Financial Disclosure and Bond Insurance

41

Financial Disclosure and Bond Insurance Angela K. Gore Charles H. Lundquist College of Business University of Oregon Eugene, Oregon 97403 email: [email protected] Kevin Sachs College of Business Administration University of Cincinnati Cincinnati, OH 45221 email: [email protected] Charles Trzcinka* Kelley School of Business Indiana University Bloomington, IN 47405 email: [email protected] March 7, 2003 *Corresponding author Acknowledgments: We are grateful to William Baber, Sudipta Basu, Walter Blacconiere, Donal Byard, Diane Del Guercio, Kimberly Dunn, Neal Galpin, Aloke Ghosh, Robert Hagerman, Shane Johnson, Brian Kluger, Steven Matsunaga, Jeffrey Mills, Dale Morse, Eric Press, Michael Rozeff, Bharat Sarath, Michael Stein, Samuel Tiras, James Wahlen, an anonymous referee, and workshop participants at Baruch College, the University of Cincinnati, SUNY at Buffalo, Temple University, Indiana University, and the 2002 annual meeting of the American Law and Economics Association for their insightful comments. We also thank Richard Balderman and the Michigan Department of Treasury Local Audit staff and Kenneth Johnson and the Pennsylvania Department of Community and Economic Development for the use of their financial reports.

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Financial Disclosure and Bond Insurance

Financial Disclosure and Bond Insurance

Angela K. Gore Charles H. Lundquist College of Business

University of Oregon Eugene, Oregon 97403

email: [email protected]

Kevin Sachs College of Business Administration

University of Cincinnati Cincinnati, OH 45221

email: [email protected]

Charles Trzcinka* Kelley School of Business

Indiana University Bloomington, IN 47405

email: [email protected]

March 7, 2003

*Corresponding author

Acknowledgments: We are grateful to William Baber, Sudipta Basu, Walter Blacconiere, Donal Byard, Diane Del Guercio, Kimberly Dunn, Neal Galpin, Aloke Ghosh, Robert Hagerman, Shane Johnson, Brian Kluger, Steven Matsunaga, Jeffrey Mills, Dale Morse, Eric Press, Michael Rozeff, Bharat Sarath, Michael Stein, Samuel Tiras, James Wahlen, an anonymous referee, and workshop participants at Baruch College, the University of Cincinnati, SUNY at Buffalo, Temple University, Indiana University, and the 2002 annual meeting of the American Law and Economics Association for the ir insightful comments. We also thank Richard Balderman and the Michigan Department of Treasury Local Audit staff and Kenneth Johnson and the Pennsylvania Department of Community and Economic Development for the use of their financial reports.

ABSTRACT: Regulators typically assume that public financial disclosure is necessary for the efficient functioning of capital markets. Economists recognize that other mechanisms, such as insurance, can mitigate problems occurring when buyers have less information than sellers. We examine whether public financial disclosures and bond insurance are substitutes. Our data are from municipal issuers in Michigan, where financial disclosure is required by the state, and Pennsylvania, where disclosure is unregulated. We study municipal issuers because they are not covered by federal securities laws and state laws often allow issuers to choose the level of financial disclosure. Overall, we find that when disclosure is unregulated, issuers substitute between disclosure and insurance. When disclosure is required by state law, issuers use less insurance. Our results imply that required accounting disclosure is not necessarily optimal since rational issuers will trade off public disclosure and insurance when free to do so.

1

I. INTRODUCTION

The current media focus on corporate accounting problems typically assumes that far-

reaching public financial disclosure is necessary for the efficient functioning of capital markets

and the protection of investors. This assumption is a cornerstone of the Securities Acts of 1933

and 1934, which require all issuers to supply audited financial statements following government-

approved rules. In contrast, economists believe that public financial disclosure is only one of

many ways to solve the problems that occur when buyers have less information than sellers. An

issuer could, for example, purchase insurance for the security or could agree to private

disclosure. Issuers face a choice of mechanisms that affect the price of the security and are likely

to choose a combination that obtains the best price at the lowest cost to the issuer. Public

disclosure is not necessarily the lowest-cost mechanism available and will not always be chosen

in a free market.

In the United States, accounting disclosures are mandated for all private issuers of public

securities. Thus it is impossible to observe the choices that private issuers would make if they

were free to combine mechanisms that reduce asymmetric information. However, government

issuers (states and cities) are not covered by federal securities laws and local laws often allow

issuers the freedom to choose the amount of public disclosure. The use of bond insurance,

coincidently or not, has become common in the municipal sector, with over 50% of new debt

issues insured. The purpose of this paper is to test whether the legal freedom to make efficient

combinations and the use of municipal bond insurance are related. We examine municipal issuers

in two states, one regulated and one unregulated, to determine if the regulation of accounting

information affects the trade-off of public disclosure and insurance.

Bond insurance is a guarantee by an insurance company to assume the principal and

interest obligations of a bond in the event of default. In addition to municipal issuers, it is also

2

used by health care organizations and firms in regulated industries, such as public utilities.

Previous studies show that bond insurance lowers the debt costs of municipal issuers.1

Issuers can also lower capital costs (that is, raise the prices of their securities) by publicly

disclosing information. Theoretical studies argue that voluntary disclosure reduces information

asymmetry among investors by reducing transactions and information costs, which in turn

increases investor confidence and therefore increases stock liquidity. 2 Research demonstrates

that a proxy for transactions costs and information costs, the bid-ask spread, is positively

correlated with a security’s expected return. Yakov Amihud and Haim Mendelson argue that this

implies that policies which reduce the bid-ask spread are likely to reduce an issuer’s capital cost3.

Studies show that in fact, public disclosure of accounting information raises the price of

securities for corporate and government issuers of public securities.4

1 David Kidwell, Eric Sorenson, & John Wachowicz, Estimating the Signaling Benefits of Debt Insurance: The Case of Municipal Bonds, 22 J. Fin. & Quant. Analysis 3, 299 (1987) find that municipal issuers that purchase bond insurance reduce their borrowing costs by 34.1 basis points, well above the average insurance premium of 11.7 basis points. In addition, Anjan Thakor, An Exploration of Competitive Signalling Equilibria with ‘Third Party’ Information Production: the Case of Debt Insurance, 37 J. Fin., 717 (1982) uses a theoretical model to show that insurance directly lowers default risk by guaranteeing payment in the event of default and indirectly lowers it by signaling new information to lenders about the underlying default risk. 2 For theoretical studies on the relationship between asymmetric information and liquidity, see Douglas Diamond & Robert Verrecchia, Disclosure, Liquidity, and the Cost of Capital, 46 J. Fin. 1325 (1991), and Oliver Kim & Robert Verrecchia, Market Liquidity and Volume Around Earnings Announcements, 17 J. Acct. & Econ. 41 (1994). Several papers find empirical evidence consistent with theoretical work. For example, Michael Welker, Disclosure Policy, Information Asymmetry and Liquidity in Equity Markets, 11 Contemp. Acct. Res. 801 (1995) finds a negative relationship between analyst's rankings of disclosure and bid-ask spreads. Other studies find that asymmetric information affects bond marketability, whereby lower-rated bond issues receive fewer bids than higher-rated issues due to underwriters' uncertainties about their value (see Michael Hopewell & George Kaufman, Commercial Bank Bidding on Municipal Revenue Bonds: New Evidence, 32 J. Fin. 1647 (1977); and Reuben Kessel, A Study of the Effects of Competition in the Tax-Exempt Bond Market, 79 J. Pol. Econ. 706 (1971)). In addition, lower-rated bond issues have larger underwriter spreads and higher variances, indicating that lower-rated issues are more difficult to price than higher-rated issues (Earl Benson, The Search for Information by Underwriters and its Impact on Municipal Interest Cost, 34 J. Fin. 871 (1979); and Eric Sorenson, An Analysis of the Relationship Between Underwriter Spread and the Pricing of Municipal Bonds, 15 J. Fin. & Quant. Analysis 435 (1980)). 3 Yakov Amihud & Haim Mendelson, Asset Pricing and the Bid-Ask Spread, 17 J. Fin. Econ. 223 (1986) establish the relationship between returns and bid-ask spreads. Yakov Amihud & Haim Mendelson, The Liquidity Route to a Lower Cost of Capital, 12 J. Applied Corp. Fin. 8 (2000) discuss using disclosure to reduce the cost of capital. 4 Studies that find public disclosure lowers the cost of capital for corporate debt, corporate equity and state government debt are, respectively: Partha Sengupta, Corporate Disclosure Quality and the Cost of Debt, 73 Acct. Rev. 4, 459 (1998); Christine Botosan, Disclosure Level and the Cost of Equity Capital, 72 Acct. Rev. 323 (1997); and Earl Benson, Barry Marks & Kumar Raman, The Effect of Voluntary GAAP Compliance and Financial Disclosure on Governmental Borrowing Costs, 6 J. Acct., Auditing, & Fin. 303 (1991).

3

Given that economists have identified two capital-cost-reducing mechanisms, we

investigate how municipal issuers choose between them. We test whether disclosure and bond

insurance are substitutes in the efforts by municipalities to lower their costs of issuing debt. Our

tests exploit the fact that not all states require municipal issuers to comply with government

rules, known as “Generally Accepted Accounting Principles” or GAAP, allowing us to

investigate how both regulated and unregulated issuers choose between the two means of

reducing debt costs.

Our first test uses a sample of municipal issuers from Pennsylvania, a state that does not

require GAAP disclosure. We find a significant negative relationship between bond insurance

and GAAP disclosure, which is consistent with substitution. However, we find no relationship

between bond insurance and “non-GAAP” disclosure, defined as disclosures beyond those

required by GAAP.

We next compare the sample of municipalities in Pennsylvania with those in Michigan, a

state that requires GAAP, and find that Michigan municipalities are significantly less likely to

insure their bonds. This result suggests GAAP regulation constrains the use of bond insurance in

Michigan. However, we also find evidence that Michigan’s GAAP requirement increases the

substitution of non-GAAP disclosure for insurance. In contrast to Pennsylvania, where we find

no relationship between non-GAAP disclosure and insurance, in Michigan we find a significant

negative relationship between non-GAAP disclosure and insurance. This finding suggests that,

given a state-mandated GAAP requirement, municipalities respond by substituting non-GAAP

information for bond insurance.

Our study contributes to the literature documenting unintended costs of securities

regulation, in this case the possible underutilization of an alternative mechanism to reduce

4

information asymmetries5. Frank Easterbrook and Daniel Fischel observe that, although many

years have passed since the passage of the securities acts, we still know very little about the

effects of mandatory disclosure or other securities regulations. They categorize the costs of

disclosure regulation as direct (for example, the costs of compiling and disseminating financial

information), and indirect (for example, the abandonment of profitable investment opportunities,

and the substitution of useless, but complying information for relevant voluntary disclosures)6.

Our evidence is of an indirect cost -- the underutilization of an alternative, but possibly more

efficient mechanism for reducing the information costs of market participants and hence, the

capital costs of the issuer.

If, as our results suggest, the net benefits of disclosure are indeed traded off against the

net benefits of bond insurance, then allowing freedom to choose enables an issuer to obtain a

better price for its securities by using the mechanism that is less costly. A possible implication of

our results is that the regulation of accounting disclosure precludes the discovery or use of more

efficient mechanisms for lowering borrowing costs and shielding investors from risk. It is at least

plausible that a less restricted bond market may benefit from future reforms7.

