013) Date Added Ticker Name Sector

ROE (%)

Debt / Equity

Yield (%) Quality

Market Val ($mn) Cost Px Price

BofAML Rating

FCF/ DIV Footnotes

4/1/2012 ADP ADP Information Tech. 22.6 0.1 2.7 A 28,784 55.19 59.29 B-1-7 2.1 Bbijopsvw 11/1/2011 BAX Baxter Health Care 32.6 0.8 2.3 A+ 37,270 53.52 67.84 B-1-7 2.2 BObijopsvw 12/1/2010 CVX Chevron Energy 19.0 0.1 3.0 A+ 225,369 82.70 115.15 A-2-7 1.5 Bbgijopsvw 1/2/2013 EMR Emerson Industrials 19.0 0.5 2.8 A+ 41,457 54.60 57.25 B-2-7 1.8 Bbijopsvw 10/1/2012 HON Honeywell Industrials 24.5 0.6 2.2 A- 53,457 60.80 68.24 B-1-7 2.5 Bbijopsvw 1/3/2012 KO Coca Cola Consumer Staples 26.5 1.0 2.7 A+ 143,644 35.07 37.24 A-1-7 1.7 BObgijopsvw 10/1/2012 LLTC Linear Tech Corp Information Tech. 56.7 1.0 3.4 A- 8,474 32.57 36.62 B-1-7 1.5 Bbijopsw 2/2/2009 MCD McDonald's Corp Consumer Disc. 40.0 1.0 3.0 A 95,669 57.90 95.29 B-1-7 1.4 Bbgijopsvw 5/3/2010 MDT Medtronic Health Care 19.1 0.7 2.2 A 47,129 44.13 46.6 A-1-7 3.7 BObgijopsvw 10/1/2012 MMM 3M Industrials 26.6 0.3 2.3 A+ 64,008 93.29 100.55 B-1-7 2.6 Bbgijopsvw 8/1/2011 MSFT Microsoft Corp Information Tech. 22.6 0.2 3.0 A- 208,080 27.27 27.45 B-1-7 2.3 Bbijopsvw 2/1/2013 PG Procter & Gamble Consumer Staples 17.4 0.5 2.9 A+ 205,505 75.16 75.16 A-1-7 2.0 Bbgijopsvw 4/1/2012 PAYX PAYX Information Tech. 34.4 0.0 4.0 A 10,555 30.99 32.65 A-2-7 1.3 Bbjopw 2/1/2013 UTX United Tech Industrials 20.3 0.9 2.3 A+ 73,841 87.57 87.57 B-1-7 2.9 BObgijopsvw 12/3/2012 WMT Wal*Mart Stores Consumer Staples 23.5 0.8 2.2 A+ 117,000 71.34 69.95 A-1-7 2.3 Bbijopsv 2/1/2012 XOM ExxonMobil Energy 27.5 0.1 2.3 A+ 410,204 83.97 89.97 A-1-7 2.8 Bbijopsvw Average 27.0 0. 5 2.7 107,294 2.1 S&P 500 benchmarks: 14.3 1.1 2.0 Source: BofA Merrill Lynch Global Research, BofA Merrill Lynch US Quantitative Strategy, FactSet, S&P Note: Calculations are based on data from the last 12 months. Financials stocks are excluded because they typically have very high Debt/Equity ratios that have nothing to do with their capital structure. We calculate the benchmark S&P 500 ROE by taking the average of the aggregate ROE (S&P 500 EPS ÷ by book value per share) and the median ROE. Disclaimer: These stocks have been selected according to the specified screening criteria and do not constitute a recommended list. Investors looking for a high quality dividend yield oriented investment can consider this analysis as one part of their decision making process, but should also consider other factors including fundamental opinions, financial risk, investment risk, management strategies and operating and financial outlooks.

International High Quality & Dividend Yield Screen (Methodology on page 9) Table 2: Global Non-US High Quality and High Dividend Yield Screen (February 2013)

Ticker ADR Company Country Sector MCAP Quality Dividend yield %

BofAML Rating

Price as of 06 Feb (US$)

ADR Px as of 6 Feb (US$) Footnotes

MEGGF MEGGY MEGGITT UK Industrials 5,395 A- 2.5% B-1-7 6.81 13.91 BNbijopqsvSBGSF SBGSY SCHNEIDER ELECTRIC France Industrials 42,128 A- 3.0% B-2-7 74.32 14.89 gijopqsvSNYNF SNY SANOFI France Health Care 129,251 A 3.7% A-1-7 93.91 47.34 BbijopsvwJCYCF JCYGY JARDINE CYCLE & CARRIAGE Singapore Retailing 14,544 A 3.0% C-1-7 41.69 83.66 iqvALFVF ALFVY ALFA LAVAL Sweden Industrials 8,952 A- 2.4% B-2-7 22.82 22.88 pqSource: BofA Merrill Lynch Global Quantitative Strategy, MSCI, IBES, S&P. Note: Dividend yields are gross of taxes. Disclaimer: These stocks have been selected according to the specified screening criteria and do not constitute a recommended list. Investors looking for a high quality dividend yield oriented investment can consider this analysis as one part of their decision making process, but should also consider other factors including fundamental opinions, financial risk, investment risk, management strategies and operating and financial outlooks.

Savita Subramanian Equity & Quant Strategist

Additional insights High Quality & Dividend Yield Screen, 01 February 2013

Nigel Tupper Quantitative Strategist

Additional insights Global Quantessential Style, 06 February 2013

Inves tment S t ra tegy 07 February 2013

5

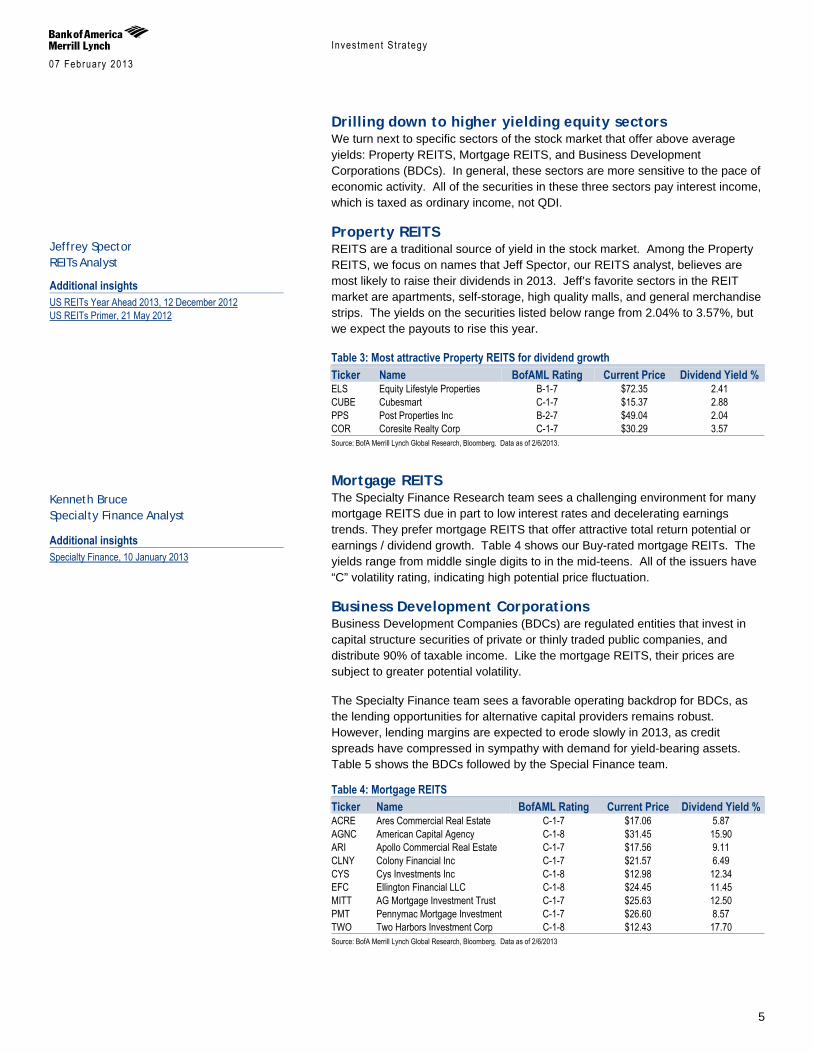

Drilling down to higher yielding equity sectors We turn next to specific sectors of the stock market that offer above average yields: Property REITS, Mortgage REITS, and Business Development Corporations (BDCs). In general, these sectors are more sensitive to the pace of economic activity. All of the securities in these three sectors pay interest income, which is taxed as ordinary income, not QDI.

Property REITS REITS are a traditional source of yield in the stock market. Among the Property REITS, we focus on names that Jeff Spector, our REITS analyst, believes are most likely to raise their dividends in 2013. Jeff’s favorite sectors in the REIT market are apartments, self-storage, high quality malls, and general merchandise strips. The yields on the securities listed below range from 2.04% to 3.57%, but we expect the payouts to rise this year. Table 3: Most attractive Property REITS for dividend growth Ticker Name BofAML Rating Current Price Dividend Yield % ELS Equity Lifestyle Properties B-1-7 $72.35 2.41 CUBE Cubesmart C-1-7 $15.37 2.88 PPS Post Properties Inc B-2-7 $49.04 2.04 COR Coresite Realty Corp C-1-7 $30.29 3.57 Source: BofA Merrill Lynch Global Research, Bloomberg. Data as of 2/6/2013.

