FDI and TNCs in Agriculture in Developing Countries

47

FDI AND TNCs IN AGRICULTURE OF DEVELOPING COUNTRIES 1 FINANCING, INVESTMENT, EXPORTS AND MARKET ACCESS Prepared for UNCTAD ZBIGNIEW ZIMNY Geneva, March 2009 1 Inputs from the paper were used in UNCTAD (2009), World Investment Report 2009. Transnational Corporations, Agricultural Production and Development, New York and Geneva: United Nations.

Transcript of FDI and TNCs in Agriculture in Developing Countries

FDI AND TNCs IN AGRICULTURE OF

DEVELOPING COUNTRIES1

FINANCING, INVESTMENT, EXPORTS AND

MARKET ACCESS

Prepared for UNCTAD

ZBIGNIEW ZIMNY

Geneva, March 2009

1 Inputs from the paper were used in UNCTAD (2009), World Investment Report 2009. Transnational

Corporations, Agricultural Production and Development, New York and Geneva: United Nations.

2

Table of Contents

Chapter I. FINANCING AND INVESTMENT ………………………………………3

A. Introduction …………………………………………………………………...3

B. Direct impacts: contributing capital and investment through FDI ……………4

C. Indirect impacts ………………………………………………………………10

D. Easing financial and investment constraints for local farmers ……………....11

E. Modernizing an industry: the case of dairy industry in Zambia ……………...15

F. Direct and indirect crowding out and crowding in …………………………...17

G. Conclusions …………………………………………………………………..21

Chapter II. EXPORTS AND MARKET ACCESS …………………………………..22

A. Background: agricultural exports of developing countries …………………..22

B. The role of TNCs in agricultural exports of developing countries ………..…25

1. Trading TNCs ………………………………………………………...26

2. TNCs as producers and exporters from host countries ……………….33

3. TNCs as coordinators of international value chains: the case of

Kenya …………………………………………………………………35

C. Conclusions …………………………………………………………………..42

References ………………………………………………………………………………44

Tables

1. Major host developing countries to FDI in agriculture: the role of FDI in

investment and value added in agriculture and the entire economy,

ratios, %, 2004-2007 …………………………………………………………7

Figures

1. Exports of traditional and non-traditional agricultural products from

developing countries, 1995 and 2005, billions of dollars ……………………24

Boxes

1. FDI in agriculture in Viet Nam …………………………………………….…9

2. FDI in agriculture in China …………………………………………………...9

3. Shortcutting coffee value chain: not easy but possible ……………………….28

4. Olam International -- a modern developing country-based trading TNC …….31

5. The role of TNCs in upgrading Africa’s exports of cashews ………………...32

6. Trade barriers to market access of developing countries’ agricultural

commodities …………………………………………………………………..37

3

Chapter I. FINANCING AND INVESTMENT

A. Introduction

TNCs can contribute to development because, while investing abroad, they deploy a

package of assets and resources that are useful for development but are often in shortage

or not at all available in developing countries. Key assets and resources include capital,

technology, skills, managerial expertise and access to international markets. When TNCs

invest abroad through undertaking FDI, then, in distinction from other sources of foreign

capital, TNC-related capital inflow always comes with investment projects. In some

industries, TNCs invest abroad through non-equity forms of FDI (such as franchising or

management contracts popular in fast food, hotel or car rental industries) or influence

local production in host countries through a variety of contractual arrangements, which

may vary according to the industry. In manufacturing, for example, this is often done

through original-equipment manufacturing arrangements (OEM). In infrastructure, build-

operate–transfer (BOT) arrangements are a widespread form of TNC-involvement in

electricity or roads building. In the latter cases an investment package does not include a

direct contribution of FDI capital, although TNC involvement can facilitate access to

capital in other forms. The composition of non-capital components of the package varies

by industry, the type of investment, the type of an agreement and often depends on

capabilities of host countries. In many cases TNCs undertake or sponsor investment

projects which could not be undertaken by domestic enterprises or, if they could, TNCs

projects are typically characterized by higher levels of efficiency than domestic ones. Of

course, TNCs invest abroad with a view to increasing their own efficiency and

competitiveness and not necessarily those of host countries. In many cases interests of

TNCs and developing countries overlap and outcomes are positive, while in others they

diverge and expected contributions of TNCs do not materialize, are too limited or

benefits are associated with negative impacts.

These impacts of TNCs occur also in the agriculture in developing countries, but in most

cases they take the form of indirect impacts, related to FDI by TNCs in food processing

and food retailing or the control of cross-border supply chains by TNCs remaining in

4

their home countries. Direct impacts through FDI in agriculture are small, but in a

growing number of host developing countries they can be significant.

B. Direct impacts: contributing capital and investment through FDI

When considering the impact of TNCs on agricultural production one should keep in

mind that the direct impact is very limited because FDI in agricultural production is very

small. It was more important several decades ago, as an inheritance from the colonial

times, when large foreign-owned plantations were quite a popular way of ensuring access

to agricultural resources. For example, early foreign investors in Latin America’s food

industry often integrated vertically, controlling vast areas of land and exporting goods

such as sugar, bananas or meat to the United States and Europe. Since the 1980s, the

multinational ownership of land has lost importance everywhere (Rama and Wilkinson,

2008, p. ; and UNCTC, 1983, p. 218). For example, in Central America, TNCs have

moved away from banana plantation production to purchasing bananas from local

farmers and providing technical advice and marketing services. The tea industry in

Kenya, originally based on the foreign-owned plantation model, has undergone a similar

transformation as did international tobacco industry (Eaton, C. and A.W. Shepherd, 2001,

chapter 1, p. 7). The process was triggered by the nationalization movement, as part of

decolonization, after World War Two. During 1960-1976, agriculture was second, after

banking and insurance, among industries affected by takeovers of foreign enterprises in

developing countries, with 272 cases of takeovers (compared to 349 cases in banking and

insurance out of the total of 1369 takeovers). In South and East Asia, nearly half of all

nationalizations took place in agriculture (United Nations, 1978, p. 233).

Nationalizations provided an initial impetus to TNC withdrawal from agricultural

production and focus on downstream activities in the value chain, while securing

increasingly inputs through contracts with local farmers in developing countries.

Subsequent transformations of agriculture towards commercialization and those of food

retail trading in developing countries, in response to rapidly growing demand for higher

value food products, urbanization and a growing entry of women into labour market,

5

have reinforced the trend towards contracting farm inputs, not only on the part of TNCs

but also local processing firms, supermarkets, and other agents.

Nowadays, there are many agribusiness TNCs in the world, but they continue to focus on

downstream activities: processing, trading and marketing of food. During 1996-2000,

only 4% of foreign affiliates of the 100 largest agricultural TNCs dealt in agriculture. As

mentioned above, there are also important TNCs in agricultural raw materials, but they

focus on trading activities, sometimes dominating international markets of individual

products. Apparently, food and commodity TNCs no longer consider agricultural

activities as their competitive advantage, trying instead to influence these activities

through controlling and coordinating supply chains going back to production, and giving

rise to a variety of indirect effects of TNCs on agriculture in host developing countries.

The emergence and a growing role of supermarket TNC chains in both developed and

developing countries have added particularly strong impetus to these developments.

Consequently, the contributions of FDI in agriculture to overall capital inflows and

investment in developing countries are small. During most of the 1990s and at the

beginning of the 21st century, FDI inflows into agriculture of developing countries

remained at a level below $2 billion annually, averaging higher only during 1994-1996,

at $3.3 billion per year. During 2004-2007, such flows amounted to $2.7 billion per year,

or a negligible 1.4% of total FDI inflows to developing countries. They may increase in

the future, as there is a growing interest on the part several developing countries (such as

China2 or countries of West Asia

3) in promoting FDI in agriculture to increase the supply

of food and commodities and an increasing number of host developing countries relaxes

restrictions on, and improves the investment climate for, FDI in agriculture.

