Evidence taken at Public Hearings 25-27 May 1992.

179

LEGISLATIVE ASSEMBLY OF QUEENSLAND PARLIAMENTARY COMMITIEE OF PUBLIC ACCOUNTS Implementation of the Public Finance Standards: Evidence taken at Public Hearings 25-27 May 1992. Parliamentary Committee of Public Accounts Report No. 19 June 1992

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Evidence taken at Public Hearings 25-27 May 1992.

LEGISLATIVE ASSEMBLY OF QUEENSLAND

PARLIAMENTARY COMMITIEE OF PUBLIC ACCOUNTS

Implementation of the Public Finance Standards:Evidence taken at Public Hearings 25-27 May1992.

Parliamentary Committee of Public Accounts Report No. 19June 1992

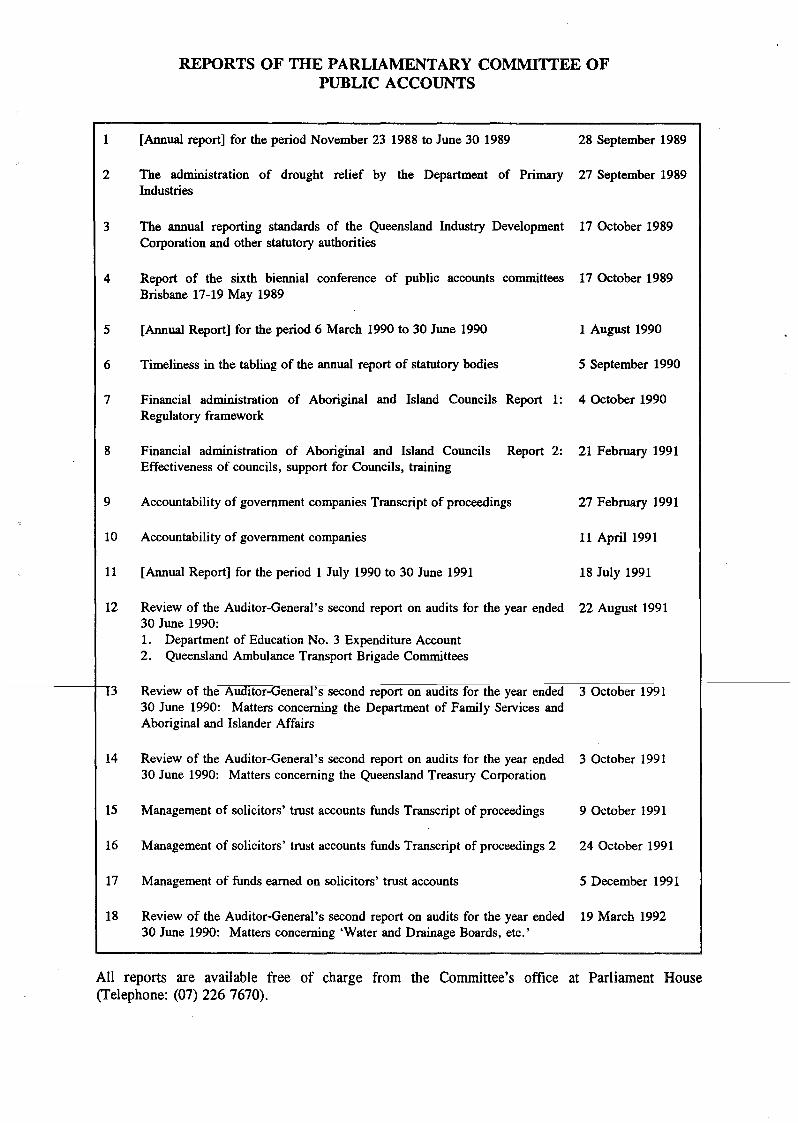

REPORTS OF THE PARLIAMENTARY COMMITTEE OFPUBLIC ACCOUNTS

1 [Annual report] for the period November 23 1988 to June 30 1989 28 September 1989

2 The administration of drought relief by the Department of Primary 27 September 1989Industries

3 The annual reporting standards of the Queensland Industry Development 17 October 1989Corporation and other statutory authorities

4 Report of the sixth biennial conference of public accounts committees 17 October 1989Brisbane 17-19 May 1989

5 [Annual Report] for the period 6 March 1990 to 30 June 1990 1 August 1990

6 Timeliness in the tabling of the annual report of statutory bodies 5 September 1990

7 Financial administration of Aboriginal and Island Councils Report 1: 4 October 1990Regulatory framework

8 Financial administration of Aboriginal and Island Councils Report 2: 21 February 1991Effectiveness of councils, support for Councils, training

9 Accountability of government companies Transcript of proceedings 27 February 1991

10 Accountability of government companies 11 April 1991

11 [Annual Report] for the period 1 July 1990 to 30 June 1991 18 July 1991

12 Review of the Auditor-General's second report on audits for the year ended 22 August 199130 June 1990:1. Department of Education No. 3 Expenditure Account2. Queensland Ambulance Transport Brigade Committees

Ij Kevlew of the Auditor-General's second report on audits for the year ended 3 October 199130 June 1990: Matters concerning the Department of Family Services andAboriginal and Islander Affairs

14 Review of the Auditor-General's second report on audits for the year ended 3 October 199130 June 1990: Matters concerning the Queensland Treasury Corporation

15 Management of solicitors' trust accounts funds Transcript of proceedings 9 October 1991

16 Management of solicitors' trust accounts funds Transcript of proceedings 2 24 October 1991

17 Management of funds earned on solicitors' trust accounts 5 December 1991

18 Review of the Auditor-General's second report on audits for the year ended 19 March 199230 June 1990: Matters concerning 'Water and Drainage Boards, etc.'

All reports are available free of charge from the Committee's office at Parliament House(Telephone: (07) 226 7670).

PARLIAMENTARY COMMITTEE OF PUBLIC ACCOUNTSOF THE FORTY-SIXTH PARLIAMENT

Dr J G Flynn MLA 1 Toowoomba NorthChairman

Mr J A Elliott MLA CunninghamDeputy Chairman

Ms L R Bird MLA Whitsunday

Mr K H Davies MLA2 Townsville

Mr K W Hayward MLA3 Caboolture

Mr P A Heath MLA4 Nundah

Mr J Pearce MLAs Broadsound

Mr T J Perrett MLA Barambah

Mr J H Sullivan MLA6 Glasshouse

Dr D J H Watson MLA Moggill

1 Appointed 17 April 1991Chainnanfrom 10 March 1992

2 Resigned 11 March 19923 Chainnan from 8 March 1990

Appointed a Minister of the Crown 16 December 19914 Resigned 9 April 19915 Appointed 10 March 19926 Appointed 11 March 1992

, CHAIRMAN'S INTRODUCTION

As part of its inquiry into the implementation of the Public Finance Standards, theParliamentary Committee of Public Accounts conducted public hearings at ParliamentHouse on 25 - 27 May 1992 at which evidence was taken from representatives of thefollowing organisations:

MONDAY 25 MAY 1992

Queensland TreasuryDepartment of Resource IndustriesDepartment of Justice

TUESDAY 26 MAY 1992

Brisbane Girls' Grammar SchoolDepartment of Primary IndustriesDepartment of Employment, Vocational Education, Training and Industrial RelationsQueensland University of Technology

WEDNESDAY 27 MAY 1992

Queensland RailUniversity of Southern QueenslandQueensland Corrective Services CommissionDepartment of the Premier, Economic and Trade Development

In accordance with Standing Order 205 the Committee is pleased to present the transcriptof proceedings of the hearings.