Mortgage REITS The Specialty Finance Research team sees a challenging environment for many mortgage REITS due in part to low interest rates and decelerating earnings trends. They prefer mortgage REITS that offer attractive total return potential or earnings / dividend growth. Table 4 shows our Buy-rated mortgage REITs. The yields range from middle single digits to in the mid-teens. All of the issuers have “C” volatility rating, indicating high potential price fluctuation.

Business Development Corporations Business Development Companies (BDCs) are regulated entities that invest in capital structure securities of private or thinly traded public companies, and distribute 90% of taxable income. Like the mortgage REITS, their prices are subject to greater potential volatility.

The Specialty Finance team sees a favorable operating backdrop for BDCs, as the lending opportunities for alternative capital providers remains robust. However, lending margins are expected to erode slowly in 2013, as credit spreads have compressed in sympathy with demand for yield-bearing assets. Table 5 shows the BDCs followed by the Special Finance team. Table 4: Mortgage REITS Ticker Name BofAML Rating Current Price Dividend Yield % ACRE Ares Commercial Real Estate C-1-7 $17.06 5.87 AGNC American Capital Agency C-1-8 $31.45 15.90 ARI Apollo Commercial Real Estate C-1-7 $17.56 9.11 CLNY Colony Financial Inc C-1-7 $21.57 6.49 CYS Cys Investments Inc C-1-8 $12.98 12.34 EFC Ellington Financial LLC C-1-8 $24.45 11.45 MITT AG Mortgage Investment Trust C-1-7 $25.63 12.50 PMT Pennymac Mortgage Investment C-1-7 $26.60 8.57 TWO Two Harbors Investment Corp C-1-8 $12.43 17.70 Source: BofA Merrill Lynch Global Research, Bloomberg. Data as of 2/6/2013

Jeffrey Spector REITs Analyst

Additional insights US REITs Year Ahead 2013, 12 December 2012 US REITs Primer, 21 May 2012

Kenneth Bruce Specialty Finance Analyst

Additional insights Specialty Finance, 10 January 2013

Inves tment S t ra tegy 07 February 2013

6

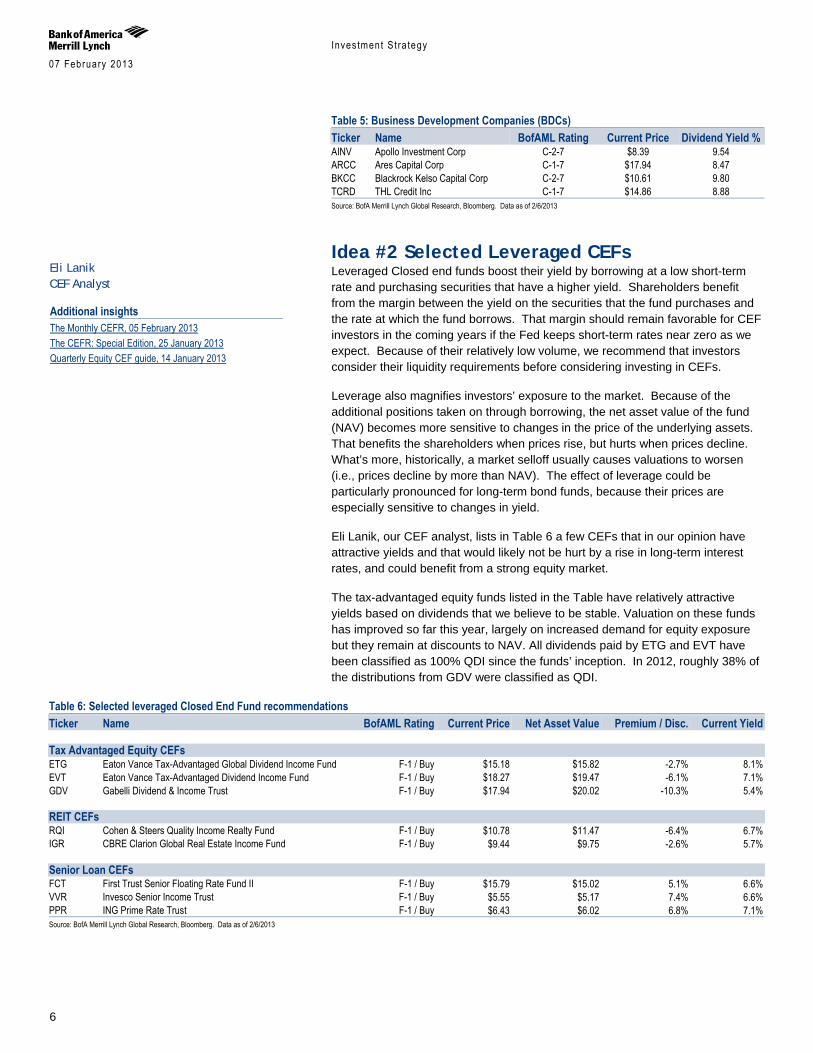

Table 5: Business Development Companies (BDCs) Ticker Name BofAML Rating Current Price Dividend Yield % AINV Apollo Investment Corp C-2-7 $8.39 9.54 ARCC Ares Capital Corp C-1-7 $17.94 8.47 BKCC Blackrock Kelso Capital Corp C-2-7 $10.61 9.80 TCRD THL Credit Inc C-1-7 $14.86 8.88 Source: BofA Merrill Lynch Global Research, Bloomberg. Data as of 2/6/2013

Idea #2 Selected Leveraged CEFs Leveraged Closed end funds boost their yield by borrowing at a low short-term rate and purchasing securities that have a higher yield. Shareholders benefit from the margin between the yield on the securities that the fund purchases and the rate at which the fund borrows. That margin should remain favorable for CEF investors in the coming years if the Fed keeps short-term rates near zero as we expect. Because of their relatively low volume, we recommend that investors consider their liquidity requirements before considering investing in CEFs.

Leverage also magnifies investors’ exposure to the market. Because of the additional positions taken on through borrowing, the net asset value of the fund (NAV) becomes more sensitive to changes in the price of the underlying assets. That benefits the shareholders when prices rise, but hurts when prices decline. What’s more, historically, a market selloff usually causes valuations to worsen (i.e., prices decline by more than NAV). The effect of leverage could be particularly pronounced for long-term bond funds, because their prices are especially sensitive to changes in yield.

Eli Lanik, our CEF analyst, lists in Table 6 a few CEFs that in our opinion have attractive yields and that would likely not be hurt by a rise in long-term interest rates, and could benefit from a strong equity market.

The tax-advantaged equity funds listed in the Table have relatively attractive yields based on dividends that we believe to be stable. Valuation on these funds has improved so far this year, largely on increased demand for equity exposure but they remain at discounts to NAV. All dividends paid by ETG and EVT have been classified as 100% QDI since the funds’ inception. In 2012, roughly 38% of the distributions from GDV were classified as QDI.

Table 6: Selected leveraged Closed End Fund recommendations Ticker Name BofAML Rating Current Price Net Asset Value Premium / Disc. Current Yield Tax Advantaged Equity CEFs ETG Eaton Vance Tax-Advantaged Global Dividend Income Fund F-1 / Buy $15.18 $15.82 -2.7% 8.1% EVT Eaton Vance Tax-Advantaged Dividend Income Fund F-1 / Buy $18.27 $19.47 -6.1% 7.1% GDV Gabelli Dividend & Income Trust F-1 / Buy $17.94 $20.02 -10.3% 5.4% REIT CEFs RQI Cohen & Steers Quality Income Realty Fund F-1 / Buy $10.78 $11.47 -6.4% 6.7% IGR CBRE Clarion Global Real Estate Income Fund F-1 / Buy $9.44 $9.75 -2.6% 5.7% Senior Loan CEFs FCT First Trust Senior Floating Rate Fund II F-1 / Buy $15.79 $15.02 5.1% 6.6% VVR Invesco Senior Income Trust F-1 / Buy $5.55 $5.17 7.4% 6.6% PPR ING Prime Rate Trust F-1 / Buy $6.43 $6.02 6.8% 7.1% Source: BofA Merrill Lynch Global Research, Bloomberg. Data as of 2/6/2013

Eli Lanik CEF Analyst

Additional insights The Monthly CEFR, 05 February 2013 The CEFR: Special Edition, 25 January 2013 Quarterly Equity CEF guide, 14 January 2013