2 By 2005, China has established production bases abroad for soybean and corn (in Russia and Central Asia

among others), crop, rubber, tropical fruit and sisal (in South-East Asia and Latin America. It has also

established several Agricultural Centres abroad: on methane in Laos, hybrid rice technology in Indonesia,

rubber nursery stock in Burma, or agriculture technology in Russia (The Survey of Foreign Investment in

China’s Agriculture Industry of 2005, 21 March 2006,

http://www.fdi.gov.cn/pub/FDI_EN/Economy/Sectors/Agriculture/Agriculture/t20080130_89294.htm

3 See on this Woertz et al., 2008.

6

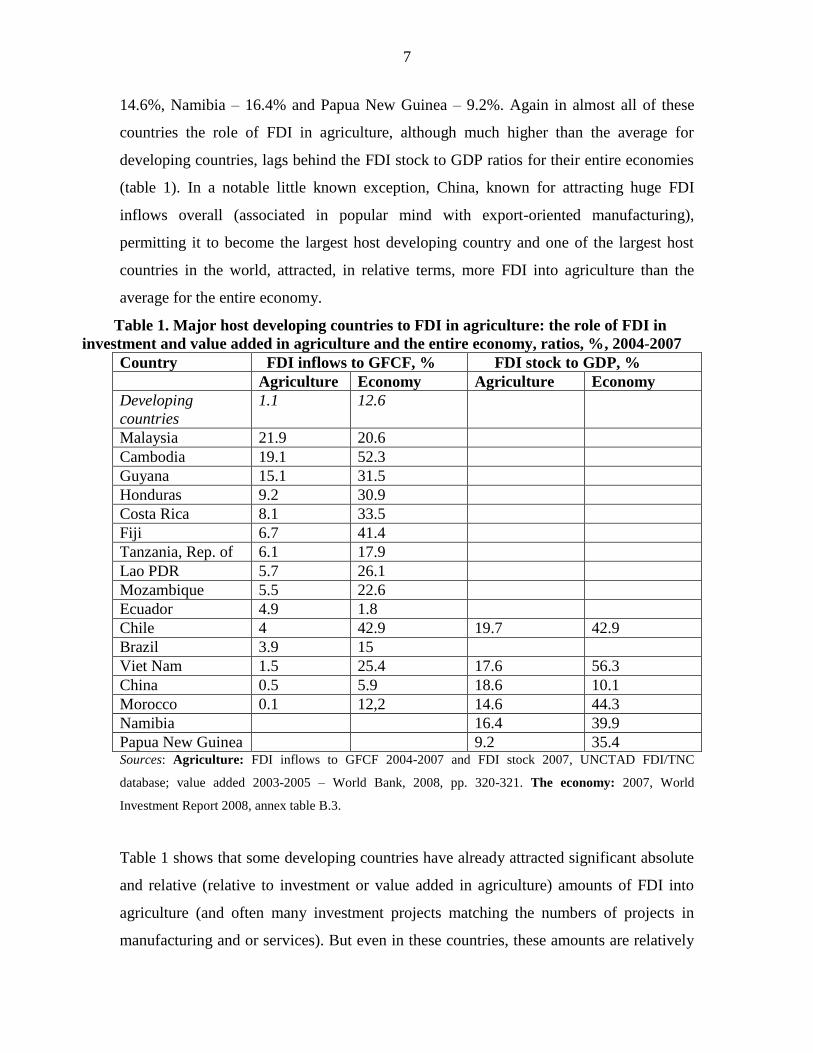

An estimated stock of agricultural FDI in developing countries was some $5 billion in

2007, or 0.8% of the total FDI stock of developing countries. This is still a negligible

amount, smaller than many individual FDI projects in services such as

telecommunications or electricity.

Equally small is the contribution of FDI to domestic investment of developing countries

in agriculture. FDI inflows into agriculture during 2004-2007 produce a negligible ratio

of FDI to gross fixed capital formation (GFCF) in agriculture of 1.1%, compared to the

ratio of 12.6% for total FDI inflows to total GFCF of developing countries in 2007. The

ratio of agricultural FDI stock to agricultural GDP of developing countries is also small –

only 1% in 2005, compared to the 26% ratio for manufacturing and 33% for services

GDP. There are, however, several developing countries, in which the importance of FDI

in domestic agricultural investment is much higher than the average for developing

countries. As regards FDI inflows to GFCF in 2004-2007, Malaysia and Cambodia take

the lead with the ratio in agriculture around one fifth, followed by Guyana (15.1%),

Honduras (9.2%) and eight countries with the ratios ranging from 4% to 8% (table 1). In

all these countries but two (Malaysia and Ecuador), the contributions of FDI to

investment in agriculture are, however, several times smaller than those of total FDI to

investment in the entire economy.

The 2004-2007 FDI inflows to GFCF ratios inform about the most recent contributions of

FDI to agricultural investment. But FDI inflows fluctuate from year to year, or from

period to period, sometimes heavily. For example, some countries (e.g. China, Viet Nam,

Egypt, Morocco) and regions (Africa) received much larger FDI inflows into agriculture

during 2000-2003 than during 2004-2007.4 Viet Nam, for example, received much more

FDI during 1995-2000 ($309 million annually) than during 2001-2007 ($102, box 1). The

ratio of FDI stock in agriculture (in 2007) to agricultural value added5 produces a couple

of additional developing countries with a significant all-time contributions of FDI capital

to national agriculture: Chile – 19.7% , China – 18.6%, Viet Nam – 17.6%, Morocco –

4 UNCTAD FDI/TNC database

5 Annual average value added in agriculture during 2003-2005 (taken from the World Bank, 2008, pp. 320-

321).

7

14.6%, Namibia – 16.4% and Papua New Guinea – 9.2%. Again in almost all of these

countries the role of FDI in agriculture, although much higher than the average for

developing countries, lags behind the FDI stock to GDP ratios for their entire economies

(table 1). In a notable little known exception, China, known for attracting huge FDI

inflows overall (associated in popular mind with export-oriented manufacturing),

permitting it to become the largest host developing country and one of the largest host

countries in the world, attracted, in relative terms, more FDI into agriculture than the

average for the entire economy.

Table 1. Major host developing countries to FDI in agriculture: the role of FDI in

investment and value added in agriculture and the entire economy, ratios, %, 2004-2007

Country FDI inflows to GFCF, % FDI stock to GDP, %

Agriculture Economy Agriculture Economy

Developing

countries

1.1 12.6

Malaysia 21.9 20.6

Cambodia 19.1 52.3

Guyana 15.1 31.5

Honduras 9.2 30.9

Costa Rica 8.1 33.5

Fiji 6.7 41.4

Tanzania, Rep. of 6.1 17.9

Lao PDR 5.7 26.1

Mozambique 5.5 22.6

Ecuador 4.9 1.8

Chile 4 42.9 19.7 42.9

Brazil 3.9 15

Viet Nam 1.5 25.4 17.6 56.3

China 0.5 5.9 18.6 10.1

Morocco 0.1 12,2 14.6 44.3

Namibia 16.4 39.9

Papua New Guinea 9.2 35.4 Sources: Agriculture: FDI inflows to GFCF 2004-2007 and FDI stock 2007, UNCTAD FDI/TNC

database; value added 2003-2005 – World Bank, 2008, pp. 320-321. The economy: 2007, World

Investment Report 2008, annex table B.3.

Table 1 shows that some developing countries have already attracted significant absolute

and relative (relative to investment or value added in agriculture) amounts of FDI into

agriculture (and often many investment projects matching the numbers of projects in

manufacturing and or services). But even in these countries, these amounts are relatively

8

small, when compared to total FDI inflows or stocks (1.2% in China’s inflows in 2004-

2007, 1.5% in Chile or 0.1% in Morocco). This suggests that one of the reasons for the

low significance of agricultural FDI in overall FDI is much lower capital intensity of

investment and the small average size of projects in agriculture compared to that in other

sectors, notably in infrastructure services, where one privatization-related project can

involve billions of dollars of investment. When, however, agricultural FDI is compared to

investment or value added in agriculture in a host country (more appropriate comparison

than that to overall FDI), or, even better, to the private investment in agriculture, then it

turns out, that such FDI can play a significant role.

