Feasibility study on waste utilization of a palm oil refinery

252

N E DO- I C-00ER25 020005089 FeasibiIity Study on Waste Utilization of a Palm Oil Refinery March. 2001 New Energy and Industrial Technologies Development Organization (NEDO) Listed Kawasaki Heavy Industries, Ltd. -6

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Feasibility study on waste utilization of a palm oil refinery

N E DO- I C-00ER25

020005089

FeasibiIity Study onWaste Utilization of a Palm Oil Refinery

March. 2001

New Energy and Industrial Technologies Development Organization (NEDO)

Listed Kawasaki Heavy Industries, Ltd.

-6

Feasibility study on waste utilization on palm oil refinery

(Entrusted) Kawasaki Heavy Industries, Ltd. March. 2001

Study purpose ;

This study intends to realize high conservation of fossil fuels consumed by the existing diesel generator & boiler and the reduction of methane gas discharged from palm waste by introducing a high-efficiency fluidized bed boiler co generation system to utilize palm waste to palm oil refinery. As a result, the much reduction of greenhouse gas can be expected.

N E DO- I C-00ER25

FeasibiIity Study onWaste Utilization of a Palm Oil Refinery

Marchx 2001

New Energy and Industrial Technologies Development Organization (NEDO)

Entrusted Kawasaki Heavy Industries, Ltd.

PREFACE

PREFACEThis report represents the results of the “Feasibility Study on Waste Utilization of a

Palm Oil Refinery”, which was carried out by KAWASAKI HEAVY INDUSTRIES, LTD.,

entrusted by New Energy and Industrial Technologies Development Organization

(NEDO), as a part of the “Basic Survey for Promotion of Joint Implementation, etc.” in

the 2000 fiscal year.

In the “Kyoto Protocol” which was adopted as the Third Conference of the Parties

(COPS) to the United Nations Framework Convention on Climate Change (UNFCCC)

held in Kyoto in December 1997, the “Targets for Greenhouse Gases Reduction” was

fixed, and as means of attaining the targets, the “Joint Implementation (JI)” system to

share among advanced countries the volume of Greenhouse Gases to be reduced, and

the system: “Clean Development Mechanism (CDM)” to be participated by both

advanced and developing countries, were also determined.

Japan, too, must take step forward to attain its targets with these systems utilized

positively. As a part of such steps, this feasibility study was carried out introducing a

co generation equipment with the fluidizer bed boiler using as fuel the palm waste

being dumped so far to the Lahad Datu works of the company: FELDA VEGETABLE

OIL PROEUCTS in Malaysia, which was intended for the promotion of energy

substantiation and which was also intended for the control of methane gas generated

from the dumped waste and was further intended for the reduction of CO2 discharge

originating from fossil fuel being used so far in the existing diesel generator and boiler,

to link it with the future CDM.

When such a co generation are introduced into FELDA VEGETABLE OIL PROEUCTS,

the subject company of this survey, the results are obtained such as it is feasible both in

technology and in economy or finance and it effect can also be expected in energy

substitution and in Green House Gases reduction, and moreover that it can contribute

to the prevention of the earth’s warming as well, with improvement in its economy.

The introduction of such co generation is expectable, in Malaysia, to other palm oil

companies, and other districts as well, because the palm oil industry holds a dominant

position in Malaysian industries and generates a great volume of palm waste, and

therefore, taking into account the conformance of such a project to the Malaysian energy

P-1

policy, such a project can be regarded as a scheme in which a great possibility of

materialization can be seen.

During the period of this survey technological interchange was made three times

between FELDA and our company and adjustments were also carried out through

hearing on technological items, field investigations at the enforcement site for the

power plant, draft making and discussions on the fundamental scheme, etc. In result,

a fundamental agreement was attained so as to direct their steps toward the realization

of the project could be reached.

March 3, 2001

KAWASAKI HEAVY INDUSTRIES, LTD.

A List of Investigators’ Names:

(KAWASAKI HEAVY INDUSTRIES, LTD.)

Role Name Belonging Sec./Dept Post• Business management /

Staff in charge of survey T.Arai Boiler Plant Dept. Senior Staff Officerimplementation

• Business management /Staff in charge of sales T. Michino Power Plant Sales Dept. 1 Senior Manager

• Business management /Assistant to staff in charge of M. Yamamoto Boiler Plant Dept. Utility Sect. Managersurvey implementation

• Supervisor in charge of engineering Y. Tsunematsu Boiler Plant Dept. Utility Sect. Staff" Officer• Supervisor in charge of sales MYamada Power Plant Sales Dept. 1 Senior Staff" Officer• Assistant to supervisor in charge TMizumoto Power Plant Sales Dept. 1 Staff Officer

of sales• Sales in charge T. Hamada Power Plant Sales Dept. 1 Attendant• Sales in charge T. Suzuki Power Plant Sales Dept. 1 Attendant• Combustion facility design YTanabe Boiler Plant Dept Utility Sect. Staff Officer• Staff in charge of overall project T. Miyoshi Boiler Plant Dept. Utility Sect. Staff'Officer

Boiler Plant Dept. Utility Sect.JL. JLkSWLiJLVX X

• Staff in charge of overall project Y.Yosino Boiler Plant Dept. Utility Sect. Attendant• Supervising of boiler facility H. Sasaki Boiler Plant Dept. Industrial

Sect.Manager

• Boiler facility planning Y.Miki Boiler Plant Dept. Industrial Sect.

Staff Officer

• Boiler facility planning in charge KSunaga Boiler Plant Dept. Industrial Sect.

Attendant

• Supervising of Control system S. Tanaka Power Plant E & C Dept Senior Manager• Control system planning T.Itoh Power Plant E &C Dept Manager• Electric and control system N. Wasada Power Plant E &C Dept Staff Officer

design in charge• Electric and control system T. Umeki Power Plant E & C Dept Assistant Manager

design• Supervising of combustion

systemN.Takahashi Research & Development

Dept.Senior Manager

• Supervising of analysis and test C. Kurata R&D Dept. Manager• Combustion system planning T.Ino R&DDept. Staff'Officer• Analysis and test in charge KTaniguchi R&D Dept Assistant Manager• Assistant to staff in charge of T.Aoki R&DDept. Attendant

engineering management• Crushing facility in charge K. Miyoshi Crushing Plant Div. R&D

Sect.Attendant

• Supervising of civil engineering H. Koike Production Control Dept Senior Managerand construction work planning

• Civil engineering and S. Ozaki Production Control Dept. Managerconstruction work planning

• Civil engineering and T. Zama Production Control Dept. Staff Officerconstruction work planning

• Supervising of tax system, etc S. Sakabe Control Dept. Senior Managersurvey

• Tax system survey and S. Sekikawa Control Dept. Assistant Managersubcontract in charge

• Cost calculation in charge T.Yasui Control Dept. Manager

CONTENTS

SUMMARY

CHAPTER 1 FUNDAMENTAL ITEMS OF THE PROJECT......... l-l1.1 Situations of Partner Country............................................................................ 1 — 11.1.1 An Outline of General Affairs........................................................................ 1 — 11.1.1.1 Territory........................................................................................................ 1 — 11.1.1.2 Location........................................................................................................... 1 — 11.1.1.3 Population....................................................................................................... 1 — 11.1.1.4 Races............................................................................................................... 1—21.1.1.5 Language ...................................................................................................... 1 — 21.1.1.6 Climate........................................................................................................... 1—21.1.1.7 Currency......................................................................................................... 1 — 21.1.1.8 Visa................................................................................................................... 1—21.1.1.9 Difference in Time ...................................................................................... 1 — 31.1.1.10 Religion............................................................................................................ 1 — 31.1.1.11 King.................................................................................................................. 1-31.1.1.12 Designations of Ranks.................................................................................. 1 — 31.1.1.13 Education........................................................................................................ 1 — 41.1.1.14 Number of Japanese Residents................................................................... 1—41.1.1.15 A Brief History............................................................................................. 1 — 51.1.2 Politics............................................................................................................. 1 — 61.1.2.1 Political System........................................................................................... 1—61.1.2.2 Federal Congress System........................................................................... 1 — 61.1.2.3 Political Parties............................................................................................. 1—61.1.2.4 Big Project Conceptions............................................................................. 1 — 71.1.2.5 Countermeasures in the Asian Currency Crisis.................................... 1 — 71.1.2.6 Mahathir Ism ............................................................................................... 1—81.1.2.7 Cabinet Members......................................................................................... 1—91.1.3 Economy................................................................................................................. 1 — 101.1.3.1 General Condition of Economy.................................................................... 1 — 101.1.3.2 Trade.................................................................................................................. 1-121.1.3.3 Recent Political and Economical Affairs................................................... 1 — 131.2 Palm Oil Industry in Malaysia........................................................................ 1 — 141.2.1 History and Present Status of Palm Oil Industry..................................... 1 — 141.2.2 Condition of Location for Palm Oil Mills..................................................... 1 — 161.2.3 Evil Influences of Palm Oil Mills and

Environmental Countermeasures................................................................. 1 — 16

— C— 1 —

1.3 Energy Conditions............................................................................................ 1 — 181.3.1 Change of Energy in Malaysia........................................................................ 1 — 181.3.2 Electric Power Situation in Malaysia............................................................ 1—201.3.2.1 Demand-and-Supply Balance of Electric Power....................................... 1 — 201.3.2.2 Controversial Points between Power Demand in Future

and Supply Reinforcing Programs................................................................ 1—201.4 Need of Project Linked with CDM, etc...................................... ...................... 1 — 221.4.1 Need of Project as Seen from Policy Side ................................................... 1 — 221.4.2 Prospect for Cooperation from Government............................................... 1 — 231.4.2.1 Pioneer Status.................................................................................................. 1—231.4.2.2 Investment Tax Allowance (ITA).................................................................. 1—231.4.2.3 Reinvestment Allowance (RA)...................................................................... 1 — 241.4.2.4 Favorable Treatment Actions for R & D ................................................... 1 — 241.4.2.5 Favorable Treatment Actions for Advanced-Technology Industry-----1 — 241.5 Necessity of Introducing Alternative Energy Technology

in the Industry as Object of Project.................................................................. 1—251.6 Meaning, Need and Effect of Project in Question and Spread in