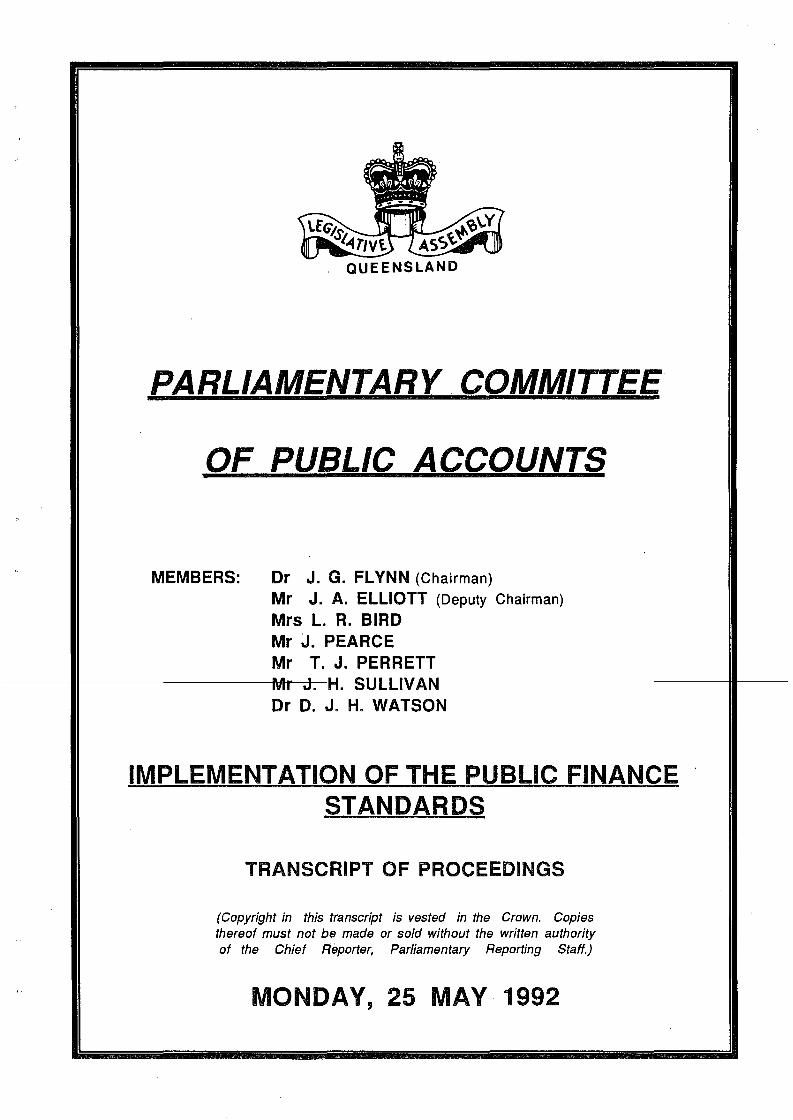

PARLIAMENTARY COMMITTEE

OF PUBLIC ACCOUNTS

MEMBERS: Dr J. G. FLYNN (Chairman)

Mr J. A. ELLIOTT (Deputy Chairman)

Mrs L. R. BIRDMr J. PEARCEMr T. J. PERRETT

Dr D. J. H. WATSON

IMPLEMENTATION OF THE PUBLIC FINANCESTANDARDS

TRANSCRIPT OF PROCEEDINGS

(Copyright in this transcript is vested in the Crown. Copiesthereof must not be made or sold without the written authorityof the Chief Reporter, Parliamentary Reporting Staff.)

MONDAY, 25 MAY 1992

The Committee commenced at 9.04 a.m.

The CHAIRMAN: I declare open this public hearing of the Parliamentary Committee of PublicAccounts. This public hearing is being held pursuant to the Public Accounts Committee Act 1988. TheCommittee has convened this hearing today to hear evidence in relation to the Committee's inquiry into theimplementation of the Public Finance Standards in the Queensland public sector. I would like to inform membersof the media and the public that tape-recording of these proceedings is not permitted.

Before you commence to give evidence, I am obliged to inform you that the proceedings here today arelegal proceedings of the Legislative Assembly and the Committee requires that your evidence be given on oathor affirmation.

HENRY ROBERT SMERDON, swom and examined:

GRAHAM JOHN CARPENTER, sworn and examined:

ROBERT ALEXANDER SHEAD, sworn and examined:

MICHAEL JOHN BOSWELL, sworn and examined:

The CHAIRMAN: Mr Smerdon, could you state your full name and the title of the position you hold?

Mr Smerdon: Henry Robert Smerdon, Under Treasurer and Under Secretary, Treasury Department.

The CHAIRMAN: Mr Carpenter, could you state your full name and the title of the position you hold?

Mr Carpenter: Graham John Carpenter, Assistant Under Treasurer, Financial Management andSystems, Queensland Treasury.

The CHAIRMAN: Mr Shead, could you state your full name and the title of the position you hold?

Mr Shead: Robert Alexander Shead, Director, Financial Management Policy, Queensland Treasury.

The CHAIRMAN: Mr Boswell, could you state your full name and the title of the position you hold?

Mr Boswell: Michael John Boswell, Director, Program Management.

The CHAIRMAN: The Parliamentary Committee of Public Accounts is an all-party Committee of theQueensland Parliament whose purpose is to scrutinise and provoke reform of the financial administration of thepublic sector and to ensure that Executive government is accountable to Parliament. The Committee conductsits business in accordance with the Public Accounts Committee Act and the Standing Rules and Orders of theLegislative Assembly relating to select committees.

The Committee is presently conducting an investigation into the implementation of the Public FinanceStandards in departments and statutory bodies. These standards are issued under the Financial Administrationand Audit Act and commenced operation on 1 July 1990. The Committee has a particular interest in therequirements of the standards relating to financial management practice manuals, position assessments,systems appraisals, program management, internal audit, and the move to general purpose financial reportingby business undertakings and statutory bodies. The use of private consultants in implementation of thestandards is also of interest to the Committee.

I inform you as witnesses that you are reqUired here today to answer all questions relevant to thesubject matter of this inquiry. The Committee would like you to answer its questions frankly, and to provide it withan accurate and clear view of your organisation's position on the issues canvassed. All members of theCommittee will be asking questions. We will direct them all to you, Mr Smerdon. You are free to answer and inviteany of your colleagues to answer, as well.

Mr Smerdon: I will probably pass to the two people on my left, who have most detailed knowledge. Iwill endeavour to answer where I can.

The CHAIRMAN: That is fine.

Mr Smerdon: In the interests of assisting the Committee, I think that those people are the mostfamiliar with the detail and would be better able to provide the answers that you seek.

The CHAIRMAN: We will direct the questions to you and you can pass them on to wherever you thinkthey should go. The Committee understands that the Public Finance Standards replaced the Treasurer'sInstructions and Minister's directions. Could you tell us why this change occurred?

Mr Smerdon': I think it goes back to what the Treasurer's Instructions had become. They wereintended as guidelines, but they became almost law in themselves. They were very detailed and veryprescriptive in what they set down. While they were intended to be all-embracing, in fact there were quite anumber of exceptions issued in them in regar.d to particular departments. At the same time, we were looking atbudget processes and endeavouring to elevate Treasury's overall role in the budget process to a higher plane so

T201 rwb~d

25/5/92- 1 - H. Smerdon/G. Carpenter

B SheadtM Boswell

that departments had much more responsibility and accountability for their own activities. What we tried to dowas to develop a system of standards so that departments or entities could operate within those broadstandards and leave it to the line managers to develop the detailed application of those standards in their ownorganisation. While we endeavoured to include a lot of accounting information, we also felt that in terms ofoverall management, accounting by itself was not sufficient. So we brought in things such as strategic planning,internal audit and a range of other matters which we felt were relevant to financial management practices in thisState. At the same time, we also included the practice statements, practice statements being areas where therewas a general application of the standards and where it would have been helpful for the guidance of departmentalaccountable officers and accounting people in their day-to-day activities. We intended to keep the practicestatements to a minimum and only where we thought it was necessary to do that sort of thing.

The CHAIRMAN: In general terms, the application of these standards in fact allows more flexibility todepartments?

Mr Smerdon: It allows more day-to-day flexibility for the departments. Being the person whodeveloped the concept, to some extent, I looked at the way the Australian accounting standards wereformulated. If you apply those to normal business practices, the idea is to provide a standard by which entitieswould comply. It is then left for auditors and others to determine whether or not those standards had beencorrectly applied. It gave managers more flexibility to comply with what we believe to be quite high standards. Infact, we believe we have regained the lead in financial management practices in the public sector as a result ofthese Public Finance Standards.

The CHAIRMAN: In what key ways do these Public Finance Standards differ from the formerTreasurer's Instructions? You have touched on that already.

Mr Smerdon: I think they are less detailed than the previous instructions. They talk more aboutconcepts and standards that should apply. They do not get down to the nitty-gritty as the old Treasurer'sInstructions used to. There is not a specific standard by which to dispose of the director-general's car, orsomething like that. They are more about what is best practice.

The CHAIRMAN: The Public Finance Standards apply to both departments and statutory bodies, andthe structure and operations of departments and statutory bodies are quite different. Could you tell us what therationale is in developing a single set of standards with common application to both departments and statutorybodies?

Mr Smerdon: From my point of view, I think, while they are different in structure, the principles shouldbe very much the same. It is all about accountability and good financial management practices. I do not think weshould distinguish between a body's particular structure in terms of applying sound financial managementpractices. That is why the concept applied both to departments and to statutory bodies.