Another reason for low FDI in agriculture in most developing countries is that in many of

these countries, which have locational advantages for such FDI (suitable climate and

available fertile land), FDI in agriculture has not been a priority sector for attracting FDI

and these countries have kept restrictions on such FDI. Countries, which lifted

restrictions on FDI entry have often not succeeded in establishing enabling FDI

framework for FDI in agriculture through, for example, resolving the issues concerning

access to land or reducing risks of investing in agriculture related to environmental or

social concerns or political opposition.

China and Viet Nam are examples of two countries, which included FDI in agriculture

among their FDI priorities and, in distinction from other developing countries which did

the same thing, attracted significant amounts of this FDI, making a clear difference for

their agriculture not only in terms of capital and investment but also in terms of

upgrading (productivity, exports, etc). Experiences of these two countries, based on

national sources, are presented in boxes 1 and 2.

Box 1. FDI in agriculture in Viet Nam

Vietnam has actively promoted FDI into agriculture since many years, providing it with

incentives. During 1988-2007, the country registered 674 FDI projects in agriculture, forestry and fishing

worth $3.9 billion of total registered capital. These projects accounted for 7% of the total number of

registered FDI projects and 4% of the total registered FDI capital (General Statistics Office of Vietnam,

2007, p. 104). But the implementation of licensed projects is much lower and, as a result, FDI stock in

agriculture was $1.7 billion in 2007. If the stock is compared with value added in agriculture or estimated

9

private investment in Vietnam’s agriculture during 1988-2007,6 then the contribution of foreign investment

becomes very significant, respectively 18% and 28% of the total. Vietnam is thus an example of a

developing country, which has relied considerably on FDI for both its agricultural development and its

private investment in agriculture. Most of this FDI originates from developing countries of Asia, with

Taiwan Province of China, being the largest home country, accounting for a quarter of FDI stock in

agriculture in Vietnam (Truong Thi Thu Trang, 2009).

Apart from bringing much needed capital to Vietnam’s agriculture, FDI projects have contributed

to the promotion of production capacity, brought about advanced technology, and contributed to increasing

the competitiveness of agro-forestry produces. Sugar production programmes, vegetable and fruit

plantation and processing programmes, reforestation programmes and new technology transfer have

produced high-yield plant and animal varieties, and other processed products of international standards.

Furthermore, “tens of thousands of jobs have been created (there have been so far 75,000 industrial

labourers working for FDI enterprises in the sector), raw materials and services produced for the processing

industry, etc. Skills for managers and technical staff have been strengthened and workers trained with

higher professional skills” (International Support Group, 2004: 5). Given all this, Vietnam is continuing its

efforts to improve the investment climate in agriculture to sustain FDI inflows (which, after reaching a peak

during the mid-1990s, fell at the beginning of the 21st century), raise the level of implementation of

registered FDI projects and promote not only resource exploitation but also FDI in advanced activities

(Truong Thi Thu Trang, 2009). The Ministry of Agriculture has prepared a programme aimed at addressing

bottlenecks for this FDI during 2008-2015.7

Box 2. FDI in agriculture in China

China, apart from promoting its own FDI in agriculture abroad, is also attracting inward FDI into

agriculture. In 1998, China opened several areas of agriculture to FDI and since that time it has attracted

significant FDI inflows, fluctuating annually from 1998 to 2008 between $600 million and over $1 billion.

(source: MOFCOM, UNCTAD Asian seminar). During the entire period China registered 10,622 FDI

projects in agriculture (or 3% of the total number of FDI projects) and nearly $10 billion of cumulated FDI

inflows (or 1.5% of total inflows). These inflows, when compared to agricultural value added, produce a

ratio of nearly 19% (table 1), putting China among the group of developing countries, which rely

significantly on FDI in its agriculture. The significance of foreign firms for agricultural investment may

be even higher. An official Chinese source estimates the amount of investment by foreign firms (“FDI

amount in contract”) at the end of 2005, at the cumulated total of $32.9 billion.8 When this amount is

compared to the total Chinese investment in fixed assets in rural areas (during 1999-2006, including both

agricultural and non-agricultural investment), the resulting ratio is 20%. It is even bigger, 57%, when

compared to fixed investment of farm households during the same period.9

FDI in China’s agriculture often breaks the traditional pattern of investment by agribusiness

TNCs, focusing on processing and trading. Japanese brewing TNC, Asahi, rented land and is planning to

cultivate cows and build greenhouses for organic farming. Heng River Fruit from Macao diversified from

selling fruits to its own citrus production and contract farming with local farmers. French Vivendi

6 Data on private investment comes from General Statistics Office of Vietnam, Statistical Yearbook of

Vietnam 2007 online,

http://www.gso.gov.vn/default_en.aspx?tabid=515&idmid=5&ItemID=8030, tables 42 and 51. 7 Vietnam. Foreign Press Center Foreign investment in agriculture remains limited, 18 December 2008,

http://www.presscenter.org.vn/en/content/view/115/44. 8 Sources for China include The Survey of Foreign Investment in China’s Agriculture Industry, various

issues from 2002 to 2006 retrieved on 22 February 2009 from

http://www.fdi.gov.cn/pub/FDI_EN/Economy/Sectors/Agriculture/Agriculture/t20080130_89294.htm. The

reported FDI refers, according to the source, to “FDI amount in contract”. 9 Data on investment in agriculture comes from National Bureau of Statistics of China, China Statistical

Yearbook 2008 online http://www.stats.gov.cn/eNgliSH/statisticaldata/yearlydata/, tables 5-26 and 5-2.

10

Universal has invested in citrus orchard base and established cooperation with local farmers. According to

the Ministry of Agriculture, FDI supplements domestic capital for investment, brings advanced

technologies and equipment, introduces new products and advanced management, promotes the

development of food processing industry, and accelerates the reform in rural areas and agriculture in

general. Half of the output of FDI firms is exported.

Pending the end of the world’s financial and economic crisis, agricultural FDI is set to

grow in the long-term. FDI in agriculture by some major home countries has recently

increased, and in some cases, quite significantly, in response to the commodity boom and

high prices during the past couple of years. For example, the United States FDI stock in

“agriculture, forestry, fishing and hunting” increased during only three past years, from

2004 to 2007, by over 60%, owing mainly to the to the increase of FDI in crop

production, by nearly 90%, from $490 million to $920 million. In addition, there is a

growing interest on the part of several developing countries (such as China or countries in

West Asia) in promoting outward FDI in agriculture to increase the supply of food and

commodities through imports from host developing countries. And finally, an increasing

number of host developing countries relaxes restrictions on, and improves the investment

climate for, FDI in agriculture.

C. Indirect impacts

Agrobusiness and supermarket TNCs rarely invest in agricultural production but they

have engaged heavily in market-seeking FDI in their respective activities in both

developed and developing countries. To secure agricultural inputs they establish local

supply chains, using contracts with local farmers. Sometimes these chains span across

borders, leading to efficiency-seeking, cross-border value chains. But efficiency-seeking

value chains are more often established by supermarkets based in developed countries,

which seek in developing countries competitive products, meeting high quality and food

safety requirements.

Contracts are used in both market-seeking FDI and in efficiency-seeking investment,

sometimes as part of very long value chains. Market-seeking FDI involves the expansion

of supermarkets and food processors in foreign markets. To the extent to which a host

11

developing country has an agricultural capacity (not all host countries have), such

expansion results in the establishment of domestic value chains. For example, Nestle

India has a retail network of some 700 outlets in India, serviced by 4,000 distributors and

covering 3,300 towns. Its products include baby food, infant milk powder, dairy

whiteners, sweetened condensed milk, ghee, UHT milk, curd and butter. In 2001 Nestle

sourced milk from over 8,500 local farmers, from larger ones directly and from smaller

ones through agents. In the latter case contracts are concluded with agents (Birthal et al.

2005, pp. 7-8). Exports of horticulture products from Kenya to the United Kingdom is an

example of the efficiency-seeking value chain. In this case the value chain is much longer

than in the case of market-seeking investment as it involves exporters in Kenya and

importers in the United Kingdom. The chain is run by supermarkets in the United

Kingdom. The agents who conclude contracts with local farmers in Kenya are not

supermarkets but exporters, most of them foreign investors (see below the section on

market access and exports).