Possibility of Similar Industry............................................................................ 1—26

CHAPTER 2 CONCRETIZATION OF PROJECT PLAN 2-12.1 Project Plan............................................................................................................ 2—12.1.1 Overview of the Project Site............................................................................ 2—12.1.1.1 Geography ........................................................................ ............................ 2—12.1.1.2 Climate and Rainfall Amount at Site ....................................................... 2—22.1.1.3 Population.......................................................................................................2—32.1.1.4 Project Site.......................................................................................................2—42.1.1.5 Power Demand...............................................................................................2—52.1.2 Contents of Project..........................................................................................2—62.1.3 Objective Green House Gases, etc. ............................................................. 2—72.2 Outline of Enforcement Site (Enterprise)..................................................... 2—82.2.1 Degree of Interest at Enforcement Site (Enterprise)...............................2—82.2.1.1 Outline of FELDA Group............................................................................ 2—82.2.1.2 Status of Earning Rate (Profit).................................................................. 2 — 102.2.1.3 Degree of Interest...........................................................................................2 — 102.2.2 Status of Applicable Facilities at Enforcement Site

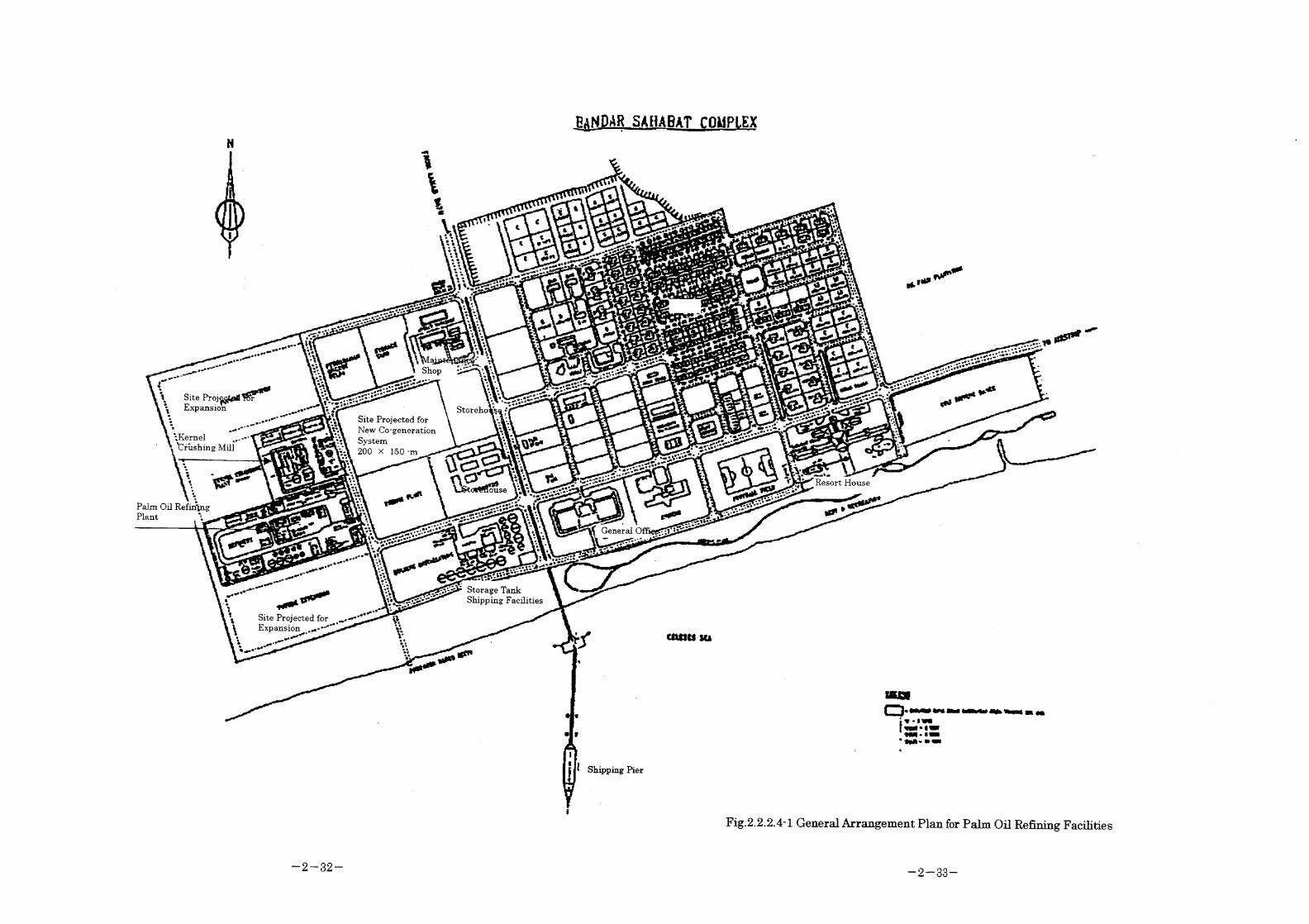

(Enterprise)(Outline. Specification and Commissioning Status).............2—122.2.2.1 Outline of Palm Oil......................................................................................... 2—122.2.2.2 Overall Image of FELDA S ARAB AT COMPLEX.................................... 2-232.2.2.3 Palm Oil Mill..................................................................................................... 2-272.2.2.4 Refining Process............................................................................................... 2—312.2.3 Capability of Project Execution at Enforcement Site (Enterprise) 2—372.2.3.1 Technological Capability.................................................................................2—372.2.3.2 Management Capability................................................................................. 2—372.2.3.3 Administrative Foundation and Administrative Capability..................2—38

— C—2—

2.2.3.4 Funds bearing Capability............................................................................. 2—382.2.3.5 Manpower-bearing Capability.....................................................................2—392.2.3.6 Enforcement Organization...........................................................................2—402.2.4 Contents of Project at Enforcement Site (Enterprise) and

Modified Specification at the Applicable Facilities.................................2—412.2.4.1 Basic Plan and Policy on Project .............................................................2—412.2.4.2 Demand and Supply Balance of Power and Plant Steam after

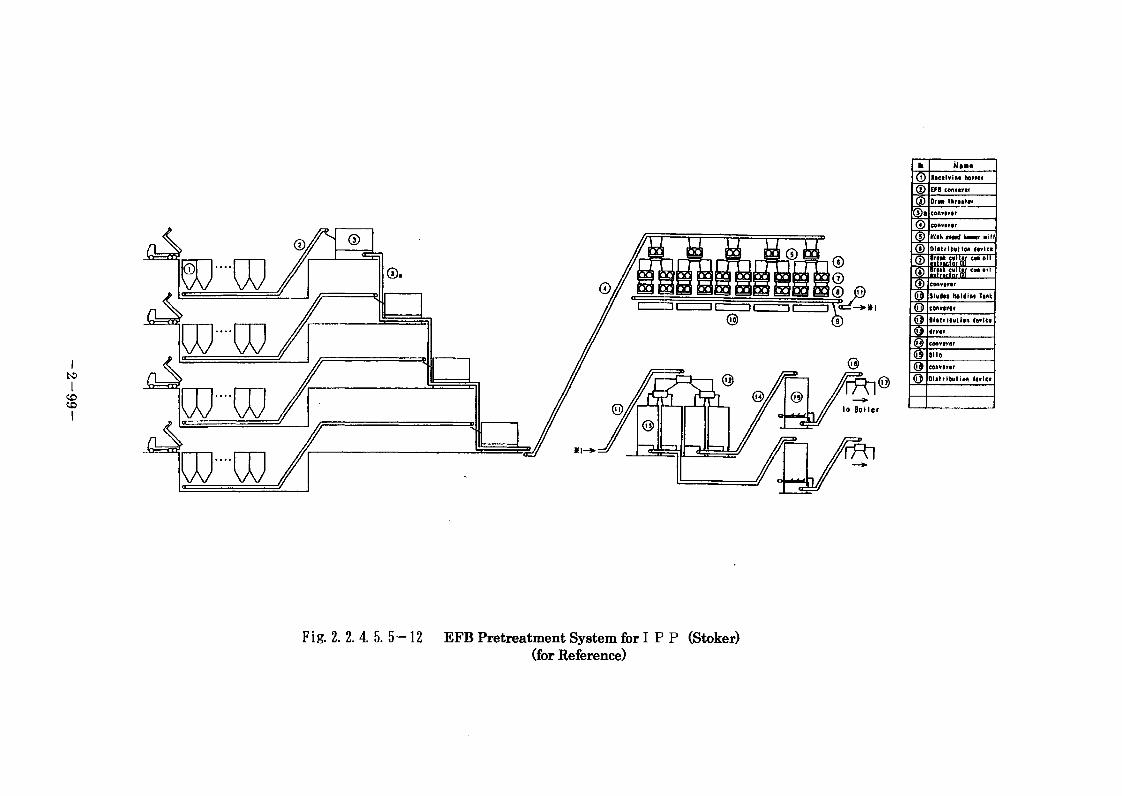

Introduction of the Co-generation System............................................... 2—452.2.4.3 Properties of Fuel (Palm Waste).................................................................2—542.2.4.4 Confirmation Test........................................................................................... 2—572.2.4.5 Specification of Planned Facilities ' ........................................................2—742.2.4.5.1 Steam Condition......................................................................................... 2—742.2.4.5.2 Boiler..............................................................................................................2—782.2.4.5.3 Turbine ..........................................................................................................2—812.2.4.5.4 Generator......................................................................................................2—832.2.4.5.5 EFB Pretreatment Equipment.................................................................2—842.2.4.5.6 Flue Gas Treatment Equipment.............................................................2—1002.2.4.5.7 Feed Water and Cooling Water Facility................................................. 1 — 1032.2.4.5.8 Electrical and Instrumentation Equipment.........................................2—1062.2.4.5.9 Estimated Performance............................................................................. 2—1112.2.4.6 Civil Engineering/Construction Works..................................................... 2—1142.2.4.7 Outline of Transportation Plan .................................................................2—1162.2.5 Scope of Supply including Fund, Facility Equipment,

