Finding the Missing Middle

44

Transcript of Finding the Missing Middle

FINDING THE MISSING MIDDLE

A Journey withFoundation for Enterprise Management

Innovations, Inc.

AIDA LICAROS VELASCO

PREFACE

Success in entrepreneurial undertaking is defined in growing and sustaining a business. Starting a business poses less of a challenge than growing and sustaining it. This book addresses the issue of helping micro enterprises grow into small and medium enterprises through credit, training, and consultancy program. Foundation for Enterprise Management Innovations, Inc. (FEMI) is an NGO that advocates growing and sustaining such enterprises called “The Missing Middle.” FEMI has shown that sustaining micro enterprises into small and medium ones can be done. The organization has helped more than 200 enterprises in their bid to grow and sustain their business through loans and business development services. It has also inculcated the culture of on-time repayment through its practice of lending with a heart. On-site visits, management consultation, monitoring of utilization of funds lent, assistance in bookkeeping and documentation of processes, and periodic training on management principles are seen by FEMI’s Benepartners as critical factors that helped them achieve a high repayment rate and sustainable growth in their business. The business development model of FEMI uses the Focus-Localize-Partner Model in achieving FEMI’s advocacy for graduating micros.

Given the effectiveness of the business model of FEMI, there is a need to expand lending activities in terms of loan amounts and the number of benepartners who can avail of the loans. This strategy will allow more micro enterprises to move to the “missing middle” niche. From there, FEMI can turn over the enterprises to the formal financial sector. . The expansion of the market will mean more funds tapped for lending through 1)partnership with financial institutions like rural banks and commercial banks; 2) tapping social investors or “angel investors” to fund business expansion that have high growth potential; and 3) building linkages with local and foreign foundations with advocacies aligned to the mission-vision of FEMI.

Published in 2011by the Foundation for Enterprise Management Innovations, Inc.29 A Magat Salamat St., Project 4Quezon City, Philippines

ISBN No. 978-971-95244-0-3

Copyright © 2011 byFoundation for Enterprise Management Innovations, Inc.

All rights reserved. No part of this book may be reproducedin any form or by any means without the permission ofthe copyright owner and the publisher.

Cover Design and Layout by Jeremy Benjamin Magnaye

Printed by Proprint Design Corner

ACKNOWLEDGEMENTS

The author would like to express her deepest gratitude to the people and organizations that made this book a reality. A sincere thank you to the following

To FEMI, whose advocacy to help the country in poverty alleviation through rural employment generation has inspired this book;

To De La Salle University for providing the training, facilities, and support staff that acted in service to the missing middle;To the management, staff and consultants of FEMI for their untiring guidance and support in data gathering and analysis; To the Benepartners for their sincerity and willingness to provide information about the case studies presented in this book;

To Jeremy Benjamin Magnaye for designing the cover and layout of the book;

To Angela Velasco for editing the book’s draft;To my family, Willy, January, and Gela for serving as my inspiration in this advocacy;

And

To God Almighty for giving the grace and inspiration in completing this project.

Market expansion will also mean more resources will be needed to support the business development services of FEMI. This will mean more consultants are to be tapped and a more formal structure of training program and business monitoring system must be designed. Development of more resources will be best achieved through equity and debt sources of financing and through human resource and management systems development. This book aims to invite others to join in FEMI’s journey in finding and growing the missing middle

Aida Licaros-Velasco

FOREWORD

Poverty alleviation is, understandably, a major goal in the Philippines. This book presents one organization’s contribution to such an effort.

The Mother Rosa Memorial Foundation started in 1998 with the goal of assisting entrepreneurs. It was turned over to theFoundation for Enterprise Management Innovations, Inc (FEMI) in 2007. FEMI’s core belief is employment as a critical ingredient to social development. Their focus is on micro enterprises that were poised for growth. The premise iss that employment generation would be the natural consequence of business expansion.From the start, therefore, FEMI had unwittingly decided to work with the segment of enterprises called the “missing middle”, a term the organization only discovered three years ago. Not having any model to follow, FEMI stumbled its way through, focusing only on one goal: helping micro enterprises expand. FEMI’s history has gone through failures as well as successes. After thirteen years, FEMI felt that it had a sustainable and effective business model that could contribute to poverty alleviation. However, it was deemed prudent to have an authoritative third person to document and validate the model. Hence, why this book was written.

Dr. Aida Licaros-Velasco, an eminent scholar and business researcher in the De La Salle University, was asked to study the FEMI experience. Her work is a welcome contribution since there is a dearth of literature on Philippine cases that discuss the “missing middle”. The FEMI experience is presented here not as a model of success or excellence, but as a springboard for learning.

FEMI would like to acknowledge DISOP, a Belgian non-government agency that has provided financial support and guidance from the start and throughout the organization’s difficult years. This book was made possible through DISOP’s generosity.

It is FEMI’s hope that this book encourages interest among the academe, non-government agencies, donors, financial institutions, and government agencies to look more closely into the “missing middle.” It is a much neglected segment in spite of its vast potential for poverty alleviation and national social development.

Manuel Quezon AvancenaPresidentFoundation for Enterprise Management Innovations, Inc.

Finding the Missing Middle

TABLE OF CONTENTS

I. Introduction

II. Foundation for Enterprise Management Innovations, Inc. (FEMI)

a. History

b. Performance

III. The FEMI Business Model

a. Operations and Marketingi. Product and Service Offeringii .Marketingiii. Lending

b. Effectivenessi. Project Outcomesii. Business Development Servicesiii. Achievements

c. Opportunities with the Missing Middlei. Potential Demandii. Competition

IV. Mapping the Future

V. The Benepartnersa. Pilipinang kay Ganda: The Case of JCF Soap Manufacturingb. May Pera sa Basura: The case of CJR Junkshopc. The Puzzle: The Case of Stanpuz Corp.d. Nang Tumilaook ang Manok: The Case of Joseldan Marketing

e. Balik Pilipinas and Pag-asa: The Case of T & L Live and Dressed Chicken

VI. FEMI and the Missing Middle

VII. The Journey Begins…a. Capital Base Expansionb. Business Consultancy Developmentc. Partnership Growth

VIII. References

IX. Appendices

Finding the Missing Middle Finding the Missing Middle

I. Introduction

The Philippines is traditionally seen as a place for low manufacturing costs. The government and industry promote the country as a good source of low cost labor. However, the development of other Asian countries like Vietnam, Indonesia, and Thailand and the present economic boom of China and India have contested this claim. Thus, the Philippines has seen the exodus of large multinational companies’ manufacturing operations in response to the low manufacturing costs being provided by other countries in Asia. The country is left with the opportunity of providing goods and services that were previously provided by large organizations to the hands of small and medium enterprises (SMEs). This resulted in the growth and development of the SMEs. These SMEs cater to the needs of the population that can no longer be served by the large corporations.

Large organizations also find the Philippines to be a poor choice to invest in because of the country’s low level of competitiveness. This low level of competitiveness results from the difficulties of doing business in the Philippines. Most of these difficulties are institutional in nature and the government is held accountable.

The Philippine Global Entrepreneurship Monitor Report for 2006-2007 has documented the profile of Filipino entrepreneur (Madarang and Habito, 2007). According to the report, 39.4% of Filipinos are engaged in entrepreneurial activities. Fifty-two percent of these entrepreneurs are engaged in early stage activity or are in business between 3 months to 3.5 years. Forty-eight percent are established businesses that have been existing for more than 3.5 years. These businesses have an average capital of P10,000.

A typical Filipino entrepreneur is male, married, 25-44 years old, a high school graduate, and comes from low income group. They are driven by necessity and more than half are engaged in retail trade. There is very little application of technology and minimal use of

1

Finding the Missing Middle Finding the Missing Middle

innovation. Seventy percent are engaged in businesses that do not generate employment since the entrepreneur assumes all the functions of the business. Most of the businesses employ less than 4 employees and very few have 20 employees or more. Filipino entrepreneurship has very poor employment generation activity. Business engagement is only done on a local basis and very few are engaged in exportation. There is very little growth and few have long-term view of the business. However, they see business opportunities and are highly confident that they have the knowledge and skills in doing business.

The present pool of Filipino entrepreneurs is driven by previous work experience (37%), exposure to family business (29%), and education and formal training (17%). Filipinos entered entrepreneurial activity as a means to support the financial needs of the family accounts for 54% of entrepreneurial motivation. Only 37% takes advantage of an opportunity. This is compounded by the problems in doing business in the Philippines namely, corruption, inefficient government bureaucracy, and inadequate infrastructure. These discourage Filipinos to enter a business and consider employment as a better source of livelihood. However, businesses can have two resources that are not easily replicated: good work ethics and the labor force’s health1.