In both cases, contracts with local farmers concluded directly by TNCs (Nestle with

larger milk suppliers) or indirectly on their behalf (by Nestle’s agents in India or by

exporters in Kenya), although not contributing to FDI inflows, exert very important

effects on agriculture in developing countries.

D. Easing financial and investment constraints for local farmers

Given relatively small contributions of FDI to capital inflows and agricultural investment

in most developing countries, contracts with local farmers concluded directly by TNCs or

indirectly on their behalf (by agents participating in value chains coordinated or

controlled by TNCs), although not representing FDI inflows, exert important effects on

agriculture in developing countries, including on easing financial and other investment

constraints for local farmers in developing countries.

This is an important contribution, as, despite the rapid development of financial services

to agriculture, a majority of small holders worldwide remain without access to these

12

services10

(World Bank, 2008: 143). There has been a demise of special credit lines to

agriculture through public programmes, state banks or export crop marketing boards,

leaving huge gaps in financial services, “still largely unfulfilled despite numerous

institutional innovations” (World Bank, 2008: 13). Some even argue, that “with the

collapse or restructuring of many agricultural banks and the closure of many export crop

marketing boards (particularly in Africa) which in the past supplied farmers with inputs

on credit, difficulties have increased rather than decreased”11

(Eaton and Shepherd, 2001,

chapter 1: 3).

Private banking and other financial institutions have not filled the gap, because they tend

to concentrate their activities in urban areas, where concentration of potential clients

(businesses and households) is higher, clients are more affluent, operating costs are lower

and contract enforcement easier than in rural areas. Where finance in rural areas has been

available (often through informal service arrangements such as money lenders,

pawnshops or families), it has been often directed at larger farms, excluding the majority

of small producers from the formal credit system.12

In this situation, the emergence of

vertically coordinated supply chains, domestic and/or international, and contract farming,

often run by TNCs, has facilitated in many cases financial intermediation for farmers,

including smallholders, which have been able to link to these chains. In addition to

facilitating or providing finance, contracts come often with several other components of

the package of resources, typically characteristic for “FDI package”, such as know-how,

the provision of inputs, training and guaranteed markets. TNCs are often in a better

10

For example in India, 87% of the surveyed households in two states had no access to formal credit and

71% had no access to a savings account in a formal financial institution (World Bank, 2008: 143-144). 11

State-sponsored financial institutions were abandoned because they did not serve well their purpose. In

many developing countries “government efforts to improve rural financial markets have a record of doing

more harm than good, heavily distorting market prices; repressing and crowding out private financial

activities; and creating centralized, inefficient, and frequently overstaffed bureaucracies captured by

politics” (World Bank, 2008: 145). While some countries ( such as the Republic of Korea or Taiwan,

China) have replaced them successfully with government-sponsored agricultural lending institutions, others

have not succeeded. 12

Difficulties in financing small agriculture originate in the lack of assets owned by smallholders which

could serve as a collateral for credit. In cases such assets are owned, there is a reluctance to use them as

collateral, as they are too vital too livelihoods. The development of microfinance, providing access to credit

without formal collateral, deals with these problems, but microfinance is still in infancy and does not yet

reach most agricultural activities.

13

position to provide finance than local firms, as one of the competitive advantages of

TNCs is their financial strength (Dunning, 1993, pp. 81-83).

Consequently, contracts, especially with large reputable TNCs can, in a number of ways,

ease financial constraints for participating local farmers in developing countries:

Contract farming usually allows farmers access to credit to finance production

inputs and/or investment. In most cases it is sponsors who advance such credit

(Eaton and Shepherd, 2001, chapter 1, p. 3; and Birthal et al., 2005, pp. 36-37).

“Working capital credit is typically supplied in kind, via input provision, by the

contracting firm” (da Silva, 2005, p. 16). Agro-industry firms have an advantage

over banks in acting as lenders because of their ability to monitor and enforce

credit contracts (Key and Runsten, 1999).13

Some bank managers see the contracts with large agro-industry firms as a

collateral substitute, enabling smallholders to obtain credit from banks, which

would not have been possible otherwise due to the lack of a collateral (Reardon

and Swinnen, 2004). Often, arrangements for credit are made with banks or

government agencies by sponsors of contracts. In these cases the contract serves

as a collateral. This is particularly important, when substantial investment by

farmers is required (in, e.g., tobacco barns or heavy machinery).”Banks will not

normally advance credit without guarantees from the sponsor” (Eaton and

Shepherd, 2001, ibid.)

Participation in contract farming strengthens the credit and investment capability

of farmers through increasing their income. Contract farmers have significantly

higher incomes than other farmers: from 10% to as much as 100% in Guatemala,

Indonesia and Kenya (World Bank, 2008, p. 127). In two contract system cases

examined in India, one concerning milk and another vegetables, revenues of

13

Though credit can be abused by farmers through selling crops to outsiders, or using material inputs for

purposes outside the contractual obligations. Therefore, many contracts include provisions concerning the

use of credit provided as part of contracts.

14

farmers were 2 to 4 times higher than those of non-contract farmers (Birthal et al.,

2005, p. 36).

Review or conceptual studies of contract farming by experts and international

organizations such as FAO or UNIDO, mentioned above, state that access to credit from

contracting firms or banks is a typical feature of contract farming (in addition to, or as

part of, the provision of other forms of assistance). Most empirical studies have

confirmed that, indeed, in addition to inputs and extension services, contracting firms

also provided credit, e.g., in Madagascar and Slovakia (World Bank, 2008, p. 128) or in

India (Birthal et al., 2005, pp. 36-36). But this does not always have to be the case. In

East Asia, for example, some smaller suppliers unable to meet contractual investment

requirements (such as labeling or packaging) were excluded from the possibilities offered

by foreign retailers such as increased sales and access to new markets (Coe and Hess,

2005, after Rama and Wilkinson, 2008, p.56). In addition, dealing with large agro-

business firms can put financial pressures on participating farmers. It is a common

supermarkets’ practice to delay payments to suppliers, for example, in the case of Latin

America’s horticulture products, by 15 to 90 days (Reardon and Berdegue, 2002, p. 381).

On the other hand, as noted in one study, “agro-business firms usually include [in

contracts with smallholders] forward payments or provision of inputs” to overcome the

problem of financial constraints faced by smallholders (Simmons, 2003, p. 18).

While the provision or facilitation of finance to local farmers through contract farming is

common, data concerning the amounts involved are typically not available. But as some

examples indicate, when large TNCs are involved, these amounts can be huge. Bunge, a

United States agro-business TNC, provided an equivalent of nearly $1 billion worth of

inputs to Brazilian soya farmers in 2004 (Greenpeace, 2006). Overall, United States'

TNCs are responsible for 60% of the total financing of soya production in Brazil

(Milieudefensie and Friends of the Earth, 2006).14

14

However, the current economic crisis appears to be reducing the availability of finance. For example,

Bunge cut advance cash payment to Brazilian farmers by 70% in 2008 ( “In Brazil, credit to farmers dries

up”, The Wall Street Journal, 29 November 2008).

15

E. Modernizing an industry: the case of dairy industry in Zambia

Dairy industry in Zambia is an example of a successful transformation of an industry with

FDI participation, leading to the structural transformation of dairy farming. Before 1991,

the industry was controlled by the state-owned Dairy Produce Board (DPB), which

implemented several programmes aimed at stimulating production and supporting

smallholders. However, these programmes were “generally unsuccessful, … milk

production remained very low and a formal dairy industry never really took off” (Neven,

et al., 2006, p. 3).

Since 1991, Zambia has liberalized and deregulated food markets and trade, privatized or

closed state-owned enterprises and encouraged FDI. Simultaneous entry of TNCs in milk

processing and in retail distribution has transformed the milk industry, introducing

modern procurement methods and the institutional, organizational and technological

changes in the entire supply chain.