Service etc. provided by both Parties required forthe Applicable Project Enforcement........................................................... 2—118

2.2.6 Conditions on the Premise of the Enforcement of the Projectand Problems to be solved ............................................................................2—122

2.2.7 Project Enforcement Schedule......................................................................2—1232.3 Concretization of Fund Plan..............................................................................2—1252.3.1 Fund Plan required for the Project Enforcement.....................................2—1252.3.1.1 Required Amount of Fund ........................................................................2—1252.3.1.2 Procurement Method....................................................................................2—1262.3.1.2.1 Ordinary Procurement................................................................................2—1262.3.1.2.2 Expansion of Enterprise as a Joint Venture (JV) .............................. 2—1262.3.1.2.3 Grant of Economical and Environmental Cooperation

with Overseas Countries............................................................................2—1272.3.1.2.4 Un tied Bank Loan Granted by Japan Bank for

International Cooperation........................................................................2—1272.3.2 Prospect of Fund Procurement (Execution Plan of Investigation

Consignee and of Enforcement Site (Enterprise))...................................2—1282.3.2.1 Execution Plan of Investigation Consignee............................................2—1282.3.2.2 Execution Plan of Enforcement Site (Enterprise)................................. 2—130

— C—3—

2.4 CDM Condition and the Relating Matters...................................................2—1332.4.1 Setting of Project Enforcement Condition based on the Actual

State at Project Enforcement Site, Division of Work etc. and Adjusting Matters with the Other Country required for the successful Materialization of CDM................................................................2—133

2.4.2 Feasibility of Agreement concluded for the CDM of the applicable Project (Requirements that the Other Country may agree with the Way of Concepts of Other Country Government and of Enforcement Site (Enterprise) concerning the CDM)..................................................... 2—137

CHAPTER 3 EFFECT OF THE PROJECT.......................................3.1 Energy Substitution Effect................................................................................3.1.1 Technological Grounds for Producing the Energy Substitution Effect3.1.2 Base Line Forming the Basis for Computation of Energy

Substitution Effect (Concepts of Estimating the Energy Consumption in the Case where the Project is Not Executed).............

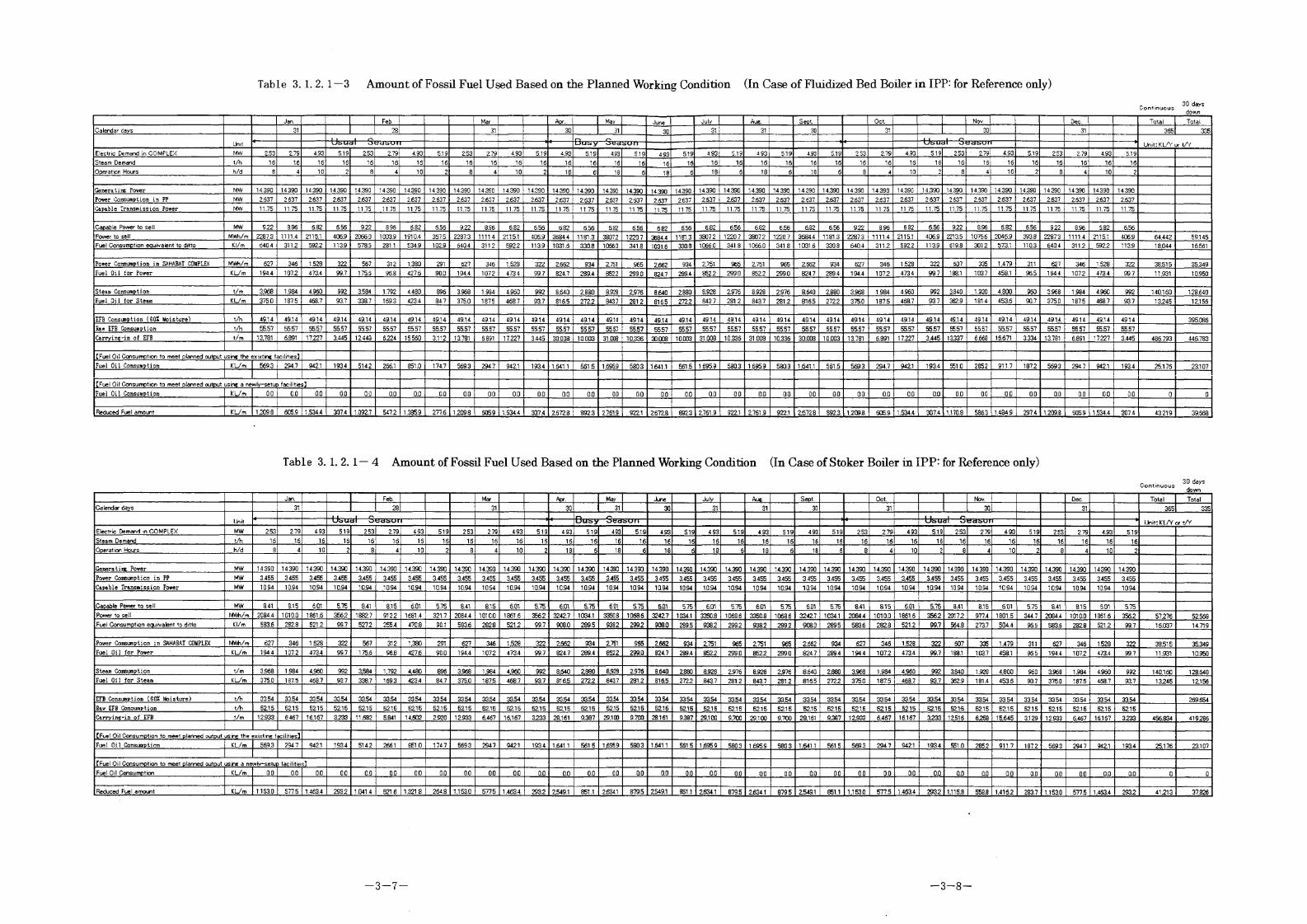

3.1.2.1 Concepts on Base Line Setting.................................................................3.1.2.2 Quantity of Fuel Used on the Base Line.................................................3.1.3 Practical Volume, Producing Period and Accumulated Volume of

Energy Substitution Effect (Effect when the Project has been executed)......................................................................................................

3.1.3.1 Concepts on Setting the Case of the Project Executed...................3.1.3.2 Practical Volume and Accumulated Volume of Energy

Substitution Effect: ................................................................................3.1.4 Practical Confirmation Method of Energy Substitution Effect3.2 Green House Gases Reduction Effect.....................................................3.2.1 Technological Grounds for Producing the Green House Gases

Reduction Effect......................................................................................3.2.2 Base Line Forming the Basis for Computation of Green House

Gases Reduction Effect (Concepts for Estimating the Discharge when the Project is not Executed)...................................

3.2.2.1 Concepts on Base Line Setting...........................................................3.2.2.2 Computation on Base Line...................................................................3.2.3 Practical Volume, Producing Period and Accumulated Volume of

Green House Gases Reduction Effect(Effect when the Project has been Executed) ....................................................................................

3.2.3.1 Concepts on Setting the Case of the Project Executed...................3.2.3.2 Practical Volume and Accumulated Volume of Green

House Gases Reduction Effect.............................................................3.2.4 Practical Confirmation Method of Green House Gases

Reduction Effect (Monitoring Method) .............................................3.3 Influence on Productivity............................................................................

3-13-13-1

3-13-1

3-103-10

3-113-173-18

3-18

3-183-183-19

3-203-20

3-22

3-273-28

— C—4—

CHAPTER 4 EARNING RATE 4-14.1 Economic Effect in Return on Investment..................................................... 4— 14.1.1 Case Patters for Trial Computation ............................................................. 4—14.1.2 Prerequisites for Trial Computation............................................................. 4—14.1.3 Results of Computation...................................................................................... 4—34.2 Effect VS. Cost ......................................................................................................4—264.2.1 Energy Substitution Effect..............................................................................4—264.2.2 Green House Gases Reduction Effect......................................................... 4—264.3 Others............................................................................ 4—27(Appended Document) Payback Period........................................................................4—28

CHAPTER 5 ASCERTAINMENT OF PROPAGATING EFFECT 5-15.1 Possibility of Technology Introduced by the Project to Spread in

the Country in Question....................................................................................5—15.2 Effect with Spread Taken into Account........................................................... 5—25.2.1 Energy Substitution Effect..............................................................................5—25.2.2 Green House Gases Reduction Effect........................................................... 5—2

CHAPTER 6 INFLUENCE OF PROJECT UPON OTHERS 6-16.1 Influence upon Environmental Aspect........................................................... 6—16.2 Influence upon Economical Aspect....................................................................6—26.3 Influence upon Social Aspect..............................................................................6—3

CHAPTER 7 OTHERS..............................................................................7-17.1 Palm Waste as a Fuel..........................................................................................7—17.1.1 Yield of FFB ......................................................................................................7-17.1.2 Yield of Palm Waste ........................................................................................7—17.1.3 Properties of Palm Waste................................................................................7—27.2 Effective Utilization of Palm Waste...............................................................7—37.2.1 Current EFB Utilization Status................................................................... 7—37.2.2 Current Palm Waste Utilization Status..................................................... 7—37.2.3 Power Generation Limit in Effective Utilization of Palm Waste.........7—47.2.4 Future Utilization Method of EFB............................................................... 7—4

CONCLUSION

LIST of REFFERENCES

APPENDIXAppendix — 1 : Report of the 1st Field Survey Appendix—2 : Report of the 2nd Field Survey Appendix—3 : Report of the 3rd Field Survey

— C—5“

SUMMARY

SUMMARY

1. Purpose of Survey

The palm oil industry in Malaysia holds a very weighty position in the country

and evils arising from the industry have also come into question.

EFB (Empty Fruit Bunches) have been disposed by incineration in palm oil mills

so far and the resultant ashes have been returned to plantations as manure.