Inves tment S t ra tegy 07 February 2013

7

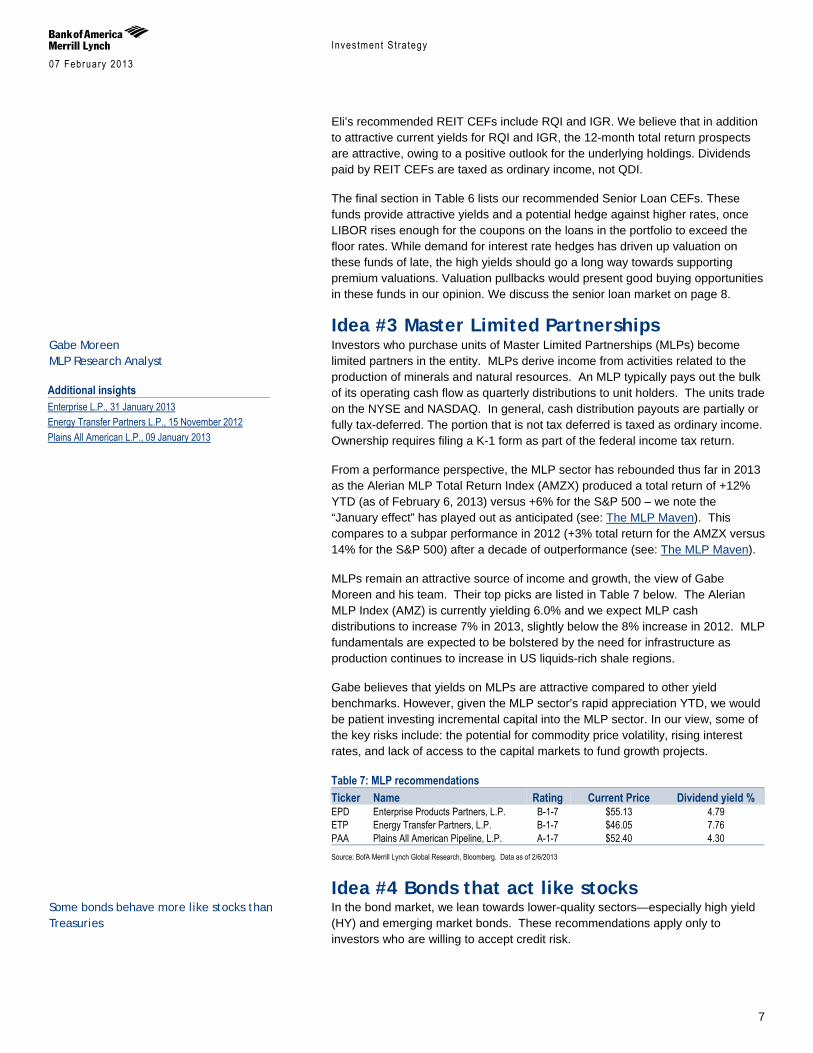

Eli’s recommended REIT CEFs include RQI and IGR. We believe that in addition to attractive current yields for RQI and IGR, the 12-month total return prospects are attractive, owing to a positive outlook for the underlying holdings. Dividends paid by REIT CEFs are taxed as ordinary income, not QDI.

The final section in Table 6 lists our recommended Senior Loan CEFs. These funds provide attractive yields and a potential hedge against higher rates, once LIBOR rises enough for the coupons on the loans in the portfolio to exceed the floor rates. While demand for interest rate hedges has driven up valuation on these funds of late, the high yields should go a long way towards supporting premium valuations. Valuation pullbacks would present good buying opportunities in these funds in our opinion. We discuss the senior loan market on page 8.

Idea #3 Master Limited Partnerships Investors who purchase units of Master Limited Partnerships (MLPs) become limited partners in the entity. MLPs derive income from activities related to the production of minerals and natural resources. An MLP typically pays out the bulk of its operating cash flow as quarterly distributions to unit holders. The units trade on the NYSE and NASDAQ. In general, cash distribution payouts are partially or fully tax-deferred. The portion that is not tax deferred is taxed as ordinary income. Ownership requires filing a K-1 form as part of the federal income tax return.

From a performance perspective, the MLP sector has rebounded thus far in 2013 as the Alerian MLP Total Return Index (AMZX) produced a total return of +12% YTD (as of February 6, 2013) versus +6% for the S&P 500 – we note the “January effect” has played out as anticipated (see: The MLP Maven). This compares to a subpar performance in 2012 (+3% total return for the AMZX versus 14% for the S&P 500) after a decade of outperformance (see: The MLP Maven).

MLPs remain an attractive source of income and growth, the view of Gabe Moreen and his team. Their top picks are listed in Table 7 below. The Alerian MLP Index (AMZ) is currently yielding 6.0% and we expect MLP cash distributions to increase 7% in 2013, slightly below the 8% increase in 2012. MLP fundamentals are expected to be bolstered by the need for infrastructure as production continues to increase in US liquids-rich shale regions.

Gabe believes that yields on MLPs are attractive compared to other yield benchmarks. However, given the MLP sector’s rapid appreciation YTD, we would be patient investing incremental capital into the MLP sector. In our view, some of the key risks include: the potential for commodity price volatility, rising interest rates, and lack of access to the capital markets to fund growth projects.

Idea #4 Bonds that act like stocks In the bond market, we lean towards lower-quality sectors—especially high yield (HY) and emerging market bonds. These recommendations apply only to investors who are willing to accept credit risk.

Gabe Moreen MLP Research Analyst

Additional insights Enterprise L.P., 31 January 2013 Energy Transfer Partners L.P., 15 November 2012 Plains All American L.P., 09 January 2013

Table 7: MLP recommendations Ticker Name Rating Current Price Dividend yield % EPD Enterprise Products Partners, L.P. B-1-7 $55.13 4.79 ETP Energy Transfer Partners, L.P. B-1-7 $46.05 7.76 PAA Plains All American Pipeline, L.P. A-1-7 $52.40 4.30 Source: BofA Merrill Lynch Global Research, Bloomberg. Data as of 2/6/2013

Some bonds behave more like stocks than Treasuries

Inves tment S t ra tegy 07 February 2013

8

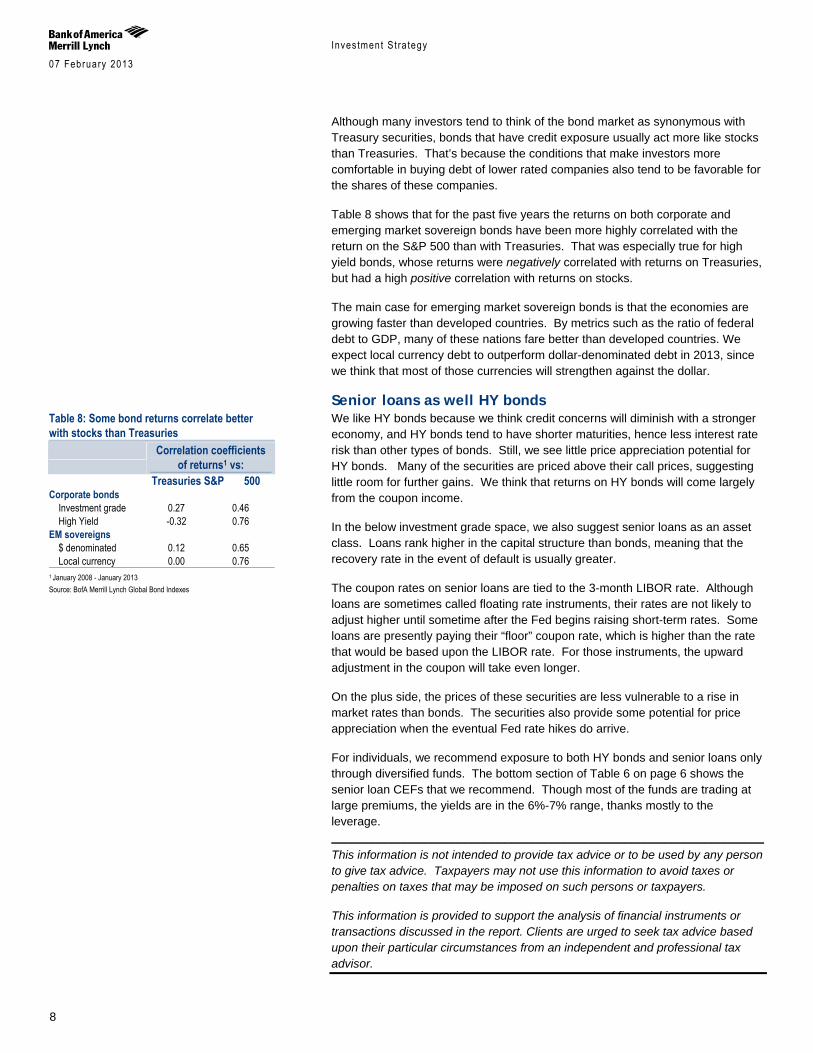

Although many investors tend to think of the bond market as synonymous with Treasury securities, bonds that have credit exposure usually act more like stocks than Treasuries. That’s because the conditions that make investors more comfortable in buying debt of lower rated companies also tend to be favorable for the shares of these companies.

Table 8 shows that for the past five years the returns on both corporate and emerging market sovereign bonds have been more highly correlated with the return on the S&P 500 than with Treasuries. That was especially true for high yield bonds, whose returns were negatively correlated with returns on Treasuries, but had a high positive correlation with returns on stocks.

The main case for emerging market sovereign bonds is that the economies are growing faster than developed countries. By metrics such as the ratio of federal debt to GDP, many of these nations fare better than developed countries. We expect local currency debt to outperform dollar-denominated debt in 2013, since we think that most of those currencies will strengthen against the dollar.

Senior loans as well HY bonds We like HY bonds because we think credit concerns will diminish with a stronger economy, and HY bonds tend to have shorter maturities, hence less interest rate risk than other types of bonds. Still, we see little price appreciation potential for HY bonds. Many of the securities are priced above their call prices, suggesting little room for further gains. We think that returns on HY bonds will come largely from the coupon income.

In the below investment grade space, we also suggest senior loans as an asset class. Loans rank higher in the capital structure than bonds, meaning that the recovery rate in the event of default is usually greater.