The rest of the paper is as follows. The hypotheses are developed in Section 2. Section 3

describes the sample of municipalities, the data sources, the model specification, and the

5 Gregg A. Jarrell, Change at the Exchange: the Causes and Effects of Deregulation, 27 J. Law & Econ. (1984); and Jay R. Ritter, The Costs of Going Public, 19 J. Fin. Econ. 269 (1987), document several unintended effects of securities regulation. 6 Frank H. Easterbrook & Daniel R. Fischel, The Economic Structure of Corporate Law (1991). Indirect municipal disclosure costs include the competitive disadvantage that disclosing information can have on the ability of a municipality to attract employers. In addition, municipalities may incur indirect costs by substituting useless, but complying information required under GAAP regulation for more relevant voluntary disclosures. For a description of the direct costs of municipal disclosure, see note 20 infra. 7 Yakov Amihud, Kenneth Garbade, & Marcel Kahn, in A New Governance Structure for Corporate Bonds, 51 Stan. L. Rev. 447 (1999), propose increasing the right of public bondholders by appointing a "supertrustee" with the duty and power to actively monitor, renegotiate, and enforce bond covenants, and with access to confidential company information, thereby overcoming the collective action problem. Although the authors focus on corporate bonds, the reform may work as well for municipal bonds.

5

variables used in the tests. Section 4 presents the results, Section 5 describes the results of

sensitivity tests, and Section 6 concludes the paper.

II. HYPOTHESIS DEVELOPMENT

A. Substitution of disclosure and insurance

Our focus is on the relationship between disclosure and the cost of capital. To develop the

theory we need two assumptions. First, we assume municipal decision makers have incentives to

lower municipal debt costs. For example, ceteris paribus, if lower debt costs lead to lower

property taxes, which translate into more votes for municipal officials, then municipal officials

will want to lower borrowing costs. Second, we assume competitive bond and insurance markets.

Competitive markets imply that issuers fully bear transaction and information costs in the form

of insurance premiums, in the case of insured debt, and higher debt costs, in the case of

uninsured debt.8 Previous research develops theory and evidence that corporate capital costs are

an increasing function of the bid-ask spread, suggesting firms can reduce capital costs through

actions that lower investors' transaction costs and information costs.9

In the municipal bond market, one such action is to insure the bond issue. For a premium,

municipal bond insurers provide policies that guarantee the repayment of principal and interest in

the event of default. Bond insurance substitutes the default risk of the insurance company for the

default risk of the issuer.10 When municipal debt is insured, it is automatically given the highest

bond rating of “AAA,” lowering the issuer’s debt cost relative to the cost of the same debt

8 Michael Jensen & William Meckling, Theory of the Firm: Managerial Behavior, Agency Costs, and Ownership Structure, 3 J. Fin. Econ. 305 (1976). 9 See Amihud & Mendelson, supra note 2. 10 If the default risk of the issuer becomes irre levant with bond insurance, disclosure policy will not influence debt-costs at the margin. However, lenders likely may bear residual transaction costs associated with municipal default, and accordingly still price the default risk of the issuer.

6

without insurance.11 Policy premiums are set based on the issuer’s default risk at the inception of

the contract, and are paid in full by the issuer at that time.

Given asymmetric information whereby investors are unable to fully determine the

default risk characteristics of uninsured issuers, insurance purchases can affect debt prices in two

ways.12 First, insurance reduces bond yields by lowering default risk through guaranteeing

payment in the event of default. Second, the insurer collects and analyzes private information

about the municipality, and uses it to set the premium, which reflects the insurer's assessment of

the true underlying default probabilities. Thus, the insurance premiums themselves reduce

information asymmetry, which improves the liquidity of the issue, lowering issuers' net

borrowing costs.13 In fact, empirical research finds that issuers subject to a high degree of price

and quality uncertainty (high information asymmetry) benefit relatively more from bond

insurance.14

A second capital-cost reducing action is to publicly release financial information.

Disclosure studies assume that, even in efficient capital markets, managers have superior

information about their organizations' expected future performance than do outside investors.

Studies that examine the economic consequences of voluntary disclosure find there are three

general types of capital market effects for firms that make extensive voluntary public

11 See Kidwell, Sorenson & Wachowicz, supra note 1, and Robert Bland & Yu Chilik, Municipal Bond Insurance: an Assessment of its Effectiveness at Lowering Interest Costs, 3 Gov't. Fin. Rev. 23 (1987). Although insured bonds are automatically rated AAA by Moody's, Standard and Poor's, and Fitch (MBIA internet home page), they typically trade at yields comparable to A-rated bonds. 12 Assuming risk-neutral market participants and complete insurance markets, insurance premiums should be competitively priced such that bond issuers are indifferent between selling bonds with or without insurance, and in theory, the net benefit of insurance would be zero. However, Kidwell, Sorensen, & Wachowicz supra note 1 at 308 find that municipalities save 22 basis points on average, net of the insurance premiums. Because the net benefit is non-zero, it implies that there are additional costs involved with issuing insurance. 13 For example, given a case where two issuers each insured their bonds and thus received a AAA bond rating, investors will not be able to discern which issuer is more likely to default by simply observing the bond rating. However, if investors observe that one issuer paid a much higher insurance premium than the other, then this would reduce the level of information asymmetry. 14 Using bond ratings to proxy for the degree of information asymmetry, Kidwell, Sorensen, & Wachowicz supra note 1 at 311 find that the net benefits of insurance increase monotonically as bond ratings decline.

7

disclosures: improved liquidity for stocks and bonds, increased following by information

intermediaries, and increased reductions in the cost of capital.15

For example, consider a municipality whose managers have better information about the

municipality’s future prospects than do outside investors. If this information asymmetry cannot

be resolved, the municipality will view making public securities offerings as costly since

investors will demand a higher return. As a consequence, managers who anticipate making

capital market transactions have incentives to provide voluntary disclosure to reduce the

information asymmetry problem, thus reducing the cost of financing.16 A similar argument is

made by Barry and Brown, who note that when disclosure is not perfect, investors bear risks in

forecasting their investments' future payoff.17 If this risk is not diversifiable, investors will

demand an incremental return for bearing the information risk.18 Managers therefore have

15 While several studies establish a link between asymmetric information and liquidity, the relationship between disclosure and information intermediaries is not as clear. The information asymmetry problem gives rise to the demand for information intermediaries such as bond rating agencies and financial analysts, who engage in private information production to uncover managers' superior information, as discussed in Paul Healy & Krishna Palepu, Information Asymmetry, Corporate Disclosure, and the Capital Markets: A Review of the Empirical Disclosure Literature, 31 J. Acct. & Econ. 405 (2001). The effect of voluntary public disclosure on the demand for information intermediaries' services is ambiguous, however, and potentially hampered by endogeneity. For example, increased public disclosure may lower financial analysts' information acquisition costs, enabling them to create valuable new information, such as improved forecasts and buy/sell recommendations, thus increasing demand for their services (see Mark Lang & Russell Lundholm, Corporate Disclosure Policy and Analyst Behavior, 71 Acct. Rev. 467 (1996)). On the other hand, voluntary public disclosure also pre-empts analysts' ability to distribute managers' private information to investors, leading to a decline in the demand for their services. 16 Stewart Myers & Nicholas Majluf, Corporate Financing and Investment Decisions When Firms Have Information that Investors do not Have, 13 J. Fin. Econ. 187 (1984). 17 Christopher Barry & Stephen Brown, Differential Information and the Small Firm Effect, 13 J. Fin. Econ. 283 (1984) and Christopher Barry & Stephen Brown, Differential Information and Security Market Equilibrium, 20 J. Fin. & Quant. Analysis 407 (1985). In the case of municipal bonds, many issues are not rated by ratings agencies, and for these unrated issues, public disclosure is especially important to help resolve information asymmetry. Empirical research such as Lisa Fairchild & Timothy Koth, The Impact of State Disclosure Requirements on Municipal Yields, 51 Nat'l Tax J. 733 (1998), finds the decrease in debt costs from public disclosure is greater for unrated issues. Even when bonds are rated, the ratings alone are not sufficient for investors to forecast risk. Bond ratings only represent a range for the probability of default, not the probability of recovery, and the ratings agencies do not assess the liquidity of the underlying assets. 18 If one assumes well-diversified investors, it then raises the question of the necessity of insurers, given investors could simply diversify risk in the same way that insurers do. However, it is an empirical question as to how well individual investors, the largest segment of municipal bond purchasers, are able to diversify a portfolio of municipal bonds. Because municipal bonds are only tax-free in the state in which the investor resides, investors would have to diversify among those bonds available within their state. Many states have a very limited number of bond issues available in a given year, making this a difficult task. Insurers, on the other hand, are not limited to one state, and are thus more easily able to diversify their portfolio. In addition, regardless of whether investors are well-

8

incentives to voluntarily disclose information to reduce investors' information risk, and hence

lower their cost of capital. The results of empirical studies bear this out, showing that public

financial disclosure reduces the cost of capital for both corporate and government issuers19.

There are therefore at least two mechanisms an issuer can use to reduce information

asymmetry and hence, its debt cost. Municipal managers seek the greatest debt-cost reduction

using most efficient combination of mechanisms available.20 The efficient combination of

financial disclosure and bond insurance depends on whether the two mechanisms are substitute

factors in debt-cost reduction.

If disclosure and bond insurance are substitutes, it implies an increase in the level of one

causes a decrease in the marginal debt-cost reduction brought about by the other. If this marginal

benefit is reduced, then ceteris paribus, a rational issuer will choose less of the mechanism, since

it chooses the level of the mechanism where marginal benefits and costs are equalized.21 This

leads to the following hypothesis.

H1 (substitution): Ceteris paribus, if public disclosure and bond insurance are substitutes, increases in the level of one will be associated with decreases in the level of the other.

diversified, David Mayers & Clifford Smith, Jr., On the Corporate Demand for Insurance, 55 J. Bus. 281 (1982) suggest that insurers may provide a monitoring function that investors cannot perfom on their own, which would lower investors' transaction costs, again giving rise to the demand for insurers. 19 See note 4 supra . 20 We assume both mechanisms are costly. In the case of insurance, issuers pay a premium to the insurer. The direct costs of public municipal disclosure include the costs of monitoring, compiling and disseminating public financial information. Due to the small size of many municipalities, these disclosure costs can be significant since they often involve hiring accountants and others to perform the services. In addition, note that issuers’ choice of less than full disclosure is consistent with public disclosure by municipalities being costly (see Angela Gore, The Effects of GAAP Regulation on Local Government Disclosure (unpublished manuscript, University of Oregon, 2003)). 21 This is an adaptation of the standard definition of substitutes in production, found in any standard price theory text. Our analysis treats bond insurance and public financial disclosure as input factors in a production process whose output can be thought of as information-risk reduction, which is priced in the bond market. In our analysis, marginal debt-cost reduction is analogous to marginal revenue product in standard producer theory.