However, since the particles of soot discharged from incinerators cause air pollution,

the palm oil mills constructed in and after 1993 have been prohibited from installing

incinerators.

Therefore most EFB discharged have been disposed by using for mulching

(composting) in plantations; however since circumferential mulching to individual

oil palm tree takes much labor, dumping on the sides of farm roads has increased,

causing secondary problems, such as spontaneous combustion n the dry season,

damage to fruits due to mass generation of beetles, etc. In contrast with the fact that

shells and boiler, as waste from palm oil mills, have already been used for boiler

burning as an electric energy and process steam source, EFB have not been used as

an effective energy source so far, because they have hard fiber and are big in shape

and appropriate pretreatment is indispensable before putting them into the furnace

owing to their water content more than 60 %, and further because the have the

property of heavy slogging due to the melting point as low as about 1,000° C of the

ash coming from them.

Such decaying treatment generates a great volume of methane as Green House

Gases.

If these EFB can be effectively used as biomass energy, such can contribute much

to the reduction of Green House Gases.

In this survey, a feasibility study was made on the project o introducing a

co generation equipment to use EFB effectively, into SAHABAT COMPLEX, SABAH

State, possessed by FELDA which is the largest company in the Malaysian palm oil

industry. The survey was carried out with a view to linking it with the Clean

Development Malaysian in this country.

Since this feasibility study conforms opportunely to the energy policy of the

Malaysian Government, the study came to be carried out not only on

Industry owned PP but also on IPP, at a request of the Ministry of Energy.

2. Objects of Survey

In this survey, a feasibility study was carried out, on the fluidized bed system and

on the stoker system, as the type of the EFB burning system for the boiler, in the

introduction of a co-generation equipment into FELDA SAHABAT COMPLEX in

SABAH State, Malaysia.

3. Results of Survey

As the result of this survey, the following became clear by introducing a

Industry-owned Power Plant having a generating-end output of 7,800 kW.

For reference, in the case of introducing a IPP co-generation having a

generating-end output of 16,000 kW the result are also represented.

1) Energy substitution effect (reduced to crude oil quantity during twenty years):

About 376 ktoe for Industry-owned PP with fluidized bed boilers!

About 363 k toe for Industry-owned PP with stoker boilers!

(for Reference)

About 695 k toe for IPP with fluidized bed boilers!

About 662 k toe for IPP with stoker boilers.

2) Green House Gases reduction effect (reduced to carbon dioxide quantity

during twenty years):

About 5,757 kt-COs for Industry owned PP with fluidized bed boilers!

About 5,478 kt -CO2 for Industry-owned PP with stoker boilers!

(for Reference)

About 11,654 kt-C02 for IPP with fluidized bed boilers!

About 10,970 kt-C02 for IPP with stoker boilers.

S-2

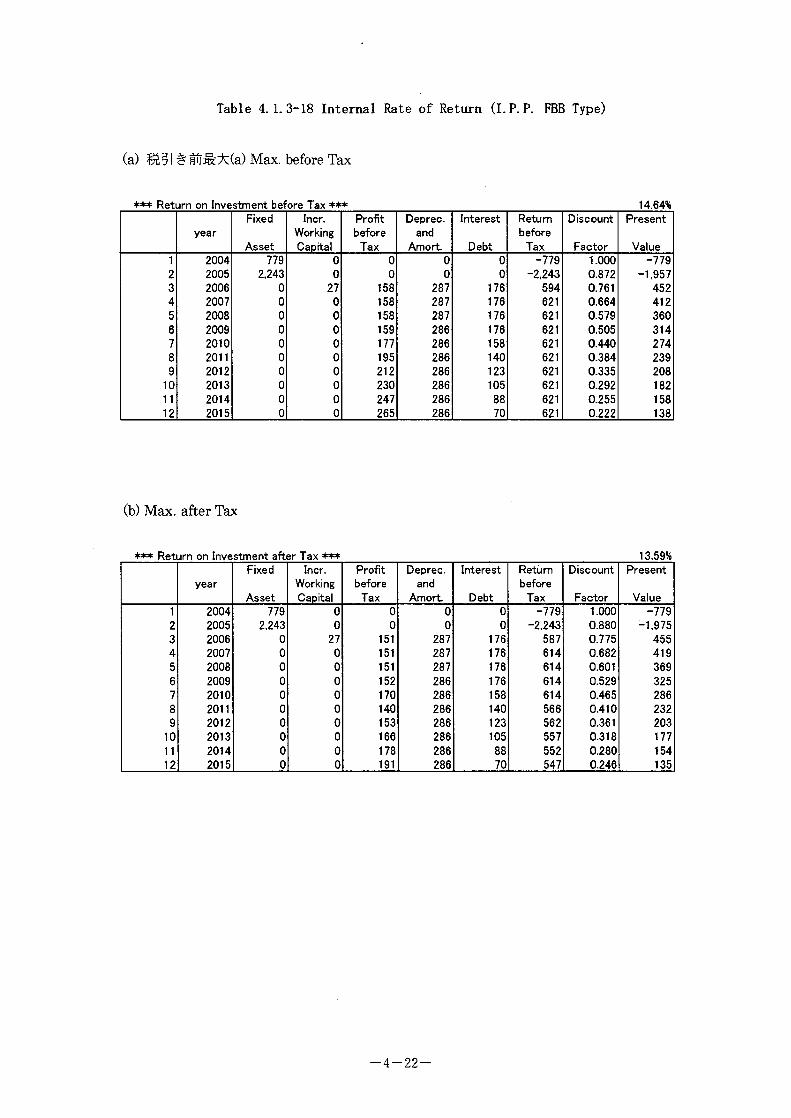

3) Profitability-

The IRR for each case before tax deduction and after tax deduction is as

shown in the following table:

Before tax deduction After tax deduction

Max. Min. Max. Min.

Industry owned

PP

Fluidized Bed Boiler 8.47% 3.32% 8.08% 3.32%

Stoker Boiler 7.50% 2.27% 7.20% 2.27%

(for Reference)

Before tax deduction After tax deduction

Max. Min. Max. Min.

IPP Fluidized Bed Boiler 14.64% 9.13% 13.59% 8.64%

Stoker Boiler 12.97% 7.71% 12.07% 7.38%

For these values, the profit life has been set ten years, as the same value as the

depreciation period for equipment in FEDLA, but realistically, the equipment in

question can be used indisputably more than ten years.

Accordingly, if the project life value is set longer, an equal amount of cash flow

will be kept for the prolonged period and the IRR will be further improved.

In Industry owned PP, all of generated energy is used within the private group,

and therefore, it is not needed to deny unconditionally the effect of investment into

the system even if the IRR value is lower than in IPP, because there is no such

indefinite factor which any third parties are concerned with, as electric energy

selling to the outside in IPP.

As shown above, the IRR for the case of IPP by the FBB system amounts to a

good value of about 14% at the maximum profit, and it amounts to a value

exceeding the open market rate even at the minimum profit.

S-3

4) Possibility of spread:

In the biomass energy policy of the Malaysian Government, many “favorable

treatment sections' are expected to be established, and taking the fact into

account, a great possibility of realization can be seen in the spread of similar

projects.

5) Influence to other aspects:

In the environmental aspect, the discharge of NOx, SOx and smoke dust can be

reduced.

IN the economical aspect, such project will contribute to industrial development

and employment promotion because more than half of required equipment in

value are expected to be supplied from Malaysia and neighboring countries, and in

addition, improvement in profitability can be promoted in the palm oil industry.

From the above, it can safely be said that to introduce in Malaysia the equipment

in question which was studied in this project, can produce a great measure of effect

in aspects, such as environmental problems, energy consumption efficiency and

cast reduction, and further that the project in question conforms to the energy

policy and environmental improvement policy of the Malaysian Government and

thus can meet various prior conditions to be required when any schemes for the

DDM are assumed.

Thus this project conforms surely to related policies in the Malaysian

Government, and when opinion was tapped on the project in question, the MOE

spoke: “Energy-sawing promotion and environmental improvement in the palm oil

industry are major items to be faced squarely by the Malaysian Government. We

are much interested in them and want to promote them together.” The DOE also

spoke: “We are much interested and will cooperate with you. Please promote them.

Let DOE serve as a monitor on the project in question.” Furthermore the Malaysian

Energy Center has also promised positively its wholehearted support toward the

realization of this project.

Also, Enforcement Site (Enterprise) has a great interest in this project.

S-4

The company is so enthusiastic that it has dispatched an investigation committee

to Denmark being an advanced country in biomass power generation, and has made

an on-site inspection of the rice hash burning power plant.

Great expectations are laid on this project which would enable the whole

company to save, even in future, the diesel oil consumed in the company, because

the whole of the area expected to be covered by power supply in this project belongs

to the same group companies.

Upon the pride as FELDA having the largest palm oil company in the world

largest palm oil country, the corporation intends to realize biomass power

generation developed from palm oil production for the first time in the world.

S-5

CHAPTER 1

FUNDAMENTAL ITEMS OF THE PROJECT

Abstract

In Malaysia, which promotes now industrial high-degree advancement and addedvalue

upgrading in line with the fundamental conception worked out by its government to

achieve its entry into the family of advanced countries before 2020, this project by which

an attempt is made to introduce the newest biomass power generation into the palm oil

industry being ranked as one of major primary products as important as crude oil in the

country, can be regarded as a very significant project conforming to the governmental

conception as well.

In executing a project, there are conditions peculiar to each country and the project can

never be realized without respect to such conditions. In this chapter, the general

situation of Malaysia, the palm oil industry and energy conditions in Malaysia, and the

meaning and needs of this project are mentioned.

CHAPTER 1 FUNDAMENTAL ITEMS OF THE PROJECT

1.1 Situations of Partner Country

1.1.1 An Outline of General Affairs

1.1.1.1 Territory

Malaysia is composed of Malay Peninsula and the northern part of Borneo Island.