Business in the Philippines is dominated by micro, small and medium enterprises; they account for 99.6% % of total business establishments as of 20092. These establishments are owned by small businesses with low capitalization. Most of these owners are from the low income class D. Statistics show that 63.2% 70% of employment is provided by micro, small, and medium industries. As of 2009, only 36.8% of employment is provided by large establishments. The onset of financial crises has seen the closure of some large establishments, and thus the reduction in employment by large establishments.

1 The World Economic Economic Global Competitiveness Report cited these two as the least reasons for not doing business in the Philippines.2 Data on Philippine SMEs are based on DTI Report on SME Statistics.

2

Most establishments into wholesale and retail trade account for 30% of employment generated by this industry. Eighty-eight percent of wholesalers and retailers are micro, small, and medium enterprises. Twenty-seven percent of employment is in manufacturing, where almost half are large business establishments.

The government has realized that economic growth can only be achieved if there are more businesses that can generate employment and income. As history has proven, it is the business sector that creates wealth for the nation and not the government. The government just creates and implements policies for business to thrive, grow, and sustain. However, the government has been harping on attracting big business that will invest in the country. Present statistics shows that they have been failing miserably. The government would also want to bid for the development of entrepreneurship based on high technology innovation, in an attempt to replicate the experience of Silicon Valley. The present conditions of technology research and product development show that the Philippines allocates a very low percentage of GNP on research and development compared to its Asian neighbors3. The present pool of entrepreneurs does not have the tenacity to adapt technology and innovation. There is a need to rethink the strategies the Philippines can adapt for the country’s economic development.

Some organizations in the Philippines see the current make-up of business establishments as an opportunity to help in the development of the country’s SMEs. Non-government institutions have been formed to specifically cater to these business enterprises through micro-finance and credit facilities offers that are not being provided by large and established financial institutions. Entrepreneurial and management training programs are being offered by some NGOs. Most of these NGOs have been in existence for more than ten years. These NGOs are catering to micro enterprises that offer credit or financial assistance for amounts less than P50,000, short-term period of less than a year, and interest ranging 2-5% per month.

3Based on WEF Global Competitiveness Report 2010-2011

3

Finding the Missing Middle Finding the Missing Middle

CORE VALUES TRUSTWORTHY We will be honest at all times. We will ensure that we have the competence necessary to deliver programs for the Benepartners.

CARINGWe will be sensitive to the feelings and needs of the stakeholders. Our primary concern is to promote the well-being of the direct and indirect beneficiaries of the program. We will reward those who excel and ensure that those in need will be cared for.

PASSIONATEWe will view work not as a job, but an opportunity to get involved in the promotion of an alternative model of poverty alleviation. We will be enthusiastic and sincere in everything we do.

COMMITTEDWe pledge to perform our mandates wholeheartedly. We will maintain creativity and innovativeness in order to deliver valuable results.

WITH INTEGRITY We will impart the moral purpose of the services we are rendering to the Benepartners. We will strictly adhere to the set policies of the organization especially in relating with our Benepartners. We will walk the talk.

PATRIOTICWe aspire that everything we do contributes to the welfare of our fellowmen and our country. We will continue advocating the model and will encourage entrepreneurs, development practitioners, socially-oriented investors, donors, funding agencies, and the academe to actively participate in our endeavour.

6 7

The mission of FEMI is hinged in helping the country alleviate the conditions of the rural area’s poor. To do this, the following objectives were set:

1. To generate/sustain rural jobs2. To increase income of people in the province3. To help minimize urban migration4. To develop employability to rural workers

FEMI envisions itself to be a “substantial contributor to driving social and economic development in the Philippines” through recruitment, development, and growing enterprises focusing on the “missing middle” niche. Attainment of FEMI’s vision hinges on the following commitment: “We want to grow your business by addressing not only your credit requirements but also your learning and development needs. Together, we will analyze your loan size requirements vis-avis the strategic path of your enterprise”. FEMI’s business model is founded on partnership for growing business with its clients. Thus, FEMI’s clients are called “benepartners.”

It takes a five-prong approach in achieving its mission. First, its mission is grounded on understanding its focused customers, and the graduating micros or micro enterprises transitioning into small or medium enterprises, but do not have access to financial resources offered by formal financial institutions. Second, FEMI takes the lead in developing and sustaining the business model of these enterprises that operate outside Metro Manila. Third, the growth of FEMI’s “Benepartners” is the foundation of all the activities and services offered. Fourth, FEMI focuses on excellence in its identified competency, financial assistance to “Benepartners” through loans, and guidance in the business operations. Fifth, FEMI is a value-based organization exemplifying trust and caring for its Benepartners, passionate and committed to all its actions, in living integrity, and in embodying patriotism in all its endeavours.

Finding the Missing Middle Finding the Missing Middle

FEMI adapts a three-pillared approach in the development of the missing middle. These are credit, learning and development, and networking. FEMI provides credit to benepartners for business expansions that will result in job creation. Loan provided ranges from P100,000 to P500,000, given for a period of one year; they are geared for working capital requirement or for the purchase of equipment, with an interest of 2%-3% per month. Soft collateral is accepted. Learning and development pillar refers to the professional training and consultancy offered by FEMI to its Benepartners. Yearly profiling and training needs assessment are conducted. Seminars are formally conducted using classroom methodology or cluster (“Kapihan”) sessions. Consultancy is provided through one-on-one business mentoring. FEMI promotes the establishment of meaningful collaboration between FEMI and its benepartners. Collaboration among benepartners is supported through the exchange of information, technology, and actual business experience.

a. History Foundation for Enterprise Management Innovations, Inc. or FEMI

was founded in 2007 as a non-stock, non-profit organization duly registered with the Securities and Exchange Commission. It started its operations in 1998 as the Tri-Center Rural Enterprises Services Project (TRESP) to contribute to the development of the rural sectors through

Capacity building – enhancing the capability of rural-based entrepreneurs and/or cooperatives in the actual product development and enterprise management Research and information technology – helping rural-based entrepreneurs and cooperatives improve products and services through research and information dissemination Processing and distribution of rural-based products – assisting in actual marketing of rural-based product

The project was triggered by FEMI’s experience with the Mother Rosa Memorial Foundation (MRMF), wherein they saw that micro enterprises can be formed and grown, but cannot meet the challenges of sustaining their growth. The social development arm of MRMF has undertaken Initiatives on helping farmers in San Simon, Pampanga to increase rice yield of farms from 50-60 cavans/hectare to 100-120 cavans/hectare. A cooperative was also set-up to help the farmers put-up post harvest facilities (warehouse and marketing). The business grew but eventually closed down due to the farmer’s lack of capacity to sustain the new growth. The assistance that MRMF extended to the farmers like simple bookkeeping, interpersonal skills, leadership training, and community development was no longer appropriate for the size of operations the farmers needed. MRMF is not equipped to guide the farmers when their business is in the growth stage. This is also the observed experience of many start-up businesses moving on to the growth stage. This phenomenon is brought about by two factors, namely, 1) the lack of resources to sustain the growth and 2) the lack of management capability to effectively and efficiently supervise the business operations. The need to provide resources to meet the challenges of moving from micro to small or medium enterprises and the development of managerial skills became the driving force in founding FEMI. The vision to help small and medium enterprises move towards the growth stage was started through the project called TRESP, which would help entrepreneurs grow and sustain their business.

TRESP was a five-year project conceptualized and was started by LIVECOR in partnership with DISOP, a Belgian NGO, and MRMF, a Philippine NGO. Funding for TRESP came from Belgian foundation DISOP. The project operated for five years from September 1998 to December 2002. In September 2000, MRMF was left to manage the project due to the withdrawal of LIVECOR. LIVECOR was closed down by the government and led to its withdrawal from the project. This left MRMF to start and manage TRESP. It was envisioned that TRESP would be owned and managed by the project beneficiaries at the end of the project.

8 9

Finding the Missing Middle Finding the Missing Middle

Although TRESP was a social project, it is envisioned to generate average annual sales of P12.3 million and annual income of P1.3 million during the five-year period. This is based on the principle that “social development and business are not mutually exclusive concerns, but they actually complement each other and could therefore be pursued at the same time”. The project started with a total funding of P10.4 million—P9.5million from DISOP and P900,000 from MRMF. Its operations consisted mainly of finished goods marketing and raw materials procurement for the beneficiaries. It served 20 enterprise beneficiaries and released loan of P7.5 million for the period from 1998 to 2002.

Revenue and income targets were not met and were scaled down

due to the lack of manpower resources to carry out the plans. The following factors affect the performance of the project:

soundness of the basic premise of the project, absence of concrete plans and programs, lack of credit assistance facilities, problems encountered in finished products marketing, and scaling down of organizational support, problems encountered in the business of beneficiaries.