The coupon rates on senior loans are tied to the 3-month LIBOR rate. Although loans are sometimes called floating rate instruments, their rates are not likely to adjust higher until sometime after the Fed begins raising short-term rates. Some loans are presently paying their “floor” coupon rate, which is higher than the rate that would be based upon the LIBOR rate. For those instruments, the upward adjustment in the coupon will take even longer.

On the plus side, the prices of these securities are less vulnerable to a rise in market rates than bonds. The securities also provide some potential for price appreciation when the eventual Fed rate hikes do arrive.

For individuals, we recommend exposure to both HY bonds and senior loans only through diversified funds. The bottom section of Table 6 on page 6 shows the senior loan CEFs that we recommend. Though most of the funds are trading at large premiums, the yields are in the 6%-7% range, thanks mostly to the leverage. _________________________________________________________________ This information is not intended to provide tax advice or to be used by any person to give tax advice. Taxpayers may not use this information to avoid taxes or penalties on taxes that may be imposed on such persons or taxpayers.

This information is provided to support the analysis of financial instruments or transactions discussed in the report. Clients are urged to seek tax advice based upon their particular circumstances from an independent and professional tax advisor.

Table 8: Some bond returns correlate better with stocks than Treasuries

Correlation coefficients

of returns1 vs: Treasuries S&P 500 Corporate bonds

Investment grade 0.27 0.46 High Yield -0.32 0.76

EM sovereigns $ denominated 0.12 0.65 Local currency 0.00 0.76

1 January 2008 - January 2013 Source: BofA Merrill Lynch Global Bond Indexes

Inves tment S t ra tegy 07 February 2013

9

Methodology: US High Quality & Dividend Yield Screen We list a screen of preferred securities that meet specified selection criteria and have relatively high yields for their credit rating and industry sector. The US High Quality & Dividend Yield Screen is not a recommended list.

Screening criteria We combined our two secular themes through the following criteria. In our view, these screening factors were likely to uncover higher-quality companies that offered relatively secure dividend yield. The stocks are selected from the S&P 500.

S&P Common Stock Rank of A+, A, or A-. The S&P Common Stock Rankings are our main measure of quality. These rankings are based primarily on the growth and stability of earnings and dividends over a 10-year period.

Return on Equity (ROE) greater than the average S&P 500 ROE.

Debt/Equity lower than the S&P 500.

Dividend yield greater than the S&P 500.

BofA Merrill Lynch Research Investment Opinion indicates Buy or Neutral as well as the likelihood that the dividend will remain the same or be increased (ie, a dividend rating of “7”).

The ratio of the last 12 months’ free cash flow to dividends must be greater than 1.0.

Methodology: International High Quality & Dividend Yield Screen We list a screen of preferred securities that meet specified selection criteria and have relatively high yields for their credit rating and industry sector. The International High Quality & Dividend Yield Screen is not a recommended list.

Screening criteria This monthly screen selects high quality and high dividend yield stocks from the MSCI AC World ex-USA Index covered by BofA Merrill Lynch Global Research. The screen uses the following criteria to uncover higher quality companies that offer relatively secure dividend yield.

S&P Common Stock Rank (quality rank) of A+, A, or A-. The S&P Common Stock rankings are our main measure of quality. These rankings are based on the stability and growth in earnings and dividends over a seven-year period for non-US companies.

Return on Equity (ROE) greater than the MSCI Index.

Debt/Equity lower than the MSCI Index.

Dividend yield greater than the MSCI Index.

BofAML Investment Opinion indicates Buy or Neutral, as well as the likelihood that the dividend will remain the same or be increased (ie, a dividend rating of 7).

The ratio of the past 12 months’ free cash flow to dividends is greater than 1.0.

Note: Please be aware that several links in this report are directed to lists that are updated on a monthly basis. There may have been updates to one or more lists. Investors should check for the latest available reports.

Inves tment S t ra tegy 07 February 2013

10

Footnote key /#/ One or more analysts responsible for covering the securities in this report owns such securities. /b/ MLPF&S or one of its affiliates acts as a market maker for the equity securities recommended in the report. /g/ MLPF&S or an affiliate was a manager of a public offering of securities of this company within the last 12 months. /i/ The company is or was, within the last 12 months, an investment banking client of MLPF&S and/or one or more of its affiliates. /j/ MLPF&S or an affiliate has received compensation from the company for non-investment banking services or products within the past 12 months. /o/ The company is or was, within the last 12 months, a securities business client (non-investment banking) of MLPF&S and/or one or more of its affiliates. /p/ The company is or was, within the last 12 months, a non-securities business client of MLPF&S and/or one or more of its affiliates. /q/ In the US, retail sales and/or distribution of this report may be made only in states where these securities are exempt from registration or have been qualified for sale. /r/ An officer, director or employee of MLPF&S or one of its affiliates is an officer or director of this company. /s/ MLPF&S or an affiliate has received compensation for investment banking services from this company within the past 12 months. /v/ MLPF&S or an affiliate expects to receive or intends to seek compensation for investment banking services from this company or an affiliate of the company within the next three months. /w/ MLPF&S together with its affiliates beneficially owns one percent or more of the common stock of this company. If this report was issued on or after the 10th day of the month, it reflects the ownership position on the last day of the previous month. Reports issued before the 10th day of a month reflect the ownership position at the end of the second month preceding the date of the report. /x/ Customers of MLPF&S in the US can receive independent, third-party research on companies covered in this report, at no cost to them, if such research is available. Customers can access this independent research at http://www.ml.com/independentresearch or can call 1-800-637-7455 to request a copy of this research. /z/ The country in which this company is organized has certain laws or regulations that limit or restrict ownership of the company's shares by nationals of other countries. /A/ One of the analysts covering the company is a former employee of the company and, in that capacity, received compensation from the company within the past 12 months. /B/ MLPF&S or one of its affiliates is willing to sell to, or buy from, clients the common equity of the company on a principal basis. /C/ Merrill Lynch is affiliated with an NYSE specialist organization that specializes in one or more securities issued by the subject companies. This affiliated NYSE specialist organization makes a market in, and may maintain a long or short position in or be on the opposite side of orders executed on the Floor of the NYSE in connection with one or more of the securities issued by these companies. /N/ The company is a corporate broking client of Merrill Lynch International in the United Kingdom. /O/ MLPF&S or one of it affiliates has a significant financial interest in the fixed income instruments of the issuer. If this report was issued on or after the 10th day of a month, it reflects a significant financial interest on the last day of the previous month. Reports issued before the 10th day of a month reflect a significant financial interest at the end of the second month preceding the date of the report.

Price objective basis & risk AG Mortgage Investment Trust, Inc. (MITT) Our $25.50 Price Objective is based on a 1.10x multiple to Q4'12e BV, in line with the hybrid mortgage REIT universes. We anticipate investors will continue to ascribe a premium valuation around 1.1x BV to MITT, given its above average dividend yield of 13% and its stable earnings and BV track record. Downside/upside risks to achieving our price objective and EPS forecast are 1) changes in the absolute level of rates resulting in higher/lower funding costs and BV pressure/strength, 2) a flattening/steepening of the yield curve causing investment spreads to decline/rise, 3) significant increases/declines in MBS spreads causing BV pressure/strength, 4) deteriorating/improving capital markets leading to higher/lower borrowing costs, 5) material increases/declines in refinance activity causing smaller/wider interest spreads and 6) adverse/favorable government intervention in the mortgage markets or GSE activity. Execution risk, namely poor asset selection, could also negatively impact shares.

American Capital Agency Corp. (AGNC) Our $33.50 price objective is based on a 1.10x to Q4'12e BV, which we believe is justified given the company's above average dividend yield of 16% and its strong earnings and BV track record. AGNC's focus on investments with low prepayment sensitivity should reduce yield compression in the low interest rate environment and suggests it will continue to trade at a premium to its peers.

Inves tment S t ra tegy 07 February 2013

11

Downside/upside risks to our price objective and EPS forecast are 1) changes in the absolute level of rates resulting in higher/lower funding costs and BV pressure/strength, 2) a flattening/steepening of the yield curve causing investment spreads to decline/rise, 3) significant increases/decreases in MBS spreads causing BV pressure/strength, 4) deteriorating/improving capital markets leading to higher/lower borrowing costs, 5) material increases/decreases in refinance activity causing smaller/wider interest spreads and 6) adverse/favorable government intervention in the mortgage markets or GSEs. Execution risk, namely poor asset selection, could also negatively impact shares.

Apollo Commercial Real Estate Finance (ARI) Our $19.00 price objective is based on a 1.15x P/BV multiple to book value. The stock currently trades at a discount to its book value. However, as its earning yield continues to rise in 2012, its valuation should improve accordingly, in our view. ARI could generate $1.60 dividend per share over the next 12 months, suggesting a yield of around 9.5% at the current share price. Downside/upside risks to our price objective or EPS and DPS forecast are a delays/faster than anticipated capital deployment, unfavorable/favorable price movements in the target asset classes, rising/falling interest rates, credit deterioration/improvement in commercial real estate mortgages, disruptions/strengthening in the capital markets and unexpected changes in government regulations of the financial markets.