9

B. Implications for Disclosure Regulation

When disclosure is unregulated, there is no mandated minimum level of public financial

disclosure. Each issuer weighs the expected costs and benefits of disclosure and insurance and

sets a policy that yields the greatest debt-cost reduction at the lowest cost. When disclosure is

mandated by regulation, it requires that each issuer disclose at least some minimum level of

financial information about itself. If the mandated minimum level exceeds an issuer's

unregulated equilibrium disclosure level, then a regulated issuer's ability to substitute disclosure

for insurance is constrained.22

The regulation of municipal financial disclosure implies the following hypothesis:

H2 (regulation): Ceteris paribus, if public disclosure and bond insurance are substitutes, then the level of bond insurance is lower under regulated disclosure than under unregulated disclosure.

III. RESEARCH DESIGN AND METHODS

A. Theory Implementation

The development of hypothesis 1 assumes that issuers form efficient combinations of

disclosure and insurance based on unbiased expectations about changes in the relative costs and

benefits of those factors. An ideal test of hypothesis 1 would be to observe changes in each

issuer’s marginal disclosure and insurance decisions over all states of nature. While we cannot

observe the states of nature or how they map into decisions, we can observe, for each issuer, the

equilibrium combination formed. Thus, most of our tests examine the relationship between the

levels of disclosure and the levels of insurance across the observed equilibrium combinations.23

22 We assume each mechanism is characterized by decreasing marginal debt-cost reduction and non-decreasing marginal costs. 23 We acknowledge that our theory makes predictions based on marginal changes, while our hypotheses use levels analysis. However, we believe our hypothesis specification is a reasonable first approximation of issuer decision-making when faced with a pricing relationship where investors price securities based on the amount of public disclosure and insurance. In addition, tests of marginal predictions using levels analysis in pricing relationships are common in finance. Bond prices are directly affected by levels of information variables such as bond ratings that

10

B. Sample Selection

In our tests, we exploit the fact that not all states require governmental GAAP. We

employ data from Pennsylvania, which does not require GAAP, and from Michigan, which

requires GAAP 24. We confine our analysis to two states to ensure that the municipalities in the

sample are as much alike with respect to non-disclosure regulatory and legal constraints as

possible. In this way, we increase the probability that the influences on disclosure are the same

for all of the municipalities in the sample. Michigan and Pennsylvania are chosen because they

closely match each other in many ways other than the level of disclosure regulation. However,

because there are only nine states that have unregulated disclosure, we control for the differences

most likely to affect disclosure levels.

The two states are similar in the following manner. Both states have city and township

governments that do not have overlapping boundaries. This ensures that the responsibility for the

financial reporting relationship is clear. Each state allows both general obligation and revenue

bonds, and allows cities to issue debt directly. We use these requirements because regulations

affecting incentives to issue debt can indirectly cause variation in disclosure. Both states require

local governments to be audited, although Pennsylvania allows the choice of an external or an

internal auditor. We use this criterion because mandated audits potentially influence the level of

GAAP disclosures. Finally, we were unable to find any differences between the two states with

regards to bond insurance regulations.

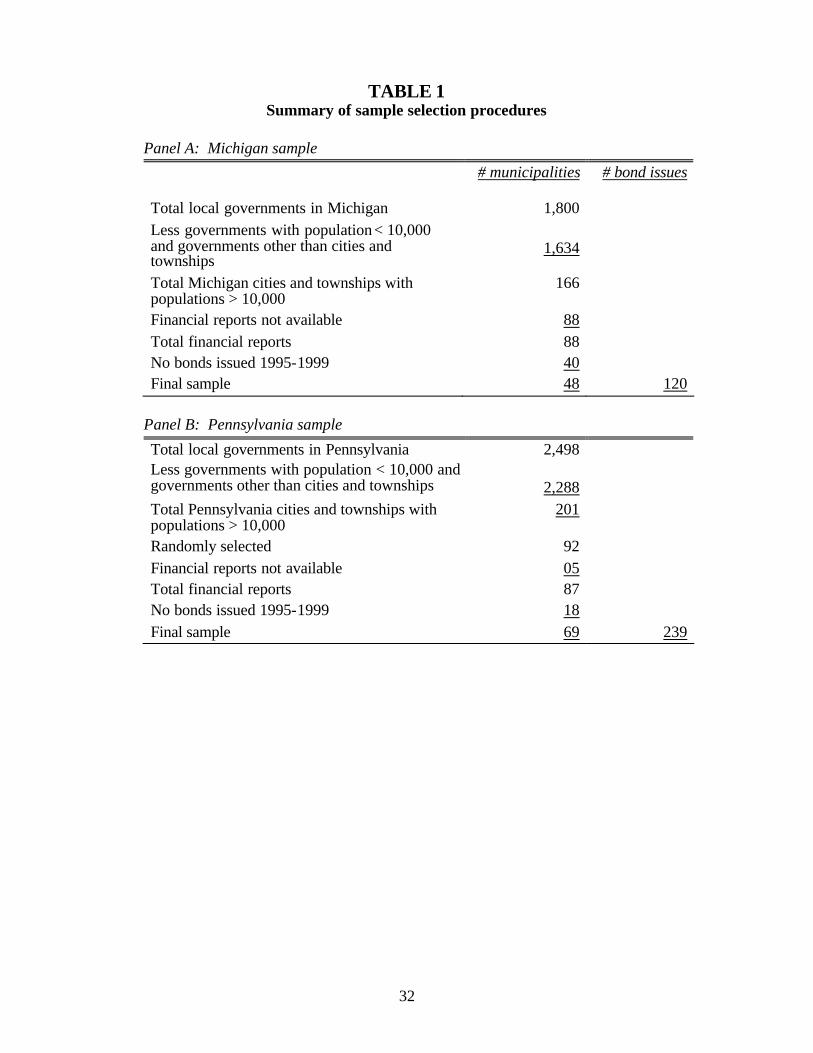

Table 1, panel A describes the selection criteria for the Michigan sample. We select the

166 municipalities with populations greater than 10,000 from the 1,800 cities and townships in

involve a marginal trade-off for the issuer. John Campbell, Andrew Lo & Craig Mackinlay, Econometrics of Financial Markets, Princeton University Press, 1997 show that bond prices are linear functions of the state variables. 24 See the survey of each state’s disclosure requirements in National Association of State Auditors, Comptrollers and Treasurers: Technical Activities and Functions (1996).

11

Michigan25. From these, we collected financial reports for 88 municipalities from the Michigan

Department of Treasury. We next eliminate 40 municipalities that did not issue any bonds

between 1995 and 1999, leaving 48 issuers in the Michigan sample. The 48 municipalities

issued 120 bonds between 1995 and 1999.

(Insert Table 1 here)

Table 1, panel B describes the selection criteria for the Pennsylvania sample. We select

the 201 municipalities with populations greater than 10,000 from the 2,498 cities and townships

in Pennsylvania. From these, we randomly selected 92 financial reports, roughly equivalent to

the number selected from Michigan. Of the 92, 65 are collected through requests to the

municipalities, and 22 are collected from the Pennsylvania Department of Community and

Economic Development. From the 87 remaining municipalities, we eliminate 18 that did not

issue any bonds between 1995 and 1999, leaving 69 municipalities in the Pennsylvania sample.

The 69 municipalities issued 239 bonds between 1995 and 199926.

Because of the high cost of hand-collecting financial disclosure data, we examine

disclosure data for only one year, 1995, and test decisions in the cross section.

C. Hypothesis Tests

We test each hypothesis in two ways — at the municipality- level and at the bond issue-

level. Both hypotheses make predictions about the relationship between disclosure policy and

the decision to insure debt. However, it is difficult to compare these variables directly since

decisions about each are made at different levels of transaction.

Disclosure policy is set largely at the organizational level, determined by expected future

debt-market activity, size, audit quality and various other organization-specific factors. It is not

25 This is based on Jerald L. Zimmerman, The Municipal Accounting Maze: an Analysis of Political Incentives, 15 J. Acct. Res. 107 (1977). 26 Our specifications tests, which examine bonds issued from 1991-1995, use some of the eliminated financial reports.

12

typically dependent on one bond issue. We therefore employ an empirical model that examines,

at the municipality- level, the relationship between a government’s disclosure level and the

percentage of insured bonds.

The insurance decision is determined largely at the individual bond- issue level,

depending on such factors as the size of the issue, and the type of bond (that is, general

obligation or revenue). Therefore, we also employ an empirical model that examines the

relationship between the decision to insure an individual bond issue and the disclosure level.

Model 1: OLS Model for Municipality- level Tests of Municipal Disclosure DISCLOSUREi = αi + β1iDEBTi + β2iAUDITSi + β3iCITYi + β4iLNPOPi + β5INSUREDi +ε i (1) Where: DISCLOSUREi is the value of the GAAP, non-GAAP, or TOTAL disclosure index in 1995 for government i. DEBTi is the total debt/population in 1995 for government i. AUDITSi is the number of municipal audits performed in 1995 by government i’s auditor. CITYi is a dummy variable for the city form of government (city = 1; town = 0). LNPOPi is the log of total population (in 000’s) in 1995 for government i. INSUREDi is the number of insured bond issues / total number of bond issues from 1995 to 1999 for government i.

The dependent variable is measured alternately using GAAP, non-GAAP, or TOTAL (the

sum of the two) disclosure indices, described in detail below. Each disclosure index measures

the number of items satisfied by the financial report. The independent variable of interest is

INSURED, which measures the propensity of a municipal issuer to insure its current and future

debt. The remaining control variables are shown in previous studies to be important

determinants of disclosure policy. For the substitution hypothesis, we test whether β5 is

significantly negative for the sample of unregulated Pennsylvania issuers. We confine our

analysis of H1 to Pennsylvania because our tests require variation in the disclosure measure, and

if GAAP is required by state law, there will presumably be little variation in disclosure. In

13

addition, we confine this test to the unregulated state to avoid the potentially confounding effects

of disclosure regulation.

We also use this model to test, by Michigan municipality, a sufficient condition of the

regulation hypothesis (described further in section IV). For this test, the variable of interest is

also INSURED.

Disclosure Indices. We construct disclosure indices to measure the level of public

disclosure by issuers27. We use the indices developed by Angela Gore; one measuring the extent

of GAAP disclosure (that is, promulgated by the Governmental Accounting Standards Board)

and one measuring non-GAAP disclosure (that is, disclosure beyond what is promulgated under

governmental GAAP)28. We also combine the two to form an index of total disclosure. The

GAAP index contains eighteen equally-weighted disclosure items (see Appendix A), so each

municipality may have a score between 0 and 18. The Non-GAAP index is comprised of

thirteen equally-weighted disclosures (see Appendix B), while the Total index is comprised of all

31 GAAP and non-GAAP items.29

Each individual disclosure item is counted if it is present, and for the GAAP index, is

substantially in compliance with GAAP requirements. For example, if a municipality includes a

financial statement footnote describing their cash deposits (GAAP disclosure item #11,

Appendix A), then this item would count toward their GAAP index score. No attempt is made to

assess the “quality” of particular disclosures, however.

27 Botosan supra note 4 uses a disclosure index for corporations. Paul Copley, The Association Between Municipal Disclosure Practices and Audit Quality, 10 J. Acct. & Pub. Policy 245 (1991) and Gore, supra note 19, develop disclosure indices for municipalities. 28 The traditional term for non-GAAP information is "voluntary disclosure" (see John Core, A Review of the Empirical Disclosure Literature: Discussion, 31 J. Acct. & Econ. 441 (2001)). However, because all disclosure is voluntary in Pennsylvania, it renders the term "voluntary" confusing in our study. 29 The use of an index that weights each disclosure item equally is supported by Walter Robbins & Kenneth Austin, Disclosure Quality in Governmental Financial Reports: an Assessment of the Appropriateness of a Compound Measure, 24 J. Acct. Res. 412 (1986). They find that variables significantly associated with disclosure using an equally-weighted index are also significantly associated with disclosure using a compound index.