At the same time, drastically reduced government support to smallholders was replaced

by initiatives of NGOs and public-private industry alliances, which helped organize

farmers into groups, build refrigerated milk collection centres, introduce and implement

new technologies and good practices at the production and collection stages and establish

formal linkages with Zambia’s leading dairy processors (Neven, et al., 2006, p. 5). These

changes facilitated the linking of many local farmers with modern supply chains brought

to Zambia by TNCs.

Initial FDI came from a South African TNC, Bonnita, which acquired processing plants

from DPB in 1996 and restructured production, closing some facilities, investing in

upgrading others and introducing modern management practices with suppliers of milk,

based on contracts and standards. Bonnita was acquired in 1998 by an Italian TNC,

Parmalat, which has continued modernization initiated by Bonnita. The industry was

further transformed in 2004 by the strategic alliance between Finta – a locally-owned

dairy processor -- and Clover, South Africa’s largest dairy processing company,

16

associated through partnerships with a French TNC, Danone, and Fonterra from New

Zealand, the world’s largest dairy cooperative. Zambia’s food retail industry has been

transformed with the entry in 1996 of major South African supermarket TNCs such as

Shoprite and SPAR. These chains have drastically increased the use of refrigeration in the

supply chain and have created a reliable and growing formal market for dairy products

taking away the market share from informal retailing.

Practices of foreign companies have been followed, to some extent and with some

success, by local players, such as Melissa, the Zambian-owned chain. A range of small

local processing firms have survived by improving production standards and responding

to the needs of a growing local market, sourcing often, however, products from abroad,

notably from South Africa. Finta, associated with foreign firms (including Clover, a

South African TNC), but locally-owned, sources raw materials from Brazil and imports

dairy products from South Africa. Melissa also often seeks cheaper imported products

(Kenny and Mather, ???, pp. 4, 6 and 8).

As a result of the entry of supermarket and milk processing TNCs in response to the

changes in Government’s policy, the dairy sector of Zambia has undergone a drastic

modernization. A long term decline of the industry has been reversed, and the production

and consumption of milk has grown rapidly. TNCs expansion in Zambia has improved

the national supply and quality of dairy products. Supermarket TNCs, more committed to

local sourcing than some local firms, have created new opportunities not only for local

farmers but also for local processing firms. Zambia has become less dependent on the

imports of powdered milk and other dairy products, while expanding production capacity

to record levels and satisfying a growing local consumer market (Kenny and Mather, ???,

p. 7).

F. Direct and indirect crowding out and crowding in

In the TNC context crowding out refers to a situation when a TNC entry makes domestic

investors give up investment projects to avoid competition with more efficient foreign

17

enterprises or it eliminates less efficient domestic firms from a market.15

Most developed

countries are not concerned with crowding out less efficient (domestic) enterprises by

more efficient (foreign) enterprises, especially if the entry takes the form of greenfield

investment (some of these countries, however, sometimes prevent foreign takeovers of

national firms, considered “strategic”). Competitive pressures mobilizing domestic firms

to increase their efficiency are seen as one of the benefits from FDI leading to better

allocation of resources and benefiting greater efficiency of the economy as a whole.

Developing countries are often concerned with crowding out effects of TNCs, seeing

them, in spite of positive effects on economic efficiency,16

as undermining domestic

enterprise development, a goal, many developing countries pursues. While foreign

affiliates that introduce new goods and services to the host economy are seen favourably,

those that undertake investments in the areas where domestic producers already exist, not

necessarily so (except in developing countries, which also see positive effects from

competition by foreign affiliates, at least in some activities).17

Crowding in takes place when investment by foreign affiliates stimulates new investment

in downstream or upstream production by other foreign or domestic producers. In many

cases, the emergence of domestic subcontractors would not be possible without foreign

15

There can also be crowding out of local firms from the financial markets, if TNCs finance their

investment through borrowing from a host country’s financial markets, and financial resources in that country are scarce (which is a typical situation in most developing countries), they can make borrowing

unaffordable for domestic firms and crowd them out of financial markets and possibly out of business. By

definition, FDI activity by TNCs can not crowd out domestic investors, as FDI comprises only funds

brought from abroad, including foreign affiliates’ financing by their parents, adding to the supply of

financial resources in host countries. The possibility of the financial crowding out occurs only if TNCs

borrow massively from the domestic market, which is rather a rare case.

16

In rigorous economic analysis, the net effect of crowding out on the host country’s economy should take

into account secondary effects such as what happens to the released resources (they may be used in other

activities in which local firms have greater competitive advantages) or how the surviving local competitors

react to TNC entry (they may take up the challenge and raise efficiency, investment and profitability). It

may also be that after initial crowding out of some (inefficient) enterprises, foreign affiliates crowd in other

(efficient) domestic firms through backward and forward linkages. 17

Developing countries, which do not want domestic enterprises to be taken over or threatened by TNC

competition, continue to keep restrictions on FDI entry or accept TNC activities in forms that do not pose a

danger to domestic enterprises. In spite of the rapid liberalization of FDI in developing countries such

restrictions are still quite common in infrastructure services, petroleum industry and certain areas of

agriculture.

18

affiliates, which provide stable long-term markets as well as access to technological

information.

Direct crowding out of local producers in agriculture by foreign affiliates engaged in

agricultural production would take place if these affiliates would undertake similar

activities as those undertaken by local farms, large and small. This may happen, but is

unlikely on a large scale.18

As mentioned earlier, FDI in agriculture is very small overall.

In countries, in which it is significant, such as Viet Nam or China, foreign affiliates are

reported to engage in new products, requiring advanced knowledge and technologies not

available to local farmers. In most cases they also bring market access beyond the reach

of local farmers. Often, direct engagement in agriculture is accompanied by establishing

linkages with local farmers through contract farming. If foreign affiliates produce similar

products as those cultivated by local farms, they typically do so at a much higher level of

efficiency and productivity, as shown in the examples above.

As mentioned earlier, there is considerable FDI in developing countries by market-

seeking supermarket chains, market-seeking and efficiency-seeking FDI by

manufacturing food processing TNCs and efficiency-seeking, export-oriented

involvement of supermarket TNCs through the control of local producers within

international value chains. The former two types of TNCs may crowd out local firms –

small retail firms, local supermarkets and processing firms. And they more often than not

do so, together with large competitive local firms, more and more often also TNCs. In

Latin America, where supermarket retailing is more developed among developing

countries, supermarkets and specialized wholesalers increasingly dominate the food

marketing industry in urban areas, marginalizing and crowding out small traders, spot

food markets and neighborhood stores (Dolan, Humphrey and Harris-Pascal, 2001;

Reardon and Berdegué, 2002).19

But such processes take place everywhere, with or

18

There are reports, for example, that some horticulture exporters (most of them foreign firms) in Kenya

engaged in production under the pressure from supermarket chains from the United Kingdom, in response

to allegations about inadequate product quality to show that they take steps to have greater control over the

production and its quality. This must have cut out several local farmers from the value chain. 19

For example, 64,198 small shops went out of business in Argentina from 1984 to 1993 and 5,240 in

Chile from 1991 to 1995.

19

without the participation of TNCs, and are symptomatic of retail market revolution,

which took place in developed countries several decades ago and now is spreading to

developing countries. TNCs may accelerate this process but they certainly did not

necessarily trigger it.

In other cases, local firms or regional developing country TNCs, if they exist and have

sufficient capabilities, undertake the challenge, often learning from developed country

TNCs and leading to better outcomes for local consumers and themselves. In China,

many TNCs entered food market during the 1990s, dominating its high-income segment.

As reported in one study (Wei and Cacho, 2001, after Rama and Wilkinson, 2008, p. 54),

“regional players …, such as President from Taiwan Province of China, Charoen

Popkhand from Thailand, Sinar Mass from Indonesia and Kerry from Malaysia were

able to benefit from their knowledge of the market, positioning themselves in the middle-

income consumer segment that is crucial for market expansion. Unable to compete in this

segment, a number of transnationals, such as Danone and Carlsberg withdrew, selling

their investments to regional competitors. …Competition was strengthened as domestic

firms learned from foreign investors, setting new quality standards and developing

reputable reputable competitive brands. Wie and Cacho conclude that the policy of

attracting FDI in China has resulted in the emergence of many strong domestic firms”.

