Financial Statements of Government Organizations - Ontario.ca

450

Treasury Board Secretariat PUBLIC ACCOUNTS OF ONTARIO Financial Statements of Government Organizations VOLUME 2B 2016–2017

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Financial Statements of Government Organizations - Ontario.ca

Treasury Board Secretariat

PUBLIC ACCOUNTSOF ONTARIO

Financial Statements of Government Organizations

VOLUME 2B 2016– 2017

TABLE OF CONTENTS

Volume 2B

Page

General

Responsible Ministry for Government Agencies .......................................................................................... iiA Guide to the Public Accounts ................................................................................................................... iv

FINANCIAL STATEMENTS

Section 1 ─ Government Organizations – Cont’d

Niagara Parks Commission ....................................................................... March 31, 2017...................... 1-11-25Northern Ontario Heritage Fund Corporation ............................................. March 31, 2017......................

Ontario Agency for Health Protection and Promotion(Public Health Ontario)................................................................. March 31, 2017...................... 1-39

1-531-731-891-1071-1271-1431-1611-1951-2051-2311-2451-2731-2871-3131-3271-3431-3631-3791-4011-429

Ontario Capital Growth Corporation........................................................... March 31, 2017......................Ontario Clean Water Agency ..................................................................... December 31, 2016 ...............Ontario Educational Communications Authority (TV Ontario) .................... March 31, 2017......................Ontario Electricity Financial Corporation.................................................... March 31, 2017......................Ontario Energy Board ................................................................................ March 31, 2017......................Ontario Financing Authority ....................................................................... March 31, 2017......................Ontario French-Language Educational Communications Authority............ March 31, 2017......................Ontario Immigrant Investor Corporation..................................................... March 31, 2017......................Ontario Infrastructure and Lands Corporation (Infrastructure Ontario)....... March 31, 2017......................Ontario Mortgage and Housing Corporation .............................................. March 31, 2017......................Ontario Northland Transportation Commission .......................................... March 31, 2017......................Ontario Place Corporation ......................................................................... December 31, 2016 ...............Ontario Securities Commission.................................................................. March 31, 2017......................Ontario Tourism Marketing Partnership Corporation.................................. March 31, 2017......................Ontario Trillium Foundation........................................................................ March 31, 2017......................Ornge......................................................................................................... March 31, 2017......................Ottawa Convention Centre Corporation ..................................................... March 31, 2017......................Province of Ontario Council for the Arts (Ontario Arts Council).................. March 31, 2017......................The Royal Ontario Museum ....................................................................... March 31, 2017......................Toronto Organizing Committee for the 2015 Pan American

and Parapan American Games (Toronto 2015) ........................... March 31, 2017...................... 1-4231-425Toronto Waterfront Revitalization Corporation (Waterfront Toronto).......... March 31, 2017......................

i

PUBLIC ACCOUNTS, 2016-2017

ii

RESPONSIBLE MINISTRY FOR GOVERNMENT BUSINESS ENTERPRISES, ORGANIZATIONS, TRUSTS & MISCELLANEOUS FINANCIAL STATEMENTS

Ministry of Agriculture, Food and Rural Affairs AgriCorp Agricultural Research Institute of Ontario

Ministry of the Attorney General Legal Aid Ontario The Public Guardian and Trustee for the Province of Ontario

Ministry of Economic Development, Employment and Infrastructure/Research and Innovation General Real Estate Portfolio Ontario Capital Growth Corporation Ontario Immigrant Investor Corporation

Toronto Waterfront Revitalization Corporation (Waterfront Toronto)

Ministry of Education Education Quality and Accountability Office Ontario Educational Communications Authority (TV Ontario) Ontario French-Language Educational Communications Authority

Ministry of Energy Brampton Distribution Holdco Inc. Hydro One Limited

Independent Electricity System Operator Ontario Energy Board Ontario Power Generation Inc.

Ministry of the Environment and Climate Change Ontario Clean Water Agency

Ministry of Finance Deposit Insurance Corporation of Ontario Liquor Control Board of Ontario Losses Deleted from the Accounts Motor Vehicle Accident Claims Fund Ontario Electricity Financial Corporation Ontario Financing Authority Ontario Lottery and Gaming Corporation Ontario Securities Commission Pension Benefits Guarantee Fund Provincial Judges Pension Fund Revenue Remissions

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

Ontario Infrastructure and Lands Corporation (Infrastructure Ontario)

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

zhangsa2

Typewritten Text

PUBLIC ACCOUNTS, 2016-2017

iii

RESPONSIBLE MINISTRY FOR GOVERNMENT BUSINESS ENTERPRISES, ORGANIZATIONS, TRUSTS & MISCELLANEOUS FINANCIAL STATEMENTS

Ministry of Health and Long-Term Care Cancer Care Ontario eHealth Ontario Local Health Integration Network – Central Local Health Integration Network – Central East Local Health Integration Network – Central West Local Health Integration Network – Champlain Local Health Integration Network – Erie St. Clair Local Health Integration Network – Hamilton Niagara Haldimand Brant Local Health Integration Network – Mississauga Halton Local Health Integration Network – North East Local Health Integration Network – North Simcoe Muskoka Local Health Integration Network – North West Local Health Integration Network – South East Local Health Integration Network – South West Local Health Integration Network – Toronto Central Local Health Integration Network – Waterloo Wellington Ontario Agency for Health Protection and Promotion (Public Health Ontario) Ornge

Ministry of Labour Workplace Safety and Insurance Board

Ministry of Municipal Affairs and Housing Ontario Mortgage and Housing Corporation

Ministry of Natural Resources and Forestry Algonquin Forestry Authority Forest Renewal Trust

Ministry of Northern Development and Mines Northern Ontario Heritage Fund Corporation Ontario Northland Transportation Commission

Ministry of Tourism, Culture and Sport The Centennial Centre of Science and Technology (Ontario Science Centre) Metropolitan Toronto Convention Centre Corporation Niagara Parks Commission Ontario Place Corporation Ontario Tourism Marketing Partnership Corporation Ontario Trillium Foundation Ottawa Convention Centre Corporation Province of Ontario Council for the Arts (Ontario Arts Council) The Royal Ontario Museum Toronto Organizing Committee for the 2015 Pan American and Parapan American Games (Toronto 2015)

Ministry of Transportation Metrolinx

Treasury Board Secretariat Ontario Pension Board

PUBLIC ACCOUNTS, 2016-2017

iv

A GUIDE TO THE PUBLIC ACCOUNTS

1. SCOPE OF THE PUBLIC ACCOUNTS

The 2016-2017 Public Accounts of the Province of Ontario comprise the Annual Report and Consolidated Financial Statements and three volumes:

Volume 1 contains ministry statements and detailed schedules of debt and other items. The ministry statements reflect the financial activities of the government’s ministries on the accrual basis of accounting, providing a comparison of appropriations with actual spending. Ministry expenses include all expenses that are subject to appropriation approved by the Legislative Assembly, but exclude adjustments arising from consolidation of government organizations whose expenses are not appropriated.

Volume 2 contains the financial statements of Government Organizations and Business Enterprises that are part of the government’s reporting entity and other miscellaneous financial statements.

Volume 3 contains the details of payments made by ministries to vendors (including sales tax) and transfer payment recipients that are not deemed to be prohibited by the Freedom of Information and Protection of Privacy Act.

2. A GUIDE TO VOLUME 2 OF THE PUBLIC ACCOUNTS

The financial statements of the selected crown corporations, boards and commissions are for fiscal periods ending within the Province’s own fiscal period April 1, 2016 to March 31, 2017. They are presented in the same detail as the approved, audited financial statements and as nearly as possible in the same form. The statements have been presented in the order shown in the Table of Contents. In addition, a listing is provided which groups the crown corporations, boards and commissions by ministerial responsibility.

GOVERNMENT ORGANIZATIONS (CONT’D)

THE NIAGARA PARKS COMMISSION

MANAGEMENT REPORT March 31, 2017

The Management of The Niagara Parks Commission are responsible for the financial statements and all other information presented in these statements. The statements have been prepared by management in accordance with the framework identified in Note 2 in the accompanying audited financial statements.

The financial statements include amounts based on best estimates and judgments. Management has determined such amounts on a reasonable basis in order to ensure that the statements are presented fairly, in all material respects.

Management maintains a system of internal accounting and administrative control that is designed to provide reasonable assurance that the financial information is relevant, reliable, accurate and that the Commission’s assets are properly accounted for and adequately safeguarded.

The Board of The Niagara Parks Commission is responsible for gaining assurance that management fulfills its responsibilities for financial reporting and is ultimately responsible for reviewing and approving the financial statements.

The Board, through the Audit and Finance Committee, meets periodically with Management to discuss financial results, auditing matters, financial reporting issues and to satisfy itself that each group is properly discharging responsibilities. The Committee reviews the financial statements before recommending approval by the Board.

The financial statements have been audited by Grant Thornton LLP, the Commission’s appointed External Auditor and in accordance with Canadian generally accepted auditing standards on behalf of the Commission, Minister of Tourism, Culture and Sport and the Provincial Auditor General. Grant Thornton LLP had direct and full access to all Commission records as well as full access to the Audit and Finance Committee with and without the presence of Management to discuss their audit and findings as to the integrity of the Commission’s financial reporting.

_________________________ ________________________________Reegan McCullough Margaret Neubauer Chief Executive Officer Senior Director, Corporate Services June 23, 2017 June 23, 2017

PUBLIC ACCOUNTS, 2016-2017 1-1

Grant Thornton LLP Suite B 222 Catharine Street, PO Box 336 Port Colborne, ON L3K 5W1

T +1 905 834 3651 F +1 905 834 5095 E [email protected] www.GrantThornton.ca

Independent auditor’s report

To The Niagara Parks Commission, the Minister of Tourism, Culture and Sport and the Auditor General of Ontario

We have audited the accompanying financial statements of The Niagara Parks Commission, which comprise the statement of financial position as at March 31, 2017, and the statements of operations, accumulated surplus, changes in net debt and cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information.

Management is responsible for the preparation of these financial statements in accordance with the basis of accounting described in Note 2 to the financial statements, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Audit • Tax • AdvisoryGrant Thornton LLP. A Canadian Member of Grant Thornton International Ltd

1-2 PUBLIC ACCOUNTS, 2016-2017

Opinion

In our opinion, the financial statements of The Niagara Parks Commission for the year ended March 31, 2017 are prepared, in all material respects, in accordance with the basis of accounting described in Note 2 to the financial statements.

Emphasis of matters Without modifying our opinion, we draw attention to Note 2 to the financial statements which describes the basis of accounting used in the preparation of these financial statements and the significant differences between such basis of accounting and Canadian public sector accounting standards.