The CHAIRMAN: When the standards were initially drafted, did Treasury consult other public sectorbodies?

Mr Smerdon: The initial consultation process was in two stages. In the first stage, there were avariety of people who we had regular dealings with-I am going back now to the time that they were beingdeveloped, in their very embryonic stage-people like Graham Henry from Arthur Andersen and other peoplewho we had dealings with who we believed were experts in this field. So the concepts were passed by thesesorts of people in the development. It then went through the second stage where there was a much more formalconsultation process which led to their issue as a draft set of standards. I must admit that I lost track of thedetail beyond the embryonic stage. Perhaps Mr Carpenter might want to comment about the process beyondthat second stage.

Mr Carpenter: As Mr Smerdon has indicated, an exposure draft was released and comments wereinvited from a wide range of interested parties. Treasury received 34 responses-three from Ministers, 11 fromdepartments, 11 from statutory bodies, three from professional bodies, four from accounting firms and twoothers. They were then collated into a working paper on the responses. The respondents showed strong supportfor these standards as then being developed. A seminar-cum-workshop was held with departmental officers andmeetings with other interested parties were also arranged and held. There was obviously a range of amendmentsmade to the previous draft. Then the revised draft was issued to a selective audience, including the PublicSector Management Commission, the. Premier's Department, Administrative Services, the Auditor-General, theInstitute of Internal Auditors, Suncorp, Queensland Railways and, am I right in saying, Public AccountsCommittee?

Mr Shead: i am not sure.

Mr Carpenter: Perhaps I had better be clear on that. Further amendments were made to that andthen the Public Finance Standards were approved and promulgated in the Gazette in mid-1990, and shortly after

T202 wro/cap25/5/92

-2- H. Smerdon/G. CarpenterR Shead/M. Boswell

that a forum was held for senior officers on 19 July 1990. So that is, in broad terms, the process that wasadopted.

Dr WATSON: There was no compulsion for departments or bodies to respond to that initial invitation?It was an invitation to comment on the standards but not a compulsion to answer?

Mr Carpenter: No. As I understand it, it was an invitation to provide comments and response.

Dr WATSON: Thirty-four out of how many potential? Would you have any idea?

Mr Carpenter: We had a different structure then, so I will turn to Mr Shead.

Mr Shead: I would say it would be a couple of hundred.

Dr WATSON: Thirty-four out of a couple of hundred, perhaps?

Mr Shead: Yes.

Mr Smerdon: Within that 200 there would have been a range of quite small bodies who were given anopportunity to comment but who probably mc;ly not have had the resources, for example, to provide a significantcomment.

Mr ELLIOTT: Of those larger bodies, what sort of percentage responded, do you think?

Mr Carpenter: We would have to provide that to you separately. I do not have that level of detail herewith me.

Mr Shead: I think most of the major ones-Suncorp, OIDC, the TAB and so on-have all responded.

The CHAIRMAN: Is there any process in place now to allow for further amendments to the PublicFinance Standards? Is there any ongoing process?

Mr Carpenter: Yes, there is an ongoing process. A set of amendments was processed in mid-1991and a further set of amendments is with the Treasurer--

Mr Shead: They were approved last week.

Mr Carpenter: They have now been approved by the Treasurer, late last week.

The CHAIRMAN: How did that come about? What is the process? Who starts it?

Mr Shead: I suppose the impetus comes from various sources, whether it is from new Australianaccounting standards which come out, responses from departments, the feedback that we get in various forumsfrom departments, or initiatives that Treasury has undertaken such as the corporate card and the new bankingtender and so on. For most of those, particularly where they are of significance, we have a consultative processand get feedback from departments at the time. We do not duplicate the consultative process with theaccounting bodies, we have already been through that in terms of an accounting standard, for example, butbasically there is a consultative process we go through, and they are drafted within Treasury and then afterinformally consulting with the Audit Office we formally seek the Auditor-General's concurrence. After that, theygo to the Treasurer for approval and promulgation.

Mr Smerdon: The concept of standards was to ensure that they were in place and remain relativelyunchanged. We would hope that the development was of such a rigorous nature that you would not want regularchange to the standards-by "regular" I mean every few months-which was a problem with the old Treasurer'sInstructions. Where they are changing is when there has been some significant development, as Mr Shead said,like the State corporate card, which needed to be incorporated in it.

The CHAIRMAN: From what date did the Public Finance Standards become operative? Has atransition period been allowed for public sector bodies to comply with any particular provisions of the standards?

Mr Carpenter: Yes, 1 July 1990 was the date of application. Yes, there are transitional periods. I willcertainly outline two, and I will look to Mr Shead if there are further. One relates to business units of departmentsand for significant statutory bodies to prepare general purpose financial reports and comply with Australianstatements of accounting concepts and Australian accounting standards. That transition period was throughuntil the financial year that commences basically on 1 July 1992. There is a clarification of that period in relationto entities that do not have a reporting year that ends on 30 June, where the 1993 calendar year will apply, whichis one of the amendments that went through last week. The other area is in terms of program evaluation, wherethere is a three-year transitional period. I will ask Mr Shead if there are other transitional periods.

Mr Shead: No, that is it.

The CHAIRMAN: That means the bodies that are required to comply with the general purposefinancial statements must have that in their report at the end of the financial year?

Mr Carpenter: That is correct.

T203lrs/cc25/5/92

-3- H, Smerdon/G, CarpenterB Shead/M Boswell

The CHAIRMAN: At the end of the 1992-93 financial year, they will have to have been complyingduring that year, and that next financial report should actually comply?

Mr Shead: That is correct. The bodies with the 31 December year-the educational institutionsparticularly would be a 1993 calendar year.

Mr Carpenter: That is one of the amendments that the Treasurer signed last week.

The CHAIRMAN: Public Finance Standard 501 deals with annual financial statements, and thetransitional arrangements provide that any "necessary changes shall be effected as early as practicable duringa transitional period up to and including the financial year ending during 1992-93." Basically, there has beensome confusion, but I think you have just clarified it. There has been some confusion in a number ofdepartments as to when they were going to have to comply. Do you think that confusion is still about?

Mr Carpenter: We hope not. We became aware of that confusion in about August/September lastyear. At that stage there was communication to agencies of the intention to clarify the Public FinanceStandards. That was held in order to put a series of amendments through this month. As I said, there was someconfusion with the previous wording in relation to, for example, those with a calendar year reporting period. Webelieve that the amendments last week clarify that.

The CHAIRMAN: Our Committee has sought advice from Ministers as to which of their departmentalfunctions and statutory bodies will be regarded as business undertakings for the purposes of preparation of theirannual financial statements. The Ministers have made varying interpretations as to what constitutes a businessundertaking. Do you think that further guidance should be provided to various departments to clarify this?

Mr Shead: Possibly, although I think in a lot of cases it is up to the Minister to determine theobjectives of a body if the body is to be treated as a commercial undertaking or a business undertaking. I am notsure if it is always up to Treasury to make the decision. At the same time, there is a whole continuum of activitieswithin departments. At one extreme, for example, it would be ridiculous to require general purpose financialstatements from some small user-charging activity. So there must be a subjective decision made in thatrespect. If we feel there are any anomalies or gross anomalies in the system, there would be no problems with usissuing guidelines. We will be carrying out a review of annual reports at the end of this financial year, aroundOctoberlNovember, to do a post mortem on how things are going. From that, we might pick up that sort of need.

The CHAIRMAN: At this stage you would leave it to the Ministers to make their own decisions and,basically, if you find any glaring anomalies you would consider any guidelines at that time?

Mr Shead: In a lot of cases, those things come out of recommendations, for example, of the PSMC,and become Government policy in terms of commercialisation and so on, as to what bodies are to be set up asbusiness undertakings.

Mr Smerdon: The Government-owned enterprise legislation will shake out some of the businessundertakings and give a much clearer picture of what is and is not a business undertaking once the GOElegislation becomes law.

The CHAIRMAN: Schedule B of the Public Finance Standards lists various statements of accountingconcepts and Australian Accounting Standards and their applicability to the public sector. Certain standards arelisted as being applicable to business undertakings. For example, AAS 4 relates to depreciation of non-currentassets and AAS 10 relates to accounting for revaluation of non-eurrent assets. Should not all entities preparingaccrual accounts and not only business undertakings comply with those standards?