The plan to form a cooperative was envisioned so that the TRESP would turn over the ownership and management of the project to its beneficiaries. On January 26, 2001, the TRESP Multi-Purpose Cooperative (TRESP-MPC) was officially registered at the Coop Development Authority. Membership of the Coop totalled to 50 members by the end of December 2002. Although the cooperative was formed, turnover of the TRESP project to the beneficiaries did not materialize due to the following reasons: a) absence of a well-defined program for the project turnover; b) more time needed to establish the groundwork for the beneficiaries formation into an entity; and c) lack of readiness on the part of the beneficiaries to take over the management of TRESP. The beneficiaries’ lack of readiness to manage TRESP can be traced to the following factors: 1) shallow commitment from majority of TRESP-MPC members ; 2) the need to enhance the cooperative’s leadership

10 11

and management skills; and 3) lack of time on the part of the identified cooperative leaders to manage the cooperative and attend to their respective business.

TRESP continued the project and was renewed for another five years through the additional funds infused by DISOP. The cooperative started to manage the lending programs for its members in 2002. TRESP and TRESP-MPC became partners in helping micro enterprises in sustaining their growth and development. TRESP-MPC members also borrow from TRESP and avail of its business training and development programs.

In 2007, TRESP’s undertaking continued under a new set-up, FEMI, which was duly registered as a non-stock, non-profit organization. It aimed to continue the principle of poverty alleviation through rural enterprise development by creating employment and job opportunities. FEMI engages in lending and training programs to its beneficiaries who are now members of the cooperative. As of today, FEMI has total assets of P19.25 million. A total of P12.10 million was lent to its beneficiaries as of August 2011. Figures 1, 2 and 3 show the performance of FEMI in terms of asset size, loans receivables and net income.

b. Performance

FEMI’s benepartners are small-scale entrepreneurs in Tarlac, Pampanga, Bataan, Bulacan, Rizal, Cavite, Laguna, and Batangas. Fifty-three percent (53%) of its Benepartners are college graduates, 22% attended college, 12% are vocational graduates and 13% completed secondary education. Majority of its Benepartners are female (59%) and 92% are married. Fifty-five percent (55%) put up a business as a result of identifying opportunity due to previous work experience, 25% inherited the business, and 20% were influenced by their friends and families to start-up a business. Fifty-four percent (54%) are engaged in manufacturing, 32% in trading, and 14% in services.

The Benepartners have an average start-up capital of P154,500,

Finding the Missing Middle Finding the Missing Middle

Figure 1. FEMI’s Total Assets (1999-August 2011)

average monthly gross sales of P314,500, and average monthly gross income of P93,500. Loan size per benepartner ranges from P100,000-500,000. Repayment rate is 95%.500,000. Repayment rate is 95%.

Figure 2. FEMI’s Loans Receivable (1999- 2011)

12 13

Figure 3. Net Income (1999-2010)

The foundation has grown considerably over the last thirteen years. Its loan releases have increased to P12.10 million as of August 2011 as a result of increased loan amounts of benepartners and increase in the number of benepartners. It has experienced fluctuating income from a loss of P1million in 1999 to an income of P561,301 at the end of August 2011. Assets increased exponentially in 2011 as a result of social investments of private individuals.

FEMI has identified its niche in the market, “The missing middle.” These are enterprises that are moving from micro enterprise to SMEs focused on sustainable growth. These enterprises have seen stable operations but the lack of financial resources limits their growth. They have yet to acquire easy access to banks and other financial institution due to lack of documentation and incapacity to meet documentation requirements of formal financial institutions. It is also difficult for the missing middle to face the challenges of growth such as an expanding market, the need for a formal and documented system, and required managerial capabilities.

Finding the Missing Middle Finding the Missing Middle14 15

Figure 4. FEMI’s Market Niche: The Missing Middle

Source: FEMI Journey 2, 2008

III. The FEMI Business Model

It is FEMI’s vision to help in the country’s poverty alleviation, specifically in the rural areas. This is to be done through generation and sustainability of jobs, increase in income, reduce urban migration, and development of capabilities and employability of rural workers. Figure 5 depicts the business model FEMI adapts.

Figure 5. FEMI Business Model

FEMI caters to micro enterprises that are in the growth stage. This growing micro enterprise is moving to become a SME. FEMI offers lending services (P100k to P500k), business development services or seminars, and management skills training. Through money borrowed from FEMI, the micro enterprise grows its business. FEMI begins its involvement with benepartners by helping them with fund requirements. It guides the benepartners on the proper use of the borrowed funds and on better management of the enterprise through seminars and management skills training. Access to higher loans offered by FEMI and provided business guidance create a synergy that helps the growing micro enterprise become a small or medium enterprise. Growth is measured by the job increase generated by the

Finding the Missing Middle Finding the Missing Middle

benepartners and the asset growth of the business. Jobs generated can be direct jobs employed by the business or external jobs generated through the creation of other businesses through its set of suppliers, distributors, wholesalers, and retailers. Asset growth of the business is another measurement of growth that will help the developing micro gain access to higher and cheaper sources of funds. The success of FEMI’s partnership with growing micros is also measured by the ability of the enterprise to access funds in established financial institutions like commercial banks.

Details of the Business Development Model of FEMI is shown in Figure 6. This model has been used by FEMI for the past 13 years. This is sustained by the FEMI’s 13-year experience with growing micros, a clear vision of serving the “missing middle”, and business partnerships with its clients. These resulted in a high repayment rate of loans and the satisfaction of its clients. In as much as FEMI would want to extend its services to more growing micros, FEMI is hindered by its limited resources, which mostly come from grants of DISOP. Opportunities to expand its pool of benepartners is supported by the growing “missing middle”, lesser regulations on NGOs, increasing interest on social entrepreneurship, and the recognized importance of SMEs in nation-building and poverty alleviation. However, the strict regulations on lending being implemented by formal financial institutions and the policies of the government hinder the achievement of FEMI’s vision of making its benepartners have access to credit provided by the banking institutions. The effectiveness of the model is supported by five case studies at the end of this book.

The Business Development Model starts with the clear identification of FEMI’s market niche, “The Missing Middle.” These are micro enterprises that are beginning to move to bigger operations with more assets and employees. They are rural based with loan needs of P50,000 to P1Million4. The market of these enterprises is growing and more market opportunities are being identified, thus supporting the need for bigger capital. These businesses have no access to funds from formal financial institutions like banks. Although some of these enterprises 4 As defined by FEMI

have assets that can be offered as collateral, these enterprises feel that they cannot meet the documentation needed and other requirements of formal financial institutions.

Management systems have been set in place. It has its own staff to take care of the daily transactions and an overall management committee that sets the direction for FEMI. The President is assisted by the Executive Director, who handles the daily transactions that ensure FEMI’s vision and mission is achieved.

16 17

Finding the Missing Middle Finding the Missing Middle

Figure 6. FEMI Business Development Model

18 19

i. Marketing

There is no formal marketing system being employed by FEMI. Benepartners are sourced through word of mouth from the current pool of borrowers, NGOs operating in strategic areas of beneficiaries, and members of cooperative. Partnership with local government units or LGUs and other government agencies is also strengthened to identify potential benepartners in the area. Potential benepartners are screened by the barangay. The office of the Department of Trade and Industry in the locality is also tapped for the list of SMEs operating in the provinces.

ii. Lending

The lending process is based on the referral system from existing beneficiaries and through the recommendation of the barangay committee (after the barangay committee has conducted initial credit investigation). Loan is extended to firms based on the loan’s purpose, interconnectedness to current business and growth potential, and repayment capabilities. The cooperative is a source of informal information in granting loans. Loans are granted based on the credit committee’s evaluation. Basis for the loan approval are the client’s capability to pay, growth potential of the business, employment generation and business partnership development. The loan repayment rate is 95%.

B. Effectiveness

i. Project outcomes

FEMI provides loans and business support through seminars and workshops that tackle better management of the enterprise for its benepartners. Since 2003, FEMI has served a total of 93 establishments availing of these services. Of these, 41 are actively engaged with FEMI

Finding the Missing Middle Finding the Missing Middle

a. Operations and Marketing

i. Product and Service Offering

FEMI lends to small5 (asset size: P3m to P15m; no. of employees: 19-99) and medium (asset size: P15m to P100; number of employees: 100-199) enterprises at a rate of 2% per month. Interest rates on loans increased as perceived risk of borrowers increases. Borrowers are classified as A-client (least risk), B-client (less risk), and C-client (high risk). Loans of A-clients bear interest of 2% per month or 24%p.a., B-client, 2.5% per month or 30% p.a., and C-client, 3% per month or 36% p.a. Loan amount ranges from P100,000 to P800,000. Loans are secured with collaterals like utility vehicles, equipment, and residential real estate. Loan repayment is at a high of 95%.