Port Colborne, Canada Chartered Professional Accountants June 23, 2017 Licensed Public Accountants

PUBLIC ACCOUNTS, 2016-2017 1-3

Audit • Tax • AdvisoryGrant Thornton LLP. A Canadian Member of Grant Thornton International Ltd

The Niagara Parks Commission Statement of Financial Position As at March 31 2017 2016

(in thousands of dollars)

Financial assetsCash and cash equivalents $ 8,207 $ 395 Accounts receivable 4,974 1,738Inventories – saleable 4,055 3,892

17,236 6,025

Liabilities Bank indebtedness (Note 3) - 2,180Accounts payable 10,977 9,041Accrued payroll 2,758 2,706Deferred revenue (Note 4) 2,283 1,316Deferred capital funding (Note 5) 28,534 26,390 Long term financing (Note 6) 26,592 28,371 Post-employment benefits (Note 7) 3,121 3,558Power plant stabilization obligation (Note 8) 29,414 29,076

103,679 102,638

Net debt (86,443) (96,613)

Non-financial assets Tangible capital assets (Note 10 and Page 23) 158,613 155,332 Inventories – other 936 1,199 Prepaid expenses 479 1,230

160,028 157,761

Accumulated surplus (Note 11) $ 73,585 $ 61,148

Commitments and contingencies (Notes 12 and 13)

On behalf of the Commission

Janice Thomson, Chair Ian Nielsen-Jones, Commissioner

See accompanying notes to the financial statements.

1-4 PUBLIC ACCOUNTS, 2016-2017

The Niagara Parks Commission Statement of Operations For the year ended March 31, 2017

Budget Actual Actual 2017 2017 2016

(in thousands of dollars)

RevenuesRevenue producing operations $ 73,088 $ 85,424 $ 76,402 Land rent 6,997 7,009 6,882 Commission, rentals and fees 14,480 14,946 12,858 Premium on United States funds – net 800 1,119 1,073 Government transfers – special projects - 520 - Sundry revenue 5 20 7

95,370 109,038 97,222

Expenses (Page 24) Revenue producing operations

Cost of goods sold 12,008 14,871 13,265 Operating 37,044 38,995 36,953 Maintenance 16,133 16,343 15,759 Administrative and police 13,689 13,838 13,584 Marketing and promotion 3,595 3,414 3,283 Special projects - 520 -

82,469 87,981 82,844 Net surplus for the year before other items 12,901 21,057 14,378

Other items Interest expense – net (Note 14) 1,483 1,282 1,502 Amortization of tangible capital assets (Note 10) 9,033 8,754 8,359

Amortization of deferred capital funding (Note 5) (1,670) (1,706) (1,498) Gain on disposal of tangible capital assets - (48) (34)

8,846 8,282 8,329

Net surplus from operations 4,055 12,775 6,049

Net increase in power plant stabilization obligation (Note 8) (705) (338) (239)

Annual surplus $ 3,350 $ 12,437 $ 5,810

See accompanying notes to the financial statements.

PUBLIC ACCOUNTS, 2016-2017 1-5

The Niagara Parks Commission Statement of Accumulated Surplus For the year ended March 31, 2017

Budget Actual Actual2017 2017 2016

(in thousands of dollars)

Accumulated surplus (Note 11) Beginning of year $ 61,148 $ 61,148 $ 55,338

Annual surplus 3,350 12,437 5,810

End of year $ 64,498 $ 73,585 $ 61,148

See accompanying notes to the financial statements.

1-6 PUBLIC ACCOUNTS, 2016-2017

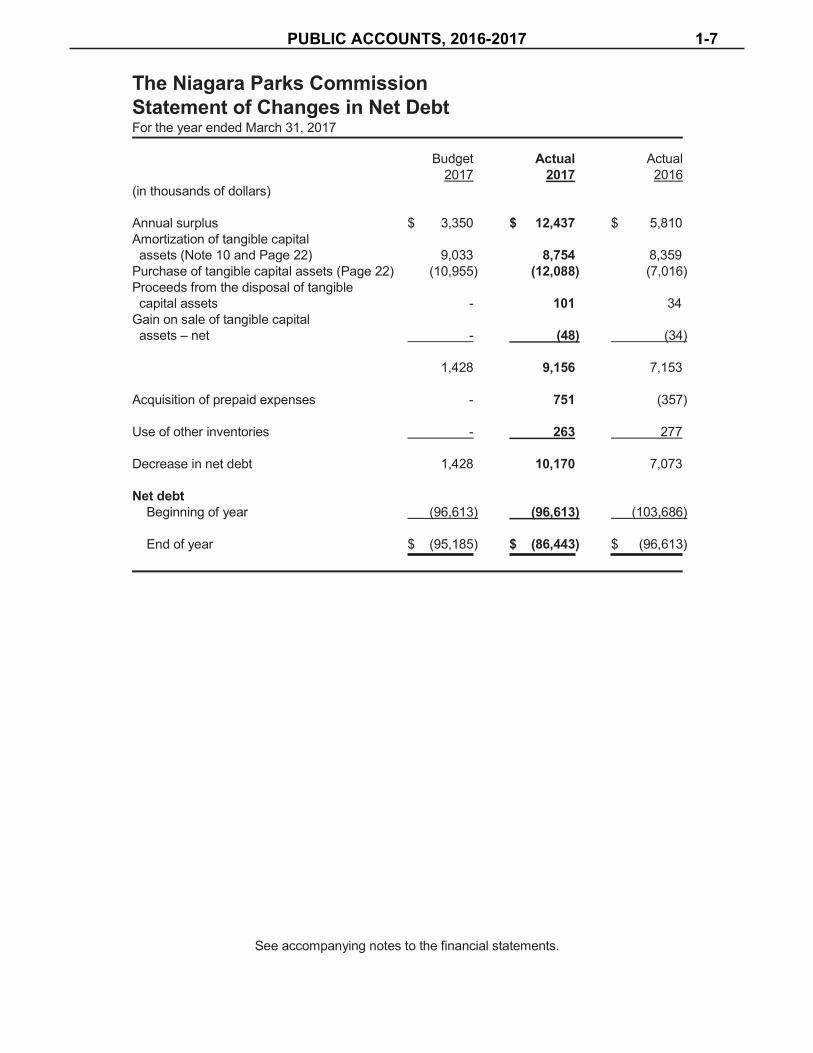

The Niagara Parks Commission Statement of Changes in Net Debt For the year ended March 31, 2017

Budget Actual Actual 2017 2017 2016

(in thousands of dollars)

Annual surplus $ 3,350 $ 12,437 $ 5,810 Amortization of tangible capital assets (Note 10 and Page 22) 9,033 8,754 8,359

Purchase of tangible capital assets (Page 22) (10,955) (12,088) (7,016)Proceeds from the disposal of tangible capital assets - 101 34Gain on sale of tangible capital assets – net - (48) (34)

1,428 9,156 7,153

Acquisition of prepaid expenses - 751 (357)

Use of other inventories - 263 277

Decrease in net debt 1,428 10,170 7,073

Net debt Beginning of year (96,613) (96,613) (103,686)

End of year $ (95,185) $ (86,443) $ (96,613)

See accompanying notes to the financial statements.

PUBLIC ACCOUNTS, 2016-2017 1-7

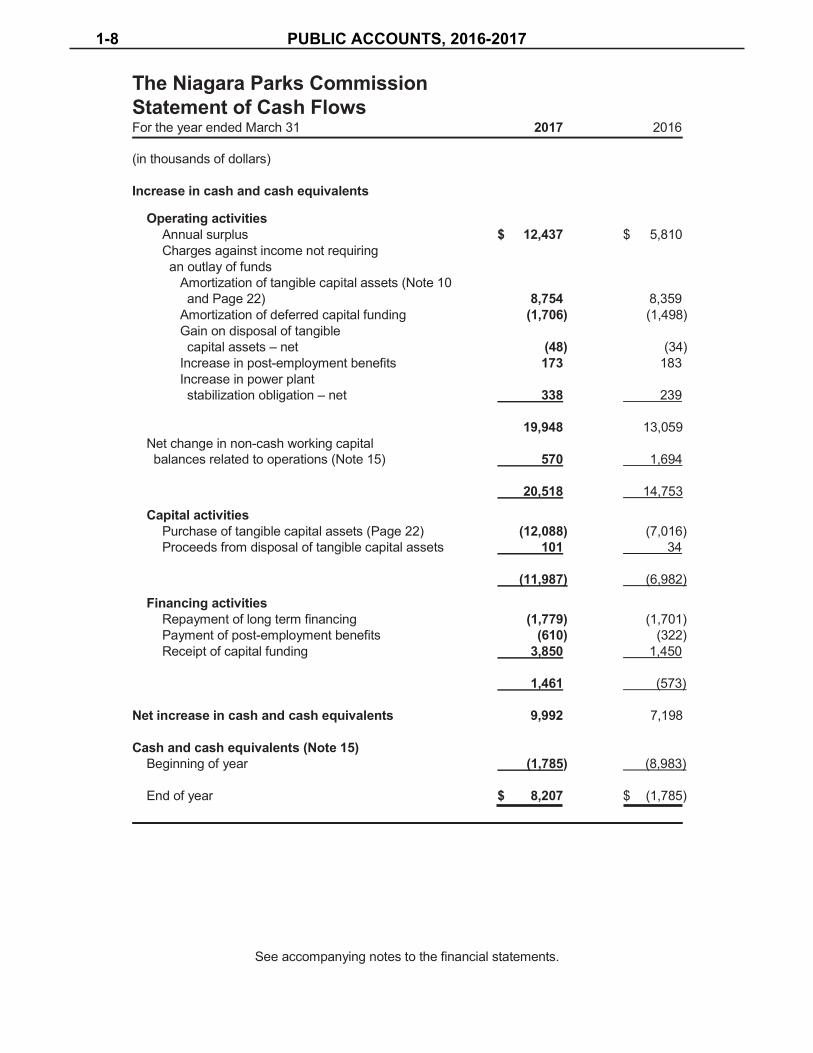

The Niagara Parks Commission Statement of Cash Flows For the year ended March 31 2017 2016

(in thousands of dollars)

Increase in cash and cash equivalents

Operating activities Annual surplus $ 12,437 $ 5,810Charges against income not requiring an outlay of funds

Amortization of tangible capital assets (Note 10 and Page 22) 8,754 8,359

Amortization of deferred capital funding (1,706) (1,498) Gain on disposal of tangible capital assets – net (48) (34)Increase in post-employment benefits 173 183 Increase in power plant stabilization obligation – net 338 239

19,948 13,059 Net change in non-cash working capital balances related to operations (Note 15) 570 1,694

20,518 14,753

Capital activities Purchase of tangible capital assets (Page 22) (12,088) (7,016) Proceeds from disposal of tangible capital assets 101 34

(11,987) (6,982)

Financing activities Repayment of long term financing (1,779) (1,701) Payment of post-employment benefits (610) (322) Receipt of capital funding 3,850 1,450

1,461 (573)

Net increase in cash and cash equivalents 9,992 7,198

Cash and cash equivalents (Note 15) Beginning of year (1,785) (8,983)

End of year $ 8,207 $ (1,785)

See accompanying notes to the financial statements.