Mr Shead: Those applicability statements are derived from the standards themselves. We have notattempted to give them any wider application than they have under the tenor of the Australian AccountingStandards. There are certain problems there, and I think that is built into the process under which they areissued by the Public Sector Accounting Standards Board. If they decide to widen their application, for example,to all reporting entities, I expect that we would follow that lead. But currently, we do not have any broader orwider application than they have under their own process.

Mr Carpenter: In that regard, the Public Sector Accounting Standards Board has an exposure draftout at the moment in regard to Government departments. That is one of the items on the agenda of the board. Asto the issue of the standards application, as Mr Shead has indicated, we are basically in line with the currentposition with regard to reporting as regards the distinction between Government departments and the statutorybody area.

Mr PERRETT: I would like to ask some questions about system appraisals. The Public FinanceStandards require that departments and statutory bodies formally appraise all of their financial systemsannually. Could you tell us the purpose of performing system appraisals?

.Mr : I guess the system appraisal is to ensure that within each of the agencies there is a

T2031rs/cc25/5/92

-4- H. SmerdonlG. CarpenterR SheadlM Boswell

review obviously at least once per annum to ensure that the agency systems and the information that flows fromthose systems can be met on a timely basis, and clearly also that those systems will safeguard against losses,fraud, misappropriation and corruption. Obviously, the systems within an agency includes a range, and not justEDP systems, to ensure that the support is provided for the program management within each of the agencies. Akey element of systems appraisal is the risk analysis that is taken within each agency.

Mr PERRETT: What level of detail and content should the system appraisal contain?

Mr Carpenter: I guess that issue has been the subject of some discussion as to what theappropriate level is. I guess it would depend upon the nature of the organisation and its complexity. However, asa central agency, we are aware of some confusion. We will be seeking to develop some guidelines in that area.We are aware of some confusion in the service-for example, the amount of detail that is required in systemsappraisal.

Mr PERRETT: How would you envisage an organisation would go about completing a systemappraisal?

Mr Carpenter: I guess you have to start from the role of the agency, looking at the strategic plan ofthe organisation and the key objectives within the program management framework. From my perspective, itwould be driven from information needs within the agency. Then you would have to assess whether the keypeople are receiving the information in order to manage within the organisation. Obviously, there are otherelements to that. There are a number of requirements in the Public Finance Standards of meeting the variousfinancial requirements, or indeed also the Act. Obviously there are some broader issues and some detailedassessments as to whether the systems provide the appropriate internal controls within that agency.

Mr Shead: There are two facets that I see to systems appraisals. The first one is in terms of ensuringthat accounting systems, financial information systems or information systems generally are producing reliableinformation for management decision making. The second one focuses on the performance of those systems,looking at the outcomes and outputs. I suppose this is really to take up the slack where the Treasurer'sInstructions concentrated on procedures step by step within a system relating to what has to be done. Now, thefocus is more on the outcomes of the system to ensure that the system is delivering in terms of what is expectedof it. I think that links in quite closely with program management in terms of concentration on outputs rather onwhat the system actually does in a procedural sense

The CHAIRMAN: Whose job would it be-and obviously that would vary too, I suppose-who wouldbe doing the system appraisal in general terms?

Mr Shead: We hope that it would be line managers taking responsibility for their systems, both theperformance of the system and the internal control structure built into the system. We are aware of someagencies who have given it to internal audit, and that was certainly an option left open when the Public FinanceStandards came down. It was certainly our preference that line managers take responsibility for their owndecisions, and formally report on that to the accountable body, whether it is the accountable officer or thestatutory body, once a year

The CHAIRMAN: Does it need to be put together in one report from all of the line managers or is it justa matter oHf various people are reporting that their area is okay, that is adequate? Does there need-to-be-<il:l--------more formal reporting process?

Mr Carpenter: We believe that it would need to come together at the corporate level. So that would beour view.

Mr Shead: Yes. We have not prescribed any form or anything like that. As Graham said, it dependson the system, whether you have got a small accounting system within a Magistrates Court or a largeraccounting system, a complex one, within say, OIC.

Mr PERRETT: For the system appraisals to be performed effectively, would it be necessary for anorganisation to have its systems and procedures documented in its financial practice manual.

Mr Carpenter: The financial management practfce manual needs to provide the framework withinwhich the organisation is operating. There needs to be a very strong manual.

Mr PERRETT: It is this Committee's interpretation that a formal process would need to be followedwhen performing each system appraisal and that the results thereof be documented. Is that what the standardsrequire?

Mr Carpenter: No, they do not go to that degree of prescription, although obviously there would needto be some documentation of the systems appraisal process.

Mr PERRETT: Should all branch officers undertaking accounting functions, or in control of assets,etc., be included in the parent agency's annual systems appraisal process.

T204jam25/5/92

-5- Mr H, SmerdonlMr G, CarpenterB SbeadlM Boswell

Mr Shead: Generally, I would say yes. If the person in charge of that branch, office, or whatever, hasresponsibility for the operation of the financial systems, then they should be involved in the process.

Mr PERRETT: Are there any arguments for not being involved in that process?

Mr Shead: I did not see any immediate-possibly-no, I cannot see any.

Mr PERRETT: Public Financial Standard 610(3) requires that internal audit determine whether or notsystem appraisals have been properly undertaken, submitted and acted upon. Bearing this in mind, would it beappropriate for the internal auditor to actually do the system appraisals?

Mr Carpenter: Our view is that it is up to management to determine the most appropriate framework,or the process for the systems appraisal, as has been indicated by Mr Shead. We are aware of some caseswhere internal auditors have been involved, but in other cases where an internal audits role is reviewing what hasbeen done.

Dr WATSON: I just ask a question, because a couple of these have come back a couple of timeswhere you have said that it is up to the line manager, and you have said that there could a fair bit of diversity inwhat is actually undertaken.

Mr Carpenter: Yes.

Dr. WATSON: What leads you to believe that there ought to be this diversity across the publicsector, and how would you tell whether the diversity is too great or whether people are just trying to, if you like,not implement the systems correctly?

Mr Carpenter: Obviously, we are dealing with a diverse range of organisations. So that is going tolead to some diversity in itself. As I said earlier, the risk analysis is what we believe to be the driving force behindthe process adopted within the agencies. So an assessment of the risks in terms of the systems, and thatobviously covers a range of risks--

Dr WATSON: Who is doing the risk analysis, though, here? It is those same managers, is it?

Mr Carpenter: Yes, We believe that part of the role of the manager is to effectively manage the risks,including those related to the systems within the organisation.

Mr Shead: I think the underlying principles are always going to be the same. The principles of internalcontrol as set out in the auditing practice statements and so on, but the design of the systems, the types ofrisks being undertaken by an organisation are going to vary, depending on its activities.

Mr Smerdon: Could I just ask Mr Shead and Mr Carpenter to comment on the role of external audit inthis process? It might be helpful.

Mr Carpenter: Obviously the role of an external audit, we would hope-and we are aware that itdoes-is to review the management within the organisations. Obviously, one of the requirements in terms ofcompliance with Public Finance Standards is to ensure that position assessment and systems appraisals arebeing adequately undertaken. So it would be, I would expect, appropriate for the external auditors to be able toassess the process adopted within the organisation, given that the role of an external audit, obviously, is basedon a risk assessment as well.

Mr Smerdon: I am sorry, but I saw a line of questioning that suggested that we should not be allowingfreedom to line managers to carry out these appraisals, but I wanted to reinforce the point, I think, that there is acheck and balance in the system which can allow freedom, but at the same time keep a good overview of what IS

happening.

Dr WATSON: You have got a role for an external auditor, you have also got a role for Treasurypresumably, in terms of developing the systems and making sure that the systems are, if you like, consistent, orwhatever, across it. My line of questioning was basically how you can determine whether or not the diversity IS

too great versus appropriate.

Mr Shead: I think Treasury has no great role in terms of specifying system across the public sector,except where we have a lead agency role, for example, with the QGFMS system, In terms of systems set upwithin individual agencies, whether it is a university, a marketing board, or whatever, that is not-we do not see itas our role.

Mr Smerdon: And we would see some difficulty with an external audit relationship. If we were to movein as a policeman-type 'thing with these system-I think we see it clearly as an external audit function. Ifsomething is drawn to our attention, or we become aware of it through other means, we will certainly act. But wedo not see ourselves as being the second policeman in the process.

Mr SULLIVAN: In answer to a question a little earlier, Mr Shead said the option was left open in thestandards for an internal audit to perform the systems appraisal and standard 610(3) indicates that an internal

T204jam25/5/92

-6- Mr H. SmerdonlMr G. CarpenterB. SheadlM Boswell

audit must determine whether those appraisals have been done properly. Do you not see any conflict there inthat internal audit could form the appraisal and then certify that it has been done properly?