Apollo Investment Corporation (AINV) Our $9.00 Price Objective is based on a 1.1x multiple to stated net asset value (NAV), which should be achievable as AINV demonstrates stable shareholder returns and investors continue to favor yield-based investments. AINV warrants a modest discount to BDC peers, as its NAV exhibits heightened sensitivity due to weakening economic fundamentals and a large legacy position in liquid mezzanine investments. Over a longer horizon, we estimate it could generate an attractive mid-teens total return, sustaining a 10% dividend yield, versus peers in the 9 - 11% range, as earnings stabilize. Downside risks to achieving our price objective and EPS forecast are 1) material weakening in credit markets, 2) a significantly slowdown in investment activity, 3) a deteriorating macroeconomic environment, 4) disruptions in the capital markets, and 5) weaker than expected investment performance.

Ares Capital Corporation (ARCC) Our $18 Price Objective is based on a 1.15x multiple to stated net asset value (NAV), which in our view is achievable in a stable operating backdrop with intensifying demand for yield bearing investments. ARCC warrants a premium to BDC peers as a best-in-class operator and stable position of senior secured investments, in our opinion. Asset values should remain largely range bound for the foreseeable future, as strong operating trends persist and investors increasingly target yield-based investments. ARCC should sustain its 9% dividend yield, versus peers in the 9-12% range, as earnings trends remain favorable biased to the upside. Downside risks to achieving our price objective and EPS forecast are 1) material weakening in credit markets, 2) a significantly slowdown in investment activity, 3) a deteriorating macroeconomic environment, 4) disruptions in the capital markets, and 5) weaker than expected investment performance.

Inves tment S t ra tegy 07 February 2013

12

Ares Commercial Real Estate Corp. (ACRE) Our $19 Price Objective is based on a 1.05x multiple to Q3'12 forecast BV of $17.99. In our view, ACRE can achieve a modest premium to its peer average, given its internal sourcing model, which tends to attract better investor interest, and its attractive potential economic returns. ACRE should achieve a 9% ROE, based on our forecast, modestly above peers. Valuations for the comparable mortgage REIT peers range between 85% and 105% of stated BV, with a significant premium applied to ACRE's closest peer, STWD. Downside risks to our price objective or EPS and DPS forecast are a delay in capital deployment, unfavorable price movement in the target asset classes, volatile interest rates, credit deterioration in commercial real estate mortgages, further disruptions in the capital markets and unexpected changes in government regulations of the financial markets.

BlackRock Kelso Capital Corporation (BKCC) Our $10.50 Price Objective is based on a 1.1x multiple to stated net asset value (NAV), which is achievable as BKCC exhibits stable earnings and NAV, and investor interest continues for yield-based investments. BKCC is well positioned to capitalize on a favorable investment backdrop, due to its majority senior holdings, as it enters a new phase of growth in higher quality investments. However, in the near term we expect potentially heightened price volatility should the economic backdrop weaken meaningfully. Over a longer horizon, BKCC should generate an attractive low-double-digit total return, sustaining an 10% dividend yield, versus peers in the 9 - 11%, as earnings stabilize. Downside risks to achieving our price objective and EPS forecast are 1) a significantly slower investment pace than anticipated, 2) a deteriorating macroeconomic environment, 3) a difficult capital market environment leading to higher borrowing costs, 4) weaker than expected portfolio company performance, and 5) poor execution and asset selection by management.

Colony Financial (CLNY) Our $23.00 price objective is based on a 1.25x multiple to book value, at the high end of the peer range, due to its proven asset sourcing and strong earnings and BV track record. CLNY should generate a long term dividend yield of 7-9%. The potential gains from its distressed loan investment could drive the buying demand over time, in our view. Based on our current financial model, the company could generate roughly $1.40 dividend per share in 2013, suggesting a yield of 7% at the current share price. Earnings could be volatile due to the back-end profit loading nature of CLNY's investments. Risks to achieving our price objective or EPS and DPS forecast are a delay in capital deployment, unfavorable price movement in the target asset classes, volatile interest rates, continued credit deterioration in commercial mortgages, further disruption in the capital markets and unexpected changes in government policies.

CoreSite Realty Corporation (COR) Our price objective of $32 for COR reflects a 7.5% premium to our 12-month forward NAV estimate. The 7.5% premium reflects COR's management expertise. The upside risks to our PO are better-than-expected operating conditions in COR's key markets. Risks to our price objective are 1) increased competition, 2) customer consolidation or bankruptcies, 3) a decrease in datacenter demand, 4)

Inves tment S t ra tegy 07 February 2013

13

execution risk and 5) conflicts of interests with majority shareholders and stock overhang. As a real estate company, COR remains exposed to excessive new supply in its markets, rising construction and capital costs, real estate values, and rising interest rates.

CubeSmart (CUBE) Our forward NAV derived PO of $16 represents a 5% premium to our 12 month forward NAV. We think the premium is justified given CUBE's improved balance sheet. Downside risks to our PO are a significant systemic negative inflection in storage fundamentals and higher interest rates, while upside risks are a loosening of the debt markets and a better-than-expected fundamental performance driven by increased consumer demand for self-storage space.

CYS Investments, Inc (CYS) Our $13.50 Price Objective is based on a 1.0x multiple to Q4'12e BV, which is in-line with the Agency mortgage REIT universe. CYS is trading at roughly 0.87x BV, likely in anticipation of earnings compression, in our opinion. Valuations on agency mortgage REIT stocks could moderate, as investors digest rising prepayment speeds and a certain amount of uncertainty in monetary policy prospectively. However, CYS' dividend yield of 13% is consistent with most agency mortgage REITs, supporting a peer-like valuation, in our view. Downside/upside risks to our price objective are: 1) changes in the absolute level of rates resulting in higher/lower funding costs and BV pressure/expansion, 2) a flattening/steepening of the yield curve causing investment spreads to decline/rise, 3) significant increases/decreases in MBS spreads causing BV pressure/expansion, 4) deteriorating/improving capital markets leading to higher/lower borrowing costs, 5) material increases/decreases in refinance activity causing smaller/larger interest spreads and 6) adverse/favorable government intervention in the mortgage markets or GSE activity. Execution risk, namely poor asset selection, could also negatively impact shares.

Ellington Financial LLC (EFC) Our $25.25 Price Objective is based on a 1.05x multiple to our Q4'12e BV, which we think is appropriate given current income at the low-end of peers and potential from trading gains. EFC is attractively valued at a discount to BV, in our view, versus hybrid mortgage REIT peers that is currently trading at a modest premium. As liquidity in the shares improves and EFC establishes a longer earnings track record, we anticipate investors will value the shares more in line with the mortgage REIT group, implying share price upside potential. Risks to achieving our price objective and EPS forecast are: 1) execution risk: poor security selection, sub-optimal portfolio construction, ineffective risk management or financing decisions lead to below comparable investment returns, 2) reduced visibility and predictability: EFC's more complex investment strategy and active management style is inherently less predictable and difficult to forecast, possibly leading to a discount valuation or increased volatility, 3) Prepayment risk: Volatile prepayments could reduced economic returns in EFC's portfolio and remain a point of earnings risk, given low interest rates and government housing policy significant increases/declines in MBS spreads causing BV pressure/strength, 4) Liquidity risk: Poor liquidity and disruptions in the REPO market could undermine EFC's portfolio returns or weigh on valuation.

Inves tment S t ra tegy 07 February 2013

14

Energy Transfer (ETP) Our $48 per LP unit PO is based on a 7.75 pct target yield on our annualized 4Q13E distribution of $3.72, which is higher than the target yields for many of ETP's large cap MLP peers. We see ETP's higher than peer average yield as justified by its less robust growth prospects than some of its large-cap MLP peers and some continued headwinds at its legacy businesses. Business risks to our price objective on ETP are execution risk around integrating recent acquisitions, lower than expected returns on growth projects, a sustained decrease in nat gas commodity prices which could curtail drilling activity around gathering systems and pipelines, or lower basis differentials. Increasing costs may also reduce the returns realized on ETP's growth projects. Upside risks include better than expected returns on ETP's growth projects, a pick-up in nat gas pricing and basis differentials, and better than expected results at ETP's recently acquired assets. The tax treatment of ETP depends on its status as a partnership for federal income tax purposes. Should ETP become subject to taxes, performance could be materially affected. From a macro perspective, financial risks are rising interest rates, a stricter regulatory environment which would increase operating and maintenance expenses, and the need for ETP to turn to the capital markets to finance growth initiatives since the partnership distributes the bulk of its operating cash flow.

Enterprise L.P. (EPD) Our $61 per LP unit PO is based on a 4.75 pct target yield on our annualized 1Q14E distribution of $2.90, which is consistent with the target yield we think appropriate for lower business risk MLPs like EPD. We consider EPD a low business risk MLP owing to its large, diverse asset base and strong organic growth outlook. Downside risks to our price objective are supply chain disruptions, the loss of key customers, a sustained period of low natural gas prices, and a severe hurricane season, any of which could negatively impact volumes at EPD's pipelines and storage facilities and demand for gathering, processing, and storage of natural gas and NGLs. A high natural gas to crude oil ratio would negatively impact natural gas processing economics, leading to lower processed volumes of natural gas, lower NGL production and lower demand for EPD's services and use of its facilities. From a macro perspective, risks are an increasing interest rate environment, EPD's need to externally finance growth initiatives since EPD distributes the bulk of its operating cash flow (as is the case for all MLPs), and a stricter regulatory environment, which would increase operating and maintenance expenses. Furthermore, the tax treatment of EPD depends on its status as a partnership for federal income tax purposes: should EPD become subject to taxes, its performance could be materially affected.