1-8 PUBLIC ACCOUNTS, 2016-2017

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

1. Nature of operations

The Niagara Parks Commission (the “Commission”) is governed by the Niagara Parks Act. Initially established in 1885, the Commission is an “Operational Enterprise” of the Province of Ontario and is responsible for maintaining, protecting and showcasing over 1,300 hectares ofparkland stretching some 56 kilometres along the Niagara River from Lake Erie to Lake Ontario. The Commission is exempt from corporate income taxes under the Income Tax Act (Canada) and Ontario Corporation Tax Act.

The Commission is also classified as an Other Government Organization by the Ministry of Finance and as such, the Commission’s audited financial statements are published as part of the Public Accounts.

2. Significant accounting policies

Basis of accounting

The financial statements have been prepared in accordance with the financial reporting provisions of the Ontario Financial Administration Act, Ontario Ministry of Tourism Memorandum of Understanding and the accounting requirements of Regulation 395/11 of the Ontario Financial Administration Act. The Ontario Ministry of Tourism Memorandum of Understanding requires that the financial statements be prepared in accordance with the Canadian public sector accounting standards. The Ontario Financial Administration Act provides that changes may be required to the application of these standards as a result of regulation.

Regulation 395/11 to the Ontario Financial Administration Act requires that contributions received or receivable for the acquisition or development of depreciable tangible capital assets and contributions of depreciable tangible capital assets for use in providing services, be recorded as deferred capital contributions and be recognized as revenue in the Statement of Operations at a rate equal to amortization charged on the related depreciable tangible capital assets. These contributions include government transfers and externally restricted contributions.

The accounting requirement under Regulation 395/11 is not consistent with the requirements of Canadian public sector accounting standards which requires that:

government transfers be recognized as revenue when approved by the transferor and theeligibility criteria have been met unless the transfer contains a stipulation that creates aliability, in which case the transfer is recognized as revenue over the period that theliability is extinguished in accordance with public sector accounting standard PS3410;externally restricted contributions be recognized as revenue in the period in which theresources are used for the purpose or purposes specified in accordance with publicsector accounting standard PS3100.

As a result revenue recognized in the Statement of Operations and certain related deferred revenues and deferred capital contributions would be recorded differently under Canadian Public Sector Accounting Standards.

PUBLIC ACCOUNTS, 2016-2017 1-9

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

2. Significant accounting policies (continued)

Basis of accounting (continued)

The significant accounting principles used in the preparation of these financial statements are summarized below.

Cash and cash equivalents

Cash and cash equivalents include cash on hand, balances with banks and short term deposits with maturities of less than three months.

Inventories

Saleable and other inventories are valued at the lower of average cost and net realizable value.

Tangible capital assets

Tangible capital assets are recorded at cost. Cost includes all directly attributable expenses in the acquisition, construction, development and/or betterment of the asset required to install the asset at the location and in the condition necessary for its intended use. Contributed tangible capital assets are capitalized at estimated fair value upon acquisition.

The Commission capitalizes an amount of interest as part of the costs of its capital works in progress and financed via long term financing.

Works of art for display in the Commission property are not included as capital assets. Works of art are held for exhibition, educational and historical interest. Such assets are deemed worthy of preservation because of the social rather than financial benefits they provide to the community. No valuation of the collection has been disclosed in the financial statements.

Leases are classified as capital or operating leases. Leases that transfer substantially all benefits incidental to ownership are accounted for as capital leases. All other leases are accounted for as operating leases and the related lease payments are charged to expenses as incurred.

Amortization is calculated on a straight-line basis to write-off the net cost of each asset over its estimated useful life for all classes except land. Land is considered to have an infinite life without amortization. Residual values of assets are assumed to be zero with any net gain or loss arising from the disposal of assets recognized in the Statement of Operations. Amortization is charged on a monthly basis. Assets under construction are not amortized until the asset is available for productive use.

Amortization is based on the following classifications and useful lives:

Classification Useful Life Land improvements, buildings, roadways and structures 7 to 40 years

Equipment and furnishings 3 to 10 years Vehicles 10 to 12 years

1-10 PUBLIC ACCOUNTS, 2016-2017

The Niagara Parks CommissionNotes to the Financial Statements For the year ended March 31, 2017

2. Significant accounting policies (continued)

Deferred revenue

Revenue that is restricted by legislation of senior governments or by agreement with external parties are deferred and reported as restricted revenues. When qualifying expenses are incurred, restricted revenues are brought into revenue at equal amounts. Revenues received in advance of expenses that will be incurred in a later period are deferred until they are earned by being matched against those expenses.

Deferred capital funding

Government transfers for capital purposes and contributed tangible capital assets are recorded as a liability, referred to as deferred capital funding, and are recognized into revenue at the same rate as the related tangible capital assets are amortized, in accordance with Regulation 395/11 to the Ontario Financial Administration Act, as disclosed above.

Post-employment benefits

The present value of the cost of providing employees with future benefit programs is expensed as employees earn these entitlements.

Liabilities for contaminated sites

Contaminated sites are a result of contamination being introduced into air, soil, water or sediment of a chemical, organic or radioactive material or live organism that exceeds an environmental standard. The liability is recorded net of any expected recoveries. A liability for remediation of contaminated sites is recognized when a site is not in productive use and all the following criteria are met:

an environmental standard exists;contamination exceeds the environmental standard;the Commission:o is directly responsible; oro accepts responsibility;it is expected that future economic benefits will be given up; anda reasonable estimate of the amount can be made.

The liability is recognized as management’s estimate of the cost of post-remediation including operation, maintenance and monitoring that are an integral part of the remediation strategy for a contaminated site.

Revenue recognition

Revenue from gift shops, restaurants and attractions are recognized when merchandise has been transferred to the customer or services have been rendered. Revenue from land rent, commissions, rentals, fees and sundry are recognized over the life of the agreement or when earned.

PUBLIC ACCOUNTS, 2016-2017 1-11

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

2. Significant accounting policies (continued)

Foreign currency translation

These financial statements are presented in Canadian dollars. Assets and liabilities denominated in foreign currencies are translated at the exchange rates in effect at the Statement of Financial Position date. Gains and losses on translation are reflected in the annual surplus (deficit).

Use of estimates and measurement uncertainty

The preparation of financial statements in accordance with Canadian public sector accounting standards requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Two areas in which estimates are used are with regards to post-employment benefits and the power plant stabilization obligation.

3. Credit facilities

The credit facilities, which have a maximum borrowing capacity of $ 15,000,000, provide for two types of loans. There is a variable rate loan facility which varies with the Canadian Imperial Bank of Commerce prime rate and there is a fixed rate operating loan facility available with a maximum term not to exceed 364 days at rates which are set relative to banker’s acceptance rates. These credit facilities are unsecured and expire on March 31, 2021, with an option of a three year renewal at the Commission’s discretion. As at March 31, 2017, $ Nil has been drawn upon for all credit facilities (2016 - $ 1,371,416). Taking into account outstanding cheques and deposits, the balance reported on the Statement of Financial Position is $ Nil(2016 - $ 2,179,628).

1-12 PUBLIC ACCOUNTS, 2016-2017

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

4. Deferred revenue 2017 2016(in thousands of dollars)

Defunct power stations (Note 8) $ 8 $ 135 Sale proceeds related to Fort Erie land transaction 314 321 Other 1,961 860

$ 2,283 $ 1,316

Fort Erie land transaction obligation

In fiscal 2009, the Commission and the Peace Bridge Authority (“PBA”) entered into an agreement to transfer parcels of land. The PBA acquired a 5.952 acre parcel located in Fort Erie from the Commission for $ 2,021,206. The Commission acquired an option for $ 670,000 plus an annual sum of $ 7,300 adjusted for inflation, to receive 1.973 acres of river front property located at the end of Jarvis Street in Fort Erie from the PBA. The agreement calls for the net proceeds to the Commission in the amount of $ 1,351,206 to be spent on a) funding improvements at Old Fort Erie which are intended for the 200th year anniversary of the War of1812 and b) returning and/or maintaining the Jarvis Street property as parkland.

The net proceeds were recorded as part of deferred revenue on the Statement of Financial Position. To date approximately $ 996,000 from these proceeds have been spent on the capital works project for the renovation of Old Fort Erie and approximately $ 47,000 has been spent on the Jarvis Street property maintenance. As of March 31, 2017, approximately $ 314,285 remains for use in 2018 and beyond.

5. Deferred capital funding 2017 2016 (in thousands of dollars)

Deferred capital funding Beginning of year $ 26,390 $ 26,438

Received during year for capital projects 3,850 1,450

Amortization (1,706) (1,498)

End of year $ 28,534 $ 26,390

PUBLIC ACCOUNTS, 2016-2017 1-13

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

6. Long term financing 2017 2016 (in thousands of dollars)

Unsecured fixed rate term loan requiring blended payments of principal and interest of $ 2,640,907 per annum, bearing interest at 5.06% through to April, 2027 $ 21,951 $ 23,400

Unsecured fixed rate term loan requiring blended first annual payment of $ 543,418 and then payments of $ 569,965 per annum thereafter, bearing interest at 5.07% through to April, 2027 4,553 4,876

The Commission has an option to purchase land requiring annual payments of $ 7,300 until January, 2028 (Note 4) 88 95

$ 26,592 $ 28,371

The principal payments of the long term financial obligations due in the next five years are as follows:

2018 $ 1,877 2019 1,972 2020 2,071 2021 2,173 2022 2,285

1-14 PUBLIC ACCOUNTS, 2016-2017

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

7. Post-employment benefits

Defined termination benefits

The Commission provides a defined employee future benefit, payable on termination to certain full time employees with a minimum of five years of service. The benefit is calculated on the basis of one week’s remuneration, at the time of termination, for every year of full time service provided to the Commission to a maximum of twenty-six weeks. The accrued benefit liability as at March 31, 2017 is $ 3,121,208 (2016 - $ 3,557,888).

The Commission requires that an actuarial valuation of the post-employment benefits be conducted every three years. The last valuation was completed for the year ended March 31, 2016 with extrapolations through to 2019 and updated on March 29, 2017. The latest valuation reflects approved changes by the Commission regarding eligibility and maximum amounts of the benefit payable upon termination.

The actual obligation as at March 31, 2017 is $ 2,331,209 (2016 - $ 2,674,097) which is the actuarial valuation for March 31, 2017 adjusted for the actual benefits paid of $ 609,558, incorporated in an actuarial update provided dated March 29, 2017.