Mr Shead: That is certainly the reason why we strongly prefer that line managers take responsibilityfor it, but I think that it is a weakness in the explanatory overview where it left it open and that we will be movingto rectify that.

Mr SULLIVAN: To make an amendment that should be made regularly?

Mr Shead: Yes.

Mr SULLIVAN: Thank you.

Mr PERRETT: Mr Smerdon, to whom, in your opinion, should the results of the completed system ofappraisals be reported?

Mr Smerdon: In general terms, it should eventually get to the top level of management, but MrCarpenter may want to comment more on that.

Mr Carpenter: The appropriate reporting line is through the accountable officer, who hasresponsibility for the management of the agency.

Mr CHAIRMAN: There is no need to go outside the agency, except as, I suppose, an external auditcheck?

Mr Shead: No, we see it as purely an internal management tool.

Mr PERRETT: Of what benefit are system appraisals to management?

Mr Carpenter: Well, we would hope that it would be an important element of the management of theorganisation to ensure that systems support the strategic direction of the organisation and provide support tothe direction as outlined in the corporate plan. Obviously, that in turn should fall in line with the program structureand the priorities laid down by the Government and, of course, satisfy compliance with the laws and regulationsof the State as well.

Mr PERRETT: Would it be practicable to issue a standard format for public sector bodies to followwhen completing their system appraisals?

Mr Carpenter: As I indicated earlier, it is our intention to carry out some further work in response tocomments from agencies, and we are looking at carrying out some workshops on that, and also drafting someguidelines, but that is as far as we see that we will go.

Mrs BIRD: I have some questions. The Public Finance Standards require the departments andstatutory bodies to complete their position assessments. They are required to be prepared quarterly, and insome instances annually. Just so that we are all on the same level, could you just give us an example and tell uswhat is a position assessment?

Mr Carpenter: The Public Finance Standards, as you will have noticed, are structured on the basisthat agencies are managing assets, liabilities, revenue and expenses as well as the equity issue, which isprimarily a statutory body or business undertaking concept. So, in terms of the position assessments, thePublic Finance Standards require agencies to assess their finanCIal position. Now, that in a number of agencieswill have already been provided through monthly reports to the board or to the accountable officer, but clearly, inothers, it is introducing some concepts for the first time, in particular for departments to have better informationon all assets and liabilities as well as the revenue and expense reporting.

Mrs B IRD: The departments have in the past been required to update periodic budget andexpenditure reviews, and statutory bodies have followed this in the process. The Committee has noted thatmany bodies regard such budget reviews as being their position assessments, and I think Mr Smerdon touchedon that earlier. Is this an appropriate attitude, or is more required by the Public Finance Standards?

Mr Carpenter: Clearly, that is part of the position assessment. The Public Finance Standards alsorequire-and I guess this is a change in particular for budget dependent agencies who work within what ispredominantly a cash-based appropriation accounting system-that cognisance be paid to the assets and,where appropriate, liabilities that are being managed within the agency, so that is a change in past practice interms of the management and in line with the structure and framework of the Public Finance Standardsthemselves.

Mrs BIRD: Well, what level of detail should, do you think, the position assessment contain?

Mr Carpenter: Again, it is obviously going to depend upon the agency that is concerned and thefinancial structure of the department or statutory body. That is obviously going to depend upon the key issues interms of the financial performance of the organisation. Perhaps I might move that to Mr Shead. Mr Shead has

T20525/5/92

-7- H. Smerdon/G. CarpenterB SheadIM Boswell

been heavily involved in a series of workshops that have been held in recent months in that particular area.

Mr Shead: We have had a series of 17 workshops early this year, covering about 200 people fromvarious departments and statutory bodies. We have walked them through the position assessment processusing a set of guidelines or a pro forma approach. Our intention was not to tell them this is what Treasury thinksthey should be doing, but to give them some sort of guidance, given that this is a new concept, and to help themthink about the issues they should be looking and should be managing. At the same time, I think those proformas did not just concentrate on financial information. I think ideally there should be a link with theperformance indicators of the organisation, particularly for Government departments where the bottom line is notjust a dollar figure; it should be the cost of their operations as well as their performance indicators and meetingsocial objectives and so on, and ideally the two should be linked together in a position assessment, butobviously that is going to take a while to develop.

Mr Smerdon: If I could just add a more general comment to that. One of the dangers that we have isgoing back to the same problem we had with the Treasurer's Instructions-being asked to prescribe formats,prescribe detail. What it is about is managers getting information out of the system that helps them managebetter, and by leaving the format somewhat open, by leaving the specification information somewhat open,hopefully managers, if they are worth their salt, will be looking at the sort of information, both financial and nonfinancial, that they need to manage the business enterprise of the department they are running. I have a greatfear that if we start prescribing things overly, we will end up getting only the information that is prescribed, and Ithink that will leave the question of whether that is the right information quite open in a number of cases. I think itis very important to stress that point.

Mrs BIRD: Given those points that you raised, how do you see organisations going about completingthe position assessment if they do not have some sort of guidelines or some--

Mr Smerdon: I will pass it back to Bob. I will just raise some general comments first.

Mrs BIRD: Did you handle that in those 17 seminars that you had?

Mr Shead: Yes, we circulated the pro formas, and in a lot of cases it was obvious that people had notconsidered a lot of issues, particularly in relation to asset management. As you were saying, a lot of the focushas been on the appropriation system and managing in terms of the cash outlays. The objective is to broadenthe focus of departmental managers in particular in terms of looking at the assets holdings and so on, andmanaging the whole picture.

Mrs BIRD: What was your advice to them on how they could complete a position assessment, or whatwas the outcome?

Mr Shead: The outcome, based on our evaluation, is that they all considered it was very successful.There was quite a high rating on the evaluation forms. The outcome was not, as I said, us telling them what to do;it was really getting them to think about the core issues, and these I think were spelt out fairly well in the proforma guidelines that we circulated at the workshops.

Mr Smerdon: Could I just follow on from that? There is a very important point that I would like tostress with the Committee. This position assessment should not be seen as a little discrete entity on its own. Itneeds be to be seen in the bigger picture of what an organisation is about. That is the reason we have MikeBoswell here today, and that is looking at strategic planning for.an organisation: what is the organisation onabout, what does it need to do, what are assets under its control, how best are those assets or funds going to beused to meet the organisation's objectives? I think a position assessment needs to be fitted into that broadcontext of seeing where a department is going, how it is managing its assets, how it is managing its budget, howit is controlling the risks, the liabilities and so forth. I would like systems appraisal position assessments to beseen in the context of the organisation as a whole-what is the big picture for the organisation--rather thantrying to focus unnecessarily on the detail of position assessments.

The CHAIRMAN: Do you think many departments are focusing on trying to include this non-financialinformation in the position assessments-linking the two? As Bob has just said, it is a desirable thing. Aredepartments aware of that and striving towards it?

Mr Shead: Certainly some statutory bodies are. We have seen some very good ones in terms ofreporting to senior management on meeting their objectives, setting things out in graphical format and so on,rather than just a schedule of actual budget breakdown. In terms of the departments-we have not had much ofa chance to have a look at what they have been doing, but I expect its going to be a more difficult process forthem, and in a lot of cases it will depend on how they go with the strategic planning and developing operationalplans with performance indicators and so on. That is really th~ first step, I think.

Mr Boswell: Certainly in terms of the review that we have just done of the implementation of programmanagement, there are a number of departments who have made significant strides in that area. There is more

T20525/5/92

- 8- H, SmerdonlG, CarpenterB. SbeadlM Boswell

work to be done, but there has been some good progress.

Mrs BIRD: The Public Finance Standards require revenue and expense position assessments toinclude a review of gains or losses arising from changes in the value of investments. This is required to be donequarterly. What would an entity with property investments need to do to satisfy this requirement?

Mr Carpenter: Has that already been specifically raised?

Mr Shead: That was one of the issues raised by the Public Trust Office in the workshops. Theyencountered some difficulties in that regard. It basically involved them looking at the market values of theirinvestment portfolio and monitoring that, at least on a quarterly basis.

Mrs BIRD: Public Finance Standard 251 deals with equity position assessments. Amongst otherthings it requires bodies that prepare general purpose financial statements to annually determine and assess"the return on equity or other appropriate base being achieved from operations". Of what relevance is thisinformation to a non-commercial statutory body?