14

The indices are composed of disclosures contained within the annual financial reports.

The GAAP disclosures are drawn from the basic financial statements and footnotes. Non-GAAP

disclosures are from the basic financial statements, footnotes, and supplementary statistical

information. In addition, the ind ices only use disclosures that apply to all municipalities.

Otherwise, the index could proxy for complexity, as larger and more complex governments

would tend to score higher.

Insurance. In order to evaluate the propensity to insure bonds, we use the portfolio of

new bonds issued by the government between 1995 and 1999. We choose the bond portfolio

definition by assuming rational issuers publicly disclose information in anticipation of future

bond-market activity. We use a multi-year horizon and treat disclosure policy as a function of

the debt-market activity of issuers from 1995, the disclosure year, to four years ahead. The

proxy we use for the level of bond insurance, INSURED, is the ratio of insured debt issues to

total debt issues between 1995 and 1999 for a given issuer.

Control Variables. We include four additional independent variables, debt, population,

audit quality, and government type, as controls. The proxy for the debt level, DEBT, is the ratio

of total debt to population, with the denominator acting as a size deflator30. Prior disclosure

studies find the log of population (LNPOP), a surrogate for size, is positively associated with

disclosure31. Studies also find that audit quality is positively associated with public financial

disclosure levels.32 Public financial disclosure is required to be audited in both Michigan and

30 This follows Copley, supra note 27 and Ingram & DeJong, The Effect of Regulation on Local Government Disclosure Practices, 6 J. Acct. & Pub. Policy 245 (1987). Gore, supra note 20, finds that the level of debt-market participation is positively associated with municipal disclosure. 31 The log of population is used as a size proxy in studies such as Robbins & Austin supra note 29 and John Evans & James Patton, An Economic Analysis of Participation in the Municipal Finance Officers Association Certificate of Conformance Program, 5 J. Acct. & Econ. 151 (1983). 32 Audit quality measures the auditor's expertise at auditing governmental entities. Prior disclosure research finds that for audits requiring specialized knowledge, such as governmental audits, there is a positive association between the number of specialized audits performed (industry specialization) and audit quality. Following Gore supra note 20, we use auditor industry specialization as a proxy for audit quality.

15

Pennsylvania, and higher-quality auditors are associated with higher disclosure levels33. Our

proxy for audit quality is AUDITS, the number of Pennsylvania or Michigan municipal audits

performed by the government's CPA firm. Finally, CITY is a dummy variable used to indicate

whether the government is a city or township 34.

With the exception of the audit quality, population, and insurance variables, we obtain all

data directly from the municipalities' 1995 financial reports. Data for the audit quality variable

are hand-collected from the Michigan Department of Treasury and the Pennsylvania Department

of Community and Economic Development. Population data are from the 1990 census, while the

remaining variables are hand-collected from the Thomson Financial Municipal Database.

Model 2: Logit Model for Bond- issue- level Tests of the Decision to Insure an Issue ISSINSUREi = αi + β1iLNAMOUNTi + β2iGOBONDi + β3iLNPOPi + β4iDEBTi + β5FREQi + β6PRIOR_INSi + β7DISCLOSUREi + ε i (2) Where: ISSINSUREi is an indicator variable equal to one if the bond issue is insured, and zero otherwise. LNAMOUNTi is the log of the issue amount (in dollars). GOBONDi is equal to one if the issue is a general obligation bond, zero if a revenue bond. LNPOPi is the log of total population (in 000’s) for government i. DEBTi is the total debt/population in 1995 for government i. FREQi is the total number of bond issues in the prior four years for government i. PRIOR_INSi is equal to one if government i issued insured debt in the prior year, and zero otherwise. DISCLOSUREi is the value of the GAAP, non-GAAP, or TOTAL disclosure index in 1995 for government i.

We use this model for bond- issue level tests to predict the decision by a municipality of

whether or not to insure an issue. The dependent variable, ISSINSURE, is an indicator variable

for whether a specific bond issue is insured. Our test of H1 examines whether, for the sample of 33 Although Pennsylvania does not require GAAP financial disclosures, they do require that municipalities have annual financial statement audits. If Pennsylvania municipalities voluntarily comply with GAAP, then auditors are required to verify the GAAP disclosures. The audit costs are directly paid by the individual municipalities in each state. Therefore, GAAP disclosure is subject to monitoring costs in both Pennsylvania and Michigan. 34 Disclosure studies such as Zimmerman, supra note 25 and Copley, supra note 27, find that the form of government is positively associated with disclosure level.

16

Pennsylvania bonds issued between 1995 and 1999, β7 is significantly negative if disclosure and

insurance are substitutes. The remaining variables are controls.

We also use model 2 to test the regulation hypothesis, using the combined sample of

Michigan and Pennsylvania bonds issued between 1995 and 1999. An indicator variable is

added to the model, STATE, that has a value of one for Michigan issuers and zero for

Pennsylvania issuers. We examine whether the estimated coefficient for STATE is significantly

negative, indicating bond issues are less likely to be insured under regulation.

Control Variables. We employ a variable measuring the dollar amount of the bond issue

(LNAMOUNT), because larger issues can be more difficult to sell, and insurance may be

employed to make them more attractive. We include the number of new bonds issued (FREQ) to

measure the frequency with which a government goes to the bond market for financing, which

may affect the likelihood of insurance. We also use two indicator variables. The first

(GOBOND) is equal to one if the bond is a general obligation bond, and zero otherwise. Non-

general obligation bonds are not backed by the full faith and credit of the municipality, which

may increase the likelihood of insurance. The second dummy variable (PRIOR_INS) is equal to

one if an insured bond is issued in the prior year, and zero otherwise. The propensity to insure

an issue may be affected by whether the municipality already has an insured issue outstanding.

In addition, we use the population, debt per capita, and disclosure index variables defined in the

municipality- level tests. All of the bond issue variables are hand-collected from the Thomson

Financial Municipal Database.

IV. RESULTS

A. Descriptive Statistics and Correlations

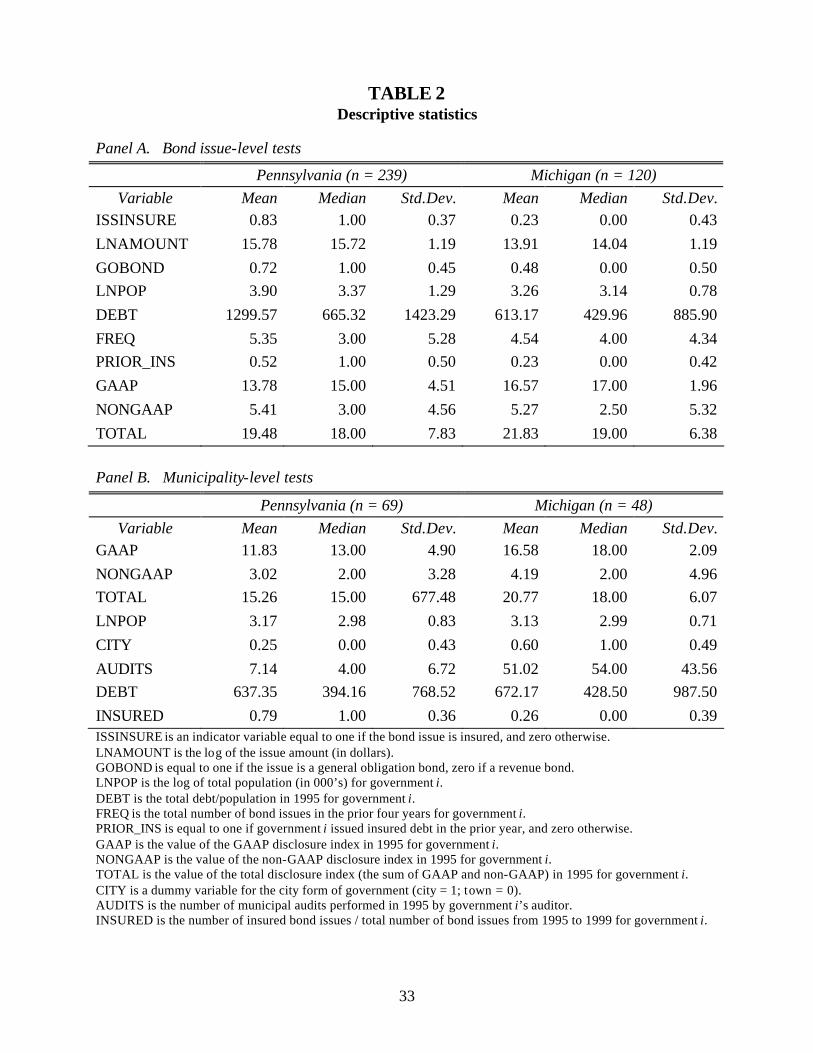

Table 2 contains descriptive statistics. Panel A presents descriptive statistics for the

bond- issue level samples from Pennsylvania and Michigan. The variable ISSINSURE indicates

17

that 83% of the Pennsylvania municipal issues between 1995 and 1999 are insured, compared to

only 23% of Michigan issues, consistent with the regulation hypothesis, although only a

univariate comparison.

(Insert Table 2 here)

Panel B of Table 2 shows descriptive statistics for the municipality- level samples from

each state. As one would expect, Michigan issuers have more GAAP disclosures (16.58 out of

18) and a smaller deviation in GAAP disclosures than do Pennsylvania issuers (11.83).35 This

finding suggests that Michigan issuers are predominantly GAAP compliant, which could

constrain their ability to substitute insurance for disclosure. The average Pennsylvania

municipality insured 79% of its debt issues between 1995 and 1999, compared to only 26% in

Michigan. This, like the similar statistic reported in Panel A, is consistent with the regulation

hypothesis. Michigan governments employ higher quality auditors than do Pennsylvania

municipalities, consistent with our reported results about GAAP compliance.

Table 3 contains correlation matrices for all tests. For the Pennsylvania municipality-

level tests (Panel A), significant Pearson partial correlations exist between the population and

city dummy variables (suggesting that larger municipalities tend to be cities), population and

debt per capita (suggesting that larger municipalities issue more debt per capita), and debt per

capita and the city dummy variable (suggesting that cities carry more debt than townships).

Panel B reports correlations for the Michigan municipality- level tests. It is notable that no

significant correlations exist in the Michigan sample except between audit quality and

population, implying that larger municipalities in Michigan employ higher quality auditors. We

checked condition indices for the two samples to ascertain whether there are problems with

35 Descriptive statistics for municipality-level variables differ between panels A and B of Table 2 because panel A weights all statistics according to the number of bond issues.

18

multicollinearity36. The condition indices are 9.1 for Panel A (GAAP only) and 3.0 for Panel B

(GAAP only), indicating only weak dependencies in these data sets.