Defined benefit plan information 2017 2016

(in thousands of dollars)

Employee benefit plan assets $ Nil $ Nil Employee benefit plan liabilities 3,121 3,558

Employee benefit plan deficit $ 3,121 $ 3,558

Benefit obligation recognized on the Statement of Financial Position

Benefit obligation, beginning of year $ 3,558 $ 3,697 Expense for the year 173 183 Benefits paid during the year (610) (322)

Benefit obligation, end of year $ 3,121 $ 3,558

PUBLIC ACCOUNTS, 2016-2017 1-15

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

7. Post-employment benefits (continued)2017 2016

(in thousands of dollars)

The net benefit expense is as follows: Current service cost $ 163 $ 170Interest cost 104 117Amortization of actuarial gain/loss (94) (104)

$ 173 $ 183

The main actuarial assumptions applied in the valuation of the defined benefit plan are as follows:

Interest (discount) rate – the accrued obligation and the expense for the year were determined using a discount rate of 4.25% (2016 - 4.25%).

Salary levels – future salary and wage levels were assumed to increase at 2% per annum.

These assumptions were reviewed in the current year.

Pension benefits

The Commission provides pension benefits for all its permanent employees (and to non-permanent employees who elect to participate) through the Public Service Pension Fund (“PSPF”) and the Ontario Public Service Employees’ Union Pension Fund (“OPSEU Pension Fund”). These are defined benefit pension plans for employees of the Province and many provincial agencies. The Province of Ontario, which is the sole sponsor of the PSPF and a joint sponsor of the OPSEU Pension Fund, determines the Commission’s annual payments to the funds. As the sponsors are responsible for ensuring that the pension funds are financially viable, any surpluses or unfunded liabilities arising from statutory actuarial funding valuations are not assets or obligations of the Commission. The Commission’s annual payments of $ 2,316,697 (2016 - $ 2,318,548), of which $ 1,158,349 (2016 - $ 1,159,274) represents the employees’ portion, are included in the administrative and police expense on the Statement of Operations.

The cost of post-employment, non-pension benefits are paid by the Province and therefore are not included in the Statement of Operations.

1-16 PUBLIC ACCOUNTS, 2016-2017

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

8. Power plant stabilization obligation

The Province of Ontario directed the Commission to accept ownership of three former electricity generating power stations all located within Commission lands.

The Toronto Power Generating Station (“TPGS”) and the Ontario Power Generating Station (“OPGS”) were transferred by Ontario Power Generation Inc. (“OPG”) to the Commission at no cost in August, 2007. As part of the terms of transfer of TPGS and OPGS, OPG was to undertake certain structural and environmental work to ensure that the buildings were no threat to the public. The Canadian Niagara Power Generating Station (“CNPGS”) previously owned by Fortis Ontario was transferred April 30, 2009.

The Ministry of Tourism engaged the services of an architectural firm (The Ventin Group Inc.) to ensure that the original Government Directive governing the initial transfer was complied with and to identify work and related costs required to “stabilize and mothball” all the facilities until an ultimate use for the buildings can be determined. The Ventin Group identified the remaining lead paint at the TPGS and OPGS as a deficiency which OPG should have resealed or encapsulated after cleaning. The Ventin Group reported that there are substantial costs required to bring the three power stations to what would be considered a “mothball” state. Therefore, additional costs would be required to bring these buildings to a “development ready” state. Further, there are in existence certain secondary structures related to TPGS and OPGS that were not accounted for in the original Government Directive that will result in additional remediation costs at some point in the future.

The Commission is of the belief that the acceptance of these power generating stations will require a significant infusion of funds that is beyond its capacity to meet. As at March 31, 2017,ongoing discussions with the Province have not resulted in any assurance that the Commission will not be responsible for any future costs. Any costs that are expected to be incurred for the purposes described above will not commence without funding received from the Province.

VFA, Inc. has reviewed the infrastructure through site visits and prepared estimates using standard engineering formulas. Further, they have provided the Commission with their assessment and a requirements list report providing costs for each component of stabilization required, as well as the timing of when these costs should be incurred. Commission engineering staff have reviewed the list and categorized the costs by year according to urgency and based on expected available funding, with the most urgent requirements addressed over the next two years. In addition, the Commission undertook several studies to determine critical underground infrastructure that needs replacing, including seismic studies, review of intake gates, geophysical and geotechnical settlement and a stability investigation.

The stabilization obligation as of March 31, 2017 has been calculated to be $ 29,414,141 (2016 - $ 29,076,363). This is an increase of $ 337,778 from 2016 and has been recorded in theStatement of Operations.

This obligation represents the Commission’s best estimate of the costs required to “stabilize and mothball” the three power stations based on the information noted above. The Commission estimates that this work could take approximately four years to complete and estimates the costs to increase by 1.5% per year, being the five year average industrial construction inflation rate according to Statistics Canada.

PUBLIC ACCOUNTS, 2016-2017 1-17

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

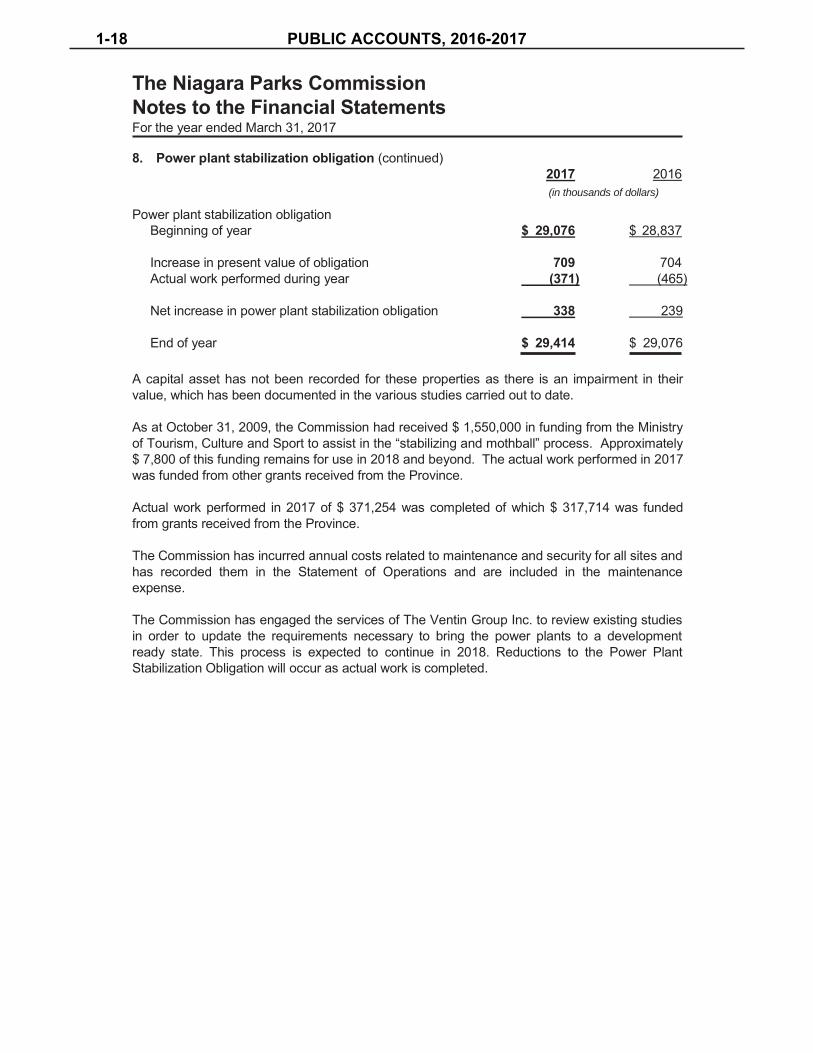

8. Power plant stabilization obligation (continued)2017 2016 (in thousands of dollars)

Power plant stabilization obligation Beginning of year $ 29,076 $ 28,837

Increase in present value of obligation 709 704 Actual work performed during year (371) (465)

Net increase in power plant stabilization obligation 338 239

End of year $ 29,414 $ 29,076

A capital asset has not been recorded for these properties as there is an impairment in their value, which has been documented in the various studies carried out to date.

As at October 31, 2009, the Commission had received $ 1,550,000 in funding from the Ministry of Tourism, Culture and Sport to assist in the “stabilizing and mothball” process. Approximately $ 7,800 of this funding remains for use in 2018 and beyond. The actual work performed in 2017 was funded from other grants received from the Province.

Actual work performed in 2017 of $ 371,254 was completed of which $ 317,714 was funded from grants received from the Province.

The Commission has incurred annual costs related to maintenance and security for all sites and has recorded them in the Statement of Operations and are included in the maintenance expense.

The Commission has engaged the services of The Ventin Group Inc. to review existing studies in order to update the requirements necessary to bring the power plants to a development ready state. This process is expected to continue in 2018. Reductions to the Power Plant Stabilization Obligation will occur as actual work is completed.

1-18 PUBLIC ACCOUNTS, 2016-2017

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

9. Liabilities for contaminated sites

The Commission reports environmental liabilities related to the management and remediationof any contaminated sites where the Commission is obligated or likely obligated to incur such costs. Currently no such contaminated sites have been identified and therefore no liability has been recorded.

The Commission’s ongoing efforts to assess contaminated sites may result in future environmental remediation liabilities related to newly identified sites, or changes in the assessments or intended use of existing sites. Any changes to the Commission’s liabilities for contaminated sites will be accrued in the year in which they are assessed as likely and reasonably estimable.

10. Tangible capital assets 2017 2016(in thousands of dollars)

Accumulated Net Net Cost Depreciation Book Value Book Value

Land $ 14,359 $ - $ 14,359 $ 14,359 Land improvements 17,135 - 17,135 17,135 Buildings, roadways and structures 241,819 121,934 119,885 118,341

Equipment and furnishings 44,148 39,406 4,742 4,297 Vehicles 4,887 3,160 1,727 975

322,348 164,500 157,848 155,107 Capital works in progress 765 - 765 225

$ 323,113 $ 164,500 $ 158,613 $ 155,332

Equipment under capital lease included above $ 69 $ 63 $ 6 $ 13

Amortization of tangible capital assets Budget Actual Actual

2017 2017 2016(in thousands of dollars)

Amortization of income producing assets $ 4,443 $ 4,230 $ 4,428 Amortization of non-income producing assets 4,590 4,524 3,931

$ 9,033 $ 8,754 $ 8,359

PUBLIC ACCOUNTS, 2016-2017 1-19

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

11. Accumulated surplus 2017 2016 (in thousands of dollars)

Operating surplus (deficit) $ 2,633 $ (6,789)

Investment in tangible capital assets 130,079 128,942

Unfunded Long term debt (26,592) (28,371) Post-employment benefits (3,121) (3,558)Power plant stabilization obligation (29,414) (29,076)

(59,127) (61,005)

Accumulated surplus $ 73,585 $ 61,148

Surplus funds

Pursuant to Section 16(2) of the Niagara Parks Act, any surplus moneys shall, on the order of the Lieutenant Governor in Council, be paid to the Minister of Finance and shall form part of the consolidated revenue fund. As of March 31, 2017 no surplus moneys have been recorded as a liability to the Minister of Finance.

12. Commitments

The Commission has committed to approximately $ 13,288,000 in capital works projects in the next year.

The Commission has two agreements with a franchisor requiring the payment of service fees of 4.5% of gross sales and advertising and marketing fees of 2.5% of gross sales. The terms of the agreements are ten years, expiring in April, 2017 and October, 2022.