The region of Malay Peninsula is called West Malaysia and consists of the special

district Kuala Lumpur as capital and 11 states. On the other hand, the northern

part of Borneo Island is called East Malaysia and consists of two states and the

Labuan district placed under federal direct control. The area of the territory is

329,758 km2, as the sum of 131,598 km2 for the peninsular region and 198,160 km2

for East Malaysia, and 70% of the total territory is forested.

Table 1.1.1.11 States of Malaysia

Name of State Name of State(West Malaysia)Kuala LumpurSelangorNegri SembilanMelakaJohorPahangPenangKedah

PerilsPerakKelantanTerengganu (East Malaysia)SabahSarawakLabuan

1.1.1.2 Location

The peninsular region is situated between 6° 43' N. (North Latitude) and 1°

16' N, and between 104° 17' E. (East Longitude) and 100° 8' E. East Malaysia

is situated between 7° 25' N. and 1° N., and between 119° 20' E. and 109°

40' E. The southernmost point is situated nearly right at the equator.

1.1.1.3 Population

The whole population is 23,250,000 by governmental estimation in 2000 and is

23,790,000 by governmental estimation in 2001. The population by ages gives a

breakdown of 33.9 % for 14 years and downward, 62.2 % for ages ranging from 15

to 64 years, and 3.9 % for 65 years and over. The population of the capital Kuala

Lumpur is about 1,280 thousand. 1-1)

— 1 — 1 —

1.1.1.4 Races

Malaysia is a multiracial country, which includes mainly people of Malayan

origin, Chinese origin and of Indian origin, and the rates of their populations are

about 60, 30 and 10 % respectively. In addition to these, there are people of

minority races including the people of European origin, the aborigines

“Orangasuli’s” in West Malaysia and the “Uru” tribesmen as natives in East

Malaysia.

1.1.1.5 Language

The national language is Malayan (provided in Article 152 of the Constitution).

In addition to this, English, Chinese and Tamil are used as official languages

among people of respective races, but English is deeply infiltrated under the

influence of the past British reign.

1.1.1.6 Climate

The country has a hot and humid tropical climate throughout the year and has a

violent squall frequently. The mean air temperature in the daytime is about 30

degree C, but it sometimes gets cold unexpectedly in the morning. There is no

sharp distinction between the rainy season and the dry season. However on the

east coast of West Malaysia, from November to February, the monsoon blows, it is

rainy and the waves are high; so that this season is usually referred to as the rainy

season. Yearly rainfall is 1,600 to 6,000 mm.

1.1.1.7 Currency

The unit for currency denominations is Malaysian Ringit (RM) or Malaysian

Dollar (M$). Since autumn of 1998, the Malaysian Government has adopted a

fixed exchange rate policy to the US dollar (the fixed rate is: 1 US$ = 3.8 RM). The

rate to the Japanese yen is 1 RM = about 32 yen (as of March 2001), but owing to

the fixed rate policy to the US dollar and a prohibitive action against overseas

carrying of RM s, RM s can not be used overseas but can be used only in Malaysia.

1.1.1.8 Visa

No visa for entry from Japan is needed if the entrant's stay is within three

months, but a six-months or longer residual validity time is required with the

passport. However for voyages with the object of conducting the operations

attended by compensations (as in the dispatch of supervisors), it is needed to

— 1 — 2 —

obtain work permits, as a rule.

1.1.1.9 Difference in Time

The difference from the Japan time is minus one hour. However it is felt as if

minus two hours, in bodily sensation, because the sun rises after seven a m. and

sets at about eight p.m. throughout the year. As a matter of fact, the difference in

time of Thailand being situated around the same east longitude as Malaysia, is

minus two hours from Japan. It is said that in Malaysia there were originally two

times: the West Malaysian time and the East Malaysian time, but that they were

standardized into them East Malaysian time which made a difference of minus

one hour from the Japan time.

1.1.1.10 Religion

The state religion is Islam believed in mainly by Malayans that account for 60 %

of the whole population. Buddhism or Christianity is believed in by people of

Chinese descent and Hinduism by people of Indian descent. Kelantan State in the

north of West Malaysia and Terengganu State situated on the east coast show an

especially marked Islamic color.

1.1.1.11 King

Of the 11 states in West Malaysia, nine states have a ruler called “sultan” each.

The title “sultan” is originally the title for the throne, which appeared in Arabia,

the birthplace of Islam. A council of the rules of the nine states is held every five

years, and one of the rulers is elected to king. It follows that the term of service as

king is five years; and fundamentally the order of undertaking this service has

been decided beforehand among the states. The king is called “Agon” in Malayan

and is a highly symbolic being like the Japanese ‘tenno" is. The king exercises his

power to appoint ministers, to open a session of the Federal Congress and to

dissolve the Congress, and his legislative power including consent to bills carried

by both Houses of the Congress, and he performs his diplomatic duties, such as

foreign travels, reception to the visits of foreign leaders, etc., and makes official

announcement on the fast which is the biggest event in Islam.

1.1.1.12 Designations of Ranks

The following designations of ranks exist in Malaysia and are still being used:

CD Tunku: put on princes, princesses & sultan's relatives in the first degree,

-1-3-

(2) Raja: given to persons blood related to the royal family

(3) Tun: the highest rank given to persons other than the members of the

royal family,

(D Tan Sri: the second rank given to persons other than the members of the

royal family,

(5) Dato, Datuk: the third rank given to persons other than the members of the

royal family,

© Haji: given to persons who made a pilgrimage to Mecca and practiced

asceticism,

(7) Encik, Tuan: meaning “Mr.”,

© Cik, Puan: meaning “Mrs.”

The designations, “Tun”, “Tan Sri” and “Dato (Datuk)” are given to persons who

contributed to the nation or region, socially or economically or otherwise, and if

such a designation is given to a married person, an equal special designation will

be given to the person’s spouse as well. As a matter related to names, Malayans

have no surname, but their names are expressed as “So-and-so (first name) son

(daughter) of so and so (parent's name)”. For instance, if a man is “Ahmad” being a

son of his father named “Dato Ismail”, his name is expressed as “Ahmad bin Dato

Ismail” (where “bin” means “son of).

1.1.1.13 Education

The educational system and the percentage of school attendance are as follows:

School Level Educationalsystem

Percentage of School Attendance

Elementary school 6 years 97%

Junior high school 3years 83%

Senior high school 2 years 55%

Preparatory course for univ./coll. 2 years 22%

U niver sity/colle ge 3years 3.7%

1.1.1.14 Number of Japanese Residents

The number of Japanese residents increased rapidly from 1990 till 1998,

amounting to 11,726 in 1998. More than 7,600 center on the capital Kuala Lumpur

and Selangor State, and secondly 1,380 live in Penang State and 1,170 in Johor

State. Seeing the number of Japanese-affiliated invading enterprises by types of

— 1 — 4 —

industry, those of the manufacturing industry account for a little under 60 % of the

whole; those of commerce amount to about 15 %', those of construction and plant

industry amount to about 8 %; and the others the rest.

As to schools for Japanese, there are three elementary/junior-high schools in the

peninsular region, a school of the same kind in East Malaysia, and only one

kindergarten in Kuala Lumpur. The number of pupils amounts to about 1,500 in

all (as of May 1999).

1.1.1.15 A Brief History

Table 1.1.1.151 A Brief History of Malaysia 12)

Year Political Power Event1405 Melaka Kingdom comes into the world.

1511 Melaka Kingdom is captured by Portugal.

1641 The territory is captured by Holland in place of Portugal

1824 The territory is captured by England in place of Holland.

1867 England colonializes the whole territory of Malaysia.

1941 With the outbreak of Pacific War, the Japanese forces capture the Malay Peninsula.

1945 The territory comes again under the rule of England (UK) with Japan’s defeat.

1957 Malay Peninsula and Singapore Island become independent as the Federation of Malaya.

1958

1963

A Rahman assumes office as the 1st Prime Minister

The northwest part of Borneo is annexed and the Federation of Malaysia comes into the world.

1965 Singapore becomes independent and the present territory is fixed.

1969 Razak assumes office as the 2nd Prime Minister

A collision takes place between people of Malayan origin and people of Chinese origin on 13th May

1976 Fseion assumes office as the 3rd Prime Minister

1981 Mahathir assumes office as the 4th Prime Minister

— 1 — 5 —

1.1.2 Politics

1.1.2.1 Political System

The political system is a constitutional monarchy and the present Mahathir Power

has been maintained for more than 19 year as the political power which has lasted

longest among the powers of incumbent leaders in Southeast Asia, since Mahathir

assumed office as the first prime minister coming from any classes other than the

royal family.

1.1.2.2 Federal Congress System

The Federal Congress of Malaysia is divided into the Upper House and the Lower

House, which are called “Dewan Negara” and “Dewan Racat” respectively. The

Upper House has 68 seats with the term of membership of six years, and is

composed of 42 intelligent members nominated by the king and 26 members

selected from state assemblies. Similarly to the House of Councilors in Japan, the

Upper House has narrower limits of power than the Lower House. The Lower

House has 193 seats and its members are elected by nation’s direct vote, like in the

House of Representatives of Japan, from 192 small electoral districts covering the

whole country. Both the election by state assemblies and the election for the Lower

House are carried out every five years.

1.1.2.3 Political Parties

The Government party in Malaysia is “Balisan National” (meaning National

Front; Abbreviation: BN), and BN holds 148 of 193 seats in the Lower House. The

parties composing BN are as follows:

UMNO BARU (meaning New Unified Malayan National Organization),

MCA (Malaysian Chinese Association),

MIC (Malaysian Indian Council),

PPP (People’s Progress Party),

GERAKAN (meaning People’s Movement Party),

HANIM (HANIM Party),

AKAR (meaning Peoples Righteous Movement Party),

PBB (meaning Sarawak Bumiputra Conservative Party),

SNAP (Sarawak National Party),

SUPP (Sarawak Unified People’s party),

— 1 —6 —

and two other parties;

Thus 12 parties in all are included.

On the other hand, nongovernment parties are DAP (Democratic Action Party)

having 10 seats, PAS (meaning All-Malaysian Islam Party) having 27 seats, PBS

(meaning Sabah Unification Party) having 3 seats and KEADILAN having 5 seats.