(Insert Table 3 here)

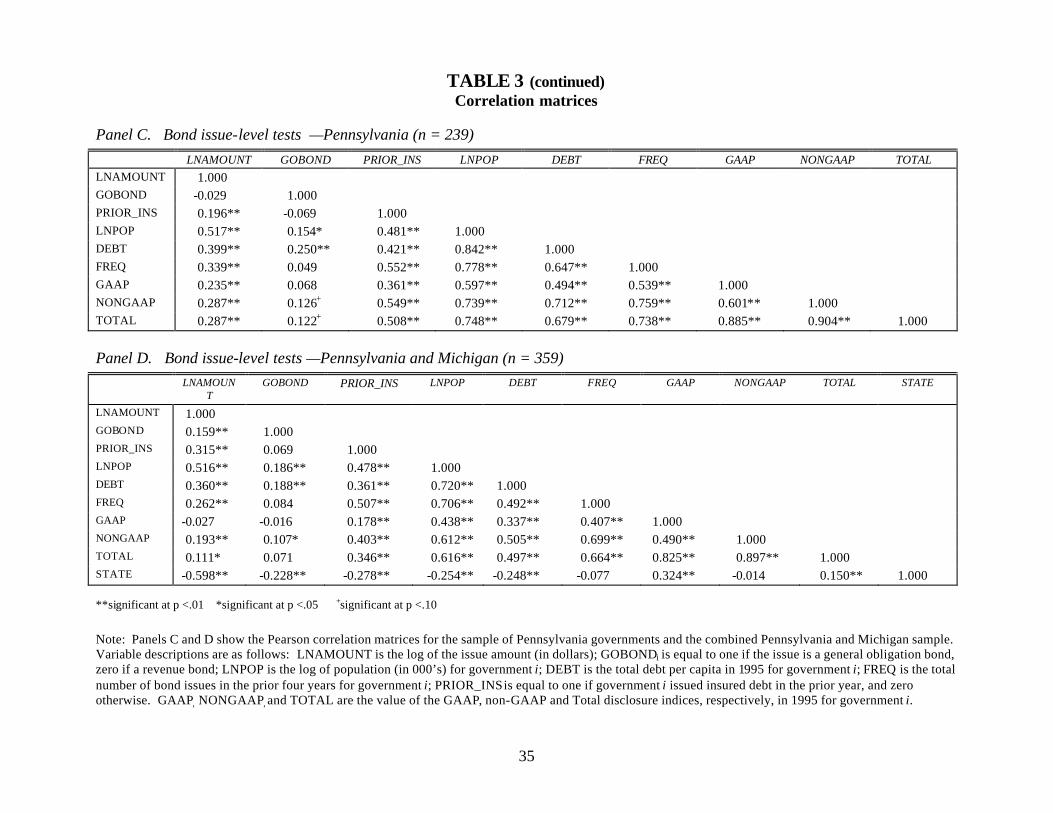

Panels C and D from Table 3 report correlations for the bond issue- level data from the

Pennsylvania and the combined Pennsylvania/Michigan samples used in tests of hypotheses 1

and 2, respectively. Pearson correlations are highly significant between almost all of the pairs of

independent variables. Condition indices for these data sets are 37.5 for Panel C (GAAP only)

and 20.5 for Panel D (GAAP only).37 Accepted econometric practice defines condition numbers

greater than 30 as indicating "moderate" multicollinearity38. We conclude that multicollinearity

is not severe in our covariance matrices.

B. Results of Hypothesis Tests

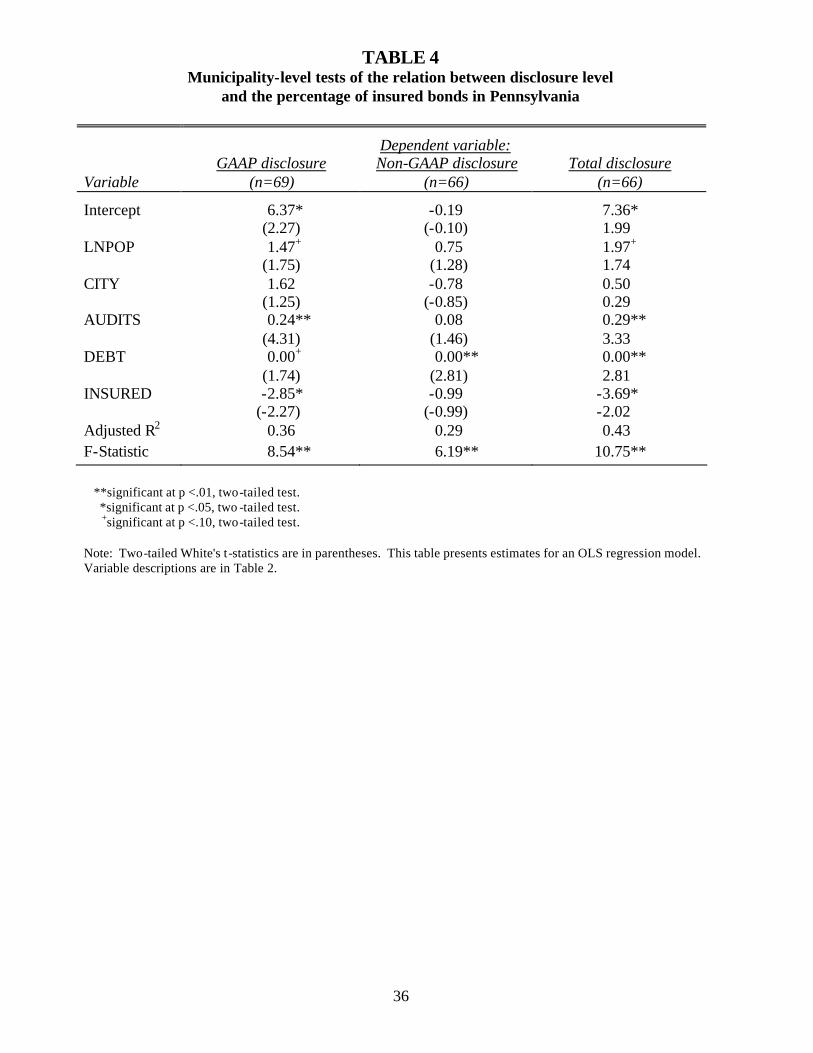

1. Hypothesis One: Substitution

The substitution hypothesis implies a negative relationship between the percentage of

insured bonds and disclosure level. Table 4 contains results of the municipality- level tests. We

examine the relationship between an issuer’s disclosure level, measured using three disclosure

indices, and the percentage of insured bonds (INSURED).

(Insert Table 4 here)

When GAAP disclosure is the dependent variable, we find a significant negative

association between disclosure and the percentage of insured bonds. This result is consistent

with substitution between GAAP disclosure and bond insurance. We find no significant

relationship, however, for non-GAAP disclosure. Debt per capita, a measure of debt-market

36 David Belsley, Edwin Kuh, & Roy Welsch, Regression Diagnostics: Identifying Influential Data and Sources of Collinearity (2000). 37 Condition indices for the non-GAAP and Total data sets are 34.8 and 21.7, respectively, in Pennsylvania and 35.6 and 21.2 in the combined sample. 38 Belsley, Kuh, & Welsch, supra note 36.

19

participation, is significantly positive for all definitions of disclosure, and noticeably more

significant for non-GAAP than for GAAP disclosures. These results imply that, although non-

GAAP disclosure is correlated with debt-market activity, consistent with borrowing cost

reductions, it is independent of the insurance decision. This could be the result of systematically

different costs and benefits between GAAP and non-GAAP disclosures. If, at the margin, non-

GAAP disclosure is more valuable than GAAP disclosure in reducing debt costs, then rational

issuers substitute GAAP disclosure for insurance before they substitute non-GAAP disclosure.

We note that the relationship between disclosure and insurance is significantly negative

for the TOTAL disclosure index as well. The TOTAL index represents the entire opportunity set

with respect to disclosures from which an unregulated issuer can choose to trade for insurance.

Therefore, this index represents the variable that comes closest to representing the actual choice

made by Pennsylvania issuers. Finally, we note audit quality is highly significant in the GAAP

disclosure decision, but not for non-GAAP, as might be expected.

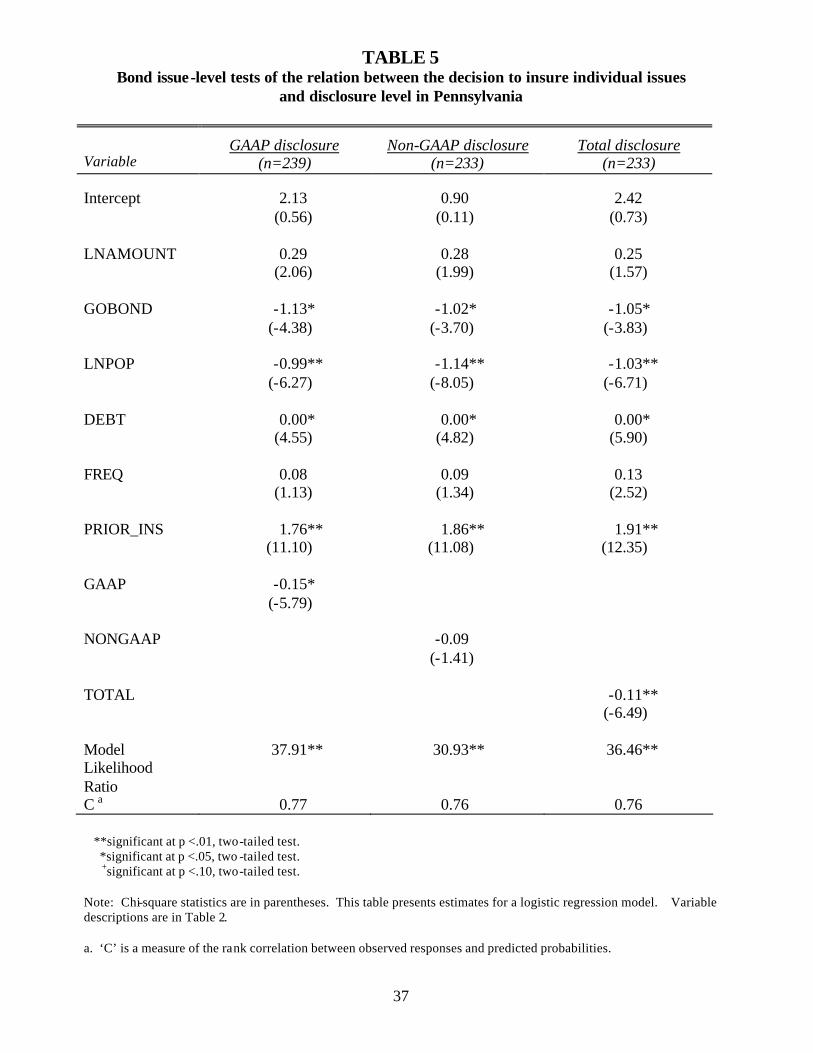

Table 5 contains logistic results of bond- issue level tests of the first hypothesis. We

include all 239 bonds issued by the Pennsylvania municipalities between 1995 and 1999. The

independent variable of interest is the disclosure variable (GAAP, non-GAAP, or TOTAL),

which is predicted to be negative if insurance and disclosure are substitutes.

(Insert Table 5 here)

Consistent with substitution and with the municipality- level test results, GAAP disclosure

is significant and negatively associated with the decision to insure. Results for non-GAAP

disclosure fail to reveal any significant negative association between the decision to insure a

bond and non-GAAP disclosure, similar to the results of the municipality- level tests.