.

All three types of services and manufacturing food TNCs affect indirectly domestic

agricultural production in host developing countries, mainly through contract farming,

producing many winners and leaving out many losers, local farmers (though not

crowding them out, as these TNCs are not directly involved in such production). Those

farmers, who meet the requirements of TNCs (such as quality and safety, logistical

requirements, adherence to private standards, volume and consistency of production, etc.)

receive their support (or that by agents acting on behalf of TNCs), undertake or increase

commercial production, often for export, and achieve higher revenues. For those who fail

to meet the requirements of supermarket chains and other TNCs, prospects are unchanged

or bleak. Their situation often deteriorates, as, for example, supermarkets crowd out small

20

local shops, spot markets and neighborhood stores, which are for these farmers

alternative outlets to sell their products.

Access to supply chains of supermarkets and processing firms is considered by farmers as

worthy and beneficial, in spite of pressures on investment and increased capabilities. But

even those farms that succeed in establishing themselves as suppliers to agro-industry

firms face a number of challenges. If they are unable to meet them, they may drop out of

the supply chain. There is a general perception that contract farming favours large and

medium-sized farms, triggering a tendency towards the exclusion of smallholders. But as

noted in one study, summarizing a number of country case studies in Latin America,

“exclusion of smallgrowers from participating [in supply chains to Latin American

supermarkets] does not appear to be in any way automatic” (Reardon and Berdegue,

2002, p. 382). Case studies of different countries themselves found both failures of

smallholders to survive in the chains as well as successes (sometimes owing to the

support from public and private institutions, ibid.). Studies on other continents have also

found rather mixed evidence in this respect. A study on India has found that “the

criticism against contract farming schemes for their bias against small producers has not

been found true. Evidence from the case studies has indicated considerable involvement

of smallholders in such schemes” (Birthal et al., 2002, p. 36). The study addressed also

another criticism of contract farming, namely, that large contracting firms facing small

producers extract from them monopsonistic rent and found it unfounded, as the contract

farmers in the study received relatively higher process than (from 4% to 25%) than non-

contract farmers (ibid.).

While there are cases of exclusion of small farmers from the supply chains, what matters

more than the farm size in other cases is farmers’ capacity to implement technologies that

result in quality improvements, higher productivity, lower costs and the ability to plant

and harvest at needed times during a year. This in turn is determined by factors such as

the level of education of farmers, access to transport and roads, irrigation (with good

21

quality water) and by access to physical assets such as wells, cold chain, greenhouses,

vehicles and packing sheds.20

G. Conclusions

TNCs in agriculture are less frequent providers of finance and investment through FDI to

developing countries than TNCs in manufacturing and services. One reason is that TNCs

in agriculture-related activities focus on their core competencies (which lie in

downstream activities such as processing, marketing and control of distribution

channels), undertaking FDI in agricultural production less frequently than do TNCs in

manufacturing and services production. Another reason is that agricultural FDI has not

been a priority sector for FDI attraction in many developing countries possessing

locational advantages in agriculture. In fact, many countries still maintain restrictions on

FDI entry into agriculture. Countries, which lifted such restrictions, have not yet been

able to provide all necessary ingredients of the enabling FDI framework encouraging

such FDI. But in some developing countries FDI has been a considerable source of

financing and investment in agriculture, especially when compared to national

agricultural investment and value added. This proves that, although a general pattern

indicates a smaller propensity of agriculture-related TNCs to engaging in agricultural

production in host countries than that of manufacturing and service TNCs, there are

enough agriculture-related TNCs – large and small – that are ready to do so, provided that

host countries create risk-free (or low risk) environment conducive to such investment. In

addition, new investors are emerging, such as TNCs from developing countries,

interested in undertaking FDI (often with the support and encouragement of their

governments, interested in raising food security) or private equity funds. As more and

more developing countries are opening to agricultural FDI and improve their investment

frameworks, FDI in agriculture is set to rise in the long-term, pending the conclusion of

the world economic crisis.

20

Reardon and Berdegue, 2007, a box prepared for World Development Report 2008 on “Whether the rise

of supermarkets excludes small farmers”.

22

Contract farming with TNC involvement is another significant source of finance, or

financial facilitation, to local farming in developing countries. It is an “agricultural”

equivalent of non-equity forms of FDI in manufacturing and services. Similarly to these

forms, contract farming often comes with other elements, characteristic for FDI package,

such as know-how, technology, training and access to markets, local or international (see

export section on the latter). In distinction from FDI-related financing and investment, it

addresses, at least partly, the issue of involving smallholders in developing countries

(those, who are able to meet contract requirements) in commercial farming.

Chapter II. EXPORTS AND MARKET ACCESS

A. Background: agricultural exports of developing countries

In the long term, the role of agriculture in the world trade has declined, reflecting the

structural shift of production and demand in the world economy away from agriculture

towards manufacturing and services. In absolute terms, both agricultural production and

trade have grown, but at a slower pace than those in manufacturing and services.

Consequently, the share of agricultural products in world exports decreased from one-

third in the early 1960s to 10% at the beginning of the 21st century (FAO, 2005, p. 12).

The increase of agricultural prices during the past couple of years, from 2004 to 2008,

has temporarily altered the declining trend, but with prices falling again in 2009, a long

term trend towards the relative decline of the importance of agriculture products in world

trade is likely to resume.

These changes have also affected developing countries, although to a different degree and

at a different pace as regards individual countries. As in the world exports, the share of

agricultural exports in overall exports of developing countries decreased significantly,

too, from over 50% to 10%, reducing a high dependence of developing countries on

agricultural exports, once considered as a barrier to development. Export dependence of

the least- developed countries on agriculture is higher, amounting to 20%. In many

individual developing countries it is much higher. In twenty nine developing countries of

23

Latin America and the Caribbean and Sub-Saharan Africa this dependence exceeds 40%

(ibid., pp. 172-176). Forty three developing countries still depend on a single agricultural

commodity (such as coffee, bananas, cotton or cocoa) for over 20% of their total export

revenues and over 50% of their agricultural export revenues (ibid., p. 128). Volatile

markets for agricultural commodities (due to the slow or no demand growth and the

emergence of new producers, both causing a long term decline in prices and short term

price fluctuations) reflect adversely on the economies of these countries, resulting in

large fluctuations and/or prolonged stagnation of export revenues and negative impacts

on income, employment and growth.

But not all agricultural products have faced stagnating demand and unfavourable prices in

world trade. Driven by the rapidly rising demand and urbanization in developed and

better-off developing countries, exports of non-traditional agricultural products, including

horticulture and fish (dubbed in the literature “high value” agricultural products), have

become much larger and have grown much more rapidly21

than those of traditional

products such as coffee, cocoa, tea, sugar, spices and nuts. At the beginning of the 21st

century exports of non-traditional products accounted for 31% of global agricultural

exports (compared to 20% in 1980), while those of traditional agricultural commodities

for 13% (down from 22% in 1980). Developing countries as a whole have capitalized on

this trend expanding rapidly non-traditional agricultural exports (figure 1), and increasing

their share in their total agricultural exports to 41% from 22% in 1980, while the share of

the latter group decreased from 40% to 19% (Humphrey, 2006, p. 2).

Another estimate broadens the range of higher value food items, including not only fresh

and processed fruits and vegetables and fish and fish products, but also meat, nuts, spices

and floriculture. Exports of all these products from developing countries were by 2000

1.5 to 2 times higher than in 1980, accelerating at the beginning of the 21st century to the

level 3 to 3.5 higher than in 1980 (World Bank, 2008, p. 13). The value of these exports

21

During 1995-2006, an annual rate of growth of world exports of fruits was 5.3% and vegetables 5.4%,

while that of coffee -1.2%, of cotton 0.1% and rice 2% [UNCTAD (2008). UNCTAD Handbook of

Statistics 2008 (Geneva and New York: United Nations), p. 144-147].

24

from developing countries amounted to $134 billion in 2004, or 43% of their total agro-

food exports.