Mr Shead: At this stage, not a lot. The return on equity is the bottom line in terms of the Government'spolicy on corporatisation, as well as other indicators. In terms of corporatisation and commercialisation return onequity, it is going to be an important factor. It is obviously not an important factor at all in a non-commercialactivity.

The CHAIRMAN: They still have to present it and show it.

Mr Shead: Or other appropriate base. Obviously, you would not know what your equity or capital baseis in terms of the current accounting set up.

Mr J. H. SULLIVAN: In relation to property again, and in relation to bodies holding property doingquarterly position assessments, are they going to have to appoint a valuer every three months to revalue theirproperties.

Mr Shead: No, there has been nothing prescribed in terms of how valuations are to be done. We arecurrently looking at a policy in terms of their recognition and valuation of non-current physical assets across theboard. That needs to link in with the work that I think Graham is involved in with GOE valuation Australiawide.There are a lot of different agendas going on around Australia in terms of asset valuations. We are currentlydeveloping a consistent policy to apply across commercial and non-commercial activities in the public sector inQueensland.

Mr J. H. SULLIVAN: So the answer is that they do not have to appoint a registered valuer everyquarter to provide a written evaluation?

Mr Shead: No.

Mrs BIRD: I get the feeling that you are suggesting that there needs to be some sort of flexibility inthe quarterly assessments.

Mr Shead: Yes, certainly.

Mr ELLIOTT: In the light of Westpac's latest move and looking at a way out, as far as some of itspotential market positions are concerned and as far as property is concerned, do you see some 01 yourstatutory bodies doing that sort of thing and looking at potential losses on property?

Mr Smerdon: I am not aware of a significant statutory body that will realise losses on property. Thebodies that I am associated with in another form regularly review the property values, not through a registeredvaluer process, but simply looking at what they are deriving from the investment they have in the building-whatis the revenue stream being generated and capitalising on that whatever the current cap rate happens to beThat is the quickest way to see whether the value in the books is the value of the property.

Mr ELLIOTT: As far as the financial management practice manuals are concerned, the PublicFinance Standards and Financial Administration and Audit Act require all departments and statutory bodIes tohave a financial management practice manual. Why is it important that organisations have a finanCialmanagement practice manual?

Mr Carpenter: There are two elements to that issue. They relate to some of our earlier commentsabout the program management framework because the financial management practice manual is not just, forexample, to cover accounting procedures. It is about the financial management framework within whichagencies operate. Prior to the Public Finance Standards there was a requirement under the FinancialAdministration Audit Act-since 1978-for accounting manuals so that the thrust as outlined earlier in terms ofwhere the Public Finance Standards are going at the broader level, is to ensure that the financial managementframework with an agency is outlined in the practice manual. Treasury also felt that the accounting manualstended to concentrate on detailed procedures, as indicated earlier, rather than the broader policy requirements.

T206 rktlsib25/5/92

-9- H, Smerdon/G, CarpenterR SheadlM Boswell

Of course, they were also deficient in that they tended just to concentrate on the accounting areas within theagency. We see the financial management practice manual as being an important framework, designedspecifically for each of the agencies to take account of their risk profile or their program managementframework, including their assessments of risks in terms of the management within the organisation. Accountingreporting framework is an element of the financial management practices within each of the agencies.

Mr PEARCE: I have a couple of questions on the practice manuals. Do you think it is necessary forvery small statutory bodies to have a practice manual, and why would you hold that view?

Mr Carpenter: In any organisation there needs to be some consistent practices in place. Obviously,developing a practice manual for a major Government department is going to be a very different exercise than fora small board of trustees of a small statutory body, but we would argue that, irrespective of the size of theagency, this does need to be brought together. Obviously there are other issues about how the appropriate staffare aware of the practices and policies within the organisation. We believe every organisation should have afinancial management practice manual.

Mr PEARCE: You would be aware of the general status of the practice manuals in departments andstatutory bodies. After looking through some of the correspondence that we have had, the Committee feels thatin many cases there is a lot to be done to bring them up to par. Would you agree with that?

Mr Carpenter: We would certainly agree with that. As part of assessing the then position with theimplementation of Public Finance Standards, we undertook a survey in September of last year and we noticed atthat stage around three-quarters of the agencies were at various stages of developing their manuals. The stafffrom within Mr Shead's area have also been working with a number of agencies who are seeking to developand/or upgrade their financial management practice manuals. We are aware that that is an area where a lot ofwork is taking place in agencies at the moment.

Mr PEARCE: I think that it is important that we come on line together across the system. Do you thinkthat the departments are keeping in touch or are some lagging behind? Is there a need to make sure that theyare up there, pushing in the same direction?

Mr Carpenter: Clearly, there are some that are further advanced than others. I am not sure if MrShead wants to add to that?

Mr Shead: We are aware of a fair bit of communication between departments developing FMPmanuals. It is certainly an issue that we have been encouraging to get them to talk to each other and show theirmanuals around. Some excellent manuals have been developed and we are encouraging them to share theirknowledge around the system.

The CHAIRMAN: What is the latest a department should have its manual completed if it is going to beready to fully comply with the standards next financial year? Do they need to have it before 31 July this year or30 June this year?

Mr Carpenter: Technically, they should have been in place prior to now. Obviously, moving from theprevious accounting manual framework to the financial management practice manual has meant that there hasbeen a great deal of work to be undertaken in most agencies. Our view would be that the sooner agencies canhave the practice manual in place, the sooner they will be protecting their own agency in terms of the programmanagement and the general development of financial management in the agency.

The CHAIRMAN: Could you actually put a date on when it is too late to be ready?

Mr Carpenter: We would hope that by the end of this calendar year most agencies would have itready.

Dr WATSON: Are they going to be into the process, though, by 1 July this financial year or nextfinancial year?

Mr Carpenter: It is when the financial management practice manual is available. Obviously, in anumber of agencies there are different component parts of that and some parts would be further advanced thanothers. One would hope that, although the component parts will be there and available within the agency earlier,my hope would be that by the end of this calendar year all agencies should have the manual together.

Mr Smerdon: That should not be an implication that somehow departments, because they have notgot a manual in place, are not complying with the spirit of the requirements. I think it is a case of somedepartments taking a view that it is a lower priority to document all this in its complete sense. Again, that doesnot mean to say that there is not substantial documentation of it already but not completed. I think there is a fairamount of work done in terms of the review process that has gone on in terms of accounting staff and other staffinvolved in the review process. I think that has delayed preparation of the manuals more than we would like. Wehave tried to take a reasonable view about resource requirements that might be required in putting these things

T207 rwbfjf25/5/92

-10 - H. Smerdon/G. CarpenterB SheadlM Boswell

together.

Mr PEARCE: That leads me on to the next question. Do you think there should be an adequate skillsbase within departments for financial management practice manuals to be prepared internally?

Mr Smerdon: Yes, in a general sense.

Mr PEARCE: Putting the Public Finance Standards aside, for how long have departments andstatutory bodies been required to have financial management practice manuals or accounting manuals, as theywere previously known?

Mr Shead: It was a requirement that came in when the Treasurer's Instructions or the FinancialAdministration and Audit Act came into force on 1 July 1978.

Mr PEARCE: We understand that public sector bodies have experienced considerable difficulty overa long period of time in preparing and maintaining up-to-date financial management practice manuals. Could youexplain why that has occurred?

Mr Shead: Originally, looking back through the old manuals that Treasury had from the late seventiesand early eighties, they were very detailed. In a lot of cases, departments were documenting everything thatmoved. That is certainly not an approach we are recommending. In many larger and complex organisations, theyare adopting a tiered approach, keeping in some places three levels or three components of the actual financialmanagement practice manual at the top level. It is best for laying high-level policies such as organisationalstructures and details of internal control systems, and putting the responsibility reporting arrangements in placeand delegations and, within that, working down the various desktop manuals or procedural manuals and so on.

Mr PEARCE: So there is a need to simplify the whole process?

Mr Shead: Certainly it is not our view that they should go out and document everything that takesplace, every flow of paper through an organisation. If it is going to be a useful tool for management, it has toconcentrate on the basics.

Mr J. H. SULLIVAN: I would like to ask some questions about internal audit. The PFS requires eachdepartment or statutory body with an internal audit function to develop an internal audit charter. Would it beappropriate to incorporate a standard audit charter in the standards and is anything being done about doingthat?

Mr Carpenter: On the issue of internal audit, as I am sure this Committee is aware, EARC hasprepared a report on public sector auditing and there are a number of recommendations in that report whichrelate to the role of internal audit. The Government, we expect, shortly will be looking at the response to theEARC report. I think I am right in saying that there is a specific recommendation in regard to internal auditcharters.