Equity LifeStyle Properties (ELS) Our $79.00 price objective for ELS represents a 5.0% premium to our forward NAV estimate. We feel this is warranted given ELS's strong balance sheet and management team. The downside risk to our price objective is economic and operating conditions in ELS' markets deteriorating beyond our expectations and higher interest rates. In addition, a reduction in GSE lending to Manufactured Housing could weigh on ELS' access to capital, borrowing costs, and direct real estate values.

PennyMac Mortgage Investment Trust (PMT) Our price objective of $30.25 is based on 1.5x Q4'12e BV, supported by forecasted earnings and dividend acceleration over the next 12 months. Our price objective implies a 9% dividend yield and 11x P/E multiple to our '13e estimates,

Inves tment S t ra tegy 07 February 2013

15

which is above PMT's mortgage REIT peers. We believe the potential earnings upside is significant as PMT expands its mortgage banking business and it continues to execute its NPL investment strategy. Risks to achieving our price objective or EPS and DPS forecast are a delay in capital deployment, unfavorable price movement in the target asset classes, volatile interest rates, continued credit deterioration in residential mortgages, further disruption in the capital markets and unexpected changes in government policies.

Plains AA (PAA) Our $55 per LP unit PO is based on a 4.5 pct target yield on our annualized 1Q14E distribution of $2.46 which is consistent with the target yield we think appropriate for lower business risk, larger market cap - yet higher growth - MLPs like PAA. We consider PAA a lower-risk business MLP owing to its diverse asset base, investment grade balance sheet, low direct commodity sensitivity, seasoned management team, and solid organic growth outlook. Business risks to our price objective on PAA are a decrease in crude oil price volatility, a decrease in domestic crude oil supply, an outright decline in demand due to higher prices, economic slowdown or other reasons, and supply chain disruptions. This would negatively affect volumes transported through PAA's pipelines and stored at its facilities. Cost inflation and project timing delays are also potential risks to the partnership's capex program, as several other expansion projects are competing with PAA for labor and materials. The tax treatment of PAA depends on its status as a partnership for federal income tax purposes. Should PAA become subject to taxes, PAA's performance could be materially affected. From a macro perspective, financial risks are rising interest rates, which would be negative for MLP valuations in general, and a stricter regulatory environment, which would increase operating and maintenance expenses.

Post Properties, Inc. (PPS) Our $55 price objective for PPS is in line with our forward NAV estimate since demand fundamentals are improving in PPS's markets, however their markets are less supply constrained. The upside risk to our price objective is better than expected employment and operating conditions in PPS's markets and lower interest rates. The downside risk to our price objective is employment and operating conditions in PPS's markets deteriorating beyond our expectations and higher interest rates. In addition, a reduction in GSE lending to the multifamily sector could weigh on PPS's access to capital, borrowing costs, and direct real estate values.

THL Credit, Inc. (TCRD) Our $15.00 price objective is based on a 1.15x multiple to stated net asset value (NAV), which in our view is achievable in a stable operating backdrop with intensifying demand for yield bearing investments. TCRD warrants a modest premium to BDC peers due to its higher yield portfolio of late-vintage assets and superior growth potential, in our opinion. Asset values should remain largely range bound for the foreseeable future, as strong operating trends persist and investors increasingly target yield-based investments. TCRD should sustain its 9% dividend yield, versus peers in the 9%-11% range, as earnings trends remain favorable biased to the upside.

Inves tment S t ra tegy 07 February 2013

16

Downside risks to achieving our price objective and EPS forecast are 1) material weakening in credit markets, 2) a significantly slowdown in investment activity, 3) a deteriorating macroeconomic environment, 4) disruptions in the capital markets, and 5) weaker than expected investment performance.

Two Harbors Investment Corp. (TWO) Our $12.25 Price Objective is based on a 1.1x multiple to Q4'12e BV, in line with the hybrid mortgage REIT universes. We anticipate investors will continue to ascribe a premium valuation around 1.1x BV to TWO, given its above average dividend yield of 12% and its stable earnings and BV track record. Downside/upside risks to achieving our price objective and EPS forecast are 1) changes in the absolute level of rates resulting in higher/lower funding costs and BV pressure/strength, 2) a flattening/steepening of the yield curve causing investment spreads to decline/rise, 3) significant increases/declines in MBS spreads causing BV pressure/strength, 4) deteriorating/improving capital markets leading to higher/lower borrowing costs, 5) material increases/declines in refinance activity causing smaller/wider interest spreads and 6) adverse/favorable government intervention in the mortgage markets or GSE activity. Execution risk, namely poor asset selection, could also negatively impact shares.

Link to Definitions Credit Click here for definitions of commonly used terms.

Energy Click here for definitions of commonly used terms.

Financials Click here for definitions of commonly used terms.

Macro Click here for definitions of commonly used terms.

Analyst Certification We, Elias Lanik, Gabe Moreen, Jeffrey Spector and Kenneth Bruce, hereby certify that the views each of us has expressed in this research report accurately reflect each of our respective personal views about the subject securities and issuers. We also certify that no part of our respective compensation was, is, or will be, directly or indirectly, related to the specific recommendations or view expressed in this research report.

Inves tment S t ra tegy 07 February 2013

17

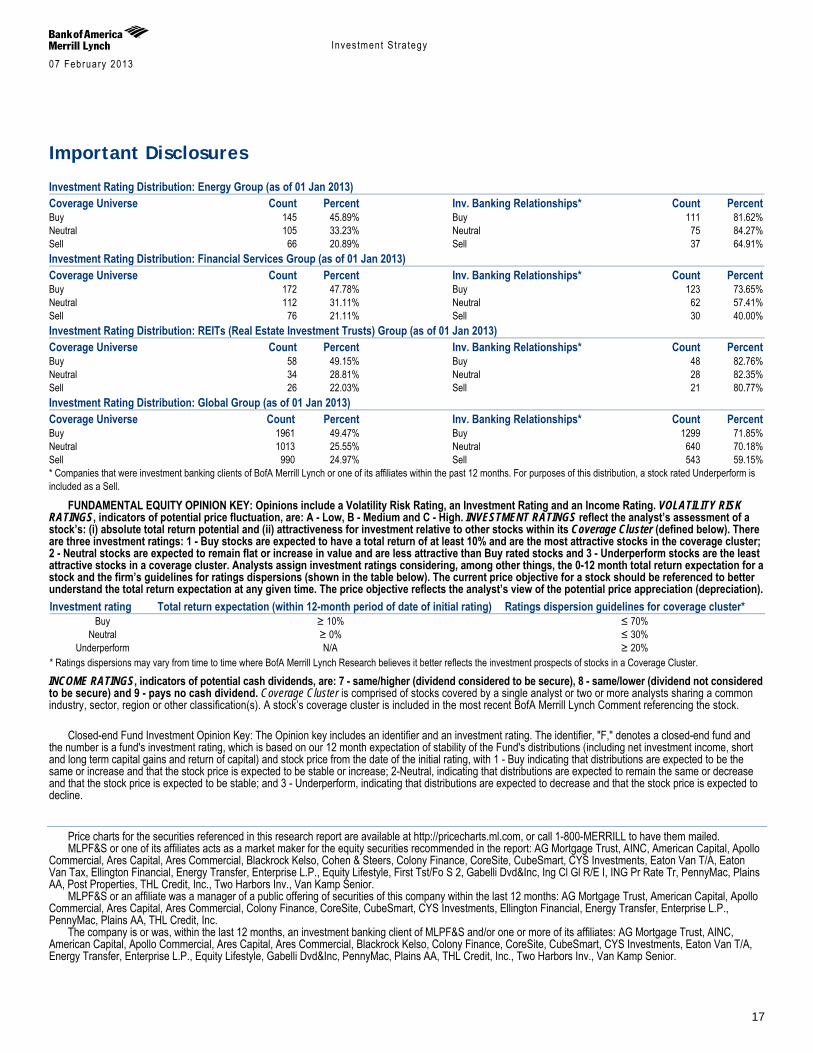

Important Disclosures Investment Rating Distribution: Energy Group (as of 01 Jan 2013) Coverage Universe Count Percent Inv. Banking Relationships* Count Percent Buy 145 45.89% Buy 111 81.62% Neutral 105 33.23% Neutral 75 84.27% Sell 66 20.89% Sell 37 64.91% Investment Rating Distribution: Financial Services Group (as of 01 Jan 2013) Coverage Universe Count Percent Inv. Banking Relationships* Count Percent Buy 172 47.78% Buy 123 73.65% Neutral 112 31.11% Neutral 62 57.41% Sell 76 21.11% Sell 30 40.00% Investment Rating Distribution: REITs (Real Estate Investment Trusts) Group (as of 01 Jan 2013) Coverage Universe Count Percent Inv. Banking Relationships* Count Percent Buy 58 49.15% Buy 48 82.76% Neutral 34 28.81% Neutral 28 82.35% Sell 26 22.03% Sell 21 80.77% Investment Rating Distribution: Global Group (as of 01 Jan 2013) Coverage Universe Count Percent Inv. Banking Relationships* Count Percent Buy 1961 49.47% Buy 1299 71.85% Neutral 1013 25.55% Neutral 640 70.18% Sell 990 24.97% Sell 543 59.15% * Companies that were investment banking clients of BofA Merrill Lynch or one of its affiliates within the past 12 months. For purposes of this distribution, a stock rated Underperform is included as a Sell.