The loan is geared for working capital needs, expansion, and fixed asset acquisition. FEMI also offers management training programs to its beneficiaries. The following training programs were given to beneficiaries:

1. Financial Managementa. Bookkeepingb. Accounts receivables managementc. Cash flow managementc. Loans and working capital

2. Operations Managementa. Kaizenb. Supply chain management

3. Human resource and development management4. Business improvement, survival, and expansion5. Strategic planning

The training programs have helped the beneficiaries in organizing

financial records and proper budgeting. It has also broadened their business perspective and improved their management style. 5SME classification is based on approved amendments to HB 1754.

though loan availments and business trainings and seminars. Thirty-two of the 41 beneficiaries have availed of loans. Loan summary for period January-July 2011 is summarized in Table 1.

AreaPampanga

Bulacan

Cavite

Tarlac

Total Region 3

Total Region 4

Bataan

Rizal

TOTAL

20

3

2

2

24

7

3

5

31

10

3

61

2

16

6

2

5

9

2

1

2

14

5

1

4

19

No. of Beneficiaries

No. of Barangays

No. of Municipalities

Table 1. Summary of Loan Granted by Area and Amount (January-July 2011)

Table 2. Employment and Supply Chain Partners (2003-2009)

The business of the benepartners has seen growth in employment and business partnership with distributors, dealers, suppliers, and sub-contractors. Table 2 shows the total number of employment generated by the businesses of FEMI’s benepartners and the number of increased partners in their supply chain.

6762361649462

2477

67622226

Total number of employeesIncreased in number of employeesNumber of Distributors

Number of Subcontractors

Number of Dealers

Total employment generated

Number of Suppliers

Total number of business partnership

6 As of 2010, FEMI has served a total of 245 enterprises through its credit facilities and business development training program. FEMI’s training and development program resulted in more than 12,000 jobs generated in benepartners’ supply chain.

20 21

Finding the Missing Middle Finding the Missing Middle

Figure 7. FEMI Loan Sizes

Figure 7 shows that most benepartners (31% or 25 establishments) availed of loan in the amount of P300,000. Ten benepartners or 26% borrowed P500,000. More than half of benepartners are in trading industry serving the local market. Majority of those that availed of the loan are engaged in food products (40% in trading and 15% in manufacturing).

Table 3. Loan Distribution by Industry and Products*

Table 4. Loan Purposes*

Products

Products

Live & dressed

Bakery

General merchandise

Novelty item

Fish

Concrete hollow blocks

Vegetable

Pork chicharon

Cycle parts

Foil heat insulation

Bakery materials

Product

Beauty care

Processed meat

Scrap materials

Herbal soap

Fingerlings

TOTAL

Hardware

Home décor

Packaging materials

Garments

Bottle cleaning

Funeral service

TOTAL

TOTAL

TRADING

MANUFACTURING

SERVICE

1,300,00.00

1,600,000.00

900,000.00

400,000.00

200,000.00

200,000.00

500,000.00

500,000.00

300,000.00

300,000.00

200,000.00

900,000.00

1,150,000.00

1,100,000.00

300,000.00

200,000.00

5,500,000.00

500,000.00

500,000.00

250,000.00

550,000.00

100,000.00

150,000.00

6,450,000.00

150,000.00

11%

13%

7%

3%

2%

2%

4%

4%

2%

2.5%

2%

7%

9.5%

9%

2.5%

2%

45%

4%

4%

2%

4.5%

1%

2%

53%

1.5%

Loan Purpose

Salaries

Plant construction and renovation

Raw Materials

Vehicle/Equipment

TOTAL

Amount (P’000)

1,250

700

7,300

600

9,850

% of Total

13

7

74

6

100

*As of July 2011

*As of 2009

Loans availed by benepartners were for working capital requirement; specifically to pay their workers’ salaries and to purchase raw materials. Loan is also allocated for expansion (plant construction and renovation) and acquisition of fixed assets like vehicles.

22 23

Finding the Missing Middle Finding the Missing Middle

Table 5. Femi’s Role in the Business of Benepartners

ii. Business Development Services

FEMI also offers training programs and seminars to its benepartners. These programs and seminars help the benepartners improve their business management and growth. These training programs have been very useful in assisting the benepartners in efficiently managing the loan proceeds and have been assuring FEMI a high repayment rate. Based on the survey conducted with FEMI benepartners, these training programs have helped them in managing and growing their business. Table 5 presents the role FEMI has played in the benepartner’s business growth and development. There were 32 participants in the workshop that was conducted.

How has FEMI helped in the growth and sustainability of your business?

FEMI helps not only in lending us money but also encourage entrepreneurs to expand the business.

First of all the added working capital helps a lot but most specially the trainings & seminars they offer which open our minds & give us right decisions, etc.

They helped by lending money for the additional of capital

Aside from meat shop– we expanded for another business like canteen

FEMI lend us capital w/ a lower interest, FEMI puts their trust to us regarding our proposal & plans

It helps a lot we provide things that especially needs in business growth

Sustain our business thru seminar

By teaching us on business forecast and decisions

Always giving a seminar in handling all kinds of business growth

Keeping myself focus, I can say I am now in the right direction, it is a matter of time & a lot of hard work and partly financially to keep the business in place.

They helped us in our financial capability

Through TRESP-MPC and of course my business partners

Malaking tulong dahil ang Femi siya ang tumulong para magkaroon kami ng puhunan at malaking tulong niya sa kabuhayan namin.

By giving additional financial support

By giving us time to listen to our business needs.They always conduct seminars and visit us personally as if we are their own relatives

24 25

The participants were divided into four groups to validate their individual response. Based on the group presentation, the best feature of FEMI is their ability to guide on managing the business and in the strict monitoring of business objectives. The management of FEMI has not only provided financial assistance but coaching as well. Benepartners look at FEMI as a parent who constantly provides guidance and as a teacher that continuously provides training and monitoring of their projects. FEMI regularly conducts site visit and meetings with the benepartners. Some of these visits and meetings are shown in Figure 8.

The benepartners also credit the management team of FEMI for providing not only financial assistance but also education through trainings and seminars. Topics of these seminars include: record keeping, accounting and report documentation, product technology development, business expansion, supply chain management, human resource management, etc. FEMI’s lending capacity and business guidance are what give its competitive advantage over financial institutions lending credit to SMEs. To the benepartners, FEMI is “caring for the small entrepreneurs to start their business and eventually lets them grow in the business.”

The benepartners, however, pointed out that FEMI should provide longer credit terms and higher loan values. This is one area of opportunity that FEMI should look into. Beneparnters have become loyal to FEMI because of facility to access loans. However, as the business grows, they need higher loan values and longer credit terms. Other services that benepartners would like FEMI to provide are as follows:

1. Business documentation for government agencies2. Rediscounting3. More guidance4. Higher loan value and longer credit terms

Finding the Missing Middle Finding the Missing Middle

Figure 8. FEMI On-Site Visit to Benepartners

Pedro Santos Woodcraft – Cue Sticks

Briones Tilapia Hatchery

Tinio’s Furniture

JCF Soap

26 27

iii. Achievements

The high repayment rate of Benepartners can be traced to three factors: a) facility to borrow; b) guidance and regulatory policies to ensure use of loan proceeds; c) partnership with benepartners in managing and growing the business through seminars, workshops, and personal site visits. During site visits, the benepartners are transparent with FEMI in discussing the business’ status as well as concerns and problems of day-to-day operations. Since most businesses are family owned and managed, family relationships are also established with FEMI. This creates a personalized manner in handling each benepartner, creating strong alliance between FEMI and the borrower. The Filipino value of “kahihiyan” becomes a powerful driving force in making the benepartners more committed to meet their loan obligations. This also helps FEMI understand the business’ financial and personal aspects. The benepartners look at FEMI as a guiding arm in the business, thus or as a parent that helps the business succeed.

Through the thirteen years that FEMI has been in operation, it has developed a strategic competency of knowing and understanding its clients. This characteristic can be called “lending with a heart.” FEMI contributes to a business’ growth by opening opportunities to more employment and creation of more business partnerships. The organization’s regular visits and training programs allow FEMI to better understand its market. Stronger partnerships have been established thanks to these visits, and has also allowed for customer focus. The training programs and advisory sessions with the Benepartners create an atmosphere of partnership between FEMI and the Benepartners. The business model of FEMI can be explained through the Focus-Localize-Partner Model as seen in Figure 9.

Finding the Missing Middle Finding the Missing Middle

Figure 9. FEMI’s Focus-Localize-Partner Model7

Although FEMI has helped its benepartners provide employment generation in the rural areas, the vision of making its benepartners tap credit facilities in the formal banking sector has not been achieved. The benepartners find it more advantageous to borrow from FEMI than to borrow from commercial banks. The interest rate that FEMI offers is acceptable to its clients, although higher than that of a commercial bank. The higher interest rate is offset by the facility to borrow from FEMI, the lesser number of document requirements, and business training and development partnership activities being offered by FEMI. Consultancy services and strategic planning activities are also provided by FEMI. This is seen by the benepartners as an important factor to improve and sustain their business’ growth.