The Commission leases vehicles, equipment and premises under operating leases expiring in 2018. The total obligation under operating leases amounts to approximately $ 8,603 in 2018.

13. Contingencies

The Commission is in litigation pertaining to certain claims for which the likelihood of loss is not determinable and the amount not reasonably estimable. Accordingly, no provision for these claims is reflected in the financial statements.

1-20 PUBLIC ACCOUNTS, 2016-2017

The Niagara Parks Commission Notes to the Financial Statements For the year ended March 31, 2017

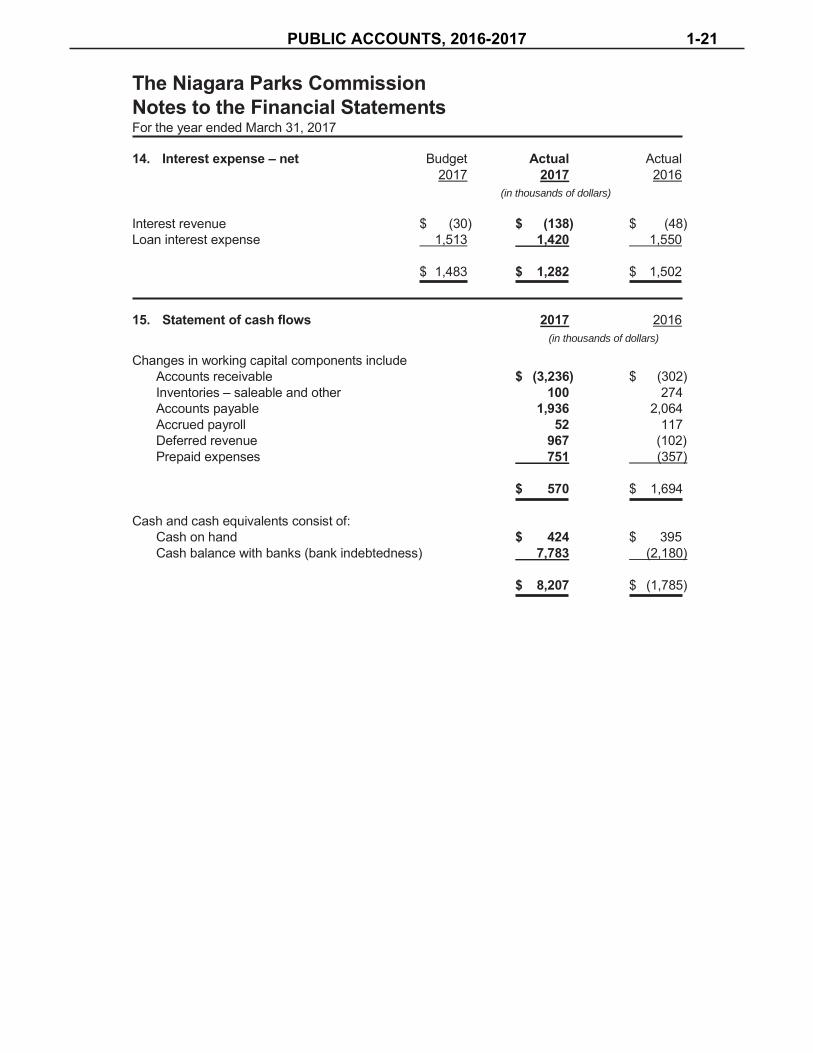

14. Interest expense – net Budget Actual Actual2017 2017 2016

(in thousands of dollars)

Interest revenue $ (30) $ (138) $ (48) Loan interest expense 1,513 1,420 1,550

$ 1,483 $ 1,282 $ 1,502

15. Statement of cash flows 2017 2016 (in thousands of dollars)

Changes in working capital components include Accounts receivable $ (3,236) $ (302) Inventories – saleable and other 100 274 Accounts payable 1,936 2,064 Accrued payroll 52 117 Deferred revenue 967 (102) Prepaid expenses 751 (357)

$ 570 $ 1,694

Cash and cash equivalents consist of: Cash on hand $ 424 $ 395Cash balance with banks (bank indebtedness) 7,783 (2,180)

$ 8,207 $ (1,785)

PUBLIC ACCOUNTS, 2016-2017 1-21

The

Niag

ara

Park

s Co

mm

issi

on

Sche

dule

of T

angi

ble

Capi

tal A

sset

s Fo

r the

yea

r end

ed M

arch

31,

201

7

Build

ings

, Eq

uipm

ent

Cap

ital

Land

R

oadw

ays

and

and

Wor

ks in

La

nd

Impr

ovem

ents

St

ruct

ures

Fu

rnis

hing

s Ve

hicl

es

Prog

ress

20

1720

16

(in th

ousa

nds

of d

olla

rs)

Cost

Be

ginn

ing

of y

ear

$ 14

,359

$

17,1

35

$ 23

3,11

7 $

42,4

96

$ 4,

086

$ 22

5$

311,

418

$ 30

4,58

2

Add

addi

tions

-

- 8,

477

1,90

993

776

512

,088

7,01

6Le

ss d

ispo

sals

- -

- (2

57)

(136

)-

(393

)(1

80)

Tran

sfer

s of

cap

ital w

orks

in

pro

gres

s -

- 22

5-

- (2

25)

--

End

of y

ear

14,3

59

17,1

35

241,

819

44,1

48

4,88

7 76

532

3,11

3 31

1,41

8

Accu

mul

ated

am

ortiz

atio

n Be

ginn

ing

of y

ear

- -

114,

776

38,1

99

3,11

1-

156,

086

147,

907

Add

amor

tizat

ion

- -

7,15

8 1,

415

181

-8,

754

8,35

9 Le

ss d

ispo

sals

- -

- (2

08)

(132

)-

(340

)(1

80)

End

of y

ear

- -

121,

934

39,4

06

3,16

0-

164,

500

156,

086

Net b

ook

valu

e$

14,3

59

$ 17

,135

$

119,

885

$ 4,

742

$ 1,

727

$ 76

5$

158,

613

$ 15

5,33

2

1-22 PUBLIC ACCOUNTS, 2016-2017

The Niagara Parks Commission Schedule of Expenses by Object For the year ended March 31, 2017

Budget Actual Actual 2017 2017 2016

(in thousands of dollars)

Cost of goods sold $ 12,008 $ 14,871 $ 13,265 Salaries, wages and benefits 47,159 48,399 46,343 Sales and other 3,448 3,950 3,466 Equipment repairs and maintenance 4,405 4,652 4,451 Materials and supplies 2,651 2,700 2,568 Advertising and promotion 2,793 3,050 2,684 Facilities 7,025 6,772 6,793 Administrative 2,980 3,067 3,274 Special projects - 520 -

$ 82,469 $ 87,981 $ 82,844

PUBLIC ACCOUNTS, 2016-2017 1-23

Suite 200, Roberta Bondar Place, 70 Foster Drive, Sault Ste. Marie, Ontario P6A 6V8Tel: (705) 945-6700 or 1-800-461-8329, Fax: (705) 945-6701 www.nohfc.com

Place Roberta Bondar, 70, promenade Foster, bureau 200, Sault Ste. Marie (Ontario) P6A 6V8 Tél. 705 945-6700 ou 1 800 461-8329, Téléc. 705 945-6701 www.nohfc.com

Northern Ontario Heritage Fund Corporation Year ended March 31, 2017

Responsibility for Financial Reporting

The accompanying financial statements of the Northern Ontario Heritage Fund Corporation (NOHFC) have been prepared in accordance with Canadian public sector accounting standards, and are the responsibility of management. The preparation of financial statements necessarily involves the use of estimates based on management’s judgment, particularly when transactions affecting the current accounting period cannot be finalized with certainty until future periods. The financial statements have been properly prepared within reasonable limits of materiality and in light of information available up to June 8, 2017.

Management is responsible for the integrity of the financial statements and maintains a system of internal controls designed to provide reasonable assurance that the assets are safeguarded and that reliable financial information is available on a timely basis. The system includes formal policies andprocedures and an organizational structure that provides for appropriate delegation of authority and segregation of responsibilities.

The Board, through the Audit Committee, is responsible for ensuring that management fulfills its responsibilities for financial reporting and internal controls. The Audit Committee, comprised of members who are not employees/officers of NOHFC generally meets periodically with management and the Office of the Auditor General to satisfy itself that each group has properly discharged its respective responsibility.

The financial statements have been audited by the Office of the Auditor General of Ontario. The Auditor’s responsibility is to express an opinion on whether the financial statements are fairly presented in accordance with Canadian public sector accounting standards. The Auditor’s Report outlines the scope of the Auditor’s examination and opinion.

_______________ ___________________ D. Bruce Strapp Melanie MuncasterExecutive Director Assistant Director NOHFC NOHFC

PUBLIC ACCOUNTS, 2016-2017 1-25

__________________ __________________ Susan Richichi, CPA, CA Jocelyn Ouellet, CPA, CMA Manager Financial Services Senior Corporate ControllerNOHFC NOHFC

__________________ Glen Vine Manager Program ServicesNOHFC

1-26 PUBLIC ACCOUNTS, 2016-2017

PUBLIC ACCOUNTS, 2016-2017 1-27

NORTHERN ONTARIO HERITAGE FUND CORPORATIONStatement of Financial Position

March 31, 2017, with comparative information for 2016

($000s) 2017 2016

Financial Assets Current assets:

Cash and cash equivalents (note 3) $ 301,466 $ 283,223 Accrued interest 488 448Loans receivable (note 4) 41,591 43,278

343,545 326,949

Financial Liabilities

Accounts payable and accrued liabilities (note 5) 10,462 13,559

Net financial assets 333,083 313,390

Non-Financial Assets

Tangible capital assets (note 6) 5 9

Commitments (note 9)

Net investment by the Province of Ontario $ 333,088 $ 313,399

See accompanying notes to financial statements.

On behalf of the Board:

______________________ Co-Chair

______________________ Co-Chair

______________________ Executive Director

1-28 PUBLIC ACCOUNTS, 2016-2017

NORTHERN ONTARIO HERITAGE FUND CORPORATION Statement of Operations

Year ended March 31, 2017, with comparative information for 2016

Budget ($000s) 2017 2017 2016

Revenue: Province of Ontario grant $ 100,000 $ 100,000 $ 100,000 Interest on cash and cash equivalents 2,355 1,933 2,163 Interest on loans receivable 2,068 2,158 2,233 Recoveries – 1,167 1,152

104,423 105,258 105,548

Expenses: Conditional contributions 81,081 74,834 74,705 Credit losses (note 7) 8,823 2,981 5,976 Administration (note 8) 9,699 7,754 7,051

99,603 85,569 87,732

Excess of revenue over expenses $ 4,820 19,689 17,816

Net investment by the Province of Ontario, beginning of year 313,399 295,583

Net investment by the Province of Ontario, end of year $ 333,088 $ 313,399

See accompanying notes to financial statements.