When TOTAL disclosure is used in the logit analysis, it is negative and significant at the

1% level. This strong result arises from the TOTAL disclosure variable’s ability to better

20

capture the disclosure opportunity set from which issuers make decisions. In each of the three

specifications, the decision to insure is positively related to the prior use of bond insurance and

debt per capita. It is negatively related to the use of general obligation bonds, and negatively

associated with population, consistent with smaller municipalities more likely to insure. All

three specifications have model likelihood ratios significant at better than 1% and classification

accuracy rates in excess of 76%.

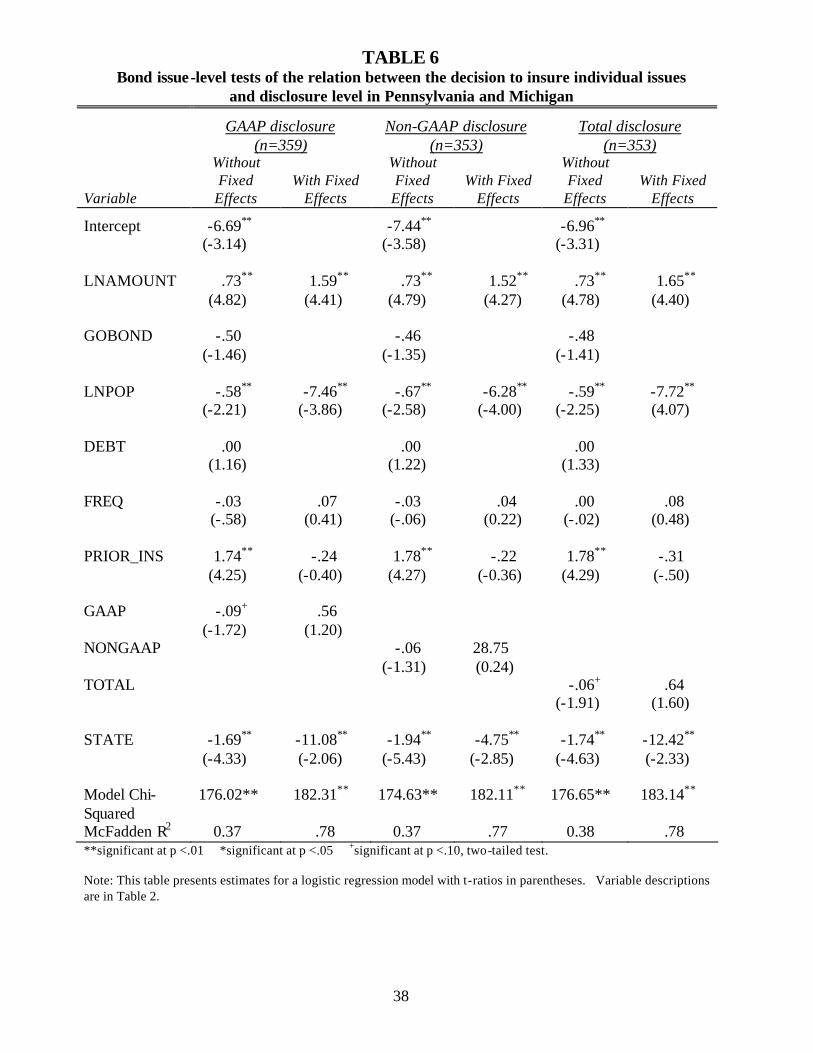

2. Hypothesis Two: Disclosure Regulation Under Substitution

In the regulation hypothesis, we argue that if disclosure and bond insurance are

substitutes then mandating a minimum level of disclosure makes bond insurance marginally less

valuable, and fewer bonds will be insured. We test this using logistic regressions at the bond

issue- level, combining 120 bond issues from Michigan (the regulated state) with the 239 issues

from Pennsylvania. Our variable of interest is STATE, coded one if the issuer is from Michigan,

and zero if from Pennsylvania. We examine whether STATE is negative, indicating that

Michigan issues are less likely to be insured, or positive, indicating issues are more likely to be

insured.39 However, using an individual bond as the dependent variable together with

independent variables that are defined at the municipality- level raises the possibility that the

residuals will not be independent across observations. To account for the influence of omitted

variables that vary by issuer we ran a “fixed effects” logit model where we specified dummy

variables for each of the issuers. This will control for the average effect of omitted variables that

vary by issuer40.

39 We do not perform combined sample tests of Model 1, where disclosure is the dependent variable, because GAAP is required in Michigan. Therefore, STATE would be significant due to the large difference in disclosure caused by Michigan’s GAAP requirement, as noted in Gore, supra note 20. 40 We used 107 (of 116 possible) dummy variables and had to drop two independent variables (DEBT and GOBOND) because of multicollinearity. With all of the independent variables and 116 dummy variables, the condition index of the matrix was 72,204,000. Belsley, Kuh & Welsch, supra note 36, argue that a condition index

21

Table 6 contains the regulation hypothesis test results. In the model without fixed effects,

for all three disclosure indices, there is a significant negative association between the state

dummy variable and the decision to insure, indicating Michigan issues are less likely to be

insured than are Pennsylvania issues. This is consistent with the scenario of insurance and

disclosure being substitutes, and insurance being less beneficial in Michigan, given the mandated

level of disclosure.

(Insert Table 6 here)

The models are all highly significant, with model likelihood ratios all significant at better

than 1%, and classification accuracy rates of better than 87%. Results on control variables are

similar to results reported for the Pennsylvania sample in Table 5. However, unlike the test of

the Pennsylvania sample, we find an insignificant coefficient on debt per capita and general

obligation bonds. We caution the reader against over- interpreting these findings, however, since

we constrain the coefficient estimates to be constant between the two states.

In the model with fixed effects, STATE is significant at the 5% level even controlling for

the influence of omitted variables on the constant of the logit model. We believe this is strong

evidence that regulation reduces the use of bond insurance. While the control variables LN

AMOUNT, LNPOP and PRIOR_INS are significant in the fixed effects model, the disclosure

variables are not. The latter may be due to the high correlation between STATE and GAAP

disclosure, since GAAP is required in Michigan, but not in Pennsylvania.

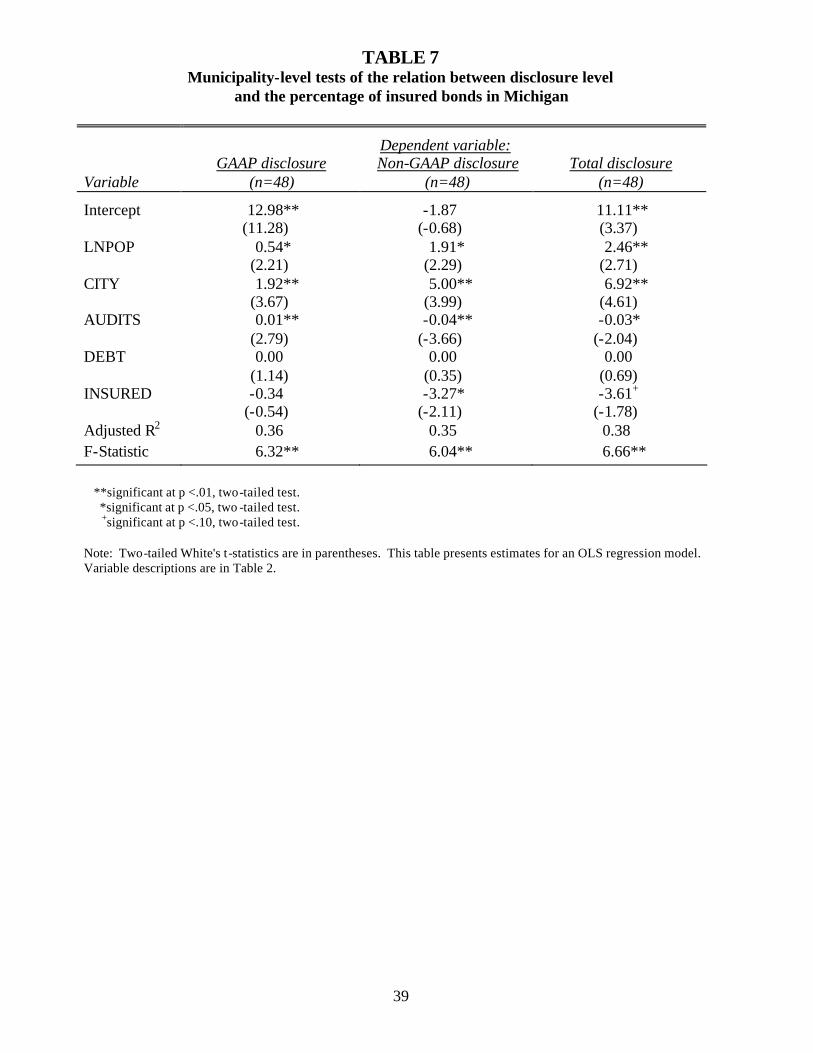

We next further explore the effects of disclosure regulation on the trade-off between

disclosure and insurance by presenting municipality- level tests of the regulation hypothesis,

of 30 indicates “moderate” multicollinearity and 100 indicates “severe” multicollinearity. We simply eliminated variables until the condition index was in the moderate range. The dummy variables were eliminated randomly, and the two independent variables were eliminated because of their high correlation with other variables.

22

confined to Michigan issuers, in Table 7.41 In doing so, we test an implication of the regulation

hypothesis: under regulation, the ability of an issuer to substitute disclosure for insurance is

constrained. In other words, for fewer bonds to be insured in the regulated state, GAAP

regulation will constrain the issuers’ ability to trade-off disclosures for insurance, thereby

rendering insurance a less attractive option. We therefore expect that INSURED will be

insignificant in the Michigan sample.

Regression results for GAAP disclosure on the INSURED variable show, as we expect,

no significant association between GAAP disclosure and the percentage of insured bonds. Note

that in spite of the GAAP requirement, we find several of the control variables are significant

(LNPOP, CITY, and AUDITS), indicating that there are GAAP violators (non-compliance) in

Michigan. The insignificant coefficient on INSURED is consistent with GAAP regulation

constraining the ability of municipal officials to substitute GAAP disclosure for insurance. We

also find a significant negative coefficient on INSURED for the non-GAAP regression. This

differs from the Pennsylvania sample results in Tables 4 and 5, where we find a significant

negative relationship between GAAP disclosure and insurance, and no relationship between non-

GAAP disclosure and insurance. Our finding is consistent with disclosure regulation

constraining the ability of issuers to substitute GAAP disclosure for insurance, but substituting

non-GAAP disclosure instead. If the ability to substitute non-GAAP for GAAP disclosure in the

trade for insurance is sufficiently large, the prediction of less insurance under regimes of GAAP

regulation will not hold. However, taken with the result that fewer Michigan issues are insured,

we interpret the combined findings to imply that, although some substitution of non-GAAP for

GAAP disclosure takes place under regulation, the overall ability to trade disclosure for 41 Although this can be construed as an additional test of H1, we restrict our initial tests of H1 to an unregulated disclosure environment (Pennsylvania) to avoid the potentially confounding effects of regulation. For example, ex ante one would expect there to be insufficient variation in GAAP disclosure to adequately test this hypothesis using Michigan data. Statistics presented in Table 2 bear this out, showing a small standard deviation in GAAP disclosure in Michigan compared to Pennsylvania.

23

insurance remains sufficiently constrained to preclude the insurance option for a significant

number of issues.