C. Opportunities with the Missing Middle

i. Potential demand

The need to develop small and medium enterprises has been

7 The FLP Model is patterned after the FLP Model being advocated by UNDP to engage the poor in doing business with large organizations.

28 29

recognized by both the private and public sector. Micro lending institutions have grown throughout the years. Banks like the Land Bank of the Philippines and Development Bank of the Philippines have been mandated to provide loans to SMEs. Commercial banks like Planters Bank, Bank of the Philippine Islands, Banco de Oro, etc. include SMEs in their loan portfolio. However, the move to serve SMEs has not been easy because banks have changed their minds with regards to serving SMEs. Past clients have been big organizations that can meet the formal documentation process and loan security usually needed by the banks. Regulatory policies imposed on banks limit banking sector serve the capital requirement needs of the SMEs. Table 6 shows the number of SMEs that can be tapped as a target market. Based on the current clients being served by FEMI, there is still a very big number of SMEs that can be given credit. Most of these SMEs rely on micro financing institutions.

Table 6. Potential SME Market for FEMI

Number of EstablishmentsSmall MediumRegion Small Medium

Number of Employed Individuals

5,759 (8.6%)

222 (7.23 %)

8,680 (12.9%)

500 (16.28%)

67,166 3,070 1,522,227 416,686

122,236 (8.03%)

30,675 (7.36%)

191,900 (12.6%)

68,778 (16.5%)

Central Luzon

Southern TagalogTotal Phils

ii. Competition

The increasing number of SMEs has seen the growth of micro lending institutions. In the formal banking sector, rural banks are the institutions that cater to the financing needs of SMEs. Based on a UN study, more than 200 commercial banks and other formal financial institutions are now engaged in providing loans for SMEs. Analysis of the competition among those providing financial services to SMEs has shown that non-formal lending institutions like NGOS have to be more adaptable to the SMEs’ needs. This is basically due to the following factors:

Finding the Missing Middle Finding the Missing Middle

There are lesser lending and depository policies on NGOs compared to banks and formal lending institutions. NGOs have more direct access to the needs of SMEs since they work closely with them on social and business issues.

NGOs direct and personal contact with SMEs create a strong, safe, and accessible payment system.NGOs have more expertise in handling loans that are not purely collateral based but are more opportunity based.

Table 7. Summary of Parameters of Lending Institutions Catering to SMEsAuthorized Activities

Type Regulated by

Owner-ship

Supervised by

Main Funding Sources

Legal Basis

Formal Institutions

Savings and Credit Coop

Savings deposits and loan to members

CDAIndividual members None Capital plus

member deposits

Cooperatives Code

NGOs Loans to individuals and groups

Annual Reports to SEC and BSP

Private trustees None Grants,

donations, commercial loans

Law on trusts and nonprofit foundations

Thrift Banks

Savings deposits and loans

BSP,PDICPrivate investors

BSP,PDIC Equity, commercial loans, deposits

Rural Banks

Savings deposits and loans

BSP,PDICPrivate investors

BSP,PDIC Equity, commercial deposits and loans

Pawnshops

Pawn loansBSP, SECPrivate investors

None Equity, commercial loans

Lending investors

LoansSECPrivate investors

None

Thrift Banks Act (1995) Law on Corporations (2001)

Rural Banks Act (1992)Law on Corporations

General Banking Law (2000)

General banking Law, Law on Corporations

Equity, commercial loans

Semiformal Institutions

Source: Financial Sector Assessment, Philippines

30 31

Microenterprises can receive products and services from microlending institutions or NGOs. Loan amount averages P3,000 –P5,000 and does not exceed P150,000. Interest rates of loan average 24-40% per year are inclusive of upfront service fees of 2-5% and weekly collections of the loan payment. Savings and credit cooperatives also offer micro financing with an interest of 18-24% per year. Collection frequency on loans is weekly, bi-weekly, or monthly. Although there is a formal sector that offers micro financing services to micro businesses, SMEs find it hard to access loan from banks and other formal lending institutions. Loan amounts between P100,000 to P1M are usually the loan requirements of SMEs. Banks, including rural banks, find this amount too low and not usually profitable given the institution’s cost consideration. This has left the SMEs that are graduating from micro enterprises to secure a loan from the informal sector. There is a large opportunity in this financial service.

Table 7 presents the summary on the lending institutions catering to SMEs. The table shows that NGOs have a more competitive advantage compared to formal lending institutions in terms of lesser regulations, private access to funds, and authorized activities. At present, there is an absence of financial institutions that cater to the graduating micros.

Finding the Missing Middle Finding the Missing Middle

IV. MAPPING THE FUTUREThe growth of SMEs opens more business opportunities for FEMI.

FEMI has defined its core value proposition: serving the community through job generation. For FEMI to support poverty alleviation through job generation, there should be more benepartners that FEMI should cater to. This will mean more funds for lending should be available.

As of August 2011, FEMI has a P12.1 million loan portfolio, 3 loan officers, and 31 clients. Average loan size is P200k and each loan officer can handle P15million loan portfolio. With the management and resource strengths and opportunities open to FEMI, they aim to loan P20 million in 2010 and increase it to P100 million in 2013. Strategic objectives that have been lined up are shown in Table 8.

Table 8. Strategic Objectives

Target Baseline (2010)

2011 2012 2013

Loan Portfolio P20m P40m P60m 100m

Number Of Clients 80 (P250k ave loan size)

133 (P300k ave. loan size)

171 (P350k ave loan size)

285 (P350k ave loan size)

Number of loan officers

2 3 4 7

Loan fund sourcesBanks P 5M P12M P 20 M P40MOther Financial Institutions

5M 10M 20M 30M

Investors 3M 10M 11M 20MFEMI Loan Fund 7M 8 M 9M 10MTotal Loan Fund P 20M P40 M P28 M P100 M

32 33

IV. THE BENEPARTNERS

The following case studies document the effectiveness of FEMI’s business model. These cases show the impact of FEMI’s loan program in the growth of the business’sales, assets, and job generation

a. Pilipinang Kay Ganda: The Case of JCF SOAP MANUFACTURING

Josephine “Josie” C. Festejo founded JIMAR Cosmetics Manufacturing in 1996. The name was later changed to JCF Soap Manufacturing. The business started with the manufacture and sale of perfume, detergent soap, and bleaching chemicals. To date, the company concentrates on the production and sale of papaya whitening soap. Josie started as a sales agent of cosmetics and beauty care products. Her knowledge of the product, the market, and networks of suppliers and manufacturers inspired her to put up her own business, which would engage in the manufacture and sales of beauty products. Her network with a chemist friend enabled her to develop beauty products like perfume, soap, and bleaching chemicals. She was able to seize an opportunity by catering to the Filipino market’s demand for skin whitening products. To further enhance her knowledge and skills in product development, she attended training programs given by TLRC on soap manufacturing. Equipped with technical knowledge on soap manufacturing, she concentrated on the sale and production of papaya soap. The company carries the brand name “Dagta” papaya soap and “Brilliant” for detergent. The company eventually phased out the production of detergent and concentrated on papaya soap. The business operates on an 8-hour shift with 8 employees. Production includes soap manufacturing, and involves raw materials preparation, mixing, forming, and packaging.

Josie Festejo started her partnership with FEMI in 2003, receiving a loan of P100,000. The business registered an annual sale of P1.68 million, with a profit margin before tax of 46.04% or P773,486. As of 2009, annual sales amounted to P2.99 million with a 48% profit margin before tax or P1.44 million. The number of employees has remained at 8 in the last four years. Today, the business has 3 distributors, 23 dealers, and 3 suppliers.

Finding the Missing Middle Finding the Missing Middle

The company borrowed a total of P750,000 during the period 2003-2005. Josie has been very active in the different seminars and workshop given by FEMI. She was one of the founders of the credit cooperative and she is very much involved in her community’s socio-civic activities. She was also elected president of the Rotary Club, Antipolo Chapter.

Figure 10. Josie Festejo and Variants of Dagta Soap

Josie attributes the growth and sustainability of her business to the financial resources provided by FEMI. Better profitability level and funds management are attributed to the training and seminar workshop on cash and working capital management; kaizen and supply chain management; marketing seminar; and a seminar on legal management. She was also able to increase the company’s asset base through the acquisition of a new vehicle, paid with a bank loan and the acquisition of additional property.