PUBLIC ACCOUNTS, 2016-2017 1-29

NORTHERN ONTARIO HERITAGE FUND CORPORATIONStatement of Changes in Net Financial Assets

Year ended March 31, 2017, with comparative information for 2016

($000s) 2017 2016

Excess of revenue over expenses $ 19,689 $ 17,816

Amortization of capital assets 4 3

Increase in net financial assets 19,693 17,819

Net financial assets beginning of year 313,390 295,571

Net financial assets, end of year $ 333,083 $ 313,390

See accompanying notes to financial statements.

1-30 PUBLIC ACCOUNTS, 2016-2017

NORTHERN ONTARIO HERITAGE FUND CORPORATIONStatement of Cash Flows

Year ended March 31, 2017 with comparative information for 2016

($000s) 2017 2016

Lending, investing and financial assistance activities: Loan disbursements $ (14,925) $ (15,923) Loan repayments and recoveries 14,802 13,028 Conditional contributions (77,197) (76,612) Interest received on loans receivable 2,175 2,285Other revenue 7 393

(75,138) (76,829)

Financing activities: Cash contributions from the Province for

lending and financial assistance activities 100,000 100,000

Operating activities: Amortization (4) (3) Interest received on cash and cash equivalents 1,867 2,882 Administration costs (8,482) (6,759)

(6,619) (3,880)

Net increase in cash and cash equivalents 18,243 19,291

Cash and cash equivalents, beginning of year 283,223 263,932

Cash and cash equivalents, end of year $ 301,466 $ 283,223

See accompanying notes to financial statements.

PUBLIC ACCOUNTS, 2016-2017 1-31

NORTHERN ONTARIO HERITAGE FUND CORPORATIONNotes to Financial Statements

Year ended March 31, 2017

1. Nature of the business:The Northern Ontario Heritage Fund Corporation (the “Corporation”) wasestablished, without share capital, on June 1, 1988 under the Northern OntarioHeritage Fund Act. The purpose of the Corporation is to fund infrastructureimprovements and economic development opportunities in Northern Ontario byproviding financial assistance by way of conditional contributions, forgivableperformance loans, and term loans. As an Ontario Crown agency, theCorporation is exempt from federal and provincial income taxes under theIncome Tax Act (Canada).The Corporation partners with communities, businesses and entrepreneursacross Northern Ontario to create jobs and strengthen the Northern economy.The Corporation delivers five targeted programs as follows: Strategic EconomicInfrastructure Program, Northern Community Capacity Building Program,Northern Innovation Program, Northern Business Opportunity Program, andNorthern Ontario Internship Program.

2. Significant accounting policies:

The significant accounting policies used to prepare these financial statementsare summarized below.(a) Basis of accounting:

The financial statements have been prepared by management in accordancewith Canadian public sector accounting standards for provincial reportingentities established by the Canadian Public Sector Accounting Board (PSAB)of the Chartered Professional Accountants of Canada.

(b) Transactions with the Province of Ontario:The Province of Ontario contributes funds to finance the lending and financialassistance activities. The net investment by the Province of Ontario isincreased (reduced) by the excess (deficiency) of revenue over expenses.

(c) Cash and cash equivalents:Cash and cash equivalents consist primarily of funds on deposit in charteredbanks and short-term investments on deposit with the Ontario FinancingAuthority, a related party.

1-32 PUBLIC ACCOUNTS, 2016-2017

NORTHERN ONTARIO HERITAGE FUND CORPORATIONNotes to Financial Statements

Year ended March 31, 2017

2. Significant accounting policies (continued):(d) Financial instruments:

Financial instruments obtained in arm’s-length transactions are initiallymeasured at their fair value. Interest free loans are discounted to fair valuewhen initially recorded. Financial instruments are subsequently measured inone of the following categories (i) fair value or (ii) cost or amortized cost. TheCorporation uses fair value for the subsequent measurement of cash andcash equivalents. The Corporation uses amortized cost for the subsequentmeasurement of loans receivable and accounts payable and accruedliabilities.

(e) Tangible capital assets:Tangible capital assets are recorded at cost, which includes all amounts thatare directly attributable to the acquisition or betterment of the asset.The cost, less residual value of the tangible capital asset, is amortized on astraight line basis over its estimated useful life as follows:

Years

Automotive 7

(f) Provision for credit losses:

Credit losses arise on loans receivable issued by the Corporation. In additionto specific write-offs and write-downs, a provision for credit losses ismaintained in an amount considered adequate to absorb anticipated credit-related losses. The provision for losses on loans consists of provisions onspecific loans and a general provision on the remaining loans and is deductedfrom loans receivable.

The amounts written off and written down in the year and changes inprovisions, are charged to credit losses in the Statement of Operations.Recoveries reflect Funds received during the year from loans provided for in aprior year and are recorded as recoveries on the Statement of Operations.

(g) Revenue recognition:Government grants are recognized when receivable, amounts aredeterminable and collectability is assured. Interest income is recognized onthe accrual basis. Interest revenue on loans receivable is recognized in thefinancial statements in an amount estimated to be recoverable. Interestrevenue ceases to be recognized on fully impaired loans.

PUBLIC ACCOUNTS, 2016-2017 1-33

NORTHERN ONTARIO HERITAGE FUND CORPORATIONNotes to Financial Statements

Year ended March 31, 2017

2. Significant accounting policies (continued):(h) Conditional contributions and forgivable loans:

The Corporation expenses conditional contributions and forgivableperformance loans when disbursed. Approved commitments are notrecognized in the financial statements until the conditions of the funding havebeen met by the recipients.

(i) Use of estimates:Preparation of the financial statements in conformity with Canadian publicsector accounting standards requires management to make estimates andassumptions that affect the reported amounts of assets and liabilities and thereported amounts of revenue and expenses during the reporting period.Actual results could differ from those estimated. Significant estimates includethe provision for credit losses and the loan discount.

3. Cash and cash equivalents:

The Northern Ontario Heritage Fund Act restricts investments to securities issuedor guaranteed by the provinces, Canada, United States, United Kingdom, theInternational Bank for Reconstruction and Development and any CanadianSchedule I or II bank, and other investments as authorized by the LieutenantGovernor in Council. The Corporation, through an Investment ManagementAgreement with the Ontario Financing Authority, invests excess funds insecurities as allowed by the Act.

Cash and cash equivalents consist of:

($000s) 2017 2016

Cash $ 100,243 $ 83,255 Short-term investments 201,223 199,969

$ 301,466 $ 283,224

Short-term investments consist of Treasury Bills (maturing within 365 days) which yielded 0.67% on average (2016 – 0.63%). All Treasury Bills are redeemable on demand.

1-34 PUBLIC ACCOUNTS, 2016-2017

NORTHERN ONTARIO HERITAGE FUND CORPORATIONNotes to Financial Statements

Year ended March 31, 2017

4. Loans receivable:

($000s) 2017 2016

Current $ 7,118 $ 7,185 Long-term 58,896 63,405 Loans in arrears and default 10,080 7,829 Provision for credit losses (34,217) (34,846) Loan discount (286) (295)

$ 41,591 $ 43,278

Generally, loans bear fixed interest rates ranging from 0% to 8.25% and are fully repayable within 20 years from the date disbursed.

The changes in the provision for credit losses are as follows:

($000s) 2017 2016

Balance, beginning of year $ 34,846 $ 56,650 Loans written off in the year (2,478) (27,099) Change in loan provision 1,849 5,295

Balance, end of year $ 34,217 $ 34,846

The change in the loan discount balances are as follows:

($000s) 2017 2016

Balance, beginning of year $ 295 $ 346Amount of loan discount written down – (2) Amount amortized to interest on loans receivable (9) (49)

Balance, end of year $ 286 $ 295

PUBLIC ACCOUNTS, 2016-2017 1-35

NORTHERN ONTARIO HERITAGE FUND CORPORATIONNotes to Financial Statements

Year ended March 31, 2017

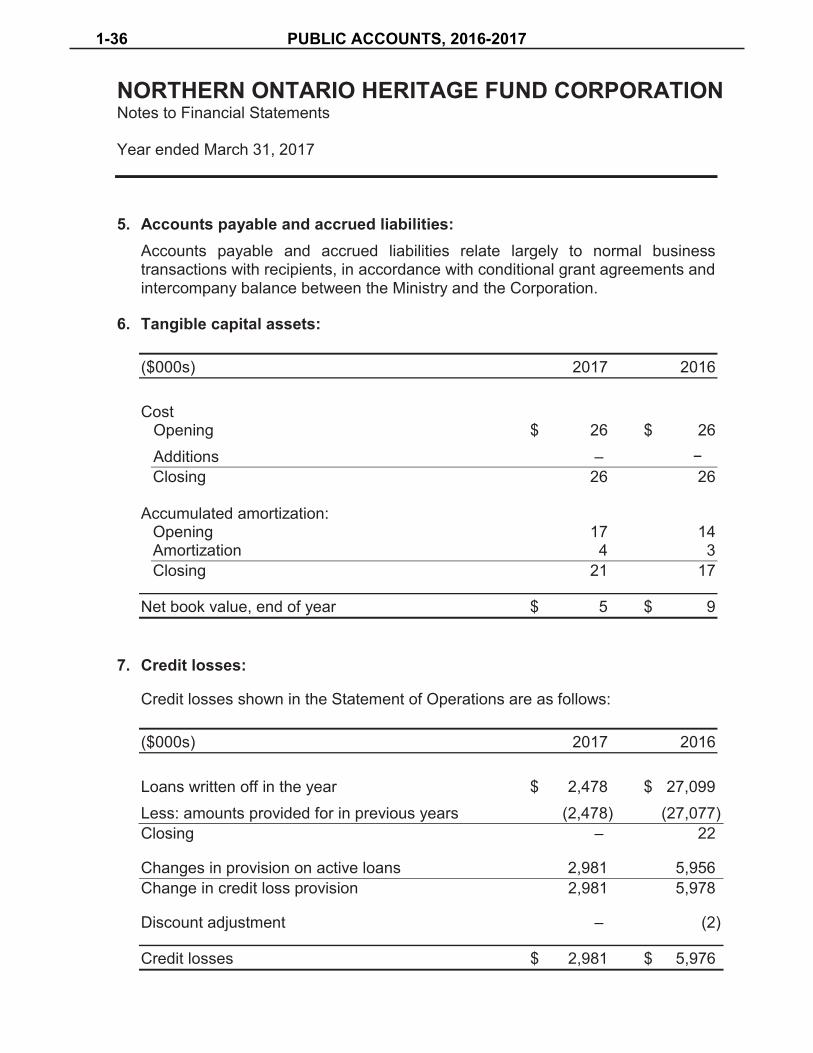

5. Accounts payable and accrued liabilities:Accounts payable and accrued liabilities relate largely to normal businesstransactions with recipients, in accordance with conditional grant agreements andintercompany balance between the Ministry and the Corporation.