FUNDAMENTAL EQUITY OPINION KEY: Opinions include a Volatility Risk Rating, an Investment Rating and an Income Rating. VOLATILITY RISK RATINGS, indicators of potential price fluctuation, are: A - Low, B - Medium and C - High. INVESTMENT RATINGS reflect the analyst’s assessment of a stock’s: (i) absolute total return potential and (ii) attractiveness for investment relative to other stocks within its Coverage Cluster (defined below). There are three investment ratings: 1 - Buy stocks are expected to have a total return of at least 10% and are the most attractive stocks in the coverage cluster; 2 - Neutral stocks are expected to remain flat or increase in value and are less attractive than Buy rated stocks and 3 - Underperform stocks are the least attractive stocks in a coverage cluster. Analysts assign investment ratings considering, among other things, the 0-12 month total return expectation for a stock and the firm’s guidelines for ratings dispersions (shown in the table below). The current price objective for a stock should be referenced to better understand the total return expectation at any given time. The price objective reflects the analyst’s view of the potential price appreciation (depreciation). Investment rating Total return expectation (within 12-month period of date of initial rating) Ratings dispersion guidelines for coverage cluster*

Buy ≥ 10% ≤ 70% Neutral ≥ 0% ≤ 30%

Underperform N/A ≥ 20% * Ratings dispersions may vary from time to time where BofA Merrill Lynch Research believes it better reflects the investment prospects of stocks in a Coverage Cluster.

INCOME RATINGS, indicators of potential cash dividends, are: 7 - same/higher (dividend considered to be secure), 8 - same/lower (dividend not considered to be secure) and 9 - pays no cash dividend. Coverage Cluster is comprised of stocks covered by a single analyst or two or more analysts sharing a common industry, sector, region or other classification(s). A stock’s coverage cluster is included in the most recent BofA Merrill Lynch Comment referencing the stock.

Closed-end Fund Investment Opinion Key: The Opinion key includes an identifier and an investment rating. The identifier, "F," denotes a closed-end fund and the number is a fund's investment rating, which is based on our 12 month expectation of stability of the Fund's distributions (including net investment income, short and long term capital gains and return of capital) and stock price from the date of the initial rating, with 1 - Buy indicating that distributions are expected to be the same or increase and that the stock price is expected to be stable or increase; 2-Neutral, indicating that distributions are expected to remain the same or decrease and that the stock price is expected to be stable; and 3 - Underperform, indicating that distributions are expected to decrease and that the stock price is expected to decline.

Price charts for the securities referenced in this research report are available at http://pricecharts.ml.com, or call 1-800-MERRILL to have them mailed. MLPF&S or one of its affiliates acts as a market maker for the equity securities recommended in the report: AG Mortgage Trust, AINC, American Capital, Apollo

Commercial, Ares Capital, Ares Commercial, Blackrock Kelso, Cohen & Steers, Colony Finance, CoreSite, CubeSmart, CYS Investments, Eaton Van T/A, Eaton Van Tax, Ellington Financial, Energy Transfer, Enterprise L.P., Equity Lifestyle, First Tst/Fo S 2, Gabelli Dvd&Inc, Ing Cl Gl R/E I, ING Pr Rate Tr, PennyMac, Plains AA, Post Properties, THL Credit, Inc., Two Harbors Inv., Van Kamp Senior.

MLPF&S or an affiliate was a manager of a public offering of securities of this company within the last 12 months: AG Mortgage Trust, American Capital, Apollo Commercial, Ares Capital, Ares Commercial, Colony Finance, CoreSite, CubeSmart, CYS Investments, Ellington Financial, Energy Transfer, Enterprise L.P., PennyMac, Plains AA, THL Credit, Inc.

The company is or was, within the last 12 months, an investment banking client of MLPF&S and/or one or more of its affiliates: AG Mortgage Trust, AINC, American Capital, Apollo Commercial, Ares Capital, Ares Commercial, Blackrock Kelso, Colony Finance, CoreSite, CubeSmart, CYS Investments, Eaton Van T/A, Energy Transfer, Enterprise L.P., Equity Lifestyle, Gabelli Dvd&Inc, PennyMac, Plains AA, THL Credit, Inc., Two Harbors Inv., Van Kamp Senior.

Inves tment S t ra tegy 07 February 2013

18

MLPF&S or an affiliate has received compensation from the company for non-investment banking services or products within the past 12 months: AG Mortgage Trust, AINC, American Capital, Ares Capital, Ares Commercial, Blackrock Kelso, Colony Finance, CoreSite, CubeSmart, CYS Investments, Eaton Van T/A, Ellington Financial, Energy Transfer, Enterprise L.P., Equity Lifestyle, ING Pr Rate Tr, PennyMac, Plains AA, THL Credit, Inc., Two Harbors Inv., Van Kamp Senior.

The company is or was, within the last 12 months, a non-securities business client of MLPF&S and/or one or more of its affiliates: AINC, American Capital, Ares Capital, Ares Commercial, Blackrock Kelso, Colony Finance, CoreSite, CubeSmart, Eaton Van T/A, Ellington Financial, Energy Transfer, Enterprise L.P., Equity Lifestyle, ING Pr Rate Tr, PennyMac, Plains AA, THL Credit, Inc., Van Kamp Senior.

MLPF&S or an affiliate has received compensation for investment banking services from this company within the past 12 months: AG Mortgage Trust, AINC, American Capital, Apollo Commercial, Ares Capital, Ares Commercial, Colony Finance, CoreSite, CubeSmart, CYS Investments, Eaton Van T/A, Energy Transfer, Enterprise L.P., Equity Lifestyle, Gabelli Dvd&Inc, PennyMac, Plains AA, THL Credit, Inc., Van Kamp Senior.

MLPF&S or an affiliate expects to receive or intends to seek compensation for investment banking services from this company or an affiliate of the company within the next three months: AG Mortgage Trust, AINC, American Capital, Ares Capital, Ares Commercial, Blackrock Kelso, Colony Finance, CoreSite, CubeSmart, CYS Investments, Eaton Van T/A, Energy Transfer, Enterprise L.P., Equity Lifestyle, PennyMac, Plains AA, THL Credit, Inc., Two Harbors Inv., Van Kamp Senior.

MLPF&S together with its affiliates beneficially owns one percent or more of the common stock of this company. If this report was issued on or after the 8th day of the month, it reflects the ownership position on the last day of the previous month. Reports issued before the 8th day of a month reflect the ownership position at the end of the second month preceding the date of the report: AG Mortgage Trust, American Capital, Apollo Commercial, Cohen & Steers, CoreSite, Eaton Van Tax, First Tst/Fo S 2, Ing Cl Gl R/E I, PennyMac, Plains AA, THL Credit, Inc., Two Harbors Inv., Van Kamp Senior.

MLPF&S or one of its affiliates is willing to sell to, or buy from, clients the common equity of the company on a principal basis: AG Mortgage Trust, AINC, American Capital, Apollo Commercial, Ares Capital, Ares Commercial, Blackrock Kelso, Cohen & Steers, Colony Finance, CoreSite, CubeSmart, CYS Investments, Eaton Van T/A, Eaton Van Tax, Ellington Financial, Energy Transfer, Enterprise L.P., Equity Lifestyle, First Tst/Fo S 2, Gabelli Dvd&Inc, Ing Cl Gl R/E I, ING Pr Rate Tr, PennyMac, Plains AA, Post Properties, THL Credit, Inc., Two Harbors Inv., Van Kamp Senior.

The company is or was, within the last 12 months, a securities business client (non-investment banking) of MLPF&S and/or one or more of its affiliates: AG Mortgage Trust, AINC, American Capital, Ares Capital, CubeSmart, CYS Investments, Eaton Van T/A, Ellington Financial, Energy Transfer, Enterprise L.P., First Tst/Fo S 2, ING Pr Rate Tr, PennyMac, Plains AA, Post Properties, Two Harbors Inv., Van Kamp Senior.

Due to the nature of strategic analysis, the issuers or securities recommended or discussed in this report are not continuously followed. Accordingly, investors must regard this report as providing stand-alone analysis and should not expect continuing analysis or additional reports relating to such issuers and/or securities.

BofA Merrill Lynch Research personnel (including the analyst(s) responsible for this report) receive compensation based upon, among other factors, the overall profitability of Bank of America Corporation, including profits derived from investment banking revenues.

BofA Merrill Lynch Global Credit Research analysts regularly interact with sales and trading desk personnel in connection with their research, including to ascertain pricing and liquidity in the fixed income markets.

Other Important Disclosures

Rule 144A securities may be offered or sold only to persons in the U.S. who are Qualified Institutional Buyers within the meaning of Rule 144A under the Securities Act of 1933, as amended.

SECURITIES DISCUSSED HEREIN MAY BE RATED BELOW INVESTMENT GRADE AND SHOULD THEREFORE ONLY BE CONSIDERED FOR INCLUSION IN ACCOUNTS QUALIFIED FOR SPECULATIVE INVESTMENT.

Recipients who are not institutional investors or market professionals should seek the advice of their independent financial advisor before considering information in this report in connection with any investment decision, or for a necessary explanation of its contents.

The securities discussed in this report may be traded over-the-counter. Retail sales and/or distribution of this report may be made only in states where these securities are exempt from registration or have been qualified for sale.