DAP is a party being based on support from urban Chinese, and PAS is a

nationwide party rich in Islamic traditional color. As the result of the 2000 election,

PAS has held a majority in Kelantan State and Terengganu State, and the

Government party is under extreme uneasiness at the fact that Terengganu State,

which is the center of oil bases supporting the obtaining of foreign money in

Malaysia, has been placed under PAS' s command.

1.1.2.4 Big Project Conceptions

In order to prevent the recurrence of the same affair as the great collision between

Chinese and Malaysian in May 1969, which was the biggest recial dispute in

Malaysian history, Premier Mahathir set forth many big project conceptions with

the view of raising people’s consciousness of brethren and their pride. The national

car “Proton”, the national bike “Modenas”, the induction of “Commonwealth

Games”, the construction of a FI circuit, the Kuala Lumpur City Center project,

MSC (Multimedia Super Corridor), etc. are good examples.

As to the “Vision 2020” to aim at Malaysia’s entry into the family of advanced

countries before 2020, the prime minister himself keep on serving as flagman

toward its success, and its slogan “Malaysia Bore” means: “It is possible if

Malaysians do it” in Malayan.

1.1.2.5 Countermeasures in the Asian Currency Crisis

On the occasion of the currency crisis and subsequent economic depression,

Premier Mahathir attracted public attention by criticizing the speculator, Mr.

George Solus, with his name designated, and he also astonished the world by

working out suddenly in 1998 a fixed exchange rate system to the US dollar and a

prohibitive policy against the overseas carrying of RM’s over a specified amount,

after declaring that economic restoration will be promoted independently without

receiving support from the International Monetary Fund (IMF). These policies are

said to be based on advice from Minister of Finance, Tun Daim Zainudin.

Though the sudden policies around criticism from foreign countries, the rate of

— 1 — 7 —

Malaysia's economic growth has been recorded as 5.8 % in 1999 and 11.9 % in the

first quarter of 2000. This shows a tendency to recover steadily in economics, and

high appraisals have been centered again on the determination of Premier

Mahathir.

1.1.2.6 Mahathir Ism

Whereas Premier Mahathir is sometimes subjected to criticism, this is owing to

his unswerving faith and self confidence, his almost too strong leadership and his

astonishing determination; and thus his high capability is beyond question and he

can be regarded as one of representative leaders in the world. The former Deputy

Prime Minister, Anwar, who had been regarded as successor of Premier Mahathir,

was dismissed and no candidate for the next Prime Minister has been fixed.

Nevertheless Premier Mahathir declares he will retire at once if his successor is

found. What is required from his successor is to succeed the powerful Mahathir Ism

to enable the realization of Malaysia’s entry into the family to advanced countries

before 2020 (though Premier Mahathir says his successor is not necessarily of the

same type as himself), and it seems the influencing power of Premier Mahathir will

not fade away from Malaysia for the time being.

-1-8-

1.1.2.7 Cabinet Members

The present cabinet members are as follows:

Table 1.1.2.7-1 Malaysian Cabinet

(As of Jan/2000)

Ministry Ministry

Prime Minister Datuk Seri Dr. Mahathir Mohamad

Deputy Prime Minister Datuk Seri Abdullah Ahmad Badawi

Special Function & Finance Tun Dain Zainuddin

T ransport Datuk Seri Dr. Ling Liong Sik

Works Datuk Seri S. Sarny Vellu

Primary Industries Datuk Seri Dr. Lim Keng Yaik

Energy, Communications & Multimedia Datuk Leo Moggie

International Trade & Industry Datuk Seri Rafidah Aziz

Defence Datuk Seri Najib Tun Razak

Science, Technology and Environment Datuk Seri Law Hieng Ding

Foreign Datuk Seri Syed Hamid Albar

Domestic Trade & Consumer Affairs Tan Sri Muhyiddin Yassin

Health Datuk Chua Jui Meng

Land and Cooperative Development Tan Sri Kasitah Gaddam

National Unity & Community Development Datuk Dr. Siti Zaharah Sulaiman

Information Tan Sri Khalil Yaacob

Culture, Arts & Tourism Datuk Abdul kadir Sheikh Fadzir

Human Resources Datuk Dr. Fong Chan Onn

Housing & Local Government Datuk Ong Ka Ting

Entrepreneur Development Datuk Nazri Abdul Aziz

Rural Development Datuk Azmi Khalid

Youth and Sports Datuk Hishamuddin Tun Hussein

Agriculture Datuk Effendi Norwawi

Education Tan Sri Musa Mohamad

Prime Minister’s Department Datuk Dr. Abdul Hamid Othman

Prime Minister’s Department Datuk Pandikar Amin Mulia

Prime Minister’s Department Tan Sri Bernard Dompok

Prime Minister’s Department Datuk Rais Yatim

— 1 — 9—

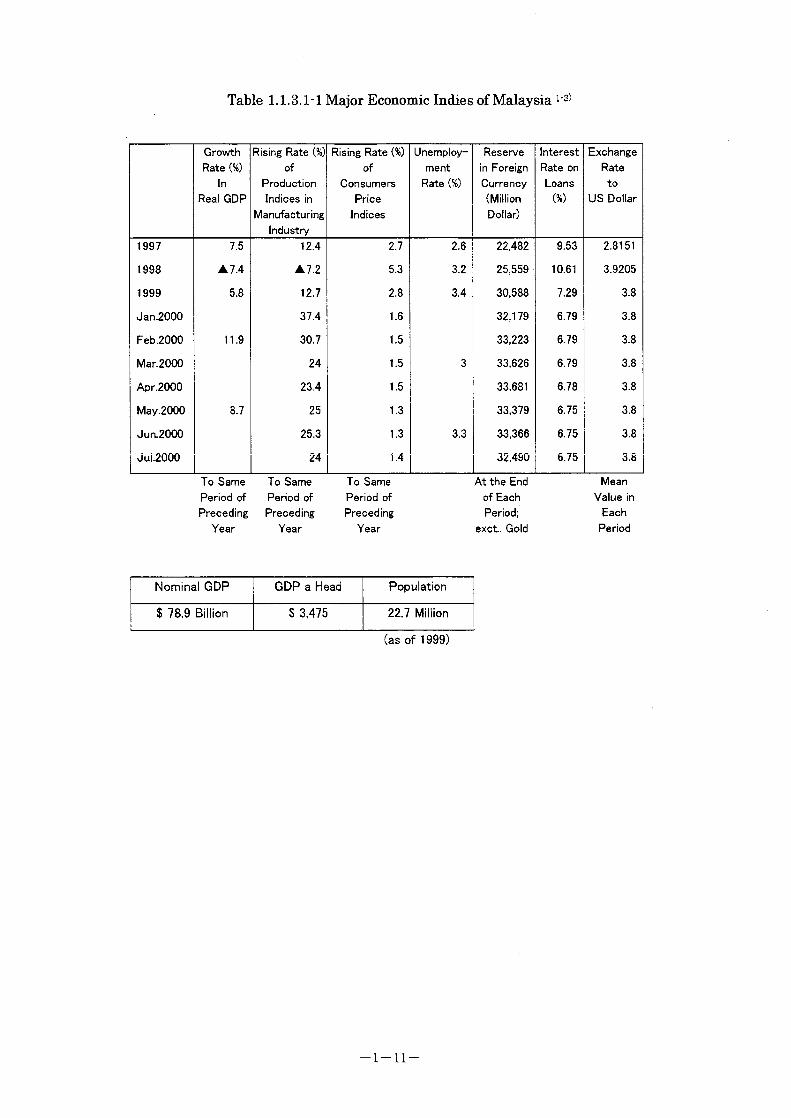

1.1.3 Economy

1.1.3.1 General Condition of Economy

The Malaysian economy attained its growth worth recording, as high as 8 to 9 % in

annual mean value, during the period from 1988 to 1997. This growth brought

about a remarkable rise in real wages, a sudden extension of the export of

industrial products, and an inflow of enormous investment by foreign investors.

Especially, into the takeover of enterprises, excessive investments suggestive of the

bubble period in Japan were made, and the financial crisis brought about from 1997

to 1998, shocked the Malaysian economy to make its footing unsteady at a heat.

The Government’s drastic introduction of the fixed exchange rate system to the US

dollar and the prohibitive action against overseas remittance, minimized damage

due to a fall in the exchange rate, while on the other hand owing to sudden

depreciation of currency and in the stock market, the national budget which was

5.5 % of GDP in 1997 was drived down to 3 % in 1998 through a strict curtailment

of expenditures, in order to reduce shortage in the current account. Accordingly the

Government determined a reduction up to 20 % of annual expenditure, a restraint

on large-sum imports and the postponement of large-scale undertakings. On

account of the Government’s reduced budget and slowdown in economic growth,

bankruptcies increased and the jobless increased in number in 1998 and 1999. The

rate of economic growth in Malaysia sinked to about 4 % in 1998 and 1999.

However the signs of economic recovery have come to be surely shown and the rate

of economic growth in 2000 forecasted by the Government is 5 %.

— 1 —10—

Table 1.1.3.11 Major Economic Indies of Malaysia v3)

Growth Rate (%)

InReal GDP

Rising Rate (%) of

ProductionIndices in

Manufacturing Industry

Rising Rate (%) of

ConsumersPrice

Indices

Unemployment

Rate (%)

Reserve in Foreign Currency (Million Dollar)

InterestRate onLoans

(%)

ExchangeRateto

US Dollar

1997 7.5 12.4 2.7 2.6 22,482 9.53 2.8151

1998 A 7.4 A7.2 5.3 3.2 25,559 10.61 3.9205

1999 5.8 12.7 2.8 3.4 30,588 7.29 3.8

Jan.2000 37.4 1.6 32,179 6.79 3.8

Feb.2000 11.9 30.7 1.5 33,223 6.79 3.8

Mar.2000 24 1.5 3 33,626 6.79 3.8

Apr.2000 23.4 1.5 33,681 6.78 3.8

May.2000 8.7 25 1.3 33,379 6.75 3.8

Jun.2000 25.3 1.3 3.3 33,366 6.75 3.8

Jul.2000 24 1.4 32,490 6.75 3.8

To Same Period of Preceding

Year

To Same Period of Preceding

Year

To Same Period of Preceding

Year

At the End Meanof Each Value inPeriod; Each

exct. Gold Period

Nominal GDP GDP a Head Population

$ 78.9 Billion $ 3,475 22.7 Million

(as of 1999)

-1-11-

1.1.3.2 Trade

The gross exports and gross imports of Malaysia in 1999 and in 2000 are as follows

according to the Government’s estimation:

In 1999, exports are 81,200 million US dollar and

Imports are 63.400 million US dollar;

In 2000, exports are 89,100 million US dollar and

Imports are 71,000 million US dollar.