6. Tangible capital assets:

($000s) 2017 2016

Cost Opening $ 26 $ 26 Additions – −Closing 26 26

Accumulated amortization: Opening 17 14Amortization 4 3 Closing 21 17

Net book value, end of year $ 5 $ 9

7. Credit losses:

Credit losses shown in the Statement of Operations are as follows:

($000s) 2017 2016

Loans written off in the year $ 2,478 $ 27,099 Less: amounts provided for in previous years (2,478) (27,077) Closing – 22

Changes in provision on active loans 2,981 5,956 Change in credit loss provision 2,981 5,978

Discount adjustment – (2)

Credit losses $ 2,981 $ 5,976

1-36 PUBLIC ACCOUNTS, 2016-2017

NORTHERN ONTARIO HERITAGE FUND CORPORATIONNotes to Financial Statements

Year ended March 31, 2017

8. Administration expenses:

Details of administration expenses in the year are as follows:

Budget ($000s) 2017 2017 2016

Salaries, wages and benefits $ 2,096 $ 1,952 $ 1,674Transportation and communications 339 386 254Services 3,153 2,214 1,688 Management fees 4,040 3,047 3,019 Marketing – 122 6 Supplies and equipment 67 29 42Financial information system – – 365Amortization on tangible capital assets 4 4 3

$ 9,699 $ 7,754 $ 7,051

The Province provides pension benefits for all of the Corporation’s permanent staff through participation in the Public Service Pension Fund and the Ontario Public Service Employees’ Union Pension Fund which are both multi-employer defined benefit pension plans established by the Province of Ontario. The costs of the pension plans, and other post-retirement non-pension benefits provided to eligible staff are paid by the Province and are not included in these financial statements.

9. Commitments:Funds committed but not disbursed as at March 31, 2017 are $252,664,593(2016 – $217,197,435).

10. Financial instruments:The main risks that the Corporation’s financial instruments are exposed to arecredit risk, liquidity risk, and market risk.

(a) Credit risk:Credit risk is the risk that the counterparty to a financial instrument may fail todischarge an obligation or commitment that it has entered into. TheCorporation provides credit to its loan portfolio clients in the normal course ofoperations. To mitigate the risk, the Corporation screens loan applicants,

PUBLIC ACCOUNTS, 2016-2017 1-37

NORTHERN ONTARIO HERITAGE FUND CORPORATIONNotes to Financial Statements

Year ended March 31, 2017

registers security on the loans and maintains provisions for contingent credit losses.

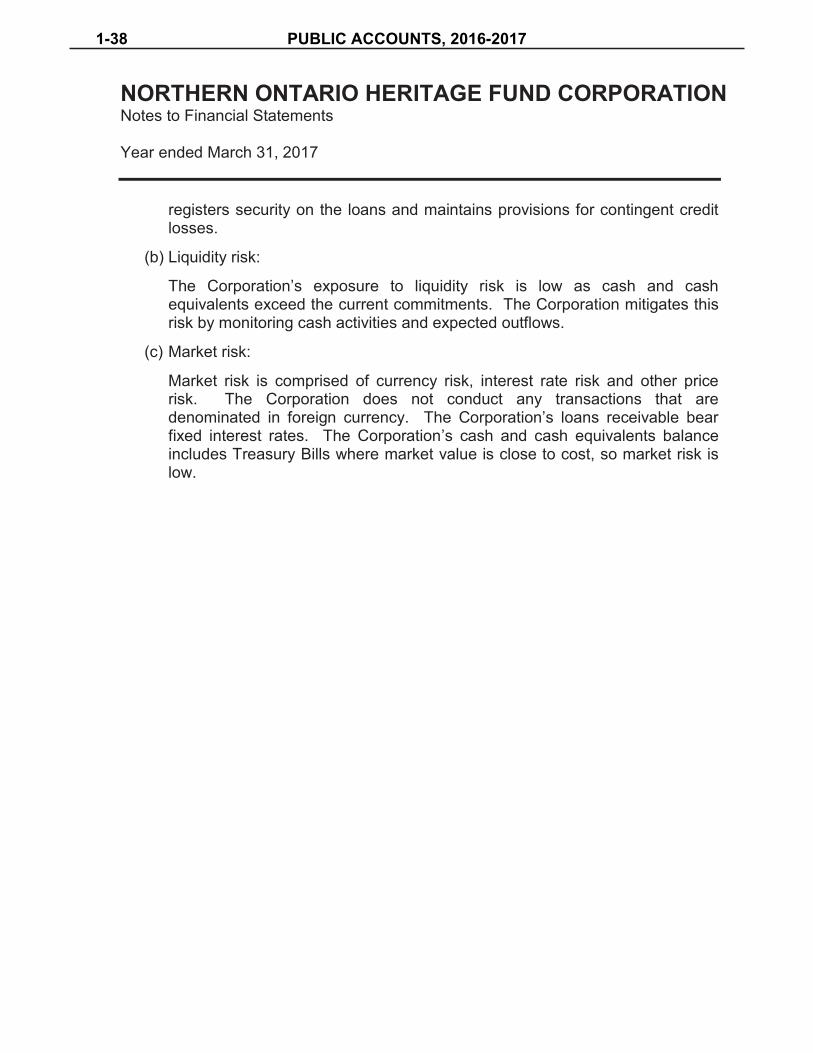

(b) Liquidity risk:

The Corporation’s exposure to liquidity risk is low as cash and cashequivalents exceed the current commitments. The Corporation mitigates thisrisk by monitoring cash activities and expected outflows.

(c) Market risk:

Market risk is comprised of currency risk, interest rate risk and other pricerisk. The Corporation does not conduct any transactions that aredenominated in foreign currency. The Corporation’s loans receivable bearfixed interest rates. The Corporation’s cash and cash equivalents balanceincludes Treasury Bills where market value is close to cost, so market risk islow.

1-38 PUBLIC ACCOUNTS, 2016-2017

PUBLIC ACCOUNTS, 2016-2017 1-39

Independent auditors’ report

To the Members of Ontario Agency for Health Protection and Promotion

We have audited the accompanying financial statements of Ontario Agency for Health Protection and Promotion [operating as Public Health Ontario], which comprise the statement of financial position as at March 31, 2017, and the statements of operations and changes in net assets and cash flows for the year thenended, and a summary of significant accounting policies and other explanatory information.

Management’s responsibility for the financial statementsManagement is responsible for the preparation and fair presentation of these financial statements in accordance with Canadian public sector accounting standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ responsibilityOur responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the financial statements present fairly, in all material respects, the financial position of Ontario Agency for Health Protection and Promotion [operating as Public Health Ontario] as at March 31, 2017, andthe results of its operations and its cash flows for the year then ended in accordance with Canadian public sectoraccounting standards.

Toronto, CanadaJune 20, 2017

1-40 PUBLIC ACCOUNTS, 2016-2017

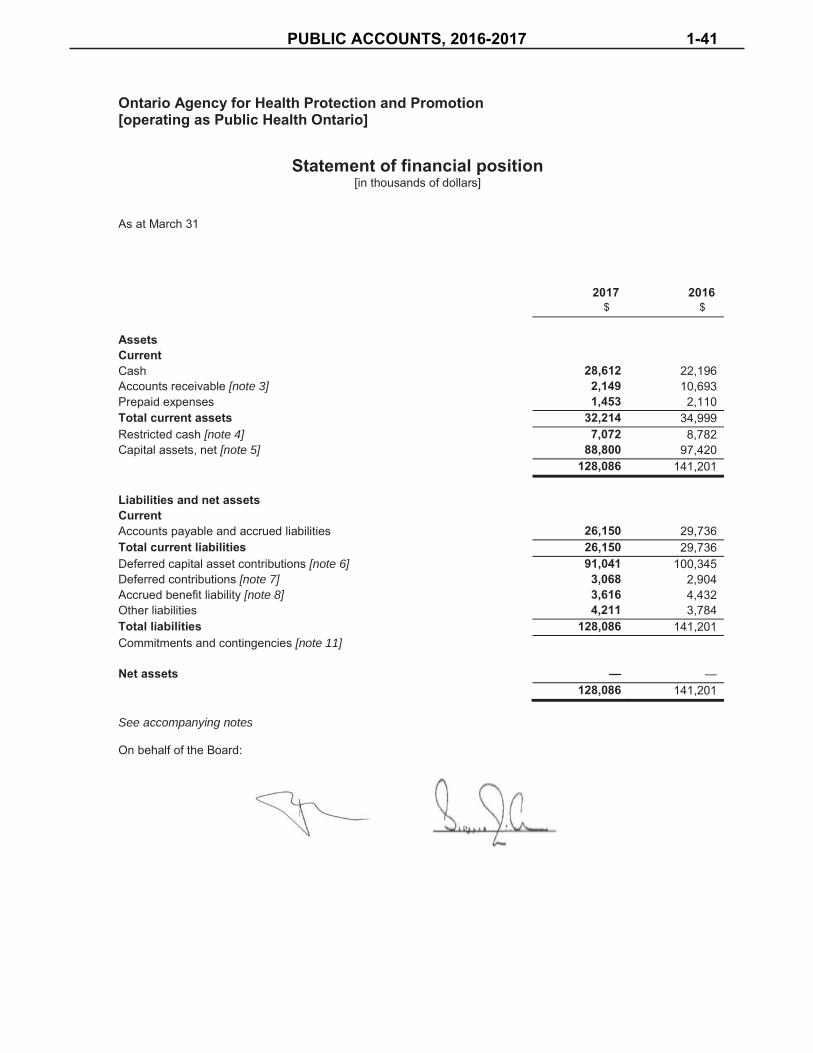

Ontario Agency for Health Protection and Promotion[operating as Public Health Ontario]

Statement of financial position [in thousands of dollars]

As at March 31

2017 2016$ $

AssetsCurrentCash 28,612 22,196Accounts receivable [note 3] 2,149 10,693Prepaid expenses 1,453 2,110Total current assets 32,214 34,999Restricted cash [note 4] 7,072 8,782Capital assets, net [note 5] 88,800 97,420

128,086 141,201

Liabilities and net assetsCurrentAccounts payable and accrued liabilities 26,150 29,736Total current liabilities 26,150 29,736Deferred capital asset contributions [note 6] 91,041 100,345Deferred contributions [note 7] 3,068 2,904Accrued benefit liability [note 8] 3,616 4,432Other liabilities 4,211 3,784Total liabilities 128,086 141,201Commitments and contingencies [note 11]

Net assets — —128,086 141,201

See accompanying notes

On behalf of the Board:

PUBLIC ACCOUNTS, 2016-2017 1-41

Ontario Agency for Health Protection and Promotion[operating as Public Health Ontario]

Statement of operations and changes in net assets

[in thousands of dollars]

Year ended March 31

2017 2016$ $

RevenueMinistry of Health and Long-Term Care

Base operations 152,960 151,437Health Promotion Resource Centre 3,573 3,573

Amortization of deferred capital asset contributions [note 6] 6,932 7,873Other grants 1,746 1,705Miscellaneous recoveries 1,787 876