(Insert Table 7 here)

V. SENSITIVITY TESTS

We examine the sensitivity of our results to alternative design specifications. We

separate the tests into two categories, alternative measures of disclosure and insurance, and

alternative functional specifications. We briefly describe the rationale for each test, and the

effects of the tests on our inferences.

A. Alternative Disclosure Measures

A key component of our research design is our measure of disclosure. Therefore, we

assess the sensitivity of our results to the disclosure proxies by using two alternative measures.

The first, a disclosure index based on Copley, 42 is considered a measure of GAAP disclosures.

The second is a dummy variable indicating whether the municipality won a Government Finance

Officers Association (GFOA) certificate of achievement. The latter variable is used in studies to

represent voluntary (non-GAAP) disclosure.43

The results of these tests do not differ significantly from those reported. Thus, we again

find a negative association between GAAP disclosure and bond insurance, and a lack of

association between non-GAAP disclosure and bond insurance.

B. Alternative Insurance Measures

Another important part of our research design is our measure of insurance. We assess

the implicit assumptions made previously in our insurance measure in several ways. First, for

the tests reported in Table 4, we assess our assumption that disclosure precedes bond issuance,

42 See Copley, supra note 27. 43 See Evans & Patton, supra note 31.

24

that is, our use of the percentage of insured bonds issued from the disclosure year, 1995, through

1999. We now assume that bond issuance precedes disclosure, and measure insurance using

bonds issued from 1991 through 1995. The results of these tests, not shown in the tables, are

generally consistent with those reported. Second, for the tests reported in Table 6, we assess our

use of the number of insured bond issues by replacing this variable with the dollar value of

insured bonds (dollar value of insured bonds / dollar value of total bonds issued). The results of

these tests, not shown in the tables, are generally consistent with those reported.

C. Alternative Functional Specifications

1. State Dummy Interaction Term

To ascertain whether the regulation hypothesis results in Table 6 are attributable to a shift

in the slope coefficients between the states, we interact the STATE dummy variable with the

remaining independent variables. Including this interactive term does not affect our inferences.

The STATE intercept dummy variable is still significantly negative.

2. Simultaneous Equations

We hypothesize that disclosure and insurance are jointly related. Testing this hypothesis

by using a simultaneous equations model assumes our hypothesis is true. However, conditional

on the above findings, we should find that a simultaneous equation system does, in fact,

represent the joint endogeneity of the insurance and disclosure variables. To support or reject our

previous findings we use two-stage least squares to estimate two equations simultaneously. The

first has disclosure as the dependent (endogenous) variable and all of the independent variables

from Model 1, including the percentage of insured bonds, as independent variables. The second

equation has the percentage of insured bonds as the dependent variable, and all of the other

independent variables from Model 1, plus disclosure, as independent variables. Using the

combined sample of Michigan and Pennsylvania municipalities, we find that there is a

25

significant, simultaneous relationship (p-value lower than .01) between the percentage of insured

bonds and disclosure, when disclosure is measured by GAAP or TOTAL. When disclosure is

measured by NONGAAP, however, the relationship is insignificant. Since disclosure and

insurance are both used by issuers to reduce debt costs, the two stage least squares results

confirm our prior findings.

3. Independence

Our regressions in Tables 5 and 6 contain incidences where individual municipalities

issue multiple bonds. The use of individual bonds as the dependent variable together with

independent variables that are defined at the municipality- level raises the possibility that the

residuals will not be independent across observations. We use a "fixed effects" model to

mitigate any dependence in the residuals, but the model may not be entirely appropriate since

over 30% of our sample contains municipalities with only one bond issue. We therefore run

regressions where we use the average of the variables shown in Tables 5 and 6, and the

percentage of insured bonds as the dependent variable, thus resulting in one observation per

municipality. The results of these tests are consistent with those presented, and demonstrate that

a lack of independence does not affect our inferences.

VI. CONCLUSION

We provide evidence on the use of alternative mechanisms to reduce the cost of capital

for municipal issuers by examining the empirical relationship between public financial disclosure

and bond insurance. We argue that if disclosure and bond insurance are substitutes, then the

effect of regulating a minimum level of disclosure is to render insurance less beneficial in debt-

cost reduction, and fewer bonds will be insured.

Our findings are strongly consistent with substitution. When municipalities are free to

choose among combinations of debt-cost reducing mechanisms, they substitute GAAP

26

disclosures with bond insurance. When disclosure is regulated, issuers insure bonds less

frequently.

An implication of our results is that the regulation of accounting disclosure can force

disclosure levels too high, thus rendering substitute mechanisms, such as bond insurance, less

beneficial at reducing debt costs. Where mandatory disclosure levels are high and regulation is

pervasive, as in the corporate sector, alternative capital-cost reducing mechanisms may not be

discovered. We also find evidence consistent with regulation inducing issuers to substitute non-

mandated disclosures for mandated disclosures in the trade-off of one debt-cost reducing

mechanism for another. An implication of this finding is if additional disclosures are made

mandatory the ability of issuers to make efficient combinations of debt-cost reducing

mechanisms will be further constrained.

Our study has limitations, however. First, we examine the relationship between the levels

of two factors, in the cross section, without reference to their costs. This choice is driven by the

unavailability of insurance premium and disclosure-cost data. Second, we utilize one year of

disclosure data collected from two states, raising the possibility that our results may not

generalize to other states or the corporate sector.

The results of our study should be cautiously extended beyond the market for municipal

debt. While mechanisms such as insurance on commercial paper exist in the corporate sector, it

is not clear whether substitution of such insurance with disclosure is important, or even

meaningful, since the same corporate issuers often have publicly traded equity capital. However,

taken as a whole, the strong evidence we find of substitution between signals given by rational

managers to the market suggests that corporate issuers would engage in similar substitutions if

allowed.

27

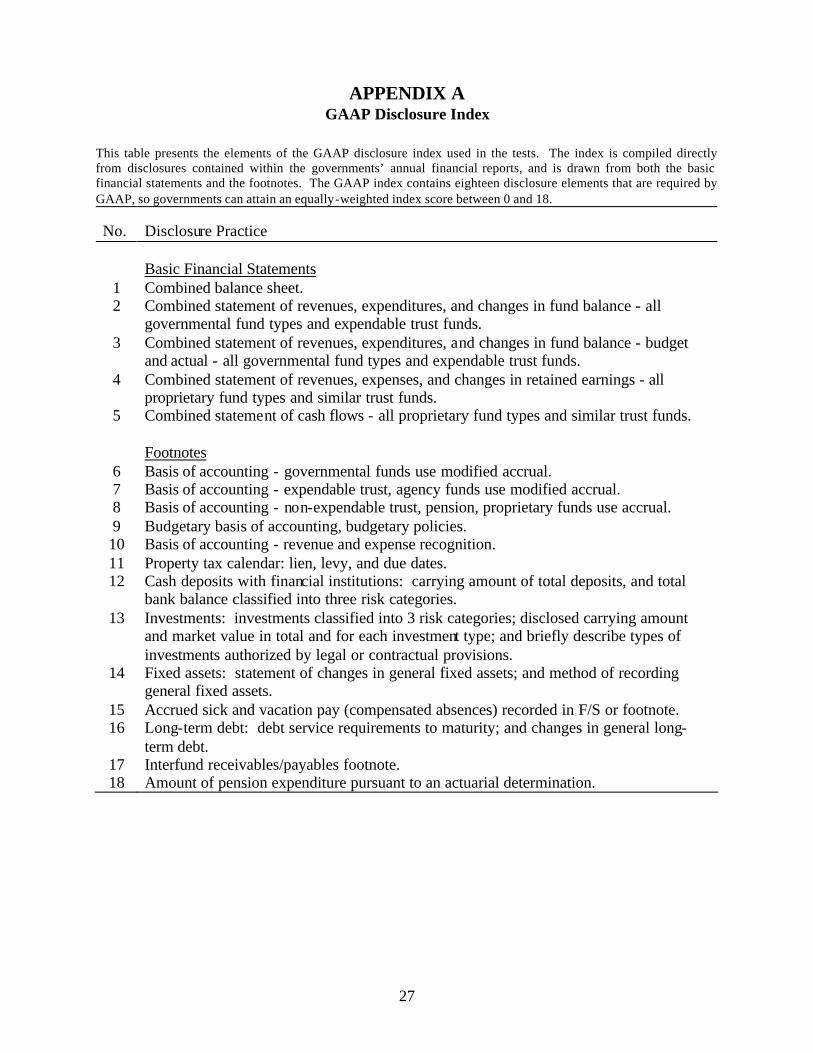

APPENDIX A GAAP Disclosure Index

This table presents the elements of the GAAP disclosure index used in the tests. The index is compiled directly from disclosures contained within the governments’ annual financial reports, and is drawn from both the basic financial statements and the footnotes. The GAAP index contains eighteen disclosure elements that are required by GAAP, so governments can attain an equally-weighted index score between 0 and 18.

No. Disclosure Practice

Basic Financial Statements 1 Combined balance sheet. 2 Combined statement of revenues, expenditures, and changes in fund balance - all

governmental fund types and expendable trust funds. 3 Combined statement of revenues, expenditures, and changes in fund balance - budget

and actual - all governmental fund types and expendable trust funds. 4 Combined statement of revenues, expenses, and changes in retained earnings - all

proprietary fund types and similar trust funds. 5 Combined statement of cash flows - all proprietary fund types and similar trust funds. Footnotes 6 Basis of accounting - governmental funds use modified accrual. 7 Basis of accounting - expendable trust, agency funds use modified accrual. 8 Basis of accounting - non-expendable trust, pension, proprietary funds use accrual. 9 Budgetary basis of accounting, budgetary policies. 10 Basis of accounting - revenue and expense recognition. 11 Property tax calendar: lien, levy, and due dates. 12 Cash deposits with financial institutions: carrying amount of total deposits, and total

bank balance classified into three risk categories. 13 Investments: investments classified into 3 risk categories; disclosed carrying amount

and market value in total and for each investment type; and briefly describe types of investments authorized by legal or contractual provisions.

14 Fixed assets: statement of changes in general fixed assets; and method of recording general fixed assets.

15 Accrued sick and vacation pay (compensated absences) recorded in F/S or footnote. 16 Long-term debt: debt service requirements to maturity; and changes in general long-

term debt. 17 Interfund receivables/payables footnote. 18 Amount of pension expenditure pursuant to an actuarial determination.