Officers of MLPF&S or one or more of its affiliates (other than research analysts) may have a financial interest in securities of the issuer(s) or in related investments.

From time to time, research analysts may conduct site visits of companies under their coverage. BofA Merrill Lynch does not accept payment or reimbursement from companies of travel expenses incurred by research analysts in connection with site visits

This report, and the securities discussed herein, may not be eligible for distribution or sale in all countries or to certain categories of investors. Information relating to Affiliates of MLPF&S and Distribution of Affiliate Research Reports: BofA Merrill Lynch includes Merrill Lynch, Pierce, Fenner & Smith Incorporated ("MLPF&S") and its affiliates. Investors should contact their BofA

Merrill Lynch representative or Merrill Lynch Global Wealth Management financial advisor if they have questions concerning this report. "BofA Merrill Lynch" and "Merrill Lynch" are each global brands for BofA Merrill Lynch Global Research.

MLPF&S distributes, or may in the future distribute, research reports of the following non-US affiliates in the US (short name: legal name): Merrill Lynch (France): Merrill Lynch Capital Markets (France) SAS; Merrill Lynch (Frankfurt): Merrill Lynch International Bank Ltd., Frankfurt Branch; Merrill Lynch (South Africa): Merrill Lynch South Africa (Pty) Ltd.; Merrill Lynch (Milan): Merrill Lynch International Bank Limited; MLI (UK): Merrill Lynch International; Merrill Lynch (Australia): Merrill Lynch Equities (Australia) Limited; Merrill Lynch (Hong Kong): Merrill Lynch (Asia Pacific) Limited; Merrill Lynch (Singapore): Merrill Lynch (Singapore) Pte Ltd.; Merrill Lynch (Canada): Merrill Lynch Canada Inc; Merrill Lynch (Mexico): Merrill Lynch Mexico, SA de CV, Casa de Bolsa; Merrill Lynch (Argentina): Merrill Lynch Argentina SA; Merrill Lynch (Japan): Merrill Lynch Japan Securities Co., Ltd.; Merrill Lynch (Seoul): Merrill Lynch International Incorporated (Seoul Branch); Merrill Lynch (Taiwan): Merrill Lynch Securities (Taiwan) Ltd.; DSP Merrill Lynch (India): DSP Merrill Lynch Limited; PT Merrill Lynch (Indonesia): PT Merrill Lynch Indonesia; Merrill Lynch (Israel): Merrill Lynch Israel Limited; Merrill Lynch (Russia): OOO Merrill Lynch Securities, Moscow; Merrill Lynch (Turkey I.B.): Merrill Lynch Yatirim Bank A.S.; Merrill Lynch (Turkey Broker): Merrill Lynch Menkul Değerler A.Ş.; Merrill Lynch (Dubai): Merrill Lynch International, Dubai Branch; MLPF&S (Zurich rep. office): MLPF&S Incorporated Zurich representative office; Merrill Lynch (Spain): Merrill Lynch Capital Markets Espana, S.A.S.V.; Merrill Lynch (Brazil): Bank of America Merrill Lynch Banco Multiplo S.A.; Merrill Lynch KSA Company, Merrill Lynch Kingdom of Saudi Arabia Company.

This research report has been approved for publication and is distributed in the United Kingdom to professional clients and eligible counterparties (as each is defined in the rules of the Financial Services Authority) by Merrill Lynch International and Banc of America Securities Limited (BASL), which are authorized and regulated by the Financial Services Authority and has been approved for publication and is distributed in the United Kingdom to retail clients (as defined in the rules of the Financial Services Authority) by Merrill Lynch International Bank Limited, London Branch, which is authorized by the Central Bank of Ireland and is subject to limited regulation by the Financial Services Authority – details about the extent of its regulation by the Financial Services Authority are available from it on request; has been considered and distributed in Japan by Merrill Lynch Japan Securities Co., Ltd., a registered securities dealer under the Financial Instruments and Exchange Act in Japan; is distributed in Hong Kong by Merrill Lynch (Asia Pacific) Limited, which is regulated by the Hong Kong SFC and the Hong Kong Monetary Authority; is issued and distributed in Taiwan by Merrill Lynch Securities (Taiwan) Ltd.; is issued and distributed in India by DSP Merrill Lynch Limited; and is issued

Inves tment S t ra tegy 07 February 2013

19

and distributed in Singapore by Merrill Lynch International Bank Limited (Merchant Bank) and Merrill Lynch (Singapore) Pte Ltd. (Company Registration No.’s F 06872E and 198602883D respectively) and Bank of America Singapore Limited (Merchant Bank). Merrill Lynch International Bank Limited (Merchant Bank) and Merrill Lynch (Singapore) Pte Ltd. are regulated by the Monetary Authority of Singapore. Bank of America N.A., Australian Branch (ARBN 064 874 531), AFS License 412901 (BANA Australia) and Merrill Lynch Equities (Australia) Limited (ABN 65 006 276 795), AFS License 235132 (MLEA) distributes this report in Australia only to 'Wholesale' clients as defined by s.761G of the Corporations Act 2001. With the exception of BANA Australia, neither MLEA nor any of its affiliates involved in preparing this research report is an Authorised Deposit-Taking Institution under the Banking Act 1959 nor regulated by the Australian Prudential Regulation Authority. No approval is required for publication or distribution of this report in Brazil and its local distribution is made by Bank of America Merrill Lynch Banco Múltiplo S.A. in accordance with applicable regulations. Merrill Lynch (Dubai) is authorized and regulated by the Dubai Financial Services Authority (DFSA). Research reports prepared and issued by Merrill Lynch (Dubai) are prepared and issued in accordance with the requirements of the DFSA conduct of business rules.

Merrill Lynch (Frankfurt) distributes this report in Germany. Merrill Lynch (Frankfurt) is regulated by BaFin. This research report has been prepared and issued by MLPF&S and/or one or more of its non-US affiliates. MLPF&S is the distributor of this research report in

the US and accepts full responsibility for research reports of its non-US affiliates distributed to MLPF&S clients in the US. Any US person receiving this research report and wishing to effect any transaction in any security discussed in the report should do so through MLPF&S and not such foreign affiliates.

General Investment Related Disclosures: This research report provides general information only. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer,

to buy or sell any securities or other financial instrument or any derivative related to such securities or instruments (e.g., options, futures, warrants, and contracts for differences). This report is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation and the particular needs of any specific person. Investors should seek financial advice regarding the appropriateness of investing in financial instruments and implementing investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Any decision to purchase or subscribe for securities in any offering must be based solely on existing public information on such security or the information in the prospectus or other offering document issued in connection with such offering, and not on this report.

Securities and other financial instruments discussed in this report, or recommended, offered or sold by Merrill Lynch, are not insured by the Federal Deposit Insurance Corporation and are not deposits or other obligations of any insured depository institution (including, Bank of America, N.A.). Investments in general and, derivatives, in particular, involve numerous risks, including, among others, market risk, counterparty default risk and liquidity risk. No security, financial instrument or derivative is suitable for all investors. In some cases, securities and other financial instruments may be difficult to value or sell and reliable information about the value or risks related to the security or financial instrument may be difficult to obtain. Investors should note that income from such securities and other financial instruments, if any, may fluctuate and that price or value of such securities and instruments may rise or fall and, in some cases, investors may lose their entire principal investment. Past performance is not necessarily a guide to future performance. Levels and basis for taxation may change.

BofA Merrill Lynch is aware that the implementation of the ideas expressed in this report may depend upon an investor's ability to "short" securities or other financial instruments and that such action may be limited by regulations prohibiting or restricting "shortselling" in many jurisdictions. Investors are urged to seek advice regarding the applicability of such regulations prior to executing any short idea contained in this report.

This report may contain a trading idea or recommendation which highlights a specific identified near-term catalyst or event impacting a security, issuer, industry sector or the market generally that presents a transaction opportunity, but does not have any impact on the analyst’s particular “Overweight” or “Underweight” rating (which is based on a three month trade horizon). Trading ideas and recommendations may differ directionally from the analyst’s rating on a security or issuer because they reflect the impact of a near-term catalyst or event.

Foreign currency rates of exchange may adversely affect the value, price or income of any security or financial instrument mentioned in this report. Investors in such securities and instruments effectively assume currency risk.

UK Readers: The protections provided by the U.K. regulatory regime, including the Financial Services Scheme, do not apply in general to business coordinated by BofA Merrill Lynch entities located outside of the United Kingdom. BofA Merrill Lynch Global Research policies relating to conflicts of interest are described at http://www.ml.com/media/43347.pdf.

Officers of MLPF&S or one or more of its affiliates (other than research analysts) may have a financial interest in securities of the issuer(s) or in related investments.

MLPF&S or one of its affiliates is a regular issuer of traded financial instruments linked to securities that may have been recommended in this report. MLPF&S or one of its affiliates may, at any time, hold a trading position (long or short) in the securities and financial instruments discussed in this report.

BofA Merrill Lynch, through business units other than BofA Merrill Lynch Global Research, may have issued and may in the future issue trading ideas or recommendations that are inconsistent with, and reach different conclusions from, the information presented in this report. Such ideas or recommendations reflect the different time frames, assumptions, views and analytical methods of the persons who prepared them, and BofA Merrill Lynch is under no obligation to ensure that such other trading ideas or recommendations are brought to the attention of any recipient of this report.