Mr Shead: That is right. EARC has recommended that the practice statements incorporate a standardinternal audit charter, which is not to say I do not think that it needs to be standardised across the entire publicsector. I think there is room for individual agencies to build on that as they like. But the intention certainly is thatthere is a core internal audit charter which ensures that internal audit focuses on the basics at least.

Mr J. H. SULLIVAN: In relatIon to that, you beheve that the Government's response to the EARCrecommendations will result in that kind of approach being taken?

Mr Carpenter: I do not think we are going to pre-empt the Government's decisions in regard to thatreport.

Mr Smerdon: As officers, it is a view to which we would subscribe.

Mr J. H. SULLIVAN: Some departments have merged their internal audit, program evaluation andother review functions. Earlier, we touched on this matter. The Committee is concerned that this type ofstructure could hinder the independence of internal audit and also that internal audit staff could be diverted fromthe internal function to perform other duties within the group, Do you think that these combined structures couldhinder the independence and effectiveness of internal audit?

Mr Shead: There is the potential there, I think, to do that. Certainly indications of experience of thelast 10 years are that some internal auditors have veered away from the intention of internal audit since it wasestablished in the eighties. On the other side, I do not think that it is necessarily something that should beprohibited. I can see advantages in it, particularly in smaller organisations. One of the reasons behind the EARCrecommendation on internal audit charter is to ensure that that unit, whatever it is called and whatever its extraresponsibilities are, does actually carry out internal audit functions as required under the Act.

Mr J. H. SULLIVAN: You would see perhaps an expansion of workload as meaning an expansion ofthat section, whatever it is called, rather than setting up separate sections as a viable possibility? Taking on

T207 rwbfjf25/5/92

- 11 - H. Smerdon/G. CarpenterR, SheadlM Boswell

functions such as systems appraisal by internal auditors will divert them away from the internal audit function,which itself is important?

Mr Shead: As we have said, we hope that internal audit sections do not get involved in doing systemsappraisals.

Mr Smerdon: As a general comment, if an organisation is big enough, it should have a separate,distinct internal audit function. It should not be confused in terms of what it does. Mr Shead was alluding to thefact that where organisations are small and may have a resource problem, it may be acceptable to have the twolinked together.

The CHAIRMAN: Whose job is it to find out ifthere is any problem in a department's internal auditsection being diverted by doing other tasks? Who identifies that?

Mr Carpenter: The accountable officer has responsibility and should address the question of theinternal audit charter being clarified. Obviously, the buck stops there with the accountable officer in terms of therole of the internal audit. Obviously, external audit has an interest in the work of internal audit-in fact, has aprofessional responsibility to consider the role of internal audit, and I guess that the Auditor-General has theopportunity to comment both to management and perhaps in public reports if he feels that internal audit is noteffectively carrying out the role that he believes is appropriate.

Mr ELLIOTT: As far as training and implementation are concerned, have many public sector bodiesasked your department to provide them with guidance in implementing the Public Finance Standards in theirorganisations?

Mr Smerdon: I think it would be "Yes", but I will ask Graham to comment in detail.

Mr Carpenter: Yes. Certainly that same survey to which I referred earlier last year was to identify theareas. As we indicated earlier, position assessments was an area that seemed to be a high priority for training,and we responded accordingly. We do also try to communicate with agencies. We do that in a number of ways.We have half-yearly departmental forums at which a number of issues, a good number of which are related toPublic Finance Standards, are the subject of discussions with senior departmental officials. There are the formalprocesses, as I said, such as position assessments and obviously ongoing interaction with a number of peoplein my division, primarily in the branch headed by Mr Shead. We have also recognised the need to not justconcentrate our efforts in Brisbane, and accordingly we have had visits outside of Brisbane and further plannedin the next couple of months.

Mr Shead: And this week.

Mr Carpenter: Right.

Mr ELLIOTI: Have these requests for guidance come from both departments and statutory bodies?

Mr Carpenter: Yes, they certainly have.

Mr ELLIOTT: Can you give us any particular instances in which any of those statutory bodies havebeen up and running faster than others, or is it pretty much line ball right across the whole scene?

Mr Carpenter: No, it is a mixed picture. For some agencies, for example in the area of generalpurpose financial reporting, a number of bodies have been reporting in line with the accounting standards for anumber of years. We, however, have others-QEC I guess is one example, and the electricity bodiesgenerally-who are moving to general purpose financial reporting from 1 July, and obviously there is a majormove there, whereas for other bodies such as the Port of Brisbane Authority, it is not such as big an impact.

Mr Shead: Other bodies such as universities and grammar schools have set up working parties tolook at the implementation in order to facilitate the implementation of the standards.

Mr ELLIOTT: What has your department done to identify areas where difficulties have beenexperienced by these public sector bodies in implementing the Public Finance Standards?

Mr Carpenter: Obviously, the survey that we undertook last year was an important process. We alsotried to move around and hear reactions, not just in my area but in other parts of Treasury as well. So we do try toget out of the Executive Building to hear views from agencies of areas of concern.

Mr PEARCE: Is there a general willingness there for people to come forward and want to talk to youabout it and invite you over to talk to them about it?

Mr Carpenter: A good number of agencies do. It does vary a bit. Some are quite willing and happy tohave us talking with them and working with them, Some others a.re not so keen,

The CHAIRMAN: What if somebody rings you up? Can you offer a full range of assistance? Ifsomebody rings you up and wants advice with the financial management practice manual or program

T208 wro/mlk25/5/92

-12 - H. SmerdonlG. CarpenterR SheadIM, Boswell

management-if they ring you about anything and seek advice-can you offer appropriate help?

Mr Carpenter: We can put them on to someone at least to answer. There is obviously a limit to theresources that we have. We do not have a large branch in the Financial Management Policy Branch, andobviously there are a number of competing priorities there with different projects. But we do try to be responsive,as I am aware that the area headed by Mr Boswell is in terms of responding to issues of interest and concern.

Mr Shead: We can cover most things in-house. Program management queries, for example, we wouldpass on to Mike Boswell's area. Some questions which touch on areas such as corporatisation we would pass onto the GOE Unit. Basically, we can offer the full range of assistance. There is a limit to our resources.

The CHAIRMAN: You can provide some direct help or advice as to where to go or what to do?

Mr Shead: Exactly.

Mr Smerdon: I think our role is essentially advisory. We would be limiting our consultancy-type role.We are not resourced enough to undertake a consultancy-type role. We certainly provide as much help as wepossibly can.

Mr ELLIOTT: Does that apply to the statutory bodies just as much as it does to the departments?

Mr Shead: Yes.

Mr ELLIOTT: Or are they not as keen to come across and get involved?

Mr Shead: The only difficulty I suppose with statutory bodies are the country ones, and they are theones we try to target in our regional visits around Queensland.

Mr Smerdon: It would be fair to say, I think, that where a statutory body has had a relationship withTreasury that has been ongoing for a number of years, it is much easier for it to come forward and seek advice.But organisations we have rarely dealt with in our history may want to continue doing their own thing. It reallydepends a little bit on the history.

Mr ELLIOTT: In November last year, the Auditor-General reported to Parliament that the majority oforganisations were unsure as to what form system appraisals and position assessments should take. He alsosaid there was an uncertainty as to the desired level of content required and of the reporting processesnecessary to allow benefit to be gained by upper management. The Auditor-General stated that gUidance byTreasury on these issues was considered essential. Did you consult the Auditor-General on these matters whendeveloping your training modules?

Mr Shead: I suppose we did not see the important factor being the form of the assessments andappraisals. It is really about managing upwards within an organisation and encouraging managers to look at theresources that they control and so on and to report to the top management, the executive level, on how theseresources are being managed. For that reason, we have not consulted with the Auditor-General on things like theform of the requirements.

Mr Smerdon: It does come back to whether we should be prescribing formats and so forth, as weused to do with the Treasurer's Instructions, whether we should allow management to be proper managers. Ifthere was a view that we should go back to the prescriptive model, I for one would be sort of saying that I do notthink that is a very good move.

Mr ELLIOTT: Really, you would like to see them using their own initiative more within the framework?

Mr Smerdon: I would think so. I think part of the problem is that in terms of external audit, the moreprescriptive the process, the easier it is for the external audit to be undertaken. I think you have got to balanceup the two.