The business sells its products through distributors. It also manufactures soap for other branded papaya soap companies, dermatologists, and derma clinics. These distributors sell the soap to various store outlets. Fifty percent of its total sales are its subcontracting arrangements with a papaya soap company; the soap is sold using company’s brand name. The papaya soap carries the brand name “Dagta.” The company sources its raw materials and supplies from three suppliers on a 30-day credit term. It sells its products on cash basis and credit terms of 30-45 days. The company does not enter into

34 35

direct distribution of its products with supermarkets due to the high cost charged for consigning the product and a long payment term of 120 days. Dagta soap is sold nationwide through distributors. It is available in Luzon, Iloilo, Cebu, Leyte, Masbate, and some parts of Mindanao. It has ten major distributors all over the country.

The company carries a wide assortment of papaya soap that addressrd different needs for skin care. The products are as follows:

Dagta Papaya Herbal Skin Whitening Soap – pure organic soap made from fresh papaya fruit, coconut oil, and minerals. It nourishes the skin and prevents skin blemishes and allergies.

Rich Katas ng Papaya Skin Bleaching Herbal Soap – skin bleaching herbal soap with coconut oil. It can be used as a bath soap to whiten the skin.

Dagta Oatmeal with Milk Soap – contains milk and oatmeal with glycerine and mineral oil that nourishes the skin and prevents white and black heads.

Dagta Akapulko-Guava Herbal Soap – anti-bacterial soap for skin diseases such as “an-an”, athlete’s foot or “alipunga”, eczema and other skin allergies. It can also be used as feminine hygiene soap.

Dagta Tawas-Papaya Herbal Skin Whitening soap – prevents body odor, skin blemishes, and allergies.

Dagta Kalamansi with Tawas Deodorizer Herbal Soap – protects the body from excessive sweating, perspiration, and body odor.

Dagta Squalene Plus Papaya Soap – anti-aging soap that contians deep-sea shark liver oil, fresh papaya fruit, coconut oil, and minerals.

Finding the Missing Middle Finding the Missing Middle

Hair Grower with Aloe Vera Herbal Soap – contains aloe vera extract that prevents hair loss

Dagta Skin Whitening Glutatione Soap with Alpha-T Acids, Vit C, and Sheep Placenta Extracts – skin whitening, anti- aging, and anti-oxidant soap

The success of JCF Manufacturing is attributed by Josie to the ability to recognize the opportunity of papaya soap, conservative fund management, and having a good quality product. The company is planning to market the product more aggressively. The company has put up a Facebook account so it can cater to a wider global market. Through the help of FEMI, the company has engaged a consultant to help expand its market and introduce its brand as “Dagta.” Marketing strategies are being developed to increase the market; one of which is the establishment of JCF’s website, http://www.dagta.tk.

In order to prepare for a more aggressive marketing strategy, JCF is also being assisted in its sales projections. It plans to borrow funds again from FEMI to support its expansion program. Although it has collateral to offer for its loan requirements, JCF is not very keen to loan from banks at a lower interest rate. This is due to the difficulty in getting a loan approval, documentation requirements, etc. Access to commercial bank’s loan facility can be very time consuming. This discourages the JCF from applying for a loan to support business expansion. JCF is also one of the SMEs being assisted by De La Salle University in the ASEAN Consulting Based Learning Program (COBLAS) for Asian Entrepreneurs (sponsored by AsiaSEED under the ASEAN Secretariat).

Figure 11. Dagta Website (www.dagta.tk)

36 37

Figure 12. SUPPLY CHAIN MAP OF JCF SOAP MANUFACTURING

Finding the Missing Middle Finding the Missing Middle

b. May Pera sa Basura: The Case of CJR Junkshop

Ms. Rosemary De Guzman and her spouse (now deceased) started operating a junkshop in 2003 with the help of two workers. The business was registered under DTI in 2006, under the name CJR Junkshop; it had an initial capitalization of P50,000. CJR buys scrap materials (plastic, metals, papers and cartons) in Cainta, Rizal and nearby areas. The business was able to triple its capital during its first year of operations. CJR was able to enter the scrap bidding for scrap materials of large establishments like hospitals and construction firms. The technique of assessing the value of scrap learned by Mr. De Guzman from his previous employment at a junkshop in Pampanga proved to be a critical success factor for CJR’s operations. The technique of assessing the value of the scrap materials is critical in this type of business.

Contracts awarded to Mrs. De Guzman were: medical hospital (P1.4M, P150K), construction firm (P1.5M), mall (P50K every 2 months), and food processing plant (P1.353M). Mrs. De Guzman used to secure her financing requirements from a financier lending at an interest of 10%. The financier managed the sales and collects the receivables until the loan and interest was paid. Through a friend’s referral, Mrs. De Guzman started borrowing from FEMI in 2008 with an initial loan of P100,000. To date, CJR Junkshop has borrowed a total of P2.4 million from FEMI. Loan payments of interest and principal are made on time. Financing requirements of CJR are all sourced from FEMI.

At present, the bulk of CJR’s business is focused on the bidding of scrap materials from different companies like hospitals, construction firms, malls, and supermarket. The latest bid awarded was from one of the big food processing companies in the country in the amount of P1,353,625. Mrs. De Guzman has an on-going bid project with the Department of Public Works and Highways for a project costing not less than P500,000.

38 39

Mrs. De Guzman attributed the success of the business to the following factors: a) tacit knowledge on assessing value of scrap materials; b) honest and fair business practices; c) management training skills development conducted by FEMI; and d) low-cost of working capital requirements provided for by FEMI. The business success in translated to an increased number of workers (from 2 in 2003 to 16 in 2010) and the acquisition of assets like trucks, land, and a residential house for the family. Business engagement with FEMI has resulted in increased profit for CJR, which went from a monthly net profit after tax of P84,000 in 2008 to P226,000 as of July 2010. Suppliers and distributors also increased as a result of more sales and winning bids of the business.

The financial success of CJR is supported by the management skills Mrs. De Guzman acquired in the last three years. She attributed the business’ success to the funds easily accessible from FEMI, the different training programs she attended, and the guidance the organization offered to her business. To date, CJR has expanded into two locations: one in Antipolo and another in Angono. As the business expands, the children are starting to take an active participation in the business. Her eldest son is now taking active participation in the management of the main shop in Cainta, while the second child is managing the new shop in Angono. CJR is also one of the SMEs being assisted by De La Salle University in the ASEAN Consultancy Based Learning Program (COBLAS) for Asian Entrepreneurs (sponsored by AsiaSEED under the ASEAN Secretariat ).

Finding the Missing Middle Finding the Missing Middle

Figure 13. Mrs. Rosemarie De Guzman meeting with AsiaSEED Consultant and DLSU Faculty

Figure 14. The CJR Junk Yard

40 41

Figure 15. SUPPLY CHAIN MAP OF CJR JUNKSHOP

Finding the Missing Middle Finding the Missing Middle

c. The Puzzle : The Case of Stanpuz Corp.

Figure 16. Mr. Danila Cuervo (center) with Mr. Ishida of AsiaSEED and Albert of FEMI

Figure 17. Stanpuz Products

Stanpuz Corp. started business operations in 1993 as a manufacturer of gifts, housewares, and novelty items. In 1997, the business was incorporated under the name Stanpuz Corp. as a closed corporation owned by the Cervo siblings. The business is managed by Mr. Danilo Cervo, an industrial technologist. The idea of putting up a business came to Mr. Cervo when he worked as a waiter in a luxury ship; there he met a Belgian co-worker who gave him the idea of putting up a business of wooden puzzle toys for export in Europe. The Belgian friend gave him an initial capital to start the business. This started the business STANPUZ, which stands for “Standing Puzzle.”

42 43

As market opportunities were discovered, Stanpuz business expanded to new product lines like laminated capiz vases, fiber glass vases with fine hand painting, home decors made of indigenous materials, and metal craft products. The business is mainly engaged in export. Like other exporters, Stanpuz has to address concerns such as the weakening dollar value, economic slowdown in Europe, competition from China, Vietnam, and Indonesia, and the rampant copying of designs by other companies. Development of new designs and expansion of European market are two strategies the company uses to face the aforementioned concerns. Major clients are Kazmar Trading and Sentimentals. Sales terms are 30% downpayment and 70% upon delivery for shipment.

The company operates 8 hours a day, 7 days a week. Stanpuz employed 24 workers (8 regular and 16 contractual) and five (5) subcontractors, with an average of 10 employees per subcontractor Aside from regular mandatory benefits like SSS, Philhealth, and medical benefits, employees are given incentive pay when they meet their target.

Stanpuz started borrowing from FEMI in 2009 with an initial loan amount of P200,000. To date, total loan availed of amounts to P1.2 million with on-time repayments. In 2008, prior to loan engagement with FEMI, total sales amounted to P4.8 million. Sales increased to P7.25 million in 2009 with the loan assistance from FEMI. Profit margin also improved from 4.8% in 2008 to 6.6% in 2009. FEMI’s seminars, networks, and consultancy services contributed to the increase in sales and profitability during the last few years. To date, FEMI’s consultancy services have been extended to the participation of Stanpuz in the ASEAN Consultancy Based Learning for Asian SMEs (COBLAS) program with De La Salle University. Students and faculty members of De La Salle University act as consultants, assisting Stanpuz in human resource related issues. The program is funded by AsiaSEED under the auspices of the ASEAN Secretariat.