The main exported goods are industrial products, palm oil, petroleum, wood and

woodwork, and rubber; and the major partner countries as destinations are ASEAN

(23.1 %), US (22.4 %), EU (15.8 %) and Japan (11.5 %).

The main imported goods are industrial semi manufactured goods, capital goods

and consumption goods; and as to the trade partners, import from ASEAN (20.8 %),

Japan (20.8 %), US (17.8 %), EU (11.5 %) is prominent.

— 1 —12 —

1.1.3.3 Recent Political and Economic Affairs

Table 1.1.3.3 -1 Recent Political and Economic Affairs 12)

Year Month Affairs

1990 Oct. A general election; the Government party UMNO gets the 2/3 stable majority. Labuan Island is designated as an Offshore Center.

1991 Feb. “Vision 2020” is released (to aim at Malaysia’s entry into the family of advanced countries before 2020).

Jun. National Development Policy (NDP) is released.1992 Dec A violence event by the sultan of Johor State is revealed and developed to an

issue on the forfeit of sultans’ privileges.1993 Mar. The Constitution is reformed on sultans’ privileges.

Nov. A staff election in UMNO; Anwar assumes office as Vice-president.Dec. Anwar assumes office as Deputy Prime Minister.

1994 Dec. The Foreign Exchange Act is amended.1995 Apr. A general election; the Government party BN wins a sweeping victory.1996 May. The 7th Malaysia Plan is released.

Aug. On “Multimedia Super Corridor”, the Government’s Keynote and the details of its favorable treatment actions are released.

Oct. A staff election in UMNO; Mahathir as President and Anwar as Vice-president are reelected without vote.

Dec. The 2nd Industrial master Plan (IMP2) is released.1997 Jul. Asian currency falls, originating from the shift of the exchange rate system for

the Thailand’s Baht to the floating system.Ringgit (RM) reaches the lowest rate in history: 4.895 RM to the US dollar, on 7th Jan. 1998.

1998 May. In the first quarter of 1998, growthrate in GDP reaches minus 1.8 %, which is the worst minus growth unprecedented since 1985.

Jun. The new international airport opens.Sep. Capital restraints are introduced; the fixed exchange rate system for the

Ringgit (RM) is introduced; the Commonwealth Games are held.Deputy Prime Minister Anwar is dismissed.

1999 Jan. Abdullah assumes office as Deputy Prime Minister.Feb. Capital restraints are relaxed in part. (Exit levy is introduced.)Sep. Capital restraints are relaxed again. (Exit levy is changed in part.)

1.2.2 Condition of Location for Palm Oil Mills

Since a large quantity of water is needed in the process of palm oil extraction, palm

oil mills are usually constructed near rivers having sufficient water. Generally, 1.5

m3 water is needed to refine one ton palm oil from FFB (Fresh Fruit Bunches).

In addition, as FFB must be efficiently collected in a wide expanse of plantation, it

is to be desired that the mill is located in the center of a plantation.

It is most important to secure wide lands, as a matter of course; therefore most

mills are necessarily located not in urban areas but in the out-of-the-way interior.

1.2.3 Evil Influences of Palm Oil Mills and Environmental Countermeasures

Since the waste water from palm oil mills include many organic matters, serious

water pollution will be aroused if the water is discharged in rivers as it is without

treatment. If a palm oil mills is located along a river, there is a fair possibility of

people living downstream to be affected by the mill.

As a countermeasure against the above, the Malaysian Government established and

the standard for waste water treatment has been set.

Another big evil influence is air pollution. After oil has been extracted from FFB,

fiber, kernels, shells and EFB (Empty Fruit Bunches) are left Fiber and shells are

used as fuel for boilers to generate steam and electricity, and kernels are hand EFB

were burnt in fields before to turn them into ashes usable as manure, but field

burning is now prohibited because it generates a large quantity of smoke and dust.

To serve as manure in place of ashes, EFB are used for mulching in plantations so

as to turn to clay slowly. However in addition to leisureliness in such a method of

disposal, EFB as much as about 23 % of FFB are generated, and thus some

producers who dump them unlawfully in other places, have begun to appear

hindered by spatial limits for mulching. Though the mills are located deep in the

mountains, such unlawful dumping are performed in places lying deeper, so as not to

be detected. In results, aborigines who keep living in traditional ways from ancient

times have been affected by the dumping, and criticism as public opinion has begun

to arise.

1-16

It is considered as an ideal solution to burn EFB without emitting smoke and dust

to utilize the heat as energy and to utilize ashes for manure.

— 1 — 17

1.3 Energy Conditions

1.3.1 Change of Energy in Malaysia

Malaysia depended on petroleum for 75 % of its total energy demand in 1990.

However in the 6th Malaysia Plan for the period from 1991 to 1995, the Government

advanced a breakaway from dependence on petroleum and a switchover to stable

and efficient energy. The aim is to slough off the biased dependence on one king of

energy source, by well-balanced utilization of four major energy sources: petroleum,

natural gas, coal and water power.

The final commercial energy demand in Malaysia, which had been dashing up the

stairs of high growth at that time, increased suddenly at a mean rate of 8.6 % per

year during the period.

Table 1.3.1-1 Final Commercial Energy Demand by Sources 16)

(1990-2000)

Source 1990 1995 2000Average Annual Growth Rate (%)

PJ % PJ % PJ % 6MP 7MP

Crude Oil & Petro. Products 414.0 74.9 561.7 67.1 777.5 60.8 6.3 6.7Natural Gas 45.7 8.3 103.5 12.4 188.1 14.7 17.8 12.7Electricity 71.8 13.0 131.4 15.7 221.8 17.3 12.8 11.0Coal & Coke 21.5 3.9 40.1 4.8 92 7.2 13.3 18.1

TOTAL 553 100 836.7 100 1279.4 100 8.6 8.9Per Capita Consumption

(gigajoules) 28.9 41.1 56.1 6.6 6.4Notes:1) Refers to the quantity of commercial energy delivered to final consumers but excluded gas, coal and

fuel oil used in electricity generation.2) Joule is the unit of energy to establish the equivalent physical heat content of each energy form.

One megajopule = 10° joules, one gigajoule (GJ) = 103 Joules and one petajoule (PJ) = 10' 5 joules and one PJ = 0.0239 million tones of oil equivalent (mtoe). One toe = 7.6 barrels.

3) Includes natural gas used as fuel and feedstock consumed by the non-electricity sector.4) 6MP: The 6th Malaysia Plan, 7MP: The 7th Malaysia Plan.

(Drawn from the 7th Malaysia Plan)

Seeing the demand by sectors, the maximum energy consumption is shown in the

sector connected with transportation, which amounts to 39.1 % of the total energy

demand in 1995 fiscal year. In the sector connected with transport, energy

consumption increased rapidly because automobiles grew in number at a rate of 7 %

per year at that time owing to success in the people’s car project. Energy

consumption in the sector of the manufacturing industry rose at a rate of 9.7 % per

— 1 —18 —

year with the pursuit of added value in the sector.

Table 1.3.1-2 Final Commercial Energy Demand by Sectors v6)

(1990-2000)

Source 1990 1995 2000Average Annual Growth Rate (%)

PJ % PJ % PJ % 6MP 7MP

Agriculture & Forestry 32.8 6.0 52.7 6.3 63.4 5.0 9.9 3.7Mining & Quarrying 25.7 4.6 34.4 4.1 50.0 3.9 6.0 7.8Manufacturing 187.8 34.0 298.7 35.7 488.7 38.2 9.7 10.3Transport 220.9 40.0 326.7 39.1 490.1 38.3 8.1 8.4Commercial 23.9 4.3 34.7 4.1 53.3 4.2 7.7 9.0Residential 43.4 7.8 51.5 6.2 64.4 5.0 3.5 4.6Non-Energy 18.5 3.3 38 4.5 69.5 5.4 15.5 12.8

TOTAL 553 100 836.7 100 1279.4 100 8.6 8.9(Drawn from the 7th Malaysia Plan)

The state-operated petroleum public corporation, Petronas, which generalizes

petroleum and natural gas operations, took rapid actions to support the

Governmental policy, with the result that switchovers among energy sources shown

in the following table has been realized.

Table 1.3.1-3 Primary Commercial Energy Supply by Sources 16)

(1990-2000)

Source 1990 1995 2000Average Annual Growth Rate (%)

PJ % PJ % PJ % 6MP 7MP

Crude Oil & Petro. Products 520.2 71.4 746.1 55.3 943.2 49.4 7.5 4.8Natural Gas 114.4 15.7 456.4 33.8 793.9 41.6 32.0 11.7Hydro 38.3 5.3 52.8 3.9 53.5 2.8 6.6 0.3Coal & Coke 55.5 7.6 93.2 7.0 117.9 6.2 10.9 4.8

TOTAL 728.9 100 1384.5 100 1908.5 100 13.1 7.2(Drawn from the 7th Malaysia Plan)

As found from the above table, worthy of special mention is the growth rate of the

switchover to natural gas. The reserves of natural gas in Malaysia are said to be

corresponding to its supply for 75 years. The abundant reserves and the execution of

the scheme of laying the natural gas pipeline through the peninsula which was

carried forward during the period, contributed greatly to the switchover to natural

gas. And coal supply which depends wholly on import, also showed high growth.