Dr WATSON: Is there not also an issue that while you do not want to be prescriptive, there has alsogot to be some kind of consistency across the public sector with respect to the amount of detail that is going tobe included-the level of the content, if you like? Some of the uncertainty that is associated with, let us say,departments and statutory bodies has to be somewhat related to how they perceive themselves vis-a-vis everyother department and how someone like Treasury, which may be concerned with resource allocation and stufflike that, views the appropriateness of the report.

Mr Smerdon: I think it comes back to the issue of practice statements being that sort of forum, andperhaps we have not been as good communicators as we might like to have been with some of the entities inexplaining the process to them. We have certainly taken steps to try to correct that.

Mr ELLIOTT: The Public Finance Standards became operative on 1 July 1990. Your department heldits first position assessment workshops in February and March 1992 and we understand that it will be conductingsystem appraisal training sessions during the latter part of this financial year. Why was there such a long delaybetween implementing the Public Finance Standards and conducting these training sessions?

T208 wro/mlk25/5/92

-13 - H. SmerdonlG. CarpenterR SheadtM Boswell

Mr Smerdon: I think it is essentially a resource issue. We were going through, at that period, a PublicSector Management Commission review. The capacity to put additional resources into that area was extremelylimited. That review showed that we needed to strengthen that area quite markedly. There was a time lapsebetween getting the resources in and then beginning this process of communication. We acknowledge that weshould have done it earlier, but I think the capacity to do it was not there at the time. Graham might have a moredetailed comment on that.

Mr Carpenter: The only comment I would make is that after they were promulgated, there was aforum held for senior officers. As the Under Treasurer has indicated, the review of Treasury by the PSMC andnow the creation of the division that I head and also the branch that Mr Shead heads were in response to arecognised need to do some more work in this area.

Mr ELLIOTT: To what extent have participants indicated that they have found the training sessionshelpful?

Mr Shead: Evaluations have been very positive. They have all marked us highly.

Mr PEARCE: So you are doing a good job, you reckon?

Mr Shead: I think so.

Dr WATSON: Are you saying you are resolving the uncertainty in those training sessions?

Mr Shead: I think we are helping them to think about how they need to manage upwards a lot better.

Dr WATSON: Who are "they"? What level are we talking about managing upwards, and where is thatuncertainty being resolved?

Mr Shead: We have had people, for example, the Public Trustee turn up. I do not think we have hadany accountable officers, but people the next level down-directors of corporate services, finance managersdown to accountants, subaccountants and so on.

Dr WATSON: So you have had no accountable officers turn up?

Mr Carpenter: We have not been targeting accountable officers. I think the reference to the PublicTrustee turning up is the style of operation of that particular person. But our target is to get I guess the middle tosenior management level within the organisation, and obviously also some of the operative levels have alsobeen involved.

Mr ELLIOTT: Have some participants of these training sessions been critical, and if so, in whatrespect? Have they found flaws or holes or made suggestions as to how this could be done better?

Mr Shead: We have had some good feedback on some problems with the standards and how they areworded. We have taken them on board. Some have been taken in in the current round of amendments, and Ithink some last year as well. We are constantly encouraging feedback in our forums. For example, around thecountry, we get quite valuable feedback and we take it on board where it is appropriate in terms of amending thestandards.

Mr ELLIOTT: What constraints has your department faced in assisting departments and statutorybodies in implementing the Public Finance Standards? Being Treasury as well, you have sort of--

Mr Smerdon: Unfortunately, I think Treasury is always the hardest upon ourselves, so we tend tounderresource the area. Certainly, having Graham and Bob on board has helped that. But that was what wasrecognised during that review process. We were a bit in limbo. It took us a little while to get the right sorts ofresources on board.

Mr Shead: I think that a second problem has been to reach the entire public sector. We found thatwith a lot of our workshops, forums and so on, the information goes to the people who are there and does notspread any further within the organisation. In many cases we rely on organisations to disseminate information.and that is not always successful.

Dr WATSON: Earlier, you talked about acting as a consultant in some of these things. In other areaspeople are hiring outside consultants. In Treasury, is there a fee for service there?

Mr Smerdon: The question is whether it is our real role to act as a consultant to departments. Ipersonally do not see it as our role to be a consultant. Essentially, I think it is a departmental matter, with usproviding advice and assistance where we can. But I have to say that I would be counselling against setting up aconsultancy service within Treasury to assist with that.

Dr WATSON: This is probably a Vf3ry naive question, but with these standards that are beingintroduced, Treasury does not see its role as providing-perhaps "consultancy service" is too broad-but what

T209lrs/jd25/5/92

-14- H. Smerdon/G. CarpenterB Shead/M Boswell

exactly is Treasury's role in the introduction of these kinds of standards right across the public service. Is therenot a role for Treasury in doing that, and therefore part of the education and consulting process, or am Imistaken?

Mr Smerdon: I hope that I did not say that we do not provide advice. Quite strongly, we provideadvice and assist in implementation issues. The point that I was addressing was the question of providing anactual consultancy-type arrangement where we did the work that the department was supposed to be doing. Weare certainly assisting with implementation. I am sure that Mike Boswell would vouch for that in the programmanagement area. He spends a lot of his time talking to departments about program structure, strategicplanning, and so on. Certainly Graham and Bob, from their side of things, would say that they are spending a lotof time-perhaps more than they would like to-assisting departments in interpretations: what does it reallymean; how do we go about it, etc.

Mr ELLIOTT: You may recall in the 1980-83 period, three people from Treasury came across fromNational Parks to assist us largely in looking at financial control. How does what you are doing now differ fromthe sort of thing that you used to do then?

Mr Smerdon: If I remember rightly, that National Parks one related to the internal operational auditservice, which was a separate entity within Treasury and which was in fact a consultancy organisation. It wasnot working with Treasury per se. It had to be located in the department, but its role was to assist theaccountable officer with operational audit issues.

Mr Carpenter: I know that we are concentrating on Public Finance Standards, but there is a separateissue with regard to the Treasury responsibilities as lead agency for Queensland Government FinancialManagement Systems. Another part of my responsibility is to see that we have available a suite of financialmanagement systems that are supportive of the direction in Public Finance Standards. In that particular area,specific consulting support is being provided, including on a cost-recovery basis.

Mr J. H. SULLIVAN: Could I take us almost back to the beginning when we spoke aboutconsultation in relation to amendments and the PFS. I understand that in March of this year some proposedamendments relating to program management were circulated by Treasury. I also understand that, in relation tothose amendments, comment was not sought from statutory bodies although it was sought from thedepartments. Whilst I appreciate what Mr Smerdon said about trying to set the standards without having toamend them all the time, I am a bit concerned about the apparent limited nature of the consultation. Could youtell me why there appears to be a limited rather than full consultation for amendments?

Mr Boswell: I do not remember that we did consult with statutory authorities.

Mr J. H. SULLIVAN: It is my understanding that they were circulated to statutory authorities butthat comment was not sought from them, although comment was sought from departments.

Mr Boswell: That was not my recollection.

Mr Smerdon: Could we take that on board and perhaps come back to you with some more specificcomment on that? Quite obviously there is some difference.

The CHAIRMAN: We are about to move on to program management, about which we have quite anumber of questions. Does anybody wish to comment on anything so far?

Mrs BIRD: I seek one point of clarification. You were talking about not being involved in consultation,but do you see yourselves in a role of perhaps providing some assistance in facilitation of the PFS?

Mr Smerdon: We have been consulting with departments very regularly. We are not into theconsultancy arrangement where a department engages us, for example, to write its manual of financialpractices. That is not our role. It is not our role to develop a specific program structure for them. We will certainlyassist and work with a department. But at the end of the day, they are big boys out there, and they get paidmoney to do certain things. We really do not want to be wasting our resources in doing the work that they shouldbe doing. We are happy to assist, but I am certainly not prepared to put in scarce resources and do the job forthe departments. There is an ownership issue here. Unless they own the end product, they are not going to abideby it in the way that we want them to. They have to put a lot of sweat and blood into that, and then they will own it.That is what we are really after. That is the way the system will work, when departments and entities out thereown this whole Public Finance Standards process.

Mr Shead: We are happy to give our advice on it. We are currently reviewing a number of manuals. Wehave given a lot of assistance-probably more than we should have-to a number of large departments. We arehappy to help to the limit that we can. At the same time, we need to make sure that it is their product.

The CHAIRMAN: As there are no iurther comments at this stage, we will adjourn and reconvene at10.45.

T209lrs/jd25/5/92

-15 - H. SmerdonlG, Carpenter8, SheadIM Boswell

The CQmmittee adjQurned at 10.27 a.m.

The CQmmittee resumed at 10 44 a m.