Figure 1. Exports of traditional and non-traditional

agricultural products from developing countries, 1995

and 2005, billions of dollars

0

5

10

15

20

25

Ric

e

Cotto

n

Coco

aTea

Coffe

e

Fruits

Veg

etab

les

Fish

Edi

ble

produ

cts

1995 2005

Source: UNCTAD, 2007, pp. 152-155.

Developing countries as a whole have performed much better in overall exports than in

those of agricultural products. Owing to the successful diversification of exports of many

developing countries towards manufacturing, and, in some cases towards tradable

services (e.g., India), the share of developing countries in total world exports increased

from 29% in 1980 to 38% in 2007.22

However, the share of developing countries in

world’s agricultural exports decreased from 40% to 30%. All developing countries’

regions except Asia experienced the declining shares, which were in the case of Africa

particularly drastic: from 10% to 3%. True, the declining position of developing countries

in agricultural exports has been partly due to the competition from the subsidized exports

of developed countries (in the case of e.g. cotton exports) and partly due to trade barriers

in developed world suppressing prices of, and/or demand for, some agricultural products

exported from developing countries. But the deteriorating agricultural export

performance reflects also, in spite of continuing comparative advantage, a

22

UNCTAD (2008). UNCTAD Handbook of Statistics 2008 (Geneva and New York: United Nations), p. 2.

25

competitiveness problem of many developing countries in reducing costs, improving

quality and accessing demanding markets for agricultural products. As principal markets

for these exports are in developed countries, in many cases of successful exports TNC

supermarket chains and other TNCs have been instrumental in helping increase these

exports through the control of cross-border supply chains and contract farming in

developing countries, as trading intermediaries and, finally, in a number of cases, as

direct foreign investors, as discussed in the following sections.23

B. The role of TNCs in agricultural exports of developing countries

The role of TNCs in agricultural exports of developing countries differs from that in

manufacturing exports. In the latter, the involvement of TNCs more often than not takes

the form of FDI, especially in the case of technologically sophisticated products. In such

a case, TNCs are both producers and exporters, providing host countries with the entire

package of FDI resources necessary for exporting. They also carry the risks of export

projects. In agriculture, TNCs more often than not are not producers of exported

products. Rarely involved in farming, as mentioned earlier (though this is changing in

many cases) they focus instead on downstream operations in the supply or value chain

such as processing, providing services necessary for exports, marketing and/or selling

products to final consumers. In many cases, they provide ingredients necessary for

successful exporting such as market information, seeds, technology, know-how, brand

names for differentiated products and, most importantly, the knowledge of, and access to,

international markets. Possessing a comparative advantage in producing an agricultural

product by a country does not automatically translate into exporting. While several

developing countries have acquired and developed capabilities and technologies needed

for successful exporting of agricultural products, simple or sophisticated ones, many

others have not, in spite of trying. Therefore the role of TNCs in increasing the

23

Demand for these products is also growing rapidly in developing countries – 6-7 per cent a year,

providing additional opportunities for domestic producers, including smallholders. Supermarkets are a key

channel between these producers and consumers, dominating domestic retail sales of agricultural products.

For example in some Latin American countries they account for 60% of these sales (World Bank, 2008, p.

12).

26

competitiveness of agricultural exports of many developing countries should not be

underestimated. This role differs by products, by host countries and by strategies of

individual TNCs. While there are some prevailing patterns as to this role, there are

always many exceptions.

1. Trading TNCs

Historically, in traditional agricultural commodities and/or products such as coffee,

cocoa, tea, rice, sugar or bananas, TNCs were often involved in exports as producers,

owning plantations and farms in many developing countries. As a result of

nationalizations of the 1960s and 1970s24

and the development of value chains, based on

contract farming and other arrangements, the prevailing form of TNCs in these

commodities is that of an international trading and/or a processing company. In the case

of some products, a few TNCs can dominate the international market. In fact, the

traditionally significant role of international trading companies, intermediaries in trade in

traditional agricultural commodities (UNCTC, 1983, p. 212-218) did not change much

and in a number of products it even increased.

In the case of coffee, typically produced for exports in most coffee-growing countries,25

approximately 80% of production worldwide originates from small-scale farms. (pp. 26-

27). A few TNCs, however, dominate downstream operations in the global coffee sector

24

During 1960-1976, agriculture was second, after banking and insurance, among industries affected by

takeovers of foreign enterprises in developing countries, with 272 cases of takeovers (compared to 349

cases in banking and insurance out of the total of 1369 takeovers). In South and East Asia, nearly half of all

nationalizations took place in agriculture (United Nations, 1978, p. 233). Nationalizations provided an

initial impetus to TNC withdrawal from agricultural production and focus on downstream activities in the

value chain, while securing increasingly inputs through contracts with local farmers in developing

countries. Subsequent transformations of agriculture towards commercialization and those of food retail

trading in developing countries, in response to rapidly growing demand for higher value food products,

urbanization and a growing entry of women into labour market, have reinforced the trend towards

contracting farm inputs, not only on the part of TNCs but also local processing firms, supermarkets, and

other agents.

25

Over 50 countries produce coffee. The largest developing country exporters include Brazil (accounting

for 29% of world exports), Viet Nam (18%), Colombia (11%), Indonesia (5%) and Peru (4%). For many

smaller exporters coffee is a major item in overall exports: Ethiopia (33%), Burundi (25%), Honduras

(21%), Uganda (20%), Rwanda and Nicaragua (17%) (Krueger and Negash, 2009, p.4).

27

(including the Neumann Kaffee Gruppe, ED&F Man, Ecom Agro-industrial Corp, and the

Groupe Louis Dreyfus) sourcing coffee from growers, often through local middlemen,

often processing it and distributing further to international buyers (Krueger and Negash,

2009, p. 12). TNCs purchase coffee from host countries’ farmers through various

contractual arrangements such as "contract framing", but also through spot market

transactions. Contracts seek to guarantee the supply of and demand for coffee, usually raw

or semi-processed coffee. They typically stipulate the quantity, price and quality of coffee

and distribute risks between the contracting parties. A typical example of a contractual

arrangement, which ties TNCs and coffee producers, is the so-called out-grower scheme.

The scheme helps farmers receive from TNCs goods and services which are necessary for

efficient export production, such as seeds, fertilizers, capital, knowledge and technology.

The TNCs receive coffee, usually raw or semi-processed, and process it further. TNCs are

responsible for marketing and managing the whole operation (ibid., p. 27), that is, “for

bringing coffee to the table” (ibid., p. 17).

TNCs can also provide, if necessary, a wider range of services to exporters, based on

management contracts. For example, ED&F Man, a Swiss-based TNC with affiliates

operating in 16 of the top 20 coffee-producing host countries, provides in Kenya (through

its affiliate, the Coffee Management Services) farm management services, based on the

latest research and technology, assisting farmers in accessing international coffee

markets.26

It also offers other services including financing, farm inputs, accountancy

services, feasibility studies (including environmental and social assessment studies),

marketing, certification compliance and farmer training.27

For the bulk of globally traded coffee, international trading houses and processing TNCs

(“roasters”, such as Eduscho, Lavazza, Jacob Suchard, Tschibo or Nestle) buy the green

coffee beans in coffee growing countries and the role of developing country participants

in the value chain usually ends there. One of the key reasons is that coffee sold to final

consumers is in most cases a branded product. Developing a coffee brand (and, for that

26

See http://www.coffeemanagement.co.ke/. 27

Namely, Brazil, Cameroon, Colombia, Costa Rica, Côte d’Ivoire, Ethiopia, Guatemala, Honduras,

Indonesia, Kenya, Tanzania, Mexico, Papua New Guinea, Peru, Uganda and Vietnam:

http://www.edfman.com/coffee.php?cs=coffee&ss=bd.

28

matter, any brand) and successfully nurturing and marketing it in intensively competitive

markets is very costly and risky. It also requires a continuous, large volume supply of

coffee of high and consistent quality. Attempts by developing countries to develop own

brands and thus shorten value chain by eliminating intermediaries more often than not

have failed, but there have been few successes, often in some association with TNCs (box

3).