— 1 —19—

1.3.2 Electric Power Situation in Malaysia

1.3.2.1 Demand and Supply Balance of Electric Power v7)

The total electric power demand in West Malaysia in the first quarter of 2000, is

about 9,700 MW at peak hours, and the total capacity of power generating facilities

is about 11,800 MW at the same point of time. About 65 % of the capacity is covered

by the facilities of the electric power company TNB (Tenaga National), and at the

rest is covered by private IPP.

It is said that about 30 % is usually appropriate for the margin rate of power

generation capability to power demand. The margin rate at the above point of time

is a low value of about 21.5 % and in addition, the real power supply capability is

lower than the capability of power generating facilities by technical or

non technical losses existing.

In Malaysia, a large-scale power outage throughout the peninsula broke out two

times in the past, and its reccurence is still apprehended. In addition to outages,

the problem of what is called the “quality of electric power”, which causes

instantaneous voltage drops frequently, is affecting production in many plants.

1.3.2.2 Controversial Points between Power Demand in Future and

Supply Reinforcing Programs

According to the power station buildup program of TNB, it has been expected that

the 30 % margin rate can be kept for the time being, if the 3rd phase (500 MW X 2)

of the construction of Kapa Power Station starts in 1998. However the construction

has been delayed largely, and the prospect for the startup of operations is still far

from certain. Granting that the operation starts sooner or later, the program has

been so formulated that there will be no increase in power generation capability

thereafter till Denkir Power Station (350 MW) starts operation in 2002. (See

Fig.1.3.2.2-1.)

However power demand in Malaysia is expected to grow at a rate of 7 to 9 % per

year, and there is much possibility of power conditions being left precarious till the

4th quarter of 2002.

— 1 — 20—

1.4 Need of Project Linked with CDM,etc.

1.4.1 Need of Project as Seen from Policy Side

The Malaysian Government has already worked out the following policies related

closely with this project:

(1) In 1991, the “Vision 2020” to aim at Malaysian’s entry in the family of

advanced countries before 2020, was released.

(2) In 1996, the 2nd Industry Master Plan (IMP2) was made up, in which the

palm oil industry was ranked as an important strategic industry.

(3) In 2000, the 8th Malaysia Plan was made, in which renewable energy

sources are prearranged to be introduced with the target year set at 2005

and among then special energy has been thrown into biomass power

generation with an action plan made on it.

For the purpose of putting these plans in action, the Malaysian Palm Oil Board

(MPOB) was established with the Palm Oil Registration and Licensing Authority

(PORLA) and the Palm Oil Research and Development Institute of Malaysia

(PORIM) united into one organization, to strengthen support to the palm oil industry,

and in addition, on the introduction of favorable treatment actions in biomass power

generation, adjustments were made among the organs concerned and mutual

consent was reached, leaded by the MOE.

Since EFB, which are disposed be caused of their unsuitability to fuel for general

boilers, have the problem of methane gas being generated in the places of disposal

and that of soot and smoke being generated from field burning, the co-generation by

effective utilization of palm waste (EFB, fiber, shell, etc are residues after oil

squeezing from FFB), which is an energy source alternative to fossil fuel in the

meaning as a disposing method of low pollution, is being marked by the Department

of Environment (DOE) as well.

Thus this project conforms surely to related policies in the Malaysian Government,

and when opinion was tapped on the project in question, the MOE spoke:

“Energy-sawing promotion and environmental improvement in the palm oil industry

are major items to be faced squarely by the Malaysian Government. We are much

interested in them and want to promote them together.” The DOE also spoke: “We

are much interested and will cooperate with you. Please promote them. Let DOE

serve as a monitor on the project in question.” Furthermore the Malaysian Energy

-1-22-

Center has also promised positively its wholehearted support toward the realization

of this project.

In this way Malaysia has fully taken into consideration the national interest of its

own country from participation in the CDM, and it can be considered that Malaysia

is ready to participate as an activity under the CDM whenever any effective project

is given.

Accordingly it may be said that the need of this project linked with the CDM is

extremely high.

1.4.2 Prospect for Cooperation from Government

As to the prospect for cooperation from the Government, various favorable

treatment policies for investment have been framed 12), and by obtaining license

from the Malaysian Industry Development Agency (MIDA), the following favorable

treatments can be received:

1.4.2.1 Pioneer Status

This is a system to be given to the encouraged businesses and encouraged

production items specified by Minister of Trade and Industry, and an enterprise

whose Pioneer Status has been approved can receive the favor of partial exemption

from taxation upon imported equipment. Particularly Sabah State where the

proposed project site: Sahabat Complex is situated, has been designated as a

specially encouraged area, and there is much possibility of an additional favorable

treatment being given. The favor in taxation is exemption for 5 years of the

cooperation tax on 70 % of the legal income.

1.4.2.2 Investment Tax Allowance (ITA)

(D Period: 5 years (Reckoning of losses may be deferred)

(2) Favor in taxation: Up to 60 % of qualified capital disbursement is deductible

from income with a limit of 70 % of the legal income. (The deductible sum

remaining after deduction in the fiscal year under review, is kept deductible in

subsequent years.)

(3) To the enterprises having Pioneer Status, which have extended their business

to the east coast of West Malaysia and/or East Malaysia in order to expend

— 1 — 23 —

industrial areas, tax exemption on 85 % of the legal income is applied for 5

years (70 % for other areas). And to the enterprises to which ITA is applied,

80 % deduction from the income tax is basically applied, and the deductible

sum in each fiscal year is raised up to 85 % of the legal income.

1.4.2.3 Reinvestment Allowance (RA)

This is approved on the projects for expansion or modernization of the present

business of for multification of business, which are executed by resident corporations

in the manufacturing industry, agriculture and fishery. This allowance amounts up

to 660 % of the qualified disbursement. In general, this allowance is limited to 70 %

of the legal income. However to companies making reinvestments in specific areas of

East Malaysia and of the east coast of West Malaysia, allowances amounting up to

100 % of the legal income are approved. The deductible sum remaining after

deduction is kept deductible in subsequent years till the total deductible sum is

deduced.

1.4.2.4 Favorable Treatment Actions for R & D

To encourage research and development (R & D), there are various favorable

treatment actions. (Double deduction for R & D, investment tax allowance,

industrial allowance, etc.)

1.4.2.5 Favorable Treatment Actions for Advanced-Technology Industry

Advanced-technology enterprises are those engaging in the encouraged business

and in manufacture of encouraged products, in the field of new advanced

technologies, and a favorable treatment system to these enterprises also exists.

Since this project can also be interpreted as a new advanced technology, the

possibility of this favorable treatment action being applied to it is also undeniable.

-1-24-

1.5 Necessity of Introducing Alternative Energy Technology in the Industry as Object of

Project

As mention the above, palm oil mills are usually located far from the national grid,

larger mills are more so, due to their physical reasons so that they have to establish

in-house power generation facilities. Necessary electric power for the oil squeezing

process depends on diesel generators while necessary steam is supplied from the

boiler that are fueled by palm fiber and shell of which easily combusting.

The squeezed oil at palm oil mills is called as crude palm oil (hereafter as CPO),

semi product situation, so that they are required to refine for the final product. CPO

is collected from each palm oil mill to a refinery factory by truck of which CPO has to

refine for being final product. However, the refinery factory doesn’t have palm shell

for boiler fuel so that it has consumed a large quantity of diesel oil for boiler that

requires to generate steam for refinery process and for operation of diesel generator

that requires for obtaining electric power. But consuming diesel oil directly reflects on

the cost of final product.

In 1999, about 10 million ton crude palm oil in all was produced from about 57

million ton FFB, and as EFB amount to approx. 23 % of FFB, it follows that about 13

million ton EFB were generated as biomass waste in 1998.

The quantity of energy to be obtained from the total volume of EFB generated in

Malaysia, amounts to 2 million ton in the quantity of alternative oils, according to

investigation by the Malaysian Palm Oil Association. It is said that this corresponds

to 6 % of the energy needed in the whole of Malaysia. It is a fair loss to the country to

nullify the source of such a large volume of energy as before, and it can be considered

that it is necessary to utilize EFB as an alternative energy source in order to

strengthen the international competitive position in prices, of Malaysian palm oil

which is an important major export item.

— 1—25 —

1.6 Meaning, Need and Effect of Project in Question and Possibility of Spread in Similar

Industry

There were 328 palm oil mills in Malaysia as of 1998: 75 % of them in West

Malaysia and 25 % in East Malaysia. The FFB processing capability is 20 to 90 ton

per hour, though it varies with mills, and more than 60 % of all mills have capability

not less than 30 ton per hour.

‘30 ton per hour' means an EFB processing capability of 260 thousand ton per year

at 24-hour and 365-day operation, with EFB generation of 60 thousand ton per year.

About 200 thousand ton EFB per year are needed for 7 MW power generation,

though it varies with generation capabilities in private power generation; therefore it

follows that needed EFB can be secured if they are collected from 4 to 5 mills with a

scale of 30 ton per hour.

If this project is successful, it is considered that there is a great possibility of spread

in future into the similar industry.

(D The fact that EFB having been so far used only for mulching can be used ass

fuel, means, in itself the realization of extraordinary cost saving, compared with

the cost of diesel oil having been used so far.

(D It is the key to secure and collect a sufficient quantity of EFB; and now that

EFB are processed, EFB are necessarily accumulated once at least in the

stripper (the process to separate them from palm fruits) of each mill. It is not

difficult to provide the 2nd transport system from there to the burning site. It is

feasible independently for such a large organization as FELD A, to secure a

sufficient quantity of EFB, and even in the case of private companies of smaller

scales can minimize risks by executing the project jointly with neighboring

plural mills.

(3) In such cases as neighboring mills consent to investment can not be obtained,

the quantity of EFB can be secured by making with them long-term contracts to

take EFB only from them. It must be feasible to make such trades favorably

with them because every company is worried about EFB disposal.

(4) Profitability of the project can be improved by selling electric energy to the

national grid on the basis of IPP. Particularly, in the case of sites near the

national grid within West Malaysia, the possible issue of bearing the cost of

transmission line laying, is easy to settle by compromise with TNB, and this is