166,998 165,464

Expenses [note 8]Public health laboratory program 102,690 100,514Science and public health programs 43,361 42,578General and administration [note 9] 14,015 14,499Amortization of capital assets 6,932 7,873

166,998 165,464Excess of revenue over expenses for the year — —

Net assets, beginning of year — —Net assets, end of year — —

See accompanying notes

1-42 PUBLIC ACCOUNTS, 2016-2017

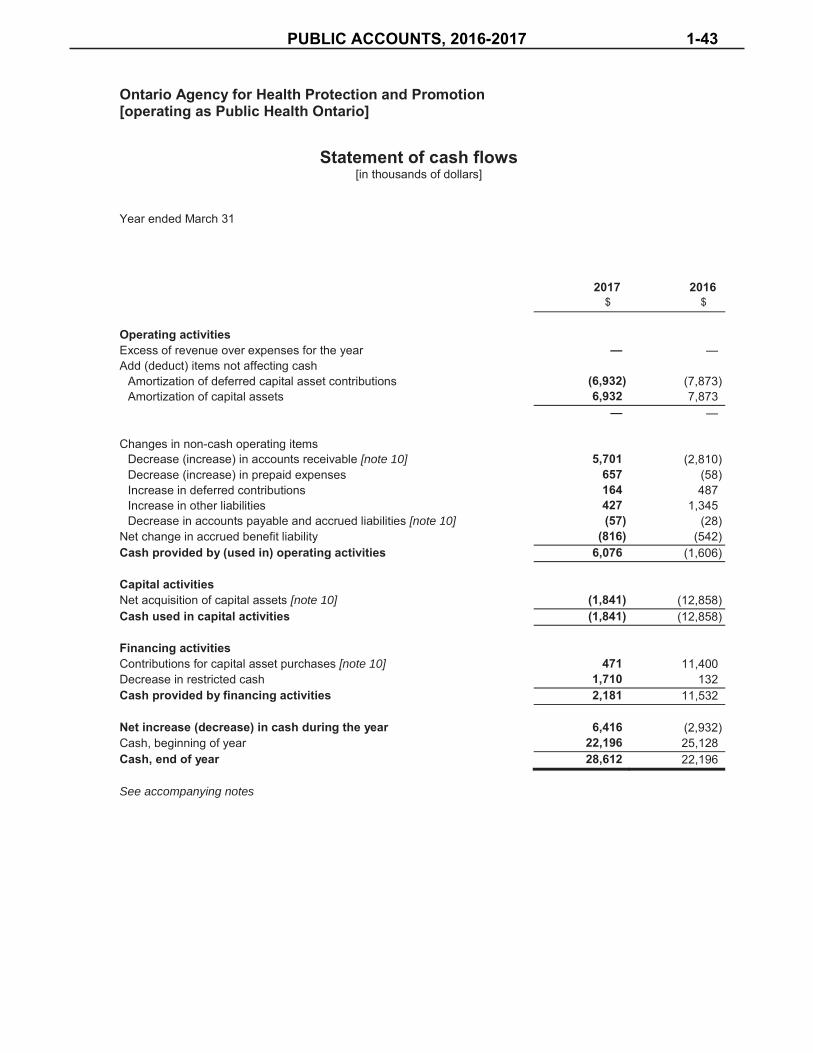

Ontario Agency for Health Protection and Promotion[operating as Public Health Ontario]

Statement of cash flows [in thousands of dollars]

Year ended March 31

2017 2016$ $

Operating activitiesExcess of revenue over expenses for the year — —Add (deduct) items not affecting cash

Amortization of deferred capital asset contributions (6,932) (7,873)Amortization of capital assets 6,932 7,873

— —

Changes in non-cash operating itemsDecrease (increase) in accounts receivable [note 10] 5,701 (2,810)Decrease (increase) in prepaid expenses 657 (58)Increase in deferred contributions 164 487Increase in other liabilities 427 1,345Decrease in accounts payable and accrued liabilities [note 10] (57) (28)

Net change in accrued benefit liability (816) (542)Cash provided by (used in) operating activities 6,076 (1,606)

Capital activitiesNet acquisition of capital assets [note 10] (1,841) (12,858)Cash used in capital activities (1,841) (12,858)

Financing activitiesContributions for capital asset purchases [note 10] 471 11,400Decrease in restricted cash 1,710 132Cash provided by financing activities 2,181 11,532

Net increase (decrease) in cash during the year 6,416 (2,932)Cash, beginning of year 22,196 25,128Cash, end of year 28,612 22,196

See accompanying notes

PUBLIC ACCOUNTS, 2016-2017 1-43

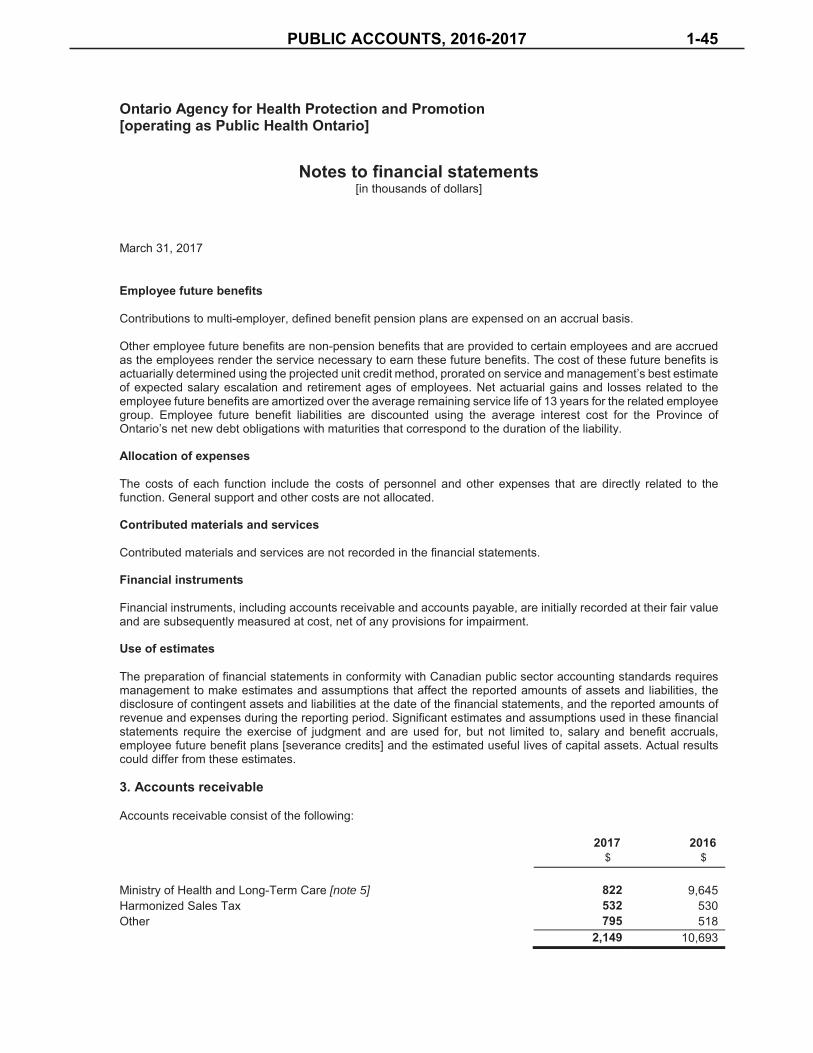

Ontario Agency for Health Protection and Promotion[operating as Public Health Ontario]

Notes to financial statements[in thousands of dollars]

March 31, 2017

1. Description of the organization

Ontario Agency for Health Protection and Promotion [“OAHPP”] [operating as Public Health Ontario] was established under the Ontario Agency for Health Protection and Promotion Act, 2007 as a corporation without share capital. OAHPP’s mandate is to enhance the protection and promotion of the health of Ontarians, contribute to efforts to reduce health inequities, provide scientific and technical advice and support to those working across sectors to protect and improve the health of Ontarians and to carry out and support activities such as population health assessment, public health research, surveillance, epidemiology, planning and evaluation.

Under the Ontario Agency for Health Protection and Promotion Act, 2007, OAHPP is primarily funded by the Province of Ontario.

OAHPP, as an agency of the Crown, is exempt from income taxes.

2. Summary of significant accounting policies

These financial statements have been prepared in accordance with Canadian public sector accounting standards as established by the Public Sector [“PS”] Accounting Board of the Chartered Professional Accountants of Canada. OAHPP has elected to follow PS 4200-4270 in the Public Sector Accounting Handbook.

Revenue recognition

Contributions are recorded in the accounts when received or receivable if the amount to be received can be reasonably estimated and collection is reasonably assured. Unrestricted contributions are recognized as revenue when initially recorded in the accounts. Externally restricted contributions are recorded as deferred contributions or deferred capital contributions when initially recorded in the accounts and recognized as revenue in the period in which the related expenses are incurred.

Capital assets

Capital assets are recorded at acquisition cost. Contributed capital assets are recorded at fair market value at thedate of contribution. Amortization is provided on a straight-line basis based upon the estimated useful service lives of the assets as follows:

Building service equipment 5-30 yearsOther equipment 5-10 yearsFurniture 5-20 yearsLeasehold improvements Over the term of the lease

Inventory and other supplies held for consumption

Inventory and other supplies held for consumption are expensed when acquired.

1-44 PUBLIC ACCOUNTS, 2016-2017

Ontario Agency for Health Protection and Promotion[operating as Public Health Ontario]

Notes to financial statements[in thousands of dollars]

March 31, 2017

Employee future benefits

Contributions to multi-employer, defined benefit pension plans are expensed on an accrual basis.

Other employee future benefits are non-pension benefits that are provided to certain employees and are accrued as the employees render the service necessary to earn these future benefits. The cost of these future benefits is actuarially determined using the projected unit credit method, prorated on service and management’s best estimate of expected salary escalation and retirement ages of employees. Net actuarial gains and losses related to the employee future benefits are amortized over the average remaining service life of 13 years for the related employee group. Employee future benefit liabilities are discounted using the average interest cost for the Province of Ontario’s net new debt obligations with maturities that correspond to the duration of the liability.

Allocation of expenses

The costs of each function include the costs of personnel and other expenses that are directly related to the function. General support and other costs are not allocated.

Contributed materials and services

Contributed materials and services are not recorded in the financial statements.

Financial instruments

Financial instruments, including accounts receivable and accounts payable, are initially recorded at their fair value and are subsequently measured at cost, net of any provisions for impairment.

Use of estimates

The preparation of financial statements in conformity with Canadian public sector accounting standards requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenue and expenses during the reporting period. Significant estimates and assumptions used in these financial statements require the exercise of judgment and are used for, but not limited to, salary and benefit accruals, employee future benefit plans [severance credits] and the estimated useful lives of capital assets. Actual results could differ from these estimates.

3. Accounts receivable

Accounts receivable consist of the following:

2017 2016$ $