________________________________________________________________________________

Box 3. Shortcutting coffee value chain: not easy but possible

One of the ways of shortcutting the coffee value chain, that is, to sell coffee through fewer intermediaries,

notably international trading companies, is to develop own brand. But this is not easy, as most brands have

been developed by “roasting” companies from developed countries, benefiting from the proximity to the

largest consumer groups and investing heavily in advertising. There are very few global coffee brands that

are owned by coffee producers. Two recent examples of "shortened value chains", in which developing

country producers take coffee directly to developed country markets, are Juan Valdez Café from Colombia

and two Ugandan coffees.

Juan Valdez Café, run by the National Federation of Coffee Growers of Colombia, a non-profit

organization, has successfully capitalized on the good reputation of Colombian coffee, particularly in the

United States. It owes 13 coffee stores in the United States Its products are also available in selected Wal-

Mart and Kroger stores, as well as online. In addition there are 7 stores in Spain, 7 in Ecuador and 6 in

Chile. Wal-Mart and other supermarket chains also sell Juan Valdez coffee in Mexico, El Salvador, Costa

Rica and Panama.28

Most of Uganda’s coffee exports go through the traditional channels of the international trading companies

(Biryabarema, 2008). But there are two exceptions. Uganda Mountain Coffee and Good African Coffee

have been launched by the Ugandan Coffee Development Authority in partnership with Coffee Legends (a

United States “roaster”), Heifer International (an NGO) and BJ's (United States retailer). Both brands are

not yet wide-spread or aggressively marketed. Good African Coffee is sold by Waitrose, one of the largest

supermarket chains in the United Kingdom (Magumba, 2008).

Another way is to by-pass branding and develop niche products such as organic coffee, with some

partnership with TNCs and/or the support of development agencies. The organic coffee-producing co-

operative of the Indigenous Peoples of the Sierra Madre of Motozintla (ISMAM) represents over 1,500

indigenous smallholder families who grow coffee at high altitudes in Southern Mexico. ISMAM formed a

partnership with German coffee roaster Niehoff and a French importer Schorn SA in late 2002, each partner

holding a stake of one third in the venture (Farmingsolutions, 2009a).29

Successful cases of exporters of

organic coffee have also emerged within the framework of the "Export Promotion of Organic Products

from Africa" programme of SIDA. In Uganda, the programme links cooperatives with Ecom's local

subsidiary Kawacom. In Tanzania the cooperatives work with a local exporter providing the market access

know-how (EPOPA, 2009). The Kaffa Forest Coffee Farmers Cooperative Union, entered into a

partnership with Original Food (a German company) and is assisted by the German development

cooperation agency GTZ. Without the latter's engagement it would not have been possible to build up the

cooperative. Coffee grown in the Kaffa Forest found a niche in Third World and Fair Trade shops as well

28

See the Juan Valdez website at http://www.juanvaldezcafe.com/procafecol/mapa/ and

http://www.juanvaldezcafe.us/Locations.asp. 29

ISMAM's coffee can - for instance - be ordered online at:

http://www.unionroasted.com/farms/farm.aspx?id=4.

29

as in Gourmet shops and restaurants. It earns the farmers up to double the price paid for conventional

coffee (Grefe, 2009).

On the other hand, there are projects that struggle with difficulties in accessing consumer markets. The

World Bank assisted Kibale Forest Wild Coffee project in Uganda seems to have failed. The main reason

was small amount of (wild) coffee per harvest. In addition, the organizers of the project had not foreseen

the very high costs of establishing a consumer brand for their specialty coffee (not only wild coffee), and

the limited interest of roasters to take on board the organically grown coffee from Kibale as a high value

addition to potential blends (World Bank, 2002).

Source: Krueger and Negash, 2009, p. 10

________________________________________________________________________________

Since the early 20th

century, banana trade has been dominated by vertically integrated

TNCs that controlled production, packing, shipping, import and ripening (Arias, et al.,

2003). Beginning in the 1970s, TNCs began to divest themselves of banana plantations

(among others, as a result of many problems and tensions surrounding banana

plantations, concerning human rights, working conditions and environmental impact) and

contract banana production out to local producers in developing countries, while still

controlling the exportation of bananas (Hall, 2008). Today, banana trade remains in the

hands of a few large TNCs (Chiquita, Dole, Del Monte and Fyffes). Some of them still

have plantations in developing countries (e.g. Chiquita, Del Monte and Dole in Ecuador,

Colombia, Costa Rica, Guatemala, Honduras and the Philippines; Del Monte and Dole in

Cameroon and Côte d’Ivoire). It is estimated that about half of the bananas sold by

Chiquita, Dole and Del Monte originate from their own plantations. Other TNCs like

Fyffes do no own any banana plantations (Liang and Pollan, 2009, p. 3). Banana exports

have increasingly come under international scrutiny, given its past history of violations of

human rights, working conditions and environmental standards. As a result, key TNCs

have increasingly embraced voluntary certification standards, giving them a further edge

over non-complying companies.

Soya is an important export item for a number of developing countries such as Brazil,

Argentina or Paraguay.30

Soya farming is largely undertaken by local farmers, large (as is

often the case in Argentina and Brazil) or small (as in China and India). Corporate

30

In Paraguay, soya accounts for 30% of total exports, in Argentina for 13% and Brazil for 6% (Ohinata

and Moussa, 2009, p. 8).

30

farming of soya by TNCs has been very rare. Four trading TNCs dominate, however, the

world trade in soya beans: Archer Daniels Midland (United States), Bunge (United

States), Cargill (United States) and Louis Dreyfus Group (France). These TNCs

significantly influence soya farming, providing resources to farmers -- loans, seeds

fertilizers and other chemicals -- in exchange for soya (and, for that matter, other

agricultural commodities) at harvest. For example, Bunge alone provided an equivalent

of nearly $1 billion worth of inputs to Brazilian farmers in 2004 (Greenpeace, 2006).

United States' TNCs are responsible for 60% of the total financing of soya production in

Brazil (Milieudefensie and Friends of the Earth, 2006).31

In Paraguay, Cargill distributes

seeds to farmers, runs the country’s largest soya bean processing plant and buys 20% of

soya beans produced (Ohinata and Moussa, 2009, p. 12).

A useful role of TNCs as intermediaries in international trade in traditional agricultural

products -- providers of market knowledge and access, logistics as well as other

ingredients necessary for exports (all reducing or eliminating transaction costs for

producers in developing countries) -- does not come without cost. A high and increasing

concentration of market power of international trading companies is said to be a key

reason behind the growing difference between world and domestic prices (that is,

developing country exporters’ export exit prices) for such products as wheat, rice or

sugar, which more than doubled between 1974 and 1994 (World Bank, 2008, p. 136).

High concentration is also held responsible for reduced benefits of developing countries

from exports of coffee, tea and cocoa. According to the World Bank, “it is generally

believed that when an industry’s CR4 [that is the share of the four largest companies in

the market] exceeds 40%, competitiveness [of markets] begins to decline, leading to

higher spreads between what consumers pay what producers receive for their produce”

(ibid.). In coffee, international trading companies, intermediating between some 25

million farmers and 500 million consumers exhibit a CR4 of 40% and coffee roasters that

of 45%. The share of revenues of major coffee producing countries in the retail price at

destination declined from one third in the early 1990s to 10% in 2002, while the sales of

31

However, the current economic crisis appears to be reducing the availability of finance. For example,

Bunge cut advance cash payment to Brazilian farmers by 70% in 2008 ( “In Brazil, credit to farmers dries

up”, The Wall Street Journal, 29 November 2008).

31

coffee doubled. Similar concentration ratios, ranging from 40% to 50%, exist in cocoa

market for trading companies, cocoa grinders and confectionary manufacturers. In tea the

ratio is much higher, as three firms control more than 80% of the world market.

Consequently, developing countries’ claim on value added declined from around 60% in

the early 1970s to less than 30% in 1998-2000 (ibid.).32

Historically, trading TNCs (and, for that matter, other agriculture-related TNCs)

originated from a few developed countries, often former colonial powers. Nowadays,