Finding the Missing Middle Finding the Missing Middle

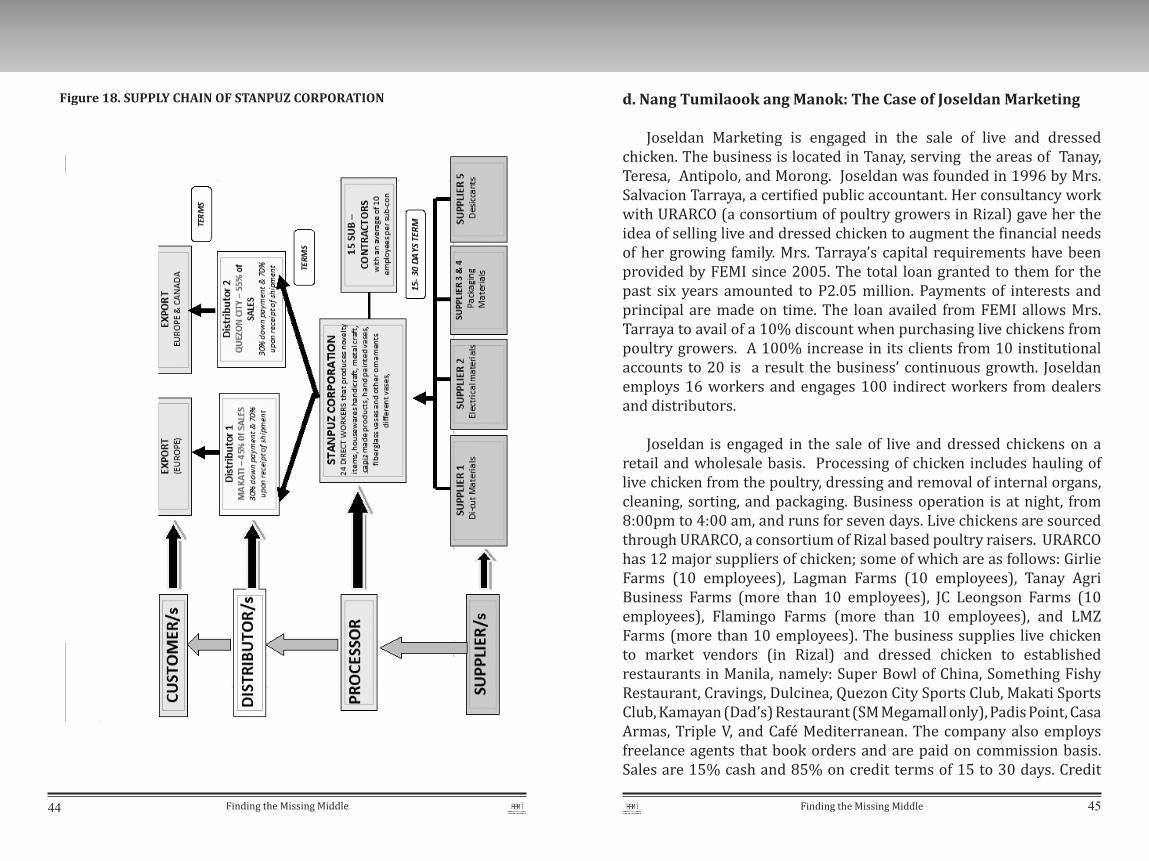

Figure 18. SUPPLY CHAIN OF STANPUZ CORPORATION

44 45

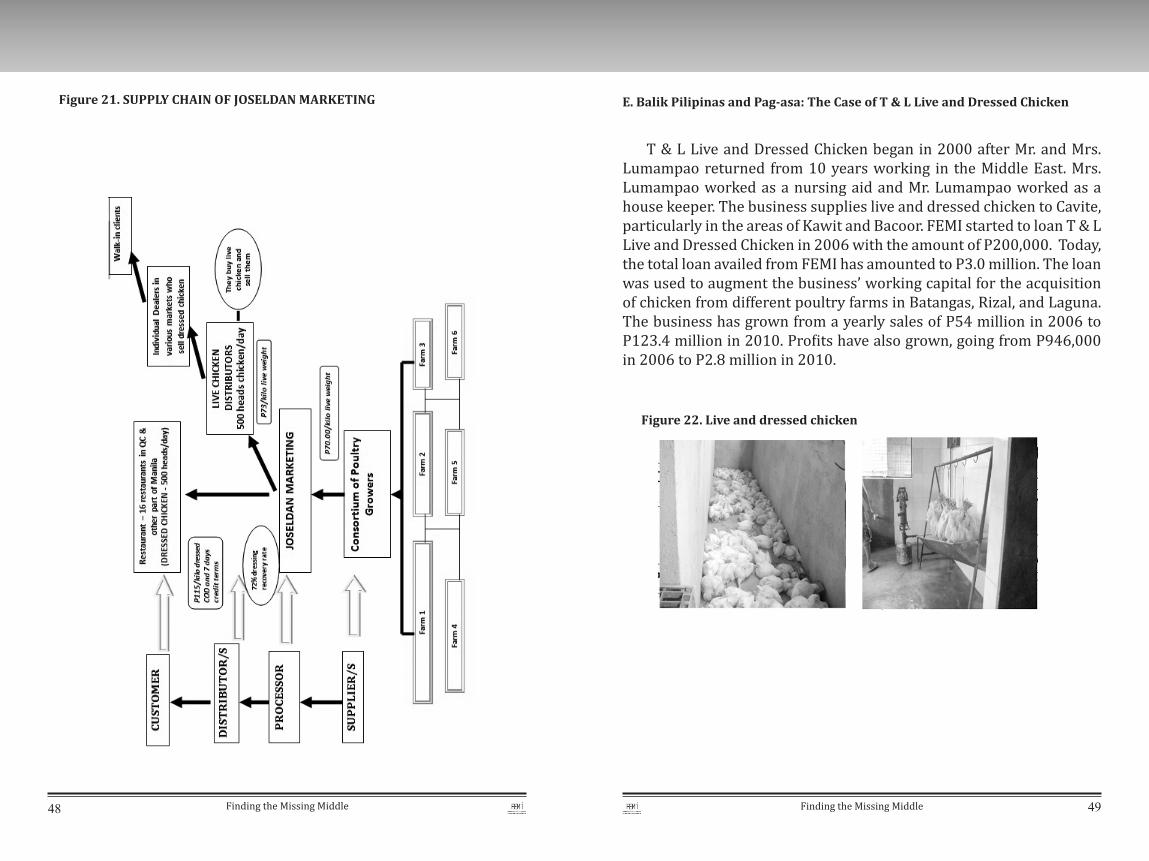

d. Nang Tumilaook ang Manok: The Case of Joseldan Marketing

Joseldan Marketing is engaged in the sale of live and dressed chicken. The business is located in Tanay, serving the areas of Tanay, Teresa, Antipolo, and Morong. Joseldan was founded in 1996 by Mrs. Salvacion Tarraya, a certified public accountant. Her consultancy work with URARCO (a consortium of poultry growers in Rizal) gave her the idea of selling live and dressed chicken to augment the financial needs of her growing family. Mrs. Tarraya’s capital requirements have been provided by FEMI since 2005. The total loan granted to them for the past six years amounted to P2.05 million. Payments of interests and principal are made on time. The loan availed from FEMI allows Mrs. Tarraya to avail of a 10% discount when purchasing live chickens from poultry growers. A 100% increase in its clients from 10 institutional accounts to 20 is a result the business’ continuous growth. Joseldan employs 16 workers and engages 100 indirect workers from dealers and distributors.

Joseldan is engaged in the sale of live and dressed chickens on a retail and wholesale basis. Processing of chicken includes hauling of live chicken from the poultry, dressing and removal of internal organs, cleaning, sorting, and packaging. Business operation is at night, from 8:00pm to 4:00 am, and runs for seven days. Live chickens are sourced through URARCO, a consortium of Rizal based poultry raisers. URARCO has 12 major suppliers of chicken; some of which are as follows: Girlie Farms (10 employees), Lagman Farms (10 employees), Tanay Agri Business Farms (more than 10 employees), JC Leongson Farms (10 employees), Flamingo Farms (more than 10 employees), and LMZ Farms (more than 10 employees). The business supplies live chicken to market vendors (in Rizal) and dressed chicken to established restaurants in Manila, namely: Super Bowl of China, Something Fishy Restaurant, Cravings, Dulcinea, Quezon City Sports Club, Makati Sports Club, Kamayan (Dad’s) Restaurant (SM Megamall only), Padis Point, Casa Armas, Triple V, and Café Mediterranean. The company also employs freelance agents that book orders and are paid on commission basis. Sales are 15% cash and 85% on credit terms of 15 to 30 days. Credit

Finding the Missing Middle Finding the Missing Middle

transactions are usually covered by post dated checks. Joseldan Per submitted in house financial statements which state that the business registers an average of P2.8 million gross monthly sales and a return on sales at 9.3%.