28

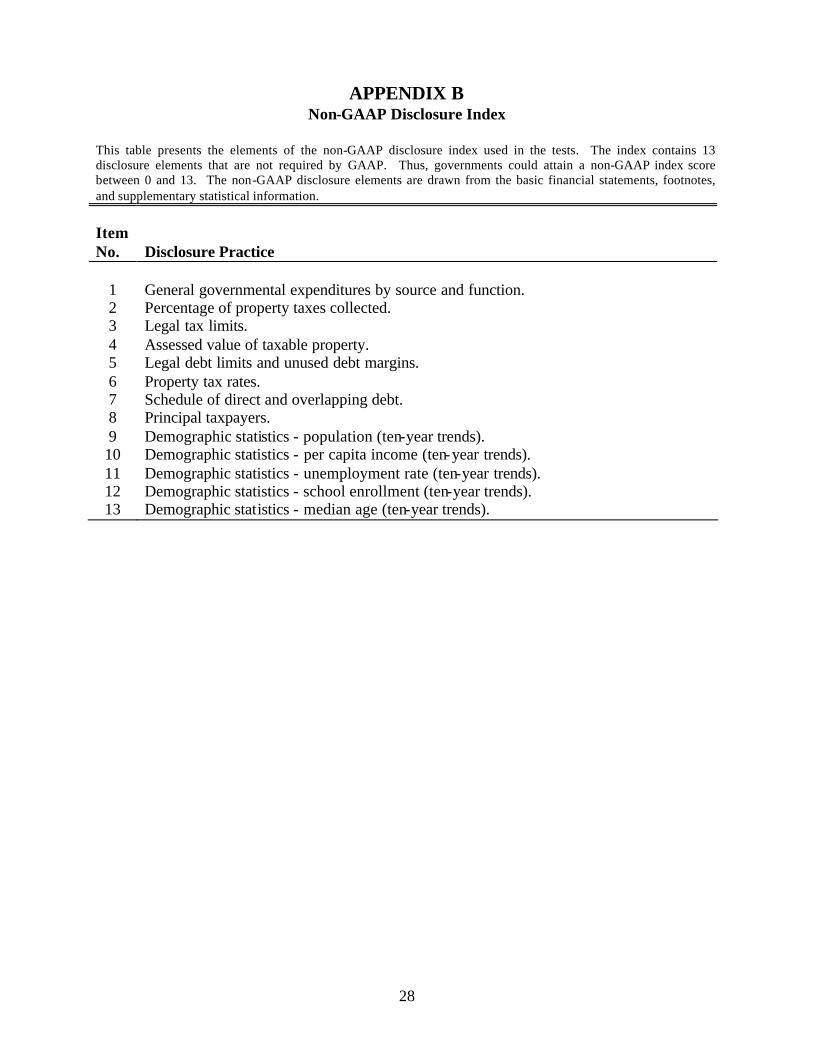

APPENDIX B Non-GAAP Disclosure Index

This table presents the elements of the non-GAAP disclosure index used in the tests. The index contains 13 disclosure elements that are not required by GAAP. Thus, governments could attain a non-GAAP index score between 0 and 13. The non-GAAP disclosure elements are drawn from the basic financial statements, footnotes, and supplementary statistical information.

Item No. Disclosure Practice

1 General governmental expenditures by source and function. 2 Percentage of property taxes collected. 3 Legal tax limits. 4 Assessed value of taxable property. 5 Legal debt limits and unused debt margins. 6 Property tax rates. 7 Schedule of direct and overlapping debt. 8 Principal taxpayers. 9 Demographic statistics - population (ten-year trends). 10 Demographic statistics - per capita income (ten-year trends). 11 Demographic statistics - unemployment rate (ten-year trends). 12 Demographic statistics - school enrollment (ten-year trends). 13 Demographic statistics - median age (ten-year trends).

29

BIBLIOGRAPHY Amihud, Yakov; Garbade, Kenneth; and Kahan, Marcel. "A New Governance Structure for

Corporate Bonds." Stanford Law Review 51 (1999): 447-492. Amihud, Yakov and Mendelson, Haim. "The Liquidity Route to a Lower Cost of Capital."

Journal of Applied Corporate Finance 12 (2000): 8-25. Amihud, Yakov and Mendelson, Haim. "Asset Pricing and the Bid-Ask Spread." Journal of

Financial Economics 17 (1986): 223-249. Barry, Christopher B. and Brown, Stephen J. "Differential Information and the Small Firm

Effect." Journal of Financial Economics 13, No. 2 (1984): 283-295. Barry, Christopher B. and Brown, Stephen J. "Differential Information and Security Market

Equilibrium." Journal of Financial and Quantitative Analysis 20 (1985): 407-422. Belsley, David; Kuh, Edwin; and Welsch, Roy. Regression Diagnostics: Identifying Influential

Data and Sources of Collinearity. New York: John Wiley & Sons, 2000. Benson, Earl D. "The Search for Information by Underwriters and its Impact on Municipal

Interest Cost." Journal of Finance 34 (1979): 871-884. Benson, Earl D.; Marks, Barry R.; and Raman, K. K. "The Effect of Voluntary GAAP

Compliance and Financial Disclosure on Governmental Borrowing Costs." Journal of Accounting, Auditing, and Finance 6 (1991): 303-319.

Bland, Robert L. and Chilik, Yu. "Municipal Bond Insurance: an Assessment of its

Effectiveness at Lowering Interest Costs." Government Finance Review 3 (1987): 23-26. Botosan, Christine. "Disclosure Level and the Cost of Equity Capital." The Accounting Review

72 (1997): 323-349. Campbell, John; Lo, Andrew; and Mackinlay, Craig. Econometrics of Financial Markets,

Princeton University Press, 1997. Copley, Paul. "The Association Between Municipal Disclosure Practices and Audit Quality."

Journal of Accounting and Public Policy 10 (1991): 245-266. Core, John. "A Review of the Empirical Disclosure Literature: Discussion." Journal of

Accounting and Economics 31 (2001): 441-456. Diamond, Douglas W. and Verrecchia, Robert E. "Disclosure, liquidity, and the Cost of Capital.

The Journal of Finance 46 (1991): 1325-1355. Easterbrook, Frank H. and Fischel, Daniel R. The Economic Structure of Corporate Law.

Cambridge, MA: Harvard University Press, 1991.

30

Evans, John and Patton, James. "An Economic Analysis of Participation in the Municipal Finance Officers Association Certificate of Conformance Program." Journal of Accounting and Economics 5, No. 2 (1983): 151-175.

Fairchild, Lisa M. and Koch, Timothy W. "The Impact of State Disclosure Requirements on

Municipal Yields." National Tax Journal, 51, 4 (1998): 733-753. Gore, Angela K. "The Effects of GAAP Regulation on Local Government Disclosure."

Unpublished working paper. University of Oregon, 2003. Healy, Paul M. and Palepu, Krishna G. "Information Asymmetry, Corporate Disclosure, and the

Capital Markets: A Review of the Empirical Disclosure Literature." Journal of Accounting and Economics 31 (2001): 405-440.

Hopewell, Michael H. and Kaufman, George G. "Commercial Bank Bidding on Municipal

Revenue Bonds: New Evidence." Journal of Finance 32 (1977): 1647-1656. Ingram, Robert and DeJong, Douglas. "The Effect of Regulation on Local Government

Disclosure Practices." Journal of Accounting and Public Policy 6 (1987): 245-270. Jarrell, Gregg. "Change at the Exchange: the Causes and Effects of Deregulation." Journal of

Law and Economics 27 (1984). Jensen, Michael, and Meckling, William. "Theory of the Firm: Managerial Behavior, Agency

Costs, and Ownership Structure." Journal of Financial Economics 3 (1976): 305-360. Kessel, Rueben A. "A Study of the Effects of Compeition in the Tax-Exempt Bond Market."

Journal of Political Economy 79 (1971): 706-738. Kidwell, David; Sorensen, Eric; and Wachowicz, John. "Estimating the Signaling Benefits of

Debt Insurance: the Case of Municipal bonds." Journal of Financial and Quantitative Analysis 22, No. 3 (1987): 299-313.

Kim, Oliver and Verrecchia, Robert E. "Market Liquidity and Volume Around Earnings

Announcements." Journal of Accounting and Economics 17 (1994): 41-68. Lang, Mark H. and Lundholm, Russell. "Corporate Disclosure Policy and Analyst Behavior."

The Accounting Review 71 (1996): 467-493. Leftwich, Richard. "Market Failure Fallacies and Accounting Information." Journal of

Accounting and Economics 2 (1980): 193-211. Mayers, David, and Smith, Jr., Clifford W. "On the Corporate Demand for Insurance." The

Journal of Business 55, No. 2 (1982): 281-296. MBIA internet home page. Myers, Stewart C. and Majluf, Nicholas S. "Corporate Financing and Investment Decisions

When Firms Have Information That Investors do not Have." Journal of Financial Economics 13 (1984): 187-222.

31

National Association of State Auditors, Comptrollers, and Treasurers (NASACT). State

Comptrollers: Technical Activities and Functions, NASACT, Lexington, KY, 1996. Ritter, Jay. "The Costs of Going Public." Journal of Financial Economics 19 (1987): 269. Robbins, Walter, and Austin, K. "Disclosure Quality in Governmental Financial Reports: an

Assessment of the Appropriateness of a Compound Measure." Journal of Accounting Research, 24, No. 2 (1986): 412-421.

Sengupta, Partha. "Corporate Disclosure Quality and the Cost of Debt." The Accounting Review

73, 4 (1998): 459-474. Sorenson, Eric. "An Analysis of the Relationship Between Underwriter Spread and the Pricing

of Municipal Bonds." Journal of Financial and Quantitative Analysis 15 (1980): 435-447. Thakor, Anjan. "An Exploration of Competitive Signalling Equilibria with ‘Third Party’

Information Production: the Case of Debt Insurance." The Journal of Finance 37 (1982): 717-739.

Watts, Ross L. and Zimmerman, Jerald L. Positive Accounting Theory. Englewood Cliffs, N.J.,

Prentice Hall, 1986. Welker, Michael. "Disclosure Policy, Information Asymmetry and Liquidity in Equity

Markets." Contemporary Accounting Research 11 (1995): 801-828. Zimmerman, Jerald L. "The Municipal Accounting Maze: an Analysis of Political Incentives."

Journal of Accounting Research 15 (Supplement) (1977): 107-144.

32

TABLE 1 Summary of sample selection procedures

Panel A: Michigan sample

# municipalities # bond issues

Total local governments in Michigan 1,800 Less governments with population < 10,000 and governments other than cities and townships

1,634

Total Michigan cities and townships with populations > 10,000

166

Financial reports not available 88 Total financial reports 88 No bonds issued 1995-1999 40 Final sample 48 120

Panel B: Pennsylvania sample

Total local governments in Pennsylvania 2,498 Less governments with population < 10,000 and governments other than cities and townships

2,288

Total Pennsylvania cities and townships with populations > 10,000

201

Randomly selected 92 Financial reports not available 05 Total financial reports 87 No bonds issued 1995-1999 18 Final sample 69 239

33

TABLE 2 Descriptive statistics

Panel A. Bond issue-level tests

Pennsylvania (n = 239) Michigan (n = 120) Variable Mean Median Std.Dev. Mean Median Std.Dev.

ISSINSURE 0.83 1.00 0.37 0.23 0.00 0.43 LNAMOUNT 15.78 15.72 1.19 13.91 14.04 1.19 GOBOND 0.72 1.00 0.45 0.48 0.00 0.50 LNPOP 3.90 3.37 1.29 3.26 3.14 0.78 DEBT 1299.57 665.32 1423.29 613.17 429.96 885.90 FREQ 5.35 3.00 5.28 4.54 4.00 4.34 PRIOR_INS 0.52 1.00 0.50 0.23 0.00 0.42 GAAP 13.78 15.00 4.51 16.57 17.00 1.96 NONGAAP 5.41 3.00 4.56 5.27 2.50 5.32 TOTAL 19.48 18.00 7.83 21.83 19.00 6.38 Panel B. Municipality-level tests

Pennsylvania (n = 69) Michigan (n = 48) Variable Mean Median Std.Dev. Mean Median Std.Dev.