Last November 25, 2010, Mrs. Tarraya was awarded FEMI’s Best Practices in Establishing Good Relationship in Various Components in Full Supply Chain. She was also the recipient of Best Benepartner in Credit Program as she was able to pay her loans on time and without any record of holding checks. Mrs. Tarraya also serves as Vice-Chairman and member of the TRESP MPCBoard of Directors.

The business of the Tarraya family has expanded from chicken to becoming an accounting consultancy firm (Tarraya and Associates Accounting and Auditing Firm) and a manpower agency. Mrs. Tarraya is slowly passing on the baton in managing the business to her children. Her eldest son, Joshua is now in charge of the daily operations of Joseldan Marketing, while her youngest son, Danny is in charge of the manpower agency.

The success of Joseldan Marketing is hinged on the strong faith of Mrs. Tarraya, which is seen in her practice of Christian based business principles. Her training as an accountant enables her to set up a system of check and balance in the business, ensuring that daily operations are smoothly and efficiently managed. The funds that Joseldan borrowed from FEMI have been very useful in securing a discounted supply of chicken and widening its client base. To better manage the business, Mrs. Tarroja attended the following training programs: credit and accounts receivables management, supply chain analysis, basic of selling, sales negotiation, working capital management, leadership seminar, good manufacturing practices, and basic strategic planning seminar. Joseldan is currently undergoing consultancy session with FEMI consultant Ronald de Dios, former general manager of Pfizer in the Animal Division, for the turnover of business management to the children of Mrs. Tarraya. Joseldan is also classified as a graduating benepartner and has been referred to a Small Business Corporation for a loan of P2 million.46 47

Figure 19. FEMI’s consultants on visit at Joseldan

Figure 20. Consultants’ Meeting with Mrs. Tarraya and son

Finding the Missing Middle Finding the Missing Middle48 49

Figure 21. SUPPLY CHAIN OF JOSELDAN MARKETING E. Balik Pilipinas and Pag-asa: The Case of T & L Live and Dressed Chicken

Figure 22. Live and dressed chicken

T & L Live and Dressed Chicken began in 2000 after Mr. and Mrs. Lumampao returned from 10 years working in the Middle East. Mrs.Lumampao worked as a nursing aid and Mr. Lumampao worked as a house keeper. The business supplies live and dressed chicken to Cavite, particularly in the areas of Kawit and Bacoor. FEMI started to loan T & L Live and Dressed Chicken in 2006 with the amount of P200,000. Today, the total loan availed from FEMI has amounted to P3.0 million. The loan was used to augment the business’ working capital for the acquisition of chicken from different poultry farms in Batangas, Rizal, and Laguna. The business has grown from a yearly sales of P54 million in 2006 to P123.4 million in 2010. Profits have also grown, going from P946,000 in 2006 to P2.8 million in 2010.

Finding the Missing Middle Finding the Missing Middle

Figure 23 Mrs. Lumampao

Mr. And Mrs. Lumampao attribute their business’ success to the capital requirements that are provided by FEMI and also to the training programs and consultancy that FEMI extends to improve the management of the growing business. As business grows, the owners realized the need for a systematic recording of transactions and proper documentation of the business financial position. Through the support (loan grants and business development services) given by FEMI to T&L, the following results were achieved:

1. Acquisition of lot (70 sq.m)2. Establishment of slaughter house in the acquired lot (concrete and 2 storey building)3. Improvement of service vehicles (3 units for deliveries)

Training programs provided by FEMI has resulted in improvements

of the management of the business namely:

Improvement in recordingsImprovement of production plant (maintaining cleanliness & orderliness)Minimizing losses thru proper management of personnelInstallation of operating systems such as daily recording of transactions, some additional benefits to personnel (SSS, free boardand lodging, and incentives) accounts receivable management.

50 51

Figure 24. SUPPLY CHAIN MAP OF T & L LIVE & DRESSED CHICKEN

Finding the Missing Middle Finding the Missing Middle

VI. FEMI AND THE MISSING MIDDLE

For the past thirteen years, FEMI has been continuously pursuing its mission of helping the country alleviate poverty through job generation in the rural area. This mission has been carried out through the strategy of focusing on the “missing middle” or “graduating micros.” FEMI has helped 274 enterprises. Direct and indirect jobs generated by these enterprises totalled to more than 12,000. These include employment generated directly through these enterprises and indirect job generation from jobs provided by the suppliers, distributors, wholesalers, retailers, and agents that are involved in the enterprise’s supply chain. The credit granted to the benepartners enabled the firms to sustain and grow their operations. The five cases previously presented attest to the success of FEMI’s business model.

Working capital requirements can easily be sourced from FEMI without having to go through the tedious procedures and documentation requirements demanded by formal credit institutions like commercial banks. The capability of the benepartners to pay is enhanced through the business services training programs and the consultancy being offered by FEMI. The benepartners have attested that these training programs and consultancies contributed to a large degree in the development of management skills. The trainings also provided the owners a more systematized way of conducting the business through better documentation process, management information systems, accounting procedures, and record keeping. All these enable the benepartners to manage the enterprise in a more organized manner. The net effect of all these programs is a high repayment rate of 95%.

The attainment of FEMI’s goal of job generation in the rural areas is a result of the strategy called Focus-Localize-Partner Model, which FEMI adapted in working with their benepartners. Focus refers to knowing the core competencies of the firm and clearly identifying its vision. FEMI has clearly identified the market called the “missing middle.” The core competency of FEMI in understanding and serving the “missing

52 53

middle” has been developed through its thirteen years of working with these benepartners. FEMI has developed a profound sensitivity to the concerns and aspirations of its market niche.

Localize strategy is carried through site visits and monitoring of business performance. This enabled FEMI to know and understand their benepartners better. The benepartners perceive this strategy as a show of concern from FEMI. The benepartners call this strategy “lending with a heart.”

Partnership with the beneficiaries has always been the driving force of FEMI’s deals with its beneficiaries. To FEMI, the clients they lend to are not just borrowers-they are also partners. Figure 9 (Focus-Localize-Partner Model) depicts the strategic model being used by FEMI in attainment of its goal. This strategic model serves as a good way of addressing the social issues of poverty and unemployment. Solving these social issues through the use of entrepreneurial ability and paradigms makes FEMI a social entrepreneurship. Partnership in FEMI’s model includes networking with local government units and other government institutions. This creates a wider source of information for identifying potential benepartners and evaluation of loan applications. Networking among benepartners is also encouraged to support each other’s business, share experiences, and information.

The Focus-Localize-Partner Model enables FEMI to carry out its role of job generation in the rural areas. FEMI has clearly identified its target market called the “missing middle,” whose needs for capital are not provided for by the microfinacing institutions and banks. The missing middle comprise 83% of the industry in the Philippines.

Finding the Missing Middle Finding the Missing Middle

Figure 25. FEMI’s Job Generation Model

Source: FEMI’s Journey 2, 2008.

Jobs generated by FEMI’s lending (credit)and business development services (BDS) is a result of FEMI’s defined role in the supply chain of its benepartners, as shown in Figure 25. Unlike traditional credit giving NGO’s and financial institutions, FEMI goes beyond the lending process by assisting its benepartners in developing management competencies through its training and consultancy programs. The BDS allows FEMI to have an open communication with its benepartners. This facilitates immediate feedback and updated information on the business performance and concerns of the benepartners. It also allows FEMI to have an updated database on its benepartners, which will generate information for the guidance, controls, and better assistance in the business’ performance. The FLP Model of FEMI is hinged on the three-pillared approach to development of the missing middle, namely, credit, business development service or learning and development, and networking. FEMI can only continue its advocacy of rural job generation and helping in the growth and development of Philippine businesses if it can have expanded capital and more resources.

54 55

VII. THE JOURNEY BEGINS...

The mission of FEMI has been carried out in the past thirteen years in spite of its meager resources. The business model of FEMI is hinged on the concept of partnership with the clients, providing a strong foundation for the organization. The commitment of FEMI to help in the poverty alleviation program bore fruits through the number of benepartners it has helped and the number of jobs the businesses have generated over the years. There are two strategic advantages FEMI has used in helping the benepartners grow and sustain their business. These are a) easy access to loans and b) business development services.

At hindsight, the loan FEMI gives to its benepartners compared